ADVANCED ISSUES IN FRANCHISOR ACQUISITIONS OF FRANCHISEES IS VERTICAL INTEGRATION IN YOUR FUTURE?

|

|

|

- Elfreda Watson

- 6 years ago

- Views:

Transcription

1 ADVANCED ISSUES IN FRANCHISOR ACQUISITIONS OF FRANCHISEES IS VERTICAL INTEGRATION IN YOUR FUTURE? Joel R. Buckberg Shareholder Commercial Transactions & Business Counseling Practice Group Chair Baker, Donelson, Bearman, Caldwell & Berkowitz, P.C. Nashville, TN Emily C. Decker Senior Vice President, General Counsel and Secretary Buffalo Wild Wings, Inc. Minneapolis, MN

2 AGENDA Review Standard Terms for Acquisitions of Franchisees Discuss Unique Aspects of These Transactions Review Best Practices for Exercising a Franchisor s Right of First Refusal Questions welcomed throughout the presentation we want to hear your experiences and thoughts

3 Business Factors Driving Vertical Deals Strategic Markets Low Interest Rates Private Equity Cash and Dry Powder Return on Investment Differential Capital Formulas and Market Values Refranchising Potential

4 Typical Franchise Acquisition Categories Owner/Operator Purchase Multi-Market Purchase Financial Seller Purchase

5 Transaction Structure Depends on Acquisition Category Deal Type Buyer Ownership Vehicle Buyer Debt Financing Options Financial Accounting for Buyer under GAAP Risk Management Purchase Price Holdback Diligence Issues Important Tax Considerations

6 Due Diligence What are the diligence requirements when a franchisor is acquiring a business that it obviously knows very well? What is available from standard records and reports? What do the field representatives know and don t write in the reports? Are discretionary reports prepared consistently with franchisor/affiliate methodology and treatment? Know before you go?

7 Due Diligence Typical Information Gaps in Franchise Reporting Books and records quality Deferred Maintenance Human Resources Compliance Tax Compliance Revenue Reporting and Cash Flow Accuracy Supply Chain Compliance Marketing Compliance Lease Compliance

8 Structure Checklist Buyer Ownership Vehicle Buyer Debt Financing Options Financial Accounting for Buyer under GAAP Risk Management Purchase Price Holdback Tax Options and Impacts Gain, Loss, Income Recapture of accelerated depreciation Basis adjustments Deferral/Installment/Shelter

9 Valuation Agreement formula Recent sales System Lore Formulas Other Factors: Outlet condition and capital expenditures needed to meet standards Geography Territorial rights Direction of outlet economics Intrabrand performance Cash Flow EBITDA

10 How to Value the Deal Unique valuation elements for purchasing franchisees Critical factors for valuation What is the goodwill value? Fair Market Value v. Fair Value Impact of franchisor call rights

11 Franchisor Call Rights Short form term sheet Consider attaching a form Purchase Agreement as an exhibit or maintain as Item 22 exhibit to FDD If triggered by change of control, consider timing discretion, right to extend right to exercise and obligation to close Specify parties to agreement like all owners and guarantors Refer to customary representations and warranties Specify indemnity and holdback concept

12 Letters of Intent Getting to yes on commercial terms Easier /Cheaper to negotiate than full agreement Sets forth structure and financing Can the parties reach agreement and develop trust? Enforceable or not? Preliminary agreement to negotiate in good faith

13 Important Deal Points Representations and Warranties Typical Provisions System Specific Materiality or Flat Sandbag or Not? Representations and Warranties Insurance Advantages Types of Policies and Key Terms Exclusions and Retention Premiums and Dispute Resolution

14 Important Deal Points, cont. Indemnification Holdbacks and Offsets Material Adverse Changes Before Closing ABA Deal Points Studies New Resource: The Impact on Deal Size on Highly Negotiated M&A Deals, Eric Rauch and Brian Burke The Business Lawyer, Summer 2016, pp

15 Key Negotiated Points of Risk Allocation Liability Cap Liability Basket Amount and Type Seller s Catch All Representation and Warranty No Undisclosed Liabilities Representation Closing Conditions

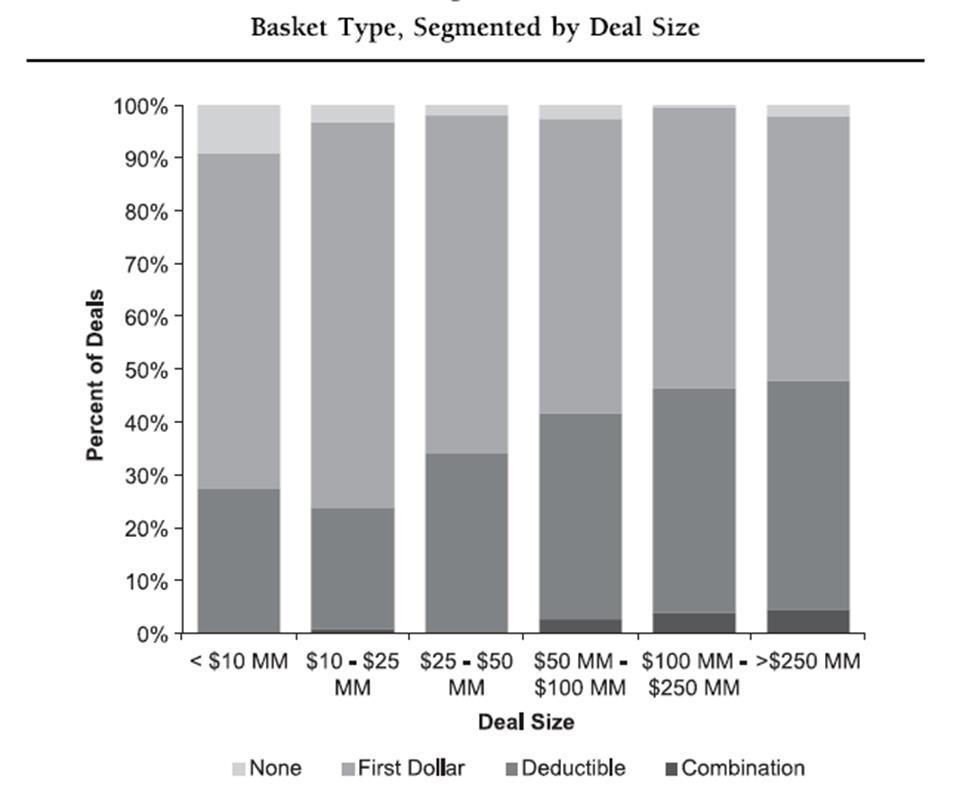

16 Definitions Liability Cap Percentage of Purchase Price exposed for nonfundamental reps and warranties breach Liability Basket Amount and Type Percentage of Purchase Price or Dollar Amount Deductible Seller liable for amount in excess of deductible Tipping Basket Seller liable from first dollar if threshold met or exceeded Combination or Partial Tipping Basket Seller liable for amount in excess of threshold and percentage of amount below threshold No Basket First Dollar Liability

17 Liability Cap

18 Baskets

19 Definitions Seller s Catch All Representation and Warranty 10b-5 type or Full 10b-5: No representation or warranty made by Seller in this Agreement and [all related disclosures] contains any untrue statement or omits to state any material fact necessary to make any of them, in light of the circumstances in which they are made, not misleading. Full Disclosure: Seller does not have any knowledge of any fact that has specific application to Seller (other than general economic or industry conditions) that may materially adversely affect the business, assets, financial condition, results of operations or prospects of the Business that has not been disclosed to Buyer in this Agreement and the [related disclosures].

