A New Look at Ratios Using Reformulated Numbers

|

|

|

- Domenic Lyons

- 5 years ago

- Views:

Transcription

1 A New Look at Ratios Using Reformulated Numbers Dr. Ron Lazer Session Topics Review Reformulation of Financial Statements: Reformulated Ratios and Decomposition Eample: Panera Bread FSA Reformulated Ratios 1

2 FSA Reformulated Ratios 2

3 Reformulated Statements of Stockholders FSA Reformulated Ratios 3

4 The Standard Balance Sheet The Typical Reformulated Balance Sheet FSA Reformulated Ratios 4

5 The Standard Income Statement The Reformulated Income Statement FSA Reformulated Ratios 5

6 The Reformulated Income Statement (cont.) Traditional ROA Return on Assets Definition of ROA: Net Profit ROA = AverageTotal Assets Net Profit = Net Income + Interest Epense (1 Ta rate) + Minority Interest in Earnings Decomposing ROA: Net Profit Sales ROA = Sales Assets ROA= Profit Margin * Assets Turnover FSA Reformulated Ratios 6

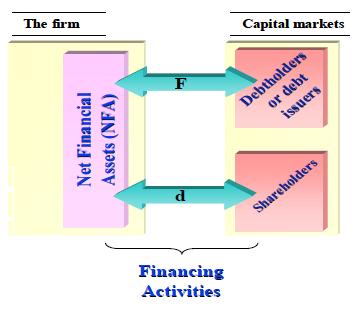

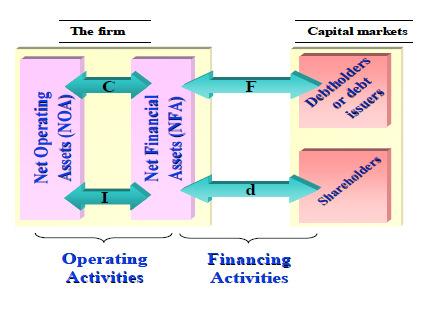

7 Problems with Traditional ROA Intermingles Financing and Operating Net Income is not Comprehensive Financial Assets are in denominator Operating Liabilities are not in denominator Return on Net Operating Assets This is the return on operating activities: (not affected by firm s level of debt, i.e. financing decisions): Net Operating Profit After Ta (NOPAT) Return on Net Operating Assets (RNOA) = Average Net Operating Assets (NOA) This is how much the firm pays for debt (financing) Net Non-operating Epense Percentage: NNEP = Net Non - Operating Epenses (NNE) Average Net Non Operating Obligations () Ron Lazer FSA Reformulated Ratios 7

8 ROA vs. RNOA Total Assets vs. NOA (Financial Assets (FA) ecluded from NOA, Operating Liabilities (OL) included) Numerator: NI adjusted for Interest vs. NOPAT RNOA usually > ROA, because NOA < Total Assets RNOA = NOPM NOAT margin effect turnover effect where NOPM = NOPAT/Sales and NOAT = Sales/NOA Value of RNOA Framework Company Comparison Benefits Changes in company s accounting over time Adjustments easy to eecute and understand impact on profitability, growth and leverage Accounting Quality Benefits Effects of manipulations that alter numerator NOPAT will have predictable and value relevant impact on denominator NOA FSA Reformulated Ratios 8

9 Value of RNOA Framework Valuation Benefits Forecasting focused on value relevant items DCF can be streamlined when scenario has path for profitability and growth Risk Analysis Benefits Useful for adjusting for off-bs items Useful when understanding a firm s coverage, solvency and liquidity ratios Traditional ROE Return on We can decompose ROE into several components: ROE = NI Sales Sales Assets Assets ROE = NI Margin * Asset Turnover * Total Leverage FSA Reformulated Ratios 9

10 Traditional ROE Problems with Decomposition The basic ROE model doesn t separate the impact of operating decisions from the impact of financing decisions on ROE. There is a tradeoff between Total Leverage and Net Operating Margin higher leverage (debt) higher interest payments lower net profit margins Hard to determine the impact of increase in leverage on ROE ROCE Reformulated ROCE = Net Income + OCI NOPAT - NNE ROCE = ROCE = ROCE = ROCE = NOPAT NOPAT NOA NOPAT NOA NNE NOA NNE + NNE Ron Lazer FSA Reformulated Ratios 10

11 ROCE Reformulated (cont.) ROCE = ROCE = ROCE = NOPAT NOA NOPAT NOA NOPAT NOA + (1 + + ) NOPAT NOA NNE NNE NNE ROCE = RNOA + RNOAFin Lev NNEPFin Lev ROCE = RNOA + (RNOA - NNEP) FLEV ROCE = RNOA + Spread FLEV Ron Lazer ROCE vs. RNOA ROCE can be restated as: RNOA + FLEV * (RNOA-NNEP) Is Financial Leverage helping or hurting a firm? Difference between RNOA and NNEP determines ROCE FSA Reformulated Ratios 11

12 The Case of Microsoft (2003) The Case of Microsoft (2003) Cont. How will the analysis change if Microsoft paid Dividends of $33B (as it did in 2004 ) FSA Reformulated Ratios 12

13 What s net? Further Profitability Analysis FSA Reformulated Ratios 13

14 Identifying Problem Company Names Best Buy FedE Caterpillar Abbot Laboratories NOPM NOAT 13.83% % % % 6.83 Panera Bread Co. FSA Reformulated Ratios 14

15 Appendi: Reformulation Terminology Appendi: Reformulation Terminology FSA Reformulated Ratios 15

Based on current ratio calculations for all companies, which company is more liquid? a. Company 1 b. Company 2 c. Company 3 d.

Chapter 5 Financial Accounting, 5 th Edition by Dyckman, Hanlon, Magee, & Pfeiffer Solutions to Practice Quiz Topic: Liquidity Ratios 1. Selected balance sheet and income statement information is presented

Chapter 5 Financial Accounting, 5 th Edition by Dyckman, Hanlon, Magee, & Pfeiffer Solutions to Practice Quiz Topic: Liquidity Ratios 1. Selected balance sheet and income statement information is presented

Tenant: Law Firm 4 NAICS: Primary Industry: Offices of lawyers

Tenant: Law Firm 4 NAICS: 541110 Primary Industry: Offices of lawyers Date: 05.25.17 Table of Contents Law Firm 4 132 Main Street TABLE OF CONTENTS TIL Score Executive Summary Tenant Score Information

Tenant: Law Firm 4 NAICS: 541110 Primary Industry: Offices of lawyers Date: 05.25.17 Table of Contents Law Firm 4 132 Main Street TABLE OF CONTENTS TIL Score Executive Summary Tenant Score Information

Gateway NACM Credit Conference Presented by: Curtis Litchfield, CCE September 20, 2018

Gateway NACM Credit Conference Presented by: Curtis Litchfield, CCE September 20, 2018 Who Receives and Analyzes Financial Statements? Why do you request them? What information are you trying to determine?

Gateway NACM Credit Conference Presented by: Curtis Litchfield, CCE September 20, 2018 Who Receives and Analyzes Financial Statements? Why do you request them? What information are you trying to determine?

