Chapter 7: Decpreciation and Income Taxes

|

|

|

- Drusilla Miller

- 5 years ago

- Views:

Transcription

1 Chapter 7: Decpreciation and Income Taxes Tsui-Ping Chung 1

2 The goal The objective of Chapter 7 is to explain how depreciation affects income taxes, and how income taxes affect economic decision making. 2

3 Depreciation is the decrease in value of physical properties with the passage of time.( 时间流逝 ) It is an accounting concept, a non-cash cost, that establishes an annual deduction against before tax income. It is intended to approximate the yearly fraction of an asset s value used in the production of income. 3

4 Property( 不动产 ) is depreciable if it is used in business or held to produce income. it has a determinable useful life, longer than one year. it is something that wears out, decays, gets used up, becomes obsolete, or loses value from natural causes. it is not inventory, stock in trade, or investment property. 4

5 Depreciable property is tangible (can be seen or touched; personal or real) or intangible (such as copyrights, patents, or franchises). depreciated, d according to a depreciation schedule, when it is put in service (when it is ready and available for its specific use). 5

6 Definition Adjusted (cost) basis Basis or cost basis Book value(bv) Market value(mv) Recovery period Recovery rate Slavage value(sv) Useful life 6

7 Straight line (SL): constant amount of depreciation each year over the depreciable life of the asset. N = depreciable life B = cost basis d k = depreciaton in k BV k = book value at end of k SV N = salvage value N 7

8 Example 7.1 Cost basis of $200, and five year depreciable life. SV=$20,000 at the end of five years Ui Using SL method Annual depreciation amounts and the book value of laser at the end of yeat. 8 N = depreciable life B = cost basis d k = depreciaton in k k BV k = book value at end of k SV N = salvage value

9 Declining-balance (DB) A constant-percentage of the remaining BV is depreciated each year. B = cost basis d k = depreciaton in k BV k = book value at end of k k The constant percentage is determined by R, where R = 2/N when 200% declining balance is being used, R = 1.5/N when 150% declining balance is being used. 9

10 Example 7.2 Cost basis of $4,000 and 10 year depreciable life. SV=$0 at the end of 10 years Ui Using DB method R=2/N (200% DB method) R=1.5/N (150% DB method) 10

11 DB with switchover to SL DB never reaches a BV of zero, and it is permissible ibl to switch from this method to the SL method. This method is used in calculating the MACRS. 11

12 12

13 The units-of-production method method can be used when the decrease in value of the assset is mostly a function of use, instead of time. The cost basis is allocated equally over the number of units produced d over the asset s life. The depreciation per unit of production is found from the formula below. Depreciation per unit of production: 13

14 Example 7.3 Cost basis of $50, and 30, hours of use. SV=$10,000 at the end of 30,000 hours Find its depreciation rate per hour of use and find its BV after 10,000 hours of operation. 14

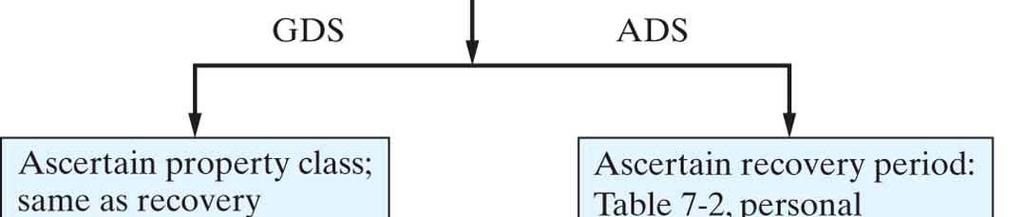

15 Modified Accelerated Cost Recovery System is the principle method for computing depreciation for property in engineering i projects. It consists of two systems, the main system called the General Depreciation System (GDS) the Alternative Depreciation System (ADS). 15

16 When an asset is depreciated using MACRS( 加速资本回收系统 ), the following information is needed to calculate deductions. Cost basis, B Date the property was placed into service The property p class and recovery yperiod The MACRS depreciation method (GDS or ADS). The time convention that applies (half year) 16

17 Property class and recovery period Two types recovery periods ADS For tangible personal property, the ADS recovery rate is almost the same as the class life Under a 12 year ADS recovery rate GDS Most tangible personal property is assigned six classes.(3, 5, 7, 10, 15, 20) real property is assigned two real property classes: nonresidential and residential 39 years for nonresidential and 27.5 years for residential 17

18 18

19 19

20 Depreciation methods, time convention and recovery rates GDS, 3, 5, 7, 10 year personal classes: The 200% DB method; then switching to SL GDS, 15, 20 year personal classes: The 1500% DB method; then switching to SL GDS nonresidential and residential: SL over the fixed GDS recovery period. ADS: SL method for both personal and real property over the fixed ADS recovery periods. 20 A half year tome convention: begin at middle of the year

21 21

22 22

23 Using MACRS(GDS) is easy! Determine the asset s s recovery period (Table 7-2). Use the appropriate column from Table 7-3 that matches the recovery period to find the recovery rate, r k, and compute the depreciation for each year as 23

24 Example 7.4 A new piece of semiconductor manufacturing equipment. The cost basis for the equipment is $100,000. Determine The depreciation charge permissible in the fourth year, The BV at the end of the fourth year, The cumulative depreciation through the third year The BV at the end of the fifth year if the equipment is disposed of at that time? 24

25 25

26 Example 7.5 Computer and peripheral equipment, used in business. BV at that time is $25,000. A new fast computer system have a MV $400, A deal was agreed to pay $325,000 What is the GDS property class of the new computer system? How much depreciation can be conducted each year based on this class life? 26

27 Example 7.6 Produced a large manufacturing of sheet metal products and placed in new computer-controlled flexible manufacturing system for $3.0 million Using ADS What depreciations can be claimed for the system? 27

28 A comprehensive depreciation example 7.7 Figure 7-2 BV Comparisons for Selected Methods of Depreciation in Example 7-7 (Note: The bus is assumed to be sold in year six for the MACRS-GDS method.) 28

29 There are many different types of taxes. Income taxes are assessed as a function of gross revenues minus allowable expenses. Property taxes are assessed as a function of the value of property owned. Sales taxes are assessed on the basis of purchase of goods or services. Excise taxes are federal taxes assessed as a function of the sale of certain goods or services often considered nonnecessities. 29

30 Taking taxes into account changes our expectations of returns on projects, so our MARR (after-tax) is lower. 30

31 The after-tax tax MARR should be at least the tax-adjusted weighted average cost of capital (WACC). 31 λ = fraction of a firm s pool of capital borrowed from lenders t = effective income tax rate as a decimal i b = before-tax interest paid on borrowed capital e a = after-tax tax cost of equity capital

32 Depreciation is not a cash flow, but it affects a corporation s taxable income, and therefore the taxes a corporation pays. Taxable income = gross income all expenses except capital invest. depreciation deductions. 32

33 Federal taxes are calculated cu ated using a set of income brackets. each applying a different tax rate on the marginal value of income. State t taxes vary widely. Tax rates are found in Table 7-5. Corporations need to know their effective tax rate,, which is a combination of federal and state taxes according to either formula below. 33

