Leases: A Comprehensive Update on the Joint Project

|

|

|

- Madlyn Knight

- 6 years ago

- Views:

Transcription

1 The Dbriefs Financial Reporting series presents: Leases: A Comprehensive Update on the Joint Project Bob Uhl, Deloitte & Touche LLP Trevor Farber, Deloitte & Touche LLP James Barker, Deloitte & Touche LLP Beth Young, Deloitte & Touche LLP April 3, 2013

2 Agenda Significant provisions Lessee accounting Lessor accounting Other considerations Question and answer

3 Keep in mind This webcast does not provide official Deloitte & Touche LLP interpretive accounting guidance Check with a qualified advisor before taking any action See later slides for information on obtaining written summaries of issues discussed today 1

4 Learning objective To enhance participants understanding of important accounting issues and developments pertaining to recent actions of the FASB, IASB and EITF. 2

5 Poll question #1 Are you a financial statement preparer, user, auditor, or other interested party? Preparer User Auditor Other

6 Significant Provisions

7 Overview and timing 6 Issued in August 2010 Original Exposure Draft (ED) Comment period ended December 2010 Over 750 letters received Revised ED Expected to be issued second quarter 2013 Final Standard Expected to be issued 2014 Effective Date Expected to be no sooner than

8 Scope Overall similar to current U.S. GAAP Exclude: Leases for the right to explore for or use minerals, oils, natural gas, and similar nonregenerative resources Leases of biological assets, including timber Intangible assets 4

9 Short-term leases Maximum possible lease term, including options to renew, that is 12 months or less Short-term leases would include leases that: Are cancellable by both the lessee and lessor with minimal termination payments, or Include renewal options that must be agreed to by both the lessee and lessor Current operating lease treatment for lessee and lessor Elective in nature by underlying asset class 5

10 Definition of a lease A contract in which the right to use a specified asset (the underlying asset) is conveyed, for a period of time, in exchange for consideration Specified asset Explicitly or implicitly identified Substitution rights must be considered Control Ability to direct the use and receive the benefit from use Rights to substantially all economic benefits from use over the lease term Taking all of the output will no longer be determinative 6

11 Poll question #2 Do you agree with the revised definition of a lease? Yes No Not sure

12 Lease term Noncancellable period + renewal period(s) for which lessee has significant economic incentive to exercise renewal options Contract Factors The terms included in the lease agreement Asset Factors Specific characteristics of the underlying asset Entity Factors The historical practice of the entity, management s intent, and common industry practice Market Factors Market rentals for comparable assets 7

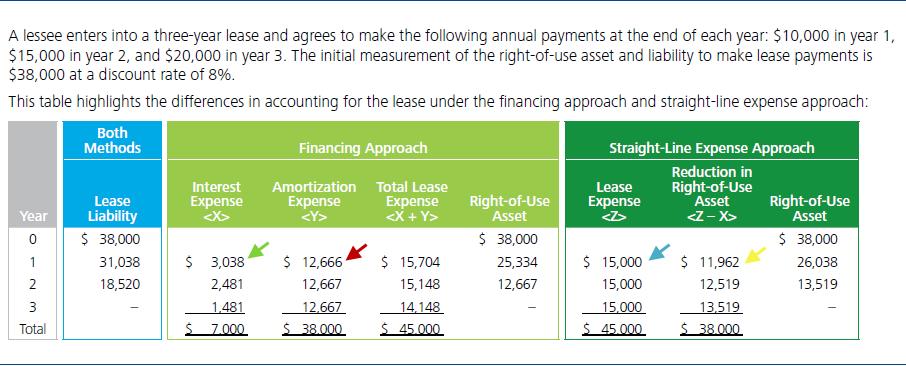

13 Lease payments Fixed lease payments Include lease payments that are to be made over the lease term For example, payments required in a period that follows a termination option are used to measure lease assets and liabilities if it is determined that the lessee has a significant economic incentive to not exercise the termination option Variable lease payments - only included if: In-substance fixed payments Payments based on index or rate 8

14 Lease payments Residual value guarantees (RVGs) Lessees Include the difference between the expected residual value and the guaranteed residual value Lessors Certain RVGs considered lease payments. All RVGs can be considered in evaluating the impairment of residual assets Purchase options Recognition, measurement and classification Termination penalties Treated consistently with the determination of the lease term 9

15 Contracts that contain lease and nonlease components Lessee Allocate transaction price based on whether or not the purchase price is observable If purchase price of each component is observable based on relative purchase price of individual components If purchase price of one or more components, but not all, is observable based on a residual method If none of the purchase prices are observable account for the entire transaction as a lease Lessor Allocate transaction price on a relative standalone selling price basis (consistent with the revenue proposal) Estimate standalone selling price if not observable Expected cost-plus margin, adjusted market assessment, or residual method (if price is highly variable or uncertain) are acceptable estimation methods 10

16 Discount rate Lessee Rate the lessor charges the lessee when available; otherwise, its incremental borrowing rate Lessor Rate the lessor charges the lessee, which could be: Lessee s incremental borrowing rate Rate implicit in the lease Yield on the property for property leases Discount rate should be reassessed when there is a change in the lease payments 11

17 Poll question #3 True or False: When determining the lease term, an entity should consider contract-related factors at both the inception of the lease and each period (reassessment). True False

18 Lessee Accounting

19 Lessee accounting Initial measurement Right-of-use asset Present value (PV) of lease payments + lessee s initial direct costs Initial direct costs: Incremental costs directly attributable to negotiating and arranging a lease Recognize lease incentives as a reduction in the right-of-use asset Lease liability PV of lease payments Subsequent measurement Right-of-use asset Amortized cost: Method of amortization depends on nature of underlying asset (see slides that follow) Impairment: Refer to existing standards (ASC 360) Lease liability Amortized cost: Use the effective interest method 12

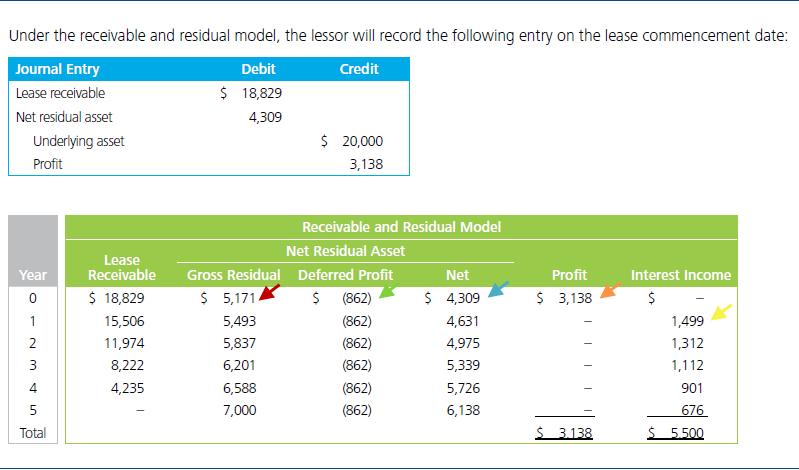

20 Lessee accounting A lessee s determination of the appropriate expense recognition pattern would be based on whether the lessee acquires and consumes more than an insignificant portion of the underlying asset Yes Is the leased asset property? No Lease term is a major portion of asset s remaining economic life OR PV of fixed lease payments accounts for substantially all of the FV Lease term is insignificant to asset s total economic life OR PV of fixed lease payments insignificant relative to asset FV? Yes No Yes No Financing Approach Straight-line Expense Approach Straight-line Expense Approach Financing Approach 13

