APPRAISER & ASSESSOR Real Estate Tax Valuation Overview and Issues

|

|

|

- Melina Waters

- 5 years ago

- Views:

Transcription

1 APPRAISER & ASSESSOR Real Estate Tax Valuation Overview and Issues James R. Johnston, MAI, SRA J. Michael Tarello, MAI, ASA, MRA May 20, 2015 BOSTON Property Advisors Vision Government Solutions

2 AGENDA Expenses Above and Below the Line Income, Rent Roll, Lease Abstracts Expenses, Ordinary and Extraordinary Cap Rate Data and Issues Land Curve Value in Use vs Highest and Best

3 AGENDA Fee Simple vs Leased Fee Mass Appraisal vs Ad Valorem Fair Cash Value 38 D & 61 A Requirements Discovery Process-Limited Data Negotiation Techniques ATB Data Direct Cap vs DCF Questions and Open Discussion

4 Expenses Above and Below the Line What line are we talking about? BOSTON Property Advisors

5 Expenses Above and Below the Line

6 Summary of DCF

7 Expenses Above and Below the Line Investors Methods per PWC/Korpacz Survey: BOSTON Property Advisors

8 Income, Rent Roll and Lease Abstracts Market Rent Contract Rent Effective Rent (After concessions) Excess Rent (Above Market) Percentage Rent (Straight Percentage) Overage Rent (Above Breakpoint) Office Rent: Gross with Base Year Oper & Tax Expense Retail Rent: Net Plus Oper & Tax Exp. and Percentage Rent Industrial Rent: Net (Direct or Pass Through Expenses)

9 Income, Rent Roll and Lease Abstracts Rent Rolls Try to get two to three years of income and expense info Provide a form that is detailed, but easy to use You want it to provide you with gross income, vacancy and effective gross income Make sure form offers area to show who pays what for expenses Have area in form for sales and cost information Lease Abstracts Lease income, date terms, options for renewal, type of lease (NNN or Gross) see sample form Percentage income, CAM contribution

10 Type of Lease NNN

11 Type of Lease Gross

12 Income & Expense Form

13 Income & Expense Form

14 Lease Abstract Form

15 Expenses BOMA Office Expense Report

16 Expenses Dollars and Cents of Shopping Centers

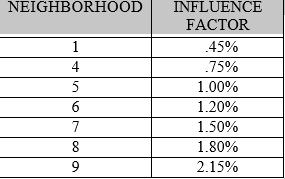

17 Vacancy Rate Source

18 Cap Rate Data Source PWC / Korpacz Investor Survey Office Rates

19 Cap Rate Data Source

20 Cap Rate Data Source

21 Johnston Tarello Investors Survey

22 Land Curve-Land Residuals Land curve developed based on market data from community or neighboring towns Land curve parameters ( based on zoning & base lot) Economy of scale Understand land to building ratio and its affects on the land curve Base prime lot (based on Zoning) Excess land, secondary lots, front foot, acreage discount Neighborhood delineation, Street or traffic adjustment Water influence factors All factors must be supported by market data

23 Land Curve Chart

24 Neighborhood Chart

25 Water Influence Factors

26 Acreage Discount Chart

27 Land Curve-Land Residuals Step One- Land and Building Rates =100% for Residential Class- One two and three family Step Two- Lower your land rates to desired median, say 95% Step Three- Run land residuals and save in excel Step Four- Lower building rates to 95% and run improved sales ratio studies By using the building rates at 100% it gives you a true indicator of what your Land Residuals are overall and for each neighborhood

28 Land Curve-Land Residuals Step One Verify sales, review data to determine any time adjustment factor Set building style rates to 100% market value based on M & S or local costs Adjust depreciation tables to current base year Based on land sales and extracted land sales, adjust land curve and neighborhood codes to 100% market value, Also determine base prime lot (usually by zoning) If limited sales available consult neighboring towns Run residuals and improved ratio studies to DOR standards and save a Copy (land residuals and ration studies should be ay 100% of MV) Step Two Lower land curve to desired median and review ratio studies for DOR requirements

29 Land Curve-Land Residuals Step Three Run the land residuals based on step two s rates In excel sort to DOR requirements Need to be run for one, two and three families Separate into neighborhood sorted by size Separate into parcels above and below primary lot acreage number to prove excess land These breakouts need to be further divided by neighborhoods, street adjustment and water influence

30 Land Curve-Land Residuals Step Four Adjust the building rates to your desired median Run all your ratio studies to meet DOR requirements Make a copy of the sales ratio studies and the Residuals These are the ratio studies you will present to the DOR rep Saving a copy of the residuals gives you a picture of all three scenarios

31 Value in Use v Highest and Best Use Assessed value based on value in use or present use 100% or 0% occupied vs market vacancy Excess or potentially developable land issue Value as of January 1 Construction permits can be Jan 1 or June 30 Reconcile both dates

32 Value in Use v Highest and Best Use Key Definitions Highest and Best Use The reasonably probable and legal use of vacant land or an improved property, which is physically possible, appropriately supported, financially feasible, that results in the highest value. The four criteria the highest and best use must meet are legal permissibility, physical possibility, financial feasibility, and maximum profitability. Highest and Best Use of Property As Improved The use that should be made of property as it exists. An existing property should be renovated or retained as is so long as it continues to contribute the total value of the property, or until the return from a new improvement would more than offset the cost of demolishing the existing building and constructing a new one. Value in use. The value a specific property has for a specific use. Use Value Assessment. An assessment based on the value of property as it is currently used, not on its market value considering alternative uses.

33 Fee Simple vs Leased Fee Fee Simple- Market rates for valuation date Leased Fee- Contract rents set for a specific time period Leased Fee rates may be lower, higher or similar to Fee Simple Reconcile leased fee rates to fee simple rates

34 Fee Simple vs Leased Fee Key Definitions Fee simple estate. Absolute ownership unencumbered by any other interest or state, subject only to the limitations imposed by the governmental powers of taxation, eminent domain, police power, and escheat. Leased fee estate. An ownership interest held by a landlord with the rights of use and occupancy conveyed by lease to others. The rights of the lessor (leased fee owner) and the leased fee a specified by contract terms contained within the lease. Leasehold estate. The interest held by a lessee (the tenant or renter) through a lease conveying the rights of use and occupancy for a stated term under certain conditions. Market rent. The rental income that a property would most probably command in the open market; indicated by the current rents paid and asked for comparable space as of the date of the appraisal. Market Value as stated herein is consistent with the term Fair Cash Value, as defined in the case of Boston Gas v. Assessors of Boston: 334 Mass (1956). "This means fair market value, which is the price an owner willing but not on the compulsion to sell from one willing but not under compulsion to buy. It means the highest price that a normal purchaser not under peculiar compulsion to pay at the time, and cannot exceed the sum which the owner after reasonable effort could obtain for his property The Fair Cash Value is the value the property would have had on January 1, of any taxable year in the hands of any owner, including the present owner."

