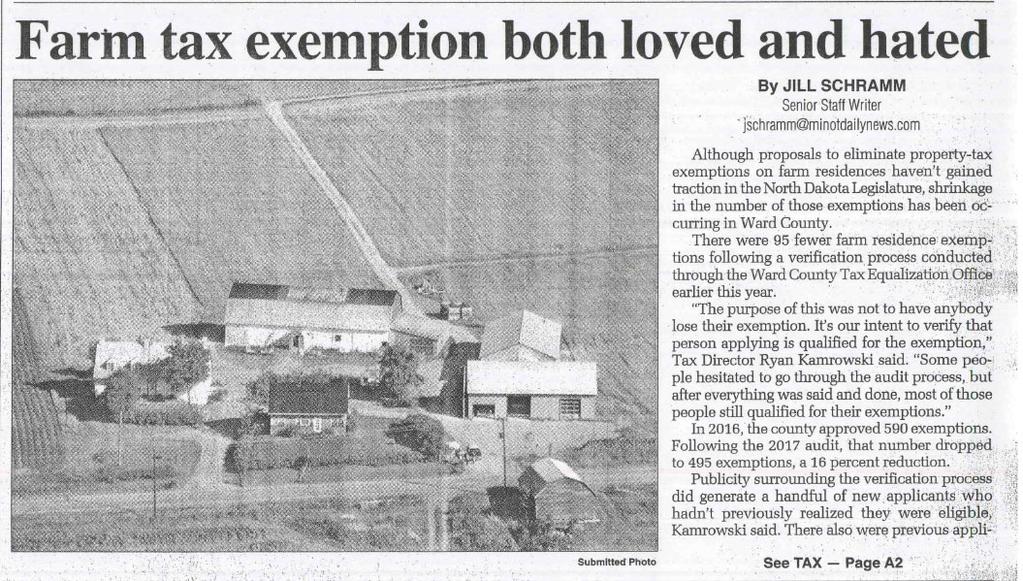

Property Tax Fairness and the Future of Further Reform

|

|

|

- Carmella Russell

- 5 years ago

- Views:

Transcription

1 Property Tax Fairness and the Future of Further Reform Ryan Kamrowski, Director of Tax Equalization, Ward County Senator Dwight Cook, Mandan (Dist. 34) Donnell Preskey Hushka, Government Affairs Specialist, NDACo

2 Ryan Kamrowski Phone: Professional Experience: 2015-present Director of Tax Equalization, Ward County Property Appraiser, Ward County Education: Bachelor of Science, Business Management, 2011 Bachelor of Science, International Business, 2011 Minot State University, Minot, ND Certification: Class I Assessor, State of ND, Office of State Tax Commissioner Professional Memberships: International Association of Assessing Officers (IAAO) 2014-Present North Dakota Association of Assessing Officers (NDAAO) 2013-Present

3 Topics of Discussion 2015 House Bill No Established new assessor education requirements Amended NDCC and , Requirements for assessors based on jurisdictional size Amended NDCC , assessments of unorganized Twp s Created NDCC , certificate classifications, education and trasition by July 31, 2017 Exemption & Credit Applications Types of Exemptions Available Types of Credits Available Impact on Local Jurisdictions Ward County s Approach to Verification and Auditing Applications.

4 Who Are Assessor/Appraisers (Video)

5 Requirements prior to 2015 House Bill No Three classifications of Assessors Tax Director Required 240 hrs of State regulated education to receive certifications Required 40 hrs of continuing education every 4 years to renew City Assessor (Jurisdiction larger than 5000 in Population) Required 200 hrs of State regulated education to receive certifications Required 40 hrs of continuing education every 4 years to renew Township/City Assessor (Jurisdictions with population less than 5000) Required 28 hrs of State Regulated Edcuation or passing grade on self-study exam Required annual attendance to minimum of 4hr class taught by County Tax Director each year.

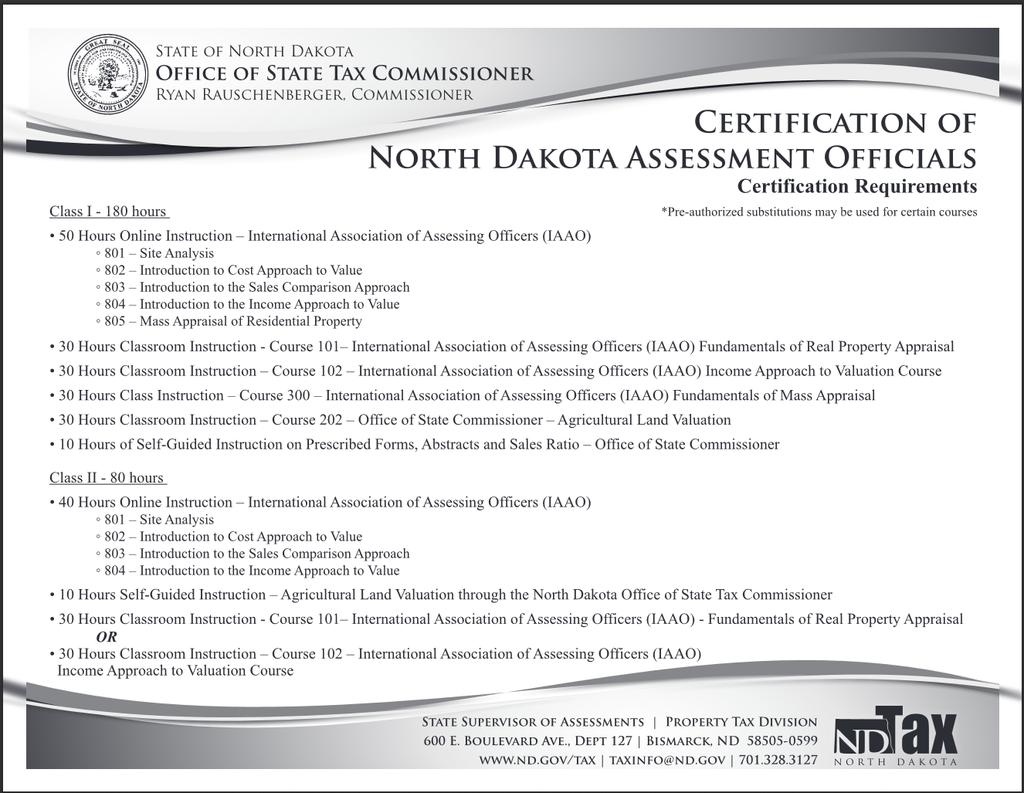

6 Requirements to Assess Property in North Dakota Under Current Law (Post HB 1059) Pursuant to N.D.C.C & : The board of county commissioners of each county shall appoint a county director of tax equalization who must be experienced in assessment and equalization procedures and techniques, and who holds a current certification as a class I assessor issued by the state supervisor of assessments. Any city with a population of under 5000 or township may, by resolution of its governing body, retain an assessor who is certified or eligible to be certified as a Class II Assessor who shall retain the powers, duties, and responsibilities of the office. Any city with a population of 5000 or greater may, by resolution of its governing body, retain an assessor who is certified or eligible to be certified as a Class I Assessor who shall retain the powers, duties, and responsibilities of the office. A person may not serve as an assessor for longer than twenty-four months before being certified by the state supervisor of assessments as having met the minimum requirements. The expenses of the city or township assessors must be paid by the city or township exercising this option.

7 Requirements to Assess Property in North Dakota Under Current Law Class 1 Assessor Class II Assessor Have a High School Diploma or its Equivalent Have a High School Diploma or its Equivalent 180 hrs of State Approved Ed. 80 hrs of State Approved Ed. An assessor certificate is valid for a term of two years An assessor certificate is valid for a term of two years Renewed if holder has completed 20 hrs of approved classroom inst. or seminars during the term of certificate. 20 hrs in 2yrs Renewed if holder has completed 10 hrs of approved classroom inst. or seminars during the term of certificate. 10hrs in 2 yrs

8

9 Jurisdictional Cost for Certification Class I Assessor 180 hrs of Education ~$2800 Salary (at median of $45,000/yr) ~$5400 Lodging and Per Diem ~$1800 Total Estimated Cost: $10,000 Cost for Recertification: $800- $2000 every 2 years Class II Assessor 80 hrs of Education ~$1500 Salary (at median of 45,000/yr) ~$1700 Lodging and Per Diem ~$450 Total Estimated Cost: $3,650 Cost for Recertification: $400- $1000 every 2 years

10 Pros & Cons Pros Cons Uniform Education Cost Higher Quality of Education $3,600 to $10,000 per assessor More Educational Opportunities On site Lack of local jurisdiction involvement Online Resource and Networking Capabilities

11 What is the Role of Assessors/Appraisers Video)

12 State Wide Implications Decrease in local assessment official Increase in county and city assessor staff IAAO (International Association of Assessing Officers) parcel count guideline for number of staff: 2500 improved parcels per certified assessor. Ex. County w/ 10,000 improved parcels should have 4 certified assessors dedicated to annual reviews and reassessments of parcels to maintain a fair and equitable valuations Increased cost to local jurisdictions that wish to retain township or city assessor, rather than revert assessments to County

13 Ward County Implications Number of Cert. Assessors in Ward County (Including City of Minot) 2013 Ward County Tax Equalization: 4 City of Minot: 4 Township & Cities under 5,000 pop.: Ward County Tax Equalization: 6 City of Minot: 5 Township & Cities under 5,000 pop.: 3

14 Ward County s Solution Increase in Certified Assessors 2 FTE added, one in 2015 & one in 2016 Evolution of Assessment Process Increased efficiency through CAMA program (Computer Aided Mass Appraisal) Utilization of Aerial Imagery Implementation and Integration of GIS software with Assessment Data