20 Definitions No Undisclosed Liabilities Full Coverage: Seller has no liabilities related to or arising from the Business except for liabilities reflected on or reserved for on the Balance Sheet and the Interim Balance Sheet. Seller Friendly Seller has no liabilities except for those of a nature required to be disclosed under GAAP or which could not reasonably be expected to have a Material Adverse Effect except for those reflected on the Balance Sheet and the Interim Balance Sheet, and those incurred in the ordinary course of business since the date of the Interim Balance Sheet.

21 Catch All Reps

22 Undisclosed Liabilities

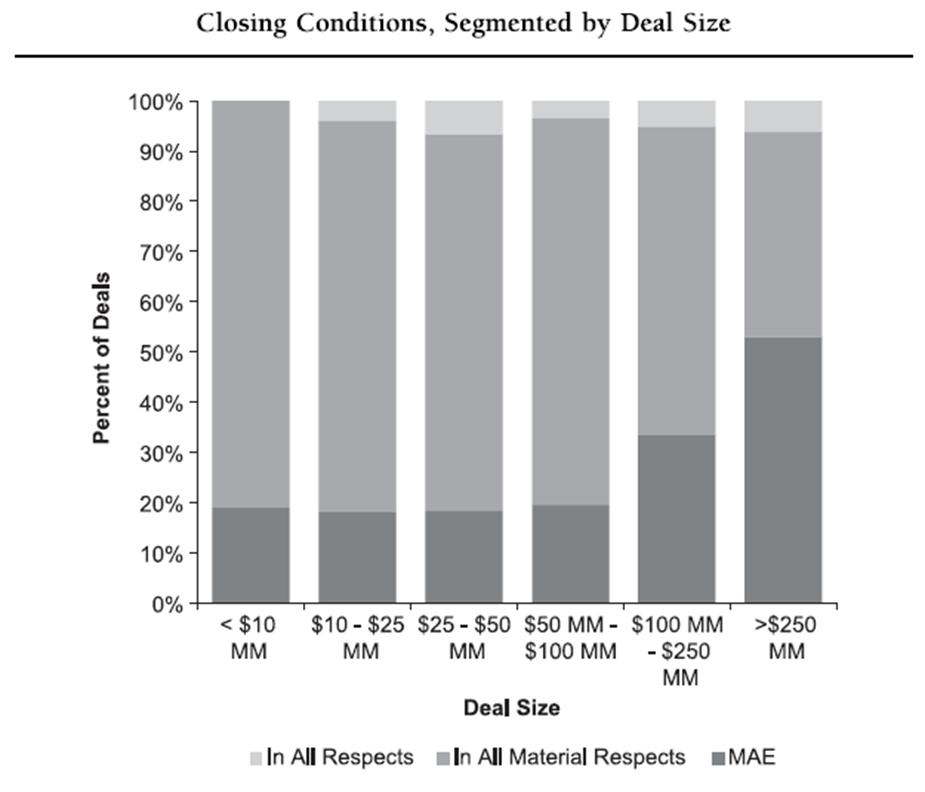

23 Closing Conditions Closing certainty affected by allowed variation of representations and warranties between signing and closing Buyer Friendly: Each of the Seller s representations and warranties shall be accurate in all respects as of the Closing Date as if made on the Closing Date Less Buyer Friendly: Each of the Seller s representations and warranties shall be accurate in all material respects as of the Closing Date as if made on the Closing Date Seller Friendly: Each of the Seller s representations and warranties shall be accurate in all respects as of the Closing Date as if made on the Closing Date, except for inaccuracies which individually and in the aggregate would not give rise to a Material Adverse Effect

24 Closing Conditions

25 Deal Points Size Matters More Seller friendly in larger deals More Buyer friendly in smaller deals Trend toward more seller friendly deals More cash chasing fewer opportunities means more competition and more buyer friendly terms

26 Franchisor Right of First Refusal Early involvement of the franchisor Transfer requirements Remodels and operational minimum standards What s for sale? Additional development rights

27 ROFR Process Notify the franchisor of a proposed transfer Triggering the ROFR Due diligence must be submitted Pros/cons of requiring a form purchase agreement Approval of the new franchisee Separate process from ROFR

28 Franchisor s Exercise Adjusting the purchase agreement for the franchisor Closing the deal Taking over the business from the franchisee Transition Services Licenses and Permits Third party consents Important accounts and relationships

29 Additional Due Diligence Issues State Tax Issues Will the target s state tax the franchisee fee revenues in that state? Was the franchisee compliant with tax laws? Federal Tax Audit Changes in 2018 Predictive Coding Document intensive diligence Contract-oriented franchise Easy to duplicate for pattern transactions

30 Conclusion Questions? Thank You Joel R. Buckberg Emily Decker

Negotiating Asset & Share Purchase Agreements: Fundamental Considerations. I. Berl Nadler Paul Lamarre

Negotiating Asset & Share Purchase Agreements: Fundamental Considerations I. Berl Nadler Paul Lamarre February 27, 2014 Negotiating Asset and Purchase Agreements Form of the Transaction: Assets vs. Shares;

Negotiating Asset & Share Purchase Agreements: Fundamental Considerations I. Berl Nadler Paul Lamarre February 27, 2014 Negotiating Asset and Purchase Agreements Form of the Transaction: Assets vs. Shares;

Center for Entrepreneurial Studies, Stanford Graduate School of Business. Summary of Primary Issues in Acquisition Transactions

September 23, 2009 TO: FROM: RE: Center for Entrepreneurial Studies, Stanford Graduate School of Business Perkins Coie LLP Summary of Primary Issues in Acquisition Transactions This memorandum provides

September 23, 2009 TO: FROM: RE: Center for Entrepreneurial Studies, Stanford Graduate School of Business Perkins Coie LLP Summary of Primary Issues in Acquisition Transactions This memorandum provides

Cross-border M&A: Comparing U.K. and U.S. Private M&A Transactions

Cross-border M&A: Comparing U.K. and U.S. Private M&A Transactions Presented by Dan Hirschovits Harold Birnbaum William Tong Elyka Anvari December 14, 2017 Davis Polk & Wardwell London LLP is a limited

Cross-border M&A: Comparing U.K. and U.S. Private M&A Transactions Presented by Dan Hirschovits Harold Birnbaum William Tong Elyka Anvari December 14, 2017 Davis Polk & Wardwell London LLP is a limited

UK M&A Deals: What A US Buyer Should Expect

UK M&A Deals: What A US Buyer Should Expect Introduction The market for M&A deals is on the rebound after a sluggish 2013, with the first and second quarters of 2014 being some of the most active quarters

UK M&A Deals: What A US Buyer Should Expect Introduction The market for M&A deals is on the rebound after a sluggish 2013, with the first and second quarters of 2014 being some of the most active quarters

Stock Purchase Agreement Commentary

Stock Purchase Agreement Commentary This is just one example of the many online resources Practical Law Company offers. PLC Corporate and Securities Commentary on key terms and conditions commonly found

Stock Purchase Agreement Commentary This is just one example of the many online resources Practical Law Company offers. PLC Corporate and Securities Commentary on key terms and conditions commonly found

roots The Substance of the Standard Contents Changes to the Accounting for Goodwill for Private Companies

The Substance of the Standard MAYER HOFFMAN MCCANN P.C. AN INDEPENDENT CPA FIRM TM A publication of the Professional Standards Group February 2014 Changes to the Accounting for Goodwill for Private Companies

The Substance of the Standard MAYER HOFFMAN MCCANN P.C. AN INDEPENDENT CPA FIRM TM A publication of the Professional Standards Group February 2014 Changes to the Accounting for Goodwill for Private Companies

5. The cost of buildings includes all necessary costs related to the purchase or construction

CHAPTER REVIEW Plant Assets 1. (S.O. 1) Plant assets are tangible resources that are used in the operations of a business and are not intended for sale to customers. Plant assets are subdivided into four

