CITY OF EAST POINT EAST POINT REDEVELOPMENT PLAN

|

|

|

- Denis Jennings

- 5 years ago

- Views:

Transcription

1 CITY OF EAST POINT EAST POINT REDEVELOPMENT PLAN TAX ALLOCATION DISTRICT #2 EAST POINT COMMERCIAL CORRIDORS AMENDED MAY 2017 PREPARED FOR: PREPARED BY:

2 TABLE OF CONTENTS Table of Contents... 2 Executive Summary... 4 Introduction... 4 The Opportunity and Vision for the Redevelopment Area... 5 Legal Basis and Qualifying Conditions for the TAD... 8 Key Redevelopment Challenges... 9 The Goal Introduction Proposal and Grounds for Exercise of Redevelopment Powers Geographic Boundaries (A) How Residents in East Point and Fulton County will Benefit Overview of Tax Allocation Districts Grounds for Exercise of Redevelopment Powers (B) Why the East Point Corridors Study Area Qualifies as a Redevelopment Area Market and Demographic Conditions Plan Vision and Goal Proposed Land Uses after Redevelopment (C) Proposed Redevelopment Projects (D) Contractual Relationships (E) Relocation Plans (F) Zoning & Land Use Compatibility (G) Method of Financing / Proposed Public Investments (H) TAD Potential of Downtown East Point Projects Assessed Valuation for TAD (I) Historic Property within Boundaries of TAD (J) Creation & Termination Dates for TAD (K) Tax Allocation Increment Base (M) Property Taxes for Computing Tax Allocation Increments (N) Tax Allocation Bond Issues (O, P, Q) Amount of Bond Issue Term of the Bond Issue or Issues Rate of Bond Issue Positive Tax Allocation Increments Property to be Pledged for Payment of the Bonds School System Impact Analysis (R) The Current Value of TAD #2 Verses the Fulton County School System s Tax Digest Implications of Status Quo Conditions to the FCSS Executive Summary 2

