$12,850,000 COUNTY OF EL DORADO COMMUNITY FACILITIES DISTRICT NO (CARSON CREEK) SPECIAL TAX BONDS SERIES 2016

|

|

|

- Shannon Short

- 6 years ago

- Views:

Transcription

1 NEW ISSUE-FULL BOOK ENTRY NOT RATED In the opinion of Jones Hall, A Professional Law Corporation, San Francisco, California, Bond Counsel, subject, however to certain qualifications described herein, under existing law, the interest on the Bonds is excluded from gross income for federal income tax purposes and such interest is not an item of tax preference for purposes of the federal alternative minimum tax imposed on individuals and corporations, although for the purpose of computing the alternative minimum tax imposed on certain corporations, such interest is taken into account in determining certain income and earnings. In the further opinion of Bond Counsel, such interest is exempt from California personal income taxes. See "TAX MATTERS" herein. $12,850,000 COUNTY OF EL DORADO COMMUNITY FACILITIES DISTRICT NO (CARSON CREEK) SPECIAL TAX BONDS SERIES 2016 Dated: Date of Delivery Due: September 1, as shown below The bonds captioned above (the "Bonds"), are being issued by the County of El Dorado (the "County") by and through its Community Facilities District No (Carson Creek) (the "District"). The Bonds are special tax obligations of the County, authorized pursuant to the Mello-Roos Community Facilities Act of 1982, as amended, being California Government Code Section 53311, et seq. (the "Act"), and are issued pursuant to a Fiscal Agent Agreement dated as of September 1, 2016 (the "Fiscal Agent Agreement") by and between the County and The Bank of New York Mellon Trust Company, N.A., as fiscal agent (the "Fiscal Agent"). The Bonds are being issued to (i) construct and acquire certain public facilities of benefit to the District, (ii) provide for the establishment of a reserve fund, and (iii) pay initial administration expenses and the costs of issuance of the Bonds. Interest on the Bonds is payable March 1, 2017, and thereafter semiannually on September 1 and March 1 of each year. The Bonds are being issued as fully registered bonds, registered in the name of Cede & Co. as nominee of The Depository Trust Company, New York, New York ("DTC"), and will be available to ultimate purchasers in the denomination of $5,000 or any integral multiple thereof, under the book-entry system maintained by DTC. See "APPENDIX G THE BOOK-ENTRY SYSTEM." The Bonds are secured by and payable from a pledge of Special Tax Revenues (as defined herein) derived from Special Taxes (as defined herein) to be levied by the County on real property within the boundaries of the District, from the proceeds of any foreclosure actions brought following a delinquency in the payment of the Special Taxes, and from amounts held in certain funds under the Fiscal Agent Agreement, all as more fully described herein. Unpaid Special Taxes do not constitute a personal indebtedness of the owners of the parcels within the District. In the event of delinquency, proceedings may be conducted only against the parcel of real property securing the delinquent Special Tax. There is no assurance the owners will be able to pay the Special Tax or that they will pay a Special Tax even though financially able to do so. To provide funds for payment of the Bonds and the interest thereon as a result of any delinquent Special Taxes, the County will establish a Reserve Fund from proceeds of the Bonds, as described herein. See "SECURITY FOR THE BONDS." Property in the District subject to the Special Tax comprises approximately 264 gross acres. Land in the District is planned for 1,059 age-restricted single family residential homes and 4 acres of multi-family use. Construction and sales of homes has commenced by Lennar Homes of California, Inc., which anticipates developing all of the single family homes in the District. See "THE DISTRICT" and "OWNERSHIP OF PROPERTY WITHIN THE DISTRICT." The Bonds are subject to optional and mandatory redemption prior to maturity as described herein. See "THE BONDS Redemption." NEITHER THE FAITH AND CREDIT NOR THE TAXING POWER OF THE COUNTY, THE STATE OF CALIFORNIA OR ANY POLITICAL SUBDIVISION THEREOF IS PLEDGED TO THE PAYMENT OF THE BONDS. THE BONDS DO NOT CONSTITUTE A DEBT OF THE COUNTY WITHIN THE MEANING OF ANY STATUTORY OR CONSTITUTIONAL DEBT LIMITATION. THE INFORMATION SET FORTH IN THIS OFFICIAL STATEMENT, INCLUDING INFORMATION UNDER THE HEADING "SPECIAL RISK FACTORS," SHOULD BE READ IN ITS ENTIRETY. This cover page contains certain information for general reference only. It is not a summary of all of the provisions of the Bonds. Prospective investors must read the entire Official Statement to obtain information essential to the making of an informed investment decision. See "SPECIAL RISK FACTORS" herein for a discussion of the special risk factors that should be considered, in addition to the other matters and risk factors set forth herein, in evaluating the investment quality of the Bonds. The Bonds are offered when, as and if issued, subject to approval as to their legality by Jones Hall, a Professional Law Corporation, San Francisco, California, Bond Counsel. Certain legal matters will also be passed on by Jones Hall, as Disclosure Counsel, and Stradling, Yocca, Carlson & Rauth, Newport Beach, California, as counsel to the Underwriter. It is anticipated that the Bonds will be available for delivery through the facilities of DTC on or about September 15, 2016 in New York, New York. The date of this Official Statement is August 23, 2016

2 Maturity Date (September 1) MATURITY SCHEDULE $5,630,000 Serial Bonds Principal Amount Interest Rate Yield Price 2017 $130, % 0.660% % HK , HL , HM , HN , HP , HQ , HR , HS , HT , HU , C HV , C HW , C HX , C HY , HZ , JA , JB , JC , JD , JE9 CUSIP (283113) $1,725, % Term Bond Due September 1, 2039; Price: %; Yield: 3.250%; CUSIP: JF6 $5,495, % Term Bond Due September 1, 2046 Price: % C ; Yield: 2.940%; CUSIP: JG4 C : Serial bonds priced to first optional redemption date of September 1, 2023 at 103%. Term Bond due September 1, 2046 priced to optional redemption date of September 1, 2024 at 102%. Copyright 2016, CUSIP Global Services, and a registered trademark of the American Bankers Association. CUSIP data is provided by CUSIP Global Services, which is managed on behalf of American Bankers Association by S&P Capital IQ. Neither the County nor the Underwriter assumes any responsibility for the accuracy of the CUSIP data.

3 COUNTY OF EL DORADO, CALIFORNIA Board of Supervisors Ron Mikulaco, District No. 1 Shiva Frentzen, District No. 2 Brian Veerkamp, District No. 3 Michael Ranalli, District No. 4 Sue Novasel, District No. 5 County Officials Karl Weiland, Assessor Joe Harn, Auditor-Controller C.L. Raffety, Treasurer-Tax Collector County Staff Don Ashton, Chief Administrative Officer Michael Ciccozzi, County Counsel Steve Pedretti, Director of Community Development Agency SPECIAL SERVICES Bond Counsel Jones Hall, A Professional Law Corporation San Francisco, California Fiscal Agent The Bank of New York Mellon Trust Company, N.A. Los Angeles, California District Administrator NBS Government Finance Group Temecula, California Appraiser Bender Rosenthal, Inc. Sacramento, California Disclosure Counsel Jones Hall, A Professional Law Corporation San Francisco, California

4 GENERAL INFORMATION ABOUT THIS OFFICIAL STATEMENT Use of Official Statement. This Official Statement is submitted in connection with the sale of the Bonds referred to herein and may not be reproduced or used, in whole or in part, for any other purpose. This Official Statement is not to be construed as a contract with the purchasers of the Bonds. Estimates and Forecasts. When used in this Official Statement and in any continuing disclosure by the County or the Developer, in any press release and in any oral statement made with the approval of an authorized officer of the County or the Developer, the words or phrases "will likely result," "are expected to", "will continue", "is anticipated", "estimate", "project," "forecast", "expect", "intend" and similar expressions identify "forward looking statements." Such statements are subject to risks and uncertainties that could cause actual results to differ materially from those contemplated in such forwardlooking statements. Any forecast is subject to such uncertainties. Inevitably, some assumptions used to develop the forecasts will not be realized and unanticipated events and circumstances may occur. Therefore, there are likely to be differences between forecasts and actual results, and those differences may be material. The information and expressions of opinion herein are subject to change without notice, and neither the delivery of this Official Statement nor any sale made hereunder shall, under any circumstances, give rise to any implication that there has been no change in the affairs of the County since the date hereof. Limit of Offering. No dealer, broker, salesperson or other person has been authorized by the County to give any information or to make any representations in connection with the offer or sale of the Bonds other than those contained herein and if given or made, such other information or representation must not be relied upon as having been authorized by the County or the Underwriter. This Official Statement does not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of the Bonds by a person in any jurisdiction in which it is unlawful for such person to make such an offer, solicitation or sale. Involvement of Underwriter. The Underwriter has provided the following sentence for inclusion in this Official Statement. The Underwriter has reviewed the information in this Official Statement in accordance with, and as a part of, their responsibilities to investors under the Federal Securities Laws as applied to the facts and circumstances of this transaction, but the Underwriter does not guarantee the accuracy or completeness of such information. The information and expressions of opinions herein are subject to change without notice and neither delivery of this Official Statement nor any sale made hereunder shall, under any circumstances, create any implication that there has been no change in the affairs of the County since the date hereof. All summaries of the documents referred to in this Official Statement, are made subject to the provisions of such documents, respectively, and do not purport to be complete statements of any or all of such provisions. IN CONNECTION WITH THIS OFFERING, THE UNDERWRITER MAY OVERALLOT OR EFFECT TRANSACTIONS WHICH STABILIZE OR MAINTAIN THE MARKET PRICE OF THE BONDS AT A LEVEL ABOVE THAT WHICH MIGHT OTHERWISE PREVAIL IN THE OPEN MARKET. SUCH STABILIZING, IF COMMENCED, MAY BE DISCONTINUED AT ANY TIME. THE BONDS HAVE NOT BEEN REGISTERED UNDER THE SECURITIES ACT OF 1933, AS AMENDED, IN RELIANCE UPON AN EXCEPTION FROM THE REGISTRATION REQUIREMENTS CONTAINED IN SUCH ACT. THE BONDS HAVE NOT BEEN REGISTERED OR QUALIFIED UNDER THE SECURITIES LAWS OF ANY STATE.

