WATERFRONT LOCAL IMPROVEMENT DISTRICT OVERVIEW. November 2017

|

|

|

- Frank Watson

- 5 years ago

- Views:

Transcription

1 WATERFRONT LOCAL IMPROVEMENT DISTRICT OVERVIEW November 2017

2 LOCAL IMPROVEMENT DISTRICT Funding tool by which property owners financially contribute to a project that will increase the value of their property Used to fund public projects in State of Washington Governed by specific state and local laws (including special benefit study) 2

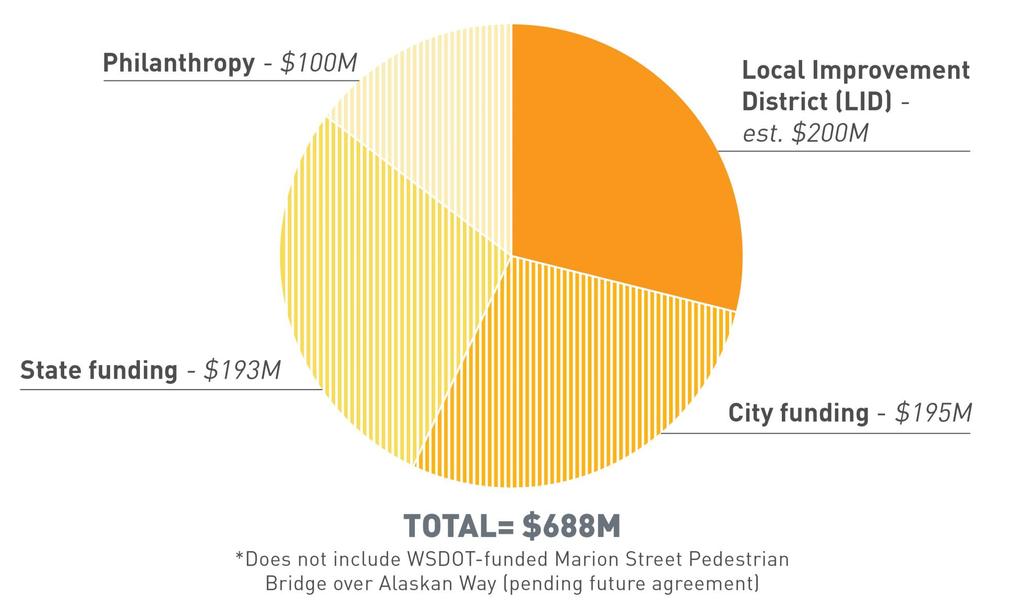

3 FUNDING 3

4 TERMINOLOGY Special benefit: Estimated increase in a property s fair market value as a result of public improvements. Special benefit study: Conducted by an independent appraisal firm to determine the LID boundary and the difference between the fair market value of each property before and immediately after the improvement. Assessment: Portion of the special benefit each property owner will pay. Cannot exceed the amount of the special benefit. Cost-benefit ratio: Portion of the special benefit each property will pay. Same ratio will apply to all assessed properties. (Determined by City Council) 4

5 STATUTORY REQUIREMENTS Total assessments not more than special benefits Total assessments not more than total cost Assessments are roughly proportionate to each other Exempt Properties: 1. Housing Authority Property 2. Farm, agricultural, or timber lands 3. Federal property 5

6 SPECIAL BENEFIT 6

7 SPECIAL BENEFIT STUDY WHY? A special benefit study is a tool consistently used with LID projects. Municipality retains an expert consultant to evaluate the project, special benefits attributable to properties and classes of property and confirms boundaries of the assessment district. Special benefit studies follow state law and judicial decisions, which provide guidance on how the appraiser conducts their analysis. The courts have ruled that assessments should be based on the proportionate special benefits received by all properties within the LID. In complex LID projects (like the Waterfront Seattle LID) where a property s highest and best use is influenced by a number of factors including zoning and multiple types of use on one parcel a special benefit study is an element of the City s formation process as well as outreach to the community within the LID. 7

8 SPECIAL BENEFIT/PROPORTIONATE STUDY Discussion points below apply to both Formation and Final Special Benefit Studies. Difference in market value without (before) versus with (after) the LID project is completed. Special benefit is defined as: the difference in the fair market value of the property without the improvement and the fair market value of the property with the improvement (commonly called before and after, more properly called without and with ).* Important Points of Study Estimate the value of parcels without ( before ) and with ( after ) the LID. The viaduct removal, Seawall, Deep Bore Tunnel, and surface road replacement are assumed to be completed as a base condition. Based on the fair market value of the fee simple interest of each individual property within the LID boundary. Market value based on highest and best use of land and improvements. Market-based research and analysis: Exterior inspection of each parcel within the LID. Study of market data and sales (Income, Vacancy, Supply/Demand, etc.). Review of other projects Vancouver, B.C, Portland, San Francisco, New York, Boston. Meetings and public hearings. Prepare narrative report for formation and final assessment roll. * Source: Local Road Improvement Districts Manual for Washington State. Sixth Edition Print. 8

9 DEFINITION MARKET VALUE Market Value is defined as: The most probable price that a property should bring in a competitive and open market under all conditions requisite to a fair sale, the buyer and seller each acting prudently and knowledgeably, and assuming the price is not affected by undue stimulus. Implicit in this definition is the consummation of a sale as of a specified date and the passing of title from seller to buyer under conditions whereby: Buyer and seller are typically motivated; Both parties are well informed or well advised, and acting in what they consider their own best interests; A reasonable time is allowed for exposure in the open market; Payment is made in terms of cash in United States dollars or in terms of financial arrangements comparable thereto; and The price represents the normal consideration for the property sold unaffected by special or creative financing or sales concessions granted by anyone associated with the sale. Source: The Dictionary of Real Estate Appraisal. Sixth edition. The Appraisal Institute, Print. 9

10 DEFINITION FEE SIMPLE INTEREST & HIGHEST AND BEST USE Fee Simple Estate is defined as: Absolute ownership unencumbered by any other interest or estate, subject only to the limitations imposed by the governmental powers of taxation, eminent domain, police power, and escheat. * Highest and Best Use is defined as: The reasonably probable use of property that results in the highest value. The four criteria that the highest and best use must meet are legal permissibility, physical possibility, financial feasibility, and maximum productivity.* Highest and Best Use As Vacant and As Improved *Source: The Dictionary of Real Estate Appraisal. Sixth edition. The Appraisal Institute, Print. 10

11 COMPLEX PROPERTIES Complex properties require more in-depth research. Special purpose properties Mixed use residential/office/retail/hotel Low income/affordable housing properties High rise office/retail buildings 11

12 REASONS WHY MARKET VALUES INCREASE Enhanced location amenities improved waterfront amenities/market appeal. Income Approach Increase in rents, lower vacancy levels/capitalization rates as well as lower perceived risk. Direct Sales Comparison Approach Higher land/overall property values and improved market perception. Above factors generally interrelated in an investor/developer/market participant thought process when buying income-generating properties similar to a number of properties in the Waterfront Seattle LID. Condominium owners typically receive an increase in market value due to enhanced location and market perception of waterfront amenities. 12

13 HOW ASSESSMENTS ARE CALCULATED Assessments are calculated by taking each property s special benefit amount and multiplying it by the cost benefit ratio. Example (for illustrative purposes only)* Property Special Benefit (SB): $5,000 Cost Benefit Ratio (determined by City Council): 50% Assessment: $2,500 *If SB = $5,000 and cost/benefit ratio is 40%, assessment would be $2,000. *If SB = $5,000 and cost/benefit ratio is 60%, assessment would be $3,000. x = 13