21 Classification of lease components Analyze agreement to determine if separate accounting is required for lease components Use of the asset depends on other assets that are readily available to the entity Use of the asset is interrelated with other assets identifiable in the contract Classification should be based on the primary asset of the lease component Land and building elements of a property lease would not need to be assessed separately 14

22 Poll question #4 Do you agree with the two model approach that the boards have proposed for lessees? Yes No Not sure

23 Lessee accounting 15

24 Lessee accounting Constituents concern about income statement effect being inconsistent with lease economics 16

25 Reassessment of lease payments 17

26 Lessor Accounting

27 Lessor accounting Receivable and residual Operating lease Derecognize Underlying asset Recognize Lease receivable Residual asset Defer profit relating to the residual asset (netted with residual asset) Continue to recognize the underlying asset and recognize lease income over the lease term 18

28 Lessor accounting A lessor s determination of the appropriate expense recognition pattern would be based on whether the lessee acquires and consumes more than an insignificant portion of the underlying asset Yes Is the leased asset property? No Lease term is a major portion of asset s remaining economic life OR PV of fixed lease payments accounts for substantially all of the FV Lease term is insignificant to asset s total economic life OR PV of fixed lease payments insignificant relative to asset FV? Yes No Yes No Receivable and Residual Approach Operating Lease Approach Operating Lease Approach Receivable and Residual Approach 19

29 Poll question #5 Variable payments are included in a lessee and lessor s calculation of lease payments when: They are based on an index or a rate They are in-substance fixed payments Both of the above None of the above

30 Lessor accounting A manufacturer leases a piece of its equipment to a lessee. The leased equipment has a carrying amount of $20,000 and a fair value of $24,000 at lease commencement. The terms of the lease are as follows: 20

31 Lessor accounting

32 Other Considerations

33 Other considerations Lease commencement Recognition, measurement and classification Build to suit transactions The guidance in ASC related to a lessee s involvement with construction (previously EITF 97-10) will not be carried forward Subleases Head lease account for assets and liabilities in accordance with guidance for lessees Sublease account for assets and liabilities in accordance with guidance for lessors 22

34 Other considerations Sale and leaseback transactions Existing guidance will not be carried forward Entities should look to the guidance on revenue recognition to determine whether the conditions of sale are met Consider whether the seller/lessee has the ability to direct the use of, and obtain substantially all of the remaining benefits from, the asset If revenue recognition conditions are met, a whole asset approach would be used in accounting for the transaction If consideration is fair value, gains and losses would not be deferred 23

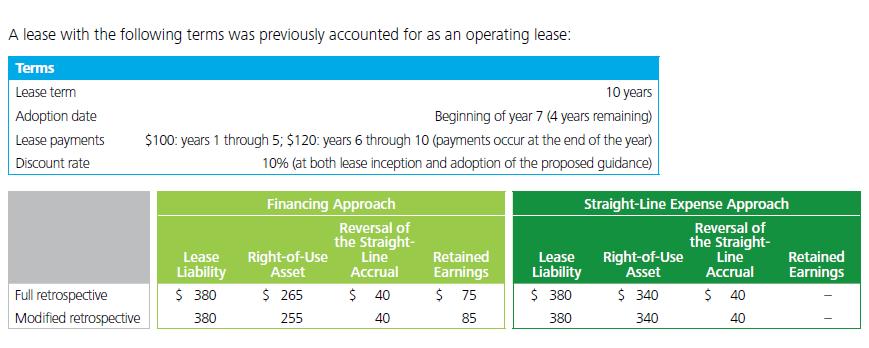

35 Transition Lessee 24 Full retrospective approach OR Modified retrospective approach Operating leases existing at beginning of earliest comparative period presented: Finance Method Recognize lease liability at PV of remaining lease payments Recognize right-of-use asset as a proportion of lease liabilities Recognize difference in retained earnings Reverse straight line accrual Straight Line Method Recognize lease liabilities at PV of remaining lease payments Recognize right-of-use asset at the amount of the related lease liability Reverse straight line accrual Capital leases existing at the beginning of earliest comparative period presented: Apply existing guidance for recognition and measurement purposes Reclassify carrying amount of lease assets and liabilities as rightof-use assets and lease liabilities

36 Transition Lessee 25

37 Poll question #6 True or False: Under the proposal, a lessee that enters into a sublease would look to the guidance for lessors to determine how to account for the transaction? True False

38 Transition Lessor Full retrospective approach OR Modified retrospective approach Operating leases existing at beginning of earliest comparative period presented: Receivable and Residual Method Recognize lease receivable asset measured at present value of remaining lease payments Recognize residual asset based on the proposed model Derecognize the leased asset Sales-type and financing leases existing at the beginning of earliest comparative period presented: Apply existing guidance for recognition and measurement purposes Reclassify the amounts recorded in accordance with the proposed presentation requirements 26

39 Operational and implementation challenges Systems New systems requirements Identification lease arrangements and capturing relevant data Changes to internal controls Business Changes Compliance with debt covenants Educating analysts Lease vs. buy decisions Financial Reporting Increased judgments Right-of-use assets will need to be evaluated for impairment Tax complexities Increased disclosures 27

40 Poll question #7 Do you or your organization plan to comment on the exposure draft? Yes No Haven t decided

41 Question and answer

42 Join us June 17at 2 PM ET as our Financial Reporting series presents: EITF Roundup: Highlights from the June Meeting

43 Eligible viewers may now download CPE certificates. Click the CPE icon in the dock at the bottom of your screen.

44 Contact info Bob Uhl James Barker Trevor Farber Beth Young

45 This presentation contains general information only and Deloitte is not, by means of this presentation, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This presentation is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte shall not be responsible for any loss sustained by any person who relies on this presentation.

46 About Deloitte Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Please see for a detailed description of the legal structure of Deloitte Touche Tohmatsu Limited and its member firms. Please see for a detailed description of the legal structure of Deloitte LLP and its subsidiaries. Certain services may not be available to attest clients under the rules and regulations of public accounting. Member of Deloitte Touche Tohmatsu Limited

Bring it on Discussing the FASB s new leases standard

The Dbriefs Financial Reporting series presents: Bring it on Discussing the FASB s new leases standard March 15, 2016 Bob Uhl, Partner, Deloitte & Touche LLP James Barker, Partner, Deloitte & Touche LLP

The Dbriefs Financial Reporting series presents: Bring it on Discussing the FASB s new leases standard March 15, 2016 Bob Uhl, Partner, Deloitte & Touche LLP James Barker, Partner, Deloitte & Touche LLP

FSA Faculty Consortium Technical Accounting Update. Bob Uhl, partner, Deloitte & Touche LLP

FSA Faculty Consortium Technical Accounting Update Bob Uhl, partner, Deloitte & Touche LLP Deloitte University May 30, 2014 Acronyms Acronym ASC ASU ED FASB IASB IFRS U.S. GAAP Full Form Accounting Standards

FSA Faculty Consortium Technical Accounting Update Bob Uhl, partner, Deloitte & Touche LLP Deloitte University May 30, 2014 Acronyms Acronym ASC ASU ED FASB IASB IFRS U.S. GAAP Full Form Accounting Standards

FASB and IASB Continue Making Decisions on Lease Accounting

Accounting Journal Entry FASB and IASB Continue Making Decisions on Lease Accounting March 28, 2011 At recent meetings, the FASB and IASB (the boards ) have continued to make progress on the leases project,

Accounting Journal Entry FASB and IASB Continue Making Decisions on Lease Accounting March 28, 2011 At recent meetings, the FASB and IASB (the boards ) have continued to make progress on the leases project,

The new accounting standard for leases. 27 March 2017

The new accounting standard for leases 27 March 2017 Disclaimer Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity.

