Lease Accounting under ASC 842

|

|

|

- Rosalyn Sims

- 5 years ago

- Views:

Transcription

1 Lease Accounting under ASC 842 Neil MacDonald CPA CMA PMP Solutions Consultant Binary Stream Software Inc

2 Introduction Neil MacDonald CPA, CMA, PMP 30+ years progressive Business, Project and IT Management, formal management and financial training, technical and industry certifications Project management and technical leadership in the delivery of IT and ERP implementations Resolution and consulting skills in applying best practices and efficiency initiatives Career History: Solutions Consultant 2011 Present Dynamics GP Consultant Mgr. IT and Process Improvements

3 Disclaimer Lease Accounting under ASC 842 ASC 842 is new. It is extensive. The guidance from FASB runs close to 200 pages long, detailed pages This webinar will only cover the high level points to get you started on ASC 842. It is in no way intended to be comprehensive, and due to the ever changing updates from FASB, is not meant to be a conclusive coverage of ASC 842 While I am a CPA CMA (Chartered Professional Accountant / Certified Management Accountant), I am not a life-long expert in leasing I am also not YOUR CPA It is your responsibility to learn as much about ASC 842 as you can, from various resources, accounting white papers and articles, as well as the relevant IASB or IFRS topics and discuss these with your own CPAs and auditors to ensure you are compliant 3

4 Session agenda Lease Accounting under ASC 842 Why are we here? Goals / objectives of this webinar What is ASC 842? Identifying and classifying your leases Lessee accounting creating Right of Use assets / lease liabilities Lease vs Non-Lease components & direct vs indirect costs Steps to prepare for ASC 842 adoption How can I be ASC 842 compliant with my leases in Dynamics GP? Q&A but feel free to ask questions any time! 4

5 Goals / Objectives Lease Accounting under ASC 842 Understanding ASC 842 Allow you to recognize if this applies to you, whether lessee or lessor Help you plan for ASC 842 adoption what do you need to know and consider? Understand what some of the industry experts and accounting firms are recommending Discuss how to handle ASC 842 in Dynamics GP 5

6 Challenges ASC 842 ASC 842 is new and comprehensive; I don t really understand it! I don t have time to read ASC 842 I have lots of leases Implementation time is too close! My ERP may not handle ASC 842 automatically

7 ASC 842 Leases aka ASU , IFRS 16 Acknowledgement is given to the following resources used to compile this presentation: New Developments Summary FASB issues new lease accounting standard Grant Thornton 10 Minutes on the new US lease standard PwC Executive Accounting Update Lessees KPMG Executive Accounting Update Lessors - KPMG Leases (Topic 842) - FASB 7

8 What is ASC 842? Updated FASB accounting standard; replaces ASC 840 IFRS updated as well (IFRS 16), but not identical Changes lease accounting for both lessors and lessees Lessor changes are minimal mainly lease classification Lessee changes are significant, so we will focus on those Key points: Lessors focus on control of the asset to determine lease type; most accounting remains similar to today s standard Lessees will show all leases longer than 12 months on the balance sheet, with a right of use asset and a corresponding liability / investment 8

9 Do I need to care about ASC 842? Who is affected by ASC 842? Topic 842 affects any entity that enters into a lease (as that term is defined in this update), with some specified scope exemptions. If your company leases as the lessor or the lessee - real property, land, computers, copiers, vehicles, trade marks etc ASC 842 applies to you! 9

10 ASC 842 timing When does ASC 842 go into effect? For public companies and some NFPs: as of fiscal periods beginning after Dec 15, 2018; option to adopt 1 year early Applies to NFPs that have issued, or are conduit bond obligators for, securities that are traded, listed or quoted on an exchange or OTC markets For private companies and all other NFPs As of fiscal periods beginning after Dec 15, 2019 Option to adopt two years early Early adoption may make sense for lessors because the changes are fewer, and while implementing ASC

11 Transition Modified Retrospective Transition Requires adjusting the accounting for any leases existing at the beginning of the earliest comparative period Typically means 2 years of retrospective adjustment (for publicly traded companies, 2019 implementation requires 2018 and 2017 comparative financials) Leases that expire before the implementation date will not require adjusting For some firms, due to the extent of their leasing activities, this might be very difficult and time consuming Many examples provided to guide both lessors and lessees: See through 254 Section has several pages covering practical expedients with illustrations 11

12 Transition BREAKING NEWS! Cumulative Update ASU , Leases (ASC 842) Targeted Improvements - Released August 2018 Allows users to apply ASC 842 at the adoption date and recognize a cumulative-effect adjustment to the opening balance of retained earnings in the period of adoption Entities that elect this method should report comparative periods in accordance with ASC 840 Lessors may also elect a practical expedient allowing them to not separate lease and non-lease components, by asset class. There are limitations to this election so read ASU to ensure it applies to you. 12

13 Identify Your Leases

14 Identify your leases Section contains a flowchart to help determine whether a contract is or contains a lease. Note that the flow chart does not include all the guidance on identifying a lease in this subtopic and is not intended as a substitute for the guidance on identifying a lease in this subtopic. 14

15 Lease, or no lease? A coffee company (customer) enters into a contract with an airport operator (supplier) to use space for it s kiosk for a three year period. Contract specifies size of space, but not location. In fact, the supplier can dictate that the kiosk be moved at its discretion. There are minimal costs to supplier to move the customer. Customer owns the kiosk, and there are many areas in the airport where the customer might be located and/or relocated. Lease or no lease? 15

16 Lease, or no lease? A utility company (customer) enters into a contract to purchase all the electricity produced by supplier s solar farm for 20 years. The solar farm is listed in the contract and the supplier cannot substitute it; the solar power cannot come from another facility. Customer designed the solar farm, hiring experts to determine the best location and engineer the equipment. Supplier built to customer s specs and must maintain the farm. Supplier receives tax credits relating to construction and ownership, customer receives renewable energy credits that accrue from use of solar farm. Lease or no lease? 16

17 Lease, or no lease? A utility company (customer) enters into a contract to purchase all the electricity produced by supplier s explicitly stated plant for 3 years. The supplier owns, maintains and operates the plant and cannot substitute it. The contract sets out the quantity and timing of the power produced. Supplier designed the power plant and built it prior to entering into contract with customer. Lease or no lease? 17

18 Lease, or no lease? Customer enters into a contract with a telecom company (supplier) for network services for 2 years. Contract requires supplier to meet a specified quality level. Supplier installs, configures and operates servers on customer s premises. Supplier determines speed and quality of data transport. Supplier can reconfigure the servers/network to meet service level. Lease or no lease? No lease! ( through 126) Contract is a service contract, with no identified asset, wherein the supplier uses equipment to meet a service level. Customer does not control the servers; level of service is specified and cannot be changed without a new/modified contract. Even though customer creates the traffic, that does not change the configuration of the network, and does not affect how and for what purpose the servers are used. Supplier makes decisions over how servers are configured and used. 18

19 Lease, or no lease? Customer enters into a contract with a telecom company (supplier) for use of a specific server for 3 years. Supplier installs, configures and maintains server on customer s premises. Supplier substitutes server only in the event of a malfunction. Customer decides what data is stored on the server and how it fits into its server farm; customer can change these decisions at any time during the contract. Lease or no lease? Lease! ( through 130) There is an identified asset, which customer has the right to use and control for three years. Customer has the right to change the use of the server; supplier does not. Customer has the right to obtain all economic benefits from use of the server; customer also has exclusive use of the server. Customer has the right to direct the use of the server and change that at any time, without consulting the supplier. 19

20 Identify your leases (continued) Lease classifications Lessees will need to distinguish between operating and financing (formerly capital) leases Lessors will need to distinguish between sales-type, direct financing and operating leases Since virtually all leases will now appear on the balance sheet, these lease types affect how lessees and lessors recognize expense / revenue on the P&L 20

21 Identify your leases (continued) Lease classifications Under ASC 842, a lease is a financing lease for a lessee, and a sales-type lease for a lessor if the lessee obtains effective control of the asset. What determines effective control? If any of the following are met ( ): The lease transfers ownership of the asset to the lessee at the end of the lease The lease has a bargain purchase option The lease term is for the major part of the remaining economic life of the asset This can be ignored if the lease begins at or near the end of the asset s useful life The present value of the lease payments, plus the guaranteed residual, amounts to substantially all of the leased asset s fair value The asset is specialized and has no alternative use to the lessor Absent any of these conditions, the lease is treated as an operating lease. 21

22 Identify your leases (continued) Lease classifications What thresholds are used to determine substantially all of the fair value or the major part of the remaining economic life? ASC uses these thresholds: 75% or more is a major part of an asset s remaining economic life 90% or more is substantially all of an asset s fair value An asset is near the end of its economic life when 25% or less of its economic life remains What about the rate used to compute present values? The discount rate is the rate implicit in the lease, or The lessees incremental borrowing rate 22