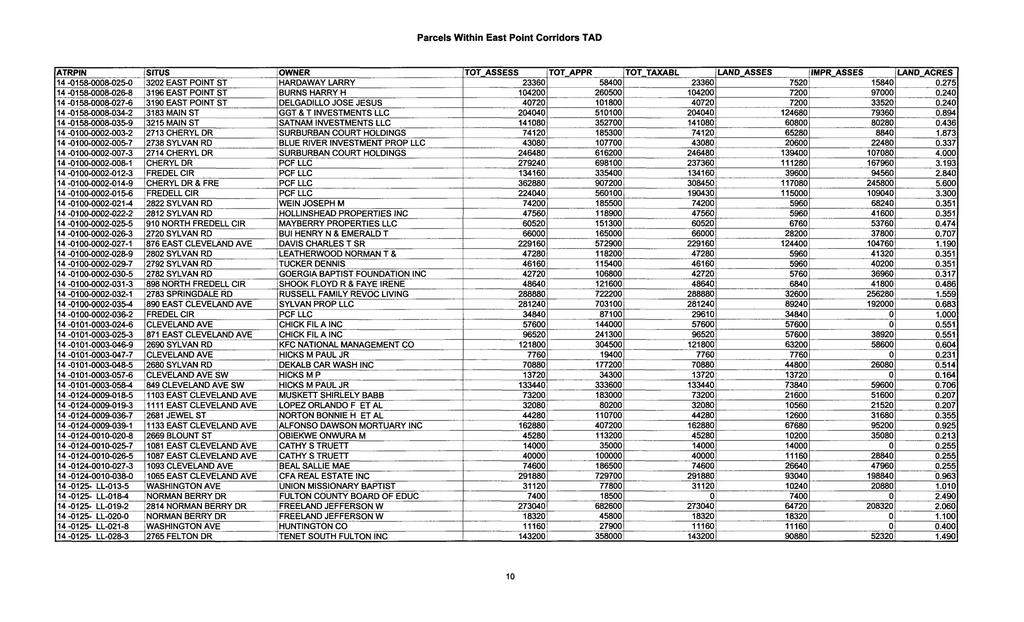

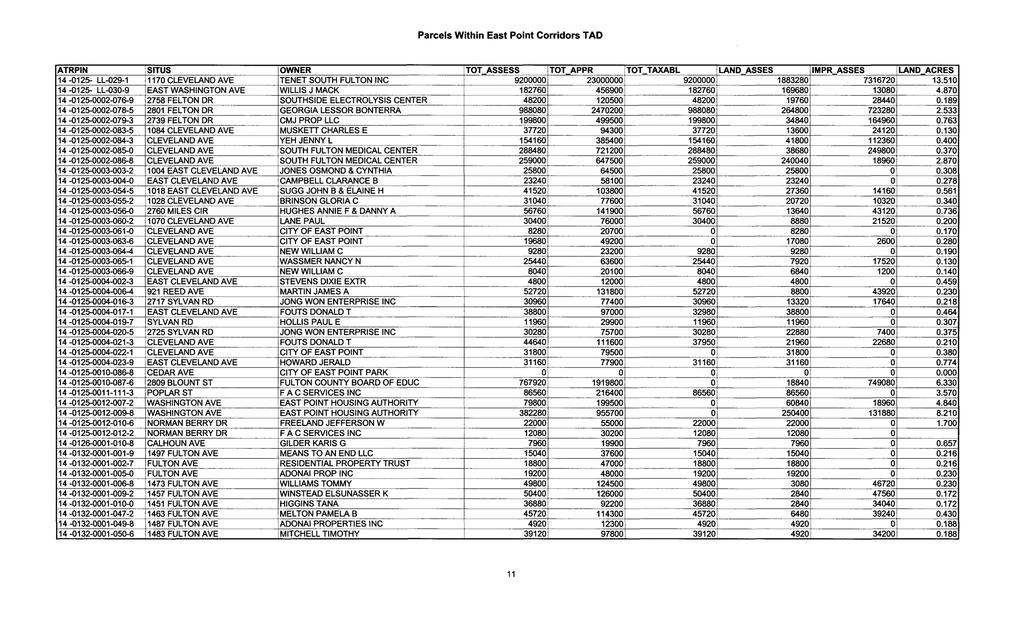

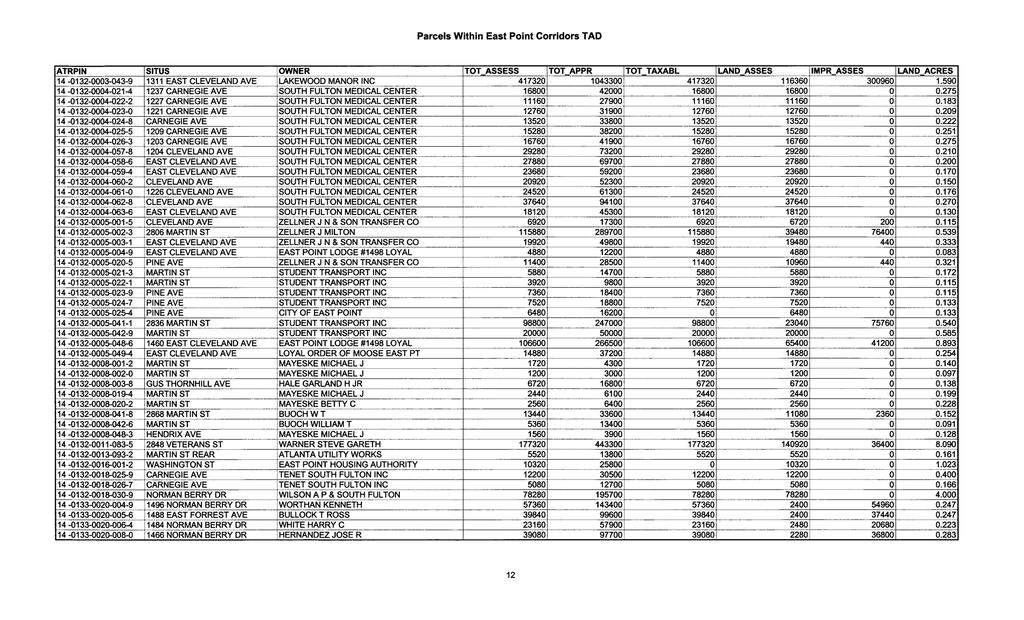

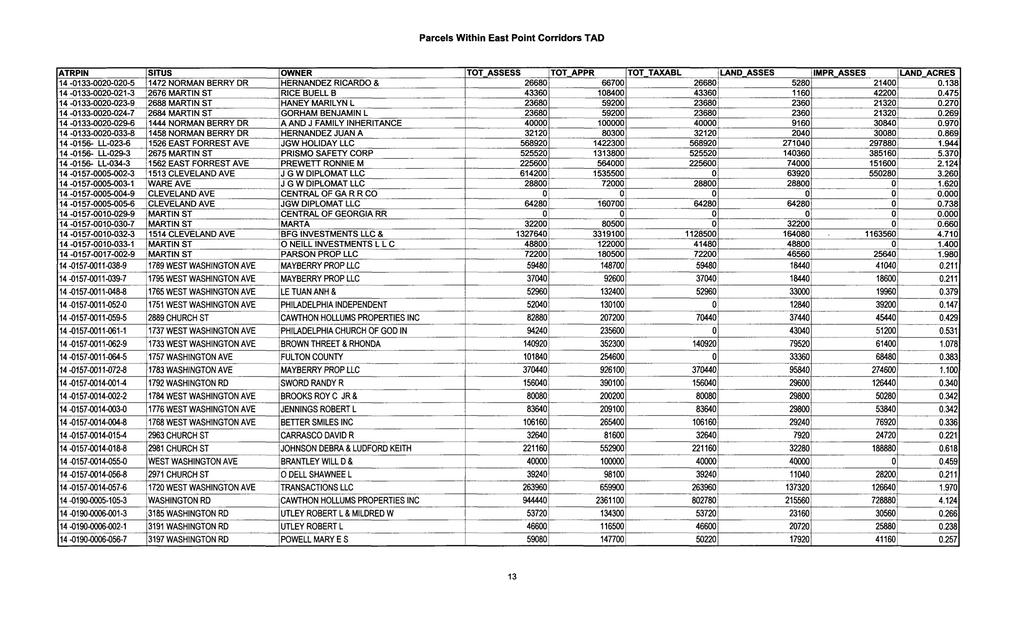

3 Proposed Redevelopment in East Point TAD # The Location of School Facilities within the Redevelopment Area An Estimate of Educational Special Purpose Local Option (ESPLOST) Sales Taxes and Incremental Business Personal Property Taxes Projected from TAD Development Conclusion Regarding School District Impacts Appendices Appendix A. LIST OF TAX PARCEL ID NUMBERS (PROPERTIES WITHIN THE TAD) Appendix B. East Point Mayor, City Council and City Manager Appendix C. Fulton County Board of Commissioners and County Manager Appendix D. Fulton County Board of Education and Superintendent of Schools * Headings followed by a letter in parenthesis [e.g. (A)] denote information required per Georgia Code Chapter 36, Title 44-3(9). Executive Summary 3

4 Tax Allocation District #2 - East Point Commercial Corridors EXECUTIVE SUMMARY INTRODUCTION In 2006, the City of East Point adopted a Redevelopment Plan (the Plan) creating Tax Allocation District #2 East Point Commercial Corridors (TAD #2). The Redevelopment Plan was prepared in conformance with the provisions of the Georgia Redevelopment Powers Law (O.C.G.A. Title 36 Chapter 44) which governs the creation of the Tax Allocation Districts in the state. 1 The Plan was prepared at the request of the City of East Point and duly adopted by resolution of the City Council. TAD #2 was later certified by the Georgia Commissioner of Revenue and became effective as of December 31, This document is intended to update and formally amend the original Plan, which is now more than 10 years old. Due in part to the impacts of the last recession, which was unforeseen at the time the original Redevelopment Plan was prepared, several of the projects upon which TAD #2 was based have failed to materialize more than a decade later. Other sites have been developed in ways different than forecast in 2006 and are no longer in play. So, while some growth has occurred within the TAD boundaries since 2006, the City is still struggling to recover fiscally from the severe economic and housing market downturn which occurred during and following the recession. The economic and fiscal justifications for creating TAD #2 are therefore more compelling in 2017 than they were when the Plan was first adopted more than a decade ago. Fulton County agreed to participate in TAD #2, but included in its consent a sunset provision which may limit the TAD s future financing capacity. The Fulton County School System s Board of Education (BOE) declined to consent to TAD #2 following its initial creation in After the BOE adopted a new policy toward Tax Allocation Districts, the City made a second, unsuccessful attempt to secure BOE consent in late Without the full participation of all three jurisdictions, the City will be unable to offer sufficient financial incentives to attract developers and implement redevelopment projects that are critical to the City s economic recovery. After several years of market inactivity, East Point has made recent progress in interesting developers to participate in its Downtown redevelopment efforts. The potential to resurrect some projects envisioned in 2006 has also increased the City s desire to obtain County and School District consent to TAD #2. Because of the market s recent improvement and emerging developer interest in TAD #2, the City has authorized the 2006 Redevelopment Plan to be amended reflect current economic conditions and present a realistic framework for County and School District participation. The scope of this plan amendment does not include changing the boundaries of or resetting the base value of TAD #2, and is limited to the following: 1. Updating the economic, demographic, and fiscal justifications for establishing TAD #2, to reflect market conditions as of early 2017; 1 The East Point Corridors Tax Allocation District and Redevelopment Plan was prepared for the City of East Point by Huntley Partners, Inc. of Atlanta, Georgia. The report was issued in December of Executive Summary (DRAFT) 4

5 2. Updating the list of potential redevelopment projects which remain possible under current economic conditions, IF adequate financial incentives can be leveraged through TAD #2 to make those projects financially feasible; 3. Reset the term the TAD will remain in effect, to preserve the option to issue TAD financing, should the City Council opt to do so; and 4. To comply with statutory changes made to the Redevelopment Powers Law since the 2006 Plan was prepared, particularly the requirements to prepare a School District Impact Analysis (Section (9)(R)). The following report contains much of the text of the original Redevelopment Plan and only updates those specific sections that have changed significantly since THE OPPORTUNITY AND VISION FOR THE REDEVELOPMENT AREA The overall purpose of the East Point Corridors Redevelopment Plan and Tax Allocation District (TAD) is to establish a financing mechanism to help facilitate recommended improvements which are outlined in this Plan. Specifically, the TAD was proposed for the following purposes: 1. To attract private, taxable redevelopment opportunities to the East Point Corridors sectors of the City of East Point. 2. To further the City s goals of improving underdeveloped urban areas as well as of attracting desirable development, including professional jobs. 3. To provide funding that, in turn, will attract additional regional, State and Federal funding to allow improvements to land use, transportation, and recreational areas. 4. To realize the full economic potential of an increasingly urbanized community. 5. To increase employment opportunities for residents of the TAD area and surrounding East Point neighborhoods. 6. To increase opportunities for market-driven residential and commercial development within the East Point Corridors area. 7. To overcome constraints to development generated by aged and obsolete commercial and residential structures, inefficient transportation infrastructure and inadequate physical connections to the surrounding community. Executive Summary 5

6 8. To achieve the basic goals that were stated in the LCI and Cleveland Avenue studies and incorporated into the redevelopment plan, as follows: Provide desirable residential product types in the central business district, preferably with an ownership preference. Provide additional retail, dining, entertainment and other commercial amenities such as better supermarkets within East Point. In addition, create a critical mass of people in the CBD sufficient to attract a destination retail market. Maximize land use advantages though the development of mixed-use projects allowing for live-work convenience to residents and closer retail in proximity to housing. Encourage development that will protect and enhance existing study area neighborhoods while connecting them to the civic and commercial center of the CBD. Enhance connectivity within and among East Point neighborhoods though the design, extension and general improvement of walking, bicycling and multi-use trails. Ensure the provision of sidewalks connecting open spaces and parks and allowing access to existing City amenities. Improve the possibilities for redevelopment of the surplus MARTA parking lot and Sylvan Road / Cleveland Avenue area. Improve the pedestrian environment (amenities, access, usability, traffic calming, lighting, personal safety) Increase usable greenspace/parks. Increase the tax base with which to fund basic city services. Create financing mechanisms, resources and incentives such as this Tax Allocation District to fund redevelopment. Create a better profile throughout Metro Atlanta with potential residents seeking unique, convenient, safe, community-oriented housing locations. Executive Summary 6

7 EAST POINT TAD #2 BOUNDARY The boundaries of the Redevelopment Area and Tax Allocation District #2 are shown on Map E-1 on the following page. The East Point Corridor TAD incorporates that portion of Cleveland Avenue stretching from the city limits of East Point and Atlanta one block west of I-85 to the Irene Kidd Parkway, where it continues to Church Street two blocks west of Main Street. The TAD also includes that portion of Main Street stretching from Vesta Avenue on the south to the City limits at Womack Avenue on the north. Additionally, the TAD incorporates the Washington Road corridor from the Central Business District to I-285, incorporating several commercial clusters along or in immediate proximity to Washington Road. MAP E-1: Executive Summary 7

8 LEGAL BASIS AND QUALIFYING CONDITIONS FOR THE TAD The City of East Point has the authority to exercise all redevelopment and other powers authorized or granted municipalities pursuant to the Redevelopment Powers Law (Chapter 44 of Title 36 of the O.C.G.A.), as approved by City voters by referendum. The redevelopment area qualifies as a TAD under the following specific definitions of the Redevelopment Powers Law under Sections (7), (A) and (B). Portions of the definition which are applicable to the East Point Corridors Redevelopment Area include the following: Criterion A: A "blighted or distressed area" is an area that is experiencing one or more conditions of blight as evidenced by: i ii iii The dilapidation, deterioration, age, or obsolescence of structures, buildings, or improvements; The presence of a predominant number of substandard, vacant, deteriorated, or deteriorating structures; the predominance of a defective or inadequate street layout or transportation facilities; or faulty lot layout in relation to size, accessibility, or usefulness Evidence of pervasive poverty defined as being greater than 10 percent of the population in the area as determined by current data from the United States Bureau of the Census, and an unemployment rate that is 10 percent higher than the state average; v. Any combination of the foregoing that substantially impairs or arrests the sound growth of the community; Criterion B: A "deteriorating area" is an area that is experiencing physical or economic decline or stagnation as evidenced by two or more of the following: i. The presence of a substantial number of structures or buildings that are 40 years old or older and have no historic significance); ii. High commercial or residential vacancies compared to the City as a whole; iii. Predominance of structures or buildings of relatively low value iv. Declining or stagnant rents ; As is discussed later in this report, East Point Corridors qualifies as a redevelopment area under the Redevelopment Powers Law due to its meeting and in most cases far exceeding the general criteria cited in the Law. Furthermore, this plan demonstrates that a continuation of the status quo is the least desirable and most costly financial outcome for the City, County, and School District. Executive Summary 8

