2010 Property Values and Assessment Practices Report (Assessment Year 2009)

|

|

|

- Nathaniel Morrison

- 6 years ago

- Views:

Transcription

1 This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project Property Values and Assessment Practices Report (Assessment Year 2009) A report submitted to the Minnesota State Legislature pursuant to Laws 2001, First Special Session, Chapter 5, Article 3, Section 92 Property Tax Division Minnesota Department of Revenue March 1, 2010

2

3 March 1, 2010 To the members of the Legislature of the State of Minnesota: I am pleased to present to you the eighth annual Property Values and Assessment Practices Report undertaken by the Department of Revenue in response to Minnesota Laws 2001, First Special Session, Chapter 5, Article 3, Section 92. This report provides a summary of assessed property values and assessment practices within the state of Minnesota. This year s report does not include summaries of market value trends by county. However, this information is available on request to the Property Tax Division. Sincerely, Ward L. Einess Commissioner i

4 Per Minnesota Statute 3.197, any report to the legislature must contain at the beginning of the report the cost of preparing the report, including any costs incurred by another agency or another level of government. The estimated cost to prepare this report was $2,800. ii

5 Table of Contents Executive Summary...1 Introduction...3 Overview of the Department of Revenue s Role...3 System Basics...4 Sales Ratio Studies and 2009 Assessment Year Results...8 Statewide values and assessment practices indicators...9 Chart 1: Growth in EMV, TMV and excluded value Charts 2-6: Average annual change in market value by property type...11 Map 1: Percent change in estimated market value Map 2: New construction as a percent of total estimated market value Maps 3-4: Median sales and trimmed coefficient of dispersion ratios by property type...15 Map 5: Fixed outlier index for residential property...17 Summary of State Board of Equalization Orders...18 Map 6: Number of property types affected by 2009 State Board Orders...20 Map 7: Percent of city/town jurisdictions affected by 2009 State Board Orders...21 Appendix 1: Summary of State Board Orders...22 Appendix 2: Glossary...28 Appendix 3: 21-month Study...30 References...31 iii

6 Executive Summary This report analyzes the assessment of 6 types of property: Residential/Seasonal, Apartments, Commercial-Industrial, Resorts, Farms, and Timber. The real estate market continued to slow down throughout Minnesota with the number of sales declining for all property classes through the fall of 2008 except for the agricultural class. These trends have continued beyond the reporting period, with the number of agricultural sales also slowing in calendar year Changes to the classification system became effective for the 2009 assessment. The change was away from the former agricultural classification system to 2a agricultural and 2b rural vacant land distinctions. The changes are described in a separate report to the legislature, Assessment and Classification Practices Report: The Agricultural Property Tax Program, Class 2a Agricultural Property and Class 2b Rural Vacant Land Property. The changes caused some property to change classification among agricultural, residential and seasonal recreational classes. Statewide assessor had to change the property classification on about 450,000 of the 2,726,507 taxable parcels. The reclassification and review is ongoing. The classification changes to agricultural, timber, seasonal residential and residential properties made it impossible to use the traditional measures of assessment performance for the 2009 assessment year. Changes in level of assessment are mingled with class shifts so that the 2008 and 2009 classes do not contain the same properties. The Department requested special reporting from the counties in order to judge whether they met the requirements that the median ratio of agricultural properties were between 90% and 105%. Counties submitted preliminary market value by parcel files which were matched with the 2008 sales data. The resulting sales ratios were used to judge the quality of assessment. In counties that were not able to supply preliminary market value files, a review of sold and a sample of unsold properties was conducted. For the 2010 assessment the Department will require preliminary market value files from all counties. Assessment quality remained relatively consistent between the 2008 and 2009 assessments. This is reflected in both of the primary measures of assessment quality, the sales ratio and the coefficient of dispersion. As a general rule, both sales ratios and coefficients of dispersion are better in classes with more sales activity. The coefficient of dispersion (COD) measures the uniformity of assessments. The coefficients generally were within the International Association of Assessing Officers (IAAO) acceptable ranges in counties that had an adequate sample of sales. The IAAO ranges are shown on page 8, in Table 4. A sales ratio measures how close assessors values are to the ultimate sales price of property. The statewide median sales ratios for the 6 property types were all in the targeted 90% to 105% range. Most ratios were down slightly from 2008 as assessors reacted to the weakening market in many areas. For agricultural, resort, and timber properties, the median in 2009 was slightly higher than in 2008 due to a continuation of strong real estate markets in those sectors. Assessors made smaller value changes for 2009 than in any year since The estimated market value for the farm and other classes was the only one that grew by more than 1%. In the period from 2000 through 2006 all values increased by at least 10% annually, but the statewide 1

7 values for residential property declined between 2007 and 2008 and have continued to decline in this study period and the period following the end of this study. Between 2008 and 2009, many counties reported market value decreases in a number of property types. See Table 1. Type Number of counties with decreased value Statewide change in value Residential % Apartment % Seasonal % Farm % Comm/Industrial % Other* % Table 1 *The overall increase in the other type is mainly due changes in public utility valuations. 2

8 2010 PROPERTY VALUES AND ASSESSMENT PRACTICES REPORT (ASSESSMENT YEAR 2009) Introduction During the 2001 special legislative session, the state legislature mandated an annual report from the Department of Revenue on property tax values and assessment practices within the state of Minnesota. This year, 2010, is the eighth annual report on such data and practices to the legislature. As outlined in Laws 2001, First Special Session, Chapter 5, Article 3, Section 92, the report contains information by major types of property on a statewide basis and at various jurisdictional levels. In accordance with that law, this report consists of: recent market value trends, including projections; trend analysis of excluded market value; shift in share analysis detailing the impact of market value trends on the proportional tax burden of major classes of property; assessment quality indicators, including sales ratios and coefficients of dispersion for counties; a summary of State Board Orders. The purpose of this report is to provide the legislature with an accurate snapshot of the current state of property tax assessment, as well as an overview of the Department of Revenue s responsibility to oversee the state s property tax assessment process. This report provides a vehicle for an ongoing, systematic collection of property value data for the purpose of monitoring and analyzing underlying value trends and assessment quality indicators. This information and analysis is used to satisfy the Department s responsibility to inform government officials and the public about valuation trends within the property tax system. Overview of the Revenue Department s Role Property taxes are an important source of revenue for all local units of government in the state (cities, townships, school districts, special taxing districts, and counties). As such, the responsibility that it be administered fairly and uniformly is a paramount responsibility of the Department of Revenue. This responsibility is reflected in the primary objective of the Property Tax Division at the Department of Revenue: to ensure the proper administration of, and compliance with, property tax laws. The Property Tax Division measures compliance with property tax laws through: 1. The State Board of Equalization, which ensures that property taxpayers pay their fair share no more and no less. The Commissioner of Revenue, acting as the State Board of Equalization, has the authority to issue orders increasing or decreasing assessed market values in order to bring about equalization; 3

9 2. Promotion of uniformity of administration among the counties, thereby ensuring that each taxpayer will be treated in the same manner regardless of where the taxpayer lives; 3. Delivery of accurate and timely aid calculations, certifications, and actual aid payments; 4. Education and information supplied to county officials, including technical manuals, bulletins, answers to specific questions, and courses taught by Division personnel. These offerings provide county officials the support and training necessary to administer the property tax laws equitably and uniformly. In addition, education and information that the Division provides to taxpayers helps ensure they pay no more and no less than the law requires. System Basics In Minnesota, property tax is an ad valorem tax (a tax in proportion to value). For most property, it is levied in one year, based on the property assessment as of January 2 nd, and becomes payable in the following calendar year. For manufactured homes classed as personal property, the tax is levied and payable in the same year. The tax on a parcel of property is based primarily on its Estimated Market Value (EMV), property class, the total value of all property within the taxing areas, and the budgets of all local governmental units located within the taxing area. Estimated Market Value (EMV) is an assessor s estimate of the property s sales price if it were to be sold on the open market in a normal arms-length transaction; i.e., in an environment in which the buyer and seller are typically motivated and without influence from special financing considerations or the like. Assessors determine the EMV of all taxable property within their jurisdiction as of January 2 nd of each year, except properties of public utilities, railroads, air-flight property and minerals, which are instead assessed by Property Tax Division personnel. The EMV is not necessarily the value on which the property is taxed. The legislature has provided various programs which may reduce the market value for certain types of property for purposes of taxation. These reductions are made by deferment, limitation or exclusion, such as Green Acres, or This Old House programs. The market value after these reductions are applied is referred to as the Taxable Market Value, or TMV. The example in Table 2 on page 5 shows a possible transition from Estimated Market Value to Taxable Market Value. 4

10 Market Value Calculation Example 2009 for taxes payable in 2010 AY Market Value Irrespective of Contaminants $480, Contamination Value 120, Estimated Market Value (EMV) [1 2] 360, Green Acres Deferment 50, Open Space Deferment NA 6. Aggregate Resource Preservation Deferment NA 7. Platted Vacant Land Exclusion NA 8. This Old House Exclusion 9, This Old Business Exclusion 15, Disabled Veterans Exclusion NA 11. Mold Damage Reduction NA 12. Lead Hazard Reduction NA 13. Taxable Market Value (TMV) [ ] $286,000 Table 2 Note: Additional examples can be found in Section of the Auditor/Treasurer Manual. This rather extreme scenario assumes that the parcel: (1) Is a split class farm homestead/commercial parcel: (2) Is contaminated and subject to the contamination tax; (3) Qualifies for the Green Acres Deferment; (4) Has qualifying improvements under This Old House ; and (5) Has qualifying improvements under This Old Business. Examples from previous years may also contain limited market value calculations as well, which expired in assessment year

