Real Estate Valuation in the Open Economy June 26, 2014 The 15 th NBER-CCER Conference CCER Beijing University Joshua Aizenman USC and the NBER

|

|

|

- Arthur Hill

- 6 years ago

- Views:

Transcription

1 Real Estate Valuation in the Open Economy June 26, 2014 The 15 th NBER-CCER Conference CCER Beijing University Joshua Aizenman USC and the NBER

2 SPA IRL UK CHI CHI GER SPA US house-prices in real term index Q Q The Economist

3 The purpose Explore the stability of the key conditioning variables accounting for the real estate valuation before and after the crisis of , in a panel of 36 countries, for the period of 2005:I -2012:IV, recognizing the crisis break. We evaluate the importance of changes of 1. Current account, 2. Credit market conditions, 3. lagged real estate appreciation [proxy for momentum] and other variables in explaining 3 the patters of real estate valuations.

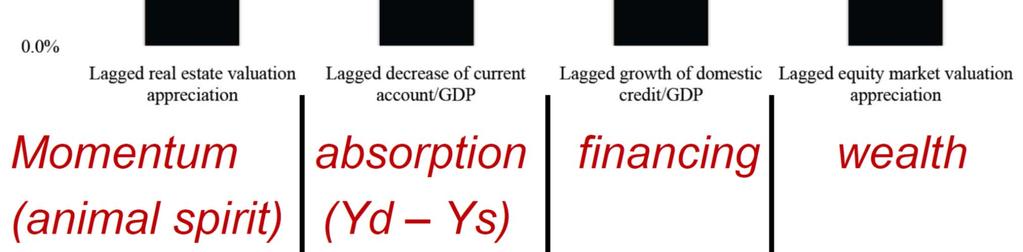

4 Main results The most economically significant variable in accounting for real estate valuation changes are 1. The lagged real estate appreciation (real estate inflation minus CPI inflation), 2. Changes of the current account/gdp, 3. Changes in domestic credit/gdp, 4. Equity market appreciation (equity market appreciation minus CPI inflation). 4

5 Results, cont. The effects are economically substantial: 1. a 1 s.d. increase in lagged real estate appreciation (REA) is associated with a 10 % increase in REA; 2. a 1 s.d. increase in lagged current account deficit is associated with a 5% higher REA; 3. a 1 s.d. increase in lagged domestic credit/gdp growth is associated with 3% higher REA. Both current account and credit growth channels are important, with the animal-spirits / momentum channels playing the most important role. 5

6 Motivation Shiller s 2005 concerns that the US housing market is overheating. Leamer (2007): Housing is the US business cycle. 6

7 Background papers Aizenman and Jinjarak (2008) The economic importance of current account variations, in accounting for the real estate valuation, exceeds that of other macro variables [41 countries, ]. The global crisis of sparked a vibrant debate Borio and Disyatat (2011) - The main causing factor to the financial crisis was the excess elasticity of the international monetary and financial system; Obstfeld (2012) - External imbalances - a symptom that deeper financial threats are gathering. Gourinchas and Obstfeld (2012) Domestic credit expansion and real currency appreciation have been the most robust 7 and significant predictors of financial crises

8 Shiller warns of "bubbly" global home prices Reuters Oct 14, 2013 In June this year, he pointed to a potential new housing bubble in some of America's largest cities. "It is up 12 percent in the last year. This is a very rapid price increase right now, and I believe that it is accelerated somewhat by the Fed's policy," he said. China, Brazil, India, Australia, Norway and Belgium, among other countries, were witnessing similar price rises. "There are so many countries that are looking bubbly," he said. 8

9 Nouriel Roubini theguardian.com, 2 December 2013 Housing bubble 2.0 can only end badly The global economy's new housing bubbles may not be about to burst just yet, because the forces feeding them especially easy money and the need to hedge against inflation are still fully operative. Now, five years later, signs of frothiness, if not outright bubbles, are reappearing in housing markets in Switzerland, Sweden, Norway, Finland, France, Germany, Canada, Australia, New Zealand, and, back for an encore, the UK (well, London). In emerging markets, bubbles are appearing in Hong Kong, Singapore, China, and Israel, and in major 9 urban centers in Turkey, India, Indonesia, and Brazil.

10 Cu. Act. and real estate linkages 1. Tomura (2010) Expectation-driven boom bust cycles in house prices in the presence of uncertainty about the duration of high growth occurs only if the economy is open to international capital flows. 2. Laibson and Mollerstrom (2010) - national asset bubbles may explain the international imbalances. A Conjecture: a two way feedback between asset valuation and current accounts. 10

11 Cu. Act. and real estate linkages, cont. 3. Gete s (2010) - an increased demand for housing may generate trade deficits without the need for wealth effects or trade in capital goods. Housing booms are larger if the country can run a trade / current account deficit. 4. Adam et al. (2011) - an open economy with subjective beliefs about price behavior, updated beliefs using Bayes' rule. Belief dynamics replicates the empirical association between Cu. Act. patterns and real estate valuations. Low interest rates a house price boom. 11

12 The current account and credit growth may impact the valuation of national real estates via different but related channels I. Growing current account deficits is a signal of a growing gap between the spending of domestic residents [absorption] and their output. As long as the demand for non-traded durable assets is positively correlated with absorption, higher current account deficits tend to be associated with higher real estate valuation. II. As most households co-finance the purchase of their dwelling thorough the banking system, greater financial depth and accelerated growth rate of credit increases the demand for houses 12 increasing the real estate valuation.

13 We explore the following issues i. Stability of the key conditioning variables accounting for the real estate valuation before and after the crisis; the relative importance of the current account and credit growth patterns. ii. The importance of momentum in the pricing of real estate, controlling for other macro factors. This issue is related to concerns about possible bubble dynamics. iii. Symmetry of the patterns during real estate appreciation versus real estate depreciation. iv. Possible two way causality between current account and real estate valuation patterns. v. The degree to which the valuation of equities is accounted by similar conditioning variables. 13

14 Data and patterns 36 countries in the sample, both developed and emerging markets, 2005:I to 2012:IV. Based on the panel unit-root and panel cointegration tests, we apply dynamic panel data estimation in first-differenced series for the real estate and macro variables in our sample. With 36 countries and over 20 quarterly periods for each country, the fixed-effect estimation are applicable. However, given that several series are highly persistent in the panel of countries, we focus in on dynamic panel estimation as our main econometric evidence. 14

15 We validates the robustness of the association between real estate valuation of lagged current account patterns both before and after the crisis. The base regression is a dynamic panel estimate of 36 countries, 2005:I -2012:IV, recognizing the crisis break. It accounts for the appreciation rate of the real estate (real estate inflation - CPI inflation) by: 1. lagged appreciation rate of the real estate valuation, 2. lagged changes in the current account/gdp, 3. lagged changes in the domestic credit/gdp, 4. lagged changes in the equity market appreciation (equity market appreciation minus CPI inflation), 5. a vector of lagged changes of macro controls [inflation, growth of industrial production, TED spreads, sovereign spreads, VIX, and international reserves]. 15

16 Empirical specification where t denotes time (quarterly); i country; CAD/GDP: current-account deficit/gdp; DCR/GDP: domestic credit/gdp; and X denotes a vector of controls in changes, including -- CPI inflation, growth of industrial production, TED spread, VIX, Sovereign CDS spread, and foreign reserve accumulation. 16

17 The most economically significant variable in accounting for real estate valuation changes 1. The lagged real estate appreciation, 2. Current account deficit/gdp, 3. Domestic credit/gdp, 4. Equity market appreciation. The first three effects are economically substantial: - a one standard deviation increase in lagged real estate appreciation is associated with a 10 % increase in the present real estate appreciation, - much larger than the impact of a one standard deviation increase in the current account deficit (5%) and that of domestic credit/gdp growth (3%). 17