35 Mass Appraisal Ad Valorem Fair Cash value Mass Appraisal based on Fair Cash Value Mass Appraisal- Values a group of properties based on equity and specific valuation date Mass Appraisal separates land building value, real estate, personal property and good will Mass Appraisal Value vs individual ad valorem fair cash value at ATB May have to reconcile difference

36 INCOME VALUE PER BED $9,288 $35,162 Nursing Home Sample INCOME ANALYSIS FOR FY xxxx Nursing Home Valuation ADDRESS: 123 HIGH ST, TOPSFIELD, MA Any Street NUMBER OF ROOMS : 123 LEVEL OF CARE: 1-41BEDS, 2-81 BEDS LAND SIZE: 7.39 AC ASSESSMENT: $4,482,200 PER BED: $36,440 ACTUAL DATA ECONOMIC DATA POTENTIAL GROSS INCOME $82, $10,141,448 $10,141,448 VACANCY 0.00% $0 $0 EGI $10,141,448 $10,141,448 EXPENCES 90.36% OF PGI $9,163, % $8,721,645 NET INCOME $977,616 $1,419,803 LESS ENTREPRENUERSHIP 7.50% $760,609 $760,609 RETURN ON GROSS INCOME R. E. EFF. GROSS INCOME $217,007 $659,194 LESS PERSONAL PROPERTY $450 $55,350 $55,350 PER BED RESERVES FOR REPLACEMENT 5.00% $10,850 $32,960 NET R.E. INCOME $150,807 $570,884 CAPITALIZATION RATE 13.20% 13.20% INCOME VALUE $1,142,478 $4,324,882

37 VALUE PER ROOM $54,526 Hotel Sample Spreadsheet Hotel ADDRESS: Any Street MBL 1/1/1 ROOMS 82 ASSESSED VALUE: $4,265,700 VALUE PER ROOM: $52,021 AVERAGE ROOM RATE: $85 GROSS INCOME: ROOMS $2,544,050 2% F&B MISC $50,881 TOTAL $2,594,931 LESS VACANCY: 45% $1,144,823 POT GROSS INCOME: $1,450,109 TOTAL DEPT EXP: 25% $362,527 UNDISTR OPER EXP 25% $362,527 FIXED EXPENSE 2% $29,002 NET INC BEFORE BUS & PP 48% $696,052 BUSINESS COMPONENT 5% $72,505 PERSONAL PROPERTY 6% $87,007 NET OPERATING INCOME $536,540 CAP RATE 12.0% TOTAL VALUE OF REAL ESTATE $4,471,168

38 38D Requirements 38 D- Assessor requests I&E info for revaluation Owner or lessee required to return info under oath within 60 days Failure to respond results in automatic dismissal of filing at ATB False statement bar from statutory appeal Res penalty of $50, comm penalty of $250 BOA must inform owner or lessee

39 61A Requirements 61 A- Assessor requests I&E info for abatement review Owner or lessee required to return info under oath within 30 days Failure to respond bar from statutory appeal Unless unable to comply for reasons beyond control or made good faith effort This also applies to 38 D

40 Discovery Process limited data negotiation technique Owner or lessee appeals to ATB Request set of Interrogatories send out immediately even if you do not have a set date Work with your attorney and appraiser to ask appropriate question If return info incomplete- conf call with ATB Request for dismissal due to incomplete response ATB will give time table for response, if not returned the case will be dismissed

41 Discovery Process limited data negotiation technique When in abatement or pre trial negotiations Do not negotiate in a position of weakness Burden of proof is with owner or rep Require supporting data Do not split the baby- your assessment is already at market (unless incorrect data) Rep is an advocate of owner- will present a low figure for settlement purposes Negotiate with equity to other properties in mind

42 Sample ATB Decision

43 Sample ATB Finding

44 DCF VS Direct Cap Direct Cap utilized for mass appraisal valuation DCF used for investment and institutional valuation DCF good tool for new construction Determines stabilize income stream in an unstable property- high vacancy or in transition type of property Also used for development projects DCF information can be useful for developing a stabilized direct cap value

45 DCF VS Direct Cap

46 Questions and Open Discussion Specific issues you deal with Difficult types of properties to assess or appraise

APPRAISER & ASSESSOR Real Estate Tax Valuation Overview and Issues

APPRAISER & ASSESSOR Real Estate Tax Valuation Overview and Issues James R. Johnston, MAI, SRA J. Michael Tarello, MAI, ASA, MRA February 11, 2015 BOSTON Property Advisors Vision Government Solutions AGENDA

APPRAISER & ASSESSOR Real Estate Tax Valuation Overview and Issues James R. Johnston, MAI, SRA J. Michael Tarello, MAI, ASA, MRA February 11, 2015 BOSTON Property Advisors Vision Government Solutions AGENDA

RESIDUAL ANALYSIS PRINCIPLES AND PROCEEDURES

RESIDUAL ANALYSIS PRINCIPLES AND PROCEEDURES OVERVIEW 1. Residual analysis or extractions, are a form of land valuation study. 2. This analysis relies on the improved sales (typically the largest group

RESIDUAL ANALYSIS PRINCIPLES AND PROCEEDURES OVERVIEW 1. Residual analysis or extractions, are a form of land valuation study. 2. This analysis relies on the improved sales (typically the largest group

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330 REVIEW NOTES by CHUCK DUNN CHAPTER 20 Copyright 2010 by the Real Estate Division and Chuck Dunn. All rights reserved CHAPTER 20 - THE INCOME

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330 REVIEW NOTES by CHUCK DUNN CHAPTER 20 Copyright 2010 by the Real Estate Division and Chuck Dunn. All rights reserved CHAPTER 20 - THE INCOME

WATERFRONT LOCAL IMPROVEMENT DISTRICT OVERVIEW. November 2017

WATERFRONT LOCAL IMPROVEMENT DISTRICT OVERVIEW November 2017 LOCAL IMPROVEMENT DISTRICT Funding tool by which property owners financially contribute to a project that will increase the value of their property

WATERFRONT LOCAL IMPROVEMENT DISTRICT OVERVIEW November 2017 LOCAL IMPROVEMENT DISTRICT Funding tool by which property owners financially contribute to a project that will increase the value of their property

MAAO Sales Ratio Committee 2013 Fall Conference Seminar

MAAO Sales Ratio Committee 2013 Fall Conference Seminar Presented By: Al Whitcomb Dakota County (Retired) John Keefe Chisago County Assessor Brent Reid City of Coon Rapids Michael Thompson Scott County

MAAO Sales Ratio Committee 2013 Fall Conference Seminar Presented By: Al Whitcomb Dakota County (Retired) John Keefe Chisago County Assessor Brent Reid City of Coon Rapids Michael Thompson Scott County

LOCAL IMPROVEMENT DISTRICT APPRAISER PRESENTATION. November 2017

LOCAL IMPROVEMENT DISTRICT APPRAISER PRESENTATION November 2017 SPECIAL BENEFIT STUDY WHY? A special benefit study is a tool consistently used with LID projects. Municipality retains an expert consultant

LOCAL IMPROVEMENT DISTRICT APPRAISER PRESENTATION November 2017 SPECIAL BENEFIT STUDY WHY? A special benefit study is a tool consistently used with LID projects. Municipality retains an expert consultant

Following is an example of an income and expense benchmark worksheet:

After analyzing income and expense information and establishing typical rents and expenses, apply benchmarks and base standards to the reappraisal area. Following is an example of an income and expense

After analyzing income and expense information and establishing typical rents and expenses, apply benchmarks and base standards to the reappraisal area. Following is an example of an income and expense

