Selling Your Ophthalmology Practice. Financial Interest Disclosure 5/2/2016. Mark E. Kropiewnicki, Esquire, LLM* Daniel M. Bernick, Esquire, MBA*

|

|

|

- Regina Reynolds

- 6 years ago

- Views:

Transcription

1 Selling Your Ophthalmology Practice Mark E. Kropiewnicki, Esquire, LLM* Daniel M. Bernick, Esquire, MBA* The Health Care Group Plymouth Meeting, PA * Financial Interest Financial Interest Disclosure We have the following financial interests or relationships to disclose: Shareholders of and Consultants with The Health Care Group, Inc. and Health Care Consulting, Inc. Shareholders of and Attorneys with Health Care Law Associates, P.C. Mark E. Kropiewnicki, Esq., LLM 1

2 Who We Are Business and legal advisors to physicians Publishers of the Goodwill Registry, used in valuation of ophthalmology and other medical practices Handle and advise re: practice buy-ins, buy-outs, sales, mergers and valuations Introduction What s Happening Now Pros and Cons of Selling Valuation of Your Practice Basic Sale Structure and Process Possible Continued Practice with Buyer After Sale What s Happening Now The pressure of demographics: Baby boom doctors reaching retirement Uncertainty in the air ACOs Budget pressure/reimbursements EMR costs Watching other doctors get out 2

3 So there are reasons to consider selling But not to panic ophthalmology has been surprisingly resilient Per MGMA, median ophthalmologist compensation has increased 13.1% from 2010 to 2014, from $330,784 to $374,201 SGR has been repealed Hospitals do not control referrals to ophthalmologists What Are My Alternatives? Outright Sale Cash and promissory note for the practice Stock sale vs. asset sale 1-12 month transition period, usually Seller usually works short term as employee or contractor Seller retires But, what if you are not ready to retire? 3

4 Close Down Low effort, no legal fees, no brokerage costs But.no value for your practice Will your patients be well cared for? Will your staff have jobs? What to do with charts? Bring on Associate for Buy-In Can yield the highest value for your practice But takes a long time (6-10 years) to fully realize that value Significant hassle, fees, negotiation It may not work out Stand Pat The comfortable decision You know what your life will look like Could ease workload and stress by dropping surgery 4

5 But Time Doesn t Stand Still You are still exposed to reimbursement cuts, overhead increases Cutting back or dropping surgery will hurt the value of your practice Your health may preclude further delay You still have to deal with EMR and ICD-10 You may have an interested buyer: Bird in the hand. Compare Outright Sale Realize some value for your practice, now But you must be ready to pull the trigger If a buyer offers you your desired purchase price today. Are you ready to go? Should I Sell My Building Too? Be flexible: sell or rent, as buyer wishes Simultaneous sale may be hard to achieve The value of your practice is perishable Not true of office building or condo 5

6 What About My ASC? ASC enhances the value of your practice for buyer (ancillary profit) If you have partners in the ASC You will need their permission to sell to buyer Give Yourself Time It always takes longer than you think Time pressures negatively affect price Time for related transactions: e.g., lease or sell office space Buyer has been found: 3-9 months Buyer not yet found: months, or more What s for Sale? The Big Three Hard Assets Equipment, leasehold improvements, supplies, software Accounts Receivable Goodwill Includes going concern value, charts, phone number, staff, seller s endorsement of buyer, seller s restrictive covenant 6

7 Book Value Hard Asset Valuation Nearly always too low Assets expensed under Section 179 These have an immediate book value of zero The rest have a book value of zero in 5-7 years Specialized Appraisal Not available for all items Needs updating frequently Modified Book Value Approach Eliminate assets no longer in use Eliminate personal assets Recalculate depreciation 8-12 year life (overall) Straight-line depreciation Floor value: 20% of original cost Generally reasonable for most items Supplies Optical frames, contact lenses, drugs Physical inventory, or Estimated value, based on prior year s expense E.g., prior year expense divided by 12 times 2 (for 2 months supply) 7

8 What s Your Practice Worth? Accounts Receivable Typically not sold in an asset sale So seller generally collects and keeps the accounts receivable What s Your Practice Worth? Goodwill: What is it? Any kind of intangible value Likelihood of patient returning to the practice Practice name, location, phone number Reputation in marketplace Value as a going concern Goodwill Valuation Methods Income Approaches Excess Earnings Discounted Cash Flow Capitalized Earnings Comparable Sales or Market 8

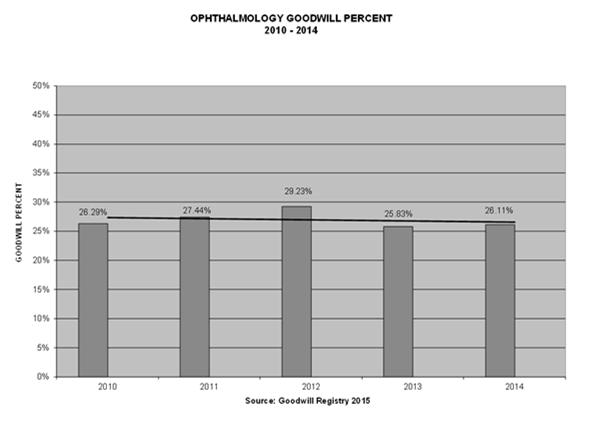

9 Comparable Sales Method Same idea as pricing a house Benchmark value, based on neighborhood comparables Adjust for individual features Good: high profit, nice location, lifestyle, modern facilities, moderate competition, good payor mix Bad: low earnings, undesirable location, closed panels Comparable Sales Method 2015 HCG Goodwill Registry Ten year average for ophthalmology is 26.72% of annual practice collections Five year average for ophthalmology is 27.2% of annual practice collections Guidelines for ophthalmology THESE ARE (LONG RUN) AVERAGES! YOURS MAY BE HIGHER OR LOWER! 9

10 Source: Goodwill Registry

11 Sealing the Deal: Nuts and Bolts Stock or Assets Sellers want stock sales (all capital gain) Buyers want asset sales Better tax treatment for buyer Avoids liabilities Buyer can cherry pick assets E.g. no purchase of accounts receivable or outdated or unwanted equipment, frames, supplies, etc. Price For what? Stock or assets? With or without accounts receivables? With or without liabilities? Develop a term sheet or letter of intent 11

12 Tax Allocation: S Corp or No Corp Item Seller Wants: Buyer Wants: Goodwill $$$$$ (cap gain) $ (slow write off) Equipment $ (ord. income) $$$$ (fast write off) Inventory $ (ord. income) $$$$$ (immed. deduct) Consulting Pay $ (ord. income + FICA) $$$$$ (immed. deduct) Non Compete $ (ord. income) $ (slow write off) Tax Allocation: Seller Has C Corp Objective: Avoid corporate double tax Funnel some of sales price outside the corporation directly to shareholder/doctor Personal goodwill or personal non-compete Talk with your tax advisor some tax risk Sample Personal Goodwill Allocation Buyer 100,000 Doctor Buyer 200,000 Corporation 300,000 Total 12