18

19 The animal-spirits and expectations channels playing the most important role in the boom and bust of real estate valuation The results are also supportive of both current account and credit growth channels. Support for a positive feedback of real estate appreciation to equity market appreciation, consistent with the wealth effects from real estate valuation to equity investment. 19

20 Sensitivity Analysis The main results hold using either 2007:III (Northern Rock event) or 2008:III (Lehman Brothers event) as an alternative turning point. We find that a reverse and positive feedback of real estate appreciation to current account deficit is not supported by the data over the crisis period. Asymmetric adjustment between appreciation and depreciation: For the real estate appreciation episode, estimation results are largely consistent with the results from the whole-sample estimation. 20

21 For the real estate depreciation episode, only lagged real estate valuation appreciation and equity market valuation appreciation are found statistically significant in the association with the real estate valuation. When real estate markets were on the rise, the real estate valuation adjusts with respect to macro variables differently from when the markets were declining. Asymmetric bubbly dynamics are evident in the real estate valuation. 21

22 Concluding remarks We confirmed a robust positive association between the appreciation of real estate valuation and increases in current account deficits and the growth rates of credit (both as fractions of the GDP) in 36 countries, covering the OECD and emerging markets, before and after the global financial crisis. While the relative impact of the current account deficit is larger than that of credit growth in our sample, one should recognize that the growth of credit/gdp is a noisy measure of the effective credit growth in the 22 real estate market.

23 Cont. Data limitations prevented us from controlling directly for the credit conditions in the real estate markets [like the stringency of credit standards, required down payment, the effective spreads in the mortgage markets, etc.] There is no reason to expect that the relative ranking of the importance of the current account versus the credit channels in accounting for real estate appreciations should be stable overtime. Yet, as theory suggests, both channels are potent and should not be ignored. 23

24 The most important factor accounting for the appreciation: the impact of momentum: the lagged quarterly appreciations in the past year. A real estate appreciation of 1% in a given quarter was associated with a projected real appreciation of more than 1% in the next three quarters. This is in line with Shiller s (2000) concerns regarding Irrational Exuberance in the USA in the early 2000s, with Case, Shiller, and Thompson (2012) s, and Glaeser, Gottlieb, and Gyourko (2013) s questioning the role of cheap credit on real estate boom. Shiller s concerns apply globally. The effects of CAD prevails both before and after 24 the crisis.

25 Follow up agenda Aizenman, Jinjarak and Huanhuan Zheng (2014) work in progress Added controls: LTV, stringency of credit standards, required down payment, the effective spreads in the mortgage markets, house price/rent I. What are the output and growth costs associated with corrections of bubbly real estate, and what factors determine these costs. II. Endogeneity issues Preliminary findings: small corrections don t have significant growth effects, faster corrections are associated with faster recoveries. 25

26 /

Housing markets, wealth and the business cycle

Housing markets, wealth and the business cycle Nathalie Girouard copyright with the author OECD Economics Department DG ECFIN workshop: Housing and mortgage markets and the EU economy Brussels, 21 November

Housing markets, wealth and the business cycle Nathalie Girouard copyright with the author OECD Economics Department DG ECFIN workshop: Housing and mortgage markets and the EU economy Brussels, 21 November

MONETARY POLICY AND HOUSING MARKET: COINTEGRATION APPROACH

MONETARY POLICY AND HOUSING MARKET: COINTEGRATION APPROACH Doh-Khul Kim, Mississippi State University - Meridian Kenneth A. Goodman, Mississippi State University - Meridian Lauren M. Kozar, Mississippi

MONETARY POLICY AND HOUSING MARKET: COINTEGRATION APPROACH Doh-Khul Kim, Mississippi State University - Meridian Kenneth A. Goodman, Mississippi State University - Meridian Lauren M. Kozar, Mississippi

The Housing Price Bubble, Monetary Policy, and the Foreclosure Crisis in the U.S.

The Housing Price Bubble, Monetary Policy, and the Foreclosure Crisis in the U.S. John F. McDonald a,* and Houston H. Stokes b a Heller College of Business, Roosevelt University, Chicago, Illinois, 60605,

The Housing Price Bubble, Monetary Policy, and the Foreclosure Crisis in the U.S. John F. McDonald a,* and Houston H. Stokes b a Heller College of Business, Roosevelt University, Chicago, Illinois, 60605,

An Assessment of Recent Increases of House Prices in Austria through the Lens of Fundamentals

An Assessment of Recent Increases of House Prices in Austria 1 Introduction Martin Schneider Oesterreichische Nationalbank The housing sector is one of the most important sectors of an economy. Since residential

An Assessment of Recent Increases of House Prices in Austria 1 Introduction Martin Schneider Oesterreichische Nationalbank The housing sector is one of the most important sectors of an economy. Since residential

Housing valuations: no bubble apparent

Housing valuations: no bubble apparent Kathleen Stephansen and Maxine Koster This analysis focuses on cross-country comparisons of housing valuations. Our main findings are: Housing markets have been generally

Housing valuations: no bubble apparent Kathleen Stephansen and Maxine Koster This analysis focuses on cross-country comparisons of housing valuations. Our main findings are: Housing markets have been generally

The Effect of House Prices on Growth

Ewald Walterskirchen The Effect of House Prices on Growth During the last decade, disparities in growth rates have been widening between the "Anglo- Scandinavian" countries and the euro area. A hypothesis

Ewald Walterskirchen The Effect of House Prices on Growth During the last decade, disparities in growth rates have been widening between the "Anglo- Scandinavian" countries and the euro area. A hypothesis

Not Your Parents Real Estate Market

NEW THINKING Not Your Parents Real Estate Market Why changing how we view residential real estate is essential in today s economy Is there a housing bubble? How long can this possibly last? I remember

NEW THINKING Not Your Parents Real Estate Market Why changing how we view residential real estate is essential in today s economy Is there a housing bubble? How long can this possibly last? I remember

Messung der Preise Schwerin, 16 June 2015 Page 1

New weighting schemes in the house price indices of the Deutsche Bundesbank How should we measure residential property prices to inform policy makers? Elena Triebskorn*, Section Business Cycle, Price and

New weighting schemes in the house price indices of the Deutsche Bundesbank How should we measure residential property prices to inform policy makers? Elena Triebskorn*, Section Business Cycle, Price and

An Assessment of Current House Price Developments in Germany 1

An Assessment of Current House Price Developments in Germany 1 Florian Kajuth 2 Thomas A. Knetsch² Nicolas Pinkwart² Deutsche Bundesbank 1 Introduction House prices in Germany did not experience a noticeable

An Assessment of Current House Price Developments in Germany 1 Florian Kajuth 2 Thomas A. Knetsch² Nicolas Pinkwart² Deutsche Bundesbank 1 Introduction House prices in Germany did not experience a noticeable

THE YIELD CURVE AS A LEADING INDICATOR ACROSS COUNTRIES AND TIME: THE EUROPEAN CASE

University of New Hampshire University of New Hampshire Scholars' Repository Honors Theses and Capstones Student Scholarship Fall 2014 THE YIELD CURVE AS A LEADING INDICATOR ACROSS COUNTRIES AND TIME:

University of New Hampshire University of New Hampshire Scholars' Repository Honors Theses and Capstones Student Scholarship Fall 2014 THE YIELD CURVE AS A LEADING INDICATOR ACROSS COUNTRIES AND TIME:

Essentials of Real Estate Economics

Essentials of Real Estate Economics SIXTH EDITION, Dennis J. McKenzie Richard M. Betts MAI, SRA, ASA (Real Estate) Property Analyst Carol A. Jensen Cabrillo College, Aptos and City College of San Francisco