Typical Valuation Approaches and How to Deal With Them

Typical Valuation Approaches and How to Deal With Them January, 2018 Anthony F. DellaPelle, Esq., CRE Shareholder, McKirdy, Riskin, Olson & DellaPelle, P.C. Morristown, New Jersey Christian F. Torgrimson,

Typical Valuation Approaches and How to Deal With Them January, 2018 Anthony F. DellaPelle, Esq., CRE Shareholder, McKirdy, Riskin, Olson & DellaPelle, P.C. Morristown, New Jersey Christian F. Torgrimson,

Chapter 8. How much would you pay today for... The Income Approach to Appraisal

How much would you pay today for... Chapter 8 One hundred dollars paid with certainty each year for five years, starting one year from now. Why would you pay less than $500 Valuation Using the Income Approach

How much would you pay today for... Chapter 8 One hundred dollars paid with certainty each year for five years, starting one year from now. Why would you pay less than $500 Valuation Using the Income Approach

Risk Management Insights

Risk Management Insights Appraisal Review Part II: Income Capitalization Approach George Mann, Managing Director and Chief Appraiser, Collateral Evaluation Services, Inc.and Nikki Griffith, MAI, CCIM,

Risk Management Insights Appraisal Review Part II: Income Capitalization Approach George Mann, Managing Director and Chief Appraiser, Collateral Evaluation Services, Inc.and Nikki Griffith, MAI, CCIM,

BUSI 331: Real Estate Investment Analysis and Advanced Income Appraisal

BUSI 331: Real Estate Investment Analysis and Advanced Income Appraisal PURPOSE AND SCOPE The Real Estate Investment Analysis and Advanced Income Appraisal course BUSI 331 is intended to build upon the

BUSI 331: Real Estate Investment Analysis and Advanced Income Appraisal PURPOSE AND SCOPE The Real Estate Investment Analysis and Advanced Income Appraisal course BUSI 331 is intended to build upon the

Chapter 8. How much would you pay today for... The Income Approach to Appraisal

How much would you pay today for... Chapter 8 One hundred dollars paid with certainty each year for five years, starting one year from now. Why would you pay less than $500 Valuation Using the Income Approach

How much would you pay today for... Chapter 8 One hundred dollars paid with certainty each year for five years, starting one year from now. Why would you pay less than $500 Valuation Using the Income Approach

Office Building. Market Value Assessment in Saskatchewan Handbook. Office Building Valuation Guide

Market Value Assessment in Saskatchewan Handbook Office Building Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass

Market Value Assessment in Saskatchewan Handbook Office Building Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass

ASSESSMENT METHODOLOGY

2018 ASSESSMENT METHODOLOGY MULTI-RESIDENTIAL MANUFACTURED HOME PARK A summary of the methods used by the City of Edmonton in determining the value of multi-residential manufactured home park land properties

2018 ASSESSMENT METHODOLOGY MULTI-RESIDENTIAL MANUFACTURED HOME PARK A summary of the methods used by the City of Edmonton in determining the value of multi-residential manufactured home park land properties

Basics of Commercial Real Estate Transactions Day Two

Basics of Commercial Real Estate Transactions Day Two John Rockwell, Partner Energy October 12, 2016 PG&E refers to the Pacific Gas and Electric Company, a subsidiary of PG&E Corporation. 2010 Pacific

Basics of Commercial Real Estate Transactions Day Two John Rockwell, Partner Energy October 12, 2016 PG&E refers to the Pacific Gas and Electric Company, a subsidiary of PG&E Corporation. 2010 Pacific

Multi-Family Methodology Analysis

Multi-Family Methodology 2018 Analysis Assessment Department February, 2018 2018 Multi-Family Assessment Methodology Property assessments in the City of Medicine Hat reflect the fee simple market value

Multi-Family Methodology 2018 Analysis Assessment Department February, 2018 2018 Multi-Family Assessment Methodology Property assessments in the City of Medicine Hat reflect the fee simple market value

ASSESSMENT METHODOLOGY

2018 ASSESSMENT METHODOLOGY COMMERCIAL FREE-STANDING PARKADE A summary of the methods used by the City of Edmonton in determining the value of free-standing parkade properties in Edmonton for assessment

2018 ASSESSMENT METHODOLOGY COMMERCIAL FREE-STANDING PARKADE A summary of the methods used by the City of Edmonton in determining the value of free-standing parkade properties in Edmonton for assessment

2016 Level I Tutorials. Income Approach to Value

2016 Level I Tutorials Income Approach to Value 1 The income approach is based on the principal that the value of an investment property reflects the quality and quantity of the income it is expected to

2016 Level I Tutorials Income Approach to Value 1 The income approach is based on the principal that the value of an investment property reflects the quality and quantity of the income it is expected to

Retail Acquisition Example

Property Information Retail Acquisition Example Project Assumptions Acquisition Assumptions Property Name Retail Acquisition Example Project Type Acquisition Location Austin, TX Acquisition Cost $1,800,000

Property Information Retail Acquisition Example Project Assumptions Acquisition Assumptions Property Name Retail Acquisition Example Project Type Acquisition Location Austin, TX Acquisition Cost $1,800,000

Understanding Mississippi Property Taxes

Understanding Mississippi Property Taxes Property tax revenues are a vital component of the budgets of Mississippi s local governments. Property tax revenues allow these governments to provide important

Understanding Mississippi Property Taxes Property tax revenues are a vital component of the budgets of Mississippi s local governments. Property tax revenues allow these governments to provide important

PREPARING FOR THE MINNESOTA INCOME PROPERTY CASE STUDY EXAM WORKSHOP

PREPARING FOR THE MINNESOTA INCOME PROPERTY CASE STUDY EXAM WORKSHOP Date: September 18, 2018 Location: Country Inn & Suites Chanhassen, MN Instructor: Bob Wilson, CAE, ASA Revised October, 2017 PREPARING

PREPARING FOR THE MINNESOTA INCOME PROPERTY CASE STUDY EXAM WORKSHOP Date: September 18, 2018 Location: Country Inn & Suites Chanhassen, MN Instructor: Bob Wilson, CAE, ASA Revised October, 2017 PREPARING

NCGS , ,

NCGS 105-283, 105-286, 105-317 Requires Counties to establish values based on current market conditions. Values should be at or near 100% of market value as of the reappraisal date. Counties MUST do a

NCGS 105-283, 105-286, 105-317 Requires Counties to establish values based on current market conditions. Values should be at or near 100% of market value as of the reappraisal date. Counties MUST do a

Chapter 8. The Income Approach to Appraisal. Two Approaches to Income Valuation. How Does DCF Differ from Direct Cap? Rationale:

The Income Approach to Appraisal Chapter 8 Valuation Using the Income Approach Rationale: Value of a property is the present value of its anticipated income. Often called income capitalization Capitalize:

The Income Approach to Appraisal Chapter 8 Valuation Using the Income Approach Rationale: Value of a property is the present value of its anticipated income. Often called income capitalization Capitalize:

REAL ESTATE INVESTMENTS

REAL ESTATE INVESTMENTS PROBLEM SET 2 1. PROBLEM The leases for space in an office building provide for limitations or stops on the lessor s liability for real estate taxes and operating expenses. Each

