Mark Prendergast Director of Trusts & Estates

|

|

|

- Shawn Turner

- 6 years ago

- Views:

Transcription

1 Mark Prendergast Director of Trusts & Estates San Antonio Estate Planners Council December 20 th, 2011

2 Dallas Headquarters $800 Million in last 12 months Founded rd Largest Auction House in the world Leader in Coins and Collectibles 400+ Employees Opened Beverly Hills saleroom in February 2010 Opened in New York City September 2010

3 Valuation and Sale of Artwork and Collectibles Recent Auction Highlights The Factors of Value Proper Appraisal Valuation Working with Auction Houses

4

5 The Art and Collectibles Market

6

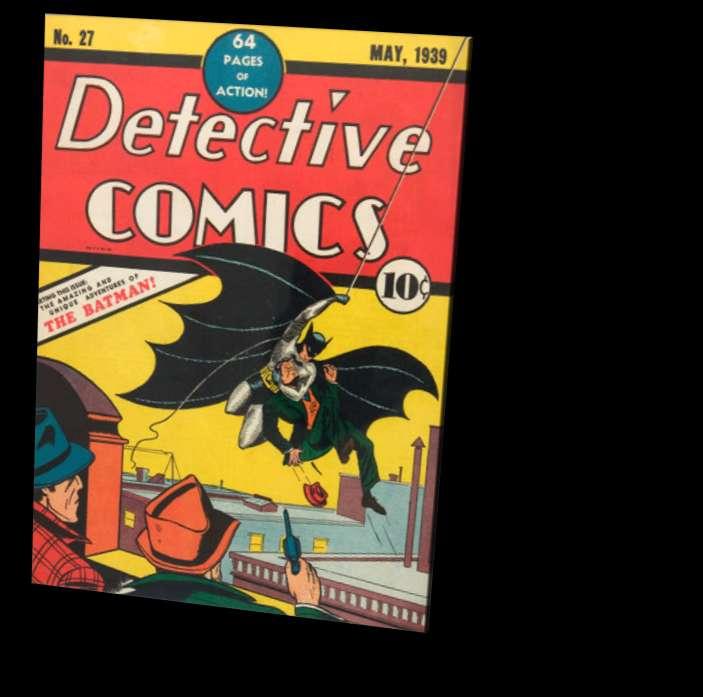

7 Recent Highlights Illustration Art Post-War Art/Contemporary Art American and Texas Paintings

8 Niche markets finding the right sources and appraisers for values.

9

10 Post-War & Contemporary Art October 2008

11

12

13 American and Texas Art

14

15

16

17 Factors that affect the value of property Provenance Rarity Quality Condition Fashion

18 Provenance

19

20

21

22 Rarity

23

24 Quality

25

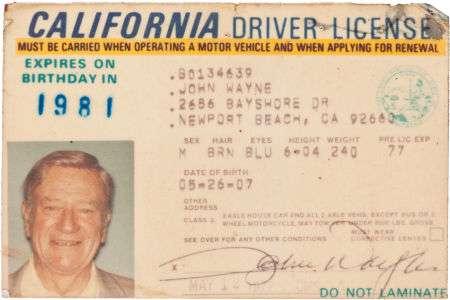

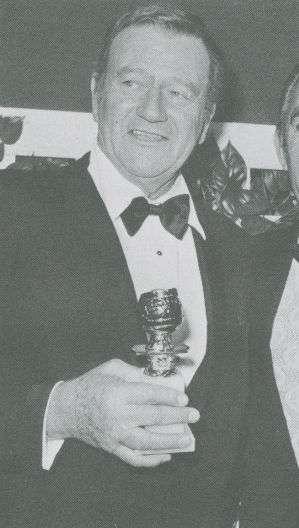

26 Condition

27

28

29

30 Fashion: Trends and styles

31

32 Combination of Factors

33 Wayne Auction

34

35 Appraisals of Tangible Property - IRS compliant written appraisals - Fair Market and Retail Replacement Value - Charitable Donation - Financial Planning - Equitable Distribution - Gift Tax - Estate Planning - Insurance - Estate Tax - Trusts/Conservatorships - Variances Charitable Donation restricted use issues, blockage discounts, fractional/partial donations, partial/joint ownership. - Timely delivery of appraisals - Costs based on number of items/scope of work not values.

36 IRS Compliance for all tax appraisals of tangible property. -very strict compliance requirements, especially for Charitable Donations own set of requirements - appraiser and appraisal must follow the USPAP guidelines - Uniform Standards of Professional Appraisal Practice -as set forth by The Appraisal Foundation -a not-for-profit organization dedicated to the advancement of professional valuation, was established by the appraisal profession in the United States in 1987 and authorized by Congress as the source of appraisal standards and appraisal qualifications

37 Fair Market Value (FMV) is the price that property would sell for on the open market. It is the price that would be agreed on between a willing buyer and a willing seller, with neither being required to act, and both having reasonable knowledge of the relevant facts. If you put a restriction on the use of property you donate, the FMV must reflect that restriction." IRS Publication 561

38 Retail Replacement Values the highest price in terms of cash or other precisely revealed terms that would be required to replace an item with another of similar age, quality, origin, appearance, provenance, and condition, within a reasonable length of time in an appropriate and relevant market

39 Auction Estimate vs. $30,000 to $50,000 Appraisal Fair Market Value Retail Replacement Cost $40,000 $70,000+ True Value = Sold for $35,000 December 2010

40 Working with an Auction House Appraisals we like to do *Estate Tax *Financial or Estate Planning Appraisals we may not do *Insurance *True/Fair Market Value * Charitable Donation disinterested qualification - can t have sold or sell in the future * Retail Replacement don t know the retail market * Divorce contentious - each side associated with an auction house and property then sold through neutral venue * No potential for sales associated Time prohibitive pulls experts away from immediate business which is primary focus

41 No Charge For a Fee For a Fee Rebated Fees NO Fees Seller s Fees Buyer s Premium Auction Estimates Auction or Purchase Evaluation Estate Walkthrough Selection For Sale/Sale Proposal Potential Value Consultation Formal Written Appraisals - $350 per hour, $2,800 per day + travel expenses and out-of-pocket costs. Estimated total costs and capped fees available for large collection or estate appraisals Verbal Appraisal contracts for Museums/Institutions/Private Collectors/Corporate Collections i.e. 10 per year for $1,500 usually for shipping/loan insurance concerns All appraisal fees can be rebated against future seller fee s based on the amount of material sold listed on the appraisal. For top clients, major estates, important collections, museums and non-profits - or with commitment to sell. Varies in categories and on value of consignment Usually 15% or less no other fees. Most other houses are higher with fees per lot for insurance, photography, and marketing. Fine Art/Dec Arts- 25% first $50,000, 20% to $1M, 12% $1M % in Comics, Historical, Sports, Movie Posters 15% in Coins and Currency

42

43 Mark Prendergast Director of Trusts & Estates San Antonio Estate Planners Council December 20 th, 2011

Research Methods APPRAISAL BASICS

APPRAISAL BASICS WHY? WHAT? HOW? WHERE? Why am I doing this appraisal? (purpose) What value am I using? (RRV, FMV, etc.) How will I find my values? (approach) Where will I find my comps? (market) Insurance

APPRAISAL BASICS WHY? WHAT? HOW? WHERE? Why am I doing this appraisal? (purpose) What value am I using? (RRV, FMV, etc.) How will I find my values? (approach) Where will I find my comps? (market) Insurance

INSURANCE VALUATIONS

INSURANCE VALUATIONS Insurance valuations reflect the cost of replacement after loss or damage. Pall Mall Art Advisors reviews valuations annually so that replacement costs reflect changing market value.

INSURANCE VALUATIONS Insurance valuations reflect the cost of replacement after loss or damage. Pall Mall Art Advisors reviews valuations annually so that replacement costs reflect changing market value.