15 1308 Organized Townships (2018) How Assessing Requirements Impacted Responsibilities Statewide ND Cities Jurisdictions Assessed by the County Jurisdictions assessed by 'local' Assessors Total Number of 'local' Assessors 2013 Townships 2018 Townships 2013 Cities 2018 Cities *2018 NDACo Study

16 Township Assessing County 37% Local 63% County 76% Local 24%

17 City Assessing County 41% Local 59% County 66% Local 34%

18 Local (Non-County) Assessors 648 City Township City Township

19 TOTAL NUMBER OF LOCAL ASSESSORS Fewer Assessors 76% Decrease

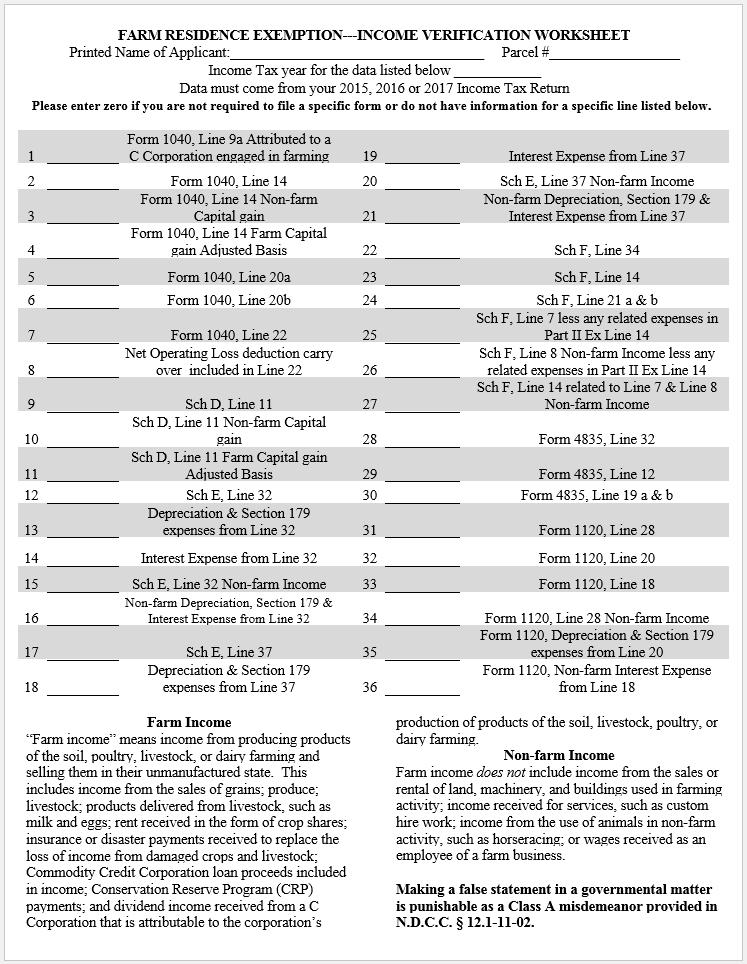

20 Summary of NDACo Statewide Survey Results 76% Decrease in Total Assessors (-493) 84% Decrease in Township Assessors (-427) 48% Decrease in City Assessors (-66) 109% Increase in assessors to County Tax Equalization Offices (+520) Statistics indicate that many County Tax Equalization Offices are currently understaffed to perform fair and equitable assessments

21 Video

22 Property Tax Exemption of a Farm Residence

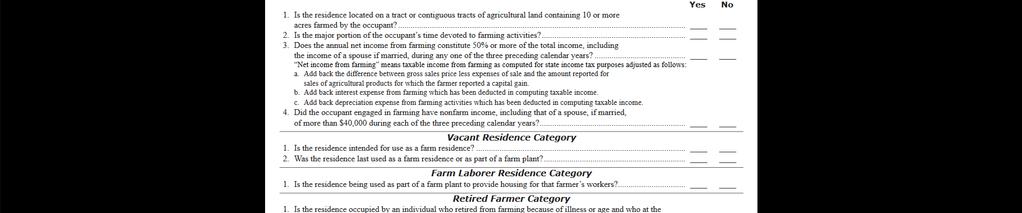

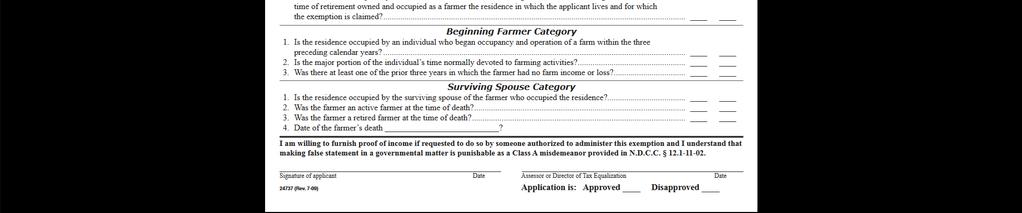

23 What is the Farm Residence Exemption Exempts, from Ad Valorem Property Taxation, the Residence of an applicant that qualifies for the exemption Applicants apply under one of six categories: Active Farmer, Retired Farmer, Beginning Farmer, Vacant, Farm Laborer, or Surviving Spouse. "Farmer" means an individual who normally devotes the major portion of time to the activities of producing products of the soil, with the exception of marijuana grown under chapter ; poultry; livestock; or dairy farming in such products unmanufactured state and has received annual net income from farming activities which is fifty percent or more of annual net income, including net income of a spouse if married, during any of the three preceding calendar years. NDCC (15b.2) In addition to any of the provisions of this subsection or any other provision of law, a residence situated on agricultural land is not exempt for the year if it is occupied by an individual engaged in farming who had nonfarm income, including that of a spouse if married, of more than forty thousand dollars during each of the three preceding calendar years. This paragraph does not apply to a retired farmer or a beginning farmer as defined in paragraph 2. NDCC (15b.5)

24 Why did Ward County Decide to Preform Audits Had several township boards and many qualifying applicants express concerns about abuse of the exemption. Every other exemption or credit required applicants to furnish income, medical, or financial documents to qualify for exemption Homestead Credit: Medical, Financial, & Income Blind and Wheelchair Exemption: Medical Disabled Veterans Credit: Medical PILOT: Financial & Income Tax Exemption: Financial & Income Farm Residence Exemption: NONE It was determined that Ward County should not show bias for one exemption over another.

25 Implementation of Audit With the Approval of the Ward County Commission, all applications were audited. Included financial audit for Active, Retired, Beginning, & Laborer categories Included physical inspection to validate vacancy for the Vacant category. Included reviewing death certificated in the recorders office for Surviving Spouse category. (only done to determine the 5 year extension of exemption for those who were active at time of passing.)

26 Implementation of Audit Mailed all applicants (both county assessed and locally assessed) a copy of the application, letter outlining the audit requirements, the state provided 3 page income verification worksheet, & affidavit to sign if prepared by individual other than applicant. ie: Accountant Requested that all applications and income verification worksheets be return prior to Feb. 1 st as noted on the top of the Exemption Application.