Essentials of Real Estate Economics SIXTH EDITION, Dennis J. McKenzie Richard M. Betts MAI, SRA, ASA (Real Estate) Property Analyst Carol A. Jensen Cabrillo College, Aptos and City College of San Francisco

INVESTMENT ANALYSIS Q1 2018

INVESTMENT ANALYSIS Q1 18 Review of the previous year Global Property Guide Financial Information for the Residential Property Buyer Global Property Guide Financial Information for the Residential Property

INVESTMENT ANALYSIS Q1 18 Review of the previous year Global Property Guide Financial Information for the Residential Property Buyer Global Property Guide Financial Information for the Residential Property

A STUDY ON IMPACT OF CONSUMER INDICES ON HOUSING PRICE INDEX AMONG BRICS NATIONS

International Journal of Civil Engineering and Technology (IJCIET) Volume 9, Issue 5, May 2018, pp. 1165 1169, Article ID: IJCIET_09_05_130 Available online at http://www.iaeme.com/ijciet/issues.asp?jtype=ijciet&vtype=9&itype=5

International Journal of Civil Engineering and Technology (IJCIET) Volume 9, Issue 5, May 2018, pp. 1165 1169, Article ID: IJCIET_09_05_130 Available online at http://www.iaeme.com/ijciet/issues.asp?jtype=ijciet&vtype=9&itype=5

How should we measure residential property prices to inform policy makers?

How should we measure residential property prices to inform policy makers? Dr Jens Mehrhoff*, Head of Section Business Cycle, Price and Property Market Statistics * Jens This Mehrhoff, presentation Deutsche

How should we measure residential property prices to inform policy makers? Dr Jens Mehrhoff*, Head of Section Business Cycle, Price and Property Market Statistics * Jens This Mehrhoff, presentation Deutsche

Housing Markets: Balancing Risks and Rewards

Housing Markets: Balancing Risks and Rewards October 14, 2015 Hites Ahir and Prakash Loungani International Monetary Fund Presentation to the International Housing Association VIEWS EXPRESSED ARE THOSE

Housing Markets: Balancing Risks and Rewards October 14, 2015 Hites Ahir and Prakash Loungani International Monetary Fund Presentation to the International Housing Association VIEWS EXPRESSED ARE THOSE

Susanne E. Cannon Department of Real Estate DePaul University. Rebel A. Cole Departments of Finance and Real Estate DePaul University

Susanne E. Cannon Department of Real Estate DePaul University Rebel A. Cole Departments of Finance and Real Estate DePaul University 2011 Annual Meeting of the Real Estate Research Institute DePaul University,

Susanne E. Cannon Department of Real Estate DePaul University Rebel A. Cole Departments of Finance and Real Estate DePaul University 2011 Annual Meeting of the Real Estate Research Institute DePaul University,

Economic and monetary developments

Box 4 House prices and the rent component of the HICP in the euro area According to the residential property price indicator, euro area house prices decreased by.% year on year in the first quarter of

Box 4 House prices and the rent component of the HICP in the euro area According to the residential property price indicator, euro area house prices decreased by.% year on year in the first quarter of

RESEARCH BRIEF TURKISH HOUSING MARKET: PRICE BUBBLE SEPTEMBER 2014 SUMMARY. A Cushman & Wakefield Research Publication OVERVIEW

RESEARCH BRIEF TURKISH HOUSING MARKET: PRICE BUBBLE SEPTEMBER 2014 SUMMARY OVERVIEW Debates on the existence of a price bubble in the Turkish housing market have continued after numerous news releases

RESEARCH BRIEF TURKISH HOUSING MARKET: PRICE BUBBLE SEPTEMBER 2014 SUMMARY OVERVIEW Debates on the existence of a price bubble in the Turkish housing market have continued after numerous news releases

London IHP Leadership Exchange

London IHP Leadership Exchange Assets Real Estate Production and Acquisition Review of Global Markets Robert Grundy, Head of Housing, Savills Tuesday 7 th October, 2014 Winckworth Sherwood, Minerva House,

London IHP Leadership Exchange Assets Real Estate Production and Acquisition Review of Global Markets Robert Grundy, Head of Housing, Savills Tuesday 7 th October, 2014 Winckworth Sherwood, Minerva House,

MARKET STRATEGY VIEWPOINT U.S. Housing Decelerating

Jan-01 Oct-01 Jul-02 Apr-03 Jan-0 Oct-0 Jul-05 Apr-0 Jan-07 Oct-07 Jul-08 Apr-09 Jan-10 Oct-10 Jul-11 Apr-12 Jan-13 Oct-13 Jul-1 Apr-15 Jan-1 Oct-1 Jul-17 Apr-18 U.S. Housing Decelerating August 27, 2018

Jan-01 Oct-01 Jul-02 Apr-03 Jan-0 Oct-0 Jul-05 Apr-0 Jan-07 Oct-07 Jul-08 Apr-09 Jan-10 Oct-10 Jul-11 Apr-12 Jan-13 Oct-13 Jul-1 Apr-15 Jan-1 Oct-1 Jul-17 Apr-18 U.S. Housing Decelerating August 27, 2018

DEPARTMENT OF ECONOMICS DISCUSSION PAPER SERIES

ISSN 1471-0498 DEPARTMENT OF ECONOMICS DISCUSSION PAPER SERIES HOW HOUSING SLUMPS END Agustin S. Benetrix, Barry Eichengreen and Kevin H. O Rourke Number 577 October 2011 Manor Road Building, Oxford OX1

ISSN 1471-0498 DEPARTMENT OF ECONOMICS DISCUSSION PAPER SERIES HOW HOUSING SLUMPS END Agustin S. Benetrix, Barry Eichengreen and Kevin H. O Rourke Number 577 October 2011 Manor Road Building, Oxford OX1

- 1 - IN HONG KONG. Prepared by Frank Leung, Kevin Chow and Gaofeng Han 1 Research Department. Abstract

- 1 - LONG-TERM AND SHORT-TERM DETERMINANTS OF PROPERTY PRICES IN HONG KONG Prepared by Frank Leung, Kevin Chow and Gaofeng Han 1 Research Department Abstract Property prices in Hong Kong increased markedly

- 1 - LONG-TERM AND SHORT-TERM DETERMINANTS OF PROPERTY PRICES IN HONG KONG Prepared by Frank Leung, Kevin Chow and Gaofeng Han 1 Research Department Abstract Property prices in Hong Kong increased markedly

The Real Estate and Land Market of Russia: Factors of the Sustainable Development

The Real Estate and Land Market of Russia: Factors of the Sustainable Development Vasily Nilipovskiy (State University of Land Use Planning, Moscow, Russia) ? &! and! &? There is no definite answer in

The Real Estate and Land Market of Russia: Factors of the Sustainable Development Vasily Nilipovskiy (State University of Land Use Planning, Moscow, Russia) ? &! and! &? There is no definite answer in

2 July 2018 FNB HOUSE PRICE INDEX RESULTS FOR JUNE 2018 ACCELERATION, BUT FOR HOW LONG?

2 July 2018 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 john.loos@fnb.co.za THULANI LUVUNO: ANALYST 087-730 2254 thulani.luvuno@fnb.co.za

2 July 2018 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 john.loos@fnb.co.za THULANI LUVUNO: ANALYST 087-730 2254 thulani.luvuno@fnb.co.za

Determination and Countermeasures of Real Estate Market Bubble in Beijing

2017 International Conference on Manufacturing Construction and Energy Engineering (MCEE 2017) ISBN: 978-1-60595-483-7 Determination and Countermeasures of Real Estate Market Bubble in Beijing Ke Sheng

2017 International Conference on Manufacturing Construction and Energy Engineering (MCEE 2017) ISBN: 978-1-60595-483-7 Determination and Countermeasures of Real Estate Market Bubble in Beijing Ke Sheng

