|

|

|

- Aldous Andrews

- 5 years ago

- Views:

Transcription

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16 AIRTEL UGANDA LIMITED NOTES TO THE FINANCIAL STATEMENTS (CONTINUED) 2. Summary of significant accounting policies (continued) (b) Changes in accounting policies (continued) Amendments to IAS 12 Income Taxes 1-Jan-2017 In January 2016, through issuing amendments to IAS 12, the IASB clarified the accounting treatment of deferred tax assets of debt instruments measured at fair value for accounting, but measured at cost for tax purposes. The amendment is effective from 1 January The company is currently evaluating the impact, but does not anticipate that adopting the amendments would have a material impact on its financial statements. Amendments to IAS 7 Statement of Cash Flows 1 January 2017 In January 2016, the IASB issued amendments to IAS 7 Statement of Cash Flows with the intention to improve disclosures of financing activities and help users to better understand the reporting entities liquidity positions. Under the new requirements, entities will need to disclose changes in their financial liabilities as a result of financing activities such as changes from cash flows and non-cash items (e.g. gains and losses due to foreign currency movements). The amendment is effective from 1 January The company is currently evaluating the impact. Amendments to IFRS 2 Classification and Measurement of Sharebased Payment Transactions 1 January 2018 The IASB issued amendments to IFRS 2 Sharebased Payment that address three main areas: the effects of vesting conditions on the measurement of a cash-settled share-based payment transaction; the classification of a share-based payment transaction with net settlement features for withholding tax obligations; and accounting where a modification to the terms and conditions of a share-based payment transaction changes its classification from cash settled to equity settled. On adoption, entities are required to apply the amendments without restating prior periods, but retrospective application is permitted if elected for all three amendments and other criteria are met. The amendments are effective for annual periods beginning on or after 1 January 2018, with early application permitted. This is not expected to have any impact on the company s financial statements. 14

17

18

19 AIRTEL UGANDA LIMITED NOTES TO THE FINANCIAL STATEMENTS (CONTINUED) 2. Summary of significant accounting policies (continued) (e) Property and equipment (continued) An item of property and equipment is derecognised upon disposal or when no future economic benefits are expected from its use or disposal. Gains and losses on disposal of property and equipment are determined by reference to their carrying amounts and are taken into account in determining profit. Following the sale of Uganda Towers Limited to Eaton Towers Uganda Limited, the towers that were not absorbed by Eaton were taken over by Airtel Uganda Limited and recorded in its plant and equipment. The Asset Retirement Obligation related to the towers is classified as liabilities directly associated with the towers. (f) Intangible assets Intangible assets acquired separately are measured on initial recognition at cost. Subsequently, intangible assets are carried at cost less accumulated amortisation and any accumulated impairment losses. Intangible assets with infinite lives are amortised over their economic useful life and assessed for impairment whenever there is an indication that the intangible asset may be impaired. The telecoms operating licence is amortised over five years whilst computer software is amortised over three years. (g) Accounting for leases The determination of whether an arrangement is, or contains a lease is based on the substance of the arrangement and involves an assessment of whether the fulfilment of the arrangement is dependent on the use of a specific asset or assets and whether or not the arrangement conveys a right to use the asset. Finance leases Finance leases, which transfer substantially all the risks and benefits incidental to ownership of the leased item to the lessee are capitalized at the inception of the lease at the fair value of the leased asset or, if lower, at the present value of the minimum lease payments. Lease payments are apportioned between the finance charges and reduction of the lease liability so as to achieve a constant rate of interest on the remaining balance of the liability. Finance charges are charged directly against income. Where a finance lease results from a sale and lease back transaction, any excess of the sale proceeds over the carrying amount of the asset is deferred and amortised over the lease term. Capitalised leased assets are depreciated over the shorter of the estimated useful lives of the assets, or the lease term if there is no reasonable certainty that the company will obtain ownership by the end of the lease term. Operating leases Operating leases are all leases that are not finance leases. Operating lease payments are recognised as expenses in the profit or loss on the straight line basis over the lease term. (h) Inventories Inventories are valued at the lower of cost and net realisable value. Cost is determined on a first-in first-out basis.net realisable value is the estimated selling price in the ordinary course of business, less applicable variable selling expenses. 17

20

21

22

23

24

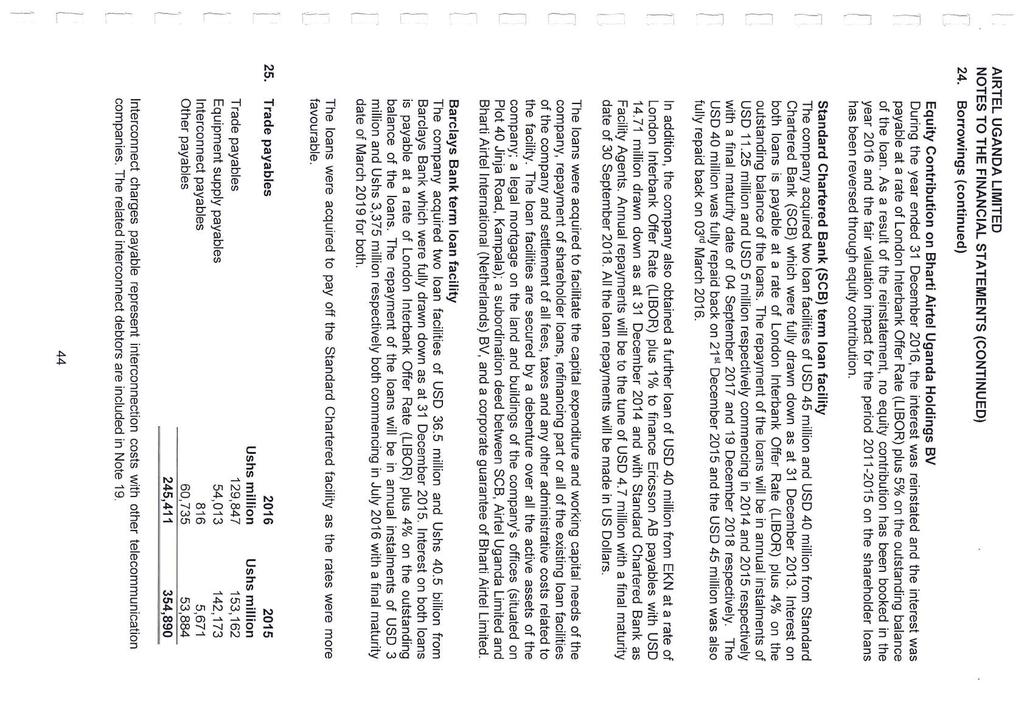

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

International Accounting Standard 17 Leases. Objective. Scope. Definitions IAS 17

International Accounting Standard 17 Leases Objective 1 The objective of this Standard is to prescribe, for lessees and lessors, the appropriate accounting policies and disclosure to apply in relation

International Accounting Standard 17 Leases Objective 1 The objective of this Standard is to prescribe, for lessees and lessors, the appropriate accounting policies and disclosure to apply in relation

LKAS 17 Sri Lanka Accounting Standard LKAS 17

Sri Lanka Accounting Standard LKAS 17 Leases CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 17 LEASES paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 4 CLASSIFICATION OF LEASES 7 LEASES IN THE FINANCIAL STATEMENTS

Sri Lanka Accounting Standard LKAS 17 Leases CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 17 LEASES paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 4 CLASSIFICATION OF LEASES 7 LEASES IN THE FINANCIAL STATEMENTS

In December 2003 the IASB issued a revised IAS 17 as part of its initial agenda of technical projects.

