Utility M&A: A Case Study in the Sale of a Utility s Service Area

|

|

|

- Sharleen Lynch

- 5 years ago

- Views:

Transcription

1 Utility M&A: A Case Study in the Sale of a Utility s Service Area NARUC Accounting and Finance Meeting, March 8, 2016 Victor Prep, P.E. Byron S. Watson, CFA Denver, Colorado ,

2 Introduction o Victor Prep, P.E. Executive Consultant BSME from OU, MBA from Univ. of PA, Wharton Registered P.E. in CO, LA, and PA, and Certified Energy Manager Retired Nuclear Submarine Naval Officer o Byron S. Watson, CFA, CRRA Senior Consultant BSEE from SMU, MBA from Emory University o Members of the Firm act as Advisors to the Council of the City of New Orleans ( Council ). Our Services as Advisors are in Certain Ways Comparable to Those of a Commission s Staff 1

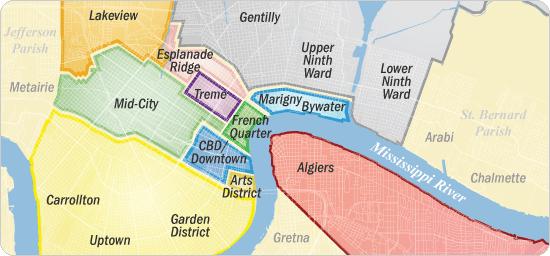

3 Introduction: Background Map of New Orleans 2

4 Introduction: Background o Prior to September 1, 2015, Retail Electric Service in the City of New Orleans was Provided by two Separate Entergy Operating Companies In the 15 th Ward of New Orleans (a.k.a. Algiers or the West Bank ), Entergy Louisiana, LLC ( ELL or Seller ) Provided Retail Electric Service to 22,187 Customers In New Orleans, Except for Algiers, Entergy New Orleans, Inc. ( ENO or Seller ) Provided Retail Electric Service to 169,856 Customers o The Council was the Retail Regulator of both Utilities Each Utility had Separate and Different Rates, a Different Allowed ROE, and Separate Rate Actions Before the Council Each Utility Owned or Contracted for its own Generating Capacity, Largely From Different Generating Units Each Utility had Separate Transmission and Distribution Plant O&M-Related Services Were Provided to Both Utilities by a Single Energy Subsidiary (Entergy Services, Inc.) 3

5 Introduction: Background o As a Result of Negotiations, Seller (ELL) Agreed to Transfer its Electric Service Operations to Buyer (ENO) and Also Sell Related Utility Plant and Rights to Generating Capacity Buyer Would Become the Single Retail Electric Utility Provider for All of New Orleans The Council Would be the Retail Regulator of One Electric Utility, the Buyer, and Would No Longer Regulate the Seller Buyer Would own, Operate, and Maintain all Electric Utility Plant Previously Owned by Seller in Algiers Franchise Rights to Operate in New Orleans Would be Transferred form Seller to Buyer Buyer Would Enter into a Purchased Power Agreement (PPA) with Seller to Continue Access to an Agreed-Upon Portion of Seller s Generating Resources 4

6 Introduction: Background o On October 30, 2014, Buyer and Seller Jointly Filed for Approval to: Sell Seller s Assets Located in Algiers to Buyer at Net Book Value Transfer all Franchise Rights to Provide Retail Service to Buyer so that Seller Would Have no Remaining Operations in New Orleans Create a New PPA Providing Buyer a Slice of Seller s Generating Fleet Capacity and Energy (1.84% of Each of Seller s Units for the Life of Each Unit) Leave Retail Base Rates Unchanged (i.e., Two Separate Rate Structures) Until a Later Combined Rate Case Could Set a New Single Set of Retail Rates for All of New Orleans Receive other Related Relief, Such as Modifications to Franchises o The Filing s Requested Relief was Collectively Called the Algiers Transaction ( Transaction ) o Separately, ELL (Seller) and Another Entergy Operating Company, Entergy Operating Company, Entergy Gulf States Louisiana, L.L.C. ( EGSL ) were Merging Closing the Merger After the Transaction was Critical 5

7 I. PUBLIC GOOD THE CASE FOR REGULATORY CONSOLIDATION 6

8 Net Ratepayer Savings o Increased Costs are Offset by Administrative Savings Averaging an Estimated $1.6 million per Year Regulation at both the FERC and in Local Jurisdiction Avoided Duplicative Rate Cases and FRP Evaluations o Annual Revenue Requirement Related to Service Algiers is Expected to Increase by Approximately $1.5 Million (Average) Algiers PPA is Based on FERC ROE of 11% vs. Seller s Allowed ROE of 9.95%. FERC May Reduce the ROE as Part of Docket ER Recovery of Transaction Implementation Costs Increased Costs Related to Changes in Participation in RTO Markets o Net Measurable and Expected Ratepayer Savings Average Approximately $0.1 Million Annually o Additional Ratepayer Savings Related to Future Regulatory Actions Difficult to Quantify 7

9 Advantages Other o Reduce Customer Confusion Relating to Differing Rates and Rate Schedules in the Same City o Eliminate Uneconomic Signals Presented by Differing Commercial and Industrial Rates in Same Geographic Area o Eliminate any Perceived Inequity due to Different Allowed ROEs o Reduce Administrative Burden on Local Regulators o Fewer Interventions at FERC Proceedings o Allow Relatively Small Algiers to Participate in Economies Available to Larger Buyer Direct Ownership of Generating Units Securitization of Storm Costs Access to A Large (i.e., $75 Million ) Storm Reserve Our Review Suggested no new Procurement Economies 8

10 II. TRANSACTION SUMMARY 9

11 Transaction: Steps o Transaction in Three Steps, Each Occurring in Immediate Sequence o Step 1: Create New Subsidiary to Receive Plant Located in Algiers o A Key Transaction Objective was to Maintain Book Value Basis for Assets Sold to Buyer 10

12 Transaction: Steps o Step 2: Seller Sells the New Subsidiary to Buyer At Assets Net-book Value 11

13 Transaction: Steps o Step 3: Merge New Subsidiary into Buyer o Transaction Maintains Book Value for Assets 12

14 Transaction Balance Sheets Algiers Asset Summary Seller Balance Sheet Illustration ($000) Seller Pre- Transaction Algiers Assets Seller Additions to Algiers Assets Algiers LLC Account Categories / Titles Utility Plant 9,947,569 88,956 1,700 90,656 Accumulated Provision for Depreciation, Amort, Depl (3,943,655) (28,527) (28,527) Nuclear Fuel - Net 147,385 Net Utility Plant 6,151,299 60,429 1,700 62,129 Other Property and Investments 1,160,798 Current and Accrued Assets 680,844 3,500 3,500 Deferred Debits (Regulatory Assets) 2,371, ,698 24,575 Total Assets 10,364,217 64,806 25,398 90,204 Common Equity and Preferred Stock 2,975,652 60,051 60,051 Long-Term Debt 2,961,670 Other Noncurrent Liabilities 664,861 2,106 2,106 Current and Accrued Liabilities 368,612 Accumulated Deferred Income Tax 2,492,629 19,150 8,501 27,651 Deferred Credits 900, Total Liabilities and Stockholder Equity 10,364,217 21,652 68,552 90,204 13

15 Transaction Balance Sheets Algiers Asset Summary Buyer Balance Sheet Illustration ($000) Buyer Pre- Transaction Algiers LLC Buyer Post- Transaction Account Categories / Titles Utility Plant 1,141,404 90,656 1,232,060 Accumulated Provision for Depreciation, Amort, Depl (532,067) (28,527) (560,594) Net Utility Plant 609,337 62, ,466 Other Property and Investments 11,533 11,533 Current and Accrued Assets 143,942 3, ,442 Accumulated Deferred Income Tax - Step-up 27,651 27,651 Deferred Debits (Regulatory Assets) 201,784 24, ,359 Total Assets 966, ,855 1,084,451 Common Equity 226,063 28, ,338 Long-Term Debt 225,944 28, ,219 Other Noncurrent Liabilities 10,253 2,106 12,359 Current and Accrued Liabilities 121, ,274 Short-Term Debt (Money Pool or Credit Facility) 3,500 3,500 Accumulated Deferred Income Tax 27,651 27,651 Intercompany Payable (due to Seller) 27,651 27,651 Deferred Credits 383, ,459 Total Liabilities and Stockholder Equity 966, ,855 1,084,451 14

