IFRS Update Guy Thomas, CPA, CA

|

|

|

- Phillip Evelyn Carter

- 5 years ago

- Views:

Transcription

1 IFRS Update Guy Thomas, CPA, CA

2 D&Co IFRS update

3 Agenda 3 new standards under IFRS IFRS 9 Financial Instruments IFRS 15 Revenue from Contracts with Customers IFRS 16 Leases

4 Agenda Some narrow scope amendments to other standards Honorable mention of: some specific industry issues (cryptocurrency and cannabis) What the Heck series

5

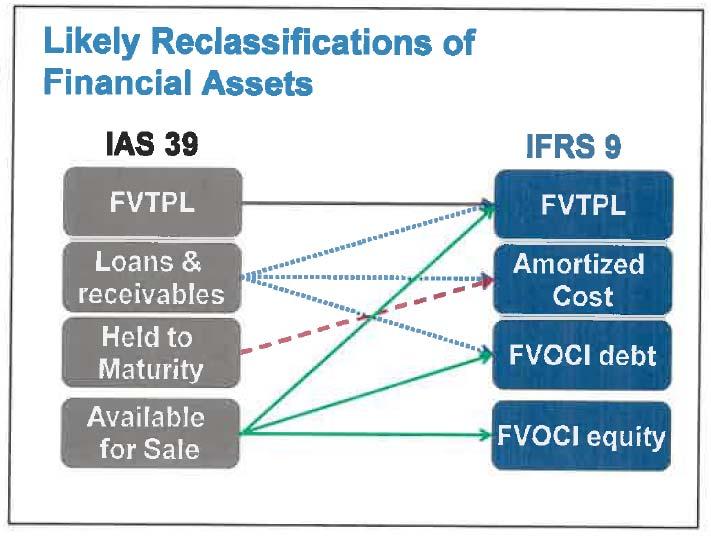

6 Overview IFRS 9 Effective for years commencing on or after January 1, 2018 Uses a business model test for assets (classifications based on how they are managed) Affects long term loans, equity investments, non vanilla financial assets and hedging

7 IFRS 9 Asset classification Now 2.5 classifications for financial assets (previously 4) 1. Amortized cost (effective interest method) assets held to collect contractual cash flows only 2. Amortized costs and for sale assets held to collect contractual cash flows and for sale 3. Fair value

8 IFRS 9 Asset classification Determine the type of asset. Is it: receivable vanilla or not Equity must be fair value For Vanilla receivable Use the business model test Business model is hold, classify as amortized cost Business model is sell, classify FVOCI For other receivable ( FVTPL )

9 IFRS 9 Asset classification If the financial asset is equity (shares in a public or private company) Elect at initial recognition for each asset purchased to recognize changes in value as FVTPL or FVOCI. (note FVOCI never hits P&L)

10 IFRS 9 Asset classification Show off your analysis to your audit committee, board of directors and your auditors

11 IFRS 9 Asset classification

12

13 IFRS 9 Measurement considerations Receivables are measured using one impairment test the Expected Credit Loss ( ECL ) approach 12 month ECL s, lifetime ECL, lifetime credit impaired ECL

14 IFRS 9 Measurement considerations

15 IFRS 9 Measurement considerations For trade receivables can use a simplified approach Record lifetime ECL s at initial recognition of trade receivable

16 IFRS 9 Asset measurement Bit of conflict on measuring complex receivables Theoretically add the fair value of the components within the instrument Guidance indicates fair value day one is based on transaction price Practically may have component values higher or lower than transaction price, particularly with valuation models.

17 IFRS 9 Financial liabilities Not a lot of change from IAS 39 Still have either of FVTPL and amortized cost Hedging Revised standard is simpler to apply

18 IFRS 9 Disclosure More! Analysis Information on credit risk Reconciliations

19 IFRS 9 Transition Should be applied retrospectively, no requirement to restate comparatives but must reconcile opening retained earnings and OCI

20

21 IFRS 15 overview Revenue from contracts with customers Effective for years commencing on or after January 1, 2018 Creates one comprehensive model to account for revenue from contracts with customers

22 IFRS 15 overview Replaces six standards IAS 18 was 9 pages long, IFRS 15 is over 50 pages

23 IFRS 15 a new way of thinking Recognize revenue upon a transfer of control of a good or service, previously risk and reward model Principles based, but there is a lot of prescriptive guidance (over 100 examples)

24 IFRS 15 a new way of thinking Document how the requirements in the standard are met Biggest impact will be on telecommunication, real estate and licensing companies Big increase in disclosure

25 IFRS 15 application 5 step model to achieve the core principle Identify the contract with the customer Identify the performance obligations Determine the transaction price Allocate the transaction price to the performance obligations Recognize revenue when the performance obligation is satisfied

26 IFRS 15 Identify the contract with the customer An agreement that creates enforceable rights and obligations May be written, verbal or based on regular customer business practices Can identify payment terms Probability of collection

27 IFRS 15 Identify the performance obligations Promises to transfer goods or services to a customer If distinct, then account for separately If not distinct, then combine

28 IFRS 15 Determine the transaction price Amount of consideration a company expects to be entitled to Could be: fixed amount variable amount ( expected amount or most likely amount )

29 IFRS 15 Allocate transaction price to the performance obligations Generally done in proportion to their stand alone prices of the good or service promised in the contract Methods for estimating stand alone prices: adjusted market assessment approach expected cost plus a margin approach residual approach

30 IFRS 15 Recognize revenue when the performance obligation is satisfied The asset is transferred when or as the customer obtains control of that asset Indicators of transfer of control Measure progress over time using one method, either of output or input method.

31 IFRS 15 Disclosure requirements Disaggregation of revenue (many) Significant judgements

32 IFRS 15 Transition approaches Full retrospective adoption; or Modified retrospective adoption

33

34 IFRS 16 Leases Effective for years commencing on or after January 1, 2019 Effect is on the Lessee, little change for Lessor Capitalizes all but immaterial and short term leases practical expedient one lease model for Lessees

35 IFRS 16 impact most companies If your company leases office/retail/ warehouse space, vehicles, equipment or other arrangements, you are affected

36 IFRS 16 exemptions Leases of non regenerative assets (mineral property, O&G interests, other) Leases of biological assets Service concession arrangements Licenses of intellectual property granted by lessor Rights held by a lessee under certain licensing arrangements Practical expedient for short term immaterial leases (which should be disclosed in FS)

37 IFRS 16 Contracts IFRS 16.9 At inception of a contract, an entity shall assess whether the contract is, or contains, a lease... if the contract conveys the right to control the use of an identified asset for a period of time in exchange for consideration.

