This Land is Your Land on the Balance Sheet. FASAB Research and Findings of the Accounting and Reporting of Government Land Project

|

|

|

- James McCarthy

- 5 years ago

- Views:

Transcription

1 This Land is Your Land on the Balance Sheet. FASAB Research and Findings of the Accounting and Reporting of Government Land Project American Society of Military Comptrollers (ASMC) San Diego, PDI 2 June 2017 Presenters: Domenic Savini and Bobby Hart

2 Disclaimer Views expressed are those of the speakers. The Board expresses its views in official publications. Roles on Task Force Dom FASAB Representative Bobby Industry Representative 1

3 What is Land? Grand Canyon, All Rights Reserved - 2

4 What is Land? Intangible IUS Immobile Land Mobile (x) Tangible (y) Real Property Building Structures Linear Structures Personal Property Watercraft Electronic Systems Helicopters Tanks Servers Manufacturing Equipment IT Equipment Office Furniture Operating Materials & Consumable Supplies Inventory Held for Sale Stockpile Pre-positioned Stock Raw Materials or work in process Paper Towels Pens Printer Toner x Axis y Axis Portability Tangibility 3

5 How Does FASAB Define Land? Land is the solid part of the surface of the earth Currently, we have 2 buckets to categorize land: SFFAS 6: General Property, Plant, and Equipment (GPP&E) Land, and SFFAS 29: Stewardship Land What assets are excluded from the land : Natural resources that are depletable such as mineral deposits and petroleum; Renewable resources such as timber, and the outer-continental shelf resources related to land. 4

6 How Do We Account for Land Now? 2 Buckets SFFAS 6 requires that land and land rights acquired for or in connection with other general PP&E are to be capitalized at the cost incurred to bring the assets to a form and condition suitable for use. SFFAS 29 defines stewardship land as land other than land acquired for or in connection with other general PP&E. It requires note disclosures regarding policies for managing land, categories of land, and physical quantity information. It is important to note that stewardship land is expensed when acquired; that is, no asset dollar amount shown on balance sheet. 5

7 How Much Land Do We Manage? 6

8 Where is Bulk of Land Located? 7

Relinquishments by Colonies Ceded by other")

9 How Did We Acquire Land? Source: GAO Speaker Series, Public Lands Foundation, America s Public Lands, Origins, History, and Future. April 7, 2016 Acquisition Era 1780s-1860s Native American Cession (1763 French & Indian War) Relinquishments by Colonies Ceded by other Countries Purchases 8

10 How Did We Acquire Land? Acquisition Area Land Water Total Acres Acres Acres Percentage of U.S. Land State Cessions ( ) 233,415,680 3,409, ,825, % $ 6,200,000 (c) Louisiana Purchase (1803) (d) 523,446,400 6,465, ,911, % $23,213,568 Red River Basin ( ) 29,066, ,040 29,601, % $ - Cession from Spain (1819) 43,342,720 2,801,920 46,144, % $ 6,674,057 Oregon Compromise (1846) 180,644,480 2,741, ,386, % $ - Mexican Cession (1848) 334,479,360 4,201, ,680, % $16,295,149 Purchase from Texas (1850) 78,842,880 83,840 78,926, % $15,496,448 Gadsden Purchase (1853) 18,961,920 26,880 18,988, % $10,000,000 Alaska Purchase (1867) 365,333,120 12,909, ,242, % $ 7,200,000 Total Public Domain 1,807,533,440 33,175,680 1,840,709, % $85,079,222 (a) Cost (b) 9

11 FASAB Land Projects Goal Our Goal - To improve the accounting and reporting for land so that information needed to meet the reporting objectives and qualitative characteristics is provided while meeting the costbenefit constraints. 10

12 FASAB Ground Rules SFFAC 1 Objectives of Federal Financial Reporting Uncle Sam is the BOSS!! Budgetary Integrity support of budget process; linking accounting and budgeting Operating Performance more meaningful data; cost/benefit and performance data Stewardship improved accountability of resources Systems and Control cost effective systems and controls Note: 64% of Task Force said we needed to enhance Land reporting relative to the BOSS. 11

13 FASAB Ground Rules SFFAC 1 Qualitative Characteristics Uncle Sam requires proper attire!! To be effective, communicating financial information in financial reports must have these 6 basic characteristics: 1. Understandability 2. Reliability 3. Relevance 4. Timeliness 5. Consistency 6. Comparability Note: 67% of Task Force said we needed to enhance Land reporting relative to the qualitative characteristics. 12

14 Land Task Force Role To serve as expert advisors that: Provide information Identify issues & alternative solutions Validate options Consensus is not required Open, intellectually-honest dialogue, and balanced viewpoints will guide our work 13

15 Project History & Timeline Staff expects that the Board will develop and expose guidance in calendar year 2017, finalizing the Statement during the early part of calendar year 2018 as follows: July 2016 Task force to reviewed results of agency one-on-on meetings and land-use categories developed by staff August 2016 April 2017 Further developed nonfinancial (for example, acreage) reporting recommendations Identified most appropriate reporting venue for nonfinancial information (for example, Basic, RSI, or OAI) Further developed measurement and recognition recommendations Began developing draft exposure draft May 2017 August 2017 Finalize and issue exposure draft December 2017 April 2018 Finalize guidance or standards 14

16 Is Land Really an Asset? SFFAC 5, Par. 22 To be an asset of the federal government, a resource must possess two characteristics: First, it embodies economic benefits or services that can be used in the future. Second, the government controls access to the economic benefits or services and, therefore, can obtain them and deny or regulate the access of other entities. 15

17 Is Land Really an Asset? Assets are expected to provide benefits that outweigh costs. SFFAC 1, Par. 64. Expected benefits often are not cash inflows but rather are the services provided by the asset. Assets & liabilities are allocations of the cost of past transactions based on assumptions about future benefit and sacrifice. SFFAC 1, Par An asset is a resource that embodies economic benefits or services that the federal government controls. Meeting the basic recognition criteria is a necessary but not a sufficient condition for recognition. Additional considerations for a recognition decision are measurement of the candidate for recognition and assessments of the materiality and benefit versus cost of the amount measured. SFFAC 5 16

18 Government-Wide Reporting 17

19 What Does GPP&E Land Look Like Government-Wide? page

20 2015 GSA FRPP* Profile for GPP&E Land = 49.6M Acres Total DOE 4% DOI 13% % of Total Acres DoD 81% DoD USDA Commerce DOE HHS DHS DOJ Labor State DOI Treasury DOT VA EPA GSA NASA NSF DoD 81.26% DOI 12.66% DOE 4.44% NASA 0.38% DOT 0.31% USDA 0.28% State 0.24% DHS 0.15% DOJ 0.10% VA 0.08% Commerce 0.04% Labor % HHS % GSA % NSF % EPA % Treasury % *GSA FRPP General Service Administration s Federal Real Property Profile 19

21 Stewardship vs. GPP&E Federal Land by Acreage (in Millions) Stewardship G-PP&E 20

22 What Does Stewardship Land Look Like Government-Wide? pages 71 and

23 Stewardship Land Comparison of Same Departments/Agencies What Do They Count? DOI (Selected) Federal Water and Related Projects National Wildlife Refuges National Fish Hatcheries National Parks USDA (Selected) National Grasslands National Forests National Preserves VA Cemeteries Archaeological Sites DoD Archaeological Sites HHS Indian Trust Land EPA Superfund Sites None or None Listed Separately By Type DOE NASA State DHS DOJ Commerce Labor GSA NSF Treasury 22

