$23,155,000 COUNTY OF SACRAMENTO COMMUNITY FACILITIES DISTRICT NO (NORTH VINEYARD STATION NO. 1) SPECIAL TAX BONDS, SERIES 2016

|

|

|

- Melissa Cain

- 5 years ago

- Views:

Transcription

1 NEW ISSUE (Book-Entry Only) NO RATING In the opinion of Orrick, Herrington & Sutcliffe LLP, Bond Counsel to the County, based upon an analysis of existing laws, regulations, rulings and court decisions, and assuming, among other matters, the accuracy of certain representations and compliance with certain covenants, interest on the 2016 Bonds is excluded from gross income for federal income tax purposes under Section 103 of the Internal Revenue Code of 1986 and is exempt from State of California personal income taxes. In the further opinion of Bond Counsel, interest on the 2016 Bonds is not a specific preference item for purposes of the federal individual or corporate alternative minimum taxes, although Bond Counsel observes that such interest is included in adjusted current earnings when calculating corporate alternative minimum taxable income. Bond Counsel expresses no opinion regarding any other tax consequences related to the ownership or disposition of, or the amount, accrual or receipt of interest on, the 2016 Bonds. See CONCLUDING INFORMATION Tax Matters. $23,155,000 COUNTY OF SACRAMENTO COMMUNITY FACILITIES DISTRICT NO (NORTH VINEYARD STATION NO. 1) SPECIAL TAX BONDS, SERIES 2016 Dated: Date of Initial Issuance Due: September 1, inside cover The County of Sacramento Community Facilities District No (North Vineyard Station No. 1) Special Tax Bonds, Series 2016 (the 2016 Bonds ) are being issued by the County of Sacramento (the County ) with respect to its Community Facilities District No (North Vineyard Station No. 1) (the District ) to provide funds to (i) refund the outstanding County of Sacramento Community Facilities District No (North Vineyard Station No. 1) Special Tax Bonds, Series 2007A, issued by the County with respect to the District, (ii) pay costs of the acquisition and construction of certain public facilities required in connection with the development of land within the District, (iii) fund a Bond Reserve Fund in the amount described herein, (iv) fund capitalized interest on a portion of the 2016 Bonds through approximately September 1, 2016, and (v) pay certain costs of issuing the 2016 Bonds. The 2016 Bonds are authorized to be issued pursuant to the Mello-Roos Community Facilities Act of 1982, as amended (Section et seq. of the Government Code of the State of California), and pursuant to Resolution No adopted by the Board of Supervisors of the County (the Board of Supervisors ) on August 7, 2007 (the Original Resolution ), as supplemented by Resolution No adopted by the Board of Supervisors on April 26, 2016 (the First Supplement and together with the Original Resolution, the Bond Resolution ). The District has been formed by and is located in the County. The 2016 Bonds are being issued in fully registered book-entry form only in denominations of $5,000 or any integral multiple thereof and, when executed and delivered, will be registered in the name of Cede & Co. as nominee of The Depository Trust Company, New York, New York ( DTC ), which will act as securities depository for the 2016 Bonds, and purchasers will not receive certificates representing their interests in the 2016 Bonds. See THE 2016 BONDS Book-Entry Only System. Interest on the 2016 Bonds is payable semiannually on each March 1 and September 1, commencing September 1, Such interest on and the principal of the 2016 Bonds is payable by the County s Director of Finance to Cede & Co., and such payments are expected to be disbursed to the beneficial owners of the 2016 Bonds through the participants of DTC. The 2016 Bonds and any additional bonds payable on a parity with them (collectively, the Bonds ) are payable from the proceeds of an annual special tax (the Special Tax ) to be levied on and collected from Parcels of Taxable Property (as defined herein) in the District. The Special Tax is to be levied according to the amended rate and method of apportionment approved by the County Board of Supervisors and by the vote of the qualified landowner-electors in the District. See APPENDIX B AMENDED RATE AND METHOD OF APPORTIONMENT OF SPECIAL TAX. The Special Tax will be collected in the same manner and at the same time as ad valorem property taxes applicable to the Parcels of Taxable Property. See SECURITY AND SOURCES OF PAYMENT FOR THE 2016 BONDS The Special Tax. The 2016 Bonds are subject to optional, mandatory and extraordinary redemption as described herein. See THE 2016 BONDS Redemption. Neither the full faith and credit nor the general taxing power of the County, the District, the State of California, or any political subdivision thereof is pledged to the payment of the 2016 Bonds. The 2016 Bonds are not general obligations of the County but are limited obligations of the County payable solely from proceeds of the Special Tax and certain funds and accounts as provided in the Bond Resolution. This cover page contains certain information for general reference only. It is not a summary of the 2016 Bonds. Prospective investors must read the entire Official Statement to obtain information essential to the making of an informed investment decision. See SPECIAL RISK FACTORS for a discussion of special risk factors that should be considered, in addition to the other matters set forth herein, in evaluating the investment quality of the 2016 Bonds. MATURITY SCHEDULE (See Inside Cover) The 2016 Bonds are offered when, as and if issued and accepted by the Underwriter, subject to the approval as to their validity by Orrick, Herrington & Sutcliffe LLP, Bond Counsel to the County, and certain other conditions. Certain legal matters will be passed on for the County by the office of County Counsel, and other legal matters will be passed upon for the County by its Disclosure Counsel, Stradling Yocca Carlson & Rauth, a Professional Corporation, Newport Beach, California and for the Underwriter by its counsel, Jones Hall, A Professional Law Corporation, San Francisco, California. It is anticipated that the 2016 Bonds in book-entry form will be available for delivery to DTC in New York, New York on or about June 8, Dated May 25, 2016.

2 $23,155,000 COUNTY OF SACRAMENTO COMMUNITY FACILITIES DISTRICT NO (NORTH VINEYARD STATION NO. 1) SPECIAL TAX BONDS, SERIES 2016 MATURITY SCHEDULE Maturity September 1 Principal Amount Interest Rate Yield CUSIP No $300, % 0.75% MY , MZ , NA , NB , NC , ND , NE , NF , NG , NH , NJ , C NK , NL , NM , NN , NP , NQ5 $7,100, % Term Bond due September 1, 2040 Yield 3.19% C CUSIP No. : NT9 $6,740, % Term Bond due September 1, 2045 Yield 3.25% C CUSIP No. : NU6 C Yield to optional redemption date of September 1, 2026, at par. CUSIP is a registered trademark of the American Bankers Association ( CUSIP Global Services (CGS) is managed on behalf of the American Bankers Association by S&P Capital IQ. Copyright 2016 CUSIP Global Services. All rights reserved. CUSIP data herein are provided for convenience of reference only. Neither the County nor the Underwriter takes any responsibility for the accuracy of the CUSIP data.

3 Investment in the 2016 Bonds involves risks which are not appropriate for certain investors. Therefore, only persons with substantial financial resources (in net worth or income) who understand (either alone or with competent investment advice) the risk of investment in the 2016 Bonds should consider such an investment. All information for investors regarding the County of Sacramento (the County ), its Community Facilities District No (North Vineyard Station No. 1) (the District ), and the 2016 Bonds is contained in this Official Statement. While the County maintains an internet website for various purposes, none of the information on that website is intended to assist investors in making any investment decision or to provide any continuing information with respect to the 2016 Bonds or any other obligations of the County or the District. No dealer, broker, salesperson or other person has been authorized by the County to provide any information or to make any representations other than as contained herein and, if given or made, such other information or representation must not be relied upon as having been authorized by the County. This Official Statement does not constitute an offer to sell or the solicitation of an offer to buy, nor shall there be any sale of the 2016 Bonds by a person in any jurisdiction in which it is unlawful for such person to make such an offer, solicitation or sale. This Official Statement is not to be construed as a contract with the purchasers of the 2016 Bonds. Statements contained in this Official Statement that involve estimates, forecasts or matters of opinion, whether or not expressly so described herein, are intended solely as such and are not to be construed as a representation of facts. The information and expressions of opinion herein are subject to change without notice; and neither delivery of this Official Statement nor any sale of securities made hereunder shall, under any circumstances, create any implication that there has been no change in the affairs of the County, the District, the property in the District, the Developer or any matters discussed herein since the date hereof. The Underwriter has provided the following sentence for inclusion in this Official Statement: The Underwriter has reviewed the information in this Official Statement in accordance with, and as part of, its responsibilities to investors under the federal securities laws as applied to the facts and circumstances of this transaction, but the Underwriter does not guarantee the accuracy or completeness of such information. CAUTIONARY INFORMATION REGARDING FORWARD-LOOKING STATEMENTS IN THIS OFFICIAL STATEMENT Certain statements included or incorporated by reference in this Official Statement constitute forward-looking statements within the meaning of the United States Private Securities Litigation Reform Act of 1995, Section 21E of the United States Exchange Act of 1934, as amended, and Section 27A of the United States Securities Act of 1933, as amended. Such statements are generally identifiable by the terminology used such as plan, expect, estimate, budget or other similar words. The achievement of certain results or other expectations contained in such forward-looking statements involves known and unknown risks, uncertainties and other factors which may cause actual results, performance or achievements described to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. No updates or revisions to those forward-looking statements are expected to be issued if or when the expectations, or events, conditions or circumstances on which such statements are based change. IN CONNECTION WITH THIS OFFERING, THE UNDERWRITER MAY OVER ALLOT OR EFFECT TRANSACTIONS WHICH STABILIZE OR MAINTAIN THE MARKET PRICE OF THE SECURITIES OFFERED HEREBY AT A LEVEL ABOVE THAT WHICH MIGHT OTHERWISE PREVAIL IN THE OPEN MARKET. SUCH STABILIZING, IF COMMENCED, MAY BE DISCONTINUED AT ANY TIME. THE UNDERWRITER MAY OFFER AND SELL SECURITIES AT PRICES LOWER THAN THE PUBLIC OFFERING PRICES SET FORTH ON THE INSIDE FRONT COVER PAGE HEREOF, SUCH PUBLIC OFFERING PRICES MAY BE CHANGED FROM TIME TO TIME BY THE UNDERWRITER. THESE SECURITIES HAVE NOT BEEN REGISTERED UNDER THE SECURITIES ACT OF 1933, AS AMENDED, IN RELIANCE UPON AN EXEMPTION CONTAINED IN SUCH ACT. THEY HAVE NOT BEEN REGISTERED OR QUALIFIED UNDER THE SECURITIES LAWS OF ANY STATE.

