PREVIEW OF CHAPTER 21-2

|

|

|

- Kerrie Austin

- 6 years ago

- Views:

Transcription

1 21-1

2 PREVIEW OF CHAPTER Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield

3 21 Accounting for Leases LEARNING OBJECTIVES After studying this chapter, you should be able to: Explain the nature, economic substance, and advantages of lease transactions. 2. Describe the accounting criteria and procedures for capitalizing leases by the lessee. 3. Contrast the operating and capitalization methods of recording leases. 4. Explain the advantages and economics of leasing to lessors and identify the classifications of leases for the lessor. 5. Describe the lessor s accounting for direct-financing leases. 6. Identify special features of lease arrangements that cause unique accounting problems. 7. Describe the effect of residual values, guaranteed and unguaranteed, on lease accounting. 8. Describe the lessor s accounting for sales-type leases. 9. List the disclosure requirements for leases.

4 THE LEASING ENVIRONMENT Who Are the Players? A lease is a contractual agreement between a lessor and a lessee, that gives the lessee the right to use specific property, owned by the lessor, for a specified period of time. Largest group of leased equipment involves: Information technology equipment Transportation (trucks, aircraft, rail) Construction Agriculture 21-4 LO 1

5 ILLUSTRATION 21-2 What Do Companies Lease? 21-5

6 THE LEASING ENVIRONMENT Who Are the Players? Banks Independents Captive Leasing Companies Credit Suisse (CHE) Chase (USA) Barclays (GBR) Deutsche Bank (DEU) 30% CNH Capital (NLD) (for CNH Global), BMW Financial Services (DEU) (for BMW) IBM Global Financing (USA) (for IBM) 44% Market Share 26% 21-6 LO 1

7 THE LEASING ENVIRONMENT Advantages of Leasing % financing at fixed rates. 2. Protection against obsolescence. 3. Flexibility. OFF-BALANCE-SHEET FINANCING 4. Less costly financing. 5. Tax advantages. 6. Off-balance-sheet financing LO 1

8 THE LEASING ENVIRONMENT Conceptual Nature of a Lease Capitalize a lease that transfers substantially all of the benefits and risks of property ownership, provided the lease is non-cancelable. Leases that do not transfer substantially all the benefits and risks of ownership are operating leases LO 1

9 21 Accounting for Leases LEARNING OBJECTIVES After studying this chapter, you should be able to: Explain the nature, economic substance, and advantages of lease transactions. 2. Describe the accounting criteria and procedures for capitalizing leases by the lessee. 3. Contrast the operating and capitalization methods of recording leases. 4. Explain the advantages and economics of leasing to lessors and identify the classifications of leases for the lessor. 5. Describe the lessor s accounting for direct-financing leases. 6. Identify special features of lease arrangements that cause unique accounting problems. 7. Describe the effect of residual values, guaranteed and unguaranteed, on lease accounting. 8. Describe the lessor s accounting for sales-type leases. 9. List the disclosure requirements for leases.

10 ACCOUNTING BY THE LESSEE If the lessee capitalizes a lease, the lessee records an asset and a liability generally equal to the present value of the rental payments. Records depreciation on the leased asset. Treats the lease payments as consisting of interest and principal. ILLUSTRATION 21-2 Journal Entries for Capitalized Lease LO 2

11 ACCOUNTING BY THE LESSEE For a finance lease, the IASB has identified four criteria. 1. Lease transfers ownership of the property to the lessee. 2. Lease contains a bargain-purchase option. 3. Lease term is for major part of the economic life of the asset. 4. Present value of the minimum lease payments amounts to substantially all of the fair value of the leased asset. One or more must be met for finance lease accounting LO 2

12 ACCOUNTING BY THE LESSEE Lease Agreement Leases that DO NOT meet any of the four criteria are accounted for as operating leases. ILLUSTRATION 21-4 Diagram of Lessee s Criteria for Lease Classification LO 2

13 ACCOUNTING BY THE LESSEE Capitalization Criteria Transfer of Ownership Test If the lease transfers ownership of the asset to the lessee, it is a finance lease. Bargain-Purchase Option Test At the inception of the lease, the difference between the option price and the expected fair market value must be large enough to make exercise of the option reasonably assured LO 2

14 ACCOUNTING BY THE LESSEE Capitalization Criteria Economic Life Test Lease term is generally considered to be the fixed, noncancelable term of the lease. Bargain-renewal option can extend this period. At the inception of the lease, the difference between the renewal rental and the expected fair rental must be great enough to make exercise of the option to renew reasonably assured LO 2

15 ACCOUNTING BY THE LESSEE Illustration: Carrefour (FRA) leases Lenovo (CHN) PCs for two years at a rental of 100 per month per computer and subsequently can lease them for 10 per month per computer for another two years. The lease clearly offers a bargain-renewal option; the lease term is considered to be four years LO 2

16 ACCOUNTING BY THE LESSEE Capitalization Criteria Recovery of Investment Test Minimum Lease Payments: Minimum rental payments Guaranteed residual value Penalty for failure to renew or extend the lease Bargain-purchase option Executory Costs: Insurance Maintenance Taxes Exclude from PV of Minimum Lease Payment Calculation LO 2

17 ACCOUNTING BY THE LESSEE Capitalization Criteria Recovery of Investment Test Discount Rate Lessee computes the present value of the minimum lease payments using the implicit interest rate. In the event it is impracticable to determine the implicit rate, the lessee should use its incremental borrowing rate LO 2

18 ACCOUNTING BY THE LESSEE Asset and Liability Accounted for Differently Asset and Liability Recorded at the lower of: 1. present value of the minimum lease payments (excluding executory costs) or 2. fair market value of the leased asset at the inception of the lease LO 2

19 ACCOUNTING BY THE LESSEE Asset and Liability Accounted for Differently Depreciation Period If lease transfers ownership, depreciate asset over the economic life of the asset. If lease does not transfer ownership, depreciate over the term of the lease LO 2

20 ACCOUNTING BY THE LESSEE Asset and Liability Accounted for Differently Effective-Interest Method Used to allocate each lease payment between principal and interest. Depreciation Concept Depreciation and the discharge of the obligation are independent accounting processes LO 2

21 ACCOUNTING BY THE LESSEE Illustration: CNH Capital (NLD) (a subsidiary of CNH Global) and Ivanhoe Mines Ltd. (CAN) sign a lease agreement dated January 1, 2015, that calls for CNH to lease a front-end loader to Ivanhoe beginning January 1, The terms and provisions of the lease agreement and other pertinent data are as follows. The term of the lease is five years. The lease agreement is non-cancelable, requiring equal rental payments of $25, at the beginning of each year (annuity-due basis). The loader has a fair value at the inception of the lease of $100,000, an estimated economic life of five years, and no residual value. Ivanhoe pays all of the executory costs directly to third parties except for the property taxes of $2,000 per year, which is included as part of its annual payments to CNH. The lease contains no renewal options. The loader reverts to CNH at the termination of the lease. Ivanhoe s incremental borrowing rate is 11 percent per year. Ivanhoe depreciates similar equipment that it owns on a straight-line basis. CNH sets the annual rental to earn a rate of return on its investment of 10 percent per year; Ivanhoe knows this fact. LO 2

22 ACCOUNTING BY THE LESSEE What type of lease is this? Explain. Capitalization Criteria: 1. Transfer of ownership 2. Bargain purchase option 3. Lease term for major part of economic life of leased property 4. Present value of minimum lease payments substantially all of FMV of property Finance Lease, #3 NO NO Lease term = 5 yrs. Economic life = 5 yrs. PV = $100,000 FMV = $100,000. YES YES LO 2

23 ACCOUNTING BY THE LESSEE Computation of Capitalized Lease Payments Payment $ 25, Property taxes (executory cost) - 2, Minimum lease payment 23, Present value factor (i=10%,n=5) x PV of minimum lease payments $ * Ivanhoe uses CNH s implicit interest rate of 10 percent instead of its incremental borrowing rate of 11 percent because (1) it is lower and (2) it knows about it. * Present value of an annuity due of 1 for 5 periods at 10% (Table 6-5) LO 2

24 ACCOUNTING BY THE LESSEE Ivanhoe records the finance lease on its books on January 1, 2015, as: Leased Equipment 100, Lease Liability 100, Ivanhoe records the first lease payment on January 1, 2015, as follows. Property Tax Expense 2, Lease Liability 23, Cash 25, LO 2

25 ACCOUNTING BY THE LESSEE ILLUSTRATION 21-6 Lease Amortization Schedule for Lessee Annuity-Due Basis LO 2

26 ACCOUNTING BY THE LESSEE ILLUSTRATION 21-6 Lease Amortization Schedule for Lessee Annuity-Due Basis Prepare the entry to record accrued interest at December 31, Ivanhoe records accrued interest on December 31, 2014 Interest Expense 7, Interest Payable 7, LO 2

27 ACCOUNTING BY THE LESSEE Prepare the required on December 31, 2015, to record depreciation for the year using the straight-line method ($100,000 5 years). Depreciation Expense 20,000 Accumulated Depreciation Leased Equipment 20,000 The liabilities section as it relates to lease transactions at December 31, ILLUSTRATION 21-7 Reporting Current and Non-Current Lease Liabilities LO 2

28 ACCOUNTING BY THE LESSEE Ivanhoe records the lease payment of January 1, 2015, as follows. ILLUSTRATION 21-6 Lease Amortization Schedule for Lessee Annuity-Due Basis Property Tax Expense 2, Interest Payable 7, Lease Liability 16, Cash 25, LO 2

29 ACCOUNTING BY THE LESSEE Operating Method (Lessee) The lessee assigns rent to the periods benefiting from the use of the asset and ignores, in the accounting, any commitments to make future payments. Illustration: Assume Ivanhoe accounts for the lease as an operating lease. Ivanhoe records the payment on January 1, 2015, as follows. Rent Expense 25, Cash 25, LO 2

30 21 Accounting for Leases LEARNING OBJECTIVES After studying this chapter, you should be able to: Explain the nature, economic substance, and advantages of lease transactions. 2. Describe the accounting criteria and procedures for capitalizing leases by the lessee. 3. Contrast the operating and capitalization methods of recording leases. 4. Explain the advantages and economics of leasing to lessors and identify the classifications of leases for the lessor. 5. Describe the lessor s accounting for direct-financing leases. 6. Identify special features of lease arrangements that cause unique accounting problems. 7. Describe the effect of residual values, guaranteed and unguaranteed, on lease accounting. 8. Describe the lessor s accounting for sales-type leases. 9. List the disclosure requirements for leases.