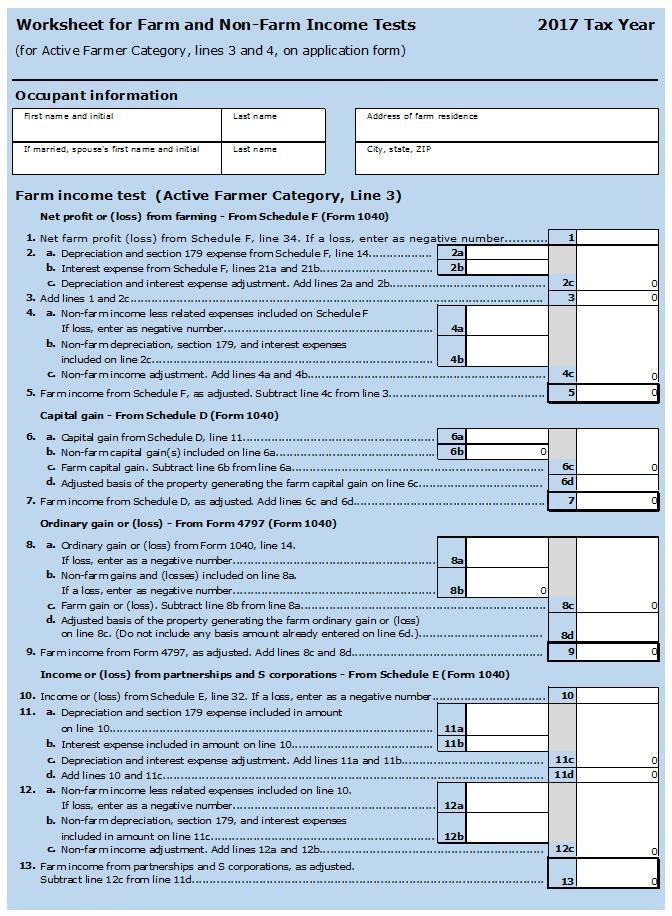

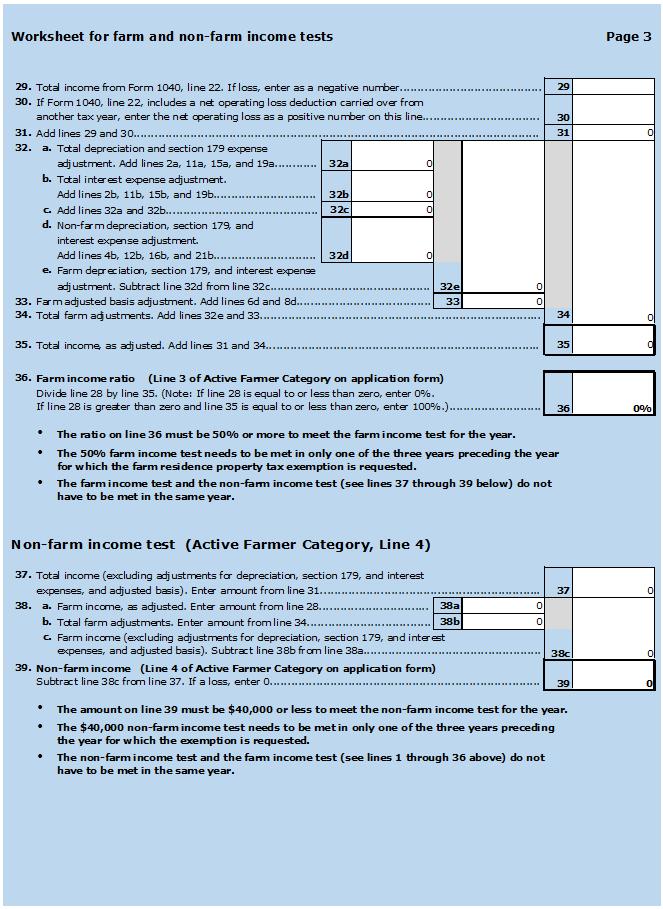

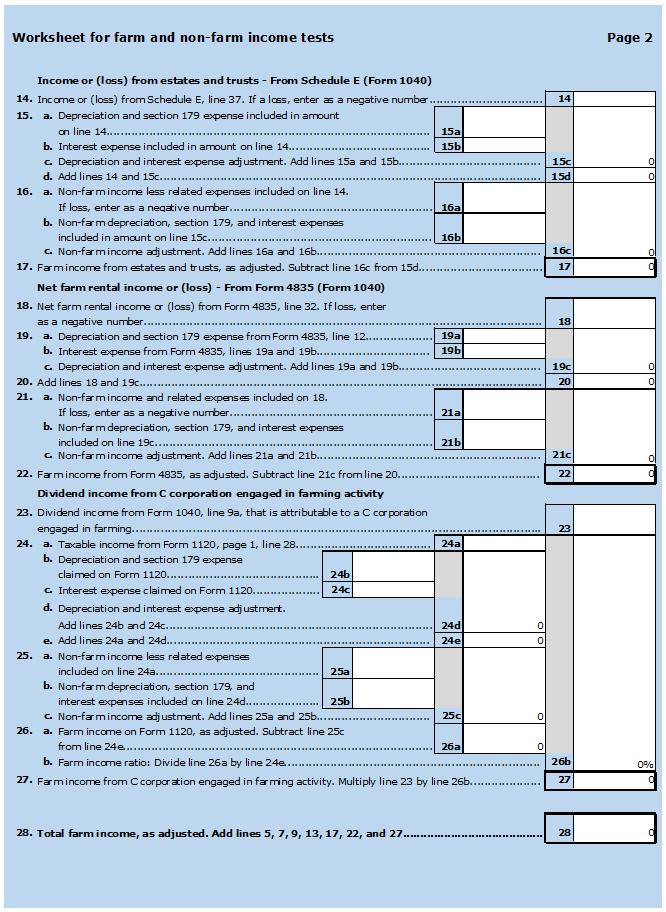

27 State Tax Dept. Worksheet

28 So What Happened? Responses from Applicants Several irate and angry phone calls, letters, & s Concerns from applicants pertaining to return date of application Response from Ward County Commissioners Unsettled by the amount of contacts pertaining to the audit process Unease on the complexity of the State Tax Dept. 3 page Worksheet Ward County Commission Suspended the Audit after 3 weeks Commission requested simplification of the audit process be done before proceeding with the audit

29

30 Audit Version 2.0 New and revised Income Verification Worksheet was generated Expanded off of a version that was created by Donald Flaherty, Dickey County Dir. of Tax Equalization 1 page, easy to read, fill in the blank format Extended Deadline for Application and Income Worksheet to township or city equalization meeting

31

32 Results of Audit Tax Year Applicants Estimated Market Value Exempt $103,250,000 Estimated Taxable Value Exempt $4,646,250 Estimated Tax Revenue Exempt Tax Year Applicants 95 applicants no longer qualified 16% Market Value Added to Tax Roll $16,474,000 Estimated Tax Revenue $1,022,000 (based on average mill levy in county of 220 mills) $163,100(based on average mill levy in county of 220 mills)

33 Moving Forward Active Farmer applicants are required to complete income verification worksheet every 3 years Example: qualified 2017 using 2016 income, will need to requalify again for 2020 using 2019 income Retired Farmers will not be audited again unless evidence is present to support otherwise. All applicants changing from Active Farmer to Retired Farmer are require to furnish proof of category reclassification Applicants of Laborer, Vacant, Beginning, & Surviving Spouse categories are reviewed yearly based off of application criteria.

34 Farm Residence Exemption NDACo Survey 11,400 Approved Farm- Residence Exemptions Reported (40/53 counties) Most Counties determine eligibility: 1-3 years 29 Counties require income verification for farm-residence exemption

35 Frequency of Utilizing Third Party Appraiser Never 10 Annually 9 Counties Using Annual Third Party Appraisers located in Western ND Once 3 On Request 20 43/53 Counties Responded

36 14 Cost to Counties for Outside Industrial Appraisal Services $1-25,000 $25,000-50,000 $50,000-75,000 $75, ,000 $100,000+

37 Counties lack expertise in industrial assessments Very expensive to outsource at taxpayer expense Counties mixed on who should handle industrial appraisals 3 rd party State Appointed Shared County Assessor Industrial Appraisals in ND NDACo Survey

38 Reflection on Property Tax Changes & Future of Property Tax Reform Senator Dwight Cook, Mandan

39 Property Tax Reform - Legislative Changes Numerous changes to increase understanding, fairness and transparency in last two sessions Major Tax Reform of Levies (2015) Repealed & Consolidated Levies Enhanced Assessor Training Requirements (2015) Uniform Property Tax Statement Reference in $ not mills Preliminary Consolidated Budget Notice (2017)

40 Preliminary Budget Notice New in 2018 Replaces current Truth in Taxation Notices Changes Dates for Centrally Assessed Properties & Reporting Requirements Shifts dates approximately 1 month earlier Penalties for late reporting

41 Preliminary Budget Notice NEW in 2018 Single, consolidated Notice- Includes budget hearing dates & locations for all taxing districts Costs to be shared

42 Preliminary Budget Notice A taxing district that fails to provide the information required under this subsection on or before August tenth may not impose a property tax levy in a greater amount of dollars than was imposed by the taxing district in the prior year. (N.D.C.C (1)) Century Code requires taxing jurisdictions to submit Preliminary Budget to County by 8/10 Failure to submit: Held at previous years budget in DOLLARS

43 Uniform Property Tax Statement

44 Typical Ward County Assessment!!! (Video)

45 QUESTIONS/COMMENTS

FLORIDA CONSTITUTION

FLORIDA CONSTITUTION (Provisions related to ad valorem property taxes and exemptions) ARTICLE VII - FINANCE AND TAXATION SECTION 2. Taxes; rate.-- All ad valorem taxation shall be at a uniform rate within

FLORIDA CONSTITUTION (Provisions related to ad valorem property taxes and exemptions) ARTICLE VII - FINANCE AND TAXATION SECTION 2. Taxes; rate.-- All ad valorem taxation shall be at a uniform rate within

Additional senior homestead exemption.

02-1 02-1 F L O R I D A H O U S E O F R E P R E S E N T A T I V E S ENROLLED CS/HJR 169 2012 Legislature 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 House Joint Resolution

02-1 02-1 F L O R I D A H O U S E O F R E P R E S E N T A T I V E S ENROLLED CS/HJR 169 2012 Legislature 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 House Joint Resolution

Duties of the Assessors

Duties of the Assessors Value Properties Determine New Growth Set Tax Rate Assess Property Taxes Abate & Exempt Taxes Manage Overlay Account Assess Local Excises 1 Value Property Assessments based on fair

Duties of the Assessors Value Properties Determine New Growth Set Tax Rate Assess Property Taxes Abate & Exempt Taxes Manage Overlay Account Assess Local Excises 1 Value Property Assessments based on fair

CS for CP0004, Second Engrossed 07-08

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 Resolution of the Taxation and Budget Reform Commission A resolution proposing an amendment to Sections 3 and 4 of Article

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 Resolution of the Taxation and Budget Reform Commission A resolution proposing an amendment to Sections 3 and 4 of Article

PROPERTY REASSESSMENT AND TAXATION. State Tax Commission Jefferson City, Missouri

PROPERTY REASSESSMENT AND TAXATION State Tax Commission Jefferson City, Missouri Revised January, 2017 INTRODUCTION Some aspects of the property tax system are confusing to many taxpayers. It is important

PROPERTY REASSESSMENT AND TAXATION State Tax Commission Jefferson City, Missouri Revised January, 2017 INTRODUCTION Some aspects of the property tax system are confusing to many taxpayers. It is important

2017 Annual Report. Fayette County Appraisal District P. O. Box 836 La Grange, TX 78945

2017 Annual Report Fayette County Appraisal District P. O. Box 836 La Grange, TX 78945 FCAD 2017 Annual Report 1 2017 ANNUAL REPORT FAYETTE COUNTY APPRAISAL DISTRICT INTRODUCTION The Fayette County Appraisal

2017 Annual Report Fayette County Appraisal District P. O. Box 836 La Grange, TX 78945 FCAD 2017 Annual Report 1 2017 ANNUAL REPORT FAYETTE COUNTY APPRAISAL DISTRICT INTRODUCTION The Fayette County Appraisal