38 IFRS 16 Identification considerations There is an identified asset (lessor cannot substitute for their own benefit) Right to obtain substantially all of the economic benefits from using the asset Right to direct how to use the asset Decisions determined during and before the period of use Protective rights

39 IFRS 16 Components Lease and non lease Account for each separately unless applying practical expedients can account for as a single lease but must disclose the practical expedient has been applied

40 IFRS 16 Portfolio approach Can use for leases with similar characteristics Practical expedient so disclose it

41 IFRS 16 Lease Measurement 1) Lease term 2) Lease payments 3) Determine Discount rates 4) Calculate PV of future lease payments

42

43 IFRS 16 Lease Measurement Term Non cancellable period together with both: Option to extend if reasonably certain to exercise that option Option to terminate if reasonably certain not to exercise that option

44 IFRS 16 Lease Measurement Payments Fixed payments and in substance (unavoidable) payments Variable payments with linked index or rate Lease incentives (deduct) Purchase option (if exercise expected) Termination penalty (if exercise expected) Residual guarantees

45 IFRS 16 Lease Measurement Discount Rate Use either Interest rate implicit in the lease, if readily determinable, otherwise Incremental borrowing rate for lessee

46 IFRS 16 Lease measurement PV NPV based on term, payment amounts and discount rate

47 IFRS 16 Right Of Use Asset Includes: Lease liability Lease payments before commencement date (less any incentives) Initial direct costs Decommissioning estimates

48 IFRS 16 Reassessment of Liability Re measure if there is a change in: lease term assessment of option to purchase amounts payable for residual guarantees index or rate related to lease payments Change is reflected in Lease Liability and the related Right Of Use asset, and likely a P&L effect as well.

49 IFRS 16 Lease modifications Re measure Account as separate lease if: Lease scope is increased by adding right of use asset(s) and Consideration increases by a commensurate stand alone price for the increased scope If not a separate lease Adjust lease liability and related right of use asset, likely P&L effect

50 IFRS 16 Presentation Statement of Financial Position Right of use assets with offsetting lease liabilities Statement of Operations Interest expense (using effective interest rate method) Accretion Depreciation Statement of Cash Flows Addbacks on non cash items Principal repayments in financing activities New estimates and judgements will be required New disclosure requirements

51 IFRS 16 Transition Choose full or modified retrospective transition approach If modified approach, just look forward. Need to show reconciliation (including cleanup of any related prepaids or accruals)

52 IFRS 16 Ongoing Watch for: changes in lease terms or estimates embedded leases within service contracts separate impairment considerations of Right Of Use assets Subleases intermediate lessor Is sublease financing or operating If financing, de recognition of part of asset but liability has different counterparties

53 IFRS 16 Internal Documentation You will need to substantiate the assessment of all contracts in the context of the standard Create a list of all leases with a summary of terms Expectations and estimations

54 IFRS 16 accounting overview Show off your analysis to your audit committee, board of directors and your auditors

55

56 Narrow scope amendments IAS 7 Statement of Cash Flows IAS 12 Income Taxes IAS 23 Borrowing Costs debt outstanding after related asset is ready for use is general borrowing IAS 28 Long Term Interests in Associates and JV s IAS 40 Investment Property

57 Narrow scope amendments IFRS 2 Share based Payments (endorsed) IFRS 3 Business Combinations Party obtaining control of a joint operation is a business combination achieved in stages with remeasurements of FV at acquisition dates IFRS 9 Financial Instruments Debt modifications result in immediate recognition of a gain or loss IFRS 11 Joint Arrangements Party obtaining joint control of a business that is a joint operation has no re measurement of FV IFRS 17 Insurance Contracts

58 Narrow scope amendments IFRIC 22 Foreign currency transactions and advance consideration IFRIC 23 Uncertainty over income tax If an entity chooses tax treatment that is not probable to be accepted by tax authorities, should recognize the uncertainty in its income tax accounting Detection risk is not considered

59 Honorable mention Cryptocurrency Industry Not an investment under IAS 39 or IFRS 9 Is it an intangible asset (IAS 38) or inventory (IAS 2) If inventory, lower or cost or NRV OR if meeting brokertrader status then FV less costs to sell Revenue recognition issues under IFRS 15 for miners Requires lots of consideration and position papers Canadian accounting bodies and Regulators are working to provide guidance within the existing IFRS framework

60 Honorable mention Cannabis Industry Biological assets under IAS 41 requires FV measurement Revenue recognition under IAS 18 and IFRS 15 Differing application of FV changes of biologiacal asset within IS Differing application of components of cost of sales No specific guidance FV changes in COGs can result in GP being higher than sales October 17, 2018 Canada reduced haze of cannabis through legalization Cross boarder considerations not legal at federal level in USA IFRS Discussion Group (IDG) considered in June, 2018 Canadian accounting bodies and Regulators are working to provide guidance within the existing IFRS framework

61 Recap IFRS 9 recap Affects all companies, at least for disclosure Two categories for financial assets (amortized cost or fair value) Classification based on business model New Impairment model Disclosure

62 Recap IFRS 15 recap Big effect on software, telecoms, real estate New criteria to recognize revenue when customer has control of the goods or services Lots of new disclosure

63 Recap IFRS 16 recap Affects almost all companies Only one type of lease (finance) with exceptions (short term leases and low dollar impact) Requires consideration of all contracts Requires lease summaries and analysis NPV calculations, lots of assumptions and disclosures Pervasive effect on financial statements

64 Final take aways Q comes quickly after the year end statements are finished What are you waiting for What The Heck

International Financial Reporting Standard 16 Leases. Objective. Scope. Recognition exemptions (paragraphs B3 B8) IFRS 16

IFRS 16") International Financial Reporting Standard 16 Leases Objective 1 This Standard sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective is to ensure

International Financial Reporting Standard 16 Leases Objective 1 This Standard sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective is to ensure

In December 2003 the IASB issued a revised IAS 17 as part of its initial agenda of technical projects.

IFRS Standard 16 Leases In April 2001 the International Accounting Standards Board (IASB) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

IFRS Standard 16 Leases In April 2001 the International Accounting Standards Board (IASB) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

IFRS 16 LEASES. Page 1 of 21

IFRS 16 LEASES OBJECTIVE The objective is to ensure that lessees and lessors provide relevant information in a manner that faithfully represents those transactions. This information gives a basis for users

IFRS 16 LEASES OBJECTIVE The objective is to ensure that lessees and lessors provide relevant information in a manner that faithfully represents those transactions. This information gives a basis for users

In December 2003 the Board issued a revised IAS 17 as part of its initial agenda of technical projects.

IFRS 16 Leases In April 2001 the International Accounting Standards Board (the Board) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

IFRS 16 Leases In April 2001 the International Accounting Standards Board (the Board) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

IFRS 16 : Lease accounting

IFRS 16 : Lease accounting Effective for accounting periods beginning on or after 1 January 2019 December 2017 IFRS 16: Lease accounting The IASB published the new IFRS 16 lease standard, in order to avoid

IFRS 16 : Lease accounting Effective for accounting periods beginning on or after 1 January 2019 December 2017 IFRS 16: Lease accounting The IASB published the new IFRS 16 lease standard, in order to avoid

New leases standard ASC 842 Lessee - operating leases. Itai Gotlieb, Partner, Professional Practice July 2017

ASC 842 Lessee - operating leases Itai Gotlieb, Partner, Professional Practice July 2017 Overview Under Accounting Standards Codification (ASC) 842, Leases, lessees recognize assets and liabilities for

ASC 842 Lessee - operating leases Itai Gotlieb, Partner, Professional Practice July 2017 Overview Under Accounting Standards Codification (ASC) 842, Leases, lessees recognize assets and liabilities for

