CITY OF OWATONNA ASSESSMENT REPORT. Steele County Assessor s Department. William G. Effertz, SAMA Steele County Assessor

|

|

|

- Shanon Pearson

- 5 years ago

- Views:

Transcription

1 2017 CITY OF OWATONNA ASSESSMENT REPORT Steele County Assessor s Department William G. Effertz, SAMA Steele County Assessor Tyler Diersen, AMA, Assistant County Assessor April 11, 2017

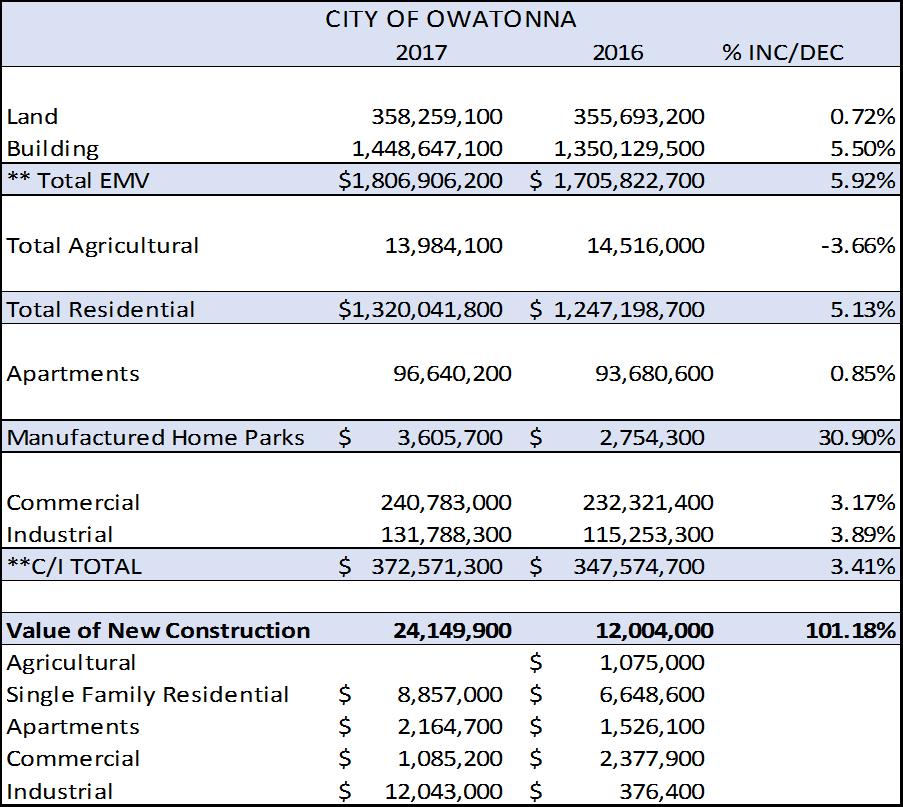

2 2017 Assessment Report City of Owatonna Assessor s Department 2017 Local Board of Appeal and Equalization Overview of the City of Owatonna 2017 Assessment The purpose of the Board of Appeal and Equalization is to provide a fair and objective forum for property owners to appeal their valuation and/or classification. The goal of the Board of Appeal and Equalization is to address property owners issues fairly and objectively. The initial meeting of the Board of Appeal and Equalization is to hear from the property owners and the assessor s will review the information and report our findings at the reconvene meeting. State law requires the assessor to value all the property at market value every year. All real property subject to taxation shall be listed and assessed every year with reference to its value on January 2. Property owners receive a Notice of Valuation every year in February or early March. Minnesota Statute states, All real property shall be valued at its market value. In estimating and determining such value, the assessor shall not adopt a lower or different standard of value because the same is to serve as a basis for taxation, nor shall adopt as criterion of value the price for which property would sell at auction or forced sale, or in the aggregate with all the property in the town or district but shall value each article or description of property to be fairly worth in money. Market value is defined as, The most probable price in terms of money which a property will bring in a competitive and open market under all conditions requisite to a fair sale, the buyer and seller, each acting prudently, knowledgeably and assuming the price is not affected by undue stimulus. The real estate tax is ad valorem (by value) and based on the value of property and not the owner s ability to pay. The assessment is updated in a uniform objective manner each year. The assessor analyzes the previous twelve months real estate sales to modify the mass appraisal system to the current market as well as to improve equalization among properties. For the 2017 City of Owatonna Assessment Report 1

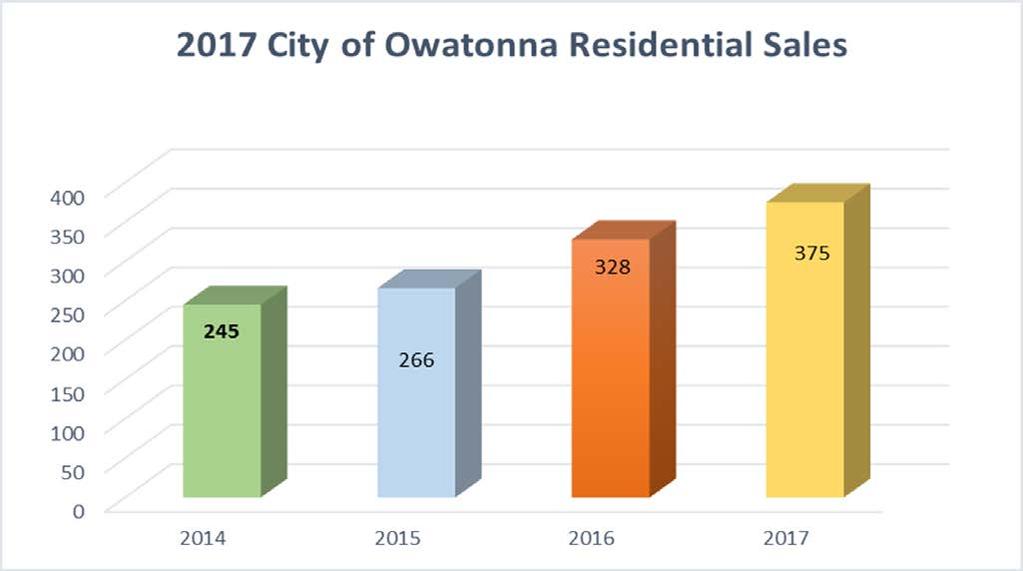

3 January 2, 2017 assessment, sales from October 1, 2015 to September 30, 2016 were analyzed both for market trends as well as the assessment to sale ratio (assessor s value divided by the sale price). There are two reasons that valuations change each year. The most common reason is due to the ever changing market conditions of the real estate market. The second reason for a valuation change is, even in a stable market, if a property value based on analysis of sales, is thought to be under or over assessed, either in relation to other properties or to a range of acceptable guidelines, the valuation may increase or decrease. Different types of real estate changes at different rates. The objective of the assessor is to be both accurate and uniform. The Commissioner of Revenue requires that all property types to be assessed between 90 to 105% of the selling price. Any assessment by aggregate property type that is outside of this range will be adjusted accordingly by the State Board of Appeal and Equalization. The 2017 Assessment: The City s assessed values expanded by 5.92% from 2016 for a total Estimated Market Value of $1.8 billion. This increase is a result of a combination of market adjustments and new construction. Residential: When considering the total housing stock in 2017, the typical home in the City of Owatonna is valued at $137,600 was constructed in 1974 and contains 1,302 square feet or $ per square foot. For the fourth consecutive year that single family residential market has shown growth. In 2017, residential market grew 5.13%. This represents the change in residential properties in total. Not all properties changed in the same manner. Each neighborhood and each property type had their own story to tell with regard to market changes. As part of the economic recovery, the number of foreclosure sales has dropped to more typical market levels that existed prior to the mortgage industry failure. The peak for the foreclosure crisis was 175 in 2010 as compared to 40 in In contrast, the number of traditional sales has increased from 245 in 2014 to 375 for the 2017 assessment, an increase of 53% more sales to analyze. As the number of sales increases, so does the reliability of the statistical analysis when measuring accuracy and uniformity. The number of foreclosures had been contributing to the (over) supply side of the buyers market. Real estate professionals report that the balance has shifted to 2017 City of Owatonna Assessment Report 2

