IFRS 16 : LEASES. M P Vijay Kumar

|

|

|

- Marion Madeline Page

- 5 years ago

- Views:

Transcription

1 IFRS 16 : LEASES M P Vijay Kumar

2 IFRS 16, LEASES AGENDA 1 Background of IFRS 16 2 Primary requirements under IAS 17, Leases 3 IFRS 16, Leases 4 High Level Summary 4.1 Lease Definition 4.2 Lessee Accounting 4.3 Modification of Leases 4.4 Sale and Lease back Transactions 4.5 Disclosures 4.6 Effective Date and Transition 4.7 Issues and Solutions 4.8 Appendix: Few examples 5 Thank you 2

3 BACKGROUND OF IFRS 16,LEASES A Long journey March IASB & FASB issued joint Discussion Paper, Aug joint Exposure Draft (ED) and May second joint ED was issued. IFRS 16 issued by IASB in Jan 2016 is effective from 1 January Though a product of joint project, some differences exist between IFRS 16 & US GAAP (Topic 840) IFRS 16 supersedes IAS 17, Leases; IFRIC 4, Determining whether an Arrangement contains a Lease; SIC-15, Operating Leases Incentives; and SIC-27, Evaluating the Substance of Transactions Involving the Legal Form of a Lease. One IASB member (Mr Wei-Guo Zhang) has given dissenting opinion. 3

4 LEASE PRIMARY REQUIREMENTS UNDER IAS 17, LEASES I AS 17 requires classification of lease between operating and finance lease Operating lease Finance lease Lease payments recognised as an expense on a straight-line basis over the lease term. Lease asset recognised in balance sheet as asset and liability at amount equal to the fair value of the leased property or, if lower, the present value of the minimum lease payments. Initial direct costs added to the amount recognised as an asset. Lease payments apportioned between the finance charge and the reduction of the outstanding liability. Finance lease gives rise to depreciation expense for depreciable assets as well as finance expense for each accounting period. 4

5 LEASE NEED FOR CHANGE IN ACCOUNTING FOR LESSEE AS ENVISAGED BY IASB/FASB Source IFRS 16 Effect Analysis by IASB 5

6 M P VIJAY KUMAR The Institute of Chartered Accountants of India 6 6

7 LEASE NEED FOR CHANGE IN ACCOUNTING FOR LESSEE AS ENVISAGED BY IASB The accounting requirements under previous lease standard failed to meet the needs of the user of financial statements since: Information reported about operating leases lacked transparency and did not meet the needs of users of financial statements. Existence of two different accounting models for leases, in which assets and liabilities associated with leases were not recognised for operating leases but were recognised for finance leases, meant that transactions that were economically similar could be accounted for very differently which reduced comparability for users of financial statements. Why a single accounting model under IFRS 16 lessee s right to use the underlying asset meets the definition of an asset lessee s obligation to make lease payments meets the definition of a liability Results in a more faithful representation of a lessee s assets and liabilities With enhanced disclosures, results in greater transparency of a lessee s financial leverage and capital employed. 7

8 EXPECTED SIGNIFICANT IMPACT OF IFRS 16 The IASB expects IFRS 16 to significantly improve the quality of financial reporting for companies with material off balance sheet leases. Applying IAS 17, most leases were not reported on a lessee s balance sheet. Consequently, a lessee did not provide a complete picture of the assets it controlled and used and the lease payments Off balance sheet lease financing numbers which are substantial will now get disclosed in financial statements. 8

9 EXPECTED SIGNIFICANT IMPACT OF IFRS 16 In an analysis conducted by the IASB, it observed that over 14,000 listed companies (of about 30,000 listed companies) disclose information about off balance sheet leases totalled US$2.86 trillion (on an undiscounted basis). IFRS 16 is expected to affect the amounts reported by almost half of listed companies. An analysis conducted by IASB shows that the use of off balance sheet leases is highly concentrated within some industry sectors and within some companies. The IASB in an analysis compared the off balance sheet leases to the total assets of 1,022 companies. 9

10 EXPECTED SIGNIFICANT IMPACT OF IFRS 16 IFRS 16 is expected to significantly improve the comparability of financial information. It will reduce opportunities to structure leasing transactions to achieve off balance sheet accounting. The IASB also expects that the exemption for leases of lowvalue assets will be of particular benefit for smaller companies that apply full IFRS. 10

11 EXPECTED IMPACT: HIGH LEVEL SUMMARY Impact Summary (as issued by IASB) There will be an impact on Three Components of financial statements viz. Statement of Financial Position, Statement of Profit and Loss and Statement of Cash Flows. Key financial metrics or ratios will change e.g. Leverage ratios, Operating ratios. The IASB expects that ü it will significantly improve the quality of financial reporting for companies with material off balance sheet leases. Applying previous standard, most leases were not reported on a lessee s balance sheet. Consequently, a lessee did not provide a complete picture of the assets it controlled and used and the lease payments. ü affect the amounts reported by many listed companies. ü significantly improve the comparability of financial information. ü exemption for leases of low-value assets will be of particular benefit for smaller companies that apply full IFRS. 11

12 IFRS 16: HIGH LEVEL SUMMARY Lessor Accounting Substantially carries forward the lessor accounting requirements in IAS 17, except disclosures which are enhanced now. Accordingly, a lessor continues to classify its leases as operating leases or finance leases, and to account for those two types of leases differently. Lessee Accounting Eliminates the classification of leases as either operating leases or finance leases as is required by IAS 17 for lessee. Introduces a single lessee accounting model whereby lessee accounts for all leases in same way. Applying single lease model, a lessee is required to recognise: ü assets and liabilities for all leases except (a) leases with a term of less than 12 months or (b), the underlying asset of low value; and ü depreciation of lease assets separately from interest on lease liabilities in the income statement. 12

13 EXPECTED IMPACT: HIGH LEVEL SUMMARY Statement of Financial Position Impact : How will it change? IAS 17 IFRS 16 Finance lease Operating lease All Leases Assets XXX XXX Liabilities XXX XXX Total XXX XXX Off balance sheet rights/obligation XXX Total Balance Sheet (B/S) Size will increase due to off B/S exposures getting recognised as on B/S assets and liabilities. 13

14 EXPECTED IMPACT: HIGH LEVEL SUMMARY Statement of Profit and Loss How will it change? IAS 17 IFRS 16 Finance lease Operating lease All Leases Revenue xxx xxx xxx Operating costs (excluding depreciation and amortisation) EBITDA --- xxx Single expense Depreciation and amortisation Depreciation --- Depreciation Operating profit Finance costs Interest --- Interest Profit before tax Net Profit/Loss is not expected to change significantly for many companies BUT Expense Line items, EBIDTA and Operating Profit/Loss will change due to reclassification of expenses. 14

15 EXPECTED IMPACT: HIGH LEVEL SUMMARY Statement of Cash Flows: How will it change? Operating Activities Investing Activities IAS 17 IFRS 16 Finance lease Operating lease All Leases Financing Activities XXX XXX (Interest + Principal Payments) XXX Net Cash Flows XXX XXX Net Cash flows will not change BUT cash flows from Operating Activities will improve and Financing Activities will increase. 15

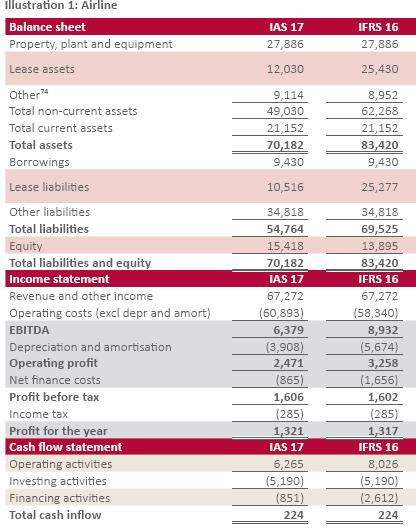

16 EXPECTED SIGNIFICANT IMPACT OF IFRS 16 A comparative analysis of IFRS 16 vs. IAS 17 in case of Airline Company is given in the next slide. 16

17 17

18 IMPACT ON P&L IFRS 16 VS IAS 17 COMPANY S EXPENSE IN $ 1,40,000 1,20,000 1,00,000 80,000 60,000 40,000 1,19,401 1,15,842 1,12,035 49,165 45,607 41,799 1,07,961 37,725 1,03,602 33,366 98,937 93,946 28,701 23,710 Depreciation expense under new standard Interest expense under new standard Column1 88,606 18,370 82,892 12,656 76,778 70,236 70,236 70,236 70,236 70,236 70,236 70,236 70,236 70,236 70,236 RENT EXPENSE in IAS 17 6,542 20, YEAR ASSUMPTIONS: YEAR LEASE 2. RENT OF $100,000 PER ANNUM 3. DISCOUNT RATE OF 7% 18