11 Sales Ratio Studies There are 87 counties, 854 cities and 1,807 townships in the state, which encompass 2,726,507 taxable real property parcels. Minnesota Statutes require all property to be assessed at fair market value annually. Compliance efforts by individual taxing jurisdictions have resulted in a combined total of approximately 75% of taxable parcels which changed in value from 2008 to In order to evaluate the accuracy and uniformity of assessments within the state (and thus to ensure compliance with property tax laws), the Property Tax Division conducts annual sales ratio studies which measure the relationship between appraised values and market values or the actual sales price. As a mathematical expression, a sales ratio is the assessor s estimated market value of a property divided by its actual sales price, as seen in the following illustration, Equation 1: SALES RATIO = Assessor s Estimated Market Value Sales Price Equation 1 The sales ratio study provides an indication of the level of assessment (how close appraisals are to market value on an overall basis), as well as the uniformity of assessment (how close individual appraisals are to the median ratio and each other). The results from the studies are then used to assist the equalizing of values within the state. The State Board of Equalization directly equalizes property by ordering jurisdictions to raise or lower values by a certain percentage for a given property type; this is known as a State Board Order. The ratios are also used in calculating state aids and levies to achieve fair distributions to schools and local governments. The ratio studies may also be used in Tax Court proceedings to support a claim that property is either fairly or unfairly assessed in a certain region. In addition, county and city assessors are able to use the results from the Division s annual studies to monitor their own jurisdictions appraisal performances, establish reappraisal priorities, identify any appraisal procedural problems, and/or adjust values between reappraisals. The basic steps involved in a sales ratio study are as follows: 1. Define the purpose and scope of the study 2. Collect and prepare appraisal and sales data 3. Match appraisal and sales data 4. Group the data by property types and geographic areas 5. Perform statistical analysis 6. Evaluate and apply results In order for the study to be accurate, there are certain considerations that must be addressed. To ensure that the study is statistically precise, the sample should be of sufficient size and representative of the population, the market data (or actual sales) must be verified and screened, 6

12 and sales price may need to be adjusted for such conditions as seller-provided financing, inflation, or deflation. The Department of Revenue conducts three sales ratio studies annually: 9- and 12-month studies are used to ensure the quality of assessment practices, and a 21-month study is used for levy and aid purposes as discussed in Appendix 3. There were approximately 102,000 Certificates of Real estate Value (CRV) received in 2009 of which 58,000 were considered good, current-year, open-market sales. These 58,000 sales provide the basis for the sales ratio studies. TWELVE-MONTH STUDY The 12-month study is used mainly to determine State Board of Equalization Orders. The 12 months encompass the period from October 1 of one year through September 30 of the next year. The dates are based on the dates of sale as indicated on the Certificate of Real Estate Value (CRV). These certificates are filled out by the buyer or seller whenever property is sold or conveyed and filed with the county. The certificates include the sales price of the property, disclosure of any special financial terms associated with the sale, and whether the sale included personal property. The actual sales price from the CRV is then compared to what the county has reported as the market value. The data contained in the report is based upon the 12-month study using sales from October 1, 2008, through September 30, These sales are compared with values from assessment year 2009, taxes payable The sale prices are adjusted for time and financial terms back to the date of the assessment, which is January 2 of each year. For this study, the sales are adjusted to January 2, In areas with few sales, it is very difficult to adjust for inflation or deflation because the sales samples are used to develop time trends. For example, based on an annual inflation rate of 6 percent (.5 percent monthly), if a house were purchased in August 2009 for $200,000, it would be adjusted back to a January 2008 value of $193,000, or the sales price would be adjusted downward by 3.5 percent for the seven-month timeframe back to January. The State Board of Equalization orders assessment changes when the level of assessment (as measured by the median sales ratio) is below 90 percent, or above 105 percent. The orders are usually on a county-, city-, or township-wide basis for a particular classification of property. All State Board Orders must be implemented by the county. The changes will be made to the current assessment under consideration, for taxes payable the following year. The equalization process (including issuing State Board Orders) is designed not only to equalize values on a county-, town-, or city-wide basis, but also to equalize values across county lines to ensure a fair valuation process across taxing districts, county lines, and property types. State Board Orders are implemented only after a review of values and sales ratios and discussions with the county assessors in the county affected by the State Board Orders, county assessors in adjacent counties, and the commissioner. 7

13 PROPERTY TYPE 2008 and 2009 Assessment Year Results FINAL ADJUSTED MEDIAN RATIO COEFFICIENT OF DISPERSION SAMPLE SIZE State Board Year Residential/Seasonal ,889 40,537 Apartment Commercial/Industrial ,550 1,225 Resorts Farm ,261 2,416 Timber Table 3 Table 3 shows median sales ratios and coefficients of dispersion (COD) by property type for 2008 and The lower the COD, the more uniform are the assessments. A high coefficient suggests a lack of equality among individual assessments, with some parcels being assessed at a considerably higher ratio than others. Note that property types with smaller sample sizes tend to have lower sales ratios and higher CODs. The International Association of Assessing Officers recommends trimming the most extreme outliers from the sample before calculating the COD. The trimming method is to exclude sales that are outside 1.5 times the inter-quartile range. This eliminates a few extreme sales that would distort the COD. Per the International Association of Assessing Officers, the acceptable ranges for the COD are as follows in Table 4: Newer, homogenous residential properties Older residential areas Rural residential and seasonal properties Income producing: larger, urban area smaller, rural area Vacant land Depressed markets Table or less 15.0 or less 20.0 or less 15.0 or less 20.0 or less 20.0 or less 25.0 or less The Property Tax Division is working collaboratively with the local assessment community to explore alternatives in bringing the actual COD to within the acceptable ranges displayed above. NINE-MONTH STUDY The nine-month study is a subset of the 12-month study and is used primarily by the Minnesota Tax Court. It is exactly the same as the 12-month study except for the sales during the fall months (October, November and December) are excluded from the study. Therefore, the latest nine-month study examines sales from January 1, 2009, through September 30, The Tax Court uses the sales ratio from the nine-month study when determining disputed market values. 8