16 Tax Considerations o Transaction had to Close Prior to The ELL/EGSL Merger to Avoid Loss of ADIT and Related Tax Recapture (i.e., Maintain Tax Deferral Represented In ADIT Balance) o ADIT as Of Transaction Close Date Associated With Algiers Assets is Retained by Seller Seller Must Eventually Pay Taxes Equal to ADIT Buyer Must Eventually Pay Taxes Equal to any new ADIT That Accumulates After Transaction Close o Buyer Records Offsetting ADIT Debits And Credits Associated With Step-Up ADIT Substantially Equal to The Algiers Assets ADIT as of The Transaction Close (i.e., Zero Effect on Owner Equity) o Zero-Interest Note Payable From Buyer to Seller Equal to Step-Up ADIT. Intercompany Payable Recreates Effect of ADIT Liability on Buyer s Books and Compensates Seller for Increased Tax Liability 15

17 III. KEY ASPECTS OF TRANSACTION 16

18 Purchase Price o Purchase Price of Seller s Assets was Net Book Value Basis of Rate Base in Ratemaking, Provides Continuity Accumulated Depreciation Represents Capital Costs Already Recovered by Ratepayers, So a Higher Amount Could Result in Double-Recovery of Costs o Sale at Net-Book Value (Gross Cost less Accumulated Book Depreciation) Raises Tax Basis Pre-Transaction, Tax Basis of Assets Were Lower Than Book Basis Tax Basis is Increased by Related ADIT (Transaction Debits Tax Basis by ADIT Amount) ADIT Debit is Paid By Zero-interest Note of Same Amount Payable to Seller. Note Amortizes as ADIT Balance Reverses Neither ADIT Debit nor Note Payable are to be Included in Buyer s Future Rate Action Cost Studies 17

19 Evaluation Issues o Prior to the Transaction, the Cost to Provide Service in Algiers was Determined in Large Part by an Allocation of the Seller s Overall Costs Throughout its Entire Service Territory Algiers Represented About 2-3% of Seller s Overall Costs of Service o Also, Seller was in the Process of Merging with EGSL Merger was Scheduled to Close After the Transaction, in Part to Prevent a Taxable Gain on ADIT Step-Up o At the Time of the Transaction, Seller s Algiers Area was Subject to a FRP, With Four Annual Evaluations Remaining o Transaction Made Such FRP Evaluations Unfeasible Merger of Algiers Assets and Operations into Buyer s Accounts Fatally Clouds any Algiers-Specific Accounting o Parties Agreed to Suspend the Algiers FRP and Freeze Rates 18

20 Transaction Conditions o Conditions on Transaction Approval to Protect the Public Interest Buyer Not to Request Rate Action that Singles Out One Service Area, to Prevent Cherry Picking Service Areas to Maximize Revenues Rate Freeze Until the Mid-2018 Combined Rate Case Filing (Discussed Later) Transaction-related Changes To Algiers Base Rate Revenue Requirement are not Reflected in Rates Until the Combined Rate Case No Algiers FRP Evaluations (Discussed Later) Regulatory Cost Reduced By Eliminating Three FRP Evaluations Previously Scheduled in Recent Rate Case Settlement o Transaction Had to Close Prior to The ELL/EGSL to Avoid Loss of ADIT and Related Tax Recapture o ADIT Step-up and Intercompany Payable not to be Included in Future Buyer Rate Action Cost Studies 19

21 Rate Making Issues o The Transaction Closed On September 1, 2015 o The First Full-year Test Year Available for a Cost Of Service Study on Buyer s Combined Operations Would be CY 2016 In Our Experience, a Split-Year Test Year had Proven to be Problematic o Seller was in The Second Step of a 4-Step Annual Algiers Retail Rate Ramp-up Scheduled to Finish In 2017 At the End of the 4-step Rate Ramp-up, Algiers Rates Will be Roughly Comparable to Those Currently Charged by Buyer o In the Interest of Rate Stability, Parties Negotiated a Rate Freeze Through 2018, When a Combined Rate Case Based on a 2017 TY For the Buyer s Combined Operations May Set New Rates 20

22 Interim Ratemaking Issues o Until New Rates can be Established for all of New Orleans Through a Combined Rate Case, the Following Interim Provisions Were Adopted A Combined Fuel Adjustment Clause Important Rate Differences Between Algiers and Buyer s Original Service Area A Combined (Blended) Environmental Adjustment Clause Separate RTO (i.e., MISO) Cost Recovery Riders Phase-in Of Previously Approved Rate Increases in Algiers to Continue Separate Energy Efficiency / DSM Program Budgets and Funding Sources 21

23 IV. ACCOUNTING METHODOLOGIES 22

24 Accounting Methodologies o Objective to Determine Net-book Value of Assets Sold to Buyer o Complications Most Distribution Assets Were Accounted for With Mass Property Accounting Where Individual Assets were not Identified The Original Cost of Most Distribution Assets Physically in Algiers was Unknowable The Sales Price of Most Distribution Assets was Established by Allocating a Portion of all Of Seller s Distribution Assets Allocation was Based on the Same Factors From the Most Recent Rate Case for Algiers Some Transmission Assets Carried Across the Boundary Between Buyer and Seller Asset Purchase Price and Related O&M was Divided Between Buyer and Seller Based on Length of Transmission on Either Side of Boundary Accounts Receivable based on Differing Billing Cycles and Different Collection Rates 23

25 Accounting Methodologies o Complications (Cont.) Seller and Buyer Have Different Depreciation Rates. Upon Close of Transaction, Algiers Assets Begin Depreciation According to Buyer s Approved Depreciation Rates Regulatory Assets Were Transferred at Their Book Value net of Amortization Property Right to Collect Securitization Bonds Servicing Costs Extends to Algiers ADIT is Substantially Eliminated on Buyer s Books due to Tax Basis Step-up Effect of ADIT is Recreated Through Intercompany Note Algiers Benefits from Buyer s Existing Storm Reserve 24

26 Compliance Filing o Within Three Months of Close of the Transaction, Buyer was Required to Make an Accounting Compliance Filing Identifying and Valuing the Algiers Assets as of Transaction Close Showing Supporting Data Showing all Assumptions and Computations, and Formulae o 60-day Review Period Following Filing of Accounting Compliance Filing Upon Completion of Review Period, Parties may File List of Unresolved Issues o 6-month Period to Resolve Issues With Accounting Compliance Filing Unresolved Issues may Call for Supplemental Procedural Schedule 25

27 V. OBSERVATIONS and Q&A 26

28 Considerations for Regulators o In M&A Activity, How is the Public Interest Determined? Determination of Regulators of Both Buyer and Seller Required How to Determine What Benefits Reasonably will Materialize o How to Treat Seller Assets That are Difficult to Physically Identify Allocate Based on Factors From Recent Rate Action Physical Plant Survey Detailed Audit of a Statistical Sample of Property Accounting Entries o How to Provide Generating Capacity to Sold Region PPA of Slice Of Seller s System PPA or Ownership Interest in Specific Generating Units Buyer to Purchase Capacity / Energy in RTO Auctions / Markets 27

29 Considerations for Regulators o What are the Tax Effects of an M&A Transaction? How to Properly Allocate Affected Tax Costs to Appropriate Party How to Avoid New Tax Expenses o Prevent Double-Recovery of Plant Investment Is Accumulated Depreciation Balance Maintained? If Purchase Price is Above Net Book Value, Should Goodwill be Recovered? o What Regulatory Assets, Including Regulatory Assets Related to Stranded Assets, are Appropriately Transferrable in Utility M&A? 28

ALGIERS RATE CASE FREQUENTLY ASKED QUESTIONS

ALGIERS RATE CASE FREQUENTLY ASKED QUESTIONS FREQUENTLY ASKED QUESTIONS Entergy Louisiana, LLC and Entergy Gulf States Louisiana, L.L.C. Rate Case 2013 How are electrical rates set for Entergy Louisiana

ALGIERS RATE CASE FREQUENTLY ASKED QUESTIONS FREQUENTLY ASKED QUESTIONS Entergy Louisiana, LLC and Entergy Gulf States Louisiana, L.L.C. Rate Case 2013 How are electrical rates set for Entergy Louisiana