Donations of Personal Property

Donations of Personal Property BENEFITS FOR ALL SANDRA TROPPER, FASA ACCREDITED SR. APPRAISER, FINE ART Personal Property Donations Presented to the National Capital Gift Planning Council Sandra Tropper,

Donations of Personal Property BENEFITS FOR ALL SANDRA TROPPER, FASA ACCREDITED SR. APPRAISER, FINE ART Personal Property Donations Presented to the National Capital Gift Planning Council Sandra Tropper,

Please find attached a brief overview of our services and an informative review of Chase Group s SBA-compliant business valuation services.

THE CHASE GROUP - Business Brokers Mergers, Acquisitions, Financing & Valuation Services 41185 Golden Gate Circle, Suite 202 Murrieta, CA 92562 951.541.0414 tel 951.303.8157 fax www.chasegroup.us 2012

THE CHASE GROUP - Business Brokers Mergers, Acquisitions, Financing & Valuation Services 41185 Golden Gate Circle, Suite 202 Murrieta, CA 92562 951.541.0414 tel 951.303.8157 fax www.chasegroup.us 2012

Tax Strategies for Purchasing Going Concern Properties

Pre-closing Purchase Price Allocations Tax Strategies for Purchasing Going Concern Properties Innovative Solutions to Taxing Problems Tax Strategies for Purchasing Going Concern Properties When a business,

Pre-closing Purchase Price Allocations Tax Strategies for Purchasing Going Concern Properties Innovative Solutions to Taxing Problems Tax Strategies for Purchasing Going Concern Properties When a business,

Appraisal Review & Advisory Opinion 20 Controversy. Presenter: Lisa Kimbro, MAI, AI-GRS

Appraisal Review & Advisory Opinion 20 Controversy Presenter: Lisa Kimbro, MAI, AI-GRS Practicing appraisers know USPAP, and appraisers that complete review work know USPAP s Standard 3. But what about

Appraisal Review & Advisory Opinion 20 Controversy Presenter: Lisa Kimbro, MAI, AI-GRS Practicing appraisers know USPAP, and appraisers that complete review work know USPAP s Standard 3. But what about

CALIFORNIA POLYTECHNIC STATE UNIVERSITY SAN LUIS OBISPO GIFT-IN-KIND ( GIK ) ACCEPTANCE PROCEDURES

ACCEPTANCE PROCEDURES") CALIFORNIA POLYTECHNIC STATE UNIVERSITY SAN LUIS OBISPO GIFT-IN-KIND ( GIK ) ACCEPTANCE PROCEDURES DEFINITIONS Accounting Standards are financial accounting rules that regulate the manner in which GIK

CALIFORNIA POLYTECHNIC STATE UNIVERSITY SAN LUIS OBISPO GIFT-IN-KIND ( GIK ) ACCEPTANCE PROCEDURES DEFINITIONS Accounting Standards are financial accounting rules that regulate the manner in which GIK

Business Valuations in the Planned Giving Context

Business Valuations in the Planned Giving Context 38 th Annual Minnesota Planned Giving Conference November 4, 2014 Presented by: Richard C. Berning, CPA/ABV/CFF, CBA, CVA, ABAR, CMA Copyright 2014: Berning

Business Valuations in the Planned Giving Context 38 th Annual Minnesota Planned Giving Conference November 4, 2014 Presented by: Richard C. Berning, CPA/ABV/CFF, CBA, CVA, ABAR, CMA Copyright 2014: Berning

12/31/2013. The Retained Life Estate An Underutilized Gift. The Retained Life Estate An Underutilized Gift. 1. Real estate gift trends

The Retained Life Estate An Underutilized Gift Planned Giving Group of New England Boston, MA January 8, 2014 Dennis P. Bidwell dbidwell@bidwelladvisors.com (413) 584-2732 www.bidwelladvisors.com 1 The

The Retained Life Estate An Underutilized Gift Planned Giving Group of New England Boston, MA January 8, 2014 Dennis P. Bidwell dbidwell@bidwelladvisors.com (413) 584-2732 www.bidwelladvisors.com 1 The

Comprehensive Appraisal Studies Program SUMMER 2017 INTENSIVE COURSE DESCRIPTIONS

SUMMER 2017 INTENSIVE COURSE DESCRIPTIONS Orientation and Meet and Greet with Linda Selvin, Executive Director, and Cynthia Herbert, AAA Appraisers Association of America Date: July 5, 9:30 a.m. 12:30

SUMMER 2017 INTENSIVE COURSE DESCRIPTIONS Orientation and Meet and Greet with Linda Selvin, Executive Director, and Cynthia Herbert, AAA Appraisers Association of America Date: July 5, 9:30 a.m. 12:30

Jacqueline Williams Snyder ISA. AM. BFA. MA. Professional Profile

Jacqueline Williams Snyder ISA. AM. BFA. MA. Appraisal and Conservation Services Phone Email: Mailing address: 12223 Highland Ave. Suite 106-325, Rancho Cucamonga, CA 91739 Insurance Appraisals * Market

Jacqueline Williams Snyder ISA. AM. BFA. MA. Appraisal and Conservation Services Phone Email: Mailing address: 12223 Highland Ave. Suite 106-325, Rancho Cucamonga, CA 91739 Insurance Appraisals * Market

PROPERTY APPRAISAL PROCEDURES. Budget, Finance & Audit Committee March 3, 2014

PROPERTY APPRAISAL PROCEDURES Budget, Finance & Audit Committee March 3, 2014 Purpose Provide overview of: City s procedures and requirements for real property appraisals Difference between City s appraisal

PROPERTY APPRAISAL PROCEDURES Budget, Finance & Audit Committee March 3, 2014 Purpose Provide overview of: City s procedures and requirements for real property appraisals Difference between City s appraisal

Hypothetical Condition. USPAP defines an Extraordinary Assumption as:

- 40 - Chapter 1: Appraisal Terminology USPAP defines an Extraordinary Assumption as: EXTRAORDINARY ASSUMPTION: an assumption, directly related to a specific assignment, as of the effective date of the

- 40 - Chapter 1: Appraisal Terminology USPAP defines an Extraordinary Assumption as: EXTRAORDINARY ASSUMPTION: an assumption, directly related to a specific assignment, as of the effective date of the

New York Agricultural Land Trust

New York Agricultural Land Trust P.O. Box 121 Preble, NY 13141 www.nyalt.org New York Agricultural Land Trust Agricultural Conservation Easements and Appraisals Introduction An agricultural conservation

New York Agricultural Land Trust P.O. Box 121 Preble, NY 13141 www.nyalt.org New York Agricultural Land Trust Agricultural Conservation Easements and Appraisals Introduction An agricultural conservation

Chapter 1: Appraisal Terminology. While USPAP does not define the term competency, it does contain a COMPETENCY RULE.

- 22 - Chapter 1: Appraisal Terminology Competency While USPAP does not define the term competency, it does contain a COMPETENCY RULE. The COMPETENCY RULE states that in all cases, the appraiser must perform

- 22 - Chapter 1: Appraisal Terminology Competency While USPAP does not define the term competency, it does contain a COMPETENCY RULE. The COMPETENCY RULE states that in all cases, the appraiser must perform

APPRAISAL TERMS AND DEFINITIONS

APPRAISAL TERMS AND DEFINITIONS ACTUAL CASH VALUE (ACV): This term refers to Market Value and is generally synonymous with payment restricted to cash. Some insurance policies also define ACV as the replacement

APPRAISAL TERMS AND DEFINITIONS ACTUAL CASH VALUE (ACV): This term refers to Market Value and is generally synonymous with payment restricted to cash. Some insurance policies also define ACV as the replacement

1972 Volkswagen Beetle 2-Door Convertible. Appraised for Bourne s Auto Center. December 30, 2017

1972 Volkswagen Beetle 2-Door Convertible Appraised for Bourne s Auto Center December 30, 2017 Auto Appraisal Group Inc. Headquarters: 800-848-2886 Fax: 888-575-9319 Page 1 of 7 AUTO APPRAISAL GROUP INC.

