TRACKING VALUE 2010 ANNUAL REPORT

|

|

|

- Dwain Todd

- 5 years ago

- Views:

Transcription

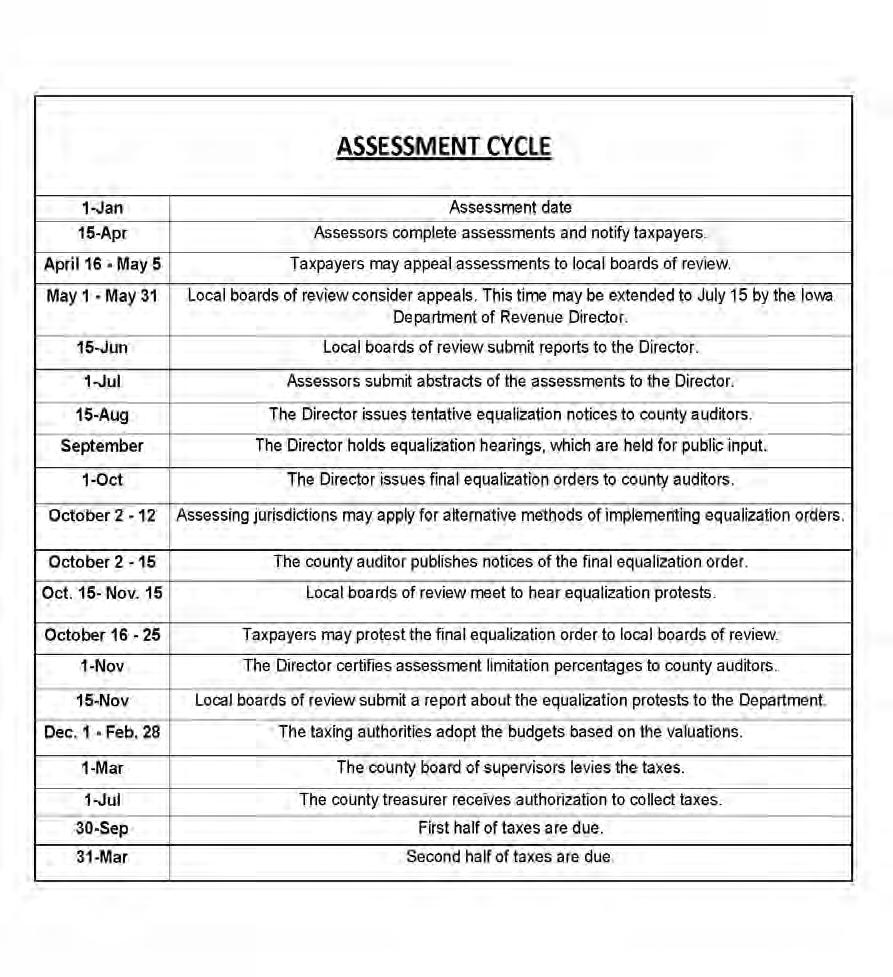

1 TRACKING VALUE 2010 ANNUAL REPORT Winneshiek County Assessor s office James Alstad, Winneshiek County Assessor What s Inside This Issue! Assessor s Message Pg. 1 Conference Board Members Pg. 2 Personnel Pg. 3 Staff Pg. 4 Conference Board Duties Pg. 5 Intro to Property Tax Pg Assessment Abstracts Pg Exempt Property Report Pg Board of Review Report Pg Statistical explanations Pg. 27 Sales Analysis Pg Statewide Data Pg New Home Analysis Pg. 40 Assessed Valuation Trend Pg. 41 Taxable Valuation Trend Pg. 42 Assessment Cycle Pg. 43

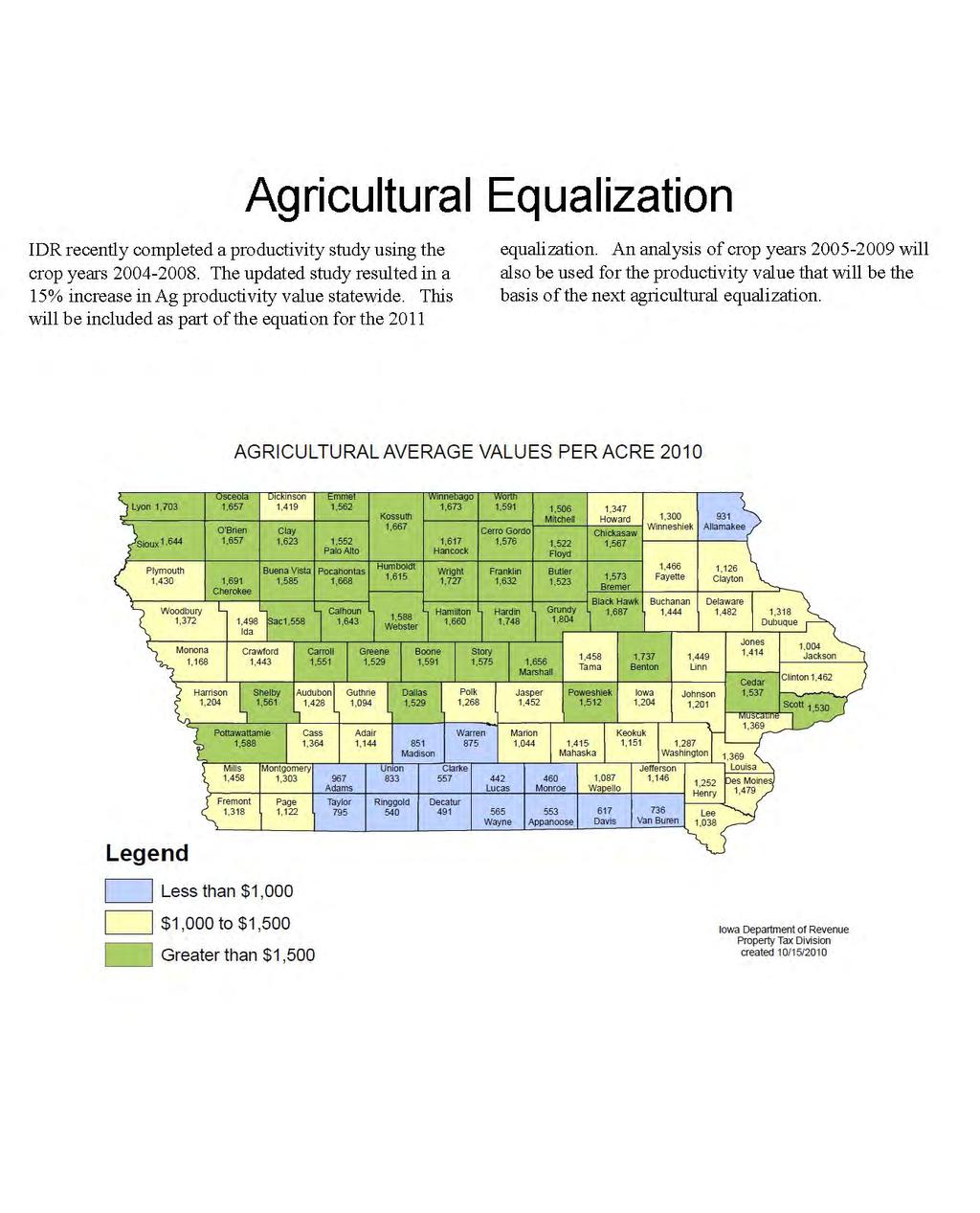

2 A Message From the Assessor Assessment Year To the Honorable Conference Board and Winneshiek County Taxpayers: Within this report you will find an overview of statistics, sales data, and information pertaining to the operations of the assessor s office for Our Staff and I continue to be dedicated to the duties of the assessor s office. I am pleased to report that we have achieved compliance with the laws governing the assessment process as set forth by the Iowa State Legislature and the Iowa Department of Revenue. On or before April 15, 2011 we will be sending out our assessment notices for the 2011 assessment year. We will soon be finishing our analysis of market data to see where our assessments need to be for commercial, industrial, residential, and agricultural properties. All early indications are that our market is stable. Changes should be minimal in order to maintain compliance with assessment laws. However, with agricultural property assessments based on productivity, we are expecting a substantial increase on our agricultural classed properties as a result of some good crop years in the formula affecting value. Legislatively there are a couple property tax issues at the forefront of Governor Branstad s spending plan. His proposal included concerns regarding property tax relief for commercial properties. Commercial property is now taxed at 100 percent of its assessed value. Branstad proposed lowering taxable values of commercial to 60 percent for new property and reducing it over five years for existing commercial properties. Cutting Corporate income taxes was also mentioned in the Governor s plan. Among the Governor s ideas to compensate lower commercial revenues is to raise the tax on casino profits, scale back funding for preschools, freeze state spending on schools for two years, and force state agencies to tighten their budgets. We ll wait and see if his goal of easing the burden on commercial will come to fruition. It s hard not to be empathetic to the commercial property owners in Iowa when it comes to property tax. I hope you find the information provided in this report helpful in understanding the assessment process. Please feel free to contact our office at anytime if you should have any questions regarding the assessment process at

3 CONFERENCE BOARD MEMBERS SCHOOL BOARD Myron Rediske: North Winneshiek School District Dr. Wendy Mihm-Herold: South Winneshiek School District Dan Schutte: Postville School District Ernest Schmitt: Turkey Valley School District Brian Petersburg: Decorah Community School District Jeff Murphy: Howard Winneshiek School District No member resides: Allamakee Community School District MAYORS Joseph McCasland: Mayor, City of Calmar Margaret Jones: Mayor, City of Castalia David Brenno: Mayor, City of Ridgeway Michael T. Klimesh: Mayor, City of Spillville Paul Herold: Mayor, City of Fort Atkinson Don Arendt: Mayor, City of Decorah Mae Schmitt: Mayor, City of Jackson Junction Charles Covell : Mayor, City of Ossian COUNTY SUPERVISORS Les Askelson: Fourth District Supervisor / Conference Board Chairman Lonnie Pierce: First District Supervisor John Logsdon: Second District Supervisor William Ibanez: Fifth District Supervisor Stephen Bouska: Third District Supervisor 2

4 OFFICE PERSONNEL Start Date Jim Alstad, Assessor December, 2001 Scott Anderson, Deputy Assessor August, 2007 Lyn White, Office Manager April, 1990 Jennifer Brooks, Mapping Technician July, 2008 BOARD OF REVIEW Term Expires Ron Hemesath December 31, 2011 Michael Kelly December 31, 2013 John L. Heying December 31, 2014 Jim Ludeking December 31, 2015 Orvin Hotvedt December 31, 2016 EXAMINING BOARD Term Expires Calvin Anderson (Supervisors) December 31, 2011 Dennis Hovden (Schools) December 31, 2011 Dave Olson (Mayors) December 31,

5 THE TEAM Deputy Assessor, Scott Anderson, is now in his 4th year working in Winneshiek County after eleven plus years as an Appraiser in Allamakee County. Office Manager, Lyn White, is now in her 20th year working for the Winneshiek County Assessors office. Mapping Technician/GIS Assistant, Jennifer Brooks, is in her 3rd year with the assessor s office with ten prior years of experience in the Winneshiek County Auditor s Office. Mission Statement: To achieve equalization among all classes of property by maintaining the highest standards in appraisal practices and law, guided by the goal of providing quality service to the public, and making a difference through effort and striving to be better. 4

6 Conference Board Duties and Procedures The Conference Board consists of three voting units which are: Board of Supervisors. Mayors of the incorporated cities of the county. One representative from the Board of Directors of each school district in the county, whom must be a resident of the county. Functions of the Conference Board: Appoints members of the Examining Board to six year terms. Appoints the Assessor and re-appoints the Assessor every six years. Determines how many Deputies an Assessor may have but the Assessor appoints the Deputies. Determines the number of employees. Establishes and adopts an annual budget for the Assessor s office. The Chairman of the Conference Board is the Chairman of the Board of Supervisors and the Clerk of the Conference Board is the Assessor for the County. Both of these positions are defined by the Code of Iowa. No action of a Conference Board shall be valid except by the vote of not less than two of the three units. The members of the Conference Board should remain in the meeting room in open session with the members of the public present to discuss the agenda items presented. Votes should be done individually by roll call vote, show of hands or some similar method, so as to clearly indicate and make public the vote of each individual member on each motion and with votes shown in the minutes. The majority votes of the members present of each unit shall be the vote of that unit. The majority votes of the units will determine whether a motion passes or fails. At least two members of each voting unit must be present in order for the unit to cast a vote. The lawmakers of Iowa set up this procedure to remove any political influence from the Assessor s office. The operation of the Assessor s office is totally separate from other forms of local government. This is why the Conference Board is a separate Board and approves a separate budget specifically for the Assessor s office. The reason for the three units is that each unit represents one of the three major local taxing bodies of the County. 5

