CBRE VIETNAM, HCMC MARKET OVERVIEW Q4/2013 PRESENTED BY: GREG OHAN, DIRECTOR, VIETNAM

|

|

|

- Horace Lane

- 5 years ago

- Views:

Transcription

1 CBRE VIETNAM, HCMC MARKET OVERVIEW Q4/2013 PRESENTED BY: GREG OHAN, DIRECTOR, VIETNAM NOVEMBER 19 TH 2013

2 CONTENTS HOW TO MAKE THE RIGHT DECISION? 1. Know The Market Overview of Vietnam Office Market 2. Know Your Business Key Considerations When Making an Office Relocation / Renewal Decision 3. Know the Future Outlook CBRE Predictions 4. Lim Tower & Hoa Lam Corporation Overview of Lim Tower Hoa Lam Corporation and Lim Tower 2 2

, led by Japan (25%) VN ranks 99th on business-friendly list (90th in 2012, 78th in 2011) Gold price decreased to VND")

3 RECENT HEADLINES Increase 66% y-o-y ($19 billion) in FDI exceed the 2013 target ($18.13 billion), led by Japan (25%) VN ranks 99th on business-friendly list (90th in 2012, 78th in 2011) Gold price decreased to VND 36.6 mil/tael. Global gold down to US$1,286/ounce VN highest car 9m/2013, increasing 18% y-o-y, led by Toyota, Ford and GM Credit growth is expected to reach 11% - 12% in 2013 Haiyan Typhoon ravaged through the Philippines causing floods, storms and damage in central VN. Is the worst behind us? 3

4 1 KNOW THE MARKET

5 MARKET OVERVIEW - HCMC Q3 SNAPSHOT OFFICE GRADE A GRADE B GRADE C TOTAL Number of properties Total supply (GFA, sm) 329, , ,437 2,123,086 New supply (properties) Net absorption (NLA,sm) Q3/ ,000 20,802 27,720 Q-o-q change (%) 207.2% 10.1% 31.1% Y-o-y change (%) 104.1% 220.1% 180.3% Vacancy rate (%) 11.8%(*) 11.3% 11.5% Q-o-q change (pp) Y-o-y change (pp) Average asking rents (US$ psm per month) Q-o-q change (%) 3.0% 3.2% 2.9% Y-o-y change (%) 6.2% 8.2% 7.0% 5

6 $80 $60 $40 $20 MARKET OVERVIEW - HCMC RENT AVERAGE ASKING RENTS Grade A Grade B Average asking rent increases. Asking rent in the Grade A and Grade B segment risen by 3.0% q-oq and 3.2% q-o-q. $ GRADE A GRADE B Number of buildings GFA (sm) 329, ,718 Mature buildings are already raising rents whilst those in the next tier down, be A- or B+, are maintaining their rents. 6

7 Vacant Space (sm) Average Asking Rent (US$ psm per month) Vacant Space (sm) Average Asking Rent (US$ psm per month) MARKET OVERVIEW - HCMC RENT & VACANCY GRADE B VACANT SPACE AND AVERAGE ASKING RENTS GRADE B VACANT SPACE AND AVERAGE ASKING RENT 120, ,000 80,000 60,000 40,000 20,000 0 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q $100 $90 $80 $70 $60 $50 $40 $30 $20 $10 $0 Vacant Space Asking Rent 100,000 GRADE A VACANT SPACE AND AVERAGE ASKING RENTS GRADE A VACANT SPACE AND AVERAGE ASKING RENT $100 80,000 $80 60,000 $60 40,000 $40 20,000 $ Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q Vacant Space Asking Rent $0

8 Area (sm, NLA) Asking rent (US$/sm/month) MARKET OVERVIEW - HCMC GRADE A VS. GRADE B PERFORMANCE HCMC Office Market Performance Grade A & B Leased Area Vacant Area Asking Rent 1,000, , , , ,000 0 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q $25 $23 $21 $19 $17 $15 RENTS CONTINUE AN UPWARD TREND Increased slightly by 2.5% q-o-q to US$21.8 psm, p/mth Vacancy rate in Grade A market declining Vacancy rate in Grade B market rising slightly owing to new buildings launched over the last quarter 8

9 MARKET OVERVIEW - HANOI RISING NEW SUPPLY AND DECREASING OCCUPANCY RATES $50 Office Asking Rents Grade A Grade B 50% Office Vacancy Grade A Grade B $40 40% $30 30% $20 20% $10 10% $0 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q % Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q ASKING RENT Grade A average asking rents decreased by 2.8% q-o-q while Grade B improved by 1.5% Grade A - downward pressure as Landlords are more competitive Grade B asking rents decreased by 14% and projected to continue VACANCY Grade A vacancy rate continued to decrease 2to 26.31% Grade B vacancy increased up to 34.7% due to the new supply of 4 grade B buildings Y-O-Y Grade A vacancy decreased 1.16 pp while Grade B increased sharply 15.5 pp 9

10 2 KNOW YOUR BUSINESS

11 TENANT PROFILING - HCMC ENQUIRIES BY ORIGIN - YTD 26% 26% Vietnam US Japan UK 6% 7% 7% 8% 19% Korea China Other Source: CBRE Strong occupier interest (26%) remains Vietnamese / local companies expanding and consolidating US continues to remain the largest foreign occupier group by country dominating enquiry levels followed by Japan and Korean based organization's respectively

12 TENANT PROFILING - HCMC ENQUIRY BY TRANSACTION YTD ENQUIRY BY INDUSTRY YTD 16% Technology Manuf acturing 20% Finance 35% Education 84% Retail 17% Relocation or extension New entrant Pharmaceutical Others 4% 5% 6% 13% Source: CBRE Demand driven by office occupiers seeking expansion / relocation Fringe / New CBD buildings have given occupiers flexibility to upgrade and consolidate. The focus 2H 2013 has been consolidation and taking advantage of limited / remaining cost effective opportunities in NEW buildings offering attractive packages to raise occupancy levels

13 TENANT PROFILING KEY FACTORS TO UNDERSTAND BEFORE MOVING 1. TYPE OF BUSINESS Industry type can define location E.g. Banking / Finance D1. Call centre non CBD 2. LENGTH OF TENANCY Current lease term length 3. REASON FOR MOVING Expansion? Consolidation? Cost Understanding current needs and whether 4. CURRENT REQUIREMENTS existing size / accommodation suitable. Current location, space, head count, expiry etc Headcount, location, space sqm, building grade 5. FUTURE REQUIREMENTS desired, operational date, operational hours, IT provider etc 6. PARKING No. of car and motorbike 7. BUDGET Monthly / p/sqm Security, Back Up Power, IT. Fire & Safety, 8. OTHER OPERATIONAL FACTORS Signage 13

14 TENANT PROFILING KEY FACTORS TO CONSIDER WHEN MOVING 1. FIT OUT Fit out : US$350 US$450 p/sqm 2. RE INSTATMENT Reinstatement : US$25 US$35 Grade A : US$6 - US$8 3. SERVICE CHARGE Grade B : US$5 - US$6 Grade C : US$3+ 4. FLOOR MEASUREMENT (Net or Gross) 5. SECURITY DEPOSITS 6. PAYMENTS TERMS 14 Gross: most common areas contained within the external walls Net: within a tenancy at each floor level measured from finishes 3 months rent +SC in cash held for the duration of lease, returned at expiry Quarterly in advance for rent +SC. Longer payment terms = lower rent 7. LEASE TERMS 2 5 years + (Negotiable) 8. PARKING COSTS 9. STANDARD OPERATING HOURS Cars: US$150 - US$250/lot/month Motorbikes: US$6 - US$20/lot/month Monday - Friday : 8.30am to 6.00pm Saturday : 8.30am to 1.00pm 10. LEASE DENOMINATION By law denominated in VND

15 MAJOR TENANTS WHO HAVE MADE THE MOVE YTD RELOCATIONS / NEW OFFICES IN Q4/2013 IT Pharma Consumer goods Pharma Pharma Pharma Finance Insurance Construction Securities Banking Conglomerate Sourcing operation 15 Electronics Construction Assurance Banking

16 3 KNOW THE FUTURE

17 ABSORPTION YTD HCMC REVIEW Net Absorption YTD Grade A 27,535 34,016 33,917 24,209 26,250 Grade B 48,140 97,744 85,367 39,921 55,058 Total 75, , ,284 64,130 81,308 Total supply YTD Grade A 134, , , , ,853 Grade B 356, , , , ,553 Total 491, , , , ,406 Net absorption in 2013 to increase by 25+ Vs Net absorption dominated by increased activity in Grade B

18 Gross Floor Area (sm) Gross Floor Area (sm) SUPPLY YTD - HCMC CURRENT & FUTURE SUPPLY 400,000 GRADE A OFFICE STOCK 300, , ,000 0 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q Exisitng space New supply Total GFA 1,000, , , , , GRADE B OFFICE STOCK Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q Existing supply New supply Total GFA

19 OPPORTUNITIES FOR TENANTS HCMC UPCOMING COMPLETED 2014 SUPPLY SGGP Building 21,700 sm GFA NTMK, D3 Vietin Bank Tower 24,315 sm GFA CBD Vietcombank Tower 55,000 sm GFA CBD Viettel Tower 65,971 sm GFA CMT8, D3 Q MB Sunny Tower 16,000 sm GFA CBD 19

20 SUPPLY PIPELINE - HCMC OUTLOOK HCMC Office Supply Forecast (Grade A & B), GFA sm 2013 to 2015 Existing Space - GFA (sm) New Space Come Online 1,600,000 Limited supply 175,346 sm 8 quarters 1,200, , ,000 0 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q Source: CBRE 2013 AND THE FIRST HALF OF 2014 WILL END WITH STABILITY FOR OFFICE SEGMENT will require a strategic approach with major occupiers NOW planning and negotiating for expiries in mid to late Asking rents in mature buildings with quality asset management services will maintain good performance even though there will be additional new supply in the next few quarters as demand for high quality and good location office space continues. Flexible leasing terms and high quality services are still the keys to attracting or retaining tenants.

