An Introduction to the Housing Tax Credit Program - Part 1

|

|

|

- Harry Burke

- 5 years ago

- Views:

Transcription

1

2 An Introduction to the Housing Tax Credit Program - Part 1 Moderator: Diana McIver, DMA Development Company, LLC Panelists: Christine Richardson, Locke Lord LLP Michael Celkis, CohnReznick LLP

3 What Today s Session Will Cover Morning Session The Basics of the Housing Tax Credit Program History Two types of credits What can be built/who can live there Legal Issues & Working with an Attorney Ownership Structures Partnership Structures Legal Considerations in the Life of a Tax Credit Deal Accounting Issues & Working with an Accountant Eligible Basis, 10% Test, and other accounting rules Coupling bonds with Credits and the 50% Test The Ta C edit P og a at 3 Afternoon Session The Tax Credit Program in Texas The QAP/Threshold & Scoring Two Case Studies The Specifics of Developing with Tax Credits both from the Developer standpoint and the Investor perspective. Two developers will each walk through a case study on a tax credit deal. Two investors will evaluate the transactions, providing feedback to the developers.

4 History of the Housing Tax Credit Program 1986 Congress through the Tax Reform Act, enacted Section 42 of the Internal Revenue Code. Section 42 created the Low Income Housing Tax Credit (LIHTC) to provide incentives to the private sector to invest in affordable housing. Credit is a dollar-for-dollar tax reduction. Credit is based on the Cost of Construction or Rehabilitation The Tax Credit program is 32 years old and is the oldest (longest lived) supply side housing program. More than 2.5 million units have been built under this program Congress made the LIHTC program permanent TDHCA e o ed the o ds Lo I o e f o the p og a a e. No i Texas it is called the Housing Tax Credit (HTC) Program Congress enacted the Housing & Economic Recovery Act of 2008 (HERA) with the most significant changes since 1986.

5 History, continued 2009 Congress enacted American Reinvestment and Recovery Act of 2009 (ARRA) which created the Tax Credit Assistance Program (TCAP) and Tax Credit Exchange (Exchange) on a temporary basis Tax Cuts and Jobs Act aka Tax Reform (December 2017) preserved housing tax credits and private activity bonds; created Opportunity Zones 2018 Omnibus Budget Bill (March 2018): 50% cap increase (over 4 years) in the 9% program and added income-averaging.

6 Two Types of Tax Credits 9% Credit Also known as the 70% present value credit In Texas, these credits are awarded annually on a competitive basis. 4% Credit Also known as the 30% present value credit A aila le /ta e e pt o ds th ough the tate s Volu e Cap Allo atio.

7 What is a 9% Credit? Each State receives a per capita allocation, adjusted annually. In 2017, the amount was $2.35 per capita. In 2018, that jumped to $2.70 per capita thanks to the Omnibus Bill. Approximately $76,677,700 is available in 2018 for Texas. 10 Year Credit (longer compliance period) New construction or substantial rehabilitation If rehab, building acquisition costs qualify only for a 4% credit

8 What is a 4% Credit? 4% Credit is used in tandem w/private Activity Bonds. States have $105 per capita limit on ALL Private Activity Bonds, also called Volume Cap. Texas receives annual allocation of approximately $2.97 billion Eligible Uses are many from sewage plants to student loans to affordable housing Approximately $654 million is reserved in Texas for multifamily housing bonds, to be issued by TDHCA, TSAHC, and Local Issuers When used with Private Activity Bonds, the 4% Credit is a 10 year Credit (Compliance is 30 years).

9 4% Credit, continued. Issuers of Bonds can be Housing Finance Agencies, Housing Authorities, Public Facility Corporations, Texas State Affordable Housing Corporation (TSAHC) or TDHCA, but only TDHCA can award the 4% tax credits and application must be filed timely. New Requirement (effective 9/1/13): Must have local resolution of NO OPPOSITION, regardless of bond issuer. No TDHCA scoring applies to 4% Tax Credits, but must meet Threshold Requirements of the QAP, including notifications, design, amenities, etc. Te as Legislatu e has esta lished de elop e t e ui e e ts fo tie s of o petitio based on affordability factors, and also provided a system for allocating bond cap throughout the 13 Regions. Undersubscribed for past nine years, but OVERSUBSCRIBED in The amount of the credit floats monthly and is not fixed at 4%.

10 Affordability Requirements 40% of the rents based on 60% Area Median Income (AMI), or 20% of the rents based on 50% AMI Must keep project affordable for at least 30 years (some states may require longer). In Texas, extra points are awarded to 9% HTC developments for keeping the housing affordable for 40 years. Credits are only awarded on the units that meet the long term affordability test. Although Market Rate units are allowed, no tax credits are available for these units. NEW: With the new income averaging, a development can get tax credits on units with rents based on 80% AMI; however, the average throughout the development cannot be greater than 60%.

11 What Can Be Built? Housing Types can be multiple types (both new construction and rehab) but must meet the definition of ualified eside tial e tal p ope t Multifamily Rental, e.g., family, workforce housing Senior Rental (age 55+) Single Room Occupancy (SROs) for Homeless

12 Who Can Live in a Tax Credit Community? Individuals or Families or Seniors or Persons with Disabilities with incomes at or below 80% of Area Median Income will soon be eligible to live in Tax Credit Housing however, since there is no rent subsidy, they must be able to afford the rent. (Existing developments will continue to have 60% AMI restrictions.) A resident with a voucher from a housing authority can live in Tax Credit Housing and pay 30% of their income for rent.

13 How Is a Tax Credit Rent Calculated? Two Bedroom Rent assumes 3 person family (1.5 persons per bedroom) Imputed income at 60% of AMI: $36,000 Multiplied by: x30% Maximum Annual Rent: $10,800 Divided by (months): 12 Maximum Monthly Rent: $900* *must include both rent and utilities e.g., if the utility allowance on 2BR is $120. Max rent would be $780.

14 Structuring a Tax Credit Deal: Legal Issues and Considerations

15 Ownership Structure The housing development is owned by a limited partnership (LP) or limited liability company (LLC). Must be a pass-through for federal income tax purposes.

16 Ownership Structure HOUSING DEVELOPMENT Owner Entity, LP or Owner Entity, LLC General Partner (for LP) Managing Member (for LLC).01% Investor Limited Partner (for LP) Investor Member (for LLC) 99.99%* *An affiliate of the investor will often act as a special limited partner/ member for administrative oversight and protection of the i esto s rights.

17 Ownership Structure: General Partner/Managing Member In an LP, the general partner is the controlling party and is responsible for the construction and operation of the housing development. In an LLC, the managing member is the functional equivalent of the general partner. General Partner/Managing Member is often structured as an LLC (but can have another form, such as a corporation, etc.) The general partner or managing member is typically an affiliate of the developer/guarantor. Compensation is usually structured as fees or distributions paid from cash flow.

18 Ownership Structure: Investor Limited Partner/Investor Member Investor limited partner in an LP; investor member in an LLC. Purchases the tax credits by making capital contributions to the Owner. Has consent rights over major decisions in order to protect its investment. Typically receives an asset management fee as compensation for its oversight activities.

19 Ownership Structure Ground Lease Used in transactions with housing authorities in order to obtain a property tax exemption. Same LP or LLC ownership structure, with key differences: The housing authority has legal title to the land and ground leases it to the LP/LLC owner LP/LLC owner develops, owns, and operates the project. Typically includes a special limited partner or member that is an affiliate of the developer/guarantor.

20 Ownership Structure (Ground Lease) Ground Lease HOUSING DEVELOPMENT Owner Entity, LP or Owner Entity, LLC General Partner/ Managing Member (Affiliate of HA).01% Investor Limited Partner/ Investor Member 99.98% Special Limited Partner/Member (Affiliate of Developer/Guarantor).01% Land owned by housing authority Fee Interest Housing Authority 100%

21 Developer Responsible for coordinating all aspects of a tax credit deal from inception through stabilized operations. Receives a developer fee (typically limited to 15% of eligible basis). Often an affiliate of the general partner/managing member (but not always). Also responsible for guaranties, either directly or through affiliates. Multiple developers can be structured as co-developers or through a fee sharing arrangement.

22 Legal Considerations In The Life of a Tax Credit Deal Site selection Tax Credit application Selection of financing partners Equity/debt closing TDHCA compliance Permanent loan closing Property disposition/year 15

23 Legal Considerations In The Life of a Tax Credit Deal Site selection Review/negotiation of purchase contract Title review Tax Credit application QAP/Rules issues Appeals Deal structuring considerations Selection of financing partners Review equity/debt term sheets Equity/debt closing Review/negotiation of financing documents Due diligence Legal opinions

24 Legal Considerations In The Life of a Tax Credit Deal TDHCA compliance Required submissions (10% test; cost certification, etc.) Compliance matters Permanent loan closing See equity/debt closing Property disposition/year 15 Structuring considerations Review/negotiation of documents TDHCA change of ownership LURA amendments

25 Trusted Advisor Project Team Role of Accountant Financial Projections analysis Deal Structuring Tax Planning Exit Strategy Keeping up with changes in the industry (Federal and State Level)

26 Compliance Role of Accountant, Cont. Audits/Tax Returns 10% Test Report (9% deals) Cost Certification Bond Specific Reports (50% test, 95/5 test, arbitrage calculation) Project Specific Requirements (cost segregation, lease testing, credit adjuster, DSCR report, qualified contract pricing) of AMI.