. 2. Increase in amount of total assets (specifically long-lived assets). 21-31 3.")

31 ACCOUNTING BY THE LESSEE ILLUSTRATION 21-8 Comparison of Charges to Operations Capital vs. Operating Leases Differences using a finance lease instead of an operating lease. 1. Increase in amount of reported debt (both short-term and long-term). 2. Increase in amount of total assets (specifically long-lived assets) Lower income early in the life of the lease, therefore lower retained earnings. LO 3

32 21 Accounting for Leases LEARNING OBJECTIVES After studying this chapter, you should be able to: Explain the nature, economic substance, and advantages of lease transactions. 2. Describe the accounting criteria and procedures for capitalizing leases by the lessee. 3. Contrast the operating and capitalization methods of recording leases. 4. Explain the advantages and economics of leasing to lessors and identify the classifications of leases for the lessor. 5. Describe the lessor s accounting for direct-financing leases. 6. Identify special features of lease arrangements that cause unique accounting problems. 7. Describe the effect of residual values, guaranteed and unguaranteed, on lease accounting. 8. Describe the lessor s accounting for sales-type leases. 9. List the disclosure requirements for leases.

33 ACCOUNTING BY THE LESSOR Benefits to the Lessor 1. Interest revenue. 2. Tax incentives. 3. Residual value profits LO 4

34 ACCOUNTING BY THE LESSOR Economics of Leasing A lessor determines the amount of the rental, basing it on the rate of return the implicit rate needed to justify leasing the asset. If a residual value is involved (whether guaranteed or not), the company would not have to recover as much from the lease payments LO 4

35 ACCOUNTING BY THE LESSOR Classification of Leases by the Lessor a. Operating leases. b. Finance leases Direct-financing leases Sales-type leases LO 4

36 ACCOUNTING BY THE LESSOR Classification of Leases by the Lessor ILLUSTRATION Diagram of Lessor s Criteria for Lease Classification LO 4

37 21 Accounting for Leases LEARNING OBJECTIVES After studying this chapter, you should be able to: Explain the nature, economic substance, and advantages of lease transactions. 2. Describe the accounting criteria and procedures for capitalizing leases by the lessee. 3. Contrast the operating and capitalization methods of recording leases. 4. Explain the advantages and economics of leasing to lessors and identify the classifications of leases for the lessor. 5. Describe the lessor s accounting for direct-financing leases. 6. Identify special features of lease arrangements that cause unique accounting problems. 7. Describe the effect of residual values, guaranteed and unguaranteed, on lease accounting. 8. Describe the lessor s accounting for sales-type leases. 9. List the disclosure requirements for leases.

38 ACCOUNTING BY THE LESSOR Direct-Financing Method (Lessor) In substance the financing of an asset purchase by the lessee. Lessor records: A lease receivable instead of a leased asset. Receivable is the present value of the minimum lease payments plus the present value of the unguaranteed residual value LO 5

39 ACCOUNTING BY THE LESSOR Illustration: Using the data from the preceding CNH/Ivanhoe example we illustrate the accounting treatment for a direct-financing lease. We repeat here the information relevant to CNH in accounting for this lease transaction. 1. The term of the lease is five years beginning January 1, 2015, non-cancelable, and requires equal rental payments of $25, at the beginning of each year. Payments include $2,000 of executory costs (property taxes). 2. The equipment (front-end loader) has a cost of $100,000 to CNH, a fair value at the inception of the lease of $100,000, an estimated economic life of five years, and no residual value CNH incurred no initial direct costs in negotiating and closing the lease transaction. (continued) LO 5

40 ACCOUNTING BY THE LESSOR We repeat here the information relevant to CNH in accounting for this lease transaction. 4. The lease contains no renewal options. The equipment reverts to CNH at the termination of the lease. 5. CNH sets the annual lease payments to ensure a rate of return of 10 percent (implicit rate) on its investment as shown. Fair market value of leased equipment $ 100, Present value of residual value (calculation below) - Amount to be recovered through lease payment 100, PV factor of annunity due (i=10%, n=5) Annual payment required $ 23, LO 5

41 ACCOUNTING BY THE LESSOR The lease meets the criteria for classification as a directfinancing lease for two reasons: 1. the lease term equals the equipment s estimated economic life, and 2. the present value of the minimum lease payments equals the equipment's fair value. It is not a sales-type lease because there is no difference between the fair value ($100,000) of the loader and CNH s cost ($100,000) LO 5

, as follows. Lease Receivable 100,000 Equipment 100,000 Companies often report the lease receivable in the statement of financial position as Net investment in finance leases.")

42 ACCOUNTING BY THE LESSOR ILLUSTRATION Computation of Lease Receivable CNH records the lease of the asset and the resulting receivable on January 1, 2015 (the inception of the lease), as follows. Lease Receivable 100,000 Equipment 100,000 Companies often report the lease receivable in the statement of financial position as Net investment in finance leases LO 5

43 ACCOUNTING BY THE LESSOR ILLUSTRATION Lease Amortization Schedule for Lessor Annuity-Due Basis LO 5

44 ACCOUNTING BY THE LESSOR ILLUSTRATION Lease Amortization Schedule for Lessor Annuity-Due Basis On January 1, 2015, CNH records receipt of the first year s lease payment as follows. Cash 25, Ivanhoe records accrued interest on December 31, 2014 Lease Receivable 23, Property Tax Expense/Property Taxes Payable 2, LO 5

45 ACCOUNTING BY THE LESSOR ILLUSTRATION Lease Amortization Schedule for Lessor Annuity-Due Basis On December 31, 2015, CNH recognizes the interest revenue earned during the first year through the following entry. Interest Receivable 7, Ivanhoe records accrued interest on December 31, 2014 Interest Revenue 7, LO 5

46 ACCOUNTING BY THE LESSOR At December 31, 2015, CNH reports the lease receivable in its statement of financial position among current assets or non-current assets, or both. It classifies the portion due within one year or the operating cycle, whichever is longer, as a current asset, and the rest with non-current assets. ILLUSTRATION Reporting Lease Transactions by Lessor LO 5

47 ACCOUNTING BY THE LESSOR ILLUSTRATION Lease Amortization Schedule for Lessor Annuity-Due Basis The following entry records the receipt of the second year's lease payment on January 1, Cash 25, Ivanhoe records accrued interest on December 31, 2014 Lease Receivable 16, Interest Receivable 7, Property Tax Expense/Property Taxes Payable 2, LO 5

48 ACCOUNTING BY THE LESSOR ILLUSTRATION Lease Amortization Schedule for Lessor Annuity-Due Basis The following entry records the recognition of interest earned on December 31, Ivanhoe Interest Receivable records accrued interest on December 5, , 2014 Interest Revenue 5, LO 5

49 ACCOUNTING BY THE LESSOR Operating Method (Lessor) Records each rental receipt as rental revenue. Depreciates leased asset in the normal manner LO 5

50 ACCOUNTING BY THE LESSOR Assuming that the direct-financing lease illustrated for CNH does not qualify as a finance lease, CNH accounts for it as an operating lease and records the cash rental receipt as follows. Cash 25, Rental Revenue 25, Depreciation is recorded as follows: ($100,000 5 years = $20,000) Depreciation Expense 20,000 Accumulated Depreciation 20, LO 5

51 21 Accounting for Leases LEARNING OBJECTIVES After studying this chapter, you should be able to: Explain the nature, economic substance, and advantages of lease transactions. 2. Describe the accounting criteria and procedures for capitalizing leases by the lessee. 3. Contrast the operating and capitalization methods of recording leases. 4. Explain the advantages and economics of leasing to lessors and identify the classifications of leases for the lessor. 5. Describe the lessor s accounting for direct-financing leases. 6. Identify special features of lease arrangements that cause unique accounting problems. 7. Describe the effect of residual values, guaranteed and unguaranteed, on lease accounting. 8. Describe the lessor s accounting for sales-type leases. 9. List the disclosure requirements for leases.