34 34

35 Example 7.9 Gross income: $5,270,000, 000 expenses: $2,927,500 Depreciation deductions: $1,874,300 What would be its taxable income and federal income tax for the tax year? 35

36 The disposal of a depreciable asset can result in a gain or loss based on the sale price (market value) and the current book value A gain is often referred to as depreciation recapture( 折旧回朔 ), and it is generally taxed as the same as ordinary income( 正常收入 ). A loss is a capital loss. An asset sold for more than it s cost basis results in a capital gain. Example

37 General procedure for making after-tax economic analysis After-tax economic analysis is generally the same as beforetax analysis, just using after-tax tax cash flows (ATCF) instead of before-tax cash flows (BTCF). The analysis a s is conducted using the after-tax ta MARR. 37

38 Cash flows are typically y determined for each year using the notation below. R k = revenues (and savings) from the project during period k E k = cash outflows during k for deductible expenses d k = sum of all noncash, or book, costs during k, such as depreciation t = effective income tax rate on ordinary income T k = income tax consequence during year k ATCF k = ATCF from the project during year k 38

39 Some important cash flow formulas. Taxable income Ordinary income tax consequences 39

40 Figure 7-4 General Format (Worksheet) for After-Tax Analysis; Determining the ATCF 40

41 Example 7-12 and 13 41

42 Figure 7-5 Spreadsheet Solution, Example

43 Economic value added (EVA) is an estimate of the profit-earning potential ti 潜在性 of proposed capital investments in engineering projects. It is the difference between a company s adjusted net operating profit after taxes (NOPAT) in a particular year its after-tax cost of capital during that year. 43

44 where, and 44

CHAPTER 7. Depreciation And Income Taxes. Created By : Eng.Maysa Gharaybeh

CHAPTER 7 Depreciation And Income Taxes Created By : Eng.Maysa Gharaybeh Depreciation Decrease in value of physical properties with passage of time and use. More specifically: Accounting concept establishing

CHAPTER 7 Depreciation And Income Taxes Created By : Eng.Maysa Gharaybeh Depreciation Decrease in value of physical properties with passage of time and use. More specifically: Accounting concept establishing

Lecture 8 (Part 2) Depreciation

Depreciation") Seg2510 Management Principles for Engineering Managers Lecture 8 (Part 2) Depreciation Department of Systems Engineering and Engineering Management The Chinese University of Hong Kong 1 Part I Review of

Seg2510 Management Principles for Engineering Managers Lecture 8 (Part 2) Depreciation Department of Systems Engineering and Engineering Management The Chinese University of Hong Kong 1 Part I Review of

Lecture 8 (Part 1) Depreciation

Depreciation") Seg2510 Management Principles for Engineering Managers Lecture 8 (Part 1) Depreciation Department of Systems Engineering and Engineering Management The Chinese University of Hong Kong 1 Depreciation Depreciation

Seg2510 Management Principles for Engineering Managers Lecture 8 (Part 1) Depreciation Department of Systems Engineering and Engineering Management The Chinese University of Hong Kong 1 Depreciation Depreciation

ILLUSTRATION 11-1 PATTERNS OF BOOK VALUE OVER LIFE OF ASSET

ILLUSTRATION 11-1 PATTERNS OF BOOK VALUE OVER LIFE OF ASSET $ Cost of asset N PR: Book value activity methods Depreciable cost SL: Book value straight line Salvage value AC: Book value accelerated S E

ILLUSTRATION 11-1 PATTERNS OF BOOK VALUE OVER LIFE OF ASSET $ Cost of asset N PR: Book value activity methods Depreciable cost SL: Book value straight line Salvage value AC: Book value accelerated S E

Week11, Chap 8 Accounting 1A, Financial Accounting

Week11, Chap 8 Accounting 1A, Financial Accounting Reporting and Interpreting Property, Plant, and Equipment;Natural Resources; and Intangibles Instructor: Michael Booth Understanding The Business Insufficient

Week11, Chap 8 Accounting 1A, Financial Accounting Reporting and Interpreting Property, Plant, and Equipment;Natural Resources; and Intangibles Instructor: Michael Booth Understanding The Business Insufficient

5. The cost of buildings includes all necessary costs related to the purchase or construction

CHAPTER REVIEW Plant Assets 1. (S.O. 1) Plant assets are tangible resources that are used in the operations of a business and are not intended for sale to customers. Plant assets are subdivided into four

CHAPTER REVIEW Plant Assets 1. (S.O. 1) Plant assets are tangible resources that are used in the operations of a business and are not intended for sale to customers. Plant assets are subdivided into four

The cost of this asset includes the purchase price, plus any taxes, commissions, and other amounts paid to make the asset ready for use.

Accounting Fundamentals Lesson 7 7.0 Long-Term Assets Plant Assets, are long-lived assets that are tangible. The cost of this asset includes the purchase price, plus any taxes, commissions, and other amounts

Accounting Fundamentals Lesson 7 7.0 Long-Term Assets Plant Assets, are long-lived assets that are tangible. The cost of this asset includes the purchase price, plus any taxes, commissions, and other amounts

Chapter 9: Long-Lived Assets and Cost Allocation

1 Chapter 9: Long-Lived Assets and Cost Allocation 2 Capitalize vs Expense Revenue Expenditures Merely maintain a given level of services Should be Expensed Debit Expense Capital Expenditures Provide future

1 Chapter 9: Long-Lived Assets and Cost Allocation 2 Capitalize vs Expense Revenue Expenditures Merely maintain a given level of services Should be Expensed Debit Expense Capital Expenditures Provide future

You may have to use Form 4562 to figure and report your depreciation. See Which Forms To Use in chapter 3. Also see Publication 946.

1 of 10 11/29/2011 2:27 AM 2. Depreciation of Rental Property Table of Contents The Basics What Rental Property Can Be Depreciated? When Does Depreciation Begin and End? Depreciation Methods Basis of Depreciable

1 of 10 11/29/2011 2:27 AM 2. Depreciation of Rental Property Table of Contents The Basics What Rental Property Can Be Depreciated? When Does Depreciation Begin and End? Depreciation Methods Basis of Depreciable

Accounting for Plant Assets and Depreciation

Ch16 Accounting for Plant Assets and Depreciation 1 Understanding PPE Acquisition of PPE (cost) Depreciation of PPE Revenue expenditure vs. capital expenditure Disposition of PPE (sale, trade, and discard)

Ch16 Accounting for Plant Assets and Depreciation 1 Understanding PPE Acquisition of PPE (cost) Depreciation of PPE Revenue expenditure vs. capital expenditure Disposition of PPE (sale, trade, and discard)

Long-lived, Revenue-producing Assets. Expected to Benefit Future Periods

Section 8 - Property, Plant, Equipment (Fixed Assets), and Depletable Resources Types of Assets Long-lived, Revenue-producing Assets 10-1 Expected to Benefit Future Periods Tangible Property, Plant, Equipment

