Chapter 11 Investments in Noncurrent Operating Assets Utilization and Retirement

|

|

|

- Sherilyn Casey

- 6 years ago

- Views:

Transcription

1 Chapter 11 Investments in Noncurrent Operating Assets Utilization and Retirement 1. The annual depreciation expense 2. The depletion of natural resources 3. The changes in estimates and methods in the computation of depreciation 4. The impairment of asset 5. The amortization or impairment for intangible assets 6. The sale of depreciable assets in exchange for cash and in exchange for other depreciable assets 7. The depreciation for partial periods 8. The MACRS income tax depreciation system 11-1

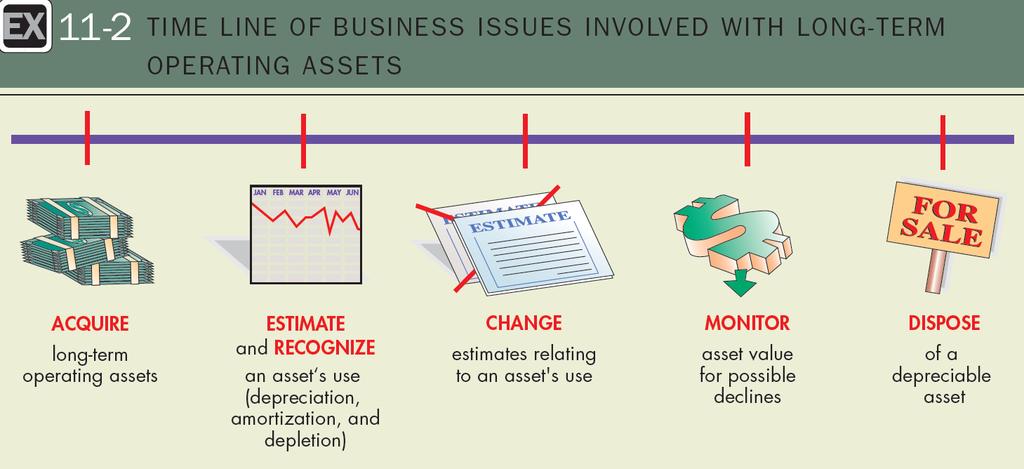

2 11-2

3 1. Use straight-line, accelerated, use-factor, and group depreciation methods to compute annual depreciation What is depreciation? Depreciation is not a process through which a company accumulates a cash fund to replace its long-lived fixed assets. Depreciation is not a way to compute the current value of long-lived assets. Depreciation is the systematic allocation of the cost of an asset over the different periods benefited by the use of the asset. 11-3

4 Factors Affecting the Periodic Depreciation Charge Four factors are taken into consideration in determining the appropriate amount of annual depreciation expense. Asset cost Residual or salvage value Useful life Pattern of use 11-4

5 Depreciation Vocabulary Asset cost is the purchase cost plus any capitalized expenditures. Residual (salvage) value of property is an estimate of the amount for which the asset can be sold when it is retired. Useful life is the expected life of the asset in years, hours of service, or per unit of output. 11-5

6 Useful Life The physical factors that limit the service life of an asset are 1) wear and tear, 2) deterioration and decay, and 3) damage or destruction. The primary functional factor limiting the useful life of assets is obsolescence. 11-6

7 Pattern of Use Depreciable Cost (Asset) To match asset cost against revenue, periodic depreciation charges should reflect as closely as possible the pattern of use. Period 1 Period 2 Period

A depreciation method is")

8 Pattern of Use Depreciable Cost (Asset) A depreciation method is selected to assign these costs to future periods. Period 1 Period 2 Period

Period 1 Period 2 Period 3")

9 Pattern of Use Depreciable Cost (Asset) Period 1 Period 2 Period

10 Pattern of Use Depreciable Cost (Asset) Period 1 Period 2 Period

11 Recording Periodic Depreciation The general form of the journal entry used to recognize depreciation is as follows: Depreciation Expense Accumulated Depreciation xx xx The accumulation of expired cost in a separate account rather than crediting the asset account permits identification of the original cost of the asset and the accumulated depreciation

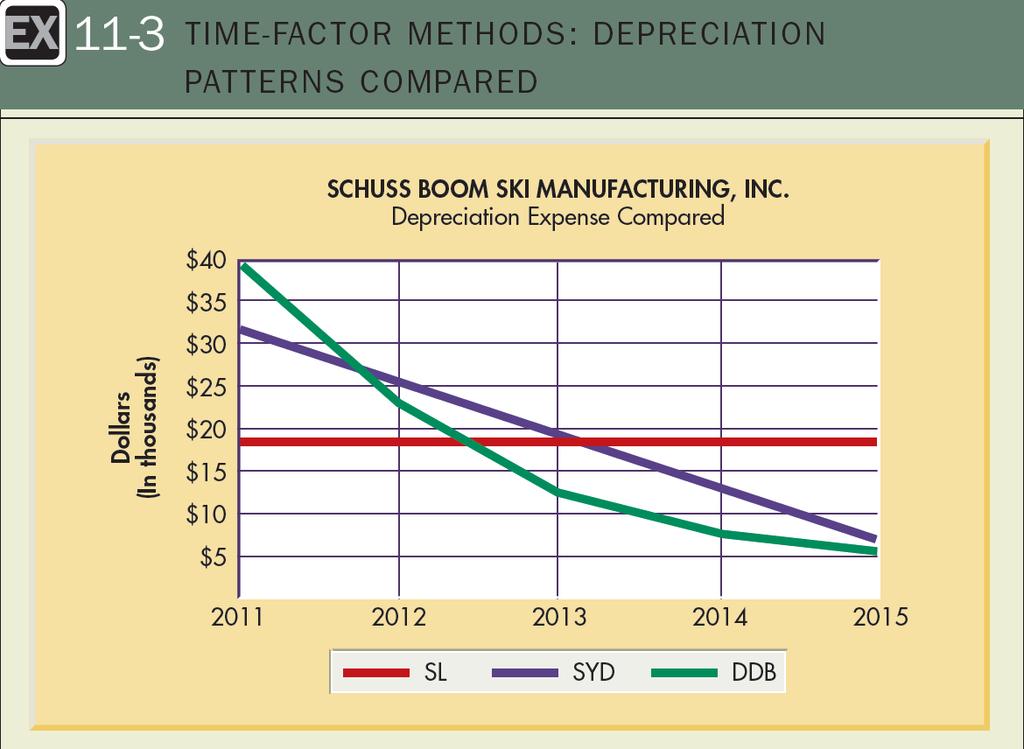

12 Depreciation Formula Symbols The examples that follow assume the acquisition of a polyurethane plastic-molding machine at the beginning of 2013 by Schuss Boom Ski Manufacturing, Inc., at a cost of $100,000 with an estimated residual value of $5,000. C = Asset cost R = Estimated residual value n = Estimated life in years, hours of service, or units of output r = Depreciation rate per period, per hour of service, or per unit of output D = Periodic depreciation charge 11-12

13 Time-Factor Methods Straight-Line Of the time-factor methods, straight-line depreciation is by far the most popular. Straight-line depreciation relates to the passage of time and recognizes equal depreciation in each year of the life of the asset. This method assumes the asset is equally useful during each time period

14 Straight-Line Depreciation Using data for the machine acquired by Schuss Boom Ski Manufacturing and assuming a 5-year life, annual depreciation is computed as follows: C R $100,000 $5,000 D = = N 5 years = $19,000 per year 11-14

15 Straight-Line Depreciation Equals the projected residual value 11-15

16 Sum-of-the-Years Digits Method The sum-of-the-years -digits depreciation method yields decreasing depreciation in each successive year. To determine the denominator, use the following formula (assuming 5 years): [n (n + 1)] SYD = 2 [5 (5 + 1)] SYD = 2 SYD = 15 Or, simple add

17 Sum-of-the-Years Digits Method Now that we know the denominator, we can determine the depreciation for the year using the following formula, where t equals years remaining at the beginning of the period. t D = SYD (C R) D = 5 15 ($100,000 $5,000) D = $31,

18 Sum-of-the-Years Digits Method For the second year, we reduce the numerator by one. t D = SYD (C R) D = 4 15 ($100,000 $5,000) D = $25,333 (continued) 11-18

19 Sum-of-the-Years Digits Method The annual depreciation for all five years: (continued) Equals the projected residual value 11-19

20 Sum-of-the-Years Digits Method $35,000 $28,000 Annual Depreciation Expense $21,000 $14,000 $7,000 Residual Value of $5,000 $

21 Declining-Balance Method The declining-balance depreciation method provides decreasing charges by applying a constant percentage rate to a declining asset book value. First, the constant percentage must be calculated. The most popular rate is two times the straightline rate, and this method is called doubledeclining balance depreciation. The percentage to be used is calculated as shown in Slide

22 Declining-Balance Method 11-22

23 Declining-Balance Method Or you can use the following formula to get the straight-line rate: 1/n Thus, the molding machine would have a straight-line rate of 20% (1/5). This number is doubled to arrive at the double-declining percentage of 40%. The chart shown on Slide demonstrates how the constant rate is applied to the remaining asset book value each year