International Accounting Standard 17 Leases In April 2001 the International Accounting Standards Board (IASB) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards

International Accounting Standard 17 Leases In April 2001 the International Accounting Standards Board (IASB) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards

WEEK 6 ACCOUNTING FOR LEASES IAS 17

WEEK 6 ACCOUNTING FOR LEASES IAS 17 Learning Objectives Discuss the Classification of Leases Understand Sale and Leaseback Transactions Explain the accounting procedure in IAS 17 Highlight the disclosure

WEEK 6 ACCOUNTING FOR LEASES IAS 17 Learning Objectives Discuss the Classification of Leases Understand Sale and Leaseback Transactions Explain the accounting procedure in IAS 17 Highlight the disclosure

Property, Plant and Equipment

International Accounting Standard 16 Property, Plant and Equipment In April 2001 the International Accounting Standards Board (IASB) adopted IAS 16 Property, Plant and Equipment, which had originally been

International Accounting Standard 16 Property, Plant and Equipment In April 2001 the International Accounting Standards Board (IASB) adopted IAS 16 Property, Plant and Equipment, which had originally been

Leases. Indian Accounting Standard (Ind AS) 17. Leases

17. Leases") Leases Indian Accounting Standard (Ind AS) 17 Leases Contents Paragraphs OBJECTIVE 1 SCOPE 2-3 DEFINITIONS 4-6 CLASSIFICATION OF LEASES 7-19 LEASES IN THE FINANCIAL STATEMENTS OF LESSEES 20-35 Finance

Leases Indian Accounting Standard (Ind AS) 17 Leases Contents Paragraphs OBJECTIVE 1 SCOPE 2-3 DEFINITIONS 4-6 CLASSIFICATION OF LEASES 7-19 LEASES IN THE FINANCIAL STATEMENTS OF LESSEES 20-35 Finance

CHAPTER TWO Concepts and principles

CHAPTER TWO Concepts and principles 2.3 GOVERNMENT AND NON-GOVERNMENT GRANTS Recognition and presentation grants and contributions 2.3.2.8 Grants and contributions, including donated assets, shall not

CHAPTER TWO Concepts and principles 2.3 GOVERNMENT AND NON-GOVERNMENT GRANTS Recognition and presentation grants and contributions 2.3.2.8 Grants and contributions, including donated assets, shall not

EN Official Journal of the European Union L 320/373

29.11.2008 EN Official Journal of the European Union L 320/373 INTERNATIONAL FINANCIAL REPORTING STANDARD 3 Business combinations OBJECTIVE 1 The objective of this IFRS is to specify the financial reporting

29.11.2008 EN Official Journal of the European Union L 320/373 INTERNATIONAL FINANCIAL REPORTING STANDARD 3 Business combinations OBJECTIVE 1 The objective of this IFRS is to specify the financial reporting

IAS 16 Property, Plant and Equipment. Uphold public interest

IAS 16 Property, Plant and Equipment Uphold public interest Background IAS 16 became operational in 1983 Major amendments have been made several times including 1998, 2003, 2008, 2012, 2013, 2014 The objective

IAS 16 Property, Plant and Equipment Uphold public interest Background IAS 16 became operational in 1983 Major amendments have been made several times including 1998, 2003, 2008, 2012, 2013, 2014 The objective

Leases. (a) the lease transfers ownership of the asset to the lessee by the end of the lease term.

the lease transfers ownership of the asset to the lessee by the end of the lease term.") Leases 1.1. Classification of leases A lease is classified as a finance lease if it transfers substantially all the risks and rewards incidental to ownership. A lease is classified as an operating lease

Leases 1.1. Classification of leases A lease is classified as a finance lease if it transfers substantially all the risks and rewards incidental to ownership. A lease is classified as an operating lease

6 The following terms are used in this Standard with the meanings specified: A bearer plant is a living plant that:

International Accounting Standard 16 Property, Plant and Equipment Objective 1 The objective of this Standard is to prescribe the accounting treatment for property, plant and equipment so that users of

International Accounting Standard 16 Property, Plant and Equipment Objective 1 The objective of this Standard is to prescribe the accounting treatment for property, plant and equipment so that users of

TOPIC 2 - IAS 40 INVESTMENT PROPERTY

TOPIC 2 - IAS 40 INVESTMENT PROPERTY Definitions: Investment Property: Property held to earn rentals or for capital appreciation or both. An entity may own land or a building as an investment rather than

TOPIC 2 - IAS 40 INVESTMENT PROPERTY Definitions: Investment Property: Property held to earn rentals or for capital appreciation or both. An entity may own land or a building as an investment rather than

International Financial Reporting Standards (IFRS)

") FACT SHEET September 2011 IAS 38 Intangible Assets (This fact sheet is based on the standard as at 1 January 2011.) Important note: This fact sheet is based on the requirements of the International Financial

FACT SHEET September 2011 IAS 38 Intangible Assets (This fact sheet is based on the standard as at 1 January 2011.) Important note: This fact sheet is based on the requirements of the International Financial

In December 2003 the Board issued a revised IAS 40 as part of its initial agenda of technical projects.

