Journey of Real estate (Past, present and Future) Speaker CA Sandesh Mundra

|

|

|

- Cynthia Morton

- 5 years ago

- Views:

Transcription

1 Journey of Real estate (Past, present and Future)

2 Goods Service Land GST on goods & Service not on land Why land is the third category? Roots in history. Lets check..!!

3 States not in control of Britishers were under Suzerainty of British Crown. Some British enclaves controlled by Portugal

4 Instruments signed by Princely States States under Britishers - Instrument of Accession -three powers to Govt. Defence, external affairs, and communications States with intermediate status signed another Instrument to preserve degree of power they had under Britishers States with substantial administration of Britishers, had a different Instrument of Accession Only leasehold rights available in some cases Kandla Port trust/navi Mumbai/NOIDA and All Industrial Development Corporations

5 How to define land? Not defined under GST / Income Tax Land Not defined in Transfer of Property Act and in General Clauses Act Some Land Revenue Codes and Land Acquisition Act - Land includes benefits to arise out of land and things attached to the earth or permanently fastened to anything attached to the earth

6 Service tax Evolution of indirect taxes on real estate Levy introduced in 1994 Levy introduced on Construction services in 2004 Levy introduced on Works Contract in 2007 Levy confirmed on Developers in 2013 in Larsen and Turbo by confirming the ratio in Raheja Corporation

7 Supply under GST All forms of supply of goods or services or both made or agreed to be made for a consideration by a person in the course or furtherance of business Activities in Schedule III not be treated as supply - Entry (5). Sale of land Goods - 2(52) goods means every kind of movable property... Services - (102) services means anything other than goods. Previous regime Service means an activity for consideration excluding immovable property.

8 Rights in land Right to mortgag e Right to develop Right to license Easemen t rights Right to resell Tenanc y rights Right to lease

9 Deemed service under Schedule II of GST Act Right to mortgag e Right to develop Right to license Easeme nt rights Right to resell Tenancy rights Right to lease

10 Development Rights Transferable development rights Non-transferable development rights - European countries in India started in Bombay in 1990 for slum Looking to the Indian Govt., private individuals also started this concept

11 Developm ent Control Regulation s Stamp Duty Income tax Developme nt rights Pre GST GST RERA

12 Treatment of development rights in pre GST era Not taxed under VAT / Service Tax However Construction/works contract service in lieu of development rights Taxable under service tax Barter cannot be taxed as per Gannon Dunkerly 1958 (SC). Negative view in M/s Sumer Corporation..Bombay High Court

13 Develop ment Control Regulatio ns Stam p Duty Income tax Developm ent rights Pre GST GST RERA

14 Stamp duty for development rights in Maharashtra Stamp duty on DR same as that on conveyance

15 Valuation rules in Greater Mumbai for Stamp duty on development agreements Transaction In case of area sharing arrangements, Higher of :- In case of revenue sharing, Higher of :- Valuation Land owner area as per construction rate + money to land owner Developer s land x Rate of Land Current Value of the land owner s share in terms of the rate of sale having regard to the permissible user thereof x monetary compensation awarded to the land owner Valuation of the whole land at the rate of land

16 Developm ent Control Regulation s Stamp Duty Income tax Developme nt rights Pre GST GST RERA

Bill, 2016 passed by Rajya Sabha 01 May, 2016 The Act is enacted 25")

17 Real Estate Regulation and Development Act 01 May, 2018 Deadline to establish an exclusive website 01 May, 2017 Deadline for Rules & Authority to be set by each state May 2008 Concept paper on regulation of real estate sector and a model law for legislation prepared 10 March, 2016 Real Estate (Regulation and Development) Bill, 2016 passed by Rajya Sabha 01 May, 2016 The Act is enacted 25 March, March, 2016 Bill passed in Lok Sabha Bill receives President s assent

18 Specific Issues relating to Joint Development Model under RERA Area Sharing Model Revenue Sharing Model

19 Specific Issues relating to Joint Development Model under RERA Land Owner or Developer liable for registration under RERA? More than one separate Bank Account? Common Collection towards land and construction? GST implications Compulsory Registration of JDA No escape from capital gains? Registration of each phase separately Merits and Demerits

20 Specific Issues relating to Joint Development Model under RERA Power of Attorney in lieu of Joint Development Agreement? Compulsory to be registered? Land Cost not in the books of Developer..filled in Form 3 by developer(ca Certificate)? Cost of Land Historical Cost or FMV or Indexed Cost?

21 Developme nt Control Regulation s Stamp Duty Income tax Developme nt rights Pre GST GST RERA

22 Development rights in income tax Section 2(47) - "transfer", in relation to a capital asset, includes, (v) any transaction referred to in S. 53A of the TPA (DR covered) or.form (vi) any transaction (whether by way of becoming a member of, or acquiring shares in, a cooperative society, company or other association of persons or by way of any agreement or any arrangement or in any other manner whatsoever) which has the effect of transferring, or enabling the enjoyment of, any immovable property..substance Transfer includes transfer of development rights and its transfer attracts capital gain in Income tax

23 Development rights in income tax 45(5A) Capital gain arises to an assessee being an individual or a HUF from transfer of capital asset, being land or building or both, under a specified agreement, (DR is land) capital gains shall be chargeable to income-tax as income of the previous year in which the certificate of completion for the whole or part of the project is issued by the competent authority; and for the purposes of section 48, the stamp duty value, on the date of issue of the said certificate, of his share, being land or building or both in the project, as increased by the consideration received in cash, if any, shall be deemed to be the full value of the consideration received or accruing as a result of the transfer of the capital asset.

24 Development rights in income tax Provided that the provisions of this sub-section shall not apply where the assessee transfers his share in the project on or before the date of issue of the said certificate of completion and capital gains shall be deemed to be income of the previous year in which such transfer takes place and the provisions of this Act, other than the provisions of this sub-section, shall apply for the purpose of determination of full value of consideration received or accruing as a result of such transfer.

25 Correlation between income tax and GST Section 45(5A) of income tax says that through the specified agreement, land or building stands transferred. Can we refer the same in GST as sale of land? In income tax and GST, deferment of point of taxation only to pure area sharing arrangements where cash inflow does not happen initially. Area sharing whether part or whole is allowed for deferring tax liability. If landowner further transferred his part of units before allotment then, no deferment

26 Developme nt Control Regulations Stamp Duty Income tax Developme nt rights Pre GST GST RERA

27 Department s view

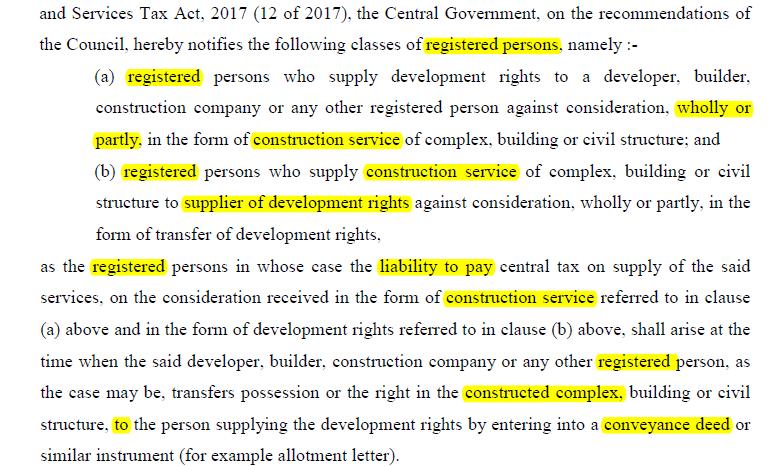

28 Notification 4/2018

29 All development rights (Taxability on text) Whether transfer of development rights/transfer of TDR are:- 1. Sale of land??? 2. Supply of services..???? Let us discuss..!!!

