SAMA Presenters: Steve Suchan Todd Treslan February 1, 2015

|

|

|

- Amberly Marshall

- 5 years ago

- Views:

Transcription

1 SAMA Presenters: Steve Suchan Todd Treslan February 1, 2015

2 Presentation Overview Part 1 - Steve SAMA Who we are and what we do Assessment legislation and principles Valuation standards (Regulated, non-regulated) Part 2 - Todd Role of Assessor vs Assessment Appraiser Right of Entry Services Provided by SAMA Three approaches to value 2017 Revaluation trends Questions and wrap-up

3 SAMA s Roles and Responsibilities AMA Act -- Board Governed Agency Governance $160B /$1.64B Ass mt / Taxes (100% Province) Policy Quality Assurance Computer System Communication Safety Net for Province Assessment Services 763 of 771 municipalities (61%Munic/39%) Annual Maintenance General Re-inspections Revaluations Support of Value

4 SAMA Board Chair: Neal Hardy (RM Hudson Bay, #395) Urban: Wade Murray (Regina) Urban: Al Heron (Eston) Rural: John Wagner (RM Piapot, #110) Rural: Murray Purcell (RM Montrose, #315) Province: Jim Angus (Harris) Province: Myron Knafelc (Watson) CEO: Irwin Blank

5 Vision and Mission Statements Vision SAMA is the recognized leader and authority on property assessment, and Saskatchewan s service provider of choice Mission SAMA develops, regulates and delivers a stable, costeffective assessment system that is accurate, up-todate, universal, equitable and understandable. Core Values Integrity, professionalism, dedication, solution focused.

6 SAMA s Strategic Directions 1. Establish a new, stakeholder supported funding model for SAMA. (ie. maint fee) 2. Simplify and streamline to improve efficiency and effectiveness. 3. Use policy, process and technology changes together to radically increase property inspections. 4. Strengthen the capabilities of all employees.

Weyburn Melfort Yorkton Swift")

7 SAMA Regions Saskatoon North Battleford Regina Moose Jaw (city) Weyburn Melfort Yorkton Swift Current

8

9 Purpose of Assessments Financial Foundation for local governments Municipal services (police, fire, streets, water, parks, recreation, libraries...) K to 12 Education What you do with it is up to the local government Local Autonomy

10 Assessment Principles Ad Valorem Property Values Property Assessments Assessments

11 Assessment Principles Mass Appraisal Base Date Four Year Updates (Revaluations) Foundation in Legislation Market Valuation Standard Regulated Property Assessment Standard Equity SAMA Board Orders

12 Assessments - Foundational Component of the Property Tax System Property Assessment SAMA Tax Classes, Percentage of Value & Exemptions Local Mill Rates & Tax Tools Municipality Property Taxes Payable GR Uniform Education Mill Rates GR

13 Assessment Legislation The Assessment Management Agency Act (AMA Act) Regulations Board Orders The Cities Act (CAct) Regulations The Municipalities Act (MAct) Regulations The Northern Municipalities Act, 2010 (NAct) Regulations

14 Assessment Legislation The Assessment Management Agency Act (s12.(1)) Prepare assessment manuals, guidelines, handbooks and other materials. Perform valuations and revaluations. Maintain a central database. Ensure public, municipal councils a government aware of assessment methods and policies. Confirm assessments of municipalities.

15 Assessment Legislation The Assessment Management Agency Act SAMA Revaluation Board Orders. January 1, 2011 for January 1, 2015 for January 1, 2019 for Are corresponding Orders for each revaluation relating to: - Market Evidence. - Quality Assurance Standard for market value properties. - Regulated Manual.

16 Assessment Legislation MAct, CAct, NAct All property in a city/municipality is subject to assessment. Assessments prepared annually. Facts, conditions and circumstances as of January 1 as if they occurred on the base date. Same base date used for four years. Annual maintenance and periodic reinspections.

17 Assessment Legislation MAct, CAct, NAct Regulated and non-regulated assessments. Regulated property assessments shall be determined according to the regulated property assessment valuation standard. Heavy industrial property Resource production equipment Pipeline and railway roadway Agricultural land Non-regulated property assessments shall be determined according to the market valuation standard. Residential and commercial property

18

19 Regulated Manual Highlights Part I Median Assessed Value to Sale Price Ratio Part II Regulated Property Valuation models are specified for regulated property. Agricultural Land Agricultural Land Mixed Use Heavy Industrial Land (includes rates) Railway Roadway (includes rates) Heavy Industrial Buildings and Structures Oil and Gas Well Resource Production Equipment Mine Resource Production Equipment Pipelines Environmental Contamination (industrial property only)

20 Regulated Manual Highlights Manual defines heavy industrial property which includes: Mines that extract a mineral resource Petroleum based industry Ethanol properties greater than 50 M liters capacity Manufacturing of fertilizer, malt, steel, steel pipe Lumber related industry including saw mills, wood products Generating power (coal, natural gas, wind turbines)

21 Assessment Legislation MAct, CAct, Nact Market Valuation Standard non-regulated property assessment" means an assessment for property other than a regulated property assessment. mass appraisal means the process of preparing assessments for a group of properties as of the base date using standard appraisal methods, employing common data and allowing for statistical testing. market value means the amount that a property should be expected to realize if the real estate in fee simple in the property is sold in a competitive and open market by a willing seller to a willing buyer, each acting prudently and knowledgeably, and assuming that the amount is not affected by undue stimuli.

22 Assessment Legislation MAct, CAct, Nact Market Valuation Standard "market valuation standard" means the standard achieved when the assessed value of property: (i) is prepared using mass appraisal; (ii) is an estimate of the market value of the estate in fee simple in the property; (iii) reflects typical market conditions for similar properties; and (iv) meets quality assurance standards established by order of the agency;

23 Market Valuation Standard Three Accepted Approaches to Value Cost Approach Sales Comparison Approach Property Income (Rental) Approach

24 Market Valuation Standard Publications Market Value Assessment in Saskatchewan Handbook (Handbook). SAMA s 2011 Cost Guide (Guide). Marshall and Swift/Boechk LLC. Marshall Valuation Service (MVS) Residential Cost Handbook (RCH)

25

26

27

28 Questions?

29 Presentation Overview Part 1 - Steve SAMA Who we are and what we do Assessment legislation and principles Valuation standards (Regulated, non-regulated) Part 2 - Todd Role of Assessor vs Assessment Appraiser Right of Entry Services Provided by SAMA Three approaches to value 2017 Revaluation trends Questions and wrap-up

30 Role of the Assessor Prepare assessment roll Determine tax class of property Determine tax status

31 Role of the Assessment Appraiser 12 (1) b of the Assessment Management Agency Act Establish, maintain and undertake valuations 293(1)(a)(i) of the Municipalities Act Determine the non-commercial portion that exemptions apply to in a rural municipality of properties that are used in both the agricultural operation of the land and a commercial use

32 Right of Entry - Legislation Section 23 of the Assessment Management Agency Act gives the right of entry to a property to the assessment appraiser. Requires Produce identification Reasonable times Reasonable request What if entry is refused?