9 The fundamental purpose of the East Point Corridors TAD Redevelopment Plan is to address the conclusion that the proposed East Point Corridors TAD area has not been subject to growth and development through private enterprise and cannot reasonably anticipate development without approval of this Plan. In addition, this area has been a long-established redevelopment priority. The East Point Corridors area has been designated as an area appropriate for redevelopment in the City of East Point Comprehensive Plan. Additionally, the City formally adopted the 2005 East Point Livable Centers Initiative plan and the 2006 Cleveland Avenue Corridor Study. The original and continuing intent of TAD #2 is to help leverage higher property tax collections within an area that was substantially under-performing in 2006 and remains under-performing in terms of property values and generation of tax revenues. The housing, retail and commercial redevelopment proposed for the tax allocation district would increase the City s existing property tax digest, by incentivizing redevelopment and helping to finance needed infrastructure improvements, which would not otherwise be financially feasible, at no additional cost to East Point taxpayers. In light of the TAD s actual performance over the past decade and the broader economic and fiscal issues facing East Point, the City has authorized the 2006 Redevelopment Plan to be amended in order to reflect current economic and market conditions. This amended redevelopment plan removes some of the original projects proposed in 2006, downsizes others, and focuses on more achievable near term opportunities that are focused primarily on MARTA-accessible downtown sites. The number and value of residential units forecast in the 2006 Plan, particularly forsale condominium products, has been substantially reduced to reflect market limitations on those products. Those housing adjustments in turn reduce population and school enrollment impacts that were forecast a decade ago. The City hopes that the County and School District will be more likely to consent to a Plan which focuses on achievable, near term projects, with more modest expectations and requiring smaller commitments of property tax increments. KEY REDEVELOPMENT CHALLENGES The City of East Point has invested substantial funds and effort to create a shared vision for its future, committing significant planning and other resources toward the revitalization and redevelopment of its Downtown and major commercial gateways into Downtown. The City s future challenge is to attract new private investment and create a density of population and economic activity that will be sufficient to support commercial success, within a city that has suffered from above average poverty and unemployment, stagnant population change and declining housing values. Older urbanized areas like Downtown East Point often suffer from surrounding development patterns, inadequate transportation facilities and antiquated infrastructure which do not support new development of a quality or character desired by community residents. The following specific observations were noted in Executive Summary 9

10 the 2006 Plan and summarize the specific challenges faced by, and reasons for designating the redevelopment area: (a) Structural Age and Deterioration: The majority of the retail buildings and apartments were constructed between 35 and 50 years ago. They have experienced only minor improvements since that time. Consequently, they are out of date and have become somewhat dilapidated due to the passage of time and frequent use. (b) Inefficient and Obsolete Commercial Design and Layout: The commercial centers and freestanding structures along the major roads within the East Point Corridors area are inefficient with respect to site use and density. Most are considered unattractive with respect to current retailer standards and obsolete with respect to consumer market appeal. Parking is inefficient, and store frontage and signage are below current market standards and design. (c) Lack of Retail Market Appeal: As reflected in both rent and sales, the limited number of retail businesses within the proposed East Point Corridors TAD do not have the brand recognition, product offerings, marketing capacity, pricing, merchandising or basic critical mass to appeal customers within either the primary or secondary retail markets. (d) Lack of Rental Revenue Generation: Commercial rental rates in the East Point Corridors Area are significantly below those achieved in developing Metro Atlanta neighborhoods. (e) Economic Underutilization of Developable Land: A significant proportion of developable land within the area is underutilized with respect to potential density, type of development and/or resulting market and taxable values. (f) Congested Access and Egress: The design and layout of the major roads and intersections within the East Point Corridors TAD contribute to traffic congestion and delays, particularly at major intersections at Cleveland Avenue and Norman Berry Drive; Irene Kidd Parkway at both Central Avenue and Main Street; Norman Berry Drive at Main Street; and Main Street at Willingham Drive. The area's internal network of feeder roadways is not conducive to the efficient flow of traffic into and out of the existing or contemplated retail, office and mixed-use projects in that area. The currently inadequate network of interior and residential streets within the area will become even less capable of handling both community and pass-through traffic. THE GOAL The creation of East Point TAD Number 2, known as East Point Commercial Corridors, is intended to provide the City with additional financial resources to attract private investment to key downtown development sites which are either served by or accessible to transit. The strategy envisioned in the TAD was to attract new development to the downtown area as a first step toward incrementally revitalizing the City s older established commercial districts. Increased future property tax revenues leveraged from Executive Summary 10

11 private investment within the TAD would also provide local funding to improve downtown streetscapes and infrastructure servicing development sites. The TAD s boundaries encompass the bulk of potential development sites in the core downtown area and, using the City s major commercial corridors, link a series of seven commercial clusters along or in close proximity to Washington Road. It was originally conceived that most of these clusters could accommodate mixed use development, and long range forecasts contained in the 2006 Plan included 1,950 residential units along with 717,000 SF of retail space, nearly 590,000 SF of office space and 200 hotel rooms. Characteristics of TAD #2 are summarized in Table E-1: Table E-1: East Point Tax Allocation District #2 - East Point Commercial Corridors - Parcel Information* Parcels (approximate)* 750 Acreage* TAD #2 Certified Base Digest $48,837, East Point Taxable (Digest) Value (M&O Portion) $911,372,181 TAD Certified Digest as a % of City s Taxable Value when created 5.4% 2016 East Point Taxable (Digest) Value (M&O Portion) $811,347,731 TAD Certified Digest as a % of City s 2016 Taxable Value 6.02% *TAD acreage and 2016 digest estimates are as reported by the Fulton County Assessor. Today, TAD#2 contains approximately 750 parcels covering nearly 295 taxable acres. In the decade following its creation in 2006, the taxable digest value of the district has increased from a base of $48.8 million to a 2016 digest of $55.6 million, according to Fulton County Assessment Department records. The total TAD digest has increased by a modest 14% over the decade, faster than the City but only a third of County and School District growth rates over the same period. The taxable real estate digest (40% value) within TAD #2 currently averages only $188,500 per acre (in 2016), far below forecast expectations made a decade ago. This low average value explains the City s desire to attract new, higher-density development into the most marketable locations along its under-valued and under-performing commercial corridors. Most importantly, the revitalization of these key areas was viewed as critical to stabilizing the value of the City s housing stock, which was aging and well below regional values when the TAD was formed. While some investment has occurred in TAD # 2 since 2006, the combination of recession and lack of financial resources has limited the TAD s value as a redevelopment incentive. The City s inability to achieve its redevelopment goals for TAD #2 has contributed to broader value declines elsewhere in the City. As illustrated in the following graphs, East Point s total taxable digest has decreased by 4% since 2000 and outside of the two TADs, digest values have fallen by more than $189 million (-22%). The fiscal implications of the status quo trends have thus been negative to all three taxing jurisdictions and there is no reason to expect that this 16-year negative growth trend will reverse itself, absent of achieving one or more game changing catalyst projects. After a decade of very limited success with the availability of City and County tax increment only, it is clear that Executive Summary 11

12 more financial assistance will be needed to attract desired development, on a sufficient scale, to positively impact existing conditions. Exhibit E-3: These graphs show the change in East Point s property tax digest by year, from 2000 through The top graph shows total Citywide digest change since The bottom compares digest growth in the City s two TAD s to the balance of the City. Digesr (40%) Value $1,200,000,000 $1,000,000,000 $800,000,000 $600,000,000 $400,000,000 Change in East Point M&O Tax Digest by Year: $200,000,000 $ Locations of Change in East Point's M&O Tax Digest by Year: $1,200,000,000 Balance of City Digest (40%) Value $1,000,000,000 $800,000,000 $600,000,000 $400,000,000 $200,000,000 $ TAD 1 TAD 2 Balance of City POTENTIAL REDEVELOPMENT PROJECTS The City had initially identified eleven potential redevelopment projects or project areas within TAD #2 where redevelopment efforts would be focused. These projects collectively represented the vision for the future of East Point as a mixed-use center and transit node, supported by attractive gateway corridors into downtown and multiple new development nodes near those commercial corridors. Together the projects involved more than 1.3 million SF of retail and office development, new hotels and more than 1,900 housing units, representing a combined construction cost of more than $500 million. Executive Summary 12