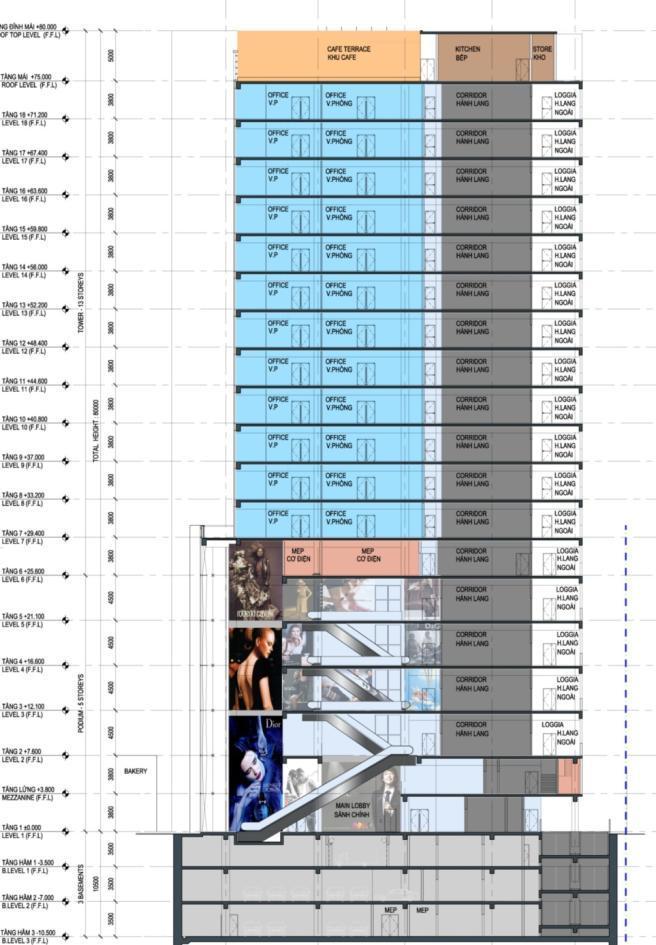

21 OPPORTUNITIES FOR TENANTS OCCUPANCY IN KEY OFFICE BUILDINGS Occupancy Area Occupancy Area Q (approx m2) Q (approx m2) Lim Tower D % % 5, President Place D % % 1, Bitexco Financial Tower D % 10, % 6, Kumho Asiana Plaza D % % Metropolitan D % % Sun Wah Tower D % 1, % 1, Diamond Plaza D % % 0.00 Saigon Centre D % % Saigon Tower D % % Me Linh Point Tower D % % A&B Tower D % % Green Power D % % Vincom Center D % 19, % 13, Centec Tower D % % 1, An Phu Plaza D % % 1, Saigon Trade Center D % 3, % 12, Maritime Bank Tower D % 2, % 4, CentrePoint PN 99.70% % E town TB 98.00% 1, % 2, Ree Tower 21 D % % TOTAL Q ,231 Q ,433

22 OPPORTUNITIES FOR TENANTS OCCUPANCY IN KEY OFFICE BUILDINGS Occupancy% Q vs Q % 80.00% 60.00% 40.00% 20.00% Q Q % 22

23 SMALL MEDIUM SIZED BUILDING PIPELINE - HCMC 23 CBRE is tracking 175 new mixed use office developments in key and fringe CBD Districts e.g. 1,3, Tan Binh and Phu Nuan

24 PLANNING FOR RELOCATION MAKING THE RIGHT MOVE In the HCMC CBD, Only 8 buildings (A and B Grade) can provide over 1,000 sqm contiguous space today. 5 of them are Grade A Lim Tower one of them. Only 4 buildings (A and B Grade) combined in the HCMC CBD have a floor plate over 1,000 sqm This means, VERY limited options for MNCs looking for seeking international standard, quality larger commercial buildings 50% of the 175+ NEW Small-Medium sized buildings are being built by SOEs and 50% are for owner occupation For any major occupier planning an occupancy solution, the opportunity is tightening with timing and planning early the key to achieving your occupancy solution 24

25 4 LIM TOWER & HOA LAM CORPORATION

26 LIM TOWER - OVERVIEW 26

27 LIM TOWER PRIME LOCATION Positioned at the corner of Le Thanh Ton and Ton Duc Thang street, the Building positioned at the gateway to District 1, is the largest Grade A office building to be completed in 2013 with a total area of over 34,000sqm, 34 floors, 550 parking spots within the building and additional parking also available in close proximity. 27

28 LIM TOWER MODERN & EFFICIENT The building design incorporates the latest architecture to create an environmentally and operationally efficient office building for Tenants Over 80% of the Building façade is covered by the latest Euro window double glazed UV protection glass Each levels features floor to ceiling glass, maximizes the best view in HCMC along with allowing additional natural light. The curtain wall glazing system at LIM reflects over 90% of external sound and heat. Saving operation cost and providing efficient and comfortable working environment. 28

29 LIM TOWER PROJECT OVERVIEW Developer Height Total Net leasable area Typical Net plate Ceiling height Total Parking Lift Mai Thanh Service Company Limited 34 levels (123m) & 2 basements; 30 floors for office 20,466 sqm Approx. 700 sqm 2.55 m (finishing to finishing) 6 levels for car and motorbike parking: 2 basements: car parking (150 lots), 3 rd 6 th floor: motorbike parking (950 lots) 9 high speed Thyssen Krupp lifts: Low zone: 4 passenger lifts (up to 20 th floor), High Zone: 4 passenger lifts (21 st floor 34 th floor) 1 service lift; 1600kg/lift Air-conditioning Centralized chiller AC system FCU/floor Security system 24 hour security and CCTV throughout Back-up power Provide 100% back-up power (2,000 KVA) Asking rent Please call Service charge $6 p/sqm Completion Q3 /

30 LIM TOWER PROJECT OVERVIEW Technique floor & Rooftop 21 st 34 th floors: Leasable area 7 th 20 th floors: Techcombank 3 rd - 6 th floor: Motorbike parking 1 st - 2 nd floors: leased by Techcombank 2 basements: car parking 30

31 LIM TOWER 2, 158 VO VAN TAN Q COMPLETION 31

32 LIM TOWER 2, 158 VO VAN TAN Q COMPLETION 32

33 OFFICE ENQUIRY HOTLINE THANK YOU 2013, CBRE, Group Inc. CBRE Limited confirms that information contained herein, including projections, has been obtained from sources believed to be reliable. While we do not doubt their accuracy, we have not verified them and make no guarantee, warranty or representation about them. It is your responsibility to confirm independently their accuracy and completeness. This information is presented exclusively for use by CBRE clients and professionals and all rights to the material are reserved and cannot be reproduced without prior written permission of CBRE. About CBRE Group, Inc. CBRE Group, Inc. (NYSE:CBG), a Fortune 500 and S&P 500 company headquartered in Los Angeles, is the world s largest commercial real estate services firm (in terms of 2011 revenue). The Company has approximately 34,000 employees (excluding affiliates), and serves real estate owners, investors and occupiers through more than 300 offices (excluding affiliates) worldwide. CBRE offers strategic advice and execution for property sales and leasing; corporate services; property, facilities and project management; mortgage banking; appraisal and valuation; development services; investment management; and research and consulting. Please visit our Web site at

CBRE Vietnam Q HCMC Tenants Evening

CBRE Vietnam Q2 2012 HCMC Tenants Evening 22 nd May 2012 Presented by: Greg Ohan Vincom Center, 47 Ly Tu Trong District 1, HCMC, Vietnam Today s Message To You!... 2 drivers in business 1. Fear 2. Greed

CBRE Vietnam Q2 2012 HCMC Tenants Evening 22 nd May 2012 Presented by: Greg Ohan Vincom Center, 47 Ly Tu Trong District 1, HCMC, Vietnam Today s Message To You!... 2 drivers in business 1. Fear 2. Greed

CBRE HCMC Office Services 2010 Tenants Evening Part I:

CBRE HCMC Office Services 2010 Tenants Evening Part I: 2010 Are we in for a happy ending? Tuesday 26th January 2010 Presented by: Mr. Chris Currie Associate Director Office Services Market Overview Q1

CBRE HCMC Office Services 2010 Tenants Evening Part I: 2010 Are we in for a happy ending? Tuesday 26th January 2010 Presented by: Mr. Chris Currie Associate Director Office Services Market Overview Q1

P R E S S R E L E A S E

P R E S S R E L E A S E FOR IMMEDIATE RELEASE Tuesday, September 30, 2014 CBRE (Vietnam) Co., Ltd Unit 1201, Me Linh Point Tower 2 Ngo Duc Ke, District 1 Ho Chi Minh City, Vietnam T 84 3 824 6125 F 84

P R E S S R E L E A S E FOR IMMEDIATE RELEASE Tuesday, September 30, 2014 CBRE (Vietnam) Co., Ltd Unit 1201, Me Linh Point Tower 2 Ngo Duc Ke, District 1 Ho Chi Minh City, Vietnam T 84 3 824 6125 F 84