The new accounting standard for leases 27 March 2017 Disclaimer Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity.

Technical Line FASB final guidance

No. 2016-09 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect health care entities In this issue: Overview... 1 Key considerations... 3 Scope and scope exceptions...

No. 2016-09 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect health care entities In this issue: Overview... 1 Key considerations... 3 Scope and scope exceptions...

Applying the new lease accounting standard

Applying the new lease accounting standard In February 26, the FASB issued Accounting Standards Update (ASU) No. 26-, Leases (codified as Accounting Standards Codification Topic (ASC) 842). ASC 842 introduces

Applying the new lease accounting standard In February 26, the FASB issued Accounting Standards Update (ASU) No. 26-, Leases (codified as Accounting Standards Codification Topic (ASC) 842). ASC 842 introduces

Technical Line FASB final guidance

No. 2019-01 3 January 2019 Technical Line FASB final guidance How the new leases standard affects automotive entities In this issue: Overview... 1 Recent standard setting activity... 2 Key considerations...

No. 2019-01 3 January 2019 Technical Line FASB final guidance How the new leases standard affects automotive entities In this issue: Overview... 1 Recent standard setting activity... 2 Key considerations...

Technical Line FASB final guidance

No. 2018-18 13 December 2018 Technical Line FASB final guidance How the new leases standard affects life sciences entities In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions...

No. 2018-18 13 December 2018 Technical Line FASB final guidance How the new leases standard affects life sciences entities In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions...

Defining Issues May 2013, No

Defining Issues May 2013, No. 13-24 FASB and IASB Issue Revised Exposure Drafts on Lease Accounting The FASB and IASB (the Boards) recently issued revised joint exposure drafts (EDs) on proposed changes

Defining Issues May 2013, No. 13-24 FASB and IASB Issue Revised Exposure Drafts on Lease Accounting The FASB and IASB (the Boards) recently issued revised joint exposure drafts (EDs) on proposed changes

Lease Accounting and Loan Covenants: What is the Impact?

Lease Accounting and Loan Covenants: What is the Impact? Monday June 26, 2017 9:15 AM 10:30 AM Presented by: Charlie Shannon Partner Moss Adams LLP 8750 N. Central Expressway, Suite 300 Dallas, TX 75231

Lease Accounting and Loan Covenants: What is the Impact? Monday June 26, 2017 9:15 AM 10:30 AM Presented by: Charlie Shannon Partner Moss Adams LLP 8750 N. Central Expressway, Suite 300 Dallas, TX 75231

Summary of IFRS Exposure Draft Leases

The International Accounting Standards Board (IASB) recently issued a revised exposure draft (ED) relating to leases. Once these proposals are finalized the new guidance will replace the IAS 17 Leases.

The International Accounting Standards Board (IASB) recently issued a revised exposure draft (ED) relating to leases. Once these proposals are finalized the new guidance will replace the IAS 17 Leases.

What private companies need to know about applying the new lease standard

What private companies need to know about applying the new lease standard In February 26, the FASB issued Accounting Standards Update (ASU) No. 26-, Leases (codified as Accounting Standards Codification

What private companies need to know about applying the new lease standard In February 26, the FASB issued Accounting Standards Update (ASU) No. 26-, Leases (codified as Accounting Standards Codification

Technical Line FASB final guidance

No. 2018-08 20 September 2018 Technical Line FASB final guidance How the new leases standard affects engineering and construction entities In this issue: Overview... 1 Key considerations... 2 Scope and

No. 2018-08 20 September 2018 Technical Line FASB final guidance How the new leases standard affects engineering and construction entities In this issue: Overview... 1 Key considerations... 2 Scope and

CPE regulations require online participants to take part in online questions

KPMG s CFO Financial Forum Webcast FASB/IASB Revised Lease Accounting Exposure Drafts A Detailed Look Part III: Lessor Accounting June 25, 2013 Administrative CPE regulations require online participants

KPMG s CFO Financial Forum Webcast FASB/IASB Revised Lease Accounting Exposure Drafts A Detailed Look Part III: Lessor Accounting June 25, 2013 Administrative CPE regulations require online participants

Leases: Overview of the new guidance

Leases: Overview of the new guidance Prepared by: Richard Stuart, Partner, National Professional Standards Group, RSM US LLP richard.stuart@rsmus.com, +1 203 905 5027 March 2, 2016 Introduction On February

Leases: Overview of the new guidance Prepared by: Richard Stuart, Partner, National Professional Standards Group, RSM US LLP richard.stuart@rsmus.com, +1 203 905 5027 March 2, 2016 Introduction On February

Consumer & Industrial Products Spotlight Proposed Changes to Lessor Accounting: The Lessor of Two Evils?

Issue 1, June 2013 Consumer & Industrial Products Spotlight Proposed Changes to Lessor Accounting: The Lessor of Two Evils? In This Issue: Background Key Issues Other Items Challenges Thinking Ahead Entities

Issue 1, June 2013 Consumer & Industrial Products Spotlight Proposed Changes to Lessor Accounting: The Lessor of Two Evils? In This Issue: Background Key Issues Other Items Challenges Thinking Ahead Entities

Leases ASU September 20, 2017

Leases ASU 2016-02 September 20, 2017 Meet the Speakers Tonisha Spratte, CPA Senior Accountant Cherry Bekaert tspratte@cbh.com Matthew Mars Senior Accountant Cherry Bekaert mmars@cbh.com Agenda What is

Leases ASU 2016-02 September 20, 2017 Meet the Speakers Tonisha Spratte, CPA Senior Accountant Cherry Bekaert tspratte@cbh.com Matthew Mars Senior Accountant Cherry Bekaert mmars@cbh.com Agenda What is

Edison Electric Institute and American Gas Association New Lease Standard

Edison Electric Institute and American Gas Association New Lease Standard May 16, 2016 Disclaimer The information contained herein is of a general nature and is not intended to address the circumstances

Edison Electric Institute and American Gas Association New Lease Standard May 16, 2016 Disclaimer The information contained herein is of a general nature and is not intended to address the circumstances

The New Lease Accounting Standard. Hunter Mink, CPA, CCIFP Brian Rosenberg, CPA, MBA

The New Lease Accounting Standard Hunter Mink, CPA, CCIFP Brian Rosenberg, CPA, MBA 1 Agenda Introduction Lease Identification and Classification Lessee Accounting Other Considerations Disclosures Impact

The New Lease Accounting Standard Hunter Mink, CPA, CCIFP Brian Rosenberg, CPA, MBA 1 Agenda Introduction Lease Identification and Classification Lessee Accounting Other Considerations Disclosures Impact

KPMG s CFO. Webcast. Administrative

KPMG s CFO Financial Forum Webcast A Detailed Look at the FASB/IASB Revised Leases Exposure Drafts Part I (Scope, Definition, and Lease Classification) June 13, 2013 Administrative CPE regulations require

KPMG s CFO Financial Forum Webcast A Detailed Look at the FASB/IASB Revised Leases Exposure Drafts Part I (Scope, Definition, and Lease Classification) June 13, 2013 Administrative CPE regulations require

Technical Line FASB final guidance

No. 2016-11 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect real estate entities In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions...