24 Agency financial reporting Illustrative Examples From FY 2014 Excerpts 23

25 What Does GPP&E Land Look Like at an Agency? Source: U.S. Army Corps of Engineers, AFR 2014, page

26 What Does GPP&E Land Look Like at an Agency? Source: U.S. Department of Energy, AFR2104, pages 49 and

27 What Does GPP&E Land Look Like at an Agency? Source: U.S. Department of the Interior, AFR 2014, page

28 What Does Stewardship Land Look Like at an Agency? Source: U.S. Department of Agriculture, AFR 2014, pages 105 and 107, respectively. 27

29 What Does Stewardship Land Look Like at an Agency? Source: U.S. Department of the Interior, AFR 2014, Stewardship Assets Note 9 on page

30 What Does Stewardship Land Look Like at an Agency? Source: U.S. Department of the Interior, AFR 2014, RSI on page

31 What Does Stewardship Land Look Like at an Agency? 30

32 Staff Round-Tables & Task Force Results 31

33 Round-Table Agencies Executive Agency Department of Defense Department of Energy Department of the Interior 32

34 Round-Table Results Topics Discussed Common Themes Land Background Accounting System General Land Policy Land Rights Land Improvements Uniform Accounting Data Integrity and Reliability Audit Challenges Assigning Fair Value Estimating Values (i.e., to include other methods besides formal appraisals) Impairment Other Notable mission differences Systems not all integrated Stabilization mode Immaterial Immaterial & SFFAS 6 OK Current distinctions = clarity Questionable Exist: RSI/OAI can mitigate Use sparingly; cost vs. benefit Debatable in-house estimates shift burden to back-end audit Immaterial & SFFAS 44 OK Avoid reporting as Basic 33

35 Some Task Force Results Deeper Dive 34

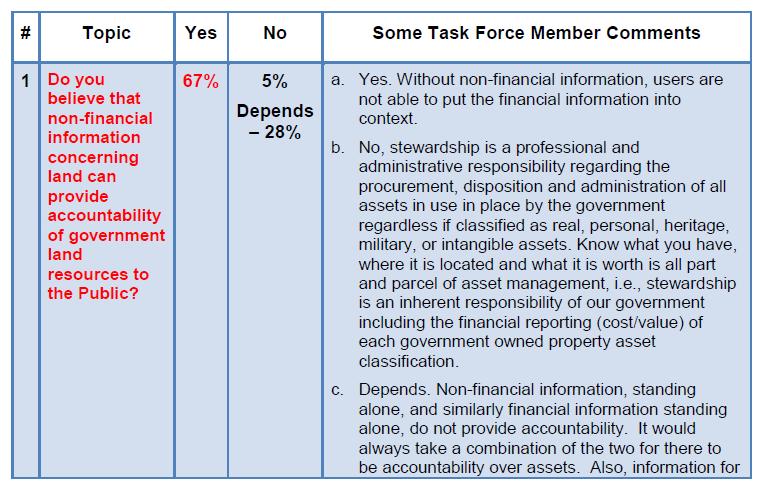

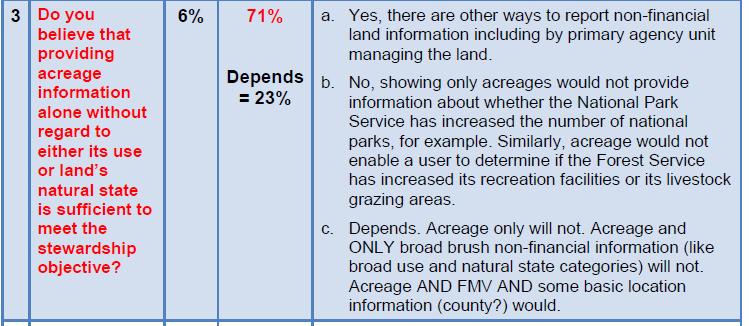

36 Q1. Do you believe that the cost of land putting aside for the moment the type of cost measurement technique used is essential for the reporting of all types of federal land managed by the government? 35

37 Exploring the Use of Non-Financial Information 36

38 Uniform Accounting for All Land 37

39 User Needs and Preparer Burden 38

40 Data Reliability and Integrity 39

41 Data Reliability and Integrity 40

42 Stewardship 41

43 Stewardship 42

44 Land Use 43

45 Tribal Land 44

46 Contact and Website Information General inquiries can be directed to Phone: Listserv Exposure Drafts Active Projects Dom Savini, CPA, CMA, MSA Bobby Hart, CPA, CMA, CFM, PMP, CGFM, CICA

July 30, Dear Ms. Payne:

July 30, 2018 Ms. Wendy M. Payne Executive Director Federal Accounting Standards Advisory Board Mailstop 6H19 441 G Street, NW, Suite 6814 Washington, DC 20548 Dear Ms. Payne: On behalf of the Association

July 30, 2018 Ms. Wendy M. Payne Executive Director Federal Accounting Standards Advisory Board Mailstop 6H19 441 G Street, NW, Suite 6814 Washington, DC 20548 Dear Ms. Payne: On behalf of the Association

It s Back Accounting for Asset Leases the new way!

It s Back Accounting for Asset Leases the new way! Kent Bettisworth BETTISWORTH & ASSOCIATES 2016 ERP Corp. All rights reserved. Controlling 2016 Conference September 12-15, 2016 in San Diego Kent Bettisworth

It s Back Accounting for Asset Leases the new way! Kent Bettisworth BETTISWORTH & ASSOCIATES 2016 ERP Corp. All rights reserved. Controlling 2016 Conference September 12-15, 2016 in San Diego Kent Bettisworth

Specialised activities

Specialised activities Agenda Accounting for specialised activities Agriculture Property development Service concession arrangements Extractive activities Biological assets Common accounting practices

Specialised activities Agenda Accounting for specialised activities Agriculture Property development Service concession arrangements Extractive activities Biological assets Common accounting practices

FASB Emerging Issues Task Force

EITF Issue No. 03-17 FASB Emerging Issues Task Force Issue No. 03-17 Title: Subsequent Accounting for Executory Contracts That Have Been Recognized on an Entity's Balance Sheet Document: Issue Summary

EITF Issue No. 03-17 FASB Emerging Issues Task Force Issue No. 03-17 Title: Subsequent Accounting for Executory Contracts That Have Been Recognized on an Entity's Balance Sheet Document: Issue Summary

Accounting and Auditing Update. Tennessee Chapter of hfma Spring Institute 2016 Presented by William C. Matheney FHFMA CPA and Meredith P.

Accounting and Auditing Update Tennessee Chapter of hfma Spring Institute 2016 Presented by William C. Matheney FHFMA CPA and Meredith P. Cate Today s Objectives Present an overview of pertinent recently

Accounting and Auditing Update Tennessee Chapter of hfma Spring Institute 2016 Presented by William C. Matheney FHFMA CPA and Meredith P. Cate Today s Objectives Present an overview of pertinent recently

NPMA and ASTM International Partners in Action

NPMA and ASTM International Partners in Action Christi Basile Bob Holcombe 1 ASTM International What is it? ASTM International is one of the largest voluntary standards development organizations in the

NPMA and ASTM International Partners in Action Christi Basile Bob Holcombe 1 ASTM International What is it? ASTM International is one of the largest voluntary standards development organizations in the

Defense Finance and Accounting Service

Defense Finance and Accounting Service DFAS 7900.4 M Financial Requirements Manual Volume 3, Property, Plant and Equipment August 2015 Strategy, Policy and Requirements ZP SUBJECT: Description of Requirement

Defense Finance and Accounting Service DFAS 7900.4 M Financial Requirements Manual Volume 3, Property, Plant and Equipment August 2015 Strategy, Policy and Requirements ZP SUBJECT: Description of Requirement

