APPRAISAL REPORT OF THE STATE OF SOUTH DAKOTA PROPERTY A ACRE SITE LOCATED AT 1501 US HIGHWAY 14 BYPASS BROOKINGS, SOUTH DAKOTA

|

|

|

- Samson Bennett

- 5 years ago

- Views:

Transcription

1 APPRAISAL REPORT OF THE STATE OF SOUTH DAKOTA PROPERTY A ACRE SITE LOCATED AT 1501 US HIGHWAY 14 BYPASS BROOKINGS, SOUTH DAKOTA CONTROL NUMBER CLIENT SOUTH DAKOTA OFFICE OF SCHOOL AND PUBLIC LANDS ATTN: MR. RYAN BRUNNER 500 EAST CAPITOL AVENUE PIERRE, SOUTH DAKOTA DATE OF VALUE NOVEMBER 20, 2018 BY SHAYKETT APPRAISAL COMPANY, INC. 601 NORTH MINNESOTA AVENUE, SUITE 100 SIOUX FALLS, SOUTH DAKOTA (605)

2 Shaykett Appraisal Company, Inc. 601 N. Minnesota Avenue, Suite 100 Sioux Falls, South Dakota Phone (605) Fax (605) Travis E. Shaykett Steven C. Shaykett, MAI George P. Stavrenos State Certified General Appraiser State Certified General Appraiser State Certified General Appraiser December 10, 2018 South Dakota Office of School and Public Lands Attn: Mr. Ryan Brunner 500 East Capitol Avenue Pierre, South Dakota RE: Appraisal Report of the State of South Dakota Property A Acre Site Located At 1501 US Highway 14 Bypass Brookings, South Dakota Control # Dear Mr. Brunner: In accordance with your request, we have prepared an Appraisal Report of the above referenced property. Purpose of the appraisal is to estimate the as is fee simple estate market value of the subject property as of November 20, Intended use of the appraisal is to assist in the disposal of the property. After viewing the subject property on November 20, 2018, as well as completing research and analysis necessary for the appraisal of the property, it is our opinion that the as is fee simple estate market value of the subject property as of November 20, 2018 was $1,860,000. ONE MILLION EIGHT HUNDRED SIXTY THOUSAND DOLLARS Analysis of the subject property and the data on which the appraisers opinions are based are set forth in the following report. Appraisal has been made in conformity with generally accepted appraisal practices in compliance with the Uniform Standards of Professional Appraisal Practice (USPAP). Appraisal is subject to all assumptions, limiting conditions, and other special limiting conditions as set forth in this report, or as specifically presented below, if any.

3

4 LIMITING CONDITIONS This appraisal report and the letter of transmittal and the certification of value are made expressly subject to the following limiting conditions, and any special limiting conditions contained elsewhere which are incorporated herein by reference. 1. This appraisal is subject to the accuracy of the legal description furnished the appraisers; however, we can assume no responsibility for matters legal in nature, nor can we render an opinion as to the title. 2. The distribution of the total valuation between land and improvements applied only under the existing program of utilization. The separate valuations for land and improvements must not be used in conjunction with any other appraisal and are invalid if so used. 3. We believe the information which was furnished to us by others is reliable, but we assume no responsibility for its accuracy. The comparable data relied upon in this appraisal is believed to be from reliable sources. However, it was not possible to view the comparables completely and it was necessary to rely on the information furnished by others as to said data. Therefore, the value conclusions are subject to the correctness of said data. 4. Unless otherwise indicated, all existing liens and encumbrances have been disregarded and the property is appraised as though it were free and clear of any such impediments that might affect value. The property is appraised as though it were under responsible ownership and competent management. 5. Subsurface rights (minerals and oil) were considered as they may contribute to the value of the surface rights unless otherwise indicated. 6. All furnishings and equipment, except those specifically indicated, have been disregarded by the appraisers. Only the real estate has been considered. 7. The appraisers have viewed, as far as possible, by observation, the land and the improvements thereon and have reported damage, if any, by termites, dry rot, wet rot, or other infestations as a matter of information. However, it was not possible to personally observe conditions beneath the soil or hidden structural components within the improvements. Viewing by the appraisers does not guarantee the lack of the presence of any hazardous materials, gases, or other materials which could be considered to pollute the environs of the subject property. Therefore, no representations are made herein as to these matters and unless specifically considered in the report, our value estimate is subject to any such conditions that could cause a loss in value. 8. Any sketches in this report are included to assist the reader in visualizing the property. We have made no survey of the property and assume no responsibility in connection with such matters.

5 LIMITING CONDITIONS 9. We are not required to give testimony or to appear in court by reason of this appraisal with reference to the property in question unless arrangements have been previously made therefore. 10. Possession of this report or a copy thereof does not carry with it the right of publication. Neither all nor any part of the contents of this report shall be conveyed to the public through advertising, public relations, news, sales or other media, nor for any purpose, without the written consent and approval of the appraisers, particularly as to valuation conclusions, the identity of the appraisers or firm with which they are connected, or any reference to the Appraisal Institute or to the MAI designation. 11. It is assumed that there is full compliance with all applicable federal, state and local environmental regulations and laws unless non-compliance is stated, defined and considered in the appraisal report. 12. The appraisers are not aware of the presence of soil contamination on the subject property, unless otherwise noted in this appraisal report. The effect upon market value, due to contamination was not considered in this appraisal, unless otherwise stated. 13. The appraisers are not aware of the presence of asbestos or other toxic contaminants in the building(s), unless otherwise noted in this report. The effect upon market value, due to contamination was not considered in this appraisal, unless otherwise stated. 14. Unless otherwise stated in this report, the existence of hazardous material, which may or may not be present on the property, was not observed by the appraisers. The appraisers have no knowledge of the existence of such materials on or in the property. The appraisers, however, are not qualified to detect such substances. The value estimate is predicated on the assumption that there is no such material on or in the property that would cause a loss in value. No responsibility is assumed for any such conditions, or for any expertise or engineering knowledge required to discover them. The client is urged to retain an expert in this field, if desired. 15. The appraisal is subject to any proposed improvements or additions being completed as set forth in the plans, specification, and representations referred to in the report, and all work being performed in a good and workmanlike manner. The appraisal is further subject to the proposed improvements or additions being constructed in accordance with the regulations of the local, county, and state authorities. The plans, specifications, and representations referred to are an integral part of the appraisal report when new construction or additions, renovation, refurbishing, or remodeling applies.

6 LIMITING CONDITIONS 16. The limit of liability of the appraisers or Shaykett Appraisal Company, Inc. is limited to the client only. Further there is no accountability, obligation or liability to any third party. If this report is placed in the hands of anyone other than the client, the client shall make such party aware of all limiting conditions and assumptions of this assignment. The appraisers are also in no way responsible for the costs to correct any physical, economic, legal or any other deficiencies of the property. In the case of any third party actions brought against the client, the client will hold the appraisers completely harmless. 17. The Americans with Disabilities Act ("ADA") became effective January 26, The appraisers have not made a specific compliance survey and analysis of this property to determine whether or not it is in conformity with the various detailed requirements of the ADA. It is possible that a compliance survey of the property, together with a detailed analysis of the requirements of the ADA, could reveal that the property is not in compliance with one or more of the requirements of the Act. If so, this fact could have a negative effect upon the value of the property. Since the appraisers have no direct evidence relating to this issue, possible noncompliance with the requirements of ADA in estimating the value of the property has not been considered. 18. Provision of an Insurable Value by the appraisers does not change the intended user or the intended purpose of the appraisal. The appraisers assume no liability for the Insurable Value estimate provided and do not guarantee that any estimate or opinion will result in the subject property being fully insured for any possible loss that may be sustained. The appraisers recommend that an insurance professional be consulted. The Insurable Value estimate may not be a reliable indication of replacement or reproduction cost for any date other than the effective date of this appraisal due to changing costs of labor and materials and due to changing building codes and governmental regulations and requirements.

7

8

9 SUMMARY OF IMPORTANT FACTS AND CONCLUSIONS Location: 1501 US Highway 14 Bypass Brookings, South Dakota Latitude & Longitude: Approximate Center of Property (Decimal Degrees) , Owner of Record: Property Rights Appraised: Land Area: Description of the Property: Zoning: State of South Dakota Fee Simple Estate Acres The property is predominately unimproved agricultural land, used by South Dakota State University for fruit tree research and various other agricultural research throughout the past twenty plus years. Improvements consist of one cold storage building and several other older storage buildings. Agricultural District, A Effective Date of Value: November 20, 2018 Highest and Best Use: Subdivision development ****** VALUATION SUMMARY ****** Fee Simple Estate Market Value: Indicated by the Cost Approach N/A Income Capitalization Approach N/A Sales Comparison Approach $1,860,000 Final Estimate of Market Value: $1,860,000

10 TABLE OF CONTENTS LETTER OF TRANSMITTAL LIMITING CONDITIONS APPRAISER CERTIFICATIONS SUMMARY OF IMPORTANT FACTS AND CONCLUSIONS IDENTIFICATION OF THE PROPERTY 1 CLIENT AND INTENDED USER 1 PURPOSE AND INTENDED USE OF THE APPRAISAL 1 PLAT MAP 2 GRAPE RESEARCH SURVEY 3 APPRAISAL REPORT OPTION 4 DATE OF VALUE AND DATE OF THE REPORT 4 DEFINITION OF MARKET VALUE 4 PROPERTY RIGHTS APPRAISED 4 PERSONAL PROPERTY 4 INTANGIBLE PROPERTY 5 HYPOTHETICAL CONDITION 5 EXTRAORDINARY ASSUMPTION 5 SCOPE OF WORK 6 AREA DATA 8 STATE MAP 9 NEIGHBORHOOD DATA 15 FUTURE LAND USE PLAN 18 NEIGHBORHOOD MAP 19 NEIGHBORHOOD AERIAL 20 MARKET CONDITIONS 21