5 TABLE OF CONTENTS Page INTRODUCTION... 1 THE BONDS... 6 Authority for Issuance... 6 Description of the Bonds... 6 Redemption... 7 Transfer or Exchange of Bonds ESTIMATED SOURCES AND USES OF FUNDS SECURITY AND SOURCES OF PAYMENT FOR THE BONDS General Special Taxes Special Tax Methodology Levy of Annual Special Tax; Maximum Special Tax Delinquent Payments of Special Tax; Covenant for Superior Court Foreclosure Reserve Fund Special Tax Fund Bond Fund Community Facilities Fund Additional Bonds DEBT SERVICE SCHEDULE THE FACILITIES Eligible Facilities Estimated Cost of the Facilities THE DISTRICT Formation of the District Location and Description of the District Planned Development in the District OWNERSHIP OF PROPERTY WITHIN THE DISTRICT APPRAISAL OF PROPERTY WITHIN THE DISTRICT The Appraisal Value to Special Tax Burden Ratios Overlapping Liens and Priority of Lien Estimated Tax Burden on Single Family Home SPECIAL RISK FACTORS Concentration of Property Ownership Failure or Inability to Complete Proposed Development on a Timely Basis Disclosures to Future Purchasers Impact Fees Litigation - Austin v. County of El Dorado Future Land Use Regulations Earthquakes Endangered Species Hazardous Substances Naturally Occurring Asbestos California Drought Conditions Potential Impact of Water Shortage Water Reports Direct and Overlapping Public Indebtedness Private Indebtedness Land Values Collection of Special Tax Maximum Special Tax Rates Exempt Properties FDIC/Federal Government Interests in Properties Bankruptcy and Foreclosure Delays No Acceleration Provision Loss of Tax Exemption Ballot Initiatives Absence of Secondary Market for the Bonds Recent Case Law Related to the Mello-Roos Act i

6 LEGAL MATTERS Legal Opinions Tax Exemption No Litigation CONTINUING DISCLOSURE NO RATINGS UNDERWRITING PROFESSIONAL FEES EXECUTION APPENDIX A - RATE AND METHOD OF APPORTIONMENT OF SPECIAL TAX APPENDIX B - THE APPRAISAL APPENDIX C - THE COUNTY OF EL DORADO APPENDIX D - FORM OF OPINION OF BOND COUNSEL APPENDIX E - FORMS OF CONTINUING DISCLOSURE UNDERTAKINGS APPENDIX F - THE BOOK ENTRY SYSTEM APPENDIX G - SUMMARY OF CERTAIN PROVISIONS OF THE FISCAL AGENT AGREEMENT ii

7 OFFICIAL STATEMENT $12,850,000 COUNTY OF EL DORADO COMMUNITY FACILITIES DISTRICT NO (CARSON CREEK) SPECIAL TAX BONDS SERIES 2016 This Official Statement, including the cover page and all Appendices hereto, is provided to furnish certain information in connection with the issuance by the County of El Dorado (the "County") by and through its Community Facilities District No (Carson Creek) (the "District") of the bonds captioned above (the "Bonds"). Any statements made in this Official Statement involving matters of opinion or of estimates, whether or not so expressly stated, are set forth as such and not as representations of fact, and no representation is made that any of the estimates will be realized. Definitions of certain terms used herein and not defined herein have the meaning set forth in the Fiscal Agent Agreement. INTRODUCTION This introduction is not a summary of this Official Statement. It is only a brief description of and guide to, and is qualified by, more complete and detailed information contained in the entire Official Statement, including the cover page and attached appendices, and the documents summarized or described in this Official Statement. A full review should be made of the entire Official Statement. The offering of the Bonds to potential investors is made only by means of the entire Official Statement. Creation of the District. On January 27, 2015, the Board of Supervisors adopted Resolution No (the "Resolution of Formation"), which formed the District and followed a Resolution of Intention adopted December 16, The District was established and authorized to incur bonded indebtedness in an aggregate principal amount not to exceed $50,000,000 at a special election in the District held on the same day. Under the provisions of the Act, since there were fewer than 12 registered voters residing within the District at any point during the 90-day period preceding the adoption of the Resolution of Formation, the qualified electors entitled to vote in the special election consisted solely of Lennar Homes of California, Inc. a California Corporation (the Developer ), the only eligible landowner/voter in the District. The landowner voted to incur the indebtedness and to approve the annual levy of Special Taxes to be collected within the District, for the purpose of paying for the Facilities, including repaying any indebtedness of the District, replenishing the Reserve Fund and paying the administrative expenses of the District. See "THE DISTRICT" herein. See "SECURITY AND SOURCES OF PAYMENT FOR THE BONDS Additional Bonds" below.

8 The Bonds are issued pursuant to the provisions of the Mello-Roos Community Facilities Act of 1982, as amended (Sections 53311, et seq., of the Government Code of the State of California) (the "Act") and pursuant to a Fiscal Agent Agreement dated as of September 1, 2016 (the "Fiscal Agent Agreement") between the County and The Bank of New York Mellon Trust Company, N.A., Los Angeles, California, as fiscal agent (the "Fiscal Agent") and Resolution No (the "Resolution") adopted on April 7, 2015 by the Board of Supervisors of the County (the "Board of Supervisors") which authorized the issuance of the Bonds payable from Special Taxes (as defined herein) levied on property within the District according to a methodology approved by the County. The Bonds represent the first series of a total of $50,000,000 of bonds authorized by the District and the issuance of additional bonds in the future are contemplated. See "SECURITY FOR THE BONDS" herein. Bond Terms. The Bonds will be dated as of and bear interest from the date of delivery thereof at the rate or rates set forth on the cover page of this Official Statement. Interest on the Bonds is payable on March 1 and September 1 of each year (each an "Interest Payment Date"), commencing March 1, The Bonds will be issued without coupons in denominations of $5,000 or any integral multiple thereof. Registration of Ownership of Bonds. The Bonds will be issued only as fully registered bonds in book-entry form, registered in the name of Cede & Co., as nominee of The Depository Trust Company ("DTC"). Ultimate purchasers of Bonds will not receive physical certificates representing their interest in the Bonds. So long as the Bonds are registered in the name of Cede & Co., as nominee of DTC, references herein to the Owners will mean Cede & Co., and will not mean the ultimate purchasers of the Bonds. Payments of the principal, premium, if any, and interest on the Bonds will be made directly to DTC, or its nominee, Cede & Co. so long as DTC or Cede & Co. is the registered owner of the Bonds. Disbursements of such payments to DTC s Participants is the responsibility of DTC and disbursements of such payments to the Beneficial Owners is the responsibility of DTC s Participants and Indirect Participants, as more fully described herein. See "APPENDIX F THE BOOK-ENTRY SYSTEM." Use of Proceeds. Proceeds of the Bonds will primarily be used to finance the costs of constructing and installing public facilities authorized to be financed by the Special Taxes (the "Facilities," as described herein). The Facilities consist generally of roadway and transportation improvements, intersection and signal improvements, sanitary sewer systems, drainage systems, potable water systems, landscaping improvements, development impact fees, and other infrastructure improvements necessary for development of property within the District, as well as park and open space improvements (which include environmental mitigation costs). Portions of the Facilities comprising backbone infrastructure are complete or nearly complete, including Carson Crossing Drive, utility infrastructure and grading, as well as a sewer lift station. Homebuilding commenced in 2015; models are open and sales are underway. See THE DISTRICT - Planned Development in the District herein. The cost of a portion of the Facilities will be reimbursed by the proceeds of the Bonds and by additional bonds expected to be issued in the future, as described below, and the Developer is required to fund any remaining shortfall. See "THE FACILITIES." Proceeds of the Bonds will also be used to establish a reserve fund (described below) available for payment on the Bonds and to provide initial administration costs and to pay cost of the issuance of the Bonds. Source of Payment of the Bonds. The Board of Supervisors has covenanted to annually levy special taxes on the property in the District (the "Special Taxes") beginning in fiscal year in accordance with the Rate and Method of Apportionment for County of El Dorado Community Facilities District No (Carson Creek) (as amended, the "Rate and Method"), which is attached as APPENDIX B to this Official Statement. The Bonds and any Additional Bonds 2