30 Two edged sword Notification 4/2018 CGST (Rate) dated Lets look at a practical case :-

31 Tax impact on affordable housing as a new business Option

32 Benefits under GST in two ways Lower rate Exemption

33 Lower rates under Notification 11/2017-CGST (Rate) dated For RAY For JNNMRU For PMAY For State Govt. Scheme For infrastructure status For Any other scheme

34 Infrastructure Status The following entry was inserted vide Notification 1/2018-Central Tax (Rate) dated Sr No 1. Original + Repair + Maintenance Particulars 12% Rate low-cost houses of carpet area of 60 square metres per house in an affordable housing project which has been given infrastructure status vide notification of Government of India, in Ministry of Finance, Department of Economic Affairs vide F. No. 13/6/2009-INF, dated the 30th March,2017; (Effective tax rate after land deduction of 1/3rd of total is 8%) (as per notification of Economic Affairs)

35 Definitions as per Notification Affordable Housing is defined as a housing project using at least 50% of the Floor Area Ratio (FAR)/Floor Space Index (FSI) for dwelling units with carpet area of not more than 60 square meters. (FAR = Total covered area / plot area) Carpet Area shall have the same meaning as assigned to it in clause (k) of section 2 of the Real Estate (Regulation and Development) Act, Calculation of FSI limit Common area treatment No tender required for this scheme

Original + Repairs + Maintenance (c) a civil structure or any other original works pertaining to the In-situ rehabilitation of existing slum dwellers using land as a")

36 In-Situ Redevelopment of existing slums Date Notificatio n No. Particulars Rate OLD /2017- Central Tax (Rate) Original + Repairs + Maintenance (c) a civil structure or any other original works pertaining to the In-situ rehabilitation of existing slum dwellers using land as a resource through private participation under the Housing for All (Urban) Mission/Pradhan Mantri Awas Yojana, only for existing slum dwellers; 12% NEW /2018- Central Tax (Rate) Original + Repairs + Maintenance (c) a civil structure or any other original works pertaining to the ln-situ redevelopment of existing slums using land as a resource, under the Housing for All (Urban) Mission/ Pradhan Mantri Awas Yojana (Urban). 12% (Effective tax rate after land deduction of 1/3rd of total considerati on is 8%)

37 Press Release stated: The Council has also recommended that the benefit of concessional rate of GST of 12% (effective GST rate of 8% after deducting value of land) applicable to houses supplied to existing slum dwellers under the in-situ redevelopment of existing slums using land as a resource component of PMAY may be extended to houses purchased by persons other than existing slum dwellers also. This would make the in-situ redevelopment of existing slums using land as a resource component of PMAY more attractive to builders as well as buyers.

38 Credit linked subsidy scheme The following entry was inserted vide Notification 1/2018-Central Tax (Rate) dated Sr No Particulars Rate 1 Original + Maintenance + Repairs a civil structure or any other original works for CLSS for EWS/ LIG/MlG-1/MlG-2 under the Housing for All (Urban) Mission/ Pradhan Mantri Awas Yojana (Urban); 12% (Effective tax rate after land deduction of 1/3rd of total consideration is 8%)

39 Passing on of Credits under Section 171 Press Release stated: The housing projects in the affordable segment in the country would now attract GST of 8% (after deducting value of land). The builder or developer will not be required to pay GST on the construction service of flats etc. in cash but would have enough ITC (input tax credits) in his books to pay the output GST, in which case, he should not recover any GST payable on the flats from the buyers. He can recover GST from the buyers of flats only if he recalibrates the cost of the flat after factoring in the full ITC available in the GST regime and reduces the ex-gst price of flats. The builders/developers are expected to follow the principles laid down under section 171 of the GST Act scrupulously.

40 Lets look at some other issues

41 Key controversies in GST and interplay with other statues like RERA, Stamp duty etc. Meaning of First occupation Deduction of land read with conditions in RERA Delhi AAR Treatment of liquidated damages Negative AAR Credit of works contract service for developer Larsen and tubro Developer is a works contractor Interchangeable words used in Notification 11/2017

42 Key controversies in GST and interplay with other statues like RERA, Stamp duty etc. Reversal of credit What?? When???? How????? For land & After BU sales Example GST on maintenance deposit/preferential Location/Parking / Cancellation / Nomination charges collected with total consideration Hyderabad FAQ Maintenance deposit cannot be taxed and rest all (other than Nomination charges treated as Composite supply with real estate)

43 Key controversies in GST and interplay with other statues like RERA, Stamp duty etc. Credit of inputs held in WIP by builders Negative Circular Credit of WIP by works contractors Notices issued by Dept. Overflow of credit not allowed to builders Credit of taxes paid on DR (if..)

44 Key controversies in GST and interplay with other statues like RERA, Stamp duty etc. Treatment of long term lease Bombay HC Judgment (Negative) & Greater Noida (Delhi CESTAT Positive) Cancellation of service post GST (and of transition period) if period to issue credit note is expired Inter-state movement of capital goods with payment of tax

45 Other controversies Claiming refund Change in definition of Net ITC Reimbursement of Electricity Charges from tenants on the basis of sub meter Reimbursement of electricity charges on sub-meter Not taxable M/s S.B Developers Ltd vs CST, New Delhi Free Issue of Material Bhayana Builders Supreme Court Composite supply Vs Mixed supply Vs works contract Back to intention regime negative advance rulings.

46 Other controversies Whether splitting allowed post GST? High seas sales No sunset clause in Article 366(29A) Credit of motor vehicle in construction industry

47 Any space for planning amid all these difficult issues?

48 Options available and financial implications How about an option contract?? How about a mortgage contract?

49 Thank you!! Any doubts??..contact us at

Indirect Tax Study Circle Meeting Wednesday, 22 nd February, Real Estate Sector - issues and Recent Developments.

THE CHAMBER OF TAX CONSULTANTS 3, Rewa Chambers, Ground Floor, 31, New Marine Lines, Mumbai - 400 020 Tel.: 2200 1787 / 2209 0423 / 2200 2455 E-mail: office@ctconline.org Website: www.ctconline.org Indirect

THE CHAMBER OF TAX CONSULTANTS 3, Rewa Chambers, Ground Floor, 31, New Marine Lines, Mumbai - 400 020 Tel.: 2200 1787 / 2209 0423 / 2200 2455 E-mail: office@ctconline.org Website: www.ctconline.org Indirect

GST Impact on Real Estate CMA Bhogavalli Mallikarjuna Gupta Founder : India-gst.in Director Business Advisory Services, Procode Softech India Pvt Ltd

GST Impact on Real Estate CMA Bhogavalli Mallikarjuna Gupta Founder : India-gst.in Director Business Advisory Services, Procode Softech India Pvt Ltd SME, Speaker, Author & Advisor - Indian GST, GCC VAT

GST Impact on Real Estate CMA Bhogavalli Mallikarjuna Gupta Founder : India-gst.in Director Business Advisory Services, Procode Softech India Pvt Ltd SME, Speaker, Author & Advisor - Indian GST, GCC VAT

Basic Division of Construction Activity

Company Logo 1 Basic Division of Construction Activity Commercial or Industrial Construction Services. 10% 10% Construction of Residential Complex Services. 20% 60% Preferential Location Services. Management,

Company Logo 1 Basic Division of Construction Activity Commercial or Industrial Construction Services. 10% 10% Construction of Residential Complex Services. 20% 60% Preferential Location Services. Management,

Redevelopment/Joint Development of Real Estate. By CA Anil Sathe

Redevelopment/Joint Development of Real Estate By SCOPE Taxation aspects of Redevelopment/Joint Development in the case of :- Owner - Individual Co-operative Housing Society Members of the Society Tenants

Redevelopment/Joint Development of Real Estate By SCOPE Taxation aspects of Redevelopment/Joint Development in the case of :- Owner - Individual Co-operative Housing Society Members of the Society Tenants

GST for Builders, Developers and Works Contractors

GST for Builders, Developers and Works Contractors CA Yashwant J. Kasar B.Com, FCA, DISA, CISA, PMP, FAIA 20 th March 2018 GST on construction activity Service Accounting Code Heading for Construction

GST for Builders, Developers and Works Contractors CA Yashwant J. Kasar B.Com, FCA, DISA, CISA, PMP, FAIA 20 th March 2018 GST on construction activity Service Accounting Code Heading for Construction

Service Tax on Real Estate A Practical Perspective (PART A) (B.COM(H), CA, CIFRS, CBV)

(B.COM(H), CA, CIFRS, CBV)") Service Tax on Real Estate A Practical Perspective (PART A) By CA. Ankit Gulgulia (B.COM(H), CA, CIFRS, CBV) This article aims to discuss few essential issues that require to be addressed in light to the

Service Tax on Real Estate A Practical Perspective (PART A) By CA. Ankit Gulgulia (B.COM(H), CA, CIFRS, CBV) This article aims to discuss few essential issues that require to be addressed in light to the

Government of Uttar Pradesh. Workshop for Housing for All Date - 09/08/2016. State Urban Development Agency

Government of Uttar Pradesh Workshop for Housing for All Date - 09/08/2016 State Urban Development Agency Overview of Scheme Housing shortage estimated at 2 Cr, out of these 2 Cr, 30 Lakh shortage is in