Broker. Investment Real Estate. Chapter 15. Copyright Gold Coast Schools 1

Broker Chapter 15 Investment Real Estate Copyright Gold Coast Schools 1 Learning Objectives Matching an investor with the right property Evaluating the sites and improvements of income properties Determining

Broker Chapter 15 Investment Real Estate Copyright Gold Coast Schools 1 Learning Objectives Matching an investor with the right property Evaluating the sites and improvements of income properties Determining

CHAPTER 18 Lease Financing and Business Valuation

Copyright 2008 by the Foundation of the American College of Healthcare Executives 6/13/07 Version 18-1 CHAPTER 18 Lease Financing and Business Valuation Lease financing Leasing basics Analysis by the lessee

Copyright 2008 by the Foundation of the American College of Healthcare Executives 6/13/07 Version 18-1 CHAPTER 18 Lease Financing and Business Valuation Lease financing Leasing basics Analysis by the lessee

An Examination of Potential Changes in Ratio Measurements Historical Cost versus Fair Value Measurement in Valuing Tangible Operational Assets

An Examination of Potential Changes in Ratio Measurements Historical Cost versus Fair Value Measurement in Valuing Tangible Operational Assets Pamela Smith Baker Texas Woman s University A fictitious property

An Examination of Potential Changes in Ratio Measurements Historical Cost versus Fair Value Measurement in Valuing Tangible Operational Assets Pamela Smith Baker Texas Woman s University A fictitious property

FASB/IASB LEASE ACCOUNTING IMPACT

FASB/IASB LEASE ACCOUNTING IMPACT PREPARED BY: DAN DOKOVIC ddokovic@intelicacre.com 15455 CONWAY ROAD ST. LOUIS, MO 63017 314.270.5991 INTELICACRE.COM 2012 Intelica CRE. All Rights Reserved. No part of

FASB/IASB LEASE ACCOUNTING IMPACT PREPARED BY: DAN DOKOVIC ddokovic@intelicacre.com 15455 CONWAY ROAD ST. LOUIS, MO 63017 314.270.5991 INTELICACRE.COM 2012 Intelica CRE. All Rights Reserved. No part of

Intermediate Accounting

Intermediate Accounting 11-1 Prepared by Coby Harmon University of California, Santa Barbara 11 Depreciation, Impairments, and Depletion Intermediate Accounting 14th Edition 11-2 Kieso, Weygandt, and Warfield

Intermediate Accounting 11-1 Prepared by Coby Harmon University of California, Santa Barbara 11 Depreciation, Impairments, and Depletion Intermediate Accounting 14th Edition 11-2 Kieso, Weygandt, and Warfield

Project Economics: The Value of Leasing. Russell Banham, Savills

ICSC European Retail Property School Project Economics: The Value of Leasing Russell Banham, Savills (Investment, Development & Asset Management) Introduction Who I am Russell Banham Over 30 years of experience

ICSC European Retail Property School Project Economics: The Value of Leasing Russell Banham, Savills (Investment, Development & Asset Management) Introduction Who I am Russell Banham Over 30 years of experience

Chapter 18. Investors have different required yields Different risk assessment Different opportunity cost of equity

Decision Making in Real Estate Centers Around Valuation Chapter 18 Investment Decisions: Ratios We examined the concept of market value in Chapters 7 & 8 As noted, professional RE appraisers are often

Decision Making in Real Estate Centers Around Valuation Chapter 18 Investment Decisions: Ratios We examined the concept of market value in Chapters 7 & 8 As noted, professional RE appraisers are often

Valbridge Valuation Advisory

Valbridge Valuation Advisory Re: Attn: Multi-Family Property Taxes Lenders and Purchasers Cash is king, and property taxes can kill the cash flow of a multi-family property. What does that mean to you?

Valbridge Valuation Advisory Re: Attn: Multi-Family Property Taxes Lenders and Purchasers Cash is king, and property taxes can kill the cash flow of a multi-family property. What does that mean to you?

Cap Rate Trends, Methodology and Analysis. Dane R. Anderson MAI, CCIM Appraisal & Litigation Services Director

Cap Rate Trends, Methodology and Analysis Dane R. Anderson MAI, CCIM Appraisal & Litigation Services Director 1 Quickly The Income Approach Basis of the Approach Present worth of future benefits Two Methods:

Cap Rate Trends, Methodology and Analysis Dane R. Anderson MAI, CCIM Appraisal & Litigation Services Director 1 Quickly The Income Approach Basis of the Approach Present worth of future benefits Two Methods:

THE ART OF BUSINESS VALUATION

BUSINESS VALUATIONS GROWING THE ART OF BUSINESS VALUATION Douglas A. Michel, CPA/ABV, CVA & Alex E. Kummer, CPA, CVA, Clark Schaefer Hackett THE VALUE OF YOUR BUSINESS Steve Lumley, LGI CFO BUY SELL AGREEMENTS

BUSINESS VALUATIONS GROWING THE ART OF BUSINESS VALUATION Douglas A. Michel, CPA/ABV, CVA & Alex E. Kummer, CPA, CVA, Clark Schaefer Hackett THE VALUE OF YOUR BUSINESS Steve Lumley, LGI CFO BUY SELL AGREEMENTS

Financial Modeling Workshop Using Excel

Financial Modeling Workshop Using Excel Page 1 of 11 Why Attend Financial modeling is crucial for taking investment decisions that can have a huge financial impact on companies. By attending this course,

Financial Modeling Workshop Using Excel Page 1 of 11 Why Attend Financial modeling is crucial for taking investment decisions that can have a huge financial impact on companies. By attending this course,

Financial Analysis Workshop. Contents are subject to change. For the latest updates visit

Financial Analysis Workshop Page 1 of 11 Why Attend In today s world, finance professionals are challenged with providing management a detailed analysis of the impact of the organization's financial decisions.

Financial Analysis Workshop Page 1 of 11 Why Attend In today s world, finance professionals are challenged with providing management a detailed analysis of the impact of the organization's financial decisions.

CFA Level 1. Financial Reporting and Analysis. Non-current Liabilities

CFA Level 1 Financial Reporting and Analysis Non-current Liabilities 2011, Associate Professor Ole Sørensen, Ph.d. Side 1 Coupon Bonds Promises two types of payments: periodic interest payments and a lumpsum

CFA Level 1 Financial Reporting and Analysis Non-current Liabilities 2011, Associate Professor Ole Sørensen, Ph.d. Side 1 Coupon Bonds Promises two types of payments: periodic interest payments and a lumpsum

Broker. Basic Business Appraisal. Chapter 9. Copyright Gold Coast Schools 1

Broker Chapter 9 Basic Business Appraisal 1 Learning Objectives Describe the characteristics of the legal entities a business appraiser may encounter List at least 5 reasons for a business appraisal List

Broker Chapter 9 Basic Business Appraisal 1 Learning Objectives Describe the characteristics of the legal entities a business appraiser may encounter List at least 5 reasons for a business appraisal List