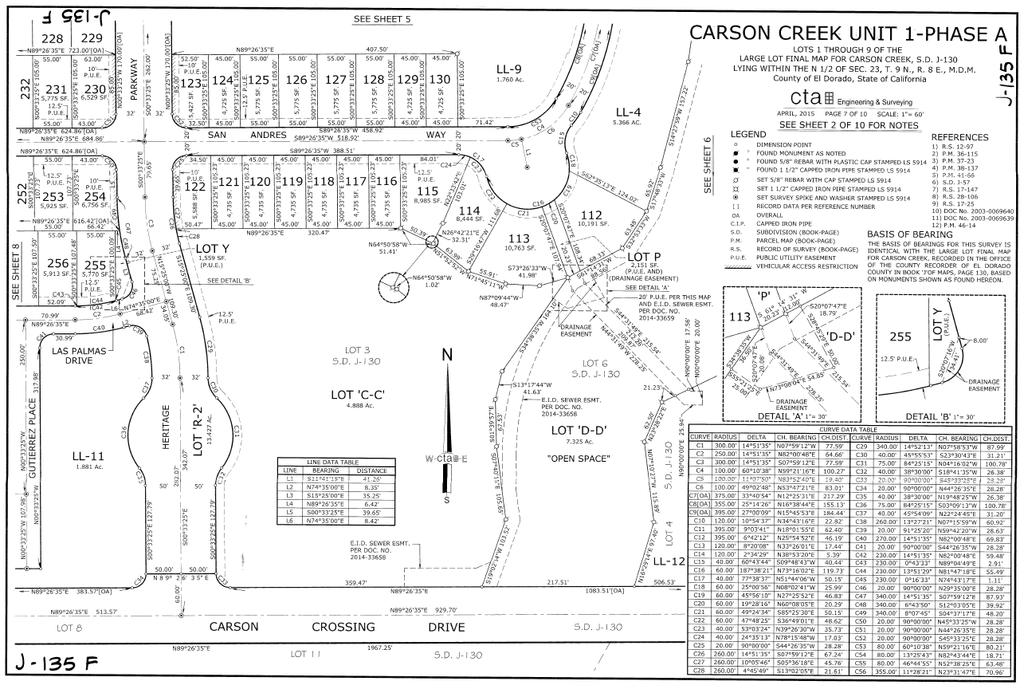

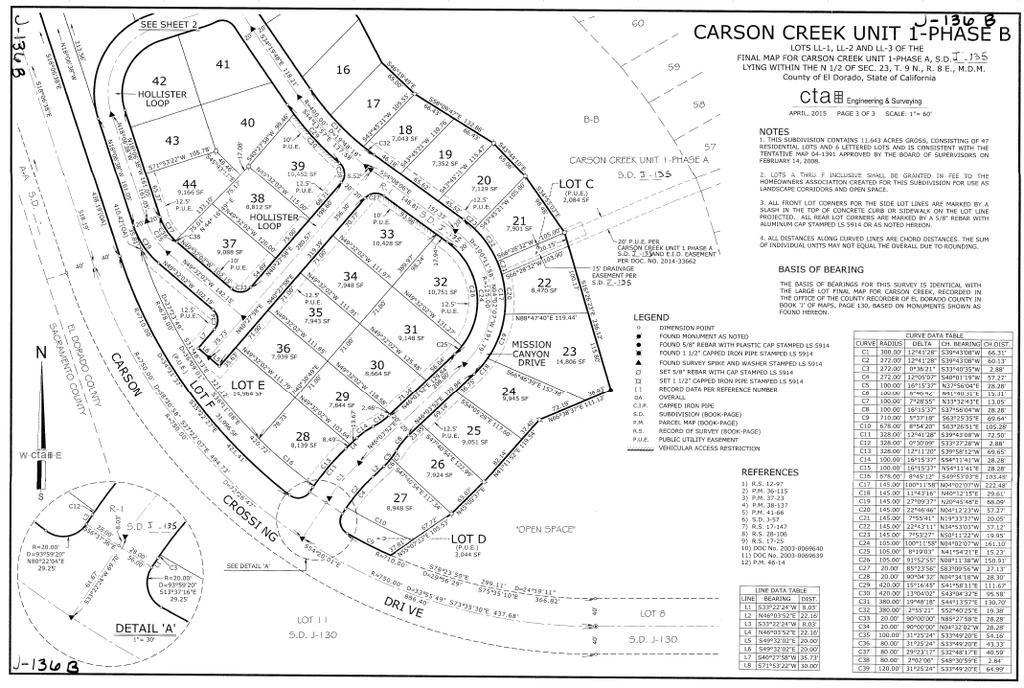

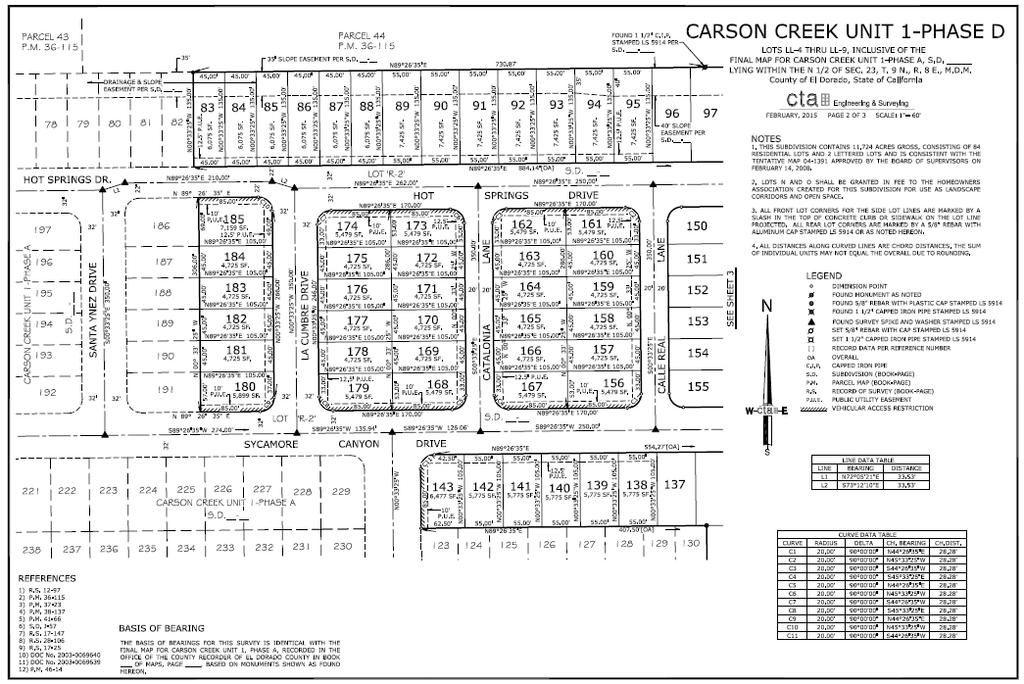

9 (as defined herein) are secured by and payable from a first pledge of "Special Tax Revenues." Special Tax Revenues are proceeds of the Special Taxes received by the County, including any scheduled payments thereof, interest and proceeds of the redemption or sale of property sold as a result of foreclosure of the lien of the Special Taxes to the amount of said interest (but not including any interest in excess of the interest due on the Bonds and the Bonds or any penalties collected in connection with any such foreclosure). Special Taxes are the special taxes levied by the County within the District pursuant to the Rate and Method under the Act, the Ordinance and the Fiscal Agent Agreement. See SECURITY AND SOURCES OF PAYMENT FOR THE BONDS Special Tax Methodology" and "APPENDIX A RATE AND METHOD OF APPORTIONMENT OF SPECIAL TAX." Pursuant to the Act, the Resolution of Formation (as defined herein), and the Fiscal Agent Agreements, so long as any Bonds are outstanding, the County will annually levy the Special Tax against all land within the District that is taxable under the Act and the Rate and Method in accordance with the proceedings for the authorization and issuance of the Bonds and to make provision for the collection of the Special Tax in amounts which will be sufficient to pay interest on, principal of and redemption premium (if any) on the Bonds as such becomes due and payable and to replenish the Reserve Fund (as defined herein) as necessary. See "SECURITY AND SOURCES OF PAYMENT FOR THE BONDS - Special Taxes" herein. Unpaid Special Taxes do not constitute a personal indebtedness of the owners of any of the parcels within the District. In the event of delinquency, proceedings may be conducted only against the real property on which the Special Tax is delinquent. The unpaid Special Taxes are not required to be paid upon sale of property within the District. Additional Bonds. The maximum authorized indebtedness for the District is $50 million; the Bonds are the first series of bonds being issued by the District and additional bonds are expected to be issued in the future. So long as the Bonds are outstanding, any future bonds issued for the District and secured on parity with the Bonds (herein, "Additional Bonds") are required to meet certain conditions of issuance as set forth in the Fiscal Agent Agreement and no bonds having a lien senior to the lien of the Bonds are allowed; see "SECURITY AND SOURCES OF PAYMENT FOR THE BONDS Additional Bonds." Reserve Fund. In the Fiscal Agent Agreement, the County directs the Fiscal Agent to establish a Reserve Fund (the "Reserve Fund") from Bond proceeds in the amount of the Reserve Requirement, which amount is available to be transferred to the Bond Fund in the event of delinquencies in the payment of the Special Taxes, to the extent of such delinquencies. The Reserve Fund is required to be maintained at the Reserve Requirement from moneys available under the Fiscal Agent Agreement. See "SECURITY AND SOURCES OF PAYMENT FOR THE BONDS Reserve Fund." If there are additional delinquencies after depletion of funds in the Reserve Fund, the County is not obligated to pay the Bonds or replenish the Reserve Fund. Covenant to Foreclose. The County has covenanted in the Fiscal Agent Agreement to cause foreclosure proceedings to be commenced and prosecuted against parcels with delinquent installments of the Special Taxes in certain circumstances. For a more detailed description of the foreclosure covenant see "SECURITY AND SOURCES OF PAYMENT FOR THE BONDS - Delinquent Payments of Special Tax; Covenant for Superior Court Foreclosure." Property Subject to the Special Tax. The land in the District is located along the southern line of White Rock Road, just east of and adjacent to the El Dorado County/Sacramento County border, within the County s ("CCSP") area. The land in the District is also known locally as "Carson Creek." Property in the District subject to the Special Tax 3

