August Company Update

|

|

|

- Denis Marshall

- 6 years ago

- Views:

Transcription

1 August Company Update 11

2 Key company highlights 1 Fully-integrated real estate investment company with significant scale in our core market 2 Well-positioned in a favourable macroeconomic and attractive real estate environment 3 High quality commercial real estate portfolio in attractive Bucharest locations 4 Robust rental income and cash flow growth 5 Large and diversified international and creditworthy tenant base 6 Experienced senior management team supported by local integrated operating platform 2 2

200 >175k 2 3 Significant scale in a fragmented segment Single counterparty for tenants")

3 1 Fully-integrated real estate investment company with significant scale in our core market Fully-integrated platform with scale in the fragmented Bucharest office market with proven capabilities in leasing out substantial space in a short time frame 1 Turn-key solutions, tailored to tenant s needs GWI cumulative leased space by month sqm Office Retail Industrial¹ Industrial¹ (tenant's option) 200 >175k 2 3 Significant scale in a fragmented segment Single counterparty for tenants Trusted real estate advisor for tenants Depth and breadth of market knowledge 0 Apr-13 Jun-13 Aug-13 Oct-13 Dec-13 Feb-14 Apr-14 Jun-14 ¹ Include expansions that tenants of the TAP asset are entitled to exercise under their lease agreements 3 3

4 2 Romania is a large CEE country with solid economic fundamentals and a legal environment favourable to investors Strong macroeconomic fundamentals GDP growth above the CEE average Favourable environment for real estate investments One of the lowest cost of labour in the EU 2.3% Romania CEE EU 3.5% 3.1% Forecast 3.8% USD per hour, 2013 data % Low unemployment (2013) Low Public debt / GDP (2013) 5.7% 10.5% 10.9% Romania CEE EU 88.4% 36.8% 49.4% Greece Portugal Czech Republic High quality infrastructure Poland Slovakia Hungary Bulgaria Romania Turkey Modern regulation Stable currency (RON/EUR) Romania CEE EU Forecast Increasing highway network Modern metro system in Bucharest Further improved certainty of property rights Further protection of landlord Source: Economist Intelligence Unit 4 4

.")

5 2 A comprehensive program of subsidies from both the national government and the EU provides substantial support to FDIs in Romania A successful track record of absorption of funds... Increase of reimbursements from the EU in 2013 compared to the period²...position Romania as a top FDI destination Increasing FDI flow ($bn) % 100% 80% 60% Romania, a European leader % 20% 0% RO IT GR NL MTBG HU CZ PT FR SE PL LV EE DE SI LU LT AT DK CY ES SK BE FI IE UK from blue-chip internationals¹...and significant new funding planned for bn of funding for with multiple objectives Long term commitment to the country is a pre-requisite to access the subsidies Technological development Shift towards low-carbon economy Sustainable transportation Access and use of quality information Education, skills and lifelong learning Promoting employment and labour mobility Source: Ministry of European Funds of Romania; EIU 1 Example of 10 blue-chip multinationals investing in Romania leveraging on the public incentives 5 ² RO: Romania, IT: Italy, GR: Greece, NL: The Netherlands, MT: Malta, BG: Bulgaria, HU: Hungary, CZ: Czech Republic, PT: Portugal, FR: France, SE: Sweden, PL: Poland, LV: Latvia, EE: Estonia, DE: Germany, SI: Slovenia, LU: Luxembourg, LT: Lithuania, AT: Austria, DK: Denmark, CY: Cyprus, ES: Spain, SK: Slovakia, BE: Belgium, FI: Finland, IE: Ireland, UK: United Kingdom 5

6 2 Favorable market dynamics position Romania among the most attractive real estate markets in the CEE region Structural supply/demand imbalance for commercial space in Bucharest , Sqm Supply Demand 06A 07A 08A 09A 10A 11A 12A 13A...with over 50% of the take up comprising new occupation / pre-leases Demand by type of transactions, 2013 Renewal / renegotiation 38% Expansion 11% Pre-leases 9% New occupation 42% Demand for high quality modern office space exceeding the supply over the last few years Majority of take-up is comprised of new occupation and pre-leases, benefiting from the favourable fundamentals for real estate operators / developers Bucharest has one of the most attractive return profiles in the region Office yields in various cities 6.0% 6.3% 7.3% 7.5% 8.3% 9.0% One of the most attractive return profiles in the region with the second highest yields Warsaw Prague Bratislava Budapest Bucharest Sofia Significant supply / demand imbalance recorded over the last few years from strong multinationals tenants demand and limited new developments, coupled with superior yields compared to other CEE capitals, and room for potential significant appreciation Source: Knight Frank, CBRE; 6 6

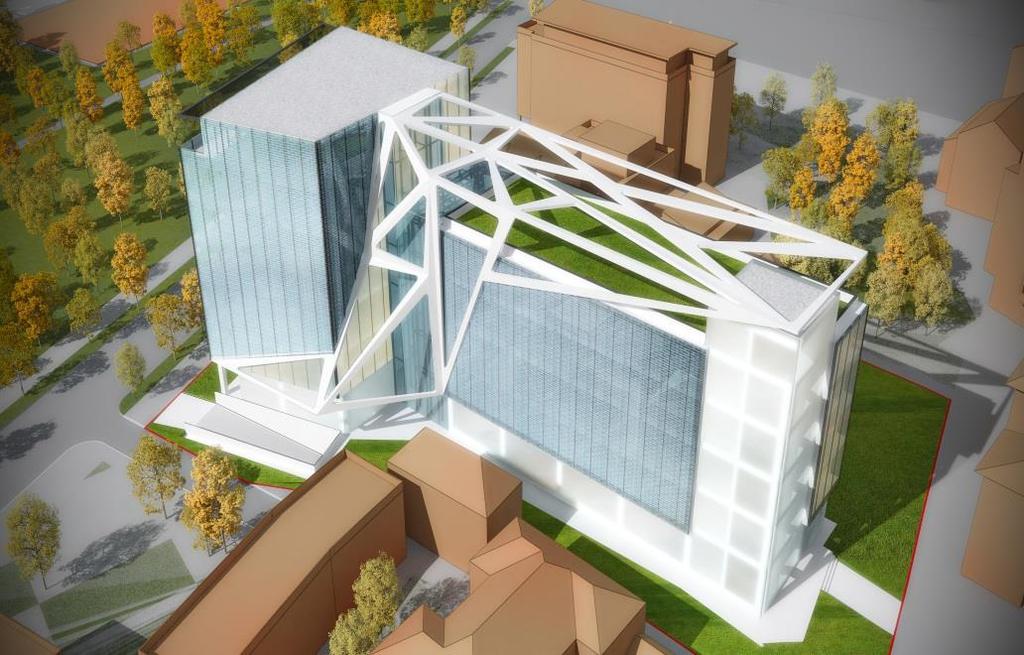

7 3 Globalworth benefits from a high quality portfolio in the most attractive Bucharest locations Majority of the portfolio located in the New CBD Newest and highest quality assets district Lower vacancy rates and higher rental levels Most sought after area for commercial real estate Excellent infrastructure access Herastrau1 TCI Bucharest One BOB BOC Globalworth Campus New CBD area Upground Towers Majority of Globalworth s portfolio i s located in the new business centre of Bucharest, New CBD The portfolio provides top quality assets that are in high demand in this sought-after district Attractive, modern, recent office stock benefitting from the immediate proximity to infrastructure (metro, tram, bus, road) as well as facing main streets Proximity to both national and international airports, natural attractions (parks, lakes), affluent residential clusters, and a new fully-leased mall create an environment conducive to a fast growing business centre TCI is a landmark asset in the historical CBD area, being the second tallest office tower in the country Excellent infrastructure access (metro, tram, bus, road) in the heart of Bucharest Overlooks Romanian central government buildings and ministries Immediate access to a large park City offices 7 Newly refurbished office stock in the South of the city centre, only two metro stops away from the heart of Bucharest, in a residential area where such stock is scarce Excellent infrastructure access (metro, tram, bus, road) 7

8 million 3 with significant value growth potential GAV upon completion¹ GAV bridge to value upon completion¹ 30% Total GAV: 887mm 1,000 Total uplift on currently owned portfolio: 355mm % % % % % 12% 400 8% 7% 5% 5% % 3% Today Remaining development cost Current portfolio including development costs Mark to market uplift Total GAV (at compeltion) ¹ Based on average appraised valuation as per Coldwell Banker and CBRE appraisals as of June Excludes Floreasca 1 asset which is in the process of being sold. 8 8