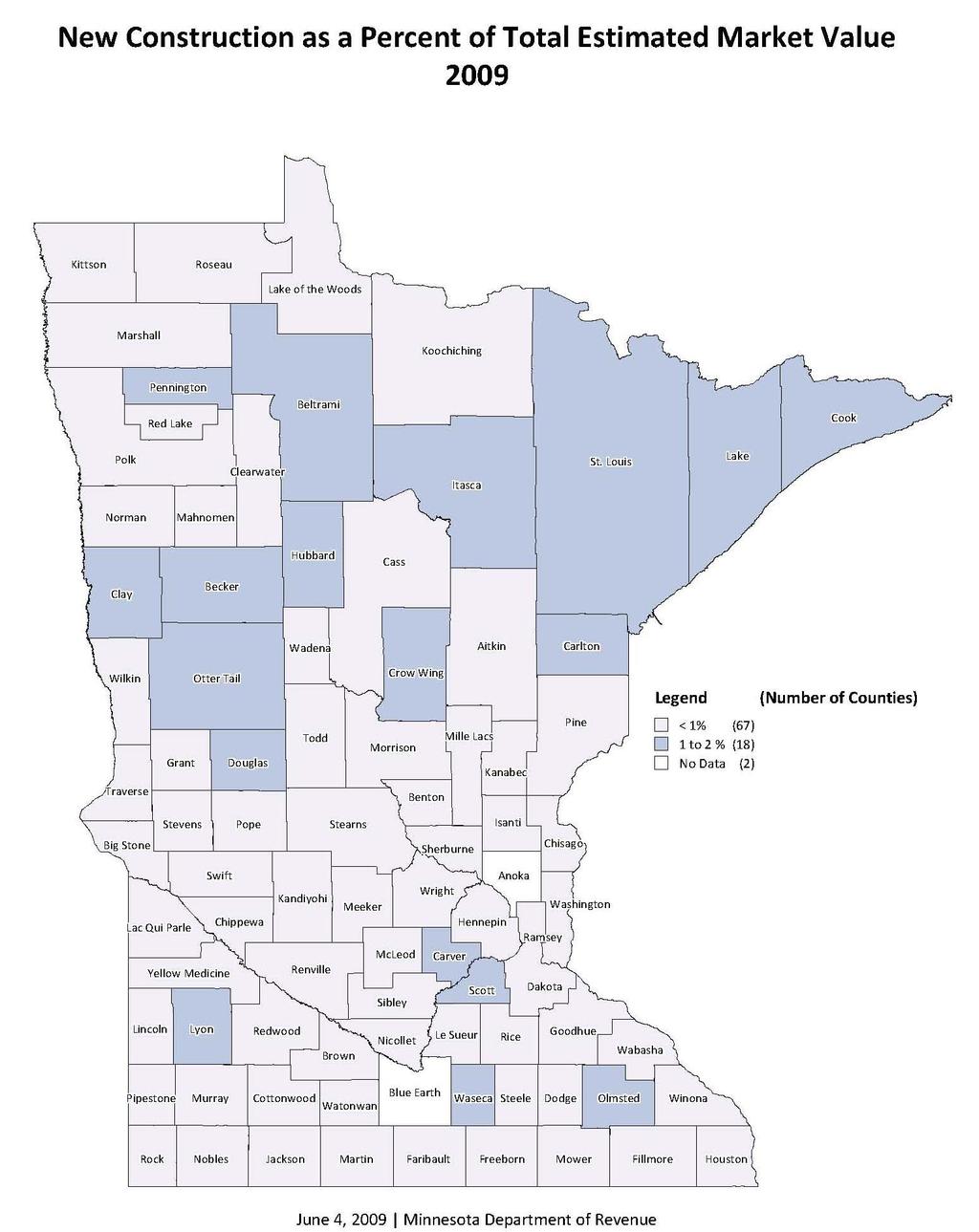

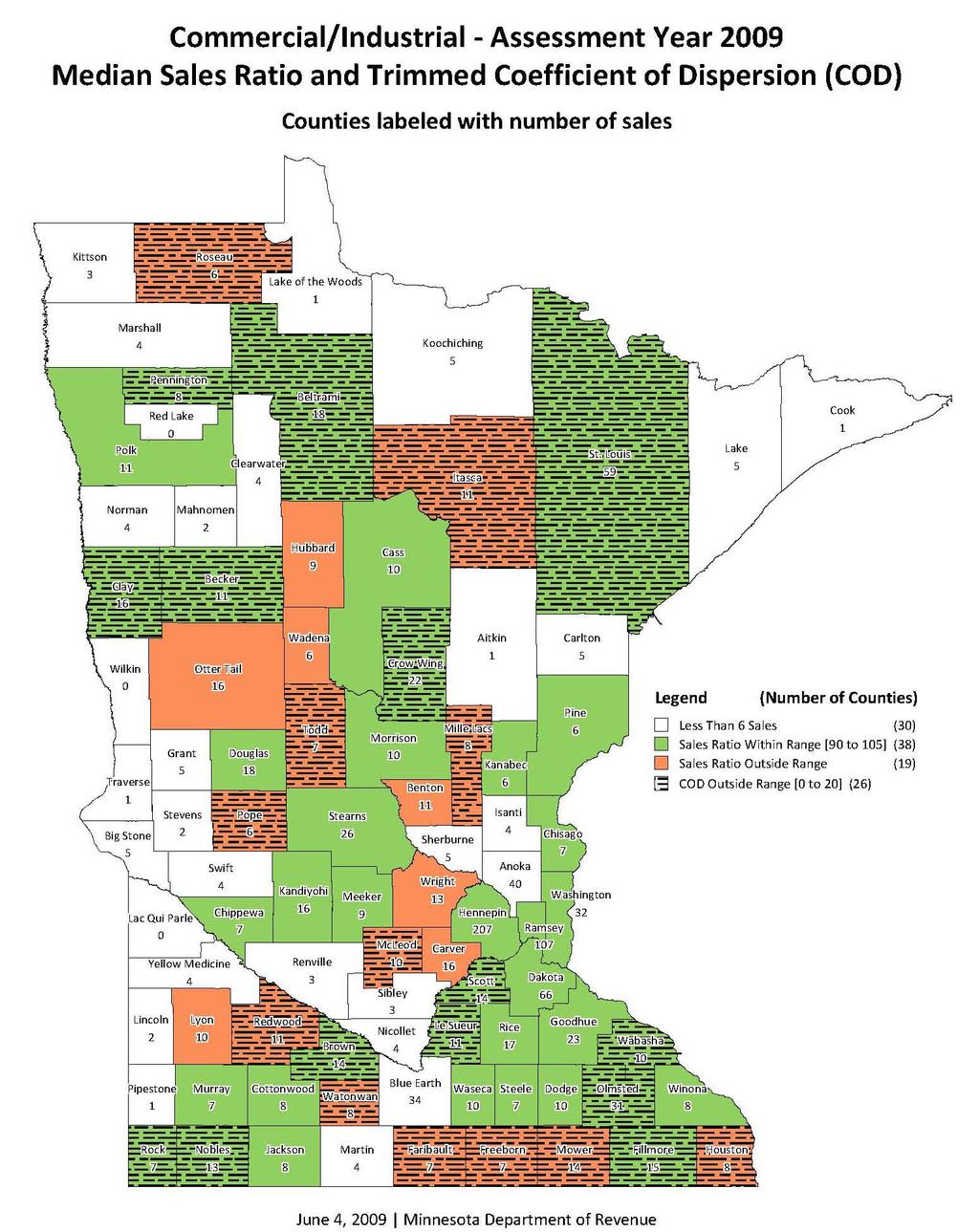

14 Statewide Values and Assessment Practices Indicators The following pages contain statewide charts and maps showing information regarding property values sales ratio measures in Minnesota. Chart 1 shows the statewide growth in estimated market and property value exclusions from 1994 through Charts 2 through 6 show the statewide growth in estimated market value by major property types from 2001 through Map 1, Percent Change in Estimated Market Value, displays the percent change from assessment years 2008 to 2009 in estimated market value for each county. Map 2, New Construction Percentage of Total Estimated Market Value, displays the average percentage that new construction composes of estimated market value for each county from assessment years 2008 to The residential and agricultural maps are not shown for the 2009 assessment because classification changes prevented local effort calculations for this study. Maps 3 and 4 show the 2009 State Board sales ratios and coefficients of dispersion (COD) for, apartment and commercial industrial property. The maps show the number of sales for the county and the shading indicates whether the median countywide sales ratio and COD were within the targeted ranges. The COD is smaller when there are more sales in a property type or when the properties are more similar. Apartment and commercial property types are within the standard range when they have CODs between 0 percent and 20 percent. It is important to remember that countywide ratios and CODs are more stable within areas that have larger samples and similar real estate markets. In counties with fewer sales spread out over large areas, different market forces may be moving sales prices in opposite directions so that it is harder to uniformly value property. In areas with small sales samples or lower priced properties the COD may be large due to a few outlier sales. For example, if an assessor is off by $5,000 on a property, the error would be 2 percent on a $250,000 sale, but 20 percent on a $25,000 sale. If most of the properties in the sales sample were higher priced properties, the average difference would be small and the COD would be within the standard range. If most of the properties were lower priced it becomes more likely that the COD would be outside the standard range. Map 5 shows the residential outlier index or percent of residential or seasonal sales that are considered outliers. Outliers are defined as sales that have ratios less than 65% or greater than 135%. The counties with darker shading have a higher percent of outliers. Counties with few sales or with sales in areas with very different markets tend to have a higher percentage of outliers than counties with large sales samples. Map 6 shows the distributions of 2009 State Board Orders by county. Map 7 shows the percent of cities or townships within a county that received a State Board Order. State Board Orders are blanket adjustments to values in a property type to get the level of assessment within the 90% to 105% acceptable range. 9

15 Growth in Total EMV, TMV and Excluded Value % 5.21% 3.63% 1.76% Billions Excluded Value as Percent of EMV 4.63% 2.01% 2.34% 3.11% 1.79% 1.57% 1.16% 7.46% 9.49% 9.39% 8.13% 7.30% n/a % % % % % % % % % % % % % % % % change in EMV from previous year Taxable Market Value Excluded Value Chart 1 10

16 Statewide Total and Residential Homestead Percent Change in Estimated Market Value Percent change from prior year Chart % 11.0% 6.0% 1.0% -4.0% 15.8% 15.1% 13.8% 13.7% 12.2% 11.7% 11.4% 11.7% 11.8% 11.3% 10.2% 8.6% 6.4% 3.7% 1.8% -0.7% -4.0% -1.1% Assessment Year Residential All Property Types Statewide Commercial-Industrial Percent Change in Estimated Market Value Percent Change from prior year 18.0% 13.0% 8.0% 3.0% -2.0% 13.8% 13.7% 12.7% 11.7% 11.7% 11.8% 11.3% 10.5% 11.1% 9.9% 7.4% 4.6% 5.3% 6.4% 6.7% 1.8% 2.5% -1.1% Assessment Year Com-Ind All Property Types Chart 3 Statewide Farm and Timber Percent Change in Estimated Market Value Percent change from prior year 18.0% 13.0% 8.0% 3.0% -2.0% 16.2% 16.0% 13.8% 13.7% 13.4% 11.7% 11.7% 11.8% 10.6% 11.3% 10.4% 8.4% 8.6% 9.3% 6.4% 6.3% 1.8% -1.1% Assessment Year Farms & Timber All Property Types Chart 4 11

17 Statewide Seasonal-Recreational Percent Change in Estimated Market Value Percent Change From Prior Year Chart % 17.0% 12.0% 7.0% 2.0% -3.0% -8.0% 20.7% 17.7% 18.4% 18.8% 18.4% 18.8% 13.8% 13.7% 11.7% 11.7% 11.8% 11.3% 13.0% 6.4% 3.8% 1.8% -7.5% -1.1% Assessment Year Seasonal- Recreational All Property Types Percent Change from prior year Chart % 13.0% 8.0% 3.0% -2.0% 17.8% Statewide Total and Rental Housing Percent Change in Estimated Market Value 19.9% 13.8% 13.7% 21.4% 19.4% 17.1% 17.0% 11.7% 11.7% 11.8% 11.3% 10.4% 6.4% 2.0% 1.8% 0.0% -1.1% Assessment Year Rental housing All Property Types 12

18 Map 1 13

19 Map 2 14

20 Map 3 15

21 Map 4 16

22 Map 5 17

23 18

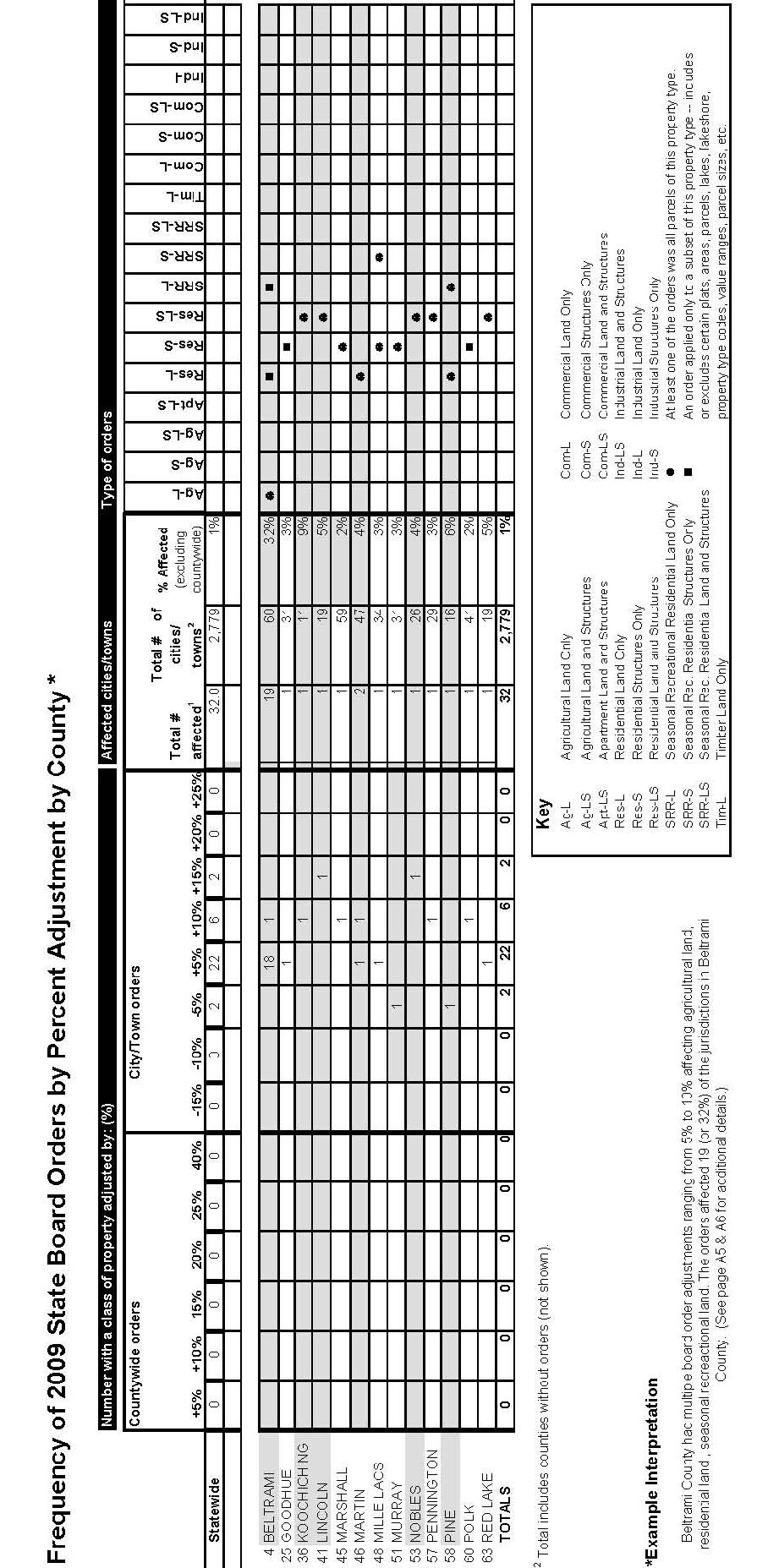

24 Summary of 2009 State Board Orders by Property Classification and Jurisdictions* PROPERTY BOARD ORDER JURISDICTIONS AFFECTED BY ORDER Percent CLASSIFICATION (% increase or decrease) Countywide City Township Total of Total Residential Subtotal % % % % % % % % Apartment Subtotal % % 0 0.0% Commercial Industrial Subtotal % % % 0 0.0% % Seasonal Recreational Subtotal % % % % % 0 0.0% % % Agricultural Subtotal % % % % % % % Timberland Subtotal % % % % % 0 0.0% Totals % *Example Interpretation Eighteen (or 51.4%) of the 35 State Board Orders issued in 2009 were + 5% adjustments to agricultural property. 19

