ProLease Release Notes

|

|

|

- Daniella Moore

- 5 years ago

- Views:

Transcription

1 IMPORTANT - This document includes all changes made to the ProLease Lease Administration Database since version 9.1. You can print only the pages you want based on the table of contents below. Version Changes Print Pages 2-14 Release date 6/23/2018 Version Changes Print Pages Release date 5/12/2018 Version 2018 Changes Print Page Release date 3/11/2018 Version Changes Print Page Release date 12/2/2017 Version Changes Print Page Release date 9/2/2017 Version Changes Print Page Release date 6/10/2017 Version 2017 Changes Print Page Release date 1/28/2017 Version Changes Print Page 48 Release date 8/7/2016 Version Changes Print Page Release date 4/30/2016 Version 2016 Changes Print Page 54 Release date 3/5/2016 Version Changes Print Page Release date 11/21/2015 Version 2015 Changes Print Page Release date 2/28/2015 Version 2014 Changes Print Page Release date 9/20/2014 Version Changes Print Page 78 Release date 9/7/2013 Version 2013 Changes Print Pages Release date 6/22/2013

2 June 2018 What s New in Version We are calling this an Interim version. We have made a number of changes to set ProLease up for the next two versions which will be: -Version Transition Journal Entries -Version Monthly Journal Entries There will be 4 sets of Transition Journal Entries. They are: -FASB Operating -FASB Finance -IASB Operating -IASB Finance There will be 3 sets of Monthly Journal Entries. They are: -FASB Operating -FASB Finance -IASB Finance IMPORTANT The ProLease transition JE s assume that you are using the easiest and most popular method of transition (outlined below) and you are applying all the practical expedients except hindsight. FASB -Prospective Transition approach IASB -Modified Retrospective approach (ii) 2

3 1) CURRENT (SHORT TERM) & NON-CURRENT (LONG TERM) LIABILITY -We have added 3 new columns (X, Y & Z) to the Monthly Segment, Monthly Schedule and Monthly portfolio level reports. They are: Col X) Current (Short Term) Liability Col Y) Non-Current (Long Term) Liability Col Z) Proof Column (X + Y = Lease Liability Closing Balance) 3

to look like this.")

4 2) MAIN OPERATING CAPITALIZATION SCHEDULE SCREEN - We have changed the main Operating capitalization schedule screen (Type B schedules) to look like this. The main changes are in the circled area below. The changes are as follows: -View Capitalization Schedule Codes 2-7 When the user clicks on this button, they will be taken to the following screen: 4

5 On the old capitalization screen, we had one field labeled Capitalization Code. This was a unique ID for every capitalization schedule. We still have that field, but it is now labeled Capitalization Schedule Code #1. On the old capitalization screen, we had a field labeled Accounting Group / Business Unit. This was nothing more than a modifiable drop down list that you could use to create a Group. You could assign schedules to different groups, then when you wanted to run a portfolio level report, you could filter the report to show only certain groups of schedules. This field (and all of your data that was in this field) still exists, but it is now called Capitalization Schedule Code #2. We have defaulted the name of this code to Group. You can change that in the Preferences section. We have also added 5 additional Capitalization Codes. All modifiable drop down boxes, bringing the total # of capitalization schedule codes to 7. You can name codes 1 through 7 in the Preferences section. Preference #5, allows you to change the name of the capitalization schedule codes. You can also filter any capitalization schedule reports by these capitalization schedule codes. 5

6 IMPORTANT The codes do not actually appear on any of the capitalization reports right now. We ran out of time and needed to get this version out. It was important to give you the ability to filter the capitalization schedule reports by these codes. In the next version we will add these codes to the logical capitalization reports where they should appear. -Schedule Transitioned? Any lease that exists on the night before your transition date and expires on or after your transition date must be transitioned as of your transition date. When you run any of the Final Transition JE reports, ProLease will put todays date in this field for every capitalization schedule that is included in that export. Once a date appears in this box, this schedule can never be included in any other transition export. IMPORTANT A capitalization schedule can only be transitioned once. Having a date in this field tells ProLease that this schedule has already been transitioned. This is a protected field. The only way to get a date in this field is to have one of the ProLease transition JE reports put the date in the field. The date will be the date the schedule was transitioned. -When we release the next version, we will also have a report that will show you all of the capitalization schedules that have / have not been transitioned. IMPORTANT In the current version, in the capitalization Preferences, there is a field for you to enter your transition date. You should go to the Preferences section and enter your transition date. See screen shot below. 6

7 -Hold Journal Entry Export This is a check box that you can check or uncheck. If you check this box, it will put this capitalization schedule on Hold. When a capitalization schedule is on Hold, it will not be included in either the Transition JE or the Monthly JE reports. 7

to look like this.")

8 3) MAIN FINANCE CAPITALIZATION SCHEDULE SCREEN - We have changed the main Finance capitalization schedule screen (Type A schedules) to look like this. -The Finance capitalization schedule screen has the same 3 changes as the Operating schedule screen: -View capitalization schedule codes 2-7 -Schedule Transitioned? -Hold Journal Entry Export 8

9 -There is also a new field on the Finance capitalization screen called Finance Schedule Board. This is a mandatory field. It is a non-modifiable drop down list. There are two choices on this list. They are: -FASB -IASB Both boards have Finance schedules so anytime you create a Finance schedule, you must specify whether the schedule is for FASB or IASB. On the previous page is an example of the FASB Finance screen as well as the IASB Finance screen. IASB Extra Fields on Finance Schedule Asset Class IASB disclosure reports make you report on the ROU Asset by Asset class. This is a mandatory field. It is a modifiable drop down list. You can add as many asset classes as you want. Lease was Previously Prior to IFRS 16, IASB companies categorized leases as either Operating or Finance. When an IASB company transitions their existing leases, they must flag each lease for the current lease type (Operating or Finance) because they will get different treatment on the transition JE reports. This field allows you to flag a schedule as either Operating or Finance, so we know which transition JE export this schedule should be included in. 9

Initial Segment -(HCJE) Initial Segment Mid Term Schedule -(HCJE) Cancellation Partial Space with Option -(HCJE) Cancellation Partial Space without Option -(HCJE) Cancellation")

10 4) HARD CODED CHOICES ON THE REASON FOR SEGMENT DROP DOWN LIST - When you look at the Reason for Segment drop down list, you will see there are some new choices as follows: -(HCJE) Initial Segment Transitioned -(HCJE) Initial Segment -(HCJE) Initial Segment Mid Term Schedule -(HCJE) Cancellation Partial Space with Option -(HCJE) Cancellation Partial Space without Option -(HCJE) Cancellation Full Space with Option -(HCJE) Cancellation Full Space without Option *(HCJE) stands for Hard Coded for Journal Entry Any choice that starts with (HCJE) cannot be changed or deleted by you. This is a standard choice on the drop down list. The significance of these choices is that in the JE reports, there are certain situations that require special accounting, by using one of these choices as a reason for segment, that tells ProLease one of these special accounting situations is occurring and ProLease will do all of the special accounting. (HCJE) Initial Segment To be Transitioned Any capitalization schedule that you create that is for a lease that is in existence on your transition date should have this reason for segment. This tells ProLease that this schedule should be included in one of the transition JE s. IMPORTANT For any schedule to be transitioned, the segment that has your transition date in it must have this choice as a Reason for Segment. (HCJE) Initial Segment For any lease that you sign after your transition date, this should be the Reason for Segment for the first segment in that schedule. 10

