TOPIC 6 - IAS 38 INTANGIBLE ASSETS

|

|

|

- Philippa Patrick

- 5 years ago

- Views:

Transcription

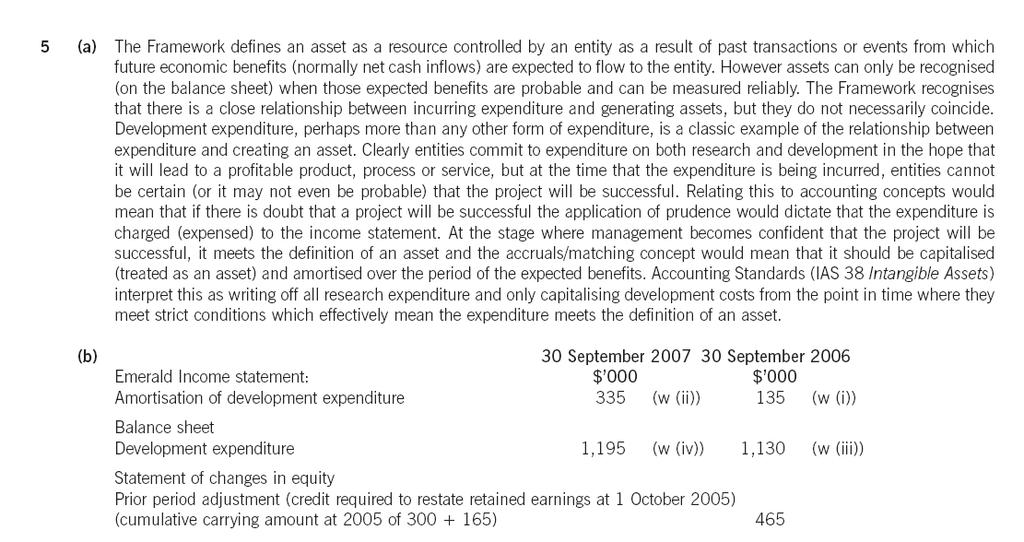

1 TOPIC 6 - IAS 38 INTANGIBLE ASSETS Objective: To set out the treatment of intangible assets that are not covered by other accounting standards - e.g. Goodwill acquired in a business combination is covered by IFRS 3 BUSINESS COMBINATIONS Most long term intangible assets are amortised over their expected useful life ( amortisation is the equivalent of depreciation) Definition: An intangible asset is an identifiable, non monetary asset without physical substance (e.g. Landing rights for an airline company) An intangible asset should be recognised if all the following criteria are met It is identifiable I It is controlled by the entity C Probable Inflow of future economic benefits P Reliable Measurement of Cost can be made RM 1

2 IAS 38 states that to be identifiable, an intangible asset Must be separable (capable of being separated or divided from the entity and sold, transferred, rented) or Must arise from contractual or other legal rights Control: An entity controls an intangible asset if it has the power to obtain the future economic benefits (usually net cash inflow) flowing from the resource e.g. Legal rights that are enforceable in court, copyrights Staff training and customers list are not intangible assets because they fail the control test staff could leave the business at any time and the customers on a customer list have no obligation to make future purchases Assets acquired as a result of a government grant (i.e. granting of Govt Licence) may be capitalised at fair value, along with a corresponding credit for the value of the grant. Asset and grant will be amortised/released over useful life. Net effect on profits is nil A testing facility built during the Development Phase is capitalised and depreciated in accordance with IAS 16 Internally Generated Intangibles: General Rule: Internally generated intangibles are generally not recognised in the financial statements due to failure of the identifiability test or its cost cannot be measured reliably Examples of Possible Intangible Assets include: Goodwill Acquired in a Business Combination Computer Software Patents Copyrights Motion Picture Films 2

3 Import Quotas Franchises Customer and Supplier Relationships In particular the following internally generated intangibles cannot be recognised Start Up, Pre Opening and Pre Operating Costs Training Costs Relocation Costs Advertising Costs Goodwill Brands Mastheads (e.g. Newspaper masthead) Publishing Titles Customer Lists Customer Relationships (whether contractual or non contractual) If some of the listed items are purchased from another business entity they might be recognised because Pass the identifiability test Cost capable of being reliably measured The exception to the ban on capitalising internally generated intangibles is Development Expenditure Research and Development Expenditure: Research: original and planned investigation undertaken to gain new scientific or technical knowledge and understanding Research Expenditure Examples Activities aimed at obtaining new knowledge 3

4 The search for, evaluation and final selection of, applications of research findings or other knowledge The search for alternatives for materials, devices, products, processes, systems or services The formulation, design, evaluation and final selection of possible alternatives for new or improved materials, devices, products, systems or services Development: the application of research findings or other knowledge to a plan or design for the production of new or substantially improved products, processes, systems or services before the start of commercial production or use Exam Note: Exam Note: If a question uses the word research then this is obviously an indicator to expense the expenditure. The overriding feature of expenditure during the research phase is that it tends to be exploratory and without a clearly defined outcome. Note: Marketing research to determine the optimal selling strategy is expensed. Development Expenditure Examples: Design, construction and testing of pre production prototypes Construction and operation of a pilot plant that is not large enough for economic commercial production Design of tools, jigs, moulds, and dies involving new technology Design, construction and testing of a chosen alternative for new or improved materials, products, processes, systems or services Accounting Treatment of Research Costs: The cost of research should not be recognised as an asset Such expenditure must be written off as an expense in the year in which incurred Accounting Treatment of Development Costs: Expenditure on development can only be capitalised as an intangible asset when all of the 6 following conditions are met 1. P robable Future Economic Benefits 2. I ntention to Complete and use/sell 4

5 3. R esources adequate to complete and use/sell 4. A bility to use/sell 5. T echnical Feasibility 6. E xpenditure can be reliably measured Memory Aid: PIRATE Failure to meet all 6 conditions means expenditure is treated as research costs Once such expenditure has been written off as an expense, it cannot subsequently be reinstated as an intangible asset N.B. Amortisation of capitalised development expenditure does not begin until the commercial use of the product, service or process has started matching concept - matching incomes from the development expenditure with expenses of development Amortisation of the capitalised development expenditure should be in accordance with the pattern in which the assets future economic benefits are consumed KEY POINT With development expenditure, as opposed to research costs, the development expenditure is incurred at a later stage in the project, and the probability of success should be more apparent - i.e. hence greater chance of assessing the probability of inflow of future economic benefits) On the other hand, because research costs are incurred earlier in a project, there is less likelihood of probable inflow of economic benefits at that stage, and part of the recognition criteria for an asset is failed and hence research costs are expensed Measurement of Intangibles: Initial measurement is at cost. For internally generated intangible asset (like development expenditure) cost is the expenditure incurred from the date when the asset first meets the recognition criteria (Exclude selling,admin & general overheads; training costs; advertising expenditure) 5

6 Subsequent Measurement Cost Model (Cost Acc Amortisation - Any Imp. Losses) or Revaluation Model (Fair Value Subsequent Acc Amortisation Subsequent Imp Losses) Rules on Revaluation gains/losses follow the guidance in IAS 16 Note, only intangible assets which can be traded in an active market where the items are homogenous, can be accounted for under the revaluation model. If an intangible asset cannot be traded in an active market (like a Trademark which is a bespoke intangible asset), then the cost model must be followed An Intangible asset which could be revalued is a Taxi Licence Amortisation & Impairment of Intangible Assets: Useful life of an intangible asset is either Finite Or Indefinite Finite Life: Intangible to be Amortised over its Useful Life Amortisation written off to profit or loss If indicators exist, then an impairment review should be carried out (As Per IAS 36 IMPAIRMENT OF ASSETS) Indefinite Life (N.B.) No Amortisation Impairment reviews to be carried out annually IAS 38 Intangible Assets 6

