IIFM PRODUCT DESCRIPTION. for. Himaayah Min Taqallub As aar Assarf or an Islamic Cross-Currency Swap (ICRCS)

|

|

|

- Chester Lindsey

- 6 years ago

- Views:

Transcription

First Leg (Party A as Buyer) & Second Leg (Party B")

1 IIFM PRODUCT DESCRIPTION for Himaayah Min Taqallub As aar Assarf or an Islamic Cross-Currency Swap (ICRCS) DFT Terms confirmation template (Wa ad - based and involving a Two Sales structure) First Leg (Party A as Buyer) & Second Leg (Party B as Buyer) 1

2 1. Introduction (product overview) ISDA and IIFM have published the DFT Terms confirmation templates to be used to document Himaayah Min Taqallub As aar Assarf or Islamic Cross- Currency Swaps under the ISDA/IIFM Tahawwut Master Agreement (the "TMA"). This explanatory memorandum explains the Islamic structures used and sets out the key features of these templates. ISDA/IIFM Tahawwut Master Agreement (the "TMA"). The TMA is a master agreement that contains the general terms and conditions agreed between the parties and under which parties may enter into "Transactions" and/or "DFT Terms Agreements" relating to "Designated Future transactions". The TMA draws a distinction between "Transactions" that have been entered into between the parties and "Designated Future transactions" that will or may be entered into between the parties in the future. This is an important distinction which is key to the different close-out mechanisms which apply to these two types of arrangement. The terms of a Transaction are evidenced by a "Confirmation". The terms of a Designated Future transaction are provided for in a DFT Terms Agreement, which is evidenced by a "DFT Terms confirmation". (The TMA uses upper and lower case "Transactions", "transactions", "Confirmations" and "confirmations" to help distinguish between the two types of arrangement and the manner in which they are documented). The exercise of an undertaking (or Wa'ad) contained in a DFT Terms Agreement leads to the entry into a Transaction. Once a Designated Future transaction is, pursuant to a DFT Terms Agreement, entered into between the parties, it becomes a "Transaction" under the TMA and should be documented using a "Confirmation". A failure to enter into a Designated Future transaction when required to do so in accordance with a DFT Terms Agreement is an Event of Default under the TMA. DFT Terms confirmations for ICRCS Each set of templates comprises two DFT Terms confirmations, one relating to the First Leg of an ICRCS; the other relating to the Second Leg of an ICRCS. In the conventional swap market, a swap, consisting of two legs (typically, one representing the purchasing one currency and one representing the purchasing of a second currency), will be treated as a single transaction and documented by a single confirmation. In the case of a Wa'ad-based ICRCS, however, instead of using a single document for both legs, there is some Shari 'ah preference for the Wa'ad (or undertaking) for each leg to be clear and distinct, and not combined with that of the other leg. Therefore, to document the ICRCS, two separate template DFT Terms confirmations are proposed, one for each leg. 2

3 2. Product Purpose An ICRCS enables parties to hedge currency risk and the profit rate risk associated with a given currency. For example, where a party has an investment in one jurisdiction in relation to which it has obtained funding denominated in the currency of that jurisdiction (for example where the party has issued sukuk in the relevant currency and it will have to make regular payments in that currency with respect to the sukuk), but the party accounts in the currency of its home jurisdiction, the ICRCS provides it with the potential to hedge its foreign currency requirements into the currency of its home jurisdiction. 3

4 3. Product Description The DFT Terms confirmation relates to Himaayah Min Taqallub As aar Assarf (Islamic cross-currency swap) ("ICRCS") implemented through arrangements whereby each party simultaneously grants to the other party a Wa ad (undertaking) to purchase Shari ah compliant assets from such other party on one or more specified future dates on the basis of Murabaha transactions to be entered into on each exercise of the Wa ad (undertaking) by such other party and where the purchase price payable in respect of such Murabaha transaction is to be determined on the basis of the cost price of the purchased Shari ah compliant assets plus a profit amount, with the purchase price payable by one party being denominated in one of the two currencies the subject of such Islamic cross-currency swap and the purchase price payable by the other party being denominated in the other of the two currencies the subject of such Islamic cross-currency swap. This DFT Terms confirmation contains a Wa ad (undertaking) granted by Party A to Party B. Under a Related DFT Terms Agreement, Party B grants a Wa ad (undertaking) to Party A. This DFT Terms Agreement and the Related DFT Terms Agreement together form an Islamic Cross Currency Swap. Two Sales Structure ICRCS The ICRCS assumes a Two Sales Structure ICRCS. For each Calculation Period in relation to the ICRCS, the two Wa'ads set out in the DFT Terms confirmations for the First Leg and for the Second Leg, respectively, will be exercisable and exercised against the undertaking party (i.e. the Buyer) by the exercising party (the Seller). Therefore, two Murabaha Sales will be entered into between the parties; one in relation to the First Leg and one in relation to the Second Leg. Accordingly, there will be two asset-flows and two cash-flows (in two different currencies) between the parties in relation to each Calculation Period for the ICRCS. A product description has been included in Part 1 of the relevant template DFT Terms confirmations describing how the Two Sales Structure should work. Each party will represent that, if Shari ah compliance is relevant for its purpose, then it has satisfied itself as to the Shari ah compliance of the Transactions and DFT Terms Agreements entered into by it under the ISDA/IIFM Tahawwut Master Agreement. 4

5 Two Sales Structure documentation architecture 5

6 4. Designated Future transactions. The parties may from time to time agree (the documents and other confirming evidence exchanged between the parties or otherwise effective for the purpose of confirming or evidencing any such agreement being a "DFT Terms confirmation" and each such agreement being a "DFT Terms Agreement") the terms of further transactions in each case being either (i) a transaction which, by such DFT Terms Agreement, the parties agree to enter into between them in the future under the TMA or (ii) a transaction which, by such DFT Terms Agreement, one party (the first party) undertakes to the other (the second party) to enter into under the TMA at the election of the second party at a future date (all of such further transactions being "Designated Future transactions"). Except as is expressly provided in the TMA, Designated Future transactions shall not constitute Transactions for the purposes of the TMA unless and until subsequently entered into, and when entered into they shall constitute Transactions, shall be confirmed by way of a Confirmation and shall cease to be Designated Future transactions. Use of Wa'ad leading to Murabaha Sale The ICRCS templates use a Wa'ad (or undertaking) structure, as is now increasingly common in Islamic finance transactions. A Wa'ad is an undertaking or promise made by one party (the Buyer of assets) to the other party (the Seller of assets) that, if required by the Seller (usually called exercise of the undertaking or Wa'ad), the Buyer will fulfil its promise, in this case, to enter into a Murabaha (or sale and purchase) contract under which it will buy from the Seller an agreed quantity of agreed Shari 'ah compliant assets at an agreed price (which may be determined by applying an agreed formula for calculating a price) on the relevant exercise date. The Wa'ad is contained in Paragraph 10 (Buyer's Undertaking) of each template DFT Terms confirmation. If and when the Buyer's Wa'ad (or undertaking) is exercised by the Seller on an Exercise Date, the Buyer is required to purchase specified assets under a Murabaha contract with the Seller and execute a Murabaha Asset Sale Confirmation. A Murabaha Sale entered into between the parties constitutes a Transaction under the TMA. The mechanics of the Murabaha Sale are set out in Paragraph 11 of each template DFT Terms confirmation, with Annex 2 providing an agreed form of Murabaha Asset Sale Confirmation to evidence and contain the operative provisions of the Murabaha Sale. 6

7 5. ICRCS specific terms A ICRCS deals primarily in the exchange of two currencies whereby one party hedges its assets or liabilities in one currency (Currency A) by buying or selling that currency for a fixed amount of another currency (Currency B). There may be an initial exchange between the parties of a fixed amount of Currency A against a fixed amount of Currency B. If such an initial exchange is made, then a further final exchange of a fixed amount of Currency A against a fixed amount of Currency B may also be made between the parties at a later date or upon termination of the ICRCS (in an opposite manner to the initial exchange). It is also possible that a party's assets or liability in one currency are linked to a benchmark or fixed profit rate related to that currency. Therefore, as well as there being an exchange of currency, there may well also be a profit rate swap built into the ICRCS which will be reflected in the resultant payment amount. In order to deal with these features, new terms have been introduced to capture the multiple elements of an ICRCS: First Currency and Second Currency: usually a cross currency swap deals with the "swapping" of two currencies. These currencies are elected in DFT terms confirmation. Specified Currency is the currency of the Payment Amount which can be the First Currency or the Second Currency. Capital Amount is the original principal amount in respect of which the exchange rate is calculated, i.e. this identifies the size of the ICRCS. Profit Type 1: means a capital amount of a Specified Currency representing the initial and final exchanges of the Specified Currencies which are the subject of the ICRCS. Profit Type 2: means: the profit element calculated in respect of a capital amount and on the basis of either a Fixed Profit Rate or Floating Profit Rate in the DFT Terms confirmation. The profit element of the purchase price may not be calculated in the same manner in respect of each Murabaha Sale i.e. the first Murabaha Sale entered into pursuant to a ICRCS may entail a profit amount that is the capital amount of one of the Specified Currencies (Profit Type 1), the payment of such capital amount representing the initial exchange of such specified currency. 7

8 Each of the other Murabaha Sales after the first one may entail a profit amount that is calculated on the basis of either a fixed rate (Profit Type 2 Fixed Profit Rate) or a benchmark profit rate (Profit Type 2 Floating Profit Rate), the payment of an amount calculated by application of a rate to the capital amount representing the payment of the profit element of the ICRCS. The final Murabaha Sale entered into may entail a profit amount that is equal to the sum of (i) a profit amount that is the capital amount of one of the specified currencies (Profit Type 1) which represents the final exchange of a Specified Currency and (ii) a profit amount that is calculated on the basis of either a fixed rate (Profit Type 2 Fixed Profit Rate) or a benchmark profit rate (Profit Type 2 Floating Profit Rate). Part 3 of the DFT Terms confirmation will specify whether, in respect of each Murabaha Sale envisaged, the profit element of the purchase price for that Murabaha Sale is "Profit Type 1", "Profit Type 2 Fixed Rate", "Profit Type 2 Floating Rate", "Profit Type 1 plus Profit Type 2 Fixed Rate" or "Profit Type 1 plus Profit Type 2 Floating Rate". The profit rate types used in the DFT Terms Agreement and a Related DFT Terms Agreement can be based on a fixed rate together with a floating rate, or two fixed rates or two floating rates as each rate represents the rate of return on a different specified currency. 8