11 (HCJE) Initial Segment Mid Term Schedule If you purchase ProLease after your transition date and we are creating all new capitalization schedules that have already been on your books, you should use this choice as the Reason for Segment for the first segment in each schedule. This will give you the data entry fields to make sure that the opening balance for the lease liability and the ROU Asset are the same as your closing balance on the night before you switch over to ProLease. IMPORTANT There is no reason to have any segment use this choice if you are using ProLease prior to your transition date. The remaining 4 choices: -(HCJE) Cancellation Partial Space with Option -(HCJE) Cancellation Partial Space without Option -(HCJE) Cancellation Full Space with Option -(HCJE) Cancellation Full Space without Option All deal with cancelling either some, or all of your space and whether you had an option or did not have an option. These choices should only be used when you are creating a new segment because the decision to cancel space has become reasonably certain regardless of whether there was an option or not. 5) MODIFICATION COLUMN In the following sections: Operating Schedule Landlord Allowance Initial Direct Costs ROU Asset Carry Over Finance Schedule Landlord Allowance Initial Direct Costs We previously had a Modification column that would allow you to enter any type of modification you want. It was a sort of catch-all that allowed you to modify the amount in any month in any one of these ROU asset components. Because we do not know what this modification is, we cannot journalize it, so we got rid of those columns. 11

12 6) LANDLORD ALLOWANCE In the Previous version, you would enter any landlord allowance that you received on or before the commencement date in section D of the capitalization data entry section shown below. This allowance would only impact the ROU Asset. Any Landlord Allowances you received after the commencement date, you need to enter into the liability section and it would also impact the ROU Asset. That would be done in the Choose Expenses section of letter A in the data entry form shown below: We have hard coded a choice on the Expense / Credit drop down list for (HC) Landlord Allowance. 12

, That amount will automatically appear in its own")

13 We have also added a new column to the Monthly Segment, Monthly Schedule and Monthly Portfolio level reports to break out these landlord allowances. If you enter a Landlord Allowance amount in the Add New Cost / Credit section using the (HC) Landlord Allowance choice on the list (See below), That amount will automatically appear in its own new column in the lease liability section shown below. 13

14 7) PRE-PAID RENT In previous versions of ProLease you were able to plug the Pre-Paid rent amount into the ROU Asset and it was combined with any other plug amount. In this version, we created a separate columns for the ROU Asset Plug amount and the Pre-Paid rent amount. There are also numerous other small changes that are too numerous and detailed to mention. We hope you enjoy using version and we thank you for your continued support. Next version will be the transition JE s. 14

15 May ) IASB DISCLOSURE REPORTING What s New in Version We have added IASB Disclosure reporting. We now have both FASB & IASB Disclosure reports. -We have also added the ability to flag a lease as either: -Expiring within 12 months of transition date -Low value asset In the real estate module, you can do this either: -When you create a new property -When you create a new subspace In the equipment module, you can do this: -When you add a new equipment lease -When you create a new asset pay schedule On all 4 of the above screens, you will see a section that looks like the below screen shot. IMPORTANT only short term leases are for both FASB & IASB. The other two choices are IASB only. IMPORTANT A lease cannot be included in more than one of the above 3 categories, hence, ProLease will not allow you to check more than one of the above 3 boxes. FYI the Short term lease category should take precedence over the low value asset 15

")

16 category. In other words, if a lease is both short term and a low value asset, you should flag it as a short term lease. As an IASB company, you can make an accounting policy election to not capitalize either: -Leases that expire within 12 months of your transition date -Leases that are of a low value (<=$5,000 USD) However, we still need to track these leases because we need to report on them in the disclosure report. ProLease will NOT automatically flag these leases / assets. You have to flag each one of these leases / assets by selecting the proper choice on the screen above. This is done on the screen shot above. For leases that expire within 12 months of the transition date, ProLease will automatically calculate the S/L rent amount for the period of this lease that is after the transition date and show that amount in the short term lease section on the IASB disclosure report. This amount will be included in the section for Short Term Leases. For leases that are of a low value, they will appear on a separate line in the IASB disclosure report. 2) FASB DISCLOSURE REPORTING In the first year after transition, you are going to need to generate quarterly disclosure reports. This is only for the first year after transition. We have added a From date field on the FASB Disclosure report filter form so you can run the FASB disclosure report for any period of time you want. 3) NEW PREFERENCES We have expanded the Preferences section for Capitalization schedules to include the following: 16

17 Preference #1 ProLease always calculates PV on a MONTHLY basis. You can choose to make this calculation assuming either a BEGINNING or END of month calculation. Preference #2 When you create a Finance Schedule in ProLease, you must flag this schedule as either a FASB Finance Schedule or an IASB Finance Schedule. This Preference will allow you to set a default as to whether the schedule will be a FASB or IASB schedule. IMPORTANT This is only a default. The user can still change this field once the schedule is created. Preference #3 Show 1 or 2 years For the IASB disclosure report, you can choose to show one or two years. This is what it will default to. Preference #4 This preference allows you to enter an amount and a currency type that you consider a low value asset. 17

18 IMPORTANT ProLease does not automatically flag a lease as a low value asset by comparing payments to this amount. This amount and currency type is used in labels to let the user know what your threshold for low value is. These are labels only. Preference #5 This Preference allows you to tell ProLease what your transition date is. When you are flagging a lease as a lease that expires within 12 months of your transition date, ProLease needs to know your transition date so it knows when to start calculating the rent to be shown on the disclosure report. This field will also be important in the next version for Journal Entries. What are we working on for the next release? -Journal Entries -Transition and Subsequent -FASB & IASB -Finance & Operating schedules 18

19 March ) FASB DISCLOSURE REPORTING What s New in Version 2018 There are two FASB Disclosure reports. They are: Report #1) Quantitative Disclosure report Report #2) 5 Year Maturity Analysis with Reconciliation In the real estate module, these new reports reside in the list of standard reports. They are report #74 & #75 as seen below. In the equipment module, the disclosure reports also reside in the list of standard reports, but they are report #40 & #41 as seen below. IMPORTANT The IASB has a different disclosure report. We are working on that report now and it will be included in the next version (v2018.1). Planned release date is April 30, Both FASB disclosure reports pull all of their information from the capitalization schedules you have set up in ProLease. If you do not have any capitalization schedules set up, you will not get any information on your disclosure reports when you run them. As long as you have either Operating or Finance schedules set up in either the real estate or equipment module, just run either of the disclosure reports and they will populate automatically and summarize your lease portfolio. 19

20 FASB QUANTITATIVE DISCLOSURE REPORT Below is an example of what the FASB quantitative disclosure report looks like: The FASB quantitative disclosure report, shows two years. IMPORTANT This report will always be run over the past two years. Meaning that on 1/1/2021, you would run it for 2019 & Columns C through F are the exact report that FASB shows a sample of in the guidance. In column H, ProLease gives you an explanation of what each row in the report represents and how it is calculated. Imagine when you run this report, every row has millions of dollars in it and you have absolutely no clue as to how these amounts were calculated or arrived at. Notice in column B, in the red font next to each row, it says Row 1, Row 2, Row 3 etc. When you run this disclosure report, ProLease will generate an Excel file with multiple Tabs. The first tab is the Quantitative disclosure report shown above. The other tabs are the backup detail information for each row (Row 1, Row 2, Row 3 etc.). Below is what the tabs in the Excel workbook looks like when you run the Quantitative Disclosure report: IMPORTANT There are more tabs in the file than what you see above. But there is not enough room to show all the tabs. 20

21 The red row # s in column B on the report, refer to the row # s on the tabs in the Excel spreadsheet. If you have a question about how Row #1 was calculated in the Excel report shown above, you would go to the tab labeled Rows 1,2,7,9,10 - Finance and it will show you every capitalization schedule that was included in the Row 1 calculation and show you how that number was derived. These detail tabs will be incredibly helpful in getting you to understand every schedule and every amount that was included in the numbers that appear on the Quantitative disclosure report. 5 YEAR MATURITY ANALYSIS WITH RECONCILIATION The purpose of this report is to show the 5 year and up remaining liability as well as reconcile it to make sure all of your schedules are created correctly. IMPORTANT Unlike the Quantitative report which is run over the past, this report gets run for the future 5 years and up. Below is an example of what this disclosure report looks like. Every record in this report represents one capitalization schedule. The above screen shot shows one record in this report. You can filter this report to show either: -Only Operating Schedules -Only Finance Schedules -Both Operating & Finance Schedules Columns A through I are identifier info that will let you know what schedule this record is for. Columns J through Q show you the 5-year and up remining liability as well as the reconciliation. Column J will show you what each row represents. Below is an explanation of what each row represents: 21