IAS 40 Investment Property In April 2001 the International Accounting Standards Board (the Board) adopted IAS 40 Investment Property, which had originally been issued by the International Accounting Standards

IAS 40 Investment Property In April 2001 the International Accounting Standards Board (the Board) adopted IAS 40 Investment Property, which had originally been issued by the International Accounting Standards

Sri Lanka Accounting Standard-LKAS 17. Leases

Sri Lanka Accounting Standard-LKAS 17 Leases -516- Sri Lanka Accounting Standard-LKAS 17 Leases Sri Lanka Accounting Standard LKAS 17 Leases is set out in paragraphs 1 69. All the paragraphs have equal

Sri Lanka Accounting Standard-LKAS 17 Leases -516- Sri Lanka Accounting Standard-LKAS 17 Leases Sri Lanka Accounting Standard LKAS 17 Leases is set out in paragraphs 1 69. All the paragraphs have equal

2 This Standard shall be applied in accounting for all leases other than:

Indian Accounting Standard (Ind AS) 17 Leases (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in bold type indicate the main

Indian Accounting Standard (Ind AS) 17 Leases (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in bold type indicate the main

Property, Plant and Equipment

IAS 16 Property, Plant and Equipment In April 2001 the International Accounting Standards Board (the Board) adopted IAS 16 Property, Plant and Equipment, which had originally been issued by the International

IAS 16 Property, Plant and Equipment In April 2001 the International Accounting Standards Board (the Board) adopted IAS 16 Property, Plant and Equipment, which had originally been issued by the International

IAS 40. Definition. Examples. Investment property. Investment Property. Examples of investment property

IAS 40 Investment property Definition Investment Property Investment property is property held by the owner to earn rentals or for capital appreciation or both. 2 Examples Examples of investment property

IAS 40 Investment property Definition Investment Property Investment property is property held by the owner to earn rentals or for capital appreciation or both. 2 Examples Examples of investment property

International Financial Reporting Standards (IFRS)

") FACT SHEET February 2011 IAS 17 Leases (This fact sheet is based on the standard as at 1 January 2011.) Important note: This fact sheet is based on the requirements of the International Financial Reporting

FACT SHEET February 2011 IAS 17 Leases (This fact sheet is based on the standard as at 1 January 2011.) Important note: This fact sheet is based on the requirements of the International Financial Reporting

SSAP 14 STATEMENT OF STANDARD ACCOUNTING PRACTICE 14 LEASES

SSAP 14 STATEMENT OF STANDARD ACCOUNTING PRACTICE 14 LEASES (Issued October 1987; revised February 2000) The standards, which have been set in bold italic type, should be read in the context of the background

SSAP 14 STATEMENT OF STANDARD ACCOUNTING PRACTICE 14 LEASES (Issued October 1987; revised February 2000) The standards, which have been set in bold italic type, should be read in the context of the background

An intangible asset is an identifiable non-monetary asset without physical substance.

Technical Summary This extract has been prepared by IASC Foundation staff and has not been approved by the IASB. For the requirements reference must be made to International Financial Reporting Standards.

Technical Summary This extract has been prepared by IASC Foundation staff and has not been approved by the IASB. For the requirements reference must be made to International Financial Reporting Standards.

NEWTOWN SCHOOL FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER

NEWTOWN SCHOOL FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2016 School Address: Mein Street, Newtown, Wellington School Postal Address: Mein Street, Newtown, WELLINGTON, 6021 School Phone: 04 389

NEWTOWN SCHOOL FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2016 School Address: Mein Street, Newtown, Wellington School Postal Address: Mein Street, Newtown, WELLINGTON, 6021 School Phone: 04 389

The new IFRS 16 Leases effective as of 1 January 2019

The new IFRS 16 Leases effective as of 1 January 2019 IFRS 16 was issued by IASB on 13 January 2016. The Standard is effective as of 1 January 2019. It has not yet been adopted by the EC. This is a Standard

The new IFRS 16 Leases effective as of 1 January 2019 IFRS 16 was issued by IASB on 13 January 2016. The Standard is effective as of 1 January 2019. It has not yet been adopted by the EC. This is a Standard

International Financial Reporting Standard 16 Leases. Objective. Scope. Recognition exemptions (paragraphs B3 B8) IFRS 16

IFRS 16") International Financial Reporting Standard 16 Leases Objective 1 This Standard sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective is to ensure

International Financial Reporting Standard 16 Leases Objective 1 This Standard sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective is to ensure

Lesson 6 International Accounting Lelio Bigogno, Stefano Santucci

Università degli studi di Pavia Facoltà di Economia a.a. 2014-2015 2015 Lesson 6 International Accounting Lelio Bigogno, Stefano Santucci 1 IAS/IFRS: Objective and definition of IAS38 2 The objective of

Università degli studi di Pavia Facoltà di Economia a.a. 2014-2015 2015 Lesson 6 International Accounting Lelio Bigogno, Stefano Santucci 1 IAS/IFRS: Objective and definition of IAS38 2 The objective of

Contents. Easy. Fairly Complicated. More Advanced. Page. Background. Background to financial reporting in South Africa... 3

Contents Easy Fairly Complicated More Advanced Background Background to financial reporting in South Africa... 3 Conceptual Framework for Financial Reporting 2010 RECENT DEVELOPMENTS REGARDING THE CONCEPTUAL

Contents Easy Fairly Complicated More Advanced Background Background to financial reporting in South Africa... 3 Conceptual Framework for Financial Reporting 2010 RECENT DEVELOPMENTS REGARDING THE CONCEPTUAL

Non-current Assets. Prof.(FH) Dr. Walter Egger

Dr. Walter Egger") Non-current Assets Prof.(FH) Dr. Walter Egger IAS 38 Intangible Assets Intangible Asset Is an identifiable non-monetary asset without physical substance Identifiability Seperable (can be seperated, divided

Non-current Assets Prof.(FH) Dr. Walter Egger IAS 38 Intangible Assets Intangible Asset Is an identifiable non-monetary asset without physical substance Identifiability Seperable (can be seperated, divided

Property, Plant and Equipment

International Accounting Standard 16 Property, Plant and Equipment In April 2001 the International Accounting Standards Board (IASB) adopted IAS 16 Property, Plant and Equipment, which had originally been

International Accounting Standard 16 Property, Plant and Equipment In April 2001 the International Accounting Standards Board (IASB) adopted IAS 16 Property, Plant and Equipment, which had originally been

New Zealand Equivalent to International Accounting Standard 17 Leases (NZ IAS 17)

") New Zealand Equivalent to International Accounting Standard 17 Leases (NZ IAS 17) Issued November 2004 and incorporates amendments up to and including 30 June 2011 This Standard was issued by the Financial

New Zealand Equivalent to International Accounting Standard 17 Leases (NZ IAS 17) Issued November 2004 and incorporates amendments up to and including 30 June 2011 This Standard was issued by the Financial

IASB Staff Paper March 2011

IASB Staff Paper March 2011 Effect of board redeliberations on Exposure Draft Leases About this staff paper This staff paper indicates how the proposals in the Exposure Draft Leases would change as a result

IASB Staff Paper March 2011 Effect of board redeliberations on Exposure Draft Leases About this staff paper This staff paper indicates how the proposals in the Exposure Draft Leases would change as a result

There are two main reasons why leases may need to be reclassified under the Code.

4.2 Leases and Lease Type Arrangements A - Reclassification of Leases The requirements of the Code in respect of lease classification are different to those of the SORP. Authorities will therefore need

4.2 Leases and Lease Type Arrangements A - Reclassification of Leases The requirements of the Code in respect of lease classification are different to those of the SORP. Authorities will therefore need

In December 2003 the IASB issued a revised IAS 40 as part of its initial agenda of technical projects.

