IFRS 15 and IFRS 16 Webinar

|

|

|

- Bertha Roberts

- 6 years ago

- Views:

Transcription

1 CPA Ireland Skillnet CPA Ireland Skillnet, is a training network that is funded by Skillnets, a state funded, enterprise led support body dedicated to the promotion and facilitation of training and up-skilling as key elements in sustaining Ireland s national competitiveness. The CPA Ireland Skillnet provides excellent value CPE (continual Professional Education) in accountancy, law, tax and strategic personal development to accountants working both in practice and in industry. However our attendees are not limited to the accountancy field as we welcome all interested parties to our events. The CPA Ireland Skillnet is funded by member companies and the Training Networks Programme, an initiative of Skillnets Ltd. funded from the Department of Education and Skills. IFRS 15 and IFRS 16 Webinar September 2016 Dublin Presenter Robert J Kirk Professor of Financial Reporting

2 IFRS 15 REVENUE FROM CONTRACTS WITH CUSTOMERS Background Joint project IASB and FASB Significant diversity in practice under IAS 18 USA had number of industry standards Boilerplate disclosure New standard concentrates on transfer of control rather than risks and rewards Introduces a 5 step approach to revenue recognition

3 Scope Exceptions Lease contracts under IAS 17 Insurance contracts under IFRS 4 Financial instruments under IFRS 9; and Group income under IFRS 10, 11 and IAS 27 and 28 Core Principle Recognise Revenue to depict transfer of promised goods or services to customers in an amount that reflects consideration to which entity expects to be entitled in exchange for those goods or services

4 Steps to achieve Core Principle Identify contract with a customer Identify separate performance obligations in contract Determine transaction price Allocate transaction price to separate performance obligations in contract Recognise revenue when entity satisfies a performance obligation Step 1: Identify Contract Contract: Agreement between two or more parties that creates enforceable rights & obligations Essentials of a Contract: - has commercial substance - has been approved by the parties (Written, Oral or Implied) & commitment to perform obligations - each party s right regarding goods/services can be identified - payment terms can be identified - Probable that consideration will be collected by vendor

5 Step 2: Identify separate performance obligations (contd.) Entity promises to transfer more than one good or service Check conditions for Non-Distinct: - goods/services are highly interrelated & transferring them to customer requires that entity also provide a significant service of integrating goods/services into combined item(s) for which customer has contracted and - bundle of goods/services is significantly modified or customised to fulfil contract Yes Combine with other promised goods/ services until a distinct bundle is identified No No Check conditions for Distinct: - sold separately on regular basis or - customer can benefit from good /service either on its own or together with other resources readily available to him Yes Account as separate performance obligation Example determining whether goods or services are distinct Construction contract goods and services are not distinct A building contractor (the vendor) enters into a contract to build a new office block for a customer. The vendor is responsible for the entire project, including procuring the construction materials, project management and associated services. The project involves site clearance, foundations, construction, piping and wiring, equipment installation and finishing. Solution Although the goods or services to be supplied are capable of being distinct (because the customer could, for example, benefit from them on their own by using, consuming or selling the goods or services, and could purchase them from other suppliers), they are not distinct in the context of the vendor s contract with its customer. This is because the vendor provides a significant service of integrating all of the inputs into the combined output (the new office block) which it has contracted to deliver to its customer.

6 Software scenario A A vendor enters into a contract with a customer to supply a licence for a standard off the shelf software package, install the software, and to provide unspecified software updates and technical support for a period of two years. The vendor sells the licence and technical support separately, and the installation service is routinely provided by a number of other unrelated vendors. The software will remain functional without the software updates and technical support. The software is delivered separately from the other goods or services, can be installed by a different third party vendor, and remains functional without the software updates and technical support. Therefore, it is concluded that the customer can benefit from each of the goods or services either on their own or together with other goods or services that are readily available. In addition, each of the promises to transfer goods or services is separately identifiable; because the installation services does not significantly modify or customise the software, the installation and software are separate outputs promised by the vendor, and not one overall combined output. Solution The following distinct goods or services are identified: Software licence Installation service Software updates and Technical support. Software scenario B The vendor s contract with its customer is the same as in scenario A, except that as part of the installation service the software is to be substantially customised in order to add significant new functionality to enable the software to interface with other software already being used by the customer. The customised installation service can be provided by a number of unrelated vendors. In this case, although the installation service could be provided by other entities, the analysis required by IFRS 15 indicates that within the context of its contract with the customer, the promise to transfer the licence is not separately identifiable from the customised installation service. In contrast and as before, the software updates and technical updates are separately identifiable. Solution The following distinct goods or services are identified: Software licence and customised installation service Software updates Technical support.

7 Software scenario C The vendor s contract with its customer is the same as in scenario B, except that: The vendor is the only supplier that is capable of carrying out the customised installation service The software updates and technical support are essential to ensure that the software continues to operate satisfactorily, and the customer s employees continue to be able to operate the related IT systems. No other entity is capable of providing the software updates or the technical support. In this case, the analysis required by IFRS 15 indicates that in the context of its contract with the customer, the promise is to transfer a combined service. Solution This combined service is identified as the single distinct good or service. Step 3: Determine Transaction Price Transaction price: Amount of consideration to which an entity expects to be entitled in exchange for transferring promised goods or services to a customer excluding amounts collected on behalf of third parties IAS 18 -At FV Variable consideration: Use expected value or most likely amount whichever can be predicted better Time Value of Money: Adjust if contract has financing component that is significant to contract (Exception: 1 year or less)

8 Step 3: Determine Transaction Price (contd.) Non-cash consideration: At FV If FV can t be estimated reasonably, measure by reference to stand-alone selling price of goods /services Consideration payable to customer: - Entity pays or expects to pay consideration to customer or other parties that purchase goods/services from customer and customer can apply that amount against amount owed to entity Reduce from Transaction Price unless payment is in exchange for distinct good/service Ignore effects of customer credit risk Step 4: Allocate Transaction Price Allocate TP to each separate PO Determine stand-alone selling price at contract inception of good/service underlying each separate PO for allocation purpose If stand-alone selling price not observable: estimation Allocation of subsequent changes in TP: - Amount allocated to a satisfied PO: Recognise as Revenue or as Reduction of Revenue - in period of subsequent change

9 Step 5: Recognise Revenue Satisfy Performance Obligation by transferring a promised good or service Customer obtains control of good or service Recognise Revenue Step 5: Recognise Revenue (Contd.) Customer Obtains Control of Good or Service: Goods and services are assets, even if only momentarily, when they are received & used (as in case of many services) Control of an asset: - ability to direct use of & obtain substantially all of the remaining benefits from asset - ability to prevent other entities from directing use of and obtaining benefits from an asset - benefits are potential cash flows that can be obtained directly or indirectly in many ways

Determine whether each Separate PO is satisfied: Over Time If either of following conditions is met: (a) entity s performance creates or enhances an asset that customer controls as asset is created")

