Enabling Strategies for Urban Housing Microfinance

|

|

|

- Milton Bryce Bell

- 5 years ago

- Views:

Transcription

1 i A National Workshop titled : Exploring enabling strategies for Urban Housing Microfinance: A crucial step towards Housing for All was organised by the Ministry of Housing and Urban Poverty Alleviation (MoHUPA) and HUDCO s HSMI on the 16 th of June, 2015 at India Habitat Centre, New Delhi. The workshop concludes that to make housing finance available, accessible and affordable to the urban poor, the following are needed: Policy interventions to improve Credit flow to low-income housing finance market; Availability of land for housing the urban poor; Customised Products and delivery mechanisms; Institutional partnerships amongst lending and anchor institutions and finally lateral support through technology and capacity building. The workshop ushered in setting up of on-line working group to take the subject of Housing microfinance towards suggestions for policy formulation. The document that follows is a policy perspective put together by the working group with its suggestions to the Ministry of Housing & Urban Poverty Alleviation. The Report of the National Workshop titled: Exploring enabling strategies for Urban Housing Microfinance:A crucial step towards Housing for All is at

and Low Income Group (LIG) urban population.")

2 Introduction Urban Housing Microfinance: A Policy Perspective Urban housing shortage in India at the end of the Eleventh Five Year Plan ( ) is estimated to be million units. This shortage is historically skewed towards the urban poor ie the Economically Weaker Sections (EWS) and Low Income Group (LIG) urban population. Resource constraints, challenges of slum redevelopment and the inclusion - exclusion errors in targeting, keep Public sector Housing interventions far from meeting the housing needs of the low income segment population. Adversely complementing this, the urban poor population, due to reasons of inadequacy of income to service the debt, informality of employment and insecurity of tenure, remain incapable of accessing the formal housing finance market. Reasons for restrictive entry of formal institutional housing finance into Microfinance is an idea whose time has come Kofi Annan the low income housing sector revolve around high transaction costs for small loans; non-applicability of traditional mortgage lien; policy restrictions in accessing cost effective long term funds by institutions like MFIs and HFCs. The Government of India s Housing for All mission for urban area will be implemented through the States/UTs under the Pradhan Mantri Awas Yojana (PMAY) with the objective of providing houses to all eligible beneficiaries by the year The mission covers all 4041 statutory towns with focus on 500 Class I cities. This mission is pillared on four verticals or implementation methodologies, namely 1) In Situ Slum Redevelopment, 2) Credit linked Subsidy Scheme 3) Affordable Housing in Partnership and 4) Subsidy for ii

3 iii Beneficiary led House construction. In-fact the Housing Microfinance (HMF) implementation approach has broadened the definition of Housing micro-finance to include the principles of both incremental housing finance based on micro-finance methods and traditional mortgage finance catering to various segments within the urban poor. This therefore gives an opportunity for HMF institutions to contribute effectively to each of the four verticals of the PMAY, and possibly in ways that conventional formal financial institutions cannot. The present Housing finance behaviour of the financial institutions on the one hand, and, the target borrowers on the other, necessitate that customized products for different segments of urban poor and institutional partnerships amongst various stakeholders be facilitated for effective implementation of the Housing For All mission. In the absence of this, there is a perceptible danger of excluding a significant target clientele, thereby dampening the objective of the Housing for All mission. Commercial institutions catering to higher income brackets may lack the aptitude and required people-centric resources for upscaling low income housing finance market. In view of this, a policy perspective to Housing Microfinance is proposed to especially enable institutions like NGO-MFIs, NBFC-MFIs, Co-operatives, HFCs and Banks experienced and interested in the sector to meet the latent housing finance demand of the urban poor and informal sector population. This perspective envisions to contribute to the Housing for All mission of the Government of India by supporting its implementation through the PMAY till 2022 while independently continuing to serve the emerging low-income housing finance market which would remain outside the scope of the PMAY. It also presupposes Government of India support for policy pre-requisites to enable upscaling Housing microfinance in India and thereby reaching housing to the urban poor. 2a. Definition Provision of housing finance to the urban poor ie households with low, irregular and informal incomes for the purpose of additions, repairs and improvements in existing housing units; purchase and construction of new house in informal, semi-formal and formal urban areas 2b. Defining features Housing microfinance is traditionally defined as the provision of unsecured microcredit to meet the demand of low-income households to repair or improve their existing homes or build their own homes over time. The

4 traditional definition has the danger of restricting HMF to incremental housing only. The definition in the HMF policy perspective document is therefore a paradigm shift and is broad-based on the following factors: Convergence of micro-mortgages and finance for micro-housing. Includes both mortgage and nonmortgage housing loan products Based on principles of both incremental (short term and repeat loans )and conventional long term housing finance Contextualize HMF with the situation of Low income Housing finance market in India Need to support Housing for All mission of the Government of India and also be a part of PMAY implementation process 3. Scope The Housing Microfinance policy should cover all urban areas of the country covering 4041 statutory and 3894 census towns of India and will include urban poor population with a minimum household monthly income of Rs. 5000/-. 4. Policy Objectives Reach housing finance to every urban poor who has the ability to repay but cannot access formal finance. Housing micro-finance must support Housing for All mission of the Government of India and be an integral part of the PMAY scheme. Facilitate all institutions (NGO- MFIs, NBFC-MFIs, HFCs, Banks and other lending institutions) to enter the low income and informal housing market. Facilitate alternative security mechanisms as surrogate to secure land tenure. Build capacities of institutions involved in delivering HMF Lateral support through Technology and Capacity Building to end-use clients 5. Guiding Principles The income definition of urban poor is as per the EWS and LIG income levels prescribed in Pradhan Mantri Awas Yojana(PMAY) scheme of the MoHUPA, Government of India. Loan products have been devised keeping in mind differing income subsets within urban poor, varying housing needs, repayment capacities, land title issues and credit appraisal processes. HMF agencies must cater to every income subset within the EWS/LIG Negligible exclusion and inclusion errors. iv