11 TABLE OF CONTENTS ZONING 24 ASSESSMENT INFORMATION AND TAX DATA 25 PROPERTY DESCRIPTION 26 PROPERTY AERIAL 29 HIGHEST AND BEST USE 31 SALES COMPARISON APPROACH 33 RECONCILIATION AND FINAL ESTIMATE OF MARKET VALUE 37 COMPARABLE SALES MAP(S) COMPARABLE LAND SALE WRITE-UPS EXHIBITS: 1 Zoning Regulations 2 Photographs of Subject Property 3 Floodplain Map ****** ADDENDA ******

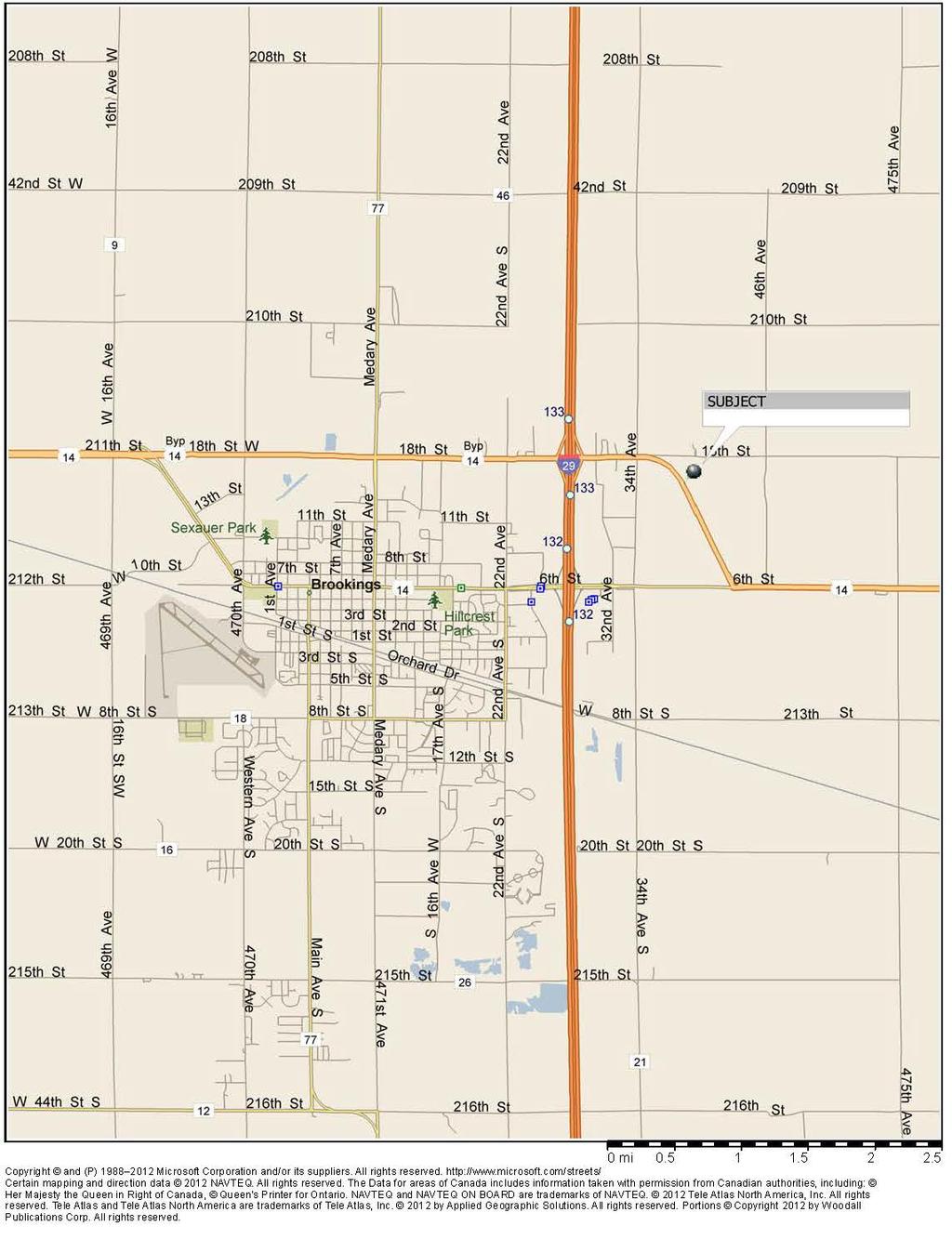

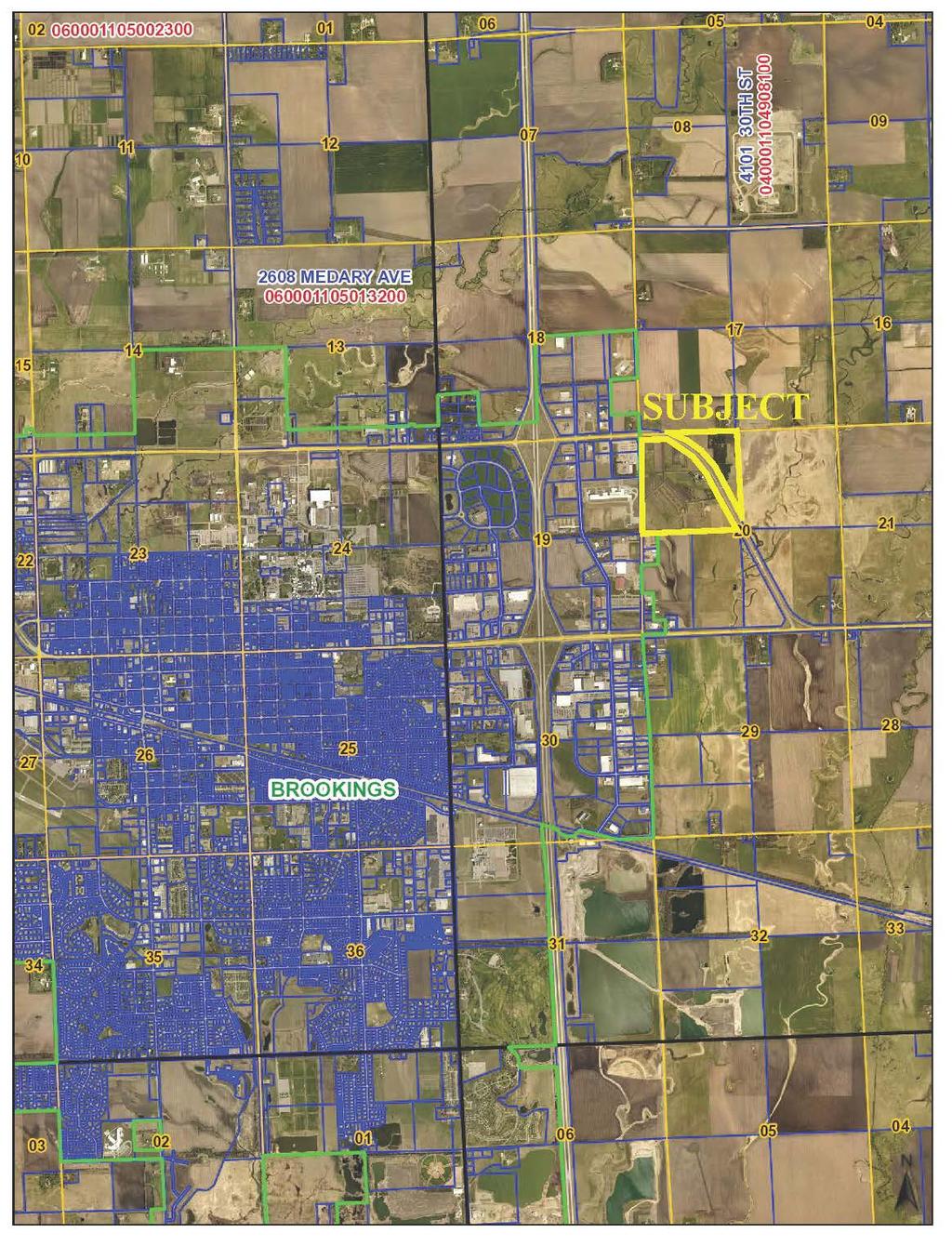

12 IDENTIFICATION OF THE PROPERTY APPRAISAL REPORT LEGAL DESCRIPTION: Legal description of the subject property, as compiled by the appraisers, is as follows. The Northwest Quarter except Lot H-1 and H-2 of Section 20, Township 110 North, Range 49 West of the 5th P.M. A plat map from the Brookings County website can be found on the following page with subject shaded in yellow. LOCATION: Subject property is located at 1501 US Highway 14 Bypass, Brookings, South Dakota. The property is not located within the City of Brookings. Site will be discussed in greater detail in later sections SITE AND IMPROVEMENTS: The property is predominately unimproved agricultural land, used by South Dakota State University for fruit tree research and various other agricultural research throughout the past twenty plus years. Improvements consist of one cold storage building and several other older storage buildings. OWNERSHIP AND HISTORY: Subject property has been under the ownership of the State of South Dakota for in excess of three years. South Dakota State University has used the property for agricultural research for the past twenty plus years. According to William Gibbons, PhD, with South Dakota State University, the university would continue to do research on the 7.5 acre parcel currently being used for grape research, which could last up to 10 years. If the property was to be sold, South Dakota State University would lease the 7.5 acre site for the duration of research, terms of the potential lease would have to be part of the negotiation of the price for the property. This will be discussed further, later in the report. A copy of the survey identifying the 7.5 acres can be found on page 3. Subject property is not listed for sale on the open market to the knowledge of the appraisers. CLIENT AND INTENDED USER Client and intended user of the appraisal is Mr. Ryan Brunner and South Dakota Office of School and Public Lands. PURPOSE AND INTENDED USE OF THE APPRAISAL Purpose of the appraisal is to estimate the as is fee simple estate market value of the subject property as of November 20, Intended use of the appraisal is to assist in the disposal of the property. 1

