IFRS 3 Business Combinations

|

|

|

- Irma McKenzie

- 6 years ago

- Views:

Transcription

1 IFRS 3 Business Combinations 0

2 Objectives Define a business combination under IFRS 3 (Revised 2008) Describe the steps in applying the acquisition method Explain the recognition and measurement principles of IFRS 3 (Revised 2008) Determine how to account for non-controlling interest in a partial acquisition Identify the key differences between IFRS 3 (Revised 2008) and Accounting Standard 14

3 Plan for session Session 1 Scope and key definitions under IFRS 3 (Revised 2008) Session 2 Acquisition Method Session 3 Key differences between IFRS 3 and Accounting Standard 14 (AS14, Accounting for Amalgamations)

4 Key aspects What constitutes a business combination? Who is the acquirer? What is the date of acquisition? What is the cost of acquisition? Contingent consideration What are the assets and liabilities acquired? Intangibles? Contingent liabilities? Treatment of bargain purchase Subsequent adjustments Accounting for income tax Accounting and presenting Non-controlling Interest (NCI)

5 Primary Literature Under IFRS: IFRS 3 (Revised 2008) Business Combinations Under Indian GAAP: AS 14 Accounting for Amalgamations

6 Scope of IFRS 3 (Revised 2008) Transactions or events that meet the definition of a Business Combination Formation of a joint venture Acquisition of an asset or group of assets not constituting a business A combination of entities or businesses under common control

7 Identifying a Business Combination An entity shall determine whether a transaction or other event is a business combination by applying the definition in this IFRS, which requires that the assets acquired and liabilities assumed constitute a business. For example, an entity may acquire a set of assets and activities that represents the ownership and management of a group of pipelines used for the transport of oil, gas and other hydrocarbons on behalf of a number of customers. The operation has a limited number of employees (mainly used in maintenance of the pipelines and billing of customers), a system used for tracking transported hydrocarbons and a minor amount of working capital. The transaction involves the transfer of employees and systems, but not the working capital. Notwithstanding that the inputs into the process are minimal, the group of pipelines will meet the definition of a business and so the transaction will be accounted for as a business combination

8 Identifying a Business Combination Contd.. If the assets acquired are not a business, the reporting entity shall account for the transaction or other event as an asset acquisition. For example, acquisition of a shell or shelf company is not a business combination as defined in IFRS 3(2008) because no business is being acquired.

9 Key Definitions Business combination A transaction or other event in which an acquirer obtains control of one or more businesses. Control The power to govern the financial and operating policies of an entity so as to obtain benefits from its activities. Business A business consists of inputs and processes applied to those inputs that have the ability to create outputs.

10 Example of a Common Control Transaction A B and C are wholly-owned subsidiaries of A. B C A transfers its equity interest in B to C. In exchange, C issues further equity shares to A. B The transaction is a common control transaction since both B and C are under the common control of A.

11 Acquisition Method All business combinations are accounted for using the acquisition method. To apply acquisition method it is required to; Stage 1 Identifying the acquirer Stage 2 Determining the acquisition date Stage 3 Recognizing and measuring the identifiable assets acquired, the liabilities assumed, and any non-controlling interest in the acquiree Stage 4 Recognizing and measuring goodwill or a gain from a bargain purchase

12 Identifying the Acquirer Guidance under IFRS 3 (Revised 2008) to identify the acquirer; Facts One of the entities has transferred cash or other assets or incurred liabilities Exchanging equity instruments Voting right in the combined entity Existence of a large minority voting interest The composition of the governing body The composition of the senior management Other terms of exchange If more than two entities involved If a new entity is formed to issue equity interest If a new entity is formed and transferred cash or other assets or incurred liabilities Acquirer The entity that transfers cash or other assets or incurs liabilities The entity that retains largest portion of the voting rights of the combined entity The single owner who retains the largest voting rights The entity that can elect and or appoint or remove a majority of the governing body members The entity whose (former) management dominates the combined management The entity that pays premium over the pre-combination fair value of the equity interests Among the other things, consider; the size of the operations of the combined entities the combined entity that has initiated the business combination One of the combining entities The new entity

13 Determining the Acquisition Date Date on which the acquirer obtains control of the acquiree. Usually, the date on which the acquirer legally transfers the consideration, acquires the assets, and assumes the liabilities of the acquiree - the closing date.

14 Acquisition Date Q&A On 1 December 20X7, Entity A acquires a 35% noncontrolling equity interest in Entity B. On 1 January 20X9 Entity A acquires 40% interest in Entity B, which gives it control of Entity B. What is the acquisition date?` a) 1 December 20X7 b) 1 January 20X9

15 Identifying and Measuring Consideration Consideration should be measured at fair value. Consideration is the sum of the acquisition-date fair values of: The assets transferred The liabilities incurred by the acquirer The equity interests issued Acquisition-related costs are generally expensed as incurred except for the costs that are incurred related to the issuance of debt or equity securities

16 Identifying and Measuring Consideration Contingent consideration Recognize at acquisition-date fair value as part of the consideration transferred. Obligation to pay contingent consideration is classified as a liability or equity Subsequent measurement: If classified as equity, no re-measurement. Subsequent settlement shall be accounted for within equity. If classified as liability and that liability is: A financial instrument within the scope of IAS 39, re-measure to fair value through earnings or comprehensive income each period until settled Not within scope of IAS 39, account for in accordance with IAS 37 or other IFRSs as appropriate

17 Consideration Paid Case Study Entity A acquired controlling interest in Entity B and issued 100,000 shares to its owners as a consideration for the acquisition. The fair value of the share issued by Entity A was as follows; Rs. 350,000 as at the date of the acquisition agreement Rs. 425,000 as at the date of the acquisition as identified by the agreement Entity A incurred the following expenses in relation with the acquisition; Legal and consulting fees of Rs. 20,000 General administrative costs of Rs. 10,000 Costs related to issuance of equity Rs. 15,000 Entity A also agrees with Entity B that if it meets certain performance based targets within next two year, an additional consideration (in cash) of Rs. 70,000 will be paid to it. Entity A determines the fair value of this additional consideration as Rs. 45,000. Compute the amount of consideration paid in the above transaction?

18 Case Study Solution Computation of consideration paid Rs. Fair value of equity issued as at the date of acquisition 425,000 Fair value of the contingent consideration 45,000 Total consideration paid 470,000 Expenses incurred in relation with the acquisition Other expenses Legal and consulting fees of Rs. 20,000 General administrative costs of Rs. 10,000 Costs related to issuance of equity Rs. 15,000 Accounting treatment To be charged to expenses as incurred To be charged to expenses as incurred To be recognized in accordance with IAS 32 and IAS 39.

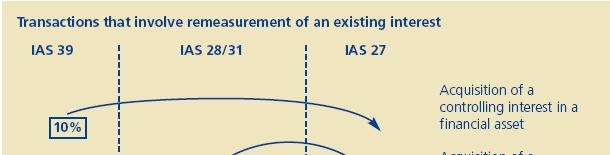

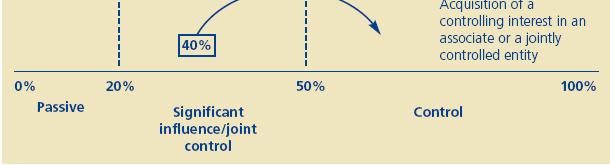

19 Recognition and Measurement Principles As of the acquisition date, the acquirer shall recognize, separately from goodwill, the identifiable assets acquired, the liabilities assumed, and any non-controlling interest in the acquiree. The acquirer shall measure the identifiable assets acquired and the liabilities assumed at their acquisition-date fair values. For each business combination, the acquirer shall measure non-controlling interest either at fair value, or at non-controlling interest s proportionate share of the acquiree s identifiable net assets.

20 Recognition and Measurement Principles Contd.. Non-controlling interest could have a negative carrying balance. If there are accumulated net losses attributable to noncontrolling interest.

21 Goodwill Measurement Goodwill= Aggregate Consideration (+) Non-controlling interest (+) Previously held equity interest (acquisition date fair value) (-) Net Identifiable assets acquired and liabilities assumed Tested for impairment and is not amortized

22 Goodwill Measurement Illustration Case facts: P pays Rs. 800 to purchase 80% of the shares of S. Fair value of 100% of S s identifiable net assets is Rs Fair value of the non-controlling interest is Rs. 185.