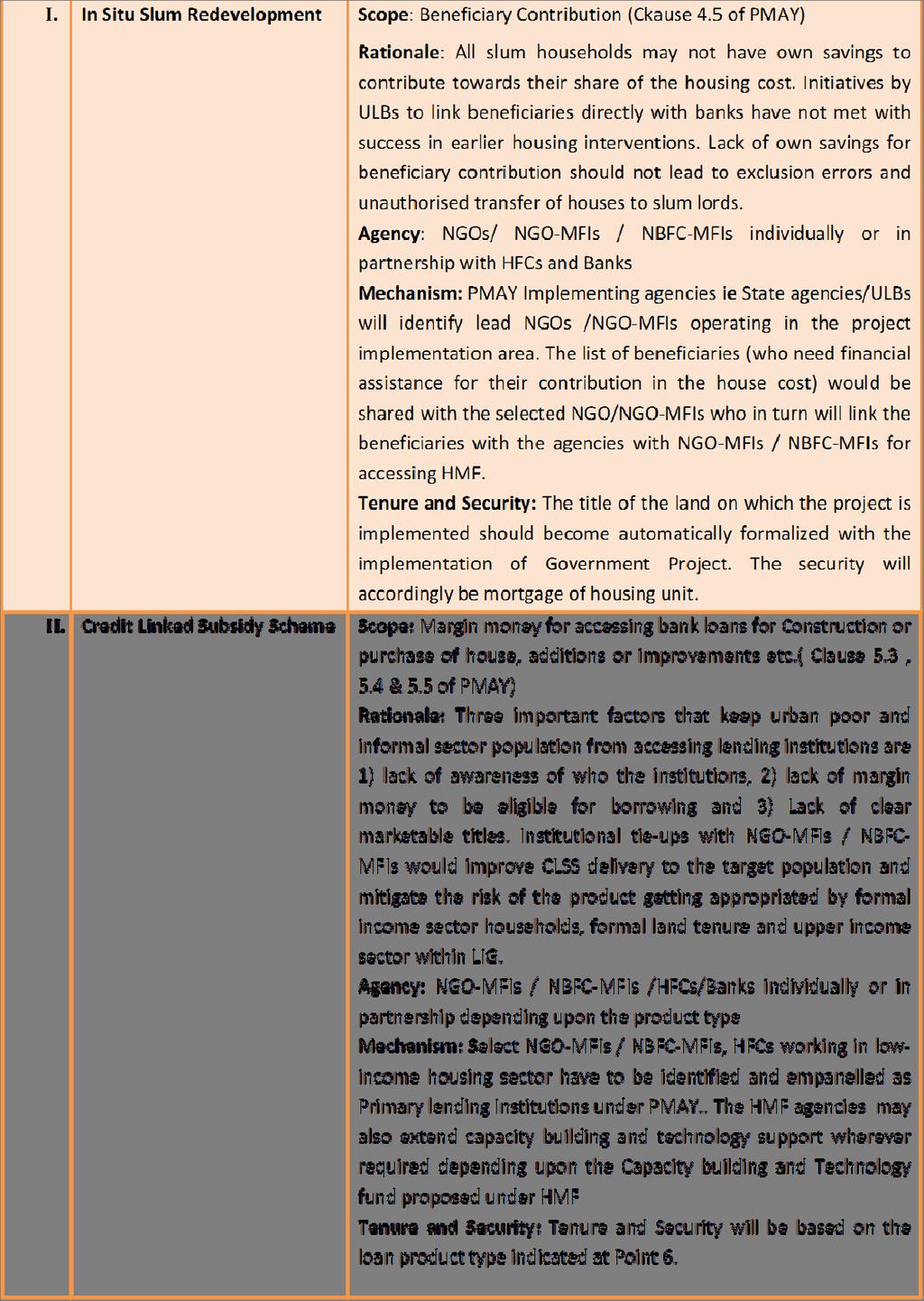

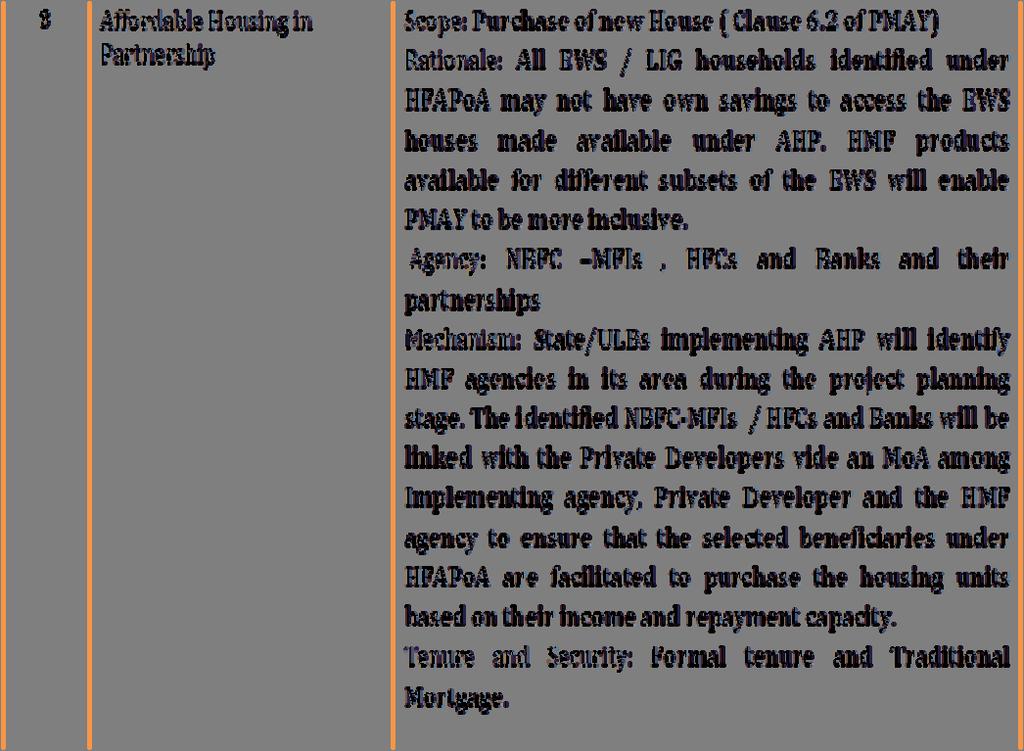

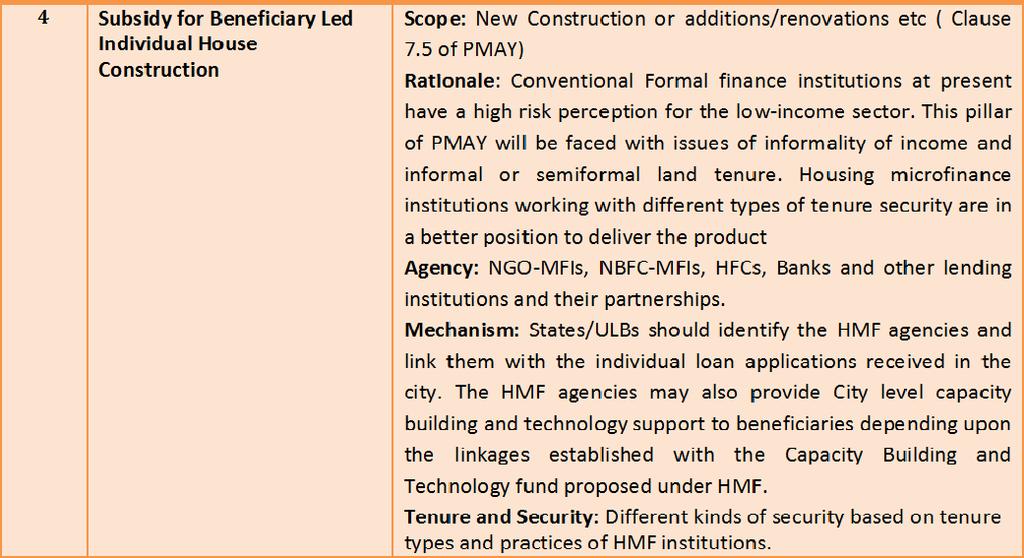

5 iv 6. HMF Products The products are based on lessons drawn both from both existing practices and principles, besides future possibilities which are subject to enhancement of credit flow to institutions that have displayed success in reaching housing finance to the poor and informal sector population.

availability of long term and cheaper funds for HMF agencies,")

6 7. Housing Microfinance Agencies 8. Policy Pre-requisites for Upscaling HMF The Urban HMF Policy approach presupposes certain policy interventions required to facilitate a) availability of long term and cheaper funds for HMF agencies, b) availability of land for low-income housing projects and 3) formalisation & legalisation of land tenure 8a Enhance credit flow to the HMF sector Setting up a corpus fund for housing microfinance HMF Corpus fund may be set up in HUDCO or NHB or any other national level apex institution. Set up a HMF single window for project appraisal and fund disbursement Support development/ restructuring of schemes within the apex institution to fund directly to MFIs and other lending institutions Identify and empanel institutional partners for HMF in different states (NGOs, NGO- MFIs, HFCs, Banks etc) Modification in RBI norms for MFIs Exclusion of HMF Loan from the maximum indebtedness Cap of Rs lakh for MFI borrower to be computed by MFI vi

7 vii Modifications in PSL Norms Low ticket housing loans of less than Rs 6.00 lakhs and loans between Rs 6.00 lakhs & Rs lakhs should be made a separate category like agricultural credit, of may be 5% each within the Overall PSL target. PSL norms for onward lending to HFIs to be modified to include MFIs without any restrictions. This is warranted as banks are not taking the direct credit risk, and the MFIs and HFCs provide a cushion of capital to underwrite the underlying risk. Banks should be allowed to issue long term bonds for financing the loans given to MFIs under the issue of Long Term Bonds by Banks Financing of Infrastructure and Affordable Housing. Relaxing wholesale lending caps for HFCs HFC wholesale lending is restricted to 15% of their net worth currently. Relaxing this credit concentration cap would improve flow of funding from HFCs to MFIs. Risk sharing /Tripartite guarantee for MFI s while funding housing projects developed by state housing boards,nodal agencies Relaxing Commercial Real Estate exposure Norms for exposure to Affordable Housing Projects Recommendations for Credit Risk Guarantee Trust Fund for HMF A dedicated credit risk guarantee fund may be created for HMF or HMF should be included in the existing Credit Risk Guarantee Fund scheme of NHB. The Government may provide partial Guarantee to cover the principal amount in default or Loss Default Guarantee to cover the first or second loss as the case may be. This would bring down the risk premium. This is especially significant for client profile that is vulnerable to economic disasters. The existing upfront fees (currently an upfront fee of 1% of outstanding portfolio) should be restructured to improve the uptake of the Credit Risk Guarantee Trust Fund managed by NHB and MoHUPA. Since default rates are lower than 1%, it prevents HFCs, Banks and MFIs from availing the benefit under the scheme.

8 Develop a customized NHB refinance scheme for NBFC -MFIs A separate refinance scheme focussed only on NBFC MFIs (which can be priced appropriately) be formulated for MFIs to enter the HMF market. NHB could take the initiative to develop a different scheme with specific eligibility criteria, portfolio benchmarks, customized internal credit rating models etc. Supply side interventions to reduce Housing Cost Fiscal and tax reliefs to lower the unit cost of the home itself, such as waiver of all stamp duties for first time home purchases of less than 6 lakhs and reduced stamp duty for home purchases priced between 6 lakhs & 10 lakhs. A methodology to refund all input taxes that go into the cost of the home has to be worked out. This would reduce the house cost by 40% depending on the location. In-built technology support and construction advisory services would lead to unit cost reduction Development Control regulations are a state subject. However if adequately modified can reduce the costs considerably and therefore make the market more accessible to the poor and low income. Costs can be considerably reduced based on the price of land, this combined with adequately priced and structured housing finance, and policy on registration (exemption from stamp duty etc.) will support the low income to cross over from de-facto tenure to legal title enabled by the market. Land Availability for Housing the low income population. a) Undertake an exercise in land inventory in the town/city (public land, under-utilized public lands; land available with Public Sector undertakings in the city and unused private lands b) Land Pooling based on the land inventory results c) Improving land delivery system by easing land legislation d) Improvements in Planning system by introducing reservations in the local urban plans based on land inventory results e) In all new developments, the reservation of land to the extent of % land area of all land layout beyond a certain land area or viii

![ix f) 20-25 % of built up area, developed by all development group [ government sector, public sector, private sector or joint sector development] g) In case of](/docs-images/89/99067143/images/9-0.jpg "existing re-development or for in-situ environmental improvement and shelter upgradation, on public or private lands, the ownership title [ patta] or /and tenurial")

![rights [ for not shifting for at least ] of 35 years. 8b.](/docs-images/89/99067143/images/9-1.jpg "Legal titles and housing microfinance Land tenure may be broadly categorised as 1) Secure Tenure 2) Defacto tenure 3) Insecure tenure.")

9 ix f) % of built up area, developed by all development group [ government sector, public sector, private sector or joint sector development] g) In case of existing re-development or for in-situ environmental improvement and shelter upgradation, on public or private lands, the ownership title [ patta] or /and tenurial rights [ for not shifting for at least ] of 35 years. 8b. Legal titles and housing microfinance Land tenure may be broadly categorised as 1) Secure Tenure 2) Defacto tenure 3) Insecure tenure. The product categorisation in the HMF policy is also based on the kind land tenure and lending practices ranging from formal to the in-formal title security. Existing Housing microfinance products are being securitized with paralegal titles, legal titles wherever available and alternative collateral. To make the Housing Microfinance policy implementable, formalisation / legalization of the land tenure in both public and private lands, following is proposed:

The integration methodology proposes Willingness of the institution, 2) a 1) Sustainable model and a 2) Pilot model.")

10 9. Implementation Methodology of HMF 9a.Integration of the products in the HFA (One or more of the PMAY verticals) The integration methodology proposes Willingness of the institution, 2) a 1) Sustainable model and a 2) Pilot model. structural and operational parameters and 3) geographical spread. A list of HMF institutions and guidelines on 9a.1 Long Term Sustainable Model The PMAY is being implemented by the States/ULBs. For integration of HMF with PMAY, the States/ULBs should parameters could be circulated by the Centre. Integrating HMF with Housing for All will be based on different possibilities create a pool of identified HMF that each of the verticals/ agencies as indicated in Point 7 above. implementation methodologies that Identification must be based on 1) PMAY has prescribed. x

11 xi

12 xii

.")