4 COUNTY OF SACRAMENTO, CALIFORNIA BOARD OF SUPERVISORS Roberta MacGlashan, Supervisor, District 4, Chair Don Nottoli, Supervisor, District 5, Vice Chair Patrick Kennedy, Supervisor, District 2 Susan Peters, Supervisor, District 3 Phil Serna, Supervisor, District 1 COUNTY STAFF Navdeep S. Gill, County Executive Britt Ferguson, Chief Financial Officer Kristen Yates, County Debt Officer Ben Lamera, Interim Director of Finance Robyn Truitt Drivon, Esq., County Counsel BOND COUNSEL Orrick, Herrington & Sutcliffe LLP FINANCIAL ADVISOR Public Financial Management, Inc. San Francisco, California DISCLOSURE COUNSEL Stradling Yocca Carlson & Rauth, a Professional Corporation Newport Beach, California SPECIAL TAX CONSULTANT Goodwin Consulting Group, Inc. Sacramento, California APPRAISER Seevers Jordan Zeigenmeyer Real Estate Appraisal and Consultation Rocklin, California VERIFICATION AGENT Causey, Demgen & Moore, P.C. Denver, Colorado

5 TABLE OF CONTENTS Page INTRODUCTION... 1 General... 1 The District... 1 Sources of Payment for the 2016 Bonds... 3 Continuing Disclosure... 4 Bond Owners Risks... 4 Other Information... 4 THE 2016 BONDS... 5 Authority for Issuance... 5 Purpose of the 2016 Bonds... 5 Description of the 2016 Bonds... 5 Limited Obligation... 6 Redemption... 6 Selection of 2016 Bonds for Redemption... 8 Notice of Redemption... 8 Book-Entry Only System... 8 ESTIMATED SOURCES AND USES OF FUNDS... 9 THE REFUNDING PLAN... 9 General... 9 Verification of Mathematical Computations DEBT SERVICE SCHEDULE AND ESTIMATED COVERAGE SECURITY AND SOURCES OF PAYMENT FOR THE 2016 BONDS General The Special Tax Special Tax Analysis Proceeds of the Special Tax Letter of Credit Agreement Letter of Credit Bank Bond Reserve Fund Covenant for Foreclosure Teeter Plan Delinquency History Property Values and the Appraisal Direct and Overlapping Bonded Indebtedness Top Taxpayers Parity Bonds THE DISTRICT General Description Lennar Development Plan Vineyard Creek Status of Entitlements Facilities THE DEVELOPER Lennar Homes of California, Inc i

6 TABLE OF CONTENTS (continued) THE DEVELOPER S FINANCING PLANS SPECIAL RISK FACTORS Introduction Concentration of Ownership Levy of Special Tax Collection of the Special Tax Teeter Plan Termination Exempt Properties Failure to Develop Properties Maximum Special Tax Payment of Special Tax Not Personal Obligation of Property Owners Disclosures to Future Purchasers Parity Taxes and Special Assessments Reductions in Property Values Bankruptcy and Legal Delays FDIC/Federal Government Interests In Properties Geologic, Topographic and Climatic Conditions Endangered Species Legal Requirements Hazardous Substances No Acceleration Provision No Obligation To Pay Debt Service Loss of Tax Exemption Audit of Tax-Exempt Bond Issues Limited Secondary Market; Potential Reductions in Bond Values Proposition Shapiro Decision Ballot Initiatives CONCLUDING INFORMATION Legality Tax Matters Continuing Disclosure No Litigation No General Obligation of the County or the District No Ratings Underwriting Financial Advisor Miscellaneous APPENDIX A APPRAISAL REPORT... A-1 APPENDIX A-1 UPDATE APPRAISAL REPORT... A-1-1 APPENDIX B AMENDED RATE AND METHOD OF APPORTIONMENT OF SPECIAL TAX... B-1 APPENDIX C FORM OF CONTINUING DISCLOSURE CERTIFICATE OF THE COUNTY... C-1 APPENDIX D INFORMATION CONCERNING THE DEPOSITORY TRUST COMPANY... D-1 APPENDIX E PROPOSED FORM OF OPINION OF BOND COUNSEL... E-1 APPENDIX F FORM OF DEVELOPER CONTINUING DISCLOSURE AGREEMENT... F-1 APPENDIX G SUMMARY OF CERTAIN PROVISIONS OF THE BOND RESOLUTION... G-1 Page ii

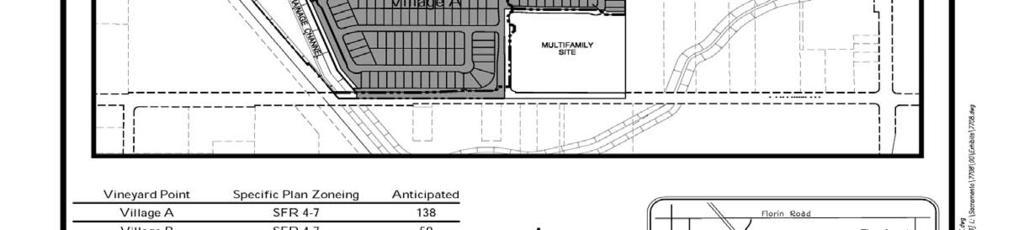

7 $23,155,000 COUNTY OF SACRAMENTO COMMUNITY FACILITIES DISTRICT NO (NORTH VINEYARD STATION NO. 1) SPECIAL TAX BONDS, SERIES 2016 INTRODUCTION General The purpose of this Official Statement, which includes the cover page and attached appendices, is to provide certain information concerning the County of Sacramento Community Facilities District No (North Vineyard Station No. 1) Special Tax Bonds, Series 2016 in the principal amount of $23,155,000 (the 2016 Bonds ). The 2016 Bonds are being issued by the County of Sacramento (the County ) with respect to its Community Facilities District No (North Vineyard Station No. 1) (the District or the CFD ) to provide funds to (i) refund the outstanding County of Sacramento Community Facilities District No (North Vineyard Station No. 1) Special Tax Bonds, Series 2007A, issued by the County with respect to the District (the 2007 Bonds ), (ii) pay costs of the acquisition and construction of certain public facilities required in connection with the development of land within the District, (iii) fund the Bond Reserve Fund in the amount of the Required Bond Reserve (each as defined herein), (iv) fund capitalized interest on a portion of the 2016 Bonds through approximately September 1, 2016, and (v) pay certain costs of issuing the 2016 Bonds. The 2016 Bonds are authorized to be issued pursuant to the Mello-Roos Community Facilities Act of 1982, as amended (Section et seq. of the Government Code of the State of California), and pursuant to Resolution No adopted by the Board of Supervisors of the County (the Board of Supervisors ) on August 7, 2007 (the Original Resolution ), as supplemented by Resolution No adopted by the Board of Supervisors on April 26, 2016 (the First Supplement and together with the Original Resolution, the Bond Resolution ). Capitalized terms that are not otherwise defined herein shall have the respective meanings ascribed to them in the Bond Resolution. The 2016 Bonds and any additional bonds issued pursuant to the Bond Resolution and payable on a parity with the 2016 Bonds ( Parity Bonds and, together with the 2016 Bonds, the Bonds ) are payable from the proceeds of an annual special tax (the Special Tax ) to be levied and collected from Parcels of Taxable Property (as defined herein) in the District. The Special Tax is to be levied according to the amended rate and method of apportionment approved by the Board of Supervisors on June 5, 2007 and by the vote of the qualified landowner-electors in the District at an election held on May 29, 2007 (the Special Tax Formula ). For purposes of the Special Tax Formula, the 2016 Bonds constitute both Vineyard Creek Bonds and Vineyard Point Bonds. See APPENDIX B AMENDED RATE AND METHOD OF APPORTIONMENT OF SPECIAL TAX. The Special Tax is expected to be collected in the same manner and at the same time as ad valorem property taxes applicable to the Parcels of Taxable Property. See SECURITY AND SOURCES OF PAYMENT FOR THE 2016 BONDS The Special Tax. The District General. The District is located within an unincorporated area in the southeastern portion of the County, approximately 13 miles southeast of downtown Sacramento and five miles north of the City of Elk Grove. More specifically, the District is situated west of Bradshaw Road, north of Gerber Road and south of Florin Road. The District consists of approximately 284 gross acres and consists of a portion of the North Vineyard Station Specific Plan ( NVSSP ) area. The District includes the master planned community known as Vineyard Point and a portion of the master planned community known as Vineyard Creek. 1