Van Zandt County Appraisal District 2017 Annual Report

Van Zandt County Appraisal District 2017 Annual Report Introduction The Van Zandt County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property

Van Zandt County Appraisal District 2017 Annual Report Introduction The Van Zandt County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property

VAN ZANDT COUNTY APPRAISAL DISTRICT 2018 ANNUAL REPORT

VAN ZANDT COUNTY APPRAISAL DISTRICT 2018 ANNUAL REPORT INTRODUCTION The Van Zandt County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property

VAN ZANDT COUNTY APPRAISAL DISTRICT 2018 ANNUAL REPORT INTRODUCTION The Van Zandt County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property

Equalization. Equalization. Statutory Duties. Statutory Authority

Equalization Citizens Board of Commissioners Administrator /Controller Statutory Duties Advise and assist the Board of Commissioners in equalizing property tax assessments on a county-wide basis. File

Equalization Citizens Board of Commissioners Administrator /Controller Statutory Duties Advise and assist the Board of Commissioners in equalizing property tax assessments on a county-wide basis. File

F L O R I D A H O U S E O F R E P R E S E N T A T I V E S

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 House Joint Resolution A joint resolution proposing an amendment to Section 6 of Article VII and the creation of a new section in Article

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 House Joint Resolution A joint resolution proposing an amendment to Section 6 of Article VII and the creation of a new section in Article

Van Zandt County Appraisal District 2015 Annual Report

Van Zandt County Appraisal District 2015 Annual Report Introduction The Van Zandt County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property

Van Zandt County Appraisal District 2015 Annual Report Introduction The Van Zandt County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property

We look forward to working with you to build on our collaboration and enhance our partnership on behalf of all Minnesotans.

Date: February 27, 2017 To: County Assessors, Auditors, and Treasurers From: Cynthia Rowley, Director Property Tax Division Subject: Property Tax Services Report The Property Tax Division of the Minnesota

Date: February 27, 2017 To: County Assessors, Auditors, and Treasurers From: Cynthia Rowley, Director Property Tax Division Subject: Property Tax Services Report The Property Tax Division of the Minnesota

UNDERSTANDING PROPERTY TAXES IN COLORADO

UNDERSTANDING PROPERTY TAXES IN COLORADO This brochure was created to provide general information on the Colorado property tax system. For more specific information on any one of these topics, please visit

UNDERSTANDING PROPERTY TAXES IN COLORADO This brochure was created to provide general information on the Colorado property tax system. For more specific information on any one of these topics, please visit

2015 Annual Report. The appraisal district is governed by a Board of Directors whose primary responsibilities are to:

Refugio County Appraisal District Mailing Address: PO Box 156, Refugio, Texas 78377-0156 Physical Location: 420 North Alamo Street, Refugio, Texas 78377 Telephone Number: 361-526-5994 Website: www.refugiocad.org

Refugio County Appraisal District Mailing Address: PO Box 156, Refugio, Texas 78377-0156 Physical Location: 420 North Alamo Street, Refugio, Texas 78377 Telephone Number: 361-526-5994 Website: www.refugiocad.org

Florida Senate CS for CS for SJR 170. By the Committees on Appropriations; and Finance and Tax; and Senators Brandes and Hutson

By the Committees on Appropriations; and Finance and Tax; and Senators Brandes and Hutson 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 Senate Joint Resolution A joint

By the Committees on Appropriations; and Finance and Tax; and Senators Brandes and Hutson 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 Senate Joint Resolution A joint

YOUR GUIDE TO THE REASSESSMENT PROGRAM

YOUR GUIDE TO THE REASSESSMENT PROGRAM Why Reassess? Reassessment is required by law. Act 208, as passed by the General Assembly in 1975, provides that all real property will be valued at its current market

YOUR GUIDE TO THE REASSESSMENT PROGRAM Why Reassess? Reassessment is required by law. Act 208, as passed by the General Assembly in 1975, provides that all real property will be valued at its current market

41 st Annual Conference Appraising Property

2017 KCCA 41 st Annual Conference Appraising Property Kansas County Commissioners Association Junction City, Kansas June 2, 2017 Topics Overview PVD s Role in the Appraisal Process Appointment of County

2017 KCCA 41 st Annual Conference Appraising Property Kansas County Commissioners Association Junction City, Kansas June 2, 2017 Topics Overview PVD s Role in the Appraisal Process Appointment of County

ASSESSMENT AND TAXATION

ABSTRACT A brief synopsis of the assessment, appeal and taxation process as implemented by the Code of Iowa and Administrative Rules. ASSESSMENT AND TAXATION Iowa State Association of Assessors General

ABSTRACT A brief synopsis of the assessment, appeal and taxation process as implemented by the Code of Iowa and Administrative Rules. ASSESSMENT AND TAXATION Iowa State Association of Assessors General

To: Property Appraisers, Taxing Authorities and Interested Parties From: James McAdams Date: June 5, 2012 Bulletin: PTO 12-04

Property Tax Oversight Bulletin: PTO 12-04 To: Property Appraisers, Taxing Authorities and Interested Parties From: James McAdams Date: Bulletin: PTO 12-04 FLORIDA DEPARTMENT OF REVENUE PROPERTY TAX INFORMATIONAL

Property Tax Oversight Bulletin: PTO 12-04 To: Property Appraisers, Taxing Authorities and Interested Parties From: James McAdams Date: Bulletin: PTO 12-04 FLORIDA DEPARTMENT OF REVENUE PROPERTY TAX INFORMATIONAL

Chapter 11: Conservation Easements

Chapter 11: Conservation Easements An * in the left margin indicates a change in the statute, rule, or text since the last publication of the manual. I. Introduction In 2008, Colorado s appraiser statutes

Chapter 11: Conservation Easements An * in the left margin indicates a change in the statute, rule, or text since the last publication of the manual. I. Introduction In 2008, Colorado s appraiser statutes

F L O R I D A H O U S E O F R E P R E S E N T A T I V E S

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 House Joint Resolution A joint resolution proposing amendments to Sections 3 and 4 of Article VII and the creation of Section 34 of

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 House Joint Resolution A joint resolution proposing amendments to Sections 3 and 4 of Article VII and the creation of Section 34 of

Ad Valorem Tax Escambia County FL Explained

Ad Valorem Tax Escambia County FL Explained What properties must be appraised? REAL PROPERTY - the physical land and appurtenances affixed to the land, e.g., structures. The term "land","real estate","realty"

Ad Valorem Tax Escambia County FL Explained What properties must be appraised? REAL PROPERTY - the physical land and appurtenances affixed to the land, e.g., structures. The term "land","real estate","realty"

CHAPTER Senate Bill No. 4-D

CHAPTER 2007-339 Senate Bill No. 4-D An act relating to ad valorem taxation; authorizing the Department of Revenue to adopt emergency rules; providing for application and renewal thereof; requiring the

CHAPTER 2007-339 Senate Bill No. 4-D An act relating to ad valorem taxation; authorizing the Department of Revenue to adopt emergency rules; providing for application and renewal thereof; requiring the

1 SB By Senator Pittman. 4 RFD: Finance and Taxation General Fund. 5 First Read: 21-FEB-17. Page 0

1 SB226 2 181182-1 3 By Senator Pittman 4 RFD: Finance and Taxation General Fund 5 First Read: 21-FEB-17 Page 0 1 181182-1:n:02/07/2017:LFO-HP/jmb 2 3 4 5 6 7 8 SYNOPSIS: Currently, residents of this state

1 SB226 2 181182-1 3 By Senator Pittman 4 RFD: Finance and Taxation General Fund 5 First Read: 21-FEB-17 Page 0 1 181182-1:n:02/07/2017:LFO-HP/jmb 2 3 4 5 6 7 8 SYNOPSIS: Currently, residents of this state

The Duties of the Iowa Assessor (ISAC New County Officers School)

") The Duties of the Iowa Assessor (ISAC New County Officers School) Wayne Schwickerath Story County Assessor January 19, 2017 Purpose of Presentation (Iowa Code Chapter 441) Assessment & Valuation of Property)

The Duties of the Iowa Assessor (ISAC New County Officers School) Wayne Schwickerath Story County Assessor January 19, 2017 Purpose of Presentation (Iowa Code Chapter 441) Assessment & Valuation of Property)

COMMERCIAL REHABILITATION ACT Act 210 of The People of the State of Michigan enact:

COMMERCIAL REHABILITATION ACT Act 210 of 2005 AN ACT to provide for the establishment of commercial rehabilitation districts in certain local governmental units; to provide for the exemption from certain

COMMERCIAL REHABILITATION ACT Act 210 of 2005 AN ACT to provide for the establishment of commercial rehabilitation districts in certain local governmental units; to provide for the exemption from certain

BASTROP CENTRAL APPRAISAL DISTRICT ANNUAL REPORT 2016

BASTROP CENTRAL APPRAISAL DISTRICT ANNUAL REPORT 2016 EXECUTIVE SUMMARY The first part of the year included gathering information on new construction and the analyzing of data for the 2016 appraisal roll.

BASTROP CENTRAL APPRAISAL DISTRICT ANNUAL REPORT 2016 EXECUTIVE SUMMARY The first part of the year included gathering information on new construction and the analyzing of data for the 2016 appraisal roll.

