Unleash The Power!

|

|

|

- Candice Thornton

- 5 years ago

- Views:

Transcription

1 Unleash The Power!

2 V a l u a t i o n P r o d u c t D e s c r i p t i o n

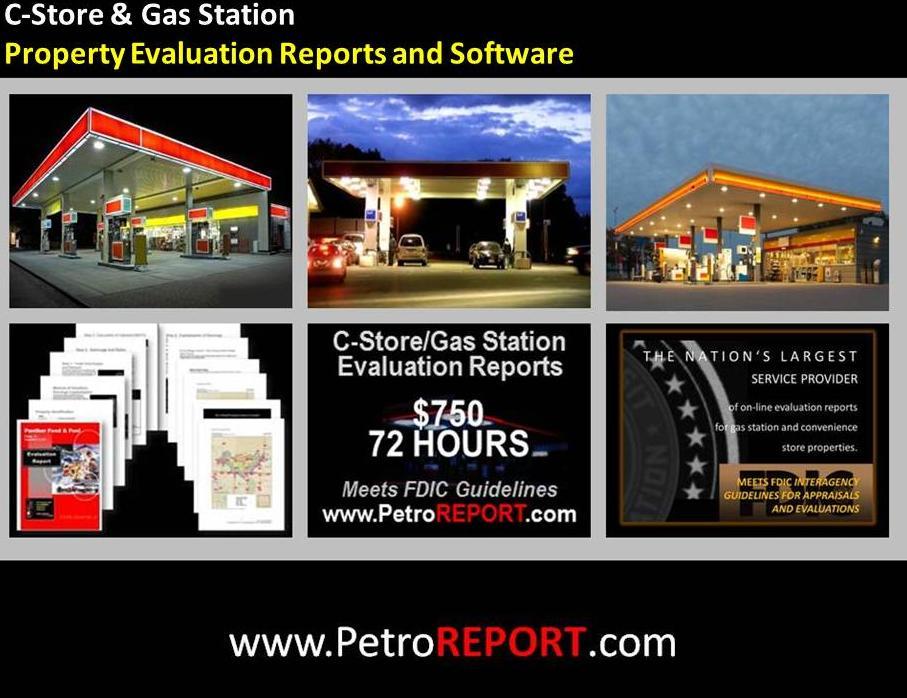

$3,500 C-Store & Gas Station Property Summary Appraisal Report MEETS USPAP AND STATE LICENSING REQUIREMENTS FOR A")

3 Choice (A) $750 C-Store & Gas Station Property Evaluation Report MEETS FDIC INTERAGENCY GUIDELINES FOR EVALUATIONS Choice (B) $950 C-Store & Gas Station Property Automated Summary Appraisal Report MEETS USPAP AND STATE LICENSING REQUIREMENTS FOR A CERTIFIED APPRAISAL Choice (C) $3,500 C-Store & Gas Station Property Summary Appraisal Report MEETS USPAP AND STATE LICENSING REQUIREMENTS FOR A CERTIFIED APPRAISAL methodology You can download samples of all three reports at the following link. SAMPLE REPORT DOWNLOADS

.")

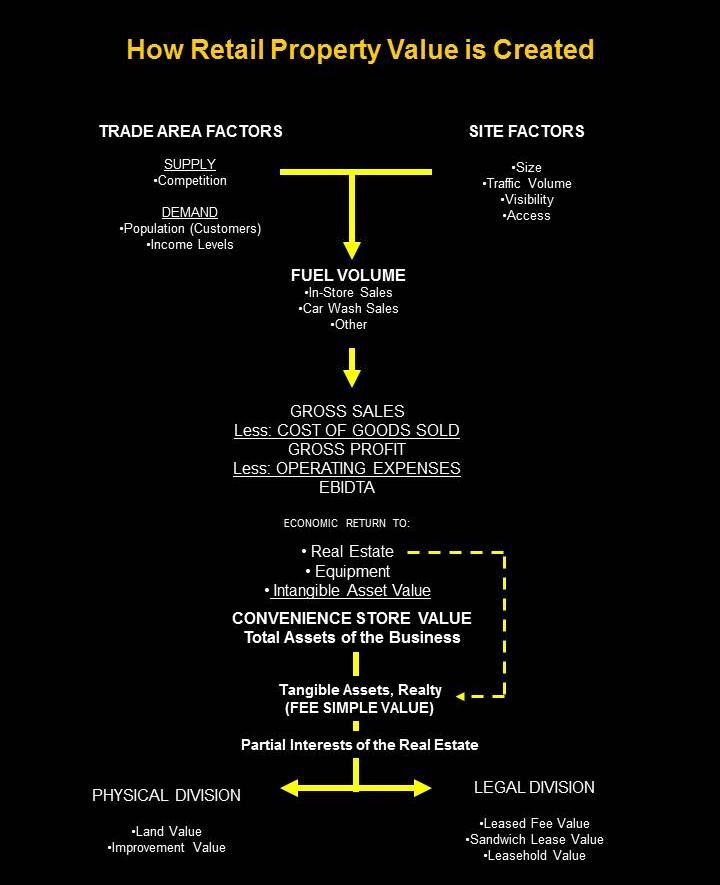

4 Choice (A) $750 C-Store & Gas Station Property Evaluation Report COMPLIANT WITH FDIC INTERAGENCY GUIDELINES FOR EVALUATIONS Delivered within 72 Hours NATIONWIDE Primary approach is the Income Approach using a Capitalization of Earnings under typical management as recommended by International Valuation Standards (IVS SR- 232). Support to the primary valuation approach from summary Cost Approach and summary Peer Group sales within the State. Projections under typical management (fee simple value) for: (a) Annual gallonage (b) In-store sales (c) Gross profit (d) Adjusted EBIDTA (e) NOI to real estate The Evaluation Reports consider and adjust the real estate value for: Supply and demand in the trade area (3-minute drive-time) Hypermarket competition Resident population demographics Reliable and supported value estimates for: Real Estate (site, store building, fuel service, car wash) Equipment (moveable personal property) Business Value (intangible assets) You can download samples of all three reports at the following link. SAMPLE REPORT DOWNLOADS 1

5 Choice (B) $950 C-Store & Gas Station Property Automated Summary Appraisal Report COMPLIANT WITH USPAP AND STATE LICENSING REQUIREMENTS FOR A CERTIFIED APPRAISAL State-Certified, Summary Appraisal Report. NATIONWIDE. Same as Choice A with the addition of certifications and licenses meeting the requirements for a state-certified, summary appraisal report. Transaction amounts greater than $1 million. Inspection option available for $1,200. You can download samples of all three reports at the following link. SAMPLE REPORT DOWNLOADS 2

You can download")

6 Choice (C) $3,500 C-Store & Gas Station Property Summary Appraisal Report COMPLIANT WITH USPAP AND STATE LICENSING REQUIREMENTS FOR A CERTIFIED APPRAISAL Subject Property Inspection Original field measurements of all improvements. Interior and exterior viewing. Access points and street visibility measurements. Trade Area Inspection Surveillance of the 3-Minute drive-time trade area (primary market). Viewing of competitive locations and hypermarkets, traffic volumes and patterns, 2-Part Appraisal Report (described on following page) You can download samples of all three reports at the following link. SAMPLE REPORT DOWNLOADS 3

