2011 ASSESSMENT RATIO REPORT

|

|

|

- Kathlyn Matthews

- 5 years ago

- Views:

Transcription

1 2011 Ratio Report

2

3 SECTION I OVERVIEW 2011 ASSESSMENT RATIO REPORT The Department of Assessments and Taxation appraises real property for the purposes of property taxation. Properties are valued using the three approaches to value generally recognized by the appraisal profession: cost, sales comparison, and (when applicable) income. Residential property characteristics include type of structure, size, quality and type of construction, condition of structure, and any new improvements. Commercial properties are reviewed for type of structure, size, type and quality of construction, condition of structure, current use of the property, any new improvements, types of tenants, and vacancy. This year we valued over 739,764 properties, which require the use of mass appraisal techniques. While a fee appraiser is concerned with valuing one property at a time, an assessor is valuing whole neighborhoods. To accomplish this, special mass appraisal procedures are used. The assessor will review the data and calculate replacement costs for improvements much like a fee appraiser. The assessor will then review the sales from the area. In Maryland, the local assessment office, except in Baltimore City, receives a copy of all deeds and property sales prices as the deed transferring the property is recorded with the clerk of the court. In Baltimore City, the Department of Public Works does the data entry and provides the data to the Department. In the assessor s review and analysis of the sales, the assessor will develop land rates, depreciation tables, and sales analysis reports. After completing the analysis, the assessor applies the factors uniformly throughout the neighborhood to value all comparable properties in a uniform manner. Rental rates, vacancy and collection loss, expense ratios and capitalization rates are analyzed, and uniformly applied for comparable income producing properties. The Department s work is reviewed by legislative auditors and is often scrutinized by individual property owners. We are continually striving for higher quality in assessment uniformity. Our quality control program begins with the individual assessor and the assessor s immediate supervisor. As work is completed, each assessor s supervisor reviews the analysis, makes recommendations, and approves the work. When the assessor completes the revaluation, the supervisor makes a random check using procedural and data editing checks. Following the completion of the revaluation, various computer edits are made to assure good valuation quality. A measurement of quality is the assessed value/sale price ratio. A ratio is the relationship of two numbers, in this case assessed value and sale price. It measures how closely our values compare to the actual sales prices. The average assessed value/sale price ratio indicates a typical level of value. Because the marketplace is not perfect, there will always be properties that sell for more or less than can be anticipated due to factors such as buyers willing to pay extra for a unique property or declining values in a buyer s market. In mass appraisal and assessment ratio studies, we are not only concerned with average assessed value/sale price levels (ratios) but also with the degree of spread (variation) from the typical ratio. The measurement of variation is called the coefficient of dispersion (COD). The lower the COD, the more uniform the assessment level.

4 In the balance of this report, Section II will give a more detailed explanation of the statistical terms as applied to assessment administration and quality control. Section III explains the International Association of Assessing Officers Standard of Performance for ratio studies. Section IV gives an overview of statewide appraisal quality for the most recent valuation of triennial Group 2, performed in December SECTION II RATIO STATISTICS The purpose of this ratio study is to test the quality of the assessment product. The quality of the assessment product is examined from both an assessment level and assessment uniformity standpoint. Assessment level examines the degree to which the assessments are performed based upon the statutory requirement of full market value. Assessment uniformity measures the degree to which different properties are assessed at equal percentages of their market values. From our most recent valuation, we perform many ratio studies examining neighborhoods, types of structures, age of structures, etc. We use as a performance gauge several measures of central tendency. Each measure of central tendency is affected differently by outliers. A ratio of assessed value to sale price is calculated for each property. The average ratio is the total of all ratios divided by the number of sales. The average (mean) ratio has a natural upward bias. This would indicate a higher level of assessment than has actually occurred. The median is the midpoint of any data listed from lowest to highest. The median ratio is the point where half the ratios fall above and half ratios fall below. The median ratio counts each ratio equally. It is less biased by extreme ratios (outliers) or by individual property values. The weighted ratio is the total of all assessed values divided by the total of all sale prices. Since the weighted ratio counts each dollar equally, it is swayed by higher priced properties. In addition to the general level of assessments, we are also concerned with the relative spread or variation that individual ratios fall from the typical. There are two measurements of variability: coefficient of dispersion and coefficient of variation. These statistics measure horizontal inequities, or the dispersion of ratios regardless of the value of the individual properties. The coefficient of dispersion is calculated by dividing the average absolute deviation by the median ratio. The average absolute deviation is calculated by subtracting the median ratio from each ratio, adding all the results but ignoring positive and negative signs, and dividing by the number of ratios. Acceptable coefficients of dispersion depend on property type but should typically be 20% or less. Coefficient of variation is calculated by dividing the standard deviation by the mean or average ratio and multiplying by 100. The variance is calculated by subtracting the mean from each ratio, squaring the differences, summing the squared differences, dividing by the total number of ratios less one. The standard deviation is calculated by taking the square root of the variance. The coefficient of dispersion is the preferable measure of variance unless a sample is normally distributed. In a normal distribution situation, coefficient of variation is the preferable measure of variance. Another statistical measure used to gauge assessment uniformity is the Price Related Differential (PRD). The PRD tests to see if higher or lower valued properties are assessed at the same level. It is calculated by dividing the average ratio by the weighted ratio. This statistic measures vertical inequities. When low-value properties are valued at a higher percentage of their market Page 2

