APPENDIX FOR THE ECONOMIC DEVELOPMENT STRATEGY CITY OF LYNN, MASSACHUSETTS. May 16, 2005

|

|

|

- Mildred Collins

- 5 years ago

- Views:

Transcription

1 APPENDIX FOR THE ECONOMIC DEVELOPMENT STRATEGY CITY OF LYNN, MASSACHUSETTS May 16, 2005 Prepared for: City of Lynn Office of Economic & Community Development Lynn City Hall 3 City Hall Square Lynn, MA Attention: Mr. Don Walker Prepared by: RKG Associates, Inc. Economic, Planning and Real Estate Consultants 277 Mast Road Durham, NH Economic Planning and Real Estate Consultants Tel: FAX: 603: Web:

2 TABLE OF CONTENTS I. APPENDIX...1 A. Economic Conditions and Trends Employment and Business Trends Transition in the Employment Base Employment by Selected Sectors Growth Sectors... 8 B. Demographic and Labor Force Characteristics Population and Households Trends and Projections Population by Age Households by Income Educational Attainment Employment in Major Industries Commuting Patterns Unemployment Rate and Labor Force Trends...14 C. Development Potential for Additional Retail and Service in Lynn, MA D. Regional Real Estate Market Conditions Office Market R & D Market Industrial Market...20 E. Commercial and Industrial Availabilities in Lynn F. Results of a Survey of Lynn Businesses and Major Employers G. Lynn s Residential Median Values and Chapter 40-B Housing H. Lynn Tax Base and Trends I. Lynn s Economic Opportunity Zones Downtown Central Lynn Lynnway GE-Riverworks/Western Avenue Broad Street/MBTA Corridor Boston Street/Western Avenue Lower Broadway Hospital...74 RKG Associates, Inc. Page i

3 I. APPENDIX This appendix contains statistics, graphs, maps and tables of data assembled by RKG Associates, Inc. (RKG) for the economic development strategy for the City of Lynn, MA. A. Economic Conditions and Trends Statistical data on employment and business trends are presented in this section for the City of Lynn and its region. For this report, the region is the South Essex Workforce Investment Area (WIA) as defined by the Massachusetts Division of Career Services (DCS) & Massachusetts Division of Unemployment Assistance (DUA), formerly known as the Massachusetts Division of Employment and Training (DETMA). The region includes the communities of Beverly, Danvers, Essex, Gloucester, Hamilton, Ipswich, Lynn, Lynnfield, Manchester, Marblehead, Middleton, Nahant, Peabody, Rockport, Salem, Saugus, Swampscott, Topsfield and Wenham. Lynn s geographical position within the region is exhibited in the map on the following page. 1. Employment and Business Trends Figure A-1: Jobs in Lynn declined by 32% between 1985 and 2004, while in the region jobs increased by 10%. In 2004, Lynn s employment (24,540) represented about 15% of the jobs in the region (166,120), a decline from 24% in This data suggest Lynn has lost its prominence as an economic center of the region, and did not benefit from the economic expansion of the late 1990s as the region did. Jobs in Lynn Employment Trends ( ) 36,000 34,000 32,000 30,000 28,000 26,000 24,000 Source: DETMA & RKG Lynn & So. Essex WIA City of Lynn So. Essex WIA 170, , , , , , ,000 Jobs in So. Essex WIA RKG Associates, Inc. Page 1

4 RKG Associates, Inc. Page 2

5 Figure A-2: Businesses in Lynn declined from a high of nearly 1,600 in 1986 to a low of 1,190 in Since 1997, the number of businesses increased to 1,390 in In comparison, businesses in the region increased from 9,100 in 1985 to 12,170 in Businesses in Lynn 1,600 1,500 1,400 1,300 1,200 Business Trends ( ) Lynn & So, Essex WIA 13,000 12,000 11,000 10,000 9,000 Businesses in So. Essex WIA 1, ,000 Source: DETMA & RKG Lynn So. Essex Appendix Table A-1 exhibits statistical data from MA DCS & DUA for Lynn and the South Essex WIA. Total employment, the number of businesses and the average wage for each year is shown. Appendix Table A-1: City of Lynn Economic Development Strategy - Employment, Businesses and Wage Data Employment Businesses Average Wage Year City of Lynn So. Essex WIA City of Lynn So. Essex WIA City of Lynn So. Essex WIA , ,044 1,452 9,095 $23,457 $18, , ,616 1,596 10,065 $24,522 $19, , ,281 1,578 10,521 $24,875 $20, , ,297 1,542 10,717 $25,732 $21, , ,005 1,549 10,917 $27,422 $22, , ,405 1,510 10,905 $28,245 $23, , ,275 1,403 10,454 $28,883 $24, , ,291 1,281 10,001 $30,096 $26, , ,867 1,273 10,233 $30,130 $26, , ,550 1,248 10,587 $30,674 $27, , ,042 1,258 10,908 $30,815 $28, , ,061 1,224 10,976 $31,946 $29, , ,388 1,188 11,341 $33,055 $30, , ,261 1,202 11,692 $34,026 $31, , ,175 1,264 12,001 $37,217 $33, , ,489 1,255 11,212 $39,289 $36, , ,141 1,301 11,490 $40,392 $37, , ,838 1,311 11,730 $42,016 $37, , ,722 1,352 12,005 $44,044 $40, [1] 24, ,121 1,391 12,169 $43,472 $39,156 [1] 2nd quarter Source: MA DCS & DUA, and RKG Associates, Inc. RKG Associates, Inc. Page 3

6 2. Transition in the Employment Base Figure A-3: The decline in employment affected the make-up of Lynn s employment base. Manufacturing jobs represented 43% of the base in 1985, but only 20% in Trade employment represented 20% of the base in 1985 but only 16% in On the other hand, the services sector increased from 21% in 1985 to 36% in Similarly, the government sector increased from 9% in 1985 to 18% in Lynn, MA: Transition in Employment by Major Industry Manufacturing Services Trade (Whs. & Ret.) 1995 Government Fin., Ins. and RE Construction 1990 Trans. Comm. & P.Util ,000 10,000 15,000 20,000 25,000 30,000 35,000 Jobs in Lynn Figure A-4: Employment in the manufacturing sector in the region declined from a 25% representation in 1985 to 12% in Services employment accounted for 33% of the regional base in 2004, as compared to 21% in Trade employment accounted for 29% of the base in 2004, similar to the 30% representation in South Essex WIA: Transition in Employment by Industry Manufacturing Services Trade (Whs. & Ret.) Government Fin., Ins. and RE Construction Trans. Comm. & P.Util. Jobs in So. Essex WIA inthousands Appendix Table A-2 details employment by selected industries for the corresponding years for Lynn and the region. RKG Associates, Inc. Page 4

7 Figure A-5: Lynn lost nearly 10,500 jobs in the manufacturing sector between 1985 and 2004, accounting for nearly 60% of the employment lost in this sector in the region. Lynn also experienced losses in the Trade and Financial Sector in comparison to gains in the region. Lynn experienced marginal growth in the Services sector in comparison to the increase in the region. Changes in Jobs by Industry Sectors 1985 to 2004 Total Employment Trans. Comm. & Util. Construction Fin., Ins. and RE Government Trade (Whs. & Ret.) Services Manufacturing So. Essex Lynn (20,000) (10,000) 0 10,000 20,000 30,000 Change in Jobs Figure A-6: Between 2000 and 2004, Lynn lost 1,550 jobs in the manufacturing sector, while the region experienced a loss of 5,580 jobs in this sector. Lynn experienced a gain of 1,660 jobs in the Services sector during this period, which accounted for more than 50% of the increase in the region. Lynn however experienced losses in all the other sectors (except construction) while gains were experienced in the region (except in Trade). Changes in Jobs by Industry Sectors 2000 to 2004 Total Employment Trans. Comm. & Util. Construction Fin., Ins. and RE Government Trade (Whs. & Ret.) Services Manufacturing So. Essex (6,000) (4,000) (2,000) 0 2,000 4,000 Change in Jobs Appendix Table A-3 exhibits the specific data on the long and short term changes in employment by the sectors. Lynn RKG Associates, Inc. Page 5

8 Appendix Table A-2: City of Lynn Economic Development Strategy Employment Trends by Major Industry Sectors for Selected Years City of Lynn [1] Manufacturing 15,482 10,240 8,000 6,554 5,010 Services 7,480 7,335 7,396 7,253 8,911 Trade (Whs. & Ret.) 7,047 6,386 4,552 4,258 3,881 Government 3,203 3,475 4,251 4,680 4,353 Fin., Ins. and RE 1,304 1, Construction ,052 Trans. Comm. & P.Util Agr., Fish & Forest TOTAL 35,820 29,682 26,271 25,214 24,537 South Essex WIA [1] Manufacturing 38,235 31,030 27,449 26,091 20,510 Services 32,397 38,935 44,781 51,537 54,772 Trade (Whs. & Ret.) 45,170 46,824 46,236 48,691 48,086 Government 18,281 19,299 19,112 21,394 22,133 Fin., Ins. and RE 5,971 7,124 6,195 7,268 7,826 Construction 5,327 4,847 4,369 5,534 6,567 Trans. Comm. & P.Util. 4,162 4,969 4,546 5,297 5,596 Agr., Fish & Forest 1,501 1,377 1,354 1, TOTAL 151, , , , ,121 [1] 2nd quarter Source: MA DCC & DUA, and RKG Associates, Inc. Appendix TableA-3: City of Lynn Economic Development Strategy - Changes in Employment by Industry Sectors (Long & Short Term) City of Lynn So. Essex WIA 1985 to 2004 # Change % Change # Change % Change Manufacturing (10,472) -67.6% (17,725) -46.4% Services 1, % 22, % Trade (Whs. & Ret.) (3,166) -44.9% 2, % Government 1, % 3, % Fin., Ins. and RE (509) -39.0% 1, % Construction % 1, % Trans. Comm. & P.Util. (6) -1.3% 1, % Agr., Fish & Forest % (870) -58.0% TOTAL (11,283) -31.5% 15, % City of Lynn So. Essex WIA 2000 to 2004 # Change % Change # Change % Change Manufacturing (1,544) -23.6% (5,581) -21.4% Services 1, % 3, % Trade (Whs. & Ret.) (377) -8.9% (605) -1.2% Government (327) -7.0% % Fin., Ins. and RE (192) -19.5% % Construction % 1, % Trans. Comm. & P.Util. (172) -27.4% % Agr., Fish & Forest (10) -11.1% (972) -60.6% TOTAL (677) -2.7% (1,294) -0.8% NOTE: 2nd quarter of 2004 Source: MA DCC & DUA, and RKG Associates, Inc. RKG Associates, Inc. Page 6