Government of Uttar Pradesh Workshop for Housing for All Date - 09/08/2016 State Urban Development Agency Overview of Scheme Housing shortage estimated at 2 Cr, out of these 2 Cr, 30 Lakh shortage is in

Development Agreement - A - Taxability and Timing perspective

Development Agreement - A - Taxability and Timing perspective S KHAITAN & ASSOCIATES SHUBHAM KHAITAN Development Agreement A Taxability and Timing perspective 1. Preamble Ever since the advent of GST,

Development Agreement - A - Taxability and Timing perspective S KHAITAN & ASSOCIATES SHUBHAM KHAITAN Development Agreement A Taxability and Timing perspective 1. Preamble Ever since the advent of GST,

INDIRECT TAX AND REAL ESTATE

2 nd February, 2013 INDIRECT TAX AND REAL ESTATE Real Estate Summit Bombay Chartered Accountants Society and Indian Merchants Chamber By Vikram Nankani 1 AGENDA 1. VAT and Real Estate K. Raheja Development

2 nd February, 2013 INDIRECT TAX AND REAL ESTATE Real Estate Summit Bombay Chartered Accountants Society and Indian Merchants Chamber By Vikram Nankani 1 AGENDA 1. VAT and Real Estate K. Raheja Development

Study Course on DTAA. other Income. Presented dby Mayur. B. Desai

Study Course on DTAA Income from Immovable property and other Income Presented dby Mayur. B. Desai Mayur B. Desai 1 Income from Immovable Property Article 6 (UN Model) Mayur B. Desai 2 Income from Immovable

Study Course on DTAA Income from Immovable property and other Income Presented dby Mayur. B. Desai Mayur B. Desai 1 Income from Immovable Property Article 6 (UN Model) Mayur B. Desai 2 Income from Immovable

S. 43CA: Tax Implications On Builders And Real Estate Developers Dr. (CA) Raj K. Agarwal & Dr. Rakesh Gupta, Advocate

Raj K. Agarwal & Dr. Rakesh Gupta, Advocate") S. 43CA: Tax Implications On Builders And Real Estate Developers Dr. (CA) Raj K. Agarwal & Dr. Rakesh Gupta, Advocate Finance Act, 2013 has inserted a new section 43CA under the Income Tax Act, 1961 which

S. 43CA: Tax Implications On Builders And Real Estate Developers Dr. (CA) Raj K. Agarwal & Dr. Rakesh Gupta, Advocate Finance Act, 2013 has inserted a new section 43CA under the Income Tax Act, 1961 which

2.2 As the builder and developer deals with immovable property, laws relating to the same are analysed and discussed first hereinafter.

INCOME TAX ISSUES IN REAL ESTATE TRANSACTIONS Chetan A. Karia Chartered Accountant 1. Introduction The issue of taxation of income from business of real estate development is refusing to settle. With the

INCOME TAX ISSUES IN REAL ESTATE TRANSACTIONS Chetan A. Karia Chartered Accountant 1. Introduction The issue of taxation of income from business of real estate development is refusing to settle. With the

Government of India Ministry of Housing and Urban Affairs National Buildings Organisation

Government of India Ministry of Housing and Urban Affairs National Buildings Organisation FORMAT Information Collection format for the Completed / Under Construction in respect of EWS/LIG (Guidelines and

Government of India Ministry of Housing and Urban Affairs National Buildings Organisation FORMAT Information Collection format for the Completed / Under Construction in respect of EWS/LIG (Guidelines and

DRAFTING AGREEMENTS UNDER MOFA, 1963 AND MAOA, 1970 PARIMAL SHROFF & CO. Advocates, Solicitors & Notary Mumbai

DRAFTING AGREEMENTS UNDER MOFA, 1963 AND MAOA, 1970 PARIMAL K.S SHROFF & CO. Advocates, Solicitors & Notary Mumbai LAWS APPLICABLE Indian Contract Act, 1872 Evidence Act, 1897 Indian Succession Act, 1925

DRAFTING AGREEMENTS UNDER MOFA, 1963 AND MAOA, 1970 PARIMAL K.S SHROFF & CO. Advocates, Solicitors & Notary Mumbai LAWS APPLICABLE Indian Contract Act, 1872 Evidence Act, 1897 Indian Succession Act, 1925

GST Guidance Note 8 Job Work

GST Guidance Note 8 Job Work What this Guidance Note contains? 8.01 Meaning of Job work 8.02 Need for registration/ declaration of the place of business of job worker as principal s additional place of

GST Guidance Note 8 Job Work What this Guidance Note contains? 8.01 Meaning of Job work 8.02 Need for registration/ declaration of the place of business of job worker as principal s additional place of

Legislative Brief The Land Acquisition, Rehabilitation and Resettlement Bill, 2011

Legislative Brief The Land Acquisition, Rehabilitation and Resettlement Bill, 2011 The Land Acquisition, Rehabilitation and Resettlement Bill, 2011 was introduced in the Lok Sabha by the Minister for Rural

Legislative Brief The Land Acquisition, Rehabilitation and Resettlement Bill, 2011 The Land Acquisition, Rehabilitation and Resettlement Bill, 2011 was introduced in the Lok Sabha by the Minister for Rural

INSTRUCTIONS TO PRIVATE DEVELOPERS

INSTRUCTIONS TO PRIVATE DEVELOPERS Government of Andhra Pradesh has established the A.P.Township and Infrastructure Development Corporation Limited(APTIDCO) to develop sustainable Townships and also creating

INSTRUCTIONS TO PRIVATE DEVELOPERS Government of Andhra Pradesh has established the A.P.Township and Infrastructure Development Corporation Limited(APTIDCO) to develop sustainable Townships and also creating

TDR FAQs FREQUENTLY ASKED QUESTIONS

1 TDR FAQs FREQUENTLY ASKED QUESTIONS Q-1. The building was constructed 25 years ago and the Co-operative Society was registered 20 yrs ago. Inspite of its members best efforts the builders have not given

1 TDR FAQs FREQUENTLY ASKED QUESTIONS Q-1. The building was constructed 25 years ago and the Co-operative Society was registered 20 yrs ago. Inspite of its members best efforts the builders have not given

AFFORDABLE HOUSING. April 2018 I Volume 32

AFFORDABLE HOUSING April 2018 I Volume 32 1 01 02 03 04 05 06 07 2 April 2018 I Volume 32 April 2018 I Volume 32 3 4 April 2018 I Volume 32 Change in Housing Prices Prices rose in 32 of 50 cities in the

AFFORDABLE HOUSING April 2018 I Volume 32 1 01 02 03 04 05 06 07 2 April 2018 I Volume 32 April 2018 I Volume 32 3 4 April 2018 I Volume 32 Change in Housing Prices Prices rose in 32 of 50 cities in the

Project Address. RERA Regd. No. Photograph. Visiting Card

Parsvnath Buildwell Pvt. Ltd. CIN: U45400DL2008PTC178395 (A JOINT VENTURE COMPANY OF PARSVNATH DEVELOPERS ) Registered Office : Parsvnath Tower, Near Shahdara Metro Station, Shahdara, Delhi - 110032 Ph.

Parsvnath Buildwell Pvt. Ltd. CIN: U45400DL2008PTC178395 (A JOINT VENTURE COMPANY OF PARSVNATH DEVELOPERS ) Registered Office : Parsvnath Tower, Near Shahdara Metro Station, Shahdara, Delhi - 110032 Ph.