13 xiii 9a. 2 Pilot Model (HMF Integration with PMAY under NHB/HUDCO) An immediate roll out for Pilot Projects only Set up a HMF revolving fund. Link the fund with Credit Risk Guarantee Fund (with modified title clauses). Set up/strengthen a dedicated window/program Management Unit (PMU) in HUDCO/NHB for HMF program management. Based on the experience of NHB/HUDCO, select and empanel Housing MFIs, HFCs and borrowing institutions with good track record. Roll out pilot initiatives with a view to start-up the HMF process by funding MFIs / HFCs for PMAY products. Monitor and Evaluate processes and results.

Structure the HMF fund Identify and")

14 9b. Market based HMF outside the scope of PMAY Urban poor falling outside the eligibility criteria of PMAY or residing in slums/ non-slum areas that have not been taken up under any of the four verticals can access any of the housing finance products from the HMF institutions. However these clients shall not be entitled for Government subsidies. In the market based approach, HMF products and processes are not restricted to Government projects alone. 9b.1 Market based Institutional Structures and partnerships for enabling and upscaling HMF Functions for Start-Up Identify equity investors (Internal and External) Structure the HMF fund Identify and empanel institutional partners for implementing HMF by HMF Apex Institution/ NHB / HUDCO / Specialised Committee constituted under MoHUPA. Determine the Structural and Operational Eligibility Parameters for the institutional partners to participate in the empanelment process for HMF (Indicative list appended at Annexure - A) Capacity Building of functionaries in the Apex Institution xiv

Develop Third Party monitoring and evaluation mechanisms 9b.")

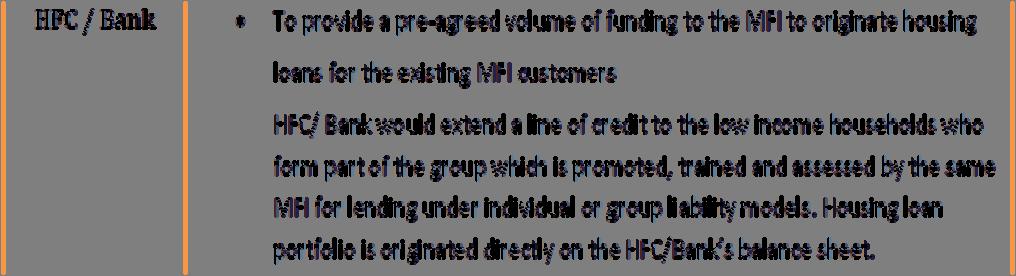

15 xiv Develop project appraisal guidelines (Indicative parameters at Annexure -B) Develop Third Party monitoring and evaluation mechanisms 9b.2 Hybrid Model (Banks/HFCs + NHB/HUDCO) To bring confidence amongst banks to lend MFIs/MFI s clients, a structure where in MFI provides first loss protection (5-10%), NHB/HUDCO provides a second loss protection (20-25%) in the form of a guarantee is proposed. In this model, role of banks/hfcs will be funding, NHB/HUDCO would provide training and technical assistance to MFI s, and MFIs will be responsible for sourcing and collection. This model can be tested with selected MFIs.

16 9b.3 Bankers Correspondent Model (MFI in partnership with HFC/Banks) xvi

17 xvii 9b.4 Setting up separate verticals for HMF within lending institutions like MUDRA Bank or Scheduled Commercial banks like BANDHAN may be explored The existing clients of enterprise loans may be targeted under such institutional arrangements Project /Construction finance: lending to developers for building low-income housing projects 10. Capacity Building & Support 10a. Capacity Building areas and mechanisms Demand Side Housing Finance Literacy and Construction practices for urban poor Using MFIs for demand aggregation by State Housing Boards/HFA implementing agencies Supply Side Developing a credit score model in collaboration with recognised CICs which draw information from both MFI and Consumer loans Development of E KYC to be made available to HFCs/Banks and MFIs 10b. Implementation Support Areas and mechanisms Industry best practice sharing Institutionalising City/town Setting up of Information bank of upcoming and available housing projects Data bank on regularised slums level utility bureau to bring about reduction in transaction cost for lending institutions

18 10c. Institutional Partners Identification of partners with Solutions, Lafarge the support of Technology Academy(India); SEWA Mutual Mission Under HFA Benefit Trust; Development Nominating the nodal agency like HSMI/BMTPC MoA to be signed with Capacity Alternatives etc Define roles and responsibilities and terms of agreement with building and Technology individual partners based on partners ( Egs. Habitat for their area of support Humanity; Micro Home 10d. Setting up a HMF Capacity Building and Technology Fund Housing financial literacy or time. Besides to meet the one time construction assistance will add to capital cost and O&M cost of administrative expenses. The expected establishing credit bureaus, information gain derived from reduced losses bank on low income housing projects cannot outweigh these costs for the and best practices, the Government of lending institutions at this point of India has to set up a dedicated fund.. xviii

19 xix Annexure - A Indicative list of Parameters for empanelling Housing Microfinance agencies 1 Governance, Management & Organization Board and Management Client relationship and credentials Operating locations 2 Systems, Processes, Technology and Human Resources Human Resources MIS & Technology Financial Management Systems Risk Management and Control Systems 3 Financial Evaluation & Portfolio Quality Profitability ratios Portfolio quality Liquidity and ALM Source Scaling up Housing Microfinance: Study by IFMR Capital in partnership with NHB and DFID.

20 Annexure- B HMF project appraisal for lending institutions Indicative Credit appraisal Parameters Applicability of HMF Model proposed Applicability of HMF Product applied Loan amount Project Cost Location details Type of land tenure ( Formal / Semi-formal / Informal) Building plan approval agency Details of housing to be funded Proof of income and identity Client Socio-Economic Profile Summary of household cash flow Client relationship with borrowing agency / partners Credit History of the borrower if any Collateral (Legal / Paralegal / alternate security) Risk mitigation measures Rate of Interest Repayment tenure Repayment schedule for end-use borrowers ( weekly / fortnightly/monthly)

21 Acknowledgements The Policy Perspective on Urban Housing Microfinance is an outcome based on discussions and feedback received from the HMF working group members. Special mention is made to K.P. Manikandan from Ashoka Innovators, Madhusudan Menon from Micro Housing Finance Corporation, Shilpa Rao & Debdoot Banerjee from Janalaksmi Financial services,, Gouri Kumar from ESAF Microfin, V Suresh, Sireesha Patnaik from SMBT, Bjal Brahmbhatt from SEWA-MHT, Rita Bhattacharya from NHB, Dr. H.S. Gill Vijaya Vasu, Debesh Chakraborty, Kanika Basu and Sangeeta Maunav from HUDCO. Contact: Readers Comments and suggestions may be reached to Dr. H S Gill at edhudco@gmail.com or to Sangeeta Maunav at sangeetamaunav73@gmail.com Disclaimer: The Policy Perspective on Urban Housing Microfinance is a compilation of ideas and suggestions backed by experience of individuals and institutions working on the subject of housing finance for the poor and informal sector population. The document does not represent the views of the Ministry of Housing & Urban Poverty Alleviation (MoHUPA)and Housing & Urban Development Corporation (HUDCO). xxi

INSTRUCTIONS TO PRIVATE DEVELOPERS

INSTRUCTIONS TO PRIVATE DEVELOPERS Government of Andhra Pradesh has established the A.P.Township and Infrastructure Development Corporation Limited(APTIDCO) to develop sustainable Townships and also creating

INSTRUCTIONS TO PRIVATE DEVELOPERS Government of Andhra Pradesh has established the A.P.Township and Infrastructure Development Corporation Limited(APTIDCO) to develop sustainable Townships and also creating

Day 1 Session 1 'Rajiv Awas Yojana - Slum Free India Mission' by P.K.Mohanty (Joint Secretary and Mission Director JNNURM, MoHUPA)

") Cities Alliance Project Output Day 1 Session 1 ' - Slum Free India Mission' by P.K.Mohanty (Joint Secretary and Mission Director JNNURM, MoHUPA) India International Workshop: Scaling up Upgrading and Affordable

Cities Alliance Project Output Day 1 Session 1 ' - Slum Free India Mission' by P.K.Mohanty (Joint Secretary and Mission Director JNNURM, MoHUPA) India International Workshop: Scaling up Upgrading and Affordable

Government of Uttar Pradesh. Workshop for Housing for All Date - 09/08/2016. State Urban Development Agency

Government of Uttar Pradesh Workshop for Housing for All Date - 09/08/2016 State Urban Development Agency Overview of Scheme Housing shortage estimated at 2 Cr, out of these 2 Cr, 30 Lakh shortage is in

Government of Uttar Pradesh Workshop for Housing for All Date - 09/08/2016 State Urban Development Agency Overview of Scheme Housing shortage estimated at 2 Cr, out of these 2 Cr, 30 Lakh shortage is in

Barrio Mio. Transforming High Risk Neighborhoods in Mixco, Guatemala. Public Private Partnerships and Applicable Financial Instruments

Barrio Mio. Transforming High Risk Neighborhoods in Mixco, Guatemala Public Private Partnerships and Applicable Financial Instruments May 29, 2014 www.pciglobal.org www.encludesolutions.com The Barrio

Barrio Mio. Transforming High Risk Neighborhoods in Mixco, Guatemala Public Private Partnerships and Applicable Financial Instruments May 29, 2014 www.pciglobal.org www.encludesolutions.com The Barrio

Scheme of Service. for. Housing Officers

REPUBLIC OF KENYA Scheme of Service for Housing Officers APPROVED BY THE PUBLIC SERVICE COMMISSION AND ISSUED BY THE PERMANENT SECRETARY MINISTRY OF STATE FOR PUBLIC SERVICE OFFICE OF THE PRIME MINISTER