13 Payment Terms 100% bank financing is best, or at least Significant $$$ upfront down payment (50%) Buyer has skin in the game Payment Terms and Security Personal guarantee of promissory note From buyer personally From buyer s spouse Collateral: all assets acquired PLUS buyer s future accounts receivable Attorney s fees, if Seller must sue buyer Life insurance on buyer Target Sale Date Leave time for buyer to get licenses, hospital/asc privileges, and payor credentials Assume that until title passes at closing, buyer may renege Therefore, no letter to patients or other irrevocable acts prior to closing 13

14 Post Sale Employment of Seller Generally not guaranteed for more than 1 year Depends on the buyer Larger group practices (3+ owners) may be able to accommodate seller Solo buyer may not Terms of Post Sale Employment Typical Pay: % of collections Duties (call? surgery?) Assignment of patients Termination rights of each party Days/hours/locations to be worked Non compete restriction What about teaching, consulting, lecturing, etc.? Lease of Space When seller is landlord Typical term 3-5 years Seller should avoid rights of first refusal or options to buy the real estate This diminishes the saleability and value of the real estate 14

15 Due Diligence Call buyer s references Can buyer be trusted to take good care of your patients? Does buyer have good business judgment? Run a lien and judgment search on buyer Does buyer pay his/her/its debts? Transition Letters to patients and referrers Not sent prior to closing Text of letter often agreed prior to sale Who prepares the mailing, actually? Who pays for the mailing? Transition Collection of seller s accounts receivable Will buyer help? Does buyer get a fee for helping with this? How long will buyer help? 15

16 Transition (cont d) Staff: What happens to staff s accrued benefits, vacation, etc.? Use of seller s name (door, brochures, etc.) How long does this continue after sale? Appropriate indemnifications to seller Custody and maintenance of medical records QUESTIONS? Mark E. Kropiewnicki, Esq., LLM 16

17 Selling Your Ophthalmology Practice Mark E. Kropiewnicki, Esquire, LLM* Daniel M. Bernick, Esquire, MBA* The Health Care Group Plymouth Meeting, PA * Financial Interest 17

Getting More Value for Your Practice

Getting More Value for Your Practice D A N I E L M. B E R N I C K, E S QUI R E, M B A T H E H E A LT H C A R E GROUP P LY M OUT H M E E T I N G, PA W W W. H E A LT H C A R E G R O U P. C O M Who We Are

Getting More Value for Your Practice D A N I E L M. B E R N I C K, E S QUI R E, M B A T H E H E A LT H C A R E GROUP P LY M OUT H M E E T I N G, PA W W W. H E A LT H C A R E G R O U P. C O M Who We Are

Exit Strategies for a Medical Practice

Exit Strategies for a Medical Practice John D. Colucci, Esq., CPA McLane Middleton, PA Jonathan P. Gorski, CPA, MBA Edelstein & Company LLP June 12, 2018 Introduction John D. Colucci, a director at McLane

Exit Strategies for a Medical Practice John D. Colucci, Esq., CPA McLane Middleton, PA Jonathan P. Gorski, CPA, MBA Edelstein & Company LLP June 12, 2018 Introduction John D. Colucci, a director at McLane

Practice Valuations. Welcome To The Digital Learning Center. Today s Presentation. Course Faculty. Presented by. What s Your Practice Worth?

Welcome To The Digital Learning Center Presented by Your Partner In Building High Performance Practices Today s Presentation Practice Valuations What s Your Practice Worth? Course Faculty R. Thomas (Tom)

Welcome To The Digital Learning Center Presented by Your Partner In Building High Performance Practices Today s Presentation Practice Valuations What s Your Practice Worth? Course Faculty R. Thomas (Tom)

WIN-WIN PRACTICE TRANSITIONS. Chester J. Gary, DDS, JD MAXIMIZE VALUE, MINIMIZE RISK

TRANSITIONS WIN-WIN PRACTICE MAXIMIZE VALUE, MINIMIZE RISK University at Buffalo Dental Alumni Association Greater Buffalo Niagara Dental Meeting November 6, 2008 Chester J. Gary, DDS, JD Dentist, Attorney,

TRANSITIONS WIN-WIN PRACTICE MAXIMIZE VALUE, MINIMIZE RISK University at Buffalo Dental Alumni Association Greater Buffalo Niagara Dental Meeting November 6, 2008 Chester J. Gary, DDS, JD Dentist, Attorney,

A PODIATRY MANAGEMENT PANEL. Questions about Buying and Selling a Podiatry Practice. Dr. David Edward Marcinko; MBA CMP

A PODIATRY MANAGEMENT PANEL Questions about Buying and Selling a Podiatry Practice Dr. David Edward Marcinko; MBA CMP What overriding factors should one consider when shopping for a podiatric medical practice?

A PODIATRY MANAGEMENT PANEL Questions about Buying and Selling a Podiatry Practice Dr. David Edward Marcinko; MBA CMP What overriding factors should one consider when shopping for a podiatric medical practice?

Considerations For Selling a Practice - Integration vs. Independent. Heather Delgado, J.D. Partner Barnes & Thornburg LLP

Considerations For Selling a Practice - Integration vs. Independent Heather Delgado, J.D. Partner Barnes & Thornburg LLP I have no relevant financial relationships with commercial interests to disclose.

Considerations For Selling a Practice - Integration vs. Independent Heather Delgado, J.D. Partner Barnes & Thornburg LLP I have no relevant financial relationships with commercial interests to disclose.

Stock Purchase Agreement Commentary

Stock Purchase Agreement Commentary This is just one example of the many online resources Practical Law Company offers. PLC Corporate and Securities Commentary on key terms and conditions commonly found

Stock Purchase Agreement Commentary This is just one example of the many online resources Practical Law Company offers. PLC Corporate and Securities Commentary on key terms and conditions commonly found

Selling to Your Employees Through an ESOP

April 18, 2008 Selling to Your Employees Through an ESOP Presented by: Mary Giganti Waldheger Coyne Dave Gustafson Moore Stephens Apple Bill Rosenberg Columbia Chemical Richard Tanner Ownership Advisors,

April 18, 2008 Selling to Your Employees Through an ESOP Presented by: Mary Giganti Waldheger Coyne Dave Gustafson Moore Stephens Apple Bill Rosenberg Columbia Chemical Richard Tanner Ownership Advisors,

11 Essential Steps to Purchasing or Selling Your Veterinary Practice

11 Essential Steps to Purchasing or Selling Your Veterinary Practice The attorneys on the Veterinary Practice team of Mandelbaum Salsburg, led by Peter Tanella, have represented many veterinarians in the

11 Essential Steps to Purchasing or Selling Your Veterinary Practice The attorneys on the Veterinary Practice team of Mandelbaum Salsburg, led by Peter Tanella, have represented many veterinarians in the

M&A STRUCTURE/ANATOMY OF A TRANSACTION PRESENTATION OUTLINE. December 6, 2016

M&A STRUCTURE/ANATOMY OF A TRANSACTION PRESENTATION OUTLINE December 6, 2016 1. HOW TO STRUCTURE A TRANSACTION DEAL TYPES AND CONSIDERATION a. Main types = Asset purchase, stock purchase and merger. Structure

M&A STRUCTURE/ANATOMY OF A TRANSACTION PRESENTATION OUTLINE December 6, 2016 1. HOW TO STRUCTURE A TRANSACTION DEAL TYPES AND CONSIDERATION a. Main types = Asset purchase, stock purchase and merger. Structure