9 3. Employment by Selected Sectors Despite the employment transition that has occurred in Lynn over the last twenty years, the City still maintains a strong and viable employment base. Nearly 92% of Lynn s private employment in 2004 (2 nd quarter) is concentrated in twenty-four major industry sectors as shown Appendix Table A-4. General Electric remains Lynn s largest employer, and most of its employment is categorized as Durable Goods Manufacturing, which accounts for 18.5% of the private employment in the City. Employment in three health-related sectors contributes another 23% of total employment in the City. In comparison, these same four sectors account for about 25% of the employment in the region. Food manufacturing is another major industry in Lynn as it represents nearly 5% of the base, as compared to the 2% representation in the region. Similarly, employment in the social assistance industry accounts for 5% of Lynn s base but only 2% of that in the region, as shown below. Appendix Table A-4: City of Lynn, MA Economic Development Strategy Employment in Selected Industry Sectors in Lynn to So. Essex WIA (2004) % of Lynn Total So. Essex WIA % of Total Durable Goods MFG 3, % 15, % Nursing & Residential Care Facilities 1, % 6, % Ambulatory Health Care Services 1, % 8, % Hospitals 1, % 6, % Food Services and Drinking Places 1, % 13, % Construction 1, % 6, % Social Assistance 1, % 2, % Food Manufacturing % 2, % Administrative and Support Services % 7, % Professional and Technical Services % 7, % Food and Beverage Stores % 6, % Finance and Insurance % 5, % Wholesalers, Durable Goods % 2, % General Merchandise Stores % 3, % Non-Durable MFG (exc. Food) % 3, % Motor Vehicle and Parts Dealers % 3, % Health and Personal Care Stores % 1, % Repair and Maintenance % 1, % Membership Organizations & Associations % 2, % Information % 2, % Real Estate % 2, % Arts, Entertainment, & Recreation % 3, % Merchant Wholesalers, Nondurable Goods % 2, % Clothing and Clothing Accessories Stores % 2, % Subtotal 18, % 120, % Total (Private Employment) 20, % 143, % Source: MA DCS & DUA, and RKG Associates, Inc. The region has higher employment representation in most retail and food service sectors, as well as financial, administrative, and professional service sectors, as shown above. This may be attributed to Lynn s location in relation to other areas of the region. RKG Associates, Inc. Page 7

10 Appendix Table A-5 exhibits the average employment and wages in Lynn for the 2 nd quarter of Appendix Table A-5: City of Lynn Economic Development Strategy City of Lynn Employment and Wage Report 2004 (2nd quarter) No. of Average Average Establish- Monthly Weekly Description ments Employment Wages Private Employment Goods-Producing Domain 184 6,061 $1,344 Construction 126 1,052 $1, Construction 126 1,052 $1,032 Manufacturing 58 5,010 $1, Manufacturing 58 5,010 $1,410 NONDUR - Non-Durable Goods Manufacturing 23 1,267 $800 Service-Providing Domain 1,183 14,122 $600 Trade, Transportation and Utilities 284 2,980 $ Utilities $ Wholesale Trade $ Retail Trade 193 2,114 $ Transportation and Warehousing $577 Information $ Information $988 Financial Activities $ Finance and Insurance $ Real Estate and Rental and Leasing $649 Professional and Business Services 180 2,172 $ Professional and Technical Services $1, Administrative and Waste Services $512 Education and Health Services 181 5,701 $ Educational Services $ Health Care and Social Assistance 171 5,629 $610 Leisure and Hospitality 152 1,359 $ Arts, Entertainment, and Recreation $ Accommodation and Food Services 136 1,144 $275 Other Services $ Other Services, Ex. Public Admin $369 Total, All Industries (PRIVATE) 1,367 20,184 $823 Federal Government $1,019 State Government $676 Local Government 10 3,294 $928 Private & Government Total 1,391 24,537 $836 Source: MA DCS & DUA and RKG Associates, Inc. 4. Growth Sectors Between 2000 and 2004, Lynn experienced growth in twenty industry sectors that accounted for an increase of nearly 1,900 jobs, as shown in Appendix Table A-6. Professional services employment experienced an increase of nearly 400 jobs during in the last four years, followed by employment growth in the hospitals sector, the administrative and support services sector, the construction industry, to name a few. RKG Associates, Inc. Page 8

11 Appendix Table A-6: City of Lynn Economic Development Strategy Employment Growth in Top Twenty Industry Sectors ( ) Lynn South Essex WIA Industry Sector Increase in Jobs % Increase Industry Sector Increase in Jobs % Increase Prof. & Tech. Services % Hospitals 1,071 21% Hospitals % Construction 1,047 19% Admin. & Support Services % Food & Beverage Stores % Construction % Prof. & Tech. Services % Nursing & Res.Care Facilities % Building Materials & Garden Equip % Social Assistance % Miscellaneous MFG % Amb.Health Care Services 128 8% Amusement, Gambling et al % Real Estate 75 43% Nursing & Res.Care Facilities % Private Households 75 74% Machinery MFG % General Merchandise 51 17% Credit Intermediation & Related Activities % Miscellaneous Retailers 26 40% Motor Vehicle & Parts Dealers % Nonstore Retailers 19 27% Personal & Laundry Services % Gasoline Stations 14 16% Food Services & Drinking Places 257 2% Repair & Maintenance 12 5% Ambulatory Health Care Services 239 3% Transit & Ground Transport 9 12% Real Estate % Wholesalers, Durable Goods 7 2% Furniture & Home Furnishings Stores % Membership Org. & Assoc. 7 3% Educational Services 233 9% Educational Services 5 7% Religious, Grantmaking, etc % Truck Transportation 4 5% Insurance Carriers & Related Activities 164 8% Performing Arts & Spectator Sports 1 6% Private Households % Total 1,894 9% Total 8,983 6% Source: MA DCS & DUA, and RKG Associates, Inc. The top twenty growth sectors in the region experienced a gain of nearly 9,000 jobs as shown above, and employment growth in hospitals, construction, food and beverage stores, and professional services sectors were among the highest. The miscellaneous and machinery manufacturing sectors also experienced gains of 900 jobs in the region over the last four years, and it is unknown if Lynn captured any growth in these sectors since the data is suppressed in the smaller geography. Despite the recession in the early 2000s, certain sectors continue to show growth and Lynn has benefited. However, it is unlikely Lynn would capture a large-scale user within the short term except for an end-user whose actions are difficult to quantify. Lynn does have a strong base in the health related industries and this sector is anticipate to grow in conjunction with the aging of the baby-boom generation. Lynn also has a strong manufacturing base such that a strategy of supporting and retaining this sector should be considered, as well as nurturing the growth of other businesses. RKG Associates, Inc. Page 9

12 B. Demographic and Labor Force Characteristics Population and household statistics are presented in this section, as well as data regarding the characteristics of the labor force in the City and the region. 1. Population and Households Trends and Projections Lynn s population was estimated at 90,400 persons in 2004, which represented a 1.5% increase since This growth rate was slightly lower than the 2% increase in the region between 2000 and 2004 as shown in Appendix Table B-1. Population in Lynn is forecasted to increase by 1,440 persons over the next five years. This gain indicates a 1.6% growth rate in Lynn, which is slightly lower than 2.2% rate forecasted for the region. Appendix Table B-1 - City of Lynn Economic Development Strategy Population, Households and Median Househols Income Trends and Projections Lynn South Essex WIA Population 81,245 89,050 90,362 91, , , , ,233 # Change -- 7,805 1,312 1, ,046 8,220 9,211 % Change % 1.5% 1.6% % 2.0% 2.2% % Racial Population 17% 32% 32% 33% 6% 11% 11% 11% % Hispanic Population 9% 18% 22% 25% 3% 6% 9% 13% Households 31,554 33,511 34,284 35, , , , ,232 # Change -- 1, ,013 4,620 5,482 % Change % 2.3% 2.7% % 2.9% 3.4% Median Household Income $28,728 $37,594 $40,261 $45,214 $38,328 $52,320 $56,174 $62,539 # Change -- $8,866 $2,667 $4, $13,992 $3,854 $6,365 % Change % 7.1% 12.3% % 7.4% 11.3% Source: US Census, Demographics NOW and RKG Associates, Inc. Referring to the previous table, Lynn s racial and Hispanic population represented 32% and 22% of the total population in 2004, which is a higher concentration than indicated in the region. Lynn s minority diversity is also forecasted to increase over the next five years. Median household income was estimated at $40,300 in 2004, representing a 7% increase since The median household income was estimated at $56,200 in the region, increasing by 7% since Median incomes in both areas are forecasted to increase over the next five years, and the anticipated growth in Lynn (12.3%) is higher than the region (11.3%). Despite this higher rate of increase, Lynn s median household income is forecasted to be about 28% lower than that for the region in This income difference can be partially attributed to a higher percentage of low-income housing in Lynn in comparison to the region. RKG Associates, Inc. Page 10

13 2. Population by Age Figure B-1: The babyboom generation (45 to 54 and 55 to 64) experienced most of the population growth in Lynn, between 2000 and 2004, followed by those in the 15 to 24 age cohort. Population declines were experienced in the other age groups. Over the next five years, continued gains are forecasted in the same three age brackets that increased over the last four years. In 2009, the elderly population (65 and up) will represent 13% of total population while those under 15 would account for 21% of Lynn s population. City of Lynn - Trends in Population by Age Groups 65 & up 55 to to to to to 24 Under 15 0% 5% 10% 15% 20% 25% Source: US Census, Demographics NOW & RKG Associates, Inc. Figure B-2: A similar trend in the growth of babyboomers (45 to 54 and 55 to-64) and the population aged 15 to 24 occurred in the region between 2000 and 2004, while declines were evident in the other age groups. Population projections indicate continued growth in the same three age sectors over the next five years. In 2009, the elderly population will represent 15% of the region s population, while persons under age 15 will account for 18% of the population. South Essex WIA - Trends in Population by Age Groups 65 & up 55 to to to to to 24 Under 15 0% 5% 10% 15% 20% 25% Source: US Census, Demographics NOW & RKG Associates, Inc. Lynn and the region will lose population in the 25 to 44 age groups and those under 15 over the next five years, but will gain population at the younger (15 to 24) and in the older cohorts (45 and older). The 55 to 64 age group in Lynn and the region will experience the most growth over the next five years. RKG Associates, Inc. Page 11