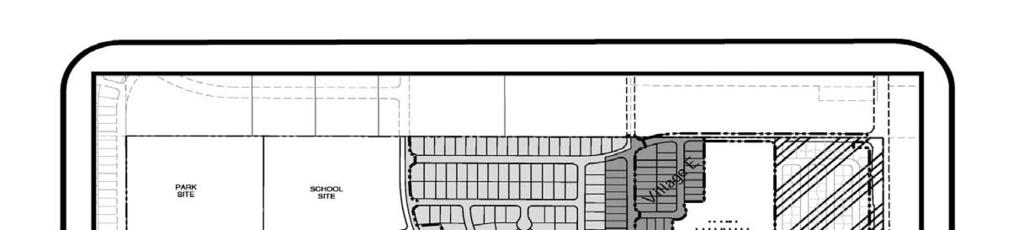

8 Planned Development. Lennar Homes of California, Inc. (the Developer or Lennar ) has completed construction within Vineyard Point with 709 completed single family homes owned by individual homeowners, including a 177-unit active adult community with a clubhouse. The Developer is actively developing the remaining parcels within the Vineyard Creek development. For development planning purposes, Lennar has divided the property that it still owns within the Vineyard Creek portion of the District into Units to be developed in phases. A map showing the location of the Units is included on page 39. The Vineyard Creek portion of the District consists of a portion of Unit 1 and Units 4, 5 and 6, planned for 383 single family detached homes, 185 of which will be part of an age-restricted community. As of March 1, 2016, Lennar had sold and closed 10 completed homes to individual homeowners, 4 completed homes were under contract to be sold, and 24 homes were under construction (13 of which were under contract to be sold) within the portion of Unit 1 of Vineyard Creek in the District. As of such date, construction had not yet commenced in Units 4, 5 or 6. The District is also planned to include a multifamily project on a site of approximately 6.77 acres. Lennar expects to either construct the multi-family project itself or sell the parcel to another merchant builder. The balance of the property within the District consists of approximately 16.6 acres for parks and related open space and trails, and approximately 90 acres for streets and public utilities. See the THE DISTRICT General Description for a summary of the current development status within the District and in CFD No CFD No The remaining portion of the Vineyard Creek development that is not included within the District is within County of Sacramento Community Facilities District No (North Vineyard Station No. 2) ( CFD No ). CFD No is located southeast of the District and is planned for 479 single family detached residential units being developed by Lennar and 94 lots currently owned by Family Real Property Limited Partnership planned for residential development. Thomas P. Winn, as trustee of his personal trust, is the majority owner of Family Real Property Limited Partnership and the sole shareholder of Tom Winn Communities, a California corporation ( Winn Communities ). Winn Communities will undertake to manage and improve the property within CFD No that is owned by Family Real Property Limited Partnership. As referenced herein, Winn shall refer to both Winn Communities and Family Real Property Limited Partnership; provided, however, Winn Communities does not own any real property within CFD No As of March 1, 2016, Lennar had closed 19 homes in CFD No to individual homeowners, had entered into contracts to sell 48 additional homes, had 18 completed homes and 37 homes under construction; the remaining property within the CFD No owned by Lennar was in various stages of development from finished lots to unimproved land and the property owned by Winn was unimproved land. The County expects to issue special tax bonds with respect to CFD No concurrently with the issuance of the 2016 Bonds. A portion of the proceeds of such bonds are expected to fund a portion of the public infrastructure costs necessary to develop the Vineyard Creek project, which includes property within the District and CFD No and the property owned by Winn which is not a part of Vineyard Creek. Special taxes levied within CFD No are not pledged to and are not available to pay the principal of and interest on the 2016 Bonds. Appraisal. An appraisal of certain Taxable Property within the District, dated March 31, 2016, and an Update Appraisal Report dated April 26, 2016 (such appraisal and the Update Appraisal Report are referred to collectively as the Appraisal ), have been prepared by Seevers Jordan Ziegenmeyer, Real Estate Appraisal and Consultation, Rocklin, California (the Appraiser ). A copy of the Appraisal is attached to this Official Statement as Appendix A and Appendix A-1. The purpose of the Appraisal is to set forth the Appraiser s opinions of value of a certain portion of the Taxable Property on the assumptions (among others) that the improvements expected to be financed with 2016 Bond proceeds were installed and that the appraised property were subject to the lien of the Special Taxes. The Appraisal is based on the status of development as of 2

9 January 20, 2016 (the Date of Value ) which, as described above and under the captions THE DISTRICT General Description and THE DEVELOPMENT PLAN, has progressed since such date. To arrive at the estimated value of the Taxable Property within the District, the Appraiser applied the following methodology: (i) for the 657 completed single family homes owned by individual homeowners within the District, as of January 1, 2015, the Appraiser used the Fiscal Year assessed values assigned by the County; (ii) for the 145 completed or partially completed single family homes without an assessed value as of January 1, 2015, the Appraiser used the sales comparison approach to estimate the market values for such homes and (iii) for the remaining Taxable Property within the District, which as of the Date of Value, consisted of 291 lots in either a mass graded or raw land condition, the Appraiser used a discounted cash flow analysis to arrive at the estimated bulk market value. The property described in (ii) and (iii) of the foregoing sentence is referred to in this Official Statement as the Appraised Property. Based on the assumptions set forth in the Appraisal, and subject to the limiting conditions described therein, the Appraiser is of the opinion that the market value of the Appraised Property was $53,610,000 (represents a rounded total of the individually appraised parcels) as of the Date of Value. In the Update Appraisal Report, the Appraiser concludes based on the assumptions and limiting conditions set forth therein that as of April 26, 2016 the value of the Appraised Property was not less than the market value as of the Date of Value. Combined with the Fiscal Year assessed value of the 657 homes within the District owned by individual homeowners as of January 1, 2015 ($178,281,801), the Appraiser is of the opinion that the cumulative (aggregate) value of the Taxable Property within the District, as of the Date of Value, was not less than $231,891,801 (the Composite Value ). This Composite Value is approximately 9.27 times the $23,155,000 principal amount of the 2016 Bonds and the $1,839,629 amount of direct and overlapping tax and assessment debt on the Taxable Property. See SECURITY AND SOURCES OF PAYMENT FOR THE 2016 BONDS Property Values and the Appraisal and Direct and Overlapping Bonded Indebtedness. The Appraisal is based upon a variety of assumptions and limiting conditions that are described in the full text of the Appraisal attached to this Official Statement as Appendix A and Appendix A-1. The Appraiser s opinions reflect conditions prevailing in the applicable market as of the Date of Value. Neither the County or the Underwriter makes any representation as to the accuracy of the Appraisal. There is no assurance that the property within the District can be sold for the amounts set forth in the Appraisal or that any parcel can be sold for a price sufficient to pay the Special Taxes for such parcel in the event of a default in payment of Special Taxes by the owner of such parcel. See the caption SPECIAL RISK FACTORS Reductions in Property Values, Appendix A and Appendix A-1. Sources of Payment for the 2016 Bonds The County is authorized to issue up to a maximum of $30,000,000 in bonded indebtedness with respect to the District. The County issued the 2007 Bonds in the aggregate principal amount of $14,415,000, leaving a remaining authorization of $15,585,000. The 2016 Bonds are the second series of bonds that may be issued by the County with respect to the District. The 2016 Bonds will refund the 2007 Bonds and include $9,745,000 allocable to finance new capital improvements; therefore, following the issuance of the 2016 Bonds $5,840,000 in bond authorization will remain. See THE REFUNDING PLAN. The 2016 Bonds are referred to in the Special Tax Formula and in the Bond Resolution as Vineyard Point Bonds and as Vineyard Creek Bonds. The County may issue one or more Series of Parity Bonds to finance the construction or acquisition of additional facilities described under the caption THE DISTRICT Facilities in a principal amount equal to the lesser of (i) the amount remaining under the $30,000,000 in bond authorization or (ii) an amount determined based upon the projected Maximum Annual Special Taxes which could be levied on Parcels of Taxable Property within the District at build-out, subject to the requirements under the Bond Resolution for the issuance of Parity Bonds. See SECURITY AND SOURCES OF PAYMENT FOR THE 2016 BONDS Special Tax Analysis. Upon the issuance of such Parity Bonds, Special Taxes would be levied on the Parcels of Taxable Property within the District to pay debt service on the 2016 Bonds and Parity Bonds. See SECURITY AND SOURCES OF PAYMENT FOR THE 2016 BONDS Parity Bonds and The Special Tax Classification of Parcels Subject to Special Tax herein. 3