27 The 10% Test What is it? A 10% Test supports Basis Incurred in a project. Basis incurred must be at least 10% of the Reasonably Expected Basis of the project on a specific date. Basis Incurred: Total osts i u ed to date hi h ep ese ts a p oje t s depreciable basis plus land. Reasonably Expected Basis: A p oje t s dep e ia le asis plus la d osts. This amount is generally stipulated by the Owner as part of the Carryover Allocation. * Note: 10% tests are only for 9% competitive credits

28 The 10% Calculation 10% Basis Incurred (land + depreciable basis) Reasonably Expected Basis (total expected land + depreciable basis)

29 Cost Certification What is it? CPA s audit of p oje t osts. Re ui ed Housi g C edit Age HCA to e tif eligibility for low income housing credits. Each HCA has specific information required to be included. Typically required: Schedules of total and eligible costs by project and building. Calculation of credits. Sources and uses of funds. Gap analysis. Project Proformas. Upon acceptance from the HCA, the Agency issues Form 8609

30 Eligible Basis Eligible Basis = adjusted basis of building at end of 1 st year credit period Includes common areas 30% Boost in QCTs or DDAs Projects located in HUD-designated Qualified Census Tracts or Difficult to Develop Areas receive a 30% increase on eligible basis.

31 Eligible Basis, Cont. Costs that ARE included: Building acquisition Engineering and architecture Appraisals Construction costs Furniture, Fixtures & Equipment Impact fees/permits Inspections Depreciable land improvement Developer fee Interest during production

32 Eligible Basis, Cont. Costs that ARE NOT included: Land Permanent loan fees Marketing and lease-up costs Tax credit fees Reserves Syndication fees Commercial or income-producing space

33 Eligible Basis, Cont. Costs that MIGHT BE included: Tenant relocation Accounting Legal Acquisition Interest Construction loan fees Real estate taxes Environmental

34 Specific Tests for Tax Exempt Bonds 50% Test The 50% Test is calculated by dividing the Bond Proceeds by the Aggregate Basis of the Project. For these purposes: Bond Proceeds: Include only the amount of bonds used to finance the acquisition, hard construction and soft costs of the project. Generally this will equal the mortgage amount. Bond Proceeds include interest earned on the bonds or bond reserve funds. Aggregate Basis: I ludes the p oje t s dep e ia le asis a d la d osts.

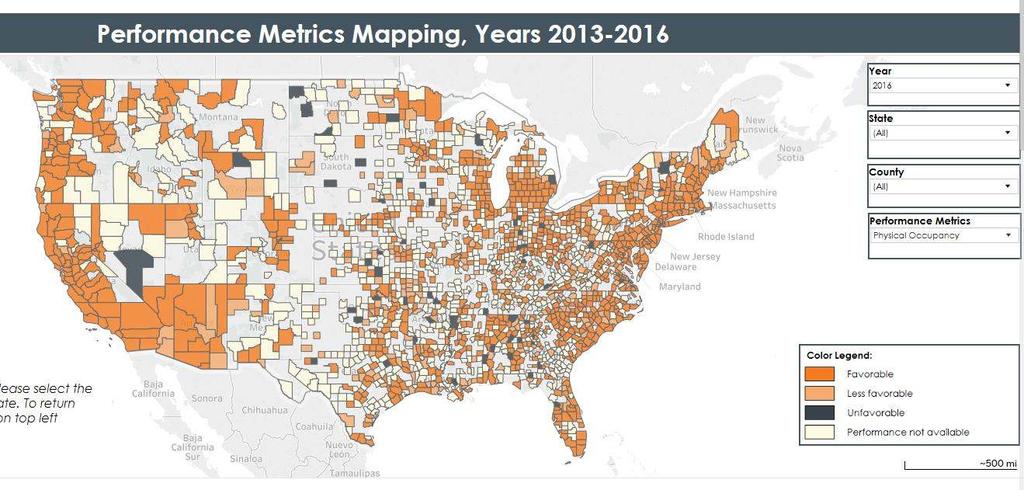

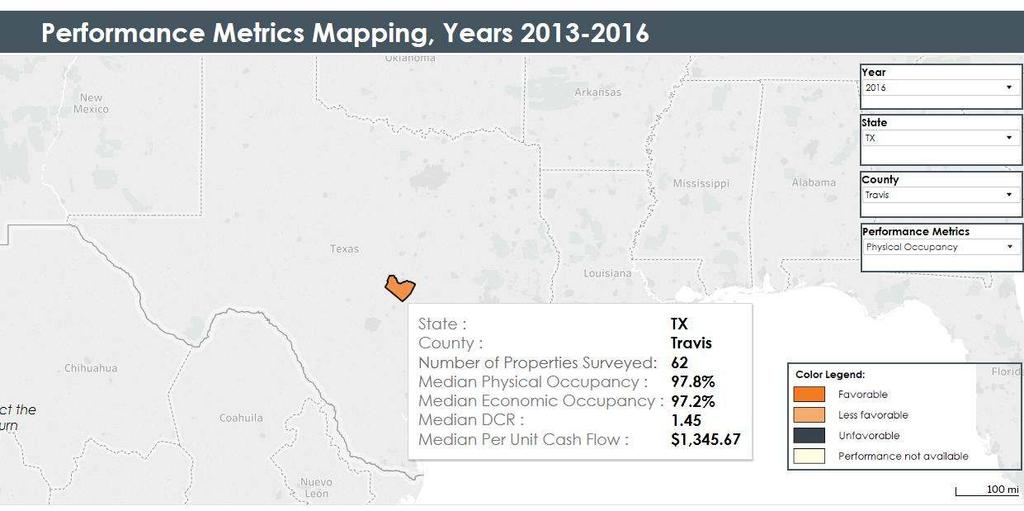

35 Meeting the 50% Test If the project meets the 50% Test, the project may claim 100% of the 4% credits on the total amount of eligible basis. EXAMPLE Volume Cap Bonds $10,000,000 Aggregate Basis $19,900,000 50% Test Ratio % Land in Aggregate Basis $2,000,000 Eligible Basis $17,900,000 Eligible Under 50% Test % Final Eligible Basis $17,900,000

36 What Happens if the 50% Test Fails? If the project does not meet the 50% Test, the project is limited to 4% credits on the amount of eligible basis times the final ratio. This has a severe impact on the available credits! EXAMPLE Volume Cap Bonds $10,000,000 Aggregate Basis $20,100,000 50% Test Ratio % Land in Aggregate Basis $2,000,000 Eligible Basis $18,100,000 Eligible Under 50% Test % Final Eligible Basis $9,004,975

37 Other Bond Rules The project must meet the 95/5 Test. This test is ofte alled the good ost / ad ost test a d is t pi all pe fo ed a i depe de t a ou ta t. Fo these purposes, some examples are: Good Costs: Building and land, common space, resident recreation and parking facilities related to the rental residential units. Bad Costs: Commercial space, financing fees, bond issuance costs.

38 Credit Adjuster Occurs when project does not meet negotiated credit delivery amounts Spelled out in the partnership/operating agreements Generally will reduce LP final equity payment Typically there are two types of adjuster calculations (Permanent and Timing)

39 Permanent Adjuster -Occurs when there is a change in eligible basis or tax credit percentage. -Can be adjusted upward or downward depending on the LPA. -A small variance in basis allocated over the life of the credits can mean a large variance between actual and expected contributions made by the investor. Federal Tax Credit Downward Basis Adjuster: Projected Aggregate Federal Tax Credits 750,000 Actual Federal Tax Credits 700,000 Variance 50,000 Adjusted for 10 years 500,000 LP ownership % 99.99% Net Variance to LP 499,950 Downward Basis Adjustment Factor 0.90 Permanent Credit Adjuster 449,955

40 Timing Adjuster Federal Tax Credit Downward Timing Adjuster: Projected Adjusted Total Estimated Credits to investor in first year 750, ,000 Actual credits delivered in first year 350, ,000 Variance (350,000) Timing Adjuster Fraction Downward Timing Adjuster (227,500)

41 The Housing Tax Credit Investment and Operating Performance Study Mike Celkis, CPA CohnReznick LLP

42 Origin of Our Performance Study So You want to see the track record? The first study was undertaken by CohnReznick professionals in 2000 when 6,250 properties were surveyed.

43 Over 22,000 properties surveyed in 2016; representing approximately 70% of actively managed LIHTC properties and $83 billion in total credits. 50 U.S. states, Guam, Puerto Rico, and U.S. Virgin Islands 92% of U.S. MSAs Data contributed by 35 participants including every active LIHTC syndicator.