9 6. Key Features of the ICRCS DFT Terms confirmations Transaction terms Each template DFT Terms confirmation (at Part 3) contains line items for specific agreed terms to be completed on the Trade Date (e.g. Effective Date, Business Day, Purchase Dates, Payment Dates, Buyer, Seller, etc.), as agreed between the parties upon entry into the relevant DFT Terms Agreement. Related confirmations/legs For the purposes of linking the two payments which are made in the currency swap, the DFT Terms confirmation for one leg of a ICRCS should identify the DFT Terms confirmation for the other leg as being related to it, as a "Related DFT Terms confirmation". Annexed pro-forma documents A form of Exercise Notice is included in each DFT Terms confirmation at Annex 1. The form of Exercise Notice is intended to be extracted, completed and used by the Seller when it wishes to exercise the Buyer's Wa'ad (or undertaking) on an Exercise Date. This form may be used multiple times over the term of the ICRCS and is not to be completed upon entry into the DFT Terms Agreement. A form of Murabaha Asset Sale Confirmation (i.e. a "Confirmation" for the purposes of the TMA) is included in Annex 2 of each DFT Terms confirmation. This form is intended to be extracted, completed and used to document entry into each Murabaha Sale (i.e. a "Transaction" for the purposes of the TMA). This form may also be used multiple times over the term of the ICRCS and is not to be completed upon entry into the DFT Terms Agreement. Once completed and executed, the Murabaha Asset Sale Confirmation will constitute a Confirmation for the purposes of the TMA and the Murabaha Sale that it confirms will constitute a Transaction under the TMA. Footnote guidance Extensive footnotes are included throughout the template DFT Terms confirmations to provide guidance to the parties (in particular in respect of the some important Shari'ah considerations) but these do not form part of the terms of the contract between the parties. 9

10 As a practical and drafting matter, a new clean version of the relevant template, without footnotes, will need to be created before the parties agree and finalise the relevant terms of their DFT Terms Agreement. Shari 'ah compliant assets Only Shari'ah compliant assets that are suitable as the subject matter of a Murabaha Sale may be sold by Buyer to Seller. "Shari'ah compliant assets" are defined generally in Part 2 of the template DFT Terms confirmations as being "any asset or assets which comply or are consistent with the principles of the Shari'ah and which, for Shari'ah purposes, are suitable as the subject matter of a Murabaha Sale". (By way of example, gold is not generally regarded as constituting Shari'ah compliant assets for these purposes.) To provide certainty of subject matter, the parties should agree and describe in detail the relevant assets in each DFT Terms confirmation relating to a leg of the ICRCS (i.e. by filling in the missing information in Part 3 of the template DFT Terms confirmation as part of the DFT Terms Agreement) and the Murabaha Asset Sale Confirmation. The expectation is that different types of assets will be specified in the two legs of the ICRCS. Definitions The ICRCS templates contain and introduce new terminologies such as, the terms "First Currency" and "Second Currency" as it was felt that these terms would be more intuitive in the context of a product that is structured using Islamic asset sales. It should be noted that the Buyer under one leg of the ICRCS will be the Seller under the other leg of the ICRCS. Agency/brokerage The template DFT Terms confirmations anticipate that the parties may wish to appoint an agent or broker to deliver, buy, sell or receive delivery of assets on its behalf. In these cases, the views of Shari'ah advisers should be sought to ensure that the use of the agent/broker and the relevant agency/brokerage procedures in the context of the particular ICRCS transaction do not fall foul of restrictions such as the prohibition on Bai Al Inah. 10

11 Execution as a Deed The usual practice in the Islamic finance market is that a Wa'ad (or undertaking) is evidenced or confirmed using a deed and, therefore, the DFT Terms confirmations provide for the Buyer to enter into a DFT Terms Agreement as a deed. The parties will need to satisfy themselves as to the correct form of words to be used in the place designated for signature by the Buyer to ensure that the DFT Terms Agreement is properly executed as a deed. 11

12 7. Product Shari ah Approval and Guidelines While IIFM's Shari'ah Board has approved the ICRCS templates after extensive consideration, it is always the responsibility of each of the parties entering to the ICRCS to ensure that, to the extent that Shari'ah compliance is relevant to its dealings and corporate governance, its use of the documents in the context of the transactions which it enters into satisfies its own Shari'ah advisers that the relevant hedging transaction is Shari'ah compliant and that the documents are suitable for, and are being used appropriately in, the context of that particular hedging transaction. In order to assist market participants with regard to the DFT Terms confirmation provided to market participants by ISDA and IIFM, the IIFM Shari ah Board have provide the following guidelines regarding Shari ah compliance: Transactions should be entered into only for the purpose of hedging actual risks of the relevant party. Transactions should not be entered into for purposes of speculation, i.e. actual settlements of assets and payments must take place. No cash settlements without concluding actual transaction on deliverable assets. The asset must be Islamicly lawful (i.e. Halal). No interest (whether called interest or an alternative name but which represents interest) is to be chargeable under a transaction. 12

13 Illustration ICRCS Two Sale Structure - Worked example 13

14 Illustration in relation to ICRCS Islamic hedging Management The following example illustrates how the ICRCS templates work through an example of Islamic hedging. Hedging liability in respect of Sukuk Imagine that: Party A will issue USD 10,000,000 Sukuk with a 12-month tenor on 1 February 2016: Sukuk pays out a capital (or principal) amount at one year maturity and periodic (monthly) floating profit amounts to investors over the course of its tenor. Party A's main operations are in Euro and Party A wishes to sell the USD it has raised under the Sukuk for Euro. Party A's main income is in fixed Euro and Party A is exposed to any changes in the currency exchange rates of Euro to USD and the profit rates in respect of USD. Party A wishes to hedge itself against the possibility that the exchange and profit rates used to calculate the USD floating amounts will increase. By entering into the ICRCS, it is looking to fix its exposure in relation to the Sukuk. Party A wishes to buy the USD it requires to repay the principal of the Sukuk on maturity. The PRS enables Party A to hedge its USD exposure under the Sukuk by converting it into a Euro exposure (i.e. Party A knows that by paying an amount of Euro to Party B, Party A will receive from Party B the USD amount necessary to pay under the Sukuk). Party B was highly dependent on Euro income and through the PRS is able to convert some of that into USD income. 14

15 The Hedging ICRCS Party A and Party B enter into ICRCS on 25 January 2016 (Trade Date), under which: Initial Exchange: Party A will pay a USD capital amount (Profit Type 1) (being the amount raised under the sukuk) under one (First) leg of the ICRCS (and receive a Euro amount under the other leg). Party B will pay a Euro capital amount (Profit Type 1) under one (Second) leg of the ICRCS (and receive a USD amount under the other leg). Interim Exchanges Party A will pay Euro fixed amounts (Profit Type 2 Fixed Profit Rate) under one (First) leg of the ICRCS (and receive USD floating amounts under the other leg). Party B will pay USD floating amounts (Profit Type 2 Floating Profit Rate) under one (Second) leg of the ICRCS (and receive the Euro fixed amounts under the other leg). Final Exchanges: Party A will pay a Euro capital amount and fixed amount (Profit Type 1 + Profit Type 2 Fixed Profit Rate) under one (First) leg of the ICRCS (and receive a USD amount under the other leg in order to repay the principal under the Sukuk). Party B will pay a USD capital amount and floating amounts (Profit Type 1 + Profit Type 2 Floating Profit Rate) under one (Second) leg of the ICRCS (and receive the Euro amount under the other leg). To achieve these payments, the parties will buy or sell Shari'ah compliant assets to each other pursuant to a Murabaha Sale to be entered into pursuant to a Wa'ad (or undertaking). 15

16 Explanation of Trade Date, Effective Date and Target Settlement Date Trade Date is the date on which the parties enter into a DFT Terms Agreement Effective Date is the date on which the DFT Terms Agreement becomes "live", i.e. the first day of the period of the hedging protection and the first day of the first Calculation Period in respect of that DFT Terms Agreement The Effective Date may be the same date as the Trade Date or it may be later than the Trade Date Why do we need both a Trade Date and an Effective Date? Because, whilst the parties may enter into a DFT Terms Agreement on a given day, that agreement may be subject to the satisfaction of conditions precedent by a certain later date in order that the agreement can become effective; and/or Because the parties may wish to have the "start date" of the DFT Terms Agreement coincide with the period for which hedging is required. Therefore, the Effective Date may fall on a later date than the Trade Date In our example, the Trade Date is 25 January 2016 this is the date when the parties enter into their DFT Terms Agreements. However, Party A requires the hedging to run from 1 February 2016 (the Effective Date) as that is the day it will issue the Sukuk in respect of which it is looking for hedging protection. Also conditions precedent must be fulfilled before 1 February 2016 (the Effective Date) in order for the DFT Terms Agreements to become effective 16

17 The ICRCS Documentation Party A and Party B have already entered into a TMA. Party A and Party B enter into the ICRCS by way of two separate DFT Term Agreements (each of which is documented in a separate DFT Terms confirmation: one in respect of the first leg of the PRS, and the other in respect of the second leg of the ICRCS). Each DFT Terms Agreement contains a Wa'ad (undertaking) to enter into one or more Designated Future transactions (if the Wa'ad is exercised). The DFT Terms Agreements are entered into on 25 January 2016 (Trade Date). The ICRS is to have a tenor of 12 months commencing 1 February 2015 (i.e. the date on which Party A is to issue the Sukuk which it is looking to hedge) so that date will be the "Effective Date" under the DFT Terms Agreement and first day of the period for which the ICRCS will provide Party A with the hedge. The ICRCS hedging period will have 12 Calculation Periods of one month each (to track the Sukuk). 17