23 Goodwill Measurement (Alternative I) If P elects to measure non-controlling interests as their proportionate interest in the net assets of S; Fair value of the considerations transferred 800 Add: Proportionate fair value of the non-controlling interest (20% of S s identifiable net assets of $ 600) Rs. 120 Sub total 920 Less: Fair value of S s identifiable net assets (600) Goodwill 320

24 Goodwill Measurement (Alternative II) If P elects to measure non-controlling interests at fair value; Fair value of the considerations transferred 800 Add: Fair value of the non-controlling interest Rs. 185 Sub total 985 Less: Fair value of S s identifiable net assets (600) Goodwill 385

25 Gain From Bargain Purchase Bargain purchase occurs if the fair value of the identifiable net assets of the acquiree exceeds the aggregate of: The consideration transferred, The non-controlling interests, and The fair value of any previously held equity interest. Gain on bargain purchase is recognized in profit or loss on the acquisition date. Reassessment required prior to recognizing a bargain purchase gain.

26 Non-control to Control Transactions

27 Non-control to Control Transactions Case Study Entity A acquired a 75% controlling interest in Entity B in two stages. In 20X4, Entity A acquired a 15% equity interest for cash consideration of Rs. 10,000. Entity A classified the interest as available-for-sale under IAS 39. From 20X4 to the end of 20X7, Entity A reported fair value increase of Rs. 2,000 in other comprehensive income (OCI). In 20X8, Entity A acquired a further 60% equity interest for cash consideration of Rs. 60,000. Entity A identifies net assets of Entity B with a fair value of Rs. 80,000. Entity A elected to measure noncontrolling interests at their share of net assets. On the date of acquisition, the previously-held 15% interest had a fair value of Rs. 12,500. Compute the goodwill and gain/ loss on account fair value changes in the investment upon acquisition of controlling interest in 20X8.

28 Case Study Solution Computation of goodwill on the second acquisition Rs. Fair value of consideration given for controlling interest 60,000 Non-controlling interest (25% * Rs. 80,000) 20,000 Fair value previously-held interest 12,500 Sub-total 92,500 Less: Fair value of net assets of acquire (80,000) Goodwill 12,500 Expenses incurred in relation with the acquisition Other expenses Legal and consulting fees of Rs. 20,000 General administrative costs of Rs. 10,000 Costs related to issuance of equity Rs. 15,000 Accounting treatment To be charged to expenses as incurred To be charged to expenses as incurred To be recognized in accordance with IAS 32 and IAS 39.

29 Case Study Solution Contd.. Computation of fair value differences on the investment Rs. Gain on disposal of 15% investment (Rs. 12,500 Rs. 12,000) 500 Gain previously reported in OCI (Rs. 12,000 Rs. 10,000) 2,000 Total gain 2,500 Entity A should include Rs. 2,500 (as computed above) in statement of comprehensive income in 20X8.

30 Business combination without the Transfer of Consideration An acquirer may obtain control of an acquiree without transferring consideration. Such as; Acquiree repurchases a sufficient number of its own shares for an existing investor (acuqirer) to obtain control; Minority veto rights lapse that previously kept the acquirer from controlling an acquiree in which the acquirer held the majority voting rights; and A business combination by contract alone. In such cases, IFRS 3 requires an acquirer to be identified, and the acquisition method be applied.

31 Measurement Period Measurement period is the period after the acquisition date during which the acquirer adjust the provisional amounts recognized for a business combination. Cannot exceed one year from the acquisition date. If the initial accounting for a business combination is incomplete by the end of reporting period, the financial statements should be prepared using the provisional values for the items for which the accounting is incomplete. Revise comparative information for prior periods. Need to adjust the income statement for changes in depreciation and amortization.

32 Separate Transactions The acquirer and the acquiree may have a pre-existing relationship or other arrangement before negotiations for the business combination began; or they may enter into an arrangement during the negotiations that is separate from the business combination. The acquirer should identify amounts that are not part of the exchange for the acquiree and should recognize only the consideration transferred for the acquiree; and the assets acquired and liabilities assumed in the exchange for the acquiree Separate transactions should be accounted for in accordance with the relevant IFRSs

33 Examples of Separate Transactions A transaction that in effect settles pre-existing relationships between the acquirer and acquiree; A transaction that remunerates employees or former owners of the acquiree for future services; and A transaction that reimburses the acquiree or its former owners for paying the acquirer's acquisition-related costs.

34 Recognition and Measurement Exceptions Recognition Exceptions Contingent liabilities Measurement Exceptions Reacquired rights Share-based payment awards Assets held for sale Recognition Measurement Both Recognition and Measurement exceptions Income taxes Employee benefits Indemnification assets

35 Measurement Considerations Other Items Reacquired Rights Initial Measurement Measure as an identifiable intangible asset apart from goodwill. Value based upon remaining contractual term. Subsequent Measurement Amortized over the remaining contractual period of the contract in which the right was granted. Contingent Liabilities Indemnification Assets Recognized at fair value if liability arises from a past event and can be measured reliably. Generally, measured at the acquisition date fair value. If related to a contingent liability, then it is not recognized at the acquisition date because its fair value is not reliably measurable at that date. If related to an asset or liability, for example, that results from an employee benefit that is measured on a basis other than acquisition-date fair value. Higher of acquisition-date fair value less cumulative amortization into income, if any, or amount based on IAS 37 (best estimate of settlement). Measured on the same basis as the indemnified liability or asset.

36 Disposal of controlling Interests Increase/ decrease in ownership percentage of subsidiary (as long as parent retains control) Recorded as equity transactions No gain or loss is recognized If the parent retains a non-controlling interest after control is lost: Non-controlling interest is remeazured to fair value on the date control is lost Recognize gain or loss in the income statement

37 Line of Difference IFRS and Indian GAAP The pooling of interests and purchase method Recognition of Assets and Liabilities Goodwill Measurement Non-Controlling interests Contingent Considerations Acquisition Related Costs

38 Key Differences IFRS Vs. Indian GAAP Topic IFRS Indian GAAP 1 Scope IFRS 3 is applicable to both amalgamations (where acquirer looses identity) and acquisitions (where acquiree continued in existence). 2 Method of accounting All business combinations have to be accounted for by applying the purchase method. 3 Measurement The identifiable assets acquired and the liabilities assumed are measured at their acquisition date fair value. 4 Noncontrolling interest At the time of acquisition, an entity may elect to measure, on a transaction to transaction basis, the non-controlling interest either at fair value or at the non-controlling interests proportionate share of the fair value of the identifiable net assets of the acquirer. AS 14 is applicable to only amalgamations. Business combinations may be accounted for using either the pooling of interests method (if certain criteria are met) (or) the purchase method. The identifiable assets acquired and the liabilities assumed are recorded at the existing carrying amounts in the books of the acquiree under pooling of interest method or at the carrying values or fair values in the case of purchase method. At the time of acquisition, minority interests are recorded based on the minority s share in the existing carrying amounts of net assets of acquiree on the date of acquisition. This is determined on the basis of information contained in the financial statements of the acquirees as on the date of investment.

39 Key Differences IFRS Vs. Indian GAAP Contd.. Topic IFRS Indian GAAP 5 Initial measurement of goodwill 6 Subsequent measurement of goodwill Measured as the difference between; the aggregate of (a) the acquisition date fair value of the consideration transferred; (b) the amount of any non-controlling interest and (c) in a business combination achieved in stages, the acquisition-date fair value of the acquirer s previously held equity interest in the acquirer; and The net of the acquisition-date fair values of the identifiable assets acquired and the liabilities assumed. If the above difference is negative, the resulting gain is recognized as a bargain purchase in the statement of comprehensive income. Goodwill is not amortized but tested for impairment on an annual basis or more frequently if events or changes in circumstance indicate impairment. Any excess of the amount of the consideration over the value of the net assets of the transferor company acquired by the transferee company is recognized in the financial statements as goodwill arising on amalgamation. If the amount of the above consideration is lower than the value of the net assets acquired, the difference is recognized as Capital Reserve, a component of sharehodlers equity. Goodwill arising on amalgamation in the nature of purchase is amortized over a period not exceeding five years. There is no guidance on goodwill arising on acquisition of subsidiary or assets and liabilities of a business. In practice such goodwill is not amortized but tested for impairment.