14 FEASIBILITY STUDY Initial estimate of overall range of total special benefit to determine feasibility Does not include parcel-by-parcel analysis and is not used to determine assessments. Total estimated range in study area: $ million 14

15 LID ANALYSIS AREAS B C D A E 15

16 SPECIAL BENEFIT STUDY AREA 16

17 LID FORMATION PROCESS 17

18 FOR MORE INFORMATION:

LOCAL IMPROVEMENT DISTRICT APPRAISER PRESENTATION. November 2017

LOCAL IMPROVEMENT DISTRICT APPRAISER PRESENTATION November 2017 SPECIAL BENEFIT STUDY WHY? A special benefit study is a tool consistently used with LID projects. Municipality retains an expert consultant

LOCAL IMPROVEMENT DISTRICT APPRAISER PRESENTATION November 2017 SPECIAL BENEFIT STUDY WHY? A special benefit study is a tool consistently used with LID projects. Municipality retains an expert consultant

Multi-Family Methodology Analysis

Multi-Family Methodology 2018 Analysis Assessment Department February, 2018 2018 Multi-Family Assessment Methodology Property assessments in the City of Medicine Hat reflect the fee simple market value

Multi-Family Methodology 2018 Analysis Assessment Department February, 2018 2018 Multi-Family Assessment Methodology Property assessments in the City of Medicine Hat reflect the fee simple market value

A Demonstration Appraisal Report. Of a. Located at. Date of Appraisal. Prepared for. Prepared by

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 W. 10 th Street Kansas

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 W. 10 th Street Kansas

A Demonstration Appraisal Report. Of a. Located at. Date of Appraisal. Prepared for. Prepared by

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 West 10 th Street Kansas

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 West 10 th Street Kansas

Avoiding Common Errors in Appraisals for Financial

Avoiding Common Errors in Appraisals for Financial Institutions Panelists: Brian Bailey, CCIM, Senior Financial Analyst Commercial Real Estate, Federal Reserve Bank of Atlanta James Murrett, MAI, Director

Avoiding Common Errors in Appraisals for Financial Institutions Panelists: Brian Bailey, CCIM, Senior Financial Analyst Commercial Real Estate, Federal Reserve Bank of Atlanta James Murrett, MAI, Director

APPRAISING COMMERCIAL INVESTMENT PROPERTY

APPRAISING COMMERCIAL INVESTMENT PROPERTY Cydney G. Bender-Reents, MAI President Jared M. Calabrese, MAI Senior Appraiser YOUR HOUSE AS SEEN BY: Yourself Your Lender YOUR HOUSE AS SEEN BY: Your Buyer Your

APPRAISING COMMERCIAL INVESTMENT PROPERTY Cydney G. Bender-Reents, MAI President Jared M. Calabrese, MAI Senior Appraiser YOUR HOUSE AS SEEN BY: Yourself Your Lender YOUR HOUSE AS SEEN BY: Your Buyer Your

PROPERTY OWNER HANDBOOK

VOLUNTARY ACQUISTION PROJECT PROPERTY OWNER HANDBOOK TABLE OF CONTENTS PROPERTY OWNER HANDBOOK A Purpose of the Handbook...1 B Eligibility for Acquisition...2 C. Acquisition Process and Timeframe...3 D.

VOLUNTARY ACQUISTION PROJECT PROPERTY OWNER HANDBOOK TABLE OF CONTENTS PROPERTY OWNER HANDBOOK A Purpose of the Handbook...1 B Eligibility for Acquisition...2 C. Acquisition Process and Timeframe...3 D.

DEMO ITEM SUBJECT COMPARABLE SOLD # 1 COMPARABLE SOLD # 2 COMPARABLE SOLD # 3

Residential Broker Price Opinion FHA CASE #: ASSIGNED LLB: PROPERTY ADDRESS: I. GENERAL MARKET CONDITIONS II. Current market condition: Depressed Slow Stable Improving Excellent Employment conditions:

Residential Broker Price Opinion FHA CASE #: ASSIGNED LLB: PROPERTY ADDRESS: I. GENERAL MARKET CONDITIONS II. Current market condition: Depressed Slow Stable Improving Excellent Employment conditions:

Interagency Appraisal and

Interagency Appraisal and Evaluation (IAEG) Workshop Purpose (77456) Supersedes the 1994 Interagency Appraisal & Evaluation Guidelines Address supervisory matters relating to real estate appraisal and

Interagency Appraisal and Evaluation (IAEG) Workshop Purpose (77456) Supersedes the 1994 Interagency Appraisal & Evaluation Guidelines Address supervisory matters relating to real estate appraisal and

APPRAISER & ASSESSOR Real Estate Tax Valuation Overview and Issues

APPRAISER & ASSESSOR Real Estate Tax Valuation Overview and Issues James R. Johnston, MAI, SRA J. Michael Tarello, MAI, ASA, MRA February 11, 2015 BOSTON Property Advisors Vision Government Solutions AGENDA

APPRAISER & ASSESSOR Real Estate Tax Valuation Overview and Issues James R. Johnston, MAI, SRA J. Michael Tarello, MAI, ASA, MRA February 11, 2015 BOSTON Property Advisors Vision Government Solutions AGENDA

To all Appraisers: Brief Overview:

To all Appraisers: As the appraisal industry continues to change, the demand for alternative valuation solutions grows. That is why is excited to announce the addition of a new product - the Desktop Appraisal

To all Appraisers: As the appraisal industry continues to change, the demand for alternative valuation solutions grows. That is why is excited to announce the addition of a new product - the Desktop Appraisal

Copyright, 1999, 2002, 2004, Freddie Mac. All Rights Reserved.

Page 1 of 13 Engineering Requirements/Chapter 12: Appraiser and Appraisal Requirements/12.1: General requirements 12.1: General requirements For all multifamily purchase programs and products, the Seller/Servicer

Page 1 of 13 Engineering Requirements/Chapter 12: Appraiser and Appraisal Requirements/12.1: General requirements 12.1: General requirements For all multifamily purchase programs and products, the Seller/Servicer

Source: Reg. Y, 55 FR 27771, July 5, 1990, unless otherwise noted.

Subpart G Appraisal Standards for Federally Related Transactions Source: Reg. Y, 55 FR 27771, July 5, 1990, unless otherwise noted. 225.61 Authority, purpose, and scope. (a) Authority. This subpart is

Subpart G Appraisal Standards for Federally Related Transactions Source: Reg. Y, 55 FR 27771, July 5, 1990, unless otherwise noted. 225.61 Authority, purpose, and scope. (a) Authority. This subpart is

FIRST AMENDMENT TO LEASE

Attachment 1 FIRST AMENDMENT TO LEASE THIS FIRST AMENDMENT TO LEASE, dated, 2013 ( First Amendment ), by and between the State of California, acting by and through its Department of General Services, (hereinafter

Attachment 1 FIRST AMENDMENT TO LEASE THIS FIRST AMENDMENT TO LEASE, dated, 2013 ( First Amendment ), by and between the State of California, acting by and through its Department of General Services, (hereinafter

[Code of Federal Regulations] [Title 12, Volume 5] [Revised as of January 1, 2004] From the U.S. Government Printing Office via GPO Access

![[Code of Federal Regulations] [Title 12, Volume 5] [Revised as of January 1, 2004] From the U.S. Government Printing Office via GPO Access](/thumbs/80/82487200.jpg "[Code of Federal Regulations] [Title 12, Volume 5] [Revised as of January 1, 2004] From the U.S. Government Printing Office via GPO Access") [Code of Federal Regulations] [Title 12, Volume 5] [Revised as of January 1, 2004] From the U.S. Government Printing Office via GPO Access TITLE 12--BANKS AND BANKING CHAPTER V--OFFICE OF THRIFT SUPERVISION,