19 PRESENTATION Balance sheet under current IAS 17 Inception Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10 Assets Liabilities Balance sheet under IFRS 16 Right of use asset $702,358 $632,122 $561,887 $491,651 $421,415 $351,179 $280,943 $210,707 $140,472 $70,236 $0 Lease liability ($702,358) ($651,523) ($597,130) ($538,929) ($476,654) ($410,020) ($338,721) ($262,432) ($180,802) ($93,458) $0 Net equity $0 ($19,401) ($35,243) ($47,278) ($55,239) ($58,841) ($57,778) ($51,724) ($40,330) ($23,222) $0 Income statement under IAS 17 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10 Operating lease expense 100, , , , , , , , , ,000 Income statement under IFRS 16 Amortisation expense $70,236 $70,236 $70,236 $70,236 $70,236 $70,236 $70,236 $70,236 $70,236 $70,236 Interest expense $49,165 $45,607 $41,799 $37,725 $33,366 $28,701 $23,710 $18,370 $12,656 $6,542 Total expense $119,401 $115,842 $112,035 $107,961 $103,602 $98,937 $93,946 $88,606 $82,892 $76, Difference (19,401) (15,842) (12,035) (7,961) (3,602) 1,063 6,054 11,394 17,108 23,222

20 LEASE : IFRS 16 DEFINES LEASE AS: A contract is, or contains, a lease if the contract conveys the right to control the use of an identified asset for a period of time in exchange for consideration. Right to control the use Right to obtain substantially all of economic benefits from use of identified asset through out the period of use; and Right to direct the use of identified asset through out the period of use. Identified Asset Specified EXPLICITLY - e.g., Specific serial number Specified IMPLICITLY - Only one asset available that is capable of being used to meet the contract terms. Portions of Assets - a portion of a bigger asset is an identified asset if it is physically distinct. eg: a floor of a building could be an identified asset. Substantive substitution rights If the supplier has a substantive right to substitute asset, there is no identified asset and no lease. Supplier has practical ability to substitute - eg: alternative assets are readily available and customer cannot prevent the substitution and Supplier would benefit economically from substituting - ie: benefits of substituting exceed costs. 20

21 PARTY THAT DIRECTS THE USE The determination of which party directs the use of the underlying asset may require judgement. Decisions regarding operating an asset are generally about the decisions about how and for what purpose an asset is used. In certain types of contracts the entity and the supplier, both may have some involvement in deciding how and for what purpose the asset is used. Therefore, the determination of which party directs the use of the underlying asset may require judgement. 21

22 SEPARATING COMPONENTS OF CONTRACT Lease component allocate consideration Non-lease (service) component Lessee: Allocate consideration on basis of relative stand-alone price. Estimation is permitted - relative stand-alone prices is not readily available. Optional practical expedient: account for a lease component and non-lease components as a single lease component. Lessor: Allocate the consideration based on requirements of IFRS 15 (paragraphs 73-90) relative stand-alone selling prices. When to separate components? a)lessee can benefit from use of asset on its own or with other resources readily available b) Items are neither highly dependent nor high interrelated 22

23 LEASE RECOGNITION BY LESSEE A. Recognition: At commencement date, recognise a right-of-use asset and a lease liability. B. Recognition exemptions: Two major optional exemptions Short term months lease term 2. apply by class of underlying asset 3. not applies to lease containing purchase option Leases of low value assets 1. apply to leases for which underlying asset is of low value 2. apply on a lease by lease basis 3. for e.g., tablet, personal computers, etc. Low value asset exemption applies: to underlying asset when new on an absolute basis irrespective of materiality Low value asset exemption cannot be applied: to head lease in case of subleases if the nature of the underlying asset, when new, is not typically low value 23

24 LEASE LEASE TERM The lease term begins at the commencement date and includes any rentfree periods provided to the lessee by the lessor. Lease term is determined together with periods covered by option to terminate or extend the lease term if lessee is reasonably certain to do so. After the commencement date, a lessee needs to reassess the lease term upon the occurrence of a significant event or change in circumstances that is within the control of lessee 24

25 LEASE MEASUREMENT BY LESSEE Right-ofuse Asset Lease liability Initial Measurement At cost which comprises the amount of the lease liability lease prepayments, less lease incentives received lessee s initial direct costs estimate of restoration, removal and dismantling costs Present value of unpaid lease payments (discounted using interest rate implicit in the lease if readily determinable; otherwise, incremental borrowing rate) which include following Fixed payments (including in-substance fixed payments) Variable lease payments that depend on index or rate Residual value guarantees Exercise price of purchase options Termination penalties Subsequent Measurement Cost model unless entity applies Revaluation model under IAS 16. Measured by Increasing carrying amount to reflect interest on lease liability; Reducing carrying amount to reflect lease payments made; and Re-measuring carrying amount to reflect any reassessment or lease modifications or to reflect revised insubstance fixed lease payments 25

26 LEASE PRESENTATION BY LESSEE Present in Balance Sheet or disclose in notes Right-of-use assets separately from other assets. If not disclosed separately, including right-of-use assets within the same line item within which the corresponding underlying assets would be presented if they were owned and disclose which line items in balance sheet include those right-of-use assets. Lease liabilities separately from other liabilities. If not disclosed separately, disclose which line items in the balance sheet include lease liabilities. Present in Statement of profit and loss Interest expense on the lease liability separately from the depreciation charge for the right-of-use asset. Interest expense on the lease liability as a component of finance costs, which as per IAS 1, Presentation of Financial Statements, requires to be presented separately in the statement of profit or loss. Classify under Statement of Cash Flows Cash payments for the principal portion of the lease liability within financing activities; Cash payments for the interest portion of the lease liability applying the requirements in IAS 7 Statement of Cash Flows for interest paid; and Short-term lease payments, payments for leases of low-value assets and variable lease payments not included in the measurement of the lease liability within operating activities. 26

27 LEASE MODIFICATION BY LESSEE Modifications accounted as a separate lease if: it increases the scope of the lease by adding the right to use one or more underlying assets; and the consideration for the lease increases by an amount commensurate with the stand-alone price for the increase in scope. If modification not accounted as a separate lease at the effective date of lease modification, lessee shall: (a) allocate consideration between lease and non-lease component (b) determine the lease term of modified lease (c) remeasure the lease liability by discounting the revised lease payments using a revised discount rate and accounting it as follows: Modification decreasing the scope of lease ü Decrease carrying amount of right-of-use asset to reflect partial or full termination ü Recognise any gain or loss in profit or loss For other modification (say lease rentals change) ü Make corresponding adjustment to carrying amount of right-of-use asset ü Adjust lease liability to reflect re-measurement 27

28 LEASE : SALE AND LEASE BACK If an entity (the seller-lessee) transfers an asset to another entity (the buyer-lessor) and leases that asset back from the buyer-lessor, both the seller-lessee and the buyer-lessor shall account for the transfer contract and the lease Determine whether transfer of asset is sale or not as per IFRS 15 when a performance obligation is satisfied. If transfer of asset is a sale- Seller lessee - measure right-of-use asset at the proportion of the previous carrying amount that relates to right-of-use retained by the seller-lessee. Hence, gain/loss recognised to the extent of rights transferred to the buyer-lessor. Buyer Lessor- account for purchase of asset with reference to applicable standards and for lease apply this standard. If transfer of asset is not a sale- Seller lessee - continue to recognise transferred asset and recognise financial liabilities equal to transfer proceeds applying IFRS 9 Buyer Lessor - transferred asset not recognised - recognise financial asset at amount equal to transfer proceeds applying IFRS 9 28

29 LEASES : DISCLOSURES (EMPHASIS HERE IS ON NEW DISCLOSURES) Lessee : IFRS 16 includes an overall disclosure objective, and requires a company to disclose: (a) Qualitative and quantitative information about nature of leasing activities assets and expenses and cash flows related to leases (link to IFRS 7 removed) except for maturity analysis of lease liabilities) ; and (b) IFRS 16 requires to disclose fact that lease is accounted for as short term leases or leases of low value assets. Lessor : IFRS 16 requires enhanced disclosures as follows and de-links these from IFRS 7 Nature or leasing activities and risk management Maturity analysis buckets changed- on annual basis for each of first 5 years & total for remaining years Disclosure of different components income- lease income and variable payments & separately for those not linked to indexes or rates 29

30 LEASES: EFFECTIVE DATE AND TRANSITION Effective Date IFRS 16 is applicable for annual reporting periods beginning on or after 1 st January, Transition Definition of lease An entity is not required to reassess whether a contract is, or contains, a lease at the date of initial application. Instead, permitted to ü Apply IFRS 16 to contracts that were previously identified as leases applying IAS 17, Leases ü Apply IFRS 16 lease IDENTIFICATION requirements only to contracts entered into after the date of transition Lessor: No adjustments on transition for leases and account for leases applying IFRS 16 from the date of initial application. 30

