ASC 842 Lease Accounting Quantitative Disclosure Requirements for Tenants You Need to Know. AUTHOR: Michael Nichols, Chief Financial Officer

|

|

|

- Camilla Bridges

- 5 years ago

- Views:

Transcription

1 ASC 842 Lease Accounting Quantitative Disclosure Requirements for Tenants You Need to Know AUTHOR: Michael Nichols, Chief Financial Officer

released the new ASC 842 and 23% of organizations have yet to assess the impact of changes.")

2 The Current State of ASC 842 CURRENT IMPACT OF THE NEW FASB REGULATIONS It s been a little over one year since the Financial Accounting Standards Board (FASB) released the new ASC 842 and 23% of organizations have yet to assess the impact of changes. While the new standard is set to take effect January 1st, 2019, the adjustment of these regulations will have a significant impact on operations and resources. The new ASC 842 essentially requires companies to build their own disclosure based on a set of proscribed requirements from FASB. According to recent progress reports conducted by Pricewaterhouse Coopers, (PWC) financial executives listed data collection and systems among their biggest challenges. In fact, an estimated 75% of respondents described their implementation issues as somewhat or very difficult likely due to the intricate calculations now required. The cost of implementing these regulations are expected to rise but Fischer s technology is empowering clients to get ahead of the challenge and save thousands of expenses in the long run. 23% Organizations Yet to Assess Changes 75% Analysts estimate there are approximately $3 trillion in off-balance sheet lease commitments alone. Previously, a large portion of lease costs were limited to the income statement and might only appear on the balance sheet as a footnote. Currently, the only disclosures you re likely to see is in the disclosure for off-balance sheet arrangements and contractual obligations within Management s Discussion and Analysis, however, this has taken a huge turn requiring a massive manual output from financial reporting. Find Implementation Somewhat of Very Difficult 43% Will Use a New Lease Management System to Handle Transition

3 ASC 842 will now require companies to put their lease obligations on the balance sheet both as a liability and asset ( Lease Liability and Right of Use Asset ). The disclosure objective as stated in ASC 842 is for entities to provide information about leases that enable users of financial statements to assess the amount, timing, AND uncertainty of cash flows arising from leases. In order to achieve this objective, lessees will need to do more than just recognize all leases on the balance sheet. Lessees and lessors will be required to disclose both quantitative and qualitative information regarding its leases and the significant judgments made when applying ASC 842, as well as the amounts recognized in the financial statements related to leases. It s no surprise that companies are investing heavy financial resources and staff into making the needed changes. PWC reported 43% of financial executive indicated they will implement a new lease management system to handle the complexities of this transition and many are allocating internal staff to implement changes. With the complex nature of ASC 842 and deadline swiftly approaching, it s safe to assume many organizations are at great risk of accelerating a process that requires much diligence. More importantly, the new regulations can help improve lease management if handled properly. For example, are you currently tracking the separate operating and financing cash flows for finance leases vs the operating cash flows for operating leases? Are you capable of building a spreadsheet to track each of the disclosure items on an individual basis for each property in your portfolio that also aggregates them for financial reporting purposes? Just months away from ASC 842 taking effect, these are the questions organizations should be assessing. Evaluating Opportunity With nearly three decades in tenant representation and customized product development, Fischer is taking lead in providing solutions to help clients leverage these changes as an opportunity. Fischer s ManagePath product is fully compliant with ASC 842 disclosure requirements and possess a streamlined system of automated calculations and workflows to help mitigate risks. To better help you understand the unusual regulations, let s examine the key changes surrounding disclosure requirements organizations must start to solve for.

Sublease income, disclosed on a gross basis,")

4 Lessee Disclosures to Be Aware of You will notice under paragraph the new issuance requires that a lessee discloses qualitative and quantitative information about its leases in addition to the significant judgements made in applying ASC 842 to those leases and the amounts recognized in the financial statements relating to those leases requires that a lessee consider the level of detail necessary to satisfy the disclosure objective to ensure it is presenting useful information that is not obscured by providing insignificant detail or by aggregating items with different characteristics. To achieve this end is very specific and requires that a lessee shall disclose significant qualitative details. Since we re focused on quantitative disclosures let s look at the requirements of , which stipulates the following information be presented: Finance lease cost, segregated between the amortization of the right-of-use assets and interest on the lease liabilities Operating lease cost determined in accordance with paragraphs (a) and Short-term lease cost, excluding expenses relating to leases with a lease term of one month or less, determined in accordance with paragraph Variable lease cost determined in accordance with paragraphs (b) and (b) Sublease income, disclosed on a gross basis, separate from the finance or operating lease expense Net gain or loss recognized from sale and leaseback transactions in accordance with paragraph Amounts segregated between those for finance and operating leases for the following items: Cash paid for amounts included in the measurement of lease liabilities, segregated between operating and financing cash flows Supplemental noncash information on lease liabilities arising from obtaining right-of-use assets Weighted-average remaining lease term Weighted-average discount rate