52 SPECIAL ACCOUNTING PROBLEMS 1. Residual values. 2. Sales-type leases (lessor). 3. Bargain-purchase options. 4. Initial direct costs. 5. Current versus non-current classification. 6. Disclosure LO 6

53 21 Accounting for Leases LEARNING OBJECTIVES After studying this chapter, you should be able to: Explain the nature, economic substance, and advantages of lease transactions. 2. Describe the accounting criteria and procedures for capitalizing leases by the lessee. 3. Contrast the operating and capitalization methods of recording leases. 4. Explain the advantages and economics of leasing to lessors and identify the classifications of leases for the lessor. 5. Describe the lessor s accounting for direct-financing leases. 6. Identify special features of lease arrangements that cause unique accounting problems. 7. Describe the effect of residual values, guaranteed and unguaranteed, on lease accounting. 8. Describe the lessor s accounting for sales-type leases. 9. List the disclosure requirements for leases.

54 SPECIAL ACCOUNTING PROBLEMS Residual Values Meaning of Residual Value - Estimated fair value of the leased asset at the end of the lease term. Guaranteed versus Unguaranteed A guaranteed residual value is when the lessee agrees to make up any deficiency below a stated amount that the lessor realizes in residual value at the end of the lease term LO 7

55 SPECIAL ACCOUNTING PROBLEMS Residual Values Lease Payments - Lessor may adjust lease payments because of the increased certainty of recovery of a guaranteed residual value. Lessee Accounting for Residual Value - The minimum lease payment includes a guaranteed residual value but excludes an unguaranteed residual value LO 7

56 Lease Payments Illustration: Assume the same data as in the CNH/Ivanhoe illustrations except that CNH estimates a residual value of $5,000 at the end of the five-year lease term. In addition, CNH assumes a 10 percent return on investment (ROI), whether the residual value is guaranteed or unguaranteed. The terms and provisions of the lease agreement and other pertinent data are as follows. The term of the lease is five years. The lease agreement is non-cancelable, requiring equal rental payments of $25, at the beginning of each year (annuity-due basis). The loader has a fair value at the inception of the lease of $100,000, an estimated economic life of five years. Ivanhoe pays all of the executory costs directly to third parties except for the property taxes of $2,000 per year, which is included as part of its annual payments to CNH. The lease contains no renewal options. The loader reverts to CNH at the termination of the lease. Ivanhoe s incremental borrowing rate is 11 percent per year. Ivanhoe depreciates similar equipment that it owns on a straight-line basis. CNH sets the annual rental to earn a rate of return on its investment of 10 percent per year; Ivanhoe knows this fact. LO 7

57 Lease Payments CNH assumes a 10 percent return on investment (ROI), whether the residual value is guaranteed or unguaranteed. CNH would compute the amount of the lease payments as follows. ILLUSTRATION Lessor s Computation of Lease Payments LO 7

58 Lease Accounting for Residual Value Guaranteed Residual Value (Lessee Accounting) An additional lease payment that the lessee will pay in property or cash, or both, at the end of the lease term. ILLUSTRATION Computation of Lessee s Capitalized Amount Guaranteed Residual Value LO 7

59 Guaranteed Residual Value (Lessee) ILLUSTRATION Lease Amortization Schedule for Lessee Guaranteed Residual Value LO 7

60 Guaranteed Residual Value (Lessee) At the end of the lease term, before the lessee transfers the asset to CNH, the lease asset and liability accounts have the following balances. ILLUSTRATION Account Balances on Lessee s Books at End of Lease Term Guaranteed Residual Value Assume that Ivanhoe depreciated the leased asset down to its residual value of $5,000 but that the fair market value of the residual value at December 31, 2019, was $3,000. Ivanhoe would make the following journal entry LO 7

454.76 Lease Liability 4,545.24 Accumulated Depreciation Leased Equipment 95,000.")

61 Guaranteed Residual Value (Lessee) ILLUSTRATION Loss on Disposal of Equipment 2, Interest Expense (or Interest Payable) Lease Liability 4, Accumulated Depreciation Leased Equipment 95, Leased Equipment 100, Cash 2, LO 7

62 Lease Accounting for Residual Value Unguaranteed Residual Value (Lessee Accounting) Assume the same facts as those above except that the $5,000 residual value is unguaranteed instead of guaranteed. CNH will recover the same amount through lease rentals that is, $96, Ivanhoe would capitalize the amount as follows: ILLUSTRATION Computation of Lessee s Capitalized Amount Unguaranteed Residual Value LO 7

63 Unguaranteed Residual Value (Lessee) ILLUSTRATION Lease Amortization Schedule for Lessee Unguaranteed Residual Value LO 7

64 Unguaranteed Residual Value (Lessee) At the end of the lease term, before Ivanhoe transfers the asset to CNH, the lease asset and liability accounts have the following balances. ILLUSTRATION Account Balances on Lessee s Books at End of Lease Term Unguaranteed Residual Value LO 7

65 Lessee Entries Involving Residual Values ILLUSTRATION Comparative Entries for Guaranteed and Unguaranteed Residual Values, Lessee Company LO 7

of $5,000. CNH determines the payments as follows.")

66 SPECIAL ACCOUNTING PROBLEMS Lessor Accounting for Residual Value The lessor works on the assumption that it will realize the residual value at the end of the lease term whether guaranteed or unguaranteed. Illustration: Assume a direct-financing lease with a residual value (either guaranteed or unguaranteed) of $5,000. CNH determines the payments as follows. ILLUSTRATION LO 7

67 Lessor Accounting for Residual Value ILLUSTRATION Lease Amortization Schedule, for Lessor Guaranteed or Unguaranteed Residual Value LO 7

68 Lessor Accounting for Residual Value CNH would make the following entry for this directfinancing lease on 1/1/15. Illustration Lease Receivable 100, Equipment 100, LO 7

69 Lessor Accounting for Residual Value CNH would make the following entry for this directfinancing lease on 1/1/15. Illustration Cash 25, Lease Receivable 23, Property Tax Expense/Property Taxes Payable 2, LO 7

70 Lessor Accounting for Residual Value CNH would make the following entry for this directfinancing lease on 12/31/15. Illustration Interest Receivable 7, Interest Revenue 7, LO 7

71 21 Accounting for Leases LEARNING OBJECTIVES After studying this chapter, you should be able to: Explain the nature, economic substance, and advantages of lease transactions. 2. Describe the accounting criteria and procedures for capitalizing leases by the lessee. 3. Contrast the operating and capitalization methods of recording leases. 4. Explain the advantages and economics of leasing to lessors and identify the classifications of leases for the lessor. 5. Describe the lessor s accounting for direct-financing leases. 6. Identify special features of lease arrangements that cause unique accounting problems. 7. Describe the effect of residual values, guaranteed and unguaranteed, on lease accounting. 8. Describe the lessor s accounting for sales-type leases. 9. List the disclosure requirements for leases.

72 SPECIAL ACCOUNTING PROBLEMS Sales-Type Leases (Lessor) Primary difference between a direct-financing lease and a sales-type lease is the manufacturer s or dealer s gross profit (or loss). Lessor records the sale price of the asset, the cost of goods sold and related inventory reduction, and the lease receivable. There is a difference in accounting for guaranteed and unguaranteed residual values LO 8

73 Sales-Type Leases (Lessor) Direct-Financing versus Sales-Type Leases ILLUSTRATION LO 8

74 Sales-Type Leases (Lessor) LEASE RECEIVABLE (also referred to as NET INVESTMENT). The present value of the minimum lease payments plus the present value of any unguaranteed residual value. The lease receivable therefore includes the present value of the residual value, whether guaranteed or not. SALES PRICE OF THE ASSET. The present value of the minimum lease payments. COST OF GOODS SOLD. The cost of the asset to the lessor, less the present value of any unguaranteed residual value LO 8

75 Sales-Type Leases (Lessor) Illustration: To illustrate a sales-type lease with a guaranteed residual value and with an unguaranteed residual value, assume the same facts as in the preceding direct-financing lease situation. The estimated residual value is $5,000 (the present value of which is $3,104.60), and the leased equipment has an $85,000 cost to the dealer, CNH. Assume that the fair market value of the residual value is $3,000 at the end of the lease term LO 8

76 Sales-Type Leases (Lessor) Computation of Lease Amounts by CNH Financial Sales-Type Lease ILLUSTRATION LO 8

77 Sales-Type Leases (Lessor) Comparative Entries Illustration

78 SPECIAL ACCOUNTING PROBLEMS Bargain Purchase Option (Lessee) Lessee must increase the present value of the minimum lease payments by the present value of the option. Only difference between the accounting treatment for a bargain-purchase option and a guaranteed residual value of identical amounts is in the computation of the annual depreciation LO 8

79 SPECIAL ACCOUNTING PROBLEMS Initial Direct Costs (Lessor) Accounting for initial direct costs: Operating leases, the lessor should defer initial direct costs. Sales-type leases, the lessor expenses the initial direct costs. Direct-financing lease, the lessor adds initial direct costs to the net investment LO 8

80 SPECIAL ACCOUNTING PROBLEMS Current versus Noncurrent Both the annuity-due and the ordinary-annuity situations report the reduction of principal for the next period as a current liability/current asset LO 8

81 Current versus Noncurrent ILLUSTRATION Lease Amortization Schedule Ordinary- Annuity Basis The current portion of the lease liability/receivable as of December 31, 2015, would be $18, LO 8

82 21 Accounting for Leases LEARNING OBJECTIVES After studying this chapter, you should be able to: Explain the nature, economic substance, and advantages of lease transactions. 2. Describe the accounting criteria and procedures for capitalizing leases by the lessee. 3. Contrast the operating and capitalization methods of recording leases. 4. Explain the advantages and economics of leasing to lessors and identify the classifications of leases for the lessor. 5. Describe the lessor s accounting for direct-financing leases. 6. Identify special features of lease arrangements that cause unique accounting problems. 7. Describe the effect of residual values, guaranteed and unguaranteed, on lease accounting. 8. Describe the lessor s accounting for sales-type leases. 9. List the disclosure requirements for leases.

