NEW ISSUE - BOOK-ENTRY-ONLY NOT RATED LIMITED OFFERING

|

|

|

- Maximilian Gibbs

- 6 years ago

- Views:

Transcription

1 NEW ISSUE - BOOK-ENTRY-ONLY NOT RATED LIMITED OFFERING In the opinion of Bond Counsel, assuming continuing compliance with certain tax covenants, interest on the Series 2004A Bonds is excluded from gross income for federal income tax purposes under existing statutes, regulations, rulings and court decisions. Interest on the Series 2004A Bonds is not an item of tax preference for purposes of the federal alternative minimum tax imposed on individuals and corporations. However, see TAX MATTERS herein for a description of the alternative minimum tax on corporations and certain other federal tax consequences of ownership of the Series 2004A Bonds. Bond Counsel is further of the opinion that the Series 2004A Bonds and income thereon, are exempt from taxation under the laws of the State of Florida, except as to estate taxes and taxes imposed by Chapter 220, Florida Statutes, on interest, income or profits on debt obligations owned by corporations as defined in Chapter 220. For a more complete discussion of tax aspects, see TAX MATTERS herein. $73,580,000 MIDTOWN MIAMI COMMUNITY DEVELOPMENT DISTRICT (Miami-Dade County, Florida) Special Assessment and Revenue Bonds, Series 2004A (Parking Garage Project) Dated: Date of Delivery Due: May 1, as shown below The Midtown Miami Community Development District (Miami-Dade County, Florida) Special Assessment and Revenue Bonds, Series 2004A (Parking Garage Project) (the Series 2004A Bonds ) are being issued by Midtown Miami Community Development District (the District ) in fully registered form, without coupons, in denominations of $5,000 and integral multiples thereof; provided, however, that the Series 2004A Bonds will be deliverable to the initial purchasers thereof only in minimum amounts of $100,000 or integral multiples of $5,000 in excess of $100,000. The Series 2004A Bonds will bear interest at the rates set forth below, calculated on the basis of a 360-day year comprised of twelve thirty-day months, payable semi-annually on each May 1 and November 1, commencing November 1, The Series 2004A Bonds, when issued, will be registered in the name of Cede & Co., as nominee of The Depository Trust Company ( DTC ), New York, New York. Purchases of beneficial interests in the Series 2004A Bonds will be made in book-entry-only form and purchasers of beneficial interests in the Series 2004A Bonds will not receive physical bond certificates. For so long as the book-entry only system is maintained, the principal of, premium, if any, and interest on the Series 2004A Bonds will be paid from the sources described herein by Wachovia Bank, National Association, as trustee (the Trustee ), to DTC as the registered owner thereof. Disbursement of such payments to the DTC Participants is the responsibility of DTC and disbursement of such payments to the beneficial owners is the responsibility of the DTC Participants and Indirect Participants, as more fully described herein. Any purchaser, as a beneficial owner of a Series 2004A Bond, must maintain an account with a broker or dealer who is, or acts through, a DTC Participant in order to receive payment of the principal of, premium, if any, and interest on such Series 2004A Bond. See BOOK-ENTRY ONLY SYSTEM herein. Proceeds of the Series 2004A Bonds will be used to provide funds for (i) the payment of a portion of the costs of the construction of certain parking facilities, public open space and other public improvements within the District (as more particularly described herein, the Series 2004A Project ), (ii) the payment of interest on the Series 2004A Bonds through November 1, 2007, (iii) the funding of the Series 2004A Debt Service Reserve Account and (iv) the payment of the costs of issuance of the Series 2004A Bonds. See PLAN OF FINANCE, THE SERIES 2004A PROJECT and APPENDIX C Form of Indenture herein. The District is a special-purpose government of the State of Florida, created in accordance with the Uniform Community Development District Act of 1980, Chapter 190, Florida Statutes, as amended (the Act ) and Section 1.10(A)(21) of the Miami-Dade Home Rule Charter, by Ordinance No , enacted by the Board of County Commissioners of Miami-Dade County, Florida on December 16, The Series 2004A Bonds are being issued pursuant to the Act, and a Master Trust Indenture dated as of July 1, 2004, as supplemented by a First Supplemental Trust Indenture dated as of July 1, 2004 (collectively, the Indenture ), both entered into by and between the District and the Trustee. Capitalized terms not otherwise defined herein will have the meaning assigned to them in the Interlocal Agreement (defined herein) or the Indenture. The Series 2004A Bonds are secured by a pledge of the Pledged Revenues. The Pledged Revenues consist of (a) all revenues received by the District under the Interlocal Agreement dated May 28, 2004 among the City of Miami, Florida (the City ), Miami-Dade County, Florida (the County ) and the District (the Interlocal Agreement ) and deposited in the Series 2004A Subaccount within the Revenue Fund pursuant to the Indenture, as further described herein, (b) all revenues received by the District from Special Assessments levied and collected on all or a portion of the District Lands with respect to the Series 2004A Bonds, including, without limitation, amounts received from any foreclosure proceeding for the enforcement of collection of such Special Assessments or from the issuance and sale of tax certificates with respect to such Special Assessments, and (c) all moneys on deposit in the Funds and Accounts established under the Indenture for the Series 2004A Bonds; provided, however, that Pledged Revenues will not include (i) any moneys transferred to the Rebate Fund, or investment earnings thereon, and (ii) special assessments levied and collected by the District under Section , Florida Statutes, for maintenance purposes or maintenance special assessments levied and collected by the District under Section (3), Florida Statutes. The lien on the Special Assessments will be on a parity with other debt of the District being issued contemporaneously with the Series 2004A Bonds, as described herein. See PLAN OF FINANCE and SECURITY FOR THE SERIES 2004A BONDS, herein. The Series 2004A Bonds are subject to optional, mandatory and extraordinary mandatory redemption at the times, in the amounts, and at the redemption prices more fully described herein under the caption DESCRIPTION OF THE SERIES 2004A BONDS Redemption Provisions. The Series 2004A Bonds authorized under the Indenture and the obligation evidenced thereby will not constitute a lien upon any property of or within the District, including, without limitation, the Series 2004A Project or any portion thereof in respect of which any such bonds are being issued, or any part thereof, but will constitute a lien only on the Pledged Revenues as set forth in the Indenture. Nothing in the Series 2004A Bonds or in the Indenture will be construed as obligating the District to pay the Series 2004A Bonds or the redemption price thereof or the interest thereon except from the Pledged Revenues, or as pledging the faith and credit of the District, the City, the County, or the State of Florida or any political subdivision thereof, or as obligating the District, the City, the County, or the State of Florida or any of its political subdivisions, directly or indirectly or contingently, to levy or to pledge any form of taxation whatever therefor. The purchase of the Series 2004A Bonds involves a degree of risk (See BONDHOLDERS RISKS herein) and is not suitable for all investors (See SUITABILITY FOR INVESTMENT herein). The Underwriter is limiting this Offering to Accredited Investors within the meaning of Chapter 517, Florida Statutes, as amended and the rules of the Florida Department of Financial Services promulgated thereunder; the limitation of the initial offering to Accredited Investors does not denote restrictions of transfer in any secondary market for the Series 2004A Bonds. The Series 2004A Bonds are not credit enhanced or rated and no application has been made for a rating with respect to the Series 2004A Bonds. Amounts, Maturities, Interest Rates, Price or Yield and Initial Cusip Numbers $25,100,000, 6.00% Term Bonds Due May 1, 2024 Price 100% Initial Cusip Number 59807P AA3 $48,480,000, 6.25% Term Bonds Due May 1, 2037 Yield 6.30% Initial Cusip Number 59807P AB1 This cover page contains certain information for quick reference only. It is not a summary of the Series 2004A Bonds. Investors must read this entire Limited Offering Memorandum to obtain information essential to the making of an informed investment decision. The Series 2004A Bonds are offered for delivery when, as and if issued by the District and accepted by the Underwriter, subject to the receipt of the opinion of Greenberg Traurig, P.A., Miami, Florida, Bond Counsel, as to the validity of the Series 2004A Bonds and the excludability of interest thereon from gross income for federal income tax purposes. Certain legal matters will be passed upon for the Underwriter by its counsel, Squire, Sanders & Dempsey L.L.P., Miami, Florida, for the District by its counsel, Billing, Cochran, Heath, Lyles, Mauro & Anderson, P.A., Fort Lauderdale, Florida for Midtown Partners, LLC by its counsel, Greenberg Traurig, P.A., Miami, Florida, for DDR Miami Avenue LLC by its counsel, Broad and Cassel, Boca Raton, Florida and for the Trustee by its counsel, Holland & Knight LLP, Miami, Florida. Dunlap & Associates, Inc., Winter Park, Florida, and Fidelity Financial Services, L.C., Hollywood, Florida, serve as co-financial advisors to the City. It is expected that the Series 2004A Bonds will be delivered in book-entry form through the facilities of DTC on or about July 28, July 16, 2004

2

3 MIDTOWN MIAMI COMMUNITY DEVELOPMENT DISTRICT BOARD OF SUPERVISORS Deborah Samuel Michael Ullian Richard Forrest Linda Nickels Aaron Newman DISTRICT MANAGER Severn Trent Services, Inc. Coral Springs, Florida COUNSEL TO THE DISTRICT Billing, Cochran, Heath, Lyles, Mauro & Anderson, P.A. Fort Lauderdale, Florida SPECIAL COUNSEL Edwards and Carstarphen Miami, Florida FINANCIAL ADVISOR Fishkind and Associates, Inc. Orlando, Florida CO-FINANCIAL ADVISOR TO CITY OF MIAMI Dunlap and Associates, Inc. Winter Park, Florida Fidelity Financial Services, L.C. Hollywood, Florida CONSULTING ENGINEER Kimley-Horn and Associates, Inc. Miami, Florida BOND COUNSEL Greenberg Traurig, P.A. Miami, Florida