No. 2016-11 14 April 2016 Technical Line FASB final guidance How the FASB s new leases standard will affect real estate entities In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions...

GASB Update. Airports Council International North America 2017 Finance Committee Workshop. Blake Rodgers, Senior Manager September 17, 2017

GASB Update Airports Council International North America 2017 Finance Committee Workshop Blake Rodgers, Senior Manager September 17, 2017 Agenda High Level Overview of GASB Statement No. 87, Leases Other

GASB Update Airports Council International North America 2017 Finance Committee Workshop Blake Rodgers, Senior Manager September 17, 2017 Agenda High Level Overview of GASB Statement No. 87, Leases Other

Lease accounting scope & impacts

Leasing Lease accounting scope & impacts Scope What s in? All industries, all entities Arrangements that meet the definition of a lease Embedded leases within other arrangements What s out? Leases of:

Leasing Lease accounting scope & impacts Scope What s in? All industries, all entities Arrangements that meet the definition of a lease Embedded leases within other arrangements What s out? Leases of:

New leases standard ASC 842 Lessee - operating leases. Itai Gotlieb, Partner, Professional Practice July 2017

ASC 842 Lessee - operating leases Itai Gotlieb, Partner, Professional Practice July 2017 Overview Under Accounting Standards Codification (ASC) 842, Leases, lessees recognize assets and liabilities for

ASC 842 Lessee - operating leases Itai Gotlieb, Partner, Professional Practice July 2017 Overview Under Accounting Standards Codification (ASC) 842, Leases, lessees recognize assets and liabilities for

Technical Line FASB final guidance

No. 2018-15 6 December 2018 Technical Line FASB final guidance How the new leases standard affects consumer products and retail entities In this issue: Overview... 1 Recent standard-setting activity...

No. 2018-15 6 December 2018 Technical Line FASB final guidance How the new leases standard affects consumer products and retail entities In this issue: Overview... 1 Recent standard-setting activity...

Click to edit Master title style REVENUE RECOGNITION Understanding the New Revenue Recognition Standard ASC 606

Click to edit Master title style REVENUE RECOGNITION Understanding the New Revenue Recognition Standard ASC 606 9/7/2017 0 Agenda Overview of ASC 606 Review of the five-step process Accounting for contract

Click to edit Master title style REVENUE RECOGNITION Understanding the New Revenue Recognition Standard ASC 606 9/7/2017 0 Agenda Overview of ASC 606 Review of the five-step process Accounting for contract

On the Horizon: Leases and Fiduciary Responsibilities

On the Horizon: Leases and Fiduciary Responsibilities Dean Michael Mead, Research Manager Florida School Finance Officers Association November 11, 2015 The views expressed in this presentation are those

On the Horizon: Leases and Fiduciary Responsibilities Dean Michael Mead, Research Manager Florida School Finance Officers Association November 11, 2015 The views expressed in this presentation are those

The joint leases project change is coming

No. 2010-4 18 June 2010 Technical Line Technical guidance on standards and practice issues The joint leases project change is coming What you need to know The proposed changes to the accounting for leases

No. 2010-4 18 June 2010 Technical Line Technical guidance on standards and practice issues The joint leases project change is coming What you need to know The proposed changes to the accounting for leases

Executive Summary. New leases standard Lessees

Executive Summary December 2018 The new leases standard focuses on increased transparency and comparability providing financial statement users with more information about an entity s leasing activities.

Executive Summary December 2018 The new leases standard focuses on increased transparency and comparability providing financial statement users with more information about an entity s leasing activities.

Proposed New Accounting Standards For Leases

Relationships backed by performance. Proposed New Accounting Standards For Leases Doug Richardson Live Seminar 9:00am 10:30am June 21 2012 Overview and Background Leases serve a vital role in many entities

Relationships backed by performance. Proposed New Accounting Standards For Leases Doug Richardson Live Seminar 9:00am 10:30am June 21 2012 Overview and Background Leases serve a vital role in many entities

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions. August 24, 2017

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions August 24, 2017 Learning objectives Define leasing implications related to recently revised FASB standard Differentiate between new

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions August 24, 2017 Learning objectives Define leasing implications related to recently revised FASB standard Differentiate between new

Technical Line FASB final guidance

No. 2018-10 11 October 2018 Technical Line FASB final guidance How the new leases standard affects airlines In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions... 2 Definition

No. 2018-10 11 October 2018 Technical Line FASB final guidance How the new leases standard affects airlines In this issue: Overview... 1 Key considerations... 2 Scope and scope exceptions... 2 Definition

4/4/2018. GASB's New Leases Standard

GASB's New Leases Standard April 4, 2018 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in a group Complete group attendance form

GASB's New Leases Standard April 4, 2018 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in a group Complete group attendance form

Lease & Finance Accountants Conference. September The Westin Charlotte Charlotte, NC

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Lessor Accounting under ASC 842 EQUIPMENT LEASING AND FINANCE ASSOCIATION Presenters Rod Hurd Chief

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Lessor Accounting under ASC 842 EQUIPMENT LEASING AND FINANCE ASSOCIATION Presenters Rod Hurd Chief

FASB/IASB Update Part II

American Accounting Association FASB/IASB Update Part II Tom Linsmeier FASB Member August 3, 2014 The views expressed in this presentation are those of the presenters. Official positions of the FASB/IASB

American Accounting Association FASB/IASB Update Part II Tom Linsmeier FASB Member August 3, 2014 The views expressed in this presentation are those of the presenters. Official positions of the FASB/IASB

IFRS 16 LEASES. Page 1 of 21

IFRS 16 LEASES OBJECTIVE The objective is to ensure that lessees and lessors provide relevant information in a manner that faithfully represents those transactions. This information gives a basis for users

IFRS 16 LEASES OBJECTIVE The objective is to ensure that lessees and lessors provide relevant information in a manner that faithfully represents those transactions. This information gives a basis for users

LEASES WHERE ARE WE? Steve Rathjen

LEASES WHERE ARE WE? Steve Rathjen 267 256-3110 srathjen@kpmg.com Agenda Project status Lease definition and classification Lessee accounting Lessor accounting Presentation, disclosures, and transition

LEASES WHERE ARE WE? Steve Rathjen 267 256-3110 srathjen@kpmg.com Agenda Project status Lease definition and classification Lessee accounting Lessor accounting Presentation, disclosures, and transition

Lease Accounting Standard Update ASU Presented by: Nicholas Hoefel, CPA Manager, Audit Services Group

Lease Accounting Standard Update ASU 2016-02 Presented by: Nicholas Hoefel, CPA Manager, Audit Services Group 1 Overview Introduction Background and current environment Effective dates and transition Key

Lease Accounting Standard Update ASU 2016-02 Presented by: Nicholas Hoefel, CPA Manager, Audit Services Group 1 Overview Introduction Background and current environment Effective dates and transition Key

Miles CPA Review: FAR Updates

Miles CPA Review: FAR - 2019 Updates Summary of updates: - FAR-4.4: s [ASC 842] effective fiscal years beginning after Dec 15, 2018 (for issuers) and effective fiscal years beginning after Dec 15, 2019