83 SPECIAL ACCOUNTING PROBLEMS Disclosing Lease Data For lessees: A general description of material leasing arrangements. A reconciliation between the total of future minimum lease payments at the end of the reporting period and their present value. The total of future minimum lease payments at the end of the reporting period, and their present value for periods (1) not later than one year, (2) later than one year and not later than five years, and (3) later than five years LO 9

84 SPECIAL ACCOUNTING PROBLEMS Disclosing Lease Data For lessors: A general description of material leasing arrangements. A reconciliation between the gross investment in the lease at the end of the reporting period, and the present value of minimum lease payments receivable at the end of the reporting period. Unearned finance income. The gross investment in the lease and the present value of minimum lease payments receivable at the end of the reporting period for periods (1) not later than one year, (2) later than one year and not later than five years, and (3) later than five years LO 9

85 Unresolved Lease Accounting Problems To avoid leased asset capitalization, companies design, write, and interpret lease agreements to prevent satisfying any of the four finance lease criteria. The real challenge lies in disqualifying the lease as a finance lease to the lessee, while having the same lease qualify as a finance (sales or financing) lease to the lessor. Unlike lessees, lessors try to avoid having lease arrangements classified as operating leases LO 9

86 GLOBAL ACCOUNTING INSIGHTS LEASE ACCOUNTING Leasing is a global business. Lessors and lessees enter into arrangements with one another without regard to national boundaries. Although U.S. GAAP and IFRS for leasing are similar, both the FASB and the IASB have decided that the existing accounting does not provide the most useful, transparent, and complete information about leasing transactions that should be provided in the financial statements

87 GLOBAL ACCOUNTING INSIGHTS Relevant Facts Following are the key similarities and differences between U.S. GAAP and IFRS related to accounting for leases. Similarities Both U.S. GAAP and IFRS share the same objective of recording leases by lessees and lessors according to their economic substance, that is, according to the definitions of assets and liabilities. Much of the terminology for lease accounting in U.S. GAAP and IFRS is the same. Under U.S. GAAP and IFRS, lessees and lessors use the same general lease capitalization criteria to determine if the risks and rewards of ownership have been transferred in the lease

88 GLOBAL ACCOUNTING INSIGHTS Relevant Facts Differences One difference in lease terminology is that finance leases are referred to as capital leases in U.S. GAAP. U.S. GAAP for leases uses bright-line criteria to determine if a lease arrangement transfers the risks and rewards of ownership; IFRS is more general in its provisions. U.S. GAAP has additional lessor criteria: payments are collectible, and there are no additional costs associated with a lease. U.S. GAAP requires use of the incremental rate unless the implicit rate is known by the lessee and the implicit rate is lower than the incremental rate. IFRS requires that lessees use the implicit rate to record a lease unless it is impractical to determine the lessor s implicit rate.

89 GLOBAL ACCOUNTING INSIGHTS Relevant Facts Differences Under U.S. GAAP, extensive disclosure of future non-cancelable lease payments is required for each of the next five years and the years thereafter. IFRS does not require it although some companies provide a year-by-year breakout of payments due in years 1 through 5. The FASB standard for leases (SFAS No. 13) has been the subject of more than 30 interpretations since its issuance. The IFRS leasing standard is IAS 17, first issued in This standard is the subject of only three interpretations. One reason for this small number of interpretations is that IFRS does not specifically address a number of leasing transactions that are covered by U.S. GAAP. Examples include lease agreements for natural resources, sale-leasebacks, real estate leases, and leveraged leases.

90 GLOBAL ACCOUNTING INSIGHTS On the Horizon Lease accounting is one of the areas identified in the IASB/FASB Memorandum of Understanding. The Boards have issued proposed rules based on right of use, which requires that all leases, regardless of their terms, be accounted for in a manner similar to how finance leases are treated today. That is, the notion of an operating lease will be eliminated, which will address the concerns under current rules in which no asset or liability is recorded for many operating leases. A final standard is expected in You can follow the lease project at the IASB website (

91 APPENDIX 21A EXAMPLES OF LEASE ARRANGEMENTS ILLUSTRATION 21A-1 Illustrative Lease Situations, Lessors LO 10 Understand and apply lease accounting concepts to various lease arrangements

92 APPENDIX 21A EXAMPLES OF LEASE ARRANGEMENTS ILLUSTRATION 21A-2 Comparative Entries for Operating Lease LO 10

93 21-93 LO 10

94 APPENDIX 21A EXAMPLES OF LEASE ARRANGEMENTS ILLUSTRATION 21A-3 Comparative Entries for Finance Lease Bargain- Purchase Option LO 10

95 APPENDIX 21A EXAMPLES OF LEASE ARRANGEMENTS LO 10

96 APPENDIX 21A EXAMPLES OF LEASE ARRANGEMENTS ILLUSTRATION 21A-4 Comparative Entries for Finance Lease LO 10

97 APPENDIX 21A EXAMPLES OF LEASE ARRANGEMENTS LO 10

98 APPENDIX 21A EXAMPLES OF LEASE ARRANGEMENTS ILLUSTRATION 21A-5 Comparative Entries for Operating Lease LO 10

99 APPENDIX 21B SALE-LEASEBACKS The term sale-leaseback describes a transaction in which the owner of the property (seller-lessee) sells the property to another and simultaneously leases it back from the new owner. Advantages: 1. Financing 2. Taxes LO 11 Describe the lessee s accounting for sale-leaseback transactions.

100 APPENDIX 21A SALE-LEASEBACKS DETERMINING ASSET USE To the extent the seller-lessee continues to use the asset after the sale, the sale-leaseback is really a form of financing. Lessor should not recognize a gain or loss on the transaction. If the seller-lessee gives up the right to the use of the asset, the transaction is in substance a sale. Gain or loss recognition is appropriate LO 11

101 APPENDIX 21A SALE-LEASEBACKS Lessee If the lease meets one of the four criteria for treatment as a finance lease, the seller-lessee should Account for the transaction as a sale and the lease as a finance lease. Defer any profit or loss it experiences from the sale of the assets that are leased back under a finance lease. Amortize profit over the lease term LO 11

102 APPENDIX 21A SALE-LEASEBACKS Lessee If none of the finance lease criteria are satisfied, the sellerlessee accounts for the transaction as a sale and the lease as an operating lease. Lessee defers such profit or loss and amortizes it in proportion to the rental payments over the period when it expects to use the assets LO 11

103 APPENDIX 21A SALE-LEASEBACKS Lessor If the lease meets one of the lease capitalization criteria, the purchaser-lessor records the transaction as a purchase and a direct-financing lease. If the lease does not meet the criteria, the purchaser-lessor records the transaction as a purchase and an operating lease LO 11

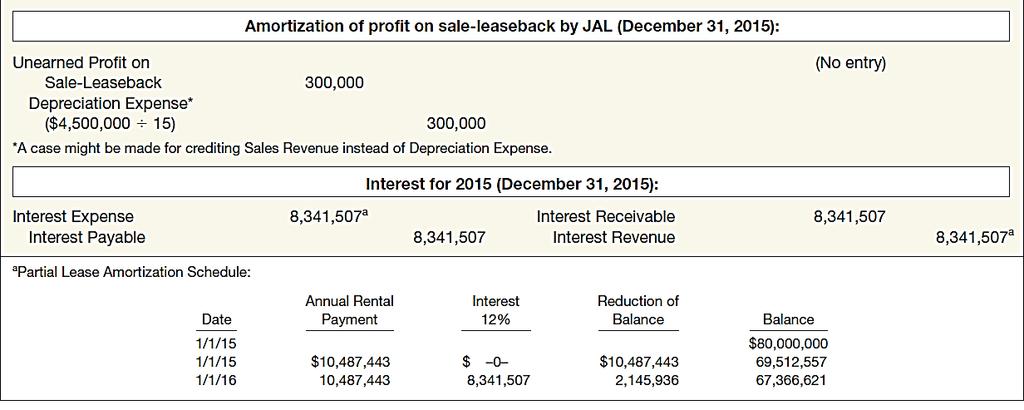

104 APPENDIX 21A SALE-LEASEBACKS SALE-LEASEBACK EXAMPLE Japan Airlines (JAL) on January 1, 2015, sells a used Boeing 757 having a carrying amount on its books of $75,500,000 to CitiCapital for $80,000,000. JAL immediately leases the aircraft back under the following conditions: 1. The term of the lease is 15 years, non-cancelable, and requires equal rental payments of $10,487,443 at the beginning of each year. 2. The aircraft has a fair value of $80,000,000 on January 1, 2015, and an estimated economic life of 15 years. 3. JAL pays all executory costs. 4. JAL depreciates similar aircraft that it owns on a straight-line basis over 15 years. 5. The annual payments assure the lessor a 12 percent return. 6. JAL s incremental borrowing rate is 12 percent LO 11

