The New Leasing Guidance and Its Impact to PeopleSoft Asset Management and Lease Administration

|

|

|

- Clarence Hamilton

- 6 years ago

- Views:

Transcription

1

2 The New Leasing Guidance and Its Impact to PeopleSoft Asset Management and Lease Administration Session Loida Chez Product Management Director PeopleSoft Asset Lifecycle Management Solutions July 19, 2017

3 Safe Harbor Statement The following is intended to outline our general product direction. It is intended for information purposes only, and may not be incorporated into any contract. It is not a commitment to deliver any material, code, or functionality, and should not be relied upon in making purchasing decisions. The development, release, and timing of any features or functionality described for Oracle s products remains at the sole discretion of Oracle. 3

4 Agenda Development Phases Configuration Considerations What s Next? Q & A 4

Phase 1 Foundation Phase 2 Foundation Phase 3 Lessee Phase 4 Migration")

5 Lease Accounting Development Approach Phased Enhancement Rollout (9.2 Only) Phase 1 Foundation Phase 2 Foundation Phase 3 Lessee Phase 4 Migration Transition 5

6 Phases 1 and 2 Preparing the Foundation for New Leasing Guidance Financials Audit Framework Supplemental Data Related Leases and Hierarchy Viewer Lease data import Accounting hierarchy Interunit transfers Lease expiration/asset retirement Interim rent Equipment leasing Finance/capital payables leases Lease classification assistant Enhanced integration with Asset Management - ChartField transfers - Recategorization - Asset cost adjustments - Asset life update/book change Non -Exhaustive 6

7 Phase 3 Payables Lease Extensions for ASC 842 and IFRS 16 Multi-asset leases More precise data capture of financial terms Allocation of lease payments Asset-level lease classification and accounting 7

8 Financial Terms Total Lease Payments = Unpaid Lease Payments + Payments Due at End of Lease ROU Asset Cost = Present Value of Lease Payments + Initial Direct Cost + Prepaids Lease Incentives Received 8

9 Financial Terms New rent types enable more precise data capture of financial terms Initial Direct Cost Lease Incentives Prepaid Rent 9

10 Financial Terms 10

11 Financial Terms Initial direct cost is reflected in the right-of-use asset 11

12 Lease Options Related actions to enter lease option payments Penalties Renewal Purchase 12

13 Lease Options Associate option to an underlying asset in a lease Evaluate if purchase option is bargain with percentage of fair value calculation Establish if option is reasonably certain to be exercised 13

14 Lease Options Options reasonably certain to be exercised are reflected total lease payments and right-of-use asset 14

15 Leased Assets Add new equipment or property asset Select asset added in Asset Management prior to lease entry 15

16 Leased Assets 16

17 Leased Assets 17

18 Leased Assets Fair value used to determine if purchase option is a bargain 18

19 Leased Assets Residual value included in lease liability 19

20 Allocation of Lease Payments Lease payment allocation basis Manual Percent Price 20

21 Allocation of Lease Payments 21

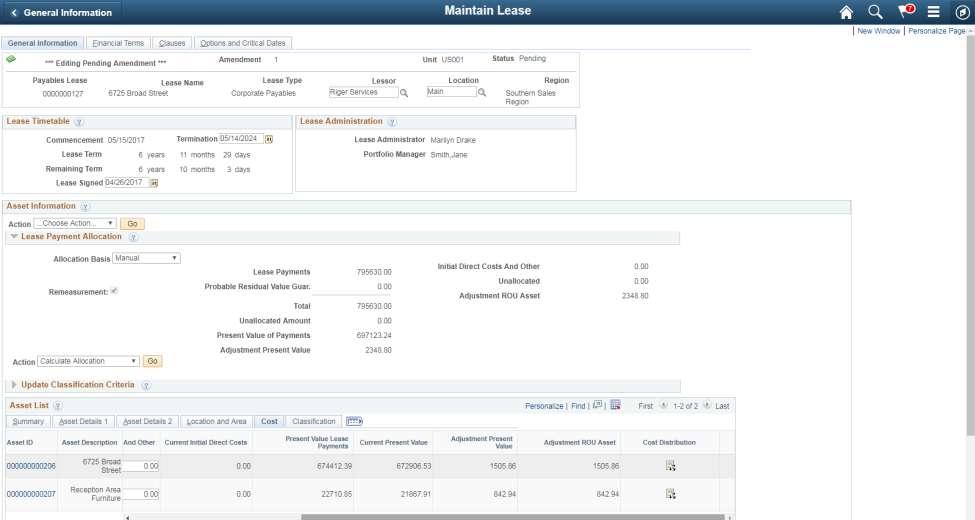

22 Lease Classification Lease classification determined by asset Classify all assets or one asset at a time 22

23 Lease Classification 23

24 Lease Classification 24

25 Lease Amendments Is the amendment the result of lease remeasurement? 25

26 Lease Amendments 26

27 Lease Amendments 27

28 Configuration Considerations Lease Administration Lease Classification, Borrowing Rate, Miscellaneous Rent, and Lease Options 28

29 Lease Administration Business Unit What is Your Organization s Accounting Policy for Lease Classification? If FASB BU, define - major part of remaining economic life of leased asset - substantially all of the fair value of the underlying asset Percentage of fair value considered bargain purchase (optional) If IFRS BU, all payables leases are finance 29

30 Borrowing Rate Optionally Configure a Default Incremental Borrowing Rate 30

31 Miscellaneous Rent Types Initial Direct Cost, Prepaid Rent, and Miscellaneous Recurring Rent New rent type identifier Initial Direct Cost Other If rent type is other specify if rent is Included in lease payments Interim or prepaid rent 31

32 Lease Options Renewal, Penalties, and Purchase Options Valid option types Renewal Purchase Penalties Other 32

33 Configuration Considerations Asset Management Asset Categories and Profiles 33

34 Asset Categories Finance versus Operating Finance Lease Categories = Depreciable Operating Lease Categories = Non-Depreciable 34

35 Asset Profiles Finance versus Operating Finance Lease Profiles = Capitalized Asset Operating Lease Profiles = Capitalized Asset 35

36 Asset Profiles Finance versus Operating Finance Lease Profiles = Depreciable Operating Lease Profiles = Non-Depreciable 36

37 Configuration Considerations Accounting Hierarchy 37

38 Lease Accounting Hierarchy Highest level in default hierarchy AM Accounting Entry Templates LA Accounting Rules CF Override 38

39")

39 Asset Management Accounting Entry Templates Evaluate Existing and Create New Review accounting entry templates for existing lease asset categories Create new accounting entry templates for new - Asset categories - Cost types Lease Incentive Lease Remeasurement Rent Expense - Lease Expense Transaction Type (LEX) 39

40 Lease Accounting Rules Evaluate Existing and Create New Review existing transaction routing codes and LA accounting rules for existing transaction groups Evaluate if new LA accounting rules are needed for new transaction groups - Lease Obligation - Lease Interest Expense - Prior Period Lease Obligation - Prior Period Interest Expense - Rent Expense - Lease Incentive 40