Cost of Service. NARUC Energy Regulatory Partnership Program

Cost of Service NARUC Energy Regulatory Partnership Program The Energy Regulatory Commission of the Republic of Macedonia and The Vermont Public Service Board by Randy Pratt Vermont Public Service Board

Cost of Service NARUC Energy Regulatory Partnership Program The Energy Regulatory Commission of the Republic of Macedonia and The Vermont Public Service Board by Randy Pratt Vermont Public Service Board

Center for Entrepreneurial Studies, Stanford Graduate School of Business. Summary of Primary Issues in Acquisition Transactions

September 23, 2009 TO: FROM: RE: Center for Entrepreneurial Studies, Stanford Graduate School of Business Perkins Coie LLP Summary of Primary Issues in Acquisition Transactions This memorandum provides

September 23, 2009 TO: FROM: RE: Center for Entrepreneurial Studies, Stanford Graduate School of Business Perkins Coie LLP Summary of Primary Issues in Acquisition Transactions This memorandum provides

Lessor Example Performance Obligation Approach

Lessor Example Performance Obligation Approach **Disclaimer The exposure draft received nearly 700 letters of comment through the comment period ended December 15, 2010. There is some expectation that

Lessor Example Performance Obligation Approach **Disclaimer The exposure draft received nearly 700 letters of comment through the comment period ended December 15, 2010. There is some expectation that

FPL Institutional Investor Information. August 2013

FPL Institutional Investor Information August 2013 What is the Earnings Surveillance Reporting (ESR)? Florida Public Service Commission (FPSC) Surveillance Reporting Monitors the reasonableness of Florida

FPL Institutional Investor Information August 2013 What is the Earnings Surveillance Reporting (ESR)? Florida Public Service Commission (FPSC) Surveillance Reporting Monitors the reasonableness of Florida

SAUL CENTERS, INC Wisconsin Avenue, Suite 1500, Bethesda, Maryland (301)

") SAUL CENTERS, INC. 7501 Wisconsin Avenue, Suite 1500, Bethesda, Maryland 20814-6522 (301) 986-6200 October 29, 2015, Bethesda, MD. Saul Centers, Inc. Reports Third Quarter 2015 Earnings Saul Centers, Inc.

SAUL CENTERS, INC. 7501 Wisconsin Avenue, Suite 1500, Bethesda, Maryland 20814-6522 (301) 986-6200 October 29, 2015, Bethesda, MD. Saul Centers, Inc. Reports Third Quarter 2015 Earnings Saul Centers, Inc.

SAUL CENTERS, INC Wisconsin Avenue, Suite 1500, Bethesda, Maryland (301)

") May 3, 2018, Bethesda, MD. SAUL CENTERS, INC. 7501 Wisconsin Avenue, Suite 1500, Bethesda, Maryland 20814-6522 (301) 986-6200 Saul Centers, Inc. Reports First Quarter 2018 Earnings Saul Centers, Inc. (NYSE:

May 3, 2018, Bethesda, MD. SAUL CENTERS, INC. 7501 Wisconsin Avenue, Suite 1500, Bethesda, Maryland 20814-6522 (301) 986-6200 Saul Centers, Inc. Reports First Quarter 2018 Earnings Saul Centers, Inc. (NYSE:

Definitions. CPI is a lease in which base rent is adjusted based on changes in a consumer price index.

Annualized Rental Income is rental revenue under our leases on Operating Properties on a straight-line basis, which includes the effect of rent escalations and any tenant concessions, such as free rent,

Annualized Rental Income is rental revenue under our leases on Operating Properties on a straight-line basis, which includes the effect of rent escalations and any tenant concessions, such as free rent,

Perry Farm Development Co.

(a not-for-profit corporation) Consolidated Financial Report December 31, 2010 Contents Report Letter 1 Consolidated Financial Statements Balance Sheet 2 Statement of Operations 3 Statement of Changes

(a not-for-profit corporation) Consolidated Financial Report December 31, 2010 Contents Report Letter 1 Consolidated Financial Statements Balance Sheet 2 Statement of Operations 3 Statement of Changes

SAUL CENTERS, INC Wisconsin Avenue, Suite 1500, Bethesda, Maryland (301)

") SAUL CENTERS, INC. 7501 Wisconsin Avenue, Suite 1500, Bethesda, Maryland 20814-6522 (301) 986-6200 Saul Centers, Inc. Reports Third Quarter 2016 Earnings November 1, 2016, Bethesda, MD. Saul Centers, Inc.

SAUL CENTERS, INC. 7501 Wisconsin Avenue, Suite 1500, Bethesda, Maryland 20814-6522 (301) 986-6200 Saul Centers, Inc. Reports Third Quarter 2016 Earnings November 1, 2016, Bethesda, MD. Saul Centers, Inc.

M&A STRUCTURE/ANATOMY OF A TRANSACTION PRESENTATION OUTLINE. December 6, 2016

M&A STRUCTURE/ANATOMY OF A TRANSACTION PRESENTATION OUTLINE December 6, 2016 1. HOW TO STRUCTURE A TRANSACTION DEAL TYPES AND CONSIDERATION a. Main types = Asset purchase, stock purchase and merger. Structure

M&A STRUCTURE/ANATOMY OF A TRANSACTION PRESENTATION OUTLINE December 6, 2016 1. HOW TO STRUCTURE A TRANSACTION DEAL TYPES AND CONSIDERATION a. Main types = Asset purchase, stock purchase and merger. Structure

SAUL CENTERS, INC Wisconsin Avenue, Suite 1500, Bethesda, Maryland (301)

") SAUL CENTERS, INC. 7501 Wisconsin Avenue, Suite 1500, Bethesda, Maryland 20814-6522 (301) 986-6200 Saul Centers, Inc. Reports Third Quarter 2017 Earnings November 2, 2017, Bethesda, MD. Saul Centers, Inc.

SAUL CENTERS, INC. 7501 Wisconsin Avenue, Suite 1500, Bethesda, Maryland 20814-6522 (301) 986-6200 Saul Centers, Inc. Reports Third Quarter 2017 Earnings November 2, 2017, Bethesda, MD. Saul Centers, Inc.

Florida Power & Light Company, P.O. Box , Miami, FL 33102

Florida Power & Light Company, P.O. Box 291, Miami, FL 3312 I=PL January 15,213 Mr. John Slemkewicz Public Utilities Supervisor Division of Economic Regulation Florida Public Sel'Vice Commission 254 Shumard

Florida Power & Light Company, P.O. Box 291, Miami, FL 3312 I=PL January 15,213 Mr. John Slemkewicz Public Utilities Supervisor Division of Economic Regulation Florida Public Sel'Vice Commission 254 Shumard

JEA s Future Opportunities and Considerations

JEA s Future Opportunities and Considerations Michael Mace, Managing Director February 14, 2018 PFM Orlando, FL Charlotte, NC pfm.com PFM 1 Discussion Topics - Introduction - Scope of the Report - Utility

JEA s Future Opportunities and Considerations Michael Mace, Managing Director February 14, 2018 PFM Orlando, FL Charlotte, NC pfm.com PFM 1 Discussion Topics - Introduction - Scope of the Report - Utility

Front Yard Residential Corporation Reports Third Quarter 2018 Results

Front Yard Residential Corporation Reports Third Quarter 2018 Results November 7, 2018 CHRISTIANSTED, U.S. Virgin Islands, Nov. 07, 2018 (GLOBE NEWSWIRE) -- Front Yard Residential Corporation ( Front Yard

Front Yard Residential Corporation Reports Third Quarter 2018 Results November 7, 2018 CHRISTIANSTED, U.S. Virgin Islands, Nov. 07, 2018 (GLOBE NEWSWIRE) -- Front Yard Residential Corporation ( Front Yard

Student Learning Outcomes

Chapter 4 Intercompany Transactions: Topic 2, Depreciable Assets; Loans and Notes Dr. Chula King Advanced Accounting The University of West Florida 1 Student Learning Outcomes Explain why transactions

Chapter 4 Intercompany Transactions: Topic 2, Depreciable Assets; Loans and Notes Dr. Chula King Advanced Accounting The University of West Florida 1 Student Learning Outcomes Explain why transactions