7 An Introduction to Iowa Property Tax Property taxes are not determined by a single individual who assesses your property and sends you a bill. The final tax rate is the result of budgets established to provide services, an assessor s assessment, a county auditor s calculations, and laws administered by the Iowa Department of Revenue. Because property assessment involves a series of events that takes 18 months from start to finish, this information will not be able to answer all your questions. It should, however, be able to explain the basic principles and events involved in calculating the property tax rate. What is the Iowa property tax? The Iowa property tax is primarily a tax on "real property," which is mostly land, buildings, structures, and other improvements that are constructed on or in the land, attached to the land, or placed upon a foundation. Typical improvements include a building, house or mobile home, fences, and paving. The following five classes of real property are evaluated: residential agricultural commercial industrial utilities/railroad [This class is assessed at the state level.] Who pays property tax? Home owners pay almost 43 percent of the property tax collected each year in Iowa. Farmers pay more than 22 percent, and businesses and industry more than 31 percent. Utility companies, including railroads, pay more than 3 percent. 6

8 How often is property assessed? State law requires that all real property be assessed every two years in odd-numbered years. Railroads and public utilities, which are assessed by the Iowa Department of Revenue, are assessed every year. Which governments collect property taxes? Property tax supports many different "taxing authorities." Cities, counties, school districts, and townships are the most common. Taxing authorities may also include community college districts, agricultural extension districts, assessor offices, hospital districts, and sanitation districts. In addition, there are associations for fire protection, drainage, and other public needs that levy taxes. Iowa has more than 2,000 taxing authorities. Most property is taxed by more than one taxing authority. 7

9 How is the rate of the property tax determined? 1. The value of property is established. The assessor (or the Iowa Department of Revenue) estimates the value of each property. This is called the "assessed value." 2. The assessments of all taxable properties are added together. The assessor totals the assessed value in each classification and reports it to the county auditor. 3. The Department examines total assessed values and equalizes them. Each assessor sends the reports, called "abstracts," to the Iowa Department of Revenue. The abstract shows the total taxable values of all real property in each jurisdiction by classification of property, not by individual property. A process called "equalization" is applied every two years to ensure that property values are comparable among jurisdictions and according to law. In addition, the "assessment limitation" is applied every year. This process is commonly called "rollback" and is used in response to inflation. 4. Budgets are established. Each taxing authority determines its own budget. The budget includes the cost of providing services, the amount of aid received from the federal and state governments, the amount of money remaining from previous years, and revenue from other charges for services. Each approved budget is submitted to the county auditor. 5. A tax rate is established. The county auditor divides the amount of the budget that is not funded by other sources by the taxable value of all the property in the taxing district. The result is referred to as "dollars per thousand." If the dollars per thousand were $10, the tax on a home valued at $50,000 would be calculated at $10 x 50. 8

10 The tax on that home would be $500 for that single taxing authority. Since more than one taxing authority is calculating a tax rate for the property, all the rates are added together, resulting in a single tax levy called a consolidated levy. This consolidated levy is always the result of two or more tax rates established by different government entities. 6. Credits are subtracted. Credits such as the Homestead Credit are subtracted before a final tax bill is sent to the taxpayer. Also.. Before you ever see your tax bill, two additional steps occur to test and adjust assessments to legal levels. Equalization In Step 3 above, the Iowa Department of Revenue is responsible for "equalizing" assessments every two years. Following is a general explanation of the purpose of equalization. The Department compares the assessors abstracts to a "sales assessment ratio study" it has completed independently of the assessors. If the assessment (by property class) is 5 percent or more above or below the sales ratio study, the Department increases or decreases the assessment. There is no sales ratio study for agricultural and industrial property. Equalization occurs on an entire class of property, not on an individual property. Also, equalization occurs on an assessing jurisdiction basis, not on a statewide basis. Equalization is important because it helps maintain equitable assessments among classes of property and among assessing jurisdictions. This contributes to a more fair distribution of state aid, such as aid to schools. It also helps to equally distribute the total tax burden within the area. 9

11 Rollbacks More than 20 years ago, residential property values were rising quickly. To help cushion the impact of high inflation, the Legislature passed an assessment limitation law called rollback. Increases in assessed values for residential and agricultural property are subject to this assessment limitation formula. If the statewide increase in values of homes and farms exceeds 4 percent due to revaluation, their values are "rolled back" so that the total increase statewide is 4 percent. Rollback is also available for industrial and commercial property when necessary. This does not mean that the assessment on your home will increase by only 4 percent. The rollback is applied on a class of property, not an individual property. This means that the statewide total taxable value can increase by only 4 percent due to revaluation. Property Tax Collections in FY08 An estimated $3,793,147,933 was collected in Iowa in fiscal year K-12 Schools: $1,592,503,527 Cities: $1,126,557,411 Counties: $824,972,727 Hospitals: $77,402,471 Merged Area Schools: $ 78,161,332 Assessors: $42,866,218 Townships: $22,477,124 Agricultural Extension District: $14,702,888 Miscellaneous: $13,504,235 10

12 What causes taxes to increase? Basically, three variables must interact to decrease or increase your property taxes: The combined budgets of the taxing authorities The total value of all the property in the taxing unit The value of your property Your taxes increase if... The budgets increase and the value of all properties remain the same. The budgets and value of property in the entire government unit remain the same but the value of the individual s property increases. The budgets and value of the individual s property remain the same but the value of the property in the entire government unit decreases. Your taxes decrease if... The budgets decrease and the values of all properties remain the same. The budgets and value of property in the entire government unit remain the same but the value of the individual s property decreases. The budgets and value of the individual s property remain the same but the value of the property in the entire government unit increases. Why might you pay higher taxes than your neighbor? The value of a house depends on land size, square footage, type of construction, age, quality, location, story height, and condition, but that s not all. Your neighbor s property may be taxed by different taxing districts than you are. For instance, districts are often divided by highways. If your neighbor s property is across the highway, it may be taxed by different districts than you are. Also, credits and exemptions such as Homestead, Ag Land, and Military could make a difference. What if you disagree with the assessed value of your property? Property owners who disagree with the assessor s estimate of the market value of their property should ask themselves, "Could I sell this property for that amount 11

13 today?" If the answer is yes, then the value is probably correct. However, every property owner has the right to appeal an assessment. Property owners may appeal their initial assessments to local boards of review by filing a written protest between April 16 and May 5 of each year. These boards meet annually in May to consider the protests. In a reassessment year a property owner may protest an assessment for one or more of the following reasons: The assessment is not comparable to others with similar properties. The property is assessed at more than its actual value. The property is exempt from taxation. There is an error in the assessment. The assessment is fraudulent A property owner may appeal the protest to the Property Assessment Appeal Board, if not satisfied with the board of review's decision. If dissatisfied with a property assessment appeal board decision, the decision may then be appealed to the district court. In the alternative, property owners may still file appeals directly with the district court and forego filing with the property assessment appeal board. Contact your assessor's office for more information. What property is exempt? Iowa offers a variety of total and partial exemptions and credits to the property tax. It is the property owner s (or renter s) responsibility to apply for these. Contact your assessor for information on the following: Agricultural land Art galleries Barn and one-room schoolhouse Cattle facility Cemeteries Data center Disabled veterans homestead Educational institutions 12

14 Family farm credit Forest cover Forest reservations Fruit tree reservations Governments: state, cities, counties, townships Historic property rehabilitation Homestead credit Impoundment structures Industrial partial (427B) Industrial machinery and equipment and computers first assessed in Iowa for 1995 and thereafter Libraries/literary societies Low-income tax credit for elderly, disabled Low-income rent reimbursement for elderly, disabled Low-rent housing Methane gas conversion Military exemption Mobile home reduced rate for low income Native prairies Open prairies Personal property Pollution control and recycling Public grounds Recreational lakes Religious, charitable, benevolent associations Rivers and streams River and stream banks Special assessments for elderly, disabled, low income Speculative shell buildings Urban revitalization War veterans associations Web search portal Wetlands Wildlife habitats Wind energy conversion 13

15 Homestead Credit The Homestead Credit is available to residential property owners. Iowans will save $100,658,781 in property taxes in fiscal year The credit is an actual reduction in the amount of property tax owed; it is not a refund. To qualify for the credit, the property owner must be a resident of Iowa and actually live on the property on July 1 and for at least six months of every year. The only exceptions are persons in the military and nursing homes who otherwise qualify. Sign-up for the credit is at the assessor s office by July 1 of the year the credit is first claimed. Once a person qualifies, the credit continues until the property is sold or until the owner no longer qualifies. Military Exemption Military veterans who (1) served on active duty and were honorably discharged or (2) members of reserve forces or Iowa National Guard who served at least 20 years qualify for this exemption. The veteran must apply with the local assessor. Once accepted, the exemption is ongoing. $2.4 million has been appropriated for fiscal year Ag Land Credit The Agricultural Land Tax Credit was originally established in 1939 to help offset higher farm taxes. The credit is available to all owners of agricultural land of 10 acres or more if the use is for agricultural or horticultural purposes. Land owners do not actually file a claim. The county auditor determines the amount of the credit for each taxpayer. In fiscal year 2010, $24,610,183 has been appropriated to agricultural land owners. Family Farm Credit Legislation was enacted in 1990 to provide $10 million for the Family Farm Tax Credit. The purpose was to give an additional property tax credit to those individual land owners who were actively engaged in farming the land. One application is required unless the ownership or a designated person changes. 14

16 Land used for agricultural or horticultural purposes in tracts of 10 contiguous acres or more qualify for this credit. Buildings and other structures do not. The application may be filed any time; however, a claim signed after November 1 is considered a claim filed for the following year. Assessors County and city assessors are not employees of the State or of the Iowa Department of Revenue. How many are there? Counties: Each of Iowa s 99 counties has one assessor. Cities: Eight Iowa cities have their own assessors. Any city with a population of more than 10,000 people may elect to have its own assessor. What do they do? An assessor s primary duty is to assess all real property, which includes residential, commercial, industrial, and agricultural. The Iowa Department of Revenue assesses public utilities and railroads. What don t they do? Collect taxes Calculate taxes Determine the tax rate How does someone become an assessor? County assessors are appointed by a conference board composed of the county board of supervisors, the mayors of all incorporated cities, and a board member from each school district who lives in the assessor s jurisdiction. City assessors are appointed by a conference board composed of the county board of supervisors, members of the city council, and all members of each school board. 15

17 Assessors are appointed to 6-year terms. To be eligible, they must have a high school diploma or GED and pass an examination administered by the Iowa Department of Revenue. To be reappointed, they must successfully complete a continuing education program equal to 150 hours of classroom instruction during their 6-year terms. How does an assessor value property? Residential, commercial and industrial real estate is assessed at 100 percent of market value The assessor must determine the fair market value of the property. To do this, the assessor generally uses three approaches. Market Approach: Find properties sold recently that are comparable to yours. Analyze sales of similar properties that were recently sold. Determine the most probable sales price of the property being appraised. Cost Approach: Estimate how much money at current labor and material prices it would take to replace the property with one similar to it. This is useful when no sales of comparable properties exist. Income Approach: If the property produces income, such as with an apartment or office building, estimate its ability to produce income. Agricultural real estate is assessed at 100 percent of productivity and net earning capacity value. The assessor considers the productivity and net earning capacity of the property. Agricultural income as reflected by production, prices, expenses, and various local conditions is taken into account. What is the role of the Iowa Department of Revenue? The Iowa Department of Revenue assists local governments in making property tax assessments fair and in compliance with the law. It does not collect or use property taxes. 16

18 It administers an examination which would-be assessors and deputy assessors must pass. It issues equalization orders to county auditors every two years for classes of property. It provides technical assistance and educational programs for assessors and members of boards of review. It issues regulations on assessors, conference boards and boards of review. It assesses all utility and railroad properties. It administers credits and exemptions to property owners. It has general supervisory authority over the operation of the assessors offices and the boards of review. 17

