50 Most Common Appraisal Review Deficiencies Webinar 9:00 AM Mountain Time

|

|

|

- Marianna Bates

- 6 years ago

- Views:

Transcription

1 50 Most Common Appraisal Review Deficiencies Webinar 9:00 AM Mountain Time All audio for this webinar is through your computer there is no separate call-in number Please ensure that you are able to receive sound through your computer and that your speakers are un-muted If you have any technical or audio issues please review the Support for Technical Issues document by clicking on the Supporting Material Button located just below this screen 1

2 Important Things to Know Question and Answer Format Utilize Ask a Question button on your screen To view response to a question, click on Answered Questions tab Audio/Technology questions utilize the Help button Supporting Material A copy of this Power Point presentation A PDF version of the presentation Frequently Asked Questions related to technical issues (PDF) If you have audio issues or the slides stop advancing simply refresh or reload the page displaying the webinar 2

3 Make Sure Pop-Up Blockers are Disabled Pop-up Blocker is turned on in Internet Explorer by default. To turn it off or to turn it on again if you've already turned it off, follow these steps: Open Internet Explorer by clicking the Start button, and then clicking Internet Explorer. Click the Tools button, and then click Pop-up Blocker. Do one of the following: To turn off Pop-up Blocker, click Turn Off Pop-up Blocker. To turn on Pop-up Blocker, click Turn On Pop-up Blocker. 3

4 Important Things to Know Archive Version (POP-UP) 4

5 The Most Common Errors Found in FHA Appraisal Reports (URAR) 5

6 Presenters Don Pearsall Karl Kaufmann 6

7 Purpose The purpose of this presentation is to acquaint the audience with the most common errors that FHA finds when reviewing appraisal reports. It introduces and explains, rather than supplants, official policy issued in Handbooks and Mortgagee Letters. If you find a discrepancy between the presentation and Handbooks, Mortgagee Letters, etc., the official policies prevail. Please note the information provided in this training is subject to change. 7

8 Energy Efficient Mortgages What is an EEM? Allows homeowners to improve the energy efficiency of their home by financing the cost of the improvements into their loan. If the savings in utility costs will more than pay for the costs of the improvement, borrower does not have to qualify for the extra costs of the energy improvements. Who is eligible? New and existing 1-4 units including condominiums and manufactured homes Purchases, streamline refinances, no cash-out refinances, 203(h) disaster loans, and 203(k) rehabilitation mortgages Homeowners How do you apply? Find a EEM lender Purchase a HERS report from an acceptable source (utility company, local state or federal agency or nonprofit) Qualify for the base mortgage before the energy efficient improvements are added No second appraisal is needed to support added costs 8

9 Energy Efficient Mortgages Want More Information? EEM Webinar is Archived See Mortgagee Letters; ML ML ML ML See HUD Handbook D.1 Department of Energy s website: _improvement_contractors#s1 9

10 Poll Question What section of HUD Manual pertains to Valuation Protocol? 10

11 Homeownership Centers Santa Ana Denver Atlanta Philadelphia 11

12 Objectives To illustrate the most common errors found in FHA appraisal reports Provide an understanding of FHA guidelines To change your mindset from Form Filler to Analytical Appraiser Answer your questions 12

13 Resources Resource Center: CALLFHA ( ) Knowledge Base: /answers 13

14 Resources Handbooks: (6/99) Valuation Analysis, with emphasis on Appendix D REV 1 (3/90) Valuation Analysis REV 2 (12/91) Architectural Processing & Inspections REV 1 (3/91) Requirements for existing 1-4 family units (7/94) Appendix K, MPS Proposed construction 1-4 family 14

15 15

16 16

17 Appraiser s Certification on the FHA Roster Application I certify that I have read and fully understand and will comply with HUD Handbook , Valuation Analysis for Home Mortgage Insurance for Single Family One- to- Four Unit Dwellings (with particular emphasis on Appendix D, Valuation Protocol ), any updates to the Handbook, Mortgagee Letters, and all other instructions and standards, in performing all appraisals on properties that will be security for HUD/FHA insured mortgages. 17

18 FHA Appraiser Oversight FHA oversight is based on the following risk factors, as established in Mortgagee Letter : High default rate on loans High volume of FHA loans Complaints Referrals Previous administrative appraiser roster actions 18

19 Review Process How does the FHA review process work? Appraisal reports are randomly selected Desk Review Risk Assessment (value and property condition) Identify possible deviation from HUD/USPAP Field review (if necessary) Completed by contract appraisers or FHA staff appraisers Rating Action or Sanction Letter 19

20 Disciplinary Actions Notice of Deficiency Education FHA Roster Removal Limited Denial of Participation (LDP) National Debarment Civil Money Penalties Civil & Criminal Actions Multiple sanctions may be pursued concurrently 20

21 Disciplinary Actions Removal or Removal w/education: Value Fraud Repairs Prior actions/sanctions and other factors These deficiencies have a direct impact on value and marketability and represent the highest level of risk. 21

22 Disciplinary Actions Education: Environmental Legal compliance Data collection & reporting Support for adjustments Prior actions/sanctions and other factors These deficiencies may impact the quality of the report; but generally do not affect value. 22

23 Disciplinary Actions Notice of Deficiency (NOD) Inaccurate reporting Omission of information Flawed data interpretation Prior actions/sanctions and other factors These deficiencies are considered gaps in due diligence and professionalism. 23

24 Appraiser s Rights Regarding Disciplinary Action Notice of Deficiency and Education cannot be appealed Roster Removal may request informal conference Limited Denial of Participation (LDP), National Debarment Civil, Criminal sanctions - remedy through Civil/Criminal Court systems 24

25 FHA Appraisal Requirements and the Most Common Errors 25

26 Subject Section URAR (FNMA 1004) 26

27 #1 Neighborhood Name Report the name of the subdivision, the commonly known neighborhood name or the name of the PUD , D-14 27

28 #2 Intended User Intended Users must be identified Lender/Client HUD/FHA must be included as Intended User It is also acceptable to add the phrase and its successors or assigns after the Lender/Client name , D-15 28

29 #3 Analyze the Listing Failure to analyze the subject s current or previous listing within the past 12 months , D-15 29

30 #3 Analyze the Listing Subject Listing History USPAP Standard Rule 1-5(a): Requires the appraiser to analyze all agreements of sale, options, and listings of the subject property current as of the effective date of the appraisal Uspap Standards 1-5(a) 30

31 #3 Analyze the Listing Definition of Analysis? The act or process of providing information, recommendations, and/or conclusions on diversified problems in real estate other than estimating value (The Dictionary of Real Estate Appraisal, Third Edition, Appraisal Institute) 31

32 #3 Analyze the Listing Examples: Twelve Month Listing History The subject is listed in the MLS Not Acceptable DOM150; Subject property was offered for sale 03/01/2012 for $150,000; price change to $140,000 on 04/01/2012. Data source is IRIS# DOMUnk; Subject property listed as FSBO on 03/01/2012 for $145, Don t forget to check for FSBO listings - 32

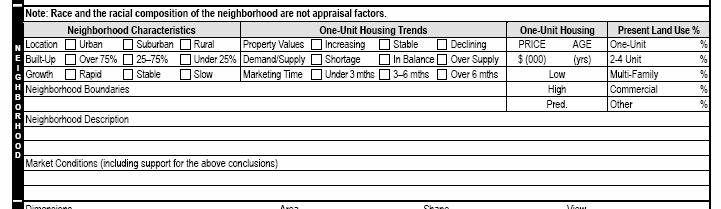

33 #4 Analyze the Sale Discuss and analyze the terms of the sale and any seller concessions that may have had an effect on the sales price of the subject property. 33

34

35 #4 - Analyze the Sale Examples: Contract provided Not Acceptable Purchase contract arms-length and typical for market Arms-length sale. Contract submitted 01/03/12 for $135,000, countered by seller on 01/03/12 for $145,000, and accepted by buyer on 01/04/12. Seller paying $2,500 in closing costs, and down payment assistance Mortgagee Letter

36 #5 - Analyze Concessions Sales Concessions The appraiser is to report any financial assistance (loan charges, sales concessions, gift or down payment assistance, etc.) paid by any party on behalf of the borrower If the sale involves personal property (e.g. above ground pool, lawn mower, furniture, etc.) it should be identified and excluded from the valuation Mortgagee Letter

37 #5 Analyze Concessions Ask yourself What would the property have sold for if there were no concessions, down payment assistance or discounts? 37

38 #6 Contract Price Contract Price Enter the final agreed upon contract price Contract Date The date of contract is the date all parties execute the sales agreement Date of Contract Enter the date of the contract. This is the date when all parties have agreed to the terms of, and signed the contract , D-16 38

39 Neighborhood 39

40 Neighborhood The appraiser must observe neighborhood characteristics and surrounding properties to make determinations that will be incorporated into the valuation of the subject property. Omission of conditions that may adversely affect the value of the property is poor appraisal practice and violates the Uniform Standards of Professional Appraisal Practice D-16 40