5. The cost of buildings includes all necessary costs related to the purchase or construction

CHAPTER REVIEW Plant Assets 1. (S.O. 1) Plant assets are tangible resources that are used in the operations of a business and are not intended for sale to customers. Plant assets are subdivided into four

CHAPTER REVIEW Plant Assets 1. (S.O. 1) Plant assets are tangible resources that are used in the operations of a business and are not intended for sale to customers. Plant assets are subdivided into four

Advanced M&A and Merger Models Quiz Questions

Advanced M&A and Merger Models Quiz Questions Transaction Assumptions and Sources & Uses Purchase Price Allocation & Balance Sheet Combination Combining the Income Statement Revenue, Expense, and CapEx

Advanced M&A and Merger Models Quiz Questions Transaction Assumptions and Sources & Uses Purchase Price Allocation & Balance Sheet Combination Combining the Income Statement Revenue, Expense, and CapEx

Week11, Chap 8 Accounting 1A, Financial Accounting

Week11, Chap 8 Accounting 1A, Financial Accounting Reporting and Interpreting Property, Plant, and Equipment;Natural Resources; and Intangibles Instructor: Michael Booth Understanding The Business Insufficient

Week11, Chap 8 Accounting 1A, Financial Accounting Reporting and Interpreting Property, Plant, and Equipment;Natural Resources; and Intangibles Instructor: Michael Booth Understanding The Business Insufficient

Two subsidaries - with land sales from parent to each subsidiary, from each subsidiary to parent, and between subsidiaries

TwoSubs.xls (c)john Bildersee 2002 Two subsidaries - with land sales from parent to each subsidiary, from each subsidiary to parent, and between subsidiaries Cost of acquisition 1,200,000 Life Percent

TwoSubs.xls (c)john Bildersee 2002 Two subsidaries - with land sales from parent to each subsidiary, from each subsidiary to parent, and between subsidiaries Cost of acquisition 1,200,000 Life Percent

THE ART OF BUSINESS VALUATION

BUSINESS VALUATIONS GROWING THE ART OF BUSINESS VALUATION Douglas A. Michel, CPA/ABV, CVA & Alex E. Kummer, CPA, CVA, Clark Schaefer Hackett THE VALUE OF YOUR BUSINESS Steve Lumley, LGI CFO BUY SELL AGREEMENTS

BUSINESS VALUATIONS GROWING THE ART OF BUSINESS VALUATION Douglas A. Michel, CPA/ABV, CVA & Alex E. Kummer, CPA, CVA, Clark Schaefer Hackett THE VALUE OF YOUR BUSINESS Steve Lumley, LGI CFO BUY SELL AGREEMENTS

Florida Power & Light Company, 700 Universe Blvd, Juno Beach FL

Florida Power & Light Company, 7 Universe Blvd, Juno Beach FL. 3348-42 I=PL April 15, 214 Mr. Bart Fletcher Public Utilities Supervisor Division of Accounting and Finance Florida Public Service Commission

Florida Power & Light Company, 7 Universe Blvd, Juno Beach FL. 3348-42 I=PL April 15, 214 Mr. Bart Fletcher Public Utilities Supervisor Division of Accounting and Finance Florida Public Service Commission

Heiwa Real Estate Co., Ltd.

To the Shareholders of Heiwa Real Estate Co., Ltd. INFORMATION DISCLOSED ON THE INTERNET UPON ISSUING NOTICE CONCERNING THE CONVOCATION OF THE 94th ORDINARY GENERAL SHAREHOLDERS MEETING THE 94th FISCAL

To the Shareholders of Heiwa Real Estate Co., Ltd. INFORMATION DISCLOSED ON THE INTERNET UPON ISSUING NOTICE CONCERNING THE CONVOCATION OF THE 94th ORDINARY GENERAL SHAREHOLDERS MEETING THE 94th FISCAL

Exit Strategies for a Medical Practice

Exit Strategies for a Medical Practice John D. Colucci, Esq., CPA McLane Middleton, PA Jonathan P. Gorski, CPA, MBA Edelstein & Company LLP June 12, 2018 Introduction John D. Colucci, a director at McLane

Exit Strategies for a Medical Practice John D. Colucci, Esq., CPA McLane Middleton, PA Jonathan P. Gorski, CPA, MBA Edelstein & Company LLP June 12, 2018 Introduction John D. Colucci, a director at McLane

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C FORM 10-Q

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q ý QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Quarterly Period Ended

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q ý QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Quarterly Period Ended

Achieved record annual revenues of $110.0 million for 2018, representing an increase of 5.8%

Clipper Realty Inc. Announces Fourth Quarter and Full-Year 2018 Results Reports Record Annual Revenues, Record Annual Income from Operations and Record Quarterly and Annual Adjusted Funds from Operations

Clipper Realty Inc. Announces Fourth Quarter and Full-Year 2018 Results Reports Record Annual Revenues, Record Annual Income from Operations and Record Quarterly and Annual Adjusted Funds from Operations

INDEPENDENT AUDITORS REPORT 1. Balance Sheets 2. Statements of Operations 3. Statements of Changes in Partners Capital 4. Statements of Cash Flows 5

Sunrise Carlisle, LP Financial Statements as of and for the Years Ended December 31, 2016 and 2015, Other Financial Information, and Independent Auditors Reports TABLE OF CONTENTS INDEPENDENT AUDITORS

Sunrise Carlisle, LP Financial Statements as of and for the Years Ended December 31, 2016 and 2015, Other Financial Information, and Independent Auditors Reports TABLE OF CONTENTS INDEPENDENT AUDITORS

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2011

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2011 Presented By: Marianne Heard, CPA, MST, Tax Director, Kevin P. Martin & Associates, P.C.

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2011 Presented By: Marianne Heard, CPA, MST, Tax Director, Kevin P. Martin & Associates, P.C.

Process. Thomas Dvorsky Director, Office of Electric, Gas and Water New York State Public Service Commission May 23, 2011

Electric Distribution Rate Setting Process Thomas Dvorsky Director, Office of Electric, Gas and Water New York State Public Service Commission May 23, 2011 Rate Case Schedule NY Public Service Law Requires

Electric Distribution Rate Setting Process Thomas Dvorsky Director, Office of Electric, Gas and Water New York State Public Service Commission May 23, 2011 Rate Case Schedule NY Public Service Law Requires

Before the Minnesota Public Utilities Commission State of Minnesota. Docket No. E002/GR Exhibit (LMC-1) Property Taxes

Property Taxes") Direct Testimony and Schedules Leanna M. Chapman Before the Minnesota Public Utilities Commission State of Minnesota In the Matter of the Application of Northern States Power Company for Authority to Increase

Direct Testimony and Schedules Leanna M. Chapman Before the Minnesota Public Utilities Commission State of Minnesota In the Matter of the Application of Northern States Power Company for Authority to Increase

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2014

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2014 Presented By: Karen Kent, CPA, Partner, Kevin P. Martin & Associates, P.C. Kenneth Lund,

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2014 Presented By: Karen Kent, CPA, Partner, Kevin P. Martin & Associates, P.C. Kenneth Lund,

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC FORM 8-K/A

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 FORM 8-K/A CURRENT REPORT Pursuant to Section 13 or 15(d) of The Securities Exchange Act of 1934 Date of Report (Date of earliest event

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 FORM 8-K/A CURRENT REPORT Pursuant to Section 13 or 15(d) of The Securities Exchange Act of 1934 Date of Report (Date of earliest event

Front Yard Residential Corporation Announces Transformative Acquisition and Reports Second Quarter 2018 Results

Front Yard Residential Corporation Announces Transformative Acquisition and Reports Second Quarter 2018 Results August 9, 2018 CHRISTIANSTED, U.S. Virgin Islands, Aug. 09, 2018 (GLOBE NEWSWIRE) -- Front

Front Yard Residential Corporation Announces Transformative Acquisition and Reports Second Quarter 2018 Results August 9, 2018 CHRISTIANSTED, U.S. Virgin Islands, Aug. 09, 2018 (GLOBE NEWSWIRE) -- Front

roots The Substance of the Standard Contents Changes to the Accounting for Goodwill for Private Companies