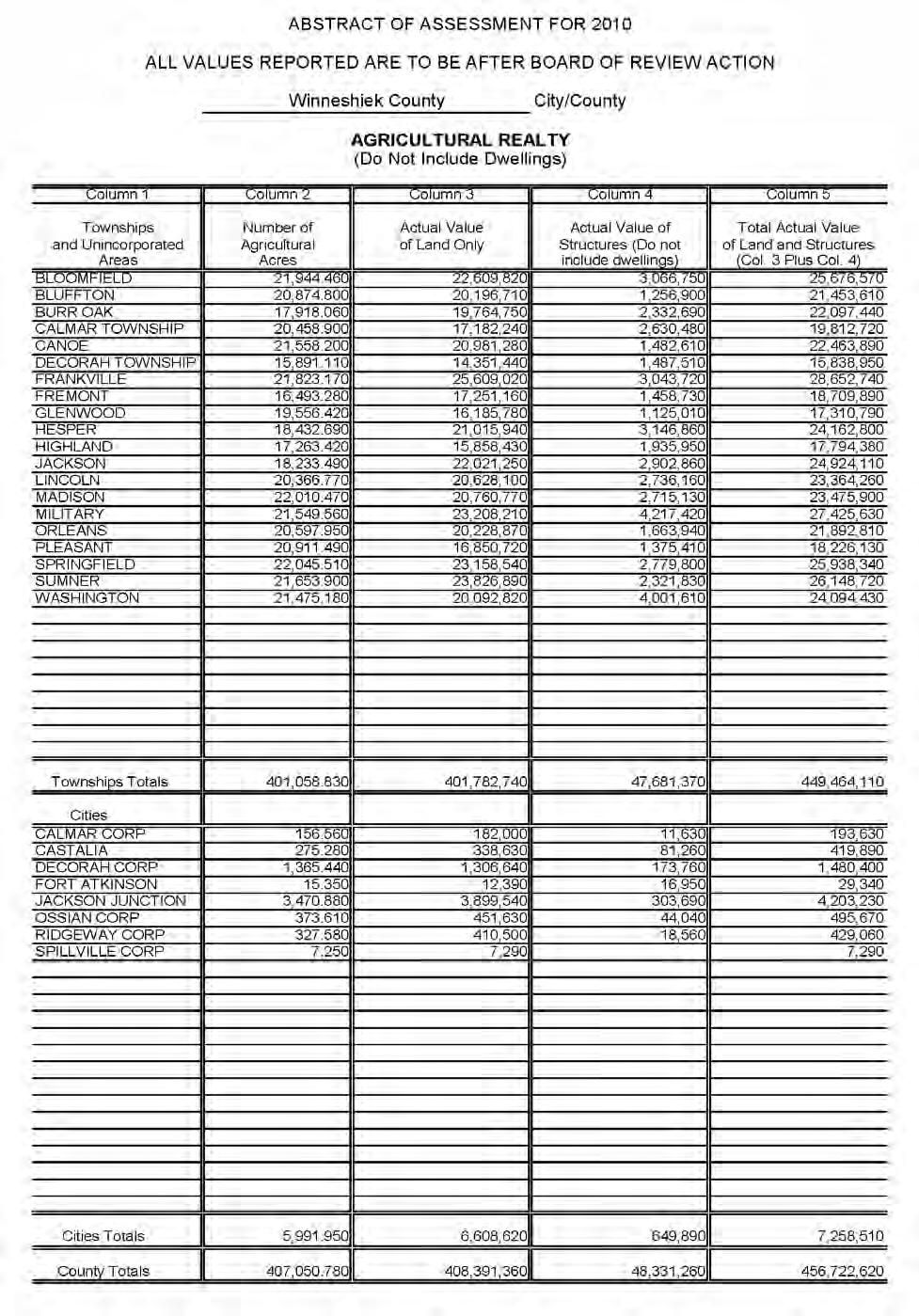

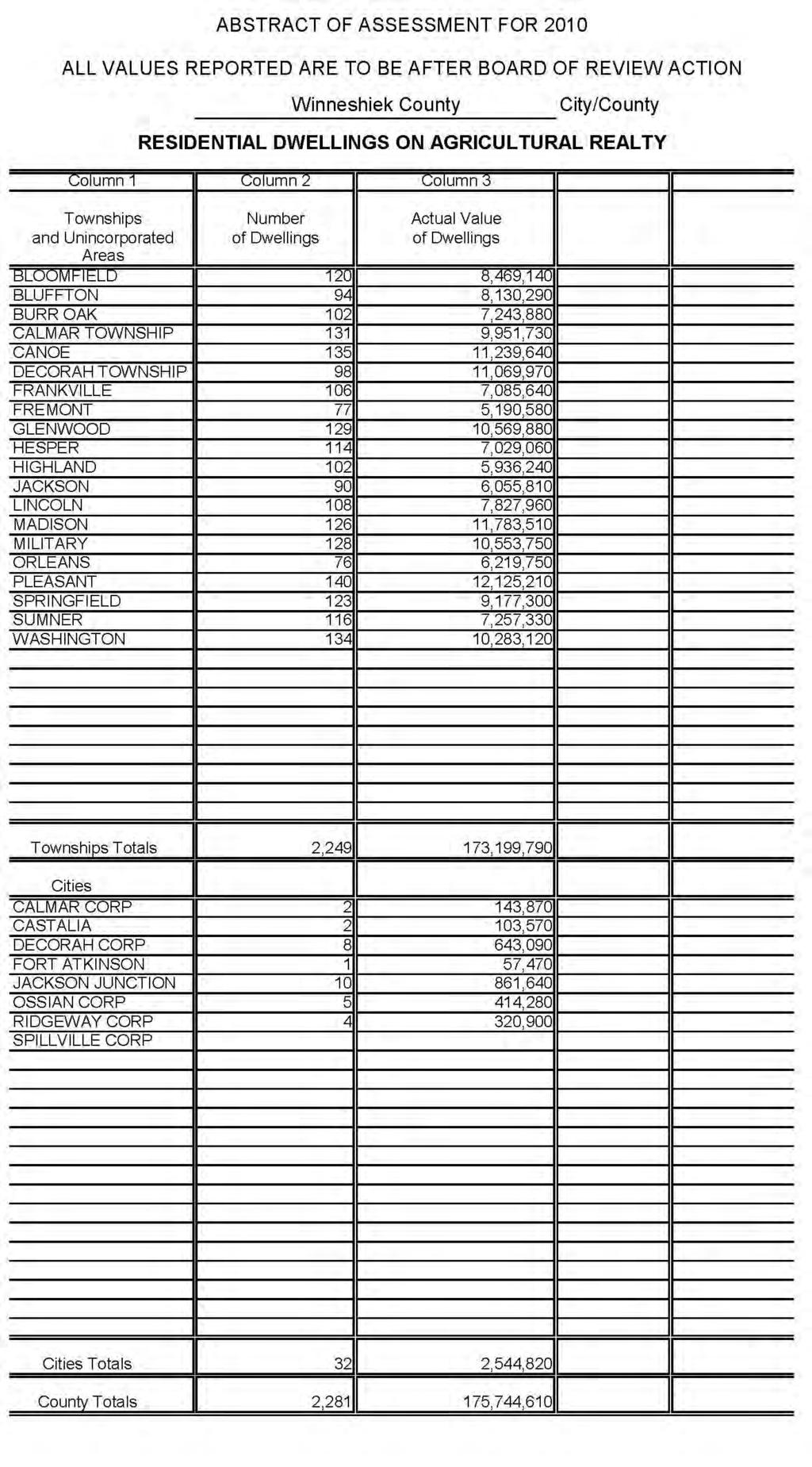

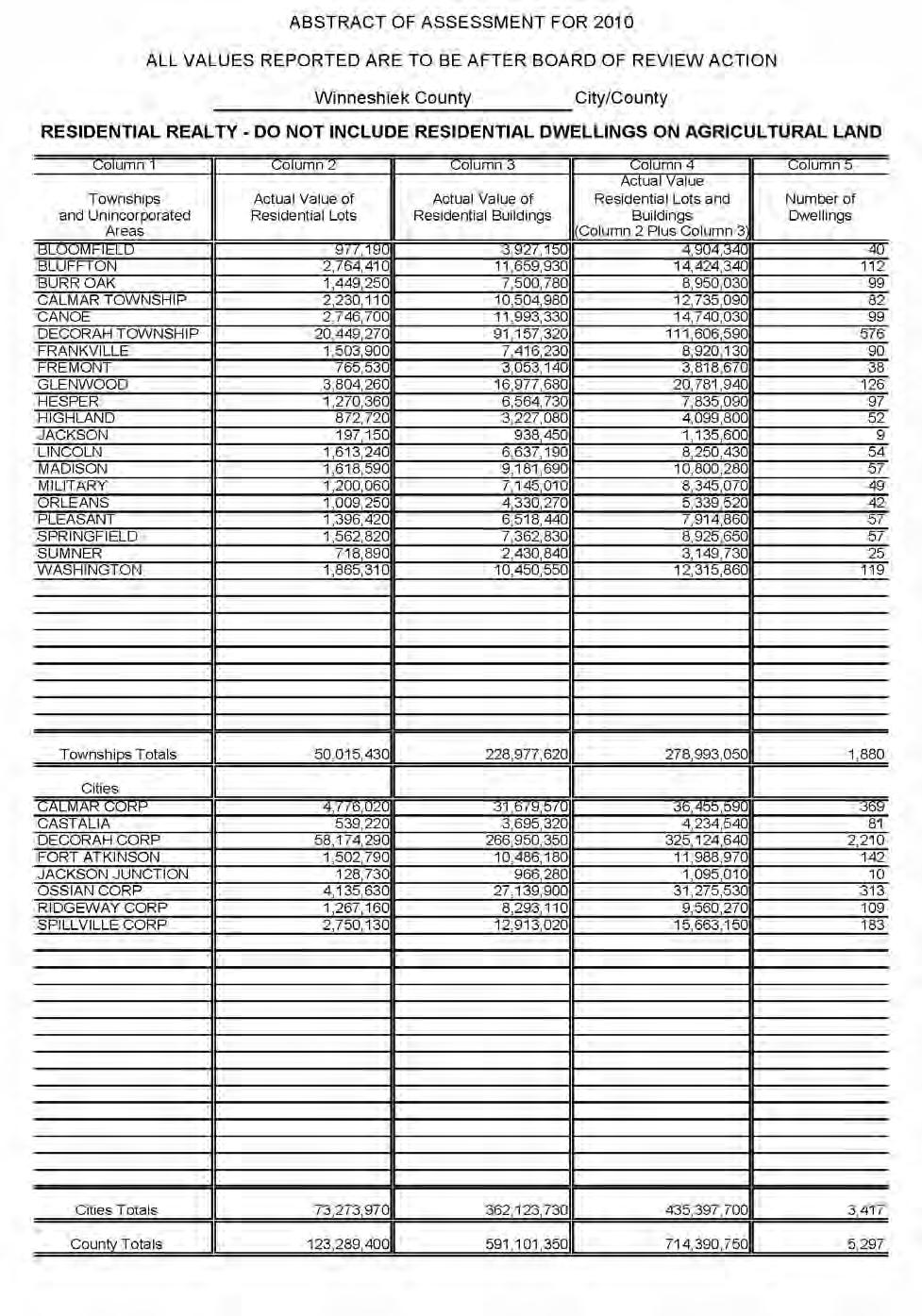

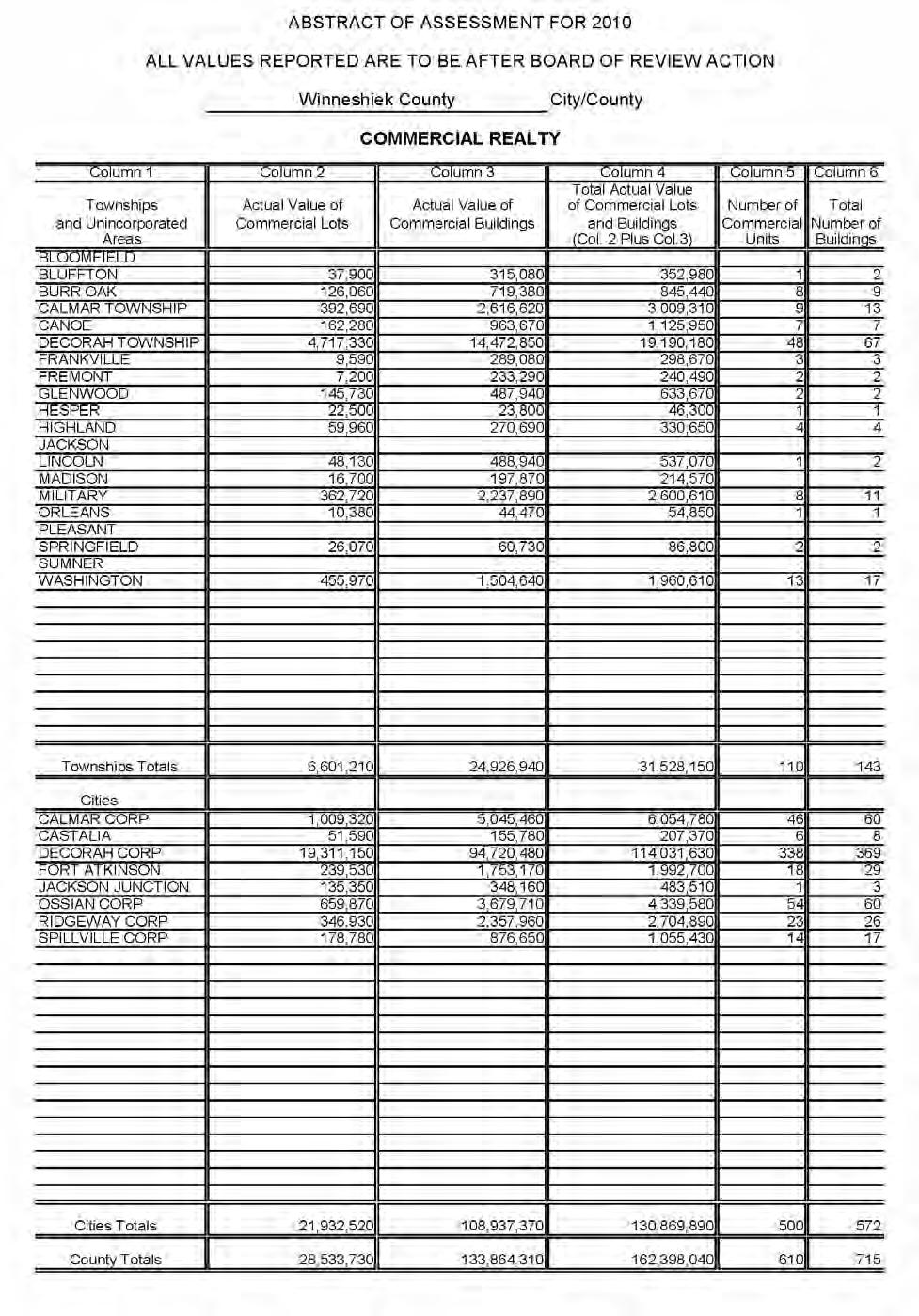

19 18

20 19

21 20

22 21

23 22

24 23

25 24

26 25

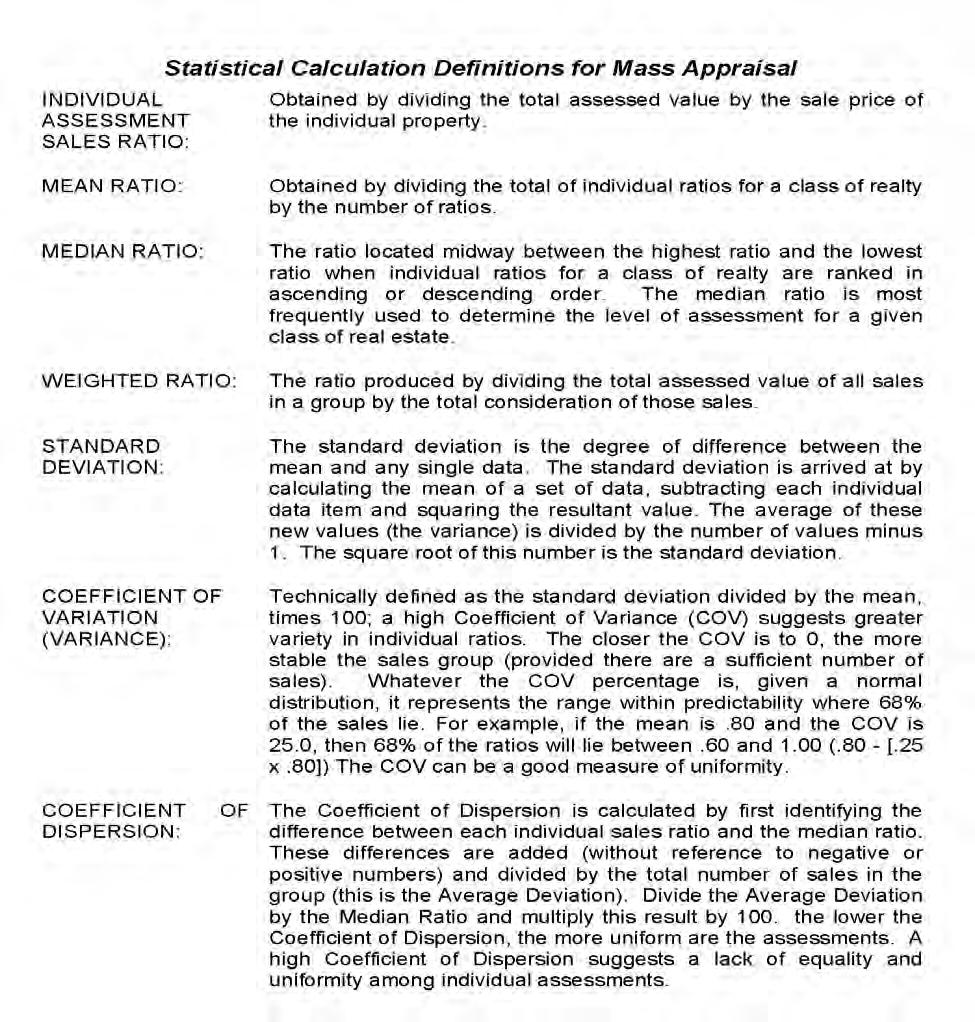

27 26

28 27

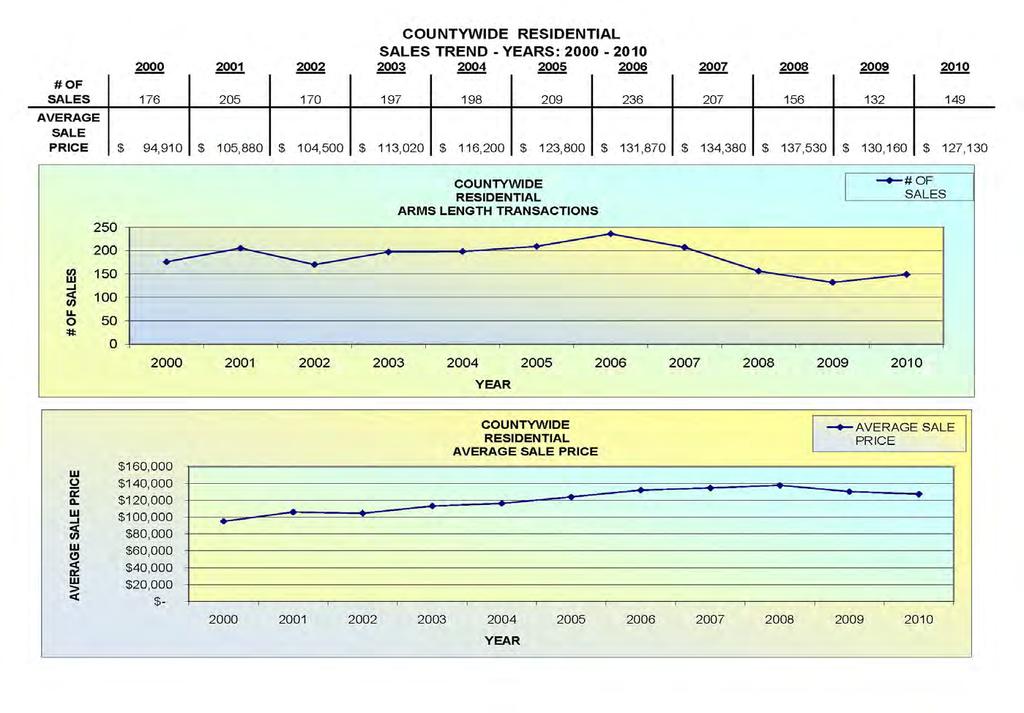

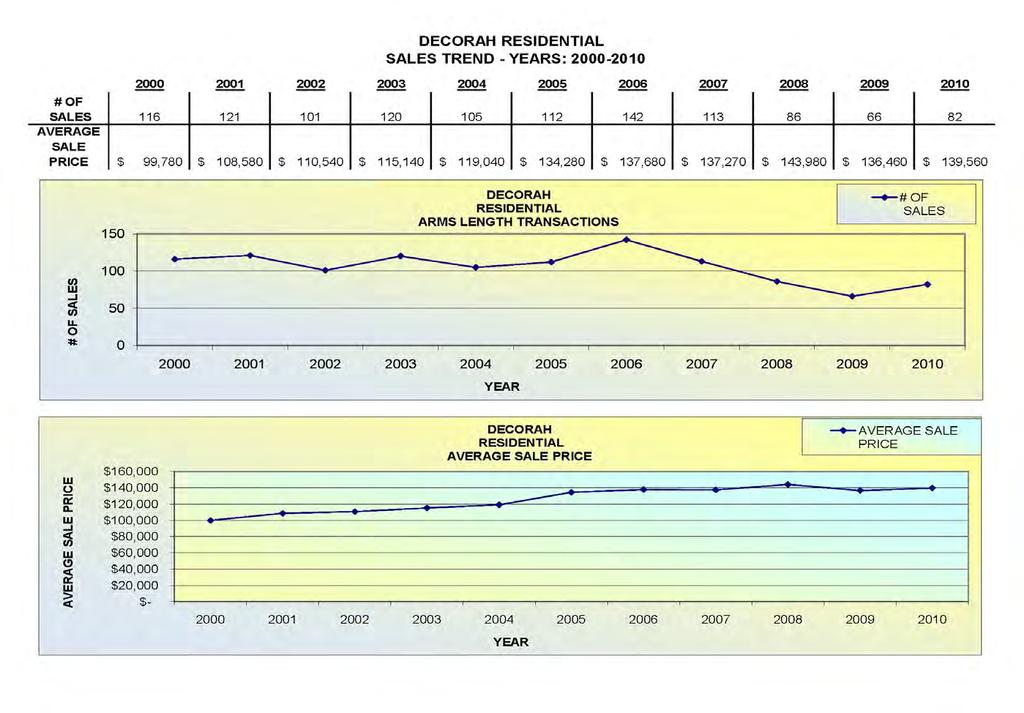

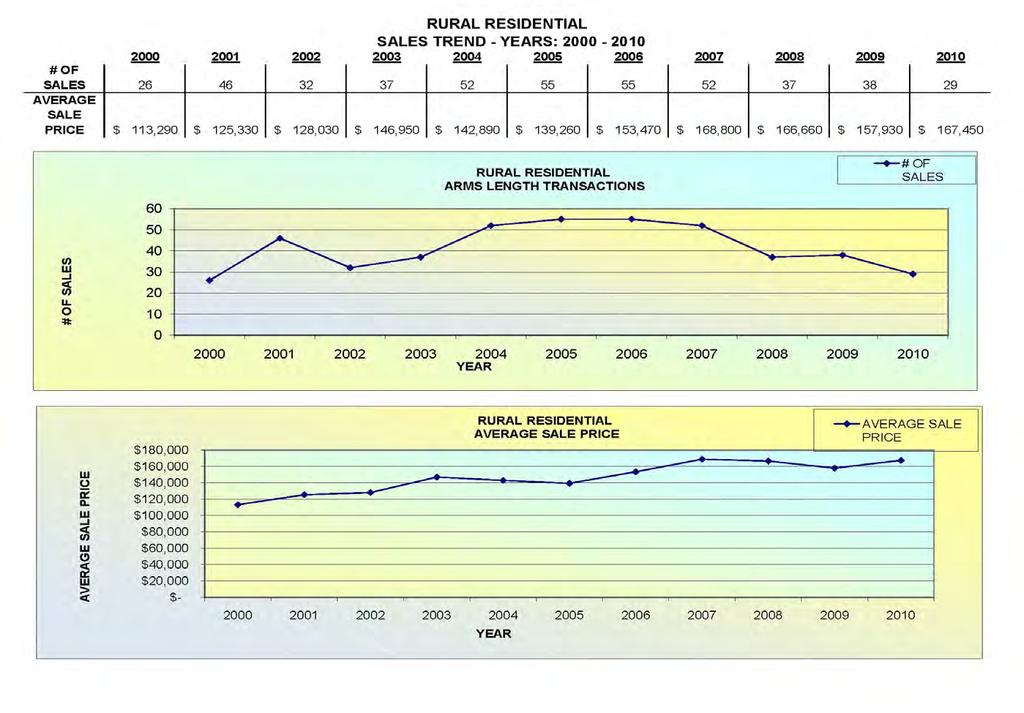

29 28 COUNTYWIDE RESIDENTIAL

30 29 COUNTYWIDE RESIDENTIAL

31 30 COUNTYWIDE RESIDENTIAL

32 31

33 32

34 33

35 34

36 35

37 36

38 37

39 38

40 39

41 40

42 41

43 42

44 43

45 I'm a great believer that any tool that enhances communication has profound effects in terms of how people can learn from each other, and how they can achieve the kind of freedoms that they're interested in. - Bill Gates