LLANO CENTRAL APPRAISAL DISTRICT REAPPRAISAL PLAN FOR TAX YEARS 2017 & 2018 AS ADOPTED BY THE BOARD OF DIRECTORS

LLANO CENTRAL APPRAISAL DISTRICT REAPPRAISAL PLAN FOR TAX YEARS 2017 & 2018 AS ADOPTED BY THE BOARD OF DIRECTORS TABLE OF CONTENTS ITEM PAGE Executive Summary 5 Revaluation Decision (Statutory or Administrative)

LLANO CENTRAL APPRAISAL DISTRICT REAPPRAISAL PLAN FOR TAX YEARS 2017 & 2018 AS ADOPTED BY THE BOARD OF DIRECTORS TABLE OF CONTENTS ITEM PAGE Executive Summary 5 Revaluation Decision (Statutory or Administrative)

We hope the trends provide additional perspective on your county s work. We know it provided valuable insight on the work we do here at Revenue.

Date: March 6, 2018 To: County Assessors, Auditors, and Treasurers From: Jon Klockziem, Acting Director Subject: Property Tax Services Report The Property Tax Division of the is pleased to provide the

Date: March 6, 2018 To: County Assessors, Auditors, and Treasurers From: Jon Klockziem, Acting Director Subject: Property Tax Services Report The Property Tax Division of the is pleased to provide the

NEIGHBORHOOD ENTERPRISE ZONE ACT Act 147 of The People of the State of Michigan enact:

NEIGHBORHOOD ENTERPRISE ZONE ACT Act 147 of 1992 AN ACT to provide for the development and rehabilitation of residential housing; to provide for the creation of neighborhood enterprise zones; to provide

NEIGHBORHOOD ENTERPRISE ZONE ACT Act 147 of 1992 AN ACT to provide for the development and rehabilitation of residential housing; to provide for the creation of neighborhood enterprise zones; to provide

TRANSMITTAL MEMORANDUM DEPARTMENT OF REVENUE RULES

T/M 05-20 Date: December 28, 2005 TRANSMITTAL MEMORANDUM DEPARTMENT OF REVENUE RULES PURPOSE: This transmittal memorandum contains instructions for filing updated material for Department of Revenue Rules.

T/M 05-20 Date: December 28, 2005 TRANSMITTAL MEMORANDUM DEPARTMENT OF REVENUE RULES PURPOSE: This transmittal memorandum contains instructions for filing updated material for Department of Revenue Rules.

The Future of Property Taxes in Florida. Amber Hughes Sr. Legislative Advocate Florida League of Cities

The Future of Property Taxes in Florida Amber Hughes Sr. Legislative Advocate Florida League of Cities 2017 Legislative Issues Non-homestead assessment limitation caps Recapture Implementation of Voter

The Future of Property Taxes in Florida Amber Hughes Sr. Legislative Advocate Florida League of Cities 2017 Legislative Issues Non-homestead assessment limitation caps Recapture Implementation of Voter

Pickens County Reassessment Program. Utilizing CAMA GIS MLS SQL

1 Pickens County 2019 Reassessment Program Utilizing CAMA GIS MLS SQL Pickens County Reassessment History 1980 Countywide Reappraisal 1990 Countywide Reappraisal 1999 Countywide Reappraisal 2004 Countywide

1 Pickens County 2019 Reassessment Program Utilizing CAMA GIS MLS SQL Pickens County Reassessment History 1980 Countywide Reappraisal 1990 Countywide Reappraisal 1999 Countywide Reappraisal 2004 Countywide

2018 Annual Report. Fayette County Appraisal District P. O. Box 836 La Grange, TX 78945

2018 Annual Report Fayette County Appraisal District P. O. Box 836 La Grange, TX 78945 FCAD 2018 Annual Report 1 2018 ANNUAL REPORT FAYETTE COUNTY APPRAISAL DISTRICT INTRODUCTION The Fayette County Appraisal

2018 Annual Report Fayette County Appraisal District P. O. Box 836 La Grange, TX 78945 FCAD 2018 Annual Report 1 2018 ANNUAL REPORT FAYETTE COUNTY APPRAISAL DISTRICT INTRODUCTION The Fayette County Appraisal

Annual Report. Les Cook, CFA Citrus County Property Appraiser. Citrus County Property Appraiser [Type here] October 2017

![Annual Report. Les Cook, CFA Citrus County Property Appraiser. Citrus County Property Appraiser [Type here] October 2017](/thumbs/86/93980936.jpg "Annual Report. Les Cook, CFA Citrus County Property Appraiser. Citrus County Property Appraiser [Type here] October 2017") 2017 Annual Report Les Cook, CFA Citrus County Property Appraiser Citrus County Property Appraiser [Type here] October 2017 A Message from Les Cook The Citrus County Property Appraiser Annual Report contains

2017 Annual Report Les Cook, CFA Citrus County Property Appraiser Citrus County Property Appraiser [Type here] October 2017 A Message from Les Cook The Citrus County Property Appraiser Annual Report contains

Terrell County Appraisal District 2018 Annual Report

Terrell County Appraisal District 2018 Annual Report Introduction The Terrell County Appraisal District is a political subdivision of the State of Texas. The Texas Constitution, Texas Property Tax Code

Terrell County Appraisal District 2018 Annual Report Introduction The Terrell County Appraisal District is a political subdivision of the State of Texas. The Texas Constitution, Texas Property Tax Code

Request for Proposals For Assessor. Charter Township of Augusta Washtenaw County

Request for Proposals For Assessor (Michigan Certified Assessing Officer) Charter Township of Augusta Washtenaw County Charter Township of Augusta 8021 Talladay Road Whittaker, MI 48190 Phone 734-461-6117

Request for Proposals For Assessor (Michigan Certified Assessing Officer) Charter Township of Augusta Washtenaw County Charter Township of Augusta 8021 Talladay Road Whittaker, MI 48190 Phone 734-461-6117

Standard on Professional Development

Standard on Professional Development Approved January 2013 International Association of Assessing Officers This standard replaces the December 2000 Standard on Professional Development. IAAO assessment

Standard on Professional Development Approved January 2013 International Association of Assessing Officers This standard replaces the December 2000 Standard on Professional Development. IAAO assessment

Gaines County Appraisal District 2016 Annual Report

Gaines County Appraisal District 2016 Annual Report Introduction The Gaines County Appraisal District is a political subdivision of the state, The Constitution of the State of Texas, the Texas Property

Gaines County Appraisal District 2016 Annual Report Introduction The Gaines County Appraisal District is a political subdivision of the state, The Constitution of the State of Texas, the Texas Property

Q. How is Agricultural property valued? A. GENERAL INFORMATION Many states have laws regarding the preferential assessment of agricultural land.

Q. How is Agricultural property valued? A. GENERAL INFORMATION Many states have laws regarding the preferential assessment of agricultural land. This means that farm and ranch assessments are usually based

Q. How is Agricultural property valued? A. GENERAL INFORMATION Many states have laws regarding the preferential assessment of agricultural land. This means that farm and ranch assessments are usually based

(35 ILCS 200/15-175) Sec General homestead exemption. (a) Except as provided in Sections and , homestead property is entitled

Sec General homestead exemption. (a) Except as provided in Sections and , homestead property is entitled") (35 ILCS 200/15-175) Sec. 15-175. General homestead exemption. (a) Except as provided in Sections 15-176 and 15-177, homestead property is entitled to an annual homestead exemption limited, except as described

(35 ILCS 200/15-175) Sec. 15-175. General homestead exemption. (a) Except as provided in Sections 15-176 and 15-177, homestead property is entitled to an annual homestead exemption limited, except as described

MINNESOTA REVENUE ASSESSMENT AND CLASSIFICATION PRACTICES REPORT

MINNESOTA REVENUE ASSESSMENT AND CLASSIFICATION PRACTICES REPORT THE AGRICULTURAL PROPERTY TAX PROGRAM, CLASS 2A AGRICULTURAL PROPERTY, AND CLASS 2B RURAL VACANT LAND PROPERTY A report submitted to the

MINNESOTA REVENUE ASSESSMENT AND CLASSIFICATION PRACTICES REPORT THE AGRICULTURAL PROPERTY TAX PROGRAM, CLASS 2A AGRICULTURAL PROPERTY, AND CLASS 2B RURAL VACANT LAND PROPERTY A report submitted to the

2018 Annual Report FINAL CERTIFICATION. Les Cook, CFA Citrus County Property Appraiser

2018 Annual Report FINAL CERTIFICATION Les Cook, CFA Citrus County Property Appraiser A Message from Les Cook The Citrus County Property Appraiser Annual Report contains an overview of the trends in the

2018 Annual Report FINAL CERTIFICATION Les Cook, CFA Citrus County Property Appraiser A Message from Les Cook The Citrus County Property Appraiser Annual Report contains an overview of the trends in the

GENERAL ASSESSMENT DEFINITIONS

21st Century Appraisals, Inc. GENERAL ASSESSMENT DEFINITIONS Ad Valorem tax. A tax levied in proportion to the value of the thing(s) being taxed. Exclusive of exemptions, use-value assessment laws, and

21st Century Appraisals, Inc. GENERAL ASSESSMENT DEFINITIONS Ad Valorem tax. A tax levied in proportion to the value of the thing(s) being taxed. Exclusive of exemptions, use-value assessment laws, and

Citrus County Property Appraiser TRIM Frequently Asked Questions

Citrus County Property Appraiser TRIM Frequently Asked Questions updated 8-13-2018 1 1 WHAT IS A TRIM NOTICE? TRIM stands for TRuth In Millage. This notice allows you to compare last year s assessed value

Citrus County Property Appraiser TRIM Frequently Asked Questions updated 8-13-2018 1 1 WHAT IS A TRIM NOTICE? TRIM stands for TRuth In Millage. This notice allows you to compare last year s assessed value

04.08 SPECIAL VALUATIONS AND DEFERRALS

04.08 SPECIAL VALUATIONS AND DEFERRALS Deferral programs recognize that market value of certain types of property may exceed the value that would be determined if the property were limited to its current

