RESTRICTED APPRAISAL OF A: Light Industrial Building located at 804 Winkle Dr., South Houston, Harris County, Texas PREPARED FOR:

|

|

|

- Daisy Gabriella Robertson

- 5 years ago

- Views:

Transcription

1 RESTRICTED APPRAISAL OF A: Light Industrial Building located at 804 Winkle Dr., South Houston, Harris County, Texas PREPARED FOR: Mr. Wayne McMillian Harmac Group, Inc Red Pheasant Ct. Houston, Texas Date of Value As Is : Date of Report: January 11, 2017 February 13, 2017 BY MB LANE & ASSOCIATES, INC Hempstead Highway, Suite 102 Houston, Texas (File No B)

2 February 13, 2017 Mr. Wayne McMillian Harmac Group, Inc Red Pheasant Ct. Houston, Texas Reference: Restricted Appraisal of a light industrial building located at 804 Winkler Dr, South Houston, Harris County, Texas Dear Mr. McMillian: In compliance with your request, we have developed an opinion of the As Is value of the subject property in Fee Simple Estate. The As Is date of value is as of the date of our site visit January 11, This is a restricted appraisal report as defined by USPAP. The persons involved in preparing this appraisal report is Michael B. Lane, MAI. We are providing a value opinion based upon a one year exposure period. The value concluded to is subject to the assumptions and contingent and limiting conditions contained within both the body of this Restricted Appraisal Report. This report presents summary discussions of the data, reasoning, and analyses that were used in the appraisal process to develop the appraiser s opinion of value. Supporting documentation concerning the data, reasoning, and analyses is retained in the appraiser s workfile. The depth of discussion retained in this report is specific to the needs of the client and for the intended use stated below. It is noted that the appraiser s opinions and conclusions set forth in the report may not be understood properly without additional information in the appraiser s workfile. The appraiser is not responsible for unauthorized use of this report. The property right appraised in this report is the Fee Simple Estate. We are providing a value opinion based upon a one year exposure period. Please review our Contingent and Limiting Conditions, beginning on Page ix, as our value is subject to these provisions. The subject property is presently improved with one metal office/warehouse building consisting of a gross leaseable area of ±12,000 square feet. The site has an overall size of acres. In our analysis, two approaches to value has been considered, that being the Market Approach- As Improved and Income Approach.

3 Mr. Wayne McMillian February 13, 2017 Harmac Group, Inc. Page 2 Based on the quality and condition of the improvements As Is as well as the current market conditions, it is the appraiser s opinion that the market value of the subject property is based on a 12 month exposure period. Therefore our opinion of the market value As Is of the Fee Simple Estate, as of January 11, 2017, of the subject property is as follows: Eight Hundred Fifteen Thousand Dollars $815,000 Market Value, as further defined in this report, is the most probable price which a property should bring in a competitive and open market under all conditions requisite to a fair sale, the buyer and seller each acting prudently and knowledgeable, and assuming the price is not affected by undue stimulus. Prior to accepting this assignment, the appraisers concluded that they have the necessary experience and/or knowledge to competently complete the appraisal, and during the preparation of the appraisal, the appraisers have not discovered any areas in the assignment requiring appraisal expertise in which we were lacking. The above statements of appraiser competency applies to knowledge and/or experience for the real estate appraisal discipline and not other areas of trades, professions or disciplines such as engineering, surveyors, attorneys, etc. We completed a drive-by inspection of the subject property only. That is, we observed the property from the street. We did not access the site or inspect the building. Any information on the interior or exterior of the building was provided by our client or our visual inspection. We did not observe, or are we aware of any natural, cultural, recreational, environmental, or scientific value influences affecting the subject property. Additionally, we have not made a specific Americans with Disabilities Act (ADA) compliance survey and analysis of this property to determine whether or not it is in conformity with the various detailed requirements of the ADA. The value estimate is predicated on the assumption that no such influences are present that would affect our value conclusions. We have no expertise in these fields and no responsibility is assumed for any such conditions or for any expertise, engineering or other special knowledge required to discover them. Such studies are required before these values can be relied on by readers of this report. The reported analyses, opinions and conclusions were developed, and this report has been prepared, in conformity with the appraisal guidelines of the Code of Professional Ethics & Standards of Professional Practice of the Appraisal Institute, which include the Uniform Standards of Professional Appraisal Practice.

4 Mr. Wayne McMillian February 13, 2017 Harmac Group, Inc. Page 3 Your attention is now directed to the following report which contains the data and analysis used in our final value opinion. If after reviewing this report, you have any questions, please do not hesitate to contact this office. Yours truly, Michael B. Lane, MAI TX G MBL:jd mbl17001 B

5 TABLE OF CONTENTS Title Page i. Letter of Transmittal ii. Table of Contents v. Certification vi. Summary of Salient Facts and Conclusions viii. Contingent and Limiting Conditions x. INTRODUCTION Scope of Work 1. Intended Use and Users of the Appraisal 3. Date of Valuation 3. Property Rights Appraised 3. Competency Statement 3. Definition of Market Value 4. FACTUAL DESCRIPTIONS Identification of the Property 6. Property History 6. Statement of Ownership 6. Area Analysis - Houston 7. Assessment and Tax Analysis 9. Site Data 10. Improvement Data 14. Zoning 16. ANALYSIS OF DATA AND OPINIONS OF THE APPRAISER Highest and Best Use 17. Market Approach to Value - Improved 18. Reconciliation and Final Value Opinion 23. ADDENDA Qualifications Improved Sale Photos Comparable Rental Map Flood Map Subject Photographs Letter of Engagement v

6 CERTIFICATION We certify that, to the best of our knowledge and belief: (1) The statements of facts contained in this report are true and correct. (2) The reported analyses, opinions, and conclusions are limited only by the reported assumptions and limiting conditions, and are our personal, impartial, and unbiased professional analyses, opinions, and conclusions. (3) We have no present (or the specified) present or prospective interest in the property that is the subject of this report, and no (or the specified) personal interest with respect to the parties involved. (4) We have no bias with respect to the property that is the subject of this report or the parties involved with this assignment. (5) Our compensation for completing this assignment is not contingent upon the development or reporting of a predetermined value or direction in value that favors the cause of the client, the amount of the value opinion, the attainment of a stipulated result, or the occurrence of a subsequent event directly related to the intended use of this appraisal. (6) Our engagement in this assignment was not contingent upon developing or reporting predetermined results. (7) Our analyses, opinions, or conclusions were developed, and this report has been prepared, in conformity with the Uniform Standards of Professional Appraisal Practice and the Code of the Professional Ethics of the Appraisal Institute. (8) This report is subject to the requirements of the Appraisal Institute relating to review by its duly authorized representatives. (9) Michael B. Lane has made personal site visits to the property that is the subject of this report. (10) No one provided significant real property appraisal assistance to the person signing this report. (11) As of the date of this report, Michael B. Lane, MAI, has completed the requirements of the continuing education program of the Appraisal Institute. (12) As of the date of this report, Michael B. Lane, MAI is a Texas State Certified General Real Estate Appraisers. vi

7 CERTIFICATION - CONTINUED (13) This appraisal assignment was NOT based on a requested minimum value, a specified valuation, or the approval of a loan. (14) MBLane and Associates has not previously performed valuation services relating to the subject property. (15) The market value As Is of the Fee Simple Estate of the subject property, as of January , is as follows: As Is Market Value $815,000 Michael B. Lane, MAI TX G vii

