CAMA System Depreciation. CAMA System Depreciation and Effective Age

|

|

|

- Kelley Wilkinson

- 6 years ago

- Views:

Transcription

1 CAMA System Depreciation and Effective Age

2 Edgar Clodfelter, VMPA NEMRC Sr. Appraiser

3

4 The goal of the Assessor is not cost, but market value. Cost is merely the avenue to market value Property Assessment Valuation IAAO Textbook.

5 Goal is Market Value Property is to be appraised at its fair market value. Fair market value is defined in 32 V.S.A as: The price which the property will bring in the market when offered for sale and purchased by another, taking into consideration all the elements of the availability of the property, its use both potential and prospective, any functional deficiencies, and all other elements such as age and condition which combine to give property a market value.

6 Cost Approach Sum of estimated land value and estimated depreciated cost of the building and other improvements. Value = Land Value + Improvement Value IV = (Replacement Cost New Depreciation) RCNLD

7 Cost Approach Works best: New Improvements Sale and Income data scarce Special Purpose Properties Industrial Properties The difficulty in using the Cost Approach with older improvements is determining Depreciation, and it s significant other, Effective Age.

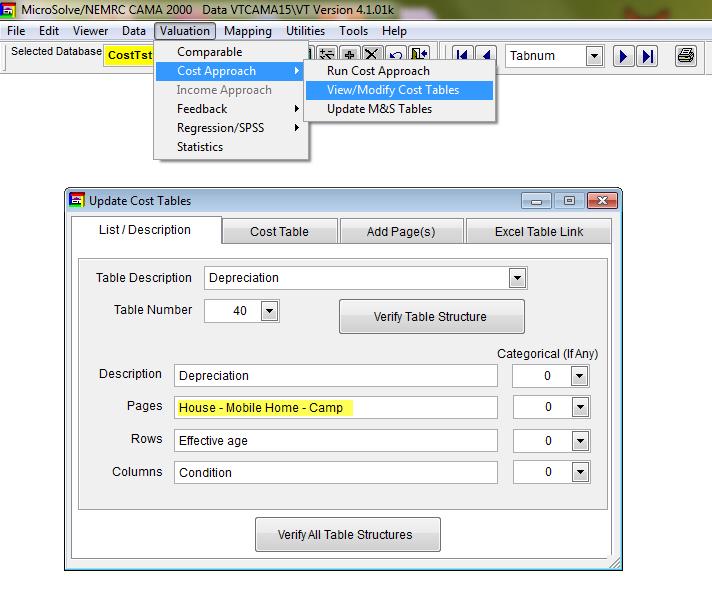

8 Replacement Cost Tables Market Adjusted Cost Approach (Base Adjusted by Time/Location) Tables 1-7 = Marshall & Swift Depreciation Table 40 = Age/Effective and Condition Land Tables (Housesite Value, Acres, Frontage) Tables 43, 44, 45, 57, 58, 59, 60 = Land Value Site Improvements Table 49 Outbuildings (Detached Structures) Table 46 = Water and Septic = Marshall & Swift

9 Market Adjusted Cost Value Land Value (Market Based) + Building Value (Town Specific Adjusted M&S Tables and Depreciation) + Outbuildings Value (M&S Tables) + Site Improvements (Water & Septic Contributory Value)

10 All structures are made up of elements that have varying economic lives. Building Element Considerations: Type ( residential, commercial, etc.) Quality ( grades, style) Structure ( foundation and framing) Exterior ( siding, style) Roof ( type, pitch, cover) Windows ( type, screens) Plumbing ( fixtures, type and grade) Heating and Air Conditioning (type and capacity) Room and Finish ( flooring, trim, walls) Bath Details ( number, type) Many are items that become worn and depreciate over time.

11 Depreciation: The loss in value, from all causes, of property having a limited economic life. Types of Depreciation: Physical Deterioration - The loss in value due to wear and tear over time. Functional Obsolescence - The loss of value due to changes in style, taste, technology, needs and demands. Economic Obsolescence - The loss of value due to factors external to the property.

12 Depreciation/Obsolescence: Curable and Incurable Curable - Repairing or replacing obsolescence or physical loss at a reasonable cost. The repair must make economic sense. Example - Replacing a furnace. Incurable - When the defect in an asset becomes too costly to repair. Example - Replacing Foundation Example Small residential dwelling on commercial strip. (Dorset street in South Burlington)

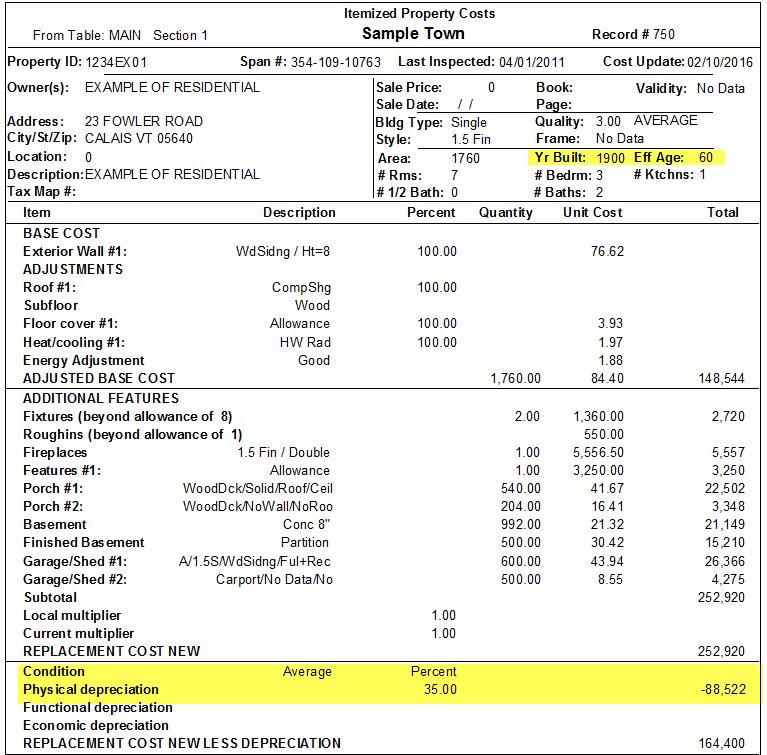

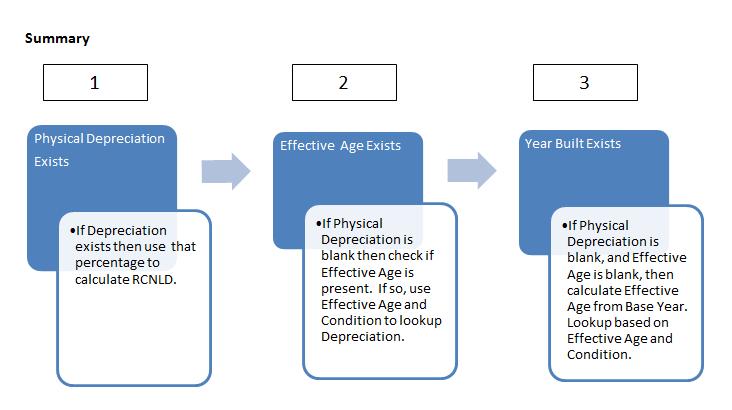

13 MicroSolve Residential Depreciation Tables The MicroSolve computer assisted mass appraisal (CAMA) system can calculate physical depreciation on residential improvements, mobile homes and camps in several ways. The following will describe how the user can utilize table lookups based on age (or effective age) and condition, or use direct input of physical depreciation.

14 I. Direct Input: Direct Input of Depreciation applied to Dwelling - Example Physical Depreciation of 10 percent entered 10 percent of the RCN value will be removed Depreciation is forced by the user Depreciation will remain until deleted from the record.