BUSINESS COMBINATIONS: CLARIFYING THE DEFINITION OF A BUSINESS

BUSINESS COMBINATIONS: CLARIFYING THE DEFINITION OF A BUSINESS Prepared by: Robert Dombrowski, Partner, National Professional Standards Group, RSM US LLP robert.dombrowski@rsmus.com, +1 847 413 6209 TABLE

BUSINESS COMBINATIONS: CLARIFYING THE DEFINITION OF A BUSINESS Prepared by: Robert Dombrowski, Partner, National Professional Standards Group, RSM US LLP robert.dombrowski@rsmus.com, +1 847 413 6209 TABLE

TOWN OF LINCOLN COUNCIL POLICY

Page 1 of 10 PURPOSE The purpose of this policy is to prescribe the accounting treatment for tangible capital assets so that users of the financial report can discern information about the investment in

Page 1 of 10 PURPOSE The purpose of this policy is to prescribe the accounting treatment for tangible capital assets so that users of the financial report can discern information about the investment in

IAG Conference Accounting Update Emerging issues in the public sector 20 November 2014 Michael Crowe Yannick Maurice

www.pwc.com.au IAG Conference Accounting Update Emerging issues in the public sector 20 November 2014 Michael Crowe Yannick Maurice Agenda Introduction Key topics o Fair value o PPP Projects Refinancing

www.pwc.com.au IAG Conference Accounting Update Emerging issues in the public sector 20 November 2014 Michael Crowe Yannick Maurice Agenda Introduction Key topics o Fair value o PPP Projects Refinancing

A New Lease on Life: The GASB s New Accounting for Leases

Tuesday, May 23, 2017 2:00 3:15PM A New Lease on Life: The GASB s New Accounting for Leases MODERATOR Frances Lee Deputy Chief Financial Officer San Francisco Public Utilities Commission SPEAKERS Stephen

Tuesday, May 23, 2017 2:00 3:15PM A New Lease on Life: The GASB s New Accounting for Leases MODERATOR Frances Lee Deputy Chief Financial Officer San Francisco Public Utilities Commission SPEAKERS Stephen

Comment on the Exposure Draft Leases

15 December 2010 International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Financial Accounting Standards Board 401 Merritt 7 PO Box 5116 Norwalk CT 06856-5116 United States

15 December 2010 International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Financial Accounting Standards Board 401 Merritt 7 PO Box 5116 Norwalk CT 06856-5116 United States

Private Land Conservation: Conservation Easements. Matt Singer Land Stewardship Manager

Private Land Conservation: Conservation Easements Matt Singer Land Stewardship Manager Galveston Bay Foundation Mission: To preserve, protect, and enhance the natural resources of the Galveston Bay estuarine

Private Land Conservation: Conservation Easements Matt Singer Land Stewardship Manager Galveston Bay Foundation Mission: To preserve, protect, and enhance the natural resources of the Galveston Bay estuarine

Accounting and Auditing. Norman Mosrie, CPA, FMFMA, CHFP James Sutherland, CPA

Accounting and Auditing Norman Mosrie, CPA, FMFMA, CHFP James Sutherland, CPA Leases (ASU 2016-02; Topic 842) A lease contract conveys the right to use an asset (the underlying asset) for a period of time

Accounting and Auditing Norman Mosrie, CPA, FMFMA, CHFP James Sutherland, CPA Leases (ASU 2016-02; Topic 842) A lease contract conveys the right to use an asset (the underlying asset) for a period of time

YOUNG COUNTY APPRAISAL DISTRICT

YOUNG COUNTY APPRAISAL DISTRICT 2016 - ANNUAL APPRAISAL REPORT AS OF 8/24/2016 1 2 TABLE OF CONTENTS ITEM PAGE Introduction 4 Purpose of Report...4 Taxing Entities, Rates & Exemptions 5 Property Types

YOUNG COUNTY APPRAISAL DISTRICT 2016 - ANNUAL APPRAISAL REPORT AS OF 8/24/2016 1 2 TABLE OF CONTENTS ITEM PAGE Introduction 4 Purpose of Report...4 Taxing Entities, Rates & Exemptions 5 Property Types

Temporary exemption from IAS 8 paragraphs 11 and 12

International Financial Reporting Standard 6 Exploration for and Evaluation of Mineral Resources Objective 1 The objective of this IFRS is to specify the financial reporting for the exploration for and

International Financial Reporting Standard 6 Exploration for and Evaluation of Mineral Resources Objective 1 The objective of this IFRS is to specify the financial reporting for the exploration for and

CPE ARTICLE. An Introduction to Lessee Accounting (Topic 842, Leases)

") CPE ARTICLE An Introduction to Lessee Accounting (Topic 842, Leases) 42 Today scpa Curriculum: Accounting and auditing Level: Basic Designed For: Public practitioners and business and industry Objectives:

CPE ARTICLE An Introduction to Lessee Accounting (Topic 842, Leases) 42 Today scpa Curriculum: Accounting and auditing Level: Basic Designed For: Public practitioners and business and industry Objectives:

Implementing the New Lease Guidance

Implementing the New Lease Guidance October 22, 2018 2018 Crowe LLP 2018 Crowe LLP Agenda Background Scope Effective dates & transition requirements Lessee accounting model Lessor accounting model Specialized

Implementing the New Lease Guidance October 22, 2018 2018 Crowe LLP 2018 Crowe LLP Agenda Background Scope Effective dates & transition requirements Lessee accounting model Lessor accounting model Specialized

Texas Parks and Wildlife Foundation Buffer Lands Program Program Description and Application

Texas Parks and Wildlife Foundation Texas Parks and Wildlife Foundation s mission is to provide private support to Texas Parks and Wildlife Department to manage and conserve the natural and cultural resources

Texas Parks and Wildlife Foundation Texas Parks and Wildlife Foundation s mission is to provide private support to Texas Parks and Wildlife Department to manage and conserve the natural and cultural resources

Accountability and Custody for Government Property and Contract Property

OUSD(AT&L) Acquisition Resources & Analysis (ARA) Property and Equipment Policy Accountability and Custody for Government Property and Contract Property Accountability for Government Property Objective:

OUSD(AT&L) Acquisition Resources & Analysis (ARA) Property and Equipment Policy Accountability and Custody for Government Property and Contract Property Accountability for Government Property Objective:

What/Who Determines that an Appraiser is Qualified in our Program?

What/Who Determines that an Appraiser is Qualified in our Program? Mike Jones, SR/WA, Maryland Certified General Appraiser Realty Specialist, FHWA Office of Real Estate Services Is it becoming tougher

What/Who Determines that an Appraiser is Qualified in our Program? Mike Jones, SR/WA, Maryland Certified General Appraiser Realty Specialist, FHWA Office of Real Estate Services Is it becoming tougher

Proposed New Accounting Standards For Leases

Relationships backed by performance. Proposed New Accounting Standards For Leases Doug Richardson Live Seminar 9:00am 10:30am June 21 2012 Overview and Background Leases serve a vital role in many entities

Relationships backed by performance. Proposed New Accounting Standards For Leases Doug Richardson Live Seminar 9:00am 10:30am June 21 2012 Overview and Background Leases serve a vital role in many entities

December 13, delivery: To: Subject: File Reference No

Email delivery: To: director@fasb.org Subject: File Reference No. Technical Director File Reference No. Financial Accounting Standards Board 401 Merritt 7 PO Box 5116 Norwalk, CT 06856-5116 Ladies and

Email delivery: To: director@fasb.org Subject: File Reference No. Technical Director File Reference No. Financial Accounting Standards Board 401 Merritt 7 PO Box 5116 Norwalk, CT 06856-5116 Ladies and