41 What s Next? 46

42 Lease Accounting Development Approach Phased Enhancement Rollout (9.2 Only) Phase 1 Foundation Phase 2 Foundation Phase 3 Lessee Phase 4 Migration Transition 47

43 What does all this mean for me? Asset Management and Lease Administration Licensed Customers No additional licenses needed; additional planned functionality already included Asset Management Only Customers Evaluate your lease portfolio. You may want to consider licensing and implementing Lease Administration for all asset types (including properties), lessee/lessor, and advanced leasing capabilities 48

44 Q&A 49

45 MW Get Connected and Stay Informed Key PeopleSoft Information Sources Oracle PeopleSoft Page Oracle PeopleSoft Development Group Blogs 50

46 51

47

PeopleSoft Asset Management and PeopleSoft Lease Administration: Adapting to Change Session Number

PeopleSoft Asset Management and PeopleSoft Lease Administration: Adapting to Change Session Number 102640 Loida Chez PeopleSoft Product Strategy James Quijas Boise Cascade Company July 18, 2018 Safe Harbor

PeopleSoft Asset Management and PeopleSoft Lease Administration: Adapting to Change Session Number 102640 Loida Chez PeopleSoft Product Strategy James Quijas Boise Cascade Company July 18, 2018 Safe Harbor

HERE WE GO AGAIN. THE NEW LEASE STANDARD (ASC TOPIC 842) February Internal Audit, Risk, Business & Technology Consulting

February Internal Audit, Risk, Business & Technology Consulting") HERE WE GO AGAIN THE NEW LEASE STANDARD (ASC TOPIC 842) February 2018 Internal Audit, Risk, Business & Technology Consulting PRESENTERS Edna Lopez Protiviti Managing Director edna.lopez@protiviti.com Scott

HERE WE GO AGAIN THE NEW LEASE STANDARD (ASC TOPIC 842) February 2018 Internal Audit, Risk, Business & Technology Consulting PRESENTERS Edna Lopez Protiviti Managing Director edna.lopez@protiviti.com Scott

New leases standard ASC 842 Lessee - operating leases. Itai Gotlieb, Partner, Professional Practice July 2017

ASC 842 Lessee - operating leases Itai Gotlieb, Partner, Professional Practice July 2017 Overview Under Accounting Standards Codification (ASC) 842, Leases, lessees recognize assets and liabilities for

ASC 842 Lessee - operating leases Itai Gotlieb, Partner, Professional Practice July 2017 Overview Under Accounting Standards Codification (ASC) 842, Leases, lessees recognize assets and liabilities for

Accounting and Auditing. Norman Mosrie, CPA, FMFMA, CHFP James Sutherland, CPA

Accounting and Auditing Norman Mosrie, CPA, FMFMA, CHFP James Sutherland, CPA Leases (ASU 2016-02; Topic 842) A lease contract conveys the right to use an asset (the underlying asset) for a period of time

Accounting and Auditing Norman Mosrie, CPA, FMFMA, CHFP James Sutherland, CPA Leases (ASU 2016-02; Topic 842) A lease contract conveys the right to use an asset (the underlying asset) for a period of time

Executive Summary. New leases standard Lessees

Executive Summary December 2018 The new leases standard focuses on increased transparency and comparability providing financial statement users with more information about an entity s leasing activities.

Executive Summary December 2018 The new leases standard focuses on increased transparency and comparability providing financial statement users with more information about an entity s leasing activities.

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions. August 24, 2017

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions August 24, 2017 Learning objectives Define leasing implications related to recently revised FASB standard Differentiate between new

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions August 24, 2017 Learning objectives Define leasing implications related to recently revised FASB standard Differentiate between new

SAP REAL ESTATE MANAGEMENT (RE-FX)

") SAP REAL ESTATE MANAGEMENT (RE-FX) New Leasing Standards at a Glance Peter Tabone Principal Consultant REAL. WORLD. EXPERIENCE. NORTH AMERICA ASIA PACIFIC MIDDLE EAST EUROPE www.vestapartners.com Vesta

SAP REAL ESTATE MANAGEMENT (RE-FX) New Leasing Standards at a Glance Peter Tabone Principal Consultant REAL. WORLD. EXPERIENCE. NORTH AMERICA ASIA PACIFIC MIDDLE EAST EUROPE www.vestapartners.com Vesta

47.1% of organizations concerned about their ability to implement

Leases: Not Just for the 1 Lease Standard - Statistics 10 year project In 2014, $3.0 trillion in off-balance sheet lease commitments 47.1% of organizations concerned about their ability to implement 2

Leases: Not Just for the 1 Lease Standard - Statistics 10 year project In 2014, $3.0 trillion in off-balance sheet lease commitments 47.1% of organizations concerned about their ability to implement 2

IFRS 16 Lease overview and EY s enabling toolkit

IFRS 16 Lease overview and EY s enabling toolkit Content Page Section I IFRS 16 overview 2 Appendix I EY Lease enabling technology suite 9 Appendix II EY Contacts 17 Page 1 IFRS 9 Classification and measurement

IFRS 16 Lease overview and EY s enabling toolkit Content Page Section I IFRS 16 overview 2 Appendix I EY Lease enabling technology suite 9 Appendix II EY Contacts 17 Page 1 IFRS 9 Classification and measurement

LeaseAccelerator,Inc All Rights Reserved.

1 LEASE ACCOUNTING - ASC 842 100 DATA FIELDS TO COLLECT FROM YOUR LEASES PAYMENTS: The following data fields impact lease payments. Changes to payments will impact how you account for your leases. Number

1 LEASE ACCOUNTING - ASC 842 100 DATA FIELDS TO COLLECT FROM YOUR LEASES PAYMENTS: The following data fields impact lease payments. Changes to payments will impact how you account for your leases. Number

ASC 842: Leases. Presented by: Maxwell Locke & Ritter LLP June 15, Maxwell Locke & Ritter

ASC 842: Leases Presented by: Maxwell Locke & Ritter LLP June 15, 2018 The New Lease Standard FASB ASC 842, Leases Supersedes FASB ASC 840, Leases Effective for calendar year-end public companies in 2019;

ASC 842: Leases Presented by: Maxwell Locke & Ritter LLP June 15, 2018 The New Lease Standard FASB ASC 842, Leases Supersedes FASB ASC 840, Leases Effective for calendar year-end public companies in 2019;

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions. August 24, 2017

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions August 24, 2017 Learning objectives Define leasing implications related to recently revised FASB standard Differentiate between new

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions August 24, 2017 Learning objectives Define leasing implications related to recently revised FASB standard Differentiate between new

PRACTICAL TIPS FOR IMPLEMENTING THE NEW LEASE ACCOUNTING STANDARD

PRACTICAL TIPS FOR IMPLEMENTING THE NEW LEASE ACCOUNTING STANDARD SHAUNA WATSON, VP, GLOBAL HEAD OF TECHNICAL ACCOUNTING MICHAEL ALLEN, PARTNER, TRANSACTION ADVISORY SERVICES 1. Overview of Accounting