31 LEASES: EFFECTIVE DATE AND TRANSITION CONTD... Lessee Decide following transition method Shall apply the method consistently to all of its leases in which it is a lessee. Full retrospective application: Apply IAS 8 Prepare financial statements as if IFRS 16 had always been applied Restate comparative information Disclose effect on each line item Cumulative catch-up: Recognise cumulative effect of initial application as an adjustment to the opening balance of retained earnings or other component of equity Do not restate comparative information Disclose effect of applying cumulative catch-up approach 31

32 LEASES: EFFECTIVE DATE AND TRANSITION CONTD... Cumulative catch-up approach to: Leases previously classified as operating leases Recognise lease liability measured at the present value of the remaining lease payments, discounted using the lessee s incremental borrowing rate at the date of initial application. Recognise a right-of-use asset at the date of initial application by measuring either a) its carrying amount as if the IFRS 16 had been applied since the commencement date, but discounted using the lessee s incremental borrowing rate at the date of initial application; or b) an amount equal to the lease liability, adjusted by the amount of any prepaid or accrued lease payments relating to that lease recognised in the balance sheet immediately before the date of initial application Leases previously classified as finance leases Carrying amount of the lease asset and lease liability measured applying IAS 17 shall become the carrying amount of the right-of-use asset and the lease liability at the date of initial application. 32

33 ISSUE : FOREIGN CURRENCY LEASE LIABILITY As a financial liability, lease liability if denominated in foreign currency is affected by foreign currency risk exposure. There is no specific requirement in IFRS 16 relating to effects of foreign currency exchange differences of lease liabilities denominated in a foreign currency. Accordingly, foreign currency exchange differences on lease liability are required to be recognised in profit or loss applying IAS 21. Issue: Recognition of foreign currency exchange differences on lease liability in profit or loss applying IAS 21 would bring volatility in profit or loss. 33

34 ISSUE : FOREIGN CURRENCY LEASE LIABILITY CONTD... Solution: Reasons for recognition of foreign currency exchange differences relating to lease liabilities in profit or loss are as follows: it is consistent with the requirements of IAS 21 for foreign exchange differences arising from other financial liabilities. it represent the economic effect of the lessee s currency exposure to the foreign exchange risk. it matches with the accounting followed by lessee entering into derivatives to hedge its exposure to foreign currency risk. subsequent changes to a foreign exchange rate should not have any effect on the cost of a non-monetary item. Consequently, it would be inappropriate to include such changes in the re-measurement of the right-of-use asset. 34

35 ISSUE : DUAL ACCOUNTING Issue: IFRS 16 requires single lease model for Lessee and accordingly Right-to-Use asset needs to be capitalised in the books of Lessee on the basis of control concept. Presentation of leased assets and liabilities in the books of lessee amounts to double accounting. Retaining dual lease model in the books of the Lessor is not appropriate. For example, in case of an arrangements which are considered as Operating leases (as per IAS 17), Lessee has to capitalise Right-to-use asset like other non-financial liabilities and Lessor also records the asset which is given to lessee on lease as other non-financial asset like Property, Plant and Equipment. In the case both lessor and lessee is capitalizing the asset and recording depreciation in Profit and loss. Response: It is not mandatory to have full mirror accounting in the books of lessor and lessee. In such cases, generally asset is obtained on lease for part of its useful life and lessee recognises right-to-use only for that portion. De-recognition of asset for part of the useful life by the lessor is not appropriate. Accordingly, recognition of asset in books of both i..e. lessor and lessee is appropriate. 35

36 ISSUE : IMPACT ON KEY FINANCIAL RATIOS Issue: EBITDA ratios will be impacted because : ü under IFRS 16 operating lease expense previously recorded on a straight line basis will be recorded as depreciation of the right-of-use asset and interest incurred on the lease liability. ü these changes to the income statement affect both the timing and nature of lease expense, which may have significant impacts to financial KPIs (key performance indicators) Solution: Under IFRS 16, pricing models may need to be adjusted if they are based on EBITDA because the new standard will have the effect of making EBITDA higher. 36

37 ISSUE : INCOME TAX IMPLICATIONS Issue: IFRS 16 may have a broad impact on the tax treatment of leasing transactions, as tax accounting for leasing is often based on accounting principles. Given that there is no uniform leasing concept for tax purposes, the effect of the proposed lease accounting model will vary significantly, depending on the tax jurisdiction. In some jurisdictions IFRS principles and/or IFRS financial statements may be relevant for determining certain tax thresholds (e.g. in the Netherlands and UK). Items that may be impacted include the applicable depreciation rules, specific rules limiting the tax deductibility of interest (for example, thin capitalisation rules for debt versus equity, percentage of EBITDA rules), and existing transfer pricing agreements, sales/indirect taxes and existing leasing tax structures (in territory and cross-border leases). Solution: A reassessment of existing and proposed leasing structures should be performed against the new standard to ensure continued tax benefits and/or management of (new) tax risks on the horizon. 37

38 ISSUE : SEPARATING LEASE AND NON- LEASE COMPONENT Issue: For contracts with multiple components, entities are required to identify and separate nonlease components (e.g., operations, maintenance services) from the lease component. Today, many entities may not focus on identifying the distinct components because their accounting treatment (i.e., the accounting for an operating lease and a service contract) is often the same. IFRS 16 does also allows lessees to recognise the lease and non-lease components as a single lease component on the balance sheet, but that would have the effect of increasing the lease obligation on the balance sheet. Solution: Lessees may find that policy attractive when the non-lease components are not a significant aspect of the arrangement. Therefore, lessees that do not elect to combine lease and non-lease components may need to put robust processes in place to identify and account for the separate components if they wish to minimise the impact of IFRS 16 on their balance sheets. 38

39 ISSUE : LEASE PAYMENTS DEPENDENT ON RATE/INDEX Issue: Lease liability to be re-measured for lease payments dependent on rate/index Standard prescribes re-measurement of the lease liability every time there is a change in the cash flows resulting from change in index/rate and to recognise the corresponding effect in right-of-use asset. In case of multiple assets on lease, lease payments may have to re-measured very frequently. Solution: Systems can be developed to re-measure the ROU and lease liability to reflect the impact of change in index. It is conceptually better as index related inflation is accounted for appropriately. 39

40 ISSUE : RECOGNITION OF SECURITY DEPOSITS Issue: On or before the date of commencement of a lease, sometimes lessee is required give interest free security deposit to the lessor. There are situations in which as per lease agreements such security deposits are for material amount and may result into lower lease rentals. Solution: Security deposit does not meet the definition of a lease payment under IFRS 16 because it is not a payment relating to the right to use the underlying asset Security deposit of this nature should be accounted for as a financial asset because it is collateral provided to the lessor. Security deposit be recognised initially at fair value in accordance with IFRS 9 Financial Instruments and will normally be measured subsequently at amortised cost, resulting in the recognition of interest revenue over the lease term for the difference between the fair value at the commencement of the lease and its nominal amount receivable at the end of the lease term. 40

41 ISSUE : RECOGNITION OF SECURITY DEPOSITS CONTD... Solution: The difference between the nominal amount of the deposit and its fair value at the commencement of the lease represents, in effect, an additional lease payment which is prepaid. Consequently, it is added to the initial carrying amount of the right-of-use asset in accordance with IFRS 16:24(b) and recognised in profit or loss over the lease term as part of the depreciation of that asset. 41

42 ISSUE : OTHER ISSUES Issue: Identifying embedded leases is the most common challenge Solution: IFRS 16 provides guidance and illustrative examples. However, the same needs to applied carefully. Issue: Establishing an appropriate Incremental Borrowing Rate (IBR): Because the interest rate implicit in a lease is often difficult to obtain by a lessee, many lessees are turning to an incremental borrowing rate instead. But determining the IBR requires significant judgment. Solution: Calculating IBR will be a recurring requirement in the future so it is essential that the process for estimating it is sound and aligns to the objective of the leases standards. With regard to tackling the IBR challenge specifically, the following may be possible ü to plan internally estimate of the IBR for each lease ü to obtain direct quotes from a lender. ü to hire a third party to help them estimate the IBR. 42

43 ISSUE : OTHER ISSUES CONTD... Issue: Integrating a lease accounting system into the existing IT system environment. Solution: Lessees need to identify system gaps and changes that may be needed in their IT environment. Entities need to implement sustainable lease software solutions that are capable of dealing with the new lease accounting requirements. 43