Miles CPA Review: FAR - 2019 Updates Summary of updates: - FAR-4.4: s [ASC 842] effective fiscal years beginning after Dec 15, 2018 (for issuers) and effective fiscal years beginning after Dec 15, 2019

GASB 87 - Leases. South Carolina Association of CPAs Fall Fest November 16, 2018 Mauldin & Jenkins

November 16, 2018 Mauldin & Jenkins 800-277-0050 www.mjcpa.com GASB 87 - Leases Effective for periods beginning after December 15, 2019 - December 31, 2020 or June 30, 2021 or September 30, 2021 Amends

November 16, 2018 Mauldin & Jenkins 800-277-0050 www.mjcpa.com GASB 87 - Leases Effective for periods beginning after December 15, 2019 - December 31, 2020 or June 30, 2021 or September 30, 2021 Amends

Gearing up for change New IFRS on Leases

Gearing up for change New IFRS on Leases In a nutshell The changes Lessee accounting Effective date: 1 January 2019 Limited changes to scope of IAS 17 Enhanced guidance on identifying a lease Lessor accounting

Gearing up for change New IFRS on Leases In a nutshell The changes Lessee accounting Effective date: 1 January 2019 Limited changes to scope of IAS 17 Enhanced guidance on identifying a lease Lessor accounting

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions. August 24, 2017

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions August 24, 2017 Learning objectives Define leasing implications related to recently revised FASB standard Differentiate between new

Preparing for the new ASC 842 Leasing Standard Challenges and Solutions August 24, 2017 Learning objectives Define leasing implications related to recently revised FASB standard Differentiate between new

Leases. Tatsumi Yamada Board Member and Partner KPMG AZSA LLC (Former Board Member of the IASB)

") Leases Tatsumi Yamada Board Member and Partner KPMG AZSA LLC (Former Board Member of the IASB) Contents Project Development Key point related to recognition of assets and liabilities Separation of service

Leases Tatsumi Yamada Board Member and Partner KPMG AZSA LLC (Former Board Member of the IASB) Contents Project Development Key point related to recognition of assets and liabilities Separation of service

IASB Staff Paper March 2011

IASB Staff Paper March 2011 Effect of board redeliberations on Exposure Draft Leases About this staff paper This staff paper indicates how the proposals in the Exposure Draft Leases would change as a result

IASB Staff Paper March 2011 Effect of board redeliberations on Exposure Draft Leases About this staff paper This staff paper indicates how the proposals in the Exposure Draft Leases would change as a result

Preview of the New Exposure Draft of the Lease Accounting Project Key elements and commentary

Preview of the New Exposure Draft of the Lease Accounting Project Key elements and commentary Prepared by Bill Bosco, Leasing 101 www.leasing-101.com The Financial Accounting Standards Board (FASB) and

Preview of the New Exposure Draft of the Lease Accounting Project Key elements and commentary Prepared by Bill Bosco, Leasing 101 www.leasing-101.com The Financial Accounting Standards Board (FASB) and

The Dbriefs Financial Reporting series presents: FAQs about the new FASB leases standard: You're not alone

The Dbriefs Financial Reporting series presents: FAQs about the new FASB leases standard: You're not alone May 8, 2017 Bob Uhl, Partner, Deloitte & Touche LLP James Barker, Partner, Deloitte & Touche LLP

The Dbriefs Financial Reporting series presents: FAQs about the new FASB leases standard: You're not alone May 8, 2017 Bob Uhl, Partner, Deloitte & Touche LLP James Barker, Partner, Deloitte & Touche LLP

Leases Refashioned. The Bottom Line. Retail & Distribution Spotlight January In This Issue

Retail & Distribution Spotlight January 2017 In This Issue Background Key Issues Challenges Thinking Ahead Contacts Leases Refashioned The Bottom Line On February 25, 2016, the FASB issued its new leases

Retail & Distribution Spotlight January 2017 In This Issue Background Key Issues Challenges Thinking Ahead Contacts Leases Refashioned The Bottom Line On February 25, 2016, the FASB issued its new leases

Heads Up. FASB Draws a Bright Line Through Operating Leases Proposed ASU Revamps Lease. Accounting. The ED, released by the FASB as a proposed

August 17, 2010 Volume 17, Issue 27 Heads Up In This Issue: Background Effective Date In a Nutshell Scope Lessee Accounting Lessor Accounting Presentation and Disclosures Transition The ED, released by

August 17, 2010 Volume 17, Issue 27 Heads Up In This Issue: Background Effective Date In a Nutshell Scope Lessee Accounting Lessor Accounting Presentation and Disclosures Transition The ED, released by

Lease Accounting Standard

Lease Accounting Standard AGA/EEI Spring Accounting Conference May 22, 2017 Lease Identification & Lease Classification Lease identification Identified asset Control over use Lease Asset is explicitly

Lease Accounting Standard AGA/EEI Spring Accounting Conference May 22, 2017 Lease Identification & Lease Classification Lease identification Identified asset Control over use Lease Asset is explicitly

Deeper Dive Leases. Overview

Deeper Dive Leases Presented by: Shaun Johnson, CPA Dingus, Zarecor & Associates PLLC Overview Effective dates Big picture Objective, impact, and implementation Applicability and definition Initial recognition

Deeper Dive Leases Presented by: Shaun Johnson, CPA Dingus, Zarecor & Associates PLLC Overview Effective dates Big picture Objective, impact, and implementation Applicability and definition Initial recognition

What Nonprofits Need to Know About the New Standards for Lease Accounting

The webcast will start at 1 p.m. Eastern Please note: Handout You can print or download the webcast handout at https://capincrouse.com/webcast-lease-accounting CPE CPE certificates will be emailed to you

The webcast will start at 1 p.m. Eastern Please note: Handout You can print or download the webcast handout at https://capincrouse.com/webcast-lease-accounting CPE CPE certificates will be emailed to you

ASC Topic 842 Leases. September 25 &

ASC Topic 842 Leases September 25 & 26 2017 This presentation is intended solely for the information and use of the EEI and AGA and is not intended to be and should not be used by anyone other than these

ASC Topic 842 Leases September 25 & 26 2017 This presentation is intended solely for the information and use of the EEI and AGA and is not intended to be and should not be used by anyone other than these

Implementing the New Lease Guidance

Implementing the New Lease Guidance October 22, 2018 2018 Crowe LLP 2018 Crowe LLP Agenda Background Scope Effective dates & transition requirements Lessee accounting model Lessor accounting model Specialized

Implementing the New Lease Guidance October 22, 2018 2018 Crowe LLP 2018 Crowe LLP Agenda Background Scope Effective dates & transition requirements Lessee accounting model Lessor accounting model Specialized

IFRS 16 Leases supplement

IFRS 16 Leases supplement Guide to annual financial statements IFRS December 2017 kpmg.com/ifrs Contents About this supplement 1 About IFRS 16 3 The Group s lease portfolio 6 Part I Modified retrospective

IFRS 16 Leases supplement Guide to annual financial statements IFRS December 2017 kpmg.com/ifrs Contents About this supplement 1 About IFRS 16 3 The Group s lease portfolio 6 Part I Modified retrospective

International Financial Reporting Standard 16 Leases. Objective. Scope. Recognition exemptions (paragraphs B3 B8) IFRS 16

IFRS 16") International Financial Reporting Standard 16 Leases Objective 1 This Standard sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective is to ensure

International Financial Reporting Standard 16 Leases Objective 1 This Standard sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective is to ensure

Something Borrowed, Something New Get Ready for the New Lease Accounting Standard

April 2016 Something Borrowed, Something New Get Ready for the New Lease Accounting Standard By Scott G. Lehman, CPA, and David E. Wentzel, CPA Audit / Tax / Advisory / Risk / Performance Smart decisions.