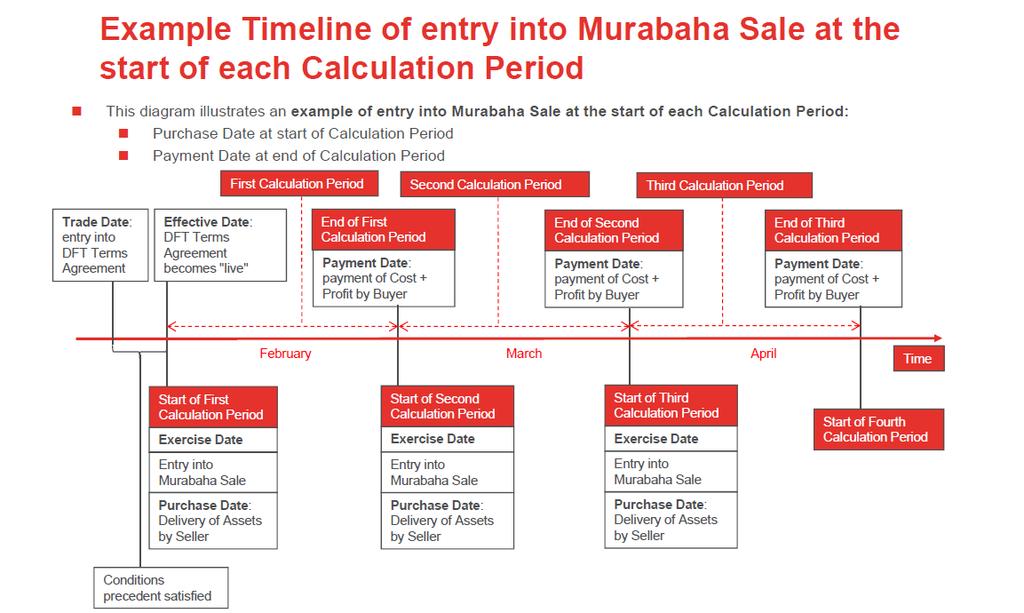

18 Terms of the ICRCS (Two Sale Structure) Terms of the ICRCS: Wa'ad in each leg of ICRCS Each DFT Terms Agreement contains a Wa'ad granted by one party to the other (by Undertaking Party to Exercising Party ), as illustrated in Figure A below. In the DFT Terms Agreement for the First Leg, Party A is the Undertaking Party. In the DFT Terms Agreement for the Second Leg, Party B is the Undertaking Party. By its Wa'ad, the Undertaking Party undertakes to purchase Shari'ah compliant assets at an agreed price from the Exercising Party, if the Exercising Party exercises the Wa'ad by notice on an Exercise Date. Wa'ad granted by each of Party A and Party B Party A First wa ad- Party A promises to purchase assets (copper), if wa'ad exercised Second wa ad - Party B promises to purchase assets (zinc), if wa ad exercised Party B Exercise of Wa'ad Party A and Party B's ICRCS will use the Two Sale Structure and two Murabaha Sales will be entered into at the start of each Calculation Period with Purchase Date at the start of the Calculation Period and Payment date at the end of the Calculation Period under each DFT Terms Agreement. 18

19 If a Wa'ad is exercised, the Undertaking Party must buy assets from the Exercising Party and execute a Murabaha Sale Confirmation evidencing the Murabaha Sale between the parties. Exercise of Wa'ad in Two Sale Structure: Consequences First Leg of ICRCS: Party A s Wa'ad to Party B has become exercisable in respect of the first Calculation Period. Accordingly, the expected order of events would be as follows: Party B exercises Party A's Wa'ad on the Exercise Date by notice to Party A. Party A and Party B enter into a Murabaha Sale (i.e. Party B sells assets to Party A). Party A and Party B execute a Murabaha Sale Confirmation. The Murabaha Sale pursuant to the First Leg of the ICRCS becomes a Transaction under the TMA. Second leg of ICRCS: Party B s Wa'ad to Party B has become exercisable in respect of the first Calculation Period. Accordingly, the expected order of events would be as follows: Party A exercises Party B's Wa'ad on the Exercise Date by notice to Party B. Party B and Party A enter into a Murabaha Sale (i.e. Party A sells assets to Party B). Party B and Party A execute a Murabaha Sale Confirmation. The Murabaha Sale pursuant to the Second Leg of the ICRCS becomes a Transaction under the TMA. 19

20 Exercise of Wa'ad in Two Sale Structure: Murabaha Sale Exercise of the Wa'ad under the First Leg requires Party A and Party B to enter into a Murabaha Sale, (i.e. Party B sells SC Assets to Party A at a purchase price consisting of Cost Price + Profit). Delivery of assets: Party B (the Seller) delivers the SC Assets (copper) to Party A on the Purchase Date, which, in this example, falls at the start of each Calculation Period. Payment of purchase price: Party A (the Buyer) pays the deferred purchase price of Cost + Profit on the Payment Date, which, in this example, falls at the end of the each Calculation Period. Cost Price under First Leg is the cost of the SC Assets (copper) to the Seller. Profit is determined by reference to the Profit Type: o Initial Exchange = Profit Type 1 (Capital Amount of USD) o Interim Exchange = Profit Type 2 Fixed Profit Rate of Euro [Capital Amount x FPR x FPR Day Count Fraction] o Final Exchange = Profit Type 1 (Capital Amount of Euro) + Profit Type 2 -Fixed Profit Rate of Euro Exercise of the Wa'ad under the Second Leg requires Party A and Party B to enter into a Murabaha Sale, (i.e. Party A sells SC Assets to Party B at a purchase price consisting of Cost Price + Profit). Delivery of assets: Party A (the Seller) delivers the SC Assets (zinc) to Party B on the Purchase Date, which, in this example, falls at the start of each Calculation Period. Payment of purchase price: Party B (the Buyer) pays the deferred purchase price of Cost + Profit on the Payment Date, which, in this example, falls at the end of the each Calculation Period. Cost Price under First Leg is the cost of the SC Assets (zinc) to the Seller. 20

21 Profit is determined by reference to the Profit Type: o Initial Exchange = Profit Type 1 (Capital Amount of Euro) o Interim Exchange = Profit Type 2 Floating Profit Rate Amount of USD [Capital Amount x FLPR x FLPR Day Count Fraction] o Final Exchange = Profit Type 1 (Capital Amount of USD) + Profit Type 2 Floating Profit Rate of USD) First Leg Party A is Undertaking Party/Buyer Party B is Exercising Party/Seller Specified Currency First Currency Second Currency Purchase Dates Payment Dates Fixed Profit Rate (FPR) First Payment Date: First Currency Second Payment Date [etc.]: Second Currency Final Payment Date : Second Currency Second Leg Specified Currency USD First Currency Euro Second Currency The first date of each Calculation Purchase Period Dates The last date of each Calculation Payment Period Dates 2% per annum Floating Profit Rate (FLPR) Party A is Exercising Party/Seller Party B is Undertaking Party/Buyer First Payment Date: First Currency Second Payment Date [etc.]: Second Currency Final Payment Date : Second Currency Euro USD The first date of each Calculation Period The last date of each Calculation Period LIBOR Shari'ah compliant assets For First Leg: Copper Spread Shari'ah compliant assets 0.5% per annum For Second Leg: Zinc 21

22 22

New product documentation for Himaayah Min Taqallub As'aar Assarf (Islamic Cross Currency Swaps)

") New product documentation for Islamic Cross Currency Swaps 1 Briefing note 26 November 2015 New product documentation for Himaayah Min Taqallub As'aar Assarf (Islamic Cross Currency Swaps) Today marks

New product documentation for Islamic Cross Currency Swaps 1 Briefing note 26 November 2015 New product documentation for Himaayah Min Taqallub As'aar Assarf (Islamic Cross Currency Swaps) Today marks

حماية من تق لب أسعار الصرف

Heading [Letterhead of Party A as Buyer of the First Leg Assets, the Undertaking provider] [Date of confirmation] DFT Terms confirmation DFT Terms Agreement for a Himaayah Min Taqallub As aar Assarf or

Heading [Letterhead of Party A as Buyer of the First Leg Assets, the Undertaking provider] [Date of confirmation] DFT Terms confirmation DFT Terms Agreement for a Himaayah Min Taqallub As aar Assarf or

[Letterhead of Buyer, the Undertaking provider] DFT Terms confirmation

![[Letterhead of Buyer, the Undertaking provider] DFT Terms confirmation](/thumbs/95/124192779.jpg "[Letterhead of Buyer, the Undertaking provider] DFT Terms confirmation") Heading [Letterhead of Buyer, the Undertaking provider] [Date of confirmation] [Name and address of Seller] DFT Terms confirmation DFT Terms Agreement for the Mu 'Addal Ribh Thabit (Fixed Profit Rate or

Heading [Letterhead of Buyer, the Undertaking provider] [Date of confirmation] [Name and address of Seller] DFT Terms confirmation DFT Terms Agreement for the Mu 'Addal Ribh Thabit (Fixed Profit Rate or

THE ISDA/IIFM TAHAWWUT MASTER AGREEMENT WORKSHOP ON IIFM STANDARDS SESSION: ISLAMIC HEDGING STANDARDS QUDEER LATIF. 10 April 2017

SESSION: ISLAMIC HEDGING STANDARDS QUDEER LATIF 10 April 2017 THE ISDA/IIFM TAHAWWUT MASTER AGREEMENT 1 ISDA/IIFM TAHAWWUT MASTER AGREEMENT Architecture Framework Agreement Multiproduct Single Agreement

SESSION: ISLAMIC HEDGING STANDARDS QUDEER LATIF 10 April 2017 THE ISDA/IIFM TAHAWWUT MASTER AGREEMENT 1 ISDA/IIFM TAHAWWUT MASTER AGREEMENT Architecture Framework Agreement Multiproduct Single Agreement

Master Terms and Conditions for an Islamic Foreign Exchange Forward (Wiqayah Min Taqallub As'aar Assarf) (Single Binding Wa'ad based structure)

(Single Binding Wa'ad based structure)") Master Terms and Conditions for an Islamic Foreign Exchange Forward (Wiqayah Min Taqallub As'aar Assarf) (Single Binding Wa'ad based structure) وقاية من تقلب أسعار الرصف قامئ عىل وعد ملزم من طرف واحد Disclaimer

Master Terms and Conditions for an Islamic Foreign Exchange Forward (Wiqayah Min Taqallub As'aar Assarf) (Single Binding Wa'ad based structure) وقاية من تقلب أسعار الرصف قامئ عىل وعد ملزم من طرف واحد Disclaimer

Sharia Compliant Treasury

IIFM Industry Seminar on Islamic Capital & Money Market th May 2014, Tower Level,Bank Indonesia, Indonesia Ismail E Dadabhoy Advisor IIFM Sharia Compliant Treasury Liquidity Management Tools Murabaha Wakala

IIFM Industry Seminar on Islamic Capital & Money Market th May 2014, Tower Level,Bank Indonesia, Indonesia Ismail E Dadabhoy Advisor IIFM Sharia Compliant Treasury Liquidity Management Tools Murabaha Wakala

2. The terms of this particular Swap Transaction to which the Confirmation relates are as follows:

From: To: Attention: Deutsche Bank A.G., London Branch Motor 2012 Plc Winchester House Mailstop 428, 1 Great Winchester Street, London. EC2N 2DB The Directors 19 September 2012 Dear Sirs, Confirmation

From: To: Attention: Deutsche Bank A.G., London Branch Motor 2012 Plc Winchester House Mailstop 428, 1 Great Winchester Street, London. EC2N 2DB The Directors 19 September 2012 Dear Sirs, Confirmation

Covered Bond Swap Confirmation

Execution Version Covered Bond Swap Confirmation March 22, 2016 To: RBC Covered Bond Guarantor Limited Partnership, acting by its managing general partner, RBC Covered Bond GP Inc. 155 Wellington Street

Execution Version Covered Bond Swap Confirmation March 22, 2016 To: RBC Covered Bond Guarantor Limited Partnership, acting by its managing general partner, RBC Covered Bond GP Inc. 155 Wellington Street

Covered Bond Swap Confirmation

Covered Bond Swap Confirmation July 15, 2016 To: Attention: CIBC Covered Bond (Legislative) Guarantor Limited Partnership, acting by its managing general partner, CIBC Covered Bond (Legislative) GP Inc.