10 Step 5: Recognise Revenue (contd.) Determine whether each Separate PO is satisfied: Over Time If either of following conditions is met: (a) entity s performance creates or enhances an asset that customer controls as asset is created or enhanced or (b) entity s performance does not create asset with an alternative use to entity & at least one of following criteria is met: - customer simultaneously receives & consumes benefits of entity s performance as it performs - another entity would not need to substantially re-perform the work entity has completed to date if that other entity were to fulfil remaining obligation to customer or - entity has right to payment for performance completed to date & it expects to fulfil contract as promised Point in time Entity to consider following indicators of transfer of control (in addition to requirements for control) to determine point in time: - entity has a present right to payment for asset - customer has legal title to asset - entity has transferred physical possession of asset - customer has significant risks and rewards of ownership of asset - customer has accepted asset Disclosure Annual disclosure requirements Disclosure type Disaggregated revenue Required information Disaggregation of revenue into categories that show how economic factors affect the nature, amount, timing, and uncertainty of revenue and cash flows Reconciliation of contract balances Opening and closing balances and revenue recognized during the period from changes in contract balances Qualitative and quantitative information about the significant changes in contract balances Performance obligations Descriptive information about an entity s performance obligations Information about the transaction price allocated to remaining performance obligations and when revenue will be recognized

11 Disclosure Annual disclosure requirements Disclosure type Required information Significant judgments Method used to recognize revenue for performance obligations satisfied over time and why the method is appropriate Significant judgments related to transfer of control for performance obligations satisfied at a point in time Information about the methods, inputs, and assumptions used to determine and allocate transaction price Costs to obtain or fulfil a contract Judgments made to determine costs to obtain or fulfill a contract, and method of amortization Closing balances of assets and amount of amortization/impairment Practical expedients Use of either of the following: The practical expedient regarding the existence of a significant financing component; The practical expedient for expensing certain costs of obtaining a contract; IFRS 16 Leases (January 2016)

12 IFRS 16 Leases (January 2016) The need for change All leases create assets and liabilities Investors and analysts frequently adjust a lessee s balance sheet Lack of comparability Lack of information

13 IFRS 16 Leases (January 2016) Scope IFRS 16 applies to all leases except: leases to explore for or use minerals, oil, natural gas and similar nonregenerative resources; leases of biological assets within the scope of IAS 41, Agriculture, held by lessees; service concession arrangements within the scope of IFRIC 12, licences of intellectual property granted by a lessor within the scope of IFRS 15, Revenue from Contracts with Customers; and rights held by lessee under licensing agreements within the scope of IAS 38, Intangible Assets, for items such as motion picture films, video recordings, plays, manuscripts, patents and copyrights. IFRS 16 Leases (January 2016) The IASB lessee accounting model In essence for all leases, the IASB model requires a lessee to: (a) recognise lease assets and liabilities on the balance sheet, initially measured at the present value of unavoidable lease payments; (b) recognise amortisation of lease assets and interest on lease liabilities over the lease term; and (c) separate the total amount of cash paid into a principal portion (presented within financing activities) and interest (presented within either operating or financing activities).

14 IFRS 16 Leases Exemptions Leases with less than 12 months Low value leases e.g. PCs, office furniture elect on lease by lease basis IFRS 16

")

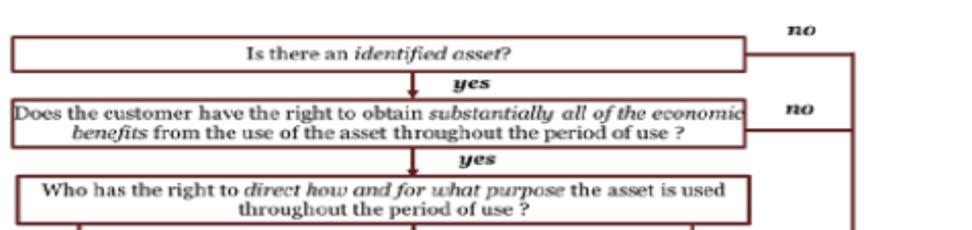

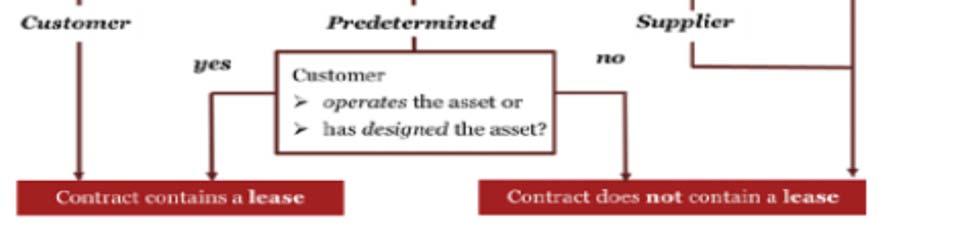

15 IFRS 16 Leases (January 2016) IFRS 16 Determining whether a contract contains a lease

")

16 IFRS 16 Leases (January 2016) IFRS 16 Leases (January 2016)

")

17 IFRS 16 Leases (January 2016) IFRS 16 Leases (January 2016)

18 Accounting by Lessees IFRS 16 Initial recognition right of use asset and lease liability Right of use asset amount of liability + initial direct costs + incentives, restoration obligations Lease liability PV discounted at implicit rate or incremental borrowing rate Presentation IFRS 16 SOFP Right-of-use asset can be presented either separately or in the same line item in which the underlying asset would be presented. Lease liability can be presented either as a separate line item or together with other financial liabilities. If the right-of-use asset and the lease liability are not presented as separate line items, must disclose in the notes the carrying amount of those items and the line item in which they are included. SOPLOCI Depreciation charge is presented in the same line item/items in which similar expenses (such as depreciation of property, plant and equipment) are shown. The interest expense on the lease liability is presented as part of finance costs. However, the amount of interest expense on lease liabilities has to be disclosed in the notes. SOCF Lease payments are classified consistently with payments on other financial liabilities: Principal portion of the lease liability - cash flow from financing activities. Interest portion of the lease liability - either as an operating cash flow or a cash flow resulting from financing activities (in accordance with the entity s accounting policy regarding the presentation of interest payments).

19 Major Disclosures IFRS 16 Right of use asset Depreciation charge (by class of underlying asset) Carrying amount (by class of underlying asset) Additions Lease liabilities Interest expense Maturity analysis in accordance with paragraph 39 and B11 of IFRS 7 Recognition and measurement exemptions Expense relating to short-term leases Expense relating to leases of low-value assets Other disclosures relating to income statement Expense relating to variable lease payments not included in lease liabilities Income from subleasing right-of-use assets Gains or losses arising from sale and leaseback transactions Disclosure IFRS 16 Total cash outflow for leases Future cash outflows from Variable lease payments (includes key variables on which payments depend and how they affect them) Extension options and termination options Residual value guarantees Leases not yet commenced to which the entity is committed Short-term lease commitments Qualitative disclosures Nature of the lessee s leasing activities Restrictions or covenants imposed by leases Sale and leaseback transactions

20 IFRS 16 Leases IFRS 16

21 END OF PRESENTATION Thank you for your kind attention Any questions?

International Financial Reporting Standard 16 Leases. Objective. Scope. Recognition exemptions (paragraphs B3 B8) IFRS 16

IFRS 16") International Financial Reporting Standard 16 Leases Objective 1 This Standard sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective is to ensure

International Financial Reporting Standard 16 Leases Objective 1 This Standard sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective is to ensure

IFRS 16 LEASES. Page 1 of 21

IFRS 16 LEASES OBJECTIVE The objective is to ensure that lessees and lessors provide relevant information in a manner that faithfully represents those transactions. This information gives a basis for users

IFRS 16 LEASES OBJECTIVE The objective is to ensure that lessees and lessors provide relevant information in a manner that faithfully represents those transactions. This information gives a basis for users

In December 2003 the Board issued a revised IAS 17 as part of its initial agenda of technical projects.