April 2016 Something Borrowed, Something New Get Ready for the New Lease Accounting Standard By Scott G. Lehman, CPA, and David E. Wentzel, CPA Audit / Tax / Advisory / Risk / Performance Smart decisions.

Lease Update. June 2017 Addison, Texas

Lease Update June 2017 Addison, Texas William Bill Schneider CPA, CGMA Bill is an Audit Director at AT&T. AT&T delivers advanced mobile services, next-generation TV, highspeed internet and smart solutions

Lease Update June 2017 Addison, Texas William Bill Schneider CPA, CGMA Bill is an Audit Director at AT&T. AT&T delivers advanced mobile services, next-generation TV, highspeed internet and smart solutions

ASC 842: Leases. Presented by: Maxwell Locke & Ritter LLP June 15, Maxwell Locke & Ritter

ASC 842: Leases Presented by: Maxwell Locke & Ritter LLP June 15, 2018 The New Lease Standard FASB ASC 842, Leases Supersedes FASB ASC 840, Leases Effective for calendar year-end public companies in 2019;

ASC 842: Leases Presented by: Maxwell Locke & Ritter LLP June 15, 2018 The New Lease Standard FASB ASC 842, Leases Supersedes FASB ASC 840, Leases Effective for calendar year-end public companies in 2019;

Technical Line FASB final guidance

No. 2018-11 11 October 2018 Technical Line FASB final guidance How the new leases standard affects telecom and media and entertainment entities In this issue: Overview... 1 Key considerations... 2 Scope

No. 2018-11 11 October 2018 Technical Line FASB final guidance How the new leases standard affects telecom and media and entertainment entities In this issue: Overview... 1 Key considerations... 2 Scope

Financial Computer Systems Inc. (203)

") Introduction to ASC 842 and EZLease Financial Computer Systems Inc. www.ezlease.net (203) 652-1375 The road to ASC 842 Begun in July 2006; joint project of FASB & IASB Primary purpose: Put lessee operating

Introduction to ASC 842 and EZLease Financial Computer Systems Inc. www.ezlease.net (203) 652-1375 The road to ASC 842 Begun in July 2006; joint project of FASB & IASB Primary purpose: Put lessee operating

How the lease accounting proposal might affect your company

Applying IFRS How the lease accounting proposal might affect your company August 2013 Contents 1. Overview... 1 2. Identifying a lease... 2 2.1 Scope exclusions... 2 2.2 Definition of a lease... 3 2.2.1

Applying IFRS How the lease accounting proposal might affect your company August 2013 Contents 1. Overview... 1 2. Identifying a lease... 2 2.1 Scope exclusions... 2 2.2 Definition of a lease... 3 2.2.1

Measuring Lease Liabilities EQUIPMENT LEASING AND FINANCE ASSOCIATION

Measuring Lease Liabilities EQUIPMENT LEASING AND FINANCE ASSOCIATION Presenters Kerrie Cadugan, Executive Director, EY Barbara Galaini, Chief Accounting Officer of the Americas, Avolon The views expressed

Measuring Lease Liabilities EQUIPMENT LEASING AND FINANCE ASSOCIATION Presenters Kerrie Cadugan, Executive Director, EY Barbara Galaini, Chief Accounting Officer of the Americas, Avolon The views expressed

Defining Issues. FASB Completes Technical Redeliberations on Leases. October 2015, No Key Facts. Key Impacts

Defining Issues October 2015, No. 15-47 FASB Completes Technical Redeliberations on Leases The FASB met on October 7 to discuss comments received and related follow-up issues on the external review of

Defining Issues October 2015, No. 15-47 FASB Completes Technical Redeliberations on Leases The FASB met on October 7 to discuss comments received and related follow-up issues on the external review of

Headline Verdana Bold The evolutions of leases accounting under IFRS 16 Mariano Bruno, Carlo Laganà, Giuseppe Ambrosio, Deloitte & Touche S.p.A.

SHIPPING AND THE LAW 7^ Edition 25-26 October 2016 NAPLES Headline Verdana Bold The evolutions of leases accounting under IFRS 16 Mariano Bruno, Carlo Laganà, Giuseppe Ambrosio, Deloitte & Touche S.p.A.

SHIPPING AND THE LAW 7^ Edition 25-26 October 2016 NAPLES Headline Verdana Bold The evolutions of leases accounting under IFRS 16 Mariano Bruno, Carlo Laganà, Giuseppe Ambrosio, Deloitte & Touche S.p.A.

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N AGENDA Leases FASB & GASB Revenue Recognition FASB 2 FASB ASU 2016-02, Leases (Topic

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N AGENDA Leases FASB & GASB Revenue Recognition FASB 2 FASB ASU 2016-02, Leases (Topic

GASB 87. OVERVIEW: Supersedes GASB s 13 and 62 (paragraphs ).

.") Leases OVERVIEW: Supersedes GASB s 13 and 62 (paragraphs 211-271). Will require significant changes from its current practice, particularly in the accounting for operating leases Effective for reporting

Leases OVERVIEW: Supersedes GASB s 13 and 62 (paragraphs 211-271). Will require significant changes from its current practice, particularly in the accounting for operating leases Effective for reporting

HKFRS 16 Leases sets out the principles for the recognition, measurement, presentation and disclosure

HKFRS 16 Leases Introduction HKFRS 16 Leases sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective of HKFRS 16 is to ensure that lessees and lessors

HKFRS 16 Leases Introduction HKFRS 16 Leases sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective of HKFRS 16 is to ensure that lessees and lessors

Impact of lease accounting changes to corporate real estate

Impact of lease accounting changes to corporate real estate Overview In February 2016, the Financial Accounting Standards Board (FASB) issued its long-awaited revision to lease accounting Accounting Standards

Impact of lease accounting changes to corporate real estate Overview In February 2016, the Financial Accounting Standards Board (FASB) issued its long-awaited revision to lease accounting Accounting Standards

IFRS Project Insights Leases

IFRS Project Insights Leases The IASB and FASB ( the Boards ) published a Discussion Paper (DP) setting out a proposed lessee accounting model in March 2009. The proposed accounting model has evolved since

IFRS Project Insights Leases The IASB and FASB ( the Boards ) published a Discussion Paper (DP) setting out a proposed lessee accounting model in March 2009. The proposed accounting model has evolved since

Topic 842- Leases Making The Transition

Topic 842- Leases Making The Transition K-deep Dhaliwal, Partner, Moss Adams LLP Adam Hite, Senior Manager, Moss Adams LLP The material appearing in this presentation is for informational purposes only

Topic 842- Leases Making The Transition K-deep Dhaliwal, Partner, Moss Adams LLP Adam Hite, Senior Manager, Moss Adams LLP The material appearing in this presentation is for informational purposes only