105 APPENDIX 21A SALE-LEASEBACKS SALE-LEASEBACK EXAMPLE This lease is a finance lease to JAL because the lease term is equal to the estimated life of the aircraft and because the present value of the lease payments is equal to the fair value of the aircraft to CitiCapital. CitiCapital should classify this lease as a direct financing lease LO 11

106 APPENDIX 21A SALE-LEASEBACKS LO 11

107 APPENDIX 21A SALE-LEASEBACKS LO 11

108 COPYRIGHT Copyright 2015 John Wiley & Sons, Inc. All rights reserved. Reproduction or translation of this work beyond that permitted in Section 117 of the 1976 United States Copyright Act without the express written permission of the copyright owner is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons, Inc. The purchaser may make back-up copies for his/her own use only and not for distribution or resale. The Publisher assumes no responsibility for errors, omissions, or damages, caused by the use of these programs or from the use of the information contained herein

Section 12 Accounting for Leases Accounting by the Lessor and Lessee

Section 12 Accounting for Leases Accounting by the Lessor and Lessee 15-1 A lease is an agreement in which the lessor conveys the right to use property, plant, or equipment, usually for a stated period

Section 12 Accounting for Leases Accounting by the Lessor and Lessee 15-1 A lease is an agreement in which the lessor conveys the right to use property, plant, or equipment, usually for a stated period

Chapter 15 Leases 15-1

Chapter 15 Leases 1. Why Leasing sometimes makes more sense 2. The accounting issues in recording a lease transaction 3. The types of contractual provisions in lease 4. The lease classification: capital

Chapter 15 Leases 1. Why Leasing sometimes makes more sense 2. The accounting issues in recording a lease transaction 3. The types of contractual provisions in lease 4. The lease classification: capital

DIRECT-FINANCING TERMS

CHAPTER 21 ALTERNATIVE LESSOR ACCOUNTING GROSS PRESENTATION This alternate discussion describes the accounting by lessors, using a gross presentation. These pages can be substituted for the discussion

CHAPTER 21 ALTERNATIVE LESSOR ACCOUNTING GROSS PRESENTATION This alternate discussion describes the accounting by lessors, using a gross presentation. These pages can be substituted for the discussion

CHAPTER 21. Accounting for Leases. *1. Rationale for leasing. 1, 2, 4 1, 2 3, 6, 7, 8, 14 5, 9, 10, 11, 12, 13 15, 16, 17, 18

CHAPTER 21 Accounting for Leases ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis *1. Rationale for leasing. 1, 2, 4 1, 2 *2. Lessees;

CHAPTER 21 Accounting for Leases ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis *1. Rationale for leasing. 1, 2, 4 1, 2 *2. Lessees;

Accounting For Leases

C hapter 21 Accounting For Leases Intermediate Accounting 10th edition Nikolai Bazley Jones An electronic presentation by Norman Sunderman Angelo State University COPYRIGHT 2007 Thomson South-Western,

C hapter 21 Accounting For Leases Intermediate Accounting 10th edition Nikolai Bazley Jones An electronic presentation by Norman Sunderman Angelo State University COPYRIGHT 2007 Thomson South-Western,

To download more slides, ebook, solutions and test bank, visit CHAPTER 21 ACCOUNTING FOR LEASES

CHAPTER 21 ACCOUNTING FOR LEASES IFRS questions are available at the end of this chapter. TRUE-FALSE Conceptual Answer No. Description T 1. Benefits of leasing. F 2. Accounting for long-term leases. F

CHAPTER 21 ACCOUNTING FOR LEASES IFRS questions are available at the end of this chapter. TRUE-FALSE Conceptual Answer No. Description T 1. Benefits of leasing. F 2. Accounting for long-term leases. F

2) All long-term leases should be capitalized in the accounts by the lessee.

All long-term leases should be capitalized in the accounts by the lessee.") Chapter 18 Leases 1) The principal attribute of finance leases is that the risks and rewards of asset ownership are deemed to remain with the lessor. LO: 18-02 List the criteria for classification of a

Chapter 18 Leases 1) The principal attribute of finance leases is that the risks and rewards of asset ownership are deemed to remain with the lessor. LO: 18-02 List the criteria for classification of a

Accounting for Leases in Public Sector (IPSAS 13 Leases)

") TRAINING WORKSHOP ON APPLICATION OF IPSASs Accounting for Leases in Public Sector (IPSAS 13 Leases) By Yona Killagane NSSF COMMERCIAL COMPLEX MOROGORO 7thApril 2017 Objectives and Scope Objective: Prescribes

TRAINING WORKSHOP ON APPLICATION OF IPSASs Accounting for Leases in Public Sector (IPSAS 13 Leases) By Yona Killagane NSSF COMMERCIAL COMPLEX MOROGORO 7thApril 2017 Objectives and Scope Objective: Prescribes

International Accounting Standard 17 Leases. Objective. Scope. Definitions IAS 17

International Accounting Standard 17 Leases Objective 1 The objective of this Standard is to prescribe, for lessees and lessors, the appropriate accounting policies and disclosure to apply in relation

International Accounting Standard 17 Leases Objective 1 The objective of this Standard is to prescribe, for lessees and lessors, the appropriate accounting policies and disclosure to apply in relation

IFRS 16 LEASES. Page 1 of 21

IFRS 16 LEASES OBJECTIVE The objective is to ensure that lessees and lessors provide relevant information in a manner that faithfully represents those transactions. This information gives a basis for users

IFRS 16 LEASES OBJECTIVE The objective is to ensure that lessees and lessors provide relevant information in a manner that faithfully represents those transactions. This information gives a basis for users

SSAP 14 STATEMENT OF STANDARD ACCOUNTING PRACTICE 14 LEASES

SSAP 14 STATEMENT OF STANDARD ACCOUNTING PRACTICE 14 LEASES (Issued October 1987; revised February 2000) The standards, which have been set in bold italic type, should be read in the context of the background

SSAP 14 STATEMENT OF STANDARD ACCOUNTING PRACTICE 14 LEASES (Issued October 1987; revised February 2000) The standards, which have been set in bold italic type, should be read in the context of the background

Leases. (a) the lease transfers ownership of the asset to the lessee by the end of the lease term.

the lease transfers ownership of the asset to the lessee by the end of the lease term.") Leases 1.1. Classification of leases A lease is classified as a finance lease if it transfers substantially all the risks and rewards incidental to ownership. A lease is classified as an operating lease

Leases 1.1. Classification of leases A lease is classified as a finance lease if it transfers substantially all the risks and rewards incidental to ownership. A lease is classified as an operating lease

International Financial Reporting Standards (IFRS)

") FACT SHEET February 2011 IAS 17 Leases (This fact sheet is based on the standard as at 1 January 2011.) Important note: This fact sheet is based on the requirements of the International Financial Reporting

FACT SHEET February 2011 IAS 17 Leases (This fact sheet is based on the standard as at 1 January 2011.) Important note: This fact sheet is based on the requirements of the International Financial Reporting

LKAS 17 Sri Lanka Accounting Standard LKAS 17

Sri Lanka Accounting Standard LKAS 17 Leases CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 17 LEASES paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 4 CLASSIFICATION OF LEASES 7 LEASES IN THE FINANCIAL STATEMENTS

Sri Lanka Accounting Standard LKAS 17 Leases CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 17 LEASES paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 4 CLASSIFICATION OF LEASES 7 LEASES IN THE FINANCIAL STATEMENTS

Lease & Finance Accountants Conference. September The Westin Charlotte Charlotte, NC

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Lessor Accounting under ASC 842 EQUIPMENT LEASING AND FINANCE ASSOCIATION Presenters Rod Hurd Chief

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Lessor Accounting under ASC 842 EQUIPMENT LEASING AND FINANCE ASSOCIATION Presenters Rod Hurd Chief

Summary of IFRS Exposure Draft Leases

The International Accounting Standards Board (IASB) recently issued a revised exposure draft (ED) relating to leases. Once these proposals are finalized the new guidance will replace the IAS 17 Leases.

The International Accounting Standards Board (IASB) recently issued a revised exposure draft (ED) relating to leases. Once these proposals are finalized the new guidance will replace the IAS 17 Leases.

(b) Computation of present value of minimum lease payments: $8,668 X * = $36,144. *Present value of an annuity due of 1 for 5 periods at 10%.