UNDERSTANDING THE DEVELOPMENT PRO FORMA

UNDERSTANDING THE DEVELOPMENT PRO FORMA March 16, 2017 ULI Urban Leadership Program Dr. Steven Webber Ryerson University/Urbanformation Consulting Pro forma Financial analysis based on Revenues Costs Return

UNDERSTANDING THE DEVELOPMENT PRO FORMA March 16, 2017 ULI Urban Leadership Program Dr. Steven Webber Ryerson University/Urbanformation Consulting Pro forma Financial analysis based on Revenues Costs Return

Credit Risk. Thinkstock. 42 May 2013 The RMA Journal Copyright 2013 by RMA

CR Credit Risk Thinkstock 42 May 2013 The RMA Journal Copyright 2013 by RMA Pitfalls in Conventional Earnings-Based DSCR Measures and a Recommended Alternative BY DAVID ANDRUKONIS, CRC FOR LENDERS, a significant

CR Credit Risk Thinkstock 42 May 2013 The RMA Journal Copyright 2013 by RMA Pitfalls in Conventional Earnings-Based DSCR Measures and a Recommended Alternative BY DAVID ANDRUKONIS, CRC FOR LENDERS, a significant

Preface Who Should Read This Book 3 Organization and Content 4 Acknowledgments 5 Contacting the Author 5 About the Author 6

Preface.................................................................... 3 Who Should Read This Book 3 Organization and Content 4 Acknowledgments 5 Contacting the Author 5 About the Author 6...........................................................

Preface.................................................................... 3 Who Should Read This Book 3 Organization and Content 4 Acknowledgments 5 Contacting the Author 5 About the Author 6...........................................................

DELTA AIR LINES, INC. URL Location: ations/annual_report_proxy_statement/

Name:Tze-Yun Chen ID: 650743660 Section C: 8-9:50 am Accy 517-Imhoff Spring 2010 DELTA AIR LINES, INC. URL Location: http://www.delta.com/about_delta/investor_rel ations/annual_report_proxy_statement/

Name:Tze-Yun Chen ID: 650743660 Section C: 8-9:50 am Accy 517-Imhoff Spring 2010 DELTA AIR LINES, INC. URL Location: http://www.delta.com/about_delta/investor_rel ations/annual_report_proxy_statement/

FSA Faculty Consortium Technical Accounting Update. Bob Uhl, partner, Deloitte & Touche LLP

FSA Faculty Consortium Technical Accounting Update Bob Uhl, partner, Deloitte & Touche LLP Deloitte University May 30, 2014 Acronyms Acronym ASC ASU ED FASB IASB IFRS U.S. GAAP Full Form Accounting Standards

FSA Faculty Consortium Technical Accounting Update Bob Uhl, partner, Deloitte & Touche LLP Deloitte University May 30, 2014 Acronyms Acronym ASC ASU ED FASB IASB IFRS U.S. GAAP Full Form Accounting Standards

Sales Associate Course

Sales Associate Course Chapter Seventeen Real Estate Investments and Business Opportunity Brokerage 1 Investment Analysis Most important consideration: Economic soundness Land use controls Zoning Deed

Sales Associate Course Chapter Seventeen Real Estate Investments and Business Opportunity Brokerage 1 Investment Analysis Most important consideration: Economic soundness Land use controls Zoning Deed

Definitions. CPI is a lease in which base rent is adjusted based on changes in a consumer price index.

Annualized Rental Income is rental revenue under our leases on Operating Properties on a straight-line basis, which includes the effect of rent escalations and any tenant concessions, such as free rent,

Annualized Rental Income is rental revenue under our leases on Operating Properties on a straight-line basis, which includes the effect of rent escalations and any tenant concessions, such as free rent,

ESOP Feasibility and Valuation Basics

ESOP Feasibility and Valuation Basics Ohio Employee Ownership Center Akron/Fairlawn Hilton Fairlawn, Ohio April 21, 2006 Richard A. Schlueter rschlueter@comstockvaluation.com C VA 1 Levee Way, Suite 3109

ESOP Feasibility and Valuation Basics Ohio Employee Ownership Center Akron/Fairlawn Hilton Fairlawn, Ohio April 21, 2006 Richard A. Schlueter rschlueter@comstockvaluation.com C VA 1 Levee Way, Suite 3109

NON-GAAP FINANCIAL MEASURES

NON-GAAP FINANCIAL MEASURES Welltower Inc. (HCN) believes that revenues, net operating income from continuing operations (NOICO), net income and net income attributable to common stockholders (NICS), as

NON-GAAP FINANCIAL MEASURES Welltower Inc. (HCN) believes that revenues, net operating income from continuing operations (NOICO), net income and net income attributable to common stockholders (NICS), as

Part 1. Estimating Land Value Using a Land Residual Technique Based on Discounted Cash Flow Analysis

Table of Contents Overview... v Seminar Schedule... ix SECTION 1 Part 1. Estimating Land Value Using a Land Residual Technique Based on Discounted Cash Flow Analysis Preview Part 1... 1 Land Residual Technique...

Table of Contents Overview... v Seminar Schedule... ix SECTION 1 Part 1. Estimating Land Value Using a Land Residual Technique Based on Discounted Cash Flow Analysis Preview Part 1... 1 Land Residual Technique...

Investor Presentation. First Quarter 2015

Investor Presentation First Quarter 2015 1 CAUTIONARY STATEMENTS Today s session and our answers to questions contain statements that constitute forward-looking statements about expected future events

Investor Presentation First Quarter 2015 1 CAUTIONARY STATEMENTS Today s session and our answers to questions contain statements that constitute forward-looking statements about expected future events

BUSINESS VALUATIONS: FUNDAMENTALS, TECHNIQUES AND THEORY (FT&T) CHAPTER 6

CHAPTER 6") Fundamentals, Techniques & Theory COMMONLY USED METHODS OF VALUATION BUSINESS VALUATIONS: FUNDAMENTALS, TECHNIQUES AND THEORY (FT&T) CHAPTER 6 REVIEW QUESTIONS 1995 2013 by National Association of Certified

Fundamentals, Techniques & Theory COMMONLY USED METHODS OF VALUATION BUSINESS VALUATIONS: FUNDAMENTALS, TECHNIQUES AND THEORY (FT&T) CHAPTER 6 REVIEW QUESTIONS 1995 2013 by National Association of Certified

Project Direction Presentation June SBM Offshore All rights reserved.