7 Part 1 of the Report The fee simple estate for the tangible and intangible assets. This value is based on market-level earnings for stores of the subject's particular physical configuration at the subject's specific location under typical management. The fee simple value does not rely on the operator s historic (actual) profit and loss statements. The fee simple value is based on how a typical operator would perform with the subject s real estate assets at the fixed location. Because this is the fee simple value, this value is irrespective of the existing brand, supply and service contracts. Approaches used in Part 1 of our appraisals: Capitalized Earnings Approach Developed for the Tangible Assets, Real Property. Excess earnings estimates, if any, applied to value estimate of Intangible Assets. Sales Comparison Approach. Developed for the Tangible Assets, Real Property. Cost Approach Developed for the Tangible Assets, Real Property. Developed for Tangible Assets, Non-Realty (FF&E). Part 2 of the Report The value Under Current Operations. This value is based on the business s ability to generate earnings under the existing supply contracts, branding agreements, and historical financial performance, and current management. Business Operating Agreements (BOA) and branding agreements for the convenience store or gas station are not part of the recorded title to the real property. Often these contracts do not automatically transfer with the sale of the real estate. In many cases, these agreements either terminate upon the transfer or are renegotiated between the new parties, if the property sells. The value Under Current Operations assumes the existing business operating agreements remain in place and that the quality and depth of management remains unchanged. This estimate is more of an economic performance measure, which can show for example, the current business s ability to satisfy the debt requirements of the fee simple interest. The value estimate of the real estate and other physical assets of the property Under Current Operations is limited in its applicability and should not be assumed to reflect transferable market value. In the event of foreclosure, the value Under Current Operations will likely not be realized by the mortgagee, or Deed of Trust beneficiary. Approaches used in Part 2 of our appraisals: Capitalized Earnings Approach Developed for the Tangible Assets, Real Property. Excess earnings estimates, if any, applied to value estimate of Intangible Assets. For the reasons above, rather than expressing a value estimate, this economic characteristic is usually included in our appraisal reports as an index. 4

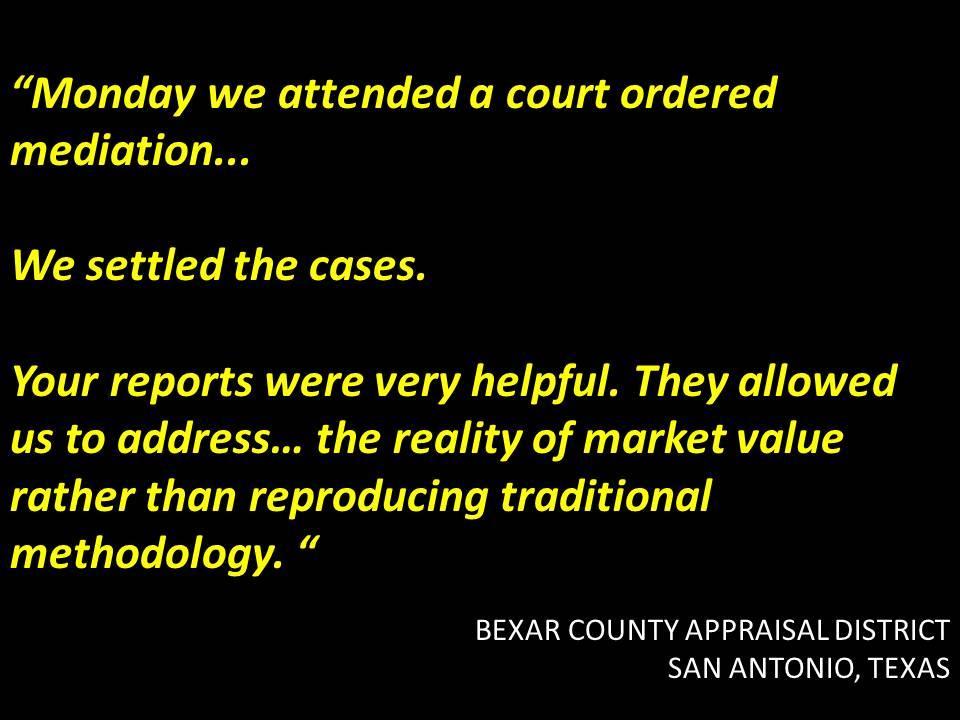

8 "We ve been very successful so far and your evaluation reports have been a big part of our success." - Property Tax Appeal, International Convenience Store Chain

9 The primary method of valuation is a capitalization of EBIDTA income approach. This method is recommended by the Appraisal Institute s Convenience Stores and Retail Fuel Properties: Essential Appraisal Issues and International Valuation Standards (IVS Guidance Note 13 and SR 232). Additional support for the valuation estimate includes a summary cost approach and local peer group NAICS 4471 sale transaction summaries. These Evaluation Reports and Automated Summary Appraisals include projections under typical management (fee simple value) for: a) Annual gallonage (b) In-store sales (c) Gross profit (d) Adjusted EBIDTA (e) NOI to real estate WE DO NOT: With c-stores and gas stations, real estate usually comprises about 90% of the value of the going concern. Most appraisers subtract the cost approach value of the real estate from the EBIDTA capitalization, which makes the real estate value a constant and leaves intangible asset value residual. This is not good appraisal practice and is simply an expression of the cost approach two times for the highest-value asset of the business. WE DO: Our Evaluation Reports and Automated Summary Appraisals leave the value of the real estate residual in the capitalized income approach so that the real estate s location strengths and weaknesses as measured by earnings potential are reflected in the value estimate. The Evaluation Reports and Automated Summary Appraisals consider and adjust the real estate value for: Supply and demand in the trade area (3-minute drive-time) Hypermarket competition Resident population demographics methodology Most appraisers do not consider or adjust for these important characteristics, even in higher costing statecertified appraisals. Our Evaluation Reports and Automated Summary Appraisals are often more accurate and reliable than many other vendors expensive state-certified appraisal reports because we follow industry-recommended valuation procedure of using a capitalization of earnings income approach for this specialized type of property. All reports include valuations of : Real Estate Equipment Business Value 6

10 7

11 8

12 7

Robert E. Bainbridge, MAI C-STORE VALUATIONS

Robert E. Bainbridge, MAI C-STORE VALUATIONS How to Appraise Your Convenience Store Yourself: A STEP-BY-STEP GUIDE Robert E. Bainbridge, MAI PUBLISHED BY C-STORE VALUATIONS, DALLAS, TEXAS LIBRARY OF CONGRESS

Robert E. Bainbridge, MAI C-STORE VALUATIONS How to Appraise Your Convenience Store Yourself: A STEP-BY-STEP GUIDE Robert E. Bainbridge, MAI PUBLISHED BY C-STORE VALUATIONS, DALLAS, TEXAS LIBRARY OF CONGRESS

Site Feasibility Report

January 6, 2016 Site Feasibility Report Your File No. N/A Proposed Pio Nono Avenue Site 1095 Pio Nono Avenue Macon GEORGIA 31204 COMPLETED FOR: Bob Fountain BobFountain (478) 747-9577 bfountain2@gmail.com

January 6, 2016 Site Feasibility Report Your File No. N/A Proposed Pio Nono Avenue Site 1095 Pio Nono Avenue Macon GEORGIA 31204 COMPLETED FOR: Bob Fountain BobFountain (478) 747-9577 bfountain2@gmail.com

Interagency Appraisal and

Interagency Appraisal and Evaluation (IAEG) Workshop Purpose (77456) Supersedes the 1994 Interagency Appraisal & Evaluation Guidelines Address supervisory matters relating to real estate appraisal and

Interagency Appraisal and Evaluation (IAEG) Workshop Purpose (77456) Supersedes the 1994 Interagency Appraisal & Evaluation Guidelines Address supervisory matters relating to real estate appraisal and

BUSI 330 Suggested Answers to Review and Discussion Questions: Lesson 10

BUSI 330 Suggested Answers to Review and Discussion Questions: Lesson 10 1. The client should give you a copy of their income and expense statements for the last 3 years showing their rental income by

BUSI 330 Suggested Answers to Review and Discussion Questions: Lesson 10 1. The client should give you a copy of their income and expense statements for the last 3 years showing their rental income by

