CHAPTER 7. Depreciation And Income Taxes. Created By : Eng.Maysa Gharaybeh

|

|

|

- Ruth Jessica Owens

- 6 years ago

- Views:

Transcription

1 CHAPTER 7 Depreciation And Income Taxes Created By : Eng.Maysa Gharaybeh

2 Depreciation Decrease in value of physical properties with passage of time and use. More specifically: Accounting concept establishing annual deduction against before-tax income to reflect effect of time and use on asset s value in firm s financial statements to match yearly fraction of value used by asset in production of income over asset s economic life

3 Property Is Depreciable if it Meets These Requirements : be used in business or held to produce income. have a determinable useful life which is longer than one year wear out, decay, get used up, become obsolete, or lose value from natural causes not be inventory, stock in trade, or investment property

4 Depreciable Property (Tangible, Intangible ) Tangible : can be seen or touched personal المنقولة) property (االموال : includes assets such as machinery, vehicles, equipment, furniture, etc... real غير المنقولة) property (االموال : anything erected on, growing on, or attached to land (Since land does not have a determinable life itself, it is not depreciable) براءات patent( Intangible : personal property, such as copyright, (إعفاء معين,امتياز) franchise or (االختراع

5 When Depreciation Starts And Stops Depreciation starts when property is placed in service for use in business or for production of income. Property is considered in service when ready and available for specific use, even if not actually used yet. Depreciation stops when cost of placing it in service has been recovered or when it is soled, whichever occurs first.

to original cost basis, used to calculate depreciation deductions Improvement of the asset increases the original cost basis Casualty or theft loss")

6 Additional Definitions Basis, or cost basis : (unadjusted cost ) initial cost of purchase an asset, plus sales tax, transportation, and normal costs of making asset serviceable Adjusted cost basis : allowable adjustment (increase or decrease) to original cost basis, used to calculate depreciation deductions Improvement of the asset increases the original cost basis Casualty or theft loss decrease the original cost basis

k = k adjusted cost basis - Σ (depreciation")

7 Additional Definitions Book Value (BV) : Worth of depreciable property as shown on company records Represents amount of capital remaining invested in property and must be recovered in future through accounting process (Book Value) k = k adjusted cost basis - Σ (depreciation deduction) j j=1

8 Additional Definitions Market Value (MV) : Amount paid by willing buyer to willing seller for property where no advantage and no compulsion to transact approximates present value of what will be received through ownership of property, including time-value of money (or profit)

under MACRS Class Life for Alternative Depreciation System (ADS) Recovery Rate :Percentage for each")

9 Additional Definitions Recovery Period :Number of years over which basis of property is recovered through accounting process. Normally the useful life for classical methods Property class for General Depreciation System (GDS) under MACRS Class Life for Alternative Depreciation System (ADS) Recovery Rate :Percentage for each year of MACRS recovery period used to calculate an annual depreciation deduction.

10 Additional Definitions Salvage Value (SV) : Estimated value of property at the end of useful life. expected selling price of property when asset can no longer be used productively net salvage value used when expenses incurred in disposing of property; cash outflows must be deducted from cash inflows for final net salvage value with classical methods of depreciation, estimated salvage value is established and used with MACRS, the salvage value of depreciable property is defined to be zero

11 Additional Definitions Useful Life : Expected (estimated) period of time property will be used in trade or business or to produce income; sometimes referred to as depreciable life.

12 The Classical Depreciation Methods N = depreciable life of the asset in years B = cost basis, including allowable adjustments d k = annual depreciation deduction in year k (1< k <N) d k* = cumulative depreciation through year k BV k = book value at the end of year k BV N = book value at the end of the depreciable (useful) life SV N = salvage value at the end of year N R = the ratio of depreciation in any one year to the BV at the beginning of the year

13 Straight-Line (SL) Method Simplest depreciation method Assumes constant amount is depreciated each year over depreciable (useful) life N = depreciable life B = cost basis d k = depreciaton in k BV k = book value at end of k SV N = salvage value

14

15 Declining Balance (DB) Method Sometimes called constant percentage method or Matheson formula Assumed annual cost of depreciation is fixed percentage of BV at beginning of year R is constant R = 2 / N when 200% declining balance OR R = 1.5 / N when 150% declining balance used d 1 = B ( R ) d k = B ( 1 - R ) k - 1 ( R ) d k* = B [ 1 - (1 - R ) k ] BV k = B ( 1 - R ) k BV N = B ( 1 - R ) N Because declining balance method never reaches BV = 0, it s permissible to switch from this to straight-line method so asset s SV N will be zero or other desired value

16

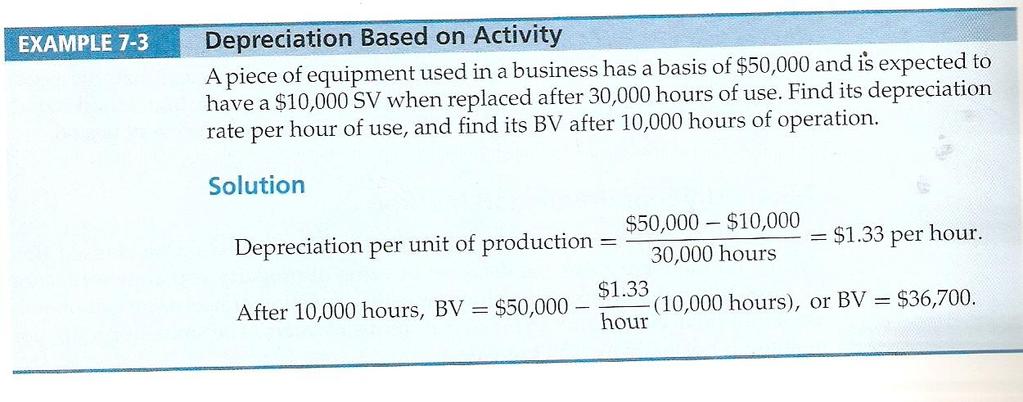

17 Units-of-Production Method Not based on the idea that decrease in value of property is a function of time Decrease in value is mostly a function of use Method results in cost basis (minus final SV) being allocated equally over the estimated number of units produced during useful life of asset. Depreciation per unit of production =

18

19 DB with Switchover to SL DB method will NEVER reach BV =0 You can switch from DB to SL The switch over occurs in the year in which a larger depreciation amount is obtained from SL method

20

1 4,000/10 years =400 2 3,200/9 year = 355.")

21 Table 7-1 page 328 d k = ( B - SVN ) / N But the basis B from Col(1)Changed every year and N is the remaining years As followes : Year (3) 1 4,000/10 years = ,200/9 year = ,560/8years = 320 And so on We select the largest depreciation amount.

22 Taxable Income (Before Taxable Income) taxable income = gross income - all expenses - depreciation

23 The disposal of a depreciable asset can result in a gain or loss based on the sale price (market value) and the current book value A gain is often referred to as depreciation recapture, and it is generally taxed as the same as ordinary income. A loss is a capital loss. An asset sold for more than it s cost basis results in a capital gain.