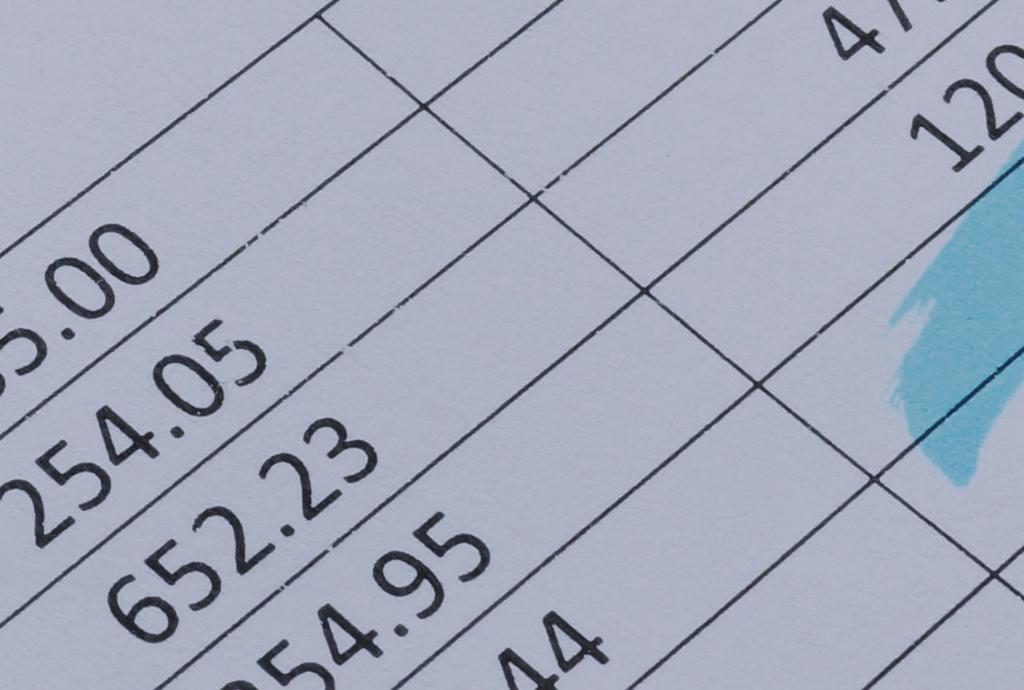

5 Understanding the Big Picture The amount of information required to meet the quantitative disclosure requirements is substantial. Even for tenants with a relatively small number of properties in their portfolio the effort required to gather, analyze and create the necessary quantitative disclosures is enormous. 43% of financial executive indicated they will implement a new lease management system. Fischer s ManagePath has a quantitative disclosure schedule built-in, enabling a simple portfolio import with each property s lease information. ManagePath handles calculations and creates a disclosure schedule that can be delivered straight to your financial reporting team. Supporting details for individual properties or groups of properties are available in the system for custom reporting or for audit support. Below is an example of Fischer s quantitative disclosure report generated directly from ManagePath using numbers from a hypothetical example portfolio loaded into the system. The disclosure report closely follows the example set forth in paragraph to ensure compliance with ASC 842 disclosure requirements. Year Ending December Lease cost Finance lease cost $ 1,708,576 $ 1,784,731 Amortization of right-of-use assets $ 898,525 $ 893,748 Interest on lease liabilities $ 810,051 $ 890,983 Operating lease cost $ 32,206,431 $ 33,287,410 Short-term lease cost $ - $ - Variable lease cost $ 1,533,379 $ 1,434,099 Sublease income $ (707,610) $ (859,550) Total lease cost $ 34,740,776 $ 35,646,690 Other information (Gains) and losses on sale and leaseback transactions, net $ - $ - Cash paid for amounts included in the measurements of lease liabilities $ 52,732,822 $ 53,901,230 Operating cash flows from finance leases $ 810,051 $ 890,983 Operating cash flows from operating leases $ 50,242,224 $ 51,454,925 Financing cash flows from finance leases $ 1,680,547 $ 1,555,322 Right-of-use assets obtained in exchange for new finance lease liabilities $ 75,180 $ - Right-of-use assets obtained in exchange for new operating lease liabilities $ 19,404,475 $ 9,140,951 Weighted-average remaining lease term--finance leases 11.7 years 12.1 years Weighted-average remaining lease term-- operating leases 7.1 years 7.4 years Weighted-average discount rate--finance leases 5.5% 5.5% Weighted-average discount rate--operating leases 5.4% 5.4% Fisher s Manage Path solution eliminates the need to create complex schedules in support of your disclosure requires. The same system used by your real estate department for managing your portfolio of leased and owned properties can also produce entries for your accounting department and disclosure reports for your financial reporting team. Policy changes are inevitable in today s volatile market but that shouldn t warrant companies to exhaust all resources to prepare. Successful implementation is about knowing what resources are best equipped to handle the job at hand. Take comfort in your compliance management and diligently source the best technology or resources to tackle the challenges. NEED A DETAILED SCHEDULE BY PROPERTY FOR AUDIT SUPPORT? MANAGEPATH PROVIDES THE BREAKDOWN NECESSARY TO SUPPORT YOUR DISCLOSURE DOCUMENT.

6 About Fischer Fischer is a leading global corporate real estate firm that provides consulting, brokerage and technology solutions to corporate real estate users looking for a conflict-free broker for their real estate needs. Founded in 1985, Fischer helps clients get the most out of their real estate portfolios and activities by applying its in-depth knowledge of strategic influences to decisions that impact every aspect of their business. Since 1986, Fischer has developed corporate real estate technology solutions and remains the technology innovation leader. Our unique blend of expertise in corporate real estate services and technology has earned us the trust and respect of some of the largest and most successful corporations in the world As exclusive tenant representatives and corporate real estate consultants for many of the world s largest companies, Fischer delivers results through deep expertise in portfolio management, strategic planning, acquisitions, dispositions, project management, transaction and construction management, capital markets, sale-leasebacks and technology.

7 Resources Ellis, Jeffrey. Leasing: Disclosures Under ASC 842. Bloomberg BNA May Hale, Vicky. Lease Disclosures: Stepping it up from ASC 840 to ASC 842. GAAP Dynamics May Wyatt, Sheri lease accounting survey: implementation progress report. PwC May Young, Michael. What exactly is a lease?. BlumShapiro May 2018.

8

Accounting Update. Anne Cloutier, CPA, FHFMA Principal March 27, 2015

Accounting Update Anne Cloutier, CPA, FHFMA Principal March 27, 2015 Current Accounting for Leases Capital leases - a lessee recognizes leased assets and liabilities on the balance sheet. Operating leases

Accounting Update Anne Cloutier, CPA, FHFMA Principal March 27, 2015 Current Accounting for Leases Capital leases - a lessee recognizes leased assets and liabilities on the balance sheet. Operating leases

Something Borrowed, Something New Get Ready for the New Lease Accounting Standard

April 2016 Something Borrowed, Something New Get Ready for the New Lease Accounting Standard By Scott G. Lehman, CPA, and David E. Wentzel, CPA Audit / Tax / Advisory / Risk / Performance Smart decisions.

April 2016 Something Borrowed, Something New Get Ready for the New Lease Accounting Standard By Scott G. Lehman, CPA, and David E. Wentzel, CPA Audit / Tax / Advisory / Risk / Performance Smart decisions.

Implementing the New Lease Guidance

Implementing the New Lease Guidance October 22, 2018 2018 Crowe LLP 2018 Crowe LLP Agenda Background Scope Effective dates & transition requirements Lessee accounting model Lessor accounting model Specialized

Implementing the New Lease Guidance October 22, 2018 2018 Crowe LLP 2018 Crowe LLP Agenda Background Scope Effective dates & transition requirements Lessee accounting model Lessor accounting model Specialized

Executive Summary. New leases standard Lessees

Executive Summary December 2018 The new leases standard focuses on increased transparency and comparability providing financial statement users with more information about an entity s leasing activities.

Executive Summary December 2018 The new leases standard focuses on increased transparency and comparability providing financial statement users with more information about an entity s leasing activities.

What private companies need to know about applying the new lease standard

What private companies need to know about applying the new lease standard In February 26, the FASB issued Accounting Standards Update (ASU) No. 26-, Leases (codified as Accounting Standards Codification

What private companies need to know about applying the new lease standard In February 26, the FASB issued Accounting Standards Update (ASU) No. 26-, Leases (codified as Accounting Standards Codification

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions. August 24, 2017

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions August 24, 2017 Learning objectives Define leasing implications related to recently revised FASB standard Differentiate between new

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions August 24, 2017 Learning objectives Define leasing implications related to recently revised FASB standard Differentiate between new

Defining Issues. FASB Completes Technical Redeliberations on Leases. October 2015, No Key Facts. Key Impacts

Defining Issues October 2015, No. 15-47 FASB Completes Technical Redeliberations on Leases The FASB met on October 7 to discuss comments received and related follow-up issues on the external review of

Defining Issues October 2015, No. 15-47 FASB Completes Technical Redeliberations on Leases The FASB met on October 7 to discuss comments received and related follow-up issues on the external review of

Implementing GASB s Lease Guidance

The effective date of the Governmental Accounting Standards Board s (GASB) new lease guidance is drawing nearer. Private sector companies also have recently adopted significantly revised lease guidance;

The effective date of the Governmental Accounting Standards Board s (GASB) new lease guidance is drawing nearer. Private sector companies also have recently adopted significantly revised lease guidance;

I ROC 2017 Financial Administrators Section Conference

I ROC 2017 Financial Administrators Section Conference September 9, 2017 kpmg.ca Presenters Chris Cornell KPMG Partner, Financial Services Steven Sharma KPMG Partner, Financial Services 2 IIROC 2017 Financial

