The Great Chinese Bubble: Justifying the High and Rapidly Rising Prices of Residential Housing Values in China

|

|

|

- Lucas Page

- 6 years ago

- Views:

Transcription

1 University of Pennsylvania ScholarlyCommons Wharton Research Scholars Wharton School The Great Chinese Bubble: Justifying the High and Rapidly Rising Prices of Residential Housing Values in China Sharon Wang University of Pennsylvania Follow this and additional works at: Part of the Business Commons Wang, Sharon, "The Great Chinese Bubble: Justifying the High and Rapidly Rising Prices of Residential Housing Values in China" (2014). Wharton Research Scholars This paper is posted at ScholarlyCommons. For more information, please contact

2 The Great Chinese Bubble: Justifying the High and Rapidly Rising Prices of Residential Housing Values in China Keywords China, residential housing Disciplines Business This working paper is available at ScholarlyCommons:

3 The Great Chinese Bubble: Justifying the high and rapidly rising prices of residential housing values in China Are China's housing prices misaligned with the fundamentals of supply and demand? By Sharon Wang Advised by Professor Joseph Gyourko of the Wharton Real Estate Department

4 Contents Purpose and Significance of Paper... 3 Major Housing Reforms... 5 Setting the Private Residential Real Estate Sector in Motion... 5 Land market Better Regulated... 5 Property Rights Better protected... 5 Current Status of Chinese Property Market... 5 Residential Property Market Segmentation... 5 Policy Intervention... 6 Rising Income Level and High Savings Rate... 7 High Homeownership Rate... 8 Leverage in the System... 9 Just what is a Bubble? So, Is There a Bubble? Escalating Land Prices Urbanization remains a key driver of demand Determining the supply curve: Flat or Steep? Methodology Nation-Wide Data City-level Data Conclusions Bibliography

5 Purpose and Significance of Paper The purpose of this paper is to examine whether China s decade of rapid growth in home prices represents a gigantic housing bubble. The United States Housing meltdown in triggered a financial crisis that progressed into the worst recession since the Great Depression. Six years later, the United States is still recovering from the impact, and home prices have just begun to reach pre-crisis levels. There are still millions of "shadow" inventory- underwater mortgages, modified mortgages, and delinquent mortgages- in the markets. As of January 2014, CoreLogic estimates that there are 2.47 million loans that are 90 days or more past due or already in foreclosure (CoreLogic, 2014). While this is the lowest level since 2008 and 23% below 2013 levels, it will take time for the market to fully absorb this shadow supply (CoreLogic, 2014). In contrast, China withstood the turmoil with a $586 billion economic stimulus package in 2008 invested in housing, infrastructure, transportation, disaster rebuilding, tax cuts, and finance. The stimulus package was welcomed by world leaders who believed that by boosting the Chinese economy, China would simultaneously help stabilize the world economy. Upon announcement of the fiscal stimulus, markets around the world jumped. However, more recently there have been concerns that Chinese banks have loosened their lending standards as a result of the stimulus, which could lead to excessive lending to home purchasers and even more rapidly rising prices. These loosened lending standards may lead to an increase in nonperforming loans. If the unjustified high prices collapse, would the Chinese government also perform a bailout, similar to the Emergency Economic Stabilization Act of 2008? Through this act, the United States government had authorized the U.S. Treasury to buy risky and nonperforming debt from various lending institution and infused $250 billion into the American banking system (US Federal Government). Despite concerns of the Chinese facing similar risks that pre-recession America faced, the likelihood of this happening is low, mainly due to the high equity levels that the Chinese tend to put into their homes relative to the rest of the world. There is an equity buffer in the Chinese market to withstand a drop in prices. It is unlikely that the Chinese government will allow prices to drop so much that it eats into the equity before implementing measures, as seen by the two decades of effective housing policy measures. Perhaps what is much more concerning is the fact that residential investment accounts for 1/6 th of China s economic growth (World Bank). China s GDP growth is already slowest in the past two decades. The direct and indirect effects on the economy outside of the banking system would be tremendous. While China continues to be the world s largest exporter, China s government is attempting to move the country away from reliance on state-led industry and exports toward larger domestic consumption, especially as the rising wages and appreciating Renminbi have been hindering the 3

6 nation s export growth (Silk, 2014). With the majority of the Chinese people's money invested in real estate, even if there is enough equity in the Chinese mortgage loans, the bursting of a housing bubble would significantly impact Chinese people's internal consumption power and slow down the economy even further. A significant slowdown in China, being the second largest global economy and a prime driver of the world economy, could trigger a downward spiral for the rest of the world. Percentage GDP Growth of China and other countries Source: World Bank Therefore, the crucial issue is whether there are housing bubbles in major cities throughout the country that are about to burst. China has experienced extraordinary growth in the housing market during the past decade, which has been accompanied by substantial increases in residential property prices. As a result, owning a home has become increasingly less affordable for most working families, despite government's efforts in implementing policies and programs that support homeownership. The government has imposed a long string of housing policy measures to slow home price increase, aiming to curb property speculation and improve affordability. While these policies have been effective to a certain extent, prices only seem to be temporarily suppressed. Furthermore, another thing of concern would be the rent levels in these cities. Rents can be an indicator of a bubble, and rents in China have not grown nearly as quickly as sales have. In fact, in Beijing and Shanghai, rent levels are well below 2008 levels (Fung, 2014). 4

7 Major Housing Reforms Setting the Private Residential Real Estate Sector in Motion From founding of People s Republic of China to 1978, all land was publicly owned. There was a welfare system in place, in which government provided low-cost but also lowquality accommodations. In 1988, the Chinese Constitution was amended to allow land transactions. In March 1998, the Communist party announced new system to encourage people to purchase their homes, using one-time subsidies and mortgage incentives. In 1994, the government implemented a rent reform, allowed the sales of public housing, introducing concepts of economically affordable houses and commodity houses. In August 1999, it was declared that any residential unit built after January 1, 1999 was to be bought, not allocated by the government. After the housing reform, the land market was better regulated and property rights better protected. (McKinsey Global Institute, 2009) Land market Better Regulated China took major steps to improve regulation of its land market through the 1) abolition of private transfer of land titles after August 2004 and 2) requirements that all sites sold by local governments must through a public listing process with transaction prices disclosed. The introduction of the new rule provided better transparency. (Li, 2013) Property Rights Better protected To protect the legal rights of owners, the National People s Congress voted in August 1007 to add a new clause to the General Principles of the Law on Management of Urban Real Estate. The clause aims to protect the legal rights of owners and to guarantee the residence conditions of private owners after resettlement. The clause allows residential land use right scan to be automatically renewed upon expiration. (Li, 2013) Current Status of Chinese Property Market Residential Property Market Segmentation These are the main types of residential properties in China. Developers mainly focus on the upper segments of the market. 1) Commodity Houses/ Private Housing Commodity houses are purchased and rented at market prices. In 2010, municipal governments limited purchase of homes by non-residents to curtail speculation. There are concerns that this may lead to distortion of prices. This is the main focus for property developers. Property titles are transferable. Private housing segment has been gaining market share, accounting for 35% of total supply in 2012 (Li, 2013). 2) Economic Housing 5

8 Economically affordable houses are set by the government to be at no more than 3-5% above total construction costs (China Index Institute, 2012). To qualify, households must have hukou and other requirements. Once purchased, cannot be sold for another 5 years. The market share of economically affordable houses has been declining sharply (See graph below). Priced at 50-70% discount below private housing prices, these used to be built by state-owned real estate enterprises, targeted at Middle-income families with residency (Li, 2013). These properties are re-saleable after 5 years. 3) Low-rent Housing Initially built by the government, these are meant for low-income families that cannot afford a house. Units are allotted to families and are non-tradable. 4) Public Rental Housing Newly introduced in , public rental housing units is targeted at the population working in the major cities but do not have residency (hukou). These are also meant for families with income constraints but not eligible to apply for economic and low-rent housing. 5) Shanty-town Resettlement Started in 2007 for the resettlement needs of shanty-town occupants. These are not re-saleable. % Share of Economically Affordable Housing in China Years Source: China National Bureau of Statistics Policy Intervention Policy intervention by the Chinese government dates as far back as The industry was highly under-regulated prior to these policies. Demand side tightening measures are more common adopted, because the Central government has limited control over housing supply due to the highly fragmented nature of industry. After the 2008 financial crisis, the government implemented monetary easing such as mortgage rate cuts, and incentives were provided by local governments for home purchases, such as with ranting of residency status in cities. 6

9 Supply-side restrictive measures Breaking down large sites into smaller sites during land sale to increase asset turnover and completion Idle Land Policy (confiscating land set idle for over two years) Land Appreciation Tax Development of affordable homes Increasing supply of small units Demand-side restrictive measures Increasing deed tax on luxury properties Forbidding resale of units before completion Capital Gain Tax on resale of units within two five years of purchase Price caps on primary construction launches Real Estate Tax in Shanghai and Chongqing House Purchase Restrictions Credit measures targeting at real estate Project LTV limited at 65% LTV limit of residential mortgages across first, second, and third time home buyers Rising Income Level and High Savings Rate Two main factors make the Chinese consumer market stand out: 1) a rapidly rising per capita income level and 2) a high savings rate. According to Boston Consulting Group, China continues to have the highest percentage increase in assets under management, at 36.8%, boosted by strong economic growth and appreciation of Renminbi. Per-capita disposable income and population of middle class expected to continue to increase, though at a slower pace. (Milkin Institute) Chinese households own about $3.2 trillion in financial wealth, which is approximately 44% of the wealth of Asia-Pacific excluding Japan. Additionally, 64% of the assets are cash holdings. (Xu L. J., 2012) National savings rate are important for the long-run health of economies. China has a National Savings Rate savings rate of 49.5% of GDP, which is ranked top 5 in the world and first amongst commodity-importing countries. This high savings rate can help the nation withstand a deterioration in global financing conditions. (Bank of America Private Wealth Management, 2012) 7

10 National savers: The Top 10 Highest Savings Rates Countries in 2012 Source: International Monetary Fund as of April 2013 High Homeownership Rate As a result, homeownership rate is very high in China. Homeownership was at 90% in 2012, which is 6th highest in the world. This can be compared to the United States homeownership rate, which has been fluctuating around 65%. It is believed that the high homeownership rate of the Chinese is due to a mix of cultural influences and limited investing opportunities for the Chinese. The Chinese government limits the amount of Chinese money invested abroad, and the Chinese stock markets are high in volatility. As the Chinese citizens' net wealth grew exponentially in the past decade, many Chinese view investing in real estate as the single most safe and feasible way to invest their money. % Homeownership in the United States

ratio is extremely low when compared to other nations.")