Advanced Real Estate Investment and Analysis REAL 240/840 Spring 2014; Room TBA (As of November 18, 2013)

") Advanced Real Estate Investment and Analysis REAL 240/840 Spring 2014; Room TBA (As of November 18, 2013) Professor Joseph Gyourko Office Hours: Monday 12N-1:30pm 1480 SH-DH and by appointment gyourko@wharton.upenn.edu

Advanced Real Estate Investment and Analysis REAL 240/840 Spring 2014; Room TBA (As of November 18, 2013) Professor Joseph Gyourko Office Hours: Monday 12N-1:30pm 1480 SH-DH and by appointment gyourko@wharton.upenn.edu

Advanced Real Estate Investment and Analysis REAL 240/840 Spring 2013; Huntsman 345 (Tentative as of November 15, 2012)

") Advanced Real Estate Investment and Analysis REAL 240/840 Spring 2013; Huntsman 345 (Tentative as of November 15, 2012) Professor Joseph Gyourko Office Hours: Monday 12N-1:30pm 1480 SH-DH and by appointment

Advanced Real Estate Investment and Analysis REAL 240/840 Spring 2013; Huntsman 345 (Tentative as of November 15, 2012) Professor Joseph Gyourko Office Hours: Monday 12N-1:30pm 1480 SH-DH and by appointment

Summary of JREI Global Property Value/Rent Indices (No. 11, Oct. 2018)

") November 29, 2018 Japan Real Estate Institute (JREI) JREI-kenkyu-madoguchi@imail.jrei.jp Summary of JREI Global Property Value/Rent Indices (No. 11, Oct. 2018) We are pleased to release a summary of the

November 29, 2018 Japan Real Estate Institute (JREI) JREI-kenkyu-madoguchi@imail.jrei.jp Summary of JREI Global Property Value/Rent Indices (No. 11, Oct. 2018) We are pleased to release a summary of the

Discussion of: The Seeds of the Crisis: the Housing Market and the Business Cycle by Marcelle Chauvet and Meichi Huang

Discussion of: The Seeds of the 2007-2009 Crisis: the Housing Market and the Business Cycle by Marcelle Chauvet and Meichi Huang Knut Are Aastveit Norges Bank The 4th Oslo Workshop on Economic Policy:

Discussion of: The Seeds of the 2007-2009 Crisis: the Housing Market and the Business Cycle by Marcelle Chauvet and Meichi Huang Knut Are Aastveit Norges Bank The 4th Oslo Workshop on Economic Policy:

Democratising Property Investments

Democratising Property Investments What I wish to share today 1. Property sector outlook 2. How theedgeproperty.com can help you make better property investment decisions Property Sector Outlook The property

Democratising Property Investments What I wish to share today 1. Property sector outlook 2. How theedgeproperty.com can help you make better property investment decisions Property Sector Outlook The property

The OeNB property market monitor of April 2015: Residential property price growth in Austria slowed down markedly in the second half of 2014

The OeNB property market monitor of April : Residential property price growth in slowed down markedly in the second half of Martin Schneider, Karin Wagner, Walter Waschiczek Residential property price

The OeNB property market monitor of April : Residential property price growth in slowed down markedly in the second half of Martin Schneider, Karin Wagner, Walter Waschiczek Residential property price

The Future and REAL Challenges of Real Estate

The Future and REAL Challenges of Real Estate David Lee Director, Sim Kee Boon Institute for Financial Economics Professor of Quantitative Finance (Practice) Singapore Management University The Future

The Future and REAL Challenges of Real Estate David Lee Director, Sim Kee Boon Institute for Financial Economics Professor of Quantitative Finance (Practice) Singapore Management University The Future

Resilience of national housing systems in times of a credit crunch

Resilience of national housing systems in times of a credit crunch Presentation at the session Global economic crisis and housing policy response Academy of Sciences of the Czech Republic Institute of

Resilience of national housing systems in times of a credit crunch Presentation at the session Global economic crisis and housing policy response Academy of Sciences of the Czech Republic Institute of

What Factors Determine the Volume of Home Sales in Texas?

What Factors Determine the Volume of Home Sales in Texas? Ali Anari Research Economist and Mark G. Dotzour Chief Economist Texas A&M University June 2000 2000, Real Estate Center. All rights reserved.

What Factors Determine the Volume of Home Sales in Texas? Ali Anari Research Economist and Mark G. Dotzour Chief Economist Texas A&M University June 2000 2000, Real Estate Center. All rights reserved.

MODELLING HOUSE PRICES AND HOME OWNERSHIP. Ian Mulheirn and Nishaal Gooroochurn

MODELLING HOUSE PRICES AND HOME OWNERSHIP Ian Mulheirn and Nishaal Gooroochurn NIESR - 1 June 2018 OBJECTIVES Explain the drivers of house prices and home ownership in the UK. Use the model to explain

MODELLING HOUSE PRICES AND HOME OWNERSHIP Ian Mulheirn and Nishaal Gooroochurn NIESR - 1 June 2018 OBJECTIVES Explain the drivers of house prices and home ownership in the UK. Use the model to explain

AGEC 603. Real Estate. Property and Capital Markets

AGEC 603 Property and Capital Markets Real Estate National of buildings, the land built on, and vacant land Value second largest component of wealth Measured both as a flow and a stock Flow value of new

AGEC 603 Property and Capital Markets Real Estate National of buildings, the land built on, and vacant land Value second largest component of wealth Measured both as a flow and a stock Flow value of new

Time Varying Trading Volume and the Economic Impact of the Housing Market

Time Varying Trading Volume and the Economic Impact of the Housing Market Norman Miller University of San Diego Liang Peng 1 University of Colorado at Boulder Mike Sklarz New City Technology First draft:

Time Varying Trading Volume and the Economic Impact of the Housing Market Norman Miller University of San Diego Liang Peng 1 University of Colorado at Boulder Mike Sklarz New City Technology First draft:

Hong Kong Prime Office Monthly Report. October 2011 RESEARCH NON-CORE DISTRICTS LEAD THE MARKET

RESEARCH October 2011 Hong Kong Prime Office Monthly Report NON-CORE DISTRICTS LEAD THE MARKET Business and investment activity slowed in Hong Kong over the past month, on the back of negative economic

RESEARCH October 2011 Hong Kong Prime Office Monthly Report NON-CORE DISTRICTS LEAD THE MARKET Business and investment activity slowed in Hong Kong over the past month, on the back of negative economic

Global Real Estate: Similarities & Differences

Global Real Estate: Similarities & Differences Robin Goodchild International Director & Head of European Strategy 24 th June 2010 How do Real Estate Markets Work? Space Market Property Market Capital Market

Global Real Estate: Similarities & Differences Robin Goodchild International Director & Head of European Strategy 24 th June 2010 How do Real Estate Markets Work? Space Market Property Market Capital Market

Discussion: Understanding the Real Estate Market in China

Discussion: Understanding the Real Estate Market in China Anna Wong Federal Reserve Board of Governors HKMA/PBoC/DRC Conference: China s Real Estate Market and Implications and Economic and Financial Stability

Discussion: Understanding the Real Estate Market in China Anna Wong Federal Reserve Board of Governors HKMA/PBoC/DRC Conference: China s Real Estate Market and Implications and Economic and Financial Stability

Summary of JREI Global Property Value/Rent Indices (No. 10, Apr. 2018)

") May 29, 2018 Japan Real Estate Institute (JREI) JREI-kenkyu-madoguchi@imail.jrei.jp Summary of JREI Global Property Value/Rent Indices (No. 10, Apr. 2018) We are pleased to release a summary of the results

May 29, 2018 Japan Real Estate Institute (JREI) JREI-kenkyu-madoguchi@imail.jrei.jp Summary of JREI Global Property Value/Rent Indices (No. 10, Apr. 2018) We are pleased to release a summary of the results

OUR GLOBAL FOOTPRINT INDEPENDENT, INTERNATIONAL, COMMERCIAL, RESIDENTIAL. Locally expert, globally connected.