Section 8 - Property, Plant, Equipment (Fixed Assets), and Depletable Resources Types of Assets Long-lived, Revenue-producing Assets 10-1 Expected to Benefit Future Periods Tangible Property, Plant, Equipment

Before Class starts.(make sure your name is on all submissions)

") Before Class starts.(make sure your name is on all submissions) March 27 exam conflicts must be resolved before Spring break. Fourth Homework due Thursday 3/6 before class. Fifth Homework due 3/20 before

Before Class starts.(make sure your name is on all submissions) March 27 exam conflicts must be resolved before Spring break. Fourth Homework due Thursday 3/6 before class. Fifth Homework due 3/20 before

Chapter 08 - Long-Term Assets. Chapter Outline

Section 1 Plant Assets I. Cost Determination Plant assets are tangible assets used in a company's operations that have a useful life of more than one accounting period. Consistent with cost principle,

Section 1 Plant Assets I. Cost Determination Plant assets are tangible assets used in a company's operations that have a useful life of more than one accounting period. Consistent with cost principle,

Before Class starts.(make sure your name is on all submissions)

") Before Class starts.(make sure your name is on all submissions) Fourth Homework due 10/27(MW) or 10/28(TR) before class. No exceptions. Help session 10/26 1:00-3:30pm in GBS130 Fifth Homework due 11/3(MW)

Before Class starts.(make sure your name is on all submissions) Fourth Homework due 10/27(MW) or 10/28(TR) before class. No exceptions. Help session 10/26 1:00-3:30pm in GBS130 Fifth Homework due 11/3(MW)

Chapter 11 Depreciation. Depreciations: Straight Line Sum of Years Digits Declining Balance

Chapter 11 Depreciation Depreciations: Straight Line Sum of Years Digits Declining Balance 1 Depreciation is important because it affects the taxes that firms pay. The taxable income is (Income expenses).

Chapter 11 Depreciation Depreciations: Straight Line Sum of Years Digits Declining Balance 1 Depreciation is important because it affects the taxes that firms pay. The taxable income is (Income expenses).

Financial Accounting. John J. Wild. Sixth Edition. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 08 Reporting and Analyzing Long-Term Assets Conceptual Learning

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 08 Reporting and Analyzing Long-Term Assets Conceptual Learning

ACCOUNTING - CLUTCH CH. 8 - LONG LIVED ASSETS.

!! www.clutchprep.com CONCEPT: INITIAL COST OF LONG-LIVED (PLANT) ASSETS Plant Assets include,,, and RULE: Initial cost includes the price plus all expenditures to make an asset When recording the initial

!! www.clutchprep.com CONCEPT: INITIAL COST OF LONG-LIVED (PLANT) ASSETS Plant Assets include,,, and RULE: Initial cost includes the price plus all expenditures to make an asset When recording the initial

Sales Associate Course

Sales Associate Course Chapter Seventeen Real Estate Investments and Business Opportunity Brokerage 1 Investment Analysis Most important consideration: Economic soundness Land use controls Zoning Deed

Sales Associate Course Chapter Seventeen Real Estate Investments and Business Opportunity Brokerage 1 Investment Analysis Most important consideration: Economic soundness Land use controls Zoning Deed

Before Class starts.(make sure your name is on all submissions)

") Before Class starts.(make sure your name is on all submissions) March 27 exam conflicts must be resolved before Spring break. Your papers Fourth Homework due Today 3/6 before class. Fifth Homework due

Before Class starts.(make sure your name is on all submissions) March 27 exam conflicts must be resolved before Spring break. Your papers Fourth Homework due Today 3/6 before class. Fifth Homework due

Agenda cont. Claiming the special depreciation allowance Figuring depreciation under MACRS Additional rules for listed property Basis of assets

Depreciation Basics Agenda What property can and cannot be depreciated When depreciation begins and ends Methods for depreciating property Basis of depreciable property How to treat repairs and improvements

Depreciation Basics Agenda What property can and cannot be depreciated When depreciation begins and ends Methods for depreciating property Basis of depreciable property How to treat repairs and improvements

Chapter 11 Investments in Noncurrent Operating Assets Utilization and Retirement

Chapter 11 Investments in Noncurrent Operating Assets Utilization and Retirement 1. The annual depreciation expense 2. The depletion of natural resources 3. The changes in estimates and methods in the

Chapter 11 Investments in Noncurrent Operating Assets Utilization and Retirement 1. The annual depreciation expense 2. The depletion of natural resources 3. The changes in estimates and methods in the

4/10/2012. Long-Lived Assets and Depreciation. Overview of Long-lived Assets. Learning Objectives (LO) Learning Objectives (LO)

Learning Objectives (LO)") Learning Objectives (LO) CHAPTER Long-Lived Assets and Depreciation 8 After studying this chapter, you should be able to 1. Distinguish a company s expenses from expenditures that it should capitalize

Learning Objectives (LO) CHAPTER Long-Lived Assets and Depreciation 8 After studying this chapter, you should be able to 1. Distinguish a company s expenses from expenditures that it should capitalize

The Cost Principle. Plant Assets. Intangible Assets. Natural Resources. Depreciation. Amortization. Depletion. Chapter 9

Plant Assets Natural Resources Intangible Assets Depreciation Depletion Amortization Chapter 9 2 Held for use in business Full cost includes several expenditures Last several years Can be sold or traded

Plant Assets Natural Resources Intangible Assets Depreciation Depletion Amortization Chapter 9 2 Held for use in business Full cost includes several expenditures Last several years Can be sold or traded

Cost Segregation Instructor Teaching Schedule (3-Hour)

") Time Topic Pages Student Objectives 8:30-8:35 Course introduction Page 2 What is cost segregation? Objective of cost segregation: to increase cash flow Benefit of cost segregation Learning objectives Page

Time Topic Pages Student Objectives 8:30-8:35 Course introduction Page 2 What is cost segregation? Objective of cost segregation: to increase cash flow Benefit of cost segregation Learning objectives Page

How To Depreciate Property

Department of the Treasury Internal Revenue Service Publication 946 Cat. No. 13081F How To Depreciate Property Section 179 Deduction MACRS Listed Property For use in preparing 1999 Returns Contents Introduction...

Department of the Treasury Internal Revenue Service Publication 946 Cat. No. 13081F How To Depreciate Property Section 179 Deduction MACRS Listed Property For use in preparing 1999 Returns Contents Introduction...

