OREO Valuations, Pitfalls, and Regulatory & Tax Considerations

|

|

|

- Daniela Palmer

- 6 years ago

- Views:

Transcription

1 OREO Valuations, Pitfalls, and Regulatory & Tax Considerations Monday, June 17, :00 PM 3:15 PM. Presented by: Michael J. Indiveri Principal Michael J. Indiveri, CPA LLC 7 Phyllis Drive Succasunna, NJ P: E: mindiveri@indivericpa.com

2 AGENDA ECONOMIC ENVIRONMENT GAAP / REGULATORY REPORTING OVERVIEW EXAMINATION CONSIDERATIONS TAX CONSIDERATIONS COMMON PITFALLS QUESTONS slide 2 Michael J. Indiveri, CPA LLC

3 ECONOMIC ENVIRONMENT slide 3

4 CURRENT CONDITIONS 1-4 Family Mortgage Market Continues to Improve Commercial Mortgage Market Faces Significant Challenges Economic Improvement is Regional Uncertainty Regarding Effect of Transition to Amortizing HELOC Payments OREO Will Likely Remain on Bank,s Balance Sheets slide 4

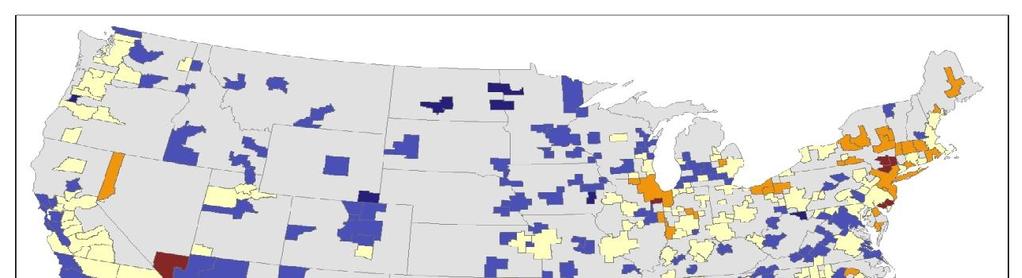

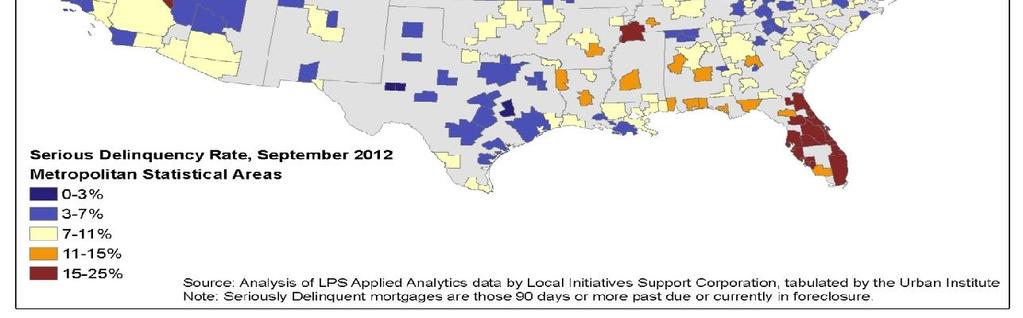

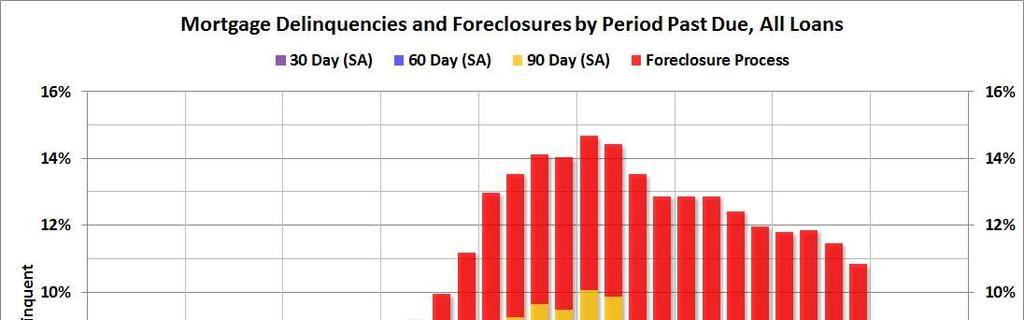

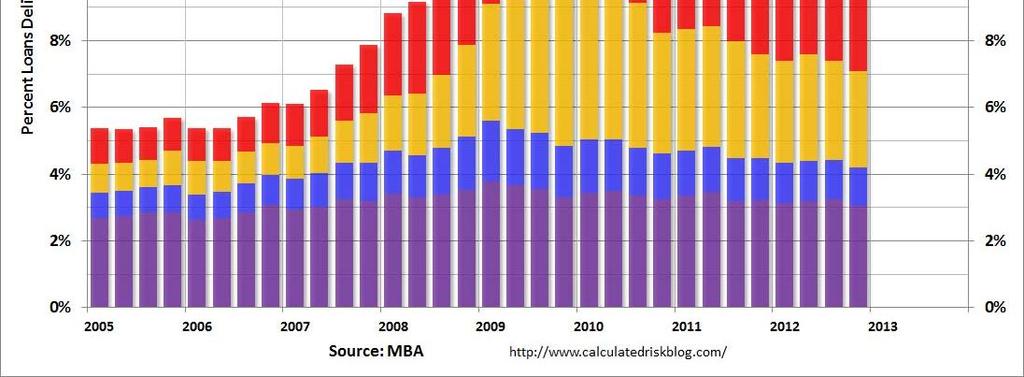

5 1-4 FAMILY MARKET Delinquency Rate fell to 7.09% at 12/31/2012, the lowest level since Serious delinquency rate, (percentage of loans 90 days or more past due or in the process of foreclosure) was 6.78 %, a decrease of 25 basis points from last quarter, and a decrease of 95 basis points from the fourth quarter of Mortgage performance has shown large improvement nationally and in almost every state. The foreclosure starts rate decreased by the largest amount ever in the MBA survey and now stands at half of its peak in 2009 The two biggest factors impacting the number of loans in the foreclosure process still are the magnitude of the problem in Florida and the judicial foreclosure systems in some states. slide 5

6 slide 6

7 slide 7

8 slide 8

9 slide 9

10 slide 10

11 GAAP / Regulatory Overview ASC establishes the guidance on accounting for and the reporting of foreclosed assets ASC establishes the guidance for the Impairment and Disposal of Long-Lived Assets ASC applies to all transactions in which the seller provides financing to the buyer of real estate 12 USC 29 - Sec. 29. establishes the regulatory authority by which a national banking association may purchase, hold, and convey real estate Most states have laws governing the acquisition and retention of such assets. slide 11

12 REGULATORY OVERVIEW For Regulatory Reporting Purposes, OREO Includes: All real estate, other than bank premises, actually owned or controlled by the bank and its consolidated subsidiaries, including real estate acquired through foreclosure or deed in lieu of foreclosure, even if the bank has not yet received title to the property; Real estate collateral in a bank's possession, regardless of whether formal foreclosure proceedings have been initiated; Foreclosed real estate sold under contract and accounted for under the deposit method of accounting Property originally acquired for future expansion but no longer intended for that purpose; and slide 12

13 REGULATORY OVERVIEW The holding period is generally limited to 5 years. A bank may receive approval to hold OREO for an additional 5 years provided: The bank can demonstrate that it made a good faith effort to dispose of the property, or Disposal within the 5 years would have been detrimental The bank must apply for approval; it is not automatic slide 13

14 Accounting for OREO (ASC ) Foreclosed properties should initially be recorded at the lower of the net amount receivable (cost) or the fair value of the property (fair value less estimated selling costs) The excess of the recorded investment in loan satisfied over the fair value fair value of the property received must be charged against the Allowance for Loan and Lease Losses ( ALLL ) If a property is sold shortly after foreclosure it may be appropriate to substitute the net sale value for the fair value and adjust the ALLL slide 14

15 Accounting for OREO Fair value should generally be determined through external appraisals, current letters of intent, broker price opinions or executed agreements of sale. The determination is made on an individual property basis After foreclosure, each foreclosed real estate parcel must be carried at the lower of: the fair value of the real estate minus the estimated costs to sell the real estate or the cost of the real estate slide 15