41 #7- Neighborhood Boundaries Neighborhood boundaries and characteristics N, S, E, & W characteristics Market conditions in the subject neighborhood Prevalence of seller and financial concessions 41

42 #7 Neighborhood Boundaries Describe the Neighborhood Boundaries and characteristics. The appraiser must clearly define the boundaries north, south, east and west of the subject s neighborhood. Providing a description of neighborhood boundaries by physical features such as streets, rail lines, other man-made barriers or well defined natural barriers (i.e. rivers, lakes, etc.) details the make up and understanding regarding neighborhood composition , D-18 42

43 #7 Neighborhood Boundaries Unacceptable Neighborhood Boundaries The neighborhood boundaries include the city limits of Fort Morgan. The neighborhood boundaries consist of the city of Ephraim and the neighboring city of Manti. Be specific in the description 43

44 #8 Marketability of the Neighborhood Discuss factors that would attract residents or cause them to reject the neighborhood. Some typical factors important to discuss include: Level of maintenance and condition of homes Housing styles, ages, sizes, etc. Land uses Proximity to employment and amenities, including travel distance and time to local employment sources and community amenities Employment stability, in terms of variety of employment opportunities and industries Overall appeal of the neighborhood as compared to competitive neighborhoods in the same market Convenience to schools and shopping with respect to distance, time and required means of transportation , D-18 44

45 #9 Market Conditions Discuss the market conditions in the subject neighborhood and the prevalence of seller and financial concessions Provide relevant information in support of conclusions relating to trends in property values, demand/supply and marketing time Provide a description of the prevalence and impact of sales and financing concessions and/or down payment assistance in the subject s market area Other areas of discussion may include days on market, list to sale price ratios, and/or financing availability , D-18 45

46 #10 Declining Markets Appraiser Responsibilities in a Declining Market Provide relevant information and specific data to support a declining conclusion including: research of local trends in property values demand/supply marketing time list-to-sale ratios Provide the data source for your information, such as MLS, standard pricing services, local and national studies, etc Mortgagee Letter

47 #11 Built-up versus Present Land Use Inaccurate or incomplete assessment of the make-up of the Neighborhood Characteristics and the Present Land Use. 47

48 #12 Inappropriate Land Use Inaccurate and misleading estimates of Present Land Use % If a portion of the land use consists of parks or other unspecified classifications, the appraiser is required to estimate the percentages as Other and provide explanation for any noted other land use (i.e. parks, undeveloped, vacant, etc.) , D-17 48

49 #13 Exposure Time Exposure time is a component of the definition for the value opinion being developed. The appraiser must also develop and state the opinion of reasonable exposure time linked to that value opinion Uspap standards 1-2(c)(iv), 2-2(b)(v) & Statement #6 49

50 #13 Exposure Time Exposure Time is the estimated length of time that the property interest being appraised would have been offered on the market prior to the hypothetical consummation of a sale at market value on the effective date of the appraisal. Exposure time is a retrospective opinion based on an analysis of past events assuming a competitive and open market. Marketing Time happens after the date of the appraisal. Marketing Time is an estimate because it is in the future. Uspap definitions pg. u3 50

51 #14 - SITE Site dimensions are not included or there are erroneous references to county records or plat maps that are not included in the appraisal. 51

52 #14 - Site Dimensions List all dimensions of the site beginning with the frontage. If the shape of the site is irregular, show the boundary dimensions (85' X 150' X 195' X 250'), or attach a property survey, site plan or plat or legal description with the comment, see attached. Do not list site area on the dimensions line , D-18 52

53 Actual Appraiser Quotes The land fill has an impact on the dwelling (improvements on the land). The land value is the land value No current market data exits for the externality. However past experience suggests a 10% reduction in the improvements due to this factor. It is noted that the information supporting this adjustment is not in our office files, but in memory. 53

54 #15 Zoning Information Zoning is missing and/or zoning description is not adequate. The appraiser is required to report the specific zoning used by the local municipality or jurisdiction. Include a general statement describing what the zoning permits Zoning descriptions such as Single Family or Residential are not adequate Describe the dominant factor for the zoning code such as site size, density, frontage, etc , D-19 54

55 #16 Well & Septic Individual Water Supply & Sewage Systems Report availability of connection to public or community water/sewer system Appraiser must identify noncompliance 55

56 #16 Well & Septic Individual Water Supply & Sewage Systems Utilities The appraiser shall indicate whether a public water or sewage disposal system is available to the site. If available, connection must be made to public or community water/sewage disposal system if connection costs are reasonable. The lender will determine whether connection is feasible , D-19 56

57 #16 Well & Septic Question: The appraiser is required to sketch well, septic, and property line distances. 57

58 #17 FEMA Maps If the property is within a Special Flood Hazard Area, mark "YES". Otherwise, mark NO Attach a copy of the flood map panel for properties located within an identified flood hazard area Enter the FEMA Zone designation Enter the FEMA Map number and map date. If it is not shown on any map, enter Not Mapped , D-20 58

59 #18 Design (Style) The appraiser is required to enter the appropriate architectural design (style) descriptor that best describes the subject property. Valid descriptions include, but are not limited to, Colonial, Rambler, Georgian, Farmhouse. Descriptors such as brick, average, conventional, traditional, or typical are not architectural styles. Design (Style) Enter a brief description of the house design style using historical or contemporary fashion. For example: Cape Cod, bi-level, split level, split foyer, colonial, town house, rowhouse, etc. Do not use builder s model name. Do not use generic descriptions such as Traditional or Conventional , D-21 59

60 #19 Year Built - New Construction For existing properties less than one year old The appraiser is required to provide both the month and year completed Provide comments and photographs pertaining to the grading and drainage for the subject To remain compliant, the appraiser is required to report this information in an alternate section of the appraisal , D-21 60

61 #19 - New Construction No comments about grading and drainage. HUD Handbook , paragraph 4-2 (B)(2)(b) - Compliance Inspections states: Final inspection report must provide a specific statement on acceptance of grading and drainage. Inadequate grading and drainage is the biggest complaint of homebuyers and should be carefully reviewed. 61

62 #20 GLA Adjustments Adjustments for GLA are not consistent The dollar per square foot adjustment is not consistent from comparable to comparable This is usually the result of cloning previous reports with residual data Use of generic canned comments in addendums do not agree with the actual adjustments , D-30 62

63 #21 - Sketch The building sketch must reflect all exterior dimensions of the improvements. This includes patios, porches, garages, breezeways, and offsets. Sketch Include a building sketch showing the Gross Living Area Above Grade, including all exterior dimensions of the house. Include patios, porches, garages, breezeways and other offsets. State covered or uncovered to indicate a roof or no roof (such as over a patio). Show calculations used to arrive at the estimated gross living area. An interior sketch or floor plan is required for properties exhibiting functional obsolescence attributable to the lay out , D-13 63

64 #21 - Sketch Sketch 64

65 #22 Subject Photos Photographs are to: Show front and rear at opposite angles to show all sides of subject property and all improvements Show street scene Be at least a single photo of each comparable property Show the grade of the vacant lot for proposed construction Be taken by appraiser (no people in photos) , D-13 65

66 #23 Photos of Improvements Provide photographs of improvements with contributory value that are not captured in either the front or rear photograph. Examples: Pool, shed, sunroom, barn, shop and detached garages , D-13 66

67 #24 Reporting the Room Count Inconsistency in the subject s room count, as compared to the building sketch, results in confusing the reader. Room count includes living room, dining room, kitchen, den, recreation room and one or more bedrooms Typically, the foyer, bath and laundry rooms are not counted as rooms , D-26 & D-27 67

68 #25 Location Map The appraiser is required to include a legible street map. Street Map Include a legible street map showing the location of the subject and each of the comparable sales utilized. If substantial distance exists between the subject and comparable sales, additional legible maps should be submitted to show the location of the comparable sales , D-13 68

69 # 25 Location Map 1 3 Location Map 2 Maps Local street map showing subject location & each comparable sale Show roadways and street names 69

70 #26 MPR & MPS Minimum Property Requirements (MPR) and Minimum Property Standards (MPS) For new construction to be eligible for FHA insurance: It must comply with HUD s Minimum Property Standards HUD Handbook Appendix K, (including 24 CFR d) Existing construction must comply with HUD s Minimum Property Requirements (HUD Handbook ) , D-2 70

71 #26 - MPR & MPS Minimum Property Requirements (MPR) and Minimum Property Standards (MPS) In the performance of an FHA appraisal: The appraiser must denote any deficiency in the appropriate section(s) (site issues in the site section, improvement issues in the improvements section) of the appraisal report The appraiser is to note those repairs necessary to make the property comply with FHA s Minimum Property Requirements (MPR) or Minimum Property Standards (MPS) together with the estimated cost to cure , D-2 71

72 #27 Comparable Selection The appraiser is required to report: The number of comparable sales in the subject neighborhood within 12 months of the effective date of the appraisal and The number of comparable properties currently offered for sale as of the effective date of the appraisal Unlike the neighborhood price data, which includes all sales, this section focuses only on those properties that are comparable to the subject, not the universe of sales , D-28 72