11 Top Homeownership Rates in the World 98% 96% 94% 92% 90% 88% 86% 84% 82% 80% 78% Source: Barclay's Research, Xinhua English News Leverage in the System In terms of financing of homes, Chinese homeowners take on very low leverage. Even without taking into consideration housing price growth, the Loan-to-Value (LTV) ratio is extremely low when compared to other nations. The average LTV ratio is around 21-30%. It is believed that the low leverage levels is due to the high savings rate of the nation (49.5% of GDP) and ceilings put on LTVs by the Housing Provident Fund. Additionally, most home loans in China are variable-rate mortgages, which can be concerning especially with the mortgage rates on the rise. The Chinese housing finance system is mainly comprised of 1) the Housing Provident Fund lending, and 2) private sector mortgage lending. Average Interest Rates on Home Mortgages Source: Standard Chartered bank (2013) 9

12 1) Housing Provident Fund ( 住房工資金 ) The Chinese has a system called the Housing Provident Fund (HPF) in place to curfew the amount of debt one can take on. The HPF is a defined contribution pension, of which contribution come from both employers and employees. Monthly contribution from both sides should be at least 5% of the employees' monthly salary, and capped at 20%. Each city has its own HPF Management center. Additionally, the max loan amount is Rmb 0.4 mn for individual and Rmb 0.8 mn for a household. The allowable loan amount is set at 15 25x HPF account amount. The max LTV for small unit (<90 square meters) is 80%, and the max LTV for a larger unit larger unit (>90 square meters) is 70%. (Housing Finance Network, 2013) 2) Private Sector Mortgage Private sector is the main source of home finance, accounting for 82% of total home mortgages last year (Li, 2013). China s private sector mortgage grew 173 times since 1998, now the second largest Asia-Pacific market (US $1.16 trillion) after Japan (US $1.29 trillion) (Housing Finance Network, 2013). China Mortgage Loan LTV Limits China Mortgage Loan Rates Source: PBoC, J.P. Morgan Equity Research Just what is a Bubble? Asset bubbles have been the cause of many economic recessions, but is there a way to empirically spot the bubble before it bursts? In New York Times, Yale economist Robert Shiller listed factors giving rise to a bubble. He argued that a bubble is a form of "psychological malfunction", and below is a checklist to determine if there is an asset bubble. (Shiller, 2010) 1) Sharp increases in the price of an asset 2) Great public excitement about said increases 3) An accompanying media frenzy 4) Stories of people earning a lot of money, causing envy among people who aren t 5) Growing interest in the asset class among the general public 10

.")

13 6) New era theories justify unprecedented price increases 7) A decline in lending standards All of the above have been seen in China's major cities. Determinants of Home prices include fundamentals of housing supply and demand (Glindro et al., 2005). Another factor (which arguably can be categorized as a fundamental) is government support and policies (Huang, 2004). As seen from the graph below from JP Morgan Asia Research, China's property market represents a highly regulated industry, and the government has significant impact on the property index. Similarly, Xu and Chen found in a paper published in 2010 that monetary policy clearly accelerated home price growth, while speculative investment inflow did not have a significant impact on home price growth after controlling for money supply growth (Xu and Chen, 2010). JP Morgan China Property index 11

14 So, Is There a Bubble? The possibility of a real estate bubble in China is hardly a trivial matter, and much research have already been done. There are mixed results from papers written so far on this issue. Most agree that there is a higher chance of a bubble existing in megametropolitan cities such as Beijing and Shanghai. Ahuja and colleagues in 2010 found that there is lack of evidence of a nationwide housing bubble, but some studies find overpricing may exist in mega-metropolitan areas such as Beijing, Shanghai, and Chongqing (Ahuja et al, 2010). In a paper by Wu, Gyourko, and Deng in 2010, it was stated that although we could not provide a definitive test with our limited data multiple parts of evidence suggest the potential for substantial mispricing in Beijing and other Chinese housing markets The magnitude of the increase in land values over the past 2 3 years in particular in Beijing is unprecedented to our knowledge (Wu, Gyourko, & Deng, 2010). In 2011, Wall Street Journal published an article titled The Great Property Bubble of China May Be Popping, suggesting that after years of housing prices gone wild, prices are finally heading downwards (Davis, 2011). World Bank economists warned in press conferences that a downturn in property prices was among the biggest economic risks that China faces. While there was a slowdown in the property markets in , especially due to government s efforts to rein in rising residential property prices and create a soft landing, such was with abovementioned demand and supply restraints. However, prices have only continued escalating upwards since Escalating Land Prices China s official data from the National Bureau of Statistics website is haunted by controversy, with widespread doubts about its accuracy. For example, independent estimates of China s GDP growth suggest that the official data might be exaggerated. But the one thing we can be certain of are the escalating land prices in China (Orlik, 2011). The government introduced in 2004 that all sites sold by local governments must go through a public listing process, enabling researchers to obtain public data on land prices. The Chinese National hedonic Land Price Index (CRLPI), an index developed by Joseph Gyourko, Jing Wu, and Yongheng Deng in 2012, tracks the real land prices of 35 city markets in China. Since the first quarter of 2004, real land prices have increased by approximately 200%. There was prices surge just before the recession and dropped during the global financial crisis. Prices quickly picked up after the 2008 stimulus was implemented. This price escalation continued until 2011 when the stimulus came off as the government once again worry about the overpriced property values and affordability of homes. Similarly for city-wide data, we see the common trend of rapidly rising land prices in each city. 12

15 Chinese National Hedonic Land Price Index (35 Markets) Hedonic Index Chinese City-level Hedonic Land Price Index Hedonic Index Beijing Tianjin Shanghai Hangzhou Wuhan Chongqing Chengdu Source: Wharton/NUS/Tsinghua Chinese Residential Land Price Indexes (CRLPI) 13

16 Urbanization remains a key driver of demand What is the cause of the escalating prices? The abovementioned high homeownership rate, high savings rate, and high income growth are all factors. Arguably the most important factor in the rapidly rising prices of homes is urbanization, which is the main demand driver for residential houses. Demand curve is very clearly shifting outwards due to urbanization and strong economic fundamentals. In fact, urban population of China is expected to increase by 26% over the next decade (Economic Intelligence Unit). This is caused by burgeoning economic success and rapidly rising standard of living. In 2011, China's urban population has already exceeded 50 % of its total population for the first time, meaning that over half of China now lives in major cities. In fact, McKinsey Global Institute found that if current trend holds, nearly 1 billion people will live in urban centers by As seen in the graph below by the Reserve Bank of Australia, urbanization rate is predicted to reach 75% of total Chinese population by Urbanization Rate, projected by Reserve Bank of Australia Source: United Nations, Reserve Bank of Australia 14

17 China Map: Population Size and Urbanization Rate by Provinces and Municipalities Source: JP Morgan Asia Pacific Research Determining the supply curve: Flat or Steep? Now that we've established with evidence the escalating prices and high demand of the Chinese property market, the shape of the supply curve in China can help determine whether there is a housing bubble in China's major cities. To justify the prices, we would hope that the supply curve slopes upwards instead of laying flat. There was a total of 3.4 billion square meter of floor space built in China in 2012 (CEIC). Arguably, the scale of construction was necessary to house 20 million annual increase in urban population. The question is not that whether prices should increase, but by how much is reasonable? It is impossible to perform a detailed econometrics study due to limited readily available data on the market cycles in China for analysis. Due to the limitations, this study performs a "back-of-the-envelope" analysis to determine whether supply might be outstripping demand. 15