International Accounting Standard 40 Investment Property In April 2001 the International Accounting Standards Board (IASB) adopted IAS 40 Investment Property, which had originally been issued by the International

International Accounting Standard 40 Investment Property In April 2001 the International Accounting Standards Board (IASB) adopted IAS 40 Investment Property, which had originally been issued by the International

In December 2003 the Board issued a revised IAS 40 as part of its initial agenda of technical projects.

IAS Standard 40 Investment Property In April 2001 the International Accounting Standards Board (the Board) adopted IAS 40 Investment Property, which had originally been issued by the International Accounting

IAS Standard 40 Investment Property In April 2001 the International Accounting Standards Board (the Board) adopted IAS 40 Investment Property, which had originally been issued by the International Accounting

Università degli studi di Pavia Facoltà di Economia a.a Lesson 8 International Accounting Lelio Bigogno, Stefano Santucci

Università degli studi di Pavia Facoltà di Economia a.a. 2013-2014 Lesson 8 International Accounting Lelio Bigogno, Stefano Santucci 1 IAS/IFRS: IAS17 Leasing 2 History of IAS17 October 1980 Exposure Draft

Università degli studi di Pavia Facoltà di Economia a.a. 2013-2014 Lesson 8 International Accounting Lelio Bigogno, Stefano Santucci 1 IAS/IFRS: IAS17 Leasing 2 History of IAS17 October 1980 Exposure Draft

IAS 38 Intangible Assets

21/12/2010, Tuesday From To Details Faculty 2:15 PM 5:30 PM IAS 38 : Intangible Assets IAS 40 : Investment Property IFRS 5 : Non Current Assets Held for Sale and Discontinued Operations CA. Chintan Patel,

21/12/2010, Tuesday From To Details Faculty 2:15 PM 5:30 PM IAS 38 : Intangible Assets IAS 40 : Investment Property IFRS 5 : Non Current Assets Held for Sale and Discontinued Operations CA. Chintan Patel,

International GAAP Holdings Limited Model financial statements for the year ended 31 December 2017 (With early adoption of IFRS 16)

") International GAAP Holdings Limited Model financial statements for the year ended 31 December 2017 (With early adoption of IFRS 16) Appendix 1: Early application of IFRS 16 Leases Introduction This Appendix

International GAAP Holdings Limited Model financial statements for the year ended 31 December 2017 (With early adoption of IFRS 16) Appendix 1: Early application of IFRS 16 Leases Introduction This Appendix

SLAS 19 (Revised 2000) Sri Lanka Accounting Standard SLAS 19 (Revised 2000) LEASES

Sri Lanka Accounting Standard SLAS 19 (Revised 2000) LEASES") Sri Lanka Accounting Standard SLAS 19 (Revised 2000) LEASES 265 Introduction This Standard (SLAS 19 (revised 2000) ) replaces Sri Lanka Accounting Standard SLAS 19, Accounting for Leases ( the original

Sri Lanka Accounting Standard SLAS 19 (Revised 2000) LEASES 265 Introduction This Standard (SLAS 19 (revised 2000) ) replaces Sri Lanka Accounting Standard SLAS 19, Accounting for Leases ( the original

Materiële Vaste Activa. 27 September 2005 Pearl Couvreur

Materiële Vaste Activa 27 September 2005 Pearl Couvreur P w C Contents 1. Principle 2. Acquisition cost 3. Subsequent costs 4. Borrowing costs 5. Assets acquired in a business combination 6. Revaluation

Materiële Vaste Activa 27 September 2005 Pearl Couvreur P w C Contents 1. Principle 2. Acquisition cost 3. Subsequent costs 4. Borrowing costs 5. Assets acquired in a business combination 6. Revaluation

This version includes amendments resulting from IFRSs issued up to 31 December 2008.

International Accounting Standard 17 Leases This version includes amendments resulting from IFRSs issued up to 31 December 2008. IAS 17 Leases was issued by the International Accounting Standards Committee

International Accounting Standard 17 Leases This version includes amendments resulting from IFRSs issued up to 31 December 2008. IAS 17 Leases was issued by the International Accounting Standards Committee

IFRS. 4Point Learning Systems Inc. 3/28/2010

4Point Learning Systems Inc. 2010 4Point Learning Systems Inc. No part of these notes may be copied stored or reproduced by any means whatsoever without the express written consent of the authors. Disclaimer:

4Point Learning Systems Inc. 2010 4Point Learning Systems Inc. No part of these notes may be copied stored or reproduced by any means whatsoever without the express written consent of the authors. Disclaimer:

WEEK 9 Investment Property IAS 40

WEEK 9 Investment Property IAS 40 Learning Objectives Define the term investment property. Explain the recognition and measurement procedures in IAS 40 Discuss how to treat disposable of an asset Discuss

WEEK 9 Investment Property IAS 40 Learning Objectives Define the term investment property. Explain the recognition and measurement procedures in IAS 40 Discuss how to treat disposable of an asset Discuss

Summary of IFRS Exposure Draft Leases

The International Accounting Standards Board (IASB) recently issued a revised exposure draft (ED) relating to leases. Once these proposals are finalized the new guidance will replace the IAS 17 Leases.

The International Accounting Standards Board (IASB) recently issued a revised exposure draft (ED) relating to leases. Once these proposals are finalized the new guidance will replace the IAS 17 Leases.

Build Toronto Inc. Consolidated Financial Statements December 31, 2015

Consolidated Financial Statements May 10, 2016 Independent Auditor s Report To the Shareholder of Build Toronto Inc. We have audited the accompanying consolidated financial statements of Build Toronto

Consolidated Financial Statements May 10, 2016 Independent Auditor s Report To the Shareholder of Build Toronto Inc. We have audited the accompanying consolidated financial statements of Build Toronto

Property, Plant and Equipment

International Accounting Standard 16 Property, Plant and Equipment This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 16 Property, Plant and Equipment was issued by

International Accounting Standard 16 Property, Plant and Equipment This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 16 Property, Plant and Equipment was issued by

Property, Plant & Equipment Intangible Assets

Property, Plant & Equipment Intangible Assets October 17, 2015 Contents: 1. Property, Plant and Equipment (Ind AS 16) - Borrowing Costs (Ind AS 23) - Stripping Costs of a Surface Mine (Appendix B to Ind

Property, Plant & Equipment Intangible Assets October 17, 2015 Contents: 1. Property, Plant and Equipment (Ind AS 16) - Borrowing Costs (Ind AS 23) - Stripping Costs of a Surface Mine (Appendix B to Ind

CNK & Associates, LLP

& Associates, LLP Accounting Standards vs Taxation - Revenue Recognition, Effect of Changes in Foreign Exchange Rates, Construction Contracts, Leases & Government Grants 8th July 2017 Gautam Nayak Himanshu