9 4 Robust rental income and cash flow growth Acquisition & Development Cost NOI ( m) Asset Name Status Investment Cost YTD ( m) 1 Remaining Development Cost ( m) Acq./Dev.Cost ( m) Current / Contracted 2 Q1 15(E) Q1 16(E) NOI Yield 3 BOB Completed % BOC Completed % Upground Towers Completed % TCI Completed % City Offices Completed/ Redevelopment % TAP 4 Completed/Development % Herastrau 1 Development % Globalworth Campus Development % Bucharest One Development % TOTAL REAL ESTATE % Asset Manager Operations % TOTAL GWI % ¹ Investment Cost YTD, represents the total acquisition cost and subsequent capex spent by GWI on each investment. 2 Contracted rent includes the pre-letting for Globalworth Campus, Bucharest One which are expected to be completed in Q1/2016 as well as c. 1.6m and 1.1m of pre-lettings associated will with TAP and City offices which are expected to be delivered in Q1/2015 and Q4/2014 respectively. 3 NOI yield based on Acquisition and Development Cost and Q1 16E NOI per property. 4 Remaining development for TAP includes c. 10.8m relating to the construction cost for the light industrial premises leased 9 to Continental to be delivered in Q and the costs for the second phase of development of Valeo and Continental 9

10 4...supported by triple-net lease terms, secure and visible cash flows Predictable, stable cash flows 1 Expenses covered by tenants secured on a long term basis Approximately 78% of the leases expire in or after 2020 Tax Insurance Maintenance Triple net lease 78% 2 Euro-denominated, matching debt currency leases Interest Rent 3 Inflation-indexed leases 4 Not material exposure to local currency Building contracts Management Few local employees RON 6% 5% 5% 1% 2% 3% >2020 Note: Lease expiry based on contracted commercial rental income and calculated on full lease life, not on first break date 10 10

11 4 and by favourable contracts terms in development projects ensuring protection against cost over-run and unexpected project delays The turn-key contracts with contractors provide the highest protection to GWI and no space for downside cash flow exposure GWI selects best-in-class contractors with a solid track-record Risk of cost over-run Risk of delays in the delivery Risk of defects External credit support Leverage over the constructor Turn-key contracts Deviations from pre-agreed specifics and price covered by the contractor Delivery date of the building contractually agreed Penalties to the contractor for delayed delivery of space Work to rectify deviations from contracted specifications covered by the contractor Bank guarantees enhance the constructor s credit worthiness, covering against: Cost over-run Delays-related penalties Defects Retention mechanism A certain % retained on all interim payments to the constructor as form of guarantee, paid upon satisfactory completion Bog Art example Strong track record Built the award winning Unicredit Tower High reputation Best constructor of the year 2013 (Construction & Investment Journal) In depth local knowledge Conservative, favourable contract features and partnerships with best-in-class contractors reinforce GWI s track record of assets delivered on time, 11 with no material defects 11

12 5 Attracting high quality, diversified tenants from around the world A highly diversified tenants base both by country of origin Belgium South Africa 4% 3% France 5% Greece 7% USA 12% UK 14% Italy 2% Other 10% Romania 20% Germany 23% Other 65% State / Government 35% and by business sector Based on annualized contracted rental income as of June 30, 2014 Based on annualized contracted rental income as of June 30, % international tenants 12 Oil&Gas 2% Utilities 2% Accounting 3% Government 4% Other 21% Conglomerate 5% Services 8% Technology 12% Telecom 24% Financial 19% 12

13 6 A top management with unique track record in the real estate sector Ioannis Papalekas Founder & CEO Andreas Papadopoulos CFO Dimitris Raptis Deputy CEO / CIO Adrian Dănoiu COO Stan Andre Deputy CIO Stamatis Sapkas Investment Director Legal Department (2 people) Finance and Accounting (11 people) Investments (2 people) Project Management (7 people) Commercial Sales & Leasing Marketing (6 people) Administrative and Human Resources (8 people) IT&C (2 people) Project Development & Facility Management (6 people) Experienced top management leading a successful investment team of 40+ professionals 13 13

14 6 and a clear, proven strategy Clear, focused strategic guidelines with a proven investment strategy Key Sector Commercial real estate assets 1 Arbitrage between the acquisition, development and management of new commercial assets, and of existing distressed / underperforming / mispriced assets that can be transitioned into high quality properties Key Region Romania, Bucharest area in particular 2 Total investment cost at an attractive discount to third party appraisal value, offering capital appreciation potential Key Tenants Multinational corporations and financial institutions 3 High quality tenant pre-lettings drive the success of the developments Key Terms Attractive long-term lease terms, EUR denominated, triple-net, inflation linked 4 Focus on CF from triple-net leases, offering attractive yields A conservative, proven strategy generating attractive risk-adjusted returns, made up of a combination of yield and capital appreciation, by investing in a diversified, internally managed portfolio of properties 14 14

15 Appendix Assets profiles 15 15

16 Current Portfolio Standing assets BOC 16 16

on 8 floors above ground and 895 parking spaces Part of")

17 Current Portfolio Standing assets BOC BOC Description Class A office building completed in 2009, located in the Northern part of Bucharest on Dimitrie Pompeiu area Offers 57,607sqm (GLA) on 8 floors above ground and 895 parking spaces Part of a wider building complex developed by the Founder between 2006 and 2011 which includes BOB and Upground Towers Tenants Stats GLA / Current Value 57,607sqm / 136mm Contracted occupancy 95.6% Remaining lease length to expiration 6.4 years Parking indoor/outdoor 842 / 53 Note: GLA refers to commercial and residential space; Average rent refers to ERV of commercial space 17 17

18 Current Portfolio Standing assets BOB 18 18

19 Current Portfolio Standing assets BOB BOB Description Class A office building, completed in 2008, located in the Northern part of Bucharest on Dimitrie Pompeiu area Offers 22,391sqm (GLA) on 7 floors above ground and 161 parking spaces Part of a wider building complex developed by the Founder between 2006 and 2011 which includes BOC and Upground Towers Tenants Stats GLA / Current Value 22,391sqm / 48mm Contracted occupancy 86.5% Remaining lease length to expiration 5.8 years Parking spaces 161 Note: GLA refers to commercial and residential space; Average rent refers to ERV of commercial space 19 19

20 Current Portfolio Standing assets TCI 20 20

21 Current Portfolio Standing assets TCI TCI Description Landmark class A building completed in 2012 centrally located in Bucharest s Historical CBD area at Victoriei Square Consists of two interconnected buildings and is currently the 2 nd tallest building in Bucharest. Comprises 22,228sqm GLA extending over 26 floors above ground Tenants Stats GLA / Current Value 22,228sqm / 73mm Contracted occupancy 97.3% Ministry of European funds Remaining lease length to expiration 4.9 years Parking indoor/outdoor 130 / 74 Note: GLA refers to commercial and residential space; Average rent refers to ERV of commercial space 21 21

22 Current Portfolio Standing assets City Offices 22 22

Note: GLA refers to commercial and")

23 Current Portfolio Standing assets City Offices City offices Description Mixed-use property comprising of two connected buildings, a Commercial Building and a Multilevel Parking (1,019 spaces) Located at the southern part of Bucharest in the densely populated area of Eroii Revolutiei Former retail mall recently re-developed/re-positioned to its current use with construction works expected to be completed in 2014 Tenants Stats GLA / Current Value 32,024sqm / 57mm Contracted occupancy 32.0% Remaining lease length to expiration 7.2 years Parking spaces 1,019 (all indoor) Note: GLA refers to commercial and residential space; Average rent refers to ERV of commercial space 23 23

24 Current Portfolio Standing assets Upground Towers 24 24

25 Current Portfolio Standing assets Upground Towers Upground Towers Description Modern residential complex located in the Northern part of Bucharest on Fabrica de Glucoza Street The complex was completed in 2009 and Globalworth currently owns 446 residential units (in 2 towers of 17 floors each), retail space of 6,589sqm and 618 parking spaces Tenants Stats GLA / Current Value 67,493 sqm / 106mm Contracted occupancy 95.0% (Retail) / 51.9% (Residential) Remaining lease length to expiration 10.2 years Parking indoor/outdoor 563 / 55 Note: GLA refers to commercial and residential space; Average rent refers to ERV of commercial space; 1 Refers to retail 25 25

26 Current Portfolio Assets under completion Bucharest One 26 26

27 Current Portfolio Assets under completion Bucharest One Bucharest One Description Flagship office development project under construction in the northern part of Bucharest in the Floreasca/Barbu Vacarescu area Upon completion, the building will be the second tallest tower in Bucharest, offering 53,923 sqm GLA over 23 floors above ground Development expected to be completed by Q Tenants Stats GLA / Current Value 53,923sqm / 55mm Contracted occupancy 44.1% Remaining lease length to expiration 9.8 years Parking indoor/ outdoor 528 / 219 Note: GLA refers to commercial and residential space; Average rent refers to ERV of commercial space 27 27