33 Right of Entry - Practice Reasonable notice Contact municipality one day in advance Knock on door to notify occupant Reasonable time Between 8:00 am and 6:00 pm Identification Sign on vehicle Wear photo ID

34 Trespassing Residential not marked Go to door, knock no answer gather information from exterior Residential Marked Go to door, knock talk to owner or occupant and ask permission If no answer then leave property without gathering information from private property If gated or secured, do not enter the property

35 Services Provided by SAMA Annual Maintenance Preparation of inspection list (properties requested by municipality and properties we have identified from previous inspections) On site inspections Preparation of revised assessments Delivery of revised assessments (hard copy and electronic form)

36 Services Provided by SAMA Support of Value (Appeals) Preparation of appeal briefs for submission to Board of Revision Attendance at Board of Revision hearing Delivery of revised assessments if required (hard copy and electronic form) SAMA will appeal decisions to the Saskatchewan Municipal Board if required Attendance at Saskatchewan Municipal Board hearings Access to Legal Counsel

37 Services Provided by SAMA Reinspection Identify assessment issues with Council Develop inspection plan Communication plan (letter to ratepayers, property confirmation forms and numbers) On site inspections of improvements (including call backs)

38 Services Provided by SAMA Reinspection Review market analysis Preparation of revised assessments Present values to Council and administration Follow up with an open house in the spring

39 Services Provided by SAMA Revaluation Update of assessments in revaluation years (currently every four years) Sales Verification Market Analysis (land and improvements) Preparation of revised assessments Delivery of revised assessments (hard copy and electronic form) Open houses in revaluation years

40 Market Valuation Standard Three Accepted Approaches to Value Cost Approach Sales Comparison Approach Property Income (Rental) Approach

41

42 Overview of the Cost Approach

43 Land Valuation Average selling prices for land As of the applicable base date (January 1, 2011)

44 Land Valuation Non-Agricultural Land Valuation Arm s length sales are collected and verified Determine units of comparison Identify neighbourhoods Determine base land rates (select median based on sales in the neighbourhood)

45 Improvement Valuation Replacement cost new determined from SAMA s 2011 Cost Guide (residential and selected commercial) or Marshall Valuation Service (commercial) Adjust for depreciation (based on the age and condition of the structure) Adjust to reflect average selling prices for comparable improvements as of the base date (January 1, 2011) by using a MAF (market adjustment factor) A MAF is calculated for each sale and the MAF applied is developed from the median of comparable sales in the neighbourhood

46 Summary of the Cost Approach Property Value = land value + building value - Vacant land sales used to estimate land value. - Buildings are costed (RCN) using standardized procedures; actual cost not used - Physical depreciation assigned - Market depreciation assigned (MAF)

47 Overview of the Sales Comparison Approach Using Multiple Regression Analysis (MRA) Techniques

48 Sales Comparison Approach Mass appraisal approach which determines the market value through a comparison of valid sales. Sale prices are used directly to identify value determining variables and ultimately calculate assessments. Preferred for single family or condo residential properties when adequate sales exist. Multiple Regression Analysis (MRA) techniques are commonly used to build sales comparison models.

49 Sales Comparison Approach MRA is a statistical process that: Is objective, Requires less property characteristics Can be recalibrated quickly There are three types of MRA models; Additive, Multiplicative and Hybrid. When properly specified and calibrated, all types achieve acceptable results.

50 Sales Comparison Approach Application by SAMA Hybrid: Moose Jaw, Humboldt, Kindersley, Martensville, Warman, Weyburn, Estevan, Yorkton, Melville, Melfort Multiplicative: Moose Jaw condominium model Provincial High Rise and Low Rise Apartment Condominium model

51 Overview of the Property Income (Rental) Approach

52 Property Income (Rental) Approach Overview One of three internationally accepted methods of valuing property; Primary valuation approach for (rental) income producing properties; Income Approach is used for mass appraisal in other jurisdictions; Only considers property or rental income. Does not consider owner s personal income.

53 Reasons for Using Income Approach Based on the Principle of Anticipation. Purchasers of an income property pay a sale price now, to receive future benefits (rental income stream) Accounts for the return on investment expected by typical purchasers of income producing properties. Primary approach used by industry as the valuator undertakes the same analysis as buyers and sellers of income producing properties.

54 SAMA s Income Approach Application for ) Multi-Residential Regular ownership, non-condo Majority of apartments province-wide 2) Accommodation Hotels and Motels located in a city 3) Shopping Malls Regional and Community Enclosed Malls province-wide 4) General Commercial Retail, Office, Warehouse, etc - Moose Jaw, Yorkton, Estevan, Weyburn and respective RM s

55 2017 Revaluation Trends Trend graph from the November/2014 SAMA Advisory Committee Meetings. Ag land trends updated January 26, 2015 Represents property type on a provincial basis. Market valuation standard property trends will vary by municipality.

56 Preliminary 2017 Revaluation Assessment Trends 2017: Sales Based 2017: Cost Based Trends 2009 Multiple 2013 Multiples Multiple Increase Prov. Trend To Be Determined Property Class

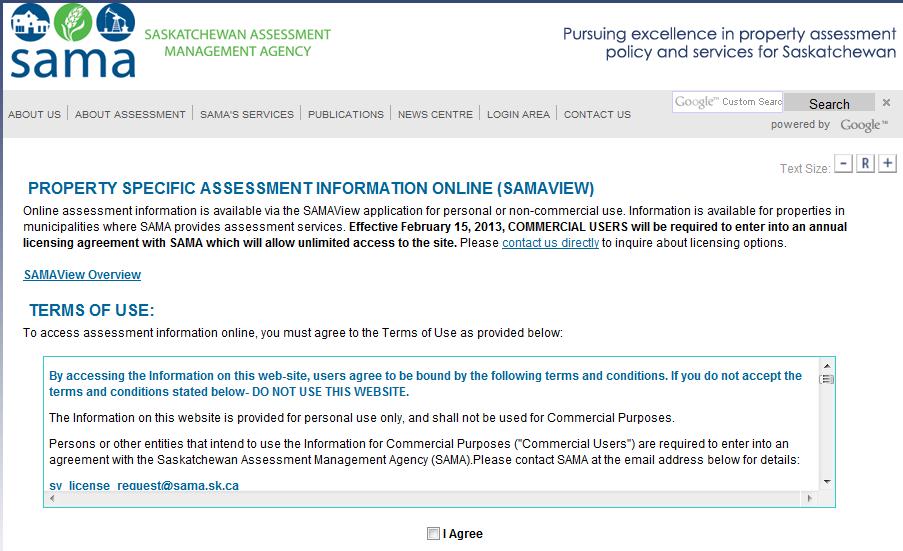

57 Additional Resources SAMA s website On-line manuals, handbooks, FAQs etc SAMAView

58 SAMA s Website

59 SAMAView

60 Questions?

SAMA Presentation February 7-15, 2013 RMAA and UMAAS Sponsored Workshop Series

SAMA Presentation February 7-15, 2013 RMAA and UMAAS Sponsored Workshop Series Presentation Overview SAMA Who we are and what we do Summary of assessment legislation and policy Valuation publications Valuation

SAMA Presentation February 7-15, 2013 RMAA and UMAAS Sponsored Workshop Series Presentation Overview SAMA Who we are and what we do Summary of assessment legislation and policy Valuation publications Valuation

Assessment Principles. Three Accepted Approaches to Value Cost Approach Sales Comparison Approach Property Income (Rental) Approach

Approach") Assessment Principles Three Accepted Approaches to Value Cost Approach Sales Comparison Approach Property Income (Rental) Approach Overview of the Cost Approach Land Valuation Average selling prices for

Assessment Principles Three Accepted Approaches to Value Cost Approach Sales Comparison Approach Property Income (Rental) Approach Overview of the Cost Approach Land Valuation Average selling prices for

Introduction. Market Value Assessment in Saskatchewan Handbook. Introduction

Market Value Assessment in Saskatchewan Handbook Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass Appraisal for

Market Value Assessment in Saskatchewan Handbook Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass Appraisal for

Date: 15/01/30 Page: 1

Formulas, Rules and Principles Subject: General Document Number 1.1.1 Summary This section describes how this Manual is to be used for the 2017 revaluation (January 1, 2017 to December 31, 2020). Regulated

Formulas, Rules and Principles Subject: General Document Number 1.1.1 Summary This section describes how this Manual is to be used for the 2017 revaluation (January 1, 2017 to December 31, 2020). Regulated

Market Value Assessment and Administration

Market Value and Administration This technical document is part of a series of draft discussion papers created by Municipal Affairs staff and stakeholders to prepare for the Municipal Government Act Review.