18 Methodology To arrive at a reliable framework to model supply and demand, we used official data from the Chinese National Bureau of Statistics (NBS) and formulated the following assumptions. We have come up with a framework to calculate supply and demand in terms of number of units. We collected both national and city data. CALCULATION OF DEMAND (IN UNITS) Average Number of Households The average number of households represents an estimate of housing demand, because household formation represents home buyers. The high homeownership rate in China suggests that most of the household formation translates to owners rather than renters. This data can be found readily available from NBS or from dividing total population with the average persons per household. Associate Professor of Community and Regional Planning at Iowa State University suggests adding a vacancy rate percentage to the demand estimate. The idea is that an efficient housing market should offer prospective buyers a variety of choices of units so they might choose which one, if any, best suits their needs. (Woods & Barta, 2000) CALCULATION OF SUPPLY (IN UNITS) Total Floor Space TTTTT FFFFF SSSSS = PPPPPPPPPP FFFFF SSSSS ppp CCCCCC DDDDDDDDDDD SSSSSS MMMMM SSSSSS MMMMM = PPPPPPP PPPPPP Average Flat Size Avvvvvv FFFF SSSS = AAAAAAA NNNNNNNN HHHHHhooo SSSS FFFFF SSSSS ppp CCCCCC SSSSSS MMMMM = PPPPPPP SSSSSS MMMMM UUUU UUUU PPPPPP Total Units TTTTT UUUUU = TTTTT FFFFF SSSSS AAAAAAA FFFF SSSS SSSSSS MMMMM UUUUU = SSSSSS MMMMM/ UUUU 16

19 Nation-Wide Data We multiplied China s Urban Population with Floor Space per Capita in Urban China. Total Floor Space is obtained by subtracting estimated demolitions from the resulting numbers. Average Flat Size was obtained by multiplying Average National Household Size with Floor Space per Capita. Total units was obtained by dividing Total Floor Space with the Average Flat Size. This is our measure of housing supply. Housing demand is measured by average number of households. DEMOLITIONS To estimate demolitions, we gathered data from State-Owned Assets Supervision and Administration Commission of the State Council. According to the commission, there was a total of 1.8 billion square meters of floor space demolished between 2008 and This implies an annual demolition rate of at least 4.5%. However, stock of dilapidated residential buildings should gradually decline as buildings are replaced with higher-quality construction. Furthermore, expropriation process is beginning to cost more due to enforcement of property rights (Henderson, 2009), which also slows down demolition rate. These numbers are in line with the depreciation rate from Chinese national accounts with average building life span of 50 years. Hence, we produced the following demolition rate chart, which will be subtracted from total floor space. 17

20 URBAN CHINA DATA Sources: National Bureau of Statistics, Australia Reserve Bank, and Sustaining China s Economic Growth after the Global Financial Crisis (Lardy) 18

SUPPLY")

21 Supply vs. Demand in Urban China ( ) SUPPLY DEMAND 19

22 Change in Supply and Demand ( ) 25.00% 20.00% 15.00% 10.00% 5.00% % Change in No of Households in Urban China % Change in No of Units in Urban China 0.00% We see that the average annual increase is 5.48% for supply but only 3.62% for demand. It may be possible that the nation started out with an incredible amount of supply shortage, but the data suggests that supply seems to be outstripping demand at the national level currently. Furthermore, Total Residential Floor Space (8.28%) is growing at a much faster pace than Total Units (5.48%). This is because while average household size has shrunk from 3.7 persons per household in 1996 to 3.02 persons per household in 2012, the average size of a residential flat in urban China has increased from 63 square meters in 1996 to 99 square meters in This led to a 193% increase in floor area per capita since

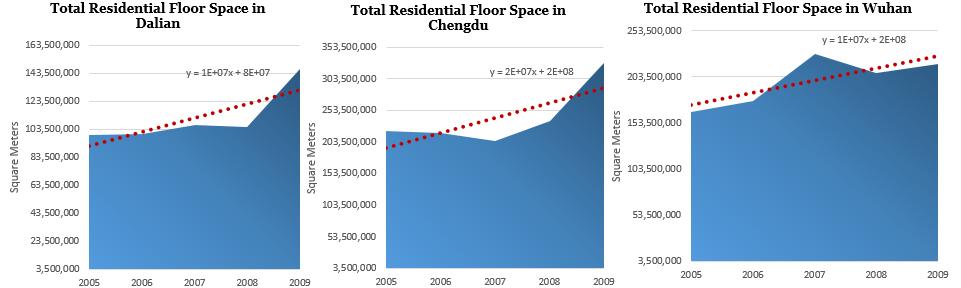

23 City-level Data Understanding that real estate markets are local, looking only at national data would be insufficient in trying to answer the question of whether there are housing bubbles in China s cities. We analyzed data from 10 major cities in China: Beijing, Shanghai, Chongqing, Tianjin, Guangzhou, Nanjing, Wuhan, Dalian, Chengdu, and Hangzhou. We calculated total residential floor space for each city for a measure of housing supply. However, we had some doubts regarding the accuracy of the data for Number of Households at the city-level from National Bureau of Statistics. Official numbers reveal that number of households in many of the 10 cities did not increase much or at all. For example, number of households in Guangzhou, Dalian, Wuhan, and Chengdu remained constant since 1995 according to official numbers. Due to the high urbanization trends over the past two decades, we know that this simply cannot be true. This misrepresentation might be a result of statistics only the Huji ( 戶籍 ) system. The Chinese relies on hukous ( 戶口 ), or residential permits, to record the number of households in a city; however, there are many city residents holding illegal hukous, and these people are not reflected in the statistics. Due to limitations of the data from National Bureau of Statistics, we were unable to perform the precise demand vs. supply analysis in terms of number of flats at the city level. Nevertheless, we use Beijing as an example for city-level data, because the official numbers reflect a slightly more accurate picture of how much number of households have risen over the years, increasing 460% since

24 BEIJING DATA 22

")

25 Supply vs. Demand in Beijing ( ) SUPPLY DEMAND 23

26 Data from NBS does not reach as far back for city-level data. We were able to calculate data for supply from Although the data for number of households is staggered, the line regression provides an estimate for household demand from Beijing has an average annual increase of 6.6% in supply, which is higher than the estimate for Urban China. On the demand side, we see an incredible average annual increase of 14.5% in number of households. This suggests that demand is exceeding supply at the Beijing city-level. Similar to national data, Total Residential Floor Space (19.7%) is growing at a much faster pace than Total Units (6.6%). This is because while average household size has shrunk from 3.1 persons per household in 1996 to 2.5 persons per household in 2012, the average size of a residential flat in urban China has been increasing at approximately 6 square meters per year. Hence, floor space per capita has been increasing at around 14% per year. However, the above information should to be taken with a grain of salt, as we only have 5 years of data for supply. 24

27 DATA FOR OTHER CITIES 25

28 Conclusions The landscape of China's property markets have changed drastically since the successful privatization of the housing sector in the 1990s. However, the years of extraordinary pricing growth give rise to concerns that pricing bubbles have formed in some cities. The collapse of these bubbles would lead to slowdown of the nation and potentially the global economy as well. To combat large bubbles in cities, Chinese policy makers have implemented a series of corrective measures after 2008 to ensure a soft landing. Required reserve ratios for banks have increased 12 times in , and interest rates at People s Bank of China have been increased to curtail housing mortgages. Facing a tightening credit market, real estate developers have begun to produce fewer units. Yet, prices continue to escalate. To better combat housing bubbles, the Milkin Institute suggests that property taxes should be better implemented in addition to the monetary policy instruments. Crowe et al. (2011) states that higher rates of property taxation can help limit housing booms as well as short-run volatility around an upward trend in prices. However, China s property tax reform faces enormous challenges including resistance from influential interest groups. Successful establishment of a property tax as a major revenue source requires not only strong assessment techniques and tax design but also political determination and administrative reform. In aggregate at the nation-level, supply seems to be exceeding demand with a higher amount of supply built each year than demanded from urbanization. Assuming data from National Bureau of Statistics is accurate, the high and escalating prices in China seem to be unjustified. Even if the cities had started with a large shortage of supply, we should have expected some slowdown in prices according to these trends. Prices do not necessarily have to fall, but an increase of 6-15% a year suggests a much stronger demand than supply, which is not the case at the national level. However, at the city-level, Beijing seems to be experiencing the opposite. With an a average annual increase of 6.6% in total residential units and an average annual increase of 14.5% in number of households, data suggest that demand is exceeding supply in Beijing. However, city-level data analysis is limited by lack of supply data pre 2005 and post With only 5 years of data for supply, we should take the results with a grain of salt. Due to inaccurate data for number of households, we could not perform a detailed supply versus demand analysis on the city-level data for the 9 other cities. However, we were able to calculate Total Residential Floor Space for the cities. It is evident through the graphs that the supply has been steadily increasing in each of the 10 major cities analyzed. 26