24 Declining-Balance Method 11-24

25 11-25

26 11-26

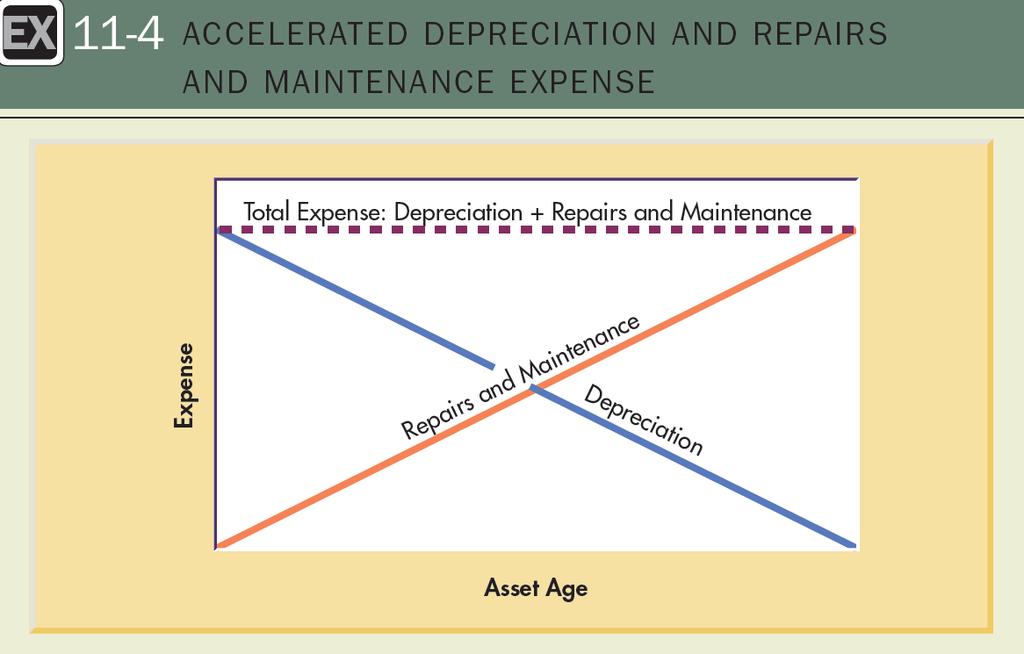

27 Factors Suggesting the Use of an Accelerated Method 1) The anticipation of a significant contribution in early periods with the extent of the contribution to be realized in later periods being less definite. 2) The possibility that inadequacy or obsolescence may result in premature retirement of the asset

28 Use-Factor Methods Use-factor depreciation methods view asset exhaustion as related primarily to asset use or output and provide periodic charges varying with the degree of such services. Service-Hours Depreciation The first use-factor method we will examine is service-hours depreciation. This method is based on the theory that the purchase of an asset represents the purchase of a number of hours of direct service

29 Service-Hours Depreciation Let s continue with the Schuss Boom Ski Manufacturing machine. It cost $100,000 and had a residual value of $5,000. It is estimated that the machine will perform for an estimated service life of 20,000 hours. Now we can determine the rate to be applied to each service hour

30 Service-Hours Depreciation C R D = n = D = $4.75 per hour $100,000 $5,000 20,000 hours Equals the projected residual value 11-30

31 Productive-Output Depreciation Productive-output depreciation is based on the theory that an asset is acquired for the service it can provide in the form of production output. The Schuss Boom asset is estimated to have a productive life of 25,000 units. Assume the company produced 3,200 units in 2013 and 5,400 units in

32 Productive-Output Depreciation r = C R n = $100,000 $5,000 25,000 units r = $3.80 per unit Annual depreciation for 2013 and 2014: 2013: 3,200 units $3.80 = $12, : 5,400 units $3.80 = $20,

33 Group and Composite Depreciation Group depreciation groups similar assets into depreciation accounts (e.g., all of a company s delivery vans). Composite depreciation refers to placing assets in the group that are related but dissimilar (e.g., all of a company s desks, chairs, and computers). The group depreciation procedure treats a collection of assets as a single group

34 Group and Composite Depreciation The rate of 12.5%, applied to the cost of existing assets, $20,000, results in annual depreciation of $2,

35 Group and Composite Depreciation Because the accumulated depreciation account applies to the entire group of assets, no book value can be calculated for any specific asset. If asset B were sold for $3,500 after two years, the following entry would be as follows: Cash 3,500 Accumulated Depreciation 2,500 Equipment 6,000 No gain or loss is recognized

36 Depreciation and IAS 16 The component approach is required under IASB standards. The following requirement is contained in IAS 16: Each part of an item of property, plant and equipment with a cost that is significant in relation to the total cost of the item shall be depreciated separately

37 Depreciation and Accretion of an Asset Retirement Obligation Bryan Beach Company purchases and erects an oil platform at a total cost of $750,000. Bryan Beach is legally obligated to dismantle and remove the platform after 10 years. It is estimated that this will cost $100,000. Assuming an 8% interest rate, the present value of the obligation is $46,319 [ (n = 10; i = 8%) $100,000]

38 Depreciation and Accretion of an Asset Retirement Obligation The journal entries to record the purchase of the oil platform and the recognition of the asset retirement obligation are as follows: Oil Platform 750,000 Cash 750,000 Oil Platform 46,319 Asset Retirement Obligation 46,

39 Depreciation and Accretion of an Asset Retirement Obligation The cost of the oil platform asset, including the estimated retirement obligation, is depreciated just like any other long-term asset. Depreciation Expense 79,632* Accumulated Depreciation Oil Platform 79,632 *Assuming straight-line depreciation [($750,000 + $46,319)/10] 11-39

40 Depreciation and Accretion of an Asset Retirement Obligation Each year an entry must be made to recognize the increase in the present value of the asset retirement obligation. Accretion Expense 3,706* Asset Retirement Obligation 3,706 * ($46,319 x 0.08) = $3,

41 2. Apply the productive-output method to the depletion of natural resources Depletion of Natural Resources Natural resources (also called wasting assets) are consumed as the physical units representing these resources are removed and sold. The computation of depletion expense is an adaption of the productive-output method of depreciation. Perhaps the most difficult problem is estimating the amount of resources available for economical removal from the land

42 Depletion of Natural Resources Land containing mineral deposits is purchased at a cost of $5,500,000. It is expected to have a residual value of $250,000. The natural resource supply is estimated at 1,000,000 tons. The unit-depletion charge and the total depletion charge for the first year, assuming the withdrawal of 80,000 tons, are calculated on Slide

43 Depletion of Natural Resources Depletion charge per ton = $5,500,000 $250,000 1,000,000 tons Depletion charge per ton = $5.25 Depletion for 2013 = $ ,000 tons = $420,

44 Depletion of Natural Resources Record the initial purchase as follows: Mineral Deposits 5,500,000 Cash 5,500,000 Record the depletion for 2013 as follows: Depletion Expense 420,000 Accumulated Depletion (or Mineral Deposits) 420,000 If only 60,000 tons are sold, $105,000 is reported as part of ending inventory

45 28. Incorporate changes in estimates and methods into the computation of depreciation for current and future periods Change in Estimated Life A company purchased $50,000 of equipment and estimated a 10-year life. Using the straightline method with no residual value, the annual depreciation would be $5,000. After four years, accumulated depreciation would amount to $20,000, and the remaining book value would be $30,000. Early in the fifth year, a reevaluation of the life indicates only four more years of service can be expected from the asset

46 Change in Estimated Life Divide the book value by the new estimated remaining life After four years, the book value is $30,000 ($50,000 $20,000) 11-46

47 Change in Estimated Units of Production A change in accounting for natural resources occurs when the estimate of the recoverable units changes as a result of further discoveries, improved extraction processes, or changes in sales prices that indicate changes in the number of units that can be extracted profitably

48 Change in Estimated Units of Production Land is purchased at a cost of $5,500,000 with estimated net residual value of $250,000. The original estimate of natural resources in the land was 1,000,000 tons. In the second year of operations, 100,000 tons of ore are withdrawn. At the end of that year appraisers indicate a remaining tonnage of 950,

49 Change in Estimated Units of Production Cost assignable to recoverable tons as of the beginning of second year: Original costs applicable to depletable resources $5,250,000 Deduct: Depletion charge for first year 420,000 Balance of cost subject to depletion $4,830,

50 Change in Estimated Units of Production Estimated recoverable tons as of the beginning of second year: Number of tons withdrawn in 2 nd year 100,000 Estimated recoverable tons as of the end of the second year 950,000 Total recoverable tons as of the beginning of the second year 1,050,000 Depletion charge per ton for second year: $4,830,000/1,050,000 = $4.60 Depletion charge for second year: 100,000 $4.60 = $460,

51 Change in Estimated Units of Production Cost assignable to recoverable tons as of the beginning of second year: Original costs applicable to depletable resources $5,250,000 Add: Additional costs incurred in 2 nd year 525,000 $5,775,000 Deduct: Depletion charge for first year 420,000 Balance of cost subject to depletion $5,355,000 Estimated recoverable tons as of the beginning of second year 1,050,000 Depletion charge per ton for second year: $5,355,000/1,050,000 = $5.10 Depletion for second year: 100,000 $5.10 = $510,

52 Change in Depreciation Method Another change in estimate occurs when the actual pattern of consumption of an asset doesn t match the pattern of consumption implicit in the depreciation method. Example: An asset is purchased for $120,000 with a 12-year expected useful life and zero salvage value. After two years of straight line depreciation, the asset has a remaining book value of $10,

53 Change in Depreciation Method The company decides the double-decliningbalance method would yield a better estimate of periodic depreciation. The straight-line depreciation rate is 10% (1/n = 1/10 = 10%). Double that rate is 20%. Year 3 depreciation is $100,000 x 0.20, or $20,

54 4. Identify whether an asset is impaired, and measure the amount of the impairment loss using both U.S. GAAP and IASB standards Accounting for Asset Impairment FASB Statement No. 144 addresses four questions: 1. When should an asset be reviewed for possible impairment? An impairment review should be conducted whenever there has been a material change in the way an asset is used or in the business environment

55 Accounting for Asset Impairment 2. When is an asset impaired? An asset is impaired when the undiscounted sum of estimated future cash flows from an asset is less than the book value of the asset

56 Accounting for Asset Impairment 3. How should an impairment loss be measured? The impairment loss is the difference between the book value of the asset and the asset s fair value. The fair value can be approximated using the present value of estimated future cash flows from the asset

57 Accounting for Asset Impairment 4. What information should be disclosed about an impairment? Disclosure should include a description of the impaired asset, reasons for the impairment, a description of the measurement assumptions, and the business segment or segments affected

58 Accounting for Asset Impairment Guangzhou Company purchased a building five years ago for $600,000. It has an expected life of 20 years and no residual value. Guangzhou has decided that the building should be evaluated for possible impairment. Guangzhou estimates that the building has a remaining useful life of 15 years, that net cash inflow from the building will be $25,000 per year, and that the fair value of the building is $230,

59 Accounting for Asset Impairment The $450,000 book value is compared to the $375,000 ($25, years) undiscounted future cash flows. An impairment loss should be recognized. The loss is $220,000 ($450,000 $230,000). The impairment loss would be recorded as follows: Accumulated Depreciation Building 150,000 Loss on Impairment of Building 220,000 Building ($600,000 $230,000) 370,