13 Table E-2: List of Proposed Projects 2006 Redevelopment Plan Corporate Office Townhomes MF Condos MF Apartments Site Retail (SF) Local Office (SF) (SF) Hotel (Rooms) (Units) (Units) (Units) 1 Buggy Works Expansion 70, , East Point Commons 52, Tri-Cities Plaza 100, MARTA South Parking Lot 50, , North Main District 25,000 25,000 50, North Main MXD 50,000 25, Central Main District 50,000 25,000 8 South Main District 50,000 10, SFMC Campus + King Bldg 175, Sylvan Road MXD Center 250,000 25, Wagon Works Expansion 20, Total 717, , , Source: East Point Corridors Tax Allocation District and Redevelopment Plan, 2006 Site With the passage of a decade and the impact of the Great Recession, most of the above list of projects are no longer financially feasible on the scale and in the time frame originally proposed. Some of these project sites have already been developed for similar or other uses or are otherwise no longer in play. In amending this redevelopment plan the City has evaluated and down-sized the original project list into six locations where redevelopment is most likely to be feasible, within a reasonable time period. Projects have also been re-scaled to reflect foreseeable, near-term market conditions and input the City has gathered from prospective developers. Residential impacts have also been substantially reduced, particularly for ownership products. Table E-3: Revised List of Proposed Projects 2017 Amended Redevelopment Plan Retail (SF) Local Office (SF) Corporate Office (SF) Hotel Townhomes (Rooms) (Units) Senior Housing (Units) MF Apartments (Units) 1 Buggy Works Expansion 50,000 25, East Point Commons 60, MARTA South Parking Lot 50,000 50, Central Main District 50,000 25,000 5 South Main District 50,000 10,000 6 Wagon Works Expansion 20,000 Total 280,000 60,000 50, The revised list of six projects appears in Table E-3. Development totals have been re-worked and focused on Downtown. If successful, these projects would still have Executive Summary 13

14 a positive economic and fiscal impact on the City, while generating minimal service costs impacts on the county and school system. The earliest of these projects to be implemented is the proposed East Point Commons, which is illustrated below the table. While the City would strongly consider proposals to invest TAD proceeds to support other redevelopment projects elsewhere in TAD #2, the following list of projects will be given priority in terms of focus and funding as it becomes available. Exhibit E-4: This exhibit shows a recent development concept for East Point Commons. The City and its Development Authority are actively negotiating to convey the assembled properties to a private developer. However, the project is not financially feasible without the investment of property tax increments contributed by all three taxing jurisdictions, through the TAD. TOTAL DEVELOPMENT POTENTIAL If these project areas are developed as forecast, BAG estimates that they could collectively support 390,000 SF of retail and office space, 120 hotel rooms and 580 residential units, including 180 units of senior housing. These estimates represent an approximate 70% reduction to both residential and commercial totals forecast in The primary adjustments made were the removal of for sale condominium units and a substantial reduction in retail and corporate office development. Revised retail totals also reflect and remove square footage that has already been developed. BAG estimates that when completed, these projects would have a full market value of nearly $126 million based on their current value. 2 The distribution the projects 2 Full market value in this context refers to the likely value assigned to completed developments by the Fulton County Tax Assessor. Full market value for tax purposes is different from, and should not be confused with, actual construction costs or sales prices. Executive Summary 14

15 market values by project and component is summarized in Table E-4. As shown, the largest investment is the East Point Commons, which accounts for nearly half of the estimated end value of the entire list. Table E-4: Estimated Full Market Value of Revised TAD Projects by Component 2017 Amended Redevelopment Plan Senior Multi-Family Project/Site Retail Office Hotel Townhomes Housing Apartments Total 1 Buggy Works Expansion $4,500,000 $2,375,000 $0 $24,000,000 $0 $0 $30,875,000 2 East Point Commons $5,400,000 $0 $0 $0 $25,200,000 $31,500,000 $62,100,000 3 MARTA South Parking Lot $4,500,000 $4,750,000 $9,600,000 $0 $0 $0 $18,850,000 4 Central Main District $4,500,000 $2,375,000 $0 $0 $0 $0 $6,875,000 5 South Main District $4,500,000 $950,000 $0 $0 $0 $0 $5,450,000 6 Wagon Works Expansion $1,800,000 $0 $0 $0 $0 $0 $1,800,000 Total $25,200,000 $10,450,000 $9,600,000 $24,000,000 $25,200,000 $31,500,000 $125,950,000 BAG further estimates that the projects listed in Table E-4 could potentially be built out over a 6 to 9-year period. The additional tax digest created by this new development, coupled with a most allowance for future appreciation and value change elsewhere in the TAD (based on historical value growth since 2006), would increase the TAD s digest from roughly $55.6 million (in 2016), to nearly $116.9 million in 10 years. Annual real estate taxes collected within the TAD by all jurisdictions would increase from $2.4 million currently to roughly $5.1 million by year 10, with approximately $2.1 million in taxes continuing to be received by the taxing jurisdictions respective general funds and the balance of nearly $3.0 million contributed as tax allocation increment to support redevelopment. This forecast appears in Table E-5. Executive Summary 15

16 Table E-5: Estimated TAD Revenues from Build Out of Revised TAD Projects 2017 Amended Redevelopment Plan Year (2017 = 1) TAD Base Digest Full Market Value of New Development Incremental Tax Digest from New Development Base Growth TOTAL TAD 2 Digest Total Tax Mils Base RE Taxes to General Funds Available Tax Allocation Increment 1 $48,837,930 $0 $0 $55,619,258 $55,619,258 $2,443,521 $2,145,597 $297,924 2 $48,837,930 $0 $0 $56,342,308 $56,342,308 $2,475,287 $2,145,597 $329,690 3 $48,837,930 $9,780,000 $3,912,000 $57,074,758 $60,986,758 $2,679,331 $2,145,597 $533,734 4 $48,837,930 $34,143,300 $13,657,320 $57,816,730 $71,474,050 $3,140,069 $2,145,597 $994,473 5 $48,837,930 $85,566,938 $34,226,775 $58,568,348 $92,795,123 $4,076,768 $2,145,597 $1,931,171 6 $48,837,930 $121,674,707 $48,669,883 $59,329,736 $107,999,619 $4,744,747 $2,145,597 $2,599,150 7 $48,837,930 $127,956,913 $51,182,765 $60,101,023 $111,283,788 $4,889,031 $2,145,597 $2,743,434 8 $48,837,930 $131,945,092 $52,778,037 $60,882,336 $113,660,373 $4,993,441 $2,145,597 $2,847,844 9 $48,837,930 $134,261,832 $53,704,733 $61,673,806 $115,378,539 $5,068,925 $2,145,597 $2,923, $48,837,930 $136,060,672 $54,424,269 $62,475,566 $116,899,835 $5,135,760 $2,145,597 $2,990, $48,837,930 $137,885,736 $55,154,294 $63,287,748 $118,442,043 $5,203,514 $2,145,597 $3,057, $48,837,930 $139,737,436 $55,894,974 $64,110,489 $120,005,464 $5,272,200 $2,145,597 $3,126, $48,837,930 $141,616,193 $56,646,477 $64,943,925 $121,590,403 $5,341,831 $2,145,597 $3,196, $48,837,930 $143,522,435 $57,408,974 $65,788,196 $123,197,170 $5,412,421 $2,145,597 $3,266, $48,837,930 $145,456,596 $58,182,638 $66,643,443 $124,826,081 $5,483,984 $2,145,597 $3,338, $48,837,930 $147,419,119 $58,967,648 $67,509,808 $126,477,455 $5,556,534 $2,145,597 $3,410, $48,837,930 $149,410,453 $59,764,181 $68,387,435 $128,151,616 $5,630,085 $2,145,597 $3,484, $48,837,930 $151,431,055 $60,572,422 $69,276,472 $129,848,894 $5,704,651 $2,145,597 $3,559, $48,837,930 $153,481,391 $61,392,556 $70,177,066 $131,569,622 $5,780,248 $2,145,597 $3,634, $48,837,930 $155,561,933 $62,224,773 $71,089,368 $133,314,141 $5,856,890 $2,145,597 $3,711, $48,837,930 $157,673,162 $63,069,265 $72,013,530 $135,082,795 $5,934,592 $2,145,597 $3,788, $48,837,930 $159,815,568 $63,926,227 $72,949,706 $136,875,933 $6,013,370 $2,145,597 $3,867, $48,837,930 $161,989,647 $64,795,859 $73,898,052 $138,693,910 $6,093,240 $2,145,597 $3,947, $48,837,930 $164,195,905 $65,678,362 $74,858,726 $140,537,088 $6,174,216 $2,145,597 $4,028, $48,837,930 $166,434,857 $66,573,943 $75,831,890 $142,405,832 $6,256,315 $2,145,597 $4,110, Year Totals $125,360,975 $53,639,919 $71,721,055 Future Revenues 6.0% $31,014,409 Source: Bleakly Advisory Group, Inc. POTENTIAL TAD FUNDING Should all three taxing jurisdictions commit their M&O millage to the TAD on the real estate (only), the above forecast could produce total estimated TAD proceeds of $71.7 million over 25 years. 3 This forecast represents an approximate 234% increase over likely tax revenues if existing conditions do not significantly change throughout the forecast. Of these estimated property tax increments pledged to the TAD, (and assuming that millage rates to not change significantly over the forecast), 3 We have used a 25-year forecast as representative of the total likely investment required of the taxing jurisdictions. The City will be requesting that the County and School District agree to extend the life of the TAD for a maximum of 30 years beginning from the City s point of signing a development agreement to provide TAD funding to a first project, or until all redevelopment costs are paid, whichever occurs first. Executive Summary 16