46

Contact Us. Forms for these credits and exemptions are included with the descriptions. Ag Land Credit. Low-Rent Housing Exemption

1 of 12 12/5/2017 2:01 PM Contact Us Home» Iowa Tax / Fee Descriptions and Rates Forms for these credits and exemptions are included with the descriptions. Ag Land Credit Barn and One-Room School House

1 of 12 12/5/2017 2:01 PM Contact Us Home» Iowa Tax / Fee Descriptions and Rates Forms for these credits and exemptions are included with the descriptions. Ag Land Credit Barn and One-Room School House

ASSESSMENT AND TAXATION

ABSTRACT A brief synopsis of the assessment, appeal and taxation process as implemented by the Code of Iowa and Administrative Rules. ASSESSMENT AND TAXATION Iowa State Association of Assessors General

ABSTRACT A brief synopsis of the assessment, appeal and taxation process as implemented by the Code of Iowa and Administrative Rules. ASSESSMENT AND TAXATION Iowa State Association of Assessors General

2014 ANNUAL REPORT Senate File 295 Property Tax Reform

TRACKING VALUE Winneshiek County Assessor s Office James Alstad, ICA Winneshiek County Assessor 2014 ANNUAL REPORT Senate File 295 Property Tax Reform ASSESSORS WEBSITE www.winneshiek.us WINNESHIEK COUNTY

TRACKING VALUE Winneshiek County Assessor s Office James Alstad, ICA Winneshiek County Assessor 2014 ANNUAL REPORT Senate File 295 Property Tax Reform ASSESSORS WEBSITE www.winneshiek.us WINNESHIEK COUNTY

PROPERTY REASSESSMENT AND TAXATION. State Tax Commission Jefferson City, Missouri

PROPERTY REASSESSMENT AND TAXATION State Tax Commission Jefferson City, Missouri Revised January, 2017 INTRODUCTION Some aspects of the property tax system are confusing to many taxpayers. It is important

PROPERTY REASSESSMENT AND TAXATION State Tax Commission Jefferson City, Missouri Revised January, 2017 INTRODUCTION Some aspects of the property tax system are confusing to many taxpayers. It is important

Property Tax Credits & Exemptions. Kay Arvidson Property Tax Division December 16, 2015

Property Tax Credits & Exemptions Kay Arvidson Property Tax Division December 16, 2015 Today s Agenda A Little About Property Taxes Definitions Credits & Exemptions Agricultural Business Economic Development

Property Tax Credits & Exemptions Kay Arvidson Property Tax Division December 16, 2015 Today s Agenda A Little About Property Taxes Definitions Credits & Exemptions Agricultural Business Economic Development

UNDERSTANDING PROPERTY TAXES IN COLORADO

UNDERSTANDING PROPERTY TAXES IN COLORADO This brochure was created to provide general information on the Colorado property tax system. For more specific information on any one of these topics, please visit

UNDERSTANDING PROPERTY TAXES IN COLORADO This brochure was created to provide general information on the Colorado property tax system. For more specific information on any one of these topics, please visit

YOUR GUIDE TO THE REASSESSMENT PROGRAM

YOUR GUIDE TO THE REASSESSMENT PROGRAM Why Reassess? Reassessment is required by law. Act 208, as passed by the General Assembly in 1975, provides that all real property will be valued at its current market

YOUR GUIDE TO THE REASSESSMENT PROGRAM Why Reassess? Reassessment is required by law. Act 208, as passed by the General Assembly in 1975, provides that all real property will be valued at its current market

Understanding Mississippi Property Taxes

Understanding Mississippi Property Taxes Property tax revenues are a vital component of the budgets of Mississippi s local governments. Property tax revenues allow these governments to provide important

Understanding Mississippi Property Taxes Property tax revenues are a vital component of the budgets of Mississippi s local governments. Property tax revenues allow these governments to provide important

LOCAL REVENUE SOURCES. Local Revenue Sources. Sources of Local Revenue: County 02/15/ County Revenue by Source

LOCAL REVENUE SOURCES Martha Walston, Fiscal Research Division February 16, 2011 Local Revenue Sources Property Tax Deed Stamp tax Sales tax: occupancy tax and meals tax Privilege tax Other local taxes

LOCAL REVENUE SOURCES Martha Walston, Fiscal Research Division February 16, 2011 Local Revenue Sources Property Tax Deed Stamp tax Sales tax: occupancy tax and meals tax Privilege tax Other local taxes

2018 Annual Appraisal Report

2018 Annual Appraisal Report SUMMARY OF APPRAISAL ACTIVITIES, EXEMPTIONS, EQUALIZATION AND TAX RATES FOR 2018 TAX YEAR Wendy Grams, RPA, CTA, CCA CENTRAL APPRAISAL DISTRICT OF BANDERA COUNTY P. O. BOX

2018 Annual Appraisal Report SUMMARY OF APPRAISAL ACTIVITIES, EXEMPTIONS, EQUALIZATION AND TAX RATES FOR 2018 TAX YEAR Wendy Grams, RPA, CTA, CCA CENTRAL APPRAISAL DISTRICT OF BANDERA COUNTY P. O. BOX

FREEDOM OF INFORMATION ACT POSTING

CHIEF COUNTY ASSESSING OFFICIAL KENDALL COUNTY ANDREW P. NICOLETTI 111 West Fox Street Rm. 303 Yorkville, Illinois 60560-1498 630-553-4146 FREEDOM OF INFORMATION ACT POSTING The purpose of the Freedom

CHIEF COUNTY ASSESSING OFFICIAL KENDALL COUNTY ANDREW P. NICOLETTI 111 West Fox Street Rm. 303 Yorkville, Illinois 60560-1498 630-553-4146 FREEDOM OF INFORMATION ACT POSTING The purpose of the Freedom

York County 2015 Reassessment Program. York County Assessor s Office 18 W. Liberty St York SC fax

York County 2015 Reassessment Program York County Assessor s Office 18 W. Liberty St York SC 29745 803-684-8526 803-628-3936 fax Re-Assessment The Reassessment Program Act 208: Act 208, as passed by the

York County 2015 Reassessment Program York County Assessor s Office 18 W. Liberty St York SC 29745 803-684-8526 803-628-3936 fax Re-Assessment The Reassessment Program Act 208: Act 208, as passed by the

The Duties of the Iowa Assessor (ISAC New County Officers School)

") The Duties of the Iowa Assessor (ISAC New County Officers School) Wayne Schwickerath Story County Assessor January 19, 2017 Purpose of Presentation (Iowa Code Chapter 441) Assessment & Valuation of Property)

The Duties of the Iowa Assessor (ISAC New County Officers School) Wayne Schwickerath Story County Assessor January 19, 2017 Purpose of Presentation (Iowa Code Chapter 441) Assessment & Valuation of Property)

We look forward to working with you to build on our collaboration and enhance our partnership on behalf of all Minnesotans.

Date: February 27, 2017 To: County Assessors, Auditors, and Treasurers From: Cynthia Rowley, Director Property Tax Division Subject: Property Tax Services Report The Property Tax Division of the Minnesota

Date: February 27, 2017 To: County Assessors, Auditors, and Treasurers From: Cynthia Rowley, Director Property Tax Division Subject: Property Tax Services Report The Property Tax Division of the Minnesota

APPEAL PROCESS GUIDE FOR THE PROPERTY OWNER

2018 APPEAL PROCESS GUIDE FOR THE PROPERTY OWNER IMPORTANT DATES TO KNOW 2018 APPEAL PROCESS TIME FRAME March 1 - assessment notices must be mailed March 15 - last day to file for owner-occupied status

2018 APPEAL PROCESS GUIDE FOR THE PROPERTY OWNER IMPORTANT DATES TO KNOW 2018 APPEAL PROCESS TIME FRAME March 1 - assessment notices must be mailed March 15 - last day to file for owner-occupied status

Brazoria County Appraisal District

Brazoria County Appraisal District Annual Report 2018 Mission Statement Our mission as public servants is to demand excellence in the services provided to the taxpayers and taxing jurisdictions of Brazoria

Brazoria County Appraisal District Annual Report 2018 Mission Statement Our mission as public servants is to demand excellence in the services provided to the taxpayers and taxing jurisdictions of Brazoria

IMPORTANT ANNOUNCEMENT: Our website is changing! Please click here for details.

IMPORTANT ANNOUNCEMENT: Our website is changing! Please click here for details. Home Search Downloads Exemptions Agriculture Maps Tangible Links Contact Home Frequently Asked Questions (FAQ) Frequently

IMPORTANT ANNOUNCEMENT: Our website is changing! Please click here for details. Home Search Downloads Exemptions Agriculture Maps Tangible Links Contact Home Frequently Asked Questions (FAQ) Frequently

Assessment Overview. Gallagher Amendment Interim Committee. July 13, 2018

Assessment Overview Gallagher Amendment Interim Committee July 13, 2018 Life s FAQs: Why is the sky blue? How does gravity work? Are we there yet? What happens in an Assessor s office.. how does property

Assessment Overview Gallagher Amendment Interim Committee July 13, 2018 Life s FAQs: Why is the sky blue? How does gravity work? Are we there yet? What happens in an Assessor s office.. how does property

Office of Legislative Services Background Report The Assessment of Real Property: Answers to Frequently Asked Questions

Office of Legislative Services Background Report The Assessment of Real Property: Answers to Frequently Asked Questions OLS Background Report No. 120 Prepared By: Local Government Date Prepared: New Jersey

Office of Legislative Services Background Report The Assessment of Real Property: Answers to Frequently Asked Questions OLS Background Report No. 120 Prepared By: Local Government Date Prepared: New Jersey

CHAPTER 2: HOUSING. 2.1 Introduction. 2.2 Existing Housing Characteristics

CHAPTER 2: HOUSING 2.1 Introduction Housing Characteristics are related to the social and economic conditions of a community s residents and are an important element of a comprehensive plan. Information

CHAPTER 2: HOUSING 2.1 Introduction Housing Characteristics are related to the social and economic conditions of a community s residents and are an important element of a comprehensive plan. Information

We hope the trends provide additional perspective on your county s work. We know it provided valuable insight on the work we do here at Revenue.

Date: March 6, 2018 To: County Assessors, Auditors, and Treasurers From: Jon Klockziem, Acting Director Subject: Property Tax Services Report The Property Tax Division of the is pleased to provide the

Date: March 6, 2018 To: County Assessors, Auditors, and Treasurers From: Jon Klockziem, Acting Director Subject: Property Tax Services Report The Property Tax Division of the is pleased to provide the

UNDERSTANDING YOUR ASSESSMENT

UNDERSTANDING YOUR ASSESSMENT An informational booklet explaining property assessments and procedures. Provided by the Town of York Assessor s Office This booklet will attempt to explain the Assessment

UNDERSTANDING YOUR ASSESSMENT An informational booklet explaining property assessments and procedures. Provided by the Town of York Assessor s Office This booklet will attempt to explain the Assessment

Assessor Ken Yazel. Ad Valorem Property Taxes In Tulsa County, OK. Prepared by the Tulsa County Assessor s Office

Assessor Ken Yazel Ad Valorem Property Taxes In Tulsa County, OK Prepared by the Tulsa County Assessor s Office Tulsa County Assessor s Office Our Commitment Ken Yazel, Assessor The Tulsa County Assessor

Assessor Ken Yazel Ad Valorem Property Taxes In Tulsa County, OK Prepared by the Tulsa County Assessor s Office Tulsa County Assessor s Office Our Commitment Ken Yazel, Assessor The Tulsa County Assessor

CHAPTER Senate Bill No. 2222

CHAPTER 98-167 Senate Bill No. 2222 An act relating to taxation; amending s. 197.122, F.S.; specifying the time within which property appraisers may correct a material mistake of fact in an appraisal;

CHAPTER 98-167 Senate Bill No. 2222 An act relating to taxation; amending s. 197.122, F.S.; specifying the time within which property appraisers may correct a material mistake of fact in an appraisal;

Q. How is Agricultural property valued? A. GENERAL INFORMATION Many states have laws regarding the preferential assessment of agricultural land.