13 PLAT MAP 2

14 GRAPE RESEARCH SURVEY 3

15 APPRAISAL REPORT OPTION Appraisal is presented in an Appraisal Report format in compliance with the Uniform Standards of Professional Appraisal Practice (USPAP). DATE OF VALUE AND DATE OF THE REPORT Effective date of value is November 20, 2018, the date the subject property was viewed by Mr. Travis E. Shaykett, State Certified General Appraiser. Date of the appraisal report is the date stated on the Appraiser Certifications. DEFINITION OF MARKET VALUE Definition of market value, as used in this report, is taken from The Dictionary of Real Estate Appraisal, 6 th Edition, published in 2015 at page 141, and reads as follows: Market Value. The most probable price, as of a specified date, in cash, or in terms equivalent to cash, or in other precisely revealed terms, for which the specified property rights should sell after reasonable exposure in a competitive market under all conditions requisite to a fair sale, with the buyer and seller each acting prudently, knowledgeably, and for self-interest, and assuming that neither is under undue duress. PROPERTY RIGHTS APPRAISED Property rights appraised are fee simple estate. Outstanding liens, mortgages, easements or other types of encumbrances are considered, but not separately addressed, unless stated elsewhere in the report. Definition of fee simple estate, as used in this report, is taken from The Dictionary of Real Estate Appraisal, 6 th Edition, published in 2015 at page 90. Fee Simple Estate. Absolute ownership unencumbered by any other interest or estate, subject only to the limitations imposed by the governmental powers of taxation, eminent domain, police power, and escheat. PERSONAL PROPERTY Typically, personal property is not included in the value of real estate. Definition of personal property is as follows: Personal Property. Identifiable tangible objects that are considered by the general public as being "personal" - for example, furnishings, artwork, antiques, gems and jewelry, collectibles, machinery and equipment; all tangible property that is not classified as real estate. (USPAP, Edition) There is no personal property included in the final value estimate. 4

16 INTANGIBLE PROPERTY Typically, intangible property is not included in the value of real estate. Definition of intangible property is as follows: Intangible Property (Intangible Assets). Nonphysical assets, including but not limited to franchises, trademarks, patents, copyrights, goodwill, equities, securities, and contracts as distinguished from physical assets such as facilities and equipment. (USPAP, Edition) There is no intangible property included in the final value estimate. HYPOTHETICAL CONDITION Hypothetical conditions are contrary to what exists. Definition of hypothetical conditions is as follows: Hypothetical Condition. A condition, directly related to a specific assignment, which is contrary to what is known by the appraiser to exist on the effective date of the assignment results, but is used for the purpose of analysis. (USPAP, Edition) Comment: Hypothetical conditions are contrary to known facts about physical, legal, or economic characteristics of the subject property; or about conditions external to the property, such as market conditions or trends; or about the integrity of data used in an analysis. There are no hypothetical conditions in this appraisal report. EXTRAORDINARY ASSUMPTION Extraordinary assumptions presume uncertain information to be factual. Definition of extraordinary assumptions is as follows: Extraordinary Assumption. An assignment-specific assumption, as of the effective date regarding uncertain information used in an analysis, which, if found to be false, could alter the appraiser s opinions or conclusions. (USPAP, ed.) Comment: Uncertain information might include physical, legal, or economic characteristics of the subject property; or conditions external to the property, such as market conditions or trends; or the integrity of data used in an analysis. There are no extraordinary assumptions in this appraisal. 5

17 SCOPE OF WORK As mentioned earlier, the University wants to continue to occupy the 7.5 acres currently devoted to grape production research. This would include the buildings at subject. Also, perimeter 6 foot high chain link fence would need to be maintained, to keep the wild life out. For the University to continue use of the 7.5 acres the issues of who would be responsible for maintaining the buildings and the fence, or installing proper fence around the 7.5 acres, as well as reasonable rent would need to be part of the purchase negotiations. This could even be some type of discount of the purchase price. Since, the actual terms of a lease or a property price discount are yet to be determined the appraisers will appraise the property as unencumbered and without any benefit of or discount for the existing vineyard. Also, in the opinion of the appraisers, due to the age, condition and design of the existing buildings would have some interim use, but they do not contribute to the highest and best use of property. The estimate of market value of a property usually calls for the employment of three approaches to value. These approaches to value are identified as follows: Cost Approach Income Capitalization Approach Sales Comparison Approach In the Cost Approach, the appraisers estimate the new replacement cost of the improvements. A deduction is made for depreciation due to wear and tear, design and plan, and neighborhood defects. The value of the land, which is estimated by direct comparison with similar vacant sites, is then added to the depreciated cost of the improvements. In the Income Capitalization Approach, the appraisers estimate the market rent, sometimes known as economic rent, from rents found in the market from similar properties. Next, there is a deduction for operating expenses to arrive at the net operating income. The net operating income is then capitalized into a value indication by means of one or more capitalization methods with data taken from the market. In the Sales Comparison Approach, the appraisers compare the subject property on a similar unit of comparison with similar sale properties. Adjustments are made for all factors of dissimilarity recognized by the market. All known sales were considered and used to develop market adjustments; however, the appraisers relied on only those considered to be most similar to the property appraised. After a thorough analysis, the data is then correlated into a final value estimate by this approach. The appraisers then correlate the indicated value estimates of the three approaches into a final value estimate. Consideration is given to the relative strengths and weaknesses of each approach, giving the most weight to the approach most commonly used by typical purchasers for the type of property appraised. Scope of work for this appraisal assignment includes the development of the Sales Comparison Approach only, since the subject property buildings are considered interim use only, so is appraised is vacant land. 6

18 SCOPE OF WORK As part of this appraisal, the appraisers have made a number of independent investigations and analysis specific to this appraisal based on data developed during the appraisal and also on data files maintained in the appraisers office and updated on an ongoing basis. Mr. Travis E. Shaykett, State Certified General Appraiser, viewed the subject property and completed most of the research, writing of the report, and development of the approaches to value. Mr. Steven C. Shaykett, MAI, State Certified General Appraiser, reviewed the appraisal as co-appraiser. Research undertaken and the major data sources used are discussed in the following paragraphs. Property Description and Analysis: Appraisers obtained pertinent information from the client, the City of Brookings, and the Brookings County Assessor s Office relating to the subject property as needed. Brookings County Courthouse records were reviewed by the appraisers for a history of transactions relating to the subject property for a period in excess of three years. Subject property was viewed by Mr. Travis E. Shaykett on November 20, 2018 along with 2 South Dakota State University employees Ms. Missy Vande Weerd, Assistant to the Director South Dakota Agricultural Experiment State at SDSU and Mr. Brett Owens, instructor of horticulture. Photographs of the subject property and the surrounding area were taken on that day. Market Data Program: Appraisers obtained data on comparable sales by researching sales occurring within the last three years which were similar in use and located in the subject area. Due to the size of subject no highly similar properties were found in this market. Research did develop sales in the Brookings area that were considered and relied upon, even though smaller in size. Search for comparable sales was expanded to other eastern South Dakota communities to assist in developing the Sales Comparison Approach. Appraisers obtained copies of deeds from the county courthouses and attempted to contact the buyers, sellers, or others knowledgeable, to verify transaction data. Details of the verified sales are included in the Addenda. Correlation and Final Value Estimate: Upon completion of all the steps to gather and analyze data, a review of the value indications is made and a final value estimate conclusion. 7

19 AREA DATA Area data is based on the intended user of the report already having a basic understanding of the economic, social, and governmental forces affecting the real estate market. Purpose of the area and neighborhood analysis is to review information on the social, governmental, and economic forces of the local economy and the expectations for the future. Data and conclusions are based on and from research maintained in the appraisers file. Appraisers have made a review of relevant data for Brookings, Brookings County, and South Dakota. Comparison will include a review of relevant demographic and economic data for similar sized cities and counties in the general region, including Aberdeen (Brown County), Watertown (Codington County), Mitchell (Davison County), Huron (Beadle County), and Yankton (Yankton County). A map of South Dakota can be found on the following page. TABLE 1 POPULATION COMPARISONS (%) CHANGE (%) CHANGE (%) CHANGE Brookings 13,717 14,951 16,270 18,504 22, % 13.73% 19.20% Brookings County 22,158 24,332 25,207 28,220 31, % 11.95% 13.27% Aberdeen 26,476 25,851 24,927 24,658 26, % -1.08% 5.81% Brown County 36,920 36,962 35,580 35,460 36, % -0.34% 3.02% Watertown 13,388 15,649 17,592 20,237 21, % 15.04% 6.15% Codington County 19,140 20,885 22,698 25,897 27, % 14.09% 5.14% Mitchell 13,425 13,916 13,798 14,558 15, % 5.51% 4.78% Davison County 17,319 17,820 17,503 18,741 19, % 7.07% 4.07% Huron 14,299 13,000 12,448 11,893 12, % -4.46% 5.88% Beadle County 20,877 19,195 18,253 17,023 17, % -6.74% 2.20% Yankton 11,919 12,011 12,703 13,528 14, % 6.49% 6.85% Yankton County 19,039 18,952 19,252 21,652 22, % 12.47% 3.63% South Dakota 665, , , , , % 8.45% 7.86% SOURCE: U.S. Census Bureau From 2000 to 2010, the city of Brookings and Brookings County showed the greatest population growth, at percent and percent respectively. The comparison cities were led by Yankton at 6.85 percent, Watertown at 6.15 percent, and Huron at 5.88 percent. The state as a whole experienced population growth of 7.86 percent. According to the U.S. Census Bureau the estimated 2017 population for Brookings is 29,938, which is an increase of percent from