4 more of a sellers market, as the number of listings has been reduced and days on the market have decreased. At the beginning of the assessment process, we analyze the residential market by comparing sale prices to the assessor s estimated market value from the previous year. This indicated a beginning median ratio of 86.8%. After our analysis and making corresponding market adjustments for the 2017 assessment, our final ratio improved to 91.9%. The statistical uniformity measurement is the coefficient of dispersion which improved to an excellent The COD measures the central tendency of all sales around the median. The median sale price was $152,500. There were 33 new single family homes constructed in This very positive economic indicator should continue to rise as the existing housing market continues to improve. Residential Vacant Land: For the 2017 assessment there were 37 vacant lot sales of these 20 were deemed to be arm s length transactions. Of the 20 sales, the median sale price was $25,900 and our ratio is 105.4%. Commercial/Industrial: There were 7 commercial and industrial sales that were included in the 2017 assessment time study. These sales indicated that the market grew by 3.41%. The all important 2017 final ratio is 96.5%. For analysis purposes, commercial/industrial market is segmented in several ways; by georgraphic area, by use type, i.e. small retail, big box retail, office, banks, restaurants, gas stations, etc. Industrial properties are also broken down based on the type of use and type of structure, i.e. warehouse, heavy and light manufacturing and distribution warehouse, etc.. Apartments/Multi-family: The market has provided a record number of sales over the last two years. This past year we had 6 arms length transactions and 9 sales in The sales data greatly improves the validity of the assessment analysis. In addition, property managers and owners are sent rental and expense surveys which also improves the accuracy and uniformity of the assessment. After modest adjustments, the assessment increasesd by 1.71% for apartments the final 2017 ratio was 96.04% City of Owatonna Assessment Report 3

5 New Construction: New construction is indication of economic conditions (growth in the assessment due to added improvements). New Construction remains robust at $24 million of added value for the 2017 assessment. New construction has a cumulative effect on the tax base, as we saw that tax base expand by $21.7 million in 2014, $18.8 million in 2015, and $12.0 million in Approximately 54% of this expansion of the tax base is from commercial/industrial properties. Conclusion: The assessor s office is in the business of gathering, analyzing and processing real estate market data. The collaborative efforts between the City of Owatonna and Steele County greatly enhances our ability to perform our statutory duties. The goal is to provide open and transparent property tax administration. All the assessment data is available to the public at the Steele County website under Tax Information and Parcel Data. The GIS interactive mapping provides a web based mapping system that interested parties can search for specific information about properties in Steele County. One of the main objectives in property tax administration is an equalized assessment (sales ratio s between %). It is important that maximum equalization be attained both among local property owners and between taxing districts because the assessment serves as a basis for: 1. Tax levies by overlapping governmental units (i.e. counties, school districts, and special taxing districts). 2. Determination of net bonded indebtedness restricted by statute to a percentage of either the local assessed value or market value. 3. Determination of authorized levies restricted by statutory tax rate limits. 4. Apportionment of state aid to governmental units via the school aid formula and the local government aid formula. An equitable distribution of the tax burden is achieved only if it is built upon a uniform assessment. The result of a non-uniform assessment is a shift in the tax burden to other property owners City of Owatonna Assessment Report 4

6 5

7 6

8 7

9 8

10 9

11 10

12 11

13 12

14 13

15 14

MINUTES LOCAL BOARD OF APPEAL & EQUALIZATION CITY OF OWATONNA. City Adm. Bldg. Owatonna, Minnesota Tuesday, April 24, :00 o clock p.m.

MINUTES LOCAL BOARD OF APPEAL & EQUALIZATION CITY OF OWATONNA City Adm. Bldg. Owatonna, Minnesota Tuesday, April 24, 2018 7:00 o clock p.m. Council Members Present: Dave Burbank, Doug Voss, Jeff Okerberg,

MINUTES LOCAL BOARD OF APPEAL & EQUALIZATION CITY OF OWATONNA City Adm. Bldg. Owatonna, Minnesota Tuesday, April 24, 2018 7:00 o clock p.m. Council Members Present: Dave Burbank, Doug Voss, Jeff Okerberg,

Past & Present Adjustments & Parcel Count Section... 13

Assessment 2017 Report This report includes specific information regarding the 2017 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

Assessment 2017 Report This report includes specific information regarding the 2017 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

Introduction. Bruce Munneke, S.A.M.A. Washington County Assessor. 3 P a g e

Assessment 2016 Report This report includes specific information regarding the 2016 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

Assessment 2016 Report This report includes specific information regarding the 2016 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

2018 Property Values and Assessment Practices Report Assessment Year 2017

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp 2018 Property Values

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp 2018 Property Values

2017 Property Values and Assessment Practices Report Assessment Year 2016

2017 Property Values and Assessment Practices Report Assessment Year 2016 Property Tax Division March 1, 2017 Per Minnesota Statutes, section 3.197, any report to the Legislature must contain, at the

2017 Property Values and Assessment Practices Report Assessment Year 2016 Property Tax Division March 1, 2017 Per Minnesota Statutes, section 3.197, any report to the Legislature must contain, at the

Board of Appeal and Equalization Handbook

Board of Appeal and Equalization Handbook This handbook was created to satisfy the training requirements of Minnesota Statutes, sections 274.014 and 274.135 Updated January 2018 Table of Contents Introduction...

Board of Appeal and Equalization Handbook This handbook was created to satisfy the training requirements of Minnesota Statutes, sections 274.014 and 274.135 Updated January 2018 Table of Contents Introduction...

DIRECTIVE # This Directive Supersedes Directive # and #92-003

Division Of Property Valuation Docking State Office Building 915 SW Harrison St., Room 400N Topeka, KS 66612-1588 Nick Jordan, Secretary David N. Harper, Director phone: 785-296-2365 fax: 785-296-2320

Division Of Property Valuation Docking State Office Building 915 SW Harrison St., Room 400N Topeka, KS 66612-1588 Nick Jordan, Secretary David N. Harper, Director phone: 785-296-2365 fax: 785-296-2320

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

ASSESSMENT AND TAXATION

ABSTRACT A brief synopsis of the assessment, appeal and taxation process as implemented by the Code of Iowa and Administrative Rules. ASSESSMENT AND TAXATION Iowa State Association of Assessors General

ABSTRACT A brief synopsis of the assessment, appeal and taxation process as implemented by the Code of Iowa and Administrative Rules. ASSESSMENT AND TAXATION Iowa State Association of Assessors General

Special Plainview City Council Meeting Board of Appeals and Equalization Meeting AGENDA Tuesday, April 16, 2019, at 6:00 P.M.