I ROC 2017 Financial Administrators Section Conference September 9, 2017 kpmg.ca Presenters Chris Cornell KPMG Partner, Financial Services Steven Sharma KPMG Partner, Financial Services 2 IIROC 2017 Financial

What Nonprofits Need to Know About the New Standards for Lease Accounting

The webcast will start at 1 p.m. Eastern Please note: Handout You can print or download the webcast handout at https://capincrouse.com/webcast-lease-accounting CPE CPE certificates will be emailed to you

The webcast will start at 1 p.m. Eastern Please note: Handout You can print or download the webcast handout at https://capincrouse.com/webcast-lease-accounting CPE CPE certificates will be emailed to you

Lease Accounting - New Changes in US, International and Government Accounting Standards

Lease Accounting - New Changes in US, International and Government Accounting Standards Roberta J. Cable, Ph.D., CMA Patricia Healy, CPA, CMA Lubin School of Business Administration, Pace University, USA

Lease Accounting - New Changes in US, International and Government Accounting Standards Roberta J. Cable, Ph.D., CMA Patricia Healy, CPA, CMA Lubin School of Business Administration, Pace University, USA

Is Your Operating Lease An Asset or Liability? It s Now Both

MFM Annual Conference Is Your Operating Lease An Asset or Liability? It s Now Both 23 May 2016-1:30 pm 2:20 pm Disclaimer These slides are for educational purposes only and are not intended, and should

MFM Annual Conference Is Your Operating Lease An Asset or Liability? It s Now Both 23 May 2016-1:30 pm 2:20 pm Disclaimer These slides are for educational purposes only and are not intended, and should

Lease Accounting and Loan Covenants: What is the Impact?

Lease Accounting and Loan Covenants: What is the Impact? Monday June 26, 2017 9:15 AM 10:30 AM Presented by: Charlie Shannon Partner Moss Adams LLP 8750 N. Central Expressway, Suite 300 Dallas, TX 75231

Lease Accounting and Loan Covenants: What is the Impact? Monday June 26, 2017 9:15 AM 10:30 AM Presented by: Charlie Shannon Partner Moss Adams LLP 8750 N. Central Expressway, Suite 300 Dallas, TX 75231

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions. August 24, 2017

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions August 24, 2017 Learning objectives Define leasing implications related to recently revised FASB standard Differentiate between new

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions August 24, 2017 Learning objectives Define leasing implications related to recently revised FASB standard Differentiate between new

Agenda. Monday, August 14, Section One The FASB s New Lease Accounting Standard. 8:30 Introduction to the new Lease Accounting Model Overview

Lease and Revenue Recognition Accounting Workshop Hosted by: Smith and Gesteland August 14 15, 2017 Madison Marriott West (This workshop qualifies for 16 hours of CPE) Monday, August 14, 2017 Agenda Section

Lease and Revenue Recognition Accounting Workshop Hosted by: Smith and Gesteland August 14 15, 2017 Madison Marriott West (This workshop qualifies for 16 hours of CPE) Monday, August 14, 2017 Agenda Section

Deeper Dive Leases. Overview

Deeper Dive Leases Presented by: Shaun Johnson, CPA Dingus, Zarecor & Associates PLLC Overview Effective dates Big picture Objective, impact, and implementation Applicability and definition Initial recognition

Deeper Dive Leases Presented by: Shaun Johnson, CPA Dingus, Zarecor & Associates PLLC Overview Effective dates Big picture Objective, impact, and implementation Applicability and definition Initial recognition

The clock is ticking. How to jumpstart your lease accounting implementation project

The clock is ticking How to jumpstart your lease accounting implementation project Lease accounting: Adopting the new standard (ASC 842) 3 Start with challenges, finish with benefits 4 Pine Hill s four

The clock is ticking How to jumpstart your lease accounting implementation project Lease accounting: Adopting the new standard (ASC 842) 3 Start with challenges, finish with benefits 4 Pine Hill s four

MONITORDAILY SPECIAL REPORT. Lease Accounting Project Update as of May 25, 2011 Prepared by Bill Bosco, Leasing 101

MONITORDAILY SPECIAL REPORT Lease Accounting Project Update as of May 25, 2011 Prepared by Bill Bosco, Leasing 101 The high volume of comment letters (780+) and numerous outreach meetings had common criticisms

MONITORDAILY SPECIAL REPORT Lease Accounting Project Update as of May 25, 2011 Prepared by Bill Bosco, Leasing 101 The high volume of comment letters (780+) and numerous outreach meetings had common criticisms

Applying the new lease accounting standard

Applying the new lease accounting standard In February 26, the FASB issued Accounting Standards Update (ASU) No. 26-, Leases (codified as Accounting Standards Codification Topic (ASC) 842). ASC 842 introduces

Applying the new lease accounting standard In February 26, the FASB issued Accounting Standards Update (ASU) No. 26-, Leases (codified as Accounting Standards Codification Topic (ASC) 842). ASC 842 introduces

GAAP UPDATE DEANA BOWDEN, CPA, MSA WHITE NELSON DIEHL EVANS LLP

GAAP UPDATE DEANA BOWDEN, CPA, MSA WHITE NELSON DIEHL EVANS LLP TOPICS 2016-02 Topic 842 Leases 2016-14 Topic 958 Not for Profits 2016-18 Topic 230 Cash Flows LEASES Current US Generally Accepted Accounting

GAAP UPDATE DEANA BOWDEN, CPA, MSA WHITE NELSON DIEHL EVANS LLP TOPICS 2016-02 Topic 842 Leases 2016-14 Topic 958 Not for Profits 2016-18 Topic 230 Cash Flows LEASES Current US Generally Accepted Accounting

GASB 87. OVERVIEW: Supersedes GASB s 13 and 62 (paragraphs ).

.") Leases OVERVIEW: Supersedes GASB s 13 and 62 (paragraphs 211-271). Will require significant changes from its current practice, particularly in the accounting for operating leases Effective for reporting

Leases OVERVIEW: Supersedes GASB s 13 and 62 (paragraphs 211-271). Will require significant changes from its current practice, particularly in the accounting for operating leases Effective for reporting

FASB s 2013 Proposal on Accounting for Leases

FASB s 2013 Proposal on Accounting for Leases Frequently Asked Questions September 2013 The project on lease accounting is a joint project of the FASB and the International Accounting Standards Board.

FASB s 2013 Proposal on Accounting for Leases Frequently Asked Questions September 2013 The project on lease accounting is a joint project of the FASB and the International Accounting Standards Board.

New Accounting Rules for Revenue and Leases

New Accounting Rules for Revenue and Leases CFMA Education Summit March 22, 2017 Presented by: Carole McNees, CPA, Partner, Plante & Moran, PLLC Recently released standards New guidance from the Financial

New Accounting Rules for Revenue and Leases CFMA Education Summit March 22, 2017 Presented by: Carole McNees, CPA, Partner, Plante & Moran, PLLC Recently released standards New guidance from the Financial

Lease Accounting Is Final Time to Prepare for Implementation

Copyright 2016 by the Construction Financial Management Association (CFMA). All rights reserved. This article first appeared in CFMA Building Profits (a member-only benefit) and is reprinted with permission.