17 approximately $24.5 million would be contributed by the City, $17.1 million by Fulton County and $30.1 million by the School District. The balance of real estate tax collections from within the TAD of approximately $53.7 million over 25 years, would continue to be used for general fund purposes, along with tax revenues associated with growth in personal property tax digest associated with future retail, office and hotel development within the TAD. Table E-6: East Point TAD #2 East Point Commercial Corridors Potential Redevelopment Sites Potential Redevelopment Residential Units (Apartments, Townhomes & Senior Units) 580 Average Full Market Value/Unit $139,100 Commercial, Retail, Office & Hotel S.F. 444,000 Average Full Market Value/SF $ Future Market Value of TAD Projects at Build-out (Year 10) $136.0 Million Total TAD #2 Taxable Digest at Completion (Year 10) $116.9 Million Net New TAD Taxable Real Estate Digest at Completion $66.5 Million Total tax allocation increment to the TAD #2 Fund (Yr 10) $2.99 million Source: Developers, City of East Point and BAG BAG also estimates that the forecasted growth in tax increments could support potential financing or bond revenues of $31.0 million (net after issuance costs and reserves) for investment in redevelopment projects and additional public improvements. (This estimate assumes that approximately 70% to 80% of forecasted tax increments could be generated quickly enough to be pledged for financing purposes.) Should the Fulton County School System refuse to consent to the TAD, the amount of net proceeds available to invest in redevelopment projects (with City and County increments only) is reduced to roughly $17.5 million. This amount is unlikely to be sufficient to incentivize the quality or density of redevelopment needed to achieve the City s objectives and reduce long term trends. POTENTIAL INVESTMENTS OF TAD PROCEEDS Table E-7 distributes the estimated future TAD proceeds to each of the project sites listed in this Plan, based on the proportional share of future tax allocation increments those projects will create. Depending on the specific situation, TAD funds could be used to make public infrastructure improvements, build structured parking or provide direct financial incentives to developers to offset construction costs. Uses of TAD proceeds will be defined by the City of East Point during negotiations with individual developers on a case by case basis. Funding decisions will be based on the amount of incremental tax revenues those projects will generate, as well as the availability of current/future tax increments available to the TAD Special Fund. The City is committed to using TAD proceeds in most effective and appropriate manner allowed under the Redevelopment Powers Law, to achieve successful results. Executive Summary 17

18 Table E-7: Potential Uses of Estimated Future Proceeds TAD #2 - East Point Commercial Corridors Estimated Build Supportable Project/Site Out Value TAD Proceeds 1 Buggy Works Expansion $30,875,000 $7,602,678 2 East Point Commons $62,100,000 $15,291,539 3 MARTA South Parking Lot $18,850,000 $4,641,635 4 Central Main District $6,875,000 $1,692,904 5 South Main District $5,450,000 $1,342,011 6 Wagon Works Expansion $1,800,000 $443,233 Total $125,950,000 $31,014,000 The City recognizes that TAD #2 encompasses a larger area than is represented by these 6 projects listed above. Other, currently unforeseen projects may arise in the future, which merit public support. Although uses of TAD proceeds will be prioritized toward the projects listed in Table E-7, the City will also consider supporting other worthwhile redevelopment projects in TAD #2, if/when such opportunities arise. SCHOOL DISTRICT IMPACTS The fiscal consequences resulting from economic decline within older sections of East Point have been very detrimental to the FCSS for nearly two decades. Annual collections of school district taxes within the City have declined since the year 2000, while the number of students enrolled in the FCSS East Point Schools has steadily increased. The FCSS currently collects only 2.1% of all local school taxes from East Point residents and businesses, while nearly 8% of total District enrollment is based in schools that are physically located within the City limits. Local economic conditions have also made the task of educating students more challenging, as evidenced by above average child poverty rates, below average rates of home ownership, high percentages of single parent households and high mobility/turnover among the student population attending East Point Schools. A continuation of existing conditions in East Point will be costly to future FCSS operations and school performance. As demonstrated by the recent success of the City s Camp Creek TAD, potential impacts to the Fulton County Public Schools from participating in the proposed TAD #2 should be positive in the short term and very positive in the long term. Increased collections of personal property taxes from new commercial development and increased future e-splost revenues should be sufficient to offset a very marginal increase in school district enrollment, even while the TAD is in effect. Once the TAD is dissolved and real property taxes accrue to the School District, the Districts tax digest will be greatly increased over what is feasible absent of the TAD. Executive Summary 18

19 Impacts on the Fulton County Public School System from participating in East Point TAD #2 are as follows: The proposed TAD will affect the future appreciation on 0.16% (sixteen onehundredths of one percent) of the School s taxable digest. All current property taxes on real estate (roughly $902,700/year) will continue to go to the school system only increases above the current amount are pledged to the TAD. The redevelopment area will potentially attract 950 new residents and fewer than 60 school-aged children at build out, achieved after several years of construction. This represents an addition of 0.8% to the current enrollment of FCSS schools located within the City limits. There is one existing Fulton County School facility located inside the TAD boundary, Parklane Elementary School, which is located at 2809 Blount Street. (Parcel ID: LL018) When fully built out within roughly 10 years, the proposed redevelopment projects could collectively generate an additional $390,000 per year in net annual e-lost funds from new residents and businesses, during years in which the e-lost is in effect. In addition, increased commercial personal property digest, which is not pledged to the TAD, could generate roughly $280,000 per year in educational property taxes. Should the FCSS not consent to TAD #2 and as a result, no major redevelopment projects are implemented, it is likely that property values would continue to grow modestly, by the same average as occurred during the first decade since TAD #2 was formed. In such a case, the FCSS would instead receive an additional $8.0 million in increased real estate taxes from future value growth within TAD #2, cumulatively, over 25 years. 4 Maintaining status quo conditions in TAD #2 will also have no impact in reversing the long-term erosion of school tax revenues generated elsewhere in the City. By comparison, forecasted cumulative gains in e-lost and commercial personal property taxes from implementing the six identified TAD projects are estimated to total nearly $14.8 million to the FCSS over the same 25-year period. Increased FCSS revenues received from participating in the TAD, while it is in effect, thus exceed the modest amount of real estate taxes that might otherwise be collected by choosing to not to consent, if such a decision results in no major redevelopment occurring, and status quo conditions continue for another decade. More detailed findings are provided in the full report. 4 This estimate represents the incremental gain of 1.3% annual digest growth compounded, over existing FCSS revenues of $902,000 per year associated with the base value of the TAD. If the FCSS was currently participating in TAD #2, its total financial commitment to the TAD Special Fund would have been roughly $125,000 in Executive Summary 19

20 Tax Allocation District #2 - East Point Commercial Corridors INTRODUCTION In 2006, the City of East Point adopted a Redevelopment Plan (the Plan) creating Tax Allocation District #2 East Point Commercial Corridors (TAD #2). That Plan presented the justification, rationale, boundaries, fiscal data, and proposed projects which, at the time, were forecast to result from the establishment of TAD #2. The Redevelopment Plan was prepared in conformance with the provisions of the Georgia Redevelopment Powers Law (O.C.G.A. Title 36 Chapter 44) which governs the creation of the Tax Allocation Districts in the state. The Plan was prepared at the request of the City of East Point and duly adopted by resolution of the City Council. TAD #2 was later certified by the Georgia Commissioner of Revenue and became effective as of December 31, This document is intended to update and formally amend the original Plan, which is now more than 10 years old. The foundations for the original Redevelopment Plan and Tax Allocation District were assembled from earlier plans and sources that were compiled in 2005 and Those sources included (1) the 2005 City of East Point Livable Centers Initiative report prepared by Pond & Company in association with The Collaborative Firm, Sizemore Group and Market+Main; (2) the 2006 Cleveland Avenue Corridor Study: Masterplan prepared by Urban Studio, Inc. in association with WK Dickson & Co., Inc. and Iteris, Inc.; (3) the 2005 East Point MARTA Development: Real Estate Development Methods study prepared by the East Point MARTA Development Consultants team, and (4) the City of East Point s 2006 Comprehensive Plan Update. The Redevelopment Plan incorporated proposed projects and development forecasts contained in those studies, which were prepared during the high point of the housing market bubble which preceded the Great Recession. Due in part to the impacts of the last recession, which was unforeseen at the time the original Redevelopment Plan was prepared, several of the projects upon which TAD #2 was based have failed to materialize more than a decade later. Some of the identified redevelopment sites in that plan are also less likely to become available for redevelopment in the near term. So, while some growth has occurred within the TAD boundaries since 2006, the City is still struggling to recover fiscally from the severe economic and housing market downturn which occurred during and following the recession. The economic and fiscal justifications for creating TAD #2 are therefore equally or more compelling in 2017 as they were when the Plan was first adopted more than a decade ago. Fulton County agreed to participate in TAD #2, but included in its consent a sunset provision which may limit the TAD s future financing capacity. The Fulton County School System s Board of Education (BOE) declined to consent to TAD #2 following its initial creation in After the BOE adopted a new policy toward Tax Allocation Districts, the City made a second, unsuccessful attempt to secure BOE consent in late Without the full participation of all three jurisdictions, the City will be unable to offer sufficient financial incentives to attract developers and implement redevelopment projects that are critical to the City s economic recovery. Introduction 20