14 3. Households by Income Figure B-3: Households with incomes of $75,000 or more increased between 2000 and 2004, while households in the lower income brackets decreased. A similar trend is forecasted over the next five years as households earning $75,000 or more are projected to increase by more than 2,100 households. Despite this increase, more than 30% of Lynn s households are forecasted to earn incomes of less than $25,000 in City of Lynn - Trends in Households by Income Cohorts $100,000 and up $75,000 to $99, $50,000 to $74, $25,000 to $49,999 Less than $25,000 0% 10% 20% 30% 40% 50% Source: US Census, Demographics NOW & RKG Associates, Inc. Figure B-4: Households in both income brackets South Essex WIA - Trends in Households by Income earning $75,000 or more Cohorts also increased between 2000 and 2004, similar to $100,000 and up Lynn, while declines were evident in the lower income $75,000 to $99,999 groups. Five-year forecasts indicate that households earning $100,000 or more $50,000 to $74,999 in the region will increase by more than 10,150, and $25,000 to $49,999 this income cohort will account for 27% of the households in the region. Less than $25,000 Households earning incomes of less than $25,000 will represent about 20% of households in Source: US Census, Demographics NOW & RKG Associates, Inc. the region in 2009, and more than 32% of the region s households earning less than $25,000 will be in Lynn % 10% 20% 30% 40% RKG Associates, Inc. Page 12

15 4. Educational Attainment Figure B-5: Nearly 47% of Lynn s population had attained a high-school education or higher, according to the US Census. This factor is lower than the 60% indicated for the region. Despite Lynn having a lower educational attainment level, approximately 55% of the businesses surveyed in conjunction with the Economic Development Strategy, indicated good labor force characteristics within the City. Graduate or Profession Degree Associate & Bachelor's Degree College-No Degree High School Graduate Source: US Census & RKG Associates, Inc. Educational Attainment (2000) 0% 5% 10% 15% 20% 25% % of Population So. Essex WIA City of Lynn 5. Employment in Major Industries Figure B-6: Most of Lynn s resident workers in 2000 were employed in the retail trade, manufacturing, health services and other services sector, according to the US Census. A majority of the region s resident labor force were similarly employed in these four sectors but to a lower degree than in Lynn with the exception of other services. The region also had a higher concentration in the finance and educational services sectors as well as in the arts and entertainment sector. Employment of Resident Workers in Major Industries (2000) Retail trade Manufacturing Health services Other Services Trans., Comm. & Util. Educational services Finance, Insur. & RE Construction Public administration Wholesale trade Arts, Entertainment et al Source: US Census & RKG Associates, Inc. 0% 5% 10% 15% 20% 25% % of Resident Workers So. Essex WIA City of Lynn 6. Commuting Patterns Commuting patterns of the resident workers in Lynn indicated that 71% of the resident workers in 2000 had jobs outside of Lynn, and the remaining 29% had jobs within the City. In comparison, 56% of the local jobs in Lynn were held by persons who commuted into the City from outside. Selected commuting data is exhibited in Appendix Table B-2. The RKG Associates, Inc. Page 13

16 middle column identifies the percentage of local Lynn s resident workers and the right column identifies the percentage of local jobs in the City. The left column identifies the community into which a Lynn resident commuted to work, or the community from which persons commuted for work in Lynn. For instance, 14% of the resident workers in Lynn commuted to Boston for work; but persons that commuted to Lynn from Boston held 2% of the jobs in Lynn. Appendix Table B-2: City of Lynn: Economic Development Strategy Commuting Patterns of Resident Workers & Holders of Local Jobs Lynn Resident Workers Lynn Local Jobs Total in Lynn 38,360 25,542 In Lynn 29% 44% Outside Lynn 71% 56% Boston 14% 2% Salem 6% 5% Peabody 6% 4% Danvers 4% 2% Saugus 3% 3% Beverly 3% 2% Cambridge 2% 0% Swampscott 2% 3% Andover 2% 0% Woburn 2% 0% Chelsea 1% 1% Marblehead 1% 2% Lawrence 1% 1% Haverhill 1% 1% Malden 1% 1% Note: Bold Communities in South Essex WIA Source: US Census and RKG Associates, Inc. 7. Unemployment Rate and Labor Force Trends Figure B-7: Lynn s unemployment rate declined to 6.6% in 2004, suggesting improving economic conditions from 2003 when the rate peaked at 7.6%. In 2000, Lynn s employment rate was 3.2% and the lowest rate during the fifteen-year period. Lynn s highest unemployment rate was 10.8% in 1992 at the end of the recession of the early 1990s. Historically, Lynn s unemployment rate is about 1% higher than indicated statewide or in the region. Unemployment Rate Trends ( ) 12% City of Lynn 10% So. Essex WIA 8% Massachusetts 6% 4% 2% 0% Source: MA DCS & DUA and RKG Associates, Inc. RKG Associates, Inc. Page 14

17 Between 1990 and 2004, Lynn s labor force increased by 7%, while the number of unemployed persons declined by nearly 6%, as shown below. However, the number of unemployed persons in Lynn more than doubled since 2000, such that in 2004 Lynn had nearly 2,800 persons unemployed or 6.6% of the labor force. Appendix Table B-3: City of Lynn Economic Development Strategy Trends in Labor Force and Unemployment ( ) Year Labor force City of Lynn Employment Unemployment Unemployment Rate Labor force South Essex WIA Employment Unemployment Unemployment Rate ,927 36,000 2, % 206, ,266 12, % ,862 33,875 3, % 202, ,739 17, % ,470 33,429 4, % 201, ,263 17, % ,783 33,991 2, % 201, ,419 13, % ,747 34,134 2, % 202, ,811 11, % ,511 35,244 2, % 200, ,952 9, % ,756 35,866 1, % 201, ,139 7, % ,018 37,154 1, % 207, ,075 7, % ,207 37,630 1, % 209, ,431 6, % ,252 37,654 1, % 209, ,936 6, % ,138 39,826 1, % 208, ,492 4, % ,986 40,152 1, % 218, ,814 7, % ,779 40,091 2, % 222, ,360 11, % ,251 39,031 3, % 218, ,774 12, % ,787 39,030 2, % 216, ,769 10, % # change ,860 3,030 (171) -0.9% 10,194 11,503 (1,309) -0.9% (796) 1, % 8,297 2,277 6, % % change % 8.4% -5.8% 4.9% 5.9% -10.7% % -2.0% 110.1% 4.0% 1.1% 122.2% Source: MA DCS & DUA and RKG Associates, Inc. Referring to the previous table, the number of unemployed persons in the region more than doubled between 2000 and 2004, such that nearly 11,000 persons were unemployed in The number of unemployed persons in Lynn represented about 25% of the available regional labor force in C. Development Potential for Additional Retail and Service in Lynn, MA The estimated demand for consumer retail goods and services, by selected merchandise line, is nearly $438.0 million from the residents of Lynn in An accompanying spreadsheet (Appendix Table C-6) at the end of this section, presents the estimated consumer demand by individual merchandise line. A summary of that demand for specific store types is presented in the following table: RKG Associates, Inc. Page 15

18 Appendix Table C-1 Estimated Consumer Demand for 2004 In $000 s for Lynn, MA Residents Store Type Est Demand Food, Grocery and Dining $232,489 Drug Store and Personal Items $41,047 Household Goods and Furniture $43,333 Apparel $70,916 Electronics $18,244 Specialty Retail $31,944 TOTAL $437,973 Source: RKG Associates, Inc. The estimated sales at stores in Lynn, by the above referenced store types, for 2004, is slightly more than $282.0 million as shown in Appendix Table C-2. Appendix Table C-2 Estimated Sales by Store Type for 2004 In $000 s for Lynn, MA Residents Store Type Est Sales Food, Grocery and Dining $161,689 Drug Store and Personal Items $44,287 Household Goods and Furniture $16,764 Apparel $23,187 Electronics $11,974 Specialty Retail $24,271 TOTAL $282,172 Source: Census of Retail Trade and RKG Associates, Inc. When comparing the data in the two previous tables, an indication of sales leakage of approximately $155.8 million is evident. Sales leakage refers to the local consumer demand for goods and services that is not being captured by the local merchants, and is exhibited by story type in Appendix Table C-3. Appendix Table C-3 Estimated Sales Leakage by Store Type for 2004 In $000 s for Lynn, MA Residents Store Type Est Leakage Food, Grocery and Dining $70,800 Drug Store and Personal Items -$3,240 Household Goods and Furniture $26,569 Apparel $47,729 Electronics $6,271 Specialty Retail $7,672 TOTAL $155,801 Source: RKG Associates, Inc. Additional store and expanded retail selection in Lynn, coupled with marketing and promotional efforts could serve to recapture a portion of this sales leakage. It is not possible to recapture 100% of sales leakage as consumers will continue to purchase items away from home, while at work or through other means such as the internet and catalog sales. This analysis take as a conservative approach in estimating that it may be possible to recapture between 35% and 45% of this sales leakage, given new development or redevelopment potential and future marketing. This potential is summarized in the following table. RKG Associates, Inc. Page 16

19 Appendix Table C-4 Estimated Recaptured Sales Leakage by Store Type In $000 s for Lynn, MA Store Type Recapture Of 35% Recapture Of 45% Food, Grocery and Dining $24,780 $31,860 Drug Store and Personal Items NA NA Household Goods and Furniture $9,299 $11,956 Apparel $16,705 $21,478 Electronics $2,195 $2,822 Specialty Retail $2,685 $3,453 Source : RKG Associates, Inc. TOTAL $55,665 $71,569 Utilizing a conservative sales estimate of $300 per square foot, the above referenced recapture of sales leakage could result in the additional, supportable development of between 185,000 SF and 240,000 SF in Lynn, as presented in the following table. Appendix Table C-5 Est. Supportable New Retail Development from Recaptured Sales Leakage by Store Type [1] Story Type Recapture Of 35% Recapture Of 45% Food, Grocery and Dining 82, ,201 Drug Store and Personal Items NA NA Household Goods and Furniture 30,998 39,854 Apparel 55,683 71,593 Electronics 7,316 9,406 Specialty Retail 8,951 11,509 TOTAL 185, ,562 [1] Factored at $300/SF Source: RKG Associates, Inc. RKG Associates, Inc. Page 17