The Substance of the Standard MAYER HOFFMAN MCCANN P.C. AN INDEPENDENT CPA FIRM TM A publication of the Professional Standards Group February 2014 Changes to the Accounting for Goodwill for Private Companies

The Substance of the Standard MAYER HOFFMAN MCCANN P.C. AN INDEPENDENT CPA FIRM TM A publication of the Professional Standards Group February 2014 Changes to the Accounting for Goodwill for Private Companies

GASBs Presented by: William Blend, CPA, CFE

GASBs 87-89 Presented by: William Blend, CPA, CFE Leases: Statement 87 Effective Date and General Implementation Effective for Florida fiscal year end 2021. Earlier application is encouraged. Leases should

GASBs 87-89 Presented by: William Blend, CPA, CFE Leases: Statement 87 Effective Date and General Implementation Effective for Florida fiscal year end 2021. Earlier application is encouraged. Leases should

Clipper Realty Inc. Announces Third Quarter 2018 Results Reports Record Revenues, Income From Operations and Adjusted Funds From Operations

Clipper Realty Inc. Announces Third Quarter 2018 Results Reports Record Revenues, Income From Operations and Adjusted Funds From Operations NEW YORK, November 1, 2018 /Business Wire/ -- Clipper Realty

Clipper Realty Inc. Announces Third Quarter 2018 Results Reports Record Revenues, Income From Operations and Adjusted Funds From Operations NEW YORK, November 1, 2018 /Business Wire/ -- Clipper Realty

Extra Space Storage Inc. Reports 2017 Fourth Quarter and Year-End Results

Extra Space Storage Inc. Reports 2017 Fourth Quarter and Year-End Results February 20, 2018 SALT LAKE CITY, Feb. 20, 2018 /PRNewswire/ -- Extra Space Storage Inc. (NYSE: EXR) (the "Company"), a leading

Extra Space Storage Inc. Reports 2017 Fourth Quarter and Year-End Results February 20, 2018 SALT LAKE CITY, Feb. 20, 2018 /PRNewswire/ -- Extra Space Storage Inc. (NYSE: EXR) (the "Company"), a leading

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2016

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2016 Presented By: Karen Kent, CPA, Partner, Kevin P. Martin & Associates, P.C. Kenneth Lund,

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2016 Presented By: Karen Kent, CPA, Partner, Kevin P. Martin & Associates, P.C. Kenneth Lund,

Why IFRS 16 matters to the shipping industry

www.pwc.no Why IFRS 16 matters to the shipping industry October 2017 Executive summary New lease standard to be effective 1 January 2019. Early implementation permitted together with IFRS 15 (effective

www.pwc.no Why IFRS 16 matters to the shipping industry October 2017 Executive summary New lease standard to be effective 1 January 2019. Early implementation permitted together with IFRS 15 (effective

EN Official Journal of the European Union L 320/373

29.11.2008 EN Official Journal of the European Union L 320/373 INTERNATIONAL FINANCIAL REPORTING STANDARD 3 Business combinations OBJECTIVE 1 The objective of this IFRS is to specify the financial reporting

29.11.2008 EN Official Journal of the European Union L 320/373 INTERNATIONAL FINANCIAL REPORTING STANDARD 3 Business combinations OBJECTIVE 1 The objective of this IFRS is to specify the financial reporting

A CASE STUDY: THE TREATMENT OF LEASES AND THE IMPACT ON FINANCIAL RATIOS UNDER THE PROPOSED NEW US GAAP LEASE REQUIREMENTS PER ASU

A CASE STUDY: THE TREATMENT OF LEASES AND THE IMPACT ON FINANCIAL RATIOS UNDER THE PROPOSED NEW US GAAP LEASE REQUIREMENTS PER ASU 842 Peter Harris, New York Institute of Technology Michael Benjamin, New

A CASE STUDY: THE TREATMENT OF LEASES AND THE IMPACT ON FINANCIAL RATIOS UNDER THE PROPOSED NEW US GAAP LEASE REQUIREMENTS PER ASU 842 Peter Harris, New York Institute of Technology Michael Benjamin, New

SECURITIES AND EXCHANGE COMMISSION. Washington, D.C FORM 8-K CURRENT REPORT

SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 8-K CURRENT REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Date of Report (Date of earliest event reported):

SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 8-K CURRENT REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Date of Report (Date of earliest event reported):

PS Business Parks, Inc. Reports Results for the Quarter Ended September 30, 2018

News Release PS Business Parks, Inc. 701 Western Avenue Glendale, CA 91201-2349 psbusinessparks.com For Release: Immediately Date: October 23, 2018 Contact: Jeff Hedges (818) 244-8080, Ext. 1649 PS Business

News Release PS Business Parks, Inc. 701 Western Avenue Glendale, CA 91201-2349 psbusinessparks.com For Release: Immediately Date: October 23, 2018 Contact: Jeff Hedges (818) 244-8080, Ext. 1649 PS Business

ADVANCED ISSUES IN FRANCHISOR ACQUISITIONS OF FRANCHISEES IS VERTICAL INTEGRATION IN YOUR FUTURE?

ADVANCED ISSUES IN FRANCHISOR ACQUISITIONS OF FRANCHISEES IS VERTICAL INTEGRATION IN YOUR FUTURE? Joel R. Buckberg Shareholder Commercial Transactions & Business Counseling Practice Group Chair Baker,

ADVANCED ISSUES IN FRANCHISOR ACQUISITIONS OF FRANCHISEES IS VERTICAL INTEGRATION IN YOUR FUTURE? Joel R. Buckberg Shareholder Commercial Transactions & Business Counseling Practice Group Chair Baker,

Real Estate Accounting

Real Estate Accounting Steven M. Bragg Chapter 1 Introduction to Accounting... 1 Learning Objectives... 1 Introduction... 1 Financial Accounting Basics... 1 Accounting Frameworks... 2 The Accounting Cycle...

Real Estate Accounting Steven M. Bragg Chapter 1 Introduction to Accounting... 1 Learning Objectives... 1 Introduction... 1 Financial Accounting Basics... 1 Accounting Frameworks... 2 The Accounting Cycle...

GASB 87. OVERVIEW: Supersedes GASB s 13 and 62 (paragraphs ).

.") Leases OVERVIEW: Supersedes GASB s 13 and 62 (paragraphs 211-271). Will require significant changes from its current practice, particularly in the accounting for operating leases Effective for reporting

Leases OVERVIEW: Supersedes GASB s 13 and 62 (paragraphs 211-271). Will require significant changes from its current practice, particularly in the accounting for operating leases Effective for reporting

7/2/2015. The Statement of Cash Flows. Learning Objectives. Learning Objectives. Chapter 16

The Statement of Cash Flows Chapter 16 2014 Pearson Education, Inc. Publishing as Prentice Hall 16-1 Learning Objectives 1. Identify the purposes of the statement of cash flows and distinguish among operating,

The Statement of Cash Flows Chapter 16 2014 Pearson Education, Inc. Publishing as Prentice Hall 16-1 Learning Objectives 1. Identify the purposes of the statement of cash flows and distinguish among operating,

Accounting and Financial Reporting Trends

Relationships backed by performance. Accounting and Financial Reporting Trends T.J. Boyle June 20, 2013 What s New Leases Revenue Recognition Derivatives Other Comprehensive Income AICPA Accounting for

Relationships backed by performance. Accounting and Financial Reporting Trends T.J. Boyle June 20, 2013 What s New Leases Revenue Recognition Derivatives Other Comprehensive Income AICPA Accounting for

Public Service Commission

State of Florida Public Service Commission CAPITAL C IHCLE OFFICE CENT ER 2540 S II U~ I ARD O AK BOULEVARD T A LLAIIASS EE, FLORIDA 32399-0850 -M-E-M-0-R-A-N-D-U-M- DATE: November 30, 20 17 TO: FROM:

State of Florida Public Service Commission CAPITAL C IHCLE OFFICE CENT ER 2540 S II U~ I ARD O AK BOULEVARD T A LLAIIASS EE, FLORIDA 32399-0850 -M-E-M-0-R-A-N-D-U-M- DATE: November 30, 20 17 TO: FROM:

GOLDFIELD CORPORATION

GOLDFIELD CORPORATION The Goldfield Corporation (Goldfield), incorporated in 1906, is engaged in electrical construction, including the placement of fiber optic cable and real estate development. The Company,

GOLDFIELD CORPORATION The Goldfield Corporation (Goldfield), incorporated in 1906, is engaged in electrical construction, including the placement of fiber optic cable and real estate development. The Company,

We are pleased to provide all owners with the King s Creek Plantation Owners Association Annual Report.