15 II. Table Lookup: Effective Age Input Depreciation Table based on Age/Effective Age and Condition Effective Age reflects condition and utility relative to actual age If Physical Depreciation blank, and Effective Age entered Table Lookup Example 150 year old Dwelling Improvements to current living standards Wiring Heating System Plumbing Updated Kitchen Modern Bath Effective Age Say 60-70

16 Input Effective Age and Condition = Table Lookup

17 Running Cost System completes Table Lookup for Effective Age and Condition. Used to calculate depreciated amount for RCNLD. Fills the field of Physical Depreciation from Table 40.

18

19 III. Table Lookup: Effective Age Calculated Effective Age based on Year Built and Base Year Base Year is year of completion of reappraisal Stored in either USIT or new Table 61

20 Old Usit Program Updated Table 61

21 Table Lookup: Effective Age Calculated If Physical Depreciation Blank And Effective Age field Blank And Year Built Exists Calculated Effective Age from Year Built and Base Year Example with Base Year 2013

22 Depreciation Table: Depreciation tables can be developed and input for: Residential Dwellings Mobile Homes Camps

23

24 Column 0 Effective Age - Row 1 through 9 Condition

25 Table 40, Page 2 - MHO Depreciation

26 Table 40, Page 3 Camp Depreciation

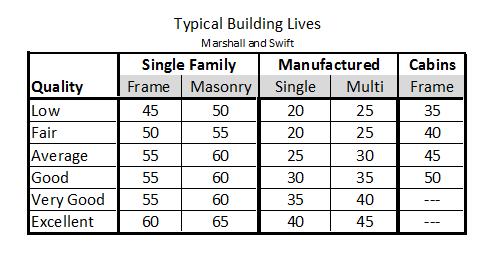

27 Depreciation Calculations: Direct Input Table Lookup: Effective Age Input Table Lookup: Effective Age Calculated

28

29 From Marshall & Swift presentation IAAO conference 2012 By curing obsolescence we are increasing the Economic Life of the Improvement

30 Effective Age What you see is what you get Consider meeting someone new. You know they are 60, but when you meet them you notice they have taken good care of themselves and appear more like 50. Their chronological age is 60, but their effective age is 50.

31 Effective Age may or may not be the same as actual or chronological age. Dependent upon: Maintenance Design Location Effective Age + Remaining Economic Life = Total Economic Life Effective Age and remaining Economic life equals the total life span of an improvement. Total Economic Life Effective Age Remaining Economic Life

32 Depreciation = Effective Age Total Economic Life Example: EA 80 / TEL 200 =.40 Calculating Total Economic Life

33

34 Effective Age Problem: 1. Older homes do not work with Typical Building Lives Tables 2. Determination is frequently based on observation. 3. Various levels of experience in application 4. Difficult to explain 5. Difficult to maintain consistency 6. Guess work Effective Age Importance 1. Critical variable used with Depreciation tables 2. Provides basis for calculation of RCNLD 3. Critical variable for use with comparable sales 4. Allows for consistency of assessments

35 Need a way to conceptually determine Effective Age for Mass Appraisal Must be simple to Implement Easy to Understand Easy to Explain Can be Consistently Applied

36 Estimating Effective Age by Unit-in-Place Method ***A Guideline*** Similar to Unit-in-Place method of Cost Approach Building components segregated into Units of construction Recognize each units contribution to overall depreciation

37 Economic Life of Improvements Long Lived Items o Basic structure components o Likely incurable deterioration Short Lived Items o Building component replaced several times o Likely curable

38

39

40

41

42 New Construction Year Built 2015 Actual Age = Effective Age

43 Year Built 1997 Actual Age = 19 Effective Age = 19

44 Year Built 1830 Actual Age = / 2 = 93 Effective Age = 90-95

45 Why Functional Depreciation?

46

47 Example

48

49

50 Summary Unit-in-Place approach provides a Guideline Importance of consistency Use with caution for high value historic properties

51 Information Sources A Mass Appraisal Approach to Developing Effective Age Tables for Residential Mass Appraisal Mary Jo Staroska, CAA 1998 Estimation and Use of Effective-Age and Evaluation of Depreciation Schedules in the Mass Appraisal Process Gary McCabe, CAE 1995 IAAO Publication

52

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330 REVIEW NOTES by CHUCK DUNN CHAPTER 19 Copyright 2010 by the Real Estate Division and Chuck Dunn. All rights reserved CHAPTER 19 - DEPRECIATION

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330 REVIEW NOTES by CHUCK DUNN CHAPTER 19 Copyright 2010 by the Real Estate Division and Chuck Dunn. All rights reserved CHAPTER 19 - DEPRECIATION

Cornerstone 2 Basic Valuation of Machinery and Equipment

INSTITUTE FOR PROFESSIONALS IN TAXATION PERSONAL PROPERTY TAX SCHOOL Cornerstone 2 Basic Valuation of Machinery and Equipment Learning Objectives At the end of this section, the learner will be able to:

INSTITUTE FOR PROFESSIONALS IN TAXATION PERSONAL PROPERTY TAX SCHOOL Cornerstone 2 Basic Valuation of Machinery and Equipment Learning Objectives At the end of this section, the learner will be able to:

Chapter 37. The Appraiser's Cost Approach INTRODUCTION

Chapter 37 The Appraiser's Cost Approach INTRODUCTION The cost approach for estimating current market value starts with the recognition that a parcel of real estate contains two components - the land and

Chapter 37 The Appraiser's Cost Approach INTRODUCTION The cost approach for estimating current market value starts with the recognition that a parcel of real estate contains two components - the land and

BUSI 330 Suggested Answers to Review and Discussion Questions: Lesson 9

BUSI 330 Suggested Answers to Review and Discussion Questions: Lesson 9 1. Students should give a brief definition of each of the following terms and provide one example which illustrates how they are

BUSI 330 Suggested Answers to Review and Discussion Questions: Lesson 9 1. Students should give a brief definition of each of the following terms and provide one example which illustrates how they are

Proving Depreciation

Institute for Professionals in Taxation 40 th Annual Property Tax Symposium Tucson, Arizona Proving Depreciation Presentation Concepts and Content: Kathy G. Spletter, ASA Stancil & Co. Irving, Texas kathy.spletter@stancilco.com

Institute for Professionals in Taxation 40 th Annual Property Tax Symposium Tucson, Arizona Proving Depreciation Presentation Concepts and Content: Kathy G. Spletter, ASA Stancil & Co. Irving, Texas kathy.spletter@stancilco.com

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330 REVIEW NOTES by CHUCK DUNN CHAPTER 17 Copyright 2010 by the Real Estate Division and Chuck Dunn. All rights reserved CHAPTER 17- THE COST APPROACH

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330 REVIEW NOTES by CHUCK DUNN CHAPTER 17 Copyright 2010 by the Real Estate Division and Chuck Dunn. All rights reserved CHAPTER 17- THE COST APPROACH

ASSESSMENT METHODOLOGY

2018 ASSESSMENT METHODOLOGY COST APPROACH A summary of the methods used by the City of Edmonton in determining the value of residential and non-residential properties valued using the cost approach in

2018 ASSESSMENT METHODOLOGY COST APPROACH A summary of the methods used by the City of Edmonton in determining the value of residential and non-residential properties valued using the cost approach in

Licensing Education STUDY GUIDE. The Manitoba Real Estate Association

Licensing Education STUDY GUIDE The Manitoba Real Estate Association NOTE: This Study Guide replaces the Assignment Booklet referred to in the Appraisal workbook. It does not have to be returned to the

Licensing Education STUDY GUIDE The Manitoba Real Estate Association NOTE: This Study Guide replaces the Assignment Booklet referred to in the Appraisal workbook. It does not have to be returned to the

The Value of Real Estate

Chapter 11 The Value of Real Estate 1 Chapter Objectives Describe how several broad factors and specific principles impact the value of property. Contrast value, price, and cost. Define the necessary factors

Chapter 11 The Value of Real Estate 1 Chapter Objectives Describe how several broad factors and specific principles impact the value of property. Contrast value, price, and cost. Define the necessary factors