Market Value and Administration This technical document is part of a series of draft discussion papers created by Municipal Affairs staff and stakeholders to prepare for the Municipal Government Act Review.

Saskatchewan Municipal Board Assessment Appeals Committee

Saskatchewan Municipal Board Assessment Appeals Committee Appeal: 2009-0089 RESPONDENT: City of Prince Albert In the matter of an appeal to the Assessment Appeals Committee, Saskatchewan Municipal Board,

Saskatchewan Municipal Board Assessment Appeals Committee Appeal: 2009-0089 RESPONDENT: City of Prince Albert In the matter of an appeal to the Assessment Appeals Committee, Saskatchewan Municipal Board,

CITY OF OWATONNA ASSESSMENT REPORT. Steele County Assessor s Department. William G. Effertz, SAMA Steele County Assessor

2017 CITY OF OWATONNA ASSESSMENT REPORT Steele County Assessor s Department William G. Effertz, SAMA Steele County Assessor Tyler Diersen, AMA, Assistant County Assessor April 11, 2017 2017 Assessment

2017 CITY OF OWATONNA ASSESSMENT REPORT Steele County Assessor s Department William G. Effertz, SAMA Steele County Assessor Tyler Diersen, AMA, Assistant County Assessor April 11, 2017 2017 Assessment

Saskatchewan Municipal Board Assessment Appeals Committee

Saskatchewan Municipal Board Assessment Appeals Committee Appeal: 2009-0039 RESPONDENT: Town of Hudson Bay In the matter of an appeal to the Assessment Appeals Committee, Saskatchewan Municipal Board,

Saskatchewan Municipal Board Assessment Appeals Committee Appeal: 2009-0039 RESPONDENT: Town of Hudson Bay In the matter of an appeal to the Assessment Appeals Committee, Saskatchewan Municipal Board,

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

RESIDENTIAL PROPERTY VALUATION PROCESS

RESIDENTIAL PROPERTY VALUATION PROCESS Introduction Gregg County is comprised of approximately 276 square miles of area. Gregg County Appraisal District (GCAD) is responsible for the appraisal of the approximately

RESIDENTIAL PROPERTY VALUATION PROCESS Introduction Gregg County is comprised of approximately 276 square miles of area. Gregg County Appraisal District (GCAD) is responsible for the appraisal of the approximately

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

Saskatchewan Assessment Management Agency Commercial Advisory Committee Meeting Minutes for April 23, 2009 Regina, Saskatchewan

Saskatchewan Assessment Management Agency Commercial Advisory Committee Meeting Minutes for April 23, 2009 Regina, Saskatchewan Joint Session with City Advisory Committee Commercial Members Present: Craig

Saskatchewan Assessment Management Agency Commercial Advisory Committee Meeting Minutes for April 23, 2009 Regina, Saskatchewan Joint Session with City Advisory Committee Commercial Members Present: Craig

Grain Elevator. Market Value Assessment in Saskatchewan Handbook. Grain Elevator Valuation Guide

Market Value Assessment in Saskatchewan Handbook Grain Elevator Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass

Market Value Assessment in Saskatchewan Handbook Grain Elevator Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass

CURRENT ISSUES IN SASKATCHEWAN PROPERTY ASSESSMENT

CURRENT ISSUES IN SASKATCHEWAN PROPERTY ASSESSMENT A report on the 2005 Revaluation Consultation Meetings held by the Saskatchewan Assessment Management Agency JANUARY 2006 TABLE OF CONTENTS Message from

CURRENT ISSUES IN SASKATCHEWAN PROPERTY ASSESSMENT A report on the 2005 Revaluation Consultation Meetings held by the Saskatchewan Assessment Management Agency JANUARY 2006 TABLE OF CONTENTS Message from

METHODOLOGY GUIDE VALUING LANDS IN TRANSITION IN ONTARIO. Valuation Date: January 1, 2016

METHODOLOGY GUIDE VALUING LANDS IN TRANSITION IN ONTARIO Valuation Date: January 1, 2016 August 2017 August 22, 2017 The Municipal Property Assessment Corporation (MPAC) is responsible for accurately assessing

METHODOLOGY GUIDE VALUING LANDS IN TRANSITION IN ONTARIO Valuation Date: January 1, 2016 August 2017 August 22, 2017 The Municipal Property Assessment Corporation (MPAC) is responsible for accurately assessing

Assessment Appeals Committee

Assessment Appeals Committee DETERMINATION OF APPEALS UNDER Section 16 of The Municipal Board Act and Section 246 of The Municipalities Act Appeal Numbers: AAC 2016-0129 (Lead), 2016-0127, 2016-0128, 2016-0130,

Assessment Appeals Committee DETERMINATION OF APPEALS UNDER Section 16 of The Municipal Board Act and Section 246 of The Municipalities Act Appeal Numbers: AAC 2016-0129 (Lead), 2016-0127, 2016-0128, 2016-0130,

LLANO CENTRAL APPRAISAL DISTRICT REAPPRAISAL PLAN FOR TAX YEARS 2017 & 2018 AS ADOPTED BY THE BOARD OF DIRECTORS

LLANO CENTRAL APPRAISAL DISTRICT REAPPRAISAL PLAN FOR TAX YEARS 2017 & 2018 AS ADOPTED BY THE BOARD OF DIRECTORS TABLE OF CONTENTS ITEM PAGE Executive Summary 5 Revaluation Decision (Statutory or Administrative)

LLANO CENTRAL APPRAISAL DISTRICT REAPPRAISAL PLAN FOR TAX YEARS 2017 & 2018 AS ADOPTED BY THE BOARD OF DIRECTORS TABLE OF CONTENTS ITEM PAGE Executive Summary 5 Revaluation Decision (Statutory or Administrative)

Chapter 27 Saskatchewan Housing Corporation Providing Social Housing to Eligible Clients 1.0 MAIN POINTS

Chapter 27 Saskatchewan Housing Corporation Providing Social Housing to Eligible Clients 1.0 MAIN POINTS By law, the responsibilities of Saskatchewan Housing Corporation include promoting, encouraging,

Chapter 27 Saskatchewan Housing Corporation Providing Social Housing to Eligible Clients 1.0 MAIN POINTS By law, the responsibilities of Saskatchewan Housing Corporation include promoting, encouraging,

METHODOLOGY GUIDE VALUING MOTELS IN ONTARIO. Valuation Date: January 1, 2016

METHODOLOGY GUIDE VALUING MOTELS IN ONTARIO Valuation Date: January 1, 2016 AUGUST 2016 August 22, 2016 The Municipal Property Assessment Corporation (MPAC) is responsible for accurately assessing and

METHODOLOGY GUIDE VALUING MOTELS IN ONTARIO Valuation Date: January 1, 2016 AUGUST 2016 August 22, 2016 The Municipal Property Assessment Corporation (MPAC) is responsible for accurately assessing and

Gas Station. Market Value Assessment in Saskatchewan Handbook. Gas Station Valuation Guide

Market Value Assessment in Saskatchewan Handbook Gas Station Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass

Market Value Assessment in Saskatchewan Handbook Gas Station Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass

WALLER COUNTY APPRAISAL DISTRICT MASS APPRAISAL REPORT APPRAISAL YEAR 2018

WALLER COUNTY APPRAISAL DISTRICT MASS APPRAISAL REPORT APPRAISAL YEAR 2018 ADDENDUM TO WCAD REAPPRAISAL PLAN FOR 2017 AND 2018 WALLER COUNTY APPRAISAL DISTRICT Uniform Standards of Professional Appraisal