Project Direction Presentation June 2013 Disclaimer Some of the statements contained in this presentation that are not historical facts are statements of future expectations and other forward-looking statements

Project Direction Presentation June 2013 Disclaimer Some of the statements contained in this presentation that are not historical facts are statements of future expectations and other forward-looking statements

Preface Table of Contents Chapter 1: Overview of the Liquor Store Industry... 13

Preface.................................................................... 3 Who Should Read This Book 3 Organization and Content 4 Chapter 4: Liquor Store Business Valuation 4 Acknowledgments 5 Contacting

Preface.................................................................... 3 Who Should Read This Book 3 Organization and Content 4 Chapter 4: Liquor Store Business Valuation 4 Acknowledgments 5 Contacting

Governance and Finance: How do they go together? Margaret Lund, Consultant Courtney Berner, UW Center for Cooperatives November 9, 2017

Governance and Finance: How do they go together? Margaret Lund, Consultant Courtney Berner, UW Center for Cooperatives November 9, 2017 Overview of session Role of the board of directors What financial

Governance and Finance: How do they go together? Margaret Lund, Consultant Courtney Berner, UW Center for Cooperatives November 9, 2017 Overview of session Role of the board of directors What financial

Georgia Tech Financial Analysis Lab 800 West Peachtree Street NW Atlanta, GA

800 West Peachtree Street NW Atlanta, GA 30308-0520 404-894 - 4395 http://www.scheller.gatech.edu/finlab Dr. Charles W. Mulford, Director Invesco Chair and Professor of Accounting charles.mulford@scheller.gatech.edu

800 West Peachtree Street NW Atlanta, GA 30308-0520 404-894 - 4395 http://www.scheller.gatech.edu/finlab Dr. Charles W. Mulford, Director Invesco Chair and Professor of Accounting charles.mulford@scheller.gatech.edu

Sector Scorecard. Proposed indicators for measuring efficiency within the sector have been developed for the following areas:

Registered Providers Working Group on Efficiency Sector Scorecard Proposed indicators for measuring efficiency within the sector have been developed for the following areas: A. Business Health B. Development

Registered Providers Working Group on Efficiency Sector Scorecard Proposed indicators for measuring efficiency within the sector have been developed for the following areas: A. Business Health B. Development

Sekisui House, Ltd. First Quarter of FY2018 (February 1, 2018 through April 30, 2018) Summary of Consolidated Financial Results

Summary of Consolidated Financial Results") Sekisui House, Ltd. First Quarter of (February 1, 2018 through April 30, 2018) Summary of Consolidated Financial 1. Overview 2. Financial Position 3. Segment Information Built to Order Supplied Housing

Sekisui House, Ltd. First Quarter of (February 1, 2018 through April 30, 2018) Summary of Consolidated Financial 1. Overview 2. Financial Position 3. Segment Information Built to Order Supplied Housing

IFRS 16 Leases consequences on the financial statements and financial indicators

Audit financiar, XV, Nr. Marian 1(145)/20, SĂCĂRIN 114-122 ISSN: 1583-5812; ISSN on-line: 1844-8801 IFRS 16 Leases consequences on the financial statements and financial indicators Abstract In January

Audit financiar, XV, Nr. Marian 1(145)/20, SĂCĂRIN 114-122 ISSN: 1583-5812; ISSN on-line: 1844-8801 IFRS 16 Leases consequences on the financial statements and financial indicators Abstract In January

Professional Certification Programs

Professional Certification Programs Participants in NDC training, including staff members of Housing and Economic Development Networks, State and Local Governments, Community Development Banks and Charitable

Professional Certification Programs Participants in NDC training, including staff members of Housing and Economic Development Networks, State and Local Governments, Community Development Banks and Charitable

Sekisui House, Ltd. Second Quarter of FY2017 (February 1, 2017 through July 31, 2017) Summary of Consolidated Financial Results. Management Direction

Summary of Consolidated Financial Results. Management Direction") Sekisui House, Ltd. Second Quarter of (February 1, 2017 through July 31, 2017) Summary of Consolidated Financial 1. Overview 2. Financial Position 3. Segment Information Built to Order Supplied Housing

Sekisui House, Ltd. Second Quarter of (February 1, 2017 through July 31, 2017) Summary of Consolidated Financial 1. Overview 2. Financial Position 3. Segment Information Built to Order Supplied Housing

PELLISSIPPI STATE TECHNICAL COMMUNITY COLLEGE MASTER SYLLABUS INCOME PROPERTY VALUATION REA 1950

PELLISSIPPI STATE TECHNICAL COMMUNITY COLLEGE MASTER SYLLABUS INCOME PROPERTY VALUATION REA 1950 Class Hours: 3.0 Credit Hours: 3.0 Laboratory Hours: 0.0 Date Revised: Fall 05 NOTE: This course is not

PELLISSIPPI STATE TECHNICAL COMMUNITY COLLEGE MASTER SYLLABUS INCOME PROPERTY VALUATION REA 1950 Class Hours: 3.0 Credit Hours: 3.0 Laboratory Hours: 0.0 Date Revised: Fall 05 NOTE: This course is not

Atwater ave Fiscal Year Beginning January 2019

10-Year After Tax Cash Flow Analysis INITIAL INVESTMENT Purchase Price + Acquisition Costs - 1st Mortgage + Total Loan Fees and Points Initial Investment $949900 $9499 $474950 $4750 $489198 MORTGAGE DATA

10-Year After Tax Cash Flow Analysis INITIAL INVESTMENT Purchase Price + Acquisition Costs - 1st Mortgage + Total Loan Fees and Points Initial Investment $949900 $9499 $474950 $4750 $489198 MORTGAGE DATA

Lease Accounting and Loan Covenants: What is the Impact?

Lease Accounting and Loan Covenants: What is the Impact? Monday June 26, 2017 9:15 AM 10:30 AM Presented by: Charlie Shannon Partner Moss Adams LLP 8750 N. Central Expressway, Suite 300 Dallas, TX 75231

Lease Accounting and Loan Covenants: What is the Impact? Monday June 26, 2017 9:15 AM 10:30 AM Presented by: Charlie Shannon Partner Moss Adams LLP 8750 N. Central Expressway, Suite 300 Dallas, TX 75231

CENTURY PROPERTIES GROUP, INC. Analysts Presentation: FY 2013 Results April 2014

CENTURY PROPERTIES GROUP, INC. Analysts Presentation: FY 2013 Results April 2014 IMPORTANT NOTICE AND DISCLAIMER These materials have been prepared by Century Properties Group Inc. (together with its subsidiaries,

CENTURY PROPERTIES GROUP, INC. Analysts Presentation: FY 2013 Results April 2014 IMPORTANT NOTICE AND DISCLAIMER These materials have been prepared by Century Properties Group Inc. (together with its subsidiaries,

Real Estate Finance and Development Syllabus

Real Estate Finance and Development Syllabus Course Description This course will provide participants with a general understanding of real estate finance and development with an emphasis on housing development

Real Estate Finance and Development Syllabus Course Description This course will provide participants with a general understanding of real estate finance and development with an emphasis on housing development

Investor Presentation December 2017

Investor Presentation December 2017 Cautionary Statement This presentation includes statements concerning our expectations, beliefs, plans, objectives, goals, strategies, future events or performance and

Investor Presentation December 2017 Cautionary Statement This presentation includes statements concerning our expectations, beliefs, plans, objectives, goals, strategies, future events or performance and

Residual Valuations & Development Appraisals

Residual Valuations & Development Appraisals Speaker: Richard Johnson Presentation to the SCSI 28 th May 2015 Savills 33 Molesworth Street, Dublin 2 T: +353 (0) 1 618 1344 E: richard.johnson@savills.ie

Residual Valuations & Development Appraisals Speaker: Richard Johnson Presentation to the SCSI 28 th May 2015 Savills 33 Molesworth Street, Dublin 2 T: +353 (0) 1 618 1344 E: richard.johnson@savills.ie