44 Appendix: Few Examples 44

45 LEASE : IDENTIFICATION (Source : IFRS 16 Leases Illustrative Examples) Example 1A : Rail Cars Contract between customer and freight carrier (supplier) that provides customer with the use of 10 rail cars of a particular type for five years. Customer determines when, where and which goods are to be transported using the cars. Rails cars when not in use are kept at customer s premises. Customer can use the cars for another purpose (for example, storage) if it so chooses. However, the contract specifies that Customer cannot transport particular types of cargo (for example, explosives). The contract also requires Supplier to provide an engine and a driver when requested by Customer. Supplier can choose to use any one of a number of engines to fulfil each of Customer s requests, and one engine could be used to transport goods of other customers but within a similar timeframe, Supplier can choose to attach up to 100 rail cars to the engine). Supplier can substitute the rail cars only for service or repair and nothing else. Right to control use of the asset Identified asset No Substitution right Contract contains lease of rail cars. Provision of engine and driver is not a lease contract. 45

46 LEASE : IDENTIFICATION (Source : IFRS 16 Leases Illustrative Examples) Example 1B : Rail Cars The contract between Customer and Supplier requires Supplier to transport a specified quantity of goods by using a specified type of rail car in accordance with a stated timetable for a period of five years. The timetable and quantity of goods specified are equivalent to Customer having the use of 10 rail cars for five years. Supplier has a large pool of similar rail cars that can be used to fulfil the requirements of the contract. Similarly, Supplier can choose to use any one of a number of engines to fulfil each of Customer s requests, and one engine could be used to transport not only Customer s goods, but also the goods of other customers. The contract also requires Supplier to provide an engine and a driver when requested by Customer. Supplier keeps the engines at its premises and provides instructions to the driver detailing Customer s requests to transport goods. Right to control use of the asset Identified asset No Substitution right Contract does not contain lease of rail cars nor engines 46

47 LEASE : IDENTIFICATION (Source : IFRS 16 Leases Illustrative Examples) Example 2A : Concession Space A coffee company (Customer) enters into a contract with an airport operator (Supplier) to use a space in the airport to sell its goods for a three-year period. The contract states the amount of space and that the space may be located at any one of several boarding areas within the airport. There are many areas in the airport that are available and that would meet the specifications for the space in the contract. Supplier has the right to change the location of the space allocated to Customer at any time during the period of use. There are minimal costs to Supplier associated with changing the space for the Customer: Customer uses a kiosk (that it owns) that can be moved easily to sell its goods. Right to control use of the asset Identified asset No Substitution right Contract does not contain lease 47

48 LEASE : IDENTIFICATION (Source : IFRS 16 Leases Illustrative Examples) Example 2B : Concession Space Retail Outlet in a Shopping Mall Customer enters into a contract with a property owner (Supplier) to use Retail Unit A ( part of a larger space) for a five-year period to operate its well-known store brand to sell its goods during the hours that the larger retail space is open. Customer makes all of the decisions about the use of the retail unit during the period of use. Supplier can require Customer to relocate to another retail unit. In that case, Supplier is required to provide Customer with a retail unit of similar quality and specifications to Retail Unit A and to pay for Customer s relocation costs. Supplier would benefit economically from relocating Customer only if a major new tenant were to decide to occupy a large amount of retail space at a rate sufficiently favourable to cover the costs of relocating Customer and other tenants in the retail space. However, although it is possible that those circumstances will arise, at inception of the contract, it is not likely that those circumstances will arise. Right to control use of the asset Identified asset No Substitution right Contract contains lease of Retail Unit Space. (for supplier it is not economically beneficial to substitute space) 48

49 SHARED CAPACITY In BC 116, it is concluded that a customer is unlikely to have the right to control the use of a capacity portion of a larger asset if that portion is not physically distinct (for example, if it is a 20 per cent capacity portion of a pipeline). customer is unlikely to have the right to control the use of its portion because decisions about the use of the asset are typically made at the larger asset level. Consequently, the IASB concluded that widening the definition to include capacity portions of a larger asset would increase complexity for little benefit. Issue: whether situations like shared capacity of network services etc will be considered as service contracts and not a lease which is change compared to existing practice? M P VIjay Kumar 49

50 LEASE : SALE AND LEASE BACK (Source : IFRS 16 Leases Illustrative Examples) An entity (Seller-lessee) sells an Aircraft to another entity (Buyer-lessor) for cash of CU1,800,000 which had book carrying amount of CU 1,000,000. It leases back the aircraft for 18 years under operating lease with annual instalment of CU 105,000. Interest rate implicit in the lease if 4.5%. Present Value of 18 annual payments will be CU 1,276,800. Now the calculation of gain/loss on sale and lease back and measurement amount for recognition of Right of Use and Financial Liability is as follows. IAS 17 IFRS 16 Sale Value 1,800,000 ROU as proportion to the previous carrying amount Carrying Value 1,000,000 1,000,000/1,800,000 x 1,276,800 = 709,333 Gain to be recognised immediately, sale is at fair value 800,000 Gain/loss relating to the ROU transferred 800,000 / 1,800,000 x (1,800,000-1,276,800) = 232,533 Dr Cash 1,800,000 Dr ROU 709,333 Cr PPE Air Craft 1,000,000 Cr Financial Liability 1,276,800 Cr Gain on sale /lease back 232,533 50

51 MY TAKE ON WINDS OF CHANGE Data is connected from the source to the ledger via cloud-based applications. Accounting is morphing into what economists call "interaction jobs", where technical knowledge is assumed and higher value is applied to a person's ability to interact with internal and external clients, identify problems, come up with alternative solutions, determine which are affordable at this point in time and communicate and influence to deliver an outcome. The successful accountants of the future will be strong communicators, possess greater IT skills combined with strategic vision and they will be devoted to ongoing professional development. Globalisation is the future of accounting as more and more businesses require real-time manufacturing and information, mobile marketing and online tools, including the cloud, to expand their customer base internationally. Thus accounting, auditing and finance professionals with knowledge of international standards and regulations will thrive. ICAI is geared to this reality and 32 overseas chapters of ICAI is a testimony apart from embracing International accounting and assurance standards. Indian Chartered Accountants, thanks to the rigorous training and enviable forward looking curriculum, possess right insights and foresight to overcome challenges and make the best use of the opportunities. 51

52 COMPARISON WITH US GAAP US GAAP and IFRS requires recognition and measurement of leases in similar manner with certain minor differences, such as: IFRS 16 allows companies to exclude leases of low-value assets considering these would be immaterial while US GAAP does not allow the same. Treatment with regard to former leases classified as operating leases is different Ø Ø IFRS requires single lease model i.e. all leases to be recognised in the same manner US GAAP requires dual lease model i.e. to continue with the previous classification and to account for the same differently. Under IFRS inflation-linked payments are reassessed when those payments change while under US GAAP these are not reassessed. 5 2

53 COMPARISON WITH US GAAP Differences with regard to disclosures Ø IFRS 16 does not include prescriptive qualitative disclosures requirements and requires companies to determine the information that would satisfy those objectives. Ø Under US GAAP specific qualitative items are required to be disclosed, e.g., terms and conditions of extension and termination options in leases. Ø It is expected that information disclosed about features in leases, such as, extension and termination options, will be different 5 3

54 Follow ICAI on Social Media

In December 2003 the IASB issued a revised IAS 17 as part of its initial agenda of technical projects.

IFRS Standard 16 Leases In April 2001 the International Accounting Standards Board (IASB) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

IFRS Standard 16 Leases In April 2001 the International Accounting Standards Board (IASB) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

IFRS 16 LEASES. Page 1 of 21

IFRS 16 LEASES OBJECTIVE The objective is to ensure that lessees and lessors provide relevant information in a manner that faithfully represents those transactions. This information gives a basis for users

IFRS 16 LEASES OBJECTIVE The objective is to ensure that lessees and lessors provide relevant information in a manner that faithfully represents those transactions. This information gives a basis for users

International Financial Reporting Standard 16 Leases. Objective. Scope. Recognition exemptions (paragraphs B3 B8) IFRS 16

IFRS 16") International Financial Reporting Standard 16 Leases Objective 1 This Standard sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective is to ensure

International Financial Reporting Standard 16 Leases Objective 1 This Standard sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective is to ensure

New Zealand Equivalent to International Financial Reporting Standard 16 Leases (NZ IFRS 16)

") New Zealand Equivalent to International Financial Reporting Standard 16 Leases (NZ IFRS 16) Issued February 2016 This Standard was issued on 11 February 2016 by the New Zealand Accounting Standards Board

New Zealand Equivalent to International Financial Reporting Standard 16 Leases (NZ IFRS 16) Issued February 2016 This Standard was issued on 11 February 2016 by the New Zealand Accounting Standards Board

In December 2003 the Board issued a revised IAS 17 as part of its initial agenda of technical projects.