& Associates, LLP Accounting Standards vs Taxation - Revenue Recognition, Effect of Changes in Foreign Exchange Rates, Construction Contracts, Leases & Government Grants 8th July 2017 Gautam Nayak Himanshu

EY s Spotlight on Telecommunications Accounting

Issue 1/2015 EY s Spotlight on Telecommunications Accounting Considerations under IFRS EY s Spotlight on Telecommunications Accounting is a bimonthly publication that addresses key industry topics and

Issue 1/2015 EY s Spotlight on Telecommunications Accounting Considerations under IFRS EY s Spotlight on Telecommunications Accounting is a bimonthly publication that addresses key industry topics and

EHLANZENI DISTRICT MUNICIPALITY ACCOUNTING POLICIES TO THE ANNUAL FINANCIAL STATEMENTS

EHLANZENI DISTRICT MUNICIPALITY ACCOUNTING POLICIES TO THE ANNUAL FINANCIAL STATEMENTS 1. OBJECT TO THE POLICY The aim of the policy is to set accounting standards in line with good international financial

EHLANZENI DISTRICT MUNICIPALITY ACCOUNTING POLICIES TO THE ANNUAL FINANCIAL STATEMENTS 1. OBJECT TO THE POLICY The aim of the policy is to set accounting standards in line with good international financial

In December 2003 the Board issued a revised IAS 17 as part of its initial agenda of technical projects.

IFRS 16 Leases In April 2001 the International Accounting Standards Board (the Board) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

IFRS 16 Leases In April 2001 the International Accounting Standards Board (the Board) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

HKAS 17 Leases 1 October 2005

HKAS 17 Leases 1 October 2005 1. Objective of HKAS 17 The objective of Hong Kong Accounting Standard (HKAS) 17 Leases is to prescribe, for lessees and lessors, the appropriate accounting policies and disclosure

HKAS 17 Leases 1 October 2005 1. Objective of HKAS 17 The objective of Hong Kong Accounting Standard (HKAS) 17 Leases is to prescribe, for lessees and lessors, the appropriate accounting policies and disclosure

Intangible Assets IAS 38, IAS 36, IFRS 3

Intangible Assets IAS 38, IAS 36, IFRS 3 Agenda 1. Introduction 2. Recognition 3. Measurement 4. Impairment of intangible assets (IAS 36) Basic concept Cash-Generating Units 5. Disclosures 2 1 Introduction

Intangible Assets IAS 38, IAS 36, IFRS 3 Agenda 1. Introduction 2. Recognition 3. Measurement 4. Impairment of intangible assets (IAS 36) Basic concept Cash-Generating Units 5. Disclosures 2 1 Introduction

International Financial Reporting Standards. Sample material

International Financial Reporting Standards Sample material Always in context guiding you all the way with summaries key points, diagrams and definitions REVENUE RECOGNITION CHAPTER CONTENTS The provisions

International Financial Reporting Standards Sample material Always in context guiding you all the way with summaries key points, diagrams and definitions REVENUE RECOGNITION CHAPTER CONTENTS The provisions

IFRS Link. Contents. Newsletter. 1 IASB 11 EU Endorsement

IFRS Link Newsletter Issue 25 Contents 1 IASB 11 EU Endorsement New standard on accounting for leases With IFRS 16 Leases, the IASB published a new standard on accounting for leases on 13 January 2016.

IFRS Link Newsletter Issue 25 Contents 1 IASB 11 EU Endorsement New standard on accounting for leases With IFRS 16 Leases, the IASB published a new standard on accounting for leases on 13 January 2016.

Financial Accounting Standards Committee

Statement of Financial Accounting Standards No. 37 20 July 2006 Translated by Chi-Chun Liu, Professor (National Taiwan University) Financial Accounting Standards Committee -605- -606- Statement of Financial

Statement of Financial Accounting Standards No. 37 20 July 2006 Translated by Chi-Chun Liu, Professor (National Taiwan University) Financial Accounting Standards Committee -605- -606- Statement of Financial

International Accounting Standard 38 Intangible Assets. Objective. Scope

International Accounting Standard 38 Intangible Assets Objective 1 The objective of this Standard is to prescribe the accounting treatment for intangible assets that are not dealt with specifically in

International Accounting Standard 38 Intangible Assets Objective 1 The objective of this Standard is to prescribe the accounting treatment for intangible assets that are not dealt with specifically in

How the lease accounting proposal might affect your company

Applying IFRS How the lease accounting proposal might affect your company August 2013 Contents 1. Overview... 1 2. Identifying a lease... 2 2.1 Scope exclusions... 2 2.2 Definition of a lease... 3 2.2.1

Applying IFRS How the lease accounting proposal might affect your company August 2013 Contents 1. Overview... 1 2. Identifying a lease... 2 2.1 Scope exclusions... 2 2.2 Definition of a lease... 3 2.2.1

ACCOUNTING STANDARDS BOARD STANDARD OF GENERALLY RECOGNISED ACCOUNTING PRACTICE LEASES (GRAP 13)

") GRAP 13 ACCOUNTING STANDARDS BOARD STANDARD OF GENERALLY RECOGNISED ACCOUNTING PRACTICE LEASES (GRAP 13) Acknowledgement This Standard of Generally Recognised Accounting Practice (GRAP) is drawn primarily

GRAP 13 ACCOUNTING STANDARDS BOARD STANDARD OF GENERALLY RECOGNISED ACCOUNTING PRACTICE LEASES (GRAP 13) Acknowledgement This Standard of Generally Recognised Accounting Practice (GRAP) is drawn primarily

SRI LANKA ACCOUNTING STANDARD

(REVISED 2005) SRI LANKA ACCOUNTING STANDARD PROPERTY, PLANT & EQUIPMENT THE INSTITUTE OF CHARTERED ACCOUNTANTS OF SRI LANKA (REVISED 2005) SRI LANKA ACCOUNTING STANDARD PROPERTY, PLANT & EQUIPMENT The

(REVISED 2005) SRI LANKA ACCOUNTING STANDARD PROPERTY, PLANT & EQUIPMENT THE INSTITUTE OF CHARTERED ACCOUNTANTS OF SRI LANKA (REVISED 2005) SRI LANKA ACCOUNTING STANDARD PROPERTY, PLANT & EQUIPMENT The

International Financial Reporting Standards (IFRS)

") FACT SHEET February 2011 IAS 40 Investment Property (This fact sheet is based on the standard as at 1 January 2011.) Important note: This fact sheet is based on the requirements of the International Financial

FACT SHEET February 2011 IAS 40 Investment Property (This fact sheet is based on the standard as at 1 January 2011.) Important note: This fact sheet is based on the requirements of the International Financial

AAT Professional Diploma in Accounting

Qualification Number: R486 04 Qualification Technical Information Version 1.1 published 13 June 2016 AAT Professional Diploma in Accounting Qualification Technical Information Units in this qualification