10 Tips for Real Estate Investors

10 Tips for Real Estate Investors FINANCIAL ADVISORS TRUSTWORTHY BY DESIGN SM When you buy a home, people often remind you it could be the biggest investment you will ever make. But should you use that

10 Tips for Real Estate Investors FINANCIAL ADVISORS TRUSTWORTHY BY DESIGN SM When you buy a home, people often remind you it could be the biggest investment you will ever make. But should you use that

Valuation Issues and Divorce

Lori Wilhelmy, ASA 513.813.4134 LWilhelmy@ComStockAdvisors.com Valuation Issues and Divorce The valuation of a closely held business for divorce purposes is based on valuation theory, state statute and

Lori Wilhelmy, ASA 513.813.4134 LWilhelmy@ComStockAdvisors.com Valuation Issues and Divorce The valuation of a closely held business for divorce purposes is based on valuation theory, state statute and

All the help you need. Succession Planning. Andrew Kerr. wilsonbrownesolicitors. wilsonbrowne.co.uk. wilsonbrownelaw

Succession Planning Andrew Kerr Legal & Commercial Process Getting the business ready for sale before the search for a buyer begins Identify who could be a potential buyer Establish the Heads of Terms

Succession Planning Andrew Kerr Legal & Commercial Process Getting the business ready for sale before the search for a buyer begins Identify who could be a potential buyer Establish the Heads of Terms

Personal vs. Enterprise Goodwill: Where Are We and How Do I Deal With It? By: Gary R. Trugman CPA/ABV, MCBA, ASA, MVS

Personal vs. Enterprise Goodwill: Where Are We and How Do I Deal With It? By: Gary R. Trugman CPA/ABV, MCBA, ASA, MVS Speaker Biography Gary R. Trugman is the President of Trugman Valuation Associates,

Personal vs. Enterprise Goodwill: Where Are We and How Do I Deal With It? By: Gary R. Trugman CPA/ABV, MCBA, ASA, MVS Speaker Biography Gary R. Trugman is the President of Trugman Valuation Associates,

Valuation Spotlight: Is that Really Worth That?

Valuation Spotlight: Is that Really Worth That? Panelist: Panelist: Panelist: HUD/ORCF: Moderator: JP LoMonaco, MAI Valuation & Information Group Colleen Blumenthal, MAI HealthTrust Michael Baldwin, MAI,

Valuation Spotlight: Is that Really Worth That? Panelist: Panelist: Panelist: HUD/ORCF: Moderator: JP LoMonaco, MAI Valuation & Information Group Colleen Blumenthal, MAI HealthTrust Michael Baldwin, MAI,

Heiwa Real Estate Co., Ltd.

To the Shareholders of Heiwa Real Estate Co., Ltd. INFORMATION DISCLOSED ON THE INTERNET UPON ISSUING NOTICE CONCERNING THE CONVOCATION OF THE 94th ORDINARY GENERAL SHAREHOLDERS MEETING THE 94th FISCAL

To the Shareholders of Heiwa Real Estate Co., Ltd. INFORMATION DISCLOSED ON THE INTERNET UPON ISSUING NOTICE CONCERNING THE CONVOCATION OF THE 94th ORDINARY GENERAL SHAREHOLDERS MEETING THE 94th FISCAL

New leases standard ASC 842 Lessee - operating leases. Itai Gotlieb, Partner, Professional Practice July 2017

ASC 842 Lessee - operating leases Itai Gotlieb, Partner, Professional Practice July 2017 Overview Under Accounting Standards Codification (ASC) 842, Leases, lessees recognize assets and liabilities for

ASC 842 Lessee - operating leases Itai Gotlieb, Partner, Professional Practice July 2017 Overview Under Accounting Standards Codification (ASC) 842, Leases, lessees recognize assets and liabilities for

Center for Entrepreneurial Studies, Stanford Graduate School of Business. Summary of Primary Issues in Acquisition Transactions

September 23, 2009 TO: FROM: RE: Center for Entrepreneurial Studies, Stanford Graduate School of Business Perkins Coie LLP Summary of Primary Issues in Acquisition Transactions This memorandum provides

September 23, 2009 TO: FROM: RE: Center for Entrepreneurial Studies, Stanford Graduate School of Business Perkins Coie LLP Summary of Primary Issues in Acquisition Transactions This memorandum provides

Accounting Of Intangible Assets Indian as- 26

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668. Volume 16, Issue 2. Ver. II (Feb. 2014), PP 40-45 Accounting Of Intangible Assets Indian as- 26 Manpreet Sharma,

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668. Volume 16, Issue 2. Ver. II (Feb. 2014), PP 40-45 Accounting Of Intangible Assets Indian as- 26 Manpreet Sharma,

Strategies For Making a Golf Course Work In Your Community

Strategies For Making a Golf Course Work In Your Community April 3, 2006 Laurence A. Hirsh, CRE, MAI, SGA Moderator Randy Addison, Esq. Thomas G. Bennison Henry DeLozier William E. Ellis William E. Ellis

Strategies For Making a Golf Course Work In Your Community April 3, 2006 Laurence A. Hirsh, CRE, MAI, SGA Moderator Randy Addison, Esq. Thomas G. Bennison Henry DeLozier William E. Ellis William E. Ellis

Executive Summary. New leases standard Lessees

Executive Summary December 2018 The new leases standard focuses on increased transparency and comparability providing financial statement users with more information about an entity s leasing activities.

Executive Summary December 2018 The new leases standard focuses on increased transparency and comparability providing financial statement users with more information about an entity s leasing activities.

Intangibles CHAPTER CHAPTER OBJECTIVES. After careful study of this chapter, you will be able to:

CHAPTER Intangibles CHAPTER OBJECTIVES After careful study of this chapter, you will be able to: 1. Explain the accounting alternatives for intangibles. 2. Record the amortization or impairment of intangibles.

CHAPTER Intangibles CHAPTER OBJECTIVES After careful study of this chapter, you will be able to: 1. Explain the accounting alternatives for intangibles. 2. Record the amortization or impairment of intangibles.

MARITAL SETTLEMENT AGREEMENT CHECKLIST

MARITAL SETTLEMENT AGREEMENT CHECKLIST This checklist reviews common issues that are addressed in a Marital Settlement Agreement. Not every issue will apply to your situation. I. Property Division a. Real

MARITAL SETTLEMENT AGREEMENT CHECKLIST This checklist reviews common issues that are addressed in a Marital Settlement Agreement. Not every issue will apply to your situation. I. Property Division a. Real

IAS Revenue. By:

IAS - 18 Revenue International Accounting Standard No 18 (IAS 18) Revenue In 1998, IAS 39, Financial Instruments: Recognition and Measurement, amended paragraph 11 of IAS 18, adding a cross-reference to

IAS - 18 Revenue International Accounting Standard No 18 (IAS 18) Revenue In 1998, IAS 39, Financial Instruments: Recognition and Measurement, amended paragraph 11 of IAS 18, adding a cross-reference to

Frequently Asked Questions:

Frequently Asked Questions: What makes a good associate dentist position? Answer: The most important factor in an associate role is how busy are you expected to be. The primary goals of most associates

Frequently Asked Questions: What makes a good associate dentist position? Answer: The most important factor in an associate role is how busy are you expected to be. The primary goals of most associates

ANNUAL REPORT 2017 Lake Country Co-operative Association Limited

ANNUAL REPORT Management's Responsibility To the Members of Lake Country Co-operative Association Limited: Management is responsible for the preparation and presentation of the accompanying financial statements,

ANNUAL REPORT Management's Responsibility To the Members of Lake Country Co-operative Association Limited: Management is responsible for the preparation and presentation of the accompanying financial statements,

Definitions. CPI is a lease in which base rent is adjusted based on changes in a consumer price index.