IFRS 16 Leases In April 2001 the International Accounting Standards Board (the Board) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

IFRS 16 Leases In April 2001 the International Accounting Standards Board (the Board) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

New leases standard ASC 842 Lessee - operating leases. Itai Gotlieb, Partner, Professional Practice July 2017

ASC 842 Lessee - operating leases Itai Gotlieb, Partner, Professional Practice July 2017 Overview Under Accounting Standards Codification (ASC) 842, Leases, lessees recognize assets and liabilities for

ASC 842 Lessee - operating leases Itai Gotlieb, Partner, Professional Practice July 2017 Overview Under Accounting Standards Codification (ASC) 842, Leases, lessees recognize assets and liabilities for

Gearing up for change New IFRS on Leases

Gearing up for change New IFRS on Leases In a nutshell The changes Lessee accounting Effective date: 1 January 2019 Limited changes to scope of IAS 17 Enhanced guidance on identifying a lease Lessor accounting

Gearing up for change New IFRS on Leases In a nutshell The changes Lessee accounting Effective date: 1 January 2019 Limited changes to scope of IAS 17 Enhanced guidance on identifying a lease Lessor accounting

Applying IFRS in consumer products and retail

Applying IFRS in consumer products and retail Leases standard Consumer products and retail Updated June 2017 Contents Overview 2 1. Identifying a lease 3 1.1 Definition of a lease 3 1.2 Identified asset

Applying IFRS in consumer products and retail Leases standard Consumer products and retail Updated June 2017 Contents Overview 2 1. Identifying a lease 3 1.1 Definition of a lease 3 1.2 Identified asset

Headline Verdana Bold The evolutions of leases accounting under IFRS 16 Mariano Bruno, Carlo Laganà, Giuseppe Ambrosio, Deloitte & Touche S.p.A.

SHIPPING AND THE LAW 7^ Edition 25-26 October 2016 NAPLES Headline Verdana Bold The evolutions of leases accounting under IFRS 16 Mariano Bruno, Carlo Laganà, Giuseppe Ambrosio, Deloitte & Touche S.p.A.

SHIPPING AND THE LAW 7^ Edition 25-26 October 2016 NAPLES Headline Verdana Bold The evolutions of leases accounting under IFRS 16 Mariano Bruno, Carlo Laganà, Giuseppe Ambrosio, Deloitte & Touche S.p.A.

A Review of IFRS 16 Leases By Tan Liong Tong

A Review of IFRS 16 Leases By Tan Liong Tong In April 2016, the MASB issued MFRS 16 Leases that is identical to IFRS 16 Leases issued by the IASB in January 2016. The effective date of this new MFRS is

A Review of IFRS 16 Leases By Tan Liong Tong In April 2016, the MASB issued MFRS 16 Leases that is identical to IFRS 16 Leases issued by the IASB in January 2016. The effective date of this new MFRS is

Exposure Draft. Indian Accounting Standard (Ind AS) 116 Leases. (Last date for Comments: August 31, 2017)

116 Leases. (Last date for Comments: August 31, 2017)") ED/Ind AS/2017/06 Exposure Draft Indian Accounting Standard (Ind AS) 116 Leases (Last date for Comments: August 31, 2017) Issued by Accounting Standards Board The Institute of Chartered Accountants of

ED/Ind AS/2017/06 Exposure Draft Indian Accounting Standard (Ind AS) 116 Leases (Last date for Comments: August 31, 2017) Issued by Accounting Standards Board The Institute of Chartered Accountants of

IFRS 16 Leases supplement

IFRS 16 Leases supplement Guide to annual financial statements IFRS December 2017 kpmg.com/ifrs Contents About this supplement 1 About IFRS 16 3 The Group s lease portfolio 6 Part I Modified retrospective

IFRS 16 Leases supplement Guide to annual financial statements IFRS December 2017 kpmg.com/ifrs Contents About this supplement 1 About IFRS 16 3 The Group s lease portfolio 6 Part I Modified retrospective

IFRS Project Insights Leases

IFRS Project Insights Leases The IASB and FASB ( the Boards ) published a Discussion Paper (DP) setting out a proposed lessee accounting model in March 2009. The proposed accounting model has evolved since

IFRS Project Insights Leases The IASB and FASB ( the Boards ) published a Discussion Paper (DP) setting out a proposed lessee accounting model in March 2009. The proposed accounting model has evolved since

HKFRS 16 Leases sets out the principles for the recognition, measurement, presentation and disclosure

HKFRS 16 Leases Introduction HKFRS 16 Leases sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective of HKFRS 16 is to ensure that lessees and lessors

HKFRS 16 Leases Introduction HKFRS 16 Leases sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective of HKFRS 16 is to ensure that lessees and lessors

The New Lease Accounting Standard. Hunter Mink, CPA, CCIFP Brian Rosenberg, CPA, MBA

The New Lease Accounting Standard Hunter Mink, CPA, CCIFP Brian Rosenberg, CPA, MBA 1 Agenda Introduction Lease Identification and Classification Lessee Accounting Other Considerations Disclosures Impact

The New Lease Accounting Standard Hunter Mink, CPA, CCIFP Brian Rosenberg, CPA, MBA 1 Agenda Introduction Lease Identification and Classification Lessee Accounting Other Considerations Disclosures Impact

The new IFRS 16 Leases effective as of 1 January 2019

The new IFRS 16 Leases effective as of 1 January 2019 IFRS 16 was issued by IASB on 13 January 2016. The Standard is effective as of 1 January 2019. It has not yet been adopted by the EC. This is a Standard

The new IFRS 16 Leases effective as of 1 January 2019 IFRS 16 was issued by IASB on 13 January 2016. The Standard is effective as of 1 January 2019. It has not yet been adopted by the EC. This is a Standard

Sri Lanka Accounting Standard - SLFRS 16. Leases

Sri Lanka Accounting Standard - SLFRS 16 Leases CONTENTS from paragraph SRI LANKA ACCOUNTING STANDARD - SLFRS 16 LEASES INTRODUCTION OBJECTIVE 1 SCOPE 3 RECOGNITION EXEMPTIONS 5 IDENTIFYING A LEASE 9 Separating

Sri Lanka Accounting Standard - SLFRS 16 Leases CONTENTS from paragraph SRI LANKA ACCOUNTING STANDARD - SLFRS 16 LEASES INTRODUCTION OBJECTIVE 1 SCOPE 3 RECOGNITION EXEMPTIONS 5 IDENTIFYING A LEASE 9 Separating

FASB/IASB Update Part II

American Accounting Association FASB/IASB Update Part II Tom Linsmeier FASB Member August 3, 2014 The views expressed in this presentation are those of the presenters. Official positions of the FASB/IASB

American Accounting Association FASB/IASB Update Part II Tom Linsmeier FASB Member August 3, 2014 The views expressed in this presentation are those of the presenters. Official positions of the FASB/IASB

Applying IFRS in Financial Services

Applying IFRS in Financial Services IASB issues new leases standard - financial services April 2016 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition of a lease

Applying IFRS in Financial Services IASB issues new leases standard - financial services April 2016 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition of a lease

International GAAP Holdings Limited Model financial statements for the year ended 31 December 2017 (With early adoption of IFRS 16)

") International GAAP Holdings Limited Model financial statements for the year ended 31 December 2017 (With early adoption of IFRS 16) Appendix 1: Early application of IFRS 16 Leases Introduction This Appendix

International GAAP Holdings Limited Model financial statements for the year ended 31 December 2017 (With early adoption of IFRS 16) Appendix 1: Early application of IFRS 16 Leases Introduction This Appendix

Applying IFRS. A closer look at the new leases standard. August 2016

Applying IFRS A closer look at the new leases standard August 2016 Contents Overview 3 1. Scope and scope exceptions 5 1.1 General 5 1.2 Determining whether an arrangement contains a lease 6 1.3 Identifying

Applying IFRS A closer look at the new leases standard August 2016 Contents Overview 3 1. Scope and scope exceptions 5 1.1 General 5 1.2 Determining whether an arrangement contains a lease 6 1.3 Identifying

IASB issues new leases standard consumer products and retail

Applying IFRS in consumer products and retail IASB issues new leases standard consumer products and retail June 2016 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition

Applying IFRS in consumer products and retail IASB issues new leases standard consumer products and retail June 2016 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition

Summary of IFRS Exposure Draft Leases

The International Accounting Standards Board (IASB) recently issued a revised exposure draft (ED) relating to leases. Once these proposals are finalized the new guidance will replace the IAS 17 Leases.

The International Accounting Standards Board (IASB) recently issued a revised exposure draft (ED) relating to leases. Once these proposals are finalized the new guidance will replace the IAS 17 Leases.

