$8,800,000 COUNTY OF SAN BERNARDINO COMMUNITY FACILITIES DISTRICT NO (LYTLE CREEK NORTH) IMPROVEMENT AREA NO. 5 SPECIAL TAX BONDS, SERIES 2017

|

|

|

- Bertina Richardson

- 5 years ago

- Views:

Transcription

1 NEW ISSUE - BOOK-ENTRY-ONLY NO RATING In the opinion of Orrick, Herrington & Sutcliffe LLP, Bond Counsel to the District, based upon an analysis of existing laws, regulations, rulings and court decisions, and assuming, among other matters, the accuracy of certain representations and compliance with certain covenants, interest on the Series 2017 Bonds is excluded from gross income for federal income tax purposes under Section 103 of the Internal Revenue Code of 1986 and is exempt from State of California personal income taxes. In the further opinion of Bond Counsel, interest on the Series 2017 Bonds is not a specific preference item for purposes of the federal individual or corporate alternative minimum taxes, although Bond Counsel observes that such interest is included in adjusted current earnings when calculating corporate alternative minimum taxable income. Bond Counsel expresses no opinion regarding any other tax consequences related to the ownership or disposition of, or the amount, accrual or receipt of interest on, the Series 2017 Bonds. See TAX MATTERS. $8,800,000 COUNTY OF SAN BERNARDINO COMMUNITY FACILITIES DISTRICT NO (LYTLE CREEK NORTH) IMPROVEMENT AREA NO. 5 SPECIAL TAX BONDS, SERIES 2017 Dated: Date of Delivery Due: September 1, as shown on the inside cover page The County of San Bernardino Community Facilities District No (Lytle Creek North) Improvement Area No. 5 Special Tax Bonds, Series 2017 (the Series 2017 Bonds ) are being issued and delivered: (i) to finance a portion of certain public facilities eligible to be financed by the District (as defined herein); (ii) to fund a reserve fund; (iii) to fund an initial deposit to an administrative expense fund; and (iv) to pay costs of issuance of the Series 2017 Bonds. The County of San Bernardino Community Facilities District No (Lytle Creek North) (the District ) has been formed by and is located in the County of San Bernardino, California (the County ). Improvement Area No. 5 ( Improvement Area No. 5 ) is located within the District. The Series 2017 Bonds are authorized to be issued pursuant to the Mello-Roos Community Facilities Act of 1982, as amended (Section et seq. of the Government Code of the State of California), and pursuant to an Indenture, dated as of December 1, 2017 (the Indenture ), by and between the District and U.S. Bank National Association, as trustee (the Trustee ). The Series 2017 Bonds are special obligations of the District and are payable solely from Net Special Tax Revenues (as defined herein) and other assets pledged therefor under the Indenture, all as further described herein. Special Taxes (as defined herein) are to be levied according to the rate and method of apportionment approved by the Board of Supervisors of the County and the qualified electors within Improvement Area No. 5 of the District, as more fully described herein. See the caption SECURITY AND SOURCES OF PAYMENT FOR THE SERIES 2017 BONDS and Appendix A. The Special Taxes will be collected in the same manner and at the same time as ad valorem property taxes. The County Board of Supervisors is the legislative body of the District. Pursuant to the Indenture, Additional Bonds payable from Net Special Tax Revenues on a parity with the Series 2017 Bonds may be issued by the District for Improvement Area No. 5, but only to refund the Series 2017 Bonds or any outstanding Additional Bonds (as defined herein). See the caption SECURITY AND SOURCES OF PAYMENT FOR THE SERIES 2017 BONDS No Additional Bonds Except for Refunding. The Series 2017 Bonds are being issued in fully registered book-entry form only in denominations of $5,000 or any integral multiple thereof; and, when issued, they will be registered in the name of Cede & Co. as nominee of The Depository Trust Company, New York, New York, which will act as securities depository for the Series 2017 Bonds. Purchasers will not receive certificates representing their interests in the Series 2017 Bonds. Interest on the Series 2017 Bonds is payable on March 1 and September 1 of each year, commencing March 1, Payment of the principal of and interest on the Series 2017 Bonds, and redemption premiums, if any, thereon will be made by the Trustee, to Cede & Co. for subsequent disbursement to DTC Participants, which are expected to remit such payments to the Beneficial Owners of the Series 2017 Bonds. See the caption THE SERIES 2017 BONDS Book Entry Only System and Appendix G. The Series 2017 Bonds are subject to optional, mandatory, and sinking fund redemption as described herein. See the caption The Series 2017 Bonds Redemption. EXCEPT FOR THE NET SPECIAL TAX REVENUES AND AMOUNTS HELD IN THE SPECIAL TAX FUND, THE BOND FUND AND THE RESERVE FUND UNDER THE INDENTURE, NO OTHER FUNDS ARE PLEDGED TO THE PAYMENT OF THE SERIES 2017 BONDS. THE SERIES 2017 BONDS ARE NOT GENERAL OR SPECIAL OBLIGATIONS OF THE COUNTY BUT ARE SPECIAL, LIMITED OBLIGATIONS OF THE DISTRICT PAYABLE SOLELY FROM THE NET SPECIAL TAX REVENUES AND AMOUNTS HELD IN THE SPECIAL TAX FUND, THE BOND FUND AND THE RESERVE FUND UNDER THE INDENTURE AS MORE FULLY DESCRIBED HEREIN. NEITHER THE FAITH AND CREDIT NOR THE TAXING POWER OF THE DISTRICT (EXCEPT TO THE LIMITED EXTENT SET FORTH IN THE INDENTURE), THE COUNTY, OR THE STATE OF CALIFORNIA, OR ANY POLITICAL SUBDIVISION THEREOF, IS PLEDGED TO THE PAYMENT OF THE SERIES 2017 BONDS. THE PURCHASE OF THE SERIES 2017 BONDS INVOLVES CERTAIN RISKS AND THE SERIES 2017 BONDS ARE NOT SUITABLE INVESTMENTS FOR ALL TYPES OF INVESTORS. SEE THE CAPTION SPECIAL RISK FACTORS FOR A DISCUSSION OF CERTAIN RISK FACTORS THAT SHOULD BE CONSIDERED, IN ADDITION TO THE OTHER MATTERS SET FORTH HEREIN, IN EVALUATING THE INVESTMENT QUALITY OF THE SERIES 2017 BONDS. This cover page contains certain information for general reference only. It is not a summary of this issue. Prospective investors must read the entire Official Statement to obtain information essential to the making of an informed investment decision. MATURITY SCHEDULE (See Inside Cover Page) The Series 2017 Bonds are offered when, as and if issued and accepted by the Underwriter, subject to approval as to their legality by Orrick, Herrington & Sutcliffe LLP, Los Angeles, California, Bond Counsel to the District, and subject to other conditions. Certain legal matters will be passed on for the County and the District by County Counsel and by Stradling Yocca Carlson & Rauth, a Professional Corporation, Newport Beach, California, as Disclosure Counsel, for Lennar Homes of California, Inc. by Holland & Knight LLP, San Francisco, California, for the Underwriter by its counsel, Jones Hall, A Professional Law Corporation, San Francisco, California, and for the Trustee by its counsel. It is anticipated that the Series 2017 Bonds in book-entry form will be available for delivery through the facilities of DTC on or about December 13, Dated: November 21, 2017

2 $8,800,000 COUNTY OF SAN BERNARDINO COMMUNITY FACILITIES DISTRICT NO (LYTLE CREEK NORTH) IMPROVEMENT AREA NO. 5 SPECIAL TAX BONDS, SERIES 2017 MATURITY SCHEDULE BASE CUSIP $4,490,000 Serial Bonds Maturity Date (September 1) Principal Amount Interest Rate Yield Price CUSIP 2018 $185, % 1.220% RM , RN , RP , RQ , RR , RS , RT , RU , RV , CC RW , C RX , C RY , C RZ , C SA , C SB , SC , SD , SE , SF , SG4 $1,730, % Term Bonds Due September 1, 2042 Yield 3.750% Price C % CUSIP SH2 $2,580, % Term Bonds Due September 1, 2048 Yield 3.800% Price C % CUSIP SJ8 CC Priced to the optional redemption date of September 1, 2024, at 103%. C Priced to the optional redemption date of September 1, 2027, at par. CUSIP is a registered trademark of the American Bankers Association. CUSIP data herein is provided by CUSIP Global Services, managed by S&P Global Market Intelligence on behalf of The American Bankers Association. This information is not intended to create a database and does not serve in any way as a substitute for the CUSIP Services Bureau. CUSIP numbers are provided for convenience of reference only. None of the County, the District or the Underwriter takes any responsibility for the accuracy of such numbers.