20 Appendix Table C- 6 : Lynn, MA - Estimated Sales Demand/Actual By Merchandise Line (2004) Est. Demand Est. Demand Est. Sales Est. Leakage Est. Leakage Est. Percent Recapture Sales $000s Pot. Retail SF ($300/SF) Merchandise Line Per Capita Total ($000s) Total ($000s) Total ($000s) Per Capita Sales Leakage 35% 45% 35% 45% FOOD AND GROCERY $ 2,876 $ 232,489 $ 161,689 $ 70,800 $ % $ 24,780 $ 31,860 82, ,201 Food $ 1,766 $ 142,728 $ 112,025 $ 30,704 $ % Food Away From Home $ 994 $ 80,366 $ 41,221 $ 39,144 $ % Alcoholic Beverages $ 116 $ 9,395 $ 8,443 $ 952 $ % MISC. PERSONAL ITEMS $ 508 $ 41,047 $ 44,287 -$ 3,240 -$ % Drugs, Medical Equipment $ 235 $ 19,030 $ 22,382 -$ 3,352 -$ % Personal Care Services, Cosmetics, etc. $ 272 $ 22,016 $ 21,905 $ 111 $ 1 0.5% HOUSEHOLD EQUIP.& SERVICES $ 536 $ 43,333 $ 16,764 $ 26,569 $ % $ 9,299 $ 11,956 30,998 39,854 Furniture $ 227 $ 18,321 $ 6,193 $ 12,128 $ % Floor Coverings $ 80 $ 6,446 $ 1,511 $ 4,934 $ % Appliances (Major & Small) $ 115 $ 9,275 $ 3,852 $ 5,423 $ % Misc. Hshld Equipment $ 115 $ 9,292 $ 5,208 $ 4,084 $ % APPAREL $ 877 $ 70,916 $ 23,187 $ 47,729 $ % $ 16,705 $ 21,478 55,683 71,593 Women's Apparel 16+ $ 362 $ 29,244 $ 9,322 $ 19,922 $ % Men's Apparel 16+ $ 199 $ 16,107 $ 5,069 $ 11,038 $ % Girl's Apparel 2 to 15 $ 41 $ 3,285 $ 959 $ 2,326 $ % Boy's Apparel 2 to 15 $ 50 $ 4,077 $ 1,193 $ 2,884 $ % Children's Apparel (<Age 2) $ 42 $ 3,359 $ 1,097 $ 2,261 $ % Footwear $ 154 $ 12,419 $ 3,877 $ 8,543 $ % Other Apparel, Acc., Svcs. $ 30 $ 2,424 $ 1,670 $ 754 $ % ELECTRONICS $ 226 $ 18,244 $ 11,974 $ 6,271 $ % $ 2,195 $ 2,822 7,316 9,406 TV, Radios, Sound Equipment $ 62 $ 5,012 $ 2,589 $ 2,423 $ % Video, CDs $ 98 $ 7,928 $ 6,149 $ 1,779 $ % Computers $ 50 $ 4,028 $ 2,751 $ 1,277 $ % Other electronics $ 16 $ 1,277 $ 485 $ 792 $ % MISCELLANEOUS $ 395 $ 31,944 $ 24,271 $ 7,672 $ % $ 2,685 $ 3,453 8,951 11,509 Reading Materials $ 139 $ 11,237 $ 8,090 $ 3,146 $ % Sporting Goods $ 57 $ 4,612 $ 3,236 $ 1,376 $ % Camera and Photo $ 42 $ 3,409 $ 4,531 -$ 1,121 -$ % Jewelry $ 59 $ 4,748 $ 3,074 $ 1,674 $ % Toys $ 98 $ 7,938 $ 5,340 $ 2,598 $ % TOTAL $ 5,418 $ 437,973 $ 282,172 $ 155,801 $ 1, % $ 55,665 $ 71, , ,562 Source: NDS/UDS Data Services, U.S. Census of Retail Trade and RKG Associates, Inc. RKG Associates, Inc. Page 18

21 D. Regional Real Estate Market Conditions Regional conditions in the office, research and development (R & D), and industrial markets are reviewed in this section. The source is a biannual survey of the Greater Boston market prepared by Spaulding and Slye Collier International (S & S). The market includes the Cities of Boston and Cambridge and seven suburban submarkets. Lynn is geographically within the North suburban market however, S & S does not track buildings in Lynn, although S & S does survey buildings in other North Shore communities such as Beverly, Danvers and Peabody. This finding is likely attributed to Lynn s location in comparison to these other communities, since they have modern business parks such as Centennial Park in Peabody, or conversions of major industrial complexes such as the Cummings Center in Beverly. Although Lynn is not included in the S & S survey, this regional review is germane to the economic development strategy since Lynn would compete for new major economic opportunities with these properties identified by S & S. It should also be added that S & S does not survey owner-occupied properties but those that are renter-occupied or investorowned. 1. Office Market Regional conditions in the office sector continue to be soft, while recovery from the recession of 2001 has been slow, and rents in 2004 are lower in many cases than in prior years. The Greater Boston market has more than 152 million square feet (m SF) of office properties, as shown in Appendix Table D-1, including 79m SF in the suburbs. The North submarket has 11.7m SF of office properties including 3.7m SF within selected towns of the Lynn region. This indicates that the Lynn region has 31% of the office supply in the North submarket. As shown below, the Lynn region has an availability rate of 29%, which is higher than indicated for the suburbs (26%) or Greater Boston (23%). Averaging asking price in the Lynn region is also lower than in the other market areas. Appendix Table D-1: Office Market Characteristics (Winter 2005) Geography Supply [1] Available [1] % Available Absorption [1,2] AVG. Asking Rent (gross) Greater Boston % 1.75 $23.43 Suburbs % 1.37 $18.57 North % (0.11) $17.78 Lynn Region % (0.09) $16.51 Beverly % (0.10) $16.81 Danvers % 0.05 $14.80 Lynnfield % (0.01) $16.50 Peabody % (0.01) $16.55 Saugus % (0.02) $19.00 [1] In millions of SF [2] Change in occupied space from prior year Source: Spaulding & Slye Office Report & RKG Associates, Inc. Absorption of office space in 2004 was negative in the Lynn region and the North submarket, as shown above. In fact, the Lynn region experienced nearly 82% of the negative absorption in the North submarket last year, with most of it occurring in Beverly. In comparison, the suburban market and the Greater Boston market experienced positive absorption in 2004, as evident by an increase of 1.4m SF and 1.8m SF in occupied office space, respectively. RKG Associates, Inc. Page 19

22 However, these are fairly weak figures in comparison to the available supply, and would suggest a fifteen to twenty-year supply of available office space within Greater Boston. 2. R & D Market The Greater Boston market has more than 49.3m SF of R & D space and 31% of it is available, as shown in Appendix Table D-2. The North submarket has 6.7m SF of R & D buildings, and the availability rate is 21%, lower than indicated for the suburbs (33%). The Lynn region has less than 25% of the North submarket supply, and the availability rate is 14%, better than indicated in the other geographies. The R& D supply in the region is fairly evenly divided between Beverly, Danvers and Peabody. Similar to the office market, asking average rental rates in the Lynn region is lower than indicated for the Greater Boston and suburban market. Appendix Table D-2: R & D Market Characteristics (Winter 2005) Geography Supply [1] Available [1] % Available Absorption [1, 2] AVG. Asking Rent (net) Greater Boston % (0.22) $9.40 Suburbs % (0.21) $9.35 North % 0.02 $8.72 Lynn Region % 0.01 $8.60 Beverly % 0.05 $12.45 Danvers % Peabody % (0.04) $8.00 [1] In millions of SF [2] Change in occupied space from prior year Source: Spaulding & Slye Office Report & RKG Associates, Inc. 3. Industrial Market The Greater Boston industrial market., as surveyed by S & S, has more than 60m SF and 23% is available, as shown in Appendix Table D-3. The North submarket has 10.5m SF or 18% of the suburban market, and the availability rate is 16% lower than indicated for Greater Boston. The Lynn region has only 10% of the North submarket, but the availability rate is higher at 25%. Interestingly, the average asking rent in the Lynn region is higher than indicated in the Greater Boston area. Absorption for industrial space was negative in 2004 in the Greater Boston areas and the suburban markets, including the North. However, absorption of industrial space in Peabody was positive, making absorption in the Lynn region also positive. Appendix Table D-3: Industrial Market Characteristics (Winter 2005) Geography Supply [1] Available [1] % Available Absorption [1,2] AVG. Asking Rent (net) Greater Boston % (1.74) 5.98 Suburbs % (1.77) 5.95 North % (0.28) 6.95 Lynn Region % 0.10 $6.19 Beverly % Danvers % (0.02) $5.50 Peabody % 0.12 $7.02 [1] In millions of SF [2] Change in occupied space from prior year Source: Spaulding & Slye Office Report & RKG Associates, Inc. RKG Associates, Inc. Page 20

23 The region has a significant supply of available space in all market sectors, and most of these properties are more modern than those available in Lynn. This supply would likely limit new construction in the near future with the exception of end-users. In addition, the Commonwealth recently announced that the Blue-Line extension to Lynn is on the 20-year transportation plan. Linking Lynn to downtown Boston via the subway system should improve the City s location as an office market destination in the future. E. Commercial and Industrial Availabilities in Lynn RKG prepared a listing of available commercial and industrial properties in Lynn from a variety of sources. One was a review of commercial and industrial property web site listings, including the one prepared by Lynn s Office of Economic and Community Development. Field observations were also utilized as well as the surveys of Lynn businesses preformed in conjunction with this project. In short, a supply of nearly 1m SF was vacant and/or available in Lynn either for-sale or for-rent, as shown in Appendix Table E-1. Listings of the individual properties are exhibited in Appendix Table E-2. Approximately 0.63m SF of industrial buildings were available in Lynn, including 0.29m SF in the Lynnway economic opportunity zone, 0.21m SF in the downtown zone, and 0.11m SF in the Central Lynn zone. Available office space represented another 24% of the available properties and nearly 75% of the office space is in the downtown. Reportedly, a portion of this available office space in the downtown was reoccupied, so the figures below may be slightly overstated. Commercial spaces including street level retail space make up the remaining 10% of the available properties, and most of the available commercial spaces are also in the downtown, as shown below. Appendix Table E-1: Building Availabilities in Lynn by Use & Economic Opportunity Zones (March 2005) Industrial Office Comm. Total Total 629, ,997 96, ,604 Lynnway 289,290 40,000 30, ,790 Downtown 214, ,047 54, ,513 Broad St/MBTA 14,000 4, ,000 Central Lynn 111,628 12,000 8, ,884 GE/Western Ave Boston/Western ,467 4,417 Lower Broadway Hospital Source: RKG Associates, Inc. Pricing for space in Lynn appears competitive with the region, as industrial space was quoted in the $4 to $6/SF range, and office and commercial space in the $10/SF to $20/SF range. The location, size, level of finish, utilities included, and amenities such as parking, can influence pricing. Lynn s downtown is currently undergoing revitalization due in part to a recent zoning change that allowed owners of existing buildings to convert the upper floors to residential use without providing on-site parking. The impact of this has created approximately 200 new RKG Associates, Inc. Page 21