4 No dealer, broker, salesperson or other person has been authorized by the District or the Underwriter to give any information or make any representations, other than those contained in this Limited Offering Memorandum, and if given or made, such other information or representations must not be relied upon as having been authorized by either of the foregoing. This Limited Offering Memorandum does not constitute an offer to sell or the solicitation of an offer to buy and there will be no offer, solicitation or sale of the Series 2004A Bonds by any person in any jurisdiction in which it is unlawful for such person to make such offer, solicitation or sale. The Underwriter has reviewed the information in this Limited Offering Memorandum in accordance with, and as part of, its responsibilities to investors under the United States federal securities laws as applied to the facts and circumstances of this transaction. The information set forth herein has been furnished by the District and obtained from sources, including the Developers, which are believed by the District and the Underwriter to be reliable, but it is not guaranteed as to accuracy or completeness, and is not to be construed as a representation of the Underwriter. The information and expressions of opinion herein are subject to change without notice, and neither the delivery of this Limited Offering Memorandum, nor any sale made hereunder, will, under any circumstances, create any implication that there has been no change in the affairs of the District or the Developers since the date hereof. The Series 2004A Bonds have not been registered under the Securities Act of 1933, nor has the Indenture been qualified under the Trust Indenture Act of 1939, in reliance upon exemptions contained in such laws. The registration or qualification of the Series 2004A Bonds under the securities laws of any jurisdiction in which they may have been registered or qualified, if any, will not be regarded as a recommendation thereof. None of such jurisdictions, or any of their agencies, have passed upon the merits of the Series 2004A Bonds or the accuracy or completeness of this Limited Offering Memorandum.

5 TABLE OF CONTENTS SUMMARY STATEMENT...iii INTRODUCTION... 1 PLAN OF FINANCE... 3 General... 3 Allocation of Series 2004 Project...5 Levy of Special Assessments... 6 Additional Security for the Parking Garage Project Bonds... 6 Anticipated Structure of the Assessment Levy... 9 DESCRIPTION OF THE SERIES 2004A BONDS... 9 General Description... 9 Redemption Provisions BOOK-ENTRY ONLY SYSTEM SECURITY FOR THE SERIES 2004A BONDS General Economic Incentive Payments Tax Increment Revenues Special Assessments Debt Service Reserve Fund Application of Pledged Revenues under Indenture Investment of Funds Additional Obligations BONDHOLDERS RISKS SOURCES AND USES OF FUNDS DEBT SERVICE REQUIREMENTS THE DISTRICT General Governance Powers and Authority The District Manager and Other Consultants THE SERIES 2004A PROJECT Overview Series 2004A Project THE DEVELOPMENTS AND DEVELOPERS Overview Development Area 1 Midtown Miami Development Area 2 Shops at Midtown Miami i Page

6 TABLE OF CONTENTS Page Infrastructure Zoning Environmental Market Appraised Value Utilities TAX MATTERS General Tax Treatment of Original Issue Discount AGREEMENT BY THE STATE LEGALITY FOR INVESTMENT SUITABILITY FOR INVESTMENT ENFORCEABILITY OF REMEDIES FINANCIAL STATEMENTS LITIGATION NO RATING CONTINUING DISCLOSURE UNDERWRITING CONSULTANTS VALIDATION FORWARD-LOOKING STATEMENTS LEGAL MATTERS AUTHORIZATION AND APPROVAL APPENDICES APPENDIX A Engineer s Report APPENDIX B Interlocal Agreement APPENDIX C Form of Indenture APPENDIX D Assessment Methodology APPENDIX E Tax Increment Report APPENDIX F Certain Information about the City APPENDIX G Certain Information about the County APPENDIX H Proposed Form of Opinion of Bond Counsel APPENDIX I Forms of Continuing Disclosure Agreements APPENDIX J Appraisal ii

7 SUMMARY STATEMENT This Summary Statement is part of this Limited Offering Memorandum, and is subject in all respects to the more complete information and definitions contained in or incorporated in this Limited Offering Memorandum. This Summary Statement should not be considered to be a complete statement of the facts material to making an investment decision. The offering by the Midtown Miami Community Development District (the District ) of its Special Assessment and Revenue Bonds, Series 2004A (Parking Garage Project) (the Series 2004A Bonds or the Parking Garage Project Bonds ) to potential investors is made only by means of this entire Limited Offering Memorandum. No person is authorized to detach this Summary Statement from this Limited Offering Memorandum or to otherwise use it without the entire Limited Offering Memorandum. Unless otherwise defined, all capitalized terms in this Summary Statement will be as defined herein, in the Interlocal Agreement (herein defined), the Indenture (herein defined). Bondholders Risks; Limited Offering An investment in the Series 2004A Bonds involves certain risks. The Series 2004A Bonds will be sold only to Accredited Investors within the meaning of Chapter 517, Florida Statutes, as amended, and the rules of the Florida Department of Financial Services promulgated thereunder, although there is no restriction upon resales of the Series 2004A Bonds. See SECURITY FOR THE SERIES 2004A BONDS, BONDHOLDERS RISKS and SUITABILITY FOR INVESTMENT herein. The District The District is a special-purpose government of the State of Florida created in accordance with the Uniform Community Development District Act of 1980, Chapter 190, Florida Statutes, as amended (the Act ), Section 1.10(A)(21) of the Miami-Dade Home Rule Charter, by Ordinance No (the Ordinance ) enacted by the Board of County Commissioners of Miami-Dade County, Florida on December 16, The land within the District (the District Lands ) consists of approximately 56 acres of land located entirely within the City of Miami, Florida (the City ), and within Miami-Dade County (the County ). For more complete information about the District, see THE DISTRICT herein. The Series 2004A Bonds The Series 2004A Bonds are being issued pursuant to the Act and a Master Trust Indenture, dated as of July 1, 2004, as supplemented by a First Supplemental Trust Indenture dated as of July 1, 2004 (collectively, the Indenture ), by and between the District and Wachovia Bank, National Association, as trustee (the Trustee ). The Indenture is reproduced herein in Appendix C Form of Indenture. The Series 2004A Bonds will be issued in fully registered form, in denominations of $5,000 and integral multiples thereof; provided, however, that the Series 2004A Bonds will be deliverable to the initial purchasers thereof only in minimum amounts of $100,000 or integral multiples of $5,000 in excess of $100,000. Interest on the Series 2004A Bonds is payable on May 1 and November 1 of each year, commencing iii

8 November 1, 2004, until maturity or prior redemption. The Series 2004A Bonds are subject to redemption prior to their stated dates of maturity, as provided herein. The Series 2004A Bonds are initially being issued in book-entry only form. See DESCRIPTION OF THE SERIES 2004A BONDS and BOOK-ENTRY ONLY SYSTEM herein. Purpose of the Series 2004A Bonds The Series 2004A Bonds are being issued in order to provide funds for (i) the payment of a portion of the costs of the Series 2004A Project, (ii) the payment of interest on the Series 2004A Bonds through November 1, 2007, (iii) the funding of the Series 2004A Debt Service Reserve Account and (iv) the payment of the costs of issuance of the Series 2004A Bonds. See THE SERIES 2004A PROJECT and Appendix C Form of Indenture herein. Plan of Finance The District s financing plan is the culmination of an agreement among the District, the City and the County, the terms of which are memorialized in the Interlocal Agreement among the District, the City and the County dated as of May 28, 2004 (the Interlocal Agreement ). The District will issue two series of bonds under the Indenture. The Series 2004A Bonds will finance the construction of certain parking facilities, public open space and other public improvements. The District also expects to issue Special Assessment Bonds, Series 2004B (Infrastructure Project Bonds) (herein the Series 2004B Bonds or the Infrastructure Project Bonds and, collectively with the Series 2004A Bonds, the Series 2004 Bonds ) to finance the construction of other infrastructure to support the Developments (defined herein), including utilities, landscaping, streetscapes and other public improvements. The bifurcation of the Series 2004 Bonds reflects the agreement of the City and the County to make certain payments to the District for the benefit of the Parking Garage Project Bonds (but not the Infrastructure Project Bonds) subject to certain development performance measures and other criteria as set forth in the Interlocal Agreement, as further discussed herein under the headings PLAN OF FINANCE and SECURITY FOR THE SERIES 2004A BONDS. The Series 2004B Bonds will not be secured by or payable from any portion of the payments from the City and the County to the District, or any other entity under the Interlocal Agreement but will be secured by a parity lien on the Special Assessments. The Developers and the Developments The lands within the District are expected to be developed as two distinct mixed-use projects, Midtown Miami and the Shops at Midtown (collectively, the Developments ). Upon completion, it is currently expected that the Developments will contain a retail shopping center, residential condominium units with retail areas, an office tower with retail areas, public plazas, rental apartments, an entertainment facility with retail areas and a multi-use facility, and parking facilities. There are two primary developer groups associated with the Developments, each controlling distinct tracts (or portions thereof) within the District and, in some cases, the developable air rights (or certain levels of air rights) over other tracts. Each of the Developers is separately responsible for the development of their respective portions of the Developments. See PLAN OF FINANCE and THE DEVELOPMENTS AND DEVELOPERS herein for additional information regarding the Developers and the Developments. iv