1972 Volkswagen Beetle 2-Door Convertible Appraised for Bourne s Auto Center December 30, 2017 Auto Appraisal Group Inc. Headquarters: 800-848-2886 Fax: 888-575-9319 Page 1 of 7 AUTO APPRAISAL GROUP INC.

2017 Reappraisal Preliminary Report. February 6, 2017

2017 Reappraisal Preliminary Report February 6, 2017 Reappraisal is required at least every 8 years per NCGS105-286 Last reappraisal was conducted for 2011 Reappraisal includes both land and improvements.

2017 Reappraisal Preliminary Report February 6, 2017 Reappraisal is required at least every 8 years per NCGS105-286 Last reappraisal was conducted for 2011 Reappraisal includes both land and improvements.

BUSINESS VALUATIONS: FUNDAMENTALS, TECHNIQUES AND THEORY (FT&T) CHAPTER 1

CHAPTER 1") Fundamentals, Techniques & Theory INTRODUCTION TO BUSINESS VALUATION BUSINESS VALUATIONS: FUNDAMENTALS, TECHNIQUES AND THEORY (FT&T) CHAPTER 1 REVIEW QUESTIONS 1995 2013 by National Association of Certified

Fundamentals, Techniques & Theory INTRODUCTION TO BUSINESS VALUATION BUSINESS VALUATIONS: FUNDAMENTALS, TECHNIQUES AND THEORY (FT&T) CHAPTER 1 REVIEW QUESTIONS 1995 2013 by National Association of Certified

Perry County. Appeal Procedures, Rules, and Regulations v.1.1

Perry County Appeal Procedures, Rules, and Regulations 2000 v.1.1 PERRY COUNTY BOARD OF ASSESSMENT APPEALS APPEAL PROCEDURES, RULES, AND REGULATIONS Property owners have the right, under Pennsylvania law,

Perry County Appeal Procedures, Rules, and Regulations 2000 v.1.1 PERRY COUNTY BOARD OF ASSESSMENT APPEALS APPEAL PROCEDURES, RULES, AND REGULATIONS Property owners have the right, under Pennsylvania law,

AICPA Valuation Services VS Section Statements on Standards for Valuation Services VS Section 100 Valuation of a Business, Business Ownership

AICPA Valuation Services VS Section Statements on Standards for Valuation Services VS Section 100 Valuation of a Business, Business Ownership Interest, Security, or Intangible Asset Calculation Engagements

AICPA Valuation Services VS Section Statements on Standards for Valuation Services VS Section 100 Valuation of a Business, Business Ownership Interest, Security, or Intangible Asset Calculation Engagements

I. FRACTIONAL INTERESTS IN GENERAL 1 II. CONTROL/DECONTROL DISCOUNTING 6

I. FRACTIONAL INTERESTS IN GENERAL 1 II. CONTROL/DECONTROL DISCOUNTING 6 A. Unity of Ownership Squelched Rev. Rul. 93-12 and its Progeny 6 B. Aggregation of Various Interests in Same Property 11 C. Stock

I. FRACTIONAL INTERESTS IN GENERAL 1 II. CONTROL/DECONTROL DISCOUNTING 6 A. Unity of Ownership Squelched Rev. Rul. 93-12 and its Progeny 6 B. Aggregation of Various Interests in Same Property 11 C. Stock

SCOPE OF WORK The problem to solve: General category of items to appraise: Ownership interest: Effective date of valuation:

SCOPE OF WORK The problem to solve: The appraiser was asked to examine a diamond ring from images and information provided by the client, and to provide a Retail Replacement Value appraisal. General category

SCOPE OF WORK The problem to solve: The appraiser was asked to examine a diamond ring from images and information provided by the client, and to provide a Retail Replacement Value appraisal. General category

Valuation Issues and Divorce

Lori Wilhelmy, ASA 513.813.4134 LWilhelmy@ComStockAdvisors.com Valuation Issues and Divorce The valuation of a closely held business for divorce purposes is based on valuation theory, state statute and

Lori Wilhelmy, ASA 513.813.4134 LWilhelmy@ComStockAdvisors.com Valuation Issues and Divorce The valuation of a closely held business for divorce purposes is based on valuation theory, state statute and

APPRAISING ART - APPRAISAL FORMAT P. 1 APPRAISING ART

APPRAISING ART - APPRAISAL FORMAT P. 1 Introduction to the Appraisal of Fine Art Appraisal Studies Program New York University SPRING 2005 Instructor: Gayle M. Skluzacek, AAA I. Types of appraisals A.

APPRAISING ART - APPRAISAL FORMAT P. 1 Introduction to the Appraisal of Fine Art Appraisal Studies Program New York University SPRING 2005 Instructor: Gayle M. Skluzacek, AAA I. Types of appraisals A.

Presentation to The New England Graduate Accounting Studies Conference June 18, 2014 Roger Winsby, President Axiom Valuation Solutions

Current Developments in Business Valuation Presentation to The New England Graduate Accounting Studies Conference June 18, 2014 Roger Winsby, President Axiom Valuation Solutions Roger M. Winsby President

Current Developments in Business Valuation Presentation to The New England Graduate Accounting Studies Conference June 18, 2014 Roger Winsby, President Axiom Valuation Solutions Roger M. Winsby President

Rare Window Onto Artwork Valuation Issues In Insolvency

Portfolio Media. Inc. 860 Broadway, 6th Floor New York, NY 10003 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com Rare Window Onto Artwork Valuation Issues In Insolvency

Portfolio Media. Inc. 860 Broadway, 6th Floor New York, NY 10003 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com Rare Window Onto Artwork Valuation Issues In Insolvency

Gifts-In-Kind Policy (Non-monetary donations)

") Gifts-In-Kind Policy (Non-monetary donations) Last revised by: Executive Committee March 27, 2012 Minute 5 Effective: September 27, 2011 Overview This policy establishes the conditions under which gifts-in-kind

Gifts-In-Kind Policy (Non-monetary donations) Last revised by: Executive Committee March 27, 2012 Minute 5 Effective: September 27, 2011 Overview This policy establishes the conditions under which gifts-in-kind

Mary Sudar Accredited Senior Appraiser American Society of Appraisers

Mary Sudar Accredited Senior Appraiser 1201 Pacific Avenue, Suite 600, 98402 Mailing address: PO Box 463, Burley, Washington 98322 253.759.9440 360.874.2062 FAX PROFESSIONAL Accredited Senior Appraiser,

Mary Sudar Accredited Senior Appraiser 1201 Pacific Avenue, Suite 600, 98402 Mailing address: PO Box 463, Burley, Washington 98322 253.759.9440 360.874.2062 FAX PROFESSIONAL Accredited Senior Appraiser,

The Influence of EU Regulation and European Valuation Standards on Real Estate Valuation

The Influence of EU Regulation and European Valuation Standards on Real Estate Valuation Thessaloniki 9 th October 2015 Krzysztof Grzesik REV Chairman TEGoVA The European Group of Valuers Associations

The Influence of EU Regulation and European Valuation Standards on Real Estate Valuation Thessaloniki 9 th October 2015 Krzysztof Grzesik REV Chairman TEGoVA The European Group of Valuers Associations

Appraisers and Assessors of Real Estate

http://www.bls.gov/oco/ocos300.htm Appraisers and Assessors of Real Estate * Nature of the Work * Training, Other Qualifications, and Advancement * Employment * Job Outlook * Projections Data * Earnings

http://www.bls.gov/oco/ocos300.htm Appraisers and Assessors of Real Estate * Nature of the Work * Training, Other Qualifications, and Advancement * Employment * Job Outlook * Projections Data * Earnings