3 SAN BERNARDINO COUNTY BOARD OF SUPERVISORS Robert A. Lovingood, Chair, First District Curt Hagman, Vice Chair, Fourth District Janice Rutherford, Supervisor, Second District James Ramos, Supervisor, Third District Josie Gonzales, Supervisor, Fifth District COUNTY OFFICIALS Gary McBride, County Executive Officer Oscar Valdez, Auditor-Controller/Treasurer/Tax Collector Vacant, Chief Financial Officer Michelle Blakemore, County Counsel Jeff Rigney, Director-Special Districts Department SPECIAL SERVICES BOND COUNSEL Orrick, Herrington & Sutcliffe LLP Los Angeles, California SPECIAL TAX CONSULTANT David Taussig and Associates, Inc. Newport Beach, California REAL ESTATE APPRAISER Harris Realty Appraisal Newport Beach, California DISCLOSURE COUNSEL Stradling Yocca Carlson & Rauth Newport Beach, California FINANCIAL ADVISOR CSG Advisors Incorporated San Francisco, California TRUSTEE U.S. Bank National Association Los Angeles, California

4 No dealer, broker, salesperson or other person has been authorized by the County, the District, the Trustee or the Underwriter to give any information or to make any representations in connection with the offer or sale of the Series 2017 Bonds other than those contained herein and, if given or made, such other information or representations must not be relied upon as having been authorized by the County, the District, the Trustee or the Underwriter. This Official Statement does not constitute an offer to sell or the solicitation of an offer to buy, nor shall there be any sale of the Series 2017 Bonds by a person in any jurisdiction in which it is unlawful for such person to make such an offer, solicitation or sale. This Official Statement is not to be construed as a contract with the purchasers or Owners of the Series 2017 Bonds. Statements contained in this Official Statement which involve estimates, forecasts or matters of opinion, whether or not expressly so described herein, are intended solely as such and are not to be construed as representations of fact. This Official Statement, including any supplement or amendment hereto, is intended to be deposited with the Electronic Municipal Market Access System of the Municipal Securities Rulemaking Board, which can be found at The Underwriter has provided the following sentence for inclusion in this Official Statement: The Underwriter has reviewed the information in this Official Statement in accordance with, and as part of, its responsibilities to investors under the federal securities laws as applied to the facts and circumstances of this transaction, but the Underwriter does not guarantee the accuracy or completeness of such information. The information set forth herein which has been obtained by the County or the District from third party sources is believed to be reliable but is not guaranteed as to accuracy or completeness by the County, the District or the Trustee. The information and expressions of opinion herein are subject to change without notice and neither the delivery of this Official Statement nor any sale made hereunder shall, under any circumstances, create any implication that there has been no change in the affairs of the County or the District, the property owners within the District or any other parties described herein since the date hereof. All summaries of the Indenture or other documents are made subject to the provisions of such documents respectively and do not purport to be complete statements of any or all of such provisions. Reference is hereby made to such documents on file with the County for further information in connection therewith. While the County maintains an internet website for various purposes, none of the information on such website is incorporated by reference herein or intended to assist investors in making any investment decision or to provide any continuing information with respect to the Series 2017 Bonds or any other bonds or obligations of the County. Any such information that is inconsistent with the information set forth in this Official Statement should be disregarded. Certain statements included or incorporated by reference in this Official Statement constitute forward-looking statements within the meaning of the United States Private Securities Litigation Reform Act of 1995, Section 21E of the United States Securities Exchange Act of 1934, as amended, and Section 27A of the United States Securities Act of 1933, as amended. Such statements are generally identifiable by the terminology used such as plan, expect, estimate, project, budget or other similar words. Such forward-looking statements include, but are not limited to, certain statements contained in the information under the captions IMPROVEMENT AREA NO. 5, DEVELOPMENT OF PROPERTY IN IMPROVEMENT AREA NO. 5 and PROPERTY OWNERSHIP. THE ACHIEVEMENT OF CERTAIN RESULTS OR OTHER EXPECTATIONS CONTAINED IN SUCH FORWARD-LOOKING STATEMENTS INVOLVES KNOWN AND UNKNOWN RISKS, UNCERTAINTIES AND OTHER FACTORS WHICH MAY CAUSE ACTUAL RESULTS, PERFORMANCE OR ACHIEVEMENTS DESCRIBED TO BE MATERIALLY DIFFERENT FROM ANY FUTURE RESULTS, PERFORMANCE OR ACHIEVEMENTS EXPRESSED OR IMPLIED BY SUCH FORWARD-LOOKING STATEMENTS. THE DISTRICT DOES NOT PLAN TO ISSUE ANY UPDATES OR REVISIONS TO THE FORWARD-LOOKING STATEMENTS SET FORTH IN THIS OFFICIAL STATEMENT. IN CONNECTION WITH THE OFFERING OF THE SERIES 2017 BONDS, THE UNDERWRITER MAY OVERALLOT OR EFFECT TRANSACTIONS WHICH STABILIZE OR MAINTAIN THE MARKET PRICE OF SUCH SERIES 2017 BONDS AT A LEVEL ABOVE THAT WHICH MIGHT OTHERWISE PREVAIL IN THE OPEN MARKET. SUCH STABILIZING, IF COMMENCED, MAY BE DISCONTINUED AT ANY TIME. THE SERIES 2017 BONDS HAVE NOT BEEN REGISTERED UNDER THE SECURITIES ACT OF 1933, AS AMENDED, IN RELIANCE UPON AN EXEMPTION CONTAINED IN SUCH ACT. THE SERIES 2017 BONDS HAVE NOT BEEN REGISTERED OR QUALIFIED UNDER THE SECURITIES LAWS OF ANY STATE.

5 TABLE OF CONTENTS Page INTRODUCTION... 1 General... 1 The District... 1 The Appraisal... 3 Sources of Payment for the Series 2017 Bonds... 4 Continuing Disclosure... 5 Bond Owners Risks... 5 Other Information... 5 ESTIMATED SOURCES AND USES OF FUNDS... 5 THE SERIES 2017 BONDS... 6 Authority for Issuance... 6 Purpose of the Series 2017 Bonds... 6 Description of the Series 2017 Bonds... 6 Book-Entry Only System... 7 Redemption... 7 DEBT SERVICE SCHEDULE SECURITY AND SOURCES OF PAYMENT FOR THE SERIES 2017 BONDS Special, Limited Obligations of the District; Pledge of Net Special Tax Revenues Special Taxes Rate and Method of Apportionment of Special Taxes Collection and Application of Special Taxes Covenant for Superior Court Foreclosure Maximum Special Tax Capacity Property Values Special Tax Fund Bond Fund Reserve Fund No Additional Bonds Except for Refunding Subordinate Obligations IMPROVEMENT AREA NO Location Description of the Authorized Facilities DEVELOPMENT OF PROPERTY IN IMPROVEMENT AREA NO Rosena Ranch Development Improvement Area No Infrastructure Development Lennar Homes Financing Plan PROPERTY OWNERSHIP Lennar Homes of California, Inc Lennar Lytle SPECIAL RISK FACTORS Risks of Real Estate Secured Investments Generally Limited Obligations Insufficiency of Special Taxes Failure to Develop Remaining Homes Soils and Seismic Conditions and Natural Disasters i

6 TABLE OF CONTENTS (Continued) Endangered Species Hazardous Substances Parity Taxes, Special Assessments and Land Development Costs Disclosures to Future Purchasers Non-Cash Payments of Special Taxes Payment of the Special Tax is Not a Personal Obligation of the Owners Property Values FDIC/Federal Government Interests in Properties Bankruptcy and Foreclosure No Acceleration Provision Loss of Tax Exemption Audit of Tax-Exempt Bond Issues Limitations on Remedies Limited Secondary Market; Potential Reductions in Bond Values Funds Invested in the County Investment Pool Potential Early Redemption of Series 2017 Bonds from Prepayments Proposition Shapiro Decision Ballot Initiatives CONTINUING DISCLOSURE TAX MATTERS FINANCIAL ADVISOR LEGAL MATTERS LITIGATION NO RATING UNDERWRITING FINANCIAL INTERESTS ADDITIONAL INFORMATION Page APPENDIX A RATE AND METHOD OF APPORTIONMENT OF SPECIAL TAXES... A-1 APPENDIX B APPRAISAL REPORT AND UPDATE APPRAISAL REPORT... B-1 APPENDIX C GENERAL INFORMATION CONCERNING SAN BERNARDINO COUNTY... C-1 APPENDIX D SUMMARY OF CERTAIN PROVISIONS OF THE INDENTURE... D-1 APPENDIX E FORM OF OPINION OF BOND COUNSEL... E-1 APPENDIX F FORM OF CONTINUING DISCLOSURE AGREEMENT... F-1 APPENDIX G BOOK-ENTRY ONLY SYSTEM... G-1 ii