Sri Lanka Accounting Standard - SLFRS 16. Leases

Sri Lanka Accounting Standard - SLFRS 16 Leases CONTENTS from paragraph SRI LANKA ACCOUNTING STANDARD - SLFRS 16 LEASES INTRODUCTION OBJECTIVE 1 SCOPE 3 RECOGNITION EXEMPTIONS 5 IDENTIFYING A LEASE 9 Separating

Sri Lanka Accounting Standard - SLFRS 16 Leases CONTENTS from paragraph SRI LANKA ACCOUNTING STANDARD - SLFRS 16 LEASES INTRODUCTION OBJECTIVE 1 SCOPE 3 RECOGNITION EXEMPTIONS 5 IDENTIFYING A LEASE 9 Separating

FSA Faculty Consortium Technical Accounting Update. Bob Uhl, partner, Deloitte & Touche LLP

FSA Faculty Consortium Technical Accounting Update Bob Uhl, partner, Deloitte & Touche LLP Deloitte University May 30, 2014 Acronyms Acronym ASC ASU ED FASB IASB IFRS U.S. GAAP Full Form Accounting Standards

FSA Faculty Consortium Technical Accounting Update Bob Uhl, partner, Deloitte & Touche LLP Deloitte University May 30, 2014 Acronyms Acronym ASC ASU ED FASB IASB IFRS U.S. GAAP Full Form Accounting Standards

HKFRS 16 Leases sets out the principles for the recognition, measurement, presentation and disclosure

HKFRS 16 Leases Introduction HKFRS 16 Leases sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective of HKFRS 16 is to ensure that lessees and lessors

HKFRS 16 Leases Introduction HKFRS 16 Leases sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective of HKFRS 16 is to ensure that lessees and lessors

New Zealand Equivalent to International Financial Reporting Standard 16 Leases (NZ IFRS 16)

") New Zealand Equivalent to International Financial Reporting Standard 16 Leases (NZ IFRS 16) Issued February 2016 This Standard was issued on 11 February 2016 by the New Zealand Accounting Standards Board

New Zealand Equivalent to International Financial Reporting Standard 16 Leases (NZ IFRS 16) Issued February 2016 This Standard was issued on 11 February 2016 by the New Zealand Accounting Standards Board

CPA COMPETENCY MAP STUDY NOTES UPDATE TO DECEMBER 31, 2018

CPA COMPETENCY MAP STUDY NOTES UPDATE TO DECEMBER 31, 2018 Please note that several of the updates relate to changes that are not effective until 2019. For 2019 PEP Module Exams and for the CFE, you are

CPA COMPETENCY MAP STUDY NOTES UPDATE TO DECEMBER 31, 2018 Please note that several of the updates relate to changes that are not effective until 2019. For 2019 PEP Module Exams and for the CFE, you are

Gearing up for change New IFRS on Leases

Gearing up for change New IFRS on Leases In a nutshell The changes Lessee accounting Effective date: 1 January 2019 Limited changes to scope of IAS 17 Enhanced guidance on identifying a lease Lessor accounting

Gearing up for change New IFRS on Leases In a nutshell The changes Lessee accounting Effective date: 1 January 2019 Limited changes to scope of IAS 17 Enhanced guidance on identifying a lease Lessor accounting

Summary of IFRS Exposure Draft Leases

The International Accounting Standards Board (IASB) recently issued a revised exposure draft (ED) relating to leases. Once these proposals are finalized the new guidance will replace the IAS 17 Leases.

The International Accounting Standards Board (IASB) recently issued a revised exposure draft (ED) relating to leases. Once these proposals are finalized the new guidance will replace the IAS 17 Leases.

Exposure Draft 64 January 2018 Comments due: June 30, Proposed International Public Sector Accounting Standard. Leases

Exposure Draft 64 January 2018 Comments due: June 30, 2018 Proposed International Public Sector Accounting Standard Leases This document was developed and approved by the International Public Sector Accounting

Exposure Draft 64 January 2018 Comments due: June 30, 2018 Proposed International Public Sector Accounting Standard Leases This document was developed and approved by the International Public Sector Accounting

IFRS 15 and IFRS 16 Webinar

CPA Ireland Skillnet CPA Ireland Skillnet, is a training network that is funded by Skillnets, a state funded, enterprise led support body dedicated to the promotion and facilitation of training and up-skilling

CPA Ireland Skillnet CPA Ireland Skillnet, is a training network that is funded by Skillnets, a state funded, enterprise led support body dedicated to the promotion and facilitation of training and up-skilling

IFRS 16 Leases supplement

IFRS 16 Leases supplement Guide to annual financial statements IFRS December 2017 kpmg.com/ifrs Contents About this supplement 1 About IFRS 16 3 The Group s lease portfolio 6 Part I Modified retrospective

IFRS 16 Leases supplement Guide to annual financial statements IFRS December 2017 kpmg.com/ifrs Contents About this supplement 1 About IFRS 16 3 The Group s lease portfolio 6 Part I Modified retrospective

LEASES WHERE ARE WE? Steve Rathjen

LEASES WHERE ARE WE? Steve Rathjen 267 256-3110 srathjen@kpmg.com Agenda Project status Lease definition and classification Lessee accounting Lessor accounting Presentation, disclosures, and transition

LEASES WHERE ARE WE? Steve Rathjen 267 256-3110 srathjen@kpmg.com Agenda Project status Lease definition and classification Lessee accounting Lessor accounting Presentation, disclosures, and transition

Click to edit Master title style REVENUE RECOGNITION Understanding the New Revenue Recognition Standard ASC 606

Click to edit Master title style REVENUE RECOGNITION Understanding the New Revenue Recognition Standard ASC 606 9/7/2017 0 Agenda Overview of ASC 606 Review of the five-step process Accounting for contract

Click to edit Master title style REVENUE RECOGNITION Understanding the New Revenue Recognition Standard ASC 606 9/7/2017 0 Agenda Overview of ASC 606 Review of the five-step process Accounting for contract

HKFRS 16 Leases. Disclaimer. Date 21 April 2017 Time 19:00 21:00 Venue Boys' and Girls' Clubs Association

HKFRS 16 Leases Date 21 April 2017 Time 19:00 21:00 Venue Boys' and Girls' Clubs Association www.zhtraining.com Disclaimer The materials of this seminar are intended only to provide general information

HKFRS 16 Leases Date 21 April 2017 Time 19:00 21:00 Venue Boys' and Girls' Clubs Association www.zhtraining.com Disclaimer The materials of this seminar are intended only to provide general information

Deeper Dive Leases. Overview

Deeper Dive Leases Presented by: Shaun Johnson, CPA Dingus, Zarecor & Associates PLLC Overview Effective dates Big picture Objective, impact, and implementation Applicability and definition Initial recognition

Deeper Dive Leases Presented by: Shaun Johnson, CPA Dingus, Zarecor & Associates PLLC Overview Effective dates Big picture Objective, impact, and implementation Applicability and definition Initial recognition

[TO BE PUBLLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (i)]

![[TO BE PUBLLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (i)]](/thumbs/95/124393322.jpg "[TO BE PUBLLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (i)]") [TO BE PUBLLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (i)] GOVERNMENT OF INDIA MINISTRY OF CORPORATE AFFAIRS NOTIFICATION New Delhi, the 30 th March, 2019 G.S.R. (E).