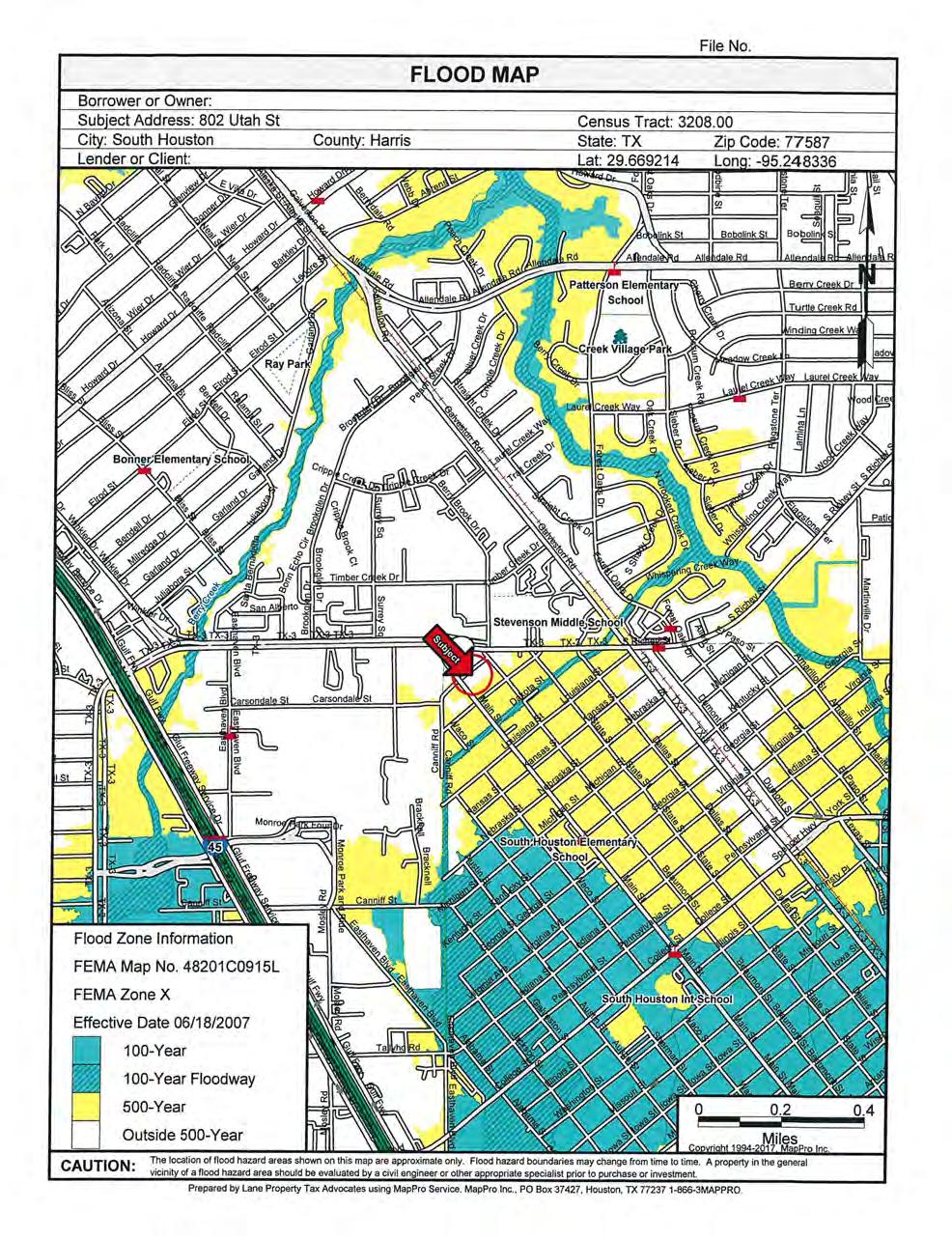

8 SUMMARY OF SALIENT FACTS AND CONCLUSIONS Key Map Location Identification Location Intended Use of the Appraisal Property Right Appraised Overall Land Size 535Z Light Industrial Building The subject property is located at the north corner of Utah Street and Main Street. It has a street address of 804 Winkle Dr., South Houston, Harris County, Texas The subject does not front on Winkler Dr., but the parent tract does have frontage on Winkler Drive. The intended use of this appraisal is to provide an opinion of the As Is market value of the herein legally described property and the improvements. Fee Simple Estate acres (35,500 square feet). Improvements Improvements include one metal office/warehouse building containing a total of ±12,000 square feet of gross building area. Supporting site improvements include a stabilized yard and fencing. Occupancy Level Highest and Best Use As Vacant As Improved Zoning Flood Plain Status 100% (Tenant Occupied) Retention until development is feasible again Light Industrial development The property is located within the city limits of South Houston. It is zoned C-1 General Commercial. According to flood maps issued by the Federal Emergency Management Agency (Community Panel FIRM #48201C0915L), effective June 18, 2007 for Harris County, it appears that the subject is located outside of the 100-year and 500-year flood plains. A copy of the flood map is included as an addendum to this report. viii

9 SUMMARY OF SALIENT FACTS AND CONCLUSIONS - CONTINUED OPINIONS OF VALUE: Sales Comparison Approach: $840,000 Income Approach $790,000 Final Opinion of Value As Is $815,000 Exposure Time: 12 Months Effective Date of Market Value As Is : January 11, 2017 Date of Report: February 13, 2017 ix

10 CONTINGENT AND LIMITING CONDITIONS This appraisal is subject to the following limiting conditions. The legal description furnished to us is assumed to be correct. We assume no responsibility for matters legal in character, nor do we render any opinion as to the title, which is assumed to be good. Any existing liens and encumbrances have been disregarded and the property appraised as though free and clear under responsible ownership and competent management, unless otherwise indicated. We have made no survey and assume no responsibility in connection with such matters. We believe the information in this report furnished by others to be reliable, but we assume no responsibility for its accuracy. This includes, but is not limited to, information obtained in regard to flood plains, wetlands, geological fault lines, sufficiency of public utilities, and land or surface subsidence. The construction and condition of the improvements mentioned in the body of this report is based on observation and no engineering study has been made, unless previously noted, which would discover latent defects. No certification as to construction or any of the physical aspects could be given unless a proper engineering study were made. No fault line, flood plain, or subsidence study has been made by the appraisal firm and could be under taken only by a qualified engineering firm. The distribution of the total valuation between land and improvements in this report applies only under the existing program of utilization. The separate valuations for land and improvements must not be used in conjunction with any other appraisal, and are invalid if so used. We are not required to give testimony or attendance in court by reason of this appraisal with reference to the property in question, unless arrangements have been made previously. Possession of this report or a copy thereof does not carry with it the right of publication. It may not be used for any purpose by anyone other than the addressee without the previous written consent of the appraiser. Neither all, nor any part of the contents of this report shall be conveyed to the public through advertising, public relations, news, sales or other media, without the consent and approval of the author, particularly as to valuation conclusions, and identity of the appraiser or firm with which he/she is connected, or any reference to the Appraisal Institute, or the MAI designation. This report is written in conformity with the professional standards of practice and code of ethics of the Appraisal Institute, the Uniform Standards of Professional Appraisal Practice and the rules of the Texas Real Estate Commission. Unless otherwise stated in this report, the existence of hazardous substances, including without limitation asbestos, polychlorinated biphenyls, petroleum leakage, or agricultural chemicals, which may or may not be present on the property, or other environmental conditions, were not called to the attention of nor did the appraiser become aware of such during the appraiser s site visit. The appraiser has no knowledge of the existence of such materials on or in the property unless otherwise stated. The appraiser, however, is not qualified to test such substances or conditions. If the presence of such substances, such as asbestos, urea formaldehyde foam insulation, or other hazardous x

11 CONTINGENT AND LIMITING CONDITIONS - CONTINUED substances or environmental conditions, may affect the value of the property, the value estimated is predicated on the assumption that there is no such condition on or in the property or in such proximity thereto that it would cause a loss in value. No responsibility is assumed for any such conditions, nor for any expertise or engineering knowledge required to discover them. The appraiser represents that he/she is not an expert to appraise insulation or other products banned by the Consumer Products Safety Commission which might render the property more or less valuable. In connection with this appraisal, the appraiser has not inspected or tested for, nor taken into consideration in any respect the presence or absence of insulation or other said products increase or decrease in the value of the property from the value placed thereon by the opinion of the appraiser. The Americans with Disabilities Act (ADA) became effective January 26, I (we) have not made a specific compliance survey and analysis of this property to determine whether or not it is in conformity with the various detailed requirements of the ADA. It is possible that a compliance survey of the property together with a detailed analysis of the requirements of the ADA could reveal that the property is not in compliance with one or more of the requirements of the act. If so, this fact could have a negative impact upon the value of the property. Since I (we) have no direct evidence relating to this issue, I (we) did not consider possible noncompliance with the requirements of ADA in estimating the value of the property. It is understood that this assignment and the payment of our fee is not dependent or contingent upon any loan commitment, sale, trial outcome, receipts of funds by you, or any other condition or contingency. The liability of MB Lane and Associates, Inc., its owner and staff, is limited to the Client only and to the amount of the fee actually paid for the services rendered, as liquidated damages, if any related dispute arises. Further, there is no accountability, obligation, or liability to any third party. If this report is placed in the hands of anyone other than Client, the Client shall make such party aware of all limiting conditions and assumptions of the assignment and related discussions. The Appraiser is in no way to be responsible for any costs incurred to discover or correct any deficiencies of any type present in the property; physically, financially, and/or legally. Client also agrees that in case of lawsuit (brought by lender, partner or part owner in any form of ownership, tenant or any party), Client will hold Appraiser(s) completely harmless from and against any liability, loss, cost or expense incurred or suffered by Appraiser(s) in any such action, regardless of its outcome. These reports may be relied upon by the CLIENT, in determining whether to make a loan evidenced by a note ( the Property Note ) which is further secured by the Property. These reports may be relied upon by the purchaser or assignee of the Property Note in determining whether to acquire the Property Note or Interest therein. In addition, these reports may be relied upon by any rating agency involved in rating the securities secured by, or representing an Interest in, the Property Note. These reports may be used in connection with materials offering for sale the Property Note, or an interest in the Property Note, and in presentations to any rating agency. With respect to the foregoing, these reports speak only as of the Origination date of these reports unless specifically updated through a supplemental report. xi

12 INTRODUCTION xii

13 SCOPE OF WORK Extent To Which The Property Was Identified. We were provided with an older survey of the subject property and we obtained a plat map from the Harris County Appraisal District (HCAD) for the identification of the subject site, its location and shape. The gross building area of the existing improvements was based on the survey provided and verified by our site visit. We did not perform a title search of the subject property. Extent To Which Tangible Property Was Visited. We visited the property and viewed the interior and exterior of the improvements. We are not engineers and are not qualified to assess structural integrity or the adequacy and condition of its mechanical, electrical, or plumbing components. This appraisal is not a property condition report, and should not be relied upon to disclose any conditions present in the property, and it does not guarantee the property to be free of defects. We are not licensed inspectors, and we did not make an inspection of the property as defined by TREC Rule for real estate inspectors. We are not qualified to detect or identify hazardous substances, which may, or may not, be present on, in, or near the subject property. The presence of hazardous materials may negatively affect market value. We have no reason to suspect the presence of hazardous substances, and we valued the subject assuming that none are present. No responsibility is assumed for any such conditions or for any expertise or engineering services of specialists for the purpose of conducting inspections, engineering studies, or environmental audits. While we refer to FEMA flood maps, we are not surveyors and not qualified to make flood plain determinations, and we recommend that a qualified party be consulted before any investment decision is made. The Type And Extent Of Data Researched. We conducted a search for sales and rental data of similar light industrial buildings in the immediate area. Our data sources were the LoopNet RecentSales and Costar data services, as well as our own internal files. Our search for data concentrated on the immediate market area and expanded through Harris County as necessary. Our search for data extended back to January, We supplemented these sources with information from knowledgeable brokers, particularly those with listings in the immediate area. Texas is a non-disclosure state. It is important that the intended users of this appraisal understand that in Texas, there is no legal requirement for grantors or grantees to disclose any information relative to a transfer of real property, other than the recording of the deed itself. In Texas, the deed contains no information about the transaction, including the purchase price. As a result, no data source provides absolute coverage of all transactions. It is possible that there are sales of which we are unaware. Our data sources provide all the data typically available to appraisers in the normal course of business. The Type And Extent Of Analysis Applied. We developed opinions of value using two of the usual approaches to value, namely the sales comparison approach-as improved and income approaches. The cost approach was not utilized as this approach is not typically used by purchasers in making investment decisions on this type property. Significant Real Property Appraisal Assistance Provided No one provided significant real 1