7 IAS 38 & IFRS 3: Deals with Purchased Goodwill created when one business acquires another Will be covered when studying consolidated accounts IAS 38 INTANGIBLE ASSETS Disclosure General An entity shall disclose the following for each class of intangible assets, distinguishing between internally generated intangible assets and other intangible assets: (a) whether the useful lives are indefinite or finite and, if finite, the useful lives or the amortisation rates used; (b) the amortisation methods used for intangible assets with finite useful lives; (c) the gross carrying amount and any accumulated amortisation (aggregated with accumulated impairment losses) at the beginning and end of the period; (d) the line item(s) of the statement of comprehensive income in which any amortisation of intangible assets is included; (e) a reconciliation of the carrying amount at the beginning and end of the period showing: (i) additions, indicating separately those from internal development, those acquired separately, and those acquired through business combinations; 7

8 (ii) assets classified as held for sale or included in a disposal group classified as held for sale in accordance with IFRS 5 and other disposals; (iii) increases or decreases during the period resulting from revaluations under paragraphs 75, 85 and 86 and from impairment losses recognised or reversed in other comprehensive income in accordance with IAS 36 (if any); (iv) impairment losses recognised in profit or loss during the period in accordance with IAS 36 (if any); (v) impairment losses reversed in profit or loss during the period in accordance with IAS 36 (if any); (vi) any amortisation recognised during the period; (vii) net exchange differences arising on the translation of the financial statements into the presentation currency, and on the translation of a foreign operation into the presentation currency of the entity; and (viii) other changes in the carrying amount during the period. An entity shall also disclose: (a) for an intangible asset assessed as having an indefinite useful life, the carrying amount of that asset and the reasons supporting the assessment of an indefinite useful life. In giving these reasons, the entity shall describe the factor(s) that played a significant role in determining that the asset has an indefinite useful life. (b) a description, the carrying amount and remaining amortisation period of 8

9 any individual intangible asset that is material to the entity s financial statements. (c) for intangible assets acquired by way of a government grant and initially recognised at fair value (see paragraph 44): (i) the fair value initially recognised for these assets; (ii) their carrying amount; and (iii) whether they are measured after recognition under the cost model or the revaluation model. (d) the existence and carrying amounts of intangible assets whose title is restricted and the carrying amounts of intangible assets pledged as security for liabilities. (e) the amount of contractual commitments for the acquisition of intangible assets. If intangible assets are accounted for at revalued amounts, an entity shall disclose the following: (a) by class of intangible assets: (i) the effective date of the revaluation; (ii) the carrying amount of revalued intangible assets; and (iii) the carrying amount that would have been recognised had the revalued class of intangible assets been measured after recognition using the cost model in paragraph 74; (b) the amount of the revaluation surplus that relates to intangible assets at 9

10 the beginning and end of the period, indicating the changes during the period and any restrictions on the distribution of the balance to shareholders; and (c) the methods and significant assumptions applied in estimating the assets fair values. Intangible Assets (other than Goodwill) Acquired as Part of Business Combination IFRS 3 Business Combinations and IAS 38 Intangible Assets addresses the recognition of separable intangible assets. Once an intangible asset of a Subsidiary is identifiable and has a reliable fair value, then it can be recognised as an Intangible Asset on the acquisition of a Subsidiary. So for example, 1m spent on a research project, and for which a reliable fair value of 1.2m has been estimated by the purchasing company directors, can be recognised as an intangible asset in the context of a business combination. Likewise, if a subsidiary has a customer list which could be sold to other companies and the fair value of this customer list can be reliably measured at 3m, then this too can be recognised as an intangible asset, but again, only in the context of a business combination So, in summary, items can be recognised as intangible assets in a business combination scenario, once they are identifiable and have a fair value which can be reliably measured Website Costs SIC 32 Intangible Assets Web Site Costs, states that an entity s own website that arises from development and is for internal or external access is an internally developed intangible asset that is subject to the requirements of IAS 38 All expenditure on developing a website solely for advertising an entity s own products and services should be recognised as an expense when incurred However, if an entity is able to demonstrate that a website is capable of generating future economic benefits (for example, orders can be placed through the website), then the related costs can be capitalised (i.e. PIRATE) 10

11 PAST EXAM QUESTIONS P1 IAS 38 PAST EXAM QUESTIONS P2 IAS 38 Q3 (1) Aug 13 Q (A) April 15 Q1,Q2 April 2011 Q (A) April 14 Q3 August 2010 Q (A) (B) Aug 13 Q1,Q2,Q4 April 2010 Q (a) Apr 2013 Q (a) Aug 2012 Question to Practice 11

12 12

13 13

14 14

15 15

Lesson 6 International Accounting Lelio Bigogno, Stefano Santucci

Università degli studi di Pavia Facoltà di Economia a.a. 2014-2015 2015 Lesson 6 International Accounting Lelio Bigogno, Stefano Santucci 1 IAS/IFRS: Objective and definition of IAS38 2 The objective of

Università degli studi di Pavia Facoltà di Economia a.a. 2014-2015 2015 Lesson 6 International Accounting Lelio Bigogno, Stefano Santucci 1 IAS/IFRS: Objective and definition of IAS38 2 The objective of

An intangible asset is an identifiable non-monetary asset without physical substance.

Technical Summary This extract has been prepared by IASC Foundation staff and has not been approved by the IASB. For the requirements reference must be made to International Financial Reporting Standards.

Technical Summary This extract has been prepared by IASC Foundation staff and has not been approved by the IASB. For the requirements reference must be made to International Financial Reporting Standards.

International Financial Reporting Standards (IFRS)

") FACT SHEET September 2011 IAS 38 Intangible Assets (This fact sheet is based on the standard as at 1 January 2011.) Important note: This fact sheet is based on the requirements of the International Financial

FACT SHEET September 2011 IAS 38 Intangible Assets (This fact sheet is based on the standard as at 1 January 2011.) Important note: This fact sheet is based on the requirements of the International Financial

IFRS Training. IAS 38 Intangible Assets. Professional Advisory Services

IFRS Training IAS 38 Intangible Assets Table of Contents Section 1 Overview 2 Introduction to Intangible Assets 3 Recognition and Initial Measurement 4 Internally Generated Intangible Assets 5 Measurement

IFRS Training IAS 38 Intangible Assets Table of Contents Section 1 Overview 2 Introduction to Intangible Assets 3 Recognition and Initial Measurement 4 Internally Generated Intangible Assets 5 Measurement

Financial Accounting Standards Committee

Statement of Financial Accounting Standards No. 37 20 July 2006 Translated by Chi-Chun Liu, Professor (National Taiwan University) Financial Accounting Standards Committee -605- -606- Statement of Financial

Statement of Financial Accounting Standards No. 37 20 July 2006 Translated by Chi-Chun Liu, Professor (National Taiwan University) Financial Accounting Standards Committee -605- -606- Statement of Financial

In May 2014 the Board amended IAS 38 to clarify when the use of a revenue-based amortisation method is appropriate.