22 -A) Total Rent to be Capitalized This row shows the total rent to be capitalized for the 5 year and up time period shown in columns K P. -B) Lease Liability Interest This row shows the interest expense on the lease liability for the time period shown. -C) New segment lease liability open balance minus closing balance If there was a modification to the schedule during any time period in this report, this row will show you the opening lease liability of the new segment minus the closing lease liability balance from the previous segment. IMPORTANT Because this report is usually run in the future, this row will almost always be blank. However, because we allow you to run this report over any time period you want, if you do run this report over any past period, there might be a modification to this schedule in which case this row will be necessary to reconcile the schedule to $0. -D) Lease Liability as of M/D/YYYY (Where M/D/YYYY is the start date of this report) This is a calculated row. It is A minus B minus C from above. This should give you the present value of the remaining liability in this schedule as of the start date of the report. -E) PV on Cap Schedule as of M/D/YYYY (Where M/D/YYYY is the start date of this report) This row will show you the PV on the capitalization schedule on the start date of this report. To reconcile this capitalization schedule, D minus E above should equal $0.00. That is what row 13 on the above screen shot shows. 22

23 2) SHORT TERM LEASES Version 2018 allows you to mark any lease that is less than 12 months in length as a Short Term Lease. You do not capitalize leases that are 12 months or less however, you still need to track these leases because on the disclosure reports you need to show the straight-line rent amount of all short-term leases. IMPORTANT - ProLease will calculate the straight-line rent of any lease that is flagged as a short-term lease automatically. You do not have to create a separate straight-line rent schedule. There are two places you can flag a cost as a short-term lease. The first is on the mandatory fields screen when you create a new property. When you enter a term that is 12 months or less, the screen will look like this: 23

?")

24 If you enter a term that is longer than 12 months, you will not be able to flag this lease as a short-term lease. The screen will look like this. Notice the short-term lease box is gone and it shows Not Applicable because the term is greater than 12 months. IMPORTANT The line labeled 2. Lease ends within 12 months of Transition Date (IASB)? is only for IASB companies. The IASB says that if the lease expires within 12 months of your transition date, you do not have to capitalize that lease however, you will still need to track these leases because they will need to appear on the IASB Disclosure reports. This is how you will mark a lease as expiring within 12 months of the transition date. FASB does not have this same exemption. This feature will be important in the next version when we have the IASB disclosure reporting completed. You can also flag a subspace as a short-term lease or a lease that expires within 12 months of your transition date. The same function outlined above appears on the subspace screen. IMPORTANT If you extend a long-term lease for 12 months or less, that is NOT considered a short-term lease. That is an extension of a long-term lease. 24

variable expense amount.")

25 3) VARIABLE EXPENSES Version 2018 also allows you to track variable expenses. This is important because the quantitative disclosure report requires you to calculate the un-booked (uncapitalized) variable expense amount. ProLease does this by tracking: -The total amount of variable expenses incurred MINUS -The variable expenses that have been booked (capitalized) EQUALS -The unbooked variable expenses. To make this calculation, you need to flag any expenses that are variable expenses. This can be done in two places: A) Modify Preferences Section - In the Preferences section, we have a new Preference called Identify Variable Expenses for Disclosure Reporting. This screen will show a list of all of the expenses you have created in ProLease. You can set, as a default, which expenses should be included in the variable expense calculation. 25

26 2) The screen below, is where you select which expenses get capitalized in each capitalization schedule. We have added new functionality that will also allow you to flag an expense as Variable. On the left side of the screen, you will see a new column labeled Variable Lease Cost. Any expense that you mark as Variable Lease Cost in the preferences section will automatically appear checked on this screen. If there are any other expenses on the left side of the screen that you want to include in the variable expense calculation, you can flag them (check them) on this screen. IMPORTANT Flagging an expense as a Variable Lease Cost does not mean that expense will be capitalized. An expense will only get capitalized if you check the Include box. Checking the Variable Lease Cost box only means this expense will be included in the Variable Expenses Incurred calculation. The only way an expense on the left side of the screen gets included in the Variable Expenses Booked calculation is if you check the box labeled Include. The right side of the screen allows you to create any additional cost you want to capitalize. Any cost you enter on the right side of the screen will automatically be booked (capitalized). You can then flag it as a Variable expense or not. When you enter an expense on the right side of the screen and mark it as Variable Lease Cost, this expense will be included in the Variable Expense Booked calculation but it will NOT be included in the Variable Expenses Incurred calculation. By checking the box labeled Incurred, the expense on the right side of the screen will be included in both the Variable Expenses Incurred and Variable Expenses Booked calculations. 26

27 Let s use CPI as an example. A FASB company never has to capitalize CPI increases unless something else causes them to modify the schedule and at the modification time, they will include any accrued to date CPI amounts in their modified capitalization schedule. The CPI escalation on the left side of the screen should be flagged as a Variable Lease Cost so the total CPI expense will be included in the Variable Expense Incurred calculation. The Include checkbox should not be checked. If you check the Include box, the CPI will be capitalized (You do not want to do that). Now let s say that in 4/1/2014 I give back some space (contract) so I modify the capitalization schedule. In addition, I am paying $2,000 per month for accrued CPI increases on the contraction date so I will modify the capitalization schedule on 4/1/2014 and on the right side of the screen I will create a line item for CPI Booked Expense that will show a $2,000 monthly payment from 4/1/2014 to the end of the term (1/31/2021) and I will flag that expense as a Variable Lease Cost. The screen will look like this: The left side of the screen will include the total CPI payments in the Variable Cost Incurred calculation. The right side of the screen will include the $2,000 per month CPI payments in the Variable Cost Booked calculation. 27

28 4) PAGINATION OF ASSETS ON THE GENERAL LEASE INFO SCREEN IN THE EQUIPMENT MODULE In the equipment module, if you have lots of assets in a single lease, it took time to draw the screen and scroll through all the assets. We have added a pagination function to make it quicker to draw all the assets and scroll through them. You can set the number of records you want to show on the screen in the Modify Preferences section. In the example below, my database is set to show 20 records at a time. When you go to the General Lease Info screen and there are more than 20 assets in a lease, the pagination function will show up as outlined below. 28

, instead of having to re-enter any additional costs or credits from the previous segment, you can click this button and it will")

NEW REPORT LIST OF ALL SEGMENTS IN A CAPITALIZATION SCHEDULE This report will detail each segment in each capitalization schedule in both the real estate module and the equipment")

29 5) NEW COPY FUNCTION We added a Copy from Previous Segment button to the Add New Cost / Credit section on the screen below. If you modify a schedule (create a new segment), instead of having to re-enter any additional costs or credits from the previous segment, you can click this button and it will automatically copy all the additional costs / credits from the previous segment to this new segment. 6) NEW REPORT LIST OF ALL SEGMENTS IN A CAPITALIZATION SCHEDULE This report will detail each segment in each capitalization schedule in both the real estate module and the equipment module. 7) ADDED LATITUDE / LONGITUDE TO THE ALL PROPERTIES REPORT We added the Latitude & Longitude for each property to the end of the all properties report. 29

30 8) DEFAULT TO EITHER OPERATING OR FINANCE SCHEDULE We have a Preference that allows you to choose when you go to a capitalization report, does the report filter form default to show Operating or Finance schedules. This Preference will now also determine, when you create a capitalization schedule, if the default will be either Operating or Finance schedule on the screen shown below. 30

31 If your default is set to Finance schedules, every time you create a new schedule, it will default to a Finance schedule. If you are set to default to Operating schedules, it will default to an Operating schedule. This will make it easy for IASB companies to set themselves up to default everything to Finance schedules and IASB companies can set a default to either Finance or Operating schedules. LEASE CAPITALIZATION MANUAL We are currently working on redoing the manual for the capitalization screen to include all the new functionality we have added in the last few versions as well as new functionality that we will be adding in the next few versions. This new functionality includes: -IASB Disclosure reports -Monthly Journal Entries -Foreign Exchange rates Redoing the manual is a monumental job and we will be updating and posting a new manual as we finish each section. Our focus is first and foremost on adding new features to the software. That is the number one priority. If you have any questions about ProLease, feel free to call our tech support line but we are aware that the manual needs updating to include all the new functionality and we will be updating is as soon as possible. 31