Vietnam Property Market Overview 2016

Vietnam Property Market Overview 2016 Economic Highlights Vietnam Economic Overview GDP Growth % 10.0 8.0 6.0 4.0 2.0 Real GDP Growth (y-o-y) 1Q16 1Q15 1Q14 Vietnam 5.5% 6.1% 5.0% HCMC 7.1% 6.9% 7.7% Hanoi

Vietnam Property Market Overview 2016 Economic Highlights Vietnam Economic Overview GDP Growth % 10.0 8.0 6.0 4.0 2.0 Real GDP Growth (y-o-y) 1Q16 1Q15 1Q14 Vietnam 5.5% 6.1% 5.0% HCMC 7.1% 6.9% 7.7% Hanoi

Construction Investment Cools In Lead Up To General Election

Phnom Penh, Q2 218 Construction Investment Cools In Lead Up To General Election Average High-end Condominium Price $3,211/SQM Prime Condominium Rent $14.3/SQM Prime Office Rent $25.5/SQM Prime Retail Mall

Phnom Penh, Q2 218 Construction Investment Cools In Lead Up To General Election Average High-end Condominium Price $3,211/SQM Prime Condominium Rent $14.3/SQM Prime Office Rent $25.5/SQM Prime Retail Mall

QUARTERLY REPORTS FOR HCMC & HANOI. Market Insights from CBRE s HCMC Quarterly Report Q4 2010

Market Insights from CBRE s HCMC Quarterly Report Q4 2010 CBRE RESEARCH & CONSULTING Presented by: Rudolf Hever Tam Le Associate Director Financial Analyst CB Richard Ellis (Vietnam) Co., Ltd. Wednesday,

Market Insights from CBRE s HCMC Quarterly Report Q4 2010 CBRE RESEARCH & CONSULTING Presented by: Rudolf Hever Tam Le Associate Director Financial Analyst CB Richard Ellis (Vietnam) Co., Ltd. Wednesday,

Da Nang City MarketView

Da Nang City MarketView Q2 213 CBRE Global Research and Consulting VN Q2 GDP 5.% HCMC Q2 GDP 8.1% DA NANG Q2 GDP 7.1% VNINDEX 24% LOCAL GOLD PRICE 19.4% TRADE BALANCE US$1.9 billion ECONOMY IS MOVING IN

Da Nang City MarketView Q2 213 CBRE Global Research and Consulting VN Q2 GDP 5.% HCMC Q2 GDP 8.1% DA NANG Q2 GDP 7.1% VNINDEX 24% LOCAL GOLD PRICE 19.4% TRADE BALANCE US$1.9 billion ECONOMY IS MOVING IN

HCMC MARKET INSIGHTS Q2/2013

HCMC MARKET INSIGHTS Q2/2013 Presented by: Dung Duong (Ms.) July 8, 2013 VIETNAM ECONOMY Q2 2013 ECONOMIC OVERVIEW Q2/2012 Q1/2013 Q2/2013 Y-o-Y Q-o-Q GDP (% y-o-y) 4.8% 4.8% 5.0% CPI (% y-o-y, e-o-p)

HCMC MARKET INSIGHTS Q2/2013 Presented by: Dung Duong (Ms.) July 8, 2013 VIETNAM ECONOMY Q2 2013 ECONOMIC OVERVIEW Q2/2012 Q1/2013 Q2/2013 Y-o-Y Q-o-Q GDP (% y-o-y) 4.8% 4.8% 5.0% CPI (% y-o-y, e-o-p)

SHANGHAI GRADE A OFFICE MARKET UPDATE Q3 2018

COLLIERS QUARTERLY Peng Jiang Senior Manager Research East China +86 21 6141 355 Peng.Jiang@colliers.com OFFICE SHANGHAI Q3 218 2 OCTOBER 218 SHANGHAI GRADE A OFFICE MARKET UPDATE Q3 218 Summary & Recommendations

COLLIERS QUARTERLY Peng Jiang Senior Manager Research East China +86 21 6141 355 Peng.Jiang@colliers.com OFFICE SHANGHAI Q3 218 2 OCTOBER 218 SHANGHAI GRADE A OFFICE MARKET UPDATE Q3 218 Summary & Recommendations

Construction investment cools down but markets remain heated

Phnom Penh, 217 Construction investment cools down but markets remain heated Average High-end Condominium Price $3,18/SQM Prime Condominium Rent $15.6/SQM Prime Office Rent $22.2/SQM Prime Retail Mall

Phnom Penh, 217 Construction investment cools down but markets remain heated Average High-end Condominium Price $3,18/SQM Prime Condominium Rent $15.6/SQM Prime Office Rent $22.2/SQM Prime Retail Mall

MARCH 2014 HCMC CENTRAL BUSINESS DISTRICT HO CHI MINH CITY. CBD MARKET Report.

MARCH 2014 HCMC CENTRAL BUSINESS DISTRICT HO CHI MINH CITY CBD MARKET Report www.colliers.com/vietnam TABLE OF CONTENTS HCMC CBD MARKET REPORT MARCH 2014 Market Highlights Page OFFICE MARKET Market Overview

MARCH 2014 HCMC CENTRAL BUSINESS DISTRICT HO CHI MINH CITY CBD MARKET Report www.colliers.com/vietnam TABLE OF CONTENTS HCMC CBD MARKET REPORT MARCH 2014 Market Highlights Page OFFICE MARKET Market Overview

Mapletree Profile: Creating Value in Asia

your premium place your premium place Mapletree Profile: Creating Value in Asia Mapletree is a leading Asia-focused real estate development, investment and capital management company headquartered in Singapore

your premium place your premium place Mapletree Profile: Creating Value in Asia Mapletree is a leading Asia-focused real estate development, investment and capital management company headquartered in Singapore

HANOI. Economics Quick Stats. Hot Topics. Hanoi s GDP (%) Hanoi s CPI (%) HANOI

Hanoi s CPI (%) HANOI") CBRE VIETNAM HANOI www.cbrevietnam.com January 2012 Economics Quick Stats Hot Topics Change from last VIETNAM 2011 Current Yr. Qtr. Real GDP Growth 5.89% Implemented FDI Exports Imports $11 bil $96.3 bil

CBRE VIETNAM HANOI www.cbrevietnam.com January 2012 Economics Quick Stats Hot Topics Change from last VIETNAM 2011 Current Yr. Qtr. Real GDP Growth 5.89% Implemented FDI Exports Imports $11 bil $96.3 bil

Quarterly Market Briefing Vietnam Q4/2016

Savills Research - Subscription form Savills Market Research Vietnam Quarterly Market Briefing Vietnam Q4/2016 Macro Indicators Value YoY Growth Rate (%) GDP growth rate (%) 6.2% -0.5ppt Retail sales (Billion

Savills Research - Subscription form Savills Market Research Vietnam Quarterly Market Briefing Vietnam Q4/2016 Macro Indicators Value YoY Growth Rate (%) GDP growth rate (%) 6.2% -0.5ppt Retail sales (Billion

HCMC Quarterly Report Q4/2012 Review and 2013 Outlook

Market Insights from CBRE HCMC Quarterly Report Q4/2012 Review and 2013 Outlook Presented by: Dung Duong Senior Manager CB Richard Ellis (Vietnam) Co., Ltd. Tuesday, January 3, 2012 VIETNAM ECONOMY 2 0

Market Insights from CBRE HCMC Quarterly Report Q4/2012 Review and 2013 Outlook Presented by: Dung Duong Senior Manager CB Richard Ellis (Vietnam) Co., Ltd. Tuesday, January 3, 2012 VIETNAM ECONOMY 2 0

GATEWAY OFFICE PLAZA. Welcome to Gateway Office Plaza. 350 Burnsville Parkway Burnsville, MN 55337

Welcome to Gateway Office Plaza Strategically located near the intersection of 35W and Burnsville Parkway, Gateway Office Plaza is a unique blend of easy access, freeway visibility and walkable amenities.

Welcome to Gateway Office Plaza Strategically located near the intersection of 35W and Burnsville Parkway, Gateway Office Plaza is a unique blend of easy access, freeway visibility and walkable amenities.

Ho Chi Minh City MarketView

Nominal GDP (VND Trillions) Growth Rate (%) Ho Chi Minh City MarketView Q3 213 CBRE Global Research and Consulting VN Q3 GDP 5.1% y-o-y HCMC Q3 GDP 1.3% y-o-y HANOI Q3 GDP 7.9% y-o-y VNINDEX 17.7% y-o-y

Nominal GDP (VND Trillions) Growth Rate (%) Ho Chi Minh City MarketView Q3 213 CBRE Global Research and Consulting VN Q3 GDP 5.1% y-o-y HCMC Q3 GDP 1.3% y-o-y HANOI Q3 GDP 7.9% y-o-y VNINDEX 17.7% y-o-y

GDP exceeded the 2017 target and at 6.8% achieved the highest growth in five years. GDP per capita was US$2,385 and increased 10% year on year (YoY).

.") GDP exceeded the 217 target and at 6.8 achieved the highest growth in five years. GDP per capita was US$2,385 and increased 1 year on year (YoY). Credit growth is estimated to reach 18 to 19 percent. Estimated

GDP exceeded the 217 target and at 6.8 achieved the highest growth in five years. GDP per capita was US$2,385 and increased 1 year on year (YoY). Credit growth is estimated to reach 18 to 19 percent. Estimated

OCTOBER 2014 HCMC CENTRAL BUSINESS DISTRICT HO CHI MINH CITY CBD MARKET REPORT.