10 comprises approximately 264 gross acres planned for 1,059 age-restricted single family residential homes and 4 acres of multifamily use expected to be developed as an assisted living facility. Construction of site improvements for the first phase of development has begun and is nearly complete, including the backbone roadway (Carson Crossing Drive), utility infrastructure and grading, and a sewer lift station. Construction of homes commenced in 2015 by the Developer, which anticipates developing all of the single family homes in the District over the next 8 years. As of July 31, 2016, 29 homes had been completed and sold to homewoners, and another 114 homes were under construction, of which 112 were in contract for sale. Non-taxable land uses within the District will incorporate various parks and open space areas, and to a lesser extent, commercial uses. Bond Sizing. The Bonds have been sized to leverage the anticipated Special Tax Revenues generated from Taxable Property in Unit 1 and in Lot 7 of Unit 3, all of which have recorded Final Maps. See Table 4 under the caption THE DISTRICT - Planned Development in the District. Appraised Value of Property. Property in the District classified as Taxable Property (as defined in the Rate and Method) is security for the Special Tax. At the County s request, Bender Rosenthal (the Appraiser ) prepared an appraisal report (the Appraisal ) and a bring forward letter for the taxable real property within the District, which sets forth a total hypothetical bulk vale of not less than $108,070,000, as of April 1, 2016, as confirmed on July 29, 2016 (the Appraised Value ). The valuation assumes completion of the Facilities funded by the Bonds (but not any Additional Bonds) and accounts for the impact of the lien of the Special Tax. However, it does not recognize the full value of the homes completed and sold to individual homeowners since April 1, See "THE FACILITIES." In considering the estimates of value evidenced by the Appraisal, it should be noted that the Appraisal is based upon a number of standard and special assumptions which affect the estimates as to value, in addition to the assumption of completion of the Facilities and other hypothetical circumstances. See "APPRAISAL OF PROPERTY WITHIN THE DISTRICT" and Appendix B. The aggregate Appraised Value is approximately 8.4 times the $12,850,000 aggregate principal amount of the Bonds, and the Appraised Value allocable to the property within Unit 1 and Lot 7 of Unit 3, the tax capacity on which the Bonds have been sized, is approximately 4.8 to 1, assuming all of the Bonds have been allotted only to property upon which Special Taxes are estimated to be levied upon in Fiscal Year See "APPRAISAL OF PROPERTY WITHIN THE DISTRICT." Risks of Investment. See the section of this Official Statement entitled "SPECIAL RISK FACTORS" for a discussion of special factors that should be considered, in addition to the other matters set forth herein, in considering the investment quality of the Bonds. Limited Obligation of the County. The general fund of the County is not liable and the full faith and credit of the County is not pledged for the payment of the interest on, or principal of or redemption premiums, if any, on the Bonds. The Bonds are not secured by a legal or equitable pledge of or charge, lien or encumbrance upon any property of the County or any of its income or receipts, except the money in the Special Tax Fund and the Reserve Fund (both described herein) established under the Fiscal Agent Agreement, and neither the payment of the interest on nor principal of or redemption premiums, if any, on the Bonds is a general debt, liability or obligation of the County. The Bonds do not constitute an indebtedness of the County within the meaning of any constitutional or statutory debt limitation or restrictions and neither the Board of Supervisors, the County nor any officer or employee thereof are liable for the payment of the interest on or principal of or redemption premiums, if any, on the Bonds other than from the proceeds of the 4

11 Special Taxes and the money in the Special Tax Fund, as provided in the Fiscal Agent Agreement. Summary of Information. Brief descriptions of certain provisions of the Fiscal Agent Agreement, the Bonds and certain other documents are included herein. The descriptions and summaries of documents herein do not purport to be comprehensive or definitive, and reference is made to each such document for the complete details of all its respective terms and conditions, copies of which are available for inspection at the office of the Finance Director of the County. All statements herein with respect to certain rights and remedies are qualified by reference to laws and principles of equity relating to or affecting creditors rights generally. Capitalized terms used in this Official Statement and not otherwise defined herein have the meanings ascribed to such terms in the Fiscal Agent Agreement. The information and expressions of opinion herein speak only as of the date of this Official Statement and are subject to change without notice. Neither delivery of this Official Statement, any sale made hereunder, nor any future use of this Official Statement shall, under any circumstances, create any implication that there has been no change in the affairs of the County or the District since the date hereof. Any statements made in this Official Statement involving matters of opinion or of estimates, whether or not so expressly stated, are set forth as such and not as representations of fact, and no representation is made that any of the estimates will be realized. 5

12 THE BONDS Authority for Issuance The Bonds are issued pursuant to the Fiscal Agent Agreement, approved by Resolutions Nos and adopted by the Board of Supervisors on March 22, 2016 and June 28, 2016, respectively, and the Act. On January 27, 2015, the Board of Supervisors adopted Resolution No (the "Resolution of Formation"), which formed the District and followed a Resolution of Intention adopted December 16, The District was established and authorized to incur bonded indebtedness in an aggregate principal amount not to exceed $50,000,000 at a special election in the District held on the same day. Under the provisions of the Act, since there were fewer than 12 registered voters residing within the District during the 90-day period preceding the adoption of the Resolution of Formation, the qualified electors entitled to vote in the special election consisted solely of the Developer, the only eligible landowner/voter in the District. The landowner voted to incur the indebtedness and to approve the annual levy of Special Taxes to be collected within the District, for the purpose of paying for the Facilities, including repaying any indebtedness of the District, replenishing the Reserve Fund and paying the administrative expenses of the District. See "THE DISTRICT" herein. See "SECURITY AND SOURCES OF PAYMENT FOR THE BONDS Additional Bonds" below. Description of the Bonds Bond Terms. The Bonds will be dated as of and bear interest from the date of delivery thereof at the rates and mature in the amounts and years, as set forth on the cover page hereof. The Bonds are being issued in the denomination of $5,000 or any integral multiple thereof. Interest on the Bonds will be payable semiannually on March 1 and September 1 of each year (each an "Interest Payment Date"), commencing March 1, The principal of the Bonds and premiums due upon the redemption thereof, if any, will be payable in lawful money of the United States of America at the principal corporate trust office of the Fiscal Agent in Los Angeles, California, or such other place as designated by the Fiscal Agent, upon presentation and surrender of the Bonds; provided that so long as any Bonds are in book-entry form, payments with respect to such Bonds will be made by wire transfer, or such other method acceptable to the Fiscal Agent, to DTC. Book-Entry Only System. The Bonds are being issued as fully registered bonds, registered in the name of Cede & Co., as nominee of The Depository Trust Company, New York, New York ("DTC"), and will be available to ultimate purchasers under the book-entry system maintained by DTC. Ultimate purchasers of Bonds will not receive physical certificates representing their interest in the Bonds. So long as the Bonds are registered in the name of Cede & Co., as nominee of DTC, references herein to the Owners will mean Cede & Co., and will not mean the ultimate purchasers of the Bonds. The Fiscal Agent will make payments of the principal, premium, if any, and interest on the Bonds directly to DTC, or its nominee, Cede & Co., so long as DTC or Cede & Co. is the registered owner of the Bonds. Disbursements of such payments to DTC s Participants is the responsibility of DTC and disbursements of such payments to the Beneficial Owners is the responsibility of DTC s Participants and Indirect Participants, as more fully described herein. See "APPENDIX G THE BOOK ENTRY SYSTEM." below. Calculation and Payment of Interest. Interest on the Bonds will be computed on the basis of a 360-day year consisting of twelve 30-day months. Interest on the Bonds (including the 6

13 final interest payment upon maturity or earlier redemption) is payable by check of the Fiscal Agent mailed on each Interest Payment Date by first class mail to the registered Owner thereof at such registered Owner s address as it appears on the registration books maintained by the Fiscal Agent at the close of business on the Record Date preceding the Interest Payment Date, or by wire transfer made on such Interest Payment Date upon written instructions received by the Fiscal Agent on or before the Record Date preceding the Interest Payment Date, of any Owner of $1,000,000 or more in aggregate principal amount of Bonds; provided that so long as any Bonds are in book-entry form, payments with respect to such Bonds will be made by wire transfer, or such other method acceptable to the Fiscal Agent, to DTC. See "APPENDIX G BOOK ENTRY SYSTEM" below. Each Bond will bear interest from the Interest Payment Date next preceding the date of authentication thereof unless (i) it is authenticated on an Interest Payment Date, in which event it will bear interest from such date of authentication, or (ii) it is authenticated prior to an Interest Payment Date and after the close of business on the Record Date preceding such Interest Payment Date, in which event it will bear interest from such Interest Payment Date, or (iii) it is authenticated prior to the Record Date preceding the first Interest Payment Date, in which event it will bear interest from the Dated Date; provided, however, that if at the time of authentication of a Bond, interest is in default thereon, such Bond will bear interest from the Interest Payment Date to which interest has previously been paid or made available for payment thereon. So long as the Bonds are registered in the name of Cede & Co., as nominee of DTC, payments of the principal, premium, if any, and interest on the Bonds will be made directly to DTC, or its nominee, Cede & Co. Disbursements of such payments to DTC s Participants is the responsibility of DTC and disbursements of such payments to the Beneficial Owners is the responsibility of DTC s Participants and Indirect Participants, as more fully described herein. See "APPENDIX G THE BOOK ENTRY SYSTEM" below. Redemption Optional Redemption. The Bonds are subject to optional redemption from any source of available funds prior to maturity at the option of the County, in whole, or in part among maturities selected by the County and by lot within a maturity, on any Interest Payment Date on or after September 1, 2023, at the following respective redemption prices (expressed as percentages of the principal amount of the Bonds to be redeemed), plus accrued interest thereon to the date of redemption: Redemption Dates Redemption Price September 1, 2023 and March 1, % September 1, 2024 and March 1, September 1, 2025 and March 1, September 1, 2026 and Interest Payment Dates thereafter 100 7