[TO BE PUBLLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (i)] GOVERNMENT OF INDIA MINISTRY OF CORPORATE AFFAIRS NOTIFICATION New Delhi, the 30 th March, 2019 G.S.R. (E).

Exposure Draft. Indian Accounting Standard (Ind AS) 116 Leases. (Last date for Comments: August 31, 2017)

116 Leases. (Last date for Comments: August 31, 2017)") ED/Ind AS/2017/06 Exposure Draft Indian Accounting Standard (Ind AS) 116 Leases (Last date for Comments: August 31, 2017) Issued by Accounting Standards Board The Institute of Chartered Accountants of

ED/Ind AS/2017/06 Exposure Draft Indian Accounting Standard (Ind AS) 116 Leases (Last date for Comments: August 31, 2017) Issued by Accounting Standards Board The Institute of Chartered Accountants of

Headline Verdana Bold The evolutions of leases accounting under IFRS 16 Mariano Bruno, Carlo Laganà, Giuseppe Ambrosio, Deloitte & Touche S.p.A.

SHIPPING AND THE LAW 7^ Edition 25-26 October 2016 NAPLES Headline Verdana Bold The evolutions of leases accounting under IFRS 16 Mariano Bruno, Carlo Laganà, Giuseppe Ambrosio, Deloitte & Touche S.p.A.

SHIPPING AND THE LAW 7^ Edition 25-26 October 2016 NAPLES Headline Verdana Bold The evolutions of leases accounting under IFRS 16 Mariano Bruno, Carlo Laganà, Giuseppe Ambrosio, Deloitte & Touche S.p.A.

Leases ASU September 20, 2017

Leases ASU 2016-02 September 20, 2017 Meet the Speakers Tonisha Spratte, CPA Senior Accountant Cherry Bekaert tspratte@cbh.com Matthew Mars Senior Accountant Cherry Bekaert mmars@cbh.com Agenda What is

Leases ASU 2016-02 September 20, 2017 Meet the Speakers Tonisha Spratte, CPA Senior Accountant Cherry Bekaert tspratte@cbh.com Matthew Mars Senior Accountant Cherry Bekaert mmars@cbh.com Agenda What is

10 TH European IFRS power and utilities roundtable

10 TH European IFRS power and utilities roundtable Victor Chan, Partner, EY 29 November 2016 European IFRS Power and Utilities roundtable IFRS 16 Leases: the journey so far November 2016 Agenda Overview

10 TH European IFRS power and utilities roundtable Victor Chan, Partner, EY 29 November 2016 European IFRS Power and Utilities roundtable IFRS 16 Leases: the journey so far November 2016 Agenda Overview

The New Lease Accounting Standard. Hunter Mink, CPA, CCIFP Brian Rosenberg, CPA, MBA

The New Lease Accounting Standard Hunter Mink, CPA, CCIFP Brian Rosenberg, CPA, MBA 1 Agenda Introduction Lease Identification and Classification Lessee Accounting Other Considerations Disclosures Impact

The New Lease Accounting Standard Hunter Mink, CPA, CCIFP Brian Rosenberg, CPA, MBA 1 Agenda Introduction Lease Identification and Classification Lessee Accounting Other Considerations Disclosures Impact

GASB 87 - Leases. South Carolina Association of CPAs Fall Fest November 16, 2018 Mauldin & Jenkins

November 16, 2018 Mauldin & Jenkins 800-277-0050 www.mjcpa.com GASB 87 - Leases Effective for periods beginning after December 15, 2019 - December 31, 2020 or June 30, 2021 or September 30, 2021 Amends

November 16, 2018 Mauldin & Jenkins 800-277-0050 www.mjcpa.com GASB 87 - Leases Effective for periods beginning after December 15, 2019 - December 31, 2020 or June 30, 2021 or September 30, 2021 Amends

Lease Accounting Standard Update ASU Presented by: Nicholas Hoefel, CPA Manager, Audit Services Group

Lease Accounting Standard Update ASU 2016-02 Presented by: Nicholas Hoefel, CPA Manager, Audit Services Group 1 Overview Introduction Background and current environment Effective dates and transition Key

Lease Accounting Standard Update ASU 2016-02 Presented by: Nicholas Hoefel, CPA Manager, Audit Services Group 1 Overview Introduction Background and current environment Effective dates and transition Key

Edison Electric Institute and American Gas Association New Lease Standard

Edison Electric Institute and American Gas Association New Lease Standard May 16, 2016 Disclaimer The information contained herein is of a general nature and is not intended to address the circumstances

Edison Electric Institute and American Gas Association New Lease Standard May 16, 2016 Disclaimer The information contained herein is of a general nature and is not intended to address the circumstances

Defining Issues May 2013, No

Defining Issues May 2013, No. 13-24 FASB and IASB Issue Revised Exposure Drafts on Lease Accounting The FASB and IASB (the Boards) recently issued revised joint exposure drafts (EDs) on proposed changes

Defining Issues May 2013, No. 13-24 FASB and IASB Issue Revised Exposure Drafts on Lease Accounting The FASB and IASB (the Boards) recently issued revised joint exposure drafts (EDs) on proposed changes

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N AGENDA Leases FASB & GASB Revenue Recognition FASB 2 FASB ASU 2016-02, Leases (Topic

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N AGENDA Leases FASB & GASB Revenue Recognition FASB 2 FASB ASU 2016-02, Leases (Topic

IFRS Link. Contents. Newsletter. 1 IASB 11 EU Endorsement

IFRS Link Newsletter Issue 25 Contents 1 IASB 11 EU Endorsement New standard on accounting for leases With IFRS 16 Leases, the IASB published a new standard on accounting for leases on 13 January 2016.

IFRS Link Newsletter Issue 25 Contents 1 IASB 11 EU Endorsement New standard on accounting for leases With IFRS 16 Leases, the IASB published a new standard on accounting for leases on 13 January 2016.