14 property appraisal assistance to the persons signing this report. General This Appraisal Report has been prepared under Standards Rule 2-2(a) of an appraisal performed under Standards Rule 1 of the Uniform Standards of Professional Appraisal Practice (USPAP). It has been our intention to prepare this appraisal in conformity with the Uniform Standards of Professional Appraisal Practice (USPAP) of the Appraisal Foundation, and the Code of Ethics and the Standards of Professional Practice of the Appraisal Institute. This appraisal is presented as a restricted use appraisal. This report presents summary discussions of the data, reasoning, and analyses that were used in the appraisal process to develop the appraiser s opinion of value. Supporting documentation concerning the data, reasoning, and analyses is retained in the appraiser s workfile. The depth of discussion retained in this report is specific to the needs of the client and for the intended use stated below. It is noted that the appraiser s opinions and conclusions set forth in the report may not be understood properly without additional information in the appraiser s workfile. The appraiser is not responsible for unauthorized use of this report. 2

15 INTENDED USE AND USERS OF THE APPRAISAL The intended use of this appraisal is to provide an opinion of the As Is market value of the Fee Simple Estate of the subject property for asset valuation services. The client also represents that the report will be used only by Harmac Group, Inc. and Mr. Wayne McMillian for the intended use set forth above. DATE OF VALUATION Our opinion of market value As Is is as of January 11, 2017, the date of our site visit to the subject property. PROPERTY RIGHTS APPRAISED The property rights being appraised in this report consist of the Fee Simple Estate of the subject property which is as instructed by the client. Fee simple estate is defined by The Dictionary of Real Estate Appraisal, Fifth Edition, copyright 2010, page 78, by the Appraisal Institute as being: Absolute ownership unencumbered by any other interest or estate, subject only to the limitations imposed by the governmental powers of taxation, eminent domain, police power and escheat. COMPETENCY STATEMENT Prior to accepting this assignment, the appraisers concluded that they have the necessary experience and/or knowledge to competently complete the appraisal, and during the preparation of the appraisal, the appraisers have not discovered any areas in the assignment requiring appraisal expertise which they were lacking. 3

16 DEFINITION OF MARKET VALUE The definition of market value is defined by Title XI of the Financial Institution Reform, Recovery, and Enforcement Act of 1989, 12 CFR, Part 323 as follows: Market Value means the most probable price which a property should bring in a competitive and open market under all conditions requisite to a fair sale, the buyer and seller each acting prudently and knowledgeable, and assuming the price is not affected by undue stimulus. Implicit in this definition is the consummation of a sale as of a specified date and the passing of title from seller to buyer under conditions whereby: 1. Buyer and seller are typically motivated; 2. Both parties are well informed or well advised, and acting in what they consider their own best interests; 3. A reasonable time is allowed for exposure in the open market; 4. Payment is made in terms of cash in U.S. Dollars or in terms of financial arrangements comparable thereto; and 5. The price represents the normal consideration for the property sold unaffected by special or creative financing or sales concessions granted by anyone associated with the sale. 4

17 FACTUAL DESCRIPTIONS OF THE PROPERTY 5

18 IDENTIFICATION OF THE PROPERTY The subject property can legally be described as acre or 35,500 square feet of land found in Lots 2-6, Block 109, South Houston R/P, South Houston, Harris County, TX. The subject property is located at the north corner of Utah Ave. and Main Street. The property has a street address of 804 Winkler Dr., South Houston, Harris County, Texas. PROPERTY HISTORY The subject property is leased to UniCoat. The lease expires April 1, The lease rate is $7,100 per month with the tenant paying all utilities and common area maintenance of the facility. The ownership indicated that the tenant is planning to move out, but he has another party interested There are no known offers to purchase the subject property and no transactions that we are aware of involving the subject property in the last three years. STATEMENT OF OWNERSHIP According to information provided to us, as of the date of this appraisal, the subject property is owned by McMillian Enterprises, LLC. 6

19 Provided upon request. HOUSTON AREA AND NEIGHBORHOOD DATA 7

20 8

21 ASSESSMENT AND TAXES The subject property is listed by the Harris County Appraisal District (HCAD) under Account Number The 2016 assessed value is estimated at $564,805, which includes $177,500 for the land and $387,305 for the improvements. The land assessment is based on an allocation of a larger parcel containing a total of 42,539 square feet at a unit value of $5.00 psf. The overall totals are shown in the following table: 2016 HCAD Assessed Value Land $177,500 Improvements $387,305 Assessed Value $564,805 The following summarizes the taxing authorities 2016 taxes based on the 2016 assessed value of $564,805. Taxing Authority 2016 Tax Rate Estimated Taxes Harris County & Related Entities $ $3,588 San Jacinto College $ $1,030 Pasadena ISD $ $7,625 City of South Houston $ $3,571 Total $ $15,813 Total assessment of the existing property is $564,805. This would equate to a tax responsibility of $15,813 or ±$1.32 per square foot. 9

22 ZONING The subject is located within the city limits of South Houston. According to the city, the subject property is zoned C-1 Commercial. Land uses under this zoning regulation include generally commercial and light industrial uses. Thus, it would appear that the subject property is a legal conforming use. 10

23 HIGHEST AND BEST USE The subject site includes a total of approximately acres or ±35,500 square feet of land which is suitable for a variety of uses. It has access to all utilities, and has what is considered to be a usable configuration with a generally level topography and is located outside the 100 and 500-year flood plains. Additionally, as indicated in the Site Data section, the City of South Houston utilizes zoning to regulate land uses. The site is zoned C-1 Commercial and is considered a legal conforming use. In our opinion, the most likely use would be light industrial development based on surrounding uses. Based on our analysis of the light industrial market in this area, this use would not be considered financially feasible on a speculative basis. In our opinion, the property s highest and best use, as vacant, is retention until development is once again financially feasible. The highest and best use, as improved, of the subject property is for continuation of its current use as a light industrial property. 11

24 MARKET APPROACH TO VALUE The market approach leans heavily upon the principle of substitution. In essence, this principle states that a prudent purchaser will pay no more for any particular property than it would cost him to acquire an equally desirable alternate property. The Market Approach utilizes the sales of properties similar to the subject as the basis for an indication of market value. Direct comparison is made between each sale and the subject on an item-by-item basis to include such factors as conditions of sale, market conditions, size, physical characteristics and economic characteristics. Adjustments are made to the sales price of the comparable property in order to arrive at an indication of what it would have sold for had it been essentially the same as the subject property. These adjusted prices are then reconciled into an indication of value for the subject. The following are comparable sales which, in our opinion, are similar to the subject. The sales included herein are felt to be the most comparable of the data uncovered in our research. The comparables used are scattered throughout Harris County. All properties were visually observed and pertinent data about each was verified. These sales were compared with each other in order to obtain appropriate adjustments. 12

25 IMPROVED SALES MAP 13

26 MARKET APPROACH TO VALUE - CONTINUED No. Location Sale Date YOC Size Land: Building Sales Price Sales Price /PSF Steelman St., Houston 8/12/ , :1 $1,200,000 $ Jeanetta, Houston 8/19/ , :1 $1,550,000 $ East Belt, Humble 12/1/ , :1 $2,325,000 $ Market St., Houston 4/28/ , :1 $1,050,000 $ Market St., Houston 12/7/ , :1 $490,000 $48.66 Sub 804 Winkle Dr , When comparing the above sales to the subject property, adjustments were considered for factors such as conditions of sale, financing terms, location and physical characteristics. Each of these factors has been addressed in the following adjustment grid. The grid below illustrates the procedure in arriving at a value for the subject property. 14

27 MARKET APPROACH TO VALUE - CONTINUED IMPROVED SALES ADJUSTMENT GRID Sale 1 Sale 2 Sale 3 Sale 4 Sale 5 Sale Price Per Unit $75.00 $95.92 $90.54 $58.79 $48.66 Financing 0% 0% 0% 0% 0% Market Conditions 0% 0% 0% 0% 0% Condition of Sale 0% 0% 0% 0% 0% Adjusted Sale Price/Unit $75.00 $95.92 $90.54 $58.79 $48.66 Location I S S I I 10% -10% -15% 15% 15% Building Size 16,000 16,160 25,680 17,860 9,500 0% 0% 5% 0% 0% Age/Condition % -5% 0% 10% 10% Corner/Access E E E E E 0% 0% 0% 0% 0% Construction Quality E E S E E 0% 0% -5% 0% 0% Land : Building % -10% -15% -5% -5% Amenities E E E E E 0% 0% 0% 0% 0% Net Adjustment -5% -25% -30% 20% 20% Indicated Value Unit $71.25 $71.94 $63.38 $70.55 $58.39 Summary of Adjustments Range of Indicated Values: $58.39 to $71.94 Average Value Unit $67.10 Indicated Value: $

28 MARKET APPROACH TO VALUE - CONTINUED Conclusions After applying all necessary adjustments, the comparable sales reflect an indicated range of value from $58.39 per square foot to $71.94 per square foot of net rentable area, with an average value per square foot of $ Considering the location, age/condition, and overall market appeal of the subject property in relation to the above sales, a value at the middle of the range, or $70.00 per square foot of gross area is appropriate. The total value indication for the subject is as follows: Gross Rentable Area Concluded Value PSF Indicated Value 12,000 $70.00 $840,000 As Is Market Value via the Sales Comparison Approach (Rounded) $840,000 16