WALLER COUNTY APPRAISAL DISTRICT MASS APPRAISAL REPORT APPRAISAL YEAR 2018 ADDENDUM TO WCAD REAPPRAISAL PLAN FOR 2017 AND 2018 WALLER COUNTY APPRAISAL DISTRICT Uniform Standards of Professional Appraisal

Course Mass Appraisal Practices and Procedures

Course 331 - Mass Appraisal Practices and Procedures Course Description This course is designed to build on the subject matter covered in Course 300 Fundamentals of Mass Appraisal and prepare the student

Course 331 - Mass Appraisal Practices and Procedures Course Description This course is designed to build on the subject matter covered in Course 300 Fundamentals of Mass Appraisal and prepare the student

ASSESSMENT METHODOLOGY

2018 ASSESSMENT METHODOLOGY COST APPROACH A summary of the methods used by the City of Edmonton in determining the value of residential and non-residential properties valued using the cost approach in

2018 ASSESSMENT METHODOLOGY COST APPROACH A summary of the methods used by the City of Edmonton in determining the value of residential and non-residential properties valued using the cost approach in

Saskatchewan Assessment Management Agency Commercial Advisory Committee Meeting Minutes for October 26, 2004 Regina, Saskatchewan

Saskatchewan Assessment Management Agency Commercial Advisory Committee Regina, Saskatchewan PRESENT: Craig Melvin, Committee Chair, SAMA Board Chair Fred Clipsham, Cities Sector Board member Sharon Armstrong,

Saskatchewan Assessment Management Agency Commercial Advisory Committee Regina, Saskatchewan PRESENT: Craig Melvin, Committee Chair, SAMA Board Chair Fred Clipsham, Cities Sector Board member Sharon Armstrong,

Saskatchewan Municipal Board Assessment Appeals Committee

Saskatchewan Municipal Board Assessment Appeals Committee Appeal: 2011-0066 JOINT RECOMMENDATION RESPONDENT: City of Saskatoon In the matter of an appeal to the Assessment Appeals Committee, Saskatchewan

Saskatchewan Municipal Board Assessment Appeals Committee Appeal: 2011-0066 JOINT RECOMMENDATION RESPONDENT: City of Saskatoon In the matter of an appeal to the Assessment Appeals Committee, Saskatchewan

Office Building. Market Value Assessment in Saskatchewan Handbook. Office Building Valuation Guide

Market Value Assessment in Saskatchewan Handbook Office Building Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass

Market Value Assessment in Saskatchewan Handbook Office Building Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass

Revaluation process ongoing in Norwalk

Revaluation process ongoing in Norwalk Property owners will have the opportunity to appeal assessment beginning December 5 (Norwalk, Conn.) The City of Norwalk is in the final phase of its revaluation

Revaluation process ongoing in Norwalk Property owners will have the opportunity to appeal assessment beginning December 5 (Norwalk, Conn.) The City of Norwalk is in the final phase of its revaluation

Past & Present Adjustments & Parcel Count Section... 13

Assessment 2017 Report This report includes specific information regarding the 2017 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

Assessment 2017 Report This report includes specific information regarding the 2017 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

Rockwall CAD. Basics of. Appraising Property. For. Property Taxation

Rockwall CAD Basics of Appraising Property For Property Taxation ROCKWALL CENTRAL APPRAISAL DISTRICT 841 Justin Rd. Rockwall, Texas 75087 972-771-2034 Fax 972-771-6871 Introduction Rockwall Central Appraisal

Rockwall CAD Basics of Appraising Property For Property Taxation ROCKWALL CENTRAL APPRAISAL DISTRICT 841 Justin Rd. Rockwall, Texas 75087 972-771-2034 Fax 972-771-6871 Introduction Rockwall Central Appraisal

GENERAL ASSESSMENT DEFINITIONS

21st Century Appraisals, Inc. GENERAL ASSESSMENT DEFINITIONS Ad Valorem tax. A tax levied in proportion to the value of the thing(s) being taxed. Exclusive of exemptions, use-value assessment laws, and

21st Century Appraisals, Inc. GENERAL ASSESSMENT DEFINITIONS Ad Valorem tax. A tax levied in proportion to the value of the thing(s) being taxed. Exclusive of exemptions, use-value assessment laws, and

Saskatchewan Municipal Board Assessment Appeals Committee

Saskatchewan Municipal Board Appeals Committee Appeal: 2011-0061 JOINT RECOMMENDATION RESPONDENT: City of Saskatoon In the matter of an appeal to the Appeals Committee, Saskatchewan Municipal Board, by:

Saskatchewan Municipal Board Appeals Committee Appeal: 2011-0061 JOINT RECOMMENDATION RESPONDENT: City of Saskatoon In the matter of an appeal to the Appeals Committee, Saskatchewan Municipal Board, by:

Introduction. Bruce Munneke, S.A.M.A. Washington County Assessor. 3 P a g e

Assessment 2016 Report This report includes specific information regarding the 2016 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

Assessment 2016 Report This report includes specific information regarding the 2016 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

We value... Fairness Integrity Efficiency

We value... Fairness Integrity Efficiency Prince George City Council Presentation Christopher Whyte Deputy Assessor John Castle Senior Appraiser May 2 nd, 2011 BC Assessment Our Mission is to: The mission

We value... Fairness Integrity Efficiency Prince George City Council Presentation Christopher Whyte Deputy Assessor John Castle Senior Appraiser May 2 nd, 2011 BC Assessment Our Mission is to: The mission

REAPPRAISAL PLAN

Brown County Appraisal District REAPPRAISAL PLAN 2019-2020 1 2 Table of Contents Executive Summary 5 Plan For Periodic Appraisal 7 Revaluation Decision 8 Performance Analysis 8 Reappraisal Year Process

Brown County Appraisal District REAPPRAISAL PLAN 2019-2020 1 2 Table of Contents Executive Summary 5 Plan For Periodic Appraisal 7 Revaluation Decision 8 Performance Analysis 8 Reappraisal Year Process

ASSESSMENT METHODOLOGY

2019 ASSESSMENT METHODOLOGY COMMERCIAL RETAIL AND OFFICE CONDOMINIUMS A summary of the methods used by the City of Edmonton in determining the value of commercial retail and office condominium properties

2019 ASSESSMENT METHODOLOGY COMMERCIAL RETAIL AND OFFICE CONDOMINIUMS A summary of the methods used by the City of Edmonton in determining the value of commercial retail and office condominium properties

2017 Reappraisal Preliminary Report. February 6, 2017

2017 Reappraisal Preliminary Report February 6, 2017 Reappraisal is required at least every 8 years per NCGS105-286 Last reappraisal was conducted for 2011 Reappraisal includes both land and improvements.

2017 Reappraisal Preliminary Report February 6, 2017 Reappraisal is required at least every 8 years per NCGS105-286 Last reappraisal was conducted for 2011 Reappraisal includes both land and improvements.