16 Accounting for OREO Any subsequent decline in the real estate s fair value, prior to disposal, must be recognized as a valuation allowance against the real estate which is created through a charge to expense The valuation allowance should thereafter be increased or decreased (but not below zero) for changes in the real estate s fair value or estimated selling costs Costs relating to the development and improvement of the OREO properties may be capitalized Operating expense, such as real estate taxes and maintenance are charged to expense as incurred Bank may also elect to treat OREO as Held for Sale and carry it at fair market value slide 16

17 Financed Sales of OREO There are five revenue recognition methods Full Accrual Method Under this method, the disposition is recorded as a sale. Any resulting profit is recognized in full and the sellerfinanced asset is reported as a loan. The following conditions must be met in order to utilize this method. A sale has been consummated, The receivable is not subject to future subordination The usual risks and rewards of ownership have been transferred, and The buyer's initial investment (down payment) and continuing investment (periodic payments) are adequate to demonstrate a commitment to pay for the property. slide 17

18 Initial Investment Guidelines slide 18

19 Financed Sales of OREO Installment Method This method recognizes a sale and corresponding loan Profits are recognized as the bank receives payments Interest income is recognized on an accrual basis, when appropriate The down payment is not adequate to allow for use of the full accrual method, but recovery of the cost of the property is reasonably assured in the event of buyer default slide 19

20 Financed Sales of OREO Cost Recovery Method A sale and corresponding loan and may apply when dispositions do not qualify under the full accrual or installment methods No profit or interest income is recognized until either the aggregate payments exceed the recorded amount of the loan or a change to another accounting method is appropriate The loan is maintained on nonaccrual status while this method is used slide 20

21 Financed Sales of OREO Reduced-Profit Method This method is appropriate in those situations where the bank receives an adequate down payment, but the loan amortization schedule does not meet the requirements of the full accrual method Any profit is recognized as payments are received Profit recognition is based on the present value of the lowest level of periodic payments required under the loan agreement Seldom used in practice because sales with adequate down payments are generally not structured with inadequate loan amortization requirements slide 21

22 Financed Sales of OREO Deposit Method The deposit method is used in situations where a sale of the real estate has not been consummated A sale is not recorded and the asset continues to be reported as OREO No profit or interest income is recognized Payments received from the borrower are reported as a liability until sufficient payments or other events have occurred which allow the use of one of the other methods slide 22

23 Income Tax Overview Charge-offs against the ALLL, due to differences in the property cost at the time of foreclosure and the fair value of the property are generally tax deductible in the same period as the foreclosure OREO valuation expenses and recoveries are generally not tax deductible until the property is sold Certain holding period expense may take on the attributes of capital improvements for tax accounting and will not be recognized until the property is sold Tax basis sales revenue recognition may be different than GAAP basis revenue recognition slide 23

24 Income Tax Overview Tax basis timing differences may generate a deferred tax asset or liability depending on the nature of the difference. It is critical that the bank maintains accurate tax basis records (Tax Books) Tax basis records should be maintained at the property level as individual properties may have different attributes Tax basis records should be reconciled to the GAAP basis records at least quarterly slide 24

25 PITFALLS Pre-acquisition Due Diligence Risks Property Related Risks Legal Risks Tax Risks Appraisal Risks Operational Risks slide 25

26 Pre-acquisition Due Diligence Risks Property Level Risks: Environmental liabilities Property may have high risk tenants (dry cleaners, gas stations, etc.) Past contamination may require expensive remediation Property violations and fines Zoning violations Fire hazards Deferred maintenance Unpaid real estate taxes and other taxes slide 26

27 Pre-acquisition Due Diligence Risks Property Level Risks: Invalid certificate of occupancy Inability to operate property as currently configured May have to vacate tenants, break leases rezone property Special license requirements Assisted living facilities, nursing homes, hospitals Unpaid property and / or other taxes Reputation Risk Schools, houses of worship, not-for-profit agencies, low income housing present special foreclosure challenges slide 27

28 Pre-acquisition Due Diligence Risks Legal Risks: Complex foreclosures require specialized legal experience Inappropriate legal vehicle for holding the property may: Expose the bank assets and shareholders to unnecessary liability Require the bank to be licensed as a bank in a foreign state Cause the bank to be in violation of its regulatory charter slide 28

29 Pre-acquisition Due Diligence Risks Tax Risks: Appropriate tax structure requires careful consideration ( C Corp, LLC, LLP) Inappropriate tax planning can expose the bank to: Higher than required income tax expense Loss of deductions Nexus in jurisdictions in which the bank or parent company does not operate slide 29

30 Pre-acquisition Due Diligence Risks Appraisal Risks: Complex properties require appraisers with specialized skills, construction valuation, environmental studies, etc. Deficient appraisals will likely expose the bank to: Criticism from auditors and regulators Challenges by tax authorities Potential restatements slide 30

31 Operational Risks Board established policies for OREO may not be effective or may not exist Management may not have adequate risk management systems in place to properly identify, classify, and track OREO The board, management and effected personnel may not possess the skills and knowledge necessary to effectively manage and execute the responsibilities related to OREO. slide 31

32 Operational Risks Management may not fully understand the contractual arrangements in place when properties are serviced by other institutions or the fiduciary responsibilities as the lead bank Control systems that safeguard assets and ensure the integrity of accounting data/financial reports may be ineffective Management may lack the skills to properly oversee retained experts (appraisers, contractors, property managers) slide 32

33 GAAP /CALL Report Presentation GAAP / SEC PRESENTATION CALL REPORT PRESENTATION OREO (1) Other Real Estate Owned RC7 Other Real Estate Owned OREO Valuation Allowance (1) Other Real Estate Owned RC7 Other Real Estate Owned Gain on sale of OREO Net Gain (Loss) Sale of OREO RI5.j Net gain (loss) OREO Loss on Sale of OREO Net Gain (Loss) Sale of OREO RI5.j Net gain (loss) OREO Income from operation of OREO properties (rent, fees, etc.) Net Income Expense of OREO RI5,5l, (3) Gross rentals and other income from all real estate reportable in RC7 OREO operating expenses Net Income Expense of OREO RI7,d.2.n Miscellaneous Expenses OREO Valuation Expense (Write downs) Net Income Expense of OREO RI5,j Net gain (loss) OREO (1) If immaterial Other Assets slide 33

34 Conclusion Foreclosure brings all the rights, privileges and liabilities of ownership Thank you Questions slide 34

ACCOUNTING FOR OTHER REAL ESTATE TRANSACTIONS CURRENT ISSUES AND EXAMINER OBSERVATIONS

ACCOUNTING FOR OTHER REAL ESTATE TRANSACTIONS CURRENT ISSUES AND EXAMINER OBSERVATIONS Paul Oseland, CPA Federal Reserve Bank of Kansas City Oklahoma City Branch Supervision and Risk Management OREO Accounting

ACCOUNTING FOR OTHER REAL ESTATE TRANSACTIONS CURRENT ISSUES AND EXAMINER OBSERVATIONS Paul Oseland, CPA Federal Reserve Bank of Kansas City Oklahoma City Branch Supervision and Risk Management OREO Accounting

BOARD OF GOVERNORS FEDERAL RESERVE SYSTEM

BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM WASHINGTON, D.C. 20551 DIVISION OF BANKING SUPERVISION AND REGULATION DIVISION OF CONSUMER AND COMMUNITY AFFAIRS SR 12-10 CA 12-9 June 28, 2012 TO THE OFFICERS

BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM WASHINGTON, D.C. 20551 DIVISION OF BANKING SUPERVISION AND REGULATION DIVISION OF CONSUMER AND COMMUNITY AFFAIRS SR 12-10 CA 12-9 June 28, 2012 TO THE OFFICERS

Center for Plain English Accounting AICPA s National A&A Resource Center available exclusively to PCPS members

Report April 19, 2017 Center for Plain English Accounting AICPA s National A&A Resource Center available exclusively to PCPS members Sale-Leaseback Transactions Involving Real Estate Navigating the Twists

Report April 19, 2017 Center for Plain English Accounting AICPA s National A&A Resource Center available exclusively to PCPS members Sale-Leaseback Transactions Involving Real Estate Navigating the Twists

ANNUAL REPORT 2017 Lake Country Co-operative Association Limited

ANNUAL REPORT Management's Responsibility To the Members of Lake Country Co-operative Association Limited: Management is responsible for the preparation and presentation of the accompanying financial statements,

ANNUAL REPORT Management's Responsibility To the Members of Lake Country Co-operative Association Limited: Management is responsible for the preparation and presentation of the accompanying financial statements,

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2011

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2011 Presented By: Marianne Heard, CPA, MST, Tax Director, Kevin P. Martin & Associates, P.C.