Special Plainview City Council Meeting Board of Appeals and Equalization Meeting AGENDA Tuesday, April 16, 2019, at 6:00 P.M. Special meetings are meetings held at a time or place that is different from

Special Plainview City Council Meeting Board of Appeals and Equalization Meeting AGENDA Tuesday, April 16, 2019, at 6:00 P.M. Special meetings are meetings held at a time or place that is different from

2017 Reappraisal Preliminary Report. February 6, 2017

2017 Reappraisal Preliminary Report February 6, 2017 Reappraisal is required at least every 8 years per NCGS105-286 Last reappraisal was conducted for 2011 Reappraisal includes both land and improvements.

2017 Reappraisal Preliminary Report February 6, 2017 Reappraisal is required at least every 8 years per NCGS105-286 Last reappraisal was conducted for 2011 Reappraisal includes both land and improvements.

City of Nashua, NH 2018 Revaluation Informational Meeting

City of Nashua, NH 2018 Revaluation Informational Meeting Legal Requirements Constitutional Duty of the City: [Art.] 6. [Valuation and Taxation.] The public charges of government, or any part thereof,

City of Nashua, NH 2018 Revaluation Informational Meeting Legal Requirements Constitutional Duty of the City: [Art.] 6. [Valuation and Taxation.] The public charges of government, or any part thereof,

REAL ESTATE MARKET AND YOUR TAX

REAL ESTATE MARKET AND YOUR TAX ASSESSMENT All of us Island property owners received our tax assessment notices from the County recently. As real estate agents we have been fielding many questions about

REAL ESTATE MARKET AND YOUR TAX ASSESSMENT All of us Island property owners received our tax assessment notices from the County recently. As real estate agents we have been fielding many questions about

UNDERSTANDING PROPERTY TAXES IN COLORADO

UNDERSTANDING PROPERTY TAXES IN COLORADO This brochure was created to provide general information on the Colorado property tax system. For more specific information on any one of these topics, please visit

UNDERSTANDING PROPERTY TAXES IN COLORADO This brochure was created to provide general information on the Colorado property tax system. For more specific information on any one of these topics, please visit

York County 2015 Reassessment Program. York County Assessor s Office 18 W. Liberty St York SC fax

York County 2015 Reassessment Program York County Assessor s Office 18 W. Liberty St York SC 29745 803-684-8526 803-628-3936 fax Re-Assessment The Reassessment Program Act 208: Act 208, as passed by the

York County 2015 Reassessment Program York County Assessor s Office 18 W. Liberty St York SC 29745 803-684-8526 803-628-3936 fax Re-Assessment The Reassessment Program Act 208: Act 208, as passed by the

Washington Department of Revenue Property Tax Division. Valid Sales Study Kitsap County 2015 Sales for 2016 Ratio Year.

P. O. Box 47471 Olympia, WA 98504-7471. Washington Department of Revenue Property Tax Division Valid Sales Study Kitsap County 2015 Sales for 2016 Ratio Year Sales from May 1, 2014 through April 30, 2015

P. O. Box 47471 Olympia, WA 98504-7471. Washington Department of Revenue Property Tax Division Valid Sales Study Kitsap County 2015 Sales for 2016 Ratio Year Sales from May 1, 2014 through April 30, 2015

41 st Annual Conference Appraising Property

2017 KCCA 41 st Annual Conference Appraising Property Kansas County Commissioners Association Junction City, Kansas June 2, 2017 Topics Overview PVD s Role in the Appraisal Process Appointment of County

2017 KCCA 41 st Annual Conference Appraising Property Kansas County Commissioners Association Junction City, Kansas June 2, 2017 Topics Overview PVD s Role in the Appraisal Process Appointment of County

SAMA Presentation February 7-15, 2013 RMAA and UMAAS Sponsored Workshop Series

SAMA Presentation February 7-15, 2013 RMAA and UMAAS Sponsored Workshop Series Presentation Overview SAMA Who we are and what we do Summary of assessment legislation and policy Valuation publications Valuation

SAMA Presentation February 7-15, 2013 RMAA and UMAAS Sponsored Workshop Series Presentation Overview SAMA Who we are and what we do Summary of assessment legislation and policy Valuation publications Valuation

We look forward to working with you to build on our collaboration and enhance our partnership on behalf of all Minnesotans.

Date: February 27, 2017 To: County Assessors, Auditors, and Treasurers From: Cynthia Rowley, Director Property Tax Division Subject: Property Tax Services Report The Property Tax Division of the Minnesota

Date: February 27, 2017 To: County Assessors, Auditors, and Treasurers From: Cynthia Rowley, Director Property Tax Division Subject: Property Tax Services Report The Property Tax Division of the Minnesota

Publication 136 April 2016

Illinois Department of Revenue Constance Beard, Director Publication 136 April 2016 Property Assessment and Equalization The information in this publication is current as of the date of the publication.

Illinois Department of Revenue Constance Beard, Director Publication 136 April 2016 Property Assessment and Equalization The information in this publication is current as of the date of the publication.

2011 ASSESSMENT RATIO REPORT

2011 Ratio Report SECTION I OVERVIEW 2011 ASSESSMENT RATIO REPORT The Department of Assessments and Taxation appraises real property for the purposes of property taxation. Properties are valued using

2011 Ratio Report SECTION I OVERVIEW 2011 ASSESSMENT RATIO REPORT The Department of Assessments and Taxation appraises real property for the purposes of property taxation. Properties are valued using

ASSESSORS ANSWER FREQUENTLY ASKED QUESTIONS ABOUT REAL PROPERTY Assessors Office, 37 Main Street

A. THE ASSESSMENT PROCESS: ASSESSORS ANSWER FREQUENTLY ASKED QUESTIONS ABOUT REAL PROPERTY Assessors Office, 37 Main Street What is mass appraisal? Assessors must value all real and personal property in

A. THE ASSESSMENT PROCESS: ASSESSORS ANSWER FREQUENTLY ASKED QUESTIONS ABOUT REAL PROPERTY Assessors Office, 37 Main Street What is mass appraisal? Assessors must value all real and personal property in

GENERAL ASSESSMENT DEFINITIONS

21st Century Appraisals, Inc. GENERAL ASSESSMENT DEFINITIONS Ad Valorem tax. A tax levied in proportion to the value of the thing(s) being taxed. Exclusive of exemptions, use-value assessment laws, and

21st Century Appraisals, Inc. GENERAL ASSESSMENT DEFINITIONS Ad Valorem tax. A tax levied in proportion to the value of the thing(s) being taxed. Exclusive of exemptions, use-value assessment laws, and

Equalization. Overview. Multiplier Basics

The purpose of this primer is to outline the Illinois Department of Revenue s (IDOR) process in the determination of Cook County s equalization factor commonly known as the multiplier. It describes how

The purpose of this primer is to outline the Illinois Department of Revenue s (IDOR) process in the determination of Cook County s equalization factor commonly known as the multiplier. It describes how

April 12, The Honorable Martin O Malley And The General Assembly of Maryland

April 12, 2011 The Honorable Martin O Malley And The General Assembly of Maryland As required by Section 2-202 of the Tax-Property Article of the Annotated Code of Maryland, I am pleased to submit the

April 12, 2011 The Honorable Martin O Malley And The General Assembly of Maryland As required by Section 2-202 of the Tax-Property Article of the Annotated Code of Maryland, I am pleased to submit the

Office of Legislative Services Background Report The Revaluation of Real Property: Answers to Frequently Asked Questions About the Revaluation Process

Office of Legislative Services Background Report The Revaluation of Real Property: Answers to Frequently Asked Questions About the Revaluation Process OLS Background Report No. 119 Prepared By: Local Government

Office of Legislative Services Background Report The Revaluation of Real Property: Answers to Frequently Asked Questions About the Revaluation Process OLS Background Report No. 119 Prepared By: Local Government

We hope the trends provide additional perspective on your county s work. We know it provided valuable insight on the work we do here at Revenue.