32 December 2017 What s New in Version ) EQUIPMENT LEASING CAPITALIZATION MODULE You can now capitalize all of your equipment leases. The equipment capitalization module works the exact same way as the real estate capitalization module. If you have capitalized a lease in the real estate module, you will be able to capitalize equipment leases day 1, out of the box. The only difference is that instead of capitalizing pieces of space in real estate, you will be capitalizing assets in equipment. You can create an unlimited number of capitalization schedules (Operating or Finance schedules) under either FASB or IFRS rules in an equipment lease. IMPORTANT You do not have to create a lease classification test to create a capitalization schedule. The test is optional. You can just create Operating or Finance schedules without creating a lease classification test. IMPORTANT If you do create a lease classification test and it returns an Operating lease, you can override that and create a Finance capitalization schedule (or vice versa). 2) EQUIPMENT LEASING NEW UPLOAD FILE We have added a new upload file that will allow you to upload any additional cost or credit into any asset. You can enter a one-time cost or a recurring cost. We have also made two other small changes to the upload process: A) You can now add a Pay Date when you are paying a cost monthly. B) You can now upload pay schedule dates completely separate from the lease dates and asset dates. 3) ENTER AN AMOUNT INTO THE ROU ASSET We have added the ability to Plug an amount into the ROU Asset at any time. If you have a deferred rent balance that is different than the ProLease balance and you need to make an adjustment or if you have pre-paid rent, this new feature will be very helpful to allow you to add a cost to the ROU Asset without affecting the lease liability. 32

33 4) NEW REPORT Report #73 Capitalization Schedule Detail Report. This new report will allow you to enter a start date and an end date. This report will show you everything you could want to know about each of your schedules between the two dates you entered on the filter form. Coming soon: Version 2018 Release Date - End of January 2018 Includes Disclosure reports. We will have 3 disclosure reports: 1) Weighted average term and discount rate for Finance & Operating schedules 2) Quantitative disclosure report 3) 5 Year maturity analysis of future rents and reconciliation Version Release Date End of March 2018 Includes Monthly Journal Entries We will have a default set of monthly journal entries, however, if you are looking to export a file that can be uploaded into your GL program, we will need to customize that export file for each client. Version Release Date May June 2018 Includes The ability to convert capitalization schedules in foreign currencies back to a home currency. This is a much more complicated process than simply applying an exchange rate to local currency amount. Below is a brief synopsis on how we will be doing this. -The rents in the local currency are PV'd to capitalize the lease. -The op lease calculations are done to produce a level P&L cost in the local currency -The ROU asset amort and the imputed interest are calculated at inception, but the monthly interest expense amounts are converted using the month's average prevailing exchange rate. -The ROU asset is converted at historic rates and the amort is not adjusted for changes in rates as it is based on the historic rate (at commencement date) 33

34 -The lease liability is converted initially at the historic rate but an FX gain/loss on the lease liability is calculated each month by applying the difference in the month's opening and closing FX conversion rates. -The Monthly P&L cost is the sum of the FX gain/loss on the liability plus the ROU asset amort and imputed interest both converted at the average prevailing FX exchange rates. 34

35 September 2017 What s New in Version ) EQUIPMENT LEASING A/P RENT PAYMENT FUNCTION We have added the same rent payment function that we have in the real estate module to the equipment module. You can now export a file containing all the monthly payments, vendor information, G/L codes, expense names etc. you need to make to you re A/P department. 3) EQUIPMENT LEASING ALLOCATIONS SCREEN We have added the Allocations screen to the equipment module. Assets can now be charged back to one or multiple Cost Centers. This function works the exact same as it does in the real estate module but rather than split out Subspaces, you split out Assets. You can break out the monthly payments in the A/P export report by Cost Center as well. 35

and a Finance Capitalization Schedule (IFRS Type A ) for the same lease.")

36 4) ACCOUNTING BOARD FIELD ProLease allows you to create multiple capitalization schedules for a single lease. You enter the lease once, then you can create both an Operating Capitalization Schedule (US GAAP FASB Type B ) and a Finance Capitalization Schedule (IFRS Type A ) for the same lease. On both an Operating Capitalization Schedule and a Finance Capitalization Schedule, we have added a new field labeled Accounting Board. You can enter either FASB or IASB for each schedule. This field is actually a modifiable drop-down list so you can add an unlimited number of categories (i.e. Germany IASB, Austrian IASB etc.). When you run reports, you can filter the reports to show only FASB schedules, Only IASB schedules, only Germany IASB schedules etc. 36

37 5) IMPAIRMENT & MODIFICATIONS We have made our Impairment feature much more flexible. In previous versions, we allowed you to impair the ROU Asset only, however the total ROU Asset is actually made up of 4 components: Landlord Allowance IDC Costs ROU Asset Carry Over ROU Asset You can now impair any or all of the ROU Asset components. You can either partially impair the component or impair it all the way down to $0. Below is a sample of the new Impairment / Modification data entry screen. We have also given you the ability to modify any component of the ROU Asset. The difference between a modification and an impairment is that on the disclosure reports they will go to different places. 37

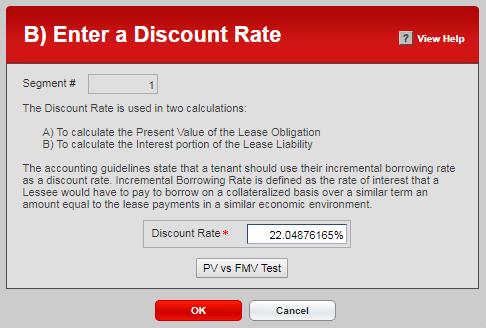

38 6) FINANCE LEASE PRESENT VALUE vs FAIR MARKET VALUE STARTING POINT CALCULATOR In a Finance capitalization schedule only, the guidance says that you should start the Lease Liability & ROU Asset with the lesser of the PV of the rents or the FMV of the asset. IMPORTANT When you calculate the PV, you should use the Lessor s implicit rate when available. If it is not available, you should use the Lessee s incremental borrowing rate. If the PV is less than the FMV, you will start the Lease Liability and ROU Asset with the PV amount. If the FMV is less than the PV, you will start the Lease Liability and the ROU Asset with the FMV amount. The problem is that you cannot just plug the starting amount to be the FMV amount. The starting amount for the lease liability must be the PV of the rents. Hence, if you want the starting amount to be the FMV, you must calculate what discount rate you need to use to make the PV of the rent payments the FMV amount. For example, suppose the PV of the rents was $100 and the FMV was $90. You would need to start the Lease Liability and the ROU Asset with $90. You would need to calculate what discount rate you would need to use to get the PV to be $90. This calculator will tell you what discount rate you need to use to get the PV of the rent payments to be the FMV amount ($90). 38

39 When you are in a Finance capitalization schedule on the data entry screen for the discount rate, you will see a button labeled PV vs FMV Test. Let s assume that your discount rate is 5.00% and the FMV of the asset is $1,000,000. We need to calculate the PV of the rent payments using the 5.00% discount rate then compare that PV amount to the $1,000,000 FMV amount. If the PV is lower than $1,000,000 FMV, we will use the PV as the starting point for the Lease Liability & ROU Asset, but if the $1,000,000 FMV is lower than the PV, then we want to use the $1,000,000 FMV as the starting amount for the Lease Liability and ROU Asset. To use this calculator, enter your % discount rate in the box above. Then click on the button labeled PV vs FMV Test. You will now be looking at the following screen: 39

40 Letter A above took the discount rate from the previous screen and populated automatically. Enter the $1,000,000 FMV amount in letter B above. Your screen should now look like this: These are the two variables you need to make this calculation. Click on the button labeled Calculate and your screen will now look like this: 40