CHAPTER REVIEW Plant Assets 1. (S.O. 1) Plant assets are tangible resources that are used in the operations of a business and are not intended for sale to customers. Plant assets are subdivided into four

May 6, 2010 Marriott Philadelphia Downtown

DELVACCA PRESENTS: Issues Surrounding Indemnity Clauses in Merger and Acquisition Agreements May 6, 2010 Marriott Philadelphia Downtown DELVACCA thanks Cozen O Connor for sponsoring this event. Determining

DELVACCA PRESENTS: Issues Surrounding Indemnity Clauses in Merger and Acquisition Agreements May 6, 2010 Marriott Philadelphia Downtown DELVACCA thanks Cozen O Connor for sponsoring this event. Determining

Advanced M&A and Merger Models Quiz Questions

Advanced M&A and Merger Models Quiz Questions Transaction Assumptions and Sources & Uses Purchase Price Allocation & Balance Sheet Combination Combining the Income Statement Revenue, Expense, and CapEx

Advanced M&A and Merger Models Quiz Questions Transaction Assumptions and Sources & Uses Purchase Price Allocation & Balance Sheet Combination Combining the Income Statement Revenue, Expense, and CapEx

Chapter 9 - REPORTING AND ANALYZING LONG-LIVED ASSETS

Revised Summer 2018 Chapter 9 Review 1 Chapter 9 - REPORTING AND ANALYZING LONG-LIVED ASSETS LO 1: Explain the accounting for plant asset expenditures. Plant Assets (Also known as Property, Plant, and

Revised Summer 2018 Chapter 9 Review 1 Chapter 9 - REPORTING AND ANALYZING LONG-LIVED ASSETS LO 1: Explain the accounting for plant asset expenditures. Plant Assets (Also known as Property, Plant, and

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2011

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2011 Presented By: Marianne Heard, CPA, MST, Tax Director, Kevin P. Martin & Associates, P.C.

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2011 Presented By: Marianne Heard, CPA, MST, Tax Director, Kevin P. Martin & Associates, P.C.

REAL ESTATE TOPICS JUNE 1, 2008 NEGOTIATING AND STRUCTURING JOINT VENTURE AND LLC AGREEMENTS

BENNETT VALLEY LAW REAL ESTATE TOPICS JUNE 1, 2008 NEGOTIATING AND STRUCTURING JOINT VENTURE AND LLC AGREEMENTS Parties negotiate joint venture agreements in the spirit of optimism. Anxious to combine

BENNETT VALLEY LAW REAL ESTATE TOPICS JUNE 1, 2008 NEGOTIATING AND STRUCTURING JOINT VENTURE AND LLC AGREEMENTS Parties negotiate joint venture agreements in the spirit of optimism. Anxious to combine

The Financial Accounting Standards Board

V A L U A T I O N How the New Leases Standard May Impact Business Valuations By Judith H. O Dell, CPA, CVA The Financial Accounting Standards Board issued the 485 page Leases Standard (Topic 842) in February,

V A L U A T I O N How the New Leases Standard May Impact Business Valuations By Judith H. O Dell, CPA, CVA The Financial Accounting Standards Board issued the 485 page Leases Standard (Topic 842) in February,

Cross-Border M&A Transactions. November 7, 2017

Cross-Border M&A Transactions November 7, 2017 Risk/reward comparison: closing adjustments vs locked box Balance Sheet date Warranty protection Signing Warranty protection (if repeated) Pre-closing covenants:

Cross-Border M&A Transactions November 7, 2017 Risk/reward comparison: closing adjustments vs locked box Balance Sheet date Warranty protection Signing Warranty protection (if repeated) Pre-closing covenants:

Thomas H. Warren Ram C. Sunkara February 22, 2011

Thomas H. Warren Ram C. Sunkara February 22, 2011 Electric Cooperative M&A Issues: Power Asset M&A Our Coop Power Project Experience In the past two years, we have assisted our Electric Cooperative clients

Thomas H. Warren Ram C. Sunkara February 22, 2011 Electric Cooperative M&A Issues: Power Asset M&A Our Coop Power Project Experience In the past two years, we have assisted our Electric Cooperative clients

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2016

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2016 Presented By: Karen Kent, CPA, Partner, Kevin P. Martin & Associates, P.C. Kenneth Lund,

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2016 Presented By: Karen Kent, CPA, Partner, Kevin P. Martin & Associates, P.C. Kenneth Lund,

RULES AND REGULATIONS FOR ADMINISTRATION OF AREA DRAINAGE PLANS

RIVERSIDE COUNTY RULES AND REGULATIONS FOR ADMINISTRATION OF AREA DRAINAGE PLANS ADOPTED JUNE 10, 1980 BY RESOLUTION NO. 80-244 AMENDMENTS RESOLUTION NO. May 26, 1981 81-148 Nov. 9, 1982 82-320 July 3,

RIVERSIDE COUNTY RULES AND REGULATIONS FOR ADMINISTRATION OF AREA DRAINAGE PLANS ADOPTED JUNE 10, 1980 BY RESOLUTION NO. 80-244 AMENDMENTS RESOLUTION NO. May 26, 1981 81-148 Nov. 9, 1982 82-320 July 3,

DUE DILIGENCE HEART OF A PRIVATE EQUITY TRANSACTION

DUE DILIGENCE HEART OF A PRIVATE EQUITY TRANSACTION DUE DILIGENCE: WHAT WHY WHO WHEN WHAT IS DUE DILIGENCE? Black s Law Dictionary defines Due Diligence as a measure of prudence or activity to be expected

DUE DILIGENCE HEART OF A PRIVATE EQUITY TRANSACTION DUE DILIGENCE: WHAT WHY WHO WHEN WHAT IS DUE DILIGENCE? Black s Law Dictionary defines Due Diligence as a measure of prudence or activity to be expected

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2014

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2014 Presented By: Karen Kent, CPA, Partner, Kevin P. Martin & Associates, P.C. Kenneth Lund,

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2014 Presented By: Karen Kent, CPA, Partner, Kevin P. Martin & Associates, P.C. Kenneth Lund,

IR RESOURCES LIMITED

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness

Week11, Chap 8 Accounting 1A, Financial Accounting

Week11, Chap 8 Accounting 1A, Financial Accounting Reporting and Interpreting Property, Plant, and Equipment;Natural Resources; and Intangibles Instructor: Michael Booth Understanding The Business Insufficient

Week11, Chap 8 Accounting 1A, Financial Accounting Reporting and Interpreting Property, Plant, and Equipment;Natural Resources; and Intangibles Instructor: Michael Booth Understanding The Business Insufficient

Exit Strategies for a Medical Practice

Exit Strategies for a Medical Practice John D. Colucci, Esq., CPA McLane Middleton, PA Jonathan P. Gorski, CPA, MBA Edelstein & Company LLP June 12, 2018 Introduction John D. Colucci, a director at McLane

Exit Strategies for a Medical Practice John D. Colucci, Esq., CPA McLane Middleton, PA Jonathan P. Gorski, CPA, MBA Edelstein & Company LLP June 12, 2018 Introduction John D. Colucci, a director at McLane

ACQUISITIONS OF SUBSIDIARIES AND DIVISIONS

ACQUISITIONS OF SUBSIDIARIES AND DIVISIONS First Run Broadcast: November 10, 2016 1:00 p.m. E.T./12:00 p.m. C.T./11:00 a.m. M.T./10:00 a.m. P.T. (60 minutes) Buying part of an operating company is entirely

ACQUISITIONS OF SUBSIDIARIES AND DIVISIONS First Run Broadcast: November 10, 2016 1:00 p.m. E.T./12:00 p.m. C.T./11:00 a.m. M.T./10:00 a.m. P.T. (60 minutes) Buying part of an operating company is entirely