7

8

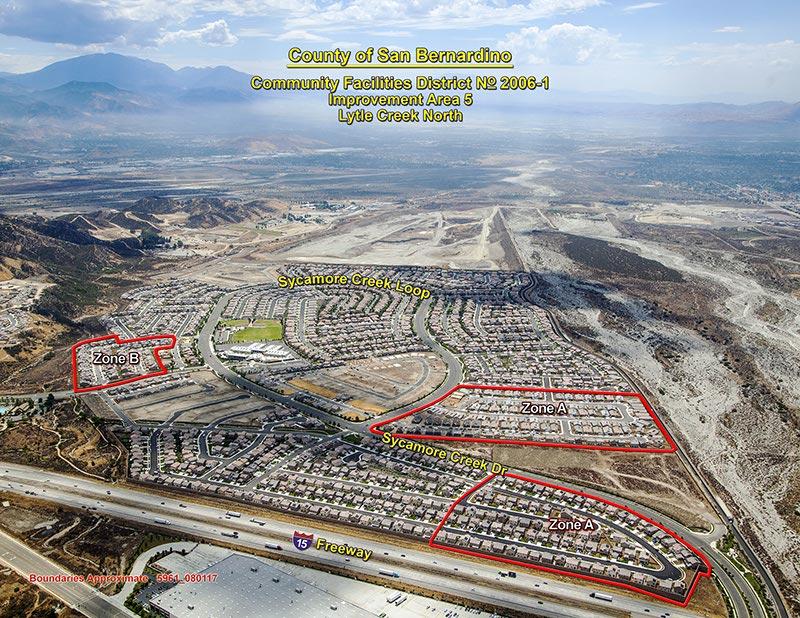

9 $8,800,000 COUNTY OF SAN BERNARDINO COMMUNITY FACILITIES DISTRICT NO (LYTLE CREEK NORTH) IMPROVEMENT AREA NO. 5 SPECIAL TAX BONDS, SERIES 2017 INTRODUCTION General This Introduction is not a summary of this Official Statement. It is only a brief description of and guide to, and is qualified by, more complete and detailed information contained in the entire Official Statement and the documents summarized or described herein. A full review should be made of the entire Official Statement. The sale and delivery of the Series 2017 Bonds to potential investors is made only by means of the entire Official Statement. All capitalized terms used in this Official Statement and not defined have the meaning set forth in Appendices A or D. The purpose of this Official Statement, which includes the cover page, inside cover page, the table of contents and the attached appendices (collectively, the Official Statement ), is to provide certain information concerning the issuance of the $8,800,000 County of San Bernardino Community Facilities District No (Lytle Creek North) Improvement Area No. 5 Special Tax Bonds, Series 2017 (the Series 2017 Bonds ). The proceeds of the Series 2017 Bonds will be used: (i) to finance a portion of certain public facilities eligible to be financed by the District (as such term is defined herein); (ii) to fund a reserve fund; (iii) to fund an initial deposit to an administrative expense fund; and (iv) to pay costs of issuance of the Series 2017 Bonds. The Series 2017 Bonds are authorized to be issued pursuant to the Mello-Roos Community Facilities Act of 1982, as amended (Section et seq. of the Government Code of the State of California) (the Act ) and an Indenture, dated as of December 1, 2017 (the Indenture ), by and between the District and U.S. Bank National Association, as trustee (the Trustee ). See the caption THE SERIES 2017 BONDS. Subject to the provisions of the Indenture permitting the application thereof for the purposes and on the terms set forth therein, the Series 2017 Bonds are secured under the Indenture by a pledge of and lien upon Net Special Tax Revenues (as such term is defined herein) and other assets pledged therefor under the Indenture. Under certain circumstances, the District may issue additional bonds on behalf of Improvement Area No. 5 (as defined below) of the District which are payable on a parity with the Series 2017 Bonds pursuant to the provisions of the Indenture (the Additional Bonds and, together with the Series 2017 Bonds, the Bonds ) provided that such Additional Bonds may be issued solely for the purposes of refunding the Series 2017 Bonds or any Additional Bonds. See the caption SECURITY AND SOURCES OF PAYMENT FOR THE SERIES 2017 BONDS No Additional Bonds Except for Refunding. The District General. The District is approximately coterminous with a master planned community being developed by Lennar Lytle, LLC ( Lennar Lytle ) known as Rosena Ranch. The Rosena Ranch development consists of approximately 386 gross acres planned for the development of 2,086 residential units. Improvement Area No. 5 (as defined below) comprises 270 of the planned units within the Rosena Ranch development and is the fifth area within the District to be developed. Formation Process. The District was formed on March 13, 2007, by the County of San Bernardino (the County ) pursuant to the Act to finance wastewater treatment facilities, road improvements, culvert crossings and traffic signals, bridge improvements, trails and trail-related landscape improvements, sanitary sewer system improvements, domestic water system improvements, landscaping improvements, storm system, 1

10 storm water retention basins, water detention basins, drainage and flood protection improvements, community park improvements, fire and police protection facilities and land, rights-of-way and easements necessary for any of such facilities (collectively, the Facilities ) and certain services, including fire protection services, maintenance of parks, parkways and open space and flood and storm protection services (collectively, the Services ). Neither the proceeds of the Series 2017 Bonds nor the proceeds of any Additional Bonds will be used to finance the Services. At the time that the District was formed, the District had designated two improvement areas within the District known as Improvement Area No. 1 of County of San Bernardino Community Facilities District No ( Improvement Area No. 1 ) and Improvement Area M of County of San Bernardino Community Facilities District No (Lytle Creek North) ( Improvement Area M ). In 2011, certain property within Improvement Area M was designated as Improvement Area No. 2 of County of San Bernardino Community Facilities District No (Lytle Creek North) ( Improvement Area No. 2 ). In 2012, certain property within Improvement Area M was designated as Improvement Area No. 3 of County of San Bernardino Community Facilities District No (Lytle Creek North) ( Improvement Area No. 3 ). In 2014, certain property within Improvement Area M was designated as Improvement Area No. 4 of County of San Bernardino Community Facilities District No (Lytle Creek North) ( Improvement Area No. 4 ). In 2016, certain property within Improvement Area M was designated as Improvement Area No. 5 of County of San Bernardino Community Facilities District No (Lytle Creek North) ( Improvement Area No. 5 ). In 2017, certain property within Improvement Area M and property annexed to the District was designated as Improvement Area No. 6 of County of San Bernardino Community Facilities District No (Lytle Creek North) ( Improvement Area No. 6 ). There is no longer any property that is expected to be developed into residential lots within Improvement Area M. This Official Statement contains information relating to the issuance of the Series 2017 Bonds on behalf of Improvement Area No. 5 only. The Series 2017 Bonds are not secured by Net Special Tax Revenues from any of Improvement Area No. 1, Improvement Area No. 2, Improvement Area No. 3, Improvement Area No. 4, or Improvement Area No. 6 but are secured solely by Net Special Tax Revenues from Improvement Area No. 5. The Act was enacted by the State of California (the State ) Legislature to provide an alternative method of financing certain public capital facilities and services, especially in developing areas of the State. Any local agency (as such term is defined in the Act) may establish a community facilities district to provide for and finance the cost of eligible public facilities and services. Generally, the legislative body of the local agency which forms a community facilities district acts on behalf of such district as its legislative body. Subject to approval by two-thirds of the votes cast at an election and compliance with the other provisions of the Act, a community facilities district may issue bonds to finance the costs of public facilities and may levy and collect a special tax within such district to repay such indebtedness. The Board of Supervisors of the County (the Board of Supervisors ) acts as the legislative body of the District. Pursuant to the Act, the Board of Supervisors adopted the necessary resolutions stating its intent to establish the District and undertook certain proceedings to designate Improvement Area No. 5 therein, to authorize the levy of special taxes on taxable property within the boundaries of the District and Improvement Area No. 5, and to have the District and Improvement Area No. 5 incur bonded indebtedness for the purpose of financing the authorized Facilities. Following public hearings conducted pursuant to the provisions of the Act, the Board of Supervisors adopted resolutions establishing the District and designating Improvement Area No. 5 therein, and calling special elections to submit the levy of the special taxes and the incurring of bonded indebtedness to the qualified voters of Improvement Area No. 5. On April 19, 2016, at an election held pursuant to the Act, the landowners who comprised the qualified voters of Improvement Area No. 5 authorized the District to incur bonded indebtedness in the aggregate principal amount not to exceed $9,000,000 for Improvement Area No. 5 and approved the Rate and Method of Apportionment for Improvement Area No. 5 of the District (the Rate and Method ), which establishes a special tax to fund the Special Tax Requirement (as such term is defined in the Rate and Method), which Special Tax Requirement includes amounts required in 2