23 Lessee accounting Let s go deeper

24 Lessee accounting If a lease is less than 12 months, and does not contain a purchase option that is reasonably expected to be exercised, a lease does not have to appear on the balance sheet, i.e. treat as an operating lease under ASC 840 (Short-term Election) If a lease renewal exists that extends the lease beyond 12 months, but is not expected to be exercised, the same treatment applies For the remaining leases, both a Right of Use (RoU) asset and a lease liability will be placed on the balance sheet Both the RoU asset and the liability will generally be recognized at the present value of the remaining lease payments Initial direct costs will also be capitalized as part of the RoU asset Operating leases payments will be recognized as rental expense on a straight-line basis over the lease term Finance Leases rental expense and interest expense will be recognized based on the interest rate, and the RoU asset will be amortized straight-line over the shorter of its useful life or the lease term 24

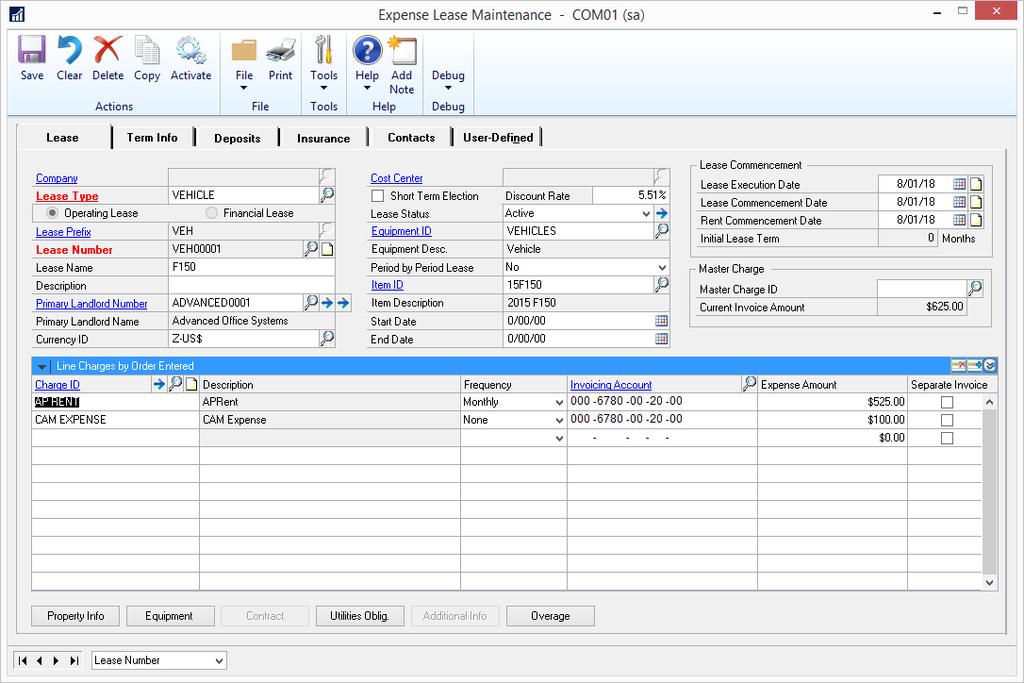

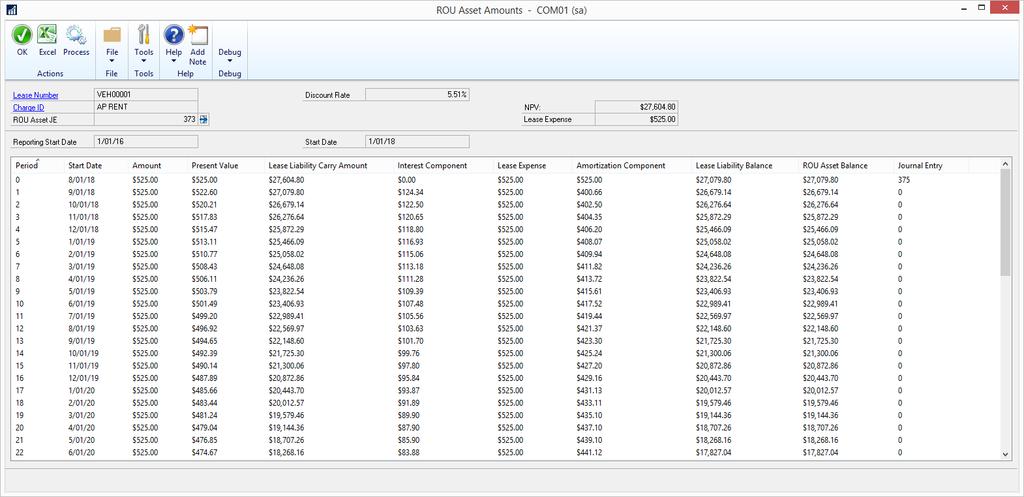

25 Implementing a lease Create a Right of Use Asset For each lease charge, calculate the Net Present Value for the sum of the flow of payments and the charge s residual value Discount Rate 5.51% Lease Payments: 100,000 Base rent at the end of year 1 110,000 Base rent at the end of year 2 125,000 Base rent at the end of year 3 NPV = 100,000/( ) ^ ,000 /( ) ^ ,000 /( ) ^3 = 94, , ,421 = 300,000 Right of Use Asset Created RoU Asset $300,000 Lease Liability $300,000 27

26 Implementing a lease (continued) Finance lease Calculate Amortization Expense based on NPV of pmts Amortization Expense (Finance Lease) = 300,000 / 3 = 100,000 Calculate Interest Expense 1st year invoice Year 1 Interest Component: 300,000 x 5.51% = 16,535 Year 2 Interest Component: (300, , ,535) x 5.51% = 11,935 Year 3 Interest Component: (300, , , , ,935) x 5.51% = 6,530 Interest Expense 16,535 1st year Interest Component Lease Liability 16,535 1st year Interest Component Amortization Expense 100,000 Amortization expense from the RoU Asset calculation RoU Asset 100,000 Amortization expense from the RoU Asset calculation Lease Liability 100,000 1st year payment AP 100,000 1st year payment 28

27 Implementing a lease (continued) Finance lease Calculate Amortization Expense based on NPV of pmts Amortization Expense (Finance Lease) = 300,000 / 3 = 100,000 Calculate Interest Expense 2nd year invoice Year 1 Interest Component: 300,000 x 5.51% = 16,535 Year 2 Interest Component: (300, , ,535) x 5.51% = 11,935 Year 3 Interest Component: (300, , , , ,935) x 5.51% = 6,530 Interest Expense 11,935 2nd year Interest Component Lease Liability 11,935 2nd year Interest Component Amortization Expense 100,000 Amortization expense from the RoU Asset calculation RoU Asset 100,000 Amortization expense from the RoU Asset calculation Lease Liability 110,000 2nd year payment AP 110,000 2nd year payment 29

28 Implementing a lease (continued) Finance lease Calculate Amortization Expense based on NPV of pmts Amortization Expense (Finance Lease) = 300,000 / 3 = 100,000 Calculate Interest Expense 3rd year invoice Year 1 Interest Component: 300,000 x 5.51% = 16,535 Year 2 Interest Component: (300, , ,535) x 5.51% = 11,935 Year 3 Interest Component: (300, , , , ,935) x 5.51% = 6,530 Interest Expense 6,530 3rd year Interest Component Lease Liability 6,530 3rd year Interest Component Amortization Expense 100,000 Amortization expense from the RoU Asset calculation RoU Asset 100,000 Amortization expense from the RoU Asset calculation Lease Liability 125,000 3rd year payment AP 125,000 3rd year payment 30

29 Implementing a lease (continued) Operating lease Calculate Straight-line Amount i.e. Lease Expense from RoU (100, , ,000)/3 = 111,667 Calculate Interest Expense Year 1 Interest Component: 300,000 x 5.51% = 16,535 Year 2 Interest Component: (300, , ,535) x 5.51% = 11,935 Year 3 Interest Component: (300, , , , ,935) x 5.51% = 6,530 Calculate Amortization Component Year 1 Amortization Component: 111,667 16,535 = 95,132 Year 2 Amortization Component: 111,667 11,935 = 99,732 Year 3 Amortization Component: 111,667 6,530 = 105,137 31

30 Implementing a lease (continued) Operating lease 1st year invoice: Lease Expense 111,667 Lease Expense from the RoU Asset calculation Lease Liability 16,535 1st year Interest Component RoU Asset 95,132 1st year Amortization Component Lease Liability 100,000 1st year payment AP 100,000 1st year payment 2nd year invoice: Lease Expense 111,667 Lease Expense from the RoU Asset calculation Lease Liability 11,935 2nd year Interest Component RoU Asset 99,732 2nd year Amortization Component Lease Liability 110,000 2nd year payment AP 110,000 2nd year payment 3rd year invoice: Lease Expense 111,667 Lease Expense Lease Liability 6,530 3 rd year Interest Component RoU Asset 105,137 3 rd year Amortization Component Lease Liability 125,000 3 rd year payment AP 125,000 3 rd year payment 32