Personal vs. Enterprise Goodwill: Where Are We and How Do I Deal With It? By: Gary R. Trugman CPA/ABV, MCBA, ASA, MVS

Personal vs. Enterprise Goodwill: Where Are We and How Do I Deal With It? By: Gary R. Trugman CPA/ABV, MCBA, ASA, MVS Speaker Biography Gary R. Trugman is the President of Trugman Valuation Associates,

Personal vs. Enterprise Goodwill: Where Are We and How Do I Deal With It? By: Gary R. Trugman CPA/ABV, MCBA, ASA, MVS Speaker Biography Gary R. Trugman is the President of Trugman Valuation Associates,

MERCER COUNTY BOARD OF ASSESSMENT APPEALS

MERCER COUNTY BOARD OF ASSESSMENT APPEALS APPEAL PROCEDURES, RULES AND REGULATIONS A property owner has the right, under Pennsylvania law, to appeal their assessments if the owner believes that the assessment

MERCER COUNTY BOARD OF ASSESSMENT APPEALS APPEAL PROCEDURES, RULES AND REGULATIONS A property owner has the right, under Pennsylvania law, to appeal their assessments if the owner believes that the assessment

Replacement Value Appraisal for Insurance Claim Settlement Purposes Appraisal Report

Replacement Value Appraisal for Insurance Claim Settlement Purposes Appraisal Report Intended user: John Panico, Heather Caraballo Affiliated Adjustment 3000 Marcus Avenue, Ste 3W3 Lake Success, NY 11042

Replacement Value Appraisal for Insurance Claim Settlement Purposes Appraisal Report Intended user: John Panico, Heather Caraballo Affiliated Adjustment 3000 Marcus Avenue, Ste 3W3 Lake Success, NY 11042

Pecos County Appraisal District. Chief Appraiser: Sam Calderon III

Pecos County Appraisal District Chief Appraiser: Sam Calderon III Meet Your Appraiser Staff Agenda The goals and objectives of this presentation is to provide Property Owner s an overview of PCAD s Appraisal

Pecos County Appraisal District Chief Appraiser: Sam Calderon III Meet Your Appraiser Staff Agenda The goals and objectives of this presentation is to provide Property Owner s an overview of PCAD s Appraisal

Guide Note 6 Consideration of Hazardous Substances in the Appraisal Process

Guide Note 6 Consideration of Hazardous Substances in the Appraisal Process Introduction The consideration of environmental conditions along with social, economic, and governmental conditions is fundamental

Guide Note 6 Consideration of Hazardous Substances in the Appraisal Process Introduction The consideration of environmental conditions along with social, economic, and governmental conditions is fundamental

THE APPRAISAL PROCESS APRIL 2014 KANSAS CITY

THE APPRAISAL PROCESS APRIL 2014 KANSAS CITY INTRODUCTION MEMBERSHIP OR EDUCATION QUESTIONS: CALL 312.981.6778 OUR AUDIENCE Professionals who rely on appraisals and accurate value information Community

THE APPRAISAL PROCESS APRIL 2014 KANSAS CITY INTRODUCTION MEMBERSHIP OR EDUCATION QUESTIONS: CALL 312.981.6778 OUR AUDIENCE Professionals who rely on appraisals and accurate value information Community

Co-Sponsored By: Person, Whitworth, Borchers and Morales, LLP

Co-Sponsored By: Person, Whitworth, Borchers and Morales, LLP "Profitable Mineral Management" BREAKFAST SERIES for Surface and Mineral Owners Admission by Invitation Only DATE: April 17, 2018 TOPIC: LOCATION:

Co-Sponsored By: Person, Whitworth, Borchers and Morales, LLP "Profitable Mineral Management" BREAKFAST SERIES for Surface and Mineral Owners Admission by Invitation Only DATE: April 17, 2018 TOPIC: LOCATION:

SUMMER VILLAGE OF YELLOWSTONE ACCOUNTING FOR TANGIBLE CAPITAL ASSETS CLASSIFICATION/CAPITALIZATION THRESHOLD/AMORTIZATION POLICY NO.

RESPONSIBILITY: C.A.O. APPROVED BY COUNCIL: DATE: September 16, 2009 PURPOSE: The objective of this policy is to prescribe the accounting treatment for tangible capital assets so that users of the financial

RESPONSIBILITY: C.A.O. APPROVED BY COUNCIL: DATE: September 16, 2009 PURPOSE: The objective of this policy is to prescribe the accounting treatment for tangible capital assets so that users of the financial

National Trust for Historic Preservation Collections Management Policy INTRODUCTION

National Trust for Historic Preservation Collections Management Policy INTRODUCTION The National Trust for Historic Preservation and its Collections. The National Trust for Historic Preservation in the

National Trust for Historic Preservation Collections Management Policy INTRODUCTION The National Trust for Historic Preservation and its Collections. The National Trust for Historic Preservation in the

NORTH COTSWOLD SALEROOM, GL54 2AR,

Catalogue 2 BOURTON-ON-THE-WATER Gloucestershire To be held at THE NORTH COTSWOLD SALEROOM, GL54 2AR, off the Village High Street, 16 miles from both Cheltenham and Cirencester, 28 miles from Oxford ANTIQUE

Catalogue 2 BOURTON-ON-THE-WATER Gloucestershire To be held at THE NORTH COTSWOLD SALEROOM, GL54 2AR, off the Village High Street, 16 miles from both Cheltenham and Cirencester, 28 miles from Oxford ANTIQUE

THE ART OF BUSINESS VALUATION

BUSINESS VALUATIONS GROWING THE ART OF BUSINESS VALUATION Douglas A. Michel, CPA/ABV, CVA & Alex E. Kummer, CPA, CVA, Clark Schaefer Hackett THE VALUE OF YOUR BUSINESS Steve Lumley, LGI CFO BUY SELL AGREEMENTS

BUSINESS VALUATIONS GROWING THE ART OF BUSINESS VALUATION Douglas A. Michel, CPA/ABV, CVA & Alex E. Kummer, CPA, CVA, Clark Schaefer Hackett THE VALUE OF YOUR BUSINESS Steve Lumley, LGI CFO BUY SELL AGREEMENTS

Conservation Easement Appraisals. Applicability. Part I: Appraisal Concepts and Methods of Valuation

Conservation Easement Appraisals 2011 Wyoming Conservation Easement Conference June 2, 2011 Laramie, Wyoming Hunsperger & Weston, Ltd. Mark Weston 5889 Greenwood Plaza Boulevard Suite 404 Greenwood Village,

Conservation Easement Appraisals 2011 Wyoming Conservation Easement Conference June 2, 2011 Laramie, Wyoming Hunsperger & Weston, Ltd. Mark Weston 5889 Greenwood Plaza Boulevard Suite 404 Greenwood Village,

Tioga County Board of Assessment Appeals Tioga County Courthouse 118 Main Street Wellsboro, PA 16901

Tioga County Appeal Procedures Rules Regulations 2008 (v.1.0) Tioga County Board of Assessment Appeals Tioga County Courthouse 118 Main Street Wellsboro, PA 16901 TIOGA COUNTY BOARD OF ASSESSMENT APPEALS

Tioga County Appeal Procedures Rules Regulations 2008 (v.1.0) Tioga County Board of Assessment Appeals Tioga County Courthouse 118 Main Street Wellsboro, PA 16901 TIOGA COUNTY BOARD OF ASSESSMENT APPEALS

ILLINOIS HOUSING DEVELOPMENT AUTHORITY APPRAISAL SCOPE AND GUIDELINES December 2015

ILLINOIS HOUSING DEVELOPMENT AUTHORITY APPRAISAL SCOPE AND GUIDELINES December 2015 As part of the Common Application for Multifamily Financing, the Illinois Housing Development Authority (IHDA) requires

ILLINOIS HOUSING DEVELOPMENT AUTHORITY APPRAISAL SCOPE AND GUIDELINES December 2015 As part of the Common Application for Multifamily Financing, the Illinois Housing Development Authority (IHDA) requires

ANTIQUE AND HOUSEHOLD FURNITURE

Catalogue 2 BOURTON-ON-THE-WATER Gloucestershire To be held at THE NORTH COTSWOLD SALEROOM, GL54 2AR, off the Village High Street, 16 miles from both Cheltenham and Cirencester, 28 miles from Oxford ANTIQUE

Catalogue 2 BOURTON-ON-THE-WATER Gloucestershire To be held at THE NORTH COTSWOLD SALEROOM, GL54 2AR, off the Village High Street, 16 miles from both Cheltenham and Cirencester, 28 miles from Oxford ANTIQUE

WESTERN ILLINOIS UNIVERSITY FOUNDATION REAL ESTATE GIFT ACCEPTANCE POLICY. As Adopted July 10,2013.