11 any Fiscal Year to pay the principal of and interest on the Series 2017 Bonds and any Additional Bonds when due. See the captions SECURITY AND SOURCES OF PAYMENT FOR THE SERIES 2017 BONDS Special Taxes and SECURITY AND SOURCES OF PAYMENT FOR THE SERIES 2017 BONDS Rate and Method of Apportionment of Special Taxes and Appendix A. At the time of the establishment of the District, a special tax was also approved for the District, including Improvement Area No. 5 to fund: (i) certain costs of fire protection ( Special Tax A ); (ii) maintenance of open space and flood and storm drain protection services ( Special Tax B ); and (iii) maintenance of parks and parkways, but only if such maintenance services are not provided by the property owner association ( Special Tax C, and together with Special Tax A and Special Tax B, collectively, the Services Special Taxes ). The Services Special Taxes are not pledged to pay the Series 2017 Bonds. Improvement Area No. 5. Improvement Area No. 5 encompasses approximately 46.4 gross acres. The property in Improvement Area No. 5 is proposed for 270 detached residential dwellings. Lennar Lytle was the original owner of the property within Improvement Area No. 5 but had previously transferred all of such property to Lennar Homes of California, Inc. ( Lennar Homes ), the developer within Improvement Area No. 5. As of August 1, 2017 (the date of value set forth in the Appraisal (defined below)), Improvement Area No. 5 had 218 completed homes owned by homeowners; 14 completed but unclosed homes owned by Lennar Homes and 38 homes in various stages of unit construction owned by Lennar Homes. As of October 1, 2017, Improvement Area No. 5 had (i) 250 completed homes owned by homeowners, (ii) five completed homes which have been sold but ownership of which had not yet transferred to individual homeowners, and (iii) 15 homes in various stages of unit construction owned by Lennar Homes, of which 14 have been sold to individual homeowners and are expected to close upon completion of home construction. See the caption DEVELOPMENT OF PROPERTY IN IMPROVEMENT AREA NO. 5. Improvement Area No. 5 is located north of the City of Fontana s northern boundary, in unincorporated San Bernardino County. Improvement Area No. 5 is bounded by Interstate 15 Freeway on the north/northwest and Lytle Creek on the south. The property is near the foot of the San Gabriel Mountains at the mouth of Lytle Creek Canyon. Ownership of the property in Improvement Area No. 5 is described under the caption PROPERTY OWNERSHIP. The Appraisal An appraisal report for the land and existing improvements within Improvement Area No. 5 was prepared by Harris Realty Appraisal, Newport Beach, California (the Appraiser ). The appraisal report (the Appraisal ), which is dated August 22, 2017, is entitled Appraisal Report County of San Bernardino Community Facilities District No Improvement Area No. 5 Lytle Creek North and establishes a date of value of August 1, 2017 (the Date of Value ). The Appraisal is set forth in Appendix B. The Appraisal provides an estimate of the minimum market value of the fee simple interest subject to special tax and special assessment liens of the property within Improvement Area No. 5 consisting of approximately 46.4 gross acres planned for development into approximately 270 detached single-family residential units. As of the Date of Value, the property within Improvement Area No. 5 was owned by the 218 individual homeowners and Lennar Homes. The Appraiser is of the opinion that the minimum market value of the land and improvements in existence within Improvement Area No. 5 as of the Date of Value, was $103,400,000. This value results in an estimated overall appraised value-to-lien ratio (including the Series 2017 Bonds and all direct and overlapping tax and assessment debt and general obligation debt) for Improvement Area No. 5 of approximately to- 1. Excluding the outstanding general obligation debt, the estimated appraised value to lien ratio would be approximately to-1. The value-to-lien ratios for individual properties in Improvement Area No. 5 vary 3

12 significantly from this overall average. See the caption SECURITY AND SOURCES OF PAYMENT FOR THE SERIES 2017 BONDS Property Values Estimated Appraised Value-to-Lien. The Appraiser has prepared an Update Appraisal Report with an effective date of October 1, 2017 (the Update Appraisal Report ) which is attached hereto as Appendix B. In the Update Appraisal Report, the Appraiser concludes that the value of the appraised properties as of the date of the Update Appraisal Report, is not less than the conclusion of value for such property set forth in the Appraisal Report. The Appraisal is based upon a variety of assumptions and limiting conditions that are described in the full text of the Appraisal attached to this Official Statement as Appendix B. The Appraiser s opinions reflect conditions prevailing in the applicable market as of the Date of Value. None of the County, the District or the Underwriter makes any representation as to the accuracy of the Appraisal. There is no assurance that the property within Improvement Area No. 5 can be sold for the amounts set forth in the Appraisal or that any parcel can be sold for a price sufficient to pay the Special Taxes for such parcel in the event of a default in payment of Special Taxes by the owner of such parcel. See the caption SPECIAL RISK FACTORS Property Values and Appendix B. Sources of Payment for the Series 2017 Bonds Under the Indenture, the District has pledged to repay the Series 2017 Bonds from Net Special Tax Revenues and other assets pledged therefor under the Indenture, subject to the provisions of the Indenture permitting the application thereof for the purposes and on the terms and conditions set forth therein. Net Special Tax Revenues consist of Special Tax Revenues less the amount required to pay Administrative Expenses. Special Tax Revenues are defined in the Indenture to include the proceeds of the Special Taxes received by or on behalf of the District for Improvement Area No. 5, including any prepayments thereof, interest and penalties thereon and proceeds of the redemption or sale of property sold as a result of foreclosure of the lien of the Special Taxes, which will be limited to the amount of said lien and interest and penalties thereon. The Services Special Taxes are not pledged to pay the Series 2017 Bonds. The Net Special Tax Revenues are the primary security for the repayment of the Series 2017 Bonds and any Additional Bonds. In the event that the Special Taxes are not paid prior to delinquency, the only sources of funds available to pay the debt service on the Series 2017 Bonds and any Additional Bonds are amounts held by the Trustee in the Special Tax Fund, the Bond Fund and the Reserve Fund. Amounts held in the Rebate Fund, the Improvement Fund and the Administrative Expense Fund are not available to pay the debt service on the Series 2017 Bonds and any Additional Bonds. See the caption SECURITY AND SOURCES OF PAYMENT FOR SERIES 2017 BONDS No Additional Bonds Except for Refunding for a description of the conditions precedent to the issuance of Additional Bonds, including, among other requirements, the requirement that Annual Debt Service in each Bond Year, calculated for all Bonds that will be Outstanding after the issuance of such Additional Bonds, will be less than or equal to Annual Debt Service in such Bond Year, calculated for all Bonds which are Outstanding immediately prior to the issuance of such Additional Bonds. EXCEPT FOR THE NET SPECIAL TAX REVENUES AND AMOUNTS HELD IN THE SPECIAL TAX FUND, THE BOND FUND AND THE RESERVE FUND UNDER THE INDENTURE, NO OTHER FUNDS ARE PLEDGED TO THE PAYMENT OF THE SERIES 2017 BONDS. THE SERIES 2017 BONDS ARE NOT GENERAL OR SPECIAL OBLIGATIONS OF THE COUNTY BUT ARE SPECIAL, LIMITED OBLIGATIONS OF THE DISTRICT PAYABLE SOLELY FROM THE NET SPECIAL TAX REVENUES AND AMOUNTS HELD IN THE SPECIAL TAX FUND, THE BOND FUND AND THE RESERVE FUND UNDER THE INDENTURE AS MORE FULLY DESCRIBED HEREIN. NEITHER THE FAITH AND CREDIT NOR THE TAXING POWER OF THE DISTRICT (EXCEPT TO THE LIMITED EXTENT SET FORTH IN THE INDENTURE), THE COUNTY, OR THE STATE OF CALIFORNIA, OR ANY POLITICAL SUBDIVISION THEREOF, IS PLEDGED TO THE PAYMENT OF THE SERIES 2017 BONDS. 4

13 Continuing Disclosure The District has agreed to provide, or cause to be provided, to the Electronic Municipal Market Access System ( EMMA ) of the Municipal Securities Rulemaking Board (the MSRB ), certain annual financial information and operating data and notice of certain enumerated events in order to assist the Underwriter in complying with Rule 15c2-12 adopted by the Securities and Exchange Commission under the Securities Exchange Act of 1934, as the same may be amended from time to time (the Rule ). See the caption CONTINUING DISCLOSURE and Appendix F for a description of the specific nature of the annual reports and enumerated event notices to be filed by the District or its representatives. Bond Owners Risks Certain events could affect the timely repayment of the principal of, premium, if any and interest on the Series 2017 Bonds when due. See the caption SPECIAL RISK FACTORS for a discussion of certain factors that should be considered, in addition to other matters set forth herein, in evaluating an investment in the Series 2017 Bonds. The Series 2017 Bonds are not being rated by any nationally recognized rating agency. Other Information This Official Statement speaks only as of its date, and the information contained herein is subject to change. Brief descriptions of the Series 2017 Bonds and the Indenture are included in this Official Statement. Such descriptions and information do not purport to be comprehensive or definitive. All references herein to the Indenture, the Series 2017 Bonds and the Constitution and laws of the State, as well as the proceedings of the Board of Supervisors, acting as the legislative body of the District, are qualified in their entirety by references to such documents, laws and proceedings, and with respect to the Series 2017 Bonds, by reference to the Indenture. Copies of the Indenture and other documents referred to herein are available for inspection and (upon request and payment to the County of a charge for copying, mailing and handling) for delivery from the Special Districts Department of the County at 157 West 5th Street, 2nd Floor, San Bernardino, California , Attention: Mr. Jeff Rigney, Director. ESTIMATED SOURCES AND USES OF FUNDS The following table sets forth the estimated sources and uses of Series 2017 Bonds proceeds: Sources Principal Amount of Bonds $ 8,800, Plus Net Original Issue Premium 236, Total Sources $ 9,036, Uses Improvement Fund $ 8,245, Reserve Fund (1) 494, Administrative Expense Fund 30, Costs of Issuance Fund (2) 176, Underwriter s Discount 90, Total Uses $ 9,036, (1) (2) An amount equal to the initial Reserve Requirement. Includes legal fees, Trustee fees, Financial Advisor fees, Special Tax Consultant fees, Appraiser fees, printing costs and certain other Series 2017 Bond issuance costs. 5