IFRS 16 Leases In April 2001 the International Accounting Standards Board (the Board) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

IFRS 16 Leases In April 2001 the International Accounting Standards Board (the Board) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

In December 2003 the IASB issued a revised IAS 17 as part of its initial agenda of technical projects.

IFRS Standard 16 Leases In April 2001 the International Accounting Standards Board (IASB) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

IFRS Standard 16 Leases In April 2001 the International Accounting Standards Board (IASB) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

IFRS 15. Revenue from Contracts with Customers. Presented by CPA Dr. Peter Njuguna

IFRS 15 Revenue from Contracts with Customers Presented by CPA Dr. Peter Njuguna Introduction Revenue is income from ordinary activities. A contract has rights and obligations between two or more parties.

IFRS 15 Revenue from Contracts with Customers Presented by CPA Dr. Peter Njuguna Introduction Revenue is income from ordinary activities. A contract has rights and obligations between two or more parties.

Sri Lanka Accounting Standard - SLFRS 16. Leases

Sri Lanka Accounting Standard - SLFRS 16 Leases CONTENTS from paragraph SRI LANKA ACCOUNTING STANDARD - SLFRS 16 LEASES INTRODUCTION OBJECTIVE 1 SCOPE 3 RECOGNITION EXEMPTIONS 5 IDENTIFYING A LEASE 9 Separating

Sri Lanka Accounting Standard - SLFRS 16 Leases CONTENTS from paragraph SRI LANKA ACCOUNTING STANDARD - SLFRS 16 LEASES INTRODUCTION OBJECTIVE 1 SCOPE 3 RECOGNITION EXEMPTIONS 5 IDENTIFYING A LEASE 9 Separating

Headline Verdana Bold The evolutions of leases accounting under IFRS 16 Mariano Bruno, Carlo Laganà, Giuseppe Ambrosio, Deloitte & Touche S.p.A.

SHIPPING AND THE LAW 7^ Edition 25-26 October 2016 NAPLES Headline Verdana Bold The evolutions of leases accounting under IFRS 16 Mariano Bruno, Carlo Laganà, Giuseppe Ambrosio, Deloitte & Touche S.p.A.

SHIPPING AND THE LAW 7^ Edition 25-26 October 2016 NAPLES Headline Verdana Bold The evolutions of leases accounting under IFRS 16 Mariano Bruno, Carlo Laganà, Giuseppe Ambrosio, Deloitte & Touche S.p.A.

HKFRS 16 Leases sets out the principles for the recognition, measurement, presentation and disclosure

HKFRS 16 Leases Introduction HKFRS 16 Leases sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective of HKFRS 16 is to ensure that lessees and lessors

HKFRS 16 Leases Introduction HKFRS 16 Leases sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective of HKFRS 16 is to ensure that lessees and lessors

Exposure Draft 64 January 2018 Comments due: June 30, Proposed International Public Sector Accounting Standard. Leases

Exposure Draft 64 January 2018 Comments due: June 30, 2018 Proposed International Public Sector Accounting Standard Leases This document was developed and approved by the International Public Sector Accounting

Exposure Draft 64 January 2018 Comments due: June 30, 2018 Proposed International Public Sector Accounting Standard Leases This document was developed and approved by the International Public Sector Accounting

IFRS 16 : Lease accounting

IFRS 16 : Lease accounting Effective for accounting periods beginning on or after 1 January 2019 December 2017 IFRS 16: Lease accounting The IASB published the new IFRS 16 lease standard, in order to avoid

IFRS 16 : Lease accounting Effective for accounting periods beginning on or after 1 January 2019 December 2017 IFRS 16: Lease accounting The IASB published the new IFRS 16 lease standard, in order to avoid

Exposure Draft. Indian Accounting Standard (Ind AS) 116 Leases. (Last date for Comments: August 31, 2017)

116 Leases. (Last date for Comments: August 31, 2017)") ED/Ind AS/2017/06 Exposure Draft Indian Accounting Standard (Ind AS) 116 Leases (Last date for Comments: August 31, 2017) Issued by Accounting Standards Board The Institute of Chartered Accountants of

ED/Ind AS/2017/06 Exposure Draft Indian Accounting Standard (Ind AS) 116 Leases (Last date for Comments: August 31, 2017) Issued by Accounting Standards Board The Institute of Chartered Accountants of

New Zealand Equivalent to International Financial Reporting Standard 16 Leases (NZ IFRS 16)

") New Zealand Equivalent to International Financial Reporting Standard 16 Leases (NZ IFRS 16) Issued February 2016 This Standard was issued on 11 February 2016 by the New Zealand Accounting Standards Board

New Zealand Equivalent to International Financial Reporting Standard 16 Leases (NZ IFRS 16) Issued February 2016 This Standard was issued on 11 February 2016 by the New Zealand Accounting Standards Board

IASB Staff Paper March 2011

IASB Staff Paper March 2011 Effect of board redeliberations on Exposure Draft Leases About this staff paper This staff paper indicates how the proposals in the Exposure Draft Leases would change as a result

IASB Staff Paper March 2011 Effect of board redeliberations on Exposure Draft Leases About this staff paper This staff paper indicates how the proposals in the Exposure Draft Leases would change as a result

Gearing up for change New IFRS on Leases

Gearing up for change New IFRS on Leases In a nutshell The changes Lessee accounting Effective date: 1 January 2019 Limited changes to scope of IAS 17 Enhanced guidance on identifying a lease Lessor accounting

Gearing up for change New IFRS on Leases In a nutshell The changes Lessee accounting Effective date: 1 January 2019 Limited changes to scope of IAS 17 Enhanced guidance on identifying a lease Lessor accounting

Applying IFRS. A closer look at the new leases standard. August 2016

Applying IFRS A closer look at the new leases standard August 2016 Contents Overview 3 1. Scope and scope exceptions 5 1.1 General 5 1.2 Determining whether an arrangement contains a lease 6 1.3 Identifying

Applying IFRS A closer look at the new leases standard August 2016 Contents Overview 3 1. Scope and scope exceptions 5 1.1 General 5 1.2 Determining whether an arrangement contains a lease 6 1.3 Identifying

IFRS Update Guy Thomas, CPA, CA

IFRS Update Guy Thomas, CPA, CA D&Co IFRS update Agenda 3 new standards under IFRS IFRS 9 Financial Instruments IFRS 15 Revenue from Contracts with Customers IFRS 16 Leases Agenda Some narrow scope amendments

IFRS Update Guy Thomas, CPA, CA D&Co IFRS update Agenda 3 new standards under IFRS IFRS 9 Financial Instruments IFRS 15 Revenue from Contracts with Customers IFRS 16 Leases Agenda Some narrow scope amendments

New IASB leases standard engineering and construction

Applying IFRS New IASB leases standard engineering and construction October 2016 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition of a lease 3 1.3 Arrangements

Applying IFRS New IASB leases standard engineering and construction October 2016 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition of a lease 3 1.3 Arrangements

Accounting Update. Anne Cloutier, CPA, FHFMA Principal March 27, 2015

Accounting Update Anne Cloutier, CPA, FHFMA Principal March 27, 2015 Current Accounting for Leases Capital leases - a lessee recognizes leased assets and liabilities on the balance sheet. Operating leases