OUR GLOBAL FOOTPRINT INDEPENDENT, INTERNATIONAL, COMMERCIAL, RESIDENTIAL. Locally expert, globally connected. ABOUT THE GROUP THERE S A HUMAN ELEMENT IN THE WORLD OF PROPERTY THAT IS TOO EASILY OVERLOOKED.

OUR GLOBAL FOOTPRINT INDEPENDENT, INTERNATIONAL, COMMERCIAL, RESIDENTIAL. Locally expert, globally connected. ABOUT THE GROUP THERE S A HUMAN ELEMENT IN THE WORLD OF PROPERTY THAT IS TOO EASILY OVERLOOKED.

Housing Price Prediction Using Search Engine Query Data. Qian Dong Research Institute of Statistical Sciences of NBS Oct. 29, 2014

Housing Price Prediction Using Search Engine Query Data Qian Dong Research Institute of Statistical Sciences of NBS Oct. 29, 2014 Outline Background Analysis of Theoretical Framework Data Description The

Housing Price Prediction Using Search Engine Query Data Qian Dong Research Institute of Statistical Sciences of NBS Oct. 29, 2014 Outline Background Analysis of Theoretical Framework Data Description The

How Severe is the Housing Shortage in Hong Kong?

(Reprinted from HKCER Letters, Vol. 42, January, 1997) How Severe is the Housing Shortage in Hong Kong? Y.C. Richard Wong Introduction Rising property prices in Hong Kong have been of great public concern

(Reprinted from HKCER Letters, Vol. 42, January, 1997) How Severe is the Housing Shortage in Hong Kong? Y.C. Richard Wong Introduction Rising property prices in Hong Kong have been of great public concern

How should we measure residential property prices to inform policy makers? 1

IFC Satellite meeting at the ISI Regional Statistics Conference on Is the household sector in Asia overleveraged: what do the data say? Kuala Lumpur, Malaysia, 15 November 2014 How should we measure residential

IFC Satellite meeting at the ISI Regional Statistics Conference on Is the household sector in Asia overleveraged: what do the data say? Kuala Lumpur, Malaysia, 15 November 2014 How should we measure residential

THE EFFECTS OF MACROPRUDENTIAL POLICY ON HOUSING MARKET: EVIDENCE FROM 30 PROVINCES IN CHINA

THE EFFECTS OF MACROPRUDENTIAL POLICY ON HOUSING MARKET: EVIDENCE FROM 30 PROVINCES IN CHINA LINA WANG Master Student of Faculty of Economics, Chulalongkron University, Bangkok, Thailand E-mail: nanathai1023@gmail.com

THE EFFECTS OF MACROPRUDENTIAL POLICY ON HOUSING MARKET: EVIDENCE FROM 30 PROVINCES IN CHINA LINA WANG Master Student of Faculty of Economics, Chulalongkron University, Bangkok, Thailand E-mail: nanathai1023@gmail.com

Dynamic Impact of Interest Rate Policy on Real Estate Market

Dynamic Impact of Interest Rate Policy on Real Estate Market Jianghong Zhang College of Economics and Management, Sichuan Agriculture University 211 Huimin Road, Wenjiang District, Chengdu 61113, China

Dynamic Impact of Interest Rate Policy on Real Estate Market Jianghong Zhang College of Economics and Management, Sichuan Agriculture University 211 Huimin Road, Wenjiang District, Chengdu 61113, China

Regional house prices cycles in the UK : a Markov switching Var. Rosen Azad Chowdhury Duncan Maclennan

Regional house prices cycles in the UK 1978-2012: a Markov switching Var Rosen Azad Chowdhury Duncan Maclennan Ripple effects, house price convergence and house price cycles The Ripple effect states that

Regional house prices cycles in the UK 1978-2012: a Markov switching Var Rosen Azad Chowdhury Duncan Maclennan Ripple effects, house price convergence and house price cycles The Ripple effect states that

Investor Update Q results. Maëlys Castella October 22, 2015

Investor Update Q3 2015 results Maëlys Castella October 22, 2015 Agenda Highlights Operational review Financial review Conclusion Questions 2 Q3 2015; Another quarter of improved performance Revenue million

Investor Update Q3 2015 results Maëlys Castella October 22, 2015 Agenda Highlights Operational review Financial review Conclusion Questions 2 Q3 2015; Another quarter of improved performance Revenue million

Released: June Commentary 2. The Numbers That Drive Real Estate 3. Recent Government Action 9. Topics for Home Buyers, Sellers, and Owners 11

Released: June 2011 Commentary 2 The Numbers That Drive Real Estate 3 Recent Government Action 9 Topics for Home Buyers, Sellers, and Owners 11 Brought to you by: KW Research Commentary The U.S. housing

Released: June 2011 Commentary 2 The Numbers That Drive Real Estate 3 Recent Government Action 9 Topics for Home Buyers, Sellers, and Owners 11 Brought to you by: KW Research Commentary The U.S. housing

HONG KONG PRIME OFFICE Monthly Report

RESEARCH February 2011 HONG KONG PRIME OFFICE Monthly Report RENTS TO SURPASS 2008 PEAKS BY YEAR-END Players in Hong Kong's office leasing market started the game of 'musical chairs' again at the beginning

RESEARCH February 2011 HONG KONG PRIME OFFICE Monthly Report RENTS TO SURPASS 2008 PEAKS BY YEAR-END Players in Hong Kong's office leasing market started the game of 'musical chairs' again at the beginning

House Prices and City Revenues

House Prices and City Revenues William Doerner & Keith Ihlanfeldt Florida State University Prepared for The Crisis in Real Estate and its Impact in Public Finance Federal Reserve Bank of Atlanta September

House Prices and City Revenues William Doerner & Keith Ihlanfeldt Florida State University Prepared for The Crisis in Real Estate and its Impact in Public Finance Federal Reserve Bank of Atlanta September

REAL ESTATE SENTIMENT INDEX 2 nd Quarter 2018

About Real Estate Sentiment Index (RESI) The Real Estate Sentiment Index (RESI) is jointly developed by the Real Estate Developers Association of Singapore (REDAS) and the Department of Real Estate (DRE),

About Real Estate Sentiment Index (RESI) The Real Estate Sentiment Index (RESI) is jointly developed by the Real Estate Developers Association of Singapore (REDAS) and the Department of Real Estate (DRE),

DETERMINANTS OF HOUSING PRICES IN METROPOLITAN CHINA: EVIDENCE FROM BEIJING AND SHANGHAI FROM 2005 to Liang Zhong

DETERMINANTS OF HOUSING PRICES IN METROPOLITAN CHINA: EVIDENCE FROM BEIJING AND SHANGHAI FROM 2005 to 2012 by Liang Zhong A dissertation submitted to the Faculty of the University of Delaware in partial

DETERMINANTS OF HOUSING PRICES IN METROPOLITAN CHINA: EVIDENCE FROM BEIJING AND SHANGHAI FROM 2005 to 2012 by Liang Zhong A dissertation submitted to the Faculty of the University of Delaware in partial

How Did Foreclosures Affect Property Values in Georgia School Districts?

Tulane Economics Working Paper Series How Did Foreclosures Affect Property Values in Georgia School Districts? James Alm Department of Economics Tulane University New Orleans, LA jalm@tulane.edu Robert

Tulane Economics Working Paper Series How Did Foreclosures Affect Property Values in Georgia School Districts? James Alm Department of Economics Tulane University New Orleans, LA jalm@tulane.edu Robert

How to Mitigate the Risk of Moral Hazard?