S ection 7 DEPRECIATION UNDER FEDERAL INCOME TAX DEPRECIATION RULES

S ection 7 UNDER FEDERAL INCOME TAX RULES Important: This section explains how to depreciate for tax purposes assets purchased in 2000 or thereafter. Prior to 2000, there were many changes in tax depreciation

S ection 7 UNDER FEDERAL INCOME TAX RULES Important: This section explains how to depreciate for tax purposes assets purchased in 2000 or thereafter. Prior to 2000, there were many changes in tax depreciation

March 23, 2006 Anderson ECON 136A 11am Class FINAL EXAM v. 1 Name

March 23, 2006 Anderson ECON 136A 11am Class FINAL EXAM v. 1 Name YOU MUST WRITE YOUR NAME ON THIS EXAM AND TURN IT IN WITH YOUR SCANTRON AND BLUE-BOOK! Complete questions #1-25 on your scantron AND WRITE

March 23, 2006 Anderson ECON 136A 11am Class FINAL EXAM v. 1 Name YOU MUST WRITE YOUR NAME ON THIS EXAM AND TURN IT IN WITH YOUR SCANTRON AND BLUE-BOOK! Complete questions #1-25 on your scantron AND WRITE

What is the depreciation for year three (3) using the Sum-of-Years Digits method? (4, all or nothing)

using the Sum-of-Years Digits method? (4, all or nothing)") Carefully read each problem before answering. Please write clearly, and show and label all formulas and/or factors used in any problem requiring mathematical calculations. 1. Based on your knowledge of

Carefully read each problem before answering. Please write clearly, and show and label all formulas and/or factors used in any problem requiring mathematical calculations. 1. Based on your knowledge of

Accounting for tangible fixed Assets

Accounting for tangible fixed Assets Fixed assets are used (not consumed) in operations of a business provide benefits beyond the current accounting period Fixed assets are either acquired or self constructed

Accounting for tangible fixed Assets Fixed assets are used (not consumed) in operations of a business provide benefits beyond the current accounting period Fixed assets are either acquired or self constructed

CHAPTER 6 - Accounting for Long-Term Operational Assets

CHAPTER 6 - Accounting for Long-Term Operational Assets ANSWERS TO QUESTIONS 1. Long-term operational assets are those assets that are used by a business to generate revenue. In contrast, investments are

CHAPTER 6 - Accounting for Long-Term Operational Assets ANSWERS TO QUESTIONS 1. Long-term operational assets are those assets that are used by a business to generate revenue. In contrast, investments are

Copyright 2009 The Learning House, Inc. Fixed and Intangible Assets Page 1 of 13

Copyright 2009 The Learning House, Inc. Fixed and Intangible Assets Page 1 of 13 Introduction This lesson focuses on the long-term assets used to operate a company. These assets can be grouped into fixed

Copyright 2009 The Learning House, Inc. Fixed and Intangible Assets Page 1 of 13 Introduction This lesson focuses on the long-term assets used to operate a company. These assets can be grouped into fixed

Plant design and economics (8)

") Plant design and economics (8) Zahra Maghsoud ٢ DEPRECIATION (Ch. 9 Peters and Timmerhaus ) The reduction in value due to physical deterioration, technological advances, economic changes, or other factors

Plant design and economics (8) Zahra Maghsoud ٢ DEPRECIATION (Ch. 9 Peters and Timmerhaus ) The reduction in value due to physical deterioration, technological advances, economic changes, or other factors

Chapter 9 - REPORTING AND ANALYZING LONG-LIVED ASSETS

Revised Summer 2018 Chapter 9 Review 1 Chapter 9 - REPORTING AND ANALYZING LONG-LIVED ASSETS LO 1: Explain the accounting for plant asset expenditures. Plant Assets (Also known as Property, Plant, and

Revised Summer 2018 Chapter 9 Review 1 Chapter 9 - REPORTING AND ANALYZING LONG-LIVED ASSETS LO 1: Explain the accounting for plant asset expenditures. Plant Assets (Also known as Property, Plant, and

John Smith Attachment to Form Statement 1

John Smith 123-45-6789 Attachment to Form 3115 Part II, Line 12a, Description of Items Being Changed Statement 1 The taxpayer is proposing to change the method of depreciation for assets used in JS Construction

John Smith 123-45-6789 Attachment to Form 3115 Part II, Line 12a, Description of Items Being Changed Statement 1 The taxpayer is proposing to change the method of depreciation for assets used in JS Construction

Plant assets are resources that have

10-1 LEARNING OBJECTIVE 1 Explain the accounting for plant asset expenditures. Plant assets are resources that have physical substance (a definite size and shape), are used in the operations of a business,

10-1 LEARNING OBJECTIVE 1 Explain the accounting for plant asset expenditures. Plant assets are resources that have physical substance (a definite size and shape), are used in the operations of a business,

Supplemental Instruction Handouts Financial Accounting Chapter 9: Property, Plant and Equipment and Intangibles Answer Key

Supplemental Instruction Handouts Financial Accounting Chapter 9: Property, Plant and Equipment and Intangibles Answer Key 1. A) Prepare a calculation to show the cost of this machine. $23,500 x 0.02 =

Supplemental Instruction Handouts Financial Accounting Chapter 9: Property, Plant and Equipment and Intangibles Answer Key 1. A) Prepare a calculation to show the cost of this machine. $23,500 x 0.02 =

Prepared by: Alex Socratous For My High School Students

Prepared by: Alex Socratous For My High School Students CHAPTER 2 CAPITAL ASSETS DEPRECIATION CAPITAL ASSETS Capital assets are long-lived assets that are used in the operations of a business and are not

Prepared by: Alex Socratous For My High School Students CHAPTER 2 CAPITAL ASSETS DEPRECIATION CAPITAL ASSETS Capital assets are long-lived assets that are used in the operations of a business and are not

Chapter 8. Accounting for Long-Term Assets

Chapter 8 Accounting for Long-Term Assets C 1 Plant Assets Tangible in Nature Actively Used in Operations Expected to Benefit Future Periods Called Property, Plant, & Equipment 8-2 C 1 Plant Assets Decline

Chapter 8 Accounting for Long-Term Assets C 1 Plant Assets Tangible in Nature Actively Used in Operations Expected to Benefit Future Periods Called Property, Plant, & Equipment 8-2 C 1 Plant Assets Decline

Accounting 1 Instructor Notes

Accounting 1 Instructor Notes CHAPTER 10 FIXED ASSETS AND INTANGIBLE ASSETS McDonald's was founded in 1955 and the company now has 22,500 restaurants in 122 countries around the world. Approximately 70

Accounting 1 Instructor Notes CHAPTER 10 FIXED ASSETS AND INTANGIBLE ASSETS McDonald's was founded in 1955 and the company now has 22,500 restaurants in 122 countries around the world. Approximately 70

Depreciation. Dr. M. S. Memon. Mehran UET, Jamshoro, Pakistan. Department of Industrial Engineering and Management

Depreciation Dr. M. S. Memon Department of Industrial Engineering and Management Mehran UET, Jamshoro, Pakistan https://msmemon.wordpress.com/scmlab/ Introduction Any equipment which is purchased today

Depreciation Dr. M. S. Memon Department of Industrial Engineering and Management Mehran UET, Jamshoro, Pakistan https://msmemon.wordpress.com/scmlab/ Introduction Any equipment which is purchased today

7/2/2015. The Statement of Cash Flows. Learning Objectives. Learning Objectives. Chapter 16

The Statement of Cash Flows Chapter 16 2014 Pearson Education, Inc. Publishing as Prentice Hall 16-1 Learning Objectives 1. Identify the purposes of the statement of cash flows and distinguish among operating,

The Statement of Cash Flows Chapter 16 2014 Pearson Education, Inc. Publishing as Prentice Hall 16-1 Learning Objectives 1. Identify the purposes of the statement of cash flows and distinguish among operating,

