Presented by Appraisal Institute Canada & Appraisal Institute

|

|

|

- Matthew Ball

- 5 years ago

- Views:

Transcription

1 VALUATION BEYOND BORDERS 2017 INTERNATIONAL CONFERENCE Presented by Appraisal Institute Canada & Appraisal Institute 1

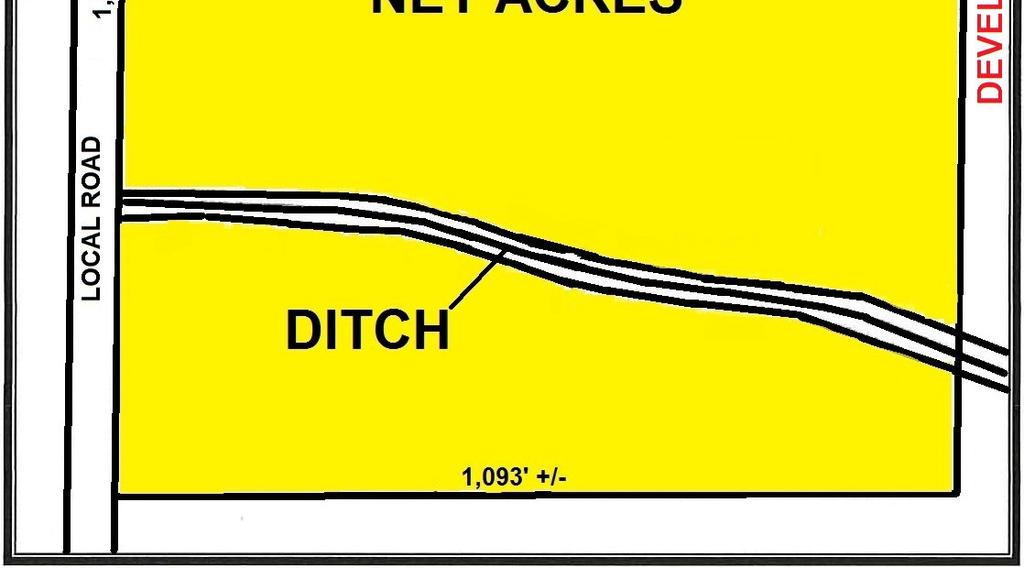

2 LITIGATION SUPPORT REVIEW CASE Subject s Basic Factors: Community: Vital, growing suburban community in the mid west Subject: acres of vacant development land Corner site Zoning: ID-2 - Research Flex District 2

3 APPRAISER S OPINIONS OF VALUE VALUATION BEFORE THE TAKING:$20,125,000 VALUATION AFTER THE TAKING: $18,568,388 DIFFERENCE: $ 1,556,612 3

4 The Subject Property 4

5 5

6 THE TAKINGS 6

7 WD = Fee simple acquisition. P = Permanent easements for utilities, grading and drainage. 7

8 APPRAISER S OPINION OF IMPACT FROM THE TAKINGS They will prohibit access on the Development Road, thereby causing a change in the Highest and Best Use of the property: the highest and best use of the residue, After the Taking, is lower-intensity commercial development land. 8

9 VALUATION BEFORE THE TAKING 9

10 "Before" Land Sale Summary Sale Location Sale Date Sale Price Acres $/Acre 1 Redacted 6/24/2011 $668, $425,000 2 Redacted 6/29/2011 $2,764, $308,000 3 Redacted 8/25/2017 $980, $629,820 4 Redacted 10/18/2011 $750, $483,559 5 Redacted 20/16/2011 $1,190, $297,500 6 Redacted 5/31/2012 $4,352, $425,000 7 Redacted 10/22/2012 $810, $243,355 8 Redacted 3/1/2013 $990, $244,264 9 Redacted 6/5/2013 $1,000, $341, Redacted 6/27/2013 $4,000, $301, Redacted 6/28/2013 $750, $251, Redacted 9/17/2013 $1,000, $159, Redacted 3/11/2014 $910, $319, Redacted 9/30/2014 $2,000, $775, Redacted 4/1/2015 $1,700, $325, Redacted 4/13/2015 $3,450, $203,720 Sub Local / State Roads Smallest Largest 10

11 VALUE CONCLUSION BEFORE THE TAKING analysis took into account the physical characteristics of the subject, as well as the surrounding development trends, with the adjusted unit values providing a reliable range in value. CONCLUSION: $20,125,000 11

12 VALUATION OF THE RESIDUE 12

13 13

14 "After" Land Sale Summary Sale Location Sale Date Sale Price Acres $/Acre 1 Redacted 6/24/2011 $668, $425,000 2 Redacted 6/29/2011 $2,764, $308,000 3 Redacted 8/25/2017 $980, $629,820 4 Redacted 10/18/2011 $750, $483,559 5 Redacted 20/16/2011 $1,190, $297,500 6 Redacted 5/31/2012 $4,352, $425,000 7 Redacted 10/22/2012 $810, $243,355 8 Redacted 3/1/2013 $990, $244,264 9 Redacted 6/5/2013 $1,000, $341, Redacted 6/27/2013 $4,000, $301, Redacted 6/28/2013 $750, $251, Redacted 9/17/2013 $1,000, $159, Redacted 3/11/2014 $910, $319, Redacted 9/30/2014 $2,000, $775, Redacted 4/1/2015 $1,700, $325, Redacted 4/13/2015 $3,450, $203,720 Sub Local / State Roads

15 AFTER VALUE ANALYSIS: Although subject is larger than the sales, a variety of uses would be reasonable.it is noted that the changes to subject indicate a slightly less intensive commercial use for a portion of the site.an overall unit value of $325,000 per acre has been selected After Value = $18,568,385 15

16 REVIEWER S ANALYSIS 16

17 A. Verification of Sales. POINTS OF DISAGREEMENT B. Relevance of Sales Comparables. C. Lack of application of systematic process in the Sales Comparison approach. D. Faulty Highest and Best Use analysis. E. Erroneous Effect of the Taking analysis. 17

18 ITEM A Sales Verification (setting forth a standard ) no information in the report or workfile that indicates that the appraiser independently verified the sale transactions with a knowledgeable party to the sale. Both the Uniform Standards of Federal Land Acquisition and the DOT require the appraiser to speak directly with a party to the transaction. they set a base level of standards prevalent in eminent domain scope of work situations, to wit: 18

19 ITEM A Sales Verification (cont.) (setting forth a standard ) Verification-A primary purpose of verifying a sale of real property is to make sure that the sale occurred under conditions that meet the definition of value used in the appraisal. The Uniform Standards of Professional Appraisal Practice require that appraisers collect, verify and analyze all information necessary to achieve credible assignment results. Page 125, The Appraisal of Real Estate, 14 th Edition, c 2013 by The Appraisal Institute 19

20 ITEM A Sales Verification (cont.) (setting forth a standard ) These items could significantly impact the comparison process. Lack of independent verification does not allow for their consideration in the analysis. The lack of verification is considered a flaw. 20

21 ITEM A VERIFICATION OF SALES STEP 3 FACTORS COMPLETENESS The comparable sales data were not thoroughly developed. ACCURACY The accuracy of the work under review is therefore, highly suspect. It does not conform to typical standards for an eminent domain appraisal. ADEQUACY The sales data were not adequately verified. Therefore, the scope of work was inadequate. 21

22 ITEM B ITEM B- Relevance Relevanceof Sales Comparables The sales data used are not comparable to subject, to wit: 1. Comps range from to ac. 2. Mean is ac. and median is ac. 3. Subject is ac. 4. Smallest sale was restaurant on ac. Implies subject could contain 37+ similar sites. 5. Largest was ac. for apartment use. Implies subject could hold 3.4 X more apartments or 1,426 units. 22

23 B. Relevance of Sales (cont.) How long would it take to absorb 37 restaurant sites or 1,420 apartment units in this market? Subject simply could not be fully used as quickly as a smaller single user site could. Therefore, a discount would be required because: development for numerous small site users would require planning, design, infrastructure, holding costs, time and entrepreneurial profit. 23

24 B. Relevance of Sales (cont.) (setting forth a standard) Following are three definitions which have applicability to this situation: site. Improved land or a lot in a finished state so that it is ready to be used for a specific purpose. raw land.land that is undeveloped; land in its natural state before grading, draining, subdivision, or the installation of utilities; land with minimal or no appurtenant constructed improvements. commercial land. Land that can be developed for a nonspecific commercial use. The Dictionary of Real Estate Appraisal 6 th Edition, c-2016 by the Appraisal Institute, pg40. The Dictionary of Real Estate Appraisal 6 th Edition, c-2016 by the Appraisal Institute, pg215. The Dictionary of Real Estate Appraisal 6 th Edition, c-2016 by the Appraisal Institute, pg