Copyright 2016 by the Construction Financial Management Association (CFMA). All rights reserved. This article first appeared in CFMA Building Profits (a member-only benefit) and is reprinted with permission.

7829 Glenwood Avenue Canal Winchester, Ohio November 19,2013

7829 Glenwood Avenue Canal Winchester, Ohio 43110 614-920-1425 November 19,2013 Technical Director File Reference Number 2013-270 Financial Standards Accounting Board 401 Merritt 7 Norwalk, Connecticut

7829 Glenwood Avenue Canal Winchester, Ohio 43110 614-920-1425 November 19,2013 Technical Director File Reference Number 2013-270 Financial Standards Accounting Board 401 Merritt 7 Norwalk, Connecticut

Gearing up for change New IFRS on Leases

Gearing up for change New IFRS on Leases In a nutshell The changes Lessee accounting Effective date: 1 January 2019 Limited changes to scope of IAS 17 Enhanced guidance on identifying a lease Lessor accounting

Gearing up for change New IFRS on Leases In a nutshell The changes Lessee accounting Effective date: 1 January 2019 Limited changes to scope of IAS 17 Enhanced guidance on identifying a lease Lessor accounting

Preparing for the new lease accounting standard What transportation, hospitality, and services companies need to know

Preparing for the new lease accounting standard What transportation, hospitality, and services companies need to know Preface 1 2 3 4 5 6 7 8 The new lease accounting standard is expected to have a significant

Preparing for the new lease accounting standard What transportation, hospitality, and services companies need to know Preface 1 2 3 4 5 6 7 8 The new lease accounting standard is expected to have a significant

presentation for October 5, 2018

presentation for October 5, 2018 Proper Lease Analysis + Proper Technology = Successful Implementation Designed by Former Big 4 Auditors Built for Audit Efficiency Key Design Principles Ease of Use & Security

presentation for October 5, 2018 Proper Lease Analysis + Proper Technology = Successful Implementation Designed by Former Big 4 Auditors Built for Audit Efficiency Key Design Principles Ease of Use & Security

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N AGENDA Leases FASB & GASB Revenue Recognition FASB 2 FASB ASU 2016-02, Leases (Topic

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N AGENDA Leases FASB & GASB Revenue Recognition FASB 2 FASB ASU 2016-02, Leases (Topic

Accounting and Auditing Update. Paul Lundy

Accounting and Auditing Update Paul Lundy Leases: Not Just for the Footnotes Anymore Significant Financial Statement Impact New lease standard generally requires all leases to be capitalized and recognized

Accounting and Auditing Update Paul Lundy Leases: Not Just for the Footnotes Anymore Significant Financial Statement Impact New lease standard generally requires all leases to be capitalized and recognized

NEW LEASE ACCOUNTING STANDARD

NEW LEASE ACCOUNTING STANDARD Accounting Standards Update (ASU) 2016-02, Leases & GASB 87, Leases LEASES Leases: Why a New Leases Standard? 1 IMPLEMENTATION TIMELINE January 2016 IASB issued IFRS 16, Leases

NEW LEASE ACCOUNTING STANDARD Accounting Standards Update (ASU) 2016-02, Leases & GASB 87, Leases LEASES Leases: Why a New Leases Standard? 1 IMPLEMENTATION TIMELINE January 2016 IASB issued IFRS 16, Leases

CPE regulations require online participants to take part in online questions

KPMG s CFO Financial Forum Webcast FASB/IASB Revised Lease Accounting Exposure Drafts A Detailed Look Part III: Lessor Accounting June 25, 2013 Administrative CPE regulations require online participants

KPMG s CFO Financial Forum Webcast FASB/IASB Revised Lease Accounting Exposure Drafts A Detailed Look Part III: Lessor Accounting June 25, 2013 Administrative CPE regulations require online participants

New Lease Accounting Standards: Love at First Sight or Heartbreak?

New Lease Accounting Standards: Love at First Sight or Heartbreak? February 14, 2019 To Receive CPE Credit Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader

New Lease Accounting Standards: Love at First Sight or Heartbreak? February 14, 2019 To Receive CPE Credit Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader

roots The Substance of the Standard Contents Changes to the Accounting for Goodwill for Private Companies

The Substance of the Standard MAYER HOFFMAN MCCANN P.C. AN INDEPENDENT CPA FIRM TM A publication of the Professional Standards Group February 2014 Changes to the Accounting for Goodwill for Private Companies

The Substance of the Standard MAYER HOFFMAN MCCANN P.C. AN INDEPENDENT CPA FIRM TM A publication of the Professional Standards Group February 2014 Changes to the Accounting for Goodwill for Private Companies

AMERICAN INTERNATIONAL GROUP, INC.

AMERICAN INTERNATIONAL GROUP, INC. Technical Director Financial Accounting Standards Board 401 Merritt 7 P.O. Box 5116 Norwalk, CT 06856-5116 Re: FASB File Reference No., Proposed Accounting Standards

AMERICAN INTERNATIONAL GROUP, INC. Technical Director Financial Accounting Standards Board 401 Merritt 7 P.O. Box 5116 Norwalk, CT 06856-5116 Re: FASB File Reference No., Proposed Accounting Standards

Re: File Reference: No , Exposure Draft: Leases (Topic 842)

") September 13, 2013 Russell G. Golden, Chairman Financial Accounting Standards Board 401 Merritt 7 PO Box 5116 Norwalk, Connecticut 06856-5116 Hans Hoogervorst, Chairman International Accounting Standards

September 13, 2013 Russell G. Golden, Chairman Financial Accounting Standards Board 401 Merritt 7 PO Box 5116 Norwalk, Connecticut 06856-5116 Hans Hoogervorst, Chairman International Accounting Standards

LEASES WHERE ARE WE? Steve Rathjen

LEASES WHERE ARE WE? Steve Rathjen 267 256-3110 srathjen@kpmg.com Agenda Project status Lease definition and classification Lessee accounting Lessor accounting Presentation, disclosures, and transition

LEASES WHERE ARE WE? Steve Rathjen 267 256-3110 srathjen@kpmg.com Agenda Project status Lease definition and classification Lessee accounting Lessor accounting Presentation, disclosures, and transition

Headline Verdana Bold The evolutions of leases accounting under IFRS 16 Mariano Bruno, Carlo Laganà, Giuseppe Ambrosio, Deloitte & Touche S.p.A.

SHIPPING AND THE LAW 7^ Edition 25-26 October 2016 NAPLES Headline Verdana Bold The evolutions of leases accounting under IFRS 16 Mariano Bruno, Carlo Laganà, Giuseppe Ambrosio, Deloitte & Touche S.p.A.

SHIPPING AND THE LAW 7^ Edition 25-26 October 2016 NAPLES Headline Verdana Bold The evolutions of leases accounting under IFRS 16 Mariano Bruno, Carlo Laganà, Giuseppe Ambrosio, Deloitte & Touche S.p.A.