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

Kitsap County Assessor

Documentation for Area 6 - Bainbridge Island Tax Year: 2019 Appraisal Date: 1/1/2018 Property Type: Office - General Office, Medical Office, and Banks Updated 5/1/2018 by CM27 Area Overview Bainbridge

Documentation for Area 6 - Bainbridge Island Tax Year: 2019 Appraisal Date: 1/1/2018 Property Type: Office - General Office, Medical Office, and Banks Updated 5/1/2018 by CM27 Area Overview Bainbridge

Kitsap County Assessor

Kitsap County Assessor Documentation for Area 5 - Bremerton and Central Kitsap East Tax Year: 2019 Appraisal Date: 1/1/2018 Property Type: Office - General Office, Medical Office, and Banks Updated 5/1/2018

Kitsap County Assessor Documentation for Area 5 - Bremerton and Central Kitsap East Tax Year: 2019 Appraisal Date: 1/1/2018 Property Type: Office - General Office, Medical Office, and Banks Updated 5/1/2018

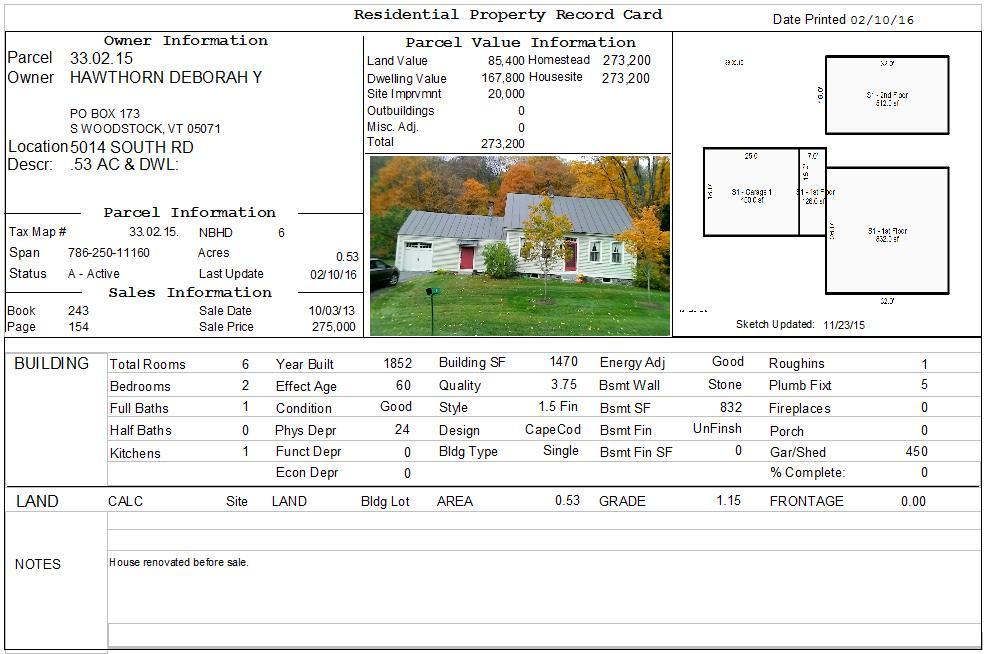

UNDERSTANDING YOUR PROPERTY RECORD CARD

UNDERSTANDING YOUR PROPERTY RECORD CARD OBJECTIVE: At first glance, the real estate property assessment record card can be intimidating. There is a wealth of information that can be difficult to read and

UNDERSTANDING YOUR PROPERTY RECORD CARD OBJECTIVE: At first glance, the real estate property assessment record card can be intimidating. There is a wealth of information that can be difficult to read and

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

ASA s 7 th Annual Equipment Valuation Conference. Cost Approach and Sales Comparison Approach: A Closer Look at Depreciation

ASA s 7 th Annual Equipment Valuation Conference Cost Approach and Sales Comparison Approach: A Closer Look at Depreciation Background Information Rick Wilichowski Managing Director, Machinery & Equipment

ASA s 7 th Annual Equipment Valuation Conference Cost Approach and Sales Comparison Approach: A Closer Look at Depreciation Background Information Rick Wilichowski Managing Director, Machinery & Equipment

IAS 4.0 Cost & Income Valuation Guide

IAS 4.0 Cost & Income Valuation Guide TABLE OF CONTENTS PREFACE... 1 ASSESSMENT ADMINISTRATION (AA) SCREENS RELATED TO VALUATION... 2 AA44 Jurisdiction Update...2 Overview... 2 To Query an Assessment Jurisdiction

IAS 4.0 Cost & Income Valuation Guide TABLE OF CONTENTS PREFACE... 1 ASSESSMENT ADMINISTRATION (AA) SCREENS RELATED TO VALUATION... 2 AA44 Jurisdiction Update...2 Overview... 2 To Query an Assessment Jurisdiction

A Demonstration Appraisal Report. Of a. Located at. Date of Appraisal. Prepared for. Prepared by

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 W. 10 th Street Kansas

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 W. 10 th Street Kansas

PROPERTY TAX SAVINGS STRATEGIES FOR NEW CONSTRUCTION DEVELOPMENTS

WOULD YOU ALLOW THE IRS TO DO YOUR TAXES? WHY ARE YOU ALLOWING THE COUNTY ASSESSOR TO DO YOURS? PROPERTY TAX SAVINGS STRATEGIES FOR NEW CONSTRUCTION DEVELOPMENTS DATE OF COMPLETION IS TYPICALLY THE DATE

WOULD YOU ALLOW THE IRS TO DO YOUR TAXES? WHY ARE YOU ALLOWING THE COUNTY ASSESSOR TO DO YOURS? PROPERTY TAX SAVINGS STRATEGIES FOR NEW CONSTRUCTION DEVELOPMENTS DATE OF COMPLETION IS TYPICALLY THE DATE

APPLICATION TO REGISTER A SUBJECT PROPERTY BUSI 398 RESIDENTIAL PROPERTY GUIDED CASE STUDY

Please fill out this form, save it to your computer, then submit it via Turnitin.com (see Submit Written Assignments and Projects on your Course Resources webpage for details) APPLICATION TO REGISTER A

Please fill out this form, save it to your computer, then submit it via Turnitin.com (see Submit Written Assignments and Projects on your Course Resources webpage for details) APPLICATION TO REGISTER A

II. STARTING THE APPRAISAL

I. UNDERSTANDING THE DEMONSTRATION NARRATIVE REPORT REQUIREMENTS A. Thoroughly read the IAAO s Guide to Real Property Demonstration Report Writing: Residential Property 2014 1. Main goal is to demonstrate

I. UNDERSTANDING THE DEMONSTRATION NARRATIVE REPORT REQUIREMENTS A. Thoroughly read the IAAO s Guide to Real Property Demonstration Report Writing: Residential Property 2014 1. Main goal is to demonstrate

MMSVP Migration Wizard

MMSVP Migration Wizard Questions? From within BS&A, go to Help>Contact Customer Support and select Request Support Phone Call or Email Support. Or, you may call us at (855) 272-7638 and ask for the appropriate

MMSVP Migration Wizard Questions? From within BS&A, go to Help>Contact Customer Support and select Request Support Phone Call or Email Support. Or, you may call us at (855) 272-7638 and ask for the appropriate

Tangible Personal Property Summation Valuation Procedures

Property Tax Valuation Insights Tangible Personal Property Summation Valuation Procedures Robert F. Reilly, CPA For ad valorem property taxation purposes, industrial and commercial taxpayer tangible personal

Property Tax Valuation Insights Tangible Personal Property Summation Valuation Procedures Robert F. Reilly, CPA For ad valorem property taxation purposes, industrial and commercial taxpayer tangible personal

Depreciation Analysis Guide

Market Value Assessment in Saskatchewan Handbook Depreciation Analysis Guide Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market

Market Value Assessment in Saskatchewan Handbook Depreciation Analysis Guide Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market

1101. Guidelines for Ascertaining the Fair Market Value of Drilling Rigs and Related Equipment

Chapter 11. Drilling Rigs and Related Equipment 1101. Guidelines for Ascertaining the Fair Market Value of Drilling Rigs and Related Equipment A. General - The standard for valuation of drilling rigs and

Chapter 11. Drilling Rigs and Related Equipment 1101. Guidelines for Ascertaining the Fair Market Value of Drilling Rigs and Related Equipment A. General - The standard for valuation of drilling rigs and

PROCEDURES TO IDENTIFY AND QUANTIFY ECONOMIC OBSOLESCENCE IN THE PROPERTY TAX VALUATION OF INDUSTRIAL AND COMMERCIAL PROPERTIES

Spring 2007 Economic Obsolescence Analysis Insights Insights 65 PROCEDURES TO IDENTIFY AND QUANTIFY ECONOMIC OBSOLESCENCE IN THE PROPERTY TAX VALUATION OF INDUSTRIAL AND COMMERCIAL PROPERTIES Robert F.