AAT Professional Diploma in Accounting

Qualification Number: R486 04 Qualification Technical Information Version 1.1 published 13 June 2016 AAT Professional Diploma in Accounting Qualification Technical Information Units in this qualification

Qualification Number: R486 04 Qualification Technical Information Version 1.1 published 13 June 2016 AAT Professional Diploma in Accounting Qualification Technical Information Units in this qualification

Deeper Dive Leases. Overview

Deeper Dive Leases Presented by: Shaun Johnson, CPA Dingus, Zarecor & Associates PLLC Overview Effective dates Big picture Objective, impact, and implementation Applicability and definition Initial recognition

Deeper Dive Leases Presented by: Shaun Johnson, CPA Dingus, Zarecor & Associates PLLC Overview Effective dates Big picture Objective, impact, and implementation Applicability and definition Initial recognition

Week11, Chap 8 Accounting 1A, Financial Accounting

Week11, Chap 8 Accounting 1A, Financial Accounting Reporting and Interpreting Property, Plant, and Equipment;Natural Resources; and Intangibles Instructor: Michael Booth Understanding The Business Insufficient

Week11, Chap 8 Accounting 1A, Financial Accounting Reporting and Interpreting Property, Plant, and Equipment;Natural Resources; and Intangibles Instructor: Michael Booth Understanding The Business Insufficient

LETTER No. 020/2010. São Paulo, December 15 th, Chief Technical Officer. Financial Accounting Standards Board. Ref.: Exposure Draft ED/2010/9

LETTER No. 020/2010 São Paulo, December 15 th, 2010. Chief Technical Officer Financial Accounting Standards Board Ref.: Exposure Draft ED/2010/9 ABEL Associação Brasileira das Empresas de Leasing (Brazilian

LETTER No. 020/2010 São Paulo, December 15 th, 2010. Chief Technical Officer Financial Accounting Standards Board Ref.: Exposure Draft ED/2010/9 ABEL Associação Brasileira das Empresas de Leasing (Brazilian

Lease Accounting Standard Update ASU Presented by: Nicholas Hoefel, CPA Manager, Audit Services Group

Lease Accounting Standard Update ASU 2016-02 Presented by: Nicholas Hoefel, CPA Manager, Audit Services Group 1 Overview Introduction Background and current environment Effective dates and transition Key

Lease Accounting Standard Update ASU 2016-02 Presented by: Nicholas Hoefel, CPA Manager, Audit Services Group 1 Overview Introduction Background and current environment Effective dates and transition Key

GASB 87: Leases. Hosted By: Ben Lindekugel, Executive Director Association of Washington Public Hospital Districts

GASB 87: Leases Hosted By: Ben Lindekugel, Executive Director Association of Washington Public Hospital Districts November 6, 2018 Presented By Tom Dingus, CPA, Partner Dingus, Zarecor & Associates PLLC

GASB 87: Leases Hosted By: Ben Lindekugel, Executive Director Association of Washington Public Hospital Districts November 6, 2018 Presented By Tom Dingus, CPA, Partner Dingus, Zarecor & Associates PLLC

LLANO CENTRAL APPRAISAL DISTRICT REAPPRAISAL PLAN FOR TAX YEARS 2017 & 2018 AS ADOPTED BY THE BOARD OF DIRECTORS

LLANO CENTRAL APPRAISAL DISTRICT REAPPRAISAL PLAN FOR TAX YEARS 2017 & 2018 AS ADOPTED BY THE BOARD OF DIRECTORS TABLE OF CONTENTS ITEM PAGE Executive Summary 5 Revaluation Decision (Statutory or Administrative)

LLANO CENTRAL APPRAISAL DISTRICT REAPPRAISAL PLAN FOR TAX YEARS 2017 & 2018 AS ADOPTED BY THE BOARD OF DIRECTORS TABLE OF CONTENTS ITEM PAGE Executive Summary 5 Revaluation Decision (Statutory or Administrative)

Lessor Example Performance Obligation Approach

Lessor Example Performance Obligation Approach **Disclaimer The exposure draft received nearly 700 letters of comment through the comment period ended December 15, 2010. There is some expectation that

Lessor Example Performance Obligation Approach **Disclaimer The exposure draft received nearly 700 letters of comment through the comment period ended December 15, 2010. There is some expectation that

roots The Substance of the Standard Contents Changes to the Accounting for Goodwill for Private Companies

The Substance of the Standard MAYER HOFFMAN MCCANN P.C. AN INDEPENDENT CPA FIRM TM A publication of the Professional Standards Group February 2014 Changes to the Accounting for Goodwill for Private Companies

The Substance of the Standard MAYER HOFFMAN MCCANN P.C. AN INDEPENDENT CPA FIRM TM A publication of the Professional Standards Group February 2014 Changes to the Accounting for Goodwill for Private Companies

CAPITAL ASSET POLICY

CAPITAL ASSET POLICY POLICY STATEMENT Morningside College, through each of its operating departments acquires and disposes of capital assets. Each department is responsible for following College procedures

CAPITAL ASSET POLICY POLICY STATEMENT Morningside College, through each of its operating departments acquires and disposes of capital assets. Each department is responsible for following College procedures

IAS 16 Property, Plant and Equipment. Uphold public interest

IAS 16 Property, Plant and Equipment Uphold public interest Background IAS 16 became operational in 1983 Major amendments have been made several times including 1998, 2003, 2008, 2012, 2013, 2014 The objective

IAS 16 Property, Plant and Equipment Uphold public interest Background IAS 16 became operational in 1983 Major amendments have been made several times including 1998, 2003, 2008, 2012, 2013, 2014 The objective

Accounting for Tangible Capital Assets

Accounting for Tangible Capital Assets Date Approved by Board: 2011.11.17 Resolution No.: 11-113 2016.05.19 16-048 Lead Role: CFO Replaces: N/A Last Review Date: N/A Next Review Date: 2019.05.19 Policy

Accounting for Tangible Capital Assets Date Approved by Board: 2011.11.17 Resolution No.: 11-113 2016.05.19 16-048 Lead Role: CFO Replaces: N/A Last Review Date: N/A Next Review Date: 2019.05.19 Policy

IPSASB Consultation Paper (CP): Financial Reporting for Heritage in the Public Sector Proposed comments from the FOCAL i working group

: Financial Reporting for Heritage in the Public Sector Proposed comments from the FOCAL i working group") IPSASB Consultation Paper (CP): Financial Reporting for Heritage in the Public Sector Proposed comments from the FOCAL i working group (Chile, Colombia, Brazil, Ecuador, Mexico, Peru, Paraguay and Panama)

IPSASB Consultation Paper (CP): Financial Reporting for Heritage in the Public Sector Proposed comments from the FOCAL i working group (Chile, Colombia, Brazil, Ecuador, Mexico, Peru, Paraguay and Panama)

Comment Letter No December 15, Merritt 7 840). assess the. impact of. should be

. assess the. impact of. should be") December 15, 2010 Financial Accounting Standards Board Attn: Technical Director File Reference No. 1850-100 401 Merritt 7 P.O. Box 5116 Norwalk, CT 06856-5116 Via e-mail to director@fasb.org Re: File Reference

December 15, 2010 Financial Accounting Standards Board Attn: Technical Director File Reference No. 1850-100 401 Merritt 7 P.O. Box 5116 Norwalk, CT 06856-5116 Via e-mail to director@fasb.org Re: File Reference

Department of Defense INSTRUCTION

Department of Defense INSTRUCTION NUMBER 5000.64 August 13, 2002 USD(AT&L) SUBJECT: Defense Property Accountability References: (a) Under Secretary of Defense (Acquisition, Technology and Logistics) and

Department of Defense INSTRUCTION NUMBER 5000.64 August 13, 2002 USD(AT&L) SUBJECT: Defense Property Accountability References: (a) Under Secretary of Defense (Acquisition, Technology and Logistics) and