IFRS Project Insights Leases

IFRS Project Insights Leases The IASB and FASB ( the Boards ) published a Discussion Paper (DP) setting out a proposed lessee accounting model in March 2009. The proposed accounting model has evolved since

IFRS Project Insights Leases The IASB and FASB ( the Boards ) published a Discussion Paper (DP) setting out a proposed lessee accounting model in March 2009. The proposed accounting model has evolved since

GASBs Presented by: William Blend, CPA, CFE

GASBs 87-89 Presented by: William Blend, CPA, CFE Leases: Statement 87 Effective Date and General Implementation Effective for Florida fiscal year end 2021. Earlier application is encouraged. Leases should

GASBs 87-89 Presented by: William Blend, CPA, CFE Leases: Statement 87 Effective Date and General Implementation Effective for Florida fiscal year end 2021. Earlier application is encouraged. Leases should

The new IFRS 16 Leases effective as of 1 January 2019

The new IFRS 16 Leases effective as of 1 January 2019 IFRS 16 was issued by IASB on 13 January 2016. The Standard is effective as of 1 January 2019. It has not yet been adopted by the EC. This is a Standard

The new IFRS 16 Leases effective as of 1 January 2019 IFRS 16 was issued by IASB on 13 January 2016. The Standard is effective as of 1 January 2019. It has not yet been adopted by the EC. This is a Standard

On the Horizon: Leases and Fiduciary Responsibilities

On the Horizon: Leases and Fiduciary Responsibilities Dean Michael Mead, Research Manager Florida School Finance Officers Association November 11, 2015 The views expressed in this presentation are those

On the Horizon: Leases and Fiduciary Responsibilities Dean Michael Mead, Research Manager Florida School Finance Officers Association November 11, 2015 The views expressed in this presentation are those

Leases: A Comprehensive Update on the Joint Project

The Dbriefs Financial Reporting series presents: Leases: A Comprehensive Update on the Joint Project Bob Uhl, Deloitte & Touche LLP Trevor Farber, Deloitte & Touche LLP James Barker, Deloitte & Touche

The Dbriefs Financial Reporting series presents: Leases: A Comprehensive Update on the Joint Project Bob Uhl, Deloitte & Touche LLP Trevor Farber, Deloitte & Touche LLP James Barker, Deloitte & Touche

Accounting and Auditing. Norman Mosrie, CPA, FMFMA, CHFP James Sutherland, CPA

Accounting and Auditing Norman Mosrie, CPA, FMFMA, CHFP James Sutherland, CPA Leases (ASU 2016-02; Topic 842) A lease contract conveys the right to use an asset (the underlying asset) for a period of time

Accounting and Auditing Norman Mosrie, CPA, FMFMA, CHFP James Sutherland, CPA Leases (ASU 2016-02; Topic 842) A lease contract conveys the right to use an asset (the underlying asset) for a period of time

IASB Staff Paper March 2011

IASB Staff Paper March 2011 Effect of board redeliberations on Exposure Draft Leases About this staff paper This staff paper indicates how the proposals in the Exposure Draft Leases would change as a result

IASB Staff Paper March 2011 Effect of board redeliberations on Exposure Draft Leases About this staff paper This staff paper indicates how the proposals in the Exposure Draft Leases would change as a result

IFRS 16 Leases. Presented by Anton van Wyk M. Com CA (SA)

") IFRS 16 Leases Presented by Anton van Wyk M. Com CA (SA) Why a new IFRS for leases? Information reported about operating leases lacked transparency and did not meet the needs of users of financial statements

IFRS 16 Leases Presented by Anton van Wyk M. Com CA (SA) Why a new IFRS for leases? Information reported about operating leases lacked transparency and did not meet the needs of users of financial statements

Accounting and Auditing Update. Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc.

Accounting and Auditing Update Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc. Agenda Overview of the standard setting agenda Revenue recognition Lease

Accounting and Auditing Update Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc. Agenda Overview of the standard setting agenda Revenue recognition Lease

Proposed New Accounting Standards For Leases

Relationships backed by performance. Proposed New Accounting Standards For Leases Doug Richardson Live Seminar 9:00am 10:30am June 21 2012 Overview and Background Leases serve a vital role in many entities

Relationships backed by performance. Proposed New Accounting Standards For Leases Doug Richardson Live Seminar 9:00am 10:30am June 21 2012 Overview and Background Leases serve a vital role in many entities

International GAAP Holdings Limited Model financial statements for the year ended 31 December 2017 (With early adoption of IFRS 16)

") International GAAP Holdings Limited Model financial statements for the year ended 31 December 2017 (With early adoption of IFRS 16) Appendix 1: Early application of IFRS 16 Leases Introduction This Appendix

International GAAP Holdings Limited Model financial statements for the year ended 31 December 2017 (With early adoption of IFRS 16) Appendix 1: Early application of IFRS 16 Leases Introduction This Appendix

GASB 87: Leases. Hosted By: Ben Lindekugel, Executive Director Association of Washington Public Hospital Districts

GASB 87: Leases Hosted By: Ben Lindekugel, Executive Director Association of Washington Public Hospital Districts November 6, 2018 Presented By Tom Dingus, CPA, Partner Dingus, Zarecor & Associates PLLC

GASB 87: Leases Hosted By: Ben Lindekugel, Executive Director Association of Washington Public Hospital Districts November 6, 2018 Presented By Tom Dingus, CPA, Partner Dingus, Zarecor & Associates PLLC

Applying IFRS in consumer products and retail

Applying IFRS in consumer products and retail Leases standard Consumer products and retail Updated June 2017 Contents Overview 2 1. Identifying a lease 3 1.1 Definition of a lease 3 1.2 Identified asset

Applying IFRS in consumer products and retail Leases standard Consumer products and retail Updated June 2017 Contents Overview 2 1. Identifying a lease 3 1.1 Definition of a lease 3 1.2 Identified asset

Accounting Update. Anne Cloutier, CPA, FHFMA Principal March 27, 2015

Accounting Update Anne Cloutier, CPA, FHFMA Principal March 27, 2015 Current Accounting for Leases Capital leases - a lessee recognizes leased assets and liabilities on the balance sheet. Operating leases

Accounting Update Anne Cloutier, CPA, FHFMA Principal March 27, 2015 Current Accounting for Leases Capital leases - a lessee recognizes leased assets and liabilities on the balance sheet. Operating leases

How the lease accounting proposal might affect your company

Applying IFRS How the lease accounting proposal might affect your company August 2013 Contents 1. Overview... 1 2. Identifying a lease... 2 2.1 Scope exclusions... 2 2.2 Definition of a lease... 3 2.2.1

Applying IFRS How the lease accounting proposal might affect your company August 2013 Contents 1. Overview... 1 2. Identifying a lease... 2 2.1 Scope exclusions... 2 2.2 Definition of a lease... 3 2.2.1

Get ready for FRS 116: Leases

Get ready for FRS 116: Leases Chetan Hans & Eng Min Lor Grant Thornton Singapore Overview of main changes Replaces FRS 17 Leases, INT FRS 104 Determining whether an Arrangement contains a Lease, INT FRS

Get ready for FRS 116: Leases Chetan Hans & Eng Min Lor Grant Thornton Singapore Overview of main changes Replaces FRS 17 Leases, INT FRS 104 Determining whether an Arrangement contains a Lease, INT FRS

IFRS : Where do we stand? Planned changes 2012 and beyond

International Financial Reporting Standards IFRS : Where do we stand? Planned changes 2012 and beyond Philippe DANJOU Board Member Warsaw, December 6, 2012 The views expressed in this presentation are

International Financial Reporting Standards IFRS : Where do we stand? Planned changes 2012 and beyond Philippe DANJOU Board Member Warsaw, December 6, 2012 The views expressed in this presentation are

IFRS 16. Changes in recognizing leases in the financial statements

IFRS 16 Changes in recognizing leases in the financial statements The new standard in a nutshell: To whom the new standard applies / Binding terms and conditions In January 2016, the International Accounting

IFRS 16 Changes in recognizing leases in the financial statements The new standard in a nutshell: To whom the new standard applies / Binding terms and conditions In January 2016, the International Accounting