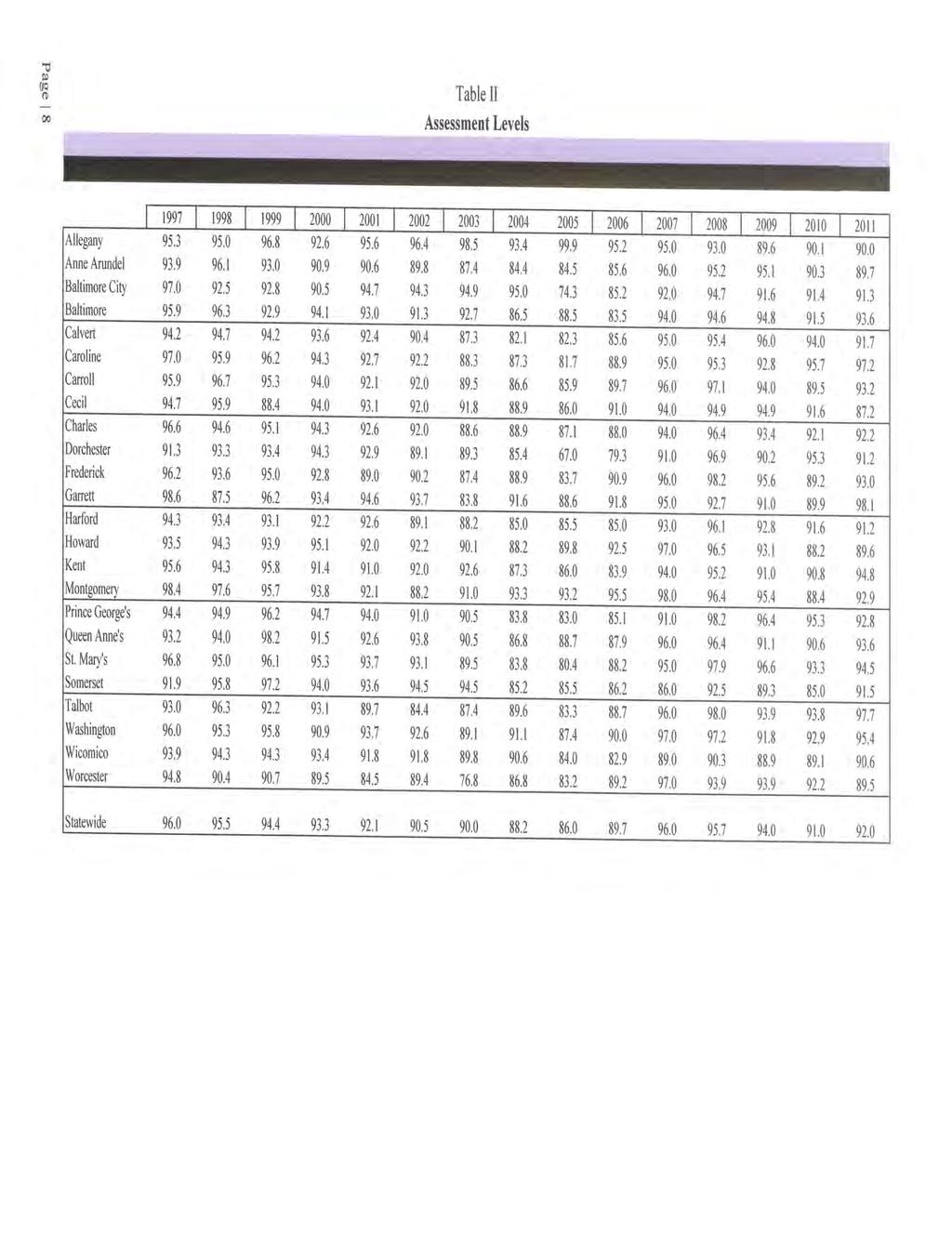

5 value, the property taxes levied against these assessments would be considered regressive. Conversely, if high-value properties are valued at a higher percentage of their market value, property taxes levied against these assessments would be considered progressive. Typically, PRDs have an upward bias because higher priced properties are more unique. PRDs should range between 0.98 and 1.03, except for very small samples. For example, a PRD of 1.03 indicates under valuation of high priced properties, while a PRD of.98 shows an under valuation of low priced properties. Other descriptive statistical methods that may be used to analyze the assessment product are histograms, frequency distributions, and scatter diagrams. Due to the scope of this report, we have not examined them here. For further information on statistics relating to assessments, please refer to the International Association of Assessing Officers publication Improving Real Property Assessment. Table I is the Fiscal Year 2012 Real Property Base/Ratio by Subdivision with assessment ratios expressed relative to full value. Table II is a history of weighted assessment ratios converted to full value (100% levels) that allows for comparison between years by adjusting for statutory changes in the assessment level. Table III displays examples of the statistical calculations used in this report. Tables IV and V show the residential and commercial 2011 Ratio Study data by jurisdiction at assessed full market value level for the area most recently assessed. Following the ratio study is Table VI of the report detailing issues of assessment and appraisal quality that are summarized in Section IV. SECTION III RATIO STUDY STANDARDS VALUES TO SALE PRICES The International Association of Assessing Officers (IAAO) is a professional organization of assessing officials which provides educational programs, assessment administration standards, and research on appraisal and tax policy issues. IAAO has developed numerous standards and texts on appraisal and assessment administration. Additionally, the organization is a founding member of the national Appraisal Foundation which developed the Uniform Standards of Professional Appraisal Practice (USPAP). IAAO s Standard on Ratio Studies was first published in September 1980 and was revised in January The Standard is advisory in nature. This Standard provides guidance to those performing ratio studies in the mass appraisal field regarding the design, statistics, performance measures and other issues related to such studies. The Maryland Department of Assessments and Taxation uses the fundamental ratio statistical measures of the Standard and has adopted IAAO s Assessment Ratio Performance Standard as the criteria to judge the performance of Maryland revaluations. Page 3

6 The IAAO Ratio Performance Standards are: Ratio Study Uniformity Standards Indicating Acceptable General Quality* General Property Class Jurisdiction Size /Profile /Market Activity Max COD Residential improved (single family dwellings, condominiums, manuf. housing, 2-4 family units) Income-producing properties (commercial, industrial, apartments,) Very large jurisdictions / densely populated / newer properties / active markets 5.0 to 10.0 Large to mid-sized jurisdictions / older & newer properties / less active markets 5.0 to 15.0 Rural or small jurisdictions / older properties / depressed market areas 5.0 to 20.0 Very large jurisdictions / densely populated / newer properties / active markets 5.0 to 15.0 Large to mid-sized jurisdictions / older & newer properties / less active markets 5.0 to 20.0 Rural or small jurisdictions / older properties / depressed market areas 5.0 to 25.0 Residential vacant land Very large jurisdictions / rapid development / active markets 5.0 to 15.0 Large to mid-sized jurisdictions / slower development / less active markets 5.0 to 20.0 Other (non-agricultural) vacant land Rural or small jurisdictions/ little development / depressed markets 5.0 to 25.0 Very large jurisdictions / rapid development / active markets 5.0 to 20.0 Large to mid-sized jurisdictions / slower development / less active markets 5.0 to 25.0 Rural or small jurisdictions/ little development / depressed markets 5.0 to 30.0 These types of property are provided for general guidance only and may not represent jurisdictional requirements. *The COD performance recommendations are based upon representative and adequate sample sizes, with outliers trimmed and a 95% level of confidence. *Appraisal level recommendation for each type of property shown should be between 0.90 and *PRD's for each type of property should be between 0.98 and 1.03 to demonstrate vertical equity. PRD standards are not absolute and may be less meaningful when samples are small or when wide variation in prices exist. In such cases, statistical tests of vertical equity hypotheses should be substituted. *CODs lower than 5.0 may indicate sales chasing or non-representative samples. Source: Standard on Ratio Studies; International Association of Assessing Officers; Kansas City, MO; January 2010; pg 33. Ratio studies may be performed for various reasons including appraisal accuracy and assessment equity studies, to judge the need for management of a reappraisal, to identify problems with appraisal procedures, to assist in market analysis, and to adjust appraised values. Many ratio study design issues must be considered depending on the purpose of the ratio study. This study considers unadjusted sales price data six months prior to and six months after the date of finality (date of valuation, January 1 st ) for which assessments have become effective so that an unbiased estimate of assessment performance can be obtained. Sales that are arms-length transactions between willing and informed buyers and sellers are used in this study. Maryland s ratio performance is good and conforms to the IAAO Standard. While several measures of central tendency are calculated (average, median, and weighted ratios), the median is less affected by extreme ratios. The IAAO observes in its Standard that the median is generally the preferred measure of central tendency for monitoring appraisal performance. For this reason, median ratios are used in this study to measure compliance with IAAO standards. Page 4