REPUBLIC OF KENYA Scheme of Service for Housing Officers APPROVED BY THE PUBLIC SERVICE COMMISSION AND ISSUED BY THE PERMANENT SECRETARY MINISTRY OF STATE FOR PUBLIC SERVICE OFFICE OF THE PRIME MINISTER

HOUSING FOR ALL (URBAN) MISSION

MISSION") HOUSING FOR ALL (URBAN) MISSION FREQUENTLY ASKED QUESTIONS (FAQs) 1. What is Housing for All (HFA), its objectives and scope? 2. What is the Coverage and duration of HFA? 3. What financial support will

HOUSING FOR ALL (URBAN) MISSION FREQUENTLY ASKED QUESTIONS (FAQs) 1. What is Housing for All (HFA), its objectives and scope? 2. What is the Coverage and duration of HFA? 3. What financial support will

Government of India Ministry of Housing and Urban Affairs National Buildings Organisation

Government of India Ministry of Housing and Urban Affairs National Buildings Organisation FORMAT Information Collection format for the Completed / Under Construction in respect of EWS/LIG (Guidelines and

Government of India Ministry of Housing and Urban Affairs National Buildings Organisation FORMAT Information Collection format for the Completed / Under Construction in respect of EWS/LIG (Guidelines and

The Affordable. Housing Finance Summit Highlights. Vinod Kothari Consultants P. Ltd. presents.

http://vinodkothari.com/events.htm Vinod Kothari Consultants P. Ltd. presents The Affordable Housing Finance Summit 2 0 1 3 22 23 January 2013, Venue TBA, Mumbai Supported By : Highlights The stakeholders

http://vinodkothari.com/events.htm Vinod Kothari Consultants P. Ltd. presents The Affordable Housing Finance Summit 2 0 1 3 22 23 January 2013, Venue TBA, Mumbai Supported By : Highlights The stakeholders

Ministry of Housing & Urban Poverty Alleviation. Ministry of Housing & Urban Poverty Alleviation Government of India. JnNURM & RAY

Government of India JnNURM & RAY Faridabad, 16 th March 2012 1 MoHUPA: Key Functions & Programmes Formulation of Housing Policy and Programs Matters related to Human Settlements & Urban Development including

Government of India JnNURM & RAY Faridabad, 16 th March 2012 1 MoHUPA: Key Functions & Programmes Formulation of Housing Policy and Programs Matters related to Human Settlements & Urban Development including

Channelling Financial Flows for Adequate and Affordable Housing

Channelling Financial Flows for Adequate and Affordable Housing Renu Sud Karnad Joint Managing Director Housing Development Finance Corporation Limited - India FIG Working Week 28 Integrating Generations

Channelling Financial Flows for Adequate and Affordable Housing Renu Sud Karnad Joint Managing Director Housing Development Finance Corporation Limited - India FIG Working Week 28 Integrating Generations

SOCIAL JUSTICE CURRENT AFFAIRS 2017 HOUSING FOR ALL -PMAY

SOCIAL JUSTICE CURRENT AFFAIRS 2017 HOUSING FOR ALL -PMAY India is undergoing a rapid urbanization now. This requires expansion of urban amenities. A major deficit is housing among urban population. National

SOCIAL JUSTICE CURRENT AFFAIRS 2017 HOUSING FOR ALL -PMAY India is undergoing a rapid urbanization now. This requires expansion of urban amenities. A major deficit is housing among urban population. National

Legislative Brief The Land Acquisition, Rehabilitation and Resettlement Bill, 2011

Legislative Brief The Land Acquisition, Rehabilitation and Resettlement Bill, 2011 The Land Acquisition, Rehabilitation and Resettlement Bill, 2011 was introduced in the Lok Sabha by the Minister for Rural

Legislative Brief The Land Acquisition, Rehabilitation and Resettlement Bill, 2011 The Land Acquisition, Rehabilitation and Resettlement Bill, 2011 was introduced in the Lok Sabha by the Minister for Rural

RECENT DEVELOPMENTS IN HOUSING FINANCE IN LITHUANIA

HOUSING AND URBAN DEVELOPMENT FOUNDATION RECENT DEVELOPMENTS IN HOUSING FINANCE IN LITHUANIA Eduardas Kazakevičius 1 SUMMARY! Macro environment conducive of housing finance development: GDP, prices, interest

HOUSING AND URBAN DEVELOPMENT FOUNDATION RECENT DEVELOPMENTS IN HOUSING FINANCE IN LITHUANIA Eduardas Kazakevičius 1 SUMMARY! Macro environment conducive of housing finance development: GDP, prices, interest

International Journal of Management Excellence Volume 8 No.2 February 2017

Perspective of Developer, Buyer, Financier and Equity Participants in Real Estate Project Development Process in India: An important constituent of Construction Industry Alok Singh Indian Institute of

Perspective of Developer, Buyer, Financier and Equity Participants in Real Estate Project Development Process in India: An important constituent of Construction Industry Alok Singh Indian Institute of

SLUMS IN DELHI ISSUES AND POLICY PERSPECTIVES

SLUMS IN DELHI ISSUES AND POLICY PERSPECTIVES SEMINAR ON URBAN GOVERNANCE IN THE CONTEXT OF JAWAHARLAL NEHRU NATIONAL URBAN RENEWAL MISSION (JNNURM) 24th-25th November 2006, New Delhi DELHI DEVELOPMENT

SLUMS IN DELHI ISSUES AND POLICY PERSPECTIVES SEMINAR ON URBAN GOVERNANCE IN THE CONTEXT OF JAWAHARLAL NEHRU NATIONAL URBAN RENEWAL MISSION (JNNURM) 24th-25th November 2006, New Delhi DELHI DEVELOPMENT

IAG Conference Accounting Update Emerging issues in the public sector 20 November 2014 Michael Crowe Yannick Maurice

www.pwc.com.au IAG Conference Accounting Update Emerging issues in the public sector 20 November 2014 Michael Crowe Yannick Maurice Agenda Introduction Key topics o Fair value o PPP Projects Refinancing

www.pwc.com.au IAG Conference Accounting Update Emerging issues in the public sector 20 November 2014 Michael Crowe Yannick Maurice Agenda Introduction Key topics o Fair value o PPP Projects Refinancing

17 CFR Ch. II ( Edition)

") 229.1110 trustee s removal, replacement or resignation, as well as how the expenses associated with changing from one trustee to another trustee will be paid. Instruction to Item 1109. If multiple trustees

229.1110 trustee s removal, replacement or resignation, as well as how the expenses associated with changing from one trustee to another trustee will be paid. Instruction to Item 1109. If multiple trustees

Ex-Ante Evaluation (for Japanese ODA Loan)

") Ex-Ante Evaluation (for Japanese ODA Loan) 1. Project name Country: Republic of the Union of Myanmar (Myanmar) Project name: Housing Finance Development Project L/A signing date: March 29, 2018 Approved

Ex-Ante Evaluation (for Japanese ODA Loan) 1. Project name Country: Republic of the Union of Myanmar (Myanmar) Project name: Housing Finance Development Project L/A signing date: March 29, 2018 Approved

Tamil Nadu Slum Clearance Board was established in September and has been implementing various Housing, Slum Development and

HOUSING AND URBAN DEVELOPMENT DEPARTMENT DEMAND NO. 26 POLICY NOTE 2015-2016 2. TAMIL NADU SLUM CLEARANCE BOARD Tamil Nadu Slum Clearance Board was established in September 1970 and has been implementing

HOUSING AND URBAN DEVELOPMENT DEPARTMENT DEMAND NO. 26 POLICY NOTE 2015-2016 2. TAMIL NADU SLUM CLEARANCE BOARD Tamil Nadu Slum Clearance Board was established in September 1970 and has been implementing

DELHI DEVELOPMENT AUTHORITY HOUSING DEPARTMENT (LIG) CIRCULAR

CIRCULAR") DELHI DEVELOPMENT AUTHORITY HOUSING DEPARTMENT (LIG) Dated: 17.01.2019 CIRCULAR LAUNCHING DATE AND TIME: 18.01.2019 AT 15.00 HRS Subject:- Launching of Online Running Scheme for disposal of old inventory

DELHI DEVELOPMENT AUTHORITY HOUSING DEPARTMENT (LIG) Dated: 17.01.2019 CIRCULAR LAUNCHING DATE AND TIME: 18.01.2019 AT 15.00 HRS Subject:- Launching of Online Running Scheme for disposal of old inventory

Presenter: Jennifer Oomen Associate Director, Center For Innovation In Shelter & Finance Habitat for Humanity International

Breakout Session 1: SCALING UP HOUSING MICROFINANCE: Global Best Practices from the Field Presenter: Jennifer Oomen Associate Director, Center For Innovation In Shelter & Finance Habitat for Humanity International

Breakout Session 1: SCALING UP HOUSING MICROFINANCE: Global Best Practices from the Field Presenter: Jennifer Oomen Associate Director, Center For Innovation In Shelter & Finance Habitat for Humanity International

c) Contact persons in the organisation d) Name of Directors/ Promoters alongwith the names of the key individuals in the controlling group

Contact persons in the organisation d) Name of Directors/ Promoters alongwith the names of the key individuals in the controlling group") PNBHF - 358 PROFORMA FOR CALLING INFORMATION FROM PRIVATE BUILDERS AND CORPORATE BODIES 1 Preliminary Information a) Name and address of the applicant undertaking the project with Tel.No. b) Constitution/Status

PNBHF - 358 PROFORMA FOR CALLING INFORMATION FROM PRIVATE BUILDERS AND CORPORATE BODIES 1 Preliminary Information a) Name and address of the applicant undertaking the project with Tel.No. b) Constitution/Status

Affordable Housing in India*

Affordable Housing in India* Rapid urbanisation and migration to cities have caused severe urban housing shortages in India, particularly for the economically weaker sections. In this context, the Government

Affordable Housing in India* Rapid urbanisation and migration to cities have caused severe urban housing shortages in India, particularly for the economically weaker sections. In this context, the Government