OCTOBER 2014 HCMC CENTRAL BUSINESS DISTRICT HO CHI MINH CITY CBD MARKET REPORT www.colliers.com/vietnam TABLE OF CONTENTS HCMC CBD MARKET REPORT OCTOBER 2014 Market Highlights Page OFFICE MARKET Market

OCTOBER 2014 HCMC CENTRAL BUSINESS DISTRICT HO CHI MINH CITY CBD MARKET REPORT www.colliers.com/vietnam TABLE OF CONTENTS HCMC CBD MARKET REPORT OCTOBER 2014 Market Highlights Page OFFICE MARKET Market

Although total registered FDI slightly decreased -1% YoY, disbursed FDI in 2018 increased 9% to over US$19 billion.

GDP growth reached 7.1, bolstered by strong manufacturing and exports. The expansion of the service sector was robust, supported by private consumption and record tourist arrivals. National retail sales

GDP growth reached 7.1, bolstered by strong manufacturing and exports. The expansion of the service sector was robust, supported by private consumption and record tourist arrivals. National retail sales

Quarterly Market Briefing Viet Nam Q3/2017

Savills Research - Subscription form Savills Market Research Vietnam Quarterly Market Briefing Viet Nam Q3/217 Macro Indicators 9M/217 Value YoY Growth Rate GDP growth rate () 6.4 +.4 ppt Retail sales

Savills Research - Subscription form Savills Market Research Vietnam Quarterly Market Briefing Viet Nam Q3/217 Macro Indicators 9M/217 Value YoY Growth Rate GDP growth rate () 6.4 +.4 ppt Retail sales

Hanoi Quarterly Report

Market Insights from CBRE s Hanoi Quarterly Report CBRE RESEARCH & CONSULTANCY Presented by: Richard Leech Thanh Tran Executive Director Senior Manager CB Richard Ellis (Vietnam) Co., Ltd. January 19 th

Market Insights from CBRE s Hanoi Quarterly Report CBRE RESEARCH & CONSULTANCY Presented by: Richard Leech Thanh Tran Executive Director Senior Manager CB Richard Ellis (Vietnam) Co., Ltd. January 19 th

Q MARKET INSIGHTS OFFICE SECTOR HANOI

Q4 215 MARKET INSIGHTS OFFICE SECTOR In 215, Vietnam has benefited from stability in the macroeconomic Gross Domestic Product (GDP) in Q4 215 increased 7.1 year on year (y-o-y), bringing the overall GDP

Q4 215 MARKET INSIGHTS OFFICE SECTOR In 215, Vietnam has benefited from stability in the macroeconomic Gross Domestic Product (GDP) in Q4 215 increased 7.1 year on year (y-o-y), bringing the overall GDP

CHICAGO CBD OFFICE INVESTMENT PROPERTIES GROUP

CHICAGO CBD OFFICE INVESTMENT PROPERTIES GROUP SECOND QUARTER NEWSLETTER 216 HOT TOPICS Capital markets remain a focus with 14 assets either under contract or sold totaling $2.6 billion, which includes

CHICAGO CBD OFFICE INVESTMENT PROPERTIES GROUP SECOND QUARTER NEWSLETTER 216 HOT TOPICS Capital markets remain a focus with 14 assets either under contract or sold totaling $2.6 billion, which includes

Serviced Apartment Overview

Serviced Apartment Overview Presented by Mr. MARC TOWNSEND Managing Director CB Richard Ellis (Vietnam) Co., Ltd. 10 August, 2010 FUNDAMENTALS FOR GROWTH NOMINAL GDP AND REAL GDP GROWTH RATE OF HCMC Nominal

Serviced Apartment Overview Presented by Mr. MARC TOWNSEND Managing Director CB Richard Ellis (Vietnam) Co., Ltd. 10 August, 2010 FUNDAMENTALS FOR GROWTH NOMINAL GDP AND REAL GDP GROWTH RATE OF HCMC Nominal

NOVEMBER 2014 HCMC CENTRAL BUSINESS DISTRICT HO CHI MINH CITY. CBD MARKET Report.

NOVEMBER 2014 HCMC CENTRAL BUSINESS DISTRICT HO CHI MINH CITY CBD MARKET Report www.colliers.com/vietnam TABLE OF CONTENTS HCMC CBD MARKET REPORT NOVEMBER 2014 Market Highlights Page OFFICE MARKET Market

NOVEMBER 2014 HCMC CENTRAL BUSINESS DISTRICT HO CHI MINH CITY CBD MARKET Report www.colliers.com/vietnam TABLE OF CONTENTS HCMC CBD MARKET REPORT NOVEMBER 2014 Market Highlights Page OFFICE MARKET Market

HANOI. Economics Quick Stats. Hot Topics. Hanoi s CPI (%)

") CBRE VIETNAM HANOI www.cbrevietnam.com Economics Quick Stats Change from last VIETNAM 211 Current Yr. Qtr. Real GDP Growth 5.89% Implemented FDI Exports Imports $11 bil $96.3 bil $15.8 bil CPI 18.58% Tourism

CBRE VIETNAM HANOI www.cbrevietnam.com Economics Quick Stats Change from last VIETNAM 211 Current Yr. Qtr. Real GDP Growth 5.89% Implemented FDI Exports Imports $11 bil $96.3 bil $15.8 bil CPI 18.58% Tourism

Market Commentary Perth CBD Office

Market Commentary Perth CBD Office November 2016 Executive Summary The vacancy rate at 3Q16 is 24.7%, reflecting a quarterly increase of 0.1 percentage points. Two office projects are under construction

Market Commentary Perth CBD Office November 2016 Executive Summary The vacancy rate at 3Q16 is 24.7%, reflecting a quarterly increase of 0.1 percentage points. Two office projects are under construction

Hanoi Quarterly Report

Market Insights from CBRE s Hanoi Quarterly Report Presented by: CBRE RESEARCH & CONSULTANCY Richard Leech Thanh Tran Executive Director Senior Manager CB Richard Ellis (Vietnam) Co., Ltd. April 12 th

Market Insights from CBRE s Hanoi Quarterly Report Presented by: CBRE RESEARCH & CONSULTANCY Richard Leech Thanh Tran Executive Director Senior Manager CB Richard Ellis (Vietnam) Co., Ltd. April 12 th

HANOI Q3 GDP 7.9% y-o-y. VNINDEX 17.7% y-o-y IMPROVING LEGISLATION AND INFRASTRUCTURE PROVIDES FURTHER IMPETUS FOR GROWTH.

Nominal GDP (VND Trillions) Growth Rate (%) Hanoi MarketView Q3 213 CBRE Global Research and Consulting VN Q3 GDP 5.1% y-o-y HCMC Q3 GDP 1.3% y-o-y HANOI Q3 GDP 7.9% y-o-y VNINDEX 17.7% y-o-y LOCAL GOLD

Nominal GDP (VND Trillions) Growth Rate (%) Hanoi MarketView Q3 213 CBRE Global Research and Consulting VN Q3 GDP 5.1% y-o-y HCMC Q3 GDP 1.3% y-o-y HANOI Q3 GDP 7.9% y-o-y VNINDEX 17.7% y-o-y LOCAL GOLD

SUPPLY, DEMAND & PIPELINE PROJECTS

VIETNAM RETAIL PROPERTY MARKET SUPPLY, DEMAND & PIPELINE PROJECTS Presented by: Mr. Richard Leech - Executive Director CB Richard Ellis (Vietnam) January 27th, 2010 Vietnam Retail Market HIGHLIGHTS Another

VIETNAM RETAIL PROPERTY MARKET SUPPLY, DEMAND & PIPELINE PROJECTS Presented by: Mr. Richard Leech - Executive Director CB Richard Ellis (Vietnam) January 27th, 2010 Vietnam Retail Market HIGHLIGHTS Another

Office Snapshot Q1 2016

Office Snapshot Q1 216 Hanoi, Vietnam HANOI OFFICE Economic Indicators Market Indicators Grade A 2 months 15 2 months 16 CPI (%).64 1.3 Inward FDI (billion US$) 1.19 2.8 Trade balance (billion US$) (.61).86

Office Snapshot Q1 216 Hanoi, Vietnam HANOI OFFICE Economic Indicators Market Indicators Grade A 2 months 15 2 months 16 CPI (%).64 1.3 Inward FDI (billion US$) 1.19 2.8 Trade balance (billion US$) (.61).86

APRIL 2014 HCMC CENTRAL BUSINESS DISTRICT HO CHI MINH CITY CBD MARKET REPORT.