Spring 2007 Economic Obsolescence Analysis Insights Insights 65 PROCEDURES TO IDENTIFY AND QUANTIFY ECONOMIC OBSOLESCENCE IN THE PROPERTY TAX VALUATION OF INDUSTRIAL AND COMMERCIAL PROPERTIES Robert F.

Kitsap County Assessor

Documentation for Area 3 South - Port Orchard and South Kitsap UGA Tax Year: 2019 Appraisal Date: 1/1/2018 Property Type: Restaurants, Bars, and Taverns Updated 5/16/2018 by CM20 Area Overview Port Orchard

Documentation for Area 3 South - Port Orchard and South Kitsap UGA Tax Year: 2019 Appraisal Date: 1/1/2018 Property Type: Restaurants, Bars, and Taverns Updated 5/16/2018 by CM20 Area Overview Port Orchard

APPLICATION TO REGISTER A SUBJECT PROPERTY BUSI 499 INCOME PROPERTY GUIDED CASE STUDY

Please fill out this form, save it to your computer, then submit it via Turnitin.com (see Submit Written Assignments and Projects on your Course Resources webpage for details) APPLICATION TO REGISTER A

Please fill out this form, save it to your computer, then submit it via Turnitin.com (see Submit Written Assignments and Projects on your Course Resources webpage for details) APPLICATION TO REGISTER A

FEMA National Floodplain Insurance Program (NFIP) Substantial Improvement/Substantial Damage Determination

Substantial Improvement/Substantial Damage Determination") Determining Structure/Market Value FEMA National Floodplain Insurance Program (NFIP) For additional clarification of requirements, please refer to FEMA Publication P-758, Substantial Improvement and Substantial

Determining Structure/Market Value FEMA National Floodplain Insurance Program (NFIP) For additional clarification of requirements, please refer to FEMA Publication P-758, Substantial Improvement and Substantial

Date: 15/01/30 Page: 1

Formulas, Rules and Principles Subject: General Document Number 1.1.1 Summary This section describes how this Manual is to be used for the 2017 revaluation (January 1, 2017 to December 31, 2020). Regulated

Formulas, Rules and Principles Subject: General Document Number 1.1.1 Summary This section describes how this Manual is to be used for the 2017 revaluation (January 1, 2017 to December 31, 2020). Regulated

ECONOMIC OBSOLESCENCE IS AN ESSENTIAL PROCEDURE

Spring 2006 Property Tax Valuation www.willamette.com 3 ECONOMIC OBSOLESCENCE IS AN ESSENTIAL PROCEDURE OF A COST APPROACH VALUATION OF INDUSTRIAL OR COMMERCIAL PROPERTIES Robert F. Reilly and Robert P.

Spring 2006 Property Tax Valuation www.willamette.com 3 ECONOMIC OBSOLESCENCE IS AN ESSENTIAL PROCEDURE OF A COST APPROACH VALUATION OF INDUSTRIAL OR COMMERCIAL PROPERTIES Robert F. Reilly and Robert P.

Gas Station. Market Value Assessment in Saskatchewan Handbook. Gas Station Valuation Guide

Market Value Assessment in Saskatchewan Handbook Gas Station Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass

Market Value Assessment in Saskatchewan Handbook Gas Station Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass

Kitsap County Assessor

Narrative for Area 3 North - Kingston and North Kitsap East Tax Year: 2018 Appraisal Date: 1/1/2017 Property Type: Office - General Office, Medical Office, and Banks Area Overview Kingston including rural

Narrative for Area 3 North - Kingston and North Kitsap East Tax Year: 2018 Appraisal Date: 1/1/2017 Property Type: Office - General Office, Medical Office, and Banks Area Overview Kingston including rural

EXPLANATION OF MARKET MODELING IN THE CURRENT KANSAS CAMA SYSTEM

EXPLANATION OF MARKET MODELING IN THE CURRENT KANSAS CAMA SYSTEM I have been asked on numerous occasions to provide a lay man s explanation of the market modeling system of CAMA. I do not claim to be an

EXPLANATION OF MARKET MODELING IN THE CURRENT KANSAS CAMA SYSTEM I have been asked on numerous occasions to provide a lay man s explanation of the market modeling system of CAMA. I do not claim to be an

A Demonstration Appraisal Report. Of a. Located at. Date of Appraisal. Prepared for. Prepared by

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 West 10 th Street Kansas

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 West 10 th Street Kansas

Residential Site Valuation and Cost Approach 2 nd Edition Hondros Learning Chapter Quiz and Work Problem Answer Key:

Residential Site Valuation and Cost Approach 2 nd Edition Hondros Learning Chapter Quiz and Work Problem Answer Key: Chapter 1 Quiz 1. A parcel of land with on-site improvements (e.g., utilities) is best

Residential Site Valuation and Cost Approach 2 nd Edition Hondros Learning Chapter Quiz and Work Problem Answer Key: Chapter 1 Quiz 1. A parcel of land with on-site improvements (e.g., utilities) is best

RAINS COUNTY APPRAISAL DISTRICT

RAINS COUNTY APPRAISAL DISTRICT 2017 MASS APPRAISAL SUMMARY REPORT mass appraisal report 2017 uspap_appr_report RAINS COUNTY APPRAISAL DISTRICT 2017 MASS APPRAISAL SUMMARY REPORT Identification of Subject:

RAINS COUNTY APPRAISAL DISTRICT 2017 MASS APPRAISAL SUMMARY REPORT mass appraisal report 2017 uspap_appr_report RAINS COUNTY APPRAISAL DISTRICT 2017 MASS APPRAISAL SUMMARY REPORT Identification of Subject:

MASS APPRAISAL- REVALUATION PLAN BRULE COUNTY, SD ASSESSOR YEARS

MASS APPRAISAL- REVALUATION PLAN BRULE COUNTY, SD ASSESSOR YEARS 2013-2017 5/5/5 Rotation to Follow 5/5/5 explained and outlined on last page Prepared 10/01/2013 Amended 10/15/2014 ESCALATED TIMELINE WAS

MASS APPRAISAL- REVALUATION PLAN BRULE COUNTY, SD ASSESSOR YEARS 2013-2017 5/5/5 Rotation to Follow 5/5/5 explained and outlined on last page Prepared 10/01/2013 Amended 10/15/2014 ESCALATED TIMELINE WAS

namib I A UniVERSITY

namib I A UniVERSITY OF SCIEnCE AnD TECHnOLOGY Faculty of Natural Resources and Spatial Sciences Department of Land and Property Sciences QUALIFICATION{S): Bachelor of Property Studies Honours Diploma

namib I A UniVERSITY OF SCIEnCE AnD TECHnOLOGY Faculty of Natural Resources and Spatial Sciences Department of Land and Property Sciences QUALIFICATION{S): Bachelor of Property Studies Honours Diploma

procedures Basic Appraisal F i n a l Examination #2 2 nd edition

F i n a l Examination #2 A n s w e r Key Page 82 1. When determining effective gross income from potential gross income, an appraiser considers a. debt service. b. depreciation. c. fixed expenses. d. vacancy