07 AFFORDABLE GREEN BUILDING HOUSING EXTENT OF PROBLEM CONFUSION OVER DEFINITION KEY GOVERNMENT INITIATIVES

AFFORDABLE HOUSING EXTENT OF PROBLEM As per Government estimates, the total housing shortage in the urban areas, at the beginning of the 11 th Plan period was around 24.71 million units (see fig 1) and

AFFORDABLE HOUSING EXTENT OF PROBLEM As per Government estimates, the total housing shortage in the urban areas, at the beginning of the 11 th Plan period was around 24.71 million units (see fig 1) and

MADE EASY WEST BENGAL CO-OPERATIVE SOCIETIES LAW

MADE EASY WEST BENGAL CO-OPERATIVE SOCIETIES LAW 1. What Act and Rules are applicable in this law? The West Bengal Co-operative Societies (Amendment) Act, 2011 as well as Rules, 2011 are applicable relating

MADE EASY WEST BENGAL CO-OPERATIVE SOCIETIES LAW 1. What Act and Rules are applicable in this law? The West Bengal Co-operative Societies (Amendment) Act, 2011 as well as Rules, 2011 are applicable relating

EXTRAORDINARY PUBLISHED BY AUTHORITY. No. 1241, CUTTACK, SATURDAY, AUGUST 22, 2015/ SRAVAN 31, 1937

EXTRAORDINARY PUBLISHED BY AUTHORITY No. 1241, CUTTACK, SATURDAY, AUGUST 22, 2015/ SRAVAN 31, 1937 [No. 20719 HUD-HU-SCH-0002-2015/HUD.] HOUSING & URBAN DEVELOPMENT DEPARTMENT RESOLUTION The 14th August,

EXTRAORDINARY PUBLISHED BY AUTHORITY No. 1241, CUTTACK, SATURDAY, AUGUST 22, 2015/ SRAVAN 31, 1937 [No. 20719 HUD-HU-SCH-0002-2015/HUD.] HOUSING & URBAN DEVELOPMENT DEPARTMENT RESOLUTION The 14th August,

DELHI DEVELOPMENT AUTHORITY OFFICE OF PR.COMMISSIONER(H,LD&CWG)

") 1 DELHI DEVELOPMENT AUTHORITY OFFICE OF PR.COMMISSIONER(H,LD&CWG) Sub: Draft Slum Rehabilitation Policy based on Mumbai s Slum Rehabilitation Policy One of the major challenges that face DDA is to handle

1 DELHI DEVELOPMENT AUTHORITY OFFICE OF PR.COMMISSIONER(H,LD&CWG) Sub: Draft Slum Rehabilitation Policy based on Mumbai s Slum Rehabilitation Policy One of the major challenges that face DDA is to handle

ROLE OF SOUTH AFRICAN GOVERNMENT IN SOCIAL HOUSING. Section 26 of the Constitution enshrines the right to housing as follows:

1 ROLE OF SOUTH AFRICAN GOVERNMENT IN SOCIAL HOUSING Constitution Section 26 of the Constitution enshrines the right to housing as follows: Everyone has the right to have access to adequate housing The

1 ROLE OF SOUTH AFRICAN GOVERNMENT IN SOCIAL HOUSING Constitution Section 26 of the Constitution enshrines the right to housing as follows: Everyone has the right to have access to adequate housing The

JHARKHAND AFFORDABLE URBAN HOUSING POLICY. Resolution

Jharkhand Affordable Urban Housing Policy - 2016 Government of Jharkhand Department of Urban Development & Housing Resolution Resolution No. - 2135 Ranchi, Dated-18/04/2016 Subject: Affordable Urban Housing

Jharkhand Affordable Urban Housing Policy - 2016 Government of Jharkhand Department of Urban Development & Housing Resolution Resolution No. - 2135 Ranchi, Dated-18/04/2016 Subject: Affordable Urban Housing

RHLF WORKSHOP The National Housing Code

RHLF WORKSHOP The National Housing Code Outline 1. Statutory requirements 2. Background- why a new Code 3. The structure of the new Code 4. National Housing Programmes 5. National Housing Programmes under

RHLF WORKSHOP The National Housing Code Outline 1. Statutory requirements 2. Background- why a new Code 3. The structure of the new Code 4. National Housing Programmes 5. National Housing Programmes under

Affordable housing in India: Case of Mumbai. Arnab Jana May 18, 2017

Affordable housing in India: Case of Mumbai Arnab Jana May 18, 2017 Introduction to housing in India Housing is a critical sector in Indian economy. It is directly linked to the construction sector that

Affordable housing in India: Case of Mumbai Arnab Jana May 18, 2017 Introduction to housing in India Housing is a critical sector in Indian economy. It is directly linked to the construction sector that

City of St. Petersburg, Florida Consolidated Plan. Priority Needs

City of St. Petersburg, Florida 2000-2005 Consolidated Plan Priority Needs Permanent supportive housing and services for homeless and special needs populations. The Pinellas County Continuum of Care 2000

City of St. Petersburg, Florida 2000-2005 Consolidated Plan Priority Needs Permanent supportive housing and services for homeless and special needs populations. The Pinellas County Continuum of Care 2000

UN-HABITAT: Philippines - Overview of the Current Housing Rights Situation and Related Activities

UN-HABITAT: Philippines - Overview of the Current Housing Rights Situation and Related Activities 1) Background and normative/institutional framework for the promotion and protection of housing rights:

UN-HABITAT: Philippines - Overview of the Current Housing Rights Situation and Related Activities 1) Background and normative/institutional framework for the promotion and protection of housing rights:

Terms of Reference for the Regional Housing Affordability Strategy

Terms of Reference for the Regional Housing Affordability Strategy Prepared by: CRD Regional Planning Services September, 2001 Purpose The Capital Region is one of the most expensive housing markets in

Terms of Reference for the Regional Housing Affordability Strategy Prepared by: CRD Regional Planning Services September, 2001 Purpose The Capital Region is one of the most expensive housing markets in

India: Capacity Building for Commercial Bank Lending for Solar Energy Projects

Completion Report Project Number: 44475-012 Technical Assistance Number: 7802 July 2015 India: Capacity Building for Commercial Bank Lending for Solar Energy Projects This document is being disclosed to

Completion Report Project Number: 44475-012 Technical Assistance Number: 7802 July 2015 India: Capacity Building for Commercial Bank Lending for Solar Energy Projects This document is being disclosed to

AFFORDABEL HOUSING FOR ALL

Raj Pal, Principal Adviser, National Housing Bank AFFORDABEL HOUSING FOR ALL There are three basic needs of human being, i.e. food, clothing and shelter. Right from the mankind evolved, he has been struggling

Raj Pal, Principal Adviser, National Housing Bank AFFORDABEL HOUSING FOR ALL There are three basic needs of human being, i.e. food, clothing and shelter. Right from the mankind evolved, he has been struggling

City of Johannesburg Approach

DEVELOPMENT OF AN APPROACH FOR THE RECOGNITION OF INFORMAL SETTLEMENTS AND TENURE IN SOUTH AFRICA WITH THE POTENTIAL FOR REGIONAL APPLICABILITY City of Johannesburg Approach December 2009 Recognition of

DEVELOPMENT OF AN APPROACH FOR THE RECOGNITION OF INFORMAL SETTLEMENTS AND TENURE IN SOUTH AFRICA WITH THE POTENTIAL FOR REGIONAL APPLICABILITY City of Johannesburg Approach December 2009 Recognition of

Tennessee Basic Principles of Real Estate and New Affiliates 90 Hour Course Outline

Tennessee Basic Principles of Real Estate and New Affiliates 90 Hour Course Outline Basic Principles of Real Estate I. The Real Estate Business Describe real estate activities Identify real estate professions

Tennessee Basic Principles of Real Estate and New Affiliates 90 Hour Course Outline Basic Principles of Real Estate I. The Real Estate Business Describe real estate activities Identify real estate professions

Rent Policy. Approved on: 9 December 2010 Board of Management Consolidated November 2015

Rent Policy Approved on: 9 December 2010 Board of Management Consolidated November 2015 BIELD HOUSING ASSOCIATION LIMITED Registered Office: 79 Hopetoun Street, Edinburgh EH7 4QF Scottish Charity No SC006878

Rent Policy Approved on: 9 December 2010 Board of Management Consolidated November 2015 BIELD HOUSING ASSOCIATION LIMITED Registered Office: 79 Hopetoun Street, Edinburgh EH7 4QF Scottish Charity No SC006878

Growing Housing Opportunities in Africa

Growing Housing Opportunities in Africa Encouraging Investment Growing the Market Simon Walley Housing Finance Program Coordinator World Bank October 9, 2012 Content 1. Affordable Housing A Global Opportunity

Growing Housing Opportunities in Africa Encouraging Investment Growing the Market Simon Walley Housing Finance Program Coordinator World Bank October 9, 2012 Content 1. Affordable Housing A Global Opportunity

Summary of Sustainable Financing of Housing Public Hearings November 2012

Summary of Sustainable Financing of Housing Public Hearings November 2012 For an Equitable Sharing of National Revenue 10 December 2012 Financial and Fiscal Commission Montrose Place (2nd Floor), Bekker

Summary of Sustainable Financing of Housing Public Hearings November 2012 For an Equitable Sharing of National Revenue 10 December 2012 Financial and Fiscal Commission Montrose Place (2nd Floor), Bekker

HOUSING FINANCE RE-EXAMINING THE SOLUTIONS TO HOUSING FINANCE. SUMMIT 3rd EDITION 18 TH SEPTEMBER 2018 SAHARA STAR, MUMBAI

HOUSING FINANCE SUMMIT 3rd EDITION 18 TH SEPTEMBER 2018 SAHARA STAR, MUMBAI RE-EXAMINING THE SOLUTIONS TO HOUSING FINANCE OVERVIEW Food, Clothing & Shelter the three major requirements of human being and

HOUSING FINANCE SUMMIT 3rd EDITION 18 TH SEPTEMBER 2018 SAHARA STAR, MUMBAI RE-EXAMINING THE SOLUTIONS TO HOUSING FINANCE OVERVIEW Food, Clothing & Shelter the three major requirements of human being and