Cost Engineering Dr. Nabil I El Sawalhi Associate professor Construction Management

Cost Engineering Dr. Nabil I El Sawalhi Associate professor Construction Management CE - L6 1 Construction Equipment CE - L6 2 Equipment can be classified as specific use or general use. Specific Use Equipment

Cost Engineering Dr. Nabil I El Sawalhi Associate professor Construction Management CE - L6 1 Construction Equipment CE - L6 2 Equipment can be classified as specific use or general use. Specific Use Equipment

Financial Accounting Chapter 10: Property, Plant and Equipment and Intangibles Answer Key

Supplemental Instruction Handouts Financial Accounting Chapter 10: Property, Plant and Equipment and Intangibles Answer Key 1. A) Prepare a calculation to show the cost of this machine. $23,500 x 0.02

Supplemental Instruction Handouts Financial Accounting Chapter 10: Property, Plant and Equipment and Intangibles Answer Key 1. A) Prepare a calculation to show the cost of this machine. $23,500 x 0.02

SOLUTIONS. Learning Goal 28

S1 Learning Goal 28 Multiple Choice 1. b 2. a 3. c 4. b However, the double-declining-balance method calculates the depreciation expense on the full asset cost until the final year of use. 5. d Total appraised

S1 Learning Goal 28 Multiple Choice 1. b 2. a 3. c 4. b However, the double-declining-balance method calculates the depreciation expense on the full asset cost until the final year of use. 5. d Total appraised

The Cost of Property, Plant, Equipment

1 The Cost of Property, Plant, Equipment The cost of property, plant, and equipment includes the purchase price of the asset and all expenditures necessary to prepare the asset for its intended use. Land.

1 The Cost of Property, Plant, Equipment The cost of property, plant, and equipment includes the purchase price of the asset and all expenditures necessary to prepare the asset for its intended use. Land.

Acquisition cost Purchase price plus all expenditures needed to prepare the asset for its intended use

CAPITAL ASSETS Issues to consider: Compute initial acquisition cost Account for subsequent costs Allocate cost to periods benefited Record disposal Acquisition cost Purchase price plus all expenditures

CAPITAL ASSETS Issues to consider: Compute initial acquisition cost Account for subsequent costs Allocate cost to periods benefited Record disposal Acquisition cost Purchase price plus all expenditures

CHAPTER 9 LONG-LIVED ASSETS SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY

CHAPTER 9 LONG-LIVED ASSETS SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 K 17. 2 K 33. 2 C 49. 3 K 65.

CHAPTER 9 LONG-LIVED ASSETS SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 K 17. 2 K 33. 2 C 49. 3 K 65.

Chapter 10 Capital Assets Solutions. (g) NA (current asset) (h) NR (i) NA (inventory) (j) I (k) I (l) NA (investment) (m) NR (n) NR (o) NR (p) I

NA (current asset) (h) NR (i) NA (inventory) (j) I (k) I (l) NA (investment) (m) NR (n) NR (o) NR (p) I") Chapter 10 Capital Assets Solutions Assigned Questions: Study Objective Textbook Pages to Read 9 p. 481-486 19 14-10 Solutions: Q1. Tangible and intangible capital assets both are long-lived assets that

Chapter 10 Capital Assets Solutions Assigned Questions: Study Objective Textbook Pages to Read 9 p. 481-486 19 14-10 Solutions: Q1. Tangible and intangible capital assets both are long-lived assets that

CAS -16 COST ACCOUNTING STANDARD ON DEPRECIATION AND AMORTISATION

Cost Accounting Standards Board CAS -16 COST ACCOUNTING STANDARD ON DEPRECIATION AND AMORTISATION The following is the COST ACCOUNTING STANDARD 16 (CAS 16) issued by the Council of The Institute of Cost

Cost Accounting Standards Board CAS -16 COST ACCOUNTING STANDARD ON DEPRECIATION AND AMORTISATION The following is the COST ACCOUNTING STANDARD 16 (CAS 16) issued by the Council of The Institute of Cost

Section 168. Accelerated Cost Recovery System

Section 168. Accelerated Cost Recovery System 26 CFR 1.168(i) 1: General asset accounts. T.D. 9132 DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Part 1 Changes in Use Under Section 168(i)(5)

Section 168. Accelerated Cost Recovery System 26 CFR 1.168(i) 1: General asset accounts. T.D. 9132 DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Part 1 Changes in Use Under Section 168(i)(5)

SOLUTIONS Learning Goal 19

S1 Learning Goal 19 Multiple Choice 1. b 2. a 3. c 4. b However, the double-declining-balance method calculates the depreciation expense on the full asset cost until the final year of use. 5. d Total appraised

S1 Learning Goal 19 Multiple Choice 1. b 2. a 3. c 4. b However, the double-declining-balance method calculates the depreciation expense on the full asset cost until the final year of use. 5. d Total appraised

Financial Leasing of Capital Assets in Pork Production

Financial Leasing of Capital Assets in Pork Production Originally published as PIH-5. Authors: Chris Hurt, Purdue University Allan E. Lines, Ohio State University Gerry Schwab, Michigan State University

Financial Leasing of Capital Assets in Pork Production Originally published as PIH-5. Authors: Chris Hurt, Purdue University Allan E. Lines, Ohio State University Gerry Schwab, Michigan State University

and Notice of Public Hearing Changes in Use Under Section 168(i)(5)

(5)") Notice of Proposed Rulemaking and Notice of Public Hearing Changes in Use Under Section 168(i)(5) REG 138499 02 AGENCY: Internal Revenue Service (IRS), Treasury. ACTION: Notice of proposed rulemaking and

Notice of Proposed Rulemaking and Notice of Public Hearing Changes in Use Under Section 168(i)(5) REG 138499 02 AGENCY: Internal Revenue Service (IRS), Treasury. ACTION: Notice of proposed rulemaking and

1. Like financial accounting, most business property must be capitalized for tax purposes.

Chapter 02 Property Acquisition and Cost Recovery True / False Questions 1. Like financial accounting, most business property must be capitalized for tax purposes. True False 2. Tax cost recovery methods

Chapter 02 Property Acquisition and Cost Recovery True / False Questions 1. Like financial accounting, most business property must be capitalized for tax purposes. True False 2. Tax cost recovery methods

Some Important Matters

Long-lived Assets 15.501/516 Accounting Spring 2004 Professor S. Roychowdhury Sloan School of Management Massachusetts Institute of Technology March 15, 2004 1 Some Important Matters Problem sets 5&6 Due

Long-lived Assets 15.501/516 Accounting Spring 2004 Professor S. Roychowdhury Sloan School of Management Massachusetts Institute of Technology March 15, 2004 1 Some Important Matters Problem sets 5&6 Due

Implications of Alternative Farm Tractor Depreciation Methods 1. Troy J. Dumler, Robert O. Burton, Jr., and Terry L. Kastens 2