PRACTICAL TIPS FOR IMPLEMENTING THE NEW LEASE ACCOUNTING STANDARD SHAUNA WATSON, VP, GLOBAL HEAD OF TECHNICAL ACCOUNTING MICHAEL ALLEN, PARTNER, TRANSACTION ADVISORY SERVICES 1. Overview of Accounting

Is Your Operating Lease An Asset or Liability? It s Now Both

MFM Annual Conference Is Your Operating Lease An Asset or Liability? It s Now Both 23 May 2016-1:30 pm 2:20 pm Disclaimer These slides are for educational purposes only and are not intended, and should

MFM Annual Conference Is Your Operating Lease An Asset or Liability? It s Now Both 23 May 2016-1:30 pm 2:20 pm Disclaimer These slides are for educational purposes only and are not intended, and should

HOW TO JUMP START YOUR ASC 842 LEASE ACCOUNTING PROJECT WEBINAR MARCH

HOW TO JUMP START YOUR ASC 842 LEASE ACCOUNTING PROJECT WEBINAR MARCH 14 2018 Today s Panelists Scott Vanlandingham Principal Consulting Iyaye Amabeoku Senior Manager Technical Accounting Michael Gregorski

HOW TO JUMP START YOUR ASC 842 LEASE ACCOUNTING PROJECT WEBINAR MARCH 14 2018 Today s Panelists Scott Vanlandingham Principal Consulting Iyaye Amabeoku Senior Manager Technical Accounting Michael Gregorski

Impact of lease accounting changes to corporate real estate

Impact of lease accounting changes to corporate real estate Overview In February 2016, the Financial Accounting Standards Board (FASB) issued its long-awaited revision to lease accounting Accounting Standards

Impact of lease accounting changes to corporate real estate Overview In February 2016, the Financial Accounting Standards Board (FASB) issued its long-awaited revision to lease accounting Accounting Standards

CPE regulations require online participants to take part in online questions

KPMG s CFO Financial Forum Webcast FASB/IASB Revised Lease Accounting Exposure Drafts A Detailed Look Part III: Lessor Accounting June 25, 2013 Administrative CPE regulations require online participants

KPMG s CFO Financial Forum Webcast FASB/IASB Revised Lease Accounting Exposure Drafts A Detailed Look Part III: Lessor Accounting June 25, 2013 Administrative CPE regulations require online participants

Edison Electric Institute and American Gas Association New Lease Standard

Edison Electric Institute and American Gas Association New Lease Standard May 16, 2016 Disclaimer The information contained herein is of a general nature and is not intended to address the circumstances

Edison Electric Institute and American Gas Association New Lease Standard May 16, 2016 Disclaimer The information contained herein is of a general nature and is not intended to address the circumstances

Center for Plain English Accounting

Report April 18, 2018 Center for Plain English Accounting AICPA s National A&A Resource Center Debits and Credits Associated with New Lease Accounting Standard CPEA Lease Standard Implementation Series

Report April 18, 2018 Center for Plain English Accounting AICPA s National A&A Resource Center Debits and Credits Associated with New Lease Accounting Standard CPEA Lease Standard Implementation Series

Guide to auditing the implementation of ASC 842, Leases

Guide to auditing the implementation of ASC 842, Leases Revised July 2018 Contents Glossary of key terms... 1 1 Introduction... 2 1.1 Overview... 2 1.2 Leases audit roadmap for lessees... 3 1.3 Summary

Guide to auditing the implementation of ASC 842, Leases Revised July 2018 Contents Glossary of key terms... 1 1 Introduction... 2 1.1 Overview... 2 1.2 Leases audit roadmap for lessees... 3 1.3 Summary

LEASES WHERE ARE WE? Steve Rathjen

LEASES WHERE ARE WE? Steve Rathjen 267 256-3110 srathjen@kpmg.com Agenda Project status Lease definition and classification Lessee accounting Lessor accounting Presentation, disclosures, and transition

LEASES WHERE ARE WE? Steve Rathjen 267 256-3110 srathjen@kpmg.com Agenda Project status Lease definition and classification Lessee accounting Lessor accounting Presentation, disclosures, and transition

The new accounting standard for leases. 27 March 2017

The new accounting standard for leases 27 March 2017 Disclaimer Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity.

The new accounting standard for leases 27 March 2017 Disclaimer Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity.

Lessor Example Performance Obligation Approach

Lessor Example Performance Obligation Approach **Disclaimer The exposure draft received nearly 700 letters of comment through the comment period ended December 15, 2010. There is some expectation that

Lessor Example Performance Obligation Approach **Disclaimer The exposure draft received nearly 700 letters of comment through the comment period ended December 15, 2010. There is some expectation that

Accounting and Auditing Update. Paul Lundy

Accounting and Auditing Update Paul Lundy Leases: Not Just for the Footnotes Anymore Significant Financial Statement Impact New lease standard generally requires all leases to be capitalized and recognized

Accounting and Auditing Update Paul Lundy Leases: Not Just for the Footnotes Anymore Significant Financial Statement Impact New lease standard generally requires all leases to be capitalized and recognized

Implementing the New Lease Guidance

Implementing the New Lease Guidance October 22, 2018 2018 Crowe LLP 2018 Crowe LLP Agenda Background Scope Effective dates & transition requirements Lessee accounting model Lessor accounting model Specialized

Implementing the New Lease Guidance October 22, 2018 2018 Crowe LLP 2018 Crowe LLP Agenda Background Scope Effective dates & transition requirements Lessee accounting model Lessor accounting model Specialized

Implementing GASB s Lease Guidance

The effective date of the Governmental Accounting Standards Board s (GASB) new lease guidance is drawing nearer. Private sector companies also have recently adopted significantly revised lease guidance;

The effective date of the Governmental Accounting Standards Board s (GASB) new lease guidance is drawing nearer. Private sector companies also have recently adopted significantly revised lease guidance;

Miles CPA Review: FAR Updates

Miles CPA Review: FAR - 2019 Updates Summary of updates: - FAR-4.4: s [ASC 842] effective fiscal years beginning after Dec 15, 2018 (for issuers) and effective fiscal years beginning after Dec 15, 2019

Miles CPA Review: FAR - 2019 Updates Summary of updates: - FAR-4.4: s [ASC 842] effective fiscal years beginning after Dec 15, 2018 (for issuers) and effective fiscal years beginning after Dec 15, 2019

presentation for October 5, 2018

presentation for October 5, 2018 Proper Lease Analysis + Proper Technology = Successful Implementation Designed by Former Big 4 Auditors Built for Audit Efficiency Key Design Principles Ease of Use & Security

presentation for October 5, 2018 Proper Lease Analysis + Proper Technology = Successful Implementation Designed by Former Big 4 Auditors Built for Audit Efficiency Key Design Principles Ease of Use & Security

REAL ESTATE LEASE ACCOUNTING

REAL ESTATE LEASE ACCOUNTING WHAT CHANGES UNDER ASC 842 2017 LeaseAccelerator Inc. Page 1 REAL ESTATE LEASE ACCOUNTING KEY POLICY ELECTIONS MARK KOPPERSMITH & SCOTT SILVER Defining Asset Classes Asset