44 Acknowledgement Formerly known as Great Lakes Capital Fund

45 Tenant Income Profile 46% of Tenants earned less than 30% of AMI, 35% earned between 30% and 50% of AMI, and the remaining 19% earned no more than 60% of AMI. 19.0% 46.0% 35.0% 50% to 60% AMI 30% to 50% AMI Less than 30% AMI

46 Portfolio Composition (% of net equity) By Developer Type By Tenancy Type 3.6% 2.5% 36.0% 26.5% 64.0% For Profit Non Profit 67.3% Family Senior Special Needs Other By Development Type By Credit Type 2.4% 2.0% 29.0% 35.7% 59.8% New construction 71.0% 9% credit 4% credit Acq/Rehab Historic Rehab Other

47 Occupancy Performance High occupancy continued Occupancy levels in LIHTC properties have been remarkably consistent from one year to the next. Performance Median Physical Occupancy Performance Median Economic Occupancy 98.0% 97.5% 97.0% 96.5% 96.0% 97.2% 96.4% 97.5% 96.9% 97.7% 97.0% 97.9% 96.9% 97.5% 97.0% 96.5% 96.0% 95.5% 95.0% 94.5% 96.3% 94.6% 96.6% 95.3% 96.9% 96.0% 97.0% 95.6% 95.5% % National TX National TX

48 Physical Occupancy by Credit Type

49 Underperformance (under 90% occupancy) Underperformance - Physical Occupancy Underperformance - Economic Occupancy 12.0% 10.0% 8.0% 6.0% 4.0% 9.9% 7.5% 8.5% 5.7% 6.7% 5.6% 4.6% 4.7% 25.0% 20.0% 15.0% 10.0% 22.6% 15.5% 15.5% 11.7% 13.1% 13.3% 10.0% 9.0% 2.0% 5.0% 0.0% % National TX National TX

50 Cash Flow Performance Improved cash flow performance sustained De t Co e age Ratios DCR s ho e ed et ee. 3 a d. 5 fo a significant portion of the last decade, before rising to 1.21 in Performance Median DCR Performance Median Per Unit Cash Flow 1.45 $ $800 $700 $698 $775 $660 $800 $ $600 $597 $571 $ $ National TX National TX

51 Per Unit Cash Flow by Credit Type:

52 Underperformance DCR under 1.0 Underperformance - DCR Underperformance - Per Unit Cash Flow 20.0% 15.0% 10.0% 18.4% 18.0% 16.9% 13.8% 14.7% 14.3% 9.9% 12.0% 25.0% 20.0% 15.0% 10.0% 20.0% 19.3% 17.8% 15.0% 15.4% 14.9% 10.5% 12.3% 5.0% 5.0% 0.0% % National TX National TX

53 Total Housing Credit Equity Volume In recent years, roughly 75% of all housing credit investments were acquired through syndication.

54 Average Capital Stack: All Credit Projects since 2012

55 Housing Tax Credit Equity Market: CRA vs Economic Volume

56 Cumulative Foreclosure Rate

57 Annual LIHTC Foreclosure Rate vs. Conventional Multifamily

58 Performance by Property Age Ninety-six percent of the properties in the portfolio were 20 years or younger.

59 Median 2016 Per Unit Operating Expenses by Development Type

60

61

62 Key Takeaways Incredible strength in affordable housing demand exists in virtually every part of the country. LIHTC property performance is strong, with all basic metrics continuing to improve. The risk profile in housing tax credit investments has fallen to an historically low level. The industry has come a long way at improving underwriting and asset management practices. Due to the fact that housing tax credit properties are, by design, underwritten with a narrow margin for error, aggressive underwriting, unexpected market condition or improper management can still result in property failures.

63 63 And thus, dear students, we have arrived at the formula for understanding the Housing Tax Credit Program...

64 Questions & Answers? Diana McIver, DMA Development Company, LLC Ch isti e. Ch is i ha dso, Locke Lord, LLP crichardson@lockelord.com Mike Celkis, CPA, CohnReznick, LLP Mike.Celkis@CohnReznick.com

Low Income Housing Tax Credits 101 (and a little beyond 101) James Lehnhoff, Municipal Advisor

James Lehnhoff, Municipal Advisor") Low Income Housing Tax Credits 101 (and a little beyond 101) James Lehnhoff, Municipal Advisor 9/29/2017 1 Affordable Housing Need What is Affordable? Overview Why do affordable housing projects need financial

Low Income Housing Tax Credits 101 (and a little beyond 101) James Lehnhoff, Municipal Advisor 9/29/2017 1 Affordable Housing Need What is Affordable? Overview Why do affordable housing projects need financial

INTRODUCTION TO FEDERAL LOW INCOME HOUSING TAX CREDITS. 1. Applicable Percentage

INTRODUCTION TO FEDERAL LOW INCOME HOUSING TAX CREDITS I. THE TAX CREDIT GENERALLY a. Established under the Tax Reform Act of 1986. Essentially an effort to partially privatize the affordable housing industry.

INTRODUCTION TO FEDERAL LOW INCOME HOUSING TAX CREDITS I. THE TAX CREDIT GENERALLY a. Established under the Tax Reform Act of 1986. Essentially an effort to partially privatize the affordable housing industry.

Tax Credits 101. Wednesday, November 7 10:45am 12:00pm

Tax Credits 101 Wednesday, November 7 10:45am 12:00pm Today s Panel Kevin Clark Ohio Housing Finance Agency (OHFA) Brian Graney Ohio Capital Corporation for Housing Meg Manley PIRHL, LLC Tim Swiney Wallick

Tax Credits 101 Wednesday, November 7 10:45am 12:00pm Today s Panel Kevin Clark Ohio Housing Finance Agency (OHFA) Brian Graney Ohio Capital Corporation for Housing Meg Manley PIRHL, LLC Tim Swiney Wallick

Opening Doors to Affordable Mixed-Use Development

Opening Doors to Affordable Mixed-Use Development 1 Housing Colorado October 5, 2016 2 Session Objectives Learn: The Basics of Low-Income and Historic Tax Credits, including recent Colorado LIHTC program

Opening Doors to Affordable Mixed-Use Development 1 Housing Colorado October 5, 2016 2 Session Objectives Learn: The Basics of Low-Income and Historic Tax Credits, including recent Colorado LIHTC program

Florida Housing Finance Corporation Qualified Allocation Plan Low Income Housing Tax Credits Program

Florida Housing Finance Corporation 2016 2017 Qualified Allocation Plan Low Income Housing Tax Credits Program I. Introduction Pursuant to Section 420.5099, Florida Statutes, the Florida Housing Finance

Florida Housing Finance Corporation 2016 2017 Qualified Allocation Plan Low Income Housing Tax Credits Program I. Introduction Pursuant to Section 420.5099, Florida Statutes, the Florida Housing Finance

Housing Tax Credit Carryover, 10 Percent Test, Evidence of Construction Start and Final Allocation Application Training Workshop. September 20, 2018

Housing Tax Credit Carryover, 10 Percent Test, Evidence of Construction Start and Final Allocation Application Training Workshop September 20, 2018 Table of Contents Topic Page Carryover Allocation Application

Housing Tax Credit Carryover, 10 Percent Test, Evidence of Construction Start and Final Allocation Application Training Workshop September 20, 2018 Table of Contents Topic Page Carryover Allocation Application

OVERVIEW OF TAX-EXEMPT AFFORDABLE HOUSING BONDS

1075 Peachtree Street, N.E. Suite 2500 Atlanta, GA 30309-3962 (404) 885-1500 Fax (404) 892-7056 www.seyfarth.com (404) 888-1883 direct danmcrae@mindspring.com dmcrae@seyfarth.com OVERVIEW OF TAX-EXEMPT

1075 Peachtree Street, N.E. Suite 2500 Atlanta, GA 30309-3962 (404) 885-1500 Fax (404) 892-7056 www.seyfarth.com (404) 888-1883 direct danmcrae@mindspring.com dmcrae@seyfarth.com OVERVIEW OF TAX-EXEMPT

The Affordable Housing Credit Improvement Act of 2017

The Affordable Housing Credit Improvement Act of 2017 Sponsored by Representatives Pat Tiberi (R-OH) and Richard Neal (D-MA), the Affordable Housing Credit Improvement Act of 2017 would enact numerous

The Affordable Housing Credit Improvement Act of 2017 Sponsored by Representatives Pat Tiberi (R-OH) and Richard Neal (D-MA), the Affordable Housing Credit Improvement Act of 2017 would enact numerous

Tax Credit Finance Primer. Tim Favaro. Partner Cannon Heyman & Weiss, LLP.

Tax Credit Finance Primer Tim Favaro Partner Cannon Heyman & Weiss, LLP tfavaro@chwattys.com New Markets Tax Credit & Historic Tax Credit 101 New Markets Tax Credit Program: Background Codified in Section

Tax Credit Finance Primer Tim Favaro Partner Cannon Heyman & Weiss, LLP tfavaro@chwattys.com New Markets Tax Credit & Historic Tax Credit 101 New Markets Tax Credit Program: Background Codified in Section

Texas State Affordable Housing Corporation

The has approved these policies and request for proposals ( RFP ) for its multifamily tax-exempt bond programs for calendar year 20162017. These policies and RFP are updated annually to inform the public

The has approved these policies and request for proposals ( RFP ) for its multifamily tax-exempt bond programs for calendar year 20162017. These policies and RFP are updated annually to inform the public

DISABILITY HOUSING NETWORK LOW INCOME HOUSING TAX CREDIT DEVELOPMENT

DISABILITY HOUSING NETWORK LOW INCOME HOUSING TAX CREDIT DEVELOPMENT OCTOBER 24, 2012 OHIO CAPITAL CORPORATION FOR HOUSING OCCH s mission is: to cause the construction, rehabilitation, and preservation

DISABILITY HOUSING NETWORK LOW INCOME HOUSING TAX CREDIT DEVELOPMENT OCTOBER 24, 2012 OHIO CAPITAL CORPORATION FOR HOUSING OCCH s mission is: to cause the construction, rehabilitation, and preservation

OVERVIEW OF HOUSING TAX CREDITS

OVERVIEW OF HOUSING TAX CREDITS Under the provisions of the Tax Reform Act of 1986, a federal Housing Tax Credit (HTC) was created to encourage the development of rental housing for limited income households.

OVERVIEW OF HOUSING TAX CREDITS Under the provisions of the Tax Reform Act of 1986, a federal Housing Tax Credit (HTC) was created to encourage the development of rental housing for limited income households.