REAL ESTATE INVESTMENTS PROBLEM SET 2 1. PROBLEM The leases for space in an office building provide for limitations or stops on the lessor s liability for real estate taxes and operating expenses. Each

Mercantile Ground Lease Parcel Acquisition. Briefing to the Economic Development and Housing Committee June 27, 2006

Mercantile Ground Lease Parcel Acquisition Briefing to the Economic Development and Housing Committee June 27, 2006 Purpose Describe the provisions of the development agreement with Forest City ( FC Merc

Mercantile Ground Lease Parcel Acquisition Briefing to the Economic Development and Housing Committee June 27, 2006 Purpose Describe the provisions of the development agreement with Forest City ( FC Merc

INSTITUTE FOR PROFESSIONALS IN TAXATION REAL PROPERTY TAX SCHOOL REVIEW AND INTRODUCTION

INSTITUTE FOR PROFESSIONALS IN TAXATION REAL PROPERTY TAX SCHOOL REVIEW AND INTRODUCTION This section is an overview of the major topics covered by IPT s Property Tax School which are directly relevant

INSTITUTE FOR PROFESSIONALS IN TAXATION REAL PROPERTY TAX SCHOOL REVIEW AND INTRODUCTION This section is an overview of the major topics covered by IPT s Property Tax School which are directly relevant

THE REVALUATION OF ROXBURY

THE REVALUATION OF ROXBURY The following is the definition of a Revaluation Program as described in the Handbook for New Jersey Assessors : A revaluation program seeks to spread the tax burden equitably

THE REVALUATION OF ROXBURY The following is the definition of a Revaluation Program as described in the Handbook for New Jersey Assessors : A revaluation program seeks to spread the tax burden equitably

WALLER COUNTY APPRAISAL DISTRICT MASS APPRAISAL REPORT APPRAISAL YEAR 2018

WALLER COUNTY APPRAISAL DISTRICT MASS APPRAISAL REPORT APPRAISAL YEAR 2018 ADDENDUM TO WCAD REAPPRAISAL PLAN FOR 2017 AND 2018 WALLER COUNTY APPRAISAL DISTRICT Uniform Standards of Professional Appraisal

WALLER COUNTY APPRAISAL DISTRICT MASS APPRAISAL REPORT APPRAISAL YEAR 2018 ADDENDUM TO WCAD REAPPRAISAL PLAN FOR 2017 AND 2018 WALLER COUNTY APPRAISAL DISTRICT Uniform Standards of Professional Appraisal

Sales Associate Course

Sales Associate Course Chapter Sixteen Appraisal 1 2 Appraiser Specific amount Impartial (non biased) Defendable Estimate (Opinion) of value Fee based on time and difficulty Must follow Uniform Standards

Sales Associate Course Chapter Sixteen Appraisal 1 2 Appraiser Specific amount Impartial (non biased) Defendable Estimate (Opinion) of value Fee based on time and difficulty Must follow Uniform Standards

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330 REVIEW NOTES by CHUCK DUNN CHAPTER 16 Copyright 2010 by the Real Estate Division and Chuck Dunn. All rights reserved CHAPTER 16 - LAND AND SITE

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330 REVIEW NOTES by CHUCK DUNN CHAPTER 16 Copyright 2010 by the Real Estate Division and Chuck Dunn. All rights reserved CHAPTER 16 - LAND AND SITE

GENERAL ASSESSMENT DEFINITIONS

21st Century Appraisals, Inc. GENERAL ASSESSMENT DEFINITIONS Ad Valorem tax. A tax levied in proportion to the value of the thing(s) being taxed. Exclusive of exemptions, use-value assessment laws, and

21st Century Appraisals, Inc. GENERAL ASSESSMENT DEFINITIONS Ad Valorem tax. A tax levied in proportion to the value of the thing(s) being taxed. Exclusive of exemptions, use-value assessment laws, and

How to Read a Real Estate Appraisal Report

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

Filing a property assessment complaint and preparing for your hearing. Alberta Municipal Affairs

Filing a property assessment complaint and preparing for your hearing Alberta Municipal Affairs Alberta s Municipal Government Act, the 2018 Matters Relating to Assessment Complaints Regulation, and the

Filing a property assessment complaint and preparing for your hearing Alberta Municipal Affairs Alberta s Municipal Government Act, the 2018 Matters Relating to Assessment Complaints Regulation, and the

GASB 87: Leases. Hosted By: Ben Lindekugel, Executive Director Association of Washington Public Hospital Districts

GASB 87: Leases Hosted By: Ben Lindekugel, Executive Director Association of Washington Public Hospital Districts November 6, 2018 Presented By Tom Dingus, CPA, Partner Dingus, Zarecor & Associates PLLC

GASB 87: Leases Hosted By: Ben Lindekugel, Executive Director Association of Washington Public Hospital Districts November 6, 2018 Presented By Tom Dingus, CPA, Partner Dingus, Zarecor & Associates PLLC

ASSESSMENT AND TAXATION

ABSTRACT A brief synopsis of the assessment, appeal and taxation process as implemented by the Code of Iowa and Administrative Rules. ASSESSMENT AND TAXATION Iowa State Association of Assessors General

ABSTRACT A brief synopsis of the assessment, appeal and taxation process as implemented by the Code of Iowa and Administrative Rules. ASSESSMENT AND TAXATION Iowa State Association of Assessors General

Shopping Centre. Market Value Assessment in Saskatchewan Handbook. Shopping Centre Valuation Guide

Market Value Assessment in Saskatchewan Handbook Shopping Centre Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass

Market Value Assessment in Saskatchewan Handbook Shopping Centre Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass

Real Estate Appraisal

Market Value Chapter 17 Real Estate Appraisal This presentation includes materials from Ling and Archer, 4 th edition, Real Estate Principles The highest price a property will bring if: Payment is made

Market Value Chapter 17 Real Estate Appraisal This presentation includes materials from Ling and Archer, 4 th edition, Real Estate Principles The highest price a property will bring if: Payment is made

In-Depth Capitalization Rate Review

In-Depth Capitalization Rate Review Leonard J. Patcella, Jr., CMI, MAI President Equity Appraisal Co., Inc. Springhouse, PA jack.equityappraisal@comcast.net David A. Schneider, Esq. Partner Archer & Greiner,

In-Depth Capitalization Rate Review Leonard J. Patcella, Jr., CMI, MAI President Equity Appraisal Co., Inc. Springhouse, PA jack.equityappraisal@comcast.net David A. Schneider, Esq. Partner Archer & Greiner,

Rockwall CAD. Basics of. Appraising Property. For. Property Taxation

Rockwall CAD Basics of Appraising Property For Property Taxation ROCKWALL CENTRAL APPRAISAL DISTRICT 841 Justin Rd. Rockwall, Texas 75087 972-771-2034 Fax 972-771-6871 Introduction Rockwall Central Appraisal

Rockwall CAD Basics of Appraising Property For Property Taxation ROCKWALL CENTRAL APPRAISAL DISTRICT 841 Justin Rd. Rockwall, Texas 75087 972-771-2034 Fax 972-771-6871 Introduction Rockwall Central Appraisal

A Demonstration Appraisal Report. Of a. Located at. Date of Appraisal. Prepared for. Prepared by