24 After Tax Economic Analysis

25 R k = revenues (and savings from the project: cash inflow from project during period k E k = cash outflows during year k for deductible expenses and interest d k = depreciation t = effective income tax rate on ordinary income (federal, state and other); assumed to remain constant during the study period T k = income taxes paid during year k BTCF k = Before Tax Cash Flow for year k ATCF k = After Tax Cash Flow for year k

26 The taxable income = ( R k E k - d k ) The income tax: T k = - t ( R k E k d k ) BTCF k = R k E k ATCF k = BTCF k + T k = (R k E k ) - t ( R k E k d k ) = (1 t)(r k E k ) + t d k

27 Example: An asset is expected to produce a net cash inflows of 70,000 per year for the six year period, where the cost basis is 260,000 and the market value is 20,000. MARR is 10% use SL method.. A) develop BTCF B)develop ATCF C) Calculate the PW for both CFs

28 BTCF 0-260, , , , , , , ,000 PW= -260, ,000 (P/A,10%,6)+ 20,000(P/F,10%,6) = -260, ,000(4.3553) +20,000 (0.5645)=56,161 PW >0 it is acceptable alternative SL = (260,000-20,000)/6 = 40,000 per year

29 ATCF EOY A BTCF B Depreciation Deduction C=A B Taxable Income D= - 0.4C Income Tax E= A+D ATCF 0-260, , ,000 40,000 30,000-12,000 58, ,000 40,000 30,000-12,000 58, ,000 40,000 30,000-12,000 58, ,000 40,000 30,000-12,000 58, ,000 40,000 30,000-12,000 58, ,000 40,000 30,000-12,000 58,000 6(market value) 20,000 20,000 20,000 PW= -260, ,000 (P/A,10%,6)+ 20,000(P/F,10%,6) = -260, ,000(4.3553) +20,000 (0.5645)= 3,897.4 PW >0 it is acceptable alternative

Chapter 7: Decpreciation and Income Taxes

Chapter 7: Decpreciation and Income Taxes Tsui-Ping Chung 1 The goal The objective of Chapter 7 is to explain how depreciation affects income taxes, and how income taxes affect economic decision making.

Chapter 7: Decpreciation and Income Taxes Tsui-Ping Chung 1 The goal The objective of Chapter 7 is to explain how depreciation affects income taxes, and how income taxes affect economic decision making.

Lecture 8 (Part 1) Depreciation

Depreciation") Seg2510 Management Principles for Engineering Managers Lecture 8 (Part 1) Depreciation Department of Systems Engineering and Engineering Management The Chinese University of Hong Kong 1 Depreciation Depreciation

Seg2510 Management Principles for Engineering Managers Lecture 8 (Part 1) Depreciation Department of Systems Engineering and Engineering Management The Chinese University of Hong Kong 1 Depreciation Depreciation

Chapter 11 Depreciation. Depreciations: Straight Line Sum of Years Digits Declining Balance

Chapter 11 Depreciation Depreciations: Straight Line Sum of Years Digits Declining Balance 1 Depreciation is important because it affects the taxes that firms pay. The taxable income is (Income expenses).

Chapter 11 Depreciation Depreciations: Straight Line Sum of Years Digits Declining Balance 1 Depreciation is important because it affects the taxes that firms pay. The taxable income is (Income expenses).

The cost of this asset includes the purchase price, plus any taxes, commissions, and other amounts paid to make the asset ready for use.

Accounting Fundamentals Lesson 7 7.0 Long-Term Assets Plant Assets, are long-lived assets that are tangible. The cost of this asset includes the purchase price, plus any taxes, commissions, and other amounts

Accounting Fundamentals Lesson 7 7.0 Long-Term Assets Plant Assets, are long-lived assets that are tangible. The cost of this asset includes the purchase price, plus any taxes, commissions, and other amounts

You may have to use Form 4562 to figure and report your depreciation. See Which Forms To Use in chapter 3. Also see Publication 946.

1 of 10 11/29/2011 2:27 AM 2. Depreciation of Rental Property Table of Contents The Basics What Rental Property Can Be Depreciated? When Does Depreciation Begin and End? Depreciation Methods Basis of Depreciable

1 of 10 11/29/2011 2:27 AM 2. Depreciation of Rental Property Table of Contents The Basics What Rental Property Can Be Depreciated? When Does Depreciation Begin and End? Depreciation Methods Basis of Depreciable

Lecture 8 (Part 2) Depreciation

Depreciation") Seg2510 Management Principles for Engineering Managers Lecture 8 (Part 2) Depreciation Department of Systems Engineering and Engineering Management The Chinese University of Hong Kong 1 Part I Review of

Seg2510 Management Principles for Engineering Managers Lecture 8 (Part 2) Depreciation Department of Systems Engineering and Engineering Management The Chinese University of Hong Kong 1 Part I Review of

Chapter 9: Long-Lived Assets and Cost Allocation

1 Chapter 9: Long-Lived Assets and Cost Allocation 2 Capitalize vs Expense Revenue Expenditures Merely maintain a given level of services Should be Expensed Debit Expense Capital Expenditures Provide future

1 Chapter 9: Long-Lived Assets and Cost Allocation 2 Capitalize vs Expense Revenue Expenditures Merely maintain a given level of services Should be Expensed Debit Expense Capital Expenditures Provide future

5. The cost of buildings includes all necessary costs related to the purchase or construction

CHAPTER REVIEW Plant Assets 1. (S.O. 1) Plant assets are tangible resources that are used in the operations of a business and are not intended for sale to customers. Plant assets are subdivided into four

CHAPTER REVIEW Plant Assets 1. (S.O. 1) Plant assets are tangible resources that are used in the operations of a business and are not intended for sale to customers. Plant assets are subdivided into four

Week11, Chap 8 Accounting 1A, Financial Accounting

Week11, Chap 8 Accounting 1A, Financial Accounting Reporting and Interpreting Property, Plant, and Equipment;Natural Resources; and Intangibles Instructor: Michael Booth Understanding The Business Insufficient

Week11, Chap 8 Accounting 1A, Financial Accounting Reporting and Interpreting Property, Plant, and Equipment;Natural Resources; and Intangibles Instructor: Michael Booth Understanding The Business Insufficient

Accounting for Plant Assets and Depreciation

Ch16 Accounting for Plant Assets and Depreciation 1 Understanding PPE Acquisition of PPE (cost) Depreciation of PPE Revenue expenditure vs. capital expenditure Disposition of PPE (sale, trade, and discard)

Ch16 Accounting for Plant Assets and Depreciation 1 Understanding PPE Acquisition of PPE (cost) Depreciation of PPE Revenue expenditure vs. capital expenditure Disposition of PPE (sale, trade, and discard)

Sales Associate Course

Sales Associate Course Chapter Seventeen Real Estate Investments and Business Opportunity Brokerage 1 Investment Analysis Most important consideration: Economic soundness Land use controls Zoning Deed

Sales Associate Course Chapter Seventeen Real Estate Investments and Business Opportunity Brokerage 1 Investment Analysis Most important consideration: Economic soundness Land use controls Zoning Deed

Before Class starts.(make sure your name is on all submissions)

") Before Class starts.(make sure your name is on all submissions) March 27 exam conflicts must be resolved before Spring break. Fourth Homework due Thursday 3/6 before class. Fifth Homework due 3/20 before

Before Class starts.(make sure your name is on all submissions) March 27 exam conflicts must be resolved before Spring break. Fourth Homework due Thursday 3/6 before class. Fifth Homework due 3/20 before

How To Depreciate Property

Department of the Treasury Internal Revenue Service Publication 946 Cat. No. 13081F How To Depreciate Property Section 179 Deduction MACRS Listed Property For use in preparing 1999 Returns Contents Introduction...