Annualized Rental Income is rental revenue under our leases on Operating Properties on a straight-line basis, which includes the effect of rent escalations and any tenant concessions, such as free rent,

Annualized Rental Income is rental revenue under our leases on Operating Properties on a straight-line basis, which includes the effect of rent escalations and any tenant concessions, such as free rent,

ADVANCED ISSUES IN FRANCHISOR ACQUISITIONS OF FRANCHISEES IS VERTICAL INTEGRATION IN YOUR FUTURE?

ADVANCED ISSUES IN FRANCHISOR ACQUISITIONS OF FRANCHISEES IS VERTICAL INTEGRATION IN YOUR FUTURE? Joel R. Buckberg Shareholder Commercial Transactions & Business Counseling Practice Group Chair Baker,

ADVANCED ISSUES IN FRANCHISOR ACQUISITIONS OF FRANCHISEES IS VERTICAL INTEGRATION IN YOUR FUTURE? Joel R. Buckberg Shareholder Commercial Transactions & Business Counseling Practice Group Chair Baker,

THE ART OF BUSINESS VALUATION

BUSINESS VALUATIONS GROWING THE ART OF BUSINESS VALUATION Douglas A. Michel, CPA/ABV, CVA & Alex E. Kummer, CPA, CVA, Clark Schaefer Hackett THE VALUE OF YOUR BUSINESS Steve Lumley, LGI CFO BUY SELL AGREEMENTS

BUSINESS VALUATIONS GROWING THE ART OF BUSINESS VALUATION Douglas A. Michel, CPA/ABV, CVA & Alex E. Kummer, CPA, CVA, Clark Schaefer Hackett THE VALUE OF YOUR BUSINESS Steve Lumley, LGI CFO BUY SELL AGREEMENTS

Sales Associate Course

Sales Associate Course Chapter Seventeen Real Estate Investments and Business Opportunity Brokerage 1 Investment Analysis Most important consideration: Economic soundness Land use controls Zoning Deed

Sales Associate Course Chapter Seventeen Real Estate Investments and Business Opportunity Brokerage 1 Investment Analysis Most important consideration: Economic soundness Land use controls Zoning Deed

Lease & Finance Accountants Conference. September The Westin Charlotte Charlotte, NC

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Basic Principles of Lessors under ASC 842 Mamta Shori, Wells Fargo Equipment Finance Joe Sebik,

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Basic Principles of Lessors under ASC 842 Mamta Shori, Wells Fargo Equipment Finance Joe Sebik,

Copyright 2009 The Learning House, Inc. Fixed and Intangible Assets Page 1 of 13

Copyright 2009 The Learning House, Inc. Fixed and Intangible Assets Page 1 of 13 Introduction This lesson focuses on the long-term assets used to operate a company. These assets can be grouped into fixed

Copyright 2009 The Learning House, Inc. Fixed and Intangible Assets Page 1 of 13 Introduction This lesson focuses on the long-term assets used to operate a company. These assets can be grouped into fixed

Chapter 11. Learning Objectives. Non-current Assets. Horngren, Best, Fraser, Willett: Accounting 6e 2010 Pearson Australia

PowerPoint to accompany Chapter 11 Non-Current Assets: Property, Plant and Equipment, and Intangibles Learning Objectives 1. Measure the cost of a non-current asset 2. Account for depreciation 3. Select

PowerPoint to accompany Chapter 11 Non-Current Assets: Property, Plant and Equipment, and Intangibles Learning Objectives 1. Measure the cost of a non-current asset 2. Account for depreciation 3. Select

Leases. (a) the lease transfers ownership of the asset to the lessee by the end of the lease term.

the lease transfers ownership of the asset to the lessee by the end of the lease term.") Leases 1.1. Classification of leases A lease is classified as a finance lease if it transfers substantially all the risks and rewards incidental to ownership. A lease is classified as an operating lease

Leases 1.1. Classification of leases A lease is classified as a finance lease if it transfers substantially all the risks and rewards incidental to ownership. A lease is classified as an operating lease

EN Official Journal of the European Union L 320/373

29.11.2008 EN Official Journal of the European Union L 320/373 INTERNATIONAL FINANCIAL REPORTING STANDARD 3 Business combinations OBJECTIVE 1 The objective of this IFRS is to specify the financial reporting

29.11.2008 EN Official Journal of the European Union L 320/373 INTERNATIONAL FINANCIAL REPORTING STANDARD 3 Business combinations OBJECTIVE 1 The objective of this IFRS is to specify the financial reporting

Building Wealth With Real Estate

Building Wealth With Real Estate - Broker/Property Manager/Loan Officer Goal of My Presentation- Understand These Topics 2 How To Build Wealth And Retire Sooner Types of Income Income Tax Rates Cash Flow

Building Wealth With Real Estate - Broker/Property Manager/Loan Officer Goal of My Presentation- Understand These Topics 2 How To Build Wealth And Retire Sooner Types of Income Income Tax Rates Cash Flow

BUYER S ACQUISITION OUTLINE

BUYER S ACQUISITION OUTLINE Preliminary Copyright 1997 by Maryann A. Waryjas Presented February, 1998 1. This outline assumes that management has engaged in a comprehensive, in depth study of the needs

BUYER S ACQUISITION OUTLINE Preliminary Copyright 1997 by Maryann A. Waryjas Presented February, 1998 1. This outline assumes that management has engaged in a comprehensive, in depth study of the needs

CHAPTER 6 - Accounting for Long-Term Operational Assets

CHAPTER 6 - Accounting for Long-Term Operational Assets ANSWERS TO QUESTIONS 1. Long-term operational assets are those assets that are used by a business to generate revenue. In contrast, investments are

CHAPTER 6 - Accounting for Long-Term Operational Assets ANSWERS TO QUESTIONS 1. Long-term operational assets are those assets that are used by a business to generate revenue. In contrast, investments are

RELOCATION LET US BE YOUR FIRST IMPRESSION. BONDNEWYORK.COM

RELOCATION LET US BE YOUR FIRST IMPRESSION. BONDNEWYORK.COM BOND RELOCATION Bond Relocation is a full-service relocation firm offering comprehensive programs designed to minimize the stress so common in

RELOCATION LET US BE YOUR FIRST IMPRESSION. BONDNEWYORK.COM BOND RELOCATION Bond Relocation is a full-service relocation firm offering comprehensive programs designed to minimize the stress so common in

Intangible Assets IAS 38, IAS 36, IFRS 3

Intangible Assets IAS 38, IAS 36, IFRS 3 Agenda 1. Introduction 2. Recognition 3. Measurement 4. Impairment of intangible assets (IAS 36) Basic concept Cash-Generating Units 5. Disclosures 2 1 Introduction

Intangible Assets IAS 38, IAS 36, IFRS 3 Agenda 1. Introduction 2. Recognition 3. Measurement 4. Impairment of intangible assets (IAS 36) Basic concept Cash-Generating Units 5. Disclosures 2 1 Introduction

INVESTING IN REAL ESTATE WITH AN IRA

INVESTING IN REAL ESTATE WITH AN IRA INVESTING IN REAL ESTATE WITH AN IRA 1 GETTING STARTED When people think of their IRA they often think that their investments must be made in bank CDs, the stock market

INVESTING IN REAL ESTATE WITH AN IRA INVESTING IN REAL ESTATE WITH AN IRA 1 GETTING STARTED When people think of their IRA they often think that their investments must be made in bank CDs, the stock market

Got too Much Space? Sublease it.