25 Map 6 20

26 Map 7 21

27 APPENDIX I Summary of State Board Orders County Aitkin Assessment District Type of Property State Board Changes Percent Percent Increase Decrease Anoka Becker Beltrami Townships of: Battle Agricultural Land Only Birch Residential Land On Water Front Parcels Only On Gilstad, Rabideau and Benjamin Lakes Only (See Attached Exhibit A) +10 Seasonal Residential Recreational Land On Water Front Parcels Only On Gilstad, Rabideau and Benjamin Lakes Only (See Attached Exhibit A) +10 Cormant Agricultural Land Only Eland Agricultural Land Only Hagali Agricultural Land Only Hines Agricultural Land Only Hornet Agricultural Land Only Kelliher Agricultural Land Only Langor Agricultural Land Only Nebish Agricultural Land Only O'Brien Agricultural Land Only Port Hope Agricultural Land Only Quiring Agricultural Land Only Red Lake Agricultural Land Only Shooks Agricultural Land Only Shotley Agricultural Land Only Summit Agricultural Land Only 22

28 County Beltrami (Continued) Assessment District Waskish Woodrow Summary of State Board Orders Type of Property Agricultural Land Only Agricultural Land Only State Board Changes Percent Percent Increase Decrease Benton Big Stone Blue Earth Brown Carlton Carver Cass Chippewa Chisago Clay Clearwater Cook Cottonwood Crow Wing Dakota Dodge Douglas 23

29 County Faribault Assessment District Summary of State Board Orders Type of Property State Board Changes Percent Percent Increase Decrease Fillmore Freeborn Goodhue City of: Wanamingo Residential Land and Structures Excluding Residential Vacant Land Parcels Grant Hennepin Houston Hubbard Isanti Itasca Jackson Kanabec Kandiyohi Kittson Koochiching City of: Northome Residential Land and Structures +10 Lac Qui Parle Lake 24

30 County Lake of the Woods Assessment District Summary of State Board Orders Type of Property State Board Changes Percent Percent Increase Decrease LeSueur Lincoln City of: Lake Benton Residential Land and Structures +15 Lyon Mahnomen Marshall Township of: Excel Residential Structures Only +10 Martin Cities of: Sherburn Residential Land Only Truman Residential Land Only +10 McLeod Meeker Mille Lacs Township of: Eastside Residential Structures Only Seasonal Residential Recreational Structures Only Morrison Mower Murray City of: Chandler Residential Structures Only -5 Nicollet Nobles City of: Rushmore Residential Land and Structures

31 County Norman Assessment District Summary of State Board Orders Type of Property State Board Changes Percent Percent Increase Decrease Olmsted Otter Tail Pennington City of: St. Hilaire Residential Land and Structures +10 Pine Township of: Pine City Residential Land Only Seasonal Residential Recreational Land Only -5-5 Pipestone Polk City of: Fosston Residential Structures Only On Properties With Total EMV of $60,000 or Greater +10 Pope Ramsey Red Lake City of: Red Lake Falls Residential Land and Structures Redwood Renville Rice Rock Roseau St. Louis 26

32 County Scott Assessment District Summary of State Board Orders Type of Property State Board Changes Percent Percent Increase Decrease Sherburne Sibley Stearns Steele Stevens Swift Todd Traverse Wabasha Wadena Waseca Washington Watonwan Wilkin Winona Wright Yellow Medicine 27

33 APPENDIX II Glossary Estimated Market Value (EMV) The estimated market value is the assessor s estimate of what a property would sell for on the open market with a typically motivated buyer and seller without special financial terms. This is the most probable price, in terms of money, that a property would bring in an open and competitive market. The EMV for a property is finalized on the assessment date, which is January 2 of each year. Certificate of Real Estate Value (CRV) A certificate of real estate value must be filed with the county auditor whenever real property is sold or conveyed in Minnesota. Information reported on the CRV includes the sales price, the value of any personal property, if any, included in the sale, and the financial terms of the sale. The CRV is eventually filed with the Property Tax Division of the Department of Revenue. Coefficient of Dispersion (COD) The coefficient of dispersion is a measurement of variability (the spread or dispersion) and provides a simple numerical value to describe the distribution of sales ratios in relationship to the median ratio of a group of properties sold. The COD is also known as the index of assessment inequality and is the percentage by which the various sales ratios differ, on average, from the median ratio. Limited Market Value (LMV) The limited market value is the market value of a property after statutory limits are imposed on the value of the property. The law surrounding the LMV is meant to limit how much the value of a property may increase from year to year. Median Ratio The median ratio is a measure of central tendency. It is the sales ratio that is the midpoint of all ratios. Half of the ratios fall above this point and the other half fall below this point. The median ratio is used for the State Board of Equalization and the Minnesota Tax Court studies after all final adjustments. Sales Ratio A sales ratio is the ratio comparing the market value of a property with the actual sales price of the property. The market value is determined by the county assessor and reported annually to the Department of Revenue. The actual sales price is reported on the Certificate of Real Estate Value (CRV). State Board of Equalization The State Board of Equalization consists of the Commissioner of Revenue, who has the power to review sales ratios for counties and make adjustments in order to bring estimated market values within the accepted range of 90 to 105 percent. State Board Order A state board order is issued by the State Board of Equalization to adjust the market values of certain property within certain jurisdictions. Taxable Market Value (TMV) The taxable market value is the value that a property is actually taxed on after all limits, deferrals, and exclusions are calculated. It may or may not be the same as the property s estimated market value or limited market value. 28

34 Trimming Method The trimming method used here is to exclude sales that are outside 1.5 times the inter-quartile range. This method starts by sorting the sample by ascending ratio then dividing the sample into quarters (quartiles). The first quarter is at the 25% point of sample. The second quartile is the 50% or median point. The third quartile is at the 75% point. The fourth quartile includes the highest ratios. The inter quartile range is the difference between the values at the first and third quartiles. This number is multiplied by 1.5 to calculate the trimming point for the upper and lower bounds when calculating the COD. Adjusted Median Ratio The adjusted median ratio is calculated by multiplying the median ratio by one plus the overall percent change in value made by the local assessor between the prior and current assessment year (as seen in Equation 2.) The change in assessor s value is also called local effort. Equation 2 Adjusted median ratio= Median ratio x (1+local effort). 29

35 APPENDIX III Twenty-One-Month Study The 21-month study is completely different from the other two studies. Its purpose is to adjust values used for state aid calculations so that all jurisdictions across the state are equalized. In order to build stability into the system, a longer term of 21 months is used. This allows for a greater number of sales. While the nine- and 12-month studies compare the actual sales to the assessor s estimated market value, the 21-month study compares actual sales to the assessor s taxable market value. As with the nine- and 12-month studies, the sale prices are adjusted for time and terms of financing. The 21-month study is used to calculate adjusted net tax capacities that are used in the foundation aid formula for school funding. It is also used to calculate tax capacities for local government aid (commonly referred to as LGA) and various smaller aids such as library aid. This study is also utilized by bonding companies to rate the fiscal capacity of different governmental jurisdictions. The adjusted net tax capacity is used to eliminate differences in levels of assessment between taxing jurisdictions for state aid distributions. All property is supposed to be valued at its selling price in an open market, but many factors make that goal hard to achieve. The sales ratio study can be used to eliminate differences caused by local markets or assessment practices. The adjusted net tax capacity is calculated by dividing the net tax capacity of a class of property by the sales ratio for the class. In the example below, the residential net tax capacity would be divided by the residential sales ratio to produce the residential adjusted net tax capacity. The process would be repeated for all of the property types. The total adjusted net tax capacity would be used in state aid calculations. Table 5 shows the calculation of adjusted net tax capacity in a school district. PROPERTY TYPE NAME TAXABLE NET TAX CAPACITY SALES RATIO ADJUSTED NET TAX CAPACITY Residential 46,907, ,321,929 Apartment 1,318, ,439,884 Seasonal/Recreational 63, ,821 Farms 2,897, ,170,714 Commercial Only 12,929, ,039,526 Industrial Only 7,173, ,360,114 Timber Public Utility 725, ,291 Railroad 58, ,374 Mineral Personal 966, ,946 TOTAL 73,041, ,177,599 Table 5 30

36 References Dornfest, Alan S Ratio Study Class. Course Manual used for the Minnesota Department of Revenue Sales Ratio Study Class, St. Paul, MN, Nov , International Association of Assessing Officers Standard on Ratio Studies. Rev. ed., Chicago, IL: International Association of Assessing Officers. Minnesota Department of Revenue Property Taxes Levied in Minnesota: 2000 Assessments Taxes Payable in St. Paul, MN: Minnesota Department of Revenue. Minnesota House of Representatives Research Department Property Tax Assessment and Sales Ratio Studies: Presentation to Property Tax Task Force. St. Paul, MN: Minnesota House of Representatives. 31

STATE LAND OFFICE: An Inventory of Its Appraisals of State Land:

MINNESOTA HISTORICAL SOCIETY Minnesota State Archives STATE LAND OFFICE: An Inventory of Its Appraisals of State Land: OVERVIEW OF THE RECORDS Agency: Series Title: Minnesota. State Land Office. Appraisals

MINNESOTA HISTORICAL SOCIETY Minnesota State Archives STATE LAND OFFICE: An Inventory of Its Appraisals of State Land: OVERVIEW OF THE RECORDS Agency: Series Title: Minnesota. State Land Office. Appraisals

2005 Property Values and Assessment Practices Report (Assessment year 2004)

") 2005 Property Values and Assessment Practices Report (Assessment year 2004) A report submitted to the Minnesota State Legislature pursuant to Laws 2001, First Special Session, Chapter 5, Article 3, Section

2005 Property Values and Assessment Practices Report (Assessment year 2004) A report submitted to the Minnesota State Legislature pursuant to Laws 2001, First Special Session, Chapter 5, Article 3, Section