31 And that is the easy part!!! Q. What happens if the lease is based on variable components, for example the escalation is based on CPI? Q. What if a lease is modified or terminated early? Typically, the RoU Asset and Lease Liability need to be restated and the difference goes to a gain or loss account 33

32 Lease vs non-lease components & direct costs

33 Lease / Non-lease components Affects both lessees and lessors Lessees Need to evaluate services, allocate consideration to each component Example: a lease might contain property taxes, and maintenance (CAM). Taxes have no identifiable benefit to the lessee, so can be included in the ROU asset. CAM is a separately identifiable benefit, so is not part of the ROU asset. Base value of non-lease components on their relative stand-alone prices. If indeterminable, might need to ask the lessor. There is a practical expedient that allows, by asset class, for lease and non-lease components to be accounted for together as a single lease component Be careful! If significant, this can dramatically increase the amounts shown on the balance sheet, which might change some financial ratios Basis for Conclusions, paragraph BC14-c, states: "Topic 842 characterizes operating lease liabilities as operating liabilities, rather than debt. Consequently, those amounts may not affect certain financial ratios that often are used in debt covenants." 35

34 Lease / Non-lease components Affects both lessees and lessors Lessors Need to evaluate services, allocate consideration to each component Example: a lease might contain property taxes, and maintenance (CAM). Taxes have no identifiable benefit to the lessee, thus are part of the lease entries & investment. CAM is a separately identifiable benefit, so is not part of the lease investment. Base the value of non-lease components on their relative stand-alone prices. Treat revenue from non-lease components under the guidance of ASC 606 Revenue from Contracts with Customers 36

35 Direct vs Indirect Costs ASC 842 changes the definition of initial direct costs : Costs to negotiate or arrange a lease that would have been incurred regardless of whether the lease was obtained, such as fixed employee salaries, are not initial direct costs. Example of costs allowed ( ) Commissions Payments made to an existing tenant to incentivize that tenant to terminate its lease Example of costs not allowed ( ) General overhead, including depreciation, occupancy and equipment costs, unsuccessful origination time or idle time Costs related to activities performed by the lessor for advertising, soliciting potential tenants, servicing existing leases Costs related to activities that occur before the lease is obtained, such as obtaining tax or legal advice, negotiating lease terms or conditions, or evaluating a potential lessee s financial condition Expensing these latter costs could result in higher expense recognition prior to the lease, as well as higher margins on lease income 37

36 What the experts are saying PwC 10 Minutes on The New Lease Standard

37 What Do I Do? With the changes to both ASC 842 Leases, and ASC 606 Revenue from Contracts with Customers, coming so close together, and the obvious link for Lessors, how do I manage adopting both? The PwC document referenced early suggests you consider these things: Since the standards are so closely aligned, especially for lessors, adopting both concurrently might make sense. This means early adoption of 842 since 606 is applicable in Are your systems and controls ready for early adoption? What are your peers/competitors doing? Will you be the only one to not adopt early? What do your investors prefer? One big change (606 & 842), or one per year (606 in 2018, 842 in 2019)? The interest rate environment do you adopt early using today s interest rate, or wait and use 2019 s? The expedients allow you to hold off certain leases until restructuring or changing leases is required. Should you wait, or do it now? Reporting requirements: both GAAP and IFRS, or just one (the standards are not identical) There are no correct (or wrong) answers, except the ones that are right for your business! 39

38 Steps to prepare PwC 10 Minutes on the New Lease Standard The same PwC document contains six steps to help you prepare: 1.Get every resource on board every department in your organization might be impacted, from IT to tax, to procurement, to operations, to treasury and investor relations. Ensure you budget both cost and resources 2. Break into the filing cabinets inspect and understand your leases, lease terms, renewal options and payments. Examine each lease, or class of lease. Be prepared in multi-asset leases to identify and account for each component as a separate lease. Understand lease and non-lease elements. 3.Assess the impact Do the practical expedients make more sense for your business? Estimate future balance sheet amounts for operating leases. Evaluate your leasing strategy, i.e lease vs buy, short vs long term 40

39 Steps to prepare PwC 10 Minutes on the New Lease Standard The same PwC document contains six steps to help you prepare: 4. Examine and understand regulatory and tax implications 5. Manage the transition do you need to redesign or invest in new systems? Don t forget that testing and implementation take time, so start early 6. Reassess agreements plan to periodically re-evaluate lease terms. Ongoing compliance costs are likely to be higher than today 41

40 Managing leases in Dynamics GP

41 What does that mean for my Dynamics ERP? Managing leases in your MS Dynamics GP ERP requires either Massive, complex Excel spreadsheets; build and track RoU assets & investments and manually JE each period Excel is useful, but cumbersome. (A recent report from the EU found over 50% of all critical spreadsheets in large organizations contained material defects!*) * - European Spreadsheet Risks Interest Group A third party, non-integrated property lease solution - has over 50 different packages What is the upgrade path? Reporting capability? How does it update your GL? Most require manual or integrated JEs to ensure GL is up to date but how up to date? ISV solution Talk to your Dynamics VAR for recommendations Ask your peers on the GPUG Forum what they are doing 43

42 Questions to Ask Yourself / Your VAR Will my ERP handle this today? Hint: GP cannot! So, do you have the Excel skills/time? Will the recommended solution automatically calculate and build the RoU asset and liability at the correct values, or do I have to do it manually? Will the recommended solution handle the new reporting requirements? Will the recommended solution assist with easing the implementation? Is the recommended solution GP integrated, or will I have to use manual integrations and journal entries to update my GL? Will the GL be up to date real time or only after a data synchronization? Can my VAR train me and support me on whatever solution I choose? No right or wrong answers except what works for you but ASK! 44

43 Binary Stream s Property Management Fully integrated lease management module for Dynamics GP (D365 F&O coming in 2019!) Designed for lessors or lessees Commercial, retail, residential applications Build and manage complex lease payment escalations Percent, or sales based, rent Common Area Maintenance reconciliation Automatic creation of Right of Use Asset and Lease Liability Adjustment and true up of RoU Asset and Lease Liability when lease terms and conditions change In-depth reporting Report Writer, or SSRS 45

44 Binary Stream s Property Management Screenshots 46

45 Summary Lease Accounting under ASC 842 Reviewed ASC 842 Lease classification examples Lessee accounting examples What you need to know to get ready! How to handle ASC 842 in Dynamics GP Binary Stream s PrM 47

46

47 For more ASC 842 information and GP solutions Cady Jackson Client Account Manager P M NexTecGroup.com

The New Lease Accounting Standard. Hunter Mink, CPA, CCIFP Brian Rosenberg, CPA, MBA

The New Lease Accounting Standard Hunter Mink, CPA, CCIFP Brian Rosenberg, CPA, MBA 1 Agenda Introduction Lease Identification and Classification Lessee Accounting Other Considerations Disclosures Impact

The New Lease Accounting Standard Hunter Mink, CPA, CCIFP Brian Rosenberg, CPA, MBA 1 Agenda Introduction Lease Identification and Classification Lessee Accounting Other Considerations Disclosures Impact

Lease Accounting and Loan Covenants: What is the Impact?

Lease Accounting and Loan Covenants: What is the Impact? Monday June 26, 2017 9:15 AM 10:30 AM Presented by: Charlie Shannon Partner Moss Adams LLP 8750 N. Central Expressway, Suite 300 Dallas, TX 75231

Lease Accounting and Loan Covenants: What is the Impact? Monday June 26, 2017 9:15 AM 10:30 AM Presented by: Charlie Shannon Partner Moss Adams LLP 8750 N. Central Expressway, Suite 300 Dallas, TX 75231

Implementing the New Lease Guidance

Implementing the New Lease Guidance October 22, 2018 2018 Crowe LLP 2018 Crowe LLP Agenda Background Scope Effective dates & transition requirements Lessee accounting model Lessor accounting model Specialized

Implementing the New Lease Guidance October 22, 2018 2018 Crowe LLP 2018 Crowe LLP Agenda Background Scope Effective dates & transition requirements Lessee accounting model Lessor accounting model Specialized

Lease Accounting Standard Update ASU Presented by: Nicholas Hoefel, CPA Manager, Audit Services Group

Lease Accounting Standard Update ASU 2016-02 Presented by: Nicholas Hoefel, CPA Manager, Audit Services Group 1 Overview Introduction Background and current environment Effective dates and transition Key

Lease Accounting Standard Update ASU 2016-02 Presented by: Nicholas Hoefel, CPA Manager, Audit Services Group 1 Overview Introduction Background and current environment Effective dates and transition Key

Lease accounting scope & impacts

Leasing Lease accounting scope & impacts Scope What s in? All industries, all entities Arrangements that meet the definition of a lease Embedded leases within other arrangements What s out? Leases of:

Leasing Lease accounting scope & impacts Scope What s in? All industries, all entities Arrangements that meet the definition of a lease Embedded leases within other arrangements What s out? Leases of:

Executive Summary. New leases standard Lessees

Executive Summary December 2018 The new leases standard focuses on increased transparency and comparability providing financial statement users with more information about an entity s leasing activities.