Computation of present value of minimum lease payments: $8,668 X * = $36,144. *Present value of an annuity due of 1 for 5 periods at 10%.") Accounting 472 Summer 2002 Chapter 22 Solutions EXERCISE 22-1 (15-20 minutes) (a) This is a capital lease to Burke since the lease term (5 years) is greater than 75% of the economic life (6 years) of the

Accounting 472 Summer 2002 Chapter 22 Solutions EXERCISE 22-1 (15-20 minutes) (a) This is a capital lease to Burke since the lease term (5 years) is greater than 75% of the economic life (6 years) of the

CA. Gopal Ji Agrawal

CA. Gopal Ji Agrawal 1. Scope 2. Key concepts 3. Accounting for leases 4. Other Lease Contracts 4. Disclosure 5. Appendix (s) 6. Questions October 1980 September 1982 IAS 17 Accounting for Leases Exposure

CA. Gopal Ji Agrawal 1. Scope 2. Key concepts 3. Accounting for leases 4. Other Lease Contracts 4. Disclosure 5. Appendix (s) 6. Questions October 1980 September 1982 IAS 17 Accounting for Leases Exposure

SLAS 19 (Revised 2000) Sri Lanka Accounting Standard SLAS 19 (Revised 2000) LEASES

Sri Lanka Accounting Standard SLAS 19 (Revised 2000) LEASES") Sri Lanka Accounting Standard SLAS 19 (Revised 2000) LEASES 265 Introduction This Standard (SLAS 19 (revised 2000) ) replaces Sri Lanka Accounting Standard SLAS 19, Accounting for Leases ( the original

Sri Lanka Accounting Standard SLAS 19 (Revised 2000) LEASES 265 Introduction This Standard (SLAS 19 (revised 2000) ) replaces Sri Lanka Accounting Standard SLAS 19, Accounting for Leases ( the original

In December 2003 the IASB issued a revised IAS 17 as part of its initial agenda of technical projects.

International Accounting Standard 17 Leases In April 2001 the International Accounting Standards Board (IASB) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards

International Accounting Standard 17 Leases In April 2001 the International Accounting Standards Board (IASB) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards

Auditing PP&E, Including Leases

Auditing PP&E, Including Leases Learning Objectives Discuss typical audit risks and special considerations. Tailor an audit plan to assessed audit risk. Explain key controls related to PP&E. Describe lease

Auditing PP&E, Including Leases Learning Objectives Discuss typical audit risks and special considerations. Tailor an audit plan to assessed audit risk. Explain key controls related to PP&E. Describe lease

In December 2003 the Board issued a revised IAS 17 as part of its initial agenda of technical projects.

IFRS 16 Leases In April 2001 the International Accounting Standards Board (the Board) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

IFRS 16 Leases In April 2001 the International Accounting Standards Board (the Board) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

International Financial Reporting Standard 16 Leases. Objective. Scope. Recognition exemptions (paragraphs B3 B8) IFRS 16

IFRS 16") International Financial Reporting Standard 16 Leases Objective 1 This Standard sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective is to ensure

International Financial Reporting Standard 16 Leases Objective 1 This Standard sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective is to ensure

Accounting Standards for Enterprises No Leases No. 3 [2006] of the Ministry of Finance

![Accounting Standards for Enterprises No Leases No. 3 [2006] of the Ministry of Finance](/thumbs/76/73123969.jpg "Accounting Standards for Enterprises No Leases No. 3 [2006] of the Ministry of Finance") Accounting Standards for Enterprises No. 21 - Leases No. 3 [2006] of the Ministry of Finance Chapter I General Provisions Article 1With a view to regulating the recognition and measurement of leases, as

Accounting Standards for Enterprises No. 21 - Leases No. 3 [2006] of the Ministry of Finance Chapter I General Provisions Article 1With a view to regulating the recognition and measurement of leases, as

In December 2003 the IASB issued a revised IAS 17 as part of its initial agenda of technical projects.

IFRS Standard 16 Leases In April 2001 the International Accounting Standards Board (IASB) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

IFRS Standard 16 Leases In April 2001 the International Accounting Standards Board (IASB) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

Intermediate Accounting

Intermediate Accounting Presenters: Amy Nelson, SVP, De Lage Landen Financial Services Theo Schuldt, Assistant Controller, GATX Corporation Agenda Lease Classification Issues Items included/excluded in

Intermediate Accounting Presenters: Amy Nelson, SVP, De Lage Landen Financial Services Theo Schuldt, Assistant Controller, GATX Corporation Agenda Lease Classification Issues Items included/excluded in

CP:

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 10-1 10-2 PREVIEW OF CHAPTER 10 10-3

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 10-1 10-2 PREVIEW OF CHAPTER 10 10-3

The new accounting standard for leases. 27 March 2017

The new accounting standard for leases 27 March 2017 Disclaimer Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity.

The new accounting standard for leases 27 March 2017 Disclaimer Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity.

Università degli studi di Pavia Facoltà di Economia a.a Lesson 8 International Accounting Lelio Bigogno, Stefano Santucci

Università degli studi di Pavia Facoltà di Economia a.a. 2013-2014 Lesson 8 International Accounting Lelio Bigogno, Stefano Santucci 1 IAS/IFRS: IAS17 Leasing 2 History of IAS17 October 1980 Exposure Draft

Università degli studi di Pavia Facoltà di Economia a.a. 2013-2014 Lesson 8 International Accounting Lelio Bigogno, Stefano Santucci 1 IAS/IFRS: IAS17 Leasing 2 History of IAS17 October 1980 Exposure Draft

Miles CPA Review: FAR Updates

Miles CPA Review: FAR - 2019 Updates Summary of updates: - FAR-4.4: s [ASC 842] effective fiscal years beginning after Dec 15, 2018 (for issuers) and effective fiscal years beginning after Dec 15, 2019

Miles CPA Review: FAR - 2019 Updates Summary of updates: - FAR-4.4: s [ASC 842] effective fiscal years beginning after Dec 15, 2018 (for issuers) and effective fiscal years beginning after Dec 15, 2019

Leases: Overview of the new guidance

Leases: Overview of the new guidance Prepared by: Richard Stuart, Partner, National Professional Standards Group, RSM US LLP richard.stuart@rsmus.com, +1 203 905 5027 March 2, 2016 Introduction On February

Leases: Overview of the new guidance Prepared by: Richard Stuart, Partner, National Professional Standards Group, RSM US LLP richard.stuart@rsmus.com, +1 203 905 5027 March 2, 2016 Introduction On February

Sri Lanka Accounting Standard-LKAS 17. Leases

Sri Lanka Accounting Standard-LKAS 17 Leases -516- Sri Lanka Accounting Standard-LKAS 17 Leases Sri Lanka Accounting Standard LKAS 17 Leases is set out in paragraphs 1 69. All the paragraphs have equal

Sri Lanka Accounting Standard-LKAS 17 Leases -516- Sri Lanka Accounting Standard-LKAS 17 Leases Sri Lanka Accounting Standard LKAS 17 Leases is set out in paragraphs 1 69. All the paragraphs have equal

Captive and Vendor Leasing

Captive and Vendor Leasing Equipment Leasing Association Lease Accountants Conference September 18, 2006 Deborah Brady James S. Brzoska Alan L. Moose Key Equipment Finance IBM Global Financing John Deere

Captive and Vendor Leasing Equipment Leasing Association Lease Accountants Conference September 18, 2006 Deborah Brady James S. Brzoska Alan L. Moose Key Equipment Finance IBM Global Financing John Deere

Leases. Indian Accounting Standard (Ind AS) 17. Leases

17. Leases") Leases Indian Accounting Standard (Ind AS) 17 Leases Contents Paragraphs OBJECTIVE 1 SCOPE 2-3 DEFINITIONS 4-6 CLASSIFICATION OF LEASES 7-19 LEASES IN THE FINANCIAL STATEMENTS OF LESSEES 20-35 Finance

Leases Indian Accounting Standard (Ind AS) 17 Leases Contents Paragraphs OBJECTIVE 1 SCOPE 2-3 DEFINITIONS 4-6 CLASSIFICATION OF LEASES 7-19 LEASES IN THE FINANCIAL STATEMENTS OF LESSEES 20-35 Finance

New Zealand Equivalent to International Financial Reporting Standard 16 Leases (NZ IFRS 16)

") New Zealand Equivalent to International Financial Reporting Standard 16 Leases (NZ IFRS 16) Issued February 2016 This Standard was issued on 11 February 2016 by the New Zealand Accounting Standards Board

New Zealand Equivalent to International Financial Reporting Standard 16 Leases (NZ IFRS 16) Issued February 2016 This Standard was issued on 11 February 2016 by the New Zealand Accounting Standards Board

Professor Authored Problem Solutions Intermediate Accounting 3. Leases. Solution to Problem 1 Lessor s computation of lease payments

Professor Authored Problem Solutions Intermediate Accounting 3 Leases Solution to Problem 1 Lessor s computation of lease payments In general, the following amounts get input into your calculator: PV!

Professor Authored Problem Solutions Intermediate Accounting 3 Leases Solution to Problem 1 Lessor s computation of lease payments In general, the following amounts get input into your calculator: PV!