60 Accounting for Asset Impairment In many cases, it is more appropriate to estimate a range of possible future cash flows rather than make a specific point estimate. It is estimated that the following two cash flow scenarios are possible: Future Cash Inflow Probability Scenario 1 $20,000 per year for 15 years 85% Scenario 2 $50,000 per year for 15 years 15% 11-60

61 Accounting for Asset Impairment Undiscounted Future Cash Inflow Probability Scenario 1 $20,000 x 15 years = $300,000 85% Scenario 2 $50,000 x 15 years = $750,000 15% Probability-Weighted Future Cash Flows Scenario 1 $255,000 Scenario 2 112,500 $367,500 The $367,500 is compared to the book value of the building, indicating impairment

62 Accounting for Asset Impairment Assume there is no observable market value of the building and that the market value must be estimated using present value techniques. If the risk-free interest rate is 6.0%, the expected present value is computed as follows: Future Cash Inflow PV (at 6%) Probability Scenario 1 $20,000 x 15 years $194,245 85% Scenario 2 $50,000 x 15 years $485,612 15% 11-62

63 Accounting for Asset Impairment Probability-Weighted Present Value Scenario 1 $165,108 Scenario 2 72,842 $237,950 The impairment loss entry would be Accumulated Depreciation Building 150,000 Loss on Impairment of Building 212,050 Building ($600,000 $237,950) 362,

64 International Accounting for Asset Impairment: IAS 36 IAS 36 requires that a company recognize an impairment loss whenever the recoverable amount of an asset is less than its book value. Recoverable amount is the higher of the selling price of the asset or the discounted future cash flows associated with the asset s use. IAS 36 allows for the reversal of an impairment loss if events in subsequent years suggest the asset is no longer impaired

65 Recognizing an Upward Asset Revaluation Using the Guangzhou Company example, assume that after five years the fair market value is $540,000. Guangzhou elects to employ the allowable alternative under international standards. The journal entry is needed to recognize the asset revaluation is as follows: Accumulated Depreciation Building 150,000 Revaluation Equity Reserve 90,000 Building ($600,000 $540,000) 60,

66 Recording the Disposal of Revalued Asset Assume that immediately after revaluing the building to $540,000, Guangzhou Company sells it for $540,000 in cash. The disposal would be recorded as follows: Cash 540,000 Building 540,000 Revaluation Equity Reserve 90,000 Retained Earnings 90,000 Note that because Guangzhou chose to revalue the asset, the gain is never reported as a gain

67 5. Discuss the issues impacting proper recognition of amortization or impairment for intangible assets Amortization and Impairment of Intangible Assets Subject to Amortization Intangible assets are to be amortized by the straight-line method unless there is strong justification for using another method. Because companies must disclose both the original cost and the accumulated amortization for an amortizable intangible, the credit should be to a separate accumulated amortization account

68 Amortization and Impairment of Intangible Assets Subject to Amortization Ethereal Company purchased a customer list for $30,000 on January 1, It is expected to have economic value for four years. The expected residual value is zero. On December 31, 2013, the following journal entry is made to recognize amortization expense: Amortization Expense ($30,000/4 years) 7,500 Accumulated Amortization Customer List 7,

69 Amortization and Impairment of Intangible Assets Subject to Amortization During 2014, before the amortization entry is made, a test for impairment is made. The future cash flow of the list is expected to be $15,000 which is less than the book value of $22,500 ($30,000 $7,500). The amount of the impairment loss is $10,500. Impairment Loss ($22,500 $12,000) 10,500 Accumulated Amortization Customer List 7,500 Customer List ($30,000 $12,000) 18,

70 Impairment of Intangibles Not Subject to Amortization The FASB describes the following examples of intangibles with indefinite lives: Broadcast licenses often have a renewal period of 10 years. Because renewal is virtually automatic, such licenses are considered to have an indefinite life. A trademark right is granted for a limited time, but can be renewed almost routinely. If economic factors suggest that the trademark will continue to have value in the foreseeable future, then its useful life is indefinite

71 Impairment of Intangibles Not Subject to Amortization Impalpable Company has a broadcast license that has no foreseeable end to its useful life. The license cost $60,000, and it was estimated that the license generated cash flows of $7,000 per year. Recent events have convinced management that the cash flow will be reduced. The weighted probability shows that the estimated fair value is $52,

72 Impairment of Intangibles Not Subject to Amortization Because the estimated fair value is less than the book value ($52,000 < $60,000), the intangible asset is impaired. The loss is recognized with the following journal entry: Impairment Loss ($60,000 $52,000) 8,000 Broadcast License 8,

73 Procedures in Testing Goodwill for Impairment The procedure in testing goodwill for impairment is a four step test. Buyer Company acquired Target Company on January 1, As part of the acquisition, $1,000 in goodwill was recognized; this goodwill was assigned to Buyer s Manufacturing unit. For 2013, earnings for the Manufacturing unit were $350. Separately traded companies with operations similar to the manufacturing reporting unit have market values approximately equal to six times earning

74 Procedures in Testing Goodwill for Impairment As of December 31, 2013, book and fair values of assets and liabilities of the Manufacturing reporting units are as follow: Book Values Fair Values Identifiable assets $3,500 $4,000 Goodwill 1,000? Liabilities 2,000 2,

75 Procedures in Testing Goodwill for Impairment 1. Compute the fair value of each reporting unit to which goodwill has been assigned. Using the earnings multiple, the fair value of the Manufacturing reporting unit is estimated to be $2,100 ($350 x 6)

76 Procedures in Testing Goodwill for Impairment 2. If the fair value of the reporting unit exceeds the net book value of the assets and liabilities of the reporting unit, the goodwill is assumed to not be impaired and no impairment is recognized. The net book value of the assets and liabilities of the Manufacturing reporting unit is $2,500 [($3,500 +$1,000) $2,000]. Since $2,100 (step 1) is less than $2,500, further computations are needed

77 Procedures in Testing Goodwill for Impairment 3. If the fair value of the reporting unit is less than the net book value of the assets and liabilities of the reporting unit, then a new fair value of goodwill is computed. Goodwill value is always a residual value. Implied fair value of goodwill is calculated as follows: Estimated fair value of Manufacturing $2,100 Fair value of identifiable assets fair value of liabilities ($4,000 $2,000) 2,000 Implied fair value of goodwill $

78 Procedures in Testing Goodwill for Impairment 4. If the implied amount of goodwill computed in (3) is less than the amount initially recorded, a goodwill impairment loss is recognized for the difference. The implied fair value of goodwill is less than the recorded amount of goodwill ($100 < $1,000). The journal entry necessary to recognize goodwill impairment loss is as follows: Goodwill Impairment Loss 900 Goodwill

79 6. Account for the sale of depreciable assets in exchange for cash and in exchange for other depreciable assets Asset Retirement by Sale On July 1, 2013, Landon Supply Co. sells machinery for $43,600 that is recorded on the books at a cost of $83,600 with accumulated depreciation as of January 1, 2013, of $50,600. Assume a 10 percent straight-line rate. Depreciation Expense Machinery 4,180 Accumulated Depreciation Machinery 4,180 To record depreciation for six months in $83,600 x.10 x 6/

80 Asset Retirement by Sale The entry to record the sale is as follows: Cash 43,600 Accumulated Depreciation Machinery 54,780 Machinery 83,600 Gain on Sale of Machinery 14,780 To record sale of machinery at a gain. [$43,600 ($83,600 $54,780)] 11-80

81 Asset Classified as Held for Sale Special accounting is required if the following conditions are satisfied: Management commits to a plan to sell a longterm operating asset. The asset is available for immediate sale. An active effort to locate a buyer is underway. It is probable that the sale will be completed within one year

82 Asset Classified as Held for Sale If the criteria are satisfied, two uncommon accounting actions are required. During the interval between being classified as held for sale and actually being sold: 1. No depreciation is to be recognized, and 2. The asset is to be reported at the lower of its book value or its fair value (less the estimated cost to sell)

83 Asset Classified as Held for Sale On July 1, 2013, Haas Company has a building that cost $100,000 and accumulated depreciation of $35,000. Haas commits to plans to sell the building by March 1, On July 1, 2013, the building has an estimated fair value of $40,000 and it is estimated that the selling costs will be $3,

84 Asset Classified as Held for Sale The following entry would be made on July 1: Building Held for Sale 37,000 Loss on Held-for-Sale Classification 28,000 Accumulated Depreciation Building 35,000 Building 100,000 If the net realizable value had been greater than the book value of $65,000 ($100,000 $35,000), no journal entry would have been made

85 Asset Classified as Held for Sale On December 31, 2013, the estimated selling price was $58,000 (with $3,000 estimated selling costs), the following journal entry would be necessary: Building Held for Sale 18,000 Gain on Recovery Value Held for Sale 18,000 ($58,000 $3,000) $37,

86 Asset Retirement by Exchange for Other Nonmonetary Assets When an operating asset is acquired in exchange for another nonmonetary asset, the new asset acquired is generally recorded at its fair market value or the fair value of the nonmonetary asset given in exchange, whichever is more clearly determinable. However, if the exchange has no real commercial substance, the asset received is sometimes recorded at the BOOK value of the asset given

87 Asset Retirement by Exchange for Other Nonmonetary Assets Delivery equipment that cost $83,600 and has accumulated depreciation of $54,780 is exchanged for delivery equipment that has a fair market value of $43,600. Delivery Equipment 43,600 Accumulated Depreciation Machinery 54,780 Machinery 83,600 Gain on Exchange of Machinery 14,

88 Asset Retirement by Exchange for Other Nonmonetary Assets Assume the delivery equipment s fair market value is not determinable, but the machinery has a market value of $25,000. The entry to record the exchange would be as follows: Delivery Equipment 25,000 Accumulated Depreciation Machinery 54,780 Loss on Exchange of Machinery 3,820 Machinery 83,

89 Asset Retirement by Exchange for Other Nonmonetary Assets Assume the delivery equipment s fair market value is not determinable, but the machinery has a market value of $25,000. In addition to the delivery equipment, cash of $3,000 was received. The entry would be as follows: Cash 3,000 Delivery Equipment 22,000 Accumulated Depreciation Mach. 54,780 Loss on Exchange of Machinery 3,820 Machinery 83,600 Fair market value of machine 11-89