PROJECT INITIATION DOCUMENT

Project Name: Housing Futures Phase Two Project Sponsor: Steve Hampson Project Manager: Denise Lewis Date Issued: 15 February 2008 Version No: 1 Background: At Full Council on 31 January 2008 the following

Project Name: Housing Futures Phase Two Project Sponsor: Steve Hampson Project Manager: Denise Lewis Date Issued: 15 February 2008 Version No: 1 Background: At Full Council on 31 January 2008 the following

Interagency Appraisal and

Interagency Appraisal and Evaluation (IAEG) Workshop Purpose (77456) Supersedes the 1994 Interagency Appraisal & Evaluation Guidelines Address supervisory matters relating to real estate appraisal and

Interagency Appraisal and Evaluation (IAEG) Workshop Purpose (77456) Supersedes the 1994 Interagency Appraisal & Evaluation Guidelines Address supervisory matters relating to real estate appraisal and

ASHOKA: HOUSING FOR ALL Building Affordable Housing Communities. MANIKANDAN KP November 2013 TERI

ASHOKA: HOUSING FOR ALL Building Affordable Housing Communities MANIKANDAN KP November 2013 TERI Ashoka Global Association of Leading Social Entrepreneurs Three Decade Old ; Sector & Regional Agnostic

ASHOKA: HOUSING FOR ALL Building Affordable Housing Communities MANIKANDAN KP November 2013 TERI Ashoka Global Association of Leading Social Entrepreneurs Three Decade Old ; Sector & Regional Agnostic

Flexible tenure. 1 Global Innovation assessment - Human Cities Coalition

Flexible tenure Decision making process: Explore to develop new mechanisms to better integrate community needs into existing city development/housing plans, in particular plans around development of new

Flexible tenure Decision making process: Explore to develop new mechanisms to better integrate community needs into existing city development/housing plans, in particular plans around development of new

COUNTY GOVERNMENT OF LAMU Department of Land, Physical Planning, Infrastructure & Urban Development

1 COUNTY GOVERNMENT OF LAMU Department of Land, Physical Planning, Infrastructure & Urban Development TERMS OF REFERENCE FOR OUTSOURCING OF CONSULTANCY SERVICES FOR SURVEY & REGULARIZATION OF KATSAIKAIKAIRU

1 COUNTY GOVERNMENT OF LAMU Department of Land, Physical Planning, Infrastructure & Urban Development TERMS OF REFERENCE FOR OUTSOURCING OF CONSULTANCY SERVICES FOR SURVEY & REGULARIZATION OF KATSAIKAIKAIRU

R E Q U E S T F O R P R O P O S A L S

P.O. Box 3209, Houghton, 2041 Block A, Riviera Office Park, 6-10 Riviera Road, Riviera R E Q U E S T F O R P R O P O S A L S M A R K E T S U R V E Y T O I N F O R M R E S I D E N T I A L H O U S I N G

P.O. Box 3209, Houghton, 2041 Block A, Riviera Office Park, 6-10 Riviera Road, Riviera R E Q U E S T F O R P R O P O S A L S M A R K E T S U R V E Y T O I N F O R M R E S I D E N T I A L H O U S I N G

Commercial Real Estate Debt Finance This course is presented in London on: 26 February 2018, 29 November 2018

Commercial Real Estate Debt Finance This course is presented in London on: 26 February 2018, 29 November 2018 The Banking and Corporate Finance Training Specialist Course Objectives Participants will:

Commercial Real Estate Debt Finance This course is presented in London on: 26 February 2018, 29 November 2018 The Banking and Corporate Finance Training Specialist Course Objectives Participants will:

Housing for All by 2022: A Big Opportunity in the Making

Harshad Borawake, Head of Research, Equity Mirae Asset Global Investments (India) MIRAE ASSET LENS Executive Summary India s urban population has grown five-fold in the last halfcentury to approximately

Harshad Borawake, Head of Research, Equity Mirae Asset Global Investments (India) MIRAE ASSET LENS Executive Summary India s urban population has grown five-fold in the last halfcentury to approximately

Localism and the future of affordable home ownership. Cornwall Council. Louise Dwelly Strategic Affordable Housing Manager

Localism and the future of affordable home ownership Cornwall Council Louise Dwelly Strategic Affordable Housing Manager Service context in Cornwall Team based within Planning Service 18 staff including

Localism and the future of affordable home ownership Cornwall Council Louise Dwelly Strategic Affordable Housing Manager Service context in Cornwall Team based within Planning Service 18 staff including

Minimum Educational Requirements

Minimum Educational Requirements (MER) For all persons elected to practice in each Member Association With effect from 1 January 2011 1 Introduction 1.1 The European Group of Valuers Associations (TEGoVA)

Minimum Educational Requirements (MER) For all persons elected to practice in each Member Association With effect from 1 January 2011 1 Introduction 1.1 The European Group of Valuers Associations (TEGoVA)

Presented by: K.Vidyadhar AMD MEPMA

Status of RAY in Andhra Pradesh: Issues and Challenges Presented by: K.Vidyadhar AMD MEPMA SLUM PROFILE OF ANDHRA PRADESH No. of ULBs - 173 Total Urban Population (2001 census) - 208.08 Lakhs Urban Population

Status of RAY in Andhra Pradesh: Issues and Challenges Presented by: K.Vidyadhar AMD MEPMA SLUM PROFILE OF ANDHRA PRADESH No. of ULBs - 173 Total Urban Population (2001 census) - 208.08 Lakhs Urban Population

Exposure Draft. Accounting Standard (AS) 40 Investment Property. Last date for the comments: November 10, 2018

40 Investment Property. Last date for the comments: November 10, 2018") Exposure Draft Accounting Standard (AS) 40 Investment Property Last date for the comments: November 10, 2018 Issued by Accounting Standards Board The Institute of Chartered Accountants of India 1 Exposure

Exposure Draft Accounting Standard (AS) 40 Investment Property Last date for the comments: November 10, 2018 Issued by Accounting Standards Board The Institute of Chartered Accountants of India 1 Exposure

Strengthening Property Rights in Pursuit of Poverty Reduction: Commentary on the 2010 Lesotho Land Reform Project

Strengthening Property Rights in Pursuit of Poverty Reduction: Commentary on the 2010 Lesotho Land Reform Project Resetselemang Clement Leduka Department of Geographical & Environmental Sciences National

Strengthening Property Rights in Pursuit of Poverty Reduction: Commentary on the 2010 Lesotho Land Reform Project Resetselemang Clement Leduka Department of Geographical & Environmental Sciences National

LOW-COST LAND INFORMATION SYSTEM FOR SUSTAINABLE URBAN DEVELOPMENT

Presented at the FIG Congress 2018, May 6-11, 2018 in Istanbul, Turkey LOW-COST LAND INFORMATION SYSTEM FOR SUSTAINABLE URBAN DEVELOPMENT Case Examples in Kenya and Zambia Presented by John Gitau Land

Presented at the FIG Congress 2018, May 6-11, 2018 in Istanbul, Turkey LOW-COST LAND INFORMATION SYSTEM FOR SUSTAINABLE URBAN DEVELOPMENT Case Examples in Kenya and Zambia Presented by John Gitau Land

Hkkjr es a vkokl dh izo`fùk,oa izxfr lecu/kh fjiksvz] twu] 2003

![Hkkjr es a vkokl dh izo`fùk,oa izxfr lecu/kh fjiksvz] twu] 2003](/thumbs/89/99586555.jpg "Hkkjr es a vkokl dh izo`fùk,oa izxfr lecu/kh fjiksvz] twu] 2003") Hkkjr es a vkokl dh izo`fùk,oa izxfr lecu/kh fjiksvz] twu] 2003 Report on Trend and Progress of Housing in India, June 2003 CHAPTER VIII RECENT DEVELOPMENTS Securitization is a tested market oriented resource

Hkkjr es a vkokl dh izo`fùk,oa izxfr lecu/kh fjiksvz] twu] 2003 Report on Trend and Progress of Housing in India, June 2003 CHAPTER VIII RECENT DEVELOPMENTS Securitization is a tested market oriented resource

Course Descriptions Real Estate and the Built Environment

CMGT REAL XRCM Construction Management Courses Real Estate Courses Executive Master Online Courses CMGT 4110 PreConstruction Integration & Planning CMGT 4120 Construction Planning & Scheduling This course

CMGT REAL XRCM Construction Management Courses Real Estate Courses Executive Master Online Courses CMGT 4110 PreConstruction Integration & Planning CMGT 4120 Construction Planning & Scheduling This course

Ind AS 115 Impact on the real estate sector and construction companies

01 Ind AS 115 Impact on the real estate sector and construction companies This article aims to: Highlight key areas of impact of Ind AS 115 on the real estate sector and construction companies. Summary

01 Ind AS 115 Impact on the real estate sector and construction companies This article aims to: Highlight key areas of impact of Ind AS 115 on the real estate sector and construction companies. Summary

Land Administration Projects Currently there are more than 70 land administration projects being implemented Many donors involved, including NGOs Thes

Governance in Land Administration: Conceptual Framework Tony Burns and Kate Dalrymple Land Equity International FIG Working Week Stockholm, Sweden June 16-19, 2008 Rationale for better LA Secure land tenure

Governance in Land Administration: Conceptual Framework Tony Burns and Kate Dalrymple Land Equity International FIG Working Week Stockholm, Sweden June 16-19, 2008 Rationale for better LA Secure land tenure

GLTN Tools and Approaches in Support of Land Policy Implementation in Africa

GLTN Tools and Approaches in Support of Land Policy Implementation in Africa Jamal Browne (UN-Habitat), Jaap Zevenbergen (ITC), Danilo Antonio (UN-Habitat), Solomon Haile (UN-Habitat) Land Policy Development

GLTN Tools and Approaches in Support of Land Policy Implementation in Africa Jamal Browne (UN-Habitat), Jaap Zevenbergen (ITC), Danilo Antonio (UN-Habitat), Solomon Haile (UN-Habitat) Land Policy Development

Standard Information / Document Request List. Application for the Authority s Consent to the Merger of MPF Schemes

The applicant should note that a person who in any document given to the Authority makes a statement that the person knows to be false or misleading in a material respect, or recklessly makes a statement

The applicant should note that a person who in any document given to the Authority makes a statement that the person knows to be false or misleading in a material respect, or recklessly makes a statement

Evaluating the award of Certificates of Right of Occupancy in urban Tanzania

Evaluating the award of Certificates of Right of Occupancy in urban Tanzania Jonathan Conning 1 Klaus Deininger 2 Justin Sandefur 3 Andrew Zeitlin 3 1 Hunter College and CUNY 2 DECRG, World Bank 3 Centre

Evaluating the award of Certificates of Right of Occupancy in urban Tanzania Jonathan Conning 1 Klaus Deininger 2 Justin Sandefur 3 Andrew Zeitlin 3 1 Hunter College and CUNY 2 DECRG, World Bank 3 Centre

SUMMARY LAND ACQUISITION PLAN. Supplementary Appendix to the. Report and Recommendation of the President to the Board of Directors.