Executive Summary December 2018 The new leases standard focuses on increased transparency and comparability providing financial statement users with more information about an entity s leasing activities.

What Nonprofits Need to Know About the New Standards for Lease Accounting

The webcast will start at 1 p.m. Eastern Please note: Handout You can print or download the webcast handout at https://capincrouse.com/webcast-lease-accounting CPE CPE certificates will be emailed to you

The webcast will start at 1 p.m. Eastern Please note: Handout You can print or download the webcast handout at https://capincrouse.com/webcast-lease-accounting CPE CPE certificates will be emailed to you

New leases standard ASC 842 Lessee - operating leases. Itai Gotlieb, Partner, Professional Practice July 2017

ASC 842 Lessee - operating leases Itai Gotlieb, Partner, Professional Practice July 2017 Overview Under Accounting Standards Codification (ASC) 842, Leases, lessees recognize assets and liabilities for

ASC 842 Lessee - operating leases Itai Gotlieb, Partner, Professional Practice July 2017 Overview Under Accounting Standards Codification (ASC) 842, Leases, lessees recognize assets and liabilities for

Edison Electric Institute and American Gas Association New Lease Standard

Edison Electric Institute and American Gas Association New Lease Standard May 16, 2016 Disclaimer The information contained herein is of a general nature and is not intended to address the circumstances

Edison Electric Institute and American Gas Association New Lease Standard May 16, 2016 Disclaimer The information contained herein is of a general nature and is not intended to address the circumstances

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions. August 24, 2017

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions August 24, 2017 Learning objectives Define leasing implications related to recently revised FASB standard Differentiate between new

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions August 24, 2017 Learning objectives Define leasing implications related to recently revised FASB standard Differentiate between new

Lease & Finance Accountants Conference. September The Westin Charlotte Charlotte, NC

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Basic Principles of Lessors under ASC 842 Mamta Shori, Wells Fargo Equipment Finance Joe Sebik,

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Basic Principles of Lessors under ASC 842 Mamta Shori, Wells Fargo Equipment Finance Joe Sebik,

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions. August 24, 2017

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions August 24, 2017 Learning objectives Define leasing implications related to recently revised FASB standard Differentiate between new

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions August 24, 2017 Learning objectives Define leasing implications related to recently revised FASB standard Differentiate between new

Leases: Overview of the new guidance

Leases: Overview of the new guidance Prepared by: Richard Stuart, Partner, National Professional Standards Group, RSM US LLP richard.stuart@rsmus.com, +1 203 905 5027 March 2, 2016 Introduction On February

Leases: Overview of the new guidance Prepared by: Richard Stuart, Partner, National Professional Standards Group, RSM US LLP richard.stuart@rsmus.com, +1 203 905 5027 March 2, 2016 Introduction On February

7/30/2018. Health Care. A CHC-Focused Plan for the New Lease Accounting Standard

Health Care A CHC-Focused Plan for the New Lease Accounting Standard July 31, 2018 1 TO RECEIVE CPE CREDIT Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader

Health Care A CHC-Focused Plan for the New Lease Accounting Standard July 31, 2018 1 TO RECEIVE CPE CREDIT Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader

Deeper Dive Leases. Overview

Deeper Dive Leases Presented by: Shaun Johnson, CPA Dingus, Zarecor & Associates PLLC Overview Effective dates Big picture Objective, impact, and implementation Applicability and definition Initial recognition

Deeper Dive Leases Presented by: Shaun Johnson, CPA Dingus, Zarecor & Associates PLLC Overview Effective dates Big picture Objective, impact, and implementation Applicability and definition Initial recognition

Center for Plain English Accounting

Report April 18, 2018 Center for Plain English Accounting AICPA s National A&A Resource Center Debits and Credits Associated with New Lease Accounting Standard CPEA Lease Standard Implementation Series

Report April 18, 2018 Center for Plain English Accounting AICPA s National A&A Resource Center Debits and Credits Associated with New Lease Accounting Standard CPEA Lease Standard Implementation Series

ASC 842 (Leases)

") ASC 842 (Leases) On February 25, 2016 the Financial Accounting Standards Board of the United States (FASB) issued substantial new guidance on the treatment of leases for both lessees and lessors. The FASB

ASC 842 (Leases) On February 25, 2016 the Financial Accounting Standards Board of the United States (FASB) issued substantial new guidance on the treatment of leases for both lessees and lessors. The FASB

Is Your Operating Lease An Asset or Liability? It s Now Both

MFM Annual Conference Is Your Operating Lease An Asset or Liability? It s Now Both 23 May 2016-1:30 pm 2:20 pm Disclaimer These slides are for educational purposes only and are not intended, and should

MFM Annual Conference Is Your Operating Lease An Asset or Liability? It s Now Both 23 May 2016-1:30 pm 2:20 pm Disclaimer These slides are for educational purposes only and are not intended, and should

Applying the new lease accounting standard

Applying the new lease accounting standard In February 26, the FASB issued Accounting Standards Update (ASU) No. 26-, Leases (codified as Accounting Standards Codification Topic (ASC) 842). ASC 842 introduces

Applying the new lease accounting standard In February 26, the FASB issued Accounting Standards Update (ASU) No. 26-, Leases (codified as Accounting Standards Codification Topic (ASC) 842). ASC 842 introduces

IMPACTS OF NEW LEASE ACCOUNTING STANDARD WHAT DOES IT MEAN TO ME? Jessica Richter, CPA.CITP, CISA Jamie Becker June 11, 2018

IMPACTS OF NEW LEASE ACCOUNTING STANDARD WHAT DOES IT MEAN TO ME? Jessica Richter, CPA.CITP, CISA Jamie Becker June 11, 2018 3 AGENDA ASC 842 Leases, ASU 2016-02 What s new Comparison with today s rules

IMPACTS OF NEW LEASE ACCOUNTING STANDARD WHAT DOES IT MEAN TO ME? Jessica Richter, CPA.CITP, CISA Jamie Becker June 11, 2018 3 AGENDA ASC 842 Leases, ASU 2016-02 What s new Comparison with today s rules

Miles CPA Review: FAR Updates

Miles CPA Review: FAR - 2019 Updates Summary of updates: - FAR-4.4: s [ASC 842] effective fiscal years beginning after Dec 15, 2018 (for issuers) and effective fiscal years beginning after Dec 15, 2019

Miles CPA Review: FAR - 2019 Updates Summary of updates: - FAR-4.4: s [ASC 842] effective fiscal years beginning after Dec 15, 2018 (for issuers) and effective fiscal years beginning after Dec 15, 2019

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N AGENDA Leases FASB & GASB Revenue Recognition FASB 2 FASB ASU 2016-02, Leases (Topic

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N AGENDA Leases FASB & GASB Revenue Recognition FASB 2 FASB ASU 2016-02, Leases (Topic

Impact of lease accounting changes to corporate real estate

Impact of lease accounting changes to corporate real estate Overview In February 2016, the Financial Accounting Standards Board (FASB) issued its long-awaited revision to lease accounting Accounting Standards

Impact of lease accounting changes to corporate real estate Overview In February 2016, the Financial Accounting Standards Board (FASB) issued its long-awaited revision to lease accounting Accounting Standards

AASB 16: Experience the Fundamental Overhaul of Lease Accounting for Lessees

AASB 16: Experience the Fundamental Overhaul of Lease Accounting for Lessees Introduction to Session This introductory session we will: Explore the Principles of AASB 16 Learn how to Identify a Lease Work

AASB 16: Experience the Fundamental Overhaul of Lease Accounting for Lessees Introduction to Session This introductory session we will: Explore the Principles of AASB 16 Learn how to Identify a Lease Work

What private companies need to know about applying the new lease standard

What private companies need to know about applying the new lease standard In February 26, the FASB issued Accounting Standards Update (ASU) No. 26-, Leases (codified as Accounting Standards Codification

What private companies need to know about applying the new lease standard In February 26, the FASB issued Accounting Standards Update (ASU) No. 26-, Leases (codified as Accounting Standards Codification

ASC 842: Leases. Presented by: Maxwell Locke & Ritter LLP June 15, Maxwell Locke & Ritter

ASC 842: Leases Presented by: Maxwell Locke & Ritter LLP June 15, 2018 The New Lease Standard FASB ASC 842, Leases Supersedes FASB ASC 840, Leases Effective for calendar year-end public companies in 2019;

ASC 842: Leases Presented by: Maxwell Locke & Ritter LLP June 15, 2018 The New Lease Standard FASB ASC 842, Leases Supersedes FASB ASC 840, Leases Effective for calendar year-end public companies in 2019;

Lease Accounting and simplease Accounting Updates. Trevor Warren & Jason Reljac

Lease Accounting and simplease Accounting Updates Trevor Warren & Jason Reljac Today s Agenda Overview Scope and Definition of a Lease Lease Classification Lessee Accounting Financial Statement Impact

Lease Accounting and simplease Accounting Updates Trevor Warren & Jason Reljac Today s Agenda Overview Scope and Definition of a Lease Lease Classification Lessee Accounting Financial Statement Impact

Accounting and Auditing Update. Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc.