April 30, 2016 Dear Owner, We are pleased to provide all owners with the King s Creek Plantation Owners Association Annual Report. The Report includes the following information: 1. The full legal name

April 30, 2016 Dear Owner, We are pleased to provide all owners with the King s Creek Plantation Owners Association Annual Report. The Report includes the following information: 1. The full legal name

CONSOLIDATED FINANCIAL STATEMENTS

CONSOLIDATED FINANCIAL STATEMENTS Dundee Real Estate Investment Trust Consolidated Balance Sheets (unaudited) June 30, December 31, (in thousands of dollars) Note 2004 2003 Assets Rental properties 3,4

CONSOLIDATED FINANCIAL STATEMENTS Dundee Real Estate Investment Trust Consolidated Balance Sheets (unaudited) June 30, December 31, (in thousands of dollars) Note 2004 2003 Assets Rental properties 3,4

Intangibles CHAPTER CHAPTER OBJECTIVES. After careful study of this chapter, you will be able to:

CHAPTER Intangibles CHAPTER OBJECTIVES After careful study of this chapter, you will be able to: 1. Explain the accounting alternatives for intangibles. 2. Record the amortization or impairment of intangibles.

CHAPTER Intangibles CHAPTER OBJECTIVES After careful study of this chapter, you will be able to: 1. Explain the accounting alternatives for intangibles. 2. Record the amortization or impairment of intangibles.

PREVIEW OF CHAPTER 21-2

21-1 PREVIEW OF CHAPTER 21 21-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 21 Accounting for Leases LEARNING OBJECTIVES After studying this chapter, you should be able to: 21-3

21-1 PREVIEW OF CHAPTER 21 21-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 21 Accounting for Leases LEARNING OBJECTIVES After studying this chapter, you should be able to: 21-3

IFRS Training. IAS 38 Intangible Assets. Professional Advisory Services

IFRS Training IAS 38 Intangible Assets Table of Contents Section 1 Overview 2 Introduction to Intangible Assets 3 Recognition and Initial Measurement 4 Internally Generated Intangible Assets 5 Measurement

IFRS Training IAS 38 Intangible Assets Table of Contents Section 1 Overview 2 Introduction to Intangible Assets 3 Recognition and Initial Measurement 4 Internally Generated Intangible Assets 5 Measurement

CC HOLDINGS GS V LLC INDEX TO FINANCIAL STATEMENTS. Consolidated Financial Statements Years Ended December 31, 2011, 2010 and 2009

INDEX TO FINANCIAL STATEMENTS Consolidated Financial Statements Years Ended December 31, 2011, 2010 and 2009 Report of PricewaterhouseCoopers LLP, Independent Auditors...................................

INDEX TO FINANCIAL STATEMENTS Consolidated Financial Statements Years Ended December 31, 2011, 2010 and 2009 Report of PricewaterhouseCoopers LLP, Independent Auditors...................................

Emerging Issues Task Force. EITF Agenda Committee Report Supplement. Mining Industry Issues November 5, 2003

1103RPTMNG Emerging Issues Task Force Agenda Committee Report Supplement Mining Industry Issues November 5, 2003 Potential New Issues Page(s) 1. Whether Mining Rights are Tangible or Intangible Assets

1103RPTMNG Emerging Issues Task Force Agenda Committee Report Supplement Mining Industry Issues November 5, 2003 Potential New Issues Page(s) 1. Whether Mining Rights are Tangible or Intangible Assets

On the Horizon: Leases and Fiduciary Responsibilities

On the Horizon: Leases and Fiduciary Responsibilities Dean Michael Mead, Research Manager Florida School Finance Officers Association November 11, 2015 The views expressed in this presentation are those

On the Horizon: Leases and Fiduciary Responsibilities Dean Michael Mead, Research Manager Florida School Finance Officers Association November 11, 2015 The views expressed in this presentation are those

Chapter 8. Accounting for Long-Term Assets

Chapter 8 Accounting for Long-Term Assets C 1 Plant Assets Tangible in Nature Actively Used in Operations Expected to Benefit Future Periods Called Property, Plant, & Equipment 8-2 C 1 Plant Assets Decline

Chapter 8 Accounting for Long-Term Assets C 1 Plant Assets Tangible in Nature Actively Used in Operations Expected to Benefit Future Periods Called Property, Plant, & Equipment 8-2 C 1 Plant Assets Decline

PS Business Parks, Inc. Reports Results for the Quarter and Year Ended December 31, 2018

News Release PS Business Parks, Inc. 701 Western Avenue Glendale, CA 91201-2349 psbusinessparks.com For Release: Immediately Date: February 20, 2019 Contact: Jeff Hedges (818) 244-8080, Ext. 1649 PS Business

News Release PS Business Parks, Inc. 701 Western Avenue Glendale, CA 91201-2349 psbusinessparks.com For Release: Immediately Date: February 20, 2019 Contact: Jeff Hedges (818) 244-8080, Ext. 1649 PS Business

Leases. (a) the lease transfers ownership of the asset to the lessee by the end of the lease term.

the lease transfers ownership of the asset to the lessee by the end of the lease term.") Leases 1.1. Classification of leases A lease is classified as a finance lease if it transfers substantially all the risks and rewards incidental to ownership. A lease is classified as an operating lease

Leases 1.1. Classification of leases A lease is classified as a finance lease if it transfers substantially all the risks and rewards incidental to ownership. A lease is classified as an operating lease

Thomas H. Warren Ram C. Sunkara February 22, 2011

Thomas H. Warren Ram C. Sunkara February 22, 2011 Electric Cooperative M&A Issues: Power Asset M&A Our Coop Power Project Experience In the past two years, we have assisted our Electric Cooperative clients

Thomas H. Warren Ram C. Sunkara February 22, 2011 Electric Cooperative M&A Issues: Power Asset M&A Our Coop Power Project Experience In the past two years, we have assisted our Electric Cooperative clients

Topic 4B: Developer Fee Elimination During Consolidation or Combination

Analysis/Input GAAP There are two approaches to eliminating developer fee income in financial statements that consolidate or combine the developer that earns the fee and a property that capitalizes the

Analysis/Input GAAP There are two approaches to eliminating developer fee income in financial statements that consolidate or combine the developer that earns the fee and a property that capitalizes the

ANNUAL REPORT 2017 Lake Country Co-operative Association Limited

ANNUAL REPORT Management's Responsibility To the Members of Lake Country Co-operative Association Limited: Management is responsible for the preparation and presentation of the accompanying financial statements,

ANNUAL REPORT Management's Responsibility To the Members of Lake Country Co-operative Association Limited: Management is responsible for the preparation and presentation of the accompanying financial statements,

~f/~~ ey S. Chronister Controller

TECC> PEOPLES GAS August 15,2016 Bart Fletcher, Public Utilities Supervisor Division of Accounting and Finance Florida Public Service Commission 2540 Shumard Oak Boulevard Tallahassee, Florida 32399-0850

TECC> PEOPLES GAS August 15,2016 Bart Fletcher, Public Utilities Supervisor Division of Accounting and Finance Florida Public Service Commission 2540 Shumard Oak Boulevard Tallahassee, Florida 32399-0850

Impact of lease accounting changes to corporate real estate

Impact of lease accounting changes to corporate real estate Overview In February 2016, the Financial Accounting Standards Board (FASB) issued its long-awaited revision to lease accounting Accounting Standards

Impact of lease accounting changes to corporate real estate Overview In February 2016, the Financial Accounting Standards Board (FASB) issued its long-awaited revision to lease accounting Accounting Standards

Getting More Value for Your Practice

Getting More Value for Your Practice D A N I E L M. B E R N I C K, E S QUI R E, M B A T H E H E A LT H C A R E GROUP P LY M OUT H M E E T I N G, PA W W W. H E A LT H C A R E G R O U P. C O M Who We Are

Getting More Value for Your Practice D A N I E L M. B E R N I C K, E S QUI R E, M B A T H E H E A LT H C A R E GROUP P LY M OUT H M E E T I N G, PA W W W. H E A LT H C A R E G R O U P. C O M Who We Are