Accounting Update Anne Cloutier, CPA, FHFMA Principal March 27, 2015 Current Accounting for Leases Capital leases - a lessee recognizes leased assets and liabilities on the balance sheet. Operating leases

New Accounting Rules for Revenue and Leases

New Accounting Rules for Revenue and Leases CFMA Education Summit March 22, 2017 Presented by: Carole McNees, CPA, Partner, Plante & Moran, PLLC Recently released standards New guidance from the Financial

New Accounting Rules for Revenue and Leases CFMA Education Summit March 22, 2017 Presented by: Carole McNees, CPA, Partner, Plante & Moran, PLLC Recently released standards New guidance from the Financial

Applying IFRS. New IASB leases standard oilfield services. December 2016

Applying IFRS New IASB leases standard oilfield services December 2016 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition of a lease 3 1.3 Identifying and separating

Applying IFRS New IASB leases standard oilfield services December 2016 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition of a lease 3 1.3 Identifying and separating

Miles CPA Review: FAR Updates

Miles CPA Review: FAR - 2019 Updates Summary of updates: - FAR-4.4: s [ASC 842] effective fiscal years beginning after Dec 15, 2018 (for issuers) and effective fiscal years beginning after Dec 15, 2019

Miles CPA Review: FAR - 2019 Updates Summary of updates: - FAR-4.4: s [ASC 842] effective fiscal years beginning after Dec 15, 2018 (for issuers) and effective fiscal years beginning after Dec 15, 2019

FSA Faculty Consortium Technical Accounting Update. Bob Uhl, partner, Deloitte & Touche LLP

FSA Faculty Consortium Technical Accounting Update Bob Uhl, partner, Deloitte & Touche LLP Deloitte University May 30, 2014 Acronyms Acronym ASC ASU ED FASB IASB IFRS U.S. GAAP Full Form Accounting Standards

FSA Faculty Consortium Technical Accounting Update Bob Uhl, partner, Deloitte & Touche LLP Deloitte University May 30, 2014 Acronyms Acronym ASC ASU ED FASB IASB IFRS U.S. GAAP Full Form Accounting Standards

IFRS Project Insights Leases

IFRS Project Insights Leases The IASB and FASB ( the Boards ) published a Discussion Paper (DP) setting out a proposed lessee accounting model in March 2009. The proposed accounting model has evolved since

IFRS Project Insights Leases The IASB and FASB ( the Boards ) published a Discussion Paper (DP) setting out a proposed lessee accounting model in March 2009. The proposed accounting model has evolved since

Defining Issues May 2013, No

Defining Issues May 2013, No. 13-24 FASB and IASB Issue Revised Exposure Drafts on Lease Accounting The FASB and IASB (the Boards) recently issued revised joint exposure drafts (EDs) on proposed changes

Defining Issues May 2013, No. 13-24 FASB and IASB Issue Revised Exposure Drafts on Lease Accounting The FASB and IASB (the Boards) recently issued revised joint exposure drafts (EDs) on proposed changes

[TO BE PUBLLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (i)]

![[TO BE PUBLLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (i)]](/thumbs/95/124393322.jpg "[TO BE PUBLLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (i)]") [TO BE PUBLLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (i)] GOVERNMENT OF INDIA MINISTRY OF CORPORATE AFFAIRS NOTIFICATION New Delhi, the 30 th March, 2019 G.S.R. (E).

[TO BE PUBLLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (i)] GOVERNMENT OF INDIA MINISTRY OF CORPORATE AFFAIRS NOTIFICATION New Delhi, the 30 th March, 2019 G.S.R. (E).

International Financial Reporting Standards (IFRS)

") FACT SHEET February 2011 IAS 17 Leases (This fact sheet is based on the standard as at 1 January 2011.) Important note: This fact sheet is based on the requirements of the International Financial Reporting

FACT SHEET February 2011 IAS 17 Leases (This fact sheet is based on the standard as at 1 January 2011.) Important note: This fact sheet is based on the requirements of the International Financial Reporting

Proposed New Accounting Standards For Leases

Relationships backed by performance. Proposed New Accounting Standards For Leases Doug Richardson Live Seminar 9:00am 10:30am June 21 2012 Overview and Background Leases serve a vital role in many entities

Relationships backed by performance. Proposed New Accounting Standards For Leases Doug Richardson Live Seminar 9:00am 10:30am June 21 2012 Overview and Background Leases serve a vital role in many entities

The New Lease Accounting Standard. Hunter Mink, CPA, CCIFP Brian Rosenberg, CPA, MBA

The New Lease Accounting Standard Hunter Mink, CPA, CCIFP Brian Rosenberg, CPA, MBA 1 Agenda Introduction Lease Identification and Classification Lessee Accounting Other Considerations Disclosures Impact

The New Lease Accounting Standard Hunter Mink, CPA, CCIFP Brian Rosenberg, CPA, MBA 1 Agenda Introduction Lease Identification and Classification Lessee Accounting Other Considerations Disclosures Impact

IFRS 16 Leases. Presented by Anton van Wyk M. Com CA (SA)

") IFRS 16 Leases Presented by Anton van Wyk M. Com CA (SA) Why a new IFRS for leases? Information reported about operating leases lacked transparency and did not meet the needs of users of financial statements

IFRS 16 Leases Presented by Anton van Wyk M. Com CA (SA) Why a new IFRS for leases? Information reported about operating leases lacked transparency and did not meet the needs of users of financial statements

Technical Line FASB final guidance

No. 2018-08 20 September 2018 Technical Line FASB final guidance How the new leases standard affects engineering and construction entities In this issue: Overview... 1 Key considerations... 2 Scope and

No. 2018-08 20 September 2018 Technical Line FASB final guidance How the new leases standard affects engineering and construction entities In this issue: Overview... 1 Key considerations... 2 Scope and

Click to edit Master title style REVENUE RECOGNITION Understanding the New Revenue Recognition Standard ASC 606

Click to edit Master title style REVENUE RECOGNITION Understanding the New Revenue Recognition Standard ASC 606 9/7/2017 0 Agenda Overview of ASC 606 Review of the five-step process Accounting for contract

Click to edit Master title style REVENUE RECOGNITION Understanding the New Revenue Recognition Standard ASC 606 9/7/2017 0 Agenda Overview of ASC 606 Review of the five-step process Accounting for contract

IFRS 16 Leases supplement

IFRS 16 Leases supplement Guide to annual financial statements IFRS December 2017 kpmg.com/ifrs Contents About this supplement 1 About IFRS 16 3 The Group s lease portfolio 6 Part I Modified retrospective

IFRS 16 Leases supplement Guide to annual financial statements IFRS December 2017 kpmg.com/ifrs Contents About this supplement 1 About IFRS 16 3 The Group s lease portfolio 6 Part I Modified retrospective

IASB issues new leases standard consumer products and retail

Applying IFRS in consumer products and retail IASB issues new leases standard consumer products and retail June 2016 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition

Applying IFRS in consumer products and retail IASB issues new leases standard consumer products and retail June 2016 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition

AASB 16: Experience the Fundamental Overhaul of Lease Accounting for Lessees

AASB 16: Experience the Fundamental Overhaul of Lease Accounting for Lessees Introduction to Session This introductory session we will: Explore the Principles of AASB 16 Learn how to Identify a Lease Work