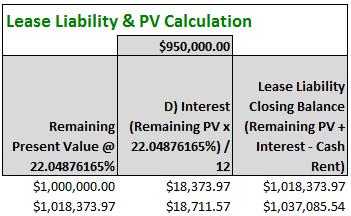

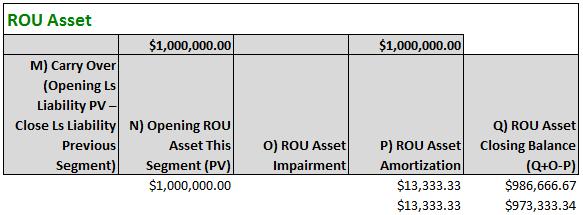

41 Letter C above shows you the % discount rate is $1,653, The FMV is $1,000,000. You should use the FMV amount to start the Lease Liability and ROU Asset in this schedule. Letter D above tells you that you need to use a discount rate of % to make the PV of this rent stream $1,000,000. Click Done on the screen above and you will be back on the Discount rate screen. Enter this new calculated discount rate and when you run the capitalization schedule, your PV starting point for the Lease Liability and the ROU Asset will be $1,000,

42 42

43 7) REPORT #72 PORTFOLIO RECONCILIATION DETAIL REPORT We changed the name of this report to Portfolio 1 Month Report. We also added some additional columns to this report. Accounting Board Reason for Schedule Segment # Reason for Segment Segment Commence Segment Expire Segment Discount Rate Segment PV on Day 1 In addition, we added all new columns for modifications and impairments on the Landlord Allowance, IDC Costs, ROU Asset. 8) OPTION STATUS DROP DOWN LIST We made the Option Status drop down list a modifiable drop-down list. 43

44 June 2017 What s New in Version There are 2 new features in version ) UPLOAD FILES FOR THE EQUIPMENT LEASING MODULE Many of our clients have thousands of equipment leases. The process of going into ProLease and manually entering each lease and asset one at a time would take way too long and be way too difficult. To solve this issue, we have created a series of 14 Excel upload templates. You can enter data into a preformatted Excel template and upload the data with the click of a button. To go to the upload file section, from the ProLease Equipment Module Main Menu, click on: GLOBAL SETTINGS 4. MODIFY PREFERENCES 19. PROLEASE EQUIPMENT UPLOAD FILES You will now be looking at the following screen: In version , we will be releasing 7 of the 14 upload files. The 7 we will be releasing are as follows: 44

45 Upload File #1 Add New Records to the Phone Book Allows you to upload new records into the phone book. You cannot edit / change or delete existing information in the phone book. You can only add new records to the phone book. Upload File #2 Add New Lease / Asset Allows you to create a new lease with one asset in it. You cannot edit / change or delete existing lease / asset information. You can only add new leases with a single asset. If you lease has multiple assets, see upload file #3 below. Upload File #3 Add New Assets to Existing Lease If your lease has multiple assets, you would use upload file #2 to create the lease and the first asset, then you would use upload file #3 to add an unlimited number of additional assets to the existing lease. You cannot edit / change or delete existing asset information. You can only add new assets to an existing lease. Upload File #4 Add New Lease Payments to Existing Assets Allows you to add new lease payments to an existing asset. You cannot edit / change or delete existing lease payment information. You can only add new lease payments to an existing asset. Upload File #9 Add Renewal Options Allows you to add an unlimited number of renewal options to an existing lease. You cannot edit / change or delete existing renewal option information. You can only add new renewal options to an existing lease. Upload File #10 Add Cancellation Options Allows you to add an unlimited number of cancellation options to an existing lease. You cannot edit / change or delete existing cancellation option information. You can only add new cancellation options to an existing lease. Upload File #11 Add Purchase Options Allows you to add an unlimited number of purchase options to an existing lease. You cannot edit / change or delete existing purchase option information. You can only add new purchase options to an existing lease. IMPORTANT You cannot upload data into the real estate module. You can only upload data into the equipment module. We will be releasing the rest of the upload files in the next few versions. 2) CAPITALIZATION SCHEDULES MID MONTH START MONTH CALCULATION If your lease begins mid-month, we have changed the calculation for the lease liability and the ROU asset to more accurately reflect the partial month period. January

46 What s New in Version 2017 Welcome to version There is absolutely nothing new in the Lease Admin Module or the Project Tracking module. Version 2017 is all about a brand-new module for Equipment Leasing. We have re-named the Lease Admin module to Real Estate and we have a new module named Equipment. The equipment module will allow you to track all non-real estate leases. This includes, cars, trucks, planes, forklifts, copiers, phone systems, computers, servers and anything else you might lease. With all the new lease accounting changes upon us, everybody wants one program to track all of their real estate leases and equipment leases. ProLease was the first software provider to offer full FASB / IASB lease capitalization capability for real estate leases. ProLease is now the first to offer both real estate and equipment lease tracking all in one program. This equipment module is the culmination of 13 months of work. We hired equipment leasing experts to work with us to help us build this module. We have shown it to over 20 companies over the last 3 months and it has received rave reviews. People told us I wish it was available today. The good news is. now it is available today. 46

47 Other software providers may tell you that you can track your equipment leases in their real estate module but that never works. There are lots of things about equipment leases that are structured completely different than real estate leases. The ProLease equipment leasing module has been created specifically for tracking all non-real estate leases. You can: Have one or more assets in a lease Assets can be added at any time during the lease term and have a different term than the lease term Payments for assets under a lease can be specified separately so if you have multiple assets under one lease they can all have different payment schedules and Pay to Company s. Track lots of detail info about each asset (manufacturer, model, year etc.) Track the location of each asset Track payment information Track lease / asset contact information Track residual value guarantee Track personal property tax Track who is the owner for purposes of income tax. If lessee, you can generate depreciation schedules based on any MACRS schedule. Track who is the lessor Track Renew, Purchase, Return this asset Track Critical Dates for all equipment leases Upload unlimited documents in each lease Run lots of reports to see all of your equipment data And lots of other great things. If you have been using the ProLease real estate module or project tracking module, you will be able to use the equipment module in no time. It works the exact same way. The navigation, searching, report filtering, expenses, critical dates, payment info, document upload etc. all work the same way. Coming soon, we are creating an upload feature that will allow you to enter data into an Excel spreadsheet and upload it into the equipment leasing module. We plan to add this feature in mid-april We have lots of other great features we plan to add to the equipment module over the next 12 months. As with our real estate module, we will never stop improving and developing. EXTREMELY IMPORTANT The equipment module is NOT a free upgrade. This is a new module that you must purchase. To schedule a demo or get pricing, please call: 47

48 August 2016 What s New in Version There are two new features in this version: 1) We have added additional functionality for IASB companies to transition their current leases to the new lease accounting guidelines. 2) On all reports that show both Local & Home amounts, when you go Direct to Excel, we have redesigned the reports so that every amount (Local & Home) is in a separate cell so you have maximum flexibility to work with data. As always, we hope you enjoy and thank you for your continued support. Alan Bushell John Unger ProCalc, Inc. Link Systems alan@procalc.com John_Unger@linksystems.com

49 April 2016 What s New in Version There are two new features in this version: We have added a Lease Classification and Decision Documentation section to our lease capitalization module. Straight line rent reports When you export them to Excel, every amount is now in a separate column in Excel. 1) LEASE CLASSIFICATION AND DECISION DOCUMENTATION Under the new accounting rules, when you sign a lease, you need to be able to perform 5 tests to see if your lease is either a Finance or Operating lease. Even if you know the lease is either a Finance Lease or an Operating lease you still need to document how you arrived at this decision so you will need to perform the 5 tests to determine the type of lease. This new lease classification and decision documentation function allows you to perform and record the results of the 5 tests. In addition, you can record your rationale for certain decisions that you will be making about this lease. For example, are we likely or not likely to exercise a renewal / cancellation option? Why are we using this discount rate? How did we arrive at the deductions we are taking? There are 5 tests you need to be able to perform to determine if a lease is a Finance lease or an Operating lease: 1. Does title transfer at end of term? 2. Is there a purchase option that is reasonably certain to be exercised? 3. Is the lease term for a major part of the remaining economic life of the asset? 4. Is the PV of the rent payments substantially all of the FMV of the asset? 5. Is the asset so specialized that at the end of the term it has no value to the lessor? #1, #2 & #5 above are Yes / No questions. They are simple enough. #2 & #3 above require calculations. You need to know: 49