2011 ASSESSMENT RATIO REPORT

2011 Ratio Report SECTION I OVERVIEW 2011 ASSESSMENT RATIO REPORT The Department of Assessments and Taxation appraises real property for the purposes of property taxation. Properties are valued using

2011 Ratio Report SECTION I OVERVIEW 2011 ASSESSMENT RATIO REPORT The Department of Assessments and Taxation appraises real property for the purposes of property taxation. Properties are valued using

Assessment Appeals Committee

Assessment Appeals Committee DETERMINATION OF AN APPEAL UNDER Section 16 of The Municipal Board Act and Section 246 of The Municipalities Act Appeal Number: AAC 2015-0156 Date and Location: April 6, 2016

Assessment Appeals Committee DETERMINATION OF AN APPEAL UNDER Section 16 of The Municipal Board Act and Section 246 of The Municipalities Act Appeal Number: AAC 2015-0156 Date and Location: April 6, 2016

City of Norwalk Revaluation Project

City of Norwalk 2018 Revaluation Project Presenter: Paul Miller Supervisor: Salim Serdah Appraisers: James Steiner, John Valente, Steve Beccio, Rich Nicolosi, and Gynt Grube. Why Revaluation? It s important

City of Norwalk 2018 Revaluation Project Presenter: Paul Miller Supervisor: Salim Serdah Appraisers: James Steiner, John Valente, Steve Beccio, Rich Nicolosi, and Gynt Grube. Why Revaluation? It s important

Duties of the Assessors

Duties of the Assessors Value Properties Determine New Growth Set Tax Rate Assess Property Taxes Abate & Exempt Taxes Manage Overlay Account Assess Local Excises 1 Value Property Assessments based on fair

Duties of the Assessors Value Properties Determine New Growth Set Tax Rate Assess Property Taxes Abate & Exempt Taxes Manage Overlay Account Assess Local Excises 1 Value Property Assessments based on fair

CITY OF JACKSONVILLE, FLORIDA

PROPERTY APPRAISER DEPARTMENT VISION: To earn the public s trust. DEPARTMENT MISSION: We will: Produce a fair, equitable and accurate tax roll as required by law. Focus on our customers the taxpayers.

PROPERTY APPRAISER DEPARTMENT VISION: To earn the public s trust. DEPARTMENT MISSION: We will: Produce a fair, equitable and accurate tax roll as required by law. Focus on our customers the taxpayers.

A Guide to the Municipal Planning Process in Saskatchewan

A Guide to the Municipal Planning Process in Saskatchewan A look at the municipal development permit and the subdivision approval process in Saskatchewan May 2008 Prepared By: Community Planning Branch

A Guide to the Municipal Planning Process in Saskatchewan A look at the municipal development permit and the subdivision approval process in Saskatchewan May 2008 Prepared By: Community Planning Branch

LITIGATING IN A MASS APPRAISAL ENVIRONMENT

11 th Mass Appraisal Valuation Symposium Innovation, Transformation, Knowledge Enhancement and Improved Efficiencies in Mass Appraisal Niagara Falls, Canada May 17-18, 2016 LITIGATING IN A MASS APPRAISAL

11 th Mass Appraisal Valuation Symposium Innovation, Transformation, Knowledge Enhancement and Improved Efficiencies in Mass Appraisal Niagara Falls, Canada May 17-18, 2016 LITIGATING IN A MASS APPRAISAL

Saskatchewan Assessment Management Agency Commercial Advisory Committee. Meeting Minutes for March 21, Regina, Saskatchewan

Saskatchewan Assessment Management Agency Commercial Advisory Committee Regina, Saskatchewan PRESENT: Fred Clipsham, Cities Sector Board member Richard Douglas, Education Sector Board member Robert (Bob)

Saskatchewan Assessment Management Agency Commercial Advisory Committee Regina, Saskatchewan PRESENT: Fred Clipsham, Cities Sector Board member Richard Douglas, Education Sector Board member Robert (Bob)

Assessment Appeals Committee

Assessment Appeals Committee DETERMINATION OF AN APPEAL UNDER Section 16 of The Municipal Board Act and Section 216 of The Cities Act Appeal Number: AAC 2016-0034 Date and Location: February 16, 2017 Saskatoon,

Assessment Appeals Committee DETERMINATION OF AN APPEAL UNDER Section 16 of The Municipal Board Act and Section 216 of The Cities Act Appeal Number: AAC 2016-0034 Date and Location: February 16, 2017 Saskatoon,

2014 Annual Report. Fayette County Appraisal District P. O. Box 836 La Grange, TX 78945

2014 Annual Report Fayette County Appraisal District P. O. Box 836 La Grange, TX 78945 FCAD 2014 Annual Report 1 2014 ANNUAL REPORT FAYETTE COUNTY APPRAISAL DISTRICT INTRODUCTION The Fayette County Appraisal

2014 Annual Report Fayette County Appraisal District P. O. Box 836 La Grange, TX 78945 FCAD 2014 Annual Report 1 2014 ANNUAL REPORT FAYETTE COUNTY APPRAISAL DISTRICT INTRODUCTION The Fayette County Appraisal

DIRECTIVE # This Directive Supersedes Directive # and #92-003

Division Of Property Valuation Docking State Office Building 915 SW Harrison St., Room 400N Topeka, KS 66612-1588 Nick Jordan, Secretary David N. Harper, Director phone: 785-296-2365 fax: 785-296-2320

Division Of Property Valuation Docking State Office Building 915 SW Harrison St., Room 400N Topeka, KS 66612-1588 Nick Jordan, Secretary David N. Harper, Director phone: 785-296-2365 fax: 785-296-2320

April 12, The Honorable Martin O Malley And The General Assembly of Maryland

April 12, 2011 The Honorable Martin O Malley And The General Assembly of Maryland As required by Section 2-202 of the Tax-Property Article of the Annotated Code of Maryland, I am pleased to submit the

April 12, 2011 The Honorable Martin O Malley And The General Assembly of Maryland As required by Section 2-202 of the Tax-Property Article of the Annotated Code of Maryland, I am pleased to submit the

Saskatchewan Assessment Management Agency Commercial Advisory Committee Meeting Minutes for November 15, 2007 Regina, Saskatchewan

Saskatchewan Assessment Management Agency Commercial Advisory Committee Meeting Minutes for November 15, 2007 Regina, Saskatchewan Joint Session with City Advisory Committee Commercial Members Present:

Saskatchewan Assessment Management Agency Commercial Advisory Committee Meeting Minutes for November 15, 2007 Regina, Saskatchewan Joint Session with City Advisory Committee Commercial Members Present:

RAINS COUNTY APPRAISAL DISTRICT

RAINS COUNTY APPRAISAL DISTRICT 2017 MASS APPRAISAL SUMMARY REPORT mass appraisal report 2017 uspap_appr_report RAINS COUNTY APPRAISAL DISTRICT 2017 MASS APPRAISAL SUMMARY REPORT Identification of Subject:

RAINS COUNTY APPRAISAL DISTRICT 2017 MASS APPRAISAL SUMMARY REPORT mass appraisal report 2017 uspap_appr_report RAINS COUNTY APPRAISAL DISTRICT 2017 MASS APPRAISAL SUMMARY REPORT Identification of Subject:

2018 Annual Report. Fayette County Appraisal District P. O. Box 836 La Grange, TX 78945

2018 Annual Report Fayette County Appraisal District P. O. Box 836 La Grange, TX 78945 FCAD 2018 Annual Report 1 2018 ANNUAL REPORT FAYETTE COUNTY APPRAISAL DISTRICT INTRODUCTION The Fayette County Appraisal

2018 Annual Report Fayette County Appraisal District P. O. Box 836 La Grange, TX 78945 FCAD 2018 Annual Report 1 2018 ANNUAL REPORT FAYETTE COUNTY APPRAISAL DISTRICT INTRODUCTION The Fayette County Appraisal

86 years in the making Caspar G Haas 1922 Sales Prices as a Basis for Estimating Farmland Value

2 Our Journey Begins 86 years in the making Caspar G Haas 1922 Sales Prices as a Basis for Estimating Farmland Value Starting at the beginning. Mass Appraisal and Single Property Appraisal Appraisal

2 Our Journey Begins 86 years in the making Caspar G Haas 1922 Sales Prices as a Basis for Estimating Farmland Value Starting at the beginning. Mass Appraisal and Single Property Appraisal Appraisal