[Code of Federal Regulations] [Title 12, Volume 5] [Revised as of January 1, 2004] From the U.S. Government Printing Office via GPO Access TITLE 12--BANKS AND BANKING CHAPTER V--OFFICE OF THRIFT SUPERVISION,

APPRAISER & ASSESSOR Real Estate Tax Valuation Overview and Issues

APPRAISER & ASSESSOR Real Estate Tax Valuation Overview and Issues James R. Johnston, MAI, SRA J. Michael Tarello, MAI, ASA, MRA May 20, 2015 BOSTON Property Advisors Vision Government Solutions AGENDA

APPRAISER & ASSESSOR Real Estate Tax Valuation Overview and Issues James R. Johnston, MAI, SRA J. Michael Tarello, MAI, ASA, MRA May 20, 2015 BOSTON Property Advisors Vision Government Solutions AGENDA

REED APPRAISAL COMPANY REAL PROPERTY APPRAISERS AND CONSULTANTS

REAL PROPERTY APPRAISERS AND CONSULTANTS 100 SOUTH KENTUCKY AVENUE #230 ip.o. BOX 1645 ilakeland, FLORIDA 33802-1645 OFFICE: (863) 688-6718 ifax: (863) 688-5993iEMAIL: stan@reedappraisalco.com TO: Henry

REAL PROPERTY APPRAISERS AND CONSULTANTS 100 SOUTH KENTUCKY AVENUE #230 ip.o. BOX 1645 ilakeland, FLORIDA 33802-1645 OFFICE: (863) 688-6718 ifax: (863) 688-5993iEMAIL: stan@reedappraisalco.com TO: Henry

Chapter 5 Fee Appraiser Responsibilities

Chapter 5 Fee Appraiser Responsibilities The fee appraiser is responsible for all aspects of the appraisal process. Important: Certain key appraisal functions may not be delegated to anyone else. Failure

Chapter 5 Fee Appraiser Responsibilities The fee appraiser is responsible for all aspects of the appraisal process. Important: Certain key appraisal functions may not be delegated to anyone else. Failure

Clark County Cooperative Management Area (CMA) Deed Modification Policy

Deed Modification Policy") Clark County Cooperative Management Area (CMA) Deed Modification Policy Policy Number: CMA-1.0 Effective Date: 5/7/13 Revised: New Subject: SUMMARY Previous CMA land that was conveyed to private parties

Clark County Cooperative Management Area (CMA) Deed Modification Policy Policy Number: CMA-1.0 Effective Date: 5/7/13 Revised: New Subject: SUMMARY Previous CMA land that was conveyed to private parties

RESTRICTED APPRAISAL REPORT

Restricted Use Appraisal Report Thomas J. Schulte & Associates Page #1 RESTRICTED APPRAISAL REPORT SUBJECT ASSIGNMENT Property City: Zip Code: County: Legal Description: Assessor's Parcel #: Tax Year:

Restricted Use Appraisal Report Thomas J. Schulte & Associates Page #1 RESTRICTED APPRAISAL REPORT SUBJECT ASSIGNMENT Property City: Zip Code: County: Legal Description: Assessor's Parcel #: Tax Year:

As Of: Prepared For: Prepared By:

of 216 SW 131st St As Of: 06/11/11 Prepared For: Prime Pacific Bank 2502 196th St SW Lynnwood WA 98036 Prepared By: Cynthia A. Nagle, CREA 922 N Cedar St Tacoma, WA 98406 RESTRICTED APPRAISAL REPORT Restriction

of 216 SW 131st St As Of: 06/11/11 Prepared For: Prime Pacific Bank 2502 196th St SW Lynnwood WA 98036 Prepared By: Cynthia A. Nagle, CREA 922 N Cedar St Tacoma, WA 98406 RESTRICTED APPRAISAL REPORT Restriction

Appraisal and Market Analysis of Indoor Waterpark Resorts

Appraisal and Market Analysis of Indoor Waterpark Resorts By David J. Sangree, MAI, CPA, ISHC An appraisal of an indoor waterpark resort is similar to other appraisals in that it is a professional appraiser

Appraisal and Market Analysis of Indoor Waterpark Resorts By David J. Sangree, MAI, CPA, ISHC An appraisal of an indoor waterpark resort is similar to other appraisals in that it is a professional appraiser

The TAUREAN Residential Valuation System An Overview

The TAUREAN Residential Valuation System An Overview By Michael L. Robbins, Ph.D., CRE Taurean Residential Valuation Services, LLC 150 N. Sunny Slope Road, Suite 225, Brookfield, WI 53005 Phone: (262)

The TAUREAN Residential Valuation System An Overview By Michael L. Robbins, Ph.D., CRE Taurean Residential Valuation Services, LLC 150 N. Sunny Slope Road, Suite 225, Brookfield, WI 53005 Phone: (262)

Topics 1. About BC Assessment 2. Valuation 3. Classification 4. Key dates 5. Assessments & taxes assessment roll 2

Overview of 2018 Assessment Roll Peace River Regional District David Keough, Deputy Assessor Tracey Love, Senior Appraiser Topics 1. About BC Assessment 2. Valuation 3. Classification 4. Key dates 5. Assessments

Overview of 2018 Assessment Roll Peace River Regional District David Keough, Deputy Assessor Tracey Love, Senior Appraiser Topics 1. About BC Assessment 2. Valuation 3. Classification 4. Key dates 5. Assessments

Village of Scarsdale

Village of Scarsdale VILLAGE HALL / 1001 POST ROAD / SCARSDALE, NY 10583 914.722.1110 / WWW.SCARSDALE.COM Village Wide Revaluation Frequently Asked Questions Q1. How was the land value for each parcel

Village of Scarsdale VILLAGE HALL / 1001 POST ROAD / SCARSDALE, NY 10583 914.722.1110 / WWW.SCARSDALE.COM Village Wide Revaluation Frequently Asked Questions Q1. How was the land value for each parcel

Introduction. Market Value Assessment in Saskatchewan Handbook. Introduction

Market Value Assessment in Saskatchewan Handbook Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass Appraisal for

Market Value Assessment in Saskatchewan Handbook Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass Appraisal for

Mike Dalton Jr. and Associates. Christina Adams INVOICE NUMBER Mike Dalton Jr. and Associates 8191 Wethersfield Drive. PB125 Germantown, TN 38138

Mike Dalton Jr. and Associates FROM: INVOICE Christina Adams INVOICE NUMBER Mike Dalton Jr. and Associates 8191 Wethersfield Drive Germantown, TN 38138 DATE 08/14/2016 Telephone Number: (901) 674-0239

Mike Dalton Jr. and Associates FROM: INVOICE Christina Adams INVOICE NUMBER Mike Dalton Jr. and Associates 8191 Wethersfield Drive Germantown, TN 38138 DATE 08/14/2016 Telephone Number: (901) 674-0239

Land and Property Terminology

513-721-LAND(5263) Land and Property Terminology What is Acreage? Acreage is more than one acre. An acre was originally an English unit of land area designating a day's plowing for a yoke of oxen, now

513-721-LAND(5263) Land and Property Terminology What is Acreage? Acreage is more than one acre. An acre was originally an English unit of land area designating a day's plowing for a yoke of oxen, now

PREPARING FOR THE MINNESOTA INCOME PROPERTY CASE STUDY EXAM WORKSHOP

PREPARING FOR THE MINNESOTA INCOME PROPERTY CASE STUDY EXAM WORKSHOP Date: September 18, 2018 Location: Country Inn & Suites Chanhassen, MN Instructor: Bob Wilson, CAE, ASA Revised October, 2017 PREPARING