21 After several years of market inactivity, the City has made recent progress in interesting developers to participate in its Downtown redevelopment efforts. The potential to resurrect some projects envisioned in 2006 has also increased the City s desire to obtain County and School District consent to TAD #2. Because of the market s recent improvement and emerging developer interest in TAD #2, the City has authorized Bleakly Advisory Group (BAG) to update and amend the 2006 Redevelopment Plan to reflect current economic conditions and present a realistic framework for County and School District participation. The scope of this plan amendment does not include changing the boundaries of or resetting the base value of TAD #2, and is limited to the following: 1. Updating the economic, demographic, and fiscal justifications for establishing TAD #2, to reflect market conditions as of early 2017; 2. Updating the list of potential redevelopment projects which remain possible under current economic conditions, IF adequate financial incentives can be leveraged through TAD #2 to make those projects financially feasible; 3. Reset the term the TAD will remain in effect, to preserve the option to issue TAD financing, should the City Council opt to do so; and 4. To comply with statutory changes made to the Redevelopment Powers Law since the 2006 Plan was prepared, particularly the requirements to prepare a School District Impact Analysis (Section (9)(R)). The following report retains much of the text of the original Redevelopment Plan and only updates those specific sections that have changed significantly since PROPOSAL AND GROUNDS FOR EXERCISE OF REDEVELOPMENT POWERS GEOGRAPHIC BOUNDARIES (A) The East Point Corridor TAD incorporates that portion of Cleveland Avenue stretching from the city limits of East Point and Atlanta one block west of I-85 to the Irene Kidd Parkway, where it continues to Church Street two blocks west of Main Street. The TAD also includes that portion of Main Street stretching from Vesta Avenue on the south to the City limits at Womack Avenue on the north. Additionally, the TAD incorporates the Washington Road corridor from the Central Business District to I-285, incorporating several commercial clusters along or in immediate proximity to Washington Road. The following series of maps show the regional setting of the Redevelopment Area, followed by the TAD boundary map and enlarged insets showing the key redevelopment opportunities / sites within the TAD. Proposal (DRAFT) 21

22 Regional Setting and Major Roadways. Proposal (DRAFT) 22

23 Tax Allocation District #2 - East Point Commercial Corridors Map 1: TAD #2 Boundary Map (L) Proposal (DRAFT) 23

North Main District (2)")

24 Tax Allocation District #2 - East Point Commercial Corridors Map 2: East Point Corridor TAD Boundaries: Enlarged Sub Areas Cleveland Avenue Corridor (1) North Main District (2) Proposal (DRAFT) 24

")

")

25 Central and South Main District (3) Washington Road Corridor - North (4) Proposal (DRAFT) 25

26 Washington Road Corridor - South (5) HOW RESIDENTS IN EAST POINT AND FULTON COUNTY WILL BENEFIT OVERVIEW OF TAX ALLOCATION DISTRICTS Tax allocation districts are Georgia s version of tax increment financing. Tax increment financing is a redevelopment funding mechanism that reinvests the future taxes from real estate development back into a project either (a) directly, as an incentive to attract new private investment into an area or (b) indirectly by paying for public improvements that could not be absorbed as a private development cost. As described by the Council of Development Finance Agencies. ( TIF was created and first used in California in Hundreds of TIF districts have helped spur urban redevelopment in cities across the country. Today, all 50 states and the District of Columbia use tax increment financing in some form. In 1985, the Georgia General Assembly authorized formation of Georgia s form of tax increment financing called Tax Allocation Districts (TADs). The purpose of a Georgia tax allocation district is similar to tax increment financing in any other state. A TAD allows increased property taxes generated by new development within the designated district to be used to finance costs related to the development, such as public infrastructure, land acquisition, relocation, demolition, parking structures, Proposal (DRAFT) 26

27 utilities, debt service and planning costs. Other allowed uses of TAD proceeds include: Sewer expansion and repair Storm drainage Street construction and expansion Water supply improvements Park improvements Bridge construction and repair Curb and sidewalk work Grading and earthwork Traffic control Cities and counties throughout Georgia have created TADs to stimulate major new construction and renovation or rehabilitation in underdeveloped or blighted areas. Nearly 80 Georgia cities and counties have either created or are considering establishing TADs in their communities. There were also several existing TAD s in Fulton County as of the end A TAD offers local governments the opportunity to promote worthwhile redevelopment projects that would otherwise not be financially viable, or are located in areas which would otherwise be unattractive to private investment. Prior to the last Recession in 2008 and 2009, other Georgia tax allocation districts such as Atlantic Station (Midtown Atlanta) and the Camp Creek Marketplace in East Point, demonstrated the economic benefits which TADs can generate. These benefits include: A stronger economic base TAD incentives can attract private development that would not otherwise have occurred absent of the District designation. The halo effect Several Georgia TADs have generated significant new investment in areas surrounding the TAD as well as within the tax allocation districts, further expanding positive economic impacts to the host taxing jurisdictions. No impact on current tax revenues Redevelopment is effectively promoted without tapping into existing general governmental revenues or levying special assessments on property owners. Expands the local tax base By stimulating economic activity, TAD s expand the local tax digest, create additional demand for retail sales and as a result, local sales taxes and SPLOST revenues. Is self-financing TADs are self-financing, since they are funded by the increased tax revenues from new development within the district. High leverage Typically TAD funds represent between 5-15% of project costs, leveraging 7-20 times their value in private investment. Proposal (DRAFT) 27

28 Tax Allocation District #2 - East Point Commercial Corridors In summary, a tax allocation district is a financing mechanism that can be used to pay for public infrastructure or reduce private development costs, to make an underutilized area attractive to private investment and development, at no additional cost to local taxpayers. Establishing a TAD does not create a tax increase for either the community or property owners within the District. Nor does a TAD reduce tax revenues to the community, below levels which existed at the time the District was certified. In many cases, TADs can increase general fund revenues from new business personal property taxes, added county sales taxes, hotel/motel taxes, business license fees and other revenues which are not pledged for redevelopment purposes and would not otherwise occur. GROUNDS FOR EXERCISE OF REDEVELOPMENT POWERS (B) Tax Allocation Districts are authorized in Georgia under the Redevelopment Powers Law, O.C.G.A. Title 36, Chapter 44. In 2009, the Redevelopment Powers Law was amended again, with the following definition of a redevelopment area. Redevelopment area means an urbanized area as determined by current data from the US Bureau of the Census or an area presently served by sewer that qualifies as a blighted or distressed area, a deteriorating area, or an area with inadequate infrastructure as follows: (A) A blighted or distressed area is an area that is experiencing one of more conditions of blight as evidenced by: (i) The presence of structures, buildings, or improvements that by reason of dilapidation; deterioration; age; obsolescence; inadequate provision for ventilation, light, air, sanitation, or open space; overcrowding; conditions which endanger life or property by fire or other causes; or any combination of such factors, are conducive to ill health, transmission of disease, infant mortality, high unemployment, juvenile delinquency, or crime and are detrimental to the public health, safety, morals, or welfare; (ii) Is substantially underutilized by containing open lots or parcels of land; (iii) Contains a predominant number of substandard, vacant, deteriorated, or deteriorating structures, the predominance of a defective or inadequate street layout, or transportation facilities; or faulty lot layout in relation to size, accessibility, or usefulness; (iv) Evidence of pervasive poverty, defined as being greater than 10 percent of the population in the area as determined by current data from the U.S. Bureau of the Census, and an unemployment rate that is 10 percent higher than the state average; (v) Adverse effects of airport or transportation related noise or environmental contamination or degradation or other adverse environmental factors that the political subdivision has determined to be impairing the redevelopment of the area; or (vi) The existence of conditions through any combination of the foregoing that substantially impair the sound growth of the community and retard the provision of housing accommodations or employment opportunities; (B) A deteriorating area is an area that is experiencing physical or economic decline or stagnation as evidenced by two or more of the following: (i) The presence of a substantial number of structures or buildings that are 40 years old or older and have no historic significance; (ii) High commercial or residential vacancies compared to the political subdivision as a whole; Method of Financing/Proposed Public Investments (DRAFT) 28

29 (iii) The predominance of structures or buildings of relatively low value compared to the value of structures or buildings in the surrounding vicinity or significantly slower growth in the property tax digest than is occurring in the political subdivision as a whole; (iv) Declining or stagnant rents or sales prices compared to the political subdivision as a whole; (v) In areas where housing exists at present or is determined by the political subdivision to be appropriate after redevelopment, there exists a shortage of safe, decent housing that is not substandard and that is affordable for persons of low and moderate income; (vi) Deteriorating or inadequate utility, transportation, or transit infrastructure; and (C) An area with inadequate infrastructure means an area characterized by: (i) Deteriorating or inadequate parking, roadways, bridges, pedestrian access, or public transportation or transit facilities incapable of handling the volume of traffic into or through the area, either at present or following redevelopment; or (ii) Deteriorating or inadequate utility infrastructure either at present or following redevelopment. -Georgia Redevelopment Powers Law WHY THE EAST POINT CORRIDORS STUDY AREA QUALIFIES AS A REDEVELOPMENT AREA The City of East Point has the authority to exercise all redevelopment and other powers authorized or granted municipalities pursuant to the Redevelopment Powers Law, as now or hereafter amended by virtue of a successful City voter referendum. The following section addresses how the proposed Redevelopment Area qualifies as meeting the conditions described in O.C.G.A. Section subsections A, B and C presented above. 5 It should be noted that the presence of substandard buildings is not necessarily prevalent throughout the entire Redevelopment Area, due in part to actions already taken. TAD#2 is envisioned as a catalyst to start new economic activity in Downtown East Point, that will eventually spread to other portions of the Redevelopment Area, and where the following conditions are prevalent: The following specific observed conditions were noted in the 2006 Plan illustrate the qualifying definition of a redevelopment area: (a) Structural Age and Deterioration: The majority of the retail buildings and apartments were constructed between 35 and 50 years ago. They have experienced only minor improvements since that time. Consequently, they are out of date and have become somewhat dilapidated due to the passage of time and frequent use. (b) Inefficient and Obsolete Commercial Design and Layout: The commercial centers and freestanding structures along the major roads within the East Point Corridors area are inefficient with respect to site use and density. Most are 5 The discussion in this section addresses the City of East Point rather than the 294-acre Redevelopment Area, which is primarily commercial in nature. Characteristics of the relatively small population that resides within TAD #2 are assumed to be similar to the City as a whole. Tax Allocation Bond Issues (O, P, Q) (DRAFT) 29