25 B. Relevance of Sales (cont.) RESULTS OF REVIEWER S INVESTIGATION: Only 3 of the 16 sales comparables and possibly 3 others were legally permitted in this zoning district. 25

26 REVIEWER'S RECONSTRUCTED LAND SALE/USE SUMMARY Sale Sale Date Acres $/Ac. Use in Report JLS ObservedUse Permitted in ID-2? 1 6/24/ $425,000 Hotel (Fairfield Inn &Suites) No 6 5/31/ $425,000 Car Mag (car dealerships) No 9 6/5/ $341,297 Office Building (retail strip center) No 10 6/27/ $301,159 Wal-Mart (Wal-Mart) No 14 9/30/ $775,194 Hotel Vacant land No 15 4/1/ $325,483 Retail Center Impvmts. To be razed No 3 8/25/ $629,820 Restaurant (Logan's Roadhouse) No. Accessory only 4 10/18/ $483,559 Restaurant (IHOP) No. Accessory only 16 4/13/ $203,720 Apartments-420 Units Vacant land No. Live-work only. 7 10/22/ $243,355 Apartments (apartments) No. Live-work only. 5 12/16/ $297,500 Nursing Home (Heartland) Possible 8 3/1/ $244,264 Senior Living (Alzheimer's Care) Possible 13 3/11/ $319,410 Commercial (Senior Citizen) Possible 2 6/29/ $308,000 Medical (urgent care facility) Yes 11 6/28/ $251,762 Office Vacant land Yes 12 9/17/ $159,847 Office/Commercial Vacant - 2 pcls. Yes 26

27 B. Relevance of Sales (cont.) Report fatally flawed because no analytical process was evident which separated the legally permitted sales from the others or to otherwise account for this difference in the analysis. 27

28 ITEM B RELEVANCE OF SALES COMPARABLES STEP 3 FACTORS Completeness not met because data was not thoroughly analyzed. Accuracy This data set does not conform to the subject. The data are certainly not correct. Adequacy improper data. Relevance the data are not relevant (applicable). Reasonableness the legally permitted uses of most sales were not reasonable (fair or proper) under the circumstances. 28

29 ITEM C: Lack of application of a systematic analytical process (Sales Comparison Approach): On page 37 the report states:.the specifics of available land sales are researched, compared to the subject site, and adjusted for any differences that may affect the price. These differences include changing market conditions or time, property interest that was transferred, location and other physical characteristics. However, there are no quantitative or qualitative adjustment charts or narrative analyses in the report or analytical notes in the workfile. The salient differences were not measured and applied to each of the sales as compared to subject. 29

30 ITEM C LACK OF SYSTEMATIC PROCESS STEP 3 FACTORS Completeness The data were not adjusted nor were they compared to subject in a meaningful analytical manner. The analyses are incomplete. Accuracy, Adequacy, Relevance and Reasonableness The very broad brush technique used misrepresents accuracy(conformity to a standard) and adequacy, as well as relevance (connected and applicable to the outcome). Therefore, the results are not reasonable (fair or proper). 30

31 ITEM D: Highest and Best Use Analyses Appraiser s Conclusion: Commercial Development Land 1. Application of the four tests (legally permissible, physically possible, economically feasible and maximally productive) are vague, incomplete and inconsistent. 2. No delineation of legally permitted uses which leads to using 10 sales which were not legally permitted. 3. Conclusion is too vague in light of raw land and site definitions. 31

32 ITEM D -Highest and Best Use Analyses Step 3 Factors Completeness the analyses were not comprehensive and were not developed in a sound and methodical manner. Accurate the data did not conform to the four tests. Adequacy the conclusion was too vague. Relevance the conclusion was not connected to the sales data used. Reasonableness the conclusion was not proper and a reasonable person would disagree. Reasonable care was not used. 32

33 ITEM E: Appraiser s Effect of the Taking Page 60 of the appraisal report: After the taking The property will have access from Local Road and via the right-in/right-out driveway on State Road. The Taking and the easements precludeaccess to/from Development Road. 33

34 ITEM E: Effect of the Taking This statement is factually incorrect. Reference is made to the legal descriptions for the takings in the addenda of the appraisal report. They clearly enumerate the extent of access rights as follows: Parcel 1-WD: WITHOUT LIMITATION OF EXISTING ACCESS RIGHTS Parcel 1-P1: Grantor/Owner, for himself and his heirs, executors, administrators, successors and assigns, reserves all existing rights of ingress and egress to and from any residual area. Parcel 1-P2: Grantor/Owner, for himself and his heirs, executors, administrators, successors and assigns, reserves all existing rights of ingress and egressto and from any residual area. 34

35 ITEM E EFFECT OF THE TAKING (change in HBU) Step 3 FACTORS ACCURACY, ADEQUACY, RELEVANCE AND REASONABLENESS No access rights have been acquired and the conclusion (page 60, 2 nd paragraph) that: the highest and best use of the residue, After the Taking, is lower-intensity commercial development land. is not accurate and is not adequate (lacks support). The conclusion is not reasonable (fair or proper). 35

36 FINAL CONCLUSIONS OF THE REVIEWER A. The analyses are not appropriate. B. The opinions and conclusions are not credible. C. The report is not appropriate and is considered to be misleading. 36

37 PRACTICAL RESULT OF REVIEW Appraisal result= $1,556,612 award to property owner. Settlement result = $227,000. (And perhaps some semblance of the Public Trust is maintained/restored.) 37

38 THE END QUESTIONS AND ANSWERS 38

39 REVIEW REPORT FUNDAMENTALS 39

40 IDENTITY OF THE WORK UNDER REVIEW: Property Identification: SEC State Road & Local Road Burgeoning Midwest City, USA Appraiser/Appraisal Firm: REDACTED Effective Date of Value: August 10, 2015 Appraisal Report Date: October 9,

41 IDENTITY OF THE APPRAISAL REVIEWER: Jefferson L. Sherman, MAI, AI-GRS Sherman-Andrzejczyk Group, Inc Chardon Road Suite 220 Willoughby Hills, Ohio DATE OF REVIEW REPORT: March 15, 2016 IDENTITY OF CLIENT AND INTENDED USERS OF THE REVIEW: Iwanna Wynn, Esq., and Doie, Cheatum & Howe, LLC INTENDED USE OF THE REVIEWER S OPINIONS AND CONCLUSIONS: Litigation preparation and potential settlement analysis. 41

42 PURPOSE OF THE REVIEW: The purpose of the appraisal review is to: a. Opine as to the report s consistency with the Uniform Standards of Professional Appraisal Practice (USPAP). b. Consider the completeness, accuracy, adequacy, relevance and reasonableness of the appraisal, and; c. Opine as to whether the analyses are appropriate within the context of requirements applicable to that work, and; d. Opine as to whether the opinions and conclusions are credible within the context of the requirements applicable for that work, and; e. Develop an opinion whether the report is appropriate and not misleading within the context of the requirements applicable to that work; and f. Develop reasons for any disagreement and; g. Not produce the reviewer s own opinions of value 42

43 EXTRAORDINARY ASSUMPTIONS OF THE REVIEW: None HYPOTHETICAL CONDITIONS OF THE APPRAISAL REVIEW: None 43

44 SCOPE OF WORK USED TO DEVELOP THIS APPRAISAL REVIEW: I read the appraisal report. I examined the contents of the appraiser s workfile as provided to me by the Client. I conducted a drive-by inspection/viewing of the subject and the comparable land sales used in the report. I did not attempt to verify the sales or subject data other than via corroboration with available public record data. I analyzed the report and workfile for consistency with the Uniform Standards of Professional Appraisal Practice, for the appraisal theory and techniques, proper before and after analysis for an eminent domain matter, mathematical accuracy, reasonableness and consistency, and as to the credibility of the analyses and conclusions. I did not communicate with the appraiser in any way during the course of this review assignment. 44

45 VALUATION BEYOND BORDERS 2017 INTERNATIONAL CONFERENCE Presented by Appraisal Institute Canada & Appraisal Institute Thank You 45

Anatomy Of An Appraisal

Anatomy Of An Appraisal Leslie A. Fields The most important thing to know about an appraisal report is how to review and critique it. Leslie A. Fields a partner with the Law Firm of Faegre & Benson LLP,

Anatomy Of An Appraisal Leslie A. Fields The most important thing to know about an appraisal report is how to review and critique it. Leslie A. Fields a partner with the Law Firm of Faegre & Benson LLP,