10 Pursuant to the Special Tax Formula, the Special Taxes are apportioned within the District first to Developed Property, then to Parcels of Final Map Property and then to Parcels of Large Lot Subdivision Map Property (as such terms are defined in the Special Tax Formula), to the extent necessary to meet the Special Tax Requirement (as defined in the Special Tax Formula). For the Fiscal Year Special Tax levy, there were 703 parcels of Developed Property (i.e., assessor s parcels for which a building permit has been issued as of June 1, 2015) within the District. Based on development status as of March 1, 2016, 749 parcels classified as Developed Property for the Fiscal Year Special Tax levy are expected to support approximately 81% of the annual debt service on the 2016 Bonds (without considering any capitalized interest). Neither the full faith and credit nor the general taxing power of the County, the District, the State of California, or any political subdivision thereof is pledged to the payment of the 2016 Bonds. The 2016 Bonds are not general obligations of the County but are limited obligations of the County payable solely from proceeds of the Special Tax and certain funds and accounts as provided in the Bond Resolution. Continuing Disclosure The County has agreed to provide, or cause to be provided, to the Electronic Municipal Market Access System ( EMMA ) of the Municipal Securities Rulemaking Board (the MSRB ), certain annual financial information and operating data and notice of certain enumerated events in order to assist the Underwriter in complying with Rule 15c2-12 adopted by the Securities and Exchange Commission under the Securities Exchange Act of 1934, as the same may be amended from time to time (the Rule ). See the caption CONCLUDING INFORMATION Continuing Disclosure and Appendix C for a description of the specific nature of the annual reports and enumerated event notices to be filed by the County or its representatives. The Underwriter does not consider the Developer to be an obligated person with respect to the 2016 Bonds for purposes of the Rule. Notwithstanding the foregoing, to assist in the marketing of the 2016 Bonds, the Developer has agreed to provide, or cause to be provided to EMMA, certain updates with respect to the development within the District and notices of certain material events. See Appendix F for a description of the specific nature of the annual reports and enumerated event notices to be filed by the Developer or its representatives. Bond Owners Risks Certain events could affect the timely repayment of the principal of, premium, if any and interest on the 2016 Bonds when due. See the caption SPECIAL RISK FACTORS for a discussion of certain factors that should be considered, in addition to other matters set forth herein, in evaluating an investment in the 2016 Bonds. The 2016 Bonds are not being rated by any nationally recognized rating agency. Other Information Brief descriptions of the 2016 Bonds, the Bond Resolution, the security for the 2016 Bonds, the Special Tax, the County and the District are included in this Official Statement together with summaries of certain provisions of the 2016 Bonds, the Bond Resolution and certain other documents. Such descriptions do not purport to be comprehensive or definitive. All references herein to the Bond Resolution and other documents are qualified in their entirety by reference to such documents, and references herein to the 2016 Bonds are qualified in their entirety by reference to the form thereof included in the Bond Resolution, copies of which are available for inspection at the office of the Clerk of the Board of Supervisors. This information speaks only as of its date, and the information contained herein is subject to change. Unless otherwise defined elsewhere in this Official Statement, capitalized terms shall have the meanings assigned to them in the Bond Resolution. 4

11 THE 2016 BONDS Authority for Issuance The Mello Roos Community Facilities Act of 1982, as amended (Sections et seq. of the California Government Code) (the Act ), was enacted by the California Legislature to provide an alternate method of financing certain public capital facilities and services, especially in developing areas of the State of California (the State ). Subject to approval by a two-thirds vote of a district s qualified electors and compliance with the provisions of the Act, a legislative body of a local agency may issue bonds for a community facilities district to finance certain public improvements and may levy and collect a special tax within such district to repay such indebtedness. The legislative body is also authorized to issue bonds to refund such indebtedness, subject to compliance with the provisions of the Act. Pursuant to the Act, the Board of Supervisors adopted on December 13, 2005, Resolution No providing for the establishment of the District and calling an election to authorize the issuance of bonds and the levying of a special tax within the District and adopted Resolution No determining the necessity to incur bonded indebtedness within the District in an amount not to exceed $30,000,000. On January 19, 2006, at an all-mailed ballot election held pursuant to the Act, the then-sole owners of land within the District, who under the terms of the Act were the only qualified electors within the District, authorized the issuance of up to $30,000,000 principal amount of special tax bonds to finance certain public facilities to serve the property within the District and approved the maximum rate and method of apportionment of the Special Tax to pay the principal of and interest on such bonds. The rate and method of apportionment was subsequently amended at a May 29, 2007 mailed ballot election. See caption SECURITY AND SOURCES OF PAYMENT FOR THE 2016 BONDS The Special Tax herein. The 2016 Bonds are being issued pursuant to the Bond Resolution adopted by the Board of Supervisors of the County on August 7, 2007, as supplemented on April 26, Purpose of the 2016 Bonds The 2016 Bonds are being issued to provide funds to (i) refund the outstanding 2007 Bonds, (ii) pay costs of the acquisition and construction of certain public facilities required in connection with the development of land within the District, (iii) fund the Bond Reserve Fund in the amount of the Required Bond Reserve (each as defined herein), (iv) fund capitalized interest on a portion of the 2016 Bonds through approximately September 1, 2016, and (v) pay certain costs of issuing the 2016 Bonds. Description of the 2016 Bonds The 2016 Bonds will be issued as fully registered bonds without coupons in denominations of $5,000, or any integral multiple thereof (not exceeding the principal amount maturing at any one time), and shall be dated the date of their initial issuance (the Dated Date ). The 2016 Bonds will mature on September 1, in the principal amounts and years, and will bear interest at the rates, shown on the inside front cover of this Official Statement. Interest on the 2016 Bonds will be computed on the basis of a 360-day year consisting of twelve 30-day months and will be payable semiannually on March 1 and September 1 of each year, commencing September 1, 2016 (each an Interest Payment Date ). Each 2016 Bond will bear interest from the Interest Payment Date next preceding the date of registration thereof, unless (i) it is registered on a day during the period from the sixteenth day of the calendar month next preceding an Interest Payment Date to such Interest Payment Date (both dates inclusive), in which event it shall bear interest from such Interest Payment Date, or (ii) it is registered on a day on or before the fifteenth day of the month preceding the first Interest Payment Date, in which event it shall bear interest from its date; provided, that if at the time of registration of any 2016 Bond interest is then in default thereon, such 2016 Bond shall bear interest from the Interest Payment Date to which interest thereon has previously been paid or made available for payment. 5