20 STATE MAP 9

21 AREA DATA Table 2 shows the breakdown of population within a specific age bracket and Table 3 shows the median age. A majority of the population in the city of Brookings and Brookings County is made up of the younger population. POPULATION BY AGE CITY OF BROOKINGS TABLE 2 POPULATION BY AGE % OF POPULATION TABLE 3 MEDIAN AGE BROOKINGS COUNTY % OF POPULATION > 20 7, % 10, % , % 4, % , % 4, % , % 6, % , % 2, % , % 3, % TOTAL 22, % 31, % SOURCE: U.S. Census Bureau, 2010 Census BROOKINGS 23.5 BROOKINGS CO ABERDEEN 36.4 BROWN CO HURON 39.8 BEADLE CO MITCHELL 36.8 DAVISON CO WATERTOWN 36.6 CODINGTON CO YANKTON 40.4 YANKTON CO SOUTH DAKOTA 36.9 SOURCE: U.S. Census Bureau, 2010 Census 10

22 AREA DATA TABLE 4 LEADING EMPLOYERS BROOKINGS EMPLOYER # OF EMPLOYEES South Dakota State University 4,463 Daktronics 1,600 3M 1,100 Larson Manufacturing 557 Brookings Health System 500 Walmart 425 Aramark 405 Brookings School District 400 Hy-Vee Food Store 450 Twin City Fan 299 Bel Brands 290 City of Brookings 282 Fishback Financial Corporation 239 Brookings Municipal Utilities 230 United Living Community 215 Swiftel Communications 213 Falcon Plastics 193 Boys and Girls Club 180 SOURCE: Brookings Economic Development Corporation U.S. Department of Housing and Urban Development compiles the median family income for all counties in South Dakota on an annual basis. A history of median family income is provided below in Table 5. Brookings County experienced a 34.2 percent increase in median family income from 2000 to 2016, and sets the low end of the range, but still shows positive growth. TABLE 5 MEDIAN FAMILY INCOME % CHANGE ANNUAL % CHANGE BROOKINGS COUNTY $46,800 $65,400 $65,700 $62, % 2.1% BROWN COUNTY $44,000 $59,900 $66,900 $66, % 3.2% CODINGTON COUNTY $45,900 $61,200 $65,500 $64, % 2.6% DAVISON COUNTY $42,200 $60,400 $67,600 $64, % 3.2% BEADLE COUNTY $43,800 $55,300 $60,600 $59, % 2.3% YANKTON COUNTY $44,400 $59,400 $71,900 $69, % 3.6% SOUTH DAKOTA $43,500 $58,900 $64,700 $62, % 2.8% SOURCE: U.S. Dept of Housing and Urban Development 11

23 AREA DATA Table 6 illustrates the new construction building permits for single family and multi-family units for the past 13 years. Number of housing starts is affected by growth, the affordability of the cost of mortgage money, and the supply of existing homes. All these factors are generally reflective of the health of a local economy. The number of housing starts is generally a good barometer of the expansion of the local economy. TABLE 6 BUILDING PERMITS YEAR SINGLE FAMILY MULTI-FAMILY- UNITS TOTAL SOURCE: SOCDS Table 7 shows the gross retail sales. This table indicates that all comparisons, except for Aberdeen, have increased in retail sales from 2011 to TABLE 7 RETAIL SALES ($000) % CHANGE ANNUAL CHANGE BROOKINGS $467,881 $480,079 $528,771 $502,766 $516,684 $547,153 $536, % 2.1% ABERDEEN $1,754,010 $1,893,199 $2,334,767 $1,802,250 $1,493,706 $1,418,252 $1,573, % -1.5% WATERTOWN $746,894 $858,419 $878,984 $891,417 $862,466 $817,140 $850, % 2.0% MITCHELL $657,014 $692,963 $715,426 $731,513 $721,371 $687,772 $667, % 0.2% HURON $407,373 $478,106 $427,403 $407,683 $434,016 $426,131 $1,258, % 29.9% YANKTON $468,738 $436,174 $459,513 $457,862 $467,593 $457,329 $472, % 0.1% SOUTH DAKOTA $25,742,464 $29,215,473 $25,122,436 $27,848,227 $27,394,724 $27,574,118 $27,553, % 1.0% SOURCE: SD Department of Revenue and Regulation 12

24 AREA DATA Appraisers have reviewed unemployment statistics for the past eight years on a local level and a state level. Table 8 shows the unemployment rates for selected South Dakota micropolitan statistical areas, as well as the state. For all comparisons, the unemployment rates have decreased from 2010 to Brookings unemployment rate for 2017 at 3.2 percent is lower than the state average. Typically, an unemployment rate around 5.0 percent is indicative of a healthy economy. TABLE 8 NON SEASONALLY ADJUSTED UNEMPLOYMENT RATE 2010 Average 2011 Average 2012 Average 2013 Average 2014 Average 2015 Average 2016 Average 2017 Average Brookings MiSA 4.7% 4.4% 3.9% 3.4% 3.1% 2.9% 2.6% 3.2% Aberdeen MiSA 3.8% 3.8% 3.5% 3.2% 2.8% 2.7% 2.5% 3.0% Watertown MiSA 5.2% 4.6% 3.9% 3.6% 3.3% 3.1% 2.9% 3.4% Mitchell MiSA 4.5% 4.1% 3.5% 3.3% 2.9% 2.7% 2.4% 3.1% Huron MiSA 4.1% 3.6% 3.3% 3.5% 3.1% 2.7% 2.8% 2.9% Yankton MiSA 5.1% 4.6% 3.8% 3.5% 3.0% 2.6% 2.4% 3.0% South Dakota 5.0% 4.7% 4.3% 3.8% 3.4% 3.1% 2.8% 3.3% SOURCE: SD Department of Labor Area Data Conclusion: Brookings and Brookings County have experienced positive, strong population growth from 1980 to 2010, at a pace higher than the state. Economic capacity of the population is increasing at a rate similar to the comparable counties. Median family income is towards the low end of the comparison counties and the state, but has shown growth. A combination of steady population growth and an increasing buying capacity has made an atmosphere of stable economic growth. Economic growth is reflected in the number of building permits issued and retail sales growth. Brookings had shown growth in both single and multi-family building permits over the past few years but shows a decline in 2017, and retail sales have increased from 2011 to However, the close proximity of Brookings to Sioux Falls, the major retail trade center in the region, may influence this factor. Currently the unemployment rate for Brookings is below the state average and is estimated to continue at this same level. Overall, the economy of Brookings has slowed, but still continues to grow at a similar pace experienced in the recent past. The ability of the local economy and population to grow will be in direct correlation to growth in the local employment sector. There are no known factors that would indicate a significant change will occur in the near future in the local economy in either a positive or negative direction in any way that is more significant than any other community in the state. 13

25 AREA DATA Educational services provide a substantial portion of the local employment. Attraction of new businesses and industries, as well as the expansion of existing businesses and industries in the market, could significantly expand the city's economy. Development of a new Multi-Plex Center was expected to increase economic activity through events held. However, this has taken longer than expected to spur economic activity. Brookings added a dairy manufacturing operation on the east side of town, which created over 200 additional jobs. The 3M Company is in the second phase of an expansion project that is anticipated to add 60 new jobs to the facility by Novita Nutrition, LLC is building a $70 million feed processing plant on the edge of Aurora and will create 34 jobs at the plant and 10 jobs at the corporate headquarters in Brookings. Overall, socioeconomic growth in Brookings has been slow for over the last 20 years. This slow growth is expected to continue in the near future and over the long term. The capacity for expansion of the socioeconomic base will be in direct relationship to the number of new businesses and industries that can be attracted to the city. Slow growth generally tends to keep demand for all types of real estate low, which in turn generally keeps real estate values at a slow growth, and at a price level commensurate with economic activity levels. 14