APRIL 2014 HCMC CENTRAL BUSINESS DISTRICT HO CHI MINH CITY CBD MARKET REPORT www.colliers.com/vietnam TABLE OF CONTENTS APRIL 2014 Market Highlights Page OFFICE MARKET Market Overview Outlook Table Map

APRIL 2014 HCMC CENTRAL BUSINESS DISTRICT HO CHI MINH CITY CBD MARKET REPORT www.colliers.com/vietnam TABLE OF CONTENTS APRIL 2014 Market Highlights Page OFFICE MARKET Market Overview Outlook Table Map

International developers driving land price appreciation

Q1 21 = 1 MARKETVIEW Phnom Penh, Q1 216 International developers driving land price appreciation Average High-end Condominium Price $3,195/SQM Prime Apartment Rent $21.9/SQM Prime Office Rent $22.7/SQM

Q1 21 = 1 MARKETVIEW Phnom Penh, Q1 216 International developers driving land price appreciation Average High-end Condominium Price $3,195/SQM Prime Apartment Rent $21.9/SQM Prime Office Rent $22.7/SQM

VIETNAM ECONOMY Q ECONOMIC OVERVIEW. Presented by: Dung Duong (Ms.) July 8, 2013 Q2/2012 Q1/2013 Q2/2013

July 8, 2013 Q2/2012 Q1/2013 Q2/2013") HCMC MARKET INSIGHTS Q2/213 Presented by: Dung Duong (Ms.) July 8, 213 VIETNAM ECONOMY Q2 213 ECONOMIC OVERVIEW Q2/212 Q1/213 Y-o-Y Q-o-Q Q2/213 GDP (% y-o-y) 4.8% 4.8% 5.% CPI (% y-o-y, e-o-p) 6.9% 6.6%

HCMC MARKET INSIGHTS Q2/213 Presented by: Dung Duong (Ms.) July 8, 213 VIETNAM ECONOMY Q2 213 ECONOMIC OVERVIEW Q2/212 Q1/213 Y-o-Y Q-o-Q Q2/213 GDP (% y-o-y) 4.8% 4.8% 5.% CPI (% y-o-y, e-o-p) 6.9% 6.6%

AUGUST 2014 HCMC CENTRAL BUSINESS DISTRICT HO CHI MINH CITY CBD MARKET REPORT.

AUGUST 2014 HCMC CENTRAL BUSINESS DISTRICT HO CHI MINH CITY CBD MARKET REPORT www.colliers.com/vietnam TABLE OF CONTENTS HCMC CBD MARKET REPORT AUGUST 2014 Market Highlights Page OFFICE MARKET Market Overview

AUGUST 2014 HCMC CENTRAL BUSINESS DISTRICT HO CHI MINH CITY CBD MARKET REPORT www.colliers.com/vietnam TABLE OF CONTENTS HCMC CBD MARKET REPORT AUGUST 2014 Market Highlights Page OFFICE MARKET Market Overview

Office Continues Stable Growth, Meanwhile. High-End Residential Market Starts To Cool

MARKETVIEW Phnom Penh, Q1 218 Office Continues Stable Growth, Meanwhile High-End Residential Market Starts To Cool Average High-end Condominium Price $3,147/SQM Prime Condominium Rent $15./SQM Prime Office

MARKETVIEW Phnom Penh, Q1 218 Office Continues Stable Growth, Meanwhile High-End Residential Market Starts To Cool Average High-end Condominium Price $3,147/SQM Prime Condominium Rent $15./SQM Prime Office

STABLE OCCUPANCY DESPITE RAMPED UP SUPPLY

COLLIERS QUARTERLY RESIDENTIAL MANILA Q3 2018 20 NOVEMBER 2018 Joey Roi Bondoc Manager Research Philippines +(632) 858 9057 Joey.Bondoc@colliers.com STABLE OCCUPANCY DESPITE RAMPED UP SUPPLY Summary &

COLLIERS QUARTERLY RESIDENTIAL MANILA Q3 2018 20 NOVEMBER 2018 Joey Roi Bondoc Manager Research Philippines +(632) 858 9057 Joey.Bondoc@colliers.com STABLE OCCUPANCY DESPITE RAMPED UP SUPPLY Summary &

Perth CBD office market

Perth CBD office market Considerations for stakeholders in today s office market July 215 Publication No. 15-1 Vacancy levels in the Perth office market are at a 2 year high and forecast to increase further.

Perth CBD office market Considerations for stakeholders in today s office market July 215 Publication No. 15-1 Vacancy levels in the Perth office market are at a 2 year high and forecast to increase further.

Sharper fall in office rents and capital values

Research & Forecast Report SINGAPORE OFFICE Q1 2016 Sharper fall in office rents and capital values Joanna Chen Manager, Research and Advisory The office market faces a critical juncture in the next few

Research & Forecast Report SINGAPORE OFFICE Q1 2016 Sharper fall in office rents and capital values Joanna Chen Manager, Research and Advisory The office market faces a critical juncture in the next few

INDEX INDEX DECEMBER 2014

A NEW BEGINNING INDEX INDEX... 3 AERIAL VIEWS.... 6 PROPERTY DESCRIPTION.... 9 EXTERIOR VIEW... 10 LOBBY ENTRANCE... 12 TYPICAL ELEVATOR LOBBY ( 1/8 = 1-0 ).... 14 TYPICAL ELEVATOR LOBBY.... 15 CORRIDOR...

A NEW BEGINNING INDEX INDEX... 3 AERIAL VIEWS.... 6 PROPERTY DESCRIPTION.... 9 EXTERIOR VIEW... 10 LOBBY ENTRANCE... 12 TYPICAL ELEVATOR LOBBY ( 1/8 = 1-0 ).... 14 TYPICAL ELEVATOR LOBBY.... 15 CORRIDOR...

DECEMBER 2015 HCMC CENTRAL BUSINESS DISTRICT CBD MONTHLY MARKET REPORT

DECEMBER 2015 HCMC CENTRAL BUSINESS DISTRICT CBD MONTHLY MARKET REPORT Accelerating success www.colliers.com/vietnam Table of Contents HCMC MARKET OVERVIEW Page Office Retail Hotel......... 3-5 6-7 8-9

DECEMBER 2015 HCMC CENTRAL BUSINESS DISTRICT CBD MONTHLY MARKET REPORT Accelerating success www.colliers.com/vietnam Table of Contents HCMC MARKET OVERVIEW Page Office Retail Hotel......... 3-5 6-7 8-9

Indianapolis MARKETBEAT. Office Q Economy. Market Overview INDIANAPOLIS OFFICE

INDIANAPOLIS OFFICE Economic Indicators Q2 17 Q2 18 MSA Employment 1.1M 1.1M MSA Unemployment 3.3% 3.0% U.S. Unemployment 4.3% 3. Market Indicators (Direct, All Classes) Q2 17 Q2 18 Total Market Vacancy

INDIANAPOLIS OFFICE Economic Indicators Q2 17 Q2 18 MSA Employment 1.1M 1.1M MSA Unemployment 3.3% 3.0% U.S. Unemployment 4.3% 3. Market Indicators (Direct, All Classes) Q2 17 Q2 18 Total Market Vacancy

RETAIL: INCREASED RENT BUT DECREASED OCCUPANCY

QMR Brief - HCMC GDP growth achieved 7.4 in Q1/218, the highest in Q1 for the last 1 years. The main driver was the industry and construction sector, followed by services. Inflation was well-controlled

QMR Brief - HCMC GDP growth achieved 7.4 in Q1/218, the highest in Q1 for the last 1 years. The main driver was the industry and construction sector, followed by services. Inflation was well-controlled

OFFICE MARKET REPORT. Northwest Arkansas. 3rd Quarter Q3 Market Trends 2016 by Xceligent, Inc. All Rights Reserved

OFFICE MARKET REPORT Northwest Arkansas 3rd Quarter 2016 Table of Contents/ Methodology of Tracked Set Xceligent is a leading provider of verified commercial real estate information which assists real

OFFICE MARKET REPORT Northwest Arkansas 3rd Quarter 2016 Table of Contents/ Methodology of Tracked Set Xceligent is a leading provider of verified commercial real estate information which assists real

Quarterly Market Briefing HCMC, Vietnam Q4/2016

Savills Research - Subscription form Savills Market Research Vietnam Quarterly Market Briefing HCMC, Vietnam Q4/2016 Macro Indicators Value YoY Growth Rate (%) GDP growth rate (%) 6.2% -0.5ppt Retail sales

Savills Research - Subscription form Savills Market Research Vietnam Quarterly Market Briefing HCMC, Vietnam Q4/2016 Macro Indicators Value YoY Growth Rate (%) GDP growth rate (%) 6.2% -0.5ppt Retail sales

LONG-TERM CONFIDENCE TRUMPS SLOWER DEMAND AS COMMERCIAL REAL ESTATE CONSTRUCTION RAMPS UP

For Immediate Release LONG-TERM CONFIDENCE TRUMPS SLOWER DEMAND AS COMMERCIAL REAL ESTATE CONSTRUCTION RAMPS UP First quarter office and industrial leasing activity slows while construction activity rises

For Immediate Release LONG-TERM CONFIDENCE TRUMPS SLOWER DEMAND AS COMMERCIAL REAL ESTATE CONSTRUCTION RAMPS UP First quarter office and industrial leasing activity slows while construction activity rises

growth in September slowed down to 0.82% m-o- m. The GDP increased by 5.76% y-o-y in first 9 months.