04.08 SPECIAL VALUATIONS AND DEFERRALS Deferral programs recognize that market value of certain types of property may exceed the value that would be determined if the property were limited to its current

Assessing Reform Proposal Summary

Assessing Reform Proposal Summary Specify minimum quality standards that every assessing district must meet, on their own, in cooperation with other local units, or through the county. Local units could

Assessing Reform Proposal Summary Specify minimum quality standards that every assessing district must meet, on their own, in cooperation with other local units, or through the county. Local units could

WALLER COUNTY APPRAISAL DISTRICT

2018 ANNUAL REPORT WALLER COUNTY APPRAISAL DISTRICT Introduction The Waller County Appraisal District is a political subdivision of the State of Texas created by the Texas Legislature in 1979. The operations

2018 ANNUAL REPORT WALLER COUNTY APPRAISAL DISTRICT Introduction The Waller County Appraisal District is a political subdivision of the State of Texas created by the Texas Legislature in 1979. The operations

Collin Central Appraisal District

Collin Central Appraisal District 2016 ANNUAL REPORT Introduction Collin Central Appraisal District ( District or CCAD ) is a political subdivision of the State of Texas. The Texas State Constitution,

Collin Central Appraisal District 2016 ANNUAL REPORT Introduction Collin Central Appraisal District ( District or CCAD ) is a political subdivision of the State of Texas. The Texas State Constitution,

KAUFMAN COUNTY APPRAISAL DISTRICT 2017 ANNUAL REPORT

KAUFMAN COUNTY APPRAISAL DISTRICT 2017 ANNUAL REPORT Introduction The Kaufman County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property

KAUFMAN COUNTY APPRAISAL DISTRICT 2017 ANNUAL REPORT Introduction The Kaufman County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property

THE OFFICE OF COUNTY ASSESSOR

CHAPTER 5 THE OFFICE OF COUNTY ASSESSOR The office of county assessor is primarily responsible for determining equitable values on both real and personal property for property tax purposes (63-207). However,

CHAPTER 5 THE OFFICE OF COUNTY ASSESSOR The office of county assessor is primarily responsible for determining equitable values on both real and personal property for property tax purposes (63-207). However,

CHAPTER Senate Bill No. 1830

CHAPTER 2013-72 Senate Bill No. 1830 An act relating to ad valorem taxation; amending s. 192.047, F.S.; providing that the postmark date of commercial mail delivery service is considered the date of filing

CHAPTER 2013-72 Senate Bill No. 1830 An act relating to ad valorem taxation; amending s. 192.047, F.S.; providing that the postmark date of commercial mail delivery service is considered the date of filing

APPRAISER / APPRAISALS NORTH DAKOTA BANKERS ASSOCIATION 65 TH LEGISLATIVE SESSION

APPRAISER / APPRAISALS NORTH DAKOTA BANKERS ASSOCIATION 65 TH LEGISLATIVE SESSION PLAN OF ACTION ISSUE Current law requires state standards to be at least as stringent set by the Appraisal Qualifications

APPRAISER / APPRAISALS NORTH DAKOTA BANKERS ASSOCIATION 65 TH LEGISLATIVE SESSION PLAN OF ACTION ISSUE Current law requires state standards to be at least as stringent set by the Appraisal Qualifications

INTRODUCTION MISSION OVERVIEW

INTRODUCTION The Austin County Appraisal District is a political subdivision of the State of Texas. The Constitution of the State of Texas, the Texas Property Tax Code, and the Rules of the Texas Comptroller

INTRODUCTION The Austin County Appraisal District is a political subdivision of the State of Texas. The Constitution of the State of Texas, the Texas Property Tax Code, and the Rules of the Texas Comptroller

2014 Annual Report. Fayette County Appraisal District P. O. Box 836 La Grange, TX 78945

2014 Annual Report Fayette County Appraisal District P. O. Box 836 La Grange, TX 78945 FCAD 2014 Annual Report 1 2014 ANNUAL REPORT FAYETTE COUNTY APPRAISAL DISTRICT INTRODUCTION The Fayette County Appraisal

2014 Annual Report Fayette County Appraisal District P. O. Box 836 La Grange, TX 78945 FCAD 2014 Annual Report 1 2014 ANNUAL REPORT FAYETTE COUNTY APPRAISAL DISTRICT INTRODUCTION The Fayette County Appraisal

Chapter 142 TAXATION ARTICLE I. ARTICLE II Exemption on Improvements for Physically Disabled. ARTICLE III Veterans Exemption

Chapter 142 TAXATION Senior Citizens Tax Exemption ARTICLE I 142-1. Exemption granted; application; qualifications. 142-2. Exemption granted. 142-3. Statutory authority. ARTICLE II Exemption on Improvements

Chapter 142 TAXATION Senior Citizens Tax Exemption ARTICLE I 142-1. Exemption granted; application; qualifications. 142-2. Exemption granted. 142-3. Statutory authority. ARTICLE II Exemption on Improvements

York County 2015 Reassessment Program. York County Assessor s Office 18 W. Liberty St York SC fax

York County 2015 Reassessment Program York County Assessor s Office 18 W. Liberty St York SC 29745 803-684-8526 803-628-3936 fax Re-Assessment The Reassessment Program Act 208: Act 208, as passed by the

York County 2015 Reassessment Program York County Assessor s Office 18 W. Liberty St York SC 29745 803-684-8526 803-628-3936 fax Re-Assessment The Reassessment Program Act 208: Act 208, as passed by the

Dear Brazos County Citizens and Property Owners,

2017 Annual Report Dear Brazos County Citizens and Property Owners, It is my pleasure to present the 2017 Annual Report of the Brazos Central Appraisal District. The annual report provides general information

2017 Annual Report Dear Brazos County Citizens and Property Owners, It is my pleasure to present the 2017 Annual Report of the Brazos Central Appraisal District. The annual report provides general information

Allegan County Equalization Department

Allegan County Equalization Department 2011 Department Report Equalization Report Recap 2010 2011 projects January 1- December 31, 2010 Blaine R. McLeod Director of Equalization 1 Message from the Director

Allegan County Equalization Department 2011 Department Report Equalization Report Recap 2010 2011 projects January 1- December 31, 2010 Blaine R. McLeod Director of Equalization 1 Message from the Director

RULES OF GEORGIA REAL ESTATE APPRAISERS BOARD TABLE OF CONTENTS

RULES OF GEORGIA REAL ESTATE APPRAISERS BOARD CHAPTER 539-1 SUBSTANTIVE REGULATIONS TABLE OF CONTENTS 539-1-.15 Experience Requirements. Amended. 539-1-.16 Appraiser Classifications and Their Education,

RULES OF GEORGIA REAL ESTATE APPRAISERS BOARD CHAPTER 539-1 SUBSTANTIVE REGULATIONS TABLE OF CONTENTS 539-1-.15 Experience Requirements. Amended. 539-1-.16 Appraiser Classifications and Their Education,

ASSESSOR. Mission. Program Summaries by Function

Mission The Assessor is responsible for discovering, inventorying and valuing all taxable property in the County, including residential, commercial, industrial and undeveloped properties, as well as personal

Mission The Assessor is responsible for discovering, inventorying and valuing all taxable property in the County, including residential, commercial, industrial and undeveloped properties, as well as personal

CHAPTER House Bill No. 963

CHAPTER 2000-401 House Bill No. 963 An act relating to Manatee County; merging the Anna Maria Fire Control District and Westside Fire Control District to create a new district; creating and establishing

CHAPTER 2000-401 House Bill No. 963 An act relating to Manatee County; merging the Anna Maria Fire Control District and Westside Fire Control District to create a new district; creating and establishing

Assembly Bill No. 489 Committee on Growth and Infrastructure CHAPTER...

Assembly Bill No. 489 Committee on Growth and Infrastructure CHAPTER... AN ACT relating to the taxation of property; providing for the partial abatement of the ad valorem taxes imposed on property; directing

Assembly Bill No. 489 Committee on Growth and Infrastructure CHAPTER... AN ACT relating to the taxation of property; providing for the partial abatement of the ad valorem taxes imposed on property; directing

The Department s Role

CITY ASSESSOR The Department s Role on the h Ci City s T Team August 21, 2013 Who we are... Micheal Lohmeier City Assessor (2012) (Commercial Appraiser 1998-2005, Assr. 2010-12) 12) Administration and

CITY ASSESSOR The Department s Role on the h Ci City s T Team August 21, 2013 Who we are... Micheal Lohmeier City Assessor (2012) (Commercial Appraiser 1998-2005, Assr. 2010-12) 12) Administration and

McLennan County Appraisal District Annual Report. MCAD Waco, TX. 1 P age

McLennan County Appraisal District Waco, TX Administration Annual Report McLennan County Appraisal District 2016 Annual Report MCAD Waco, TX 1 P age Appraisal District Overview The McLennan County Appraisal

McLennan County Appraisal District Waco, TX Administration Annual Report McLennan County Appraisal District 2016 Annual Report MCAD Waco, TX 1 P age Appraisal District Overview The McLennan County Appraisal

ASSESSORS ANSWER FREQUENTLY ASKED QUESTIONS ABOUT REAL PROPERTY Assessors Office, 37 Main Street

A. THE ASSESSMENT PROCESS: ASSESSORS ANSWER FREQUENTLY ASKED QUESTIONS ABOUT REAL PROPERTY Assessors Office, 37 Main Street What is mass appraisal? Assessors must value all real and personal property in

A. THE ASSESSMENT PROCESS: ASSESSORS ANSWER FREQUENTLY ASKED QUESTIONS ABOUT REAL PROPERTY Assessors Office, 37 Main Street What is mass appraisal? Assessors must value all real and personal property in

2018 Annual Appraisal Report

2018 Annual Appraisal Report SUMMARY OF APPRAISAL ACTIVITIES, EXEMPTIONS, EQUALIZATION AND TAX RATES FOR 2018 TAX YEAR Wendy Grams, RPA, CTA, CCA CENTRAL APPRAISAL DISTRICT OF BANDERA COUNTY P. O. BOX

2018 Annual Appraisal Report SUMMARY OF APPRAISAL ACTIVITIES, EXEMPTIONS, EQUALIZATION AND TAX RATES FOR 2018 TAX YEAR Wendy Grams, RPA, CTA, CCA CENTRAL APPRAISAL DISTRICT OF BANDERA COUNTY P. O. BOX

CONSOLIDATION INCENTIVE AID

CONSOLIDATION INCENTIVE AID Objective: State assistance funds for NYS cities or towns or constituent municipalities of a consolidated assessing unit for efficiencies in Real Property Tax Administration.