IAS 38 Intangible Assets In April 2001 the International Accounting Standards Board (Board) adopted IAS 38 Intangible Assets, which had originally been issued by the International Accounting Standards

IAS 38 Intangible Assets In April 2001 the International Accounting Standards Board (Board) adopted IAS 38 Intangible Assets, which had originally been issued by the International Accounting Standards

International Accounting Standard 38 Intangible Assets. Objective. Scope

International Accounting Standard 38 Intangible Assets Objective 1 The objective of this Standard is to prescribe the accounting treatment for intangible assets that are not dealt with specifically in

International Accounting Standard 38 Intangible Assets Objective 1 The objective of this Standard is to prescribe the accounting treatment for intangible assets that are not dealt with specifically in

Non-current Assets. Prof.(FH) Dr. Walter Egger

Dr. Walter Egger") Non-current Assets Prof.(FH) Dr. Walter Egger IAS 38 Intangible Assets Intangible Asset Is an identifiable non-monetary asset without physical substance Identifiability Seperable (can be seperated, divided

Non-current Assets Prof.(FH) Dr. Walter Egger IAS 38 Intangible Assets Intangible Asset Is an identifiable non-monetary asset without physical substance Identifiability Seperable (can be seperated, divided

TOPIC 2 - IAS 40 INVESTMENT PROPERTY

TOPIC 2 - IAS 40 INVESTMENT PROPERTY Definitions: Investment Property: Property held to earn rentals or for capital appreciation or both. An entity may own land or a building as an investment rather than

TOPIC 2 - IAS 40 INVESTMENT PROPERTY Definitions: Investment Property: Property held to earn rentals or for capital appreciation or both. An entity may own land or a building as an investment rather than

Accounting for Intangible Assets

Accounting for Intangible Assets 1 Examples: Goodwill- internally generated and acquired Trade mark and brand names- internally generated and acquired Patents Copyright Franchise Licenses Customer loyalty

Accounting for Intangible Assets 1 Examples: Goodwill- internally generated and acquired Trade mark and brand names- internally generated and acquired Patents Copyright Franchise Licenses Customer loyalty

L 320/252 EN Official Journal of the European Union

L 320/252 EN Official Journal of the European Union 29.11.2008 INTERNATIONAL ACCOUNTING STANDARD 38 Intangible assets OBJECTIVE 1 The objective of this standard is to prescribe the accounting treatment

L 320/252 EN Official Journal of the European Union 29.11.2008 INTERNATIONAL ACCOUNTING STANDARD 38 Intangible assets OBJECTIVE 1 The objective of this standard is to prescribe the accounting treatment

Intangible Assets (HKAS 38) 20 December Nelson Lam CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA 2005 Nelson 1

20 December Nelson Lam CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA 2005 Nelson 1") Intangible Assets (HKAS 38) 20 December 2005 Nelson Lam CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA 2005 Nelson 1 Today s Agenda Simple but Comprehensive 1. Objective and Scope Contentious 2. Definition

Intangible Assets (HKAS 38) 20 December 2005 Nelson Lam CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA 2005 Nelson 1 Today s Agenda Simple but Comprehensive 1. Objective and Scope Contentious 2. Definition

University of Economics, Prague. Non-current tangible and intangible assets (IAS 16 & IAS 38)

") University of Economics, Prague Faculty of Finance and Accounting Department of Financial Accounting and Auditing Non-current tangible and intangible assets (IAS 16 & IAS 38) 1FU486 IFRS David Procházka

University of Economics, Prague Faculty of Finance and Accounting Department of Financial Accounting and Auditing Non-current tangible and intangible assets (IAS 16 & IAS 38) 1FU486 IFRS David Procházka

Indian Accounting Standard (Ind AS) 38

38") Indian Accounting Standard (Ind AS) 38 Intangible Assets (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in bold type indicate

Indian Accounting Standard (Ind AS) 38 Intangible Assets (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in bold type indicate

Sri Lanka Accounting Standard LKAS 38. Intangible Assets

Sri Lanka Accounting Standard LKAS 38 Intangible Assets CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 38 INTANGIBLE ASSETS paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 8 Intangible assets 9 Identifiability

Sri Lanka Accounting Standard LKAS 38 Intangible Assets CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 38 INTANGIBLE ASSETS paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 8 Intangible assets 9 Identifiability

Distinctive Financial Reporting

Distinctive Financial Reporting FAC3702 Study unit 4 Intangible assets Overview Terminology Recognition & initial measurement of intangible assets Cost of internally generated intangible asset Recognition

Distinctive Financial Reporting FAC3702 Study unit 4 Intangible assets Overview Terminology Recognition & initial measurement of intangible assets Cost of internally generated intangible asset Recognition

Workshop on IND AS Intangible assets WIRC of the ICAI April 23, 2016

Workshop on IND AS Intangible assets WIRC of the ICAI April 23, 2016 Contents Background and Scope Definitions Recognition & Measurement Amortization Disclosure requirements Differences with existing AS

Workshop on IND AS Intangible assets WIRC of the ICAI April 23, 2016 Contents Background and Scope Definitions Recognition & Measurement Amortization Disclosure requirements Differences with existing AS

Intellectual Property Rights - Accounting aspects

Intellectual Property Rights - Accounting aspects Presented by: CA Vijay Mathur 10 August 2013 Agenda Intellectual Property Rights (IPR) - some definitions IPR accounting relevance and challenges Accounting

Intellectual Property Rights - Accounting aspects Presented by: CA Vijay Mathur 10 August 2013 Agenda Intellectual Property Rights (IPR) - some definitions IPR accounting relevance and challenges Accounting

Intangible Assets & Service Concession 19 March MBA MSc BBA ACA ACS CFA CPA(Aust.) CPA(US) FCCA FCPA(Practising) MSCA Nelson 1

CPA(US) FCCA FCPA(Practising) MSCA Nelson 1") Intangible Assets & Service Concession 19 March 2008 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust.) CPA(US) FCCA FCPA(Practising) MSCA 2005-08 Nelson 1 Today s Agenda Intangible Assets (HKAS 38) Service

Intangible Assets & Service Concession 19 March 2008 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust.) CPA(US) FCCA FCPA(Practising) MSCA 2005-08 Nelson 1 Today s Agenda Intangible Assets (HKAS 38) Service

Intangible Assets. Contents. Accounting Standard (AS) 26 (issued 2002)

26 (issued 2002)") Accounting Standard (AS) 26 (issued 2002) Intangible Assets Contents OBJECTIVE SCOPE Paragraphs 1-5 DEFINITIONS 6-18 Intangible Assets 7-18 Identifiability 11-13 Control 14-17 Future Economic Benefits

Accounting Standard (AS) 26 (issued 2002) Intangible Assets Contents OBJECTIVE SCOPE Paragraphs 1-5 DEFINITIONS 6-18 Intangible Assets 7-18 Identifiability 11-13 Control 14-17 Future Economic Benefits

Intangible Assets IAS 38, IAS 36, IFRS 3

Intangible Assets IAS 38, IAS 36, IFRS 3 Agenda 1. Introduction 2. Recognition 3. Measurement 4. Impairment of intangible assets (IAS 36) Basic concept Cash-Generating Units 5. Disclosures 2 1 Introduction

Intangible Assets IAS 38, IAS 36, IFRS 3 Agenda 1. Introduction 2. Recognition 3. Measurement 4. Impairment of intangible assets (IAS 36) Basic concept Cash-Generating Units 5. Disclosures 2 1 Introduction

PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 31 INTANGIBLE ASSETS (PBE IPSAS 31)

") PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 31 INTANGIBLE ASSETS (PBE IPSAS 31) This Standard was issued on 11 September 2014 by the New Zealand Accounting Standards Board of

PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 31 INTANGIBLE ASSETS (PBE IPSAS 31) This Standard was issued on 11 September 2014 by the New Zealand Accounting Standards Board of

Intangible Assets Web Site Costs

SIC-32 Material published to accompany SIC Interpretation 32 Intangible Assets Web Site Costs The text of the unaccompanied Interpretation is contained in Part A of this edition. Its effective date when

SIC-32 Material published to accompany SIC Interpretation 32 Intangible Assets Web Site Costs The text of the unaccompanied Interpretation is contained in Part A of this edition. Its effective date when

7 Days Intensive Workshop on IFRS ICAI Tower, BKC, Mumbai. IAS 16 Property, Plant & Equipments

7 Days Intensive Workshop on IFRS ICAI Tower, BKC, Mumbai 01-July-14, Tuesday From To Details Faculty 10:00 AM 1:15 PM IAS 16 : Property, Plant & Equipments IAS 38 : Intangible Assets Ind AS 40:Investment

7 Days Intensive Workshop on IFRS ICAI Tower, BKC, Mumbai 01-July-14, Tuesday From To Details Faculty 10:00 AM 1:15 PM IAS 16 : Property, Plant & Equipments IAS 38 : Intangible Assets Ind AS 40:Investment

Financial Accounting. Intangible Assets

Financial Accounting Intangible Assets Disclaimer The online video lectures and related study material (consisting of Powerpoint slides, summary modules, integrated question banks and other academic material)

Financial Accounting Intangible Assets Disclaimer The online video lectures and related study material (consisting of Powerpoint slides, summary modules, integrated question banks and other academic material)

Intangible Assets. Contents. Accounting Standard (AS) 26

26") 501 Accounting Standard (AS) 26 (issued 2002) Intangible Assets Contents OBJECTIVE SCOPE Paragraphs 1-5 DEFINITIONS 6-18 Intangible Assets 7-18 Identifiability 11-13 Control 14-17 Future Economic Benefits

501 Accounting Standard (AS) 26 (issued 2002) Intangible Assets Contents OBJECTIVE SCOPE Paragraphs 1-5 DEFINITIONS 6-18 Intangible Assets 7-18 Identifiability 11-13 Control 14-17 Future Economic Benefits

INTANGIBLE ASSETS (IAS 38) OBJECTIVE The objective of this IAS is to prescribe the accounting treatment of intangible assets not dealt in any other

OBJECTIVE The objective of this IAS is to prescribe the accounting treatment of intangible assets not dealt in any other") INTANGIBLE ASSETS (IAS 38) OBJECTIVE The objective of this IAS is to prescribe the accounting treatment of intangible assets not dealt in any other IAS. SCOPE This IAS shall be applied in accounting for

INTANGIBLE ASSETS (IAS 38) OBJECTIVE The objective of this IAS is to prescribe the accounting treatment of intangible assets not dealt in any other IAS. SCOPE This IAS shall be applied in accounting for

HKAS 38 Intangible Assets 1 January 2006

HKAS 38 Intangible Assets 1 January 2006 1. Objective of HKAS 38 The objective of Hong Kong Accounting Standard (HKAS) 38 Intangible Assets is to prescribe the accounting treatment for intangible assets

HKAS 38 Intangible Assets 1 January 2006 1. Objective of HKAS 38 The objective of Hong Kong Accounting Standard (HKAS) 38 Intangible Assets is to prescribe the accounting treatment for intangible assets

CHAPTER TWO Concepts and principles

CHAPTER TWO Concepts and principles 2.3 GOVERNMENT AND NON-GOVERNMENT GRANTS Recognition and presentation grants and contributions 2.3.2.8 Grants and contributions, including donated assets, shall not

CHAPTER TWO Concepts and principles 2.3 GOVERNMENT AND NON-GOVERNMENT GRANTS Recognition and presentation grants and contributions 2.3.2.8 Grants and contributions, including donated assets, shall not

In December 2003 the Board issued a revised IAS 40 as part of its initial agenda of technical projects.

IAS Standard 40 Investment Property In April 2001 the International Accounting Standards Board (the Board) adopted IAS 40 Investment Property, which had originally been issued by the International Accounting

IAS Standard 40 Investment Property In April 2001 the International Accounting Standards Board (the Board) adopted IAS 40 Investment Property, which had originally been issued by the International Accounting

In December 2003 the IASB issued a revised IAS 40 as part of its initial agenda of technical projects.

International Accounting Standard 40 Investment Property In April 2001 the International Accounting Standards Board (IASB) adopted IAS 40 Investment Property, which had originally been issued by the International

International Accounting Standard 40 Investment Property In April 2001 the International Accounting Standards Board (IASB) adopted IAS 40 Investment Property, which had originally been issued by the International

EN Official Journal of the European Union L 320/373

29.11.2008 EN Official Journal of the European Union L 320/373 INTERNATIONAL FINANCIAL REPORTING STANDARD 3 Business combinations OBJECTIVE 1 The objective of this IFRS is to specify the financial reporting

29.11.2008 EN Official Journal of the European Union L 320/373 INTERNATIONAL FINANCIAL REPORTING STANDARD 3 Business combinations OBJECTIVE 1 The objective of this IFRS is to specify the financial reporting

IAS 38 Intangible Assets

21/12/2010, Tuesday From To Details Faculty 2:15 PM 5:30 PM IAS 38 : Intangible Assets IAS 40 : Investment Property IFRS 5 : Non Current Assets Held for Sale and Discontinued Operations CA. Chintan Patel,

21/12/2010, Tuesday From To Details Faculty 2:15 PM 5:30 PM IAS 38 : Intangible Assets IAS 40 : Investment Property IFRS 5 : Non Current Assets Held for Sale and Discontinued Operations CA. Chintan Patel,

Intangible Assets Web Site Costs

HK(SIC)-Int 32 Revised May 2014 September 2018 Effective for annual periods beginning on or after 1 January 2005 Hong Kong (SIC) Interpretation 32 Intangible Assets Web Site Costs COPYRIGHT Copyright 2018

HK(SIC)-Int 32 Revised May 2014 September 2018 Effective for annual periods beginning on or after 1 January 2005 Hong Kong (SIC) Interpretation 32 Intangible Assets Web Site Costs COPYRIGHT Copyright 2018

In December 2003 the Board issued a revised IAS 40 as part of its initial agenda of technical projects.