14 Mandatory Redemption From Prepayments. The Bonds are subject to mandatory redemption from prepayments of the Special Tax by property owners, in whole or in part among maturities on a pro rata basis among the Bonds and any series of Additional Bonds and by lot within a maturity, on any Interest Payment Date, at the following respective redemption prices (expressed as percentages of the principal amount of the Bonds to be redeemed), plus accrued interest thereon to the date of redemption: Redemption Dates Redemption Price March 1, 2017 and Interest Payment Dates through March 1, % September 1, 2024 and March 1, September 1, 2025 and March 1, September 1, 2026 and Interest Payment Dates thereafter 100 Mandatory Sinking Fund Redemption. The Term Bonds maturing September 1, 2039 and September 1, 2046 are subject to mandatory sinking payment redemption in part on September 1, 2037 and September 1, 2040, respectively, and on each September 1 thereafter to maturity, by lot, at a redemption price equal to 100% of the principal amount thereof to be redeemed, without premium, in the aggregate respective principal amounts as set forth in the following tables: Term Bonds of September 1, 2039 Sinking Fund Redemption Date (September 1) Sinking Payments 2037 $540, , (maturity) 610,000 Term Bonds of September 1, 2046 Sinking Fund Redemption Date (September 1) Sinking Payments 2040 $645, , , , , , (maturity) 935,000 The amounts in the foregoing tables will be reduced pro rata, in order to maintain substantially level debt service, as a result of any prior partial optional redemption or mandatory redemption of the Bonds. Purchase In Lieu of Redemption. In lieu of redemption, moneys in the Bond Fund may be used and withdrawn by the Fiscal Agent for purchase of Outstanding Bonds, upon the filing with the Fiscal Agent of an Officer s Certificate requesting such purchase, at public or private sale as and when, and at such prices (including brokerage and other charges) as such Officer s Certificate may provide, but in no event may Bonds be purchased at a price in excess of the principal amount thereof, plus interest accrued to the date of purchase and any premium which would otherwise be due if such Bonds were to be redeemed in accordance with the Fiscal Agent Agreement. 8

15 Redemption Procedure by Fiscal Agent. The Fiscal Agent will cause notice of any redemption to be mailed by first class mail, postage prepaid, at least 30 days but not more than 60 days prior to the date fixed for redemption, to the Securities Depositories and to one or more Information Services, and to the respective registered Owners of any Bonds designated for redemption, at their addresses appearing on the Bond registration books in the Principal Office of the Fiscal Agent; but such mailing is not a condition precedent to such redemption and failure to mail or to receive any such notice, or any defect therein, will not affect the validity of the proceedings for the redemption of such Bonds. Such notice will state the redemption date and the redemption price and, if less than all of the then Outstanding Bonds are to be called for redemption, shall state as to any Bond called in part the principal amount thereof to be redeemed, and shall require that such Bonds be then surrendered at the Principal Office of the Fiscal Agent for redemption at the said redemption price, and shall state that further interest on such Bonds will not accrue from and after the redemption date. The cost of mailing any such redemption notice and any expenses incurred by the Fiscal Agent in connection therewith shall be paid by the County. The County shall have the right to rescind any notice of prepayment delivered by the Fiscal Agent prior to the date fixed for redemption. Whenever provision is made in the Fiscal Agent Agreement for the redemption of less than all of the Bonds of any maturity or any given portion thereof, the Fiscal Agent will select the Bonds to be redeemed, from all Bonds or such given portion thereof not previously called for redemption, by lot in any manner which the Fiscal Agent in its sole discretion shall deem appropriate; provided, however, that if Bonds are to be redeemed as a result of the prepayment of Special Taxes, Bonds shall be selected for redemption on a pro-rata basis among maturities. Upon surrender of Bonds redeemed in part only, the County will execute and the Fiscal Agent will authenticate and deliver to the registered Owner, at the expense of the County, a new Bond or Bonds, of the same series and maturity, of authorized denominations in aggregate principal amount equal to the unredeemed portion of the Bond or Bonds. Effect of Redemption. From and after the date fixed for redemption, if funds available for the payment of the principal of, and interest and any premium on, the Bonds so called for redemption are deposited in the Bond Fund, such Bonds so called will cease to be entitled to any benefit under the Fiscal Agent Agreement other than the right to receive payment of the redemption price, and no interest will accrue thereon on or after the redemption date specified in such notice. 9

16 Transfer or Exchange of Bonds So long as the Bonds are registered in the name of Cede & Co., as nominee of DTC, transfers and exchanges of Bonds will be made in accordance with DTC procedures. See "Appendix F THE BOOK ENTRY SYSTEM." Any Bond may, in accordance with its terms, be transferred or exchanged by the person in whose name it is registered, in person or by his duly authorized attorney, upon surrender of such Bond for cancellation, accompanied by delivery of a duly written instrument of transfer in a form approved by the Fiscal Agent. Whenever any Bond or Bonds are surrendered for transfer or exchange, the County will execute and the Fiscal Agent will authenticate and deliver a new Bond or Bonds, for a like aggregate principal amount of Bonds of authorized denominations and of the same maturity. The cost for any services rendered or any expenses incurred by the Fiscal Agent in connection with any such transfer or exchange will be paid by the County. The Fiscal Agent will collect from the Owner requesting such transfer any tax or other governmental charge required to be paid with respect to such transfer or exchange. No transfers or exchanges of Bonds will be required to be made (i) within 15 days prior to the date established by the Fiscal Agent for selection of Bonds for redemption or (ii) with respect to a Bond after such Bond has been selected for redemption. ESTIMATED SOURCES AND USES OF FUNDS A summary of the estimated sources and uses of funds associated with the sale of the Bonds follows: Estimated Sources of Funds: Principal Amount of Bonds $12,850, Plus Net Premium 567, Total $13,417, Estimated Uses of Funds: Acquisition and Construction Fund $12,032, Reserve Fund 927, Costs of Issuance (1) 456, Total $13,417, (1) Includes fees of bond and disclosure counsel, initial fees, expenses and charges of the Fiscal Agent, costs of printing the Official Statement, administrative fees of the County, special tax consultant, appraiser, Underwriter s discount, and other costs of issuance. 10

17 SECURITY AND SOURCES OF PAYMENT FOR THE BONDS General Pursuant to the Act, the Rate and Method, the Resolution of Formation and the Fiscal Agent Agreement, the County will annually levy the Special Taxes in an amount sufficient to pay the principal of and interest on the Bonds. The Bonds are secured by and payable from a first pledge of "Special Tax Revenues. Special Tax Revenues are proceeds of the Special Taxes received by the County, including any scheduled payments or prepayments thereof, interest and proceeds of the redemption or sale of property sold as a result of foreclosure of the lien of the Special Taxes to the amount of said interest, but shall not include any interest in excess of the interest due on the Bonds or any penalties collected in connection with any such foreclosure. Special Taxes are the special taxes levied by the County within the District under the Act, pursuant to the Rate and Method, the Ordinance and the Fiscal Agent Agreement. The Bonds are further secured by a first pledge of all moneys deposited in the Bond Fund and the Reserve Fund, both of which are established for the Bonds under the Fiscal Agent Agreement. Furthermore, on a semi-annual basis, until disbursed as provided in the Fiscal Agent Agreement, the Bonds are secured by a first pledge of all moneys in the Special Tax Fund. The Special Tax Revenues and all moneys deposited into such funds are dedicated to the payment of the principal of, and interest and any premium on, the Bonds as provided in the Fiscal Agent Agreement, until all of the Bonds have been paid and retired or until moneys or Federal Securities (as defined in the Fiscal Agent Agreement) have been set aside irrevocably for that purpose. Amounts to be transferred into the Administrative Expense Fund established under the Fiscal Agent Agreement are to be made on a subordinate basis to amounts necessary to be paid on the Bonds. The Facilities financed with the proceeds of the Bonds are not in any way pledged to pay the debt service on the Bonds. Any proceeds of condemnation, destruction or other disposition of any such facilities are not pledged to pay the debt service on the Bonds and are free and clear of any lien or obligation imposed under the Fiscal Agent Agreement. Special Taxes The County has covenanted in the Fiscal Agent Agreement to comply with all requirements of the Act so as to assure the timely collection of Special Tax Revenues, including without limitation, the collection of delinquent Special Taxes through foreclosure proceedings. The Fiscal Agent Agreement provides that the Special Taxes shall be payable and be collected in the same manner and at the same time and in the same installment as the general taxes on real property are payable, and have the same priority, become delinquent at the same times and in the same proportionate amounts and bear the same proportionate penalties and interest after delinquency as do the general taxes on real property. Because the Special Tax levy is limited to the maximum Special Tax rates set forth in the Rate and Method, no assurance can be given that, in the event of Special Tax delinquencies, the receipts of Special Taxes will, in fact, be collected in sufficient amounts in any given year to pay the Bonds. In addition, Section 53321(d) of the Act provides that the special tax levied against any parcel for which an occupancy permit for private residential use has been issued may not be increased as a consequence of delinquency or default by the owner of any other parcel within a community facilities district by more than 11