14 THE SERIES 2017 BONDS Authority for Issuance The Series 2017 Bonds are being issued pursuant to the Act and the Indenture. The Act was adopted by the State Legislature to provide an alternate method of financing certain public capital facilities and services. Once duly established by a local governmental agency, a community facilities district is itself a legally constituted governmental entity, with the governing board or legislative body of the local agency that established it constituting the legislative body of the community facilities district. Subject to approval by a two-thirds vote of a community facilities district s qualified electors and compliance with the provisions of the Act, the legislative body may authorize the issuance of bonds for the community facilities district in order to finance certain public improvements, and the legislative body may levy and collect a special tax within such community facilities district to repay such indebtedness. The total aggregate principal amount of the Series 2017 Bonds and any Additional Bonds will at no time exceed $9,000,000. The District has covenanted not to issue any Additional Bonds except for refunding purposes. See the caption SECURITY AND SOURCES OF PAYMENT FOR THE SERIES 2017 BONDS No Additional Bonds Except for Refunding and Appendix D. Purpose of the Series 2017 Bonds The Series 2017 Bonds are being issued to provide funds to: (i) to finance a portion of certain public facilities eligible to be financed by the District; (ii) to fund a reserve fund; (iii) fund an initial deposit to an administrative expense fund; and (iv) to pay costs of issuance of the Series 2017 Bonds. See the caption ESTIMATED SOURCES AND USES OF FUNDS. Description of the Series 2017 Bonds The Series 2017 Bonds will be issued in fully registered form without coupons in denominations of $5,000 or any integral multiple thereof ( Authorized Denominations ) and will be dated the date of issuance thereof. The Series 2017 Bonds are scheduled to mature on September 1 in the years and in the principal amounts and will bear interest at the rates shown on the inside front cover page of this Official Statement. Interest on the Series 2017 Bonds will be computed on the basis of a 360-day year consisting of twelve 30-day months and will be payable semiannually on March 1 and September 1 of each year, commencing March 1, 2018 (each, an Interest Payment Date ). Interest on each Series 2017 Bond will be payable from the Interest Payment Date next preceding the date of authentication thereof unless: (i) such Series 2017 Bond is authenticated on or before an Interest Payment Date and after the close of business on the preceding Record Date (the fifteenth calendar day of the month preceding each Interest Payment Date, whether or not such day is a Business Day), in which event interest thereon will be payable from such Interest Payment Date, (ii) such Series 2017 Bond is authenticated on or before the first Record Date, in which event interest thereon will be payable from the Closing Date or (iii) interest on such Series 2017 Bond is in default as of the date of authentication thereof, in which event interest thereon will be payable from the date to which interest has been previously paid or duly provided for. The interest on and principal of and redemption premiums, if any, on the Series 2017 Bonds are payable in lawful money of the United States on each Interest Payment Date. Interest will be paid by check of the Trustee mailed by first class mail, postage prepaid, on each Interest Payment Date to the Owners of the Series 2017 Bonds at their respective addresses shown on the Registration Books as of the close of business on the preceding Record Date. Notwithstanding the foregoing, interest on any Series 2017 Bond which is not punctually paid or duly provided for on any Interest Payment Date will, if and to the extent that amounts subsequently become available therefor, be paid on a payment date established by the Trustee to the Person in whose name the ownership of such Series 2017 Bond is registered on the Registration Books at the close of business on a special record date to be established by the Trustee for the payment of such defaulted interest, 6

15 notice of which will be given to such Owner not less than ten days prior to such special record date. The principal of the Series 2017 Bonds will be payable in lawful money of the United States of America upon presentation and surrender thereof upon maturity or earlier redemption at the Office of the Trustee. The Series 2017 Bonds are not general obligations of the District but are special, limited obligations of the District payable solely from Net Special Tax Revenues and the other assets pledged therefor under the Indenture. Neither the faith and credit nor the taxing power of the County, the District (except to the limited extent set forth in the Indenture), the State or any political subdivision thereof is pledged to the payment of the Series 2017 Bonds. See the caption SPECIAL RISK FACTORS Limited Obligations. Book-Entry Only System Except as otherwise provided in the Indenture, the registered Owner of all of the Series 2017 Bonds while they are in book-entry form will be DTC. As long as DTC is the registered owner of the Series 2017 Bonds, references in this Official Statement to the Owners of the Series 2017 Bonds refer to DTC and not to the Beneficial Owners (as such term is defined in Appendix G) of the Series 2017 Bonds. None of the District, the County, or the Trustee gives any assurance that DTC, its Participants or others will distribute payments with respect to the Series 2017 Bonds or notices with respect thereto to the Beneficial Owners thereof or that DTC will otherwise serve and act in the manner described in this Official Statement. See Appendix G for a further description of DTC and its book-entry system. The information presented therein is based solely on material provided by DTC. Redemption Optional Redemption. The Series 2017 Bonds maturing on or after September 1, 2025, shall be subject to optional redemption, in whole, or in part in Authorized Denominations, on any Interest Payment Date on or after September 1, 2024, from any source of available funds, at the following respective Redemption Prices (expressed as percentages of the principal amount of the Series 2017 Bonds to be redeemed), plus accrued interest thereon to the date of redemption: Redemption Dates Redemption Price September 1, 2024 and March 1, % September 1, 2025 and March 1, September 1, 2026 and March 1, September 1, 2027 and any Interest Payment Date thereafter 100 Mandatory Redemption from Special Tax Prepayments. The Series 2017 Bonds shall be subject to mandatory redemption, in whole, or in part in Authorized Denominations, on any Interest Payment Date, from and to the extent of prepaid Special Taxes required to be applied thereto pursuant to the Indenture, at the following respective Redemption Prices (expressed as percentages of the principal amount of the Series 2017 Bonds to be redeemed), plus accrued interest thereon to the date of redemption: Redemption Dates Redemption Price March 1, 2018 through March 1, % September 1, 2025 and March 1, September 1, 2026 and March 1, September 1, 2027 and any Interest Payment Date thereafter 100 Mandatory Sinking Fund Redemption. The Series 2017 Bonds maturing September 1, 2042, (the 2042 Term Bonds ) are subject to mandatory sinking fund redemption, in part, on September 1 in each year, commencing September 1, 2038, at a Redemption Price equal to the principal amount of the 2042 Term Bonds 7

16 to be redeemed, without premium, plus accrued interest thereon to the date of redemption, in the aggregate respective principal amounts in the respective years as follows: * Maturity. Sinking Fund Redemption Date (September 1) Principal Amount to Be Redeemed 2038 $320, , , , * 375,000 The Series 2017 Bonds maturing September 1, 2048, (the 2048 Term Bonds and, together with the 2042 Term Bonds, the Term Bonds ) are subject to mandatory sinking fund redemption, in part, on September 1 in each year, commencing September 1, 2043, at a Redemption Price equal to the principal amount of the 2048 Term Bonds to be redeemed, without premium, plus accrued interest thereon to the date of redemption, in the aggregate respective principal amounts in the respective years as follows: * Maturity. Sinking Fund Redemption Date (September 1) Principal Amount to Be Redeemed 2043 $390, , , , , * 475,000 If some but not all of the Term Bonds of a maturity are optionally redeemed, as described above under the caption Optional Redemption, the principal amount of such Term Bonds to be subsequently redeemed from mandatory sinking fund payments will be reduced by the aggregate principal amount of such Term Bonds so optionally redeemed, such reduction to be allocated among redemption dates in amounts of $5,000 or integral multiples thereof, as designated by the District in a Written Certificate of the District filed with the Trustee. If some but not all of the Term Bonds of a maturity are redeemed pursuant to mandatory redemption from Special Tax prepayments, as described above under the caption Mandatory Redemption from Special Tax Prepayments, the principal amount of such Term Bonds to be subsequently redeemed from mandatory sinking fund payments will be reduced by the aggregate principal amount of such Term Bonds so redeemed from Special Tax prepayments, such reduction to be allocated among redemption dates as nearly as practicable on a pro rata basis in amounts of $5,000 or integral multiples thereof, as determined by the Trustee, notice of which determination will be given by the Trustee to the District. Selection of Series 2017 Bonds for Redemption. Whenever provision is made in the Indenture for the redemption of less than all of the Series 2017 Bonds, the Trustee will select the Series 2017 Bonds to be redeemed from all Series 2017 Bonds not previously called for redemption: (a) with respect to any optional redemption of Series 2017 Bonds, among maturities of Series 2017 Bonds as directed in a Written Request by the District; (b) with respect to any redemption from prepayment of Special Taxes and the corresponding 8