Department of the Treasury Internal Revenue Service Publication 946 Cat. No. 13081F How To Depreciate Property Section 179 Deduction MACRS Listed Property For use in preparing 1999 Returns Contents Introduction...

Copyright 2009 The Learning House, Inc. Fixed and Intangible Assets Page 1 of 13

Copyright 2009 The Learning House, Inc. Fixed and Intangible Assets Page 1 of 13 Introduction This lesson focuses on the long-term assets used to operate a company. These assets can be grouped into fixed

Copyright 2009 The Learning House, Inc. Fixed and Intangible Assets Page 1 of 13 Introduction This lesson focuses on the long-term assets used to operate a company. These assets can be grouped into fixed

Chapter 11 Investments in Noncurrent Operating Assets Utilization and Retirement

Chapter 11 Investments in Noncurrent Operating Assets Utilization and Retirement 1. The annual depreciation expense 2. The depletion of natural resources 3. The changes in estimates and methods in the

Chapter 11 Investments in Noncurrent Operating Assets Utilization and Retirement 1. The annual depreciation expense 2. The depletion of natural resources 3. The changes in estimates and methods in the

Before Class starts.(make sure your name is on all submissions)

") Before Class starts.(make sure your name is on all submissions) Fourth Homework due 10/27(MW) or 10/28(TR) before class. No exceptions. Help session 10/26 1:00-3:30pm in GBS130 Fifth Homework due 11/3(MW)

Before Class starts.(make sure your name is on all submissions) Fourth Homework due 10/27(MW) or 10/28(TR) before class. No exceptions. Help session 10/26 1:00-3:30pm in GBS130 Fifth Homework due 11/3(MW)

Plant design and economics (8)

") Plant design and economics (8) Zahra Maghsoud ٢ DEPRECIATION (Ch. 9 Peters and Timmerhaus ) The reduction in value due to physical deterioration, technological advances, economic changes, or other factors

Plant design and economics (8) Zahra Maghsoud ٢ DEPRECIATION (Ch. 9 Peters and Timmerhaus ) The reduction in value due to physical deterioration, technological advances, economic changes, or other factors

Chapter 08 - Long-Term Assets. Chapter Outline

Section 1 Plant Assets I. Cost Determination Plant assets are tangible assets used in a company's operations that have a useful life of more than one accounting period. Consistent with cost principle,

Section 1 Plant Assets I. Cost Determination Plant assets are tangible assets used in a company's operations that have a useful life of more than one accounting period. Consistent with cost principle,

Long-lived, Revenue-producing Assets. Expected to Benefit Future Periods

Section 8 - Property, Plant, Equipment (Fixed Assets), and Depletable Resources Types of Assets Long-lived, Revenue-producing Assets 10-1 Expected to Benefit Future Periods Tangible Property, Plant, Equipment

Section 8 - Property, Plant, Equipment (Fixed Assets), and Depletable Resources Types of Assets Long-lived, Revenue-producing Assets 10-1 Expected to Benefit Future Periods Tangible Property, Plant, Equipment

ILLUSTRATION 11-1 PATTERNS OF BOOK VALUE OVER LIFE OF ASSET

ILLUSTRATION 11-1 PATTERNS OF BOOK VALUE OVER LIFE OF ASSET $ Cost of asset N PR: Book value activity methods Depreciable cost SL: Book value straight line Salvage value AC: Book value accelerated S E

ILLUSTRATION 11-1 PATTERNS OF BOOK VALUE OVER LIFE OF ASSET $ Cost of asset N PR: Book value activity methods Depreciable cost SL: Book value straight line Salvage value AC: Book value accelerated S E

Prepared by: Alex Socratous For My High School Students

Prepared by: Alex Socratous For My High School Students CHAPTER 2 CAPITAL ASSETS DEPRECIATION CAPITAL ASSETS Capital assets are long-lived assets that are used in the operations of a business and are not

Prepared by: Alex Socratous For My High School Students CHAPTER 2 CAPITAL ASSETS DEPRECIATION CAPITAL ASSETS Capital assets are long-lived assets that are used in the operations of a business and are not

4/10/2012. Long-Lived Assets and Depreciation. Overview of Long-lived Assets. Learning Objectives (LO) Learning Objectives (LO)

Learning Objectives (LO)") Learning Objectives (LO) CHAPTER Long-Lived Assets and Depreciation 8 After studying this chapter, you should be able to 1. Distinguish a company s expenses from expenditures that it should capitalize

Learning Objectives (LO) CHAPTER Long-Lived Assets and Depreciation 8 After studying this chapter, you should be able to 1. Distinguish a company s expenses from expenditures that it should capitalize

ACCOUNTING - CLUTCH CH. 8 - LONG LIVED ASSETS.

!! www.clutchprep.com CONCEPT: INITIAL COST OF LONG-LIVED (PLANT) ASSETS Plant Assets include,,, and RULE: Initial cost includes the price plus all expenditures to make an asset When recording the initial

!! www.clutchprep.com CONCEPT: INITIAL COST OF LONG-LIVED (PLANT) ASSETS Plant Assets include,,, and RULE: Initial cost includes the price plus all expenditures to make an asset When recording the initial

STUDY OBJECTIVE 1 CAPITAL ASSETS

Collaboratively Created Collection of Chapter 10 Content STUDY OBJECTIVE 1 CAPITAL ASSETS Capital Assets are used throughout many cycles of a business and are reused over and over again. These assets are

Collaboratively Created Collection of Chapter 10 Content STUDY OBJECTIVE 1 CAPITAL ASSETS Capital Assets are used throughout many cycles of a business and are reused over and over again. These assets are

Before Class starts.(make sure your name is on all submissions)

") Before Class starts.(make sure your name is on all submissions) March 27 exam conflicts must be resolved before Spring break. Your papers Fourth Homework due Today 3/6 before class. Fifth Homework due

Before Class starts.(make sure your name is on all submissions) March 27 exam conflicts must be resolved before Spring break. Your papers Fourth Homework due Today 3/6 before class. Fifth Homework due

Chapter 9 - REPORTING AND ANALYZING LONG-LIVED ASSETS

Revised Summer 2018 Chapter 9 Review 1 Chapter 9 - REPORTING AND ANALYZING LONG-LIVED ASSETS LO 1: Explain the accounting for plant asset expenditures. Plant Assets (Also known as Property, Plant, and

Revised Summer 2018 Chapter 9 Review 1 Chapter 9 - REPORTING AND ANALYZING LONG-LIVED ASSETS LO 1: Explain the accounting for plant asset expenditures. Plant Assets (Also known as Property, Plant, and

Agenda cont. Claiming the special depreciation allowance Figuring depreciation under MACRS Additional rules for listed property Basis of assets

Depreciation Basics Agenda What property can and cannot be depreciated When depreciation begins and ends Methods for depreciating property Basis of depreciable property How to treat repairs and improvements

Depreciation Basics Agenda What property can and cannot be depreciated When depreciation begins and ends Methods for depreciating property Basis of depreciable property How to treat repairs and improvements