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 West 10 th Street Kansas

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 West 10 th Street Kansas

New leases standard ASC 842 Lessee - operating leases. Itai Gotlieb, Partner, Professional Practice July 2017

ASC 842 Lessee - operating leases Itai Gotlieb, Partner, Professional Practice July 2017 Overview Under Accounting Standards Codification (ASC) 842, Leases, lessees recognize assets and liabilities for

ASC 842 Lessee - operating leases Itai Gotlieb, Partner, Professional Practice July 2017 Overview Under Accounting Standards Codification (ASC) 842, Leases, lessees recognize assets and liabilities for

concepts and techniques

concepts and techniques S a m p l e Timed Outline Topic Area DAY 1 Reference(s) Learning Objective The student will learn Teaching Method Time Segment (Minutes) Chapter 1: Introduction to Sales Comparison

concepts and techniques S a m p l e Timed Outline Topic Area DAY 1 Reference(s) Learning Objective The student will learn Teaching Method Time Segment (Minutes) Chapter 1: Introduction to Sales Comparison

Requirements for International Standards in Valuation & Surveying

Requirements for International Standards in Valuation & Surveying Jonathan Harris CBE DLitt(Hon), FRICS, FInstCPD, CRE President of RICS 2000-2001 Member of REM Glossary of Terms for International Valuation

Requirements for International Standards in Valuation & Surveying Jonathan Harris CBE DLitt(Hon), FRICS, FInstCPD, CRE President of RICS 2000-2001 Member of REM Glossary of Terms for International Valuation

Property Tax and Real Estate Appraisal Services

Property Tax and Real Estate Appraisal Services Appraisers/Consultants Micheal R. Lohmeier, ASA, MAI Certified General Real Estate Appraiser Direct: 248.368.8873 E: MLohmeier@virchowkrause.com Micheal

Property Tax and Real Estate Appraisal Services Appraisers/Consultants Micheal R. Lohmeier, ASA, MAI Certified General Real Estate Appraiser Direct: 248.368.8873 E: MLohmeier@virchowkrause.com Micheal

LITIGATING IN A MASS APPRAISAL ENVIRONMENT

11 th Mass Appraisal Valuation Symposium Innovation, Transformation, Knowledge Enhancement and Improved Efficiencies in Mass Appraisal Niagara Falls, Canada May 17-18, 2016 LITIGATING IN A MASS APPRAISAL

11 th Mass Appraisal Valuation Symposium Innovation, Transformation, Knowledge Enhancement and Improved Efficiencies in Mass Appraisal Niagara Falls, Canada May 17-18, 2016 LITIGATING IN A MASS APPRAISAL

City of Nashua, NH 2018 Revaluation Informational Meeting

City of Nashua, NH 2018 Revaluation Informational Meeting Legal Requirements Constitutional Duty of the City: [Art.] 6. [Valuation and Taxation.] The public charges of government, or any part thereof,

City of Nashua, NH 2018 Revaluation Informational Meeting Legal Requirements Constitutional Duty of the City: [Art.] 6. [Valuation and Taxation.] The public charges of government, or any part thereof,

Lease Accounting and Loan Covenants: What is the Impact?

Lease Accounting and Loan Covenants: What is the Impact? Monday June 26, 2017 9:15 AM 10:30 AM Presented by: Charlie Shannon Partner Moss Adams LLP 8750 N. Central Expressway, Suite 300 Dallas, TX 75231

Lease Accounting and Loan Covenants: What is the Impact? Monday June 26, 2017 9:15 AM 10:30 AM Presented by: Charlie Shannon Partner Moss Adams LLP 8750 N. Central Expressway, Suite 300 Dallas, TX 75231

For the Property Owner who wants to know!

For the Property Owner who wants to know! Answers to frequently asked questions concerning PROPERTY ASSESSMENTS and PROCEDURES. Provided by the Town of York Assessor s Office This booklet will attempt

For the Property Owner who wants to know! Answers to frequently asked questions concerning PROPERTY ASSESSMENTS and PROCEDURES. Provided by the Town of York Assessor s Office This booklet will attempt

ASSESSORS ANSWER FREQUENTLY ASKED QUESTIONS ABOUT REAL PROPERTY Assessors Office, 37 Main Street

A. THE ASSESSMENT PROCESS: ASSESSORS ANSWER FREQUENTLY ASKED QUESTIONS ABOUT REAL PROPERTY Assessors Office, 37 Main Street What is mass appraisal? Assessors must value all real and personal property in

A. THE ASSESSMENT PROCESS: ASSESSORS ANSWER FREQUENTLY ASKED QUESTIONS ABOUT REAL PROPERTY Assessors Office, 37 Main Street What is mass appraisal? Assessors must value all real and personal property in

Heiwa Real Estate Co., Ltd.

To the Shareholders of Heiwa Real Estate Co., Ltd. INFORMATION DISCLOSED ON THE INTERNET UPON ISSUING NOTICE CONCERNING THE CONVOCATION OF THE 94th ORDINARY GENERAL SHAREHOLDERS MEETING THE 94th FISCAL

To the Shareholders of Heiwa Real Estate Co., Ltd. INFORMATION DISCLOSED ON THE INTERNET UPON ISSUING NOTICE CONCERNING THE CONVOCATION OF THE 94th ORDINARY GENERAL SHAREHOLDERS MEETING THE 94th FISCAL

YOUNG COUNTY APPRAISAL DISTRICT

YOUNG COUNTY APPRAISAL DISTRICT 2017 - ANNUAL APPRAISAL REPORT AS OF 10/6/2017 1 2 TABLE OF CONTENTS ITEM PAGE Introduction 4 Purpose of Report...4 Taxing Entities, Rates & Exemptions 5 Property Types

YOUNG COUNTY APPRAISAL DISTRICT 2017 - ANNUAL APPRAISAL REPORT AS OF 10/6/2017 1 2 TABLE OF CONTENTS ITEM PAGE Introduction 4 Purpose of Report...4 Taxing Entities, Rates & Exemptions 5 Property Types

SAMA Presentation February 7-15, 2013 RMAA and UMAAS Sponsored Workshop Series

SAMA Presentation February 7-15, 2013 RMAA and UMAAS Sponsored Workshop Series Presentation Overview SAMA Who we are and what we do Summary of assessment legislation and policy Valuation publications Valuation

SAMA Presentation February 7-15, 2013 RMAA and UMAAS Sponsored Workshop Series Presentation Overview SAMA Who we are and what we do Summary of assessment legislation and policy Valuation publications Valuation

We look forward to working with you to build on our collaboration and enhance our partnership on behalf of all Minnesotans.