9 Security for the Series 2004A Bonds The Series 2004A Bonds are secured by a pledge of the Pledged Revenues under the Indenture. The Pledged Revenues consist of (a) all revenues received by the District under the Interlocal Agreement and deposited in the Series 2004A Account within the Revenue Fund pursuant to the Indenture, as further described herein, (b) all revenues received by the District from Special Assessments levied and collected on all or a portion of the District Lands with respect to the Series 2004A Bonds, including, without limitation, amounts received from any foreclosure proceeding for the enforcement of collection of such Special Assessments or from the issuance and sale of tax certificates with respect to such Special Assessments, and (c) all moneys on deposit in the Funds and Accounts established under the Indenture for the Series 2004A Bonds; provided, however, that Pledged Revenues will not include (i) any moneys transferred to the Rebate Fund, or investment earnings thereon, and (ii) special assessments levied and collected by the District under Section , Florida Statutes, for maintenance purposes or maintenance special assessments levied and collected by the District under Section (3), Florida Statutes. The lien on and pledge of the Special Assessments is on a parity with the lien thereon in favor of the Series 2004B Bonds expected to be issued contemporaneously with the Series 2004A Bonds. See PLAN OF FINANCE and SECURITY FOR THE SERIES 2004A BONDS herein. The Series 2004A Bonds authorized under the Indenture and the obligation evidenced thereby will not constitute a lien upon any property of or within the District, including, without limitation, the Series 2004A Project or any portion thereof in respect of which any such bonds are being issued, or any part thereof, but will constitute a lien only on the Pledged Revenues as set forth in the Indenture. Nothing in the Series 2004A Bonds or in the Indenture will be construed as obligating the District to pay the Series 2004A Bonds or the redemption price thereof or the interest thereon except from the Pledged Revenues, or as pledging the faith and credit of the District, the City, the County or the State of Florida or any political subdivision thereof, or as obligating the District, the City, the County, or the State of Florida or any of its political subdivisions, directly or indirectly or contingently, to levy or to pledge any form of taxation whatever therefor. Debt Service Reserve Fund A Series 2004A Debt Service Reserve Account will be created under the Indenture within the Debt Service Reserve Fund for the benefit of the Series 2004A Bonds. Pursuant to the Indenture, Series 2004A Debt Service Reserve Requirement will mean with respect to the Series 2004A Bonds, an amount equal to the least of (i) the maximum annual Debt Service Requirement for the Outstanding Series 2004A Bonds, (ii) 125% of the average annual Debt Service Requirement for the Outstanding Series 2004A Bonds, or (iii) 10% of the original proceeds (within the meaning of the Code) of the Series 2004A Bonds. See SECURITY FOR THE SERIES 2004A BONDS Debt Service Reserve Fund herein. Additional Obligations As stated above, concurrently with the issuance of the Series 2004A Bonds, the District expects to issue the Series 2004B Bonds in an aggregate principal amount of $30,020,000, v

10 payable on a parity from the Special Assessments but not payable from the Interlocal Agreement Revenues. The District will not issue any obligations, other than the Series 2004 Bonds, payable from Pledged Revenues, nor voluntarily create or cause to be created any debt, lien, pledge, assignment, encumbrance or other charge, payable from Pledged Revenues, except in the ordinary course of business; provided, however, that the District may issue bonds to refund all or a portion of the Series 2004 Bonds. See SECURITY FOR THE SERIES 2004A BONDS Additional Obligations herein. vi

11 LIMITED OFFERING MEMORANDUM relating to $73,580,000 MIDTOWN MIAMI COMMUNITY DEVELOPMENT DISTRICT (MIAMI-DADE COUNTY, FLORIDA) SPECIAL ASSESSMENT AND REVENUE BONDS, SERIES 2004A (PARKING GARAGE PROJECT) INTRODUCTION The purpose of this Limited Offering Memorandum, including the cover page, summary statement and appendices hereto, is to provide certain information in connection with the issuance and sale by the Midtown Miami Community Development District (the District ) of its $73,580,000 Special Assessment and Revenue Bonds, Series 2004A (Parking Garage Project) (the Series 2004A Bonds ). PROSPECTIVE INVESTORS SHOULD BE AWARE OF CERTAIN RISK FACTORS, ANY ONE OR MORE OF WHICH, IF MATERIALIZED TO A SUFFICIENT DEGREE, COULD DELAY OR PREVENT PAYMENT OF PRINCIPAL OF, PREMIUM, IF ANY, AND/OR INTEREST ON THE SERIES 2004A BONDS. THE SERIES 2004A BONDS ARE NOT A SUITABLE INVESTMENT FOR ALL INVESTORS. THE SERIES 2004A BONDS ARE BEING OFFERED INITIALLY ONLY TO ACCREDITED INVESTORS WITHIN THE MEANING OF CHAPTER 517, FLORIDA STATUTES, AS AMENDED, AND THE RULES OF THE FLORIDA DEPARTMENT OF FINANCIAL SERVICES PROMULGATED THEREUNDER. See SUITABILITY FOR INVESTMENT and BONDHOLDERS RISKS herein. The District is a local unit of special-purpose government of the State of Florida (the State ), created pursuant to the Uniform Community Development District Act of 1980, Chapter 190, Florida Statutes, as amended (the Act ), Section 1.10(A)(21) of the Miami-Dade Home Rule Charter, by Ordinance No (the Ordinance ) enacted by the Board of County Commissioners of Miami-Dade County, Florida on December 16, The District was established for the purpose of financing the acquisition and construction of and managing the maintenance and operation of the infrastructure necessary for development of the lands within the District. The Act authorizes the District to issue bonds for several purposes, including, but not limited to, financing the cost of acquisition and construction of parking facilities, roadways, water and sewer facilities, a stormwater management system, streetscape and landscape improvements. The District encompasses approximately 56 gross acres of land (the District Lands ) located entirely within the City of Miami, Florida (the City ) and within Miami-Dade County, Florida (the County ). For more complete information about the District, its Board of Supervisors and the District Manager, see THE DISTRICT herein. 1

12 The District Lands are expected to be developed as two distinct mixed-use projects: Midtown Miami and the Shops at Midtown (collectively, the Developments ). Upon completion, it is currently expected that the Developments will contain a retail shopping center, residential condominium units with retail areas, rental apartments, an entertainment facility with retail areas, a multi-use facility, and parking facilities. There are two primary developer groups associated with the Developments, each controlling distinct tracts (or portions thereof) within the District and, in some instances, the developable air rights (or certain levels of air rights) over other tracts. Each of the Developers is separately responsible for the development of their respective portion of the Developments. See PLAN OF FINANCE, THE DEVELOPMENTS AND DEVELOPERS herein for additional information regarding the Developers and the Developments. The Series 2004A Bonds are being issued pursuant to the Act, a Master Trust Indenture dated as of July 1, 2004, as supplemented by a First Supplemental Trust Indenture dated as of July 1, 2004 (collectively, the Indenture ) both by and between the District and Wachovia Bank, National Association, as trustee (the Trustee ). Reference is made to the Indenture for a full statement of the authority for, and the terms and provisions of, the Series 2004A Bonds. All capitalized terms used in this Limited Offering Memorandum that are not defined herein will have the respective meanings set forth in the Interlocal Agreement (defined below) or the Indenture. See Appendix B Interlocal Agreement and Appendix C Form of Indenture herein. The District s financing plan is the culmination of an agreement among the District, the City and the County, the terms of which are memorialized in the Interlocal Agreement among the District, the City and the County dated as of May 28, 2004 (the Interlocal Agreement ). The District will issue two separate series of bonds under the Indenture. The Series 2004A Bonds (sometimes called the Parking Garage Project Bonds herein) will finance the construction of certain parking facilities and public open space (the Series 2004A Project ). Concurrently with the issuance of the Series 2004A Bonds, the District expects to issue Special Assessment Bonds Series 2004B (Infrastructure Project Bonds) (herein the Series 2004B Bonds or the Infrastructure Project Bonds and, collectively with the Series 2004A Bonds, the Series 2004 Bonds ) to finance the construction of other infrastructure to support the Developments, including utilities, landscaping, streetscapes and other public improvements (the Series 2004B Project and collectively, with the Series 2004A Project, the Series 2004 Project ). The Series 2004B Bonds will be secured on a parity with the 2004A Bonds with respect to the Special Assessments. The bifurcation of the Series 2004 Bonds reflects the agreement of the City and the County to make certain payments for the benefit of the Parking Garage Project Bonds (but not the Infrastructure Project Bonds) subject to certain development performance measures and other criteria as set forth in the Interlocal Agreement, as further discussed herein under the headings PLAN OF FINANCE and SECURITY FOR THE SERIES 2004A BONDS. The Series 2004B Bonds will not be secured by or payable from any portion of the payments from the City and the County to the District or any other entity under the Interlocal Agreement. The Series 2004A Bonds are being issued in order to provide funds for (i) the payment of the cost of the Series 2004A Project, (ii) the payment of interest on the Series 2004A Bonds through November 1, 2007, (iii) the funding of the Series 2004A Debt Service Reserve Account, 2