Investor. Investment Service Centre. Listed Companies Information. YANGTZEKIANG<00294> - Results Announcement

Investor Investment Service Centre Listed Companies Information YANGTZEKIANG - Results Announcement Yangtzekiang Garment Limited announced on 16/12/2005: (stock code: 00294 ) Year end date: 31/03/2006

Investor Investment Service Centre Listed Companies Information YANGTZEKIANG - Results Announcement Yangtzekiang Garment Limited announced on 16/12/2005: (stock code: 00294 ) Year end date: 31/03/2006

Topic 14 IAS 18 - Revenue

Topic 14 IAS 18 - Revenue International Accounting Standard 18 (IAS 18) Scope of IAS 18 To prescribe the accounting treatment of revenue arising from: (a) (b) (c) (d) sale of goods; rendering of services;

Topic 14 IAS 18 - Revenue International Accounting Standard 18 (IAS 18) Scope of IAS 18 To prescribe the accounting treatment of revenue arising from: (a) (b) (c) (d) sale of goods; rendering of services;

RECENT TRENDS AND LEGAL DEVELOPMENTS IN M&A AND RELATED TRANSACTIONS

RECENT TRENDS AND LEGAL DEVELOPMENTS IN M&A AND RELATED TRANSACTIONS Steven N. Haas, Esq. Anna M. McDonough, Esq. Cozen O Connor Cozen O Connor 1900 Market Street 1900 Market Street Philadelphia, PA 19103

RECENT TRENDS AND LEGAL DEVELOPMENTS IN M&A AND RELATED TRANSACTIONS Steven N. Haas, Esq. Anna M. McDonough, Esq. Cozen O Connor Cozen O Connor 1900 Market Street 1900 Market Street Philadelphia, PA 19103

Due diligence - Hits & Misses. CA Rajesh S Shetty January 2018

Due diligence - Hits & Misses CA Rajesh S Shetty January 2018 Contents Need of due diligence What is due diligence? Types of due diligence The process Focus areas Key benefits Limitations 2 Need of Due

Due diligence - Hits & Misses CA Rajesh S Shetty January 2018 Contents Need of due diligence What is due diligence? Types of due diligence The process Focus areas Key benefits Limitations 2 Need of Due

I ROC 2017 Financial Administrators Section Conference

I ROC 2017 Financial Administrators Section Conference September 9, 2017 kpmg.ca Presenters Chris Cornell KPMG Partner, Financial Services Steven Sharma KPMG Partner, Financial Services 2 IIROC 2017 Financial

I ROC 2017 Financial Administrators Section Conference September 9, 2017 kpmg.ca Presenters Chris Cornell KPMG Partner, Financial Services Steven Sharma KPMG Partner, Financial Services 2 IIROC 2017 Financial

Presenting a live 90-minute webinar with interactive Q&A. Today s faculty features:

Presenting a live 90-minute webinar with interactive Q&A Getting M&A Deals Done: Legal Risks and Effective Strategies Managing Changes and Mitigating Risks Between Signing the Acquisition Agreement and

Presenting a live 90-minute webinar with interactive Q&A Getting M&A Deals Done: Legal Risks and Effective Strategies Managing Changes and Mitigating Risks Between Signing the Acquisition Agreement and

Plant assets are resources that have

10-1 LEARNING OBJECTIVE 1 Explain the accounting for plant asset expenditures. Plant assets are resources that have physical substance (a definite size and shape), are used in the operations of a business,

10-1 LEARNING OBJECTIVE 1 Explain the accounting for plant asset expenditures. Plant assets are resources that have physical substance (a definite size and shape), are used in the operations of a business,

MERGERS & ACQUISITIONS: HOW TO BUY OR SELL A BUSINESS. Prepared by Neil M. Kaufman, Esq.

December 19, 2012 I. Evaluating Potential Buyers and Sellers. MERGERS & ACQUISITIONS: HOW TO BUY OR SELL A BUSINESS Prepared by Neil M. Kaufman, Esq. A. Preparing to sell the Company: 1. Sellers should:

December 19, 2012 I. Evaluating Potential Buyers and Sellers. MERGERS & ACQUISITIONS: HOW TO BUY OR SELL A BUSINESS Prepared by Neil M. Kaufman, Esq. A. Preparing to sell the Company: 1. Sellers should:

Accounting Of Intangible Assets Indian as- 26

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668. Volume 16, Issue 2. Ver. II (Feb. 2014), PP 40-45 Accounting Of Intangible Assets Indian as- 26 Manpreet Sharma,

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668. Volume 16, Issue 2. Ver. II (Feb. 2014), PP 40-45 Accounting Of Intangible Assets Indian as- 26 Manpreet Sharma,

EN Official Journal of the European Union L 320/373

29.11.2008 EN Official Journal of the European Union L 320/373 INTERNATIONAL FINANCIAL REPORTING STANDARD 3 Business combinations OBJECTIVE 1 The objective of this IFRS is to specify the financial reporting

29.11.2008 EN Official Journal of the European Union L 320/373 INTERNATIONAL FINANCIAL REPORTING STANDARD 3 Business combinations OBJECTIVE 1 The objective of this IFRS is to specify the financial reporting

Implementing the New Lease Guidance

Implementing the New Lease Guidance October 22, 2018 2018 Crowe LLP 2018 Crowe LLP Agenda Background Scope Effective dates & transition requirements Lessee accounting model Lessor accounting model Specialized

Implementing the New Lease Guidance October 22, 2018 2018 Crowe LLP 2018 Crowe LLP Agenda Background Scope Effective dates & transition requirements Lessee accounting model Lessor accounting model Specialized

Selling the Privately Held Company

Selling the Privately Held Company Tuesday, January 15, 2013 Boston Bar Association Continuing Legal Education www.bostonbar.org/edu/cle SELLING THE PRIVATELY HELD COMPANY By: Steven C. Browne, Gitte J.

Selling the Privately Held Company Tuesday, January 15, 2013 Boston Bar Association Continuing Legal Education www.bostonbar.org/edu/cle SELLING THE PRIVATELY HELD COMPANY By: Steven C. Browne, Gitte J.

M&A in Canada: Private Company Acquisitions

M&A in Canada: Private Company Acquisitions Stikeman Elliott LLP M&A in Canada: Private Company Acquisitions Asset Purchase or Share Purchase?... 2 Non-tax considerations... 2 Tax considerations... 3 Legal

M&A in Canada: Private Company Acquisitions Stikeman Elliott LLP M&A in Canada: Private Company Acquisitions Asset Purchase or Share Purchase?... 2 Non-tax considerations... 2 Tax considerations... 3 Legal

The Sliding Scale of Representations and Warranties Negotiating Representations and Warranties when Buying or Selling a Business (or Real Property)

") The Sliding Scale of Representations and Warranties Negotiating Representations and Warranties when Buying or Selling a Business (or Real Property) Ty Hunter Sheehan, Esq. Hornberger Sheehan Fuller & Garza

The Sliding Scale of Representations and Warranties Negotiating Representations and Warranties when Buying or Selling a Business (or Real Property) Ty Hunter Sheehan, Esq. Hornberger Sheehan Fuller & Garza

Report on 2018 Second Quarter Operating and Financial Results

Report on 2018 Second Quarter Operating and Financial Results Forward-Looking Statements This press release includes "forward-looking statements." These statements are subject to a number of risks, uncertainties

Report on 2018 Second Quarter Operating and Financial Results Forward-Looking Statements This press release includes "forward-looking statements." These statements are subject to a number of risks, uncertainties