Lease accounting scope & impacts

Leasing Lease accounting scope & impacts Scope What s in? All industries, all entities Arrangements that meet the definition of a lease Embedded leases within other arrangements What s out? Leases of:

Leasing Lease accounting scope & impacts Scope What s in? All industries, all entities Arrangements that meet the definition of a lease Embedded leases within other arrangements What s out? Leases of:

AASB 16: Experience the Fundamental Overhaul of Lease Accounting for Lessees

AASB 16: Experience the Fundamental Overhaul of Lease Accounting for Lessees Introduction to Session This introductory session we will: Explore the Principles of AASB 16 Learn how to Identify a Lease Work

AASB 16: Experience the Fundamental Overhaul of Lease Accounting for Lessees Introduction to Session This introductory session we will: Explore the Principles of AASB 16 Learn how to Identify a Lease Work

IFRS 15. Revenue from Contracts with Customers. Presented by CPA Dr. Peter Njuguna

IFRS 15 Revenue from Contracts with Customers Presented by CPA Dr. Peter Njuguna Introduction Revenue is income from ordinary activities. A contract has rights and obligations between two or more parties.

IFRS 15 Revenue from Contracts with Customers Presented by CPA Dr. Peter Njuguna Introduction Revenue is income from ordinary activities. A contract has rights and obligations between two or more parties.

IFRS 16 Lease overview and EY s enabling toolkit

IFRS 16 Lease overview and EY s enabling toolkit Content Page Section I IFRS 16 overview 2 Appendix I EY Lease enabling technology suite 9 Appendix II EY Contacts 17 Page 1 IFRS 9 Classification and measurement

IFRS 16 Lease overview and EY s enabling toolkit Content Page Section I IFRS 16 overview 2 Appendix I EY Lease enabling technology suite 9 Appendix II EY Contacts 17 Page 1 IFRS 9 Classification and measurement

FASB/IASB Update Part II

American Accounting Association FASB/IASB Update Part II Tom Linsmeier FASB Member August 3, 2014 The views expressed in this presentation are those of the presenters. Official positions of the FASB/IASB

American Accounting Association FASB/IASB Update Part II Tom Linsmeier FASB Member August 3, 2014 The views expressed in this presentation are those of the presenters. Official positions of the FASB/IASB

Is Your Operating Lease An Asset or Liability? It s Now Both

MFM Annual Conference Is Your Operating Lease An Asset or Liability? It s Now Both 23 May 2016-1:30 pm 2:20 pm Disclaimer These slides are for educational purposes only and are not intended, and should

MFM Annual Conference Is Your Operating Lease An Asset or Liability? It s Now Both 23 May 2016-1:30 pm 2:20 pm Disclaimer These slides are for educational purposes only and are not intended, and should

IFRS 15 Revenue from contracts with customers Presentation by: CPA Freda Mitambo Partner, Deloitte & Touche

IFRS 15 Revenue from contracts with customers Presentation by: CPA Freda Mitambo Partner, Deloitte & Touche Uphold public interest Why IFRS 15 is important What does it mean for clients? Revenue recognition

IFRS 15 Revenue from contracts with customers Presentation by: CPA Freda Mitambo Partner, Deloitte & Touche Uphold public interest Why IFRS 15 is important What does it mean for clients? Revenue recognition

Lease Update. June 2017 Addison, Texas

Lease Update June 2017 Addison, Texas William Bill Schneider CPA, CGMA Bill is an Audit Director at AT&T. AT&T delivers advanced mobile services, next-generation TV, highspeed internet and smart solutions

Lease Update June 2017 Addison, Texas William Bill Schneider CPA, CGMA Bill is an Audit Director at AT&T. AT&T delivers advanced mobile services, next-generation TV, highspeed internet and smart solutions

GASB Update. Airports Council International North America 2017 Finance Committee Workshop. Blake Rodgers, Senior Manager September 17, 2017

GASB Update Airports Council International North America 2017 Finance Committee Workshop Blake Rodgers, Senior Manager September 17, 2017 Agenda High Level Overview of GASB Statement No. 87, Leases Other

GASB Update Airports Council International North America 2017 Finance Committee Workshop Blake Rodgers, Senior Manager September 17, 2017 Agenda High Level Overview of GASB Statement No. 87, Leases Other

Leases: Overview of the new guidance

Leases: Overview of the new guidance Prepared by: Richard Stuart, Partner, National Professional Standards Group, RSM US LLP richard.stuart@rsmus.com, +1 203 905 5027 March 2, 2016 Introduction On February

Leases: Overview of the new guidance Prepared by: Richard Stuart, Partner, National Professional Standards Group, RSM US LLP richard.stuart@rsmus.com, +1 203 905 5027 March 2, 2016 Introduction On February

The new accounting standard for leases. 27 March 2017

The new accounting standard for leases 27 March 2017 Disclaimer Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity.

The new accounting standard for leases 27 March 2017 Disclaimer Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity.

Lease & Finance Accountants Conference. September The Westin Charlotte Charlotte, NC

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Basic Principles of Lessors under ASC 842 Mamta Shori, Wells Fargo Equipment Finance Joe Sebik,

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Basic Principles of Lessors under ASC 842 Mamta Shori, Wells Fargo Equipment Finance Joe Sebik,

GASB 87 Leases. GASB 87 Scope and Effective Date

GASB 87 Leases December 12, 2017 GASB 87 Scope and Effective Date Effective date reporting period beginning after December 15, 2019 How does this improve accounting and financial reporting? Establishes

GASB 87 Leases December 12, 2017 GASB 87 Scope and Effective Date Effective date reporting period beginning after December 15, 2019 How does this improve accounting and financial reporting? Establishes

International Accounting Standard 17 Leases. Objective. Scope. Definitions IAS 17

International Accounting Standard 17 Leases Objective 1 The objective of this Standard is to prescribe, for lessees and lessors, the appropriate accounting policies and disclosure to apply in relation

International Accounting Standard 17 Leases Objective 1 The objective of this Standard is to prescribe, for lessees and lessors, the appropriate accounting policies and disclosure to apply in relation

4/4/2018. GASB's New Leases Standard

GASB's New Leases Standard April 4, 2018 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in a group Complete group attendance form

GASB's New Leases Standard April 4, 2018 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in a group Complete group attendance form

Technical Line FASB final guidance

No. 2016-09 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect health care entities In this issue: Overview... 1 Key considerations... 3 Scope and scope exceptions...

No. 2016-09 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect health care entities In this issue: Overview... 1 Key considerations... 3 Scope and scope exceptions...