The Urban Municipality Assessment and Taxation Regulations

1 The Urban Municipality Assessment and Taxation Regulations Repealed by Chapter M-36.1 Reg 1 (effective January 1, 2006). Formerly Chapter U-11 Reg 14 (sections 1 and 2 effective October 9, 1996; sections

1 The Urban Municipality Assessment and Taxation Regulations Repealed by Chapter M-36.1 Reg 1 (effective January 1, 2006). Formerly Chapter U-11 Reg 14 (sections 1 and 2 effective October 9, 1996; sections

Residential Revaluation Report

Residential Revaluation Report 2012 Mass Appraisal of Region 5 for 2013 Property Taxes Prepared For Steven J. Drew Thurston County Assessor TABLE OF CONTENTS Page No. CERTIFICATE OF APPRAISAL... 3 APPRAISAL

Residential Revaluation Report 2012 Mass Appraisal of Region 5 for 2013 Property Taxes Prepared For Steven J. Drew Thurston County Assessor TABLE OF CONTENTS Page No. CERTIFICATE OF APPRAISAL... 3 APPRAISAL

APPRAISER & ASSESSOR Real Estate Tax Valuation Overview and Issues

APPRAISER & ASSESSOR Real Estate Tax Valuation Overview and Issues James R. Johnston, MAI, SRA J. Michael Tarello, MAI, ASA, MRA February 11, 2015 BOSTON Property Advisors Vision Government Solutions AGENDA

APPRAISER & ASSESSOR Real Estate Tax Valuation Overview and Issues James R. Johnston, MAI, SRA J. Michael Tarello, MAI, ASA, MRA February 11, 2015 BOSTON Property Advisors Vision Government Solutions AGENDA

The Honorable Larry Hogan And The General Assembly of Maryland

2015 Ratio Report The Honorable Larry Hogan And The General Assembly of Maryland As required by Section 2-202 of the Tax-Property Article of the Annotated Code of Maryland, I am pleased to submit the Department

2015 Ratio Report The Honorable Larry Hogan And The General Assembly of Maryland As required by Section 2-202 of the Tax-Property Article of the Annotated Code of Maryland, I am pleased to submit the Department

Joint Information Session With The Commercial Advisory Committee

Saskatchewan Assessment Management Agency City Advisory Committee Conference Centre, Ramada Hotel Regina, Saskatchewan Joint Information Session With The Commercial Advisory Committee City Advisory Committee

Saskatchewan Assessment Management Agency City Advisory Committee Conference Centre, Ramada Hotel Regina, Saskatchewan Joint Information Session With The Commercial Advisory Committee City Advisory Committee

Residential Revaluation Report

Residential Revaluation Report 2013 Mass Appraisal of Mobile Homes In Courts for 2014 Property Taxes Prepared For Steven J. Drew Thurston County Assessor TABLE of CONTENTS page. CERTIFICATE OF APPRAISAL...

Residential Revaluation Report 2013 Mass Appraisal of Mobile Homes In Courts for 2014 Property Taxes Prepared For Steven J. Drew Thurston County Assessor TABLE of CONTENTS page. CERTIFICATE OF APPRAISAL...

Assessment Year 2016 Assessment Valuations / Mass Appraisal Summary Report

Assessment Year 2016 Assessment Valuations / Mass Appraisal Summary Report Overview Following up on last year s work, additional work was done cleaning up the sales data. The land valuation model was further

Assessment Year 2016 Assessment Valuations / Mass Appraisal Summary Report Overview Following up on last year s work, additional work was done cleaning up the sales data. The land valuation model was further

Hidalgo County Appraisal District Re-Appraisal Plan Approved By: Hidalgo County Appraisal District Board of Directors September 12, 2018

Hidalgo County Appraisal District Re-Appraisal Plan 2019-2020 Approved By: Hidalgo County Appraisal District Board of Directors September 12, 2018 Table of Contents Executive Summary 1 Plan for Periodic

Hidalgo County Appraisal District Re-Appraisal Plan 2019-2020 Approved By: Hidalgo County Appraisal District Board of Directors September 12, 2018 Table of Contents Executive Summary 1 Plan for Periodic

INTRODUCTION MISSION OVERVIEW

INTRODUCTION The Austin County Appraisal District is a political subdivision of the State of Texas. The Constitution of the State of Texas, the Texas Property Tax Code, and the Rules of the Texas Comptroller

INTRODUCTION The Austin County Appraisal District is a political subdivision of the State of Texas. The Constitution of the State of Texas, the Texas Property Tax Code, and the Rules of the Texas Comptroller

Assessment Appeals Committee

Assessment Appeals Committee DETERMINATION OF AN APPEAL UNDER Section 16 of The Municipal Board Act and Section 246 of The Municipalities Act Appeal Number: AAC 2015-0115 Date and Location: February 23,

Assessment Appeals Committee DETERMINATION OF AN APPEAL UNDER Section 16 of The Municipal Board Act and Section 246 of The Municipalities Act Appeal Number: AAC 2015-0115 Date and Location: February 23,

Swisher County Appraisal District 2017 Mass Appraisal Report

Swisher County Appraisal District 2017 Mass Appraisal Report Prepared Pursuant to Standard 6 of the Uniform Standards of Professional Appraisal Practice 1 TABLE OF CONTENTS Introduction 3 Listing of Taxing

Swisher County Appraisal District 2017 Mass Appraisal Report Prepared Pursuant to Standard 6 of the Uniform Standards of Professional Appraisal Practice 1 TABLE OF CONTENTS Introduction 3 Listing of Taxing

DALLAS CENTRAL APPRAISAL DISTRICT DCAD VALUATION PROCESSES

DALLAS CENTRAL APPRAISAL DISTRICT DCAD VALUATION PROCESSES DALLAS CENTRAL APPRAISAL DISTRICT DCAD DCAD appraisers appraise a large universe of properties by developing appraisal models DCAD appraisers

DALLAS CENTRAL APPRAISAL DISTRICT DCAD VALUATION PROCESSES DALLAS CENTRAL APPRAISAL DISTRICT DCAD DCAD appraisers appraise a large universe of properties by developing appraisal models DCAD appraisers

Equity from the Assessor s Perspective

Institute of Municipal Assessors 55th Annual Conference Equity from the Assessor s Perspective Andy Anstett Legislation & Policy Support Services MPAC June 7th, 2011 Key Aspects of Equity Test Defining

Institute of Municipal Assessors 55th Annual Conference Equity from the Assessor s Perspective Andy Anstett Legislation & Policy Support Services MPAC June 7th, 2011 Key Aspects of Equity Test Defining

PREPARING FOR THE MINNESOTA INCOME PROPERTY CASE STUDY EXAM WORKSHOP

PREPARING FOR THE MINNESOTA INCOME PROPERTY CASE STUDY EXAM WORKSHOP Date: September 18, 2018 Location: Country Inn & Suites Chanhassen, MN Instructor: Bob Wilson, CAE, ASA Revised October, 2017 PREPARING

PREPARING FOR THE MINNESOTA INCOME PROPERTY CASE STUDY EXAM WORKSHOP Date: September 18, 2018 Location: Country Inn & Suites Chanhassen, MN Instructor: Bob Wilson, CAE, ASA Revised October, 2017 PREPARING

Course Commerical/Industrial Modeling Concepts Learning Objectives

Course 312 - Commerical/Industrial Modeling Concepts Learning Objectives Course Description Course 312 presents a detailed study of the mass appraisal process as applied to income-producing property. Topics

Course 312 - Commerical/Industrial Modeling Concepts Learning Objectives Course Description Course 312 presents a detailed study of the mass appraisal process as applied to income-producing property. Topics

Mass Appraisal of Income-Producing Properties

Chapter 10 Mass Appraisal of Income-Producing Properties Whether valuing income-producing property or residential property, you can use similar information and methods for collecting and analyzing data