40 Key Differences IFRS Vs. Indian GAAP Contd.. Topic IFRS Indian GAAP 6 Contingent consideration 7 Subsequent adjustment of fair values 8 Acquisition related costs Consideration for the acquisition includes the acquisition-date fair value of contingent consideration. Changes to contingent consideration resulting from events after the end of the reporting period are recognized in profit or loss. Any subsequent adjustments of fair value determined on a provisional basis can be adjusted against goodwill if conditions are fulfilled. Acquisition related costs such as finder s fee, due diligence costs, etc. are accounted for as expenses in the period in which the costs are incurred and the services are received. No specific guidance. No specific guidance. No specific guidance.

41 Effective Date and Transition Effective date Business combinations for which the acquisition date is on or after the beginning of the first annual reporting period beginning on or after July 1, 2009 Transition Early adoption permitted but only for annual reporting periods beginning on or after June 30, 2007 Must disclose this fact and also apply IAS 27 (Revised 2008) from that date. Early Adoption Permitted Mandatory Adoption 04/01/ /01/ /31/ /31/ /01/2009

42

The entity that obtains control of the acquiree. The business or businesses that the acquirer obtains control of in a business combination.

IFRS 3 IFRS 3 Business Combination INTRODUCTION Background DEFINITIONS Business combination Business Acquisition date Acquirer Acquiree IFRS 3 Business Combinations outlines the accounting when an acquirer

IFRS 3 IFRS 3 Business Combination INTRODUCTION Background DEFINITIONS Business combination Business Acquisition date Acquirer Acquiree IFRS 3 Business Combinations outlines the accounting when an acquirer

Business Combinations

Business Combinations Indian Accounting Standard (Ind AS) 103 Business Combinations Contents Paragraphs OBJECTIVE 1 SCOPE 2 IDENTIFYING A BUSINESS COMBINATION 3 THE ACQUISITION METHOD 4 53 Identifying

Business Combinations Indian Accounting Standard (Ind AS) 103 Business Combinations Contents Paragraphs OBJECTIVE 1 SCOPE 2 IDENTIFYING A BUSINESS COMBINATION 3 THE ACQUISITION METHOD 4 53 Identifying

Business Combinations

International Financial Reporting Standard 3 Business Combinations This version was issued in January 2008. Its effective date is 1 July 2009. It includes amendments resulting from IFRSs issued up to 31

International Financial Reporting Standard 3 Business Combinations This version was issued in January 2008. Its effective date is 1 July 2009. It includes amendments resulting from IFRSs issued up to 31

Business Combinations IFRS 3

CA Sandesh Mundra Business Combinations IFRS 3 For many men, the acquisition of wealth does not end their troubles, it only changes them. - Lucius Annaeus Seneca Lets get some of the basics correct.. We

CA Sandesh Mundra Business Combinations IFRS 3 For many men, the acquisition of wealth does not end their troubles, it only changes them. - Lucius Annaeus Seneca Lets get some of the basics correct.. We

EN Official Journal of the European Union L 320/373

29.11.2008 EN Official Journal of the European Union L 320/373 INTERNATIONAL FINANCIAL REPORTING STANDARD 3 Business combinations OBJECTIVE 1 The objective of this IFRS is to specify the financial reporting

29.11.2008 EN Official Journal of the European Union L 320/373 INTERNATIONAL FINANCIAL REPORTING STANDARD 3 Business combinations OBJECTIVE 1 The objective of this IFRS is to specify the financial reporting

IFRS 3 Business Combinations

IFRS 3 Business Combinations What constitutes a business? an integrated set of activities and assets that is capable of being conducted and managed for the purpose of providing a return in the form of

IFRS 3 Business Combinations What constitutes a business? an integrated set of activities and assets that is capable of being conducted and managed for the purpose of providing a return in the form of

Business Combination. CA Yagnesh Desai. Compiled by CA Yagnesh 1

Business Combination CA Yagnesh Desai ymdesaiandco@gmail.com 093222 44770 09820133227 yagnesh@caymd.com 1 Indicators Not necessarily Limits by the Standard Above 50 % Control Hence Consolidate Control

Business Combination CA Yagnesh Desai ymdesaiandco@gmail.com 093222 44770 09820133227 yagnesh@caymd.com 1 Indicators Not necessarily Limits by the Standard Above 50 % Control Hence Consolidate Control

HKAS 27 and HKFRS 3 (Revised) 9 August 2010

9 August 2010") HKAS 27 and HKFRS 3 (Revised) 9 August 2010 Nelson Lam 林智遠 MBA MSc BBA ACA ACIS CFA CPA(Aust.) CPA(US) FCCA FCPA FHKIoD FTIHK MSCA 2005-10 Nelson Consulting Limited 1 Today s Agenda Consolidated and Separate

HKAS 27 and HKFRS 3 (Revised) 9 August 2010 Nelson Lam 林智遠 MBA MSc BBA ACA ACIS CFA CPA(Aust.) CPA(US) FCCA FCPA FHKIoD FTIHK MSCA 2005-10 Nelson Consulting Limited 1 Today s Agenda Consolidated and Separate

EXECUTIVE SUMMARY A GUIDE TO ACCOUNTING FOR BUSINESS COMBINATIONS

EXECUTIVE SUMMARY A GUIDE TO ACCOUNTING FOR BUSINESS COMBINATIONS This Executive Summary is part of RSM US LLP s A Guide to Accounting for Business Combinations and should be read in conjunction with that

EXECUTIVE SUMMARY A GUIDE TO ACCOUNTING FOR BUSINESS COMBINATIONS This Executive Summary is part of RSM US LLP s A Guide to Accounting for Business Combinations and should be read in conjunction with that

IFRS - 3. Business Combinations. By:

IFRS - 3 Business Combinations Objective 1. The purpose of this IFRS is to specify to disclose financial information by an entity when carrying out a business combination. In particular, specifies that

IFRS - 3 Business Combinations Objective 1. The purpose of this IFRS is to specify to disclose financial information by an entity when carrying out a business combination. In particular, specifies that

Frequently asked questions on business combinations

23 Frequently asked questions on business combinations This article aims to: Highlight some of the key examples discussed in the education material on Ind AS 103. Background Ind AS 103, Business Combinations

23 Frequently asked questions on business combinations This article aims to: Highlight some of the key examples discussed in the education material on Ind AS 103. Background Ind AS 103, Business Combinations

A guide to. accounting for. Second Edition. Assurance Tax Consulting

A guide to accounting for Business Combinations Second Edition Assurance Tax Consulting A guide to accounting for Business Combinations Second Edition January 2012 This publication is provided as an information

A guide to accounting for Business Combinations Second Edition Assurance Tax Consulting A guide to accounting for Business Combinations Second Edition January 2012 This publication is provided as an information

AUDIT A GUIDE TO ACCOUNTING FOR BUSINESS COMBINATIONS. Third Edition

AUDIT A GUIDE TO ACCOUNTING FOR BUSINESS COMBINATIONS Third Edition A GUIDE TO ACCOUNTING FOR BUSINESS COMBINATIONS THIRD EDITION June 2016 A GUIDE TO ACCOUNTING FOR BUSINESS COMBINATIONS Prepared by:

AUDIT A GUIDE TO ACCOUNTING FOR BUSINESS COMBINATIONS Third Edition A GUIDE TO ACCOUNTING FOR BUSINESS COMBINATIONS THIRD EDITION June 2016 A GUIDE TO ACCOUNTING FOR BUSINESS COMBINATIONS Prepared by:

Mergers & Acquisitions (Accounting Implications) By N Jayendran

By N Jayendran") Mergers & Acquisitions (Accounting Implications) By N Jayendran Existing Standards Under previous IGAAP:- AS 14 Accounting for Amalgamation Under Ind AS: Ind AS 103 Business Combination Accounting for

Mergers & Acquisitions (Accounting Implications) By N Jayendran Existing Standards Under previous IGAAP:- AS 14 Accounting for Amalgamation Under Ind AS: Ind AS 103 Business Combination Accounting for