Accounting and Auditing Update Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc. Agenda Overview of the standard setting agenda Revenue recognition Lease

Accounting and Auditing Update Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc. Agenda Overview of the standard setting agenda Revenue recognition Lease

GAAP UPDATE DEANA BOWDEN, CPA, MSA WHITE NELSON DIEHL EVANS LLP

GAAP UPDATE DEANA BOWDEN, CPA, MSA WHITE NELSON DIEHL EVANS LLP TOPICS 2016-02 Topic 842 Leases 2016-14 Topic 958 Not for Profits 2016-18 Topic 230 Cash Flows LEASES Current US Generally Accepted Accounting

GAAP UPDATE DEANA BOWDEN, CPA, MSA WHITE NELSON DIEHL EVANS LLP TOPICS 2016-02 Topic 842 Leases 2016-14 Topic 958 Not for Profits 2016-18 Topic 230 Cash Flows LEASES Current US Generally Accepted Accounting

Accounting and Auditing. Norman Mosrie, CPA, FMFMA, CHFP James Sutherland, CPA

Accounting and Auditing Norman Mosrie, CPA, FMFMA, CHFP James Sutherland, CPA Leases (ASU 2016-02; Topic 842) A lease contract conveys the right to use an asset (the underlying asset) for a period of time

Accounting and Auditing Norman Mosrie, CPA, FMFMA, CHFP James Sutherland, CPA Leases (ASU 2016-02; Topic 842) A lease contract conveys the right to use an asset (the underlying asset) for a period of time

Brad Bonde, CPA Senior Manager, HC Services/Audit & Advisory

Brad Bonde, CPA Senior Manager, HC Services/Audit & Advisory Overview Background Improving Lease Accounting Scope Accounting Models Disclosures Effective Dates 2 Background Source - FASB 3 QUIZ What amount

Brad Bonde, CPA Senior Manager, HC Services/Audit & Advisory Overview Background Improving Lease Accounting Scope Accounting Models Disclosures Effective Dates 2 Background Source - FASB 3 QUIZ What amount

Lease & Finance Accountants Conference. September The Westin Charlotte Charlotte, NC

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S EQUIPMENT LEASING AND FINANCE ASSOCIATION Transitioning to the ASC 842 Guidance Lessee Requirements

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S EQUIPMENT LEASING AND FINANCE ASSOCIATION Transitioning to the ASC 842 Guidance Lessee Requirements

47.1% of organizations concerned about their ability to implement

Leases: Not Just for the 1 Lease Standard - Statistics 10 year project In 2014, $3.0 trillion in off-balance sheet lease commitments 47.1% of organizations concerned about their ability to implement 2

Leases: Not Just for the 1 Lease Standard - Statistics 10 year project In 2014, $3.0 trillion in off-balance sheet lease commitments 47.1% of organizations concerned about their ability to implement 2

Grant Thornton October Leases. Navigating the guidance in ASC 842

Grant Thornton October 2018 Leases Navigating the guidance in ASC 842 This publication was created for general information purposes, and does not constitute professional advice on facts and circumstances

Grant Thornton October 2018 Leases Navigating the guidance in ASC 842 This publication was created for general information purposes, and does not constitute professional advice on facts and circumstances

presentation for October 5, 2018

presentation for October 5, 2018 Proper Lease Analysis + Proper Technology = Successful Implementation Designed by Former Big 4 Auditors Built for Audit Efficiency Key Design Principles Ease of Use & Security

presentation for October 5, 2018 Proper Lease Analysis + Proper Technology = Successful Implementation Designed by Former Big 4 Auditors Built for Audit Efficiency Key Design Principles Ease of Use & Security

Click to edit Master title style REVENUE RECOGNITION Understanding the New Revenue Recognition Standard ASC 606

Click to edit Master title style REVENUE RECOGNITION Understanding the New Revenue Recognition Standard ASC 606 9/7/2017 0 Agenda Overview of ASC 606 Review of the five-step process Accounting for contract

Click to edit Master title style REVENUE RECOGNITION Understanding the New Revenue Recognition Standard ASC 606 9/7/2017 0 Agenda Overview of ASC 606 Review of the five-step process Accounting for contract

It s Back Accounting for Asset Leases the new way!

It s Back Accounting for Asset Leases the new way! Kent Bettisworth BETTISWORTH & ASSOCIATES 2016 ERP Corp. All rights reserved. Controlling 2016 Conference September 12-15, 2016 in San Diego Kent Bettisworth

It s Back Accounting for Asset Leases the new way! Kent Bettisworth BETTISWORTH & ASSOCIATES 2016 ERP Corp. All rights reserved. Controlling 2016 Conference September 12-15, 2016 in San Diego Kent Bettisworth

GASB 87: Leases. Hosted By: Ben Lindekugel, Executive Director Association of Washington Public Hospital Districts

GASB 87: Leases Hosted By: Ben Lindekugel, Executive Director Association of Washington Public Hospital Districts November 6, 2018 Presented By Tom Dingus, CPA, Partner Dingus, Zarecor & Associates PLLC

GASB 87: Leases Hosted By: Ben Lindekugel, Executive Director Association of Washington Public Hospital Districts November 6, 2018 Presented By Tom Dingus, CPA, Partner Dingus, Zarecor & Associates PLLC

The Financial Accounting Standards Board

V A L U A T I O N How the New Leases Standard May Impact Business Valuations By Judith H. O Dell, CPA, CVA The Financial Accounting Standards Board issued the 485 page Leases Standard (Topic 842) in February,

V A L U A T I O N How the New Leases Standard May Impact Business Valuations By Judith H. O Dell, CPA, CVA The Financial Accounting Standards Board issued the 485 page Leases Standard (Topic 842) in February,

REAL ESTATE PERSPECTIVE ON NEW LEASE ACCOUNTING STANDARDS

VALUATION & ADVISORY REAL ESTATE PERSPECTIVE ON NEW LEASE ACCOUNTING STANDARDS BY JOHN CORBETT, MAI, ASA, FRICS AND MARC R. SHAPIRO, MAI, MRICS INTRODUCTION The Financial Accounting Standards Board (FASB)

VALUATION & ADVISORY REAL ESTATE PERSPECTIVE ON NEW LEASE ACCOUNTING STANDARDS BY JOHN CORBETT, MAI, ASA, FRICS AND MARC R. SHAPIRO, MAI, MRICS INTRODUCTION The Financial Accounting Standards Board (FASB)

Summary of IFRS Exposure Draft Leases

The International Accounting Standards Board (IASB) recently issued a revised exposure draft (ED) relating to leases. Once these proposals are finalized the new guidance will replace the IAS 17 Leases.

The International Accounting Standards Board (IASB) recently issued a revised exposure draft (ED) relating to leases. Once these proposals are finalized the new guidance will replace the IAS 17 Leases.

HERE WE GO AGAIN. THE NEW LEASE STANDARD (ASC TOPIC 842) February Internal Audit, Risk, Business & Technology Consulting

February Internal Audit, Risk, Business & Technology Consulting") HERE WE GO AGAIN THE NEW LEASE STANDARD (ASC TOPIC 842) February 2018 Internal Audit, Risk, Business & Technology Consulting PRESENTERS Edna Lopez Protiviti Managing Director edna.lopez@protiviti.com Scott

HERE WE GO AGAIN THE NEW LEASE STANDARD (ASC TOPIC 842) February 2018 Internal Audit, Risk, Business & Technology Consulting PRESENTERS Edna Lopez Protiviti Managing Director edna.lopez@protiviti.com Scott

Something Borrowed, Something New Get Ready for the New Lease Accounting Standard

April 2016 Something Borrowed, Something New Get Ready for the New Lease Accounting Standard By Scott G. Lehman, CPA, and David E. Wentzel, CPA Audit / Tax / Advisory / Risk / Performance Smart decisions.