30 considered unattractive with respect to current retailer standards and obsolete with respect to consumer market appeal. Parking is inefficient, and store frontage and signage are below current market standards and design. (c) Lack of Retail Market Appeal: As reflected in both rent and sales, the limited number of retail businesses within the proposed East Point Corridors TAD do not have the brand recognition, product offerings, marketing capacity, pricing, merchandising or basic critical mass to appeal customers within either the primary or secondary retail markets. (d) Lack of Rental Revenue Generation: Commercial rental rates in the East Point Corridors Area are significantly below those achieved in developing Metro Atlanta neighborhoods. (e) Economic Underutilization of Developable Land: A significant proportion of developable land within the area is underutilized with respect to potential density, type of development and/or resulting market and taxable values. (f) Congested Access and Egress: The design and layout of the major roads and intersections within the East Point Corridors TAD contribute to traffic congestion and delays, particularly at major intersections at Cleveland Avenue and Norman Berry Drive; Irene Kidd Parkway at both Central Avenue and Main Street; Norman Berry Drive at Main Street; and Main Street at Willingham Drive. The area's internal network of feeder roadways are not conducive to the efficient flow of traffic into and out of the existing or contemplated retail, office and mixed-use projects in that area. The currently inadequate network of interior and residential streets within the area will become even less capable of handling both community and pass-through traffic. (g) City Redevelopment Priority: The East Point Corridors area has been designated as an area appropriate for redevelopment in the City of East Point Comprehensive Plan. Additionally, the City formally adopted the 2005 East Point Livable Centers Initiative plan and the 2006 Cleveland Avenue Corridor Study. The Comprehensive Plan is updated on an annual basis, and the recommendations of this plan are anticipated to be considered during the update process. (h) Pervasive Poverty and High Unemployment: The redevelopment area is primarily nonresidential in character, with more than 89% of the TAD s taxable land area classified as commercial or industrial property. Poverty and resident unemployment data were not collected for the small population that resides within the redevelopment area. However, City-wide data are likely to be a conservative reflection of localized conditions, as the redevelopment area s population is likely to be less affluent that the City as a whole. The 2017 median household income in East Point is estimated to be $40,340, which is 34% lower than the median household income in Fulton County ($61,084), or the median income for the Metro-Atlanta region ($60,749). More than 19% of the City s 14,700 households are estimated to currently earn incomes below $15,000 per year, a higher percentage than Fulton County (14%) and all Metro-Atlanta households (11%) within this same income bracket. And, according to the US Tax Allocation Bond Issues (O, P, Q) (DRAFT) 30

31 Census Bureau s American Community Survey, nearly 28% of the City s population earned incomes below the poverty level in 2015, roughly double the State average. This number included nearly 19% of all families with children. The unemployment rate among East Point residents was estimated in late 2016 at 7.7%, two full percentage points above Georgia s 5.2% unemployment. The redevelopment area therefore greatly exceeds both minimum thresholds for satisfying the statutory definition of pervasive poverty and high unemployment. Comparative historic unemployment rates. Source: Civic Dashboards, from US Bureau of Labor Statistics, Local Area Unemployment Statistics. (i) According to Claritas, Inc., approximately 28% of the housing supply in East Point consists of multi-family units and 52% of all existing housing is estimated to be renter occupied. The median age of existing housing is 46 years and 64% of all housing is estimated to have been built prior to The median value of owner occupied housing is estimated at $107,121, only 39% of the current median value of all owner-occupied housing in Fulton County ($276,825) and 56% of the Metro Atlanta median value of $191,671. As these numbers indicate, East Point possesses the presence of a substantial number of structures or buildings that are 40 years old or older and have no historic significance; and the predominance of structures or buildings of relatively low value compared to the value of structures or buildings in the surrounding vicinity. The City s housing stock also exhibits declining or stagnant rents or sales prices. Tax Allocation Bond Issues (O, P, Q) (DRAFT) 31

32 In summary, East Point Corridors qualifies as a redevelopment area under the Redevelopment Powers Law due to its meeting and in most cases exceeding the general criteria cited in the Law. The overall purpose of TAD #2 is to address and resolve the key challenges, conditions and barriers to private investment. East Point envisions its downtown to be a significantly larger, higher-density, mixed-use node which combines residential, retail, office, and public uses, served by transit. Improvement of the major gateways to downtown, represents an essential building block to support revitalization of this business district, consistent with the community s vision. If successful, a revitalized and growing downtown is expected to make other portions of the redevelopment area more viable economically and create opportunities to make comparable improvements to those areas. Absent of TAD #2, East Point lacks alternative resources to finance parking, build infrastructure and improve public amenities, which are essential to drawing private investment to the City. The following photos were taken within the East Point Corridors redevelopment area back in These conditions remain representative of the conditions cited above, that qualify the area as a TAD under the Redevelopment Powers Law. Tax Allocation Bond Issues (O, P, Q) (DRAFT) 32

33 Tax Allocation Bond Issues (O, P, Q) (DRAFT) 33

34 Tax Allocation Bond Issues (O, P, Q) (DRAFT) 34

35 MARKET AND DEMOGRAPHIC CONDITIONS According to Fulton County assessment data, as of 2016 TAD #2 contained 4.2% of the City s land area, and contributed a slightly higher percentage (6.9%) of the City s total tax digest. This is due to the fact that only 10.6% of TAD #2 s land area is residential, whereas Citywide, 59% of all taxable acreage is residentially classified. On a per acre basis, the taxable digest of residential property classifications in East Point average only $57,600 per acre, compared to nearly $239,000 of tax digest generated per acre of commercial land use. Within TAD #2, residential development has a slightly higher value of $63,000 per acre, because of higher residential density within the district. In terms of commercial tax digest, the value of real estate in TAD #2 averages roughly $220,400 per acre, compared to a City average of more than $238, Adjusted for the omission of personal property digest from TAD #2, commercial real estate values are comparable to the City average. However, it should be noted that with few exceptions, the value of taxable property in most East Point locations is very low compared to Fulton County and the Atlanta Region. Excluding the Camp Creek Marketplace in TAD #1, most developed commercial buildings in East Point are old and under-performing. In several respects, most of the City meets the definition of a redevelopment area under the statute. For that reason, the following trend data are reported City wide and demonstrate the City s fiscal challenges and resulting consequences to the County and School District. Demographic Characteristics TAD #2 Real Estate Digesr (40%) Value $70,000,000 $60,000,000 $50,000,000 $40,000,000 $30,000,000 $20,000,000 $10,000,000 $0 Change in East Point Corridors TAD #2 Tax Digest: Base Exhibit 3: The taxable real estate digest of TAD #2 resumed growth after bottoming out in Current values are still below the TAD s 2008 peak. Relevant characteristics of the City and the Redevelopment Area are summarized in the following paragraphs. 6 Commercial digest calculations are not strictly comparable. City-wide digest calculations include personal property value, while the TAD digest does not. Personal property tax increment is not pledged to either of East Point s two existing Tax Allocation Districts. Tax Allocation Bond Issues (O, P, Q) (DRAFT) 35

36 Population - The City of East Point has experienced dramatic population losses since 2000, in stark contrast to a growing County and Metro-Area. 7 From 2000 to 2017, East Point s population declined by more than 2,500 residents (-7%), while Fulton County s population grew by nearly 216,000 (26%) and the Metro-Atlanta region added nearly 1.6 million new residents. The City s recovery from population losses prior to 2010 has been slowed by Table 1: Population and Household Trends Population East Point Fulton County Atlanta Metro 2000 Census 39, ,971 4,263, Census 33, ,581 5,286, Estimate 36,506 1,031,774 5,843, Projection 38,230 1,101,874 6,234,160 CAGR Growth % 1.4% 1.9% CAGR (Fcst) % 1.3% 1.3% Households East Point Fulton County Atlanta Metro 2000 Census 14, ,218 1,559, Census 13, ,377 1,943, Estimate 14, ,714 2,158, Projection 15, ,688 2,307,874 CAGR Growth % 1.7% 1.9% CAGR (Fcst) % 1.5% 1.3% New Households , , Est. Average Household Size high vacancy rates created during the Great Recession, and the absence of new residential construction during this decade. The City s population is projected to resume nominal growth over the next five years, but remain well below county and regional averages. Households - The City has gained only 400 net new households since From 2000 to 2010, the City of East Point lost 1,000 households, and has only recently recovered those losses. During the same period the number of households in Fulton County increased by more nearly 107,500 (33%) and the number of households in the Atlanta region grew by nearly 38%. Modest household growth has resumed within the City since 2010, due to a reduction in rental market vacancy rates and the transition of foreclosed single family homes to rental housing. Sustaining future household growth over the next decade will require a resumption of new housing construction. Using TAD incentives to incentivize transit oriented development presents the best (and possibly only) opportunity for East Point to create any new housing within TAD #2. 7 Data reported in this section was obtained from the Nielson Company (Pop-Facts Demographic Snapshot 2017 Report). Tax Allocation Bond Issues (O, P, Q) (DRAFT) 36