CONSOLIDATION INCENTIVE AID Objective: State assistance funds for NYS cities or towns or constituent municipalities of a consolidated assessing unit for efficiencies in Real Property Tax Administration.

TAX ROLL CERTIFICATION FLORIDA DEPARTMENT OF REVENUE

DR-489, R. 6/11 TAX ROLL CERTIFICATION I,, Property Appraiser of County certify that: The real property tax roll of this county and that of the taxing authorities therein, included in these recapitulations,

DR-489, R. 6/11 TAX ROLL CERTIFICATION I,, Property Appraiser of County certify that: The real property tax roll of this county and that of the taxing authorities therein, included in these recapitulations,

2018 Budget Presentation Assessor s Office. Steve Schleiker, El Paso County Assessor Presentation Date: November 9, 2017

2018 Budget Presentation Assessor s Office Steve Schleiker, El Paso County Assessor Presentation Date: November 9, 2017 Organizational Chart Assessor s Office 2 Operations County Assessor Is responsible

2018 Budget Presentation Assessor s Office Steve Schleiker, El Paso County Assessor Presentation Date: November 9, 2017 Organizational Chart Assessor s Office 2 Operations County Assessor Is responsible

Contact Us. Forms for these credits and exemptions are included with the descriptions. Ag Land Credit. Low-Rent Housing Exemption

1 of 12 12/5/2017 2:01 PM Contact Us Home» Iowa Tax / Fee Descriptions and Rates Forms for these credits and exemptions are included with the descriptions. Ag Land Credit Barn and One-Room School House

1 of 12 12/5/2017 2:01 PM Contact Us Home» Iowa Tax / Fee Descriptions and Rates Forms for these credits and exemptions are included with the descriptions. Ag Land Credit Barn and One-Room School House

Assessment Overview. Gallagher Amendment Interim Committee. July 13, 2018

Assessment Overview Gallagher Amendment Interim Committee July 13, 2018 Life s FAQs: Why is the sky blue? How does gravity work? Are we there yet? What happens in an Assessor s office.. how does property

Assessment Overview Gallagher Amendment Interim Committee July 13, 2018 Life s FAQs: Why is the sky blue? How does gravity work? Are we there yet? What happens in an Assessor s office.. how does property

APPLICATION FOR FIVE-YEAR AD VALOREM TAX EXEMPTION FOR OKLAHOMA MANUFACTURING OR RESEARCH & DEVELOPMENT FACILITIES

APPLICATION FOR FIVE-YEAR AD VALOREM TAX EXEMPTION FOR OKLAHOMA MANUFACTURING OR RESEARCH & DEVELOPMENT FACILITIES Revised Aug. 2009 OTC FORM 900XM-R0008/09 INCOMPLETE APPLICATIONS WILL BE NULL AND VOID

APPLICATION FOR FIVE-YEAR AD VALOREM TAX EXEMPTION FOR OKLAHOMA MANUFACTURING OR RESEARCH & DEVELOPMENT FACILITIES Revised Aug. 2009 OTC FORM 900XM-R0008/09 INCOMPLETE APPLICATIONS WILL BE NULL AND VOID

INTERNATIONAL ASSOCIATION OF ASSESSING OFFICERS STATEMENT OF COMPLIANCE

INTERNATIONAL ASSOCIATION OF ASSESSING OFFICERS STATEMENT OF COMPLIANCE Re: Criteria for Appraisal Sponsorship in The Appraisal Foundation (TAF) As a founding, sponsoring organization of TAF, the International

INTERNATIONAL ASSOCIATION OF ASSESSING OFFICERS STATEMENT OF COMPLIANCE Re: Criteria for Appraisal Sponsorship in The Appraisal Foundation (TAF) As a founding, sponsoring organization of TAF, the International

Thornton Township Assessor s Office 2017 Property Tax FORUM

Thornton Township Assessor s Office 2017 Property Tax FORUM 333 East 162 nd Street, South Holland, IL 60473 (708) 596-6040 x3175 * cholbert@thorntontwp.com * Fax (708) 596-7082 Dear Taxpayer, Welcome to

Thornton Township Assessor s Office 2017 Property Tax FORUM 333 East 162 nd Street, South Holland, IL 60473 (708) 596-6040 x3175 * cholbert@thorntontwp.com * Fax (708) 596-7082 Dear Taxpayer, Welcome to

MAP. METHODS AND ASSISTANCE PROGRAM 2015 REPORT El Paso Central Appraisal District. Glenn Hegar Texas Comptroller of Public Accounts

MAP METHODS AND ASSISTANCE PROGRAM 2015 REPORT El Paso Central Appraisal District Glenn Hegar Texas Comptroller of Public Accounts El Paso Central Appraisal District Mandatory Requirements PASS/FAIL 1.

MAP METHODS AND ASSISTANCE PROGRAM 2015 REPORT El Paso Central Appraisal District Glenn Hegar Texas Comptroller of Public Accounts El Paso Central Appraisal District Mandatory Requirements PASS/FAIL 1.

Property Tax Overview. Budget, Finance, & Audit Committee January 3, 2017

Property Tax Overview Budget, Finance, & Audit Committee January 3, 2017 Briefing Outline Property tax base values Property tax rate Property tax exemptions Legislative Session 2 Overview Ad valorem taxes

Property Tax Overview Budget, Finance, & Audit Committee January 3, 2017 Briefing Outline Property tax base values Property tax rate Property tax exemptions Legislative Session 2 Overview Ad valorem taxes

CHAPTER Senate Bill No. 2222

CHAPTER 98-167 Senate Bill No. 2222 An act relating to taxation; amending s. 197.122, F.S.; specifying the time within which property appraisers may correct a material mistake of fact in an appraisal;

CHAPTER 98-167 Senate Bill No. 2222 An act relating to taxation; amending s. 197.122, F.S.; specifying the time within which property appraisers may correct a material mistake of fact in an appraisal;

MAP. METHODS AND ASSISTANCE PROGRAM 2013 REPORT Liberty County Central Appraisal District. Susan Combs Texas Comptroller of Public Accounts

MAP METHODS AND ASSISTANCE PROGRAM 2013 REPORT Liberty County Central Appraisal District Susan Combs Texas Comptroller of Public Accounts January 22, 2014 Chief Appraiser County Appraisal District Board

MAP METHODS AND ASSISTANCE PROGRAM 2013 REPORT Liberty County Central Appraisal District Susan Combs Texas Comptroller of Public Accounts January 22, 2014 Chief Appraiser County Appraisal District Board

2016 Annual Report. Carmen Ottmer, Chief Appraiser AUSTIN COUNTY APPRAISAL DISTRICT 906 E. AMELIA ST., BELLVILLE, TEXAS 77418

2016 Annual Report Carmen Ottmer, Chief Appraiser AUSTIN COUNTY APPRAISAL DISTRICT 906 E. AMELIA ST., BELLVILLE, TEXAS 77418 INTRODUCTION The Austin County Appraisal District is a political subdivision

2016 Annual Report Carmen Ottmer, Chief Appraiser AUSTIN COUNTY APPRAISAL DISTRICT 906 E. AMELIA ST., BELLVILLE, TEXAS 77418 INTRODUCTION The Austin County Appraisal District is a political subdivision

MAP. METHODS AND ASSISTANCE PROGRAM 2013 REPORT Hood County Appraisal District. Susan Combs Texas Comptroller of Public Accounts

MAP METHODS AND ASSISTANCE PROGRAM 2013 REPORT Hood County Appraisal District Susan Combs Texas Comptroller of Public Accounts January 22, 2014 Chief Appraiser County Appraisal District Board of Directors

MAP METHODS AND ASSISTANCE PROGRAM 2013 REPORT Hood County Appraisal District Susan Combs Texas Comptroller of Public Accounts January 22, 2014 Chief Appraiser County Appraisal District Board of Directors

*SB0046* S.B. 46 S.B AGRICULTURE SUSTAINABILITY ACT. LEGISLATIVE GENERAL COUNSEL 6 Approved for Filing: V. Ashby :38 AM 6

LEGISLATIVE GENERAL COUNSEL 6 Approved for Filing: V. Ashby 6 6 01-27-12 10:38 AM 6 S.B. 46 1 AGRICULTURE SUSTAINABILITY ACT 2 2012 GENERAL SESSION 3 STATE OF UTAH 4 Chief Sponsor: Scott K. Jenkins 5 House

LEGISLATIVE GENERAL COUNSEL 6 Approved for Filing: V. Ashby 6 6 01-27-12 10:38 AM 6 S.B. 46 1 AGRICULTURE SUSTAINABILITY ACT 2 2012 GENERAL SESSION 3 STATE OF UTAH 4 Chief Sponsor: Scott K. Jenkins 5 House