24 housing units that are under-development or recently completed. Changing demographics within the downtown will eventually create new business opportunities for retail, restaurants and professional service. The City also recently completed a Lynn Downtown Workshop that identified short and long-term opportunities, and some of them are being achieved. Appendix Table E-4: Building Availabilities in Lynn (March 2005) Eco. Opp Zone Use Bldg SF Address Boston/Western Comm. 2, Franklin St Boston/Western Comm. 1, Chestnut St Boston/Western Office Chestnut St. Central Lynn Comm. 6, N. Common Central Lynn Comm. 2, Neptune Central Lynn Industrial 64, Federal St (GE Factory-Future) Central Lynn Industrial 47,000 Carr Leather Central Lynn Office 12, N. Common Diamond Dist Industrial 14, Sanderson Ave Diamond Dist Office 4, Sanderson Ave Downtown Comm. 8, Exchange Downtown Comm. 4, Exchange St Downtown Comm. 4,000 Central SQ/Mayo Downtown Comm. 6,000 Mt Vernon St under T Downtown Comm. 3,000 Fabens Building Downtown Comm. 5,000 Scattered on Union Downtown Comm. 5, Central/Olsen Downtown Comm. 5, Central/Mayo Downtown Comm. 5,000 Keith Building Downtown Comm. 1, Oxford St. Downtown Comm. 5,000 Goldblock Downtown Comm. 2, Oxford St Downtown Industrial 100,000 C Bain Downtown Industrial 53, Mt. Vernon St Downtown Industrial 50,000 Prime Bldg (537 Wash) Downtown Industrial 11, Broad St Downtown Office 5, Exchange (Edison) Downtown Office 10, Washington St Downtown Office 2, Union St Downtown Office 38, Market St (Eastern Bank) Downtown Office 105, Union St (Eastern Bank) Downtown Office 1,800 1 Market St Downtown Office 9, Oxford (Bank) Lynnway Retail 27, Lynnway Lynnway Retail 3, Lynnway Lynnway Industrial 77, Pleasant St Lynnway Industrial 100,000 Clocktower Lynnway Industrial 6, Alley St Lynnway Industrial 49, Alley St Lynnway Industrial 7, Marine Blvd Lynnway Industrial 48, Lynnway Lynnway Office 40,000 Clocktower Total 955,604 Source: Lynn Economic & Community Development website & RKG Associates, Inc. RKG Associates, Inc. Page 22

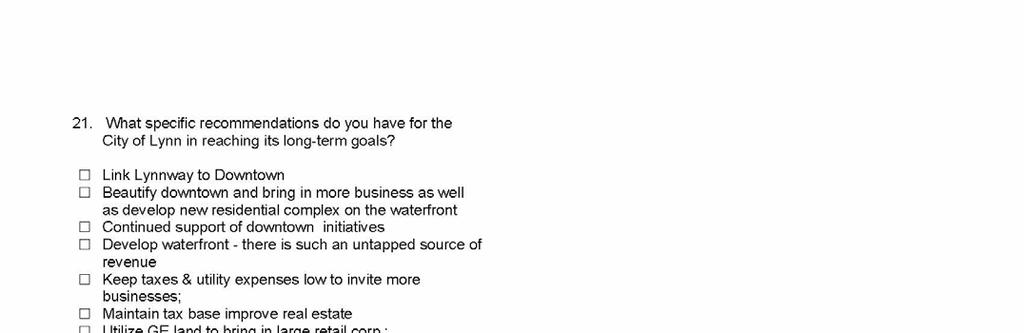

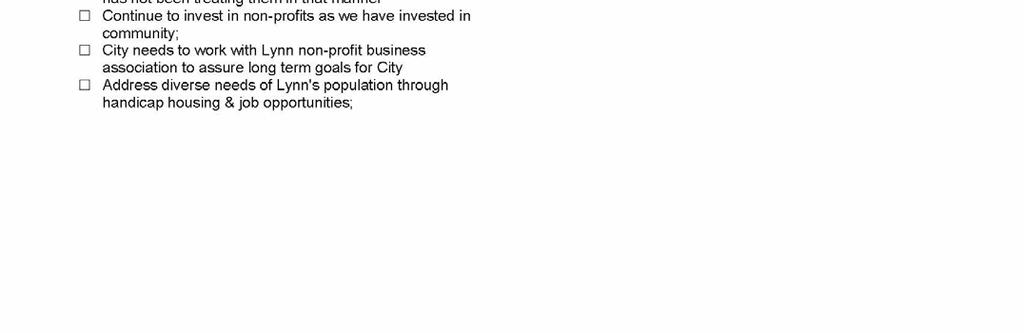

25 F. Results of a Survey of Lynn Businesses and Major Employers RKG Associates, Inc. Page 23

26 RKG Associates, Inc. Page 24

27 RKG Associates, Inc. Page 25

28 G. Lynn s Residential Median Values and Chapter 40-B Housing Figure G-1: Median values for single-family homes was $292,000 in March 2005, reflecting a 21% increase in the last year. The median condominium value was $174,900 in March 2005, which was 4% higher than the prior years. Lynn s median values have increased steadily over the last 10 or so years, but single-family value appreciated at a faster pace after 2000 such that the difference in price between single family and condominiums was much greater in 2005 than in prior years. $300,000 $250,000 $200,000 $150,000 $100,000 $50,000 MARCH City of Lynn, MA: Trends in Residential Values $ Single-Family Condominium Source: Warren Information Services & RKG Associates, inc Lynn median value for residential properties in March 2005 was lower than indicated in select communities within the region as shown below. In addition, values for both singlefamily homes and condominiums in Lynn showed continued appreciation in the last year, while median values in some communities were lower in March 2004 than in March In short, median residential values in Lynn are competitive and more affordable than in the region. Appendix Table G-1: City of Lynn Economic Development Strategy Median Residential Values in Select Communities in the Region (March, 2005) City/Town Single Family Change From 3/04 Condominium Change From 3/04 Lynn $292,000 21% $174,900 4% Beverly $348,250-4% $301,000-11% Danvers $575,000 72% $260,250-8% Lynnfield $451,000-9% N/A N/A Nahant $635,000 N/A N/A N/A Peabody $355,000 0% $208,500-17% Salem $350,000 10% $274,500 10% Saugus $377,000 6% $235,000 N/A Swampscott $430,000 19% $256,500-1% Source: Warren Information Services & RKG Associates, Inc. Chapter 40-B and Affordable Housing: Lynn had 4,479 Chapter 40B subsidized housing units, according to a May 2, 2005 subsidized housing inventory prepared by the Massachusetts Department of Housing and Community Development (DHCD). This equated to 13.0% of Lynn s year round housing supply, and indicated that Lynn exceeded the Commonwealth s goal of 10% under the provisions of Chapter 40B. It was reported in the Lynn Housing Market Study dated July 29, 2003, that there were also 2,630 households RKG Associates, Inc. Page 26

29 that leased housing in Lynn with rental vouchers or Section 8 certificates. These households in turn equate to another 7.6% of the non-seasonal housing units in Lynn. In total, more than 20% of the housing in Lynn would be considered affordable to low-income households. A review of Project Based Chapter 40B units in Table 17 on page 63 in the Lynn Housing Market Study indicate that there are six projects in downtown Lynn whose use restriction may expire between 2010 and These developments are identified in Appendix Table G-2. Exploring the conversion of these properties to market rate housing should be considered as part of the economic development strategy, since the City has exceeded the Commonwealth s goal of 10%. The market rate supply of housing would have to increase by approximately 10,000 units for the current supply of Chapter 40B to represent 10% of the housing. Alternatively, if the Chapter 40B supply were to be reduced by 1,000 units the percentage would decline to 10%. Appendix Table G-2: Selected Chapter 40-B Developments in Downtown Lynn Project Address Total Elderly Non-Elderly Exp. Year Owner Rolfe House 7 Willow St Rolfe House LP C/O SHP Mgmt. Fabens Building Union St Fabens C/O WINN Harbor Loft 7 Liberty & 678 Wash EDIC (Land) Silbseee Towers 67 Silsbee Silsbee Tower Assoc. Pinkham Apts 75 Silsbee St Unk. Greater Lynn SN Assoc Willow Apt Trust 19 Willow St EUR Willow Apt. Assoc. While the supply of Chapter 40B units represent 13% of Lynn s housing stock, the real estate taxes generated from these properties accounts for 3.3% of the residential real estate taxes. This is due in part to the tax-exempt status of the various non-profits that own these properties. Exploring ways for these tax-exempt properties to contribute to the City s tax base is recommended as a way to offset municipal service costs. H. Lynn Tax Base and Trends Lynn s tax base has been adversely impact by the changes in the City s employment base. In FY-2005, residential assessment totaled $5.55 billion and accounted for nearly 89% of the taxable assessment, as shown in Appendix Table H-1. Residential properties also generated about $56.5 million in real estate taxes or 79% of the tax levy in the City. As shown below, commercial properties represented about 7% of taxable assessment and generated 13% of the tax levy. Industrial properties contribute another 2.5% of assessment and nearly 5% of real estate taxes. Appendix Table H-1: Lynn's Tax Base in FY-2005 Assessment % of Taxable RE TAXES [1] % of Taxes Residential $5,550,211, % $56,501, % Commercial $440,961, % $9,560, % Industrial $156,419, % $3,391, % Personalty $101,672, % $2,204, % Taxable $6,249,264, % $71,656, % Tax Exempt $624,788,830 Total $6,874,053,750 [1] $10.18/1000 and $21.68/1000 Source: Lynn's Assessor's Office and RIKG Associates, Inc. RKG Associates, Inc. Page 27