13 and (iv) the payment of the costs of issuance of the Series 2004A Bonds. See THE SERIES 2004A PROJECT and Appendix C Form of Indenture herein. The Series 2004A Bonds authorized under the Indenture and the obligation evidenced thereby will not constitute a lien upon any property of or within the District, including, without limitation, the Series 2004A Project or any portion thereof in respect of which any such bonds are being issued, or any part thereof, but will constitute a lien only on the Pledged Revenues as set forth in the Indenture and described herein. Nothing in the Series 2004A Bonds authorized under the Indenture or in the Indenture will be construed as obligating the District to pay the Series 2004A Bonds or the redemption price thereof or the interest thereon except from the Pledged Revenues, or as pledging the faith and credit of the District, the City, the County or the State or any political subdivision thereof, or as obligating the District, the City, the County or the State or any of its political subdivisions, directly or indirectly or contingently, to levy or to pledge any form of taxation whatever therefor. Set forth herein are brief descriptions of the District, the Developments, the Developers and the Series 2004A Project, together with summaries of terms of the Series 2004A Bonds, the Interlocal Agreement, the Indenture and certain provisions of the Act. All references herein to the Interlocal Agreement, the Indenture and the Act are qualified in their entirety by reference to such documents and all references to the Series 2004A Bonds are qualified by reference to the definitive forms thereof and the information with respect thereto contained in the Indenture. Copies of those documents not attached hereto may be obtained during the period of the offering of the Series 2004A Bonds from the Underwriter at Banc of America Securities LLC, 250 South Park Avenue, Suite 400, Winter Park, Florida 32789, and thereafter from the District Manager at Severn Trent Services, Inc., N.W. 11 th Manor, Coral Springs, Florida upon payment of any costs for reproduction and mailing. The full text of the Interlocal Agreement appears as Appendix B and the full text of the Indenture appears as Appendix C attached hereto. General PLAN OF FINANCE The District Lands are planned for two distinct developments: the Shops at Midtown, primarily retail in nature with certain apartments and live/work units incorporated therein, and Midtown Miami, primarily residential in nature with some retail, as well as office, hotel and entertainment components. Upon completion, it is currently expected that the Developments will contain a retail shopping center, public plazas, residential condominium units with retail areas, rental apartments, a hotel, an entertainment facility with retail areas and a spa, and parking facilities. The District was established for the purpose of financing the acquisition and construction of and managing the maintenance and operation of the infrastructure necessary for development of the District Lands. The Act authorizes the District to issue bonds for purposes, among others, of financing the cost of acquisition and construction of parking facilities, roadways, water and sewer facilities, a stormwater management system and streetscape and landscape improvements. 3

14 The District s financing plan is the culmination of an agreement between the District, the City and the County, the terms of which are memorialized in the Interlocal Agreement. The District expects to issue two separate series of bonds under the Indenture, the Series 2004A Bonds (the Parking Garage Project Bonds) to finance the Series 2004A Project and the Series 2004B Bonds (the Infrastructure Project Bonds) to finance the Series 2004B Project. The bifurcation of the Series 2004 Bonds reflects the agreement of the City and the County to make certain payments to the District for the benefit of the Parking Garage Project Bonds (but not the Infrastructure Project Bonds) subject to development performance measures and other criteria as set forth in the Interlocal Agreement, as further discussed below and herein under the heading SECURITY FOR THE SERIES 2004A BONDS. The Infrastructure Project Bonds will not be secured by or payable from any portion of the payments to the District from the City and County or any other entity under the Interlocal Agreement, but will be secured by a parity lien on the Special Assessments as further described herein. [Remainder of Page Intentionally Left Blank] 4