Broker. Basic Business Appraisal. Chapter 9. Copyright Gold Coast Schools 1

Broker Chapter 9 Basic Business Appraisal 1 Learning Objectives Describe the characteristics of the legal entities a business appraiser may encounter List at least 5 reasons for a business appraisal List

Broker Chapter 9 Basic Business Appraisal 1 Learning Objectives Describe the characteristics of the legal entities a business appraiser may encounter List at least 5 reasons for a business appraisal List

Always Accurate, Always on Time

Always Accurate, Always on Time Clearing the Air: Going-Concern Valuation vs General Valuation Knowing When you Can be Better Served by a More In-depth Valuation Expert Jan, 2015 Clearing the Air: Going-Concern

Always Accurate, Always on Time Clearing the Air: Going-Concern Valuation vs General Valuation Knowing When you Can be Better Served by a More In-depth Valuation Expert Jan, 2015 Clearing the Air: Going-Concern

Appraisals & Evaluations. Association of Appraiser Regulatory Officials

Appraisals & Evaluations Association of Appraiser Regulatory Officials Agenda Appraisals Evaluations Review Referrals Reference Materials 2 Appraisals Part 323 requires an appraisal for real estate (RE)

Appraisals & Evaluations Association of Appraiser Regulatory Officials Agenda Appraisals Evaluations Review Referrals Reference Materials 2 Appraisals Part 323 requires an appraisal for real estate (RE)

All Interested Parties. Rick Baumgardner, Chair Appraisal Practices Board. Date: September 9, Background

TO: FROM: RE: All Interested Parties Rick Baumgardner, Chair Appraisal Practices Board Concept Paper Valuation Issues in Separating Tangible and Intangible Assets Date: September 9, 2013 Background Those

TO: FROM: RE: All Interested Parties Rick Baumgardner, Chair Appraisal Practices Board Concept Paper Valuation Issues in Separating Tangible and Intangible Assets Date: September 9, 2013 Background Those

concepts and techniques

concepts and techniques S a m p l e Timed Outline Topic Area DAY 1 Reference(s) Learning Objective The student will learn Teaching Method Time Segment (Minutes) Chapter 1: Introduction to Sales Comparison

concepts and techniques S a m p l e Timed Outline Topic Area DAY 1 Reference(s) Learning Objective The student will learn Teaching Method Time Segment (Minutes) Chapter 1: Introduction to Sales Comparison

BUSINESS VALUATIONS: FUNDAMENTALS, TECHNIQUES AND THEORY (FT&T) CHAPTER 6

CHAPTER 6") Fundamentals, Techniques & Theory COMMONLY USED METHODS OF VALUATION BUSINESS VALUATIONS: FUNDAMENTALS, TECHNIQUES AND THEORY (FT&T) CHAPTER 6 REVIEW QUESTIONS 1995 2013 by National Association of Certified

Fundamentals, Techniques & Theory COMMONLY USED METHODS OF VALUATION BUSINESS VALUATIONS: FUNDAMENTALS, TECHNIQUES AND THEORY (FT&T) CHAPTER 6 REVIEW QUESTIONS 1995 2013 by National Association of Certified

Always Accurate, Always on Time

Always Accurate, Always on Time U.S. Small Business Administration (SBA) Recent Changes to Standards of Operating Procedures (SOP) Qualified Appraiser and Remaining Economic Life June, 2015 Retail Petroleum

Always Accurate, Always on Time U.S. Small Business Administration (SBA) Recent Changes to Standards of Operating Procedures (SOP) Qualified Appraiser and Remaining Economic Life June, 2015 Retail Petroleum

Part 1. Introduction to the Fundamentals of Separating Real Property, Personal Property, and Intangible Business Assets. Preview...

Table of Contents Overview... ix Course Schedule... xiii SECTION 1 Part 1. Introduction to the Fundamentals of Separating Real Property, Personal Property, and Intangible Business Assets Preview... 1 Course

Table of Contents Overview... ix Course Schedule... xiii SECTION 1 Part 1. Introduction to the Fundamentals of Separating Real Property, Personal Property, and Intangible Business Assets Preview... 1 Course

California Real Estate License Exam Prep: Unlocking the DRE Salesperson and Broker Exam 4th Edition

California Real Estate License Exam Prep: Unlocking the DRE Salesperson and Broker Exam 4th Edition ANSWER SHEET INSTRUCTIONS: The exam consists of multiple choice questions. Multiple choice questions

California Real Estate License Exam Prep: Unlocking the DRE Salesperson and Broker Exam 4th Edition ANSWER SHEET INSTRUCTIONS: The exam consists of multiple choice questions. Multiple choice questions

Appraisal Review & Advisory Opinion 20 Controversy. Presenter: Lisa Kimbro, MAI, AI-GRS

Appraisal Review & Advisory Opinion 20 Controversy Presenter: Lisa Kimbro, MAI, AI-GRS Practicing appraisers know USPAP, and appraisers that complete review work know USPAP s Standard 3. But what about

Appraisal Review & Advisory Opinion 20 Controversy Presenter: Lisa Kimbro, MAI, AI-GRS Practicing appraisers know USPAP, and appraisers that complete review work know USPAP s Standard 3. But what about

Asset management. Presented by Koenraad De Bruyne Retail Director Tas-Helat Marketing Co Ltd Kuala Lumpur March 2010

Asset management Presented by Koenraad De Bruyne Retail Director Tas-Helat Marketing Co Ltd Kuala Lumpur March 2010 What is asset management? What is an asset?* Business Asset, something possessed by a

Asset management Presented by Koenraad De Bruyne Retail Director Tas-Helat Marketing Co Ltd Kuala Lumpur March 2010 What is asset management? What is an asset?* Business Asset, something possessed by a

BUSI 452 Case Studies in Appraisal II

BUSI 452 Case Studies in Appraisal II PURPOSE AND SCOPE The Case Studies in Appraisal II course (BUSI 452) is a continuation of BUSI 442. This course is intended to introduce further practical applications

BUSI 452 Case Studies in Appraisal II PURPOSE AND SCOPE The Case Studies in Appraisal II course (BUSI 452) is a continuation of BUSI 442. This course is intended to introduce further practical applications

Interagency Guidelines Web seminar, February 10, 2011

Interagency Guidelines Web seminar, February 10, 2011 Questions from participants. The answers here are suggestive guidance only and should not be treated or considered legal or regulatory advice. You

Interagency Guidelines Web seminar, February 10, 2011 Questions from participants. The answers here are suggestive guidance only and should not be treated or considered legal or regulatory advice. You

GSE FOCUS. Visit WorkflowGeeks.com for more free titles. Sponsored by Mercury Network

GSE FOCUS Visit WorkflowGeeks.com for more free titles. Sponsored by Mercury Network The SaaS Vendor Management Platform chosen by over 600 of the nation s lenders and AMCs to power more than 20,000 appraisals

GSE FOCUS Visit WorkflowGeeks.com for more free titles. Sponsored by Mercury Network The SaaS Vendor Management Platform chosen by over 600 of the nation s lenders and AMCs to power more than 20,000 appraisals

METHODOLOGY GUIDE VALUING MOTELS IN ONTARIO. Valuation Date: January 1, 2016

METHODOLOGY GUIDE VALUING MOTELS IN ONTARIO Valuation Date: January 1, 2016 AUGUST 2016 August 22, 2016 The Municipal Property Assessment Corporation (MPAC) is responsible for accurately assessing and

METHODOLOGY GUIDE VALUING MOTELS IN ONTARIO Valuation Date: January 1, 2016 AUGUST 2016 August 22, 2016 The Municipal Property Assessment Corporation (MPAC) is responsible for accurately assessing and

INTANGIBLE VALUE FACT OR FICTION

1 Define Intangible OUTLINE Outline Appraisal Concepts, Definitions and Issues Examine Legal Framework Examine Case Study Provoke Debate Declare Winning Argument (But the points don t matter) 2 One of