New Zealand Equivalent to International Accounting Standard 17 Leases (NZ IAS 17)

") New Zealand Equivalent to International Accounting Standard 17 Leases (NZ IAS 17) Issued November 2004 and incorporates amendments up to and including 30 June 2011 This Standard was issued by the Financial

New Zealand Equivalent to International Accounting Standard 17 Leases (NZ IAS 17) Issued November 2004 and incorporates amendments up to and including 30 June 2011 This Standard was issued by the Financial

Sri Lanka Accounting Standard - SLFRS 16. Leases

Sri Lanka Accounting Standard - SLFRS 16 Leases CONTENTS from paragraph SRI LANKA ACCOUNTING STANDARD - SLFRS 16 LEASES INTRODUCTION OBJECTIVE 1 SCOPE 3 RECOGNITION EXEMPTIONS 5 IDENTIFYING A LEASE 9 Separating

Sri Lanka Accounting Standard - SLFRS 16 Leases CONTENTS from paragraph SRI LANKA ACCOUNTING STANDARD - SLFRS 16 LEASES INTRODUCTION OBJECTIVE 1 SCOPE 3 RECOGNITION EXEMPTIONS 5 IDENTIFYING A LEASE 9 Separating

HKAS 17 Revised February 2014January Hong Kong Accounting Standard 17. Leases

HKAS 17 Revised February 2014January 2017 Hong Kong Accounting Standard 17 Leases HKAS 17 COPYRIGHT Copyright 2017 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial Reporting

HKAS 17 Revised February 2014January 2017 Hong Kong Accounting Standard 17 Leases HKAS 17 COPYRIGHT Copyright 2017 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial Reporting

HKAS 17 Revised January 2017September Hong Kong Accounting Standard 17. Leases

HKAS 17 Revised January 2017September 2018 Hong Kong Accounting Standard 17 Leases HKAS 17 COPYRIGHT Copyright 2018 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial Reporting

HKAS 17 Revised January 2017September 2018 Hong Kong Accounting Standard 17 Leases HKAS 17 COPYRIGHT Copyright 2018 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial Reporting

Heads Up. FASB Draws a Bright Line Through Operating Leases Proposed ASU Revamps Lease. Accounting. The ED, released by the FASB as a proposed

August 17, 2010 Volume 17, Issue 27 Heads Up In This Issue: Background Effective Date In a Nutshell Scope Lessee Accounting Lessor Accounting Presentation and Disclosures Transition The ED, released by

August 17, 2010 Volume 17, Issue 27 Heads Up In This Issue: Background Effective Date In a Nutshell Scope Lessee Accounting Lessor Accounting Presentation and Disclosures Transition The ED, released by

Accounting for Leases

Office: Business Services Procedure Contact: Director of Business Services Related Policy or Policies: Noted within procedure statement Revision History Revision Number: Change: Date: 001 Update content

Office: Business Services Procedure Contact: Director of Business Services Related Policy or Policies: Noted within procedure statement Revision History Revision Number: Change: Date: 001 Update content

Exposure Draft 64 January 2018 Comments due: June 30, Proposed International Public Sector Accounting Standard. Leases

Exposure Draft 64 January 2018 Comments due: June 30, 2018 Proposed International Public Sector Accounting Standard Leases This document was developed and approved by the International Public Sector Accounting

Exposure Draft 64 January 2018 Comments due: June 30, 2018 Proposed International Public Sector Accounting Standard Leases This document was developed and approved by the International Public Sector Accounting

The New Lease Accounting Standard. Hunter Mink, CPA, CCIFP Brian Rosenberg, CPA, MBA

The New Lease Accounting Standard Hunter Mink, CPA, CCIFP Brian Rosenberg, CPA, MBA 1 Agenda Introduction Lease Identification and Classification Lessee Accounting Other Considerations Disclosures Impact

The New Lease Accounting Standard Hunter Mink, CPA, CCIFP Brian Rosenberg, CPA, MBA 1 Agenda Introduction Lease Identification and Classification Lessee Accounting Other Considerations Disclosures Impact

CFA Level 1. Financial Reporting and Analysis. Non-current Liabilities

CFA Level 1 Financial Reporting and Analysis Non-current Liabilities 2011, Associate Professor Ole Sørensen, Ph.d. Side 1 Coupon Bonds Promises two types of payments: periodic interest payments and a lumpsum

CFA Level 1 Financial Reporting and Analysis Non-current Liabilities 2011, Associate Professor Ole Sørensen, Ph.d. Side 1 Coupon Bonds Promises two types of payments: periodic interest payments and a lumpsum

Accounting for Leases

Accounting for Leases Publication Date: July 2016 Accounting for Leases Copyright 2016 by DELTACPE LLC All rights reserved. No part of this course may be reproduced in any form or by any means, without

Accounting for Leases Publication Date: July 2016 Accounting for Leases Copyright 2016 by DELTACPE LLC All rights reserved. No part of this course may be reproduced in any form or by any means, without

2 This Standard shall be applied in accounting for all leases other than:

Indian Accounting Standard (Ind AS) 17 Leases (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in bold type indicate the main

Indian Accounting Standard (Ind AS) 17 Leases (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in bold type indicate the main

Original SSAP and Current Authoritative Guidance: SSAP No. 22

Statutory Issue Paper No. 22 Leases STATUS Finalized March 16, 1998 Original SSAP and Current Authoritative Guidance: SSAP No. 22 Type of Issue: Common Area SUMMARY OF ISSUE 1. Current statutory accounting

Statutory Issue Paper No. 22 Leases STATUS Finalized March 16, 1998 Original SSAP and Current Authoritative Guidance: SSAP No. 22 Type of Issue: Common Area SUMMARY OF ISSUE 1. Current statutory accounting

Lease Accounting Standard Update ASU Presented by: Nicholas Hoefel, CPA Manager, Audit Services Group

Lease Accounting Standard Update ASU 2016-02 Presented by: Nicholas Hoefel, CPA Manager, Audit Services Group 1 Overview Introduction Background and current environment Effective dates and transition Key

Lease Accounting Standard Update ASU 2016-02 Presented by: Nicholas Hoefel, CPA Manager, Audit Services Group 1 Overview Introduction Background and current environment Effective dates and transition Key

Technical Line FASB final guidance

No. 2016-09 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect health care entities In this issue: Overview... 1 Key considerations... 3 Scope and scope exceptions...

No. 2016-09 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect health care entities In this issue: Overview... 1 Key considerations... 3 Scope and scope exceptions...

MONITORDAILY SPECIAL REPORT. Lease Accounting Project Update as of May 25, 2011 Prepared by Bill Bosco, Leasing 101

MONITORDAILY SPECIAL REPORT Lease Accounting Project Update as of May 25, 2011 Prepared by Bill Bosco, Leasing 101 The high volume of comment letters (780+) and numerous outreach meetings had common criticisms

MONITORDAILY SPECIAL REPORT Lease Accounting Project Update as of May 25, 2011 Prepared by Bill Bosco, Leasing 101 The high volume of comment letters (780+) and numerous outreach meetings had common criticisms

Teresa Gordon s Recommended Alternative to Accounting for Leases

Teresa Gordon s Recommended Alternative to Accounting for Leases Key features: Leases with title transfer and bargain purchase options would not be excluded from the scope. Leases with title transfer or

Teresa Gordon s Recommended Alternative to Accounting for Leases Key features: Leases with title transfer and bargain purchase options would not be excluded from the scope. Leases with title transfer or

Lease & Finance Accountants Conference. September The Westin Charlotte Charlotte, NC

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Basic Principles of Lessors under ASC 842 Mamta Shori, Wells Fargo Equipment Finance Joe Sebik,

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Basic Principles of Lessors under ASC 842 Mamta Shori, Wells Fargo Equipment Finance Joe Sebik,

Impact on Financial Statements of New Accounting Model for Leases

University of Connecticut DigitalCommons@UConn Honors Scholar Theses Honors Scholar Program Spring 5-8-2011 Impact on Financial Statements of New Accounting Model for Leases Wenqi Ma University of Connecticut

University of Connecticut DigitalCommons@UConn Honors Scholar Theses Honors Scholar Program Spring 5-8-2011 Impact on Financial Statements of New Accounting Model for Leases Wenqi Ma University of Connecticut

The joint leases project change is coming

No. 2010-4 18 June 2010 Technical Line Technical guidance on standards and practice issues The joint leases project change is coming What you need to know The proposed changes to the accounting for leases

No. 2010-4 18 June 2010 Technical Line Technical guidance on standards and practice issues The joint leases project change is coming What you need to know The proposed changes to the accounting for leases

Preview of the New Exposure Draft of the Lease Accounting Project Key elements and commentary

Preview of the New Exposure Draft of the Lease Accounting Project Key elements and commentary Prepared by Bill Bosco, Leasing 101 www.leasing-101.com The Financial Accounting Standards Board (FASB) and

Preview of the New Exposure Draft of the Lease Accounting Project Key elements and commentary Prepared by Bill Bosco, Leasing 101 www.leasing-101.com The Financial Accounting Standards Board (FASB) and

New leases standard ASC 842 Lessee - operating leases. Itai Gotlieb, Partner, Professional Practice July 2017

ASC 842 Lessee - operating leases Itai Gotlieb, Partner, Professional Practice July 2017 Overview Under Accounting Standards Codification (ASC) 842, Leases, lessees recognize assets and liabilities for

ASC 842 Lessee - operating leases Itai Gotlieb, Partner, Professional Practice July 2017 Overview Under Accounting Standards Codification (ASC) 842, Leases, lessees recognize assets and liabilities for

Exposure Draft. Indian Accounting Standard (Ind AS) 116 Leases. (Last date for Comments: August 31, 2017)

116 Leases. (Last date for Comments: August 31, 2017)") ED/Ind AS/2017/06 Exposure Draft Indian Accounting Standard (Ind AS) 116 Leases (Last date for Comments: August 31, 2017) Issued by Accounting Standards Board The Institute of Chartered Accountants of

ED/Ind AS/2017/06 Exposure Draft Indian Accounting Standard (Ind AS) 116 Leases (Last date for Comments: August 31, 2017) Issued by Accounting Standards Board The Institute of Chartered Accountants of

In December 2003 the Board issued a revised IAS 40 as part of its initial agenda of technical projects.