WESTERN ILLINOIS UNIVERSITY FOUNDATION REAL ESTATE GIFT ACCEPTANCE POLICY As Adopted July 10,2013. Purpose - This policy sets forth the requirements and guidelines governing acceptance ofreal estate gifts

WESTERN ILLINOIS UNIVERSITY FOUNDATION REAL ESTATE GIFT ACCEPTANCE POLICY As Adopted July 10,2013. Purpose - This policy sets forth the requirements and guidelines governing acceptance ofreal estate gifts

Goodwill Industries of Northern Michigan G.W. Homeless Services of Northern Michigan\ Gift Acceptance Policy Adopted 8/2009

Goodwill Industries of Northern Michigan G.W. Homeless Services of Northern Michigan\ Gift Acceptance Policy Adopted 8/2009 Goodwill Industries of Northern Michigan and G.W. Homeless Services of Northern

Goodwill Industries of Northern Michigan G.W. Homeless Services of Northern Michigan\ Gift Acceptance Policy Adopted 8/2009 Goodwill Industries of Northern Michigan and G.W. Homeless Services of Northern

Intent: To establish a policy and guidelines for all procurement activities in the city. SECTION I: Purpose of Purchasing Policies...

Policy Number: Appendix C Subject: Revised: 03/26/2012 Issued: 02/10/97 Page: 1 of 10 Intent: To establish a policy and guidelines for all procurement activities in the city. Applies to: All City Employees

Policy Number: Appendix C Subject: Revised: 03/26/2012 Issued: 02/10/97 Page: 1 of 10 Intent: To establish a policy and guidelines for all procurement activities in the city. Applies to: All City Employees

1946 Jaguar Mark IV 4-Door Sedan. Appraised for Albemarle Limousine. April 30, 2018

1946 Jaguar Mark IV 4-Door Sedan Appraised for Albemarle Limousine April 30, 2018 Auto Appraisal Group Inc. Headquarters: 800-848-2886 Fax: 888-575-9319 Page 1 of 7 AUTO APPRAISAL GROUP INC. www.autoappraisal.com

1946 Jaguar Mark IV 4-Door Sedan Appraised for Albemarle Limousine April 30, 2018 Auto Appraisal Group Inc. Headquarters: 800-848-2886 Fax: 888-575-9319 Page 1 of 7 AUTO APPRAISAL GROUP INC. www.autoappraisal.com

Single-family Properties Activities Pgs. 1-5

Table of Contents Single-family Properties Activities Pgs. 1-5... 1 Seller and Buyer Rights and Responsibilities... 1 Voluntary Sale Disclosures... 2 Estimated Market Value... 3 Uniform Relocation Assistance...

Table of Contents Single-family Properties Activities Pgs. 1-5... 1 Seller and Buyer Rights and Responsibilities... 1 Voluntary Sale Disclosures... 2 Estimated Market Value... 3 Uniform Relocation Assistance...

PRESERVATION EASEMENT

PRESERVATION EASEMENT Policies and Procedures for Donations The Preservation Resource Center s easement donation program enables a property ownertaxpayer to claim a charitable deduction on his or her tax

PRESERVATION EASEMENT Policies and Procedures for Donations The Preservation Resource Center s easement donation program enables a property ownertaxpayer to claim a charitable deduction on his or her tax

DETERMINING AGENCY VALUE PART 2

DETERMINING AGENCY VALUE PART 2 NORMALIZING THE INCOME STATEMENT By: Chuck Coyne, ASA This month we continue our discussion of how to determine an agency s value. Last month we briefly discussed some of

DETERMINING AGENCY VALUE PART 2 NORMALIZING THE INCOME STATEMENT By: Chuck Coyne, ASA This month we continue our discussion of how to determine an agency s value. Last month we briefly discussed some of

Market Value What Does It Really Mean?

Market Value What Does It Really Mean? K. Erik Friess, Esq. Allen Matkins Philip D. Kopp, Esq. Newmeyer & Dillion, LLP Moderator Michael V. Sanders, MAI, SRA Coastline Realty Advisors 50 th Annual Litigation

Market Value What Does It Really Mean? K. Erik Friess, Esq. Allen Matkins Philip D. Kopp, Esq. Newmeyer & Dillion, LLP Moderator Michael V. Sanders, MAI, SRA Coastline Realty Advisors 50 th Annual Litigation

Tennessee Bar Association Webcast August 23, 2018

Tennessee Bar Association Webcast August 23, 2018 The Essentials of Business Valuation For Tennessee Attorneys (Why are the Experts so Far Apart?) As Presented to the 2018 Tennessee Judicial Conference,

Tennessee Bar Association Webcast August 23, 2018 The Essentials of Business Valuation For Tennessee Attorneys (Why are the Experts so Far Apart?) As Presented to the 2018 Tennessee Judicial Conference,

National Association of REALTORS Member Profile National Association of realtors

National Association of REALTORS 2013 Member Profile 2013 National Association of realtors National Association of REALTORS Introduction In 2012, many areas of the country started to see both home sales

National Association of REALTORS 2013 Member Profile 2013 National Association of realtors National Association of REALTORS Introduction In 2012, many areas of the country started to see both home sales

January 21, Re: Third Exposure Draft of Proposed Changes for the Edition of the Uniform Standards of Professional Appraisal Practice

National Association of Certified Valuators and Analysts NACVA January 21, 2013 Appraisal Standards Board The Appraisal Foundation 1155 15 th Street NW, Suite 1111 Washington, DC 20005 Re: Third Exposure

National Association of Certified Valuators and Analysts NACVA January 21, 2013 Appraisal Standards Board The Appraisal Foundation 1155 15 th Street NW, Suite 1111 Washington, DC 20005 Re: Third Exposure

RESIDENTIAL PROPERTY VALUATION PROCESS

RESIDENTIAL PROPERTY VALUATION PROCESS Introduction Gregg County is comprised of approximately 276 square miles of area. Gregg County Appraisal District (GCAD) is responsible for the appraisal of the approximately

RESIDENTIAL PROPERTY VALUATION PROCESS Introduction Gregg County is comprised of approximately 276 square miles of area. Gregg County Appraisal District (GCAD) is responsible for the appraisal of the approximately

Whipple Appraisal 5255 Owera Point Cazenovia, NY NYS Certified Residential Real Estate Appraiser # (09/91)

") Mark Whipple Whipple Appraisal 5255 Owera Point Cazenovia, NY 13035 mark@whippleappraisal.com LICENSES & CERTIFICATION NYS Certified Residential Real Estate Appraiser #45000012549 (09/91) PROFESSIONAL

Mark Whipple Whipple Appraisal 5255 Owera Point Cazenovia, NY 13035 mark@whippleappraisal.com LICENSES & CERTIFICATION NYS Certified Residential Real Estate Appraiser #45000012549 (09/91) PROFESSIONAL

Can I Deduct That? An Introduction to Appraisals. Stuart Lutz

Can I Deduct That? An Introduction to Appraisals Stuart Lutz I was recently called to perform the following potential appraisals: A very famous, older athlete wanted to donate to a museum his personal

Can I Deduct That? An Introduction to Appraisals Stuart Lutz I was recently called to perform the following potential appraisals: A very famous, older athlete wanted to donate to a museum his personal

What is Fair Market Value in the Timber Industry?