Implications of Alternative Farm Tractor Depreciation Methods 1 Troy J. Dumler, Robert O. Burton, Jr., and Terry L. Kastens 2 1 Selected paper at the annual meeting of the American Agricultural Economics

Implications of Alternative Farm Tractor Depreciation Methods 1 Troy J. Dumler, Robert O. Burton, Jr., and Terry L. Kastens 2 1 Selected paper at the annual meeting of the American Agricultural Economics

William & Mary Law School Scholarship Repository

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 1971 Leasing Arrangements Lawrence P. Roesen

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 1971 Leasing Arrangements Lawrence P. Roesen

B EXERCISES E11-1B (Depreciation Computations SL, SYD, DDB) Instructions (a) (b) (c) E11-2B (Depreciation Conceptual Understanding) Instructions (a)

Instructions (a) (b) (c) E11-2B (Depreciation Conceptual Understanding) Instructions (a)") B EXERCISES E11-1B (Depreciation Computations SL, SYD, DDB) Vaughn Company purchases equipment on January 1, Year 1, at a cost of $500,000. The asset is expected to have a service life of 10 years and

B EXERCISES E11-1B (Depreciation Computations SL, SYD, DDB) Vaughn Company purchases equipment on January 1, Year 1, at a cost of $500,000. The asset is expected to have a service life of 10 years and

1. Like financial accounting, most business property must be capitalized for tax purposes.

Taxation of Business Entities 6th Edition Spilker Test Bank Full Download: http://testbanklive.com/download/taxation-of-business-entities-6th-edition-spilker-test-bank/ Chapter 02 Property Acquisition

Taxation of Business Entities 6th Edition Spilker Test Bank Full Download: http://testbanklive.com/download/taxation-of-business-entities-6th-edition-spilker-test-bank/ Chapter 02 Property Acquisition

Capital Assets. Apply cost principle to compute the cost of capital assets.

Capital Assets Objectives : Describe capital assets and issues accounting for them. Apply cost principle to compute the cost of capital assets. Amortization methods: straight-line, units-ofproduction,

Capital Assets Objectives : Describe capital assets and issues accounting for them. Apply cost principle to compute the cost of capital assets. Amortization methods: straight-line, units-ofproduction,

STUDY OBJECTIVE 1 CAPITAL ASSETS

Collaboratively Created Collection of Chapter 10 Content STUDY OBJECTIVE 1 CAPITAL ASSETS Capital Assets are used throughout many cycles of a business and are reused over and over again. These assets are

Collaboratively Created Collection of Chapter 10 Content STUDY OBJECTIVE 1 CAPITAL ASSETS Capital Assets are used throughout many cycles of a business and are reused over and over again. These assets are

1. Like financial accounting, most business property must be capitalized for tax purposes.

Chapter 02 Property Acquisition and Cost Recovery True / False Questions 1. Like financial accounting, most business property must be capitalized for tax purposes. True False 2. Tax cost recovery methods

Chapter 02 Property Acquisition and Cost Recovery True / False Questions 1. Like financial accounting, most business property must be capitalized for tax purposes. True False 2. Tax cost recovery methods

Reporting and Analyzing Long-Term Operating Assets. Learning Objectives coverage by question 12, 13, 16, 18

Chapter 8 Reporting and Analyzing Long-Term Operating Assets Learning Objectives coverage by question Miniexercises Exercises Problems Cases LO1 Describe and distinguish between tangible and intangible

Chapter 8 Reporting and Analyzing Long-Term Operating Assets Learning Objectives coverage by question Miniexercises Exercises Problems Cases LO1 Describe and distinguish between tangible and intangible

1. Like financial accounting, most business property must be capitalized for tax purposes.

Chapter 02 Property Acquisition and Cost Recovery True / False Questions 1. Like financial accounting, most business property must be capitalized for tax purposes. True False 2. Tax cost recovery methods

Chapter 02 Property Acquisition and Cost Recovery True / False Questions 1. Like financial accounting, most business property must be capitalized for tax purposes. True False 2. Tax cost recovery methods

1. Like financial accounting, most business property must be capitalized for tax purposes.

Chapter 02 Property Acquisition and Cost Recovery True / False Questions 1. Like financial accounting, most business property must be capitalized for tax purposes. True False 2. Tax cost recovery methods

Chapter 02 Property Acquisition and Cost Recovery True / False Questions 1. Like financial accounting, most business property must be capitalized for tax purposes. True False 2. Tax cost recovery methods

Long-Term Assets C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM

Long-Term Assets E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information, in addition to the material

Long-Term Assets E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information, in addition to the material

Fill-in-the-Blank Equations. Exercises

Chapter 9 Long-Term Assets: Fixed and Intangible Study Guide Solutions 1. Residual value 2. Useful life 3. Straight-line rate 4. Total estimated units of activity 5. Straight-line rate 6. Depletion rate

Chapter 9 Long-Term Assets: Fixed and Intangible Study Guide Solutions 1. Residual value 2. Useful life 3. Straight-line rate 4. Total estimated units of activity 5. Straight-line rate 6. Depletion rate

Lease-Versus-Buy. By Steven R. Price, CCIM

Lease-Versus-Buy Cost Analysis By Steven R. Price, CCIM Steven R. Price, CCIM, Benson Price Commercial, Colorado Springs, Colorado, has a national tenant representation and consulting practice. He was

Lease-Versus-Buy Cost Analysis By Steven R. Price, CCIM Steven R. Price, CCIM, Benson Price Commercial, Colorado Springs, Colorado, has a national tenant representation and consulting practice. He was

Advanced M&A and Merger Models Quiz Questions

Advanced M&A and Merger Models Quiz Questions Transaction Assumptions and Sources & Uses Purchase Price Allocation & Balance Sheet Combination Combining the Income Statement Revenue, Expense, and CapEx

Advanced M&A and Merger Models Quiz Questions Transaction Assumptions and Sources & Uses Purchase Price Allocation & Balance Sheet Combination Combining the Income Statement Revenue, Expense, and CapEx

Oregon State University Extension Service

-----, E55 6 0-713 Cop. Oregon State University Extension Service Computer Software LEASE-BUY? DESCRIPTION: LEASE-BUY? is a spreadsheet template designed to show the least-cost option when deciding whether

-----, E55 6 0-713 Cop. Oregon State University Extension Service Computer Software LEASE-BUY? DESCRIPTION: LEASE-BUY? is a spreadsheet template designed to show the least-cost option when deciding whether

CHAPTER 9. Plant Assets, Natural Resources, and Intangible Assets 6, 7, 8, 24, 25, 26 3, 4, 5, 6, 7 11, , 17, 18, 19, 20, 21, 22

CHAPTER 9 Plant Assets, Natural Resources, and Intangible Assets ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems 1. Describe how the cost

CHAPTER 9 Plant Assets, Natural Resources, and Intangible Assets ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems 1. Describe how the cost

Fill-in-the-Blank Equations. Exercises

Chapter 10 Fixed Assets and Intangible Assets Study Guide Solutions 1. Residual value 2. Useful life 3. Straight-line rate 4. Total units of output 5. Straight-line rate 6. Depletion rate 7. Fixed asset

Chapter 10 Fixed Assets and Intangible Assets Study Guide Solutions 1. Residual value 2. Useful life 3. Straight-line rate 4. Total units of output 5. Straight-line rate 6. Depletion rate 7. Fixed asset

2017 Tax Act. Cost Recovery (Depreciation and Expensing)

") 2017 Tax Act Cost Recovery (Depreciation and Expensing) 1 Cost Recovery, Generally Under 263, 263A, and general tax principles, a taxpayer generally must capitalize the acquisition and production costs

2017 Tax Act Cost Recovery (Depreciation and Expensing) 1 Cost Recovery, Generally Under 263, 263A, and general tax principles, a taxpayer generally must capitalize the acquisition and production costs

Louisiana Bankers Association CFO Conference. Baton Rouge Renaissance Hotel. Benny Jeansonne, CPA Partner Silas Simmons, LLP.