AASB 16: Experience the Fundamental Overhaul of Lease Accounting for Lessees Introduction to Session This introductory session we will: Explore the Principles of AASB 16 Learn how to Identify a Lease Work

How the lease accounting proposal might affect your company

Applying IFRS How the lease accounting proposal might affect your company August 2013 Contents 1. Overview... 1 2. Identifying a lease... 2 2.1 Scope exclusions... 2 2.2 Definition of a lease... 3 2.2.1

Applying IFRS How the lease accounting proposal might affect your company August 2013 Contents 1. Overview... 1 2. Identifying a lease... 2 2.1 Scope exclusions... 2 2.2 Definition of a lease... 3 2.2.1

Applying IFRS in consumer products and retail

Applying IFRS in consumer products and retail Leases standard Consumer products and retail Updated June 2017 Contents Overview 2 1. Identifying a lease 3 1.1 Definition of a lease 3 1.2 Identified asset

Applying IFRS in consumer products and retail Leases standard Consumer products and retail Updated June 2017 Contents Overview 2 1. Identifying a lease 3 1.1 Definition of a lease 3 1.2 Identified asset

International Accounting Standard 17 Leases. Objective. Scope. Definitions IAS 17

International Accounting Standard 17 Leases Objective 1 The objective of this Standard is to prescribe, for lessees and lessors, the appropriate accounting policies and disclosure to apply in relation

International Accounting Standard 17 Leases Objective 1 The objective of this Standard is to prescribe, for lessees and lessors, the appropriate accounting policies and disclosure to apply in relation

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions. August 24, 2017

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions August 24, 2017 Learning objectives Define leasing implications related to recently revised FASB standard Differentiate between new

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions August 24, 2017 Learning objectives Define leasing implications related to recently revised FASB standard Differentiate between new

GASB 87. OVERVIEW: Supersedes GASB s 13 and 62 (paragraphs ).

.") Leases OVERVIEW: Supersedes GASB s 13 and 62 (paragraphs 211-271). Will require significant changes from its current practice, particularly in the accounting for operating leases Effective for reporting

Leases OVERVIEW: Supersedes GASB s 13 and 62 (paragraphs 211-271). Will require significant changes from its current practice, particularly in the accounting for operating leases Effective for reporting

CPA Stephen Obock November 2017

FINANCIAL REPORTING WORKSHOP New Developments on revenue recognition: IFRS 15, IPSAS 9 and IPSAS 23 Presentation by: CPA Stephen Obock November 2017 Uphold public interest Agenda 1. IFRS 15- Revenue from

FINANCIAL REPORTING WORKSHOP New Developments on revenue recognition: IFRS 15, IPSAS 9 and IPSAS 23 Presentation by: CPA Stephen Obock November 2017 Uphold public interest Agenda 1. IFRS 15- Revenue from

These FAQs reflect current views and understanding of the IASB project.

FAQ 14 SEPTEMBER 2010 IASB PROJECT ON LEASE ACCOUNTING These FAQs reflect current views and understanding of the IASB project. In August 2010, the International Accounting Standards Board (IASB) and the

FAQ 14 SEPTEMBER 2010 IASB PROJECT ON LEASE ACCOUNTING These FAQs reflect current views and understanding of the IASB project. In August 2010, the International Accounting Standards Board (IASB) and the

Leases ASU September 20, 2017

Leases ASU 2016-02 September 20, 2017 Meet the Speakers Tonisha Spratte, CPA Senior Accountant Cherry Bekaert tspratte@cbh.com Matthew Mars Senior Accountant Cherry Bekaert mmars@cbh.com Agenda What is

Leases ASU 2016-02 September 20, 2017 Meet the Speakers Tonisha Spratte, CPA Senior Accountant Cherry Bekaert tspratte@cbh.com Matthew Mars Senior Accountant Cherry Bekaert mmars@cbh.com Agenda What is

Applying IFRS in Financial Services

Applying IFRS in Financial Services IASB issues new leases standard - financial services April 2016 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition of a lease

Applying IFRS in Financial Services IASB issues new leases standard - financial services April 2016 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition of a lease

Technical Line FASB final guidance

No. 2019-01 3 January 2019 Technical Line FASB final guidance How the new leases standard affects automotive entities In this issue: Overview... 1 Recent standard setting activity... 2 Key considerations...

No. 2019-01 3 January 2019 Technical Line FASB final guidance How the new leases standard affects automotive entities In this issue: Overview... 1 Recent standard setting activity... 2 Key considerations...

COMMITTEE OF EUROPEAN SECURITIES REGULATORS

COMMITTEE OF EUROPEAN SECURITIES REGULATORS IASB 30 Cannon Street LONDON EC4M 6XH United Kingdom Date: 29 November 2010 Ref.: CESR/10-1518 RE: the IASB s Exposure Draft Leases The Committee of European

COMMITTEE OF EUROPEAN SECURITIES REGULATORS IASB 30 Cannon Street LONDON EC4M 6XH United Kingdom Date: 29 November 2010 Ref.: CESR/10-1518 RE: the IASB s Exposure Draft Leases The Committee of European

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N AGENDA Leases FASB & GASB Revenue Recognition FASB 2 FASB ASU 2016-02, Leases (Topic

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N AGENDA Leases FASB & GASB Revenue Recognition FASB 2 FASB ASU 2016-02, Leases (Topic

Accounting and Auditing Update. Tennessee Chapter of hfma Spring Institute 2016 Presented by William C. Matheney FHFMA CPA and Meredith P.

Accounting and Auditing Update Tennessee Chapter of hfma Spring Institute 2016 Presented by William C. Matheney FHFMA CPA and Meredith P. Cate Today s Objectives Present an overview of pertinent recently

Accounting and Auditing Update Tennessee Chapter of hfma Spring Institute 2016 Presented by William C. Matheney FHFMA CPA and Meredith P. Cate Today s Objectives Present an overview of pertinent recently

Executive Summary. New leases standard Lessees

Executive Summary December 2018 The new leases standard focuses on increased transparency and comparability providing financial statement users with more information about an entity s leasing activities.

Executive Summary December 2018 The new leases standard focuses on increased transparency and comparability providing financial statement users with more information about an entity s leasing activities.

Summary of IFRS Exposure Draft Leases

The International Accounting Standards Board (IASB) recently issued a revised exposure draft (ED) relating to leases. Once these proposals are finalized the new guidance will replace the IAS 17 Leases.

The International Accounting Standards Board (IASB) recently issued a revised exposure draft (ED) relating to leases. Once these proposals are finalized the new guidance will replace the IAS 17 Leases.

Applying IFRS. New IASB leases standard Mining and Metals October 2016

Applying IFRS New IASB leases standard Mining and Metals October 2016 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition of a lease 4 1.3 Arrangements entered into

Applying IFRS New IASB leases standard Mining and Metals October 2016 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition of a lease 4 1.3 Arrangements entered into

Technical Line FASB final guidance

No. 2016-09 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect health care entities In this issue: Overview... 1 Key considerations... 3 Scope and scope exceptions...

No. 2016-09 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect health care entities In this issue: Overview... 1 Key considerations... 3 Scope and scope exceptions...