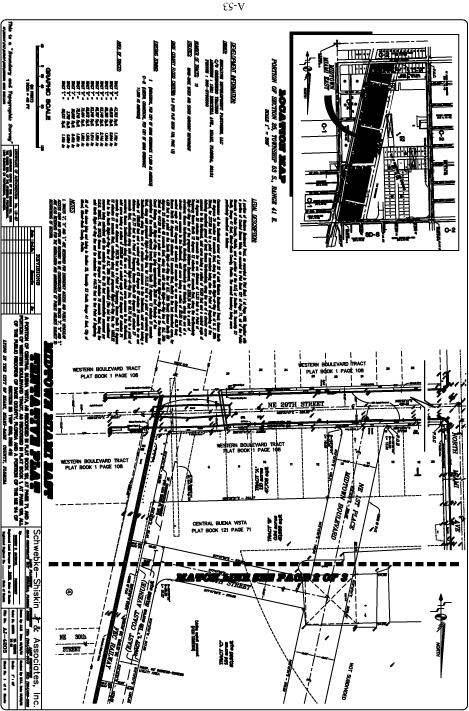

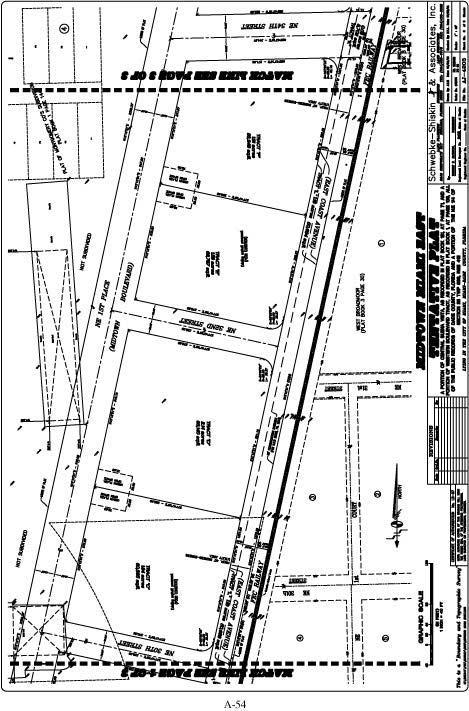

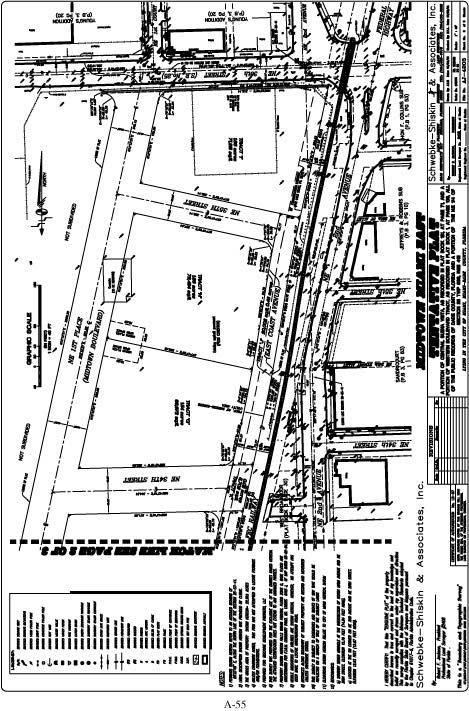

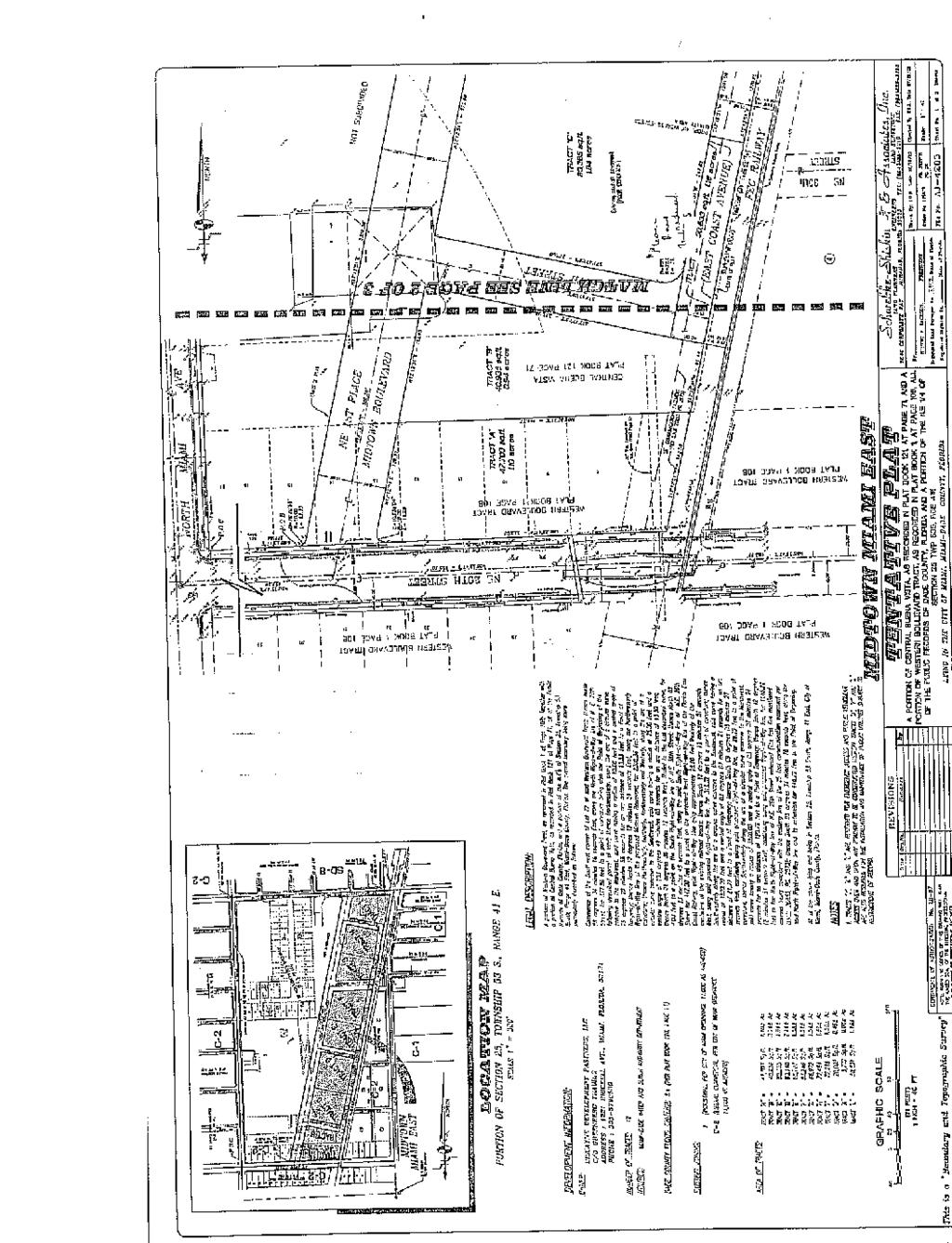

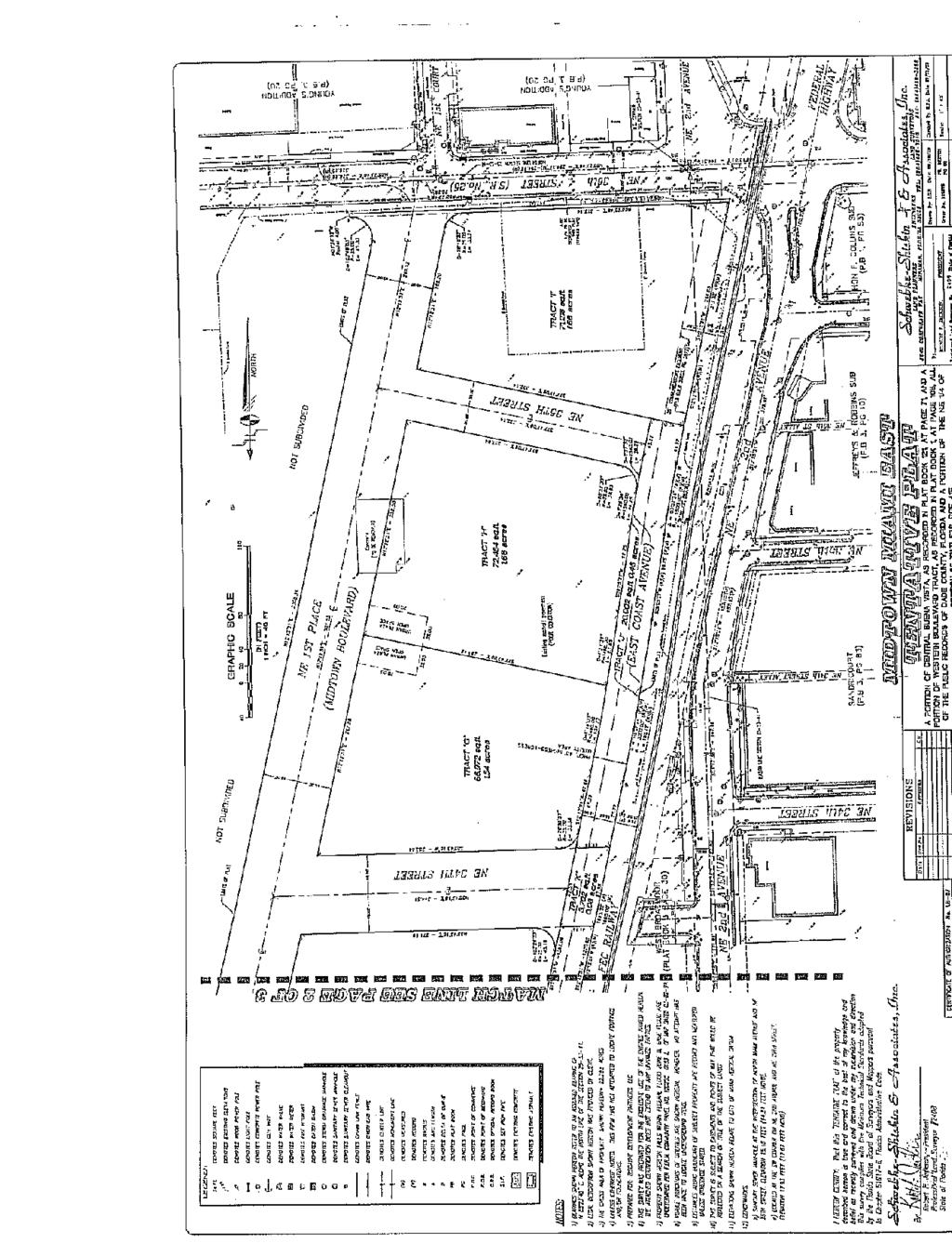

15 Allocation of Series 2004 Project The purpose of the Series 2004 Bonds is to provide funds for a portion of the acquisition and construction costs of the Series 2004 Project, which includes both the Series 2004A Project and the Series 2004B Project. The Series 2004 Project consists of public improvements to be acquired or constructed by the District, all as described in the Amended Engineer s Report dated April 21, 2004 (the Engineer s Report ) prepared for the District by Kimley-Horn and Associates, Inc. (the District Engineer ). See Appendix A - Engineer s Report. The table below sets forth the allocation of the Series 2004 Project costs and their source of funding. As shown below, a portion of the costs associated with the Parking Improvements and the Mid Block Plaza and Other Public Improvements will be funded from the sale of the Parking Garage Project Bonds. The balance of the Series 2004 Project will be funded by a combination of the sale of the Infrastructure Project Bonds and contribution by the Developers pursuant to the Completion Agreements which contribution may be offset by state or local grant moneys, as summarized herein. Allocation of Project Cost by Source of Funding Parking Infrastructure Total (1) Project Project Summary of Project Costs (1) Roadway Improvements $5,597,737 $ $5,597,737 Water and Sewer Systems 2,290,822-2,290,822 Stormwater Management Systems 2,791,286-2,791,286 Landscaping and Streetscaping 6,387,668-6,387,668 Irrigation 510, ,013 Plaza at Entertainment Block 3,617,019-3,617,019 Miscellaneous Public Improvements 5,136,166-5,136,166 Parking Improvements 45,337,889 45,337,889 - Mid Block Plaza and Other Public Improvements 5,866,130 5,866,130 - Project Costs $77,534,730 $51,204,019 $26,330,711 Sources of Funds Parking Garage Project Bonds (2) $51,204,019 $51,204,019 Infrastructure Project Bonds (2) 20,600,000 - $20,600,000 Developers Completion Agreements (3) 5,730,711-5,730,711 Sources of Funds $77,534,730 $51,204,019 $26,330,711 Notes: (1) From the Engineer s Report. See Appendix A - Engineer s Report herein. (2) These amounts represent the total expected to be funded by the Series 2004 Bonds, both include projected interest earnings on the funds held by the District and invested assuming an earnings rate of 0.5%/year. (3) Pursuant to the Completion Agreements (herein defined), the Developers will be required to contribute these funds if necessary to complete the installation of the improvements for the Series 2004 Project. The Developers have applied for certain federal, state and local grants which, if received, would be contributed to the District, thereby reducing the Developers required contribution by a like dollar amount. There is no assurance that the Developers will be successful in their pursuit of this grant funding. 5

16 Levy of Special Assessments The District will levy Special Assessments, as defined herein, in the principal amount of the Series 2004 Bonds on the District Lands benefiting from the Series 2004 Project. See THE SECURITY FOR THE SERIES 2004A BONDS Special Assessments and Appendix D - Assessment Methodology. This assessment lien is a parity lien shared ratably between the Parking Garage Project Bonds and the Infrastructure Project Bonds. The District has the power, in each year for the full term of the Series 2004 Bonds, to collect annual installments against this assessment lien in an amount equal to the aggregate annual debt service on the Series 2004 Bonds. As further described herein, the District does not intend to collect the full amount of the Special Assessments with respect to the Series 2004A Project to the extent it receives Interlocal Agreement Revenues. Additional Security for the Parking Garage Project Bonds Generally. Pursuant to the Interlocal Agreement, the City and the County have agreed to make certain contributions to the District, subject to the completion of certain development performance thresholds. These contributions relate only to the Series 2004A Project and the District has pledged all amounts received under the Interlocal Agreement to the payment of debt service on the Parking Garage Project Bonds only and not with respect to the Infrastructure Project Bonds. It is the intent and expectation that when, and if, the Stage 1 and 2 performance thresholds under the Interlocal Agreement have been met, as summarized below, the City and the County will make contributions to the District that are expected to be equal to the debt service requirements for the Parking Garage Project Bonds and will, subject to their replacement with another contribution source, as described below under Tax Increment Revenues, remain payable and in effect for the full term of the Parking Garage Project Bonds. The Developers expect that the Stage 1 performance threshold will be met by December 31, 2006, and that the Stage 2 performance threshold will be met by December 31, 2007; provided, however, no assurance can be given that there will be no delays in reaching either of such thresholds. Failure to meet either of such thresholds would result in a delay in the payment of certain Economic Incentive Payments (defined herein) and/or Tax Increment Revenues (defined herein) for a full year or more. [The Remainder of this Page is Intentionally Left Blank] 6

17 Performance Thresholds. The conditions precedent to the County and City contributions as set forth in the Interlocal Agreement are generally broken down into two stages. Stage 1 sets forth the minimum level of development necessary to require the City and the County to begin making any contributions to the District under the Interlocal Agreement. Stage 2 sets forth the minimum level of development necessary to require the City and the County to increase the initial level of contribution to an amount anticipated to cover the annual debt service requirement on the Parking Garage Project Bonds. The following table sets forth the anticipated development and the performance thresholds for Stages 1 and 2. Anticipated Development STAGE 1 a. Retail minimum 600,000 sq. ft. of retail space b. Public Improvements Parking and Midtown Plaza, both as described in the Engineer s Report c. Residential Condominium The first tower with residential and retail spaces 374,500 sq. ft. Stage 1 DUs Subtotal STAGE 2 a. Hotel/Spa - 235,000 sq. ft. of planned hotel/spa development b. Apartments - 292,000 sq. ft.. of improved area c. Office - minimum 150,000 sq. ft. of improved office space d. Residential Condominium The second tower with residential and retail spaces 395,500 sq. ft. Equivalent Development Units ( DU ) , Performance Thresholds Stage 1 Performance Threshold is defined to be: Certificates of Occupancy, as defined in the Interlocal Agreement ( COs ) must be issued for at least 90% of Stage 1 DUs (1, DUs); and The above COs requirement must include at least 600,000 sq. ft. of retail space Stage 2 Performance Threshold is defined to be: Stage 1 performance measure met; and COs must be issued for at least 90% of Stage 1 & 2 cumulative DUs (2, DUs); and The above COs requirement must include at least 150,000 sq. ft. of office space Stage 2 DUs Subtotal Stage 1&2 Cumulative DUs Total 1, , The Interlocal Agreement provides flexibility to substitute different product types from those set forth in Stage 1 and 2 so long as the cumulative DU totals at either stage are greater than or equal to 90% of the development units totals for each stage. However, two absolute requirements exist at each stage: (1) Stage 1 must include the issuance of a CO for the retail component; and (2) Stage 2 must include the issuance of a CO for the office (unless certain circumstances arise making the completion of the office impossible). 7