F i n a l Examination #2 A n s w e r Key Page 82 1. When determining effective gross income from potential gross income, an appraiser considers a. debt service. b. depreciation. c. fixed expenses. d. vacancy

Mass Appraisal of Income-Producing Properties

Chapter 10 Mass Appraisal of Income-Producing Properties Whether valuing income-producing property or residential property, you can use similar information and methods for collecting and analyzing data

Chapter 10 Mass Appraisal of Income-Producing Properties Whether valuing income-producing property or residential property, you can use similar information and methods for collecting and analyzing data

2. The, and Act, also known as FIRREA, requires that states set standards for all appraisers.

CHAPTER 4 SHORT-ANSWER QUESTIONS 1. An appraisal is an or of value. 2. The, and Act, also known as FIRREA, requires that states set standards for all appraisers. 3. Value in real estate is the "present

CHAPTER 4 SHORT-ANSWER QUESTIONS 1. An appraisal is an or of value. 2. The, and Act, also known as FIRREA, requires that states set standards for all appraisers. 3. Value in real estate is the "present

Broker. Sales Comparison, Cost Depreciation and Income Approaches. Chapter 7. Copyright Gold Coast Schools 1

Broker Chapter 7 Sales Comparison, Cost Depreciation and Income Approaches 1 Learning Objectives Describe the assumptions underlying the sales comparison approach Calculate the various adjustments necessary

Broker Chapter 7 Sales Comparison, Cost Depreciation and Income Approaches 1 Learning Objectives Describe the assumptions underlying the sales comparison approach Calculate the various adjustments necessary

Sales Associate Course

Sales Associate Course Chapter Sixteen Appraisal 1 2 Appraiser Specific amount Impartial (non biased) Defendable Estimate (Opinion) of value Fee based on time and difficulty Must follow Uniform Standards

Sales Associate Course Chapter Sixteen Appraisal 1 2 Appraiser Specific amount Impartial (non biased) Defendable Estimate (Opinion) of value Fee based on time and difficulty Must follow Uniform Standards

TECHNICAL INFORMATION PAPER - MARKET VALUE OF PROPERTY, PLANT & EQUIPMENT IN A BUSINESS

TECHNICAL INFORMATION PAPER - MARKET VALUE OF PROPERTY, PLANT & EQUIPMENT IN A BUSINESS Please view the video for this Technical Information Paper Reference ANZVTIP 2 Effective 1 st July 2015 Owner National

TECHNICAL INFORMATION PAPER - MARKET VALUE OF PROPERTY, PLANT & EQUIPMENT IN A BUSINESS Please view the video for this Technical Information Paper Reference ANZVTIP 2 Effective 1 st July 2015 Owner National

Schedule. SECTION 1. Cost Approach Principles and Cost Estimation (Morning Day 1) Overview 8:00 8:30 Registration Classroom Rules and Procedures

Overview 8:00 8:30 Registration Classroom Rules and Procedures") Schedule SECTION 1. Cost Approach Principles and Cost Estimation (Morning Day 1) Overview 8:00 8:30 Registration Classroom Rules and Procedures Introduction Cost Approach Pretest Part 1. Introduction to

Schedule SECTION 1. Cost Approach Principles and Cost Estimation (Morning Day 1) Overview 8:00 8:30 Registration Classroom Rules and Procedures Introduction Cost Approach Pretest Part 1. Introduction to

PREPARING FOR THE MINNESOTA RESIDENTIAL CASE STUDY EXAM. Minnesota Association of Assessing Officers Minnesota State Board of Assessors

PREPARING FOR THE MINNESOTA RESIDENTIAL CASE STUDY EXAM Minnesota Association of Assessing Officers Minnesota State Board of Assessors Best Western-Kelly Inn, St. Cloud, MN July 16, 2018 Overview MINNESOTA

PREPARING FOR THE MINNESOTA RESIDENTIAL CASE STUDY EXAM Minnesota Association of Assessing Officers Minnesota State Board of Assessors Best Western-Kelly Inn, St. Cloud, MN July 16, 2018 Overview MINNESOTA

Kitsap County Assessor

Kitsap County Assessor Narrative for Area 5 - Bremerton and Central Kitsap East Tax Year: 2018 Appraisal Date: 1/1/2017 Property Type: Restaurants, Bars, and Taverns Updated 6/5/2017 by CM20 Area Overview

Kitsap County Assessor Narrative for Area 5 - Bremerton and Central Kitsap East Tax Year: 2018 Appraisal Date: 1/1/2017 Property Type: Restaurants, Bars, and Taverns Updated 6/5/2017 by CM20 Area Overview

1. When is a CLA not a CLA?? 2. Annual Meeting and Town Fair. 3. Phony Parcels Creeping onto Grand Lists. 4. MyVTax system in development by PVR

1. When is a CLA not a CLA?? 2. Annual Meeting and Town Fair 3. Phony Parcels Creeping onto Grand Lists 4. MyVTax system in development by PVR VALA SUMMER 2016 Is the CLA Still a CLA in a Reappraisal Year?

1. When is a CLA not a CLA?? 2. Annual Meeting and Town Fair 3. Phony Parcels Creeping onto Grand Lists 4. MyVTax system in development by PVR VALA SUMMER 2016 Is the CLA Still a CLA in a Reappraisal Year?

Kitsap County Assessor

Narrative for Area 1 - Silverdale/Central Kitsap West Tax Year: 2018 Appraisal Date: 1/1/2017 Property Type: Restaurants, Bars, and Taverns Updated 6/5/2017 by CM20 Area Overview Silverdale including rural

Narrative for Area 1 - Silverdale/Central Kitsap West Tax Year: 2018 Appraisal Date: 1/1/2017 Property Type: Restaurants, Bars, and Taverns Updated 6/5/2017 by CM20 Area Overview Silverdale including rural

Collateral Underwriter, Regression Models, Statistics, Gambling with your License

Collateral Underwriter, Regression Models, Statistics, Gambling with your License Keith Wolf, SRA, AI-RRS Kwolf Consulting Inc. Kwolf1021@gmail.com 05/20/2015 There are Lies, Damned Lies and Statistics

Collateral Underwriter, Regression Models, Statistics, Gambling with your License Keith Wolf, SRA, AI-RRS Kwolf Consulting Inc. Kwolf1021@gmail.com 05/20/2015 There are Lies, Damned Lies and Statistics

VALUE FINDING APPRAISAL REPORT

RE 90 Rev. 01-2014 VALUE FINDING APPRAISAL REPORT (Compensation not to exceed $65,000) COUNTY John Doe 2880 Lancaster-Newark Rd. (SR 37), Pleasant Twp., 43030 Owner Mailing Address of Owner East side of

RE 90 Rev. 01-2014 VALUE FINDING APPRAISAL REPORT (Compensation not to exceed $65,000) COUNTY John Doe 2880 Lancaster-Newark Rd. (SR 37), Pleasant Twp., 43030 Owner Mailing Address of Owner East side of

SAS at Los Angeles County Assessor s Office

SAS at Los Angeles County Assessor s Office WUSS 2015 Educational Forum and Conference Anthony Liu, P.E. September 9-11, 2015 Los Angeles County Assessor s Office in 2015 Oversees 4,083 square miles of

SAS at Los Angeles County Assessor s Office WUSS 2015 Educational Forum and Conference Anthony Liu, P.E. September 9-11, 2015 Los Angeles County Assessor s Office in 2015 Oversees 4,083 square miles of

Current State of Property. Taxation in the Netherlands. Council for Real Estate Assessment (English) Waarderingskamer (Dutch)

Waarderingskamer (Dutch)") Current State of Property WAARDERINGSKAMER Taxation in the Netherlands Council for Real Estate Assessment (English) Waarderingskamer (Dutch) Council for real estate assessment Main task: quality control

Current State of Property WAARDERINGSKAMER Taxation in the Netherlands Council for Real Estate Assessment (English) Waarderingskamer (Dutch) Council for real estate assessment Main task: quality control