Date: March 6, 2018 To: County Assessors, Auditors, and Treasurers From: Jon Klockziem, Acting Director Subject: Property Tax Services Report The Property Tax Division of the is pleased to provide the

Date: March 6, 2018 To: County Assessors, Auditors, and Treasurers From: Jon Klockziem, Acting Director Subject: Property Tax Services Report The Property Tax Division of the is pleased to provide the

Revaluation process ongoing in Norwalk

Revaluation process ongoing in Norwalk Property owners will have the opportunity to appeal assessment beginning December 5 (Norwalk, Conn.) The City of Norwalk is in the final phase of its revaluation

Revaluation process ongoing in Norwalk Property owners will have the opportunity to appeal assessment beginning December 5 (Norwalk, Conn.) The City of Norwalk is in the final phase of its revaluation

Multi-Family Methodology Analysis

Multi-Family Methodology 2018 Analysis Assessment Department February, 2018 2018 Multi-Family Assessment Methodology Property assessments in the City of Medicine Hat reflect the fee simple market value

Multi-Family Methodology 2018 Analysis Assessment Department February, 2018 2018 Multi-Family Assessment Methodology Property assessments in the City of Medicine Hat reflect the fee simple market value

How the Montgomery Central Appraisal District Appraises Residential Property

How the Montgomery Central Appraisal District Appraises Residential Property The following presentation is provided to educate Montgomery County residential property owners about the Analysis & Valuation

How the Montgomery Central Appraisal District Appraises Residential Property The following presentation is provided to educate Montgomery County residential property owners about the Analysis & Valuation

Cook County Assessor s Office: 2019 North Triad Assessment. Norwood Park Residential Assessment Narrative March 11, 2019

Cook County Assessor s Office: 2019 North Triad Assessment Norwood Park Residential Assessment Narrative March 11, 2019 1 Norwood Park Residential Properties Executive Summary This is the current CCAO

Cook County Assessor s Office: 2019 North Triad Assessment Norwood Park Residential Assessment Narrative March 11, 2019 1 Norwood Park Residential Properties Executive Summary This is the current CCAO

Appraisal and Market Analysis of Indoor Waterpark Resorts

Appraisal and Market Analysis of Indoor Waterpark Resorts By David J. Sangree, MAI, CPA, ISHC An appraisal of an indoor waterpark resort is similar to other appraisals in that it is a professional appraiser

Appraisal and Market Analysis of Indoor Waterpark Resorts By David J. Sangree, MAI, CPA, ISHC An appraisal of an indoor waterpark resort is similar to other appraisals in that it is a professional appraiser

Pickens County Reassessment Program. Utilizing CAMA GIS MLS SQL

1 Pickens County 2019 Reassessment Program Utilizing CAMA GIS MLS SQL Pickens County Reassessment History 1980 Countywide Reappraisal 1990 Countywide Reappraisal 1999 Countywide Reappraisal 2004 Countywide

1 Pickens County 2019 Reassessment Program Utilizing CAMA GIS MLS SQL Pickens County Reassessment History 1980 Countywide Reappraisal 1990 Countywide Reappraisal 1999 Countywide Reappraisal 2004 Countywide

GOVERNANCE OF ASSESSOR

GOVERNANCE OF ASSESSOR State of NH Constitution NH State Statutes (RSA) State Supreme Court Case Law NH Assessing Standard Board Rules NH Department of Revenue Rules Professional Code of Conduct (USPAP)

GOVERNANCE OF ASSESSOR State of NH Constitution NH State Statutes (RSA) State Supreme Court Case Law NH Assessing Standard Board Rules NH Department of Revenue Rules Professional Code of Conduct (USPAP)

The Honorable Larry Hogan And The General Assembly of Maryland

2015 Ratio Report The Honorable Larry Hogan And The General Assembly of Maryland As required by Section 2-202 of the Tax-Property Article of the Annotated Code of Maryland, I am pleased to submit the Department

2015 Ratio Report The Honorable Larry Hogan And The General Assembly of Maryland As required by Section 2-202 of the Tax-Property Article of the Annotated Code of Maryland, I am pleased to submit the Department

EXPLAINING MASS APPRAISAL

EXPLAINING MASS APPRAISAL PROMOTING THE ROLE OF THE ASSESSOR MAAO SUMMER CONFERENCE, JUNE 24, 2015 RICHARD W. FINNEGAN, MAA Please excuse the length of this letter. I didn t have time to write a short

EXPLAINING MASS APPRAISAL PROMOTING THE ROLE OF THE ASSESSOR MAAO SUMMER CONFERENCE, JUNE 24, 2015 RICHARD W. FINNEGAN, MAA Please excuse the length of this letter. I didn t have time to write a short

SAMA Presenters: Steve Suchan Todd Treslan February 1, 2015

SAMA Presenters: Steve Suchan Todd Treslan February 1, 2015 Presentation Overview Part 1 - Steve SAMA Who we are and what we do Assessment legislation and principles Valuation standards (Regulated, non-regulated)

SAMA Presenters: Steve Suchan Todd Treslan February 1, 2015 Presentation Overview Part 1 - Steve SAMA Who we are and what we do Assessment legislation and principles Valuation standards (Regulated, non-regulated)

Citizens Guide Town of Yarmouth Reassessment Program reassessment

Citizens Guide Town of Yarmouth Reassessment Program - 2017 reassessment 1 P a g e town manager s message A townwide reassessment of all real properties located in the Town of Yarmouth will occur for tax

Citizens Guide Town of Yarmouth Reassessment Program - 2017 reassessment 1 P a g e town manager s message A townwide reassessment of all real properties located in the Town of Yarmouth will occur for tax

Property Appraisal Division Finance Department Anchorage: Performance Value Results

Anchorage: Performance Value Results Mission Provide fair and equitable basis for taxation in the Municipality of Anchorage in conformance with State law and professional standards. Core Services Valuation

Anchorage: Performance Value Results Mission Provide fair and equitable basis for taxation in the Municipality of Anchorage in conformance with State law and professional standards. Core Services Valuation

Saskatchewan Municipal Board Assessment Appeals Committee

Saskatchewan Municipal Board Assessment Appeals Committee Appeal: 2009-0039 RESPONDENT: Town of Hudson Bay In the matter of an appeal to the Assessment Appeals Committee, Saskatchewan Municipal Board,

Saskatchewan Municipal Board Assessment Appeals Committee Appeal: 2009-0039 RESPONDENT: Town of Hudson Bay In the matter of an appeal to the Assessment Appeals Committee, Saskatchewan Municipal Board,

Property Appraisal Division Finance Department Anchorage: Performance. Value. Results.