Statement of Cash Flows

CA BUSINESS SCHOOL EXECUTIVE DIPLOMA IN BUSINESS AND ACCOUNTING SEMESTER 1 : Preparation of Financial Statements Statement of Cash Flows M B G Wimalarathna (FCA, FCMA, MCIM, FMAAT, MCPM)(MBA PIM/USJ) Introduction

CA BUSINESS SCHOOL EXECUTIVE DIPLOMA IN BUSINESS AND ACCOUNTING SEMESTER 1 : Preparation of Financial Statements Statement of Cash Flows M B G Wimalarathna (FCA, FCMA, MCIM, FMAAT, MCPM)(MBA PIM/USJ) Introduction

Real Estate & REIT Modeling: Course Outline

Real Estate & REIT Modeling: Course Outline Click Here to Sign Up Now for the BIWS Real Estate & REIT Modeling Course The topics in Real Estate & REIT Modeling teach you everything you need to know about

Real Estate & REIT Modeling: Course Outline Click Here to Sign Up Now for the BIWS Real Estate & REIT Modeling Course The topics in Real Estate & REIT Modeling teach you everything you need to know about

AZRIELI GROUP. Conference Call Presentation. Financial Statements March 31, 2016

AZRIELI GROUP Conference Call Presentation Financial Statements March 31, 2016 Disclaimer The information included in this presentation is a summary only and does not exhaust all of the information on

AZRIELI GROUP Conference Call Presentation Financial Statements March 31, 2016 Disclaimer The information included in this presentation is a summary only and does not exhaust all of the information on

Project Finance Ratios Tutorial February 2017

Project Finance Ratios Tutorial February 2017 1.0 General Pease note the following guidance and instruction is to be used as an accompaniment to the Project Finance Ratios Excel file. Please feel free

Project Finance Ratios Tutorial February 2017 1.0 General Pease note the following guidance and instruction is to be used as an accompaniment to the Project Finance Ratios Excel file. Please feel free

Power Analy$I$ Maximizing Inve$tment Return$ With Your Computer

Power Analy$I$ Maximizing Inve$tment Return$ With Your Computer New Version 10.0 Developed by: James F. Little, MBA, CCIM www.1031.com JamesFLittle@MSN.com Introduction New Version 10.0 The following screen

Power Analy$I$ Maximizing Inve$tment Return$ With Your Computer New Version 10.0 Developed by: James F. Little, MBA, CCIM www.1031.com JamesFLittle@MSN.com Introduction New Version 10.0 The following screen

Deal Analyzer for Rentals

for Rentals Preview Of What You Will Learn Sections: Introduction... 6 Section 1: Inputs... 10 Section 2: Core Numbers... 13 Section 3: First-Year Operating Projection... 15 Section 4: Five-Year Operating

for Rentals Preview Of What You Will Learn Sections: Introduction... 6 Section 1: Inputs... 10 Section 2: Core Numbers... 13 Section 3: First-Year Operating Projection... 15 Section 4: Five-Year Operating

THE ELUSIVE CAP RATE Finding & Supporting Cap Rates in Uncertain Times

THE ELUSIVE CAP RATE Finding & Supporting Cap Rates in Uncertain Times Presented May 14, 2013 at the New Hampshire Association of Assessing Officers in Concord, NH by Peter F. Korpacz, MAI, CRE, FRICS

THE ELUSIVE CAP RATE Finding & Supporting Cap Rates in Uncertain Times Presented May 14, 2013 at the New Hampshire Association of Assessing Officers in Concord, NH by Peter F. Korpacz, MAI, CRE, FRICS

Lease accounting 2019 IFRS and US GAAP Preparing for a smooth landing

Lease accounting 2019 IFRS and US GAAP Preparing for a smooth landing What s next? Q4 2017 Summary As you may already be aware, the accounting standards for lease accounting will change. This means that

Lease accounting 2019 IFRS and US GAAP Preparing for a smooth landing What s next? Q4 2017 Summary As you may already be aware, the accounting standards for lease accounting will change. This means that

Business Valuation More Art Than Science

Business Valuation More Art Than Science One of the more difficult aspects of business planning is business valuation. It is also one of the more important aspects. While owners of closely held businesses

Business Valuation More Art Than Science One of the more difficult aspects of business planning is business valuation. It is also one of the more important aspects. While owners of closely held businesses

Syllabus. PRINCIPLES OF BUSINESS VALUATION Bachelor level

Coordinator: Svetlana A. Grigorieva Syllabus PRINCIPLES OF BUSINESS VALUATION Bachelor level Lecturers: Svetlana A. Grigorieva, Elvina R. Bayburina, Edgars Ragels (E&Y), Alexander E. Skorniakov (E&Y),

Coordinator: Svetlana A. Grigorieva Syllabus PRINCIPLES OF BUSINESS VALUATION Bachelor level Lecturers: Svetlana A. Grigorieva, Elvina R. Bayburina, Edgars Ragels (E&Y), Alexander E. Skorniakov (E&Y),

BUSI 452 Case Studies in Appraisal II

BUSI 452 Case Studies in Appraisal II PURPOSE AND SCOPE The Case Studies in Appraisal II course (BUSI 452) is a continuation of BUSI 442. This course is intended to introduce further practical applications

BUSI 452 Case Studies in Appraisal II PURPOSE AND SCOPE The Case Studies in Appraisal II course (BUSI 452) is a continuation of BUSI 442. This course is intended to introduce further practical applications

SAUL CENTERS, INC Wisconsin Avenue, Suite 1500, Bethesda, Maryland (301)

") SAUL CENTERS, INC. 7501 Wisconsin Avenue, Suite 1500, Bethesda, Maryland 20814-6522 (301) 986-6200 October 29, 2015, Bethesda, MD. Saul Centers, Inc. Reports Third Quarter 2015 Earnings Saul Centers, Inc.

SAUL CENTERS, INC. 7501 Wisconsin Avenue, Suite 1500, Bethesda, Maryland 20814-6522 (301) 986-6200 October 29, 2015, Bethesda, MD. Saul Centers, Inc. Reports Third Quarter 2015 Earnings Saul Centers, Inc.