73 #27 - Comparable Selection Comparable Listings Enter the number of comparable properties currently offered for sale, including those under contract, within the subject neighborhood together with the price range Comparable Sales Enter the number of comparable sales that occurred within the 12-month period preceding the effective date of the appraisal, and within the subject neighborhood, together with the price range 73

74 #27 Comparable Selection 74

75 #27 - Comparable Selection 75

76 #28 - Bracketing Bracketing the sales price and dwelling size In selecting comparable properties, the appraiser is required to use the bracketing method, as defined in The Dictionary of Real Estate Appraisal, Fourth Edition, Appraisal Institute. It is advisable to bracket the subject property with sales using both dwelling size and sales price whenever possible. If bracketing is not possible, the appraiser should explain why , D-6 76

77 Poll Question Which of the following is a verification source(s) a. MLS b. Listing Agent c. Zillow d. a. and c. 77

78 #29 Verification of Data Know the difference between a data source and a verification source. 78

79 #29 Verification of Data Data Sources versus Verification Sources Examples of Data Sources Multiple Listing Services Appraisal Files County (Public) Records Examples of Verification Sources Broker Listing Agent Buyer Seller 79

80 #29 - Verification of Data Failure to verify the sales data with a third party to the transaction in accordance with HUD requirements. Verification Source(s) Enter verification source(s), the document or party from which the additional proof was obtained. MLS by itself is not considered a verification source. Contacting someone with first-hand knowledge of the transaction (agent, broker, buyer, seller, etc.), especially where it involves confirmation of seller concessions, is the preferred method of verification. A single source may be used if the quality of data is such that sales data are confirmed and verified by settled transactions. Information provided should permit the reader of the report to locate the data from the sources cited , D-29 80

81 #30 - Verification and Analysis of Concessions 81

82 #30 Verification and Analysis of Concessions Complete an analysis to determine whether or not the concessions had an effect upon the sales price Sales or Financing Concessions Report the type of financing such as Conventional, FHA or VA, etc. Report the type and amount of sales concession for each comparable sale listed. If no concessions exist, the appraiser must note none. The appraiser is required to make market-based adjustments to the comparable sales for any sales or financing concessions that may have affected the sales price. The adjustment for such affected comparable sales must reflect the difference between the sales price with the sales concessions and what the property would have sold for without the concessions , D-29, Mortgagee Letter

83 #31 Use of comparables 6 and 12 months old Only closed (settled) sales may be used as comparable sales 1, 2 or 3. If a sale over six months is used, an explanation must be provided In general, sales over one year old should be identified as comparable sale(s) 4, 5 or 6 with an explanation as to why they are included If your best comparable is over 12 months old, include it and provide an explanation why it was necessary , D-6 & D7 83

84 #32 Quality & Condition The appraiser must indicate the Quality rating that best describes the Quality and Condition of the subject property and each comparable property. These ratings must be UAD compliant , D-30, Mortgagee Letter

85 #33 Age Actual age of the subject and comparables The appraiser is required to enter only the actual age of the subject and each comparable property. If the actual age is estimated, an explanation must be provided. Actual Age Enter only the actual age of the subject and each comparable sale , D-30 85

86 #34 - Adjustments HUD requires the appraiser to: Report specific data pertaining to the comparable properties Make adjustments to them that reflect the market s reaction to the differences between the subject property and the comparable properties Make adjustments to them that reflect the market s reaction to the differences. 86

87 #34 - Adjustments Adjustments must be supportable and reasonable Adjustments to Comparable Sales I have reported adjustments to the comparable sales that reflect the market's reaction to the differences between the subject property and the comparable sales. Appraiser s certification #9 87

88 #35 Adjustment Guidelines 88

89 #35 Adjustment Guidelines Adjusted Sale Price of Comparables Adjustments exceeding recommended guidelines Total all of the adjustments and add them to or subtract them from the sales price of each comparable. Generally, adjustments should not exceed 10% for line items, 15% for net adjustments and 25% for gross adjustments. If any adjustments exceed stated guidelines an explanation must be provided including reasons for not using more similar comparable sales , D-31 89

90 #36 List-to-Sale Price Ratios HUD requires the appraiser to: Reconcile the adjusted values of active listings or pending sales with the adjusted values of the settled sales provided If the adjusted values of the settled comparables are higher than the adjusted values of the active listings or pending sales, the appraiser must determine if a market condition adjustment is appropriate The list-to-sale price ratio adjustments must be consistent with the data entered in the Market Conditions Addendum to the Appraisal Report (Fannie Mae Form 1004MC) 90

91 #36 List Price to Sale Price Ratios Consistent list-to-sale price ratio adjustments Each listing or pending comparable sale must be adjusted consistently with the current Median Sale Price as a percentage of List Price data in the 1004MC. 91

92 #37 - Weighting The appraiser is required to weight the comparable sales in the sales comparison approach Summary of Sales Comparison Approach Explain comparable selection and any necessary explanation of adjustments. Explain any adjustments exceeding guidelines. Explain which comparable sale or sales is/are given most weight or consideration and why , D-33 92

93 #38 - Photos MLS photos are not allowed as primary photos Photos depicting the front view of each comparable sale used must be those taken by the appraiser The photos taken by the appraiser are considered evidence of compliance with the Scope of Work of having inspected each comparable sale from the street Use of MLS photos to exhibit comparable condition at the time of sale is acceptable; however, the appraiser must include their photos as well to document compliance , D-13 93

94 #38 Photos Photos reflecting silhouettes or Black Blobs are unacceptable Imaged photos and documents must also be clear 94

95 #39 - Reconciliation The appraiser is required to reconcile all three approaches to value, or provide explanation for exclusion of an approach. USPAP, Standard 2-2(b)(viii), states, in relevant part: summarize the information analyzed, the appraisal methods and techniques employed, and the reasoning that supports the analyses, opinions, and conclusions; exclusion of the sales comparison approach, cost approach, or income approach must be explained. 95

96 #40 Appraisal Conditions The appraiser is required to select the appropriate appraisal condition(s) and if necessary, provide a cost to cure for appraisals made subject to repair. Mark this box as is when: There is/are no repair(s), alteration(s) or required inspection condition(s) noted. Establishing the as is value for a regular 203(k) when needed. The property is ineligible for FHA insurance and is being rejected. The property is an REO or Pre-Foreclosure sale , D-33 96

97 #40 Appraisal Conditions Selecting the appropriate appraisal condition(s) Mark this box per plans & specs when the appraisal involves: Proposed construction, or Under construction, less than 90% complete, or A 203(k) with a Plan Review and Specification of Repairs prepared by a 203(k) Consultant , D-33 97

98 #40 Appraisal Conditions Selecting the appropriate appraisal condition(s) Mark this box subject to repairs or alterations When the appraisal involves existing housing, or new construction more than 90% complete with only buyer preference items remaining (floor coverings, appliances, landscaping packages (soil must be stabilized to prevent erosion)), requiring repairs or alterations to: Protect the health and safety of the occupants Protect the security of the property Correct physical deficiencies or conditions affecting structural integrity Complete buyer preference items for new homes, or to Complete repairs/improvements noted in work order or contractor estimates for the Streamline K Meet FHA Minimum Property Requirements , D-34 98

99 #40 Appraisal Conditions Selecting the appropriate appraisal condition(s) Indicate the reasoning for any required inspections and note this in the appropriate section of the appraisal report listing the required inspections. Mark this box subject to a required inspection when the appraisal calls for a required inspection to: Certify the condition and/or status of a mechanical or structural element of the property Protect the health and safety of the occupants Protect the security of the property Meet FHA Minimum Property Requirements or Minimum Property Standards , D-34 99

100 Cost Approach 100

101 #41 Site Value Provide support for site value Support for opinion of site value Provide a summary of the comparable land sales or other methods (abstraction, allocation, land residual, extraction) of estimating site value in support of the opinion of site value , D

102 #42 Cost Data The appraiser is required to provide the name of the cost service and reference page numbers of cost tables or factors, as the user must be able to replicate the cost conclusions. Source of Cost Data Provide the name of the cost service and reference page numbers of cost tables or factors. Reviewer or reader must be able to replicate , D

103 #43 Economic Life Remaining Economic Life State the Remaining Economic Life as a single number or as a range. This line must be completed for every FHA appraisal whether or not the cost approach is completed. An explanation is required if the remaining economic life is less than 30 years , D

104 #44 Roster Appraiser Must Inspect The assigned appraiser must inspect the property Mortgagee Letter 94-54, section VII states: HUD policy requires the appraiser who is assigned the appraisal to perform the site inspection of the subject property, all the comparables and to sign the appraisal Appraiser s Certification #2 states: I performed a complete visual inspection of the interior and exterior areas of the subject property Mortgagee Letter 94 54, Appraisers certification #2 104