90 Nonmonetary Exchange without Commercial Substance Example 1 No Cash Involved Republic Manufacturing Company owns a molding machine that it decided to exchange for a machine owned by Logan Square Company. The following cost and market data relate to the two machines: 11-90

91 Nonmonetary Exchange without Commercial Substance The entry on Republic s books to record the exchange will be: Machinery (new) 14,000 Accumulated Depreciation Machinery (old) 32,000 Machinery 46,000 The entry on Logan s books to record the exchange will be: Machinery (new) 16,000 Accumulated Depreciation Machinery (old) 37,700 Loss on Exchange of Machinery 300 Machinery (old) 54,

92 Nonmonetary Exchange without Commercial Substance Example 2 Small Amount of Cash Involved Assume the same facts as Example 1, except that it is agreed that Republic s machine has a market value of $16,000 and Logan s machine is worth $17,000. Republic pays Logan $1,000 cash. 17,

93 Nonmonetary Exchange without Commercial Substance The entry on Republic s books to record the exchange will be: Machinery (new) 15,000 Accumulated Depreciation Machinery (old) 32,000 Machinery (old) 46,000 Cash 1,000 The book value of Logan s machine is less than the fair value, indicating a $700 gain ($17,000 $16,300). A portion of the gain should be recognized as having been earned

94 Nonmonetary Exchange without Commercial Substance The amount to be recognized is computed using the following formula: Recognized gain For Logan: = Cash received Cash received + Fair value of x acquired asset Recognized $1,000 gain = x $700 = $41 $1,000 + $16,000 Total indicated gain 11-94

95 Nonmonetary Exchange without Commercial Substance The entry on Logan s books to record the exchange is as follows: Cash 1,000 Machinery (new) 15,341 Accumulated Depreciation Machinery (old) 37,700 Machinery (old) 54,000 Gain on Exchange of Machinery

96 Nonmonetary Exchange without Commercial Substance Example 3 Large Amount of Cash Involved Assume the same facts as in Example 2, except that it is agreed that Republic s machine has a fair value of $12,750 and Logan s machine has a fair value of $17,000. Republic pays Logan $4,250 cash

97 Nonmonetary Exchange without Commercial Substance The entry on Republic s books to record the exchange will be: Machinery (new) 17,000 Accumulated Depreciation Machinery (old) 32,000 Loss on Exchange of Machinery 1,250 Machinery (old) 46,000 Cash 4,250 The entry on Logan s books: Cash 4,250 Machinery (new) 12,750 Accumulated Depreciation Machinery (old) 37,700 Machinery (old) 54,000 Gain on Exchange of Machinery

98 7. Compute depreciation for partial periods, using both straight-line and accelerated methods Depreciation for Partial Periods 1. Nearest whole month 2. Nearest whole year 3. Half-year convention Makes the most intuitive sense 4. No depreciation in year of acquisition; full year depreciation in year of retirement. 5. Full year depreciation in year of acquisition; no depreciation in year of retirement

99 Depreciation for Partial Periods From this point, each year s depreciation will be $6,333 less than the previous year s depreciation

100 Depreciation for Partial Periods Sum-of-the-Years -Digits Method

101 Depreciation for Partial Periods Declining-Balance Method If the asset was purchased three-fourths of the way through the fiscal year and the firm uses the double-declining-balance depreciation, the annual expense for depreciation is shown on the following slide

102 Depreciation for Partial Periods Declining-Balance Method

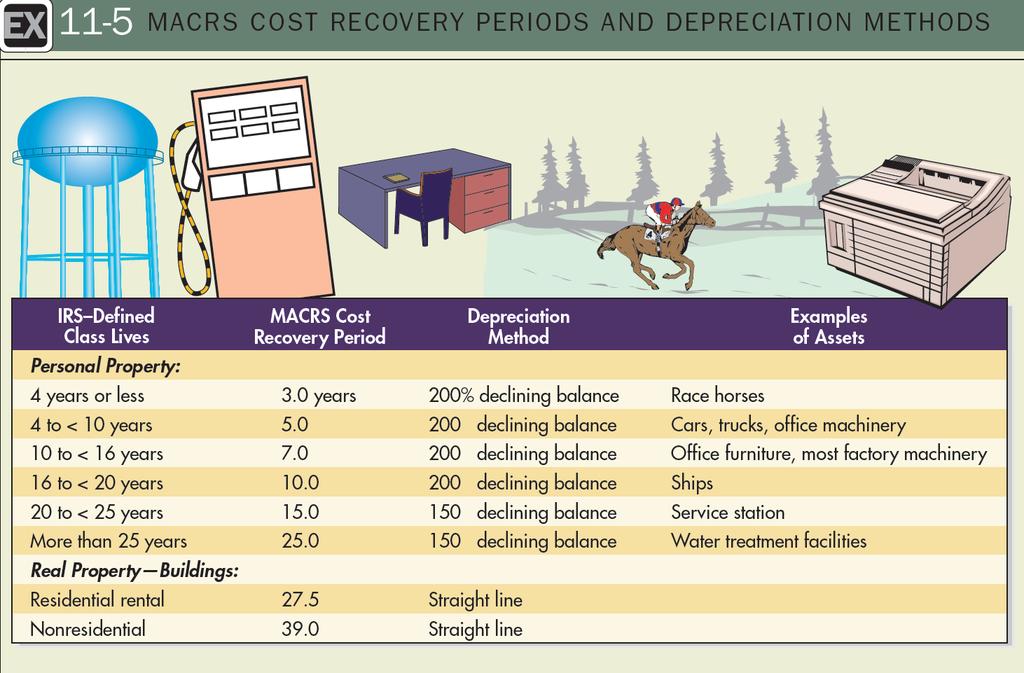

103 8. Understand the depreciation methods underlying the MACRS income tax depreciation system Income Tax Depreciation The term cost recovery was used in the tax regulations to emphasize that ACRS is not a standard depreciation method because the system is not based strictly on asset life or pattern of use. Salvage values are ignored. Depreciate over three to five years

104 11-104

105 Income Tax Depreciation The MACRS method for personal property also incorporates a half-year convention, meaning that one-half of a year s depreciation is recognized on all assets purchased or sold during the year

106 Income Tax Depreciation Office equipment is purchased for $100,000 on October 1, It has an estimated residual value of $5,

Chapter 08 - Long-Term Assets. Chapter Outline

Section 1 Plant Assets I. Cost Determination Plant assets are tangible assets used in a company's operations that have a useful life of more than one accounting period. Consistent with cost principle,

Section 1 Plant Assets I. Cost Determination Plant assets are tangible assets used in a company's operations that have a useful life of more than one accounting period. Consistent with cost principle,

4/10/2012. Long-Lived Assets and Depreciation. Overview of Long-lived Assets. Learning Objectives (LO) Learning Objectives (LO)

Learning Objectives (LO)") Learning Objectives (LO) CHAPTER Long-Lived Assets and Depreciation 8 After studying this chapter, you should be able to 1. Distinguish a company s expenses from expenditures that it should capitalize

Learning Objectives (LO) CHAPTER Long-Lived Assets and Depreciation 8 After studying this chapter, you should be able to 1. Distinguish a company s expenses from expenditures that it should capitalize

Long-lived, Revenue-producing Assets. Expected to Benefit Future Periods

Section 8 - Property, Plant, Equipment (Fixed Assets), and Depletable Resources Types of Assets Long-lived, Revenue-producing Assets 10-1 Expected to Benefit Future Periods Tangible Property, Plant, Equipment

Section 8 - Property, Plant, Equipment (Fixed Assets), and Depletable Resources Types of Assets Long-lived, Revenue-producing Assets 10-1 Expected to Benefit Future Periods Tangible Property, Plant, Equipment

An intangible asset is an identifiable non-monetary asset without physical substance.

Technical Summary This extract has been prepared by IASC Foundation staff and has not been approved by the IASB. For the requirements reference must be made to International Financial Reporting Standards.

Technical Summary This extract has been prepared by IASC Foundation staff and has not been approved by the IASB. For the requirements reference must be made to International Financial Reporting Standards.

Intermediate Accounting

Intermediate Accounting 11-1 Prepared by Coby Harmon University of California, Santa Barbara 11 Depreciation, Impairments, and Depletion Intermediate Accounting 14th Edition 11-2 Kieso, Weygandt, and Warfield

Intermediate Accounting 11-1 Prepared by Coby Harmon University of California, Santa Barbara 11 Depreciation, Impairments, and Depletion Intermediate Accounting 14th Edition 11-2 Kieso, Weygandt, and Warfield

Accounting for Plant Assets and Depreciation

Ch16 Accounting for Plant Assets and Depreciation 1 Understanding PPE Acquisition of PPE (cost) Depreciation of PPE Revenue expenditure vs. capital expenditure Disposition of PPE (sale, trade, and discard)

Ch16 Accounting for Plant Assets and Depreciation 1 Understanding PPE Acquisition of PPE (cost) Depreciation of PPE Revenue expenditure vs. capital expenditure Disposition of PPE (sale, trade, and discard)

5. The cost of buildings includes all necessary costs related to the purchase or construction

CHAPTER REVIEW Plant Assets 1. (S.O. 1) Plant assets are tangible resources that are used in the operations of a business and are not intended for sale to customers. Plant assets are subdivided into four

CHAPTER REVIEW Plant Assets 1. (S.O. 1) Plant assets are tangible resources that are used in the operations of a business and are not intended for sale to customers. Plant assets are subdivided into four

University of Economics, Prague. Non-current tangible and intangible assets (IAS 16 & IAS 38)

") University of Economics, Prague Faculty of Finance and Accounting Department of Financial Accounting and Auditing Non-current tangible and intangible assets (IAS 16 & IAS 38) 1FU486 IFRS David Procházka

University of Economics, Prague Faculty of Finance and Accounting Department of Financial Accounting and Auditing Non-current tangible and intangible assets (IAS 16 & IAS 38) 1FU486 IFRS David Procházka

A 1: It( SPECIFIC ITEMS SECTION 3061 property, plant and equipment. Additional Resources. Page 1 of6. Knotia - CICA Handbook - Accounting A2-14