Map Franklin County ASSESSMENTS FOR 2017 TAX COLLECTION STEVE MARKS ASSESSOR

Map Franklin County 1909 2016 ASSESSMENTS FOR 2017 TAX COLLECTION STEVE MARKS ASSESSOR 2 Mission Statement We, the employee s of the Franklin County Assessor s Office have a primary mission to maintain

Map Franklin County 1909 2016 ASSESSMENTS FOR 2017 TAX COLLECTION STEVE MARKS ASSESSOR 2 Mission Statement We, the employee s of the Franklin County Assessor s Office have a primary mission to maintain

November 2017 Legal Calendar

1 Sheriff, Clerk of the District, Clerk, County Board Sheriff or such person in charge of the administration of the jail must file jail report with the clerk of the district court and the county clerk,

1 Sheriff, Clerk of the District, Clerk, County Board Sheriff or such person in charge of the administration of the jail must file jail report with the clerk of the district court and the county clerk,

RULES OF TENNESSEE REAL ESTATE APPRAISER COMMISSION CHAPTER GENERAL PROVISIONS TABLE OF CONTENTS

RULES OF TENNESSEE REAL ESTATE APPRAISER COMMISSION CHAPTER 1255-01 GENERAL PROVISIONS TABLE OF CONTENTS 1255-01-.01 Purpose 1255-01-.09 Denial of License or Certificate 1255-01-.02 Definitions 1255-01-.10

RULES OF TENNESSEE REAL ESTATE APPRAISER COMMISSION CHAPTER 1255-01 GENERAL PROVISIONS TABLE OF CONTENTS 1255-01-.01 Purpose 1255-01-.09 Denial of License or Certificate 1255-01-.02 Definitions 1255-01-.10

CITY OF JACKSONVILLE, FLORIDA

PROPERTY APPRAISER DEPARTMENT VISION: To earn the public s trust. DEPARTMENT MISSION: We will: Produce a fair, equitable and accurate tax roll as required by law. Focus on our customers the taxpayers.

PROPERTY APPRAISER DEPARTMENT VISION: To earn the public s trust. DEPARTMENT MISSION: We will: Produce a fair, equitable and accurate tax roll as required by law. Focus on our customers the taxpayers.

TAX ROLL CERTIFICATION

TAX ROLL CERTIFICATION DR-43, R. 6/11 FAC Rule 12D-16.2 I,, the Property Appraiser of County, Florida, certify that all data reported on this form and accompanying forms DR-43V, DR-43CC, DR-43BM, DR-43PC,

TAX ROLL CERTIFICATION DR-43, R. 6/11 FAC Rule 12D-16.2 I,, the Property Appraiser of County, Florida, certify that all data reported on this form and accompanying forms DR-43V, DR-43CC, DR-43BM, DR-43PC,

CITY OF JACKSONVILLE, FLORIDA

PROPERTY APPRAISER DEPARTMENT VISION: To earn the public s trust. DEPARTMENT MISSION: We will: Produce a fair, equitable and accurate tax roll as required by law. Focus on our customers the taxpayers.

PROPERTY APPRAISER DEPARTMENT VISION: To earn the public s trust. DEPARTMENT MISSION: We will: Produce a fair, equitable and accurate tax roll as required by law. Focus on our customers the taxpayers.

Burleson County Appraisal District Annual Report

December 2017 111 E. Fawn St. P. O. Box 1000 Caldwell, TX 77836 Burleson County Appraisal District December 2017 It is my pleasure to present the of the Burleson County Appraisal District (BCAD). This

December 2017 111 E. Fawn St. P. O. Box 1000 Caldwell, TX 77836 Burleson County Appraisal District December 2017 It is my pleasure to present the of the Burleson County Appraisal District (BCAD). This

WYOMING DEPARTMENT OF REVENUE CHAPTER 13 PROPERTY TAX APPRAISER EDUCATION AND CERTIFICATION

CHAPTER 13 PROPERTY TAX APPRAISER EDUCATION AND CERTIFICATION Section 1. Authority. These rules are promulgated by the Wyoming Department of Revenue under authority of W.S. 18-3-201, W.S. 18-3-204, and

CHAPTER 13 PROPERTY TAX APPRAISER EDUCATION AND CERTIFICATION Section 1. Authority. These rules are promulgated by the Wyoming Department of Revenue under authority of W.S. 18-3-201, W.S. 18-3-204, and

FreestoneCentralAppraisalDistrict 2018 AnnualR eport

FreestoneCentralAppraisalDistrict 218 AnnualR eport Introduction The Freestone Central Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property

FreestoneCentralAppraisalDistrict 218 AnnualR eport Introduction The Freestone Central Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property

MAP. METHODS AND ASSISTANCE PROGRAM 2013 REPORT McLennan County Appraisal District. Susan Combs Texas Comptroller of Public Accounts

MAP METHODS AND ASSISTANCE PROGRAM 2013 REPORT McLennan County Appraisal District Susan Combs Texas Comptroller of Public Accounts January 22, 2014 Chief Appraiser County Appraisal District Board of Directors

MAP METHODS AND ASSISTANCE PROGRAM 2013 REPORT McLennan County Appraisal District Susan Combs Texas Comptroller of Public Accounts January 22, 2014 Chief Appraiser County Appraisal District Board of Directors

Throckmorton Central Appraisal District 144 N Minter Ave PO Box 788 Throckmorton, TX

Throckmorton Central Appraisal District 144 N Minter Ave PO Box 788 Throckmorton, TX 76483 940-849-5691 1 THIS PAGE IS INTENTIONALLY LEFT BLANK 2 EXECUTIVE SUMMARY Throckmorton Central Appraisal District

Throckmorton Central Appraisal District 144 N Minter Ave PO Box 788 Throckmorton, TX 76483 940-849-5691 1 THIS PAGE IS INTENTIONALLY LEFT BLANK 2 EXECUTIVE SUMMARY Throckmorton Central Appraisal District

Equalization Department

Equalization Department Citizens Board of Commissioners Administrator /Controller Equalization Director Statutory Authority Michigan Compiled Law 211.34 (3) The County Board of Commissioners of a county

Equalization Department Citizens Board of Commissioners Administrator /Controller Equalization Director Statutory Authority Michigan Compiled Law 211.34 (3) The County Board of Commissioners of a county

NOTICE OF POSITION VACANCY ASSESSOR FOR REAL ESTATE COUNTY OF KING WILLIAM, VIRGINIA

King William County Est. 1702 NOTICE OF POSITION VACANCY ASSESSOR FOR REAL ESTATE COUNTY OF KING WILLIAM, VIRGINIA King William County, Virginia (pop. 16,000+) is presently accepting applications with

King William County Est. 1702 NOTICE OF POSITION VACANCY ASSESSOR FOR REAL ESTATE COUNTY OF KING WILLIAM, VIRGINIA King William County, Virginia (pop. 16,000+) is presently accepting applications with

DELTA COUNTY APPRAISAL DISTRICT 2014 ANNUAL APPRAISAL REPORT

DELTA COUNTY APPRAISAL DISTRICT 2014 ANNUAL APPRAISAL REPORT Introduction The Delta County Appraisal District is a political subdivision of the State of Texas. The Constitution of the State of Texas, the

DELTA COUNTY APPRAISAL DISTRICT 2014 ANNUAL APPRAISAL REPORT Introduction The Delta County Appraisal District is a political subdivision of the State of Texas. The Constitution of the State of Texas, the

A BILL TO BE ENTITLED AN ACT

12 LC 34 3484S/AP House Bill 386 (AS PASSED HOUSE AND SENATE) By: Representatives Channell of the 116th, O`Neal of the 146th, Jones of the 46th, and Peake of the 137th A BILL TO BE ENTITLED AN ACT To amend

12 LC 34 3484S/AP House Bill 386 (AS PASSED HOUSE AND SENATE) By: Representatives Channell of the 116th, O`Neal of the 146th, Jones of the 46th, and Peake of the 137th A BILL TO BE ENTITLED AN ACT To amend

Gaines County Appraisal District 2013 Annual Report

Gaines County Appraisal District 2013 Annual Report Introduction The Gaines County Appraisal District is a political subdivision of the state, The Constitution of the State of Texas, the Texas Property

Gaines County Appraisal District 2013 Annual Report Introduction The Gaines County Appraisal District is a political subdivision of the state, The Constitution of the State of Texas, the Texas Property

ARLINGTON COUNTY CODE. Chapter 20 REAL ESTATE ASSESSMENT. Article I. In General

ARLINGTON COUNTY CODE Chapter 20 Article I. In General 20-1. Department of Real Estate Assessments Established. 20-2. Board of Equalization of Real Estate Assessments Established; Powers; Compensation.

ARLINGTON COUNTY CODE Chapter 20 Article I. In General 20-1. Department of Real Estate Assessments Established. 20-2. Board of Equalization of Real Estate Assessments Established; Powers; Compensation.

YOUNG COUNTY APPRAISAL DISTRICT

YOUNG COUNTY APPRAISAL DISTRICT 2017 - ANNUAL APPRAISAL REPORT AS OF 10/6/2017 1 2 TABLE OF CONTENTS ITEM PAGE Introduction 4 Purpose of Report...4 Taxing Entities, Rates & Exemptions 5 Property Types

YOUNG COUNTY APPRAISAL DISTRICT 2017 - ANNUAL APPRAISAL REPORT AS OF 10/6/2017 1 2 TABLE OF CONTENTS ITEM PAGE Introduction 4 Purpose of Report...4 Taxing Entities, Rates & Exemptions 5 Property Types