3. Income from House Property

3. Income from House Property Quick review of the chapter Sections Sec. 22 Income from House Property Chargeability and Basis of Charge Sec. 23(1)(a), (b) & (c) Annual Value, how determined Explanation

3. Income from House Property Quick review of the chapter Sections Sec. 22 Income from House Property Chargeability and Basis of Charge Sec. 23(1)(a), (b) & (c) Annual Value, how determined Explanation

The GST, the QST and Residential Complexes

Ministère du Revenu du Québec www.revenu.gouv.qc.ca The GST, the QST and Residential Complexes Construction or Renovation This publication is provided for information purposes only. It does not constitute

Ministère du Revenu du Québec www.revenu.gouv.qc.ca The GST, the QST and Residential Complexes Construction or Renovation This publication is provided for information purposes only. It does not constitute

Recent Decision on Stamp Duty on Debt Assignment

Recent Decision on Stamp Duty on Debt Assignment February 13, 2018 M U M B A I I D E L H I I B E N G A L U R U I K O L K A T A MUMBAI I DELHI I BENGALURU I KOLKATA I CHENNAI Introduction Assignment of

Recent Decision on Stamp Duty on Debt Assignment February 13, 2018 M U M B A I I D E L H I I B E N G A L U R U I K O L K A T A MUMBAI I DELHI I BENGALURU I KOLKATA I CHENNAI Introduction Assignment of

GST on trading of Transferable Development Rights (TDR s)

") DISCLAIMER: GST on trading of Transferable Development Rights (TDR s) The views expressed in this article are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe

DISCLAIMER: GST on trading of Transferable Development Rights (TDR s) The views expressed in this article are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe

CONDITIONS OF PURCHASE (GOODS AND SERVICES) DOMESTIC AND INTERNATIONAL

DOMESTIC AND INTERNATIONAL") CONDITIONS OF PURCHASE (GOODS AND SERVICES) DOMESTIC AND INTERNATIONAL 1. DEFINITIONS For the purposes of these Conditions of Purchase: Agreement means the Order together with these Conditions of Purchase;

CONDITIONS OF PURCHASE (GOODS AND SERVICES) DOMESTIC AND INTERNATIONAL 1. DEFINITIONS For the purposes of these Conditions of Purchase: Agreement means the Order together with these Conditions of Purchase;

DELHI DEVELOPMENT AUTHORITY OFFICE OF PR.COMMISSIONER(H,LD&CWG)

") 1 DELHI DEVELOPMENT AUTHORITY OFFICE OF PR.COMMISSIONER(H,LD&CWG) Sub: Draft Slum Rehabilitation Policy based on Mumbai s Slum Rehabilitation Policy One of the major challenges that face DDA is to handle

1 DELHI DEVELOPMENT AUTHORITY OFFICE OF PR.COMMISSIONER(H,LD&CWG) Sub: Draft Slum Rehabilitation Policy based on Mumbai s Slum Rehabilitation Policy One of the major challenges that face DDA is to handle

REAL ESTATE TRANSACTIONS PURUSHOTHAMAN.J

REAL ESTATE TRANSACTIONS PURUSHOTHAMAN.J 25-01-2017 PROVISION AND RULES RELATING TO REAL ESTATE TRANSACTIONS CA PURUSHOTHAMAN J 1/30/17 2 Categories of Services covered Construction of complex services

REAL ESTATE TRANSACTIONS PURUSHOTHAMAN.J 25-01-2017 PROVISION AND RULES RELATING TO REAL ESTATE TRANSACTIONS CA PURUSHOTHAMAN J 1/30/17 2 Categories of Services covered Construction of complex services

CLARIFICATIONS ON CA CERTIFICATION

CLARIFICATIONS ON CA CERTIFICATION Legal Alert 14/2017 5 th July, 2017 Through MahaRERA Circular No.7/2017, dated 4 th July 2017, w.e.f. 1 st May 2017 the Maharashtra Real Estate Regulatory Authority has

CLARIFICATIONS ON CA CERTIFICATION Legal Alert 14/2017 5 th July, 2017 Through MahaRERA Circular No.7/2017, dated 4 th July 2017, w.e.f. 1 st May 2017 the Maharashtra Real Estate Regulatory Authority has

WHEATHER RENTING OF PROPERTY IS SERVICE AND THUS LIABLE TO SERVICE TAX?

1 WHEATHER RENTING OF PROPERTY IS SERVICE AND THUS LIABLE TO SERVICE TAX? By: MUKUL GUPTA, Tax Advocate R-13/24, Raj Nagar, Ghaziabad Tel :+91120-2820380, 2821407 Mobile: +919811023739 e-mail: mukuladv@hotmail.com

1 WHEATHER RENTING OF PROPERTY IS SERVICE AND THUS LIABLE TO SERVICE TAX? By: MUKUL GUPTA, Tax Advocate R-13/24, Raj Nagar, Ghaziabad Tel :+91120-2820380, 2821407 Mobile: +919811023739 e-mail: mukuladv@hotmail.com

Registration of Cooperative Housing Society

Lecture on Registration of Cooperative Housing Society under Maharashtra Cooperative Societies Act, 1960 By Shri Sunil Deshmukh Important Provisions of MSC Act, 1960 4. Societies which may be registered.

Lecture on Registration of Cooperative Housing Society under Maharashtra Cooperative Societies Act, 1960 By Shri Sunil Deshmukh Important Provisions of MSC Act, 1960 4. Societies which may be registered.

Subject: Clarification on CA Certificates

Emblem MahaREA MAHARASHTRA REAL ESTATE REGULATORY AUTHORITY No.MahaRERA/Secy/FileNo.27/115/2017 Circular No.7/2017 Dated: 4 th July 2017 Subject: Clarification on CA Certificates Whereas, under section

Emblem MahaREA MAHARASHTRA REAL ESTATE REGULATORY AUTHORITY No.MahaRERA/Secy/FileNo.27/115/2017 Circular No.7/2017 Dated: 4 th July 2017 Subject: Clarification on CA Certificates Whereas, under section

REAL ESTATE IN INDIA 2017

Now Available REAL ESTATE IN INDIA 2017 Segment Analysis, Outlook and Opportunities Report (PDF) Data-set (Excel) India Infrastructure Research Real Estate in India 2017 Table of Contents SECTION I: MARKET

Now Available REAL ESTATE IN INDIA 2017 Segment Analysis, Outlook and Opportunities Report (PDF) Data-set (Excel) India Infrastructure Research Real Estate in India 2017 Table of Contents SECTION I: MARKET

CONDITIONS OF PURCHASE (GOODS AND SERVICES) DOMESTIC AND INTERNATIONAL

DOMESTIC AND INTERNATIONAL") CONDITIONS OF PURCHASE (GOODS AND SERVICES) DOMESTIC AND INTERNATIONAL 1. DEFINITIONS For the purposes of these Conditions of Purchase: Agreement means the Order together with these Conditions of Purchase;

CONDITIONS OF PURCHASE (GOODS AND SERVICES) DOMESTIC AND INTERNATIONAL 1. DEFINITIONS For the purposes of these Conditions of Purchase: Agreement means the Order together with these Conditions of Purchase;

Promoters

projects as well. The question has assumed particular significance in respect of obligation to deposit 70% of realization in the separate bank account. 1.3 Answer to Q. 2,5 and 12 of the Additional FAQ

projects as well. The question has assumed particular significance in respect of obligation to deposit 70% of realization in the separate bank account. 1.3 Answer to Q. 2,5 and 12 of the Additional FAQ

[Taxation of Real Estate Transactions under Direct Taxes]

![[Taxation of Real Estate Transactions under Direct Taxes]](/thumbs/95/123324353.jpg "[Taxation of Real Estate Transactions under Direct Taxes]") Ca.bhupendrashah******9322507220 CA.BHUPENDRASHAH PRESENTS [Taxation of Real Estate Transactions under Direct Taxes] [Recent Issues ] At Hotel Vits bhupendrashahca@hotmail.com *globalindiancas@yahoogroups.com

Ca.bhupendrashah******9322507220 CA.BHUPENDRASHAH PRESENTS [Taxation of Real Estate Transactions under Direct Taxes] [Recent Issues ] At Hotel Vits bhupendrashahca@hotmail.com *globalindiancas@yahoogroups.com

Income from House Property-

CONCEPT 1: Charging Section of Income from House Property (Section 22) What is taxable under Income from House Property? The Net annual value (NAV) of a property consisting of any buildings or lands appurtenant

CONCEPT 1: Charging Section of Income from House Property (Section 22) What is taxable under Income from House Property? The Net annual value (NAV) of a property consisting of any buildings or lands appurtenant

DELHI DEVELOPMENT AUTHORITY HOUSING DEPARTMENT (LIG) CIRCULAR

CIRCULAR") DELHI DEVELOPMENT AUTHORITY HOUSING DEPARTMENT (LIG) Dated: 17.01.2019 CIRCULAR LAUNCHING DATE AND TIME: 18.01.2019 AT 15.00 HRS Subject:- Launching of Online Running Scheme for disposal of old inventory

DELHI DEVELOPMENT AUTHORITY HOUSING DEPARTMENT (LIG) Dated: 17.01.2019 CIRCULAR LAUNCHING DATE AND TIME: 18.01.2019 AT 15.00 HRS Subject:- Launching of Online Running Scheme for disposal of old inventory

Terms and Conditions of Appointment

Terms and Conditions of Appointment Terms and Conditions of Appointment Definitions Agreement refers to the Terms of Business between the Agent and the Client The Agent refers to SurreyLets Ltd Client

Terms and Conditions of Appointment Terms and Conditions of Appointment Definitions Agreement refers to the Terms of Business between the Agent and the Client The Agent refers to SurreyLets Ltd Client