Housing Credit Modernization Becomes Law

Housing Credit Modernization Becomes Law July 30, 2008 President Bush today signed into law the most significant modernization of Low Income Housing Tax Credits since 1989, as part of the Housing and Economic

Housing Credit Modernization Becomes Law July 30, 2008 President Bush today signed into law the most significant modernization of Low Income Housing Tax Credits since 1989, as part of the Housing and Economic

The Affordable Housing Credit Improvement Act of 2016

The Affordable Improvement Act of 2016 S. 3237 Sponsored by Senator Maria Cantwell (D-WA) and co-sponsored by Senate Finance Committee Chairman Orrin Hatch (R-UT) and Ranking Member Ron Wyden (D-OR), the

The Affordable Improvement Act of 2016 S. 3237 Sponsored by Senator Maria Cantwell (D-WA) and co-sponsored by Senate Finance Committee Chairman Orrin Hatch (R-UT) and Ranking Member Ron Wyden (D-OR), the

MFA 2019 Qualified Allocation Plan and Application Workshop. Part V: TAX CREDIT PROGRAM OVERVIEW. Presentation Overview. Housing Priorities

Presentation Overview MFA 2019 Qualified Allocation Plan and Application Workshop Part I: Part II: Part III: Part IV: Part V: Tax Credit Program Overview Staying in Compliance 2019 QAP Review Application

Presentation Overview MFA 2019 Qualified Allocation Plan and Application Workshop Part I: Part II: Part III: Part IV: Part V: Tax Credit Program Overview Staying in Compliance 2019 QAP Review Application

EXHIBIT E LOW INCOME HOUSING TAX CREDIT APPLICATION REQUIREMENTS

EXHIBIT E LOW INCOME HOUSING TAX CREDIT APPLICATION REQUIREMENTS A. Application for Tax Credit Reservation or Tax-Exempt Bond Conditional Commitment shall Include: 1. Complete application form (current

EXHIBIT E LOW INCOME HOUSING TAX CREDIT APPLICATION REQUIREMENTS A. Application for Tax Credit Reservation or Tax-Exempt Bond Conditional Commitment shall Include: 1. Complete application form (current

Investment and Operational Performance

Housing Tax Credit Investments: Investment and Operational Performance A CohnReznick LLP Report Tax Credit Investment Services APRIL 2018 Introduction This is the seventh in a series of periodic reports

Housing Tax Credit Investments: Investment and Operational Performance A CohnReznick LLP Report Tax Credit Investment Services APRIL 2018 Introduction This is the seventh in a series of periodic reports

RFP REQUEST FOR PROPOSAL. for TAX CREDIT ADVISOR SERVICES. for BOULDER HOUSING PARTNERS. March 6, 2012 Requested Return: March 15, 2010

RFP 06-2012 REQUEST FOR PROPOSAL for TAX CREDIT ADVISOR SERVICES for BOULDER HOUSING PARTNERS March 6, 2012 Requested Return: March 15, 2010 Boulder Housing Partners 4800 Broadway Boulder, CO 80304 (720)

RFP 06-2012 REQUEST FOR PROPOSAL for TAX CREDIT ADVISOR SERVICES for BOULDER HOUSING PARTNERS March 6, 2012 Requested Return: March 15, 2010 Boulder Housing Partners 4800 Broadway Boulder, CO 80304 (720)

DIFFERENCES BETWEEN THE HISTORIC REHABILITATION TAX CREDIT AND THE LOW-INCOME HOUSING TAX CREDIT

DIFFERENCES BETWEEN THE HISTORIC REHABILITATION TAX CREDIT AND THE LOW-INCOME HOUSING TAX CREDIT Andrew S. Potts NIXON PEABODY LLP 401 Ninth Street NW Washington, D.C. 20004 apotts@nixonpeabody.com. 202-585-8337

DIFFERENCES BETWEEN THE HISTORIC REHABILITATION TAX CREDIT AND THE LOW-INCOME HOUSING TAX CREDIT Andrew S. Potts NIXON PEABODY LLP 401 Ninth Street NW Washington, D.C. 20004 apotts@nixonpeabody.com. 202-585-8337

The Affordable Housing Credit Improvement Act of 2017 (S. 548)

") The Affordable Improvement Act of 2017 (S. 548) Sponsored by Senator Maria Cantwell (D-WA) and co-sponsored by Senate Finance Committee Chairman Orrin Hatch (R-UT) and Ranking Member Ron Wyden (D-OR),

The Affordable Improvement Act of 2017 (S. 548) Sponsored by Senator Maria Cantwell (D-WA) and co-sponsored by Senate Finance Committee Chairman Orrin Hatch (R-UT) and Ranking Member Ron Wyden (D-OR),

Multifamily Finance Division Frequently Asked Questions 4% Housing Tax Credit Developments financed with Private Activity Bonds

Multifamily Finance Division Frequently Asked Questions 4% Housing Tax Credit Developments financed with Private Activity Bonds 1. What is a Private Activity Bond? What is a Housing Tax Credit? These are

Multifamily Finance Division Frequently Asked Questions 4% Housing Tax Credit Developments financed with Private Activity Bonds 1. What is a Private Activity Bond? What is a Housing Tax Credit? These are

Housing Consortium of Everett and Snohomish County 2013 Affordable Housing 101. Paul Purcell President, Beacon Development Group

Housing Consortium of Everett and Snohomish County 2013 Affordable Housing 101 Paul Purcell President, Beacon Development Group Session Outline 1. What is affordable housing? How is it defined? Who does

Housing Consortium of Everett and Snohomish County 2013 Affordable Housing 101 Paul Purcell President, Beacon Development Group Session Outline 1. What is affordable housing? How is it defined? Who does

UNIT INFORMATION (Complete the yellow-shaded areas) Gross monthly rent per. # of baths

Gross monthly rent per. # of baths") Project Name: Project #: UNIT INFORMATION (Complete the yellowshaded areas) Residential Finished Sq. Ft. per unit* Gross monthly rent per Less tenant paid Net monthly rent per # of bedrooms per unit #

Project Name: Project #: UNIT INFORMATION (Complete the yellowshaded areas) Residential Finished Sq. Ft. per unit* Gross monthly rent per Less tenant paid Net monthly rent per # of bedrooms per unit #

UNIFIED FUNDING 2017 QUESTIONS AND ANSWERS

UNIFIED FUNDING 2017 QUESTIONS AND ANSWERS Project Financing: Q1: Are HDC bond financed projects eligible for other sources besides HWF if they are not applied for in conjunction with HWF? Is HWF the sole

UNIFIED FUNDING 2017 QUESTIONS AND ANSWERS Project Financing: Q1: Are HDC bond financed projects eligible for other sources besides HWF if they are not applied for in conjunction with HWF? Is HWF the sole

Housing 101: Getting Started Development Finance Basics

Housing 101: Getting Started Development Finance Basics 23 rd Annual Statewide Housing Conference February 26, 2014 1 Challenges to Developing Affordable Housing Costs the same to develop whether rents

Housing 101: Getting Started Development Finance Basics 23 rd Annual Statewide Housing Conference February 26, 2014 1 Challenges to Developing Affordable Housing Costs the same to develop whether rents

Affordable Housing Gap and Economic Analysis

Affordable Housing Gap and Economic Analysis Town of Chapel Hill April 4, 2017 DAVID PAUL ROSEN & ASSOCIATES D EVELOPMENT, FINANCE AND POLICY ADVISORS Town of Chapel Hill PREPARED FOR: Town of Chapel Hill

Affordable Housing Gap and Economic Analysis Town of Chapel Hill April 4, 2017 DAVID PAUL ROSEN & ASSOCIATES D EVELOPMENT, FINANCE AND POLICY ADVISORS Town of Chapel Hill PREPARED FOR: Town of Chapel Hill

Agenda. District of Columbia Housing Finance Agency Before Stimulus and Current Market Conditions. DCHFA Deal Types DCHFA Team

Doing Business with the NEW DCHFA Harry D. Sewell, Executive Director May 25, 2010 Agenda Before Stimulus and Current Market Conditions New Issue Bond Program DCHFA Deal Types DCHFA Team Getting Started

Doing Business with the NEW DCHFA Harry D. Sewell, Executive Director May 25, 2010 Agenda Before Stimulus and Current Market Conditions New Issue Bond Program DCHFA Deal Types DCHFA Team Getting Started

CHAPTER TAX CREDITS AND SUBSIDY LAYERING. The Table of Contents

UNIT 12.0 PRESERVATION CHAPTER 12.10 TAX CREDITS AND SUBSIDY LAYERING The Table of Contents 12.10.1 Purpose.. I-1 12.10.2 Applicability.. I-2 12.10.3 Definitions and Acronyms... I-2 12.10.4 LIHTC s and

UNIT 12.0 PRESERVATION CHAPTER 12.10 TAX CREDITS AND SUBSIDY LAYERING The Table of Contents 12.10.1 Purpose.. I-1 12.10.2 Applicability.. I-2 12.10.3 Definitions and Acronyms... I-2 12.10.4 LIHTC s and

DATE: TO OWNER: Washington State Housing Finance Commission Low-Income Housing Tax Credit Program 1000 Second Avenue Suite 2700 Seattle WA

INDEPENDENT CERTIFIED PUBLIC ACCOUNTANT'S REPORT on CARRYOVER ALLOCATION BASIS PURSUANT TO IRS SECTION 42 (h)(1)(e)(ii) and AMERICAN RECOVERY AND REINVESTMENT ACT (ARRA) EXCHANGE PROGRAM 30% TEST PURSUANT