Real Estate Funds. 22 nd June Presented by : Mr. Harish Gagwani Sr. Investment Manager. CA. Rajeev Saraogi Investment Manager

Real Estate Funds Cracking Intrinsic " Value in Housing 22 nd June 2012 Presented by : Mr. Harish Gagwani Sr. Investment Manager CA. Rajeev Saraogi Investment Manager 1 Index Index Page No. How Private

Real Estate Funds Cracking Intrinsic " Value in Housing 22 nd June 2012 Presented by : Mr. Harish Gagwani Sr. Investment Manager CA. Rajeev Saraogi Investment Manager 1 Index Index Page No. How Private

PROJECT FINANCE & APPRAISAL Translating the Value of Regenerative Design into Real Estate Speak. Matt Macko Environmental Building Strategies

PROJECT FINANCE & APPRAISAL Translating the Value of Regenerative Design into Real Estate Speak Matt Macko Environmental Building Strategies The Developer Role Understand your client! How a developer thinks

PROJECT FINANCE & APPRAISAL Translating the Value of Regenerative Design into Real Estate Speak Matt Macko Environmental Building Strategies The Developer Role Understand your client! How a developer thinks

The Financial Accounting Standards Board

V A L U A T I O N How the New Leases Standard May Impact Business Valuations By Judith H. O Dell, CPA, CVA The Financial Accounting Standards Board issued the 485 page Leases Standard (Topic 842) in February,

V A L U A T I O N How the New Leases Standard May Impact Business Valuations By Judith H. O Dell, CPA, CVA The Financial Accounting Standards Board issued the 485 page Leases Standard (Topic 842) in February,

Cockpit Statistics Residential Agent Turnover 1) Net Commission Plan (Year) Settings / Personal

Net Commission Plan (Year) Settings / Personal") Cockpit Statistics Residential Agent Turnover 1) Net Commission Plan (Year) 2) Net Commission Plan YTD (Net Commission Plan) x (No. of days since beginning of year) / 365 How much commission would the

Cockpit Statistics Residential Agent Turnover 1) Net Commission Plan (Year) 2) Net Commission Plan YTD (Net Commission Plan) x (No. of days since beginning of year) / 365 How much commission would the

The course meets the undergraduate experiential education (EE) requirement.

requirement.") THE UNIVERSITY of NORTH CAROLINA at CHAPEL HILL DEPARTMENT of CITY and REGIONAL PLANNING CAMPUS BOX 3140 T 919-962-3983 NEW EAST BUILDING F 919-962-5206 CHAPEL HILL, NC 27599-3140 www.planning.unc.edu

THE UNIVERSITY of NORTH CAROLINA at CHAPEL HILL DEPARTMENT of CITY and REGIONAL PLANNING CAMPUS BOX 3140 T 919-962-3983 NEW EAST BUILDING F 919-962-5206 CHAPEL HILL, NC 27599-3140 www.planning.unc.edu

SECURITIES AND EXCHANGE COMMISSION. Washington, D.C FORM 8-K CURRENT REPORT

SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 8-K CURRENT REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Date of Report (Date of earliest event reported):

SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 8-K CURRENT REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Date of Report (Date of earliest event reported):

REITS and Financial Covenants: A Delicate Balance

REITS and Financial Covenants: A Delicate Balance Pauline M. Stevens * This article describes how the nancial covenants imposed on real estate investment trusts ( REITs ) di er from standard formulations

REITS and Financial Covenants: A Delicate Balance Pauline M. Stevens * This article describes how the nancial covenants imposed on real estate investment trusts ( REITs ) di er from standard formulations

Fully Stabilized 24-Unit Property at 11% Cap Rate!

Fully Stabilized 24-Unit Property at 11% Cap Rate! To Insert a Picture here, click inside this box with your mouse, then click on "INSERT PIC" button on the right and select the picture 24 Units consisting

Fully Stabilized 24-Unit Property at 11% Cap Rate! To Insert a Picture here, click inside this box with your mouse, then click on "INSERT PIC" button on the right and select the picture 24 Units consisting

Classify and describe basic forms of real estate investments.

LOS 43.a 2017 CFA Exam SS 15 Classify and describe basic forms of real estate investments. Card 1 of 52 LOS 43.a There are four basic forms of real estate investment; private equity (direct ownership),

LOS 43.a 2017 CFA Exam SS 15 Classify and describe basic forms of real estate investments. Card 1 of 52 LOS 43.a There are four basic forms of real estate investment; private equity (direct ownership),

Public Storage Reports Results for the Quarter Ended March 31, 2017

News Release Public Storage 701 Western Avenue Glendale, CA 91201-2349 www.publicstorage.com For Release Immediately Date April 26, 2017 Contact Clemente Teng (818) 244-8080, Ext. 1141 Public Storage Reports

News Release Public Storage 701 Western Avenue Glendale, CA 91201-2349 www.publicstorage.com For Release Immediately Date April 26, 2017 Contact Clemente Teng (818) 244-8080, Ext. 1141 Public Storage Reports

The course meets the undergraduate experiential education (EE) requirement.

requirement.") THE UNIVERSITY of NORTH CAROLINA at CHAPEL HILL DEPARTMENT of CITY and REGIONAL PLANNING CAMPUS BOX 3140 T 919-962-3983 NEW EAST BUILDING F 919-962-5206 CHAPEL HILL, NC 27599-3140 www.planning.unc.edu

THE UNIVERSITY of NORTH CAROLINA at CHAPEL HILL DEPARTMENT of CITY and REGIONAL PLANNING CAMPUS BOX 3140 T 919-962-3983 NEW EAST BUILDING F 919-962-5206 CHAPEL HILL, NC 27599-3140 www.planning.unc.edu

Lessor Example Performance Obligation Approach

Lessor Example Performance Obligation Approach **Disclaimer The exposure draft received nearly 700 letters of comment through the comment period ended December 15, 2010. There is some expectation that

Lessor Example Performance Obligation Approach **Disclaimer The exposure draft received nearly 700 letters of comment through the comment period ended December 15, 2010. There is some expectation that

1. On page 2 of the Prospectus the Section is renamed to Historical Financial Information.

The following amendments to the Prospectus are made by this Supplement: 1. On page 2 of the Prospectus the Section 4.14.1 is renamed to Historical Financial Information. 2. On page 4 of the Prospectus

The following amendments to the Prospectus are made by this Supplement: 1. On page 2 of the Prospectus the Section 4.14.1 is renamed to Historical Financial Information. 2. On page 4 of the Prospectus

SAUL CENTERS, INC Wisconsin Avenue, Suite 1500, Bethesda, Maryland (301)

") SAUL CENTERS, INC. 7501 Wisconsin Avenue, Suite 1500, Bethesda, Maryland 20814-6522 (301) 986-6200 Saul Centers, Inc. Reports Third Quarter 2016 Earnings November 1, 2016, Bethesda, MD. Saul Centers, Inc.

SAUL CENTERS, INC. 7501 Wisconsin Avenue, Suite 1500, Bethesda, Maryland 20814-6522 (301) 986-6200 Saul Centers, Inc. Reports Third Quarter 2016 Earnings November 1, 2016, Bethesda, MD. Saul Centers, Inc.