Applying IFRS. Presentation and disclosure requirements of IFRS 16 Leases. November 2018

Applying IFRS Presentation and disclosure requirements of IFRS 16 Leases November 2018 Contents 1. Overview 2 2. What is changing from current IFRS? 4 2.1 Presentation 4 2.2 Lessee disclosures 5 3. Presentation

Applying IFRS Presentation and disclosure requirements of IFRS 16 Leases November 2018 Contents 1. Overview 2 2. What is changing from current IFRS? 4 2.1 Presentation 4 2.2 Lessee disclosures 5 3. Presentation

HERE WE GO AGAIN. THE NEW LEASE STANDARD (ASC TOPIC 842) February Internal Audit, Risk, Business & Technology Consulting

February Internal Audit, Risk, Business & Technology Consulting") HERE WE GO AGAIN THE NEW LEASE STANDARD (ASC TOPIC 842) February 2018 Internal Audit, Risk, Business & Technology Consulting PRESENTERS Edna Lopez Protiviti Managing Director edna.lopez@protiviti.com Scott

HERE WE GO AGAIN THE NEW LEASE STANDARD (ASC TOPIC 842) February 2018 Internal Audit, Risk, Business & Technology Consulting PRESENTERS Edna Lopez Protiviti Managing Director edna.lopez@protiviti.com Scott

Proposed New Accounting Standards For Leases

Relationships backed by performance. Proposed New Accounting Standards For Leases Doug Richardson Live Seminar 9:00am 10:30am June 21 2012 Overview and Background Leases serve a vital role in many entities

Relationships backed by performance. Proposed New Accounting Standards For Leases Doug Richardson Live Seminar 9:00am 10:30am June 21 2012 Overview and Background Leases serve a vital role in many entities

IFRS 16 Leases supplement

IFRS 16 Leases supplement Guide to annual financial statements IFRS December 2017 kpmg.com/ifrs Contents About this supplement 1 About IFRS 16 3 The Group s lease portfolio 6 Part I Modified retrospective

IFRS 16 Leases supplement Guide to annual financial statements IFRS December 2017 kpmg.com/ifrs Contents About this supplement 1 About IFRS 16 3 The Group s lease portfolio 6 Part I Modified retrospective

The New Lease Accounting Standard. Hunter Mink, CPA, CCIFP Brian Rosenberg, CPA, MBA

The New Lease Accounting Standard Hunter Mink, CPA, CCIFP Brian Rosenberg, CPA, MBA 1 Agenda Introduction Lease Identification and Classification Lessee Accounting Other Considerations Disclosures Impact

The New Lease Accounting Standard Hunter Mink, CPA, CCIFP Brian Rosenberg, CPA, MBA 1 Agenda Introduction Lease Identification and Classification Lessee Accounting Other Considerations Disclosures Impact

Edison Electric Institute and American Gas Association New Lease Standard

Edison Electric Institute and American Gas Association New Lease Standard May 16, 2016 Disclaimer The information contained herein is of a general nature and is not intended to address the circumstances

Edison Electric Institute and American Gas Association New Lease Standard May 16, 2016 Disclaimer The information contained herein is of a general nature and is not intended to address the circumstances

GASB 87: Leases. Hosted By: Ben Lindekugel, Executive Director Association of Washington Public Hospital Districts

GASB 87: Leases Hosted By: Ben Lindekugel, Executive Director Association of Washington Public Hospital Districts November 6, 2018 Presented By Tom Dingus, CPA, Partner Dingus, Zarecor & Associates PLLC

GASB 87: Leases Hosted By: Ben Lindekugel, Executive Director Association of Washington Public Hospital Districts November 6, 2018 Presented By Tom Dingus, CPA, Partner Dingus, Zarecor & Associates PLLC

ARE YOU READY TO ADOPT ASC 842? February 28, 2018

ARE YOU READY TO ADOPT ASC 842? February 28, 2018 Webcast notes Resources List: Download today s slides and access other helpful links by clicking the icon Q & A: Have a question? Click the icon Polling

ARE YOU READY TO ADOPT ASC 842? February 28, 2018 Webcast notes Resources List: Download today s slides and access other helpful links by clicking the icon Q & A: Have a question? Click the icon Polling

IFRS 15. Revenue from Contracts with Customers. Presented by CPA Dr. Peter Njuguna

IFRS 15 Revenue from Contracts with Customers Presented by CPA Dr. Peter Njuguna Introduction Revenue is income from ordinary activities. A contract has rights and obligations between two or more parties.

IFRS 15 Revenue from Contracts with Customers Presented by CPA Dr. Peter Njuguna Introduction Revenue is income from ordinary activities. A contract has rights and obligations between two or more parties.

Miles CPA Review: FAR Updates

Miles CPA Review: FAR - 2019 Updates Summary of updates: - FAR-4.4: s [ASC 842] effective fiscal years beginning after Dec 15, 2018 (for issuers) and effective fiscal years beginning after Dec 15, 2019

Miles CPA Review: FAR - 2019 Updates Summary of updates: - FAR-4.4: s [ASC 842] effective fiscal years beginning after Dec 15, 2018 (for issuers) and effective fiscal years beginning after Dec 15, 2019

HOW TO JUMP START YOUR ASC 842 LEASE ACCOUNTING PROJECT WEBINAR MARCH

HOW TO JUMP START YOUR ASC 842 LEASE ACCOUNTING PROJECT WEBINAR MARCH 14 2018 Today s Panelists Scott Vanlandingham Principal Consulting Iyaye Amabeoku Senior Manager Technical Accounting Michael Gregorski

HOW TO JUMP START YOUR ASC 842 LEASE ACCOUNTING PROJECT WEBINAR MARCH 14 2018 Today s Panelists Scott Vanlandingham Principal Consulting Iyaye Amabeoku Senior Manager Technical Accounting Michael Gregorski

ManagePath: Your Solution for the New Lease Accounting Rules

ManagePath: Your Solution or the New Lease Accounting Rules ManagePath: Your Solution or the New Lease Accounting Rules CONTENTS Key Changes The ManagePath Solution Determining the Lease Term Lease Liability

ManagePath: Your Solution or the New Lease Accounting Rules ManagePath: Your Solution or the New Lease Accounting Rules CONTENTS Key Changes The ManagePath Solution Determining the Lease Term Lease Liability

Accounting and Auditing Update. Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc.

Accounting and Auditing Update Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc. Agenda Overview of the standard setting agenda Revenue recognition Lease

Accounting and Auditing Update Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc. Agenda Overview of the standard setting agenda Revenue recognition Lease

Lease Accounting Standard Update ASU Presented by: Nicholas Hoefel, CPA Manager, Audit Services Group

Lease Accounting Standard Update ASU 2016-02 Presented by: Nicholas Hoefel, CPA Manager, Audit Services Group 1 Overview Introduction Background and current environment Effective dates and transition Key

Lease Accounting Standard Update ASU 2016-02 Presented by: Nicholas Hoefel, CPA Manager, Audit Services Group 1 Overview Introduction Background and current environment Effective dates and transition Key

Liquidity and Availability of Resources Disclosures and other Upcoming FASB Requirements

Liquidity and Availability of Resources Disclosures and other Upcoming FASB Requirements Agenda ASU 2016-14 Liquidity Disclosures ASU 2014-09 Revenue Recognition Subscriptions and Membership Dues ASU 2016-02

Liquidity and Availability of Resources Disclosures and other Upcoming FASB Requirements Agenda ASU 2016-14 Liquidity Disclosures ASU 2014-09 Revenue Recognition Subscriptions and Membership Dues ASU 2016-02

Leases ASU September 20, 2017

Leases ASU 2016-02 September 20, 2017 Meet the Speakers Tonisha Spratte, CPA Senior Accountant Cherry Bekaert tspratte@cbh.com Matthew Mars Senior Accountant Cherry Bekaert mmars@cbh.com Agenda What is