Covered Bond Swap Confirmation July 15, 2016 To: Attention: CIBC Covered Bond (Legislative) Guarantor Limited Partnership, acting by its managing general partner, CIBC Covered Bond (Legislative) GP Inc.

Covered Bond Swap Confirmation

Covered Bond Swap Confirmation April 2, 2015 To: TD Covered Bond (Legislative) Guarantor Limited Partnership, acting by its managing general partner, TD Covered Bond (Legislative) GP Inc. 66 Wellington

Covered Bond Swap Confirmation April 2, 2015 To: TD Covered Bond (Legislative) Guarantor Limited Partnership, acting by its managing general partner, TD Covered Bond (Legislative) GP Inc. 66 Wellington

Covered Bond Swap Confirmation. Scotiabank Covered Bond Guarantor Limited Partnership

Covered Bond Swap Confirmation September 20, 2016 To: Scotiabank Covered Bond Guarantor Limited Partnership c/o The Bank of Nova Scotia Scotia Plaza 44 King Street West Toronto, Ontario M5H 1H1 Attn: Managing

Covered Bond Swap Confirmation September 20, 2016 To: Scotiabank Covered Bond Guarantor Limited Partnership c/o The Bank of Nova Scotia Scotia Plaza 44 King Street West Toronto, Ontario M5H 1H1 Attn: Managing

Covered Bond Swap Confirmation

Covered Bond Swap Confirmation September 27, 2016 To: Attention: NBC Covered Bond (Legislative) Guarantor Limited Partnership, acting by its managing general partner, NBC Covered Bond (Legislative) GP

Covered Bond Swap Confirmation September 27, 2016 To: Attention: NBC Covered Bond (Legislative) Guarantor Limited Partnership, acting by its managing general partner, NBC Covered Bond (Legislative) GP

ISDA INTERNATIONAL SWAPS AND DERIVATIVES ASSOCIATION, INC.

2004 ISDA Novation Definitions ISDA INTERNATIONAL SWAPS AND DERIVATIVES ASSOCIATION, INC. Copyright 2004 by INTERNATIONAL SWAPS AND DERIVATIVES ASSOCIATION, INC. 360 Madison Avenue One New Change 16th

2004 ISDA Novation Definitions ISDA INTERNATIONAL SWAPS AND DERIVATIVES ASSOCIATION, INC. Copyright 2004 by INTERNATIONAL SWAPS AND DERIVATIVES ASSOCIATION, INC. 360 Madison Avenue One New Change 16th

Ring-fencing Transfer Scheme

IN THE HIGH COURT OF JUSTICE CLAIM NO: FS-2017-000004 BUSINESS AND PROPERTY COURTS OF ENGLAND AND WALES BUSINESS LIST (ChD) Financial Services and Regulatory LLOYDS BANK PLC - and - BANK OF SCOTLAND PLC

IN THE HIGH COURT OF JUSTICE CLAIM NO: FS-2017-000004 BUSINESS AND PROPERTY COURTS OF ENGLAND AND WALES BUSINESS LIST (ChD) Financial Services and Regulatory LLOYDS BANK PLC - and - BANK OF SCOTLAND PLC

DAR AL ARKAN REAL ESTATE DEVELOPMENT COMPANY SAUDI JOINT STOCK COMPANY

DAR AL ARKAN REAL ESTATE DEVELOPMENT COMPANY INTERIM CONSOLIDATED FINANCIAL STATEMENTS AND AUDITORS LIMITED REVIEW REPORT FOR THE NINE-MONTH PERIOD ENDED 30 SEPTEMBER INTERIM CONSOLIDATED FINANCIAL STATEMENTS

DAR AL ARKAN REAL ESTATE DEVELOPMENT COMPANY INTERIM CONSOLIDATED FINANCIAL STATEMENTS AND AUDITORS LIMITED REVIEW REPORT FOR THE NINE-MONTH PERIOD ENDED 30 SEPTEMBER INTERIM CONSOLIDATED FINANCIAL STATEMENTS

Covered Bond Swap Confirmation

Covered Bond Swap Confirmation July 29, 2013 To: RBC Covered Bond Guarantor Limited Partnership, acting by its managing general partner, RBC Covered Bond GP Inc. 155 Wellington Street West, 14th Floor

Covered Bond Swap Confirmation July 29, 2013 To: RBC Covered Bond Guarantor Limited Partnership, acting by its managing general partner, RBC Covered Bond GP Inc. 155 Wellington Street West, 14th Floor

Covered Bond Swap Confirmation

Covered Bond Swap Confirmation December 14, 2015 To: Attention: CIBC Covered Bond (Legislative) Guarantor Limited Partnership, acting by its managing general partner, CIBC Covered Bond (Legislative) GP

Covered Bond Swap Confirmation December 14, 2015 To: Attention: CIBC Covered Bond (Legislative) Guarantor Limited Partnership, acting by its managing general partner, CIBC Covered Bond (Legislative) GP

Covered Bond Swap Confirmation

Covered Bond Swap Confirmation October 30, 2018 To: Attention: CIBC Covered Bond (Legislative) Guarantor Limited Partnership, acting by its managing general partner, CIBC Covered Bond (Legislative) GP

Covered Bond Swap Confirmation October 30, 2018 To: Attention: CIBC Covered Bond (Legislative) Guarantor Limited Partnership, acting by its managing general partner, CIBC Covered Bond (Legislative) GP

BMO Covered Bond Guarantor Limited Partnership c/o,bank of Montreal. Senior Manager, Securitization Finance and Operations

Confirmation - Series CBL2 Covered Bond Canadian Dollar to Euro Currency Swap From: To: Attention: Bank of Montreal BMO Covered Bond Guarantor Limited Partnership c/o,bank of Montreal Senior Manager, Securitization

Confirmation - Series CBL2 Covered Bond Canadian Dollar to Euro Currency Swap From: To: Attention: Bank of Montreal BMO Covered Bond Guarantor Limited Partnership c/o,bank of Montreal Senior Manager, Securitization

Covered Bond Swap Confirmation

Covered Bond Swap Confirmation September 25, 2014 To: TD Covered Bond (Legislative) Guarantor Limited Partnership, acting by its managing general partner, TD Covered Bond (Legislative) GP Inc. 66 Wellington

Covered Bond Swap Confirmation September 25, 2014 To: TD Covered Bond (Legislative) Guarantor Limited Partnership, acting by its managing general partner, TD Covered Bond (Legislative) GP Inc. 66 Wellington

Covered Bond Swap Confirmation. Scotiabank Covered Bond Guarantor Limited Partnership

Covered Bond Swap Confirmation January 14, 2016 To: Scotiabank Covered Bond Guarantor Limited Partnership c/o The Bank of Nova Scotia Scotia Plaza 44 King Street West Toronto, Ontario M5H 1H1 Attn: Managing

Covered Bond Swap Confirmation January 14, 2016 To: Scotiabank Covered Bond Guarantor Limited Partnership c/o The Bank of Nova Scotia Scotia Plaza 44 King Street West Toronto, Ontario M5H 1H1 Attn: Managing

Covered Bond Swap Confirmation

Covered Bond Swap Confirmation February 3, 2016 To: TD Covered Bond (Legislative) Guarantor Limited Partnership, acting by its managing general partner, TD Covered Bond (Legislative) GP Inc. 66 Wellington

Covered Bond Swap Confirmation February 3, 2016 To: TD Covered Bond (Legislative) Guarantor Limited Partnership, acting by its managing general partner, TD Covered Bond (Legislative) GP Inc. 66 Wellington

Covered Bond Swap Confirmation

Covered Bond Swap Confirmation December 8, 2017 To: RBC Covered Bond Guarantor Limited Partnership, acting by its managing general partner, RBC Covered Bond GP Inc. 155 Wellington Street West, 14th Floor

Covered Bond Swap Confirmation December 8, 2017 To: RBC Covered Bond Guarantor Limited Partnership, acting by its managing general partner, RBC Covered Bond GP Inc. 155 Wellington Street West, 14th Floor

Covered Bond Swap Confirmation

Covered Bond Swap Confirmation January 15, 2019 To: Attention: NBC Covered Bond (Legislative) Guarantor Limited Partnership, acting by its managing general partner, NBC Covered Bond (Legislative) GP Inc.

Covered Bond Swap Confirmation January 15, 2019 To: Attention: NBC Covered Bond (Legislative) Guarantor Limited Partnership, acting by its managing general partner, NBC Covered Bond (Legislative) GP Inc.