86 years in the making Caspar G Haas 1922 Sales Prices as a Basis for Estimating Farmland Value

2 Our Journey Begins 86 years in the making Caspar G Haas 1922 Sales Prices as a Basis for Estimating Farmland Value Starting at the beginning. Mass Appraisal and Single Property Appraisal Appraisal

2 Our Journey Begins 86 years in the making Caspar G Haas 1922 Sales Prices as a Basis for Estimating Farmland Value Starting at the beginning. Mass Appraisal and Single Property Appraisal Appraisal

SAMA Presentation February 7-15, 2013 RMAA and UMAAS Sponsored Workshop Series

SAMA Presentation February 7-15, 2013 RMAA and UMAAS Sponsored Workshop Series Presentation Overview SAMA Who we are and what we do Summary of assessment legislation and policy Valuation publications Valuation

SAMA Presentation February 7-15, 2013 RMAA and UMAAS Sponsored Workshop Series Presentation Overview SAMA Who we are and what we do Summary of assessment legislation and policy Valuation publications Valuation

Recommendations for COD Standards. Robert J. Gloudemans Almy, Gloudemans, Jacobs & Denne. for. New York State Office of Real Property Services

Recommendations for COD Standards Robert J. Gloudemans Almy, Gloudemans, Jacobs & Denne for New York State Office of Real Property Services March 12, 2009 Recommendations for COD Standards Robert J. Gloudemans

Recommendations for COD Standards Robert J. Gloudemans Almy, Gloudemans, Jacobs & Denne for New York State Office of Real Property Services March 12, 2009 Recommendations for COD Standards Robert J. Gloudemans

APPRAISAL REPORT PROFESSIONAL OFFICE BUILDING LOCATED AT 6400 NORTH W STREET IN PENSACOLA, FLORIDA AS OF AUGUST 7, B&A File #OG14BB8056

APPRAISAL REPORT PROFESSIONAL OFFICE BUILDING LOCATED AT 6400 NORTH W STREET IN PENSACOLA, FLORIDA 32505 AS OF AUGUST 7, 2014 B&A File #OG14BB8056 PREPARED FOR ESCAMBIA COUNTY REAL ESTATE ACQUISITION DEPARTMENT

APPRAISAL REPORT PROFESSIONAL OFFICE BUILDING LOCATED AT 6400 NORTH W STREET IN PENSACOLA, FLORIDA 32505 AS OF AUGUST 7, 2014 B&A File #OG14BB8056 PREPARED FOR ESCAMBIA COUNTY REAL ESTATE ACQUISITION DEPARTMENT

San Patricio County Appraisal District. Reappraisal Plan For. Tax Years 2013 & 2014

San Patricio County Appraisal District Reappraisal Plan For Tax Years 2013 & 2014 (adopted by SPCAD Board of Directors on September 11 th, 2012) 1 TABLE OF CONTENTS ITEM PAGE Executive Summary 4 Revaluation

San Patricio County Appraisal District Reappraisal Plan For Tax Years 2013 & 2014 (adopted by SPCAD Board of Directors on September 11 th, 2012) 1 TABLE OF CONTENTS ITEM PAGE Executive Summary 4 Revaluation

Tax Year 2018 Mass Appraisal of Properties

The Office of the Chief Appraiser David Luther, RPA, RTA, CCA Registered Professional Appraiser, TDLR #1306 Registered Texas Assessor, TDLR #1306 Mass Appraisal Report for Tax Year 2018 Mass Appraisal

The Office of the Chief Appraiser David Luther, RPA, RTA, CCA Registered Professional Appraiser, TDLR #1306 Registered Texas Assessor, TDLR #1306 Mass Appraisal Report for Tax Year 2018 Mass Appraisal

COST SEGREGATION UNCOVERING HIDDEN CASH FLOW

1800 Avenue of the Stars Suite 310 Century City, CA 90067 (310) 798-3123 info@braunco.com COST SEGREGATION UNCOVERING HIDDEN CASH FLOW Why not recover at least 5 to 10 cents for every dollar you spend

1800 Avenue of the Stars Suite 310 Century City, CA 90067 (310) 798-3123 info@braunco.com COST SEGREGATION UNCOVERING HIDDEN CASH FLOW Why not recover at least 5 to 10 cents for every dollar you spend

DALLAS CENTRAL APPRAISAL DISTRICT DCAD VALUATION PROCESSES

DALLAS CENTRAL APPRAISAL DISTRICT DCAD VALUATION PROCESSES DALLAS CENTRAL APPRAISAL DISTRICT DCAD DCAD appraisers appraise a large universe of properties by developing appraisal models DCAD appraisers

DALLAS CENTRAL APPRAISAL DISTRICT DCAD VALUATION PROCESSES DALLAS CENTRAL APPRAISAL DISTRICT DCAD DCAD appraisers appraise a large universe of properties by developing appraisal models DCAD appraisers

Grain Elevator. Market Value Assessment in Saskatchewan Handbook. Grain Elevator Valuation Guide

Market Value Assessment in Saskatchewan Handbook Grain Elevator Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass

Market Value Assessment in Saskatchewan Handbook Grain Elevator Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass

Who s Afraid of the Big, Bad Cost Approach? William D. Shepherd General Counsel Hillsborough County Property Appraiser

Who s Afraid of the Big, Bad Cost Approach? William D. Shepherd General Counsel Hillsborough County Property Appraiser 1 Cost Approach? Eww!! 2 3 Reasons for the Cost Approach s Bad Reputation: Poor job

Who s Afraid of the Big, Bad Cost Approach? William D. Shepherd General Counsel Hillsborough County Property Appraiser 1 Cost Approach? Eww!! 2 3 Reasons for the Cost Approach s Bad Reputation: Poor job

NEW LONDON, NEW HAMPSHIRE 375 MAIN STREET NEW LONDON, NH

TOWN OF NEW LONDON, NEW HAMPSHIRE 375 MAIN STREET NEW LONDON, NH 03257 WWW.NL-NH.COM READING YOUR PROPERTY RECORD CARD Vision Appraisal Technology 1.) Property Location: The actual physical location of

TOWN OF NEW LONDON, NEW HAMPSHIRE 375 MAIN STREET NEW LONDON, NH 03257 WWW.NL-NH.COM READING YOUR PROPERTY RECORD CARD Vision Appraisal Technology 1.) Property Location: The actual physical location of

Chapter 6: Auto and RV Dealership Asset Valuation (Equipment)

") Chapter 6: Auto and RV Dealership Asset Valuation (Equipment) Knowing how much the dealership s furniture, fixtures and equipment are worth will determine the amount of goodwill that is being paid as part

Chapter 6: Auto and RV Dealership Asset Valuation (Equipment) Knowing how much the dealership s furniture, fixtures and equipment are worth will determine the amount of goodwill that is being paid as part

Course Mass Appraisal Practices and Procedures

Course 331 - Mass Appraisal Practices and Procedures Course Description This course is designed to build on the subject matter covered in Course 300 Fundamentals of Mass Appraisal and prepare the student

Course 331 - Mass Appraisal Practices and Procedures Course Description This course is designed to build on the subject matter covered in Course 300 Fundamentals of Mass Appraisal and prepare the student

LLANO CENTRAL APPRAISAL DISTRICT REAPPRAISAL PLAN FOR TAX YEARS 2017 & 2018 AS ADOPTED BY THE BOARD OF DIRECTORS

LLANO CENTRAL APPRAISAL DISTRICT REAPPRAISAL PLAN FOR TAX YEARS 2017 & 2018 AS ADOPTED BY THE BOARD OF DIRECTORS TABLE OF CONTENTS ITEM PAGE Executive Summary 5 Revaluation Decision (Statutory or Administrative)

LLANO CENTRAL APPRAISAL DISTRICT REAPPRAISAL PLAN FOR TAX YEARS 2017 & 2018 AS ADOPTED BY THE BOARD OF DIRECTORS TABLE OF CONTENTS ITEM PAGE Executive Summary 5 Revaluation Decision (Statutory or Administrative)