28 Current Portfolio Assets under completion Globalworth Campus 28 28

29 Current Portfolio Assets under completion Globalworth Campus Globalworth Campus Description Globalworth Campus project is set to become upon completion one of the largest business parks in Romania offers 105,000sqm (GLA) and 1,500 parking spaces Unique development to be constructed on top of one of the busiest metro stations in Bucharest Development of three towers, one in advanced stage of negotiations with a large multinational tenant for approx. 25,000sqm, offering office and retail space Tenants Stats Advanced stage of negotiations with a large multinational tenant for approx. 25,000sqm GLA / Current Value 105,000sqm / 29mm Contracted occupancy 23.8% Remaining lease length to expiration 10.0 years Parking spaces 1,500 Note: GLA refers to commercial and residential space; Average rent refers to ERV of commercial space 29 29

30 Current Portfolio Assets under completion Herastrau

31 Current Portfolio Assets under completion Herastrau 1 Herastrau 1 Description Herastrau 1 is an office development project to be constructed in the northern part of Bucharest on Nordului Road across from Herastrau Park Most of the site was acquired out of insolvency in 2012 The building is expected to have seven floors above ground The development is currently at conceptual phase and is expected to be completed in 2016 Tenants Stats Currently under negotiation with potential tenants GLA / Current Value Contracted occupancy Remaining lease length to expiration 12,166 sqm / 7mm n.m. n.m. Parking spaces 132 (all indoor) Note: GLA refers to commercial and residential space; Average rent refers to ERV of commercial space 31 31

32 Current Portfolio Timisoara Airport Park 32 32

Description Industrial project located in the North-East")

and a second leased to Continental")

New phases would be 100%")

33 Current Portfolio Timisoara Airport Park Timisoara Airport Park (TAP) Description Industrial project located in the North-East of Timisoara in the vicinity of the international airport Benefits of easy access towards the 4th European Corridor Comprises of one logistics warehouse leased to Valeo (completed, 27,474 sqm) and a second leased to Continental (development, 45,361 sqm), both on long term contracts Both Valeo and Continetal have the option to further expand in the property with additional warehouses to be developed upon exercise of this option (40,503 sqm) New phases would be 100% pre-let Tenants Stats GLA / Current Value 72,835 sqm / 21mm Contracted occupancy 100.0% Remaining lease length to expiration Parking indoor/outdoor 13.0 Outdoor area leased / used as parking Note: GLA refers to commercial and residential space; Average rent refers to ERV of commercial space 33 33

Real Estate were. August 2007

Real Estate were Europe grows August 2007 Topics I. Middle Europe Investments III. Fund management V. Organization structure VII. The CEE Real Estate Market I. Middle Europe Investments Middle Europe Investments

Real Estate were Europe grows August 2007 Topics I. Middle Europe Investments III. Fund management V. Organization structure VII. The CEE Real Estate Market I. Middle Europe Investments Middle Europe Investments

Office Rents map EUROPE, MIDDLE EAST AND AFRICA. Accelerating success.

Office Rents map EUROPE, MIDDLE EAST AND AFRICA Accelerating success. FINLAND NORWAY EMEA Office Rents H1 2012 Oslo 35.9 5.50% 7.6% 311,000 SWEDEN Stockholm 43.7 4.75% 4.0% 80,000 Tallinn 13.4 65,000 ESTONIA

Office Rents map EUROPE, MIDDLE EAST AND AFRICA Accelerating success. FINLAND NORWAY EMEA Office Rents H1 2012 Oslo 35.9 5.50% 7.6% 311,000 SWEDEN Stockholm 43.7 4.75% 4.0% 80,000 Tallinn 13.4 65,000 ESTONIA

Globalworth Real Estate Investments Limited

Globalworth Real Estate Investments Limited Investor Presentation November 2017 Disclaimer IMPORTANT NOTICE NOT FOR RELEASE, PUBLICATION OR DISTRIBUTION, IN WHOLE OR IN PART, DIRECTLY OR INDIRECTLY, IN

Globalworth Real Estate Investments Limited Investor Presentation November 2017 Disclaimer IMPORTANT NOTICE NOT FOR RELEASE, PUBLICATION OR DISTRIBUTION, IN WHOLE OR IN PART, DIRECTLY OR INDIRECTLY, IN

Industrial and Logistics Rents map EUROPE, MIDDLE EAST AND AFRICA. Accelerating success.

Industrial and Logistics Rents map EUROPE, MIDDLE EAST AND AFRICA Accelerating success. FINLAND EMEA Industrial and Logistics Rents H2 2012 NORWAY Oslo 13.6 11.6 6.50% SWEDEN Stockholm 8.4 10.0 7.5 Helsinki

Industrial and Logistics Rents map EUROPE, MIDDLE EAST AND AFRICA Accelerating success. FINLAND EMEA Industrial and Logistics Rents H2 2012 NORWAY Oslo 13.6 11.6 6.50% SWEDEN Stockholm 8.4 10.0 7.5 Helsinki

Industrial and Logistics Rents map EUROPE, MIDDLE EAST AND AFRICA. Accelerating success.

Industrial and Logistics Rents map EUROPE, MIDDLE EAST AND AFRICA Accelerating success. FINLAND EMEA Industrial and Logistics Rents H1 2013 NORWAY Oslo 12.7 10.8 6.50% SWEDEN Stockholm 8.3 10.0 7.5 Helsinki

Industrial and Logistics Rents map EUROPE, MIDDLE EAST AND AFRICA Accelerating success. FINLAND EMEA Industrial and Logistics Rents H1 2013 NORWAY Oslo 12.7 10.8 6.50% SWEDEN Stockholm 8.3 10.0 7.5 Helsinki

Proposal for a COMMISSION REGULATION

Proposal for a COMMISSION REGULATION (EC) No / of [ ] amending Regulation (EC) No 802/2004 implementing Council Regulation (EC) No 139/2004 on the control of concentrations between undertakings (Text with

Proposal for a COMMISSION REGULATION (EC) No / of [ ] amending Regulation (EC) No 802/2004 implementing Council Regulation (EC) No 139/2004 on the control of concentrations between undertakings (Text with

Economic and monetary developments

Box 4 House prices and the rent component of the HICP in the euro area According to the residential property price indicator, euro area house prices decreased by.% year on year in the first quarter of

Box 4 House prices and the rent component of the HICP in the euro area According to the residential property price indicator, euro area house prices decreased by.% year on year in the first quarter of

More affordable housing is needed Ostrava March

More affordable housing is needed Ostrava March 14 2018 Researcher President International Union of Tenants svenbergen@telia.com I will talk about Trends in Europe Housing differs from any other market

More affordable housing is needed Ostrava March 14 2018 Researcher President International Union of Tenants svenbergen@telia.com I will talk about Trends in Europe Housing differs from any other market

EEA Nationals: Right to Reside for Welfare Benefits & Housing. Kelly-Marie Jones Hammersmith & Fulham Law Centre January 2016

EEA Nationals: Right to Reside for Welfare Benefits & Housing Kelly-Marie Jones Hammersmith & Fulham Law Centre January 2016 European Economic Area Austria Belgium Bulgaria Croatia Cyprus Czech Republic

EEA Nationals: Right to Reside for Welfare Benefits & Housing Kelly-Marie Jones Hammersmith & Fulham Law Centre January 2016 European Economic Area Austria Belgium Bulgaria Croatia Cyprus Czech Republic

Deloitte Property Index Overview of European residential markets Residential property prices increase

Deloitte Property Index 2015 - Overview of European residential markets Residential property prices increase Michal Melc Senior Manager Audit Deloitte 30 Deloitte s Property Index, an overview of European

Deloitte Property Index 2015 - Overview of European residential markets Residential property prices increase Michal Melc Senior Manager Audit Deloitte 30 Deloitte s Property Index, an overview of European

STATISTICAL REFLECTIONS

STATISTICAL REFLECTIONS 9 November 2018 Contents Summary...1 Changes in property transactions...1 Annual price index...1 Quarterly pure price index...2 Distribution of existing home transactions...2 Regional

STATISTICAL REFLECTIONS 9 November 2018 Contents Summary...1 Changes in property transactions...1 Annual price index...1 Quarterly pure price index...2 Distribution of existing home transactions...2 Regional

MONICA FLAMAROPOL

MONICA FLAMAROPOL + 40 721 290 550 monica_flamaropol@yahoo.com DEVELOPMENT STRATEGIST PROPERTY MANAGEMENT EXPERT ASSET MANAGER Enhance real estate operations through strategic development. More than a

MONICA FLAMAROPOL + 40 721 290 550 monica_flamaropol@yahoo.com DEVELOPMENT STRATEGIST PROPERTY MANAGEMENT EXPERT ASSET MANAGER Enhance real estate operations through strategic development. More than a

OUR GLOBAL FOOTPRINT INDEPENDENT, INTERNATIONAL, COMMERCIAL, RESIDENTIAL. Locally expert, globally connected.