BankafAmenca Merrill Lynch

BankafAmenca Merrill Lynch r Execution Copy To: SAN DIEGO COUNTY REGIONAL TRANSPORTATION COMMISSION 401 B Street, Suite 800 San Diego, California 92101 Attn: Gallegos, Gary Telephone: (619) 595-5300 Fax:

BankafAmenca Merrill Lynch r Execution Copy To: SAN DIEGO COUNTY REGIONAL TRANSPORTATION COMMISSION 401 B Street, Suite 800 San Diego, California 92101 Attn: Gallegos, Gary Telephone: (619) 595-5300 Fax:

IFRS INTERPRETATIONS COMMITTEE - AGENDA DECISIONS (JANUARY AND MARCH 2018)

") IFRS INTERPRETATIONS COMMITTEE - AGENDA DECISIONS (JANUARY AND MARCH 2018) INTERNATIONAL FINANCIAL REPORTING BULLETIN 2018/01 Background This Bulletin summarises issues that the IFRS Interpretations Committee

IFRS INTERPRETATIONS COMMITTEE - AGENDA DECISIONS (JANUARY AND MARCH 2018) INTERNATIONAL FINANCIAL REPORTING BULLETIN 2018/01 Background This Bulletin summarises issues that the IFRS Interpretations Committee

Covered Bond Swap Confirmation

Covered Bond Swap Confirmation June 19, 2014 To: RBC Covered Bond Guarantor Limited Partnership, acting by its managing general partner, RBC Covered Bond GP Inc. 155 Wellington Street West, 14th Floor

Covered Bond Swap Confirmation June 19, 2014 To: RBC Covered Bond Guarantor Limited Partnership, acting by its managing general partner, RBC Covered Bond GP Inc. 155 Wellington Street West, 14th Floor

IMPORTANT NOTICE. Credit Derivatives Product Management Simon Todd

IMPORTANT NOTICE #: MS#78 ; TIW#104 Date: January 28, 2011 To: Distribution From: Legal Department Subject: Revisions to the MarkitSERV Operating Procedures and the Warehouse Trust Operating Procedures

IMPORTANT NOTICE #: MS#78 ; TIW#104 Date: January 28, 2011 To: Distribution From: Legal Department Subject: Revisions to the MarkitSERV Operating Procedures and the Warehouse Trust Operating Procedures

Presentation Outline Copyright Bank Nizwa. All Rights Reserved. 2

Presentation Outline Key Products and Services Section 1 Murabaha Section 2 Ijara Section 3 Musharaka Section 4 Islamic Banks VS Conventional Banks Section 5 2017 Copyright Bank Nizwa. All Rights Reserved.

Presentation Outline Key Products and Services Section 1 Murabaha Section 2 Ijara Section 3 Musharaka Section 4 Islamic Banks VS Conventional Banks Section 5 2017 Copyright Bank Nizwa. All Rights Reserved.

Covered Bond Swap Confirmation

Covered Bond Swap Confirmation April 19, 2016 To: Attention: CIBC Covered Bond (Legislative) Guarantor Limited Partnership, acting by its managing general partner, CIBC Covered Bond (Legislative) GP Inc.

Covered Bond Swap Confirmation April 19, 2016 To: Attention: CIBC Covered Bond (Legislative) Guarantor Limited Partnership, acting by its managing general partner, CIBC Covered Bond (Legislative) GP Inc.

Covered Bond Swap Confirmation

Covered Bond Swap Confirmation October 22, 2014 To: Attention: CCDQ Covered Bond (Legislative) Guarantor Limited Partnership, acting by its managing general partner, CCDQ CB (Legislative) Managing GP Inc.

Covered Bond Swap Confirmation October 22, 2014 To: Attention: CCDQ Covered Bond (Legislative) Guarantor Limited Partnership, acting by its managing general partner, CCDQ CB (Legislative) Managing GP Inc.

CONFIRMATION. Attention: WMTT-IRPConfirmations Fax:

CONFIRMATION From: LLOYDS BANK PLC 10 Gresham Street London EC2V 7AE Attention: WMTT-IRPConfirmations Fax: 020 7158 3122 Email: WMTT-IRPConfirmations@Lloydsbanking.com Trade ID: 10147291LS UTI: 1030466833SMTSWAP000000000000000010147291LS

CONFIRMATION From: LLOYDS BANK PLC 10 Gresham Street London EC2V 7AE Attention: WMTT-IRPConfirmations Fax: 020 7158 3122 Email: WMTT-IRPConfirmations@Lloydsbanking.com Trade ID: 10147291LS UTI: 1030466833SMTSWAP000000000000000010147291LS

Covered Bond Swap Confirmation

Covered Bond Swap Confirmation November 6, 2014 To: TD Covered Bond (Legislative) Guarantor Limited Partnership, acting by its managing general partner, TD Covered Bond (Legislative) GP Inc. 66 Wellington

Covered Bond Swap Confirmation November 6, 2014 To: TD Covered Bond (Legislative) Guarantor Limited Partnership, acting by its managing general partner, TD Covered Bond (Legislative) GP Inc. 66 Wellington

INTERNATIONAL SALE CONTRACT MODEL INTERNATION SALE CONTRACT

INTERNATIONAL SALE CONTRACT MODEL This model of International Sale Contract is designed for the international sale of different types of products: raw materials, manufacturing parts, consumer goods, equipment/machinery,

INTERNATIONAL SALE CONTRACT MODEL This model of International Sale Contract is designed for the international sale of different types of products: raw materials, manufacturing parts, consumer goods, equipment/machinery,

Covered Bond Swap Confirmation

Covered Bond Swap Confirmation April 2, 2014 To: Scotiabank Covered Bond Guarantor Limited Partnership c/o The Bank of Nova Scotia Scotia Plaza 44 King Street West Toronto, Ontario M5H 1H1 Attn: Managing

Covered Bond Swap Confirmation April 2, 2014 To: Scotiabank Covered Bond Guarantor Limited Partnership c/o The Bank of Nova Scotia Scotia Plaza 44 King Street West Toronto, Ontario M5H 1H1 Attn: Managing

Consumer Finance - Common Glossary of Important Terms

Consumer Finance - Common Glossary of Important Terms Additional Rent means the component of rent representing the cost of maintenance and monitoring charges of the tracker equipment installed in the Lease

Consumer Finance - Common Glossary of Important Terms Additional Rent means the component of rent representing the cost of maintenance and monitoring charges of the tracker equipment installed in the Lease

EXHIBIT A RESOLUTION NO.

Stradling Yocca Carlson & Rauth Draft of 8/27/14 EXHIBIT A RESOLUTION NO. RESOLUTION OF THE BOARD OF DIRECTORS OF EASTERN MUNICIPAL WATER DISTRICT MAKING CERTAIN FINDINGS WITH RESPECT TO TWO INTEREST RATE

Stradling Yocca Carlson & Rauth Draft of 8/27/14 EXHIBIT A RESOLUTION NO. RESOLUTION OF THE BOARD OF DIRECTORS OF EASTERN MUNICIPAL WATER DISTRICT MAKING CERTAIN FINDINGS WITH RESPECT TO TWO INTEREST RATE

Technical Line SEC staff guidance

No. 2013-20 Updated 27 August 2015 Technical Line SEC staff guidance How to apply S-X Rule 3-14 to real estate acquisitions In this issue: Overview... 1 Applicability of Rule 3-14... 2 Measuring significance...

No. 2013-20 Updated 27 August 2015 Technical Line SEC staff guidance How to apply S-X Rule 3-14 to real estate acquisitions In this issue: Overview... 1 Applicability of Rule 3-14... 2 Measuring significance...

ASX LISTING RULES Guidance Note 23

QUARTERLY CASH FLOW REPORTS The purpose of this Guidance Note The main points it covers To assist listed entities subject to the quarterly cash flow reporting regime in Listing Rules 4.7B and 5.5 and Appendices

QUARTERLY CASH FLOW REPORTS The purpose of this Guidance Note The main points it covers To assist listed entities subject to the quarterly cash flow reporting regime in Listing Rules 4.7B and 5.5 and Appendices

12 September Mr Hans Hoogervorst Chairman The International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom

12 September 2013 Mr Hans Hoogervorst Chairman The International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Email: commentletters@ifrs.org. Dear Hans Exposure Draft ED/2013/6

12 September 2013 Mr Hans Hoogervorst Chairman The International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Email: commentletters@ifrs.org. Dear Hans Exposure Draft ED/2013/6

[Letterhead of Landlord] OFFICE EXCLUSIVE RIGHT TO LEASE Version. [Date of agreement]

![[Letterhead of Landlord] OFFICE EXCLUSIVE RIGHT TO LEASE Version. [Date of agreement]](/thumbs/83/87599795.jpg "[Letterhead of Landlord] OFFICE EXCLUSIVE RIGHT TO LEASE Version. [Date of agreement]") [Letterhead of Landlord] OFFICE EXCLUSIVE RIGHT TO LEASE Version [Date of agreement] [Name and address of broker] Re: [Insert address of subject space, including floor(s) if applicable] Gentlemen and Ladies:

[Letterhead of Landlord] OFFICE EXCLUSIVE RIGHT TO LEASE Version [Date of agreement] [Name and address of broker] Re: [Insert address of subject space, including floor(s) if applicable] Gentlemen and Ladies:

MASTER CONFIRMATION AGREEMENT FOR NON-DELIVERABLE CURRENCY OPTION TRANSACTIONS (EUROPEAN STYLE)

") MASTER CONFIRMATION AGREEMENT FOR NON-DELIVERABLE CURRENCY OPTION TRANSACTIONS (EUROPEAN STYLE) dated as of, (the Effective Date ) between ( Party A ) and ( Party B ) The parties wish to facilitate the

MASTER CONFIRMATION AGREEMENT FOR NON-DELIVERABLE CURRENCY OPTION TRANSACTIONS (EUROPEAN STYLE) dated as of, (the Effective Date ) between ( Party A ) and ( Party B ) The parties wish to facilitate the

Reg. Section 15a.453-1(c)(2) Installment method reporting for sales of real property and casual sales of personal property

(2) Installment method reporting for sales of real property and casual sales of personal property") CLICK HERE to return to the home page Reg. Section 15a.453-1(c)(2) Installment method reporting for sales of real property and casual sales of personal property... (c)contingent payment sales. (1)In general.

CLICK HERE to return to the home page Reg. Section 15a.453-1(c)(2) Installment method reporting for sales of real property and casual sales of personal property... (c)contingent payment sales. (1)In general.