12 Interest on the 2016 Bonds will be payable in lawful money of the United States only to the Holders thereof at the close of business as of the fifteenth day of the month next preceding each Interest Payment Date (the Record Date ), whether or not such day is a business day. Such interest shall be paid by check mailed on each such Interest Payment Date to such Holders at their addresses as they appear in the registration books required to be kept by the County s Director of Finance (sometimes referred to as the Paying Agent ), except that in the case of a Holder of $1,000,000 or more in aggregate principal amount of the 2016 Bonds then Outstanding, payment on any Interest Payment Date shall be made at such Holder s option by wire transfer of immediately available funds according to instructions provided by such owner to the Paying Agent not later than the applicable Record Date. Payment of the principal of a 2016 Bond will be made only to the person whose name appears as the registered owner thereof in the registration books to be kept by the Paying Agent and only on the surrender thereof at the office of the Paying Agent. See Book-Entry Only System herein. Limited Obligation The 2016 Bonds are not general obligations of the County but are limited obligations of the County payable solely from the proceeds of the Special Tax and certain funds and accounts as provided in the Bond Resolution. Neither the full faith and credit nor the general taxing power of the County, the State of California or any political subdivision thereof is pledged to the payment of the 2016 Bonds. See SPECIAL RISK FACTORS No Obligation to Pay Debt Service and CONCLUDING INFORMATION No General Obligation of the County or the District. Redemption Mandatory Sinking Fund Redemption. The Bond Resolution authorizes the provision of certain amounts (the Minimum Sinking Fund Account Payments ) for the mandatory redemption and payment of the 2016 Bonds that are Term Bonds. Minimum Sinking Fund Account Payments are to be deposited in the Sinking Fund Account in the Bond Redemption Fund to be used and withdrawn by the County at any time for the mandatory redemption or payment of the principal of the Term Bonds or for the purchase of Term Bonds at public or private sale as and when and at such prices (including brokerage and other charges, but excluding accrued interest, which is payable from the Bond Redemption Fund) as it may in its discretion determine, but not to exceed the principal amount of such Term Bonds. The Term Bonds maturing on September 1, 2040 are subject to mandatory redemption in part on any September 1 on or after September 1, 2034, upon mailed notice as provided in the Bond Resolution, at the principal amount thereof called for redemption together with accrued interest thereon to the date of redemption, on September 1 of each year, beginning on September 1, 2034, in the following amounts: Year Ending September 1 Minimum Sinking Fund Account Payments Term Bonds Maturing September 1, 2040 Minimum Sinking Fund Account Payment 2034 $ 915, , ,060, ,135, , ,000, (Maturity) 1,080,000 The Term Bonds maturing on September 1, 2045 are subject to mandatory redemption in part on any September 1 on or after September 1, 2041, upon mailed notice as provided in the Bond Resolution, at the 6

13 principal amount thereof called for redemption together with accrued interest thereon to the date of redemption, on September 1 of each year, beginning on September 1, 2041, in the following amounts: Year Ending September 1 Minimum Sinking Fund Account Payments Term Bonds Maturing September 1, 2045 Minimum Sinking Fund Account Payment 2041 $ 1,160, ,250, ,345, ,440, (Maturity) 1,545,000 In the event of a partial redemption of any of the Term Bonds (other than as a result of the application of Minimum Sinking Fund Account Payments) the amounts of the Minimum Sinking Fund Account Payments shown in the foregoing table will be reduced proportionately by the principal amount of all such Term Bonds which are redeemed by such partial redemption. Optional Redemption. The 2016 Bonds maturing by their terms on or after September 1, 2027 are subject to optional redemption by the County prior to their respective stated maturity dates on any date on or after September 1, 2026, in whole or in part, from funds derived by the County from any source (including the proceeds of bonds issued in order to refund the 2016 Bonds) other than Minimum Sinking Fund Account Payments or prepayments of the Special Tax, upon notice mailed as provided in the Bond Resolution and described under Notice of Redemption below, at a redemption price equal to the principal amount of the 2016 Bonds or portions thereof called for redemption together with accrued interest thereon to the date fixed for redemption, without premium. Extraordinary Redemption from Prepayment of Special Tax. The 2016 Bonds are subject to extraordinary redemption by the County prior to their respective stated maturity dates on any Interest Payment Date, in whole or in part, from funds derived by the County solely from prepayments of the Special Tax, upon notice mailed as provided in the Bond Resolution and described under Notice of Redemption below, at the following redemption prices (computed upon the principal amount of the 2016 Bonds or portions thereof called for redemption) together with accrued interest thereon to the date of redemption: Redemption Date Redemption Price September 1, 2016 and any Interest Payment Date through March 1, % September 1, 2024 and March 1, September 1, 2025 and March 1, September 1, 2026 and any Interest Payment Date thereafter 100 The 2016 Bonds and any Parity Bonds subject to extraordinary redemption from prepayments of Special Taxes shall be redeemed pro rata (as nearly as possible given minimum authorized denominations) in proportion to the total principal amount Outstanding of each Series at the time of Redemption. Transfers of property ownership and certain other circumstances could result in prepayments of the Special Tax applicable to particular parcels. Such prepayments would result in redemption of the 2016 Bonds prior to their stated maturity, at the redemption prices corresponding to the redemption dates as shown above, and could cause a reduction of the amount on deposit in the Bond Reserve Fund. 7

14 Selection of 2016 Bonds for Redemption If less than all the Outstanding 2016 Bonds are to be redeemed at any one time, the County shall select the maturity date or dates of the 2016 Bonds to be redeemed, and if less than all the Outstanding 2016 Bonds of any maturity are to be redeemed at any one time, the Director of Finance shall select the 2016 Bonds or the portions thereof of such maturity date to be redeemed in integral multiples of five thousand dollars ($5,000) in any manner that the Director of Finance deems appropriate and fair; provided, that any such partial redemption will result in the least disturbance of the proportionality of Annual Debt Service on the Bonds in each Bond Year (except the last Bond Year after such redemption) unless the Paying Agent has first received a report from an Independent Financial Consultant to the effect that the proceeds of the Special Taxes that would be available to the County if the Special Taxes were to be levied and collected at their maximum rate and amount on all Parcels of Taxable Property in the District, based upon the Special Tax Formula as applied on the date of the proposed partial redemption, would be equal to at least one hundred ten percent (110%) of the Maximum Annual Debt Service on the Bonds (after giving effect to such partial redemption). Notice of Redemption The Paying Agent will mail a notice of redemption to the respective Holders of all 2016 Bonds selected for redemption in whole or in part not less than 30 days and not more than 60 days prior to the date of redemption. Any notice of optional or extraordinary redemption given with respect to the 2016 Bonds may be rescinded by written notice given to the Paying Agent by the County no later than five (5) Business Days prior to the date specified for redemption. The Paying Agent will give notice of such rescission as soon as practicable thereafter in the same manner, and to the same recipients, as notice of such redemption was given. With respect to any notice of optional or extraordinary redemption of 2016 Bonds, unless, upon the giving of such notice, the 2016 Bonds to be redeemed have been deemed to have been paid within the meaning of the Bond Resolution, the redemption notice shall state that the redemption will be conditional upon the receipt by the Paying Agent on or before the date fixed for redemption of amounts sufficient to pay the principal of, and premium, if any, and interest on, such 2016 Bonds to be redeemed, and that if those amounts have not been so received the notice will be of no force and effect and the County will not be required to redeem the 2016 Bonds specified in the redemption notice. If any such notice of redemption contains such a condition and such amounts are not so received, the redemption will not be made and the Paying Agent will within a reasonable time thereafter give notice to the Holders of the Series 2016 Bonds specified in the redemption notice to the effect that the amounts were not so received and the redemption was not made, the notice to be given by the Paying Agent in the manner in which the notice of redemption was given. The failure to redeem Series 2016 Bonds pursuant to the Bond Resolution due to the failure of a condition of redemption will not constitute an event of default under the Bond Resolution. Book-Entry Only System The 2016 Bonds are to be initially registered in the name of Cede & Co., as nominee of The Depository Trust Company of New York, New York ( DTC ). One fully registered 2016 Bond will be issued for each maturity of the 2016 Bonds in the aggregate principal amount of such maturity and will be deposited with DTC. So long as Cede & Co. is the registered owner of the 2016 Bonds, references herein to the Holders of the 2016 Bonds shall refer to Cede & Co. and shall not refer to the beneficial owners of such 2016 Bonds. The County does not give any assurance that DTC, its participants or others will distribute payments with respect to the 2016 Bonds or notices concerning the 2016 Bonds to the beneficial owners thereof or that DTC or its participants will otherwise serve and act in the manner described in this Official Statement. See Appendix D for a further description of DTC and its book-entry system. The information presented therein is based solely on information provided by DTC. 8