Applying IFRS in Financial Services

Applying IFRS in Financial Services IASB issues new leases standard - financial services April 2016 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition of a lease

Applying IFRS in Financial Services IASB issues new leases standard - financial services April 2016 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition of a lease

Accounting and Auditing Update. Paul Lundy

Accounting and Auditing Update Paul Lundy Leases: Not Just for the Footnotes Anymore Significant Financial Statement Impact New lease standard generally requires all leases to be capitalized and recognized

Accounting and Auditing Update Paul Lundy Leases: Not Just for the Footnotes Anymore Significant Financial Statement Impact New lease standard generally requires all leases to be capitalized and recognized

FRS 116 Leases: Through the Eyes of Auditors. Ng Kian Hui, Head of Audit & Assurance BDO LLP

FRS 116 Leases: Through the Eyes of Auditors Ng Kian Hui, Head of Audit & Assurance BDO LLP OUTLINE 1. FRS 116 Leases General Overview 2. Identifying a Lease 3. Determining the Lease Term 4. Recognition

FRS 116 Leases: Through the Eyes of Auditors Ng Kian Hui, Head of Audit & Assurance BDO LLP OUTLINE 1. FRS 116 Leases General Overview 2. Identifying a Lease 3. Determining the Lease Term 4. Recognition

CPE regulations require online participants to take part in online questions

KPMG s CFO Financial Forum Webcast FASB/IASB Revised Lease Accounting Exposure Drafts A Detailed Look Part III: Lessor Accounting June 25, 2013 Administrative CPE regulations require online participants

KPMG s CFO Financial Forum Webcast FASB/IASB Revised Lease Accounting Exposure Drafts A Detailed Look Part III: Lessor Accounting June 25, 2013 Administrative CPE regulations require online participants

Defining Issues. FASB Completes Technical Redeliberations on Leases. October 2015, No Key Facts. Key Impacts

Defining Issues October 2015, No. 15-47 FASB Completes Technical Redeliberations on Leases The FASB met on October 7 to discuss comments received and related follow-up issues on the external review of

Defining Issues October 2015, No. 15-47 FASB Completes Technical Redeliberations on Leases The FASB met on October 7 to discuss comments received and related follow-up issues on the external review of

A Review of IFRS 16 Leases By Tan Liong Tong

A Review of IFRS 16 Leases By Tan Liong Tong In April 2016, the MASB issued MFRS 16 Leases that is identical to IFRS 16 Leases issued by the IASB in January 2016. The effective date of this new MFRS is

A Review of IFRS 16 Leases By Tan Liong Tong In April 2016, the MASB issued MFRS 16 Leases that is identical to IFRS 16 Leases issued by the IASB in January 2016. The effective date of this new MFRS is

Implementing the New Lease Guidance

Implementing the New Lease Guidance October 22, 2018 2018 Crowe LLP 2018 Crowe LLP Agenda Background Scope Effective dates & transition requirements Lessee accounting model Lessor accounting model Specialized

Implementing the New Lease Guidance October 22, 2018 2018 Crowe LLP 2018 Crowe LLP Agenda Background Scope Effective dates & transition requirements Lessee accounting model Lessor accounting model Specialized

Technical Line FASB final guidance

No. 2016-11 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect real estate entities In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions...

No. 2016-11 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect real estate entities In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions...

A New Lease on Life: The GASB s New Accounting for Leases

Tuesday, May 23, 2017 2:00 3:15PM A New Lease on Life: The GASB s New Accounting for Leases MODERATOR Frances Lee Deputy Chief Financial Officer San Francisco Public Utilities Commission SPEAKERS Stephen

Tuesday, May 23, 2017 2:00 3:15PM A New Lease on Life: The GASB s New Accounting for Leases MODERATOR Frances Lee Deputy Chief Financial Officer San Francisco Public Utilities Commission SPEAKERS Stephen

ASC 842: Leases. Presented by: Maxwell Locke & Ritter LLP June 15, Maxwell Locke & Ritter

ASC 842: Leases Presented by: Maxwell Locke & Ritter LLP June 15, 2018 The New Lease Standard FASB ASC 842, Leases Supersedes FASB ASC 840, Leases Effective for calendar year-end public companies in 2019;

ASC 842: Leases Presented by: Maxwell Locke & Ritter LLP June 15, 2018 The New Lease Standard FASB ASC 842, Leases Supersedes FASB ASC 840, Leases Effective for calendar year-end public companies in 2019;

Impact of lease accounting changes to corporate real estate

Impact of lease accounting changes to corporate real estate Overview In February 2016, the Financial Accounting Standards Board (FASB) issued its long-awaited revision to lease accounting Accounting Standards

Impact of lease accounting changes to corporate real estate Overview In February 2016, the Financial Accounting Standards Board (FASB) issued its long-awaited revision to lease accounting Accounting Standards

IASB issues new leases standard consumer products and retail

Applying IFRS in consumer products and retail IASB issues new leases standard consumer products and retail June 2016 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition

Applying IFRS in consumer products and retail IASB issues new leases standard consumer products and retail June 2016 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition

These FAQs reflect current views and understanding of the IASB project.

FAQ 14 SEPTEMBER 2010 IASB PROJECT ON LEASE ACCOUNTING These FAQs reflect current views and understanding of the IASB project. In August 2010, the International Accounting Standards Board (IASB) and the

FAQ 14 SEPTEMBER 2010 IASB PROJECT ON LEASE ACCOUNTING These FAQs reflect current views and understanding of the IASB project. In August 2010, the International Accounting Standards Board (IASB) and the

Sri Lanka Accounting Standard-LKAS 17. Leases

Sri Lanka Accounting Standard-LKAS 17 Leases -516- Sri Lanka Accounting Standard-LKAS 17 Leases Sri Lanka Accounting Standard LKAS 17 Leases is set out in paragraphs 1 69. All the paragraphs have equal

Sri Lanka Accounting Standard-LKAS 17 Leases -516- Sri Lanka Accounting Standard-LKAS 17 Leases Sri Lanka Accounting Standard LKAS 17 Leases is set out in paragraphs 1 69. All the paragraphs have equal

NEED TO KNOW. Leases A Project Update

NEED TO KNOW Leases A Project Update 2 LEASES - A PROJECT UPDATE TABLE OF CONTENTS Introduction 3 Existing guidance and the rationale for change 4 The IASB/FASB project to date 5 The main proposals 6 Definition

NEED TO KNOW Leases A Project Update 2 LEASES - A PROJECT UPDATE TABLE OF CONTENTS Introduction 3 Existing guidance and the rationale for change 4 The IASB/FASB project to date 5 The main proposals 6 Definition

IASB update. Philippe DANJOU. Board Member. IMA France 2 Octobre International Financial Reporting Standards

International Financial Reporting Standards IASB update Philippe DANJOU Board Member IMA France 2 Octobre 2012 The views expressed in this presentation are those of the presenter, not necessarily those

International Financial Reporting Standards IASB update Philippe DANJOU Board Member IMA France 2 Octobre 2012 The views expressed in this presentation are those of the presenter, not necessarily those

LKAS 17 Sri Lanka Accounting Standard LKAS 17

Sri Lanka Accounting Standard LKAS 17 Leases CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 17 LEASES paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 4 CLASSIFICATION OF LEASES 7 LEASES IN THE FINANCIAL STATEMENTS

Sri Lanka Accounting Standard LKAS 17 Leases CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 17 LEASES paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 4 CLASSIFICATION OF LEASES 7 LEASES IN THE FINANCIAL STATEMENTS

Technical Line FASB final guidance

No. 2018-18 13 December 2018 Technical Line FASB final guidance How the new leases standard affects life sciences entities In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions...