Integrated Damage Assessment Model. FEMA District IV Individual Assistance (IA) Conference

Conference") Integrated Damage Assessment Model FEMA District IV Individual Assistance (IA) Conference Presenter: Morgan B. Gilreath, Jr. Volusia County Property Appraiser IDAM is a computerized Damage Estimating

Integrated Damage Assessment Model FEMA District IV Individual Assistance (IA) Conference Presenter: Morgan B. Gilreath, Jr. Volusia County Property Appraiser IDAM is a computerized Damage Estimating

Table of Contents 2013 Commercial Revaluation Report

Table of Contents Commercial Revaluation Report 1. Commercial & Industrial Valuation Summary Introduction Uniform Standards Approaches to Value Land Valuation Land to Building Ratios Parking to Building

Table of Contents Commercial Revaluation Report 1. Commercial & Industrial Valuation Summary Introduction Uniform Standards Approaches to Value Land Valuation Land to Building Ratios Parking to Building

Kitsap County Assessor

Kitsap County Assessor Narrative for Countywide Model Tax Year: 2018 Appraisal Date: 1/1/2017 Property Type: Hangar - Airplane Area Overview Countywide models are for properties located throughout Kitsap

Kitsap County Assessor Narrative for Countywide Model Tax Year: 2018 Appraisal Date: 1/1/2017 Property Type: Hangar - Airplane Area Overview Countywide models are for properties located throughout Kitsap

MAAO Sales Ratio Committee 2013 Fall Conference Seminar

MAAO Sales Ratio Committee 2013 Fall Conference Seminar Presented By: Al Whitcomb Dakota County (Retired) John Keefe Chisago County Assessor Brent Reid City of Coon Rapids Michael Thompson Scott County

MAAO Sales Ratio Committee 2013 Fall Conference Seminar Presented By: Al Whitcomb Dakota County (Retired) John Keefe Chisago County Assessor Brent Reid City of Coon Rapids Michael Thompson Scott County

ARTICLE 18 NONCONFORMING USES, LOTS, OR STRUCTURES (entire Article amended February 6, 2009)

") ARTICLE 18 NONCONFORMING USES, LOTS, OR STRUCTURES (entire Article amended February 6, 2009) 18.01 INTENT AND PURPOSE A. Nonconforming Uses: It is the intent of this Article to allow nonconforming uses

ARTICLE 18 NONCONFORMING USES, LOTS, OR STRUCTURES (entire Article amended February 6, 2009) 18.01 INTENT AND PURPOSE A. Nonconforming Uses: It is the intent of this Article to allow nonconforming uses

Typical Valuation Approaches and How to Deal With Them

Typical Valuation Approaches and How to Deal With Them January, 2018 Anthony F. DellaPelle, Esq., CRE Shareholder, McKirdy, Riskin, Olson & DellaPelle, P.C. Morristown, New Jersey Christian F. Torgrimson,

Typical Valuation Approaches and How to Deal With Them January, 2018 Anthony F. DellaPelle, Esq., CRE Shareholder, McKirdy, Riskin, Olson & DellaPelle, P.C. Morristown, New Jersey Christian F. Torgrimson,

Chapter 8 Qualifying Property

The 3 "Cs" of Lending Capacity to Pay does the borrower make enough money to repay loan? lenders use qualifying ratios Creditworthiness [Character] is the borrower likely to repay loan on time? lenders

The 3 "Cs" of Lending Capacity to Pay does the borrower make enough money to repay loan? lenders use qualifying ratios Creditworthiness [Character] is the borrower likely to repay loan on time? lenders

Urban Land. Overview 2.1

Overview 2.1 This chapter contains the valuation procedures for determining the assessed value for residential and commercial land valued using the cost approach. SAMA s 2015 Cost Guide provides direction

Overview 2.1 This chapter contains the valuation procedures for determining the assessed value for residential and commercial land valued using the cost approach. SAMA s 2015 Cost Guide provides direction

A Guide Tax Assessment. George M. Durgin Middletown Tax Assessor August 4, 2016

A Guide Tax Assessment George M. Durgin Middletown Tax Assessor August 4, 2016 A Guide to Tax Assessment Legal Basis Valuation Land Value Building Value Appeal Process Legal Basis Rhode Island General

A Guide Tax Assessment George M. Durgin Middletown Tax Assessor August 4, 2016 A Guide to Tax Assessment Legal Basis Valuation Land Value Building Value Appeal Process Legal Basis Rhode Island General

The Three Approaches to Value

Chapter 6 The Three Approaches to Value The appraiser considers three approaches to develop indications of value. These are: Cost approach; Sales comparison (market) approach; and Income approach. All

Chapter 6 The Three Approaches to Value The appraiser considers three approaches to develop indications of value. These are: Cost approach; Sales comparison (market) approach; and Income approach. All

Assessment Principles. Three Accepted Approaches to Value Cost Approach Sales Comparison Approach Property Income (Rental) Approach

Approach") Assessment Principles Three Accepted Approaches to Value Cost Approach Sales Comparison Approach Property Income (Rental) Approach Overview of the Cost Approach Land Valuation Average selling prices for

Assessment Principles Three Accepted Approaches to Value Cost Approach Sales Comparison Approach Property Income (Rental) Approach Overview of the Cost Approach Land Valuation Average selling prices for

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330 REVIEW NOTES by CHUCK DUNN CHAPTER 12 Copyright 2010 by the Real Estate Division and Chuck Dunn. All rights reserved ARE 3 RD EDITION REVIEW

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330 REVIEW NOTES by CHUCK DUNN CHAPTER 12 Copyright 2010 by the Real Estate Division and Chuck Dunn. All rights reserved ARE 3 RD EDITION REVIEW

LITIGATING IN A MASS APPRAISAL ENVIRONMENT

11 th Mass Appraisal Valuation Symposium Innovation, Transformation, Knowledge Enhancement and Improved Efficiencies in Mass Appraisal Niagara Falls, Canada May 17-18, 2016 LITIGATING IN A MASS APPRAISAL

11 th Mass Appraisal Valuation Symposium Innovation, Transformation, Knowledge Enhancement and Improved Efficiencies in Mass Appraisal Niagara Falls, Canada May 17-18, 2016 LITIGATING IN A MASS APPRAISAL

Caldwell County Appraisal District

Caldwell County Appraisal District Reappraisal Plan for Tax Years 2019 and 2020 INTRODUCTION Scope of Responsibility The Caldwell County Appraisal District has prepared and published this reappraisal plan

Caldwell County Appraisal District Reappraisal Plan for Tax Years 2019 and 2020 INTRODUCTION Scope of Responsibility The Caldwell County Appraisal District has prepared and published this reappraisal plan

Assessing Reform Proposal Summary

Assessing Reform Proposal Summary Specify minimum quality standards that every assessing district must meet, on their own, in cooperation with other local units, or through the county. Local units could

Assessing Reform Proposal Summary Specify minimum quality standards that every assessing district must meet, on their own, in cooperation with other local units, or through the county. Local units could

Plant design and economics (8)

") Plant design and economics (8) Zahra Maghsoud ٢ DEPRECIATION (Ch. 9 Peters and Timmerhaus ) The reduction in value due to physical deterioration, technological advances, economic changes, or other factors

Plant design and economics (8) Zahra Maghsoud ٢ DEPRECIATION (Ch. 9 Peters and Timmerhaus ) The reduction in value due to physical deterioration, technological advances, economic changes, or other factors

SECURITYNATIONAL MORTGAGE COMPANY

SECURITYNATIONAL MORTGAGE COMPANY INFORMATION ON FNMA S LOAN QUALITY INITIATIVE OVERVIEW ON UMDP STANDARDIZED MORTGAGE DATA AND FILE FORMAT STANDARDS SecurityNational Mortgage Company Internal use only

SECURITYNATIONAL MORTGAGE COMPANY INFORMATION ON FNMA S LOAN QUALITY INITIATIVE OVERVIEW ON UMDP STANDARDIZED MORTGAGE DATA AND FILE FORMAT STANDARDS SecurityNational Mortgage Company Internal use only