Got too Much Space? Sublease it. Vincent Bajardi, CCIM Senior Advisor (314) 719-2069 vbajardi@gundakercommercial.com For those of us who have been in the real estate business during challenging economic

Got too Much Space? Sublease it. Vincent Bajardi, CCIM Senior Advisor (314) 719-2069 vbajardi@gundakercommercial.com For those of us who have been in the real estate business during challenging economic

12/31/2013. The Retained Life Estate An Underutilized Gift. The Retained Life Estate An Underutilized Gift. 1. Real estate gift trends

The Retained Life Estate An Underutilized Gift Planned Giving Group of New England Boston, MA January 8, 2014 Dennis P. Bidwell dbidwell@bidwelladvisors.com (413) 584-2732 www.bidwelladvisors.com 1 The

The Retained Life Estate An Underutilized Gift Planned Giving Group of New England Boston, MA January 8, 2014 Dennis P. Bidwell dbidwell@bidwelladvisors.com (413) 584-2732 www.bidwelladvisors.com 1 The

2) All long-term leases should be capitalized in the accounts by the lessee.

All long-term leases should be capitalized in the accounts by the lessee.") Chapter 18 Leases 1) The principal attribute of finance leases is that the risks and rewards of asset ownership are deemed to remain with the lessor. LO: 18-02 List the criteria for classification of a

Chapter 18 Leases 1) The principal attribute of finance leases is that the risks and rewards of asset ownership are deemed to remain with the lessor. LO: 18-02 List the criteria for classification of a

An Agent s Guide to Pre-Sale Renovation

An Agent s Guide to Pre-Sale Renovation 844-944-2629 Why work with Curbio? Nationwide, sellers give up $28 billion dollars each year by selling cheap to flippers, investors, and wholesalers. Many sellers

An Agent s Guide to Pre-Sale Renovation 844-944-2629 Why work with Curbio? Nationwide, sellers give up $28 billion dollars each year by selling cheap to flippers, investors, and wholesalers. Many sellers

SELLING THE FAMILY BUSINESS

SELLING THE FAMILY BUSINESS For owners of family businesses, the process of selling their businesses can be one of life's most stressful events. Often the owners have close emotional connections to their

SELLING THE FAMILY BUSINESS For owners of family businesses, the process of selling their businesses can be one of life's most stressful events. Often the owners have close emotional connections to their

Chapter 1 Economics of Net Leases and Sale-Leasebacks

Chapter 1 Economics of Net Leases and Sale-Leasebacks 1:1 What Is a Net Lease? 1:2 Types of Net Leases 1:2.1 Bond Lease 1:2.2 Absolute Net Lease 1:2.3 Triple Net Lease 1:2.4 Double Net Lease 1:2.5 The

Chapter 1 Economics of Net Leases and Sale-Leasebacks 1:1 What Is a Net Lease? 1:2 Types of Net Leases 1:2.1 Bond Lease 1:2.2 Absolute Net Lease 1:2.3 Triple Net Lease 1:2.4 Double Net Lease 1:2.5 The

Public Storage Reports Results for the Quarter Ended March 31, 2017

News Release Public Storage 701 Western Avenue Glendale, CA 91201-2349 www.publicstorage.com For Release Immediately Date April 26, 2017 Contact Clemente Teng (818) 244-8080, Ext. 1141 Public Storage Reports

News Release Public Storage 701 Western Avenue Glendale, CA 91201-2349 www.publicstorage.com For Release Immediately Date April 26, 2017 Contact Clemente Teng (818) 244-8080, Ext. 1141 Public Storage Reports

Team Roetter ACTION PLAN

ACTION PLAN Introduction MORE EXPOSURE. MORE KNOWLEDGE. MORE SALES. Thank you for the opportunity to present our qualifications and marketing plan to sell your property. ENCLOSED PLEASE FIND: 1. Why Hire

ACTION PLAN Introduction MORE EXPOSURE. MORE KNOWLEDGE. MORE SALES. Thank you for the opportunity to present our qualifications and marketing plan to sell your property. ENCLOSED PLEASE FIND: 1. Why Hire

Principles of Accounting II Chapter 21: Record and Communicate Operational Investments

Principles of Accounting II Chapter 21: Record and Communicate Operational Investments Multiple Asset Purchases Allocate total purchase price among assets based on relative. Suppose you buy a building

Principles of Accounting II Chapter 21: Record and Communicate Operational Investments Multiple Asset Purchases Allocate total purchase price among assets based on relative. Suppose you buy a building

RESI Update 4 th Quarter 2016

RESI Update 4 th Quarter 2016 Supplemental Investor Information George Ellison, CEO Robin Lowe, CFO 2017 Altisource Residential Corporation. All rights reserved. Forward Looking Statements This presentation

RESI Update 4 th Quarter 2016 Supplemental Investor Information George Ellison, CEO Robin Lowe, CFO 2017 Altisource Residential Corporation. All rights reserved. Forward Looking Statements This presentation

4/10/2012. Long-Lived Assets and Depreciation. Overview of Long-lived Assets. Learning Objectives (LO) Learning Objectives (LO)

Learning Objectives (LO)") Learning Objectives (LO) CHAPTER Long-Lived Assets and Depreciation 8 After studying this chapter, you should be able to 1. Distinguish a company s expenses from expenditures that it should capitalize

Learning Objectives (LO) CHAPTER Long-Lived Assets and Depreciation 8 After studying this chapter, you should be able to 1. Distinguish a company s expenses from expenditures that it should capitalize

60-HR FL Real Estate Broker Post-Licensing Learning Objectives by Lesson

Lesson 1: Starting a Real Estate Office SECTION 1: BROKERAGE OFFICE ESSENTIALS Recall the characteristics of business entities that may register as a real estate brokerage and the rules involved to operate

Lesson 1: Starting a Real Estate Office SECTION 1: BROKERAGE OFFICE ESSENTIALS Recall the characteristics of business entities that may register as a real estate brokerage and the rules involved to operate

IFRS Training. IAS 38 Intangible Assets. Professional Advisory Services

IFRS Training IAS 38 Intangible Assets Table of Contents Section 1 Overview 2 Introduction to Intangible Assets 3 Recognition and Initial Measurement 4 Internally Generated Intangible Assets 5 Measurement

IFRS Training IAS 38 Intangible Assets Table of Contents Section 1 Overview 2 Introduction to Intangible Assets 3 Recognition and Initial Measurement 4 Internally Generated Intangible Assets 5 Measurement

Practice Acquisition and Start-up Guidelines

Practice Acquisition and Start-up Guidelines 3279 Ramos Circle Sacramento, CA 95827 (800) 327-2628 www.visionone.org VISION ONE CREDIT UNION Guidelines - Practice Acquisition and Start-up Vision One Credit