Date: February 27, 2017 To: County Assessors, Auditors, and Treasurers From: Cynthia Rowley, Director Property Tax Division Subject: Property Tax Services Report The Property Tax Division of the Minnesota

Date: February 27, 2017 To: County Assessors, Auditors, and Treasurers From: Cynthia Rowley, Director Property Tax Division Subject: Property Tax Services Report The Property Tax Division of the Minnesota

SAMPLE CASE STUDY. Beaver Bay Office Building

SAMPLE CASE STUDY Beaver Bay Office Building Marks PURPOSE: Find the current market value of the subject property. DATE OF APPRAISAL: July 1, 2013 SPECIFIC INSTRUCTIONS 10 1. Estimate the market rent of

SAMPLE CASE STUDY Beaver Bay Office Building Marks PURPOSE: Find the current market value of the subject property. DATE OF APPRAISAL: July 1, 2013 SPECIFIC INSTRUCTIONS 10 1. Estimate the market rent of

Residual Valuations & Development Appraisals

Residual Valuations & Development Appraisals Speaker: Richard Johnson Presentation to the SCSI 28 th May 2015 Savills 33 Molesworth Street, Dublin 2 T: +353 (0) 1 618 1344 E: richard.johnson@savills.ie

Residual Valuations & Development Appraisals Speaker: Richard Johnson Presentation to the SCSI 28 th May 2015 Savills 33 Molesworth Street, Dublin 2 T: +353 (0) 1 618 1344 E: richard.johnson@savills.ie

Sales Associate Course

Sales Associate Course Chapter Seventeen Real Estate Investments and Business Opportunity Brokerage 1 Investment Analysis Most important consideration: Economic soundness Land use controls Zoning Deed

Sales Associate Course Chapter Seventeen Real Estate Investments and Business Opportunity Brokerage 1 Investment Analysis Most important consideration: Economic soundness Land use controls Zoning Deed

Special Purpose Properties. Special Valuation Considerations

Special Purpose Properties Special Valuation Considerations 2017 Case Study in Ottawa: New Automobile Dealership Many brand-specific specialties Cost: $4,000,000 (including land and a developer fee) Sales

Special Purpose Properties Special Valuation Considerations 2017 Case Study in Ottawa: New Automobile Dealership Many brand-specific specialties Cost: $4,000,000 (including land and a developer fee) Sales

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

Sample Exam 2 Textbook Rationales

Sample Exam 2 Textbook Rationales 1. d The agreement between landlord and tenant here is a tenancy at will. The tenant is free to move out at any time, and the landlord can tell the tenant it s time to

Sample Exam 2 Textbook Rationales 1. d The agreement between landlord and tenant here is a tenancy at will. The tenant is free to move out at any time, and the landlord can tell the tenant it s time to

Chapter 1 Economics of Net Leases and Sale-Leasebacks

Chapter 1 Economics of Net Leases and Sale-Leasebacks 1:1 What Is a Net Lease? 1:2 Types of Net Leases 1:2.1 Bond Lease 1:2.2 Absolute Net Lease 1:2.3 Triple Net Lease 1:2.4 Double Net Lease 1:2.5 The

Chapter 1 Economics of Net Leases and Sale-Leasebacks 1:1 What Is a Net Lease? 1:2 Types of Net Leases 1:2.1 Bond Lease 1:2.2 Absolute Net Lease 1:2.3 Triple Net Lease 1:2.4 Double Net Lease 1:2.5 The

The Three Approaches to Value

Chapter 6 The Three Approaches to Value The appraiser considers three approaches to develop indications of value. These are: Cost approach; Sales comparison (market) approach; and Income approach. All

Chapter 6 The Three Approaches to Value The appraiser considers three approaches to develop indications of value. These are: Cost approach; Sales comparison (market) approach; and Income approach. All

Chapter 18. Investors have different required yields Different risk assessment Different opportunity cost of equity

Decision Making in Real Estate Centers Around Valuation Chapter 18 Investment Decisions: Ratios We examined the concept of market value in Chapters 7 & 8 As noted, professional RE appraisers are often

Decision Making in Real Estate Centers Around Valuation Chapter 18 Investment Decisions: Ratios We examined the concept of market value in Chapters 7 & 8 As noted, professional RE appraisers are often

Real Estate 63-Hour Sales Associate Pre-Licensing Course. Topics Covered & Learning Objectives

Real Estate 63-Hour Sales Associate Pre-Licensing Course Topics Covered & Learning Objectives Lesson 1: Administrative Matters And Course Overview; The Real Estate Business Describe the various activities

Real Estate 63-Hour Sales Associate Pre-Licensing Course Topics Covered & Learning Objectives Lesson 1: Administrative Matters And Course Overview; The Real Estate Business Describe the various activities

BUSI 330 Suggested Answers to Review and Discussion Questions: Lesson 10

BUSI 330 Suggested Answers to Review and Discussion Questions: Lesson 10 1. The client should give you a copy of their income and expense statements for the last 3 years showing their rental income by

BUSI 330 Suggested Answers to Review and Discussion Questions: Lesson 10 1. The client should give you a copy of their income and expense statements for the last 3 years showing their rental income by

Published in Spring 1986 Issue The Real Estate Appraiser & Analyst Society of Real Estate Appraisers 1

(1) Published in Spring 1986 Issue The Real Estate Appraiser & Analyst Society of Real Estate Appraisers 1 Alternative Valuation Methods for Leasehold Properties By Tony Sevelka, AACI, SREA, MAI, CRE Introduction

(1) Published in Spring 1986 Issue The Real Estate Appraiser & Analyst Society of Real Estate Appraisers 1 Alternative Valuation Methods for Leasehold Properties By Tony Sevelka, AACI, SREA, MAI, CRE Introduction

METHODOLOGY GUIDE VALUING LONG-TERM CARE HOMES IN ONTARIO. Valuation Date: January 1, 2016

METHODOLOGY GUIDE VALUING LONG-TERM CARE HOMES IN ONTARIO Valuation Date: January 1, 2016 AUGUST 2016 August 22, 2016 The Municipal Property Assessment Corporation (MPAC) is responsible for accurately

METHODOLOGY GUIDE VALUING LONG-TERM CARE HOMES IN ONTARIO Valuation Date: January 1, 2016 AUGUST 2016 August 22, 2016 The Municipal Property Assessment Corporation (MPAC) is responsible for accurately

ASSESSMENT METHODOLOGY

2018 ASSESSMENT METHODOLOGY MULTI-RESIDENTIAL FOUR-PLEX A summary of the methods used by the City of Edmonton in determining the value of multi-residential four-plex properties in Edmonton for assessment

2018 ASSESSMENT METHODOLOGY MULTI-RESIDENTIAL FOUR-PLEX A summary of the methods used by the City of Edmonton in determining the value of multi-residential four-plex properties in Edmonton for assessment

Cap Rate Trends, Methodology and Analysis. Dane R. Anderson MAI, CCIM Appraisal & Litigation Services Director

Cap Rate Trends, Methodology and Analysis Dane R. Anderson MAI, CCIM Appraisal & Litigation Services Director 1 Quickly The Income Approach Basis of the Approach Present worth of future benefits Two Methods:

Cap Rate Trends, Methodology and Analysis Dane R. Anderson MAI, CCIM Appraisal & Litigation Services Director 1 Quickly The Income Approach Basis of the Approach Present worth of future benefits Two Methods:

RAINS COUNTY APPRAISAL DISTRICT

RAINS COUNTY APPRAISAL DISTRICT 2017 MASS APPRAISAL SUMMARY REPORT mass appraisal report 2017 uspap_appr_report RAINS COUNTY APPRAISAL DISTRICT 2017 MASS APPRAISAL SUMMARY REPORT Identification of Subject:

RAINS COUNTY APPRAISAL DISTRICT 2017 MASS APPRAISAL SUMMARY REPORT mass appraisal report 2017 uspap_appr_report RAINS COUNTY APPRAISAL DISTRICT 2017 MASS APPRAISAL SUMMARY REPORT Identification of Subject:

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

STEVEN J. DREW Assessor OFFICE OF THE ASSESSOR Service, Integrity, Fairness, Internationally Recognized for Excellence OVERVIEW OF RESIDENTIAL APPRAISAL PROCESS And Cost Valuation Report Introduction The

Capital Layer Evaluations: Hotels and More

Peer-Reviewed Article Capital Layer Evaluations: Hotels and More by Tom Troll Abstract Historically, the valuation of hotels, nursing homes, and other types of complex properties has been constrained because

Peer-Reviewed Article Capital Layer Evaluations: Hotels and More by Tom Troll Abstract Historically, the valuation of hotels, nursing homes, and other types of complex properties has been constrained because

The rental levels will be based upon contract rent for the leases in place and is provided below:

PROJECT 1: TWIN PINES FINANCIAL DATA Leases The potential income relates to rentals being obtained from tenants occupying space in the project. A current rent roll was provided, and it is assumed that

PROJECT 1: TWIN PINES FINANCIAL DATA Leases The potential income relates to rentals being obtained from tenants occupying space in the project. A current rent roll was provided, and it is assumed that

PROTECTING FEE SIMPLE VALUE FROM A LEASED FEE ANALYSIS: WHY YOUR PROPERTY MAY BE NEXT

PROTECTING FEE SIMPLE VALUE FROM A LEASED FEE ANALYSIS: WHY YOUR PROPERTY MAY BE NEXT Adam C. Strasser, Esq. Senior Tax Manager Walgreens Deerfield, IL adam.strasser@walgreens.com Anthony Barna, MAI Appraiser

PROTECTING FEE SIMPLE VALUE FROM A LEASED FEE ANALYSIS: WHY YOUR PROPERTY MAY BE NEXT Adam C. Strasser, Esq. Senior Tax Manager Walgreens Deerfield, IL adam.strasser@walgreens.com Anthony Barna, MAI Appraiser

A Guide Tax Assessment. George M. Durgin Middletown Tax Assessor August 4, 2016

A Guide Tax Assessment George M. Durgin Middletown Tax Assessor August 4, 2016 A Guide to Tax Assessment Legal Basis Valuation Land Value Building Value Appeal Process Legal Basis Rhode Island General

A Guide Tax Assessment George M. Durgin Middletown Tax Assessor August 4, 2016 A Guide to Tax Assessment Legal Basis Valuation Land Value Building Value Appeal Process Legal Basis Rhode Island General

Professional Certification Programs

Professional Certification Programs Participants in NDC training, including staff members of Housing and Economic Development Networks, State and Local Governments, Community Development Banks and Charitable

Professional Certification Programs Participants in NDC training, including staff members of Housing and Economic Development Networks, State and Local Governments, Community Development Banks and Charitable

ASSESSMENT REVIEW BOARD

ASSESSMENT REVIEW BOARD MAIN FLOOR CITY HALL 1 SIR WINSTON CHURCHILL SQUARE EDMONTON AB T5J 2R7 (780) 496-5026 FAX (780) 496-8199 NOTICE OF DECISION 0098 248/10 Altus Group Ltd. The City of Edmonton 17327

ASSESSMENT REVIEW BOARD MAIN FLOOR CITY HALL 1 SIR WINSTON CHURCHILL SQUARE EDMONTON AB T5J 2R7 (780) 496-5026 FAX (780) 496-8199 NOTICE OF DECISION 0098 248/10 Altus Group Ltd. The City of Edmonton 17327

Past & Present Adjustments & Parcel Count Section... 13

Assessment 2017 Report This report includes specific information regarding the 2017 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

Assessment 2017 Report This report includes specific information regarding the 2017 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

Cost Segregation Instructor Teaching Schedule (3-Hour)

") Time Topic Pages Student Objectives 8:30-8:35 Course introduction Page 2 What is cost segregation? Objective of cost segregation: to increase cash flow Benefit of cost segregation Learning objectives Page

Time Topic Pages Student Objectives 8:30-8:35 Course introduction Page 2 What is cost segregation? Objective of cost segregation: to increase cash flow Benefit of cost segregation Learning objectives Page

Introduction. Market Value Assessment in Saskatchewan Handbook. Introduction

Market Value Assessment in Saskatchewan Handbook Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass Appraisal for

Market Value Assessment in Saskatchewan Handbook Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass Appraisal for

Part 1. Estimating Land Value Using a Land Residual Technique Based on Discounted Cash Flow Analysis

Table of Contents Overview... v Seminar Schedule... ix SECTION 1 Part 1. Estimating Land Value Using a Land Residual Technique Based on Discounted Cash Flow Analysis Preview Part 1... 1 Land Residual Technique...

Table of Contents Overview... v Seminar Schedule... ix SECTION 1 Part 1. Estimating Land Value Using a Land Residual Technique Based on Discounted Cash Flow Analysis Preview Part 1... 1 Land Residual Technique...

Four (4) Factors in Investment Definition: Investment

Factors in Investment Definition: Investment") Introductions Your name Where you work Your job responsibilities How long you have been in the industry What you hope to get from this class Chapter 1: Investments Agenda 2 Investments Adding Value to

Introductions Your name Where you work Your job responsibilities How long you have been in the industry What you hope to get from this class Chapter 1: Investments Agenda 2 Investments Adding Value to

Table of Contents 2017 Commercial Revaluation Report

Table of Contents 07 Commercial Revaluation Report 07 Commercial & Industrial Valuation Summary Introduction Uniform Standards Approaches to Value Land Valuation Land to Building Ratios Parking to Building

Table of Contents 07 Commercial Revaluation Report 07 Commercial & Industrial Valuation Summary Introduction Uniform Standards Approaches to Value Land Valuation Land to Building Ratios Parking to Building

7401 PACIFIC BLVD. HUNTINGTON PARK, CA 90255

OFFERING MEMORANDUM $1,295,000 7401 PACIFIC BLVD. HUNTINGTON PARK, CA 90255 90% FINANCING AVAILABLE STRIP CENTER - MTM TENANCY 1 This Memorandum ( Offering Memorandum ) has been prepared by Brookfield

OFFERING MEMORANDUM $1,295,000 7401 PACIFIC BLVD. HUNTINGTON PARK, CA 90255 90% FINANCING AVAILABLE STRIP CENTER - MTM TENANCY 1 This Memorandum ( Offering Memorandum ) has been prepared by Brookfield

Introduction. Bruce Munneke, S.A.M.A. Washington County Assessor. 3 P a g e

Assessment 2016 Report This report includes specific information regarding the 2016 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

Assessment 2016 Report This report includes specific information regarding the 2016 assessment as well as general information about both the appeals and assessment processes. Contents Introduction... 3

DIRECTIVE # This Directive Supersedes Directive # and #92-003

Division Of Property Valuation Docking State Office Building 915 SW Harrison St., Room 400N Topeka, KS 66612-1588 Nick Jordan, Secretary David N. Harper, Director phone: 785-296-2365 fax: 785-296-2320

Division Of Property Valuation Docking State Office Building 915 SW Harrison St., Room 400N Topeka, KS 66612-1588 Nick Jordan, Secretary David N. Harper, Director phone: 785-296-2365 fax: 785-296-2320

EXPLAINING MASS APPRAISAL

EXPLAINING MASS APPRAISAL PROMOTING THE ROLE OF THE ASSESSOR MAAO SUMMER CONFERENCE, JUNE 24, 2015 RICHARD W. FINNEGAN, MAA Please excuse the length of this letter. I didn t have time to write a short

EXPLAINING MASS APPRAISAL PROMOTING THE ROLE OF THE ASSESSOR MAAO SUMMER CONFERENCE, JUNE 24, 2015 RICHARD W. FINNEGAN, MAA Please excuse the length of this letter. I didn t have time to write a short

Valuation models for low-income housing: How does income approach reduce ambiguity of assessing property tax?