M&A STRUCTURE/ANATOMY OF A TRANSACTION PRESENTATION OUTLINE. December 6, 2016

M&A STRUCTURE/ANATOMY OF A TRANSACTION PRESENTATION OUTLINE December 6, 2016 1. HOW TO STRUCTURE A TRANSACTION DEAL TYPES AND CONSIDERATION a. Main types = Asset purchase, stock purchase and merger. Structure

M&A STRUCTURE/ANATOMY OF A TRANSACTION PRESENTATION OUTLINE December 6, 2016 1. HOW TO STRUCTURE A TRANSACTION DEAL TYPES AND CONSIDERATION a. Main types = Asset purchase, stock purchase and merger. Structure

$450,000 $63,425 $39, % PURCHASE PRICE NET OPERATING INCOME ANNUAL CASH FLOW CAP RATE

Executive Summary Key Property Metrics $450,000 $63,425 $39,143 14.1% PURCHASE PRICE NET OPERATING INCOME ANNUAL CASH FLOW CAP RATE $70,000 $60,000 $50,000 $40,000 $30,000 Annual Cash Flow Repairs, 8%

Executive Summary Key Property Metrics $450,000 $63,425 $39,143 14.1% PURCHASE PRICE NET OPERATING INCOME ANNUAL CASH FLOW CAP RATE $70,000 $60,000 $50,000 $40,000 $30,000 Annual Cash Flow Repairs, 8%

DISCLOSEABLE TRANSACTION

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness

Business Valuations in the Planned Giving Context

Business Valuations in the Planned Giving Context 38 th Annual Minnesota Planned Giving Conference November 4, 2014 Presented by: Richard C. Berning, CPA/ABV/CFF, CBA, CVA, ABAR, CMA Copyright 2014: Berning

Business Valuations in the Planned Giving Context 38 th Annual Minnesota Planned Giving Conference November 4, 2014 Presented by: Richard C. Berning, CPA/ABV/CFF, CBA, CVA, ABAR, CMA Copyright 2014: Berning

11 Essential Steps to Purchasing or Selling Your Veterinary Practice

11 Essential Steps to Purchasing or Selling Your Veterinary Practice The attorneys on the Veterinary Practice team of Mandelbaum Salsburg, led by Peter Tanella, have represented many veterinarians in the

11 Essential Steps to Purchasing or Selling Your Veterinary Practice The attorneys on the Veterinary Practice team of Mandelbaum Salsburg, led by Peter Tanella, have represented many veterinarians in the

EDGEFRONT REALTY CORP. MANAGEMENT S DISCUSSION AND ANALYSIS For the three-month period ended March 31, 2013

EDGEFRONT REALTY CORP. MANAGEMENT S DISCUSSION AND ANALYSIS For the three-month period ended March 31, 2013 May 30, 2013 MANAGEMENT S DISCUSSION AND ANALYSIS The following management s discussion and analysis

EDGEFRONT REALTY CORP. MANAGEMENT S DISCUSSION AND ANALYSIS For the three-month period ended March 31, 2013 May 30, 2013 MANAGEMENT S DISCUSSION AND ANALYSIS The following management s discussion and analysis

IFRS - 3. Business Combinations. By:

IFRS - 3 Business Combinations Objective 1. The purpose of this IFRS is to specify to disclose financial information by an entity when carrying out a business combination. In particular, specifies that

IFRS - 3 Business Combinations Objective 1. The purpose of this IFRS is to specify to disclose financial information by an entity when carrying out a business combination. In particular, specifies that

EARNOUT PROVISIONS Bridging the Valuation Gap April 28, 2014

EARNOUT PROVISIONS Bridging the Valuation Gap April 28, 2014 Erik A. Lopez AGENDA Earnout Provisions I. Introduction II. Determining Whether to Use an Earnout III. How to Measure Performance IV. Payment

EARNOUT PROVISIONS Bridging the Valuation Gap April 28, 2014 Erik A. Lopez AGENDA Earnout Provisions I. Introduction II. Determining Whether to Use an Earnout III. How to Measure Performance IV. Payment

Intangibles CHAPTER CHAPTER OBJECTIVES. After careful study of this chapter, you will be able to:

CHAPTER Intangibles CHAPTER OBJECTIVES After careful study of this chapter, you will be able to: 1. Explain the accounting alternatives for intangibles. 2. Record the amortization or impairment of intangibles.

CHAPTER Intangibles CHAPTER OBJECTIVES After careful study of this chapter, you will be able to: 1. Explain the accounting alternatives for intangibles. 2. Record the amortization or impairment of intangibles.

Intangible Assets IAS 38, IAS 36, IFRS 3

Intangible Assets IAS 38, IAS 36, IFRS 3 Agenda 1. Introduction 2. Recognition 3. Measurement 4. Impairment of intangible assets (IAS 36) Basic concept Cash-Generating Units 5. Disclosures 2 1 Introduction

Intangible Assets IAS 38, IAS 36, IFRS 3 Agenda 1. Introduction 2. Recognition 3. Measurement 4. Impairment of intangible assets (IAS 36) Basic concept Cash-Generating Units 5. Disclosures 2 1 Introduction

Tenant: Law Firm 4 NAICS: Primary Industry: Offices of lawyers

Tenant: Law Firm 4 NAICS: 541110 Primary Industry: Offices of lawyers Date: 05.25.17 Table of Contents Law Firm 4 132 Main Street TABLE OF CONTENTS TIL Score Executive Summary Tenant Score Information

Tenant: Law Firm 4 NAICS: 541110 Primary Industry: Offices of lawyers Date: 05.25.17 Table of Contents Law Firm 4 132 Main Street TABLE OF CONTENTS TIL Score Executive Summary Tenant Score Information

Technical Line SEC staff guidance

No. 2013-20 Updated 27 August 2015 Technical Line SEC staff guidance How to apply S-X Rule 3-14 to real estate acquisitions In this issue: Overview... 1 Applicability of Rule 3-14... 2 Measuring significance...

No. 2013-20 Updated 27 August 2015 Technical Line SEC staff guidance How to apply S-X Rule 3-14 to real estate acquisitions In this issue: Overview... 1 Applicability of Rule 3-14... 2 Measuring significance...

AUDIT A GUIDE TO ACCOUNTING FOR BUSINESS COMBINATIONS. Third Edition

AUDIT A GUIDE TO ACCOUNTING FOR BUSINESS COMBINATIONS Third Edition A GUIDE TO ACCOUNTING FOR BUSINESS COMBINATIONS THIRD EDITION June 2016 A GUIDE TO ACCOUNTING FOR BUSINESS COMBINATIONS Prepared by:

AUDIT A GUIDE TO ACCOUNTING FOR BUSINESS COMBINATIONS Third Edition A GUIDE TO ACCOUNTING FOR BUSINESS COMBINATIONS THIRD EDITION June 2016 A GUIDE TO ACCOUNTING FOR BUSINESS COMBINATIONS Prepared by:

STAATSKOERANT, 6 MEI 2015 No CODE SERIES 100: THE MEASUREMENT OF THE OWNERSHIP ELEMENT OF BROAD- BASED BLACK ECONOMIC EMPOWERMENT

STAATSKOERANT, 6 MEI 2015 No. 38766 23 CODE SERIES 100: THE MEASUREMENT OF THE OWNERSHIP ELEMENT OF BROAD- BASED BLACK ECONOMIC EMPOWERMENT STATEMENT 102: RECOGNITION OF THE SALE OF ASSETS, EQUITY INSTRUMENTS,

STAATSKOERANT, 6 MEI 2015 No. 38766 23 CODE SERIES 100: THE MEASUREMENT OF THE OWNERSHIP ELEMENT OF BROAD- BASED BLACK ECONOMIC EMPOWERMENT STATEMENT 102: RECOGNITION OF THE SALE OF ASSETS, EQUITY INSTRUMENTS,

IFRS 3 Business Combinations

IFRS 3 Business Combinations 0 Objectives Define a business combination under IFRS 3 (Revised 2008) Describe the steps in applying the acquisition method Explain the recognition and measurement principles

IFRS 3 Business Combinations 0 Objectives Define a business combination under IFRS 3 (Revised 2008) Describe the steps in applying the acquisition method Explain the recognition and measurement principles

Definitions. CPI is a lease in which base rent is adjusted based on changes in a consumer price index.