OUR GLOBAL FOOTPRINT INDEPENDENT, INTERNATIONAL, COMMERCIAL, RESIDENTIAL. Locally expert, globally connected. ABOUT THE GROUP THERE S A HUMAN ELEMENT IN THE WORLD OF PROPERTY THAT IS TOO EASILY OVERLOOKED.

OUR GLOBAL FOOTPRINT INDEPENDENT, INTERNATIONAL, COMMERCIAL, RESIDENTIAL. Locally expert, globally connected. ABOUT THE GROUP THERE S A HUMAN ELEMENT IN THE WORLD OF PROPERTY THAT IS TOO EASILY OVERLOOKED.

HOUSING MARKET DEVELOPMENTS

EUROPEAN SEMESTER THEMATIC FACTSHEET HOUSING MARKET DEVELOPMENTS 1. INTRODUCTION Housing market developments in the years preceding the financial crisis, and notably the accompanying rise in household

EUROPEAN SEMESTER THEMATIC FACTSHEET HOUSING MARKET DEVELOPMENTS 1. INTRODUCTION Housing market developments in the years preceding the financial crisis, and notably the accompanying rise in household

State of the Kazakhstan economy and 2008 development forecast

State of the Kazakhstan economy and 28 development forecast 118 116 114 112 113,7 11 18 16 14 % 14 13 12 11 1 9 8 115,8 114,1 Jan.26 GDP Volume Index, Production of goods and services in the 1st half of

State of the Kazakhstan economy and 28 development forecast 118 116 114 112 113,7 11 18 16 14 % 14 13 12 11 1 9 8 115,8 114,1 Jan.26 GDP Volume Index, Production of goods and services in the 1st half of

Leasing to Finance Innovation Jurgita Bucyte Senior Adviser in Statistics & Economic Affairs, Leaseurope

Leasing to Finance Innovation Jurgita Bucyte Senior Adviser in Statistics & Economic Affairs, Leaseurope AGORADA 2016 Brussels 27 May 2016 About Leaseurope Leaseurope represents the European leasing &

Leasing to Finance Innovation Jurgita Bucyte Senior Adviser in Statistics & Economic Affairs, Leaseurope AGORADA 2016 Brussels 27 May 2016 About Leaseurope Leaseurope represents the European leasing &

INVESTOR PRESENTATION. September 2011

INVESTOR PRESENTATION September 2011 Disclaimer This document does not constitute or form part of and should not be construed as, an offer to sell or issue or the solicitation of an offer to buy or acquire

INVESTOR PRESENTATION September 2011 Disclaimer This document does not constitute or form part of and should not be construed as, an offer to sell or issue or the solicitation of an offer to buy or acquire

Student Property Global Contacts. Connecting people & property, perfectly.

Student Property Global Contacts. Connecting people & property, perfectly. Global Contacts Europe Asia PAC James Pullan Partner, Department Head +44 207 861 5422 james.pullan@knightfrank.com Emily Fell

Student Property Global Contacts. Connecting people & property, perfectly. Global Contacts Europe Asia PAC James Pullan Partner, Department Head +44 207 861 5422 james.pullan@knightfrank.com Emily Fell

IS IRELAND 25 YEARS INTO A 100-YEAR HOUSING CRISIS?

IS IRELAND 25 YEARS INTO A 100-YEAR HOUSING CRISIS? Ronan Lyons, Department of Economics, Trinity College Dublin Dublin Economics Workshop Annual Conference Wexford, September 2017 DEW Annual Conference,

IS IRELAND 25 YEARS INTO A 100-YEAR HOUSING CRISIS? Ronan Lyons, Department of Economics, Trinity College Dublin Dublin Economics Workshop Annual Conference Wexford, September 2017 DEW Annual Conference,

First Financial Results 21 Oct to 31 Dec Released 25 January 2011

First Financial Results 21 Oct to 31 Dec 2010 Released 25 January 2011 MAPLETREE INDUSTRIAL TRUST ( MIT( MIT ) 1 FIRST FINANCIAL RESULTS - KEY HIGHLIGHTS DPU of 1.52 cents for period 21 Oct to 31 Dec 2010

First Financial Results 21 Oct to 31 Dec 2010 Released 25 January 2011 MAPLETREE INDUSTRIAL TRUST ( MIT( MIT ) 1 FIRST FINANCIAL RESULTS - KEY HIGHLIGHTS DPU of 1.52 cents for period 21 Oct to 31 Dec 2010

UNECE workshop on: Cadastral and real estate registration systems: Economic information for real estate markets in the UNECE region

UNECE workshop on: Cadastral and real estate registration systems: Economic information for real estate markets in the UNECE region Roma, 5-65 6 May 2011 Maurizio Festa Agenzia del Territorio Head of Statistics

UNECE workshop on: Cadastral and real estate registration systems: Economic information for real estate markets in the UNECE region Roma, 5-65 6 May 2011 Maurizio Festa Agenzia del Territorio Head of Statistics

OUR TRACK RECORD EUROPEAN VALUATIONS

OUR TRACK RECORD EUROPEAN VALUATIONS WELCOME Our brochure provides an overview of Knight Frank European Valuations coverage, services, track record and key personnel. We have invested in the expansion

OUR TRACK RECORD EUROPEAN VALUATIONS WELCOME Our brochure provides an overview of Knight Frank European Valuations coverage, services, track record and key personnel. We have invested in the expansion

Automated Valuation Model

Automated Valuation Model An innovative tool for Market Intelligence and Risk Management June 2015 Regulated by RICS EPS - Introduction Established presence in SEE: Greece (since 2000) & Romania, Bulgaria

Automated Valuation Model An innovative tool for Market Intelligence and Risk Management June 2015 Regulated by RICS EPS - Introduction Established presence in SEE: Greece (since 2000) & Romania, Bulgaria

Economy. Denmark Market Report Q Weak economic growth. Annual real GDP growth

Denmark Market Report Q 1 Economy Weak economic growth In 13, the economic growth in Denmark ended with a modest growth of. % after a weak fourth quarter with a decrease in the activity. So Denmark is

Denmark Market Report Q 1 Economy Weak economic growth In 13, the economic growth in Denmark ended with a modest growth of. % after a weak fourth quarter with a decrease in the activity. So Denmark is

Interim report presentation

Interim report presentation 13 July, 2017 Anders Nissen, CEO Liia Nõu, CFO Forward-looking statements This presentation contains forwardlooking statements. Such statements are subject to risks and uncertainties

Interim report presentation 13 July, 2017 Anders Nissen, CEO Liia Nõu, CFO Forward-looking statements This presentation contains forwardlooking statements. Such statements are subject to risks and uncertainties

Good underlying growth

Good underlying growth Interim report January-March 2016 Stockholm, 3 May 2016 Anders Nissen, CEO Liia Nõu, CFO Agenda Introduction Financial review Market and business Q&A Anders Nissen Liia Nõu Anders

Good underlying growth Interim report January-March 2016 Stockholm, 3 May 2016 Anders Nissen, CEO Liia Nõu, CFO Agenda Introduction Financial review Market and business Q&A Anders Nissen Liia Nõu Anders

ATRIUM COMPANY PRESENTATION

ATRIUM COMPANY PRESENTATION THE LEADING OWNER & MANAGER OF CENTRAL EASTERN EUROPEAN SHOPPING CENTRES May 2017 / Based on 2016 full-year results ATRIUM LEADING OWNER & MANAGER OF CEE SHOPPING CENTRES Strong

ATRIUM COMPANY PRESENTATION THE LEADING OWNER & MANAGER OF CENTRAL EASTERN EUROPEAN SHOPPING CENTRES May 2017 / Based on 2016 full-year results ATRIUM LEADING OWNER & MANAGER OF CEE SHOPPING CENTRES Strong

Strong progress for Property Management

Strong progress for Property Management Interim report January-June 2016 Stockholm, 18 August 2016 Anders Nissen, CEO Liia Nõu, CFO Forward-looking statements PANDOX EXCELLENCE IN HOTEL OWNERSHIP & OPERATIONS

Strong progress for Property Management Interim report January-June 2016 Stockholm, 18 August 2016 Anders Nissen, CEO Liia Nõu, CFO Forward-looking statements PANDOX EXCELLENCE IN HOTEL OWNERSHIP & OPERATIONS

Dreaming about excellent office space?

Dreaming about excellent office space? prime location l modern l high quality l advanced technologies l high standard l cutting-edge design l energy saving l environmentally friendly A STRIKING NEW OFFICE

Dreaming about excellent office space? prime location l modern l high quality l advanced technologies l high standard l cutting-edge design l energy saving l environmentally friendly A STRIKING NEW OFFICE

How Europeans live and what it costs them Is renting a dwelling a profitable investment?