105 #45 Professional Assistance The appraiser must identify the specific work performed by an assistant. Pursuant to Appraiser s Certification No. 19, if the appraiser relied on significant assistance from any individual in the performance of the appraisal, that individual should be named as such and the specific tasks performed reported. APPRAISER S CERTIFICATION #19 105

106 #45 Professional Assistance Example of Specific Professional Assistance Not Appropriate: Kathy Jones provided significant assistance in the performance of this appraisal. Appropriate: Kathy Jones provided the following assistance in the performance of this appraisal: 1. Research of comparable sales. 2. Filling out portions of the URAR 3. Drawing the sketch from my notes. APPRAISER S CERTIFICATION #19 106

107 #46 - Modifying the Limiting Conditions Modifications, additions, or deletions to the intended use, intended user, definition of market value, or assumptions and limiting conditions are not permitted. The appraiser may expand the scope of work to include any additional research or analysis necessary based on the complexity of the appraisal assignment. Limiting an appraiser s liability is in direct conflict with the Appraiser s Certification No. 25. NOTE: Statements such as The appraiser s liability shall be limited to the fee paid constitute modifying the Limiting Conditions and are not allowed , D-7, APPRAISER S CERTIFICATION #15 &

108 #47 - Services performed within 3 years An appraiser must disclose any services regarding the subject property performed by the appraiser within the three year period immediately preceding acceptance of the assignment, as an appraiser or in any other capacity. USPAP Ethics Rule, pg. U8 108

109 #48 Conflicting Statements Statements in the appraisal addendums conflict with other information. Inclusion of boilerplate addendums often have information and data that conflicts with the information in other parts of the report. Including generic statements in addendums that would apply to any appraisal often result in a misleading report. Uspap ethics rule, standards rule 1-1(c) 109

110 #49 Name Enter the appraiser s name as it appears on the license If your appraiser s license states John J. Jones, you must type your name correctly, and not John Jones or Jack Jones. USPAP Ethics Rule, , D

111 #50 USPAP Compliant Report FHA requires appraisers to produce a credible, non-misleading report The appraiser is required to not render an appraisal service in a careless or negligent manner, such as by making a series of errors that, although individually might not significantly affect the results of the appraisal, in the aggregate affects the credibility of those results. 111

112 #50 - USPAP Compliant Report Knowingly Withholding Information The appraiser must not knowingly withhold any significant information from the appraisal report and to the best of their knowledge, all statements and information in this appraisal report are true and correct. Appraiser s certification #15 112

113 Top 10 Reasons to be an FHA Appraiser 8. You ll become an expert at being invisible while driving through bad neighborhoods. 9. You ll see that some people really do hang those black velveteen pictures of Elvis on their living room walls. 10. Your juggling skills will improve as you balance clipboard, tape, pens, camera, and other gadgets while inspecting homes and slowly backing away from Fido. 113

114 Top 10 Reasons to be an FHA Appraiser 5. You ll get inside homes that will make you feel much better about yours. 6. You ll see some of the most wonderful homes you ll never be able to afford. 7. You ll know where the cleanest public bathrooms in the county are. 114

115 Top 10 Reasons to be an FHA Appraiser 2. You ll dazzle your friends with your knowledge of external obsolescence. 3. You ll be really good at showing no fear when that pit-bull who has never bitten anyone" bares his teeth and heads your way. 4. You ll become a well-rounded individual from all the part-time jobs you have to take to pay the bills. 115

116 Top 10 Reasons to be an FHA Appraiser And the number one reason to be an FHA appraiser is. 1. You ll see places in people's homes that usually require a search warrant. 116

117 Have your expectations been met? CALLFHA ( ) Knowledge Base: /answers 117

118 Watch For Changes Check Mortgagee Letters and Message Boards for the Latest Information on. Get on the FHA List by sending an to: 118

119 Do not hesitate to call Call FHA ( ) 119

UNIFORM APPRAISAL DATASET (UAD) FHA SPOTLIGHT - SELECTION AND VERIFICATION OF COMPARABLE SALES

FHA SPOTLIGHT - SELECTION AND VERIFICATION OF COMPARABLE SALES") Spring 2011 Issue 3 FHA APPRAISER In This Issue: Welcome to the third issue of the Federal Housing Administration Appraiser Roster Newsletter. We hope you will find it informative. Uniform Appraisal Dataset

Spring 2011 Issue 3 FHA APPRAISER In This Issue: Welcome to the third issue of the Federal Housing Administration Appraiser Roster Newsletter. We hope you will find it informative. Uniform Appraisal Dataset

Underwriting the FHA Appraisal

Disclosure The purpose of this presentation is an overview of the subject matter with summation and explanation of recent changes in FHA policy. It introduces and explains, rather than supplants, official

Disclosure The purpose of this presentation is an overview of the subject matter with summation and explanation of recent changes in FHA policy. It introduces and explains, rather than supplants, official

APPENDIX A: VALUATION OF REAL ESTATE OWNED PROPERTIES A-1 REAL ESTATE OWNED (REO)

") APPENDIX A: VALUATION OF REAL ESTATE OWNED PROPERTIES 4150.2 A-1 REAL ESTATE OWNED (REO) FHA s Real Estate Owned (REO) properties are a result of paying a claim to a lending institution and the lender

APPENDIX A: VALUATION OF REAL ESTATE OWNED PROPERTIES 4150.2 A-1 REAL ESTATE OWNED (REO) FHA s Real Estate Owned (REO) properties are a result of paying a claim to a lending institution and the lender

All audio for this webinar is through your computer there is no separate call-in number

All audio for this webinar is through your computer there is no separate call-in number Please ensure that you are able to receive sound through your computer and that your speakers are un-muted If you

All audio for this webinar is through your computer there is no separate call-in number Please ensure that you are able to receive sound through your computer and that your speakers are un-muted If you

SIRVA Mortgage Order Instructions

SIRVA Mortgage Order Instructions Appraiser Trainees: This client does not permit Trainees to sign the appraisal report, however USPAP requirements apply when significant assistance has been provided by

SIRVA Mortgage Order Instructions Appraiser Trainees: This client does not permit Trainees to sign the appraisal report, however USPAP requirements apply when significant assistance has been provided by

Appraisal Review Reminders

Use the following list of reminders as a tool when underwriting the appraisal report. For complete information on appraisal requirements, refer to the Freddie Mac Seller/Servicer Guide (Guide) Chapter

Use the following list of reminders as a tool when underwriting the appraisal report. For complete information on appraisal requirements, refer to the Freddie Mac Seller/Servicer Guide (Guide) Chapter

Appraisal Engagement Instructions

Appraisal Engagement Instructions OVERVIEW The appraisal report must be prepared by a state licensed or certified appraiser and must comply with the Appraiser Independence Requirements (AIR), Uniform Standards

Appraisal Engagement Instructions OVERVIEW The appraisal report must be prepared by a state licensed or certified appraiser and must comply with the Appraiser Independence Requirements (AIR), Uniform Standards

Appraisal Review: Analyzing the 1004

Appraisal Review: Analyzing the 1004 1 LIVE ONLINE PARTICIPANT GUIDE Version: 8.12 Table of Contents The Purpose of the Appraisal... 3 Define Market Value... 3 Scenario 1 (John Johnson report) - 1004 Uniform

Appraisal Review: Analyzing the 1004 1 LIVE ONLINE PARTICIPANT GUIDE Version: 8.12 Table of Contents The Purpose of the Appraisal... 3 Define Market Value... 3 Scenario 1 (John Johnson report) - 1004 Uniform

Chapter 5 Fee Appraiser Responsibilities

Chapter 5 Fee Appraiser Responsibilities The fee appraiser is responsible for all aspects of the appraisal process. Important: Certain key appraisal functions may not be delegated to anyone else. Failure

Chapter 5 Fee Appraiser Responsibilities The fee appraiser is responsible for all aspects of the appraisal process. Important: Certain key appraisal functions may not be delegated to anyone else. Failure

Appraisal Review Reminders

Use the following list of reminders as a tool when underwriting the appraisal report. For complete information on appraisal requirements, refer to the Freddie Mac Seller/Servicer Guide (Guide) Chapter

Use the following list of reminders as a tool when underwriting the appraisal report. For complete information on appraisal requirements, refer to the Freddie Mac Seller/Servicer Guide (Guide) Chapter

Evaluating Your Appraisal

Evaluating Your Appraisal April 28, 2011 Presented by: Brady W. Meadows Mortgage Compliance Advisors Instructions Because of the large number of registrants, the lines will be muted. To ask a question,

Evaluating Your Appraisal April 28, 2011 Presented by: Brady W. Meadows Mortgage Compliance Advisors Instructions Because of the large number of registrants, the lines will be muted. To ask a question,

APPRAISAL REQUIREMENTS FOR SUNTENDER VALUATIONS, INC. Updated 03/26/2018

APPRAISAL REQUIREMENTS FOR SUNTENDER VALUATIONS, INC. Updated 03/26/2018 STOP Call Suntender Valuations if subject is a refinance transaction however it has been listed for sale in the past 3 months, unless

APPRAISAL REQUIREMENTS FOR SUNTENDER VALUATIONS, INC. Updated 03/26/2018 STOP Call Suntender Valuations if subject is a refinance transaction however it has been listed for sale in the past 3 months, unless

Land, Agricultural Improvements, CAFO, Rural Residence, Farm

*--FSA Appraisal Guidelines Land, Agricultural Improvements, CAFO, Rural Residence, Farm The following information elements and content descriptions are provided as guidelines to assist lenders and appraisers

*--FSA Appraisal Guidelines Land, Agricultural Improvements, CAFO, Rural Residence, Farm The following information elements and content descriptions are provided as guidelines to assist lenders and appraisers

The ATA Board of Directors concurred that this information be shared with not only ATA members, but all of the Appraisers in Texas.