Qualification Number: R486 04 Qualification Technical Information Version 1.1 published 13 June 2016 AAT Professional Diploma in Accounting Qualification Technical Information Units in this qualification

CONSULTATION DRAFT SMALL AND MEDIUM-SIZED ENTITY FINANCIAL REPORTING STANDARD (SME-FRS) CONTENTS

CONTENTS") CONSULTATION DRAFT SMALL AND MEDIUM-SIZED ENTITY FINANCIAL REPORTING STANDARD (SME-FRS) CONTENTS Section Definitions 1 Presentation of Financial Statements 2 Accounting Policies 3 Property, Plant and Equipment

CONSULTATION DRAFT SMALL AND MEDIUM-SIZED ENTITY FINANCIAL REPORTING STANDARD (SME-FRS) CONTENTS Section Definitions 1 Presentation of Financial Statements 2 Accounting Policies 3 Property, Plant and Equipment

IFRS 16 Leases supplement

IFRS 16 Leases supplement Guide to annual financial statements IFRS December 2017 kpmg.com/ifrs Contents About this supplement 1 About IFRS 16 3 The Group s lease portfolio 6 Part I Modified retrospective

IFRS 16 Leases supplement Guide to annual financial statements IFRS December 2017 kpmg.com/ifrs Contents About this supplement 1 About IFRS 16 3 The Group s lease portfolio 6 Part I Modified retrospective

IFRS Project Insights Leases

IFRS Project Insights Leases The IASB and FASB ( the Boards ) published a Discussion Paper (DP) setting out a proposed lessee accounting model in March 2009. The proposed accounting model has evolved since

IFRS Project Insights Leases The IASB and FASB ( the Boards ) published a Discussion Paper (DP) setting out a proposed lessee accounting model in March 2009. The proposed accounting model has evolved since

In May 2014 the Board amended IAS 38 to clarify when the use of a revenue-based amortisation method is appropriate.

IAS 38 Intangible Assets In April 2001 the International Accounting Standards Board (Board) adopted IAS 38 Intangible Assets, which had originally been issued by the International Accounting Standards

IAS 38 Intangible Assets In April 2001 the International Accounting Standards Board (Board) adopted IAS 38 Intangible Assets, which had originally been issued by the International Accounting Standards

31 July 2014 Japan s Modified International Standards (JMIS): Accounting Standards Comprising IFRSs and the ASBJ Modifications

: Accounting Standards Comprising IFRSs and the ASBJ Modifications") 31 July 2014 Japan s Modified International Standards (JMIS): Accounting Standards Comprising IFRSs and the ASBJ Modifications ASBJ Modification Accounting Standard Exposure Draft No. 1 Accounting for

31 July 2014 Japan s Modified International Standards (JMIS): Accounting Standards Comprising IFRSs and the ASBJ Modifications ASBJ Modification Accounting Standard Exposure Draft No. 1 Accounting for

New Zealand Equivalent to International Accounting Standard 40 Investment Property (NZ IAS 40)

") New Zealand Equivalent to International Accounting Standard 40 Investment Property (NZ IAS 40) Issued November 2004 and incorporates amendments to 28 February 2017 other than consequential amendments resulting

New Zealand Equivalent to International Accounting Standard 40 Investment Property (NZ IAS 40) Issued November 2004 and incorporates amendments to 28 February 2017 other than consequential amendments resulting

HKAS 17 Revised February 2014January Hong Kong Accounting Standard 17. Leases

HKAS 17 Revised February 2014January 2017 Hong Kong Accounting Standard 17 Leases HKAS 17 COPYRIGHT Copyright 2017 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial Reporting

HKAS 17 Revised February 2014January 2017 Hong Kong Accounting Standard 17 Leases HKAS 17 COPYRIGHT Copyright 2017 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial Reporting

HKAS 17 Revised January 2017September Hong Kong Accounting Standard 17. Leases

HKAS 17 Revised January 2017September 2018 Hong Kong Accounting Standard 17 Leases HKAS 17 COPYRIGHT Copyright 2018 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial Reporting

HKAS 17 Revised January 2017September 2018 Hong Kong Accounting Standard 17 Leases HKAS 17 COPYRIGHT Copyright 2018 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial Reporting

Latest Development of IFRS (and HKFRS) 10 January 2011

10 January 2011") Latest Development of IFRS (and HKFRS) 10 January 2011 Nelson Lam 林智遠 MBA MSc BBA ACA ACIS CFA CPA(Aust.) CPA(US) CTA FCCA FCPA FTIHK MSCA 2008-11 Nelson Consulting Limited 1 Effective for 2010 Dec. Year-End

Latest Development of IFRS (and HKFRS) 10 January 2011 Nelson Lam 林智遠 MBA MSc BBA ACA ACIS CFA CPA(Aust.) CPA(US) CTA FCCA FCPA FTIHK MSCA 2008-11 Nelson Consulting Limited 1 Effective for 2010 Dec. Year-End

PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 13 LEASES (PBE IPSAS 13)

") PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 13 LEASES (PBE IPSAS 13) This Standard was issued on 11 September 2014 by the New Zealand Accounting Standards Board of the External

PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 13 LEASES (PBE IPSAS 13) This Standard was issued on 11 September 2014 by the New Zealand Accounting Standards Board of the External

IFRS 16 LEASES. Page 1 of 21

IFRS 16 LEASES OBJECTIVE The objective is to ensure that lessees and lessors provide relevant information in a manner that faithfully represents those transactions. This information gives a basis for users

IFRS 16 LEASES OBJECTIVE The objective is to ensure that lessees and lessors provide relevant information in a manner that faithfully represents those transactions. This information gives a basis for users

IFRS and HKFRS Update and Challenge 1 June 2011

IFRS and HKFRS Update and Challenge 1 June 2011 Lam Chi Yuen, Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) CTA FCCA FCPA FHKIoD FTIHK MHKSI MSCA 2008-11 Nelson Consulting Limited 1 Effective for

IFRS and HKFRS Update and Challenge 1 June 2011 Lam Chi Yuen, Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) CTA FCCA FCPA FHKIoD FTIHK MHKSI MSCA 2008-11 Nelson Consulting Limited 1 Effective for

This version includes amendments resulting from IFRSs issued up to 31 December 2009.

International Accounting Standard 40 Investment Property This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 40 Investment Property was issued by the International

International Accounting Standard 40 Investment Property This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 40 Investment Property was issued by the International

In December 2003 the IASB issued a revised IAS 17 as part of its initial agenda of technical projects.