Appraisal Review & Advisory Opinion 20 Controversy. Presenter: Lisa Kimbro, MAI, AI-GRS

Appraisal Review & Advisory Opinion 20 Controversy Presenter: Lisa Kimbro, MAI, AI-GRS Practicing appraisers know USPAP, and appraisers that complete review work know USPAP s Standard 3. But what about

Appraisal Review & Advisory Opinion 20 Controversy Presenter: Lisa Kimbro, MAI, AI-GRS Practicing appraisers know USPAP, and appraisers that complete review work know USPAP s Standard 3. But what about

How to Read a Real Estate Appraisal Report

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

Appraisal Review for Appraiser Regulators

Appraisal Review for Appraiser Regulators Amy C. McClellan, SRA, MBA Stephen S. Wagner, MAI, SRA, AI GRS October 14, 2017 Presentation Highlights How appraisal regulators can use appraisal reviews Types

Appraisal Review for Appraiser Regulators Amy C. McClellan, SRA, MBA Stephen S. Wagner, MAI, SRA, AI GRS October 14, 2017 Presentation Highlights How appraisal regulators can use appraisal reviews Types

2018 SCCAI RESIDENTIAL SYMPOSIUM USPAP OF THE FUTURE. Paula Konikoff, JD, MAI, AI GRS

USPAP OF THE FUTURE Paula Konikoff, JD, MAI, AI GRS WHERE WE ARE NOW 2 Joint task force for Improvement of USPAP Appraisal Institute and Appraisal Foundation develop USPAP Optimization Concept 3 When unnecessary

USPAP OF THE FUTURE Paula Konikoff, JD, MAI, AI GRS WHERE WE ARE NOW 2 Joint task force for Improvement of USPAP Appraisal Institute and Appraisal Foundation develop USPAP Optimization Concept 3 When unnecessary

UNDERSTANDING HOW USPAP APPLIES TO REAL PROPERTY APPRAISAL PRACTICE USPAP Matrix

UNDERSTANDING HOW USPAP APPLIES TO REAL PROPERTY APPRAISAL PRACTICE - 2014-2015 USPAP Matrix This matrix assumes an Appraisal Report Format under S. R. 2-2(a). *Last updated 9/11/14* GENERAL Violation

UNDERSTANDING HOW USPAP APPLIES TO REAL PROPERTY APPRAISAL PRACTICE - 2014-2015 USPAP Matrix This matrix assumes an Appraisal Report Format under S. R. 2-2(a). *Last updated 9/11/14* GENERAL Violation

Guide Note 15 Assumptions and Hypothetical Conditions

Guide Note 15 Assumptions and Hypothetical Conditions Introduction Appraisal and review opinions are often premised on certain stated conditions. These include assumptions (general, and special or extraordinary)

Guide Note 15 Assumptions and Hypothetical Conditions Introduction Appraisal and review opinions are often premised on certain stated conditions. These include assumptions (general, and special or extraordinary)

RevuPro Appraisal Review

RevuPro Appraisal Review Getting It Right ELLIOTT introduces its flagship review product RevuPro, as an independent appraisal review service. Q. What is it and what does it do? A. RevuPro is a fast, economical

RevuPro Appraisal Review Getting It Right ELLIOTT introduces its flagship review product RevuPro, as an independent appraisal review service. Q. What is it and what does it do? A. RevuPro is a fast, economical

PREPARATION OF THE DEMONSTRATION APPRAISAL REPORT

PREPARATION OF THE DEMONSTRATION APPRAISAL REPORT INTRODUCTION The preparation of the demonstration appraisal report is one of the critical components of the accreditation process. The objective of the

PREPARATION OF THE DEMONSTRATION APPRAISAL REPORT INTRODUCTION The preparation of the demonstration appraisal report is one of the critical components of the accreditation process. The objective of the

VALUE FINDING APPRAISAL REPORT

RE 90 Rev. 01-2014 VALUE FINDING APPRAISAL REPORT (Compensation not to exceed $65,000) COUNTY John Doe 2880 Lancaster-Newark Rd. (SR 37), Pleasant Twp., 43030 Owner Mailing Address of Owner East side of

RE 90 Rev. 01-2014 VALUE FINDING APPRAISAL REPORT (Compensation not to exceed $65,000) COUNTY John Doe 2880 Lancaster-Newark Rd. (SR 37), Pleasant Twp., 43030 Owner Mailing Address of Owner East side of

Uniform Residential Appraisal Report (URAR) Model Appraisal

Model Appraisal") Basic Appraisal Procedures Residential Applications & Model Appraisals 15-13 Uniform Residential Appraisal Report (URAR) Model Appraisal On the following pages are examples of a completed Fannie Mae/Freddie

Basic Appraisal Procedures Residential Applications & Model Appraisals 15-13 Uniform Residential Appraisal Report (URAR) Model Appraisal On the following pages are examples of a completed Fannie Mae/Freddie

First Exposure Draft of proposed changes for the edition of the Uniform Standards of Professional Appraisal Practice

TO: FROM: RE: All Interested Parties J. Carl Schultz, Jr., Chair Appraisal Standards Board First Exposure Draft of proposed changes for the 2014-15 edition of the Uniform Standards of Professional Appraisal

TO: FROM: RE: All Interested Parties J. Carl Schultz, Jr., Chair Appraisal Standards Board First Exposure Draft of proposed changes for the 2014-15 edition of the Uniform Standards of Professional Appraisal

Yellow highlighting emphases added by A.L. Appraisal Co.

1 2 3 4 5 6 7 8 9 10 11 (AO-11) This communication by the Appraisal Standards Board (ASB) does not establish new standards or interpret existing standards. Advisory Opinions are issued to illustrate the

1 2 3 4 5 6 7 8 9 10 11 (AO-11) This communication by the Appraisal Standards Board (ASB) does not establish new standards or interpret existing standards. Advisory Opinions are issued to illustrate the

Land, Agricultural Improvements, CAFO, Rural Residence, Farm

*--FSA Appraisal Guidelines Land, Agricultural Improvements, CAFO, Rural Residence, Farm The following information elements and content descriptions are provided as guidelines to assist lenders and appraisers

*--FSA Appraisal Guidelines Land, Agricultural Improvements, CAFO, Rural Residence, Farm The following information elements and content descriptions are provided as guidelines to assist lenders and appraisers

Page 1 of 5 STANDARD 3: APPRAISAL REVIEW, DEVELOPMENT AND REPORTING In performing an appraisal review, an appraiser acting as a reviewer must develop and report a credible opinion as to the quality of

Page 1 of 5 STANDARD 3: APPRAISAL REVIEW, DEVELOPMENT AND REPORTING In performing an appraisal review, an appraiser acting as a reviewer must develop and report a credible opinion as to the quality of

619 STANDARD 2: REAL PROPERTY APPRAISAL, REPORTING

619 STANDARD 2: REAL PROPERTY APPRAISAL, REPORTING 620 In reporting the results of a real property appraisal, an appraiser must communicate each analysis, 621 opinion, and conclusion in a manner that is

619 STANDARD 2: REAL PROPERTY APPRAISAL, REPORTING 620 In reporting the results of a real property appraisal, an appraiser must communicate each analysis, 621 opinion, and conclusion in a manner that is

First Exposure Draft of proposed changes for the edition of the Uniform Standards of Professional Appraisal Practice

TO: FROM: RE: All Interested Parties Sandra Guilfoil, Chair Appraisal Standards Board First Exposure Draft of proposed changes for the 2012-13 edition of the Uniform Standards of Professional Appraisal

TO: FROM: RE: All Interested Parties Sandra Guilfoil, Chair Appraisal Standards Board First Exposure Draft of proposed changes for the 2012-13 edition of the Uniform Standards of Professional Appraisal

Restricted Use Appraisal Report Residential

Client File #: Appraisal File #: Restricted Use Appraisal Report Residential Appraisal Company: Address: Form 200.04* Phone: Fax: Website: Appraiser: Co-Appraiser: AI Membership (if any): SRA MAI SRPA

Client File #: Appraisal File #: Restricted Use Appraisal Report Residential Appraisal Company: Address: Form 200.04* Phone: Fax: Website: Appraiser: Co-Appraiser: AI Membership (if any): SRA MAI SRPA

USPAP Q&A USPAP Q&A Issue Date: December 19, 2017

USPAP Q&A 2018-19 USPAP Q&A Issue Date: December 19, 2017 The Appraisal Standards Board (ASB) of The Appraisal Foundation develops, interprets, and amends the Uniform Standards of Professional Appraisal