April 2016 Something Borrowed, Something New Get Ready for the New Lease Accounting Standard By Scott G. Lehman, CPA, and David E. Wentzel, CPA Audit / Tax / Advisory / Risk / Performance Smart decisions.

LEASES WHERE ARE WE? Steve Rathjen

LEASES WHERE ARE WE? Steve Rathjen 267 256-3110 srathjen@kpmg.com Agenda Project status Lease definition and classification Lessee accounting Lessor accounting Presentation, disclosures, and transition

LEASES WHERE ARE WE? Steve Rathjen 267 256-3110 srathjen@kpmg.com Agenda Project status Lease definition and classification Lessee accounting Lessor accounting Presentation, disclosures, and transition

Re: File Reference: No , Exposure Draft: Leases (Topic 842)

") September 13, 2013 Russell G. Golden, Chairman Financial Accounting Standards Board 401 Merritt 7 PO Box 5116 Norwalk, Connecticut 06856-5116 Hans Hoogervorst, Chairman International Accounting Standards

September 13, 2013 Russell G. Golden, Chairman Financial Accounting Standards Board 401 Merritt 7 PO Box 5116 Norwalk, Connecticut 06856-5116 Hans Hoogervorst, Chairman International Accounting Standards

Topic 842- Leases Making The Transition

Topic 842- Leases Making The Transition K-deep Dhaliwal, Partner, Moss Adams LLP Adam Hite, Senior Manager, Moss Adams LLP The material appearing in this presentation is for informational purposes only

Topic 842- Leases Making The Transition K-deep Dhaliwal, Partner, Moss Adams LLP Adam Hite, Senior Manager, Moss Adams LLP The material appearing in this presentation is for informational purposes only

Transition Requirements Under the New Lease Accounting Rules

Accounting Policy & Practice Report: News Archive 2017 December 12/28/2017 BNA Insights Transition Requirements Under the New Lease Accounting Rules By Jeffrey Ellis Jeffrey Ellis is a Senior Managing

Accounting Policy & Practice Report: News Archive 2017 December 12/28/2017 BNA Insights Transition Requirements Under the New Lease Accounting Rules By Jeffrey Ellis Jeffrey Ellis is a Senior Managing

PRACTICAL TIPS FOR IMPLEMENTING THE NEW LEASE ACCOUNTING STANDARD

PRACTICAL TIPS FOR IMPLEMENTING THE NEW LEASE ACCOUNTING STANDARD SHAUNA WATSON, VP, GLOBAL HEAD OF TECHNICAL ACCOUNTING MICHAEL ALLEN, PARTNER, TRANSACTION ADVISORY SERVICES 1. Overview of Accounting

PRACTICAL TIPS FOR IMPLEMENTING THE NEW LEASE ACCOUNTING STANDARD SHAUNA WATSON, VP, GLOBAL HEAD OF TECHNICAL ACCOUNTING MICHAEL ALLEN, PARTNER, TRANSACTION ADVISORY SERVICES 1. Overview of Accounting

Defining Issues. FASB Completes Technical Redeliberations on Leases. October 2015, No Key Facts. Key Impacts

Defining Issues October 2015, No. 15-47 FASB Completes Technical Redeliberations on Leases The FASB met on October 7 to discuss comments received and related follow-up issues on the external review of

Defining Issues October 2015, No. 15-47 FASB Completes Technical Redeliberations on Leases The FASB met on October 7 to discuss comments received and related follow-up issues on the external review of

Technical Line FASB final guidance

No. 2016-09 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect health care entities In this issue: Overview... 1 Key considerations... 3 Scope and scope exceptions...

No. 2016-09 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect health care entities In this issue: Overview... 1 Key considerations... 3 Scope and scope exceptions...

Accounting and Auditing Update. Paul Lundy

Accounting and Auditing Update Paul Lundy Leases: Not Just for the Footnotes Anymore Significant Financial Statement Impact New lease standard generally requires all leases to be capitalized and recognized

Accounting and Auditing Update Paul Lundy Leases: Not Just for the Footnotes Anymore Significant Financial Statement Impact New lease standard generally requires all leases to be capitalized and recognized

NEW LEASE ACCOUNTING STANDARD

NEW LEASE ACCOUNTING STANDARD Accounting Standards Update (ASU) 2016-02, Leases & GASB 87, Leases LEASES Leases: Why a New Leases Standard? 1 IMPLEMENTATION TIMELINE January 2016 IASB issued IFRS 16, Leases

NEW LEASE ACCOUNTING STANDARD Accounting Standards Update (ASU) 2016-02, Leases & GASB 87, Leases LEASES Leases: Why a New Leases Standard? 1 IMPLEMENTATION TIMELINE January 2016 IASB issued IFRS 16, Leases

Financial Computer Systems Inc. (203)

") Introduction to ASC 842 and EZLease Financial Computer Systems Inc. www.ezlease.net (203) 652-1375 The road to ASC 842 Begun in July 2006; joint project of FASB & IASB Primary purpose: Put lessee operating

Introduction to ASC 842 and EZLease Financial Computer Systems Inc. www.ezlease.net (203) 652-1375 The road to ASC 842 Begun in July 2006; joint project of FASB & IASB Primary purpose: Put lessee operating

Lease Accounting Is Final Time to Prepare for Implementation

Copyright 2016 by the Construction Financial Management Association (CFMA). All rights reserved. This article first appeared in CFMA Building Profits (a member-only benefit) and is reprinted with permission.

Copyright 2016 by the Construction Financial Management Association (CFMA). All rights reserved. This article first appeared in CFMA Building Profits (a member-only benefit) and is reprinted with permission.

Lease Update. June 2017 Addison, Texas

Lease Update June 2017 Addison, Texas William Bill Schneider CPA, CGMA Bill is an Audit Director at AT&T. AT&T delivers advanced mobile services, next-generation TV, highspeed internet and smart solutions

Lease Update June 2017 Addison, Texas William Bill Schneider CPA, CGMA Bill is an Audit Director at AT&T. AT&T delivers advanced mobile services, next-generation TV, highspeed internet and smart solutions

MONITORDAILY SPECIAL REPORT. Lease Accounting Project Update as of May 25, 2011 Prepared by Bill Bosco, Leasing 101

MONITORDAILY SPECIAL REPORT Lease Accounting Project Update as of May 25, 2011 Prepared by Bill Bosco, Leasing 101 The high volume of comment letters (780+) and numerous outreach meetings had common criticisms

MONITORDAILY SPECIAL REPORT Lease Accounting Project Update as of May 25, 2011 Prepared by Bill Bosco, Leasing 101 The high volume of comment letters (780+) and numerous outreach meetings had common criticisms

Why IFRS 16 matters to the shipping industry

www.pwc.no Why IFRS 16 matters to the shipping industry October 2017 Executive summary New lease standard to be effective 1 January 2019. Early implementation permitted together with IFRS 15 (effective

www.pwc.no Why IFRS 16 matters to the shipping industry October 2017 Executive summary New lease standard to be effective 1 January 2019. Early implementation permitted together with IFRS 15 (effective

Technical Line FASB final guidance

No. 2016-11 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect real estate entities In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions...

No. 2016-11 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect real estate entities In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions...

Technical Line FASB final guidance

No. 2018-08 20 September 2018 Technical Line FASB final guidance How the new leases standard affects engineering and construction entities In this issue: Overview... 1 Key considerations... 2 Scope and

No. 2018-08 20 September 2018 Technical Line FASB final guidance How the new leases standard affects engineering and construction entities In this issue: Overview... 1 Key considerations... 2 Scope and

Implementing GASB s Lease Guidance

The effective date of the Governmental Accounting Standards Board s (GASB) new lease guidance is drawing nearer. Private sector companies also have recently adopted significantly revised lease guidance;

The effective date of the Governmental Accounting Standards Board s (GASB) new lease guidance is drawing nearer. Private sector companies also have recently adopted significantly revised lease guidance;

File Reference No Re: Proposed Accounting Standards Update, Leases (Topic 842): Targeted Improvements

: Targeted Improvements") Deloitte & Touche LLP 695 East Main Street Stamford, CT 06901-2141 Tel: + 1 203 708 4000 Fax: + 1 203 708 4797 www.deloitte.com Ms. Susan M. Cosper Technical Director Financial Accounting Standards Board

Deloitte & Touche LLP 695 East Main Street Stamford, CT 06901-2141 Tel: + 1 203 708 4000 Fax: + 1 203 708 4797 www.deloitte.com Ms. Susan M. Cosper Technical Director Financial Accounting Standards Board

Applying IFRS in consumer products and retail

Applying IFRS in consumer products and retail Leases standard Consumer products and retail Updated June 2017 Contents Overview 2 1. Identifying a lease 3 1.1 Definition of a lease 3 1.2 Identified asset