General Announcement 11 19 2013 Subject: FHA Seminars in Texas Points of Misunderstanding On September 12, 2013, several ATA members contacted the ATA about contradictory statements which has caused some

General Announcement 11 19 2013 Subject: FHA Seminars in Texas Points of Misunderstanding On September 12, 2013, several ATA members contacted the ATA about contradictory statements which has caused some

March 23, 2009 MORTGAGEE LETTER

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER March 23, 2009 MORTGAGEE LETTER 2009-09 TO: SUBJECT: ALL APPROVED

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER March 23, 2009 MORTGAGEE LETTER 2009-09 TO: SUBJECT: ALL APPROVED

UNDERSTANDING HOW USPAP APPLIES TO REAL PROPERTY APPRAISAL PRACTICE USPAP Matrix

UNDERSTANDING HOW USPAP APPLIES TO REAL PROPERTY APPRAISAL PRACTICE - 2014-2015 USPAP Matrix This matrix assumes an Appraisal Report Format under S. R. 2-2(a). *Last updated 9/11/14* GENERAL Violation

UNDERSTANDING HOW USPAP APPLIES TO REAL PROPERTY APPRAISAL PRACTICE - 2014-2015 USPAP Matrix This matrix assumes an Appraisal Report Format under S. R. 2-2(a). *Last updated 9/11/14* GENERAL Violation

Demonstration Appraisal Report Utilizing a Form Report

Demonstration Appraisal Report Utilizing a Form Report National Association of Independent Fee Appraisers 330 North Wabash Avenue, Suite 2000 Chicago, IL 60611 Phone: (312) 321-6830 Fax: (312) 673-6652

Demonstration Appraisal Report Utilizing a Form Report National Association of Independent Fee Appraisers 330 North Wabash Avenue, Suite 2000 Chicago, IL 60611 Phone: (312) 321-6830 Fax: (312) 673-6652

What issues regarding FHA lending have been raise throughout this chapter and which ones place great responsibility on the appraiser?

The FHA & VA Appraiser: Thriving and Surviving (7 hour CE) This course will provide you with an understanding of the historical and present needs for FHA and VA programs. It focuses on the most current

The FHA & VA Appraiser: Thriving and Surviving (7 hour CE) This course will provide you with an understanding of the historical and present needs for FHA and VA programs. It focuses on the most current

Uniform Appraisal Dataset (UAD) Frequently Asked Questions

Frequently Asked Questions") Uniform Appraisal Dataset (UAD) Frequently Asked Questions July 13, 2014 Updated for formatting May 15, 2017 The following provides answers to questions frequently asked about Fannie Mae s and Freddie

Uniform Appraisal Dataset (UAD) Frequently Asked Questions July 13, 2014 Updated for formatting May 15, 2017 The following provides answers to questions frequently asked about Fannie Mae s and Freddie

How to Read a Real Estate Appraisal Report

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

How to Read a Real Estate Appraisal Report Much of the private, corporate and public wealth of the world consists of real estate. The magnitude of this fundamental resource creates a need for informed

2. Is the information in the contract section complete and accurate? Yes No Not Applicable If Yes, provide a brief summary.

The purpose of this appraisal field review report is to provide the lender/client with an opinion on the accuracy of the appraisal report under review. Property Address City State Zip Code Borrower Owner

The purpose of this appraisal field review report is to provide the lender/client with an opinion on the accuracy of the appraisal report under review. Property Address City State Zip Code Borrower Owner

Exterior Only Inspection Residential Appraisal Report File #

SUBJECT Summary Appraisal Report Brian J. Davis & Associates Exterior Only Inspection Residential Appraisal Report File # Page #3 The purpose of this summary appraisal report is to provide the lender/client

SUBJECT Summary Appraisal Report Brian J. Davis & Associates Exterior Only Inspection Residential Appraisal Report File # Page #3 The purpose of this summary appraisal report is to provide the lender/client

Individual Condominium Unit Appraisal Report

The purpose of this summary appraisal report is to provide the lender/client with an accurate, and adequately supported, opinion of the market value of the subject property. SUBJECT Property Address Unit

The purpose of this summary appraisal report is to provide the lender/client with an accurate, and adequately supported, opinion of the market value of the subject property. SUBJECT Property Address Unit

APPRAISAL OF REAL PROPERTY

Home Appraisals, Inc. (866) 533-7173 APPRAISAL OF REAL PROPERTY File # LOCATED AT Field Review Form Sample FOR OPINION OF VALUE 35, AS OF 11/1/7 TABLE OF CONTENTS One-Unit Field Review... 1 General Text

Home Appraisals, Inc. (866) 533-7173 APPRAISAL OF REAL PROPERTY File # LOCATED AT Field Review Form Sample FOR OPINION OF VALUE 35, AS OF 11/1/7 TABLE OF CONTENTS One-Unit Field Review... 1 General Text

Colorado Appraisal Consultants

Colorado Appraisal Consultants SUBJECT Individual Condominium Unit Appraisal Report File # The purpose of this summary appraisal report is to provide the lender/client with an accurate, and adequately

Colorado Appraisal Consultants SUBJECT Individual Condominium Unit Appraisal Report File # The purpose of this summary appraisal report is to provide the lender/client with an accurate, and adequately

Uniform Residential Appraisal Report (URAR) Model Appraisal

Model Appraisal") Basic Appraisal Procedures Residential Applications & Model Appraisals 15-13 Uniform Residential Appraisal Report (URAR) Model Appraisal On the following pages are examples of a completed Fannie Mae/Freddie

Basic Appraisal Procedures Residential Applications & Model Appraisals 15-13 Uniform Residential Appraisal Report (URAR) Model Appraisal On the following pages are examples of a completed Fannie Mae/Freddie

Copyright, 1999, 2002, 2004, Freddie Mac. All Rights Reserved.

Page 1 of 13 Engineering Requirements/Chapter 12: Appraiser and Appraisal Requirements/12.1: General requirements 12.1: General requirements For all multifamily purchase programs and products, the Seller/Servicer

Page 1 of 13 Engineering Requirements/Chapter 12: Appraiser and Appraisal Requirements/12.1: General requirements 12.1: General requirements For all multifamily purchase programs and products, the Seller/Servicer

FHA Handbook, Appendix D (January 2006) - PDF Page 1

- PDF Page 1") APPENDIX D: VALUATION PROTOCOL FHA Handbook, Appendix D (January 2006) - PDF Page 1 The appraisal process is the lender s tool for determining if a property meets the minimum requirements and eligibility

APPENDIX D: VALUATION PROTOCOL FHA Handbook, Appendix D (January 2006) - PDF Page 1 The appraisal process is the lender s tool for determining if a property meets the minimum requirements and eligibility

GAAR Harness the Power of Technology to Create the BEST Appraisal Reviews Possible

GAAR Harness the Power of Technology to Create the BEST Appraisal Reviews Possible Presented by FNC March 21, 2012 INTRODUCTION General Information: Conference Web Page Audio & Supporting Documents Submit

GAAR Harness the Power of Technology to Create the BEST Appraisal Reviews Possible Presented by FNC March 21, 2012 INTRODUCTION General Information: Conference Web Page Audio & Supporting Documents Submit

Training the Next Generation of Appraisers The S.T.A.R.T. Program - Standards to Assure Responsible Training:

Training the Next Generation of Appraisers The S.T.A.R.T. Program - Standards to Assure Responsible Training: An Industry Solution to the Declining Number of Appraisers Entering the Profession and Practical

Training the Next Generation of Appraisers The S.T.A.R.T. Program - Standards to Assure Responsible Training: An Industry Solution to the Declining Number of Appraisers Entering the Profession and Practical

Appraisal and Property Related Frequently Asked Questions (FAQs) Updated September 2014

Updated September 2014") Appraisal and Property Related Frequently Asked Questions (FAQs) Updated September 2014 This FAQ document provides responses to common questions related to Fannie Mae s property eligibility and appraisal

Appraisal and Property Related Frequently Asked Questions (FAQs) Updated September 2014 This FAQ document provides responses to common questions related to Fannie Mae s property eligibility and appraisal

Residential Evaluation Report (RER) April, 2016

April, 2016") Residential Evaluation Report (RER) ensuring compliance with the Interagency Guidelines (IAG) and USPAP April, 2016 Definitions RER shall mean a Residential Evaluation Report and is deemed to be a restricted