USPAP Q&A 2018-19 USPAP Q&A Issue Date: December 19, 2017 The Appraisal Standards Board (ASB) of The Appraisal Foundation develops, interprets, and amends the Uniform Standards of Professional Appraisal

Conservation Easement Appraisals. Applicability. Part I: Appraisal Concepts and Methods of Valuation

Conservation Easement Appraisals 2011 Wyoming Conservation Easement Conference June 2, 2011 Laramie, Wyoming Hunsperger & Weston, Ltd. Mark Weston 5889 Greenwood Plaza Boulevard Suite 404 Greenwood Village,

Conservation Easement Appraisals 2011 Wyoming Conservation Easement Conference June 2, 2011 Laramie, Wyoming Hunsperger & Weston, Ltd. Mark Weston 5889 Greenwood Plaza Boulevard Suite 404 Greenwood Village,

APPRAISAL REVIEW REPORT

APPRAISAL REVIEW REPORT REVIEW OF APPRAISALS BY BECCARIA & WEBER, INC. RE: BUENA VISTA MOBILE HOME PARK PALO AL TO, CALIFORNIA REVIEWED BY JAMES BRABANT, MAI PREPARED FOR Law Foundation of Silicon Valley,

APPRAISAL REVIEW REPORT REVIEW OF APPRAISALS BY BECCARIA & WEBER, INC. RE: BUENA VISTA MOBILE HOME PARK PALO AL TO, CALIFORNIA REVIEWED BY JAMES BRABANT, MAI PREPARED FOR Law Foundation of Silicon Valley,

Second Exposure Draft of proposed changes for the edition of the Uniform Standards of Professional Appraisal Practice

TO: FROM: RE: All Interested Parties Sandra Guilfoil, Chair Appraisal Standards Board Second Exposure Draft of proposed changes for the 2012-13 edition of the Uniform Standards of Professional Appraisal

TO: FROM: RE: All Interested Parties Sandra Guilfoil, Chair Appraisal Standards Board Second Exposure Draft of proposed changes for the 2012-13 edition of the Uniform Standards of Professional Appraisal

Is Across-the-Fence Value Equal to Market Value?

Is Across-the-Fence Value Equal to Market Value? IRWA Educational Conference San Diego, California June 16, 2015 John T. Schmick Shenehon Company 2 What is the goal of valuation assignments? Market Value

Is Across-the-Fence Value Equal to Market Value? IRWA Educational Conference San Diego, California June 16, 2015 John T. Schmick Shenehon Company 2 What is the goal of valuation assignments? Market Value

Guide Note 6 Consideration of Hazardous Substances in the Appraisal Process

Guide Note 6 Consideration of Hazardous Substances in the Appraisal Process Introduction The consideration of environmental conditions along with social, economic, and governmental conditions is fundamental

Guide Note 6 Consideration of Hazardous Substances in the Appraisal Process Introduction The consideration of environmental conditions along with social, economic, and governmental conditions is fundamental

ILLINOIS HOUSING DEVELOPMENT AUTHORITY APPRAISAL SCOPE AND GUIDELINES December 2015

ILLINOIS HOUSING DEVELOPMENT AUTHORITY APPRAISAL SCOPE AND GUIDELINES December 2015 As part of the Common Application for Multifamily Financing, the Illinois Housing Development Authority (IHDA) requires

ILLINOIS HOUSING DEVELOPMENT AUTHORITY APPRAISAL SCOPE AND GUIDELINES December 2015 As part of the Common Application for Multifamily Financing, the Illinois Housing Development Authority (IHDA) requires

SUBJECT: The Appraisal of Real Property That May Be Impacted by Environmental Contamination

1 ADVISORY OPINION 9 (AO-9) 1 2 3 4 This communication by the Appraisal Standards Board (ASB) does not establish new standards or interpret existing standards. Advisory Opinions are issued to illustrate

1 ADVISORY OPINION 9 (AO-9) 1 2 3 4 This communication by the Appraisal Standards Board (ASB) does not establish new standards or interpret existing standards. Advisory Opinions are issued to illustrate

concepts and techniques

concepts and techniques S a m p l e Timed Outline Topic Area DAY 1 Reference(s) Learning Objective The student will learn Teaching Method Time Segment (Minutes) Chapter 1: Introduction to Sales Comparison

concepts and techniques S a m p l e Timed Outline Topic Area DAY 1 Reference(s) Learning Objective The student will learn Teaching Method Time Segment (Minutes) Chapter 1: Introduction to Sales Comparison

Restricted Use Appraisal Report Residential

Client File #: Appraisal File #: Restricted Use Appraisal Report Residential Form 200.04 * Appraiser: AI Membership (if any): SRA MAI SRPA AI Affiliation (if any): Candidate for Designation Practicing

Client File #: Appraisal File #: Restricted Use Appraisal Report Residential Form 200.04 * Appraiser: AI Membership (if any): SRA MAI SRPA AI Affiliation (if any): Candidate for Designation Practicing

Real Estate Appraisal Professional Standards

Real Estate Appraisal Professional Standards Summary This proposal is to amend the Florida Administrative Code (FAC) to allow a Certified Residential Appraiser or a Certified General Appraiser to use standards

Real Estate Appraisal Professional Standards Summary This proposal is to amend the Florida Administrative Code (FAC) to allow a Certified Residential Appraiser or a Certified General Appraiser to use standards

THE WAIVER OF APPRAISAL

THE WAIVER OF APPRAISAL Succinct Explanation of the RW Process When rights of way are needed for a highway project, the owner of the property needed for the project is offered compensation (FMVE). Then

THE WAIVER OF APPRAISAL Succinct Explanation of the RW Process When rights of way are needed for a highway project, the owner of the property needed for the project is offered compensation (FMVE). Then

Common Errors and Issues in Review

Common Errors and Issues in Review February 1, 2018 Copyright 2018 Appraisal Institute. All rights reserved. Printed in the United States of America. No part of this publication may be reproduced, stored

Common Errors and Issues in Review February 1, 2018 Copyright 2018 Appraisal Institute. All rights reserved. Printed in the United States of America. No part of this publication may be reproduced, stored

Appraisal Review Update: Trends and Best Practices for Lenders and Appraisers

Appraisal Review Update: Trends and Best Practices for Lenders and Appraisers Presenters: Eric Schwartz, MAI, SRA, AI-GRS Rob Moorman, MAI, SRA, AI-GRS AI Connect July 2016 Charlotte, N.C. 1 2 Meet the

Appraisal Review Update: Trends and Best Practices for Lenders and Appraisers Presenters: Eric Schwartz, MAI, SRA, AI-GRS Rob Moorman, MAI, SRA, AI-GRS AI Connect July 2016 Charlotte, N.C. 1 2 Meet the

Data Verification. Professional Excellence Bulletin [PP-14-E] February 1995

![Data Verification. Professional Excellence Bulletin [PP-14-E] February 1995](/thumbs/90/101597168.jpg "Data Verification. Professional Excellence Bulletin [PP-14-E] February 1995") Professional Excellence Bulletin [PP-14-E] February 1995 Although obviously a cornerstone of appraisal practice, data verification has not been considered a major problem to real estate appraisers in the

Professional Excellence Bulletin [PP-14-E] February 1995 Although obviously a cornerstone of appraisal practice, data verification has not been considered a major problem to real estate appraisers in the

HIGHEST & BEST USE CHALLENGES AND SUPPORTING ADJUSTMENTS 6/11/2018 KEN MROZEK, MAI, SRA, ASA HIGHEST AND BEST USE CHALLENGES AND

HIGHEST & BEST USE CHALLENGES AND SUPPORTING ADJUSTMENTS KEN MROZEK, MAI, SRA, ASA KEN MROZEK, MAI, SRA, ASA Appraiser for 15 years Commercial and Residential Appraisals Partner and President of ARC Appraisals

HIGHEST & BEST USE CHALLENGES AND SUPPORTING ADJUSTMENTS KEN MROZEK, MAI, SRA, ASA KEN MROZEK, MAI, SRA, ASA Appraiser for 15 years Commercial and Residential Appraisals Partner and President of ARC Appraisals

Misconceptions about Across-the-Fence Methodology

Misconceptions about Across-the-Fence Methodology BY JOHN SCHMICK Across-the-fence methodology (ATF) is an appraisal tool frequently used in valuation assignments where the subject is part of railroad

Misconceptions about Across-the-Fence Methodology BY JOHN SCHMICK Across-the-fence methodology (ATF) is an appraisal tool frequently used in valuation assignments where the subject is part of railroad