New leases standard ASC 842 Lessee - operating leases. Itai Gotlieb, Partner, Professional Practice July 2017

ASC 842 Lessee - operating leases Itai Gotlieb, Partner, Professional Practice July 2017 Overview Under Accounting Standards Codification (ASC) 842, Leases, lessees recognize assets and liabilities for

ASC 842 Lessee - operating leases Itai Gotlieb, Partner, Professional Practice July 2017 Overview Under Accounting Standards Codification (ASC) 842, Leases, lessees recognize assets and liabilities for

Key Data (as on November 2013)

") Key Data (as on November 2013) Month- November, 2013 Current Price- Rs. 300 Recommendation- BUY Current P/E-10 Target- 100% return within 1 year or so. ISIN-INE951D01010 Portfolio Allocation- Allocate

Key Data (as on November 2013) Month- November, 2013 Current Price- Rs. 300 Recommendation- BUY Current P/E-10 Target- 100% return within 1 year or so. ISIN-INE951D01010 Portfolio Allocation- Allocate

CONSOLIDATED STATEMENT OF INCOME

CONSOLIDATED STATEMENT OF INCOME (unaudited, data converted from the Euro to the US Dollar (for information concerning this restatement, see Note 11 to these Consolidated Financial Statements)) 1 st quarter

CONSOLIDATED STATEMENT OF INCOME (unaudited, data converted from the Euro to the US Dollar (for information concerning this restatement, see Note 11 to these Consolidated Financial Statements)) 1 st quarter

Front Yard Residential Corporation Announces Transformative Acquisition and Reports Second Quarter 2018 Results

Front Yard Residential Corporation Announces Transformative Acquisition and Reports Second Quarter 2018 Results August 9, 2018 CHRISTIANSTED, U.S. Virgin Islands, Aug. 09, 2018 (GLOBE NEWSWIRE) -- Front

Front Yard Residential Corporation Announces Transformative Acquisition and Reports Second Quarter 2018 Results August 9, 2018 CHRISTIANSTED, U.S. Virgin Islands, Aug. 09, 2018 (GLOBE NEWSWIRE) -- Front

Financial Bootcamp. Participant Guide SAMPLE

Financial Bootcamp Participant Guide September 2017 2017 National Apartment Association 2 Table of Contents Section 1: Welcome... 6 Participant Introductions... 6 Learning Goals and Objectives... 6 Section

Financial Bootcamp Participant Guide September 2017 2017 National Apartment Association 2 Table of Contents Section 1: Welcome... 6 Participant Introductions... 6 Learning Goals and Objectives... 6 Section

FASB/IASB Update Part II

American Accounting Association FASB/IASB Update Part II Tom Linsmeier FASB Member August 3, 2014 The views expressed in this presentation are those of the presenters. Official positions of the FASB/IASB

American Accounting Association FASB/IASB Update Part II Tom Linsmeier FASB Member August 3, 2014 The views expressed in this presentation are those of the presenters. Official positions of the FASB/IASB

Benchmarking Your CCRC

Benchmarking Your CCRC Presented by: Moore Stephens Lovelace, P.A. Objectives Provide information on how ratios can provide insight into financial statements Give information about key ratios and what

Benchmarking Your CCRC Presented by: Moore Stephens Lovelace, P.A. Objectives Provide information on how ratios can provide insight into financial statements Give information about key ratios and what

Corporate Presentation

October 2018 Corporate Presentation (NYSE: SAFE) Forward-Looking Statements and Other Matters This release may contain forward-looking statements. All statements other than statements of historical fact

October 2018 Corporate Presentation (NYSE: SAFE) Forward-Looking Statements and Other Matters This release may contain forward-looking statements. All statements other than statements of historical fact

PROPOSED ACCOUNTING STANDARD REQUIRES CAPITALIZATION OF ALL LONG-TERM LEASES FOR LESSEES

PROPOSED ACCOUNTING STANDARD REQUIRES CAPITALIZATION OF ALL LONG-TERM LEASES FOR LESSEES Mark G. McCarthy, East Carolina University Brett Cotten, Columbus State University Douglas K. Schneider, East Carolina

PROPOSED ACCOUNTING STANDARD REQUIRES CAPITALIZATION OF ALL LONG-TERM LEASES FOR LESSEES Mark G. McCarthy, East Carolina University Brett Cotten, Columbus State University Douglas K. Schneider, East Carolina

Rental income, SEK million 1,071 1,014 4,122 4,109 Growth in rental income comparable properties, percent

Akelius Residential Property AB (publ) year-end report January to December summary Oct Dec Oct Dec Jan Dec Jan Dec Rental income, SEK million 1,071 1,014 4,122 4,109 Growth in rental income comparable

Akelius Residential Property AB (publ) year-end report January to December summary Oct Dec Oct Dec Jan Dec Jan Dec Rental income, SEK million 1,071 1,014 4,122 4,109 Growth in rental income comparable

Registration Course Description Classroom Rules & Procedures

Course Schedule SECTION 1. (Day 1 Morning) Introduction Part 1. Introduction and Overview Registration Course Description Classroom Rules & Procedures Part 2. Components of Discounted Cash Flow Analysis

Course Schedule SECTION 1. (Day 1 Morning) Introduction Part 1. Introduction and Overview Registration Course Description Classroom Rules & Procedures Part 2. Components of Discounted Cash Flow Analysis

Alaska Air Group, Inc. Accounting for the Costs of Returning Leased Aircraft

Alaska Air Group, Inc. Accounting for the Costs of Returning Leased Aircraft Note: During the second quarter of 2002, Alaska Air Group revised its accounting practices relating to accruals for the costs

Alaska Air Group, Inc. Accounting for the Costs of Returning Leased Aircraft Note: During the second quarter of 2002, Alaska Air Group revised its accounting practices relating to accruals for the costs

Retail Opportunity Investments Corp. Reports Strong First Quarter Results & Raises FFO Guidance

April 27, 2016 Retail Opportunity Investments Corp. Reports Strong First Quarter Results & Raises FFO Guidance $17.4% increase in FFO Per Diluted Share 7.6% Increase in Same-Center Cash Net Operating Income

April 27, 2016 Retail Opportunity Investments Corp. Reports Strong First Quarter Results & Raises FFO Guidance $17.4% increase in FFO Per Diluted Share 7.6% Increase in Same-Center Cash Net Operating Income

Interim statement from the Board of Directors for the first quarter of 2015

Regulated information - under embargo until 05/05/2015, 8 a.m. Antwerp, 5 May 2015 Interim statement from the Board of Directors Acquisition of a modern logistics site of approximately 52.000 m² in a prime

Regulated information - under embargo until 05/05/2015, 8 a.m. Antwerp, 5 May 2015 Interim statement from the Board of Directors Acquisition of a modern logistics site of approximately 52.000 m² in a prime

Understanding the Economics & Financing Structures of Moderately Priced Life Plan Communities

Understanding the Economics & Financing Structures of Moderately Priced Life Plan Communities 2 Today s Presenters Wayne Olson, Executive Vice President, Volunteers of America National Services Steve Kuhns,

Understanding the Economics & Financing Structures of Moderately Priced Life Plan Communities 2 Today s Presenters Wayne Olson, Executive Vice President, Volunteers of America National Services Steve Kuhns,

Highwoods Reports Third Quarter 2017 Results

FOR IMMEDIATE RELEASE Ref: 17-20 Contact: Brendan Maiorana Senior Vice President, Finance and Investor Relations 919-431-1529 Highwoods Reports Third Quarter 2017 Results $0.55 Net Income per Share $0.86

FOR IMMEDIATE RELEASE Ref: 17-20 Contact: Brendan Maiorana Senior Vice President, Finance and Investor Relations 919-431-1529 Highwoods Reports Third Quarter 2017 Results $0.55 Net Income per Share $0.86

IFRS 16. Changes in recognizing leases in the financial statements

IFRS 16 Changes in recognizing leases in the financial statements The new standard in a nutshell: To whom the new standard applies / Binding terms and conditions In January 2016, the International Accounting