30 In FY-1985, residential assessment represented about 75% of total assessment, while commercial properties accounted for another 12%, as shown in Appendix Table H-2. Personalty (personal property) also accounted for 4% of total assessment in 1985, in comparison to less than 2% in Appendix Table H-2: City of Lynn, MA Trends in Assessments by Type Property Type Assessed Value % of Total Assessed Value % of Total % Change Compounded % Change Residential $1,140,346, % $5,550,211, % 387% 8.2% Commercial $174,566, % $440,961, % 153% 4.7% Industrial $145,763, % $156,419, % 7% 0.4% Personalty $61,605, % $101,672, % 65% 2.5% Total $1,522,282, % $6,249,264, % 311% 7.3% Source: MA DLS, Lynn's Assessor Office & RKG Associates, Inc. Referring to the previous table, residential values increased by 387% between 1985 and This also equated to a compounded rate of 8.2% per year. Commercial properties increased at a much lower rate over the last twenty years, as shown above, while industrial properties experienced hardly any appreciation in value between 1985 and Personal property experienced 2.5% compounded increase in value. By way of comparison, the Consumer Price Index increased by 100% during this period, or a compounded annual rate of 3.5%. Figure H-1: Assessed values in Lynn increased from $1.5 billion in 1985 to $3.4 billion in 1991 and 1992 (127%), and then declined to $2.27 billion (- 33%) in In 2002 assessed values increased to a new high level of $3.8 billion (67%), and set new high levels in the subsequent years, including $6.25 billion in Most if not all the increase can be attributed to the residential portion of the tax base, which represented about 89% of taxable assessment in Billions $7 $6 $5 $4 $3 $2 $1 $ City of Lynn, MA Trends in Assessments (FY: ) 1987 Personalty Industrial Commercial Residential RKG Associates, Inc. Page 28

31 I. Lynn s Economic Opportunity Zones RKG identified eight economic opportunity zones within Lynn where the focus of future economic development would like be concentrated. Within these zones, nearly all of Lynn s commercial and industrial properties exist. These zones encompass about 1,610 acres representing 18% of the City s land area, and generate about 38% of the real property taxes in the City. There are nearly 12.2m SF of commercial and industrial building area, and nearly 1.0m SF is available or vacant. As shown below, 557 acres in the economic opportunity zones are residential and improved with 20.5m SF of building area, which equates to about 32% of the total residential building area in the City. However, the assessed values of residential properties in the economic development zones represent only 27% of the City s residential assessment, and average residential values in the economic zones ($74/SF) are 15% lower than the citywide standard ($87/SF). This lower value may also be attributed to a higher density (FAR) of residential properties in the economic opportunity zones (84%) versus the citywide standard (28%). Appendix Table I-1: Assessment Summary of the City of Lynn and the Economic Opportunity Zones City of Lynn Use Acres Gross Bldg SF Assessment RE Taxes Assmt/SF FAR [1] Residential 5,279 63,910,862 $5,550,211,903 $56,501,157 $87 28% Commercial 441 7,254,460 $440,961,667 $9,560,049 $61 38% Industrial 470 6,226,448 $156,419,200 $3,391,168 $25 30% Tax-Exempt 2,811 7,655,841 $624,788,830 $0 $82 6% Total 9,001 85,047,611 $6,772,381,600 $69,452,374 $80 22% Economic Opportunity Zones Use Acres Gross Bldg SF Assessment RE Taxes Assmt/SF FAR [1] Residential ,486,778 $1,517,584,200 $15,449,007 $74 84% Commercial 329 6,072,202 $362,985,600 $7,869,528 $60 42% Industrial 411 6,159,506 $147,572,700 $3,199,376 $24 34% Tax-Exempt 311 5,061,511 $323,135,000 $0 $64 37% Total 1,608 37,779,997 $2,351,277,500 $26,517,911 $62 54% Economic Opportunity Zones as % of City and Difference from City Standard Use Acres Gross Bldg SF Assessment RE Taxes Assmt/SF FAR [1] Residential 11% 32% 27% 27% -15% 204% Commercial 75% 84% 82% 82% -2% 12% Industrial 88% 99% 94% 94% -5% 13% Tax-Exempt 11% 66% 52% % 497% Total 18% 44% 35% 38% -22% 149% [1] FAR-Floor area ratio is an indication of density (the higher the % the more built-out) Source: Lynn's Assessors Office and RKG Associates, inc. The commercial properties in the economic opportunity zones consist of 329 acres and more than 6.0m SF of building area, and have an assessed value of $363.0 million. Commercial properties in the economic opportunity zones represent 75% of the city s commercial land area, and 85% of the city s commercial building area, and 82% of the City s commercial assessment and real estate taxes. The average commercial assessed value per SF in the opportunity zones is 2% lower than the citywide standard, and density or FAR is about 12% higher. RKG Associates, Inc. Page 29

32 Industrial properties in the economic opportunity zones consist of 411 acres, and 6.2m SF of building area, and have an assessed value of $147.6 million. Industrial properties in these eight zones represent 88% of the industrial land area in the City, and 99% of the industrial building area. The industrial assessment in the eight zones and the real estate taxes generated from industrial properties represent 94% of the citywide industrial tax levy. The economic opportunity zones contain more than 310 acres of properties owned by taxexempt entities including the City of Lynn, the Commonwealth, churches and religious organizations and non-profits entities. This land is improved with 5.5 million SF of building area that has an assessed value of $202.9 million although real property taxes are not generated from these properties. These properties contain nearly two-thirds of the taxexempt building area in the City. Appendix Table I-2: Assessment Summary of the Economic Opportunity Zones Economic Opp. Zones Acres Gross Bldg SF Total Assessment RE TAX Assmt/SF FAR Downtown 168 5,482,870 $282,518,400 $3,426,080 $52 75% Central Lynn ,296,815 $742,537,700 $6,860,142 $66 71% Lynnway 370 3,414,826 $200,999,600 $3,895,885 $59 21% GE/Western Ave ,850,516 $172,583,900 $2,330,083 $36 45% Broad St/MBTA 150 5,848,928 $397,602,000 $3,960,161 $68 89% Boston/Western 187 4,713,689 $355,740,300 $4,339,886 $75 58% Lower Broadway 74 1,581,133 $139,172,100 $1,368,237 $88 49% Hospital ,220 $60,123,500 $337,438 $102 28% Total 1,608 37,779,997 $2,351,277,500 $26,517,911 $62 54% Economic Opportunity Zones as % of City and Difference from City Standard Economic Opp. Zones Acres Gross Bldg SF Total Assessment RE TAX Assmt/SF FAR Downtown 1.9% 6.4% 4.2% 4.9% -35% 246% Central Lynn 4.1% 13.3% 11.0% 9.9% -17% 228% Lynnway 4.1% 4.0% 3.0% 5.6% -26% -2% GE/Western Ave. 2.7% 5.7% 2.5% 3.4% -55% 108% Broad St/MBTA 1.7% 6.9% 5.9% 5.7% -15% 311% Boston/Western 2.1% 5.5% 5.3% 6.2% -5% 167% Lower Broadway 0.8% 1.9% 2.1% 2.0% 11% 127% Hospital 0.5% 0.7% 0.9% 0.5% 28% 31% Total 17.9% 44.4% 34.7% 38.2% -22% 149% Source: Lynn's Assessors Office and RKG Associates, inc. Non-profits organizations are another part of Lynn s tax base, and according to the assessor s classification codes, charitable organizations (906) are listed as the owners of more than 0.5 million square feet (SF) of building area having an assessed value of nearly $34.0 million, although they are exempt from real estate taxes. The Downtown economic opportunity zone contains 168 acres, or 2% of the city s acreage. It is improved with 5.48m SF of building area or 6.4% of the city s building supply. The average assessed value per SF in the downtown is 35% lower than the citywide standard, as show in Table I-2. The downtown generates about 5% of the City s real property tax levy. Residential uses are improved on 14% of the acreage in the downtown, while accounting for 25% of the building area. Residential uses contribute about 25% of the taxes generated RKG Associates, Inc. Page 30

33 downtown, although the average residential value is about 28% below the citywide standard as shown in Appendix Table I-3. Commercial uses are improved on 42%of the downtown acreage, and commercial buildings account for 40% of the building area in the downtown, but the real estate taxes from commercial properties contribute 68% of the total from the downtown, despite the fact that commercial assessment per SF are 19% lower than the citywide standard, as shown below. Appendix Table I-3: Assessment Summary of the Downtown Economic Opportunity Zone Use Acres Gross Bldg SF Assessment RE Taxes Assmt/SF FAR Residential 24 1,379,825 $86,557,300 $881,153 $63 135% Commercial 71 2,177,925 $107,885,900 $2,338,966 $50 70% Industrial 6 404,926 $9,500,000 $205,960 $23 166% Tax-Exempt 67 1,520,194 $78,575,200 $0 $52 52% Total 168 5,482,870 $282,518,400 $3,426,080 $52 75% Downtown Opportunity Zones as % of City and Difference from City Standard Use Acres Gross Bldg SF Assessment RE Taxes Assmt/SF FAR Residential 0% 2% 2% 2% -28% 384% Commercial 16% 30% 24% 24% -19% 86% Industrial 1% 7% 6% 6% -7% 446% Tax-Exempt 2% 20% 13% % 730% Total 2% 6% 4% 5% -35% 246% Source: Lynn's Assessors Office and RKG Associates, inc. Tax-exempt properties utilized 40% of the land area in the downtown, and they are improved with 27% of the building area. These properties however don t contribute taxes. The Central Lynn economic opportunity zone contains 4% of the city s land area, and 13% of the building area, as shown below. Real estate taxes from Central Lynn account for 10% of total taxes, and the average assessed value per SF is 17% lower than the citywide average. Appendix Table I-4: Assessment Summary of the Central Lynn Economic Opportunity Zone Use Acres Gross Bldg SF Assessment RE Taxes Assmt/SF FAR Residential 194 7,776,195 $546,931,900 $5,567,767 $70 92% Commercial ,793 $42,027,300 $911,152 $50 56% Industrial ,097 $17,584,100 $381,223 $31 34% Tax-Exempt 99 2,121,730 $135,994,400 $0 $64 49% Total ,296,815 $742,537,700 $6,860,142 $66 71% Central Lynn Opportunity Zone as % of City and Difference from City Standard Use Acres Gross Bldg SF Assessment RE Taxes Assmt/SF FAR Residential 4% 12% 10% 10% -19% 232% Commercial 8% 12% 10% 10% -17% 48% Industrial 8% 9% 11% 11% 25% 13% Tax-Exempt 4% 28% 22% % 683% Total 4% 13% 11% 10% -17% 228% Source: Lynn's Assessors Office and RKG Associates, inc. Residential properties in Central Lynn are improved on 52% of the acreage and residential buildings represent 69% of the building area. Residential taxes generate about 81% of the taxes in Central Lynn, although the average residential value is about 19% lower than the citywide standard. RKG Associates, Inc. Page 31