15 ESTIMATED SOURCES AND USES OF FUNDS The estimated sources and uses of funds in connection with the issuance of the 2016 Bonds are shown in the following table: Estimated Sources and Uses of Funds Estimated Sources of Funds Principal Amount $ 23,155, Plus: Net Original Issue Premium 2,425, Less: Underwriter s Discount (158,210.37) Funds Related to 2007 Bonds (1) 2,137, Total Sources of Funds $ 27,559, Estimated Uses of Funds Escrow Fund $ 15,071, Acquisition and Construction Fund 10,362, Bond Reserve Fund 1,679, Costs of Issuance Fund (2) 221, Capitalized Interest Account (3) 224, Total Uses of Funds $ 27,559, (1) (2) (3) Includes funds held under the bond redemption fund and bond reserve fund with respect to the 2007 Bonds. Includes financial advisor s fees, legal fees, Appraiser fees, Special Tax Consultant fees, printing costs, and other costs of issuance. Represents capitalized interest on a portion of the Bonds through approximately September 1, THE REFUNDING PLAN General The County issued the 2007 Bonds pursuant the Bond Resolution in the aggregate principal amount of $14,415,000, which 2007 Bonds are currently outstanding in the aggregate principal amount of $13,965,000. The County plans to apply a portion of the proceeds of the 2016 Bonds to refund the outstanding 2007 Bonds. To effect such refunding, the County will cause a portion of the proceeds of the 2016 Bonds, together with other funds to be deposited into the Escrow Fund (the Escrow Fund ) established under the Escrow Agreement dated as of May 1, 2016 (the Escrow Agreement ), by and between County and The Bank of New York Mellon Trust Company, N.A., as escrow agent (the Escrow Agent ). Such amounts will be held in cash or invested in direct non-callable obligations of the United States of America (the Defeasance Obligations ). Cash and certain Defeasance Obligations deposited in the Escrow Fund will be scheduled to mature in such amounts and at such times and bear interest at such rates as to provide amounts sufficient to pay all regularly scheduled payments of principal of and interest on the refunded 2007 Bonds through and including September 1, 2017 and to redeem on September 1, 2017, the refunded 2007 Bonds maturing on and after September 1, 2018 at a redemption price equal to the principal amount to be redeemed, without premium. All cash and Defeasance Obligations in the Escrow Fund will be irrevocably pledged to secure, when due, the payment of the principal, interest and premium due on the refunded 2007 Bonds and will not be available to pay the principal of and interest on the 2016 Bonds. The sufficiency of the cash and Defeasance Obligations to pay such amounts will be verified by Causey, Demgen & Moore, P.C., Denver, Colorado (the Verification Agent ). See the caption Verification of Mathematical Computations below. 9

16 Verification of Mathematical Computations Upon delivery of the 2016 Bonds, the Verification Agent, a firm of independent public accountants, will deliver a report on the mathematical accuracy of certain computations based upon certain information and assertions provided to them by the Underwriter relating to: (a) the adequacy of the maturing principal of and interest earned on the Defeasance Obligations, together with the cash to be concurrently deposited in the Escrow Fund, to pay all regularly scheduled payments of principal of and interest on the refunded 2007 Bonds through and including September 1, 2017 and to redeem on September 1, 2017, the refunded 2007 Bonds maturing on and after September 1, 2018 at a redemption price equal to the principal amount to be redeemed, without premium; and (b) the computations of yield of the Bonds and the Defeasance Obligations which support Bond Counsel s opinion that interest on the 2016 Bonds is excluded from gross income for federal income tax purposes. DEBT SERVICE SCHEDULE AND ESTIMATED COVERAGE The following is the debt service schedule and estimated coverage of annual debt service on the 2016 Bonds. The coverage amounts in the table below also assume no delinquencies in the payment of Special Taxes and that no 2016 Bonds are redeemed except from Minimum Sinking Fund Account payments. Based on development status as of March 1, 2016, Special Tax revenues from Taxable Parcels of Developed Property and Final Map Property are expected to produce coverage on the 2016 Bonds of not less than 110%. Pursuant to the Act, the Special Tax levied against any Taxable Parcel for which an occupancy permit for private residential use has been issued may not be increased as a consequence of delinquency or default by the owner of any other Taxable Parcel within the District by more than 10% above the amount that would have been levied in such Fiscal Year had there never been any such delinquencies or defaults. As a result, it is possible that the County may not be able to increase the tax levy to the Maximum Special Tax rate in all years. Investors should not assume actual coverage from Special Taxes in excess of 110% of debt service. See SPECIAL RISK FACTORS Levy of Special Tax. In addition, coverage could be reduced upon the issuance of Parity Bonds. See Parity Bonds below for a description of the conditions precedent to the issuance of Parity Bonds. 10

17 Debt Service Schedule and Estimated Coverage Bond Year (Ending September 1) Principal Interest Total Annual Debt Service (1) Maximum Special Tax Levy on Developed Property (2) Maximum Special Tax Levy on Developed Property and Final Map Property (2) Estimated Net Maximum Special Tax at Build-Out (2)(3) From Maximum Special Tax Levy on Developed Property Debt Service Coverage (4) From Maximum Special Tax Levy on Developed Property and Final Map Property From Estimated Net Maximum Special Tax at Build-Out 2016 $ 224,440 (1) $ 1,208,671 $ 1,131,292 $ 1,575,249 $ 1,665,426 94% 130% 138% 2017 $ 300, ,475 1,273,475 1,153,918 1,606,754 1,698, , ,475 1,292,475 1,176,997 1,638,890 1,732, , ,725 1,307,725 1,200,536 1,671,667 1,767, , ,725 1,325,725 1,224,547 1,705,101 1,802, , ,225 1,343,225 1,249,038 1,739,203 1,838, , ,225 1,360,225 1,274,019 1,773,987 1,875, , ,725 1,376,725 1,299,499 1,809,467 1,913, , ,225 1,399,225 1,325,489 1,845,656 1,951, , ,325 1,414,325 1,351,999 1,882,569 1,990, , ,625 1,437,625 1,379,039 1,920,220 2,030, , ,875 1,454,875 1,406,620 1,958,625 2,070, , ,675 1,478,675 1,434,752 1,997,797 2,112, , ,675 1,496,675 1,463,447 2,037,753 2,154, , ,700 1,517,700 1,492,716 2,078,508 2,197, , ,800 1,540,800 1,522,571 2,120,078 2,241, , ,550 1,562,550 1,553,022 2,162,480 2,286, , ,950 1,582,950 1,584,082 2,205,730 2,331, , ,000 1,607,000 1,615,764 2,249,844 2,378, , ,250 1,631,250 1,648,079 2,294,841 2,426, ,060, ,000 1,657,000 1,681,041 2,340,738 2,474, ,135, ,000 1,679,000 1,714,662 2,387,553 2,524, , ,250 1,412,250 1,748,955 2,435,304 2,574, ,000, ,000 1,441,000 1,783,934 2,484,010 2,626, ,080, ,000 1,471,000 1,819,613 2,533,690 2,678, ,160, ,000 1,497,000 1,856,005 2,584,364 2,732, ,250, ,000 1,529,000 1,893,125 2,636,051 2,786, ,345, ,500 1,561,500 1,930,988 2,688,772 2,842, ,440, ,250 1,589,250 1,969,607 2,742,548 2,899, ,545,000 77,250 1,622,250 2,008,999 2,797,398 2,957, Total $ 23,155,000 $ 19,931,915 $ 44,071,146 $ 45,894,357 $ 63,904,846 $ 67,563,139 (footnotes on next page) 11

18 (1) (2) (3) (4) Interest on a portion of the 2016 Bonds through approximately September 1, 2016 will be funded from capitalized interest. Includes debt service on the 2007 Bonds due in the Bond Year ending September 1, See ESTIMATED SOURCES AND USES OF FUNDS. Based on revenues from Maximum Special Tax levy, escalating at 2% per year, and development status as of March 1, Amounts reflect a reduction in each year of 15% of the Maximum Special Tax revenues at build-out of property in the Vineyard Creek portion of the District. Pursuant to the Act, the Special Tax levied against any Taxable Parcel for which an occupancy permit for private residential use has been issued may not be increased as a consequence of delinquency or default by the owner of any other Taxable Parcel within the District by more than 10% above the amount that would have been levied in such Fiscal Year had there never been any such delinquencies or defaults. As a result, it is possible that the County may not be able to increase the tax levy to the Maximum Special Tax rate in all years. See the caption SPECIAL RISK FACTORS Levy of the Special Tax. 12