Chapter 35. The Appraiser's Sales Comparison Approach INTRODUCTION

Chapter 35 The Appraiser's Sales Comparison Approach INTRODUCTION The most commonly used appraisal technique is the sales comparison approach. The fundamental concept underlying this approach is that market

Chapter 35 The Appraiser's Sales Comparison Approach INTRODUCTION The most commonly used appraisal technique is the sales comparison approach. The fundamental concept underlying this approach is that market

Business Personal Property February 1, 2012 Revenue Laws

Business Personal Property February 1, 2012 Revenue Laws David Baker, Director Local Government Division N.C. Department of Revenue 919-733-7711 David.baker@dornc.com Fair Market Value N.C.G.S. 105-283:

Business Personal Property February 1, 2012 Revenue Laws David Baker, Director Local Government Division N.C. Department of Revenue 919-733-7711 David.baker@dornc.com Fair Market Value N.C.G.S. 105-283:

Homeowner s Exemption (HOE)

") Homeowner s Exemption (HOE) Table of Contents CHEAT SHEETS... 3 Add HOE to a Parcel...3 Edit HOE Record...3 Remove HOE from a Parcel...3 Find the HOE Amount...3 Who is getting the exemption?...4 New Application

Homeowner s Exemption (HOE) Table of Contents CHEAT SHEETS... 3 Add HOE to a Parcel...3 Edit HOE Record...3 Remove HOE from a Parcel...3 Find the HOE Amount...3 Who is getting the exemption?...4 New Application

Kitsap County Assessor

Narrative for Countywide Model Tax Year: 2018 Appraisal Date: 1/1/2017 Property Type: Land Leases for Cell Sites, Espresso Sites, ATM Sites, and Billboard Sites Updated 6/8/2017 by CM20 Area Overview Countywide

Narrative for Countywide Model Tax Year: 2018 Appraisal Date: 1/1/2017 Property Type: Land Leases for Cell Sites, Espresso Sites, ATM Sites, and Billboard Sites Updated 6/8/2017 by CM20 Area Overview Countywide

Henderson County Appraisal District Mass Appraisal Report

Henderson County Appraisal District 2016 Mass Appraisal Report 1 Purpose The purpose of this report is to better inform the property owners within the boundaries of the Henderson County Appraisal District

Henderson County Appraisal District 2016 Mass Appraisal Report 1 Purpose The purpose of this report is to better inform the property owners within the boundaries of the Henderson County Appraisal District

AP444 Computer Assisted Mass Appraisal

AP444 Computer Assisted Mass Appraisal 3 Credits Instructor: Kenneth Rutherford Phone: 780 871 5768 Original Developer: Patty Pidruchney Current Developer: Kenneth Rutherford Reviewer: Al Motley Created:

AP444 Computer Assisted Mass Appraisal 3 Credits Instructor: Kenneth Rutherford Phone: 780 871 5768 Original Developer: Patty Pidruchney Current Developer: Kenneth Rutherford Reviewer: Al Motley Created:

ASSESSMENT METHODOLOGY

2019 ASSESSMENT METHODOLOGY COMMERCIAL RETAIL AND OFFICE CONDOMINIUMS A summary of the methods used by the City of Edmonton in determining the value of commercial retail and office condominium properties

2019 ASSESSMENT METHODOLOGY COMMERCIAL RETAIL AND OFFICE CONDOMINIUMS A summary of the methods used by the City of Edmonton in determining the value of commercial retail and office condominium properties

Understanding Mississippi Property Taxes

Understanding Mississippi Property Taxes Property tax revenues are a vital component of the budgets of Mississippi s local governments. Property tax revenues allow these governments to provide important

Understanding Mississippi Property Taxes Property tax revenues are a vital component of the budgets of Mississippi s local governments. Property tax revenues allow these governments to provide important

Village of Scarsdale

Village of Scarsdale VILLAGE HALL / 1001 POST ROAD / SCARSDALE, NY 10583 914.722.1110 / WWW.SCARSDALE.COM Village Wide Revaluation Frequently Asked Questions Q1. How was the land value for each parcel

Village of Scarsdale VILLAGE HALL / 1001 POST ROAD / SCARSDALE, NY 10583 914.722.1110 / WWW.SCARSDALE.COM Village Wide Revaluation Frequently Asked Questions Q1. How was the land value for each parcel

New Models for Property Data Verification and Valuation

New Models for Property Data Verification and Valuation for 2006 IAAO Councils and Sections Joint Seminar May 9-11, 2006 Charleston, South Carolina Presented by George Donatello, CMS Principal Consultant

New Models for Property Data Verification and Valuation for 2006 IAAO Councils and Sections Joint Seminar May 9-11, 2006 Charleston, South Carolina Presented by George Donatello, CMS Principal Consultant

ADDENDUM #2_RFP # Computer Mass Appraisal (CAMA) Software for HC Assessor Department

Software for HC Assessor Department") Horry County Government PROCUREMENT DEPARTMENT www.horrycounty.org Horry County Office of Procurement 3230 Hwy. 319 E. Conway, South Carolina 29526 Phone 843.915.5380 Fax 843.365.9861 TO: FROM: ALL INTERESTED

Horry County Government PROCUREMENT DEPARTMENT www.horrycounty.org Horry County Office of Procurement 3230 Hwy. 319 E. Conway, South Carolina 29526 Phone 843.915.5380 Fax 843.365.9861 TO: FROM: ALL INTERESTED

Table of Contents 2015 Commercial Revaluation Report

Table of Contents 05 Commercial Revaluation Report 05 Commercial & Industrial Valuation Summary Introduction Uniform Standards Approaches to Value Land Valuation Land to Building Ratios Parking to Building

Table of Contents 05 Commercial Revaluation Report 05 Commercial & Industrial Valuation Summary Introduction Uniform Standards Approaches to Value Land Valuation Land to Building Ratios Parking to Building

FEMA has the only computerized damage assessment

The Assessor as an Integral Partner in Disaster Planning, Response, and Recovery: 2. Demonstration of an Integrated Damage Assessment Model By Morgan B. Gilreath, Jr. This article is the second in a two-part

The Assessor as an Integral Partner in Disaster Planning, Response, and Recovery: 2. Demonstration of an Integrated Damage Assessment Model By Morgan B. Gilreath, Jr. This article is the second in a two-part

Rockwall CAD. Basics of. Appraising Property. For. Property Taxation

Rockwall CAD Basics of Appraising Property For Property Taxation ROCKWALL CENTRAL APPRAISAL DISTRICT 841 Justin Rd. Rockwall, Texas 75087 972-771-2034 Fax 972-771-6871 Introduction Rockwall Central Appraisal

Rockwall CAD Basics of Appraising Property For Property Taxation ROCKWALL CENTRAL APPRAISAL DISTRICT 841 Justin Rd. Rockwall, Texas 75087 972-771-2034 Fax 972-771-6871 Introduction Rockwall Central Appraisal

Regression + For Real Estate Professionals with Market Conditions Module

USER MANUAL 1 Automated Valuation Technologies, Inc. Regression + For Real Estate Professionals with Market Conditions Module This Regression + software program and this user s manual have been created

USER MANUAL 1 Automated Valuation Technologies, Inc. Regression + For Real Estate Professionals with Market Conditions Module This Regression + software program and this user s manual have been created

2017 Reappraisal. March 10, 2017

2017 Reappraisal March 10, 2017 Today s Presenters Cheyenne Johnson, Assessor Charles Blow, CAE Robert Trouy, TMA David Baker, Certified General Appraiser Joshua Forbes Shawn Lynch, JD Together, as professional

2017 Reappraisal March 10, 2017 Today s Presenters Cheyenne Johnson, Assessor Charles Blow, CAE Robert Trouy, TMA David Baker, Certified General Appraiser Joshua Forbes Shawn Lynch, JD Together, as professional