Out of Reach 2013 Minnesota

Out of Reach 2013 Minnesota In Minnesota, the Fair Market Rent (FMR) for a two-bedroom apartment is $836. In order to afford this level of rent and utilities without paying more than 30% of on housing

Out of Reach 2013 Minnesota In Minnesota, the Fair Market Rent (FMR) for a two-bedroom apartment is $836. In order to afford this level of rent and utilities without paying more than 30% of on housing

Foreclosures in Minnesota: A Report Based on County Sheriff s Sale Data

Foreclosures in Minnesota: A Report Based on County Sheriff s Sale Data February 26, 2009 Supplement Published by: Prepared by: 600 18 th Avenue North Minneapolis, MN 55411 Telephone: 612-522-2500 Facsimile:

Foreclosures in Minnesota: A Report Based on County Sheriff s Sale Data February 26, 2009 Supplement Published by: Prepared by: 600 18 th Avenue North Minneapolis, MN 55411 Telephone: 612-522-2500 Facsimile:

Annual Report on the Minnesota Housing Market

X0A0T Annual Report on the Minnesota Housing Market FOR RESIDENTIAL REAL ESTATE ACTIVITY IN THE STATE OF MINNESOTA X1A0T 2018 Annual Report on the Minnesota Housing Market FOR RESIDENTIAL REAL ESTATE ACTIVITY

X0A0T Annual Report on the Minnesota Housing Market FOR RESIDENTIAL REAL ESTATE ACTIVITY IN THE STATE OF MINNESOTA X1A0T 2018 Annual Report on the Minnesota Housing Market FOR RESIDENTIAL REAL ESTATE ACTIVITY

2006 Property Values and Assessment Practices Report (Assessment Year 2005)

") 2006 Property Values and Assessment Practices Report (Assessment Year 2005) A report submitted to the Minnesota State Legislature pursuant to Laws 2001, First Special Session, Chapter 5, Article 3, Section

2006 Property Values and Assessment Practices Report (Assessment Year 2005) A report submitted to the Minnesota State Legislature pursuant to Laws 2001, First Special Session, Chapter 5, Article 3, Section

Annual Report on the Minnesota Housing Market FOR RESIDENTIAL REAL ESTATE ACTIVITY IN THE STATE OF MINNESOTA

Annual Report on the Minnesota Housing Market FOR RESIDENTIAL REAL ESTATE ACTIVITY IN THE STATE OF MINNESOTA FOR RESIDENTIAL REAL ESTATE ACTIVITY IN THE STATE OF MINNESOTA With a new U.S. president from

Annual Report on the Minnesota Housing Market FOR RESIDENTIAL REAL ESTATE ACTIVITY IN THE STATE OF MINNESOTA FOR RESIDENTIAL REAL ESTATE ACTIVITY IN THE STATE OF MINNESOTA With a new U.S. president from

Out of. Reach. The growing gap between. Minnesota 2017 WAGES AND RENT. An annual report from

Out of Reach Minnesota 2017 The growing gap between WAGES AND RENT An annual report from Executive Summary When families pay too much for rent, they re forced to sacrifice to make ends meet cutting back

Out of Reach Minnesota 2017 The growing gap between WAGES AND RENT An annual report from Executive Summary When families pay too much for rent, they re forced to sacrifice to make ends meet cutting back

EVICTIONS IN GREATER MINNESOTA

EVICTIONS IN GREATER MINNESOTA HOME Line - May 2018 Contents Report Summary... 2 Context and Purpose... 2 Overview and Key Findings... 2 Conclusions and a Call to Action... 3 Notes about the Data... 4

EVICTIONS IN GREATER MINNESOTA HOME Line - May 2018 Contents Report Summary... 2 Context and Purpose... 2 Overview and Key Findings... 2 Conclusions and a Call to Action... 3 Notes about the Data... 4

2004 Property Values and Assessment Practices Report

2004 Property Values and Assessment Practices Report A report submitted to the Minnesota State Legislature pursuant to Laws 2001, First Special Session, Chapter 5, Article 3, Section 92. Property Tax Division

2004 Property Values and Assessment Practices Report A report submitted to the Minnesota State Legislature pursuant to Laws 2001, First Special Session, Chapter 5, Article 3, Section 92. Property Tax Division

2017 Property Values and Assessment Practices Report Assessment Year 2016

2017 Property Values and Assessment Practices Report Assessment Year 2016 Property Tax Division March 1, 2017 Per Minnesota Statutes, section 3.197, any report to the Legislature must contain, at the

2017 Property Values and Assessment Practices Report Assessment Year 2016 Property Tax Division March 1, 2017 Per Minnesota Statutes, section 3.197, any report to the Legislature must contain, at the

2018 Property Values and Assessment Practices Report Assessment Year 2017

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp 2018 Property Values

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp 2018 Property Values

[A!] [N] rn ~ Lr~ DEPARTMENT OF NATURAL RESOURCES 500 LAFAYETIE ROAD ST. PAUL, MINNESOTA , _

![[A!] [N] rn ~ Lr~ DEPARTMENT OF NATURAL RESOURCES 500 LAFAYETIE ROAD ST. PAUL, MINNESOTA , _](/thumbs/93/112559545.jpg "[A!] [N] rn ~ Lr~ DEPARTMENT OF NATURAL RESOURCES 500 LAFAYETIE ROAD ST. PAUL, MINNESOTA , _") This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp 950217 ~ STATE OF [A!]

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp 950217 ~ STATE OF [A!]

CITY OF OWATONNA ASSESSMENT REPORT. Steele County Assessor s Department. William G. Effertz, SAMA Steele County Assessor

2017 CITY OF OWATONNA ASSESSMENT REPORT Steele County Assessor s Department William G. Effertz, SAMA Steele County Assessor Tyler Diersen, AMA, Assistant County Assessor April 11, 2017 2017 Assessment

2017 CITY OF OWATONNA ASSESSMENT REPORT Steele County Assessor s Department William G. Effertz, SAMA Steele County Assessor Tyler Diersen, AMA, Assistant County Assessor April 11, 2017 2017 Assessment

EDA President Krant, EDA Board Members, and Interim Administrator Meyer

MEMORANDUM DATE: April 9, 2018 TO: FROM: RE: EDA President Krant, EDA Board Members, and Interim Administrator Meyer Cynthia Smith Strack, Community Development Director Item 5.2 Meeting with Area Realtors

MEMORANDUM DATE: April 9, 2018 TO: FROM: RE: EDA President Krant, EDA Board Members, and Interim Administrator Meyer Cynthia Smith Strack, Community Development Director Item 5.2 Meeting with Area Realtors

Past & Present Adjustments & Parcel Count Section... 13

Assessment 2017 Report This report includes specific information regarding the 2017 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

Assessment 2017 Report This report includes specific information regarding the 2017 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

Introduction. Bruce Munneke, S.A.M.A. Washington County Assessor. 3 P a g e

Assessment 2016 Report This report includes specific information regarding the 2016 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

Assessment 2016 Report This report includes specific information regarding the 2016 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

The Honorable Larry Hogan And The General Assembly of Maryland

2015 Ratio Report The Honorable Larry Hogan And The General Assembly of Maryland As required by Section 2-202 of the Tax-Property Article of the Annotated Code of Maryland, I am pleased to submit the Department

2015 Ratio Report The Honorable Larry Hogan And The General Assembly of Maryland As required by Section 2-202 of the Tax-Property Article of the Annotated Code of Maryland, I am pleased to submit the Department

April 12, The Honorable Martin O Malley And The General Assembly of Maryland

April 12, 2011 The Honorable Martin O Malley And The General Assembly of Maryland As required by Section 2-202 of the Tax-Property Article of the Annotated Code of Maryland, I am pleased to submit the

April 12, 2011 The Honorable Martin O Malley And The General Assembly of Maryland As required by Section 2-202 of the Tax-Property Article of the Annotated Code of Maryland, I am pleased to submit the

We look forward to working with you to build on our collaboration and enhance our partnership on behalf of all Minnesotans.

Date: February 27, 2017 To: County Assessors, Auditors, and Treasurers From: Cynthia Rowley, Director Property Tax Division Subject: Property Tax Services Report The Property Tax Division of the Minnesota

Date: February 27, 2017 To: County Assessors, Auditors, and Treasurers From: Cynthia Rowley, Director Property Tax Division Subject: Property Tax Services Report The Property Tax Division of the Minnesota

MINNESOTA REVENUE ASSESSMENT AND CLASSIFICATION PRACTICES REPORT

MINNESOTA REVENUE ASSESSMENT AND CLASSIFICATION PRACTICES REPORT THE AGRICULTURAL PROPERTY TAX PROGRAM, CLASS 2A AGRICULTURAL PROPERTY, AND CLASS 2B RURAL VACANT LAND PROPERTY A report submitted to the

MINNESOTA REVENUE ASSESSMENT AND CLASSIFICATION PRACTICES REPORT THE AGRICULTURAL PROPERTY TAX PROGRAM, CLASS 2A AGRICULTURAL PROPERTY, AND CLASS 2B RURAL VACANT LAND PROPERTY A report submitted to the

Board of Appeal and Equalization Handbook

Board of Appeal and Equalization Handbook This handbook was created to satisfy the training requirements of Minnesota Statutes, sections 274.014 and 274.135 Updated January 2018 Table of Contents Introduction...

Board of Appeal and Equalization Handbook This handbook was created to satisfy the training requirements of Minnesota Statutes, sections 274.014 and 274.135 Updated January 2018 Table of Contents Introduction...

2011 ASSESSMENT RATIO REPORT

2011 Ratio Report SECTION I OVERVIEW 2011 ASSESSMENT RATIO REPORT The Department of Assessments and Taxation appraises real property for the purposes of property taxation. Properties are valued using

2011 Ratio Report SECTION I OVERVIEW 2011 ASSESSMENT RATIO REPORT The Department of Assessments and Taxation appraises real property for the purposes of property taxation. Properties are valued using

Special Plainview City Council Meeting Board of Appeals and Equalization Meeting AGENDA Tuesday, April 16, 2019, at 6:00 P.M.