18 Economic Incentive Payments. Pursuant to the Interlocal Agreement, the City and the County have each agreed to make fixed annual payments ( Economic Incentive Payments or EIP ) each year beginning in the calendar year following the year in which the Stage 1 performance thresholds are met and continuing through the term of the Parking Garage Project Bonds. The City and the County have secured their separate commitments to make Economic Incentive Payments by a covenant of the respective governments to budget and appropriate legally available Non-Ad Valorem Revenues (as hereinafter defined) each year in an amount sufficient to pay that entity s respective portion of the EIP. See SECURITY FOR THE SERIES 2004A BONDS Economic Incentive Payments, herein. When Stage 1 performance thresholds have been met, the City s and the County s collective EIP level will equal $2,559,680 per year. When Stage 2 performance thresholds have been met, the City s and the County s collective EIP level will increase to the lesser of $5,999,360 per year or the annual debt service requirements of the Parking Garage Project Bonds. The County is responsible for the payment of 40.9% of the EIP and the City is responsible for the payment of 59.1% of the EIP. Under certain circumstances the County s and City s obligation to contribute EIP may be extinguished and replaced by Tax Increment Revenues, described below. See SECURITY FOR THE SERIES 2004A BONDS Economic Incentive Payments, herein. Tax Increment Revenues. The Interlocal Agreement also provides a method to replace the EIP with tax increment revenues to be derived from the implementation of a community redevelopment plan by a community redevelopment agency pursuant to Chapter 163, Florida Statutes, expected to be created by the County and the City and to provide for a community redevelopment area that has boundaries coterminous with those of the District (the Midtown CRA Agency and the Midtown CRA, respectively). Under the Interlocal Agreement, Tax Increment Revenues means the incremental increase in ad valorem tax revenues generated within the Midtown CRA as a result of the Developments. The Interlocal Agreement also sets forth the agreement that the County and the City (a) intend to create the Midtown CRA Agency and the Midtown CRA, (b) and once created, will cause the Midtown CRA to remain in effect and the Tax Increment Revenues to remain unencumbered (except as contemplated under the Interlocal Agreement) for so long as the Parking Garage Project Bonds are outstanding, and (c) will cause the Midtown CRA Agency, subject to the performance thresholds, to contribute the maximum legally available Tax Increment Revenues to the District annually (but in an amount not to exceed annual debt service on the Parking Garage Project Bonds). See SECURITY FOR THE SERIES 2004A BONDS Tax Increment Revenues, herein. Termination of EIP. Under the Interlocal Agreement, the obligation of the City and the County to contribute EIP will terminate under two scenarios. First, if the Midtown CRA and the Redevelopment Trust Fund (as defined in the Interlocal Agreement) is established no later than June 30, 2005 and (a) the Interlocal Agreement is amended to include the Midtown CRA Agency as a party, and (b) the District, the City and the County agree that the percentage of Tax Increment Revenues to be contributed by the County and the City in each calendar year while the Parking Garage Project Bonds are outstanding under the Indenture, will be equal to the lesser of (i) the maximum percentage authorized by Section , Florida Statutes, which currently is 95% (the Maximum Percentage ), or (ii) a percentage less than the Maximum Percentage but sufficient to enable the Midtown CRA Agency to pay to the District in each calendar year Tax Increment Revenues equal to the debt service on the Parking Garage Project Bonds in each such year for the remaining term of the Parking Garage Project Bonds. If the Midtown CRA is 8

19 created prior to June 30, 2005, the base year value for calculating Tax Increment Revenues will be established based on the state of development reflected in the 2004/2005 tax roll established by the County Tax Appraiser s office. The assessed value for the District Lands, as of January 1, 2004, is not yet available. Second, in the event that the Midtown CRA and the Redevelopment Trust Fund (as defined in the Interlocal Agreement) is created after June 30, 2005, the obligation to contribute EIP will terminate, when and if, the following conditions are met (a) the County and the City are current on all EIP due under the Interlocal Agreement; (b) the Interlocal Agreement is amended to include the Midtown CRA Agency as a party, (c) the City, the County and the District agree that the percentage of Tax Increment Revenues to be contributed by the County and the City in each calendar year while the Parking Garage Project Bonds are outstanding under the Indenture, will be equal to the lesser of (i) the Maximum Percentage or (ii) a percentage less than the Maximum Percentage but sufficient to enable the Midtown CRA Agency to pay to the District in each calendar year Tax Increment Revenues equal to the debt service on the Parking Garage Project Bonds in each such year for the remaining term of the Parking Garage Project Bonds; and (d) an independent financial advisor certifies in writing to the District, the City, the County and the Trustee, that funds on deposit in the Midtown CRA redevelopment trust fund are at least equal to the Maximum Annual Debt Service on the Parking Garage Bonds. The City and County have represented to the District that they have initiated the steps necessary to create the Midtown CRA. See SECURITY FOR THE 2004A BONDS Tax Increment Revenues, herein. Anticipated Structure of the Assessment Levy The District has taken the appropriate legal steps to levy the full amount of the Special Assessments. In each year, prior to the certification of the District s assessment roll, the District will determine what level of EIP and/or Tax Increment Revenues are expected to be available. The amount of the assessments to be collected in each year for the Parking Garage Project Bonds will be reduced and offset by an amount equal to the EIP and/or Tax Increment Revenues expected in that year. All EIP and Tax Increment Revenues received by the District will be held by the Trustee under the Indenture for the benefit of only the Parking Garage Project Bonds. The Special Assessments levied in each year will secure both the Parking Garage Project Bonds and the Infrastructure Project Bonds, ratably, measured by the requirements of each Series in that particular year, regardless of the level of EIP and/or Tax Increment Revenues received or to be received by the District. General Description DESCRIPTION OF THE SERIES 2004A BONDS The Series 2004A Bonds will be dated, will bear interest at the rates per annum (computed on the basis of a 360-day year consisting of twelve thirty-day months) and, subject to the redemption provisions set forth below, will mature on the dates and in the amounts set forth on the cover page of this Limited Offering Memorandum. Interest on the Series 2004A Bonds will be payable semi-annually on each May 1 and November 1 commencing November 1,

20 until maturity or prior redemption. Wachovia Bank, National Association, is the initial Trustee, Paying Agent and Registrar for the Series 2004A Bonds. The Series 2004A Bonds will be issued in fully registered form, without coupons, in denominations of $5,000 and integral multiples thereof; provided, however, that the Series 2004A Bonds will be deliverable to the initial purchasers thereof only in minimum amounts of $100,000 or integral multiples of $5,000 in excess of $100,000. Upon initial issuance, the ownership of the Series 2004A Bonds will be registered in the name of Cede & Co., as nominee for The Depository Trust Company, New York, New York ( DTC ), and purchases of beneficial interests in the Series 2004A Bonds will be made in book-entry only form. The Series 2004A Bonds will initially be offered and sold only to Accredited Investors within the meaning of Chapter 517, Florida Statutes, as amended, and the rules of the Florida Department of Financial Services promulgated thereunder, although there is no limitation on resales of the Series 2004A Bonds. See BOOK-ENTRY ONLY SYSTEM and SUITABILITY FOR INVESTMENT below. Redemption Provisions Optional Redemption. The Series 2004A Bonds may, at the option of the District, be called for redemption prior to maturity, in whole or in part, at any time on or after May 1, 2014 (less than all Series 2004A Bonds to be selected by lot), at a Redemption Price equal to 100% of the principal amount to be redeemed, plus accrued interest from the most recent Interest Payment Date to the redemption date. Extraordinary Mandatory Redemption. The Series 2004A Bonds are subject to extraordinary mandatory redemption prior to maturity by the District in whole, on any date, or in part, on any Interest Payment Date, at an extraordinary mandatory redemption price equal to 100% of the principal amount of the Series 2004A Bonds to be redeemed, plus interest accrued to the redemption date, as follows: (i) from prepayments of Special Assessments allocable to the Series 2004A Bonds, including any excess moneys in the Series 2004A Debt Service Reserve Account resulting from such Special Assessment prepayments. (ii) from moneys on deposit in the Series 2004A Accounts and Subaccounts in the Series 2004 Funds and Accounts (other than the Rebate Fund) to the extent sufficient to pay and redeem all Outstanding Series 2004A Bonds (including accrued interest) and to pay all amounts owed to Persons under the Master Indenture. (iii) on or after the Completion Date of the Series 2004A Project, from excess moneys remaining in the Series 2004A Acquisition and Construction Account of the Acquisition and Construction Fund; and on or after the later of November 1, 2007 or the Completion Date, from moneys remaining in the Series 2004A Capitalized Interest Subaccount. (iv) on an annual basis, from excess moneys in the Series 2004A Revenue Subaccount not applied to the payment of regular debt service on the 10