REAL ESTATE LEASE ACCOUNTING WHAT CHANGES UNDER ASC 842 2017 LeaseAccelerator Inc. Page 1 REAL ESTATE LEASE ACCOUNTING KEY POLICY ELECTIONS MARK KOPPERSMITH & SCOTT SILVER Defining Asset Classes Asset

REAL ESTATE PERSPECTIVE ON NEW LEASE ACCOUNTING STANDARDS

VALUATION & ADVISORY REAL ESTATE PERSPECTIVE ON NEW LEASE ACCOUNTING STANDARDS BY JOHN CORBETT, MAI, ASA, FRICS AND MARC R. SHAPIRO, MAI, MRICS INTRODUCTION The Financial Accounting Standards Board (FASB)

VALUATION & ADVISORY REAL ESTATE PERSPECTIVE ON NEW LEASE ACCOUNTING STANDARDS BY JOHN CORBETT, MAI, ASA, FRICS AND MARC R. SHAPIRO, MAI, MRICS INTRODUCTION The Financial Accounting Standards Board (FASB)

The joint leases project change is coming

No. 2010-4 18 June 2010 Technical Line Technical guidance on standards and practice issues The joint leases project change is coming What you need to know The proposed changes to the accounting for leases

No. 2010-4 18 June 2010 Technical Line Technical guidance on standards and practice issues The joint leases project change is coming What you need to know The proposed changes to the accounting for leases

Defining Issues May 2013, No

Defining Issues May 2013, No. 13-24 FASB and IASB Issue Revised Exposure Drafts on Lease Accounting The FASB and IASB (the Boards) recently issued revised joint exposure drafts (EDs) on proposed changes

Defining Issues May 2013, No. 13-24 FASB and IASB Issue Revised Exposure Drafts on Lease Accounting The FASB and IASB (the Boards) recently issued revised joint exposure drafts (EDs) on proposed changes

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N AGENDA Leases FASB & GASB Revenue Recognition FASB 2 FASB ASU 2016-02, Leases (Topic

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N AGENDA Leases FASB & GASB Revenue Recognition FASB 2 FASB ASU 2016-02, Leases (Topic

Measuring Lease Liabilities EQUIPMENT LEASING AND FINANCE ASSOCIATION

Measuring Lease Liabilities EQUIPMENT LEASING AND FINANCE ASSOCIATION Presenters Kerrie Cadugan, Executive Director, EY Barbara Galaini, Chief Accounting Officer of the Americas, Avolon The views expressed

Measuring Lease Liabilities EQUIPMENT LEASING AND FINANCE ASSOCIATION Presenters Kerrie Cadugan, Executive Director, EY Barbara Galaini, Chief Accounting Officer of the Americas, Avolon The views expressed

10 TH European IFRS power and utilities roundtable

10 TH European IFRS power and utilities roundtable Victor Chan, Partner, EY 29 November 2016 European IFRS Power and Utilities roundtable IFRS 16 Leases: the journey so far November 2016 Agenda Overview

10 TH European IFRS power and utilities roundtable Victor Chan, Partner, EY 29 November 2016 European IFRS Power and Utilities roundtable IFRS 16 Leases: the journey so far November 2016 Agenda Overview

In February 2016, FASB issued Accounting Standards. An Analysis of the New Sale and Leaseback Guidance. DEPARTMENTS I Accounting.

An Analysis of the New Sale and Leaseback Guidance By Josef Rashty In February 2016, FASB issued Accounting Standards Update (ASU) 2016-02, Leases (Topic 842). Topic 842 will supersede the existing lease

An Analysis of the New Sale and Leaseback Guidance By Josef Rashty In February 2016, FASB issued Accounting Standards Update (ASU) 2016-02, Leases (Topic 842). Topic 842 will supersede the existing lease

Leases ASU September 20, 2017

Leases ASU 2016-02 September 20, 2017 Meet the Speakers Tonisha Spratte, CPA Senior Accountant Cherry Bekaert tspratte@cbh.com Matthew Mars Senior Accountant Cherry Bekaert mmars@cbh.com Agenda What is

Leases ASU 2016-02 September 20, 2017 Meet the Speakers Tonisha Spratte, CPA Senior Accountant Cherry Bekaert tspratte@cbh.com Matthew Mars Senior Accountant Cherry Bekaert mmars@cbh.com Agenda What is

Clay L. Pilgrim, CPA, CFE, CFF. What Financial Statement Preparers Need to Know About GASB s New Lease Accounting Proposal.

Clay L. Pilgrim, CPA, CFE, CFF What Financial Statement Preparers Need to Know About GASB s New Lease Accounting Proposal Today s Presenter Clay Pilgrim, CPA, CFE, CFF is a partner with Rushton & Company,

Clay L. Pilgrim, CPA, CFE, CFF What Financial Statement Preparers Need to Know About GASB s New Lease Accounting Proposal Today s Presenter Clay Pilgrim, CPA, CFE, CFF is a partner with Rushton & Company,

IFRS 16 Leases. An overview. March 9, kpmg.com/ca/leases

IFRS 16 Leases An overview March 9, 2016 kpmg.com/ca/leases Today s presenters Mag Stewart Jason Bower Jeff King Andy Brown Partner Professional Practice 416 777 8177 magstewart@kpmg.ca Partner Audit 604

IFRS 16 Leases An overview March 9, 2016 kpmg.com/ca/leases Today s presenters Mag Stewart Jason Bower Jeff King Andy Brown Partner Professional Practice 416 777 8177 magstewart@kpmg.ca Partner Audit 604

What private companies need to know about applying the new lease standard

What private companies need to know about applying the new lease standard In February 26, the FASB issued Accounting Standards Update (ASU) No. 26-, Leases (codified as Accounting Standards Codification

What private companies need to know about applying the new lease standard In February 26, the FASB issued Accounting Standards Update (ASU) No. 26-, Leases (codified as Accounting Standards Codification

Defining Issues. FASB and IASB Take Divergent Paths on Key Aspects of Lease Accounting. March 2014, No Key Facts

Defining Issues March 2014, No. 14-17 FASB and IASB Take Divergent Paths on Key Aspects of Lease Accounting At their March 18-19 meeting to redeliberate the proposals in their 2013 exposure drafts (EDs)

Defining Issues March 2014, No. 14-17 FASB and IASB Take Divergent Paths on Key Aspects of Lease Accounting At their March 18-19 meeting to redeliberate the proposals in their 2013 exposure drafts (EDs)

Accounting and Auditing Update. Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc.