PREPARING FOR THE MINNESOTA INCOME PROPERTY CASE STUDY EXAM WORKSHOP Date: September 18, 2018 Location: Country Inn & Suites Chanhassen, MN Instructor: Bob Wilson, CAE, ASA Revised October, 2017 PREPARING

BUSI 330 Suggested Answers to Review and Discussion Questions: Lesson 1

BUSI 330 Suggested Answers to Review and Discussion Questions: Lesson 1 1. The three characteristics necessary to gain professional recognition are: Integrity, Competence, and Provide Quality Work. Students

BUSI 330 Suggested Answers to Review and Discussion Questions: Lesson 1 1. The three characteristics necessary to gain professional recognition are: Integrity, Competence, and Provide Quality Work. Students

Discussing Green Building & Property Valuation U.S. Green Building Council Washington, D.C. -- September 16, 2014

Discussing Green Building & Property Valuation U.S. Green Building Council Washington, D.C. -- September 16, 2014 M. Lance Coyle, MAI, SRA, CCIM 2015 President of the Appraisal Institute About the Appraisal

Discussing Green Building & Property Valuation U.S. Green Building Council Washington, D.C. -- September 16, 2014 M. Lance Coyle, MAI, SRA, CCIM 2015 President of the Appraisal Institute About the Appraisal

Uniform Agricultural Appraisal Report

File No. Uniform Agricultural Appraisal Report Prepared For: Intended User: Prepared By: Date Prepared: UAAR Agri management Uniform Agricultural Appraisal Report File No # Property Identification Owner/Occupant:

File No. Uniform Agricultural Appraisal Report Prepared For: Intended User: Prepared By: Date Prepared: UAAR Agri management Uniform Agricultural Appraisal Report File No # Property Identification Owner/Occupant:

HUNTING LEASES AND TERMS By Carr Gibson and Tom Keith, MAI

HUNTING LEASES AND TERMS By Carr Gibson and Tom Keith, MAI 2012 Tom J. Keith & Associates, Inc. Some of the terms and conditions affecting hunting lease rates are outlined in the following discussion.

HUNTING LEASES AND TERMS By Carr Gibson and Tom Keith, MAI 2012 Tom J. Keith & Associates, Inc. Some of the terms and conditions affecting hunting lease rates are outlined in the following discussion.

ZELL & ASSOCIATES Real Estate Appraisers and Counselors

ZELL & ASSOCIATES Real Estate Appraisers and Counselors A Complete Appraisal Report of: 7.47 Acres of Land Known as the: SE Division Property Located At: 15004 SE Division Street Portland OR, 97236 Prepared

ZELL & ASSOCIATES Real Estate Appraisers and Counselors A Complete Appraisal Report of: 7.47 Acres of Land Known as the: SE Division Property Located At: 15004 SE Division Street Portland OR, 97236 Prepared

Restricted Use Appraisal Report Of a development site

A development site Located at: 700' E of SEC of 6th Avenue and 328 St Homestead, Florida As of November 7, 2017 Restricted Use Appraisal Report Of a development site Restricted Use Appraisal Report Of

A development site Located at: 700' E of SEC of 6th Avenue and 328 St Homestead, Florida As of November 7, 2017 Restricted Use Appraisal Report Of a development site Restricted Use Appraisal Report Of

UPDATED MARKET VALUE APPRAISAL. Day Care/Senior Center Property and Excess Parcel Governors Drive Olympia Fields, Illnois.

J _,i UPDATED MARKET VALUE APPRASAL Day Care/Senior Center Property and Excess Parcel 20080 Governors Drive Olympia Fields, llnois _ as of: March 16, 2007 Prepared for: Mr. Steve Townsend, Vice President

J _,i UPDATED MARKET VALUE APPRASAL Day Care/Senior Center Property and Excess Parcel 20080 Governors Drive Olympia Fields, llnois _ as of: March 16, 2007 Prepared for: Mr. Steve Townsend, Vice President

APPRAISAL REPORT. Vacant Commercial Land SW 268 th Street Miami, FL Cruz Appraisals, Inc SW 72 nd Street, Suite 263 Miami, FL 33173

APPRAISAL REPORT Prepared for Mr Jorge Palomeras Jpal Marketing Corporation Property Appraised Vacant Commercial Land 12711 SW 268 th Street Miami, FL 33032 Date of Valuation October 6, 2017 Prepared by

APPRAISAL REPORT Prepared for Mr Jorge Palomeras Jpal Marketing Corporation Property Appraised Vacant Commercial Land 12711 SW 268 th Street Miami, FL 33032 Date of Valuation October 6, 2017 Prepared by

Market Value What Does It Really Mean?

Market Value What Does It Really Mean? K. Erik Friess, Esq. Allen Matkins Philip D. Kopp, Esq. Newmeyer & Dillion, LLP Moderator Michael V. Sanders, MAI, SRA Coastline Realty Advisors 50 th Annual Litigation

Market Value What Does It Really Mean? K. Erik Friess, Esq. Allen Matkins Philip D. Kopp, Esq. Newmeyer & Dillion, LLP Moderator Michael V. Sanders, MAI, SRA Coastline Realty Advisors 50 th Annual Litigation

MIAMI-DADE EXPRESSWAY AUTHORITY PROPERTY ACQUISITION POLICY

MIAMI-DADE EXPRESSWAY AUTHORITY PROPERTY ACQUISITION POLICY PURPOSE It is the policy of the Miami-Dade Expressway Authority to acquire property in an economical and efficient manner pursuant to MDX s statutorily

MIAMI-DADE EXPRESSWAY AUTHORITY PROPERTY ACQUISITION POLICY PURPOSE It is the policy of the Miami-Dade Expressway Authority to acquire property in an economical and efficient manner pursuant to MDX s statutorily

Special Purpose Properties. Special Valuation Considerations

Special Purpose Properties Special Valuation Considerations 2017 Case Study in Ottawa: New Automobile Dealership Many brand-specific specialties Cost: $4,000,000 (including land and a developer fee) Sales

Special Purpose Properties Special Valuation Considerations 2017 Case Study in Ottawa: New Automobile Dealership Many brand-specific specialties Cost: $4,000,000 (including land and a developer fee) Sales

EvaluePro Real Estate Restricted Appraisal Report

EvaluePro Real Estate Restricted Appraisal Report EvaluePro Highlights Property Street: 1000 Main Street City: Anytown State: NC Zip: 12345 Property Owner: Mr. & Mrs. Property Owner Estimated Market Value:

EvaluePro Real Estate Restricted Appraisal Report EvaluePro Highlights Property Street: 1000 Main Street City: Anytown State: NC Zip: 12345 Property Owner: Mr. & Mrs. Property Owner Estimated Market Value:

LAND APPRAISAL REPORT

IDENTIFICATION LAND APPRAISAL REPORT Page #1 File No. Borrower None Census Tract * Map Reference 462820011000315 Property Address NWC Gaar and Pleasant View Roads City Richmond County Wayne State IN Zip

IDENTIFICATION LAND APPRAISAL REPORT Page #1 File No. Borrower None Census Tract * Map Reference 462820011000315 Property Address NWC Gaar and Pleasant View Roads City Richmond County Wayne State IN Zip

Revaluation process ongoing in Norwalk

Revaluation process ongoing in Norwalk Property owners will have the opportunity to appeal assessment beginning December 5 (Norwalk, Conn.) The City of Norwalk is in the final phase of its revaluation

Revaluation process ongoing in Norwalk Property owners will have the opportunity to appeal assessment beginning December 5 (Norwalk, Conn.) The City of Norwalk is in the final phase of its revaluation

Colorado Appraisal Consultants

Colorado Appraisal Consultants SUBJECT Individual Condominium Unit Appraisal Report File # The purpose of this summary appraisal report is to provide the lender/client with an accurate, and adequately

Colorado Appraisal Consultants SUBJECT Individual Condominium Unit Appraisal Report File # The purpose of this summary appraisal report is to provide the lender/client with an accurate, and adequately

Individual Condominium Unit Appraisal Report

The purpose of this summary appraisal report is to provide the lender/client with an accurate, and adequately supported, opinion of the market value of the subject property. SUBJECT Property Address Unit

The purpose of this summary appraisal report is to provide the lender/client with an accurate, and adequately supported, opinion of the market value of the subject property. SUBJECT Property Address Unit

1. Governmental powers over private property rights include a. power of taxation. b. power of escheat. c. police power. d.