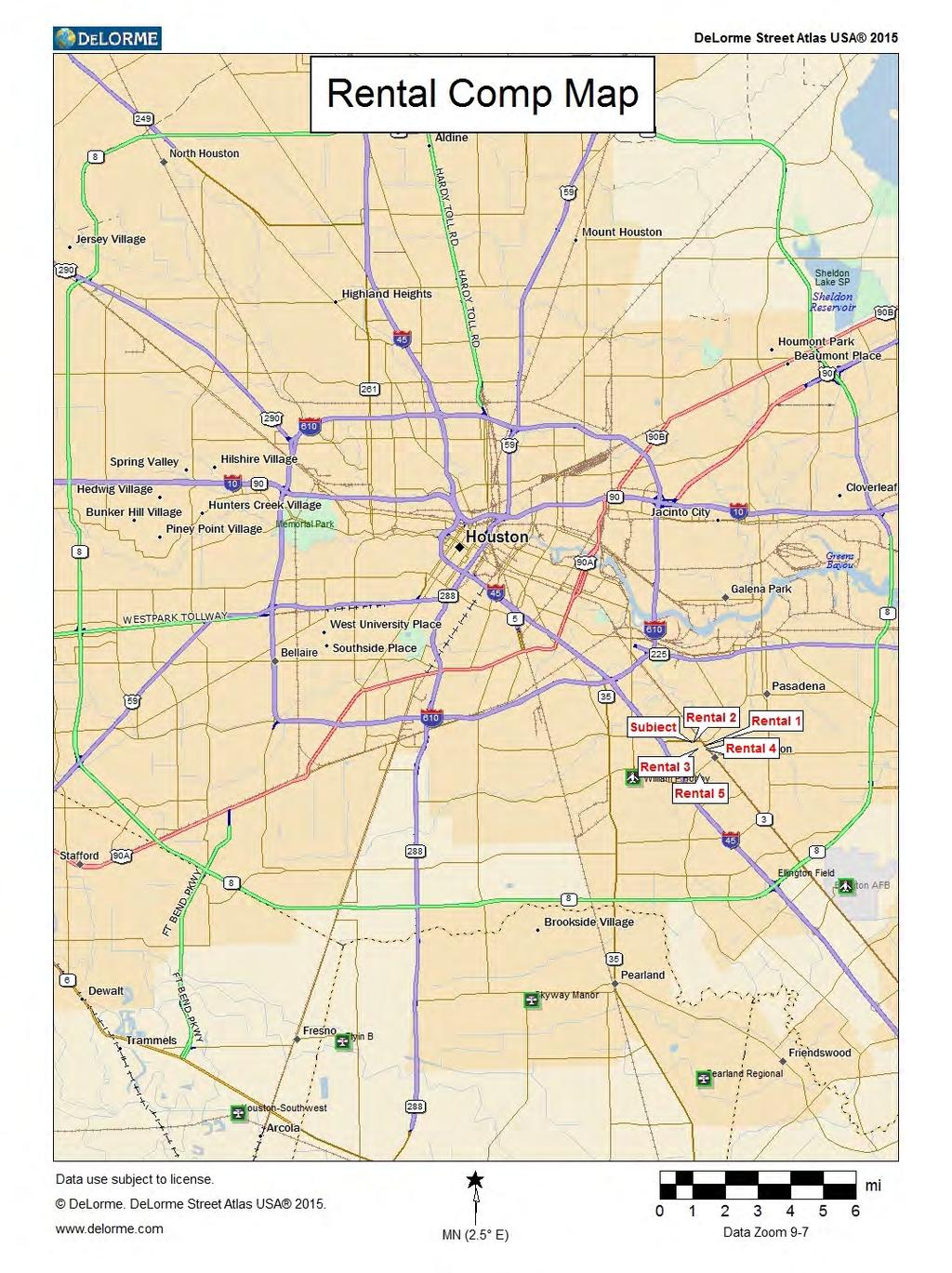

29 INCOME CAPITALIZATION APPROACH The principle assumption of the Income Approach is that there is a definite relationship between a property's value and the income it can produce. The premise behind the Income Approach is that it discounts to present worth the future income benefits the property will produce during a projected term of ownership for the typical purchaser. In this approach, gross income and various expenses are analyzed and obtained by a market data comparison with the resulting series of net incomes discounted to present value at an appropriate rate which would attract investors in this type of property. Gross revenue is obtained by analyzing facilities in competition with the subject property so as to estimate the appropriate average daily rate. Once the market rent and stabilized occupancy are determined, the appropriate expenses are deducted. The resulting net income can then either be capitalized into a value indication by an appropriate rate or discounted to present value utilizing a time line. In this instance, the net income is capitalized into a value by an appropriate rate. Rental Analysis and Economic Rental Rate Opinion. All of the rents listed on the below include office properties which are competitive to the subject property. Typically, within the income approach section of an improved property appraisal, we consider gross rental income with deductions made for various expenses and capitalize the resulting net operating income into value at an appropriate rate, resulting in an opinion of market value via the income approach. When comparing the rents to the subject, we have considered adjustments for location, construction quality, size, visibility and surrounding properties. The following chart summarizes pertinent data regarding the comparable rental items: SUMMARY OF COMPARABLE RENTALS No. Address Year Built Size SF NRA % Off. Occ. CAM PSF/Yr Rent PSF/Mo. Rent PSF/Yr Nebraska St ,200 7% 0% NNN $0.60 $ Montana St ,350 10% 100% NNN $0.71 $ Kansas St ,800 8% 100% IG $0.50 $ Kentucky ,000 2% 0% IG $0.44 $ Illinois St ,200 0% 0% NNN $0.52 $6.24 Subj. 804 Winkle Dr ,000 These properties are considered to be the best rental comparables available for comparison to the subject property. Review of the rental comparables indicate a range of annual base rental rates from $5.28 to $8.52 per square foot per year. Rentals 3 and 4 are leased on an industrial gross basis in which the tenant is responsible for utilities and maintenance, and the landlord is responsible for all other expenses associated with the property. Rentals 1, 2 and 5 are leased on a triple net basis in which the tenant is responsible for taxes, insurance, and maintenance. Subject Contract Rental Information. The subject is currently 100% occupied by a single tenant. The lease expires in April 1, The lease is on an industrial gross basis, with the tenant paying 17

30 INCOME APPROACH TO VALUE - CONTINUED for maintenance and electricity and the landlord being responsible for all other expenses relating to the property. The base rent is $85,200 a year ($7,100 a month, or $7.10 psf/yr). In our analysis, we have been asked to provide a value of the fee simple estate versus the lease fee estate, therefore, our analysis is based on an estimate of market rent. Market Rent Estimate. Based on our study and analysis of the rentals, as well as the location, quality, and interior build-out, it is our opinion that the market rental rate for the subject is $7.20 per square foot per year on a industrial gross basis. The following schedule includes our estimate of potential gross income: POTENTIAL RENT INCOME NRA (SF) Rent PSF Potential Rent Income Contract Rent 12,000 $7.20 $86,400 Total $86,400 Vacancy/Collection Loss. The condition of the property and skill of the management team can dramatically impact the occupancy rate within the subject s submarket. While trends in this area are not expected to change significantly in the near future, it is reasonable to assume that over a typical investor holding period of eight to ten years, there will be losses of income due to vacancy, tenant turnover and/or collection problems. The comparable rentals all are 0% to 100% occupied. Per CoStar Houston Industrial Market Survey, the subject is within the Southeast Outer Loop Industrial submarket, which as of 4 th Quarter 2016, reported an average vacancy for warehouse properties of 2.9%, and an overall vacancy for the Houston MSA of 5.5%. This includes older facilities and single-tenant facilities. A stabilized occupancy level of 95% (4% vacancy and 1% collection loss, or 5% total) is used in calculation of the effective gross income and net operating income. Effective Gross Income. Effective gross income is found by subtracting vacancy/collection loss from potential gross income. Effective gross income for the subject property is calculated in the table below: EFFECTIVE GROSS INCOME PGI $86,400 Less Vac. 5% $4,320 EGI $82,080 18

31 INCOME APPROACH TO VALUE - CONTINUED OPERATING EXPENSES No historical income or expense statements were presented for review, although actual property insurance expense was provided. Also, we considered expense information on similarly improved properties, obtained from conversations with owners and brokers/agents active in the area, and from information in our files, was useful in arriving at expense estimates that would reasonably be incurred in the operation of the subject property as a landlord. As indicated, the subject rent is based on an industrial gross basis with the tenant being responsible for utilities and common area maintenance. The landlord is responsible for all other expenses including taxes, insurance, management, and reserves. The subject expenses are analyzed on a stabilized occupancy basis. Ad Valorem Taxes. Property tax expense is the cost of ad valorem property taxes for the subject property. Typical tax expenses for buildings similar in use as the subject typically range from $0.45 to $1.45 psf/yr. Based on the our assessed value analysis in the Assessment and Taxes section of this report, the estimated stabilized tax liability is $15,813, or $1.32 psf/yr. Insurance. Discussions with individuals and insurance agents in this market indicated that typical insurance costs range from $0.20 to $0.40 per square foot annually, depending on, among other categories, the size of the facility. Actual insurance was reported at $3,930 or $0.33 psf/yr. For the purposes of this analysis, we have utilized an insurance expense of $0.33 psf/yr, or $3,930 for the subject property. Management, Administrative and Leasing. This expense item includes such components as a managerial fee, legal fees, accounting fees, leasing commissions, and other professional expenses. This charge is an allowance to compensate the owner and/or professional management firm for time involved in the management of the project, above and beyond the day-to-day operations. In the greater Houston retail market, professional management companies generally charge 2.0% to 8.0% of effective gross income at stabilized occupancy to manage projects similar to the subject. Typical administrative and leasing expenses range from 2% to 5% of effective gross income. Considering the size of the subject, that the subject is 100% occupied by a single tenant, and the subject is owner managed, a percentage of 2.0% of effective rental income at stabilized occupancy is considered appropriate for the subject and is calculated as follows: $82,080 x 2.0% = $1,642 Reserves for Replacement. This expense item allows for a sinking fund to be set aside to cover repairs or replacement of building component items whose physical useful life expectancy is less than the building, but longer than the typical investor holding period (replacement of shorter life items would be considered maintenance). The theory is that prudent management would allocate an annual charge sufficient for the periodic replacement of these items. The short life building component items with life expectancies greater than the typical holding period were identified in the cost approach. The subject s historical expenses does not indicate an expense in this category. Considering the size, quality and age of the subject property improvements, we have utilized an amount of $0.10 psf/yr, or $1,200 for this expense item in the income approach. This amount is 19