Chapter 10 Mass Appraisal of Income-Producing Properties Whether valuing income-producing property or residential property, you can use similar information and methods for collecting and analyzing data

2016 Annual Report. Carmen Ottmer, Chief Appraiser AUSTIN COUNTY APPRAISAL DISTRICT 906 E. AMELIA ST., BELLVILLE, TEXAS 77418

2016 Annual Report Carmen Ottmer, Chief Appraiser AUSTIN COUNTY APPRAISAL DISTRICT 906 E. AMELIA ST., BELLVILLE, TEXAS 77418 INTRODUCTION The Austin County Appraisal District is a political subdivision

2016 Annual Report Carmen Ottmer, Chief Appraiser AUSTIN COUNTY APPRAISAL DISTRICT 906 E. AMELIA ST., BELLVILLE, TEXAS 77418 INTRODUCTION The Austin County Appraisal District is a political subdivision

Urban Land. Overview 2.1

Overview 2.1 This chapter contains the valuation procedures for determining the assessed value for residential and commercial land valued using the cost approach. SAMA s 2015 Cost Guide provides direction

Overview 2.1 This chapter contains the valuation procedures for determining the assessed value for residential and commercial land valued using the cost approach. SAMA s 2015 Cost Guide provides direction

2017 Annual Report. Fayette County Appraisal District P. O. Box 836 La Grange, TX 78945

2017 Annual Report Fayette County Appraisal District P. O. Box 836 La Grange, TX 78945 FCAD 2017 Annual Report 1 2017 ANNUAL REPORT FAYETTE COUNTY APPRAISAL DISTRICT INTRODUCTION The Fayette County Appraisal

2017 Annual Report Fayette County Appraisal District P. O. Box 836 La Grange, TX 78945 FCAD 2017 Annual Report 1 2017 ANNUAL REPORT FAYETTE COUNTY APPRAISAL DISTRICT INTRODUCTION The Fayette County Appraisal

Valuing Diamonds in the Rough: Utilizing Highest and Best Use Valuation Principles in a Mass Appraisal Environment

Valuing Diamonds in the Rough: Utilizing Highest and Best Use Valuation Principles in a Mass Appraisal Environment Topics of Discussion Revaluation of a former industrial district at the height of a building

Valuing Diamonds in the Rough: Utilizing Highest and Best Use Valuation Principles in a Mass Appraisal Environment Topics of Discussion Revaluation of a former industrial district at the height of a building

The Municipal Property Assessment

Combined Residential and Commercial Models for a Sparsely Populated Area BY ROBERT J. GLOUDEMANS, BRIAN G. GUERIN, AND SHELLEY GRAHAM This material was originally presented on October 9, 2006, at the International

Combined Residential and Commercial Models for a Sparsely Populated Area BY ROBERT J. GLOUDEMANS, BRIAN G. GUERIN, AND SHELLEY GRAHAM This material was originally presented on October 9, 2006, at the International

Filing a property assessment complaint and preparing for your hearing. Alberta Municipal Affairs

Filing a property assessment complaint and preparing for your hearing Alberta Municipal Affairs Alberta s Municipal Government Act, the 2018 Matters Relating to Assessment Complaints Regulation, and the

Filing a property assessment complaint and preparing for your hearing Alberta Municipal Affairs Alberta s Municipal Government Act, the 2018 Matters Relating to Assessment Complaints Regulation, and the

How to Read a Real Estate Appraisal Report

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

EXPLAINING MASS APPRAISAL

EXPLAINING MASS APPRAISAL PROMOTING THE ROLE OF THE ASSESSOR MAAO SUMMER CONFERENCE, JUNE 24, 2015 RICHARD W. FINNEGAN, MAA Please excuse the length of this letter. I didn t have time to write a short

EXPLAINING MASS APPRAISAL PROMOTING THE ROLE OF THE ASSESSOR MAAO SUMMER CONFERENCE, JUNE 24, 2015 RICHARD W. FINNEGAN, MAA Please excuse the length of this letter. I didn t have time to write a short

Standard on Mass Appraisal of Real Property

Standard on Mass Appraisal of Real Property Approved July 2017 International Association of Assessing Officers This standard replaces the January 2012 Standard on Mass Appraisal of Real Property and is

Standard on Mass Appraisal of Real Property Approved July 2017 International Association of Assessing Officers This standard replaces the January 2012 Standard on Mass Appraisal of Real Property and is

Current State of Property. Taxation in the Netherlands. Council for Real Estate Assessment (English) Waarderingskamer (Dutch)

Waarderingskamer (Dutch)") Current State of Property WAARDERINGSKAMER Taxation in the Netherlands Council for Real Estate Assessment (English) Waarderingskamer (Dutch) Council for real estate assessment Main task: quality control

Current State of Property WAARDERINGSKAMER Taxation in the Netherlands Council for Real Estate Assessment (English) Waarderingskamer (Dutch) Council for real estate assessment Main task: quality control

Strip Commercial. Market Value Assessment in Saskatchewan Handbook. Strip Commercial Properties Valuation Guide

Market Value Assessment in Saskatchewan Handbook Strip Commercial Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and

Market Value Assessment in Saskatchewan Handbook Strip Commercial Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and

Reappraisal Plan. and. Mass Appraisal Report

Reappraisal Plan and Mass Appraisal Report ADOPTED September 13, 2012 REVISED May 23, 2013 Bastrop CAD Board of Directors Reappraisal Plan and Mass Appraisal Report FORWARD Outlook for 2013 2014 The Reappraisal

Reappraisal Plan and Mass Appraisal Report ADOPTED September 13, 2012 REVISED May 23, 2013 Bastrop CAD Board of Directors Reappraisal Plan and Mass Appraisal Report FORWARD Outlook for 2013 2014 The Reappraisal

CONSOLIDATION INCENTIVE AID

CONSOLIDATION INCENTIVE AID Objective: State assistance funds for NYS cities or towns or constituent municipalities of a consolidated assessing unit for efficiencies in Real Property Tax Administration.

CONSOLIDATION INCENTIVE AID Objective: State assistance funds for NYS cities or towns or constituent municipalities of a consolidated assessing unit for efficiencies in Real Property Tax Administration.

YOUNG COUNTY APPRAISAL DISTRICT

YOUNG COUNTY APPRAISAL DISTRICT 2017 - ANNUAL APPRAISAL REPORT AS OF 10/6/2017 1 2 TABLE OF CONTENTS ITEM PAGE Introduction 4 Purpose of Report...4 Taxing Entities, Rates & Exemptions 5 Property Types

YOUNG COUNTY APPRAISAL DISTRICT 2017 - ANNUAL APPRAISAL REPORT AS OF 10/6/2017 1 2 TABLE OF CONTENTS ITEM PAGE Introduction 4 Purpose of Report...4 Taxing Entities, Rates & Exemptions 5 Property Types

Guide to property assessment and taxation in Alberta

Guide to property assessment and taxation in Alberta table of contents pg. i pg. iii Preface iii preface pg. 1 8 Chapter 1: Overview of Alberta s property assessment and taxation system 1 chapter 1 Overview

Guide to property assessment and taxation in Alberta table of contents pg. i pg. iii Preface iii preface pg. 1 8 Chapter 1: Overview of Alberta s property assessment and taxation system 1 chapter 1 Overview

2017 Reappraisal. March 10, 2017

2017 Reappraisal March 10, 2017 Today s Presenters Cheyenne Johnson, Assessor Charles Blow, CAE Robert Trouy, TMA David Baker, Certified General Appraiser Joshua Forbes Shawn Lynch, JD Together, as professional

2017 Reappraisal March 10, 2017 Today s Presenters Cheyenne Johnson, Assessor Charles Blow, CAE Robert Trouy, TMA David Baker, Certified General Appraiser Joshua Forbes Shawn Lynch, JD Together, as professional