IAS 40 Investment Property In April 2001 the International Accounting Standards Board (the Board) adopted IAS 40 Investment Property, which had originally been issued by the International Accounting Standards

IAS 40 Investment Property In April 2001 the International Accounting Standards Board (the Board) adopted IAS 40 Investment Property, which had originally been issued by the International Accounting Standards

A Review of IFRS 16 Leases By Tan Liong Tong

A Review of IFRS 16 Leases By Tan Liong Tong In April 2016, the MASB issued MFRS 16 Leases that is identical to IFRS 16 Leases issued by the IASB in January 2016. The effective date of this new MFRS is

A Review of IFRS 16 Leases By Tan Liong Tong In April 2016, the MASB issued MFRS 16 Leases that is identical to IFRS 16 Leases issued by the IASB in January 2016. The effective date of this new MFRS is

Something Borrowed, Something New Get Ready for the New Lease Accounting Standard

April 2016 Something Borrowed, Something New Get Ready for the New Lease Accounting Standard By Scott G. Lehman, CPA, and David E. Wentzel, CPA Audit / Tax / Advisory / Risk / Performance Smart decisions.

April 2016 Something Borrowed, Something New Get Ready for the New Lease Accounting Standard By Scott G. Lehman, CPA, and David E. Wentzel, CPA Audit / Tax / Advisory / Risk / Performance Smart decisions.

FASB and IASB Continue Making Decisions on Lease Accounting

Accounting Journal Entry FASB and IASB Continue Making Decisions on Lease Accounting March 28, 2011 At recent meetings, the FASB and IASB (the boards ) have continued to make progress on the leases project,

Accounting Journal Entry FASB and IASB Continue Making Decisions on Lease Accounting March 28, 2011 At recent meetings, the FASB and IASB (the boards ) have continued to make progress on the leases project,

IASB Staff Paper March 2011

IASB Staff Paper March 2011 Effect of board redeliberations on Exposure Draft Leases About this staff paper This staff paper indicates how the proposals in the Exposure Draft Leases would change as a result

IASB Staff Paper March 2011 Effect of board redeliberations on Exposure Draft Leases About this staff paper This staff paper indicates how the proposals in the Exposure Draft Leases would change as a result

LEASES WHERE ARE WE? Steve Rathjen

LEASES WHERE ARE WE? Steve Rathjen 267 256-3110 srathjen@kpmg.com Agenda Project status Lease definition and classification Lessee accounting Lessor accounting Presentation, disclosures, and transition

LEASES WHERE ARE WE? Steve Rathjen 267 256-3110 srathjen@kpmg.com Agenda Project status Lease definition and classification Lessee accounting Lessor accounting Presentation, disclosures, and transition

IFRS 16: Leases; a New Era of Lease Accounting!

The journal is running a series of updates on IFRS, IAS, IFRIC and SIC. The updates mostly collected from different sources of IASB publication, seminars, workshop & IFRS website. This issue is based on

The journal is running a series of updates on IFRS, IAS, IFRIC and SIC. The updates mostly collected from different sources of IASB publication, seminars, workshop & IFRS website. This issue is based on

Technical Line FASB final guidance

No. 2016-11 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect real estate entities In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions...

No. 2016-11 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect real estate entities In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions...

Accounting. Stock Market Strategies. Jae K. Shim. The CPE Store, Inc

Accounting Stock Market for Strategies Leases Jae K. Shim The CPE Store, Inc. www.cpestore.com 1-800-910-2755 Accounting for Leases Jae K. Shim Copyright 2013 by Delta Publishing. All rights reserved.

Accounting Stock Market for Strategies Leases Jae K. Shim The CPE Store, Inc. www.cpestore.com 1-800-910-2755 Accounting for Leases Jae K. Shim Copyright 2013 by Delta Publishing. All rights reserved.

Leases ASU September 20, 2017

Leases ASU 2016-02 September 20, 2017 Meet the Speakers Tonisha Spratte, CPA Senior Accountant Cherry Bekaert tspratte@cbh.com Matthew Mars Senior Accountant Cherry Bekaert mmars@cbh.com Agenda What is

Leases ASU 2016-02 September 20, 2017 Meet the Speakers Tonisha Spratte, CPA Senior Accountant Cherry Bekaert tspratte@cbh.com Matthew Mars Senior Accountant Cherry Bekaert mmars@cbh.com Agenda What is

The new IFRS 16 Leases effective as of 1 January 2019

The new IFRS 16 Leases effective as of 1 January 2019 IFRS 16 was issued by IASB on 13 January 2016. The Standard is effective as of 1 January 2019. It has not yet been adopted by the EC. This is a Standard

The new IFRS 16 Leases effective as of 1 January 2019 IFRS 16 was issued by IASB on 13 January 2016. The Standard is effective as of 1 January 2019. It has not yet been adopted by the EC. This is a Standard

Leases DEFINITION OF A LEASE INTRODUCTION CHAPTER 18

Source: (Globe and money) Vstock LLC/Getty Images RF; (Skyscrapers) Arpad Benedek/Getty Images RF; (Canadian flag) BjArn Kindler/Getty Images RF; (Tablet, pen, keyboard) John Lamb/Getty Images RF. CHAPTER

Source: (Globe and money) Vstock LLC/Getty Images RF; (Skyscrapers) Arpad Benedek/Getty Images RF; (Canadian flag) BjArn Kindler/Getty Images RF; (Tablet, pen, keyboard) John Lamb/Getty Images RF. CHAPTER

Impact of lease accounting changes to corporate real estate

Impact of lease accounting changes to corporate real estate Overview In February 2016, the Financial Accounting Standards Board (FASB) issued its long-awaited revision to lease accounting Accounting Standards

Impact of lease accounting changes to corporate real estate Overview In February 2016, the Financial Accounting Standards Board (FASB) issued its long-awaited revision to lease accounting Accounting Standards

Lessor Example Performance Obligation Approach

Lessor Example Performance Obligation Approach **Disclaimer The exposure draft received nearly 700 letters of comment through the comment period ended December 15, 2010. There is some expectation that

Lessor Example Performance Obligation Approach **Disclaimer The exposure draft received nearly 700 letters of comment through the comment period ended December 15, 2010. There is some expectation that

This version includes amendments resulting from IFRSs issued up to 31 December 2008.

International Accounting Standard 17 Leases This version includes amendments resulting from IFRSs issued up to 31 December 2008. IAS 17 Leases was issued by the International Accounting Standards Committee

International Accounting Standard 17 Leases This version includes amendments resulting from IFRSs issued up to 31 December 2008. IAS 17 Leases was issued by the International Accounting Standards Committee

Intermediate Accounting

Intermediate Accounting 11-1 Prepared by Coby Harmon University of California, Santa Barbara 11 Depreciation, Impairments, and Depletion Intermediate Accounting 14th Edition 11-2 Kieso, Weygandt, and Warfield

Intermediate Accounting 11-1 Prepared by Coby Harmon University of California, Santa Barbara 11 Depreciation, Impairments, and Depletion Intermediate Accounting 14th Edition 11-2 Kieso, Weygandt, and Warfield

WEEK 6 ACCOUNTING FOR LEASES IAS 17

WEEK 6 ACCOUNTING FOR LEASES IAS 17 Learning Objectives Discuss the Classification of Leases Understand Sale and Leaseback Transactions Explain the accounting procedure in IAS 17 Highlight the disclosure

WEEK 6 ACCOUNTING FOR LEASES IAS 17 Learning Objectives Discuss the Classification of Leases Understand Sale and Leaseback Transactions Explain the accounting procedure in IAS 17 Highlight the disclosure

PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 13 LEASES (PBE IPSAS 13)

") PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 13 LEASES (PBE IPSAS 13) This Standard was issued on 11 September 2014 by the New Zealand Accounting Standards Board of the External

PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 13 LEASES (PBE IPSAS 13) This Standard was issued on 11 September 2014 by the New Zealand Accounting Standards Board of the External

GASB 87. OVERVIEW: Supersedes GASB s 13 and 62 (paragraphs ).

.") Leases OVERVIEW: Supersedes GASB s 13 and 62 (paragraphs 211-271). Will require significant changes from its current practice, particularly in the accounting for operating leases Effective for reporting

Leases OVERVIEW: Supersedes GASB s 13 and 62 (paragraphs 211-271). Will require significant changes from its current practice, particularly in the accounting for operating leases Effective for reporting

HKAS 17 Leases 1 October 2005

HKAS 17 Leases 1 October 2005 1. Objective of HKAS 17 The objective of Hong Kong Accounting Standard (HKAS) 17 Leases is to prescribe, for lessees and lessors, the appropriate accounting policies and disclosure

HKAS 17 Leases 1 October 2005 1. Objective of HKAS 17 The objective of Hong Kong Accounting Standard (HKAS) 17 Leases is to prescribe, for lessees and lessors, the appropriate accounting policies and disclosure

ABRAHAM E. HASPEL CPA

ABRAHAM E. HASPEL CPA Comments on the Financial Accounting Standard Board s: Proposed Accounting Standard Update Leases (Topic 840) (ED) I am pleased to submit the following comments in response to the

ABRAHAM E. HASPEL CPA Comments on the Financial Accounting Standard Board s: Proposed Accounting Standard Update Leases (Topic 840) (ED) I am pleased to submit the following comments in response to the

Defining Issues May 2013, No