CBRE VIETNAM HANOI www.cbrevietnam.com October 2011 Economics Quick Stats Hot Topics Change from last VIETNAM Current Yr. Qtr. Real GDP Growth 5.76% Implemented FDI Exports Imports $2.9 bil $27.7 bil $27.9

CBRE VIETNAM HANOI www.cbrevietnam.com October 2011 Economics Quick Stats Hot Topics Change from last VIETNAM Current Yr. Qtr. Real GDP Growth 5.76% Implemented FDI Exports Imports $2.9 bil $27.7 bil $27.9

COLLIERS INTERNATIONAL 2019 LANDLORD SENTIMENT SURVEY

COLLIERS INTERNATIONAL 2019 LANDLORD SENTIMENT SURVEY Colliers International 2019 Landlord Sentiment Survey 1 SURVEY OVERVIEW Colliers International s survey of landlords was conducted and completed between

COLLIERS INTERNATIONAL 2019 LANDLORD SENTIMENT SURVEY Colliers International 2019 Landlord Sentiment Survey 1 SURVEY OVERVIEW Colliers International s survey of landlords was conducted and completed between

Red Hot Rents & Cooling Vacancy

Research & Forecast Report NORTH I-680 CORRIDOR OFFICE Q3 2017 Red Hot Rents & Cooling Vacancy > > Office Inventory: 16,926,446 Square Feet > > Vacancy: 12.9 percent > > Net absorption: (380,946) Square

Research & Forecast Report NORTH I-680 CORRIDOR OFFICE Q3 2017 Red Hot Rents & Cooling Vacancy > > Office Inventory: 16,926,446 Square Feet > > Vacancy: 12.9 percent > > Net absorption: (380,946) Square

Americas Office Trends Report

AMERICAS OFFICE TRENDS REPORT Americas Office Trends Report Summary The overall national office market recovery slowed slightly in the first quarter of 2016 amid financial market volatility. However, as

AMERICAS OFFICE TRENDS REPORT Americas Office Trends Report Summary The overall national office market recovery slowed slightly in the first quarter of 2016 amid financial market volatility. However, as

REAL ESTATE Highlights

RESEARCH Q1/2011 REAL ESTATE Highlights Ho chi minh city Knight Frank HIGHLIGHTS The HCMC real estate market was subdued in Q1/2011 due to a tightening monetary policy and a stagnant period before the

RESEARCH Q1/2011 REAL ESTATE Highlights Ho chi minh city Knight Frank HIGHLIGHTS The HCMC real estate market was subdued in Q1/2011 due to a tightening monetary policy and a stagnant period before the

Vacancy Edges Lower in Fourth Quarter

Research & Forecast Report FAIRFIELD OFFICE Q4 Vacancy Edges Lower in Fourth Quarter > > Office Inventory: 5,067,112 > > Current Vacancy: 14.2% > > Net Absorption: 63,610 The vacancy rate for office space

Research & Forecast Report FAIRFIELD OFFICE Q4 Vacancy Edges Lower in Fourth Quarter > > Office Inventory: 5,067,112 > > Current Vacancy: 14.2% > > Net Absorption: 63,610 The vacancy rate for office space

DA NANG CITY. Economics Quick Stats. Hot Topics. Real GDP Growth Rate & GDP per Capita Da Nang

CB RICHARD ELLIS VIETNAM DA NANG CITY www.cbrevietnam.com April 211 Economics Quick Stats Hot Topics ECONOMY: Da Nang ranked as having the best economic governance in the Provincial Competitive Index 21

CB RICHARD ELLIS VIETNAM DA NANG CITY www.cbrevietnam.com April 211 Economics Quick Stats Hot Topics ECONOMY: Da Nang ranked as having the best economic governance in the Provincial Competitive Index 21

HANOI. Economics Quick Stats. Hot Topics. Real GDP Growth Rate & GDP per Capita in Vietnam & Hanoi

CB RICHARD ELLIS VIETNAM HANOI www.cbrevietnam.com April 211 Economics Quick Stats Change from last VIETNAM Current Yr. Qtr. Real GDP Growth 5.4% FDI Exports Imports Hot Topics $2.37 bil $19.25 bil $22.27

CB RICHARD ELLIS VIETNAM HANOI www.cbrevietnam.com April 211 Economics Quick Stats Change from last VIETNAM Current Yr. Qtr. Real GDP Growth 5.4% FDI Exports Imports Hot Topics $2.37 bil $19.25 bil $22.27

Melbourne Industrial Vacancy October 2016

Kimberley Paterson +61 3 9604 4608 Kimberley.Paterson@au.knightfr ank.com Matt Whitby +61 418 404 854 Matt.Whitby@au.knightfrank.co m Melbourne Industrial Vacancy October 2016 Despite gross take-up being

Kimberley Paterson +61 3 9604 4608 Kimberley.Paterson@au.knightfr ank.com Matt Whitby +61 418 404 854 Matt.Whitby@au.knightfrank.co m Melbourne Industrial Vacancy October 2016 Despite gross take-up being

VIETNAM REAL ESTATE - TIME TO RECALIBRATE Presented by: Marc Townsend Managing Director, CBRE Vietnam 2 nd July, 2015

VIETNAM REAL ESTATE - TIME TO RECALIBRATE Presented by: Marc Townsend Managing Director, CBRE Vietnam 2 nd July, 2015 2 CBRE VIETNAM REAL ESTATE TIME TO RECALIBRATE JULY 2015 *All the above articles were

VIETNAM REAL ESTATE - TIME TO RECALIBRATE Presented by: Marc Townsend Managing Director, CBRE Vietnam 2 nd July, 2015 2 CBRE VIETNAM REAL ESTATE TIME TO RECALIBRATE JULY 2015 *All the above articles were

Weighing Options NORTH I-680 CORRIDOR OFFICE Q % Research & Forecast Report. Market Indicators

Research & Forecast Report NORTH I-680 CORRIDOR OFFICE Q4 2018 Weighing Options > > Office Inventory: 16,966,736 square feet > > Vacancy: 15 percent > > Net absorption: (35,823) square feet, year to date

Research & Forecast Report NORTH I-680 CORRIDOR OFFICE Q4 2018 Weighing Options > > Office Inventory: 16,966,736 square feet > > Vacancy: 15 percent > > Net absorption: (35,823) square feet, year to date

The Industrial Market Cooled Off in Q1

Research & Forecast Report Long Island industrial MARKET Q1 2016 The Industrial Market Cooled Off in Q1 Rose Liu Director of Finance & Research Long Island Takeaways > > Long Island industrial market slowed

Research & Forecast Report Long Island industrial MARKET Q1 2016 The Industrial Market Cooled Off in Q1 Rose Liu Director of Finance & Research Long Island Takeaways > > Long Island industrial market slowed

Creswick Property Factsheet

Creswick Property Factsheet 1st Half 2018 OVERVIEW Creswick, located 129km north west of Melbourne is 430m above sea level. A population of 3,170 was recorded in the 2016 ABS census. The area provides

Creswick Property Factsheet 1st Half 2018 OVERVIEW Creswick, located 129km north west of Melbourne is 430m above sea level. A population of 3,170 was recorded in the 2016 ABS census. The area provides

Caution: Vacancy Increases Ahead

MARKET REPORT DISTRICT OF COLUMBIA OFFICE Fourth Quarter 2016 Caution: Vacancy Increases Ahead Market Indicators Q4 2016 2017 (Projected) NET Despite year-to-date negative absorption, the Washington, DC

MARKET REPORT DISTRICT OF COLUMBIA OFFICE Fourth Quarter 2016 Caution: Vacancy Increases Ahead Market Indicators Q4 2016 2017 (Projected) NET Despite year-to-date negative absorption, the Washington, DC

Leasing cools, but deal flow consistent

MARKETVIEW Downtown Manhattan Office, Q3 216 Leasing cools, but deal flow consistent Leasing Activity.85 MSF Net Absorption (.12) MSF Availability Rate 11.7 Vacancy Rate 9.3 Average Asking Rent $57.5 PSF

MARKETVIEW Downtown Manhattan Office, Q3 216 Leasing cools, but deal flow consistent Leasing Activity.85 MSF Net Absorption (.12) MSF Availability Rate 11.7 Vacancy Rate 9.3 Average Asking Rent $57.5 PSF

JULY 2014 HCMC CENTRAL BUSINESS DISTRICT HO CHI MINH CITY CBD MARKET REPORT.

JULY 2014 HCMC CENTRAL BUSINESS DISTRICT HO CHI MINH CITY CBD MARKET REPORT www.colliers.com/vietnam TABLE OF CONTENTS HCMC CBD MARKET REPORT JULY 2014 Market Highlights Page OFFICE MARKET Market Overview

JULY 2014 HCMC CENTRAL BUSINESS DISTRICT HO CHI MINH CITY CBD MARKET REPORT www.colliers.com/vietnam TABLE OF CONTENTS HCMC CBD MARKET REPORT JULY 2014 Market Highlights Page OFFICE MARKET Market Overview

Leasing strength concentrated in new assets

MARKETVIEW Midtown Manhattan Office, Q4 216 Leasing strength concentrated in new assets Leasing Activity 4.25 MSF Net Absorption.62 MSF Availability Rate 11.8% Vacancy Rate 7.9% Average Asking Rent $8.18

MARKETVIEW Midtown Manhattan Office, Q4 216 Leasing strength concentrated in new assets Leasing Activity 4.25 MSF Net Absorption.62 MSF Availability Rate 11.8% Vacancy Rate 7.9% Average Asking Rent $8.18

Research Report April Vietnam Property Market Brief Q

Research Report April 218 Vietnam Property Market Brief Q1 218 www.joneslanglasalle.com.vn Contents ECONOMY OF VIETNAM 3 HO CHI MINH CITY 5 Office 5 Supply slightly increases Positive demand Rent keeps

Research Report April 218 Vietnam Property Market Brief Q1 218 www.joneslanglasalle.com.vn Contents ECONOMY OF VIETNAM 3 HO CHI MINH CITY 5 Office 5 Supply slightly increases Positive demand Rent keeps

Record leasing activity in the Melbourne CBD office market

Record leasing activity in the Melbourne CBD office market June 215 Summary The recovery in the Melbourne CBD office leasing started in 214 and the momentum in leasing enquiry gathered pace in 215. We

Record leasing activity in the Melbourne CBD office market June 215 Summary The recovery in the Melbourne CBD office leasing started in 214 and the momentum in leasing enquiry gathered pace in 215. We

ECONOMIC OVERVIEW 2018/H1. YoY Growth Rate

ECONOMIC OVERVIEW 2018/H1 Value YoY Growth Rate Evolving Retail SUPPLY million m 2 Unchanged QoQ 5% YoY No new project PERFORMANCE Occupancy Gross rent 92% Stable QoQ (2)ppts YoY US$50/m 2 /mth 1% QoQ

ECONOMIC OVERVIEW 2018/H1 Value YoY Growth Rate Evolving Retail SUPPLY million m 2 Unchanged QoQ 5% YoY No new project PERFORMANCE Occupancy Gross rent 92% Stable QoQ (2)ppts YoY US$50/m 2 /mth 1% QoQ

Office Market Continues to Improve

Research & Forecast Report LAS VEGAS OFFICE Q3 2016 Office Market Continues to Improve > > Southern Nevada s office market is improving at a steady rate > > Net absorption has been positive in twelve of

Research & Forecast Report LAS VEGAS OFFICE Q3 2016 Office Market Continues to Improve > > Southern Nevada s office market is improving at a steady rate > > Net absorption has been positive in twelve of

Presentation for REITs Symposium 2016

Presentation for REITs Symposium 2016 4 June 2016 Important Notice This presentation shall be read in conjunction with OUE Commercial REIT s Financial Results announcement for 1Q 2016 dated 10 May 2016.