Chapter 15 Leases 15-1

Chapter 15 Leases 1. Why Leasing sometimes makes more sense 2. The accounting issues in recording a lease transaction 3. The types of contractual provisions in lease 4. The lease classification: capital

Chapter 15 Leases 1. Why Leasing sometimes makes more sense 2. The accounting issues in recording a lease transaction 3. The types of contractual provisions in lease 4. The lease classification: capital

Sunrise Stratford, LP

Sunrise Stratford, LP Financial Statements as of and for the Years Ended December 31, 2017 and 2016, Other Financial Information, and Independent Auditors Reports TABLE OF CONTENTS INDEPENDENT AUDITORS

Sunrise Stratford, LP Financial Statements as of and for the Years Ended December 31, 2017 and 2016, Other Financial Information, and Independent Auditors Reports TABLE OF CONTENTS INDEPENDENT AUDITORS

... ARMADA HOFFLER PROPERTIES REPORTS FOURTH QUARTER 2013 RESULTS

PRESS RELEASE.......................................... ARMADA HOFFLER PROPERTIES REPORTS FOURTH QUARTER 2013 RESULTS Core FFO of $7.1 Million, $0.22 Per Diluted Share Operating Property Portfolio at 94.4%

PRESS RELEASE.......................................... ARMADA HOFFLER PROPERTIES REPORTS FOURTH QUARTER 2013 RESULTS Core FFO of $7.1 Million, $0.22 Per Diluted Share Operating Property Portfolio at 94.4%

STAG INDUSTRIAL ANNOUNCES SECOND QUARTER 2018 RESULTS

STAG INDUSTRIAL ANNOUNCES SECOND QUARTER 2018 RESULTS Boston, MA July 31, 2018 - STAG Industrial, Inc. (the Company ) (NYSE:STAG), today announced its financial and operating results for the quarter ended

STAG INDUSTRIAL ANNOUNCES SECOND QUARTER 2018 RESULTS Boston, MA July 31, 2018 - STAG Industrial, Inc. (the Company ) (NYSE:STAG), today announced its financial and operating results for the quarter ended

GASB 69: Government Combinations

GASB 69: Government Combinations Table of Contents EXECUTIVE SUMMARY... 3 BACKGROUND... 3 KEY PROVISIONS... 3 OVERVIEW & SCOPE... 3 MERGER & TRANSFER OF OPERATIONS... 4 Mergers... 4 Transfers of Operations...

GASB 69: Government Combinations Table of Contents EXECUTIVE SUMMARY... 3 BACKGROUND... 3 KEY PROVISIONS... 3 OVERVIEW & SCOPE... 3 MERGER & TRANSFER OF OPERATIONS... 4 Mergers... 4 Transfers of Operations...

RESI Update 4 th Quarter 2016

RESI Update 4 th Quarter 2016 Supplemental Investor Information George Ellison, CEO Robin Lowe, CFO 2017 Altisource Residential Corporation. All rights reserved. Forward Looking Statements This presentation

RESI Update 4 th Quarter 2016 Supplemental Investor Information George Ellison, CEO Robin Lowe, CFO 2017 Altisource Residential Corporation. All rights reserved. Forward Looking Statements This presentation

The new accounting standard for leases. 27 March 2017

The new accounting standard for leases 27 March 2017 Disclaimer Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity.

The new accounting standard for leases 27 March 2017 Disclaimer Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity.

A new era for lease accounting plantemoran.com

A new era for lease accounting Your balance sheet may never look the same A new era for lease accounting 1 plantemoran.com Overview On Feb. 25, 2016, the Financial Accounting Standards Board (FASB) issued

A new era for lease accounting Your balance sheet may never look the same A new era for lease accounting 1 plantemoran.com Overview On Feb. 25, 2016, the Financial Accounting Standards Board (FASB) issued

Copyright 2009 The Learning House, Inc. Fixed and Intangible Assets Page 1 of 13

Copyright 2009 The Learning House, Inc. Fixed and Intangible Assets Page 1 of 13 Introduction This lesson focuses on the long-term assets used to operate a company. These assets can be grouped into fixed

Copyright 2009 The Learning House, Inc. Fixed and Intangible Assets Page 1 of 13 Introduction This lesson focuses on the long-term assets used to operate a company. These assets can be grouped into fixed

PRACTICAL TIPS FOR IMPLEMENTING THE NEW LEASE ACCOUNTING STANDARD

PRACTICAL TIPS FOR IMPLEMENTING THE NEW LEASE ACCOUNTING STANDARD SHAUNA WATSON, VP, GLOBAL HEAD OF TECHNICAL ACCOUNTING MICHAEL ALLEN, PARTNER, TRANSACTION ADVISORY SERVICES 1. Overview of Accounting

PRACTICAL TIPS FOR IMPLEMENTING THE NEW LEASE ACCOUNTING STANDARD SHAUNA WATSON, VP, GLOBAL HEAD OF TECHNICAL ACCOUNTING MICHAEL ALLEN, PARTNER, TRANSACTION ADVISORY SERVICES 1. Overview of Accounting

General Growth Properties, Inc.

General Growth Properties, Inc. Supplemental Financial Information For the Three and Nine Months Ended September 30, 2009 This presentation contains forward-looking statements. Actual results may differ

General Growth Properties, Inc. Supplemental Financial Information For the Three and Nine Months Ended September 30, 2009 This presentation contains forward-looking statements. Actual results may differ

The Financial Accounting Standards Board

V A L U A T I O N How the New Leases Standard May Impact Business Valuations By Judith H. O Dell, CPA, CVA The Financial Accounting Standards Board issued the 485 page Leases Standard (Topic 842) in February,

V A L U A T I O N How the New Leases Standard May Impact Business Valuations By Judith H. O Dell, CPA, CVA The Financial Accounting Standards Board issued the 485 page Leases Standard (Topic 842) in February,

FOR IMMEDIATE RELEASE: Equity One Reports Fourth Quarter and Year End 2014 Operating Results

Equity One, Inc. For additional information: 410 Park Avenue, Suite 1220 Mark Langer, EVP and New York, NY 10022 Chief Financial Officer 212-796-1760 FOR IMMEDIATE RELEASE: Equity One Reports Fourth Quarter

Equity One, Inc. For additional information: 410 Park Avenue, Suite 1220 Mark Langer, EVP and New York, NY 10022 Chief Financial Officer 212-796-1760 FOR IMMEDIATE RELEASE: Equity One Reports Fourth Quarter

Reinvesting With 1031 Exchange

Reinvesting With 1031 Exchange SEMINAR OUTLINE: Introduction and Learning Objectives... 2 1031 Exchange Rules: Myth or Fact?... 2 Non-Qualifying Replacement Property... 3 Exchanges with Special Challenges...

Reinvesting With 1031 Exchange SEMINAR OUTLINE: Introduction and Learning Objectives... 2 1031 Exchange Rules: Myth or Fact?... 2 Non-Qualifying Replacement Property... 3 Exchanges with Special Challenges...

Consolidated Financial Statements of ECOTRUST CANADA. Year ended December 31, 2016

Consolidated Financial Statements of ECOTRUST CANADA KPMG Enterprise TM Metro Tower I 4710 Kingsway, Suite 2400 Burnaby BC V5H 4M2 Canada Telephone (604) 527-3600 Fax (604) 527-3636 INDEPENDENT AUDITORS

Consolidated Financial Statements of ECOTRUST CANADA KPMG Enterprise TM Metro Tower I 4710 Kingsway, Suite 2400 Burnaby BC V5H 4M2 Canada Telephone (604) 527-3600 Fax (604) 527-3636 INDEPENDENT AUDITORS

MERGERS ACQUISITIONS! C onsider this: you have worked for years to build a BNA, LAW REPORT. Earn-Outs: Bridge the Gap, With Caution INC.