IFRS 16 Lease overview and EY s enabling toolkit

IFRS 16 Lease overview and EY s enabling toolkit Content Page Section I IFRS 16 overview 2 Appendix I EY Lease enabling technology suite 9 Appendix II EY Contacts 17 Page 1 IFRS 9 Classification and measurement

IFRS 16 Lease overview and EY s enabling toolkit Content Page Section I IFRS 16 overview 2 Appendix I EY Lease enabling technology suite 9 Appendix II EY Contacts 17 Page 1 IFRS 9 Classification and measurement

Edison Electric Institute and American Gas Association New Lease Standard

Edison Electric Institute and American Gas Association New Lease Standard May 16, 2016 Disclaimer The information contained herein is of a general nature and is not intended to address the circumstances

Edison Electric Institute and American Gas Association New Lease Standard May 16, 2016 Disclaimer The information contained herein is of a general nature and is not intended to address the circumstances

IFRS 16 Leases. PICPA IFRS: New Standards and Updates Dubai. 28 April 2017

IFRS 16 Leases PICPA IFRS: New Standards and Updates Dubai 28 April 2017 1 More transparent lease accounting IFRS 16 will bring most leases on-balance sheet from 2019. All companies that lease assets for

IFRS 16 Leases PICPA IFRS: New Standards and Updates Dubai 28 April 2017 1 More transparent lease accounting IFRS 16 will bring most leases on-balance sheet from 2019. All companies that lease assets for

HKFRS 16 Leases. Disclaimer. Date 21 April 2017 Time 19:00 21:00 Venue Boys' and Girls' Clubs Association

HKFRS 16 Leases Date 21 April 2017 Time 19:00 21:00 Venue Boys' and Girls' Clubs Association www.zhtraining.com Disclaimer The materials of this seminar are intended only to provide general information

HKFRS 16 Leases Date 21 April 2017 Time 19:00 21:00 Venue Boys' and Girls' Clubs Association www.zhtraining.com Disclaimer The materials of this seminar are intended only to provide general information

AASB 16: Experience the Fundamental Overhaul of Lease Accounting for Lessees

AASB 16: Experience the Fundamental Overhaul of Lease Accounting for Lessees Introduction to Session This introductory session we will: Explore the Principles of AASB 16 Learn how to Identify a Lease Work

AASB 16: Experience the Fundamental Overhaul of Lease Accounting for Lessees Introduction to Session This introductory session we will: Explore the Principles of AASB 16 Learn how to Identify a Lease Work

IFRS Link. Contents. Newsletter. 1 IASB 11 EU Endorsement

IFRS Link Newsletter Issue 25 Contents 1 IASB 11 EU Endorsement New standard on accounting for leases With IFRS 16 Leases, the IASB published a new standard on accounting for leases on 13 January 2016.

IFRS Link Newsletter Issue 25 Contents 1 IASB 11 EU Endorsement New standard on accounting for leases With IFRS 16 Leases, the IASB published a new standard on accounting for leases on 13 January 2016.

Leases: Overview of the new guidance

Leases: Overview of the new guidance Prepared by: Richard Stuart, Partner, National Professional Standards Group, RSM US LLP richard.stuart@rsmus.com, +1 203 905 5027 March 2, 2016 Introduction On February

Leases: Overview of the new guidance Prepared by: Richard Stuart, Partner, National Professional Standards Group, RSM US LLP richard.stuart@rsmus.com, +1 203 905 5027 March 2, 2016 Introduction On February

Defining Issues. FASB Completes Technical Redeliberations on Leases. October 2015, No Key Facts. Key Impacts

Defining Issues October 2015, No. 15-47 FASB Completes Technical Redeliberations on Leases The FASB met on October 7 to discuss comments received and related follow-up issues on the external review of

Defining Issues October 2015, No. 15-47 FASB Completes Technical Redeliberations on Leases The FASB met on October 7 to discuss comments received and related follow-up issues on the external review of

IFRS 16 Leases Breakfast Briefing Deloitte Financial Reporting Advisory

IFRS 16 Leases Breakfast Briefing Deloitte Financial Reporting Advisory Introduction & Agenda Session # Topic Sub-Topic 1 Overview of IFRS 16 - Introduction - Definition of a lease - Measurement of asset

IFRS 16 Leases Breakfast Briefing Deloitte Financial Reporting Advisory Introduction & Agenda Session # Topic Sub-Topic 1 Overview of IFRS 16 - Introduction - Definition of a lease - Measurement of asset

FRS 116 Leases: Through the Eyes of Auditors. Ng Kian Hui, Head of Audit & Assurance BDO LLP

FRS 116 Leases: Through the Eyes of Auditors Ng Kian Hui, Head of Audit & Assurance BDO LLP OUTLINE 1. FRS 116 Leases General Overview 2. Identifying a Lease 3. Determining the Lease Term 4. Recognition

FRS 116 Leases: Through the Eyes of Auditors Ng Kian Hui, Head of Audit & Assurance BDO LLP OUTLINE 1. FRS 116 Leases General Overview 2. Identifying a Lease 3. Determining the Lease Term 4. Recognition

IFRS 16 : Lease accounting

IFRS 16 : Lease accounting Effective for accounting periods beginning on or after 1 January 2019 December 2017 IFRS 16: Lease accounting The IASB published the new IFRS 16 lease standard, in order to avoid

IFRS 16 : Lease accounting Effective for accounting periods beginning on or after 1 January 2019 December 2017 IFRS 16: Lease accounting The IASB published the new IFRS 16 lease standard, in order to avoid

Exposure Draft 64 January 2018 Comments due: June 30, Proposed International Public Sector Accounting Standard. Leases

Exposure Draft 64 January 2018 Comments due: June 30, 2018 Proposed International Public Sector Accounting Standard Leases This document was developed and approved by the International Public Sector Accounting

Exposure Draft 64 January 2018 Comments due: June 30, 2018 Proposed International Public Sector Accounting Standard Leases This document was developed and approved by the International Public Sector Accounting

Defining Issues May 2013, No

Defining Issues May 2013, No. 13-24 FASB and IASB Issue Revised Exposure Drafts on Lease Accounting The FASB and IASB (the Boards) recently issued revised joint exposure drafts (EDs) on proposed changes

Defining Issues May 2013, No. 13-24 FASB and IASB Issue Revised Exposure Drafts on Lease Accounting The FASB and IASB (the Boards) recently issued revised joint exposure drafts (EDs) on proposed changes

Lease Accounting Standard Update ASU Presented by: Nicholas Hoefel, CPA Manager, Audit Services Group

Lease Accounting Standard Update ASU 2016-02 Presented by: Nicholas Hoefel, CPA Manager, Audit Services Group 1 Overview Introduction Background and current environment Effective dates and transition Key

Lease Accounting Standard Update ASU 2016-02 Presented by: Nicholas Hoefel, CPA Manager, Audit Services Group 1 Overview Introduction Background and current environment Effective dates and transition Key

In-depth A look at current financial reporting issues

inform.pwc.com In-depth A look at current financial reporting issues No. INT2018-08 What s inside: Overview... 2 Is the contract a lease?... 3 Components, contract consideration and allocation... 5 Initial

inform.pwc.com In-depth A look at current financial reporting issues No. INT2018-08 What s inside: Overview... 2 Is the contract a lease?... 3 Components, contract consideration and allocation... 5 Initial

How the lease accounting proposal might affect your company

Applying IFRS How the lease accounting proposal might affect your company August 2013 Contents 1. Overview... 1 2. Identifying a lease... 2 2.1 Scope exclusions... 2 2.2 Definition of a lease... 3 2.2.1

Applying IFRS How the lease accounting proposal might affect your company August 2013 Contents 1. Overview... 1 2. Identifying a lease... 2 2.1 Scope exclusions... 2 2.2 Definition of a lease... 3 2.2.1

IFRS 15. Revenue from Contracts with Customers. Presented by CPA Dr. Peter Njuguna

IFRS 15 Revenue from Contracts with Customers Presented by CPA Dr. Peter Njuguna Introduction Revenue is income from ordinary activities. A contract has rights and obligations between two or more parties.

IFRS 15 Revenue from Contracts with Customers Presented by CPA Dr. Peter Njuguna Introduction Revenue is income from ordinary activities. A contract has rights and obligations between two or more parties.