Presentation for REITs Symposium 2016 4 June 2016 Important Notice This presentation shall be read in conjunction with OUE Commercial REIT s Financial Results announcement for 1Q 2016 dated 10 May 2016.

717 EAST 1ST STREET LONG BEACH, CA 90802

LONG BEACH, CA 90802 MULTI-FAMILY INVESTMENTS LONG BEACH, CA 90802 Sale Price: $1,249,000 Sale Price/SF: $319.93 Sale Price/Unit: $312,250 Rentable SF: 3,904 SF Lot Size SF: 7,511 SF Units: 4 Floors: 2

LONG BEACH, CA 90802 MULTI-FAMILY INVESTMENTS LONG BEACH, CA 90802 Sale Price: $1,249,000 Sale Price/SF: $319.93 Sale Price/Unit: $312,250 Rentable SF: 3,904 SF Lot Size SF: 7,511 SF Units: 4 Floors: 2

Hong Kong Office MarketView

Core Fringe Core Midtown Decentralised Core Fringe Core Kowloon East Decentralised Hong Kong Office MarketView Q2 2013 Global Research and Consulting OVERALL HONG KONG Rents +0.3% q-o-q CENTRAL Rents -0.2%

Core Fringe Core Midtown Decentralised Core Fringe Core Kowloon East Decentralised Hong Kong Office MarketView Q2 2013 Global Research and Consulting OVERALL HONG KONG Rents +0.3% q-o-q CENTRAL Rents -0.2%

Homestretch: Office Market Set to Finish Strong

Research & Forecast Report RENO OFFICE Q3 2016 Homestretch: Office Market Set to Finish Strong >> Vacancy drops significantly the largest drop quarter over quarter in 2016 >> Rental rates are not increasing

Research & Forecast Report RENO OFFICE Q3 2016 Homestretch: Office Market Set to Finish Strong >> Vacancy drops significantly the largest drop quarter over quarter in 2016 >> Rental rates are not increasing

INDUSTRIAL MARKET REPORT. San Antonio. 4th Quarter Q4 Market Trends 2016 by Xceligent, Inc. All Rights Reserved

INDUSTRIAL MARKET REPORT San Antonio 4th Quarter 2015 Table of Contents/ Methodology of Tracked Set Xceligent is a leading provider of verified commercial real estate information which assists real estate

INDUSTRIAL MARKET REPORT San Antonio 4th Quarter 2015 Table of Contents/ Methodology of Tracked Set Xceligent is a leading provider of verified commercial real estate information which assists real estate

The Rise of the Gold Coast

Research & Forecast Report Long Island OFFICE MARKET Q1 2015 The Rise of the Gold Coast Rose Liu Research & Financial Analyst Long Island Takeaways Class A & B In the first quarter of 2015, Long Island

Research & Forecast Report Long Island OFFICE MARKET Q1 2015 The Rise of the Gold Coast Rose Liu Research & Financial Analyst Long Island Takeaways Class A & B In the first quarter of 2015, Long Island

Limited new supply pushes vacancy level down

Photo credit: Mukusalas business centre Riga Offices, Q 7 Limited new supply pushes vacancy level down 68, sq m.8 % 4,5 sq m 4,695 sq m 6.8 Picture: TELE Shared Service Centre: Teraudlietuves biroji, nd

Photo credit: Mukusalas business centre Riga Offices, Q 7 Limited new supply pushes vacancy level down 68, sq m.8 % 4,5 sq m 4,695 sq m 6.8 Picture: TELE Shared Service Centre: Teraudlietuves biroji, nd

ASIA PACIFIC OFFICE OVERVIEW April - June 2017

ASIA PACIFIC OFFICE OVERVIEW April - June A CUSHMAN & WAKEFIELD QUARTERLY RESEARCH PUBLICATION INSIGHTS INTO ACTION ASIA PACIFIC OFFICE OVERVIEW OCCUPIER CONDITIONS INDIA Delhi-NCR GREATER CHINA Chongqing

ASIA PACIFIC OFFICE OVERVIEW April - June A CUSHMAN & WAKEFIELD QUARTERLY RESEARCH PUBLICATION INSIGHTS INTO ACTION ASIA PACIFIC OFFICE OVERVIEW OCCUPIER CONDITIONS INDIA Delhi-NCR GREATER CHINA Chongqing

The Improvement of the Industrial Market

Research & Forecast Report Long Island industrial MARKET Q2 2015 The Improvement of the Industrial Market Rose Liu Research & Financial Analyst Long Island Takeaways The overall economy on Long Island

Research & Forecast Report Long Island industrial MARKET Q2 2015 The Improvement of the Industrial Market Rose Liu Research & Financial Analyst Long Island Takeaways The overall economy on Long Island

HANOI 9M GDP 7.9% SLUGGISH GDP GROWTH AS FEARS OF INFLATION RESURFACE INDUSTRIAL PRODUCTION SHOWING CONTINUED GROWTH

HCMC MarketView Q3 2012 CBRE Global Research and Consulting VN 9M GDP 4.7% HCMC 9M GDP 8.7% HANOI 9M GDP 7.9% VN 9M PMI 49.2 e-o-p VN CONSUMER CONFIDENCE SLUGGISH GDP GROWTH AS FEARS OF INFLATION RESURFACE

HCMC MarketView Q3 2012 CBRE Global Research and Consulting VN 9M GDP 4.7% HCMC 9M GDP 8.7% HANOI 9M GDP 7.9% VN 9M PMI 49.2 e-o-p VN CONSUMER CONFIDENCE SLUGGISH GDP GROWTH AS FEARS OF INFLATION RESURFACE

ECONOMIC OVERVIEW Q3/2013 Key Economic Indicators. Presented by: Ngoc Le (Ms.) Thursday, 3rd October, 2013

Thursday, 3rd October, 2013") HCMC MARKET INSIGHTS Q3/2013 Presented by: Ngoc Le (Ms.) Thursday, 3rd October, 2013 ECONOMIC OVERVIEW Q3/2013 Key Economic Indicators Q3/2012 Q2/2013 Q3/2013 Y-o-Y Q-o-Q Y-o-Y GDP (% y-o-y) 5.1% 4.8%

HCMC MARKET INSIGHTS Q3/2013 Presented by: Ngoc Le (Ms.) Thursday, 3rd October, 2013 ECONOMIC OVERVIEW Q3/2013 Key Economic Indicators Q3/2012 Q2/2013 Q3/2013 Y-o-Y Q-o-Q Y-o-Y GDP (% y-o-y) 5.1% 4.8%

urrent difficult economic condition and the sustainable development remain key economic tasks in Export turnover reached US$96.

CB RICHARD ELLIS VIETNAM DA www.cbrevietnam.com January 212 Economics Quick Stats Change from last VIETNAM Current Yr. Qtr. Real GDP Growth 5.89% Implemented FDI Exports Imports $2.8 bil $26.2 bil $28.9

CB RICHARD ELLIS VIETNAM DA www.cbrevietnam.com January 212 Economics Quick Stats Change from last VIETNAM Current Yr. Qtr. Real GDP Growth 5.89% Implemented FDI Exports Imports $2.8 bil $26.2 bil $28.9

THE COLLABORATIVE MARKET ST. & FRANCE AVE. EDINA

THE COLLABORATIVE MARKET ST. & FRANCE AVE. EDINA THE COLLABORATIVE PROJECT The Collaborative comprises a redevelopment of approximately 3 acres at 50th & France in Edina and will transform stand-alone

THE COLLABORATIVE MARKET ST. & FRANCE AVE. EDINA THE COLLABORATIVE PROJECT The Collaborative comprises a redevelopment of approximately 3 acres at 50th & France in Edina and will transform stand-alone

CBRE Houston ViewPoint

CBRE Houston ViewPoint DOWNTOWN HOUSTON: THE NEW GATEWAY MARKET? by Sara R. Rutledge Director, Research and Analysis INTRODUCTION Investor interest from both domestic and foreign sources has revived in

CBRE Houston ViewPoint DOWNTOWN HOUSTON: THE NEW GATEWAY MARKET? by Sara R. Rutledge Director, Research and Analysis INTRODUCTION Investor interest from both domestic and foreign sources has revived in

Monthly Market Update

Monthly Market Update December 2015 New York City Office Outlook February 2016 M A N H A T T A N Class A Asking Rents M A N H A T T A N Class A Vacancy Rates $100.00 Jan-14 Jan-15 Jan-16 20.0% Jan-14 Jan-15