21 Series 2004A Bonds or transferred to the Series 2004A Acquisition and Construction Account. (v) from proceeds of any condemnation award (or sale proceeds if the sale was under threat of condemnation) in respect of all or any portion of the Series 2004A Project which are not to be used to rebuild, replace or restore the taken portion of the Series 2004 Project. (vi) from amounts paid to the District following the damage or destruction of all or substantially all of the Series 2004A Project to such extent that, in the reasonable opinion of the District, the repair and restoration thereof would not be economical or would be impracticable; provided, however, that at least 45 days prior to such extraordinary mandatory redemption, the District is required to deliver to the Trustee (x) notice setting forth the redemption date and (y) a certificate of the Consulting Engineer confirming that the repair and restoration of the Series 2004A Project would not be economical or would be impracticable. (vii) from amounts on deposit in the Series 2004A Debt Service Reserve Account in excess of the Series 2004A Debt Service Reserve Requirement. See Appendix C Form of Indenture. [The Remainder of this Page is Intentionally Left Blank] 11

22 Mandatory Sinking Fund Redemption. The Series 2004A Bonds are subject to mandatory redemption in part by the District by lot prior to their scheduled maturity from moneys in the Series 2004A Sinking Fund Account established under the Indenture in satisfaction of applicable Amortization Installments at the Redemption Price of 100% of the principal amount thereof, without premium, together with accrued interest to the date of redemption on May 1 of the years and in the principal amounts set forth below: 2024 Term Bonds 2037 Term Bonds Year (May 1) Principal Amount Year (May 1) Principal Amount 2008 $ 250, $2,495, , ,655, ,015, ,825, ,075, ,010, ,140, ,200, ,215, ,410, ,285, ,630, ,365, ,865, ,450, ,110, ,540, ,380, ,635, ,660, ,735, ,960, ,845, * 5,280, ,960, ,080, ,210, * 2,345,000 * Maturity. Notice of Redemption. When required to redeem the Series 2004A Bonds under any provision of the Indenture or directed to do so by the District, the Trustee will cause notice of the redemption, either in whole or in part, to be mailed at least 30, but not more than 60, days prior to the redemption date to all Owners of Series 2004A Bonds to be redeemed (as such Owners appear on the Bond Register on the 5 th day prior to such mailing), at their registered addresses, but failure to mail any such notice or defect in the notice or in the mailing thereof will not affect the validity of the redemption of the Series 2004A Bonds for which notice was duly mailed in accordance with the Indenture. Effect of Notice of Redemption. Any Series 2004A Bonds duly called for redemption, for which funds have been deposited with the Trustee, will cease to bear interest from the specified redemption date, will no longer be secured by the Indenture and will be considered no longer Outstanding under the provisions of the Indenture. 12

23 BOOK-ENTRY ONLY SYSTEM The Series 2004A Bonds will be available only in book-entry form initially in the principal amounts of $100,000 and integral multiples of $5,000 in excess thereof and thereafter in denominations of $5,000 and integral multiples thereof. Purchasers of the Series 2004A Bonds will not receive certificates representing their interests in the Series 2004A Bonds purchased. The District will enter into a letter of representations (the Book-Entry Agreement ) with DTC providing for such book-entry system. The Depository Trust Company ( DTC ), New York, NY, will act as securities depository for the Series 2004A Bonds. The Series 2004A Bonds will be issued as fullyregistered securities registered in the name of Cede & Co. (DTC s partnership nominee) or such other name as may be requested by an authorized representative of DTC. One fully-registered Bond certificate will be issued for the Series 2004A Bonds, in the aggregate principal amount of such issue, and will be deposited with DTC. DTC, the world s largest depository, is a limited-purpose trust company organized under the New York Banking Law, a banking organization within the meaning of the New York Banking Law, a member of the Federal Reserve System, a clearing corporation within the meaning of the New York Uniform Commercial Code, and a clearing agency registered pursuant to the provisions of Section 17A of the Securities Exchange Act of DTC holds and provides asset servicing for over 2 million issues of U.S. and non-u.s. equity issues, corporate and municipal debt issues, and money market instruments from over 85 countries that DTC s participants ( Direct Participants ) deposit with DTC. DTC also facilitates the post-trade settlement among Direct Participants of sales and other securities transactions in deposited securities, through electronic computerized book-entry transfers and pledges between Direct Participants accounts. This eliminates the need for physical movement of securities certificates. Direct Participants include both U.S. and non-u.s. securities brokers and dealers, banks, trust companies, clearing corporations, and certain other organizations. DTC is a wholly-owned subsidiary of The Depository Trust & Clearing Corporation ( DTCC ). DTCC, in turn, is owned by a number of Direct Participants of DTC and Members of the National Securities Clearing Corporation, Government Securities Clearing Corporation, MBS Clearing Corporation, and Emerging Markets Clearing Corporation, (NSCC, GSCC, MBSCC, and EMCC, also subsidiaries of DTCC), as well as by the New York Stock Exchange, Inc., the American Stock Exchange LLC, and the National Association of Securities Dealers, Inc. Access to the DTC system is also available to others such as both U.S. and non-u.s. securities brokers and dealers, banks, trust companies, and clearing corporations that clear through or maintain a custodial relationship with a Direct Participant, either directly or indirectly ( Indirect Participants ). DTC has Standard & Poor s highest rating: AAA. The DTC Rules applicable to its Participants are on file with the Securities and Exchange Commission. More information about DTC can be found at Purchases of the Series 2004A Bonds under the DTC system must be made by or through Direct Participants, which will receive a credit for the Series 2004A Bonds on DTC s records. The ownership interest of each actual purchaser of each Bond ( Beneficial Owner ) is in turn to be recorded on the Direct and Indirect Participants records. Beneficial Owners will not receive written confirmation from DTC of their purchase. Beneficial Owners are, however, expected to 13

24 receive written confirmations providing details of the transaction, as well as periodic statements of their holdings, from the Direct or Indirect Participant through which the Beneficial Owner entered into the transaction. Transfers of ownership interests in the Series 2004A Bonds are to be accomplished by entries made on the books of Direct and Indirect Participants acting on behalf of Beneficial Owners. Beneficial Owners will not receive certificates representing their ownership interests in the Series 2004A Bonds, except in the event that use of the book-entry system for the Series 2004A Bonds is discontinued. To facilitate subsequent transfers, all the Series 2004A Bonds deposited by Direct Participants with DTC are registered in the name of DTC s partnership nominee, Cede & Co., or such other name as may be requested by an authorized representative of DTC. The deposit of the Series 2004A Bonds with DTC and their registration in the name of Cede & Co. or such other DTC nominee do not effect any change in beneficial ownership. DTC has no knowledge of the actual Beneficial Owners of the Series 2004A Bonds; DTC s records reflect only the identity of the Direct Participants to whose accounts the Series 2004A Bonds are credited, which may or may not be the Beneficial Owners. The Direct and Indirect Participants will remain responsible for keeping account of their holdings on behalf of their customers. Conveyance of notices and other communications by DTC to Direct Participants, by Direct Participants to Indirect Participants, and by Direct Participants and Indirect Participants to Beneficial Owners will be governed by arrangements among them, subject to any statutory or regulatory requirements as may be in effect from time to time. Beneficial Owners of the Series 2004A Bonds may wish to take certain steps to augment the transmission to them of notices of significant events with respect to the Series 2004A Bonds, such as redemptions, tenders, defaults, and proposed amendments to the bond documents. For example, Beneficial Owners of the Series 2004A Bonds may wish to ascertain that the nominee holding the Series 2004A Bonds for their benefit has agreed to obtain and transmit notices to Beneficial Owners. In the alternative, Beneficial Owners may wish to provide their names and addresses to the registrar and request that copies of notices be provided directly to them. Redemption notices will be sent to DTC. If less than all of the Series 2004A Bonds within an issue are being redeemed, DTC s practice is to determine by lot the amount of the interest of each Direct Participant in such issue to be redeemed. Neither DTC nor Cede & Co. (nor any other DTC nominee) will consent or vote with respect to the Series 2004A Bonds unless authorized by a Direct Participant in accordance with DTC s Procedures. Under its usual procedures, DTC mails an Omnibus Proxy to the District as soon as possible after the record date. The Omnibus Proxy assigns Cede & Co. s consenting or voting rights to those Direct Participants to whose accounts the Series 2004A Bonds are credited on the record date (identified in a listing attached to the Omnibus Proxy). Redemption proceeds, distributions, and dividend payments on the Series 2004A Bonds will be made to Cede & Co., or such other nominee as may be requested by an authorized representative of DTC. DTC s practice is to credit Direct Participants accounts upon DTC s receipt of funds and corresponding detail information from the District or their Agent, on payable date in accordance with their respective holdings shown on DTC s records. Payments by Participants to Beneficial Owners will be governed by standing instructions and customary 14

25 practices, as is the case with securities held for the accounts of customers in bearer form or registered in street name, and will be the responsibility of such Participant and not of DTC nor its nominee, Agent, or the District, subject to any statutory or regulatory requirements as maybe in effect from time to time. Payment of redemption proceeds, distributions, and dividend payments to Cede & Co. (or such other nominee as may be requested by an authorized representative of DTC) is the responsibility of the District or Agent, disbursement of such payments to Direct Participants will be the responsibility of DTC, and disbursement of such payments to the Beneficial Owners will be the responsibility of Direct and Indirect Participants. DTC may discontinue providing its services as depository with respect to the Series 2004A Bonds at any time by giving reasonable notice to the District or Agent. Under such circumstances, in the event that a successor depository is not obtained, Bond certificates are required to be printed and delivered. The District may decide to discontinue use of the system of book-entry transfers through DTC (or a successor securities depository); provided the District complies with the rules and regulations of DTC. In that event, Bond certificates will be printed and delivered. The information in this section concerning DTC and DTC s book-entry system has been obtained from sources that the District believes to be reliable, but the District takes no responsibility for the accuracy thereof. Neither the District nor the Trustee will have any responsibility or obligation to the Direct or Indirect Participants or the persons for whom they act as nominee with respect to the payments to or the providing of notice for the Direct Participants, the Indirect Participants or the Beneficial Owners of the Series 2004A Bonds. The District cannot and does not give any assurances that DTC, the DTC participants or others will distribute payments of principal of or interest on the Series 2004A Bonds paid to DTC or its nominee, as the registered owner, or provide any notices to the Beneficial Owners or that they will do so on a timely basis, or that DTC will act in the manner described in this Limited Offering Memorandum. General SECURITY FOR THE SERIES 2004A BONDS The Series 2004A Bonds authorized under the Indenture and the obligation evidenced thereby will not constitute a lien upon any property of or within the District, including, without limitation, the Series 2004A Project or any portion thereof in respect of which any such bonds are being issued, or any part thereof, but will constitute a lien only on the Pledged Revenues as set forth in the Indenture. Nothing in the Series 2004A Bonds or in the Indenture will be construed as obligating the District to pay the bonds or the redemption price thereof or the interest thereon except from the Pledged Revenues, or as pledging the faith and credit of the District, the City, the County or the State or any political subdivision thereof, or as obligating the District, the City, the County or the State or any of its political subdivisions, directly or indirectly or contingently, to levy or to pledge any form of taxation whatever therefor. 15