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2011 Presented By: Marianne Heard, CPA, MST, Tax Director, Kevin P. Martin & Associates, P.C.

Real Estate Syndication Income 19,451 NOTE

Real Estate Syndication Income 19,451 Section 10,500 Statement of Position 92-1 Accounting for Real Estate Syndication Income February 6, 1992 NOTE Statements of Position of the Accounting Standards Division

Real Estate Syndication Income 19,451 Section 10,500 Statement of Position 92-1 Accounting for Real Estate Syndication Income February 6, 1992 NOTE Statements of Position of the Accounting Standards Division

Mountain Equipment Co-operative

Mountain Equipment Co-operative Consolidated Financial Statements, and December 28, 2009 April 11, 2012 Independent Auditor s Report To the Members of Mountain Equipment Co-operative We have audited the

Mountain Equipment Co-operative Consolidated Financial Statements, and December 28, 2009 April 11, 2012 Independent Auditor s Report To the Members of Mountain Equipment Co-operative We have audited the

EDGEFRONT REALTY CORP. MANAGEMENT S DISCUSSION AND ANALYSIS For the three-month period ended March 31, 2013

EDGEFRONT REALTY CORP. MANAGEMENT S DISCUSSION AND ANALYSIS For the three-month period ended March 31, 2013 May 30, 2013 MANAGEMENT S DISCUSSION AND ANALYSIS The following management s discussion and analysis

EDGEFRONT REALTY CORP. MANAGEMENT S DISCUSSION AND ANALYSIS For the three-month period ended March 31, 2013 May 30, 2013 MANAGEMENT S DISCUSSION AND ANALYSIS The following management s discussion and analysis

EN Official Journal of the European Union L 320/373

29.11.2008 EN Official Journal of the European Union L 320/373 INTERNATIONAL FINANCIAL REPORTING STANDARD 3 Business combinations OBJECTIVE 1 The objective of this IFRS is to specify the financial reporting

29.11.2008 EN Official Journal of the European Union L 320/373 INTERNATIONAL FINANCIAL REPORTING STANDARD 3 Business combinations OBJECTIVE 1 The objective of this IFRS is to specify the financial reporting

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2016

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2016 Presented By: Karen Kent, CPA, Partner, Kevin P. Martin & Associates, P.C. Kenneth Lund,

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2016 Presented By: Karen Kent, CPA, Partner, Kevin P. Martin & Associates, P.C. Kenneth Lund,

NEW LEASE ACCOUNTING STANDARD

NEW LEASE ACCOUNTING STANDARD Accounting Standards Update (ASU) 2016-02, Leases & GASB 87, Leases LEASES Leases: Why a New Leases Standard? 1 IMPLEMENTATION TIMELINE January 2016 IASB issued IFRS 16, Leases

NEW LEASE ACCOUNTING STANDARD Accounting Standards Update (ASU) 2016-02, Leases & GASB 87, Leases LEASES Leases: Why a New Leases Standard? 1 IMPLEMENTATION TIMELINE January 2016 IASB issued IFRS 16, Leases

Rehabilitation Tax Credits

Rehabilitation Tax Credits Selected Issues in Master Lease Pass-Through Transactions Steven L. Paul Nicholas Romanos February 1, 2010 REHABILITATION TAX CREDITS Selected Issues in Master Lease Pass-Through

Rehabilitation Tax Credits Selected Issues in Master Lease Pass-Through Transactions Steven L. Paul Nicholas Romanos February 1, 2010 REHABILITATION TAX CREDITS Selected Issues in Master Lease Pass-Through

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2014

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2014 Presented By: Karen Kent, CPA, Partner, Kevin P. Martin & Associates, P.C. Kenneth Lund,

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2014 Presented By: Karen Kent, CPA, Partner, Kevin P. Martin & Associates, P.C. Kenneth Lund,

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C FORM 10-Q

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q ý QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Quarterly Period Ended

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q ý QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Quarterly Period Ended

Something Borrowed, Something New Get Ready for the New Lease Accounting Standard

April 2016 Something Borrowed, Something New Get Ready for the New Lease Accounting Standard By Scott G. Lehman, CPA, and David E. Wentzel, CPA Audit / Tax / Advisory / Risk / Performance Smart decisions.

April 2016 Something Borrowed, Something New Get Ready for the New Lease Accounting Standard By Scott G. Lehman, CPA, and David E. Wentzel, CPA Audit / Tax / Advisory / Risk / Performance Smart decisions.

The Impact of the New Revenue Standard on Real Estate Sales

The Impact of the New Revenue Standard on Real Estate Sales Wing W. Poon Montclair State University In May 2014, the FASB and the IASB jointly issued significantly revised standard on revenue recognition.

The Impact of the New Revenue Standard on Real Estate Sales Wing W. Poon Montclair State University In May 2014, the FASB and the IASB jointly issued significantly revised standard on revenue recognition.

CONSOLIDATED STATEMENT OF INCOME

CONSOLIDATED STATEMENT OF INCOME 1 st quarter (a) 2017 4 th quarter Sales 41,183 42,275 32,841 Excise taxes (5,090) (5,408) (5,319) Revenues from sales 36,093 36,867 27,522 Purchases, net of inventory

CONSOLIDATED STATEMENT OF INCOME 1 st quarter (a) 2017 4 th quarter Sales 41,183 42,275 32,841 Excise taxes (5,090) (5,408) (5,319) Revenues from sales 36,093 36,867 27,522 Purchases, net of inventory

Table of Contents PAGE MIADOCS

Table of Contents PAGE CONSOLIDATED FINANCIAL STATEMENTS Independent Auditor's Report 2 Pro-Forma Consolidated Balance Sheets as of December 31, 2017 and 2016 3 Pro-Forma Consolidated Statements of Operations

Table of Contents PAGE CONSOLIDATED FINANCIAL STATEMENTS Independent Auditor's Report 2 Pro-Forma Consolidated Balance Sheets as of December 31, 2017 and 2016 3 Pro-Forma Consolidated Statements of Operations

The Substance of the Standard

The Substance of the Standard Mayer Hoffman McCann P.C. An Independent CPA Firm TM A publication of the Professional Standards Group April 2014 Accounting Election for Common Control Leasing Arrangements

The Substance of the Standard Mayer Hoffman McCann P.C. An Independent CPA Firm TM A publication of the Professional Standards Group April 2014 Accounting Election for Common Control Leasing Arrangements

CC HOLDINGS GS V LLC INDEX TO FINANCIAL STATEMENTS. Consolidated Financial Statements Years Ended December 31, 2011, 2010 and 2009

INDEX TO FINANCIAL STATEMENTS Consolidated Financial Statements Years Ended December 31, 2011, 2010 and 2009 Report of PricewaterhouseCoopers LLP, Independent Auditors...................................

INDEX TO FINANCIAL STATEMENTS Consolidated Financial Statements Years Ended December 31, 2011, 2010 and 2009 Report of PricewaterhouseCoopers LLP, Independent Auditors...................................