NEW LEASE ACCOUNTING STANDARD

NEW LEASE ACCOUNTING STANDARD Accounting Standards Update (ASU) 2016-02, Leases & GASB 87, Leases LEASES Leases: Why a New Leases Standard? 1 IMPLEMENTATION TIMELINE January 2016 IASB issued IFRS 16, Leases

NEW LEASE ACCOUNTING STANDARD Accounting Standards Update (ASU) 2016-02, Leases & GASB 87, Leases LEASES Leases: Why a New Leases Standard? 1 IMPLEMENTATION TIMELINE January 2016 IASB issued IFRS 16, Leases

FISCAL POLICIES MANUAL... 1

FISCAL POLICIES MANUAL... 1 CAPITAL ASSETS...1 PREFACE... 1 DEFINITIONS... 1 POLICY... 5 ASSET IDENTIFICATION...5 CAPITAL ASSETS...6 CAPITALIZED ASSETS...6 INTANGIBLE ASSETS...7 DEPRECIATION AND AMORTIZATION...9

FISCAL POLICIES MANUAL... 1 CAPITAL ASSETS...1 PREFACE... 1 DEFINITIONS... 1 POLICY... 5 ASSET IDENTIFICATION...5 CAPITAL ASSETS...6 CAPITALIZED ASSETS...6 INTANGIBLE ASSETS...7 DEPRECIATION AND AMORTIZATION...9

Business Combinations IFRS 3

CA Sandesh Mundra Business Combinations IFRS 3 For many men, the acquisition of wealth does not end their troubles, it only changes them. - Lucius Annaeus Seneca Lets get some of the basics correct.. We

CA Sandesh Mundra Business Combinations IFRS 3 For many men, the acquisition of wealth does not end their troubles, it only changes them. - Lucius Annaeus Seneca Lets get some of the basics correct.. We

BUSI 398 Residential Property Guided Case Study

BUSI 398 Residential Property Guided Case Study PURPOSE AND SCOPE The Residential Property Guided Case Study course BUSI 398 is intended to give the real estate appraisal student a working knowledge of

BUSI 398 Residential Property Guided Case Study PURPOSE AND SCOPE The Residential Property Guided Case Study course BUSI 398 is intended to give the real estate appraisal student a working knowledge of

Exposure Draft ED/2010/9 - Leases

December 15 th, 2010 International Accounting Standards Board 30 Cannon Street, London EC4M 6XH United Kingdom Dear Madam/Sir, Exposure Draft ED/2010/9 - Leases The Israel Accounting Standards Board is

December 15 th, 2010 International Accounting Standards Board 30 Cannon Street, London EC4M 6XH United Kingdom Dear Madam/Sir, Exposure Draft ED/2010/9 - Leases The Israel Accounting Standards Board is

MARK TWAIN LAKE MASTER PLAN CLARENCE CANNON DAM AND MARK TWAIN LAKE MONROE CITY, MISSOURI

MARK TWAIN LAKE MASTER PLAN CLARENCE CANNON DAM AND MARK TWAIN LAKE MONROE CITY, MISSOURI CHAPTER 4 LAND ALLOCATION, LAND CLASSIFICATION, WATER SURFACE, AND EASEMENT LANDS This Master Plan is a land use

MARK TWAIN LAKE MASTER PLAN CLARENCE CANNON DAM AND MARK TWAIN LAKE MONROE CITY, MISSOURI CHAPTER 4 LAND ALLOCATION, LAND CLASSIFICATION, WATER SURFACE, AND EASEMENT LANDS This Master Plan is a land use

CFA UK response to the Exposure Draft on Leases

David Humphreys Practice Fellow International Accounting Standards Board 30 Cannon Street London EC4M 6XH 20 th December 2010 Dear David, Thank you for the opportunity to respond to the IASB Exposure Draft

David Humphreys Practice Fellow International Accounting Standards Board 30 Cannon Street London EC4M 6XH 20 th December 2010 Dear David, Thank you for the opportunity to respond to the IASB Exposure Draft

EITF Issue No EITF Issue No Working Group Report No. 1, p. 1

EITF Issue No. 03-9 The views in this report are not Generally Accepted Accounting Principles until a consensus is reached and it is FASB Emerging Issues Task Force Issue No. 03-9 Title: Interaction of

EITF Issue No. 03-9 The views in this report are not Generally Accepted Accounting Principles until a consensus is reached and it is FASB Emerging Issues Task Force Issue No. 03-9 Title: Interaction of

IMPAIRMENT TESTING OF LONG-LIVED ASSETS TO BE HELD AND USED

IMPAIRMENT TESTING OF LONG-LIVED ASSETS TO BE HELD AND USED Prepared by: Rick Day, Partner, National Director of Accounting, RSM US LLP rick.day@rsmus.com, +1 563 888 4017 TABLE OF CONTENTS Introduction...

IMPAIRMENT TESTING OF LONG-LIVED ASSETS TO BE HELD AND USED Prepared by: Rick Day, Partner, National Director of Accounting, RSM US LLP rick.day@rsmus.com, +1 563 888 4017 TABLE OF CONTENTS Introduction...

Accounting Of Intangible Assets Indian as- 26

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668. Volume 16, Issue 2. Ver. II (Feb. 2014), PP 40-45 Accounting Of Intangible Assets Indian as- 26 Manpreet Sharma,

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668. Volume 16, Issue 2. Ver. II (Feb. 2014), PP 40-45 Accounting Of Intangible Assets Indian as- 26 Manpreet Sharma,

Camp Central Appraisal District LEGAL AND ADMINISTRATIVE REQUIREMENTS

Camp Central Appraisal District LEGAL AND ADMINISTRATIVE REQUIREMENTS Counties are responsible for creating and establishing an Appraisal District. As a political subdivision of the state the major responsibility

Camp Central Appraisal District LEGAL AND ADMINISTRATIVE REQUIREMENTS Counties are responsible for creating and establishing an Appraisal District. As a political subdivision of the state the major responsibility

YOUNG COUNTY APPRAISAL DISTRICT

YOUNG COUNTY APPRAISAL DISTRICT 2017 - ANNUAL APPRAISAL REPORT AS OF 10/6/2017 1 2 TABLE OF CONTENTS ITEM PAGE Introduction 4 Purpose of Report...4 Taxing Entities, Rates & Exemptions 5 Property Types

YOUNG COUNTY APPRAISAL DISTRICT 2017 - ANNUAL APPRAISAL REPORT AS OF 10/6/2017 1 2 TABLE OF CONTENTS ITEM PAGE Introduction 4 Purpose of Report...4 Taxing Entities, Rates & Exemptions 5 Property Types

OREGON ASSOCIATION OF REALTORS

OREGON ASSOCIATION OF REALTORS 2017/2018 LEGISLATIVE POLICIES Presented to the Board of Directors September 28, 2016 1 OREGON ASSOCIATION OF REALTORS 2017/2018 LEGISLATIVE POLICY STATEMENTS GENERAL The

OREGON ASSOCIATION OF REALTORS 2017/2018 LEGISLATIVE POLICIES Presented to the Board of Directors September 28, 2016 1 OREGON ASSOCIATION OF REALTORS 2017/2018 LEGISLATIVE POLICY STATEMENTS GENERAL The

Technical Information Paper No

Environmental Condition of Property (ECOP) Investigations Technical Information Paper No. 38-001-0312 PURPOSE. To provide information on ECOP investigations for Federal real property transactions and military

Environmental Condition of Property (ECOP) Investigations Technical Information Paper No. 38-001-0312 PURPOSE. To provide information on ECOP investigations for Federal real property transactions and military