IAS 40 Investment Property In April 2001 the International Accounting Standards Board (the Board) adopted IAS 40 Investment Property, which had originally been issued by the International Accounting Standards

IAS 40 Investment Property In April 2001 the International Accounting Standards Board (the Board) adopted IAS 40 Investment Property, which had originally been issued by the International Accounting Standards

6 The following terms are used in this Standard with the meanings specified: A bearer plant is a living plant that:

International Accounting Standard 16 Property, Plant and Equipment Objective 1 The objective of this Standard is to prescribe the accounting treatment for property, plant and equipment so that users of

International Accounting Standard 16 Property, Plant and Equipment Objective 1 The objective of this Standard is to prescribe the accounting treatment for property, plant and equipment so that users of

IND AS 38 Intangible Assets

IND AS 38 Intangible Assets 1 What do you mean by Intangible Assets An intangible assets is an identifiable nonmonetary assets without physical substance held for use in the production or supply of goods

IND AS 38 Intangible Assets 1 What do you mean by Intangible Assets An intangible assets is an identifiable nonmonetary assets without physical substance held for use in the production or supply of goods

Intangible Assets Web Site Costs

SIC Interpretation 32 Intangible Assets Web Site Costs In March 2002 the International Accounting Standards Board issued SIC-32 Intangible Assets Web Site Costs, which had originally been developed by

SIC Interpretation 32 Intangible Assets Web Site Costs In March 2002 the International Accounting Standards Board issued SIC-32 Intangible Assets Web Site Costs, which had originally been developed by

Property, Plant and Equipment

IAS 16 Property, Plant and Equipment In April 2001 the International Accounting Standards Board (the Board) adopted IAS 16 Property, Plant and Equipment, which had originally been issued by the International

IAS 16 Property, Plant and Equipment In April 2001 the International Accounting Standards Board (the Board) adopted IAS 16 Property, Plant and Equipment, which had originally been issued by the International

EUROPEAN UNION ACCOUNTING RULE 7 PROPERTY, PLANT & EQUIPMENT

EUROPEAN UNION ACCOUNTING RULE 7 PROPERTY, PLANT & EQUIPMENT Page 2 of 10 I N D E X 1. Objective... 3 2. Scope... 3 3. Definitions... 3 4. Recognition... 4 4.1 General recognition principle... 4 4.2 Initial

EUROPEAN UNION ACCOUNTING RULE 7 PROPERTY, PLANT & EQUIPMENT Page 2 of 10 I N D E X 1. Objective... 3 2. Scope... 3 3. Definitions... 3 4. Recognition... 4 4.1 General recognition principle... 4 4.2 Initial

New Zealand Equivalent to International Accounting Standard 40 Investment Property (NZ IAS 40)

") New Zealand Equivalent to International Accounting Standard 40 Investment Property (NZ IAS 40) Issued November 2004 and incorporates amendments up to and inlcuding 28 February 2014 This Standard was issued

New Zealand Equivalent to International Accounting Standard 40 Investment Property (NZ IAS 40) Issued November 2004 and incorporates amendments up to and inlcuding 28 February 2014 This Standard was issued

Property, Plant & Equipment Intangible Assets

Property, Plant & Equipment Intangible Assets October 17, 2015 Contents: 1. Property, Plant and Equipment (Ind AS 16) - Borrowing Costs (Ind AS 23) - Stripping Costs of a Surface Mine (Appendix B to Ind

Property, Plant & Equipment Intangible Assets October 17, 2015 Contents: 1. Property, Plant and Equipment (Ind AS 16) - Borrowing Costs (Ind AS 23) - Stripping Costs of a Surface Mine (Appendix B to Ind

Sri Lanka Accounting Standard LKAS 40. Investment Property

Sri Lanka Accounting Standard LKAS 40 Investment Property LKAS 40 CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 40 INVESTMENT PROPERTY paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 5 CLASSIFICATION OF PROPERTY

Sri Lanka Accounting Standard LKAS 40 Investment Property LKAS 40 CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 40 INVESTMENT PROPERTY paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 5 CLASSIFICATION OF PROPERTY

International Financial Reporting Standards. Sample material

International Financial Reporting Standards Sample material Always in context guiding you all the way with summaries key points, diagrams and definitions REVENUE RECOGNITION CHAPTER CONTENTS The provisions

International Financial Reporting Standards Sample material Always in context guiding you all the way with summaries key points, diagrams and definitions REVENUE RECOGNITION CHAPTER CONTENTS The provisions

IAS 16 Property, Plant and Equipment. Uphold public interest

IAS 16 Property, Plant and Equipment Uphold public interest Background IAS 16 became operational in 1983 Major amendments have been made several times including 1998, 2003, 2008, 2012, 2013, 2014 The objective

IAS 16 Property, Plant and Equipment Uphold public interest Background IAS 16 became operational in 1983 Major amendments have been made several times including 1998, 2003, 2008, 2012, 2013, 2014 The objective

Exposure Draft. Accounting Standard (AS) 40 Investment Property. Last date for the comments: November 10, 2018

40 Investment Property. Last date for the comments: November 10, 2018") Exposure Draft Accounting Standard (AS) 40 Investment Property Last date for the comments: November 10, 2018 Issued by Accounting Standards Board The Institute of Chartered Accountants of India 1 Exposure

Exposure Draft Accounting Standard (AS) 40 Investment Property Last date for the comments: November 10, 2018 Issued by Accounting Standards Board The Institute of Chartered Accountants of India 1 Exposure

Property, Plant and Equipment

International Accounting Standard 16 Property, Plant and Equipment In April 2001 the International Accounting Standards Board (IASB) adopted IAS 16 Property, Plant and Equipment, which had originally been

International Accounting Standard 16 Property, Plant and Equipment In April 2001 the International Accounting Standards Board (IASB) adopted IAS 16 Property, Plant and Equipment, which had originally been

31 July 2014 Japan s Modified International Standards (JMIS): Accounting Standards Comprising IFRSs and the ASBJ Modifications

: Accounting Standards Comprising IFRSs and the ASBJ Modifications") 31 July 2014 Japan s Modified International Standards (JMIS): Accounting Standards Comprising IFRSs and the ASBJ Modifications ASBJ Modification Accounting Standard Exposure Draft No. 1 Accounting for

31 July 2014 Japan s Modified International Standards (JMIS): Accounting Standards Comprising IFRSs and the ASBJ Modifications ASBJ Modification Accounting Standard Exposure Draft No. 1 Accounting for

AAT Professional Diploma in Accounting

Qualification Number: R486 04 Qualification Technical Information Version 1.1 published 13 June 2016 AAT Professional Diploma in Accounting Qualification Technical Information Units in this qualification

Qualification Number: R486 04 Qualification Technical Information Version 1.1 published 13 June 2016 AAT Professional Diploma in Accounting Qualification Technical Information Units in this qualification

This version includes amendments resulting from IFRSs issued up to 31 December 2009.

International Accounting Standard 40 Investment Property This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 40 Investment Property was issued by the International

International Accounting Standard 40 Investment Property This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 40 Investment Property was issued by the International

EN Official Journal of the European Union L 320/323

29.11.2008 EN Official Journal of the European Union L 320/323 INTERNATIONAL ACCOUNTING STANDARD 40 Investment property OBJECTIVE 1 The objective of this standard is to prescribe the accounting treatment

29.11.2008 EN Official Journal of the European Union L 320/323 INTERNATIONAL ACCOUNTING STANDARD 40 Investment property OBJECTIVE 1 The objective of this standard is to prescribe the accounting treatment

Property, Plant and Equipment

International Accounting Standard 16 Property, Plant and Equipment In April 2001 the International Accounting Standards Board (IASB) adopted IAS 16 Property, Plant and Equipment, which had originally been

International Accounting Standard 16 Property, Plant and Equipment In April 2001 the International Accounting Standards Board (IASB) adopted IAS 16 Property, Plant and Equipment, which had originally been

These notes will be appropriate both for both students who have chosen financial reporting as a depth area as well as those who have not.