No. 2018-18 13 December 2018 Technical Line FASB final guidance How the new leases standard affects life sciences entities In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions...

The joint leases project change is coming

No. 2010-4 18 June 2010 Technical Line Technical guidance on standards and practice issues The joint leases project change is coming What you need to know The proposed changes to the accounting for leases

No. 2010-4 18 June 2010 Technical Line Technical guidance on standards and practice issues The joint leases project change is coming What you need to know The proposed changes to the accounting for leases

IFRS 16: Leases; a New Era of Lease Accounting!

The journal is running a series of updates on IFRS, IAS, IFRIC and SIC. The updates mostly collected from different sources of IASB publication, seminars, workshop & IFRS website. This issue is based on

The journal is running a series of updates on IFRS, IAS, IFRIC and SIC. The updates mostly collected from different sources of IASB publication, seminars, workshop & IFRS website. This issue is based on

ASC Topic 842 Leases. September 25 &

ASC Topic 842 Leases September 25 & 26 2017 This presentation is intended solely for the information and use of the EEI and AGA and is not intended to be and should not be used by anyone other than these

ASC Topic 842 Leases September 25 & 26 2017 This presentation is intended solely for the information and use of the EEI and AGA and is not intended to be and should not be used by anyone other than these

In December 2003 the Board issued a revised IAS 40 as part of its initial agenda of technical projects.

IAS 40 Investment Property In April 2001 the International Accounting Standards Board (the Board) adopted IAS 40 Investment Property, which had originally been issued by the International Accounting Standards

IAS 40 Investment Property In April 2001 the International Accounting Standards Board (the Board) adopted IAS 40 Investment Property, which had originally been issued by the International Accounting Standards

IFRS Update for Financial Services

IFRS Update for Financial Services KPMG AG, Zurich 19 April 2018 Agenda IFRS 16 Leases Challenges of the new standard IFRS 9 Financial instruments Pre-transition and interim disclosures News from the IASB

IFRS Update for Financial Services KPMG AG, Zurich 19 April 2018 Agenda IFRS 16 Leases Challenges of the new standard IFRS 9 Financial instruments Pre-transition and interim disclosures News from the IASB

Technical Line FASB final guidance

No. 2018-08 20 September 2018 Technical Line FASB final guidance How the new leases standard affects engineering and construction entities In this issue: Overview... 1 Key considerations... 2 Scope and

No. 2018-08 20 September 2018 Technical Line FASB final guidance How the new leases standard affects engineering and construction entities In this issue: Overview... 1 Key considerations... 2 Scope and

Applying IFRS. IASB issues a new leases standard tank terminals. February 2017

Applying IFRS IASB issues a new leases standard tank terminals February 2017 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition of a lease 3 1.3 Identifying and

Applying IFRS IASB issues a new leases standard tank terminals February 2017 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition of a lease 3 1.3 Identifying and

2 This Standard shall be applied in accounting for all leases other than:

Indian Accounting Standard (Ind AS) 17 Leases (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in bold type indicate the main

Indian Accounting Standard (Ind AS) 17 Leases (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in bold type indicate the main

GASB 87. OVERVIEW: Supersedes GASB s 13 and 62 (paragraphs ).

.") Leases OVERVIEW: Supersedes GASB s 13 and 62 (paragraphs 211-271). Will require significant changes from its current practice, particularly in the accounting for operating leases Effective for reporting

Leases OVERVIEW: Supersedes GASB s 13 and 62 (paragraphs 211-271). Will require significant changes from its current practice, particularly in the accounting for operating leases Effective for reporting

PRACTICAL TIPS FOR IMPLEMENTING THE NEW LEASE ACCOUNTING STANDARD

PRACTICAL TIPS FOR IMPLEMENTING THE NEW LEASE ACCOUNTING STANDARD SHAUNA WATSON, VP, GLOBAL HEAD OF TECHNICAL ACCOUNTING MICHAEL ALLEN, PARTNER, TRANSACTION ADVISORY SERVICES 1. Overview of Accounting

PRACTICAL TIPS FOR IMPLEMENTING THE NEW LEASE ACCOUNTING STANDARD SHAUNA WATSON, VP, GLOBAL HEAD OF TECHNICAL ACCOUNTING MICHAEL ALLEN, PARTNER, TRANSACTION ADVISORY SERVICES 1. Overview of Accounting

Technical Line FASB final guidance

No. 2019-01 3 January 2019 Technical Line FASB final guidance How the new leases standard affects automotive entities In this issue: Overview... 1 Recent standard setting activity... 2 Key considerations...

No. 2019-01 3 January 2019 Technical Line FASB final guidance How the new leases standard affects automotive entities In this issue: Overview... 1 Recent standard setting activity... 2 Key considerations...

Executive Summary. New leases standard Lessees

Executive Summary December 2018 The new leases standard focuses on increased transparency and comparability providing financial statement users with more information about an entity s leasing activities.

Executive Summary December 2018 The new leases standard focuses on increased transparency and comparability providing financial statement users with more information about an entity s leasing activities.

REAL ESTATE PERSPECTIVE ON NEW LEASE ACCOUNTING STANDARDS

VALUATION & ADVISORY REAL ESTATE PERSPECTIVE ON NEW LEASE ACCOUNTING STANDARDS BY JOHN CORBETT, MAI, ASA, FRICS AND MARC R. SHAPIRO, MAI, MRICS INTRODUCTION The Financial Accounting Standards Board (FASB)

VALUATION & ADVISORY REAL ESTATE PERSPECTIVE ON NEW LEASE ACCOUNTING STANDARDS BY JOHN CORBETT, MAI, ASA, FRICS AND MARC R. SHAPIRO, MAI, MRICS INTRODUCTION The Financial Accounting Standards Board (FASB)

In depth A look at current financial reporting issues for PNG

www.pwc.com/pg inform.pwc.com In depth A look at current financial reporting issues for PNG February 2016 What s inside? At a glance 1 Scope 2 Identifying a lease 2 Lessee accounting 10 Lessor accounting

www.pwc.com/pg inform.pwc.com In depth A look at current financial reporting issues for PNG February 2016 What s inside? At a glance 1 Scope 2 Identifying a lease 2 Lessee accounting 10 Lessor accounting

Financial reporting developments. A comprehensive guide. Lease accounting. Accounting Standards Codification 842, Leases.

Financial reporting developments A comprehensive guide Lease accounting Accounting Standards Codification 842, Leases October 2018 To our clients and other friends Accounting Standard Codification (ASC)

Financial reporting developments A comprehensive guide Lease accounting Accounting Standards Codification 842, Leases October 2018 To our clients and other friends Accounting Standard Codification (ASC)

IFRS 16 Leases. PICPA IFRS: New Standards and Updates Dubai. 28 April 2017

IFRS 16 Leases PICPA IFRS: New Standards and Updates Dubai 28 April 2017 1 More transparent lease accounting IFRS 16 will bring most leases on-balance sheet from 2019. All companies that lease assets for

IFRS 16 Leases PICPA IFRS: New Standards and Updates Dubai 28 April 2017 1 More transparent lease accounting IFRS 16 will bring most leases on-balance sheet from 2019. All companies that lease assets for