'" Knotia - CICA Handbook - Accounting»Accounting»Accounting Handbook»Accounting Standards»Specific items [Sections 3000-3870]»3061 - Property, Plant and Eauipment Page 1 of6 A 1: It( A2-14 SPECIFIC ITEMS

'" Knotia - CICA Handbook - Accounting»Accounting»Accounting Handbook»Accounting Standards»Specific items [Sections 3000-3870]»3061 - Property, Plant and Eauipment Page 1 of6 A 1: It( A2-14 SPECIFIC ITEMS

Acquisition cost Purchase price plus all expenditures needed to prepare the asset for its intended use

CAPITAL ASSETS Issues to consider: Compute initial acquisition cost Account for subsequent costs Allocate cost to periods benefited Record disposal Acquisition cost Purchase price plus all expenditures

CAPITAL ASSETS Issues to consider: Compute initial acquisition cost Account for subsequent costs Allocate cost to periods benefited Record disposal Acquisition cost Purchase price plus all expenditures

Week11, Chap 8 Accounting 1A, Financial Accounting

Week11, Chap 8 Accounting 1A, Financial Accounting Reporting and Interpreting Property, Plant, and Equipment;Natural Resources; and Intangibles Instructor: Michael Booth Understanding The Business Insufficient

Week11, Chap 8 Accounting 1A, Financial Accounting Reporting and Interpreting Property, Plant, and Equipment;Natural Resources; and Intangibles Instructor: Michael Booth Understanding The Business Insufficient

STUDY OBJECTIVE 1 CAPITAL ASSETS

Collaboratively Created Collection of Chapter 10 Content STUDY OBJECTIVE 1 CAPITAL ASSETS Capital Assets are used throughout many cycles of a business and are reused over and over again. These assets are

Collaboratively Created Collection of Chapter 10 Content STUDY OBJECTIVE 1 CAPITAL ASSETS Capital Assets are used throughout many cycles of a business and are reused over and over again. These assets are

Prepared by: Alex Socratous For My High School Students

Prepared by: Alex Socratous For My High School Students CHAPTER 2 CAPITAL ASSETS DEPRECIATION CAPITAL ASSETS Capital assets are long-lived assets that are used in the operations of a business and are not

Prepared by: Alex Socratous For My High School Students CHAPTER 2 CAPITAL ASSETS DEPRECIATION CAPITAL ASSETS Capital assets are long-lived assets that are used in the operations of a business and are not

B EXERCISES E11-1B (Depreciation Computations SL, SYD, DDB) Instructions (a) (b) (c) E11-2B (Depreciation Conceptual Understanding) Instructions (a)

Instructions (a) (b) (c) E11-2B (Depreciation Conceptual Understanding) Instructions (a)") B EXERCISES E11-1B (Depreciation Computations SL, SYD, DDB) Vaughn Company purchases equipment on January 1, Year 1, at a cost of $500,000. The asset is expected to have a service life of 10 years and

B EXERCISES E11-1B (Depreciation Computations SL, SYD, DDB) Vaughn Company purchases equipment on January 1, Year 1, at a cost of $500,000. The asset is expected to have a service life of 10 years and

Accounting for tangible fixed Assets

Accounting for tangible fixed Assets Fixed assets are used (not consumed) in operations of a business provide benefits beyond the current accounting period Fixed assets are either acquired or self constructed

Accounting for tangible fixed Assets Fixed assets are used (not consumed) in operations of a business provide benefits beyond the current accounting period Fixed assets are either acquired or self constructed

IAS 16 Property, Plant and Equipment. Uphold public interest

IAS 16 Property, Plant and Equipment Uphold public interest Background IAS 16 became operational in 1983 Major amendments have been made several times including 1998, 2003, 2008, 2012, 2013, 2014 The objective

IAS 16 Property, Plant and Equipment Uphold public interest Background IAS 16 became operational in 1983 Major amendments have been made several times including 1998, 2003, 2008, 2012, 2013, 2014 The objective

Non-current Assets. Prof.(FH) Dr. Walter Egger

Dr. Walter Egger") Non-current Assets Prof.(FH) Dr. Walter Egger IAS 38 Intangible Assets Intangible Asset Is an identifiable non-monetary asset without physical substance Identifiability Seperable (can be seperated, divided

Non-current Assets Prof.(FH) Dr. Walter Egger IAS 38 Intangible Assets Intangible Asset Is an identifiable non-monetary asset without physical substance Identifiability Seperable (can be seperated, divided

Intangibles CHAPTER CHAPTER OBJECTIVES. After careful study of this chapter, you will be able to:

CHAPTER Intangibles CHAPTER OBJECTIVES After careful study of this chapter, you will be able to: 1. Explain the accounting alternatives for intangibles. 2. Record the amortization or impairment of intangibles.

CHAPTER Intangibles CHAPTER OBJECTIVES After careful study of this chapter, you will be able to: 1. Explain the accounting alternatives for intangibles. 2. Record the amortization or impairment of intangibles.

The Cost Principle. Plant Assets. Intangible Assets. Natural Resources. Depreciation. Amortization. Depletion. Chapter 9

Plant Assets Natural Resources Intangible Assets Depreciation Depletion Amortization Chapter 9 2 Held for use in business Full cost includes several expenditures Last several years Can be sold or traded

Plant Assets Natural Resources Intangible Assets Depreciation Depletion Amortization Chapter 9 2 Held for use in business Full cost includes several expenditures Last several years Can be sold or traded

CHAPTER 6 - Accounting for Long-Term Operational Assets

CHAPTER 6 - Accounting for Long-Term Operational Assets ANSWERS TO QUESTIONS 1. Long-term operational assets are those assets that are used by a business to generate revenue. In contrast, investments are

CHAPTER 6 - Accounting for Long-Term Operational Assets ANSWERS TO QUESTIONS 1. Long-term operational assets are those assets that are used by a business to generate revenue. In contrast, investments are

Copyright 2009 The Learning House, Inc. Fixed and Intangible Assets Page 1 of 13

Copyright 2009 The Learning House, Inc. Fixed and Intangible Assets Page 1 of 13 Introduction This lesson focuses on the long-term assets used to operate a company. These assets can be grouped into fixed

Copyright 2009 The Learning House, Inc. Fixed and Intangible Assets Page 1 of 13 Introduction This lesson focuses on the long-term assets used to operate a company. These assets can be grouped into fixed

Chapter 9: Long-Lived Assets and Cost Allocation

1 Chapter 9: Long-Lived Assets and Cost Allocation 2 Capitalize vs Expense Revenue Expenditures Merely maintain a given level of services Should be Expensed Debit Expense Capital Expenditures Provide future

1 Chapter 9: Long-Lived Assets and Cost Allocation 2 Capitalize vs Expense Revenue Expenditures Merely maintain a given level of services Should be Expensed Debit Expense Capital Expenditures Provide future

TOWN OF LINCOLN COUNCIL POLICY

Page 1 of 10 PURPOSE The purpose of this policy is to prescribe the accounting treatment for tangible capital assets so that users of the financial report can discern information about the investment in

Page 1 of 10 PURPOSE The purpose of this policy is to prescribe the accounting treatment for tangible capital assets so that users of the financial report can discern information about the investment in

Auditing PP&E, Including Leases

Auditing PP&E, Including Leases Learning Objectives Discuss typical audit risks and special considerations. Tailor an audit plan to assessed audit risk. Explain key controls related to PP&E. Describe lease

Auditing PP&E, Including Leases Learning Objectives Discuss typical audit risks and special considerations. Tailor an audit plan to assessed audit risk. Explain key controls related to PP&E. Describe lease

Chapter 9 - REPORTING AND ANALYZING LONG-LIVED ASSETS

Revised Summer 2018 Chapter 9 Review 1 Chapter 9 - REPORTING AND ANALYZING LONG-LIVED ASSETS LO 1: Explain the accounting for plant asset expenditures. Plant Assets (Also known as Property, Plant, and

Revised Summer 2018 Chapter 9 Review 1 Chapter 9 - REPORTING AND ANALYZING LONG-LIVED ASSETS LO 1: Explain the accounting for plant asset expenditures. Plant Assets (Also known as Property, Plant, and

7 Days Intensive Workshop on IFRS ICAI Tower, BKC, Mumbai. IAS 16 Property, Plant & Equipments

7 Days Intensive Workshop on IFRS ICAI Tower, BKC, Mumbai 01-July-14, Tuesday From To Details Faculty 10:00 AM 1:15 PM IAS 16 : Property, Plant & Equipments IAS 38 : Intangible Assets Ind AS 40:Investment

7 Days Intensive Workshop on IFRS ICAI Tower, BKC, Mumbai 01-July-14, Tuesday From To Details Faculty 10:00 AM 1:15 PM IAS 16 : Property, Plant & Equipments IAS 38 : Intangible Assets Ind AS 40:Investment

Fill-in-the-Blank Equations. Exercises

Chapter 10 Fixed Assets and Intangible Assets Study Guide Solutions 1. Residual value 2. Useful life 3. Straight-line rate 4. Total units of output 5. Straight-line rate 6. Depletion rate 7. Fixed asset

Chapter 10 Fixed Assets and Intangible Assets Study Guide Solutions 1. Residual value 2. Useful life 3. Straight-line rate 4. Total units of output 5. Straight-line rate 6. Depletion rate 7. Fixed asset

Accounting for Intangible Assets

Accounting for Intangible Assets 1 Examples: Goodwill- internally generated and acquired Trade mark and brand names- internally generated and acquired Patents Copyright Franchise Licenses Customer loyalty

Accounting for Intangible Assets 1 Examples: Goodwill- internally generated and acquired Trade mark and brand names- internally generated and acquired Patents Copyright Franchise Licenses Customer loyalty

ACCOUNTING - CLUTCH CH. 8 - LONG LIVED ASSETS.