APPRAISAL REVIEW REPORT. April 7, Yasmi Govin, Director of Business and Property Management Broward County Aviation Department

Public Works Department Facilities Management Division REAL PROPERTY SECTION 115 S. Andrews Avenue, Room 501 Fort Lauderdale, Florida 33301 954-357-6808 FAX 954-357-6292 APPRAISAL REVIEW REPORT April 7,

Public Works Department Facilities Management Division REAL PROPERTY SECTION 115 S. Andrews Avenue, Room 501 Fort Lauderdale, Florida 33301 954-357-6808 FAX 954-357-6292 APPRAISAL REVIEW REPORT April 7,

PINECREST ACADEMY OF NEVADA

NOTICE OF PUBLIC MEETING of the Board of Directors of PINECREST ACADEMY OF NEVADA tice is hereby given that the Board of Directors of Pinecrest Academy of Nevada, a public charter school, will conduct

NOTICE OF PUBLIC MEETING of the Board of Directors of PINECREST ACADEMY OF NEVADA tice is hereby given that the Board of Directors of Pinecrest Academy of Nevada, a public charter school, will conduct

OHIO DEPARTMENT OF TRANSPORTATION OFFICE OF REAL ESTATE

OHIO DEPARTMENT OF TRANSPORTATION OFFICE OF REAL ESTATE DATE: April 3, 2017 TO: FROM: RE: Users of the Real Estate Manual Jared Miller, Manager Appraisal Unit Changes and Updates to the Real Estate Manual

OHIO DEPARTMENT OF TRANSPORTATION OFFICE OF REAL ESTATE DATE: April 3, 2017 TO: FROM: RE: Users of the Real Estate Manual Jared Miller, Manager Appraisal Unit Changes and Updates to the Real Estate Manual

Individual Cooperative Interest Appraisal Report

PURPOSE Individual Cooperative Interest Appraisal Report The purpose of this appraisal report is to provide the client with a credible opinion of the defined value of the subject property, given the intended

PURPOSE Individual Cooperative Interest Appraisal Report The purpose of this appraisal report is to provide the client with a credible opinion of the defined value of the subject property, given the intended

Exposure Draft of Proposed Changes to ADVISORY OPINION 21 (AO-21), USPAP Compliance

, USPAP Compliance") TO: FROM: RE: All Interested Parties Barry J. Shea, Chair Appraisal Standards Board Exposure Draft of Proposed Changes to ADVISORY OPINION 21 (AO-21), USPAP Compliance DATE: February 22, 2013 The goal

TO: FROM: RE: All Interested Parties Barry J. Shea, Chair Appraisal Standards Board Exposure Draft of Proposed Changes to ADVISORY OPINION 21 (AO-21), USPAP Compliance DATE: February 22, 2013 The goal

Second Exposure Draft of proposed changes for the edition of the Uniform Standards of Professional Appraisal Practice

TO: FROM: RE: All Interested Parties Barry J. Shea, Chair Appraisal Standards Board Second Exposure Draft of proposed changes for the 2016-17 edition of the Uniform Standards of Professional Appraisal

TO: FROM: RE: All Interested Parties Barry J. Shea, Chair Appraisal Standards Board Second Exposure Draft of proposed changes for the 2016-17 edition of the Uniform Standards of Professional Appraisal

Paragraph s 8, 9, and 10 from NACVA. Letter of October 27, 2016

Paragraph s 8, 9, and 10 from NACVA Letter of October 27, 2016 Re: Comments Regarding Proposed Treasury Regulation (REG. 163113-02) (to be used also as an Outline of Topics to be Discussed at the Public

Paragraph s 8, 9, and 10 from NACVA Letter of October 27, 2016 Re: Comments Regarding Proposed Treasury Regulation (REG. 163113-02) (to be used also as an Outline of Topics to be Discussed at the Public

Guide to Appraisal Reports

Guide to Appraisal Reports What is an appraisal? An appraisal is an independent valuation of real property prepared by a qualified Appraiser and fully documented in a report. Based on a series of appraisal

Guide to Appraisal Reports What is an appraisal? An appraisal is an independent valuation of real property prepared by a qualified Appraiser and fully documented in a report. Based on a series of appraisal

AI General Demonstration Grading Sheet

AI General Demonstration Grading Sheet Traditional Report - Fundamental Market Analysis Option Account # Candidate Subject Property Address Grader Date Mailed to Grader Original Submission If original

AI General Demonstration Grading Sheet Traditional Report - Fundamental Market Analysis Option Account # Candidate Subject Property Address Grader Date Mailed to Grader Original Submission If original

CRN Presentation Review

CRN Presentation Review Collateral Risk Network June 18, 2013 Scott Sparks VP, Consumer Chief Real Estate Appraiser Fifth Third Bank Greg Stephens SVP, Appraisal Operations and Compliance Metro-West Appraisal

CRN Presentation Review Collateral Risk Network June 18, 2013 Scott Sparks VP, Consumer Chief Real Estate Appraiser Fifth Third Bank Greg Stephens SVP, Appraisal Operations and Compliance Metro-West Appraisal

SUBJECT: Unacceptable Assignment Conditions in Real Property Appraisal Assignments

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 ADVISORY OPINION 19 (AO-19) This communication by the Appraisal Standards Board (ASB) does not establish new standards

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 ADVISORY OPINION 19 (AO-19) This communication by the Appraisal Standards Board (ASB) does not establish new standards

Demonstration Appraisal Report Utilizing a Form Report

Demonstration Appraisal Report Utilizing a Form Report National Association of Independent Fee Appraisers 330 North Wabash Avenue, Suite 2000 Chicago, IL 60611 Phone: (312) 321-6830 Fax: (312) 673-6652

Demonstration Appraisal Report Utilizing a Form Report National Association of Independent Fee Appraisers 330 North Wabash Avenue, Suite 2000 Chicago, IL 60611 Phone: (312) 321-6830 Fax: (312) 673-6652

Appraisal Stream Restricted Use Residential Appraisal Report

Appraisal Stream Restricted Use Residential Appraisal Report File No. 769kemplin This report is limited to the sole and exclusive use of the client. The appraiser's opinions and conclusions set forth in

Appraisal Stream Restricted Use Residential Appraisal Report File No. 769kemplin This report is limited to the sole and exclusive use of the client. The appraiser's opinions and conclusions set forth in

To all Appraisers: Brief Overview:

To all Appraisers: As the appraisal industry continues to change, the demand for alternative valuation solutions grows. That is why is excited to announce the addition of a new product - the Desktop Appraisal

To all Appraisers: As the appraisal industry continues to change, the demand for alternative valuation solutions grows. That is why is excited to announce the addition of a new product - the Desktop Appraisal

Property Tax and Real Estate Appraisal Services

Property Tax and Real Estate Appraisal Services Appraisers/Consultants Micheal R. Lohmeier, ASA, MAI Certified General Real Estate Appraiser Direct: 248.368.8873 E: MLohmeier@virchowkrause.com Micheal

Property Tax and Real Estate Appraisal Services Appraisers/Consultants Micheal R. Lohmeier, ASA, MAI Certified General Real Estate Appraiser Direct: 248.368.8873 E: MLohmeier@virchowkrause.com Micheal

Residential Evaluation Report (RER) April, 2016

April, 2016") Residential Evaluation Report (RER) ensuring compliance with the Interagency Guidelines (IAG) and USPAP April, 2016 Definitions RER shall mean a Residential Evaluation Report and is deemed to be a restricted

Residential Evaluation Report (RER) ensuring compliance with the Interagency Guidelines (IAG) and USPAP April, 2016 Definitions RER shall mean a Residential Evaluation Report and is deemed to be a restricted

Appraisal Institute Education Programs (Last updated December 2017)

") Appraisal Institute Education Programs (Last updated December 2017) Education program descriptions This comprehensive catalog provides descriptions, total classroom/online hours, AI CE points, and state

Appraisal Institute Education Programs (Last updated December 2017) Education program descriptions This comprehensive catalog provides descriptions, total classroom/online hours, AI CE points, and state

MODULE 7-A: APPRAISALS, BPOS AND USPAP

MODULE 7-A: APPRAISALS, BPOS AND USPAP LEARNING OBJECTIVES One of the most challenging aspects of the real estate business is the development of prices or values of the rights to real estate. Buyers and

MODULE 7-A: APPRAISALS, BPOS AND USPAP LEARNING OBJECTIVES One of the most challenging aspects of the real estate business is the development of prices or values of the rights to real estate. Buyers and