Louisiana Bankers Association CFO Conference May 21,2015 Baton Rouge Renaissance Hotel Benny Jeansonne, CPA Partner Silas Simmons, LLP Agenda Depreciation I. Current Law II. Cost Segregation III. Code

Louisiana Bankers Association CFO Conference May 21,2015 Baton Rouge Renaissance Hotel Benny Jeansonne, CPA Partner Silas Simmons, LLP Agenda Depreciation I. Current Law II. Cost Segregation III. Code

Chapter 02 Property Acquisition and Cost Recovery

Chapter 02 Property Acquisition and Cost Recovery True / False Questions 1. Like financial accounting, most business property must be capitalized for tax purposes. True False 2. Tax cost recovery methods

Chapter 02 Property Acquisition and Cost Recovery True / False Questions 1. Like financial accounting, most business property must be capitalized for tax purposes. True False 2. Tax cost recovery methods

Reading 3.6. UNSW Business School, Depreciation of property, plant and equipment, UNSW Sydney.

WARNING This material has been reproduced and communicated to you by or on behalf of the University of New South Wales in accordance with Section 113P of the Copyright Act 1968 (Act). The material in this

WARNING This material has been reproduced and communicated to you by or on behalf of the University of New South Wales in accordance with Section 113P of the Copyright Act 1968 (Act). The material in this

FACT SHEET. Depreciation of Farm Drainage Tile. Agriculture and Natural Resources OAM-1-12

FACT SHEET Agriculture and Natural Resources OAM-1-12 Depreciation of Farm Drainage Tile Wm. Bruce Clevenger OSU Extension Educator and Assistant Professor Introduction Agriculture is one of Ohio s largest

FACT SHEET Agriculture and Natural Resources OAM-1-12 Depreciation of Farm Drainage Tile Wm. Bruce Clevenger OSU Extension Educator and Assistant Professor Introduction Agriculture is one of Ohio s largest

Principles of Accounting II Chapter 21: Record and Communicate Operational Investments

Principles of Accounting II Chapter 21: Record and Communicate Operational Investments Multiple Asset Purchases Allocate total purchase price among assets based on relative. Suppose you buy a building

Principles of Accounting II Chapter 21: Record and Communicate Operational Investments Multiple Asset Purchases Allocate total purchase price among assets based on relative. Suppose you buy a building

Chapter 11. Learning Objectives. Non-current Assets. Horngren, Best, Fraser, Willett: Accounting 6e 2010 Pearson Australia

PowerPoint to accompany Chapter 11 Non-Current Assets: Property, Plant and Equipment, and Intangibles Learning Objectives 1. Measure the cost of a non-current asset 2. Account for depreciation 3. Select

PowerPoint to accompany Chapter 11 Non-Current Assets: Property, Plant and Equipment, and Intangibles Learning Objectives 1. Measure the cost of a non-current asset 2. Account for depreciation 3. Select

Chapter 10: Fixed Assets and Intangible Assets

Chapter 10: Fixed Assets and Intangible Assets Nature of Fixed Assets Fixed assets are long-term or relatively permanent assets, such as equipment, machinery, buildings, and land. Other descriptive titles

Chapter 10: Fixed Assets and Intangible Assets Nature of Fixed Assets Fixed assets are long-term or relatively permanent assets, such as equipment, machinery, buildings, and land. Other descriptive titles

Definitions. CPI is a lease in which base rent is adjusted based on changes in a consumer price index.

Annualized Rental Income is rental revenue under our leases on Operating Properties on a straight-line basis, which includes the effect of rent escalations and any tenant concessions, such as free rent,

Annualized Rental Income is rental revenue under our leases on Operating Properties on a straight-line basis, which includes the effect of rent escalations and any tenant concessions, such as free rent,

Balance at Retirements Balance at Beginning Additions and End of ($ in thousands) of Year 3 at Cost Transfers Year 3

of Year 3 at Cost Transfers Year 3") CHAPTER 10 Long-Lived Assets and Depreciation 10-1 ShopKo Stores, Inc. (ShopKo) is a leading regional discount store chain operating 109 discount retail stores in 13 states. ShopKo stores carry a wide

CHAPTER 10 Long-Lived Assets and Depreciation 10-1 ShopKo Stores, Inc. (ShopKo) is a leading regional discount store chain operating 109 discount retail stores in 13 states. ShopKo stores carry a wide

State of Mexicali Ad Valorem Taxation of Property Statutes, Rules and Regulations

STATUTES CODE OF MEXICALI OF 2000, TITLE 50 REVENUE AND TAXATION, CHAPTER 7 AD VALOREM TAXATION OF PROPERTY Sec. 50-7-1. Legislative intent The intent and purpose of the tax laws of this state are to have

STATUTES CODE OF MEXICALI OF 2000, TITLE 50 REVENUE AND TAXATION, CHAPTER 7 AD VALOREM TAXATION OF PROPERTY Sec. 50-7-1. Legislative intent The intent and purpose of the tax laws of this state are to have

CHAPTER 10 FIXED ASSETS AND INTANGIBLE ASSETS

1. a. Property, plant, and equipment or Fixed assets b. Current assets (merchandise inventory) 2. Real estate acquired as speculation should be listed in the balance sheet under the caption Investments,

1. a. Property, plant, and equipment or Fixed assets b. Current assets (merchandise inventory) 2. Real estate acquired as speculation should be listed in the balance sheet under the caption Investments,

Digital Splash. Problem 17: Plant Assets Acquisition, Disposal, and Depreciation. Zeke s Pedalorium. Algorithmic Problems and Simulations

Digital Splash Algorithmic Problems and Simulations 1 st Web- Based Edition Problem 17: Plant Assets Acquisition, Disposal, and Depreciation Zeke s Pedalorium NBE Achievement Standard: 2) Apply GAAP to

Digital Splash Algorithmic Problems and Simulations 1 st Web- Based Edition Problem 17: Plant Assets Acquisition, Disposal, and Depreciation Zeke s Pedalorium NBE Achievement Standard: 2) Apply GAAP to

Work4Me Accounting Simulations. Problem Fourteen

Work4Me Accounting Simulations 3 rd Web-Based Edition Problem Fourteen Plant Acquisition and Disposal Page 1 INTRODUCTION The Deco-Block Company buys decorative pre-cast cement blocks for retaining walls