Chapter 4 Multiple Choice Questions / Page 1 Chapter 4 Multiple Choice Questions 1. Governmental powers over private property rights include a. power of taxation. b. power of escheat. c. police power.

Chapter 4 Multiple Choice Questions / Page 1 Chapter 4 Multiple Choice Questions 1. Governmental powers over private property rights include a. power of taxation. b. power of escheat. c. police power.

Fannie Mae Selling Guide (04/12/2002) Part XI - Property and Appraisal Guidelines

Part XI - Property and Appraisal Guidelines") Fannie Mae Selling Guide (04/12/2002) Part XI - Property and Appraisal Guidelines This Part-Property and Appraisal Guidelines-details our general requirements for analyzing the property appraisal aspects

Fannie Mae Selling Guide (04/12/2002) Part XI - Property and Appraisal Guidelines This Part-Property and Appraisal Guidelines-details our general requirements for analyzing the property appraisal aspects

HIGHEST & BEST USE CHALLENGES AND SUPPORTING ADJUSTMENTS 6/11/2018 KEN MROZEK, MAI, SRA, ASA HIGHEST AND BEST USE CHALLENGES AND

HIGHEST & BEST USE CHALLENGES AND SUPPORTING ADJUSTMENTS KEN MROZEK, MAI, SRA, ASA KEN MROZEK, MAI, SRA, ASA Appraiser for 15 years Commercial and Residential Appraisals Partner and President of ARC Appraisals

HIGHEST & BEST USE CHALLENGES AND SUPPORTING ADJUSTMENTS KEN MROZEK, MAI, SRA, ASA KEN MROZEK, MAI, SRA, ASA Appraiser for 15 years Commercial and Residential Appraisals Partner and President of ARC Appraisals

Multifamily Seller/Servicer Guide Chapter 12: Appraiser and Appraisal Requirements

Multifamily Seller/Servicer Guide Chapter 12: Appraiser and Appraisal Requirements Please contact Marty Skolnik at Martin_Skolnik@freddiemac.com if you have questions about Freddie Mac s appraisal requirements.

Multifamily Seller/Servicer Guide Chapter 12: Appraiser and Appraisal Requirements Please contact Marty Skolnik at Martin_Skolnik@freddiemac.com if you have questions about Freddie Mac s appraisal requirements.

March 20, TO: All MAAO Members FROM: MAAO President Stephen C. Behrenbrinker, CAE, RE: MAAO-DOR Foreclosure Advisory Document

March 20, 2008 TO: All MAAO Members FROM: MAAO President Stephen C. Behrenbrinker, CAE, RE: MAAO-DOR Foreclosure Advisory Document Greetings! On behalf of the Minnesota Association of Assessing Officers

March 20, 2008 TO: All MAAO Members FROM: MAAO President Stephen C. Behrenbrinker, CAE, RE: MAAO-DOR Foreclosure Advisory Document Greetings! On behalf of the Minnesota Association of Assessing Officers

CITY OF OWATONNA ASSESSMENT REPORT. Steele County Assessor s Department. William G. Effertz, SAMA Steele County Assessor

2017 CITY OF OWATONNA ASSESSMENT REPORT Steele County Assessor s Department William G. Effertz, SAMA Steele County Assessor Tyler Diersen, AMA, Assistant County Assessor April 11, 2017 2017 Assessment

2017 CITY OF OWATONNA ASSESSMENT REPORT Steele County Assessor s Department William G. Effertz, SAMA Steele County Assessor Tyler Diersen, AMA, Assistant County Assessor April 11, 2017 2017 Assessment

APPRAISAL OF REAL PROPERTY LOCATED AT: FOR: AS OF: BY:

APPRAISAL OF REAL PROPERTY LOCATED AT: 489 MEADOWS EDGE COURT DEED BOOK 2896, PAGE 2759 CLEMMONS, NC 27012 FOR: ESTATE OF WILLIAM C. McINTOSH % BAILEY & THOMAS P.O. BOX 52 WINSTON-SALEM, NC 27102 AS OF:

APPRAISAL OF REAL PROPERTY LOCATED AT: 489 MEADOWS EDGE COURT DEED BOOK 2896, PAGE 2759 CLEMMONS, NC 27012 FOR: ESTATE OF WILLIAM C. McINTOSH % BAILEY & THOMAS P.O. BOX 52 WINSTON-SALEM, NC 27102 AS OF:

Office Building. Market Value Assessment in Saskatchewan Handbook. Office Building Valuation Guide

Market Value Assessment in Saskatchewan Handbook Office Building Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass

Market Value Assessment in Saskatchewan Handbook Office Building Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass

METHODOLOGY GUIDE VALUING LANDS IN TRANSITION IN ONTARIO. Valuation Date: January 1, 2016

METHODOLOGY GUIDE VALUING LANDS IN TRANSITION IN ONTARIO Valuation Date: January 1, 2016 August 2017 August 22, 2017 The Municipal Property Assessment Corporation (MPAC) is responsible for accurately assessing

METHODOLOGY GUIDE VALUING LANDS IN TRANSITION IN ONTARIO Valuation Date: January 1, 2016 August 2017 August 22, 2017 The Municipal Property Assessment Corporation (MPAC) is responsible for accurately assessing

What is Fair Market Value in the Timber Industry?

What is Fair Market Value in the Timber Industry? Roger Lord Principal Mason, Bruce & Girard www.masonbruce.com Presented at 2014 OSCPA Forest Products Conference June 27, 2014 Eugene, Oregon Natural Natural

What is Fair Market Value in the Timber Industry? Roger Lord Principal Mason, Bruce & Girard www.masonbruce.com Presented at 2014 OSCPA Forest Products Conference June 27, 2014 Eugene, Oregon Natural Natural

APPRAISAL REPORT OF THE REAL PROPERTY LOCATED AT. Enterprise Rd Dillon, SC Ronnie Gardner. March 1, 2018

APPRAISAL REPORT OF THE REAL PROPERTY LOCATED AT Dillon, SC 29536 for as of March 1, 2018 by David McLaurin 105 West Harrison Street Dillon, SC 29536 IDENTIFICATION NEIGHBORHOOD SITE MARKET DATA ANALYSIS

APPRAISAL REPORT OF THE REAL PROPERTY LOCATED AT Dillon, SC 29536 for as of March 1, 2018 by David McLaurin 105 West Harrison Street Dillon, SC 29536 IDENTIFICATION NEIGHBORHOOD SITE MARKET DATA ANALYSIS

SUMMARY APPRAISAL REPORT

File No. SUMMARY APPRAISAL REPORT OF THE REAL PROPERTY LOCATED AT 6332 Middlebelt Road Garden City, MI 48135-2163 for Mr. Edgar J. Dietrich 15001 Charlevoix Grosse Pointe Park, MI 48230 as of February

File No. SUMMARY APPRAISAL REPORT OF THE REAL PROPERTY LOCATED AT 6332 Middlebelt Road Garden City, MI 48135-2163 for Mr. Edgar J. Dietrich 15001 Charlevoix Grosse Pointe Park, MI 48230 as of February

APPRAISAL REPORT OF ±1,519 ACRES OF VACANT LAND LOCATED IN BABCOCK RANCH ALVA, FLORIDA

APPRAISAL REPORT OF ±1,519 ACRES OF VACANT LAND LOCATED IN BABCOCK RANCH ALVA, FLORIDA FOR LEE COUNTY - DEPARTMENT OF COUNTY LANDS CONSERVATION 20/20 PARCEL 450-3 NOVEMBER 2018 Diversified Appraisal, Inc.