What is Fair Market Value in the Timber Industry? Roger Lord Principal Mason, Bruce & Girard www.masonbruce.com Presented at 2014 OSCPA Forest Products Conference June 27, 2014 Eugene, Oregon Natural Natural

What is Fair Market Value in the Timber Industry? Roger Lord Principal Mason, Bruce & Girard www.masonbruce.com Presented at 2014 OSCPA Forest Products Conference June 27, 2014 Eugene, Oregon Natural Natural

PROMOTIONAL LITERATURE MACHINERY & EQUIPMENT VALUATION & CONSULTING SERVICES

Valuation and Consulting Specialists PROMOTIONAL LITERATURE MACHINERY & EQUIPMENT VALUATION & CONSULTING SERVICES Page 2 of 7 Description of Business KATS M & E, LLC is a professional multi disciplinary

Valuation and Consulting Specialists PROMOTIONAL LITERATURE MACHINERY & EQUIPMENT VALUATION & CONSULTING SERVICES Page 2 of 7 Description of Business KATS M & E, LLC is a professional multi disciplinary

KEY ISSUES IN BUSINESS VALUATIONS FOR DOMESTIC MATTERS A VALUATION EXPERT S PERSPECTIVE. February 14 21, 2015 MSBA Punta Cana, Dominican Republic

KEY ISSUES IN BUSINESS VALUATIONS FOR DOMESTIC MATTERS A VALUATION EXPERT S PERSPECTIVE February 14 21, 2015 MSBA Punta Cana, Dominican Republic Presented by: R. Christopher Rosenthal, CPA /ABV, ASA, CFF,

KEY ISSUES IN BUSINESS VALUATIONS FOR DOMESTIC MATTERS A VALUATION EXPERT S PERSPECTIVE February 14 21, 2015 MSBA Punta Cana, Dominican Republic Presented by: R. Christopher Rosenthal, CPA /ABV, ASA, CFF,

Voluntary Sales Disclosure URA Environmental Review Sample Forms. Table of Contents

Table of Contents SINGLE-FAMILY ACTIVITES... 1 Seller and Buyer Rights and Responsibilities... 1 Environmental Review ( ER )... 2 Estimated Market Value... 4 Uniform Relocation Assistance... 5 MULTI-FAMILY

Table of Contents SINGLE-FAMILY ACTIVITES... 1 Seller and Buyer Rights and Responsibilities... 1 Environmental Review ( ER )... 2 Estimated Market Value... 4 Uniform Relocation Assistance... 5 MULTI-FAMILY

DALLAS CENTRAL APPRAISAL DISTRICT DCAD VALUATION PROCESSES

DALLAS CENTRAL APPRAISAL DISTRICT DCAD VALUATION PROCESSES DALLAS CENTRAL APPRAISAL DISTRICT DCAD DCAD appraisers appraise a large universe of properties by developing appraisal models DCAD appraisers

DALLAS CENTRAL APPRAISAL DISTRICT DCAD VALUATION PROCESSES DALLAS CENTRAL APPRAISAL DISTRICT DCAD DCAD appraisers appraise a large universe of properties by developing appraisal models DCAD appraisers

Single-family Properties Activities Pgs. 1-5

Contents Single-family Properties Activities Pgs. 1-5... 1 Seller and Buyer Rights and Responsibilities... 1 Voluntary Sale Disclosures... 2 Property Valuation Method and Estimated Market Value... 3 Uniform

Contents Single-family Properties Activities Pgs. 1-5... 1 Seller and Buyer Rights and Responsibilities... 1 Voluntary Sale Disclosures... 2 Property Valuation Method and Estimated Market Value... 3 Uniform

USPAP Q&A USPAP Q&A Issue Date: December 19, 2017

USPAP Q&A 2018-19 USPAP Q&A Issue Date: December 19, 2017 The Appraisal Standards Board (ASB) of The Appraisal Foundation develops, interprets, and amends the Uniform Standards of Professional Appraisal

USPAP Q&A 2018-19 USPAP Q&A Issue Date: December 19, 2017 The Appraisal Standards Board (ASB) of The Appraisal Foundation develops, interprets, and amends the Uniform Standards of Professional Appraisal

Accounting for Tangible Capital Assets

Accounting for Tangible Capital Assets Date Approved by Board: 2011.11.17 Resolution No.: 11-113 2016.05.19 16-048 Lead Role: CFO Replaces: N/A Last Review Date: N/A Next Review Date: 2019.05.19 Policy

Accounting for Tangible Capital Assets Date Approved by Board: 2011.11.17 Resolution No.: 11-113 2016.05.19 16-048 Lead Role: CFO Replaces: N/A Last Review Date: N/A Next Review Date: 2019.05.19 Policy

Duties of the Assessors

Duties of the Assessors Value Properties Determine New Growth Set Tax Rate Assess Property Taxes Abate & Exempt Taxes Manage Overlay Account Assess Local Excises 1 Value Property Assessments based on fair

Duties of the Assessors Value Properties Determine New Growth Set Tax Rate Assess Property Taxes Abate & Exempt Taxes Manage Overlay Account Assess Local Excises 1 Value Property Assessments based on fair

Valuation Issues. Lindsey Sutton Novogradac & Company LLP. Brad Weinberg Novogradac & Company LLP

Valuation Issues PANELISTS Lindsey Sutton Novogradac & Company LLP Brad Weinberg Novogradac & Company LLP Visit www.crowdmics.online/novocolihtc to send questions to the moderator Valuation Issues How

Valuation Issues PANELISTS Lindsey Sutton Novogradac & Company LLP Brad Weinberg Novogradac & Company LLP Visit www.crowdmics.online/novocolihtc to send questions to the moderator Valuation Issues How

THE APPRAISAL STANDARDS BOARD & USPAP

THE APPRAISAL STANDARDS BOARD & USPAP INFORMATION FOR APPRAISERS AND THEIR CLIENTS A PPRAISAL S TANDARDS B OARD A MESSAGE FROM THE ASB This brochure is intended to help appraisers and users of appraisal

THE APPRAISAL STANDARDS BOARD & USPAP INFORMATION FOR APPRAISERS AND THEIR CLIENTS A PPRAISAL S TANDARDS B OARD A MESSAGE FROM THE ASB This brochure is intended to help appraisers and users of appraisal

The statements on these two pages are certified by the appraiser and her firm to be true to the best of their knowledge and belief.