31 July 2014 Japan s Modified International Standards (JMIS): Accounting Standards Comprising IFRSs and the ASBJ Modifications

: Accounting Standards Comprising IFRSs and the ASBJ Modifications") 31 July 2014 Japan s Modified International Standards (JMIS): Accounting Standards Comprising IFRSs and the ASBJ Modifications ASBJ Modification Accounting Standard Exposure Draft No. 1 Accounting for

31 July 2014 Japan s Modified International Standards (JMIS): Accounting Standards Comprising IFRSs and the ASBJ Modifications ASBJ Modification Accounting Standard Exposure Draft No. 1 Accounting for

Workshop on IND AS Intangible assets WIRC of the ICAI April 23, 2016

Workshop on IND AS Intangible assets WIRC of the ICAI April 23, 2016 Contents Background and Scope Definitions Recognition & Measurement Amortization Disclosure requirements Differences with existing AS

Workshop on IND AS Intangible assets WIRC of the ICAI April 23, 2016 Contents Background and Scope Definitions Recognition & Measurement Amortization Disclosure requirements Differences with existing AS

International Financial Reporting Standards (IFRS)

") FACT SHEET September 2011 IAS 31 Interests in joint ventures (This fact sheet is based on the standard as at 1 January 2011.) Important note: This fact sheet is based on the requirements of the International

FACT SHEET September 2011 IAS 31 Interests in joint ventures (This fact sheet is based on the standard as at 1 January 2011.) Important note: This fact sheet is based on the requirements of the International

Accounting for Amalgamations

Bangalore Branch of SIRC of ICAI Study Circle Meeting - Agenda/Contents Introduction Definitions Types of amalgamations Methods of accounting for amalgamations Consideration Treatment of goodwill arising

Bangalore Branch of SIRC of ICAI Study Circle Meeting - Agenda/Contents Introduction Definitions Types of amalgamations Methods of accounting for amalgamations Consideration Treatment of goodwill arising

FASB Emerging Issues Task Force

EITF Issue No. 09-4 FASB Emerging Issues Task Force Issue No. 09-4 Title: Seller Accounting for Contingent Consideration Document: Issue Summary No. 1, Supplement No. 1 Date prepared: August 21, 2009 FASB

EITF Issue No. 09-4 FASB Emerging Issues Task Force Issue No. 09-4 Title: Seller Accounting for Contingent Consideration Document: Issue Summary No. 1, Supplement No. 1 Date prepared: August 21, 2009 FASB

Navigating FASB's New Pushdown Rules for Acquired Entities

Navigating FASB's New Pushdown Rules for Acquired Entities Evaluating Whether and How to Adopt Pushdown Accounting on Subsidiary Financial Statements THURSDAY, APRIL 23, 2015, 1:00-2:50 pm Eastern IMPORTANT

Navigating FASB's New Pushdown Rules for Acquired Entities Evaluating Whether and How to Adopt Pushdown Accounting on Subsidiary Financial Statements THURSDAY, APRIL 23, 2015, 1:00-2:50 pm Eastern IMPORTANT

Latest Development of IFRS (and HKFRS) 10 January 2011

10 January 2011") Latest Development of IFRS (and HKFRS) 10 January 2011 Nelson Lam 林智遠 MBA MSc BBA ACA ACIS CFA CPA(Aust.) CPA(US) CTA FCCA FCPA FTIHK MSCA 2008-11 Nelson Consulting Limited 1 Effective for 2010 Dec. Year-End

Latest Development of IFRS (and HKFRS) 10 January 2011 Nelson Lam 林智遠 MBA MSc BBA ACA ACIS CFA CPA(Aust.) CPA(US) CTA FCCA FCPA FTIHK MSCA 2008-11 Nelson Consulting Limited 1 Effective for 2010 Dec. Year-End

The Western India Regional Council. Business Combinations

The Western India Regional Council Impact Analysis of Indian Accounting Standards ( Ind AS ) and Income Computation and Disclosure Standards ( ICDS ) on Business Combinations Presentation by: Paresh Clerk

The Western India Regional Council Impact Analysis of Indian Accounting Standards ( Ind AS ) and Income Computation and Disclosure Standards ( ICDS ) on Business Combinations Presentation by: Paresh Clerk

ACCOUNTING FOR ACQUISITIONS RESULTING IN COMBINATIONS OF ENTITIES OR OPERATIONS

Institute of Chartered Accountants of New Zealand FINANCIAL REPORTING NO. 36 OCTOBER 2001 ACCOUNTING FOR ACQUISITIONS RESULTING IN COMBINATIONS OF ENTITIES OR OPERATIONS Issued by the Financial Reporting

Institute of Chartered Accountants of New Zealand FINANCIAL REPORTING NO. 36 OCTOBER 2001 ACCOUNTING FOR ACQUISITIONS RESULTING IN COMBINATIONS OF ENTITIES OR OPERATIONS Issued by the Financial Reporting

In December 2003 the Board issued a revised IAS 40 as part of its initial agenda of technical projects.

IAS 40 Investment Property In April 2001 the International Accounting Standards Board (the Board) adopted IAS 40 Investment Property, which had originally been issued by the International Accounting Standards

IAS 40 Investment Property In April 2001 the International Accounting Standards Board (the Board) adopted IAS 40 Investment Property, which had originally been issued by the International Accounting Standards

In December 2003 the IASB issued a revised IAS 40 as part of its initial agenda of technical projects.

International Accounting Standard 40 Investment Property In April 2001 the International Accounting Standards Board (IASB) adopted IAS 40 Investment Property, which had originally been issued by the International

International Accounting Standard 40 Investment Property In April 2001 the International Accounting Standards Board (IASB) adopted IAS 40 Investment Property, which had originally been issued by the International

Accounting for Amalgamations

198 Accounting Standard (AS) 14 (issued 1994) Accounting for Amalgamations Contents INTRODUCTION Paragraphs 1-3 Definitions 3 EXPLANATION 4-27 Types of Amalgamations 4-6 Methods of Accounting for Amalgamations

198 Accounting Standard (AS) 14 (issued 1994) Accounting for Amalgamations Contents INTRODUCTION Paragraphs 1-3 Definitions 3 EXPLANATION 4-27 Types of Amalgamations 4-6 Methods of Accounting for Amalgamations

IFRS and HKFRS Update and Challenge 1 June 2011

IFRS and HKFRS Update and Challenge 1 June 2011 Lam Chi Yuen, Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) CTA FCCA FCPA FHKIoD FTIHK MHKSI MSCA 2008-11 Nelson Consulting Limited 1 Effective for

IFRS and HKFRS Update and Challenge 1 June 2011 Lam Chi Yuen, Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) CTA FCCA FCPA FHKIoD FTIHK MHKSI MSCA 2008-11 Nelson Consulting Limited 1 Effective for

Definitions. CPI is a lease in which base rent is adjusted based on changes in a consumer price index.

Annualized Rental Income is rental revenue under our leases on Operating Properties on a straight-line basis, which includes the effect of rent escalations and any tenant concessions, such as free rent,

Annualized Rental Income is rental revenue under our leases on Operating Properties on a straight-line basis, which includes the effect of rent escalations and any tenant concessions, such as free rent,

In December 2003 the Board issued a revised IAS 40 as part of its initial agenda of technical projects.

IAS Standard 40 Investment Property In April 2001 the International Accounting Standards Board (the Board) adopted IAS 40 Investment Property, which had originally been issued by the International Accounting

IAS Standard 40 Investment Property In April 2001 the International Accounting Standards Board (the Board) adopted IAS 40 Investment Property, which had originally been issued by the International Accounting

IASB Staff Paper March 2011

IASB Staff Paper March 2011 Effect of board redeliberations on Exposure Draft Leases About this staff paper This staff paper indicates how the proposals in the Exposure Draft Leases would change as a result

IASB Staff Paper March 2011 Effect of board redeliberations on Exposure Draft Leases About this staff paper This staff paper indicates how the proposals in the Exposure Draft Leases would change as a result

Accounting for Amalgamations

Accounting Standard (AS) 14 (revised 2016) Accounting for Amalgamations Contents INTRODUCTION Paragraphs 1-3 Definitions 3 EXPLANATION 4-27 Types of Amalgamations 4-6 Methods of Accounting for Amalgamations

Accounting Standard (AS) 14 (revised 2016) Accounting for Amalgamations Contents INTRODUCTION Paragraphs 1-3 Definitions 3 EXPLANATION 4-27 Types of Amalgamations 4-6 Methods of Accounting for Amalgamations

An intangible asset is an identifiable non-monetary asset without physical substance.