SP Energy Networks Fee Scale

SP Energy Networks Fee Scale Introduction SP Energy Networks (the Company), which is formed by the licensed and regulated companies known as SP Distribution Plc, SP Transmission Plc and SP Manweb Plc,

SP Energy Networks Fee Scale Introduction SP Energy Networks (the Company), which is formed by the licensed and regulated companies known as SP Distribution Plc, SP Transmission Plc and SP Manweb Plc,

The YMCA of Greater Vancouver Properties Foundation

Financial statements The YMCA of Greater Vancouver Properties Foundation Independent auditors report To the Directors of The YMCA of Greater Vancouver Properties Foundation Report on the financial statements

Financial statements The YMCA of Greater Vancouver Properties Foundation Independent auditors report To the Directors of The YMCA of Greater Vancouver Properties Foundation Report on the financial statements

Standard for the acquisition of land under the Public Works Act 1981 LINZS15005

Standard for the acquisition of land under the Public Works Act 1981 LINZS15005 Version date: 20 February 2014 Table of contents Terms and definitions... 5 Foreword... 6 Introduction... 6 Purpose... 6

Standard for the acquisition of land under the Public Works Act 1981 LINZS15005 Version date: 20 February 2014 Table of contents Terms and definitions... 5 Foreword... 6 Introduction... 6 Purpose... 6

ISDA. International Swaps and Derivatives Association, Inc. CREDIT SUPPORT ANNEX. between. ... and... relating to the

ISDA International Swaps and Derivatives Association, Inc. CREDIT SUPPORT ANNEX between... and... ("Party A") ("Party B") relating to the [1992/2002] ISDA Master Agreement dated as of... between Party

ISDA International Swaps and Derivatives Association, Inc. CREDIT SUPPORT ANNEX between... and... ("Party A") ("Party B") relating to the [1992/2002] ISDA Master Agreement dated as of... between Party

U.S.$500,000, (ISIN: XS )

") EIB Sukuk Company Ltd. U.S.$2,500,000,000 Trust Certificate Issuance Programme U.S.$500,000,000 Trust Certificates due 2018 (ISIN: XS0803231827) Trust Certificate Issuance Programme On 15 September 2011,

EIB Sukuk Company Ltd. U.S.$2,500,000,000 Trust Certificate Issuance Programme U.S.$500,000,000 Trust Certificates due 2018 (ISIN: XS0803231827) Trust Certificate Issuance Programme On 15 September 2011,

ISDA. International Swaps and Derivatives Association, Inc. CREDIT SUPPORT ANNEX. to the Schedule to the. Covered Bond 2002 Master Agreement

ISDA International Swaps and Derivatives Association, Inc. CREDIT SUPPORT ANNEX to the Schedule to the Covered Bond 2002 Master Agreement (Series CBL14) dated as of June 8, 2016 between The Toronto-Dominion

ISDA International Swaps and Derivatives Association, Inc. CREDIT SUPPORT ANNEX to the Schedule to the Covered Bond 2002 Master Agreement (Series CBL14) dated as of June 8, 2016 between The Toronto-Dominion

APPLICABLE FINAL TERMS. EIB Sukuk Company Ltd. Issue of U.S.$500,000,000 Trust Certificates due 2018 under the

APPLICABLE FINAL TERMS 10 July 2012 EIB Sukuk Company Ltd. Issue of U.S.$500,000,000 Trust Certificates due 2018 under the U.S.$1,000,000,000 Trust Certificate Issuance Programme PART A CONTRACTUAL TERMS

APPLICABLE FINAL TERMS 10 July 2012 EIB Sukuk Company Ltd. Issue of U.S.$500,000,000 Trust Certificates due 2018 under the U.S.$1,000,000,000 Trust Certificate Issuance Programme PART A CONTRACTUAL TERMS

Debashis Dey, Partner, Clifford Chance LLP. Sukuk Structures, Default and Assets

Debashis Dey, Partner, Clifford Chance LLP Sukuk Structures, Default and Assets Overview Treatment of Assets transferred and Balance Sheet of Obligor Differences from Conventional Bond Structures Role

Debashis Dey, Partner, Clifford Chance LLP Sukuk Structures, Default and Assets Overview Treatment of Assets transferred and Balance Sheet of Obligor Differences from Conventional Bond Structures Role

Agenda Item 11: Revenue and Non-Exchange Expenses

Agenda Item 11: Revenue and Non-Exchange Expenses David Bean, Anthony Heffernan, and Amy Shreck IPSASB Meeting June 21-24, 2016 Toronto, Canada Page 1 Proprietary and Copyrighted Information Agenda Item

Agenda Item 11: Revenue and Non-Exchange Expenses David Bean, Anthony Heffernan, and Amy Shreck IPSASB Meeting June 21-24, 2016 Toronto, Canada Page 1 Proprietary and Copyrighted Information Agenda Item

CONTRACT RULES: ICE FUTURES GILT FUTURES CONTRACTS SECTION RRRR - CONTRACT RULES: ICE FUTURES GILT FUTURES CONTRACTS

CONTRACT RULES: ICE FUTURES GILT FUTURES CONTRACTS RRRR SECTION RRRR - CONTRACT RULES: ICE FUTURES GILT FUTURES CONTRACTS RRRR.1 Interpretation RRRR.2 Contract Specification RRRR.3 List of Deliverable

CONTRACT RULES: ICE FUTURES GILT FUTURES CONTRACTS RRRR SECTION RRRR - CONTRACT RULES: ICE FUTURES GILT FUTURES CONTRACTS RRRR.1 Interpretation RRRR.2 Contract Specification RRRR.3 List of Deliverable

Exposure Draft 64 January 2018 Comments due: June 30, Proposed International Public Sector Accounting Standard. Leases

Exposure Draft 64 January 2018 Comments due: June 30, 2018 Proposed International Public Sector Accounting Standard Leases This document was developed and approved by the International Public Sector Accounting

Exposure Draft 64 January 2018 Comments due: June 30, 2018 Proposed International Public Sector Accounting Standard Leases This document was developed and approved by the International Public Sector Accounting

JPMorgan. Confirmation. Swap Transaction (Revision) The purpose of this Confirmation is to confirm the terms and conditions of the Swap Transaction

The purpose of this Confirmation is to confirm the terms and conditions of the Swap Transaction") ~.. JPMorgan Confirmation Swap Transaction (Revision) Date: December 16, 2004 Airport Commission of the City and County of San Francisco San Francisco International Airport International Terminal O. Box

~.. JPMorgan Confirmation Swap Transaction (Revision) Date: December 16, 2004 Airport Commission of the City and County of San Francisco San Francisco International Airport International Terminal O. Box

Sri Lanka Accounting Standard LKAS 40. Investment Property

Sri Lanka Accounting Standard LKAS 40 Investment Property LKAS 40 CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 40 INVESTMENT PROPERTY paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 5 CLASSIFICATION OF PROPERTY

Sri Lanka Accounting Standard LKAS 40 Investment Property LKAS 40 CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 40 INVESTMENT PROPERTY paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 5 CLASSIFICATION OF PROPERTY

Determining whether an Arrangement contains a Lease

IFRIC Interpretation 4 Determining whether an Arrangement contains a Lease This version includes amendments resulting from IFRSs issued up to 31 December 2010. IFRIC 4 Determining whether an Arrangement

IFRIC Interpretation 4 Determining whether an Arrangement contains a Lease This version includes amendments resulting from IFRSs issued up to 31 December 2010. IFRIC 4 Determining whether an Arrangement

By Dr. M. Anas Zarka*

Challenges in Making Sukuk Shariah Compliant By Dr. M. Anas Zarka* The International Investor Company,Kuwait *(views expressed are personal) Presented to International Islamic Financial Markets Conference

Challenges in Making Sukuk Shariah Compliant By Dr. M. Anas Zarka* The International Investor Company,Kuwait *(views expressed are personal) Presented to International Islamic Financial Markets Conference

Going global. Trouble ahead. Ongoing major projects. Where next?

Where now for IFRS? Gavin Aspden FCA ICAEW Director, Qualifications Going global Trouble ahead Ongoing major projects Where next? 1 Going global Trouble ahead Ongoing major projects Where next? IFRS jurisdictions

Where now for IFRS? Gavin Aspden FCA ICAEW Director, Qualifications Going global Trouble ahead Ongoing major projects Where next? 1 Going global Trouble ahead Ongoing major projects Where next? IFRS jurisdictions

Nottingham City Council Development Department

Nottingham City Council Development Department SUPPLEMENTARY PLANNING " GUIDANCE Planning Guidelines For the Provision of Local Open Space in New Residential Development original date: October 1997 UPDATE:July

Nottingham City Council Development Department SUPPLEMENTARY PLANNING " GUIDANCE Planning Guidelines For the Provision of Local Open Space in New Residential Development original date: October 1997 UPDATE:July

1 INTRODUCTION. 1.1 It is proposed that Lloyds Bank plc and Bank of Scotland plc (together, the Transferors )

") SUMMARY OF THE PROPOSED SCHEME FOR THE TRANSFER OF PART OF THE BANKING BUSINESS OF LLOYDS BANK PLC AND BANK OF SCOTLAND PLC TO LLOYDS BANK CORPORATE MARKETS PLC 1 INTRODUCTION 1.1 It is proposed that Lloyds

SUMMARY OF THE PROPOSED SCHEME FOR THE TRANSFER OF PART OF THE BANKING BUSINESS OF LLOYDS BANK PLC AND BANK OF SCOTLAND PLC TO LLOYDS BANK CORPORATE MARKETS PLC 1 INTRODUCTION 1.1 It is proposed that Lloyds

ACCOUNTING STANDARDS BOARD INTERPRETATION OF THE STANDARDS OF GENERALLY RECOGNISED ACCOUNTING PRACTICE

ACCOUNTING STANDARDS BOARD INTERPRETATION OF THE STANDARDS OF GENERALLY RECOGNISED ACCOUNTING PRACTICE DETERMINING WHETHER AN ARRANGEMENT CONTAINS A LEASE (IGRAP 3) Issued by the Accounting Standards Board

ACCOUNTING STANDARDS BOARD INTERPRETATION OF THE STANDARDS OF GENERALLY RECOGNISED ACCOUNTING PRACTICE DETERMINING WHETHER AN ARRANGEMENT CONTAINS A LEASE (IGRAP 3) Issued by the Accounting Standards Board

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC FORM 8-K/A

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 FORM 8-K/A CURRENT REPORT Pursuant to Section 13 or 15(d) of The Securities Exchange Act of 1934 Date of Report (Date of earliest event

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 FORM 8-K/A CURRENT REPORT Pursuant to Section 13 or 15(d) of The Securities Exchange Act of 1934 Date of Report (Date of earliest event

ESSENTIAL SHARIAH AND FIQH RULINGS IN ISLAMIC COMMERCIAL CONTRACTS. By: Assoc. Prof Dr. Azman bin Mohd Noor

ESSENTIAL SHARIAH AND FIQH RULINGS IN ISLAMIC COMMERCIAL CONTRACTS By: Assoc. Prof Dr. Azman bin Mohd Noor www.drazman.net 1 CLASIFICATION OF CONTRACTS Bai Murabahah (Mark-Up Sale) Bai Istisna (Manufacturing

ESSENTIAL SHARIAH AND FIQH RULINGS IN ISLAMIC COMMERCIAL CONTRACTS By: Assoc. Prof Dr. Azman bin Mohd Noor www.drazman.net 1 CLASIFICATION OF CONTRACTS Bai Murabahah (Mark-Up Sale) Bai Istisna (Manufacturing