Leases ASU 2016-02 September 20, 2017 Meet the Speakers Tonisha Spratte, CPA Senior Accountant Cherry Bekaert tspratte@cbh.com Matthew Mars Senior Accountant Cherry Bekaert mmars@cbh.com Agenda What is

IFRS 15 and IFRS 16 Webinar

CPA Ireland Skillnet CPA Ireland Skillnet, is a training network that is funded by Skillnets, a state funded, enterprise led support body dedicated to the promotion and facilitation of training and up-skilling

CPA Ireland Skillnet CPA Ireland Skillnet, is a training network that is funded by Skillnets, a state funded, enterprise led support body dedicated to the promotion and facilitation of training and up-skilling

IASB/FASB Exposure Draft on Leases. Accounting in the Retail Industry A new view of lease accounting emerges

IASB/FASB Exposure Draft on Leases Accounting in the Retail Industry A new view of lease accounting emerges Contents Introduction 1 Issue 1 Impact of capitalisation of all leases on financial statements

IASB/FASB Exposure Draft on Leases Accounting in the Retail Industry A new view of lease accounting emerges Contents Introduction 1 Issue 1 Impact of capitalisation of all leases on financial statements

File Reference No : Leases (Topic 842): a Revision of the 2010 Proposed Accounting Standards Update, Leases (Topic 840)

: a Revision of the 2010 Proposed Accounting Standards Update, Leases (Topic 840)") September 13, 2013 Technical Director Financial Accounting Standards Board 401 Merritt 7 P.O. Box 5116 Norwalk, CT 06856-5116 Via email: director@fasb.org File Reference No. 2013-270: Leases (Topic 842):

September 13, 2013 Technical Director Financial Accounting Standards Board 401 Merritt 7 P.O. Box 5116 Norwalk, CT 06856-5116 Via email: director@fasb.org File Reference No. 2013-270: Leases (Topic 842):

Leases make their way onto the balance sheet

February 2016 IFRS Practical Matters France Leases make their way onto the balance sheet Navigating the journey for a smooth landing What you need to know The IASB issued a new standard for leases that

February 2016 IFRS Practical Matters France Leases make their way onto the balance sheet Navigating the journey for a smooth landing What you need to know The IASB issued a new standard for leases that

ABRAHAM E. HASPEL CPA

ABRAHAM E. HASPEL CPA Comments on the Financial Accounting Standard Board s: Proposed Accounting Standard Update Leases (Topic 840) (ED) I am pleased to submit the following comments in response to the

ABRAHAM E. HASPEL CPA Comments on the Financial Accounting Standard Board s: Proposed Accounting Standard Update Leases (Topic 840) (ED) I am pleased to submit the following comments in response to the

ASC 842 (Leases)

") ASC 842 (Leases) On February 25, 2016 the Financial Accounting Standards Board of the United States (FASB) issued substantial new guidance on the treatment of leases for both lessees and lessors. The FASB

ASC 842 (Leases) On February 25, 2016 the Financial Accounting Standards Board of the United States (FASB) issued substantial new guidance on the treatment of leases for both lessees and lessors. The FASB

Lease accounting scope & impacts

Leasing Lease accounting scope & impacts Scope What s in? All industries, all entities Arrangements that meet the definition of a lease Embedded leases within other arrangements What s out? Leases of:

Leasing Lease accounting scope & impacts Scope What s in? All industries, all entities Arrangements that meet the definition of a lease Embedded leases within other arrangements What s out? Leases of:

Re: File Reference No , Comment Letter on the Proposed Accounting Standard Update (revised): Leases (Topic 842)

: Leases (Topic 842)") September 13, 2013 Tyco International Victor von Bruns-Strasse 8212 Neuhausen Switzerland Tel: +41 52 633 01 44 Fax: +41 52 633 02 59 www.tyco.com Russell G. Golden, Chairman Financial Accounting Standards

September 13, 2013 Tyco International Victor von Bruns-Strasse 8212 Neuhausen Switzerland Tel: +41 52 633 01 44 Fax: +41 52 633 02 59 www.tyco.com Russell G. Golden, Chairman Financial Accounting Standards

IFRS 16 Leases: Overview

IFRS Foundation IFRS 16 Leases: Overview Nairobi, Kenya Darrel Scott, IASB Member The views expressed in this presentation are those of the presenter, not necessarily those of the International Accounting

IFRS Foundation IFRS 16 Leases: Overview Nairobi, Kenya Darrel Scott, IASB Member The views expressed in this presentation are those of the presenter, not necessarily those of the International Accounting

New leases standard ASC 842 Lessee - operating leases. Itai Gotlieb, Partner, Professional Practice July 2017

ASC 842 Lessee - operating leases Itai Gotlieb, Partner, Professional Practice July 2017 Overview Under Accounting Standards Codification (ASC) 842, Leases, lessees recognize assets and liabilities for

ASC 842 Lessee - operating leases Itai Gotlieb, Partner, Professional Practice July 2017 Overview Under Accounting Standards Codification (ASC) 842, Leases, lessees recognize assets and liabilities for

FASB Proposed Accounting Standards Update (Revised), Leases (Topic 842) and IASB Exposure Draft ED/2013/6, Leases

, Leases (Topic 842) and IASB Exposure Draft ED/2013/6, Leases") September 13, 2013 Technical Director, File Reference No. International Accounting Standards Board Financial Accounting Standards Board 30 Cannon Street 401 Merritt 7 London, EC4M 6XH P.O. Box 5116 United

September 13, 2013 Technical Director, File Reference No. International Accounting Standards Board Financial Accounting Standards Board 30 Cannon Street 401 Merritt 7 London, EC4M 6XH P.O. Box 5116 United

Impact of lease accounting changes to corporate real estate

Impact of lease accounting changes to corporate real estate Overview In February 2016, the Financial Accounting Standards Board (FASB) issued its long-awaited revision to lease accounting Accounting Standards

Impact of lease accounting changes to corporate real estate Overview In February 2016, the Financial Accounting Standards Board (FASB) issued its long-awaited revision to lease accounting Accounting Standards

Technical Line FASB final guidance

No. 2018-08 20 September 2018 Technical Line FASB final guidance How the new leases standard affects engineering and construction entities In this issue: Overview... 1 Key considerations... 2 Scope and

No. 2018-08 20 September 2018 Technical Line FASB final guidance How the new leases standard affects engineering and construction entities In this issue: Overview... 1 Key considerations... 2 Scope and

Current accounting and reporting developments webcast series. March 15, 2017

Current accounting and reporting developments webcast series March 15, 2017 Q1 Q2 Q3 Q4 Welcome Beth Paul Accounting Services Group Team Leader National Professional Services Group LinkedIn Diane Howell

Current accounting and reporting developments webcast series March 15, 2017 Q1 Q2 Q3 Q4 Welcome Beth Paul Accounting Services Group Team Leader National Professional Services Group LinkedIn Diane Howell

Leases: Overview of the new guidance

Leases: Overview of the new guidance Prepared by: Richard Stuart, Partner, National Professional Standards Group, RSM US LLP richard.stuart@rsmus.com, +1 203 905 5027 March 2, 2016 Introduction On February

Leases: Overview of the new guidance Prepared by: Richard Stuart, Partner, National Professional Standards Group, RSM US LLP richard.stuart@rsmus.com, +1 203 905 5027 March 2, 2016 Introduction On February

The new accounting standard for leases. 27 March 2017

The new accounting standard for leases 27 March 2017 Disclaimer Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity.