34 Tax-exempt uses are developed on 27% of the land in Central Lynn, and have 19% of the building area. However, these properties don t generate real estate taxes. Commercial properties utilize another 9% of the land area, and they are improved with 7% of the building area in Central Lynn. The real estate taxes from commercial properties account for 13% of the taxes from Central Lynn, although commercial values are 17% lower than citywide. The Lynnway economic opportunity zone also contains about 4% of the city s land area and 4% of the building area. The Lynnway generates about 6% of the real estate taxes, although values here are 26% lower than the citywide standard. The FAR in the Lynnway (21%) is the lowest among the eight opportunity zones, indicating this zone is the most underdeveloped in comparison to the others. Appendix Table I-5: Assessment Summary of the Lynnway Economic Opportunity Zone Use Acres Gross Bldg SF Assessment RE Taxes Assmt/SF FAR Residential 7 196,040 $15,389,200 $156,662 $79 63% Commercial 114 1,716,820 $107,923,600 $2,339,784 $63 35% Industrial 203 1,372,108 $64,549,800 $1,399,440 $47 16% Tax-Exempt ,858 $13,137,000 $0 $101 6% Total 370 3,414,826 $200,999,600 $3,895,885 $59 21% Lynnway Opportunity Zone as % of City and Difference from City Standard Use Acres Gross Bldg SF Assessment RE Taxes Assmt/SF FAR Residential 0% 0% 0% 0% -10% 126% Commercial 26% 24% 24% 24% 3% -8% Industrial 43% 22% 41% 41% 87% -49% Tax-Exempt 2% 2% 2% -- 24% 4% Total 4% 4% 3% 6% -26% -2% Source: Lynn's Assessors Office and RKG Associates, inc. Nearly 55% of the land area in the Lynnway is industrial properties and industrial properties in the Lynnway generated 41% of the industrial real estate taxes in the City as shown above. Industrial values in the Lynnway are 87% higher than the citywide standard. In comparison, commercial values are only 3% higher than commercial values citywide. The GE-Riverworks/Western Avenue economic opportunity zone consists of 247 acres of 3% of the city s acreage, as shown in the following table. This zone is improved with more than 4.85m SF of building area, or 6% of the building area in the City. The taxes generated from this zone represent 3% of those in the City, and average assessed values per SF are 55% lower than the citywide standard as shown in Appendix Table I-6. Industrial properties represent 61% of the land area in this zone and 65% of the building area. The real estate taxes from industrial properties in this zone account for more than 27% of the industrial taxes in the City, although the average assessed value per SF for industrial properties is 46% lower than indicated citywide. Residential properties represent 18% of the land area and 29% of the building area. The taxes from residential uses account for 48% of the taxes generated in this zone. However, residential values are 8% lower than the citywide standard. RKG Associates, Inc. Page 32

35 Appendix Table I-6: Assessment Summary of the GE-Riverworks/Western Ave. Economic Opportunity Zone Use Acres Gross Bldg SF Assessment RE Taxes Assmt/SF FAR Residential 45 1,386,448 $110,311,500 $1,122,971 $80 70% Commercial ,007 $13,295,700 $288,251 $71 12% Industrial 150 3,152,947 $42,382,900 $918,861 $13 48% Tax-Exempt ,114 $6,593,800 $0 $54 19% Total 247 4,850,516 $172,583,900 $2,330,083 $36 45% GE-Riverwork/Western Ave. Opportunity Zone as % of City and Difference from City Standard Use Acres Gross Bldg SF Assessment RE Taxes Assmt/SF FAR Residential 1% 2% 2% 2% -8% 153% Commercial 8% 3% 3% 3% 16% -69% Industrial 32% 51% 27% 27% -46% 59% Tax-Exempt 1% 2% 1% % 197% Total 3% 6% 3% 3% -55% 108% Source: Lynn's Assessors Office and RKG Associates, inc. The Broad Street/MBTA Corridor economic opportunity zone contains 150 acres, or 2% of the city, which are improved with 5.8 million SF or 7% of the City s building area. The taxes generated from this economic opportunity zone represent 6% of total taxes in the City. This zone has the highest FAR (89%) and average assessed value per SF is 15% lower than the citywide standard. Appendix Table I-7: Assessment Summary of the Broad Street/MBTA Corridor Economic Opportunity Zone Use Acres Gross Bldg SF Assessment RE Taxes Assmt/SF FAR Residential 108 4,704,490 $348,228,600 $3,544,967 $74 100% Commercial 9 210,410 $12,294,500 $266,545 $58 53% Industrial ,648 $6,856,500 $148,649 $16 98% Tax-Exempt ,380 $30,222,400 $0 $60 50% Total 150 5,848,928 $397,602,000 $3,960,161 $68 89% Broad St./MBTA Opportunity Zone as % of City and Difference from City Standard Use Acres Gross Bldg SF Assessment RE Taxes Assmt/SF FAR Residential 2% 7% 6% 6% -15% 260% Commercial 2% 3% 3% 3% -4% 39% Industrial 2% 7% 4% 4% -37% 221% Tax-Exempt 1% 7% 5% % 694% Total 2% 7% 6% 6% -15% 311% Source: Lynn's Assessors Office and RKG Associates, inc. Residential properties utilize 72% of the land area and contain 80% of the building area. However, residential values are 15% below citywide standards in this zone. Tax exempt uses own 15% of the land area, and these properties are improved with 9% of the building area. Industrial uses are contained on 7% of the land area in this zone, and contribute less than 4% of the real estate taxes generated in this zone. The industrial taxes from these properties also represent 4% of the industrial taxes citywide. The Boston Street/Western Avenue economic opportunity zone contains 187 acres, or 2% of the city, and it is improved with 4.7m SF of building area. The real estate taxes generated from here represent 6% of those in the city. The average assessed value per SF is about 5% lower than the citywide standard. However, the average assessed value for commercial properties in this zone are 38% higher than the citywide standard, and the average for industrial properties in the zone is about 13% higher, as shown below. RKG Associates, Inc. Page 33

36 Appendix Table I-8: Assessment Summary of the Boston St./Western Ave. Economic Opportunity Zone Use Acres Gross Bldg SF Assessment RE Taxes Assmt/SF FAR Residential 103 3,527,977 $268,124,600 $2,729,508 $76 78% Commercial ,331 $67,606,000 $1,465,698 $84 32% Industrial 6 235,780 $6,673,400 $144,679 $28 97% Tax-Exempt ,601 $13,336,300 $0 $91 16% Total 187 4,713,689 $355,740,300 $4,339,886 $75 58% Boston St./Western Ave. Opportunity Zone as % of City and Difference from City Standard Use Acres Gross Bldg SF Assessment RE Taxes Assmt/SF FAR Residential 2% 6% 5% 5% -12% 182% Commercial 13% 11% 15% 15% 38% -14% Industrial 1% 4% 4% 4% 13% 219% Tax-Exempt 1% 2% 2% -- 11% 154% Total 2% 6% 5% 6% -5% 167% Source: Lynn's Assessors Office and RKG Associates, inc. Tax-exempt properties utilize 11% of the land area in the Boston Street/Western Avenue opportunity zone, but they do not contribute any real estate taxes. The Lower Broadway economic opportunity zone consists of 74 acres or less than 1% of the City, which is improved with 1.58m SF of building area, or 2% of the city s building area, as shown above. The real estate taxes generated from this economic opportunity zone represents 2% of the City. The average assessed value per SF is 11% higher in this zone than the citywide standard. Appendix Table I-9: Assessment Summary of the Lower Broadway Economic Opportunity Zone Use Acres Gross Bldg SF Assessment RE Taxes Assmt/SF FAR Residential 49 1,216,936 $111,267,900 $1,132,707 $91 57% Commercial 5 123,981 $10,837,900 $234,966 $87 53% Industrial 0 0 $26,000 $ % Tax-Exempt ,216 $17,040,300 $0 $71 29% Total 74 1,581,133 $139,172,100 $1,368,237 $88 49% Lower Broadway Opportunity Zone as % of City and Difference from City Standard Use Acres Gross Bldg SF Assessment RE Taxes Assmt/SF FAR Residential 1% 2% 2% 2% 5% 105% Commercial 1% 2% 2% 2% 44% 41% Industrial 0% 0% 0% 0% Tax-Exempt 1% 3% 3% % 358% Total 1% 2% 2% 2% 11% 127% Source: Lynn's Assessors Office and RKG Associates, inc. Residential properties utilize about 66% of the land area in this zone, and 77% of the building area. The average residential value in this zone is about 5% higher than citywide. Commercial properties account for 7% of the land area, and 8% of the building area in this zone, but contribute more than 17% of the real property taxes generated in this zone. The average commercial value per SF in the Lower Broadway zone is 44% higher than the citywide standard. Tax-exempt properties utilize 26% of the land area in the Lower Broadway zone, but don t contribute to the real estate tax levy. RKG Associates, Inc. Page 34

37 The Hospital economic opportunity zone contains 48 acres and 0.59m SF of building area. Residential uses account for 56% of the land area and 51% of the building area. Real estate taxes from residential uses account for 93% of the property taxes from this zone, and the real estate taxes generated from this zone equates to less than 1% of the city s real property tax levy, as shown below. Appendix Table I-10: Assessment Summary of the Hospital Economic Opportunity Zone Use Acres Gross Bldg SF Assessment RE Taxes Assmt/SF FAR Residential ,867 $30,773,200 $313,271 $103 25% Commercial 1 14,935 $1,114,700 $24,167 $75 24% Industrial 0 0 $0 $ Tax-Exempt ,418 $28,235,600 $0 $102 33% Total ,220 $60,123,500 $337,438 $102 28% Hospital Opportunity Zone as % of City and Difference from City Standard Use Acres Gross Bldg SF Assessment RE Taxes Assmt/SF FAR Residential 1% 0% 1% 1% 19% -8% Commercial 0% 0% 0% 0% 23% -37% Industrial 0% 0% 0% 0% Tax-Exempt 1% 4% 5% -- 25% 422% Total 1% 1% 1% 0% 28% 31% Source: Lynn's Assessors Office and RKG Associates, inc. The next pages contain two maps of the City of Lynn. This first illustrates the current land uses and the location of these eight economic opportunity zones. The second map exhibits the zoning districts in the City and the eight economic opportunity zones. These maps are followed by the base maps for the individual economic opportunity zones. Each zone has a map exhibiting land use characteristics, existing zoning districts and an aerial photograph. Two additional maps are included in the Central Lynn, GE-Riverworks/Western Avenue, Broad Street/MBTA Corridor and Boston Street/Western Avenue opportunity zones. The first one identifies the residential characteristics by type in each of these four zones, and the second identifies the range in value difference from the citywide standards of the residential properties. These additional maps are intended to assist the Office of Economic and Community Development in their neighborhood revitalization strategy. Tables identifying the land use characteristics in each zone are included in the following sections. A listing of available buildings in each economic opportunity zone is also presented, as well as a table summarizing the number of residential properties by the range of deviation in building value from the citywide standard in those specific zones. RKG Associates, Inc. Page 35