How to Mitigate the Risk of Moral Hazard? Tito Boeri Università Bocconi, Fondazione Rodolfo Debenedetti October, 11st 2013, Bertelsmann Stiftung, Brussels Boeri (Bocconi, FRDB) Let s think off the ground

How to Mitigate the Risk of Moral Hazard? Tito Boeri Università Bocconi, Fondazione Rodolfo Debenedetti October, 11st 2013, Bertelsmann Stiftung, Brussels Boeri (Bocconi, FRDB) Let s think off the ground

Real Estate Booms and Endogenous Productivity Growth

Real Estate Booms and Endogenous Productivity Growth author: Yu Shi (IMF) discussant: Arpit Gupta (NYU Stern) April 11, 2018 IMF Macro-Financial Research Conference 2018 Summary Key Argument: Real Estate

Real Estate Booms and Endogenous Productivity Growth author: Yu Shi (IMF) discussant: Arpit Gupta (NYU Stern) April 11, 2018 IMF Macro-Financial Research Conference 2018 Summary Key Argument: Real Estate

Presented at the FIG Congress 2018, May 6-11, 2018 in Istanbul, Turkey

Presented at the FIG Congress 2018, May 6-11, 2018 in Istanbul, Turkey 5 Bibliometric Analysis of Articles Presented Under Commission 7: A Case of the 25th Fig Congress in Malaysia in 2014 Zeynel Abidin

Presented at the FIG Congress 2018, May 6-11, 2018 in Istanbul, Turkey 5 Bibliometric Analysis of Articles Presented Under Commission 7: A Case of the 25th Fig Congress in Malaysia in 2014 Zeynel Abidin

Relationship between Proportion of Private Housing Completions, Amount of Private Housing Completions, and Property Prices in Hong Kong

Relationship between Proportion of Private Housing Completions, Amount of Private Housing Completions, and Property Prices in Hong Kong Bauhinia Foundation Research Centre May 2014 Background Tackling

Relationship between Proportion of Private Housing Completions, Amount of Private Housing Completions, and Property Prices in Hong Kong Bauhinia Foundation Research Centre May 2014 Background Tackling

This PDF is a selection from a published volume from the National Bureau of Economic Research

This PDF is a selection from a published volume from the National Bureau of Economic Research Volume Title: NBER Macroeconomics Annual 2015, Volume 30 Volume Author/Editor: Martin Eichenbaum and Jonathan

This PDF is a selection from a published volume from the National Bureau of Economic Research Volume Title: NBER Macroeconomics Annual 2015, Volume 30 Volume Author/Editor: Martin Eichenbaum and Jonathan

Causes & Consequences of Evictions in Britain October 2016

I. INTRODUCTION Causes & Consequences of Evictions in Britain October 2016 Across England, the private rental sector has become more expensive and less secure. Tenants pay an average of 47% of their net

I. INTRODUCTION Causes & Consequences of Evictions in Britain October 2016 Across England, the private rental sector has become more expensive and less secure. Tenants pay an average of 47% of their net

Student Property Global Contacts. Connecting people & property, perfectly.

Student Property Global Contacts. Connecting people & property, perfectly. Global Contacts Europe Asia PAC James Pullan Partner, Department Head +44 207 861 5422 james.pullan@knightfrank.com Emily Fell

Student Property Global Contacts. Connecting people & property, perfectly. Global Contacts Europe Asia PAC James Pullan Partner, Department Head +44 207 861 5422 james.pullan@knightfrank.com Emily Fell

Determinants of residential property valuation

Determinants of residential property valuation Author: Ioana Cocos Coordinator: Prof. Univ. Dr. Ana-Maria Ciobanu Abstract: The aim of this thesis is to understand and know in depth the factors that cause

Determinants of residential property valuation Author: Ioana Cocos Coordinator: Prof. Univ. Dr. Ana-Maria Ciobanu Abstract: The aim of this thesis is to understand and know in depth the factors that cause

Linkages Between Chinese and Indian Economies and American Real Estate Markets

Linkages Between Chinese and Indian Economies and American Real Estate Markets Like everything else, the real estate market is affected by global forces. ANTHONY DOWNS IN THE 2004 presidential campaign,

Linkages Between Chinese and Indian Economies and American Real Estate Markets Like everything else, the real estate market is affected by global forces. ANTHONY DOWNS IN THE 2004 presidential campaign,

Stockton Unified School District Instructional Guide for Economics Traditional Schedule

Instructional Window and Testing Dates UNIT 1 Intro to Economics Ch. 1 Ch. 2 Ch. 3 4 weeks Teacher choice Content Standards and Big Ideas Orientation, setting expectations, and classroom organization.

Instructional Window and Testing Dates UNIT 1 Intro to Economics Ch. 1 Ch. 2 Ch. 3 4 weeks Teacher choice Content Standards and Big Ideas Orientation, setting expectations, and classroom organization.

86 years in the making Caspar G Haas 1922 Sales Prices as a Basis for Estimating Farmland Value

2 Our Journey Begins 86 years in the making Caspar G Haas 1922 Sales Prices as a Basis for Estimating Farmland Value Starting at the beginning. Mass Appraisal and Single Property Appraisal Appraisal

2 Our Journey Begins 86 years in the making Caspar G Haas 1922 Sales Prices as a Basis for Estimating Farmland Value Starting at the beginning. Mass Appraisal and Single Property Appraisal Appraisal

'A study of the relationship between changes in housing values and variations in macroeconomic factors. A Research Report.

'A study of the relationship between changes in housing values and variations in macroeconomic factors. A Research Report presented to the Graduate School of Business Leadership University of South Africa.

'A study of the relationship between changes in housing values and variations in macroeconomic factors. A Research Report presented to the Graduate School of Business Leadership University of South Africa.

The Predictability of Real Estate Capitalization Rates

The Predictability of Real Estate Capitalization Rates by Vinod Chandrashekaran Manager, Equity Risk Model Research BARRA Inc. 2100 Milvia Street Berkeley, California 94704 phone: 510-649-4689 / fax: 510-548-1709

The Predictability of Real Estate Capitalization Rates by Vinod Chandrashekaran Manager, Equity Risk Model Research BARRA Inc. 2100 Milvia Street Berkeley, California 94704 phone: 510-649-4689 / fax: 510-548-1709

Change on the Horizon:

Change on the Horizon: An overview of the economy and its impact on commercial real estate By Elliot M. Shirwo, Founder and Principal BridgeCore Capital, Inc. Commercial real estate is intrinsically linked

Change on the Horizon: An overview of the economy and its impact on commercial real estate By Elliot M. Shirwo, Founder and Principal BridgeCore Capital, Inc. Commercial real estate is intrinsically linked

ECONOMIC COMMENTARY. Housing Recovery: How Far Have We Come? Daniel Hartley and Kyle Fee

ECONOMIC COMMENTARY Number 13-11 October, 13 Housing Recovery: How Far Have We Come? Daniel Hartley and Kyle Fee Four years into the economic recovery, housing markets have fi nally started to improve.

ECONOMIC COMMENTARY Number 13-11 October, 13 Housing Recovery: How Far Have We Come? Daniel Hartley and Kyle Fee Four years into the economic recovery, housing markets have fi nally started to improve.

IS IRELAND 25 YEARS INTO A 100-YEAR HOUSING CRISIS?