Anchorage: Performance. Value. Results. Mission Provide a fair and equitable basis for taxation in the Municipality of Anchorage in conformance with State law and professional standards. Core Services

Anchorage: Performance. Value. Results. Mission Provide a fair and equitable basis for taxation in the Municipality of Anchorage in conformance with State law and professional standards. Core Services

Equity from the Assessor s Perspective

Institute of Municipal Assessors 55th Annual Conference Equity from the Assessor s Perspective Andy Anstett Legislation & Policy Support Services MPAC June 7th, 2011 Key Aspects of Equity Test Defining

Institute of Municipal Assessors 55th Annual Conference Equity from the Assessor s Perspective Andy Anstett Legislation & Policy Support Services MPAC June 7th, 2011 Key Aspects of Equity Test Defining

Cranes in the air! Amari & Locallo

Cranes in the air! If you work, live in or visit Chicago s Central Business District (CBD) you cannot help but notice many construction cranes in the air heralding the beginnings of new real estate. You

Cranes in the air! If you work, live in or visit Chicago s Central Business District (CBD) you cannot help but notice many construction cranes in the air heralding the beginnings of new real estate. You

MINNESOTA REVENUE ASSESSMENT AND CLASSIFICATION PRACTICES REPORT

MINNESOTA REVENUE ASSESSMENT AND CLASSIFICATION PRACTICES REPORT THE AGRICULTURAL PROPERTY TAX PROGRAM, CLASS 2A AGRICULTURAL PROPERTY, AND CLASS 2B RURAL VACANT LAND PROPERTY A report submitted to the

MINNESOTA REVENUE ASSESSMENT AND CLASSIFICATION PRACTICES REPORT THE AGRICULTURAL PROPERTY TAX PROGRAM, CLASS 2A AGRICULTURAL PROPERTY, AND CLASS 2B RURAL VACANT LAND PROPERTY A report submitted to the

To: Property Appraisers, Taxing Authorities and Interested Parties From: James McAdams Date: June 5, 2012 Bulletin: PTO 12-04

Property Tax Oversight Bulletin: PTO 12-04 To: Property Appraisers, Taxing Authorities and Interested Parties From: James McAdams Date: Bulletin: PTO 12-04 FLORIDA DEPARTMENT OF REVENUE PROPERTY TAX INFORMATIONAL

Property Tax Oversight Bulletin: PTO 12-04 To: Property Appraisers, Taxing Authorities and Interested Parties From: James McAdams Date: Bulletin: PTO 12-04 FLORIDA DEPARTMENT OF REVENUE PROPERTY TAX INFORMATIONAL

Rockwall CAD. Basics of. Appraising Property. For. Property Taxation

Rockwall CAD Basics of Appraising Property For Property Taxation ROCKWALL CENTRAL APPRAISAL DISTRICT 841 Justin Rd. Rockwall, Texas 75087 972-771-2034 Fax 972-771-6871 Introduction Rockwall Central Appraisal

Rockwall CAD Basics of Appraising Property For Property Taxation ROCKWALL CENTRAL APPRAISAL DISTRICT 841 Justin Rd. Rockwall, Texas 75087 972-771-2034 Fax 972-771-6871 Introduction Rockwall Central Appraisal

A Panel Discussion of Developments, Trends and Issues Affecting Commercial Property Iowa Commercial Real Estate Expo

A Panel Discussion of Developments, Trends and Issues Affecting Commercial Property By Bryon Tack, MAI, CAE Polk County Deputy Assessor January 1 : Assessment of property (appraisal date) Historical data

A Panel Discussion of Developments, Trends and Issues Affecting Commercial Property By Bryon Tack, MAI, CAE Polk County Deputy Assessor January 1 : Assessment of property (appraisal date) Historical data

METHODOLOGY GUIDE VALUING MOTELS IN ONTARIO. Valuation Date: January 1, 2016

METHODOLOGY GUIDE VALUING MOTELS IN ONTARIO Valuation Date: January 1, 2016 AUGUST 2016 August 22, 2016 The Municipal Property Assessment Corporation (MPAC) is responsible for accurately assessing and

METHODOLOGY GUIDE VALUING MOTELS IN ONTARIO Valuation Date: January 1, 2016 AUGUST 2016 August 22, 2016 The Municipal Property Assessment Corporation (MPAC) is responsible for accurately assessing and

Village of Scarsdale

Village of Scarsdale VILLAGE HALL / 1001 POST ROAD / SCARSDALE, NY 10583 914.722.1110 / WWW.SCARSDALE.COM Village Wide Revaluation Frequently Asked Questions Q1. How was the land value for each parcel

Village of Scarsdale VILLAGE HALL / 1001 POST ROAD / SCARSDALE, NY 10583 914.722.1110 / WWW.SCARSDALE.COM Village Wide Revaluation Frequently Asked Questions Q1. How was the land value for each parcel

Table of Contents 2013 Commercial Revaluation Report

Table of Contents Commercial Revaluation Report 1. Commercial & Industrial Valuation Summary Introduction Uniform Standards Approaches to Value Land Valuation Land to Building Ratios Parking to Building

Table of Contents Commercial Revaluation Report 1. Commercial & Industrial Valuation Summary Introduction Uniform Standards Approaches to Value Land Valuation Land to Building Ratios Parking to Building

ESTIMATED FULL VALUE OF REAL PROPERTY IN COOK COUNTY:

ESTIMATED FULL VALUE OF REAL PROPERTY IN COOK COUNTY: 2003-2012 August 14, 2014 ESTIMATED FULL VALUE OF PROPERTY IN COOK COUNTY: Civic Federation Methodology CALCULATION OF ESTIMATED FULL VALUE The full

ESTIMATED FULL VALUE OF REAL PROPERTY IN COOK COUNTY: 2003-2012 August 14, 2014 ESTIMATED FULL VALUE OF PROPERTY IN COOK COUNTY: Civic Federation Methodology CALCULATION OF ESTIMATED FULL VALUE The full

LLANO CENTRAL APPRAISAL DISTRICT REAPPRAISAL PLAN FOR TAX YEARS 2017 & 2018 AS ADOPTED BY THE BOARD OF DIRECTORS

LLANO CENTRAL APPRAISAL DISTRICT REAPPRAISAL PLAN FOR TAX YEARS 2017 & 2018 AS ADOPTED BY THE BOARD OF DIRECTORS TABLE OF CONTENTS ITEM PAGE Executive Summary 5 Revaluation Decision (Statutory or Administrative)

LLANO CENTRAL APPRAISAL DISTRICT REAPPRAISAL PLAN FOR TAX YEARS 2017 & 2018 AS ADOPTED BY THE BOARD OF DIRECTORS TABLE OF CONTENTS ITEM PAGE Executive Summary 5 Revaluation Decision (Statutory or Administrative)

COMMITTEE OF THE WHOLE AGENDA April 18, :30 PM City Hall Council Chambers

COMMITTEE OF THE WHOLE AGENDA April 18, 2016-5:30 PM City Hall Council Chambers Committee of the Whole Meeting 1. Presentation Bluestem and TPAS - Kathy Anderson, Executive Director 2. 2016 Board of Appeals

COMMITTEE OF THE WHOLE AGENDA April 18, 2016-5:30 PM City Hall Council Chambers Committee of the Whole Meeting 1. Presentation Bluestem and TPAS - Kathy Anderson, Executive Director 2. 2016 Board of Appeals

IMPORTANT ANNOUNCEMENT: Our website is changing! Please click here for details.