Applying IFRS in consumer products and retail Leases standard Consumer products and retail Updated June 2017 Contents Overview 2 1. Identifying a lease 3 1.1 Definition of a lease 3 1.2 Identified asset

Technical Line FASB final guidance

No. 2016-03 31 March 2016 Technical Line FASB final guidance A closer look at the new leases standard The new leases standard requires lessees to recognize most leases on their balance sheets. What you

No. 2016-03 31 March 2016 Technical Line FASB final guidance A closer look at the new leases standard The new leases standard requires lessees to recognize most leases on their balance sheets. What you

THE NEW LEASE Topic 842

THE NEW LEASE Topic 842 AND WHAT IT MEANS FOR YOU FASB Topic 842 Provides New Standards for Operating Leases Operating lease information will soon be moving from the footnotes of your financial statements

THE NEW LEASE Topic 842 AND WHAT IT MEANS FOR YOU FASB Topic 842 Provides New Standards for Operating Leases Operating lease information will soon be moving from the footnotes of your financial statements

Lease Accounting - New Changes in US, International and Government Accounting Standards

Lease Accounting - New Changes in US, International and Government Accounting Standards Roberta J. Cable, Ph.D., CMA Patricia Healy, CPA, CMA Lubin School of Business Administration, Pace University, USA

Lease Accounting - New Changes in US, International and Government Accounting Standards Roberta J. Cable, Ph.D., CMA Patricia Healy, CPA, CMA Lubin School of Business Administration, Pace University, USA

THE NEW LEASE ACCOUNTING STANDARD

THE NEW LEASE ACCOUNTING STANDARD May 30, 2018 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee, and forms part

THE NEW LEASE ACCOUNTING STANDARD May 30, 2018 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee, and forms part

The joint leases project change is coming

No. 2010-4 18 June 2010 Technical Line Technical guidance on standards and practice issues The joint leases project change is coming What you need to know The proposed changes to the accounting for leases

No. 2010-4 18 June 2010 Technical Line Technical guidance on standards and practice issues The joint leases project change is coming What you need to know The proposed changes to the accounting for leases

Defining Issues May 2013, No

Defining Issues May 2013, No. 13-24 FASB and IASB Issue Revised Exposure Drafts on Lease Accounting The FASB and IASB (the Boards) recently issued revised joint exposure drafts (EDs) on proposed changes

Defining Issues May 2013, No. 13-24 FASB and IASB Issue Revised Exposure Drafts on Lease Accounting The FASB and IASB (the Boards) recently issued revised joint exposure drafts (EDs) on proposed changes

FASB and IASB Continue Making Decisions on Lease Accounting

Accounting Journal Entry FASB and IASB Continue Making Decisions on Lease Accounting March 28, 2011 At recent meetings, the FASB and IASB (the boards ) have continued to make progress on the leases project,

Accounting Journal Entry FASB and IASB Continue Making Decisions on Lease Accounting March 28, 2011 At recent meetings, the FASB and IASB (the boards ) have continued to make progress on the leases project,

IFRS 16 LEASES. Page 1 of 21

IFRS 16 LEASES OBJECTIVE The objective is to ensure that lessees and lessors provide relevant information in a manner that faithfully represents those transactions. This information gives a basis for users

IFRS 16 LEASES OBJECTIVE The objective is to ensure that lessees and lessors provide relevant information in a manner that faithfully represents those transactions. This information gives a basis for users

HOW TO JUMP START YOUR ASC 842 LEASE ACCOUNTING PROJECT WEBINAR MARCH

HOW TO JUMP START YOUR ASC 842 LEASE ACCOUNTING PROJECT WEBINAR MARCH 14 2018 Today s Panelists Scott Vanlandingham Principal Consulting Iyaye Amabeoku Senior Manager Technical Accounting Michael Gregorski

HOW TO JUMP START YOUR ASC 842 LEASE ACCOUNTING PROJECT WEBINAR MARCH 14 2018 Today s Panelists Scott Vanlandingham Principal Consulting Iyaye Amabeoku Senior Manager Technical Accounting Michael Gregorski

New Developments Summary

September 11, 2018 NDS 2018-11 New Developments Summary Implementation costs in a hosting arrangement ASU 2018-15 addresses customer accounting Summary The FASB issued ASU 2018-15, Customer s Accounting

September 11, 2018 NDS 2018-11 New Developments Summary Implementation costs in a hosting arrangement ASU 2018-15 addresses customer accounting Summary The FASB issued ASU 2018-15, Customer s Accounting

The Substance of the Standard

The Substance of the Standard Mayer Hoffman McCann P.C. An Independent CPA Firm TM A publication of the Professional Standards Group April 2014 Accounting Election for Common Control Leasing Arrangements

The Substance of the Standard Mayer Hoffman McCann P.C. An Independent CPA Firm TM A publication of the Professional Standards Group April 2014 Accounting Election for Common Control Leasing Arrangements

The clock is ticking. How to jumpstart your lease accounting implementation project

The clock is ticking How to jumpstart your lease accounting implementation project Lease accounting: Adopting the new standard (ASC 842) 3 Start with challenges, finish with benefits 4 Pine Hill s four

The clock is ticking How to jumpstart your lease accounting implementation project Lease accounting: Adopting the new standard (ASC 842) 3 Start with challenges, finish with benefits 4 Pine Hill s four

Leases ASU September 20, 2017

Leases ASU 2016-02 September 20, 2017 Meet the Speakers Tonisha Spratte, CPA Senior Accountant Cherry Bekaert tspratte@cbh.com Matthew Mars Senior Accountant Cherry Bekaert mmars@cbh.com Agenda What is

Leases ASU 2016-02 September 20, 2017 Meet the Speakers Tonisha Spratte, CPA Senior Accountant Cherry Bekaert tspratte@cbh.com Matthew Mars Senior Accountant Cherry Bekaert mmars@cbh.com Agenda What is

The new accounting standard for leases. 27 March 2017

The new accounting standard for leases 27 March 2017 Disclaimer Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity.

The new accounting standard for leases 27 March 2017 Disclaimer Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity.

Headline Verdana Bold The evolutions of leases accounting under IFRS 16 Mariano Bruno, Carlo Laganà, Giuseppe Ambrosio, Deloitte & Touche S.p.A.

SHIPPING AND THE LAW 7^ Edition 25-26 October 2016 NAPLES Headline Verdana Bold The evolutions of leases accounting under IFRS 16 Mariano Bruno, Carlo Laganà, Giuseppe Ambrosio, Deloitte & Touche S.p.A.

SHIPPING AND THE LAW 7^ Edition 25-26 October 2016 NAPLES Headline Verdana Bold The evolutions of leases accounting under IFRS 16 Mariano Bruno, Carlo Laganà, Giuseppe Ambrosio, Deloitte & Touche S.p.A.

IFRS Update Guy Thomas, CPA, CA

IFRS Update Guy Thomas, CPA, CA D&Co IFRS update Agenda 3 new standards under IFRS IFRS 9 Financial Instruments IFRS 15 Revenue from Contracts with Customers IFRS 16 Leases Agenda Some narrow scope amendments

IFRS Update Guy Thomas, CPA, CA D&Co IFRS update Agenda 3 new standards under IFRS IFRS 9 Financial Instruments IFRS 15 Revenue from Contracts with Customers IFRS 16 Leases Agenda Some narrow scope amendments

Accounting and Auditing Update. Tennessee Chapter of hfma Spring Institute 2016 Presented by William C. Matheney FHFMA CPA and Meredith P.

Accounting and Auditing Update Tennessee Chapter of hfma Spring Institute 2016 Presented by William C. Matheney FHFMA CPA and Meredith P. Cate Today s Objectives Present an overview of pertinent recently

Accounting and Auditing Update Tennessee Chapter of hfma Spring Institute 2016 Presented by William C. Matheney FHFMA CPA and Meredith P. Cate Today s Objectives Present an overview of pertinent recently

Lease Accounting Standard

Lease Accounting Standard AGA/EEI Spring Accounting Conference May 22, 2017 Lease Identification & Lease Classification Lease identification Identified asset Control over use Lease Asset is explicitly

Lease Accounting Standard AGA/EEI Spring Accounting Conference May 22, 2017 Lease Identification & Lease Classification Lease identification Identified asset Control over use Lease Asset is explicitly

CPE regulations require online participants to take part in online questions

KPMG s CFO Financial Forum Webcast FASB/IASB Revised Lease Accounting Exposure Drafts A Detailed Look Part III: Lessor Accounting June 25, 2013 Administrative CPE regulations require online participants

KPMG s CFO Financial Forum Webcast FASB/IASB Revised Lease Accounting Exposure Drafts A Detailed Look Part III: Lessor Accounting June 25, 2013 Administrative CPE regulations require online participants

Leases: A Comprehensive Update on the Joint Project

The Dbriefs Financial Reporting series presents: Leases: A Comprehensive Update on the Joint Project Bob Uhl, Deloitte & Touche LLP Trevor Farber, Deloitte & Touche LLP James Barker, Deloitte & Touche

The Dbriefs Financial Reporting series presents: Leases: A Comprehensive Update on the Joint Project Bob Uhl, Deloitte & Touche LLP Trevor Farber, Deloitte & Touche LLP James Barker, Deloitte & Touche

Technical Line FASB final guidance

No. 2019-01 3 January 2019 Technical Line FASB final guidance How the new leases standard affects automotive entities In this issue: Overview... 1 Recent standard setting activity... 2 Key considerations...