Revenue recognition for real estate developers Indian GAAP vs ICDS

Revenue recognition for real estate developers Indian GAAP vs ICDS - Published on August 2, 2016 Authors - CA Vivek Newatia - Email - vnewatia@sjaykishan.com - Ph. No. - +91 98310 88818 Revenue recognition

Revenue recognition for real estate developers Indian GAAP vs ICDS - Published on August 2, 2016 Authors - CA Vivek Newatia - Email - vnewatia@sjaykishan.com - Ph. No. - +91 98310 88818 Revenue recognition

SCHEME OF AMALGAMATION BETWEEN FUTURE AGROVET LIMITED WITH FUTURE CONSUMER ENTERPRISE LIMITED AND THEIR RESPECTIVE SHAREHOLDERS

SCHEME OF AMALGAMATION BETWEEN FUTURE AGROVET LIMITED WITH FUTURE CONSUMER ENTERPRISE LIMITED AND THEIR RESPECTIVE SHAREHOLDERS (A) PREAMBLE This Scheme of Amalgamation ( Scheme ) is presented under Sections

SCHEME OF AMALGAMATION BETWEEN FUTURE AGROVET LIMITED WITH FUTURE CONSUMER ENTERPRISE LIMITED AND THEIR RESPECTIVE SHAREHOLDERS (A) PREAMBLE This Scheme of Amalgamation ( Scheme ) is presented under Sections

PROFESSIONAL OPPORTUNITY FOR CA IN CO-OPERATIVE SECTOR AND HOUSING SOCIETIES.

Seminar on Elections in Cooperatives & Professional Opportunities PROFESSIONAL OPPORTUNITY FOR CA IN CO-OPERATIVE SECTOR AND HOUSING SOCIETIES. CA. RAMESH S. PRABHU 24/12/2016, COOP COMMITTEE(MAHARASHTRA)

Seminar on Elections in Cooperatives & Professional Opportunities PROFESSIONAL OPPORTUNITY FOR CA IN CO-OPERATIVE SECTOR AND HOUSING SOCIETIES. CA. RAMESH S. PRABHU 24/12/2016, COOP COMMITTEE(MAHARASHTRA)

REPUBLIC OF VANUATU STAMP DUTIES (AMENDMENT) ACT NO. 36 OF Arrangement of Sections

ACT NO. 36 OF Arrangement of Sections") REPUBLIC OF VANUATU STAMP DUTIES (AMENDMENT) ACT NO. 36 OF 2009 Arrangement of Sections 1 Amendment... 2 Commencement... Stamp Duties (Amendment) Act No. 36 of 2009 1 Assent: 19/10/2009 Commencement: 16/11/2009

REPUBLIC OF VANUATU STAMP DUTIES (AMENDMENT) ACT NO. 36 OF 2009 Arrangement of Sections 1 Amendment... 2 Commencement... Stamp Duties (Amendment) Act No. 36 of 2009 1 Assent: 19/10/2009 Commencement: 16/11/2009

1 S. K H A I T A N A N D A S S O C I A T E S

- S KHAITAN & ASSOCIATES SHUBHAM KHAITAN Works contract under GST The Pandora s box yet to be opened Under the current tax regime, there have been few bigger disputes than the classification of works contract.

- S KHAITAN & ASSOCIATES SHUBHAM KHAITAN Works contract under GST The Pandora s box yet to be opened Under the current tax regime, there have been few bigger disputes than the classification of works contract.

CAPITAL GAINS PROPERTY DEVELOPMENT AGREEMENTS-When Chargeable to Tax

CAPITAL GAINS PROPERTY DEVELOPMENT AGREEMENTS-When Chargeable to Tax CAPITAL GAINS- CHARGEABILITY Sec 45(1) : Capital Gains tax liability arises only when the following conditions are satisfied:- A. There

CAPITAL GAINS PROPERTY DEVELOPMENT AGREEMENTS-When Chargeable to Tax CAPITAL GAINS- CHARGEABILITY Sec 45(1) : Capital Gains tax liability arises only when the following conditions are satisfied:- A. There

Revenue Recognition- Real Estate Companies

Revenue Recognition- Real Estate Companies CTC 25 NOVEMBER ZFB & ASSOCIATES, Chartered Accountants 1 Accounting for Real Estate Transactions Introduction Scope Revenue Recognition Criteria Project Project

Revenue Recognition- Real Estate Companies CTC 25 NOVEMBER ZFB & ASSOCIATES, Chartered Accountants 1 Accounting for Real Estate Transactions Introduction Scope Revenue Recognition Criteria Project Project

Study on the application of Value Added Tax to the property sector

Study on the application of Value Added Tax to the property sector Executive summary and Country overviews N XXI/96/CB-3021 Introduction This binder contains the Executive summary, conclusions and recommendations

Study on the application of Value Added Tax to the property sector Executive summary and Country overviews N XXI/96/CB-3021 Introduction This binder contains the Executive summary, conclusions and recommendations

Land Acquisitions Act 1894 (1of 1894)

") Acquisition and Requisition of Immovable Properties-Enactments : Land Acquisitions Act 1894 (1of 1894) 1 ANNAMALAI UNIVERSITY Date : 06.03.2018 2 Acquisition and Requisition of Immovable Properties-Enactments

Acquisition and Requisition of Immovable Properties-Enactments : Land Acquisitions Act 1894 (1of 1894) 1 ANNAMALAI UNIVERSITY Date : 06.03.2018 2 Acquisition and Requisition of Immovable Properties-Enactments

Presented by: K.Vidyadhar AMD MEPMA

Status of RAY in Andhra Pradesh: Issues and Challenges Presented by: K.Vidyadhar AMD MEPMA SLUM PROFILE OF ANDHRA PRADESH No. of ULBs - 173 Total Urban Population (2001 census) - 208.08 Lakhs Urban Population

Status of RAY in Andhra Pradesh: Issues and Challenges Presented by: K.Vidyadhar AMD MEPMA SLUM PROFILE OF ANDHRA PRADESH No. of ULBs - 173 Total Urban Population (2001 census) - 208.08 Lakhs Urban Population

IAS Revenue. By:

IAS - 18 Revenue International Accounting Standard No 18 (IAS 18) Revenue In 1998, IAS 39, Financial Instruments: Recognition and Measurement, amended paragraph 11 of IAS 18, adding a cross-reference to

IAS - 18 Revenue International Accounting Standard No 18 (IAS 18) Revenue In 1998, IAS 39, Financial Instruments: Recognition and Measurement, amended paragraph 11 of IAS 18, adding a cross-reference to

GST/HST New Residential Rental Property Rebate

GST/HST New Residential Rental Property Rebate Includes Forms GST524 and GST525 RC4231(E) Rev.06 Before you start What s new Effective July 1, 2006, under proposed legislation, the GST rate will be reduced

GST/HST New Residential Rental Property Rebate Includes Forms GST524 and GST525 RC4231(E) Rev.06 Before you start What s new Effective July 1, 2006, under proposed legislation, the GST rate will be reduced

If GST is included as part of consideration, stamp duty is payable on the GST inclusive amount (Section 15A).

.") INTRODUCTION This guide has been prepared to assist in calculating the stamp duty payable on the documents available for self-stamping on RevenueSA Online or through the RevenueSA Periodic Return Arrangement.

INTRODUCTION This guide has been prepared to assist in calculating the stamp duty payable on the documents available for self-stamping on RevenueSA Online or through the RevenueSA Periodic Return Arrangement.

SHRI GANESHAY NAMAHA

SHRI GANESHAY NAMAHA Er & Vr. KEDAR CHIKODI M.Val. in Plant & Machinery B.E.Civil, MRICS (London),FIV, MPVAI, FIIV, MCVSRTA, AMIE, MPEATA, MISSE, MICA. GOVT. APPROVED VALUER, CHARTERED ENGINEER & STRUCTURAL

SHRI GANESHAY NAMAHA Er & Vr. KEDAR CHIKODI M.Val. in Plant & Machinery B.E.Civil, MRICS (London),FIV, MPVAI, FIIV, MCVSRTA, AMIE, MPEATA, MISSE, MICA. GOVT. APPROVED VALUER, CHARTERED ENGINEER & STRUCTURAL

SALE DEED FOR SUPERSTRUCTURE OF RESIDENTIAL UNIT AND SUB-LEASE- DEED FOR LAND. Sale consideration Rs. Super Area Sq. Mtrs. Stamp Duty Rs.