AMERICAN SOCIETY OF APPRAISERS. Procedural Guidelines. PG-2 Valuation of Partial Ownership Interests

AMERICAN SOCIETY OF APPRAISERS Procedural Guidelines PG-2 Valuation of Partial Ownership Interests I. Preamble A. Business valuation professionals are frequently engaged as independent financial appraisers

AMERICAN SOCIETY OF APPRAISERS Procedural Guidelines PG-2 Valuation of Partial Ownership Interests I. Preamble A. Business valuation professionals are frequently engaged as independent financial appraisers

Consolidated Financial Statements of ECOTRUST CANADA. Year ended December 31, 2016

Consolidated Financial Statements of ECOTRUST CANADA KPMG Enterprise TM Metro Tower I 4710 Kingsway, Suite 2400 Burnaby BC V5H 4M2 Canada Telephone (604) 527-3600 Fax (604) 527-3636 INDEPENDENT AUDITORS

Consolidated Financial Statements of ECOTRUST CANADA KPMG Enterprise TM Metro Tower I 4710 Kingsway, Suite 2400 Burnaby BC V5H 4M2 Canada Telephone (604) 527-3600 Fax (604) 527-3636 INDEPENDENT AUDITORS

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC FORM 8-K/A

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 FORM 8-K/A CURRENT REPORT Pursuant to Section 13 or 15(d) of The Securities Exchange Act of 1934 Date of Report (Date of earliest event

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 FORM 8-K/A CURRENT REPORT Pursuant to Section 13 or 15(d) of The Securities Exchange Act of 1934 Date of Report (Date of earliest event

HABITAT FOR HUMANITY KANSAS CITY, INC. FINANCIAL STATEMENTS

HABITAT FOR HUMANITY KANSAS CITY, INC. FINANCIAL STATEMENTS Year Ended December 31, 2015 Mayer Hoffman McCann P.C. An Independent CPA Firm 700 West 47th Street, Suite 1100 Kansas City, MO 64112 Main: 816.945.5600

HABITAT FOR HUMANITY KANSAS CITY, INC. FINANCIAL STATEMENTS Year Ended December 31, 2015 Mayer Hoffman McCann P.C. An Independent CPA Firm 700 West 47th Street, Suite 1100 Kansas City, MO 64112 Main: 816.945.5600

IFRS - 3. Business Combinations. By:

IFRS - 3 Business Combinations Objective 1. The purpose of this IFRS is to specify to disclose financial information by an entity when carrying out a business combination. In particular, specifies that

IFRS - 3 Business Combinations Objective 1. The purpose of this IFRS is to specify to disclose financial information by an entity when carrying out a business combination. In particular, specifies that

A-LF. Comptroller of the Currency Administrator of National Banks. Lease Financing. Comptroller s Handbook. January A Assets

A-LF Comptroller of the Currency Administrator of National Banks January 1998 A Assets Table of Contents Introduction...1 Background...1 Statutory and Regulatory Authority for Leasing...2 Subpart A ) General

A-LF Comptroller of the Currency Administrator of National Banks January 1998 A Assets Table of Contents Introduction...1 Background...1 Statutory and Regulatory Authority for Leasing...2 Subpart A ) General

HABITAT FOR HUMANITY OF BROWARD, INC.

FINANCIAL STATEMENTS CONTENTS Independent Auditors Report... 1-3 Financial Statements Statement of Financial Position...4 Statement of Activities and Changes in Net Assets...5 Statement of Cash Flows...6

FINANCIAL STATEMENTS CONTENTS Independent Auditors Report... 1-3 Financial Statements Statement of Financial Position...4 Statement of Activities and Changes in Net Assets...5 Statement of Cash Flows...6

HABITAT FOR HUMANITY OF BROWARD, INC.

FINANCIAL STATEMENTS CONTENTS Independent Auditors Report... 1-3 Financial Statements Statement of Financial Position...4 Statement of Activities and Changes in Net Assets...5 Statement of Cash Flows...6

FINANCIAL STATEMENTS CONTENTS Independent Auditors Report... 1-3 Financial Statements Statement of Financial Position...4 Statement of Activities and Changes in Net Assets...5 Statement of Cash Flows...6

Topic 842 Technical Corrections Summary of Comments Received

Contact(s) David Hoyer Co-Author Ext. 462 Andy Bologna Co-Author Ext. 356 Thomas Faineteau Co-Author Ext. 362 Chris Roberge Co-Author Ext. 274 Amy Park Co-Author Ext. 476 Shayne Kuhaneck Assistant Director

Contact(s) David Hoyer Co-Author Ext. 462 Andy Bologna Co-Author Ext. 356 Thomas Faineteau Co-Author Ext. 362 Chris Roberge Co-Author Ext. 274 Amy Park Co-Author Ext. 476 Shayne Kuhaneck Assistant Director

Sec. 48 Investment Credit: Eligible property and special rules; Rehabilitation expenditures; Rehabilitation credit passthroughs

Private Letter Ruling 8943074 Sec. 48 Investment Credit: Eligible property and special rules; Rehabilitation expenditures; Rehabilitation credit passthroughs This is in response to a letter dated January

Private Letter Ruling 8943074 Sec. 48 Investment Credit: Eligible property and special rules; Rehabilitation expenditures; Rehabilitation credit passthroughs This is in response to a letter dated January

VISTA POINT PROPERTIES PROPERTY MANAGEMENT AGREEMENT

VISTA POINT PROPERTIES PROPERTY MANAGEMENT AGREEMENT This Property Management Agreement (hereafter referred to as Agreement ), dated, 4/4/2017 is entered into and between Vista Point Properties (hereafter

VISTA POINT PROPERTIES PROPERTY MANAGEMENT AGREEMENT This Property Management Agreement (hereafter referred to as Agreement ), dated, 4/4/2017 is entered into and between Vista Point Properties (hereafter

Intangibles Goodwill and Other (Topic 350), Business Combinations (Topic 805), and Not-for-Profit Entities (Topic 958)

, Business Combinations (Topic 805), and Not-for-Profit Entities (Topic 958)") Proposed Accounting Standards Update Issued: December 20, 2018 Comments Due: February 18, 2019 Intangibles Goodwill and Other (Topic 350), Business Combinations (Topic 805), and Not-for-Profit Entities

Proposed Accounting Standards Update Issued: December 20, 2018 Comments Due: February 18, 2019 Intangibles Goodwill and Other (Topic 350), Business Combinations (Topic 805), and Not-for-Profit Entities

Broadstone Asset Management, LLC

Broadstone Asset Management, LLC 800 Clinton Square Rochester, NY 14604 Phone: 585-287-6500 www.broadstone.com Firm CRD#: 281847 Date: March 29, 2018 This brochure provides information about the qualifications

Broadstone Asset Management, LLC 800 Clinton Square Rochester, NY 14604 Phone: 585-287-6500 www.broadstone.com Firm CRD#: 281847 Date: March 29, 2018 This brochure provides information about the qualifications

I ROC 2017 Financial Administrators Section Conference

I ROC 2017 Financial Administrators Section Conference September 9, 2017 kpmg.ca Presenters Chris Cornell KPMG Partner, Financial Services Steven Sharma KPMG Partner, Financial Services 2 IIROC 2017 Financial

I ROC 2017 Financial Administrators Section Conference September 9, 2017 kpmg.ca Presenters Chris Cornell KPMG Partner, Financial Services Steven Sharma KPMG Partner, Financial Services 2 IIROC 2017 Financial

FASB and IASB Continue Making Decisions on Lease Accounting

Accounting Journal Entry FASB and IASB Continue Making Decisions on Lease Accounting March 28, 2011 At recent meetings, the FASB and IASB (the boards ) have continued to make progress on the leases project,

Accounting Journal Entry FASB and IASB Continue Making Decisions on Lease Accounting March 28, 2011 At recent meetings, the FASB and IASB (the boards ) have continued to make progress on the leases project,

METRO BROKERS Checklist for Commercial Real Estate Professionals

METRO BROKERS Checklist for Commercial Real Estate Professionals 2017 Metro Brokers, Inc. All Rights Reserved 1 WHAT DUE DILIGENCE IS DUE? The scope, intensity and focus of any due diligence investigation

METRO BROKERS Checklist for Commercial Real Estate Professionals 2017 Metro Brokers, Inc. All Rights Reserved 1 WHAT DUE DILIGENCE IS DUE? The scope, intensity and focus of any due diligence investigation

FPP Committee Meeting Proposed COA Changes. June 8, 2018

FPP Committee Meeting Proposed COA Changes June 8, 2018 Agenda Visit various GASB Statements COA changes needed GASB #84 Fiduciary Activities Statement No. 84 Fiduciary Activities How many currently report