Annualized Rental Income is rental revenue under our leases on Operating Properties on a straight-line basis, which includes the effect of rent escalations and any tenant concessions, such as free rent,

Annualized Rental Income is rental revenue under our leases on Operating Properties on a straight-line basis, which includes the effect of rent escalations and any tenant concessions, such as free rent,

CHOICE PROPERTIES REAL ESTATE INVESTMENT TRUST. Management s Discussion and Analysis of Financial Condition and Results of Operations

CHOICE PROPERTIES REAL ESTATE INVESTMENT TRUST Management s Discussion and Analysis of Financial Condition and Results of Operations (in thousands of Canadian dollars except where otherwise indicated)

CHOICE PROPERTIES REAL ESTATE INVESTMENT TRUST Management s Discussion and Analysis of Financial Condition and Results of Operations (in thousands of Canadian dollars except where otherwise indicated)

Carve-Out Transactions: Strategies for Due Diligence and Structuring the Deal

Presenting a live 90-minute webinar with interactive Q&A Carve-Out Transactions: Strategies for Due Diligence and Structuring the Deal WEDNESDAY, JUNE 28, 2017 1pm Eastern 12pm Central 11am Mountain 10am

Presenting a live 90-minute webinar with interactive Q&A Carve-Out Transactions: Strategies for Due Diligence and Structuring the Deal WEDNESDAY, JUNE 28, 2017 1pm Eastern 12pm Central 11am Mountain 10am

M&A ACADEMY REPRESENTATIONS AND WARRANTIES TRAINING. Presenters: Gitte Blanchet & Erin Morley November 10, 2015

M&A ACADEMY REPRESENTATIONS AND WARRANTIES TRAINING Presenters: Gitte Blanchet & Erin Morley November 10, 2015 2015 Morgan, Lewis & Bockius LLP Topics to Be Covered 1. The Basics Understanding representations

M&A ACADEMY REPRESENTATIONS AND WARRANTIES TRAINING Presenters: Gitte Blanchet & Erin Morley November 10, 2015 2015 Morgan, Lewis & Bockius LLP Topics to Be Covered 1. The Basics Understanding representations

Accounting B LECTURE 1: NON-CURRENT ASSETS. Recording, expensing and reporting non-current assets

Accounting B LECTURE 1: NON-CURRENT ASSETS Recording, expensing and reporting non-current assets - Asset: a resource controlled by an entity because of past events and from which future economic benefits

Accounting B LECTURE 1: NON-CURRENT ASSETS Recording, expensing and reporting non-current assets - Asset: a resource controlled by an entity because of past events and from which future economic benefits

Mergers & Acquisitions

Mergers & Acquisitions A new approach to professional services Oury Clark Page 1 Mergers & Acquisitions Successfully growing, selling or restructuring a business can The successful execution of corporate

Mergers & Acquisitions A new approach to professional services Oury Clark Page 1 Mergers & Acquisitions Successfully growing, selling or restructuring a business can The successful execution of corporate

NEGOTIATING M&A ESCROW AGREEMENTS

CHECKLISTS NEGOTIATING M&A ESCROW AGREEMENTS This Checklist sets out the key negotiated issues between a buyer and seller in an escrow agreement entered into in connection with an M&A transaction. It also

CHECKLISTS NEGOTIATING M&A ESCROW AGREEMENTS This Checklist sets out the key negotiated issues between a buyer and seller in an escrow agreement entered into in connection with an M&A transaction. It also

Introduction. Due Diligence

Introduction When purchasing a business or company, the prospective purchaser must turn his or her mind to a number of preliminary issues. This introduction is intended to point out those issues and highlight

Introduction When purchasing a business or company, the prospective purchaser must turn his or her mind to a number of preliminary issues. This introduction is intended to point out those issues and highlight

Current Developments. FASB, AICPA and SEC. Jim Brendel, CPA, CFE March 1, 2013

Current Developments FASB, AICPA and SEC Jim Brendel, CPA, CFE March 1, 2013 Agenda FASB Developments Selected Projects and Initiatives Revenue Recognition Leases Impairment of Intangible Assets Other

Current Developments FASB, AICPA and SEC Jim Brendel, CPA, CFE March 1, 2013 Agenda FASB Developments Selected Projects and Initiatives Revenue Recognition Leases Impairment of Intangible Assets Other

Purchase Price Allocations ASC 805 Business Combinations

Purchase Price Allocations Introduction Mergers, acquisitions, and other business transactions have numerous accounting and tax implications. Buyers generally identify and report the fair values of the

Purchase Price Allocations Introduction Mergers, acquisitions, and other business transactions have numerous accounting and tax implications. Buyers generally identify and report the fair values of the

Business Combinations IFRS 3

CA Sandesh Mundra Business Combinations IFRS 3 For many men, the acquisition of wealth does not end their troubles, it only changes them. - Lucius Annaeus Seneca Lets get some of the basics correct.. We

CA Sandesh Mundra Business Combinations IFRS 3 For many men, the acquisition of wealth does not end their troubles, it only changes them. - Lucius Annaeus Seneca Lets get some of the basics correct.. We

(Incorporated in the Cayman Islands with limited liability) (Stock Code: 896) MAJOR TRANSACTION

(Stock Code: 896) MAJOR TRANSACTION") Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness

Topic 842 Technical Corrections Summary of Comments Received

Contact(s) David Hoyer Co-Author Ext. 462 Andy Bologna Co-Author Ext. 356 Thomas Faineteau Co-Author Ext. 362 Chris Roberge Co-Author Ext. 274 Amy Park Co-Author Ext. 476 Shayne Kuhaneck Assistant Director

Contact(s) David Hoyer Co-Author Ext. 462 Andy Bologna Co-Author Ext. 356 Thomas Faineteau Co-Author Ext. 362 Chris Roberge Co-Author Ext. 274 Amy Park Co-Author Ext. 476 Shayne Kuhaneck Assistant Director

BALTIC M&A DEAL POINTS STUDY 2018

BALTIC M&A DEAL POINTS STUDY Baltic M&A Deal Points Study This fifth edition of the Baltic M&A Deal Points Study is conducted by the legal and regulatory committees and working groups of the: Estonian

BALTIC M&A DEAL POINTS STUDY Baltic M&A Deal Points Study This fifth edition of the Baltic M&A Deal Points Study is conducted by the legal and regulatory committees and working groups of the: Estonian

Achieved record annual revenues of $110.0 million for 2018, representing an increase of 5.8%

Clipper Realty Inc. Announces Fourth Quarter and Full-Year 2018 Results Reports Record Annual Revenues, Record Annual Income from Operations and Record Quarterly and Annual Adjusted Funds from Operations

Clipper Realty Inc. Announces Fourth Quarter and Full-Year 2018 Results Reports Record Annual Revenues, Record Annual Income from Operations and Record Quarterly and Annual Adjusted Funds from Operations

the property situated at 51 Shipyard Crescent Singapore (the Property ); and

; and") PROPOSED ACQUISITION OF ASSETS 1. INTRODUCTION 1.1 The board of directors (the Board ) of T T J Holdings Limited (the Company, and together with its subsidiaries, the Group ) wishes to announce that T