INDEPENDENT CERTIFIED PUBLIC ACCOUNTANT'S REPORT on CARRYOVER ALLOCATION BASIS PURSUANT TO IRS SECTION 42 (h)(1)(e)(ii) and AMERICAN RECOVERY AND REINVESTMENT ACT (ARRA) EXCHANGE PROGRAM 30% TEST PURSUANT

Billing Code DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT. [Docket No. FR-6129-N-01]

![Billing Code DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT. [Docket No. FR-6129-N-01]](/thumbs/90/102186154.jpg "Billing Code DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT. [Docket No. FR-6129-N-01]") This document is scheduled to be published in the Federal Register on 10/22/2018 and available online at https://federalregister.gov/d/2018-23000, and on govinfo.gov Billing Code 4210-67 DEPARTMENT OF

This document is scheduled to be published in the Federal Register on 10/22/2018 and available online at https://federalregister.gov/d/2018-23000, and on govinfo.gov Billing Code 4210-67 DEPARTMENT OF

Section 8: Low Income Housing Tax Credit Program Description and Requirements

Section 8: Low Income Housing Tax Credit Program Description and Requirements 2010 Consolidated Funding Cycle Application LIHTC Program Description & Requirements - Page 1 of 25 LOW INCOME HOUSING TAX

Section 8: Low Income Housing Tax Credit Program Description and Requirements 2010 Consolidated Funding Cycle Application LIHTC Program Description & Requirements - Page 1 of 25 LOW INCOME HOUSING TAX

UPDATED FINAL 2017 LIHTC QAP Online Application Q & A

2017 QAP 2.2.1 Nonprofit Set-Aside If a Project is awarded under the Nonprofit set-aside with 2 Co-General Partners, of which one is the qualified Nonprofit, could these 2 Co-General Partners be combined

2017 QAP 2.2.1 Nonprofit Set-Aside If a Project is awarded under the Nonprofit set-aside with 2 Co-General Partners, of which one is the qualified Nonprofit, could these 2 Co-General Partners be combined

Community Revitalization Efforts 2016 Thresholds and Scoring Criteria

s 2016 Thresholds and Scoring Criteria Definitions: a deliberate, concerted, and locally approved plan or documented interconnected series of local approvals and events intended to improve and enhance

s 2016 Thresholds and Scoring Criteria Definitions: a deliberate, concerted, and locally approved plan or documented interconnected series of local approvals and events intended to improve and enhance

9/9/2015. VitalSpirit LLC. Project Planning. Determine Housing Needs Population. Determine Housing Needs New Construction

Low Income Housing Tax Credits Program Setup: Finance Workshop Southwest Tribal Housing Alliance 7 th Annual Housing Forum Casino Del Sol Resort Tucson, AZ July 30, 2015 VitalSpirit LLC Team of six professionals

Low Income Housing Tax Credits Program Setup: Finance Workshop Southwest Tribal Housing Alliance 7 th Annual Housing Forum Casino Del Sol Resort Tucson, AZ July 30, 2015 VitalSpirit LLC Team of six professionals

U.S. Housing Act of 1937

SERC/NAHRO Conference Norfolk, Virginia June 25, 2018 U.S. Housing Act of 1937 Another New Deal initiative designed to relieve conditions in the nation's housing stock This was the beginning of Public

SERC/NAHRO Conference Norfolk, Virginia June 25, 2018 U.S. Housing Act of 1937 Another New Deal initiative designed to relieve conditions in the nation's housing stock This was the beginning of Public

2014 LIHTC PROGRAM UPDATE

2014 LIHTC PROGRAM UPDATE City Council Workshop July 29, 2013 LIHTC Program in Des Moines Significant impact on Des Moines development 89 projects/5,000 units in Des Moines (1989-2012) 30 projects/1,850

2014 LIHTC PROGRAM UPDATE City Council Workshop July 29, 2013 LIHTC Program in Des Moines Significant impact on Des Moines development 89 projects/5,000 units in Des Moines (1989-2012) 30 projects/1,850

APPENDIX B DESCRIPTION OF MAJOR FEDERAL LOW-INCOME HOUSING ASSISTANCE PROGRAMS

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org February 24, 2009 APPENDIX B DESCRIPTION OF MAJOR FEDERAL LOW-INCOME HOUSING ASSISTANCE

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org February 24, 2009 APPENDIX B DESCRIPTION OF MAJOR FEDERAL LOW-INCOME HOUSING ASSISTANCE

2017 Uniform Multifamily Application Templates

2017 Uniform Multifamily Application Templates 221 East 11 th Street Austin, TX 78701 Table of Contents Template Overview... 3 Using the Templates... 4 Public Notification Template... 5 Twice the State

2017 Uniform Multifamily Application Templates 221 East 11 th Street Austin, TX 78701 Table of Contents Template Overview... 3 Using the Templates... 4 Public Notification Template... 5 Twice the State

Multifamily Housing Revenue Bond Rules

Multifamily Housing Revenue Bond Rules 12.1. General. (a) Authority. The rules in this chapter apply to the issuance of multifamily housing revenue bonds ("Bonds") by the Texas Department of Housing and

Multifamily Housing Revenue Bond Rules 12.1. General. (a) Authority. The rules in this chapter apply to the issuance of multifamily housing revenue bonds ("Bonds") by the Texas Department of Housing and

Financing Historic Theaters Historic Preservation Tax Credits

Financing Historic Theaters Historic Preservation Tax Credits Heritage Ohio Annual Revitalization and Preservation Conference October 6, 2015 Chad Arfons, McDonald Hopkins LLC Federal Historic Preservation

Financing Historic Theaters Historic Preservation Tax Credits Heritage Ohio Annual Revitalization and Preservation Conference October 6, 2015 Chad Arfons, McDonald Hopkins LLC Federal Historic Preservation

This document is available via in a Microsoft Word format upon request. LOW INCOME HOUSING TAX CREDIT PROGRAM APPLICATION

This document is available via e-mail in a Microsoft Word format upon request. Development Name: LOW INCOME HOUSING TAX CREDIT PROGRAM APPLICATION DELAWARE STATE HOUSING AUTHORITY STATE OF DELAWARE Part

This document is available via e-mail in a Microsoft Word format upon request. Development Name: LOW INCOME HOUSING TAX CREDIT PROGRAM APPLICATION DELAWARE STATE HOUSING AUTHORITY STATE OF DELAWARE Part

Analyzing the Impact of the Financial Crisis on LIHTC Property Values. National Council of Affordable Housing Marketing Analysts November 9, 2009

Analyzing the Impact of the Financial Crisis on LIHTC Property Values National Council of Affordable Housing Marketing Analysts November 9, 2009 David Fournier dfournier@arausa.com THE CLIFF Total Apartments

Analyzing the Impact of the Financial Crisis on LIHTC Property Values National Council of Affordable Housing Marketing Analysts November 9, 2009 David Fournier dfournier@arausa.com THE CLIFF Total Apartments

Treasury Regulations 1.42

Treasury Regulations 1.42 1.42-1 [Reserved] 1.42-1T Limitation on low-income housing credit allowed with respect to qualified lowincome buildings receiving housing credit allocations from a State or local

Treasury Regulations 1.42 1.42-1 [Reserved] 1.42-1T Limitation on low-income housing credit allowed with respect to qualified lowincome buildings receiving housing credit allocations from a State or local

October Housing Affordability in Colorado. federal resources

October 2018 Housing Affordability in Colorado federal resources Contents Government-sponsored Enterprises 2 (GSEs) Fannie Mae, Freddie Mac, and Federal Home Loan Banks U.S. Department of Housing and 2

October 2018 Housing Affordability in Colorado federal resources Contents Government-sponsored Enterprises 2 (GSEs) Fannie Mae, Freddie Mac, and Federal Home Loan Banks U.S. Department of Housing and 2

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2016

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2016 Presented By: Karen Kent, CPA, Partner, Kevin P. Martin & Associates, P.C. Kenneth Lund,

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2016 Presented By: Karen Kent, CPA, Partner, Kevin P. Martin & Associates, P.C. Kenneth Lund,

2017 SECTION 42 HOUSING TAX CREDIT PROGRAM COMPLIANCE MANUAL for

MINNEAPOLIS COMMUNITY PLANNING ECONOMIC DEVELOPMENT AGENCY 2017 SECTION 42 HOUSING TAX CREDIT PROGRAM COMPLIANCE MANUAL for MINNEAPOLIS - SAINT PAUL HOUSING FINANCE BOARD Minneapolis CPED Contact: Mr.

MINNEAPOLIS COMMUNITY PLANNING ECONOMIC DEVELOPMENT AGENCY 2017 SECTION 42 HOUSING TAX CREDIT PROGRAM COMPLIANCE MANUAL for MINNEAPOLIS - SAINT PAUL HOUSING FINANCE BOARD Minneapolis CPED Contact: Mr.

TDHCA Question/Answer on Housing Tax Credits

TDHCA Question/Answer on Housing Tax Credits Q. What are Housing Tax Credits? A. The federal housing tax credit program is a means of directing private capital toward the creation of affordable rental

TDHCA Question/Answer on Housing Tax Credits Q. What are Housing Tax Credits? A. The federal housing tax credit program is a means of directing private capital toward the creation of affordable rental

U.S. Department of Housing and Urban Development Community Planning and Development

U.S. Department of Housing and Urban Development Community Planning and Development Special Attention of: Notice: CPD 98-1 All Secretary's Representatives All State/Area Coordinators Issued: January 22,

U.S. Department of Housing and Urban Development Community Planning and Development Special Attention of: Notice: CPD 98-1 All Secretary's Representatives All State/Area Coordinators Issued: January 22,

DAKOTA COUNTY CDA HOUSING TAX CREDIT 2017 PROCEDURAL MANUAL

DAKOTA COUNTY CDA HOUSING TAX CREDIT 2017 PROCEDURAL MANUAL MINNESOTA/2003654.0013/13965864.1 HOUSING TAX CREDIT PROGRAM 2017 TABLE OF CONTENTS I. INTRODUCTION... 4 II. AGENCY MISSION STATEMENT... 5 III.