FPP Committee Meeting Proposed COA Changes June 8, 2018 Agenda Visit various GASB Statements COA changes needed GASB #84 Fiduciary Activities Statement No. 84 Fiduciary Activities How many currently report

CHAPTER TWO Concepts and principles

CHAPTER TWO Concepts and principles 2.3 GOVERNMENT AND NON-GOVERNMENT GRANTS Recognition and presentation grants and contributions 2.3.2.8 Grants and contributions, including donated assets, shall not

CHAPTER TWO Concepts and principles 2.3 GOVERNMENT AND NON-GOVERNMENT GRANTS Recognition and presentation grants and contributions 2.3.2.8 Grants and contributions, including donated assets, shall not

White Paper on Adjusted Cashflow From Operations (ACFO) for IFRS. February, 2018

for IFRS. February, 2018") White Paper on Adjusted Cashflow From Operations (ACFO) for IFRS February, 2018 Copyright REALPAC is the owner of all copyright in this publication. All rights reserved. No part of this document may be

White Paper on Adjusted Cashflow From Operations (ACFO) for IFRS February, 2018 Copyright REALPAC is the owner of all copyright in this publication. All rights reserved. No part of this document may be

EITF ABSTRACTS. Title: Subsequent Accounting for Executory Contracts That Have Been Recognized on an Entity s Balance Sheet

EITF ABSTRACTS Issue No. 03-17 Title: Subsequent Accounting for Executory Contracts That Have Been Recognized on an Entity s Balance Sheet Date Discussed: November 12 13, 2003 References: FASB Statement

EITF ABSTRACTS Issue No. 03-17 Title: Subsequent Accounting for Executory Contracts That Have Been Recognized on an Entity s Balance Sheet Date Discussed: November 12 13, 2003 References: FASB Statement

EN Official Journal of the European Union L 320/323

29.11.2008 EN Official Journal of the European Union L 320/323 INTERNATIONAL ACCOUNTING STANDARD 40 Investment property OBJECTIVE 1 The objective of this standard is to prescribe the accounting treatment

29.11.2008 EN Official Journal of the European Union L 320/323 INTERNATIONAL ACCOUNTING STANDARD 40 Investment property OBJECTIVE 1 The objective of this standard is to prescribe the accounting treatment

HABITAT FOR HUMANITY OF THE MIDDLE KEYS, INC. Financial Statements. December 31, (With Independent Auditors Report Thereon)

") Financial Statements (With Independent Auditors Report Thereon) TABLE OF CONTENTS PAGE Independent Auditors Report 1-2 Financial Statements for the year ended Statement of Financial Position 3 Statement

Financial Statements (With Independent Auditors Report Thereon) TABLE OF CONTENTS PAGE Independent Auditors Report 1-2 Financial Statements for the year ended Statement of Financial Position 3 Statement

Current Developments. FASB, AICPA and SEC. Jim Brendel, CPA, CFE March 1, 2013

Current Developments FASB, AICPA and SEC Jim Brendel, CPA, CFE March 1, 2013 Agenda FASB Developments Selected Projects and Initiatives Revenue Recognition Leases Impairment of Intangible Assets Other

Current Developments FASB, AICPA and SEC Jim Brendel, CPA, CFE March 1, 2013 Agenda FASB Developments Selected Projects and Initiatives Revenue Recognition Leases Impairment of Intangible Assets Other

IFRS Update Guy Thomas, CPA, CA

IFRS Update Guy Thomas, CPA, CA D&Co IFRS update Agenda 3 new standards under IFRS IFRS 9 Financial Instruments IFRS 15 Revenue from Contracts with Customers IFRS 16 Leases Agenda Some narrow scope amendments

IFRS Update Guy Thomas, CPA, CA D&Co IFRS update Agenda 3 new standards under IFRS IFRS 9 Financial Instruments IFRS 15 Revenue from Contracts with Customers IFRS 16 Leases Agenda Some narrow scope amendments

CONSOLIDATED FINANCIAL STATEMENTS

CONSOLIDATED FINANCIAL STATEMENTS Dundee Real Estate Investment Trust Consolidated Balance Sheets (unaudited) June 30, December 31, (in thousands of dollars) Note 2004 2003 Assets Rental properties 3,4

CONSOLIDATED FINANCIAL STATEMENTS Dundee Real Estate Investment Trust Consolidated Balance Sheets (unaudited) June 30, December 31, (in thousands of dollars) Note 2004 2003 Assets Rental properties 3,4

HOUSE AMENDMENT Bill No. CS/HB 411

Senate CHAMBER ACTION 1.... House 2.. 3.. 4 5 ORIGINAL STAMP BELOW 6 7 8 9 10 11 The Committee on Agriculture & Consumer Affairs offered the 12 following: 13 14 Amendment (with title amendment) 15 Remove

Senate CHAMBER ACTION 1.... House 2.. 3.. 4 5 ORIGINAL STAMP BELOW 6 7 8 9 10 11 The Committee on Agriculture & Consumer Affairs offered the 12 following: 13 14 Amendment (with title amendment) 15 Remove

will not unbalance the ratio of debt to equity.

paragraph 2-12-3. c.) and prime commercial paper. All these restrictions are designed to assure that debt proceeds (including Title VII funds disbursed from escrow), equity contributions and operating

paragraph 2-12-3. c.) and prime commercial paper. All these restrictions are designed to assure that debt proceeds (including Title VII funds disbursed from escrow), equity contributions and operating

SHOPOFF PROPERTIES TRUST, INC.

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

FASB Update. FASB Exempts Private Companies from Variable Interest Entity Guidance Affects: Private Companies

FASB Update New Guidance Raises the Threshold for Discontinued Operations On April 10, the FASB issued ASU 2014-08, Reporting Discontinued Operations and Disclosures of Disposals of Components of an Entity,

FASB Update New Guidance Raises the Threshold for Discontinued Operations On April 10, the FASB issued ASU 2014-08, Reporting Discontinued Operations and Disclosures of Disposals of Components of an Entity,

CONSOLIDATED STATEMENT OF INCOME

CONSOLIDATED STATEMENT OF INCOME (unaudited, data converted from the Euro to the US Dollar (for information concerning this restatement, see Note 11 to these Consolidated Financial Statements)) 1 st quarter

CONSOLIDATED STATEMENT OF INCOME (unaudited, data converted from the Euro to the US Dollar (for information concerning this restatement, see Note 11 to these Consolidated Financial Statements)) 1 st quarter

Re: FASB Exposure Draft, Proposed Statement of Financial Accounting Standards, "Business Combinations, a replacement of FASB Statement No.

Letter of Comment No: lo%" File Reference: 1204-001 October 28, 2005 Mr. Robert Herz Chairman Financial Accounting Standards Board 40 I Merritt 7 P.O. Box 5116 Norwalk, CT 06856-5116 File Reference No.

Letter of Comment No: lo%" File Reference: 1204-001 October 28, 2005 Mr. Robert Herz Chairman Financial Accounting Standards Board 40 I Merritt 7 P.O. Box 5116 Norwalk, CT 06856-5116 File Reference No.

.01 The objective of this Standard is to prescribe the accounting treatment for investment property and related disclosure requirements.

COMPARISON OF GRAP 16 WITH IAS 40 GRAP 16 IAS 40 DIFFERENCES Objective.01 The objective of this Standard is to prescribe the accounting treatment for investment property and related disclosure requirements.

COMPARISON OF GRAP 16 WITH IAS 40 GRAP 16 IAS 40 DIFFERENCES Objective.01 The objective of this Standard is to prescribe the accounting treatment for investment property and related disclosure requirements.

Heiwa Real Estate Co., Ltd.