APPRAISAL REPORT OF ±1,519 ACRES OF VACANT LAND LOCATED IN BABCOCK RANCH ALVA, FLORIDA FOR LEE COUNTY - DEPARTMENT OF COUNTY LANDS CONSERVATION 20/20 PARCEL 450-3 NOVEMBER 2018 Diversified Appraisal, Inc.

BADGER Appraisals, LLC

BADGER Appraisals, LLC PO Box 2222 Appleton, WI 54912 T (920) 687-9000 / F (920) 687-9244 info@badgerappraisals.com www.badgerappraisals.com Residential Appraisal Service Brown * Calumet * Outagamie *

BADGER Appraisals, LLC PO Box 2222 Appleton, WI 54912 T (920) 687-9000 / F (920) 687-9244 info@badgerappraisals.com www.badgerappraisals.com Residential Appraisal Service Brown * Calumet * Outagamie *

PURCHASE PRICE ALLOCATION IN REAL ESTATE TRANSACTIONS: Does A + B + C Always Equal Value?

PURCHASE PRICE ALLOCATION IN REAL ESTATE TRANSACTIONS: Does A + B + C Always Equal Value? Morris A. Ellison, Esq. 1 Womble Carlyle Sandridge & Rice, LLP Nancy L. Haggerty, Esq. Michael Best & Friedrich,

PURCHASE PRICE ALLOCATION IN REAL ESTATE TRANSACTIONS: Does A + B + C Always Equal Value? Morris A. Ellison, Esq. 1 Womble Carlyle Sandridge & Rice, LLP Nancy L. Haggerty, Esq. Michael Best & Friedrich,

What is an Appraisal? Equity Valuations and Consulting Services Ltd.

What is an Appraisal? Equity Valuations and Consulting Services Ltd. Reid Umlah AACI designation since 1993 Principal of Equity Valuations and Consulting Services Ltd. Experience with First Nations Lands

What is an Appraisal? Equity Valuations and Consulting Services Ltd. Reid Umlah AACI designation since 1993 Principal of Equity Valuations and Consulting Services Ltd. Experience with First Nations Lands

FILED: NEW YORK COUNTY CLERK 05/31/ :25 AM INDEX NO /2017 NYSCEF DOC. NO. 1 RECEIVED NYSCEF: 05/31/2017

SUPREME COURT OF THE STATE OF NEW YORK COUNTY OF NEW YORK -------------------------------------------------------------------x THE CITY OF NEW YORK, - against - Plaintiff, FC 42ND STREET ASSOCIATES, L.P.,

SUPREME COURT OF THE STATE OF NEW YORK COUNTY OF NEW YORK -------------------------------------------------------------------x THE CITY OF NEW YORK, - against - Plaintiff, FC 42ND STREET ASSOCIATES, L.P.,

THE CORPORATION OF THE CITY OF WINDSOR POLICY

THE CORPORATION OF THE CITY OF WINDSOR POLICY Service Area: Office of the City Solicitor Policy No.: Department: Legal Approval Date: February 3, 2014 Division: Real Estate Approved By: CR 30/2014 Effective

THE CORPORATION OF THE CITY OF WINDSOR POLICY Service Area: Office of the City Solicitor Policy No.: Department: Legal Approval Date: February 3, 2014 Division: Real Estate Approved By: CR 30/2014 Effective

California Real Estate License Exam Prep: Unlocking the DRE Salesperson and Broker Exam 4th Edition

California Real Estate License Exam Prep: Unlocking the DRE Salesperson and Broker Exam 4th Edition ANSWER SHEET INSTRUCTIONS: The exam consists of multiple choice questions. Multiple choice questions

California Real Estate License Exam Prep: Unlocking the DRE Salesperson and Broker Exam 4th Edition ANSWER SHEET INSTRUCTIONS: The exam consists of multiple choice questions. Multiple choice questions

Modeling your Appraisal Report to Meet your Client's Needs in the Commercial Marketplace

Modeling your Appraisal Report to Meet your Client's Needs in the Commercial Marketplace Myth #1 The Final Estimate of Value is the Only Area of the Report Anyone Reads Financial Institutions -Interagency

Modeling your Appraisal Report to Meet your Client's Needs in the Commercial Marketplace Myth #1 The Final Estimate of Value is the Only Area of the Report Anyone Reads Financial Institutions -Interagency

Saskatchewan Municipal Board Assessment Appeals Committee

Saskatchewan Municipal Board Assessment Appeals Committee Appeal: 2009-0039 RESPONDENT: Town of Hudson Bay In the matter of an appeal to the Assessment Appeals Committee, Saskatchewan Municipal Board,

Saskatchewan Municipal Board Assessment Appeals Committee Appeal: 2009-0039 RESPONDENT: Town of Hudson Bay In the matter of an appeal to the Assessment Appeals Committee, Saskatchewan Municipal Board,

Dear Valuation Professional

Dear Valuation Professional First American Mortgage Solutions LLC has a new product offering that we would like you to consider adding to your list of services with us - (Property Assessment Collateral

Dear Valuation Professional First American Mortgage Solutions LLC has a new product offering that we would like you to consider adding to your list of services with us - (Property Assessment Collateral

Sales Associate Course

Sales Associate Course Chapter Sixteen Appraisal 1 2 Appraiser Specific amount Impartial (non biased) Defendable Estimate (Opinion) of value Fee based on time and difficulty Must follow Uniform Standards

Sales Associate Course Chapter Sixteen Appraisal 1 2 Appraiser Specific amount Impartial (non biased) Defendable Estimate (Opinion) of value Fee based on time and difficulty Must follow Uniform Standards

Appraisal Review: Analyzing the 1004

Appraisal Review: Analyzing the 1004 1 LIVE ONLINE PARTICIPANT GUIDE Version: 8.12 Table of Contents The Purpose of the Appraisal... 3 Define Market Value... 3 Scenario 1 (John Johnson report) - 1004 Uniform

Appraisal Review: Analyzing the 1004 1 LIVE ONLINE PARTICIPANT GUIDE Version: 8.12 Table of Contents The Purpose of the Appraisal... 3 Define Market Value... 3 Scenario 1 (John Johnson report) - 1004 Uniform

The Value of Real Estate

Chapter 11 The Value of Real Estate 1 Chapter Objectives Describe how several broad factors and specific principles impact the value of property. Contrast value, price, and cost. Define the necessary factors

Chapter 11 The Value of Real Estate 1 Chapter Objectives Describe how several broad factors and specific principles impact the value of property. Contrast value, price, and cost. Define the necessary factors

APPRAISAL OF 1117 MONROE STREET, VICKSBURG, MS 39180

APPRAISAL OF 1117 MONROE STREET, VICKSBURG, MS 39180 CLIENT/INTENDED USER: GLENN TRIPLETT INTENDED USE/USER: TO ASSIST THE CLIENT IN MAKING A PURCHASING DECISION. THIS REPORT IS NOT INTENDED FOR ANY OTHER

APPRAISAL OF 1117 MONROE STREET, VICKSBURG, MS 39180 CLIENT/INTENDED USER: GLENN TRIPLETT INTENDED USE/USER: TO ASSIST THE CLIENT IN MAKING A PURCHASING DECISION. THIS REPORT IS NOT INTENDED FOR ANY OTHER

If It s Property Tax Exempt, Tax It Anyway!