!! www.clutchprep.com CONCEPT: INITIAL COST OF LONG-LIVED (PLANT) ASSETS Plant Assets include,,, and RULE: Initial cost includes the price plus all expenditures to make an asset When recording the initial

!! www.clutchprep.com CONCEPT: INITIAL COST OF LONG-LIVED (PLANT) ASSETS Plant Assets include,,, and RULE: Initial cost includes the price plus all expenditures to make an asset When recording the initial

IFRS Training. IAS 38 Intangible Assets. Professional Advisory Services

IFRS Training IAS 38 Intangible Assets Table of Contents Section 1 Overview 2 Introduction to Intangible Assets 3 Recognition and Initial Measurement 4 Internally Generated Intangible Assets 5 Measurement

IFRS Training IAS 38 Intangible Assets Table of Contents Section 1 Overview 2 Introduction to Intangible Assets 3 Recognition and Initial Measurement 4 Internally Generated Intangible Assets 5 Measurement

Financial Accounting. John J. Wild. Sixth Edition. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 08 Reporting and Analyzing Long-Term Assets Conceptual Learning

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 08 Reporting and Analyzing Long-Term Assets Conceptual Learning

SOLUTIONS Learning Goal 19

S1 Learning Goal 19 Multiple Choice 1. b 2. a 3. c 4. b However, the double-declining-balance method calculates the depreciation expense on the full asset cost until the final year of use. 5. d Total appraised

S1 Learning Goal 19 Multiple Choice 1. b 2. a 3. c 4. b However, the double-declining-balance method calculates the depreciation expense on the full asset cost until the final year of use. 5. d Total appraised

SOLUTIONS. Learning Goal 28

S1 Learning Goal 28 Multiple Choice 1. b 2. a 3. c 4. b However, the double-declining-balance method calculates the depreciation expense on the full asset cost until the final year of use. 5. d Total appraised

S1 Learning Goal 28 Multiple Choice 1. b 2. a 3. c 4. b However, the double-declining-balance method calculates the depreciation expense on the full asset cost until the final year of use. 5. d Total appraised

Reporting and Analyzing Long-Term Operating Assets. Learning Objectives coverage by question 12, 13, 16, 18

Chapter 8 Reporting and Analyzing Long-Term Operating Assets Learning Objectives coverage by question Miniexercises Exercises Problems Cases LO1 Describe and distinguish between tangible and intangible

Chapter 8 Reporting and Analyzing Long-Term Operating Assets Learning Objectives coverage by question Miniexercises Exercises Problems Cases LO1 Describe and distinguish between tangible and intangible

Fill-in-the-Blank Equations. Exercises

Chapter 9 Long-Term Assets: Fixed and Intangible Study Guide Solutions 1. Residual value 2. Useful life 3. Straight-line rate 4. Total estimated units of activity 5. Straight-line rate 6. Depletion rate

Chapter 9 Long-Term Assets: Fixed and Intangible Study Guide Solutions 1. Residual value 2. Useful life 3. Straight-line rate 4. Total estimated units of activity 5. Straight-line rate 6. Depletion rate

Accounting Of Intangible Assets Indian as- 26

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668. Volume 16, Issue 2. Ver. II (Feb. 2014), PP 40-45 Accounting Of Intangible Assets Indian as- 26 Manpreet Sharma,

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668. Volume 16, Issue 2. Ver. II (Feb. 2014), PP 40-45 Accounting Of Intangible Assets Indian as- 26 Manpreet Sharma,

Chapter 8. Accounting for Long-Term Assets

Chapter 8 Accounting for Long-Term Assets C 1 Plant Assets Tangible in Nature Actively Used in Operations Expected to Benefit Future Periods Called Property, Plant, & Equipment 8-2 C 1 Plant Assets Decline

Chapter 8 Accounting for Long-Term Assets C 1 Plant Assets Tangible in Nature Actively Used in Operations Expected to Benefit Future Periods Called Property, Plant, & Equipment 8-2 C 1 Plant Assets Decline

Lesson 6 International Accounting Lelio Bigogno, Stefano Santucci

Università degli studi di Pavia Facoltà di Economia a.a. 2014-2015 2015 Lesson 6 International Accounting Lelio Bigogno, Stefano Santucci 1 IAS/IFRS: Objective and definition of IAS38 2 The objective of

Università degli studi di Pavia Facoltà di Economia a.a. 2014-2015 2015 Lesson 6 International Accounting Lelio Bigogno, Stefano Santucci 1 IAS/IFRS: Objective and definition of IAS38 2 The objective of

Intangible Assets IAS 38, IAS 36, IFRS 3

Intangible Assets IAS 38, IAS 36, IFRS 3 Agenda 1. Introduction 2. Recognition 3. Measurement 4. Impairment of intangible assets (IAS 36) Basic concept Cash-Generating Units 5. Disclosures 2 1 Introduction

Intangible Assets IAS 38, IAS 36, IFRS 3 Agenda 1. Introduction 2. Recognition 3. Measurement 4. Impairment of intangible assets (IAS 36) Basic concept Cash-Generating Units 5. Disclosures 2 1 Introduction

Long-Term Assets C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM

Long-Term Assets E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information, in addition to the material

Long-Term Assets E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information, in addition to the material

SRI LANKA ACCOUNTING STANDARD

(REVISED 2005) SRI LANKA ACCOUNTING STANDARD PROPERTY, PLANT & EQUIPMENT THE INSTITUTE OF CHARTERED ACCOUNTANTS OF SRI LANKA (REVISED 2005) SRI LANKA ACCOUNTING STANDARD PROPERTY, PLANT & EQUIPMENT The

(REVISED 2005) SRI LANKA ACCOUNTING STANDARD PROPERTY, PLANT & EQUIPMENT THE INSTITUTE OF CHARTERED ACCOUNTANTS OF SRI LANKA (REVISED 2005) SRI LANKA ACCOUNTING STANDARD PROPERTY, PLANT & EQUIPMENT The

Financial Accounting Standards Committee

Statement of Financial Accounting Standards No. 37 20 July 2006 Translated by Chi-Chun Liu, Professor (National Taiwan University) Financial Accounting Standards Committee -605- -606- Statement of Financial

Statement of Financial Accounting Standards No. 37 20 July 2006 Translated by Chi-Chun Liu, Professor (National Taiwan University) Financial Accounting Standards Committee -605- -606- Statement of Financial

CHAPTER 9. Plant Assets, Natural Resources, and Intangible Assets 6, 7, 8, 24, 25, 26 3, 4, 5, 6, 7 11, , 17, 18, 19, 20, 21, 22

CHAPTER 9 Plant Assets, Natural Resources, and Intangible Assets ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems 1. Describe how the cost

CHAPTER 9 Plant Assets, Natural Resources, and Intangible Assets ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems 1. Describe how the cost

Defining Issues May 2013, No

Defining Issues May 2013, No. 13-24 FASB and IASB Issue Revised Exposure Drafts on Lease Accounting The FASB and IASB (the Boards) recently issued revised joint exposure drafts (EDs) on proposed changes

Defining Issues May 2013, No. 13-24 FASB and IASB Issue Revised Exposure Drafts on Lease Accounting The FASB and IASB (the Boards) recently issued revised joint exposure drafts (EDs) on proposed changes

Before Class starts.(make sure your name is on all submissions)

") Before Class starts.(make sure your name is on all submissions) Fourth Homework due 10/27(MW) or 10/28(TR) before class. No exceptions. Help session 10/26 1:00-3:30pm in GBS130 Fifth Homework due 11/3(MW)

Before Class starts.(make sure your name is on all submissions) Fourth Homework due 10/27(MW) or 10/28(TR) before class. No exceptions. Help session 10/26 1:00-3:30pm in GBS130 Fifth Homework due 11/3(MW)

Plant assets are resources that have

10-1 LEARNING OBJECTIVE 1 Explain the accounting for plant asset expenditures. Plant assets are resources that have physical substance (a definite size and shape), are used in the operations of a business,

10-1 LEARNING OBJECTIVE 1 Explain the accounting for plant asset expenditures. Plant assets are resources that have physical substance (a definite size and shape), are used in the operations of a business,

IAS 38 Intangible Assets

21/12/2010, Tuesday From To Details Faculty 2:15 PM 5:30 PM IAS 38 : Intangible Assets IAS 40 : Investment Property IFRS 5 : Non Current Assets Held for Sale and Discontinued Operations CA. Chintan Patel,

21/12/2010, Tuesday From To Details Faculty 2:15 PM 5:30 PM IAS 38 : Intangible Assets IAS 40 : Investment Property IFRS 5 : Non Current Assets Held for Sale and Discontinued Operations CA. Chintan Patel,

ILLUSTRATION 11-1 PATTERNS OF BOOK VALUE OVER LIFE OF ASSET

ILLUSTRATION 11-1 PATTERNS OF BOOK VALUE OVER LIFE OF ASSET $ Cost of asset N PR: Book value activity methods Depreciable cost SL: Book value straight line Salvage value AC: Book value accelerated S E

ILLUSTRATION 11-1 PATTERNS OF BOOK VALUE OVER LIFE OF ASSET $ Cost of asset N PR: Book value activity methods Depreciable cost SL: Book value straight line Salvage value AC: Book value accelerated S E

TANGIBLE CAPITAL ASSETS

Administrative Procedure 535 Background TANGIBLE CAPITAL ASSETS The Division will follow a prescribed procedure to record and manage the tangible capital assets (TCA) owned by the Division. The treatment

Administrative Procedure 535 Background TANGIBLE CAPITAL ASSETS The Division will follow a prescribed procedure to record and manage the tangible capital assets (TCA) owned by the Division. The treatment

Property, Plant & Equipment Intangible Assets

Property, Plant & Equipment Intangible Assets October 17, 2015 Contents: 1. Property, Plant and Equipment (Ind AS 16) - Borrowing Costs (Ind AS 23) - Stripping Costs of a Surface Mine (Appendix B to Ind

Property, Plant & Equipment Intangible Assets October 17, 2015 Contents: 1. Property, Plant and Equipment (Ind AS 16) - Borrowing Costs (Ind AS 23) - Stripping Costs of a Surface Mine (Appendix B to Ind

The cost of this asset includes the purchase price, plus any taxes, commissions, and other amounts paid to make the asset ready for use.