18 10% above the amount that would have been levied in such Fiscal Year had there never been any such delinquencies or defaults. A Special Tax applicable to each taxable parcel in the District will be levied and collected according to the tax liability determined by the Board of Supervisors through the application of the Rate and Method prepared by NBS, Temecula, California (the "Special Tax Consultant") and set forth in APPENDIX B hereto for all taxable properties in the District. Interest and principal on the Bonds is payable from the annual Special Taxes to be levied and collected on taxable property within the District, from amounts held in the funds and accounts established under the Fiscal Agent Agreement (other than the Rebate Fund) and from the proceeds, if any, from the sale of such property for delinquency of such Special Taxes. The Special Taxes are exempt from the property tax limitation of Article XIIIA of the California Constitution, pursuant to Section 4 thereof, as a "special tax" authorized by a two-thirds vote of the qualified electors. The levy of the Special Taxes was authorized by the County pursuant to the Act in an amount determined according to the Rate and Method approved by the County as approved by a two-thirds vote of the qualified electors. See "Special Tax Methodology" below and "APPENDIX B - Rate and Method of Apportionment." The amount of Special Taxes that may be levied in any year, and from which principal and interest on the Bonds is to be paid, is strictly limited by the maximum rates set forth as the annual "Maximum Special Tax" in the Rate and Method. Under the Rate and Method, Special Taxes for the purpose of making payments on the Bonds will be levied annually in an amount, not in excess of the annual Maximum Special Tax. The Special Taxes and any interest earned on the Special Taxes constitute a trust fund for the principal of and interest on the Bonds pursuant to the Fiscal Agent Agreement and, so long as the principal of and interest on these obligations remains unpaid, the Special Taxes and investment earnings thereon will not be used for any other purpose, except as permitted by the Fiscal Agent Agreement, and will be held in trust for the benefit of the owners thereof and will be applied pursuant to the Fiscal Agent Agreement. The Rate and Method apportions the Special Tax Requirement (as defined in the Rate and Method and described below) among the taxable parcels of real property within the District according to the rate and methodology set forth in the Rate and Method. See "- Special Tax Methodology" below. See also "APPENDIX B - Rate and Method of Apportionment." The County has covenanted to annually levy the Special Taxes in an amount at least sufficient to satisfy the Special Tax Requirement (as defined below). Because each Special Tax levy is limited to the annual Maximum Special Tax rates authorized as set forth in the Rate and Method, no assurance can be given that, in the event of Special Tax delinquencies, the amount of the Special Tax Requirement will in fact be collected in any given year. See "SPECIAL RISK FACTORS Collection of Special Taxes" herein. The Special Taxes are collected for the County by the District in the same manner and at the same time as ad valorem property taxes. 12

19 Special Tax Methodology The Special Tax authorized under the Act applicable to land within the District will be levied and collected according to the tax liability determined by the County through the application of the appropriate amount or rate as described in the Rate and Method set forth in "APPENDIX B - Rate and Method of Apportionment." Capitalized terms set forth in this section and not otherwise defined have the meanings set forth in the Rate and Method. The discussion below incorporates summaries of certain provisions of the Rate and Method, the complete text of which appears in APPENDIX B. The Rate and Method provides that the Special Tax levy each fiscal year is calculated by first determining the "Special Tax Requirement" for the fiscal year. The Special Tax Requirement is defined in the Rate and Method to be the total required to (i) pay debt service which is due in the calendar year that commences in such fiscal year; (ii) pay periodic costs related to bonds; (iii) pay administrative expenses, (iv) pay amounts needed to establish or replenish any reserve funds; and (v) pay any amounts needed for pay-as-you-go expenditures eligble to be funded by the District to the extent that the inclusion of such amount does not increase the Special Tax levy on Undedeloped Property; (vi) an amount equal to the amount of delinquencies in payments of Special Taxes levied in the previous fiscal year, less any credit from earnings on the Reserve Fund, less (vii) a credit for funds available to reduce the annual Special Tax levy. Pursuant to the Rate and Method, the County will prepare a list of the County Assessor's parcels based on the equalized tax rolls as of each January 1 (the "Parcels"). Such rolls reflect ownership of taxable parcels as of January 1 of each year. No Special Tax will be assigned to parcels classified as tax-exempt parcels, i.e. parcels that are, or are intended to be publicly owned and are exempt from the levy of general ad valorem property taxes, such as Public Property or a parcel for which the Special Tax has been prepaid in full. Certain privately owned parcels also may be exempt, including common areas owned by homeowner s associations or property owner associations, wetlands, detention basins, water quality ponds and open space, as determined by the Disrict administrator. Each year, taxable parcels are divided into Developed Property (defined in the Rate and Method as being all Taxable Property in each Fiscal Year for which a Building Permit was issued on or before April 30 of the prior Fiscal Year), Final Map Property (defined in the Rate and Method as being all Taxable Property for which a Final Map has been recorded on or before April 30 of the prior Fiscal Year) or Undeveloped Property (defined in the Rate and Method as being all Taxable Property not classifed as Developed Property or Final Map Property), and shall be subject to allocation of Special Taxes in accordance with the Rate and Method. See APPENDIX B. The County will cause the Special Tax to be levied each Fiscal Year in an amount equal to the Special Tax Requirement by levying parcels in the following priority First: The Special Tax shall be levied on each Assessor s Parcel of Developed Property at up to 100% of the applicable Maximum Special Tax for such Fiscal Year. Second: If additional monies are needed to satisfy the Special Tax Requirement after the first step has been completed, the Special Tax shall be levied Proportionately on each Assessor s Parcel of Final Map Property at up to 100% of the Maximum Special Tax for Final Map Property; Third: If additional monies are needed to satisfy the Special Tax Requirement after the first and second step have been completed, the Special Tax shall be levied Proportionately on each 13

20 Assessor s Parcel of Undeveloped Property at up to 100% of the Maximum Special Tax for Undeveloped Property; The Rate and Method provides that the funding of Facilities can also be made from collections of the Special Tax available as the "pay-as-you-go" component of Special Taxes. Under no circumstances can the Special Tax levied against any parcel for which an occupancy permit for private residential use has been issued be increased as a consequence of delinquency or default by the owner of any other parcel wihtin the District by more than 10% above the amount that would have been levied in such Fiscal Year had there never been any such delinquencies or defaults. The annual Maximum Special Tax as prescribed by the Rate and Method is increased annually at a rate of 2% per year. 14