1 Define Intangible OUTLINE Outline Appraisal Concepts, Definitions and Issues Examine Legal Framework Examine Case Study Provoke Debate Declare Winning Argument (But the points don t matter) 2 One of

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330 REVIEW NOTES by CHUCK DUNN CHAPTER 20 Copyright 2010 by the Real Estate Division and Chuck Dunn. All rights reserved CHAPTER 20 - THE INCOME

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330 REVIEW NOTES by CHUCK DUNN CHAPTER 20 Copyright 2010 by the Real Estate Division and Chuck Dunn. All rights reserved CHAPTER 20 - THE INCOME

Hotel / Motel. Market Value Assessment in Saskatchewan Handbook. Hotel / Motel Valuation Guide

Market Value Assessment in Saskatchewan Handbook Hotel / Motel Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass

Market Value Assessment in Saskatchewan Handbook Hotel / Motel Saskatchewan Assessment Management Agency 2012 This document is a derivative work based upon a handbook entitled the "Market Value and Mass

86 years in the making Caspar G Haas 1922 Sales Prices as a Basis for Estimating Farmland Value

2 Our Journey Begins 86 years in the making Caspar G Haas 1922 Sales Prices as a Basis for Estimating Farmland Value Starting at the beginning. Mass Appraisal and Single Property Appraisal Appraisal

2 Our Journey Begins 86 years in the making Caspar G Haas 1922 Sales Prices as a Basis for Estimating Farmland Value Starting at the beginning. Mass Appraisal and Single Property Appraisal Appraisal

Broker. Sales Comparison, Cost Depreciation and Income Approaches. Chapter 7. Copyright Gold Coast Schools 1

Broker Chapter 7 Sales Comparison, Cost Depreciation and Income Approaches 1 Learning Objectives Describe the assumptions underlying the sales comparison approach Calculate the various adjustments necessary

Broker Chapter 7 Sales Comparison, Cost Depreciation and Income Approaches 1 Learning Objectives Describe the assumptions underlying the sales comparison approach Calculate the various adjustments necessary

Residential Evaluation Report (RER) April, 2016

April, 2016") Residential Evaluation Report (RER) ensuring compliance with the Interagency Guidelines (IAG) and USPAP April, 2016 Definitions RER shall mean a Residential Evaluation Report and is deemed to be a restricted

Residential Evaluation Report (RER) ensuring compliance with the Interagency Guidelines (IAG) and USPAP April, 2016 Definitions RER shall mean a Residential Evaluation Report and is deemed to be a restricted

TOWN OF LINCOLN COUNCIL POLICY

Page 1 of 10 PURPOSE The purpose of this policy is to prescribe the accounting treatment for tangible capital assets so that users of the financial report can discern information about the investment in

Page 1 of 10 PURPOSE The purpose of this policy is to prescribe the accounting treatment for tangible capital assets so that users of the financial report can discern information about the investment in

TANGIBLE CAPITAL ASSETS

Administrative Procedure 535 Background TANGIBLE CAPITAL ASSETS The Division will follow a prescribed procedure to record and manage the tangible capital assets (TCA) owned by the Division. The treatment

Administrative Procedure 535 Background TANGIBLE CAPITAL ASSETS The Division will follow a prescribed procedure to record and manage the tangible capital assets (TCA) owned by the Division. The treatment

Announcement March 24, 2005

Announcement 05-02 March 24, 2005 Amends these Guides: Selling Final Appraisal Report Forms Part XI: Property and Appraisal Analysis Guidelines In Lender Announcement 04-07 dated November 8, 2004, we released

Announcement 05-02 March 24, 2005 Amends these Guides: Selling Final Appraisal Report Forms Part XI: Property and Appraisal Analysis Guidelines In Lender Announcement 04-07 dated November 8, 2004, we released

General Market Analysis and Highest & Best Use. Learning Objectives

General Market Analysis and Highest & Best Use Learning Objectives Module & Title Module 1 Real Estate Markets and Analysis Module 2 Types and Levels of Market Analysis Module 3 The Six-Step Process and

General Market Analysis and Highest & Best Use Learning Objectives Module & Title Module 1 Real Estate Markets and Analysis Module 2 Types and Levels of Market Analysis Module 3 The Six-Step Process and

Appraisal Review Update: Trends and Best Practices for Lenders and Appraisers

Appraisal Review Update: Trends and Best Practices for Lenders and Appraisers Presenters: Eric Schwartz, MAI, SRA, AI-GRS Rob Moorman, MAI, SRA, AI-GRS AI Connect July 2016 Charlotte, N.C. 1 2 Meet the

Appraisal Review Update: Trends and Best Practices for Lenders and Appraisers Presenters: Eric Schwartz, MAI, SRA, AI-GRS Rob Moorman, MAI, SRA, AI-GRS AI Connect July 2016 Charlotte, N.C. 1 2 Meet the

AMERICAN SOCIETY OF APPRAISERS. Procedural Guidelines. PG-2 Valuation of Partial Ownership Interests

AMERICAN SOCIETY OF APPRAISERS Procedural Guidelines PG-2 Valuation of Partial Ownership Interests I. Preamble A. Business valuation professionals are frequently engaged as independent financial appraisers

AMERICAN SOCIETY OF APPRAISERS Procedural Guidelines PG-2 Valuation of Partial Ownership Interests I. Preamble A. Business valuation professionals are frequently engaged as independent financial appraisers

ASSESSMENT METHODOLOGY

2018 ASSESSMENT METHODOLOGY MULTI-RESIDENTIAL MANUFACTURED HOME PARK A summary of the methods used by the City of Edmonton in determining the value of multi-residential manufactured home park land properties

2018 ASSESSMENT METHODOLOGY MULTI-RESIDENTIAL MANUFACTURED HOME PARK A summary of the methods used by the City of Edmonton in determining the value of multi-residential manufactured home park land properties

Homebuyer Guide. Coldwell Banker. RIVIERA REALTY, INC

Coldwell Banker WWW.RivieraRealty.com Homebuyer Guide INC Finding and Financing A Home Made Simple Buying Your New Home When using a Coldwell Banker Riviera Realty Sales Associate, you can be confident

Coldwell Banker WWW.RivieraRealty.com Homebuyer Guide INC Finding and Financing A Home Made Simple Buying Your New Home When using a Coldwell Banker Riviera Realty Sales Associate, you can be confident

Automation for easy compliance

Three common appraisal compliance challenges: Automation for easy compliance 1-800-434-7260 Appraisals: Three compliance challenges 1. Appraiser independence requirements (AIR): There can be no pressure

Three common appraisal compliance challenges: Automation for easy compliance 1-800-434-7260 Appraisals: Three compliance challenges 1. Appraiser independence requirements (AIR): There can be no pressure

Please find attached a brief overview of our services and an informative review of Chase Group s SBA-compliant business valuation services.