DONEE S NAME, LOCATION ARTIST S NAME SCULPTURE PAGE 1 OF 21 APPRAISER S CERTIFICATION Abigail Hartmann Associates is a registered firm of appraisers qualified to appraise personal property including fine

DONEE S NAME, LOCATION ARTIST S NAME SCULPTURE PAGE 1 OF 21 APPRAISER S CERTIFICATION Abigail Hartmann Associates is a registered firm of appraisers qualified to appraise personal property including fine

Council Policy Name: Policy Statement and Rationale: Scope: Council Policy No.: C205 CAO 044. Date Approved by Council: May 26, 2015

Council Policy No.: C205 CAO 044 Council Policy Name: Date Approved by Council: May 26, 2015 Date revision approved by Council: Related SOP, Management Directive, Council Policy, Form Policy Statement

Council Policy No.: C205 CAO 044 Council Policy Name: Date Approved by Council: May 26, 2015 Date revision approved by Council: Related SOP, Management Directive, Council Policy, Form Policy Statement

YOUNG COUNTY APPRAISAL DISTRICT

YOUNG COUNTY APPRAISAL DISTRICT 2017 - ANNUAL APPRAISAL REPORT AS OF 10/6/2017 1 2 TABLE OF CONTENTS ITEM PAGE Introduction 4 Purpose of Report...4 Taxing Entities, Rates & Exemptions 5 Property Types

YOUNG COUNTY APPRAISAL DISTRICT 2017 - ANNUAL APPRAISAL REPORT AS OF 10/6/2017 1 2 TABLE OF CONTENTS ITEM PAGE Introduction 4 Purpose of Report...4 Taxing Entities, Rates & Exemptions 5 Property Types

Significance of USPAP

Page 1 of 10 USPAP and the Personal Property Appraiser by David J. Maloney, Jr., AOA CM and William M. Novotny, ISA AM, GCA Originally published in the Journal of Advanced Appraisal Studies All professions,

Page 1 of 10 USPAP and the Personal Property Appraiser by David J. Maloney, Jr., AOA CM and William M. Novotny, ISA AM, GCA Originally published in the Journal of Advanced Appraisal Studies All professions,

IMPORTANT UPDATED ADVISORY ON TAX SHELTER ABUSE INVOLVING CONSERVATION DONATIONS

IMPORTANT UPDATED ADVISORY ON TAX SHELTER ABUSE INVOLVING CONSERVATION DONATIONS All Land Trust Alliance (the Alliance ) member land trusts adopt and commit to implement Land Trust Standards and Practices

IMPORTANT UPDATED ADVISORY ON TAX SHELTER ABUSE INVOLVING CONSERVATION DONATIONS All Land Trust Alliance (the Alliance ) member land trusts adopt and commit to implement Land Trust Standards and Practices

WHAT EVERY ATTORNEY NEEDS TO KNOW ABOUT BUSINESS VALUATION AND WHY

NEEDS TO KNOW ABOUT BUSINESS VALUATION ALAN L. TOLMAS, CPA/ABV/CFF, ASA PRINCIPAL/FOUNDER 972.931.1800 atolmas@texff.com SOLO & SMALL FIRM SECTION FEBRUARY 1, 2012 LUNCHEON MEETING NEEDS TO KNOW ABOUT

NEEDS TO KNOW ABOUT BUSINESS VALUATION ALAN L. TOLMAS, CPA/ABV/CFF, ASA PRINCIPAL/FOUNDER 972.931.1800 atolmas@texff.com SOLO & SMALL FIRM SECTION FEBRUARY 1, 2012 LUNCHEON MEETING NEEDS TO KNOW ABOUT

Valuation Presentation for the Residents of the Central Hill Estate

Valuation Presentation for the Residents of the Central Hill Estate Introduction Jeremy Perceval FRICS RPR Founder and Managing Director of SFP Property Jeremy is a fellow of the Royal Institution of Chartered

Valuation Presentation for the Residents of the Central Hill Estate Introduction Jeremy Perceval FRICS RPR Founder and Managing Director of SFP Property Jeremy is a fellow of the Royal Institution of Chartered

Hidden Treasures Antiques & Fine Arts - Terms and Conditions of Sale

Hidden Treasures Antiques & Fine Arts - Terms and Conditions of Sale CONDITIONS OF SALE: 1. BINDING TERMS The catalogue and auction offered through Invaluable Live located at www.invaluable.com, the catalogue

Hidden Treasures Antiques & Fine Arts - Terms and Conditions of Sale CONDITIONS OF SALE: 1. BINDING TERMS The catalogue and auction offered through Invaluable Live located at www.invaluable.com, the catalogue

ESOP Feasibility and Valuation Basics

ESOP Feasibility and Valuation Basics Ohio Employee Ownership Center Akron/Fairlawn Hilton Fairlawn, Ohio April 21, 2006 Richard A. Schlueter rschlueter@comstockvaluation.com C VA 1 Levee Way, Suite 3109

ESOP Feasibility and Valuation Basics Ohio Employee Ownership Center Akron/Fairlawn Hilton Fairlawn, Ohio April 21, 2006 Richard A. Schlueter rschlueter@comstockvaluation.com C VA 1 Levee Way, Suite 3109

3 things about Livingstone s Guide to Business Valuation

Book Information 3 things about Livingstone s Guide to Business Valuation 1. Designed to provide an introduction for students not experienced with the subject 2. Also serves as a refresher for those familiar

Book Information 3 things about Livingstone s Guide to Business Valuation 1. Designed to provide an introduction for students not experienced with the subject 2. Also serves as a refresher for those familiar

MARKETING LISTING CONSULTATION. This presentation is property of Michael Lewis

MARKETING LISTING CONSULTATION This presentation is property of Michael Lewis. 310-801-6040 PROFESSIONAL PROFILE Mike Nichols Mike Nichols Exp Realty Born and raised in the Sacramento area, Mike has a

MARKETING LISTING CONSULTATION This presentation is property of Michael Lewis. 310-801-6040 PROFESSIONAL PROFILE Mike Nichols Mike Nichols Exp Realty Born and raised in the Sacramento area, Mike has a

DEALING WITH APPRAISERS AND OTHER EXPERTS:

DEALING WITH APPRAISERS AND OTHER EXPERTS: Challenges In Professionalism, Ethics and Related Issues Charles N. Pursley, Jr., Esquire Pursley Lowery Meeks LLP 260 Peachtree Street, Suite 2000 Atlanta, Georgia

DEALING WITH APPRAISERS AND OTHER EXPERTS: Challenges In Professionalism, Ethics and Related Issues Charles N. Pursley, Jr., Esquire Pursley Lowery Meeks LLP 260 Peachtree Street, Suite 2000 Atlanta, Georgia

Richard J. DiBaggio, SRA

Richard J. DiBaggio, SRA 9211 Trailing Fern State/ASC License Number 1327197 Helotes, TX 78023 Texas Certified Residential Appraiser Office (210) 218-3757 VA, FHA and Conventional Fax (866) 941-5065 RD@sun50.com

Richard J. DiBaggio, SRA 9211 Trailing Fern State/ASC License Number 1327197 Helotes, TX 78023 Texas Certified Residential Appraiser Office (210) 218-3757 VA, FHA and Conventional Fax (866) 941-5065 RD@sun50.com

Paragraph s 8, 9, and 10 from NACVA. Letter of October 27, 2016

Paragraph s 8, 9, and 10 from NACVA Letter of October 27, 2016 Re: Comments Regarding Proposed Treasury Regulation (REG. 163113-02) (to be used also as an Outline of Topics to be Discussed at the Public

Paragraph s 8, 9, and 10 from NACVA Letter of October 27, 2016 Re: Comments Regarding Proposed Treasury Regulation (REG. 163113-02) (to be used also as an Outline of Topics to be Discussed at the Public

Valuation for Compulsory Land Acquisition for Public Use. Okky Danuza Indonesian Society of Appraisers (MAPPI)

") Valuation for Compulsory Land Acquisition for Public Use Okky Danuza Indonesian Society of Appraisers (MAPPI) Introduction Logically a person would give up his/her rights if the compensation he/she receives

Valuation for Compulsory Land Acquisition for Public Use Okky Danuza Indonesian Society of Appraisers (MAPPI) Introduction Logically a person would give up his/her rights if the compensation he/she receives

All Interested Parties. Rick Baumgardner, Chair Appraisal Practices Board. Date: September 9, Background

TO: FROM: RE: All Interested Parties Rick Baumgardner, Chair Appraisal Practices Board Concept Paper Valuation Issues in Separating Tangible and Intangible Assets Date: September 9, 2013 Background Those

TO: FROM: RE: All Interested Parties Rick Baumgardner, Chair Appraisal Practices Board Concept Paper Valuation Issues in Separating Tangible and Intangible Assets Date: September 9, 2013 Background Those