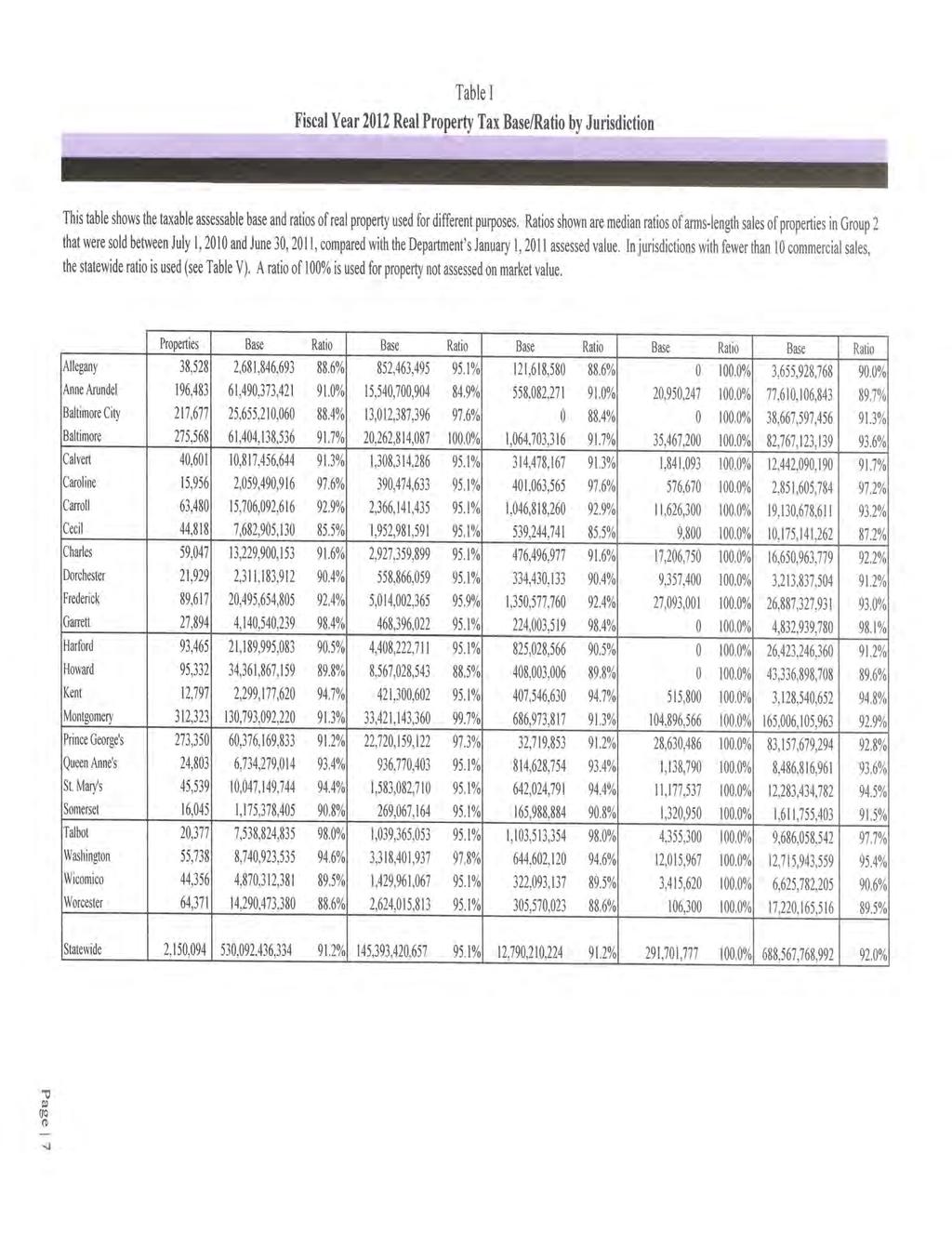

7 As a proxy for time adjustments, this report uses sales from six months before the date of finality to six months after the date of finality. Under normal circumstances, with steadily changing property values, these sales will balance. In unusual circumstances, when property values are rapidly changing, this will affect the ratio statistics. On average, the residential values in this group have decreased by 22%, while commercial property values decreased by 1%. Property value changes varied by region in the state since the last triennial revaluation in January, The largest percentage of decrease in residential property was in Charles, Dorchester, Frederick, Prince George s, and Wicomico Counties. Statewide, the Department met the IAAO standard for coefficient of dispersion indicating an overall uniformity of assessments. Commercial properties are generally less similar than residential properties. Many commercial properties are income producing and are valued using the income approach to value. Most commercial uses are cyclical in nature. Various segments of the commercial real estate market may be ascending in value as a class, while others may be declining in market popularity. Because of the uniqueness of commercial and industrial properties, measures of central tendency tend to vary more widely than with residential properties. The number of commercial properties is small compared to the number of residential properties. In several jurisdictions, the number of commercial properties which have sold is so small that the statistical measures are prone to bias. Allegany, Calvert, Caroline, Carroll, Cecil, Charles Dorchester, Garrett, Harford, Kent, Queen Anne s, St. Mary s, Somerset, Talbot, Wicomico and Worcester Counties all had fewer than 10 arms-length commercial transfers for Group 2. In those jurisdictions, individual statistical measures would be unreliable due to sample size. The number of commercial sales increased from 207 statewide in the 2010 Ratio Report to 303 statewide in the 2011 Ratio Report. SECTION IV STATEWIDE COMPARISON OF DEPARTMENT S VALUES TO SALE PRICE Quality is the degree of excellence of a product or service; the extent to which it measures up to certain standards. In this case, a measure of quality is the ratio study measuring whether the assessor appraised properties uniformly at market value. The ratio study conducted in this report is based upon sales data occurring, for the most part, after the time period of sales used by the assessor in the group of properties being reassessed. Assuming the assessor applied the mass appraisal model uniformly to all properties, this ratio study should show uniformity of assessment. This ratio study is a cross check by Department management to assure quality of the mass appraisal work product. The ratio statistics for each county in Table IV was conducted on 13,853 improved residential property sales from July 1, 2010 to June 30, 2011 and compares the Department s valuations to sale prices. Page 5

8 The frequency distribution in Table VI and statistics following present a statewide ratio analysis of improved residential property sales from July 1, 2010 to June 30, 2011 comparing the Department s values to sales prices. The measures of central tendency indicate that properties are valued at approximately 93% of sale price and that on average all other properties have very similar ratios as indicated by the 9.69 Coefficient of Dispersion. Additionally, higher valued properties are assessed at a similar level to lower valued properties as indicated by a Price Related Differential statistic of A price related differential of 1.00 indicates vertical uniformity across all strata of property values. The analysis from Table VI and the following descriptive statistics indicates that values determined by assessors for the most recent triennial Group 2 valuation attained a uniform and appropriate level of value. At the time of valuation, the assessments were close to the sale price. In summary, the data shows that properties throughout the State are assessed uniformly as required by law. Page 6

9

10

11

12

13

14

15

The Honorable Larry Hogan And The General Assembly of Maryland

2015 Ratio Report The Honorable Larry Hogan And The General Assembly of Maryland As required by Section 2-202 of the Tax-Property Article of the Annotated Code of Maryland, I am pleased to submit the Department

2015 Ratio Report The Honorable Larry Hogan And The General Assembly of Maryland As required by Section 2-202 of the Tax-Property Article of the Annotated Code of Maryland, I am pleased to submit the Department

April 12, The Honorable Martin O Malley And The General Assembly of Maryland

April 12, 2011 The Honorable Martin O Malley And The General Assembly of Maryland As required by Section 2-202 of the Tax-Property Article of the Annotated Code of Maryland, I am pleased to submit the

April 12, 2011 The Honorable Martin O Malley And The General Assembly of Maryland As required by Section 2-202 of the Tax-Property Article of the Annotated Code of Maryland, I am pleased to submit the

DEPARTMENT OF ASSESSMENTS AND TAXATION 2008 RATIO REPORT

DEPARTMENT OF ASSESSMENTS AND TAXATION 2008 RATIO REPORT State of Maryland Department of Assessments and Taxation Office of the Director Martin O'Malley Governor C. John Sullivan Jr. Director June 30,

DEPARTMENT OF ASSESSMENTS AND TAXATION 2008 RATIO REPORT State of Maryland Department of Assessments and Taxation Office of the Director Martin O'Malley Governor C. John Sullivan Jr. Director June 30,

City of Nashua, NH 2018 Revaluation Informational Meeting

City of Nashua, NH 2018 Revaluation Informational Meeting Legal Requirements Constitutional Duty of the City: [Art.] 6. [Valuation and Taxation.] The public charges of government, or any part thereof,

City of Nashua, NH 2018 Revaluation Informational Meeting Legal Requirements Constitutional Duty of the City: [Art.] 6. [Valuation and Taxation.] The public charges of government, or any part thereof,

Washington Department of Revenue Property Tax Division. Valid Sales Study Kitsap County 2015 Sales for 2016 Ratio Year.

P. O. Box 47471 Olympia, WA 98504-7471. Washington Department of Revenue Property Tax Division Valid Sales Study Kitsap County 2015 Sales for 2016 Ratio Year Sales from May 1, 2014 through April 30, 2015

P. O. Box 47471 Olympia, WA 98504-7471. Washington Department of Revenue Property Tax Division Valid Sales Study Kitsap County 2015 Sales for 2016 Ratio Year Sales from May 1, 2014 through April 30, 2015

Rockwall CAD. Basics of. Appraising Property. For. Property Taxation

Rockwall CAD Basics of Appraising Property For Property Taxation ROCKWALL CENTRAL APPRAISAL DISTRICT 841 Justin Rd. Rockwall, Texas 75087 972-771-2034 Fax 972-771-6871 Introduction Rockwall Central Appraisal

Rockwall CAD Basics of Appraising Property For Property Taxation ROCKWALL CENTRAL APPRAISAL DISTRICT 841 Justin Rd. Rockwall, Texas 75087 972-771-2034 Fax 972-771-6871 Introduction Rockwall Central Appraisal

Past & Present Adjustments & Parcel Count Section... 13

Assessment 2017 Report This report includes specific information regarding the 2017 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

Assessment 2017 Report This report includes specific information regarding the 2017 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

Introduction. Bruce Munneke, S.A.M.A. Washington County Assessor. 3 P a g e

Assessment 2016 Report This report includes specific information regarding the 2016 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

Assessment 2016 Report This report includes specific information regarding the 2016 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

MAAO Sales Ratio Committee 2013 Fall Conference Seminar

MAAO Sales Ratio Committee 2013 Fall Conference Seminar Presented By: Al Whitcomb Dakota County (Retired) John Keefe Chisago County Assessor Brent Reid City of Coon Rapids Michael Thompson Scott County

MAAO Sales Ratio Committee 2013 Fall Conference Seminar Presented By: Al Whitcomb Dakota County (Retired) John Keefe Chisago County Assessor Brent Reid City of Coon Rapids Michael Thompson Scott County

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

Town of Fairfield 2015 Revaluation Informational Meeting

www.vgsi.com Town of Fairfield 2015 Revaluation Informational Meeting Fairfield Revaluation Cycle Ct. Law states revaluations take place every 5 years Fairfield s last Revaluation was in 2010 All property

www.vgsi.com Town of Fairfield 2015 Revaluation Informational Meeting Fairfield Revaluation Cycle Ct. Law states revaluations take place every 5 years Fairfield s last Revaluation was in 2010 All property