37 Table 2: Household Income Distribution Household Income East Point Fulton County Atlanta Metro 2017 Est. Median Household Income $ 40,340 $ 61,084 $ 60,749 % of County Median Income Households by Income 66% 101% 100% HH with income >$15K 2,811 19% 58,621 14% 226,770 11% HH with income $15K - $35K 3,738 25% 74,867 17% 394,543 18% HH with income $35K - $50K 2,236 15% 50,766 12% 291,638 14% HH with income $50K - $100K 4,198 29% 111,245 26% 651,527 30% HH with income > $100K 1,707 12% 133,215 31% 594,100 28% Household Incomes Income levels among households living in East Point are substantially below those of the County and surrounding Region. The City s median household income is estimated at only $40,340 in 2017, 34% lower than the Fulton County median ($61,084). At the same time,19% of City households earn annual incomes of below $15,000 and only 12% earned incomes of more than $100,000 per year, the near opposite income distribution that is present in Fulton County. This lower income distribution appears to be attributable to the fact that more than half of East Point households are renters and the household population is slightly younger that the surrounding region. Many of these households are also living below the poverty level. Households Characteristics East Point has a smaller percentage of married couple families, a smaller percentage of families with children and a significantly higher percentage of female-headed households (both with and without children living at home) than either Fulton County or the Metro Atlanta Region. The smaller percentage of married, dual income households partly explains the income disparity shown in Table 2. Tax Allocation Bond Issues (O, P, Q) (DRAFT) 37

38 Table 3: Selected Household Characteristics Household Characteristics 2017 Est. Households by Household Size City of East Point 14,690 Fulton County 428,714 Metro Atlanta 2,158,578 1-person 5,056 34% 157,538 37% 559,953 26% 2-person 4,161 28% 123,514 29% 641,720 30% 3-person 2,361 16% 62,008 14% 373,946 17% 4-person 1,510 10% 48,309 11% 316,280 15% 5-person 800 5% 22,145 5% 155,860 7% 6-person 423 3% 9,129 2% 66,687 3% 7-or-more-person 379 3% 6,071 1% 44,132 2% 2017 Est. Average Household Size Est. Family HH Type by Presence of Own Child. 8, ,303 1,467,253 Married-Couple Family, own children 1,507 18% 71,763 30% 498,728 34% Married-Couple Family, no own children 2,227 26% 79,494 34% 536,547 37% Male Householder, own children 393 5% 7,539 3% 48,466 3% Male Householder, no own children 595 7% 10,203 4% 55,820 4% Female Householder, own children 2,049 24% 38,113 16% 189,337 13% Female Householder, no own children 1,790 21% 28,191 12% 138,355 9% 2017 Est. Households by Presence of People Under 18 14, ,714 2,158,578 Households with 1 or More People under Age 18: 4,882 33% 130,675 30% 823,068 38% Married-Couple Family 1,738 36% 75,216 58% 531,504 65% Other Family, Male Householder % 9,118 7% 59,365 7% Other Family, Female Householder 2,578 53% 45,387 35% 225,393 27% Nonfamily, Male Householder 32 1% 602 0% 4,816 1% Nonfamily, Female Householder 20 0% 352 0% 1,990 0% Households with No People under Age 18: 9,808 67% 298,039 70% 1,335,510 62% Married-Couple Family 1,995 20% 76,044 26% 503,733 38% Other Family, Male Householder 473 5% 8,616 3% 45,011 3% Other Family, Female Householder 1,257 13% 20,918 7% 102,268 8% Nonfamily, Male Householder 2,952 30% 92,298 31% 317,827 24% Nonfamily, Female Householder 3,131 32% 100,163 34% 366,671 27% Housing Tenure East Point has a dramatically lower rate of home ownership than the County and Region. Only 48% of existing housing in East Point is estimated to be owner-occupied in The percentage of homeowners is lower than Fulton County, where more than 53% of all housing is owneroccupied, even including the City of Atlanta, and substantially lower than the Atlanta Region, where only 34% of all households are renters. In addition, roughly 32% of the City s existing housing inventory (more than 5,900 units) is found in large multi-family buildings containing 5 or more units, while nearly 7,700 households are renters, suggesting that a significant percentage of these households rent single family homes rather than apartments. Housing Value Owner occupied housing in East Point is older and much lower valued than the County and Region. The median age of all owneroccupied housing in 2017 is estimated at 47 years, with only 27% of all units constructed since By comparison, the median age of all homes in Fulton County is only 25 years and 35% of the total inventory has been constructed since The age distribution of homes in East Point also translates to lower Tax Allocation Bond Issues (O, P, Q) (DRAFT) 38

39 average home values, with a median value of $107,121 and 46% of the inventory valued below $100,000. This median value is 2.6 times below that of Fulton County ($276,285), where only 17% of owner housing is valued below $100,000. Table 4: Selected Housing Characteristics Housing Characteristics Tenure % Owners East Point 48% Fulton County 53% Atlanta Metro 66% % Renters 52% 47% 34% Total Occupied Housing Units 14, ,714 2,158,578 Renter-Occupied Units 7, , ,934 Owner-Occupied Units 7, ,790 1,421,644 Owner Units Valued < $100K 3,250 46% 37,825 17% 269,687 19% Owner Units Val $100K-$200K 2,675 38% 48,073 21% 479,757 34% Owner Units Val $200K-$500K % 88,063 38% 530,111 37% Owner Units Val > $500K 159 2% 54,829 24% 142,089 10% Age of Housing Units Built since ,181 27% 175,017 32% 855,503 31% Units Built ,591 8% 141,473 26% 868,474 31% Units built pre ,760 65% 237,095 43% 1,054,550 38% Median age of housing unit (Years) Type of Housing 1 Unit Detatched (SF) 10,152 55% 233,682 48% 1,592,775 69% 1 Unit Attached (TH) 639 3% 32,536 7% 123,354 5% Small Multi-Family (2-4 Units/Bldg.) 1,762 10% 27,341 6% 97,981 4% Lg Multi-Family (5+ Units/Bldg.) 5,949 32% 194,267 40% 508,127 22% Development Density and Tax Revenues East Point is substantially underperforming in terms of its economic value and contribution of property tax revenues to the County and School District. Even though the City is largely built out and well located with respect to highway access, transit service and proximity to Hartsfield Jackson International Airport, the taxable digest within the entire city averages approximately $114,500 per acre. On a per acre basis, East Point produced an average of only $5,032 in combined City, County and School District general fund taxes in Tax values are also lower today than a decade ago when TAD #2 was created. The City is clearly under-performing its economic/fiscal potential as defined in the Redevelopment Powers Law, a factor which is equally true of the redevelopment area, with resulting negative fiscal consequences to both the County and School District. Specific revenue implications to the FCSS are discussed in the School District impact analysis section of this report. SUMMARY OF MARKET CONDITIONS RELATING TO THE QUALIFICATION AS A REDEVELOPMENT AREA In summary, designation of TAD #2 as a Redevelopment Area was fully justified in 2006, based on the statutory criteria at the time. Economic and fiscal conditions in East Point have not improved since the TAD was created and remain equally or more valid today. The experience of the past decade provides strong evidence to Tax Allocation Bond Issues (O, P, Q) (DRAFT) 39

40 suggest that the City s is unlikely to be successful in improving existing conditions within the TAD, absent of support from both the County and School District. PLAN VISION AND GOAL The overall purpose of the East Point Corridors Redevelopment Plan and Tax Allocation District (TAD) is to establish a financing mechanism to help facilitate recommended improvements which are outlined in this Plan. Specifically, the TAD is proposed for the following purposes: 1. To attract private, taxable redevelopment opportunities to the East Point Corridors sectors of the City of East Point. 2. To further the City s goals of improving underdeveloped urban areas as well as of attracting desirable development, including professional jobs. 3. To provide funding that, in turn, will attract additional regional, State and Federal funding to allow improvements to land use, transportation, and recreational areas. 4. To realize the full economic potential of an increasingly urbanized community. 5. To increase employment opportunities for residents of the TAD area and surrounding East Point neighborhoods. 6. To increase opportunities for market-driven residential and commercial development within the East Point Corridors area. 7. To overcome constraints to development generated by aged and obsolete commercial and residential structures, inefficient transportation infrastructure and inadequate physical connections to the surrounding community. 8. To maximize the tax revenue potential of the TAD area while achieving the following basic goals that were reiterated in the LCI and Cleveland Avenue studies and incorporated into the redevelopment plan, as follows: Provide desirable residential product types in the central business district, preferably with an ownership preference. Provide additional retail, dining, entertainment and other commercial amenities such as better supermarkets within East Point. In addition, create a critical mass of people in the CBD sufficient to attract a destination retail market. The boundaries of those study areas are shown on the following maps. Tax Allocation Bond Issues (O, P, Q) (DRAFT) 40

41 East Point LCI Study Area Many of the findings of the East Point LCI and Cleveland Avenue Corridor studies were incorporated into the findings of the 2006 TAD Redevelopment Plan. The Study Areas of those reports are indicated in these accompanying maps. Cleveland Avenue Corridor Study Area Tax Allocation Bond Issues (O, P, Q) (DRAFT) 41