IS IRELAND 25 YEARS INTO A 100-YEAR HOUSING CRISIS? Ronan Lyons, Department of Economics, Trinity College Dublin Dublin Economics Workshop Annual Conference Wexford, September 2017 DEW Annual Conference,

IS IRELAND 25 YEARS INTO A 100-YEAR HOUSING CRISIS? Ronan Lyons, Department of Economics, Trinity College Dublin Dublin Economics Workshop Annual Conference Wexford, September 2017 DEW Annual Conference,

Asian Journal of Empirical Research

2016 Asian Economic and Social Society. All rights reserved ISSN (P): 2306-983X, ISSN (E): 2224-4425 Volume 6, Issue 3 pp. 77-83 Asian Journal of Empirical Research http://www.aessweb.com/journals/5004

2016 Asian Economic and Social Society. All rights reserved ISSN (P): 2306-983X, ISSN (E): 2224-4425 Volume 6, Issue 3 pp. 77-83 Asian Journal of Empirical Research http://www.aessweb.com/journals/5004

Australian Dwelling Prices and Tobin's q

Australian Dwelling Prices and Tobin's q Presentation to UNSW Business School Real Estate Symposium Peter Jolly, Global Head of Research September 2016 Tobin's q q = Market Value for an asset Replacement

Australian Dwelling Prices and Tobin's q Presentation to UNSW Business School Real Estate Symposium Peter Jolly, Global Head of Research September 2016 Tobin's q q = Market Value for an asset Replacement

CPI Growth (%)

") INFLATION, INFLATION, INFLATION - ARE REITS THE ANSWER? Steven Burton, Managing Director, ING Clarion Real Estate Securities & Indraneel Karlekar, Head of Global Research and Strategy, ING Clarion Real

INFLATION, INFLATION, INFLATION - ARE REITS THE ANSWER? Steven Burton, Managing Director, ING Clarion Real Estate Securities & Indraneel Karlekar, Head of Global Research and Strategy, ING Clarion Real

Hong Kong Monetary Authority

Hong Kong Monetary Authority Research Memorandum 1/22 3 July 22 WHAT DRIVES PROPERTY PRICES IN HONG KONG? Key Points: This paper studies the determinants of property prices in Hong Kong. The estimates

Hong Kong Monetary Authority Research Memorandum 1/22 3 July 22 WHAT DRIVES PROPERTY PRICES IN HONG KONG? Key Points: This paper studies the determinants of property prices in Hong Kong. The estimates

HOUSING SUPPLY IN OECD COUNTRIES: RESPONSIVENESS AND ECONOMIC CONSEQUENCES

HOUSING SUPPLY IN OECD COUNTRIES: RESPONSIVENESS AND ECONOMIC CONSEQUENCES Christophe André OECD Economics Department Workshop Macroeconomic Implications of Housing Markets 30 November 2016 European Commission,

HOUSING SUPPLY IN OECD COUNTRIES: RESPONSIVENESS AND ECONOMIC CONSEQUENCES Christophe André OECD Economics Department Workshop Macroeconomic Implications of Housing Markets 30 November 2016 European Commission,

The Texas Office Market:

The Texas Office Market: Through the Eyes of the Sublease Market February 2017 In Millions The Texas Office Market An office market can be analyzed from many different viewpoints, but the number one rule

The Texas Office Market: Through the Eyes of the Sublease Market February 2017 In Millions The Texas Office Market An office market can be analyzed from many different viewpoints, but the number one rule

NATIONAL ASSOCIATION of REALTORS RESEARCH DIVISION. Prepared for Florida REALTORS

NATIONAL ASSOCIATION of REALTORS RESEARCH DIVISION Prepared for Florida REALTORS NATIONAL ASSOCIATION OF REALTORS RESEARCH DIVISION Page 1 Page 3 Page 4 Page 6 Page 7 Page 8 Page 9 Page 10 Page 11 Page

NATIONAL ASSOCIATION of REALTORS RESEARCH DIVISION Prepared for Florida REALTORS NATIONAL ASSOCIATION OF REALTORS RESEARCH DIVISION Page 1 Page 3 Page 4 Page 6 Page 7 Page 8 Page 9 Page 10 Page 11 Page

DEMAND FR HOUSING IN PROVINCE OF SINDH (PAKISTAN)

") 19 Pakistan Economic and Social Review Volume XL, No. 1 (Summer 2002), pp. 19-34 DEMAND FR HOUSING IN PROVINCE OF SINDH (PAKISTAN) NUZHAT AHMAD, SHAFI AHMAD and SHAUKAT ALI* Abstract. The paper is an analysis

19 Pakistan Economic and Social Review Volume XL, No. 1 (Summer 2002), pp. 19-34 DEMAND FR HOUSING IN PROVINCE OF SINDH (PAKISTAN) NUZHAT AHMAD, SHAFI AHMAD and SHAUKAT ALI* Abstract. The paper is an analysis

The State of the Commercial Real Estate Industry: Mid-Year 2011 Retail Review & Outlook

The State of the Commercial Real Estate Industry: Mid-Year 2011 Retail Review & Outlook Copyright 2011 CoStar Realty Information, Inc. No reproduction or distribution without permission. The following

The State of the Commercial Real Estate Industry: Mid-Year 2011 Retail Review & Outlook Copyright 2011 CoStar Realty Information, Inc. No reproduction or distribution without permission. The following

Rethinking Housing Affordability: Speculative Boom or Structural Burden?

Rethinking Housing Affordability: Speculative Boom or Structural Burden? Terry Rawnsley Affordable Housing Australasia Melbourne 14 th 16 th November 2016 Overview Housing is a multidimensional topic (social,

Rethinking Housing Affordability: Speculative Boom or Structural Burden? Terry Rawnsley Affordable Housing Australasia Melbourne 14 th 16 th November 2016 Overview Housing is a multidimensional topic (social,

GLOBAL ECONOMY, REAL ESTATE MARKETS & THE CYCLE

GLOBAL ECONOMY, REAL ESTATE MARKETS & THE CYCLE Professor Richard Barkham, PhD MRICS CRE, Global Chief Economist April 2016 HOW CLOSE ARE WE TO THE END OF THIS CYCLE? Jan-70 Jan-71 Jan-72 Jan-73 Jan-74

GLOBAL ECONOMY, REAL ESTATE MARKETS & THE CYCLE Professor Richard Barkham, PhD MRICS CRE, Global Chief Economist April 2016 HOW CLOSE ARE WE TO THE END OF THIS CYCLE? Jan-70 Jan-71 Jan-72 Jan-73 Jan-74

Meeting of Group of Experts on CPI 30 May 1 June 2012

Meeting of Group of Experts on CPI 30 May 1 June 2012 Content Introduction and Objective of study Data Source and Coverage Methodology Results Limitations of the study and recommendation Introduction House

Meeting of Group of Experts on CPI 30 May 1 June 2012 Content Introduction and Objective of study Data Source and Coverage Methodology Results Limitations of the study and recommendation Introduction House

Evaluating risks in the French office market with new sources of data on commercial property prices 1

IFC-National Bank of Belgium Workshop on "Data needs and Statistics compilation for macroprudential analysis" Brussels, Belgium, 18-19 May 2017 Evaluating risks in the French office market with new sources

IFC-National Bank of Belgium Workshop on "Data needs and Statistics compilation for macroprudential analysis" Brussels, Belgium, 18-19 May 2017 Evaluating risks in the French office market with new sources

86M 4.2% Executive Summary. Valuation Whitepaper. The purposes of this paper are threefold: At a Glance. Median absolute prediction error (MdAPE)

") Executive Summary HouseCanary is developing the most accurate, most comprehensive valuations for residential real estate. Accurate valuations are the result of combining the best data with the best models.

Executive Summary HouseCanary is developing the most accurate, most comprehensive valuations for residential real estate. Accurate valuations are the result of combining the best data with the best models.