19 SECURITY AND SOURCES OF PAYMENT FOR THE 2016 BONDS General The 2016 Bonds are limited obligations of the County and, except as otherwise provided in the Bond Resolution, the interest on and principal of the 2016 Bonds are payable solely from the Special Tax which is to be levied annually against the property in the District. Neither the full faith and credit nor the general taxing power of the County, the District, the State of California, or any political subdivision thereof is pledged to the payment of the 2016 Bonds. Although the Special Tax constitutes a lien on property subject to taxation in the District, it does not constitute a personal indebtedness of the owners of such property. There is no assurance that the owners will be financially able to pay the annual Special Tax or that they will pay such tax even if financially able to do so. The risk of nonpayment by property owners is more fully described in SPECIAL RISK FACTORS Collection of the Special Tax. The Special Tax In accordance with the provisions of the Act, the Board of Supervisors established the District on December 13, 2005 for the purpose of providing for the financing of certain public facilities in and for the District. At an all-mailed ballot election conducted on January 19, 2006, the landowner-electors within the District authorized both the issuance of up to $30,000,000 principal amount of special tax bonds for the purpose of financing such public facilities and the annual levy of the Special Tax to be used for the purpose, among others, of paying the interest on and principal of and redemption premiums, if any, on such bonds. On March 20, 2007, the Board of Supervisors adopted Resolution No declaring its intent to amend the special tax formula and to annex certain additional property (the Annexed Parcels ) to the District. Following a public hearing conducted on May 8, 2007, the Board of Supervisors adopted Resolution No calling an election for May 29, 2007 on the annexation of the Annexed Parcels to the District and the amendment to the special tax formula. On May 29, 2007 at an all-mailed ballot election held pursuant to the Act, El Dorado Corners, LLC, as the owner of the Annexed Parcels, approved the annexation of Annexed Parcels to the District, and the Developer, Standard Pacific Corp., North Vineyard Investors and El Dorado Corners, LLC as the sole owners of land within the District, who under the terms of the Act were the only qualified electors within the District, authorized the amendment to the special tax formula (as amended, the Special Tax Formula ). A copy of the Special Tax Formula is attached as Appendix B hereto. Pursuant to the Bond Resolution, so long as any Bonds are outstanding, the County is required to annually levy the Special Tax against Parcels of Taxable Property (as defined in the Special Tax Formula) in the District in accordance with the Special Tax Formula and make provision for the collection of the Special Tax in amounts which will be sufficient, together with the money then on deposit in the Bond Redemption Fund, after making allowance for contingencies and errors in the estimates, to yield proceeds equal to the amounts required for compliance with the agreements, conditions, covenants and terms contained in the Bond Resolution, and (i) to pay the interest on and the principal of and Minimum Sinking Fund Account Payments for and redemption premiums, if any, on the Bonds as they respectively become due and payable, (ii) to replenish the Bond Reserve Fund, and (iii) to pay all current Expenses as they become due and payable in accordance with the provisions of the Bond Resolution. The Special Tax Formula annually allocates the Special Tax required among the Parcels of Taxable Property based upon location, land uses and development status. The Special Tax Formula involves a number of separate steps to be performed by the County which are described in Appendix B and summarized below. For purposes of this section only, terms with initial capital letters not otherwise defined in this Official Statement shall have the meanings assigned to them in Appendix B. 13

20 Classification of Parcels Subject to Special Tax. On or about July 1 of each Fiscal Year, the Administrator shall identify the current Assessor s Parcel numbers for all Parcels of Taxable Property. The Administrator shall also determine: (i) whether each Assessor s Parcel of Taxable Property is Developed Property, Final Map Property, Large Lot Subdivision Map Property, Vineyard Creek Tentative Map Property, Vineyard Point Tentative Map Property or Annexation Property, (ii) for Developed Property, which Parcels are Single Family Detached Property, Single Family Attached Property, Multifamily Property and Other Property, (iii) for Parcels of Single Family Attached Property, the number of Residential Units on each Parcel, (iv) the Specific Plan Land Use Designation for each Parcel, and (v) the Special Tax Requirement. For Single Family Attached Property, the number of Residential Units shall be determined by referencing the site plan, condominium plan, or other development plan. In any Fiscal Year, if it is determined that: (i) a parcel map for property in the District was recorded after January 1 of the prior Fiscal Year (or any other date after which the Assessor will not incorporate the newly-created Parcels into the then current tax roll), (ii) because of the date the parcel map was recorded, the Assessor does not yet recognize the new Parcels created by the parcel map, and (iii) one or more of the newly-created parcels is in a different Development Class than other parcels created by the subdivision, the Administrator shall calculate the Special Tax for the property affected by recordation of the parcel map by determining the Special Tax that applies separately to the property within each Development Class, then applying the sum of the individual Special Taxes to the Parcel that was subdivided by recordation of the parcel map. For purposes of making the classification described above, Developed Property means all Parcels for which building permits have been issued on or prior to June 1 of the preceding Fiscal Year. Final Map Property means in any Fiscal Year, all Single Family Detached Property for which a Final Map had been recorded prior to June 1 of the preceding Fiscal Year and which had not yet become Developed Property. Large Lot Subdivision Map Property means, in any Fiscal Year, all Single Family Detached Property included within a Large Lot Subdivision Map that was recorded by June 1 of the prior Fiscal Year, and which has not yet become Final Map Property. Vineyard Creek Tentative Map means the vesting tentative map for the Vineyard Creek project approved by the Board of Supervisors on November 10, Vineyard Point Tentative Map means the vesting tentative map for the Vineyard Point project approved by the Board of Supervisors on November 10, Additionally, the Special Tax Formula exempts up to acres of Public Property from the levy of the Special Tax and acres identified as Parcel 3 on Attachment 1 to the Special Tax Formula (the Exempt Parcel ). The table below shows the maximum Special Tax capacity for Fiscal Year based on development status as of March 1,

21 (1) (2) (3) (4) Table 1 County of Sacramento Community Facilities District No (North Vineyard Station No. 1) Estimated Fiscal Year Maximum Special Tax Revenue Based on Land Uses at Build-Out (Development Status as of March 1, 2016) Estimated Fiscal Year Special Tax Category (1) Fiscal Year Maximum Special Tax Rate Planned Units/Acres Maximum Special Tax Revenue at Build-Out (3) Vineyard Point Developed Property SFR 3-5 $ 1, units $ 496,105 SFR 4-7 1, units 383,892 MDR , units 209,074 Clubhouse 11, acres 4,607 Total Vineyard Point 709 units $ 1,093,678 Vineyard Creek Developed Property Existing Farmhouse (2) MDR 7-12 $ 1,181 1 unit $ 1,181 Unit 1 SFR 4-7 1, units 59,060 Total $ 60,242 Final Map Property (3) Unit 1 SFR 4-7 $1, units $ 102,579 Unit 4 SFR 3-5 1, units 203,664 Clubhouse Other Property 11, acres 21,262 Unit 5 SFR 3-5 1, units 125,332 Total $ 452,836 Large Lot Map Property (4) Unit 6 SFR 3-5 1, units 156,665 Multi-Family Parcel MFR , acres 42,088 Total $ 198,753 Total Vineyard Creek 384 units $ 711,831 Total 1,093 units $1,805,508 Pursuant to the Special Tax Formula, Developed Property includes Taxable Property for which a building permit was issued as of June 1 of the prior Fiscal Year. Final Map Property is Single Family Detached Property for which a Final Map had recorded prior to June 1 of the preceding Fiscal Year and which has not yet become Developed Property. Parcel is entitled for medium density, however, such parcel is currently occupied and used as an existing farmhouse and is not owned by Lennar. The County is not aware of any plans to develop such parcel. However, the County can make no assurances that this property will not be subdivided and developed in the future. See Attachment 1 to the Rate and Method attached hereto as Appendix B for the location of the existing farmhouse which is located on the Remainder A Parcel. Development status is as of March 1, 2016 except that the final maps recorded for Units 4 and 5 in April 2016 are reflected. Excludes the Remainder B parcel owned by Douglas B/Anne R Bayless Revocable Living Trust, which is subject to the Special Tax levy but has no planned development at build-out and was not appraised. Source: Goodwin Consulting Group, Inc. Method of Apportionment of the Annual Special Tax. The Special Tax is to be levied each Fiscal Year in accordance with the following procedures until the amount of the levy equals the Special Tax 15

22 Requirement for that Fiscal Year. The Special Tax Requirement is the amount necessary in any Fiscal Year to: (i) pay principal and interest on Bonds that is due in the calendar year that begins in such Fiscal Year; (ii) create and/or replenish reserve funds for the Bonds; (iii) cure any delinquencies in the payment of principal or interest on Bonds which have occurred in the prior Fiscal Year or, based on existing delinquencies in the payment of Special Taxes, are expected to occur in the Fiscal Year in which the tax will be collected; (iv) pay Administrative Expenses; and (v) pay the costs of public improvements and public infrastructure authorized to be financed by the District. The amounts referred to in clauses (i) and (ii) of the preceding sentence may be reduced in any Fiscal Year by: (i) interest earnings on or surplus balances in funds and accounts for the Bonds to the extent that such earnings or balances are available to apply against debt service pursuant to a Bond Resolution or other legal document that sets forth these terms; (ii) proceeds received by the District from the collection of penalties associated with delinquent Special Taxes; and (iii) any other revenues available to pay debt service on the Bonds as determined by the Administrator. The Administrator shall determine the Special Tax Requirement to be collected each Fiscal Year, and the Special Tax shall be levied according to the steps outlined below. Upon the issuance of the 2016 Bonds, both Vineyard Point Bonds and Vineyard Creek Bonds (as such terms are defined in the Special Tax Formula) will have been issued. In accordance with the Special Tax Formula, the method under Alternative 3 will be as described below will be used to determine the Special Tax levy. Step 1: Step 2: Step 3: Step 4: Step 5: The Special Tax shall be levied proportionately on each Parcel of Developed Property within the District up to 100% of the Maximum Special Tax for each Parcel for such Fiscal Year until the amount levied on Developed Property is equal to the Special Tax Requirement prior to applying any Capitalized Interest that is available in the District accounts. If additional revenue is needed after Step 1, and after applying Capitalized Interest to the Special Tax Requirement, the Special Tax shall be levied proportionately on each Assessor s Parcel of Final Map Property within the District, up to 100% of the Maximum Special Tax for Final Map Property for such Fiscal Year. If additional revenue is needed after applying the first two steps, the Special Tax shall be levied proportionately on each Parcel of Large Lot Subdivision Map Property within the District, up to 100% of the Maximum Special Tax for Large Lot Subdivision Map Property for such Fiscal Year. If additional revenue is needed after applying the first three steps, the Special Tax shall be levied proportionately on each Parcel of Vineyard Creek Tentative Map Property, Vineyard Point Tentative Map Property, and Annexation Property, up to 100% of the Maximum Special Tax for such property for such Fiscal Year. If additional revenue is needed after applying the first four steps, the Special Tax shall be levied proportionately on each Assessor s Parcel of Excess Public Property, up to 100% of the Maximum Special Tax for Vineyard Creek Tentative Map Property and Vineyard Point Tentative Map Property for such Fiscal Year. Prepayment of Special Tax. The Special Tax obligation applicable to an Assessor s Parcel in the District may be prepaid and the obligation of the Assessor s Parcel to pay the Special Tax permanently satisfied as described in APPENDIX B AMENDED RATE AND METHOD OF APPORTIONMENT OF SPECIAL TAX, provided that a prepayment may be made only if there are no delinquent Special Taxes with respect to such Assessor s Parcel at the time of prepayment. Any prepayment of the Special Tax will result in an extraordinary redemption of Bonds. See THE 2016 BONDS Redemption Extraordinary Redemption from Prepayment of Special Tax. Limitations. In general, the Special Tax shall be levied and collected until principal and interest on Bonds have been repaid, costs of constructing or acquiring authorized facilities from Special Tax proceeds 16