Accounting and Auditing Update Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc. Agenda Overview of the standard setting agenda Revenue recognition Lease

Accounting and Auditing Update Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc. Agenda Overview of the standard setting agenda Revenue recognition Lease

Leases: Overview of the new guidance

Leases: Overview of the new guidance Prepared by: Richard Stuart, Partner, National Professional Standards Group, RSM US LLP richard.stuart@rsmus.com, +1 203 905 5027 March 2, 2016 Introduction On February

Leases: Overview of the new guidance Prepared by: Richard Stuart, Partner, National Professional Standards Group, RSM US LLP richard.stuart@rsmus.com, +1 203 905 5027 March 2, 2016 Introduction On February

In December 2003 the IASB issued a revised IAS 17 as part of its initial agenda of technical projects.

IFRS Standard 16 Leases In April 2001 the International Accounting Standards Board (IASB) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

IFRS Standard 16 Leases In April 2001 the International Accounting Standards Board (IASB) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

Accounting and Auditing Update. Tennessee Chapter of hfma Spring Institute 2016 Presented by William C. Matheney FHFMA CPA and Meredith P.

Accounting and Auditing Update Tennessee Chapter of hfma Spring Institute 2016 Presented by William C. Matheney FHFMA CPA and Meredith P. Cate Today s Objectives Present an overview of pertinent recently

Accounting and Auditing Update Tennessee Chapter of hfma Spring Institute 2016 Presented by William C. Matheney FHFMA CPA and Meredith P. Cate Today s Objectives Present an overview of pertinent recently

Applying the new lease accounting standard

Applying the new lease accounting standard In February 26, the FASB issued Accounting Standards Update (ASU) No. 26-, Leases (codified as Accounting Standards Codification Topic (ASC) 842). ASC 842 introduces

Applying the new lease accounting standard In February 26, the FASB issued Accounting Standards Update (ASU) No. 26-, Leases (codified as Accounting Standards Codification Topic (ASC) 842). ASC 842 introduces

Navigating the New Lease Accounting Standards for Audit Advisers Preparing Clients for the Transition to the Joint Project Lease Reporting

Navigating the New Lease Accounting Standards for Audit Advisers Preparing Clients for the Transition to the Joint Project Lease Reporting TUESDAY, JANUARY 12, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Navigating the New Lease Accounting Standards for Audit Advisers Preparing Clients for the Transition to the Joint Project Lease Reporting TUESDAY, JANUARY 12, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

FSA Faculty Consortium Technical Accounting Update. Bob Uhl, partner, Deloitte & Touche LLP

FSA Faculty Consortium Technical Accounting Update Bob Uhl, partner, Deloitte & Touche LLP Deloitte University May 30, 2014 Acronyms Acronym ASC ASU ED FASB IASB IFRS U.S. GAAP Full Form Accounting Standards

FSA Faculty Consortium Technical Accounting Update Bob Uhl, partner, Deloitte & Touche LLP Deloitte University May 30, 2014 Acronyms Acronym ASC ASU ED FASB IASB IFRS U.S. GAAP Full Form Accounting Standards

ASC Topic 842 Leases. September 25 &

ASC Topic 842 Leases September 25 & 26 2017 This presentation is intended solely for the information and use of the EEI and AGA and is not intended to be and should not be used by anyone other than these

ASC Topic 842 Leases September 25 & 26 2017 This presentation is intended solely for the information and use of the EEI and AGA and is not intended to be and should not be used by anyone other than these

Financial reporting developments. A comprehensive guide. Lease accounting. Accounting Standards Codification 842, Leases.

Financial reporting developments A comprehensive guide Lease accounting Accounting Standards Codification 842, Leases January 2019 To our clients and other friends Accounting Standard Codification (ASC)

Financial reporting developments A comprehensive guide Lease accounting Accounting Standards Codification 842, Leases January 2019 To our clients and other friends Accounting Standard Codification (ASC)

Bring it on Discussing the FASB s new leases standard

The Dbriefs Financial Reporting series presents: Bring it on Discussing the FASB s new leases standard March 15, 2016 Bob Uhl, Partner, Deloitte & Touche LLP James Barker, Partner, Deloitte & Touche LLP

The Dbriefs Financial Reporting series presents: Bring it on Discussing the FASB s new leases standard March 15, 2016 Bob Uhl, Partner, Deloitte & Touche LLP James Barker, Partner, Deloitte & Touche LLP

REVENUE RECOGNITION AND LEASE ACCOUNTING

REVENUE RECOGNITION AND LEASE ACCOUNTING DALLAS INSTITUTE OF INTERNAL AUDITORS CONFERENCE October 2017 TABLE OF CONTENTS I. REVENUE RECOGNITION OVERVIEW II. III. IV. LEASE ACCOUNTING OVERVIEW IMPLEMENTATION

REVENUE RECOGNITION AND LEASE ACCOUNTING DALLAS INSTITUTE OF INTERNAL AUDITORS CONFERENCE October 2017 TABLE OF CONTENTS I. REVENUE RECOGNITION OVERVIEW II. III. IV. LEASE ACCOUNTING OVERVIEW IMPLEMENTATION

Lease modifications. Accounting for changes to lease contracts IFRS 16. September kpmg.com/ifrs

Lease modifications Accounting for changes to lease contracts IFRS 16 September 2018 kpmg.com/ifrs Contents Contents Accounting for changes 1 1 At a glance 2 1.1 Key facts 2 1.2 Key impacts 3 2 Key concepts

Lease modifications Accounting for changes to lease contracts IFRS 16 September 2018 kpmg.com/ifrs Contents Contents Accounting for changes 1 1 At a glance 2 1.1 Key facts 2 1.2 Key impacts 3 2 Key concepts

IFRS Update Guy Thomas, CPA, CA

IFRS Update Guy Thomas, CPA, CA D&Co IFRS update Agenda 3 new standards under IFRS IFRS 9 Financial Instruments IFRS 15 Revenue from Contracts with Customers IFRS 16 Leases Agenda Some narrow scope amendments

IFRS Update Guy Thomas, CPA, CA D&Co IFRS update Agenda 3 new standards under IFRS IFRS 9 Financial Instruments IFRS 15 Revenue from Contracts with Customers IFRS 16 Leases Agenda Some narrow scope amendments

Lease Accounting and Loan Covenants: What is the Impact?

Lease Accounting and Loan Covenants: What is the Impact? Monday June 26, 2017 9:15 AM 10:30 AM Presented by: Charlie Shannon Partner Moss Adams LLP 8750 N. Central Expressway, Suite 300 Dallas, TX 75231

Lease Accounting and Loan Covenants: What is the Impact? Monday June 26, 2017 9:15 AM 10:30 AM Presented by: Charlie Shannon Partner Moss Adams LLP 8750 N. Central Expressway, Suite 300 Dallas, TX 75231

In December 2003 the Board issued a revised IAS 17 as part of its initial agenda of technical projects.