17 provisions of any Supplemental Indenture pursuant to which Additional Bonds are issued, among maturities of all Series of Bonds on a pro rata basis as nearly as practicable, and (c) with respect to any other redemption of Additional Bonds, among maturities as provided in the Supplemental Indenture pursuant to which such Additional Bonds are issued, and by lot among Bonds of the same Series with the same maturity in any manner which the Trustee in its sole discretion shall deem appropriate. For purposes of such selection, all Series 2017 Bonds will be deemed to be comprised of separate $5,000 denominations and such separate denominations will be treated as separate Series 2017 Bonds which may be separately redeemed. Notice of Redemption. If the Series 2017 Bonds are held in book-entry form, notice of redemption will be mailed to DTC and not to the Beneficial Owners of the Series 2017 Bonds under the DTC book-entry system. Neither the District nor the Trustee is responsible for giving notice of redemption to the Beneficial Owners. See the caption Book-Entry Only System and Appendix G. The Indenture provides that the Trustee will mail (by first class mail) notice of any redemption to the respective Owners of any Series 2017 Bonds designated for redemption at their respective addresses appearing on the Registration Books, at least 30 but not more than 60 days prior to the date fixed for redemption. Such notice must state the date of the notice, the redemption date, the redemption place and the Redemption Price and designate the CUSIP numbers, if any, the Series 2017 Bond numbers and the maturity or maturities of the Series 2017 Bonds to be redeemed (except in the event of redemption of all of the Series 2017 Bonds of such maturity or maturities in whole), and must require that such Series 2017 Bonds be then surrendered at the Office of the Trustee for redemption at the Redemption Price, giving notice also that further interest on such Series 2017 Bonds will not accrue from and after the date fixed for redemption. Neither the failure to receive any notice so mailed, nor any defect in such notice, will affect the validity of the proceedings for the redemption of the Series 2017 Bonds or the cessation of accrual of interest thereon from and after the date fixed for redemption. With respect to any notice of any optional redemption of Series 2017 Bonds, unless at the time such notice is given the Series 2017 Bonds to be redeemed will be deemed to have been paid within the meaning of the Indenture, such notice will state that such redemption is conditional upon receipt by the Trustee, on or prior to the date fixed for such redemption, of moneys that, together with other available amounts held by the Trustee, are sufficient to pay the Redemption Price of, and accrued interest on, the Series 2017 Bonds to be redeemed, and that if such moneys have not been so received said notice will be of no force and effect and the District will not be required to redeem such Series 2017 Bonds. In the event that a notice of redemption of Series 2017 Bonds contains such a condition and such moneys are not so received, the redemption of Series 2017 Bonds as described in the conditional notice of redemption will not be made and the Trustee will, within a reasonable time after the date on which such redemption was to occur, give notice to the Persons and in the manner in which the notice of redemption was given, that such moneys were not so received and that there will be no redemption of Series 2017 Bonds pursuant to such notice of redemption. Partial Redemption of Series 2017 Bonds. Upon surrender of any Series 2017 Bonds redeemed in part only, the District will execute and the Trustee will authenticate and deliver to the Owner thereof, at the expense of the District, a new Series 2017 Bond or Series 2017 Bonds in Authorized Denominations in an aggregate principal amount equal to the unredeemed portion of the Series 2017 Bonds surrendered. Effect of Notice of Redemption. Notice having been mailed as described under the caption Notice of Redemption, and moneys for the Redemption Price, and the interest to the applicable date fixed for redemption, having been set aside with the Trustee, the Series 2017 Bonds will become due and payable on said date, and, upon presentation and surrender thereof at the Office of the Trustee, such Series 2017 Bonds will be paid at the Redemption Price thereof, together with interest accrued and unpaid to said date. If, on the date fixed for redemption, moneys for the Redemption Price of all the Series 2017 Bonds to be redeemed, together with interest to said date, will be held by the Trustee so as to be available therefor on such date, and, if notice of redemption thereof has been mailed as aforesaid and not canceled, then, from and after said date, interest on such Series 2017 Bonds will cease to accrue and become payable. All moneys held 9

18 by or on behalf of the Trustee for the redemption of Series 2017 Bonds will be held in trust for the account of the Owners of the Series 2017 Bonds so to be redeemed without liability to such Owners for interest thereon. All Series 2017 Bonds paid at maturity or redeemed prior to maturity pursuant to the provisions of the Indenture will be canceled upon surrender thereof and destroyed. Registration of Exchange or Transfer. So long as the Series 2017 Bonds remain in book-entry form, transfer and exchange of any of the Series 2017 Bonds will be accomplished in accordance with the provisions of such book-entry system. In the event and only in the event of termination of such book-entry system with respect to the Series 2017 Bonds, the Series 2017 Bonds may be transferred and exchanged in accordance with the terms of the Indenture. See Appendix D. DEBT SERVICE SCHEDULE The following is the annual debt service schedule for the Series 2017 Bonds, assuming that no Series 2017 Bonds are redeemed prior to maturity except from mandatory sinking fund redemption. Bond Year Ending September 1 Principal (1) Interest Total Annual Debt Service 2018 $ 185,000 $ 239, $ 424, , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , ,000 87, , ,000 71, , ,000 54, , ,000 37, , ,000 19, , Total $ 8,800,000 $ 6,383, $ 15,183, (1) Includes mandatory sinking fund redemption. 10

19 SECURITY AND SOURCES OF PAYMENT FOR THE SERIES 2017 BONDS Special, Limited Obligations of the District; Pledge of Net Special Tax Revenues EXCEPT FOR THE NET SPECIAL TAX REVENUES AND AMOUNTS HELD IN THE SPECIAL TAX FUND, THE BOND FUND AND THE RESERVE FUND UNDER THE INDENTURE, NO OTHER FUNDS ARE PLEDGED TO THE PAYMENT OF THE BONDS. THE SERIES 2017 BONDS ARE NOT GENERAL OR SPECIAL OBLIGATIONS OF THE COUNTY BUT ARE SPECIAL, LIMITED OBLIGATIONS OF THE DISTRICT PAYABLE SOLELY FROM THE NET SPECIAL TAX REVENUES AND AMOUNTS HELD IN THE SPECIAL TAX FUND, THE BOND FUND AND THE RESERVE FUND UNDER THE INDENTURE, AS MORE FULLY DESCRIBED HEREIN. NEITHER THE FAITH AND CREDIT NOR THE TAXING POWER OF THE DISTRICT (EXCEPT TO THE LIMITED EXTENT SET FORTH IN THE INDENTURE), THE COUNTY, OR THE STATE OF CALIFORNIA, OR ANY POLITICAL SUBDIVISION THEREOF, IS PLEDGED TO THE PAYMENT OF THE SERIES 2017 BONDS. Subject only to the provisions of the Indenture permitting the application thereof for the purposes and on the terms and conditions set forth therein, in order to secure the payment of the principal of, premium, if any, and interest on the Bonds in accordance with their terms and with the provisions of the Indenture and the Act, the District will pledge to the Owners, and grant thereto a lien on and a security interest in, all of the Net Special Tax Revenues with respect to Improvement Area No. 5 and any other amounts held in the Special Tax Fund, the Bond Fund and the Reserve Fund. Such pledge constitutes a first lien on and security interest in such assets, which will immediately attach to such assets and be effective, binding and enforceable against the District, its successors, purchasers of any of such assets, creditors and all others asserting rights therein, to the extent set forth in and in accordance with the Indenture, irrespective of whether those parties have notice of the pledge of, lien on and security interest in such assets and without the need for any physical delivery, recordation, filing or further act. The Net Special Tax Revenues are the primary security for the repayment of the Bonds. In the event that the Special Taxes are not paid prior to delinquency, the only sources of funds available to pay the debt service on the Bonds are amounts held by the Trustee in the Special Tax Fund, the Bond Fund and the Reserve Fund. Amounts held in the Rebate Fund, the Improvement Fund and the Administrative Expense Fund are not available to pay the debt service on the Bonds. Special taxes levied on property within the District outside of Improvement Area No. 5 are not available to pay debt service on the Bonds. Special Taxes Pursuant to the Indenture, the District will fix and levy the amount of Special Taxes within Improvement Area No. 5 in each Fiscal Year in accordance with the Rate and Method and, subject to the limitations in the Rate and Method as to the maximum Special Tax that may be levied, in an amount sufficient to yield Special Tax Revenues in the amount required for: (i) the payment of principal of and interest on any Outstanding Bonds becoming due and payable during the Corresponding Bond Year; (ii) any necessary replenishment of the Reserve Fund; and (iii) the payment of Administrative Expenses estimated to be paid from such Special Tax Revenues, taking into account the balances in the funds and accounts established under the Indenture. Notwithstanding the foregoing, the amount of Special Taxes actually collected each year may be less than the amount described for a variety of different reasons. See the caption SPECIAL RISK FACTORS Insufficiency of Special Taxes. The Special Taxes are expected to be payable and collected in the same manner and at the same time and in the same installments as general taxes on real property are payable (or in such other manner as the Board of Supervisors will determine, including direct billing of the affected property owners). Although the applicable Special Tax constitutes a lien on each Assessor s Parcel of Taxable Property within Improvement Area No. 5, it does not constitute the personal indebtedness of the owner of such Assessor s Parcel. There is 11