PROPOSED ACQUISITION OF ASSETS 1. INTRODUCTION 1.1 The board of directors (the Board ) of T T J Holdings Limited (the Company, and together with its subsidiaries, the Group ) wishes to announce that T

United States Negotiated M&A Guide

United States Negotiated M&A Guide Corporate and M&A Law Committee Contact Donald E. Batterson Jenner & Block LLP Chicago, USA dbatterson@jenner.com Legal Framework The statutory law and common law (that

United States Negotiated M&A Guide Corporate and M&A Law Committee Contact Donald E. Batterson Jenner & Block LLP Chicago, USA dbatterson@jenner.com Legal Framework The statutory law and common law (that

COMMERCIAL REAL ESTATE PURCHASE AGREEMENT AND DEPOSIT RECEIPT. This Real Estate Purchase Agreement and Deposit Receipt ( Agreement ) is made between:

is made between:") LOSS REALTY GROUP COMMERCIAL REAL ESTATE PURCHASE AGREEMENT AND DEPOSIT RECEIPT This Real Estate Purchase Agreement and Deposit Receipt ( Agreement ) is made between: a(n), having an address of ( Buyer

LOSS REALTY GROUP COMMERCIAL REAL ESTATE PURCHASE AGREEMENT AND DEPOSIT RECEIPT This Real Estate Purchase Agreement and Deposit Receipt ( Agreement ) is made between: a(n), having an address of ( Buyer

Business Combination. CA Yagnesh Desai. Compiled by CA Yagnesh 1

Business Combination CA Yagnesh Desai ymdesaiandco@gmail.com 093222 44770 09820133227 yagnesh@caymd.com 1 Indicators Not necessarily Limits by the Standard Above 50 % Control Hence Consolidate Control

Business Combination CA Yagnesh Desai ymdesaiandco@gmail.com 093222 44770 09820133227 yagnesh@caymd.com 1 Indicators Not necessarily Limits by the Standard Above 50 % Control Hence Consolidate Control

Long-Term Assets C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM

Long-Term Assets E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information, in addition to the material

Long-Term Assets E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information, in addition to the material

Buying and Selling Commercial Property

Building & Construction Level 5, Evandale Place Buying and Selling Commercial Property Buying and Selling Commercial Property Purchasing or selling commercial property can be complex. Consideration needs

Building & Construction Level 5, Evandale Place Buying and Selling Commercial Property Buying and Selling Commercial Property Purchasing or selling commercial property can be complex. Consideration needs

Historic Tax Credit Presentation Date: March 22, 2016

Historic Tax Credit Presentation Date: March 22, 2016 Today s Presenter(s): Lynn Wickham Hartman (319) 896-4083 lhartman@simmonsperrine.com Matthew J. Hektoen (319) 896-4030 mhektoen@simmonsperrine.com

Historic Tax Credit Presentation Date: March 22, 2016 Today s Presenter(s): Lynn Wickham Hartman (319) 896-4083 lhartman@simmonsperrine.com Matthew J. Hektoen (319) 896-4030 mhektoen@simmonsperrine.com

U.S. Department of Housing and Urban Development Community Planning and Development

U.S. Department of Housing and Urban Development Community Planning and Development Special Attention of: Notice: CPD 98-1 All Secretary's Representatives All State/Area Coordinators Issued: January 22,

U.S. Department of Housing and Urban Development Community Planning and Development Special Attention of: Notice: CPD 98-1 All Secretary's Representatives All State/Area Coordinators Issued: January 22,

Capital Assets, Supplies, Equipment, and Intangible Property

Capital Assets, Supplies, Equipment, and Intangible Property 1 Uniform Guidance vs. OMB Circulars Prior to the Uniform Guidance, requirements governing cost Designed for DOL-ETA direct principles, administrative

Capital Assets, Supplies, Equipment, and Intangible Property 1 Uniform Guidance vs. OMB Circulars Prior to the Uniform Guidance, requirements governing cost Designed for DOL-ETA direct principles, administrative

VALUATION OF GOODWILL FOR TAX PURPOSES

1 VALUATION OF GOODWILL FOR TAX PURPOSES James P. Catty President, Corporate Valuation Services Limited Chair, International Association of Consultants, Valuators and Analysts 2 All businesses have these

1 VALUATION OF GOODWILL FOR TAX PURPOSES James P. Catty President, Corporate Valuation Services Limited Chair, International Association of Consultants, Valuators and Analysts 2 All businesses have these

Trends in M&A Provisions: Sandbagging and Anti-Sandbagging Provisions

Trends in M&A Provisions: Sandbagging and Anti-Sandbagging Provisions March 5, 2018 Bloomberg Law Reproduced with permission from Bloomberg Law. Copyright 2018 by The Bureau of National Affairs, Inc. (800-372-1033)

Trends in M&A Provisions: Sandbagging and Anti-Sandbagging Provisions March 5, 2018 Bloomberg Law Reproduced with permission from Bloomberg Law. Copyright 2018 by The Bureau of National Affairs, Inc. (800-372-1033)

DEAL LAWYERS. Assessing the Locked Box Approach to Purchase Price Adjustments

DEAL LAWYERS Vol. 6, No. 2 Assessing the Locked Box Approach to Purchase Price Adjustments By William Lawlor and Eric Siegel, Partners of Dechert LLP Certainty? In this world nothing is certain except

DEAL LAWYERS Vol. 6, No. 2 Assessing the Locked Box Approach to Purchase Price Adjustments By William Lawlor and Eric Siegel, Partners of Dechert LLP Certainty? In this world nothing is certain except

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N AGENDA Leases FASB & GASB Revenue Recognition FASB 2 FASB ASU 2016-02, Leases (Topic

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N AGENDA Leases FASB & GASB Revenue Recognition FASB 2 FASB ASU 2016-02, Leases (Topic

THE ART OF BUSINESS VALUATION

BUSINESS VALUATIONS GROWING THE ART OF BUSINESS VALUATION Douglas A. Michel, CPA/ABV, CVA & Alex E. Kummer, CPA, CVA, Clark Schaefer Hackett THE VALUE OF YOUR BUSINESS Steve Lumley, LGI CFO BUY SELL AGREEMENTS

BUSINESS VALUATIONS GROWING THE ART OF BUSINESS VALUATION Douglas A. Michel, CPA/ABV, CVA & Alex E. Kummer, CPA, CVA, Clark Schaefer Hackett THE VALUE OF YOUR BUSINESS Steve Lumley, LGI CFO BUY SELL AGREEMENTS

Leases. (a) the lease transfers ownership of the asset to the lessee by the end of the lease term.

the lease transfers ownership of the asset to the lessee by the end of the lease term.") Leases 1.1. Classification of leases A lease is classified as a finance lease if it transfers substantially all the risks and rewards incidental to ownership. A lease is classified as an operating lease

Leases 1.1. Classification of leases A lease is classified as a finance lease if it transfers substantially all the risks and rewards incidental to ownership. A lease is classified as an operating lease

AMENDED FINAL PURCHASE AND SALE AGREEMENT

AMENDED FINAL PURCHASE AND SALE AGREEMENT THIS PURCHASE AGREEMENT (the Agreement ) is dated for reference the 6th day of September, 2012 (the Effective Date ) and supersedes all other agreements made between

AMENDED FINAL PURCHASE AND SALE AGREEMENT THIS PURCHASE AGREEMENT (the Agreement ) is dated for reference the 6th day of September, 2012 (the Effective Date ) and supersedes all other agreements made between

The Allure And Pitfalls Of Earnouts: Part 2

Portfolio Media. Inc. 111 West 19 th Street, 5th Floor New York, NY 10011 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com The Allure And Pitfalls Of Earnouts: Part