IFRS Standard 16 Leases In April 2001 the International Accounting Standards Board (IASB) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

IFRS Standard 16 Leases In April 2001 the International Accounting Standards Board (IASB) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

Property, Plant & Equipment and Leases 18 October 2012

Property, Plant & Equipment and s 18 October 2012 LAM Chi Yuen Nelson 林智遠 MBA MSc BBA ACA ACS CFA FCPA(Aust.) CPA(US) CTA FCCA FCPA FHKIoD FTIHK MHKSI MSCA 2005-12 Nelson Consulting Limited 1 Today s Agenda

Property, Plant & Equipment and s 18 October 2012 LAM Chi Yuen Nelson 林智遠 MBA MSc BBA ACA ACS CFA FCPA(Aust.) CPA(US) CTA FCCA FCPA FHKIoD FTIHK MHKSI MSCA 2005-12 Nelson Consulting Limited 1 Today s Agenda

New Zealand Equivalent to International Accounting Standard 17 Leases (NZ IAS 17)

") New Zealand Equivalent to International Accounting Standard 17 Leases (NZ IAS 17) Issued November 2004 and incorporates amendments to 31 December 2016 This Standard was issued by the New Zealand Accounting

New Zealand Equivalent to International Accounting Standard 17 Leases (NZ IAS 17) Issued November 2004 and incorporates amendments to 31 December 2016 This Standard was issued by the New Zealand Accounting

IFRS for Hospitality and Gaming Industry (Part 1) 25 May 2010

25 May 2010") IFRS for Hospitality and Gaming Industry (Part 1) 25 May 2010 Nelson Lam 林智遠 MBA MSc BBA ACA ACIS CFA CPA(Aust.) CPA(US) FCCA FCPA FHKIoD MSCA 2006-10 Nelson Consulting Limited 1 Workshop Agenda Property,

IFRS for Hospitality and Gaming Industry (Part 1) 25 May 2010 Nelson Lam 林智遠 MBA MSc BBA ACA ACIS CFA CPA(Aust.) CPA(US) FCCA FCPA FHKIoD MSCA 2006-10 Nelson Consulting Limited 1 Workshop Agenda Property,

CA. Gopal Ji Agrawal

CA. Gopal Ji Agrawal 1. Scope 2. Key concepts 3. Accounting for leases 4. Other Lease Contracts 4. Disclosure 5. Appendix (s) 6. Questions October 1980 September 1982 IAS 17 Accounting for Leases Exposure

CA. Gopal Ji Agrawal 1. Scope 2. Key concepts 3. Accounting for leases 4. Other Lease Contracts 4. Disclosure 5. Appendix (s) 6. Questions October 1980 September 1982 IAS 17 Accounting for Leases Exposure

Sri Lanka Accounting Standard LKAS 40. Investment Property

Sri Lanka Accounting Standard LKAS 40 Investment Property LKAS 40 CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 40 INVESTMENT PROPERTY paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 5 CLASSIFICATION OF PROPERTY

Sri Lanka Accounting Standard LKAS 40 Investment Property LKAS 40 CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 40 INVESTMENT PROPERTY paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 5 CLASSIFICATION OF PROPERTY

EN Official Journal of the European Union L 320/323

29.11.2008 EN Official Journal of the European Union L 320/323 INTERNATIONAL ACCOUNTING STANDARD 40 Investment property OBJECTIVE 1 The objective of this standard is to prescribe the accounting treatment

29.11.2008 EN Official Journal of the European Union L 320/323 INTERNATIONAL ACCOUNTING STANDARD 40 Investment property OBJECTIVE 1 The objective of this standard is to prescribe the accounting treatment

New HKFRS for NPO/NGO 16 March 2005

New HKFRS for NPO/NGO 16 March 2005 HKFRS Nelson Lam CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA 2006 Nelson 1 Today s Agenda Property, plant and equipment (HKAS 16) Investment property (HKAS 40)

New HKFRS for NPO/NGO 16 March 2005 HKFRS Nelson Lam CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA 2006 Nelson 1 Today s Agenda Property, plant and equipment (HKAS 16) Investment property (HKAS 40)

Exposure Draft. Amendments to Ind AS 40, Investment Property. (Last date for the comments: July 11, 2018)

") ED/ Ind AS/2018/07 Exposure Draft Amendments to Ind AS 40, Investment Property (Last date for the comments: July 11, 2018) Issued by Accounting Standards Board The Institute of Chartered Accountants of

ED/ Ind AS/2018/07 Exposure Draft Amendments to Ind AS 40, Investment Property (Last date for the comments: July 11, 2018) Issued by Accounting Standards Board The Institute of Chartered Accountants of

Meet Definition of. Be investment property. & Follow FV Model. Earn Rentals

Meet Definition of Requirements It s Property Held to Use in Production Process Or Admin Purpose Earn Capital Appreciation Earn Rentals & Follow Model Instead of And Available on Property By Property Basis

Meet Definition of Requirements It s Property Held to Use in Production Process Or Admin Purpose Earn Capital Appreciation Earn Rentals & Follow Model Instead of And Available on Property By Property Basis

CAS -16 COST ACCOUNTING STANDARD ON DEPRECIATION AND AMORTISATION

Cost Accounting Standards Board CAS -16 COST ACCOUNTING STANDARD ON DEPRECIATION AND AMORTISATION The following is the COST ACCOUNTING STANDARD 16 (CAS 16) issued by the Council of The Institute of Cost

Cost Accounting Standards Board CAS -16 COST ACCOUNTING STANDARD ON DEPRECIATION AND AMORTISATION The following is the COST ACCOUNTING STANDARD 16 (CAS 16) issued by the Council of The Institute of Cost

New Zealand Equivalent to International Accounting Standard 40 Investment Property (NZ IAS 40)

") New Zealand Equivalent to International Accounting Standard 40 Investment Property (NZ IAS 40) Issued November 2004 and incorporates amendments up to and inlcuding 28 February 2014 This Standard was issued

New Zealand Equivalent to International Accounting Standard 40 Investment Property (NZ IAS 40) Issued November 2004 and incorporates amendments up to and inlcuding 28 February 2014 This Standard was issued

Business Combinations

Business Combinations Indian Accounting Standard (Ind AS) 103 Business Combinations Contents Paragraphs OBJECTIVE 1 SCOPE 2 IDENTIFYING A BUSINESS COMBINATION 3 THE ACQUISITION METHOD 4 53 Identifying

Business Combinations Indian Accounting Standard (Ind AS) 103 Business Combinations Contents Paragraphs OBJECTIVE 1 SCOPE 2 IDENTIFYING A BUSINESS COMBINATION 3 THE ACQUISITION METHOD 4 53 Identifying

NEED TO KNOW. Leases A Project Update

NEED TO KNOW Leases A Project Update 2 LEASES - A PROJECT UPDATE TABLE OF CONTENTS Introduction 3 Existing guidance and the rationale for change 4 The IASB/FASB project to date 5 The main proposals 6 Definition

NEED TO KNOW Leases A Project Update 2 LEASES - A PROJECT UPDATE TABLE OF CONTENTS Introduction 3 Existing guidance and the rationale for change 4 The IASB/FASB project to date 5 The main proposals 6 Definition