29 It seems that we are not the only ones realizing that the rising prices of residential prices in China's cities might be reaching a plateau. Big real estate players in China have begun to realize that the Chinese property market appears to be softening along with the rest of the country's economy. According to Cushman & Wakefield Research, the average yields for property transactions in Beijing has declined from 12.5% in 2004 to 6% in Similarly, property prices in Shanghai used to see average yields of 9% in 2004, which has decreased to 6% in Those who think that values have peaked have cut back on Chinese investing and are looking abroad to invest in foreign estates (Fung, 2014). However, not all developers think this way. For every transaction, there is both a buyer and a seller. Where smaller cities in China are facing swelling inventories and falling prices, Beijing is still seeing major constructions where investors believe the market is healthy and prices justified by fundamentals. Despite the findings of this study, our view on the Chinese housing market is still cautiously positive. China has several factors in place that the US did not have during the housing meltdown in The Chinese government requires high down payments and limits the LTV on property purchases. Most of the homeowners have enough equity in their properties to withstand a price drop. Essentially, China has accumulated a large enough cushion against the possibility of a crash in their housing markets. Furthermore, the Chinese government's debt level is low at approximately 40% of GDP, compared to 92% in the United States (Li, 2013). China could also call in the $3 trillion in foreign exchange reserves and $700 billion in required reserves in People's Bank of China when they do need it. Consequently, China is arguably less vulnerable to a liquidity crunch than most other nations. Therefore, while our study suggests that supply might be exceeding demand at the national level, a financial crisis the magnitude of the US Housing Crisis of is unlikely to occur. However, the Chinese will face direct effects of the reduced residential investments as developers go bankrupt and mortgages default. The phenomenon of ghost cities will be more prevalent. The reduced property investments will have spillover effects in industries such as rugs, lamps, and lightning fixtures. We can also expect new construction to drop to very low levels. While China is more protected than U.S. was from the bursting of property bubbles, we do not need a financial crisis to happen for this to be important to China and the rest of the world. Lastly, it is essential for China to compile consistent home price indices at both the local and national level. Regulators of China should improve the data collection practices to better access the effectiveness of current housing policies and to spot the early signs of a housing bubble. 27

30 Bibliography Bach, S. (2011). Adapting Land Taxation to Chinese Institutions. Retrieved from Schalken Bach: Bank of America Private Wealth Management. (2012). 101 Things Every Investor Should Know About the Global Economy. Bank, World. (2002). China National Development and Sub-National Finance: A Review of Provincial Expenditures. Report No CHA. China Index Institute. (2012). Impact of property taxes on land transfer fees. CoreLogic. (2014). CoreLogic Reports U.S. Foreclosure Inventory Down 35 Percent Nationally From a Year Ago. National Foreclosure Report. Davis, B. (2011). The Great Property Bubble of China May Be Popping. Wall Street Journal. Economic Intelligence Unit. (2011). The Sustainability of China's Housing Boom. Fung, E. (2013, July 18). China Stumbles on Property-Tax Plan. Retrieved from Wall Street Journal: 28 Fung, E. (2014). In Chinese Property, Smart Players Are Selling. Wall Street Journal. Gao, L. (n.d.). Achievements and Challenges: 30 Years of Housing Reforms in the People's Republic of China. Asian Development Bank Economic Working Paper Series. Glindro, E., Subhaij, T., Szeto, J., & Zhu, H. (2008). Determinants of House Prices in Nine Asia- Pacific Economies. Bank for International Settlements. Green, S., & Shen, L. (2012). China- Housing Inventories: Today, Tomorrow, and Ever After. Standard Chartered Global Research. Housing Finance Network. (2013). China Housing Finance Market Overview. Huang, Y. (2012). Lack of Affordable Housing Threatens China's Urban Dream. Igan, D., & Kang, H. (n.d.). Do Loan-to-Value and Debt-To-Income Limits Work? Evidence from Korea. IMF Working Paper. International Monetary Fund Global Financial Stability Report. (2011). Grappling ith Crisis Legacies. IMF Working Papers. 28

31 Li, L. K. (2013). Asia Real Estate Handbook. Asia Pacific Equity Research. Man, J. Y. (2011). China's local public finance in transition. Lincoln Institute of Land Policy. McKinsey Global Institute. (2009). Preparing for China's Urban Billion. Orlik, T. (2011). Chinese GDP Data: How Reliable? Wall Street Journal. Rongrong Ren, S. Z. (2011). China's housing reform and outcomes. Lincoln Institute of Land Policy. Shiller, R. (2010). How to Diagnose the Next Bubble. Silk, R. (2014). China Exports to Face Tough 2014 as Yuan Climbs. US Census. (2010). Average Length of Time from Start to Completion of New Privately Owned Residential Buildings. Wang, H. W. (2012). What is Unique about Chinese Real Estate Markets? JRER. Wang, Y. (n.d.). Urban Housing Reform and Finance in China: A Case Study of Beijing". Urban Affairs Reviews. Wen, Y. Y. (2005). The effect of Property Tax on Real Estate Prices. Zhongguo Wujia. Woo, C. W. (1995). Fiscal Management and Economic Reform in the People's Republic of China. Oxford University Press. Woods, M., & Barta, S. (2000). Estimating Supply and Demand in Your Local Housing Makret. Wu, J., Gyourko, J., & Deng, Y. (2010). Evaluating Conditions in Major Chinese Housing Markets. Nber Working Paper Series. Wu, X. (2011, 1 28). Property taxes kick off in Shanghia, Chongqing. Retrieved from The Standard : Xu, L. J. (2012). Foreign banks eye nation's growing wealth. Xu, X., & Chen, T. (2010). The Effect of Monetary Policy on Real Estate Price Growth in China. Yao, A. W. (2013). China's Third-Quarter GDP Growth Fastest This Year, but Outlook Dim. Retrieved from Liu, Zuo (2006). Taxation in China. Cengage Learning Asia. ISBN Zenou, Y. (2010). Housing Policy in China: Issues and Options. 29

32 30

China: Housing Market and Municipal Debt Risks

China: Housing Market and Municipal Debt Risks Wisconsin Real Estate & Economic Outlook Conference: The Shifting Landscape: What s Driving Change? Gregory Ingram Lincoln Institute of Land Policy and Peking

China: Housing Market and Municipal Debt Risks Wisconsin Real Estate & Economic Outlook Conference: The Shifting Landscape: What s Driving Change? Gregory Ingram Lincoln Institute of Land Policy and Peking

Nothing Draws a Crowd Like a Crowd: The Outlook for Home Sales

APRIL 2018 Nothing Draws a Crowd Like a Crowd: The Outlook for Home Sales The U.S. economy posted strong growth with fourth quarter 2017 Real Gross Domestic Product (real GDP) growth revised upwards to

APRIL 2018 Nothing Draws a Crowd Like a Crowd: The Outlook for Home Sales The U.S. economy posted strong growth with fourth quarter 2017 Real Gross Domestic Product (real GDP) growth revised upwards to

THE ANNUAL SPRING REAL

The Great Housing Price Showdown Last January China s central government finally introduced measures strong enough to slow housing price increases. Speculators, developers, local governments and simple

The Great Housing Price Showdown Last January China s central government finally introduced measures strong enough to slow housing price increases. Speculators, developers, local governments and simple

Linkages Between Chinese and Indian Economies and American Real Estate Markets

Linkages Between Chinese and Indian Economies and American Real Estate Markets Like everything else, the real estate market is affected by global forces. ANTHONY DOWNS IN THE 2004 presidential campaign,

Linkages Between Chinese and Indian Economies and American Real Estate Markets Like everything else, the real estate market is affected by global forces. ANTHONY DOWNS IN THE 2004 presidential campaign,

Comparative Study on Affordable Housing Policies of Six Major Chinese Cities. Xiang Cai

Comparative Study on Affordable Housing Policies of Six Major Chinese Cities Xiang Cai 1 Affordable Housing Policies of China's Six Major Chinese Cities Abstract: Affordable housing aims at providing low

Comparative Study on Affordable Housing Policies of Six Major Chinese Cities Xiang Cai 1 Affordable Housing Policies of China's Six Major Chinese Cities Abstract: Affordable housing aims at providing low

Market Insights & Strategy Global Markets

Market Insights & Strategy Global Markets UAE Real Estate Review 2016 Q2 Please find below a quick snapshot of the key topics covered in this note: Pricing trends - Sales In June 2016, monthly average

Market Insights & Strategy Global Markets UAE Real Estate Review 2016 Q2 Please find below a quick snapshot of the key topics covered in this note: Pricing trends - Sales In June 2016, monthly average

The cost of increasing social and affordable housing supply in New South Wales

The cost of increasing social and affordable housing supply in New South Wales Prepared for Shelter NSW Date December 2014 Prepared by Emilio Ferrer 0412 2512 701 eferrer@sphere.com.au 1 Contents 1 Background

The cost of increasing social and affordable housing supply in New South Wales Prepared for Shelter NSW Date December 2014 Prepared by Emilio Ferrer 0412 2512 701 eferrer@sphere.com.au 1 Contents 1 Background

Housing Markets: Balancing Risks and Rewards

Housing Markets: Balancing Risks and Rewards October 14, 2015 Hites Ahir and Prakash Loungani International Monetary Fund Presentation to the International Housing Association VIEWS EXPRESSED ARE THOSE

Housing Markets: Balancing Risks and Rewards October 14, 2015 Hites Ahir and Prakash Loungani International Monetary Fund Presentation to the International Housing Association VIEWS EXPRESSED ARE THOSE

The New Housing Crisis Not Enough Rental Homes?