Technical Summary This extract has been prepared by IASC Foundation staff and has not been approved by the IASB. For the requirements reference must be made to International Financial Reporting Standards.

Technical Summary This extract has been prepared by IASC Foundation staff and has not been approved by the IASB. For the requirements reference must be made to International Financial Reporting Standards.

GASB 69: Government Combinations

GASB 69: Government Combinations Table of Contents EXECUTIVE SUMMARY... 3 BACKGROUND... 3 KEY PROVISIONS... 3 OVERVIEW & SCOPE... 3 MERGER & TRANSFER OF OPERATIONS... 4 Mergers... 4 Transfers of Operations...

GASB 69: Government Combinations Table of Contents EXECUTIVE SUMMARY... 3 BACKGROUND... 3 KEY PROVISIONS... 3 OVERVIEW & SCOPE... 3 MERGER & TRANSFER OF OPERATIONS... 4 Mergers... 4 Transfers of Operations...

AAT Professional Diploma in Accounting

Qualification Number: R486 04 Qualification Technical Information Version 1.1 published 13 June 2016 AAT Professional Diploma in Accounting Qualification Technical Information Units in this qualification

Qualification Number: R486 04 Qualification Technical Information Version 1.1 published 13 June 2016 AAT Professional Diploma in Accounting Qualification Technical Information Units in this qualification

IFRS-5: Non-current Assets Held for Sale and Discontinued Operations

The journal is running a series of updates on IFRS, IAS, IFRIC and SIC. The updates mostly collected from different sources of IASB publication, seminars, workshop & IFRS website. This issue is based on

The journal is running a series of updates on IFRS, IAS, IFRIC and SIC. The updates mostly collected from different sources of IASB publication, seminars, workshop & IFRS website. This issue is based on

Intangibles Goodwill and Other (Topic 350), Business Combinations (Topic 805), and Not-for-Profit Entities (Topic 958)

, Business Combinations (Topic 805), and Not-for-Profit Entities (Topic 958)") Proposed Accounting Standards Update Issued: December 20, 2018 Comments Due: February 18, 2019 Intangibles Goodwill and Other (Topic 350), Business Combinations (Topic 805), and Not-for-Profit Entities

Proposed Accounting Standards Update Issued: December 20, 2018 Comments Due: February 18, 2019 Intangibles Goodwill and Other (Topic 350), Business Combinations (Topic 805), and Not-for-Profit Entities

IAS 38 Intangible Assets

21/12/2010, Tuesday From To Details Faculty 2:15 PM 5:30 PM IAS 38 : Intangible Assets IAS 40 : Investment Property IFRS 5 : Non Current Assets Held for Sale and Discontinued Operations CA. Chintan Patel,

21/12/2010, Tuesday From To Details Faculty 2:15 PM 5:30 PM IAS 38 : Intangible Assets IAS 40 : Investment Property IFRS 5 : Non Current Assets Held for Sale and Discontinued Operations CA. Chintan Patel,

roots The Substance of the Standard Contents Changes to the Accounting for Goodwill for Private Companies

The Substance of the Standard MAYER HOFFMAN MCCANN P.C. AN INDEPENDENT CPA FIRM TM A publication of the Professional Standards Group February 2014 Changes to the Accounting for Goodwill for Private Companies

The Substance of the Standard MAYER HOFFMAN MCCANN P.C. AN INDEPENDENT CPA FIRM TM A publication of the Professional Standards Group February 2014 Changes to the Accounting for Goodwill for Private Companies

Financial statement presentation. March 2007

March 2007 IASB Update is published as a convenience for the Board's constituents. All conclusions reported are tentative and may be changed or modified at future Board meetings. Decisions become final

March 2007 IASB Update is published as a convenience for the Board's constituents. All conclusions reported are tentative and may be changed or modified at future Board meetings. Decisions become final

Notice to Readers of this Summary of FASB Tentative Decisions on Business Combinations as of July 27, 2004

Notice to Readers of this Summary of FASB Tentative Decisions on Business Combinations as of July 27, 2004 The FASB and the IASB (the Boards ) plan to develop common Exposure Drafts of their proposed Statements

Notice to Readers of this Summary of FASB Tentative Decisions on Business Combinations as of July 27, 2004 The FASB and the IASB (the Boards ) plan to develop common Exposure Drafts of their proposed Statements

Accounting for Real Estate Transactions

Accounting for Real Estate Transactions A Guide for Public Accountants and Corporate Financial Professionals Second Edition MARIA K. DAVIS WILEY John Wiley & Sons, Inc. Contents Preface About the Author

Accounting for Real Estate Transactions A Guide for Public Accountants and Corporate Financial Professionals Second Edition MARIA K. DAVIS WILEY John Wiley & Sons, Inc. Contents Preface About the Author

WHITE PAPER ON FUNDS FROM OPERATIONS

WHITE PAPER ON FUNDS FROM OPERATIONS FOR IFRS REVISED: SEPTEMBER 2010 Page 1 of 17 I. Introduction and Background TABLE OF CONTENTS II. III. IV. Intended use of FFO FFO Definition Discussion of FFO Definition

WHITE PAPER ON FUNDS FROM OPERATIONS FOR IFRS REVISED: SEPTEMBER 2010 Page 1 of 17 I. Introduction and Background TABLE OF CONTENTS II. III. IV. Intended use of FFO FFO Definition Discussion of FFO Definition

.01 The objective of this Standard is to prescribe the accounting treatment for investment property and related disclosure requirements.

COMPARISON OF GRAP 16 WITH IAS 40 GRAP 16 IAS 40 DIFFERENCES Objective.01 The objective of this Standard is to prescribe the accounting treatment for investment property and related disclosure requirements.

COMPARISON OF GRAP 16 WITH IAS 40 GRAP 16 IAS 40 DIFFERENCES Objective.01 The objective of this Standard is to prescribe the accounting treatment for investment property and related disclosure requirements.

International Accounting Standard 17 Leases. Objective. Scope. Definitions IAS 17

International Accounting Standard 17 Leases Objective 1 The objective of this Standard is to prescribe, for lessees and lessors, the appropriate accounting policies and disclosure to apply in relation

International Accounting Standard 17 Leases Objective 1 The objective of this Standard is to prescribe, for lessees and lessors, the appropriate accounting policies and disclosure to apply in relation

Business Combinations and Consolidations

Stock Market Strategies Business Combinations and Consolidations Mitch Zacks Steven M. Bragg CPE Edition Distributed by The CPE Store www.cpestore.com 1-800-910-2755 Business Combinations and Consolidations

Stock Market Strategies Business Combinations and Consolidations Mitch Zacks Steven M. Bragg CPE Edition Distributed by The CPE Store www.cpestore.com 1-800-910-2755 Business Combinations and Consolidations

IAS 16 Property, Plant and Equipment. Uphold public interest

IAS 16 Property, Plant and Equipment Uphold public interest Background IAS 16 became operational in 1983 Major amendments have been made several times including 1998, 2003, 2008, 2012, 2013, 2014 The objective

IAS 16 Property, Plant and Equipment Uphold public interest Background IAS 16 became operational in 1983 Major amendments have been made several times including 1998, 2003, 2008, 2012, 2013, 2014 The objective

International Financial Reporting Standard 16 Leases. Objective. Scope. Recognition exemptions (paragraphs B3 B8) IFRS 16

IFRS 16") International Financial Reporting Standard 16 Leases Objective 1 This Standard sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective is to ensure

International Financial Reporting Standard 16 Leases Objective 1 This Standard sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective is to ensure

Intangible Assets IAS 38, IAS 36, IFRS 3

Intangible Assets IAS 38, IAS 36, IFRS 3 Agenda 1. Introduction 2. Recognition 3. Measurement 4. Impairment of intangible assets (IAS 36) Basic concept Cash-Generating Units 5. Disclosures 2 1 Introduction

Intangible Assets IAS 38, IAS 36, IFRS 3 Agenda 1. Introduction 2. Recognition 3. Measurement 4. Impairment of intangible assets (IAS 36) Basic concept Cash-Generating Units 5. Disclosures 2 1 Introduction

These notes will be appropriate both for both students who have chosen financial reporting as a depth area as well as those who have not.