The new accounting standard for leases 27 March 2017 Disclaimer Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity.

Lease Update. June 2017 Addison, Texas

Lease Update June 2017 Addison, Texas William Bill Schneider CPA, CGMA Bill is an Audit Director at AT&T. AT&T delivers advanced mobile services, next-generation TV, highspeed internet and smart solutions

Lease Update June 2017 Addison, Texas William Bill Schneider CPA, CGMA Bill is an Audit Director at AT&T. AT&T delivers advanced mobile services, next-generation TV, highspeed internet and smart solutions

Comment Letter No December 15, Merritt 7 840). assess the. impact of. should be

. assess the. impact of. should be") December 15, 2010 Financial Accounting Standards Board Attn: Technical Director File Reference No. 1850-100 401 Merritt 7 P.O. Box 5116 Norwalk, CT 06856-5116 Via e-mail to director@fasb.org Re: File Reference

December 15, 2010 Financial Accounting Standards Board Attn: Technical Director File Reference No. 1850-100 401 Merritt 7 P.O. Box 5116 Norwalk, CT 06856-5116 Via e-mail to director@fasb.org Re: File Reference

Implementing IFRS 16. Jianqiao Lu, IASB Member. Singapore, November International Accounting Standards Board, IFRS Foundation

IFRS Foundation Implementing IFRS 16 Jianqiao Lu, IASB Member International Accounting Standards Board, Singapore, November 2018 The views expressed in this presentation are those of the presenter, not

IFRS Foundation Implementing IFRS 16 Jianqiao Lu, IASB Member International Accounting Standards Board, Singapore, November 2018 The views expressed in this presentation are those of the presenter, not

June 28, Technical Director File Reference No Financial Accounting Standards Board 401 Merritt 7 P.O. Box 5116 Norwalk, CT

Technical Director File Reference No. 2016-200 401 Merritt 7 P.O. Box 5116 Norwalk, CT 06856-5116 Comments by the Edison Electric Institute and the American Gas Association Regarding the Accounting for

Technical Director File Reference No. 2016-200 401 Merritt 7 P.O. Box 5116 Norwalk, CT 06856-5116 Comments by the Edison Electric Institute and the American Gas Association Regarding the Accounting for

Defining Issues. FASB and IASB Take Divergent Paths on Key Aspects of Lease Accounting. March 2014, No Key Facts

Defining Issues March 2014, No. 14-17 FASB and IASB Take Divergent Paths on Key Aspects of Lease Accounting At their March 18-19 meeting to redeliberate the proposals in their 2013 exposure drafts (EDs)

Defining Issues March 2014, No. 14-17 FASB and IASB Take Divergent Paths on Key Aspects of Lease Accounting At their March 18-19 meeting to redeliberate the proposals in their 2013 exposure drafts (EDs)

In December 2003 the IASB issued a revised IAS 17 as part of its initial agenda of technical projects.

IFRS Standard 16 Leases In April 2001 the International Accounting Standards Board (IASB) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

IFRS Standard 16 Leases In April 2001 the International Accounting Standards Board (IASB) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

The joint leases project change is coming

No. 2010-4 18 June 2010 Technical Line Technical guidance on standards and practice issues The joint leases project change is coming What you need to know The proposed changes to the accounting for leases

No. 2010-4 18 June 2010 Technical Line Technical guidance on standards and practice issues The joint leases project change is coming What you need to know The proposed changes to the accounting for leases

Annual Accounting and Auditing Update. 11 December 2015

Annual Accounting and Auditing Update 11 December 2015 Disclaimer The views expressed by panelists are not necessarily those of Ernst & Young LLP. These slides are for educational purposes only and are

Annual Accounting and Auditing Update 11 December 2015 Disclaimer The views expressed by panelists are not necessarily those of Ernst & Young LLP. These slides are for educational purposes only and are

IS YOUR LEASE SOLUTION FASB READY? It s here!

IS YOUR LEASE SOLUTION FASB READY? It s here! Hello! Jaron Banks Sr. Sales Engineer Accruent Chris Smart Manager, Product Management Accruent Accruent Confidential and Proprietary 2016 2 Agenda Brief background

IS YOUR LEASE SOLUTION FASB READY? It s here! Hello! Jaron Banks Sr. Sales Engineer Accruent Chris Smart Manager, Product Management Accruent Accruent Confidential and Proprietary 2016 2 Agenda Brief background

Lease Accounting Changes: Pain or Gain for Equipment Lessors?

Corporate Finance & Restructuring Lease Accounting Changes: Pain or Gain for Equipment Lessors? By Pablo Wangermann Alison Mason Bill Trent In August 2010, the International Accounting Standards Board

Corporate Finance & Restructuring Lease Accounting Changes: Pain or Gain for Equipment Lessors? By Pablo Wangermann Alison Mason Bill Trent In August 2010, the International Accounting Standards Board

Bring it on Discussing the FASB s new leases standard

The Dbriefs Financial Reporting series presents: Bring it on Discussing the FASB s new leases standard March 15, 2016 Bob Uhl, Partner, Deloitte & Touche LLP James Barker, Partner, Deloitte & Touche LLP

The Dbriefs Financial Reporting series presents: Bring it on Discussing the FASB s new leases standard March 15, 2016 Bob Uhl, Partner, Deloitte & Touche LLP James Barker, Partner, Deloitte & Touche LLP

International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom. September 13, 2013

International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom September 13, 2013 Technical Director File Reference No. 2013-270 Financial Accounting Standards Board 401 Merritt

International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom September 13, 2013 Technical Director File Reference No. 2013-270 Financial Accounting Standards Board 401 Merritt

Thank you for the opportunity to comment on the above referenced Exposure Draft.

International Accounting Standards Board 1 st Floor 30 Cannon Street London, EC4M 6XH United Kingdom Financial Accounting Standards Board 401 Merritt 7 PO Box 5116 Norwalk, CT 06856 5116 United States

International Accounting Standards Board 1 st Floor 30 Cannon Street London, EC4M 6XH United Kingdom Financial Accounting Standards Board 401 Merritt 7 PO Box 5116 Norwalk, CT 06856 5116 United States

Lease Accounting Project Update and Commentary as of November 29, 2011 Prepared by: NRTA member Bill Bosco, Leasing 101

Lease Accounting Project Update and Commentary as of November 29, 2011 Prepared by: NRTA member Bill Bosco, Leasing 101 www.leasing-101.com What is new since October: - Slippage in the issuance of the

Lease Accounting Project Update and Commentary as of November 29, 2011 Prepared by: NRTA member Bill Bosco, Leasing 101 www.leasing-101.com What is new since October: - Slippage in the issuance of the

Accounting and Auditing. Norman Mosrie, CPA, FMFMA, CHFP James Sutherland, CPA

Accounting and Auditing Norman Mosrie, CPA, FMFMA, CHFP James Sutherland, CPA Leases (ASU 2016-02; Topic 842) A lease contract conveys the right to use an asset (the underlying asset) for a period of time

Accounting and Auditing Norman Mosrie, CPA, FMFMA, CHFP James Sutherland, CPA Leases (ASU 2016-02; Topic 842) A lease contract conveys the right to use an asset (the underlying asset) for a period of time

It s Back Accounting for Asset Leases the new way!