IMPORTANT ANNOUNCEMENT: Our website is changing! Please click here for details. Home Search Downloads Exemptions Agriculture Maps Tangible Links Contact Home Frequently Asked Questions (FAQ) Frequently

IMPORTANT ANNOUNCEMENT: Our website is changing! Please click here for details. Home Search Downloads Exemptions Agriculture Maps Tangible Links Contact Home Frequently Asked Questions (FAQ) Frequently

Date: March 2018 TOWN OF WATERFORD Department of Assessment

Date: March 2018 TOWN OF WATERFORD 1. Overview: The purpose of this workshop is to explain the Assessment Disclosure Notice, how assessments are derived and how to challenge your assessment if you do not

Date: March 2018 TOWN OF WATERFORD 1. Overview: The purpose of this workshop is to explain the Assessment Disclosure Notice, how assessments are derived and how to challenge your assessment if you do not

Duties of the Assessors

Duties of the Assessors Value Properties Determine New Growth Set Tax Rate Assess Property Taxes Abate & Exempt Taxes Manage Overlay Account Assess Local Excises 1 Value Property Assessments based on fair

Duties of the Assessors Value Properties Determine New Growth Set Tax Rate Assess Property Taxes Abate & Exempt Taxes Manage Overlay Account Assess Local Excises 1 Value Property Assessments based on fair

A GUIDE TO THE PROPERTY VALUATION APPEAL PROCESS - EQUALIZATION APPEALS*

A GUIDE TO THE PROPERTY VALUATION APPEAL PROCESS - EQUALIZATION APPEALS* LAND AND BUILIDNGS USED FOR RESIDENTIAL AND COMMERICAL PURPOSES (*IN COUNTIES WITHOUT HEARING OFFICER/PANELS) (Rev. 08/2016) Kansas

A GUIDE TO THE PROPERTY VALUATION APPEAL PROCESS - EQUALIZATION APPEALS* LAND AND BUILIDNGS USED FOR RESIDENTIAL AND COMMERICAL PURPOSES (*IN COUNTIES WITHOUT HEARING OFFICER/PANELS) (Rev. 08/2016) Kansas

City of Norwalk Revaluation Project

City of Norwalk 2018 Revaluation Project Presenter: Paul Miller Supervisor: Salim Serdah Appraisers: James Steiner, John Valente, Steve Beccio, Rich Nicolosi, and Gynt Grube. Why Revaluation? It s important

City of Norwalk 2018 Revaluation Project Presenter: Paul Miller Supervisor: Salim Serdah Appraisers: James Steiner, John Valente, Steve Beccio, Rich Nicolosi, and Gynt Grube. Why Revaluation? It s important

Monthly Market Watch for the Prescott Quad City Area. Provided by Keller Williams Check Realty Statistics from August 2012 Prescott MLS

August 2012 Monthly Market Watch for the Prescott Quad City Area Provided by Keller Williams Check Realty Statistics from August 2012 Prescott MLS Report Overview: This report includes MLS data for the

August 2012 Monthly Market Watch for the Prescott Quad City Area Provided by Keller Williams Check Realty Statistics from August 2012 Prescott MLS Report Overview: This report includes MLS data for the

ESTIMATED FULL VALUE OF REAL PROPERTY IN COOK COUNTY:

ESTIMATED FULL VALUE OF REAL PROPERTY IN COOK COUNTY: 2007-2016 May 21, 2018 MAJOR FINDINGS This report provides an estimate of the full market value of property in Cook County between tax years 2007 and

ESTIMATED FULL VALUE OF REAL PROPERTY IN COOK COUNTY: 2007-2016 May 21, 2018 MAJOR FINDINGS This report provides an estimate of the full market value of property in Cook County between tax years 2007 and

Minnesota Department of Revenue 2012 Sales Ratio Study Criteria

Minnesota Department of Revenue 2012 Sales Ratio Study Criteria Special Notes Forward-Adjusted Methodology Transition In the 2012 sales ratio study, the Department of Revenue will use a forward-adjusted

Minnesota Department of Revenue 2012 Sales Ratio Study Criteria Special Notes Forward-Adjusted Methodology Transition In the 2012 sales ratio study, the Department of Revenue will use a forward-adjusted

Course Mass Appraisal Practices and Procedures

Course 331 - Mass Appraisal Practices and Procedures Course Description This course is designed to build on the subject matter covered in Course 300 Fundamentals of Mass Appraisal and prepare the student

Course 331 - Mass Appraisal Practices and Procedures Course Description This course is designed to build on the subject matter covered in Course 300 Fundamentals of Mass Appraisal and prepare the student

VAN ZANDT COUNTY APPRAISAL DISTRICT 2018 ANNUAL REPORT

VAN ZANDT COUNTY APPRAISAL DISTRICT 2018 ANNUAL REPORT INTRODUCTION The Van Zandt County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property

VAN ZANDT COUNTY APPRAISAL DISTRICT 2018 ANNUAL REPORT INTRODUCTION The Van Zandt County Appraisal District is a political subdivision of the state. The Constitution of the State of Texas, the Texas Property

Introduction. Market Value Assessment in Saskatchewan Handbook. Introduction

Market Value Assessment in Saskatchewan Handbook Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass Appraisal for

Market Value Assessment in Saskatchewan Handbook Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass Appraisal for

Property Appraisal Division Finance Department Anchorage: Performance. Value. Results.

Anchorage: Performance. Value. Results. Mission Provide a fair and equitable basis for taxation in the Municipality of Anchorage in conformance with State law and professional standards. Core Services

Anchorage: Performance. Value. Results. Mission Provide a fair and equitable basis for taxation in the Municipality of Anchorage in conformance with State law and professional standards. Core Services

Kitsap County Assessor

Kitsap County Assessor Narrative for Countywide Model Tax Year: 2018 Appraisal Date: 1/1/2017 Property Type: Condominium Boat Slip Updated 6/8/2017 by CM20 Area Overview Countywide models are for properties

Kitsap County Assessor Narrative for Countywide Model Tax Year: 2018 Appraisal Date: 1/1/2017 Property Type: Condominium Boat Slip Updated 6/8/2017 by CM20 Area Overview Countywide models are for properties

YOUNG COUNTY APPRAISAL DISTRICT

YOUNG COUNTY APPRAISAL DISTRICT 2017 - ANNUAL APPRAISAL REPORT AS OF 10/6/2017 1 2 TABLE OF CONTENTS ITEM PAGE Introduction 4 Purpose of Report...4 Taxing Entities, Rates & Exemptions 5 Property Types

YOUNG COUNTY APPRAISAL DISTRICT 2017 - ANNUAL APPRAISAL REPORT AS OF 10/6/2017 1 2 TABLE OF CONTENTS ITEM PAGE Introduction 4 Purpose of Report...4 Taxing Entities, Rates & Exemptions 5 Property Types

METHODOLOGY GUIDE VALUING LANDS IN TRANSITION IN ONTARIO. Valuation Date: January 1, 2016

METHODOLOGY GUIDE VALUING LANDS IN TRANSITION IN ONTARIO Valuation Date: January 1, 2016 August 2017 August 22, 2017 The Municipal Property Assessment Corporation (MPAC) is responsible for accurately assessing

METHODOLOGY GUIDE VALUING LANDS IN TRANSITION IN ONTARIO Valuation Date: January 1, 2016 August 2017 August 22, 2017 The Municipal Property Assessment Corporation (MPAC) is responsible for accurately assessing

Sales Ratio: Alternative Calculation Methods

For Discussion: Summary of proposals to amend State Board of Equalization sales ratio calculations June 3, 2010 One of the primary purposes of the sales ratio study is to measure how well assessors track