50 What the PV of the rent stream is What the lease term is (total months) What is the useful life of the asset (total months) What is the FMV of the asset ProLease will automatically calculate The PV of the rent stream and length of your lease term. You will enter the useful life of the asset (in months) and the FMV of the asset. ProLease will then apply the 75% and 90% bright lines test to tell you if this is a Finance lease or an Operating lease. FYI The 75% and 90% bright lines test are standards in current guidance. Under the new lease accounting changes, they have changed the language to say: Is the lease term for a major part of the remaining economic life? (used to be 75%) AND Is the PV of the rent payments substantially all of the FMV of the asset? Used to be 90%) The guidance suggests that we still use the 75% and 90% bright lines but these numbers may change in the future. ProLease has built in the flexibility to allow you to change these amounts at any time. 50

51 Below is a screen shot of the new Lease Classification and Decision Documentation feature. You can see how it performs each of the 5 tests individually and makes a final lease classification as to whether this is a Finance lease or an Operating lease. ProLease automatically calculates your lease term and PV. All you have to do is plug in the Useful life of the asset and the FMV of the asset. IMPORTANT LEASE ACCOUNTING CHANGES Both the FASB and the IASB have signed off on the new lease accounting changes. As they say in the accounting world, it is now between the leather. In a very short period of time, everybody will be capitalizing operating leases (most real estate leases) and putting them on the balance sheet. Nobody, in the history of commercial real estate has ever done this before. It is a complex, time consuming process. Are you up to speed on all of these changes? You need to be. Make no mistake about it. The way we negotiate leases changed on February 25, 2016 when FASB signed off on the new rules (IASB signed off 1/2016). Any lease you sign today will be capitalized in the near future and most leases in your current portfolio will be capitalized and put on your balance sheet as well. There is a new bullet point that has been added to the job description of the corporate real estate executive and the broker. It is: Your job is to optimize the real estate portfolio to minimize the impact on the balance sheet. 51

52 There is going to be a great need for people who have the knowledge to do this. There is no reason why that person should not be you!!! ProLease has a 3-hour training session that will teach you everything you need to know about capitalizing both Finance & Operating leases. Sample topics covered include: Why are we capitalizing leases? When do we start capitalizing leases? What leases need to get capitalized? Understanding Finance & Operating leases. Determining if a lease is a Finance lease or an Operating lease. What does it mean to put a lease on the balance sheet? How do we put a lease on the balance sheet (Capitalizing a lease)? Debt vs no debt What costs are subject to capitalization? What deductions can we take to reduce the rent to be capitalized? What discount rate do we use to capitalize the lease? How do we calculate the PV? How to create a lease liability and an ROU Asset What is the effect on the P & L? How to negotiate / structure future real estate transactions so you can minimize the impact on the balance sheet How to look at existing leases and renegotiate them to reduce the impact on the balance sheet What is the effect on key ratios, debt covenants etc. In addition, you will get to see what an actual capitalization schedule looks like and get the actual roadmap as to the calculations behind every component of the schedule. You will be able to prove every number on the capitalization schedule by the end of this training session. Guaranteed! If you are interested in having us do a lease capitalization training session for your company, please call Alan Bushell alan@procalc.com. 52

53 2) STRAIGHT LINE RENT REPORTS In the last version we released (V 2016) we completely overhauled the Direct to Excel function and made the Excel version of the reports much, much, much better. We received hundreds of phone calls telling us how great the new Direct to Excel function was. However, we did have a few complaints about the straight-line rent reports because there were some cells that had multiple amounts in them and the user could not edit the fields. In version , we have changed all the straight-line rent reports to have every amount in a separate field. As always, we hope you enjoy and thank you for your continued support. Alan Bushell John Unger ProCalc, Inc. Link Systems alan@procalc.com John_Unger@linksystems.com

54 March 2016 What s New in Version 2016 There are 2 new features in this upgrade. Both of them deal with the Direct to Excel reports. 1) REPORT FORMATTING In previous versions of ProLease, when you exported a report Direct to Excel, we had very little control of the formatting in Excel. This caused Excel to automatically merge cells and it was very difficult to navigate around the report and manipulate the data. We found a new tool that gives us the ability to control the formatting in Excel to the extent that when you use the Direct to Excel function, all report column headings will appear in one row and the data will start in the row below the column headings. There will not be any more merged cells in the data portion of the report. Each piece of information will be in its own cell and you will have total flexibility to manipulate the data. 2) COMMENTS IN REPORT In Direct to Excel reports where comments used to go under each record making it impossible to manipulate the data, we have moved the comments to be in a column at the end of the report. Again, making it much easier to manipulate the data. 3) EXPORT REPORTS TO PDF You can now print ProLease reports directly to PDF. When you run the HTML report, click on FILE, EXPORT REPORT TO PDF. As always, we hope you enjoy and thank you for your continued support. Alan Bushell John Unger ProCalc, Inc. Link Systems alan@procalc.com John_Unger@linksystems.com

55 November 2015 What s New in Version This version contains mostly accounting changes. 1) CAPITALIZATION OF LEASES ProLease is now fully FASB / IASB compatible. We can capitalize Type A leases (Capital / Finance Leases) or Type B Leases (Operating Leases). We can also capitalize subtenant leases. ProLease will create a lease liability and an ROU Asset. We have a monthly export function that will export all of your monthly info to a file that can be uploaded by your finance department. You can get your balance sheet info as well as your P & L info. We have reports that can be run across one capitalization schedule, a few schedules or all of your schedules. Our reports explain the calculations in each column so you can prove any calculation anywhere in the process. Our help file gives you 4 different deals to do so you can practice and make sure you are capitalizing the lease correctly. What can I say other than this is the culmination of 5 years of work. It is totally, totally, totally awesome. Anybody can now capitalize leases. You have to see this to believe exactly how easy it is. Don t forget to schedule us to do a training session to teach you how to capitalize leases. FASB and the IASB are expected to sign off on this project in January Implementation is January 2019 retroactive to January This gives you one year (2016) to look at your portfolio and renegotiate leases that do not have favorable clauses. The goal is to have your portfolio optimized by January 2017 to make your balance sheet look good. The entire industry is about to change. Adoption is mandatory. The way we negotiate deals is about to change. Time to get busy. 2) STRAIGHT LINE RENT SUBTENANT LEASES You now have the ability to straight line subtenant rent in the new straight-line rent function. 55

56 3) NEW IMPROVED STRAIGHT-LINE RENT REPORTS We have made some really great changes to the straight-line rent reports from both a formatting perspective as well as a content perspective. 4) OTHER CHANGES As with any other ProLease release there are lots of small insignificant changes that will make the overall ProLease experience better but they are too small and numerous to list here. Enjoy and thank you for your continued support. Alan Bushell John Unger ProCalc, Inc. Link Systems alan@procalc.com John_Unger@linksystems.com

57 February 2015 What s New in Version 2015 There are not a lot of changes in this version but boy are these awesome changes. We know you are going to love them. 1) STRAIGHT LINE RENT CALCULATION UPDATED We have completely overhauled the straight-line rent calculation in Version Don t panic. The old system is still in place so you can continue using the Old S/L rent calculations and reports but when you see what the New straight line rent calculation does, we know that you are going to want to switch over to the New S/L rent system ASAP There were 2 major issues with the old S/L rent calculations that needed to be resolved. They are: A. TI PAYMENTS FROM LANDLORD (OR ANY OTHER ADJUSTMENT DURING THE TERM) - The correct way to calculate S/L rent when you are receiving one or more TI Payments from a landlord is that every time you receive a TI payment from the landlord, you recalculate your S/L rent from the date you receive the payment till the end of the term. You will reduce the remaining rent to be straight lined by the amount of the TI Payment from the landlord. There will be no change to any rent / straight line rent / deferred rent calculation in any month prior to the date you received the TI payment. Version 2015 now allows you to have an unlimited number of TI payments (or any other adjustment) at any time of the lease. ProLease will recalculate the rent / straight line rent / deferred rent going forward only. All previous calculations remain the same. B. RENEWING A LEASE - If you are in a 5-year lease (60 months), and you renew the lease in month 54 for another 5 years, you must stop the current S/L rent schedule in month 54, create a new schedule for 66 months (the remaining 6 in the initial term plus the new 60-month renewal term). In addition, you must carry over any deferred rent balance from the first S/L rent schedule to the second S/L rent schedule. Version 2015 allows you to do this very easily. If your accounting department is not using ProLease to generate all their S/L rent calculations each month, you MUST, MUST, MUST show them 57