Workshop on IND AS Intangible assets WIRC of the ICAI April 23, 2016

Workshop on IND AS Intangible assets WIRC of the ICAI April 23, 2016 Contents Background and Scope Definitions Recognition & Measurement Amortization Disclosure requirements Differences with existing AS

Workshop on IND AS Intangible assets WIRC of the ICAI April 23, 2016 Contents Background and Scope Definitions Recognition & Measurement Amortization Disclosure requirements Differences with existing AS

PROPERTY MANAGEMENT OFFICER 1 PROPERTY MANAGEMENT OFFICER 2

L017 L018 Established 11-22-91 PROPERTY MANAGEMENT OFFICER 1 PROPERTY MANAGEMENT OFFICER 2 DEFINITION To perform technical and professional duties related to the appraisal, acquisition, disposition and

L017 L018 Established 11-22-91 PROPERTY MANAGEMENT OFFICER 1 PROPERTY MANAGEMENT OFFICER 2 DEFINITION To perform technical and professional duties related to the appraisal, acquisition, disposition and

IAS Revenue. By:

IAS - 18 Revenue International Accounting Standard No 18 (IAS 18) Revenue In 1998, IAS 39, Financial Instruments: Recognition and Measurement, amended paragraph 11 of IAS 18, adding a cross-reference to

IAS - 18 Revenue International Accounting Standard No 18 (IAS 18) Revenue In 1998, IAS 39, Financial Instruments: Recognition and Measurement, amended paragraph 11 of IAS 18, adding a cross-reference to

Accounting and Auditing Update. Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc.

Accounting and Auditing Update Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc. Agenda Overview of the standard setting agenda Revenue recognition Lease

Accounting and Auditing Update Staci L. Brogan, CPA, Shareholder Patricia R. Giudici, CPA, Senior Manager Schneider Downs & Co. Inc. Agenda Overview of the standard setting agenda Revenue recognition Lease

Exposure Draft 64 January 2018 Comments due: June 30, Proposed International Public Sector Accounting Standard. Leases

Exposure Draft 64 January 2018 Comments due: June 30, 2018 Proposed International Public Sector Accounting Standard Leases This document was developed and approved by the International Public Sector Accounting

Exposure Draft 64 January 2018 Comments due: June 30, 2018 Proposed International Public Sector Accounting Standard Leases This document was developed and approved by the International Public Sector Accounting

Gearing up for change New IFRS on Leases

Gearing up for change New IFRS on Leases In a nutshell The changes Lessee accounting Effective date: 1 January 2019 Limited changes to scope of IAS 17 Enhanced guidance on identifying a lease Lessor accounting

Gearing up for change New IFRS on Leases In a nutshell The changes Lessee accounting Effective date: 1 January 2019 Limited changes to scope of IAS 17 Enhanced guidance on identifying a lease Lessor accounting

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N AGENDA Leases FASB & GASB Revenue Recognition FASB 2 FASB ASU 2016-02, Leases (Topic

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N AGENDA Leases FASB & GASB Revenue Recognition FASB 2 FASB ASU 2016-02, Leases (Topic

FASB Updates Business Definition

On January 5, 2017, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 2017-01, s (Topic 805): Clarifying the Definition of a Business. This definition is significant

On January 5, 2017, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 2017-01, s (Topic 805): Clarifying the Definition of a Business. This definition is significant

IAS 40 Investment Property

IAS 40 Investment Property Scope Applies in the: recognition, measurement and disclosure of investment property measurement in a lessee s financial statements of investment property interests held under

IAS 40 Investment Property Scope Applies in the: recognition, measurement and disclosure of investment property measurement in a lessee s financial statements of investment property interests held under

Measuring the Scope of Federal Land Ownership

Measuring the Scope of Federal Land Ownership Angela Logomasini During much of American history, landuse regulation was not a federal issue. The American system was biased against an active federal role

Measuring the Scope of Federal Land Ownership Angela Logomasini During much of American history, landuse regulation was not a federal issue. The American system was biased against an active federal role

Welcome to Webinar: Implementing FASB s Updated Lease Accounting Standard ASU (Topic 842)

") Welcome to Webinar: Implementing FASB s Updated Lease Accounting Standard ASU 2016-02 (Topic 842) Presented by: Gelman, Rosenberg & Freedman CPAs Please note: Use the Question panel to speak with the administrator

Welcome to Webinar: Implementing FASB s Updated Lease Accounting Standard ASU 2016-02 (Topic 842) Presented by: Gelman, Rosenberg & Freedman CPAs Please note: Use the Question panel to speak with the administrator

The joint leases project change is coming

No. 2010-4 18 June 2010 Technical Line Technical guidance on standards and practice issues The joint leases project change is coming What you need to know The proposed changes to the accounting for leases

No. 2010-4 18 June 2010 Technical Line Technical guidance on standards and practice issues The joint leases project change is coming What you need to know The proposed changes to the accounting for leases

Internal Audit Report

Internal Audit Report TxDOT Internal Audit Division Objective To determine if objectives are being met and are in compliance with current regulations. Opinion Based on the audit scope areas reviewed, control

Internal Audit Report TxDOT Internal Audit Division Objective To determine if objectives are being met and are in compliance with current regulations. Opinion Based on the audit scope areas reviewed, control

New Developments Summary

September 11, 2018 NDS 2018-11 New Developments Summary Implementation costs in a hosting arrangement ASU 2018-15 addresses customer accounting Summary The FASB issued ASU 2018-15, Customer s Accounting

September 11, 2018 NDS 2018-11 New Developments Summary Implementation costs in a hosting arrangement ASU 2018-15 addresses customer accounting Summary The FASB issued ASU 2018-15, Customer s Accounting

CAPITAL ASSETS MVECA. Presented by: Larry Weeks, CPA

CAPITAL ASSETS MVECA Presented by: Larry Weeks, CPA Capital Assets Overarching theory of MATERIALITY GAAP need not be applied to immaterial amounts. 2 GASB Codification Section 1400 Reporting Capital Assets

CAPITAL ASSETS MVECA Presented by: Larry Weeks, CPA Capital Assets Overarching theory of MATERIALITY GAAP need not be applied to immaterial amounts. 2 GASB Codification Section 1400 Reporting Capital Assets

The new accounting standard for leases. 27 March 2017

The new accounting standard for leases 27 March 2017 Disclaimer Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity.

The new accounting standard for leases 27 March 2017 Disclaimer Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity.

Auditing PP&E, Including Leases

Auditing PP&E, Including Leases Learning Objectives Discuss typical audit risks and special considerations. Tailor an audit plan to assessed audit risk. Explain key controls related to PP&E. Describe lease

Auditing PP&E, Including Leases Learning Objectives Discuss typical audit risks and special considerations. Tailor an audit plan to assessed audit risk. Explain key controls related to PP&E. Describe lease

CENTRAL GOVERNMENT ACCOUNTING STANDARDS

CENTRAL GOVERNMENT ACCOUNTING STANDARDS NOVEMBER 2016 STANDARD 4 Requirements STANDARD 5 INTANGIBLE ASSETS INTRODUCTION... 75 I. CENTRAL GOVERNMENT S SPECIALISED ASSETS... 75 I.1. The collection of sovereign

CENTRAL GOVERNMENT ACCOUNTING STANDARDS NOVEMBER 2016 STANDARD 4 Requirements STANDARD 5 INTANGIBLE ASSETS INTRODUCTION... 75 I. CENTRAL GOVERNMENT S SPECIALISED ASSETS... 75 I.1. The collection of sovereign

Emerging Issues Task Force. EITF Agenda Committee Report Supplement. Mining Industry Issues November 5, 2003

1103RPTMNG Emerging Issues Task Force Agenda Committee Report Supplement Mining Industry Issues November 5, 2003 Potential New Issues Page(s) 1. Whether Mining Rights are Tangible or Intangible Assets

1103RPTMNG Emerging Issues Task Force Agenda Committee Report Supplement Mining Industry Issues November 5, 2003 Potential New Issues Page(s) 1. Whether Mining Rights are Tangible or Intangible Assets

Clay L. Pilgrim, CPA, CFE, CFF. What Financial Statement Preparers Need to Know About GASB s New Lease Accounting Proposal.