SALE DEED FOR SUPERSTRUCTURE OF RESIDENTIAL UNIT AND SUB-LEASE- DEED FOR LAND Sale consideration Rs. Super Area ------ Sq. Mtrs. Stamp Duty Rs. There is no facility of Club, Swimming Pool, Gymnasium and

SALE DEED FOR SUPERSTRUCTURE OF RESIDENTIAL UNIT AND SUB-LEASE- DEED FOR LAND Sale consideration Rs. Super Area ------ Sq. Mtrs. Stamp Duty Rs. There is no facility of Club, Swimming Pool, Gymnasium and

GST/HST New Residential Rental Property Rebate

GST/HST New Residential Rental Property Rebate Includes Forms GST524 and GST525 RC4231(E) Rev.09 Is this guide for you? T his guide provides information for landlords of new residential rental properties

GST/HST New Residential Rental Property Rebate Includes Forms GST524 and GST525 RC4231(E) Rev.09 Is this guide for you? T his guide provides information for landlords of new residential rental properties

HOW TO AVAIL OF MAXIMUM BENEFIT U/S 80-IB(10) OF THE INCOME TAX ACT

OF THE INCOME TAX ACT") 1 HOW TO AVAIL OF MAXIMUM BENEFIT U/S 80-IB(10) OF THE INCOME TAX ACT [In respect of undertaking(s) engaged in the development and construction of Housing Project(s)] - By S.K. Tyagi [ Published in CTR

1 HOW TO AVAIL OF MAXIMUM BENEFIT U/S 80-IB(10) OF THE INCOME TAX ACT [In respect of undertaking(s) engaged in the development and construction of Housing Project(s)] - By S.K. Tyagi [ Published in CTR

Day 1 Session 1 'Rajiv Awas Yojana - Slum Free India Mission' by P.K.Mohanty (Joint Secretary and Mission Director JNNURM, MoHUPA)

") Cities Alliance Project Output Day 1 Session 1 ' - Slum Free India Mission' by P.K.Mohanty (Joint Secretary and Mission Director JNNURM, MoHUPA) India International Workshop: Scaling up Upgrading and Affordable

Cities Alliance Project Output Day 1 Session 1 ' - Slum Free India Mission' by P.K.Mohanty (Joint Secretary and Mission Director JNNURM, MoHUPA) India International Workshop: Scaling up Upgrading and Affordable

Real estate market has an eye on stamp duty

Real estate market has an eye on stamp duty Introduction Stamp duty is a form of tax that is imposed on instruments 1 by which right or liability is or purports to be created, transferred, limited, extended,

Real estate market has an eye on stamp duty Introduction Stamp duty is a form of tax that is imposed on instruments 1 by which right or liability is or purports to be created, transferred, limited, extended,

Housing for All by 2022: A Big Opportunity in the Making

Harshad Borawake, Head of Research, Equity Mirae Asset Global Investments (India) MIRAE ASSET LENS Executive Summary India s urban population has grown five-fold in the last halfcentury to approximately

Harshad Borawake, Head of Research, Equity Mirae Asset Global Investments (India) MIRAE ASSET LENS Executive Summary India s urban population has grown five-fold in the last halfcentury to approximately

DELHI DEVELOPMENT AUTHORITY NOTIFICATION

DELHI DEVELOPMENT AUTHORITY NOTIFICATION S. O.... - In exercise of the powers conferred by sub-section (1) of Section 57 of the Delhi Development Act, 1957, the Delhi Development Authority, with the previous

DELHI DEVELOPMENT AUTHORITY NOTIFICATION S. O.... - In exercise of the powers conferred by sub-section (1) of Section 57 of the Delhi Development Act, 1957, the Delhi Development Authority, with the previous

CA. RAMESH S. PRABHU (CHAIRMAN) MSWA

MSWA") CA. RAMESH S. PRABHU (CHAIRMAN) MSWA INTRODUCTION Co-operative movement in our country shall not only stay but also grow in times to come. In spite of the drawbacks experienced in the working and administration

CA. RAMESH S. PRABHU (CHAIRMAN) MSWA INTRODUCTION Co-operative movement in our country shall not only stay but also grow in times to come. In spite of the drawbacks experienced in the working and administration

Presentation on RFCTLARR Act, March 22, 2018

Presentation on RFCTLARR Act, 2013 March 22, 2018 Hukum Singh Meena IAS, Joint Secretary Department of Land Resources Ministry of Rural Development Government of India The Right to Fair Compensation and

Presentation on RFCTLARR Act, 2013 March 22, 2018 Hukum Singh Meena IAS, Joint Secretary Department of Land Resources Ministry of Rural Development Government of India The Right to Fair Compensation and

THE KIAMBU COUNTY VALUATION AND RATING BILL, 2015 ARRANGEMENT OF CLAUSES PART I PRELIMINARY PART II ADMINISTRATION PART III- VALUATION

THE KIAMBU COUNTY VALUATION AND RATING BILL, 2015 ARRANGEMENT OF CLAUSES Clause PART I PRELIMINARY 1- Short title. 2- Interpretation. 3- Purpose of the Act. PART II ADMINISTRATION 4- Functions of the Department.

THE KIAMBU COUNTY VALUATION AND RATING BILL, 2015 ARRANGEMENT OF CLAUSES Clause PART I PRELIMINARY 1- Short title. 2- Interpretation. 3- Purpose of the Act. PART II ADMINISTRATION 4- Functions of the Department.

Retail Leases Amendment Act 2005 No 90

New South Wales Retail Leases Amendment Act 2005 No 90 Contents Page 1 Name of Act 2 2 Commencement 2 3 Amendment of Retail Leases Act 1994 No 46 2 4 Amendment of Fines Act 1996 No 99 2 Schedule 1 Amendment

New South Wales Retail Leases Amendment Act 2005 No 90 Contents Page 1 Name of Act 2 2 Commencement 2 3 Amendment of Retail Leases Act 1994 No 46 2 4 Amendment of Fines Act 1996 No 99 2 Schedule 1 Amendment

Intensive Study Course on Conveyance / Deemed Conveyance

Intensive Study Course on Conveyance / Deemed Conveyance Organised by WIRC of ICAI On 14 th January, 2017 at Mumbai Presented by CA.Ramesh Prabhu, Chairman, M S WA/ 1. Meaning of real estate 2. Real estate

Intensive Study Course on Conveyance / Deemed Conveyance Organised by WIRC of ICAI On 14 th January, 2017 at Mumbai Presented by CA.Ramesh Prabhu, Chairman, M S WA/ 1. Meaning of real estate 2. Real estate

COMMERCIAL TENANCY AGREEMENT

COMMERCIAL TENANCY AGREEMENT (F I R S T E D I T I O N) revised Copyright Member Office Printed by Realw orks Live PARTIES Landlord: Tenant: Date: THIS AGREEMENT COMPRISES THE REFERENCE SCHEDULE AND COMMERCIAL

COMMERCIAL TENANCY AGREEMENT (F I R S T E D I T I O N) revised Copyright Member Office Printed by Realw orks Live PARTIES Landlord: Tenant: Date: THIS AGREEMENT COMPRISES THE REFERENCE SCHEDULE AND COMMERCIAL

Capital gains relating to slump sale & Recent Developments

Capital gains relating to slump sale & Recent Developments Praful Poladia 16 April 2011 Contents Introduction Pre-section 50B position Section 50B : Overview Slump sale Undertaking Cost of acquisition

Capital gains relating to slump sale & Recent Developments Praful Poladia 16 April 2011 Contents Introduction Pre-section 50B position Section 50B : Overview Slump sale Undertaking Cost of acquisition

Supporting Older People Conference

Supporting Older People Conference OS7: Are you being served? Update on service charges Speaker: S:\Dept\Conferences\2010-11\Finance 2011\Marketing\Handbook Derek Rawson Chartered Surveyor and Housing

Supporting Older People Conference OS7: Are you being served? Update on service charges Speaker: S:\Dept\Conferences\2010-11\Finance 2011\Marketing\Handbook Derek Rawson Chartered Surveyor and Housing

Signature(s)... (Stamp required in case of firm/ company)

... (Stamp required in case of firm/ company)") APPLICATION FORM Application Date:... To, DWARKADHIS PROJECTS PVT. LTD. (Hereinafter called the Developer ) Regd. Off.: PD- 4A, Pitampura, New Delhi - 110088 Corp. Off: Bldg # 2007, Main Road, Sector 45

APPLICATION FORM Application Date:... To, DWARKADHIS PROJECTS PVT. LTD. (Hereinafter called the Developer ) Regd. Off.: PD- 4A, Pitampura, New Delhi - 110088 Corp. Off: Bldg # 2007, Main Road, Sector 45