SUMMARY LAND ACQUISITION PLAN Supplementary Appendix to the Report and Recommendation of the President to the Board of Directors on the RURAL ROADS SECTOR I PROJECT in INDIA Ministry of Rural Development

SUMMARY LAND ACQUISITION PLAN Supplementary Appendix to the Report and Recommendation of the President to the Board of Directors on the RURAL ROADS SECTOR I PROJECT in INDIA Ministry of Rural Development

SOCIAL HOUSING THE WAY FORWARD

Social Housing Policy - The implementation process Kobus van Wyk, NMMU CONTENTS 1. BACKGROUND AND INTRODUCTION 2.WHAT THE POLICY SET OUT TO ACHIEVE 3.HOW IT HAD TO BE ACHIEVED AND BY WHO 4.IMPLEMENTING

Social Housing Policy - The implementation process Kobus van Wyk, NMMU CONTENTS 1. BACKGROUND AND INTRODUCTION 2.WHAT THE POLICY SET OUT TO ACHIEVE 3.HOW IT HAD TO BE ACHIEVED AND BY WHO 4.IMPLEMENTING

P r o c e d u r e F o r V e n d o r R e g i s t r a t i o n

P r o c e d u r e F o r V e n d o r R e g i s t r a t i o n Procedure for Vendor Registration: (A) Process for the New Vendor registration / addition of item / Shifting of premises / Name Change Application

P r o c e d u r e F o r V e n d o r R e g i s t r a t i o n Procedure for Vendor Registration: (A) Process for the New Vendor registration / addition of item / Shifting of premises / Name Change Application

CRISIL s criteria for rating debt backed by lease rentals of commercial real estate properties. May 2018

CRISIL s criteria for rating debt backed by lease rentals of commercial real estate properties May 2018 Criteria contacts Somasekhar Vemuri Senior Director Rating Criteria and Product Development Email:

CRISIL s criteria for rating debt backed by lease rentals of commercial real estate properties May 2018 Criteria contacts Somasekhar Vemuri Senior Director Rating Criteria and Product Development Email:

CMC Firm. An ICMCI Project STANDARD DOCUMENTATION

CMC Firm An ICMCI Project STANDARD DOCUMENTATION Table of Contents 1. Introduction... 1 2. Benefits of the CMC Firm scheme... 1 3. How to become a CMC Firm... 3 4. List of CMC Firms... 4 5. Business Model...

CMC Firm An ICMCI Project STANDARD DOCUMENTATION Table of Contents 1. Introduction... 1 2. Benefits of the CMC Firm scheme... 1 3. How to become a CMC Firm... 3 4. List of CMC Firms... 4 5. Business Model...

Subject. Date: 2016/10/25. Originator s file: CD.06.AFF. Chair and Members of Planning and Development Committee

Date: 2016/10/25 Originator s file: To: Chair and Members of Planning and Development Committee CD.06.AFF From: Edward R. Sajecki, Commissioner of Planning and Building Meeting date: 2016/11/14 Subject

Date: 2016/10/25 Originator s file: To: Chair and Members of Planning and Development Committee CD.06.AFF From: Edward R. Sajecki, Commissioner of Planning and Building Meeting date: 2016/11/14 Subject

Social Housing at the Crossroads: Possibilities for Investment, Provision and Cost Rental

ACKNOWLEDGEMENTS vii Social Housing at the Crossroads: Possibilities for Investment, Provision and Cost Rental Executive Summary No. 138 June 2014 ix Executive Summary x Ireland s approach to social housing

ACKNOWLEDGEMENTS vii Social Housing at the Crossroads: Possibilities for Investment, Provision and Cost Rental Executive Summary No. 138 June 2014 ix Executive Summary x Ireland s approach to social housing

Implementing Innovative Land Tenure Tools In East-Africa: SWOT-Analysis Of Land Governance

Presented at the FIG Working Week 2017, May 29 - June 2, 2017 in Helsinki, Finland Implementing Innovative Land Tenure Tools In East-Africa: SWOT-Analysis Of Land Governance Ine BUNTINX, Joep CROMPVOETS,

Presented at the FIG Working Week 2017, May 29 - June 2, 2017 in Helsinki, Finland Implementing Innovative Land Tenure Tools In East-Africa: SWOT-Analysis Of Land Governance Ine BUNTINX, Joep CROMPVOETS,

Community Housing Federation of Victoria Inclusionary Zoning Position and Capability Statement

Community Housing Federation of Victoria Inclusionary Zoning Position and Capability Statement December 2015 Introduction The Community Housing Federation of Victoria (CHFV) strongly supports the development

Community Housing Federation of Victoria Inclusionary Zoning Position and Capability Statement December 2015 Introduction The Community Housing Federation of Victoria (CHFV) strongly supports the development

The introduction of the LHA cap to the social rented sector: impact on young people in Scotland

The introduction of the LHA cap to the social rented sector: impact on young people in Scotland Brought to you by the Chartered Institute of Housing Executive Summary About the research This research was

The introduction of the LHA cap to the social rented sector: impact on young people in Scotland Brought to you by the Chartered Institute of Housing Executive Summary About the research This research was

NSW Affordable Housing Guidelines. August 2012

August 2012 NSW AFFORDABLE HOUSING GUIDELINES TABLE OF CONTENTS 1.0 INTRODUCTION... 1 2.0 DEFINITION OF KEY TERMS... 1 3.0 APPLICATION OF GUIDELINES... 2 4.0 PRINCIPLES... 2 4.1 Relationships and partnerships...

August 2012 NSW AFFORDABLE HOUSING GUIDELINES TABLE OF CONTENTS 1.0 INTRODUCTION... 1 2.0 DEFINITION OF KEY TERMS... 1 3.0 APPLICATION OF GUIDELINES... 2 4.0 PRINCIPLES... 2 4.1 Relationships and partnerships...

TABLE OF CONTENTS. CHAPTER I Preliminary Short Title and Commencement... 3 Power to make rules and procedures... 3 Definitions...

Regulations for Functioning of Central Registry in Bhutan, 2013 TABLE OF CONTENTS CHAPTER I Preliminary Short Title and Commencement... 3 Power to make rules and procedures... 3 Definitions... 3 CHAPTER

Regulations for Functioning of Central Registry in Bhutan, 2013 TABLE OF CONTENTS CHAPTER I Preliminary Short Title and Commencement... 3 Power to make rules and procedures... 3 Definitions... 3 CHAPTER

REAL ESTATE IN INDIA 2017

Now Available REAL ESTATE IN INDIA 2017 Segment Analysis, Outlook and Opportunities Report (PDF) Data-set (Excel) India Infrastructure Research Real Estate in India 2017 Table of Contents SECTION I: MARKET

Now Available REAL ESTATE IN INDIA 2017 Segment Analysis, Outlook and Opportunities Report (PDF) Data-set (Excel) India Infrastructure Research Real Estate in India 2017 Table of Contents SECTION I: MARKET

LAND REFORM IN MALAWI

LAND REFORM IN MALAWI Presented at the Annual Meeting for FIG Commission 7 In Pretoria, South Africa, Held From 4 th 8 th November, 2002 by Daniel O. C. Gondwe 1.0 BACKGROUND Malawi is a landlocked country

LAND REFORM IN MALAWI Presented at the Annual Meeting for FIG Commission 7 In Pretoria, South Africa, Held From 4 th 8 th November, 2002 by Daniel O. C. Gondwe 1.0 BACKGROUND Malawi is a landlocked country

Connecticut Housing Finance Authority

Connecticut Housing Finance Authority Multifamily Rental Housing Program Guideline 2018 This Guideline is Effective Table of Contents I. Preface... 4 II. Background... 4 III. Pre-Application... 4 IV. Application

Connecticut Housing Finance Authority Multifamily Rental Housing Program Guideline 2018 This Guideline is Effective Table of Contents I. Preface... 4 II. Background... 4 III. Pre-Application... 4 IV. Application

Housing Reset :: Creative Advisory Accelerating Non-Profit / City Partnerships What We Heard

Final Version Date: Feb 8, 2017 Housing Reset :: Creative Advisory Accelerating Non-Profit / City Partnerships What We Heard Purpose This Creative Advisory was formed as part of the Housing Reset to generate

Final Version Date: Feb 8, 2017 Housing Reset :: Creative Advisory Accelerating Non-Profit / City Partnerships What We Heard Purpose This Creative Advisory was formed as part of the Housing Reset to generate

Fannie Mae Update. July 30, AI Annual Conference Fannie Mae.