To the Shareholders of Heiwa Real Estate Co., Ltd. INFORMATION DISCLOSED ON THE INTERNET UPON ISSUING NOTICE CONCERNING THE CONVOCATION OF THE 94th ORDINARY GENERAL SHAREHOLDERS MEETING THE 94th FISCAL

To the Shareholders of Heiwa Real Estate Co., Ltd. INFORMATION DISCLOSED ON THE INTERNET UPON ISSUING NOTICE CONCERNING THE CONVOCATION OF THE 94th ORDINARY GENERAL SHAREHOLDERS MEETING THE 94th FISCAL

FASB Emerging Issues Task Force

EITF Issue No. 09-4 FASB Emerging Issues Task Force Issue No. 09-4 Title: Seller Accounting for Contingent Consideration Document: Issue Summary No. 1, Supplement No. 1 Date prepared: August 21, 2009 FASB

EITF Issue No. 09-4 FASB Emerging Issues Task Force Issue No. 09-4 Title: Seller Accounting for Contingent Consideration Document: Issue Summary No. 1, Supplement No. 1 Date prepared: August 21, 2009 FASB

GASB 69: Government Combinations

GASB 69: Government Combinations Table of Contents EXECUTIVE SUMMARY... 3 BACKGROUND... 3 KEY PROVISIONS... 3 OVERVIEW & SCOPE... 3 MERGER & TRANSFER OF OPERATIONS... 4 Mergers... 4 Transfers of Operations...

GASB 69: Government Combinations Table of Contents EXECUTIVE SUMMARY... 3 BACKGROUND... 3 KEY PROVISIONS... 3 OVERVIEW & SCOPE... 3 MERGER & TRANSFER OF OPERATIONS... 4 Mergers... 4 Transfers of Operations...

Section B Conforming Amendments Related to Revenue from Contracts with Customers: Amendments to the Accounting Standards Codification

Section B Conforming Amendments Related to Revenue from Contracts with Customers: Amendments to the Accounting Codification Amendments to Master Glossary 8. Supersede the following Master Glossary terms,

Section B Conforming Amendments Related to Revenue from Contracts with Customers: Amendments to the Accounting Codification Amendments to Master Glossary 8. Supersede the following Master Glossary terms,

FASB Updates Business Definition

On January 5, 2017, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 2017-01, s (Topic 805): Clarifying the Definition of a Business. This definition is significant

On January 5, 2017, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 2017-01, s (Topic 805): Clarifying the Definition of a Business. This definition is significant

60-HR FL Real Estate Broker Post-Licensing Learning Objectives by Lesson

Lesson 1: Starting a Real Estate Office SECTION 1: BROKERAGE OFFICE ESSENTIALS Recall the characteristics of business entities that may register as a real estate brokerage and the rules involved to operate

Lesson 1: Starting a Real Estate Office SECTION 1: BROKERAGE OFFICE ESSENTIALS Recall the characteristics of business entities that may register as a real estate brokerage and the rules involved to operate

Sunrise Stratford, LP

Sunrise Stratford, LP Financial Statements as of and for the Years Ended December 31, 2017 and 2016, Other Financial Information, and Independent Auditors Reports TABLE OF CONTENTS INDEPENDENT AUDITORS

Sunrise Stratford, LP Financial Statements as of and for the Years Ended December 31, 2017 and 2016, Other Financial Information, and Independent Auditors Reports TABLE OF CONTENTS INDEPENDENT AUDITORS

EITF ABSTRACTS. Title: Applying the Conditions in Paragraph 42 of FASB Statement No. 144 in Determining Whether to Report Discontinued Operations

EITF ABSTRACTS Title: Applying the Conditions in Paragraph 42 of FASB Statement No. 144 in Determining Whether to Report Discontinued Operations Issue No. 03-13 Dates Discussed: November 12 13, 2003; March

EITF ABSTRACTS Title: Applying the Conditions in Paragraph 42 of FASB Statement No. 144 in Determining Whether to Report Discontinued Operations Issue No. 03-13 Dates Discussed: November 12 13, 2003; March

ALLIED PROPERTIES REAL ESTATE INVESTMENT TRUST. Financial Statements. Year Ended December 31, 2004

ALLIED PROPERTIES REAL ESTATE INVESTMENT TRUST Financial Statements Year Ended December 31, 2004 Auditors' Report To the Unitholders of Allied Properties Real Estate Investment Trust We have audited the

ALLIED PROPERTIES REAL ESTATE INVESTMENT TRUST Financial Statements Year Ended December 31, 2004 Auditors' Report To the Unitholders of Allied Properties Real Estate Investment Trust We have audited the

FIRST INDUSTRIAL REALTY TRUST REPORTS FIRST QUARTER 2018 RESULTS

First Industrial Realty Trust, Inc. 311 South Wacker Drive Suite 3900 Chicago, IL 60606 312/344-4300 FAX: 312/922-9851 MEDIA RELEASE FIRST INDUSTRIAL REALTY TRUST REPORTS FIRST QUARTER 2018 RESULTS Occupancy

First Industrial Realty Trust, Inc. 311 South Wacker Drive Suite 3900 Chicago, IL 60606 312/344-4300 FAX: 312/922-9851 MEDIA RELEASE FIRST INDUSTRIAL REALTY TRUST REPORTS FIRST QUARTER 2018 RESULTS Occupancy

The clock is ticking. How to jumpstart your lease accounting implementation project

The clock is ticking How to jumpstart your lease accounting implementation project Lease accounting: Adopting the new standard (ASC 842) 3 Start with challenges, finish with benefits 4 Pine Hill s four

The clock is ticking How to jumpstart your lease accounting implementation project Lease accounting: Adopting the new standard (ASC 842) 3 Start with challenges, finish with benefits 4 Pine Hill s four

On the Horizon: Leases and Fiduciary Responsibilities

On the Horizon: Leases and Fiduciary Responsibilities Dean Michael Mead, Research Manager Florida School Finance Officers Association November 11, 2015 The views expressed in this presentation are those

On the Horizon: Leases and Fiduciary Responsibilities Dean Michael Mead, Research Manager Florida School Finance Officers Association November 11, 2015 The views expressed in this presentation are those

Stock Purchase Agreement Commentary

Stock Purchase Agreement Commentary This is just one example of the many online resources Practical Law Company offers. PLC Corporate and Securities Commentary on key terms and conditions commonly found

Stock Purchase Agreement Commentary This is just one example of the many online resources Practical Law Company offers. PLC Corporate and Securities Commentary on key terms and conditions commonly found

Brixmor Residual Holding LLC and Subsidiaries Years Ended December 31, 2013 and 2012 With Report of Independent Auditors

C ONSOLIDATED F INANCIAL S TATEMENTS Brixmor Residual Holding LLC and Subsidiaries Years Ended December 31, 2013 and 2012 With Report of Independent Auditors Ernst & Young LLP 1403-1211259 Consolidated

C ONSOLIDATED F INANCIAL S TATEMENTS Brixmor Residual Holding LLC and Subsidiaries Years Ended December 31, 2013 and 2012 With Report of Independent Auditors Ernst & Young LLP 1403-1211259 Consolidated

Materiële Vaste Activa. 27 September 2005 Pearl Couvreur

Materiële Vaste Activa 27 September 2005 Pearl Couvreur P w C Contents 1. Principle 2. Acquisition cost 3. Subsequent costs 4. Borrowing costs 5. Assets acquired in a business combination 6. Revaluation

Materiële Vaste Activa 27 September 2005 Pearl Couvreur P w C Contents 1. Principle 2. Acquisition cost 3. Subsequent costs 4. Borrowing costs 5. Assets acquired in a business combination 6. Revaluation

ESOP Feasibility and Valuation Basics

ESOP Feasibility and Valuation Basics Ohio Employee Ownership Center Akron/Fairlawn Hilton Fairlawn, Ohio April 21, 2006 Richard A. Schlueter rschlueter@comstockvaluation.com C VA 1 Levee Way, Suite 3109

ESOP Feasibility and Valuation Basics Ohio Employee Ownership Center Akron/Fairlawn Hilton Fairlawn, Ohio April 21, 2006 Richard A. Schlueter rschlueter@comstockvaluation.com C VA 1 Levee Way, Suite 3109

Topic 842- Leases Making The Transition

Topic 842- Leases Making The Transition K-deep Dhaliwal, Partner, Moss Adams LLP Adam Hite, Senior Manager, Moss Adams LLP The material appearing in this presentation is for informational purposes only

Topic 842- Leases Making The Transition K-deep Dhaliwal, Partner, Moss Adams LLP Adam Hite, Senior Manager, Moss Adams LLP The material appearing in this presentation is for informational purposes only