26 NEIGHBORHOOD DATA Subject property is located along the US Highway 14 Bypass south of 18 th Street and east of 34 th Street. Location of subject property northeast of Brookings just outside the city limits. U.S. Highway 14 runs east of Brookings to the Minnesota state line and to the west of Brookings continues approximately 330 miles until it connects with Interstate 90 near Wall, South Dakota. US Highway 14 Bypass runs east and west along the northern edge of the city limits. Interstate 29 is several blocks west of subject property. Interstate 29 is the primary access to Brookings and connects to Sioux Falls approximately 48 miles to the south and Fargo, North Dakota approximately 185 miles to the north. Brookings has one high school, one middle school, and three elementary schools. There are recreational amenities located within one mile of the subject neighborhood, including a golf course, shopping centers, and extensive walking and bike paths. Centers of employment are found mainly at the commercial uses along 6 th Street and industrial uses in the southeast and southwest quadrants of Brookings. Access to other parts of the city is average; however, all areas of the city can be accessed within 5 to 10 minutes driving time from the subject neighborhood. Appraisers have also reviewed the enrollment of South Dakota State University (SDSU), a land grant heritage university that was founded in According to South Dakota State University enrollment for the year was 12,107 students which was down slightly from the previous year, by 420 students. However, SDSU has been able to maintain an enrollment over 12,000 students for more than of 10 years. Although subject property is not within the city limits of Brookings, subject s neighborhood is considered to be the entire town, since all areas are dependent on goods and service providers throughout the community without overlap of primary services, such as schools, hospitals, government services, and infrastructure. Immediate neighborhood is the commercial area east of Interstate 29. A neighborhood map and aerial photograph can be found at the end of this section. Subject s immediate neighborhood and surrounding uses consist of industrial, manufacturing uses and agricultural uses. Subject neighborhood has average convenience to schools and shopping, as does most areas of the city. The commercial growth of Brookings has been around 6 th Street and Interstate 29. This neighborhood has been the primary area of commercial growth for Brookings consisting of businesses such as Lowes, Runnings Farm and Fleet, Wal-Mart, Daktronics, ProBuild, hotels, restaurants, and convenience stores. The Lowe s retail center was built in 2005, just north of 6 th Street and to the west of Interstate 29. A Super Wal-Mart opened in 2005 near the northwest quadrant of Interstate 29 and 6 th Street replacing a smaller store on 6 th Street, which is now a Runnings Farm and Fleet Store. Within the last several years, three franchise fast food restaurants have opened, and a strip mall was built along 6 th Street west of Interstate 29, other recent openings include a Taco Bell just north of Lowe s along with a Comfort Suites hotel. Commercial development east of Interstate 29 has been slower then development west of Interstate 29. Within the last several years on the east side of Interstate 29 one franchise restaurant has opened along with a new hotel. Also located in this neighborhood east of the interstate is the Swiftel Event Center and Larson Ice Center. 15

27 NEIGHBORHOOD DATA The 3M Company is in the second phase of a $70 million expansion of its plant that will be completed in phases through 2018 and is anticipated to create almost 90 new jobs. Falcon Plastics completed a 60,000 square foot addition in early Bell Brands opened a $120 million cheese manufacturing plant on the east side of Interstate 29 and south of the U.S. Highway 14 bypass intersection in October Bell Brands makes Laughing Cow Cheese. This created more than 200 jobs in 2014, and a second phase could bring an additional 200 jobs if the market demand is favorable for expansion. Novita Nutrition, LLC in 2015 completed a $70 million livestock feed processing plant on the edge of Aurora and that created 34 jobs at the plant and 10 jobs at the corporate headquarters in Brookings. Majority of the commercial and industrial development for Brookings over the last 30 years has been in the corridor with Interstate 29 on the west and 34 th Avenue on the east. Area south of 6 th Street in this corridor is fully developed, however there are several redevelopment projects that have been completed or are in the process. Area north of 6 th Street and South of 18 th Street, also known as, US Highway 14 Bypass, is nearly fully developed. Subject s location east of 34 th Avenue and along US Highway 14 Bypass is the logical expansion of this commercial/industrial district. Subject and the large vacant tract to the south of subject down to 6 th Street represent a size equal to about half the size of the corridor that has been developed over the last 30 years. However, much of the area south of subject is within the floodplain. Areas east of Interstate 29 typically have not experienced residential growth, as majority of residential development has been to the south end of Brookings. However, development in southern Brookings is nearing capacity. Appraisers reviewed the Brookings Comprehensive Plan, Planning for 2040, as adopted April Based on a review of this plan, the city of Brookings has limited direction of growth due to floodplains on all sides of the city and South Dakota State University to the north. However, there is some areas to the northeast and northwest of the city that are not within the floodplain or development could jump the floodplain. New developments in other parts of the city will begin transition to development land as developments in the south part of the city near capacity. A future land use map within this study indicates subject property west of Highway 14 Bypass would be best suited for Urban Medium Intensity while subject property east of Highway 14 Bypass is indicated to be Urban Reserve. Urban Medium Intensity would include single-family dwellings district; townhouse district; office district; local retail district; mixed use residential/business. Appraisers could find no explanation for Urban Reserve within the study. But is assumed to be long range residential. A copy of the future land use plan can be found at the end of this section. Appraisers also interviewed Mr. Mike Struck, Community Development Direct for the City of Brookings, about the comprehensive plan. According to Mr. Struck, if growth continues at similar trends as current, the need for development north of Highway 14 is anticipated to be 15 to 20 years. However, there is a trend of redevelopment within the current city limits that could extend the time frame of expansion past 20 years. According to Mr. Struck, future use of subject property would most likely be commercial development due to existing neighborhood uses and limited access from Highway 14 Bypass road. Existing neighborhood uses consist of Bel Brands which can create an occasional odor due to the cheese manufacturing process, other uses consist of implement dealerships, Swiftel Center, and other industrial and commercial uses. Additionally, according to Mr. Struck the City of Brookings and SD DOT have had conversations about limiting access along this portion of the Highway 14 Bypass due to the 16

28 NEIGHBORHOOD DATA curve and large amount of truck traffic. This would limit the access to 34 th Street, which is also access to the commercial areas directly to the west of subject. The South Dakota Department of Transportation recently completed a redevelopment of 6 th Street. Redevelopment was from the east city limits to just west of 22 nd Avenue and consisted of building a seven-lane road with a center median and new overpass over Interstate 29. Conclusion: Subject neighborhood is in the northeast section of Brookings, east of Interstate 29 along US Highway 14 Bypass. A future land use map indicates future use of subject to be mixed use with residential and low intensity commercial, however according to the community development director the most likely use would be commercial, due to existing neighborhood uses. Current commercial growth is along 6 th Street west of Interstate 29 and current residential growth is in the south end of the city but anticipated residential growth north of Highway 14 is 15 to 20 years or greater. Subject area is a mix of commercial and industrial uses transitioning to agricultural uses. Accessibility to and from the site is good from outside of the city, as well as to the residential areas of the city. 17

29 FUTURE LAND USE PLAN 18

30 NEIGHBORHOOD MAP 19

31 NEIGHBORHOOD AERIAL 20

32 MARKET CONDITIONS General overall economic conditions were discussed and summarized in the Area Data and Neighborhood Data sections of the report. This section relates specifically to the commercial/industrial real estate segment and to the subject properties as relating to exposure time and marketing period. Following paragraphs are taken directly from Advisory Opinion AO-7 of the Uniform Standards of Professional Appraisal Practice, 2018 Edition. These paragraphs help explain marketing time and methods to estimate. The reasonable marketing time is an opinion of the amount of time it might take to sell a real or personal property interest at the concluded market value level during the period immediately after the effective date of an appraisal. Marketing time differs from exposure time, which is always presumed to precede the effective date of an appraisal. Rationale and Method for Developing a Marketing Time Opinion The development of a marketing time opinion uses some of the same data analyzed in the process of developing a reasonable exposure time opinion as part of the appraisal process and is not intended to be a prediction of a date of sale or a one-line statement. It is an integral part of the analyses conducted during the appraisal assignment. The opinion may be a range and can be based on one or more of the following: * Statistical information about days on market, * Information gathered through sales verification, * Interviews of market participants, and * Anticipated changes in market conditions. Related information garnered through this process includes other market conditions that may affect marketing time, such as the identification of typical buyers and sellers for the type of real or personal property involved and typical equity investment levels and/or financing terms. The reasonable marketing time is a function of price, time, use, and anticipated market conditions, such as changes in the cost and availability of funds, and is not an isolated opinion of time alone. Exposure Time: Exposure time is presumed to precede the effective date of the appraisal. Exposure time relative to subject is estimated at 12 months or less. Basis for this estimated exposure time is conversation with brokers, as well as County and City personnel who track movement of sites and commercial/industrial properties in this market. Sales of commercial/industrial properties in Brookings, as evidenced by the sales reviewed by the appraisers, have remained at a steady pace over the past several years. Broker conversations indicated if the property was correctly priced, average marketing time is typically under 12 months. 21

33 MARKET CONDITIONS Appraisers reviewed a recent auction of 2,600 acres, that were sold in 18 tracts, of which four were similar locations as subject, the remaining properties were agricultural land in Brookings County. This auction was by private sealed bid due by November 7, 2018 with a private auction of the highest five bidders on November 16, According to the Clay Anderson broker representing the seller, the four tracts that had similar location to subject were not sold at the live auction due to auction prices not meeting the seller s expectations and several buyers not completing the due diligence in time for the auction, therefore they were unable to bid. These four tracts were identified as Tracts 13, 14, 15, and 16 for the sale. Tract 13 is located one half mile north of subject and is currently listed for $9,750 per acre. Tract 14 is located on the east side of Interstate 29 and one half mile north of Highway 34 and is currently listed for sale at $12,500 per acre. Tract 15 is located directly south of subject and is currently listed for $8,000 per acre. Tract 16 is located on the east side of 34 th Street and one-half mile south of 6 th Street and is currently listed for $6,500 per acre. Tract 14 is most similar to subject, as the most likely future use is commercial/industrial, while Tract 13 is long term residential. Tracts 15 and 16 are located within the 100-year flood plain and the wellhead protection area and are not indicated as being any future development potential. The map below shows the location of the four tracts that are now listed for sale and the current asking price. 22