Fannie Mae Update July 30, 2018 Disclaimer While every effort has been made to ensure the reliability of the session content, Fannie Mae s Selling and Servicing Guides and their updates, including Guide

Fannie Mae Update July 30, 2018 Disclaimer While every effort has been made to ensure the reliability of the session content, Fannie Mae s Selling and Servicing Guides and their updates, including Guide

Equal Credit Opportunity Act (ECOA) Valuations Rule

Valuations Rule") OCTOBER 3, 2013 Equal Credit Opportunity Act (ECOA) Valuations Rule SMALL ENTITY COMPLIANCE GUIDE The Bureau recently finalized changes to this rule. The October 2013 Final Rule amends the final rule published

OCTOBER 3, 2013 Equal Credit Opportunity Act (ECOA) Valuations Rule SMALL ENTITY COMPLIANCE GUIDE The Bureau recently finalized changes to this rule. The October 2013 Final Rule amends the final rule published

UK Housing Awards 2011

UK Housing Awards 2011 Excellence in Housing Finance and Development: Winner Rettie & Co, Springfield Properties and DCHA: Resonance at Moray Apartments, Edinburgh Summary In this climate of constrained

UK Housing Awards 2011 Excellence in Housing Finance and Development: Winner Rettie & Co, Springfield Properties and DCHA: Resonance at Moray Apartments, Edinburgh Summary In this climate of constrained

EMPANELMENT OF PROFESSIONAL REAL ESTATE CONSULTANTS TO ADVISE LIC OF INDIA ON VARIOUS REAL ESTATE MATTERS.

Estates and Office Services Department LIC of India, South Central Zonal Office Jeevan Bhagya, Saifabad HYDERABAD 500063 E-mail id: scz_estates@licindia.com EMPANELMENT OF PROFESSIONAL REAL ESTATE CONSULTANTS

Estates and Office Services Department LIC of India, South Central Zonal Office Jeevan Bhagya, Saifabad HYDERABAD 500063 E-mail id: scz_estates@licindia.com EMPANELMENT OF PROFESSIONAL REAL ESTATE CONSULTANTS

Findings: City of Johannesburg

Findings: City of Johannesburg What s inside High-level Market Overview Housing Performance Index Affordability and the Housing Gap Leveraging Equity Understanding Housing Markets in Johannesburg, South

Findings: City of Johannesburg What s inside High-level Market Overview Housing Performance Index Affordability and the Housing Gap Leveraging Equity Understanding Housing Markets in Johannesburg, South

Cork Planning Authorities Joint Housing Strategy. Managers Joint Report on the submissions received and issues raised.

Joint Housing Strategy Managers Joint Report on the submissions received and issues raised. June 2013 Introduction This is a joint report which reviews the submissions received during the public consultation

Joint Housing Strategy Managers Joint Report on the submissions received and issues raised. June 2013 Introduction This is a joint report which reviews the submissions received during the public consultation

SLUM UPGRADATION. By Kanchan Joneja, Sonal Takkar, Sukriti Thukral

SLUM UPGRADATION By Kanchan Joneja, Sonal Takkar, Sukriti Thukral WHAT IS SLUM UPGRADING Slum upgrading is a process through which informal areas are gradually improved, formalised and incorporated into

SLUM UPGRADATION By Kanchan Joneja, Sonal Takkar, Sukriti Thukral WHAT IS SLUM UPGRADING Slum upgrading is a process through which informal areas are gradually improved, formalised and incorporated into

Participants of the Ministerial Meeting on Housing and Land Management on 8 October 2013 in Geneva

Summary At its meeting on 2 April 2012, the Bureau of the Committee on Housing and Land Management of the United Nations Economic Commission for Europe agreed on the need for a Strategy for Sustainable

Summary At its meeting on 2 April 2012, the Bureau of the Committee on Housing and Land Management of the United Nations Economic Commission for Europe agreed on the need for a Strategy for Sustainable

MINNEAPOLIS SMALL AND MEDIUM MULTIFAMILY ACQUISITION LOAN PROGRAM GUIDELINES (SMMF Pilot)

") I. PURPOSE OF PROGRAM MINNEAPOLIS SMALL AND MEDIUM MULTIFAMILY ACQUISITION LOAN PROGRAM GUIDELINES (SMMF Pilot) The SMMF Pilot loan program is designed to be a pilot partnership between the Land Bank Twin

I. PURPOSE OF PROGRAM MINNEAPOLIS SMALL AND MEDIUM MULTIFAMILY ACQUISITION LOAN PROGRAM GUIDELINES (SMMF Pilot) The SMMF Pilot loan program is designed to be a pilot partnership between the Land Bank Twin

South African Council for Town and Regional Planners

TARIFF OF FEES South African Council for Town and Regional Planners PLEASE NOTE : THE TARIFF OF FEES WAS APPROVED BY THE COUNCIL CHAPTER 10 : TARIFF OF FEES 10.1 INTRODUCTION 10.1.1 General This tariff

TARIFF OF FEES South African Council for Town and Regional Planners PLEASE NOTE : THE TARIFF OF FEES WAS APPROVED BY THE COUNCIL CHAPTER 10 : TARIFF OF FEES 10.1 INTRODUCTION 10.1.1 General This tariff

Implementing Agency Department of Housing, Ministry of Local Government, Urban Development, Housing and Environment

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized PROJECT INFORMATION DOCUMENT (PID) IDENTIFICATION/CONCEPT STAGE Report No.: PIDC56649

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized PROJECT INFORMATION DOCUMENT (PID) IDENTIFICATION/CONCEPT STAGE Report No.: PIDC56649

Discussion paper RSLs and homelessness in Scotland

Discussion paper RSLs and homelessness in Scotland From the Shelter policy library April 2009 www.shelter.org.uk 2009 Shelter. All rights reserved. This document is only for your personal, non-commercial

Discussion paper RSLs and homelessness in Scotland From the Shelter policy library April 2009 www.shelter.org.uk 2009 Shelter. All rights reserved. This document is only for your personal, non-commercial

CONTENTS. List of tables 9 List of figures 11 Glossary of abbreviations 13 Preface and acknowledgements 15 1 INTRODUCTION...19

CONTENTS List of tables 9 List of figures 11 Glossary of abbreviations 13 Preface and acknowledgements 15 1 INTRODUCTION...19 1.1 Research scope and purpose...19 1.1.1 The cases...20 1.1.2 The period of

CONTENTS List of tables 9 List of figures 11 Glossary of abbreviations 13 Preface and acknowledgements 15 1 INTRODUCTION...19 1.1 Research scope and purpose...19 1.1.1 The cases...20 1.1.2 The period of

GM Global Techies Town

GM Global Techies Town Current Grading: Bangalore 5 Star out of 7 Star (Reaffirmed in May 2018) Earlier Grading: Bangalore 5 Star out of 7 Star (Assigned in February 2017) Valid till May 3, 2019 Project

GM Global Techies Town Current Grading: Bangalore 5 Star out of 7 Star (Reaffirmed in May 2018) Earlier Grading: Bangalore 5 Star out of 7 Star (Assigned in February 2017) Valid till May 3, 2019 Project

City of Brandon Brownfield Strategy

City of Brandon Brownfield Strategy 2017 Executive Summary A brownfield is a property, the expansion, redevelopment, or reuse of which may be complicated by the presence or potential presence of a hazardous

City of Brandon Brownfield Strategy 2017 Executive Summary A brownfield is a property, the expansion, redevelopment, or reuse of which may be complicated by the presence or potential presence of a hazardous

HAVEBURY HOUSING PARTNERSHIP

HS0025 HAVEBURY HOUSING PARTNERSHIP POLICY HOME PURCHASE POLICY Controlling Authority Director of Resources Policy Number HS025 Issue No. 3 Status Final Date November 2013 Review date November 2016 Equality

HS0025 HAVEBURY HOUSING PARTNERSHIP POLICY HOME PURCHASE POLICY Controlling Authority Director of Resources Policy Number HS025 Issue No. 3 Status Final Date November 2013 Review date November 2016 Equality

ENABLING AFFORDABLE HOUSING IN LOCAL GOVERNMENT AREAS. Discussion Paper COMMONEQUITY.COM.AU

ENABLING AFFORDABLE HOUSING IN LOCAL GOVERNMENT AREAS Discussion Paper COMMONEQUITY.COM.AU ENABLING AFFORDABLE HOUSING IN LOCAL GOVERNMENT AREAS Discussion Paper 42 Initiatives to facilitate affordable

ENABLING AFFORDABLE HOUSING IN LOCAL GOVERNMENT AREAS Discussion Paper COMMONEQUITY.COM.AU ENABLING AFFORDABLE HOUSING IN LOCAL GOVERNMENT AREAS Discussion Paper 42 Initiatives to facilitate affordable

The post-2005 period has seen in India intensive discussions on the alternative approaches to addressing issues of slums and affordable housing.

The post-2005 period has seen in India intensive discussions on the alternative approaches to addressing issues of slums and affordable housing. Discussions have involved a cross-section of experts including

The post-2005 period has seen in India intensive discussions on the alternative approaches to addressing issues of slums and affordable housing. Discussions have involved a cross-section of experts including

CHAUTAUQUA COUNTY LAND BANK CORPORATION

EXHIBIT H CHAUTAUQUA COUNTY LAND BANK CORPORATION LAND ACQUISITION AND DISPOSITION POLICIES AND PRIORITIES November 14, 2012 *This document is intended to provide guidance to the Chautauqua County Land

EXHIBIT H CHAUTAUQUA COUNTY LAND BANK CORPORATION LAND ACQUISITION AND DISPOSITION POLICIES AND PRIORITIES November 14, 2012 *This document is intended to provide guidance to the Chautauqua County Land

Land Tools for Tenure Security for All

Land Tools for Tenure Security for All PROF. JAAP ZEVENBERGEN UNIVERSITY OF TWENTE - ITC 1 ST JUNE 2017 HELSINKI, FINLAND GLOBAL LAND CHALLENGES 70 % Dealing with the affordability issue - how to modernize

Land Tools for Tenure Security for All PROF. JAAP ZEVENBERGEN UNIVERSITY OF TWENTE - ITC 1 ST JUNE 2017 HELSINKI, FINLAND GLOBAL LAND CHALLENGES 70 % Dealing with the affordability issue - how to modernize

BUSINESS PLAN Part 1

BUSINESS PLAN 2016-17 Part 1 Contents Executive Summary... 1 Objectives... 2 Company Formation... 3 Governance and Management Structure... 4 Decision Making... 6 Operational Management... 7 Market Overview...

BUSINESS PLAN 2016-17 Part 1 Contents Executive Summary... 1 Objectives... 2 Company Formation... 3 Governance and Management Structure... 4 Decision Making... 6 Operational Management... 7 Market Overview...