Clay L. Pilgrim, CPA, CFE, CFF What Financial Statement Preparers Need to Know About GASB s New Lease Accounting Proposal Today s Presenter Clay Pilgrim, CPA, CFE, CFF is a partner with Rushton & Company,

Clay L. Pilgrim, CPA, CFE, CFF What Financial Statement Preparers Need to Know About GASB s New Lease Accounting Proposal Today s Presenter Clay Pilgrim, CPA, CFE, CFF is a partner with Rushton & Company,

No Land, No Water: Solutions and Programs for Mitigating Land Loss

No Land, No Water: Solutions and Programs for Mitigating Land Loss Alamo Area Council of Governments Blair Calvert Fitzsimons, Chief Executive Officer Texas Agricultural Land Trust May 27, 2015 1 Outline

No Land, No Water: Solutions and Programs for Mitigating Land Loss Alamo Area Council of Governments Blair Calvert Fitzsimons, Chief Executive Officer Texas Agricultural Land Trust May 27, 2015 1 Outline

Appendix 1 Exposure Draft: ED/2013/8 Agriculture: Bearer Plants Proposed amendments to IAS 16 and IAS 41

Appendix 1 Exposure Draft: ED/2013/8 Agriculture: Bearer Plants Proposed amendments to IAS 16 and IAS 41 Questions for respondents Question 1 Scope of the amendments The IASB proposes to restrict the scope

Appendix 1 Exposure Draft: ED/2013/8 Agriculture: Bearer Plants Proposed amendments to IAS 16 and IAS 41 Questions for respondents Question 1 Scope of the amendments The IASB proposes to restrict the scope

Lease Accounting - New Changes in US, International and Government Accounting Standards

Lease Accounting - New Changes in US, International and Government Accounting Standards Roberta J. Cable, Ph.D., CMA Patricia Healy, CPA, CMA Lubin School of Business Administration, Pace University, USA

Lease Accounting - New Changes in US, International and Government Accounting Standards Roberta J. Cable, Ph.D., CMA Patricia Healy, CPA, CMA Lubin School of Business Administration, Pace University, USA

60-HR FL Real Estate Broker Post-Licensing Learning Objectives by Lesson

Lesson 1: Starting a Real Estate Office SECTION 1: BROKERAGE OFFICE ESSENTIALS Recall the characteristics of business entities that may register as a real estate brokerage and the rules involved to operate

Lesson 1: Starting a Real Estate Office SECTION 1: BROKERAGE OFFICE ESSENTIALS Recall the characteristics of business entities that may register as a real estate brokerage and the rules involved to operate

IFRS 16 : Lease accounting

IFRS 16 : Lease accounting Effective for accounting periods beginning on or after 1 January 2019 December 2017 IFRS 16: Lease accounting The IASB published the new IFRS 16 lease standard, in order to avoid

IFRS 16 : Lease accounting Effective for accounting periods beginning on or after 1 January 2019 December 2017 IFRS 16: Lease accounting The IASB published the new IFRS 16 lease standard, in order to avoid

APPENDIX B. Fee Simple v. Conservation Easement Acquisitions NTCOG Water Quality Greenprint - Training Workshops

APPENDIX B Fee Simple v. Conservation Easement Acquisitions NTCOG Water Quality Greenprint - Training Workshops Lake Arlington Watershed and Lewisville Lake East Watershed June 21, 2011 Presenter Talking

APPENDIX B Fee Simple v. Conservation Easement Acquisitions NTCOG Water Quality Greenprint - Training Workshops Lake Arlington Watershed and Lewisville Lake East Watershed June 21, 2011 Presenter Talking

FASB and IASB Continue Making Decisions on Lease Accounting

Accounting Journal Entry FASB and IASB Continue Making Decisions on Lease Accounting March 28, 2011 At recent meetings, the FASB and IASB (the boards ) have continued to make progress on the leases project,

Accounting Journal Entry FASB and IASB Continue Making Decisions on Lease Accounting March 28, 2011 At recent meetings, the FASB and IASB (the boards ) have continued to make progress on the leases project,

July 17, Technical Director File Reference No Re:

July 17, 2009 Technical Director File Reference No. 1680-100 Re: Financial Accounting Standards Board ( FASB ) and International Accounting Standards Board ( IASB ) Discussion Paper titled Leases: Preliminary

July 17, 2009 Technical Director File Reference No. 1680-100 Re: Financial Accounting Standards Board ( FASB ) and International Accounting Standards Board ( IASB ) Discussion Paper titled Leases: Preliminary

INTRODUCTION MISSION OVERVIEW

INTRODUCTION The Austin County Appraisal District is a political subdivision of the State of Texas. The Constitution of the State of Texas, the Texas Property Tax Code, and the Rules of the Texas Comptroller

INTRODUCTION The Austin County Appraisal District is a political subdivision of the State of Texas. The Constitution of the State of Texas, the Texas Property Tax Code, and the Rules of the Texas Comptroller

A 1: It( SPECIFIC ITEMS SECTION 3061 property, plant and equipment. Additional Resources. Page 1 of6. Knotia - CICA Handbook - Accounting A2-14

'" Knotia - CICA Handbook - Accounting»Accounting»Accounting Handbook»Accounting Standards»Specific items [Sections 3000-3870]»3061 - Property, Plant and Eauipment Page 1 of6 A 1: It( A2-14 SPECIFIC ITEMS

'" Knotia - CICA Handbook - Accounting»Accounting»Accounting Handbook»Accounting Standards»Specific items [Sections 3000-3870]»3061 - Property, Plant and Eauipment Page 1 of6 A 1: It( A2-14 SPECIFIC ITEMS

International Accounting Standards Board Press Release

International Accounting Standards Board Press Release 31 March 2004 IASB ISSUES STANDARDS ON BUSINESS COMBINATIONS, GOODWILL AND INTANGIBLE ASSETS The International Accounting Standards Board (IASB) today

International Accounting Standards Board Press Release 31 March 2004 IASB ISSUES STANDARDS ON BUSINESS COMBINATIONS, GOODWILL AND INTANGIBLE ASSETS The International Accounting Standards Board (IASB) today

CURRENT THROUGH PL , APPROVED 11/11/2009

CURRENT THROUGH PL 111-98, APPROVED 11/11/2009 TITLE 10. ARMED FORCES SUBTITLE A. GENERAL MILITARY LAW PART IV. SERVICE, SUPPLY, AND PROCUREMENT CHAPTER 159. REAL PROPERTY; RELATED PERSONAL PROPERTY; AND

CURRENT THROUGH PL 111-98, APPROVED 11/11/2009 TITLE 10. ARMED FORCES SUBTITLE A. GENERAL MILITARY LAW PART IV. SERVICE, SUPPLY, AND PROCUREMENT CHAPTER 159. REAL PROPERTY; RELATED PERSONAL PROPERTY; AND

4/4/2018. GASB's New Leases Standard

GASB's New Leases Standard April 4, 2018 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in a group Complete group attendance form

GASB's New Leases Standard April 4, 2018 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in a group Complete group attendance form