34 MARKET CONDITIONS Appraisers also reviewed several development land sales in the south side of Brookings. Sale 1 consists of acres that sold in June of 2016 to a local developer for $1,575,000. Based on interview with the buyer, the sale included a house and three acres that they parceled out for his personal residence. The buyer indicated they valued the remaining development land at around $36,000 per acre. The development land was within the immediate growth pattern of Brookings; therefore, the buyer was able to annex into city limits, had immediate access to utilities, and commenced residential development shortly after purchase. The second sale reviewed by the appraisers consists of acres that sold in August of 2017 to a local development group, Advantage Investments Group. Sale price was $970,000, which is $29,016 per acre. This sale is located adjacent to a new public school on the south end of the city and had good access to public utilities and was located within the city limits. Both of these sales occurred in the south end of the city where residential growth is the most predominate. Both sales had access to utilities and were in or could be annexed within the city limits immediately. Additionally, both of these sales are some of the last vacant development land in this part of the city. Also, these sales are considerably smaller than the subject property, which typically smaller sales sell for greater price per unit. It is difficult to estimate the exposure time of commercial/industrial properties in the Brookings market without a central service that tabulates this type of information. However, research by the appraisers and broker conversations support the conclusion that the subject market exposure time would be under 12 months. Appraisers have estimated that subject, properly priced and advertised, would have an exposure time of less than one year. Marketing time reflects the period after the value date required to sell the property at market value. This is heavily influenced by historical exposure time, but tempered by current economic conditions and by the pricing of the property. Brookings market area has maintained a stable real estate market, with current conditions reasonably similar to the last 12 months. Interest rates have remained low and are expected to favorably affect the feasibility of most projects. Demand appears to remain good in most areas of the market. Appraisers estimate the marketing time for subject at one year or less. The City of Brookings has had an increasing population for over twenty years. The Brookings market has well established manufacturing base and has continued to attract new employers over the past several years. Subject property is located in a community with a diversified economic base that will likely support stable to increasing demand for all types of real estate, which helps to maintain or increase rental rates and values. Subject s immediate neighborhood has experienced growth in commercial and residential demand in recent years and is expected to continue at similar trends. Overall, the subject neighborhood is considered to have average marketability for the area. 23

35 ZONING According to information obtained from the Brookings County Planning and Zoning Office, the subject property is not within the city limits Brookings and is zoned Agricultural District, A. Location of subject is within the Brookings County and City of Brookings Joint Jurisdiction Area; therefore, any zoning change would require approval by the City of Brookings and Brookings County. A copy of the zoning regulations can be found in the Addenda as Exhibit 1. Agricultural District, A allows predominately agricultural uses and a few commercial uses allowed by special exception. A complete list of allowable uses can be found in the Addenda as Exhibit 1. In the course of this appraisal, the appraisers have not been provided with or acquired on their own a legal opinion as to the zoning and private restrictions at the subject property. Interpretations of the zoning ordinance are based upon an examination of the zoning ordinance as applied to the subject property by the appraisers, and should not be construed to represent a legal opinion of the zoning ordinance as applied to the subject property. Also, the appraisers review of the courthouse records should not be construed to represent a legal opinion of the private restrictions at the subject property. Such legal opinions could be obtained by consulting an attorney, and such consultation is recommended by the appraisers. Conclusion: Current use is an allowed use within current zoning. Any development of subject consistent with existing neighborhood uses and trends would require a change in zoning. 24

36 ASSESSMENT INFORMATION AND TAX DATA Subject property is owned by a state agency, so is not subject to real estate taxes, and therefore shows no assessed values in the Brookings County Assessor s Office. However, if subject were sold for private development it would be subject to taxation. 25

37 PROPERTY DESCRIPTION Subject property is an irregular shaped site of acres, according to public records. The property is divided by US Highway 14 Bypass. An aerial photograph of the subject property can be found at the end of this section. Photographs of subject property can be found in the Addenda as Exhibit 2. Sizes shown below are estimated by appraisers based on aerial maps. Property east of highway acres Property west of highway acres Total Property Size acres The property on each side of the highway has access from one drive-way approach from US Highway 14 Bypass. The east property also has one drive-way approach from 211 th Street. General access to the neighborhood is from Interstate 29, 6 th Street also known as US Highway 14 and 18 th Street also known as US Highway 14 Bypass. The property on the west side of the highway has approximately 3,745 feet of frontage along US Highway 14 Bypass. This property also has about half mile of frontage on 34 th Avenue. This provides good access and exposure to the existing commercial/industrial district. The property on the east side of the highway has 3,170 feet along US Highway 14 Bypass and 1,975 feet of frontage along the south side of 211 th Street. All of these streets and highways are hard surfaced and would provide sites with developed street frontage at no cost to a developer. Appraisers have not been provided with a copy of the soil tests for the subject site, but other developments in the area show typical site preparation. This area has generally flat topography, with some mature trees and small rolling hills. Topography of the subject is fairly level to gently rolling, generally sloping towards the southeast. As described earlier the property has been used by South Dakota State University for agricultural research for 20 plus years. Research done on the property ranged from fruit tree studies to row crop studies. Within the west property are areas with mature dense tree groves used for various studies, trees range from fruit trees, other deciduous type trees, and coniferous type trees. The trees have not been used for research for several years and have had minimal pruning and maintenance. The perimeter of the west property is lined with mature coniferous type trees. Based on aerial maps there is approximately 30 acres of trees on the west property. Cropland research plots ranged from less than one acre up to five acres. On the east side of the highway the property has one large tree grove that consists of dense mature coniferous type trees and several smaller pockets with similar type trees, approximately 15 acres of the east property is trees. The balance of the east property is used as hay land. Currently the only research being done on the property is grape research on the west property. As shown on page 3 the vineyard and building site has been surveyed. As part of the potential sale of the property South Dakota State University would lease back the 7.5 acre surveyed area for up to 10 years, however research could be completed in a shorter time. According to a review of available flood maps from Site to Do Business, approximately acres on the west property and 0.65 acres on the east property are located within Zone A, which is an area inundated by 100 year flooding. A copy of the floodplain map is located in the Addenda as Exhibit 3. Map number for the subject property is 46011C0455C. 26

38 PROPERTY DESCRIPTION Improvements: The improvements at subject are limited to three buildings. Building 1 is a storage/office building with a walk-in cooler attached. Buildings 2 and 3 are wood post frame storage buildings. Actual age of the buildings is unknown, but effective age is estimated by the appraisers. Building 1: Use & Size: Storage/Office: 48x40=1,920 square feet Cooler Storage: 20x28= 560 square feet Total Size: 2,480 square feet Estimated Effective Age: 20 Years Expected Life: 35 Years Height: Storage/Office 12 feet eve height Cooler Storage: 12 foot side walls Construction: Storage/Office: Steel Frame Cooler Storage Stainless Steel Panels Description: Storage/Office Exterior walls are prefinished steel panels with similar roof. Interior of the storage/office area consists of shop space, office area, bathrooms, and storage. Shop space consists of concrete floor and walls and ceilings have exposed insulation and steel framing. The office area is less than 10 percent of the total size, the walls and ceilings of the office area and bathroom are painted panels walls and ceilings. The bathroom consists of 2 fixtures and one shower stall. The storage area is an old refrigerator storage that does not work. The storage/office area is heated by a fuel oil furnace. There is one 12 foot wide by 10 foot high overhead door on the south side of the building and a similar overhead door to the cooler. Cooler Storage The cooler storage is attached to the storage/office area by an enclosed walk way that is not heated. The cooler storage is on a concrete foundation. Walls and ceilings are stainless steel panel construction typical of most walk-in coolers. The cooler does have the ability to set to freeze also. Building 2: Use & Size: Storage 29x24= 696 square feet Shop 35x24= 840 square feet Total Size: 1,536 square feet Estimated Effective Age: 20 Years Expected Life: 20 Years Height: 10 feet eve height Construction: Wood Post Description: Exterior of the building is galvanized steel panels. The roof is galvanized panels with gable ends. The shop area has concrete floor and plywood walls and ceiling. There is one 10 foot by 10 foot overhead door. The shop area is heated by reznor heater suspended from the ceiling. The storage area consists of dirt floor and exposed framing. Access to the storage area is from sliding doors. 27

39 PROPERTY DESCRIPTION Building 3: Use & Size: Storage 64x30=1,920 square feet Estimated Effective Age: 20 Years Expected Life: 20 Years Height: 10 feet eve height Construction: Wood Post Description: Exterior of the building is galvanized steel panels. The roof is galvanized panels with gable ends. The interior area consists of dirt floor and exposed framing. Access to the storage area is from sliding doors. Based on conversation with maintenance personnel, there is one well that has been filled in with concrete and one well that is used to irrigate research plots. There is an unknown feet of irrigation pipe underground that supplies approximately 19 irrigation risers throughout the property. A map provided by the client can be found at the end of this section showing the approximate location of irrigation well and irrigation risers. Utilities: Water and Sewer - Natural Gas - Electricity - Telecommunications - Private well and septic system Northwestern Energy - None at site Sioux Valley Swiftel Communications- None at site According to personnel with Brookings Utilities office city water and sewer are located in 34 th Avenue, which runs along the west property line. Information regarding utilities is provided as general information, and not as a statement of fact. Only a detailed evaluation by a qualified person would determine adequacy and acceptability for the development of a property of this size. Conclusion: Subject property is located in a transitional area northeast of Brookings. Location of subject has good frontage along US Highway 14 Bypass, which is also known as 18 th Street in Brookings, and is located less than one mile from Interstate 29. Eighteenth Street and 6 th Street are the only roads that have overpasses over Interstate 29. This provides easy access to the rest of the city street network, and to center of employment and shopping. Total size of subject is acres, but is divided by US Highway 14 Bypass. Both sides are adequate size for development. Public utilities are available in the neighborhood. Topography of the property is typical to most development land in the area. Subject site has approximately 45 acres of dense mature trees, which is not typical to most development sites. Site preparation cost could be greater than most development sites in the area due to the number and size of trees on the property, additionally removal of irrigation system would increase cost. Improvements on the property consist of three storage buildings as described above. Building 1 is newer than Buildings 2 and 3, however overall usefulness of the buildings would be minimal to most developers and would contribute minimal value to the overall property. Additionally, the buildings are within the area that would be leased by the State of South Dakota for grape research. 28