32 INCOME APPROACH TO VALUE - CONTINUED considered reasonable in comparison to industry averages. Total Expenses. Total stabilized annual operating expenses for the subject property are estimated at $22,585, which translates to approximately $1.88 psf/yr of net rentable area. This amount is considered reasonable based on the size, condition, and location of the property. Net Operating Income The net operating income is the difference between effective gross income and total expenses. The net operating income is $59,495, or $4.96 per square foot, as indicated below: PROFORMA INCOME SCHEDULE Subject Property SF 12,000 Potential Gross Rental Income Estimate $86,400 Less Vacancy/Collection Loss 5% ($4,320) Effective Gross Income Estimate $82,080 Less Expenses % EGI PSF Real Estate Taxes $15, % $1.32 Insurance $3, % $0.33 Management $1, ?%? $0.14 Reserves $1, % $0.10 Total Expenses $22, % $1.88 $22,585 Net Operating Income $59,495 Direct Capitalization. This technique provides an opinion of value based upon the direct inference between income and value, using the formula I/R = V, where I is the net operating income, R is the overall capitalization rate and V equals value. This technique is based on an accrual accounting model, which addresses the initial year's operating statement stabilized after achieving a 95% occupancy level. Capitalization Rate Analysis. The estimation of the overall capitalization rate was approached through analysis of data from two primary sources; i.e., Market Extraction and a Mortgage-Equity analysis (or Band of Investment) based upon typical third party financing currently available in the market place. Market Extraction Method. In this case, we have developed an overall rate from an analysis of the market sales considered in the Sales Comparison Approach section of this report. An overall rate was derived by dividing the estimated net operating income of the sale property by its sale price. This technique involves constant dollars and stabilized operating expenses. The sales are generally 20

33 INCOME APPROACH TO VALUE - CONTINUED considered representative of typical capitalization rates for this property type. All of the Improved Sales were purchased by an owner-user. As such, no capitalization rate could be extracted from these sales. According to the 2 st Quarter 2016 PricewaterhouseCoopers (PwC) Real Estate Investor Survey Report, going-in capitalization rates for the National Warehouse market ranged from 3.00% to 7.00% with an average of 5.38%. This average is down 14 basis points over the 1 st Quarter 2015 survey, in which going-in capitalization rates for the National Warehouse market averaged 5.52%. Band of Investment Method. For purposes of this report, we have also used the band of investment technique and the debt coverage ratio techniques to estimate the appropriate overall rate (OAR). Both investment techniques presume that financing plays a major role in determining the OAR. This technique of developing a capitalization rate basically involves a synthesis between a mortgage constant and an equity dividend rate, each weighted by its percentage of contribution. The mortgage portion of this rate includes an allowance for both interest on and amortization of the mortgage component. The following is a summary of data from information published in the RealtyRates.com 3 rd Quarter 2016 Investor Survey: RealtyRates.com Investment Survey - Warehouses and Distribution Centers Minimum Maximum Average Interest Rate 2.86% 6.00% 4.43% Amortization (years) Mortgage Constant Loan to Value Ratio 60% 90% 75% Equity Dividend 7.39% 15.38% 10.99% Our research, including reviews of information published above and conversations with local lenders, revealed that mortgage terms for this type of property are being quoted to a credit-worthy customer in the range of 2.86% to 6.00%. The typical amortization period is 28 years. Additionally, the typical loan to value ratio is 75%. Assuming an 4.75% interest rate and a 25-year amortization, the annual mortgage constant is calculated to be Also, assuming a loan to value ratio of 75%, the remainder of the total value (i.e. 25%) is attributable to the equity contribution. Equity dividend rates for this type of investment have typically ranged from 7.39% to 15.38%. The calculations used to develop a capitalization rate via the Band of Investment technique is illustrated as follows: 21

34 Band of Investment Mortgage Portion 75.00% x % Equity Portion 25.00% x % Indicated Overall Rate % % (Say) 7.63% Capitalization Rate Conclusion. Based on the above and considering the rental rate for the subject at a market rate, an 7.50% capitalization rate has been utilized in the following schedule to finalize the value for the subject via the Income Approach. Utilizing the indicated (OAR) of 7.50%, an indication of value As Is market value can be derived through the formula NOI/R o = V. The following schedule details the value indications via the income approach: Stabilized Net Operating Income: $59,495 Overall Capitalization Rate: 7.50% Indicated Value: $793,267 As Is Market Value via the Income Approach: $790,000 22

35 RECONCILIATION AND FINAL VALUE OPINION The Reconciliation involves weighing the value indications provided by each method in light of its dependability as a reflection of the probable actions of users and investors in the market place. The appraiser s final conclusion of value may coincide with one of the approaches or it may reflect a weighing of relative merits of each of the approaches in leading to a final conclusion. Two methods of property valuation was used in this appraisal, the Market Approach-Improvements Only, and this final sector is the discussion of the value indication provided by this approach. Consideration of the relative merits of each value indication involves reviewing each approach with respect to: 1) reliability of the data used; 2) the applicability of the approach to the type of property being appraised; and 3) the applicability of the approach in light of the definition of value sought. Market Approach The Market Approach was used in this appraisal to provide an opinion of the land value of the property and the value of the property as improved, which takes into account the improvements. The strength of the sales comparison approach in any appraisal is that if comparable market data is available, it should accurately reflect the attitudes of typical buyers and sellers in the market place. In other words, sales of comparable properties or improvements can be analyzed and compared to the subject with adjustments being made for various different characteristics. The resulting As Is value indication via the Market Approach is as follows: $840,000 Income Approach The Income Approach method of property valuation was utilized in this report. In this approach, comparable rental information as well as expense information is extracted from the market place. We have used the direct capitalization technique to arrive at a value indication. The strength of this approach is that revenue projections, expense projections and the capitalization rate contained herein are supported by actual contract rates and market data. The value indication via the Income Approach is as follows: $790,000 Final Value Opinion. We valued the subject property utilizing the Sales Comparison and Income Approaches. We did not utilized the Cost Approach as this approach is not typically used by purchasers in making investment decisions on this type of property. We placed emphasis on both approaches. It is our opinion the subject property, if properly marketed, could be sold within a 12 month exposure period and a 12 month marketing period. The As Is Market Value of the Fee Simple Estate for the subject property as of the effective date of January 11, 2017 as follows: $815,000 23

36 ADDENDA

37 QUALIFICATIONS

38 QUALIFICATIONS OF MICHAEL B. LANE, MAI Business MB LANE & ASSOCIATES, INC. Telephone: (713) Hempstead Highway, Suite 102 Fax: (713) Houston, Texas Employment History 1999 to Present MBLane & Associates, Inc President Houston, TX 1997 to 1999 First Union Capital Markets Group Vice President Houston, TX 1994 to 1997 Banc One Capital Markets Group Underwriter Houston, TX 1986 to 1994 Edward B. Schulz & Company Senior Appraiser Houston, TX Education University of Arkansas Bachelor of Business Administration Major: Finance & Real Estate 1985 Certifications General Real Estate Appraiser in the State of Texas Certification Number: TX G Licensed Real Estate Broker in the State of Texas License Number: Member - Appraisal Institute (MAI) Current - December 31, 2016 Training (1989 to Present) Appraisal Reporting Basic Valuation Procedures Capitalization Theory & Techniques, Part A Capitalization Theory & Techniques, Part B Case Studies in Real Estate Valuation Defensible Appraisal Demonstration Report Writing Fundamentals of Separating Real Property, Personal Property & Intangible Business Assets General Market Analysis and Highest & Best Use Interagency Rules of Banks & Credit Unions National USPAP Update Property Tax Real Estate Appraisal Principles Report Writing and Valuation Analysis Sales Comparison-Adjustment Process Standards of Professional Practice, Part A Standards of Professional Practice, Part B Write It Up

39 QUALIFICATIONS OF MICHAEL B. LANE, MAI - CONTINUED Types of Real Estate Appraised & Consulting Assignments Partial List of Representative Clients Assisted Living Facilities Allegiance Bank Lowery Bank Automobile Dealership Alliance Bank Members Choice Credit Union Automotive Repair Facilities Bancorp South Moody National Bank Business Parks BB&T Patriot Bank Churches BBVA Compass Plains State Bank Condemnation Beal Bank Post Oak Bank Convenience Stores CBB Bank Prosperity Bank Fast-Food Franchises Chase/JP Morgan Q10 Kinghorn, Driver, Hough & Co. Garden Apartments Citizens State Bank Regions Bank Greenhouse/Nurseries City Bank Texas Smart Financial Credit Union Industrial & Manufacturing Coamerica Bank StanCorp Mortgage Investors Leasehold Valuation Community First Bank & Trust Stearns Bank Manual & Full Service Car Washes East West Bank Symetra Financial Medical Office Buildings Evolve Bank & Trust Synergy Bank Mini-Warehouses Fidelity Bank Texas Advantage Community Bank Mobile Home Parks GE Capital Texas Gulf Bank Motels & Hotels Guaranty Bank & Trust Tradition Bank Nursing Homes Heritage Bank Trustmark Bank Office Buildings IBC Bank US Bank Recreational Vehicle Park Independence Bank ValueBank Texas Resort and Recreational Development Independent Bank of Texas Wells Fargo Bank Restaurants/Bars Iron Stone Bank Wilshire State Bank Service Stations Shopping Centers Various Types of Studies Single-Family Subdivisions Environmental Impact Studies Special Purpose Properties Feasibility Studies Time Share Project Highest and Best Use Studies Townhouse Developments Market Studies Vacant Land