When it comes to the Financial Reporting competency, the challenge that many students face is the tremendous amount of technical knowledge included in this competency, especially in light of the fact that

When it comes to the Financial Reporting competency, the challenge that many students face is the tremendous amount of technical knowledge included in this competency, especially in light of the fact that

International Financial Reporting Standards (IFRS)

") FACT SHEET February 2011 IAS 40 Investment Property (This fact sheet is based on the standard as at 1 January 2011.) Important note: This fact sheet is based on the requirements of the International Financial

FACT SHEET February 2011 IAS 40 Investment Property (This fact sheet is based on the standard as at 1 January 2011.) Important note: This fact sheet is based on the requirements of the International Financial

Intangibles CHAPTER CHAPTER OBJECTIVES. After careful study of this chapter, you will be able to:

CHAPTER Intangibles CHAPTER OBJECTIVES After careful study of this chapter, you will be able to: 1. Explain the accounting alternatives for intangibles. 2. Record the amortization or impairment of intangibles.

CHAPTER Intangibles CHAPTER OBJECTIVES After careful study of this chapter, you will be able to: 1. Explain the accounting alternatives for intangibles. 2. Record the amortization or impairment of intangibles.

Property, Plant and Equipment

International Accounting Standard 16 Property, Plant and Equipment This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 16 Property, Plant and Equipment was issued by

International Accounting Standard 16 Property, Plant and Equipment This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 16 Property, Plant and Equipment was issued by

SRI LANKA ACCOUNTING STANDARD

(REVISED 2005) SRI LANKA ACCOUNTING STANDARD PROPERTY, PLANT & EQUIPMENT THE INSTITUTE OF CHARTERED ACCOUNTANTS OF SRI LANKA (REVISED 2005) SRI LANKA ACCOUNTING STANDARD PROPERTY, PLANT & EQUIPMENT The

(REVISED 2005) SRI LANKA ACCOUNTING STANDARD PROPERTY, PLANT & EQUIPMENT THE INSTITUTE OF CHARTERED ACCOUNTANTS OF SRI LANKA (REVISED 2005) SRI LANKA ACCOUNTING STANDARD PROPERTY, PLANT & EQUIPMENT The

Accounting Of Intangible Assets Indian as- 26

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668. Volume 16, Issue 2. Ver. II (Feb. 2014), PP 40-45 Accounting Of Intangible Assets Indian as- 26 Manpreet Sharma,

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668. Volume 16, Issue 2. Ver. II (Feb. 2014), PP 40-45 Accounting Of Intangible Assets Indian as- 26 Manpreet Sharma,

Temporary exemption from IAS 8 paragraphs 11 and 12

International Financial Reporting Standard 6 Exploration for and Evaluation of Mineral Resources Objective 1 The objective of this IFRS is to specify the financial reporting for the exploration for and

International Financial Reporting Standard 6 Exploration for and Evaluation of Mineral Resources Objective 1 The objective of this IFRS is to specify the financial reporting for the exploration for and

WEEK 9 Investment Property IAS 40

WEEK 9 Investment Property IAS 40 Learning Objectives Define the term investment property. Explain the recognition and measurement procedures in IAS 40 Discuss how to treat disposable of an asset Discuss

WEEK 9 Investment Property IAS 40 Learning Objectives Define the term investment property. Explain the recognition and measurement procedures in IAS 40 Discuss how to treat disposable of an asset Discuss

IND AS 38 Intangible Assets. By Hanmandas Bajaj B.Com; ACA, LLB

IND AS 38 Intangible Assets By Hanmandas Bajaj B.Com; ACA, LLB IAS 38:Intangible Assets Agenda Objective and Scope Key Definitions Recognition and Measurement Disclosures IND AS vs IFRS Objective of IND

IND AS 38 Intangible Assets By Hanmandas Bajaj B.Com; ACA, LLB IAS 38:Intangible Assets Agenda Objective and Scope Key Definitions Recognition and Measurement Disclosures IND AS vs IFRS Objective of IND

Materiële Vaste Activa. 27 September 2005 Pearl Couvreur

Materiële Vaste Activa 27 September 2005 Pearl Couvreur P w C Contents 1. Principle 2. Acquisition cost 3. Subsequent costs 4. Borrowing costs 5. Assets acquired in a business combination 6. Revaluation

Materiële Vaste Activa 27 September 2005 Pearl Couvreur P w C Contents 1. Principle 2. Acquisition cost 3. Subsequent costs 4. Borrowing costs 5. Assets acquired in a business combination 6. Revaluation

CAS -16 COST ACCOUNTING STANDARD ON DEPRECIATION AND AMORTISATION

Cost Accounting Standards Board CAS -16 COST ACCOUNTING STANDARD ON DEPRECIATION AND AMORTISATION The following is the COST ACCOUNTING STANDARD 16 (CAS 16) issued by the Council of The Institute of Cost

Cost Accounting Standards Board CAS -16 COST ACCOUNTING STANDARD ON DEPRECIATION AND AMORTISATION The following is the COST ACCOUNTING STANDARD 16 (CAS 16) issued by the Council of The Institute of Cost

CENTRAL GOVERNMENT ACCOUNTING STANDARDS

CENTRAL GOVERNMENT ACCOUNTING STANDARDS NOVEMBER 2016 STANDARD 4 Requirements STANDARD 5 INTANGIBLE ASSETS INTRODUCTION... 75 I. CENTRAL GOVERNMENT S SPECIALISED ASSETS... 75 I.1. The collection of sovereign

CENTRAL GOVERNMENT ACCOUNTING STANDARDS NOVEMBER 2016 STANDARD 4 Requirements STANDARD 5 INTANGIBLE ASSETS INTRODUCTION... 75 I. CENTRAL GOVERNMENT S SPECIALISED ASSETS... 75 I.1. The collection of sovereign

IFRS - 3. Business Combinations. By:

IFRS - 3 Business Combinations Objective 1. The purpose of this IFRS is to specify to disclose financial information by an entity when carrying out a business combination. In particular, specifies that

IFRS - 3 Business Combinations Objective 1. The purpose of this IFRS is to specify to disclose financial information by an entity when carrying out a business combination. In particular, specifies that

Sri Lanka Accounting Standard-LKAS 40. Investment Property

Sri Lanka Accounting Standard-LKAS 40 Investment Property CONTENTS SRI LANKA ACCOUNTING STANDARD-LKAS 40 INVESTMENT PROPERTY paragraphs OBJECTIVE 1 SCOPE 2-4 DEFINITIONS 5-15 RECOGNITION 16-19 MEASUREMENT

Sri Lanka Accounting Standard-LKAS 40 Investment Property CONTENTS SRI LANKA ACCOUNTING STANDARD-LKAS 40 INVESTMENT PROPERTY paragraphs OBJECTIVE 1 SCOPE 2-4 DEFINITIONS 5-15 RECOGNITION 16-19 MEASUREMENT

Hong Kong Accounting Standard 16 Property, Plant and Equipment

Hong Kong Accounting Standard 16 Property, Plant and Equipment 1 Contents Hong Kong Accounting Standard 16 Property, Plant and Equipment paragraphs OBJECTIVE 1 SCOPE 2-5 DEFINITIONS 6 RECOGNITION 7-14

Hong Kong Accounting Standard 16 Property, Plant and Equipment 1 Contents Hong Kong Accounting Standard 16 Property, Plant and Equipment paragraphs OBJECTIVE 1 SCOPE 2-5 DEFINITIONS 6 RECOGNITION 7-14

Exposure Draft. Amendments to Ind AS 40, Investment Property. (Last date for the comments: July 11, 2018)

") ED/ Ind AS/2018/07 Exposure Draft Amendments to Ind AS 40, Investment Property (Last date for the comments: July 11, 2018) Issued by Accounting Standards Board The Institute of Chartered Accountants of