20 no assurance that the owner of such Assessor s Parcel will be financially able to pay the applicable Special Taxes or that such owner will do so, even if it is financially able to make such payment. See the caption SPECIAL RISK FACTORS Payment of the Special Tax is Not a Personal Obligation of the Owners. Neither the Services Special Taxes nor the special taxes levied in Improvement Area No. 1, Improvement Area No. 2, Improvement Area No. 3, Improvement Area No. 4, or Improvement Area No. 6 within the District are available to pay debt service on the Series 2017 Bonds. Rate and Method of Apportionment of Special Taxes The District is legally authorized and has covenanted to cause the levy of the Special Taxes for Improvement Area No. 5 in an amount determined according to a methodology, i.e., the Rate and Method, which the Board of Supervisors and the qualified electors within Improvement Area No. 5 have approved. The Rate and Method apportions the total amount of Special Taxes to be collected among the taxable parcels in Improvement Area No. 5 as more particularly described below. The Rate and Method does not address any other special taxes which may be levied on the property in Improvement Area No. 5, such as Services Special Taxes (which are not available to pay the Series 2017 Bonds). The following is a summary of the provisions of the Rate and Method and is not intended to be a full recitation of the provisions thereof. The full text of the Rate and Method is set forth in Appendix A. The meanings of the defined terms used below are as set forth in Appendix A. The summary below is qualified by more complete and detailed information contained in the Rate and Method. Each Fiscal Year, all Taxable Property within Improvement Area No. 5 will be classified as Developed Property, Other Taxable Property or Undeveloped Property and will be subject to Special Taxes in accordance with the Rate and Method. Developed Property will be classified as Residential Property or Non- Residential Property. The Assigned Special Tax rates are set forth in Table 1 and Table 2 of Section C of the Rate and Method attached hereto as Appendix A. Pursuant to Section D of the Rate and Method, at least 30 days before the first series of Bonds are expected to be issued, if the Total Effective Tax Rate for any Plan Type in a Land Use Class exceeds 1.95%, the Assigned Special Tax rate for such Land Use Class will be reduced such that the Total Effective Tax Rate will not exceed 1.95%. In order to satisfy the requirement of the Rate and Method, the District engaged Empire Economics, Inc. to conduct a Price Point Study (the Price Point Study ) to determine the current base prices for the homes within Improvement Area No. 5. Based on the Price Point Study, the District has determined that there was no Plan Type in any Land Use Class for which the Total Effective Tax Rate exceeded 1.95% (based on a levy at 100% of the Assigned Special Tax rate). Therefore, the Assigned Special Tax rates will not be reduced pursuant to Section D of the Rate and Method. The Rate and Method only requires the foregoing analysis and the preparation of the Price Point Study prior to the issuance of the initial series of Bonds. Under the Act, under no circumstances will the Special Tax levied in any Fiscal Year against any taxable parcel of residential property within Improvement Area No. 5 be increased by more than 10% as a consequence of a delinquency or default by the owner of any other parcel within Improvement Area No. 5 above the amount that would have been levied in that Fiscal Year had there never been any such delinquencies or defaults. Such limitation would not apply to increases in Special Taxes levied for other purposes, such as the issuance of Additional Bonds or to pay directly for the acquisition or construction of the Facilities as authorized by the Rate and Method. In Fiscal Year , the District is levying the Special Tax at 100% of the Assigned Special Tax rates on Developed Property, as set forth in the Rate and Method. See Appendix A. Maximum Special Tax, Assigned Special Tax and Backup Special Tax. The Maximum Special Tax, Assigned Special Tax and Backup Special Tax in the Rate and Method are as follows: 12

21 Developed Property. The Maximum Special Tax for each Assessor s Parcel classified as Developed Property will be the greater of: (i) the amount derived by application of the Assigned Special Tax; or (ii) the amount derived by application of the Backup Special Tax. Assigned Special Tax. The Assigned Special Tax for each Land Use Class within Zone A and Zone B is listed in Table 1 and Table 2, respectively, of Section C of the Rate and Method. The Assigned Special Tax applicable to an Assessor s Parcel classified as Developed Property and Residential Property ranges: (i) in Zone A from $1,825 per unit for units with a Residential Floor Area less than 1,301 square feet to $2,366 per unit for units with a Residential Floor Area greater than 2,900 square feet; and (ii) in Zone B from $2,020 per unit for units with a Residential Floor Area of less than 1,901 square feet to $2,563 per unit for units with a Residential Floor Area greater than 3,500 square feet. The Assigned Special Tax applicable to an Assessor s Parcel classified as Non- Residential Property: (I) for Zone A is $17,407 per Acre; and (II) for Zone B is $15,010 per Acre. Backup Special Tax. The Backup Special Tax attributable to Developed Property within a Final Map for Zone A is $17,407 per acre and for Zone B is $15,010 per Acre. Undeveloped and Other Taxable Property. The Maximum Special Tax for Undeveloped Property and Other Taxable Property will be $17,407 per Acre for Property in Zone A and $15,010 per Acre for Property in Zone B. Method of Apportionment of Special Tax. For each Fiscal Year, the Board of Supervisors will determine the Special Tax Requirement and, subject to the Maximum Special Tax rates described above, will levy the Special Tax until the total Special Tax levy equals the Special Tax Requirement. The Special Tax will be levied each Fiscal Year as follows: First: The Special Tax will be levied Proportionately on each Assessor s Parcel of Developed Property at up to 100% of the Assigned Special Tax for Developed Property. Notwithstanding the foregoing, under no circumstances will the Special Tax levied in any Fiscal Year against any Assessor s Parcel of Residential Property be increased as a consequence of delinquency or default by owner or owners of any other Assessor s Parcel(s) within Improvement Area No. 5 by more than 10% above the amount that would have been levied in that Fiscal Year had there never been any such delinquencies or defaults. To the extent that the levy of the Special Tax on Residential Property is limited by the provision in the previous sentence, the levy of the Special Tax on each Assessor s Parcel of Non-Residential Property will continue in equal percentages at up to 100% of the Assigned Special Tax; Second: If additional moneys are needed to satisfy the Special Tax Requirement after the first step has been completed, the Special Tax will be levied Proportionately on each Assessor s Parcel of Undeveloped Property at up to 100% of the Maximum Special Tax for Undeveloped Property; Third: If additional moneys are needed to satisfy the Special Tax Requirement after the first two steps have been completed, then the levy of the Special Tax on each Assessor s Parcel of Developed Property whose Maximum Special Tax is determined through the application of the Backup Special Tax will be increased in equal percentages from the Assigned Special Tax up to the Maximum Special Tax for each such Assessor s Parcel. Notwithstanding the foregoing, under no circumstances will the Special Tax levied in any Fiscal Year against any Assessor s Parcel of Residential Property be increased as a consequence of delinquency or default by owner or owners of any other Assessor s Parcel(s) within Improvement Area No. 5 by more than 10% above the amount that would have been levied in that Fiscal Year had there never been any such delinquencies or defaults. To the extent that the levy of the Special Tax on Residential Property is limited by the provision in the previous sentence, the levy of the Special Tax on each Assessor s Parcel of Non- 13

22 Residential Property will continue in equal percentages from the Assigned Special Tax up to the Maximum Special Tax; and Fourth: If additional moneys are needed to satisfy the Special Tax Requirement after the first three steps have been completed, then the Special Tax will be levied Proportionately on each Assessor s Parcel of Other Taxable Property at up to the Maximum Special Tax for Other Taxable Property. Pursuant to the Rate and Method (as stated above) and under the Act, under no circumstances will the Special Tax levied in any Fiscal Year against any taxable parcel of residential property within Improvement Area No. 5 be increased by more than 10% as a consequence of a delinquency or default by the owner of any other parcel within Improvement Area No. 5 above the amount that would have been levied in that Fiscal Year had there never been any such delinquencies or defaults. Such limitation would not apply to increases in Special Taxes levied for other purposes, such as the issuance of Additional Bonds or the acquisition of Facilities. See Appendix A. Prepayment of Special Taxes. The obligation of an Assessor s Parcel to pay the Special Tax may be prepaid and permanently satisfied as described in the Rate and Method; provided that a prepayment may be made only for Assessor s Parcels of Developed Property or Undeveloped Property for which a building permit has been issued, and only if there are no delinquent Special Taxes with respect to such Assessor s Parcel at the time of prepayment, provided that the terms set forth under Section I of the Rate and Method are satisfied. The Prepayment Amount is calculated based on the Bond Redemption Amount, plus Redemption Premium, plus the Future Facilities Amount, plus Defeasance Amount, plus Administrative Fees and Expenses, less a credit for the resulting reduction in the Reserve Requirement for the Bonds (if any), all as specified in Appendix A. See the captions THE SERIES 2017 BONDS Redemption Mandatory Redemption from Special Tax Prepayments and SPECIAL RISK FACTORS Potential Early Redemption of Series 2017 Bonds from Prepayments. Exempt Property. No Special Taxes may be levied on Property Owner Association Property and Public Property, so long as the Acreage of Taxable Property within Improvement Area No. 5 is at least Acres within Zone A and 9.84 Acres within Zone B. Tax-exempt status will be assigned by the District Administrator in the chronological order in which property becomes Property Owner Association Property or Public Property. However, should an Assessor s Parcel no longer be classified as Property Owner Association Property or Public Property, its tax-exempt status will be revoked. To the extent that the exemption of an Assessor s Parcel of Property Owner Association Property or Public Property would reduce the Acreage of Taxable Property within Improvement Area No. 5 below Acres in Zone A or 9.84 Acres in Zone B, such Assessor s Parcel will be classified as Taxable Property Owner Association Property or Taxable Public Property, as applicable, and will be subject to the levy of the Special Tax and will be taxed as part of the Fourth step described above under the caption Method of Apportionment of Special Tax, at up to 100% of the applicable Maximum Special Tax for Other Taxable Property. Collection and Application of Special Taxes The Special Taxes are levied and collected by the Treasurer-Tax Collector of the County in the same manner and at the same time as ad valorem property taxes; provided, however, that the District may directly bill the Special Taxes, may collect Special Taxes at a different time or in a different manner if necessary to meet its financial obligations, and may covenant to foreclose and may actually foreclose on delinquent Assessor s Parcels as permitted by the Act. The District has made certain covenants in the Indenture for the purpose of ensuring that the current maximum rates and method of collection of the Special Taxes are not altered in a manner that would impair the District s ability to collect sufficient Special Taxes to pay debt service on the Bonds and Administrative 14