IFRS Update Guy Thomas, CPA, CA

IFRS Update Guy Thomas, CPA, CA D&Co IFRS update Agenda 3 new standards under IFRS IFRS 9 Financial Instruments IFRS 15 Revenue from Contracts with Customers IFRS 16 Leases Agenda Some narrow scope amendments

IFRS Update Guy Thomas, CPA, CA D&Co IFRS update Agenda 3 new standards under IFRS IFRS 9 Financial Instruments IFRS 15 Revenue from Contracts with Customers IFRS 16 Leases Agenda Some narrow scope amendments

NEED TO KNOW. Leases A Project Update

NEED TO KNOW Leases A Project Update 2 LEASES - A PROJECT UPDATE TABLE OF CONTENTS Introduction 3 Existing guidance and the rationale for change 4 The IASB/FASB project to date 5 The main proposals 6 Definition

NEED TO KNOW Leases A Project Update 2 LEASES - A PROJECT UPDATE TABLE OF CONTENTS Introduction 3 Existing guidance and the rationale for change 4 The IASB/FASB project to date 5 The main proposals 6 Definition

Financial reporting developments. A comprehensive guide. Lease accounting. Accounting Standards Codification 842, Leases.

Financial reporting developments A comprehensive guide Lease accounting Accounting Standards Codification 842, Leases October 2018 To our clients and other friends Accounting Standard Codification (ASC)

Financial reporting developments A comprehensive guide Lease accounting Accounting Standards Codification 842, Leases October 2018 To our clients and other friends Accounting Standard Codification (ASC)

MONITORDAILY SPECIAL REPORT. Lease Accounting Project Update as of May 25, 2011 Prepared by Bill Bosco, Leasing 101

MONITORDAILY SPECIAL REPORT Lease Accounting Project Update as of May 25, 2011 Prepared by Bill Bosco, Leasing 101 The high volume of comment letters (780+) and numerous outreach meetings had common criticisms

MONITORDAILY SPECIAL REPORT Lease Accounting Project Update as of May 25, 2011 Prepared by Bill Bosco, Leasing 101 The high volume of comment letters (780+) and numerous outreach meetings had common criticisms

Brad Bonde, CPA Senior Manager, HC Services/Audit & Advisory

Brad Bonde, CPA Senior Manager, HC Services/Audit & Advisory Overview Background Improving Lease Accounting Scope Accounting Models Disclosures Effective Dates 2 Background Source - FASB 3 QUIZ What amount

Brad Bonde, CPA Senior Manager, HC Services/Audit & Advisory Overview Background Improving Lease Accounting Scope Accounting Models Disclosures Effective Dates 2 Background Source - FASB 3 QUIZ What amount

Lease Accounti ng Standar

Lease Accounti ng Standar AGA Accounting Principles Committee August 14, 2017 AGENDA - INTRODUCTION - LEASE IDENTIFICATION/CLASSIFICATION - (Easement and Lateral Discussion) - LEASE vs NON LEASE - LEASE

Lease Accounti ng Standar AGA Accounting Principles Committee August 14, 2017 AGENDA - INTRODUCTION - LEASE IDENTIFICATION/CLASSIFICATION - (Easement and Lateral Discussion) - LEASE vs NON LEASE - LEASE

IFRS industry insights

IFRS Global Office September 2011 IFRS industry insights The Leases Project An update for the consumer business industry The tentative decision to limit the extent to which variable payments are estimated

IFRS Global Office September 2011 IFRS industry insights The Leases Project An update for the consumer business industry The tentative decision to limit the extent to which variable payments are estimated

REAL ESTATE PERSPECTIVE ON NEW LEASE ACCOUNTING STANDARDS

VALUATION & ADVISORY REAL ESTATE PERSPECTIVE ON NEW LEASE ACCOUNTING STANDARDS BY JOHN CORBETT, MAI, ASA, FRICS AND MARC R. SHAPIRO, MAI, MRICS INTRODUCTION The Financial Accounting Standards Board (FASB)

VALUATION & ADVISORY REAL ESTATE PERSPECTIVE ON NEW LEASE ACCOUNTING STANDARDS BY JOHN CORBETT, MAI, ASA, FRICS AND MARC R. SHAPIRO, MAI, MRICS INTRODUCTION The Financial Accounting Standards Board (FASB)

Leases. January 25, 2016 Comments Due: May 31, Proposed Statement of the Governmental Accounting Standards Board

January 25, 2016 Comments Due: May 31, 2016 Proposed Statement of the Governmental Accounting Standards Board Leases This Exposure Draft of a proposed Statement of Governmental Accounting Standards is

January 25, 2016 Comments Due: May 31, 2016 Proposed Statement of the Governmental Accounting Standards Board Leases This Exposure Draft of a proposed Statement of Governmental Accounting Standards is

Lease & Finance Accountants Conference. September The Westin Charlotte Charlotte, NC

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S EQUIPMENT LEASING AND FINANCE ASSOCIATION Transitioning to the ASC 842 Guidance Lessee Requirements

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S EQUIPMENT LEASING AND FINANCE ASSOCIATION Transitioning to the ASC 842 Guidance Lessee Requirements

A New Lease on Life: The GASB s New Accounting for Leases

Tuesday, May 23, 2017 2:00 3:15PM A New Lease on Life: The GASB s New Accounting for Leases MODERATOR Frances Lee Deputy Chief Financial Officer San Francisco Public Utilities Commission SPEAKERS Stephen

Tuesday, May 23, 2017 2:00 3:15PM A New Lease on Life: The GASB s New Accounting for Leases MODERATOR Frances Lee Deputy Chief Financial Officer San Francisco Public Utilities Commission SPEAKERS Stephen

LEASES: NEW ACCOUNTING REQUIREMENTS FOR LESSEES

Prepared by: Richard Stuart, Partner, National Professional Standards Group, RSM US LLP richard.stuart@rsmus.com, +1 203 905 5027 Contributions by: Teresa Dimattia, Senior Director, National Professional

Prepared by: Richard Stuart, Partner, National Professional Standards Group, RSM US LLP richard.stuart@rsmus.com, +1 203 905 5027 Contributions by: Teresa Dimattia, Senior Director, National Professional

Financial reporting developments. A comprehensive guide. Lease accounting. Accounting Standards Codification 842, Leases.

Financial reporting developments A comprehensive guide Lease accounting Accounting Standards Codification 842, Leases January 2019 To our clients and other friends Accounting Standard Codification (ASC)

Financial reporting developments A comprehensive guide Lease accounting Accounting Standards Codification 842, Leases January 2019 To our clients and other friends Accounting Standard Codification (ASC)

47.1% of organizations concerned about their ability to implement

Leases: Not Just for the 1 Lease Standard - Statistics 10 year project In 2014, $3.0 trillion in off-balance sheet lease commitments 47.1% of organizations concerned about their ability to implement 2

Leases: Not Just for the 1 Lease Standard - Statistics 10 year project In 2014, $3.0 trillion in off-balance sheet lease commitments 47.1% of organizations concerned about their ability to implement 2

PRACTICAL TIPS FOR IMPLEMENTING THE NEW LEASE ACCOUNTING STANDARD

PRACTICAL TIPS FOR IMPLEMENTING THE NEW LEASE ACCOUNTING STANDARD SHAUNA WATSON, VP, GLOBAL HEAD OF TECHNICAL ACCOUNTING MICHAEL ALLEN, PARTNER, TRANSACTION ADVISORY SERVICES 1. Overview of Accounting