Accounting Fundamentals Lesson 7 7.0 Long-Term Assets Plant Assets, are long-lived assets that are tangible. The cost of this asset includes the purchase price, plus any taxes, commissions, and other amounts

Accounting Fundamentals Lesson 7 7.0 Long-Term Assets Plant Assets, are long-lived assets that are tangible. The cost of this asset includes the purchase price, plus any taxes, commissions, and other amounts

CHAPTER 9 LONG-LIVED ASSETS SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY

CHAPTER 9 LONG-LIVED ASSETS SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 K 17. 2 K 33. 2 C 49. 3 K 65.

CHAPTER 9 LONG-LIVED ASSETS SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 K 17. 2 K 33. 2 C 49. 3 K 65.

Accounting for Tangible Capital Assets

Accounting for Tangible Capital Assets Date Approved by Board: 2011.11.17 Resolution No.: 11-113 2016.05.19 16-048 Lead Role: CFO Replaces: N/A Last Review Date: N/A Next Review Date: 2019.05.19 Policy

Accounting for Tangible Capital Assets Date Approved by Board: 2011.11.17 Resolution No.: 11-113 2016.05.19 16-048 Lead Role: CFO Replaces: N/A Last Review Date: N/A Next Review Date: 2019.05.19 Policy

Leases. (a) the lease transfers ownership of the asset to the lessee by the end of the lease term.

the lease transfers ownership of the asset to the lessee by the end of the lease term.") Leases 1.1. Classification of leases A lease is classified as a finance lease if it transfers substantially all the risks and rewards incidental to ownership. A lease is classified as an operating lease

Leases 1.1. Classification of leases A lease is classified as a finance lease if it transfers substantially all the risks and rewards incidental to ownership. A lease is classified as an operating lease

Depreciation. Dr. M. S. Memon. Mehran UET, Jamshoro, Pakistan. Department of Industrial Engineering and Management

Depreciation Dr. M. S. Memon Department of Industrial Engineering and Management Mehran UET, Jamshoro, Pakistan https://msmemon.wordpress.com/scmlab/ Introduction Any equipment which is purchased today

Depreciation Dr. M. S. Memon Department of Industrial Engineering and Management Mehran UET, Jamshoro, Pakistan https://msmemon.wordpress.com/scmlab/ Introduction Any equipment which is purchased today

Before Class starts.(make sure your name is on all submissions)

") Before Class starts.(make sure your name is on all submissions) March 27 exam conflicts must be resolved before Spring break. Fourth Homework due Thursday 3/6 before class. Fifth Homework due 3/20 before

Before Class starts.(make sure your name is on all submissions) March 27 exam conflicts must be resolved before Spring break. Fourth Homework due Thursday 3/6 before class. Fifth Homework due 3/20 before

Chapter 11. Learning Objectives. Non-current Assets. Horngren, Best, Fraser, Willett: Accounting 6e 2010 Pearson Australia

PowerPoint to accompany Chapter 11 Non-Current Assets: Property, Plant and Equipment, and Intangibles Learning Objectives 1. Measure the cost of a non-current asset 2. Account for depreciation 3. Select

PowerPoint to accompany Chapter 11 Non-Current Assets: Property, Plant and Equipment, and Intangibles Learning Objectives 1. Measure the cost of a non-current asset 2. Account for depreciation 3. Select

Property, Plant and Equipment

International Accounting Standard 16 Property, Plant and Equipment In April 2001 the International Accounting Standards Board (IASB) adopted IAS 16 Property, Plant and Equipment, which had originally been

International Accounting Standard 16 Property, Plant and Equipment In April 2001 the International Accounting Standards Board (IASB) adopted IAS 16 Property, Plant and Equipment, which had originally been

DIRECT-FINANCING TERMS

CHAPTER 21 ALTERNATIVE LESSOR ACCOUNTING GROSS PRESENTATION This alternate discussion describes the accounting by lessors, using a gross presentation. These pages can be substituted for the discussion

CHAPTER 21 ALTERNATIVE LESSOR ACCOUNTING GROSS PRESENTATION This alternate discussion describes the accounting by lessors, using a gross presentation. These pages can be substituted for the discussion

UPDATE MATERIALS INTERMEDIATE ACCOUNTING, 10 TH EDITION

UPDATE MATERIALS INTERMEDIATE ACCOUNTING, 10 TH EDITION This document contains several discussions of the effects of new accounting standards as they relate to the materials in Intermediate Accounting,

UPDATE MATERIALS INTERMEDIATE ACCOUNTING, 10 TH EDITION This document contains several discussions of the effects of new accounting standards as they relate to the materials in Intermediate Accounting,

Summary of IFRS Exposure Draft Leases

The International Accounting Standards Board (IASB) recently issued a revised exposure draft (ED) relating to leases. Once these proposals are finalized the new guidance will replace the IAS 17 Leases.

The International Accounting Standards Board (IASB) recently issued a revised exposure draft (ED) relating to leases. Once these proposals are finalized the new guidance will replace the IAS 17 Leases.

Property, Plant and Equipment

International Accounting Standard 16 Property, Plant and Equipment This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 16 Property, Plant and Equipment was issued by

International Accounting Standard 16 Property, Plant and Equipment This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 16 Property, Plant and Equipment was issued by

Chapter 10: Fixed Assets and Intangible Assets

Chapter 10: Fixed Assets and Intangible Assets Nature of Fixed Assets Fixed assets are long-term or relatively permanent assets, such as equipment, machinery, buildings, and land. Other descriptive titles

Chapter 10: Fixed Assets and Intangible Assets Nature of Fixed Assets Fixed assets are long-term or relatively permanent assets, such as equipment, machinery, buildings, and land. Other descriptive titles

International Financial Reporting Standards (IFRS)

") FACT SHEET September 2011 IAS 38 Intangible Assets (This fact sheet is based on the standard as at 1 January 2011.) Important note: This fact sheet is based on the requirements of the International Financial

FACT SHEET September 2011 IAS 38 Intangible Assets (This fact sheet is based on the standard as at 1 January 2011.) Important note: This fact sheet is based on the requirements of the International Financial

International Financial Reporting Standards. Sample material

International Financial Reporting Standards Sample material Always in context guiding you all the way with summaries key points, diagrams and definitions REVENUE RECOGNITION CHAPTER CONTENTS The provisions

International Financial Reporting Standards Sample material Always in context guiding you all the way with summaries key points, diagrams and definitions REVENUE RECOGNITION CHAPTER CONTENTS The provisions

CAS -16 COST ACCOUNTING STANDARD ON DEPRECIATION AND AMORTISATION

Cost Accounting Standards Board CAS -16 COST ACCOUNTING STANDARD ON DEPRECIATION AND AMORTISATION The following is the COST ACCOUNTING STANDARD 16 (CAS 16) issued by the Council of The Institute of Cost

Cost Accounting Standards Board CAS -16 COST ACCOUNTING STANDARD ON DEPRECIATION AND AMORTISATION The following is the COST ACCOUNTING STANDARD 16 (CAS 16) issued by the Council of The Institute of Cost

Depreciation and Depletion

Principles Depreciation and Depletion Prof.Sherif Sabry Spring 2009 1 Depreciation and Depletion Lecture outline Concept of depreciation What depreciation is not for Depreciation methods Asset impairment

Principles Depreciation and Depletion Prof.Sherif Sabry Spring 2009 1 Depreciation and Depletion Lecture outline Concept of depreciation What depreciation is not for Depreciation methods Asset impairment

MPEEM The New and Improved Residual Technique of Reserve Valuation

MPEEM The New and Improved Residual Technique of Reserve Valuation Prepared by Alan K. Stagg, PG, CMA Stagg Resource Consultants, Inc. Cross Lanes, West Virginia ABSTRACT The residual technique of reserve

MPEEM The New and Improved Residual Technique of Reserve Valuation Prepared by Alan K. Stagg, PG, CMA Stagg Resource Consultants, Inc. Cross Lanes, West Virginia ABSTRACT The residual technique of reserve

IND AS 38 Intangible Assets

IND AS 38 Intangible Assets 1 What do you mean by Intangible Assets An intangible assets is an identifiable nonmonetary assets without physical substance held for use in the production or supply of goods

IND AS 38 Intangible Assets 1 What do you mean by Intangible Assets An intangible assets is an identifiable nonmonetary assets without physical substance held for use in the production or supply of goods

Chapter 10 Capital Assets Solutions. (g) NA (current asset) (h) NR (i) NA (inventory) (j) I (k) I (l) NA (investment) (m) NR (n) NR (o) NR (p) I

NA (current asset) (h) NR (i) NA (inventory) (j) I (k) I (l) NA (investment) (m) NR (n) NR (o) NR (p) I") Chapter 10 Capital Assets Solutions Assigned Questions: Study Objective Textbook Pages to Read 9 p. 481-486 19 14-10 Solutions: Q1. Tangible and intangible capital assets both are long-lived assets that

Chapter 10 Capital Assets Solutions Assigned Questions: Study Objective Textbook Pages to Read 9 p. 481-486 19 14-10 Solutions: Q1. Tangible and intangible capital assets both are long-lived assets that

IFRS 16 LEASES. Page 1 of 21

IFRS 16 LEASES OBJECTIVE The objective is to ensure that lessees and lessors provide relevant information in a manner that faithfully represents those transactions. This information gives a basis for users

IFRS 16 LEASES OBJECTIVE The objective is to ensure that lessees and lessors provide relevant information in a manner that faithfully represents those transactions. This information gives a basis for users

6 The following terms are used in this Standard with the meanings specified: A bearer plant is a living plant that:

International Accounting Standard 16 Property, Plant and Equipment Objective 1 The objective of this Standard is to prescribe the accounting treatment for property, plant and equipment so that users of

International Accounting Standard 16 Property, Plant and Equipment Objective 1 The objective of this Standard is to prescribe the accounting treatment for property, plant and equipment so that users of

IASB Staff Paper March 2011

IASB Staff Paper March 2011 Effect of board redeliberations on Exposure Draft Leases About this staff paper This staff paper indicates how the proposals in the Exposure Draft Leases would change as a result

IASB Staff Paper March 2011 Effect of board redeliberations on Exposure Draft Leases About this staff paper This staff paper indicates how the proposals in the Exposure Draft Leases would change as a result

roots The Substance of the Standard Contents Changes to the Accounting for Goodwill for Private Companies