Sri Lanka Accounting Standard-LKAS 17. Leases

Sri Lanka Accounting Standard-LKAS 17 Leases -516- Sri Lanka Accounting Standard-LKAS 17 Leases Sri Lanka Accounting Standard LKAS 17 Leases is set out in paragraphs 1 69. All the paragraphs have equal

Sri Lanka Accounting Standard-LKAS 17 Leases -516- Sri Lanka Accounting Standard-LKAS 17 Leases Sri Lanka Accounting Standard LKAS 17 Leases is set out in paragraphs 1 69. All the paragraphs have equal

Cimmaron II Apartments Limited Partnership. Financial Statements Years Ended December 31, 2015 and 2014

Financial Statements Years Ended December 31, 2015 and 2014 And Supplementary Information Year Ended December 31, 2015 Table of Contents Page Independent Auditor's Report...1-2 Financial Statements Balance

Financial Statements Years Ended December 31, 2015 and 2014 And Supplementary Information Year Ended December 31, 2015 Table of Contents Page Independent Auditor's Report...1-2 Financial Statements Balance

Chapter 15 Leases 15-1

Chapter 15 Leases 1. Why Leasing sometimes makes more sense 2. The accounting issues in recording a lease transaction 3. The types of contractual provisions in lease 4. The lease classification: capital

Chapter 15 Leases 1. Why Leasing sometimes makes more sense 2. The accounting issues in recording a lease transaction 3. The types of contractual provisions in lease 4. The lease classification: capital

Technical Line SEC staff guidance

No. 2013-20 Updated 27 August 2015 Technical Line SEC staff guidance How to apply S-X Rule 3-14 to real estate acquisitions In this issue: Overview... 1 Applicability of Rule 3-14... 2 Measuring significance...

No. 2013-20 Updated 27 August 2015 Technical Line SEC staff guidance How to apply S-X Rule 3-14 to real estate acquisitions In this issue: Overview... 1 Applicability of Rule 3-14... 2 Measuring significance...

Perry Farm Development Co.

(a not-for-profit corporation) Consolidated Financial Report December 31, 2010 Contents Report Letter 1 Consolidated Financial Statements Balance Sheet 2 Statement of Operations 3 Statement of Changes

(a not-for-profit corporation) Consolidated Financial Report December 31, 2010 Contents Report Letter 1 Consolidated Financial Statements Balance Sheet 2 Statement of Operations 3 Statement of Changes

Public Storage Reports Results for the Quarter Ended March 31, 2017

News Release Public Storage 701 Western Avenue Glendale, CA 91201-2349 www.publicstorage.com For Release Immediately Date April 26, 2017 Contact Clemente Teng (818) 244-8080, Ext. 1141 Public Storage Reports

News Release Public Storage 701 Western Avenue Glendale, CA 91201-2349 www.publicstorage.com For Release Immediately Date April 26, 2017 Contact Clemente Teng (818) 244-8080, Ext. 1141 Public Storage Reports

CHAUTAUQUA COUNTY LAND BANK CORPORATION

EXHIBIT H CHAUTAUQUA COUNTY LAND BANK CORPORATION LAND ACQUISITION AND DISPOSITION POLICIES AND PRIORITIES November 14, 2012 *This document is intended to provide guidance to the Chautauqua County Land

EXHIBIT H CHAUTAUQUA COUNTY LAND BANK CORPORATION LAND ACQUISITION AND DISPOSITION POLICIES AND PRIORITIES November 14, 2012 *This document is intended to provide guidance to the Chautauqua County Land

IFRS 3 Business Combinations

IFRS 3 Business Combinations 0 Objectives Define a business combination under IFRS 3 (Revised 2008) Describe the steps in applying the acquisition method Explain the recognition and measurement principles

IFRS 3 Business Combinations 0 Objectives Define a business combination under IFRS 3 (Revised 2008) Describe the steps in applying the acquisition method Explain the recognition and measurement principles

Internal Audit Report

Internal Audit Report TxDOT Internal Audit Division Objective To determine if objectives are being met and are in compliance with current regulations. Opinion Based on the audit scope areas reviewed, control

Internal Audit Report TxDOT Internal Audit Division Objective To determine if objectives are being met and are in compliance with current regulations. Opinion Based on the audit scope areas reviewed, control

DIRECT-FINANCING TERMS

CHAPTER 21 ALTERNATIVE LESSOR ACCOUNTING GROSS PRESENTATION This alternate discussion describes the accounting by lessors, using a gross presentation. These pages can be substituted for the discussion

CHAPTER 21 ALTERNATIVE LESSOR ACCOUNTING GROSS PRESENTATION This alternate discussion describes the accounting by lessors, using a gross presentation. These pages can be substituted for the discussion

WE MAKE YOUR HEALTHCARE REAL ESTATE WORK FOR YOU COMMON TRANSACTIONAL COMPLIANCE PITFALLS INVOLVING HEALTHCARE REAL ESTATE

WE MAKE YOUR HEALTHCARE REAL ESTATE WORK FOR YOU COMMON TRANSACTIONAL COMPLIANCE PITFALLS INVOLVING HEALTHCARE REAL ESTATE Common Transactional Compliance Pitfalls Involving Healthcare Real Estate Table

WE MAKE YOUR HEALTHCARE REAL ESTATE WORK FOR YOU COMMON TRANSACTIONAL COMPLIANCE PITFALLS INVOLVING HEALTHCARE REAL ESTATE Common Transactional Compliance Pitfalls Involving Healthcare Real Estate Table

Delavaco Residential Properties Corp.

Delavaco Residential Properties Corp. Management Discussion and Analysis For the Quarter Ended June 30, 2015 Table of Contents 1/ FORWARD- LOOKING STATEMENTS... 1 1.1/ INTRODUCTION... 1 1.2/ KEY PERFORMANCE

Delavaco Residential Properties Corp. Management Discussion and Analysis For the Quarter Ended June 30, 2015 Table of Contents 1/ FORWARD- LOOKING STATEMENTS... 1 1.1/ INTRODUCTION... 1 1.2/ KEY PERFORMANCE

USOPF REAL ESTATE ACCEPTANCE POLICY

USOPF REAL ESTATE ACCEPTANCE POLICY The United States Olympic and Paralympic Foundation ( USOPF ) is a not-for-profit organization under the laws of the State of Colorado organized to encourage, solicit

USOPF REAL ESTATE ACCEPTANCE POLICY The United States Olympic and Paralympic Foundation ( USOPF ) is a not-for-profit organization under the laws of the State of Colorado organized to encourage, solicit

Sri Lanka Accounting Standard-LKAS 40. Investment Property

Sri Lanka Accounting Standard-LKAS 40 Investment Property CONTENTS SRI LANKA ACCOUNTING STANDARD-LKAS 40 INVESTMENT PROPERTY paragraphs OBJECTIVE 1 SCOPE 2-4 DEFINITIONS 5-15 RECOGNITION 16-19 MEASUREMENT

Sri Lanka Accounting Standard-LKAS 40 Investment Property CONTENTS SRI LANKA ACCOUNTING STANDARD-LKAS 40 INVESTMENT PROPERTY paragraphs OBJECTIVE 1 SCOPE 2-4 DEFINITIONS 5-15 RECOGNITION 16-19 MEASUREMENT

OPTIBASE LTD. ANNOUNCES THIRD QUARTER RESULTS

Media Contacts: Amir Philips, CEO, Optibase Ltd. 011-972-73-7073-700 info@optibase-holdings.com Investor Relations Contact: Marybeth Csaby, for Optibase +1-917-664-3055 Marybeth.Csaby@gmail.com OPTIBASE

Media Contacts: Amir Philips, CEO, Optibase Ltd. 011-972-73-7073-700 info@optibase-holdings.com Investor Relations Contact: Marybeth Csaby, for Optibase +1-917-664-3055 Marybeth.Csaby@gmail.com OPTIBASE

DUE DILIGENCE CHECKLIST For: [PROPERTY NAME]