ED/ Ind AS/2018/07 Exposure Draft Amendments to Ind AS 40, Investment Property (Last date for the comments: July 11, 2018) Issued by Accounting Standards Board The Institute of Chartered Accountants of

New Zealand Equivalent to International Accounting Standard 40 Investment Property (NZ IAS 40)

") New Zealand Equivalent to International Accounting Standard 40 Investment Property (NZ IAS 40) Issued November 2004 and incorporates amendments to 28 February 2017 other than consequential amendments resulting

New Zealand Equivalent to International Accounting Standard 40 Investment Property (NZ IAS 40) Issued November 2004 and incorporates amendments to 28 February 2017 other than consequential amendments resulting

LEARNING UNIT 2 IAS40 INVESTMENT PROPERTY. Disclaimer. Recognition and measurement

LEARNING UNIT 2 IAS40 INVESTMENT PROPERTY Disclaimer The information contained in the summary is to highlight important aspects in applying the principles of the applicable statements. The summary is in

LEARNING UNIT 2 IAS40 INVESTMENT PROPERTY Disclaimer The information contained in the summary is to highlight important aspects in applying the principles of the applicable statements. The summary is in

AIRTEL UGANDA LIMITED NOTES TO THE FINANCIAL STATEMENTS (CONTINUED) 2. Summary of significant accounting policies (continued) (b) Changes in accounting policies (continued) Amendments to IAS 12 Income

AIRTEL UGANDA LIMITED NOTES TO THE FINANCIAL STATEMENTS (CONTINUED) 2. Summary of significant accounting policies (continued) (b) Changes in accounting policies (continued) Amendments to IAS 12 Income

Business Combination. CA Yagnesh Desai. Compiled by CA Yagnesh 1

Business Combination CA Yagnesh Desai ymdesaiandco@gmail.com 093222 44770 09820133227 yagnesh@caymd.com 1 Indicators Not necessarily Limits by the Standard Above 50 % Control Hence Consolidate Control

Business Combination CA Yagnesh Desai ymdesaiandco@gmail.com 093222 44770 09820133227 yagnesh@caymd.com 1 Indicators Not necessarily Limits by the Standard Above 50 % Control Hence Consolidate Control

EXPOSURE DRAFT. Hong Kong Accounting Standard 40. Investment Property

EXPOSURE DRAFT Hong Kong Accounting Standard 40 Investment Property 1 Contents Hong Kong Accounting Standard 40 Investment Property paragraphs OBJECTIVE 1 SCOPE 2-4 DEFINITIONS 5-15 RECOGNITION 16-19 MEASUREMENT

EXPOSURE DRAFT Hong Kong Accounting Standard 40 Investment Property 1 Contents Hong Kong Accounting Standard 40 Investment Property paragraphs OBJECTIVE 1 SCOPE 2-4 DEFINITIONS 5-15 RECOGNITION 16-19 MEASUREMENT

Business Combinations

Business Combinations Indian Accounting Standard (Ind AS) 103 Business Combinations Contents Paragraphs OBJECTIVE 1 SCOPE 2 IDENTIFYING A BUSINESS COMBINATION 3 THE ACQUISITION METHOD 4 53 Identifying

Business Combinations Indian Accounting Standard (Ind AS) 103 Business Combinations Contents Paragraphs OBJECTIVE 1 SCOPE 2 IDENTIFYING A BUSINESS COMBINATION 3 THE ACQUISITION METHOD 4 53 Identifying

Business Combinations

International Financial Reporting Standard 3 Business Combinations This version was issued in January 2008. Its effective date is 1 July 2009. It includes amendments resulting from IFRSs issued up to 31

International Financial Reporting Standard 3 Business Combinations This version was issued in January 2008. Its effective date is 1 July 2009. It includes amendments resulting from IFRSs issued up to 31

International Accounting Standard 17 Leases. Objective. Scope. Definitions IAS 17

International Accounting Standard 17 Leases Objective 1 The objective of this Standard is to prescribe, for lessees and lessors, the appropriate accounting policies and disclosure to apply in relation

International Accounting Standard 17 Leases Objective 1 The objective of this Standard is to prescribe, for lessees and lessors, the appropriate accounting policies and disclosure to apply in relation

Business Combinations IFRS 3

CA Sandesh Mundra Business Combinations IFRS 3 For many men, the acquisition of wealth does not end their troubles, it only changes them. - Lucius Annaeus Seneca Lets get some of the basics correct.. We

CA Sandesh Mundra Business Combinations IFRS 3 For many men, the acquisition of wealth does not end their troubles, it only changes them. - Lucius Annaeus Seneca Lets get some of the basics correct.. We

Leases. (a) the lease transfers ownership of the asset to the lessee by the end of the lease term.

the lease transfers ownership of the asset to the lessee by the end of the lease term.") Leases 1.1. Classification of leases A lease is classified as a finance lease if it transfers substantially all the risks and rewards incidental to ownership. A lease is classified as an operating lease

Leases 1.1. Classification of leases A lease is classified as a finance lease if it transfers substantially all the risks and rewards incidental to ownership. A lease is classified as an operating lease

Financial Reporting Matters

Financial Reporting Matters January 2005 Issue 4 A UDIT In this edition, we discuss some challenges that may be encountered in applying the latest standard on business combinations. In addition, we highlight

Financial Reporting Matters January 2005 Issue 4 A UDIT In this edition, we discuss some challenges that may be encountered in applying the latest standard on business combinations. In addition, we highlight

International Financial Reporting Standard 16 Leases. Objective. Scope. Recognition exemptions (paragraphs B3 B8) IFRS 16

IFRS 16") International Financial Reporting Standard 16 Leases Objective 1 This Standard sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective is to ensure

International Financial Reporting Standard 16 Leases Objective 1 This Standard sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective is to ensure

.01 The objective of this Standard is to prescribe the accounting treatment for investment property and related disclosure requirements.

COMPARISON OF GRAP 16 WITH IAS 40 GRAP 16 IAS 40 DIFFERENCES Objective.01 The objective of this Standard is to prescribe the accounting treatment for investment property and related disclosure requirements.

COMPARISON OF GRAP 16 WITH IAS 40 GRAP 16 IAS 40 DIFFERENCES Objective.01 The objective of this Standard is to prescribe the accounting treatment for investment property and related disclosure requirements.

KEY DIFFERENCES- AS VS. IND AS

KEY DIFFERENCES- AS VS. IND AS October 2016 1 Titre de la présentation AGENDA Property, Plant and Equipment (PP&E) Intangible Assets Investment Property Non-current Assets Held for Sale and Discontinued

KEY DIFFERENCES- AS VS. IND AS October 2016 1 Titre de la présentation AGENDA Property, Plant and Equipment (PP&E) Intangible Assets Investment Property Non-current Assets Held for Sale and Discontinued

HKAS 40 Revised January 2017April Hong Kong Accounting Standard 40. Investment Property

HKAS 40 Revised January 2017April 2017 Hong Kong Accounting Standard 40 Investment Property HKAS 40 COPYRIGHT Copyright 2017 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial

HKAS 40 Revised January 2017April 2017 Hong Kong Accounting Standard 40 Investment Property HKAS 40 COPYRIGHT Copyright 2017 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial

Financial Accounting. Investment Property

Financial Accounting Investment Property Disclaimer The DVD lectures and related study material (consisting of Powerpoint slides, summary modules, integrated question banks and other academic material)

Financial Accounting Investment Property Disclaimer The DVD lectures and related study material (consisting of Powerpoint slides, summary modules, integrated question banks and other academic material)