THE CHASE GROUP - Business Brokers Mergers, Acquisitions, Financing & Valuation Services 41185 Golden Gate Circle, Suite 202 Murrieta, CA 92562 951.541.0414 tel 951.303.8157 fax www.chasegroup.us 2012

THE CHASE GROUP - Business Brokers Mergers, Acquisitions, Financing & Valuation Services 41185 Golden Gate Circle, Suite 202 Murrieta, CA 92562 951.541.0414 tel 951.303.8157 fax www.chasegroup.us 2012

Modeling your Appraisal Report to Meet your Client's Needs in the Commercial Marketplace

Modeling your Appraisal Report to Meet your Client's Needs in the Commercial Marketplace Myth #1 The Final Estimate of Value is the Only Area of the Report Anyone Reads Financial Institutions -Interagency

Modeling your Appraisal Report to Meet your Client's Needs in the Commercial Marketplace Myth #1 The Final Estimate of Value is the Only Area of the Report Anyone Reads Financial Institutions -Interagency

Anatomy Of An Appraisal

Anatomy Of An Appraisal Leslie A. Fields The most important thing to know about an appraisal report is how to review and critique it. Leslie A. Fields a partner with the Law Firm of Faegre & Benson LLP,

Anatomy Of An Appraisal Leslie A. Fields The most important thing to know about an appraisal report is how to review and critique it. Leslie A. Fields a partner with the Law Firm of Faegre & Benson LLP,

Basic Appraisal Procedures

Hondros Learning Basic Appraisal Procedures Timed Outline Topic Area Reference(s) Learning Objectives The student will be able to identify and/or apply: Teaching Method Time Segment (Minutes) Day 1 Chapter

Hondros Learning Basic Appraisal Procedures Timed Outline Topic Area Reference(s) Learning Objectives The student will be able to identify and/or apply: Teaching Method Time Segment (Minutes) Day 1 Chapter

Certificate in Commercial Real Estate

Certificate in Commercial Real Estate Duration: 9 months Price: 1,465 + VAT (members), 1,745 + VAT (non-members) Course Summary Commercial real estate serves a vast array of purposes, supporting public

Certificate in Commercial Real Estate Duration: 9 months Price: 1,465 + VAT (members), 1,745 + VAT (non-members) Course Summary Commercial real estate serves a vast array of purposes, supporting public

Part 2. Measures of Central Tendency: Mean, Median, and Mode

Table of Contents Overview... vii Schedule... xi SECTION 1 Introduction... 1 Part 1. Introduction to Statistics Preview Part 1... 3 Why Is Knowledge of Statistics Useful to the Appraiser?... 5 How Does

Table of Contents Overview... vii Schedule... xi SECTION 1 Introduction... 1 Part 1. Introduction to Statistics Preview Part 1... 3 Why Is Knowledge of Statistics Useful to the Appraiser?... 5 How Does

Introducing Transparency and Rationality into the Home Buying Process A RESNET Policy Proposal October 2013

Introducing Transparency and Rationality into the Home Buying Process A RESNET Policy Proposal October 2013 Published by: Residential Energy Services Network, Inc. http://resnet.us Copyright, Residential

Introducing Transparency and Rationality into the Home Buying Process A RESNET Policy Proposal October 2013 Published by: Residential Energy Services Network, Inc. http://resnet.us Copyright, Residential

Index of Examples. Chapter 1 Letter of Transmittal Chapter 2 General Assumptions and Limiting Conditions... 19

Index of Examples Chapter 1 Letter of Transmittal... 1 Example 1A Detailed Letter of Transmittal... 2 Example 1B Detailed Letter of Transmittal with Risk Factors and Assumptions... 6 Example 1C Brief Letter

Index of Examples Chapter 1 Letter of Transmittal... 1 Example 1A Detailed Letter of Transmittal... 2 Example 1B Detailed Letter of Transmittal with Risk Factors and Assumptions... 6 Example 1C Brief Letter

Land, Agricultural Improvements, CAFO, Rural Residence, Farm

*--FSA Appraisal Guidelines Land, Agricultural Improvements, CAFO, Rural Residence, Farm The following information elements and content descriptions are provided as guidelines to assist lenders and appraisers

*--FSA Appraisal Guidelines Land, Agricultural Improvements, CAFO, Rural Residence, Farm The following information elements and content descriptions are provided as guidelines to assist lenders and appraisers

October 1, Mr. Wayne Miller, Chair Appraiser Qualifications Board The Appraisal Foundation th Street, NW, Suite 1111 Washington, DC 20005

October 1, 2015 Mr. Wayne Miller, Chair Appraiser Qualifications Board The Appraisal Foundation 1155 15th Street, NW, Suite 1111 Washington, DC 20005 Dear Mr. Miller, I am honored to have the opportunity

October 1, 2015 Mr. Wayne Miller, Chair Appraiser Qualifications Board The Appraisal Foundation 1155 15th Street, NW, Suite 1111 Washington, DC 20005 Dear Mr. Miller, I am honored to have the opportunity

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330 REVIEW NOTES by CHUCK DUNN CHAPTER 16 Copyright 2010 by the Real Estate Division and Chuck Dunn. All rights reserved CHAPTER 16 - LAND AND SITE

THE APPRAISAL OF REAL ESTATE 3 RD CANADIAN EDITION BUSI 330 REVIEW NOTES by CHUCK DUNN CHAPTER 16 Copyright 2010 by the Real Estate Division and Chuck Dunn. All rights reserved CHAPTER 16 - LAND AND SITE

Retail Properties: Characteristics and Analysis Clifford J. Bogart CCIM. Welcome to Today s Simulcast!

Welcome to Today s Simulcast! Please Note: Remember to sign in (and don t forget to sign out)! Sit as close to the front as possible in the assigned seating area. Read and sign MetroTex Course Policies

Welcome to Today s Simulcast! Please Note: Remember to sign in (and don t forget to sign out)! Sit as close to the front as possible in the assigned seating area. Read and sign MetroTex Course Policies

H.K.Bentley, APPRAISERS MARYLAND VIRGINIA DISTRICT OF COLUMBIA WEST VIRGINIA DELAWARE NEVADA NATIONALLY THROUGH OUR SISTER COMPANY, BENTLEY NATIONAL

H.K. BENTLEY R E A L E S T A T E A P P R A I S E R S H.K.Bentley, APPRAISERS MARYLAND VIRGINIA DISTRICT OF COLUMBIA WEST VIRGINIA DELAWARE NEVADA NATIONALLY THROUGH OUR SISTER COMPANY, BENTLEY NATIONAL

H.K. BENTLEY R E A L E S T A T E A P P R A I S E R S H.K.Bentley, APPRAISERS MARYLAND VIRGINIA DISTRICT OF COLUMBIA WEST VIRGINIA DELAWARE NEVADA NATIONALLY THROUGH OUR SISTER COMPANY, BENTLEY NATIONAL

Canadian Standards and Quality Valuations an AIC Advantage. Dan Brewer AACI, P. App AIC President

1 Canadian Standards and Quality Valuations an AIC Advantage Dan Brewer AACI, P. App AIC President 2 Canadian Uniform Standards of Professional Appraisal Practice - CUSPAP AIC has published CUSPAP for

1 Canadian Standards and Quality Valuations an AIC Advantage Dan Brewer AACI, P. App AIC President 2 Canadian Uniform Standards of Professional Appraisal Practice - CUSPAP AIC has published CUSPAP for

WALLER COUNTY APPRAISAL DISTRICT MASS APPRAISAL REPORT APPRAISAL YEAR 2018

WALLER COUNTY APPRAISAL DISTRICT MASS APPRAISAL REPORT APPRAISAL YEAR 2018 ADDENDUM TO WCAD REAPPRAISAL PLAN FOR 2017 AND 2018 WALLER COUNTY APPRAISAL DISTRICT Uniform Standards of Professional Appraisal

WALLER COUNTY APPRAISAL DISTRICT MASS APPRAISAL REPORT APPRAISAL YEAR 2018 ADDENDUM TO WCAD REAPPRAISAL PLAN FOR 2017 AND 2018 WALLER COUNTY APPRAISAL DISTRICT Uniform Standards of Professional Appraisal

Re: Request for Comments on Proposal to Increase the Real Estate Appraisal Threshold

Sharon L. Whitaker, Vice President Commercial Real Estate & Finance Mortgage Markets, Financial Management & Public Policy (202) 663-5321 SWhitaker@aba.com Ann E. Misback, Secretary, Board of Governors

Sharon L. Whitaker, Vice President Commercial Real Estate & Finance Mortgage Markets, Financial Management & Public Policy (202) 663-5321 SWhitaker@aba.com Ann E. Misback, Secretary, Board of Governors

Direct Capital Value Comparison (Sales Comparison Approach)