38 Current Land Use Conditions and Opportunity Zones City of Lynn, Massachusetts L Y N N F I E L D P E A B O D Y Hospital Zone # S A L E M Lower Broadway Zone # S W A M P S C O T T Boston Street/Western Avenue Zone S A U G U S # Broad Street/MBTA Corridor Zone Central Lynn Zone # # Legend Residential Industrial Utilities Office/Bank/Medical Retail/Services Auto Sales/Service Parking Facilities Open Space/Park/Cemetary Church/Non-Profit/School/Colleg Government Undeveloped Land Saleable/Tax Title Opportunity Zone GE-Riverworks/Western Avenue Zone # Lynnway Zone # L y n n H a r b o r # W Downtown Zone N S E N a h a n t B a y State Route Water Body Land Use and Opportunity Zone Map prepared by RKG Associates, Inc. May, 2005 Map data provided by MASSGIS and the City of Lynn

39 Zoning Districts City of Lynn, Massachusetts L Y N N F I E L D P E A B O D Y Hospital Zone # S A L E M Lower Broadway Zone # S W A M P S C O T T Boston Street/Western Avenue Zone S A U G U S # Broad Street/MBTA Corridor Zone Central Lynn Zone # # GE-Riverworks/Western Avenue Zone # N a h a n t B a y # Legend # L y n n H a r b o r Downtown Zone Business District Business District Class 3 Central Business District Heavy Industry District Light Industry District Park/Cemetary District Single Family District General Residential District Apartment House Class 1 Apartment House Class 2 High Rise District Opportunity Zone Waterfront Incentive Overlay District CBD Overlay Zone Water Body Lynnway Zone W Zoning District Map prepared by RKG Associates, Inc. Base map data provided by the City of Lynn Zoning data provided by MASSGIS and the City of Lynn Zoning district data current as of 1999 N S E

40 1. Downtown a) Current Land Uses Current Land Use by Type in the Downtown Economic Opportunity Zone Use Acres % of Total Bldg SF % of Total Assessed Value % of Total AV/SF FAR Residential [1] % 1,783, % $106,511, % $60 166% Industrial 7 4.0% 479, % $10,535, % $22 162% Utilities 1 0.7% 70, % $2,219, % $31 147% Banks, Office, Medical % 943, % $47,444, % $50 135% Retail, Services % 1,016, % $40,245, % $40 86% Auto Sales, Services 4 2.2% 50, % $3,809, % $75 31% Parking Garages, Lots % 354, % $14,493, % $41 51% Undeveloped Land % 7, % $9,483, % -- 1% Non-Profits 5 2.7% 267, % $8,762, % $33 135% Schools & Colleges % 137, % $20,109, % $147 21% Religious Properties 1 0.9% 59, % $2,254, % $38 94% Tax-Title Properties % 0 0.0% $547, % -- 0% Government % 275, % $16,533, % $60 33% Open Space 6 3.8% 21, % $1,914, % $91 8% Total % 5,482, % $282,518, % $52 75% [1] Includes tax-exempt residential Source: Lynn's Assessors Office and RKG Associates, Inc. b) Building Availabilities Building Availabilities in the Downtown Economic Opportunity Zone Industrial Office Comm/Retail Bldg SF Address Bldg SF Address Bldg SF Address 100,000 C Bain 5, Exchange (Edison) 8, Exchange 53, Mt. Vernon St 10, Washington St 4, Exchange St 50,000 Prime Bldg (537 Wash) 2, Union St 4,000 Central SQ/Mayo 11, Broad St 38, Market St (Eastern Bank) 6,000 Mt Vernon St under T 105, Union St (Eastern Bank) 3,000 Fabens Building 1,800 1 Market St 5,000 Scattered on Union 9, Oxford (Bank) 5, Central/Olsen 5, Central/Mayo 5,000 Keith Building 1, Oxford St. 5,000 Goldblock 2, Oxford St RKG Associates, Inc. Page 38

41 Current Land Use Downtown Opportunity Zone City of Lynn, Massachusetts Legend Residential Industrial Utilities Office/Bank/Medical Retail/Services Auto Sales/Service Parking Facilities Open Space/Park/Cemetary Church/Non-Profit/School/Colleg Government Undeveloped Land Saleable/Tax Title Opportunity Zone Boundary Building Water Body Central Avenue Market Street MBTA Rail Line Lynnway Broad Street W N S E Miles Opportunity Zone map prepared by RKG Associates, Inc. May, 2005 Map data provided by the City of Lynn

42 Zoning Districts Downtown Opportunity Zone City of Lynn, Massachusetts Central Avenue Market Street Legend Business District Business District Class 3 Central Business District Heavy Industry District Light Industry District Park/Cemetary District Single Family District General Residential District Apartment House Class 1 Apartment House Class 2 High Rise District Building Opportunity Zone Boundary MBTA Rail Line Lynnway Broad Street W N S E Miles Zoning District map prepared by RKG Associates, Inc. May, 2005 Map data provided by MASSGIS and the City of Lynn

43 Zoning Districts Downtown Opportunity Zone City of Lynn, Massachusetts Central Avenue Market Street Legend Business District Business District Class 3 Central Business District Heavy Industry District Light Industry District Park/Cemetary District Single Family District General Residential District Apartment House Class 1 Apartment House Class 2 High Rise District Building Opportunity Zone Boundary MBTA Rail Line Lynnway Broad Street W N S E Miles Zoning District map prepared by RKG Associates, Inc. May, 2005 Map data provided by MASSGIS and the City of Lynn

44 2. Central Lynn a) Current Land Uses Current Land Uses by Type in the Central Lynn Economic Opportunity Zone Use Acres % of Total Bldg SF % of Total Assessed Value % of Total AV/SF FAR Residential [1] % 8,387, % $588,831, % $70 93% Industrial % 786, % $22,018, % $28 51% Utilities 0 0.0% 0 0.0% $39, % Banks, Office, Medical 4 1.2% 125, % $7,771, % $62 68% Retail, Services % 375, % $19,971, % $53 78% Auto Sales, Services 6 1.7% 99, % $5,418, % $55 38% Parking Garages, Lots 4 1.1% 0 0.0% $2,073, % Undeveloped Land % 0 0.0% $1,724, % Tax-Title Properties 0 0.0% 0 0.0% $90, % Non-Profits 4 1.0% 110, % $5,535, % $50 68% Schools & Colleges % 820, % $54,113, % $66 62% Churches % 362, % $22,049, % $61 62% Government 9 2.4% 223, % $8,111, % $36 58% Open Space, Parks, Cemeteries % 4, % $4,789, % Total % 11,296, % $742,537, % $66 71% Source: Lynn's Assessors Office and RKG Associates, Inc. b) Building Availabilities Building Availabilities in the Central Lynn Economic Opportunity Zone Industrial Office Comm/Retail Bldg SF Address Bldg SF Address Bldg SF Address 64, Federal St (GE FofF) 12, N. Common 6, N. Common 47,000 Carr Leather 2, Neptune c) Residential Properties by Assessed Values Residential Parcels in Central Lynn Economic Opportunity Areas by Building Assessed Values Range in Difference from City AVG/SF [1] Mixed S/F 2/F 3/F Multiple 4 to 8 9 or + Boarding Other Conc. Total % of Total 26% or More % 11% to 25% % 10% to -10% % -25% to -11% % -26% or more % Total , % % of Total 3% 38% 25% 24% 1% 6% 3% 0% 0% 100% [1] Citywide average value per SF is mixed use ($61); S/F ($105); 2/F ($92); 3/F ($89); Multiple ($93); 4 to 8 ($73); 9 or more ($48); Boarding ($54); other ($34) Source: Lynn's Assessors Office and RKG Associates, Inc. RKG Associates, Inc. Page 42

45 Boston Street Current Land Use Central Lynn Opportunity Zone City of Lynn, Massachusetts Harwood Street Federal Street Legend Waterhill Street Residential Industrial Utilities Office/Bank/Medical Retail/Services Auto Sales/Service Parking Facilities Open Space/Park/Cemetary Church/Non-Profit/School/Colleg Government Undeveloped Land Saleable/Tax Title Opportunity Zone Boundary Building Water Body Western Avenue Summer Street North Common Street South Common Street Neptune Street Commercial Street Blossom Street N W S E Miles Opportunity Zone map prepared by RKG Associates, Inc. May, 2005 Map data provided by the City of Lynn

46 Boston Street Zoning Districts Central Lynn Opportunity Zone City of Lynn, Massachusetts Harwood Street Federal Street Legend Waterhill Street North Common Street South Common Street Blossom Street Business District Business District Class 3 Central Business District Heavy Industry District Light Industry District Park/Cemetary District Single Family District General Residential District Apartment House Class 1 Apartment House Class 2 High Rise District Building Opportunity Zone Boundary Western Avenue Summer Street Neptune Street Commercial Street W N S E Miles Zoning District map prepared by RKG Associates, Inc. May, 2005 Map data provided by MASSGIS and the City of Lynn

47 Blossom Street W Aerial Photograph Central Lynn Opportunity Zone City of Lynn, Massachusetts N E S Miles Opportunity Zone graphic prepared by RKG Associates, Inc. May, 2005 Graphic data provided by MASSGIS Harwood Street Boston Street Federal Street Waterhill Street North Common Street South Common Street Commercial Street Summer Street Neptune Street Western Avenue

48 Boston Street Residential Property Type Central Lynn Opportunity Zone City of Lynn, Massachusetts Harwood Street Federal Street Waterhill Street Common Street South Common Street Blossom Street Type of Residential Use Single Family 2 to 3 Units 4 to 8 Units 9 or More Units Mutiple Housing Mixed Use Boarding House Other Congregate Central Lynn Zone Boundary Western Avenue Summer Street NorthCommercial Street Neptune Street N W S E Miles Residential Property map prepared by RKG Associates, Inc. May, 2005 Map data provided by the City of Lynn

49 Boston Street North Common Street South Common Street Comparison of Residential Building Value (per Square Foot) to Citywide Standard Central Lynn Opportunity Zone City of Lynn, Massachusetts Harwood Street Federal Street Blossom Street Waterhill Street % Deviation from Citywide Average 26% or More 11% to 25% 10% to -10% -11% to -25% -26% or More Central Lynn Zone Boundary Western Avenue Summer Street Neptune Street Commercial Street N W S E Miles Building Value map prepared by RKG Associates, Inc. May, 2005 Map data provided by the City of Lynn