DAKOTA COUNTY CDA HOUSING TAX CREDIT 2017 PROCEDURAL MANUAL MINNESOTA/2003654.0013/13965864.1 HOUSING TAX CREDIT PROGRAM 2017 TABLE OF CONTENTS I. INTRODUCTION... 4 II. AGENCY MISSION STATEMENT... 5 III.

The Low-Income Housing Tax Credit and the Hurricane Katrina Relief Effort

TO: FROM: Senate Committee on Finance Hurricane Katrina: Community Rebuilding Needs and Effectiveness of Past Proposals September 28, 2005 Affordable Housing Tax Credit Coalition c/o Hunton & Williams

TO: FROM: Senate Committee on Finance Hurricane Katrina: Community Rebuilding Needs and Effectiveness of Past Proposals September 28, 2005 Affordable Housing Tax Credit Coalition c/o Hunton & Williams

Novogradac LIHTC 101: The Basics Webinar Copyright 2016 Novogradac & Company LLP

Wayne Michael, CPA, NPCC, HCCP Director of Eternal Education Novogradac & Company LLP wayne.michael@novoco.com Tom Schneider, CPA Manager Novogradac & Company LLP tom.schneider@novoco.com 10-minute break

Wayne Michael, CPA, NPCC, HCCP Director of Eternal Education Novogradac & Company LLP wayne.michael@novoco.com Tom Schneider, CPA Manager Novogradac & Company LLP tom.schneider@novoco.com 10-minute break

HOME Program Basic Facts

HOME Program Basic Facts WHAT IS HOME? HOME is short for "HOME Investment Partnership Program", which became law in 1990. HOME provides an annual formula-based federal grant to the City of San Diego for

HOME Program Basic Facts WHAT IS HOME? HOME is short for "HOME Investment Partnership Program", which became law in 1990. HOME provides an annual formula-based federal grant to the City of San Diego for

Valuation Issues. Lindsey Sutton Novogradac & Company LLP. Brad Weinberg Novogradac & Company LLP

Valuation Issues PANELISTS Lindsey Sutton Novogradac & Company LLP Brad Weinberg Novogradac & Company LLP Visit www.crowdmics.online/novocolihtc to send questions to the moderator Valuation Issues How

Valuation Issues PANELISTS Lindsey Sutton Novogradac & Company LLP Brad Weinberg Novogradac & Company LLP Visit www.crowdmics.online/novocolihtc to send questions to the moderator Valuation Issues How

(a)-(g) [Reserved]. For further guidance, see T(a) through (g).

![(a)-(g) [Reserved]. For further guidance, see T(a) through (g).](/thumbs/93/111110189.jpg "(a)-(g) [Reserved]. For further guidance, see T(a) through (g).") 1.42-1 Limitation on low-income housing credit allowed with respect to qualified lowincome buildings receiving housing credit allocations from a State or local housing credit agency. (a)-(g) [Reserved].

1.42-1 Limitation on low-income housing credit allowed with respect to qualified lowincome buildings receiving housing credit allocations from a State or local housing credit agency. (a)-(g) [Reserved].

MONTANA BOARD OF HOUSING LOW INCOME HOUSING TAX CREDIT PROGRAM. - Summary of Low Income Housing Tax Credits

MONTANA BOARD OF HOUSING LOW INCOME HOUSING TAX CREDIT PROGRAM 2004 - Summary of Low Income Housing Tax Credits - Administrative Process, Eligible Competitions, and Fee Schedule - Montana Board of Housing

MONTANA BOARD OF HOUSING LOW INCOME HOUSING TAX CREDIT PROGRAM 2004 - Summary of Low Income Housing Tax Credits - Administrative Process, Eligible Competitions, and Fee Schedule - Montana Board of Housing

SUMMARY OF HPD AND HDC TERM SHEETS

SUMMARY OF HPD AND HDC TERM SHEETS This document is current as of 5/21/2015. Readers should refer to the official HPD and HDC term sheets for full program details: HPD: http://www.nyc.gov/html/hpd/html/developers/term-sheets.shtml

SUMMARY OF HPD AND HDC TERM SHEETS This document is current as of 5/21/2015. Readers should refer to the official HPD and HDC term sheets for full program details: HPD: http://www.nyc.gov/html/hpd/html/developers/term-sheets.shtml

Multifamily Housing Development Notice of Funding Availability

Multifamily Housing Development Notice of Funding Availability A Briefing to the Housing Committee Housing/Community Services Department December 5, 2016 Purpose Discuss the Notice of Funding Availability

Multifamily Housing Development Notice of Funding Availability A Briefing to the Housing Committee Housing/Community Services Department December 5, 2016 Purpose Discuss the Notice of Funding Availability

DSHA Underwriting Guidelines

DSHA Underwriting Guidelines NOTE: All applicants must utilize DSHA s LIHTC Application Part II - Pro Forma. No addition of tabs, changes to formulas, or manipulations of any kind are allowed. Any deviations

DSHA Underwriting Guidelines NOTE: All applicants must utilize DSHA s LIHTC Application Part II - Pro Forma. No addition of tabs, changes to formulas, or manipulations of any kind are allowed. Any deviations

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2014

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2014 Presented By: Karen Kent, CPA, Partner, Kevin P. Martin & Associates, P.C. Kenneth Lund,

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2014 Presented By: Karen Kent, CPA, Partner, Kevin P. Martin & Associates, P.C. Kenneth Lund,

Request for Proposals Wake County Affordable Housing Development Program for Tax Credit Developments

2015 Request for Proposals Wake County Affordable Housing Development Program for Tax Credit Developments 1) STATEMENT OF PURPOSE AND PROGRAM SUMMARY Wake County s Department of Housing and Community Revitalization

2015 Request for Proposals Wake County Affordable Housing Development Program for Tax Credit Developments 1) STATEMENT OF PURPOSE AND PROGRAM SUMMARY Wake County s Department of Housing and Community Revitalization

II. NEBRASKA INVESTMENT FINANCE AUTHORITY (NIFA) LOW INCOME HOUSING TAX CREDIT PROGRAM ALLOCATION PLAN

LOW INCOME HOUSING TAX CREDIT PROGRAM ALLOCATION PLAN") II. NEBRASKA INVESTMENT FINANCE AUTHORITY (NIFA) LOW INCOME HOUSING TAX CREDIT PROGRAM ALLOCATION PLAN 2004 LOW INCOME HOUSING TAX CREDIT PROGRAM 2004 Allocation Plan Table of Contents Page Available Low

II. NEBRASKA INVESTMENT FINANCE AUTHORITY (NIFA) LOW INCOME HOUSING TAX CREDIT PROGRAM ALLOCATION PLAN 2004 LOW INCOME HOUSING TAX CREDIT PROGRAM 2004 Allocation Plan Table of Contents Page Available Low

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2011

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2011 Presented By: Marianne Heard, CPA, MST, Tax Director, Kevin P. Martin & Associates, P.C.

Massachusetts Housing Investment Corporation Accounting, Audit & Tax Workshop For the Year Ended December 31, 2011 Presented By: Marianne Heard, CPA, MST, Tax Director, Kevin P. Martin & Associates, P.C.

REVISED REPORT TO THE HOUSING AUTHORITY OF SAN DIEGO

REVISED REPORT TO THE HOUSING AUTHORITY OF SAN DIEGO DATE ISSUED: October 3, 2016 REPORT NO: HAR16-035 ATTENTION: SUBJECT: Chair and Members of the Housing Authority of the City of San Diego For the Agenda

REVISED REPORT TO THE HOUSING AUTHORITY OF SAN DIEGO DATE ISSUED: October 3, 2016 REPORT NO: HAR16-035 ATTENTION: SUBJECT: Chair and Members of the Housing Authority of the City of San Diego For the Agenda

DECLARATION OF LAND USE RESTRICTIVE COVENANTS FOR LOW-INCOME HOUSING TAX CREDITS 2019 ALLOCATION YEAR

DECLARATION OF LAND USE RESTRICTIVE COVENANTS FOR LOW-INCOME HOUSING TAX CREDITS 2019 ALLOCATION YEAR THIS DECLARATION OF LAND USE RESTRICTIVE COVENANTS ( AGREEMENT or LURA ) dated as of, by, a, and its

DECLARATION OF LAND USE RESTRICTIVE COVENANTS FOR LOW-INCOME HOUSING TAX CREDITS 2019 ALLOCATION YEAR THIS DECLARATION OF LAND USE RESTRICTIVE COVENANTS ( AGREEMENT or LURA ) dated as of, by, a, and its

Developer Non Managing Member- Historic Tax Credit Investor. Managing Member- Developer. Developer Fee Capital Contribution Tax Capital Contributions

Developer Managing Member- Developer Non Managing Member- Historic Tax Credit Investor Developer Fee Capital Contribution Tax Credits Capital Contributions Building Owner LLC/ Master Landlord Managing

Developer Managing Member- Developer Non Managing Member- Historic Tax Credit Investor Developer Fee Capital Contribution Tax Credits Capital Contributions Building Owner LLC/ Master Landlord Managing