Objectives Chapter 12

Objectives Chapter 12 You should be able to Explain valuation and amortization of intangible assets Distinguish between amortization, expensing, and impairment Categorize specifically identifiable intangible

Objectives Chapter 12 You should be able to Explain valuation and amortization of intangible assets Distinguish between amortization, expensing, and impairment Categorize specifically identifiable intangible

WHITE PAPER ON FUNDS FROM OPERATIONS

WHITE PAPER ON FUNDS FROM OPERATIONS FOR IFRS REVISED: SEPTEMBER 2010 Page 1 of 17 I. Introduction and Background TABLE OF CONTENTS II. III. IV. Intended use of FFO FFO Definition Discussion of FFO Definition

WHITE PAPER ON FUNDS FROM OPERATIONS FOR IFRS REVISED: SEPTEMBER 2010 Page 1 of 17 I. Introduction and Background TABLE OF CONTENTS II. III. IV. Intended use of FFO FFO Definition Discussion of FFO Definition

Chapter 08 - Long-Term Assets. Chapter Outline

Section 1 Plant Assets I. Cost Determination Plant assets are tangible assets used in a company's operations that have a useful life of more than one accounting period. Consistent with cost principle,

Section 1 Plant Assets I. Cost Determination Plant assets are tangible assets used in a company's operations that have a useful life of more than one accounting period. Consistent with cost principle,

ACCOUNTING STANDARDS BOARD INTERPRETATION OF THE STANDARDS OF GENERALLY RECOGNISED ACCOUNTING PRACTICE

ACCOUNTING STANDARDS BOARD INTERPRETATION OF THE STANDARDS OF GENERALLY RECOGNISED ACCOUNTING PRACTICE INTANGIBLE ASSETS WEBSITE COSTS (IGRAP 16) Issued by the Accounting Standards Board March 2012 Acknowledgment

ACCOUNTING STANDARDS BOARD INTERPRETATION OF THE STANDARDS OF GENERALLY RECOGNISED ACCOUNTING PRACTICE INTANGIBLE ASSETS WEBSITE COSTS (IGRAP 16) Issued by the Accounting Standards Board March 2012 Acknowledgment

HONG KONG SOCIETY OF ACCOUNTANTS. Financial Accounting Standards Committee. Urgent Issues & Interpretations Sub-Committee

HONG KONG SOCIETY OF ACCOUNTANTS Financial Accounting Standards Committee Urgent Issues & Interpretations Sub-Committee Interpretation 12 Business combinations - Subsequent adjustment of fair values and

HONG KONG SOCIETY OF ACCOUNTANTS Financial Accounting Standards Committee Urgent Issues & Interpretations Sub-Committee Interpretation 12 Business combinations - Subsequent adjustment of fair values and

Meet Definition of. Be investment property. & Follow FV Model. Earn Rentals

Meet Definition of Requirements It s Property Held to Use in Production Process Or Admin Purpose Earn Capital Appreciation Earn Rentals & Follow Model Instead of And Available on Property By Property Basis

Meet Definition of Requirements It s Property Held to Use in Production Process Or Admin Purpose Earn Capital Appreciation Earn Rentals & Follow Model Instead of And Available on Property By Property Basis

In December 2003 the Board issued a revised IAS 17 as part of its initial agenda of technical projects.

IFRS 16 Leases In April 2001 the International Accounting Standards Board (the Board) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

IFRS 16 Leases In April 2001 the International Accounting Standards Board (the Board) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

IFRS 16 LEASES. Page 1 of 21

IFRS 16 LEASES OBJECTIVE The objective is to ensure that lessees and lessors provide relevant information in a manner that faithfully represents those transactions. This information gives a basis for users

IFRS 16 LEASES OBJECTIVE The objective is to ensure that lessees and lessors provide relevant information in a manner that faithfully represents those transactions. This information gives a basis for users

The Differences between full IFRS and FRS 102

CPA Ireland Skillnet CPA Ireland Skillnet, is a training network that is funded by Skillnets, a state funded, enterprise led support body dedicated to the promotion and facilitation of training and up-skilling

CPA Ireland Skillnet CPA Ireland Skillnet, is a training network that is funded by Skillnets, a state funded, enterprise led support body dedicated to the promotion and facilitation of training and up-skilling

New Zealand Equivalent to International Accounting Standard 16 Property, Plant and Equipment (NZ IAS 16)

") New Zealand Equivalent to International Accounting Standard 16 Property, Plant and Equipment () Issued November 2004 and incorporates amendments to 31 December 2016 other than consequential amendments

New Zealand Equivalent to International Accounting Standard 16 Property, Plant and Equipment () Issued November 2004 and incorporates amendments to 31 December 2016 other than consequential amendments

Chapter 11. Learning Objectives. Non-current Assets. Horngren, Best, Fraser, Willett: Accounting 6e 2010 Pearson Australia

PowerPoint to accompany Chapter 11 Non-Current Assets: Property, Plant and Equipment, and Intangibles Learning Objectives 1. Measure the cost of a non-current asset 2. Account for depreciation 3. Select

PowerPoint to accompany Chapter 11 Non-Current Assets: Property, Plant and Equipment, and Intangibles Learning Objectives 1. Measure the cost of a non-current asset 2. Account for depreciation 3. Select

In December 2003 the IASB issued a revised IAS 17 as part of its initial agenda of technical projects.

IFRS Standard 16 Leases In April 2001 the International Accounting Standards Board (IASB) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

IFRS Standard 16 Leases In April 2001 the International Accounting Standards Board (IASB) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

LKAS 17 Sri Lanka Accounting Standard LKAS 17

Sri Lanka Accounting Standard LKAS 17 Leases CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 17 LEASES paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 4 CLASSIFICATION OF LEASES 7 LEASES IN THE FINANCIAL STATEMENTS

Sri Lanka Accounting Standard LKAS 17 Leases CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 17 LEASES paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 4 CLASSIFICATION OF LEASES 7 LEASES IN THE FINANCIAL STATEMENTS

International Financial Reporting Standards (IFRSs ) 2004

2004") International Financial Reporting Standards (IFRSs ) 2004 including International Accounting Standards (IASs ) and Interpretations as at 31 March 2004 The IASB, the IASCF, the authors and the publishers

International Financial Reporting Standards (IFRSs ) 2004 including International Accounting Standards (IASs ) and Interpretations as at 31 March 2004 The IASB, the IASCF, the authors and the publishers

There are two main reasons why leases may need to be reclassified under the Code.

4.2 Leases and Lease Type Arrangements A - Reclassification of Leases The requirements of the Code in respect of lease classification are different to those of the SORP. Authorities will therefore need

4.2 Leases and Lease Type Arrangements A - Reclassification of Leases The requirements of the Code in respect of lease classification are different to those of the SORP. Authorities will therefore need

ACCOUNTING FOR ACQUISITIONS RESULTING IN COMBINATIONS OF ENTITIES OR OPERATIONS

Institute of Chartered Accountants of New Zealand FINANCIAL REPORTING NO. 36 OCTOBER 2001 ACCOUNTING FOR ACQUISITIONS RESULTING IN COMBINATIONS OF ENTITIES OR OPERATIONS Issued by the Financial Reporting

Institute of Chartered Accountants of New Zealand FINANCIAL REPORTING NO. 36 OCTOBER 2001 ACCOUNTING FOR ACQUISITIONS RESULTING IN COMBINATIONS OF ENTITIES OR OPERATIONS Issued by the Financial Reporting