The Cost Principle. Plant Assets. Intangible Assets. Natural Resources. Depreciation. Amortization. Depletion. Chapter 9

Plant Assets Natural Resources Intangible Assets Depreciation Depletion Amortization Chapter 9 2 Held for use in business Full cost includes several expenditures Last several years Can be sold or traded

Plant Assets Natural Resources Intangible Assets Depreciation Depletion Amortization Chapter 9 2 Held for use in business Full cost includes several expenditures Last several years Can be sold or traded

Plant assets are resources that have

10-1 LEARNING OBJECTIVE 1 Explain the accounting for plant asset expenditures. Plant assets are resources that have physical substance (a definite size and shape), are used in the operations of a business,

10-1 LEARNING OBJECTIVE 1 Explain the accounting for plant asset expenditures. Plant assets are resources that have physical substance (a definite size and shape), are used in the operations of a business,

CAS -16 COST ACCOUNTING STANDARD ON DEPRECIATION AND AMORTISATION

Cost Accounting Standards Board CAS -16 COST ACCOUNTING STANDARD ON DEPRECIATION AND AMORTISATION The following is the COST ACCOUNTING STANDARD 16 (CAS 16) issued by the Council of The Institute of Cost

Cost Accounting Standards Board CAS -16 COST ACCOUNTING STANDARD ON DEPRECIATION AND AMORTISATION The following is the COST ACCOUNTING STANDARD 16 (CAS 16) issued by the Council of The Institute of Cost

CHAPTER 6 - Accounting for Long-Term Operational Assets

CHAPTER 6 - Accounting for Long-Term Operational Assets ANSWERS TO QUESTIONS 1. Long-term operational assets are those assets that are used by a business to generate revenue. In contrast, investments are

CHAPTER 6 - Accounting for Long-Term Operational Assets ANSWERS TO QUESTIONS 1. Long-term operational assets are those assets that are used by a business to generate revenue. In contrast, investments are

Accounting for tangible fixed Assets

Accounting for tangible fixed Assets Fixed assets are used (not consumed) in operations of a business provide benefits beyond the current accounting period Fixed assets are either acquired or self constructed

Accounting for tangible fixed Assets Fixed assets are used (not consumed) in operations of a business provide benefits beyond the current accounting period Fixed assets are either acquired or self constructed

SOLUTIONS. Learning Goal 28

S1 Learning Goal 28 Multiple Choice 1. b 2. a 3. c 4. b However, the double-declining-balance method calculates the depreciation expense on the full asset cost until the final year of use. 5. d Total appraised

S1 Learning Goal 28 Multiple Choice 1. b 2. a 3. c 4. b However, the double-declining-balance method calculates the depreciation expense on the full asset cost until the final year of use. 5. d Total appraised

What is the depreciation for year three (3) using the Sum-of-Years Digits method? (4, all or nothing)

using the Sum-of-Years Digits method? (4, all or nothing)") Carefully read each problem before answering. Please write clearly, and show and label all formulas and/or factors used in any problem requiring mathematical calculations. 1. Based on your knowledge of

Carefully read each problem before answering. Please write clearly, and show and label all formulas and/or factors used in any problem requiring mathematical calculations. 1. Based on your knowledge of

Chapter 8. Accounting for Long-Term Assets

Chapter 8 Accounting for Long-Term Assets C 1 Plant Assets Tangible in Nature Actively Used in Operations Expected to Benefit Future Periods Called Property, Plant, & Equipment 8-2 C 1 Plant Assets Decline

Chapter 8 Accounting for Long-Term Assets C 1 Plant Assets Tangible in Nature Actively Used in Operations Expected to Benefit Future Periods Called Property, Plant, & Equipment 8-2 C 1 Plant Assets Decline

SOLUTIONS Learning Goal 19

S1 Learning Goal 19 Multiple Choice 1. b 2. a 3. c 4. b However, the double-declining-balance method calculates the depreciation expense on the full asset cost until the final year of use. 5. d Total appraised

S1 Learning Goal 19 Multiple Choice 1. b 2. a 3. c 4. b However, the double-declining-balance method calculates the depreciation expense on the full asset cost until the final year of use. 5. d Total appraised

Financial Accounting. John J. Wild. Sixth Edition. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 08 Reporting and Analyzing Long-Term Assets Conceptual Learning

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 08 Reporting and Analyzing Long-Term Assets Conceptual Learning

John Smith Attachment to Form Statement 1

John Smith 123-45-6789 Attachment to Form 3115 Part II, Line 12a, Description of Items Being Changed Statement 1 The taxpayer is proposing to change the method of depreciation for assets used in JS Construction

John Smith 123-45-6789 Attachment to Form 3115 Part II, Line 12a, Description of Items Being Changed Statement 1 The taxpayer is proposing to change the method of depreciation for assets used in JS Construction

The Cost of Property, Plant, Equipment

1 The Cost of Property, Plant, Equipment The cost of property, plant, and equipment includes the purchase price of the asset and all expenditures necessary to prepare the asset for its intended use. Land.

1 The Cost of Property, Plant, Equipment The cost of property, plant, and equipment includes the purchase price of the asset and all expenditures necessary to prepare the asset for its intended use. Land.

State of Mexicali Ad Valorem Taxation of Property Statutes, Rules and Regulations

STATUTES CODE OF MEXICALI OF 2000, TITLE 50 REVENUE AND TAXATION, CHAPTER 7 AD VALOREM TAXATION OF PROPERTY Sec. 50-7-1. Legislative intent The intent and purpose of the tax laws of this state are to have

STATUTES CODE OF MEXICALI OF 2000, TITLE 50 REVENUE AND TAXATION, CHAPTER 7 AD VALOREM TAXATION OF PROPERTY Sec. 50-7-1. Legislative intent The intent and purpose of the tax laws of this state are to have

CHAPTER 9. Plant Assets, Natural Resources, and Intangible Assets 6, 7, 8, 24, 25, 26 3, 4, 5, 6, 7 11, , 17, 18, 19, 20, 21, 22

CHAPTER 9 Plant Assets, Natural Resources, and Intangible Assets ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems 1. Describe how the cost

CHAPTER 9 Plant Assets, Natural Resources, and Intangible Assets ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems 1. Describe how the cost

FACT SHEET. Depreciation of Farm Drainage Tile. Agriculture and Natural Resources OAM-1-12

FACT SHEET Agriculture and Natural Resources OAM-1-12 Depreciation of Farm Drainage Tile Wm. Bruce Clevenger OSU Extension Educator and Assistant Professor Introduction Agriculture is one of Ohio s largest

FACT SHEET Agriculture and Natural Resources OAM-1-12 Depreciation of Farm Drainage Tile Wm. Bruce Clevenger OSU Extension Educator and Assistant Professor Introduction Agriculture is one of Ohio s largest

Chapter 10 Capital Assets Solutions. (g) NA (current asset) (h) NR (i) NA (inventory) (j) I (k) I (l) NA (investment) (m) NR (n) NR (o) NR (p) I

NA (current asset) (h) NR (i) NA (inventory) (j) I (k) I (l) NA (investment) (m) NR (n) NR (o) NR (p) I") Chapter 10 Capital Assets Solutions Assigned Questions: Study Objective Textbook Pages to Read 9 p. 481-486 19 14-10 Solutions: Q1. Tangible and intangible capital assets both are long-lived assets that