Taxation of Real Estate Transactions Under Income Tax and Service Tax

Written by: CA S N Kedia B.com(H), FCA, DISA(ICAI) Taxation of Real Estate Transactions Under Income Tax and Service Tax Introduction We see a boom in construction of real estate and bank/ financial institutions

Written by: CA S N Kedia B.com(H), FCA, DISA(ICAI) Taxation of Real Estate Transactions Under Income Tax and Service Tax Introduction We see a boom in construction of real estate and bank/ financial institutions

THE MAHARASHTRA APARTMENT OWNERSHIP ACT, 1970

THE MAHARASHTRA APARTMENT OWNERSHIP ACT, 1970 MAHARASHTRA ACT NO. XV OF 1971 1 [Received the assent of the President on the 12 th day of February, 1971; assent was first published in the Maharashtra Government

THE MAHARASHTRA APARTMENT OWNERSHIP ACT, 1970 MAHARASHTRA ACT NO. XV OF 1971 1 [Received the assent of the President on the 12 th day of February, 1971; assent was first published in the Maharashtra Government

REAL ESTATE SECTOR IN INDIA

REAL ESTATE SECTOR IN INDIA - Certain Tax And Regulatory Aspects Includes The Real Estate (Regulation and Development) Bill, 2013 Accounting Standards (including Guidance Note issued by ICAI) Foreign Investment

REAL ESTATE SECTOR IN INDIA - Certain Tax And Regulatory Aspects Includes The Real Estate (Regulation and Development) Bill, 2013 Accounting Standards (including Guidance Note issued by ICAI) Foreign Investment

Transfer of Business

This document should be read in conjunction with section 20(2)(c) of the Vat Consolidation Act 2010. (VATCA 2010) Document last reviewed December 2017 Table of Contents Introduction...1 2 What are transfers

This document should be read in conjunction with section 20(2)(c) of the Vat Consolidation Act 2010. (VATCA 2010) Document last reviewed December 2017 Table of Contents Introduction...1 2 What are transfers

Fully Managed Landlord Agreement The Landlord and the Agent hereby agree to enter into a Contract under the following terms and conditions.

Fully Managed Landlord Agreement The Landlord and the Agent hereby agree to enter into a Contract under the following terms and conditions. Date: Parties:. The Landlord:. Of.. The Agent: Ellen Kay Lettings

Fully Managed Landlord Agreement The Landlord and the Agent hereby agree to enter into a Contract under the following terms and conditions. Date: Parties:. The Landlord:. Of.. The Agent: Ellen Kay Lettings

SALE DEED. THIS INDENTURE OF SALE DEED (hereinafter referred Sale Deed ) is made and entered into at, on day of,

is made and entered into at, on day of,") SALE DEED THIS INDENTURE OF SALE DEED (hereinafter referred Sale Deed ) is made and entered into at, on day of, BETWEEN: of aged yrs., an Indian inhabitant of Mumbai, residing at, hereinafter called as

SALE DEED THIS INDENTURE OF SALE DEED (hereinafter referred Sale Deed ) is made and entered into at, on day of, BETWEEN: of aged yrs., an Indian inhabitant of Mumbai, residing at, hereinafter called as

CBDT issues draft ICDS on real estate transactions

Flash News 15 May 2017 CBDT issues draft on real estate transactions On 31 March 2015, the Ministry of Finance (MoF) issued 10 Income Computation and Disclosure Standards () operationalising a new framework

Flash News 15 May 2017 CBDT issues draft on real estate transactions On 31 March 2015, the Ministry of Finance (MoF) issued 10 Income Computation and Disclosure Standards () operationalising a new framework

Guide to Farming Taxation Measures in Finance Act Income Averaging (section 657 Taxes Consolidation Act 1997)

") Guide to Farming Taxation Measures in Finance Act 2014 Note: This Guide reflects the legislation in place as at 1 January 2015 only. For further information on the up to date position please refer to the

Guide to Farming Taxation Measures in Finance Act 2014 Note: This Guide reflects the legislation in place as at 1 January 2015 only. For further information on the up to date position please refer to the

The Cantonments (Requisitioning of Immovable Property) Ordinance,1948.

Ordinance,1948.") The Cantonments (Requisitioning of Immovable Property) Ordinance,1948. THE CANTONMENTS (REQUISITIONING OF IMMOVABLE PROPERTY) ORDINANCE 1948. (Ordinance No. IV of 1948) (28th January 1948) Whereas an emergency

The Cantonments (Requisitioning of Immovable Property) Ordinance,1948. THE CANTONMENTS (REQUISITIONING OF IMMOVABLE PROPERTY) ORDINANCE 1948. (Ordinance No. IV of 1948) (28th January 1948) Whereas an emergency

THE DELHI APARTMENT OWNERSHIP ACT, 1986 ARRANGEMENT OF SECTIONS

SECTIONS THE DELHI APARTMENT OWNERSHIP ACT, 1986 1. Short title, extent and commencement. 2. Application. 3. Definitions. ARRANGEMENT OF SECTIONS CHAPTER I PRELIMINARY CHAPTER II OWNERSHIP, HERITABILITY

SECTIONS THE DELHI APARTMENT OWNERSHIP ACT, 1986 1. Short title, extent and commencement. 2. Application. 3. Definitions. ARRANGEMENT OF SECTIONS CHAPTER I PRELIMINARY CHAPTER II OWNERSHIP, HERITABILITY

S L U M R E H A B I L I T A T I O N A U T H O R I T Y M U M B A I M A H A R A S H T R A I N D I A M A R C H 2 1 ST

S L U M R E H A B I L I T A T I O N A U T H O R I T Y M U M B A I M A H A R A S H T R A I N D I A M A R C H 2 1 ST 2 0 1 8 BACKGROUND Since beginning of 20th century slums existed in Mumbai e.g. Dharavi,

S L U M R E H A B I L I T A T I O N A U T H O R I T Y M U M B A I M A H A R A S H T R A I N D I A M A R C H 2 1 ST 2 0 1 8 BACKGROUND Since beginning of 20th century slums existed in Mumbai e.g. Dharavi,

The Bill is called the Land Acquisition, Rehabilitation and Resettlement Act, 2011

The Land Acquisition, Rehabilitation and Resettlement Bill, 2011 was introduced in Lok Sabha on September 7, 2011. On December 17, 2012, during the winter session of Parliament, the government circulated

The Land Acquisition, Rehabilitation and Resettlement Bill, 2011 was introduced in Lok Sabha on September 7, 2011. On December 17, 2012, during the winter session of Parliament, the government circulated

Article. What is immovable property? The law relating to fixtures to land and building. Vinod Kothari

What is immovable property? The law relating to fixtures to land and building Vinod Kothari vinod@vinodkothari.com Nidhi Ladha corplaw@vinodkothari.com Check at: http://india-financing.com/staff-publications.html

What is immovable property? The law relating to fixtures to land and building Vinod Kothari vinod@vinodkothari.com Nidhi Ladha corplaw@vinodkothari.com Check at: http://india-financing.com/staff-publications.html

The Western India Regional Council. Business Combinations

The Western India Regional Council Impact Analysis of Indian Accounting Standards ( Ind AS ) and Income Computation and Disclosure Standards ( ICDS ) on Business Combinations Presentation by: Paresh Clerk

The Western India Regional Council Impact Analysis of Indian Accounting Standards ( Ind AS ) and Income Computation and Disclosure Standards ( ICDS ) on Business Combinations Presentation by: Paresh Clerk

Tackling unfair practices in the leasehold market: A consultation paper Response from NAEA Propertymark September 2017

Background Tackling unfair practices in the leasehold market: A consultation paper Response from NAEA Propertymark September 2017 1. NAEA Propertymark (National Association of Estate Agents) is the UK

Background Tackling unfair practices in the leasehold market: A consultation paper Response from NAEA Propertymark September 2017 1. NAEA Propertymark (National Association of Estate Agents) is the UK

Leasehold home ownership: buying your freehold or extending your lease. Law Commission Consultation Paper

Leasehold home ownership: buying your freehold or extending your lease Law Commission Consultation Paper @Law_Commission www.lawcom.gov.uk Our role The Law Commission is a statutory independent body created

Leasehold home ownership: buying your freehold or extending your lease Law Commission Consultation Paper @Law_Commission www.lawcom.gov.uk Our role The Law Commission is a statutory independent body created

CBDT issues Draft ICDS on real estate transactions: public comments invited by 26 May, 2017

from India Tax & Regulatory Services CBDT issues Draft ICDS on real estate transactions: public comments invited by 26 May, 2017 May 15, 2017 In brief On 29 September, 2016, the Ministry of Finance notified

from India Tax & Regulatory Services CBDT issues Draft ICDS on real estate transactions: public comments invited by 26 May, 2017 May 15, 2017 In brief On 29 September, 2016, the Ministry of Finance notified

EXPLANATORY MEMORANDUM TO THE HOUSING (SERVICE CHARGE LOANS) (AMENDMENT) (WALES) REGULATIONS 2011 SI 2011 No.