When it comes to the Financial Reporting competency, the challenge that many students face is the tremendous amount of technical knowledge included in this competency, especially in light of the fact that

When it comes to the Financial Reporting competency, the challenge that many students face is the tremendous amount of technical knowledge included in this competency, especially in light of the fact that

Sri Lanka Accounting Standard LKAS 40. Investment Property

Sri Lanka Accounting Standard LKAS 40 Investment Property LKAS 40 CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 40 INVESTMENT PROPERTY paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 5 CLASSIFICATION OF PROPERTY

Sri Lanka Accounting Standard LKAS 40 Investment Property LKAS 40 CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 40 INVESTMENT PROPERTY paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 5 CLASSIFICATION OF PROPERTY

New Accounting Rules for Nonfinancial Asset Sales

On February 22, 2017, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 2017-05, Other Income Gains and Losses from the Derecognition of Nonfinancial Assets (Subtopic

On February 22, 2017, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 2017-05, Other Income Gains and Losses from the Derecognition of Nonfinancial Assets (Subtopic

New Zealand Equivalent to International Accounting Standard 40 Investment Property (NZ IAS 40)

") New Zealand Equivalent to International Accounting Standard 40 Investment Property (NZ IAS 40) Issued November 2004 and incorporates amendments up to and inlcuding 28 February 2014 This Standard was issued

New Zealand Equivalent to International Accounting Standard 40 Investment Property (NZ IAS 40) Issued November 2004 and incorporates amendments up to and inlcuding 28 February 2014 This Standard was issued

Real Estate Accounting

Real Estate Accounting Steven M. Bragg Chapter 1 Introduction to Accounting... 1 Learning Objectives... 1 Introduction... 1 Financial Accounting Basics... 1 Accounting Frameworks... 2 The Accounting Cycle...

Real Estate Accounting Steven M. Bragg Chapter 1 Introduction to Accounting... 1 Learning Objectives... 1 Introduction... 1 Financial Accounting Basics... 1 Accounting Frameworks... 2 The Accounting Cycle...

Exposure Draft. Amendments to Ind AS 40, Investment Property. (Last date for the comments: July 11, 2018)

") ED/ Ind AS/2018/07 Exposure Draft Amendments to Ind AS 40, Investment Property (Last date for the comments: July 11, 2018) Issued by Accounting Standards Board The Institute of Chartered Accountants of

ED/ Ind AS/2018/07 Exposure Draft Amendments to Ind AS 40, Investment Property (Last date for the comments: July 11, 2018) Issued by Accounting Standards Board The Institute of Chartered Accountants of

Financial Accounting Series

Financial Accounting Series NO. 221-C JUNE 2001 Statement of Financial Accounting Standards No. 142 Goodwill and Other Intangible Assets Financial Accounting Standards Board of the Financial Accounting

Financial Accounting Series NO. 221-C JUNE 2001 Statement of Financial Accounting Standards No. 142 Goodwill and Other Intangible Assets Financial Accounting Standards Board of the Financial Accounting

Japan s Modified International Standards (JMIS): Accounting Standards Comprising IFRSs and the ASBJ Modifications

: Accounting Standards Comprising IFRSs and the ASBJ Modifications") Japan s Modified International Standards (JMIS): Accounting Standards Comprising IFRSs and the ASBJ Modifications ASBJ Modification Accounting Standard No. 1 Accounting for Goodwill 30 June 2015 Amended

Japan s Modified International Standards (JMIS): Accounting Standards Comprising IFRSs and the ASBJ Modifications ASBJ Modification Accounting Standard No. 1 Accounting for Goodwill 30 June 2015 Amended

FRS 102 A New Era for UK & Irish GAAP

CPA Ireland Skillnet, is a training network that is funded by Skillnets, a state funded, enterprise led support body dedicated to the promotion and facilitation of training and up-skilling as key elements

CPA Ireland Skillnet, is a training network that is funded by Skillnets, a state funded, enterprise led support body dedicated to the promotion and facilitation of training and up-skilling as key elements

Chapter 3 Business Valuation Report

CHAPTER 3: BUSINESS VALUATION REPORT Chapter 3 Business Valuation Report A1. Pre-IPO Valuation Need Company Restructuring and Financing It is not unusual that companies undergo series of restructuring

CHAPTER 3: BUSINESS VALUATION REPORT Chapter 3 Business Valuation Report A1. Pre-IPO Valuation Need Company Restructuring and Financing It is not unusual that companies undergo series of restructuring

EN Official Journal of the European Union L 320/323

29.11.2008 EN Official Journal of the European Union L 320/323 INTERNATIONAL ACCOUNTING STANDARD 40 Investment property OBJECTIVE 1 The objective of this standard is to prescribe the accounting treatment

29.11.2008 EN Official Journal of the European Union L 320/323 INTERNATIONAL ACCOUNTING STANDARD 40 Investment property OBJECTIVE 1 The objective of this standard is to prescribe the accounting treatment

The Differences between full IFRS and FRS 102

CPA Ireland Skillnet CPA Ireland Skillnet, is a training network that is funded by Skillnets, a state funded, enterprise led support body dedicated to the promotion and facilitation of training and up-skilling

CPA Ireland Skillnet CPA Ireland Skillnet, is a training network that is funded by Skillnets, a state funded, enterprise led support body dedicated to the promotion and facilitation of training and up-skilling

IAG Conference Accounting Update Emerging issues in the public sector 20 November 2014 Michael Crowe Yannick Maurice

www.pwc.com.au IAG Conference Accounting Update Emerging issues in the public sector 20 November 2014 Michael Crowe Yannick Maurice Agenda Introduction Key topics o Fair value o PPP Projects Refinancing

www.pwc.com.au IAG Conference Accounting Update Emerging issues in the public sector 20 November 2014 Michael Crowe Yannick Maurice Agenda Introduction Key topics o Fair value o PPP Projects Refinancing

IFRS Training. IAS 38 Intangible Assets. Professional Advisory Services

IFRS Training IAS 38 Intangible Assets Table of Contents Section 1 Overview 2 Introduction to Intangible Assets 3 Recognition and Initial Measurement 4 Internally Generated Intangible Assets 5 Measurement

IFRS Training IAS 38 Intangible Assets Table of Contents Section 1 Overview 2 Introduction to Intangible Assets 3 Recognition and Initial Measurement 4 Internally Generated Intangible Assets 5 Measurement

Investor. Investment Service Centre. Listed Companies Information. YANGTZEKIANG<00294> - Results Announcement

Investor Investment Service Centre Listed Companies Information YANGTZEKIANG - Results Announcement Yangtzekiang Garment Limited announced on 16/12/2005: (stock code: 00294 ) Year end date: 31/03/2006

Investor Investment Service Centre Listed Companies Information YANGTZEKIANG - Results Announcement Yangtzekiang Garment Limited announced on 16/12/2005: (stock code: 00294 ) Year end date: 31/03/2006

IFRS 3 Business combinations. Cases. Cases Véronique Weets

Cases IFRS 3 Business combinations Cases Véronique Weets Instituut van de Bedrijfsrevisoren 1 Cases TABLE OF CONTENT Table of content... 2 IFRS 3 Business combinations... 3 Identifying the acquirer...

Cases IFRS 3 Business combinations Cases Véronique Weets Instituut van de Bedrijfsrevisoren 1 Cases TABLE OF CONTENT Table of content... 2 IFRS 3 Business combinations... 3 Identifying the acquirer...