IFRS 16 Leases In April 2001 the International Accounting Standards Board (the Board) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

IFRS 16 Leases In April 2001 the International Accounting Standards Board (the Board) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

HKFRS 16 Leases. Disclaimer. Date 21 April 2017 Time 19:00 21:00 Venue Boys' and Girls' Clubs Association

HKFRS 16 Leases Date 21 April 2017 Time 19:00 21:00 Venue Boys' and Girls' Clubs Association www.zhtraining.com Disclaimer The materials of this seminar are intended only to provide general information

HKFRS 16 Leases Date 21 April 2017 Time 19:00 21:00 Venue Boys' and Girls' Clubs Association www.zhtraining.com Disclaimer The materials of this seminar are intended only to provide general information

Lease accounting scope & impacts

Leasing Lease accounting scope & impacts Scope What s in? All industries, all entities Arrangements that meet the definition of a lease Embedded leases within other arrangements What s out? Leases of:

Leasing Lease accounting scope & impacts Scope What s in? All industries, all entities Arrangements that meet the definition of a lease Embedded leases within other arrangements What s out? Leases of:

On the Horizon: Leases and Fiduciary Responsibilities

On the Horizon: Leases and Fiduciary Responsibilities Dean Michael Mead, Research Manager Florida School Finance Officers Association November 11, 2015 The views expressed in this presentation are those

On the Horizon: Leases and Fiduciary Responsibilities Dean Michael Mead, Research Manager Florida School Finance Officers Association November 11, 2015 The views expressed in this presentation are those

EITF ABSTRACTS. [Nullified by FIN 46 and FIN 46(R) for entities within the scope of FIN 46 or FIN 46(R)]

![EITF ABSTRACTS. [Nullified by FIN 46 and FIN 46(R) for entities within the scope of FIN 46 or FIN 46(R)]](/thumbs/83/87695858.jpg "EITF ABSTRACTS. [Nullified by FIN 46 and FIN 46(R) for entities within the scope of FIN 46 or FIN 46(R)]") EITF ABSTRACTS Issue No. 90-15 Title: Impact of Nonsubstantive Lessors, Residual Value Guarantees, and Other Provisions in Leasing Transactions [Nullified by FIN 46 and FIN 46(R) for entities within the

EITF ABSTRACTS Issue No. 90-15 Title: Impact of Nonsubstantive Lessors, Residual Value Guarantees, and Other Provisions in Leasing Transactions [Nullified by FIN 46 and FIN 46(R) for entities within the

Leases. Asset to be abandoned or subleased Supplement to KPMG s Handbook, Leases US GAAP. June kpmg.com/us/frv

Leases Asset to be abandoned or subleased Supplement to KPMG s Handbook, Leases US GAAP June 2018 kpmg.com/us/frv Contents Foreword... 1 About this publication... 2 1. The concepts... 3 Q&A 1.1: Has a

Leases Asset to be abandoned or subleased Supplement to KPMG s Handbook, Leases US GAAP June 2018 kpmg.com/us/frv Contents Foreword... 1 About this publication... 2 1. The concepts... 3 Q&A 1.1: Has a

Financial Computer Systems Inc. (203)

") Introduction to ASC 842 and EZLease Financial Computer Systems Inc. www.ezlease.net (203) 652-1375 The road to ASC 842 Begun in July 2006; joint project of FASB & IASB Primary purpose: Put lessee operating

Introduction to ASC 842 and EZLease Financial Computer Systems Inc. www.ezlease.net (203) 652-1375 The road to ASC 842 Begun in July 2006; joint project of FASB & IASB Primary purpose: Put lessee operating

Lease Accounting Standard Update ASU Presented by: Nicholas Hoefel, CPA Manager, Audit Services Group

Lease Accounting Standard Update ASU 2016-02 Presented by: Nicholas Hoefel, CPA Manager, Audit Services Group 1 Overview Introduction Background and current environment Effective dates and transition Key

Lease Accounting Standard Update ASU 2016-02 Presented by: Nicholas Hoefel, CPA Manager, Audit Services Group 1 Overview Introduction Background and current environment Effective dates and transition Key

Financial reporting developments. A comprehensive guide. Lease accounting. Accounting Standards Codification 842, Leases.

Financial reporting developments A comprehensive guide Lease accounting Accounting Standards Codification 842, Leases October 2018 To our clients and other friends Accounting Standard Codification (ASC)

Financial reporting developments A comprehensive guide Lease accounting Accounting Standards Codification 842, Leases October 2018 To our clients and other friends Accounting Standard Codification (ASC)

Gearing up for change New IFRS on Leases

Gearing up for change New IFRS on Leases In a nutshell The changes Lessee accounting Effective date: 1 January 2019 Limited changes to scope of IAS 17 Enhanced guidance on identifying a lease Lessor accounting

Gearing up for change New IFRS on Leases In a nutshell The changes Lessee accounting Effective date: 1 January 2019 Limited changes to scope of IAS 17 Enhanced guidance on identifying a lease Lessor accounting

Summary of IFRS Exposure Draft Leases

The International Accounting Standards Board (IASB) recently issued a revised exposure draft (ED) relating to leases. Once these proposals are finalized the new guidance will replace the IAS 17 Leases.

The International Accounting Standards Board (IASB) recently issued a revised exposure draft (ED) relating to leases. Once these proposals are finalized the new guidance will replace the IAS 17 Leases.

Accounting Update. Anne Cloutier, CPA, FHFMA Principal March 27, 2015

Accounting Update Anne Cloutier, CPA, FHFMA Principal March 27, 2015 Current Accounting for Leases Capital leases - a lessee recognizes leased assets and liabilities on the balance sheet. Operating leases

Accounting Update Anne Cloutier, CPA, FHFMA Principal March 27, 2015 Current Accounting for Leases Capital leases - a lessee recognizes leased assets and liabilities on the balance sheet. Operating leases

The New Lease Accounting Standard. Hunter Mink, CPA, CCIFP Brian Rosenberg, CPA, MBA

The New Lease Accounting Standard Hunter Mink, CPA, CCIFP Brian Rosenberg, CPA, MBA 1 Agenda Introduction Lease Identification and Classification Lessee Accounting Other Considerations Disclosures Impact

The New Lease Accounting Standard Hunter Mink, CPA, CCIFP Brian Rosenberg, CPA, MBA 1 Agenda Introduction Lease Identification and Classification Lessee Accounting Other Considerations Disclosures Impact

Applying IFRS. Presentation and disclosure requirements of IFRS 16 Leases. November 2018

Applying IFRS Presentation and disclosure requirements of IFRS 16 Leases November 2018 Contents 1. Overview 2 2. What is changing from current IFRS? 4 2.1 Presentation 4 2.2 Lessee disclosures 5 3. Presentation

Applying IFRS Presentation and disclosure requirements of IFRS 16 Leases November 2018 Contents 1. Overview 2 2. What is changing from current IFRS? 4 2.1 Presentation 4 2.2 Lessee disclosures 5 3. Presentation

IFRS 16 Leases. PICPA IFRS: New Standards and Updates Dubai. 28 April 2017

IFRS 16 Leases PICPA IFRS: New Standards and Updates Dubai 28 April 2017 1 More transparent lease accounting IFRS 16 will bring most leases on-balance sheet from 2019. All companies that lease assets for

IFRS 16 Leases PICPA IFRS: New Standards and Updates Dubai 28 April 2017 1 More transparent lease accounting IFRS 16 will bring most leases on-balance sheet from 2019. All companies that lease assets for