Second Exposure Draft of Proposed Changes for the Edition of the Uniform Standards of Professional Appraisal Practice

TO: FROM: RE: All Interested Parties Margaret Hambleton, Chair Appraisal Standards Board Second Exposure Draft of Proposed Changes for the 2018-19 Edition of the Uniform Standards of Professional Appraisal

TO: FROM: RE: All Interested Parties Margaret Hambleton, Chair Appraisal Standards Board Second Exposure Draft of Proposed Changes for the 2018-19 Edition of the Uniform Standards of Professional Appraisal

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330 REVIEW NOTES by CHUCK DUNN CHAPTER 12 Copyright 2010 by the Real Estate Division and Chuck Dunn. All rights reserved ARE 3 RD EDITION REVIEW

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330 REVIEW NOTES by CHUCK DUNN CHAPTER 12 Copyright 2010 by the Real Estate Division and Chuck Dunn. All rights reserved ARE 3 RD EDITION REVIEW

Land / Site Valuation A Basic Review. Leslie G. Pruitt Certified General Appraiser

Land / Site Valuation A Basic Review Leslie G. Pruitt Certified General Appraiser Whose is the land, it is to the sky and the depth Whose is the land, it is to the sky and the depth This ancient maxim

Land / Site Valuation A Basic Review Leslie G. Pruitt Certified General Appraiser Whose is the land, it is to the sky and the depth Whose is the land, it is to the sky and the depth This ancient maxim

APPRAISAL REPORT OF GROSS ACRES/17.72± USABLE ACRES OF VACANT COMMERCIAL LAND

APPRAISAL REPORT OF 20.22 GROSS ACRES/17.72± USABLE ACRES OF VACANT COMMERCIAL LAND LOCATED AT NORTHWEST CORNER OF LAND O LAKES BOULEVARD & SUNTERRA DRIVE LAND O LAKES, FLORIDA 34638 Job No.: 14-0227 Prepared

APPRAISAL REPORT OF 20.22 GROSS ACRES/17.72± USABLE ACRES OF VACANT COMMERCIAL LAND LOCATED AT NORTHWEST CORNER OF LAND O LAKES BOULEVARD & SUNTERRA DRIVE LAND O LAKES, FLORIDA 34638 Job No.: 14-0227 Prepared

REPORTING GUIDELINES FOR REAL ESTATE APPRAISAL REPORTS

Property Tax Valuation Reporting REPORTING GUIDELINES FOR REAL ESTATE APPRAISAL REPORTS Robert F. Reilly and Robert P. Schweihs 43 INTRODUCTION Appraisal reports become important documents in property

Property Tax Valuation Reporting REPORTING GUIDELINES FOR REAL ESTATE APPRAISAL REPORTS Robert F. Reilly and Robert P. Schweihs 43 INTRODUCTION Appraisal reports become important documents in property

General Market Analysis and Highest & Best Use. Learning Objectives

General Market Analysis and Highest & Best Use Learning Objectives Module & Title Module 1 Real Estate Markets and Analysis Module 2 Types and Levels of Market Analysis Module 3 The Six-Step Process and

General Market Analysis and Highest & Best Use Learning Objectives Module & Title Module 1 Real Estate Markets and Analysis Module 2 Types and Levels of Market Analysis Module 3 The Six-Step Process and

Summary of Assignment. Identification of Property and Appraisal

Summary of Assignment My assignment is to review an appraisal of the Athow Property owned by Lewis and Janice Athow. The property is located near the mouth of the Dungeness River in Clallam County, Washington

Summary of Assignment My assignment is to review an appraisal of the Athow Property owned by Lewis and Janice Athow. The property is located near the mouth of the Dungeness River in Clallam County, Washington

BUSI 352 Learning Objectives

BUSI 352 Learning Objectives Purpose and Scope of the Course The Case Studies in Residential Appraisal course (BUSI 352) explores the depth and breadth of knowledge around the valuation of residential

BUSI 352 Learning Objectives Purpose and Scope of the Course The Case Studies in Residential Appraisal course (BUSI 352) explores the depth and breadth of knowledge around the valuation of residential

ASA MTS CANDIDATE REPORT REVIEW CHECKLIST INSTRUCTIONS (Effective as of January 01, 2018) Basic Report Requirements and General Report Quality

Basic Report Requirements and General Report Quality") ASA MTS CANDIDATE REPORT REVIEW CHECKLIST INSTRUCTIONS (Effective as of January 01, 2018) Basic Report Requirements and General Report Quality This checklist was designed to be a useful resource tool by

ASA MTS CANDIDATE REPORT REVIEW CHECKLIST INSTRUCTIONS (Effective as of January 01, 2018) Basic Report Requirements and General Report Quality This checklist was designed to be a useful resource tool by

Index of Examples. Chapter 1 Letter of Transmittal Chapter 2 General Assumptions and Limiting Conditions... 19

Index of Examples Chapter 1 Letter of Transmittal... 1 Example 1A Detailed Letter of Transmittal... 2 Example 1B Detailed Letter of Transmittal with Risk Factors and Assumptions... 6 Example 1C Brief Letter

Index of Examples Chapter 1 Letter of Transmittal... 1 Example 1A Detailed Letter of Transmittal... 2 Example 1B Detailed Letter of Transmittal with Risk Factors and Assumptions... 6 Example 1C Brief Letter

REQUEST FOR PROPOSAL (RFP) RFP AS. Appraisal Services Valuation of DBHA Properties

RFP AS. Appraisal Services Valuation of DBHA Properties") REQUEST FOR PROPOSAL (RFP) RFP 2019-01AS Appraisal Services Valuation of DBHA Properties Daytona Beach Housing Authority (DBHA) 211 N Ridgewood Ave Suite 300 Daytona Beach, FL 32114 (386) 253-5653 Terril

REQUEST FOR PROPOSAL (RFP) RFP 2019-01AS Appraisal Services Valuation of DBHA Properties Daytona Beach Housing Authority (DBHA) 211 N Ridgewood Ave Suite 300 Daytona Beach, FL 32114 (386) 253-5653 Terril

Mike Dalton Jr. and Associates. Christina Adams INVOICE NUMBER Mike Dalton Jr. and Associates 8191 Wethersfield Drive. PB125 Germantown, TN 38138

Mike Dalton Jr. and Associates FROM: INVOICE Christina Adams INVOICE NUMBER Mike Dalton Jr. and Associates 8191 Wethersfield Drive Germantown, TN 38138 DATE 08/14/2016 Telephone Number: (901) 674-0239

Mike Dalton Jr. and Associates FROM: INVOICE Christina Adams INVOICE NUMBER Mike Dalton Jr. and Associates 8191 Wethersfield Drive Germantown, TN 38138 DATE 08/14/2016 Telephone Number: (901) 674-0239

Evaluating Your Appraisal

Evaluating Your Appraisal April 28, 2011 Presented by: Brady W. Meadows Mortgage Compliance Advisors Instructions Because of the large number of registrants, the lines will be muted. To ask a question,

Evaluating Your Appraisal April 28, 2011 Presented by: Brady W. Meadows Mortgage Compliance Advisors Instructions Because of the large number of registrants, the lines will be muted. To ask a question,

Uniform Standards of Professional Appraisal Practice Business Valuation 7 Hour Course

Uniform Standards of Professional Appraisal Practice Business Valuation 7 Hour Course Carla G Glass, FASA Jay E Fishman, FASA Introduction USPAP Introduction Definitions Preamble Rules Standards 9 and

Uniform Standards of Professional Appraisal Practice Business Valuation 7 Hour Course Carla G Glass, FASA Jay E Fishman, FASA Introduction USPAP Introduction Definitions Preamble Rules Standards 9 and

Developing a Reviewer s Mentality... 1

Table of Contents Overview... ix Course Schedule... xiii SECTION 1 Introduction Developing a Reviewer s Mentality... 1 Part 1. Role of the Reviewer Preview Part 1... 5 Defining Review... 9 Why Clients

Table of Contents Overview... ix Course Schedule... xiii SECTION 1 Introduction Developing a Reviewer s Mentality... 1 Part 1. Role of the Reviewer Preview Part 1... 5 Defining Review... 9 Why Clients

FORENSIC REPORT EXAMINER

WHAT CAN A DO FOR YOU? TELL YOU WHAT YOU DON T KNOW! ANTHONY F. MOLLICA, MAI, CRE, ASA 1601 Bethel Road, Columbus, Ohio 43220 (614) 459-1140 AFMollica@AOL.COM -1- ANTHONY F. MOLLICA, MAI, CRE, ASA The