AUSTRALIAN HOUSING: HIPSTER BREAKFAST CHOICES OR A NATION OF SPECULATING SPIVS? Housing is a human right

AUSTRALIAN HOUSING: HIPSTER BREAKFAST CHOICES OR A NATION OF SPECULATING SPIVS? A SERIES OF QUESTIONS Is Australia in a housing bubble that will inevitably burst? What drives housing inflation in Australia?

AUSTRALIAN HOUSING: HIPSTER BREAKFAST CHOICES OR A NATION OF SPECULATING SPIVS? A SERIES OF QUESTIONS Is Australia in a housing bubble that will inevitably burst? What drives housing inflation in Australia?

ECONOMIC PERSPECTIVES

June 2018 ECONOMIC PERSPECTIVES HOME PRICE GAINS DEPEND ON LOCATION AND INFLATION; TOO EARLY TO CALL A TOP IN HOME VALUES Authored by Brian Jones, FHLBNY Financial Economist HIGHLIGHTS:» Home Prices Have

June 2018 ECONOMIC PERSPECTIVES HOME PRICE GAINS DEPEND ON LOCATION AND INFLATION; TOO EARLY TO CALL A TOP IN HOME VALUES Authored by Brian Jones, FHLBNY Financial Economist HIGHLIGHTS:» Home Prices Have

III. RECENT HOUSE PRICE DEVELOPMENTS: THE ROLE OF FUNDAMENTALS

III. RECENT HOUSE PRICE DEVELOPMENTS: THE ROLE OF FUNDAMENTALS INTRODUCTION AND SUMMARY Real house prices increased unusually rapidly in recent years This paper examines... several aspects of the current

III. RECENT HOUSE PRICE DEVELOPMENTS: THE ROLE OF FUNDAMENTALS INTRODUCTION AND SUMMARY Real house prices increased unusually rapidly in recent years This paper examines... several aspects of the current

Volume 35, Issue 1. Real Interest Rate and House Prices in Malaysia: An Empirical Study

Volume 35, Issue 1 Real Interest Rate and House Prices in Malaysia: An Empirical Study Tuck Cheong Tang Department of Economics, Faculty of Economics and Administration, University of Malaya Pei Pei Tan

Volume 35, Issue 1 Real Interest Rate and House Prices in Malaysia: An Empirical Study Tuck Cheong Tang Department of Economics, Faculty of Economics and Administration, University of Malaya Pei Pei Tan

Property. Mashreq. Economic Overview. Wealth Gauge. Exceptional. Individual.

Exceptional. Individual. Volume 14 October Economic Overview United Arab Emirates has continued to benefit its safe-heaven status. The economic recovery has been strong which is well supported by tourism,

Exceptional. Individual. Volume 14 October Economic Overview United Arab Emirates has continued to benefit its safe-heaven status. The economic recovery has been strong which is well supported by tourism,

House Prices in Denmark and Sweden *

House Prices in Denmark and Sweden * By U. Michael Bergman Department of Economics, University of Copenhagen Øster Farimagsgade 5, Building 26, DK-1353 Copenhagen K, Denmark Michael.Bergman@econ.ku.dk

House Prices in Denmark and Sweden * By U. Michael Bergman Department of Economics, University of Copenhagen Øster Farimagsgade 5, Building 26, DK-1353 Copenhagen K, Denmark Michael.Bergman@econ.ku.dk

Hong Kong Prime Office Monthly Report. August 2011 RESEARCH LEASING ACTIVITY ROBUST DESPITE VOLITILITY

RESEARCH August 2011 Hong Kong Prime Office Monthly Report LEASING ACTIVITY ROBUST DESPITE VOLITILITY Sentiment in the office sales market weakened over the past month. The slowdown was triggered by a

RESEARCH August 2011 Hong Kong Prime Office Monthly Report LEASING ACTIVITY ROBUST DESPITE VOLITILITY Sentiment in the office sales market weakened over the past month. The slowdown was triggered by a

AN EMPIRICAL ANALYSIS OF THE NORWEGIAN HOUSING MARKET

AN EMPIRICAL ANALYSIS OF THE NORWEGIAN HOUSING MARKET Are there indications pointing towards a housing bubble in the Norwegian market? Written by Karen Høvring Maiken Ludt Parmo Master s thesis, May 2016

AN EMPIRICAL ANALYSIS OF THE NORWEGIAN HOUSING MARKET Are there indications pointing towards a housing bubble in the Norwegian market? Written by Karen Høvring Maiken Ludt Parmo Master s thesis, May 2016

CANADA ECONOMICS FOCUS

CANADA ECONOMICS FOCUS House prices likely to fall for several years 3 rd Feb. 211 The recent housing boom has resulted in the largest rises in house prices ever seen in Canada, which have been similar

CANADA ECONOMICS FOCUS House prices likely to fall for several years 3 rd Feb. 211 The recent housing boom has resulted in the largest rises in house prices ever seen in Canada, which have been similar

Office market report

research Q2 2014 Office market report highlights As of Q2 2014, there were approximately 4,555,271 square metres of office space in Bangkok. 87,898 square metres of new supply filled in 2014 (The Nine

research Q2 2014 Office market report highlights As of Q2 2014, there were approximately 4,555,271 square metres of office space in Bangkok. 87,898 square metres of new supply filled in 2014 (The Nine

A Rational Explanation for Boom-and-Bust Price Patterns in Real Estate Markets

257 Rational Explanation for Boom-and-Bust Price Patterns INTERNATIONAL REAL ESTATE REVIEW 2011 Vol. 14 No. 3: pp. 257 282 A Rational Explanation for Boom-and-Bust Price Patterns in Real Estate Markets

257 Rational Explanation for Boom-and-Bust Price Patterns INTERNATIONAL REAL ESTATE REVIEW 2011 Vol. 14 No. 3: pp. 257 282 A Rational Explanation for Boom-and-Bust Price Patterns in Real Estate Markets

House Prices and Economic Growth

J Real Estate Finan Econ (2011) 42:522 541 DOI 10.1007/s11146-009-9197-8 House Prices and Economic Growth Norman Miller & Liang Peng & Michael Sklarz Published online: 11 July 2009 # Springer Science +

J Real Estate Finan Econ (2011) 42:522 541 DOI 10.1007/s11146-009-9197-8 House Prices and Economic Growth Norman Miller & Liang Peng & Michael Sklarz Published online: 11 July 2009 # Springer Science +

The Effects of Monetary Policy on Real Estate Price Dynamics: An Asset Substitutability Perspective

The Effects of Monetary Policy on Real Estate Price Dynamics: An Asset Substitutability Perspective Hai-Feng Hu Associate Professor Department of Business Administration, Wenzao Ursuline College of Languages,

The Effects of Monetary Policy on Real Estate Price Dynamics: An Asset Substitutability Perspective Hai-Feng Hu Associate Professor Department of Business Administration, Wenzao Ursuline College of Languages,

Are Asia-Pacific Housing Prices Too High for Comfort?

Are Asia-Pacific Housing Prices Too High for Comfort? Bank of Thailand Workshop Bangkok, Thailand Tientip Subhanij* Date 23 November 2007 * Joint research project of the BOT (Tientip Subhanij), BSP (Eloisa

Are Asia-Pacific Housing Prices Too High for Comfort? Bank of Thailand Workshop Bangkok, Thailand Tientip Subhanij* Date 23 November 2007 * Joint research project of the BOT (Tientip Subhanij), BSP (Eloisa

A statistical system for. Residential Property Price Indices. David Fenwick

A statistical system for Residential Property Price Indices Eurostat IAOS IFC Conference on Residential Property Price Indices Hosted by the Bank for International Settlements 11-12 November 2009, Basle

A statistical system for Residential Property Price Indices Eurostat IAOS IFC Conference on Residential Property Price Indices Hosted by the Bank for International Settlements 11-12 November 2009, Basle