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions. August 24, 2017

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions August 24, 2017 Learning objectives Define leasing implications related to recently revised FASB standard Differentiate between new

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions August 24, 2017 Learning objectives Define leasing implications related to recently revised FASB standard Differentiate between new

CA. Gopal Ji Agrawal

CA. Gopal Ji Agrawal 1. Scope 2. Key concepts 3. Accounting for leases 4. Other Lease Contracts 4. Disclosure 5. Appendix (s) 6. Questions October 1980 September 1982 IAS 17 Accounting for Leases Exposure

CA. Gopal Ji Agrawal 1. Scope 2. Key concepts 3. Accounting for leases 4. Other Lease Contracts 4. Disclosure 5. Appendix (s) 6. Questions October 1980 September 1982 IAS 17 Accounting for Leases Exposure

The Differences between full IFRS and FRS 102

CPA Ireland Skillnet CPA Ireland Skillnet, is a training network that is funded by Skillnets, a state funded, enterprise led support body dedicated to the promotion and facilitation of training and up-skilling

CPA Ireland Skillnet CPA Ireland Skillnet, is a training network that is funded by Skillnets, a state funded, enterprise led support body dedicated to the promotion and facilitation of training and up-skilling

Deeper Dive Leases. Overview

Deeper Dive Leases Presented by: Shaun Johnson, CPA Dingus, Zarecor & Associates PLLC Overview Effective dates Big picture Objective, impact, and implementation Applicability and definition Initial recognition

Deeper Dive Leases Presented by: Shaun Johnson, CPA Dingus, Zarecor & Associates PLLC Overview Effective dates Big picture Objective, impact, and implementation Applicability and definition Initial recognition

GASBs Presented by: William Blend, CPA, CFE

GASBs 87-89 Presented by: William Blend, CPA, CFE Leases: Statement 87 Effective Date and General Implementation Effective for Florida fiscal year end 2021. Earlier application is encouraged. Leases should

GASBs 87-89 Presented by: William Blend, CPA, CFE Leases: Statement 87 Effective Date and General Implementation Effective for Florida fiscal year end 2021. Earlier application is encouraged. Leases should

CPA COMPETENCY MAP STUDY NOTES UPDATE TO DECEMBER 31, 2018

CPA COMPETENCY MAP STUDY NOTES UPDATE TO DECEMBER 31, 2018 Please note that several of the updates relate to changes that are not effective until 2019. For 2019 PEP Module Exams and for the CFE, you are

CPA COMPETENCY MAP STUDY NOTES UPDATE TO DECEMBER 31, 2018 Please note that several of the updates relate to changes that are not effective until 2019. For 2019 PEP Module Exams and for the CFE, you are

Thank you for the opportunity to comment on the above referenced Exposure Draft.

International Accounting Standards Board 1 st Floor 30 Cannon Street London, EC4M 6XH United Kingdom Financial Accounting Standards Board 401 Merritt 7 PO Box 5116 Norwalk, CT 06856 5116 United States

International Accounting Standards Board 1 st Floor 30 Cannon Street London, EC4M 6XH United Kingdom Financial Accounting Standards Board 401 Merritt 7 PO Box 5116 Norwalk, CT 06856 5116 United States

Applying IFRS. IASB issues a new leases standard Oil and Gas. February 2017

Applying IFRS IASB issues a new leases standard Oil and Gas February 2017 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition of a lease 4 1.3 Arrangements entered

Applying IFRS IASB issues a new leases standard Oil and Gas February 2017 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition of a lease 4 1.3 Arrangements entered

The new IFRS 16 Leases effective as of 1 January 2019

The new IFRS 16 Leases effective as of 1 January 2019 IFRS 16 was issued by IASB on 13 January 2016. The Standard is effective as of 1 January 2019. It has not yet been adopted by the EC. This is a Standard

The new IFRS 16 Leases effective as of 1 January 2019 IFRS 16 was issued by IASB on 13 January 2016. The Standard is effective as of 1 January 2019. It has not yet been adopted by the EC. This is a Standard

LEASES WHERE ARE WE? Steve Rathjen

LEASES WHERE ARE WE? Steve Rathjen 267 256-3110 srathjen@kpmg.com Agenda Project status Lease definition and classification Lessee accounting Lessor accounting Presentation, disclosures, and transition

LEASES WHERE ARE WE? Steve Rathjen 267 256-3110 srathjen@kpmg.com Agenda Project status Lease definition and classification Lessee accounting Lessor accounting Presentation, disclosures, and transition

A Review of IFRS 16 Leases By Tan Liong Tong

A Review of IFRS 16 Leases By Tan Liong Tong In April 2016, the MASB issued MFRS 16 Leases that is identical to IFRS 16 Leases issued by the IASB in January 2016. The effective date of this new MFRS is

A Review of IFRS 16 Leases By Tan Liong Tong In April 2016, the MASB issued MFRS 16 Leases that is identical to IFRS 16 Leases issued by the IASB in January 2016. The effective date of this new MFRS is

2 This Standard shall be applied in accounting for all leases other than:

Indian Accounting Standard (Ind AS) 17 Leases (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in bold type indicate the main

Indian Accounting Standard (Ind AS) 17 Leases (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in bold type indicate the main

Leases: A Comprehensive Update on the Joint Project

The Dbriefs Financial Reporting series presents: Leases: A Comprehensive Update on the Joint Project Bob Uhl, Deloitte & Touche LLP Trevor Farber, Deloitte & Touche LLP James Barker, Deloitte & Touche

The Dbriefs Financial Reporting series presents: Leases: A Comprehensive Update on the Joint Project Bob Uhl, Deloitte & Touche LLP Trevor Farber, Deloitte & Touche LLP James Barker, Deloitte & Touche

ACCOUNTING Wayne Basford Partner - BDO

ACCOUNTING 2020 Wayne Basford Partner - BDO ACCOUNTING 2020 Do you intend to still be an accountant involved in financial reporting in 2020? 1. How many new standards are becoming applicable before 2020?

ACCOUNTING 2020 Wayne Basford Partner - BDO ACCOUNTING 2020 Do you intend to still be an accountant involved in financial reporting in 2020? 1. How many new standards are becoming applicable before 2020?

Accounting and Auditing Update. Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc.

Accounting and Auditing Update Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc. Agenda Overview of the standard setting agenda Revenue recognition Lease

Accounting and Auditing Update Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc. Agenda Overview of the standard setting agenda Revenue recognition Lease

IFRS Link. Contents. Newsletter. 1 IASB 11 EU Endorsement

IFRS Link Newsletter Issue 25 Contents 1 IASB 11 EU Endorsement New standard on accounting for leases With IFRS 16 Leases, the IASB published a new standard on accounting for leases on 13 January 2016.

IFRS Link Newsletter Issue 25 Contents 1 IASB 11 EU Endorsement New standard on accounting for leases With IFRS 16 Leases, the IASB published a new standard on accounting for leases on 13 January 2016.

Applying IFRS. IASB issues a new leases standard tank terminals. February 2017

Applying IFRS IASB issues a new leases standard tank terminals February 2017 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition of a lease 3 1.3 Identifying and

Applying IFRS IASB issues a new leases standard tank terminals February 2017 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition of a lease 3 1.3 Identifying and

Technical Line FASB final guidance

No. 2018-18 13 December 2018 Technical Line FASB final guidance How the new leases standard affects life sciences entities In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions...

No. 2018-18 13 December 2018 Technical Line FASB final guidance How the new leases standard affects life sciences entities In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions...

Technical Line FASB final guidance

No. 2017-17 29 June 2017 Technical Line FASB final guidance How the new revenue standard affects operating real estate entities In this issue: Overview... 1 Real estate sales... 2 Property management services...