CALIFORNIA POLYTECHNIC STATE UNIVERSITY SAN LUIS OBISPO GIFT-IN-KIND ( GIK ) ACCEPTANCE PROCEDURES

ACCEPTANCE PROCEDURES") CALIFORNIA POLYTECHNIC STATE UNIVERSITY SAN LUIS OBISPO GIFT-IN-KIND ( GIK ) ACCEPTANCE PROCEDURES DEFINITIONS Accounting Standards are financial accounting rules that regulate the manner in which GIK

CALIFORNIA POLYTECHNIC STATE UNIVERSITY SAN LUIS OBISPO GIFT-IN-KIND ( GIK ) ACCEPTANCE PROCEDURES DEFINITIONS Accounting Standards are financial accounting rules that regulate the manner in which GIK

The Financial Accounting Standards Board

V A L U A T I O N How the New Leases Standard May Impact Business Valuations By Judith H. O Dell, CPA, CVA The Financial Accounting Standards Board issued the 485 page Leases Standard (Topic 842) in February,

V A L U A T I O N How the New Leases Standard May Impact Business Valuations By Judith H. O Dell, CPA, CVA The Financial Accounting Standards Board issued the 485 page Leases Standard (Topic 842) in February,

Restoring the Past U.E.P.C. Building the Future

Brussels, 14.12.2010 Dear Sirs, Madam, Re: Exposure Draft Leases On behalf of the European Union of Developers and House Builders (Union Europeénne des Promoteurs-Constructeurs - UEPC), I am writing to

Brussels, 14.12.2010 Dear Sirs, Madam, Re: Exposure Draft Leases On behalf of the European Union of Developers and House Builders (Union Europeénne des Promoteurs-Constructeurs - UEPC), I am writing to

Theme Strategic Plan for Cadastral Theme

Theme Strategic Plan for Cadastral Theme Bureau of Land Management Cadastral Survey Federal Geographic Data Committee (FGDC) 2017 2021 April 2017 - Progress and Update Cadastral Theme Implementation Plan

Theme Strategic Plan for Cadastral Theme Bureau of Land Management Cadastral Survey Federal Geographic Data Committee (FGDC) 2017 2021 April 2017 - Progress and Update Cadastral Theme Implementation Plan

Finishing strong in the ASC 606 marathon: An in-depth look at Step 5 and contract costs

Finishing strong in the ASC 606 marathon: An in-depth look at Step 5 and contract costs Please disable popup blocking software before viewing this webcast Original Publication Date: May 23, 2017 CPE Credit

Finishing strong in the ASC 606 marathon: An in-depth look at Step 5 and contract costs Please disable popup blocking software before viewing this webcast Original Publication Date: May 23, 2017 CPE Credit

COMAL APPRAISAL DISTRICT ANNUAL APPRAISAL REPORT

COMAL APPRAISAL DISTRICT 2016 ANNUAL APPRAISAL REPORT TABLE OF CONTENTS Introduction..2 Mission Statement... 2 Purpose of Report...2 Entities Served..2 Legislative Changes.3 Property Types.3 Appraisal

COMAL APPRAISAL DISTRICT 2016 ANNUAL APPRAISAL REPORT TABLE OF CONTENTS Introduction..2 Mission Statement... 2 Purpose of Report...2 Entities Served..2 Legislative Changes.3 Property Types.3 Appraisal

Accounting Update. Anne Cloutier, CPA, FHFMA Principal March 27, 2015

Accounting Update Anne Cloutier, CPA, FHFMA Principal March 27, 2015 Current Accounting for Leases Capital leases - a lessee recognizes leased assets and liabilities on the balance sheet. Operating leases

Accounting Update Anne Cloutier, CPA, FHFMA Principal March 27, 2015 Current Accounting for Leases Capital leases - a lessee recognizes leased assets and liabilities on the balance sheet. Operating leases

brief introduction to the research projects (paragraphs 5 7); and

; and") STAFF PAPER FASB IASB Meeting Project Paper topic Goodwill and Impairment research project Cover paper June 2018 This paper has been prepared for discussion at a public educational meeting of the US Financial

STAFF PAPER FASB IASB Meeting Project Paper topic Goodwill and Impairment research project Cover paper June 2018 This paper has been prepared for discussion at a public educational meeting of the US Financial

EFRAG s Letter to the European Commission Regarding Endorsement of Transfers of Investment Property

Regarding Endorsement of Transfers of Investment Property Olivier Guersent Director General, Financial Stability, Financial Services and Capital Markets Union European Commission 1049 Brussels 6 April

Regarding Endorsement of Transfers of Investment Property Olivier Guersent Director General, Financial Stability, Financial Services and Capital Markets Union European Commission 1049 Brussels 6 April

New Phase I Requirements for Real Estate Transactions: Implications of the New All Appropriate Inquiries Rule

New Phase I Requirements for Real Estate Transactions: Implications of the New All Appropriate Inquiries Rule Helen Currie Foster Graves, Dougherty, Hearon & Moody, P.C. 1 State Bar of Texas 28 th Annual

New Phase I Requirements for Real Estate Transactions: Implications of the New All Appropriate Inquiries Rule Helen Currie Foster Graves, Dougherty, Hearon & Moody, P.C. 1 State Bar of Texas 28 th Annual

Board Meeting Handout ACCOUNTING FOR CONTINGENCIES September 6, 2007

PURPOSE Board Meeting Handout ACCOUNTING FOR CONTINGENCIES September 6, 2007 At today s meeting, the Board will discuss whether to add to its technical agenda a project considering whether to revise the

PURPOSE Board Meeting Handout ACCOUNTING FOR CONTINGENCIES September 6, 2007 At today s meeting, the Board will discuss whether to add to its technical agenda a project considering whether to revise the

EFRAG s Draft Letter to the European Commission Regarding Endorsement of Transfers of Investment Property

Regarding Endorsement of Transfers of Investment Property Olivier Guersent Director General, Financial Stability, Financial Services and Capital Markets Union European Commission 1049 Brussels [dd Month]

Regarding Endorsement of Transfers of Investment Property Olivier Guersent Director General, Financial Stability, Financial Services and Capital Markets Union European Commission 1049 Brussels [dd Month]

IAS 40 - Investment Property. Shareholder, Mayer Hoffman McCann P.C. October 25, 2012

MHM Executive Education Series: IAS 40 - Investment Property Presented by: Keith Peterka Shareholder, Mayer Hoffman McCann P.C. October 25, 2012 Today s Agenda IAS 40 Investment Properties U.S. GAAP Project

MHM Executive Education Series: IAS 40 - Investment Property Presented by: Keith Peterka Shareholder, Mayer Hoffman McCann P.C. October 25, 2012 Today s Agenda IAS 40 Investment Properties U.S. GAAP Project

KEY DIFFERENCES- AS VS. IND AS

KEY DIFFERENCES- AS VS. IND AS October 2016 1 Titre de la présentation AGENDA Property, Plant and Equipment (PP&E) Intangible Assets Investment Property Non-current Assets Held for Sale and Discontinued

KEY DIFFERENCES- AS VS. IND AS October 2016 1 Titre de la présentation AGENDA Property, Plant and Equipment (PP&E) Intangible Assets Investment Property Non-current Assets Held for Sale and Discontinued

4/10/2012. Long-Lived Assets and Depreciation. Overview of Long-lived Assets. Learning Objectives (LO) Learning Objectives (LO)

Learning Objectives (LO)") Learning Objectives (LO) CHAPTER Long-Lived Assets and Depreciation 8 After studying this chapter, you should be able to 1. Distinguish a company s expenses from expenditures that it should capitalize

Learning Objectives (LO) CHAPTER Long-Lived Assets and Depreciation 8 After studying this chapter, you should be able to 1. Distinguish a company s expenses from expenditures that it should capitalize