Practice Acquisition and Start-up Guidelines 3279 Ramos Circle Sacramento, CA 95827 (800) 327-2628 www.visionone.org VISION ONE CREDIT UNION Guidelines - Practice Acquisition and Start-up Vision One Credit

Chapter 13 Purchase or Inheritance Buyer/Beneficiary Side Outside Basis Purchase: Amount Paid to Seller + Share of Php. Debt

Chapter 13 Purchase or Inheritance Buyer/Beneficiary Side 1 Outside Basis Purchase: Amount Paid to Seller + Share of Php. Debt 2 13-3 Example 13-1 S sells to B 3 In Year 1, A, C, and S form the ACS Limited

Chapter 13 Purchase or Inheritance Buyer/Beneficiary Side 1 Outside Basis Purchase: Amount Paid to Seller + Share of Php. Debt 2 13-3 Example 13-1 S sells to B 3 In Year 1, A, C, and S form the ACS Limited

Accounting and Auditing Update. Paul Lundy

Accounting and Auditing Update Paul Lundy Leases: Not Just for the Footnotes Anymore Significant Financial Statement Impact New lease standard generally requires all leases to be capitalized and recognized

Accounting and Auditing Update Paul Lundy Leases: Not Just for the Footnotes Anymore Significant Financial Statement Impact New lease standard generally requires all leases to be capitalized and recognized

Section 12 Accounting for Leases Accounting by the Lessor and Lessee

Section 12 Accounting for Leases Accounting by the Lessor and Lessee 15-1 A lease is an agreement in which the lessor conveys the right to use property, plant, or equipment, usually for a stated period

Section 12 Accounting for Leases Accounting by the Lessor and Lessee 15-1 A lease is an agreement in which the lessor conveys the right to use property, plant, or equipment, usually for a stated period

ASC 842 (Leases)

") ASC 842 (Leases) On February 25, 2016 the Financial Accounting Standards Board of the United States (FASB) issued substantial new guidance on the treatment of leases for both lessees and lessors. The FASB

ASC 842 (Leases) On February 25, 2016 the Financial Accounting Standards Board of the United States (FASB) issued substantial new guidance on the treatment of leases for both lessees and lessors. The FASB

Lease Accounting: Gather your data now and understand tax implications. Tuesday, December 5, 2017

Lease Accounting: Gather your data now and understand tax implications Tuesday, December 5, 2017 Presenters Chris Stephenson Principal, Business Consulting & Technology chris.stephenson@us.gt.com Rebekah

Lease Accounting: Gather your data now and understand tax implications Tuesday, December 5, 2017 Presenters Chris Stephenson Principal, Business Consulting & Technology chris.stephenson@us.gt.com Rebekah

roots The Substance of the Standard Contents Changes to the Accounting for Goodwill for Private Companies

The Substance of the Standard MAYER HOFFMAN MCCANN P.C. AN INDEPENDENT CPA FIRM TM A publication of the Professional Standards Group February 2014 Changes to the Accounting for Goodwill for Private Companies

The Substance of the Standard MAYER HOFFMAN MCCANN P.C. AN INDEPENDENT CPA FIRM TM A publication of the Professional Standards Group February 2014 Changes to the Accounting for Goodwill for Private Companies

IFRS 16 LEASES. Page 1 of 21

IFRS 16 LEASES OBJECTIVE The objective is to ensure that lessees and lessors provide relevant information in a manner that faithfully represents those transactions. This information gives a basis for users

IFRS 16 LEASES OBJECTIVE The objective is to ensure that lessees and lessors provide relevant information in a manner that faithfully represents those transactions. This information gives a basis for users

IAS 16 Property, Plant and Equipment. Uphold public interest

IAS 16 Property, Plant and Equipment Uphold public interest Background IAS 16 became operational in 1983 Major amendments have been made several times including 1998, 2003, 2008, 2012, 2013, 2014 The objective

IAS 16 Property, Plant and Equipment Uphold public interest Background IAS 16 became operational in 1983 Major amendments have been made several times including 1998, 2003, 2008, 2012, 2013, 2014 The objective

Perry Farm Development Co.

(a not-for-profit corporation) Consolidated Financial Report December 31, 2010 Contents Report Letter 1 Consolidated Financial Statements Balance Sheet 2 Statement of Operations 3 Statement of Changes

(a not-for-profit corporation) Consolidated Financial Report December 31, 2010 Contents Report Letter 1 Consolidated Financial Statements Balance Sheet 2 Statement of Operations 3 Statement of Changes

Chapter 16: Selling a Business: Finishing Steps

Chapter 16: Selling a Business: Finishing Steps This section presents an overview of the steps needed to complete a sale. The letter of intent and purchase/sale agreements are some of the most important

Chapter 16: Selling a Business: Finishing Steps This section presents an overview of the steps needed to complete a sale. The letter of intent and purchase/sale agreements are some of the most important

WHEN A PUBLIC AGENCY IS INTERESTED IN ACQUIRING AN EASEMENT

Form 6-H When a Public Agency is interested in Acquiring an Easement Booklet WHEN A PUBLIC AGENCY IS INTERESTED IN ACQUIRING AN EASEMENT Introduction This booklet describes important features of the Uniform

Form 6-H When a Public Agency is interested in Acquiring an Easement Booklet WHEN A PUBLIC AGENCY IS INTERESTED IN ACQUIRING AN EASEMENT Introduction This booklet describes important features of the Uniform

NON U.S. RESIDENT INVESTOR GUIDE

GETTING READY NON U.S. RESIDENT INVESTOR GUIDE To be prepared to act in a speed appropriate to the New York City real estate market, it is suggested that you follow these steps prior to your visit: Define

GETTING READY NON U.S. RESIDENT INVESTOR GUIDE To be prepared to act in a speed appropriate to the New York City real estate market, it is suggested that you follow these steps prior to your visit: Define

VALUATION OF GOODWILL FOR TAX PURPOSES

1 VALUATION OF GOODWILL FOR TAX PURPOSES James P. Catty President, Corporate Valuation Services Limited Chair, International Association of Consultants, Valuators and Analysts 2 All businesses have these

1 VALUATION OF GOODWILL FOR TAX PURPOSES James P. Catty President, Corporate Valuation Services Limited Chair, International Association of Consultants, Valuators and Analysts 2 All businesses have these

Impact of lease accounting changes to corporate real estate

Impact of lease accounting changes to corporate real estate Overview In February 2016, the Financial Accounting Standards Board (FASB) issued its long-awaited revision to lease accounting Accounting Standards

Impact of lease accounting changes to corporate real estate Overview In February 2016, the Financial Accounting Standards Board (FASB) issued its long-awaited revision to lease accounting Accounting Standards

GAAP UPDATE DEANA BOWDEN, CPA, MSA WHITE NELSON DIEHL EVANS LLP

GAAP UPDATE DEANA BOWDEN, CPA, MSA WHITE NELSON DIEHL EVANS LLP TOPICS 2016-02 Topic 842 Leases 2016-14 Topic 958 Not for Profits 2016-18 Topic 230 Cash Flows LEASES Current US Generally Accepted Accounting