") 1. Introduction: It is the commonly used method and most accurate It is frequently used in the valuation of residential property for sale purpose and rental valuation for commercial properties. Require

1. Introduction: It is the commonly used method and most accurate It is frequently used in the valuation of residential property for sale purpose and rental valuation for commercial properties. Require

Proving Depreciation

Institute for Professionals in Taxation 40 th Annual Property Tax Symposium Tucson, Arizona Proving Depreciation Presentation Concepts and Content: Kathy G. Spletter, ASA Stancil & Co. Irving, Texas kathy.spletter@stancilco.com

Institute for Professionals in Taxation 40 th Annual Property Tax Symposium Tucson, Arizona Proving Depreciation Presentation Concepts and Content: Kathy G. Spletter, ASA Stancil & Co. Irving, Texas kathy.spletter@stancilco.com

How to Read a Real Estate Appraisal Report

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

An Examination of Potential Changes in Ratio Measurements Historical Cost versus Fair Value Measurement in Valuing Tangible Operational Assets

An Examination of Potential Changes in Ratio Measurements Historical Cost versus Fair Value Measurement in Valuing Tangible Operational Assets Pamela Smith Baker Texas Woman s University A fictitious property

An Examination of Potential Changes in Ratio Measurements Historical Cost versus Fair Value Measurement in Valuing Tangible Operational Assets Pamela Smith Baker Texas Woman s University A fictitious property

2. The, and Act, also known as FIRREA, requires that states set standards for all appraisers.

CHAPTER 4 SHORT-ANSWER QUESTIONS 1. An appraisal is an or of value. 2. The, and Act, also known as FIRREA, requires that states set standards for all appraisers. 3. Value in real estate is the "present

CHAPTER 4 SHORT-ANSWER QUESTIONS 1. An appraisal is an or of value. 2. The, and Act, also known as FIRREA, requires that states set standards for all appraisers. 3. Value in real estate is the "present

Mass Appraisal of Income-Producing Properties

Chapter 10 Mass Appraisal of Income-Producing Properties Whether valuing income-producing property or residential property, you can use similar information and methods for collecting and analyzing data

Chapter 10 Mass Appraisal of Income-Producing Properties Whether valuing income-producing property or residential property, you can use similar information and methods for collecting and analyzing data

The Financial Accounting Standards Board

V A L U A T I O N How the New Leases Standard May Impact Business Valuations By Judith H. O Dell, CPA, CVA The Financial Accounting Standards Board issued the 485 page Leases Standard (Topic 842) in February,

V A L U A T I O N How the New Leases Standard May Impact Business Valuations By Judith H. O Dell, CPA, CVA The Financial Accounting Standards Board issued the 485 page Leases Standard (Topic 842) in February,

Guide to Appraisal Reports

Guide to Appraisal Reports What is an appraisal? An appraisal is an independent valuation of real property prepared by a qualified Appraiser and fully documented in a report. Based on a series of appraisal

Guide to Appraisal Reports What is an appraisal? An appraisal is an independent valuation of real property prepared by a qualified Appraiser and fully documented in a report. Based on a series of appraisal

Chapter 6: Auto and RV Dealership Asset Valuation (Equipment)

") Chapter 6: Auto and RV Dealership Asset Valuation (Equipment) Knowing how much the dealership s furniture, fixtures and equipment are worth will determine the amount of goodwill that is being paid as part

Chapter 6: Auto and RV Dealership Asset Valuation (Equipment) Knowing how much the dealership s furniture, fixtures and equipment are worth will determine the amount of goodwill that is being paid as part

Guide Note 15 Assumptions and Hypothetical Conditions

Guide Note 15 Assumptions and Hypothetical Conditions Introduction Appraisal and review opinions are often premised on certain stated conditions. These include assumptions (general, and special or extraordinary)

Guide Note 15 Assumptions and Hypothetical Conditions Introduction Appraisal and review opinions are often premised on certain stated conditions. These include assumptions (general, and special or extraordinary)

Appraisal Review: Analyzing the 1004

Appraisal Review: Analyzing the 1004 1 LIVE ONLINE PARTICIPANT GUIDE Version: 8.12 Table of Contents The Purpose of the Appraisal... 3 Define Market Value... 3 Scenario 1 (John Johnson report) - 1004 Uniform

Appraisal Review: Analyzing the 1004 1 LIVE ONLINE PARTICIPANT GUIDE Version: 8.12 Table of Contents The Purpose of the Appraisal... 3 Define Market Value... 3 Scenario 1 (John Johnson report) - 1004 Uniform

A Demonstration Appraisal Report. Of a. Located at. Date of Appraisal. Prepared for. Prepared by

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 West 10 th Street Kansas

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 West 10 th Street Kansas

Core Element 6 Appropriate Regulation

Core Element 6 Appropriate Regulation While this crisis had many causes, it is clear now that the government could have done more to prevent many of these problems from growing out of control and threatening

Core Element 6 Appropriate Regulation While this crisis had many causes, it is clear now that the government could have done more to prevent many of these problems from growing out of control and threatening

Proposed New Accounting Standards For Leases

Relationships backed by performance. Proposed New Accounting Standards For Leases Doug Richardson Live Seminar 9:00am 10:30am June 21 2012 Overview and Background Leases serve a vital role in many entities

Relationships backed by performance. Proposed New Accounting Standards For Leases Doug Richardson Live Seminar 9:00am 10:30am June 21 2012 Overview and Background Leases serve a vital role in many entities

Appraiser Qualifications Board. Real Property Appraiser Qualification Criteria Interpretation Changing a Credential

Appraiser Qualifications Board Appraiser Qualifications Board Real Property Appraiser Qualification Criteria Interpretation Changing a Credential This communication is for the purpose of issuing an Interpretation

Appraiser Qualifications Board Appraiser Qualifications Board Real Property Appraiser Qualification Criteria Interpretation Changing a Credential This communication is for the purpose of issuing an Interpretation

Land Value Estimates and Forecasts for Reston. Prepared for Reston Community Center April 2013

Land Value Estimates and Forecasts for Reston Prepared for Reston Community Center April 2013 LAND VALUE ESTIMATES AND FORECASTS FOR RESTON COMMUNITY CENTER Purpose of the Analysis RCLCO (Robert Charles

Land Value Estimates and Forecasts for Reston Prepared for Reston Community Center April 2013 LAND VALUE ESTIMATES AND FORECASTS FOR RESTON COMMUNITY CENTER Purpose of the Analysis RCLCO (Robert Charles

AMC Track Presentation Austin Christensen Founder & CCO - Validox. Appraisal Manager Compliance Techniques

AMC Track Presentation Austin Christensen Founder & CCO - Validox Appraisal Manager Compliance Techniques Who Is An Appraisal Manager? 1. Staff at an Appraisal Management Company 2. Chief Appraiser 3.

AMC Track Presentation Austin Christensen Founder & CCO - Validox Appraisal Manager Compliance Techniques Who Is An Appraisal Manager? 1. Staff at an Appraisal Management Company 2. Chief Appraiser 3.

Lease accounting 2019 IFRS and US GAAP Preparing for a smooth landing

Lease accounting 2019 IFRS and US GAAP Preparing for a smooth landing What s next? Q4 2017 Summary As you may already be aware, the accounting standards for lease accounting will change. This means that

Lease accounting 2019 IFRS and US GAAP Preparing for a smooth landing What s next? Q4 2017 Summary As you may already be aware, the accounting standards for lease accounting will change. This means that

RESIDUAL ANALYSIS PRINCIPLES AND PROCEEDURES

RESIDUAL ANALYSIS PRINCIPLES AND PROCEEDURES OVERVIEW 1. Residual analysis or extractions, are a form of land valuation study. 2. This analysis relies on the improved sales (typically the largest group

RESIDUAL ANALYSIS PRINCIPLES AND PROCEEDURES OVERVIEW 1. Residual analysis or extractions, are a form of land valuation study. 2. This analysis relies on the improved sales (typically the largest group

AVM Validation. Evaluating AVM performance

AVM Validation Evaluating AVM performance The responsible use of Automated Valuation Models in any application begins with a thorough understanding of the models performance in absolute and relative terms.