Leases Refashioned. The Bottom Line. Retail & Distribution Spotlight January In This Issue

Retail & Distribution Spotlight January 2017 In This Issue Background Key Issues Challenges Thinking Ahead Contacts Leases Refashioned The Bottom Line On February 25, 2016, the FASB issued its new leases

Retail & Distribution Spotlight January 2017 In This Issue Background Key Issues Challenges Thinking Ahead Contacts Leases Refashioned The Bottom Line On February 25, 2016, the FASB issued its new leases

IFRS 16 LEASES. Page 1 of 21

IFRS 16 LEASES OBJECTIVE The objective is to ensure that lessees and lessors provide relevant information in a manner that faithfully represents those transactions. This information gives a basis for users

IFRS 16 LEASES OBJECTIVE The objective is to ensure that lessees and lessors provide relevant information in a manner that faithfully represents those transactions. This information gives a basis for users

New Zealand Equivalent to International Financial Reporting Standard 16 Leases (NZ IFRS 16)

") New Zealand Equivalent to International Financial Reporting Standard 16 Leases (NZ IFRS 16) Issued February 2016 This Standard was issued on 11 February 2016 by the New Zealand Accounting Standards Board

New Zealand Equivalent to International Financial Reporting Standard 16 Leases (NZ IFRS 16) Issued February 2016 This Standard was issued on 11 February 2016 by the New Zealand Accounting Standards Board

Leases Discount rates

Leases Discount rates What s the correct rate? IFRS 16 September 2017 kpmg.com/ifrs Contents Contents Determining the correct rate 1 1 At a glance 2 1.1 Key facts 2 1.2 Key impacts 3 2 Lessor discount

Leases Discount rates What s the correct rate? IFRS 16 September 2017 kpmg.com/ifrs Contents Contents Determining the correct rate 1 1 At a glance 2 1.1 Key facts 2 1.2 Key impacts 3 2 Lessor discount

CPE ARTICLE. An Introduction to Lessee Accounting (Topic 842, Leases)

") CPE ARTICLE An Introduction to Lessee Accounting (Topic 842, Leases) 42 Today scpa Curriculum: Accounting and auditing Level: Basic Designed For: Public practitioners and business and industry Objectives:

CPE ARTICLE An Introduction to Lessee Accounting (Topic 842, Leases) 42 Today scpa Curriculum: Accounting and auditing Level: Basic Designed For: Public practitioners and business and industry Objectives:

IFRS 16 Leases supplement

IFRS 16 Leases supplement Guide to annual financial statements IFRS December 2017 kpmg.com/ifrs Contents About this supplement 1 About IFRS 16 3 The Group s lease portfolio 6 Part I Modified retrospective

IFRS 16 Leases supplement Guide to annual financial statements IFRS December 2017 kpmg.com/ifrs Contents About this supplement 1 About IFRS 16 3 The Group s lease portfolio 6 Part I Modified retrospective

Annual Accounting and Auditing Update. 11 December 2015

Annual Accounting and Auditing Update 11 December 2015 Disclaimer The views expressed by panelists are not necessarily those of Ernst & Young LLP. These slides are for educational purposes only and are

Annual Accounting and Auditing Update 11 December 2015 Disclaimer The views expressed by panelists are not necessarily those of Ernst & Young LLP. These slides are for educational purposes only and are

Preview of the New Exposure Draft of the Lease Accounting Project Key elements and commentary

Preview of the New Exposure Draft of the Lease Accounting Project Key elements and commentary Prepared by Bill Bosco, Leasing 101 www.leasing-101.com The Financial Accounting Standards Board (FASB) and

Preview of the New Exposure Draft of the Lease Accounting Project Key elements and commentary Prepared by Bill Bosco, Leasing 101 www.leasing-101.com The Financial Accounting Standards Board (FASB) and

provide the Board with a summary of the matter and the staff s analysis and conclusions; and

IASB Agenda ref 12 STAFF PAPER IASB Meeting May 2018 Project Paper topic IFRS 16 Leases Lease incentives Annual Improvement CONTACT(S) Nicolette Lange nlange@ifrs.org +44 (0) 20 7246 6924 This paper has

IASB Agenda ref 12 STAFF PAPER IASB Meeting May 2018 Project Paper topic IFRS 16 Leases Lease incentives Annual Improvement CONTACT(S) Nicolette Lange nlange@ifrs.org +44 (0) 20 7246 6924 This paper has

IASB Staff Paper March 2011

IASB Staff Paper March 2011 Effect of board redeliberations on Exposure Draft Leases About this staff paper This staff paper indicates how the proposals in the Exposure Draft Leases would change as a result

IASB Staff Paper March 2011 Effect of board redeliberations on Exposure Draft Leases About this staff paper This staff paper indicates how the proposals in the Exposure Draft Leases would change as a result

Lease & Finance Accountants Conference. September The Westin Charlotte Charlotte, NC

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Lessor Accounting under ASC 842 EQUIPMENT LEASING AND FINANCE ASSOCIATION Presenters Rod Hurd Chief

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Lessor Accounting under ASC 842 EQUIPMENT LEASING AND FINANCE ASSOCIATION Presenters Rod Hurd Chief

International Financial Reporting Standard 16 Leases. Objective. Scope. Recognition exemptions (paragraphs B3 B8) IFRS 16

IFRS 16") International Financial Reporting Standard 16 Leases Objective 1 This Standard sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective is to ensure

International Financial Reporting Standard 16 Leases Objective 1 This Standard sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective is to ensure

It s Back Accounting for Asset Leases the new way!

It s Back Accounting for Asset Leases the new way! Kent Bettisworth BETTISWORTH & ASSOCIATES 2016 ERP Corp. All rights reserved. Controlling 2016 Conference September 12-15, 2016 in San Diego Kent Bettisworth

It s Back Accounting for Asset Leases the new way! Kent Bettisworth BETTISWORTH & ASSOCIATES 2016 ERP Corp. All rights reserved. Controlling 2016 Conference September 12-15, 2016 in San Diego Kent Bettisworth

New Lease Accounting Standards: Love at First Sight or Heartbreak?