Special Plainview City Council Meeting Board of Appeals and Equalization Meeting AGENDA Tuesday, April 16, 2019, at 6:00 P.M. Special meetings are meetings held at a time or place that is different from

Special Plainview City Council Meeting Board of Appeals and Equalization Meeting AGENDA Tuesday, April 16, 2019, at 6:00 P.M. Special meetings are meetings held at a time or place that is different from

Sales Ratio: Alternative Calculation Methods

For Discussion: Summary of proposals to amend State Board of Equalization sales ratio calculations June 3, 2010 One of the primary purposes of the sales ratio study is to measure how well assessors track

For Discussion: Summary of proposals to amend State Board of Equalization sales ratio calculations June 3, 2010 One of the primary purposes of the sales ratio study is to measure how well assessors track

Manufactured Home Parks Handbook

The Manufactured Home Parks Handbook From the Office of Minnesota Attorney General Mike Hatch www.ag.state.mn.us 1 The Manufactured Home Parks Handbook This handbook explains the Minnesota laws concerning

The Manufactured Home Parks Handbook From the Office of Minnesota Attorney General Mike Hatch www.ag.state.mn.us 1 The Manufactured Home Parks Handbook This handbook explains the Minnesota laws concerning

We hope the trends provide additional perspective on your county s work. We know it provided valuable insight on the work we do here at Revenue.

Date: March 6, 2018 To: County Assessors, Auditors, and Treasurers From: Jon Klockziem, Acting Director Subject: Property Tax Services Report The Property Tax Division of the is pleased to provide the

Date: March 6, 2018 To: County Assessors, Auditors, and Treasurers From: Jon Klockziem, Acting Director Subject: Property Tax Services Report The Property Tax Division of the is pleased to provide the

2015 SSTS Annual Report Subsurface Sewage Treatment Systems in Minnesota

Kwq- 2015 SSTS Annual Report Subsurface Sewage Treatment Systems in Minnesota October 2016 Author Cody Robinson Contributors/acknowledgements (MPCA) Subsurface Sewage Treatment Systems (SSTS) staff would

Kwq- 2015 SSTS Annual Report Subsurface Sewage Treatment Systems in Minnesota October 2016 Author Cody Robinson Contributors/acknowledgements (MPCA) Subsurface Sewage Treatment Systems (SSTS) staff would

MINNESOTA ASSOCIATION OF COUNTY AUDITORS TREASURERS AND FINANCE OFFICERS 2016 COMMITTEE LIST. Committee Name County Address

MINNESOTA ASSOCIATION OF COUNTY AUDITORS TREASURERS AND FINANCE OFFICERS 2016 COMMITTEE LIST Committee Name County Email Address Executive Committee President Laurie Davies Carver ldavies@co.carver.mn.us

MINNESOTA ASSOCIATION OF COUNTY AUDITORS TREASURERS AND FINANCE OFFICERS 2016 COMMITTEE LIST Committee Name County Email Address Executive Committee President Laurie Davies Carver ldavies@co.carver.mn.us

Assessment-To-Sales Ratio Study for Division III Equalization Funding: 1999 Project Summary. State of Delaware Office of the Budget

Assessment-To-Sales Ratio Study for Division III Equalization Funding: 1999 Project Summary prepared for the State of Delaware Office of the Budget by Edward C. Ratledge Center for Applied Demography and

Assessment-To-Sales Ratio Study for Division III Equalization Funding: 1999 Project Summary prepared for the State of Delaware Office of the Budget by Edward C. Ratledge Center for Applied Demography and

Potential Right of Way Conveyance Parcels. March 2015

Potential Right of Way Conveyance Parcels March 205 Prepared by The Minnesota Department of Transportation 395 John Ireland Boulevard Saint Paul, Minnesota 5555-899 Phone: 65-296-3000 Toll-Free: -800-657-3774

Potential Right of Way Conveyance Parcels March 205 Prepared by The Minnesota Department of Transportation 395 John Ireland Boulevard Saint Paul, Minnesota 5555-899 Phone: 65-296-3000 Toll-Free: -800-657-3774

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

Committee Name County Address

MINNESOTA ASSOCIATION OF COUNTY AUDITORS TREASURERS AND FINANCE OFFICERS 2018 COMMITTEE LIST Executive Committee President Michelle Knutson Big Stone michelle.knutson@co.big-stone.mn.us First Vice President

MINNESOTA ASSOCIATION OF COUNTY AUDITORS TREASURERS AND FINANCE OFFICERS 2018 COMMITTEE LIST Executive Committee President Michelle Knutson Big Stone michelle.knutson@co.big-stone.mn.us First Vice President

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

Allegan County Equalization Department

Allegan County Equalization Department 2011 Department Report Equalization Report Recap 2010 2011 projects January 1- December 31, 2010 Blaine R. McLeod Director of Equalization 1 Message from the Director

Allegan County Equalization Department 2011 Department Report Equalization Report Recap 2010 2011 projects January 1- December 31, 2010 Blaine R. McLeod Director of Equalization 1 Message from the Director

DIRECTIVE # This Directive Supersedes Directive # and #92-003

Division Of Property Valuation Docking State Office Building 915 SW Harrison St., Room 400N Topeka, KS 66612-1588 Nick Jordan, Secretary David N. Harper, Director phone: 785-296-2365 fax: 785-296-2320

Division Of Property Valuation Docking State Office Building 915 SW Harrison St., Room 400N Topeka, KS 66612-1588 Nick Jordan, Secretary David N. Harper, Director phone: 785-296-2365 fax: 785-296-2320

Terrell County Appraisal District 2018 Annual Report

Terrell County Appraisal District 2018 Annual Report Introduction The Terrell County Appraisal District is a political subdivision of the State of Texas. The Texas Constitution, Texas Property Tax Code

Terrell County Appraisal District 2018 Annual Report Introduction The Terrell County Appraisal District is a political subdivision of the State of Texas. The Texas Constitution, Texas Property Tax Code

UNDERSTANDING PROPERTY TAXES IN COLORADO

UNDERSTANDING PROPERTY TAXES IN COLORADO This brochure was created to provide general information on the Colorado property tax system. For more specific information on any one of these topics, please visit

UNDERSTANDING PROPERTY TAXES IN COLORADO This brochure was created to provide general information on the Colorado property tax system. For more specific information on any one of these topics, please visit

Minnesota Department of Revenue 2012 Sales Ratio Study Criteria

Minnesota Department of Revenue 2012 Sales Ratio Study Criteria Special Notes Forward-Adjusted Methodology Transition In the 2012 sales ratio study, the Department of Revenue will use a forward-adjusted

Minnesota Department of Revenue 2012 Sales Ratio Study Criteria Special Notes Forward-Adjusted Methodology Transition In the 2012 sales ratio study, the Department of Revenue will use a forward-adjusted

GENERAL ASSESSMENT DEFINITIONS

21st Century Appraisals, Inc. GENERAL ASSESSMENT DEFINITIONS Ad Valorem tax. A tax levied in proportion to the value of the thing(s) being taxed. Exclusive of exemptions, use-value assessment laws, and

21st Century Appraisals, Inc. GENERAL ASSESSMENT DEFINITIONS Ad Valorem tax. A tax levied in proportion to the value of the thing(s) being taxed. Exclusive of exemptions, use-value assessment laws, and

Equalization. Overview. Multiplier Basics

The purpose of this primer is to outline the Illinois Department of Revenue s (IDOR) process in the determination of Cook County s equalization factor commonly known as the multiplier. It describes how

The purpose of this primer is to outline the Illinois Department of Revenue s (IDOR) process in the determination of Cook County s equalization factor commonly known as the multiplier. It describes how

Washington Department of Revenue Property Tax Division. Valid Sales Study Kitsap County 2015 Sales for 2016 Ratio Year.

P. O. Box 47471 Olympia, WA 98504-7471. Washington Department of Revenue Property Tax Division Valid Sales Study Kitsap County 2015 Sales for 2016 Ratio Year Sales from May 1, 2014 through April 30, 2015

P. O. Box 47471 Olympia, WA 98504-7471. Washington Department of Revenue Property Tax Division Valid Sales Study Kitsap County 2015 Sales for 2016 Ratio Year Sales from May 1, 2014 through April 30, 2015

PROPERTY ASSESSMENT AND TAXATION

History of the Community and Service Area Structure Juneau's existing City and Borough concept was adopted in 1970 with the unification of the Cities of Juneau and Douglas and the Greater Juneau Borough.

History of the Community and Service Area Structure Juneau's existing City and Borough concept was adopted in 1970 with the unification of the Cities of Juneau and Douglas and the Greater Juneau Borough.

ASSESSMENT AND TAXATION

ABSTRACT A brief synopsis of the assessment, appeal and taxation process as implemented by the Code of Iowa and Administrative Rules. ASSESSMENT AND TAXATION Iowa State Association of Assessors General

ABSTRACT A brief synopsis of the assessment, appeal and taxation process as implemented by the Code of Iowa and Administrative Rules. ASSESSMENT AND TAXATION Iowa State Association of Assessors General

Assessment Year 2016 Assessment Valuations / Mass Appraisal Summary Report

Assessment Year 2016 Assessment Valuations / Mass Appraisal Summary Report Overview Following up on last year s work, additional work was done cleaning up the sales data. The land valuation model was further

Assessment Year 2016 Assessment Valuations / Mass Appraisal Summary Report Overview Following up on last year s work, additional work was done cleaning up the sales data. The land valuation model was further

REPORT # O L A OFFICE OF THE LEGISLATIVE AUDITOR STATE OF MINNESOTA A BEST PRACTICES REVIEW. Preserving Housing

O L A REPORT # 03-05 OFFICE OF THE LEGISLATIVE AUDITOR STATE OF MINNESOTA A BEST PRACTICES REVIEW Preserving Housing APRIL 2003 Program Evaluation Division The Minnesota Office of the Legislative Auditor

O L A REPORT # 03-05 OFFICE OF THE LEGISLATIVE AUDITOR STATE OF MINNESOTA A BEST PRACTICES REVIEW Preserving Housing APRIL 2003 Program Evaluation Division The Minnesota Office of the Legislative Auditor

Minnesota s School Trust Lands

Minnesota s School Trust Lands Biennial Report Fiscal Years 2010-2011 (7/1/2009-6/30/2011) Minnesota Department of Natural Resources March 2012 i Table of Contents Executive Summary... iv 1. History of

Minnesota s School Trust Lands Biennial Report Fiscal Years 2010-2011 (7/1/2009-6/30/2011) Minnesota Department of Natural Resources March 2012 i Table of Contents Executive Summary... iv 1. History of

DEPARTMENT OF ASSESSMENTS AND TAXATION 2008 RATIO REPORT

DEPARTMENT OF ASSESSMENTS AND TAXATION 2008 RATIO REPORT State of Maryland Department of Assessments and Taxation Office of the Director Martin O'Malley Governor C. John Sullivan Jr. Director June 30,

DEPARTMENT OF ASSESSMENTS AND TAXATION 2008 RATIO REPORT State of Maryland Department of Assessments and Taxation Office of the Director Martin O'Malley Governor C. John Sullivan Jr. Director June 30,

Publication 136 April 2016

Illinois Department of Revenue Constance Beard, Director Publication 136 April 2016 Property Assessment and Equalization The information in this publication is current as of the date of the publication.