40 PROPERTY AERIAL 29

41 IRRIGATION SYSTEM MAP 30

42 HIGHEST AND BEST USE Real estate is appraised in its highest and best use. In concluding a highest and best use of a property, consideration must be given to the land as if vacant and then considering the improvements and land together as the improved property. First, it is necessary to define highest and best use. In this appraisal, the appraisers have relied on the definition of highest and best use as defined in The Dictionary of Real Estate Appraisal, 6 th Edition, published in 2015 at page 109. Highest and Best Use. The reasonably probable use of property that results in the highest value. The four criteria that the highest and best use must meet are legal permissibility, physical possibility, financial feasibility, and maximum productivity. Legal Permissibility: Analysis of the legal permissibility, in relation to the highest and best use, examines those legal factors which could preclude the development of certain uses of the subject site or improvements. Development of the subject site or property to its highest and best use can be limited by long term leases, zoning, private deed restrictions, building codes, historic district controls, or environmental regulations. Physical Possibility: Physical possibility in relationship to the highest and best use examines the physical features of the subject site or improvements, which can preclude development of certain uses of the subject site or improvements. Development of the subject site to its highest and best use can be limited by the size, configuration, location and availability of utilities, and terrain of the site. Development of the subject improvements to their highest and best use can be limited by the size, design, type, and condition of the improvement(s). Financial Feasibility: In evaluating the financially feasible uses of the subject site or improvement, the analysis considers those applications to the subject site which would yield a positive return on investment in consideration of the constraints of legal permissibility and physical possibilities of the subject site or improvements. To estimate if potential developments of the vacant site or uses of the existing improvements provide for a market acceptable return on investment, an analysis is completed of the demand and supply in a neighborhood for the indicated physically possible and financially feasible uses. For a vacant site, the demand and supply of a given use must be at an equilibrium price level adequate enough to provide for returns that would be market acceptable to be financially feasible. For a developed property, the financially feasible uses are those uses which provide for a positive economic income stream to the property. Maximum Productivity: In the evaluation of the maximum productive uses of the subject site or improvements, the utilization which produces the greatest return is considered to be the highest and best use of the improved site. HIGHEST AND BEST USE OF THE SUBJECT PROPERTY: Subject property is within the Agricultural District, A zoning as defined by Brookings County. Zoning allows for a wide range of commercial uses and other uses, as stated in the Zoning section. A complete list of uses can be found in the Addenda as Exhibit 1. However, given the location subject is within the joint jurisdiction, so City of Brookings essentially controls future 31

43 HIGHEST AND BEST USE use. Also, it is assumed that subject would be annexed into the city and would be developed under the appropriated mixed use zoning to maximize potential of subject. There are no other private restrictions that would further restrict use, beyond the zoning, to the knowledge of the appraisers. Physical possibility considerations are those presented in the Property Description section. Subject property is located along US Highway 14 Bypass northeast of Brookings. US Highway 14 Bypass is known as 18 th Street within Brookings and location is less than a mile from Interstate 29. Subject location provides average access to all areas of the city. Subject site is divided by the highway, however both sides have acceptable size and site preparation. There are no legally permissible uses that would be restricted by physical features of the property. As described earlier subject property has been used for agricultural research for 20 plus years. The site consists of nearly 32 percent of mature trees that are a mix of fruit trees, coniferous trees and deciduous trees. These could either be removed, or become part of a well-planned attractive mixed use development park. Current zoning limits the use of the property to agricultural use or single family use. Due to the size of the trees and number of tree groves on both properties typical row crop farming would not be feasible due to the overall poor farmability. The fruit trees could provide potential economic return as an orchard, however not all the trees are fruit trees and the trees have not been maintained for fruit production for several years. Additionally, is speculative if the return from an orchard use would be greater than an alternative use. As described in the market conditions, the Brookings market has experienced good growth over the past several years. The growth has been attributed the Brookings market being able to maintain large manufacturing business and draw new business to the community along with the growth of South Dakota State University, all of which have created new jobs and have created new development. The appraisers have not made a detailed survey of the area, but based on discussion with real estate professionals there is demand for development land, especially east of Interstate 29. Timing of development is difficult to estimate and beyond the scope of work for this report. Compared to farmland that is purchased for future development purchases, subject site provides minimal alternative uses that provide an economic return during the holding period due the trees, irrigation system, and lease of 7.5 acres to South Dakota State University to complete grape research. This element could potentially have a negative effect on value if it does not provide acceptable return to the purchaser. Frontage along 34 th Avenue could provide competitive sites in a short time to help with holding cost. According to flood maps approximately acres west of the highway and 0.65 acres on the east side of the highway are located within the 100-year floodplain. Overall, this is a small portion of the site, as there is adequate area not in the floodplain and these areas can be incorporated into the design of the development. Market has demonstrated demand for development land and for this type of location at a fairly consistent price level, even for a wide range of uses. Due to location of subject property to the City of Brookings and physical features, the highest and best use of the subject property is considered to be subdivision development with interim agricultural use. 32

44 SALES COMPARISON APPROACH In the Sales Comparison Approach to value, the subject property is compared to sales of similar properties. Sales Comparison Approach is based upon the premise that the value of a property is directly correlated to the price paid for similar properties in the market. In estimating the market value of the subject property by the Sales Comparison Approach to value, the appraisers have made a search of the market for recent sales of similar properties in the Brookings market. Due to limited number of sales of similar size and similar development potential the appraisers expanded their research to include similar communities. From the review of these sales, the appraisers have selected three sales for direct comparison which best represent the range of value potential for the subject property. UNIT OF COMPARISON: Unit of comparison is the measure utilized in the market to compare properties. Based upon discussions with individuals involved in the sale of the comparable properties, the method that was most often utilized to compare development land for a purchase or sale decision was the price per acre, price per square foot, or the price per unit. Based upon this, the appraisers have compared the subject property to the comparable sales based upon price per acre due to the size. A write-up of each of the comparable sales can be found in the Addenda, as well as a map showing the location of the sales. Although the comparable sales are considered equivalent to the subject property in many aspects, adjustments to the sales were required to utilize these sales for direct comparison. Grid analysis for this comparison can be found on the following page. A discussion of the subject property and the adjustments made to the sale properties to provide an indicated value for subject is as follows. In making the comparison of subject to the sales, the following elements of comparison are considered and shown in the sequential order of their application: 1. Property Rights Conveyed 2. Financing 3. Conditions of Sale 4. Market Conditions (Time) 5. Location 6. Physical Characteristics 7. Income Characteristics Property Rights Conveyed: Subject property is appraised in fee simple estate. All of the sales were fee simple estate equivalent at sale time. No adjustment has been made for property rights conveyed. Financing: All of the sales were sold for cash, so were at terms considered equivalent to cash. No adjustment has been made for financing. 33