The New Housing Crisis Not Enough Rental Homes? August 1, 2016 by Lance Roberts of Real Investment Advice The has been a rash of articles as of late suggesting there is a new housing crisis afoot. The

The New Housing Crisis Not Enough Rental Homes? August 1, 2016 by Lance Roberts of Real Investment Advice The has been a rash of articles as of late suggesting there is a new housing crisis afoot. The

Estimating National Levels of Home Improvement and Repair Spending by Rental Property Owners

Joint Center for Housing Studies Harvard University Estimating National Levels of Home Improvement and Repair Spending by Rental Property Owners Abbe Will October 2010 N10-2 2010 by Abbe Will. All rights

Joint Center for Housing Studies Harvard University Estimating National Levels of Home Improvement and Repair Spending by Rental Property Owners Abbe Will October 2010 N10-2 2010 by Abbe Will. All rights

Findings: City of Johannesburg

Findings: City of Johannesburg What s inside High-level Market Overview Housing Performance Index Affordability and the Housing Gap Leveraging Equity Understanding Housing Markets in Johannesburg, South

Findings: City of Johannesburg What s inside High-level Market Overview Housing Performance Index Affordability and the Housing Gap Leveraging Equity Understanding Housing Markets in Johannesburg, South

The Sustainability of China's Residential Market

WHARTON REAL ESTATE REVIEW SPRING 2012 The Sustainability of China's Residential Market JAMES MACDONALD FRANCESCO MUSSITA RAND SOBCZAK JR. The foundations of China's current residential real estate market

WHARTON REAL ESTATE REVIEW SPRING 2012 The Sustainability of China's Residential Market JAMES MACDONALD FRANCESCO MUSSITA RAND SOBCZAK JR. The foundations of China's current residential real estate market

Affordable Housing in South Africa How is the market doing?

1 Affordable Housing in South Africa How is the market doing? Kecia Rust & Adelaide Steedley International Housing Solutions Industry Conference 2013 19 September 2013, Johannesburg 2 Overview Mapping

1 Affordable Housing in South Africa How is the market doing? Kecia Rust & Adelaide Steedley International Housing Solutions Industry Conference 2013 19 September 2013, Johannesburg 2 Overview Mapping

Using Historical Employment Data to Forecast Absorption Rates and Rents in the Apartment Market

Using Historical Employment Data to Forecast Absorption Rates and Rents in the Apartment Market BY CHARLES A. SMITH, PH.D.; RAHUL VERMA, PH.D.; AND JUSTO MANRIQUE, PH.D. INTRODUCTION THIS ARTICLE PRESENTS

Using Historical Employment Data to Forecast Absorption Rates and Rents in the Apartment Market BY CHARLES A. SMITH, PH.D.; RAHUL VERMA, PH.D.; AND JUSTO MANRIQUE, PH.D. INTRODUCTION THIS ARTICLE PRESENTS

Young-Adult Housing Demand Continues to Slide, But Young Homeowners Experience Vastly Improved Affordability

Young-Adult Housing Demand Continues to Slide, But Young Homeowners Experience Vastly Improved Affordability September 3, 14 The bad news is that household formation and homeownership among young adults

Young-Adult Housing Demand Continues to Slide, But Young Homeowners Experience Vastly Improved Affordability September 3, 14 The bad news is that household formation and homeownership among young adults

China s Housing Market

December 212 China s Housing Market Is a Bubble About to Burst? James R. Barth, Michael Lea, and Tong Li December 212 China s Housing Market Is a Bubble About to Burst? James R. Barth, Michael Lea, and

December 212 China s Housing Market Is a Bubble About to Burst? James R. Barth, Michael Lea, and Tong Li December 212 China s Housing Market Is a Bubble About to Burst? James R. Barth, Michael Lea, and

16 April 2018 KEY POINTS

16 April 2018 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST FNB HOME LOANS 087-328 0151 john.loos@fnb.co.za THULANI LUVUNO: STATISTICIAN 087-730 2254

16 April 2018 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST FNB HOME LOANS 087-328 0151 john.loos@fnb.co.za THULANI LUVUNO: STATISTICIAN 087-730 2254

REGIONAL. Rental Housing in San Joaquin County

Lodi 12 EBERHARDT SCHOOL OF BUSINESS Business Forecasting Center in partnership with San Joaquin Council of Governments 99 26 5 205 Tracy 4 Lathrop Stockton 120 Manteca Ripon Escalon REGIONAL analyst april

Lodi 12 EBERHARDT SCHOOL OF BUSINESS Business Forecasting Center in partnership with San Joaquin Council of Governments 99 26 5 205 Tracy 4 Lathrop Stockton 120 Manteca Ripon Escalon REGIONAL analyst april

The Uneven Housing Recovery

AP PHOTO/BETH J. HARPAZ The Uneven Housing Recovery Michela Zonta and Sarah Edelman November 2015 W W W.AMERICANPROGRESS.ORG Introduction and summary The Great Recession, which began with the collapse

AP PHOTO/BETH J. HARPAZ The Uneven Housing Recovery Michela Zonta and Sarah Edelman November 2015 W W W.AMERICANPROGRESS.ORG Introduction and summary The Great Recession, which began with the collapse

THE IMPACT OF RESIDENTIAL REAL ESTATE MARKET BY PROPERTY TAX Zhanshe Yang 1, a, Jing Shan 2,b

THE IMPACT OF RESIDENTIAL REAL ESTATE MARKET BY PROPERTY TAX Zhanshe Yang 1, a, Jing Shan 2,b 1 School of Management, Xi'an University of Architecture and Technology, China710055 2 School of Management,

THE IMPACT OF RESIDENTIAL REAL ESTATE MARKET BY PROPERTY TAX Zhanshe Yang 1, a, Jing Shan 2,b 1 School of Management, Xi'an University of Architecture and Technology, China710055 2 School of Management,

State of the Nation s Housing 2008: A Preview

State of the Nation s Housing 28: A Preview Eric S. Belsky Remodeling Futures Conference April 15, 28 www.jchs.harvard.edu The Housing Market Has Suffered Steep Declines Percent Change Median Existing

State of the Nation s Housing 28: A Preview Eric S. Belsky Remodeling Futures Conference April 15, 28 www.jchs.harvard.edu The Housing Market Has Suffered Steep Declines Percent Change Median Existing

SELF-STORAGE REPORT VIEWPOINT 2017 / COMMERCIAL REAL ESTATE TRENDS. By: Steven J. Johnson, MAI, Senior Managing Director, IRR-Metro LA. irr.

SELF-STORAGE REPORT VIEWPOINT 2017 / COMMERCIAL REAL ESTATE TRENDS By: Steven J. Johnson, MAI, Senior Managing Director, IRR-Metro LA The Self Storage Story The self-storage sector has been enjoying solid

SELF-STORAGE REPORT VIEWPOINT 2017 / COMMERCIAL REAL ESTATE TRENDS By: Steven J. Johnson, MAI, Senior Managing Director, IRR-Metro LA The Self Storage Story The self-storage sector has been enjoying solid

Housing as an Investment Greater Toronto Area

Housing as an Investment Greater Toronto Area Completed by: Will Dunning Inc. For: Trinity Diversified North America Limited February 2009 Housing as an Investment Greater Toronto Area Overview We are

Housing as an Investment Greater Toronto Area Completed by: Will Dunning Inc. For: Trinity Diversified North America Limited February 2009 Housing as an Investment Greater Toronto Area Overview We are

ON THE HAZARDS OF INFERRING HOUSING PRICE TRENDS USING MEAN/MEDIAN PRICES

ON THE HAZARDS OF INFERRING HOUSING PRICE TRENDS USING MEAN/MEDIAN PRICES Chee W. Chow, Charles W. Lamden School of Accountancy, San Diego State University, 5500 Campanile Drive, San Diego, CA 92182, chow@mail.sdsu.edu

ON THE HAZARDS OF INFERRING HOUSING PRICE TRENDS USING MEAN/MEDIAN PRICES Chee W. Chow, Charles W. Lamden School of Accountancy, San Diego State University, 5500 Campanile Drive, San Diego, CA 92182, chow@mail.sdsu.edu

Released: February 8, 2011

Released: February 8, 2011 Commentary 2 The Numbers That Drive Real Estate 3 Recent Government Action 10 Topics for Home Buyers, Sellers, and Owners 13 Brought to you by: KW Research Commentary Gradual

Released: February 8, 2011 Commentary 2 The Numbers That Drive Real Estate 3 Recent Government Action 10 Topics for Home Buyers, Sellers, and Owners 13 Brought to you by: KW Research Commentary Gradual

HOUSING MARKET OUTLOOK: SAN LUIS OBISPO, CA AND SURROUNDING AREA

HOUSING MARKET OUTLOOK: SAN LUIS OBISPO, CA AND SURROUNDING AREA GABE RANDALL SCOTT KELTING April15, 2009 National Market Overview April 15, 2009 2008: A Year in Review Starting between 1999 and 2000,

HOUSING MARKET OUTLOOK: SAN LUIS OBISPO, CA AND SURROUNDING AREA GABE RANDALL SCOTT KELTING April15, 2009 National Market Overview April 15, 2009 2008: A Year in Review Starting between 1999 and 2000,

Vesteda Market Watch Q

Vesteda Market Watch Q1 2018 7.6 Housing Market Indicator 1 Housing Market Indicator The Housing Market Indicator in the first quarter of 2018 hits a level of 7.6. This score clearly reflects the positive

Vesteda Market Watch Q1 2018 7.6 Housing Market Indicator 1 Housing Market Indicator The Housing Market Indicator in the first quarter of 2018 hits a level of 7.6. This score clearly reflects the positive

Research on Real Estate Bubble Measurement and Prevention Countermeasures in Guangzhou City

Open Journal of Social Sciences, 2018, 6, 28-39 http://www.scirp.org/journal/jss ISSN Online: 2327-5960 ISSN Print: 2327-5952 Research on Real Estate Bubble Measurement and Prevention Countermeasures in

Open Journal of Social Sciences, 2018, 6, 28-39 http://www.scirp.org/journal/jss ISSN Online: 2327-5960 ISSN Print: 2327-5952 Research on Real Estate Bubble Measurement and Prevention Countermeasures in