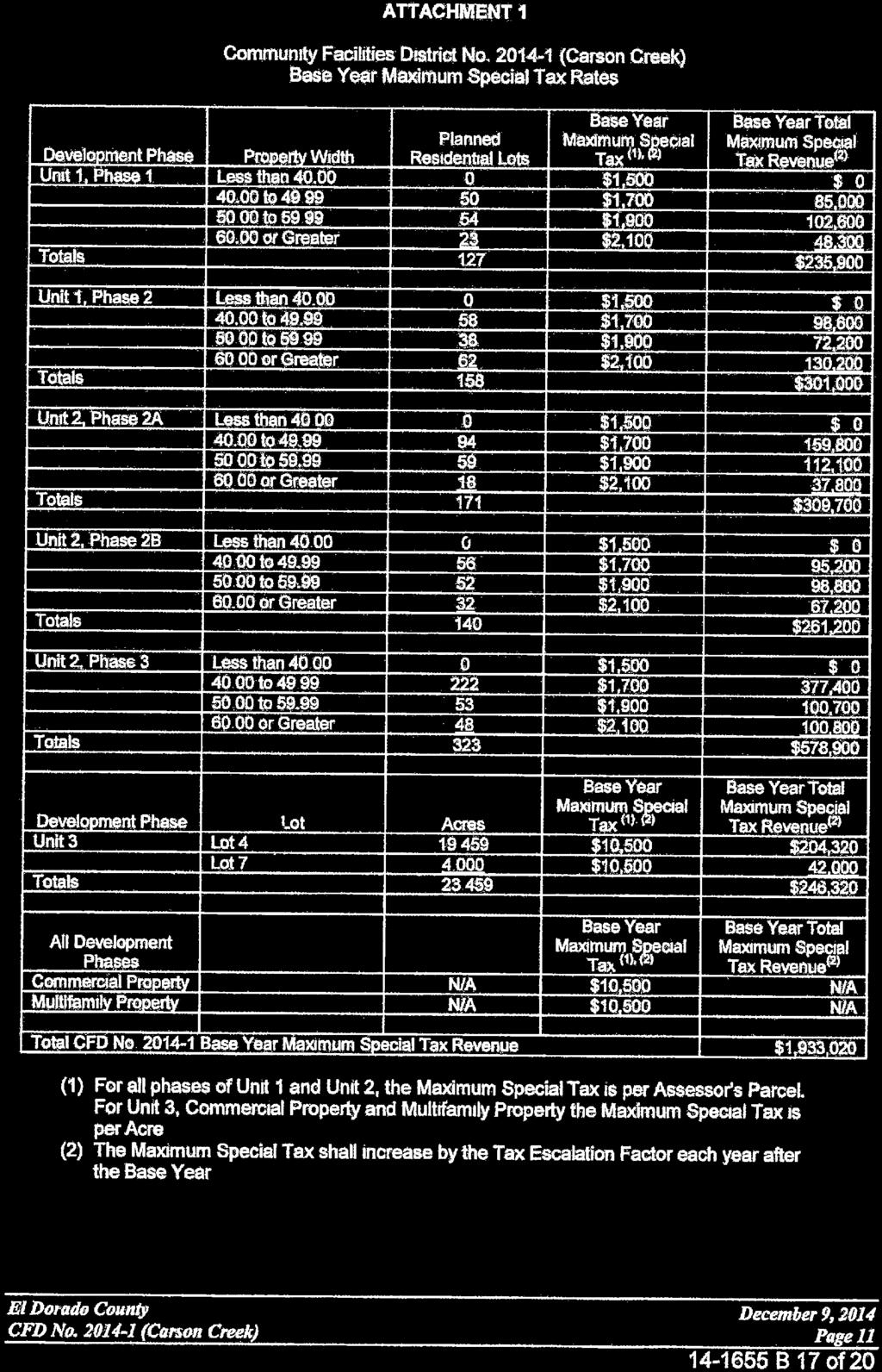

21 TABLE 1 COUNTY OF EL DORADO Community Facilities District No (Carson Creek) Special Tax Bonds Series 2016 Fiscal Year Maximum Special Tax Rates and Anticipated Levy (1) Planned Residential Lots Maximum Special Tax Rates Maximum Special Tax Revenue at Buildout Estimated Special Tax Levy Development Phase Property Width Unit 1 Per Unit IA to $1,769 $95,509 $95, to , , , or Greater 26 2,185 56,806 56,806 IB or Greater 47 2, , ,687 IC to ,977 35,582 35, or Greater 2 2,185 4,370 4,370 ID to ,769 86,665 86, to ,977 41,512 41, or Greater 14 2,185 30,588 30,588 Subtotal , ,463 Unit 2 (2) 2A to , , to , , or Greater 18 2,185 39, B to ,769 99, to , , or Greater 32 2,185 69, Phase to , , to , , or Greater 48 2, , Subtotal 634 1,196, Unit 3 Acres Per Acre Lot , , Lot N/A 10,924 44,483 44,483 Subtotal ,271 44,483 Total 1,059 $2,012,986 $604,947 (1) Based on development status and development plans as of May 2016 (2) Estimated based on the planned residential lot information provided by the Developer. Source: NBS and the Developer Prepayment of Special Tax. Property owners may permanently satisfy the Special Tax obligation of a parcel by a cash settlement with the County as permitted under Government Code Section The procedure for permanently satisfying the Special Tax obligation is set forth in the Rate and Method. See APPENDIX B. Pursuant to the Fiscal Agent Agreement, the County is required to transfer amounts received as prepayments of the Special Tax to the Fiscal Agent to be used to redeem Bonds or portions thereof. See also THE BONDS - Redemption. In addition to payment of the Special Tax, the property owners within the District will also be obligated to pay ad valorem property taxes levied against such property, certain other taxes and assessments, and taxes and assessments to pay existing and any additional overlapping debt for which the property within the District may become obligated. (See THE DISTRICT - Direct and Overlapping Governmental Obligations ). The actual amount of these taxes, which may be levied or assessed in the future, will vary depending upon a number of factors, including the assessed 15

22 value of the property within the District at such time, the actual amount of the Special Tax that is levied annually in the future and the existence of additional taxes and assessments levied in the future. Levy of Annual Special Tax; Maximum Special Tax The Act provides that the Special Tax shall be collected in the same manner as ordinary ad valorem property taxes are collected and shall be subject to the same penalties and the same procedure, sale, and lien priority in case of delinquency as is provided for ad valorem taxes. The County may deduct the reasonable administrative costs incurred in collecting the Special Tax. In the Resolution of Formation, the Board has reserved the right to utilize any method of collecting the Special Tax which it will from time to time determine to be in the best interests of the County. In the Fiscal Agent Agreement the County has covenanted for the Special Taxes to be levied annually on the ad valorem property tax bills prepared by the County Tax Collector for taxable parcels and to be collected in the same manner and, except with respect to foreclosure as provided below under Delinquent Payments of Special Tax; Covenant for Foreclosure, subject to the same penalties and the same procedure, sale, and lien priority in case of delinquency as is provided for ad valorem property taxes. The Fiscal Agent Agreement also authorizes the County to collect the Special Tax on an as-needed basis through direct billing to property owners. Section 4701 et seq. of the California Revenue and Taxation Code authorizes counties, at their option, to adopt an Alternative Method of Distribution of Tax Levies and Collections and of Tax Sale Proceeds specified therein (the Teeter Plan ) to simplify the tax-levying and apportioning process and increase flexibility in the use of available cash resources. For so long as a Teeter Plan is in effect in a particular county, each entity levying property taxes of a class covered by such county s Teeter Plan may draw on the uncollected taxes and assessments credited by the county to such entity s fund following completion of the tax roll whether or not the amount credited has actually been collected. Penalties and collection costs, when received, will be credited to various County-maintained funds rather than to the participating levying entity. The County has a Teeter Plan in effect with respect to the collection of the 1% base ad valorem property tax and with respect to general obligation bonds, but not with respect to special taxes or special assessments. The result is that the amount of the Special Tax that may be drawn upon by the District will be limited to actual collections credited to the Special Tax Fund (as defined herein) rather than amounts allocated to such fund in anticipation of collections as provided for with respect to Teeter Plan levies. For information concerning limits on ad valorem property taxes and the existence of other public and private debt encumbering property within the District, see THE DISTRICT - Direct and Overlapping Governmental Obligations. Pursuant to the Fiscal Agent Agreement, the County is required, upon receipt of Special Taxes, to deposit such proceeds in the Special Tax Fund, which is held by the County. Moneys in the Special Tax Fund are to be disbursed, as received and as needed, as provided in the Fiscal Agent Agreement. 16

23 Delinquent Payments of Special Tax; Covenant for Superior Court Foreclosure Bills for property taxes on the secured roll are mailed annually by the first of September. Such taxes are due in two installments, on November 1 and February 1 of each Fiscal Year. If unpaid, such taxes become delinquent on December 10 and April. 10, respectively, and a 10% penalty attaches to any delinquent payment. Property on the secured roll with respect to which taxes are delinquent becomes tax-defaulted on or about June 30 of the fiscal year. Such property may thereafter be redeemed by payment of a penalty of 1.5% per month to the time of redemption, plus costs and a redemption fee. Pursuant to Section 3691 of the California Revenue and Taxation Code, tax defaulted property not so redeemed within five years after it has become tax-defaulted becomes subject to sale by the County Tax Collector. The Act provides the additional remedy of judicial foreclosure for delinquencies in the payment of a special tax for so long as debt secured by the special tax is outstanding. Pursuant to the Act, the Board may order the institution of a superior court action to foreclose the lien securing a delinquent Special Tax within four years after the due date of the last installment of the principal thereof. A judgment in such an action will include the amount of the delinquency for each parcel to be foreclosed, reasonable attorneys fees, interest, penalties, and other authorized charges and costs and will order the parcel to be sold on execution as in other cases of the sale of real property by process of the court. Such judicial foreclosure action is not mandatory. However, the Board has covenanted for the benefit of the owners of the Bonds that the County Auditor-Controller will review the County s records in connection with the collection of the Special Tax not later than October 1 of each year to determine the amount of the Special Tax collected in the prior fiscal year. The County will annually on or before October 1 of each year review the public records of the County relating to the collection of the Special Tax in order to determine the amount of the Special Tax collected in the prior Fiscal Year, and (a) on the basis of such review the County will, not later than the succeeding December 1, institute foreclosure proceedings as authorized by the Act against all parcels that are delinquent in the payment of such Special Tax in such Fiscal Year by two thousand five hundred dollars ($2,500) or more in order to enforce the lien of all such delinquent installments of such Special Tax, and will diligently prosecute and pursue such foreclosure proceedings to judgment and sale, and (b) on the further basis of such review, if the County determines that the total amount so collected is less than ninety-five per cent (95%) of the total amount of the special tax levied in such Fiscal Year, the County will, not later than the succeeding December 1, institute foreclosure proceedings as authorized by the Act against all parcels that are delinquent in the payment of such Special Tax in such Fiscal Year to enforce the lien of all the delinquent installments of such Special Tax, and will diligently prosecute and pursue such foreclosure proceedings to judgment and sale; provided, that any actions taken to enforce delinquent Special Tax liens shall be taken only consistent with Sections through , both inclusive, of the Government Code of the State of California.. Pursuant to the Act, the property foreclosed upon may not be sold for less than the amount of the judgment in the foreclosure action (which may include reasonable attorneys fees, interest, penalties, and other authorized charges and costs), plus post-judgment interest and authorized costs; provided, however, that the County may, based upon certain determinations set forth in the Act, waive delinquent penalties and redemption penalties. The County has covenanted not to exercise rights under the Act to waive delinquency and redemption penalties related to or to declare an amnesty program with respect to such delinquency and redemption penalties related to the Special Taxes if to do so would materially and adversely affect the interests of the Bondholders. The County has further covenanted not to permit the tender of Bonds in payment of any Special Taxes except upon receipt of a certificate of an independent certified public accountant that to accept such tender will not result in the County having 17