If It s Property Tax Exempt, Tax It Anyway! How Local Jurisdictions Tax Publicly Owned Properties Cutchin Powell Principal Ryan, LLC Washington, DC cutchin.powell@ryan.com Colin Fraser Associate Greenberg

If It s Property Tax Exempt, Tax It Anyway! How Local Jurisdictions Tax Publicly Owned Properties Cutchin Powell Principal Ryan, LLC Washington, DC cutchin.powell@ryan.com Colin Fraser Associate Greenberg

2013 Updates Assessment Quality Minister s Guidelines and Recording and Reporting Information for Assessment Audit and Equalized Assessment Manual

IB Bulletin No. 13-03 October 2013 2013 Updates Assessment Quality Minister s Guidelines and Recording and Reporting Information for Assessment Audit and Equalized Assessment Manual The Minister of Municipal

IB Bulletin No. 13-03 October 2013 2013 Updates Assessment Quality Minister s Guidelines and Recording and Reporting Information for Assessment Audit and Equalized Assessment Manual The Minister of Municipal

How to Read a Real Estate Appraisal Report

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

BADGER Appraisals, LLC

BADGER Appraisals, LLC PO Box 2222 Appleton, WI 54912 T (920) 687-9000 / F (920) 687-9244 info@badgerappraisals.com www.badgerappraisals.com Appraisal Service Brown * Calumet * Outagamie * Winnebago APPRAISAL

BADGER Appraisals, LLC PO Box 2222 Appleton, WI 54912 T (920) 687-9000 / F (920) 687-9244 info@badgerappraisals.com www.badgerappraisals.com Appraisal Service Brown * Calumet * Outagamie * Winnebago APPRAISAL

Invesco Real Estate Acquisitions

Acquisitions With the corporate office centrally located in Dallas, Texas and regional acquisitions offices in New York, San Francisco and Orange County, Invesco is able to effectively source acquisition

Acquisitions With the corporate office centrally located in Dallas, Texas and regional acquisitions offices in New York, San Francisco and Orange County, Invesco is able to effectively source acquisition

AG-AMERICA COMMERCIAL FARM AND RANCH COLLATERAL VALUATION GUIDE

AG-AMERICA COMMERCIAL FARM AND RANCH COLLATERAL VALUATION GUIDE Table of Contents CHAPTER CV101 COLLATERAL VALUATION STANDARDS AND GUIDES... 1 CV101.1 Overview... 1 General Guidance on Terms:... 1 CHAPTER

AG-AMERICA COMMERCIAL FARM AND RANCH COLLATERAL VALUATION GUIDE Table of Contents CHAPTER CV101 COLLATERAL VALUATION STANDARDS AND GUIDES... 1 CV101.1 Overview... 1 General Guidance on Terms:... 1 CHAPTER

DEMONSTRATION APPRAISAL REPORT OFA SINGLE-FAMILY RESIDENCE LOCATED AT Clear Spring Road Minnetonka MN Prepared for

DEMONSTRATION APPRAISAL REPORT OFA SINGLE-FAMILY RESIDENCE LOCATED AT 4932 Clear Spring Road Minnetonka MN 55345 Prepared for International Association of Assessing Officers 314 West 10th Street Kansas

DEMONSTRATION APPRAISAL REPORT OFA SINGLE-FAMILY RESIDENCE LOCATED AT 4932 Clear Spring Road Minnetonka MN 55345 Prepared for International Association of Assessing Officers 314 West 10th Street Kansas

APPRAISAL OF REAL PROPERTY

Main File No. Busick 1706 Page #1 APPRAISAL OF REAL PROPERTY LOCATED AT Burnsville, NC Deed Book 725 Page 505 FOR 8777 Holiday Springs Rd Rockledge, FL 32955 OPINION OF VALUE 660,000 AS OF 06/26/2017 BY

Main File No. Busick 1706 Page #1 APPRAISAL OF REAL PROPERTY LOCATED AT Burnsville, NC Deed Book 725 Page 505 FOR 8777 Holiday Springs Rd Rockledge, FL 32955 OPINION OF VALUE 660,000 AS OF 06/26/2017 BY

Exterior Only Inspection Residential Appraisal Report File #

SUBJECT Summary Appraisal Report Brian J. Davis & Associates Exterior Only Inspection Residential Appraisal Report File # Page #3 The purpose of this summary appraisal report is to provide the lender/client

SUBJECT Summary Appraisal Report Brian J. Davis & Associates Exterior Only Inspection Residential Appraisal Report File # Page #3 The purpose of this summary appraisal report is to provide the lender/client

Basic Appraisal Procedures

Hondros Learning Basic Appraisal Procedures Timed Outline Topic Area Reference(s) Learning Objectives The student will be able to identify and/or apply: Teaching Method Time Segment (Minutes) Day 1 Chapter

Hondros Learning Basic Appraisal Procedures Timed Outline Topic Area Reference(s) Learning Objectives The student will be able to identify and/or apply: Teaching Method Time Segment (Minutes) Day 1 Chapter

MODULE 7-A: APPRAISALS, BPOS AND USPAP

MODULE 7-A: APPRAISALS, BPOS AND USPAP LEARNING OBJECTIVES One of the most challenging aspects of the real estate business is the development of prices or values of the rights to real estate. Buyers and

MODULE 7-A: APPRAISALS, BPOS AND USPAP LEARNING OBJECTIVES One of the most challenging aspects of the real estate business is the development of prices or values of the rights to real estate. Buyers and

METHODOLOGY GUIDE VALUING MOTELS IN ONTARIO. Valuation Date: January 1, 2016

METHODOLOGY GUIDE VALUING MOTELS IN ONTARIO Valuation Date: January 1, 2016 AUGUST 2016 August 22, 2016 The Municipal Property Assessment Corporation (MPAC) is responsible for accurately assessing and

METHODOLOGY GUIDE VALUING MOTELS IN ONTARIO Valuation Date: January 1, 2016 AUGUST 2016 August 22, 2016 The Municipal Property Assessment Corporation (MPAC) is responsible for accurately assessing and

Understanding and Appealing Your Property Tax Bill

Understanding and Appealing Your Property Tax Bill Presented by: John Trowbridge Assessor Lisle Township Jean Kelly Assessor DuPage Township Gregory A. Boltz Assessor DG Township Hosted By: Basic Assessment

Understanding and Appealing Your Property Tax Bill Presented by: John Trowbridge Assessor Lisle Township Jean Kelly Assessor DuPage Township Gregory A. Boltz Assessor DG Township Hosted By: Basic Assessment

APPRAISAL REPORT 7.64 ACRE SHOVEL READY SITE 24 ASPEN PARK BOULEVARD TOWN OF DEWITT ONONDAGA COUNTY, NEW YORK

APPRAISAL REPORT 7.64 ACRE SHOVEL READY SITE 24 ASPEN PARK BOULEVARD TOWN OF DEWITT ONONDAGA COUNTY, NEW YORK APPRAISAL REPORT 7.64 ACRE SHOVEL READY SITE 24 ASPEN PARK BOULEVARD TOWN OF DEWITT ONONDAGA

APPRAISAL REPORT 7.64 ACRE SHOVEL READY SITE 24 ASPEN PARK BOULEVARD TOWN OF DEWITT ONONDAGA COUNTY, NEW YORK APPRAISAL REPORT 7.64 ACRE SHOVEL READY SITE 24 ASPEN PARK BOULEVARD TOWN OF DEWITT ONONDAGA