58 version 15. This does it all and does it easier than anything you have ever seen. The New S/L rent system is consolidated on screen # 10. Notice the word New in parentheses at the top of the screen. There are also all new S/L rent reports to go with screen #10. Notice how the new reports all have the word NEW in front of them. 58

59 The Old straight line rent system is still working however; the screens and reports are clearly labeled Old. For example, on the base rent screen you will see: And the Old reports have been labeled OLD as you can see below. Nothing you do on the New screen will affect the Old reports. Conversely, nothing you do on the Old screens will affect the New reports. The old & new systems are two completely different sets of calculations and they do not touch each other. We have made sure to label any screen / button or function New or Old so you won t be confused. To read about how the New S/L rent system works, check out the help file on screen #10 or give us a call with any questions. 59

60 2) STRAIGHT LINE RENT EXPORT In version 2015 we have also created a new S/L rent export that will allow you to export your monthly S/L rent info so that it can be uploaded into your accounting software. The S/L rent export file is an Excel file that has the following columns: Primary Property Code Address City State S/L Rent Schedule Code Schedule Commence Date Schedule Expire date Total months in term Current Month # in schedule Base Rent Straight Line Base Rent Landlord TI & Other Adjustments Straight Line TI & Other Adjustments Total Straight-Line Rent (B + D) Monthly Difference (A E) Deferred rent from day 1 IMPORTANT We can customize a different export file for you if you like. We can export the data in any file type (text file, XML file,.csv file, pipe delimited file, Excel file etc.) and include any other info you need. The above is what the default export includes. 3) IMPORT FOREIGN EXCHANGE RATES We have created a new foreign exchange rate import. If you do not want to use the ProLease foreign exchange rates you can now upload your own rates very easily at any time for any month. From the ProLease Main Menu: Click on GLOBAL SETTINGS Click on 10. Import Foreign Exchange Rates 60

61 You will now be looking at the following screen: To upload your own exchange rates, you must create an Excel spreadsheet in a specific format. To see a sample of that format, click on the button in the upper right corner labeled Sample File Format To Be Uploaded. This will open an Excel file that looks like this: This Excel file explains the details of how to create the FX Rates upload file. Once you have created this upload file, follow the instructions on the screen to upload the rates. I very often get asked where does ProLease get its exchange rates from. I thought I would take this opportunity to explain where we get our FX rates from and when your rates get updated. ProLease keeps a master list of every currency in the world. 61

62 ProLease imports exchange rates every day at shortly after 5pm EST from XE.COM, however, this does not mean that your rates are updated every day. You determine how often you want your exchange rates updated in the Preferences section of ProLease. Your rates can be updated either: Everyday The first day of every month The last day of every month Pick any other day of the month (i.e. the 5 th, the 12, the 18 th etc.) If you do not want to use our rates you can now upload your own rates very easily. if you have any questions, please feel free to call us. We thank you all for your continuous support. Have a great day. Alan Bushell John Unger ProCalc, Inc. Link Systems alan@procalc.com John_Unger@linksystems.com

63 September ) DATABASE IS LOCKED MESSAGE What s New in Version 2014 In previous versions of ProLease, when you go into any property and you start to type in a field you get a message that says: You cannot edit data while the database is locked. Would you like to unlock it now? We have gotten rid of this message. When you go into a property you can just start typing. 2) DELETING CRITICAL DATES In previous versions of ProLease the only way to delete a critical date out of the critical date system was to go to the critical date alarm screen and delete it there. In version 2014 you can now delete any critical date right form the data entry screen where you entered the date. For example: When looking at the renewal option screen above, you will see the new Delete & Restore buttons. You can now delete any of these dates right from this screen by clicking on the Delete button. If you click on a delete button to delete a date you will still get a red warning prompt letting you know the date has been deleted. We have also added to that prompt WHO deleted the date (See screen shot below). 63

64 You can also Restore the date simply by clicking on the Restore button. This will put the date back into the critical date system so everybody will get an alert for this date and get rid of the red warning prompt. This will make it a lot easier for you when you exercise a renewal option and you want to delete the future LL Notify Date and Active Date so that nobody will receive alerts going forward about this option. 3) NEW ACTIVITIES SCREEN We have created a new screen called 9. Activities. 64

65 The purpose of this screen is to allow you to enter an unlimited number of random Activities. An activity can be anything you want (i.e. correspondence with the landlord, a vendor, electrical issue, construction issue, maintenance issue etc.). Each entry on this screen is date stamped. You can categorize each entry by Activity Type and you can filter the screen to only show only one specific activity type. To create an entry, click on the button labeled Add New Activity and you will be at the following screen: Activity Type This is a modifiable drop-down box so you can add as many Activity Types as you want. Activity Date Enter a date for this record. Comments Self-explanatory. You can filter the main screen to show only certain Activity Types which will make it easy for you to read through an activity. We have also created an Activities report that you can run across either one property, a few properties or the entire portfolio. 65

66 4) COPYING LEASE LEVEL INFORMATION We have created a lease level copy function that will allow you to copy lease info from one lease to another. The lease you are copying From can either be in the same property or in a completely different property. On the General Lease Info screen, in the red bar at the top is a new button labeled Copy info from Another Lease. IMPORTANT You must be in the lease you want to copy TO to use this function. Click this button and you will be at the following screen: You will select a Property to copy From. Once you have selected a property you will be given a list of all leases in that property and you will select a Lease to copy From. Once the property and lease to copy From have been selected, click on the button labeled Copy Data and all the lease level info will copy to the lease you are currently in. 66

67 5) CAPITALIZATION OF LEASES A. This is huge!!! Many of you already know that we have been working very closely with members of the working committee for FASB and IASB for the last 4 years on the leases project. We have had many, many, many face to face sit down meetings and discussions with them. We are extremely proud to announce that ProLease now has the ability to capitalize commercial real estate leases using the Type B method (SLE Method) of capitalization as per the last exposure draft. You will not believe how user-friendly ProLease has made the process of capitalizing leases. It CANNOT be any simpler than ProLease makes it. IMPORTANT As simple as we have made the process of capitalizing a lease, you still need to understand and learn the concepts of how to capitalize a lease. This includes: What information you need to track How to enter the data How the calculations are made What reports your finance department will require to see capitalized costs. ProLease has it all. Because capitalizing commercial real estate leases has never been common practice before, and most people have never done it, we cannot put this functionality out there and give everybody the ability to call our tech support line and ask us to teach them how to capitalize leases. It is for this reason that there is an additional charge for us to open up this module for each client. We are NOT charging you for the software. We are charging you for a training session. Once your company has been through the training session we will open up the capitalization module for you and you will be able to call for tech support. Please call Alan Bushell at for details about training on the capitalization of leases. EXTREMELY IMPORTANT - While we are on the topic of Lease Accounting I just want to mention that we are already working on the next version (Version 2015) and we expect to release it in January We are overhauling our current FASB Straight Line functionality to allow you to do everything you need it to do. For example: Realizing Landlord TI Payments when you receive them Realizing renewals when they are signed (As opposed to when they start) Being able to keep old straight-line calculations (deferred Rent) when things change and only change the calculations going forward. 67