40 IMPROVED SALES AND MAP

41 Sale 1 Sale 2 Sale 3

42 Sale 4 Sale 5

43 RENTAL MAP

44

45 \ FLOOD MAP

46

47 SUBJECT PHOTOGRAPHS

48 VIEWS OF THE SUBJECT PROPERTY

49 INTERIOR VIEWS

50 NORTHEASTERLY VIEW ALONG UTAH ST. WITH THE SUBJECT TO THE LEFT NORTHWESTERLY VIEW ALONG UTAH ST. WITH THE SUBJECT TO THE RIGHT

A Demonstration Appraisal Report. Of a. Located at. Date of Appraisal. Prepared for. Prepared by

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 West 10 th Street Kansas

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 West 10 th Street Kansas

A Demonstration Appraisal Report. Of a. Located at. Date of Appraisal. Prepared for. Prepared by

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 W. 10 th Street Kansas

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 W. 10 th Street Kansas

RESTRICTED APPRAISAL REPORT

Restricted Use Appraisal Report Thomas J. Schulte & Associates Page #1 RESTRICTED APPRAISAL REPORT SUBJECT ASSIGNMENT Property City: Zip Code: County: Legal Description: Assessor's Parcel #: Tax Year:

Restricted Use Appraisal Report Thomas J. Schulte & Associates Page #1 RESTRICTED APPRAISAL REPORT SUBJECT ASSIGNMENT Property City: Zip Code: County: Legal Description: Assessor's Parcel #: Tax Year:

To all Appraisers: Brief Overview:

To all Appraisers: As the appraisal industry continues to change, the demand for alternative valuation solutions grows. That is why is excited to announce the addition of a new product - the Desktop Appraisal

To all Appraisers: As the appraisal industry continues to change, the demand for alternative valuation solutions grows. That is why is excited to announce the addition of a new product - the Desktop Appraisal

EvaluePro Real Estate Restricted Appraisal Report

EvaluePro Real Estate Restricted Appraisal Report EvaluePro Highlights Property Street: 1000 Main Street City: Anytown State: NC Zip: 12345 Property Owner: Mr. & Mrs. Property Owner Estimated Market Value:

EvaluePro Real Estate Restricted Appraisal Report EvaluePro Highlights Property Street: 1000 Main Street City: Anytown State: NC Zip: 12345 Property Owner: Mr. & Mrs. Property Owner Estimated Market Value:

Copyright, 1999, 2002, 2004, Freddie Mac. All Rights Reserved.

Page 1 of 13 Engineering Requirements/Chapter 12: Appraiser and Appraisal Requirements/12.1: General requirements 12.1: General requirements For all multifamily purchase programs and products, the Seller/Servicer

Page 1 of 13 Engineering Requirements/Chapter 12: Appraiser and Appraisal Requirements/12.1: General requirements 12.1: General requirements For all multifamily purchase programs and products, the Seller/Servicer

Appraisal Stream Restricted Use Residential Appraisal Report

Appraisal Stream Restricted Use Residential Appraisal Report File No. 769kemplin This report is limited to the sole and exclusive use of the client. The appraiser's opinions and conclusions set forth in

Appraisal Stream Restricted Use Residential Appraisal Report File No. 769kemplin This report is limited to the sole and exclusive use of the client. The appraiser's opinions and conclusions set forth in

619 STANDARD 2: REAL PROPERTY APPRAISAL, REPORTING

619 STANDARD 2: REAL PROPERTY APPRAISAL, REPORTING 620 In reporting the results of a real property appraisal, an appraiser must communicate each analysis, 621 opinion, and conclusion in a manner that is

619 STANDARD 2: REAL PROPERTY APPRAISAL, REPORTING 620 In reporting the results of a real property appraisal, an appraiser must communicate each analysis, 621 opinion, and conclusion in a manner that is

Anatomy Of An Appraisal

Anatomy Of An Appraisal Leslie A. Fields The most important thing to know about an appraisal report is how to review and critique it. Leslie A. Fields a partner with the Law Firm of Faegre & Benson LLP,

Anatomy Of An Appraisal Leslie A. Fields The most important thing to know about an appraisal report is how to review and critique it. Leslie A. Fields a partner with the Law Firm of Faegre & Benson LLP,

As Of: Prepared For: Prepared By:

of 216 SW 131st St As Of: 06/11/11 Prepared For: Prime Pacific Bank 2502 196th St SW Lynnwood WA 98036 Prepared By: Cynthia A. Nagle, CREA 922 N Cedar St Tacoma, WA 98406 RESTRICTED APPRAISAL REPORT Restriction

of 216 SW 131st St As Of: 06/11/11 Prepared For: Prime Pacific Bank 2502 196th St SW Lynnwood WA 98036 Prepared By: Cynthia A. Nagle, CREA 922 N Cedar St Tacoma, WA 98406 RESTRICTED APPRAISAL REPORT Restriction

UPDATED MARKET VALUE APPRAISAL. Day Care/Senior Center Property and Excess Parcel Governors Drive Olympia Fields, Illnois.

J _,i UPDATED MARKET VALUE APPRASAL Day Care/Senior Center Property and Excess Parcel 20080 Governors Drive Olympia Fields, llnois _ as of: March 16, 2007 Prepared for: Mr. Steve Townsend, Vice President

J _,i UPDATED MARKET VALUE APPRASAL Day Care/Senior Center Property and Excess Parcel 20080 Governors Drive Olympia Fields, llnois _ as of: March 16, 2007 Prepared for: Mr. Steve Townsend, Vice President

How to Read a Real Estate Appraisal Report

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

AN APPRAISAL OF Acre Residential Site Northwest Corner Pleasant View Road & Gaar Road Richmond, Indiana 47374

AN APPRAISAL OF 3.75 Acre Residential Site Northwest Corner Pleasant View Road & Gaar Road Richmond, Indiana 47374 American United Appraisal Company, Inc. Real Estate Appraisers Jay E. Allardt, SRA August

AN APPRAISAL OF 3.75 Acre Residential Site Northwest Corner Pleasant View Road & Gaar Road Richmond, Indiana 47374 American United Appraisal Company, Inc. Real Estate Appraisers Jay E. Allardt, SRA August

Guide Note 6 Consideration of Hazardous Substances in the Appraisal Process

Guide Note 6 Consideration of Hazardous Substances in the Appraisal Process Introduction The consideration of environmental conditions along with social, economic, and governmental conditions is fundamental

Guide Note 6 Consideration of Hazardous Substances in the Appraisal Process Introduction The consideration of environmental conditions along with social, economic, and governmental conditions is fundamental

ILLINOIS HOUSING DEVELOPMENT AUTHORITY APPRAISAL SCOPE AND GUIDELINES December 2015

ILLINOIS HOUSING DEVELOPMENT AUTHORITY APPRAISAL SCOPE AND GUIDELINES December 2015 As part of the Common Application for Multifamily Financing, the Illinois Housing Development Authority (IHDA) requires

ILLINOIS HOUSING DEVELOPMENT AUTHORITY APPRAISAL SCOPE AND GUIDELINES December 2015 As part of the Common Application for Multifamily Financing, the Illinois Housing Development Authority (IHDA) requires

concepts and techniques

concepts and techniques S a m p l e Timed Outline Topic Area DAY 1 Reference(s) Learning Objective The student will learn Teaching Method Time Segment (Minutes) Chapter 1: Introduction to Sales Comparison

concepts and techniques S a m p l e Timed Outline Topic Area DAY 1 Reference(s) Learning Objective The student will learn Teaching Method Time Segment (Minutes) Chapter 1: Introduction to Sales Comparison

RAINS COUNTY APPRAISAL DISTRICT

RAINS COUNTY APPRAISAL DISTRICT 2017 MASS APPRAISAL SUMMARY REPORT mass appraisal report 2017 uspap_appr_report RAINS COUNTY APPRAISAL DISTRICT 2017 MASS APPRAISAL SUMMARY REPORT Identification of Subject:

RAINS COUNTY APPRAISAL DISTRICT 2017 MASS APPRAISAL SUMMARY REPORT mass appraisal report 2017 uspap_appr_report RAINS COUNTY APPRAISAL DISTRICT 2017 MASS APPRAISAL SUMMARY REPORT Identification of Subject:

REED APPRAISAL COMPANY REAL PROPERTY APPRAISERS AND CONSULTANTS

REAL PROPERTY APPRAISERS AND CONSULTANTS 100 SOUTH KENTUCKY AVENUE #230 ip.o. BOX 1645 ilakeland, FLORIDA 33802-1645 OFFICE: (863) 688-6718 ifax: (863) 688-5993iEMAIL: stan@reedappraisalco.com TO: Henry

REAL PROPERTY APPRAISERS AND CONSULTANTS 100 SOUTH KENTUCKY AVENUE #230 ip.o. BOX 1645 ilakeland, FLORIDA 33802-1645 OFFICE: (863) 688-6718 ifax: (863) 688-5993iEMAIL: stan@reedappraisalco.com TO: Henry

APPRAISAL REPORT. Vacant Commercial Land SW 268 th Street Miami, FL Cruz Appraisals, Inc SW 72 nd Street, Suite 263 Miami, FL 33173

APPRAISAL REPORT Prepared for Mr Jorge Palomeras Jpal Marketing Corporation Property Appraised Vacant Commercial Land 12711 SW 268 th Street Miami, FL 33032 Date of Valuation October 6, 2017 Prepared by

APPRAISAL REPORT Prepared for Mr Jorge Palomeras Jpal Marketing Corporation Property Appraised Vacant Commercial Land 12711 SW 268 th Street Miami, FL 33032 Date of Valuation October 6, 2017 Prepared by

FIRST AMENDMENT TO LEASE

Attachment 1 FIRST AMENDMENT TO LEASE THIS FIRST AMENDMENT TO LEASE, dated, 2013 ( First Amendment ), by and between the State of California, acting by and through its Department of General Services, (hereinafter

Attachment 1 FIRST AMENDMENT TO LEASE THIS FIRST AMENDMENT TO LEASE, dated, 2013 ( First Amendment ), by and between the State of California, acting by and through its Department of General Services, (hereinafter