WHAT CAN A DO FOR YOU? TELL YOU WHAT YOU DON T KNOW! ANTHONY F. MOLLICA, MAI, CRE, ASA 1601 Bethel Road, Columbus, Ohio 43220 (614) 459-1140 AFMollica@AOL.COM -1- ANTHONY F. MOLLICA, MAI, CRE, ASA The

Across-the-Fence Value and Hostage Occupancy Agreements

Across-the-Fence Value and Hostage Occupancy Agreements EUCI Conference: Electric Transmission Projects San Diego, California September 19, 2016 John T. Schmick Shenehon Company 2 What is the goal of valuation

Across-the-Fence Value and Hostage Occupancy Agreements EUCI Conference: Electric Transmission Projects San Diego, California September 19, 2016 John T. Schmick Shenehon Company 2 What is the goal of valuation

Appraisal Review: Analyzing the 1004

Appraisal Review: Analyzing the 1004 1 LIVE ONLINE PARTICIPANT GUIDE Version: 8.12 Table of Contents The Purpose of the Appraisal... 3 Define Market Value... 3 Scenario 1 (John Johnson report) - 1004 Uniform

Appraisal Review: Analyzing the 1004 1 LIVE ONLINE PARTICIPANT GUIDE Version: 8.12 Table of Contents The Purpose of the Appraisal... 3 Define Market Value... 3 Scenario 1 (John Johnson report) - 1004 Uniform

January 11, 2017 MEMORANDUM. Issue. Background. Commissioner s Recommendation

State Board of Regents Board of Regents Building, The Gateway 60 South 400 West Salt Lake City, Utah 84101-1284 TAB Q Phone 801.321.7101 Fax 801.321.7199 TDD 801.321.7130 www.higheredutah.org January 11,

State Board of Regents Board of Regents Building, The Gateway 60 South 400 West Salt Lake City, Utah 84101-1284 TAB Q Phone 801.321.7101 Fax 801.321.7199 TDD 801.321.7130 www.higheredutah.org January 11,

What/Who Determines that an Appraiser is Qualified in our Program?

What/Who Determines that an Appraiser is Qualified in our Program? Mike Jones, SR/WA, Maryland Certified General Appraiser Realty Specialist, FHWA Office of Real Estate Services Is it becoming tougher

What/Who Determines that an Appraiser is Qualified in our Program? Mike Jones, SR/WA, Maryland Certified General Appraiser Realty Specialist, FHWA Office of Real Estate Services Is it becoming tougher

Special Purpose Properties. Special Valuation Considerations

Special Purpose Properties Special Valuation Considerations 2017 Case Study in Ottawa: New Automobile Dealership Many brand-specific specialties Cost: $4,000,000 (including land and a developer fee) Sales

Special Purpose Properties Special Valuation Considerations 2017 Case Study in Ottawa: New Automobile Dealership Many brand-specific specialties Cost: $4,000,000 (including land and a developer fee) Sales

AG-AMERICA COMMERCIAL FARM AND RANCH COLLATERAL VALUATION GUIDE

AG-AMERICA COMMERCIAL FARM AND RANCH COLLATERAL VALUATION GUIDE Table of Contents CHAPTER CV101 COLLATERAL VALUATION STANDARDS AND GUIDES... 1 CV101.1 Overview... 1 General Guidance on Terms:... 1 CHAPTER

AG-AMERICA COMMERCIAL FARM AND RANCH COLLATERAL VALUATION GUIDE Table of Contents CHAPTER CV101 COLLATERAL VALUATION STANDARDS AND GUIDES... 1 CV101.1 Overview... 1 General Guidance on Terms:... 1 CHAPTER

Training the Next Generation of Appraisers The S.T.A.R.T. Program - Standards to Assure Responsible Training:

Training the Next Generation of Appraisers The S.T.A.R.T. Program - Standards to Assure Responsible Training: An Industry Solution to the Declining Number of Appraisers Entering the Profession and Practical

Training the Next Generation of Appraisers The S.T.A.R.T. Program - Standards to Assure Responsible Training: An Industry Solution to the Declining Number of Appraisers Entering the Profession and Practical

RESTRICTED APPRAISAL REPORT

Restricted Use Appraisal Report Thomas J. Schulte & Associates Page #1 RESTRICTED APPRAISAL REPORT SUBJECT ASSIGNMENT Property City: Zip Code: County: Legal Description: Assessor's Parcel #: Tax Year:

Restricted Use Appraisal Report Thomas J. Schulte & Associates Page #1 RESTRICTED APPRAISAL REPORT SUBJECT ASSIGNMENT Property City: Zip Code: County: Legal Description: Assessor's Parcel #: Tax Year:

EvaluePro Real Estate Restricted Appraisal Report

EvaluePro Real Estate Restricted Appraisal Report EvaluePro Highlights Property Street: 1000 Main Street City: Anytown State: NC Zip: 12345 Property Owner: Mr. & Mrs. Property Owner Estimated Market Value:

EvaluePro Real Estate Restricted Appraisal Report EvaluePro Highlights Property Street: 1000 Main Street City: Anytown State: NC Zip: 12345 Property Owner: Mr. & Mrs. Property Owner Estimated Market Value:

REED APPRAISAL COMPANY REAL PROPERTY APPRAISERS AND CONSULTANTS

REAL PROPERTY APPRAISERS AND CONSULTANTS 100 SOUTH KENTUCKY AVENUE #230 ip.o. BOX 1645 ilakeland, FLORIDA 33802-1645 OFFICE: (863) 688-6718 ifax: (863) 688-5993iEMAIL: stan@reedappraisalco.com TO: Henry

REAL PROPERTY APPRAISERS AND CONSULTANTS 100 SOUTH KENTUCKY AVENUE #230 ip.o. BOX 1645 ilakeland, FLORIDA 33802-1645 OFFICE: (863) 688-6718 ifax: (863) 688-5993iEMAIL: stan@reedappraisalco.com TO: Henry

2. Is the information in the contract section complete and accurate? Yes No Not Applicable If Yes, provide a brief summary.

The purpose of this appraisal field review report is to provide the lender/client with an opinion on the accuracy of the appraisal report under review. Property Address City State Zip Code Borrower Owner

The purpose of this appraisal field review report is to provide the lender/client with an opinion on the accuracy of the appraisal report under review. Property Address City State Zip Code Borrower Owner

BUSI 452 Case Studies in Appraisal II

BUSI 452 Case Studies in Appraisal II PURPOSE AND SCOPE The Case Studies in Appraisal II course (BUSI 452) is a continuation of BUSI 442. This course is intended to introduce further practical applications

BUSI 452 Case Studies in Appraisal II PURPOSE AND SCOPE The Case Studies in Appraisal II course (BUSI 452) is a continuation of BUSI 442. This course is intended to introduce further practical applications

THE TENSION BETWEEN EXPERT WITNESSES AND COUNSEL

THE TENSION BETWEEN EXPERT WITNESSES AND COUNSEL 1 Paula K. Konikoff, JD, MAI, AI-GRS Michael Rubin, Esq. Rutan & Tucker Moderator Valeo Schultz, MAI Cushman & Wakefield 49 th Annual Litigation Seminar

THE TENSION BETWEEN EXPERT WITNESSES AND COUNSEL 1 Paula K. Konikoff, JD, MAI, AI-GRS Michael Rubin, Esq. Rutan & Tucker Moderator Valeo Schultz, MAI Cushman & Wakefield 49 th Annual Litigation Seminar

Division of Real Estate. Summary of BOREA Investigations

Division of Real Estate Summary of BOREA Investigations Complaint Stats for Prior 12 Months BOREA Checklist for Investigations Generally follows the FNMA 1004 layout Neighborhood and Market Analyses Site

Division of Real Estate Summary of BOREA Investigations Complaint Stats for Prior 12 Months BOREA Checklist for Investigations Generally follows the FNMA 1004 layout Neighborhood and Market Analyses Site

UNIFORM APPRAISAL DATASET (UAD) FHA SPOTLIGHT - SELECTION AND VERIFICATION OF COMPARABLE SALES

FHA SPOTLIGHT - SELECTION AND VERIFICATION OF COMPARABLE SALES") Spring 2011 Issue 3 FHA APPRAISER In This Issue: Welcome to the third issue of the Federal Housing Administration Appraiser Roster Newsletter. We hope you will find it informative. Uniform Appraisal Dataset

Spring 2011 Issue 3 FHA APPRAISER In This Issue: Welcome to the third issue of the Federal Housing Administration Appraiser Roster Newsletter. We hope you will find it informative. Uniform Appraisal Dataset