REflexions magazine issue 46 Section title goes here REflexions magazine issue REflexions 4 Section magazine title goes issue here 6 Deloitte Property Index 2017 How Europeans live and what it costs them

REflexions magazine issue 46 Section title goes here REflexions magazine issue REflexions 4 Section magazine title goes issue here 6 Deloitte Property Index 2017 How Europeans live and what it costs them

The Architectural Profession in Europe. - A Sector Study Commissioned by the Architects Council of Europe

The Architectural Profession in Europe - A Sector Study Commissioned by the Architects Council of Europe F I N A L 18 December 2008 Mirza & Nacey F I N A L The Architectural Profession in Europe Contents

The Architectural Profession in Europe - A Sector Study Commissioned by the Architects Council of Europe F I N A L 18 December 2008 Mirza & Nacey F I N A L The Architectural Profession in Europe Contents

4.2% 2.3% 4.7% Unemployment rate Q Inflation H GDP Growth Q Retail Sales Q Average gross wage growth Q1 2017

City Report Q2 217 4.2% 2.3% 4.7% GDP Growth Q1 217 Inflation H1 217 Unemployment rate Q1 217 1,87 3.4% 1.7% Spending power, 215, Warsaw Agglomeration Retail Sales Q1 217 Average gross wage growth Q1 217

City Report Q2 217 4.2% 2.3% 4.7% GDP Growth Q1 217 Inflation H1 217 Unemployment rate Q1 217 1,87 3.4% 1.7% Spending power, 215, Warsaw Agglomeration Retail Sales Q1 217 Average gross wage growth Q1 217

How to get housing for all households Reimagining Ireland s Future housing, wealth and inequality Dublin 26 October 2018

How to get housing for all households Reimagining Ireland s Future housing, wealth and inequality Dublin 26 October 2018 Researcher President International Union of Tenants svenbergen@telia.com I will

How to get housing for all households Reimagining Ireland s Future housing, wealth and inequality Dublin 26 October 2018 Researcher President International Union of Tenants svenbergen@telia.com I will

Third Quarter 2011 Results

Third Quarter 2011 Results 10 November 2011 Platinium Business Park, Warsaw, Poland 1 Agenda Office Center Jarosova, Bratislava, Slovakia Q3 highlights Management key focus points Q3 main events Market

Third Quarter 2011 Results 10 November 2011 Platinium Business Park, Warsaw, Poland 1 Agenda Office Center Jarosova, Bratislava, Slovakia Q3 highlights Management key focus points Q3 main events Market

YTAA 2018 Exhibition Dossier

YTAA 2018 Exhibition Dossier Organised by: Founding partner: In partnership with: Partner in Venice: Sponsored by: With the support of: Contents Presentation YTAA - EU Mies Award YTAA 2018 Exhibition The

YTAA 2018 Exhibition Dossier Organised by: Founding partner: In partnership with: Partner in Venice: Sponsored by: With the support of: Contents Presentation YTAA - EU Mies Award YTAA 2018 Exhibition The

Capital market presentation August 2017

Capital market presentation August 2017 About Developer of income generating properties Total GLA* 458,000 m 2 Operating in Israel and in 8 countries in Europe Public company since 2004 listed on TA-90

Capital market presentation August 2017 About Developer of income generating properties Total GLA* 458,000 m 2 Operating in Israel and in 8 countries in Europe Public company since 2004 listed on TA-90

An Assessment of Recent Increases of House Prices in Austria through the Lens of Fundamentals

An Assessment of Recent Increases of House Prices in Austria 1 Introduction Martin Schneider Oesterreichische Nationalbank The housing sector is one of the most important sectors of an economy. Since residential

An Assessment of Recent Increases of House Prices in Austria 1 Introduction Martin Schneider Oesterreichische Nationalbank The housing sector is one of the most important sectors of an economy. Since residential

HONG KONG PRIME OFFICE Monthly Report

RESEARCH MARCH 2010 HONG KONG PRIME OFFICE Monthly Report Office market rally continues Hong Kong s economy showed further signs of recovery this past month, benefiting from a revival in regional trade,

RESEARCH MARCH 2010 HONG KONG PRIME OFFICE Monthly Report Office market rally continues Hong Kong s economy showed further signs of recovery this past month, benefiting from a revival in regional trade,

Make!t

stramatakis UNIL Make!t Happen@Lausanne Algeria Austria Belgium Bulgaria Croatia Cyprus Czech R Denmark Egypt Estonia Finland France Germany Grece Hungary Ireland Italy Jordan Latvia Lebanon Lithuania

stramatakis UNIL Make!t Happen@Lausanne Algeria Austria Belgium Bulgaria Croatia Cyprus Czech R Denmark Egypt Estonia Finland France Germany Grece Hungary Ireland Italy Jordan Latvia Lebanon Lithuania

HONG KONG PRIME OFFICE Monthly Report

RESEARCH April 2010 HONG KONG PRIME OFFICE Monthly Report Corporate sector eager to expand Hong Kong s office sales market continued to be active this past month. About 240 sales transactions were recorded

RESEARCH April 2010 HONG KONG PRIME OFFICE Monthly Report Corporate sector eager to expand Hong Kong s office sales market continued to be active this past month. About 240 sales transactions were recorded

How to define threshold households in different big German and European cities?

Presented at the FIG Working Week 2017, May 29 - June 2, 2017 in Helsinki, Finland How to define threshold households in different big German and European cities? FIG Working Week 2017 Helsinki Finland

Presented at the FIG Working Week 2017, May 29 - June 2, 2017 in Helsinki, Finland How to define threshold households in different big German and European cities? FIG Working Week 2017 Helsinki Finland

THE CASE FOR EUROPEAN LONG LEASE REAL ESTATE: CONTRIBUTING TO MORE CERTAIN INVESTMENT OUTCOMES

This document is for professional/qualified investors only. It is not to be distributed to or relied on by retail clients. THE CASE FOR EUROPEAN LONG LEASE REAL ESTATE: CONTRIBUTING TO MORE CERTAIN INVESTMENT

This document is for professional/qualified investors only. It is not to be distributed to or relied on by retail clients. THE CASE FOR EUROPEAN LONG LEASE REAL ESTATE: CONTRIBUTING TO MORE CERTAIN INVESTMENT

REAL ESTATE PRACTICE GROUP

REAL ESTATE PRACTICE GROUP Corporate and Commercial Law Mergers and Acquisitions Antitrust, EU and Public Procurement Real Estate and Construction Environment and Energy Labour Law Banking and Finance

REAL ESTATE PRACTICE GROUP Corporate and Commercial Law Mergers and Acquisitions Antitrust, EU and Public Procurement Real Estate and Construction Environment and Energy Labour Law Banking and Finance

2017 FULL YEAR 16 FEBRUARY 2018

FULL YEAR RESULTS 16 FEBRUARY 2018 : Delivering in line with strategy 1.1 billion invested Asset acquisitions 610m Development capex 414m Land acquisitions 92m 525 million disposals Asset sales 432m Land

FULL YEAR RESULTS 16 FEBRUARY 2018 : Delivering in line with strategy 1.1 billion invested Asset acquisitions 610m Development capex 414m Land acquisitions 92m 525 million disposals Asset sales 432m Land

Interim presentation. 13 July, Anders Nissen, CEO Liia Nõu, CFO

Interim presentation 13 July, 2018 Anders Nissen, CEO Liia Nõu, CFO Profitable growth 20% R12M Return on equity 2 1 2 3 Profitable acquisitions in new large markets Continued strong development in Brussels

Interim presentation 13 July, 2018 Anders Nissen, CEO Liia Nõu, CFO Profitable growth 20% R12M Return on equity 2 1 2 3 Profitable acquisitions in new large markets Continued strong development in Brussels

The use of conservation easements in the EU. Inga Račinska, Siim Vahtrus a report to NABU

The use of conservation easements in the EU Inga Račinska, Siim Vahtrus a report to NABU What is a conservation easement? A conservation easement, also known as a conservation restriction or conservation

The use of conservation easements in the EU Inga Račinska, Siim Vahtrus a report to NABU What is a conservation easement? A conservation easement, also known as a conservation restriction or conservation

Interim presentation. 24 April, Anders Nissen, CEO Liia Nõu, CFO

Interim presentation 24 April, 2018 Anders Nissen, CEO Liia Nõu, CFO A stable earnings development 21% Return on equity 2 1 2 3 Profitable acquisitions Positive effects from product development A seasonally

Interim presentation 24 April, 2018 Anders Nissen, CEO Liia Nõu, CFO A stable earnings development 21% Return on equity 2 1 2 3 Profitable acquisitions Positive effects from product development A seasonally

Hong Kong Prime Office Monthly Report. October 2011 RESEARCH NON-CORE DISTRICTS LEAD THE MARKET

RESEARCH October 2011 Hong Kong Prime Office Monthly Report NON-CORE DISTRICTS LEAD THE MARKET Business and investment activity slowed in Hong Kong over the past month, on the back of negative economic

RESEARCH October 2011 Hong Kong Prime Office Monthly Report NON-CORE DISTRICTS LEAD THE MARKET Business and investment activity slowed in Hong Kong over the past month, on the back of negative economic

Interim report presentation

Interim report presentation 10 November, 2017 Anders Nissen, CEO Liia Nõu, CFO Forward-looking statements This presentation contains forwardlooking statements. Such statements are subject to risks and

Interim report presentation 10 November, 2017 Anders Nissen, CEO Liia Nõu, CFO Forward-looking statements This presentation contains forwardlooking statements. Such statements are subject to risks and

Hong Kong Prime Office Monthly Report. September 2011 RESEARCH NON-CORE DISTRICTS LEAD THE MARKET

RESEARCH September 2011 Hong Kong Prime Office Monthly Report NON-CORE DISTRICTS LEAD THE MARKET Sentiment in the office market remained mixed over the past month. The sales market was relatively quiet,

RESEARCH September 2011 Hong Kong Prime Office Monthly Report NON-CORE DISTRICTS LEAD THE MARKET Sentiment in the office market remained mixed over the past month. The sales market was relatively quiet,

LAPACO PAPER PRODUCTS LTD.