AFFORDABLE HOUSING 101. Jimmy McCune - OCCH Tim Swiney Wallick Communities Roy Lowenstein Lowenstein Development

AFFORDABLE HOUSING 101 Jimmy McCune - OCCH Tim Swiney Wallick Communities Roy Lowenstein Lowenstein Development Affordability in Housing Defined Generally refers to housing affordable to those who earn

AFFORDABLE HOUSING 101 Jimmy McCune - OCCH Tim Swiney Wallick Communities Roy Lowenstein Lowenstein Development Affordability in Housing Defined Generally refers to housing affordable to those who earn

The State of Affordable Housing 2017

The State of Affordable Housing 2017 Panel 1: Federal Updates Moderator: Jay Harris Peter Lawrence, Novogradac Marion Mollegen McFadden, Enterprise Mike Hawkins, VHDA State of Affordable Housing 2017 Alliance

The State of Affordable Housing 2017 Panel 1: Federal Updates Moderator: Jay Harris Peter Lawrence, Novogradac Marion Mollegen McFadden, Enterprise Mike Hawkins, VHDA State of Affordable Housing 2017 Alliance

Cost Segregation Instructor Teaching Schedule (3-Hour)

") Time Topic Pages Student Objectives 8:30-8:35 Course introduction Page 2 What is cost segregation? Objective of cost segregation: to increase cash flow Benefit of cost segregation Learning objectives Page

Time Topic Pages Student Objectives 8:30-8:35 Course introduction Page 2 What is cost segregation? Objective of cost segregation: to increase cash flow Benefit of cost segregation Learning objectives Page

Qualified Contract Process

Qualified Contract Process Summary The Omnibus Budget Reconciliation Act of 1989 required that all properties receiving an allocation of Housing Credit after December 31, 1989 are subject to an "extended

Qualified Contract Process Summary The Omnibus Budget Reconciliation Act of 1989 required that all properties receiving an allocation of Housing Credit after December 31, 1989 are subject to an "extended

Connecticut Housing Finance Authority

Connecticut Housing Finance Authority Low-Income Housing Tax Credit Qualified Allocation Plan 2013 Application Year Table of Contents Table of Contents I. FEDERAL REQUIREMENTS... 3 II. STATE HOUSING PLANS...

Connecticut Housing Finance Authority Low-Income Housing Tax Credit Qualified Allocation Plan 2013 Application Year Table of Contents Table of Contents I. FEDERAL REQUIREMENTS... 3 II. STATE HOUSING PLANS...

Housing Committee April 6, 2015

Deaf Action Center Martha's Vineyard Place Housing Committee April 6, 2015 Purpose Provide background information on the Deaf Action Center s Martha Vineyard project Seek Housing Committee approval for

Deaf Action Center Martha's Vineyard Place Housing Committee April 6, 2015 Purpose Provide background information on the Deaf Action Center s Martha Vineyard project Seek Housing Committee approval for

DRAFT FOR PUBLIC COMMENT

WASHINGTON COUNTY CDA SELF-SCORING WORKSHEET 2020 LOW INCOME HOUSING TAX CREDIT PROGRAM Development Name Address/City Owner Name MINIMUM THRESHOLD REQUIREMENTS All Round 1 applicants for 9% LIHTC must

WASHINGTON COUNTY CDA SELF-SCORING WORKSHEET 2020 LOW INCOME HOUSING TAX CREDIT PROGRAM Development Name Address/City Owner Name MINIMUM THRESHOLD REQUIREMENTS All Round 1 applicants for 9% LIHTC must

FUNDING SOURCES FOR AFFORDABLE HOUSING IN HANCOCK COUNTY, MAINE

FUNDING SOURCES FOR AFFORDABLE HOUSING IN HANCOCK COUNTY, MAINE March 2013 Prepared by: Hancock County Planning Commission, 395 State Street Ellsworth, ME 04605 www.hcpcme.org voice: 207-667-7131 Fax:

FUNDING SOURCES FOR AFFORDABLE HOUSING IN HANCOCK COUNTY, MAINE March 2013 Prepared by: Hancock County Planning Commission, 395 State Street Ellsworth, ME 04605 www.hcpcme.org voice: 207-667-7131 Fax:

Analysis of a Troubled Deal. Keith Broadnax Joshua Ghena David Helm Josh White

Analysis of a Troubled Deal Keith Broadnax Joshua Ghena David Helm Josh White Identifying a Troubled Deal How to Spot and Fix Problem Deals Introduction to Presenters Josh Ghena- Lansing MI Director Special

Analysis of a Troubled Deal Keith Broadnax Joshua Ghena David Helm Josh White Identifying a Troubled Deal How to Spot and Fix Problem Deals Introduction to Presenters Josh Ghena- Lansing MI Director Special

Draft Roosevelt Income Restricted Housing Analysis

APPENDIX F Draft Roosevelt Income Restricted Housing Analysis Prepared for: Presented by: Sound Transit May 5, 2016 C/o Jeff Lehman, KPFF 1601 5th Avenue, Suite1600 Seattle, WA 98101 (206) 622 5822 Jeff.Lehman@kpff.com

APPENDIX F Draft Roosevelt Income Restricted Housing Analysis Prepared for: Presented by: Sound Transit May 5, 2016 C/o Jeff Lehman, KPFF 1601 5th Avenue, Suite1600 Seattle, WA 98101 (206) 622 5822 Jeff.Lehman@kpff.com

Differences, Procurement and

U.S. Department of Housing and Urban Development Developers and Subrecipients: Differences, Procurement and Other Rules July 24, 2012 2:00 PM EDT Community Planning and Development Purpose of Webinar To

U.S. Department of Housing and Urban Development Developers and Subrecipients: Differences, Procurement and Other Rules July 24, 2012 2:00 PM EDT Community Planning and Development Purpose of Webinar To

NATIONAL HOUSING TRUST FUND PROGRAM FFY 2018

1 NATIONAL HOUSING TRUST FUND PROGRAM FFY 2018 STATE OF NEW JERSEY GOVERNOR, PHILIP D. MURPHY DEPARTMENT OF COMMUNITY AFFAIRS LT. GOVERNOR, SHEILA Y. OLIVER - COMMISSIONER 1/17/2018 NHTF Summary 2 NHTF

1 NATIONAL HOUSING TRUST FUND PROGRAM FFY 2018 STATE OF NEW JERSEY GOVERNOR, PHILIP D. MURPHY DEPARTMENT OF COMMUNITY AFFAIRS LT. GOVERNOR, SHEILA Y. OLIVER - COMMISSIONER 1/17/2018 NHTF Summary 2 NHTF

WYOMING COMMUNITY DEVELOPMENT AUTHORITY. Affordable Rental Housing Compliance Manual For Tax Credit, Bond and HOME Projects

WYOMING COMMUNITY DEVELOPMENT AUTHORITY Affordable Rental Housing Compliance Manual For Tax Credit, Bond and HOME Projects Effective January 1, 2013 TABLE OF CONTENTS 1. Introduction A. The Purpose of

WYOMING COMMUNITY DEVELOPMENT AUTHORITY Affordable Rental Housing Compliance Manual For Tax Credit, Bond and HOME Projects Effective January 1, 2013 TABLE OF CONTENTS 1. Introduction A. The Purpose of

Glossary of Terms Low-Income Housing Tax Credit Program

Glossary of Terms 2017 Low-Income Housing Tax Credit Program AMGI: Area Median Gross Income as defined by HUD. AMI: Area Median Income as defined by HUD. BIN: The state credit agency assigns a Building

Glossary of Terms 2017 Low-Income Housing Tax Credit Program AMGI: Area Median Gross Income as defined by HUD. AMI: Area Median Income as defined by HUD. BIN: The state credit agency assigns a Building

STATE OF ALASKA ALASKA HOUSING FINANCE CORPORATION GOAL PROGRAM. (Greater Opportunities for Affordable Living Program) RATING AND AWARD CRITERIA PLAN

RATING AND AWARD CRITERIA PLAN") STATE OF ALASKA ALASKA HOUSING FINANCE CORPORATION GOAL PROGRAM (Greater Opportunities for Affordable Living Program) RATING AND AWARD CRITERIA PLAN (Qualified Allocation Plan) Effective May 25, 2016 Low-Income

STATE OF ALASKA ALASKA HOUSING FINANCE CORPORATION GOAL PROGRAM (Greater Opportunities for Affordable Living Program) RATING AND AWARD CRITERIA PLAN (Qualified Allocation Plan) Effective May 25, 2016 Low-Income

The Legal and Financial Facets of Historic Tax Credits

California Preservation Foundation From Dollars & Cents to Success: Financial Incentive Programs for Historic Preservation February 10, 2016 The Legal and Financial Facets of Historic Tax Credits Roy Chou,

California Preservation Foundation From Dollars & Cents to Success: Financial Incentive Programs for Historic Preservation February 10, 2016 The Legal and Financial Facets of Historic Tax Credits Roy Chou,

CHAPTER V: IMPLEMENTING THE PLAN

CHAPTER V: IMPLEMENTING THE PLAN A range of resources is available to fund the improvements included in the Action Plan. These resources include existing commitments of County funding, redevelopment-related

CHAPTER V: IMPLEMENTING THE PLAN A range of resources is available to fund the improvements included in the Action Plan. These resources include existing commitments of County funding, redevelopment-related

Welcome to the 9 th Annual Spring Housing Conference

Welcome to the 9 th Annual Spring Housing Conference Session One: The Washington Update 1 Opportunity In Focus: Latest Pronouncements from RAD/FHA Update Session Two: QOZ s Optimizing Opportunities 2 Qualified