Since 1978, the Chinese government. Affordable Housing in China. Joyce Yanyun Man

Affordable Housing in China The Huilongguan affordable project is a large community of middle- and low-income families, including civil servants and teachers. It is located in the northeastern part of

Affordable Housing in China The Huilongguan affordable project is a large community of middle- and low-income families, including civil servants and teachers. It is located in the northeastern part of

NEW CHALLENGES IN URBAN GOVERNANCE AND FINANCE

Final International Conference Paris January 15-16, 2015 NEW CHALLENGES IN URBAN GOVERNANCE AND FINANCE Zhi Liu Peking University Lincoln Institute of Land Policy Center for Urban Development and Land

Final International Conference Paris January 15-16, 2015 NEW CHALLENGES IN URBAN GOVERNANCE AND FINANCE Zhi Liu Peking University Lincoln Institute of Land Policy Center for Urban Development and Land

Seattle Housing Market Overview January 2019

Seattle Housing Market Overview January 2019 A review of recent trends and thoughts about the future of the Seattle housing market. Bill King President, Chief Valuation Officer Real Info, Inc. City of

Seattle Housing Market Overview January 2019 A review of recent trends and thoughts about the future of the Seattle housing market. Bill King President, Chief Valuation Officer Real Info, Inc. City of

Ontario Rental Market Study:

Ontario Rental Market Study: Renovation Investment and the Role of Vacancy Decontrol October 2017 Prepared for the Federation of Rental-housing Providers of Ontario by URBANATION Inc. Page 1 of 11 TABLE

Ontario Rental Market Study: Renovation Investment and the Role of Vacancy Decontrol October 2017 Prepared for the Federation of Rental-housing Providers of Ontario by URBANATION Inc. Page 1 of 11 TABLE

Soaring Demand Drives US Industrial Market to New Heights

Soaring Demand Drives US Industrial Market to New Heights Capitas (DIFC) Limited I June Issue: 2017 THIS ISSUE COVERS: The Amazon Factor a seismic shift in the way people shop Industrial real estate hitting

Soaring Demand Drives US Industrial Market to New Heights Capitas (DIFC) Limited I June Issue: 2017 THIS ISSUE COVERS: The Amazon Factor a seismic shift in the way people shop Industrial real estate hitting

Housing Indicators in Tennessee

Housing Indicators in l l l By Joe Speer, Megan Morgeson, Bettie Teasley and Ceagus Clark Introduction Looking at general housing-related indicators across the state of, substantial variation emerges but

Housing Indicators in l l l By Joe Speer, Megan Morgeson, Bettie Teasley and Ceagus Clark Introduction Looking at general housing-related indicators across the state of, substantial variation emerges but

By several measures, homebuilding made a comeback in 2012 (Figure 6). After falling another 8.6 percent in 2011, single-family

. After falling another 8.6 percent in 2011, single-family") 2 Housing Markets With sales picking up, low inventories of both new and existing homes helped to firm prices and spur new single-family construction in 212. Multifamily markets posted another strong year,

2 Housing Markets With sales picking up, low inventories of both new and existing homes helped to firm prices and spur new single-family construction in 212. Multifamily markets posted another strong year,

Housing Bulletin Monthly Report

August 21 Housing Bulletin Monthly Report 1 C a n a da s P r e li m i n a ry H o u s i n g S ta r t s s l i p i n J u ly Preliminary Housing St arts in Albert a* and Canada* July 28 to July 21 25, Canada

August 21 Housing Bulletin Monthly Report 1 C a n a da s P r e li m i n a ry H o u s i n g S ta r t s s l i p i n J u ly Preliminary Housing St arts in Albert a* and Canada* July 28 to July 21 25, Canada

ECONOMIC CURRENTS. Vol. 5 Issue 2 SOUTH FLORIDA ECONOMIC QUARTERLY. Key Findings, 2 nd Quarter, 2015

ECONOMIC CURRENTS THE Introduction SOUTH FLORIDA ECONOMIC QUARTERLY Economic Currents provides an overview of the South Florida regional economy. The report presents current employment, economic and real

ECONOMIC CURRENTS THE Introduction SOUTH FLORIDA ECONOMIC QUARTERLY Economic Currents provides an overview of the South Florida regional economy. The report presents current employment, economic and real

Beijing s New Challenge: China s Post-Crisis Housing Bubble

Beijing s New Challenge: China s Post-Crisis Housing Bubble June 30, 2010 Pieter Bottelier Summary China s residential property bubble (concentrated in major eastern cities) is mainly the result of excessive

Beijing s New Challenge: China s Post-Crisis Housing Bubble June 30, 2010 Pieter Bottelier Summary China s residential property bubble (concentrated in major eastern cities) is mainly the result of excessive

Cycle Monitor Real Estate Market Cycles Third Quarter 2017 Analysis

Cycle Monitor Real Estate Market Cycles Third Quarter 2017 Analysis Real Estate Physical Market Cycle Analysis of Five Property Types in 54 Metropolitan Statistical Areas (MSAs). Income-producing real

Cycle Monitor Real Estate Market Cycles Third Quarter 2017 Analysis Real Estate Physical Market Cycle Analysis of Five Property Types in 54 Metropolitan Statistical Areas (MSAs). Income-producing real

HK Monetary Policy and Housing Affordability

Workshop on Social Model, PolyU Hong Kong 29 Nov 2013 HK Monetary Policy and Housing Affordability by Dr Edward CY Yiu Associate Professor Dept of Geography and Resource Management, Chinese University

Workshop on Social Model, PolyU Hong Kong 29 Nov 2013 HK Monetary Policy and Housing Affordability by Dr Edward CY Yiu Associate Professor Dept of Geography and Resource Management, Chinese University

CONSUMER CONFIDENCE AND REAL ESTATE MARKET PERFORMANCE GO HAND-IN-HAND

CONSUMER CONFIDENCE AND REAL ESTATE MARKET PERFORMANCE GO HAND-IN-HAND The job market, mortgage interest rates and the migration balance are often considered to be the main determinants of real estate

CONSUMER CONFIDENCE AND REAL ESTATE MARKET PERFORMANCE GO HAND-IN-HAND The job market, mortgage interest rates and the migration balance are often considered to be the main determinants of real estate

things to consider if you are selling your house

things to consider if you are selling your house KEEPINGCURRENTMATTERS.COM WINTER 2012 EDITION PAGE TABLE OF CONTENTS 1 3 5 7 9 House Prices: Where They Will Be in the Spring Understanding the Impact OF

things to consider if you are selling your house KEEPINGCURRENTMATTERS.COM WINTER 2012 EDITION PAGE TABLE OF CONTENTS 1 3 5 7 9 House Prices: Where They Will Be in the Spring Understanding the Impact OF

The Relationship between Interest Rates, Income, GDP Growth. and House Prices

Research in Economics and Management ISSN 2470-4407 (Print) ISSN 2470-4393 (Online) Vol. 2, No. 1, 2017 www.scholink.org/ojs/index.php/rem The Relationship between Interest Rates, Income, GDP Growth and

Research in Economics and Management ISSN 2470-4407 (Print) ISSN 2470-4393 (Online) Vol. 2, No. 1, 2017 www.scholink.org/ojs/index.php/rem The Relationship between Interest Rates, Income, GDP Growth and

CHINA: UNDERSTANDING THE RESIDENTIAL REAL ESTATE MARKET

CHINA: UNDERSTANDING THE RESIDENTIAL REAL ESTATE MARKET August 2016 M. Chivakul, R. Lam, X. Liu, W. Maliszewski, A. Schipke The views expressed in this presentation are those of the speaker and do not

CHINA: UNDERSTANDING THE RESIDENTIAL REAL ESTATE MARKET August 2016 M. Chivakul, R. Lam, X. Liu, W. Maliszewski, A. Schipke The views expressed in this presentation are those of the speaker and do not

2016 Multifamily Outlook: Another Year of Opportunity

2016 Multifamily Outlook: Another Year of Opportunity A BERKSHIRE RESEARCH VIEWPOINT February 2016 2016 Multifamily Outlook: A Year of Opportunity A BERKSHIRE RESEARCH VIEWPOINT February 2016 2 2016 MULTIFAMILY

2016 Multifamily Outlook: Another Year of Opportunity A BERKSHIRE RESEARCH VIEWPOINT February 2016 2016 Multifamily Outlook: A Year of Opportunity A BERKSHIRE RESEARCH VIEWPOINT February 2016 2 2016 MULTIFAMILY

analyst REGIONAL San Joaquin County Housing: Current Challenges, Future Needs Stockton

Lodi 12 EBERHARDT SCHOOL OF BUSINESS Business Forecasting Center in partnership with San Joaquin Council of Governments 99 26 5 205 Tracy 4 Lathrop Stockton 120 Manteca Ripon Escalon REGIONAL analyst december

Lodi 12 EBERHARDT SCHOOL OF BUSINESS Business Forecasting Center in partnership with San Joaquin Council of Governments 99 26 5 205 Tracy 4 Lathrop Stockton 120 Manteca Ripon Escalon REGIONAL analyst december

Median Income and Median Home Price

Homeownership Remains Unaffordable; Rental Affordability Showing Signs of Improvement Richard E. Taylor, Research Manager at MaineHousing MaineHousing has released the 217 Maine Homeownership and Rental