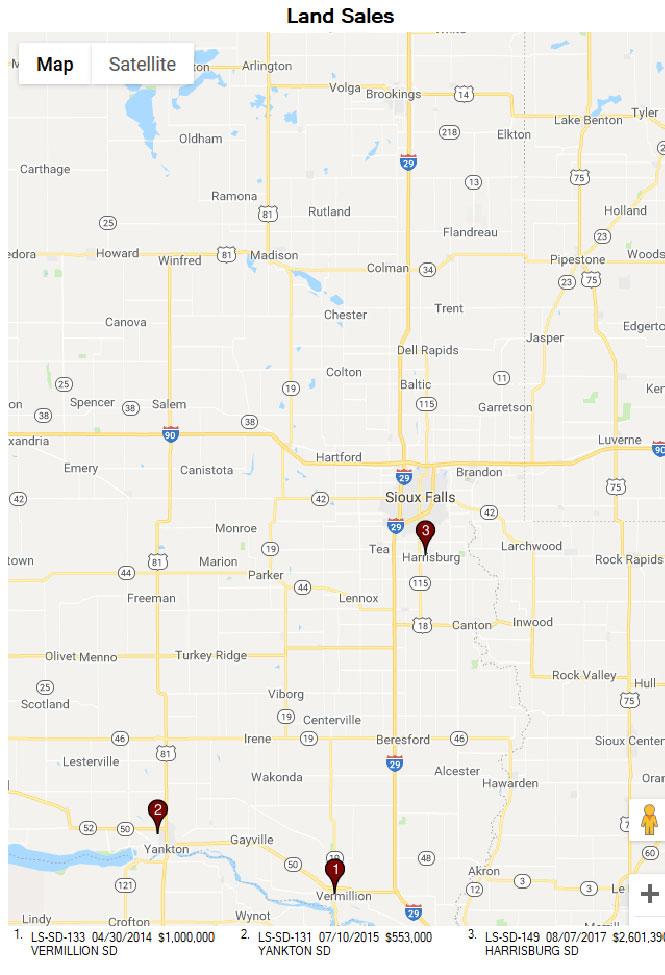

45 LAND SALE GRID Control Number Subject Land Sale 1 Land Sale 2 Land Sale 3 File Number LS-SD-133 LS-SD-131 LS-SD-149 Sale Date 11/20/2018 4/30/2014 7/10/2015 8/7/2017 Location 1501 US HIGHWAY 14 BYPASS TBD-SEE COMMENTS AND MAP TBD W. CITY LIMITS ROAD NORTH SIDE OF WILLOW STREET AND WEST SIDE OF CLIFF AVENUE BROOKINGS, SD VERMILLION, SD YANKTON, SD HARRISBURG, SD Site Size - Acres Sale Price $1,000,000 $553,000 $2,601,390 Price Per Acre $22,222 $17,839 $16,300 Zoning AGRICULTURAL, A PLANNED DEVELOPMENT SINGLE FAMILY A-1, AGRICULTURAL Real Property Rights FEE SIMPLE FEE SIMPLE FEE SIMPLE FEE SIMPLE Adjustment $0 $0 $0 Adjusted Sale Price $22,222 $17,839 $16,300 Financing Terms MARKET MARKET MARKET MARKET Adjustment $0 $0 $0 Adjusted Sale Price $22,222 $17,839 $16,300 Conditions of Sale MARKET MARKET MARKET MARKET Adjustment $0 $0 $0 Adjusted Sale Price $22,222 $17,839 $16,300 Time Differential (Years) Annual Time Adjustment Factor 3.00% 3.00% 3.00% 6.00% Adjustment $3,250 $1,890 $1,304 Adjusted Sale Price $25,472 $19,729 $17,605 Market Conditions CURRENT SIMILAR SIMILAR SIMILAR Adjustment $0 $0 $0 Adjusted Sale Price $25,472 $19,729 $17,605 Location AVERAGE SUPERIOR SUPERIOR SIMILAR Dollar Adjustment -$5,000 -$1,000 $0 Adjusted Sale Price $20,472 $18,729 $17,605 Physical Features AVERAGE SUPERIOR SUPERIOR SUPERIOR Adjustment -$2,000 -$2,000 -$2,000 Adjusted Sale Price $18,472 $16,729 $15,605 Size AVERAGE SUPERIOR SUPERIOR SIMILAR Dollar Adjustment -$4,000 -$4,000 $0 Adjusted Sale Price $14,472 $12,729 $15,605 Utility/Other AVERAGE SIMILAR SIMILAR SIMILAR Dollar Adjustment $0 $0 $0 Adjusted Sale Price $14,472 $12,729 $15,605 INDICATED VALUE $14,472 $12,729 $15,605 34

46 SALES COMPARISON APPROACH Conditions of Sale: Adjustments for conditions of sale usually reflect the motivation of the buyers and sellers. There are no unusual conditions of sale known to the appraisers for any of the sales. As best the appraisers can determine, the sales were negotiated between a knowledgeable buyer and seller, often represented by real estate professionals, with circumstances common to this market. No adjustment has been made for conditions of sale. Market Conditions (Time): Date of sale for the comparable sales is from April 2014 to August Historically, commercial land sales in Brookings and similar communities similar to Brookings have shown slow appreciation over time. Appraisers have made a plus 3.0 percent annual adjustment to Sales 1 and 2. Sale 3 is located in a community that is affected by the growth of Sioux Falls, which has shown greater appreciation than Brookings, therefore a 6 percent adjustment was made for time to Sale 3. Location: Through the analysis of the sales, the market generally recognizes some differences in location. Location of subject is an area of commercial growth of Brookings. Sale 1 is located along the western edge of the Vermillion city limits. Location of Sale 1 offers a mix of development features, such as residential development with good views along a bluff and potential commercial development along a frontage street. Additionally, Sale 1 has utilities readily available to the site. Overall location of Sale 1 is considered superior to subject, therefore a minus $5,000 per acre adjustment was made to Sale 1 for these elements. Sale 2 is located along the western edge of the city limits of Yankton. Location of Sale 2 is within the city limits in a developing residential neighborhood. Sale 2 is considered superior to subject due to location within the city limits and access to utilities. A minus adjustment of $1,000 per acre was made to Sale 2 for this element. Sale 3 is located at the corner of Cliff Avenue and Willow Street. Location of Sale 3 was not within the city limits of Harrisburg at time of sale but was annexed in shortly after. Overall location of Sale 3 is considered similar to subject and no adjustment was made for location to Sale 3. Physical Characteristics: Adjustments for physical features include factors such as size, shape, topography, frontage, accessibility, utilities, and physical features. Any adjustment for size will be presented separately. Subject property is a large tract that would require special consideration in the development of the property. Topography of the property ranges from fairly level to gently rolling. The sales were adjusted for accessibility and utilities in the location adjustment. As described in the property description section approximately 45 acres of the property is covered in trees. Additionally, there is an underground irrigation system throughout the property. All of the comparables were vacant farm land at time of sale with a fairly level topography. Additionally, all the comparables were one tract, whereas the subject property is divided by US Highway 14 Bypass. All of the comparables are superior to subject due to the cost of removing all the trees, irrigation system, and general clean-up of the site and the site being divided by the highway. A minus $2,000 per acre adjustment was made for these elements. A small portion of subject property is located within the floodplain, however all the comparables either have areas within the floodplain or areas that have similar design challenges. 35

47 SALES COMPARISON APPROACH Size: Typically, smaller sites sell for more on a per acre basis; however, not all sales follow this trend. A minus adjustment of $4,000 per acre adjustment was made to Sales 1 and 2 for this element. Sales 3 is considered similar size as subject and no adjustment is required for size. Utility/Other: Subject property has several storage buildings on the property. Improvements are one storage building with cooler storage and two older storage buildings. None of the sales have a similar improvement as subject; however, due to age and use of the improvements no adjustment was made for these elements. Additionally, the improvements would be within the 7.5 acre lease to South Dakota State University for grape research and would not be able to be used by the new buyer until lease has expired. No other adjustments have been made to any of the comparable sales. Conclusion: After adjustments, the sales indicate a range in value from $12,729 per acre up to $15,605 per acre. Sales shown are the best comparables available in the market. These sales provide a range of market demonstrated prices. Appraisers have not placed more emphasis on one sale versus another in estimating value. Subject s large property size limits the number of potential users in the Brookings market, so would be purchased for mixed use subdivision development. Appraisers have not made a detailed survey of existing developments within Brookings, but general search indicates there is adequate land in both finished sites and undeveloped land west of Interstate 29, but minimal development land east of Interstate 29. In consideration of the sales relied upon and other sales known to the appraisers, it is the judgment of the appraisers that the data indicates a value for the subject property at $13,000 per acre, which is $1,857,960, rounded to $1,860,

48 RECONCILIATION AND FINAL ESTIMATE OF MARKET VALUE Correlation of the data and the indicated value estimate is the final step in the appraisal process. Sufficient data has been assembled and analyzed for the purpose of judging the reactions of typical purchasers in the market place. Purpose of the appraisal was to estimate the as is fee simple estate market value of the subject property, and to that end the data was studied and processed by the use of one of the three approaches to value. Value estimate indicated is as follows: Cost Approach N/A Income Capitalization Approach N/A Sales Comparison Approach $1,860,000 In the correlation process, the greatest weight should be given to that approach to value most commonly used by typical purchasers for the type of property being appraised. Consideration is given to that approach to value in which the appraisers have the highest degree of confidence and which has been processed with a minimum of assumptions. Also important is the reasonableness of the data and the reliability of that data. In consideration of the above, and for the reasons and conclusions contained in this report, sole weight is given to the Sales Comparison Approach. It is the opinion of the appraisers that the as is fee simple estate market value of the subject property located in Brookings, South Dakota as of November 20, 2018 was $1,860,

49 APPRAISER QUALIFICATIONS STEVEN C. SHAYKETT, MAI EDUCATION: College: B.S. Degree, University of South Dakota, 1975 Appraisal Education: Completed required 165 hours of educational instruction, appraisal experience and comprehensive examination to be awarded Member Appraisal Institute (MAI) from the Appraisal Institute in May Continuing Education: Complete listing found at the end of this section SPECIALIZED EDUCATION: - Successfully completed the Valuation of Conservation Easements Certificate Program - Successfully completed the Appraisal Institute s Fundamentals of Separating Real Property, Personal Property and Intangible Business Assets Course for Small Business Administration (SBA) Appraisals ASSOCIATION MEMBERSHIP: Appraisal Institute - MAI Member # North Star Chapter President 2012 State Certified General Appraiser - State of South Dakota (#155CG-2019) - State of Iowa (#CG01446) - State of Minnesota (# ) Licensed Real Estate Broker - State of South Dakota Appraisers Advisory Council Member - South Dakota Appraisers Certification Program to 2001 EXPERIENCE: Mr. Shaykett has been owner of Shaykett Appraisal Company, Inc. since 1979, which was located in Prairie Village, Kansas from August 1979 to June 1984, and since June 1984 in Sioux Falls, South Dakota. Mr. Shaykett was also a partner in the firm of Shaykett Agency in Miller, South Dakota from August 1979 to June 1984, when the two offices were consolidated. Mr. Shaykett has been qualified as an expert valuation witness in a number of Circuit Courts in South Dakota, as well as Johnson County, Kansas; Cass County, Missouri; and in Federal District Court, Western Division of Missouri. 38