NORTH LEEDS MATTER 2. Response to Leeds Sites and Allocations DPD Examination Inspector s Questions. August 2017

NORTH LEEDS MATTER 2 Response to Leeds Sites and Allocations DPD Examination Inspector s Questions August 2017 CLIENT: TAYLOR WIMPEY, ADEL REFERENCE NO: CONTENTS 1.0 INTRODUCTION 2.0 TEST OF SOUNDNESS

NORTH LEEDS MATTER 2 Response to Leeds Sites and Allocations DPD Examination Inspector s Questions August 2017 CLIENT: TAYLOR WIMPEY, ADEL REFERENCE NO: CONTENTS 1.0 INTRODUCTION 2.0 TEST OF SOUNDNESS

DAR AL ARKAN REAL ESTATE DEVELOPMENT COMPANY SAUDI JOINT STOCK COMPANY

DAR AL ARKAN REAL ESTATE DEVELOPMENT COMPANY INTERIM CONSOLIDATEDFINANCIAL STATEMENTS ANDAUDITORS LIMITED REVIEW REPORT FOR THE NINE-MONTH PERIODENDED30 SEPTEMBER INTERIM CONSOLIDATED FINANCIAL STATEMENTS

DAR AL ARKAN REAL ESTATE DEVELOPMENT COMPANY INTERIM CONSOLIDATEDFINANCIAL STATEMENTS ANDAUDITORS LIMITED REVIEW REPORT FOR THE NINE-MONTH PERIODENDED30 SEPTEMBER INTERIM CONSOLIDATED FINANCIAL STATEMENTS

1 Case Study 1: Ijara Contract 1.1 LEARNING OUTCOMES. After working through Case Study 1 you should be able to do the following:

1 Case Study 1: Ijara Contract 1.1 LEARNING OUTCOMES After working through Case Study 1 you should be able to do the following: Define the Ijara contract. Define the Ijara wa Iqtina contract. Distinguish

1 Case Study 1: Ijara Contract 1.1 LEARNING OUTCOMES After working through Case Study 1 you should be able to do the following: Define the Ijara contract. Define the Ijara wa Iqtina contract. Distinguish

Real Estate Syndication Income 19,451 NOTE

Real Estate Syndication Income 19,451 Section 10,500 Statement of Position 92-1 Accounting for Real Estate Syndication Income February 6, 1992 NOTE Statements of Position of the Accounting Standards Division

Real Estate Syndication Income 19,451 Section 10,500 Statement of Position 92-1 Accounting for Real Estate Syndication Income February 6, 1992 NOTE Statements of Position of the Accounting Standards Division

ARTICLES CLASSIFICATION

Article ARTICLES CLASSIFICATION ON THE SALE OF REAL ESTATE PROPERTY (SPECIAL PERFORMANCE) ACT THAT ABOLISHES AND REPLACES ON THE SALE OF LAND (SPECIAL PERFORMANCE) ACT 1. Heading summary 2. Interpretation

Article ARTICLES CLASSIFICATION ON THE SALE OF REAL ESTATE PROPERTY (SPECIAL PERFORMANCE) ACT THAT ABOLISHES AND REPLACES ON THE SALE OF LAND (SPECIAL PERFORMANCE) ACT 1. Heading summary 2. Interpretation

IFRS 16 Leases supplement

IFRS 16 Leases supplement Guide to annual financial statements IFRS December 2017 kpmg.com/ifrs Contents About this supplement 1 About IFRS 16 3 The Group s lease portfolio 6 Part I Modified retrospective

IFRS 16 Leases supplement Guide to annual financial statements IFRS December 2017 kpmg.com/ifrs Contents About this supplement 1 About IFRS 16 3 The Group s lease portfolio 6 Part I Modified retrospective

GENERAL SALES CONTRACT no.

GENERAL SALES CONTRACT no. SELLER: BUYER: KOVINOPLASTIKA LOŽ d.o.o. Lož, Cesta 19. oktobra 57 1386 Stari trg pri Ložu, represented by Borut Flander, CEO (hereinafter referred to as the Seller) (hereinafter

GENERAL SALES CONTRACT no. SELLER: BUYER: KOVINOPLASTIKA LOŽ d.o.o. Lož, Cesta 19. oktobra 57 1386 Stari trg pri Ložu, represented by Borut Flander, CEO (hereinafter referred to as the Seller) (hereinafter

27 September Hans Hoogervorst IFRS Foundation 30 Cannon Street, London EC4M 6XH. Dear Hans IASB ED/2013/6: LEASES

27 September 2013 Hans Hoogervorst IFRS Foundation 30 Cannon Street, London EC4M 6XH Dear Hans IASB ED/2013/6: LEASES IMA represents the asset management industry operating in the UK. Our members include

27 September 2013 Hans Hoogervorst IFRS Foundation 30 Cannon Street, London EC4M 6XH Dear Hans IASB ED/2013/6: LEASES IMA represents the asset management industry operating in the UK. Our members include

ANZVGN 7 THE VALUATION OF PARTIAL INTERESTS IN PROPERTY HELD WITHIN CO-OWNERSHIP STRUCTURES

8.7 ANZ VALUATION GUIDANCE NOTE 7 ANZVGN 7 THE VALUATION OF PARTIAL INTERESTS IN PROPERTY HELD WITHIN CO-OWNERSHIP STRUCTURES 1.0 Introduction 1.1 Purpose The purpose of this Guidance Note is to provide

8.7 ANZ VALUATION GUIDANCE NOTE 7 ANZVGN 7 THE VALUATION OF PARTIAL INTERESTS IN PROPERTY HELD WITHIN CO-OWNERSHIP STRUCTURES 1.0 Introduction 1.1 Purpose The purpose of this Guidance Note is to provide

GENERAL CONDITIONS OF SALE BETWEEN PROFESSIONALS PARIS GASTRONOMY DISTRIBUTION

GENERAL CONDITIONS OF SALE BETWEEN PROFESSIONALS PARIS GASTRONOMY DISTRIBUTION SA (Company) with a Board of Directors and capital of 60.000 RCS CRETEIL n 408 980 027 Registered Office : 3, rue de la Corderie.

GENERAL CONDITIONS OF SALE BETWEEN PROFESSIONALS PARIS GASTRONOMY DISTRIBUTION SA (Company) with a Board of Directors and capital of 60.000 RCS CRETEIL n 408 980 027 Registered Office : 3, rue de la Corderie.

CONSOLIDATED FINANCIAL STATEMENTS

CONSOLIDATED FINANCIAL STATEMENTS Dundee Real Estate Investment Trust Consolidated Balance Sheets (unaudited) June 30, December 31, (in thousands of dollars) Note 2004 2003 Assets Rental properties 3,4

CONSOLIDATED FINANCIAL STATEMENTS Dundee Real Estate Investment Trust Consolidated Balance Sheets (unaudited) June 30, December 31, (in thousands of dollars) Note 2004 2003 Assets Rental properties 3,4

ISDA. International Swaps and Derivatives Association, Inc. CREDIT SUPPORT ANNEX. to the Schedule to the. Interest Rate Swap ISDA Master Agreement

AMENDED AND RESTATED ISDA International Swaps and Derivatives Association, Inc. CREDIT SUPPORT ANNEX to the Schedule to the Interest Rate Swap ISDA Master Agreement dated as of September 30, 2013 between

AMENDED AND RESTATED ISDA International Swaps and Derivatives Association, Inc. CREDIT SUPPORT ANNEX to the Schedule to the Interest Rate Swap ISDA Master Agreement dated as of September 30, 2013 between

ANNEXURE A. Referred to in the Contract For Sale of Land by Offer and Acceptance. made between as Buyer

Drover s Retreat Stage 1 R5 Special Residential Lots - Pre-sales 2011 Page 1 of 8 ANNEXURE A Referred to in the Contract For Sale of Land by Offer and Acceptance made between as Buyer and Ardross Estates

Drover s Retreat Stage 1 R5 Special Residential Lots - Pre-sales 2011 Page 1 of 8 ANNEXURE A Referred to in the Contract For Sale of Land by Offer and Acceptance made between as Buyer and Ardross Estates

Lease payments. What s included in the lease liability? IFRS 16. November kpmg.com/ifrs

Lease payments What s included in the lease liability? IFRS 16 November 2017 kpmg.com/ifrs Contents Contents Determining the lease liability 1 1 At a glance 2 1.1 Key facts 2 1.2 Key impacts 3 2 Lease

Lease payments What s included in the lease liability? IFRS 16 November 2017 kpmg.com/ifrs Contents Contents Determining the lease liability 1 1 At a glance 2 1.1 Key facts 2 1.2 Key impacts 3 2 Lease

To: Moody s Investors Service, Ltd. Attention: CDO Monitoring Team By

NOTICE FROM THE ISSUER TO THE TRUSTEE / NOTEHOLDERS / RATING AGENCIES (REGARDING THE AMENDED TRANSACTION DOCUMENTS) To: Fitch Ratings, Ltd Attention: CDO Surveillance By email: london.cdosurveillance@fitchratings.com;

NOTICE FROM THE ISSUER TO THE TRUSTEE / NOTEHOLDERS / RATING AGENCIES (REGARDING THE AMENDED TRANSACTION DOCUMENTS) To: Fitch Ratings, Ltd Attention: CDO Surveillance By email: london.cdosurveillance@fitchratings.com;

GASB 69: Government Combinations

GASB 69: Government Combinations Table of Contents EXECUTIVE SUMMARY... 3 BACKGROUND... 3 KEY PROVISIONS... 3 OVERVIEW & SCOPE... 3 MERGER & TRANSFER OF OPERATIONS... 4 Mergers... 4 Transfers of Operations...

GASB 69: Government Combinations Table of Contents EXECUTIVE SUMMARY... 3 BACKGROUND... 3 KEY PROVISIONS... 3 OVERVIEW & SCOPE... 3 MERGER & TRANSFER OF OPERATIONS... 4 Mergers... 4 Transfers of Operations...