GAAP UPDATE DEANA BOWDEN, CPA, MSA WHITE NELSON DIEHL EVANS LLP TOPICS 2016-02 Topic 842 Leases 2016-14 Topic 958 Not for Profits 2016-18 Topic 230 Cash Flows LEASES Current US Generally Accepted Accounting

New Developments Summary

September 11, 2018 NDS 2018-11 New Developments Summary Implementation costs in a hosting arrangement ASU 2018-15 addresses customer accounting Summary The FASB issued ASU 2018-15, Customer s Accounting

September 11, 2018 NDS 2018-11 New Developments Summary Implementation costs in a hosting arrangement ASU 2018-15 addresses customer accounting Summary The FASB issued ASU 2018-15, Customer s Accounting

Plant assets are resources that have

10-1 LEARNING OBJECTIVE 1 Explain the accounting for plant asset expenditures. Plant assets are resources that have physical substance (a definite size and shape), are used in the operations of a business,

10-1 LEARNING OBJECTIVE 1 Explain the accounting for plant asset expenditures. Plant assets are resources that have physical substance (a definite size and shape), are used in the operations of a business,

Lessor Example Performance Obligation Approach

Lessor Example Performance Obligation Approach **Disclaimer The exposure draft received nearly 700 letters of comment through the comment period ended December 15, 2010. There is some expectation that

Lessor Example Performance Obligation Approach **Disclaimer The exposure draft received nearly 700 letters of comment through the comment period ended December 15, 2010. There is some expectation that

Broker. Basic Business Appraisal. Chapter 9. Copyright Gold Coast Schools 1

Broker Chapter 9 Basic Business Appraisal 1 Learning Objectives Describe the characteristics of the legal entities a business appraiser may encounter List at least 5 reasons for a business appraisal List

Broker Chapter 9 Basic Business Appraisal 1 Learning Objectives Describe the characteristics of the legal entities a business appraiser may encounter List at least 5 reasons for a business appraisal List

Buyers & Sellers: A Guide to Practice Transition

AAO Practice Transition Seminar San Diego, CA April 21, 2017 Buyers & Sellers: A Guide to Practice Transition Thomas F. Ziegler, DDS, MS, JD Orthodontist / Attorney Presentation Bio for Thomas F. Ziegler,

AAO Practice Transition Seminar San Diego, CA April 21, 2017 Buyers & Sellers: A Guide to Practice Transition Thomas F. Ziegler, DDS, MS, JD Orthodontist / Attorney Presentation Bio for Thomas F. Ziegler,

MONITORDAILY SPECIAL REPORT. Lease Accounting Project Update as of May 25, 2011 Prepared by Bill Bosco, Leasing 101

MONITORDAILY SPECIAL REPORT Lease Accounting Project Update as of May 25, 2011 Prepared by Bill Bosco, Leasing 101 The high volume of comment letters (780+) and numerous outreach meetings had common criticisms

MONITORDAILY SPECIAL REPORT Lease Accounting Project Update as of May 25, 2011 Prepared by Bill Bosco, Leasing 101 The high volume of comment letters (780+) and numerous outreach meetings had common criticisms

5. The cost of buildings includes all necessary costs related to the purchase or construction

CHAPTER REVIEW Plant Assets 1. (S.O. 1) Plant assets are tangible resources that are used in the operations of a business and are not intended for sale to customers. Plant assets are subdivided into four

CHAPTER REVIEW Plant Assets 1. (S.O. 1) Plant assets are tangible resources that are used in the operations of a business and are not intended for sale to customers. Plant assets are subdivided into four

Advanced M&A and Merger Models Quiz Questions

Advanced M&A and Merger Models Quiz Questions Transaction Assumptions and Sources & Uses Purchase Price Allocation & Balance Sheet Combination Combining the Income Statement Revenue, Expense, and CapEx

Advanced M&A and Merger Models Quiz Questions Transaction Assumptions and Sources & Uses Purchase Price Allocation & Balance Sheet Combination Combining the Income Statement Revenue, Expense, and CapEx

Chapter 08 - Long-Term Assets. Chapter Outline

Section 1 Plant Assets I. Cost Determination Plant assets are tangible assets used in a company's operations that have a useful life of more than one accounting period. Consistent with cost principle,

Section 1 Plant Assets I. Cost Determination Plant assets are tangible assets used in a company's operations that have a useful life of more than one accounting period. Consistent with cost principle,

Typical Valuation Approaches and How to Deal With Them

Typical Valuation Approaches and How to Deal With Them January, 2018 Anthony F. DellaPelle, Esq., CRE Shareholder, McKirdy, Riskin, Olson & DellaPelle, P.C. Morristown, New Jersey Christian F. Torgrimson,

Typical Valuation Approaches and How to Deal With Them January, 2018 Anthony F. DellaPelle, Esq., CRE Shareholder, McKirdy, Riskin, Olson & DellaPelle, P.C. Morristown, New Jersey Christian F. Torgrimson,

Chapter 9 - REPORTING AND ANALYZING LONG-LIVED ASSETS

Revised Summer 2018 Chapter 9 Review 1 Chapter 9 - REPORTING AND ANALYZING LONG-LIVED ASSETS LO 1: Explain the accounting for plant asset expenditures. Plant Assets (Also known as Property, Plant, and

Revised Summer 2018 Chapter 9 Review 1 Chapter 9 - REPORTING AND ANALYZING LONG-LIVED ASSETS LO 1: Explain the accounting for plant asset expenditures. Plant Assets (Also known as Property, Plant, and

Chapter 09. Chapter 9 Learning Objectives. Housing Alternatives by life stage. The Decision: Factors and Finances

Chapter 09 The Decision: Factors and Finances McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. 9-1 Chapter 9 Learning Objectives 1. Evaluate available housing alternatives

Chapter 09 The Decision: Factors and Finances McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. 9-1 Chapter 9 Learning Objectives 1. Evaluate available housing alternatives

EXECUTIVE SUMMARY A GUIDE TO ACCOUNTING FOR BUSINESS COMBINATIONS

EXECUTIVE SUMMARY A GUIDE TO ACCOUNTING FOR BUSINESS COMBINATIONS This Executive Summary is part of RSM US LLP s A Guide to Accounting for Business Combinations and should be read in conjunction with that

EXECUTIVE SUMMARY A GUIDE TO ACCOUNTING FOR BUSINESS COMBINATIONS This Executive Summary is part of RSM US LLP s A Guide to Accounting for Business Combinations and should be read in conjunction with that

Prepared by: Alex Socratous For My High School Students

Prepared by: Alex Socratous For My High School Students CHAPTER 2 CAPITAL ASSETS DEPRECIATION CAPITAL ASSETS Capital assets are long-lived assets that are used in the operations of a business and are not

Prepared by: Alex Socratous For My High School Students CHAPTER 2 CAPITAL ASSETS DEPRECIATION CAPITAL ASSETS Capital assets are long-lived assets that are used in the operations of a business and are not

Before Class starts.(make sure your name is on all submissions)

") Before Class starts.(make sure your name is on all submissions) March 27 exam conflicts must be resolved before Spring break. Fourth Homework due Thursday 3/6 before class. Fifth Homework due 3/20 before

Before Class starts.(make sure your name is on all submissions) March 27 exam conflicts must be resolved before Spring break. Fourth Homework due Thursday 3/6 before class. Fifth Homework due 3/20 before