PRACTICAL TIPS FOR IMPLEMENTING THE NEW LEASE ACCOUNTING STANDARD SHAUNA WATSON, VP, GLOBAL HEAD OF TECHNICAL ACCOUNTING MICHAEL ALLEN, PARTNER, TRANSACTION ADVISORY SERVICES 1. Overview of Accounting

Is Your Operating Lease An Asset or Liability? It s Now Both

MFM Annual Conference Is Your Operating Lease An Asset or Liability? It s Now Both 23 May 2016-1:30 pm 2:20 pm Disclaimer These slides are for educational purposes only and are not intended, and should

MFM Annual Conference Is Your Operating Lease An Asset or Liability? It s Now Both 23 May 2016-1:30 pm 2:20 pm Disclaimer These slides are for educational purposes only and are not intended, and should

Sri Lanka Accounting Standard - SLFRS 16. Leases

Sri Lanka Accounting Standard - SLFRS 16 Leases CONTENTS from paragraph SRI LANKA ACCOUNTING STANDARD - SLFRS 16 LEASES INTRODUCTION OBJECTIVE 1 SCOPE 3 RECOGNITION EXEMPTIONS 5 IDENTIFYING A LEASE 9 Separating

Sri Lanka Accounting Standard - SLFRS 16 Leases CONTENTS from paragraph SRI LANKA ACCOUNTING STANDARD - SLFRS 16 LEASES INTRODUCTION OBJECTIVE 1 SCOPE 3 RECOGNITION EXEMPTIONS 5 IDENTIFYING A LEASE 9 Separating

In December 2003 the IASB issued a revised IAS 17 as part of its initial agenda of technical projects.

IFRS Standard 16 Leases In April 2001 the International Accounting Standards Board (IASB) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

IFRS Standard 16 Leases In April 2001 the International Accounting Standards Board (IASB) adopted IAS 17 Leases, which had originally been issued by the International Accounting Standards Committee (IASC)

Exposure Draft 64 January 2018 Comments due: June 30, Proposed International Public Sector Accounting Standard. Leases

Exposure Draft 64 January 2018 Comments due: June 30, 2018 Proposed International Public Sector Accounting Standard Leases This document was developed and approved by the International Public Sector Accounting

Exposure Draft 64 January 2018 Comments due: June 30, 2018 Proposed International Public Sector Accounting Standard Leases This document was developed and approved by the International Public Sector Accounting

Financial reporting developments. A comprehensive guide. Lease accounting. Accounting Standards Codification 842, Leases.

Financial reporting developments A comprehensive guide Lease accounting Accounting Standards Codification 842, Leases January 2018 To our clients and other friends Accounting Standard Codification (ASC)

Financial reporting developments A comprehensive guide Lease accounting Accounting Standards Codification 842, Leases January 2018 To our clients and other friends Accounting Standard Codification (ASC)

Lease & Finance Accountants Conference. September The Westin Charlotte Charlotte, NC

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Basic Principles of Lessors under ASC 842 Mamta Shori, Wells Fargo Equipment Finance Joe Sebik,

Lease & Finance Accountants Conference September 11-13 The Westin Charlotte Charlotte, NC H A N D O U T S Basic Principles of Lessors under ASC 842 Mamta Shori, Wells Fargo Equipment Finance Joe Sebik,

by Trevor Farber and Scott Streaser, Deloitte & Touche LLP FASB Accounting Standards Update No , Revenue From Contracts With Customers.

July 2, 2014 Volume 21, Issue 17 Heads Up In This Issue: Background Key Accounting Issues Effective Date and Transition Challenges for Entities That Account for Real Estate Transactions Thinking Ahead

July 2, 2014 Volume 21, Issue 17 Heads Up In This Issue: Background Key Accounting Issues Effective Date and Transition Challenges for Entities That Account for Real Estate Transactions Thinking Ahead

IFRS in Focus. On track for a revised exposure draft on leases. IFRS Global office October Contents

IFRS Global office October 2012 IFRS in Focus On track for a revised exposure draft on leases Contents Introduction Scope Definition of a lease Short-term leases Inception verses commencement Lease term

IFRS Global office October 2012 IFRS in Focus On track for a revised exposure draft on leases Contents Introduction Scope Definition of a lease Short-term leases Inception verses commencement Lease term

AASB 16: Experience the Fundamental Overhaul of Lease Accounting for Lessees

AASB 16: Experience the Fundamental Overhaul of Lease Accounting for Lessees Introduction to Session This introductory session we will: Explore the Principles of AASB 16 Learn how to Identify a Lease Work

AASB 16: Experience the Fundamental Overhaul of Lease Accounting for Lessees Introduction to Session This introductory session we will: Explore the Principles of AASB 16 Learn how to Identify a Lease Work

7/30/2018. Health Care. A CHC-Focused Plan for the New Lease Accounting Standard

Health Care A CHC-Focused Plan for the New Lease Accounting Standard July 31, 2018 1 TO RECEIVE CPE CREDIT Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader

Health Care A CHC-Focused Plan for the New Lease Accounting Standard July 31, 2018 1 TO RECEIVE CPE CREDIT Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader

GASBs Presented by: William Blend, CPA, CFE

GASBs 87-89 Presented by: William Blend, CPA, CFE Leases: Statement 87 Effective Date and General Implementation Effective for Florida fiscal year end 2021. Earlier application is encouraged. Leases should

GASBs 87-89 Presented by: William Blend, CPA, CFE Leases: Statement 87 Effective Date and General Implementation Effective for Florida fiscal year end 2021. Earlier application is encouraged. Leases should

Dataline A look at current financial reporting issues

Dataline A look at current financial reporting issues No. 2013-13 June 13, 2013 What s inside: Overview... 1 At a glance... 1 Background of the project... 1 Key changes from existing GAAP... 2 The proposed

Dataline A look at current financial reporting issues No. 2013-13 June 13, 2013 What s inside: Overview... 1 At a glance... 1 Background of the project... 1 Key changes from existing GAAP... 2 The proposed

Tracking IFRS Exposure draft on Leases

Issue 3 September 2010 Tracking IFRS Exposure draft on Leases 1. Introduction On 17 August 2010, the International Accounting Standards Board (IASB) and the US Financial Accounting Standards Board (FASB)

Issue 3 September 2010 Tracking IFRS Exposure draft on Leases 1. Introduction On 17 August 2010, the International Accounting Standards Board (IASB) and the US Financial Accounting Standards Board (FASB)

IFRS 16 : Lease accounting

IFRS 16 : Lease accounting Effective for accounting periods beginning on or after 1 January 2019 December 2017 IFRS 16: Lease accounting The IASB published the new IFRS 16 lease standard, in order to avoid

IFRS 16 : Lease accounting Effective for accounting periods beginning on or after 1 January 2019 December 2017 IFRS 16: Lease accounting The IASB published the new IFRS 16 lease standard, in order to avoid

IASB Exposure Draft ED/2013/6 - Leases

ACAG AUSTRALASIAN COUNCIL OF AUDITORS GENERAL 13 September 2013 Mr Hans Hoogervorst Chairman International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Dear Mr Hoogervorst

ACAG AUSTRALASIAN COUNCIL OF AUDITORS GENERAL 13 September 2013 Mr Hans Hoogervorst Chairman International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Dear Mr Hoogervorst