Mike Dalton Jr. and Associates. Christina Adams INVOICE NUMBER Mike Dalton Jr. and Associates 8191 Wethersfield Drive. PB125 Germantown, TN 38138

Mike Dalton Jr. and Associates FROM: INVOICE Christina Adams INVOICE NUMBER Mike Dalton Jr. and Associates 8191 Wethersfield Drive Germantown, TN 38138 DATE 08/14/2016 Telephone Number: (901) 674-0239

Mike Dalton Jr. and Associates FROM: INVOICE Christina Adams INVOICE NUMBER Mike Dalton Jr. and Associates 8191 Wethersfield Drive Germantown, TN 38138 DATE 08/14/2016 Telephone Number: (901) 674-0239

LOCAL IMPROVEMENT DISTRICT APPRAISER PRESENTATION. November 2017

LOCAL IMPROVEMENT DISTRICT APPRAISER PRESENTATION November 2017 SPECIAL BENEFIT STUDY WHY? A special benefit study is a tool consistently used with LID projects. Municipality retains an expert consultant

LOCAL IMPROVEMENT DISTRICT APPRAISER PRESENTATION November 2017 SPECIAL BENEFIT STUDY WHY? A special benefit study is a tool consistently used with LID projects. Municipality retains an expert consultant

Individual Cooperative Interest Appraisal Report

PURPOSE Individual Cooperative Interest Appraisal Report The purpose of this appraisal report is to provide the client with a credible opinion of the defined value of the subject property, given the intended

PURPOSE Individual Cooperative Interest Appraisal Report The purpose of this appraisal report is to provide the client with a credible opinion of the defined value of the subject property, given the intended

Uniform Agricultural Appraisal Report

File No. Uniform Agricultural Appraisal Report Prepared For: Intended User: Prepared By: Date Prepared: UAAR Agri management Uniform Agricultural Appraisal Report File No # Property Identification Owner/Occupant:

File No. Uniform Agricultural Appraisal Report Prepared For: Intended User: Prepared By: Date Prepared: UAAR Agri management Uniform Agricultural Appraisal Report File No # Property Identification Owner/Occupant:

Restricted Use Appraisal Report Of a development site

A development site Located at: 700' E of SEC of 6th Avenue and 328 St Homestead, Florida As of November 7, 2017 Restricted Use Appraisal Report Of a development site Restricted Use Appraisal Report Of

A development site Located at: 700' E of SEC of 6th Avenue and 328 St Homestead, Florida As of November 7, 2017 Restricted Use Appraisal Report Of a development site Restricted Use Appraisal Report Of

WATERFRONT LOCAL IMPROVEMENT DISTRICT OVERVIEW. November 2017

WATERFRONT LOCAL IMPROVEMENT DISTRICT OVERVIEW November 2017 LOCAL IMPROVEMENT DISTRICT Funding tool by which property owners financially contribute to a project that will increase the value of their property

WATERFRONT LOCAL IMPROVEMENT DISTRICT OVERVIEW November 2017 LOCAL IMPROVEMENT DISTRICT Funding tool by which property owners financially contribute to a project that will increase the value of their property

Interagency Appraisal and

Interagency Appraisal and Evaluation (IAEG) Workshop Purpose (77456) Supersedes the 1994 Interagency Appraisal & Evaluation Guidelines Address supervisory matters relating to real estate appraisal and

Interagency Appraisal and Evaluation (IAEG) Workshop Purpose (77456) Supersedes the 1994 Interagency Appraisal & Evaluation Guidelines Address supervisory matters relating to real estate appraisal and

RevuPro Appraisal Review

RevuPro Appraisal Review Getting It Right ELLIOTT introduces its flagship review product RevuPro, as an independent appraisal review service. Q. What is it and what does it do? A. RevuPro is a fast, economical

RevuPro Appraisal Review Getting It Right ELLIOTT introduces its flagship review product RevuPro, as an independent appraisal review service. Q. What is it and what does it do? A. RevuPro is a fast, economical

2. Is the information in the contract section complete and accurate? Yes No Not Applicable If Yes, provide a brief summary.

The purpose of this appraisal field review report is to provide the lender/client with an opinion on the accuracy of the appraisal report under review. Property Address City State Zip Code Borrower Owner

The purpose of this appraisal field review report is to provide the lender/client with an opinion on the accuracy of the appraisal report under review. Property Address City State Zip Code Borrower Owner

MODULE 7-A: APPRAISALS, BPOS AND USPAP

MODULE 7-A: APPRAISALS, BPOS AND USPAP LEARNING OBJECTIVES One of the most challenging aspects of the real estate business is the development of prices or values of the rights to real estate. Buyers and

MODULE 7-A: APPRAISALS, BPOS AND USPAP LEARNING OBJECTIVES One of the most challenging aspects of the real estate business is the development of prices or values of the rights to real estate. Buyers and

Table of Contents. Chapter 1: Introduction (Mobile Technology Evolution) 1

1") Chapter 1: Introduction (Mobile Technology Evolution) 1 I. WHY APPRAISAL IS IMPORTANT (p. 3) II. DEFINITION OF APPRAISAL (p. 4) A. Opinion (p. 4) B. Value (p. 5) C. Appraisal Art or Science? (p. 5) D.

Chapter 1: Introduction (Mobile Technology Evolution) 1 I. WHY APPRAISAL IS IMPORTANT (p. 3) II. DEFINITION OF APPRAISAL (p. 4) A. Opinion (p. 4) B. Value (p. 5) C. Appraisal Art or Science? (p. 5) D.

Dear Valuation Professional

Dear Valuation Professional First American Mortgage Solutions LLC has a new product offering that we would like you to consider adding to your list of services with us - (Property Assessment Collateral

Dear Valuation Professional First American Mortgage Solutions LLC has a new product offering that we would like you to consider adding to your list of services with us - (Property Assessment Collateral

[Code of Federal Regulations] [Title 12, Volume 5] [Revised as of January 1, 2004] From the U.S. Government Printing Office via GPO Access

![[Code of Federal Regulations] [Title 12, Volume 5] [Revised as of January 1, 2004] From the U.S. Government Printing Office via GPO Access](/thumbs/80/82487200.jpg "[Code of Federal Regulations] [Title 12, Volume 5] [Revised as of January 1, 2004] From the U.S. Government Printing Office via GPO Access") [Code of Federal Regulations] [Title 12, Volume 5] [Revised as of January 1, 2004] From the U.S. Government Printing Office via GPO Access TITLE 12--BANKS AND BANKING CHAPTER V--OFFICE OF THRIFT SUPERVISION,

[Code of Federal Regulations] [Title 12, Volume 5] [Revised as of January 1, 2004] From the U.S. Government Printing Office via GPO Access TITLE 12--BANKS AND BANKING CHAPTER V--OFFICE OF THRIFT SUPERVISION,

BADGER Appraisals, LLC

BADGER Appraisals, LLC PO Box 2222 Appleton, WI 54912 T (920) 687-9000 / F (920) 687-9244 info@badgerappraisals.com www.badgerappraisals.com Residential Appraisal Service Brown * Calumet * Outagamie *

BADGER Appraisals, LLC PO Box 2222 Appleton, WI 54912 T (920) 687-9000 / F (920) 687-9244 info@badgerappraisals.com www.badgerappraisals.com Residential Appraisal Service Brown * Calumet * Outagamie *

Sales Associate Course

Sales Associate Course Chapter Sixteen Appraisal 1 2 Appraiser Specific amount Impartial (non biased) Defendable Estimate (Opinion) of value Fee based on time and difficulty Must follow Uniform Standards

Sales Associate Course Chapter Sixteen Appraisal 1 2 Appraiser Specific amount Impartial (non biased) Defendable Estimate (Opinion) of value Fee based on time and difficulty Must follow Uniform Standards

Real Estate Appraisal Professional Standards

Real Estate Appraisal Professional Standards Summary This proposal is to amend the Florida Administrative Code (FAC) to allow a Certified Residential Appraiser or a Certified General Appraiser to use standards

Real Estate Appraisal Professional Standards Summary This proposal is to amend the Florida Administrative Code (FAC) to allow a Certified Residential Appraiser or a Certified General Appraiser to use standards

LAND APPRAISAL REPORT

IDENTIFICATION LAND APPRAISAL REPORT Page #1 File No. Borrower None Census Tract * Map Reference 462820011000315 Property Address NWC Gaar and Pleasant View Roads City Richmond County Wayne State IN Zip

IDENTIFICATION LAND APPRAISAL REPORT Page #1 File No. Borrower None Census Tract * Map Reference 462820011000315 Property Address NWC Gaar and Pleasant View Roads City Richmond County Wayne State IN Zip

William K. Boyd, Inc.