Residential Evaluation Report (RER) ensuring compliance with the Interagency Guidelines (IAG) and USPAP April, 2016 Definitions RER shall mean a Residential Evaluation Report and is deemed to be a restricted

Basic Appraisal Procedures

Hondros Learning Basic Appraisal Procedures Timed Outline Topic Area Reference(s) Learning Objectives The student will be able to identify and/or apply: Teaching Method Time Segment (Minutes) Day 1 Chapter

Hondros Learning Basic Appraisal Procedures Timed Outline Topic Area Reference(s) Learning Objectives The student will be able to identify and/or apply: Teaching Method Time Segment (Minutes) Day 1 Chapter

Single Family Housing Policy Handbook: FHA Connection 203k Calculator and Other System Enhancements

Office of Single Family Program Development Single Family Housing Policy Handbook: FHA Connection 203k Calculator and Other System Enhancements April 28, 2016 Last Updated: 4/27/16 Presented by: Kevin

Office of Single Family Program Development Single Family Housing Policy Handbook: FHA Connection 203k Calculator and Other System Enhancements April 28, 2016 Last Updated: 4/27/16 Presented by: Kevin

Announcement March 24, 2005

Announcement 05-02 March 24, 2005 Amends these Guides: Selling Final Appraisal Report Forms Part XI: Property and Appraisal Analysis Guidelines In Lender Announcement 04-07 dated November 8, 2004, we released

Announcement 05-02 March 24, 2005 Amends these Guides: Selling Final Appraisal Report Forms Part XI: Property and Appraisal Analysis Guidelines In Lender Announcement 04-07 dated November 8, 2004, we released

As Of: Prepared For: Prepared By:

of 216 SW 131st St As Of: 06/11/11 Prepared For: Prime Pacific Bank 2502 196th St SW Lynnwood WA 98036 Prepared By: Cynthia A. Nagle, CREA 922 N Cedar St Tacoma, WA 98406 RESTRICTED APPRAISAL REPORT Restriction

of 216 SW 131st St As Of: 06/11/11 Prepared For: Prime Pacific Bank 2502 196th St SW Lynnwood WA 98036 Prepared By: Cynthia A. Nagle, CREA 922 N Cedar St Tacoma, WA 98406 RESTRICTED APPRAISAL REPORT Restriction

Guidance for Lenders and Appraisers April 2009

Guidance for Lenders and Appraisers April 2009 Fannie Mae views lenders as our partners in ensuring the continued viability of the residential lending market and the continued availability of affordable

Guidance for Lenders and Appraisers April 2009 Fannie Mae views lenders as our partners in ensuring the continued viability of the residential lending market and the continued availability of affordable

FHA Reference Materials for This Seminar... 1 Primary Audience for This Seminar... 1 Not Yet Approved for FHA Appraisal Assignments?...

Table of Contents Overview... vii Seminar Schedule... xi Section 1 Introduction FHA Reference Materials for This Seminar... 1 Primary Audience for This Seminar... 1 Not Yet Approved for FHA Appraisal Assignments?...

Table of Contents Overview... vii Seminar Schedule... xi Section 1 Introduction FHA Reference Materials for This Seminar... 1 Primary Audience for This Seminar... 1 Not Yet Approved for FHA Appraisal Assignments?...

RESTRICTED APPRAISAL REPORT

Restricted Use Appraisal Report Thomas J. Schulte & Associates Page #1 RESTRICTED APPRAISAL REPORT SUBJECT ASSIGNMENT Property City: Zip Code: County: Legal Description: Assessor's Parcel #: Tax Year:

Restricted Use Appraisal Report Thomas J. Schulte & Associates Page #1 RESTRICTED APPRAISAL REPORT SUBJECT ASSIGNMENT Property City: Zip Code: County: Legal Description: Assessor's Parcel #: Tax Year:

SUBJECT: Unacceptable Assignment Conditions in Real Property Appraisal Assignments

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 ADVISORY OPINION 19 (AO-19) This communication by the Appraisal Standards Board (ASB) does not establish new standards

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 ADVISORY OPINION 19 (AO-19) This communication by the Appraisal Standards Board (ASB) does not establish new standards

Uniform Residential Appraisal Report File #

D.S. Murphy & Associates FHA/VA Case No. SUBJECT The purpose of this summary appraisal report is to provide the lender/client with an accurate, and adequately supported, opinion of the market value of

D.S. Murphy & Associates FHA/VA Case No. SUBJECT The purpose of this summary appraisal report is to provide the lender/client with an accurate, and adequately supported, opinion of the market value of

Appraisal Stream Restricted Use Residential Appraisal Report

Appraisal Stream Restricted Use Residential Appraisal Report File No. 769kemplin This report is limited to the sole and exclusive use of the client. The appraiser's opinions and conclusions set forth in

Appraisal Stream Restricted Use Residential Appraisal Report File No. 769kemplin This report is limited to the sole and exclusive use of the client. The appraiser's opinions and conclusions set forth in

Kathy Coon, SRA Appraisal Review: CSI Style ( )

") Appraisal Review: CSI Style Southern California Chapter Appraisal Institute July 16, 2009 Kathy Coon, SRA Chief Appraiser/Director-Appraisal Appraisal Quality Control FNC, Inc. www.fncinc.com com When

Appraisal Review: CSI Style Southern California Chapter Appraisal Institute July 16, 2009 Kathy Coon, SRA Chief Appraiser/Director-Appraisal Appraisal Quality Control FNC, Inc. www.fncinc.com com When

Chapter 35. The Appraiser's Sales Comparison Approach INTRODUCTION

Chapter 35 The Appraiser's Sales Comparison Approach INTRODUCTION The most commonly used appraisal technique is the sales comparison approach. The fundamental concept underlying this approach is that market

Chapter 35 The Appraiser's Sales Comparison Approach INTRODUCTION The most commonly used appraisal technique is the sales comparison approach. The fundamental concept underlying this approach is that market

Freddie Mac UCDP Proprietary Messages

UCDP Proprietary Messages -specific feedback messages for appraisals submitted to in the Uniform Collateral Data Portal (UCDP ). The content in brackets represents dynamic values. *Message text updated

UCDP Proprietary Messages -specific feedback messages for appraisals submitted to in the Uniform Collateral Data Portal (UCDP ). The content in brackets represents dynamic values. *Message text updated

BPO Best Practices Guide

BPO Best Practices Guide A Step by Step Guide for Completing BPO Reports Version: 1.0.0 Published: 03/01/2011 Global DMS, 1555 Bustard Road, Suite 300, Lansdale, PA 19446 2014, All Rights Reserved. Table

BPO Best Practices Guide A Step by Step Guide for Completing BPO Reports Version: 1.0.0 Published: 03/01/2011 Global DMS, 1555 Bustard Road, Suite 300, Lansdale, PA 19446 2014, All Rights Reserved. Table

Chapter 8 Qualifying Property

The 3 "Cs" of Lending Capacity to Pay does the borrower make enough money to repay loan? lenders use qualifying ratios Creditworthiness [Character] is the borrower likely to repay loan on time? lenders

The 3 "Cs" of Lending Capacity to Pay does the borrower make enough money to repay loan? lenders use qualifying ratios Creditworthiness [Character] is the borrower likely to repay loan on time? lenders

Interagency Appraisal and

Interagency Appraisal and Evaluation (IAEG) Workshop Purpose (77456) Supersedes the 1994 Interagency Appraisal & Evaluation Guidelines Address supervisory matters relating to real estate appraisal and

Interagency Appraisal and Evaluation (IAEG) Workshop Purpose (77456) Supersedes the 1994 Interagency Appraisal & Evaluation Guidelines Address supervisory matters relating to real estate appraisal and

Pro-Series Webinar: Fannie Mae Update Collateral Policy and Technology Guidance For Appraisers

Pro-Series Webinar: Fannie Mae Update Collateral Policy and Technology Guidance For Appraisers March 29, 2017 Presenters: Julie Jones & Jeremy Staudenmaier Webinar Audio (phone only): 1 - (866) 218-8865

Pro-Series Webinar: Fannie Mae Update Collateral Policy and Technology Guidance For Appraisers March 29, 2017 Presenters: Julie Jones & Jeremy Staudenmaier Webinar Audio (phone only): 1 - (866) 218-8865

Restricted Use Appraisal Report Residential

Client File #: Appraisal File #: Restricted Use Appraisal Report Residential Appraisal Company: Address: Form 200.04* Phone: Fax: Website: Appraiser: Co-Appraiser: AI Membership (if any): SRA MAI SRPA

Client File #: Appraisal File #: Restricted Use Appraisal Report Residential Appraisal Company: Address: Form 200.04* Phone: Fax: Website: Appraiser: Co-Appraiser: AI Membership (if any): SRA MAI SRPA

Fannie Mae Selling Guide (04/12/2002) Part XI - Property and Appraisal Guidelines

Part XI - Property and Appraisal Guidelines") Fannie Mae Selling Guide (04/12/2002) Part XI - Property and Appraisal Guidelines This Part-Property and Appraisal Guidelines-details our general requirements for analyzing the property appraisal aspects