Portfolio Media. Inc. 111 West 19 th Street, 5th Floor New York, NY 10011 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com The Allure And Pitfalls Of Earnouts: Part

Negative Goodwill and Bargain Purchases in Merger Models. An Extraordinary Gain to Go, Please

Negative Goodwill and Bargain Purchases in Merger Models An Extraordinary Gain to Go, Please Negative Goodwill and Bargain Purchases Can you explain what happens in an M&A deal if the Equity Purchase Price

Negative Goodwill and Bargain Purchases in Merger Models An Extraordinary Gain to Go, Please Negative Goodwill and Bargain Purchases Can you explain what happens in an M&A deal if the Equity Purchase Price

ARTICLE III. COMPUTATION OF EBITDA

Earnout Agreement 125 No interest is included on the deferred payments under this Agreement. A seller may wish to bargain for interest from the closing date on the basis that the earnout payments represent

Earnout Agreement 125 No interest is included on the deferred payments under this Agreement. A seller may wish to bargain for interest from the closing date on the basis that the earnout payments represent

CONSOLIDATED FINANCIAL STATEMENTS

CONSOLIDATED FINANCIAL STATEMENTS Dundee Real Estate Investment Trust Consolidated Balance Sheets (unaudited) June 30, December 31, (in thousands of dollars) Note 2004 2003 Assets Rental properties 3,4

CONSOLIDATED FINANCIAL STATEMENTS Dundee Real Estate Investment Trust Consolidated Balance Sheets (unaudited) June 30, December 31, (in thousands of dollars) Note 2004 2003 Assets Rental properties 3,4

Accounting for Tangible Capital Assets

Accounting for Tangible Capital Assets Date Approved by Board: 2011.11.17 Resolution No.: 11-113 2016.05.19 16-048 Lead Role: CFO Replaces: N/A Last Review Date: N/A Next Review Date: 2019.05.19 Policy

Accounting for Tangible Capital Assets Date Approved by Board: 2011.11.17 Resolution No.: 11-113 2016.05.19 16-048 Lead Role: CFO Replaces: N/A Last Review Date: N/A Next Review Date: 2019.05.19 Policy

SECURITIES AND EXCHANGE COMMISSION. Washington, D.C FORM 8-K CURRENT REPORT

SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 8-K CURRENT REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Date of Report (Date of earliest event reported):

SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 8-K CURRENT REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Date of Report (Date of earliest event reported):

The Value of a Master Lease

The Value of a Master Lease January 05, 2009 In today's economic climate, commercial real estate owners are finding themselves forced to creatively position their properties to entice buyers or satisfy

The Value of a Master Lease January 05, 2009 In today's economic climate, commercial real estate owners are finding themselves forced to creatively position their properties to entice buyers or satisfy

Selling Your Ophthalmology Practice. Financial Interest Disclosure 5/2/2016. Mark E. Kropiewnicki, Esquire, LLM* Daniel M. Bernick, Esquire, MBA*

Selling Your Ophthalmology Practice Mark E. Kropiewnicki, Esquire, LLM* Daniel M. Bernick, Esquire, MBA* The Health Care Group Plymouth Meeting, PA www.healthcaregroup.com * Financial Interest Financial

Selling Your Ophthalmology Practice Mark E. Kropiewnicki, Esquire, LLM* Daniel M. Bernick, Esquire, MBA* The Health Care Group Plymouth Meeting, PA www.healthcaregroup.com * Financial Interest Financial

Preparing for Negotiations: The Environmental Lawyer s Checklist In Oil and Gas Transactions

Preparing for Negotiations: The Environmental Lawyer s Checklist In Oil and Gas Transactions Presented by Jim Morriss Thompson & Knight LLP james.morriss@tklaw.com The Process Drives the Checklist Confidentiality

Preparing for Negotiations: The Environmental Lawyer s Checklist In Oil and Gas Transactions Presented by Jim Morriss Thompson & Knight LLP james.morriss@tklaw.com The Process Drives the Checklist Confidentiality

Rehabilitation Tax Credits

Rehabilitation Tax Credits Selected Issues in Master Lease Pass-Through Transactions Steven L. Paul Nicholas Romanos February 1, 2010 REHABILITATION TAX CREDITS Selected Issues in Master Lease Pass-Through

Rehabilitation Tax Credits Selected Issues in Master Lease Pass-Through Transactions Steven L. Paul Nicholas Romanos February 1, 2010 REHABILITATION TAX CREDITS Selected Issues in Master Lease Pass-Through

CHECKLIST Sale & Purchase of Business

CHECKLIST Sale & Purchase of Business Buying a business isn t as easy as it sounds. Whether you re buying or selling, make sure you deal with these essential tasks. Our team of commercial lawyers have

CHECKLIST Sale & Purchase of Business Buying a business isn t as easy as it sounds. Whether you re buying or selling, make sure you deal with these essential tasks. Our team of commercial lawyers have

$450,000 $63,425 $33, % PURCHASE PRICE NET OPERATING INCOME ANNUAL CASH FLOW CAP RATE

Executive Summary Key Property Metrics $450,000 $63,425 $33,431 14.1% PURCHASE PRICE NET OPERATING INCOME ANNUAL CASH FLOW CAP RATE $60,000 $50,000 $40,000 $30,000 Annual Cash Flow Maintenance & Repairs,

Executive Summary Key Property Metrics $450,000 $63,425 $33,431 14.1% PURCHASE PRICE NET OPERATING INCOME ANNUAL CASH FLOW CAP RATE $60,000 $50,000 $40,000 $30,000 Annual Cash Flow Maintenance & Repairs,

Utility M&A: A Case Study in the Sale of a Utility s Service Area

Utility M&A: A Case Study in the Sale of a Utility s Service Area NARUC Accounting and Finance Meeting, March 8, 2016 Victor Prep, P.E. Byron S. Watson, CFA Denver, Colorado www.ergconsulting.com 2016,

Utility M&A: A Case Study in the Sale of a Utility s Service Area NARUC Accounting and Finance Meeting, March 8, 2016 Victor Prep, P.E. Byron S. Watson, CFA Denver, Colorado www.ergconsulting.com 2016,

Chapter 8 VALUATION OF AND INFORMATION ON PROPERTIES. Definitions

Chapter 8 VALUATION OF AND INFORMATION ON PROPERTIES Definitions 8.01 In this Chapter:- (1) carrying amount means, for an applicant, the amount at which an asset is recognised in the most recent audited

Chapter 8 VALUATION OF AND INFORMATION ON PROPERTIES Definitions 8.01 In this Chapter:- (1) carrying amount means, for an applicant, the amount at which an asset is recognised in the most recent audited

Center for Plain English Accounting AICPA s National A&A Resource Center available exclusively to PCPS members

REPORT February 22, 2017 Center for Plain English Accounting AICPA s National A&A Resource Center available exclusively to PCPS members ASU 2017-04: Goodwill Simplifications Implementation Considerations

REPORT February 22, 2017 Center for Plain English Accounting AICPA s National A&A Resource Center available exclusively to PCPS members ASU 2017-04: Goodwill Simplifications Implementation Considerations

Clipper Realty Inc. Announces Third Quarter 2018 Results Reports Record Revenues, Income From Operations and Adjusted Funds From Operations

Clipper Realty Inc. Announces Third Quarter 2018 Results Reports Record Revenues, Income From Operations and Adjusted Funds From Operations NEW YORK, November 1, 2018 /Business Wire/ -- Clipper Realty

Clipper Realty Inc. Announces Third Quarter 2018 Results Reports Record Revenues, Income From Operations and Adjusted Funds From Operations NEW YORK, November 1, 2018 /Business Wire/ -- Clipper Realty