23 have been paid, and all Administrative Expenses have been reimbursed. However, in no event shall a Special Tax be levied after Fiscal Year Pursuant to the Act, under no circumstances will the Special Tax levied in any Fiscal Year against any Taxable Parcel for which an occupancy permit for private residential use has been issued within the District be increased by more than 10% as a consequence of a delinquency or default by the owner of any other parcel within the District above the amount that would have been levied in that Fiscal Year had there never been any such delinquencies or defaults. Interpretation. The County reserves the right to make minor administrative and technical changes to the Special Tax Formula that do not materially affect the rate and method of apportioning Special Taxes. In addition, the County may, in its discretion, interpret and apply the Special Tax Formula. Special Tax Analysis The Special Tax is exempt from the tax rate limitation of California Constitution Article XIIIA pursuant to Section 4 thereof as a special tax authorized by a two-thirds vote of the qualified electors as set forth in the Act. Consequently, the County has the power and is obligated to cause the levy and collection of the Special Tax in an amount determined according to the Special Tax Formula. The Act prohibits the Board of Supervisors from adopting a resolution to reduce the rate of the Special Tax or terminate the levy of the Special Tax unless the Board of Supervisors determines that the reduction or termination of the Special Tax would not interfere with the timely retirement of the outstanding Bonds. California Constitution Article XIIIC, which removed certain limitations on the initiative power, provides that the initiative power shall not be prohibited or otherwise limited in matters of reducing or repealing any local tax, assessment, fee or charge. Although the matter is not free from doubt, it is likely that the exercise by the voters of the initiative power referred to in Article XIIIC to reduce the Special Tax is subject to the same restrictions as are applicable to the Board of Supervisors pursuant to the Act. See SPECIAL RISK FACTORS Proposition 218. Although the Special Tax constitutes a lien on property subject to taxation within the District, it does not constitute a personal indebtedness of the current owners of such property or of their successors. There is no assurance that the owners will be financially able to pay the annual Special Tax or that they will pay such tax even if financially able to do so. Subject to the covenant by the County to pursue accelerated foreclosure proceedings under certain circumstances as described under Delinquent Payments of Special Tax; Covenant for Foreclosure below, the Special Tax is expected to be collected in the same manner and at the same time as ad valorem property taxes are collected; and it will be subject to the same penalties and the same procedure, sale and lien priority in case of delinquency as is provided for ad valorem property taxes. See SPECIAL RISK FACTORS Collection of the Special Tax. Pursuant to Section of the Act, properties or entities of federal, state or local governments are exempt from the Special Tax except that, under Section of the Act, property not otherwise exempt which is acquired by a public entity through a negotiated transaction, or by gift or demise, remains subject to the Special Tax. (Notwithstanding the foregoing statutory exceptions, property owned by the federal government may be exempt from the Special Tax regardless of the manner in which it was acquired.) It is not clear under the Act whether property acquired by a public entity following a tax sale or foreclosure based upon failure of a non-exempt person or entity to pay property taxes would remain subject to the Special Tax under Section of the Act or would become exempt from the Special Tax under Section of the Act. Pursuant to Section of the Act, if property subject to the Special Tax is acquired by a public entity through eminent domain proceedings, the obligation to pay the Special Tax with respect to that property is to be treated as if it were a special annual assessment. For this purpose, the present value of the obligation to pay the Special Tax to pay principal and interest on any Bonds Outstanding prior to the date of apportionment is to be treated the same as a fixed lien special annual assessment. The Act further provides that no other properties or entities are exempt from the Special Tax unless the properties or entities are expressly exempted in a resolution of consideration to levy a new tax under the Act or to alter the rate or method of apportionment of an existing tax under the Act. See SPECIAL RISK FACTORS Exempt Properties. 17

24 Neither the faith and credit nor the general taxing authority of the County, the State or any political subdivision of any of the foregoing is pledged to the payment of the 2016 Bonds. The County is to establish tax rates, within the limits of the Maximum Annual Special Tax for each Parcel of Taxable Property set forth in the Special Tax Formula, to be used to levy and apportion the Special Tax against Parcels of Taxable Property within the District on an annual basis. The actual amount of the Special Tax that could be levied and collected against property within the District during any future Fiscal Year will depend upon a number of factors, including without limitation the land use categories then in effect in the District, the tax rates imposed pursuant to the Special Tax Formula (subject to the Maximum Annual Special Tax rates) and the level of delinquent Special Tax installments. See SPECIAL RISK FACTORS Collection of the Special Tax. Annual Debt Service for the Bonds has been structured so that, based on development status within the District as of March 1, 2016 and assuming no delinquencies, Special Taxes levied on Developed Property and Final Map Property, will generate in each Fiscal Year not less than 110% of debt service payable with respect to the Bonds in each Bond Year. Pursuant to the Special Tax Formula, the Special Taxes are apportioned first to Developed Property, then to Parcels of Final Map Property, then to Parcels of Large Lot Subdivision Map Property, then to Parcels of Vineyard Creek Tentative Map Property, Vineyard Point Tentative Map Property and Annexation Property, and finally to Excess Public Property, to the extent necessary to meet the Special Tax Requirement. Pursuant to the Act, the Special Tax levied against any Taxable Parcel for which an occupancy permit for private residential use has been issued may not be increased as a consequence of delinquency or default by the owner of any other Taxable Parcel within the District by more than 10% above the amount that would have been levied in such Fiscal Year had there never been any such delinquencies or defaults. Investors should not assume actual coverage from Special Taxes in excess of 110% of debt service. The actual amount of the Special Tax that could be levied and collected against Parcels of Taxable Property during any future year will depend upon a number of factors, including without limitation the land use categories then in effect in the District, the tax rates imposed pursuant to the Special Tax Formula (subject to the Maximum Annual Special Tax rates) and the level of delinquent Special Tax installments. See SPECIAL RISK FACTORS Collection of the Special Tax herein. Additionally, pursuant to the terms of the Bond Resolution, the County may issue Parity Bonds pursuant to certain conditions precedent. See SECURITY AND SOURCES OF PAYMENT FOR THE 2016 BONDS Parity Bonds herein. In addition to payment of the Special Tax, the property within the District will also be obligated to pay ad valorem property taxes levied against such property and special assessments and special taxes levied to pay certain existing and any additional overlapping debt for which the property within the District is or may become obligated. See Direct And Overlapping Bonded Indebtedness herein. The actual amount of those taxes and assessments which may be levied or assessed in the future will vary depending upon a number of factors, including without limitation the assessed valuation of the property within the District at such time, the actual amount of the Special Tax that is levied annually in the future against such property and the existence of additional bonded and overlapping debt in the future. Special taxes and special assessments may also be levied to pay for the costs of certain services and/or to maintain certain public improvements. Proceeds of the Special Tax The County has covenanted in the Bond Resolution that all proceeds of the Special Tax, when and as received, will be immediately deposited in the County of Sacramento Community Facilities District No (North Vineyard Station No. 1) Special Tax Fund, established in the treasury of the County (the Special Tax Fund ). All money in the Special Tax Fund is to be held by the County in trust under the Bond Resolution and is to be disbursed, allocated and applied solely to the uses and purposes set forth in the Bond 18