RAIS RESEARCH ASSOCIATION for INTERDISCIPLINARY OCTOBER 2017 STUDIES Valuation models for low-income housing: How does income approach reduce ambiguity of assessing property tax? Yelin (Jenny) Li Salem

RAIS RESEARCH ASSOCIATION for INTERDISCIPLINARY OCTOBER 2017 STUDIES Valuation models for low-income housing: How does income approach reduce ambiguity of assessing property tax? Yelin (Jenny) Li Salem

Kitsap County Assessor

Narrative for Area 5 - Bremerton and Central Kitsap East Tax Year: 2018 Appraisal Date: 1/1/2017 Property Type: Retail - Strip Retail and Small Single Tenant Retail Updated 6/5/2017 by CM20 Area Overview

Narrative for Area 5 - Bremerton and Central Kitsap East Tax Year: 2018 Appraisal Date: 1/1/2017 Property Type: Retail - Strip Retail and Small Single Tenant Retail Updated 6/5/2017 by CM20 Area Overview

SAMA Presenters: Steve Suchan Todd Treslan February 1, 2015

SAMA Presenters: Steve Suchan Todd Treslan February 1, 2015 Presentation Overview Part 1 - Steve SAMA Who we are and what we do Assessment legislation and principles Valuation standards (Regulated, non-regulated)

SAMA Presenters: Steve Suchan Todd Treslan February 1, 2015 Presentation Overview Part 1 - Steve SAMA Who we are and what we do Assessment legislation and principles Valuation standards (Regulated, non-regulated)

Village of Scarsdale

Village of Scarsdale VILLAGE HALL / 1001 POST ROAD / SCARSDALE, NY 10583 914.722.1110 / WWW.SCARSDALE.COM Village Wide Revaluation Frequently Asked Questions Q1. How was the land value for each parcel

Village of Scarsdale VILLAGE HALL / 1001 POST ROAD / SCARSDALE, NY 10583 914.722.1110 / WWW.SCARSDALE.COM Village Wide Revaluation Frequently Asked Questions Q1. How was the land value for each parcel

Fully Stabilized 24-Unit Property at 11% Cap Rate!

Fully Stabilized 24-Unit Property at 11% Cap Rate! To Insert a Picture here, click inside this box with your mouse, then click on "INSERT PIC" button on the right and select the picture 24 Units consisting

Fully Stabilized 24-Unit Property at 11% Cap Rate! To Insert a Picture here, click inside this box with your mouse, then click on "INSERT PIC" button on the right and select the picture 24 Units consisting

TALK REAL. Now that you ve received your property assessment ASSESSMENTS, ROLLBACKS AND YOUR PROPERTY TAXES

REAL TALK FROM THE POLK COUNTY ASSESSOR www.assess.co.polk.ia.us SPRING 2013 ASSESSMENTS, ROLLBACKS AND YOUR PROPERTY TAXES Now that you ve received your property assessment for 2013, you re likely wondering

REAL TALK FROM THE POLK COUNTY ASSESSOR www.assess.co.polk.ia.us SPRING 2013 ASSESSMENTS, ROLLBACKS AND YOUR PROPERTY TAXES Now that you ve received your property assessment for 2013, you re likely wondering

Business Valuation More Art Than Science

Business Valuation More Art Than Science One of the more difficult aspects of business planning is business valuation. It is also one of the more important aspects. While owners of closely held businesses

Business Valuation More Art Than Science One of the more difficult aspects of business planning is business valuation. It is also one of the more important aspects. While owners of closely held businesses

2015 Polk County Assessor s Office. Ankeny Economic Development Corp. October 15, 2015

2015 Polk County Assessor s Office Ankeny Economic Development Corp. October 15, 2015 2015 Rollback Commercial - 90% Industrial - 90% Multiresidential 86.25% Residential 55.1976% (Projected) How is the

2015 Polk County Assessor s Office Ankeny Economic Development Corp. October 15, 2015 2015 Rollback Commercial - 90% Industrial - 90% Multiresidential 86.25% Residential 55.1976% (Projected) How is the

Duties of the Assessors

Duties of the Assessors Value Properties Determine New Growth Set Tax Rate Assess Property Taxes Abate & Exempt Taxes Manage Overlay Account Assess Local Excises 1 Value Property Assessments based on fair

Duties of the Assessors Value Properties Determine New Growth Set Tax Rate Assess Property Taxes Abate & Exempt Taxes Manage Overlay Account Assess Local Excises 1 Value Property Assessments based on fair

NSP Rental Basics: A Primer on Using Rental Projects to Meet NSP Obligation and 25% Set-Aside Requirement. About this Tool

NSP Rental Basics: A Primer on Using Rental Projects to Meet NSP Obligation and 25% Set-Aside Requirement About this Tool Description: This tool is intended for NSP grantees and their partners seeking

NSP Rental Basics: A Primer on Using Rental Projects to Meet NSP Obligation and 25% Set-Aside Requirement About this Tool Description: This tool is intended for NSP grantees and their partners seeking

How to Petition for a Review of Your Property Taxes: County Board of Equalization

How to Petition for a Review of Your Property Taxes: County Board of Equalization Talk with the Assessor There are several reasons why you may want to petition for a review of your property taxes. Whatever

How to Petition for a Review of Your Property Taxes: County Board of Equalization Talk with the Assessor There are several reasons why you may want to petition for a review of your property taxes. Whatever

GASB 87, Leases. Ali H. Hijazi, Senior Manager

GASB 87, Leases Ali H. Hijazi, Senior Manager Agenda Timing Defining Our Terms Accounting and Disclosure Requirements Preparation Recommendations Examples 2 Timing Timing The requirements of this standard

GASB 87, Leases Ali H. Hijazi, Senior Manager Agenda Timing Defining Our Terms Accounting and Disclosure Requirements Preparation Recommendations Examples 2 Timing Timing The requirements of this standard

ASSESSMENT METHODOLOGY

2018 ASSESSMENT METHODOLOGY MULTI-RESIDENTIAL HIGH-RISE APARTMENT A summary of the methods used by the City of Edmonton in determining the value of multi-residential high-rise properties in Edmonton for

2018 ASSESSMENT METHODOLOGY MULTI-RESIDENTIAL HIGH-RISE APARTMENT A summary of the methods used by the City of Edmonton in determining the value of multi-residential high-rise properties in Edmonton for

Strip Commercial. Market Value Assessment in Saskatchewan Handbook. Strip Commercial Properties Valuation Guide

Market Value Assessment in Saskatchewan Handbook Strip Commercial Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and

Market Value Assessment in Saskatchewan Handbook Strip Commercial Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and