GENERAL ASSESSMENT DEFINITIONS

21st Century Appraisals, Inc. GENERAL ASSESSMENT DEFINITIONS Ad Valorem tax. A tax levied in proportion to the value of the thing(s) being taxed. Exclusive of exemptions, use-value assessment laws, and

21st Century Appraisals, Inc. GENERAL ASSESSMENT DEFINITIONS Ad Valorem tax. A tax levied in proportion to the value of the thing(s) being taxed. Exclusive of exemptions, use-value assessment laws, and

Assessment Year 2016 Assessment Valuations / Mass Appraisal Summary Report

Assessment Year 2016 Assessment Valuations / Mass Appraisal Summary Report Overview Following up on last year s work, additional work was done cleaning up the sales data. The land valuation model was further

Assessment Year 2016 Assessment Valuations / Mass Appraisal Summary Report Overview Following up on last year s work, additional work was done cleaning up the sales data. The land valuation model was further

DIRECTIVE # This Directive Supersedes Directive # and #92-003

Division Of Property Valuation Docking State Office Building 915 SW Harrison St., Room 400N Topeka, KS 66612-1588 Nick Jordan, Secretary David N. Harper, Director phone: 785-296-2365 fax: 785-296-2320

Division Of Property Valuation Docking State Office Building 915 SW Harrison St., Room 400N Topeka, KS 66612-1588 Nick Jordan, Secretary David N. Harper, Director phone: 785-296-2365 fax: 785-296-2320

Cook County Assessor s Office: 2019 North Triad Assessment. Norwood Park Residential Assessment Narrative March 11, 2019

Cook County Assessor s Office: 2019 North Triad Assessment Norwood Park Residential Assessment Narrative March 11, 2019 1 Norwood Park Residential Properties Executive Summary This is the current CCAO

Cook County Assessor s Office: 2019 North Triad Assessment Norwood Park Residential Assessment Narrative March 11, 2019 1 Norwood Park Residential Properties Executive Summary This is the current CCAO

Dear Brazos County Citizens and Property Owners,

2017 Annual Report Dear Brazos County Citizens and Property Owners, It is my pleasure to present the 2017 Annual Report of the Brazos Central Appraisal District. The annual report provides general information

2017 Annual Report Dear Brazos County Citizens and Property Owners, It is my pleasure to present the 2017 Annual Report of the Brazos Central Appraisal District. The annual report provides general information

Department of Legislative Services Maryland General Assembly 2007 Session FISCAL AND POLICY NOTE

Department of Legislative Services Maryland General Assembly 2007 Session SB 641 FISCAL AND POLICY NOTE Senate Bill 641 (Senator Raskin) Judicial Proceedings and Budget and Taxation Condominiums - Conversion

Department of Legislative Services Maryland General Assembly 2007 Session SB 641 FISCAL AND POLICY NOTE Senate Bill 641 (Senator Raskin) Judicial Proceedings and Budget and Taxation Condominiums - Conversion

Table of Contents 2015 Commercial Revaluation Report

Table of Contents 05 Commercial Revaluation Report 05 Commercial & Industrial Valuation Summary Introduction Uniform Standards Approaches to Value Land Valuation Land to Building Ratios Parking to Building

Table of Contents 05 Commercial Revaluation Report 05 Commercial & Industrial Valuation Summary Introduction Uniform Standards Approaches to Value Land Valuation Land to Building Ratios Parking to Building

GOVERNANCE OF ASSESSOR

GOVERNANCE OF ASSESSOR State of NH Constitution NH State Statutes (RSA) State Supreme Court Case Law NH Assessing Standard Board Rules NH Department of Revenue Rules Professional Code of Conduct (USPAP)

GOVERNANCE OF ASSESSOR State of NH Constitution NH State Statutes (RSA) State Supreme Court Case Law NH Assessing Standard Board Rules NH Department of Revenue Rules Professional Code of Conduct (USPAP)

Course Residential Modeling Concepts

Course 311 - Residential Modeling Concepts Course Description Course 311 presents a detailed study of the mass appraisal process as applied to residential property. Topics covered include a comparison

Course 311 - Residential Modeling Concepts Course Description Course 311 presents a detailed study of the mass appraisal process as applied to residential property. Topics covered include a comparison

Publication 136 April 2016

Illinois Department of Revenue Constance Beard, Director Publication 136 April 2016 Property Assessment and Equalization The information in this publication is current as of the date of the publication.

Illinois Department of Revenue Constance Beard, Director Publication 136 April 2016 Property Assessment and Equalization The information in this publication is current as of the date of the publication.

Assessment Quality: Sales Ratio Analysis Update for Residential Properties in Indiana

Center for Business and Economic Research About the Authors Dagney Faulk, PhD, is director of research and a research professor at Ball State CBER. Her research focuses on state and local tax policy and

Center for Business and Economic Research About the Authors Dagney Faulk, PhD, is director of research and a research professor at Ball State CBER. Her research focuses on state and local tax policy and

LLANO CENTRAL APPRAISAL DISTRICT REAPPRAISAL PLAN FOR TAX YEARS 2017 & 2018 AS ADOPTED BY THE BOARD OF DIRECTORS

LLANO CENTRAL APPRAISAL DISTRICT REAPPRAISAL PLAN FOR TAX YEARS 2017 & 2018 AS ADOPTED BY THE BOARD OF DIRECTORS TABLE OF CONTENTS ITEM PAGE Executive Summary 5 Revaluation Decision (Statutory or Administrative)

LLANO CENTRAL APPRAISAL DISTRICT REAPPRAISAL PLAN FOR TAX YEARS 2017 & 2018 AS ADOPTED BY THE BOARD OF DIRECTORS TABLE OF CONTENTS ITEM PAGE Executive Summary 5 Revaluation Decision (Statutory or Administrative)

How the Montgomery Central Appraisal District Appraises Residential Property

How the Montgomery Central Appraisal District Appraises Residential Property The following presentation is provided to educate Montgomery County residential property owners about the Analysis & Valuation

How the Montgomery Central Appraisal District Appraises Residential Property The following presentation is provided to educate Montgomery County residential property owners about the Analysis & Valuation

Recommendations for COD Standards. Robert J. Gloudemans Almy, Gloudemans, Jacobs & Denne. for. New York State Office of Real Property Services

Recommendations for COD Standards Robert J. Gloudemans Almy, Gloudemans, Jacobs & Denne for New York State Office of Real Property Services March 12, 2009 Recommendations for COD Standards Robert J. Gloudemans

Recommendations for COD Standards Robert J. Gloudemans Almy, Gloudemans, Jacobs & Denne for New York State Office of Real Property Services March 12, 2009 Recommendations for COD Standards Robert J. Gloudemans

CABARRUS COUNTY 2016 APPRAISAL MANUAL

STATISTICS AND THE APPRAISAL PROCESS PREFACE Like many of the technical aspects of appraising, such as income valuation, you have to work with and use statistics before you can really begin to understand

STATISTICS AND THE APPRAISAL PROCESS PREFACE Like many of the technical aspects of appraising, such as income valuation, you have to work with and use statistics before you can really begin to understand

IREDELL COUNTY 2015 APPRAISAL MANUAL

STATISTICS AND THE APPRAISAL PROCESS INTRODUCTION Statistics offer a way for the appraiser to qualify many of the heretofore qualitative decisions which he has been forced to use in assigning values. In

STATISTICS AND THE APPRAISAL PROCESS INTRODUCTION Statistics offer a way for the appraiser to qualify many of the heretofore qualitative decisions which he has been forced to use in assigning values. In

Table of Contents 2017 Commercial Revaluation Report

Table of Contents 07 Commercial Revaluation Report 07 Commercial & Industrial Valuation Summary Introduction Uniform Standards Approaches to Value Land Valuation Land to Building Ratios Parking to Building

Table of Contents 07 Commercial Revaluation Report 07 Commercial & Industrial Valuation Summary Introduction Uniform Standards Approaches to Value Land Valuation Land to Building Ratios Parking to Building

Table of Contents 2013 Commercial Revaluation Report

Table of Contents Commercial Revaluation Report 1. Commercial & Industrial Valuation Summary Introduction Uniform Standards Approaches to Value Land Valuation Land to Building Ratios Parking to Building

Table of Contents Commercial Revaluation Report 1. Commercial & Industrial Valuation Summary Introduction Uniform Standards Approaches to Value Land Valuation Land to Building Ratios Parking to Building

Standard on Mass Appraisal of Real Property

Standard on Mass Appraisal of Real Property Approved July 2017 International Association of Assessing Officers This standard replaces the January 2012 Standard on Mass Appraisal of Real Property and is