Homeownership Remains Unaffordable; Rental Affordability Showing Signs of Improvement Richard E. Taylor, Research Manager at MaineHousing MaineHousing has released the 217 Maine Homeownership and Rental

The Seattle MD Apartment Market Report

The Seattle MD Apartment Market Report Volume 16 Issue 2, December 2016 The Nation s Crane Capital Seattle continues to experience an apartment boom which requires constant construction of new units. At

The Seattle MD Apartment Market Report Volume 16 Issue 2, December 2016 The Nation s Crane Capital Seattle continues to experience an apartment boom which requires constant construction of new units. At

Rapid recovery from the Great Recession, buoyed

Game of Homes The Supply-Demand Struggle Laila Assanie, Sarah Greer, and Luis B. Torres October 4, 2016 Publication 2143 Rapid recovery from the Great Recession, buoyed by the shale oil boom, has fueled

Game of Homes The Supply-Demand Struggle Laila Assanie, Sarah Greer, and Luis B. Torres October 4, 2016 Publication 2143 Rapid recovery from the Great Recession, buoyed by the shale oil boom, has fueled

Sekisui House, Ltd. < Presentation >

Sekisui House, Ltd. Transcript for Earnings Results Briefing for the Second Quarter of FY2018 (Telephone Conference) Date: Participants: September 6 th, 2018, Thursday 17:00 18:00 JPT Shiro Inagaki, Representative

Sekisui House, Ltd. Transcript for Earnings Results Briefing for the Second Quarter of FY2018 (Telephone Conference) Date: Participants: September 6 th, 2018, Thursday 17:00 18:00 JPT Shiro Inagaki, Representative

STRENGTHENING RENTER DEMAND

5 Rental Housing Rental housing markets experienced another strong year in 2012, with the number of renter households rising by over 1.1 million and marking a decade of unprecedented growth. New construction

5 Rental Housing Rental housing markets experienced another strong year in 2012, with the number of renter households rising by over 1.1 million and marking a decade of unprecedented growth. New construction

How Severe is the Housing Shortage in Hong Kong?

(Reprinted from HKCER Letters, Vol. 42, January, 1997) How Severe is the Housing Shortage in Hong Kong? Y.C. Richard Wong Introduction Rising property prices in Hong Kong have been of great public concern

(Reprinted from HKCER Letters, Vol. 42, January, 1997) How Severe is the Housing Shortage in Hong Kong? Y.C. Richard Wong Introduction Rising property prices in Hong Kong have been of great public concern

Filling the Gaps: Active, Accessible, Diverse. Affordable and other housing markets in Johannesburg: September, 2012 DRAFT FOR REVIEW

Affordable Land and Housing Data Centre Understanding the dynamics that shape the affordable land and housing market in South Africa. Filling the Gaps: Affordable and other housing markets in Johannesburg:

Affordable Land and Housing Data Centre Understanding the dynamics that shape the affordable land and housing market in South Africa. Filling the Gaps: Affordable and other housing markets in Johannesburg:

Single Family Sales Maine: Units

Maine Home Connection 19 Commercial St Portland, Maine 04101 MaineHomeConnection.com Office: (207) 517-3100 Email: Info@MaineHomeConnection.com For the fourth consecutive year, Maine home sales set a new

Maine Home Connection 19 Commercial St Portland, Maine 04101 MaineHomeConnection.com Office: (207) 517-3100 Email: Info@MaineHomeConnection.com For the fourth consecutive year, Maine home sales set a new

RENTAL PRODUCTION AND SUPPLY

RENTAL PRODUCTION AND SUPPLY Despite a sharp uptick in the number of renter households, construction of multifamily units for rent declined in 27 for the fifth straight year. Even so, growth in the rental

RENTAL PRODUCTION AND SUPPLY Despite a sharp uptick in the number of renter households, construction of multifamily units for rent declined in 27 for the fifth straight year. Even so, growth in the rental

Some Thoughts on Massive Affordable Housing Schemes under the Pressure of Commodity Housing Inventory in China s Cities

Open Access Library Journal 2017, Volume 4, e3722 ISSN Online: 2333-9721 ISSN Print: 2333-9705 Some Thoughts on Massive Affordable Housing Schemes under the Pressure of Commodity Housing Inventory in China

Open Access Library Journal 2017, Volume 4, e3722 ISSN Online: 2333-9721 ISSN Print: 2333-9705 Some Thoughts on Massive Affordable Housing Schemes under the Pressure of Commodity Housing Inventory in China

Trends in Affordable Home Ownership in Calgary

Trends in Affordable Home Ownership in Calgary 2006 July www.calgary.ca Call 3-1-1 PUBLISHING INFORMATION TITLE: AUTHOR: STATUS: TRENDS IN AFFORDABLE HOME OWNERSHIP CORPORATE ECONOMICS FINAL PRINTING DATE:

Trends in Affordable Home Ownership in Calgary 2006 July www.calgary.ca Call 3-1-1 PUBLISHING INFORMATION TITLE: AUTHOR: STATUS: TRENDS IN AFFORDABLE HOME OWNERSHIP CORPORATE ECONOMICS FINAL PRINTING DATE:

Single-Family vs. Multi-Family? Dietrich Heidtmann, Managing Director

U.S. Rented Residential Sector Single-Family vs. Multi-Family? Dietrich Heidtmann, Managing Director Demand: U.S. Household Formations Are Returning to Normalized Levels and the Entry of Millenials Continues

U.S. Rented Residential Sector Single-Family vs. Multi-Family? Dietrich Heidtmann, Managing Director Demand: U.S. Household Formations Are Returning to Normalized Levels and the Entry of Millenials Continues

Keppel Land in China. May 2006

1 Keppel Land in China May 2006 Presentation Outline Introduction Market Update City Updates Shanghai Tianjin Beijing Wuxi Chengdu Residential Township Development 2 3 Introduction KLL s Steps in China

1 Keppel Land in China May 2006 Presentation Outline Introduction Market Update City Updates Shanghai Tianjin Beijing Wuxi Chengdu Residential Township Development 2 3 Introduction KLL s Steps in China

Filling the Gaps: Stable, Available, Affordable. Affordable and other housing markets in Ekurhuleni: September, 2012 DRAFT FOR REVIEW

Affordable Land and Housing Data Centre Understanding the dynamics that shape the affordable land and housing market in South Africa. Filling the Gaps: Affordable and other housing markets in Ekurhuleni:

Affordable Land and Housing Data Centre Understanding the dynamics that shape the affordable land and housing market in South Africa. Filling the Gaps: Affordable and other housing markets in Ekurhuleni:

Democratising Property Investments

Democratising Property Investments What I wish to share today 1. Property sector outlook 2. How theedgeproperty.com can help you make better property investment decisions Property Sector Outlook The property

Democratising Property Investments What I wish to share today 1. Property sector outlook 2. How theedgeproperty.com can help you make better property investment decisions Property Sector Outlook The property

Residential May Karl L. Guntermann Fred E. Taylor Professor of Real Estate. Adam Nowak Research Associate

Residential May 2008 Karl L. Guntermann Fred E. Taylor Professor of Real Estate Adam Nowak Research Associate The use of repeat sales is the most reliable way to estimate price changes in the housing market

Residential May 2008 Karl L. Guntermann Fred E. Taylor Professor of Real Estate Adam Nowak Research Associate The use of repeat sales is the most reliable way to estimate price changes in the housing market

NAB COMMERCIAL PROPERTY SURVEY Q4 2017

EMBARGOED UNTIL 11.30 AM WEDNESDAY 21 FEBRUARY 2018 NAB COMMERCIAL PROPERTY SURVEY Q4 2017 Date February 2018 NAB Behavioural & Industry Economics KEY FINDINGS The NAB Commercial Property Index (a measure

EMBARGOED UNTIL 11.30 AM WEDNESDAY 21 FEBRUARY 2018 NAB COMMERCIAL PROPERTY SURVEY Q4 2017 Date February 2018 NAB Behavioural & Industry Economics KEY FINDINGS The NAB Commercial Property Index (a measure

Fantasia Holdings Group Announces 2010 Interim Results

Fantasia Holdings Group Announces 2010 Interim Results Urban complexes fuel sales growth Total revenue and net profit increase 42.8% and 74.5% respectively In the first half of 2010, total sales and net

Fantasia Holdings Group Announces 2010 Interim Results Urban complexes fuel sales growth Total revenue and net profit increase 42.8% and 74.5% respectively In the first half of 2010, total sales and net

CONTENTS. Executive Summary 1. Southern Nevada Economic Situation 2 Household Sector 5 Tourism & Hospitality Industry

CONTENTS Executive Summary 1 Southern Nevada Economic Situation 2 Household Sector 5 Tourism & Hospitality Industry Residential Trends 7 Existing Home Sales 11 Property Management Market 12 Foreclosure

CONTENTS Executive Summary 1 Southern Nevada Economic Situation 2 Household Sector 5 Tourism & Hospitality Industry Residential Trends 7 Existing Home Sales 11 Property Management Market 12 Foreclosure

Appendix 1: Gisborne District Quarterly Market Indicators Report April National Policy Statement on Urban Development Capacity

Appendix 1: Gisborne District Quarterly Market Indicators Report April 2018 National Policy Statement on Urban Development Capacity Quarterly Market Indicators Report April 2018 1 Executive Summary This