LAPACO PAPER PRODUCTS LTD. 5200 J.A. Bombardier Street Longueuil, Quebec TABLE OF CONTENTS Section Photographs & Location Maps 1 Project Summary 2 The Location 3 Lapaco Paper Products Ltd. 4 Investment

LAPACO PAPER PRODUCTS LTD. 5200 J.A. Bombardier Street Longueuil, Quebec TABLE OF CONTENTS Section Photographs & Location Maps 1 Project Summary 2 The Location 3 Lapaco Paper Products Ltd. 4 Investment

Property Index Overview of European Residential Markets

Property Index Overview of European Residential Markets Rental market Is renting a dwelling a profitable investment? 6th edition, July 2017 Introduction Introduction 03 Highlights 05 Economic Development

Property Index Overview of European Residential Markets Rental market Is renting a dwelling a profitable investment? 6th edition, July 2017 Introduction Introduction 03 Highlights 05 Economic Development

BANK OF AMERICA PLAZA

BANK OF AMERICA PLAZA LITTLE ROCK, ARKANSAS High-Rise Office Tower Exceptional Repositioning or Redevelopment Opportunity Little Rock Central Business District EXECUTIVE SUMMARY THE OFFERING CBRE, as exclusive

BANK OF AMERICA PLAZA LITTLE ROCK, ARKANSAS High-Rise Office Tower Exceptional Repositioning or Redevelopment Opportunity Little Rock Central Business District EXECUTIVE SUMMARY THE OFFERING CBRE, as exclusive

April 13 th -16 th 2016 ITALY - DRO (TN) CENTRALE di FIES

CENTRALE di FIES") April 13 th -16 th 2016 ITALY - DRO (TN) CENTRALE di FIES by MACRO DESIGN STUDIO and LIVING BUILDING CHALLENGE COLLABORATIVE: ITALY With INTERNATIONAL LIVING FUTURE INSTITUTE What It is a design workshop

April 13 th -16 th 2016 ITALY - DRO (TN) CENTRALE di FIES by MACRO DESIGN STUDIO and LIVING BUILDING CHALLENGE COLLABORATIVE: ITALY With INTERNATIONAL LIVING FUTURE INSTITUTE What It is a design workshop

OECD Affordable Housing Database OECD - Social Policy Division - Directorate of Employment, Labour and Social Affairs

HM1.3 HOUSING TENURES Definitions and methodology Housing tenure refers to the arrangements under which the household occupies all or part of a housing unit. Different types of housing tenure can be distinguished,

HM1.3 HOUSING TENURES Definitions and methodology Housing tenure refers to the arrangements under which the household occupies all or part of a housing unit. Different types of housing tenure can be distinguished,

Transit-Oriented Development Specialized Real Estate Services

COLLIERS INTERNATIONAL Transit-Oriented Development Specialized Real Estate Services Accelerating success. Colliers International transit-oriented development GROUP P. 1 2 transit-oriented development

COLLIERS INTERNATIONAL Transit-Oriented Development Specialized Real Estate Services Accelerating success. Colliers International transit-oriented development GROUP P. 1 2 transit-oriented development

KEEGAN & COPPIN COMPANY, INC.

Commercial Real Estate Services PROMINENT DOWNTOWN LOCATION 757± - 954± sf of office space available with 4th Street frontage 757± sf: Open floor plan with 3 cubicles 954± sf: Open floor plan, private

Commercial Real Estate Services PROMINENT DOWNTOWN LOCATION 757± - 954± sf of office space available with 4th Street frontage 757± sf: Open floor plan with 3 cubicles 954± sf: Open floor plan, private

CZECH REPUBLIC RESEARCH & FORECAST REPORT Q Accelerating success.

CZECH REPUBLIC RESEARCH & FORECAST REPORT Accelerating success. RESEARCH & FORECAST REPORT CZECH REPUBLIC PRAGUE OFFICE PROPERTY MARKET SUPPLY METRIC KEY OFFICE FIGURES MEASURE Total Stock 2,773,296 m

CZECH REPUBLIC RESEARCH & FORECAST REPORT Accelerating success. RESEARCH & FORECAST REPORT CZECH REPUBLIC PRAGUE OFFICE PROPERTY MARKET SUPPLY METRIC KEY OFFICE FIGURES MEASURE Total Stock 2,773,296 m

Ecosystem. a member of the ECHAlliance International Ecosystem Network. Brian O Connor, Chair, European Connected Health Alliance

Ecosystem a member of the ECHAlliance International Ecosystem Network Brian O Connor, Chair, European Connected Health Alliance Permanent International Ecosystem Network ECOSYSTEMS break down silos, transform

Ecosystem a member of the ECHAlliance International Ecosystem Network Brian O Connor, Chair, European Connected Health Alliance Permanent International Ecosystem Network ECOSYSTEMS break down silos, transform

CAPABILITY STATEMENT. Knight Frank Poland

CAPABILITY STATEMENT Knight Frank Poland CONTENTS Knight Frank worldwide Knight Frank in Poland Scope of services Milestones Asset Management Capital Markets Commercial Agency Market Research Property

CAPABILITY STATEMENT Knight Frank Poland CONTENTS Knight Frank worldwide Knight Frank in Poland Scope of services Milestones Asset Management Capital Markets Commercial Agency Market Research Property

Behind the Scenes: Washington REIT 2.0. Presentation to NAIOP Members

Behind the Scenes: Washington REIT 2.0 Presentation to NAIOP Members February 23, 2016 They always say time changes things, but you actually have to change them yourself. - Andy Warhol The Oldest REIT

Behind the Scenes: Washington REIT 2.0 Presentation to NAIOP Members February 23, 2016 They always say time changes things, but you actually have to change them yourself. - Andy Warhol The Oldest REIT

ABOUT ROMANIA AND BRAȘOV

ABOUT ROMANIA AND BRAȘOV ROMANIA has one of the fastest growing economies in the EU. In 2016, Romania recorded a 4.8% annual economic growth, ranking 1st among all European countries. The financial predictions

ABOUT ROMANIA AND BRAȘOV ROMANIA has one of the fastest growing economies in the EU. In 2016, Romania recorded a 4.8% annual economic growth, ranking 1st among all European countries. The financial predictions

DEVELOPMENT OF THE DWELLING CONSTRUCTION AND REAL ESTATE MARKET DURING THE LAST DECADE

DEVELOPMENT OF THE DWELLING CONSTRUCTION AND REAL ESTATE MARKET DURING THE LAST DECADE Olga Smirnova, Merike Sinisaar Statistics Estonia Construction and real estate are the fields of activity many people

DEVELOPMENT OF THE DWELLING CONSTRUCTION AND REAL ESTATE MARKET DURING THE LAST DECADE Olga Smirnova, Merike Sinisaar Statistics Estonia Construction and real estate are the fields of activity many people

Property Index Overview of European Residential Markets. European housing 2012

Property Index Overview of European Residential Markets European housing 2012 2nd edition, May 2013 Table of Contents Introduction 3 Economic Development in Europe 4 Residential Markets in Europe 5 Housing

Property Index Overview of European Residential Markets European housing 2012 2nd edition, May 2013 Table of Contents Introduction 3 Economic Development in Europe 4 Residential Markets in Europe 5 Housing

QRE ADVISORY SERVICES QRE. St. Martin s House, Waterloo Road, Dublin 4. Prepared by:

QRE ADVISORY SERVICES Prepared by: QRE St. Martin s House, Waterloo Road, Dublin 4 QRE QRE is a wholly owned subsidiary of the Space Property Group and was established to drive the innovations needed in

QRE ADVISORY SERVICES Prepared by: QRE St. Martin s House, Waterloo Road, Dublin 4 QRE QRE is a wholly owned subsidiary of the Space Property Group and was established to drive the innovations needed in