IFRS 16 Changes in recognizing leases in the financial statements The new standard in a nutshell: To whom the new standard applies / Binding terms and conditions In January 2016, the International Accounting

Portfolio Management Association of Canada. April 24, IFRS 16: Key impacts

Portfolio Management Association of Canada April 24, 2018 IFRS 16: Key impacts Almost all leases on balance sheet right of use asset and lease liability, with significant impacts for gearing in certain

Portfolio Management Association of Canada April 24, 2018 IFRS 16: Key impacts Almost all leases on balance sheet right of use asset and lease liability, with significant impacts for gearing in certain

Commercial Real Estate Debt Finance This course is presented in London on: 26 February 2018, 29 November 2018

Commercial Real Estate Debt Finance This course is presented in London on: 26 February 2018, 29 November 2018 The Banking and Corporate Finance Training Specialist Course Objectives Participants will:

Commercial Real Estate Debt Finance This course is presented in London on: 26 February 2018, 29 November 2018 The Banking and Corporate Finance Training Specialist Course Objectives Participants will:

FLORIDA BROKER PRELICENSE (FREC II) (V2)

(V2)") FLORIDA BROKER PRELICENSE (FREC II) (V2) TIME CONTENT OUTLINE LEARNING OBJECTIVES -- After this segment, the Licensing 7 hours 45 mins. License Law and Rules 1 explain the purpose of the license law describe

FLORIDA BROKER PRELICENSE (FREC II) (V2) TIME CONTENT OUTLINE LEARNING OBJECTIVES -- After this segment, the Licensing 7 hours 45 mins. License Law and Rules 1 explain the purpose of the license law describe

Lease accounting survey Preparing for implementation

Lease accounting survey Preparing for implementation Executive summary The new lease accounting standard proposed by the Financial Accounting Standards Board (FASB) fundamentally changes the rules that

Lease accounting survey Preparing for implementation Executive summary The new lease accounting standard proposed by the Financial Accounting Standards Board (FASB) fundamentally changes the rules that

Front Yard Residential Corporation Reports Third Quarter 2018 Results

Front Yard Residential Corporation Reports Third Quarter 2018 Results November 7, 2018 CHRISTIANSTED, U.S. Virgin Islands, Nov. 07, 2018 (GLOBE NEWSWIRE) -- Front Yard Residential Corporation ( Front Yard

Front Yard Residential Corporation Reports Third Quarter 2018 Results November 7, 2018 CHRISTIANSTED, U.S. Virgin Islands, Nov. 07, 2018 (GLOBE NEWSWIRE) -- Front Yard Residential Corporation ( Front Yard

Modeling your Appraisal Report to Meet your Client's Needs in the Commercial Marketplace

Modeling your Appraisal Report to Meet your Client's Needs in the Commercial Marketplace Myth #1 The Final Estimate of Value is the Only Area of the Report Anyone Reads Financial Institutions -Interagency

Modeling your Appraisal Report to Meet your Client's Needs in the Commercial Marketplace Myth #1 The Final Estimate of Value is the Only Area of the Report Anyone Reads Financial Institutions -Interagency

$450,000 $63,425 $39, % PURCHASE PRICE NET OPERATING INCOME ANNUAL CASH FLOW CAP RATE

Executive Summary Key Property Metrics $450,000 $63,425 $39,143 14.1% PURCHASE PRICE NET OPERATING INCOME ANNUAL CASH FLOW CAP RATE $70,000 $60,000 $50,000 $40,000 $30,000 Annual Cash Flow Repairs, 8%

Executive Summary Key Property Metrics $450,000 $63,425 $39,143 14.1% PURCHASE PRICE NET OPERATING INCOME ANNUAL CASH FLOW CAP RATE $70,000 $60,000 $50,000 $40,000 $30,000 Annual Cash Flow Repairs, 8%

Presentation Outline Copyright Bank Nizwa. All Rights Reserved. 2

Presentation Outline Key Products and Services Section 1 Murabaha Section 2 Ijara Section 3 Musharaka Section 4 Islamic Banks VS Conventional Banks Section 5 2017 Copyright Bank Nizwa. All Rights Reserved.

Presentation Outline Key Products and Services Section 1 Murabaha Section 2 Ijara Section 3 Musharaka Section 4 Islamic Banks VS Conventional Banks Section 5 2017 Copyright Bank Nizwa. All Rights Reserved.

Sunway Berhad TP: RM3.27 (+10.6%) Acquires Industrial Land Parcels in Selangor

Acquires Industrial Land Parcels in Selangor") A Member of the TA Group MENARA TA ONE, 22 JALAN P. RAMLEE, 50250 KUALA LUMPUR, MALAYSIA TEL: +603-20721277 / FAX: +603-20325048 C O M P A N Y U P D A T E Monday, 22 February 2016 FBMKLCI: 1,674.88 Sector:

A Member of the TA Group MENARA TA ONE, 22 JALAN P. RAMLEE, 50250 KUALA LUMPUR, MALAYSIA TEL: +603-20721277 / FAX: +603-20325048 C O M P A N Y U P D A T E Monday, 22 February 2016 FBMKLCI: 1,674.88 Sector:

Introduction. Survey on Real Estate Financing and Distressed Real Estate Debt 16 October 2013

Index Executive summary Page 3-6 Introduction Page 7 Methodology Page 8 Financing Situation for Commercial Real Estate Pages 9-32 Situation of Distressed Real Estate Debt Pages 33-40 2 Introduction This

Index Executive summary Page 3-6 Introduction Page 7 Methodology Page 8 Financing Situation for Commercial Real Estate Pages 9-32 Situation of Distressed Real Estate Debt Pages 33-40 2 Introduction This

Analysis Prepared by David L. Sjoquist and Robert J. Eger III

GEORGIA STATE UNIVERSITY ANDREW YOUNG SCHOOL OF POLICY STUDIES FISCAL RESEARCH CENTER DECEMBER 1, 2006 SUBJECT: Estimated Effects of Population Growth on Atlanta Public School s Revenue and Expenditures

GEORGIA STATE UNIVERSITY ANDREW YOUNG SCHOOL OF POLICY STUDIES FISCAL RESEARCH CENTER DECEMBER 1, 2006 SUBJECT: Estimated Effects of Population Growth on Atlanta Public School s Revenue and Expenditures

ANALYTICS & MANAGEMENT OF MIXED INCOME PROPERTY

MIXED INCOME PROPERTY CFO FORUM NEIGHBORWORKS AMERICA TRAINING INSTITUTE KANSAS CITY, MISSOURI Presented by Len Tatem (Tatem Consulting LLC) & John Kelley (CNAHS/HRI Cambridge, MA) DEFINING MIXED-INCOME

MIXED INCOME PROPERTY CFO FORUM NEIGHBORWORKS AMERICA TRAINING INSTITUTE KANSAS CITY, MISSOURI Presented by Len Tatem (Tatem Consulting LLC) & John Kelley (CNAHS/HRI Cambridge, MA) DEFINING MIXED-INCOME