Q. How is Agricultural property valued? A. GENERAL INFORMATION Many states have laws regarding the preferential assessment of agricultural land. This means that farm and ranch assessments are usually based

Q. How is Agricultural property valued? A. GENERAL INFORMATION Many states have laws regarding the preferential assessment of agricultural land. This means that farm and ranch assessments are usually based

Board of Appeal and Equalization Handbook

Board of Appeal and Equalization Handbook This handbook was created to satisfy the training requirements of Minnesota Statutes, sections 274.014 and 274.135 Updated January 2018 Table of Contents Introduction...

Board of Appeal and Equalization Handbook This handbook was created to satisfy the training requirements of Minnesota Statutes, sections 274.014 and 274.135 Updated January 2018 Table of Contents Introduction...

1. How can I change my mailing address? Can you change my mailing address by phone?

GENERAL FAQ s 1. How can I change my mailing address? Can you change my mailing address by phone? Please request address changes in writing indicating the new mailing address for your property and a daytime

GENERAL FAQ s 1. How can I change my mailing address? Can you change my mailing address by phone? Please request address changes in writing indicating the new mailing address for your property and a daytime

April 7, B. Notice of Assessment - Taxpayers receive annual notices of assessment in accordance with , VA Code, Ann.

COUNTY OF PRINCE WILLIAM 4379 Ridgewood Center Drive, Prince William, Suite 203. Virginia 22192-5308 Real Estate Assessments Office (703) 792-6780 Metro 631-1703 Ext. 6780 FAX: (703) 792-6775 http://www.pwcgov.org/finance

COUNTY OF PRINCE WILLIAM 4379 Ridgewood Center Drive, Prince William, Suite 203. Virginia 22192-5308 Real Estate Assessments Office (703) 792-6780 Metro 631-1703 Ext. 6780 FAX: (703) 792-6775 http://www.pwcgov.org/finance

Request for Proposals For Assessor. Charter Township of Augusta Washtenaw County

Request for Proposals For Assessor (Michigan Certified Assessing Officer) Charter Township of Augusta Washtenaw County Charter Township of Augusta 8021 Talladay Road Whittaker, MI 48190 Phone 734-461-6117

Request for Proposals For Assessor (Michigan Certified Assessing Officer) Charter Township of Augusta Washtenaw County Charter Township of Augusta 8021 Talladay Road Whittaker, MI 48190 Phone 734-461-6117

Ad Valorem Tax Escambia County FL Explained

Ad Valorem Tax Escambia County FL Explained What properties must be appraised? REAL PROPERTY - the physical land and appurtenances affixed to the land, e.g., structures. The term "land","real estate","realty"

Ad Valorem Tax Escambia County FL Explained What properties must be appraised? REAL PROPERTY - the physical land and appurtenances affixed to the land, e.g., structures. The term "land","real estate","realty"

WALLER COUNTY APPRAISAL DISTRICT

2018 ANNUAL REPORT WALLER COUNTY APPRAISAL DISTRICT Introduction The Waller County Appraisal District is a political subdivision of the State of Texas created by the Texas Legislature in 1979. The operations

2018 ANNUAL REPORT WALLER COUNTY APPRAISAL DISTRICT Introduction The Waller County Appraisal District is a political subdivision of the State of Texas created by the Texas Legislature in 1979. The operations

FLORIDA CONSTITUTION

FLORIDA CONSTITUTION (Provisions related to ad valorem property taxes and exemptions) ARTICLE VII - FINANCE AND TAXATION SECTION 2. Taxes; rate.-- All ad valorem taxation shall be at a uniform rate within

FLORIDA CONSTITUTION (Provisions related to ad valorem property taxes and exemptions) ARTICLE VII - FINANCE AND TAXATION SECTION 2. Taxes; rate.-- All ad valorem taxation shall be at a uniform rate within

Reappraisal Important Property Tax Information

Reappraisal 2013 Important Property Tax Information Spartanburg County Assessor PO Box 5762 Spartanburg, SC 29304 Telephone: (864)596-2544 Fax: (864)596-2940 Fax: (864)596-2223 www.spartanburgcounty.org

Reappraisal 2013 Important Property Tax Information Spartanburg County Assessor PO Box 5762 Spartanburg, SC 29304 Telephone: (864)596-2544 Fax: (864)596-2940 Fax: (864)596-2223 www.spartanburgcounty.org

November 2017 Legal Calendar

1 Sheriff, Clerk of the District, Clerk, County Board Sheriff or such person in charge of the administration of the jail must file jail report with the clerk of the district court and the county clerk,

1 Sheriff, Clerk of the District, Clerk, County Board Sheriff or such person in charge of the administration of the jail must file jail report with the clerk of the district court and the county clerk,

Special Plainview City Council Meeting Board of Appeals and Equalization Meeting AGENDA Tuesday, April 16, 2019, at 6:00 P.M.

Special Plainview City Council Meeting Board of Appeals and Equalization Meeting AGENDA Tuesday, April 16, 2019, at 6:00 P.M. Special meetings are meetings held at a time or place that is different from

Special Plainview City Council Meeting Board of Appeals and Equalization Meeting AGENDA Tuesday, April 16, 2019, at 6:00 P.M. Special meetings are meetings held at a time or place that is different from

The Texas Constitution sets out five basic rules for property taxes in our state:

Why does the appraisal district look at values each year? The Texas Constitution sets out five basic rules for property taxes in our state: 1. Taxation must be equal and uniform. No single property or

Why does the appraisal district look at values each year? The Texas Constitution sets out five basic rules for property taxes in our state: 1. Taxation must be equal and uniform. No single property or

Pickens County Reassessment Program. Utilizing CAMA GIS MLS SQL

1 Pickens County 2019 Reassessment Program Utilizing CAMA GIS MLS SQL Pickens County Reassessment History 1980 Countywide Reappraisal 1990 Countywide Reappraisal 1999 Countywide Reappraisal 2004 Countywide

1 Pickens County 2019 Reassessment Program Utilizing CAMA GIS MLS SQL Pickens County Reassessment History 1980 Countywide Reappraisal 1990 Countywide Reappraisal 1999 Countywide Reappraisal 2004 Countywide

SIOUX COUNTY CONFERENCE BOARD

Annual Report of the SIOUX COUNTY ASSESSOR to the SIOUX COUNTY CONFERENCE BOARD February 6, 2018 SIOUX COUNTY CONFERENCE BOARD JANUARY 1, 2018 BOARD OF SUPERVISORS Allen Bloemendaal John Degen Arlyn Kleinwolterink

Annual Report of the SIOUX COUNTY ASSESSOR to the SIOUX COUNTY CONFERENCE BOARD February 6, 2018 SIOUX COUNTY CONFERENCE BOARD JANUARY 1, 2018 BOARD OF SUPERVISORS Allen Bloemendaal John Degen Arlyn Kleinwolterink

OFFICIAL PROCEEDINGS City of Williston Local Board of Equalization May 3, :00 pm City Hall Williston, North Dakota

1. Roll Call of Commissioners OFFICIAL PROCEEDINGS City of Williston Local Board of Equalization May 3, 2017 6:00 pm City Hall Williston, North Dakota COMMISSIONERS PRESENT: Deanette Piesik, Tate Cymbaluk,

1. Roll Call of Commissioners OFFICIAL PROCEEDINGS City of Williston Local Board of Equalization May 3, 2017 6:00 pm City Hall Williston, North Dakota COMMISSIONERS PRESENT: Deanette Piesik, Tate Cymbaluk,

VAN ZANDT COUNTY APPRAISAL DISTRICT 2018 ANNUAL REPORT

VAN ZANDT COUNTY APPRAISAL DISTRICT 2018 ANNUAL REPORT INTRODUCTION The Van Zandt County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property

VAN ZANDT COUNTY APPRAISAL DISTRICT 2018 ANNUAL REPORT INTRODUCTION The Van Zandt County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property

SF 295 Overview. Lucas Beenken Public Policy Specialist Iowa State Association of Counties

SF 295 Overview Lucas Beenken Public Policy Specialist Iowa State Association of Counties Property Tax Reform SF 295 Business Property Tax Credit Commercial/Industrial Rollback Property Assessment Limitation

SF 295 Overview Lucas Beenken Public Policy Specialist Iowa State Association of Counties Property Tax Reform SF 295 Business Property Tax Credit Commercial/Industrial Rollback Property Assessment Limitation

COOKE COUNTY APPRAISAL DISTRICT ANNUAL REPORT CCAD Mission Statement

COOKE COUNTY APPRAISAL DISTRICT ANNUAL REPORT 2013 This Annual Report for 2013 endeavors to provide specific information about the operations of the CCAD. The report has been designed to provide the reader

COOKE COUNTY APPRAISAL DISTRICT ANNUAL REPORT 2013 This Annual Report for 2013 endeavors to provide specific information about the operations of the CCAD. The report has been designed to provide the reader

Map Franklin County ASSESSMENTS FOR 2017 TAX COLLECTION STEVE MARKS ASSESSOR

Map Franklin County 1909 2016 ASSESSMENTS FOR 2017 TAX COLLECTION STEVE MARKS ASSESSOR 2 Mission Statement We, the employee s of the Franklin County Assessor s Office have a primary mission to maintain

Map Franklin County 1909 2016 ASSESSMENTS FOR 2017 TAX COLLECTION STEVE MARKS ASSESSOR 2 Mission Statement We, the employee s of the Franklin County Assessor s Office have a primary mission to maintain

ASSESSORS ANSWER FREQUENTLY ASKED QUESTIONS ABOUT REAL PROPERTY Assessors Office, 37 Main Street

A. THE ASSESSMENT PROCESS: ASSESSORS ANSWER FREQUENTLY ASKED QUESTIONS ABOUT REAL PROPERTY Assessors Office, 37 Main Street What is mass appraisal? Assessors must value all real and personal property in

A. THE ASSESSMENT PROCESS: ASSESSORS ANSWER FREQUENTLY ASKED QUESTIONS ABOUT REAL PROPERTY Assessors Office, 37 Main Street What is mass appraisal? Assessors must value all real and personal property in

Amendment U Exempt Certain Possessory Interests From Property Taxes. Amendment U proposes amending the Colorado Constitution to:

Amendment U Exempt Certain Possessory Interests From Property Taxes Final Draft Amendment U proposes amending the Colorado Constitution to: beginning with tax year 0, eliminate property taxes for individuals

Amendment U Exempt Certain Possessory Interests From Property Taxes Final Draft Amendment U proposes amending the Colorado Constitution to: beginning with tax year 0, eliminate property taxes for individuals

February 2014 Legal Calendar

1 Clerk Report list of county officers to the Secretary of State. 23-1306 1 Assessor Last date for owners, lessees and/or managers of any aircraft hangars or land upon which aircraft are parked to report

1 Clerk Report list of county officers to the Secretary of State. 23-1306 1 Assessor Last date for owners, lessees and/or managers of any aircraft hangars or land upon which aircraft are parked to report

Date: March 2018 TOWN OF WATERFORD Department of Assessment

Date: March 2018 TOWN OF WATERFORD 1. Overview: The purpose of this workshop is to explain the Assessment Disclosure Notice, how assessments are derived and how to challenge your assessment if you do not

Date: March 2018 TOWN OF WATERFORD 1. Overview: The purpose of this workshop is to explain the Assessment Disclosure Notice, how assessments are derived and how to challenge your assessment if you do not

Gaines County Appraisal District 2013 Annual Report

Gaines County Appraisal District 2013 Annual Report Introduction The Gaines County Appraisal District is a political subdivision of the state, The Constitution of the State of Texas, the Texas Property

Gaines County Appraisal District 2013 Annual Report Introduction The Gaines County Appraisal District is a political subdivision of the state, The Constitution of the State of Texas, the Texas Property

Duties of the Assessors

Duties of the Assessors Value Properties Determine New Growth Set Tax Rate Assess Property Taxes Abate & Exempt Taxes Manage Overlay Account Assess Local Excises 1 Value Property Assessments based on fair

Duties of the Assessors Value Properties Determine New Growth Set Tax Rate Assess Property Taxes Abate & Exempt Taxes Manage Overlay Account Assess Local Excises 1 Value Property Assessments based on fair

Assembly Bill No. 489 Committee on Growth and Infrastructure CHAPTER...