(AMENDMENT) (WALES) REGULATIONS 2011 SI 2011 No.") EXPLANATORY MEMORANDUM TO THE HOUSING (SERVICE CHARGE LOANS) (AMENDMENT) (WALES) REGULATIONS 2011 SI 2011 No. AND THE HOUSING (PURCHASE OF EQUITABLE INTERESTS) (WALES) REGULATIONS 2011 SI 2011 No. This

EXPLANATORY MEMORANDUM TO THE HOUSING (SERVICE CHARGE LOANS) (AMENDMENT) (WALES) REGULATIONS 2011 SI 2011 No. AND THE HOUSING (PURCHASE OF EQUITABLE INTERESTS) (WALES) REGULATIONS 2011 SI 2011 No. This

IMMOVABLE PROPERTY (SPECIFIC PERFORMANCE) ORDINANCE 2012

ORDINANCE 2012") Ordinance 16 of 2012 Published in Gazette No. 1657 of 25th June 2012 IMMOVABLE PROPERTY (SPECIFIC PERFORMANCE) ORDINANCE 2012 Contents 1. Short title and commencement 2. Interpretation 3. Formalities necessary

Ordinance 16 of 2012 Published in Gazette No. 1657 of 25th June 2012 IMMOVABLE PROPERTY (SPECIFIC PERFORMANCE) ORDINANCE 2012 Contents 1. Short title and commencement 2. Interpretation 3. Formalities necessary

WHITE PAPER REAL ESTATE

WHITE PAPER REAL ESTATE 1. BIRD S EYE VIEW. The Real Estate sector is one of the most critical sectors of the Indian economy, with no regularized norm or rather lack of transparency and accountability.

WHITE PAPER REAL ESTATE 1. BIRD S EYE VIEW. The Real Estate sector is one of the most critical sectors of the Indian economy, with no regularized norm or rather lack of transparency and accountability.

CHAPTER III : STAMP DUTY AND REGISTRATION FEES

CHAPTER III : STAMP DUTY AND REGISTRATION FEES 3.1 Results of audit Test check of the records of the stamp duty and registration fee conducted during the year 2008-09, indicated non-levy/short levy of

CHAPTER III : STAMP DUTY AND REGISTRATION FEES 3.1 Results of audit Test check of the records of the stamp duty and registration fee conducted during the year 2008-09, indicated non-levy/short levy of

THE HARYANA APARTMENT OWERSHP ACT, (Haryana Act No. 10 of 1983)

") THE HARYANA APARTMENT OWERSHP ACT, 1983 (Haryana Act No. 10 of 1983) Table of Contents Sections: 1.Short Title and Commencement. 2. Application of Act. 3. Definitions. 4. Status of apartments. 5. Ownership

THE HARYANA APARTMENT OWERSHP ACT, 1983 (Haryana Act No. 10 of 1983) Table of Contents Sections: 1.Short Title and Commencement. 2. Application of Act. 3. Definitions. 4. Status of apartments. 5. Ownership

Rental. National. Affordability. the Questus Residential Investment Fund. National Rental Affordability Scheme and NRAS

and the Questus Residential Investment Fund National Rental Affordability Scheme NRAS A GOVERNMENT INCENTIVE NATIONAL RENTAL AFFORDABILITY SCHEME 105 Railway Road Subiaco WA 6008 PO Box 1533 Subiaco WA

and the Questus Residential Investment Fund National Rental Affordability Scheme NRAS A GOVERNMENT INCENTIVE NATIONAL RENTAL AFFORDABILITY SCHEME 105 Railway Road Subiaco WA 6008 PO Box 1533 Subiaco WA

GST/HST New Residential Rental Property Rebate

GST/HST New Residential Rental Property Rebate Includes Forms GST524 and GST525 RC4231(E) Rev. 10 Is this guide for you? T his guide provides information for landlords of new residential rental properties

GST/HST New Residential Rental Property Rebate Includes Forms GST524 and GST525 RC4231(E) Rev. 10 Is this guide for you? T his guide provides information for landlords of new residential rental properties

Update. Key changes made by way of Maharashtra Stamp (Amendment) Act, Niddhi Parmar Vinod Kothari & Company

Act, Niddhi Parmar Vinod Kothari & Company") Key changes made by way of Maharashtra Stamp (Amendment) Act, 2015 Niddhi Parmar mt@vinodkothari.com Vinod Kothari & Company Corporate Law Services Group corplaw@vinodkothari.com May 16, 2015 Check at:

Key changes made by way of Maharashtra Stamp (Amendment) Act, 2015 Niddhi Parmar mt@vinodkothari.com Vinod Kothari & Company Corporate Law Services Group corplaw@vinodkothari.com May 16, 2015 Check at:

Services connected with Immovable Property

Services connected with Immovable Property Services connected with Immovable Property This document should be read in conjunction with section 33(2) and section 34(c) of the VAT Consolidation Act 2010

Services connected with Immovable Property Services connected with Immovable Property This document should be read in conjunction with section 33(2) and section 34(c) of the VAT Consolidation Act 2010

INSTITUTION OF VALUERS

INSTITUTION OF VALUERS Plot No. 3, Parwana Road, Pitampura, New Delhi - 110 034 VALUATION OF REAL ESTATE SIX MONTHS COURSE GENERAL INFORMATION Name of the course : Six Month Course on Valuation of Real

INSTITUTION OF VALUERS Plot No. 3, Parwana Road, Pitampura, New Delhi - 110 034 VALUATION OF REAL ESTATE SIX MONTHS COURSE GENERAL INFORMATION Name of the course : Six Month Course on Valuation of Real

GST/HST Memoranda Series

GST/HST Memoranda Series 19.2.1 Residential Real Property Sales Overview This section of Chapter 19 examines the tax status of most types of residential real property sales. Leases of residential real

GST/HST Memoranda Series 19.2.1 Residential Real Property Sales Overview This section of Chapter 19 examines the tax status of most types of residential real property sales. Leases of residential real

TENDER FOR PURCHASE OF BUILDINGS/BUILT UP FLOOR(S)

") TENDER FOR PURCHASE OF BUILDINGS/BUILT UP FLOOR(S) The Institute of Company Secretaries of India herein after referred as Institute is a statutory body constituted under an Act of Parliament, i.e. the

TENDER FOR PURCHASE OF BUILDINGS/BUILT UP FLOOR(S) The Institute of Company Secretaries of India herein after referred as Institute is a statutory body constituted under an Act of Parliament, i.e. the

TERMS AND CONDITIONS OF EQUIPMENT LEASE / RENTAL

TERMS AND CONDITIONS OF EQUIPMENT LEASE / RENTAL 1. Law and jurisdiction 1.1 Governing law This document is governed by the law in force in the country in which the document is signed. 1.2 Submission to

TERMS AND CONDITIONS OF EQUIPMENT LEASE / RENTAL 1. Law and jurisdiction 1.1 Governing law This document is governed by the law in force in the country in which the document is signed. 1.2 Submission to

SHAPATH HEXA. Please affix your photograph. Please affix your photograph. Please affix your photograph

Corporate Office: B-900, Shapath - 4, Opp: Karnavati Club,S. G. Highway, Ahmedabad - 380051. Tel: 079-40002900 Fax: 079-40002929 Email: marketing@savvygroup.in web:www.savvygroup.in OFFICE NO. Date: /

Corporate Office: B-900, Shapath - 4, Opp: Karnavati Club,S. G. Highway, Ahmedabad - 380051. Tel: 079-40002900 Fax: 079-40002929 Email: marketing@savvygroup.in web:www.savvygroup.in OFFICE NO. Date: /

TDR - Lessons from Mumbai

The Use of ADRs & TDRs in Slum Upgrading Mathew Chandy CHF International World Bank Fourth Urban Research Forum May 2007 CHF International TDR - Lessons from Mumbai CHF International has worked in over

The Use of ADRs & TDRs in Slum Upgrading Mathew Chandy CHF International World Bank Fourth Urban Research Forum May 2007 CHF International TDR - Lessons from Mumbai CHF International has worked in over