![DUE DILIGENCE CHECKLIST For: [PROPERTY NAME]](/thumbs/82/84902906.jpg "DUE DILIGENCE CHECKLIST For: [PROPERTY NAME]") DUE DILIGENCE CHECKLIST For: [PROPERTY NAME] Page 1 / 10 1. List and describe ownership interests 2. A List required third party consents and releases (i.e., mortgages, regulatory) 3. Send authorization

DUE DILIGENCE CHECKLIST For: [PROPERTY NAME] Page 1 / 10 1. List and describe ownership interests 2. A List required third party consents and releases (i.e., mortgages, regulatory) 3. Send authorization

Business Combination. CA Yagnesh Desai. Compiled by CA Yagnesh 1

Business Combination CA Yagnesh Desai ymdesaiandco@gmail.com 093222 44770 09820133227 yagnesh@caymd.com 1 Indicators Not necessarily Limits by the Standard Above 50 % Control Hence Consolidate Control

Business Combination CA Yagnesh Desai ymdesaiandco@gmail.com 093222 44770 09820133227 yagnesh@caymd.com 1 Indicators Not necessarily Limits by the Standard Above 50 % Control Hence Consolidate Control

Click to edit Master title style REVENUE RECOGNITION Understanding the New Revenue Recognition Standard ASC 606

Click to edit Master title style REVENUE RECOGNITION Understanding the New Revenue Recognition Standard ASC 606 9/7/2017 0 Agenda Overview of ASC 606 Review of the five-step process Accounting for contract

Click to edit Master title style REVENUE RECOGNITION Understanding the New Revenue Recognition Standard ASC 606 9/7/2017 0 Agenda Overview of ASC 606 Review of the five-step process Accounting for contract

Navigating FASB's New Pushdown Rules for Acquired Entities

Navigating FASB's New Pushdown Rules for Acquired Entities Evaluating Whether and How to Adopt Pushdown Accounting on Subsidiary Financial Statements THURSDAY, APRIL 23, 2015, 1:00-2:50 pm Eastern IMPORTANT

Navigating FASB's New Pushdown Rules for Acquired Entities Evaluating Whether and How to Adopt Pushdown Accounting on Subsidiary Financial Statements THURSDAY, APRIL 23, 2015, 1:00-2:50 pm Eastern IMPORTANT

The YMCA of Greater Vancouver Properties Foundation

Financial statements The YMCA of Greater Vancouver Properties Foundation Independent auditors report To the Directors of The YMCA of Greater Vancouver Properties Foundation Report on the financial statements

Financial statements The YMCA of Greater Vancouver Properties Foundation Independent auditors report To the Directors of The YMCA of Greater Vancouver Properties Foundation Report on the financial statements

Retail Opportunity Investments Corp. Reports Strong First Quarter Results & Raises FFO Guidance

April 27, 2016 Retail Opportunity Investments Corp. Reports Strong First Quarter Results & Raises FFO Guidance $17.4% increase in FFO Per Diluted Share 7.6% Increase in Same-Center Cash Net Operating Income

April 27, 2016 Retail Opportunity Investments Corp. Reports Strong First Quarter Results & Raises FFO Guidance $17.4% increase in FFO Per Diluted Share 7.6% Increase in Same-Center Cash Net Operating Income

In December 2003 the Board issued a revised IAS 40 as part of its initial agenda of technical projects.

IAS 40 Investment Property In April 2001 the International Accounting Standards Board (the Board) adopted IAS 40 Investment Property, which had originally been issued by the International Accounting Standards

IAS 40 Investment Property In April 2001 the International Accounting Standards Board (the Board) adopted IAS 40 Investment Property, which had originally been issued by the International Accounting Standards

Sansiri Public Company Limited and its subsidiaries Report and consolidated financial statements 31 December 2017

Sansiri Public Company Limited and its subsidiaries Report and consolidated financial statements 31 December 2017 Independent Auditor's Report To the Shareholders of Sansiri Public Company Limited Opinion

Sansiri Public Company Limited and its subsidiaries Report and consolidated financial statements 31 December 2017 Independent Auditor's Report To the Shareholders of Sansiri Public Company Limited Opinion

Top 10 Real Estate Issues in Not-for-Profit Organizations

Top 10 Real Estate Issues in Not-for-Profit Organizations OCTOBER 3, 2017 MARIE BRILMYER, CPA, MACC DONNA JENKINS, CPA ADAM SCHULTZ, CPA Introduction Welcome Overview of the Webinar Introduction to Panelists

Top 10 Real Estate Issues in Not-for-Profit Organizations OCTOBER 3, 2017 MARIE BRILMYER, CPA, MACC DONNA JENKINS, CPA ADAM SCHULTZ, CPA Introduction Welcome Overview of the Webinar Introduction to Panelists

This version includes amendments resulting from IFRSs issued up to 31 December 2009.

International Accounting Standard 40 Investment Property This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 40 Investment Property was issued by the International

International Accounting Standard 40 Investment Property This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 40 Investment Property was issued by the International

NEWS RELEASE For immediate release

NEWS RELEASE For immediate release Laura Clark 904 598 7831 LauraClark@RegencyCenters.com Regency Centers Reports Second Quarter 2018 Results JACKSONVILLE, FL. (August 2, 2018) Regency Centers Corporation

NEWS RELEASE For immediate release Laura Clark 904 598 7831 LauraClark@RegencyCenters.com Regency Centers Reports Second Quarter 2018 Results JACKSONVILLE, FL. (August 2, 2018) Regency Centers Corporation

LEASES WHERE ARE WE? Steve Rathjen

LEASES WHERE ARE WE? Steve Rathjen 267 256-3110 srathjen@kpmg.com Agenda Project status Lease definition and classification Lessee accounting Lessor accounting Presentation, disclosures, and transition

LEASES WHERE ARE WE? Steve Rathjen 267 256-3110 srathjen@kpmg.com Agenda Project status Lease definition and classification Lessee accounting Lessor accounting Presentation, disclosures, and transition

Great Elm Capital Group, Inc. An Introduction to the Fort Myers Transaction & GEC s Real Estate Strategy

Great Elm Capital Group, Inc. An Introduction to the Fort Myers Transaction & GEC s Real Estate Strategy March 6, 2018 2018 Great Elm Capital Group, Inc. Disclaimer Statements in this presentation that

Great Elm Capital Group, Inc. An Introduction to the Fort Myers Transaction & GEC s Real Estate Strategy March 6, 2018 2018 Great Elm Capital Group, Inc. Disclaimer Statements in this presentation that

BUSINESS COMBINATIONS: CLARIFYING THE DEFINITION OF A BUSINESS

BUSINESS COMBINATIONS: CLARIFYING THE DEFINITION OF A BUSINESS Prepared by: Robert Dombrowski, Partner, National Professional Standards Group, RSM US LLP robert.dombrowski@rsmus.com, +1 847 413 6209 TABLE

BUSINESS COMBINATIONS: CLARIFYING THE DEFINITION OF A BUSINESS Prepared by: Robert Dombrowski, Partner, National Professional Standards Group, RSM US LLP robert.dombrowski@rsmus.com, +1 847 413 6209 TABLE

NC STATE UNIVERSITY PARTNERSHIP CORPORATION AND AFFILIATES CONSOLIDATED FINANCIAL REPORT. JUNE 30, 2016 and 2015

NC STATE UNIVERSITY PARTNERSHIP CORPORATION AND AFFILIATES CONSOLIDATED FINANCIAL REPORT JUNE 30, 2016 and 2015 NC State University Partnership Corporation and Affiliates Consolidated Financial Statements

NC STATE UNIVERSITY PARTNERSHIP CORPORATION AND AFFILIATES CONSOLIDATED FINANCIAL REPORT JUNE 30, 2016 and 2015 NC State University Partnership Corporation and Affiliates Consolidated Financial Statements

LKAS 17 Sri Lanka Accounting Standard LKAS 17

Sri Lanka Accounting Standard LKAS 17 Leases CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 17 LEASES paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 4 CLASSIFICATION OF LEASES 7 LEASES IN THE FINANCIAL STATEMENTS

Sri Lanka Accounting Standard LKAS 17 Leases CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 17 LEASES paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 4 CLASSIFICATION OF LEASES 7 LEASES IN THE FINANCIAL STATEMENTS