Chapter 10 Capital Assets Solutions Assigned Questions: Study Objective Textbook Pages to Read 9 p. 481-486 19 14-10 Solutions: Q1. Tangible and intangible capital assets both are long-lived assets that

March 23, 2006 Anderson ECON 136A 11am Class FINAL EXAM v. 1 Name

March 23, 2006 Anderson ECON 136A 11am Class FINAL EXAM v. 1 Name YOU MUST WRITE YOUR NAME ON THIS EXAM AND TURN IT IN WITH YOUR SCANTRON AND BLUE-BOOK! Complete questions #1-25 on your scantron AND WRITE

March 23, 2006 Anderson ECON 136A 11am Class FINAL EXAM v. 1 Name YOU MUST WRITE YOUR NAME ON THIS EXAM AND TURN IT IN WITH YOUR SCANTRON AND BLUE-BOOK! Complete questions #1-25 on your scantron AND WRITE

Accounting 1 Instructor Notes

Accounting 1 Instructor Notes CHAPTER 10 FIXED ASSETS AND INTANGIBLE ASSETS McDonald's was founded in 1955 and the company now has 22,500 restaurants in 122 countries around the world. Approximately 70

Accounting 1 Instructor Notes CHAPTER 10 FIXED ASSETS AND INTANGIBLE ASSETS McDonald's was founded in 1955 and the company now has 22,500 restaurants in 122 countries around the world. Approximately 70

Supplemental Instruction Handouts Financial Accounting Chapter 9: Property, Plant and Equipment and Intangibles Answer Key

Supplemental Instruction Handouts Financial Accounting Chapter 9: Property, Plant and Equipment and Intangibles Answer Key 1. A) Prepare a calculation to show the cost of this machine. $23,500 x 0.02 =

Supplemental Instruction Handouts Financial Accounting Chapter 9: Property, Plant and Equipment and Intangibles Answer Key 1. A) Prepare a calculation to show the cost of this machine. $23,500 x 0.02 =

A 1: It( SPECIFIC ITEMS SECTION 3061 property, plant and equipment. Additional Resources. Page 1 of6. Knotia - CICA Handbook - Accounting A2-14

'" Knotia - CICA Handbook - Accounting»Accounting»Accounting Handbook»Accounting Standards»Specific items [Sections 3000-3870]»3061 - Property, Plant and Eauipment Page 1 of6 A 1: It( A2-14 SPECIFIC ITEMS

'" Knotia - CICA Handbook - Accounting»Accounting»Accounting Handbook»Accounting Standards»Specific items [Sections 3000-3870]»3061 - Property, Plant and Eauipment Page 1 of6 A 1: It( A2-14 SPECIFIC ITEMS

Chapter 10: Fixed Assets and Intangible Assets

Chapter 10: Fixed Assets and Intangible Assets Nature of Fixed Assets Fixed assets are long-term or relatively permanent assets, such as equipment, machinery, buildings, and land. Other descriptive titles

Chapter 10: Fixed Assets and Intangible Assets Nature of Fixed Assets Fixed assets are long-term or relatively permanent assets, such as equipment, machinery, buildings, and land. Other descriptive titles

Long-Term Assets C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM

Long-Term Assets E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information, in addition to the material

Long-Term Assets E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information, in addition to the material

Installment Sales. Installment Method under Section 453 Allows for a gain on sale as well as the accompanying tax liability to be deferred

1 Installment Sales 2 Ordinarily recognize gain or loss when property is sold under section 1001 Amount realized less adjusted basis Typically, the entire amount of the sale or exchange will be recognized

1 Installment Sales 2 Ordinarily recognize gain or loss when property is sold under section 1001 Amount realized less adjusted basis Typically, the entire amount of the sale or exchange will be recognized

Acquisition cost Purchase price plus all expenditures needed to prepare the asset for its intended use

CAPITAL ASSETS Issues to consider: Compute initial acquisition cost Account for subsequent costs Allocate cost to periods benefited Record disposal Acquisition cost Purchase price plus all expenditures

CAPITAL ASSETS Issues to consider: Compute initial acquisition cost Account for subsequent costs Allocate cost to periods benefited Record disposal Acquisition cost Purchase price plus all expenditures

Leases. (a) the lease transfers ownership of the asset to the lessee by the end of the lease term.

the lease transfers ownership of the asset to the lessee by the end of the lease term.") Leases 1.1. Classification of leases A lease is classified as a finance lease if it transfers substantially all the risks and rewards incidental to ownership. A lease is classified as an operating lease

Leases 1.1. Classification of leases A lease is classified as a finance lease if it transfers substantially all the risks and rewards incidental to ownership. A lease is classified as an operating lease

VALUATION OF GOODWILL FOR TAX PURPOSES

1 VALUATION OF GOODWILL FOR TAX PURPOSES James P. Catty President, Corporate Valuation Services Limited Chair, International Association of Consultants, Valuators and Analysts 2 All businesses have these

1 VALUATION OF GOODWILL FOR TAX PURPOSES James P. Catty President, Corporate Valuation Services Limited Chair, International Association of Consultants, Valuators and Analysts 2 All businesses have these

Cost Segregation Instructor Teaching Schedule (3-Hour)

") Time Topic Pages Student Objectives 8:30-8:35 Course introduction Page 2 What is cost segregation? Objective of cost segregation: to increase cash flow Benefit of cost segregation Learning objectives Page

Time Topic Pages Student Objectives 8:30-8:35 Course introduction Page 2 What is cost segregation? Objective of cost segregation: to increase cash flow Benefit of cost segregation Learning objectives Page

1. Like financial accounting, most business property must be capitalized for tax purposes.

Chapter 02 Property Acquisition and Cost Recovery True / False Questions 1. Like financial accounting, most business property must be capitalized for tax purposes. True False 2. Tax cost recovery methods

Chapter 02 Property Acquisition and Cost Recovery True / False Questions 1. Like financial accounting, most business property must be capitalized for tax purposes. True False 2. Tax cost recovery methods

1. Like financial accounting, most business property must be capitalized for tax purposes.

Chapter 02 Property Acquisition and Cost Recovery True / False Questions 1. Like financial accounting, most business property must be capitalized for tax purposes. True False 2. Tax cost recovery methods

Chapter 02 Property Acquisition and Cost Recovery True / False Questions 1. Like financial accounting, most business property must be capitalized for tax purposes. True False 2. Tax cost recovery methods

Depreciation. Dr. M. S. Memon. Mehran UET, Jamshoro, Pakistan. Department of Industrial Engineering and Management

Depreciation Dr. M. S. Memon Department of Industrial Engineering and Management Mehran UET, Jamshoro, Pakistan https://msmemon.wordpress.com/scmlab/ Introduction Any equipment which is purchased today

Depreciation Dr. M. S. Memon Department of Industrial Engineering and Management Mehran UET, Jamshoro, Pakistan https://msmemon.wordpress.com/scmlab/ Introduction Any equipment which is purchased today

Chapter 02 Property Acquisition and Cost Recovery

Chapter 02 Property Acquisition and Cost Recovery True / False Questions 1. Like financial accounting, most business property must be capitalized for tax purposes. True False 2. Tax cost recovery methods

Chapter 02 Property Acquisition and Cost Recovery True / False Questions 1. Like financial accounting, most business property must be capitalized for tax purposes. True False 2. Tax cost recovery methods

CHAPTER 9 LONG-LIVED ASSETS SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY

CHAPTER 9 LONG-LIVED ASSETS SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 K 17. 2 K 33. 2 C 49. 3 K 65.