TOPIC 2 - IAS 40 INVESTMENT PROPERTY

TOPIC 2 - IAS 40 INVESTMENT PROPERTY Definitions: Investment Property: Property held to earn rentals or for capital appreciation or both. An entity may own land or a building as an investment rather than

TOPIC 2 - IAS 40 INVESTMENT PROPERTY Definitions: Investment Property: Property held to earn rentals or for capital appreciation or both. An entity may own land or a building as an investment rather than

HONG KONG SOCIETY OF ACCOUNTANTS. Financial Accounting Standards Committee. Urgent Issues & Interpretations Sub-Committee

HONG KONG SOCIETY OF ACCOUNTANTS Financial Accounting Standards Committee Urgent Issues & Interpretations Sub-Committee Interpretation 12 Business combinations - Subsequent adjustment of fair values and

HONG KONG SOCIETY OF ACCOUNTANTS Financial Accounting Standards Committee Urgent Issues & Interpretations Sub-Committee Interpretation 12 Business combinations - Subsequent adjustment of fair values and

WHITE PAPER ON FUNDS FROM OPERATIONS

WHITE PAPER ON FUNDS FROM OPERATIONS FOR IFRS REVISED: NOVEMBER 2012 Page 1 of 16 I. Introduction and Background TABLE OF CONTENTS II. III. IV. Intended use of FFO FFO Definition Discussion of FFO Definition

WHITE PAPER ON FUNDS FROM OPERATIONS FOR IFRS REVISED: NOVEMBER 2012 Page 1 of 16 I. Introduction and Background TABLE OF CONTENTS II. III. IV. Intended use of FFO FFO Definition Discussion of FFO Definition

Translation Of Financial Statements Originally Issued In Arabic

PALM HILLS DEVELOPMENTS COMPANY (An Egyptian Joint Stock Company) Consolidated Financial Statements For The Six Months Ended Together With Review Report PALM HILLS DEVELOPMENTS COMPANY S.A.E CONSOLIDATED

PALM HILLS DEVELOPMENTS COMPANY (An Egyptian Joint Stock Company) Consolidated Financial Statements For The Six Months Ended Together With Review Report PALM HILLS DEVELOPMENTS COMPANY S.A.E CONSOLIDATED

Re: FASB Exposure Draft, Proposed Statement of Financial Accounting Standards, "Business Combinations, a replacement of FASB Statement No.

Letter of Comment No: lo%" File Reference: 1204-001 October 28, 2005 Mr. Robert Herz Chairman Financial Accounting Standards Board 40 I Merritt 7 P.O. Box 5116 Norwalk, CT 06856-5116 File Reference No.

Letter of Comment No: lo%" File Reference: 1204-001 October 28, 2005 Mr. Robert Herz Chairman Financial Accounting Standards Board 40 I Merritt 7 P.O. Box 5116 Norwalk, CT 06856-5116 File Reference No.

AGC Financial Issues Committee

AGC Financial Issues Committee FASB Update Cullen D. Walsh, FASB Assistant Director January 8, 2015 The views expressed in this presentation are those of the presenter and are intended for discussion purposes

AGC Financial Issues Committee FASB Update Cullen D. Walsh, FASB Assistant Director January 8, 2015 The views expressed in this presentation are those of the presenter and are intended for discussion purposes

Applying IFRS for the real estate industry

www.pwc.co.uk Applying IFRS for the real estate industry 12 December 2018 Contents Introduction to applying IFRS for the real estate industry 1 1. Real estate value chain 2 1.1. Overview of the investment

www.pwc.co.uk Applying IFRS for the real estate industry 12 December 2018 Contents Introduction to applying IFRS for the real estate industry 1 1. Real estate value chain 2 1.1. Overview of the investment

International Financial Reporting Standards (IFRS)

") FACT SHEET September 2011 IAS 38 Intangible Assets (This fact sheet is based on the standard as at 1 January 2011.) Important note: This fact sheet is based on the requirements of the International Financial

FACT SHEET September 2011 IAS 38 Intangible Assets (This fact sheet is based on the standard as at 1 January 2011.) Important note: This fact sheet is based on the requirements of the International Financial

WEEK 9 Investment Property IAS 40

WEEK 9 Investment Property IAS 40 Learning Objectives Define the term investment property. Explain the recognition and measurement procedures in IAS 40 Discuss how to treat disposable of an asset Discuss

WEEK 9 Investment Property IAS 40 Learning Objectives Define the term investment property. Explain the recognition and measurement procedures in IAS 40 Discuss how to treat disposable of an asset Discuss

IFRS 16 Leases supplement

IFRS 16 Leases supplement Guide to annual financial statements IFRS December 2017 kpmg.com/ifrs Contents About this supplement 1 About IFRS 16 3 The Group s lease portfolio 6 Part I Modified retrospective

IFRS 16 Leases supplement Guide to annual financial statements IFRS December 2017 kpmg.com/ifrs Contents About this supplement 1 About IFRS 16 3 The Group s lease portfolio 6 Part I Modified retrospective

Detailed competency map: Knowledge requirements. (AAT examination)

") Detailed competency map: Knowledge requirements (AAT examination) Fields of competency The items listed are shown with an indicator of the minimum acceptable level of competency, based on a three-point

Detailed competency map: Knowledge requirements (AAT examination) Fields of competency The items listed are shown with an indicator of the minimum acceptable level of competency, based on a three-point

In December 2003 the Board issued a revised IAS 17 as part of its initial agenda of technical projects.

IFRS 16 Leases In April 2001 the International Accounting Standards Board (the Board) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

IFRS 16 Leases In April 2001 the International Accounting Standards Board (the Board) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

Defining Issues May 2013, No

Defining Issues May 2013, No. 13-24 FASB and IASB Issue Revised Exposure Drafts on Lease Accounting The FASB and IASB (the Boards) recently issued revised joint exposure drafts (EDs) on proposed changes

Defining Issues May 2013, No. 13-24 FASB and IASB Issue Revised Exposure Drafts on Lease Accounting The FASB and IASB (the Boards) recently issued revised joint exposure drafts (EDs) on proposed changes

Accounting for Intangible Assets

Accounting for Intangible Assets 1 Examples: Goodwill- internally generated and acquired Trade mark and brand names- internally generated and acquired Patents Copyright Franchise Licenses Customer loyalty

Accounting for Intangible Assets 1 Examples: Goodwill- internally generated and acquired Trade mark and brand names- internally generated and acquired Patents Copyright Franchise Licenses Customer loyalty

ANNUAL REPORT 2017 Lake Country Co-operative Association Limited

ANNUAL REPORT Management's Responsibility To the Members of Lake Country Co-operative Association Limited: Management is responsible for the preparation and presentation of the accompanying financial statements,

ANNUAL REPORT Management's Responsibility To the Members of Lake Country Co-operative Association Limited: Management is responsible for the preparation and presentation of the accompanying financial statements,

KEY DIFFERENCES- AS VS. IND AS

KEY DIFFERENCES- AS VS. IND AS October 2016 1 Titre de la présentation AGENDA Property, Plant and Equipment (PP&E) Intangible Assets Investment Property Non-current Assets Held for Sale and Discontinued

KEY DIFFERENCES- AS VS. IND AS October 2016 1 Titre de la présentation AGENDA Property, Plant and Equipment (PP&E) Intangible Assets Investment Property Non-current Assets Held for Sale and Discontinued

FSA Faculty Consortium Technical Accounting Update. Bob Uhl, partner, Deloitte & Touche LLP

FSA Faculty Consortium Technical Accounting Update Bob Uhl, partner, Deloitte & Touche LLP Deloitte University May 30, 2014 Acronyms Acronym ASC ASU ED FASB IASB IFRS U.S. GAAP Full Form Accounting Standards

FSA Faculty Consortium Technical Accounting Update Bob Uhl, partner, Deloitte & Touche LLP Deloitte University May 30, 2014 Acronyms Acronym ASC ASU ED FASB IASB IFRS U.S. GAAP Full Form Accounting Standards

ORIGINAL PRONOUNCEMENTS

Financial Accounting Standards Board ORIGINAL PRONOUNCEMENTS AS AMENDED Statement of Financial Accounting Standards No. 142 Goodwill and Other Intangible Assets Copyright 2008 by Financial Accounting Standards

Financial Accounting Standards Board ORIGINAL PRONOUNCEMENTS AS AMENDED Statement of Financial Accounting Standards No. 142 Goodwill and Other Intangible Assets Copyright 2008 by Financial Accounting Standards