A BNA, MERGERS INC. & ACQUISITIONS! LAW REPORT Reproduced with permission from Mergers & Acquisitions Law Report, 12 MALR 581, 06/15/2009. Copyright 2009 by The Bureau of National Affairs, Inc. (800-372-1033)

A BNA, MERGERS INC. & ACQUISITIONS! LAW REPORT Reproduced with permission from Mergers & Acquisitions Law Report, 12 MALR 581, 06/15/2009. Copyright 2009 by The Bureau of National Affairs, Inc. (800-372-1033)

Installment Sales. Installment Method under Section 453 Allows for a gain on sale as well as the accompanying tax liability to be deferred

1 Installment Sales 2 Ordinarily recognize gain or loss when property is sold under section 1001 Amount realized less adjusted basis Typically, the entire amount of the sale or exchange will be recognized

1 Installment Sales 2 Ordinarily recognize gain or loss when property is sold under section 1001 Amount realized less adjusted basis Typically, the entire amount of the sale or exchange will be recognized

GENERAL GROWTH PROPERTIES, INC. (Exact name of registrant as specified in its charter)

") UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q X Quarterly report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 For the quarterly period ended

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q X Quarterly report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 For the quarterly period ended

Chapter 08 - Long-Term Assets. Chapter Outline

Section 1 Plant Assets I. Cost Determination Plant assets are tangible assets used in a company's operations that have a useful life of more than one accounting period. Consistent with cost principle,

Section 1 Plant Assets I. Cost Determination Plant assets are tangible assets used in a company's operations that have a useful life of more than one accounting period. Consistent with cost principle,

The Impact of the New Revenue Standard on Real Estate Sales

The Impact of the New Revenue Standard on Real Estate Sales Wing W. Poon Montclair State University In May 2014, the FASB and the IASB jointly issued significantly revised standard on revenue recognition.

The Impact of the New Revenue Standard on Real Estate Sales Wing W. Poon Montclair State University In May 2014, the FASB and the IASB jointly issued significantly revised standard on revenue recognition.

4/_~=-- TECO., ..,., .. ~ (.{) ,... :c> February 15, r:.- <

,... :c> February 15, r:.- <") TECO., PEOPLES GAS AN EMERA COMPANY February 15, 2018 Bart Fletcher, Public Utilities Supervisor Division of Accounting and Finance Florida Public Service Commission 2540 Shumard Oak Boulevard Tallahassee,

TECO., PEOPLES GAS AN EMERA COMPANY February 15, 2018 Bart Fletcher, Public Utilities Supervisor Division of Accounting and Finance Florida Public Service Commission 2540 Shumard Oak Boulevard Tallahassee,

Retail Acquisition Example

Property Information Retail Acquisition Example Project Assumptions Acquisition Assumptions Property Name Retail Acquisition Example Project Type Acquisition Location Austin, TX Acquisition Cost $1,800,000

Property Information Retail Acquisition Example Project Assumptions Acquisition Assumptions Property Name Retail Acquisition Example Project Type Acquisition Location Austin, TX Acquisition Cost $1,800,000

SEC Reg. G Compliance - Non-GAAP Financial Measures

SEC Reg. G Compliance - Non-GAAP Financial Measures Funds From Operations (FFO) Reconciliation, Including Non-Cash Items 1 ($ in 000s, except per share amounts) Tentative Estimates Preliminary and Midpoint

SEC Reg. G Compliance - Non-GAAP Financial Measures Funds From Operations (FFO) Reconciliation, Including Non-Cash Items 1 ($ in 000s, except per share amounts) Tentative Estimates Preliminary and Midpoint

Accounting for Tangible Capital Assets

Accounting for Tangible Capital Assets Date Approved by Board: 2011.11.17 Resolution No.: 11-113 2016.05.19 16-048 Lead Role: CFO Replaces: N/A Last Review Date: N/A Next Review Date: 2019.05.19 Policy

Accounting for Tangible Capital Assets Date Approved by Board: 2011.11.17 Resolution No.: 11-113 2016.05.19 16-048 Lead Role: CFO Replaces: N/A Last Review Date: N/A Next Review Date: 2019.05.19 Policy

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C FORM 10-Q

10-Q 1 clpr20180930_10q.htm FORM 10-Q UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

10-Q 1 clpr20180930_10q.htm FORM 10-Q UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

Public Storage Reports Results for the Quarter Ended March 31, 2017

News Release Public Storage 701 Western Avenue Glendale, CA 91201-2349 www.publicstorage.com For Release Immediately Date April 26, 2017 Contact Clemente Teng (818) 244-8080, Ext. 1141 Public Storage Reports

News Release Public Storage 701 Western Avenue Glendale, CA 91201-2349 www.publicstorage.com For Release Immediately Date April 26, 2017 Contact Clemente Teng (818) 244-8080, Ext. 1141 Public Storage Reports

T H E O R Y O F A C C O U N T S

2011 NATIONAL CPA MOCK BOARD EXAMINATION In partnership with the Professional Review & Training Center, Inc. and Isla Lipana & Co. T H E O R Y O F A C C O U N T S INSTRUCTIONS: Select the best answer for

2011 NATIONAL CPA MOCK BOARD EXAMINATION In partnership with the Professional Review & Training Center, Inc. and Isla Lipana & Co. T H E O R Y O F A C C O U N T S INSTRUCTIONS: Select the best answer for

ALLIED PROPERTIES REAL ESTATE INVESTMENT TRUST. Financial Statements. For the Period Ended March 31, 2004

Financial Statements For the Period Ended March 31, 2004 BALANCE SHEET At March 31, 2004 INDEX Page Balance Sheet 1 Statement of Unitholders' Equity 2 Statement of Earnings 3 Statement of Cash Flows 4

Financial Statements For the Period Ended March 31, 2004 BALANCE SHEET At March 31, 2004 INDEX Page Balance Sheet 1 Statement of Unitholders' Equity 2 Statement of Earnings 3 Statement of Cash Flows 4

Balance at Retirements Balance at Beginning Additions and End of ($ in thousands) of Year 3 at Cost Transfers Year 3

of Year 3 at Cost Transfers Year 3") CHAPTER 10 Long-Lived Assets and Depreciation 10-1 ShopKo Stores, Inc. (ShopKo) is a leading regional discount store chain operating 109 discount retail stores in 13 states. ShopKo stores carry a wide

CHAPTER 10 Long-Lived Assets and Depreciation 10-1 ShopKo Stores, Inc. (ShopKo) is a leading regional discount store chain operating 109 discount retail stores in 13 states. ShopKo stores carry a wide

Table of Contents PAGE MIADOCS

Table of Contents PAGE CONSOLIDATED FINANCIAL STATEMENTS Independent Auditor's Report 2 Pro-Forma Consolidated Balance Sheets as of December 31, 2017 and 2016 3 Pro-Forma Consolidated Statements of Operations

Table of Contents PAGE CONSOLIDATED FINANCIAL STATEMENTS Independent Auditor's Report 2 Pro-Forma Consolidated Balance Sheets as of December 31, 2017 and 2016 3 Pro-Forma Consolidated Statements of Operations

Accounting and Auditing Update. Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc.

Accounting and Auditing Update Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc. Agenda Overview of the standard setting agenda Revenue recognition Lease

Accounting and Auditing Update Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc. Agenda Overview of the standard setting agenda Revenue recognition Lease

TWENTY SIXTH AMENDMENT TO THE OFFERING PLAN A PLAN TO CONVERT TO COOPERATIVE OWNERSHIP PREMISES AT 350 BLEECKER STREET, NEW YORK, NEW YORK

TWENTY SIXTH AMENDMENT TO THE OFFERING PLAN A PLAN TO CONVERT TO COOPERATIVE OWNERSHIP PREMISES AT 350 BLEECKER STREET, NEW YORK, NEW YORK The Offering Plan, dated December 31, 1984, as amended by the

TWENTY SIXTH AMENDMENT TO THE OFFERING PLAN A PLAN TO CONVERT TO COOPERATIVE OWNERSHIP PREMISES AT 350 BLEECKER STREET, NEW YORK, NEW YORK The Offering Plan, dated December 31, 1984, as amended by the

Cost Segregation Instructor Teaching Schedule (3-Hour)

") Time Topic Pages Student Objectives 8:30-8:35 Course introduction Page 2 What is cost segregation? Objective of cost segregation: to increase cash flow Benefit of cost segregation Learning objectives Page

Time Topic Pages Student Objectives 8:30-8:35 Course introduction Page 2 What is cost segregation? Objective of cost segregation: to increase cash flow Benefit of cost segregation Learning objectives Page