23 Expenses when due. First, the District has covenanted that, to the extent that it is legally permitted to do so, it will not initiate proceedings under the Act to modify the Rate and Method if such modification would adversely affect the security for the Bonds and that, if an initiative is adopted that purports to modify the Rate and Method in a manner that would adversely affect the security for the Bonds, the District will, to the extent permitted by law, commence and pursue reasonable legal actions to prevent the modification of the Rate and Method in a manner that would adversely affect the security for the Bonds. See the caption SPECIAL RISK FACTORS Proposition 218. Second, the District has covenanted not to authorize owners of taxable parcels within Improvement Area No. 5 to satisfy Special Tax obligations by the tender of Bonds unless the District has first obtained a report of an Independent Consultant certifying that doing so would not result in the District having insufficient Special Tax Revenues to pay the principal of and interest on all Outstanding Bonds when due. See the caption SPECIAL RISK FACTORS Non-Cash Payments of Special Taxes. Although the Special Taxes constitute liens on Taxable Property within Improvement Area No. 5, they do not constitute a personal indebtedness of the owners of such property within Improvement Area No. 5. Moreover, other liens for taxes and assessments already exist on the property located within Improvement Area No. 5 and other such liens could come into existence in the future in certain situations without the consent or knowledge of the County or the landowners therein. See the caption SPECIAL RISK FACTORS Parity Taxes, Special Assessments and Land Development Costs. There is no assurance that property owners will be financially able to pay the annual Special Taxes or that they will pay such taxes even if financially able to do so, all as more fully described in under the caption SPECIAL RISK FACTORS. Under the terms of the Indenture, the Trustee will establish and maintain a separate fund designated the Special Tax Fund. No later than 10 Business Days after the receipt of any Special Tax Revenues, the District will transfer such Special Tax Revenues to the Trustee for deposit in the Special Tax Fund; provided, however, that with respect to any such Special Tax Revenues that represent prepaid Special Taxes, the provisions described under the captions Special Tax Fund and THE SERIES 2017 BONDS Redemption Mandatory Redemption from Special Tax Prepayment apply. Covenant for Superior Court Foreclosure In the event of a delinquency in the payment of any installment of Special Taxes, the District is authorized by the Act to institute an action in the County Superior Court to foreclose any lien therefor. In such action, the real property subject to the Special Taxes may be sold at a judicial foreclosure sale. Such judicial foreclosure proceedings are not mandatory. However, in the Indenture, the District has covenanted for the benefit of the Owners of the Bonds that it will determine or cause to be determined, no later than September 15 of each year, whether or not any owners of property within Improvement Area No. 5 are delinquent in the payment of Special Taxes and, if such delinquencies exist, the District will order and cause to be commenced no later than November 1, and thereafter diligently prosecute, an action in the County Superior Court to foreclose the lien of any Special Taxes or installment thereof not paid when due; provided, however, that the District is not required to order the commencement of foreclosure proceedings if: (a) the total Special Tax delinquency in Improvement Area No. 5 for such Fiscal Year is less than 5% of the total Special Tax levied in such Fiscal Year; and (b) the amount then on deposit in the Reserve Fund is equal to the Reserve Requirement. Notwithstanding the foregoing, if the District determines that any single property owner in Improvement Area No. 5 is delinquent in excess of $3,500 in the payment of the Special Tax, then the District will diligently institute, prosecute and pursue foreclosure proceedings against such property owner. The mere commencement of foreclosure proceedings will not assure a prompt and favorable resolution of Special Tax delinquencies. The ability of the District to foreclose the lien of delinquent unpaid Special Taxes may be limited. See the captions SPECIAL RISK FACTORS Bankruptcy and Foreclosure and SPECIAL RISK FACTORS FDIC/Federal Government Interests in Properties. Moreover, even if a judgment of foreclosure and order of sale is obtained, the District must cause a notice of levy to be issued. Under current law, the property owner has 120 days from the date of service of the notice of levy in which to 15

24 redeem the subject property. If the property owner fails to redeem the property and it is sold, the property owner s only remedy is an action to set aside the sale, which action must be brought within 90 days of the date of sale. If such an action results in the setting aside of the foreclosure sale, the judgment is revived, and the District would be entitled to receive interest on the revived judgment as if the sale had not been made. Under former law a property owner had a period of one year within which to redeem property to be sold, and the constitutionality of the legislation that eliminated the one year redemption period has not been tested. There can be no assurance that, even if the subject property is sold, the proceeds from such sale will be sufficient to pay the delinquent installments of the Special Tax. The Act does not require the District or any other governmental agency to purchase or otherwise acquire any Assessor s Parcel being sold if there is no other purchaser at such sale. The Act does require that property being sold pursuant to foreclosure under the Act must be sold for not less than the judgment amount (which must include reasonable attorneys fees, together with interest, penalties, and other authorized charges and costs) plus post-judgment interest and authorized costs, unless a lower bid price is authorized by the Owners of at least 75% by value of the Bonds Outstanding. Maximum Special Tax Capacity The following Table 1 shows debt service coverage capacity on the Series 2017 Bonds from Net Special Tax Revenues levied at the Assigned Special Tax rate on Developed Property. For Fiscal Year , the Undeveloped Property Special Taxes is shown as $0.00 due to the fact that there is no actual levy on Undeveloped Property. For the Fiscal Year Special Tax levy, all 270 parcels within Improvement Area No. 5 will be classified as Developed Property. In Table 1 below, the Developed Property Special Taxes for Fiscal Year and thereafter assume a levy at 100% of the Assigned Special Tax rate on 270 parcels of Developed Property. The District expects to levy the Special Taxes in order to pay debt service on the Series 2017 Bonds and estimated administrative expenses, which levy is expected to be less than 100% of the Assigned Special Tax rate. Pursuant to the Act, under no circumstances will the Special Tax levied in any Fiscal Year against any taxable parcel of residential property within Improvement Area No. 5 be increased by more than 10% as a consequence of a delinquency or default by the owner of any other parcel within Improvement Area No. 5 above the amount that would have been levied in that Fiscal Year had there never been any such delinquencies or defaults. Investors should not assume actual capacity from Assigned Special Taxes on Developed Property in excess of 110% of debt service plus administrative expenses. 16

25 Fiscal Year TABLE 1 COUNTY OF SAN BERNARDINO COMMUNITY FACILITIES DISTRICT NO (LYTLE CREEK NORTH) IMPROVEMENT AREA NO. 5 DEBT SERVICE COVERAGE CAPACITY Special Tax Revenues (1) Administrative Expenses (2) Net Special Tax Revenues Series 2017 Bonds Debt Service (3) Debt Service Coverage Capacity 2018 $ 467,658 $ 0 $ 467,658 $ 424, % ,121 30, , , ,121 30, , , ,121 30, , , ,121 30, , , ,121 30, , , ,121 30, , , ,121 30, , , ,121 30, , , ,121 30, , , ,121 30, , , ,121 30, , , ,121 30, , , ,121 30, , , ,121 30, , , ,121 30, , , ,121 30, , , ,121 30, , , ,121 30, , , ,121 30, , , ,121 30, , , ,121 30, , , ,121 30, , , ,121 30, , , ,121 30, , , ,121 30, , , ,121 30, , , ,121 30, , , ,121 30, , , ,121 30, , , ,121 30, , , TOTAL $ 17,691,288 $ 900,000 $ 16,791,288 $ 15,183,633 (1) For Fiscal Year , Developed Property Special Tax Revenues are equal to 100% of the Assigned Special Tax on 220 parcels of Developed Property. The District did not levy Special Taxes on Undeveloped Property in Fiscal Year All 270 parcels within Improvement Area No. 5 will be classified as Developed Property for the Fiscal Year Special Tax levy. Fiscal Year and thereafter reflect a Special Tax levy at 100% of the Assigned Special Tax rate on all 270 parcels of Developed Property. (2) Based on the estimated administrative expenses of $30,000 in Fiscal Year and thereafter. (3) May not sum due to rounding. Source: David Taussig & Associates, Inc. Property Values Assessed Values. According to the County of San Bernardino Assessor, the property within Improvement Area No. 5 had a Fiscal Year net assessed value of $40,588,845, based on a January 1, 2017 lien date. 17