AVM Validation Evaluating AVM performance The responsible use of Automated Valuation Models in any application begins with a thorough understanding of the models performance in absolute and relative terms.

2018 SCCAI RESIDENTIAL SYMPOSIUM USPAP OF THE FUTURE. Paula Konikoff, JD, MAI, AI GRS

USPAP OF THE FUTURE Paula Konikoff, JD, MAI, AI GRS WHERE WE ARE NOW 2 Joint task force for Improvement of USPAP Appraisal Institute and Appraisal Foundation develop USPAP Optimization Concept 3 When unnecessary

USPAP OF THE FUTURE Paula Konikoff, JD, MAI, AI GRS WHERE WE ARE NOW 2 Joint task force for Improvement of USPAP Appraisal Institute and Appraisal Foundation develop USPAP Optimization Concept 3 When unnecessary

FOR SALE: 1236 White Oaks

FOR SALE: 1236 White Oaks free standing retail bldg Confidential This confidential ( Memorandum ) is being given to you for the sole purpose of evaluating the possible purchase of 1236 White Oaks, Campbell,

FOR SALE: 1236 White Oaks free standing retail bldg Confidential This confidential ( Memorandum ) is being given to you for the sole purpose of evaluating the possible purchase of 1236 White Oaks, Campbell,

Sales Associate Course

Sales Associate Course Chapter Seventeen Real Estate Investments and Business Opportunity Brokerage 1 Investment Analysis Most important consideration: Economic soundness Land use controls Zoning Deed

Sales Associate Course Chapter Seventeen Real Estate Investments and Business Opportunity Brokerage 1 Investment Analysis Most important consideration: Economic soundness Land use controls Zoning Deed

San Patricio County Appraisal District. Reappraisal Plan For. Tax Years 2013 & 2014

San Patricio County Appraisal District Reappraisal Plan For Tax Years 2013 & 2014 (adopted by SPCAD Board of Directors on September 11 th, 2012) 1 TABLE OF CONTENTS ITEM PAGE Executive Summary 4 Revaluation

San Patricio County Appraisal District Reappraisal Plan For Tax Years 2013 & 2014 (adopted by SPCAD Board of Directors on September 11 th, 2012) 1 TABLE OF CONTENTS ITEM PAGE Executive Summary 4 Revaluation

Streamlining Appraisal Services in Encompass

Streamlining Appraisal Services in Encompass A Checklist For Choosing The Most Integrated Partner Ellie Mae's Encompass(r) Digital Mortgage Management Solution is used by lenders across the country to

Streamlining Appraisal Services in Encompass A Checklist For Choosing The Most Integrated Partner Ellie Mae's Encompass(r) Digital Mortgage Management Solution is used by lenders across the country to

Exposure Draft 64 January 2018 Comments due: June 30, Proposed International Public Sector Accounting Standard. Leases

Exposure Draft 64 January 2018 Comments due: June 30, 2018 Proposed International Public Sector Accounting Standard Leases This document was developed and approved by the International Public Sector Accounting

Exposure Draft 64 January 2018 Comments due: June 30, 2018 Proposed International Public Sector Accounting Standard Leases This document was developed and approved by the International Public Sector Accounting

RPR Product Overview RPR National Property Data Sets Reporting Features... 3

Table of Contents RPR Product Overview... 2 RPR National Property Data Sets... 3 Reporting Features... 3 Features only available with MLS/CIE data included in RPR... 4 Why Include MLS/CIE Data into RPR?...

Table of Contents RPR Product Overview... 2 RPR National Property Data Sets... 3 Reporting Features... 3 Features only available with MLS/CIE data included in RPR... 4 Why Include MLS/CIE Data into RPR?...

D DAVID PUBLISHING. Mass Valuation and the Implementation Necessity of GIS (Geographic Information System) in Albania

in Albania") Journal of Civil Engineering and Architecture 9 (2015) 1506-1512 doi: 10.17265/1934-7359/2015.12.012 D DAVID PUBLISHING Mass Valuation and the Implementation Necessity of GIS (Geographic Elfrida Shehu

Journal of Civil Engineering and Architecture 9 (2015) 1506-1512 doi: 10.17265/1934-7359/2015.12.012 D DAVID PUBLISHING Mass Valuation and the Implementation Necessity of GIS (Geographic Elfrida Shehu

PRIVATE ANNUITY AGREEMENT

PRIVATE ANNUITY AGREEMENT FOR FINANCIAL PROFESSIONAL USE ONLY-NOT FOR PUBLIC DISTRIBUTION. Specimen documents are made available for educational purposes only. This specimen form may be given to a client

PRIVATE ANNUITY AGREEMENT FOR FINANCIAL PROFESSIONAL USE ONLY-NOT FOR PUBLIC DISTRIBUTION. Specimen documents are made available for educational purposes only. This specimen form may be given to a client

Practice Valuations. Welcome To The Digital Learning Center. Today s Presentation. Course Faculty. Presented by. What s Your Practice Worth?

Welcome To The Digital Learning Center Presented by Your Partner In Building High Performance Practices Today s Presentation Practice Valuations What s Your Practice Worth? Course Faculty R. Thomas (Tom)

Welcome To The Digital Learning Center Presented by Your Partner In Building High Performance Practices Today s Presentation Practice Valuations What s Your Practice Worth? Course Faculty R. Thomas (Tom)

Table of Contents SECTION 1. Overview... ix. Course Schedule... xiii. Introduction. Part 1. Introduction to the Income Capitalization Approach

Table of Contents Overview... ix Course Schedule... xiii SECTION 1 Introduction Part 1. Introduction to the Income Capitalization Approach Preview Part 1... 1 Market Value... 3 Anticipation and Other Relevant

Table of Contents Overview... ix Course Schedule... xiii SECTION 1 Introduction Part 1. Introduction to the Income Capitalization Approach Preview Part 1... 1 Market Value... 3 Anticipation and Other Relevant

The Evolution of the AVM

The Evolution of the AVM William E. King Veros Real Estate Solutions Director of Valuation Initiatives AVMs as we know them today were introduced in the 1990s, but the birth of the computer-generated valuation

The Evolution of the AVM William E. King Veros Real Estate Solutions Director of Valuation Initiatives AVMs as we know them today were introduced in the 1990s, but the birth of the computer-generated valuation

NDS offers a single source Default Services Company with SSAE16 nationwide.

ABOUT NDS Internally managing a default or REO portfolio can be challenging. Identifying, retaining and coordinating the activities of various attorneys, trustees, real estate agents and title companies

ABOUT NDS Internally managing a default or REO portfolio can be challenging. Identifying, retaining and coordinating the activities of various attorneys, trustees, real estate agents and title companies

Chapter 3 Business Valuation Report

CHAPTER 3: BUSINESS VALUATION REPORT Chapter 3 Business Valuation Report A1. Pre-IPO Valuation Need Company Restructuring and Financing It is not unusual that companies undergo series of restructuring

CHAPTER 3: BUSINESS VALUATION REPORT Chapter 3 Business Valuation Report A1. Pre-IPO Valuation Need Company Restructuring and Financing It is not unusual that companies undergo series of restructuring

An Introduction to RPX INTRODUCTION

An Introduction to RPX INTRODUCTION Radar Logic is a real estate information company based in New York. We convert public residential closing data into information about the state and prospects for the

An Introduction to RPX INTRODUCTION Radar Logic is a real estate information company based in New York. We convert public residential closing data into information about the state and prospects for the

Table of Contents. Chapter 1: Introduction (Mobile Technology Evolution) 1

1") Chapter 1: Introduction (Mobile Technology Evolution) 1 I. WHY APPRAISAL IS IMPORTANT (p. 3) II. DEFINITION OF APPRAISAL (p. 4) A. Opinion (p. 4) B. Value (p. 5) C. Appraisal Art or Science? (p. 5) D.