Fannie Mae Selling Guide (04/12/2002) Part XI - Property and Appraisal Guidelines This Part-Property and Appraisal Guidelines-details our general requirements for analyzing the property appraisal aspects

VALUE FINDING APPRAISAL REPORT

RE 90 Rev. 01-2014 VALUE FINDING APPRAISAL REPORT (Compensation not to exceed $65,000) COUNTY John Doe 2880 Lancaster-Newark Rd. (SR 37), Pleasant Twp., 43030 Owner Mailing Address of Owner East side of

RE 90 Rev. 01-2014 VALUE FINDING APPRAISAL REPORT (Compensation not to exceed $65,000) COUNTY John Doe 2880 Lancaster-Newark Rd. (SR 37), Pleasant Twp., 43030 Owner Mailing Address of Owner East side of

ILLINOIS HOUSING DEVELOPMENT AUTHORITY APPRAISAL SCOPE AND GUIDELINES December 2015

ILLINOIS HOUSING DEVELOPMENT AUTHORITY APPRAISAL SCOPE AND GUIDELINES December 2015 As part of the Common Application for Multifamily Financing, the Illinois Housing Development Authority (IHDA) requires

ILLINOIS HOUSING DEVELOPMENT AUTHORITY APPRAISAL SCOPE AND GUIDELINES December 2015 As part of the Common Application for Multifamily Financing, the Illinois Housing Development Authority (IHDA) requires

Division of Real Estate. Summary of BOREA Investigations

Division of Real Estate Summary of BOREA Investigations Complaint Stats for Prior 12 Months BOREA Checklist for Investigations Generally follows the FNMA 1004 layout Neighborhood and Market Analyses Site

Division of Real Estate Summary of BOREA Investigations Complaint Stats for Prior 12 Months BOREA Checklist for Investigations Generally follows the FNMA 1004 layout Neighborhood and Market Analyses Site

The High Performance Appraisal Process Unveiled By Sandra K. Adomatis, SRA, LEED Green Associate

The High Performance Appraisal Process Unveiled By Sandra K. Adomatis, SRA, LEED Green Associate Email: Adomatis@Hotmail.com Twitter: https://twitter.com/sadomatis Web: www.adomatisappraisalservice.com

The High Performance Appraisal Process Unveiled By Sandra K. Adomatis, SRA, LEED Green Associate Email: Adomatis@Hotmail.com Twitter: https://twitter.com/sadomatis Web: www.adomatisappraisalservice.com

To all Appraisers: Brief Overview:

To all Appraisers: As the appraisal industry continues to change, the demand for alternative valuation solutions grows. That is why is excited to announce the addition of a new product - the Desktop Appraisal

To all Appraisers: As the appraisal industry continues to change, the demand for alternative valuation solutions grows. That is why is excited to announce the addition of a new product - the Desktop Appraisal

Small Residential Income Property Appraisal Report File #

SUBJECT Summary Appraisal Report Brian J. Davis & Associates Small Residential Income Property Appraisal Report File # Page #4 The purpose of this summary appraisal report is to provide the lender/client

SUBJECT Summary Appraisal Report Brian J. Davis & Associates Small Residential Income Property Appraisal Report File # Page #4 The purpose of this summary appraisal report is to provide the lender/client

Overall Trend Section Example Seller Concessions Foreclosure Sales and Summary/Analysis of Data... 13

Appraisal and Property-Related Frequently Asked Questions (FAQs) This FAQ document provides responses to common questions related to Fannie Mae s property eligibility and appraisal policies. Following

Appraisal and Property-Related Frequently Asked Questions (FAQs) This FAQ document provides responses to common questions related to Fannie Mae s property eligibility and appraisal policies. Following

A Demonstration Appraisal Report. Of a. Located at. Date of Appraisal. Prepared for. Prepared by

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 W. 10 th Street Kansas

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 W. 10 th Street Kansas

Interagency Guidelines Web seminar, February 10, 2011

Interagency Guidelines Web seminar, February 10, 2011 Questions from participants. The answers here are suggestive guidance only and should not be treated or considered legal or regulatory advice. You

Interagency Guidelines Web seminar, February 10, 2011 Questions from participants. The answers here are suggestive guidance only and should not be treated or considered legal or regulatory advice. You

APPRAISAL OF LOCATED AT:

APPRAISAL OF LOCATED AT: 5905 S County Road K South Range, WI 54874 February 18, 2015 In accordance with your request, I have appraised the real property at: 5905 S County Road K South Range, WI 54874

APPRAISAL OF LOCATED AT: 5905 S County Road K South Range, WI 54874 February 18, 2015 In accordance with your request, I have appraised the real property at: 5905 S County Road K South Range, WI 54874

A Demonstration Appraisal Report. Of a. Located at. Date of Appraisal. Prepared for. Prepared by

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 West 10 th Street Kansas

A Demonstration Appraisal Report Of a Located at Date of Appraisal Prepared for Prepared by International Association of Assessing Officers Professional Designation Subcommittee 314 West 10 th Street Kansas

APPRAISAL OF REAL PROPERTY LOCATED AT: FOR: AS OF: BY:

APPRAISAL OF REAL PROPERTY LOCATED AT: 489 MEADOWS EDGE COURT DEED BOOK 2896, PAGE 2759 CLEMMONS, NC 27012 FOR: ESTATE OF WILLIAM C. McINTOSH % BAILEY & THOMAS P.O. BOX 52 WINSTON-SALEM, NC 27102 AS OF:

APPRAISAL OF REAL PROPERTY LOCATED AT: 489 MEADOWS EDGE COURT DEED BOOK 2896, PAGE 2759 CLEMMONS, NC 27012 FOR: ESTATE OF WILLIAM C. McINTOSH % BAILEY & THOMAS P.O. BOX 52 WINSTON-SALEM, NC 27102 AS OF:

Announcement July 13, Collateral Valuation Practices and Declining Markets

Announcement 07-11 July 13, 2007 Amends these Guides: Selling Collateral Valuation Practices and Declining Markets Introduction An accurate value for the property securing a mortgage loan is important

Announcement 07-11 July 13, 2007 Amends these Guides: Selling Collateral Valuation Practices and Declining Markets Introduction An accurate value for the property securing a mortgage loan is important

Restricted Use Appraisal Report Residential

Client File #: Appraisal File #: Restricted Use Appraisal Report Residential Form 200.04 * Appraiser: AI Membership (if any): SRA MAI SRPA AI Affiliation (if any): Candidate for Designation Practicing

Client File #: Appraisal File #: Restricted Use Appraisal Report Residential Form 200.04 * Appraiser: AI Membership (if any): SRA MAI SRPA AI Affiliation (if any): Candidate for Designation Practicing

Individual Cooperative Interest Appraisal Report

PURPOSE Individual Cooperative Interest Appraisal Report The purpose of this appraisal report is to provide the client with a credible opinion of the defined value of the subject property, given the intended

PURPOSE Individual Cooperative Interest Appraisal Report The purpose of this appraisal report is to provide the client with a credible opinion of the defined value of the subject property, given the intended

SUBJECT: The Appraisal of Real Property That May Be Impacted by Environmental Contamination

1 ADVISORY OPINION 9 (AO-9) 1 2 3 4 This communication by the Appraisal Standards Board (ASB) does not establish new standards or interpret existing standards. Advisory Opinions are issued to illustrate

1 ADVISORY OPINION 9 (AO-9) 1 2 3 4 This communication by the Appraisal Standards Board (ASB) does not establish new standards or interpret existing standards. Advisory Opinions are issued to illustrate

If you want even more information, look for the advanced training, which includes more use cases and demonstrates CU s full functionality.