New Lease Accounting Standards: Love at First Sight or Heartbreak? February 14, 2019 To Receive CPE Credit Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader

New Lease Accounting Standards: Love at First Sight or Heartbreak? February 14, 2019 To Receive CPE Credit Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader

Defining Issues. FASB Completes Technical Redeliberations on Leases. October 2015, No Key Facts. Key Impacts

Defining Issues October 2015, No. 15-47 FASB Completes Technical Redeliberations on Leases The FASB met on October 7 to discuss comments received and related follow-up issues on the external review of

Defining Issues October 2015, No. 15-47 FASB Completes Technical Redeliberations on Leases The FASB met on October 7 to discuss comments received and related follow-up issues on the external review of

AASB 16 Leases. Modifications and implementation. 23 October 2018

AASB 16 Leases Modifications and implementation 23 October 2018 Your facilitators are Patricia Stebbens Hayley Pang Michael Voogt Daina Klunder 2 Setting the scene Date of initial application is almost

AASB 16 Leases Modifications and implementation 23 October 2018 Your facilitators are Patricia Stebbens Hayley Pang Michael Voogt Daina Klunder 2 Setting the scene Date of initial application is almost

Lease & Finance Accountants Conference. September The Westin Charlotte Charlotte, NC

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Basic Principles of Lessors under ASC 842 Mamta Shori, Wells Fargo Equipment Finance Joe Sebik,

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Basic Principles of Lessors under ASC 842 Mamta Shori, Wells Fargo Equipment Finance Joe Sebik,

Sri Lanka Accounting Standard - SLFRS 16. Leases

Sri Lanka Accounting Standard - SLFRS 16 Leases CONTENTS from paragraph SRI LANKA ACCOUNTING STANDARD - SLFRS 16 LEASES INTRODUCTION OBJECTIVE 1 SCOPE 3 RECOGNITION EXEMPTIONS 5 IDENTIFYING A LEASE 9 Separating

Sri Lanka Accounting Standard - SLFRS 16 Leases CONTENTS from paragraph SRI LANKA ACCOUNTING STANDARD - SLFRS 16 LEASES INTRODUCTION OBJECTIVE 1 SCOPE 3 RECOGNITION EXEMPTIONS 5 IDENTIFYING A LEASE 9 Separating

ROCKFORD AREA HABITAT FOR HUMANITY, INC. FINANCIAL STATEMENTS and INDEPENDENT AUDITOR S REPORT. For the years ended June 30, 2014 and 2013

FINANCIAL STATEMENTS and INDEPENDENT AUDITOR S REPORT For the years ended June 30, 2014 and 2013 TABLE OF CONTENTS Independent Auditor s Report 1 Statements of Financial Position 2 Statements of Activities

FINANCIAL STATEMENTS and INDEPENDENT AUDITOR S REPORT For the years ended June 30, 2014 and 2013 TABLE OF CONTENTS Independent Auditor s Report 1 Statements of Financial Position 2 Statements of Activities

The new IFRS 16 Leases effective as of 1 January 2019

The new IFRS 16 Leases effective as of 1 January 2019 IFRS 16 was issued by IASB on 13 January 2016. The Standard is effective as of 1 January 2019. It has not yet been adopted by the EC. This is a Standard

The new IFRS 16 Leases effective as of 1 January 2019 IFRS 16 was issued by IASB on 13 January 2016. The Standard is effective as of 1 January 2019. It has not yet been adopted by the EC. This is a Standard

7/30/2018. Health Care. A CHC-Focused Plan for the New Lease Accounting Standard

Health Care A CHC-Focused Plan for the New Lease Accounting Standard July 31, 2018 1 TO RECEIVE CPE CREDIT Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader

Health Care A CHC-Focused Plan for the New Lease Accounting Standard July 31, 2018 1 TO RECEIVE CPE CREDIT Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader

IASB update. Philippe DANJOU. Board Member. IMA France 2 Octobre International Financial Reporting Standards

International Financial Reporting Standards IASB update Philippe DANJOU Board Member IMA France 2 Octobre 2012 The views expressed in this presentation are those of the presenter, not necessarily those

International Financial Reporting Standards IASB update Philippe DANJOU Board Member IMA France 2 Octobre 2012 The views expressed in this presentation are those of the presenter, not necessarily those

Technical Line FASB final guidance

No. 2018-18 13 December 2018 Technical Line FASB final guidance How the new leases standard affects life sciences entities In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions...

No. 2018-18 13 December 2018 Technical Line FASB final guidance How the new leases standard affects life sciences entities In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions...

Deloitte & Touche LLP

695 East Main Street Stamford, CT 06901-2141 Tel: + 1 203 708 4000 Fax: + 1 203 708 4797 www.deloitte.com Ms. Susan M. Cosper Technical Director Financial Accounting Standards Board 401 Merritt 7 P.O.

695 East Main Street Stamford, CT 06901-2141 Tel: + 1 203 708 4000 Fax: + 1 203 708 4797 www.deloitte.com Ms. Susan M. Cosper Technical Director Financial Accounting Standards Board 401 Merritt 7 P.O.

Technical Line FASB final guidance

No. 2016-09 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect health care entities In this issue: Overview... 1 Key considerations... 3 Scope and scope exceptions...

No. 2016-09 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect health care entities In this issue: Overview... 1 Key considerations... 3 Scope and scope exceptions...

County of Riverside OFFICE OF THE AUDITOR-CONTROLLER STANDARD PRACTICE MANUAL

County of Riverside OFFICE OF THE AUDITOR-CONTROLLER STANDARD PRACTICE MANUAL SECTION: 5 POLICY NUMBER: 511 SUBJECT: CATEGORY: CAPITAL LEASES CAPITAL ASSET POLICIES REVISED DATE: 07/01/17 APPROVED BY:

County of Riverside OFFICE OF THE AUDITOR-CONTROLLER STANDARD PRACTICE MANUAL SECTION: 5 POLICY NUMBER: 511 SUBJECT: CATEGORY: CAPITAL LEASES CAPITAL ASSET POLICIES REVISED DATE: 07/01/17 APPROVED BY:

Financial reporting developments. A comprehensive guide. Lease accounting. Accounting Standards Codification 842, Leases.

Financial reporting developments A comprehensive guide Lease accounting Accounting Standards Codification 842, Leases January 2018 To our clients and other friends Accounting Standard Codification (ASC)

Financial reporting developments A comprehensive guide Lease accounting Accounting Standards Codification 842, Leases January 2018 To our clients and other friends Accounting Standard Codification (ASC)

IS YOUR LEASE SOLUTION FASB READY? It s here!

IS YOUR LEASE SOLUTION FASB READY? It s here! Hello! Jaron Banks Sr. Sales Engineer Accruent Chris Smart Manager, Product Management Accruent Accruent Confidential and Proprietary 2016 2 Agenda Brief background

IS YOUR LEASE SOLUTION FASB READY? It s here! Hello! Jaron Banks Sr. Sales Engineer Accruent Chris Smart Manager, Product Management Accruent Accruent Confidential and Proprietary 2016 2 Agenda Brief background

ABRAHAM E. HASPEL CPA

ABRAHAM E. HASPEL CPA Comments on the Financial Accounting Standard Board s: Proposed Accounting Standard Update Leases (Topic 840) (ED) I am pleased to submit the following comments in response to the

ABRAHAM E. HASPEL CPA Comments on the Financial Accounting Standard Board s: Proposed Accounting Standard Update Leases (Topic 840) (ED) I am pleased to submit the following comments in response to the

AASB 16: Experience the Fundamental Overhaul of Lease Accounting for Lessees

AASB 16: Experience the Fundamental Overhaul of Lease Accounting for Lessees Introduction to Session This introductory session we will: Explore the Principles of AASB 16 Learn how to Identify a Lease Work

AASB 16: Experience the Fundamental Overhaul of Lease Accounting for Lessees Introduction to Session This introductory session we will: Explore the Principles of AASB 16 Learn how to Identify a Lease Work