Appendix 1: Gisborne District Quarterly Market Indicators Report April 2018 National Policy Statement on Urban Development Capacity Quarterly Market Indicators Report April 2018 1 Executive Summary This

CANADA ECONOMICS FOCUS

CANADA ECONOMICS FOCUS House prices likely to fall for several years 3 rd Feb. 211 The recent housing boom has resulted in the largest rises in house prices ever seen in Canada, which have been similar

CANADA ECONOMICS FOCUS House prices likely to fall for several years 3 rd Feb. 211 The recent housing boom has resulted in the largest rises in house prices ever seen in Canada, which have been similar

Attorneys Title Insurance Fund 2009 Real Estate Forecast Southeast Florida MSA (Broward, Miami-Dade and Palm Beach)

") Attorneys Title Insurance Fund 29 Real Estate Forecast Southeast Florida MSA (Broward, Miami-Dade and Palm Beach) Prepared by Hank Fishkind, Ph.D. Chief Economist for The Fund and Principal, Fishkind &

Attorneys Title Insurance Fund 29 Real Estate Forecast Southeast Florida MSA (Broward, Miami-Dade and Palm Beach) Prepared by Hank Fishkind, Ph.D. Chief Economist for The Fund and Principal, Fishkind &

Connecticut Full Year Housing Report

Connecticut 2014 Full Year Housing Report As 2014 Closes, Increasing Market Confidence Predicts a Solid Start to 2015 With an influx of Millennial, Gen X and Baby Boomer buyers, a strong spring market

Connecticut 2014 Full Year Housing Report As 2014 Closes, Increasing Market Confidence Predicts a Solid Start to 2015 With an influx of Millennial, Gen X and Baby Boomer buyers, a strong spring market

Hamilton s Housing Market and Economy

Hamilton s Housing Market and Economy Growth Indicator Report November 2016 hamilton.govt.nz Contents 3. 4. 5. 6. 7. 7. 8. 9. 10. 11. Introduction New Residential Building Consents New Residential Sections

Hamilton s Housing Market and Economy Growth Indicator Report November 2016 hamilton.govt.nz Contents 3. 4. 5. 6. 7. 7. 8. 9. 10. 11. Introduction New Residential Building Consents New Residential Sections

The state of the nation s Housing 2011

The state of the nation s Housing 2011 Fact Sheet PURPOSE The State of the Nation s Housing report has been released annually by Harvard University s Joint Center for Housing Studies since 1988. Now in

The state of the nation s Housing 2011 Fact Sheet PURPOSE The State of the Nation s Housing report has been released annually by Harvard University s Joint Center for Housing Studies since 1988. Now in

The Corcoran Report 3Q17 MANHATTAN

The Corcoran Report 3Q17 MANHATTAN Contents Third Quarter 2017 4/7 12/23 3 Overview 8 9 10 Market Wide 11 Luxury 24 4 Sales / Days on Market 5 Inventory / Months of Supply 6 7 Market Share Resale Co-ops

The Corcoran Report 3Q17 MANHATTAN Contents Third Quarter 2017 4/7 12/23 3 Overview 8 9 10 Market Wide 11 Luxury 24 4 Sales / Days on Market 5 Inventory / Months of Supply 6 7 Market Share Resale Co-ops

6 April 2018 KEY POINTS

6 April 2018 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 john.loos@fnb.co.za THULANI LUVUNO: STATISTICIAN 087-730 2254 thulani.luvuno@fnb.co.za

6 April 2018 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 john.loos@fnb.co.za THULANI LUVUNO: STATISTICIAN 087-730 2254 thulani.luvuno@fnb.co.za

Housing Market Outlook Trois-Rivières CMA

H o u s i n g M a r k e t I n f o r m a t i o n Housing Market Outlook C a n a d a M o r t g a g e a n d H o u s i n g C o r p o r a t i o n Date Released: Fall 2011 Activity to remain strong in 2011 and

H o u s i n g M a r k e t I n f o r m a t i o n Housing Market Outlook C a n a d a M o r t g a g e a n d H o u s i n g C o r p o r a t i o n Date Released: Fall 2011 Activity to remain strong in 2011 and

MARKET STRATEGY VIEWPOINT U.S. Housing Decelerating

Jan-01 Oct-01 Jul-02 Apr-03 Jan-0 Oct-0 Jul-05 Apr-0 Jan-07 Oct-07 Jul-08 Apr-09 Jan-10 Oct-10 Jul-11 Apr-12 Jan-13 Oct-13 Jul-1 Apr-15 Jan-1 Oct-1 Jul-17 Apr-18 U.S. Housing Decelerating August 27, 2018

Jan-01 Oct-01 Jul-02 Apr-03 Jan-0 Oct-0 Jul-05 Apr-0 Jan-07 Oct-07 Jul-08 Apr-09 Jan-10 Oct-10 Jul-11 Apr-12 Jan-13 Oct-13 Jul-1 Apr-15 Jan-1 Oct-1 Jul-17 Apr-18 U.S. Housing Decelerating August 27, 2018

Multifamily Market Commentary December 2015 Single-Family Rental Sector Attracting Institutional Investment

Multifamily Market Commentary December 2015 Single-Family Rental Sector Attracting Institutional Investment Prior to the Great Recession, the cratering of single-family home prices, and declines in the

Multifamily Market Commentary December 2015 Single-Family Rental Sector Attracting Institutional Investment Prior to the Great Recession, the cratering of single-family home prices, and declines in the

ANALYSIS OF THE CENTRAL VIRGINIA AREA HOUSING MARKET 1st quarter 2013 By Lisa A. Sturtevant, PhD George Mason University Center for Regional Analysis

ANALYSIS OF THE CENTRAL VIRGINIA AREA HOUSING MARKET 1st quarter By Lisa A. Sturtevant, PhD George Mason University Center for Regional Analysis Economic Overview Key economic factors in the first quarter

ANALYSIS OF THE CENTRAL VIRGINIA AREA HOUSING MARKET 1st quarter By Lisa A. Sturtevant, PhD George Mason University Center for Regional Analysis Economic Overview Key economic factors in the first quarter

Residential Commentary - Perth Apartment Market

Residential Commentary - Perth Apartment Market March 2016 Executive Summary The Greater Perth apartment market has attracted considerable interest from local and offshore developers. Projects under construction

Residential Commentary - Perth Apartment Market March 2016 Executive Summary The Greater Perth apartment market has attracted considerable interest from local and offshore developers. Projects under construction

An Assessment of Recent Increases of House Prices in Austria through the Lens of Fundamentals

An Assessment of Recent Increases of House Prices in Austria 1 Introduction Martin Schneider Oesterreichische Nationalbank The housing sector is one of the most important sectors of an economy. Since residential

An Assessment of Recent Increases of House Prices in Austria 1 Introduction Martin Schneider Oesterreichische Nationalbank The housing sector is one of the most important sectors of an economy. Since residential

Residential September 2010

Residential September 2010 Karl L. Guntermann Fred E. Taylor Professor of Real Estate Adam Nowak Research Associate For the first time since March, house prices turned down slightly in August (-2 percent)

Residential September 2010 Karl L. Guntermann Fred E. Taylor Professor of Real Estate Adam Nowak Research Associate For the first time since March, house prices turned down slightly in August (-2 percent)

The Knox County HOUSING MARKET

T E C H REPORT SERIES The Knox HOUSING MARKET Date: August 2007 For more information: MPC Contact Person: Bryan Berry 215-2500 MPC Website and e-mail www.knoxmpc.org contact@knoxmpc.org INTRODUCTION In

T E C H REPORT SERIES The Knox HOUSING MARKET Date: August 2007 For more information: MPC Contact Person: Bryan Berry 215-2500 MPC Website and e-mail www.knoxmpc.org contact@knoxmpc.org INTRODUCTION In

RESIDENTIAL MARKET ANALYSIS

RESIDENTIAL MARKET ANALYSIS CLANCY TERRY RMLS Student Fellow Master of Real Estate Development Candidate Oregon and national housing markets both demonstrated shifting trends in the first quarter of 2015

RESIDENTIAL MARKET ANALYSIS CLANCY TERRY RMLS Student Fellow Master of Real Estate Development Candidate Oregon and national housing markets both demonstrated shifting trends in the first quarter of 2015

Multifamily Market Commentary February 2017

Multifamily Market Commentary February 2017 Affordable Multifamily Outlook Incremental Improvement Expected in 2017 We expect momentum in the overall multifamily sector to slow in 2017 due to elevated

Multifamily Market Commentary February 2017 Affordable Multifamily Outlook Incremental Improvement Expected in 2017 We expect momentum in the overall multifamily sector to slow in 2017 due to elevated

MULTIFAMILY MARKET REPORT GREATER TORONTO AREA FALL 2017

MULTIFAMILY MARKET REPORT GREATER TORONTO AREA FALL 2017 Table of Contents 1.0 Demand Indicators 2.0 Economic Snapshot 3.0 Multifamily Housing Market Summary 4.0 Rental Market Summary 5.0 Secondary Rental

MULTIFAMILY MARKET REPORT GREATER TORONTO AREA FALL 2017 Table of Contents 1.0 Demand Indicators 2.0 Economic Snapshot 3.0 Multifamily Housing Market Summary 4.0 Rental Market Summary 5.0 Secondary Rental

This PDF is a selection from a published volume from the National Bureau of Economic Research