Restoring the Past U.E.P.C. Building the Future

Brussels, 14.12.2010 Dear Sirs, Madam, Re: Exposure Draft Leases On behalf of the European Union of Developers and House Builders (Union Europeénne des Promoteurs-Constructeurs - UEPC), I am writing to

Brussels, 14.12.2010 Dear Sirs, Madam, Re: Exposure Draft Leases On behalf of the European Union of Developers and House Builders (Union Europeénne des Promoteurs-Constructeurs - UEPC), I am writing to

NEED TO KNOW. Leases A Project Update

NEED TO KNOW Leases A Project Update 2 LEASES - A PROJECT UPDATE TABLE OF CONTENTS Introduction 3 Existing guidance and the rationale for change 4 The IASB/FASB project to date 5 The main proposals 6 Definition

NEED TO KNOW Leases A Project Update 2 LEASES - A PROJECT UPDATE TABLE OF CONTENTS Introduction 3 Existing guidance and the rationale for change 4 The IASB/FASB project to date 5 The main proposals 6 Definition

IFRS 16. Changes in recognizing leases in the financial statements

IFRS 16 Changes in recognizing leases in the financial statements The new standard in a nutshell: To whom the new standard applies / Binding terms and conditions In January 2016, the International Accounting

IFRS 16 Changes in recognizing leases in the financial statements The new standard in a nutshell: To whom the new standard applies / Binding terms and conditions In January 2016, the International Accounting

IASB Exposure Draft ED/2013/6 - Leases

ACAG AUSTRALASIAN COUNCIL OF AUDITORS GENERAL 13 September 2013 Mr Hans Hoogervorst Chairman International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Dear Mr Hoogervorst

ACAG AUSTRALASIAN COUNCIL OF AUDITORS GENERAL 13 September 2013 Mr Hans Hoogervorst Chairman International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Dear Mr Hoogervorst

Lease Accounting and Loan Covenants: What is the Impact?

Lease Accounting and Loan Covenants: What is the Impact? Monday June 26, 2017 9:15 AM 10:30 AM Presented by: Charlie Shannon Partner Moss Adams LLP 8750 N. Central Expressway, Suite 300 Dallas, TX 75231

Lease Accounting and Loan Covenants: What is the Impact? Monday June 26, 2017 9:15 AM 10:30 AM Presented by: Charlie Shannon Partner Moss Adams LLP 8750 N. Central Expressway, Suite 300 Dallas, TX 75231

New IASB leases standard engineering and construction

Applying IFRS New IASB leases standard engineering and construction October 2016 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition of a lease 3 1.3 Arrangements

Applying IFRS New IASB leases standard engineering and construction October 2016 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition of a lease 3 1.3 Arrangements

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N AGENDA Leases FASB & GASB Revenue Recognition FASB 2 FASB ASU 2016-02, Leases (Topic

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N AGENDA Leases FASB & GASB Revenue Recognition FASB 2 FASB ASU 2016-02, Leases (Topic

The IASB s Exposure Draft on Leases

The Chair Date: 9 September 2013 ESMA/2013/1245 Francoise Flores EFRAG Square de Meeus 35 1000 Brussels Belgium The IASB s Exposure Draft on Leases Dear Ms Flores, The European Securities and Markets Authority

The Chair Date: 9 September 2013 ESMA/2013/1245 Francoise Flores EFRAG Square de Meeus 35 1000 Brussels Belgium The IASB s Exposure Draft on Leases Dear Ms Flores, The European Securities and Markets Authority

LEASE ACCOUNTING UNDER IFRS 16 AND IAS 17 A COMPARATIVE APPROACH

78 LEASE ACCOUNTING UNDER IFRS 16 AND IAS 17 A COMPARATIVE APPROACH Lecturer PhD. Cristina Aurora BUNEA-BONTAȘ Constantin Brancoveanu University of Pitesti, Romania Email: bontasc@yahoo.com Abstract: In

78 LEASE ACCOUNTING UNDER IFRS 16 AND IAS 17 A COMPARATIVE APPROACH Lecturer PhD. Cristina Aurora BUNEA-BONTAȘ Constantin Brancoveanu University of Pitesti, Romania Email: bontasc@yahoo.com Abstract: In

Technical Line FASB final guidance

No. 2016-03 31 March 2016 Technical Line FASB final guidance A closer look at the new leases standard The new leases standard requires lessees to recognize most leases on their balance sheets. What you

No. 2016-03 31 March 2016 Technical Line FASB final guidance A closer look at the new leases standard The new leases standard requires lessees to recognize most leases on their balance sheets. What you

Applying IFRS. New IASB leases standard oilfield services. December 2016

Applying IFRS New IASB leases standard oilfield services December 2016 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition of a lease 3 1.3 Identifying and separating

Applying IFRS New IASB leases standard oilfield services December 2016 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition of a lease 3 1.3 Identifying and separating

[TO BE PUBLLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (i)]

![[TO BE PUBLLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (i)]](/thumbs/95/124393322.jpg "[TO BE PUBLLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (i)]") [TO BE PUBLLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (i)] GOVERNMENT OF INDIA MINISTRY OF CORPORATE AFFAIRS NOTIFICATION New Delhi, the 30 th March, 2019 G.S.R. (E).

[TO BE PUBLLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (i)] GOVERNMENT OF INDIA MINISTRY OF CORPORATE AFFAIRS NOTIFICATION New Delhi, the 30 th March, 2019 G.S.R. (E).

IASB Staff Paper March 2011

IASB Staff Paper March 2011 Effect of board redeliberations on Exposure Draft Leases About this staff paper This staff paper indicates how the proposals in the Exposure Draft Leases would change as a result

IASB Staff Paper March 2011 Effect of board redeliberations on Exposure Draft Leases About this staff paper This staff paper indicates how the proposals in the Exposure Draft Leases would change as a result

IFRS 16: Leases; a New Era of Lease Accounting!

The journal is running a series of updates on IFRS, IAS, IFRIC and SIC. The updates mostly collected from different sources of IASB publication, seminars, workshop & IFRS website. This issue is based on

The journal is running a series of updates on IFRS, IAS, IFRIC and SIC. The updates mostly collected from different sources of IASB publication, seminars, workshop & IFRS website. This issue is based on

Lease accounting scope & impacts

Leasing Lease accounting scope & impacts Scope What s in? All industries, all entities Arrangements that meet the definition of a lease Embedded leases within other arrangements What s out? Leases of:

Leasing Lease accounting scope & impacts Scope What s in? All industries, all entities Arrangements that meet the definition of a lease Embedded leases within other arrangements What s out? Leases of:

The new accounting standard for leases. 27 March 2017

The new accounting standard for leases 27 March 2017 Disclaimer Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity.

The new accounting standard for leases 27 March 2017 Disclaimer Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity.

Dear members of the International Accounting Standards Board,

International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Our ref : IASB 442 D Direct dial : (+31) 20 301 0391 Date : Amsterdam, 10 September 2013 Re : Comment on Exposure

International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Our ref : IASB 442 D Direct dial : (+31) 20 301 0391 Date : Amsterdam, 10 September 2013 Re : Comment on Exposure

Applying IFRS. IASB issues a new leases standard tank terminals. February 2017

Applying IFRS IASB issues a new leases standard tank terminals February 2017 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition of a lease 3 1.3 Identifying and

Applying IFRS IASB issues a new leases standard tank terminals February 2017 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition of a lease 3 1.3 Identifying and

Defining Issues. FASB and IASB Enter Home Stretch in Redeliberations on Lease Accounting but on Different Tracks. Key Facts. October 2014, No.

Defining Issues October 2014, No. 14-46 FASB and IASB Enter Home Stretch in Redeliberations on Lease Accounting but on Different Tracks At their July and October joint meetings, the FASB and the IASB (the

Defining Issues October 2014, No. 14-46 FASB and IASB Enter Home Stretch in Redeliberations on Lease Accounting but on Different Tracks At their July and October joint meetings, the FASB and the IASB (the

Lease accounting is changing An insight with sectoral impacts

Lease accounting is changing An insight with sectoral impacts I Lease accounting is changing An insight with sectoral impacts February 2019 KPMG.com/in Foreword The International Accounting Standards Board

Lease accounting is changing An insight with sectoral impacts I Lease accounting is changing An insight with sectoral impacts February 2019 KPMG.com/in Foreword The International Accounting Standards Board

Accounting and Auditing Update. Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc.

Accounting and Auditing Update Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc. Agenda Overview of the standard setting agenda Revenue recognition Lease

Accounting and Auditing Update Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc. Agenda Overview of the standard setting agenda Revenue recognition Lease

LEASES WHERE ARE WE? Steve Rathjen

LEASES WHERE ARE WE? Steve Rathjen 267 256-3110 srathjen@kpmg.com Agenda Project status Lease definition and classification Lessee accounting Lessor accounting Presentation, disclosures, and transition

LEASES WHERE ARE WE? Steve Rathjen 267 256-3110 srathjen@kpmg.com Agenda Project status Lease definition and classification Lessee accounting Lessor accounting Presentation, disclosures, and transition

LEASES CONTINUING FORWARD IFRS NEWSLETTER

IFRS NEWSLETTER LEASES Issue 15, June 2014 Despite the significant divergence on key aspects of their lease proposals earlier this year, the Boards appear determined to finalise this long running project

IFRS NEWSLETTER LEASES Issue 15, June 2014 Despite the significant divergence on key aspects of their lease proposals earlier this year, the Boards appear determined to finalise this long running project

Executive Summary. New leases standard Lessees

Executive Summary December 2018 The new leases standard focuses on increased transparency and comparability providing financial statement users with more information about an entity s leasing activities.