No. 2017-17 29 June 2017 Technical Line FASB final guidance How the new revenue standard affects operating real estate entities In this issue: Overview... 1 Real estate sales... 2 Property management services...

LKAS 17 Sri Lanka Accounting Standard LKAS 17

Sri Lanka Accounting Standard LKAS 17 Leases CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 17 LEASES paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 4 CLASSIFICATION OF LEASES 7 LEASES IN THE FINANCIAL STATEMENTS

Sri Lanka Accounting Standard LKAS 17 Leases CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 17 LEASES paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 4 CLASSIFICATION OF LEASES 7 LEASES IN THE FINANCIAL STATEMENTS

Leases: Overview of the new guidance

Leases: Overview of the new guidance Prepared by: Richard Stuart, Partner, National Professional Standards Group, RSM US LLP richard.stuart@rsmus.com, +1 203 905 5027 March 2, 2016 Introduction On February

Leases: Overview of the new guidance Prepared by: Richard Stuart, Partner, National Professional Standards Group, RSM US LLP richard.stuart@rsmus.com, +1 203 905 5027 March 2, 2016 Introduction On February

Leases. January 25, 2016 Comments Due: May 31, Proposed Statement of the Governmental Accounting Standards Board

January 25, 2016 Comments Due: May 31, 2016 Proposed Statement of the Governmental Accounting Standards Board Leases This Exposure Draft of a proposed Statement of Governmental Accounting Standards is

January 25, 2016 Comments Due: May 31, 2016 Proposed Statement of the Governmental Accounting Standards Board Leases This Exposure Draft of a proposed Statement of Governmental Accounting Standards is

HKFRS 16 Leases. Disclaimer. Date 21 April 2017 Time 19:00 21:00 Venue Boys' and Girls' Clubs Association

HKFRS 16 Leases Date 21 April 2017 Time 19:00 21:00 Venue Boys' and Girls' Clubs Association www.zhtraining.com Disclaimer The materials of this seminar are intended only to provide general information

HKFRS 16 Leases Date 21 April 2017 Time 19:00 21:00 Venue Boys' and Girls' Clubs Association www.zhtraining.com Disclaimer The materials of this seminar are intended only to provide general information

No February Leases (Topic 842) An Amendment of the FASB Accounting Standards Codification

An Amendment of the FASB Accounting Standards Codification") No. 2016-02 February 2016 Leases (Topic 842) An Amendment of the FASB Accounting Standards Codification The FASB Accounting Standards Codification is the source of authoritative generally accepted accounting

No. 2016-02 February 2016 Leases (Topic 842) An Amendment of the FASB Accounting Standards Codification The FASB Accounting Standards Codification is the source of authoritative generally accepted accounting

Applying IFRS. Presentation and disclosure requirements of IFRS 16 Leases. November 2018

Applying IFRS Presentation and disclosure requirements of IFRS 16 Leases November 2018 Contents 1. Overview 2 2. What is changing from current IFRS? 4 2.1 Presentation 4 2.2 Lessee disclosures 5 3. Presentation

Applying IFRS Presentation and disclosure requirements of IFRS 16 Leases November 2018 Contents 1. Overview 2 2. What is changing from current IFRS? 4 2.1 Presentation 4 2.2 Lessee disclosures 5 3. Presentation

NEED TO KNOW. Leases A Project Update

NEED TO KNOW Leases A Project Update 2 LEASES - A PROJECT UPDATE TABLE OF CONTENTS Introduction 3 Existing guidance and the rationale for change 4 The IASB/FASB project to date 5 The main proposals 6 Definition

NEED TO KNOW Leases A Project Update 2 LEASES - A PROJECT UPDATE TABLE OF CONTENTS Introduction 3 Existing guidance and the rationale for change 4 The IASB/FASB project to date 5 The main proposals 6 Definition

SSAP 14 STATEMENT OF STANDARD ACCOUNTING PRACTICE 14 LEASES

SSAP 14 STATEMENT OF STANDARD ACCOUNTING PRACTICE 14 LEASES (Issued October 1987; revised February 2000) The standards, which have been set in bold italic type, should be read in the context of the background

SSAP 14 STATEMENT OF STANDARD ACCOUNTING PRACTICE 14 LEASES (Issued October 1987; revised February 2000) The standards, which have been set in bold italic type, should be read in the context of the background

Sri Lanka Accounting Standard-LKAS 17. Leases

Sri Lanka Accounting Standard-LKAS 17 Leases -516- Sri Lanka Accounting Standard-LKAS 17 Leases Sri Lanka Accounting Standard LKAS 17 Leases is set out in paragraphs 1 69. All the paragraphs have equal

Sri Lanka Accounting Standard-LKAS 17 Leases -516- Sri Lanka Accounting Standard-LKAS 17 Leases Sri Lanka Accounting Standard LKAS 17 Leases is set out in paragraphs 1 69. All the paragraphs have equal

GASB 87 - Leases. South Carolina Association of CPAs Fall Fest November 16, 2018 Mauldin & Jenkins

November 16, 2018 Mauldin & Jenkins 800-277-0050 www.mjcpa.com GASB 87 - Leases Effective for periods beginning after December 15, 2019 - December 31, 2020 or June 30, 2021 or September 30, 2021 Amends

November 16, 2018 Mauldin & Jenkins 800-277-0050 www.mjcpa.com GASB 87 - Leases Effective for periods beginning after December 15, 2019 - December 31, 2020 or June 30, 2021 or September 30, 2021 Amends

Lease Accounting and Loan Covenants: What is the Impact?

Lease Accounting and Loan Covenants: What is the Impact? Monday June 26, 2017 9:15 AM 10:30 AM Presented by: Charlie Shannon Partner Moss Adams LLP 8750 N. Central Expressway, Suite 300 Dallas, TX 75231

Lease Accounting and Loan Covenants: What is the Impact? Monday June 26, 2017 9:15 AM 10:30 AM Presented by: Charlie Shannon Partner Moss Adams LLP 8750 N. Central Expressway, Suite 300 Dallas, TX 75231

IFRS 15 Revenue from contracts with customers Presentation by: CPA Freda Mitambo Partner, Deloitte & Touche

IFRS 15 Revenue from contracts with customers Presentation by: CPA Freda Mitambo Partner, Deloitte & Touche Uphold public interest Why IFRS 15 is important What does it mean for clients? Revenue recognition

IFRS 15 Revenue from contracts with customers Presentation by: CPA Freda Mitambo Partner, Deloitte & Touche Uphold public interest Why IFRS 15 is important What does it mean for clients? Revenue recognition

Lease accounting scope & impacts

Leasing Lease accounting scope & impacts Scope What s in? All industries, all entities Arrangements that meet the definition of a lease Embedded leases within other arrangements What s out? Leases of:

Leasing Lease accounting scope & impacts Scope What s in? All industries, all entities Arrangements that meet the definition of a lease Embedded leases within other arrangements What s out? Leases of:

Technical Line FASB final guidance

No. 2016-11 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect real estate entities In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions...

No. 2016-11 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect real estate entities In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions...