Work4Me Accounting Simulations 3 rd Web-Based Edition Problem Fourteen Plant Acquisition and Disposal Page 1 INTRODUCTION The Deco-Block Company buys decorative pre-cast cement blocks for retaining walls

CONSOLIDATED STATEMENT OF INCOME

CONSOLIDATED STATEMENT OF INCOME 1 st quarter (a) 2017 4 th quarter Sales 41,183 42,275 32,841 Excise taxes (5,090) (5,408) (5,319) Revenues from sales 36,093 36,867 27,522 Purchases, net of inventory

CONSOLIDATED STATEMENT OF INCOME 1 st quarter (a) 2017 4 th quarter Sales 41,183 42,275 32,841 Excise taxes (5,090) (5,408) (5,319) Revenues from sales 36,093 36,867 27,522 Purchases, net of inventory

ACCT 100 Chapter 5 - Adjusting Entries and the Worksheet Prof. Johnson

ACCT 100 Chapter 5 - Adjusting Entries and the Worksheet Prof. Johnson Where We've Been We've been working our way through a complete accounting cycle. Specifically, we have learned to: Analyze business

ACCT 100 Chapter 5 - Adjusting Entries and the Worksheet Prof. Johnson Where We've Been We've been working our way through a complete accounting cycle. Specifically, we have learned to: Analyze business

Contents. Deductions? MACRS

Department of the Treasury Internal Revenue Service Publication 946 Cat. No. 13081F Contents What s New for 2011... 2 What s New for 2012... 2 Reminders... 2 Introduction... 2 How To 1. Overview of Depreciation...

Department of the Treasury Internal Revenue Service Publication 946 Cat. No. 13081F Contents What s New for 2011... 2 What s New for 2012... 2 Reminders... 2 Introduction... 2 How To 1. Overview of Depreciation...

Accounting B LECTURE 1: NON-CURRENT ASSETS. Recording, expensing and reporting non-current assets

Accounting B LECTURE 1: NON-CURRENT ASSETS Recording, expensing and reporting non-current assets - Asset: a resource controlled by an entity because of past events and from which future economic benefits

Accounting B LECTURE 1: NON-CURRENT ASSETS Recording, expensing and reporting non-current assets - Asset: a resource controlled by an entity because of past events and from which future economic benefits

Depreciation, Part I Session 19

Basic Income Tax Depreciation, Part I 19-1 Depreciation, Part I Session 19 A A A AI OMB No 1545-0172 Form Department of the Treasury Attachment Internal Revenue Service (99) Sequence No Cost (business

Basic Income Tax Depreciation, Part I 19-1 Depreciation, Part I Session 19 A A A AI OMB No 1545-0172 Form Department of the Treasury Attachment Internal Revenue Service (99) Sequence No Cost (business

Graded Project OVERVIEW INSTRUCTIONS. Step 1: Create a Loan Amortization Schedule

OVERVIEW This project integrates quite a few components of your course. The most imptant thing to keep in mind, as you progress through this project, is to take one step at a time. Do not rush through

OVERVIEW This project integrates quite a few components of your course. The most imptant thing to keep in mind, as you progress through this project, is to take one step at a time. Do not rush through

A 1: It( SPECIFIC ITEMS SECTION 3061 property, plant and equipment. Additional Resources. Page 1 of6. Knotia - CICA Handbook - Accounting A2-14

'" Knotia - CICA Handbook - Accounting»Accounting»Accounting Handbook»Accounting Standards»Specific items [Sections 3000-3870]»3061 - Property, Plant and Eauipment Page 1 of6 A 1: It( A2-14 SPECIFIC ITEMS

'" Knotia - CICA Handbook - Accounting»Accounting»Accounting Handbook»Accounting Standards»Specific items [Sections 3000-3870]»3061 - Property, Plant and Eauipment Page 1 of6 A 1: It( A2-14 SPECIFIC ITEMS

Intermediate Accounting

Intermediate Accounting 11-1 Prepared by Coby Harmon University of California, Santa Barbara 11 Depreciation, Impairments, and Depletion Intermediate Accounting 14th Edition 11-2 Kieso, Weygandt, and Warfield

Intermediate Accounting 11-1 Prepared by Coby Harmon University of California, Santa Barbara 11 Depreciation, Impairments, and Depletion Intermediate Accounting 14th Edition 11-2 Kieso, Weygandt, and Warfield

CHAPTER 10 Capital Assets

CHAPTER 10 Capital Assets ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Exercises Problems Set A Problems Set B 1. Distinguish between tangible and intangible capital assets.

CHAPTER 10 Capital Assets ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Exercises Problems Set A Problems Set B 1. Distinguish between tangible and intangible capital assets.

IFRS 16 LEASES. Page 1 of 21

IFRS 16 LEASES OBJECTIVE The objective is to ensure that lessees and lessors provide relevant information in a manner that faithfully represents those transactions. This information gives a basis for users

IFRS 16 LEASES OBJECTIVE The objective is to ensure that lessees and lessors provide relevant information in a manner that faithfully represents those transactions. This information gives a basis for users

University of Nizwa / Dept. of Architecture / ARCH 506: Building Specification & Estimation / VALUATION / Ravishankar. KR / 5, January 2011.

Property Valuation Building Estimation and Costing Building Estimation and Costing Building Estimation and Costing is a vital part of Civil Engineering. No project can begin without the total Building

Property Valuation Building Estimation and Costing Building Estimation and Costing Building Estimation and Costing is a vital part of Civil Engineering. No project can begin without the total Building

Taxes and Land Preservation Computing the Capital Gains Tax

Fact Sheet 780 Taxes and Land Preservation Computing the Capital Gains Tax Many farmers have their wealth tied up in their land and would like to convert some of this land value into cash. Others want

Fact Sheet 780 Taxes and Land Preservation Computing the Capital Gains Tax Many farmers have their wealth tied up in their land and would like to convert some of this land value into cash. Others want

CONSOLIDATED STATEMENT OF INCOME

CONSOLIDATED STATEMENT OF INCOME (unaudited, data converted from the Euro to the US Dollar (for information concerning this restatement, see Note 11 to these Consolidated Financial Statements)) 1 st quarter

CONSOLIDATED STATEMENT OF INCOME (unaudited, data converted from the Euro to the US Dollar (for information concerning this restatement, see Note 11 to these Consolidated Financial Statements)) 1 st quarter

[03.01] User Cost Method. International Comparison Program. Global Office. 2 nd Regional Coordinators Meeting. April 14-16, 2010.

![[03.01] User Cost Method. International Comparison Program. Global Office. 2 nd Regional Coordinators Meeting. April 14-16, 2010.](/thumbs/89/100772946.jpg "[03.01] User Cost Method. International Comparison Program. Global Office. 2 nd Regional Coordinators Meeting. April 14-16, 2010.") Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized International Comparison Program [03.01] User Cost Method Global Office 2 nd Regional

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized International Comparison Program [03.01] User Cost Method Global Office 2 nd Regional