DATE: TO OWNER: Washington State Housing Finance Commission Low-Income Housing Tax Credit Program 1000 Second Avenue Suite 2700 Seattle WA

INDEPENDENT CERTIFIED PUBLIC ACCOUNTANT'S REPORT on CARRYOVER ALLOCATION BASIS PURSUANT TO IRS SECTION 42 (h)(1)(e)(ii) and AMERICAN RECOVERY AND REINVESTMENT ACT (ARRA) EXCHANGE PROGRAM 30% TEST PURSUANT

INDEPENDENT CERTIFIED PUBLIC ACCOUNTANT'S REPORT on CARRYOVER ALLOCATION BASIS PURSUANT TO IRS SECTION 42 (h)(1)(e)(ii) and AMERICAN RECOVERY AND REINVESTMENT ACT (ARRA) EXCHANGE PROGRAM 30% TEST PURSUANT

Applying IFRS. Presentation and disclosure requirements of IFRS 16 Leases. November 2018

Applying IFRS Presentation and disclosure requirements of IFRS 16 Leases November 2018 Contents 1. Overview 2 2. What is changing from current IFRS? 4 2.1 Presentation 4 2.2 Lessee disclosures 5 3. Presentation

Applying IFRS Presentation and disclosure requirements of IFRS 16 Leases November 2018 Contents 1. Overview 2 2. What is changing from current IFRS? 4 2.1 Presentation 4 2.2 Lessee disclosures 5 3. Presentation

Covered Bond Swap Confirmation

Execution Version Covered Bond Swap Confirmation April 26, 2016 To: RBC Covered Bond Guarantor Limited Partnership, acting by its managing general partner, RBC Covered Bond GP Inc. 155 Wellington Street

Execution Version Covered Bond Swap Confirmation April 26, 2016 To: RBC Covered Bond Guarantor Limited Partnership, acting by its managing general partner, RBC Covered Bond GP Inc. 155 Wellington Street

Determining whether an Arrangement contains a Lease

Accounting Standards Interpretation (ASI) 3 Determining whether an Arrangement contains a Lease 1 CONTENTS ASI 3 DETERMINING WHETHER AN ARRANGEMENT CONTAINS A LEASE REFERENCES paragraphs BACKGROUND 1 3

Accounting Standards Interpretation (ASI) 3 Determining whether an Arrangement contains a Lease 1 CONTENTS ASI 3 DETERMINING WHETHER AN ARRANGEMENT CONTAINS A LEASE REFERENCES paragraphs BACKGROUND 1 3

Annexure 1 TRANSACTION DIAGRAM OF THE SUKUK IJARAH PROGRAMME AND EXPLANATORY NOTES

Annexure 1 TRANSACTION DIAGRAM OF THE SUKUK IJARAH PROGRAMME AND EXPLANATORY NOTES Declares Trust and Issue Sukuk Ijarah 6 Sale Undertaking 6 Purchase Undertaking 2 2 Enter into Ijarah Agreement KDU (as

Annexure 1 TRANSACTION DIAGRAM OF THE SUKUK IJARAH PROGRAMME AND EXPLANATORY NOTES Declares Trust and Issue Sukuk Ijarah 6 Sale Undertaking 6 Purchase Undertaking 2 2 Enter into Ijarah Agreement KDU (as

Classification: Public. Heathrow Expansion. Land Acquisition and Compensation Policies. Interim Property Hardship Scheme 1.

Heathrow Expansion Land Acquisition and Compensation Policies Interim Property Hardship Scheme 1 Policy Terms 1 Introduction 1.1 This document sets out the terms of the Interim Property Hardship Scheme

Heathrow Expansion Land Acquisition and Compensation Policies Interim Property Hardship Scheme 1 Policy Terms 1 Introduction 1.1 This document sets out the terms of the Interim Property Hardship Scheme

Basic Diploma in Conveyancing Practice

Basic Diploma in Conveyancing Practice Purpose of the basic diploma course To provide step-by-step updated and thoroughly researched knowledge and skills to anyone from a beginner to a conveyancing typist

Basic Diploma in Conveyancing Practice Purpose of the basic diploma course To provide step-by-step updated and thoroughly researched knowledge and skills to anyone from a beginner to a conveyancing typist

Lease modifications. Accounting for changes to lease contracts IFRS 16. September kpmg.com/ifrs

Lease modifications Accounting for changes to lease contracts IFRS 16 September 2018 kpmg.com/ifrs Contents Contents Accounting for changes 1 1 At a glance 2 1.1 Key facts 2 1.2 Key impacts 3 2 Key concepts

Lease modifications Accounting for changes to lease contracts IFRS 16 September 2018 kpmg.com/ifrs Contents Contents Accounting for changes 1 1 At a glance 2 1.1 Key facts 2 1.2 Key impacts 3 2 Key concepts

Covered Bond Swap Confirmation

Execution Version Covered Bond Swap Confirmation March 23, 2015 To: RBC Covered Bond Guarantor Limited Partnership, acting by its managing general partner, RBC Covered Bond GP Inc. 155 Wellington Street

Execution Version Covered Bond Swap Confirmation March 23, 2015 To: RBC Covered Bond Guarantor Limited Partnership, acting by its managing general partner, RBC Covered Bond GP Inc. 155 Wellington Street

ISDA 2016 VARIATION MARGIN PROTOCOL QUESTIONNAIRE

International Swaps and Derivatives Association, Inc. ISDA 2016 VARIATION MARGIN PROTOCOL QUESTIONNAIRE published on August 16, 2016, by the International Swaps and Derivatives Association, Inc. Annotated

International Swaps and Derivatives Association, Inc. ISDA 2016 VARIATION MARGIN PROTOCOL QUESTIONNAIRE published on August 16, 2016, by the International Swaps and Derivatives Association, Inc. Annotated

AMENDMENT CREDIT SUPPORT ANNEX

Supplementary Exhibit En-SUPP 4 NEW This Supplementary Exhibit to the ISDA 2016 Variation Margin Protocol is applicable if the Agreed Method is New CSA Method and the CSA Type is English CSA. International

Supplementary Exhibit En-SUPP 4 NEW This Supplementary Exhibit to the ISDA 2016 Variation Margin Protocol is applicable if the Agreed Method is New CSA Method and the CSA Type is English CSA. International

Group Company A together with its subsidiaries

HKEX LISTING DECISION HKEX-LD43-3 (First Quarter of 2005, updated in November 2011, August, November and December 2012, November 2013, April 2014, August 2015, and February and April 2018) Name of Parties

HKEX LISTING DECISION HKEX-LD43-3 (First Quarter of 2005, updated in November 2011, August, November and December 2012, November 2013, April 2014, August 2015, and February and April 2018) Name of Parties

Exposure Draft. Indian Accounting Standard (Ind AS) 116 Leases. (Last date for Comments: August 31, 2017)

116 Leases. (Last date for Comments: August 31, 2017)") ED/Ind AS/2017/06 Exposure Draft Indian Accounting Standard (Ind AS) 116 Leases (Last date for Comments: August 31, 2017) Issued by Accounting Standards Board The Institute of Chartered Accountants of

ED/Ind AS/2017/06 Exposure Draft Indian Accounting Standard (Ind AS) 116 Leases (Last date for Comments: August 31, 2017) Issued by Accounting Standards Board The Institute of Chartered Accountants of

Easy Legals Avoiding the costly mistakes most people make when buying a property including buyer s checklist

Easy Legals Avoiding the costly mistakes most people make when buying a property including buyer s checklist Our Experience is Your Advantage 1. Why is this guide important? Thank you for ordering this

Easy Legals Avoiding the costly mistakes most people make when buying a property including buyer s checklist Our Experience is Your Advantage 1. Why is this guide important? Thank you for ordering this

In December 2003 the Board issued a revised IAS 40 as part of its initial agenda of technical projects.

IAS 40 Investment Property In April 2001 the International Accounting Standards Board (the Board) adopted IAS 40 Investment Property, which had originally been issued by the International Accounting Standards

IAS 40 Investment Property In April 2001 the International Accounting Standards Board (the Board) adopted IAS 40 Investment Property, which had originally been issued by the International Accounting Standards

Consolidated Financial Statements of ECOTRUST CANADA. Year ended December 31, 2016

Consolidated Financial Statements of ECOTRUST CANADA KPMG Enterprise TM Metro Tower I 4710 Kingsway, Suite 2400 Burnaby BC V5H 4M2 Canada Telephone (604) 527-3600 Fax (604) 527-3636 INDEPENDENT AUDITORS

Consolidated Financial Statements of ECOTRUST CANADA KPMG Enterprise TM Metro Tower I 4710 Kingsway, Suite 2400 Burnaby BC V5H 4M2 Canada Telephone (604) 527-3600 Fax (604) 527-3636 INDEPENDENT AUDITORS

Guidelines for Islamic Real Estate Investment Trusts

Guidelines for Islamic Real Estate Investment Trusts Date Issued: 21 November 2005 1 Introduction 1. These are the guidelines as outlined by the Syariah Advisory Council (SAC) of the Securities Commission

Guidelines for Islamic Real Estate Investment Trusts Date Issued: 21 November 2005 1 Introduction 1. These are the guidelines as outlined by the Syariah Advisory Council (SAC) of the Securities Commission

Heathrow Expansion. Land Acquisition and Compensation Policies. Interim Property Hardship Scheme. Policy Terms

1 Introduction Heathrow Expansion Land Acquisition and Compensation Policies Interim Property Hardship Scheme Policy Terms 1.1 This document sets out the terms of the Interim Property Hardship Scheme (the

1 Introduction Heathrow Expansion Land Acquisition and Compensation Policies Interim Property Hardship Scheme Policy Terms 1.1 This document sets out the terms of the Interim Property Hardship Scheme (the

Memorandum for the Subsidised Housing Committee of the Hong Kong Housing Authority

PAPER NO. SHC 53/2012 Memorandum for the Subsidised Housing Committee of the Hong Kong Housing Authority Sale of Remaining Surplus Home Ownership Scheme Flats and New Home Ownership Scheme Flats PURPOSE

PAPER NO. SHC 53/2012 Memorandum for the Subsidised Housing Committee of the Hong Kong Housing Authority Sale of Remaining Surplus Home Ownership Scheme Flats and New Home Ownership Scheme Flats PURPOSE

Duties Amendment (Land Rich) Act 2004 No 96

Act 2004 No 96") New South Wales Duties Amendment (Land Rich) Act 2004 No 96 Contents Page 1 Name of Act 2 2 Commencement 2 3 Amendment of Duties Act 1997 No 123 2 Schedule 1 Land rich amendments 3 Schedule 2 Other amendments

New South Wales Duties Amendment (Land Rich) Act 2004 No 96 Contents Page 1 Name of Act 2 2 Commencement 2 3 Amendment of Duties Act 1997 No 123 2 Schedule 1 Land rich amendments 3 Schedule 2 Other amendments