Assembly Bill No. 489 Committee on Growth and Infrastructure CHAPTER... AN ACT relating to the taxation of property; providing for the partial abatement of the ad valorem taxes imposed on property; directing

Assembly Bill No. 489 Committee on Growth and Infrastructure CHAPTER... AN ACT relating to the taxation of property; providing for the partial abatement of the ad valorem taxes imposed on property; directing

Thornton Township Assessor s Office 2017 Property Tax FORUM

Thornton Township Assessor s Office 2017 Property Tax FORUM 333 East 162 nd Street, South Holland, IL 60473 (708) 596-6040 x3175 * cholbert@thorntontwp.com * Fax (708) 596-7082 Dear Taxpayer, Welcome to

Thornton Township Assessor s Office 2017 Property Tax FORUM 333 East 162 nd Street, South Holland, IL 60473 (708) 596-6040 x3175 * cholbert@thorntontwp.com * Fax (708) 596-7082 Dear Taxpayer, Welcome to

Map Franklin County ASSESSMENTS FOR 2018 TAX COLLECTION STEVE MARKS ASSESSOR

Map Franklin County 1909 2017 ASSESSMENTS FOR 2018 TAX COLLECTION STEVE MARKS ASSESSOR 2 Mission Statement We, the employee s of the Franklin County Assessor s Office have a primary mission to maintain

Map Franklin County 1909 2017 ASSESSMENTS FOR 2018 TAX COLLECTION STEVE MARKS ASSESSOR 2 Mission Statement We, the employee s of the Franklin County Assessor s Office have a primary mission to maintain

Florida Amendment 1. Impact on Pinellas County

Florida Amendment 1 Impact on Pinellas County Ballot Overview What s on the ballot? Amendment 1 Third Homestead Exemption (proposed additional exemption up to $25,000 of Assessed Value for some homeowners)

Florida Amendment 1 Impact on Pinellas County Ballot Overview What s on the ballot? Amendment 1 Third Homestead Exemption (proposed additional exemption up to $25,000 of Assessed Value for some homeowners)

GENERAL ASSESSMENT DEFINITIONS

21st Century Appraisals, Inc. GENERAL ASSESSMENT DEFINITIONS Ad Valorem tax. A tax levied in proportion to the value of the thing(s) being taxed. Exclusive of exemptions, use-value assessment laws, and

21st Century Appraisals, Inc. GENERAL ASSESSMENT DEFINITIONS Ad Valorem tax. A tax levied in proportion to the value of the thing(s) being taxed. Exclusive of exemptions, use-value assessment laws, and

MCLENNAN COUNTY APPRAISAL DISTRICT PROPERTY VALUATION WORKSHOP

MCLENNAN COUNTY APPRAISAL DISTRICT PROPERTY VALUATION WORKSHOP WORKSHOP OBJECTIVES To understand: Property Tax System The valuation process What is Market Value Market Trends Time frame for protesting

MCLENNAN COUNTY APPRAISAL DISTRICT PROPERTY VALUATION WORKSHOP WORKSHOP OBJECTIVES To understand: Property Tax System The valuation process What is Market Value Market Trends Time frame for protesting

Susan Combs Texas Comptroller of Public Accounts. Property Tax Basics. Texas Property Tax

2013 Susan Combs Texas Comptroller of Public Accounts Property Tax Basics Texas Property Tax This publication is intended to provide customer assistance to taxpayers. It does not address all aspects of

2013 Susan Combs Texas Comptroller of Public Accounts Property Tax Basics Texas Property Tax This publication is intended to provide customer assistance to taxpayers. It does not address all aspects of

TITLE 7. WATERSHED PROTECTION AND RESTORATION PROGRAM

Print Anne Arundel County Code, 2005 TITLE 7. WATERSHED PROTECTION AND RESTORATION PROGRAM Section 13 7 101. Definitions. 13 7 102. Watershed Protection and Restoration Program. 13 7 103. Stormwater remediation

Print Anne Arundel County Code, 2005 TITLE 7. WATERSHED PROTECTION AND RESTORATION PROGRAM Section 13 7 101. Definitions. 13 7 102. Watershed Protection and Restoration Program. 13 7 103. Stormwater remediation

February 2, 2012 BOARD MATTER C - 1 WYOMING LAND AND IMPROVEMENT COMPANY, PROPOSAL TO ACQUIRE REAL PROPERTY IN ALBANY COUNTY, WYOMING

February 2, 2012 BOARD MATTER C - 1 ACTION: WYOMING LAND AND IMPROVEMENT COMPANY, PROPOSAL TO ACQUIRE REAL PROPERTY IN ALBANY COUNTY, WYOMING AUTHORITY: W.S. 9-4-715(k); Rules Chapter 26, Section 3 ALTERNATIVES:

February 2, 2012 BOARD MATTER C - 1 ACTION: WYOMING LAND AND IMPROVEMENT COMPANY, PROPOSAL TO ACQUIRE REAL PROPERTY IN ALBANY COUNTY, WYOMING AUTHORITY: W.S. 9-4-715(k); Rules Chapter 26, Section 3 ALTERNATIVES:

LIMITED-SCOPE PERFORMANCE AUDIT REPORT

LIMITED-SCOPE PERFORMANCE AUDIT REPORT Agricultural Land Valuation: Evaluating the Potential Impact of Changing How Agricultural Land is Valued in the State AUDIT ABSTRACT State law requires the value

LIMITED-SCOPE PERFORMANCE AUDIT REPORT Agricultural Land Valuation: Evaluating the Potential Impact of Changing How Agricultural Land is Valued in the State AUDIT ABSTRACT State law requires the value

Be It Enacted by the Legislature of the State of Florida:

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 A bill to be entitled An act relating to ad valorem taxation; amending s. 193.023, F.S.; revising authority of the property appraiser

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 A bill to be entitled An act relating to ad valorem taxation; amending s. 193.023, F.S.; revising authority of the property appraiser

Van Zandt County Appraisal District 2017 Annual Report

Van Zandt County Appraisal District 2017 Annual Report Introduction The Van Zandt County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property

Van Zandt County Appraisal District 2017 Annual Report Introduction The Van Zandt County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property

Property Tax Overview. Budget, Finance, & Audit Committee January 3, 2017

Property Tax Overview Budget, Finance, & Audit Committee January 3, 2017 Briefing Outline Property tax base values Property tax rate Property tax exemptions Legislative Session 2 Overview Ad valorem taxes

Property Tax Overview Budget, Finance, & Audit Committee January 3, 2017 Briefing Outline Property tax base values Property tax rate Property tax exemptions Legislative Session 2 Overview Ad valorem taxes

Athens County Auditor, Jill Thompson provides homeowners answers to the most commonly asked questions about the countywide 2014 reappraisal

Contact: Jill Thompson Athens County Auditor Phone 740.592.3223 Fax 740.594.3270 15 S. Court Street, Room 330 Athens, Ohio 45701 www.athenscountyauditor.org Jill Thompson Athens County Auditor Property

Contact: Jill Thompson Athens County Auditor Phone 740.592.3223 Fax 740.594.3270 15 S. Court Street, Room 330 Athens, Ohio 45701 www.athenscountyauditor.org Jill Thompson Athens County Auditor Property

CHAPTER Senate Bill No. 4-D

CHAPTER 2007-339 Senate Bill No. 4-D An act relating to ad valorem taxation; authorizing the Department of Revenue to adopt emergency rules; providing for application and renewal thereof; requiring the

CHAPTER 2007-339 Senate Bill No. 4-D An act relating to ad valorem taxation; authorizing the Department of Revenue to adopt emergency rules; providing for application and renewal thereof; requiring the

INTRODUCTION MISSION OVERVIEW

INTRODUCTION The Austin County Appraisal District is a political subdivision of the State of Texas. The Constitution of the State of Texas, the Texas Property Tax Code, and the Rules of the Texas Comptroller

INTRODUCTION The Austin County Appraisal District is a political subdivision of the State of Texas. The Constitution of the State of Texas, the Texas Property Tax Code, and the Rules of the Texas Comptroller

Accounts in Brazoria County have two primary Identification numbers. The two forms of Identification are as follows:

Accounts in Brazoria County have two primary Identification numbers. The two forms of Identification are as follows: Property ID: This is a six digit number that is generated sequentially as accounts are

Accounts in Brazoria County have two primary Identification numbers. The two forms of Identification are as follows: Property ID: This is a six digit number that is generated sequentially as accounts are

TALK REAL. Now that you ve received your property assessment ASSESSMENTS, ROLLBACKS AND YOUR PROPERTY TAXES

REAL TALK FROM THE POLK COUNTY ASSESSOR www.assess.co.polk.ia.us SPRING 2013 ASSESSMENTS, ROLLBACKS AND YOUR PROPERTY TAXES Now that you ve received your property assessment for 2013, you re likely wondering

REAL TALK FROM THE POLK COUNTY ASSESSOR www.assess.co.polk.ia.us SPRING 2013 ASSESSMENTS, ROLLBACKS AND YOUR PROPERTY TAXES Now that you ve received your property assessment for 2013, you re likely wondering

Property Tax Overview. Economic Development Committee January 17, 2017

Property Tax Overview Economic Development Committee January 17, 2017 Briefing Outline Property tax base values Property tax rate Property tax exemptions Legislative session Next steps Appendix A: Miscellaneous

Property Tax Overview Economic Development Committee January 17, 2017 Briefing Outline Property tax base values Property tax rate Property tax exemptions Legislative session Next steps Appendix A: Miscellaneous

2017 Annual Report. Fayette County Appraisal District P. O. Box 836 La Grange, TX 78945

2017 Annual Report Fayette County Appraisal District P. O. Box 836 La Grange, TX 78945 FCAD 2017 Annual Report 1 2017 ANNUAL REPORT FAYETTE COUNTY APPRAISAL DISTRICT INTRODUCTION The Fayette County Appraisal

2017 Annual Report Fayette County Appraisal District P. O. Box 836 La Grange, TX 78945 FCAD 2017 Annual Report 1 2017 ANNUAL REPORT FAYETTE COUNTY APPRAISAL DISTRICT INTRODUCTION The Fayette County Appraisal

2016 Annual Report. Carmen Ottmer, Chief Appraiser AUSTIN COUNTY APPRAISAL DISTRICT 906 E. AMELIA ST., BELLVILLE, TEXAS 77418

2016 Annual Report Carmen Ottmer, Chief Appraiser AUSTIN COUNTY APPRAISAL DISTRICT 906 E. AMELIA ST., BELLVILLE, TEXAS 77418 INTRODUCTION The Austin County Appraisal District is a political subdivision

2016 Annual Report Carmen Ottmer, Chief Appraiser AUSTIN COUNTY APPRAISAL DISTRICT 906 E. AMELIA ST., BELLVILLE, TEXAS 77418 INTRODUCTION The Austin County Appraisal District is a political subdivision

41 st Annual Conference Appraising Property

2017 KCCA 41 st Annual Conference Appraising Property Kansas County Commissioners Association Junction City, Kansas June 2, 2017 Topics Overview PVD s Role in the Appraisal Process Appointment of County

2017 KCCA 41 st Annual Conference Appraising Property Kansas County Commissioners Association Junction City, Kansas June 2, 2017 Topics Overview PVD s Role in the Appraisal Process Appointment of County

2015 Annual Report. The appraisal district is governed by a Board of Directors whose primary responsibilities are to:

Refugio County Appraisal District Mailing Address: PO Box 156, Refugio, Texas 78377-0156 Physical Location: 420 North Alamo Street, Refugio, Texas 78377 Telephone Number: 361-526-5994 Website: www.refugiocad.org

Refugio County Appraisal District Mailing Address: PO Box 156, Refugio, Texas 78377-0156 Physical Location: 420 North Alamo Street, Refugio, Texas 78377 Telephone Number: 361-526-5994 Website: www.refugiocad.org

ASSESSOR. Mission. Assessor Financial Summary

Mission The Assessor is responsible for discovering, inventorying and valuing all taxable property in the County, including residential, commercial, industrial and undeveloped properties, as well as personal

Mission The Assessor is responsible for discovering, inventorying and valuing all taxable property in the County, including residential, commercial, industrial and undeveloped properties, as well as personal

Fannin Central Appraisal District Annual Appraisal Report

Fannin Central Appraisal District Introduction The Fannin Central Appraisal District is a political subdivision of the state. The jurisdictional boundary of the Appraisal District covers 899 square miles.