Chapter 1: Introduction (Mobile Technology Evolution) 1 I. WHY APPRAISAL IS IMPORTANT (p. 3) II. DEFINITION OF APPRAISAL (p. 4) A. Opinion (p. 4) B. Value (p. 5) C. Appraisal Art or Science? (p. 5) D.

Assessment and Taxation Department Service de l évaluation et des taxes VALUATION OF HOTELS General Assessment

Assessment and Taxation Department Service de l évaluation et des taxes VALUATION OF HOTELS 2012 General Assessment City of Winnipeg Assessment and Taxation Department May 4, 2011 TABLE OF CONTENTS INTRODUCTION...

Assessment and Taxation Department Service de l évaluation et des taxes VALUATION OF HOTELS 2012 General Assessment City of Winnipeg Assessment and Taxation Department May 4, 2011 TABLE OF CONTENTS INTRODUCTION...

For legal reasons, we cannot and will not respond to messages asking for more information about a property.

About Us About Our Company USA-Foreclosure.com is the nation s largest non-subscription based Web site publicizing property scheduled for foreclosure auction. The site serves as a reliable source for those

About Us About Our Company USA-Foreclosure.com is the nation s largest non-subscription based Web site publicizing property scheduled for foreclosure auction. The site serves as a reliable source for those

ASSESSMENT METHODOLOGY

2019 ASSESSMENT METHODOLOGY COMMERCIAL RETAIL AND OFFICE CONDOMINIUMS A summary of the methods used by the City of Edmonton in determining the value of commercial retail and office condominium properties

2019 ASSESSMENT METHODOLOGY COMMERCIAL RETAIL AND OFFICE CONDOMINIUMS A summary of the methods used by the City of Edmonton in determining the value of commercial retail and office condominium properties

What Raters Need To Know About Appraisals

What Raters Need To Know About Appraisals Presented by: Sandra K. Adomatis, SRA, LEED Green Associate, NAR GREEN RESNET 2018 Conference February 27, 2018 4:00 pm 5:30 pm Copyright 2018 Sandra K. Adomatis

What Raters Need To Know About Appraisals Presented by: Sandra K. Adomatis, SRA, LEED Green Associate, NAR GREEN RESNET 2018 Conference February 27, 2018 4:00 pm 5:30 pm Copyright 2018 Sandra K. Adomatis

BOARD OF ZONING ADJUSTMENT STAFF REPORT Date: April 1, 2019

BOARD OF ZONING ADJUSTMENT STAFF REPORT Date: April 1, 2019 CASE NUMBER 6248/5842 APPLICANT NAME LOCATION VARIANCE REQUEST ZONING ORDINANCE REQUIREMENT ZONING AREA OF PROPERTY ENGINEERING COMMENTS TRAFFIC

BOARD OF ZONING ADJUSTMENT STAFF REPORT Date: April 1, 2019 CASE NUMBER 6248/5842 APPLICANT NAME LOCATION VARIANCE REQUEST ZONING ORDINANCE REQUIREMENT ZONING AREA OF PROPERTY ENGINEERING COMMENTS TRAFFIC

Creating Reliable Valuations

Two Case Studies Creating Reliable Valuations Mark Polon, CCIM Polon Consulting www.polonconsulting.com

Two Case Studies Creating Reliable Valuations Mark Polon, CCIM Polon Consulting www.polonconsulting.com

COMPLETE GUIDE TO BUYING A HOME IN SAN ANTONIO

COMPLETE GUIDE TO BUYING A HOME IN SAN ANTONIO Buying a home is a big deal. While the process is exciting, it can also be overwhelming. At KW Portfolio we are committed to making sure buyers have all the

COMPLETE GUIDE TO BUYING A HOME IN SAN ANTONIO Buying a home is a big deal. While the process is exciting, it can also be overwhelming. At KW Portfolio we are committed to making sure buyers have all the

A 1: It( SPECIFIC ITEMS SECTION 3061 property, plant and equipment. Additional Resources. Page 1 of6. Knotia - CICA Handbook - Accounting A2-14

'" Knotia - CICA Handbook - Accounting»Accounting»Accounting Handbook»Accounting Standards»Specific items [Sections 3000-3870]»3061 - Property, Plant and Eauipment Page 1 of6 A 1: It( A2-14 SPECIFIC ITEMS

'" Knotia - CICA Handbook - Accounting»Accounting»Accounting Handbook»Accounting Standards»Specific items [Sections 3000-3870]»3061 - Property, Plant and Eauipment Page 1 of6 A 1: It( A2-14 SPECIFIC ITEMS

Collateral Risk Network. The Language of Data. April Elizabeth Green

Collateral Risk Network April 2012 www.rel-e-vant.com The Language of Data Elizabeth Green 1 2 CRN April 2012 Appraisal Prose? I came to explore the wreck. The words are purposes. The words are maps. I

Collateral Risk Network April 2012 www.rel-e-vant.com The Language of Data Elizabeth Green 1 2 CRN April 2012 Appraisal Prose? I came to explore the wreck. The words are purposes. The words are maps. I

Capital Layer Evaluations: Hotels and More

Peer-Reviewed Article Capital Layer Evaluations: Hotels and More by Tom Troll Abstract Historically, the valuation of hotels, nursing homes, and other types of complex properties has been constrained because

Peer-Reviewed Article Capital Layer Evaluations: Hotels and More by Tom Troll Abstract Historically, the valuation of hotels, nursing homes, and other types of complex properties has been constrained because

Tax Strategies for Purchasing Going Concern Properties

Pre-closing Purchase Price Allocations Tax Strategies for Purchasing Going Concern Properties Innovative Solutions to Taxing Problems Tax Strategies for Purchasing Going Concern Properties When a business,

Pre-closing Purchase Price Allocations Tax Strategies for Purchasing Going Concern Properties Innovative Solutions to Taxing Problems Tax Strategies for Purchasing Going Concern Properties When a business,

Sales Associate Course

Sales Associate Course Chapter Sixteen Appraisal 1 2 Appraiser Specific amount Impartial (non biased) Defendable Estimate (Opinion) of value Fee based on time and difficulty Must follow Uniform Standards

Sales Associate Course Chapter Sixteen Appraisal 1 2 Appraiser Specific amount Impartial (non biased) Defendable Estimate (Opinion) of value Fee based on time and difficulty Must follow Uniform Standards

DIRECTIVE # This Directive Supersedes Directive # and #92-003

Division Of Property Valuation Docking State Office Building 915 SW Harrison St., Room 400N Topeka, KS 66612-1588 Nick Jordan, Secretary David N. Harper, Director phone: 785-296-2365 fax: 785-296-2320

Division Of Property Valuation Docking State Office Building 915 SW Harrison St., Room 400N Topeka, KS 66612-1588 Nick Jordan, Secretary David N. Harper, Director phone: 785-296-2365 fax: 785-296-2320

Part 1. Estimating Land Value Using a Land Residual Technique Based on Discounted Cash Flow Analysis

Table of Contents Overview... v Seminar Schedule... ix SECTION 1 Part 1. Estimating Land Value Using a Land Residual Technique Based on Discounted Cash Flow Analysis Preview Part 1... 1 Land Residual Technique...

Table of Contents Overview... v Seminar Schedule... ix SECTION 1 Part 1. Estimating Land Value Using a Land Residual Technique Based on Discounted Cash Flow Analysis Preview Part 1... 1 Land Residual Technique...