68 We are extremely excited about all the new straight-line rent functionality in the next version and we know you will be as well. EXTREMELY IMPORTANT FYI - We have also been working on an equipment leasing module which is not ready yet but will most likely be released 2 nd half of With all the new capitalization rules coming, companies want one program to enter all their leases into (real estate leases as well as equipment leases) and ProLease will be ready. We will also be adding in the capitalization of equipment leases at a later date. 5B) Although we are overhauling the straight-line rent function in the next version, we did add one feature in this version that will help you calculate your straight line rent when you need to add a carryover amount to be straight lined (i.e. early renewal). On the Base Rent screen, if you click on the button labeled: You will now be at the following screen: The left side of this screen has always been there. The right side of the screen is what is new. You can enter any amount (Positive or negative) in the box and it will add it to the beginning rent of this subspace and straight line it over the term. This function will be very helpful when you renew a lease early. 68

69 6) ADDITIONAL CLAUSES AUTO POPULATE LIST Many clients have called and asked us to give them the ability to create an Auto- Populate list for the Additional Clauses screen. They have a standard list of additional clauses in all properties and they would like to click a single button and have all those clauses get created. We aim to please. Check it out: A. When you go to the Preferences section you will see a new preference aptly named Additional Clauses Auto-Populate List. You can put an unlimited number of Additional Clauses on this list. B. When you go into any property, go to the Additional Clause screen you will see a button labeled Auto-Populate Standard Clauses. When you click this button, it will populate this screen with the choices you have in the Preferences. 69

70 Your screen will now look like this: You can now go into each clause and type in comments and add critical dates if necessary. 7) MULTIPLE TI CONTRIBUTIONS You can now enter multiple TI contributions and track all the payments from landlord at any time. 70

71 This feature is extremely helpful when you have an initial 5-year lease with a TI that you enter at the beginning of the term. Then when the 5-year term expires, you renew for another 5 years and you get another TI, you can easily enter the new TI and differentiate it from the initial TI and track all the payments for each TI separately. 8) DOCUMENTS SCREEN We added a new filter to the top of this screen that will allow you to filter all the documents by Document type. This will make it very easy for you to look through the documents. A. We also added a new column on the Documents report to show the date the document was uploaded. 9) HEADCOUNT / KEY METRICS On the Key metrics screen, we have added 2 new calculations based on Capacity. They are: Average Cost Per Capacity / Year RSF per Capacity 71

72 10) DOCUMENT BOOKMARKING FUNCTION On all screens that previously had a field for Page #, now allows you to link a button to a page of a.pdf file on the documents screen. For example: You will now click on the button labeled Op. Hours Page # and you will be at the following screen: You will type in the Page #, then click on the drop-down list titled Link to this.pdf. You will now see a list of PDF documents on the document screen. Select the document you want. Click OK and you will go back to the original screen and it will look like this: 72

NEW REPORT Report #9 Lease Summary Report is a new")

73 Notice the new View Doc button. Click this button and it will open the.pdf and take you directly to the page you entered. IMPORTANT You can only link to a.pdf file. You cannot link to any other file type. 11) NEW REPORT Report #9 Lease Summary Report is a new critical date report. The columns in the report are as follows: This report can be filtered to show either: 73

74 There are a few really great features to this report: A. It will show you how many future renewal and cancellation options you have but if you have multiple options remaining it will only show you the Landlord Notify Date for the next option. So rather than repeating the lease 3x because you have 3 renewal options, you will only see the lease once and all the options are included in the one record. B. It will show you the current month s expense. C. It will show you the number of months remaining on the term. D. It will show you the total cost remaining to the end of the term. E. It will calculate the Average Remaining Cost PSF for the rest of the term. The calculation for this column is: (((The remaining total cost / # of months remaining) * 12) / Rentable Area) This is NOT a cost that represents what you are actually paying. It is an average cost per sq ft (or whatever the rentable area is in this property) for the remaining term. 74

75 12) HEADCOUNT BY ALLOCATIONS (COST CENTER) In previous versions of ProLease you had the ability to enter headcount by Allocations on the Key Metrics screen. This would be done in the section labeled View Allocation Key Metrics (Circled below). If you click on the button labeled View Allocation Key Metrics you had the ability to enter Headcount based on Cost Centers. We have now given you the ability to enter Capacity on that screen as well: 75

76 In addition, we have created 2 new reports that will allow you to report on Allocation Key Metrics by headcount and Capacity. They are report # s 81 & ) BREAKPOINT REPORT (FOR RETAILERS) In previous versions of ProLease, when you ran the breakpoint report it showed you every breakpoint period in the term. This could include lots of entries from the past and made the report hard to work with. We now have a start and end date on the filter form and it will only show you breakpoints for the time period you request. This report is much more useful now. 14) ADDED COMMENTS FIELDS The following screens did not have a General Comments field. We have added a general comments field to these screens: Vendors Tenant & LL Send Official Notices To Amendments Maintenance & Repair Documents 15) ADDED LEASE CODES TO OWNED PROPERTIES We have added lease codes 1-12 to owned properties. If you are using a lease code to track certain data that is also in an owned property, this will allow you to categorize the owned property the same way with the lease codes. 16) COMPATIBLE BROWSERS ProLease is now compatible with Chrome on the Mac and Android tablets. Below is a list of all browsers / operating systems that ProLease will work in: Internet Explorer 8 or higher on Windows Chrome (Windows) Chrome (Mac) Safari on Mac or ipad Android tablet 76

77 17) 2 NEW CHOICES ON THE HELP MENU From any screen you can click on the HELP menu and we have added 2 new choices. G Do I Have The Current Version. This will tell you if you are on the current version or not. H - ProLease What s New Doc This choice will launch our What s New document that will show you all the upgrades we have made since version 9.1. There are also many, many, many smaller changes that are too numerous to mention in this document but we are sure they will al enhance your experience with ProLease. If you have any questions, please do not hesitate to call our tech support line. We hope you enjoy all the new features in Version Thank you for choosing ProLease. EXTREMELY IMPORTANT If you are using Chrome, it is a good idea to clear your cache before using this new version. To clear your cache, follow these steps: A) Close down ProLease and open the Chrome browser. Click on the 3 bars in the upper right corner of your screen: B) A menu will drop down, click on TOOLS C) Then click on CLEAR BROWSING DATA D) Then check CACHED IMAGES AND FILES E) At the top of the screen click on OBLITERATE FROM THE BEGINNING OF TIME You are done! Close Chrome and now go back into ProLease. 77

78 September 2013 What s New in Version Version is a small upgrade but many will find useful. 1) ProLease is now compatible with Chrome. 2) The mapping has been sped up by reformatting the balloons slightly. 3) The ProLease Main Menu has been slightly redesigned to allow more people to know about Mapping, Charts and the Dashboard. In addition, the frame has been made slightly larger to accommodate new tabs for our new Maintenance module that will be released September 14 and the new Equipment Leasing Module that will be released sometime next year (2014). As always, we hope you enjoy. We thank you for your continued support. Alan Bushell John Unger ProCalc, Inc. Link Systems alan@procalc.com john_unger@linksystems.com 78

79 June 2013 What s New in Version 2013 Version 2013 does not have a lot of new features but rather two popularly requested features. The ability to create Graphs / Charts and the ability to create a personalized dashboard that can show charts or mini reports. We hope you like these new features and as always, if you have any questions, please do not hesitate to give us a call. CAPITALIZING LEASES There is nothing in this new version that relates to capitalizing leases but now that I have your attention I thought this would be a great time to remind all of our clients we have been working very closely for the last 2+ years with a member of the working committee of FASB and the IFRS on implementing the new accounting changes. The first step in this process is to add a new ProLease module for Equipment leases. This will allow you to have all of your leases (Real estate and equipment leases) in one program. This module is approximately 70% complete and will be released before the end of this year. The schedule is currently calling for the new rules to be finalized in the first quarter of next year. Once the rules are finalized we will begin building the lease capitalization process into both the real estate lease and equipment lease modules. If you have any questions regarding the new rules or would like to talk about how you can better prepare for these upcoming changes, please feel free to call us. 1) CHARTING ProLease now gives you the ability to create charts (Graphs). When you are on the ProLease Main Menu click on Other Options and you will see the following: 79