Welcome to the 9 th Annual Spring Housing Conference Session One: The Washington Update 1 Opportunity In Focus: Latest Pronouncements from RAD/FHA Update Session Two: QOZ s Optimizing Opportunities 2 Qualified

Innovations in Solar Financing for Non-Profits and Affordable Housing CESA Workshop on Deploying Solar in Public and Affordable Housing

Innovations in Solar Financing for Non-Profits and Affordable Housing CESA Workshop on Deploying Solar in Public and Affordable Housing Bracken Hendricks CEO, Urban Ingenuity October 17, 2017 Ingenuity

Innovations in Solar Financing for Non-Profits and Affordable Housing CESA Workshop on Deploying Solar in Public and Affordable Housing Bracken Hendricks CEO, Urban Ingenuity October 17, 2017 Ingenuity

2019 9% Competitive Housing Credit Application

2019 9% Competitive Housing Credit Application Application Checklist This checklist includes all the items from the CFA application and the LIHTC Addendum that are required for the 2019 9% Application

2019 9% Competitive Housing Credit Application Application Checklist This checklist includes all the items from the CFA application and the LIHTC Addendum that are required for the 2019 9% Application

CHICAGO LOW-INCOME HOUSING TRUST FUND MAUI Program Guide and Application (Capital Investment)

") 2019 MAUI Capital Investment Application CHICAGO LOW-INCOME HOUSING TRUST FUND MAUI Program Guide and Application (Capital Investment) (Rev. 12-31-18) Chicago Low-Income Housing Trust Fund Since 1989,

2019 MAUI Capital Investment Application CHICAGO LOW-INCOME HOUSING TRUST FUND MAUI Program Guide and Application (Capital Investment) (Rev. 12-31-18) Chicago Low-Income Housing Trust Fund Since 1989,

2016 Governor s Housing Conference WELCOME. Ed Yandell, Senior Housing Credit Advisor. Low-Income Housing Tax Credit Program

2016 Governor s Housing Conference WELCOME Ed Yandell, Senior Housing Credit Advisor Partnership between private and public sectors Credit against federal income tax liability each year for 10 years Low-Income

2016 Governor s Housing Conference WELCOME Ed Yandell, Senior Housing Credit Advisor Partnership between private and public sectors Credit against federal income tax liability each year for 10 years Low-Income

National Housing Trust Fund Implementation. Virginia Housing Alliance

National Housing Trust Fund Implementation Virginia Housing Alliance June 16, 2016 Ed Gramlich National Low Income Housing Coalition 1 What Is the National Housing Trust Fund? National Housing Trust Fund

National Housing Trust Fund Implementation Virginia Housing Alliance June 16, 2016 Ed Gramlich National Low Income Housing Coalition 1 What Is the National Housing Trust Fund? National Housing Trust Fund

QUALIFIED ALLOCATION PLAN

STATE OF NEW MEXICO HOUSING TAX CREDIT PROGRAM QUALIFIED ALLOCATION PLAN Effective as of January 1, 2019 NEW MEXICO MORTGAGE FINANCE AUTHORITY Approved by Board of Directors on 11-16-2018 Approved by the

STATE OF NEW MEXICO HOUSING TAX CREDIT PROGRAM QUALIFIED ALLOCATION PLAN Effective as of January 1, 2019 NEW MEXICO MORTGAGE FINANCE AUTHORITY Approved by Board of Directors on 11-16-2018 Approved by the

FY 2018 Notice of Funding Availability (NOFA) for Affordable Housing Investment Funds (AHIF) and Federal Loan Funds

for Affordable Housing Investment Funds (AHIF) and Federal Loan Funds") FY 08 Notice of Funding Availability (NOFA) for Affordable Housing Investment Funds (AHIF) and Federal Loan Funds Overview Arlington County Department of Community Planning, Housing, and Development (CPHD)

FY 08 Notice of Funding Availability (NOFA) for Affordable Housing Investment Funds (AHIF) and Federal Loan Funds Overview Arlington County Department of Community Planning, Housing, and Development (CPHD)

STATE OF RHODE ISLAND 2013 QUALIFIED ALLOCATION PLAN. Qualified Allocation Plan

STATE OF RHODE ISLAND 2013 QUALIFIED ALLOCATION PLAN Qualified Allocation Plan 2013 1 State of Rhode Island Revised 2013 Qualified Allocation Plan For the Low-Income Housing Tax Credit Program INTRODUCTION

STATE OF RHODE ISLAND 2013 QUALIFIED ALLOCATION PLAN Qualified Allocation Plan 2013 1 State of Rhode Island Revised 2013 Qualified Allocation Plan For the Low-Income Housing Tax Credit Program INTRODUCTION

FLORIDA HOUSING FINANCE CORPORATION Tax Credit Assistance Program Project Selection Process and Criteria

FLORIDA HOUSING FINANCE CORPORATION Tax Credit Assistance Program Project Selection Process and Criteria On February 17, 2009, President Obama signed the American Recovery and Reinvestment Act of 2009

FLORIDA HOUSING FINANCE CORPORATION Tax Credit Assistance Program Project Selection Process and Criteria On February 17, 2009, President Obama signed the American Recovery and Reinvestment Act of 2009

Neighborhood Stabilization Program

Neighborhood Stabilization Program Neighborhood Stabilization Program What is the Neighborhood Stabilization Program? NSP was funded in 3 rounds to provide assistance to state and local governments to

Neighborhood Stabilization Program Neighborhood Stabilization Program What is the Neighborhood Stabilization Program? NSP was funded in 3 rounds to provide assistance to state and local governments to

Administered by. The Multifamily Programs Division of Tennessee Housing Development Agency. Ralph M. Perrey, Executive Director

Administered by The Multifamily Programs Division of Tennessee Housing Development Agency Ralph M. Perrey, Executive Director Section 1 Introduction and Disclaimers Section 2 Definitions Section 3 State

Administered by The Multifamily Programs Division of Tennessee Housing Development Agency Ralph M. Perrey, Executive Director Section 1 Introduction and Disclaimers Section 2 Definitions Section 3 State

THE NSP SUBSTANTIAL AMENDMENT

THE NSP SUBSTANTIAL AMENDMENT AMENDED DRAFT AUGUST 29, 2009 Jurisdiction(s): Town of Babylon (located in Suffolk County New York) Jurisdiction Web Address: www.townofbabylon.com NSP Contact Person: Theresa

THE NSP SUBSTANTIAL AMENDMENT AMENDED DRAFT AUGUST 29, 2009 Jurisdiction(s): Town of Babylon (located in Suffolk County New York) Jurisdiction Web Address: www.townofbabylon.com NSP Contact Person: Theresa

Washington County Housing and Redevelopment Authority. Housing Tax Credit Program Procedural Manual

Washington County Housing and Redevelopment Authority Housing Tax Credit Program 2017 Procedural Manual TABLE OF CONTENTS INTRODUCTION...1 CHAPTER 1 AUTHORITY MISSION STATEMENT...2 CHAPTER 2 ROLE OF THE

Washington County Housing and Redevelopment Authority Housing Tax Credit Program 2017 Procedural Manual TABLE OF CONTENTS INTRODUCTION...1 CHAPTER 1 AUTHORITY MISSION STATEMENT...2 CHAPTER 2 ROLE OF THE

REPORT. DATE ISSUED: December 19, 2014 REPORT NO: HCR Chair and Members of the San Diego Housing Commission For the Agenda of January 16, 2015

REPORT DATE ISSUED: December 19, 2014 REPORT NO: HCR15-008 ATTENTION: SUBJECT: Chair and Members of the San Diego Housing Commission For the Agenda of January 16, 2015 COUNCIL DISTRICT: 9 REQUESTED ACTION

REPORT DATE ISSUED: December 19, 2014 REPORT NO: HCR15-008 ATTENTION: SUBJECT: Chair and Members of the San Diego Housing Commission For the Agenda of January 16, 2015 COUNCIL DISTRICT: 9 REQUESTED ACTION

HC FINAL COST CERTIFICATION FORM AND INSTRUCTIONS

HC FINAL COST CERTIFICATION FORM AND INSTRUCTIONS The Final Cost Certification Application (FCCA) must be completed by the Applicant and returned to Florida Housing along with an unqualified audit report

HC FINAL COST CERTIFICATION FORM AND INSTRUCTIONS The Final Cost Certification Application (FCCA) must be completed by the Applicant and returned to Florida Housing along with an unqualified audit report

N.C. Housing Finance Agency

N.C. Housing Finance Agency A. Robert Kucab Executive Director Joint Appropriations Subcommittee on General Government N.C. Housing Finance Agency Established in G.S. Chapter 122A Created in 1973 Self-supporting

N.C. Housing Finance Agency A. Robert Kucab Executive Director Joint Appropriations Subcommittee on General Government N.C. Housing Finance Agency Established in G.S. Chapter 122A Created in 1973 Self-supporting

VHFA FEDERAL HOUSING CREDIT APPLICATION & VERMONT STATE AFFORDABLE HOUSING TAX CREDIT APPLICATION SUPPLEMENT

VHFA FEDERAL HOUSING CREDIT APPLICATION & VERMONT STATE AFFORDABLE HOUSING TAX CREDIT APPLICATION SUPPLEMENT Syndication Information Provide information below concerning syndication and estimated proceeds

VHFA FEDERAL HOUSING CREDIT APPLICATION & VERMONT STATE AFFORDABLE HOUSING TAX CREDIT APPLICATION SUPPLEMENT Syndication Information Provide information below concerning syndication and estimated proceeds