26 The principal of, premium, if any, and interest on the Series 2004A Bonds are secured by a pledge of and a first lien upon the Pledged Revenues, as provided in the Indenture. As set forth in the Indenture, the Pledged Revenues consist of: (a) all Interlocal Agreement Revenues, as defined below (including Economic Incentive Payments and Tax Increment Revenues), (b) all revenues received by the District from Special Assessments levied and collected on all or a portion of the District Lands with respect to the Series 2004A Bonds, including, without limitation, amounts received from any foreclosure proceeding for the enforcement of collection of such Special Assessments or from the issuance and sale of tax certificates with respect to such Special Assessments, and (c) all moneys on deposit in the Funds and Accounts established under the Indenture for the Series 2004A Bonds; provided, however, that the Pledged Revenues will not include (i) any moneys transferred to the Rebate Fund, or investment earnings thereon, and (ii) special assessments levied and collected by the District under Section , Florida Statutes, for maintenance purposes or maintenance special assessments levied and collected by the District under Section (3), Florida Statutes. The lien on Special Assessments is on a parity with the lien thereon securing the Series 2004B Bonds expected to be issued contemporaneously with the Series 2004A Bonds. See PLAN OF FINANCE and Special Assessments, herein. Under the Interlocal Agreement, subject to certain conditions (including the performance thresholds discussed above under the heading PLAN OF FINANCE Additional Security for the Series 2004A Bonds ), the District will receive the Economic Incentive Payments from the City and the County and/or Tax Increment Revenues from the Midtown CRA Agency. The payment from the Midtown CRA Agency will be based upon the incremental increase in ad valorem taxes within the District as a result of the Developments (the Tax Increment Revenues and, collectively with the Economic Incentive Payments, the Interlocal Agreement Revenues ). The receipt of these funds is subject to certain conditions, and the City s and County s obligation to contribute Economic Incentive Payments may terminate under certain circumstances. In no event will the Interlocal Agreement Revenues exceed either the Annual Debt Service Requirement on the Series 2004A Bonds or the specific amounts set forth in the Interlocal Agreement, whichever is less. See PLAN OF FINANCE, herein. Additionally, the District has approved the levy of Special Assessments to provide for the payment of the Series 2004 Project (including both the Series 2004A Project and the Series 2004B Project). The amount of Special Assessments relating to the Series 2004A Project collected by the District in each year will be offset by the Interlocal Agreement Revenues to be received by the District. See PLAN OF FINANCE, herein. For certain risks inherent in an investment in bonds secured by the Pledged Revenues, see BONDHOLDERS RISKS herein. Economic Incentive Payments General. As described above under the heading PLAN OF FINANCE, and subject to the provisions described below under Covenant to Budget and Appropriate and Release of Economic Incentive Payments, the City and the County have each agreed in the Interlocal Agreement to make the Economic Incentive Payments to the District for each completed performance threshold in the amounts set forth in the Interlocal Agreement, provided that such 16

27 Economic Incentive Payments do not exceed the corresponding Annual Debt Service requirements for the Series 2004A Bonds. These development components (or performance thresholds) are discussed above under the heading PLAN OF FINANCE Additional Security for Parking Garage Project Bonds Performance Thresholds Payment of Economic Incentive Payments. No later than January 31 st of each year during the term of the Interlocal Agreement, the Interlocal Agreement requires the District to submit a progress report to the City, the County and the Midtown CRA Agency setting forth the completed development components, if any, as of January 1 of that year (the Progress Report ). For each completed development component identified in such Progress Report, the City will verify that a Certificate of Occupancy was issued for each. No later than December 31 st of that same year, the City and the County are required to pay to the District the Economic Incentive Payments due for each completed development component described in the Progress Report, as well as for all completed development components described in all prior Progress Reports, through the term of the Series 2004A Bonds or until the EIP is released, as described below. The District will use the Economic Incentive Payments received from the City and the County solely to pay corresponding annual debt service requirement on the Series 2004A Bonds. The Economic Incentive Payments for each completed development component as set forth in the Interlocal Agreement will become payable to the District annually as described below, commencing as follows: (i) Economic Incentive Payments for the completed development components for Stage 1 (referred to as Phase I in the Interlocal Agreement) will commence in the calendar year following the calendar year in which Certificates of Occupancy have been issued for at least ninety percent (90%) of the development components for Stage 1, which must include the retail component, continuing each and every year thereafter through the term of the Interlocal Agreement, subject to reduction and elimination under circumstances described in the Interlocal Agreement, (ii) Economic Incentive Payments for completed development components for Stage 2 (referred to as Phase II in the Interlocal Agreement) will commence in the calendar year following the calendar year in which Certificates of Occupancy have been issued for at least ninety percent (90%) of the development components for Stage 2, which must include the office component unless development of the office component is subject to the occurrence of an Event of Impossibility (as defined in the Interlocal Agreement), continuing each and every year thereafter through the term of the Interlocal Agreement, subject to reduction and elimination under circumstances described in the Interlocal Agreement. Pursuant to the Interlocal Agreement, the aggregate amount of Economic Incentive Payments contributed by the County and the City to the District in each year will not exceed the Annual Debt Service requirement for that year. Offset of Tax Increment Revenues Against Economic Incentive Payments. Until released, as described below, the amount of the Economic Incentive Payments payable by the City and the County in each year will be reduced or offset by the amount of Tax Increment Revenues paid to the District by the Midtown CRA Agency in such years, if established as described below. In no event, will the sum of the Tax Increment Revenues and the Economic Incentive Payments contributed to the District in any year exceed the total scheduled Economic Incentive Payments due to the District in that year pursuant to the Interlocal Agreement or the corresponding Annual Debt Service requirement on the Series 2004A Bonds, whichever is less. 17

28 Covenant to Budget and Appropriate. The City and the County have each covenanted and agreed in the Interlocal Agreement to appropriate in their respective annual budgets, by amendment, if necessary, from Non-Ad Valorem Revenues (defined below) lawfully available in each Fiscal Year, amounts sufficient to pay their respective portion of the Economic Incentive Payments when due pursuant to the Interlocal Agreement. Such covenant and agreement on the part of the City and the County to budget and appropriate Non-Ad Valorem Revenues will be cumulative to the extent Economic Incentive Payments pursuant to the Interlocal Agreement remain unpaid, and will continue until such Economic Incentive Payments are paid, provided, however, such covenant and agreement will terminate once the obligations of the County and the City to make Economic Incentive Payments are extinguished pursuant to the Interlocal Agreement. Pursuant to the Interlocal Agreement, Non-Ad Valorem Revenues mean, with respect to the City and the County, as applicable, all revenues of the City and the County derived from any source whatsoever, other than ad valorem taxation on real or personal property, which is legally available to make the Economic Incentive Payments required in the Interlocal Agreement, but only after provision has been made by the City or the County to pay for services and programs which are necessary for essential public purposes affecting the health, welfare and safety of the inhabitants of the City or the County or which are legally mandated by applicable law. The City and the County have not covenanted to maintain any services or programs, now provided or maintained by either the City or the County, which generate Non-Ad Valorem Revenues. Such covenant to budget and appropriate does not create any lien upon or pledge of Non- Ad Valorem Revenues, nor does it preclude the County or the City from pledging in the future their Non-Ad Valorem Revenues, nor does it require the City or the County to levy and collect any particular Non-Ad Valorem Revenues, nor does it give the District a prior claim on the Non- Ad Valorem Revenues of the City and the County as opposed to claims of general creditors of the City or the County. Such covenant of the City and the County to appropriate Non-Ad Valorem Revenues is subject in all respects to the payment of any obligations secured by a pledge of Non-Ad Valorem Revenues prior or subsequent to the date of the Interlocal Agreement (including the payment of debt service on bonds and other debt instruments of the City and/or County). However, the covenant to budget and appropriate in the City s and the County s general annual budget for the purposes and in the manner stated in the Interlocal Agreement shall have the effect of making available in the manner described in the Interlocal Agreement, Non-Ad Valorem Revenues and placing on the City and the County a positive duty to appropriate and budget, by amendment, if necessary, amounts sufficient to meet their respective obligations of making the Economic Incentive Payments, to the extent required by the Interlocal Agreement, subject, however, in all respects to the restrictions of Section , Florida Statutes, and Section , Florida Statues, which provide, in part, that the governing body of each such municipality and county, respectively, make appropriations for each fiscal year which, in any one fiscal year, shall not exceed the amount to be received from taxation or other revenue sources, and subject further, to payments for services and programs which are essential public purposes affecting the health, welfare and safety of the inhabitants of the County and the City or which are legally mandated by applicable law. 18