For Discussion: Summary of proposals to amend State Board of Equalization sales ratio calculations June 3, 2010 One of the primary purposes of the sales ratio study is to measure how well assessors track

Kitsap County Assessor

Kitsap County Assessor Narrative for Countywide Model Tax Year: 2018 Appraisal Date: 1/1/2017 Property Type: Hangar - Airplane Area Overview Countywide models are for properties located throughout Kitsap

Kitsap County Assessor Narrative for Countywide Model Tax Year: 2018 Appraisal Date: 1/1/2017 Property Type: Hangar - Airplane Area Overview Countywide models are for properties located throughout Kitsap

General Market Analysis and Highest & Best Use. Learning Objectives

General Market Analysis and Highest & Best Use Learning Objectives Module & Title Module 1 Real Estate Markets and Analysis Module 2 Types and Levels of Market Analysis Module 3 The Six-Step Process and

General Market Analysis and Highest & Best Use Learning Objectives Module & Title Module 1 Real Estate Markets and Analysis Module 2 Types and Levels of Market Analysis Module 3 The Six-Step Process and

Assessment Report 2017

Assessment Report 217 Hennepin County Assessor s Office James Atchison, County Assessor, CAE, SAMA 217 TABLE OF CONTENTS Last modified (4-17-17) Table of Contents....3 Introduction and Overview of the

Assessment Report 217 Hennepin County Assessor s Office James Atchison, County Assessor, CAE, SAMA 217 TABLE OF CONTENTS Last modified (4-17-17) Table of Contents....3 Introduction and Overview of the

Panama City Beach Fire Service Assessment Information

Panama City Beach Fire Service Assessment Information On November 9, 2017, the City of Panama City Beach scheduled a public hearing for January 11, 2018 to consider the adoption of a special assessment

Panama City Beach Fire Service Assessment Information On November 9, 2017, the City of Panama City Beach scheduled a public hearing for January 11, 2018 to consider the adoption of a special assessment

Town of Fairfield 2015 Revaluation Informational Meeting

www.vgsi.com Town of Fairfield 2015 Revaluation Informational Meeting Fairfield Revaluation Cycle Ct. Law states revaluations take place every 5 years Fairfield s last Revaluation was in 2010 All property

www.vgsi.com Town of Fairfield 2015 Revaluation Informational Meeting Fairfield Revaluation Cycle Ct. Law states revaluations take place every 5 years Fairfield s last Revaluation was in 2010 All property

Assessment Year 2016 Assessment Valuations / Mass Appraisal Summary Report

Assessment Year 2016 Assessment Valuations / Mass Appraisal Summary Report Overview Following up on last year s work, additional work was done cleaning up the sales data. The land valuation model was further

Assessment Year 2016 Assessment Valuations / Mass Appraisal Summary Report Overview Following up on last year s work, additional work was done cleaning up the sales data. The land valuation model was further

2018 Assessment Report

2018 Assessment Report The Assessing Division: 952-939-8220 or assessor@eminnetonka.com Table of Contents Table of Contents... 2 Summary... 3 2018 Assessment from a Historical Perspective... 4 Tax Capacity...

2018 Assessment Report The Assessing Division: 952-939-8220 or assessor@eminnetonka.com Table of Contents Table of Contents... 2 Summary... 3 2018 Assessment from a Historical Perspective... 4 Tax Capacity...

WYOMING DEPARTMENT OF REVENUE CHAPTER 7 PROPERTY TAX VALUATION METHODOLOGY AND ASSESSMENT (DEPARTMENT ASSESSMENTS)

") CHAPTER 7 PROPERTY TAX VALUATION METHODOLOGY AND ASSESSMENT (DEPARTMENT ASSESSMENTS) Section 1. Authority. These Rules are promulgated under the authority of W.S. 39-11-102(b). Section 2. Purpose of Rules.

CHAPTER 7 PROPERTY TAX VALUATION METHODOLOGY AND ASSESSMENT (DEPARTMENT ASSESSMENTS) Section 1. Authority. These Rules are promulgated under the authority of W.S. 39-11-102(b). Section 2. Purpose of Rules.

Referred to Committee on Revenue and Economic Development. FISCAL NOTE: Effect on Local Government: May have Fiscal Impact. Effect on the State: Yes.

SENATE JOINT RESOLUTION NO. SENATORS SETTELMEYER, GUSTAVSON; AND GOICOECHEA MARCH, 0 Referred to Committee on Revenue and Economic Development S.J.R. SUMMARY Proposes to amend the Nevada Constitution to

SENATE JOINT RESOLUTION NO. SENATORS SETTELMEYER, GUSTAVSON; AND GOICOECHEA MARCH, 0 Referred to Committee on Revenue and Economic Development S.J.R. SUMMARY Proposes to amend the Nevada Constitution to

Allegan County Equalization Department

Allegan County Equalization Department 2011 Department Report Equalization Report Recap 2010 2011 projects January 1- December 31, 2010 Blaine R. McLeod Director of Equalization 1 Message from the Director

Allegan County Equalization Department 2011 Department Report Equalization Report Recap 2010 2011 projects January 1- December 31, 2010 Blaine R. McLeod Director of Equalization 1 Message from the Director

The Department s Role

CITY ASSESSOR The Department s Role on the h Ci City s T Team August 21, 2013 Who we are... Micheal Lohmeier City Assessor (2012) (Commercial Appraiser 1998-2005, Assr. 2010-12) 12) Administration and

CITY ASSESSOR The Department s Role on the h Ci City s T Team August 21, 2013 Who we are... Micheal Lohmeier City Assessor (2012) (Commercial Appraiser 1998-2005, Assr. 2010-12) 12) Administration and

City of Manassas Park, Virginia

DATE: MARCH 24, 2008 City of Manassas Park, Virginia MEMORANDUM TO: FROM: GARY FIELDS, FINANCE DIRECTOR RICHARD SANDERSON, CITY ASSESSOR SUBJECT: CY 2008 REAL PROPERTY ASSESSMENT REPORT The purpose of

DATE: MARCH 24, 2008 City of Manassas Park, Virginia MEMORANDUM TO: FROM: GARY FIELDS, FINANCE DIRECTOR RICHARD SANDERSON, CITY ASSESSOR SUBJECT: CY 2008 REAL PROPERTY ASSESSMENT REPORT The purpose of

PROPERTY ASSESSMENT AND TAXATION

History of the Community and Service Area Structure Juneau's existing City and Borough concept was adopted in 1970 with the unification of the Cities of Juneau and Douglas and the Greater Juneau Borough.

History of the Community and Service Area Structure Juneau's existing City and Borough concept was adopted in 1970 with the unification of the Cities of Juneau and Douglas and the Greater Juneau Borough.