APPRAISER & ASSESSOR Real Estate Tax Valuation Overview and Issues

APPRAISER & ASSESSOR Real Estate Tax Valuation Overview and Issues James R. Johnston, MAI, SRA J. Michael Tarello, MAI, ASA, MRA May 20, 2015 BOSTON Property Advisors Vision Government Solutions AGENDA

APPRAISER & ASSESSOR Real Estate Tax Valuation Overview and Issues James R. Johnston, MAI, SRA J. Michael Tarello, MAI, ASA, MRA May 20, 2015 BOSTON Property Advisors Vision Government Solutions AGENDA

New Models for Property Data Verification and Valuation

New Models for Property Data Verification and Valuation for 2006 IAAO Councils and Sections Joint Seminar May 9-11, 2006 Charleston, South Carolina Presented by George Donatello, CMS Principal Consultant

New Models for Property Data Verification and Valuation for 2006 IAAO Councils and Sections Joint Seminar May 9-11, 2006 Charleston, South Carolina Presented by George Donatello, CMS Principal Consultant

Delivering the 2016 Assessment Update

Delivering the 2016 Assessment Update Municipality of Port Hope Public Information Meeting May 18, 2016 Catherine Barr - Account Manager and Bert Moline Manager Valuations & Customer Relation PROPERTY

Delivering the 2016 Assessment Update Municipality of Port Hope Public Information Meeting May 18, 2016 Catherine Barr - Account Manager and Bert Moline Manager Valuations & Customer Relation PROPERTY

Part 1. Estimating Land Value Using a Land Residual Technique Based on Discounted Cash Flow Analysis

Table of Contents Overview... v Seminar Schedule... ix SECTION 1 Part 1. Estimating Land Value Using a Land Residual Technique Based on Discounted Cash Flow Analysis Preview Part 1... 1 Land Residual Technique...

Table of Contents Overview... v Seminar Schedule... ix SECTION 1 Part 1. Estimating Land Value Using a Land Residual Technique Based on Discounted Cash Flow Analysis Preview Part 1... 1 Land Residual Technique...

Depreciation Analysis Guide

Market Value Assessment in Saskatchewan Handbook Depreciation Analysis Guide Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market

Market Value Assessment in Saskatchewan Handbook Depreciation Analysis Guide Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market

Henderson County Appraisal District Mass Appraisal Report

Henderson County Appraisal District 2016 Mass Appraisal Report 1 Purpose The purpose of this report is to better inform the property owners within the boundaries of the Henderson County Appraisal District

Henderson County Appraisal District 2016 Mass Appraisal Report 1 Purpose The purpose of this report is to better inform the property owners within the boundaries of the Henderson County Appraisal District

Recommendations for COD Standards. Robert J. Gloudemans Almy, Gloudemans, Jacobs & Denne. for. New York State Office of Real Property Services

Recommendations for COD Standards Robert J. Gloudemans Almy, Gloudemans, Jacobs & Denne for New York State Office of Real Property Services March 12, 2009 Recommendations for COD Standards Robert J. Gloudemans

Recommendations for COD Standards Robert J. Gloudemans Almy, Gloudemans, Jacobs & Denne for New York State Office of Real Property Services March 12, 2009 Recommendations for COD Standards Robert J. Gloudemans

Basic Appraisal Procedures

Hondros Learning Basic Appraisal Procedures Timed Outline Topic Area Reference(s) Learning Objectives The student will be able to identify and/or apply: Teaching Method Time Segment (Minutes) Day 1 Chapter

Hondros Learning Basic Appraisal Procedures Timed Outline Topic Area Reference(s) Learning Objectives The student will be able to identify and/or apply: Teaching Method Time Segment (Minutes) Day 1 Chapter

To: Property Appraisers, Taxing Authorities and Interested Parties From: James McAdams Date: June 5, 2012 Bulletin: PTO 12-04

Property Tax Oversight Bulletin: PTO 12-04 To: Property Appraisers, Taxing Authorities and Interested Parties From: James McAdams Date: Bulletin: PTO 12-04 FLORIDA DEPARTMENT OF REVENUE PROPERTY TAX INFORMATIONAL

Property Tax Oversight Bulletin: PTO 12-04 To: Property Appraisers, Taxing Authorities and Interested Parties From: James McAdams Date: Bulletin: PTO 12-04 FLORIDA DEPARTMENT OF REVENUE PROPERTY TAX INFORMATIONAL

The Assessment Management Agency Act

Consolidated to March 15, 2013 1 The Assessment Management Agency Act being Chapter A-28.1 of the Statutes of Saskatchewan, 1986 (consult Table of Saskatchewan Statutes for effective date) as amended by

Consolidated to March 15, 2013 1 The Assessment Management Agency Act being Chapter A-28.1 of the Statutes of Saskatchewan, 1986 (consult Table of Saskatchewan Statutes for effective date) as amended by

We look forward to working with you to build on our collaboration and enhance our partnership on behalf of all Minnesotans.

Date: February 27, 2017 To: County Assessors, Auditors, and Treasurers From: Cynthia Rowley, Director Property Tax Division Subject: Property Tax Services Report The Property Tax Division of the Minnesota

Date: February 27, 2017 To: County Assessors, Auditors, and Treasurers From: Cynthia Rowley, Director Property Tax Division Subject: Property Tax Services Report The Property Tax Division of the Minnesota

ASSESSMENT METHODOLOGY

2018 ASSESSMENT METHODOLOGY MULTI-RESIDENTIAL MANUFACTURED HOME PARK A summary of the methods used by the City of Edmonton in determining the value of multi-residential manufactured home park land properties

2018 ASSESSMENT METHODOLOGY MULTI-RESIDENTIAL MANUFACTURED HOME PARK A summary of the methods used by the City of Edmonton in determining the value of multi-residential manufactured home park land properties

Caldwell County Appraisal District

Caldwell County Appraisal District Reappraisal Plan for Tax Years 2019 and 2020 INTRODUCTION Scope of Responsibility The Caldwell County Appraisal District has prepared and published this reappraisal plan

Caldwell County Appraisal District Reappraisal Plan for Tax Years 2019 and 2020 INTRODUCTION Scope of Responsibility The Caldwell County Appraisal District has prepared and published this reappraisal plan

Saskatchewan Municipal Board Assessment Appeals Committee

Saskatchewan Municipal Board Assessment Appeals Committee RESPONDENT: Rural Municipality of Prince Albert No. 461 Appeal: 0310/2005 In the matter of an appeal to the Assessment Appeals Committee, Saskatchewan

Saskatchewan Municipal Board Assessment Appeals Committee RESPONDENT: Rural Municipality of Prince Albert No. 461 Appeal: 0310/2005 In the matter of an appeal to the Assessment Appeals Committee, Saskatchewan

Golf Course. Market Value Assessment in Saskatchewan Handbook. Golf Course Valuation Guide

Market Value Assessment in Saskatchewan Handbook Golf Course Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass

Market Value Assessment in Saskatchewan Handbook Golf Course Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass

2016 MASS APPRAISAL REPORT

THROCKMORTON CENTRAL APPRAISAL DISTRICT 2016 MASS APPRAISAL REPORT WEBSITE HOMEPAGE http://www.throckmortoncad.org 2016 MASS APPRAISAL REPORT PG 1 ORGANIZATION http://www.throckmortoncad.org/organization

THROCKMORTON CENTRAL APPRAISAL DISTRICT 2016 MASS APPRAISAL REPORT WEBSITE HOMEPAGE http://www.throckmortoncad.org 2016 MASS APPRAISAL REPORT PG 1 ORGANIZATION http://www.throckmortoncad.org/organization