Build Toronto Inc. Consolidated Financial Statements December 31, 2015

Consolidated Financial Statements May 10, 2016 Independent Auditor s Report To the Shareholder of Build Toronto Inc. We have audited the accompanying consolidated financial statements of Build Toronto

Consolidated Financial Statements May 10, 2016 Independent Auditor s Report To the Shareholder of Build Toronto Inc. We have audited the accompanying consolidated financial statements of Build Toronto

Business Combinations [Group /Consolidation FS]

![Business Combinations [Group /Consolidation FS]](/thumbs/83/87107649.jpg "Business Combinations [Group /Consolidation FS]") CA BUSINESS SCHOOL POSTGRADUATE DIPLOMA IN BUSINESS FINANCE AND STRATEGY SEMESTER 1: Financial Statements Analysis Business Combinations [Group /Consolidation FS] M B G Wimalarathna (FCA, FCMA, MCIM, FMAAT,

CA BUSINESS SCHOOL POSTGRADUATE DIPLOMA IN BUSINESS FINANCE AND STRATEGY SEMESTER 1: Financial Statements Analysis Business Combinations [Group /Consolidation FS] M B G Wimalarathna (FCA, FCMA, MCIM, FMAAT,

Letter of Comment No: a S-I 'File Reference:

Karl Hoffmann 61462 Konigstein, 20. Oct. 2005 Hardtgrundweg 28 GernJany International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Letter of Comment No: a S-I 'File Reference:

Karl Hoffmann 61462 Konigstein, 20. Oct. 2005 Hardtgrundweg 28 GernJany International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Letter of Comment No: a S-I 'File Reference:

The Substance of the Standard

The Substance of the Standard Mayer Hoffman McCann P.C. An Independent CPA Firm TM A publication of the Professional Standards Group April 2014 Accounting Election for Common Control Leasing Arrangements

The Substance of the Standard Mayer Hoffman McCann P.C. An Independent CPA Firm TM A publication of the Professional Standards Group April 2014 Accounting Election for Common Control Leasing Arrangements

AIRTEL UGANDA LIMITED NOTES TO THE FINANCIAL STATEMENTS (CONTINUED) 2. Summary of significant accounting policies (continued) (b) Changes in accounting policies (continued) Amendments to IAS 12 Income

AIRTEL UGANDA LIMITED NOTES TO THE FINANCIAL STATEMENTS (CONTINUED) 2. Summary of significant accounting policies (continued) (b) Changes in accounting policies (continued) Amendments to IAS 12 Income

Accounting and Auditing Update. Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc.

Accounting and Auditing Update Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc. Agenda Overview of the standard setting agenda Revenue recognition Lease

Accounting and Auditing Update Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc. Agenda Overview of the standard setting agenda Revenue recognition Lease

Request for Information Post-implementation Review: IFRS 3 Business Combinations

Ernst & Young Global Limited Becket House 1 Lambeth Palace Road London SE1 7EU Tel: +44 [0]20 7980 0000 Fax: +44 [0]20 7980 0275 ey.com International Accounting Standards Board 30 Cannon Street London

Ernst & Young Global Limited Becket House 1 Lambeth Palace Road London SE1 7EU Tel: +44 [0]20 7980 0000 Fax: +44 [0]20 7980 0275 ey.com International Accounting Standards Board 30 Cannon Street London

Determining whether an Arrangement contains a Lease

IFRIC Interpretation 4 Determining whether an Arrangement contains a Lease This version includes amendments resulting from IFRSs issued up to 31 December 2010. IFRIC 4 Determining whether an Arrangement

IFRIC Interpretation 4 Determining whether an Arrangement contains a Lease This version includes amendments resulting from IFRSs issued up to 31 December 2010. IFRIC 4 Determining whether an Arrangement

FASB Updates Business Definition

On January 5, 2017, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 2017-01, s (Topic 805): Clarifying the Definition of a Business. This definition is significant

On January 5, 2017, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 2017-01, s (Topic 805): Clarifying the Definition of a Business. This definition is significant

International Accounting Standard 38 Intangible Assets. Objective. Scope

International Accounting Standard 38 Intangible Assets Objective 1 The objective of this Standard is to prescribe the accounting treatment for intangible assets that are not dealt with specifically in

International Accounting Standard 38 Intangible Assets Objective 1 The objective of this Standard is to prescribe the accounting treatment for intangible assets that are not dealt with specifically in

Chapter 02 Consolidation of Financial Information Answer Key Multiple Choice Questions

TEST BANK FOR FUNDAMENTALS OF ADVANCED ACCOUNTING 6TH EDITION BY HOYLE Link download full: https://digitalcontentmarket.org/download/test-bank-forfundamentals-of-advanced-accounting-6th-edition-by-hoyle

TEST BANK FOR FUNDAMENTALS OF ADVANCED ACCOUNTING 6TH EDITION BY HOYLE Link download full: https://digitalcontentmarket.org/download/test-bank-forfundamentals-of-advanced-accounting-6th-edition-by-hoyle

ASSURANCE AND ACCOUNTING ASPE - IFRS: A Comparison Investment Property

ASSURANCE AND ACCOUNTING ASPE - IFRS: A Comparison Investment Property In this publication we will examine the key differences between Accounting Standards for Private Enterprises (ASPE) and International

ASSURANCE AND ACCOUNTING ASPE - IFRS: A Comparison Investment Property In this publication we will examine the key differences between Accounting Standards for Private Enterprises (ASPE) and International

Financial Reporting Matters

Financial Reporting Matters January 2005 Issue 4 A UDIT In this edition, we discuss some challenges that may be encountered in applying the latest standard on business combinations. In addition, we highlight

Financial Reporting Matters January 2005 Issue 4 A UDIT In this edition, we discuss some challenges that may be encountered in applying the latest standard on business combinations. In addition, we highlight

17 July International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom. Dear Sir/Madam

Organismo Italiano di Contabilità OIC (The Italian Standard Setter) Italy, 00187 Roma, Via Poli 29 Tel. 0039/06/6976681 fax 0039/06/69766830 e-mail: presidenza@fondazioneoic.it 17 July 2014 International

Organismo Italiano di Contabilità OIC (The Italian Standard Setter) Italy, 00187 Roma, Via Poli 29 Tel. 0039/06/6976681 fax 0039/06/69766830 e-mail: presidenza@fondazioneoic.it 17 July 2014 International

This version includes amendments resulting from IFRSs issued up to 31 December 2009.

International Accounting Standard 40 Investment Property This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 40 Investment Property was issued by the International

International Accounting Standard 40 Investment Property This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 40 Investment Property was issued by the International

7 Days Intensive Workshop on IFRS ICAI Tower, BKC, Mumbai. IAS 16 Property, Plant & Equipments

7 Days Intensive Workshop on IFRS ICAI Tower, BKC, Mumbai 01-July-14, Tuesday From To Details Faculty 10:00 AM 1:15 PM IAS 16 : Property, Plant & Equipments IAS 38 : Intangible Assets Ind AS 40:Investment

7 Days Intensive Workshop on IFRS ICAI Tower, BKC, Mumbai 01-July-14, Tuesday From To Details Faculty 10:00 AM 1:15 PM IAS 16 : Property, Plant & Equipments IAS 38 : Intangible Assets Ind AS 40:Investment

Center for Plain English Accounting AICPA s National A&A Resource Center available exclusively to PCPS members

Report April 19, 2017 Center for Plain English Accounting AICPA s National A&A Resource Center available exclusively to PCPS members Sale-Leaseback Transactions Involving Real Estate Navigating the Twists

Report April 19, 2017 Center for Plain English Accounting AICPA s National A&A Resource Center available exclusively to PCPS members Sale-Leaseback Transactions Involving Real Estate Navigating the Twists

Auditing PP&E, Including Leases

Auditing PP&E, Including Leases Learning Objectives Discuss typical audit risks and special considerations. Tailor an audit plan to assessed audit risk. Explain key controls related to PP&E. Describe lease

Auditing PP&E, Including Leases Learning Objectives Discuss typical audit risks and special considerations. Tailor an audit plan to assessed audit risk. Explain key controls related to PP&E. Describe lease