Standard on Mass Appraisal of Real Property Approved July 2017 International Association of Assessing Officers This standard replaces the January 2012 Standard on Mass Appraisal of Real Property and is

December Commissioner. Robert D. Plattner

December Assessment Equity in New York: Resultss from the Marke et Value Survey Thomas H. Mattox Commissioner Robert D. Plattner Deputy Commissioner Contents Introduction 1 Market Value Survey Data and

December Assessment Equity in New York: Resultss from the Marke et Value Survey Thomas H. Mattox Commissioner Robert D. Plattner Deputy Commissioner Contents Introduction 1 Market Value Survey Data and

Executive Summary. Review of the Indiana County, Pennsylvania, Reassessment of For. The Indiana County Commissioners

Executive Summary ***** Review of the Indiana County, Pennsylvania, Reassessment of 2015 For The Indiana County Commissioners ***** Property Taxation and Assessment Consultants 7630 North 10 th Avenue

Executive Summary ***** Review of the Indiana County, Pennsylvania, Reassessment of 2015 For The Indiana County Commissioners ***** Property Taxation and Assessment Consultants 7630 North 10 th Avenue

Department of Legislative Services Maryland General Assembly 2012 Session

Department of Legislative Services Maryland General Assembly 2012 Session SB 123 FISCAL AND POLICY NOTE Revised Senate Bill 123 (Chair, Judicial Proceedings Committee)(By Request - Departmental - Assessments

Department of Legislative Services Maryland General Assembly 2012 Session SB 123 FISCAL AND POLICY NOTE Revised Senate Bill 123 (Chair, Judicial Proceedings Committee)(By Request - Departmental - Assessments

2017 Property Values and Assessment Practices Report Assessment Year 2016

2017 Property Values and Assessment Practices Report Assessment Year 2016 Property Tax Division March 1, 2017 Per Minnesota Statutes, section 3.197, any report to the Legislature must contain, at the

2017 Property Values and Assessment Practices Report Assessment Year 2016 Property Tax Division March 1, 2017 Per Minnesota Statutes, section 3.197, any report to the Legislature must contain, at the

Cook County Assessor s Office: 2019 North Triad Assessment. Elk Grove Residential Assessment Narrative April 16th, 2019

Cook County Assessor s Office: 2019 North Triad Assessment Elk Grove Residential Assessment Narrative April 16th, 2019 1 Elk Grove Residential Properties Executive Summary Since the 2016 re-assessment,

Cook County Assessor s Office: 2019 North Triad Assessment Elk Grove Residential Assessment Narrative April 16th, 2019 1 Elk Grove Residential Properties Executive Summary Since the 2016 re-assessment,

ASSESSMENT METHODOLOGY

2018 ASSESSMENT METHODOLOGY MULTI-RESIDENTIAL MANUFACTURED HOME PARK A summary of the methods used by the City of Edmonton in determining the value of multi-residential manufactured home park land properties

2018 ASSESSMENT METHODOLOGY MULTI-RESIDENTIAL MANUFACTURED HOME PARK A summary of the methods used by the City of Edmonton in determining the value of multi-residential manufactured home park land properties

2018 Property Values and Assessment Practices Report Assessment Year 2017

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp 2018 Property Values

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp 2018 Property Values

Course Mass Appraisal Practices and Procedures

Course 331 - Mass Appraisal Practices and Procedures Course Description This course is designed to build on the subject matter covered in Course 300 Fundamentals of Mass Appraisal and prepare the student

Course 331 - Mass Appraisal Practices and Procedures Course Description This course is designed to build on the subject matter covered in Course 300 Fundamentals of Mass Appraisal and prepare the student

concepts and techniques

concepts and techniques S a m p l e Timed Outline Topic Area DAY 1 Reference(s) Learning Objective The student will learn Teaching Method Time Segment (Minutes) Chapter 1: Introduction to Sales Comparison

concepts and techniques S a m p l e Timed Outline Topic Area DAY 1 Reference(s) Learning Objective The student will learn Teaching Method Time Segment (Minutes) Chapter 1: Introduction to Sales Comparison

City of Norwalk Revaluation Project

City of Norwalk 2018 Revaluation Project Presenter: Paul Miller Supervisor: Salim Serdah Appraisers: James Steiner, John Valente, Steve Beccio, Rich Nicolosi, and Gynt Grube. Why Revaluation? It s important

City of Norwalk 2018 Revaluation Project Presenter: Paul Miller Supervisor: Salim Serdah Appraisers: James Steiner, John Valente, Steve Beccio, Rich Nicolosi, and Gynt Grube. Why Revaluation? It s important

Fundamentals of Real Estate APPRAISAL. 10th Edition. William L. Ventolo, Jr. Martha R. Williams, JD

A Fundamentals of Real Estate APPRAISAL 10th Edition William L. Ventolo, Jr. Martha R. Williams, JD Dennis S. Tosh, PhD William B. Rayburn, PhD, MAI, CFA Consulting Editors Dearb rri Real Estate Education

A Fundamentals of Real Estate APPRAISAL 10th Edition William L. Ventolo, Jr. Martha R. Williams, JD Dennis S. Tosh, PhD William B. Rayburn, PhD, MAI, CFA Consulting Editors Dearb rri Real Estate Education

Automated Valuation Model

Automated Valuation Model An innovative tool for Market Intelligence and Risk Management June 2015 Regulated by RICS EPS - Introduction Established presence in SEE: Greece (since 2000) & Romania, Bulgaria

Automated Valuation Model An innovative tool for Market Intelligence and Risk Management June 2015 Regulated by RICS EPS - Introduction Established presence in SEE: Greece (since 2000) & Romania, Bulgaria

GREGG APPRAISAL DISTRICT

GREGG APPRAISAL DISTRICT 2017 Annual Report TABLE OF CONTENTS Page General Information 1 Certified Market Value.. 2 Certified Taxable Value. 3 Property Categories and Descriptions 4-6 Value by Classification..

GREGG APPRAISAL DISTRICT 2017 Annual Report TABLE OF CONTENTS Page General Information 1 Certified Market Value.. 2 Certified Taxable Value. 3 Property Categories and Descriptions 4-6 Value by Classification..

Dear Assessor Berrios, President Preckwinkle, Commissioner Cabonargi, Commissioner Patlak, and Commissioner Rogers:

February 15, 2018 The Honorable Joseph Berrios The Honorable Toni Preckwinkle The Honorable Michael Cabonargi The Honorable Dan Patlak The Honorable Larry R. Rogers, Jr. Dear Assessor Berrios, President

February 15, 2018 The Honorable Joseph Berrios The Honorable Toni Preckwinkle The Honorable Michael Cabonargi The Honorable Dan Patlak The Honorable Larry R. Rogers, Jr. Dear Assessor Berrios, President

ASSESSMENT REVIEW BOARD. The City of Edmonton JASPER AVENUE Assessment and Taxation Branch

ASSESSMENT REVIEW BOARD Churchill Building 10019 103 Avenue Edmonton AB T5J 0G9 Phone: (780) 496-5026 NOTICE OF DECISION NO. 0098 101/11 CVG The City of Edmonton 1200-10665 JASPER AVENUE Assessment and

ASSESSMENT REVIEW BOARD Churchill Building 10019 103 Avenue Edmonton AB T5J 0G9 Phone: (780) 496-5026 NOTICE OF DECISION NO. 0098 101/11 CVG The City of Edmonton 1200-10665 JASPER AVENUE Assessment and

ASSESSMENT METHODOLOGY

2019 ASSESSMENT METHODOLOGY COMMERCIAL RETAIL AND OFFICE CONDOMINIUMS A summary of the methods used by the City of Edmonton in determining the value of commercial retail and office condominium properties

2019 ASSESSMENT METHODOLOGY COMMERCIAL RETAIL AND OFFICE CONDOMINIUMS A summary of the methods used by the City of Edmonton in determining the value of commercial retail and office condominium properties

Appraisers and Assessors of Real Estate

http://www.bls.gov/oco/ocos300.htm Appraisers and Assessors of Real Estate * Nature of the Work * Training, Other Qualifications, and Advancement * Employment * Job Outlook * Projections Data * Earnings

http://www.bls.gov/oco/ocos300.htm Appraisers and Assessors of Real Estate * Nature of the Work * Training, Other Qualifications, and Advancement * Employment * Job Outlook * Projections Data * Earnings

Cook County Assessor s Office: 2019 North Triad Assessment. Evanston Residential Assessment Narrative Updated: April 8 th, 2019

Cook County Assessor s Office: 2019 North Triad Assessment Evanston Residential Assessment Narrative Updated: April 8 th, 2019 1 Updates to this report A previous version of this report was rendered in