Illinois Department of Revenue Constance Beard, Director Publication 136 April 2016 Property Assessment and Equalization The information in this publication is current as of the date of the publication.

YOUNG COUNTY APPRAISAL DISTRICT

YOUNG COUNTY APPRAISAL DISTRICT 2017 - ANNUAL APPRAISAL REPORT AS OF 10/6/2017 1 2 TABLE OF CONTENTS ITEM PAGE Introduction 4 Purpose of Report...4 Taxing Entities, Rates & Exemptions 5 Property Types

YOUNG COUNTY APPRAISAL DISTRICT 2017 - ANNUAL APPRAISAL REPORT AS OF 10/6/2017 1 2 TABLE OF CONTENTS ITEM PAGE Introduction 4 Purpose of Report...4 Taxing Entities, Rates & Exemptions 5 Property Types

Pickens County Reassessment Program. Utilizing CAMA GIS MLS SQL

1 Pickens County 2019 Reassessment Program Utilizing CAMA GIS MLS SQL Pickens County Reassessment History 1980 Countywide Reappraisal 1990 Countywide Reappraisal 1999 Countywide Reappraisal 2004 Countywide

1 Pickens County 2019 Reassessment Program Utilizing CAMA GIS MLS SQL Pickens County Reassessment History 1980 Countywide Reappraisal 1990 Countywide Reappraisal 1999 Countywide Reappraisal 2004 Countywide

Chapter 12 Changes Since This is just a brief and cursory comparison. More analysis will be done at a later date.

Chapter 12 Changes Since 1986 This approach to Fiscal Analysis was first done in 1986 for the City of Anoka. It was the first of its kind and was recognized by the National Science Foundation (NSF). Geographic

Chapter 12 Changes Since 1986 This approach to Fiscal Analysis was first done in 1986 for the City of Anoka. It was the first of its kind and was recognized by the National Science Foundation (NSF). Geographic

2016 Assessment Report. Hennepin County. Assessor s Department

216 Assessment Report Hennepin County Assessor s Department James R. Atchison, CAE, SAMA County Assessor Created: 6-8-216 Page 2 of 51 216 TABLE OF CONTENTS Last modified (6-9-16) Table of Contents (2

216 Assessment Report Hennepin County Assessor s Department James R. Atchison, CAE, SAMA County Assessor Created: 6-8-216 Page 2 of 51 216 TABLE OF CONTENTS Last modified (6-9-16) Table of Contents (2

Cook County Assessor s Office: 2019 North Triad Assessment. Norwood Park Residential Assessment Narrative March 11, 2019

Cook County Assessor s Office: 2019 North Triad Assessment Norwood Park Residential Assessment Narrative March 11, 2019 1 Norwood Park Residential Properties Executive Summary This is the current CCAO

Cook County Assessor s Office: 2019 North Triad Assessment Norwood Park Residential Assessment Narrative March 11, 2019 1 Norwood Park Residential Properties Executive Summary This is the current CCAO

Estimate of the Percentage of Rent that Constitutes Property Taxes in Minnesota. Based on Rent and Property Taxes Paid in 2016

Estimate of the Percentage of Rent that Constitutes Property Taxes in Minnesota Based on Rent and Property Taxes Paid in 2016 March 1, 2018 Minnesota Statute 3.197 requires any report to the Legislature

Estimate of the Percentage of Rent that Constitutes Property Taxes in Minnesota Based on Rent and Property Taxes Paid in 2016 March 1, 2018 Minnesota Statute 3.197 requires any report to the Legislature

Duties of the Assessors

Duties of the Assessors Value Properties Determine New Growth Set Tax Rate Assess Property Taxes Abate & Exempt Taxes Manage Overlay Account Assess Local Excises 1 Value Property Assessments based on fair

Duties of the Assessors Value Properties Determine New Growth Set Tax Rate Assess Property Taxes Abate & Exempt Taxes Manage Overlay Account Assess Local Excises 1 Value Property Assessments based on fair

The Department s Role

CITY ASSESSOR The Department s Role on the h Ci City s T Team August 21, 2013 Who we are... Micheal Lohmeier City Assessor (2012) (Commercial Appraiser 1998-2005, Assr. 2010-12) 12) Administration and

CITY ASSESSOR The Department s Role on the h Ci City s T Team August 21, 2013 Who we are... Micheal Lohmeier City Assessor (2012) (Commercial Appraiser 1998-2005, Assr. 2010-12) 12) Administration and

Limited Market Value Report

Limited Market Value Report 2005 Assessment Year Tax Research Division March 1, 2006 This report is available on the web at http://www.taxes.state.mn.us/taxes/legal_policy/index.shtml March 1, 2006 To

Limited Market Value Report 2005 Assessment Year Tax Research Division March 1, 2006 This report is available on the web at http://www.taxes.state.mn.us/taxes/legal_policy/index.shtml March 1, 2006 To

ASSESSMENT AND CLASSIFICATION PRACTICES REPORT LANDS ENROLLED IN STATE OR FEDERAL CONSERVATION PROGRAMS

ASSESSMENT AND CLASSIFICATION PRACTICES REPORT LANDS ENROLLED IN STATE OR FEDERAL CONSERVATION PROGRAMS A report submitted to the Minnesota State Legislature pursuant to Minnesota Laws 2005, First Special

ASSESSMENT AND CLASSIFICATION PRACTICES REPORT LANDS ENROLLED IN STATE OR FEDERAL CONSERVATION PROGRAMS A report submitted to the Minnesota State Legislature pursuant to Minnesota Laws 2005, First Special

How the Montgomery Central Appraisal District Appraises Residential Property

How the Montgomery Central Appraisal District Appraises Residential Property The following presentation is provided to educate Montgomery County residential property owners about the Analysis & Valuation

How the Montgomery Central Appraisal District Appraises Residential Property The following presentation is provided to educate Montgomery County residential property owners about the Analysis & Valuation

GOVERNANCE OF ASSESSOR

GOVERNANCE OF ASSESSOR State of NH Constitution NH State Statutes (RSA) State Supreme Court Case Law NH Assessing Standard Board Rules NH Department of Revenue Rules Professional Code of Conduct (USPAP)

GOVERNANCE OF ASSESSOR State of NH Constitution NH State Statutes (RSA) State Supreme Court Case Law NH Assessing Standard Board Rules NH Department of Revenue Rules Professional Code of Conduct (USPAP)

LIMITED-SCOPE PERFORMANCE AUDIT REPORT

LIMITED-SCOPE PERFORMANCE AUDIT REPORT Agricultural Land Valuation: Evaluating the Potential Impact of Changing How Agricultural Land is Valued in the State AUDIT ABSTRACT State law requires the value

LIMITED-SCOPE PERFORMANCE AUDIT REPORT Agricultural Land Valuation: Evaluating the Potential Impact of Changing How Agricultural Land is Valued in the State AUDIT ABSTRACT State law requires the value

City of Nashua, NH 2018 Revaluation Informational Meeting

City of Nashua, NH 2018 Revaluation Informational Meeting Legal Requirements Constitutional Duty of the City: [Art.] 6. [Valuation and Taxation.] The public charges of government, or any part thereof,

City of Nashua, NH 2018 Revaluation Informational Meeting Legal Requirements Constitutional Duty of the City: [Art.] 6. [Valuation and Taxation.] The public charges of government, or any part thereof,

REAL ESTATE MARKET AND YOUR TAX

REAL ESTATE MARKET AND YOUR TAX ASSESSMENT All of us Island property owners received our tax assessment notices from the County recently. As real estate agents we have been fielding many questions about

REAL ESTATE MARKET AND YOUR TAX ASSESSMENT All of us Island property owners received our tax assessment notices from the County recently. As real estate agents we have been fielding many questions about

ASSESSORS ANSWER FREQUENTLY ASKED QUESTIONS ABOUT REAL PROPERTY Assessors Office, 37 Main Street

A. THE ASSESSMENT PROCESS: ASSESSORS ANSWER FREQUENTLY ASKED QUESTIONS ABOUT REAL PROPERTY Assessors Office, 37 Main Street What is mass appraisal? Assessors must value all real and personal property in

A. THE ASSESSMENT PROCESS: ASSESSORS ANSWER FREQUENTLY ASKED QUESTIONS ABOUT REAL PROPERTY Assessors Office, 37 Main Street What is mass appraisal? Assessors must value all real and personal property in

YOUR GUIDE TO THE REASSESSMENT PROGRAM

YOUR GUIDE TO THE REASSESSMENT PROGRAM Why Reassess? Reassessment is required by law. Act 208, as passed by the General Assembly in 1975, provides that all real property will be valued at its current market

YOUR GUIDE TO THE REASSESSMENT PROGRAM Why Reassess? Reassessment is required by law. Act 208, as passed by the General Assembly in 1975, provides that all real property will be valued at its current market

Dear Brazos County Citizens and Property Owners,

2017 Annual Report Dear Brazos County Citizens and Property Owners, It is my pleasure to present the 2017 Annual Report of the Brazos Central Appraisal District. The annual report provides general information

2017 Annual Report Dear Brazos County Citizens and Property Owners, It is my pleasure to present the 2017 Annual Report of the Brazos Central Appraisal District. The annual report provides general information

Athens County Auditor, Jill Thompson provides homeowners answers to the most commonly asked questions about the countywide 2014 reappraisal

Contact: Jill Thompson Athens County Auditor Phone 740.592.3223 Fax 740.594.3270 15 S. Court Street, Room 330 Athens, Ohio 45701 www.athenscountyauditor.org Jill Thompson Athens County Auditor Property

Contact: Jill Thompson Athens County Auditor Phone 740.592.3223 Fax 740.594.3270 15 S. Court Street, Room 330 Athens, Ohio 45701 www.athenscountyauditor.org Jill Thompson Athens County Auditor Property

2018 Annual Appraisal Report

2018 Annual Appraisal Report SUMMARY OF APPRAISAL ACTIVITIES, EXEMPTIONS, EQUALIZATION AND TAX RATES FOR 2018 TAX YEAR Wendy Grams, RPA, CTA, CCA CENTRAL APPRAISAL DISTRICT OF BANDERA COUNTY P. O. BOX

2018 Annual Appraisal Report SUMMARY OF APPRAISAL ACTIVITIES, EXEMPTIONS, EQUALIZATION AND TAX RATES FOR 2018 TAX YEAR Wendy Grams, RPA, CTA, CCA CENTRAL APPRAISAL DISTRICT OF BANDERA COUNTY P. O. BOX