Sri Lanka Accounting Standard - SLFRS 16. Leases

Sri Lanka Accounting Standard - SLFRS 16 Leases CONTENTS from paragraph SRI LANKA ACCOUNTING STANDARD - SLFRS 16 LEASES INTRODUCTION OBJECTIVE 1 SCOPE 3 RECOGNITION EXEMPTIONS 5 IDENTIFYING A LEASE 9 Separating

Sri Lanka Accounting Standard - SLFRS 16 Leases CONTENTS from paragraph SRI LANKA ACCOUNTING STANDARD - SLFRS 16 LEASES INTRODUCTION OBJECTIVE 1 SCOPE 3 RECOGNITION EXEMPTIONS 5 IDENTIFYING A LEASE 9 Separating

IFRS Update Guy Thomas, CPA, CA

IFRS Update Guy Thomas, CPA, CA D&Co IFRS update Agenda 3 new standards under IFRS IFRS 9 Financial Instruments IFRS 15 Revenue from Contracts with Customers IFRS 16 Leases Agenda Some narrow scope amendments

IFRS Update Guy Thomas, CPA, CA D&Co IFRS update Agenda 3 new standards under IFRS IFRS 9 Financial Instruments IFRS 15 Revenue from Contracts with Customers IFRS 16 Leases Agenda Some narrow scope amendments

Business Combinations

International Financial Reporting Standard 3 Business Combinations This version was issued in January 2008. Its effective date is 1 July 2009. It includes amendments resulting from IFRSs issued up to 31

International Financial Reporting Standard 3 Business Combinations This version was issued in January 2008. Its effective date is 1 July 2009. It includes amendments resulting from IFRSs issued up to 31

7 Days Intensive Workshop on IFRS ICAI Tower, BKC, Mumbai. IAS 16 Property, Plant & Equipments

7 Days Intensive Workshop on IFRS ICAI Tower, BKC, Mumbai 01-July-14, Tuesday From To Details Faculty 10:00 AM 1:15 PM IAS 16 : Property, Plant & Equipments IAS 38 : Intangible Assets Ind AS 40:Investment

7 Days Intensive Workshop on IFRS ICAI Tower, BKC, Mumbai 01-July-14, Tuesday From To Details Faculty 10:00 AM 1:15 PM IAS 16 : Property, Plant & Equipments IAS 38 : Intangible Assets Ind AS 40:Investment

Leases (HKAS 17) June 2006

June 2006") s (HKAS 17) June 2006 Nelson Lam CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA 2005-06 Nelson 1 s Case Star Cruises Ltd. (2005) stated: The adoption of HKAS 17 requires the Group to classify the land

s (HKAS 17) June 2006 Nelson Lam CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA 2005-06 Nelson 1 s Case Star Cruises Ltd. (2005) stated: The adoption of HKAS 17 requires the Group to classify the land

HKFRS 16 Leases. Disclaimer. Date 21 April 2017 Time 19:00 21:00 Venue Boys' and Girls' Clubs Association

HKFRS 16 Leases Date 21 April 2017 Time 19:00 21:00 Venue Boys' and Girls' Clubs Association www.zhtraining.com Disclaimer The materials of this seminar are intended only to provide general information

HKFRS 16 Leases Date 21 April 2017 Time 19:00 21:00 Venue Boys' and Girls' Clubs Association www.zhtraining.com Disclaimer The materials of this seminar are intended only to provide general information

CPA COMPETENCY MAP STUDY NOTES UPDATE TO DECEMBER 31, 2018

CPA COMPETENCY MAP STUDY NOTES UPDATE TO DECEMBER 31, 2018 Please note that several of the updates relate to changes that are not effective until 2019. For 2019 PEP Module Exams and for the CFE, you are

CPA COMPETENCY MAP STUDY NOTES UPDATE TO DECEMBER 31, 2018 Please note that several of the updates relate to changes that are not effective until 2019. For 2019 PEP Module Exams and for the CFE, you are

HKFRS 16 Leases sets out the principles for the recognition, measurement, presentation and disclosure

HKFRS 16 Leases Introduction HKFRS 16 Leases sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective of HKFRS 16 is to ensure that lessees and lessors

HKFRS 16 Leases Introduction HKFRS 16 Leases sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective of HKFRS 16 is to ensure that lessees and lessors

IFRS 15. Revenue from Contracts with Customers. Presented by CPA Dr. Peter Njuguna

IFRS 15 Revenue from Contracts with Customers Presented by CPA Dr. Peter Njuguna Introduction Revenue is income from ordinary activities. A contract has rights and obligations between two or more parties.

IFRS 15 Revenue from Contracts with Customers Presented by CPA Dr. Peter Njuguna Introduction Revenue is income from ordinary activities. A contract has rights and obligations between two or more parties.

A Review of IFRS 16 Leases By Tan Liong Tong

A Review of IFRS 16 Leases By Tan Liong Tong In April 2016, the MASB issued MFRS 16 Leases that is identical to IFRS 16 Leases issued by the IASB in January 2016. The effective date of this new MFRS is

A Review of IFRS 16 Leases By Tan Liong Tong In April 2016, the MASB issued MFRS 16 Leases that is identical to IFRS 16 Leases issued by the IASB in January 2016. The effective date of this new MFRS is

HKFRS for Not-For-Profit Entity 11 January 2005

HKFRS for Not-For-Profit Entity 11 January 2005 HKFRS Nelson Lam CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA 2006 Nelson 1 Today s Agenda Introduction Non-current Assets Summary of of Convergence

HKFRS for Not-For-Profit Entity 11 January 2005 HKFRS Nelson Lam CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA 2006 Nelson 1 Today s Agenda Introduction Non-current Assets Summary of of Convergence

COUNCIL FINANCIAL STATEMENTS

COUNCIL FINANCIAL STATEMENTS Includes: Statement of Accounting Policies Prospective Financial Statements Funding Impact Statement Supporting Document for Long Term Plan Consultation Document 2018 CONTENTS

COUNCIL FINANCIAL STATEMENTS Includes: Statement of Accounting Policies Prospective Financial Statements Funding Impact Statement Supporting Document for Long Term Plan Consultation Document 2018 CONTENTS

Exposure Draft. Accounting Standard (AS) 40 Investment Property. Last date for the comments: November 10, 2018

40 Investment Property. Last date for the comments: November 10, 2018") Exposure Draft Accounting Standard (AS) 40 Investment Property Last date for the comments: November 10, 2018 Issued by Accounting Standards Board The Institute of Chartered Accountants of India 1 Exposure

Exposure Draft Accounting Standard (AS) 40 Investment Property Last date for the comments: November 10, 2018 Issued by Accounting Standards Board The Institute of Chartered Accountants of India 1 Exposure