We value... Fairness Integrity Efficiency

We value... Fairness Integrity Efficiency Prince George City Council Presentation Christopher Whyte Deputy Assessor John Castle Senior Appraiser May 2 nd, 2011 BC Assessment Our Mission is to: The mission

We value... Fairness Integrity Efficiency Prince George City Council Presentation Christopher Whyte Deputy Assessor John Castle Senior Appraiser May 2 nd, 2011 BC Assessment Our Mission is to: The mission

OFFICIAL PROCEEDINGS City of Williston Local Board of Equalization May 3, :00 pm City Hall Williston, North Dakota

1. Roll Call of Commissioners OFFICIAL PROCEEDINGS City of Williston Local Board of Equalization May 3, 2017 6:00 pm City Hall Williston, North Dakota COMMISSIONERS PRESENT: Deanette Piesik, Tate Cymbaluk,

1. Roll Call of Commissioners OFFICIAL PROCEEDINGS City of Williston Local Board of Equalization May 3, 2017 6:00 pm City Hall Williston, North Dakota COMMISSIONERS PRESENT: Deanette Piesik, Tate Cymbaluk,

86 years in the making Caspar G Haas 1922 Sales Prices as a Basis for Estimating Farmland Value

2 Our Journey Begins 86 years in the making Caspar G Haas 1922 Sales Prices as a Basis for Estimating Farmland Value Starting at the beginning. Mass Appraisal and Single Property Appraisal Appraisal

2 Our Journey Begins 86 years in the making Caspar G Haas 1922 Sales Prices as a Basis for Estimating Farmland Value Starting at the beginning. Mass Appraisal and Single Property Appraisal Appraisal

Office of Legislative Services Background Report The Assessment of Real Property: Answers to Frequently Asked Questions

Office of Legislative Services Background Report The Assessment of Real Property: Answers to Frequently Asked Questions OLS Background Report No. 120 Prepared By: Local Government Date Prepared: New Jersey

Office of Legislative Services Background Report The Assessment of Real Property: Answers to Frequently Asked Questions OLS Background Report No. 120 Prepared By: Local Government Date Prepared: New Jersey

FINANCIAL IMPACTS REPORT

TULSA INTERNATIONAL AIRPORT ECONOMIC DEVELOPMENT PROJECT PLAN FINANCIAL IMPACTS REPORT A PROJECT OF: THE CITY OF TULSA IN COOPERATION WITH: TULSA COUNTY TULSA INTERNATIONAL AIRPORT DEVELOPMENT TRUST TULSA

TULSA INTERNATIONAL AIRPORT ECONOMIC DEVELOPMENT PROJECT PLAN FINANCIAL IMPACTS REPORT A PROJECT OF: THE CITY OF TULSA IN COOPERATION WITH: TULSA COUNTY TULSA INTERNATIONAL AIRPORT DEVELOPMENT TRUST TULSA

COMAL APPRAISAL DISTRICT ANNUAL APPRAISAL REPORT

COMAL APPRAISAL DISTRICT 2016 ANNUAL APPRAISAL REPORT TABLE OF CONTENTS Introduction..2 Mission Statement... 2 Purpose of Report...2 Entities Served..2 Legislative Changes.3 Property Types.3 Appraisal

COMAL APPRAISAL DISTRICT 2016 ANNUAL APPRAISAL REPORT TABLE OF CONTENTS Introduction..2 Mission Statement... 2 Purpose of Report...2 Entities Served..2 Legislative Changes.3 Property Types.3 Appraisal

Table of Contents 2015 Commercial Revaluation Report

Table of Contents 05 Commercial Revaluation Report 05 Commercial & Industrial Valuation Summary Introduction Uniform Standards Approaches to Value Land Valuation Land to Building Ratios Parking to Building

Table of Contents 05 Commercial Revaluation Report 05 Commercial & Industrial Valuation Summary Introduction Uniform Standards Approaches to Value Land Valuation Land to Building Ratios Parking to Building

PAYMENT UNDER PROTEST APPEAL GUIDE

PAYMENT UNDER PROTEST APPEAL GUIDE In Kansas you have two opportunities to appeal the value of your property. If you appeal at the time of paying taxes, it is called a Payment Under Protest. This guide

PAYMENT UNDER PROTEST APPEAL GUIDE In Kansas you have two opportunities to appeal the value of your property. If you appeal at the time of paying taxes, it is called a Payment Under Protest. This guide

PVD Foreclosure Related Sales Guidelines

Introduction PVD Foreclosure Related Sales Guidelines The purpose of this paper is to provide guidance to county appraisers in dealing with the high volume of foreclosure related sales, also known as REO

Introduction PVD Foreclosure Related Sales Guidelines The purpose of this paper is to provide guidance to county appraisers in dealing with the high volume of foreclosure related sales, also known as REO

Mass Appraisal of Income-Producing Properties

Chapter 10 Mass Appraisal of Income-Producing Properties Whether valuing income-producing property or residential property, you can use similar information and methods for collecting and analyzing data

Chapter 10 Mass Appraisal of Income-Producing Properties Whether valuing income-producing property or residential property, you can use similar information and methods for collecting and analyzing data

DEPARTMENT OF ASSESSMENTS AND TAXATION 2008 RATIO REPORT

DEPARTMENT OF ASSESSMENTS AND TAXATION 2008 RATIO REPORT State of Maryland Department of Assessments and Taxation Office of the Director Martin O'Malley Governor C. John Sullivan Jr. Director June 30,

DEPARTMENT OF ASSESSMENTS AND TAXATION 2008 RATIO REPORT State of Maryland Department of Assessments and Taxation Office of the Director Martin O'Malley Governor C. John Sullivan Jr. Director June 30,

Camp Central Appraisal District LEGAL AND ADMINISTRATIVE REQUIREMENTS

Camp Central Appraisal District LEGAL AND ADMINISTRATIVE REQUIREMENTS Counties are responsible for creating and establishing an Appraisal District. As a political subdivision of the state the major responsibility

Camp Central Appraisal District LEGAL AND ADMINISTRATIVE REQUIREMENTS Counties are responsible for creating and establishing an Appraisal District. As a political subdivision of the state the major responsibility

COMAL APPRAISAL DISTRICT ANNUAL APPRAISAL REPORT

COMAL APPRAISAL DISTRICT 2017 ANNUAL APPRAISAL REPORT TABLE OF CONTENTS Introduction..2 Mission Statement... 2 Purpose of Report...2 Entities Served..2 Legislative Changes.3 Property Types.3 Appraisal

COMAL APPRAISAL DISTRICT 2017 ANNUAL APPRAISAL REPORT TABLE OF CONTENTS Introduction..2 Mission Statement... 2 Purpose of Report...2 Entities Served..2 Legislative Changes.3 Property Types.3 Appraisal

Equalization Department

Equalization Department Citizens Board of Commissioners Administrator /Controller Equalization Director Statutory Authority Michigan Compiled Law 211.34 (3) The County Board of Commissioners of a county

Equalization Department Citizens Board of Commissioners Administrator /Controller Equalization Director Statutory Authority Michigan Compiled Law 211.34 (3) The County Board of Commissioners of a county

How to Read a Real Estate Appraisal Report

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

YOUR GUIDE TO THE REASSESSMENT PROGRAM

YOUR GUIDE TO THE REASSESSMENT PROGRAM Why Reassess? Reassessment is required by law. Act 208, as passed by the General Assembly in 1975, provides that all real property will be valued at its current market

YOUR GUIDE TO THE REASSESSMENT PROGRAM Why Reassess? Reassessment is required by law. Act 208, as passed by the General Assembly in 1975, provides that all real property will be valued at its current market

PROPERTY REASSESSMENT AND TAXATION. State Tax Commission Jefferson City, Missouri

PROPERTY REASSESSMENT AND TAXATION State Tax Commission Jefferson City, Missouri Revised January, 2017 INTRODUCTION Some aspects of the property tax system are confusing to many taxpayers. It is important

PROPERTY REASSESSMENT AND TAXATION State Tax Commission Jefferson City, Missouri Revised January, 2017 INTRODUCTION Some aspects of the property tax system are confusing to many taxpayers. It is important