October 1, Mr. Wayne Miller, Chair Appraiser Qualifications Board The Appraisal Foundation th Street, NW, Suite 1111 Washington, DC 20005

October 1, 2015 Mr. Wayne Miller, Chair Appraiser Qualifications Board The Appraisal Foundation 1155 15th Street, NW, Suite 1111 Washington, DC 20005 Dear Mr. Miller, I am honored to have the opportunity

October 1, 2015 Mr. Wayne Miller, Chair Appraiser Qualifications Board The Appraisal Foundation 1155 15th Street, NW, Suite 1111 Washington, DC 20005 Dear Mr. Miller, I am honored to have the opportunity

USPAP Update & The Difficult and Unusual RW Appraisal Assignments

USPAP Update & The Difficult and Unusual RW Appraisal Assignments Presented by Michael C. McCall, MAI Chief Appraiser, VDOT April 15, 2013 USPAP Update On November 30 th, 2012, the Appraisal Standards

USPAP Update & The Difficult and Unusual RW Appraisal Assignments Presented by Michael C. McCall, MAI Chief Appraiser, VDOT April 15, 2013 USPAP Update On November 30 th, 2012, the Appraisal Standards

Table of Contents SECTION 1. Overview... ix. Schedule...xiii. Part 1. Origins of Eminent Domain

Table of Contents Overview... ix Schedule...xiii SECTION 1 Part 1. Origins of Eminent Domain Preview Part 1... 1 Origins of Eminent Domain... 3 Definitions... 4 Sources of Eminent Domain Law... 6 Agencies

Table of Contents Overview... ix Schedule...xiii SECTION 1 Part 1. Origins of Eminent Domain Preview Part 1... 1 Origins of Eminent Domain... 3 Definitions... 4 Sources of Eminent Domain Law... 6 Agencies

Chapter 35. The Appraiser's Sales Comparison Approach INTRODUCTION

Chapter 35 The Appraiser's Sales Comparison Approach INTRODUCTION The most commonly used appraisal technique is the sales comparison approach. The fundamental concept underlying this approach is that market

Chapter 35 The Appraiser's Sales Comparison Approach INTRODUCTION The most commonly used appraisal technique is the sales comparison approach. The fundamental concept underlying this approach is that market

Part 1. Estimating Land Value Using a Land Residual Technique Based on Discounted Cash Flow Analysis

Table of Contents Overview... v Seminar Schedule... ix SECTION 1 Part 1. Estimating Land Value Using a Land Residual Technique Based on Discounted Cash Flow Analysis Preview Part 1... 1 Land Residual Technique...

Table of Contents Overview... v Seminar Schedule... ix SECTION 1 Part 1. Estimating Land Value Using a Land Residual Technique Based on Discounted Cash Flow Analysis Preview Part 1... 1 Land Residual Technique...

Industrial and Commercial Real Estate Appraisal Procedures

Property Valuation Thought Leadership Industrial and Commercial Real Estate Appraisal Procedures John C. Ramirez The application of the asset-based approach to business valuation often involves the appraisal

Property Valuation Thought Leadership Industrial and Commercial Real Estate Appraisal Procedures John C. Ramirez The application of the asset-based approach to business valuation often involves the appraisal

The purpose of the appraisal was to determine the value of this six that is located in the Town of St. Mary s.

The purpose of the appraisal was to determine the value of this six that is located in the Town of St. Mary s. The subject property was originally acquired by Michael and Bonnie Etta Mattiussi in August

The purpose of the appraisal was to determine the value of this six that is located in the Town of St. Mary s. The subject property was originally acquired by Michael and Bonnie Etta Mattiussi in August

APPRAISAL OF REAL PROPERTY

Home Appraisals, Inc. (866) 533-7173 APPRAISAL OF REAL PROPERTY File # LOCATED AT Field Review Form Sample FOR OPINION OF VALUE 35, AS OF 11/1/7 TABLE OF CONTENTS One-Unit Field Review... 1 General Text

Home Appraisals, Inc. (866) 533-7173 APPRAISAL OF REAL PROPERTY File # LOCATED AT Field Review Form Sample FOR OPINION OF VALUE 35, AS OF 11/1/7 TABLE OF CONTENTS One-Unit Field Review... 1 General Text

Table of Contents SECTION 1. Overview... ix. Schedule...xiii. Part 1. Origins of Eminent Domain

Table of Contents Overview... ix Schedule...xiii SECTION 1 Part 1. Origins of Eminent Domain Preview Part 1... 1 Origins of Eminent Domain... 3 Definitions... 4 Sources of Eminent Domain Law... 5 Agencies

Table of Contents Overview... ix Schedule...xiii SECTION 1 Part 1. Origins of Eminent Domain Preview Part 1... 1 Origins of Eminent Domain... 3 Definitions... 4 Sources of Eminent Domain Law... 5 Agencies

BUSI 398 Residential Property Guided Case Study

BUSI 398 Residential Property Guided Case Study PURPOSE AND SCOPE The Residential Property Guided Case Study course BUSI 398 is intended to give the real estate appraisal student a working knowledge of

BUSI 398 Residential Property Guided Case Study PURPOSE AND SCOPE The Residential Property Guided Case Study course BUSI 398 is intended to give the real estate appraisal student a working knowledge of

Origins of Eminent Domain Definitions Sources of Eminent Domain Law Agencies with Power to Condemn Limitations on Condemnation Examples of Takings

Course Schedule SECTION 1. (Day 1 Morning) Overview Registration Orientation (Classroom Rules and Procedures) Part 1. Origins of Eminent Domain Origins of Eminent Domain Definitions Sources of Eminent

Course Schedule SECTION 1. (Day 1 Morning) Overview Registration Orientation (Classroom Rules and Procedures) Part 1. Origins of Eminent Domain Origins of Eminent Domain Definitions Sources of Eminent

The Official Guide to the Demonstration of Knowledge Requirement: Residential

The Official Guide to the Demonstration of Knowledge Requirement: Residential Effective June 7, 2017 Appraisal Institute advocates equal opportunity and nondiscrimination in the appraisal professional

The Official Guide to the Demonstration of Knowledge Requirement: Residential Effective June 7, 2017 Appraisal Institute advocates equal opportunity and nondiscrimination in the appraisal professional

Basic Appraisal Procedures

Hondros Learning Basic Appraisal Procedures Timed Outline Topic Area Reference(s) Learning Objectives The student will be able to identify and/or apply: Teaching Method Time Segment (Minutes) Day 1 Chapter

Hondros Learning Basic Appraisal Procedures Timed Outline Topic Area Reference(s) Learning Objectives The student will be able to identify and/or apply: Teaching Method Time Segment (Minutes) Day 1 Chapter

procedures Basic Appraisal F i n a l Examination #2 2 nd edition

F i n a l Examination #2 A n s w e r Key Page 82 1. When determining effective gross income from potential gross income, an appraiser considers a. debt service. b. depreciation. c. fixed expenses. d. vacancy

F i n a l Examination #2 A n s w e r Key Page 82 1. When determining effective gross income from potential gross income, an appraiser considers a. debt service. b. depreciation. c. fixed expenses. d. vacancy

ASSESSMENT REVIEW BOARD. The City of Edmonton JASPER AVENUE Assessment and Taxation Branch

ASSESSMENT REVIEW BOARD Churchill Building 10019 103 Avenue Edmonton AB T5J 0G9 Phone: (780) 496-5026 NOTICE OF DECISION NO. 0098 101/11 CVG The City of Edmonton 1200-10665 JASPER AVENUE Assessment and

ASSESSMENT REVIEW BOARD Churchill Building 10019 103 Avenue Edmonton AB T5J 0G9 Phone: (780) 496-5026 NOTICE OF DECISION NO. 0098 101/11 CVG The City of Edmonton 1200-10665 JASPER AVENUE Assessment and

Table of Contents. Chapter 1: Introduction (Mobile Technology Evolution) 1

1") Chapter 1: Introduction (Mobile Technology Evolution) 1 I. WHY APPRAISAL IS IMPORTANT (p. 3) II. DEFINITION OF APPRAISAL (p. 4) A. Opinion (p. 4) B. Value (p. 5) C. Appraisal Art or Science? (p. 5) D.

Chapter 1: Introduction (Mobile Technology Evolution) 1 I. WHY APPRAISAL IS IMPORTANT (p. 3) II. DEFINITION OF APPRAISAL (p. 4) A. Opinion (p. 4) B. Value (p. 5) C. Appraisal Art or Science? (p. 5) D.