Tax Court Market Occupancy v. Dark Store Theory. James Atchison Judy Engel Marc Manderscheid

Tax Court Market Occupancy v. Dark Store Theory James Atchison Judy Engel Marc Manderscheid Minnesota Case Law and Dark Store Theory Concepts Presented by: Marc Manderscheid Minnesota Case Law and Dark

Tax Court Market Occupancy v. Dark Store Theory James Atchison Judy Engel Marc Manderscheid Minnesota Case Law and Dark Store Theory Concepts Presented by: Marc Manderscheid Minnesota Case Law and Dark

Selling Part VII - Property and Appraisal Analysis

Selling Part VII - Property and Appraisal Analysis This Part--Property and Appraisal Analysis--details our general requirements for analyzing the property appraisal aspects of conventional mortgages secured

Selling Part VII - Property and Appraisal Analysis This Part--Property and Appraisal Analysis--details our general requirements for analyzing the property appraisal aspects of conventional mortgages secured

NCGS , ,

NCGS 105-283, 105-286, 105-317 Requires Counties to establish values based on current market conditions. Values should be at or near 100% of market value as of the reappraisal date. Counties MUST do a

NCGS 105-283, 105-286, 105-317 Requires Counties to establish values based on current market conditions. Values should be at or near 100% of market value as of the reappraisal date. Counties MUST do a

Water Investigation Zone No. 2 Fee Analysis Report Fiscal Year

SAN JOAQUIN COUNTY FLOOD CONTROL & WATER CONSERVATION DISTRICT Water Investigation Zone No. 2 Fee Analysis Report Fiscal Year 2017-2018 Prepared by: San Joaquin County Department of Public Works Water

SAN JOAQUIN COUNTY FLOOD CONTROL & WATER CONSERVATION DISTRICT Water Investigation Zone No. 2 Fee Analysis Report Fiscal Year 2017-2018 Prepared by: San Joaquin County Department of Public Works Water

60-HR FL Real Estate Broker Post-Licensing Learning Objectives by Lesson

Lesson 1: Starting a Real Estate Office SECTION 1: BROKERAGE OFFICE ESSENTIALS Recall the characteristics of business entities that may register as a real estate brokerage and the rules involved to operate

Lesson 1: Starting a Real Estate Office SECTION 1: BROKERAGE OFFICE ESSENTIALS Recall the characteristics of business entities that may register as a real estate brokerage and the rules involved to operate

BUSI 352 Learning Objectives

BUSI 352 Learning Objectives Purpose and Scope of the Course The Case Studies in Residential Appraisal course (BUSI 352) explores the depth and breadth of knowledge around the valuation of residential

BUSI 352 Learning Objectives Purpose and Scope of the Course The Case Studies in Residential Appraisal course (BUSI 352) explores the depth and breadth of knowledge around the valuation of residential

AVA. Accredited Valuation Analyst - AVA Exam.

NACVA AVA Accredited Valuation Analyst - AVA Exam TYPE: DEMO http://www.examskey.com/ava.html Examskey NACVA AVA exam demo product is here for you to test the quality of the product. This NACVA AVA demo

NACVA AVA Accredited Valuation Analyst - AVA Exam TYPE: DEMO http://www.examskey.com/ava.html Examskey NACVA AVA exam demo product is here for you to test the quality of the product. This NACVA AVA demo

Staff Analysis and Economic Impact Statement

Staff Analysis and Economic Impact Statement Measure: SR 13 REFERENCE: ACTION: Sponsor: Subject: Finance and Tax Committee Just Valuation of Property 1. FTC 2. TBRC Favorable Pre-meeting Date: March 13,

Staff Analysis and Economic Impact Statement Measure: SR 13 REFERENCE: ACTION: Sponsor: Subject: Finance and Tax Committee Just Valuation of Property 1. FTC 2. TBRC Favorable Pre-meeting Date: March 13,

Impact of Wind Turbines on Market Value of Texas Rural Land

Impact of Wind Turbines on Market Value of Texas Rural Land Gardner Appraisal Group Inc. Derry T. Gardner 147 E. Mistletoe Avenue San Antonio, TX 78212 www.gardnerappraisalgroup.com Prepared for the South

Impact of Wind Turbines on Market Value of Texas Rural Land Gardner Appraisal Group Inc. Derry T. Gardner 147 E. Mistletoe Avenue San Antonio, TX 78212 www.gardnerappraisalgroup.com Prepared for the South

Chapter 8 Qualifying Property

The 3 "Cs" of Lending Capacity to Pay does the borrower make enough money to repay loan? lenders use qualifying ratios Creditworthiness [Character] is the borrower likely to repay loan on time? lenders

The 3 "Cs" of Lending Capacity to Pay does the borrower make enough money to repay loan? lenders use qualifying ratios Creditworthiness [Character] is the borrower likely to repay loan on time? lenders

RESIDENTIAL APPRAISAL SUMMARY REPORT

SUBJECT ASSIGNMENT MARKET AREA DESCRIPTION Property City: Zip Code: County: Legal Description: Assessor's Parcel #: Tax Year: R.E. Taxes: $ Special Assessments: $ Borrower (if applicable): Current Owner

SUBJECT ASSIGNMENT MARKET AREA DESCRIPTION Property City: Zip Code: County: Legal Description: Assessor's Parcel #: Tax Year: R.E. Taxes: $ Special Assessments: $ Borrower (if applicable): Current Owner

TRAYNOR & ASSOCIATES, INC East 75 th Street Indianapolis, Indiana 46250

SUMMARY APPRAISAL REPORT November 15, 2013 11634 Maple Street Fishers, Indiana (Hamilton County) 13500 Effective Date of Valuation: As Is November 12, 2013 Appraisers: Joseph C. Traynor, MRICS, GAA Indiana

SUMMARY APPRAISAL REPORT November 15, 2013 11634 Maple Street Fishers, Indiana (Hamilton County) 13500 Effective Date of Valuation: As Is November 12, 2013 Appraisers: Joseph C. Traynor, MRICS, GAA Indiana

CITY OF JACKSONVILLE, FLORIDA

PROPERTY APPRAISER DEPARTMENT VISION: To earn the public s trust. DEPARTMENT MISSION: We will: Produce a fair, equitable and accurate tax roll as required by law. Focus on our customers the taxpayers.

PROPERTY APPRAISER DEPARTMENT VISION: To earn the public s trust. DEPARTMENT MISSION: We will: Produce a fair, equitable and accurate tax roll as required by law. Focus on our customers the taxpayers.

Board of Appeal and Equalization Handbook

Board of Appeal and Equalization Handbook This handbook was created to satisfy the training requirements of Minnesota Statutes, sections 274.014 and 274.135 Updated January 2018 Table of Contents Introduction...

Board of Appeal and Equalization Handbook This handbook was created to satisfy the training requirements of Minnesota Statutes, sections 274.014 and 274.135 Updated January 2018 Table of Contents Introduction...

$7,700,000. Airport Business Center FOR SALE PROPERTY NE 80th Ave, 7820 NE Holman Ave, 6130 NE 78th Ct Portland, OR 97218

$7,700,000 PROPERTY THOMAS MCDOWELL 503.225.8473 TomM@norris-stevens.com RAYMOND DUCHEK 503.225.8492 RaymondD@norris-stevens.com ±48,756 Rentable Square Feet 3 Building Complex Class B with Amenities Convenient

$7,700,000 PROPERTY THOMAS MCDOWELL 503.225.8473 TomM@norris-stevens.com RAYMOND DUCHEK 503.225.8492 RaymondD@norris-stevens.com ±48,756 Rentable Square Feet 3 Building Complex Class B with Amenities Convenient