Cook County Assessor s Office: 2019 North Triad Assessment Evanston Residential Assessment Narrative Updated: April 8 th, 2019 1 Updates to this report A previous version of this report was rendered in

Course Commerical/Industrial Modeling Concepts Learning Objectives

Course 312 - Commerical/Industrial Modeling Concepts Learning Objectives Course Description Course 312 presents a detailed study of the mass appraisal process as applied to income-producing property. Topics

Course 312 - Commerical/Industrial Modeling Concepts Learning Objectives Course Description Course 312 presents a detailed study of the mass appraisal process as applied to income-producing property. Topics

2018 Annual Appraisal Report

2018 Annual Appraisal Report SUMMARY OF APPRAISAL ACTIVITIES, EXEMPTIONS, EQUALIZATION AND TAX RATES FOR 2018 TAX YEAR Wendy Grams, RPA, CTA, CCA CENTRAL APPRAISAL DISTRICT OF BANDERA COUNTY P. O. BOX

2018 Annual Appraisal Report SUMMARY OF APPRAISAL ACTIVITIES, EXEMPTIONS, EQUALIZATION AND TAX RATES FOR 2018 TAX YEAR Wendy Grams, RPA, CTA, CCA CENTRAL APPRAISAL DISTRICT OF BANDERA COUNTY P. O. BOX

Initial sales ratio to determine the current overall level of value. Number of sales vacant and improved, by neighborhood.

Introduction The International Association of Assessing Officers (IAAO) defines the market approach: In its broadest use, it might denote any valuation procedure intended to produce an estimate of market

Introduction The International Association of Assessing Officers (IAAO) defines the market approach: In its broadest use, it might denote any valuation procedure intended to produce an estimate of market

Klickitat County Assessor's Office Mass Appraisal Report

Klickitat County Assessor's Office Mass Appraisal Report Appraisal Date: January 1, 2012 for 2013 Property Taxes Report Date: Aug 14, 2012 Prepared For: Darlene R. Johnson, Klickitat County Assessor By:

Klickitat County Assessor's Office Mass Appraisal Report Appraisal Date: January 1, 2012 for 2013 Property Taxes Report Date: Aug 14, 2012 Prepared For: Darlene R. Johnson, Klickitat County Assessor By:

Definitions ad valorem tax Adaptive Estimation Procedure (AEP) - additive model - adjustments - algorithm - amenities appraisal appraisal schedules

- additive model - adjustments - algorithm - amenities appraisal appraisal schedules") Definitions ad valorem tax - in reference to property, a tax based upon the value of the property. Adaptive Estimation Procedure (AEP) - A computerized, iterative, self-referential procedure using properties

Definitions ad valorem tax - in reference to property, a tax based upon the value of the property. Adaptive Estimation Procedure (AEP) - A computerized, iterative, self-referential procedure using properties

2003 Commercial Ratio Study of St. Louis County

P U B L I C P O L I C Y R E S E A R C H C E N T E R UNIVERSITY OF MISSOURI - ST. LOUIS 2003 Commercial Ratio Study of St. Louis County Prepared by Public Policy Research Center University of Missouri St.

P U B L I C P O L I C Y R E S E A R C H C E N T E R UNIVERSITY OF MISSOURI - ST. LOUIS 2003 Commercial Ratio Study of St. Louis County Prepared by Public Policy Research Center University of Missouri St.

Midland Central Appraisal District BIENNIAL REAPPRAISAL PLAN

BIENNIAL REAPPRAISAL PLAN FOR THE TAX YEARS 2015 AND 2016 BY THE MIDLAND CENTRAL APPRAISAL DISTRICT BOARD OF DIRECTORS September 10, 2014 TABLE OF CONTENTS ITEM PAGE Executive Summary... 4 General Overview

BIENNIAL REAPPRAISAL PLAN FOR THE TAX YEARS 2015 AND 2016 BY THE MIDLAND CENTRAL APPRAISAL DISTRICT BOARD OF DIRECTORS September 10, 2014 TABLE OF CONTENTS ITEM PAGE Executive Summary... 4 General Overview

INFLUENCED BY ECONOMIC AND INSTITUTIONAL

AN ANALYSIS OF INDIANA PROPERTY TAX REFORM: EQUITY AND COST CONSIDERATIONS Olha Krupa, Indiana University INTRODUCTION INFLUENCED BY ECONOMIC AND INSTITUTIONAL cycles, property tax is a primary source

AN ANALYSIS OF INDIANA PROPERTY TAX REFORM: EQUITY AND COST CONSIDERATIONS Olha Krupa, Indiana University INTRODUCTION INFLUENCED BY ECONOMIC AND INSTITUTIONAL cycles, property tax is a primary source

Residential Revaluation Report

Residential Revaluation Report 2013 Mass Appraisal of Mobile Homes In Courts for 2014 Property Taxes Prepared For Steven J. Drew Thurston County Assessor TABLE of CONTENTS page. CERTIFICATE OF APPRAISAL...

Residential Revaluation Report 2013 Mass Appraisal of Mobile Homes In Courts for 2014 Property Taxes Prepared For Steven J. Drew Thurston County Assessor TABLE of CONTENTS page. CERTIFICATE OF APPRAISAL...

CITY OF OWATONNA ASSESSMENT REPORT. Steele County Assessor s Department. William G. Effertz, SAMA Steele County Assessor

2017 CITY OF OWATONNA ASSESSMENT REPORT Steele County Assessor s Department William G. Effertz, SAMA Steele County Assessor Tyler Diersen, AMA, Assistant County Assessor April 11, 2017 2017 Assessment

2017 CITY OF OWATONNA ASSESSMENT REPORT Steele County Assessor s Department William G. Effertz, SAMA Steele County Assessor Tyler Diersen, AMA, Assistant County Assessor April 11, 2017 2017 Assessment

Revaluation Explained

Revaluation Explained Northeast Revaluation Group, LLC 615 Jefferson Blvd., Suite 203, Warwick, RI 02886 401-737-0300 support@nereval.com Revaluation Process in a Nutshell 1. Take a group of properties

Revaluation Explained Northeast Revaluation Group, LLC 615 Jefferson Blvd., Suite 203, Warwick, RI 02886 401-737-0300 support@nereval.com Revaluation Process in a Nutshell 1. Take a group of properties

The purpose of the appraisal was to determine the value of this six that is located in the Town of St. Mary s.

The purpose of the appraisal was to determine the value of this six that is located in the Town of St. Mary s. The subject property was originally acquired by Michael and Bonnie Etta Mattiussi in August

The purpose of the appraisal was to determine the value of this six that is located in the Town of St. Mary s. The subject property was originally acquired by Michael and Bonnie Etta Mattiussi in August

Duties of the Assessors

Duties of the Assessors Value Properties Determine New Growth Set Tax Rate Assess Property Taxes Abate & Exempt Taxes Manage Overlay Account Assess Local Excises 1 Value Property Assessments based on fair

Duties of the Assessors Value Properties Determine New Growth Set Tax Rate Assess Property Taxes Abate & Exempt Taxes Manage Overlay Account Assess Local Excises 1 Value Property Assessments based on fair

VAN ZANDT COUNTY APPRAISAL DISTRICT 2018 ANNUAL REPORT

VAN ZANDT COUNTY APPRAISAL DISTRICT 2018 ANNUAL REPORT INTRODUCTION The Van Zandt County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property

VAN ZANDT COUNTY APPRAISAL DISTRICT 2018 ANNUAL REPORT INTRODUCTION The Van Zandt County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property

1. There must be a useful number of qualified transactions to infer from. 2. The circumstances surrounded each transaction should be known.