The Substance of the Standard MAYER HOFFMAN MCCANN P.C. AN INDEPENDENT CPA FIRM TM A publication of the Professional Standards Group February 2014 Changes to the Accounting for Goodwill for Private Companies

The Substance of the Standard MAYER HOFFMAN MCCANN P.C. AN INDEPENDENT CPA FIRM TM A publication of the Professional Standards Group February 2014 Changes to the Accounting for Goodwill for Private Companies

Financial Accounting Series

Financial Accounting Series NO. 221-C JUNE 2001 Statement of Financial Accounting Standards No. 142 Goodwill and Other Intangible Assets Financial Accounting Standards Board of the Financial Accounting

Financial Accounting Series NO. 221-C JUNE 2001 Statement of Financial Accounting Standards No. 142 Goodwill and Other Intangible Assets Financial Accounting Standards Board of the Financial Accounting

Materiële Vaste Activa. 27 September 2005 Pearl Couvreur

Materiële Vaste Activa 27 September 2005 Pearl Couvreur P w C Contents 1. Principle 2. Acquisition cost 3. Subsequent costs 4. Borrowing costs 5. Assets acquired in a business combination 6. Revaluation

Materiële Vaste Activa 27 September 2005 Pearl Couvreur P w C Contents 1. Principle 2. Acquisition cost 3. Subsequent costs 4. Borrowing costs 5. Assets acquired in a business combination 6. Revaluation

Hong Kong Accounting Standard 16 Property, Plant and Equipment

Hong Kong Accounting Standard 16 Property, Plant and Equipment 1 Contents Hong Kong Accounting Standard 16 Property, Plant and Equipment paragraphs OBJECTIVE 1 SCOPE 2-5 DEFINITIONS 6 RECOGNITION 7-14

Hong Kong Accounting Standard 16 Property, Plant and Equipment 1 Contents Hong Kong Accounting Standard 16 Property, Plant and Equipment paragraphs OBJECTIVE 1 SCOPE 2-5 DEFINITIONS 6 RECOGNITION 7-14

EITF Issue No EITF Issue No Working Group Report No. 1, p. 1

EITF Issue No. 03-9 The views in this report are not Generally Accepted Accounting Principles until a consensus is reached and it is FASB Emerging Issues Task Force Issue No. 03-9 Title: Interaction of

EITF Issue No. 03-9 The views in this report are not Generally Accepted Accounting Principles until a consensus is reached and it is FASB Emerging Issues Task Force Issue No. 03-9 Title: Interaction of

Property, Plant and Equipment

IAS 16 Property, Plant and Equipment In April 2001 the International Accounting Standards Board (the Board) adopted IAS 16 Property, Plant and Equipment, which had originally been issued by the International

IAS 16 Property, Plant and Equipment In April 2001 the International Accounting Standards Board (the Board) adopted IAS 16 Property, Plant and Equipment, which had originally been issued by the International

Plant Assets, Natural Resources, and Intangible Assets

10 Plant Assets, Natural Resources, and Intangible Assets Learning Objectives 1 Explain the accounting for plant asset expenditures. 2 Apply depreciation methods to plant assets. 10-1 3 4 5 Explain how

10 Plant Assets, Natural Resources, and Intangible Assets Learning Objectives 1 Explain the accounting for plant asset expenditures. 2 Apply depreciation methods to plant assets. 10-1 3 4 5 Explain how

CHAPTER 10 Capital Assets

CHAPTER 10 Capital Assets ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Exercises Problems Set A Problems Set B 1. Distinguish between tangible and intangible capital assets.

CHAPTER 10 Capital Assets ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Exercises Problems Set A Problems Set B 1. Distinguish between tangible and intangible capital assets.

International Financial Reporting Standard 16 Leases. Objective. Scope. Recognition exemptions (paragraphs B3 B8) IFRS 16

IFRS 16") International Financial Reporting Standard 16 Leases Objective 1 This Standard sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective is to ensure

International Financial Reporting Standard 16 Leases Objective 1 This Standard sets out the principles for the recognition, measurement, presentation and disclosure of leases. The objective is to ensure

Property, Plant and Equipment

International Accounting Standard 16 Property, Plant and Equipment In April 2001 the International Accounting Standards Board (IASB) adopted IAS 16 Property, Plant and Equipment, which had originally been

International Accounting Standard 16 Property, Plant and Equipment In April 2001 the International Accounting Standards Board (IASB) adopted IAS 16 Property, Plant and Equipment, which had originally been

Distinctive Financial Reporting

Distinctive Financial Reporting FAC3702 Study unit 4 Intangible assets Overview Terminology Recognition & initial measurement of intangible assets Cost of internally generated intangible asset Recognition

Distinctive Financial Reporting FAC3702 Study unit 4 Intangible assets Overview Terminology Recognition & initial measurement of intangible assets Cost of internally generated intangible asset Recognition

Chapter 15 Leases 15-1

Chapter 15 Leases 1. Why Leasing sometimes makes more sense 2. The accounting issues in recording a lease transaction 3. The types of contractual provisions in lease 4. The lease classification: capital

Chapter 15 Leases 1. Why Leasing sometimes makes more sense 2. The accounting issues in recording a lease transaction 3. The types of contractual provisions in lease 4. The lease classification: capital

IFRS-5: Non-current Assets Held for Sale and Discontinued Operations

The journal is running a series of updates on IFRS, IAS, IFRIC and SIC. The updates mostly collected from different sources of IASB publication, seminars, workshop & IFRS website. This issue is based on

The journal is running a series of updates on IFRS, IAS, IFRIC and SIC. The updates mostly collected from different sources of IASB publication, seminars, workshop & IFRS website. This issue is based on

International Accounting Standard 17 Leases. Objective. Scope. Definitions IAS 17

International Accounting Standard 17 Leases Objective 1 The objective of this Standard is to prescribe, for lessees and lessors, the appropriate accounting policies and disclosure to apply in relation

International Accounting Standard 17 Leases Objective 1 The objective of this Standard is to prescribe, for lessees and lessors, the appropriate accounting policies and disclosure to apply in relation

CPE regulations require online participants to take part in online questions

KPMG s CFO Financial Forum Webcast FASB/IASB Revised Lease Accounting Exposure Drafts A Detailed Look Part III: Lessor Accounting June 25, 2013 Administrative CPE regulations require online participants

KPMG s CFO Financial Forum Webcast FASB/IASB Revised Lease Accounting Exposure Drafts A Detailed Look Part III: Lessor Accounting June 25, 2013 Administrative CPE regulations require online participants

March 23, 2006 Anderson ECON 136A 11am Class FINAL EXAM v. 1 Name

March 23, 2006 Anderson ECON 136A 11am Class FINAL EXAM v. 1 Name YOU MUST WRITE YOUR NAME ON THIS EXAM AND TURN IT IN WITH YOUR SCANTRON AND BLUE-BOOK! Complete questions #1-25 on your scantron AND WRITE

March 23, 2006 Anderson ECON 136A 11am Class FINAL EXAM v. 1 Name YOU MUST WRITE YOUR NAME ON THIS EXAM AND TURN IT IN WITH YOUR SCANTRON AND BLUE-BOOK! Complete questions #1-25 on your scantron AND WRITE

EUROPEAN UNION ACCOUNTING RULE 7 PROPERTY, PLANT & EQUIPMENT

EUROPEAN UNION ACCOUNTING RULE 7 PROPERTY, PLANT & EQUIPMENT Page 2 of 10 I N D E X 1. Objective... 3 2. Scope... 3 3. Definitions... 3 4. Recognition... 4 4.1 General recognition principle... 4 4.2 Initial

EUROPEAN UNION ACCOUNTING RULE 7 PROPERTY, PLANT & EQUIPMENT Page 2 of 10 I N D E X 1. Objective... 3 2. Scope... 3 3. Definitions... 3 4. Recognition... 4 4.1 General recognition principle... 4 4.2 Initial

EN Official Journal of the European Union L 320/373

29.11.2008 EN Official Journal of the European Union L 320/373 INTERNATIONAL FINANCIAL REPORTING STANDARD 3 Business combinations OBJECTIVE 1 The objective of this IFRS is to specify the financial reporting

29.11.2008 EN Official Journal of the European Union L 320/373 INTERNATIONAL FINANCIAL REPORTING STANDARD 3 Business combinations OBJECTIVE 1 The objective of this IFRS is to specify the financial reporting

AAT Professional Diploma in Accounting

Qualification Number: R486 04 Qualification Technical Information Version 1.1 published 13 June 2016 AAT Professional Diploma in Accounting Qualification Technical Information Units in this qualification

Qualification Number: R486 04 Qualification Technical Information Version 1.1 published 13 June 2016 AAT Professional Diploma in Accounting Qualification Technical Information Units in this qualification

In May 2014 the Board amended IAS 38 to clarify when the use of a revenue-based amortisation method is appropriate.

IAS 38 Intangible Assets In April 2001 the International Accounting Standards Board (Board) adopted IAS 38 Intangible Assets, which had originally been issued by the International Accounting Standards

IAS 38 Intangible Assets In April 2001 the International Accounting Standards Board (Board) adopted IAS 38 Intangible Assets, which had originally been issued by the International Accounting Standards

Section 12 Accounting for Leases Accounting by the Lessor and Lessee

Section 12 Accounting for Leases Accounting by the Lessor and Lessee 15-1 A lease is an agreement in which the lessor conveys the right to use property, plant, or equipment, usually for a stated period

Section 12 Accounting for Leases Accounting by the Lessor and Lessee 15-1 A lease is an agreement in which the lessor conveys the right to use property, plant, or equipment, usually for a stated period

Chapter 9 Question Review 1

Chapter 9 Question Review 1 Chapter 9 Questions Multiple Choice 1. The calculation of depreciation using the declining-balance method a. ignores salvage value in determining the amount to which a constant

Chapter 9 Question Review 1 Chapter 9 Questions Multiple Choice 1. The calculation of depreciation using the declining-balance method a. ignores salvage value in determining the amount to which a constant

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N

2018 Accounting & Auditing Update P R E S E N T E D B Y : D A N I E L L E Z I M M E R M A N & A N D R E A S A R T I N AGENDA Leases FASB & GASB Revenue Recognition FASB 2 FASB ASU 2016-02, Leases (Topic