Cairn Homes plc Preliminary Results

Cairn Homes plc Preliminary Results 29 February 2016 1 Disclaimer This presentation document (hereinafter this document has been prepared by Cairn Homes Plc (the Company ). This document has been prepared

Cairn Homes plc Preliminary Results 29 February 2016 1 Disclaimer This presentation document (hereinafter this document has been prepared by Cairn Homes Plc (the Company ). This document has been prepared

SEGRO plc Cunard House T +44 (0) Regent Street F +44 (0) London SW1Y 4LR

Regent Street F +44 (0) London SW1Y 4LR") 1 SEGRO plc Cunard House T +44 (0) 20 7451 9100 15 Regent Street F +44 (0) 20 7451 9150 London SW1Y 4LR www.segro.com/investors 2018 FULL YEAR PROPERTY ANALYSIS REPORT 2 ABOUT SEGRO 3 Overview 5 Combined

1 SEGRO plc Cunard House T +44 (0) 20 7451 9100 15 Regent Street F +44 (0) 20 7451 9150 London SW1Y 4LR www.segro.com/investors 2018 FULL YEAR PROPERTY ANALYSIS REPORT 2 ABOUT SEGRO 3 Overview 5 Combined

NRE: Creating Value for Shareholders. March 13, 2018

NRE: Creating Value for Shareholders March 13, 2018 Forward Looking Statement This presentation may contain certain forward-looking statements within the meaning of the Private Securities Litigation Reform

NRE: Creating Value for Shareholders March 13, 2018 Forward Looking Statement This presentation may contain certain forward-looking statements within the meaning of the Private Securities Litigation Reform

Frasers Centrepoint Limited and Frasers Commercial Trust to jointly acquire Farnborough Business Park

Frasers Centrepoint Limited and Frasers Commercial Trust to jointly acquire Farnborough Business Park 50:50 joint venture between Frasers Centrepoint Limited and Frasers Commercial Trust to acquire Farnborough

Frasers Centrepoint Limited and Frasers Commercial Trust to jointly acquire Farnborough Business Park 50:50 joint venture between Frasers Centrepoint Limited and Frasers Commercial Trust to acquire Farnborough

Residential Real Estate in CEE. Supply Shortage: Clear Driver for Sustainability

Residential Real Estate in CEE Supply Shortage: Clear Driver for Sustainability May 28 Index 4 Regional overview Quantitative and qualitative gap in supply: clear driver for sustainability 14 Survey on

Residential Real Estate in CEE Supply Shortage: Clear Driver for Sustainability May 28 Index 4 Regional overview Quantitative and qualitative gap in supply: clear driver for sustainability 14 Survey on

THE OFFICE MARKET IN THE BEGINNNING OF 2015

OFFICE MARKET HIGHLIGHTS OFFICE SUPPLY IN THE BEGINNING OF 2015 TRANSACTIONS COMPLETED IN 2014 2014 vs. 2013 Office buildings (A, B and C class) 878,000 sqm Take-Up 233,133 sqm + 28% (From which offices

OFFICE MARKET HIGHLIGHTS OFFICE SUPPLY IN THE BEGINNING OF 2015 TRANSACTIONS COMPLETED IN 2014 2014 vs. 2013 Office buildings (A, B and C class) 878,000 sqm Take-Up 233,133 sqm + 28% (From which offices

NCC Group plc. Preliminary Annual Results for the year ended 31 May 2010 July 2010

NCC Group plc Preliminary Annual Results for the year ended 31 May 2010 July 2010 Agenda Highlights Growth track record Group structure Group financials Group strategy Group sector concentrations Acquisitions

NCC Group plc Preliminary Annual Results for the year ended 31 May 2010 July 2010 Agenda Highlights Growth track record Group structure Group financials Group strategy Group sector concentrations Acquisitions

Douja Promotion Groupe Addoha. An African leader of Real Estate Development

Douja Promotion Groupe Addoha An African leader of Real Estate Development Summary I II III IV V Addoha Group: Strong fundamentals & a clear focus Development in Morocco Development in Africa Key highlights

Douja Promotion Groupe Addoha An African leader of Real Estate Development Summary I II III IV V Addoha Group: Strong fundamentals & a clear focus Development in Morocco Development in Africa Key highlights

BUCHAREST PREMIUM SALES MARKET RESIDENTIAL APARTMENTS

BUCHAREST PREMIUM SALES MARKET RESIDENTIAL APARTMENTS February 2016 2015 Disclaimer This report should not be relied upon as a basis for entering into transactions without seeking specific, qualified,

BUCHAREST PREMIUM SALES MARKET RESIDENTIAL APARTMENTS February 2016 2015 Disclaimer This report should not be relied upon as a basis for entering into transactions without seeking specific, qualified,

Real estate development significant growth driver Company profile and business model High-quality Investment Portfolio

STRATEGY Over three decades of continual development, CA Immo has become distinctly competitive and secured an excellent market position in Central Europe. By letting, managing and developing high quality

STRATEGY Over three decades of continual development, CA Immo has become distinctly competitive and secured an excellent market position in Central Europe. By letting, managing and developing high quality

Property is Our Business COMPANY PROFILE. Corporate Profile

Property is Our Business COMPANY PROFILE Corporate Profile Who we are PROPERTY ONE is a leading property house founded and established in the Kingdom of Bahrain in 2008, holding commercial registration

Property is Our Business COMPANY PROFILE Corporate Profile Who we are PROPERTY ONE is a leading property house founded and established in the Kingdom of Bahrain in 2008, holding commercial registration

Five Oaks Investment Corp.

Five Oaks Investment Corp. Investor Presentation May 2018 Disclaimer & Name Change This presentation contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933,

Five Oaks Investment Corp. Investor Presentation May 2018 Disclaimer & Name Change This presentation contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933,

Resilience of national housing systems in times of a credit crunch

Resilience of national housing systems in times of a credit crunch Presentation at the session Global economic crisis and housing policy response Academy of Sciences of the Czech Republic Institute of

Resilience of national housing systems in times of a credit crunch Presentation at the session Global economic crisis and housing policy response Academy of Sciences of the Czech Republic Institute of

NORTH PARK CORPORATE CENTER

PHASE II / SAN ANTONIO, TEXAS INVESTMENT SUMMARY THE OFFERING HFF is pleased to offer the opportunity to purchase North Park Corporate Center Phase II (the Property ), a high-quality project consisting

PHASE II / SAN ANTONIO, TEXAS INVESTMENT SUMMARY THE OFFERING HFF is pleased to offer the opportunity to purchase North Park Corporate Center Phase II (the Property ), a high-quality project consisting

Hungarian real estate market in the stage of European integration

Hungarian real estate market in the stage of European integration László Gönczi CEO Metropolis International Ltd Hungary President of the Hungarian Chapter of FIABCI Summary The Central and Eastern European

Hungarian real estate market in the stage of European integration László Gönczi CEO Metropolis International Ltd Hungary President of the Hungarian Chapter of FIABCI Summary The Central and Eastern European

GENERAL CONDITIONS OF SALE POST TRADITION S.R.L.

The following text is a faithful translation of the Italian text GENERAL CONDITIONS OF SALE POST TRADITION S.R.L. 1. DEFINITIONS 1.1. The Seller is Post Tradition S.r.l., with registered seat in Vicenza,

The following text is a faithful translation of the Italian text GENERAL CONDITIONS OF SALE POST TRADITION S.R.L. 1. DEFINITIONS 1.1. The Seller is Post Tradition S.r.l., with registered seat in Vicenza,

Hong Kong Prime Office Monthly Report. August 2011 RESEARCH LEASING ACTIVITY ROBUST DESPITE VOLITILITY

RESEARCH August 2011 Hong Kong Prime Office Monthly Report LEASING ACTIVITY ROBUST DESPITE VOLITILITY Sentiment in the office sales market weakened over the past month. The slowdown was triggered by a

RESEARCH August 2011 Hong Kong Prime Office Monthly Report LEASING ACTIVITY ROBUST DESPITE VOLITILITY Sentiment in the office sales market weakened over the past month. The slowdown was triggered by a

POSSIBLE EFFECTS ON EU LAND MARKETS OF NEW CAP DIRECT PAYMENTS

DIRECTORATE-GENERAL FOR INTERNAL POLICIES POLICY DEPARTMENT B: STRUCTURAL AND COHESION POLICIES AGRICULTURE AND RURAL DEVELOPMENT POSSIBLE EFFECTS ON EU LAND MARKETS OF NEW CAP DIRECT PAYMENTS STUDY This

DIRECTORATE-GENERAL FOR INTERNAL POLICIES POLICY DEPARTMENT B: STRUCTURAL AND COHESION POLICIES AGRICULTURE AND RURAL DEVELOPMENT POSSIBLE EFFECTS ON EU LAND MARKETS OF NEW CAP DIRECT PAYMENTS STUDY This

ATRIUM Q RESULTS ANALYST AND INVESTOR CALL. 18 May 2016

ATRIUM Q1 2016 RESULTS ANALYST AND INVESTOR CALL 18 May 2016 KEY EVENTS IN 2016 YTD OPERATIONAL PERFORMANCE Core Markets¹: NRI increased 1.2% to 36.3m; LFL NRI remained stable at 31.4m Russia continues

ATRIUM Q1 2016 RESULTS ANALYST AND INVESTOR CALL 18 May 2016 KEY EVENTS IN 2016 YTD OPERATIONAL PERFORMANCE Core Markets¹: NRI increased 1.2% to 36.3m; LFL NRI remained stable at 31.4m Russia continues

At Knight Frank Occupier Solutions, we make it our business to know your business.