Direct Comparison Approach The Direct Comparison Approach is based on the premise of the "Principle of Substitution" which implies that a rational investor or purchaser will pay no more for a particular

Direct Comparison Approach The Direct Comparison Approach is based on the premise of the "Principle of Substitution" which implies that a rational investor or purchaser will pay no more for a particular

YOUNG COUNTY APPRAISAL DISTRICT

YOUNG COUNTY APPRAISAL DISTRICT 2017 - ANNUAL APPRAISAL REPORT AS OF 10/6/2017 1 2 TABLE OF CONTENTS ITEM PAGE Introduction 4 Purpose of Report...4 Taxing Entities, Rates & Exemptions 5 Property Types

YOUNG COUNTY APPRAISAL DISTRICT 2017 - ANNUAL APPRAISAL REPORT AS OF 10/6/2017 1 2 TABLE OF CONTENTS ITEM PAGE Introduction 4 Purpose of Report...4 Taxing Entities, Rates & Exemptions 5 Property Types

Article Where in Connecticut is the Best Location for a Split Tax? An Analysis of Land Assessment Equity in Several Cities

Article Where in Connecticut is the Best Location for a Split Tax? An Analysis of Land Assessment Equity in Several Cities Jeffrey P. Cohen 1, * and Michael J. Fedele 2 1 Center for Real Estate and Urban

Article Where in Connecticut is the Best Location for a Split Tax? An Analysis of Land Assessment Equity in Several Cities Jeffrey P. Cohen 1, * and Michael J. Fedele 2 1 Center for Real Estate and Urban

Date: March 2018 TOWN OF WATERFORD Department of Assessment

Date: March 2018 TOWN OF WATERFORD 1. Overview: The purpose of this workshop is to explain the Assessment Disclosure Notice, how assessments are derived and how to challenge your assessment if you do not

Date: March 2018 TOWN OF WATERFORD 1. Overview: The purpose of this workshop is to explain the Assessment Disclosure Notice, how assessments are derived and how to challenge your assessment if you do not

Property Appraisal Division Finance Department Anchorage: Performance. Value. Results.

Anchorage: Performance. Value. Results. Mission Provide a fair and equitable basis for taxation in the Municipality of Anchorage in conformance with State law and professional standards. Core Services

Anchorage: Performance. Value. Results. Mission Provide a fair and equitable basis for taxation in the Municipality of Anchorage in conformance with State law and professional standards. Core Services

ASSESSMENT AND TAXATION

ABSTRACT A brief synopsis of the assessment, appeal and taxation process as implemented by the Code of Iowa and Administrative Rules. ASSESSMENT AND TAXATION Iowa State Association of Assessors General

ABSTRACT A brief synopsis of the assessment, appeal and taxation process as implemented by the Code of Iowa and Administrative Rules. ASSESSMENT AND TAXATION Iowa State Association of Assessors General

March 25, Mr. Craig V. Dovel Chief County Assessment Officer DuPage County Center 421 N. County Farm Road Wheaton IL Dear Mr.

March 25, 2011 Illinois Department of Revenue Office of Local Government Services Equalization and Review Section 101 W. Jefferson Street PO Box 19033 Springfield, IL 62794-9033 (217) 785-6619 Mr. Craig

March 25, 2011 Illinois Department of Revenue Office of Local Government Services Equalization and Review Section 101 W. Jefferson Street PO Box 19033 Springfield, IL 62794-9033 (217) 785-6619 Mr. Craig

Minnesota Department of Revenue 2012 Sales Ratio Study Criteria

Minnesota Department of Revenue 2012 Sales Ratio Study Criteria Special Notes Forward-Adjusted Methodology Transition In the 2012 sales ratio study, the Department of Revenue will use a forward-adjusted

Minnesota Department of Revenue 2012 Sales Ratio Study Criteria Special Notes Forward-Adjusted Methodology Transition In the 2012 sales ratio study, the Department of Revenue will use a forward-adjusted

The Municipal Property Assessment

Combined Residential and Commercial Models for a Sparsely Populated Area BY ROBERT J. GLOUDEMANS, BRIAN G. GUERIN, AND SHELLEY GRAHAM This material was originally presented on October 9, 2006, at the International

Combined Residential and Commercial Models for a Sparsely Populated Area BY ROBERT J. GLOUDEMANS, BRIAN G. GUERIN, AND SHELLEY GRAHAM This material was originally presented on October 9, 2006, at the International

METHODOLOGY GUIDE VALUING LANDS IN TRANSITION IN ONTARIO. Valuation Date: January 1, 2016

METHODOLOGY GUIDE VALUING LANDS IN TRANSITION IN ONTARIO Valuation Date: January 1, 2016 August 2017 August 22, 2017 The Municipal Property Assessment Corporation (MPAC) is responsible for accurately assessing

METHODOLOGY GUIDE VALUING LANDS IN TRANSITION IN ONTARIO Valuation Date: January 1, 2016 August 2017 August 22, 2017 The Municipal Property Assessment Corporation (MPAC) is responsible for accurately assessing

2019 Revaluation Update. Presented by the Mecklenburg County Assessor s Office

2019 Revaluation Update Presented by the Mecklenburg County Assessor s Office Progress to Date 203,933 Parcels Completed 914 Residential Neighborhoods Completed (57%) All neighborhoods will be completed

2019 Revaluation Update Presented by the Mecklenburg County Assessor s Office Progress to Date 203,933 Parcels Completed 914 Residential Neighborhoods Completed (57%) All neighborhoods will be completed

Village of Scarsdale

Village of Scarsdale VILLAGE HALL / 1001 POST ROAD / SCARSDALE, NY 10583 914.722.1110 / WWW.SCARSDALE.COM Village Wide Revaluation Frequently Asked Questions Q1. How was the land value for each parcel

Village of Scarsdale VILLAGE HALL / 1001 POST ROAD / SCARSDALE, NY 10583 914.722.1110 / WWW.SCARSDALE.COM Village Wide Revaluation Frequently Asked Questions Q1. How was the land value for each parcel

Lee Central Appraisal District

Lee Central Appraisal District 2015 Mass Appraisal Report 1 INTRODUCTION Scope of Responsibility The Lee Central Appraisal District has prepared and published this report to provide citizens and taxpayers

Lee Central Appraisal District 2015 Mass Appraisal Report 1 INTRODUCTION Scope of Responsibility The Lee Central Appraisal District has prepared and published this report to provide citizens and taxpayers

Office of Legislative Services Background Report The Revaluation of Real Property: Answers to Frequently Asked Questions About the Revaluation Process

Office of Legislative Services Background Report The Revaluation of Real Property: Answers to Frequently Asked Questions About the Revaluation Process OLS Background Report No. 119 Prepared By: Local Government

Office of Legislative Services Background Report The Revaluation of Real Property: Answers to Frequently Asked Questions About the Revaluation Process OLS Background Report No. 119 Prepared By: Local Government

DELTA COUNTY APPRAISAL DISTRICT 2014 ANNUAL APPRAISAL REPORT

DELTA COUNTY APPRAISAL DISTRICT 2014 ANNUAL APPRAISAL REPORT Introduction The Delta County Appraisal District is a political subdivision of the State of Texas. The Constitution of the State of Texas, the

DELTA COUNTY APPRAISAL DISTRICT 2014 ANNUAL APPRAISAL REPORT Introduction The Delta County Appraisal District is a political subdivision of the State of Texas. The Constitution of the State of Texas, the

Property Appraisal Division Finance Department Anchorage: Performance Value Results

Anchorage: Performance Value Results Mission Provide fair and equitable basis for taxation in the Municipality of Anchorage in conformance with State law and professional standards. Core Services Valuation

Anchorage: Performance Value Results Mission Provide fair and equitable basis for taxation in the Municipality of Anchorage in conformance with State law and professional standards. Core Services Valuation

METHODOLOGY GUIDE VALUING MOTELS IN ONTARIO. Valuation Date: January 1, 2016

METHODOLOGY GUIDE VALUING MOTELS IN ONTARIO Valuation Date: January 1, 2016 AUGUST 2016 August 22, 2016 The Municipal Property Assessment Corporation (MPAC) is responsible for accurately assessing and

METHODOLOGY GUIDE VALUING MOTELS IN ONTARIO Valuation Date: January 1, 2016 AUGUST 2016 August 22, 2016 The Municipal Property Assessment Corporation (MPAC) is responsible for accurately assessing and

Residential Revaluation Report

Residential Revaluation Report 2010 Mass Appraisal of Region 8 for 2011 Property Taxes Prepared For Patricia Costello Thurston County Assessor TABLE OF CONTENTS Page No. CERTIFICATE OF APPRAISAL...3 APPRAISAL

Residential Revaluation Report 2010 Mass Appraisal of Region 8 for 2011 Property Taxes Prepared For Patricia Costello Thurston County Assessor TABLE OF CONTENTS Page No. CERTIFICATE OF APPRAISAL...3 APPRAISAL

Equity from the Assessor s Perspective

Institute of Municipal Assessors 55th Annual Conference Equity from the Assessor s Perspective Andy Anstett Legislation & Policy Support Services MPAC June 7th, 2011 Key Aspects of Equity Test Defining

Institute of Municipal Assessors 55th Annual Conference Equity from the Assessor s Perspective Andy Anstett Legislation & Policy Support Services MPAC June 7th, 2011 Key Aspects of Equity Test Defining