Executive Summary December 2018 The new leases standard focuses on increased transparency and comparability providing financial statement users with more information about an entity s leasing activities.

Defining Issues. FASB and IASB Continue Discussions on Lease Accounting. Key Facts. June 2014, No

Defining Issues June 2014, No. 14-29 FASB and IASB Continue Discussions on Lease Accounting During the second quarter of 2014, the FASB and IASB (the Boards) continued redeliberations on the proposals

Defining Issues June 2014, No. 14-29 FASB and IASB Continue Discussions on Lease Accounting During the second quarter of 2014, the FASB and IASB (the Boards) continued redeliberations on the proposals

Leases Discount rates

Leases Discount rates What s the correct rate? IFRS 16 September 2017 kpmg.com/ifrs Contents Contents Determining the correct rate 1 1 At a glance 2 1.1 Key facts 2 1.2 Key impacts 3 2 Lessor discount

Leases Discount rates What s the correct rate? IFRS 16 September 2017 kpmg.com/ifrs Contents Contents Determining the correct rate 1 1 At a glance 2 1.1 Key facts 2 1.2 Key impacts 3 2 Lessor discount

AASB 16 Leases A fundamental overhaul of lessee accounting effective 2019

AASB 16 Leases A fundamental overhaul of lessee accounting effective 2019 kpmg.com.au Understanding the impact to your company A new leasing standard AASB 16 Leases removes the concept of operating and

AASB 16 Leases A fundamental overhaul of lessee accounting effective 2019 kpmg.com.au Understanding the impact to your company A new leasing standard AASB 16 Leases removes the concept of operating and

Shipping insights briefing

TRANSPORT Shipping insights briefing A view of the future: 2017 bigger balance sheets! kpmg.com Nearly two and a half years ago we issued a Shipping Insights Briefing, highlighting proposed changes to

TRANSPORT Shipping insights briefing A view of the future: 2017 bigger balance sheets! kpmg.com Nearly two and a half years ago we issued a Shipping Insights Briefing, highlighting proposed changes to

IASB/FASB Exposure Draft on Leases. Accounting in the Retail Industry A new view of lease accounting emerges

IASB/FASB Exposure Draft on Leases Accounting in the Retail Industry A new view of lease accounting emerges Contents Introduction 1 Issue 1 Impact of capitalisation of all leases on financial statements

IASB/FASB Exposure Draft on Leases Accounting in the Retail Industry A new view of lease accounting emerges Contents Introduction 1 Issue 1 Impact of capitalisation of all leases on financial statements

International Accounting Standard 17 Leases. Objective. Scope. Definitions IAS 17

International Accounting Standard 17 Leases Objective 1 The objective of this Standard is to prescribe, for lessees and lessors, the appropriate accounting policies and disclosure to apply in relation

International Accounting Standard 17 Leases Objective 1 The objective of this Standard is to prescribe, for lessees and lessors, the appropriate accounting policies and disclosure to apply in relation

Technical Line FASB final guidance

No. 2016-09 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect health care entities In this issue: Overview... 1 Key considerations... 3 Scope and scope exceptions...

No. 2016-09 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect health care entities In this issue: Overview... 1 Key considerations... 3 Scope and scope exceptions...

IFRS Update Guy Thomas, CPA, CA

IFRS Update Guy Thomas, CPA, CA D&Co IFRS update Agenda 3 new standards under IFRS IFRS 9 Financial Instruments IFRS 15 Revenue from Contracts with Customers IFRS 16 Leases Agenda Some narrow scope amendments

IFRS Update Guy Thomas, CPA, CA D&Co IFRS update Agenda 3 new standards under IFRS IFRS 9 Financial Instruments IFRS 15 Revenue from Contracts with Customers IFRS 16 Leases Agenda Some narrow scope amendments

Is Your Operating Lease An Asset or Liability? It s Now Both

MFM Annual Conference Is Your Operating Lease An Asset or Liability? It s Now Both 23 May 2016-1:30 pm 2:20 pm Disclaimer These slides are for educational purposes only and are not intended, and should

MFM Annual Conference Is Your Operating Lease An Asset or Liability? It s Now Both 23 May 2016-1:30 pm 2:20 pm Disclaimer These slides are for educational purposes only and are not intended, and should

Why IFRS 16 matters to the shipping industry

www.pwc.no Why IFRS 16 matters to the shipping industry October 2017 Executive summary New lease standard to be effective 1 January 2019. Early implementation permitted together with IFRS 15 (effective

www.pwc.no Why IFRS 16 matters to the shipping industry October 2017 Executive summary New lease standard to be effective 1 January 2019. Early implementation permitted together with IFRS 15 (effective

Real estate leases. How will IFRS 16 impact real estate entities? May 2016

Real estate leases How will IFRS 16 impact real estate entities? May 2016 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition of a lease 3 1.3 Identifying and separating

Real estate leases How will IFRS 16 impact real estate entities? May 2016 Contents Overview 2 1. Key considerations 3 1.1 Scope and scope exclusions 3 1.2 Definition of a lease 3 1.3 Identifying and separating

The joint leases project change is coming

No. 2010-4 18 June 2010 Technical Line Technical guidance on standards and practice issues The joint leases project change is coming What you need to know The proposed changes to the accounting for leases

No. 2010-4 18 June 2010 Technical Line Technical guidance on standards and practice issues The joint leases project change is coming What you need to know The proposed changes to the accounting for leases

Technical Line FASB final guidance

No. 2018-08 20 September 2018 Technical Line FASB final guidance How the new leases standard affects engineering and construction entities In this issue: Overview... 1 Key considerations... 2 Scope and

No. 2018-08 20 September 2018 Technical Line FASB final guidance How the new leases standard affects engineering and construction entities In this issue: Overview... 1 Key considerations... 2 Scope and

Technical Line FASB final guidance

No. 2019-01 3 January 2019 Technical Line FASB final guidance How the new leases standard affects automotive entities In this issue: Overview... 1 Recent standard setting activity... 2 Key considerations...

No. 2019-01 3 January 2019 Technical Line FASB final guidance How the new leases standard affects automotive entities In this issue: Overview... 1 Recent standard setting activity... 2 Key considerations...

Implementing IFRS 16. Jianqiao Lu, IASB Member. Singapore, November International Accounting Standards Board, IFRS Foundation

IFRS Foundation Implementing IFRS 16 Jianqiao Lu, IASB Member International Accounting Standards Board, Singapore, November 2018 The views expressed in this presentation are those of the presenter, not

IFRS Foundation Implementing IFRS 16 Jianqiao Lu, IASB Member International Accounting Standards Board, Singapore, November 2018 The views expressed in this presentation are those of the presenter, not

Get ready for FRS 116: Leases

Get ready for FRS 116: Leases Chetan Hans & Eng Min Lor Grant Thornton Singapore Overview of main changes Replaces FRS 17 Leases, INT FRS 104 Determining whether an Arrangement contains a Lease, INT FRS

Get ready for FRS 116: Leases Chetan Hans & Eng Min Lor Grant Thornton Singapore Overview of main changes Replaces FRS 17 Leases, INT FRS 104 Determining whether an Arrangement contains a Lease, INT FRS

IFRS 15 and IFRS 16 Webinar

CPA Ireland Skillnet CPA Ireland Skillnet, is a training network that is funded by Skillnets, a state funded, enterprise led support body dedicated to the promotion and facilitation of training and up-skilling

CPA Ireland Skillnet CPA Ireland Skillnet, is a training network that is funded by Skillnets, a state funded, enterprise led support body dedicated to the promotion and facilitation of training and up-skilling

Implementing the New Lease Guidance

Implementing the New Lease Guidance October 22, 2018 2018 Crowe LLP 2018 Crowe LLP Agenda Background Scope Effective dates & transition requirements Lessee accounting model Lessor accounting model Specialized

Implementing the New Lease Guidance October 22, 2018 2018 Crowe LLP 2018 Crowe LLP Agenda Background Scope Effective dates & transition requirements Lessee accounting model Lessor accounting model Specialized

2 This Standard shall be applied in accounting for all leases other than:

Indian Accounting Standard (Ind AS) 17 Leases (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in bold type indicate the main

Indian Accounting Standard (Ind AS) 17 Leases (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in bold type indicate the main

IFRS 16 Leases: Overview

IFRS Foundation IFRS 16 Leases: Overview Nairobi, Kenya Darrel Scott, IASB Member The views expressed in this presentation are those of the presenter, not necessarily those of the International Accounting