No. 2019-01 3 January 2019 Technical Line FASB final guidance How the new leases standard affects automotive entities In this issue: Overview... 1 Recent standard setting activity... 2 Key considerations...

IFRS 16 Leases. An overview. March 9, kpmg.com/ca/leases

IFRS 16 Leases An overview March 9, 2016 kpmg.com/ca/leases Today s presenters Mag Stewart Jason Bower Jeff King Andy Brown Partner Professional Practice 416 777 8177 magstewart@kpmg.ca Partner Audit 604

IFRS 16 Leases An overview March 9, 2016 kpmg.com/ca/leases Today s presenters Mag Stewart Jason Bower Jeff King Andy Brown Partner Professional Practice 416 777 8177 magstewart@kpmg.ca Partner Audit 604

The New Lease Accounting Standards

The New Lease Accounting Standards 4 CPE Hours d PDH Academy PO Box 449 Pewaukee, WI 53072 www.pdhacademy.com pdhacademy@gmail.com 888-564-9098 CONTINUING EDUCATION for Certified Public Accountants THE

The New Lease Accounting Standards 4 CPE Hours d PDH Academy PO Box 449 Pewaukee, WI 53072 www.pdhacademy.com pdhacademy@gmail.com 888-564-9098 CONTINUING EDUCATION for Certified Public Accountants THE

New Lease Accounting Standards: Love at First Sight or Heartbreak?

New Lease Accounting Standards: Love at First Sight or Heartbreak? February 14, 2019 To Receive CPE Credit Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader

New Lease Accounting Standards: Love at First Sight or Heartbreak? February 14, 2019 To Receive CPE Credit Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader

Guide to auditing the implementation of ASC 842, Leases

Guide to auditing the implementation of ASC 842, Leases Revised July 2018 Contents Glossary of key terms... 1 1 Introduction... 2 1.1 Overview... 2 1.2 Leases audit roadmap for lessees... 3 1.3 Summary

Guide to auditing the implementation of ASC 842, Leases Revised July 2018 Contents Glossary of key terms... 1 1 Introduction... 2 1.1 Overview... 2 1.2 Leases audit roadmap for lessees... 3 1.3 Summary

Technical Line FASB final guidance

No. 2018-18 13 December 2018 Technical Line FASB final guidance How the new leases standard affects life sciences entities In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions...

No. 2018-18 13 December 2018 Technical Line FASB final guidance How the new leases standard affects life sciences entities In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions...

Applying IFRS in Financial Services

Applying IFRS in Financial Services IASB issues new leases standard - financial services April 2016 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition of a lease

Applying IFRS in Financial Services IASB issues new leases standard - financial services April 2016 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition of a lease

Bring it on Discussing the FASB s new leases standard

The Dbriefs Financial Reporting series presents: Bring it on Discussing the FASB s new leases standard March 15, 2016 Bob Uhl, Partner, Deloitte & Touche LLP James Barker, Partner, Deloitte & Touche LLP

The Dbriefs Financial Reporting series presents: Bring it on Discussing the FASB s new leases standard March 15, 2016 Bob Uhl, Partner, Deloitte & Touche LLP James Barker, Partner, Deloitte & Touche LLP

Measuring Lease Liabilities EQUIPMENT LEASING AND FINANCE ASSOCIATION

Measuring Lease Liabilities EQUIPMENT LEASING AND FINANCE ASSOCIATION Presenters Kerrie Cadugan, Executive Director, EY Barbara Galaini, Chief Accounting Officer of the Americas, Avolon The views expressed

Measuring Lease Liabilities EQUIPMENT LEASING AND FINANCE ASSOCIATION Presenters Kerrie Cadugan, Executive Director, EY Barbara Galaini, Chief Accounting Officer of the Americas, Avolon The views expressed

Topic 842 Technical Corrections Summary of Comments Received

Contact(s) David Hoyer Co-Author Ext. 462 Andy Bologna Co-Author Ext. 356 Thomas Faineteau Co-Author Ext. 362 Chris Roberge Co-Author Ext. 274 Amy Park Co-Author Ext. 476 Shayne Kuhaneck Assistant Director

Contact(s) David Hoyer Co-Author Ext. 462 Andy Bologna Co-Author Ext. 356 Thomas Faineteau Co-Author Ext. 362 Chris Roberge Co-Author Ext. 274 Amy Park Co-Author Ext. 476 Shayne Kuhaneck Assistant Director

Lessor Example Performance Obligation Approach

Lessor Example Performance Obligation Approach **Disclaimer The exposure draft received nearly 700 letters of comment through the comment period ended December 15, 2010. There is some expectation that

Lessor Example Performance Obligation Approach **Disclaimer The exposure draft received nearly 700 letters of comment through the comment period ended December 15, 2010. There is some expectation that

GASBs Presented by: William Blend, CPA, CFE

GASBs 87-89 Presented by: William Blend, CPA, CFE Leases: Statement 87 Effective Date and General Implementation Effective for Florida fiscal year end 2021. Earlier application is encouraged. Leases should

GASBs 87-89 Presented by: William Blend, CPA, CFE Leases: Statement 87 Effective Date and General Implementation Effective for Florida fiscal year end 2021. Earlier application is encouraged. Leases should

AMERICAN INTERNATIONAL GROUP, INC.

AMERICAN INTERNATIONAL GROUP, INC. Technical Director Financial Accounting Standards Board 401 Merritt 7 P.O. Box 5116 Norwalk, CT 06856-5116 Re: FASB File Reference No., Proposed Accounting Standards

AMERICAN INTERNATIONAL GROUP, INC. Technical Director Financial Accounting Standards Board 401 Merritt 7 P.O. Box 5116 Norwalk, CT 06856-5116 Re: FASB File Reference No., Proposed Accounting Standards

Your Speakers Today: 10/25/2017. Christopher Garland, CHAE Principal Consultant at Mission Hospitality Solutions

1 Your Speakers Today: Christopher Garland, CHAE Principal Consultant at Mission Hospitality Solutions HFTP Global Director Chair of Hotel Advisory Council AH&LA Finance Committee Retired Senior Vice President

1 Your Speakers Today: Christopher Garland, CHAE Principal Consultant at Mission Hospitality Solutions HFTP Global Director Chair of Hotel Advisory Council AH&LA Finance Committee Retired Senior Vice President

Accounting Standards Update

Duquesne University 6th Annual Accounting CPE Conference Accounting Standards Update Amy Park, FASB Practice Fellow November 16, 2017 The views expressed in this presentation are those of the presenter.

Duquesne University 6th Annual Accounting CPE Conference Accounting Standards Update Amy Park, FASB Practice Fellow November 16, 2017 The views expressed in this presentation are those of the presenter.

Applying IFRS. A closer look at the new leases standard. August 2016

Applying IFRS A closer look at the new leases standard August 2016 Contents Overview 3 1. Scope and scope exceptions 5 1.1 General 5 1.2 Determining whether an arrangement contains a lease 6 1.3 Identifying

Applying IFRS A closer look at the new leases standard August 2016 Contents Overview 3 1. Scope and scope exceptions 5 1.1 General 5 1.2 Determining whether an arrangement contains a lease 6 1.3 Identifying

Accounting Update. Anne Cloutier, CPA, FHFMA Principal March 27, 2015

Accounting Update Anne Cloutier, CPA, FHFMA Principal March 27, 2015 Current Accounting for Leases Capital leases - a lessee recognizes leased assets and liabilities on the balance sheet. Operating leases

Accounting Update Anne Cloutier, CPA, FHFMA Principal March 27, 2015 Current Accounting for Leases Capital leases - a lessee recognizes leased assets and liabilities on the balance sheet. Operating leases

10 TH European IFRS power and utilities roundtable

10 TH European IFRS power and utilities roundtable Victor Chan, Partner, EY 29 November 2016 European IFRS Power and Utilities roundtable IFRS 16 Leases: the journey so far November 2016 Agenda Overview

10 TH European IFRS power and utilities roundtable Victor Chan, Partner, EY 29 November 2016 European IFRS Power and Utilities roundtable IFRS 16 Leases: the journey so far November 2016 Agenda Overview