Lease & Finance Accountants Conference. September The Westin Charlotte Charlotte, NC

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Lessor Accounting under ASC 842 EQUIPMENT LEASING AND FINANCE ASSOCIATION Presenters Rod Hurd Chief

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Lessor Accounting under ASC 842 EQUIPMENT LEASING AND FINANCE ASSOCIATION Presenters Rod Hurd Chief

Agenda. Monday, August 14, Section One The FASB s New Lease Accounting Standard. 8:30 Introduction to the new Lease Accounting Model Overview

Lease and Revenue Recognition Accounting Workshop Hosted by: Smith and Gesteland August 14 15, 2017 Madison Marriott West (This workshop qualifies for 16 hours of CPE) Monday, August 14, 2017 Agenda Section

Lease and Revenue Recognition Accounting Workshop Hosted by: Smith and Gesteland August 14 15, 2017 Madison Marriott West (This workshop qualifies for 16 hours of CPE) Monday, August 14, 2017 Agenda Section

The new accounting standard for leases. 27 March 2017

The new accounting standard for leases 27 March 2017 Disclaimer Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity.

The new accounting standard for leases 27 March 2017 Disclaimer Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity.

Università degli studi di Pavia Facoltà di Economia a.a Lesson 8 International Accounting Lelio Bigogno, Stefano Santucci

Università degli studi di Pavia Facoltà di Economia a.a. 2013-2014 Lesson 8 International Accounting Lelio Bigogno, Stefano Santucci 1 IAS/IFRS: IAS17 Leasing 2 History of IAS17 October 1980 Exposure Draft

Università degli studi di Pavia Facoltà di Economia a.a. 2013-2014 Lesson 8 International Accounting Lelio Bigogno, Stefano Santucci 1 IAS/IFRS: IAS17 Leasing 2 History of IAS17 October 1980 Exposure Draft

Get ready for IFRS 15

Recognising revenue in the real estate and construction industries The IASB and FASB have issued their new Standard on revenue recognition IFRS 15 Revenue from Contracts with Customers (ASU 2014-09 in

Recognising revenue in the real estate and construction industries The IASB and FASB have issued their new Standard on revenue recognition IFRS 15 Revenue from Contracts with Customers (ASU 2014-09 in

Real estate leases. How will IFRS 16 impact real estate entities? May 2016

Real estate leases How will IFRS 16 impact real estate entities? May 2016 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition of a lease 3 1.3 Identifying and separating

Real estate leases How will IFRS 16 impact real estate entities? May 2016 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition of a lease 3 1.3 Identifying and separating

IFRS 16. Changes in recognizing leases in the financial statements

IFRS 16 Changes in recognizing leases in the financial statements The new standard in a nutshell: To whom the new standard applies / Binding terms and conditions In January 2016, the International Accounting

IFRS 16 Changes in recognizing leases in the financial statements The new standard in a nutshell: To whom the new standard applies / Binding terms and conditions In January 2016, the International Accounting

FRS 116: LEASES. Ng Eng Juan Professor and Head of Accountancy Program Singapore University of Social Sciences

FRS 116: LEASES Ng Eng Juan Professor and Head of Accountancy Program Singapore University of Social Sciences Agenda: Introduction Impact of FRS 116 Definition of a lease Some salient points Conclusion

FRS 116: LEASES Ng Eng Juan Professor and Head of Accountancy Program Singapore University of Social Sciences Agenda: Introduction Impact of FRS 116 Definition of a lease Some salient points Conclusion

SLAS 19 (Revised 2000) Sri Lanka Accounting Standard SLAS 19 (Revised 2000) LEASES

Sri Lanka Accounting Standard SLAS 19 (Revised 2000) LEASES") Sri Lanka Accounting Standard SLAS 19 (Revised 2000) LEASES 265 Introduction This Standard (SLAS 19 (revised 2000) ) replaces Sri Lanka Accounting Standard SLAS 19, Accounting for Leases ( the original

Sri Lanka Accounting Standard SLAS 19 (Revised 2000) LEASES 265 Introduction This Standard (SLAS 19 (revised 2000) ) replaces Sri Lanka Accounting Standard SLAS 19, Accounting for Leases ( the original

In depth A look at current financial reporting issues for PNG

www.pwc.com/pg inform.pwc.com In depth A look at current financial reporting issues for PNG February 2016 What s inside? At a glance 1 Scope 2 Identifying a lease 2 Lessee accounting 10 Lessor accounting

www.pwc.com/pg inform.pwc.com In depth A look at current financial reporting issues for PNG February 2016 What s inside? At a glance 1 Scope 2 Identifying a lease 2 Lessee accounting 10 Lessor accounting

The IASB s Exposure Draft on Leases

The Chair Date: 9 September 2013 ESMA/2013/1245 Francoise Flores EFRAG Square de Meeus 35 1000 Brussels Belgium The IASB s Exposure Draft on Leases Dear Ms Flores, The European Securities and Markets Authority

The Chair Date: 9 September 2013 ESMA/2013/1245 Francoise Flores EFRAG Square de Meeus 35 1000 Brussels Belgium The IASB s Exposure Draft on Leases Dear Ms Flores, The European Securities and Markets Authority

ACCOUNTING. IASB releases six new standards. edition. may The IASB in mid-may released six new Accounting Standards.

may 2011 www.bdo.com.au ACCOUNTING news IASB releases six new standards The IASB in mid-may released six new Accounting Standards. IFRS 13 Fair Value Measurement is the result of the IASB s and FASB s

may 2011 www.bdo.com.au ACCOUNTING news IASB releases six new standards The IASB in mid-may released six new Accounting Standards. IFRS 13 Fair Value Measurement is the result of the IASB s and FASB s

EFRAG s Letter to the European Commission Regarding Endorsement of IFRS 16 Leases

EFRAG s Letter to the European Commission Regarding Endorsement of IFRS 16 Leases Olivier Guersent Director General, Financial Stability, Financial Services and Capital Markets Union European Commission

EFRAG s Letter to the European Commission Regarding Endorsement of IFRS 16 Leases Olivier Guersent Director General, Financial Stability, Financial Services and Capital Markets Union European Commission

CPE regulations require online participants to take part in online questions

KPMG s CFO Financial Forum Webcast FASB/IASB Revised Lease Accounting Exposure Drafts A Detailed Look Part III: Lessor Accounting June 25, 2013 Administrative CPE regulations require online participants

KPMG s CFO Financial Forum Webcast FASB/IASB Revised Lease Accounting Exposure Drafts A Detailed Look Part III: Lessor Accounting June 25, 2013 Administrative CPE regulations require online participants

(a) fulfillment of the contract depends on the use of an identified asset; and

fulfillment of the contract depends on the use of an identified asset; and") Exposure Draft Leases Comments to be received by 13 September 2013 Securities and Exchange Board of India (SEBI) welcomes the opportunity to respond to the above exposure draft. Question 1: identifying

Exposure Draft Leases Comments to be received by 13 September 2013 Securities and Exchange Board of India (SEBI) welcomes the opportunity to respond to the above exposure draft. Question 1: identifying

Exposure Draft ED/2010/9 - Leases

December 15 th, 2010 International Accounting Standards Board 30 Cannon Street, London EC4M 6XH United Kingdom Dear Madam/Sir, Exposure Draft ED/2010/9 - Leases The Israel Accounting Standards Board is

December 15 th, 2010 International Accounting Standards Board 30 Cannon Street, London EC4M 6XH United Kingdom Dear Madam/Sir, Exposure Draft ED/2010/9 - Leases The Israel Accounting Standards Board is