CHAPTER 9 LONG-LIVED ASSETS SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 K 17. 2 K 33. 2 C 49. 3 K 65.

Paper 1: Accounting. Accounting Standards. Contents: AS 6 AS 10 As 9. CA Shruthi BN

Paper 1: Accounting Accounting Standards Contents: CA Shruthi BN AS 6 AS 10 As 9 AS 6 Depreciation Accounting DEPRECIATION Meaning 2 It is a measure of wearing out, consumption or other loss of value of

Paper 1: Accounting Accounting Standards Contents: CA Shruthi BN AS 6 AS 10 As 9 AS 6 Depreciation Accounting DEPRECIATION Meaning 2 It is a measure of wearing out, consumption or other loss of value of

Louisiana Bankers Association CFO Conference. Baton Rouge Renaissance Hotel. Benny Jeansonne, CPA Partner Silas Simmons, LLP.

Louisiana Bankers Association CFO Conference May 21,2015 Baton Rouge Renaissance Hotel Benny Jeansonne, CPA Partner Silas Simmons, LLP Agenda Depreciation I. Current Law II. Cost Segregation III. Code

Louisiana Bankers Association CFO Conference May 21,2015 Baton Rouge Renaissance Hotel Benny Jeansonne, CPA Partner Silas Simmons, LLP Agenda Depreciation I. Current Law II. Cost Segregation III. Code

Reporting and Analyzing Long-Term Operating Assets. Learning Objectives coverage by question 12, 13, 16, 18

Chapter 8 Reporting and Analyzing Long-Term Operating Assets Learning Objectives coverage by question Miniexercises Exercises Problems Cases LO1 Describe and distinguish between tangible and intangible

Chapter 8 Reporting and Analyzing Long-Term Operating Assets Learning Objectives coverage by question Miniexercises Exercises Problems Cases LO1 Describe and distinguish between tangible and intangible

Principles of Accounting II Chapter 21: Record and Communicate Operational Investments

Principles of Accounting II Chapter 21: Record and Communicate Operational Investments Multiple Asset Purchases Allocate total purchase price among assets based on relative. Suppose you buy a building

Principles of Accounting II Chapter 21: Record and Communicate Operational Investments Multiple Asset Purchases Allocate total purchase price among assets based on relative. Suppose you buy a building

Intangibles CHAPTER CHAPTER OBJECTIVES. After careful study of this chapter, you will be able to:

CHAPTER Intangibles CHAPTER OBJECTIVES After careful study of this chapter, you will be able to: 1. Explain the accounting alternatives for intangibles. 2. Record the amortization or impairment of intangibles.

CHAPTER Intangibles CHAPTER OBJECTIVES After careful study of this chapter, you will be able to: 1. Explain the accounting alternatives for intangibles. 2. Record the amortization or impairment of intangibles.

Partner s Share of Partnership Debt

PARTNER S SHARE OF PARTNERSHIP DEBT; DISPOSTION OF A PARTNERSHIP INTEREST Accounting 551T - Lecture 4 Manolakas: Chapters 10, 11 and 12 Robert A. Scharlach Partner s Share of Partnership Debt Basis of

PARTNER S SHARE OF PARTNERSHIP DEBT; DISPOSTION OF A PARTNERSHIP INTEREST Accounting 551T - Lecture 4 Manolakas: Chapters 10, 11 and 12 Robert A. Scharlach Partner s Share of Partnership Debt Basis of

Financial Accounting Chapter 10: Property, Plant and Equipment and Intangibles Answer Key

Supplemental Instruction Handouts Financial Accounting Chapter 10: Property, Plant and Equipment and Intangibles Answer Key 1. A) Prepare a calculation to show the cost of this machine. $23,500 x 0.02

Supplemental Instruction Handouts Financial Accounting Chapter 10: Property, Plant and Equipment and Intangibles Answer Key 1. A) Prepare a calculation to show the cost of this machine. $23,500 x 0.02

1. Like financial accounting, most business property must be capitalized for tax purposes.

Chapter 02 Property Acquisition and Cost Recovery True / False Questions 1. Like financial accounting, most business property must be capitalized for tax purposes. True False 2. Tax cost recovery methods

Chapter 02 Property Acquisition and Cost Recovery True / False Questions 1. Like financial accounting, most business property must be capitalized for tax purposes. True False 2. Tax cost recovery methods

Non-current Assets. Prof.(FH) Dr. Walter Egger

Dr. Walter Egger") Non-current Assets Prof.(FH) Dr. Walter Egger IAS 38 Intangible Assets Intangible Asset Is an identifiable non-monetary asset without physical substance Identifiability Seperable (can be seperated, divided

Non-current Assets Prof.(FH) Dr. Walter Egger IAS 38 Intangible Assets Intangible Asset Is an identifiable non-monetary asset without physical substance Identifiability Seperable (can be seperated, divided

1. Like financial accounting, most business property must be capitalized for tax purposes.

Chapter 02 Property Acquisition and Cost Recovery True / False Questions 1. Like financial accounting, most business property must be capitalized for tax purposes. True False 2. Tax cost recovery methods

Chapter 02 Property Acquisition and Cost Recovery True / False Questions 1. Like financial accounting, most business property must be capitalized for tax purposes. True False 2. Tax cost recovery methods

Depreciation & Sale of Assets!

Depreciation & Sale of Assets! Presented for Latino Tax Professionals Association By Ricardo V. Rivas, EA "#$%&'(!"#)%*!+%*!,--.!%.!-.&(//-'!%0-.1!*#.$-!23345!%6-&!+-!+%'! 7(&8-'!#.!1+-!1%9!:&(;-**#(.!;(&!()-&!1-.!-!#*!%!:&(?'!@-@,-&!(;!

Depreciation & Sale of Assets! Presented for Latino Tax Professionals Association By Ricardo V. Rivas, EA "#$%&'(!"#)%*!+%*!,--.!%.!-.&(//-'!%0-.1!*#.$-!23345!%6-&!+-!+%'! 7(&8-'!#.!1+-!1%9!:&(;-**#(.!;(&!()-&!1-.!-!#*!%!:&(?'!@-@,-&!(;!

CHAPTER 10 Capital Assets

CHAPTER 10 Capital Assets ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Exercises Problems Set A Problems Set B 1. Distinguish between tangible and intangible capital assets.

CHAPTER 10 Capital Assets ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Exercises Problems Set A Problems Set B 1. Distinguish between tangible and intangible capital assets.