Monthly Market Update December 2015 New York City Office Outlook February 2016 M A N H A T T A N Class A Asking Rents M A N H A T T A N Class A Vacancy Rates $100.00 Jan-14 Jan-15 Jan-16 20.0% Jan-14 Jan-15

HISTORICAL VACANCY VS RENTS. Downtown Los Angeles Office Market Q Q RENTS VACANCY $31 2Q10 2Q11 2Q12 2Q13 2Q14

www.colliers.com/losangeles OFFICE LOS ANGELES MARKET REPORT Rate Decrease Below 20% As Market Activity Remains Flat MARKET OVERVIEW MARKET INDICATORS - VACANCY 19.5% The Downtown Los Angeles market in

www.colliers.com/losangeles OFFICE LOS ANGELES MARKET REPORT Rate Decrease Below 20% As Market Activity Remains Flat MARKET OVERVIEW MARKET INDICATORS - VACANCY 19.5% The Downtown Los Angeles market in

inflationary control policy. Inflation in Q1/2011 stood at 12.8% y-o-y, or 2.2% m-o-m rter, with State Bank raising both its discount

CB RICHARD ELLIS VIETNAM HO www.cbrevietnam.com April 211 Economics Quick Stats Change from last VIETNAM Current Yr. Qtr. Real GDP Growth 5.4% FDI Exports Imports $2.37 bil $19.25 bil $22.27 bil CPI (average)

CB RICHARD ELLIS VIETNAM HO www.cbrevietnam.com April 211 Economics Quick Stats Change from last VIETNAM Current Yr. Qtr. Real GDP Growth 5.4% FDI Exports Imports $2.37 bil $19.25 bil $22.27 bil CPI (average)

VIETNAM REAL ESTATE MARKET

2Q 212 RESEARCH & FORECAST REPORT VIETNAM REAL ESTATE MARKET Property Sector Overview MARKET INDICATORS ECONOMY OFFICE RETAIL APARTMENT The Vietnamese economy has shown signs of recovery over the second

2Q 212 RESEARCH & FORECAST REPORT VIETNAM REAL ESTATE MARKET Property Sector Overview MARKET INDICATORS ECONOMY OFFICE RETAIL APARTMENT The Vietnamese economy has shown signs of recovery over the second

MANHATTAN OFFICE 2017

Research Report MANHATTAN OFFICE 2017 Accelerating success. % $ ± Market Indicators Full Year 2016 Full Year 2017 Y-O-Y Change AVAILABILITY RATE 10.3% 10.0% -0.3pp AVERAGE ASKING RENT ($/SF/YR) $73.24

Research Report MANHATTAN OFFICE 2017 Accelerating success. % $ ± Market Indicators Full Year 2016 Full Year 2017 Y-O-Y Change AVAILABILITY RATE 10.3% 10.0% -0.3pp AVERAGE ASKING RENT ($/SF/YR) $73.24

Bargara Property Factsheet

Bargara Property Factsheet 1st Half 2018 OVERVIEW Bargara* is located in the Bundaberg Region of south-east Queensland, approximately 384km north of Brisbane s CBD. Over the last 7 years the population

Bargara Property Factsheet 1st Half 2018 OVERVIEW Bargara* is located in the Bundaberg Region of south-east Queensland, approximately 384km north of Brisbane s CBD. Over the last 7 years the population

Shrinking Supply Continues To Push Rates

Research & Forecast Report STOCKTON SAN JOAQUIN COUNTY OFFICE Q1 2017 Shrinking Supply Continues To Push Rates > Office inventory: 8,221,819 > Vacancy: 10.5 percent > Net absorption: 49,103 year-to-date

Research & Forecast Report STOCKTON SAN JOAQUIN COUNTY OFFICE Q1 2017 Shrinking Supply Continues To Push Rates > Office inventory: 8,221,819 > Vacancy: 10.5 percent > Net absorption: 49,103 year-to-date

City office rental values fall for second month in May

MARKETVIEW United Kingdom Monthly Index, May 217 City office rental values fall for second month in May All Property.9 All Offices 1. All Retail.8 All Industrials.9 *Arrows indicate the rate of change

MARKETVIEW United Kingdom Monthly Index, May 217 City office rental values fall for second month in May All Property.9 All Offices 1. All Retail.8 All Industrials.9 *Arrows indicate the rate of change

Vacancy Increased Slightly During the First Quarter

Research & Forecast Report STOCKTON SAN JOAQUIN COUNTY OFFICE Q1 2016 Vacancy Increased Slightly During the First Quarter > Vacancy rates have been steadily declining since the fourth quarter of 2011.

Research & Forecast Report STOCKTON SAN JOAQUIN COUNTY OFFICE Q1 2016 Vacancy Increased Slightly During the First Quarter > Vacancy rates have been steadily declining since the fourth quarter of 2011.

>> 2016 Off to A Good Start for Tri-Cities

Research & Forecast Report TRI-CITIES OFFICE Q1 216 Accelerating success. >> 216 Off to A Good Start for Tri-Cities Key Takeaways > The Tri-Cities office market saw vacancy decline for the seventh consecutive

Research & Forecast Report TRI-CITIES OFFICE Q1 216 Accelerating success. >> 216 Off to A Good Start for Tri-Cities Key Takeaways > The Tri-Cities office market saw vacancy decline for the seventh consecutive

Stronger Office Market Looking Into Future

Research & Forecast Report Long Island OFFICE MARKET Q2 2015 Stronger Office Market Looking Into Future Rose Liu Research & Financial Analyst Long Island Takeaways Class A & B Long Island economic and

Research & Forecast Report Long Island OFFICE MARKET Q2 2015 Stronger Office Market Looking Into Future Rose Liu Research & Financial Analyst Long Island Takeaways Class A & B Long Island economic and

Attached for release to the market is a Canberra Update booklet that was provided today as part of an Analyst and Investor tour of Canberra.

23 June 2010 MIRVAC GROUP CANBERRA Attached for release to the market is a Canberra Update booklet that was provided today as part of an Analyst and Investor tour of Canberra. For further information please

23 June 2010 MIRVAC GROUP CANBERRA Attached for release to the market is a Canberra Update booklet that was provided today as part of an Analyst and Investor tour of Canberra. For further information please

Has The Office Market Reached A Peak? Vacancy. Rental Rate. Net Absorption. Construction. *Projected $3.65 $3.50 $3.35 $3.20 $3.05 $2.90 $2.

Research & Forecast Report OAKLAND METROPOLITAN AREA OFFICE Q1 Has The Office Market Reached A Peak? > > Vacancy remained low at 5. > > Net Absorption was positive 8,399 in the first quarter > > Gross

Research & Forecast Report OAKLAND METROPOLITAN AREA OFFICE Q1 Has The Office Market Reached A Peak? > > Vacancy remained low at 5. > > Net Absorption was positive 8,399 in the first quarter > > Gross

Perth CBD Office Market

SPRING 2016 MARKET TRENDS New supply has moderated. There is no new supply forecast until 2018. Demand weakened in the first half of 2016. Vacancy rates continued to rise in the first half of 2016. Face

SPRING 2016 MARKET TRENDS New supply has moderated. There is no new supply forecast until 2018. Demand weakened in the first half of 2016. Vacancy rates continued to rise in the first half of 2016. Face

>> Orange County Vacancy Continues to Decline

Research & Forecast Report ORANGE COUNTY OFFICE Accelerating success. >> Orange County Continues to Decline Key Takeaways > The South County submarket led the Orange County market in overall net absorption

Research & Forecast Report ORANGE COUNTY OFFICE Accelerating success. >> Orange County Continues to Decline Key Takeaways > The South County submarket led the Orange County market in overall net absorption

HO CHI MINH QUARTERLY KNOWLEDGE REPORT. Q Accelerating success

HO CHI MINH QUARTERLY KNOWLEDGE REPORT Q4 216 Accelerating success www.colliers.com/vietnam TABLE OF CONTENTS Page ECONOMIC OVERVIEW... VIETNAM... HO CHI MINH CITY... HA NOI... 4-5 4 5 5 HO CHI MINH CITY

HO CHI MINH QUARTERLY KNOWLEDGE REPORT Q4 216 Accelerating success www.colliers.com/vietnam TABLE OF CONTENTS Page ECONOMIC OVERVIEW... VIETNAM... HO CHI MINH CITY... HA NOI... 4-5 4 5 5 HO CHI MINH CITY

Presented by Corporate Visions Pte Ltd

Our Vision : To be the leading consultancy in commercial and industrial properties Our Mission: To provide professional, value-added and cost effective business space solutions Presented by Corporate Visions

Our Vision : To be the leading consultancy in commercial and industrial properties Our Mission: To provide professional, value-added and cost effective business space solutions Presented by Corporate Visions

Cambridge Office/Lab MarketView

Cambridge Office/Lab MarketView CBRE Global Research and Consulting U.S. UNEMPLOYMENT 6.7% MA UNEMPLOYMENT 6.3% OCCUPIED SQ. FT. 19.4M OFFICE AVAIL. 10.0% LAB AVAIL. 18.4% UNDER CONSTRUCTION 1.8MSF *Arrows

Cambridge Office/Lab MarketView CBRE Global Research and Consulting U.S. UNEMPLOYMENT 6.7% MA UNEMPLOYMENT 6.3% OCCUPIED SQ. FT. 19.4M OFFICE AVAIL. 10.0% LAB AVAIL. 18.4% UNDER CONSTRUCTION 1.8MSF *Arrows