Real Estate Appraisers & Consultants Main Office 1564 Lakeview Drive Sebring, FL 33870 Satellite Office 410 Northwest 2 nd St Okeechobee, FL 34972 Phone: 863 385-6192 Fax: 866-384-0258 November 22, 2017

Real Estate Appraisers & Consultants Main Office 1564 Lakeview Drive Sebring, FL 33870 Satellite Office 410 Northwest 2 nd St Okeechobee, FL 34972 Phone: 863 385-6192 Fax: 866-384-0258 November 22, 2017

MARKET VALUE BASIS OF VALUATION

4.2 INTERNATIONAL VALUATION STANDARDS 1 MARKET VALUE BASIS OF VALUATION This Standard should be read in the context of the background material and implementation guidance contained in General Valuation

4.2 INTERNATIONAL VALUATION STANDARDS 1 MARKET VALUE BASIS OF VALUATION This Standard should be read in the context of the background material and implementation guidance contained in General Valuation

COMMERCIAL PROPERTY SUMMARY APPRAISAL REPORT

Redwood Appraisal (650) 533-4065 COMMERCIAL PROPERTY SUMMARY APPRAISAL REPORT Property Address: City: State: Zip: County: Legal Description: Page #1 SUBJECT Building Name (if applicable): Parcel ID #(s):

Redwood Appraisal (650) 533-4065 COMMERCIAL PROPERTY SUMMARY APPRAISAL REPORT Property Address: City: State: Zip: County: Legal Description: Page #1 SUBJECT Building Name (if applicable): Parcel ID #(s):

Demonstration Appraisal Report Utilizing a Form Report

Demonstration Appraisal Report Utilizing a Form Report National Association of Independent Fee Appraisers 330 North Wabash Avenue, Suite 2000 Chicago, IL 60611 Phone: (312) 321-6830 Fax: (312) 673-6652

Demonstration Appraisal Report Utilizing a Form Report National Association of Independent Fee Appraisers 330 North Wabash Avenue, Suite 2000 Chicago, IL 60611 Phone: (312) 321-6830 Fax: (312) 673-6652

MARKET RENTAL ANALYSIS OF A: MEDICAL OFFICE SPACE LOCATED AT XXXXXXXX SUITE XXXX NEW YORK, NEW YORK DATE OF RENTAL VALUE: DECEMBER 3, 2014

MARKET RENTAL ANALYSIS OF A: MEDICAL OFFICE SPACE LOCATED AT XXXXXXXX SUITE XXXX NEW YORK, NEW YORK 10017 DATE OF RENTAL VALUE: DECEMBER 3, 2014 DATE OF REPORT: DECEMBER 10, 2014 PREPARED FOR: XXXXXXXXXXXXXX

MARKET RENTAL ANALYSIS OF A: MEDICAL OFFICE SPACE LOCATED AT XXXXXXXX SUITE XXXX NEW YORK, NEW YORK 10017 DATE OF RENTAL VALUE: DECEMBER 3, 2014 DATE OF REPORT: DECEMBER 10, 2014 PREPARED FOR: XXXXXXXXXXXXXX

Summary of Assignment. Identification of Property and Appraisal

Summary of Assignment My assignment is to review an appraisal of the Athow Property owned by Lewis and Janice Athow. The property is located near the mouth of the Dungeness River in Clallam County, Washington

Summary of Assignment My assignment is to review an appraisal of the Athow Property owned by Lewis and Janice Athow. The property is located near the mouth of the Dungeness River in Clallam County, Washington

Source: Reg. Y, 55 FR 27771, July 5, 1990, unless otherwise noted.

Subpart G Appraisal Standards for Federally Related Transactions Source: Reg. Y, 55 FR 27771, July 5, 1990, unless otherwise noted. 225.61 Authority, purpose, and scope. (a) Authority. This subpart is

Subpart G Appraisal Standards for Federally Related Transactions Source: Reg. Y, 55 FR 27771, July 5, 1990, unless otherwise noted. 225.61 Authority, purpose, and scope. (a) Authority. This subpart is

Page 1 of 5 STANDARD 3: APPRAISAL REVIEW, DEVELOPMENT AND REPORTING In performing an appraisal review, an appraiser acting as a reviewer must develop and report a credible opinion as to the quality of

Page 1 of 5 STANDARD 3: APPRAISAL REVIEW, DEVELOPMENT AND REPORTING In performing an appraisal review, an appraiser acting as a reviewer must develop and report a credible opinion as to the quality of

Appraisal and Market Analysis of Indoor Waterpark Resorts

Appraisal and Market Analysis of Indoor Waterpark Resorts By David J. Sangree, MAI, CPA, ISHC An appraisal of an indoor waterpark resort is similar to other appraisals in that it is a professional appraiser

Appraisal and Market Analysis of Indoor Waterpark Resorts By David J. Sangree, MAI, CPA, ISHC An appraisal of an indoor waterpark resort is similar to other appraisals in that it is a professional appraiser

APPRAISAL OF 1117 MONROE STREET, VICKSBURG, MS 39180

APPRAISAL OF 1117 MONROE STREET, VICKSBURG, MS 39180 CLIENT/INTENDED USER: GLENN TRIPLETT INTENDED USE/USER: TO ASSIST THE CLIENT IN MAKING A PURCHASING DECISION. THIS REPORT IS NOT INTENDED FOR ANY OTHER

APPRAISAL OF 1117 MONROE STREET, VICKSBURG, MS 39180 CLIENT/INTENDED USER: GLENN TRIPLETT INTENDED USE/USER: TO ASSIST THE CLIENT IN MAKING A PURCHASING DECISION. THIS REPORT IS NOT INTENDED FOR ANY OTHER

Real Property Appraisal Summary Report of an Existing Office Condominium Unit

Real Property Appraisal Summary Report of an Existing Office Condominium Unit Located at: Morlake Executive Suites Condominium Complex 114 Morlake Drive, Suite 202 Mooresville, Iredell County, North Carolina,

Real Property Appraisal Summary Report of an Existing Office Condominium Unit Located at: Morlake Executive Suites Condominium Complex 114 Morlake Drive, Suite 202 Mooresville, Iredell County, North Carolina,

BADGER Appraisals, LLC

BADGER Appraisals, LLC PO Box 2222 Appleton, WI 54912 T (920) 687-9000 / F (920) 687-9244 info@badgerappraisals.com www.badgerappraisals.com Appraisal Service Brown * Calumet * Outagamie * Winnebago APPRAISAL

BADGER Appraisals, LLC PO Box 2222 Appleton, WI 54912 T (920) 687-9000 / F (920) 687-9244 info@badgerappraisals.com www.badgerappraisals.com Appraisal Service Brown * Calumet * Outagamie * Winnebago APPRAISAL

Office of the Comptroller of the Currency Federal Deposit Insurance Corporation Federal Reserve Board Office of Thrift Supervision

Office of the Comptroller of the Currency Federal Deposit Insurance Corporation Federal Reserve Board Office of Thrift Supervision Purpose Interagency Appraisal and Evaluation Guidelines October 27, 1994

Office of the Comptroller of the Currency Federal Deposit Insurance Corporation Federal Reserve Board Office of Thrift Supervision Purpose Interagency Appraisal and Evaluation Guidelines October 27, 1994

APPRAISAL OF REAL PROPERTY LOCATED AT: FOR: AS OF: BY:

APPRAISAL OF REAL PROPERTY LOCATED AT: 489 MEADOWS EDGE COURT DEED BOOK 2896, PAGE 2759 CLEMMONS, NC 27012 FOR: ESTATE OF WILLIAM C. McINTOSH % BAILEY & THOMAS P.O. BOX 52 WINSTON-SALEM, NC 27102 AS OF:

APPRAISAL OF REAL PROPERTY LOCATED AT: 489 MEADOWS EDGE COURT DEED BOOK 2896, PAGE 2759 CLEMMONS, NC 27012 FOR: ESTATE OF WILLIAM C. McINTOSH % BAILEY & THOMAS P.O. BOX 52 WINSTON-SALEM, NC 27102 AS OF:

Swisher County Appraisal District 2017 Mass Appraisal Report

Swisher County Appraisal District 2017 Mass Appraisal Report Prepared Pursuant to Standard 6 of the Uniform Standards of Professional Appraisal Practice 1 TABLE OF CONTENTS Introduction 3 Listing of Taxing

Swisher County Appraisal District 2017 Mass Appraisal Report Prepared Pursuant to Standard 6 of the Uniform Standards of Professional Appraisal Practice 1 TABLE OF CONTENTS Introduction 3 Listing of Taxing

VHDA Low Income Housing Tax Credit Manual Version: K. Appraisal Guidelines

VHDA Low Income Housing Tax Credit Manual Version: 2018.1 K. Appraisal Guidelines VHDA LIHTC Program Page 119 Last Modified: 11/30/2017 Appraisal Information Appraisals are required to be submitted with

VHDA Low Income Housing Tax Credit Manual Version: 2018.1 K. Appraisal Guidelines VHDA LIHTC Program Page 119 Last Modified: 11/30/2017 Appraisal Information Appraisals are required to be submitted with

Land, Agricultural Improvements, CAFO, Rural Residence, Farm

*--FSA Appraisal Guidelines Land, Agricultural Improvements, CAFO, Rural Residence, Farm The following information elements and content descriptions are provided as guidelines to assist lenders and appraisers

*--FSA Appraisal Guidelines Land, Agricultural Improvements, CAFO, Rural Residence, Farm The following information elements and content descriptions are provided as guidelines to assist lenders and appraisers

Avoiding Common Errors in Appraisals for Financial

Avoiding Common Errors in Appraisals for Financial Institutions Panelists: Brian Bailey, CCIM, Senior Financial Analyst Commercial Real Estate, Federal Reserve Bank of Atlanta James Murrett, MAI, Director

Avoiding Common Errors in Appraisals for Financial Institutions Panelists: Brian Bailey, CCIM, Senior Financial Analyst Commercial Real Estate, Federal Reserve Bank of Atlanta James Murrett, MAI, Director

2015 Appraisal Guidelines

2015 Appraisal Guidelines Pursuant to Section 13 VAC 10-180-60 of the QAP, appraisals are required for all acquisition, acquisition/rehab and adaptive reuse developments, where the applicant is seeking

2015 Appraisal Guidelines Pursuant to Section 13 VAC 10-180-60 of the QAP, appraisals are required for all acquisition, acquisition/rehab and adaptive reuse developments, where the applicant is seeking

APPRAISAL REPORT OF GROSS ACRES/17.72± USABLE ACRES OF VACANT COMMERCIAL LAND

APPRAISAL REPORT OF 20.22 GROSS ACRES/17.72± USABLE ACRES OF VACANT COMMERCIAL LAND LOCATED AT NORTHWEST CORNER OF LAND O LAKES BOULEVARD & SUNTERRA DRIVE LAND O LAKES, FLORIDA 34638 Job No.: 14-0227 Prepared

APPRAISAL REPORT OF 20.22 GROSS ACRES/17.72± USABLE ACRES OF VACANT COMMERCIAL LAND LOCATED AT NORTHWEST CORNER OF LAND O LAKES BOULEVARD & SUNTERRA DRIVE LAND O LAKES, FLORIDA 34638 Job No.: 14-0227 Prepared

YOUNG CENTRAL APPRAISAL DISTRICT