41 st Annual Conference Appraising Property

2017 KCCA 41 st Annual Conference Appraising Property Kansas County Commissioners Association Junction City, Kansas June 2, 2017 Topics Overview PVD s Role in the Appraisal Process Appointment of County

2017 KCCA 41 st Annual Conference Appraising Property Kansas County Commissioners Association Junction City, Kansas June 2, 2017 Topics Overview PVD s Role in the Appraisal Process Appointment of County

The Minnesota Rural Real Estate Market in by Jon Brekke, Hung-Lin Tao and Philip M. Raup

The Minnesota Rural Real Estate Market in 1992 by Jon Brekke, Hung-Lin Tao and Philip M. Raup University of Minnesota St. Paul, MN 55108 Economic Report ER 93-5 July, 1993 Including Special Studies Of:

The Minnesota Rural Real Estate Market in 1992 by Jon Brekke, Hung-Lin Tao and Philip M. Raup University of Minnesota St. Paul, MN 55108 Economic Report ER 93-5 July, 1993 Including Special Studies Of:

Town of Fairfield 2015 Revaluation Informational Meeting

www.vgsi.com Town of Fairfield 2015 Revaluation Informational Meeting Fairfield Revaluation Cycle Ct. Law states revaluations take place every 5 years Fairfield s last Revaluation was in 2010 All property

www.vgsi.com Town of Fairfield 2015 Revaluation Informational Meeting Fairfield Revaluation Cycle Ct. Law states revaluations take place every 5 years Fairfield s last Revaluation was in 2010 All property

VAN ZANDT COUNTY APPRAISAL DISTRICT 2018 ANNUAL REPORT

VAN ZANDT COUNTY APPRAISAL DISTRICT 2018 ANNUAL REPORT INTRODUCTION The Van Zandt County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property

VAN ZANDT COUNTY APPRAISAL DISTRICT 2018 ANNUAL REPORT INTRODUCTION The Van Zandt County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property

DELTA COUNTY APPRAISAL DISTRICT 2016 ANNUAL APPRAISAL REPORT

DELTA COUNTY APPRAISAL DISTRICT 2016 ANNUAL APPRAISAL REPORT Introduction The Delta County Appraisal District is a political subdivision of the State of Texas. The Constitution of the State of Texas, the

DELTA COUNTY APPRAISAL DISTRICT 2016 ANNUAL APPRAISAL REPORT Introduction The Delta County Appraisal District is a political subdivision of the State of Texas. The Constitution of the State of Texas, the

Assessment Report 2017

Assessment Report 217 Hennepin County Assessor s Office James Atchison, County Assessor, CAE, SAMA 217 TABLE OF CONTENTS Last modified (4-17-17) Table of Contents....3 Introduction and Overview of the

Assessment Report 217 Hennepin County Assessor s Office James Atchison, County Assessor, CAE, SAMA 217 TABLE OF CONTENTS Last modified (4-17-17) Table of Contents....3 Introduction and Overview of the

Sales Ratio Study Criteria

Sales Ratio Study Criteria Minnesota Department of Revenue Study Year 2016 Approved May 2016 The Sales Ratio Study is required by Minnesota Statute 270.12 and is used primarily to equalize assessments

Sales Ratio Study Criteria Minnesota Department of Revenue Study Year 2016 Approved May 2016 The Sales Ratio Study is required by Minnesota Statute 270.12 and is used primarily to equalize assessments

DELTA COUNTY APPRAISAL DISTRICT 2014 ANNUAL APPRAISAL REPORT

DELTA COUNTY APPRAISAL DISTRICT 2014 ANNUAL APPRAISAL REPORT Introduction The Delta County Appraisal District is a political subdivision of the State of Texas. The Constitution of the State of Texas, the

DELTA COUNTY APPRAISAL DISTRICT 2014 ANNUAL APPRAISAL REPORT Introduction The Delta County Appraisal District is a political subdivision of the State of Texas. The Constitution of the State of Texas, the

Midland Central Appraisal District BIENNIAL REAPPRAISAL PLAN

BIENNIAL REAPPRAISAL PLAN FOR THE TAX YEARS 2015 AND 2016 BY THE MIDLAND CENTRAL APPRAISAL DISTRICT BOARD OF DIRECTORS September 10, 2014 TABLE OF CONTENTS ITEM PAGE Executive Summary... 4 General Overview

BIENNIAL REAPPRAISAL PLAN FOR THE TAX YEARS 2015 AND 2016 BY THE MIDLAND CENTRAL APPRAISAL DISTRICT BOARD OF DIRECTORS September 10, 2014 TABLE OF CONTENTS ITEM PAGE Executive Summary... 4 General Overview

Rockwall CAD. Basics of. Appraising Property. For. Property Taxation

Rockwall CAD Basics of Appraising Property For Property Taxation ROCKWALL CENTRAL APPRAISAL DISTRICT 841 Justin Rd. Rockwall, Texas 75087 972-771-2034 Fax 972-771-6871 Introduction Rockwall Central Appraisal

Rockwall CAD Basics of Appraising Property For Property Taxation ROCKWALL CENTRAL APPRAISAL DISTRICT 841 Justin Rd. Rockwall, Texas 75087 972-771-2034 Fax 972-771-6871 Introduction Rockwall Central Appraisal

METHODOLOGY GUIDE VALUING MOTELS IN ONTARIO. Valuation Date: January 1, 2016

METHODOLOGY GUIDE VALUING MOTELS IN ONTARIO Valuation Date: January 1, 2016 AUGUST 2016 August 22, 2016 The Municipal Property Assessment Corporation (MPAC) is responsible for accurately assessing and

METHODOLOGY GUIDE VALUING MOTELS IN ONTARIO Valuation Date: January 1, 2016 AUGUST 2016 August 22, 2016 The Municipal Property Assessment Corporation (MPAC) is responsible for accurately assessing and

ESTIMATED FULL VALUE OF REAL PROPERTY IN COOK COUNTY:

ESTIMATED FULL VALUE OF REAL PROPERTY IN COOK COUNTY: 2003-2012 August 14, 2014 ESTIMATED FULL VALUE OF PROPERTY IN COOK COUNTY: Civic Federation Methodology CALCULATION OF ESTIMATED FULL VALUE The full

ESTIMATED FULL VALUE OF REAL PROPERTY IN COOK COUNTY: 2003-2012 August 14, 2014 ESTIMATED FULL VALUE OF PROPERTY IN COOK COUNTY: Civic Federation Methodology CALCULATION OF ESTIMATED FULL VALUE The full

Biennial Report on the Potential Right of Way Conveyance Parcels

2017-2018 Biennial Report on the Potential Right of Way Conveyance Parcels March 2019 Prepared by: The Minnesota Department of Transportation 395 John Ireland Boulevard Saint Paul, Minnesota 55155-1899

2017-2018 Biennial Report on the Potential Right of Way Conveyance Parcels March 2019 Prepared by: The Minnesota Department of Transportation 395 John Ireland Boulevard Saint Paul, Minnesota 55155-1899

YOUNG COUNTY APPRAISAL DISTRICT

YOUNG COUNTY APPRAISAL DISTRICT 2016 - ANNUAL APPRAISAL REPORT AS OF 8/24/2016 1 2 TABLE OF CONTENTS ITEM PAGE Introduction 4 Purpose of Report...4 Taxing Entities, Rates & Exemptions 5 Property Types

YOUNG COUNTY APPRAISAL DISTRICT 2016 - ANNUAL APPRAISAL REPORT AS OF 8/24/2016 1 2 TABLE OF CONTENTS ITEM PAGE Introduction 4 Purpose of Report...4 Taxing Entities, Rates & Exemptions 5 Property Types

2018 Assessment Report

2018 Assessment Report The Assessing Division: 952-939-8220 or assessor@eminnetonka.com Table of Contents Table of Contents... 2 Summary... 3 2018 Assessment from a Historical Perspective... 4 Tax Capacity...

2018 Assessment Report The Assessing Division: 952-939-8220 or assessor@eminnetonka.com Table of Contents Table of Contents... 2 Summary... 3 2018 Assessment from a Historical Perspective... 4 Tax Capacity...

Assembly Bill No. 489 Committee on Growth and Infrastructure CHAPTER...

Assembly Bill No. 489 Committee on Growth and Infrastructure CHAPTER... AN ACT relating to the taxation of property; providing for the partial abatement of the ad valorem taxes imposed on property; directing

Assembly Bill No. 489 Committee on Growth and Infrastructure CHAPTER... AN ACT relating to the taxation of property; providing for the partial abatement of the ad valorem taxes imposed on property; directing

Property Tax Fairness and the Future of Further Reform

Property Tax Fairness and the Future of Further Reform Ryan Kamrowski, Director of Tax Equalization, Ward County Senator Dwight Cook, Mandan (Dist. 34) Donnell Preskey Hushka, Government Affairs Specialist,

Property Tax Fairness and the Future of Further Reform Ryan Kamrowski, Director of Tax Equalization, Ward County Senator Dwight Cook, Mandan (Dist. 34) Donnell Preskey Hushka, Government Affairs Specialist,

COMAL APPRAISAL DISTRICT ANNUAL APPRAISAL REPORT

COMAL APPRAISAL DISTRICT 2016 ANNUAL APPRAISAL REPORT TABLE OF CONTENTS Introduction..2 Mission Statement... 2 Purpose of Report...2 Entities Served..2 Legislative Changes.3 Property Types.3 Appraisal

COMAL APPRAISAL DISTRICT 2016 ANNUAL APPRAISAL REPORT TABLE OF CONTENTS Introduction..2 Mission Statement... 2 Purpose of Report...2 Entities Served..2 Legislative Changes.3 Property Types.3 Appraisal

Understanding Mississippi Property Taxes

Understanding Mississippi Property Taxes Property tax revenues are a vital component of the budgets of Mississippi s local governments. Property tax revenues allow these governments to provide important

Understanding Mississippi Property Taxes Property tax revenues are a vital component of the budgets of Mississippi s local governments. Property tax revenues allow these governments to provide important

2019 Revaluation Update. Presented by the Mecklenburg County Assessor s Office

2019 Revaluation Update Presented by the Mecklenburg County Assessor s Office Progress to Date 203,933 Parcels Completed 914 Residential Neighborhoods Completed (57%) All neighborhoods will be completed

2019 Revaluation Update Presented by the Mecklenburg County Assessor s Office Progress to Date 203,933 Parcels Completed 914 Residential Neighborhoods Completed (57%) All neighborhoods will be completed

2017 SSTS Annual Report Subsurface Sewage Treatment Systems in Minnesota