Thank you for attending the Collateral Underwriter user interface basic training. My name is Steve Jones and I will be taking you through the course. Our objective today is to provide a foundational understanding

Thank you for attending the Collateral Underwriter user interface basic training. My name is Steve Jones and I will be taking you through the course. Our objective today is to provide a foundational understanding

OHIO DEPARTMENT OF TRANSPORTATION OFFICE OF REAL ESTATE

OHIO DEPARTMENT OF TRANSPORTATION OFFICE OF REAL ESTATE DATE: April 3, 2017 TO: FROM: RE: Users of the Real Estate Manual Jared Miller, Manager Appraisal Unit Changes and Updates to the Real Estate Manual

OHIO DEPARTMENT OF TRANSPORTATION OFFICE OF REAL ESTATE DATE: April 3, 2017 TO: FROM: RE: Users of the Real Estate Manual Jared Miller, Manager Appraisal Unit Changes and Updates to the Real Estate Manual

203K Standard Renovation Loan

203K Standard Renovation Loan RI Mortgage Broker Licene # 20082309LB MA Mortgage Broker License # MB3915 FL Mortgage Broker License # MBR475 PA Mortgage Broker License # 60246 Atlantic Mortgage & Finance

203K Standard Renovation Loan RI Mortgage Broker Licene # 20082309LB MA Mortgage Broker License # MB3915 FL Mortgage Broker License # MBR475 PA Mortgage Broker License # 60246 Atlantic Mortgage & Finance

FHA -203K And Renovation Loans

FHA -203K And Renovation Loans What is a 203K FHA Loan or a Renovation Loan? Both loan types enable homebuyers and homeowners to finance both the purchase (or refinancing) of a house and the cost of its

FHA -203K And Renovation Loans What is a 203K FHA Loan or a Renovation Loan? Both loan types enable homebuyers and homeowners to finance both the purchase (or refinancing) of a house and the cost of its

Residential Appraising What Lenders Want

Residential Appraising What Lenders Want Introductions Ken DeFeo 25 years appraising have worked for lenders for 20 years Lets get to know a little about the audience How many appraisers do we have? How

Residential Appraising What Lenders Want Introductions Ken DeFeo 25 years appraising have worked for lenders for 20 years Lets get to know a little about the audience How many appraisers do we have? How

BPOSG BROKER PRICE OPINION. Guidelines. Version 3.1 May 20, BSB BPO Standards Board

BPOSG BROKER PRICE OPINION Standards & Version 3.1 May 20, 2009 BSB BPO Standards Board BSB BPO Standards Board 6619 North Scottsdale Road Scottsdale, Arizona 85250 Standards and : BPOSG is a compilation

BPOSG BROKER PRICE OPINION Standards & Version 3.1 May 20, 2009 BSB BPO Standards Board BSB BPO Standards Board 6619 North Scottsdale Road Scottsdale, Arizona 85250 Standards and : BPOSG is a compilation

EMPLOYEE RELOCATION COUNCIL SUMMARY APPRAISAL REPORT

EMPLOYEE RELOCATION COUNCIL SUMMARY APPRAISAL REPORT Client: Client File #: Client Address: Suite #: Homeowner: Subject Property Address: County: Appraiser Company Name: TOMAINO APPRAISAL Appraiser File

EMPLOYEE RELOCATION COUNCIL SUMMARY APPRAISAL REPORT Client: Client File #: Client Address: Suite #: Homeowner: Subject Property Address: County: Appraiser Company Name: TOMAINO APPRAISAL Appraiser File

Mass Appraisal of Income-Producing Properties

Chapter 10 Mass Appraisal of Income-Producing Properties Whether valuing income-producing property or residential property, you can use similar information and methods for collecting and analyzing data

Chapter 10 Mass Appraisal of Income-Producing Properties Whether valuing income-producing property or residential property, you can use similar information and methods for collecting and analyzing data

Selling Part VII - Property and Appraisal Analysis

Selling Part VII - Property and Appraisal Analysis This Part--Property and Appraisal Analysis--details our general requirements for analyzing the property appraisal aspects of conventional mortgages secured

Selling Part VII - Property and Appraisal Analysis This Part--Property and Appraisal Analysis--details our general requirements for analyzing the property appraisal aspects of conventional mortgages secured

Table of Contents. Chapter 1: Introduction (Mobile Technology Evolution) 1

1") Chapter 1: Introduction (Mobile Technology Evolution) 1 I. WHY APPRAISAL IS IMPORTANT (p. 3) II. DEFINITION OF APPRAISAL (p. 4) A. Opinion (p. 4) B. Value (p. 5) C. Appraisal Art or Science? (p. 5) D.

Chapter 1: Introduction (Mobile Technology Evolution) 1 I. WHY APPRAISAL IS IMPORTANT (p. 3) II. DEFINITION OF APPRAISAL (p. 4) A. Opinion (p. 4) B. Value (p. 5) C. Appraisal Art or Science? (p. 5) D.

SPARC ROUND 8 (FY 10)

") SINGLE FAMILY SPARC ROUND 8 (FY 10) Sponsoring Partnerships and Revitalizing Communities June 2009 Single Family SPARC The Single Family SPARC (Sponsoring Partnership and Revitalizing Communities) program

SINGLE FAMILY SPARC ROUND 8 (FY 10) Sponsoring Partnerships and Revitalizing Communities June 2009 Single Family SPARC The Single Family SPARC (Sponsoring Partnership and Revitalizing Communities) program

Dear Valuation Professional

Dear Valuation Professional First American Mortgage Solutions LLC has a new product offering that we would like you to consider adding to your list of services with us - (Property Assessment Collateral

Dear Valuation Professional First American Mortgage Solutions LLC has a new product offering that we would like you to consider adding to your list of services with us - (Property Assessment Collateral

Avoiding Common Errors in Appraisals for Financial

Avoiding Common Errors in Appraisals for Financial Institutions Panelists: Brian Bailey, CCIM, Senior Financial Analyst Commercial Real Estate, Federal Reserve Bank of Atlanta James Murrett, MAI, Director

Avoiding Common Errors in Appraisals for Financial Institutions Panelists: Brian Bailey, CCIM, Senior Financial Analyst Commercial Real Estate, Federal Reserve Bank of Atlanta James Murrett, MAI, Director

54 System Design Collaborate: Agent Task Instructions

1 54 System Design Collaborate: Agent Task Instructions Version Date Description By 1.0 1/25/2013 Final Lizette Patterson Table of Contents Profile information... 2 Agent (Listing) Confirmation Task...

1 54 System Design Collaborate: Agent Task Instructions Version Date Description By 1.0 1/25/2013 Final Lizette Patterson Table of Contents Profile information... 2 Agent (Listing) Confirmation Task...

Collateral Underwriter Overview. National Association of REALTORS January 23, 2015

Collateral Underwriter Overview National Association of REALTORS January 23, 2015 2014 Fannie Mae. Trademarks of Fannie Mae. Introduction to Collateral Underwriter I January 2015 What Is Collateral Underwriter?

Collateral Underwriter Overview National Association of REALTORS January 23, 2015 2014 Fannie Mae. Trademarks of Fannie Mae. Introduction to Collateral Underwriter I January 2015 What Is Collateral Underwriter?

Anatomy Of An Appraisal

Anatomy Of An Appraisal Leslie A. Fields The most important thing to know about an appraisal report is how to review and critique it. Leslie A. Fields a partner with the Law Firm of Faegre & Benson LLP,

Anatomy Of An Appraisal Leslie A. Fields The most important thing to know about an appraisal report is how to review and critique it. Leslie A. Fields a partner with the Law Firm of Faegre & Benson LLP,

Guide to Appraisal Reports

Guide to Appraisal Reports What is an appraisal? An appraisal is an independent valuation of real property prepared by a qualified Appraiser and fully documented in a report. Based on a series of appraisal

Guide to Appraisal Reports What is an appraisal? An appraisal is an independent valuation of real property prepared by a qualified Appraiser and fully documented in a report. Based on a series of appraisal

Joe Metzler, NMLS

Joe Metzler, NMLS 274132 How do you turn a fixer upper into your dream home? The Solution the FHA 203(k) Loan! The purchase of a house that needs repair is often a catch-22 situation, because the bank

Joe Metzler, NMLS 274132 How do you turn a fixer upper into your dream home? The Solution the FHA 203(k) Loan! The purchase of a house that needs repair is often a catch-22 situation, because the bank

procedures Basic Appraisal F i n a l Examination #2 2 nd edition

F i n a l Examination #2 A n s w e r Key Page 82 1. When determining effective gross income from potential gross income, an appraiser considers a. debt service. b. depreciation. c. fixed expenses. d. vacancy

F i n a l Examination #2 A n s w e r Key Page 82 1. When determining effective gross income from potential gross income, an appraiser considers a. debt service. b. depreciation. c. fixed expenses. d. vacancy

Fannie Mae Single Family/2007 Selling Guide/Part XI: Property and Appraisal Guidelines/Part XI: Property and Appraisal Guidelines

Fannie Mae Single Family/2007 Selling Guide/Part XI: Property and Appraisal Guidelines/Part XI: Property and Appraisal Guidelines Part XI: Property and Appraisal Guidelines Copyright, 2001-2007, Fannie

Fannie Mae Single Family/2007 Selling Guide/Part XI: Property and Appraisal Guidelines/Part XI: Property and Appraisal Guidelines Part XI: Property and Appraisal Guidelines Copyright, 2001-2007, Fannie

10454 South Green Bay Avenue Chicago, IL Client and Order Detail. Subject Property Information

Client and Order Detail Client: Address: 10454 South Green Bay Avenue Client Loan Number: C/S/Z: Order Number: 0290016663 County: Cook Inspection Type: BPO-Interior BPO Agent: Lopez, Leo Mortgagor's Name:

Client and Order Detail Client: Address: 10454 South Green Bay Avenue Client Loan Number: C/S/Z: Order Number: 0290016663 County: Cook Inspection Type: BPO-Interior BPO Agent: Lopez, Leo Mortgagor's Name:

Measuring GLA Mixing ANSI Standards with Local Custom

Measuring GLA Mixing ANSI Standards with Local Custom Let s face it, if you put 2 or more of any profession in the same room and ask for an opinion, the number and variations of that opinion will probably