INTRODUCTION MISSION OVERVIEW

INTRODUCTION The Austin County Appraisal District is a political subdivision of the State of Texas. The Constitution of the State of Texas, the Texas Property Tax Code, and the Rules of the Texas Comptroller

INTRODUCTION The Austin County Appraisal District is a political subdivision of the State of Texas. The Constitution of the State of Texas, the Texas Property Tax Code, and the Rules of the Texas Comptroller

The High Performance Appraisal Process Unveiled By Sandra K. Adomatis, SRA, LEED Green Associate

The High Performance Appraisal Process Unveiled By Sandra K. Adomatis, SRA, LEED Green Associate Email: Adomatis@Hotmail.com Twitter: https://twitter.com/sadomatis Web: www.adomatisappraisalservice.com

The High Performance Appraisal Process Unveiled By Sandra K. Adomatis, SRA, LEED Green Associate Email: Adomatis@Hotmail.com Twitter: https://twitter.com/sadomatis Web: www.adomatisappraisalservice.com

TERMS OF ENGAGEMENT Name of the firm. Previous involvement with the property or parties to the case:

The headings contained in this framework for terms of engagement are based directly upon the list of mandatory required content set out in VPS 1 para 3.1, page 39 and the commentary which follows on pages

The headings contained in this framework for terms of engagement are based directly upon the list of mandatory required content set out in VPS 1 para 3.1, page 39 and the commentary which follows on pages

WALLER COUNTY APPRAISAL DISTRICT MASS APPRAISAL REPORT APPRAISAL YEAR 2018

WALLER COUNTY APPRAISAL DISTRICT MASS APPRAISAL REPORT APPRAISAL YEAR 2018 ADDENDUM TO WCAD REAPPRAISAL PLAN FOR 2017 AND 2018 WALLER COUNTY APPRAISAL DISTRICT Uniform Standards of Professional Appraisal

WALLER COUNTY APPRAISAL DISTRICT MASS APPRAISAL REPORT APPRAISAL YEAR 2018 ADDENDUM TO WCAD REAPPRAISAL PLAN FOR 2017 AND 2018 WALLER COUNTY APPRAISAL DISTRICT Uniform Standards of Professional Appraisal

IAS Revenue. By:

IAS - 18 Revenue International Accounting Standard No 18 (IAS 18) Revenue In 1998, IAS 39, Financial Instruments: Recognition and Measurement, amended paragraph 11 of IAS 18, adding a cross-reference to

IAS - 18 Revenue International Accounting Standard No 18 (IAS 18) Revenue In 1998, IAS 39, Financial Instruments: Recognition and Measurement, amended paragraph 11 of IAS 18, adding a cross-reference to

NEW MEXICO. Appraisal LICENSING & CONTINUING EDUCATION NEW NAME. NEW LOOK. SAME GREAT EDUCATION. is NOW Brightwood Real Estate Education

JANUARY DECEMBER 2018 NEW MEXICO Appraisal Offered by Brightwood College, San Antonio (Ingram) LICENSING & CONTINUING EDUCATION is NOW Brightwood Real Estate Education NEW NAME. NEW LOOK. SAME GREAT EDUCATION.

JANUARY DECEMBER 2018 NEW MEXICO Appraisal Offered by Brightwood College, San Antonio (Ingram) LICENSING & CONTINUING EDUCATION is NOW Brightwood Real Estate Education NEW NAME. NEW LOOK. SAME GREAT EDUCATION.

Property Tax and Real Estate Appraisal Services

Property Tax and Real Estate Appraisal Services Appraisers/Consultants Micheal R. Lohmeier, ASA, MAI Certified General Real Estate Appraiser Direct: 248.368.8873 E: MLohmeier@virchowkrause.com Micheal

Property Tax and Real Estate Appraisal Services Appraisers/Consultants Micheal R. Lohmeier, ASA, MAI Certified General Real Estate Appraiser Direct: 248.368.8873 E: MLohmeier@virchowkrause.com Micheal

VALUATION REPORT IN RESPECT OF CAR PARK 4, DIRECT PARKING MURRAY STREET PAISLEY GLASGOW PA3 1QW

VALUATION REPORT IN RESPECT OF CAR PARK 4, DIRECT PARKING MURRAY STREET PAISLEY GLASGOW PA3 1QW Prepared by: AJP Surveyors Ltd Piccadilly House 49 Piccadilly Manchester M1 2AP on 9 February 2015 Page 1

VALUATION REPORT IN RESPECT OF CAR PARK 4, DIRECT PARKING MURRAY STREET PAISLEY GLASGOW PA3 1QW Prepared by: AJP Surveyors Ltd Piccadilly House 49 Piccadilly Manchester M1 2AP on 9 February 2015 Page 1

APPRAISAL MANAGEMENT COMPANY

APPRAISAL MANAGEMENT COMPANY STANDARDS OF GOOD PRACTICE IN APPRAISAL MANAGEMENT JANUARY 6, 2010 POST OFFICE BOX 1196 WEXFORD, PA 15090 (P) 724-934-1420 (F) 724-934-0057 (W) WWW.TAVMA.ORG APPRAISAL MANAGEMENT

APPRAISAL MANAGEMENT COMPANY STANDARDS OF GOOD PRACTICE IN APPRAISAL MANAGEMENT JANUARY 6, 2010 POST OFFICE BOX 1196 WEXFORD, PA 15090 (P) 724-934-1420 (F) 724-934-0057 (W) WWW.TAVMA.ORG APPRAISAL MANAGEMENT

GIFT ACCEPTANCE AND COUNTING POLICIES

1 Florida State University Policy 8-1 2 3 4 TITLE OF POLICY: Responsible Executive: Approving Official: GIFT ACCEPTANCE AND COUNTING POLICIES Vice President of University Advancement Vice President of

1 Florida State University Policy 8-1 2 3 4 TITLE OF POLICY: Responsible Executive: Approving Official: GIFT ACCEPTANCE AND COUNTING POLICIES Vice President of University Advancement Vice President of

NORTH COTSWOLD SALEROOM, GL54 2AR,

Catalogue 2 BOURTON-ON-THE-WATER Gloucestershire To be held at THE NORTH COTSWOLD SALEROOM, GL54 2AR, off the Village High Street, 16 miles from both Cheltenham and Cirencester, 28 miles from Oxford ANTIQUE

Catalogue 2 BOURTON-ON-THE-WATER Gloucestershire To be held at THE NORTH COTSWOLD SALEROOM, GL54 2AR, off the Village High Street, 16 miles from both Cheltenham and Cirencester, 28 miles from Oxford ANTIQUE

ARKANSAS ALCB APPROVED QUALIFYING APPRAISAL EDUCATION

ARKANSAS ALCB APPROVED QUALIFYING APPRAISAL EDUCATION APPRAISAL INSTITUTE Chicago, Illinois 330 Apartment Appraisal: Concepts & Applications 04/10 16 410 National USPAP Course, (Part A) (2010-11) 04/10

ARKANSAS ALCB APPROVED QUALIFYING APPRAISAL EDUCATION APPRAISAL INSTITUTE Chicago, Illinois 330 Apartment Appraisal: Concepts & Applications 04/10 16 410 National USPAP Course, (Part A) (2010-11) 04/10

INTERNATIONAL ASSOCIATION OF ASSESSING OFFICERS STATEMENT OF COMPLIANCE

INTERNATIONAL ASSOCIATION OF ASSESSING OFFICERS STATEMENT OF COMPLIANCE Re: Criteria for Appraisal Sponsorship in The Appraisal Foundation (TAF) As a founding, sponsoring organization of TAF, the International

INTERNATIONAL ASSOCIATION OF ASSESSING OFFICERS STATEMENT OF COMPLIANCE Re: Criteria for Appraisal Sponsorship in The Appraisal Foundation (TAF) As a founding, sponsoring organization of TAF, the International