Purchase Price Allocations ASC 805 Business Combinations

Purchase Price Allocations Introduction Mergers, acquisitions, and other business transactions have numerous accounting and tax implications. Buyers generally identify and report the fair values of the

Purchase Price Allocations Introduction Mergers, acquisitions, and other business transactions have numerous accounting and tax implications. Buyers generally identify and report the fair values of the

Chapter 15 Leases 15-1

Chapter 15 Leases 1. Why Leasing sometimes makes more sense 2. The accounting issues in recording a lease transaction 3. The types of contractual provisions in lease 4. The lease classification: capital

Chapter 15 Leases 1. Why Leasing sometimes makes more sense 2. The accounting issues in recording a lease transaction 3. The types of contractual provisions in lease 4. The lease classification: capital

Obstacles to Closing Your Real Estate Deal

Obstacles to Closing Your Real Estate Deal Coni S. Rathbone coni@zupgroup.com James D. Zupancic jim@zupgroup.com Your Goal Get to Closing! Why? Closing = Commission 1031 DELAY = Closing Obstacles Can Be

Obstacles to Closing Your Real Estate Deal Coni S. Rathbone coni@zupgroup.com James D. Zupancic jim@zupgroup.com Your Goal Get to Closing! Why? Closing = Commission 1031 DELAY = Closing Obstacles Can Be

Business Valuation More Art Than Science

Business Valuation More Art Than Science One of the more difficult aspects of business planning is business valuation. It is also one of the more important aspects. While owners of closely held businesses

Business Valuation More Art Than Science One of the more difficult aspects of business planning is business valuation. It is also one of the more important aspects. While owners of closely held businesses

REAL ESTATE INVESTING GUIDE. Combine IRA tax advantages with real estate investment opportunities.

REAL ESTATE INVESTING GUIDE Combine IRA tax advantages with real estate investment opportunities. INTRODUCTION The IRS allows an IRA, Solo 401(k), or HSA to acquire real estate as an asset without penalty

REAL ESTATE INVESTING GUIDE Combine IRA tax advantages with real estate investment opportunities. INTRODUCTION The IRS allows an IRA, Solo 401(k), or HSA to acquire real estate as an asset without penalty

Office of Community Planning and Development. Introduction

WHEN A PUBLIC AGENCY ACQUIRES YOUR PROPERTY www.hud.gov/relocation U.S. Department of Housing and Urban Development Office of Community Planning and Development Introduction This booklet describes important

WHEN A PUBLIC AGENCY ACQUIRES YOUR PROPERTY www.hud.gov/relocation U.S. Department of Housing and Urban Development Office of Community Planning and Development Introduction This booklet describes important

LindaWright SERVING TAMPA FAMILIES SINCE Preparing for a Successful Home Sale

LindaWright SERVING TAMPA FAMILIES SINCE 2007 Preparing for a Successful Home Sale Welcome, I realize that you have a choice when hiring an agent to help you sell your Home and truly appreciate the opportunity

LindaWright SERVING TAMPA FAMILIES SINCE 2007 Preparing for a Successful Home Sale Welcome, I realize that you have a choice when hiring an agent to help you sell your Home and truly appreciate the opportunity

SRI LANKA ACCOUNTING STANDARD

(REVISED 2005) SRI LANKA ACCOUNTING STANDARD PROPERTY, PLANT & EQUIPMENT THE INSTITUTE OF CHARTERED ACCOUNTANTS OF SRI LANKA (REVISED 2005) SRI LANKA ACCOUNTING STANDARD PROPERTY, PLANT & EQUIPMENT The

(REVISED 2005) SRI LANKA ACCOUNTING STANDARD PROPERTY, PLANT & EQUIPMENT THE INSTITUTE OF CHARTERED ACCOUNTANTS OF SRI LANKA (REVISED 2005) SRI LANKA ACCOUNTING STANDARD PROPERTY, PLANT & EQUIPMENT The

Carter Validus Mission Critical REIT, Inc. Reports Second Quarter 2016 Results

Carter Validus Mission Critical REIT, Inc. Reports Second Quarter 2016 Results TAMPA, FL (September 1, 2016) - Carter Validus Mission Critical REIT, Inc. (the Company ) announced today its operating results

Carter Validus Mission Critical REIT, Inc. Reports Second Quarter 2016 Results TAMPA, FL (September 1, 2016) - Carter Validus Mission Critical REIT, Inc. (the Company ) announced today its operating results

Palm Taft Professional Building

Palm Taft Professional Building Office Suites 1601 North Palm Avenue Pembroke Pines, Florida Memorial Hospital Pembroke table of contents Highlights... 3 Property Information... 4 Property Location...

Palm Taft Professional Building Office Suites 1601 North Palm Avenue Pembroke Pines, Florida Memorial Hospital Pembroke table of contents Highlights... 3 Property Information... 4 Property Location...

Acquisition IOWA 2015 CDBG MANAGEMENT GUIDE APPENDIX 2 PAGE: 79

Acquisition IOWA 2015 CDBG MANAGEMENT GUIDE APPENDIX 2 PAGE: 79 WHEN A PUBLIC AGENCY ACQUIRES YOUR PROPERTY Introduction U.S. Department of Housing And Urban Development Office of Community Planning and

Acquisition IOWA 2015 CDBG MANAGEMENT GUIDE APPENDIX 2 PAGE: 79 WHEN A PUBLIC AGENCY ACQUIRES YOUR PROPERTY Introduction U.S. Department of Housing And Urban Development Office of Community Planning and

Negative Goodwill and Bargain Purchases in Merger Models. An Extraordinary Gain to Go, Please

Negative Goodwill and Bargain Purchases in Merger Models An Extraordinary Gain to Go, Please Negative Goodwill and Bargain Purchases Can you explain what happens in an M&A deal if the Equity Purchase Price

Negative Goodwill and Bargain Purchases in Merger Models An Extraordinary Gain to Go, Please Negative Goodwill and Bargain Purchases Can you explain what happens in an M&A deal if the Equity Purchase Price

How Selling Your House to a Real Estate Investor Stacks Up Against Your Other Options

How Selling Your House to a Real Estate Investor Stacks Up Against Your Other Options Pros, cons, costs, and timeline of each option So, you need to sell your house. Selling in a market like today s can

How Selling Your House to a Real Estate Investor Stacks Up Against Your Other Options Pros, cons, costs, and timeline of each option So, you need to sell your house. Selling in a market like today s can

Chapter 9: Long-Lived Assets and Cost Allocation

1 Chapter 9: Long-Lived Assets and Cost Allocation 2 Capitalize vs Expense Revenue Expenditures Merely maintain a given level of services Should be Expensed Debit Expense Capital Expenditures Provide future

1 Chapter 9: Long-Lived Assets and Cost Allocation 2 Capitalize vs Expense Revenue Expenditures Merely maintain a given level of services Should be Expensed Debit Expense Capital Expenditures Provide future

International Accounting Standard 17 Leases. Objective. Scope. Definitions IAS 17

International Accounting Standard 17 Leases Objective 1 The objective of this Standard is to prescribe, for lessees and lessors, the appropriate accounting policies and disclosure to apply in relation

International Accounting Standard 17 Leases Objective 1 The objective of this Standard is to prescribe, for lessees and lessors, the appropriate accounting policies and disclosure to apply in relation