Fannin Central Appraisal District Introduction The Fannin Central Appraisal District is a political subdivision of the state. The jurisdictional boundary of the Appraisal District covers 899 square miles.

Gaines County Appraisal District 2016 Annual Report

Gaines County Appraisal District 2016 Annual Report Introduction The Gaines County Appraisal District is a political subdivision of the state, The Constitution of the State of Texas, the Texas Property

Gaines County Appraisal District 2016 Annual Report Introduction The Gaines County Appraisal District is a political subdivision of the state, The Constitution of the State of Texas, the Texas Property

FYI For Your Information

TAXPAYER SERVICE DIVISION FYI For Your Information Gross Conservation Easement Credit OVERVIEW An income tax credit is available for tax years beginning on or after January 1, 2000, for the donation of

TAXPAYER SERVICE DIVISION FYI For Your Information Gross Conservation Easement Credit OVERVIEW An income tax credit is available for tax years beginning on or after January 1, 2000, for the donation of

CALLAHAN COUNTY APPRAISAL DISTRICT 2017 ANNUAL APPRAISAL REPORT

CALLAHAN COUNTY APPRAISAL DISTRICT 2017 ANNUAL APPRAISAL REPORT Introduction The Callahan County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the

CALLAHAN COUNTY APPRAISAL DISTRICT 2017 ANNUAL APPRAISAL REPORT Introduction The Callahan County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the

OPERATIONAL PLAN BUSINESS IMPROVEMENT DISTRICT DOWNTOWN SUN PRAIRIE

2016 OPERATIONAL PLAN BUSINESS IMPROVEMENT DISTRICT DOWNTOWN SUN PRAIRIE December 3 rd, 2015 1 A. Introduction The following is the 2016 operating plan for the Business Improvement District (BID) in downtown

2016 OPERATIONAL PLAN BUSINESS IMPROVEMENT DISTRICT DOWNTOWN SUN PRAIRIE December 3 rd, 2015 1 A. Introduction The following is the 2016 operating plan for the Business Improvement District (BID) in downtown

Office of the City Auditor. Audit of the Office of the Real Estate Assessor

Report Date: August 28, 2015 Office of the City Auditor 2401 Courthouse Drive, Room 344 Virginia Beach, Virginia 23456 757.385.5870 Promoting Accountability and Integrity in City Operations Contact Information

Report Date: August 28, 2015 Office of the City Auditor 2401 Courthouse Drive, Room 344 Virginia Beach, Virginia 23456 757.385.5870 Promoting Accountability and Integrity in City Operations Contact Information

MAP. METHODS AND ASSISTANCE PROGRAM 2013 REPORT McLennan County Appraisal District. Susan Combs Texas Comptroller of Public Accounts

MAP METHODS AND ASSISTANCE PROGRAM 2013 REPORT McLennan County Appraisal District Susan Combs Texas Comptroller of Public Accounts January 22, 2014 Chief Appraiser County Appraisal District Board of Directors

MAP METHODS AND ASSISTANCE PROGRAM 2013 REPORT McLennan County Appraisal District Susan Combs Texas Comptroller of Public Accounts January 22, 2014 Chief Appraiser County Appraisal District Board of Directors

ARKANSAS PROPERTY TAX EQUALIZATION AND APPEAL SYSTEM A SYNOPSIS. Compiled for Equalization Board Members. by the ASSESSMENT COORDINATION DEPARTMENT

ARKANSAS PROPERTY TAX EQUALIZATION AND APPEAL SYSTEM 2015 A SYNOPSIS Compiled for Equalization Board Members by the ASSESSMENT COORDINATION DEPARTMENT STATE OF ARKANSAS TABLE OF CONTENTS Constitution...1

ARKANSAS PROPERTY TAX EQUALIZATION AND APPEAL SYSTEM 2015 A SYNOPSIS Compiled for Equalization Board Members by the ASSESSMENT COORDINATION DEPARTMENT STATE OF ARKANSAS TABLE OF CONTENTS Constitution...1

WICHITA APPRAISAL DISTRICT ANNUAL REPORT

WICHITA APPRAISAL DISTRICT 2017 ANNUAL REPORT Appraised s Wichita Appraisal District is responsible for local property tax appraisal and exemption administration for the twelve taxing jurisdictions within

WICHITA APPRAISAL DISTRICT 2017 ANNUAL REPORT Appraised s Wichita Appraisal District is responsible for local property tax appraisal and exemption administration for the twelve taxing jurisdictions within

Property Tax Fairness and the Future of Further Reform

Property Tax Fairness and the Future of Further Reform Ryan Kamrowski, Director of Tax Equalization, Ward County Senator Dwight Cook, Mandan (Dist. 34) Donnell Preskey Hushka, Government Affairs Specialist,

Property Tax Fairness and the Future of Further Reform Ryan Kamrowski, Director of Tax Equalization, Ward County Senator Dwight Cook, Mandan (Dist. 34) Donnell Preskey Hushka, Government Affairs Specialist,

Van Zandt County Appraisal District 2015 Annual Report

Van Zandt County Appraisal District 2015 Annual Report Introduction The Van Zandt County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property

Van Zandt County Appraisal District 2015 Annual Report Introduction The Van Zandt County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property

MAP. METHODS AND ASSISTANCE PROGRAM 2013 REPORT Hood County Appraisal District. Susan Combs Texas Comptroller of Public Accounts

MAP METHODS AND ASSISTANCE PROGRAM 2013 REPORT Hood County Appraisal District Susan Combs Texas Comptroller of Public Accounts January 22, 2014 Chief Appraiser County Appraisal District Board of Directors

MAP METHODS AND ASSISTANCE PROGRAM 2013 REPORT Hood County Appraisal District Susan Combs Texas Comptroller of Public Accounts January 22, 2014 Chief Appraiser County Appraisal District Board of Directors

ASSESSOR. Mission. Program Summaries by Function

Mission The Assessor is responsible for discovering, inventorying and valuing all taxable property in the County, including residential, commercial, industrial and undeveloped properties, as well as personal

Mission The Assessor is responsible for discovering, inventorying and valuing all taxable property in the County, including residential, commercial, industrial and undeveloped properties, as well as personal

PROPERTY ASSESSMENT AND TAXATION

History of the Community and Service Area Structure Juneau's existing City and Borough concept was adopted in 1970 with the unification of the Cities of Juneau and Douglas and the Greater Juneau Borough.

History of the Community and Service Area Structure Juneau's existing City and Borough concept was adopted in 1970 with the unification of the Cities of Juneau and Douglas and the Greater Juneau Borough.

THE OFFICE OF COUNTY ASSESSOR

CHAPTER 5 THE OFFICE OF COUNTY ASSESSOR The office of county assessor is primarily responsible for determining equitable values on both real and personal property for property tax purposes (63-207). However,

CHAPTER 5 THE OFFICE OF COUNTY ASSESSOR The office of county assessor is primarily responsible for determining equitable values on both real and personal property for property tax purposes (63-207). However,

Burleson County Appraisal District Annual Report

December 2017 111 E. Fawn St. P. O. Box 1000 Caldwell, TX 77836 Burleson County Appraisal District December 2017 It is my pleasure to present the of the Burleson County Appraisal District (BCAD). This

December 2017 111 E. Fawn St. P. O. Box 1000 Caldwell, TX 77836 Burleson County Appraisal District December 2017 It is my pleasure to present the of the Burleson County Appraisal District (BCAD). This

Board of County Commissioners

Board of County Commissioners A board of commissioners consisting of three elected people governs each county (except Marion County). In all except Lake and St. Joseph counties, the commissioners are elected

Board of County Commissioners A board of commissioners consisting of three elected people governs each county (except Marion County). In all except Lake and St. Joseph counties, the commissioners are elected

ARLINGTON COUNTY CODE. Chapter 20 REAL ESTATE ASSESSMENT. Article I. In General

ARLINGTON COUNTY CODE Chapter 20 Article I. In General 20-1. Department of Real Estate Assessments Established. 20-2. Board of Equalization of Real Estate Assessments Established; Powers; Compensation.

ARLINGTON COUNTY CODE Chapter 20 Article I. In General 20-1. Department of Real Estate Assessments Established. 20-2. Board of Equalization of Real Estate Assessments Established; Powers; Compensation.

The Future of Property Taxes in Florida. Amber Hughes Sr. Legislative Advocate Florida League of Cities

The Future of Property Taxes in Florida Amber Hughes Sr. Legislative Advocate Florida League of Cities 2017 Legislative Issues Non-homestead assessment limitation caps Recapture Implementation of Voter

The Future of Property Taxes in Florida Amber Hughes Sr. Legislative Advocate Florida League of Cities 2017 Legislative Issues Non-homestead assessment limitation caps Recapture Implementation of Voter

Past & Present Adjustments & Parcel Count Section... 13

Assessment 2017 Report This report includes specific information regarding the 2017 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

Assessment 2017 Report This report includes specific information regarding the 2017 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

Referred to Committee on Revenue and Economic Development. FISCAL NOTE: Effect on Local Government: May have Fiscal Impact. Effect on the State: Yes.

SENATE JOINT RESOLUTION NO. SENATORS SETTELMEYER, GUSTAVSON; AND GOICOECHEA MARCH, 0 Referred to Committee on Revenue and Economic Development S.J.R. SUMMARY Proposes to amend the Nevada Constitution to

SENATE JOINT RESOLUTION NO. SENATORS SETTELMEYER, GUSTAVSON; AND GOICOECHEA MARCH, 0 Referred to Committee on Revenue and Economic Development S.J.R. SUMMARY Proposes to amend the Nevada Constitution to

FreestoneCentralAppraisalDistrict 2018 AnnualR eport

FreestoneCentralAppraisalDistrict 218 AnnualR eport Introduction The Freestone Central Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property

FreestoneCentralAppraisalDistrict 218 AnnualR eport Introduction The Freestone Central Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property

Introduction. Bruce Munneke, S.A.M.A. Washington County Assessor. 3 P a g e

Assessment 2016 Report This report includes specific information regarding the 2016 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

Assessment 2016 Report This report includes specific information regarding the 2016 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

2018 Annual Report. Fayette County Appraisal District P. O. Box 836 La Grange, TX 78945

2018 Annual Report Fayette County Appraisal District P. O. Box 836 La Grange, TX 78945 FCAD 2018 Annual Report 1 2018 ANNUAL REPORT FAYETTE COUNTY APPRAISAL DISTRICT INTRODUCTION The Fayette County Appraisal

2018 Annual Report Fayette County Appraisal District P. O. Box 836 La Grange, TX 78945 FCAD 2018 Annual Report 1 2018 ANNUAL REPORT FAYETTE COUNTY APPRAISAL DISTRICT INTRODUCTION The Fayette County Appraisal

CITY OF JACKSONVILLE, FLORIDA

PROPERTY APPRAISER DEPARTMENT VISION: To earn the public s trust. DEPARTMENT MISSION: We will: Produce a fair, equitable and accurate tax roll as required by law. Focus on our customers the taxpayers.

PROPERTY APPRAISER DEPARTMENT VISION: To earn the public s trust. DEPARTMENT MISSION: We will: Produce a fair, equitable and accurate tax roll as required by law. Focus on our customers the taxpayers.

Open Space Taxation Act

Open Space Taxation Act WASHINGTON STATE DEPARTMENT OF REVENUE JUNE 2007 The information and instructions in this brochure are to be used when applying for assessment on the basis of current use under

Open Space Taxation Act WASHINGTON STATE DEPARTMENT OF REVENUE JUNE 2007 The information and instructions in this brochure are to be used when applying for assessment on the basis of current use under

GOVERNANCE OF ASSESSOR

GOVERNANCE OF ASSESSOR State of NH Constitution NH State Statutes (RSA) State Supreme Court Case Law NH Assessing Standard Board Rules NH Department of Revenue Rules Professional Code of Conduct (USPAP)

GOVERNANCE OF ASSESSOR State of NH Constitution NH State Statutes (RSA) State Supreme Court Case Law NH Assessing Standard Board Rules NH Department of Revenue Rules Professional Code of Conduct (USPAP)