1 At Knight Frank Occupier Solutions, we make it our business to know your business. Your organisation is your passion, and your objectives are paramount. At Knight Frank Occupier Solutions, we take the

1 At Knight Frank Occupier Solutions, we make it our business to know your business. Your organisation is your passion, and your objectives are paramount. At Knight Frank Occupier Solutions, we take the

HONG KONG PRIME OFFICE Monthly Report

RESEARCH February 2011 HONG KONG PRIME OFFICE Monthly Report RENTS TO SURPASS 2008 PEAKS BY YEAR-END Players in Hong Kong's office leasing market started the game of 'musical chairs' again at the beginning

RESEARCH February 2011 HONG KONG PRIME OFFICE Monthly Report RENTS TO SURPASS 2008 PEAKS BY YEAR-END Players in Hong Kong's office leasing market started the game of 'musical chairs' again at the beginning

PROJECT INFORMATION DOCUMENT (PID) APPRAISAL STAGE

APPRAISAL STAGE") Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Project Name PROJECT INFORMATION DOCUMENT (PID) APPRAISAL STAGE Cadastre Modernization

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Project Name PROJECT INFORMATION DOCUMENT (PID) APPRAISAL STAGE Cadastre Modernization

International project development

International project development At home in numerous asset classes STRABAG Real Estate and Mischek have decades of experience in the project development and as real estate developers. Numerous projects

International project development At home in numerous asset classes STRABAG Real Estate and Mischek have decades of experience in the project development and as real estate developers. Numerous projects

RESIDENTIAL RESEARCH MARKET ACTIVITY REPORT FOR AUSTRALIAN CAPITAL CITIES & REGIONAL CENTRES

RESIDENTIAL RESEARCH MARKET ACTIVITY REPORT FOR AUSTRALIAN CAPITAL CITIES & REGIONAL CENTRES Jun-16 Sep-16 Dec-16 Aug-16 Nov-16 Feb-17 Aug-16 Nov-16 Mar-17 The official cash rate target remained at 1.5

RESIDENTIAL RESEARCH MARKET ACTIVITY REPORT FOR AUSTRALIAN CAPITAL CITIES & REGIONAL CENTRES Jun-16 Sep-16 Dec-16 Aug-16 Nov-16 Feb-17 Aug-16 Nov-16 Mar-17 The official cash rate target remained at 1.5

Office market report

research Q2 2014 Office market report highlights As of Q2 2014, there were approximately 4,555,271 square metres of office space in Bangkok. 87,898 square metres of new supply filled in 2014 (The Nine

research Q2 2014 Office market report highlights As of Q2 2014, there were approximately 4,555,271 square metres of office space in Bangkok. 87,898 square metres of new supply filled in 2014 (The Nine

This document is a preview generated by EVS

EESTI STANDARD EVS-EN 1116:2004 Kitchen furniture - Co-ordinating sizes for kitchen furniture and kitchen appliances Kitchen furniture - Co-ordinating sizes for kitchen furniture and kitchen appliances

EESTI STANDARD EVS-EN 1116:2004 Kitchen furniture - Co-ordinating sizes for kitchen furniture and kitchen appliances Kitchen furniture - Co-ordinating sizes for kitchen furniture and kitchen appliances

Dublin Property Day. April 2018 Information as at 31 December Cover: Clancy Quay Ph I and II with CGI of Ph III

April 08 Information as at 3 December 07 Cover: Clancy Quay Ph I and II with CGI of Ph III Disclaimer/Forward-Looking Statements Statements made by us in this presentation and in other reports and statements

April 08 Information as at 3 December 07 Cover: Clancy Quay Ph I and II with CGI of Ph III Disclaimer/Forward-Looking Statements Statements made by us in this presentation and in other reports and statements

Market update Q3 2017

Market update Q3 2017 1 Rikshem in brief Total property value SEK 40.3 bn Portfolio comprising c. 600 properties with c. 28,000 apartments. Lettable area c. 2.2 million sqm Annual rental income 2016 was

Market update Q3 2017 1 Rikshem in brief Total property value SEK 40.3 bn Portfolio comprising c. 600 properties with c. 28,000 apartments. Lettable area c. 2.2 million sqm Annual rental income 2016 was

Galicia 2009 Regional Workshop on Land Tenure and Land Consolidation. FAO s Experience with Land Development Instruments in Europe

Galicia 2009 Regional Workshop on Land Tenure and Land Consolidation FAO s Experience with Land Development Instruments in Europe Santiago de Compostela Galicia 9-11 of February 2009 Richard Eberlin Land

Galicia 2009 Regional Workshop on Land Tenure and Land Consolidation FAO s Experience with Land Development Instruments in Europe Santiago de Compostela Galicia 9-11 of February 2009 Richard Eberlin Land

International Real Estate Society Conference 99 REAL ESTATE INVESTMENTS: THE CASE OF BELARUS

International Real Estate Society Conference 99 Co-sponsors: Pacific Rim Real Estate Society (PRRES) Asian Real Estate Society (AsRES) Kuala Lumpur, 26-30 January 1999 REAL ESTATE INVESTMENTS: THE CASE

International Real Estate Society Conference 99 Co-sponsors: Pacific Rim Real Estate Society (PRRES) Asian Real Estate Society (AsRES) Kuala Lumpur, 26-30 January 1999 REAL ESTATE INVESTMENTS: THE CASE

RESIDENTIAL RESEARCH MARKET ACTIVITY REPORT FOR AUSTRALIAN CAPITAL CITIES & REGIONAL CENTRES

RESIDENTIAL RESEARCH MARKET ACTIVITY REPORT FOR AUSTRALIAN CAPITAL CITIES & REGIONAL CENTRES Mar-16 Jun-16 Sep-16 Jun-16 Sep-16 Dec-16 The official cash rate target remained at 1.5 on 6 December 2016.

RESIDENTIAL RESEARCH MARKET ACTIVITY REPORT FOR AUSTRALIAN CAPITAL CITIES & REGIONAL CENTRES Mar-16 Jun-16 Sep-16 Jun-16 Sep-16 Dec-16 The official cash rate target remained at 1.5 on 6 December 2016.

Office Market Snapshot Podgorica H1 2017

Economy The main macroeconomic indicators of Montenegro, having highlighted only four of them, show a diversified picture of the current trends of the Montenegrin economy. The consumer prices increased

Economy The main macroeconomic indicators of Montenegro, having highlighted only four of them, show a diversified picture of the current trends of the Montenegrin economy. The consumer prices increased

Opportunities and Hurdles for Investors in Light Industrial Properties

Opportunities and Hurdles for Investors in Light Industrial Properties Experiences from the German Market Tom de Witte CFRO Geneba Properties NV Sommerconferenz Darmstadt, 7 July 2016 15.07.16 Contents

Opportunities and Hurdles for Investors in Light Industrial Properties Experiences from the German Market Tom de Witte CFRO Geneba Properties NV Sommerconferenz Darmstadt, 7 July 2016 15.07.16 Contents

ING Lease. Leasing, Your Best Partner in Business? Hans Hoogendijk General Manager, ING Lease (C.R.), s.r.o.

, s.r.o.") ING Lease Leasing, Your Best Partner in Business? Hans Hoogendijk General Manager, ING Lease (C.R.), s.r.o. Truck Europe Forum 2007 Prague, May 15, 2007 Contents Roadmap to ING Lease in CE Europe ING Lease

ING Lease Leasing, Your Best Partner in Business? Hans Hoogendijk General Manager, ING Lease (C.R.), s.r.o. Truck Europe Forum 2007 Prague, May 15, 2007 Contents Roadmap to ING Lease in CE Europe ING Lease

London IHP Leadership Exchange

London IHP Leadership Exchange Assets Real Estate Production and Acquisition Review of Global Markets Robert Grundy, Head of Housing, Savills Tuesday 7 th October, 2014 Winckworth Sherwood, Minerva House,

London IHP Leadership Exchange Assets Real Estate Production and Acquisition Review of Global Markets Robert Grundy, Head of Housing, Savills Tuesday 7 th October, 2014 Winckworth Sherwood, Minerva House,