Depreciation, Part I Session 19

Basic Income Tax Depreciation, Part I 19-1 Depreciation, Part I Session 19 A A A AI OMB No 1545-0172 Form Department of the Treasury Attachment Internal Revenue Service (99) Sequence No Cost (business

Basic Income Tax Depreciation, Part I 19-1 Depreciation, Part I Session 19 A A A AI OMB No 1545-0172 Form Department of the Treasury Attachment Internal Revenue Service (99) Sequence No Cost (business

1. Like financial accounting, most business property must be capitalized for tax purposes.

Taxation of Business Entities 6th Edition Spilker Test Bank Full Download: http://testbanklive.com/download/taxation-of-business-entities-6th-edition-spilker-test-bank/ Chapter 02 Property Acquisition

Taxation of Business Entities 6th Edition Spilker Test Bank Full Download: http://testbanklive.com/download/taxation-of-business-entities-6th-edition-spilker-test-bank/ Chapter 02 Property Acquisition

CA - INTER LEASING

CA - INTER LEASING 1.1 LEASING LOS 1 : Introduction Leasing is an important source of medium-term financing or leasing is the process of financing the cost of an asset. It is an arrangement under which

CA - INTER LEASING 1.1 LEASING LOS 1 : Introduction Leasing is an important source of medium-term financing or leasing is the process of financing the cost of an asset. It is an arrangement under which

Question #2 (AICPA FAR)

") Exam Results Question #1 (AI.110579FAR) Four years ago on January 2, Randall Co. purchased a long-lived asset. The purchase price of the asset was $250,000, with no salvage value. The estimated useful

Exam Results Question #1 (AI.110579FAR) Four years ago on January 2, Randall Co. purchased a long-lived asset. The purchase price of the asset was $250,000, with no salvage value. The estimated useful

Accounting for Tangible Capital Assets

Accounting for Tangible Capital Assets Date Approved by Board: 2011.11.17 Resolution No.: 11-113 2016.05.19 16-048 Lead Role: CFO Replaces: N/A Last Review Date: N/A Next Review Date: 2019.05.19 Policy

Accounting for Tangible Capital Assets Date Approved by Board: 2011.11.17 Resolution No.: 11-113 2016.05.19 16-048 Lead Role: CFO Replaces: N/A Last Review Date: N/A Next Review Date: 2019.05.19 Policy

Test Code F1 Branch (MULTIPLE) (Date : )

(Date : )") FINAL CA May 2018 ACCOUNTING STANDARDS (PART 1) Test Code F1 Branch (MULTIPLE) (Date : 03.12.2017) (50 Marks) compulsory. Note: All questions are Question 1 (5 marks) As per para 10 of AS 2 Valuation of

FINAL CA May 2018 ACCOUNTING STANDARDS (PART 1) Test Code F1 Branch (MULTIPLE) (Date : 03.12.2017) (50 Marks) compulsory. Note: All questions are Question 1 (5 marks) As per para 10 of AS 2 Valuation of

EXERCISES. a. Yes. All expenditures incurred for the purpose of making the land suitable for its intended use should be debited to the land account.

EXERCISES Ex. 9 1 a. New printing press: 1, 2, 3, 4, 5 b. Used printing press: 7, 8, 9, 10 Ex. 9 2 a. Yes. All expenditures incurred for the purpose of making the land suitable for its intended use should

EXERCISES Ex. 9 1 a. New printing press: 1, 2, 3, 4, 5 b. Used printing press: 7, 8, 9, 10 Ex. 9 2 a. Yes. All expenditures incurred for the purpose of making the land suitable for its intended use should

Adopted: November 2013 MSBA/MASA Model Policy 704 Orig Revised: May 2015 Rev. 2009

Adopted: November 2013 MSBA/MASA Model Policy 704 Orig. 1995 Revised: May 2015 Rev. 2009 704 DEVELOPMENT AND MAINTENANCE OF AN INVENTORY OF FIXED ASSETS AND A FIXED ASSET ACCOUNTING SYSTEM I. PURPOSE The

Adopted: November 2013 MSBA/MASA Model Policy 704 Orig. 1995 Revised: May 2015 Rev. 2009 704 DEVELOPMENT AND MAINTENANCE OF AN INVENTORY OF FIXED ASSETS AND A FIXED ASSET ACCOUNTING SYSTEM I. PURPOSE The

TOWN OF LINCOLN COUNCIL POLICY

Page 1 of 10 PURPOSE The purpose of this policy is to prescribe the accounting treatment for tangible capital assets so that users of the financial report can discern information about the investment in

Page 1 of 10 PURPOSE The purpose of this policy is to prescribe the accounting treatment for tangible capital assets so that users of the financial report can discern information about the investment in

Some Important Matters

Long-lived Assets 15.501/516 Accounting Spring 2004 Professor S. Roychowdhury Sloan School of Management Massachusetts Institute of Technology March 15, 2004 1 Some Important Matters Problem sets 5&6 Due

Long-lived Assets 15.501/516 Accounting Spring 2004 Professor S. Roychowdhury Sloan School of Management Massachusetts Institute of Technology March 15, 2004 1 Some Important Matters Problem sets 5&6 Due

Accounting B LECTURE 1: NON-CURRENT ASSETS. Recording, expensing and reporting non-current assets

Accounting B LECTURE 1: NON-CURRENT ASSETS Recording, expensing and reporting non-current assets - Asset: a resource controlled by an entity because of past events and from which future economic benefits

Accounting B LECTURE 1: NON-CURRENT ASSETS Recording, expensing and reporting non-current assets - Asset: a resource controlled by an entity because of past events and from which future economic benefits

Chapter 11. Learning Objectives. Non-current Assets. Horngren, Best, Fraser, Willett: Accounting 6e 2010 Pearson Australia

PowerPoint to accompany Chapter 11 Non-Current Assets: Property, Plant and Equipment, and Intangibles Learning Objectives 1. Measure the cost of a non-current asset 2. Account for depreciation 3. Select

PowerPoint to accompany Chapter 11 Non-Current Assets: Property, Plant and Equipment, and Intangibles Learning Objectives 1. Measure the cost of a non-current asset 2. Account for depreciation 3. Select

Implications of Alternative Farm Tractor Depreciation Methods 1. Troy J. Dumler, Robert O. Burton, Jr., and Terry L. Kastens 2

Implications of Alternative Farm Tractor Depreciation Methods 1 Troy J. Dumler, Robert O. Burton, Jr., and Terry L. Kastens 2 1 Selected paper at the annual meeting of the American Agricultural Economics

Implications of Alternative Farm Tractor Depreciation Methods 1 Troy J. Dumler, Robert O. Burton, Jr., and Terry L. Kastens 2 1 Selected paper at the annual meeting of the American Agricultural Economics

Chapter 13 Purchase or Inheritance Buyer/Beneficiary Side Outside Basis Purchase: Amount Paid to Seller + Share of Php. Debt

Chapter 13 Purchase or Inheritance Buyer/Beneficiary Side 1 Outside Basis Purchase: Amount Paid to Seller + Share of Php. Debt 2 13-3 Example 13-1 S sells to B 3 In Year 1, A, C, and S form the ACS Limited

Chapter 13 Purchase or Inheritance Buyer/Beneficiary Side 1 Outside Basis Purchase: Amount Paid to Seller + Share of Php. Debt 2 13-3 Example 13-1 S sells to B 3 In Year 1, A, C, and S form the ACS Limited

University of Nizwa / Dept. of Architecture / ARCH 506: Building Specification & Estimation / VALUATION / Ravishankar. KR / 5, January 2011.