24 insufficient Special Tax revenues to pay the principal of and interest on the Bonds that will remain outstanding following such tender. In the event that sales or foreclosures of property are necessary, there could be a delay in payments to owners of the Bonds (if the Reserve Fund has first been depleted) pending such sales or the prosecution of such foreclosure proceedings and receipt by the County of the proceeds of sale. However, within the limits of the Rate and Method, the Board may adjust the Special Tax levied on all property within the District, subject to the annual Maximum Special Tax, to provide an amount required to pay interest on and principal of and minimum sinking fund payments for the Bonds, the amount, if any, necessary to replenish the Reserve Fund to an amount equal to the Reserve Requirement, and the amount required to pay all current annual expenses. There is, however, no assurance that the annual Maximum Special Tax, or that collections of the Special Tax at such annual Maximum Special Tax rates, will be at all times sufficient to pay the amounts required to be paid by the Fiscal Agent Agreement. See - Limitations on Increases in Special Tax Levy and SPECIAL RISK FACTORS - annual Maximum Special Tax Rates. For residential property of four or fewer units, a period of 120 days must elapse after the property is levied upon and before the notice of sale of such parcel can be given (for other property the 120 day period may be shortened to 20 days). Furthermore, if the purchaser at the sale is the judgment creditor, i.e. the County, an action may be commenced by the delinquent property owner within 90 days after the date of sale to set aside such sale. If, as a result of such an action, a foreclosure sale is set aside, the judgment is revived and the judgment creditor is entitled to interest on the revived judgment as if the sale had not been made. If the purchaser at the sale is other than the judgment creditor, the sale can not be set aside. No assurances can be given that the real property subject to foreclosure sale will be sold or, if sold, that the proceeds of sale will be sufficient to pay any delinquent Special Tax installment. The Act does not require the County to purchase or otherwise acquire any lot or parcel of property sold if there is no other purchaser at such sale. Section of the Act requires that property sold pursuant to foreclosure under the Act be sold for not less than the amount of judgment in the foreclosure action, plus post-judgment interest and authorized costs, unless the consent of the owners of 75% of the outstanding Bonds is obtained. However, under Section of the Act, the District, as judgment creditor, is entitled to purchase any property sold at foreclosure using a credit bid, where the District could submit a bid crediting all or part of the amount required to satisfy the judgment for the delinquent amount of the Special Tax. If the District becomes the purchaser under a credit bid, the District must pay the amount of its credit bid into the redemption fund established for the Bonds, but this payment may be made up to 24 months after the date of the foreclosure sale. Special Tax Enforcement and Collection Procedures. The County could receive additional funds for the payment of debt service through foreclosure sales of delinquent property, but no assurance can be given as to the amount foreclosure sale proceeds or when foreclosure sale proceeds would be received. The County has covenanted in the Fiscal Agent Agreement to take certain enforcement actions and commence and pursue foreclosure proceedings against delinquent parcels under the terms and conditions described in this Official Statement. See SECURITY FOR THE BONDS Delinquent Payments of Special Tax; Covenant for Superior Court Foreclosure. Foreclosure actions would include, among other steps, formal Board of Supervisors action to authorize commencement of foreclosure proceedings, mailing multiple demand letters to the record owners of the delinquent parcels advising them of the consequences of failing to pay the 18

25 applicable special taxes and contacting secured lenders to obtain payment. If these efforts were unsuccessful, they would be followed (as needed) by the filing of an action to foreclose in superior court against each parcel that remained delinquent. Limitations on Increases in Special Tax Levy. If owners are delinquent in the payment of Special Taxes, the County may not increase Special Tax levies to make up for delinquencies for prior Fiscal Years above the Maximum Special Tax rates specified for each category of property within the District. See SECURITY FOR THE BONDS Special Tax Methodology. In addition, due to Section 53321(d) of the Act, the Rate and Method provides that the special tax levied against any parcel for which an occupancy permit for private residential use has been issued may not be increased as a consequence of delinquency or default by the owner of any other parcel within a community facilities district by more than 10% above the amount that would have been levied in such Fiscal Year had there never been any such delinquences or defaults.in cases of significant delinquency, these factors may result in defaults in the payment of principal of and interest on the Bonds. See SPECIAL RISK FACTORS. Reserve Fund In order to further secure the payment of principal of and interest on the Bonds, a separate Reserve Fund, to be held by the Fiscal Agent, will be established for the Bonds pursuant to the Fiscal Agent Agreement. The amount on deposit in the Reserve Fund will be established in the amount of the Reserve Requirement for the Bonds, which is the least of 10% of the initial offering price to the public of the Bonds, 100% of maximum annual debt service on the Bonds, or 125% of average annual debt service as of the date of issuance of of the Bonds. If, at any time, the Reserve Fund is funded in whole or in part with cash, the County has the right at any time to cause the Fiscal Agent to release funds from the Reserve Fund, in whole or in part, by tendering to the Fiscal Agent: (1) a Qualified Reserve Account Credit Instrument, as defined in the Fiscal Agent Agreement, and (2) an opinion of Bond Counsel stating that such release will not, of itself, cause the portion of the proceeds of the Bonds designated as and comprising interest to become includable in gross income for purposes of federal income taxation. Upon tender of such items to the Fiscal Agent, the Fiscal Agent will transfer such funds from the Reserve Fund to the County to be used for any authorized District purpose. The County is required to maintain an amount of money, derived from available Special Tax collections, or other security equal to the Reserve Requirement at all times that the Bonds are outstanding. All amounts deposited in the Reserve Fund will be used and withdrawn by the Fiscal Agent solely for the purpose of making transfers to the Bond Fund in the event of any deficiency at any time in the Bond Fund of the amount then required for payment of the principal of, and interest and any premium on, the Bonds or, in accordance with the provisions of the Fiscal Agent Agreement, for the purpose of redeeming Bonds from the Bond Fund, or in the event of a prepayment of the Special Tax, as a credit in accordance with the Rate and Method. Whenever transfer is made from the Reserve Fund to the Bond Fund due to a deficiency in the Bond Fund, the Fiscal Agent will provide written notice thereof to the County. Whenever, on any Interest Payment Date, the amount in the Reserve Fund exceeds the Reserve Requirement, the Fiscal Agent is authorized to transfer an amount equal to the excess from the Reserve Fund to the Bond Fund, except that investment earnings on amounts in the Reserve Fund may be withdrawn from the Reserve Fund for purposes of making payment to the Federal government to comply with rebate requirements. 19

26 Moneys in the Reserve Fund will be invested and deposited in accordance with the Fiscal Agent Agreement. Interest earnings and profits resulting from the investment of moneys in the Reserve Fund and other moneys in the Reserve Fund will remain therein until the balance exceeds the Reserve Requirement. Whenever on or before any Interest Payment Date, the balance in the Reserve Fund exceeds the amount required to redeem or pay the Outstanding Bonds, including interest accrued to the date of payment or redemption and premium, if any, due upon redemption, and make any other transfer required under the Fiscal Agent Agreement, the Fiscal Agent will transfer the amount in the Reserve Fund to the Bond Fund to be applied, on the next succeeding Interest Payment Date, to the payment and redemption of all of the Outstanding Bonds. If the amount so transferred from the Reserve Fund to the Bond Fund exceeds the amount required to pay and redeem the Outstanding Bonds, the balance in the Reserve Fund will be transferred to the County, after payment of any amounts due the Fiscal Agent, to be used for any lawful purpose of the District. In connection with the issuance of Additional Bonds, the Reserve Fund shall be increased (or a separate reserve fund established) at or prior to the time the Additional Bonds to an amount at least equal to the Reserve Requirement on all then Outstanding Bonds (exclusive of the Additional Bonds) and such Additional Bonds. See - Additional Bonds below. Special Tax Fund Pursuant to the Fiscal Agent Agreement, the County establishes a separate fund to be held by the Auditor-Controller, to the credit of which the Auditor-Controller is required to deposit all Special Tax Revenue received by the County. Moneys in the Special Tax Fund will be held by the Auditor-Controller for the benefit of the County and the Owners of the Bonds, will be disbursed as provided in the Fiscal Agent Agreement, as provided below, and, pending any disbursement, are subject to a first lien in favor of the Owners of the Bonds. Disbursements. As soon as practicable after the receipt by the County of any Special Tax Revenues or the transfer of other amounts under the Fiscal Agent Agreement, the Auditor- Controller shall withdraw from the Special Tax Fund and transfer in the following order of priority: (i) to the Fiscal Agent for deposit in the Bond Fund, (a) an amount necessary to pay any principal or interest on the Bonds not paid when due, together with additional interest at the interest rate of the Bonds to the expected date of payment from the date such payment was due, plus (b) an amount, taking into account any amounts then on deposit in the Bond Fund for payment of the Bonds, such that the amount in the Bond Fund equals the principal, premium, if any, and interest due on the Bonds on the next two Interest Payment Dates with respect to Special Tax Revenues received during the period from September 1 through the last day of August in any calendar year in which the fiscal year commences, and on the next Interest Payment Date with respect to Special Tax Revenues received during the period from March 1 through the last day of August in any calendar year in which the fiscal year commences; (ii) to the Fiscal Agent an amount, taking into account amounts then on deposit in the Reserve Fund, so that the amount in the Reserve Fund equals the Reserve Requirement; (iii) provided any amounts needed for payment of the Bonds is sufficiently provided for, to the Administrative Expense Fund; and 20

27 (iv) after the foregoing disbursements, on September 1 of each year, any moneys remaining in the Special Tax Fund shall be transferred to the Community Facilities Fund and free of the pledge for payment of the Bonds. Bond Fund Moneys in the Bond Fund established pursuant to the Fiscal Agent Agreement will be held by the Fiscal Agent for the benefit of the Owners of the Bonds. At least 10 Business Days before each Interest Payment Date, the Fiscal Agent will notify the Auditor-Controller in writing as to the principal and premium, if any, and interest due on the Bonds on the next Interest Payment Date. At least 5 Business Days prior to each Interest Payment Date, the Fiscal Agent will determine if the amounts then on deposit in the Bond Fund are sufficient to pay the debt service due on the Bonds on the next Interest Payment Date. On each Interest Payment Date, the Fiscal Agent will withdraw from the Bond Fund and pay to the Owners of the Bonds the principal of, and interest and any premium, due and payable on such Interest Payment Date on the Bonds. In the event that amounts in the Bond Fund are insufficient for such purpose with respect to any Interest Payment Date, the Fiscal Agent shall withdraw from the Reserve Fund to the extent of any funds or Permitted Investments therein, amounts to cover the amount of such Bond Fund insufficiency. If, after the foregoing transfers, there are insufficient funds in the Bond Fund to make such payments, the Fiscal Agent shall apply the available funds first to the payment of interest on the Bonds, then to the payment of principal due on the Bonds other than by reason of sinking payments, if any. The County covenants in the Fiscal Agent Agreement to increase the levy of the Special Taxes in the next Fiscal Year (subject to the maximum amount authorized by the Rate and Method and the Act) in accordance with the procedures set forth in the Rate and Method for the purpose of curing any Bond Fund deficiencies. 21