How to Read a Real Estate Appraisal Report

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

Collateral Underwriter, Regression Models, Statistics, Gambling with your License

Collateral Underwriter, Regression Models, Statistics, Gambling with your License Keith Wolf, SRA, AI-RRS Kwolf Consulting Inc. Kwolf1021@gmail.com 05/20/2015 There are Lies, Damned Lies and Statistics

Collateral Underwriter, Regression Models, Statistics, Gambling with your License Keith Wolf, SRA, AI-RRS Kwolf Consulting Inc. Kwolf1021@gmail.com 05/20/2015 There are Lies, Damned Lies and Statistics

ATASCOSA COUNTY APPRAISAL DISTRICT 2014 MASS APPRAISAL REPORT

ATASCOSA COUNTY APPRAISAL DISTRICT 2014 MASS APPRAISAL REPORT INTRODUCTION Scope of Responsibility The Atascosa County Appraisal District (CAD) has prepared and published this report to provide our citizens

ATASCOSA COUNTY APPRAISAL DISTRICT 2014 MASS APPRAISAL REPORT INTRODUCTION Scope of Responsibility The Atascosa County Appraisal District (CAD) has prepared and published this report to provide our citizens

AVM Validation. Evaluating AVM performance

AVM Validation Evaluating AVM performance The responsible use of Automated Valuation Models in any application begins with a thorough understanding of the models performance in absolute and relative terms.

AVM Validation Evaluating AVM performance The responsible use of Automated Valuation Models in any application begins with a thorough understanding of the models performance in absolute and relative terms.

Pickens County Reassessment Program. Utilizing CAMA GIS MLS SQL

1 Pickens County 2019 Reassessment Program Utilizing CAMA GIS MLS SQL Pickens County Reassessment History 1980 Countywide Reappraisal 1990 Countywide Reappraisal 1999 Countywide Reappraisal 2004 Countywide

1 Pickens County 2019 Reassessment Program Utilizing CAMA GIS MLS SQL Pickens County Reassessment History 1980 Countywide Reappraisal 1990 Countywide Reappraisal 1999 Countywide Reappraisal 2004 Countywide

COMAL APPRAISAL DISTRICT ANNUAL APPRAISAL REPORT

COMAL APPRAISAL DISTRICT 2016 ANNUAL APPRAISAL REPORT TABLE OF CONTENTS Introduction..2 Mission Statement... 2 Purpose of Report...2 Entities Served..2 Legislative Changes.3 Property Types.3 Appraisal

COMAL APPRAISAL DISTRICT 2016 ANNUAL APPRAISAL REPORT TABLE OF CONTENTS Introduction..2 Mission Statement... 2 Purpose of Report...2 Entities Served..2 Legislative Changes.3 Property Types.3 Appraisal

Following is an example of an income and expense benchmark worksheet:

After analyzing income and expense information and establishing typical rents and expenses, apply benchmarks and base standards to the reappraisal area. Following is an example of an income and expense

After analyzing income and expense information and establishing typical rents and expenses, apply benchmarks and base standards to the reappraisal area. Following is an example of an income and expense

2005 Commercial Ratio Study of St. Louis County

P U B L I C P O L I C Y R E S E A R C H C E N T E R U N I V E R S I T Y O F M I S S O U R I - S T. L O U I S 2005 Commercial Ratio Study of St. Louis County Prepared by Public Policy Research Center University

P U B L I C P O L I C Y R E S E A R C H C E N T E R U N I V E R S I T Y O F M I S S O U R I - S T. L O U I S 2005 Commercial Ratio Study of St. Louis County Prepared by Public Policy Research Center University

DELTA COUNTY APPRAISAL DISTRICT 2016 ANNUAL APPRAISAL REPORT

DELTA COUNTY APPRAISAL DISTRICT 2016 ANNUAL APPRAISAL REPORT Introduction The Delta County Appraisal District is a political subdivision of the State of Texas. The Constitution of the State of Texas, the

DELTA COUNTY APPRAISAL DISTRICT 2016 ANNUAL APPRAISAL REPORT Introduction The Delta County Appraisal District is a political subdivision of the State of Texas. The Constitution of the State of Texas, the

Property Appraisal Division Finance Department Anchorage: Performance. Value. Results.

Anchorage: Performance. Value. Results. Mission Provide a fair and equitable basis for taxation in the Municipality of Anchorage in conformance with State law and professional standards. Core Services

Anchorage: Performance. Value. Results. Mission Provide a fair and equitable basis for taxation in the Municipality of Anchorage in conformance with State law and professional standards. Core Services

COMAL APPRAISAL DISTRICT ANNUAL APPRAISAL REPORT

COMAL APPRAISAL DISTRICT 2017 ANNUAL APPRAISAL REPORT TABLE OF CONTENTS Introduction..2 Mission Statement... 2 Purpose of Report...2 Entities Served..2 Legislative Changes.3 Property Types.3 Appraisal

COMAL APPRAISAL DISTRICT 2017 ANNUAL APPRAISAL REPORT TABLE OF CONTENTS Introduction..2 Mission Statement... 2 Purpose of Report...2 Entities Served..2 Legislative Changes.3 Property Types.3 Appraisal

Residential Revaluation Report

Residential Revaluation Report 2012 Mass Appraisal of Region 5 for 2013 Property Taxes Prepared For Steven J. Drew Thurston County Assessor TABLE OF CONTENTS Page No. CERTIFICATE OF APPRAISAL... 3 APPRAISAL

Residential Revaluation Report 2012 Mass Appraisal of Region 5 for 2013 Property Taxes Prepared For Steven J. Drew Thurston County Assessor TABLE OF CONTENTS Page No. CERTIFICATE OF APPRAISAL... 3 APPRAISAL

The Baltimore City Property Tax Study

The Baltimore City Property Tax Study DEPARTMENT OF LEGISLATIVE SERVICES 2014 Baltimore City Property Tax Study Department of Legislative Services Office of Policy Analysis Annapolis, Maryland December

The Baltimore City Property Tax Study DEPARTMENT OF LEGISLATIVE SERVICES 2014 Baltimore City Property Tax Study Department of Legislative Services Office of Policy Analysis Annapolis, Maryland December

Standard on Automated Valuation Models (AVMs)

") Standard on Automated Valuation Models (AVMs) Approved September 2003 Revised approved July, 2018 Contents 1. Scope...4 2. Principles...4 3. Introduction...5 3.1 Definition of automated valuation model

Standard on Automated Valuation Models (AVMs) Approved September 2003 Revised approved July, 2018 Contents 1. Scope...4 2. Principles...4 3. Introduction...5 3.1 Definition of automated valuation model

LIMITED-SCOPE PERFORMANCE AUDIT REPORT

LIMITED-SCOPE PERFORMANCE AUDIT REPORT Agricultural Land Valuation: Evaluating the Potential Impact of Changing How Agricultural Land is Valued in the State AUDIT ABSTRACT State law requires the value

LIMITED-SCOPE PERFORMANCE AUDIT REPORT Agricultural Land Valuation: Evaluating the Potential Impact of Changing How Agricultural Land is Valued in the State AUDIT ABSTRACT State law requires the value

ASSESSMENT REVIEW BOARD

ASSESSMENT REVIEW BOARD MAIN FLOOR CITY HALL 1 SIR WINSTON CHURCHILL SQUARE EDMONTON AB T5J 2R7 (780) 496-5026 FAX (780) 496-8199 NOTICE OF DECISION 0098 248/10 Altus Group Ltd. The City of Edmonton 17327

ASSESSMENT REVIEW BOARD MAIN FLOOR CITY HALL 1 SIR WINSTON CHURCHILL SQUARE EDMONTON AB T5J 2R7 (780) 496-5026 FAX (780) 496-8199 NOTICE OF DECISION 0098 248/10 Altus Group Ltd. The City of Edmonton 17327

ASSESSMENT METHODOLOGY

2018 ASSESSMENT METHODOLOGY COST APPROACH A summary of the methods used by the City of Edmonton in determining the value of residential and non-residential properties valued using the cost approach in

2018 ASSESSMENT METHODOLOGY COST APPROACH A summary of the methods used by the City of Edmonton in determining the value of residential and non-residential properties valued using the cost approach in

Chapter 35. The Appraiser's Sales Comparison Approach INTRODUCTION

Chapter 35 The Appraiser's Sales Comparison Approach INTRODUCTION The most commonly used appraisal technique is the sales comparison approach. The fundamental concept underlying this approach is that market

Chapter 35 The Appraiser's Sales Comparison Approach INTRODUCTION The most commonly used appraisal technique is the sales comparison approach. The fundamental concept underlying this approach is that market