Property Valuation Building Estimation and Costing Building Estimation and Costing Building Estimation and Costing is a vital part of Civil Engineering. No project can begin without the total Building

Property Valuation Building Estimation and Costing Building Estimation and Costing Building Estimation and Costing is a vital part of Civil Engineering. No project can begin without the total Building

Cost Engineering Dr. Nabil I El Sawalhi Associate professor Construction Management

Cost Engineering Dr. Nabil I El Sawalhi Associate professor Construction Management CE - L6 1 Construction Equipment CE - L6 2 Equipment can be classified as specific use or general use. Specific Use Equipment

Cost Engineering Dr. Nabil I El Sawalhi Associate professor Construction Management CE - L6 1 Construction Equipment CE - L6 2 Equipment can be classified as specific use or general use. Specific Use Equipment

Final Repair Regulations and the Impact on Owners of Investment Real Estate

Tom Scarpello Managing Partner 877.410.5040 Final Repair Regulations and the Impact on Owners of Investment Real Estate On September 13, 2013, the IRS released final regulations providing comprehensive

Tom Scarpello Managing Partner 877.410.5040 Final Repair Regulations and the Impact on Owners of Investment Real Estate On September 13, 2013, the IRS released final regulations providing comprehensive

Contents. Deductions? MACRS

Department of the Treasury Internal Revenue Service Publication 946 Cat. No. 13081F Contents What s New for 2011... 2 What s New for 2012... 2 Reminders... 2 Introduction... 2 How To 1. Overview of Depreciation...

Department of the Treasury Internal Revenue Service Publication 946 Cat. No. 13081F Contents What s New for 2011... 2 What s New for 2012... 2 Reminders... 2 Introduction... 2 How To 1. Overview of Depreciation...

LTR Report Number 1677, April 22, 2009 IRS REF: Symbol: CC:ITA:B07-PLR [Code Secs. 42, 167, 168, 263 and 263A]

![LTR Report Number 1677, April 22, 2009 IRS REF: Symbol: CC:ITA:B07-PLR [Code Secs. 42, 167, 168, 263 and 263A]](/thumbs/81/84579531.jpg "LTR Report Number 1677, April 22, 2009 IRS REF: Symbol: CC:ITA:B07-PLR [Code Secs. 42, 167, 168, 263 and 263A]") LTR-RUL, UIL No. 0263A.02-10 Capitalization and inclusion in inventory costs of certain expenses; Exceptions; Substantially constructed selfconstructed property., IRS Letter Ruling 200916007,, (January

LTR-RUL, UIL No. 0263A.02-10 Capitalization and inclusion in inventory costs of certain expenses; Exceptions; Substantially constructed selfconstructed property., IRS Letter Ruling 200916007,, (January

B EXERCISES E11-1B (Depreciation Computations SL, SYD, DDB) Instructions (a) (b) (c) E11-2B (Depreciation Conceptual Understanding) Instructions (a)

Instructions (a) (b) (c) E11-2B (Depreciation Conceptual Understanding) Instructions (a)") B EXERCISES E11-1B (Depreciation Computations SL, SYD, DDB) Vaughn Company purchases equipment on January 1, Year 1, at a cost of $500,000. The asset is expected to have a service life of 10 years and

B EXERCISES E11-1B (Depreciation Computations SL, SYD, DDB) Vaughn Company purchases equipment on January 1, Year 1, at a cost of $500,000. The asset is expected to have a service life of 10 years and

Advanced M&A and Merger Models Quiz Questions

Advanced M&A and Merger Models Quiz Questions Transaction Assumptions and Sources & Uses Purchase Price Allocation & Balance Sheet Combination Combining the Income Statement Revenue, Expense, and CapEx

Advanced M&A and Merger Models Quiz Questions Transaction Assumptions and Sources & Uses Purchase Price Allocation & Balance Sheet Combination Combining the Income Statement Revenue, Expense, and CapEx

Fundamental Accounting Principles, Volume 2

SOLUTIONS MANUAL to accompany Fundamental Accounting Principles, Volume 2 15 th Canadian Edition by Larson/Jensen/Dieckmann Prepared by: Laura Dallas, Kwantlen Polytechnic University Technical checks by:

SOLUTIONS MANUAL to accompany Fundamental Accounting Principles, Volume 2 15 th Canadian Edition by Larson/Jensen/Dieckmann Prepared by: Laura Dallas, Kwantlen Polytechnic University Technical checks by:

The objective of this policy is to outline the accounting and reporting requirements for tangible capital assets.

BYLAW #01-09 Purpose: The objective of this policy is to outline the accounting and reporting requirements for tangible capital assets. Scope: This policy applies to all village departments, boards, and

BYLAW #01-09 Purpose: The objective of this policy is to outline the accounting and reporting requirements for tangible capital assets. Scope: This policy applies to all village departments, boards, and

UNCORRECTED SAMPLE PAGES

339 Chapter 13 Accounting for non-current assets 1 Where are we headed? After completing this chapter, you should be able to: identify the characteristics of a depreciable noncurrent asset define depreciation,

339 Chapter 13 Accounting for non-current assets 1 Where are we headed? After completing this chapter, you should be able to: identify the characteristics of a depreciable noncurrent asset define depreciation,

CHAPTER 10 FIXED ASSETS AND INTANGIBLE ASSETS

1. a. Property, plant, and equipment or Fixed assets b. Current assets (merchandise inventory) 2. Real estate acquired as speculation should be listed in the balance sheet under the caption Investments,

1. a. Property, plant, and equipment or Fixed assets b. Current assets (merchandise inventory) 2. Real estate acquired as speculation should be listed in the balance sheet under the caption Investments,

DIRECT-FINANCING TERMS

CHAPTER 21 ALTERNATIVE LESSOR ACCOUNTING GROSS PRESENTATION This alternate discussion describes the accounting by lessors, using a gross presentation. These pages can be substituted for the discussion

CHAPTER 21 ALTERNATIVE LESSOR ACCOUNTING GROSS PRESENTATION This alternate discussion describes the accounting by lessors, using a gross presentation. These pages can be substituted for the discussion

Fill-in-the-Blank Equations. Exercises

Chapter 9 Long-Term Assets: Fixed and Intangible Study Guide Solutions 1. Residual value 2. Useful life 3. Straight-line rate 4. Total estimated units of activity 5. Straight-line rate 6. Depletion rate

Chapter 9 Long-Term Assets: Fixed and Intangible Study Guide Solutions 1. Residual value 2. Useful life 3. Straight-line rate 4. Total estimated units of activity 5. Straight-line rate 6. Depletion rate

Chapter 4: Accounting for Depreciation

Chapter 4: The Concept of 4.1 The Concept of Depreciable assets are physical objects that retain their size and shape but that eventually wear out or become obsolete. They are not physically consumed,

Chapter 4: The Concept of 4.1 The Concept of Depreciable assets are physical objects that retain their size and shape but that eventually wear out or become obsolete. They are not physically consumed,

Lease-Versus-Buy. By Steven R. Price, CCIM

Lease-Versus-Buy Cost Analysis By Steven R. Price, CCIM Steven R. Price, CCIM, Benson Price Commercial, Colorado Springs, Colorado, has a national tenant representation and consulting practice. He was

Lease-Versus-Buy Cost Analysis By Steven R. Price, CCIM Steven R. Price, CCIM, Benson Price Commercial, Colorado Springs, Colorado, has a national tenant representation and consulting practice. He was