It s Back Accounting for Asset Leases the new way! Kent Bettisworth BETTISWORTH & ASSOCIATES 2016 ERP Corp. All rights reserved. Controlling 2016 Conference September 12-15, 2016 in San Diego Kent Bettisworth

It s Back Accounting for Asset Leases the new way! Kent Bettisworth BETTISWORTH & ASSOCIATES 2016 ERP Corp. All rights reserved. Controlling 2016 Conference September 12-15, 2016 in San Diego Kent Bettisworth

FSA Faculty Consortium Technical Accounting Update. Bob Uhl, partner, Deloitte & Touche LLP

FSA Faculty Consortium Technical Accounting Update Bob Uhl, partner, Deloitte & Touche LLP Deloitte University May 30, 2014 Acronyms Acronym ASC ASU ED FASB IASB IFRS U.S. GAAP Full Form Accounting Standards

FSA Faculty Consortium Technical Accounting Update Bob Uhl, partner, Deloitte & Touche LLP Deloitte University May 30, 2014 Acronyms Acronym ASC ASU ED FASB IASB IFRS U.S. GAAP Full Form Accounting Standards

Current Developments. FASB, AICPA and SEC. Jim Brendel, CPA, CFE March 1, 2013

Current Developments FASB, AICPA and SEC Jim Brendel, CPA, CFE March 1, 2013 Agenda FASB Developments Selected Projects and Initiatives Revenue Recognition Leases Impairment of Intangible Assets Other

Current Developments FASB, AICPA and SEC Jim Brendel, CPA, CFE March 1, 2013 Agenda FASB Developments Selected Projects and Initiatives Revenue Recognition Leases Impairment of Intangible Assets Other

Lease Accounting Survey June 2016

www.pwc.com/us/leasingsurvey Lease Accounting Survey About this survey What will be the impacts from the sweeping changes to lease accounting finalized by the Financial Accounting Standards Board (FASB)

www.pwc.com/us/leasingsurvey Lease Accounting Survey About this survey What will be the impacts from the sweeping changes to lease accounting finalized by the Financial Accounting Standards Board (FASB)

Transition Requirements Under the New Lease Accounting Rules

Accounting Policy & Practice Report: News Archive 2017 December 12/28/2017 BNA Insights Transition Requirements Under the New Lease Accounting Rules By Jeffrey Ellis Jeffrey Ellis is a Senior Managing

Accounting Policy & Practice Report: News Archive 2017 December 12/28/2017 BNA Insights Transition Requirements Under the New Lease Accounting Rules By Jeffrey Ellis Jeffrey Ellis is a Senior Managing

Leases: A Comprehensive Update on the Joint Project

The Dbriefs Financial Reporting series presents: Leases: A Comprehensive Update on the Joint Project Bob Uhl, Deloitte & Touche LLP Trevor Farber, Deloitte & Touche LLP James Barker, Deloitte & Touche

The Dbriefs Financial Reporting series presents: Leases: A Comprehensive Update on the Joint Project Bob Uhl, Deloitte & Touche LLP Trevor Farber, Deloitte & Touche LLP James Barker, Deloitte & Touche

Accounting and Auditing Update. Tennessee Chapter of hfma Spring Institute 2016 Presented by William C. Matheney FHFMA CPA and Meredith P.

Accounting and Auditing Update Tennessee Chapter of hfma Spring Institute 2016 Presented by William C. Matheney FHFMA CPA and Meredith P. Cate Today s Objectives Present an overview of pertinent recently

Accounting and Auditing Update Tennessee Chapter of hfma Spring Institute 2016 Presented by William C. Matheney FHFMA CPA and Meredith P. Cate Today s Objectives Present an overview of pertinent recently

Investor Advisory Committee 401 Merritt 7, P.O. Box 5116, Norwalk, Connecticut Phone: Fax:

401 Merritt 7, P.O. Box 5116, Norwalk, Connecticut 06856-5116 Phone: 203 956-5207 Fax: 203 849-9714 Via Email November 5, 2014 Technical Director Financial Accounting Standards Board File Reference No.

401 Merritt 7, P.O. Box 5116, Norwalk, Connecticut 06856-5116 Phone: 203 956-5207 Fax: 203 849-9714 Via Email November 5, 2014 Technical Director Financial Accounting Standards Board File Reference No.

Lease & Finance Accountants Conference. September The Westin Charlotte Charlotte, NC

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Basic Principles of Lessors under ASC 842 Mamta Shori, Wells Fargo Equipment Finance Joe Sebik,

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Basic Principles of Lessors under ASC 842 Mamta Shori, Wells Fargo Equipment Finance Joe Sebik,

FASB Updates Business Definition

On January 5, 2017, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 2017-01, s (Topic 805): Clarifying the Definition of a Business. This definition is significant

On January 5, 2017, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 2017-01, s (Topic 805): Clarifying the Definition of a Business. This definition is significant

Technical Line FASB final guidance

No. 2016-09 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect health care entities In this issue: Overview... 1 Key considerations... 3 Scope and scope exceptions...

No. 2016-09 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect health care entities In this issue: Overview... 1 Key considerations... 3 Scope and scope exceptions...

Countdown to MFRS 16 Are you ready?

Volume 6 - Issue 3 8 June 018 Countdown to MFRS 16 Are you ready? MFRS 16 sets a new turning point for lease accounting. With the requirement for most operating leases to be recognized on the balance sheet,

Volume 6 - Issue 3 8 June 018 Countdown to MFRS 16 Are you ready? MFRS 16 sets a new turning point for lease accounting. With the requirement for most operating leases to be recognized on the balance sheet,

CFA UK response to the Exposure Draft on Leases

David Humphreys Practice Fellow International Accounting Standards Board 30 Cannon Street London EC4M 6XH 20 th December 2010 Dear David, Thank you for the opportunity to respond to the IASB Exposure Draft

David Humphreys Practice Fellow International Accounting Standards Board 30 Cannon Street London EC4M 6XH 20 th December 2010 Dear David, Thank you for the opportunity to respond to the IASB Exposure Draft

Re: Comments re: Joint board meeting of January 23, 2014 on the re-deliberation plan for the Leases Project

LEASING 101 17 Lancaster Dr. Suffern, NY 10901 Phone: 914-522-3233 Fax: 845-357-4113 wbleasing101@aol.com www.leasing-101.com Mr. Russell Golden, Chairman Financial Accounting Standards Board 401 Merritt

LEASING 101 17 Lancaster Dr. Suffern, NY 10901 Phone: 914-522-3233 Fax: 845-357-4113 wbleasing101@aol.com www.leasing-101.com Mr. Russell Golden, Chairman Financial Accounting Standards Board 401 Merritt

Lease Accounting: Gather your data now and understand tax implications. Tuesday, December 5, 2017

Lease Accounting: Gather your data now and understand tax implications Tuesday, December 5, 2017 Presenters Chris Stephenson Principal, Business Consulting & Technology chris.stephenson@us.gt.com Rebekah

Lease Accounting: Gather your data now and understand tax implications Tuesday, December 5, 2017 Presenters Chris Stephenson Principal, Business Consulting & Technology chris.stephenson@us.gt.com Rebekah